Sandwich Boosting for Accurate Estimation in Partially Linear Models for Grouped Data

Abstract

We study partially linear models in settings where observations are arranged in independent groups but may exhibit within-group dependence. Existing approaches estimate linear model parameters through weighted least squares, with optimal weights (given by the inverse covariance of the response, conditional on the covariates) typically estimated by maximising a (restricted) likelihood from random effects modelling or by using generalised estimating equations. We introduce a new ‘sandwich loss’ whose population minimiser coincides with the weights of these approaches when the parametric forms for the conditional covariance are well-specified, but can yield arbitrarily large improvements in linear parameter estimation accuracy when they are not. Under relatively mild conditions, our estimated coefficients are asymptotically Gaussian and enjoy minimal variance among estimators with weights restricted to a given class of functions, when user-chosen regression methods are used to estimate nuisance functions. We further expand the class of functional forms for the weights that may be fitted beyond parametric models by leveraging the flexibility of modern machine learning methods within a new gradient boosting scheme for minimising the sandwich loss. We demonstrate the effectiveness of both the sandwich loss and what we call ‘sandwich boosting’ in a variety of settings with simulated and real-world data.

1 Introduction

Grouped data are commonplace in many scientific, econometric and sociological disciplines. Prime examples include: repeated measures data (e.g. multiple readings of patient data), longitudinal data (e.g. where weekly sales are recorded across multiple stores), and hierarchical data (e.g. educational datasets clustered by school and potentially further sub-clustered by classroom).

To fix ideas, consider a regression setting where we have available grouped data for , with a vector of responses and predictors separated out into a covariate , whose contribution to the response we are particularly interested in, and remaining covariates ; for instance may be a treatment whose effect we wish to assess after controlling for additional covariates. In total therefore we have observations, though typically not all independent. A simple but popular approach to modelling this data in practice is via a linear model of the form

| (1) |

Here is a vector of errors such that and are regression coefficients to be estimated, with our primary target of inference.

A challenge in such settings is properly accounting for potential correlations between components of in order to obtain accurate estimates of the parameters. This may be achieved through a weighted least squares regression yielding estimates

| (2) |

in terms of weight matrices to be chosen. The optimal choice results in semiparametric efficient estimation of . A variety of approaches have been proposed for constructing the . Among the most popular are multilevel models (also known as random or mixed effects models) [Pinheiro and Bates, 2000, Fahrmeir and Tutz, 2001], which additionally make distributional assumptions on the errors , typically that of Gaussianity, and implicitly specify a particular parametrisation of in terms of the covariates through the introduction of latent random coefficients. Parameters are typically estimated through (restricted) maximum likelihood estimation [Hartley and Rao, 1967, Corbeil and Searle, 1976, Pinheiro and Bates, 2000]. An alternative is the marginal models framework [Heagerty and Zeger, 2000, Diggle et al., 2013, Fahrmeir and Tutz, 2001], which directly models the conditional covariance through a parametric form often estimated via generalised estimating equations [Liang and Zeger, 1986, Hardin and Hilbe, 2003, Ziegler, 2011]. Provided the forms of the conditional covariance are well-specified, any of these approaches will result in efficient estimates for and .

It is however well-known that all models are wrong [Box, 1976], and it is of interest to understand, under misspecification, which approaches remain useful. Below we discuss the consequences of the two potential sources of misspecification, that of the conditional covariance , and the conditional mean .

1.1 Conditional covariance misspecification

Misspecification of the conditional covariance has been given a good deal of attention in the literature. The generalised estimating equation approach that has come to be known as GEE1 [Liang et al., 1992] explicitly recognises the possibility of misspecification, and instead specifies what is referred to as a working model for the conditional covariance, with which to construct the weights. Valid inference is guaranteed even with arbitrary (fixed) weights as the estimator (1) is unbiased and standard errors may be based on a sandwich estimate of the variance of [Huber, 1967, Gourieroux et al., 1984, Royall, 1986, Liang and Zeger, 1986],

| (3) |

The idea behind the working covariance model however is to approximate the ground truth sufficiently well such that the resulting has reasonably low variance; various estimation methods have been proposed for this purpose [Prentice and Zhao, 1991, Crowder, 1995, Lumley, 1996, Halekoh et al., 2006].

While this intuition is basically well-founded, perhaps surprisingly, for a given model for the covariance, the success of these approaches depends crucially on the method of estimation, as we now demonstrate with two simple examples; specific details for these are given in Appendix A.2.

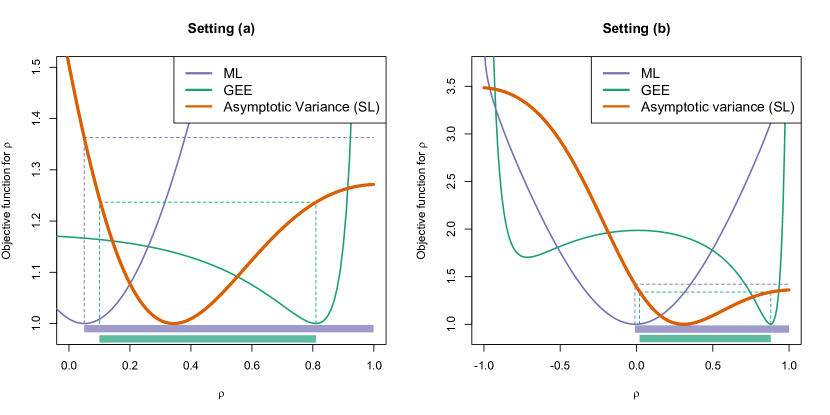

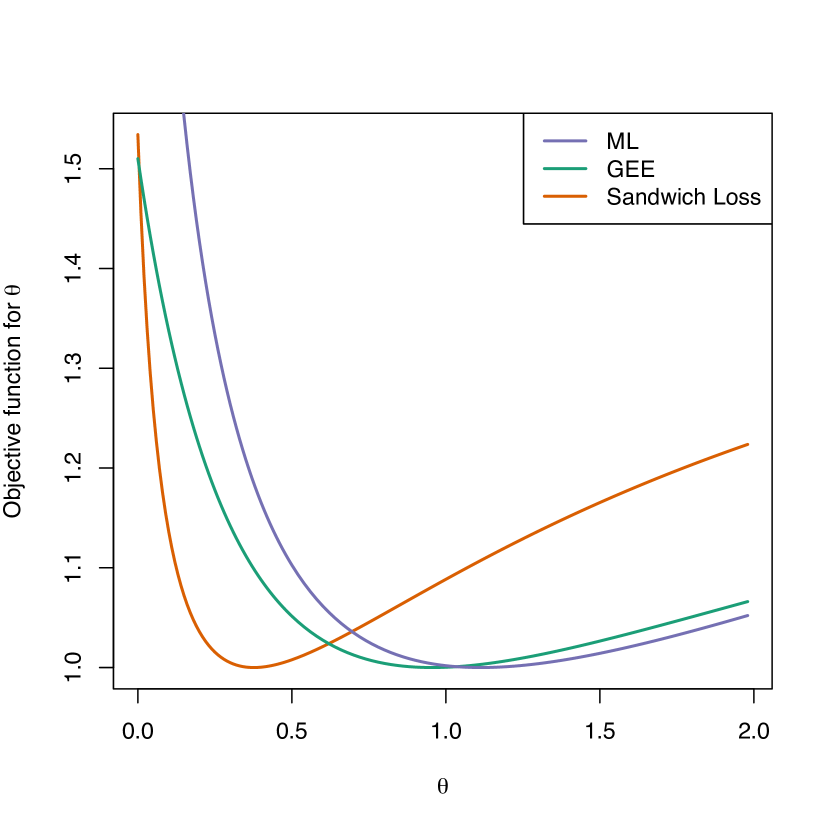

Example 1 (Conditional correlation misspecification).

Consider a version of (1) with omitted for simplicity, and each error vector given by the first realisations of an model. Suppose the weights are estimated in the parametric class consisting of inverses of the covariance matrices of processes, indexed by a single autoregressive parameter ; note that the scale of the weights does not affect the resulting so we do not consider this as a parameter. We consider two specific settings within this general setup. Figure 1 plots the objective functions that are minimised for two well-established methods for constructing weights based on estimates of

The so-called quasi pseudo maximum likelihood approach (ML) [Gourieroux and Monfort, 1993, McCullagh and Nelder, 1989, Ziegler, 2011] treats the errors as if they were normally distributed with correlation matrix given by the process for a given , and proceeds to maximise jointly over the unknown and variance , what would be the likelihood were this model to hold.

Motivated by the moment equation , a second approach (GEE) falling within the GEE1 framework estimates by the minimiser of

| (4) |

here the are the residuals from an initial unweighted least squares regression of on .

We also plot in orange the asymptotic variance (equivalent to the mean squared error), i.e., the population equivalent of (3), of the -estimator weighted by an working correlation for a given value of (the nomenclature ‘SL’ in the legend is explained in Section 1.3). In Setting (a), we see that optimising either of these objectives can result in suboptimal weights in terms of the resulting mean squared error, and any choice of would result in improved -estimation. Setting (b) tells a similar story, but also illustrates issues that can arise due to local minima of the objective functions, which, in particular are typically not guaranteed to be convex. Attempting to optimise the GEE objective by initialising at results in gradient descent converging to the highly suboptimal local optimum on the left as the derivative of the objective at is slightly positive (see also Table 4 in Appendix A.1). The resulting asymptotic variance of this final is substantially worse than even that of the unweighted choice corresponding to .

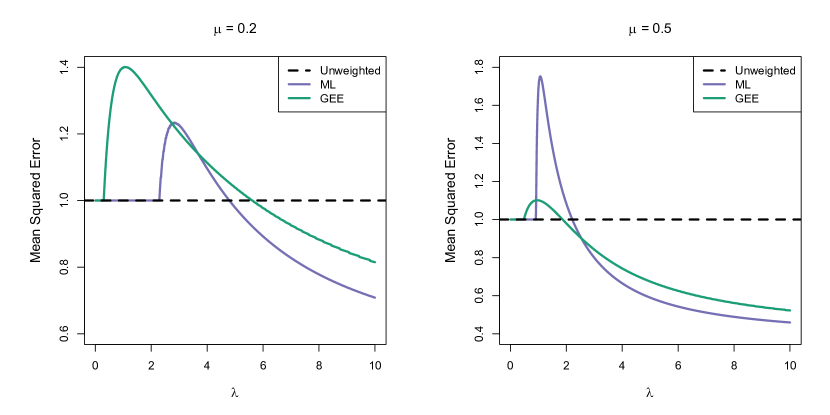

Example 2 (Conditional variance misspecification).

Consider an instance of model (1) with , so the data are ungrouped, and . Suppose the distribution of the data is such that the true conditional variance with ; we shall consider different settings for the pair of parameters . Consider using a misspecified class of functions of the form

| (5) |

where , so the smooth curve of the function is to be approximated by a step function.

Figure 2 plots the relative asymptotic mean squared errors of the weighted least squares estimates of , given by the first component of (2), for quasi pseudo maximum likelihood (ML) and GEE1-based approaches (GEE) for constructing weights based on estimates of . The former involves treating the errors as if they were normally distributed with standard deviation for some while the latter estimates by the minimiser of the sum of the squared differences between the squared residuals from an initial least squares regression of on , and ; see also Robinson [1987], Carroll [1982], Tsiatis [2006], You et al. [2007] for examples of estimation of the conditional variance through a similar least squares approach for improving -estimation in (partially) linear models.

We compare these strategies to a naive unweighted estimator, that is (2) with constant, which makes no attempt to take advantage of the heteroscedasticity in the errors to improve estimation. Note that such weights are permitted in the model class (5) used by ML and GEE in this example by taking large, so (5) for some necessarily gives a better approximation to the ground truth compared to the unweighted approach.

A first interesting observation is the quite different behaviour of the ML and GEE approaches here, with none appearing to be uniformly preferable to the other across all parameter settings. Perhaps more surprising however is the fact that for certain values of , the performances of these more sophisticated approaches lead to an inflation of the variance over an unweighted estimator (of up to almost 80%). This worrying behaviour can obfuscate model selection via AIC or BIC, as even at the population level they can favour models that result in poorer estimation of the parameter of interest .

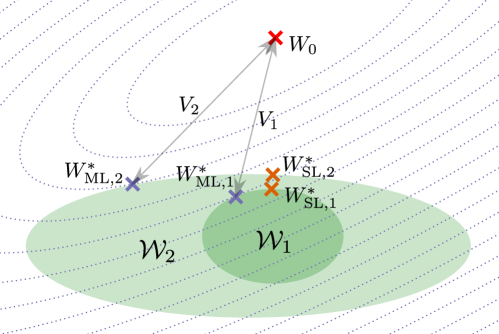

To resolve this apparent paradox, notice that although the model classes used by ML and GEE here are richer, the optimal ‘projections’ of the nuisance function (and corresponding optimal weight function ) relating to their respective losses do not necessarily coincide with the optimal projection in the sense of the mean squared error of ; in fact in general there is no reason for them to do so, as illustrated schematically in Figure 3 (see also Proposition 1 and Theorem 2 for a formalisation of this phenomenon). We return to these issues in Section 1.3, but first turn our attention to misspecification of the conditional mean .

1.2 Conditional mean misspecification

When the conditional expectation of the response given is not necessarily expected to be linear, a popular model to consider is the partially linear model

| (6) |

Here are as in (1); and are potentially nonlinear row-wise functions, that is e.g. , and writing for the th row of matrix , with a slight abuse of notation is then defined via ; and error in the on regression satisfies . Note that the model entails the conditional mean independence assumptions that

Nevertheless, the model is flexible enough to well-approximate a wide variety of data generating processes, yet still permits easy interpretation of the contribution of to the response. The second equation serves to model confounding due to . In the ungrouped setting, i.e. where , estimating in addition to forms a key part of the double / debiased machine learning (DML) framework [Chernozhukov et al., 2018] for inference about , which in recent years has emerged as the dominant approach for estimation in partially linear models. The popularity of this paradigm is due to the fact that it accommodates the use of arbitrary machine learning methods for estimating the nuisance functions and , and requires only a relatively slow rate of for the product of the corresponding mean squared errors in order to yield estimates of that converge at the parametric rate.

Emmenegger and Bühlmann [2023] recently extended this approach to the grouped data setting with , assuming a parametric form of the covariance governed by a random effects model. To estimate , they considered regressing each of and on using some independent auxiliary data and, with the resulting estimated regression functions, formed corresponding residuals and to give

| (7) |

Here the weight matrices are formed as the inverse conditional covariances estimated using (restricted) maximum likelihood. In practice, sample-splitting and cross-fitting are used in place of auxiliary data, permitting semiparametric efficient estimates, provided the model is well-specified.

However, the flexibility in modelling the conditional mean afforded by DML comes with implications for potential misspecification of the conditional covariance. One key requirement of the approach above is that, in addition to assuming a parametric form for the conditional covariance, it should also not depend on , i.e. we must have . This restriction is in fact a fundamental limitation of approaches based on DML. It comes as a consequence of requiring Neyman orthogonality, a certain first-order insensitivity to plugging in potentially biased machine learning estimators. Writing and for the corresponding regression estimate, in our case, this entails

| (8) |

being approximately zero, which may not hold unless is a function of alone. Thus misspecification of the conditional covariance, and the worrying consequences this may bring, deserve even greater attention when modelling the conditional mean in a flexible fashion through a partially linear model.

1.3 An overview of our contributions

To address the difficulties resulting from (inevitable) misspecification of the conditional covariance, we introduce a new approach for determining weight matrices in weighted least squares estimators (2) or the DML estimator in a partially linear model setting (7). Our proposal is to minimise a sandwich estimate of the variance of (i.e. (3) or the equivalent for the DML estimate) over a given parametrisation of weight matrices, thereby directly targeting the primary objective of interest: the estimation performance of . We thus treat this sandwich estimate of the variance as a loss function—the ‘sandwich loss’ (SL)—by which we determine the weights.

The asypmtotic variance plotted in Figure 1 is precisely the population version of this sandwich loss, and minimising this will, by the very definition of the loss, deliver an estimator of of minimal asymptotic variance among those considered. Returning to Example 2, Table 1 demonstrates that although ML and GEE are to be preferred in terms of estimating the true variance function , they are worse when estimating compared to our choice of weights tailored specifically for this purpose.

| Objective function | Asymptotic MSE of | Asymptotic integrated MSE of |

|---|---|---|

| GEE | 4.47 | 0.63 |

| ML | 6.82 | 0.87 |

| Sandwich loss | 4.10 | 1.10 |

While in these simple examples, the performances of the different methods are noticeably, but not radically different, we show later in Theroem 4 that there exist data generating distributions for which for a large class of misspecified working covariance models, the ratio of the variance for the -estimators between either GEE or ML and our optimal weighting scheme can be arbitrarily large.

One key message of our paper therefore is that particularly when there is a high risk of misspecification of the conditional covariance, the sandwich loss may be preferable over existing criteria when inference on the (partially) linear model parameter is of primary interest. In fact, even in the case that the conditional covariance is well-specified, there is a danger that ML or GEE approaches could converge to weights that are only locally optimal for their respective losses. Since it is only the global optima of these losses that correspond to weights with favourable properties for estimation of , their is no guarantee that the weights obtained are even locally optimal in terms of the resulting asymptotic variances. In this sense GEE and ML approaches may be more vulnerable to the consequences of local optima in their objective functions, compared to the sandwich loss; see Section 5.1.1.

A second main aim of our work is to introduce a new modelling strategy for working conditional covariances that can harness the power and flexibility of machine learning methods, similarly to how DML uses machine learning to accurately estimate nuisance functions. A challenge however is that standard regression methods cannot be directly deployed to construct weight matrices. In order to make use of these, we first decompose the inverse of the weights into a working conditional variance of each entry of , and a working correlation that we model parametrically. We introduce a new gradient boosting approach for estimating these two components through minimising our sandwich loss; this takes as input a user-chosen regression method that is used within the boosting procedure to estimate the conditional variances. We demonstrate the favourable performance of our resulting ‘sandwich boosting’ method in a variety of numerical experiments.

In Section 2 we introduce the sandwich loss and compare its population version to ML and GEE-based equivalents. In Section 2.3 we verify that despite the unusual form of the sandwich loss, under relatively mild conditions, we can expect a minimiser of the sample version to converge to its population counterpart (Theorem 3). We introduce our general cross-fitted weighted estimation approach in Section 3.1 before describing our proposed sandwich boosting scheme in Section 3.2. Section 4 presents theory showing that our resulting estimator for the partially linear model coefficient is asymptotically Gaussian under relatively mild conditions on the predictive ability of nuisance function estimators, permitting the construction of honest confidence intervals for . In contrast to existing results in this context, our theory permits the group sizes to grow with the number of groups , and importantly accommodates misspecification of the conditional covariance. We present the results of a variety of numerical experiments on simulated and real-world data in Section 5 that further explore the themes hinted at in Examples 1 and A.2, and demonstrate the effectiveness of our sandwich boosting approach. We conclude with a discussion in Section 6 outlining avenues for further work, including a sketch of an extension to estimating a coefficient function in a version of (6) with replaced by a function that is a linear combination of known basis functions, using a generalisation of the sandwich loss. The appendix contains the proofs of all results presented in the main text, additional theoretical results, further details on the examples and numerical experiments, and a detailed computational analysis of the sandwich boosting methodology. Our sandwich boosting methodology is implemented in the R package sandwich.boost111https://github.com/elliot-young/sandwich.boost/. Below we briefly review some related work not necessarily covered elsewhere in the introduction, and collect together some notation used throughout the paper.

1.4 Other related literature

As indicated in the previous sections, our work connects to a vast literature on mixed effects models, also known as multilevel models or hierarchical models, and generalised estimating equations. Some recent developments in this area have looked at such models in high-dimensional contexts. In particular Li et al. [2022] considers using a particular proxy conditional covariance parametrised by a single parameter for computational simplicity. Li et al. [2018] considers a flexible conditional covariance specification through selecting from high-dimensional random effects via regularising terms in the Cholesky decomposition of the covariance matrix of the random effects.

Most closely related to our setup here however is the work of Emmenegger and Bühlmann [2023] who consider partially linear mixed effect models [Zeger and Diggle, 1994] in the double machine learning (DML) framework, popularised by Chernozhukov et al. [2018]; see also Kennedy [2022] for a recent review of this broad topic. Earlier work considered specific nonparametric estimators for in the (grouped) partially linear model framework, for example Huang et al. [2007] use regression splines to estimate and a GEE approach for estimating weights. Within the DML area, work related to the setting of the (ungrouped) partially linear model includes Vansteelandt and Dukes [2022] who propose new targets of inference and DML estimation strategies in potentially misspecified generalised partial linear models, and Emmenegger and Bühlmann [2021] who look at estimation in partially linear models with unobserved confounding in an instrumental variables setting using a DML approach and additional regularisation to reduce variance.

Boosting [Schapire, 1990, Freund and Schapire, 1996], on which our sandwich boosting proposal is built, has received a lot of interest in recent years due to its success on modern datasets of interests. A long line of work (see for example Breiman [1999], Mason et al. [1999], Friedman et al. [2000], and Bühlmann and Hothorn [2007] for a review) in machine learning has resulted in the functional gradient descent perspective of boosting, which we make use of in developing our sandwich boosting proposal.

In general terms, our use of the sandwich loss involves selecting among estimators (in our case determined by weight functions) based on estimates of their quality (in our case, their MSEs). In this sense it is related to a number of statistical approaches, including, for example cross-validation. Of particular note is the recent work of Park and Kang [2021] who look at average treatment effect estimation in multilevel studies and pick from among a family of estimators based on augmented inverse propensity weighting [Robins et al., 1994, Robins and Rotnitzky, 1995], one minimising an estimate of their variance.

1.5 Notation

We denote the maximum and minimum eigenvalues of a matrix by and respectively. Let denote the cumulative distribution function of a standard Gaussian distribution. We will also use the shorthand . For the uniform convergence results we will present, it will be helpful to write, for a law governing the distribution of a random vector , for its expectation and for any measurable . Further, given a sequence of families of probability distributions , and for a sequence of families of real-valued random variables (which we note are permitted to depend on ), we write if for all , for a given function if , and if for any there exists such that .

2 The sandwich loss

In this section, we first outline a general weighted least squares framework for estimating , within which we formally introduce the notion of the sandwich loss. In Section 2.2 we study properties of the sandwich loss at the population level, compared to the ML and GEE-based approaches described in Section 1.1. In Section 2.3 we then study the behaviour of the sample version of the sandwich loss and show that under mild conditions, a minimiser will converge in probability to the population minimiser. For the remainder of this paper, we will work in the setting of the partially linear model (6), which includes as a special case, the linear model (1).

2.1 Weighted estimation

Here we outline a general strategy for weighted estimation of , with which we will introduce our proposed sandwich loss. For simplicity, we describe our approach in terms of an auxiliary dataset, independent of our main data. In practice however, we use sample splitting and cross-fitting to construct our estimator, as described in Section 3.1. As in the approach of Emmenegger and Bühlmann [2023], we begin by regressing each of and onto using our main data to give estimates and of the row-wise conditional expectations and . With these we form respective vectors of residuals and . With these, we find an initial estimate of using (7) with the set to identity matrices:

We then form ‘estimates’ of the errors and given by and to obtain a sandwich estimate of ( times) the variance of a -estimator utilising given weight matrices :

| (9) |

In the above, is a function that given for any , outputs a matrix . The sandwich loss views the variance estimate as a function of , and specifically as a measure of the quality of the weights , somewhat analogously to how the likelihood views the density of the data as a function of parameters to be determined. Given a class of functions , we then propose to find an (approximate) minimiser of over (see Section 3.2 for our sandwich boosting approach for carrying this out). While the sandwich loss is thus a rather trivial (re-)definition, as we try to demonstrate in the present work, this shift in perspective from variance estimate to a loss function to be minimised, can lead to non-trivial improvements in terms of estimating . Note that the sandwich loss is unaffected by any positive scaling of : this is to be expected since the resulting is equally invariant.

On the auxiliary data, we then set , and form a weighted -estimate of the form (7). Our should then deliver a low variance estimate of since this is precisely the way in which it was constructed. Indeed, we show in Section 4 that the variance estimate (9) consistently estimates the true variance (times ).

Note that although we have introduced the sandwich loss via a specific construction of the error estimates and , it is applicable more broadly to other such estimates. For example, in the simpler linear model setting, applying the Woodbury matrix identity shows that the sandwich variance estimate (2) also takes the form given in (9), for certain error estimates formed through weighted least squares regressions.

In the following section, we compare the sandwich loss to the ML and GEE-based approaches outlined in Section 1.1 theoretically by studying population versions of these.

2.2 Population level analysis

The examples in Section 1.1 hint at potential issues with the ML and GEE-based approaches, which unlike the sandwich loss, are not explicitly geared towards minimising the variance of the resulting : whilst when the conditional covariance is well-specified, their goals coincide with those of the sandwich loss, in the case of misspecification, this need not be the case. Recall that since the weight matrices are restricted to be functions of alone due to the requirement of Neyman orthogonality, it is plausible that some form of misspecification is unavoidable.

To study the properties of the approaches under potential misspecification, we work for simplicity in a setting where we observe iid instances of the partially linear model (6) with fixed finite group size , and consider population versions of the respective losses:

Here and are to be understood as generic versions of their counterparts with subscript satisfying , and almost surely for some . The weight function is in

| (10) |

where is some arbitrarily small constant. Note that the GEE loss is defined here with respect to an arbitrary matrix norm derived from an inner product, such as the Frobenius norm.

Let us write and for the infimum of over . Proposition 1 below shows that is the asymptotic variance of both the ML and GEE losses, and gives a condition under which this coincides with .

Proposition 1.

-

(a)

and are both minimised over (10) by .

-

(b)

The asymptotic variance of the sandwich loss satisfies , with equality if and only if

(11)

Note the condition (11) holds in the instance that ; but given variable is considered here to be important enough for its associated parameter to be the target of our inference, it is not inconceivable that the errors depend on them after conditioning on . In such settings, it is possible for the ratio to be arbitrarily large, as Theorem 2 below shows.

Theorem 2.

Suppose is not almost surely constant. Then for all , and for all pairs of positive definite matrices that are functions of , there exists a law on satisfying the conditions of the model (6) with , and

While the discrepancy between and is not always expected to be very large, it is nevertheless potentially a cause for concern that this can happen even when and are identity matrices, for example.

2.3 Sample level considerations

The previous section illustrated some of the advantages of the sandwich loss at the population level. The sandwich loss (9) we propose however is unusual in the sense that it is not composed of a sum of independent terms typical of the objective functions of M-estimators. A further complication is that involves estimates of the errors and , rather than these errors themselves. The classical theory of M-estimation [van der Vaart, 1998, Chap. 5] is therefore not immediately applicable here, and it is not clear whether the useful advantages of the population level sandwich loss transfer over to its empirical counterpart. The result below however shows that under relatively mild conditions, minimisation of over a parametric class yields convergence in probability to the minimiser of . We continue to work in the setup of the previous section, where our data consist of iid groups of finite size following the partially linear model (6).

Theorem 3.

Let be some compact set and

Suppose is such that for all , . Assume the regularity conditions set out in Appendix B.3, and additionally that for estimates of the error terms either

-

(a)

, or

-

(b)

.

Then any sequence of approximate minimisers with satisfies

3 Methodology

In this section we present our sandwich boosting weighted regression procedure. We first describe the basic outline of our approach for generic weight matrices employing cross-fitting in Section 3.1 and then in Section 3.2 present our boosting strategy to approximately optimise the sandwich loss within a flexible class of working covariance models.

3.1 Cross-fitting

In Section 2.1, we outlined a simplified approach for estimating in the partially linear model (6) involving first obtaining ‘estimates’ and of the errors and with which to determine a weight function through minimising the sandwich loss (9). The second stage involved forming on an independent dataset, an estimate through (7), so in particular, conditioning on the initial dataset, would be fixed. In practice, only a single dataset would be available, and we construct the two independent datasets through sample splitting, employing a -fold cross-fitting scheme to recover the loss in efficiency in using only part of the data to construct the final estimator.

Cross-fitting is a popular approach in semiparametric problems for ensuring the independence of nuisance parameter estimates from the data on which the final estimate of the target parameter is formed. This independence means that certain empirical process terms can be controlled straightforwardly even when arbitrary nuisance parameter estimators are used. Chernozhukov et al. [2018] and Emmenegger and Bühlmann [2023] use such cross-fitting in the regular and grouped partially linear models respectively, where the nuisance function estimates in question are and . In our case, cross-fitting additionally serves to guarantee independence of the weight function estimates.

Algorithm 1 details our method, with observation groups indexed by playing the roles of the initial datasets for , and those indexed by involved in the construction of the final estimator . Note that rather than forming separate estimates of corresponding to each , we instead form sets of residuals and , finally forming using these via (7), an approach known as DML2 [Chernozhukov et al., 2018]. As well as obtaining an estimate , we also calculate a sandwich estimate of the variance, with which an approximate -level confidence interval may be constructed.

3.2 Sandwich boosting

Algorithm 1 introduced a generic approach for incorporating weight functions learnt from the data into an estimator for via approximately minimising the sandwich loss over some class of functions . We now introduce an approach for performing this approximate minimisation over a class defined implicitly through a user-chosen regression method.

To introduce our approach, it is helpful to consider a class of proxy conditional covariances parametrised as

| (12) |

where, given an input , the functions and output

Here, and for (where is some closed convex set) are proxy conditional standard deviation and correlation functions that are to be modelled nonparametricaly and parametrically respectively. Note that the working covariances (12) have the property that the th entry depends only on and ; this need not be the case for for example, but is nevertheless a reasonable simplification.

Redefining , the corresponding weight class consists of functions of the form

| (13) |

understanding, up to an arbitrary positive scale factor. As an example, an equicorrelated working correlation may be parametrised as

for , with corresponding correlation given by . We also consider a version for nested group structures permitting two constant correlations and an autoregressive form suitable for longitudinal data where ; see Appendix C. Such inverse working correlations are among the classes of weights considered in the GEE1 framework [Liang and Zeger, 1986, Zeger and Liang, 1986, Ziegler, 2011]. A key difference here however is the greater flexibility afforded by learning the working inverse standard deviation function through through a boosting scheme, as we now explain. We also outline in Section 3.2.1 how our boosting scheme may be initialised at estimated weight functions derived using existing ML or GEE-based methods, for example, thereby increasing the flexibility of the functional forms considered.

Boosting has emerged as one of the most successful learning methods, with the XGBoost implementation [Chen and Guestrin, 2016] in particular dominating machine learning competitions such as those hosted on Kaggle [Bojer and Meldgaard, 2021]. Since its introduction in the work of Schapire [1990], it has been generalised and reinterpreted as a form of functional gradient descent of an objective function based on the data [Friedman et al., 2000, Mason et al., 1999, Bühlmann and Yu, 2003, Bühlmann and Hothorn, 2007]. For an objective function applied to function , an individual boosting iteration involves perturbing the -function by a step in the ‘direction’ of the -score

| (14) |

where is the indicator function at . Procedurally, the -score is evaluated at the data points and the regressed onto the data using a user-chosen ‘base learner’.

Typically takes the form of an empirical risk, so for some loss function and predictor–response pairs . The corresponding -score evaluated at the data point then takes the simple form , a function of the th observation alone. This allows for -score calculation in linear time, as well as the possibility of parallelising computations for large data sets as exploited by XGBoost. In our case however where we wish to minimise the sandwich loss (which recall is defined in terms of estimates and of the errors) over weight functions parametrised by (13), we obtain as the -score

| (15) |

where and

Thus the -score at is a function of all the data points. Nevertheless, it may be computed for all at a cost of . However, as we show in Appendix C, for the equicorrelated, nested and autoregressive working correlation structures, this cost is reduced to and may be parallelised similarly to the standard setting of minimising an empirical risk. The critical factors in allowing this are: (a) that computing the matrix inverse present in , which for an arbitrary correlation may take time, has a simple closed form; and (b) computation of the terms and involving the sparse matrix can be arranged to be by precomputing other terms appropriately.

Along with updating by regressing the -score above onto the and taking a step in the direction of the negative of this fitted regression function, we may also perform a regular projected gradient descent update for using the -score vector

| (16) |

which may be computed at no greater cost than the -score above.

With these scores, our sandwich boosting algorithm is summarised in Algorithm 2; note denotes projection onto the set . Recall that in our cross-fitting scheme (Algorithm 1), we envisage applying boosting to approximately minimise a version of the sandwich loss corresponding to subsets of the observation indices. As is standard in boosting, the algorithm requires a choice of initialisers (in our case and ) and a base learner. In all of our numerical experiments, we take , and use additive penalised cubic regression splines implemented in the R package mgcv [Wood, 2017]. We select the number of boosting iterations by cross-validation, as recommended by [Bühlmann and Hothorn, 2007], though using our sandwich loss as the evaluation criterion. Note that the algorithm is stated for fixed step sizes and for simplicity; in Appendix E, we describe the specific choices and variable step size schemes used in our numerical results.

3.2.1 Initialising from other weighting schemes

The classes of weight functions that may be fitting using our computationally efficient boosting schemes with equicorrelated, autoregressive or nested correlations can be rather rich when used in conjunction with a flexible base learner. However, these classes would not encompass all those available using classical mixed effects modelling, for example. In order to further broaden the classes of weight functions that may be considered, one can start with an initial estimated weight or conditional covariance function estimated through GEE or ML-based approaches, and fit a weight function of the form

where is of the form given by (13), using sandwich boosting. The boosting algorithm then serves to push the initial in a better direction for the purposes of estimating . This may be carried out easily by running Algorithm 2 on transformed error estimates and similarly for . In fact, one can use multiple initialisers in this way, and pick among the best sandwich-boosted versions via cross-validation with the sandwich loss as the quality criterion.

4 Theory

In this section we present results on asymptotic normality of the -estimator of Algorithm 1, and coverage guarantees for the confidence interval construction therein. Recalling the setup of Section 3.2, we consider the case where the estimated weight functions are such that takes the form (12). Let us define and by

and write .

For simplicity of the exposition, similarly to Sections 2.2, here we consider the case where our data are iid copies of the group of observations following the partially linear model (6). Recall that is a matrix whose rows, denoted , are not necessarily independenent or identically distributed. We also relax the iid assumption at the group level to permit non-identically distributed groups of unequal size in Appendix D.

Our results here are based in part on Emmenegger and Bühlmann [2023], but build on them in two key ways. Firstly, we permit the conditional covariance to be misspecified, i.e., for the (likely) possibility that the probability limit of the is not some multiple of its inverse. Secondly, we consider asymptotic regimes that allow the group size to diverge with the total number of observations at rates we will formalise later. Throughout, we assume that the number of folds used in cross-fitting is finite.

We state our results as uniform convergence results over the sequence of classes of distributions such that for all sufficiently large and for all , the following hold. Note that in the below, , , , , and are to be thought of as constants, not depending on . The values of these are not relevant in the case where the group size is finite, but play a role in the rate of growth permitted when it is diverging. Moreover denotes for constant not depending on . We have however suppressed the dependence on in , etc.

Assumption A1 (Moment assumptions).

-

(A1.1)

There exists such that and .

-

(A1.2)

The covariance matrices and satisfy and almost surely. Further, and almost surely for some .

Lower values of and will permit faster rates of divergence of (see Appendix D). Note that when is close to the equal correlation working covariance of Section 3.2, we can expect . For our simplified result in Corollary 5 we set .

Assumption A2 (Accuracy of regression function estimators).

Define the maximum within group estimation errors of regression functions and :

Then the errors of these nuisance function estimators satisfy:

-

(A2.1)

,

-

(A2.2)

,

-

(A2.3)

and

.

The assumptions on the regression function estimates are relatively weak and identical to those in Emmenegger and Bühlmann [2023], with what is typically the strongest requirement ((A2.1)) permitting nonparametric rates of for each of and . Faster rates than this however weaken conditions on how may diverge; see Corollary 5 below.

Assumption A3 (Stability of weight function estimates).

Suppose there also exists deterministic functions and whose estimators satisfy:

-

(A3.1)

where , -

(A3.2)

.

Further suppose the associated weights satisfy

-

(A3.3)

and for some almost surely.

-

(A3.4)

and for some and almost surely.

Assumptions (A3.1) and (A3.2) require a probabilistic limit for our estimates of the weight function, but this need not correspond closely to the inverse of . The eigenvalue assumption (A3.4) however does loosely quantify the discrepancy between these, and and impact the permitted divergence rate of . The reason for introducing the is that the estimated weights need not be on the same scale as (recall that the sandwich loss is invariant to positive scaling of its argument).

Theorem 4.

Consider Algorithm 1. Let the sequence of distribution families for be such that for all sufficiently large, and for all , Assumptions A1, A2 and A3 are satisfied. Further, suppose that the group size is either finite, or diverges at a rate satisfying Assumption A4 in Appendix D. Then defining

we have that is uniformly asymptotically Gaussian

and moreover the above holds with replaced by .

The result shows in particular that constructed in Algorithm 1 is an asymptotic -level honest confidence interval, under the given assumptions. Corollary 5 below specialises a version of Theorem 4 for diverging group sizes for two cases of interest where relatively simple forms of (conservative) rate requirements on are available.

Corollary 5.

Adopt the setup and notation of Theorem 4 but suppose in (A1.1) and (A2.3), and additionally that . Suppose the estimated weight functions are constructed to fall with classes (see Section 3.2) corresponding to one of the following two settings:

-

(i)

Equicorrelated working correlation, but where the true conditional correlation may be arbitrary;

-

(ii)

Autoregressive working correlation and when (see (A1.2)).

Then the conclusions of Theorem 4 holds for diverging group sizes at the following rates:

| Equicorrelated (i): | |||

| Autoregressive (ii): |

We discuss each of the cases (i) and (ii) in turn. Case (i) places few restrictions on the true conditional covariance and so results in a more stringent requirement on the growth rate of . Recall that the middle term is required to be by (A2.1) and small values of the parameter indicate better approximation of in (A3.4). Case (ii) enforces that : this occurs for instance when the true correlation function is upper bounded by an exponentially decaying function with separation (satisfied e.g. for ARMA processes). As such, this condition may be appropriate for longitudinal data. The rate requirement on is relatively weak: both and need only satisfy a rate requirement weaker than that on entailed by (A2.1) in order for to be permitted to grow at any rate .

5 Numerical experiments

In this section we explore the empirical properties of the sandwich boosting estimator on a number of simulated and real-world datasets. In all cases where covariates are available in addition to our covariate of interest , we fit partially linear models using the approach of Algorithm 1, estimating nuisance regression functions and using cubic regression splines implemented in the mgcv package [Wood, 2017]; however in addition to using weight functions selected using sandwich boosting, we also compare to versions with these selected using quasi pseudo Gaussian maximum likelihood (ML) and GEE1 (GEE) based methods. Note that the use of Algorithm 1 with ML is essentially the approach of Emmenegger and Bühlmann [2023] but using a robust sandwich estimate of the variance.

Section 5.1 explores four simulated settings with varying degrees of misspecification of the conditional covariance. Section 5.2 looks at two datasets: the first, on orange juice sales grouped by store, highlights the benefits of flexible variance modelling via the nonparametric component in our sandwich boosting scheme (Section 3.2); and the second, a longitudinal study on women’s wages, provides a real-life example of the phenomena seen in Examples 1 and 2 where more complex conditional covariance models can lead to poorer -estimation when weights are selected using ML or GEE-based approaches, and where the minimiser of the sandwich loss is rather different to those corresponding to the ML and GEE objectives.

5.1 Simulated data

We look at four simulated scenarios, and in each case consider different weight classes : we describe these classes below in terms of their implied working covariances i.e. in terms of the inverses of the weight matrices. For all the approaches we use the cross-fitting scheme (Algorithm 1) with folds.

-

•

Homoscedastic: Depending on the setting, this consists of either equicorrelated or autoregressive working correlations scaled by a constant variance, with the single parameter estimated either by maximising a Gaussian likelihood (ML), an approach of the form given in (4) (GEE) or minimising the sandwich loss through projected gradient descent (only used in the setting of Section 5.1.3).

-

•

Heteroscedastic: This uses the same working correlations as in the homoscedastic case, but allows for more flexibility in the working conditional variance function with specifics depending on the estimation method used.

-

–

ML: We model the logarithm of the conditional variance function with a polynomial basis in the covariate with the number of basis functions (restricted to at most to avoid numerical instabilities) determined by cross-validation using Gaussian log-likelihood loss. This is carried out using the nlme package [Pinheiro et al., 2022].

- –

-

–

Sandwich loss: We use sandwich boosting as described in Section 3.2.

-

–

Section 5.1.1 considers a well-specified setting where the optimal true conditional covariance weights can in principle be replicated by the heteroscedastic weight estimators; Section 5.1.2 looks at a misspecified setting where the optimal weights depend on and varies the degree of misspecification; and Sections 5.1.3 and 5.1.4 explore the effect of varying group sizes in a settings with mildly misspecified conditional correlation and variance respectively. In all cases, we simulate data with equal independent and identically distributed groups of equal size , which we vary across the settings. The mean squared errors of -estimators corresponding to each method and setting pair, averaged over 500 repetitions, are shown in Figure 4.

5.1.1 Increasing model complexity

Consider iid instances of the partially linear model (6) with group size where is the target parameter of interest, is componentwise iid uniform , , (with the and functions applied component-wise), and with covariance matrices given by

Here is the Lipschitz constant (complexity parameter) of the conditional variance function , that we will vary. We use homoscedastic and heteroscedastic working covariance classes with equicorrelated working correlation (noting that the true correlation is also constant here). As , by Proposition 1 population minimiser of the sandwich loss and those corresponding to the ML and GEE approaches should all coincide, and so from this perspective, the former should have no clear advantage in terms of the performance of the resulting -estimator, and one might expect all heteroscedastic methods to perform similarly here since they need only model the conditional variance sufficiently well to yield the semiparametrically optimal MSE (referred to as the oracle MSE).

The top left panel of Figure 4 shows that this appears to be the case when , but for larger values of the complexity parameter, both ML and GEE approaches appear to struggle. The latter displays a somewhat erratic trajectory, peaking at an MSE 9 times that of the oracle, and even greatly exceeding that of its homoscedastic counterpart (note that the curves for the homoscedastic GEE and ML estimators almost coincide). This behaviour seems likely to be due to the GEE approach finding local optima, which recall, need not be local optima for the asymptotic MSE objective, i.e., sandwich loss; see also Example 1 Setting (b) and Appendix A.1 for a similar phenomenon. The sandwich boosted estimator in comparison remains relatively robust to this increase in model complexity, maintaining performance comparable to the oracle estimator.

5.1.2 Increasing covariance misspecification

We consider instances of the partially linear model (6) with , , and . Errors are generated by introducing an unobserved confounder between and inspired by the proof of Theorem 2 as follows:

Here acts as ‘misspecification parameter’, with larger values indicating greater confounding and violation of the condition (11) for equivalence of the ML, GEE and sandwich losses. Note that denotes the mean of the entries .

As we see in the top right panel of Figure 4, the performances of the heteroscedastic ML and GEE estimators deteriorate with increasing and yield worse MSEs than even an unweighted least squares estimator as the extent of covariance misspecification increases. In contrast, despite being equally restricted to use a misspecified class of weights that are a function of alone, the sandwich boosted has a substantially smaller MSE compared to the approaches considered, with its advantage increasing with increasing .

5.1.3 Mild conditional correlation misspecification

We consider the simple setting of (grouped) linear regression:

where and are the autoregressive and moving average parameters respectively. We take and iid Gaussian innovations for the ARMA process. We consider settings with and group sizes . To demonstrate the effect of correlation misspecification, we use a constant working variance and fit all models with an working correlation, and thus we have a misspecified correlation for group sizes . Example 1, setting (a) corresponds to this setting with . The bottom left panel of Figure 4 shows that the sandwich loss here outperforms the competing approaches, with the GEE aproach leading to an inflation in MSE over an unweighted approach for moderate group sizes.

5.1.4 Mild conditional variance misspecification

We generate iid instances of the the partially linear model (6) via

for and taking . Note therefore that as , the optimal weights that depend also on are not in the weight classes considered. All methods are fit using an equicorrelated working correlation. We again see in the bottom right Figure 4 superior performance of sandwich boosting over the competitors here.

5.2 Real-world data analyses

Here we present analyses of two datasets. We fit GEE and (heteroscedastic) sandwich boosting approaches as in the previous section, but use mixed effects models (MEM) to give a family of (working) conditional covariance functions in the ML framework by taking certain covariates as random effects. We continue to use these within Algorithm 1, using the lme4 package [Bates et al., 2015] to obtain the weights in the MEM case as in Emmenegger and Bühlmann [2023], but reporting robust sandwich estimates of the variance of the constructed. We use folds for cross-fitting. To mitigate the randomness of the resulting estimators on the sample splits themselves we aggregate the and variance estimators obtained over 50 random independent sample splits using the approach of Chernozhukov et al. [2018], Emmenegger and Bühlmann [2023]; see Appendix E for details.

5.2.1 Orange juice price elasticity

We analyse historical data on orange juice sales, available from the James M. Kilts Center, University of Chicago Booth School of Business [James M. Kilts Center, Accessed: 2022]. The dataset is composed of grouped store-level scanner price and sales data over a 121 week period from 83 Dominick’s Finer Foods stores and consists of observations.

Our goal is to estimate the price elasticity of a brand of orange juice (Tropicana) during this time period. We do this via a partially linear model (6) of the logarithm of the quantity of sales () on the logarithm of the price () accounting for confounding by events in time (), the coefficient of giving the price elasticity.

| Method |

|

||||

|---|---|---|---|---|---|

| Sandwich Boosting | 30.9 | 26.0 | |||

| Homoscedastic GEE | |||||

| Heteroscedastic GEE | |||||

| Intercept only MEM | |||||

| Intercept + Time MEM |

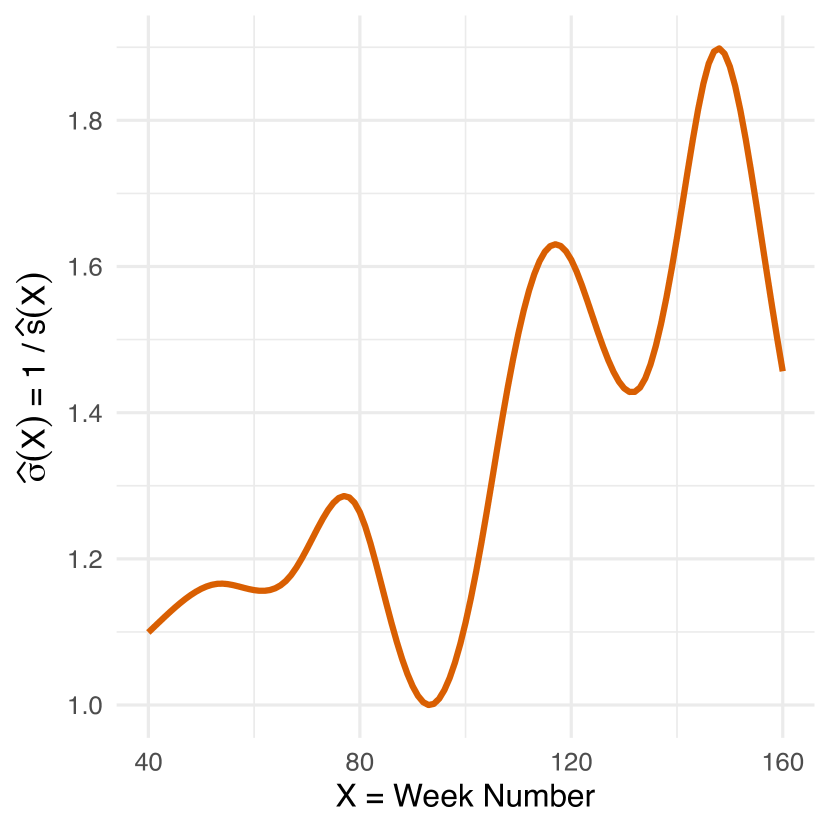

Table 2 shows the price elasticity estimators and associated sandwich variances estimates ; note GEE and sandwich boosting approaches here use an equicorrelated working correlation. We see that our sandwich boosting estimator has a 26.0% reduction in variance compared to the second best homoscedastic GEE estimator. Note that in the cases of both the mixed effects models (MEM) and GEE estimators, as a broader weight class is used, we observe poorer performance in estimating the price elasticity, illustrating the phenomenon described in Figure 3. Also note that the sandwich boosted and heteroscedastic GEE estimators model weights in the same class. However, whilst the heteroscedastic GEE estimator does not usefully model any heteroscedasticity in the data (and in fact exhibits the worst performance out of all the estimators considered), sandwich boosting successfully estimates a helpful weighting scheme. Figure 5(a) demonstrates an -function output from sandwich boosting, effectively capturing the general and seasonal trends in volatility that are not learned by the other estimators.

5.2.2 National longitudinal survey of young working women

Here we consider a dataset from the National Longitudinal Survey of Young Women [Bureau of Labor Statistics, 2004] containing the wages of 4711 young working women, each measured at approximately 6 time points per woman, totalling observations. We measure the effect of work experience in their current related sector () on the logarithm of wages (), controlling for age and tenure (), with weights a function of , using an equicorrelated working correlation for sandwich boosting and GEE approaches.

| Method |

|

||||

|---|---|---|---|---|---|

| Sandwich Boosting | 0.040 | 0.083 | 7.4 | ||

| Homoscedastic GEE | 0.040 | 0.089 | |||

| Heteroscedastic GEE | 0.039 | 0.091 | |||

| Intercept only MEM | 0.040 | 0.092 | |||

| Intercept + Age + Tenure MEM | 0.042 | 0.120 |

Table 3 gives the -estimators and associated variances for the approaches considered. Similarly to the orange juice price elasticity analysis, we see that the broader model classes of the mixed effects model and heteroscedastic GEE estimators yield larger variances than their respective homoscedastic counterparts. The sandwich boosting estimator gives a modest 7.4% reduction in variance over the second smallest homoscedastic GEE variance. Interestingly however, this improvement is entirely due to the sandwich loss rather than the potentially richer model class used by sandwich boosting: the function output by sandwich boosting is almost constant, and so it effectively uses a constant working variance and estimates a single working correlation parameter. The sandwich loss objective for this correlation (parametrised in terms of ; see Section 3.2) is plotted in Figure 5(b) alongside the objectives corresponding to the homoscedastic GEE and intercept only MEM approaches. We see that the respective -minimisers differ substantially, with the asymptotic variance (the sandwich loss) evaluated at the minimisers of the GEE and MEM approaches being larger than the asymptotic variance evaluated at any , corresponding to any working correlation in the range .

6 Discussion

In this work we have highlighted and clarified the shortcomings of some popular classical methods in the estimation of weights for weighted least squares-type estimators in partially linear models when the conditional covariance is misspecified. We instead advocate for choosing weights to minimise a sandwich estimate of the variance, what we call the sandwich loss in this context. A main contribution of ours, in the spirit of the trend towards using machine learning methods for the purposes of statistical inference, is a practical gradient boosting scheme for approximately minimising this loss over a potentially flexible family of functions defined implicitly through a user-chosen base-learner. Despite the unusual form of our loss that does not decompose as a sum over data points as with the standard case of the empirical risk, we show that for certain versions of our algorithm, the boosting updates can be performed in linear time.

Our work offers a number of directions for future research. On the computational side, it would be useful to investigate broader classes of working correlations that could be accommodated within sandwich boosting to yield linear time updates. In could also be fruitful to consider the use of the sandwich loss in other classes of models, for example it would be of interest to develop these ideas in the context of generalised (partially) linear marginal models, and beyond.

Thus far we have only considered estimator of a single scalar quantity. In other situations, one may be interested in estimating several parameters simultaneously, and in such cases there are several modifications of the basic sandwich loss that may be helpful to explore. For example, consider the following generalisation of the partially linear model (6):

| (17) |

Here denotes the Hadamard product, is a row-wise function of , and all other terms are as before; thus the response of the th observation within the th group satisfies (with a slight abuse of notation) the mean function relationship . We suppose admits the basis expansion

| (18) |

for some known basis functions (also row-wise functions of ), and unknown vector of parameters to be estimated. For example, the model where corresponds in the classical linear model setting to fitting an ‘interaction term’ between and . Given a consistent estimator of , the mean squared error of the resulting plug-in function estimator satisfies

| (19) |

This suggests the following approach. Consider a class of weighted -estimators where is a weight function among a class of , similarly to our previous framework in Section 2.1 of weighted -estimators. Then given estimates of and of , we can consider a generalised sandwich loss of the form

| (20) |

which we may attempt to minimise using a sandwich boosting approach; further details are given in Appendix F.

Our sandwich loss is defined with respect to estimated errors and derived from initial regressions, which in particular, take no advantage of the dependence structure in the data, unlike the final estimate . Clearly initial weighted regressions could deliver improved estimates of the errors, in turn giving an improved estimate of . This suggests a scheme with weights and residuals being updated iteratively, analogous to iterative generalised least squares [Goldstein, 1986, 1989]. In the simple linear model setting, where the residuals are derived from linear regressions, a generalised sandwich loss of the form (20) may be appropriate for delivering accurate estimates of the errors. How to do this for a general regression is less clear but would certainly be worthy of further investigation.

References

- Bates et al. [2015] D. Bates, M. Mächler, B. Bolker, and S. Walker. Fitting linear mixed-effects models using lme4. Journal of Statistical Software, 67(1):1–48, 2015. doi: 10.18637/jss.v067.i01.

- Bojer and Meldgaard [2021] C. S. Bojer and J. P. Meldgaard. Kaggle forecasting competitions: An overlooked learning opportunity. International Journal of Forecasting, 37(2):587–603, 2021. ISSN 0169-2070. doi: https://doi.org/10.1016/j.ijforecast.2020.07.007. URL https://www.sciencedirect.com/science/article/pii/S0169207020301114.

- Box [1976] G. E. P. Box. Science and statistics. Journal of the American Statistical Association, 71(356):791–799, 1976. doi: 10.1080/01621459.1976.10480949.

- Breiman [1999] L. Breiman. Prediction Games and Arcing Algorithms. Neural Computation, 11(7):1493–1517, 10 1999. doi: 10.1162/089976699300016106.

- Bühlmann and Hothorn [2007] P. Bühlmann and T. Hothorn. Boosting Algorithms: Regularization, Prediction and Model Fitting. Statistical Science, 22(4):477 – 505, 2007. doi: 10.1214/07-STS242.

- Bühlmann and Yu [2003] P. Bühlmann and B. Yu. Boosting with the l2 loss. Journal of the American Statistical Association, 98(462):324–339, 2003. doi: 10.1198/016214503000125.

- Bureau of Labor Statistics [2004] U. D. o. L. Bureau of Labor Statistics. National longitudinal survey of young women, 1968-1988 (rounds 1-15). Produced and distributed by the Center for Human Resource Research (CHRR), The Ohio State University, 2004. URL https://www.stata-press.com/data/r10/nlswork.dta.

- Carroll [1982] R. J. Carroll. Adapting for Heteroscedasticity in Linear Models. The Annals of Statistics, 10(4):1224 – 1233, 1982. doi: 10.1214/aos/1176345987.

- Chen and Guestrin [2016] T. Chen and C. Guestrin. Xgboost: A scalable tree boosting system. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 785–794. Association for Computing Machinery, 2016. doi: 10.1145/2939672.2939785.

- Chernozhukov et al. [2018] V. Chernozhukov, D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68, 2018. doi: 10.1111/ectj.12097.

- Corbeil and Searle [1976] R. R. Corbeil and S. R. Searle. Restricted maximum likelihood (reml) estimation of variance components in the mixed model. Technometrics, 18(1):31–38, 1976.

- Crowder [1995] M. Crowder. On the use of a working correlation matrix in using generalised linear models for repeated measures. Biometrika, 82(2):407–410, 1995.

- Diggle et al. [2013] P. Diggle, P. Heagerty, K.-Y. Liang, and S. Zeger. Analysis of Longitudinal Data, volume Second edition of Oxford Statistical Science Series. OUP Oxford, Oxford, 2013.

- Emmenegger and Bühlmann [2021] C. Emmenegger and P. Bühlmann. Regularizing double machine learning in partially linear endogenous models. Electronic Journal of Statistics, 15(2):6461–6543, 2021.

- Emmenegger and Bühlmann [2023] C. Emmenegger and P. Bühlmann. Plug-in machine learning for partially linear mixed-effects models with repeated measurements. Scandinavian Journal of Statistics, 2023. doi: 10.1111/sjos.12639.

- Fahrmeir and Tutz [2001] L. Fahrmeir and G. Tutz. Multivariate Statistical Modelling Based on Generalized Linear Models. Springer Series in Statistics. Springer, 2 edition, 2001.

- Freund and Schapire [1996] Y. Freund and R. E. Schapire. Experiments with a new boosting algorithm. In International Conference on Machine Learning, pages 148–156, 1996.

- Friedman et al. [2000] J. Friedman, T. Hastie, and R. Tibshirani. Additive logistic regression: a statistical view of boosting (with discussion and a rejoinder by the authors). The Annals of Statistics, 28(2):337 – 407, 2000. doi: 10.1214/aos/1016218223.

- Goldstein [1986] H. Goldstein. Multilevel mixed linear model analysis using iterative generalized least squares. Biometrika, 73(1):43–56, 1986.

- Goldstein [1989] H. Goldstein. Restricted unbiased iterative generalized least-squares estimation. Biometrika, 76(3):622–623, 1989.

- Gourieroux and Monfort [1993] C. Gourieroux and A. Monfort. Pseudo-likelihood methods. In Econometrics, volume 11 of Handbook of Statistics, pages 335–362. Elsevier, 1993.

- Gourieroux et al. [1984] C. Gourieroux, A. Monfort, and A. Trognon. Pseudo maximum likelihood methods: Theory. Econometrica, 52(3):681–700, 1984.

- Halekoh et al. [2006] U. Halekoh, S. Højsgaard, and J. Yan. The r package geepack for generalized estimating equations. Journal of Statistical Software, 15/2:1–11, 2006.

- Hardin and Hilbe [2003] J. W. Hardin and J. M. Hilbe. Generalized estimating equations. Chapman and Hall, 2003.

- Hartley and Rao [1967] H. O. Hartley and J. N. K. Rao. Maximum-likelihood estimation for the mixed analysis of variance model. Biometrika, 54(1/2):93–108, 1967.

- Heagerty and Zeger [2000] P. J. Heagerty and S. L. Zeger. Marginalized multilevel models and likelihood inference. Statistical Science, 15(1):1–19, 2000.

- Huang et al. [2007] J. Z. Huang, L. Zhang, and L. Zhou. Efficient estimation in marginal partially linear models for longitudinal/clustered data using splines. Scandinavian Journal of Statistics, 34(3):451–477, 2007.

- Huber [1967] P. J. Huber. The behaviour of maximum likelihood estimates under nonstandard conditions. Proceedings of the Fifth Berkeley Symposium, pages 221–223, 1967.

- James M. Kilts Center [Accessed: 2022] U. o. C. B. S. o. B. James M. Kilts Center. Dominick’s finer foods dataset. Available from Chicago Booth Research Data Center: https://www.chicagobooth.edu/research/kilts/research-data/dominicks, Accessed: 2022.

- Jennrich [1969] R. I. Jennrich. Asymptotic Properties of Non-Linear Least Squares Estimators. The Annals of Mathematical Statistics, 40(2):633 – 643, 1969. doi: 10.1214/aoms/1177697731.

- Kennedy [2022] E. H. Kennedy. Semiparametric doubly robust targeted double machine learning: a review. arXiv preprint arXiv:2203.06469, 2022.

- Li et al. [2022] S. Li, T. T. Cai, and H. Li. Inference for high-dimensional linear mixed-effects models: A quasi-likelihood approach. Journal of the American Statistical Association, 117(540):1835–1846, 2022.

- Li et al. [2018] Y. Li, S. Wang, P. X.-K. Song, N. Wang, L. Zhou, and J. Zhu. Doubly regularized estimation and selection in linear mixed-effects models for high-dimensional longitudinal data. Statistics and its Interface, 11(4):721, 2018.

- Liang and Zeger [1986] K.-Y. Liang and S. L. Zeger. Longitudinal data analysis using generalized linear models. Biometrika, 73(1):13–22, 1986.

- Liang et al. [1992] K.-Y. Liang, S. L. Zeger, and B. Qaqish. Multivariate regression analyses for categorical data. Journal of the Royal Statistical Society. Series B (Methodological), 54(1):3–40, 1992.

- Lumley [1996] T. Lumley. Generalized estimating equations for ordinal data: A note on working correlation structures. Biometrics, 52(1):354–361, 1996.

- Lundborg et al. [2022] A. R. Lundborg, I. Kim, R. D. Shah, and R. J. Samworth. The projected covariance measure for assumption-lean variable significance testing. arXiv preprint arXiv:2211.02039, 2022.

- Mason et al. [1999] L. Mason, J. Baxter, P. Bartlett, and M. Frean. Boosting algorithms as gradient descent. In Advances in Neural Information Processing Systems, volume 12. MIT Press, 1999.

- McCullagh and Nelder [1989] P. McCullagh and J. A. Nelder. Generalized linear models. Monographs on statistics and applied probability (Series) ; 37. Chapman and Hall, London, 2 edition, 1989.

- Park and Kang [2021] C. Park and H. Kang. A more efficient, doubly robust, nonparametric estimator of treatment effects in multilevel studies. arXiv preprint arXiv:2110.07740, 2021.

- Pinheiro et al. [2022] J. Pinheiro, D. Bates, and R Core Team. nlme: Linear and Nonlinear Mixed Effects Models, 2022. URL https://CRAN.R-project.org/package=nlme. R package version 3.1-161.

- Pinheiro and Bates [2000] J. C. Pinheiro and D. M. Bates. Mixed-Effects Models in S and S-PLUS, volume 1 of Springer Statistics and Computing. Springer, New York, 2000.

- Prentice and Zhao [1991] R. L. Prentice and L. P. Zhao. Estimating equations for parameters in means and covariances of multivariate discrete and continuous responses. Biometrics, 47(3):825–839, 1991.

- Robins and Rotnitzky [1995] J. M. Robins and A. Rotnitzky. Semiparametric efficiency in multivariate regression models with missing data. Journal of the American Statistical Association, 90(429):122–129, 1995.

- Robins et al. [1994] J. M. Robins, A. Rotnitzky, and L. P. Zhao. Estimation of regression coefficients when some regressors are not always observed. Journal of the American statistical Association, 89(427):846–866, 1994.

- Robinson [1987] P. Robinson. Asymptotically efficient estimation in the presence of heteroskedasticity of unknown form. Econometrica, 55(4):875–891, 1987.

- Royall [1986] R. M. Royall. Model robust confidence intervals using maximum likelihood estimators. International Statistical Review / Revue Internationale de Statistique, 54(2):221–226, 1986.

- Schapire [1990] R. E. Schapire. The strength of weak learnability. Machine Learning, 5(2):197–227, 1990. doi: 10.1007/BF00116037.

- Shah and Peters [2020] R. D. Shah and J. Peters. The hardness of conditional independence testing and the generalised covariance measure. The Annals of Statistics, 48(3), June 2020. doi: 10.1214/19-aos1857.

- Tsiatis [2006] A. A. Tsiatis. Semiparametric theory and missing data, volume 1 of Springer series in statistics. Springer, New York, 2006.

- van der Vaart [1998] A. W. van der Vaart. Asymptotic Statistics. Cambridge University Press, 1998.

- Vansteelandt and Dukes [2022] S. Vansteelandt and O. Dukes. Assumption-lean inference for generalised linear model parameters. Journal of the Royal Statistical Society Series B: Statistical Methodology, 84(3):657–685, 2022.

- Wood [2017] S. Wood. Generalized Additive Models: An Introduction with R. Chapman and Hall/CRC, 2 edition, 2017.

- You et al. [2007] J. You, G. Chen, and Y. Zhou. Statistical inference of partially linear regression models with heteroscedastic errors. Journal of Multivariate Analysis, 98(8):1539–1557, 2007. doi: 10.1016/j.jmva.2007.06.011.

- Zeger and Diggle [1994] S. L. Zeger and P. J. Diggle. Semiparametric models for longitudinal data with application to cd4 cell numbers in hiv seroconverters. Biometrics, pages 689–699, 1994.

- Zeger and Liang [1986] S. L. Zeger and K.-Y. Liang. Longitudinal data analysis for discrete and continuous outcomes. Biometrics, 42(1):121–130, 1986.

- Ziegler [2011] A. Ziegler. Generalized estimating equations. Lecture notes in statistics (Springer-Verlag). Springer, New York, 2011.

Appendix A Supplementary material relating to Section 1

A.1 Further details for Example 1

Recall that in Example 1 we consider the grouped linear model

where are iid; note that since we plot the population level objective functions of the ML and GEE approaches, along with the asymptotic variance of the resulting for each given value of , there is no need to specify the total number of groups . In Setting (a), we take and as the first realisations of an model with unit variance and autoregressive parameters and moving average parameter . Further, we take .

In Setting (b), we take and the model parameters , . Compared to the Setting (a), the working correlation model is less severely misspecified. In this setting, the obtained by minimising the ML objective results in a that has the same asymptotic mean squared error (MSE) as the unweighted estimator (obtained by setting in this working correlation model, i.e. not attempting to model the correlation at all). The GEE objective is also non-convex in , and in fact a gradient descent procedure minimising the GEE objective initialised at (as in the geepack package [Halekoh et al., 2006]) will incorrectly estimate at the local minimum at . Using this estimate for results in a with MSE times that of the unweighted estimator (and times that of the resulting from minimising the sandwich loss); see Table 4.

| Objective function |

|

|||

|---|---|---|---|---|

| Unweighted | 1.4 | |||

| GEE (geepack) | 3.4 | |||

| ML (gls) | 1.4 | |||

| Sandwich loss (sandwich.boosting) | 1.0 |

A.2 Further details on Example 2

We give further details on misspecified conditional variance motivating example in Section 1.1. Note specifically this example compares the three loss functions considered at the population level (and not the sample level) therefore exploring asymptotic properties of each loss function. We consider the ungrouped () setting where the random variables satisfy

for some (arbitrary) and where , and for constants and .

We consider using a misspecified class of functions of the form

where , with estimates of an optimal minimising one of the ML, GEE or SL losses (each method discussed in Section 1). At the population level for this example these losses can be expressed as

The model class considered is therefore parametrised by a single parameter , with each loss function minimised either analytically or via a line search.

Given a minimising of one the three losses, the (scaled) mean squared errors of the -estimator and -estimator (weighted using the -estimator) can be calculated analytically as

respectively, with results as given in Table 1

Appendix B Proof of results in Section 3

B.1 Proof of Proposition 1

We first show that is minimised over by ; this follows immediately from the decomposition of as

Note this result holds for any matrix norm derived from an inner product.

We now show that is minimised over by . Noting that where

we aim to minimise the function for arbitrary . We define by . Then given some fixed and we define the function for . The second order Taylor expansion of then gives

for some . Now, by Jacobi’s formula,

and so

Further, by direct calculation

where denotes the Frobenius norm, and with equality holding if and only if . Therefore whenever ,

and so is minimised over by .

Finally, we will show that

This can be shown by noting that

by using the identities and (for vectors and matrix ), where denotes the Kronecker product, and the Cauchy–Schwarz inequality. Equality holds in the above if and only if

Therefore with equality if and only if the condition

holds. Using the identity (for matrices ) this condition is equivalent to

completing the proof.

B.2 Proof of Theorem 2

As is almost surely non-constant there exists measurable such that . With this, we define the random variables for some to be determined later, and where with . Further, define and where and .

One can then verify that and hence and . Further, we can show that:

and

Therefore, using the forms of , and derived in the proof of Proposition 1 (also noting that ),

taking .

B.3 Regularity conditions for Theorem 3

For the statement of Theorem 3 we also impose the following regularity conditions:

-

(i)

The map is continuous for all .

-

(ii)

.

-

(iii)

The errors satisfy the moment bounds and for finite constants .

B.4 Proof of Theorem 3

Using Theorem 5.7 of van der Vaart [1998] it suffices to show

| (21) |

Define the error terms

and subsequently the terms

Then we can decompose

First we claim that . This follows by the uniform law of large numbers [Jennrich, 1969], which may be applied as due to Assumption (iii). It can similarly be shown that . Now,

and so by Markov’s inequality, . Further,

by the triangle equality. We proceed by showing that each term on the right hand side is . In the case of Assumption (a) we have

by the Cauchy–Schwarz inequality (twice). We can similarly show (again by multiple uses of the Cauchy–Schwarz inequality) that . It then follows by Markov’s inequality (alongside Lemma 12) that , and so . If alternatively Assumption (b) holds then we consider each term separately:

Term :

the first inequality follows as for any , the second follows by Hölder’s inequality, and the third by the Cauchy–Schwarz inequality.

Term :

where the first inequality follows as for any , the second follows by the Cauchy–Schwarz inequality, and the third by Hölder’s inequality.

Term :

by for any and using the Cauchy–Schwarz inequality.

Term :

By applying Markov’s inequality to each of the above terms we have , and therefore with Lemma 12 we have .

Therefore, combining the results above with the triangle inequality

| (22) |

Now, by the triangle inequality

We have already shown that and it is similarly straightforward to show that . Therefore, it remains to show that

| (23) |

To show this, it will be helpful to define

Then, further defining it follows that

| where | ||||

| where | ||||

| by (22). |

The penultimate step follows by solving the quadratic inequality in . This proves the claim (23) and hence (21), completing the proof.

Appendix C Further details on sandwich boosting

C.1 Working correlation structures that exhibit computational benefits

We outline three common working correlation structures that allow for computationally fast sandwich boosting, at computational order as opposed to .

Equicorrelated:

The equicorrelated working correlation structure (and its scaled inverse) is given by