Contagious McKean–Vlasov problems with common noise: from smooth to singular feedback through hitting times

Abstract

We consider a family of McKean-Vlasov equations arising as the large particle limit of a system of interacting particles on the positive half-line with common noise and feedback. Such systems are motivated by structural models for systemic risk with contagion. This contagious interaction is such that when a particle hits zero, the impact is to move all the others toward the origin through a kernel which smooths the impact over time. We study a rescaling of the impact kernel under which it converges to the Dirac delta function so that the interaction happens instantaneously and the limiting singular McKean–Vlasov equation can exhibit jumps. Our approach provides a novel method to construct solutions to such singular problems that allows for more general drift and diffusion coefficients and we establish weak convergence to relaxed solutions in this setting. With more restrictions on the coefficients we can establish an almost sure version showing convergence to strong solutions. Under some regularity conditions on the contagion, we also show a rate of convergence up to the time the regularity of the contagion breaks down. Lastly, we perform some numerical experiments to investigate the sharpness of our bounds for the rate of convergence.

1 Introduction

In this paper, we study the limiting behaviour of the family of conditional McKean-Vlasov equations

| (1.1) |

as tends towards zero. Here and are independent standard Brownian motions, and is a rescaled mollifier which converges to the Dirac delta as converges. Motivated by their origin as the limit of a particle system, is usually referred to as the idiosyncratic noise (of a representative particle) and as the common noise. Also for the same reason, is referred to as the loss process and quantifies the amount of mass that has crossed the boundary at zero by time . A solution to this system is the random probability measure and the loss process , conditional on .

In addition to the more classical measure dependence of the coefficients that characterise McKean–Vlasov equations, there is a further feedback mechanism through the loss process : depending on the value of , pushes towards zero causing the value of to increase, hence pushing even closer to 0. The integral kernel , which is parameterised by some , is a key element of the model and captures a latency in the transmission of to present in real-world systems. Precise conditions on the coefficient functions will be given later.

One motivation for this model arises in systemic risk, where represents the distance-to-default of a prototypical institution in a financial network with infinite entities, see for example [17]. In this setting denotes the proportion of institutions that have defaulted by time and is the cause of endogenous contagion through the feedback mechanism. In this model, we use the kernel to capture feedback where, when a financial institution defaults and their positions are unwound, the counterparties experience a gradual decrease in the value of their assets over time.

This kernel structure has also been used in other settings. A model for bank runs with common noise and smooth transmission of boundary losses was analysed in [3]. Moreover, [19] study a related mean-field model for neurons interacting gradually through threshold hitting times, albeit without common noise.

If the support of is contained in the interval with , then the transmission of shocks is almost instantaneous as the integral is then approximately equal to . In this article, we prove convergence in the following sense: if we fix a kernel and rescale it with a variable by , then we have convergence in the M1-topology of to , where is a (relaxed) solution to

| (1.2) |

It is well known that equations of the form (1.2) may develop jump discontinuities. Without common noise, given suitable assumptions, for sufficiently large a jump must occur, [16, Theorem 1.1]. And with common noise, there is a set of paths of positive probability where a jump must happen, [24, Theorem 2.1]. This motivates our use of the M1-topology as it is rich enough to facilitate the convergence of continuous functions to ones that jump. The equation, (1.1), has been posed in slightly more generality (with ) in [17]. As the convergence is strictly in the M1-topology, not J1, we only consider to be of the form . If we considered it to also be a function of and/or , then we cannot expect to obtain an equation of the form (1.2) in the limit as , due to and having jumps at the same time.

Intuitively, (1.1) is a smoothed approximation to (1.2). From a mathematical perspective, the advantage of smoothing out the interactions is that the well-posedness of (1.1) is well understood, see [17]. On the other hand, for the formulation (1.2) with instantaneous feedback, various questions concerning existence are yet to be addressed, and uniqueness remains a completely open problem. Even with constant coefficients, one cannot rely on the methods from [10], where uniqueness was treated successfully in the case of no common noise () and constant coefficients. Further discussion of the issue of existence of solutions to (1.2) will follow later, while we do not address uniqueness.

From a modelling perspective, the smoothing naturally captures the latency in real-world systems. Our motivation for taking the limit as to 0 is to investigate the convergence to the system where the feedback is felt instantaneously. This captures the situation when the latency is small compared to the time scale of interest. The instantaneous transmission model has been used in applications to systemic risk, the supercooled Stefan problem, and leaky integrate-and-fire models in neuroscience.

Variants and special cases of (1.2) have been the subject of extensive research in the field. In the simplest scenario, where and are both zero, equal to , and is a positive constant, we obtain the probabilistic formulation of the supercooled Stefan problem. A version of the Stefan problem, introduced by Stefan in [31], can be described as follows:

| (1.3) |

The solution to the partial differential equation (PDE) describes the temperature and the boundary of a material undergoing a phase transition, typically from a solid to a liquid. The supercooled Stefan problem describes the freezing of a supercooled liquid (i.e. a liquid which is below its freezing point) on the semi-infinite strip . Here is the location of the liquid-solid boundary at time . In the PDE literature, it was first established in [30] that may explode in finite time, i.e, there exists a such that . While many authors constructed classical solutions to (1.3) for , [14, 12, 13, 23, 18], from the PDE perspective it was unclear how to restart a given solution after a finite time blow-up of .

Under suitable assumptions on the initial condition (see [28]), the process admits a density on the interval , which satisfies the PDE:

By setting , we recover the classical formulation of the Stefan problem. The probabilistic reformulation provided a way to restart the system following a blow-up. Blow-ups of correspond to jumps in the probabilistic setting.

From a probabilistic perspective, when and are both zero, equal to , and is a positive constant, the stochastic differential equation (SDE) presented here yields a succinct model for studying contagion in large financial networks. With this motivation, extensive research has been conducted to investigate various properties of physical solutions to this equation [28, 27, 16, 25, 24, 26, 21, 8]. The paper [10] establishes that when possesses a bounded density that changes monotonicity finitely many times, then is unique, and for any , is continuously differentiable on for some . Additionally, in [16], it is demonstrated that for an initial condition with a bounded density that is Hölder continuous near the boundary, is unique, continuous and has a weak derivative until some explosion time. The work in [25] extends these results by showing that if the initial condition possesses an density, then we have uniqueness for a short time after the explosion time. Moreover, irrespective of the initial condition, there exists a minimal loss process that will be dominated by any other loss process that solves the equation [8].

For arbitrary initial conditions, see [16, Example 2.2], there may be infinitely many solutions. Furthermore, different solutions will take different jump sizes. Hence, it may be possible for two solutions to be equal up to the first jump time and then take jumps of different sizes. To address this ambiguity that arises at a jump time, a condition is typically imposed to restrict to admissible jump sizes. This condition is known as the physical jump condition, defined as:

| (1.4) |

where .The intuitive interpretation of (1.4) is that if we take the density of and displace it an amount towards , then the mass of the system below zero is exactly . So it is the minimal amount that we may displace our density such that the displacement and the mass below zero correspond. From a modelling perspective, the physical jump condition is the preferred choice of jump sizes due to its economic and physical interpretations. It has been established that minimal solutions are physical, [8, Theorem 6.5]. However, it remains unclear whether physical solutions are necessarily minimal due to the lack of uniqueness for general initial conditions.

Returning to (1.2), recent advances have been made in the study of general coefficients, specifically , , and , in the presence of common noise. In Remark 2.5 from [27], a generalized Schauder fixed-point argument is presented to construct strong solutions in this setting. Strong solutions refer to the property , indicating that the random probability measure is adapted to the -algebra generated by the common noise. In [24], an underlying finite particle system was shown to converge to relaxed (or weak) solutions (see 2.1), satisfying the aforementioned physical jump condition (with coeffiecients , , and ). Weak/relaxed solutions are characterised by having , instead of , see 2.1. As the empirical distributions of the finite particle systems converge weakly to , there is no guarantee that will be adapted to the -algebra generated by the common noise. As regards strong solutions in the sense just discussed, existence of strong solutions for the common noise problem satisfying the physical jump condition (1.4) has not yet been addressed in the literature.

The main contributions and structure of this paper are as follows:

-

•

Firstly, in Section 2, we prove Theorem 2.4 and Corollary 2.5 showing the weak convergence of solutions of (1.1) to relaxed solutions of (1.2) as , i.e., as the gradual feedback mechanism becomes instantaneous in the limit. As a by-product, this gives a novel method for establishing the existence of solutions to (1.2), avoiding time regularity assumptions on as needed in [24]. Furthermore, we derive an upper bound on the jump sizes, Theorem 2.4, and, under additional assumptions on the coefficients, Corollary 2.5, show that the loss process satisfies the physical jump condition (1.4).

-

•

Secondly, in Section 3, we show in Theorem 3.8 that, if the coefficients depend solely on time and is a constant, then we may upgrade our mode of convergence from weak to almost sure. As a consequence of the method employed, we can guarantee that the limiting loss process will be -measurable and satisfy the physical jump condition. In addition, we have the existence of strong solutions in this setting.

-

•

Lastly, in Section 4, for constant coefficients and without common noise, we provide in Proposition 4.1 an explicit rate of convergence of the smoothed approximations to the singular system prior to the first time the regularity of the loss function breaks down. We also give numerical tests of the convergence order in scenarios of different regularity, with and without common noise.

2 Weak convergence of smoothed feedback systems

Fix a finite time horizon and let denote the set of probability measures on a measurable space . When is a metric space, denotes the Borel -algebra. Let further denote the space of sub-probability measures, which we shall endow with the topology of weak convergence. For any interval and metric space , let denote the space of continuous functions from to . Similarly, denotes the space of càdlàg functions from to .

For every , we fix a probability space that supports two independent Brownian motions. To simplify the notation, we will denote these Brownian motions by and , however, it is important to note that they may not be equal for different values of . Similarly, we adopt the simplified notations and to refer to and the expectation under the measure respectively. In this section, we characterise the weak limit of the system given by the following equation as tends to zero:

| (2.1) |

where . The coefficient (, or respectively) is a measurable map from (, or respectively) into . The initial condition, denoted by , is assumed to be independent of the Brownian motions and positive almost surely. Finally, we define .

One way to view is as the mean-field limit of an interacting particle system where particles interact through their first hitting time of zero. The interactions among particles are smoothed out over time by convolving with the kernel . As approaches zero, the effect of interactions occurs over increasingly smaller time intervals. As is a mollifier, it is natural to expect that, as tends to zero, to converge to the instantaneous loss at time . That is to say, along a suitable subsequence, the random tuple would have a limit point where and solves

| (2.2) |

with . In this system, the feedback is felt instantaneously and is characterised by the common noise . In what follows, for technical reasons, we construct an extension of the process . For an arbitrary stochastic process , we define its extended version as follows,

| (2.3) |

We artificially extend the processes to be constant on and by a pure Brownian noise term on . Therefore, the extension to is . Consequently, the random measure remains -measurable. We show that the collection of measures is tight, hence there exists a subsequence that converges to zero such that converges weakly to the random measure . However, as the mode of convergence is weak, we cannot expect that the limit point is also measurable with respect to .

Hence, we relax our notion of solution to (2.2), which leads to the definition of relaxed solutions employed in the literature when studying the mean-field limit of particle systems with common noise [24] and also in the mean-field game literature with common source of noise [4].

Definition 2.1 (Relaxed solutions).

Let the coefficient functions , and be given along with the initial condition at time . We define a relaxed solution to (2.2) as a family on a filtered probability space such that

| (2.4) |

with , , , and , where is a two dimensional Brownian motion, is a càdlàg process, and is a random probability measure on the space of càdlàg paths .

As the drift and correlation function depend on a flow of measures, we still want them to satisfy some notion of linear growth and Lipschitzness in the measure component. We will also require some spatial and temporal regularity such that (2.1) is well-posed. We will suppose that our coefficients , and satisfy the following assumptions.

Assumption 2.2.

-

(i)

(Regularity of ) For all and , the map is . Moreover, there exists a constant such that

where

for any .

-

(ii)

(Space/time regularity of ) The map is . Moreover, there exists a constant such that

-

(iii)

(-Lipschitzness of ) For all , there exists a constant s.t.

where

for any .

-

(iv)

(Non-degeneracy) For all , , and , the constants and assumed above is such that and .

-

(v)

(Temporal regularity of ) The map is and increasing with .

-

(vi)

(Sub-Gaussian initial law) The initial law, is sub-Gaussian,

and has a density s.t. .

-

(vii)

(Regularity of mollifier) The function , the Sobolev space with one weak derivative in and zero at , such that is non-negative, and .

Solutions of (2.1) are the matter of study in [17]. Under 2.2, the existence and uniqueness of solutions are guaranteed.

Theorem 2.3 ([17, Theorem 2.7]).

Let be the unique strong solution to the SPDE

where the coefficients , and satisfy 2.2, and , the set of Schwartz functions that are zero at . Then, for any Brownian motion , we have

where is the solution to the conditional McKean-Vlasov diffusion

with initial condition .

The existence of solutions to (2.1) allows us introduce the main result of this section, showing that solutions to (2.4) exist as limit points of the collection of smoothed equations.

Theorem 2.4 (Existence and convergence generalised).

Let be the extended version of in (2.1) and set . Then, the family of random tuples is tight. Any subsequence , for a positive sequence which converges to zero, has a further subsequence which converges weakly to some . and are standard Brownian motions, is a random probability measure and is independent of .

Given this limit point, there is a background space which preserves the independence and carries a stochastic process such that is a relaxed solution to (2.4). Moreover, we have the upper bound

| (2.5) |

for all .

The notation stands for the conditional law of given , which indeed defines a random -measurable probability measure on . Under stronger assumptions, namely and be of the form , , and is a positive constant, there are established results in the literature for a lower bound on the jumps of the loss function. By Proposition 3.5 in [24], the jumps of the loss satisfy

Due to the generality of the coefficients, we were not able to establish if (2.5) holds with equality. The primary reason is the lack of independence between the term driven by the idiosyncratic noise and the remainder of the terms that is composed of. Hence the technique employed in [24, Proposition 3.5] may not be readily applied or extended to our setting. Regardless, given these two results, under stronger assumptions, we have the following existence result.

Corollary 2.5 (Existence of physical solutions).

Let the coefficients and be of the form , , and satisfy 2.2. Then provided and constant, there exists a relaxed solution to

| (2.6) |

Moreover, we have the minimal jump constraint

for all . This determines the jump sizes of .

This work presents a minor generalisation of the results in [24]. In their work, the authors imposed the condition that must be Hölder continuous with an exponent strictly greater than . Here we have made no explicit assumptions on the regularity of , only requiring it to be non-degenerate. Consequently, we can consider Corollary 2.5 as an extension to Theorem 3.2 in [24].

2.1 Limit points of the smoothed system

In order to show the existence of a limit point of , we must first choose a suitable topology to establish convergence. By Theorem 2.4 in [17], is continuous for every , but the loss of the limiting process may in fact jump. Skorohod’s M1-topology is sufficiently rich to facilitate the convergence of continuous functions to those with jumps.

The theory in [32] requires our càdlàg processes to be uniformly right-continuous at the initial time point and left-continuous at the terminal time point, when working with functions on compact time domains. As we are starting from an arbitrary initial condition which is positive almost surely, the limiting process may exhibit a jump immediately at time given sufficient mass near the boundary. For this reason, we shall embed the process from into , where , using the extension defined in (2.3). Unless stated otherwise, for notational convenience we shall denote the latter space, , by . Recall, is defined to be the law of conditional on . That is .

To show tightness and convergence of the collection of random measures , we shall follow the ideas in [9] and [24]. To begin, we first derive a Gronwall-type estimate of the smoothed system uniformly in . These estimates are necessary to show the tightness of and the existence of a limiting random measure. In the following Proposition and its sequels, will denote a constant that may change from line to line and we will denote the dependencies on the value of in its subscript. To further simplify notation, we shall use , and to denote

respectively. We shall use , and to denote their corresponding extensions as defined in (2.3).

Proposition 2.6 (Gronwall upper bound).

For any and , there is a independent of such that

| (2.7) |

Proof.

By the linear growth condition on and the triangle inequality,

By [17, Lemma A.3], for any . Therefore, a simple application of Gronwall’s inequality shows that

By (vi) in 2.2, has finite moments for every . Furthermore by employing Burkholder-Davis-Gundy inequality to control , we may deduce that for all and . Now observing that , we have by the monotonicity of expectation and Jensen’s inequality

Taking expectations and applying Fubini’s Theorem followed by Gronwall’s inequality, we obtain

| (2.8) |

Lastly, by Burkholder-Davis-Gundy inequality and (ii) from 2.2, we may bound (2.8) independent of . This completes the proof. ∎

The collection of measures are -valued random measures. To show that this collection of random variables is tight, we will need to look for compact sets in . In fact, it will be sufficient to show that is tight in . Due to the extension of the process, the tightness of the collection of measures follows easily from the properties of the M1-topology and [1, Theorem 1].

Proposition 2.7 (Tightness of smoothed random measures).

Let denote the topology of weak convergence on induced by the M1-topology on . Then the collection is tight on under 2.2.

Proof.

Define . By [32, Theorem 12.12.3], we need to verify two conditions to show the tightness of the measures on endowed with the M1-topology:

-

(i)

.

-

(ii)

For any , we have where is the oscillatory function of the M1-topology, defined as [32, Equation 12.2, Section 424].

To show the first condition we observe that by definition of the extension of our process, we have

Then, it is clear by Markov’s inequality and Proposition 2.6 that for any

uniformly in . Therefore by taking the supremum over and then over , the first condition holds. We shall not show the second condition directly. By [1, Theorem 1], the second condition is equivalent to showing

-

(I)

There is some , uniformly in , such that for all and where .

-

(II)

for all .

Note that by 2.2 we have is non-decreasing and non-negative. Therefore by the properties of Lebesgue-Stielitjes integration, is non-decreasing. As monotone functions are immaterial to the M1 modulus of continuity

where is given by

for and for . Hence to show (I), it is sufficient to bound the increments of . Note that when , is constant. Therefore, trivially we have for any . When by the formula above for we have that

| (2.9) |

Employing the linear growth condition on and Proposition 2.6,

| (2.10) |

uniformly in . By Burkholder-Davis-Gundy and the upper bound on , it is clear that

| (2.11) |

uniformly in . Therefore by Markov’s inequality,

where all the constants hold uniformly in . To verify the second condition, we observe that for any and

uniformly in . Hence we have shown that

Therefore together, conditions (I) and (II) show

for all uniformly in . This shows condition (ii). Lastly, we shall employ Markov’s inequality and Prokhorov Theorem to construct a compact set in to conclude that are tight. To begin, fix a . Now for any , we may find a such that

We define . By [32, Theorem 12.12.2], has compact closure in the M1-topology. The closure of is denoted by . Furthermore by construction . By the subadditivity of measures and Markov’s inequality

| (2.12) |

Finally, we consider the set . As endowed with the topology is a Polish space, therefore Prokhorov Theorem may be applied and it will be sufficient to show that the set of measures is tight, hence will then have compact closure in by Prokhorov Theorem. It is clear by construction that the set of measure are tight as the sets are compact in endowed with the topology. By (2.12), we have , uniformly in . As was arbitrary, this completes the proof. ∎

2.2 Continuity of hitting times

Note that is a Polish space by [32, Theorem 12.8.1] and its Borel -algebra is generated by the marginal projections, [32, Theorem 11.5.2]. Hence, the topological space is also a Polish space. Therefore, by invoking Prokhorov Theorem, [2, Theorem 5.1], tightness is equivalent to being sequentially pre-compact. So, we may choose a weakly convergent subsequence for a positive sequence which converges to zero. Let denote the limit point of this sequence. Using this limit point, we will construct a probability space and a stochastic process that will be a solution to (2.6).

Before doing this, we seek to show that for a co-countable set of times , converges weakly , where is a function on whose value is the first hitting time of . To be explicit

and

| (2.13) |

with the convention that . Our first result is that for -almost every measure , -almost every path is constant on the interval .

Lemma 2.8.

For -almost every measure , is supported on the set of paths such that .

Proof.

As is a Polish space, we may apply Skorohod’s Representation Theorem [2, Theorem 6.7]. Hence there exists a common probability space, and -valued random variables and such that

It is straight forward to see-by [32, Theorem 13.4.1]-the following maps from into itself

are continuous. Now for a the maps and from onto such that

are continuous. Therefore, by the Continuous Mapping Theorem, and almost surely in .

Fix an , then by Portmanteau Theorem and Fatou’s lemma

where the last equality follows from the embedding of from into . So by continuity of measure and the Monotone Convergence Theorem, as was arbitrary,

Similarly . ∎

As is fundamentally a time-changed Brownian motion with drift, it is not hard to show that, with probability one, will take a negative value on any open neighbourhood of its first hitting time of zero. This property is preserved by weak convergence for almost every realisation of . Furthermore, as the Lebesgue-Stieltjes integral takes non-negative values, by weak convergence we expect almost every realisation of to be supported on paths that only jump downwards.

Lemma 2.9 (Strong crossing property).

For any

| (2.14) | ||||

| (2.15) |

Proof.

As with the space of càdlàg functions, we shall employ the short hand notaiton for this proof to denote . Now, as is non-degenerate and bounded by assumption, by Kolmogorov-Chentsov Tightness Criterion, [22] and [7], we have that is tight. Additionally we define the random variable . By definition of , . Therefore is uniformly bounded by Proposition 2.6 and hence is tight on .

As marginal tightness implies joint tightness, we have is tight in by Proposition 2.7. Given a suitable subsequence, also denoted by for simplicity, we have and . Here and are used to denote the first and second marginal respectively.

Intuitively, and should have the same law as we are averaging over the stochasticity inherited by the common noise. By definition of and , for any continuous bounded function , we have

As is a Polish space, by a Montone Class Theorem argument and Dykin’s Lemma, we have

| (2.16) |

Define the canonical processes , and on , where for , and . By considering the parametric representations, the map is M1-continuous for any . Hence, by the linear growth condition on , the Continuous Mapping Theorem, and the Portmanteau Theorem, for any with and

| (2.17) | ||||

The last equality follows by the fact that for any

Sending countably and employing the right continuity of and , we deduce

Furthermore, for all -almost surely. By Lemma A.1, is a continuous local martingale with respect to the filtration generated by . It is clear that is a stopping time with respect to the filtration generated by . So the claim follows by Lemma A.2 if and . For the former condition, it is sufficient to show

As , then by Skohorod’s Representation Theorem, there exists a and on a common probability space such that , , and almost surely in . By the Portmanteau Theorem, for any

as has a -density by 2.2 (vi). So . By Lemma 2.8 and (2.16)

Therefore, is supported on paths such that for every -almost surely. Hence almost surely. Furthermore as is an M1-continuous map, follows from a simple application of the Continuous Mapping Theorem and Proposition 2.6. Therefore we deduce,

where and the final equality is due to Lemma A.2. ∎

Now we have all the ingredients to show that is an M1-continuous map.

Corollary 2.10 (Hitting time continuity).

For -almost every measure , we have that the hitting time map is continuous in the M1-topology for -almost every .

Proof.

By Lemma 2.9, for -almost every measure is supported on the set of paths where only jumps downwards and one of the following conditions hold:

-

(i)

and takes a negative value on any neighbourhood of ,

-

(ii)

and ,

-

(iii)

and .

If (i) holds, then by Lemma A.3 is M1-continuous at . If (ii) holds- and -then for any approximating sequence in the M1-topology, we must have eventually as the parametric representations get arbitrarily close in the uniform topology. Therefore as eventually, by definition eventually. Therefore is M1-continuous at . If (iii) holds, when and , then for any , with being a continuity point. We must have because only jumps downwards. So for any approximating sequence in the M1-topology, eventually . Hence, eventually . So as can be made arbitrarily close to zero, by definition . Therefore is M1-continuous at . ∎

With the result stating the hitting time is an M1-continuous map, weak convergence of the loss function follows immediately.

Lemma 2.11 (Continuity of conditional feedback).

For -almost every measure the map is continuous with respect to for all . is the set of continuity points of .

Proof.

Suppose in where is in the support of . We may assume is such that is M1-continuous for -almost every . By Skohorod’s Representation Theorem,

where is continuous for almost all paths and almost surely in . Now, for any , by the Monotone Convergence Theorem

| (2.18) |

Therefore, employing the continuity of and (2.18),

by the Dominated Convergence Theorem. So, we conclude

∎

Furthermore, we have weak convergence of the mollified loss to the singular loss.

Corollary 2.12 (Convergence of delayed loss).

For -almost every measure , converges to for any and that conveges to in .

Proof.

By Lemma 2.11, converges to for any when is supported on such that is M1-continuous map. Such measures have full support by Corollary 2.10. Furthermore, for every such ,

| (2.19) |

in the M1-topology as functions from as the functions are non-decreasing, [32, Corollary 12.5.1]. Now, for any ,

For any , we observe

As M1-convergence implies local uniform convergence at continuity points, [32, Theorem 12.5.1], and is a continuity point, by setting and sending , we have and all go to zero. ∎

2.3 Martingale arguments and convergence

As marginal tightness implies joint tightness, is tight in where is shorthand notation for , the space of continuous functions from to endowed with the topology of uniform convergence. From now on we fix a weak limit point along a subsequence for which converges to zero. Although we fixed a limit point, all the following results will hold for any limit point.

Let and . So . For completeness, we will define the probability space where and is the corresponding Borel -algebra. Define the random variables and on such that for any tuple ,

Hence the joint law of is and . We also define the limiting loss function and the co-countable set of times

| (2.20) |

Looking at the approximating system, we know for any . Even though is the weak limit of -measuable random variable, weak convergence does not all us to guarantee that limit points will be -measurable. Regardless, we may exploit the independence from the approximating system to deduce the independence of and in the limit. To fix the notation, let denote the projection of the measure onto its first two coordinates and denote the projection onto its final coordinate. then we intuitively expect .

Lemma 2.13 (Independence from idiosyncratic noise).

Let and be random variable on the probability space defined above. Then, is independent of .

Proof.

As and are Polish spaces, it is sufficient to show for any and that

| (2.21) |

The result follows by employing the Dominated Convergence Theorem and Dynkin’s Lemma. Now (2.21) follows readily by weak convergence and the Portmanteau Theorem as

The equality in the second line follows from the independence of from . ∎

We shall use to construct a probability space where we can define a process that will solve (2.2) in the sense of 2.1. Prior to that, we need to define the map employed in the martingale arguments that follow. This allows us to deduce that the process we construct will be of the correct form. For any , we define the following functionals

| (2.22) | ||||

| (2.23) |

where for any ,

and satisfies 2.2. For any with and we define the function

| (2.24) |

for arbitrary . We define the functionals

| (2.25) |

Lastly, we set the corresponding functionals without the mollification denoted by and . They are defined in exactly the same way as and with replaced by .

Remark 1 (Measurability of measure flows).

Using Corollary 2.12, we have the following proposition.

Proposition 2.14 (Functional Continuity I Generalised).

For -almost every measure , we have and converges to and respectively, whenever in , along a sequence for which is bounded for some and that converges to zero.

Proof.

By Lemma 2.9 and the definition of , we have a set of ’s that have full measure, such that

for any , and . First, we shall show that converges to . By Corollary 2.12, converges to . It is well-known that for any Borel measurable functions and of finite variation, we have for any

This together with the continuous differentiability of implies

As , by Skorohod’s Representation Theorem, there exists a and defined on a common probability space such that and almost surely in . Hence,

By Lemma A.6,

| (2.26) |

almost surely for any . Since contains all of the almost sure continuity points of , by the properties of M1-convergence and (2.26), we have

almost surely for any . Hence, we deduce converges almost surely to in . Lastly, we observe

| (2.27) |

for some constant that depends on and only but is uniform in . Therefore, is uniformly bounded as

and where the latter is uniformly bounded in for some by (2.27) and assumption. Therefore by Vitali’s Convergence Theorem, it follows that converges to .

The convergence of and to and respectively follows by similar arguments. As and are totally bounded by 2.2 (ii) and (iv), and are uniform in bounded. The continuity of and the almost sure convergence of to in the M1-topology ensures that

almost surely for all . Lastly, by the bounds on the and the boundness of , a straightforward computation shows

Therefore, the functions and satisfy 2.2 (i). Now we may apply Lemma A.6 and conclude

almost surely for all . ∎

The remainder of this section aims to show that the conditional law of converges weakly to a random variable which will have the dynamics defined in (2.6). This is achieved in the following two steps,

-

(i)

First, we construct a probability space such that , and defined as in (2.23), are continuous martingales.

- (ii)

To this end, we now proceed to show the above two claims. We begin by defining the probability space where and is the Borel -algebra . We define the probability measure

| (2.28) |

for any . Observe by construction, for any

Furthermore under , and are still Brownian motions and is independent of . This is immediate as for any ,

Given these ingredients, we may now show our first claim.

Proposition 2.15.

Let be given as in (2.23). Then , , and are all continuous martingales on , where

Proof.

If is continuous, then the continuity of the other processes follows from the continuity of and the continuity of integration. For simplicity, we shall use to denote any one of , or . Hence to show that is a martingale, it is sufficient by a Monotone Class argument that

| (2.29) |

To begin, recall where and . By Skohorod’s Representation Theorem, we may find and defined on some common probabilty space such that , and almost surely in . By definition of , for any

| (2.30) |

where the constant is from Proposition 2.6.

By (2.30), . Furthermore, by employing the Borel-Cantelli Lemma, we may deduce . So, we have a set of probability one,

such that almost surely for any and . By definition of , for any

| (2.31) |

where the constant depends on the constant from applying Burkholder-Davis-Gundy, , and the bounds on but is independent of . Hence uniformly in .

Employing Proposition 2.15 and Vitali’s Convergence Theorem

where is used to represent one of , , , or depending on . Recall for arbitrary , . So

| (2.32) |

where is either one of , or depending on the choice of . By the boundness assumption on , 2.2 (ii), is a martingale. As , we have (2.32) equals zero by the tower property. Hence, we have shown (2.29).

Lastly, to see the continuity of , define the function

for . As before, define the functionals

Following the same proof of Proposition 2.14, we have for -almost every measure , convegres to whenever in along a sequence for which

for some . We have finite moments for any , by (2.30). Therefore, by functional continuity and Vitali’s convergence theorem for any we have

By definition of and Burkholder-Davis-Gundy,

where the constant is uniform in . As is dense, by Kolmogorov’s Criterion, there is a continuous process that is a modification of . As is right continuous and is dense, these two processes are indistinguishable. Hence has a continuous version. ∎

Now, we have all ingredients to prove Theorem 2.4.

Proof of Theorem 2.4.

By Proposition 2.7, is tight. By Prokhorov Theorem, tightness on Polish spaces is equivalent to being sequentially precompact. Therefore for any subsequence , where is a positive sequence that converges to zero, we have a convergent sub-subsequence. Fix a limit point of this subsequence. As we have fixed , we define the probability space exactly as in (2.28). Now, define the càdlàg process by

Then, by the construction of and that by Lemma 2.13, for all

and . Consequently,

By Proposition 2.15,

is a continuous local martingale with

where . As and are standard independent Brownian Motions, by Levy’s Characterisation Theorem we have that

Now, as , the map is -almost surely continuous for -almost every measure . A simple application of the Portmanteau Theorem shows that . By Lemma 2.8, . The independence between and follows by Lemma 2.13. A similar argument as one employed in Lemma 2.13 shows . Lastly by Lemma A.9,

for all . ∎

3 Stronger mode of convergence

One of the limitations of the method in Section 2 is that it fails to yield a strong solution. That is, is not equal to . This is due to the mode of convergence employed being weak. To the best of our knowledge, there are no results in the existing literature relating to the existence of strong physical solutions in the setting with common noise. By Remark 2.5 from [27], the existence of strong solutions in the setting when , and are functions of time only is shown; however, it remains unclear whether these solutions are physical or not.

The work introduced in [8] provided an alternative framework to construct solutions to systems with simplified dynamics and without common noise. This is done by a fixed-point approach. Notably, the constructed solutions possess a minimality property, meaning that any alternative solution to the system will dominate the solution obtained in [8]. By utilising the mean-field limit of a perturbed finite particle system approximation, the authors deduce that minimal solutions are in fact physical.

This section extends this work to the case with common noise. Provided more restrictive assumptions on the coefficients than those introduced in 2.2, we provide an algorithm to construct minimal -measurable solutions to the singular and smoothed system. Furthermore, we get almost sure convergence of the smoothed minimal system towards the singular minimal system. As a consequence, we are able to conclude that the minimal -measurable solution is, in fact, physical. This provides an alternative method to show minimal solutions are physical in the setting of [8].

We fix a filtered probability space that satisfies the usual conditions and supports two independent Brownian motions. This differs from Section 2 as the filtered probability space may change as we change . The mode of convergence was weak in Section 2, therefore the smoothed systems needed not be defined on the same probability space. In this section, to be able to show a stronger mode of convergence, we require that our probability space and our Brownian motions are fixed because our methods employ a comparison principle approach.

We would like the loss process to be adapted and measurable with respect to the common noise. Hence, for measurability reasons, we define as the -algebra generated by and augmented to contain all -null sets. We define to be the right continuous filtration generated by that contains all the information up to time and augmented to contain all -null sets. To be precise, that is

As Brownian motion is continuous and has independent increments, is still a standard Brownian motion under the filtration .

We now propose our alternative method of solution construction. We will be considering the equation

| (3.1) |

where is a constant. The coefficients , , and are a measurable maps from into satisfying 2.2. The system starts at time with initial condition which is almost surely positive. We require no further assumptions on the initial condition.

Given any solution to (3.1), we may view the paths of living in the space

is the space of cumulative density functions on the extended real line. We endow with the topology induced by the Lévy-metric

The Lévy-metric metricizes weak convergence, hence we are endowing with the topology of weak convergence as we can associate each with a distribution . Hence as is endowed with the topology of weak convergence, then we observe that in if and only if for all . With this topology, is a compact Polish space. As in the previous section, we will let denote the space of càdlàg functions from to and we endow with the M1 topology. As elements in are increasing, then convergence in is equivalent to convergence in .

3.1 Properties of and existence of strong solutions

For any -measureable process that takes values in , we may define the operator as

By the independence of increments of Brownian motion, . Therefore, we may always choose a version of such that is a -measurable process with càdlàg paths. By artificially setting , has paths in . First, we observe that is a continuous operator.

Proposition 3.1 (Continuity of ).

Let and be a sequence of adapted -measurable processes that take values in such that almost surely in . Then almost surely in .

Proof.

For simplicity, we shall denote by and by . As done previously, we may artificially extend and to be càdlàg processes on by

By the coupling, for every . Hence trivially in . As convergence in is equivalent to convergence in the M1-topology, almost surely in . Addition is a M1-continuous map for functions that have jumps of common sign, [32, Theorem 12.7.3], therefore almost surely in . It is clear that for any and

for any by Lemma A.2. Hence, is an M1-continuous map at almost every path of by Lemma A.3. By the Conditional Dominated Convergence Theorem, for any we have

| (3.2) |

almost surely. Now, we fix a such that is countable and dense in . By (3.2), we may find a of full measure such that if we fix then (3.2) holds at for all . Now we fix a , and such that . By continuity, there is a such that and

| (3.3) |

Therefore for by monotonicity of and the above we have

for all large. In the case when is a continuity point, we set . Hence we have convergence of to at the continuity points of . Therefore, by definition, converges to in . As is a set of full measure, the result follows. ∎

We also observe that the map also preserves almost sure monotonicity of the input processes.

Lemma 3.2 (Monotonicity of ).

Let and be -measurable processes with paths in such that almost surely, then almost surely.

Proof.

As almost surely, then we have almost surely. It follows that almost surely. By monotonicity of conditional expectation,

almost surely for any . As and are càdlàg , we deduce for any almost surely. ∎

With these two results in hand, we have all the ingredients to construct -measurable solutions to (3.1).

Proposition 3.3.

Proof.

For any , we define inductively

with and is the application of -times to the function . By Lemma 3.2, almost surely for any . As these processes are càdlàg, we deduce for any almost surely. Let denote the set of full measure where the monotonicity holds for every and we fix a that is countable and dense. As is increasing and bounded above, let

It is clear for any , is -measurable. Therefore we define

By construction, is a càdlàg -measurable process with paths in . A similar proof as that used in the end of Proposition 3.1, shows that almost surely in . Hence by Proposition 3.1, . As and are càdlàg -measurable processes that are limits of , we may conclude that almost surely. Lastly, if is any càdlàg -measurable process that solves (3.1), then by Lemma 3.2 we have for all almost surely. Taking limit, we deduce almost surely. ∎

We now turn our attention to the smoothed version of (3.1). We will work on the same filtered probability space as in (3.1) that satisfies the usual conditions and supports two independent Brownian motions. For an , we consider the McKean–Vlasov problem

| (3.4) |

where is a constant. The coefficients , , and are a measurable maps from into satisfying 2.2. The system starts at time with the same initial condition, , as in (3.1). As the assumptions on is more general than those imposed in Section 2, we may not apply Theorem 2.3 to guarantee existence of solutions to (3.1). So, we propose an alternative proof to show existence of solutions. The proof follows in the same faith as Proposition 3.3. We define the operator

Therefore, solutions to (3.4) are equivalent to finding almost sure fixed points of . A simple consequence of Proposition 3.1, is that is also continuous.

Corollary 3.4 (Continuity of ).

Let and be a sequence of adapted -measurable processes that take values in such that almost surely in . Then almost surely in .

Proof.

By Proposition 3.1, it is sufficient to show that the map is continuous on . It is clear that if we implicitly define the value of to be at , then it is an element of . Let and be deterministic functions in such that in . That is, we have pointwise convergence on the continuity points of . As , it has a continuous representative. So without loss of generality, we take to be this representative. Hence is bounded on compacts, so an easy application of the Dominated Convergence Theorem gives

∎

As convolution with non-negative functions preserves monotonicity, we further deduce that is also monotonic by Lemma 3.2.

Corollary 3.5.

Let and be -measurable processes with paths in such that almost surely, then almost surely.

With monotonicity and continuity of the operator in hand, we have all the necessary results to deduce the existence of solutions to (3.4).

Proposition 3.6.

Proof.

By employing Corollary 3.4 and Corollary 3.5, this proof is verbatim to that of Proposition 3.3. ∎

The purpose of in (3.4) is two-fold. Firstly, it smoothens the effect of the feedback component on the system, hence preventing the system from jumping and making it continuous. Secondly, it delays the effect of of the system. Intuitively, one would expect that the system with instantaneous feedback, i.e. (3.1), will be dominated by that with delayed feedback. Furthermore, intuitively as we decrease , then the system with the smaller value of should be dominated by one with a larger value. This is because as decreases, the rate at which the feedback is felt by the system increases.

Lemma 3.7.

For any such that , it holds that

almost surely.

Proof.

For any deterministic functions such that , then a straight forward computation shows that and . The claim now follows from the monotonicity of Proposition 3.1 and Lemma 3.2. ∎

3.2 Convergence of minimal solutions

From now on, we will fix a sequence of positive real numbers that converge to zero. As we have established that is a decreasing process in by Lemma 3.7, we shall exploit this structure to construct a solution to (3.1). This will be a -measurable solution that will be dominated by every other -measurable solution. Therefore, we may conclude that this solution must coincide with on a set of full measure.

Theorem 3.8 (Almost sure convergence).

Let be a sequence of positive real numbers that converges to zero. Let denote the -measurable solution to (3.4) constructed in Proposition 3.6, and denote the -measurable solution to (3.1) constructed in Proposition 3.3. Then by considering the extended system

we have almost surely in . Furthermore, converges to almost surely in and satisfies the physical jump condition.

Proof.

As is a bounded sequence of reals converging to zero, we may find a decreasing subsequence which converges to zero. We fix a that is countable and dense in and by Lemma 3.7 we may find a such that for any . By the boundness of and Lemma 3.7,

is well defined for any . Furthermore by Lemma 3.7, we may deduce that

for any . It is clear by construction that is -measurable. Lastly, we define

It is immediate that is a càdlàg -measurable process. Following the similar procedure as at the end of Proposition 3.1 with the obvious changes, we obtain that almost surely in . For simplicity, we will denote by simply and let

Then almost surely in . As for every almost surely and

for any , we have that is M1-continuous at almost every path of . Therefore we deduce is a -measurable solution to (3.1). By Lemma 3.7, we have that almost surely. By Proposition 3.3, we must have almost surely and hence almost surely in . As converges to almost surely in , then by the Conditional Dominated Convergence Theorem in . By Lemma A.9 and [24, Proposition 3.5], we have

for all . ∎

Remark 2 (Propagation of minimality).

This result is parallel to Theorem 6.6 in [8], which states that minimal solutions to the finite particle system approximation will converge in probability to the limiting equation provided a unique physical solution exists. The above shows that the -measurable minimal solutions to the smoothed system will converge to the -measurable minimal solution of the limiting system without needing to assume the existence of a unique physical solution.

All of the results in this section only required non-negativity of the initial condition. Moreover, we only established the existence of solutions to (3.1) and (3.4) but made no comments and have no results regarding the number of solutions in such a general setting. However, if we assume that the initial condition satisfies 2.2 (vi), then there is a unique solution to (3.4). In other words, the we constructed is the only solution. Furthermore, if we further assume that the initial condition satisfies

then is an almost sure continuity point of . Therefore these observations along with Theorem 3.8 allow us to deduce the following result.

4 Rates of convergence

One of the limitations of the previous arguments is that they fail to yield a rate at which the convergence will occur. Provided the system is simple enough, that is in the case of no drift, no common noise and a volatility parameter set to , we employ a coupling argument to show the speed of convergence, which depends on the regularity of .

The regularity of the loss process, , has been established in the literature, [10, 16], for a suitable class of initial conditions. In this setting, we not only have almost-sure convergence of the stochastic process along a subsequence, but we will have uniform convergence on any time domain before the time that the regularity of decays. These results are in some sense parallel to those presented [20] but the difference lies in the fact that we are looking at the rate of convergence of systems with smoothed loss to the limiting system as opposed to the convergence of numerical schemes that approximate the limiting system. To be precise, we will be considering the following system of equations

| (4.1) |

where , is a standard Brownian motion, is a function from to satisfying 2.2 and .

4.1 Theoretical estimates on rates of convergence

The main result of this section is the following:

Proposition 4.1.

Let be a physical solution to (4.1) with initial condition . Suppose further that admits a bounded initial density s.t.

where are constants with . Then, for any there exists a constant s.t.

where

| (4.2) |

Proof.

By assumption, we are in the setting of [16, Theorem 1.8]. Hence, we have a unique solution, , to (4.1) up to the time defined as in (4.2). Also, for all there exists s.t. where

Step 1: Regularity of . Choose . As , for Lebesgue a.e. we may write

where the last inequality is from with . This implies

The last inequality is due to the subadditivity of concave functions. Therefore, is almost everywhere - Hölder continuous.

Step 2: Decomposition of into an integral form.

We may write as

Observe

Therefore

| (4.3) |

Step 3: Comparison between the delayed loss and instantaneous loss. By Lemma 3.7, we have that , therefore by following in the same spirit as [16, Proposition 3.1] we have

where and the second inequality follows by (4.3). As , we have

By (4.3), we may find a constant such that the second term above is bounded by . Therefore,

| (4.4) |

where

Step 4: Bounds on

As depends on and , we may not immediately apply Gronwall’s lemma or any of its generalisations. Hence we construct upper bounds to relax the dependence of on and via the function and this allows us to apply a generalisation of Gronwall’s lemma. Recall , hence in the case when

where we used the substitution . In the case when , as the support of is in

Step 5: Gronwall type argument

Now that we have sufficiently decoupled from , we may put (4.4) into a form where we may apply a generalised Gronwall Lemma. By step 4 case 1 and (4.4), we have for

By the second case of step 4 and (4.4), we have for

where the last line follows from applying Taylor’s Theorem and the Monotone Convergence Theorem. We note is summable. Now we turn our attention onto the expression in the penultimate line. In the case when ,

where the first inequality follows from the fact that as and for . In the case when , we observe that

and

Therefore, we have shown that

for all . As and are bounded by , we have independent of being greater or less than ,

for any . Lastly, by Proposition A.10, using and , then as and

where the last equality follows from the fact that . This completes the proof. ∎

The works of Fasano et al. [14, 12], Di Benedetto et al. [11], and Chayes et al. [5, 6] extensively investigate the supercooled Stefan cooling problem, focusing on the existence of a unique solution without blow-ups for all time or until the entire liquid freezes. Recently, Delarue et al. [10] established global uniqueness for the system described in (4.1), under the condition that the density of the initial condition undergoes only a finite number of changes in monotonicity. In fact, under this assumption, the loss is continuously differentiable on for some . Moreover, if the initial density has sufficient regularity, the loss will be continuously differentiable from the start. Motivated by these results, we next investigate the rate of convergence when the loss function is differentiable.

Proposition 4.2.

Suppose we have a unique physical solution to (4.1) such that for some . Then for any , there exists a constant such that

Proof.

See appendix. ∎

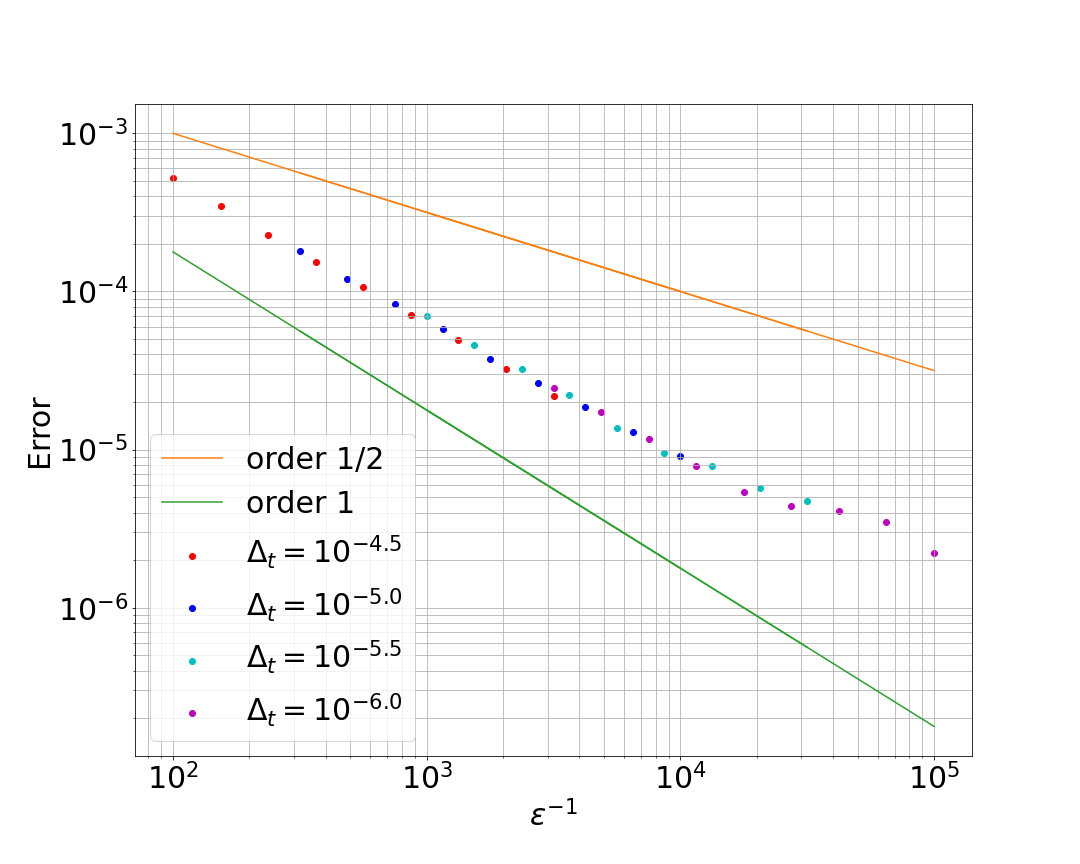

4.2 Numerical simulations

Lastly, we investigate the convergence rate of the smoothed loss function towards the singular loss function through numerical simulations. The aforementioned estimates, for the case without common noise, provide insights into the pace at which the smoothed system will approach the singular system, prior to the decline in regularity of the singular loss function. The proofs employed in the analysis utilised relatively crude upper bounds, prompting the question of whether the obtained rates are optimal.

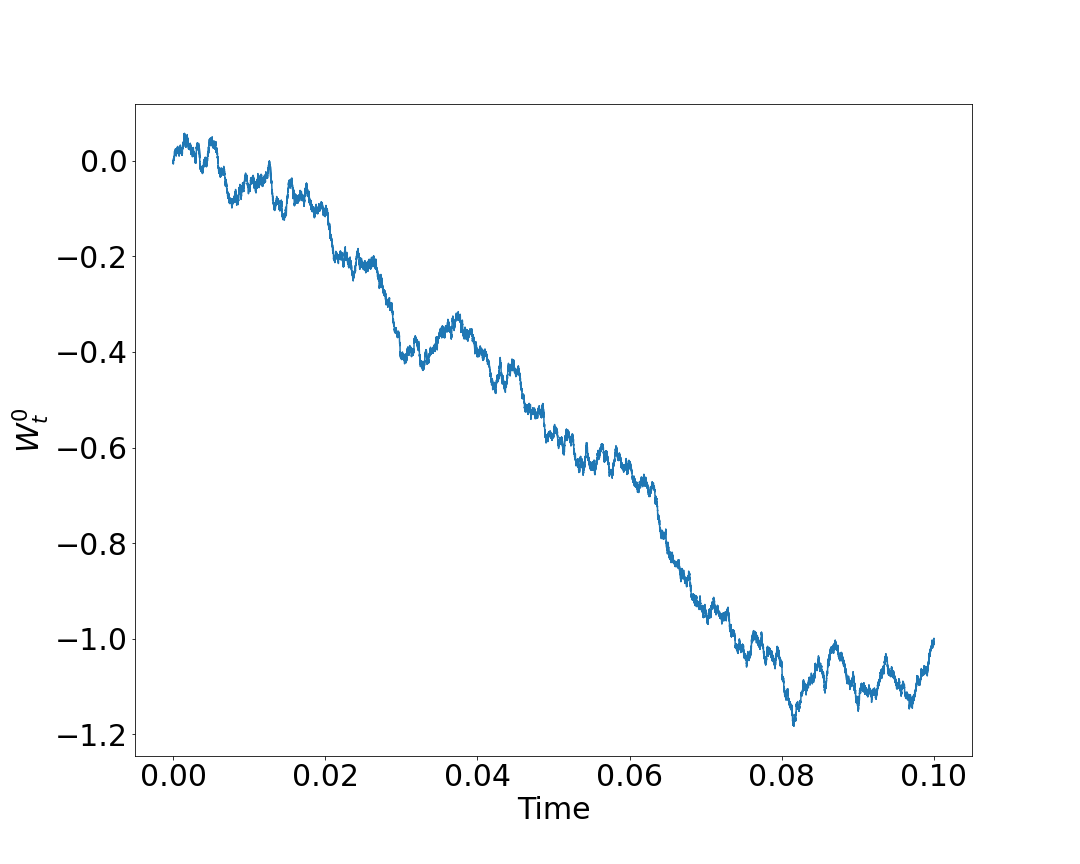

To the best of our knowledge, there is no existing literature on the regularity of the loss process in the presence of common noise. Consequently, the theoretical methods employed earlier may not be applicable in this scenario. Nevertheless, we can still explore the convergence rate in this context as well. We consider the simplest setting with common noise,

| (4.5) |

where is a fixed constant. We propose a numerical scheme that employs a particle system approximation to compute both the limiting and smoothed loss functions. Instead of employing numerical integration to compute the mollified loss of , the system will feel the impulse from a particle hitting the boundary at a random time in the future sampled from a random variable whose probability density function is the mollification kernel. The scheme is given in Algorithm 1.

By setting to zero, the algorithm approximates the loss in the setting without common noise. To compute the limiting loss function we set to zero. In the case when and , we recover the numerical scheme proposed in [20, 21]. In the numerical experiments below, we employed particles and used a uniform time discretisation of size , where is the set of delay values used for the rate of convergence plots, so that in Algorithm 1.

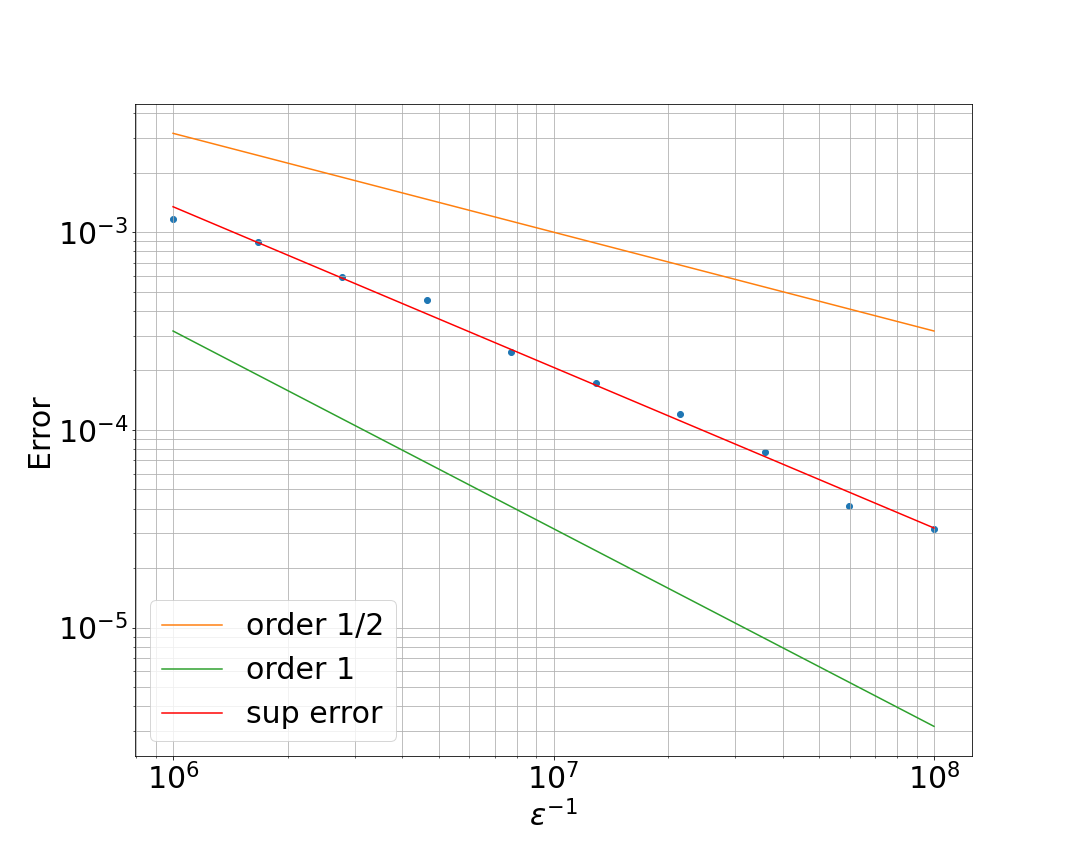

Overall, given sufficient regularity of the loss function, a rate of convergence close to is observed. In the other cases studied with Hölder initial data, with the possibility of there being a jump after the test interval, and with common noise, the rate of convergence appears to be between and . See Appendix B for further analysis regarding the rate of convergence and further examples exploring how affects the estimated rate.

4.3 Initial density vanishing at zero and no discontinuity or common noise

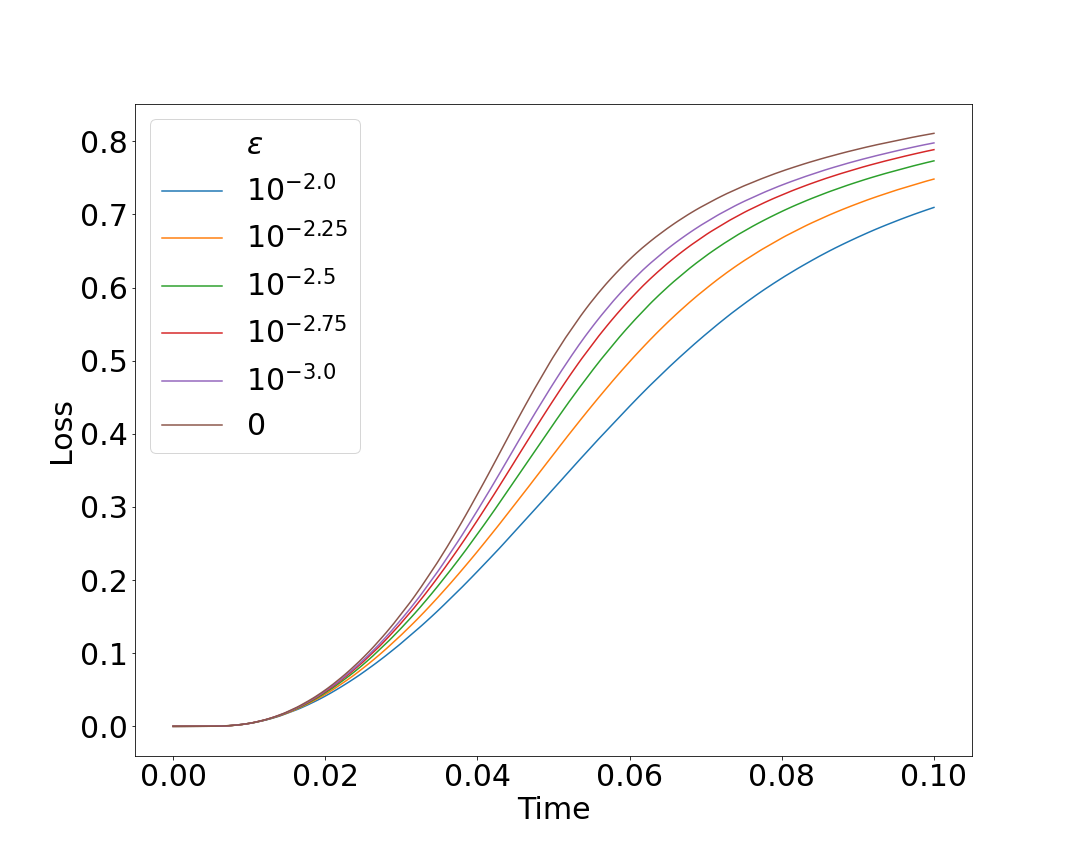

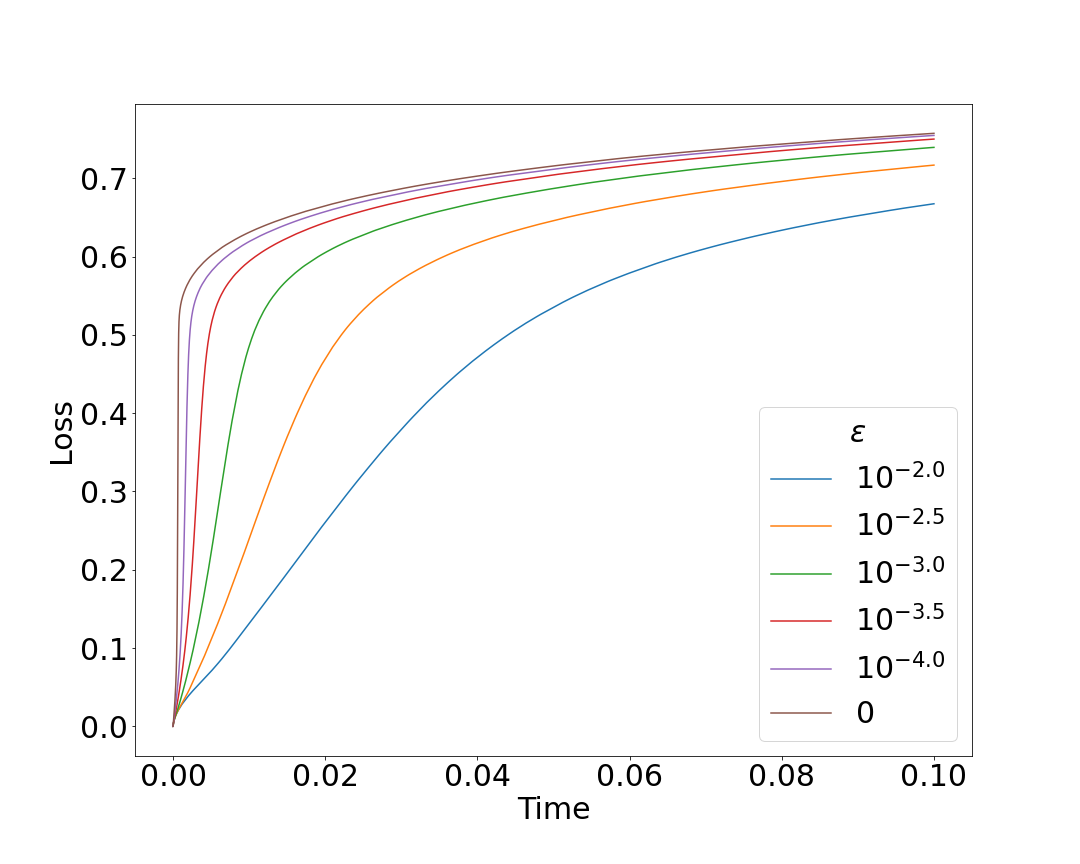

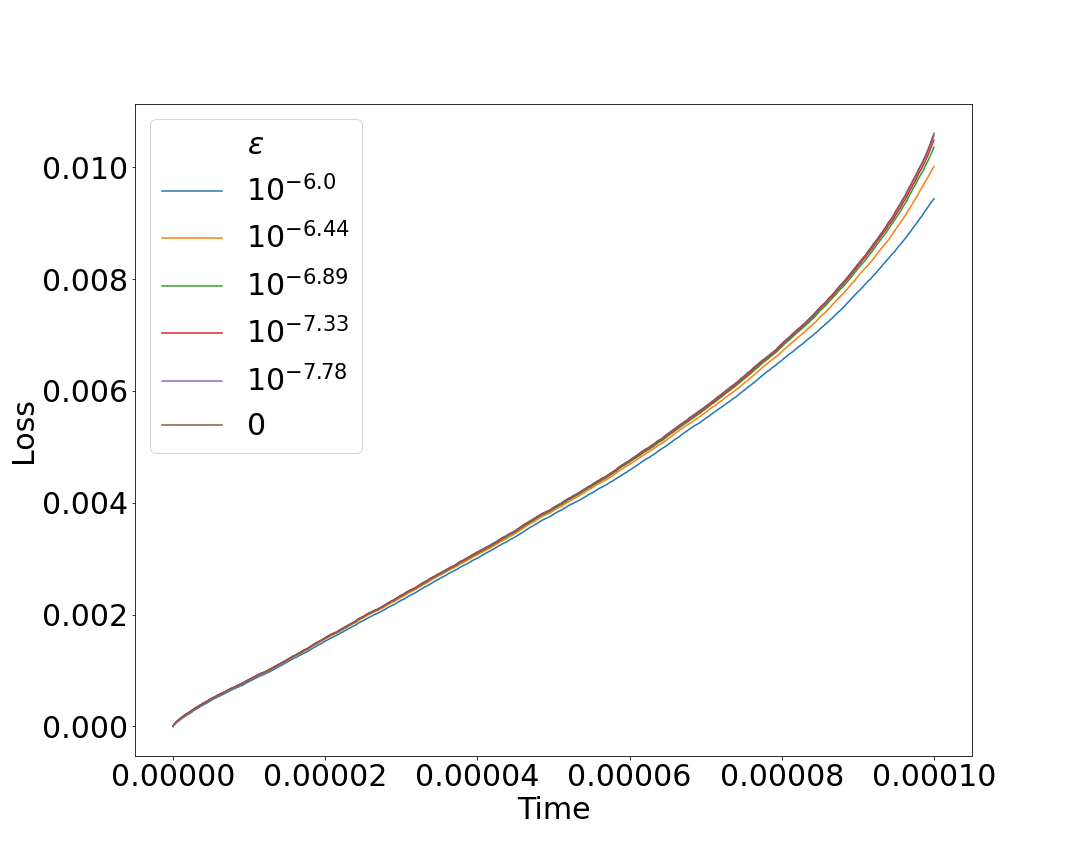

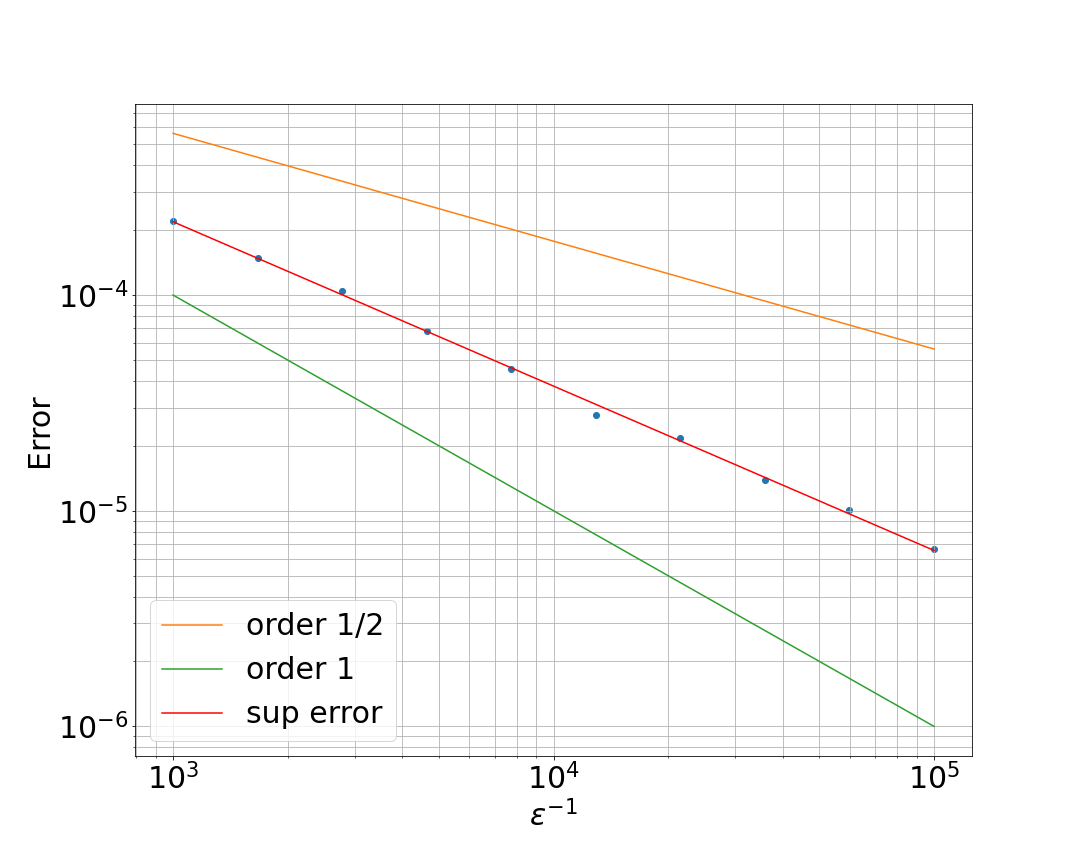

Two different initial conditions were examined in our experimental analysis, and no discontinuity was observed in either case. In the first simulation, we set to follow a uniform distribution on , with assigned a value of . In the second scenario, was generated from a gamma distribution with parameters , with was set to . Interestingly, the data from Fig. 1(b) indicate a convergence rate of in both cases. This exceeds the predicted convergence rate of .

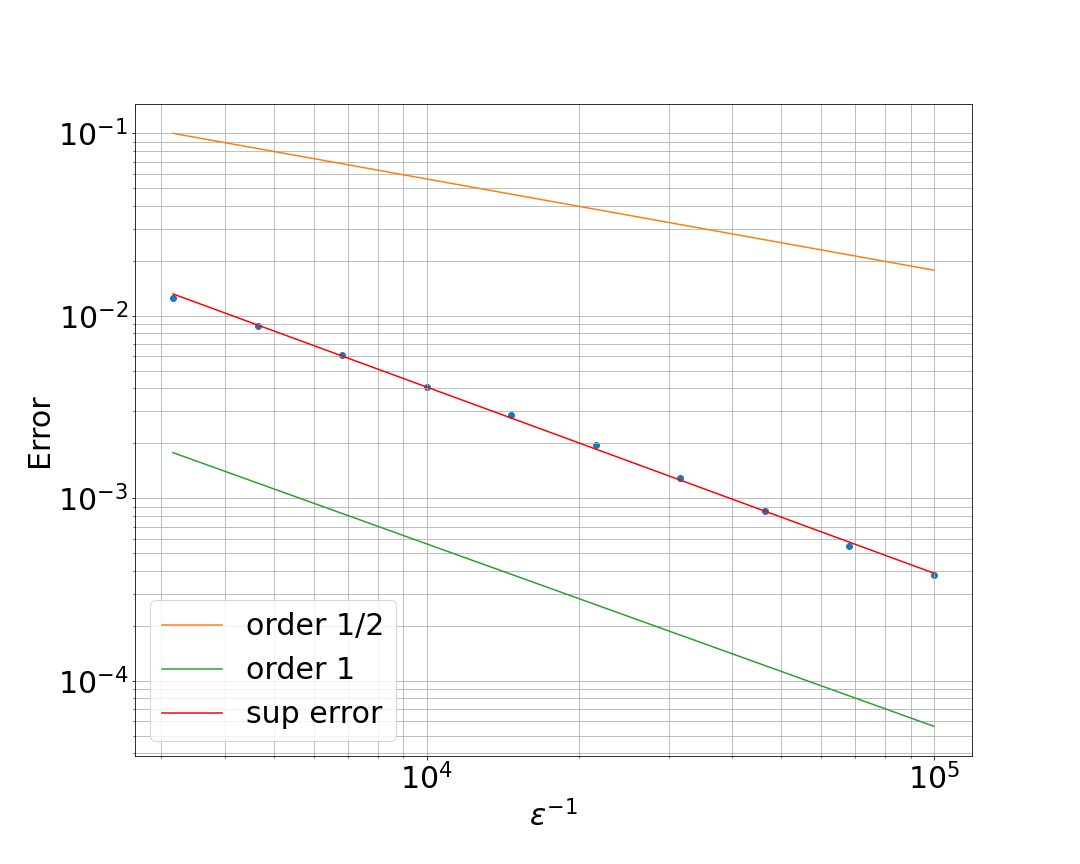

4.4 Setting with discontinuity and without common noise

To simulate a setting where we would see a systemic event, we changed the parameters of the Gamma distribution such that most of the mass will be near the boundary and made sufficiently large. In Fig. 2(c), we conducted simulations using two different initial conditions. In the first case, we set to follow a Gamma distribution with parameters and assigned a value of 0.9. In the second case, was generated from a Gamma distribution with parameters , and was set to 2. Within this particular setup, we observe a convergence rate between and prior to the occurrence of the first jump. The rate appears to be unaffected by the characteristics of the density of near the boundary, despite the theoretical estimates relying on such information. Moreover, the theoretical estimates consistently predicted a convergence rate strictly below in all scenarios involving an initial condition of this form, in contrast to our empirical results, which indicate a convergence rate greater than .

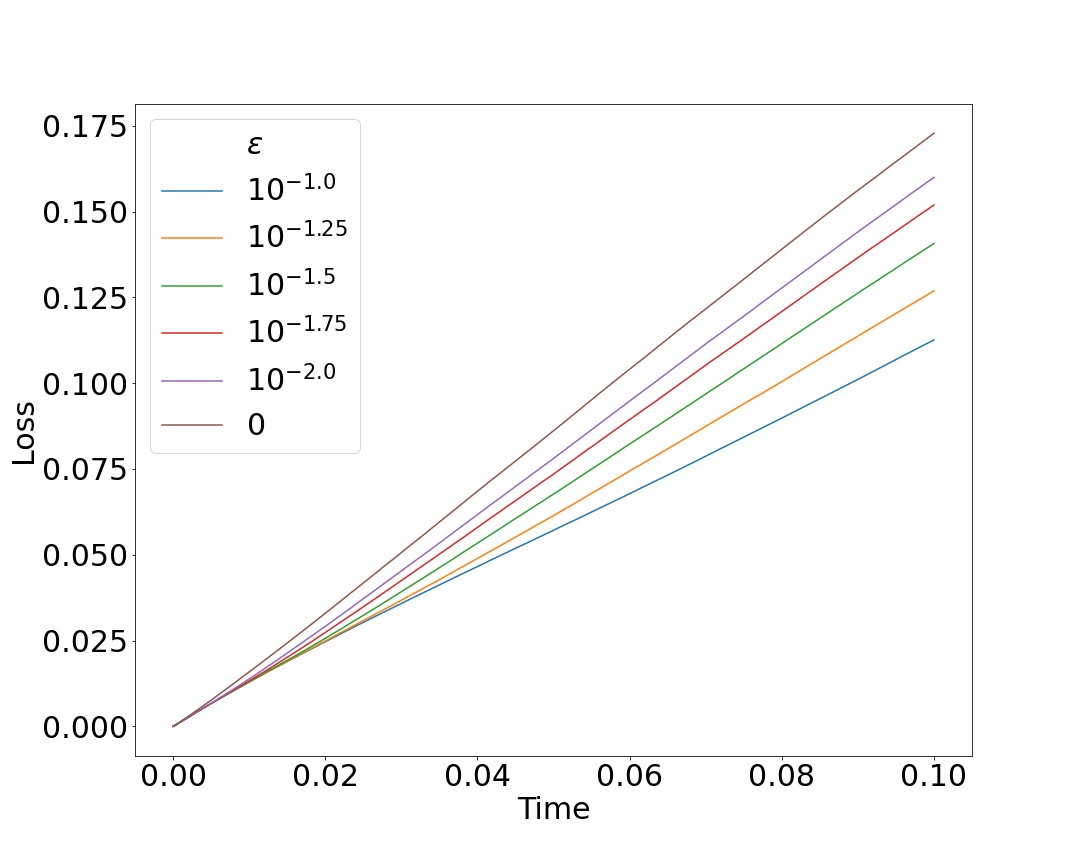

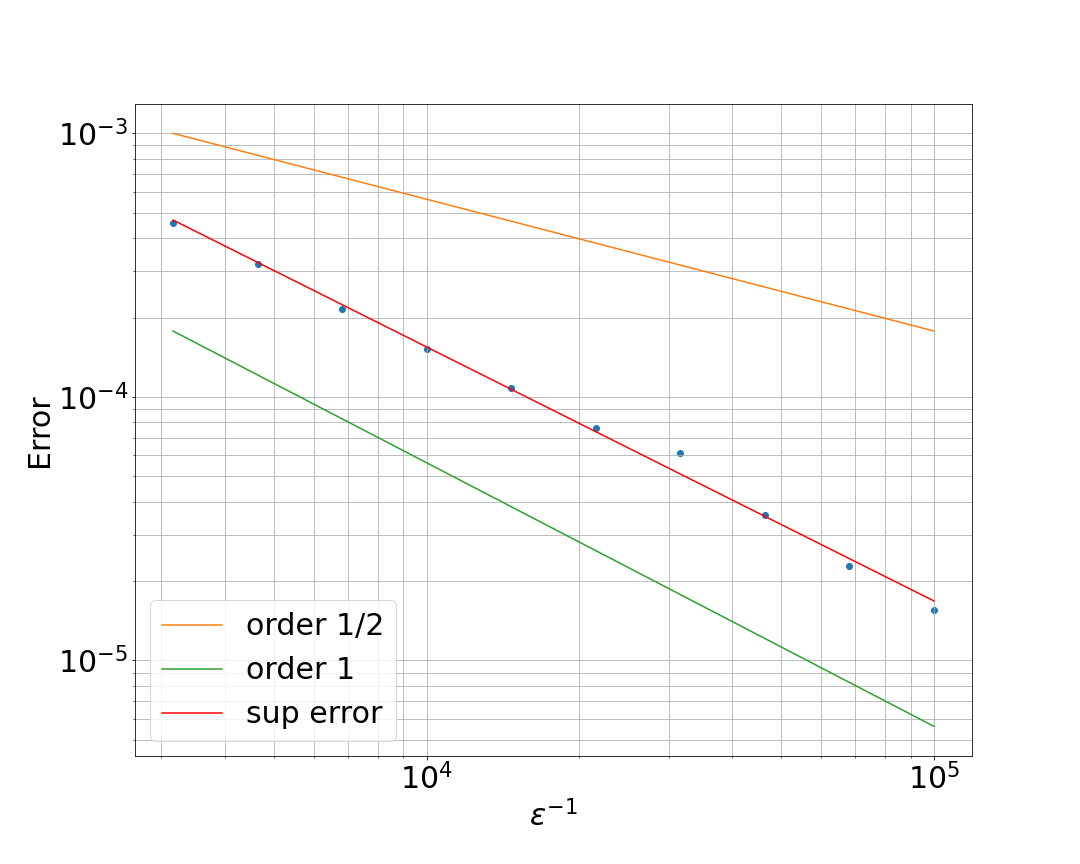

4.5 Simulations with common noise

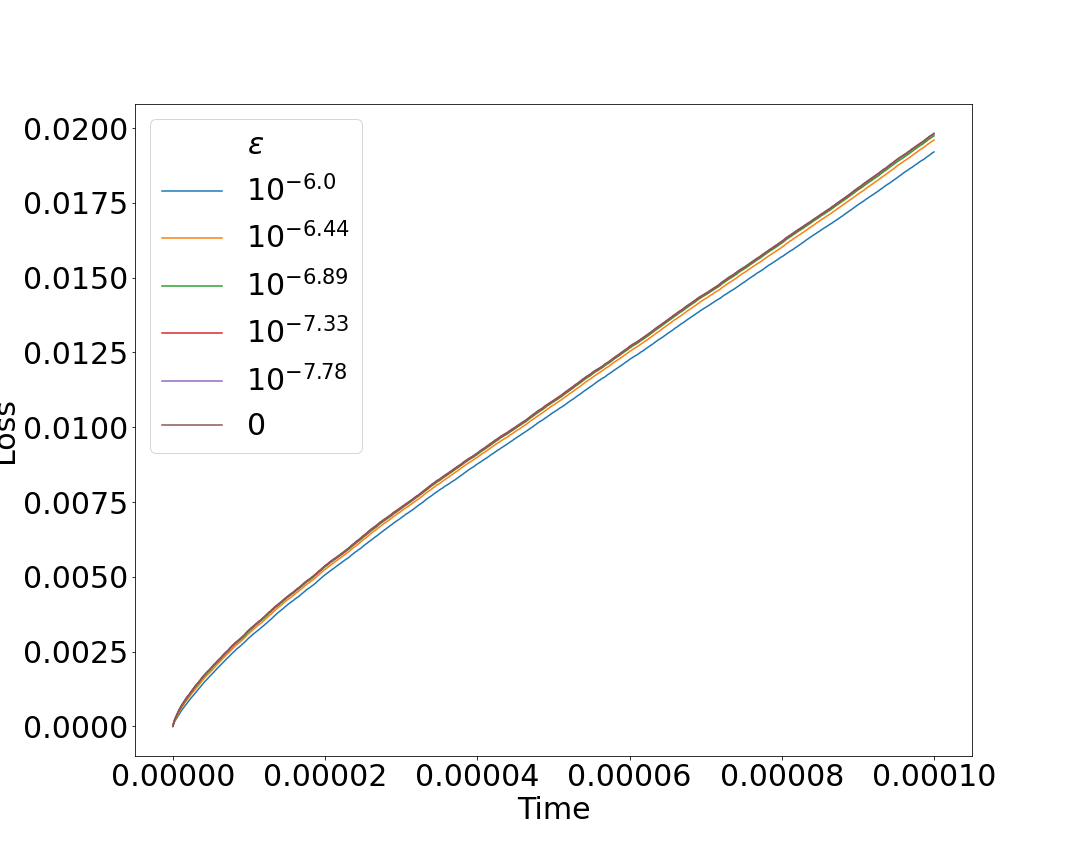

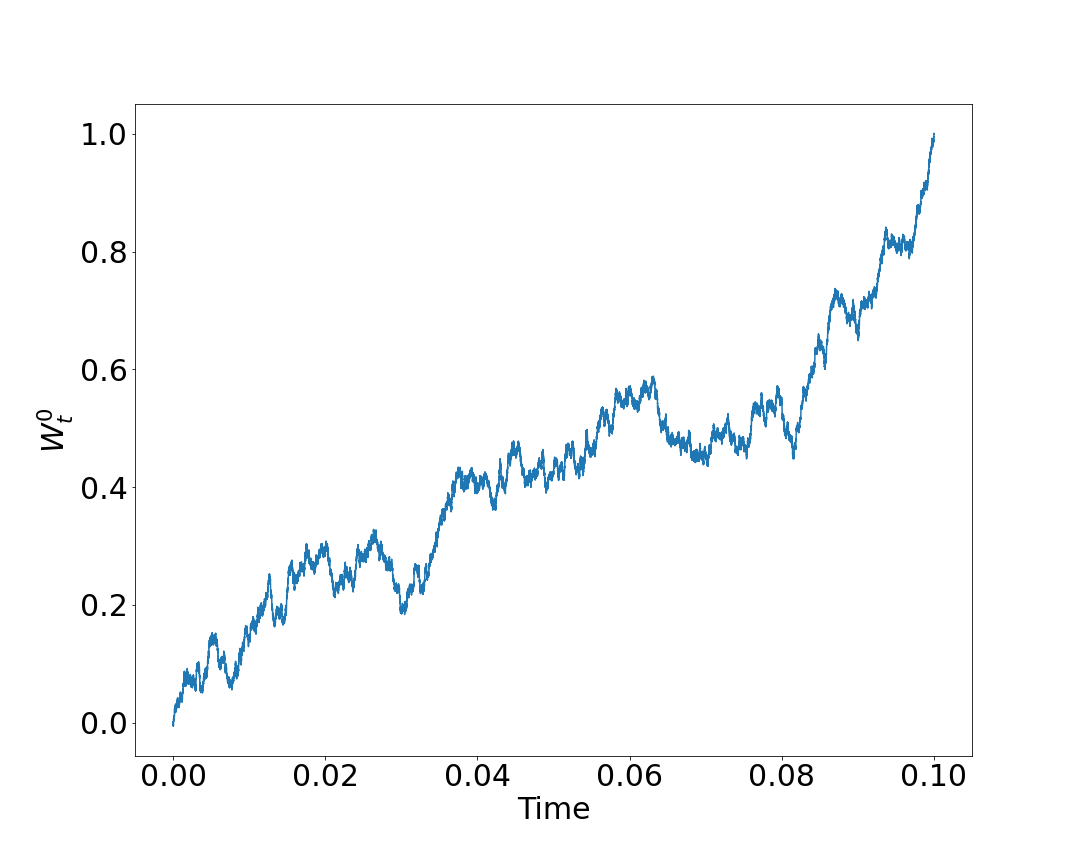

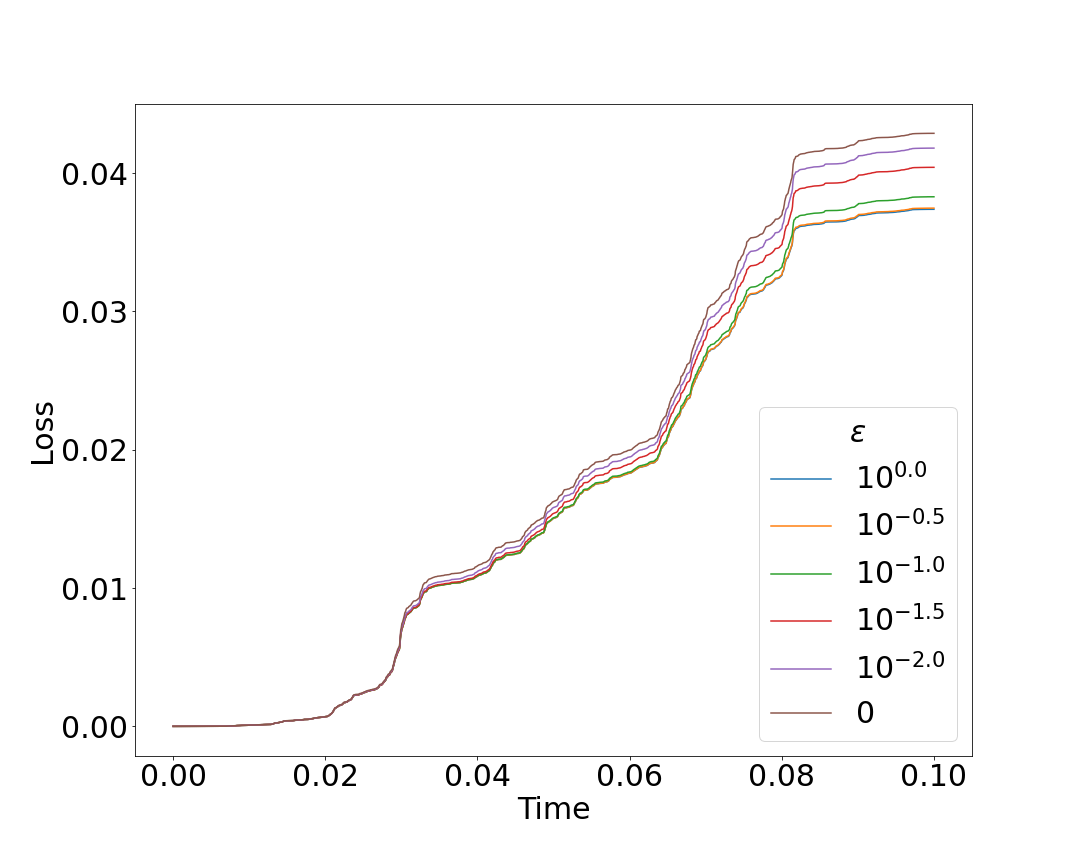

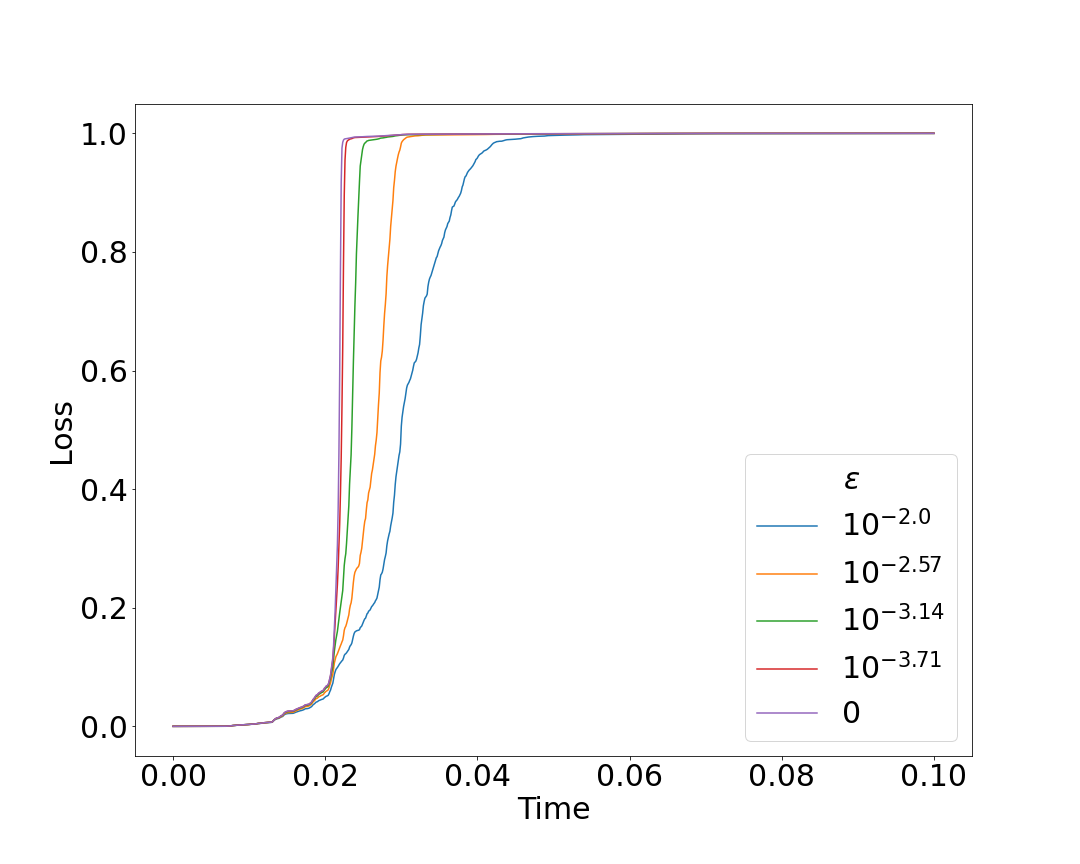

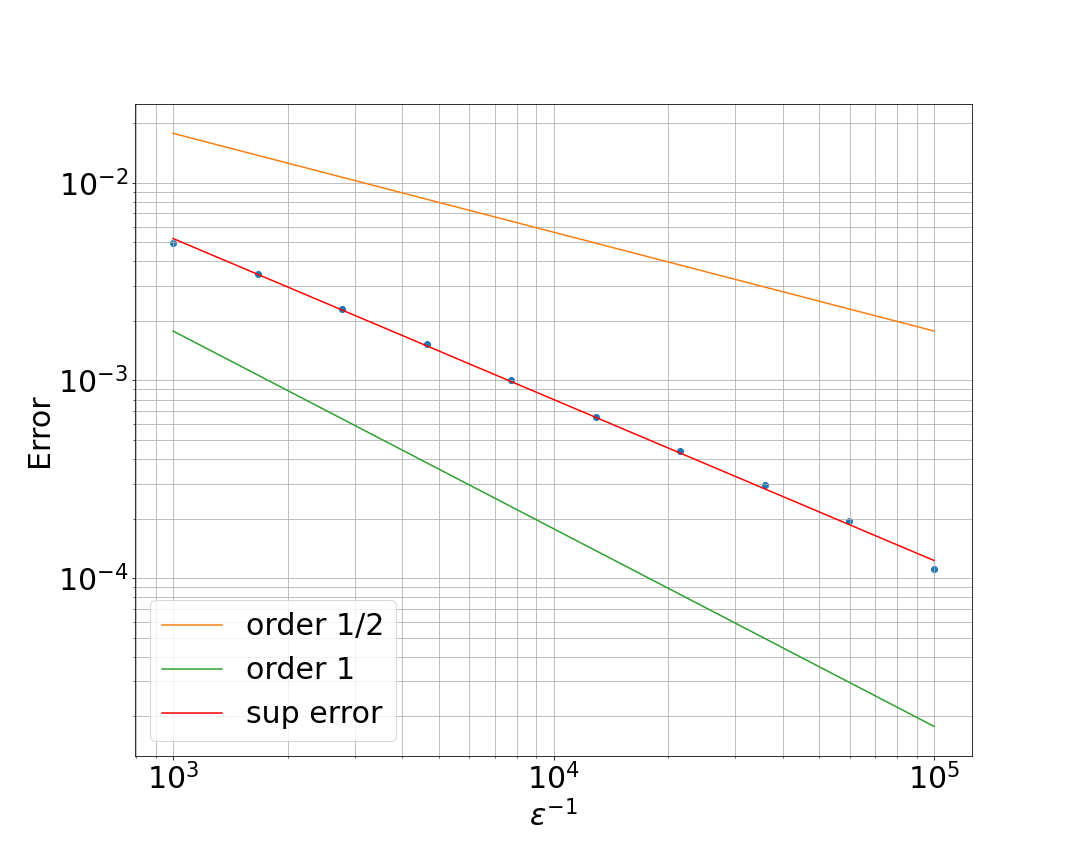

Similar to the previous subsections, we conducted two experiments. In both experiments, we assigned a uniform distribution over the interval , set to and to . This initial condition is the same as in Section 4.3. However, we used different common noise paths for each experiment. In the first simulation, the common noise path increases to over the time domain. This led to the loss process becoming rougher than the loss in the previous setting. In the second simulation, the common noise path decreases to . This induces a systemic event due to the rapid loss of mass. Despite the differences between the scenarios, we observed a similar rate of convergence between and as illustrated in Fig. 3(c).

Acknowledgement

This research has been supported by the EPSRC Centre for Doctoral Training in Mathematics of Random Systems: Analysis, Modelling and Simulation (EP/S023925/1). AP thanks Philipp Jettkant for discussions on this material.

Appendix A Technical lemmas

Lemma A.1.

Suppose that converges weakly in where and is the extension of and . Let and be the canonical processes on such that for , and . Then is a martingale with respect to the filtration generated by with quadratic variation

Proof.

Set to be the limit point of and

Now for any with and , we define the function

for arbitrary . In order to show that is a martingale, it is sufficient to show that

As , then by Skohorod’s Representation Theorem, see [2, Theorem 7.6], there are and defined on the same background space such that converges to almost surely in with and . Now for any ,

where is a constant that changes from line to line and depends only on and the ’s but is independent of . Therefore is uniformly bounded. For , it is an almost sure continuity point of . Therefore by the properties of M1-convergence, converges to almost surely. Hence we have almost sure convergence of to . Vitali’s Convergence Theorem states that almost sure convergence and uniform integrability implies convergence of means, hence

where the last inequality follows from the fact for all as is a martingale. Therefore by a monotone class theorem argument, is a continuous local martingale.

Recall almost surely in , hence we have pointwise convergence at the continuity points of , see [32, Theorem 12.5.1]. As is in by 2.2, there is a set of full probability such that for a set of ’s that have full Lebesgue measure in . Furthermore, as is bounded, by the Bounded Convergence Theorem

| (A.1) |

almost surely for any . Set

where is anyone of or and is the respective or . Employing Eq. A.1,

Also by above and the boundness of by 2.2, is uniformly bounded in . Hence by Vitali’s Convergence Theorem,

where the last inequality follows from the fact that is true martingale from the boundness of . This completes the proof. ∎

Lemma A.2.

Consider the process for where is a continuous local martingale with for any almost surely and is a non-negative random variable such that . Then for any stopping time where almost surely, then

for and .

Proof.

In the case when is simply a Brownian motion, the result readily follows by the Stong Markov Property and standard properties of Brownian motion. As is a continuous local martingale, we may view it as a (random) time-changed Brownian motion. We exploit this fact to show the claim. To begin, fix a , and set . Then conditioning on the event and its complement

| (A.2) |

Focussing on the first term, we observe

By the Dubins-Schwarz Theorem, is a time-changed Brownian motion. Therefore there exists a Brownian Motion such that

Now as almost surely, for any almost surely. So

By the reflection principle of Brownian motion, we have

In conclusion, we have shown

Setting , then by continuity of measure and the above, the expression in (A.2) converges to 0 as we send to zero. This completes the proof. ∎

Lemma A.3 (Convergence of Stopping Times).

Consider a sequence of functions in converging towards some with respect to the -topology. We assume that has the following crossing property:

| (A.3) |

where is defined as in Eq. 2.13 and for all . Then we have

Proof.

The proof is composed of two steps. We shall show that . Hence we will have equality and the claim follows.

Step 1:

We define the set of continuity points of to be . We remark that is co-countable by [2, Section 13]. As , by (A.3) for any fixed there exists a such that . Now, as is a continuity point of , by [32, Theorem 12.5.1], we have that in as . Therefore for large , hence

As was arbitrary, the claim follows.

Step 2:

As in the -topology, we may find a sequence of parametric representations of which converges uniformly to a parametric representation of , see [32, Theorem 12.5.1]. Therefore, we may find a such that . By step 1, since , we have have

Therefore by the finiteness of and compactness of , we may find a subsequence such that and for some . By the uniform convergence of the parametric representations

As , we may find such that . We also note as . Lastly as for all , we have . Therefore, . This completes the proof. ∎

Lemma A.4 (Functional Continuity II).

Let be any measure such that

| (A.4) |

for any . Then for any sequence of measures such that in , we have

in , the space of sub-probability measures on endowed with the topology of weak convergence, for and such that and .

Proof.

The proof is an application of the Continuous Mapping Theorem, [2, Theorem 2.7]. We only need to construct -almost sure continuous maps.

Step 1: Projection of measures from to

Consider the map

| (A.5) |

(A.5) is a -almost sure continuous map. Choose a such that and is in the complement of the event in (A.4). Such ’shave full measure under . M1-convergence implies pointwise convergence at continuity points, [32, Theorem 12.5.1], therefore is M1-continuous for every such . Also by Lemma 2.11, since (A.4) holds, is an M1-continuous map at . As , is M1-continuous at . Hence, is a -almost sure continuous map. By the Continuous Mapping Theorem,

Step 2: Weak convergence of sub-probability measures

For any , define the map

It is clear . By step 1,

But by definition, and . So . The conclusion now follows by Portmanteau’s Theorem. ∎

Lemma A.5 (Weak convergence of sub-probability measures).

Suppose that on for a positive sequence which converges to zero. Set

Then for any ,

Proof.

By definition of and Lemma 2.9. for any there is a set of ’s of full -measure such that

| (A.6) |

Lemma A.6 (Functional Continuity III).

Proof.

By 2.2,

| (A.8) |

The R.H.S of (A.8) is finite because in and by assumption. So it is sufficient to show converges to on a set of full Lebesgue measure. The conclusion then follows by the Dominated Convergence Theorem.

Choose an . The by Lemma A.4, . By Skohorod’s Representation Theorem, there exists a defined on a common probability space such that and almost surely in . For any with and ,

By assumption,

uniformly in for some . So is uniformly -bounded and converges to zero almost surely. Therefore, by Vitali’s Convergence Theorem,

| (A.9) |

Lastly by 2.2,

As , the first term converges to zero as in . By assumption and (A.9), the second term converges to zero as . This completes the proof. ∎

Lemma A.7.

Fix any . There is a constant independent of and such that for any we have

Proof.

To begin, fix a such that and fix a . Then we define the event

where is the constant from the linear growth condition on . Now fix . By the continuity of the loss process, [17, Theorem 2.4], there exists a such that . Employing the integration by parts formula, we observe for any

where to establish upper bounds we use the fact that is non-negative and non-decreasing, and for any . Therefore for any

Therefore as is measurable and conditioning on fixes , we have

Now, for any fixed , set . We define the event

Then on the event

Therefore on the same event

Consequently, we deduce

Therefore if we have control over the mass , we may estimate the mass with respect to that is near the boundary. Therefore, defining the event we deduce on

The last inequality follows from the fact that . Now we only need to find a independent of and such that . By application of Markov’s inequality twice

where depends on the constant from Proposition 2.6, the constant from Burkholder-Davis-Gundy to bound the second term and the uniform bounds on , but is notably independent of . Therefore, setting completes the proof. ∎

Lemma A.8.

Suppose that on for a positive sequence which converges to zero. Set

Then for any and such that we have

Proof.

As , by employing Skohorod’s Representation Theorem, there exists a and such that , and almost surely in . As -almost every measure satisfy Eq. A.4 by Lemma 2.9, then by Lemma A.4 almost surely for any . Furthermore for any , by Lemma 2.11 and Corollary 2.12, we have

almost surely. Therefore for simplicity and notational convenience for the remainder of this proof, we may suppose

Recall by Lemma A.7,

for any . It is well known that the Levy-Prokhorov metric, , metricizes weak convergence, [29, Theorem 1.11]. Fixing , we define the event

Therefore

Sending , then by the Dominated Convergence Theorem as we have almost sure convergence. Lasts by sending one at a time and in order, then by employing continuity of measure we may conclude

∎

Lemma A.9.

Suppose that on for a positive sequence which converges to zero. Then we have

| (A.10) |

almost surely for any .

Proof.

It is clear that Lemma A.9 holds for any . Hence we must only show the upper bound for . We first consider the case when . The case when will be treated separately. Now as is dense in , we may find a such that , and . Now by the Borel-Cantelli Lemma, we have a set of full measure such that

| (A.11) |

for all (possibly stochastic) large. Furthermore, by the dominated convergence theorem, we have

| (A.12) |

-almost surely in as for any

So on an event of full measure where Eq. A.11 and Eq. A.12 holds, by Portmanteau Theorem for any ,

This holds as and . Sending to zero shows the claim for every .

Proposition A.10 (Gronwall Type Inequality I).

Suppose such that . Suppose is a nonnegative, nondecreasing continuous function defined on , (constant), and suppose is nonnegative and bounded on with

on this interval. Then

where

Proof.

Let , , for localling integrable functions . Then implies

Let us prove that

| (A.13) |

and as for each t in .

Step 1: .

For ,

Now, suppose the claim is true for , then for

Hence the claim is true by the principle of induction.

Step 2:

We observe that is monotone, that is if , then by the nonnegativity of we have . Also by the linearity of integration, we see also that is a linear operator. Therefore,

Therefore, by linearity, monotonicity and step 1

Step 3: Summability of . By Gautschi’s inequality, [15], we have that for all and

Therefore,

Hence and . Hence by the ratio test, we have that is summable.

Step 4: Summability of .

By step , we have that

Therefore by the ratio test then the comparison test, we have that is summable. Hence as .

Step 5:

As , then it is clear by the Principle of Induction, by using the monotonicity and linearity of , we have . Hence taking limiting as , by step 1 and step 4, we conclude . The proof is now complete.

∎

Proof of Proposition 4.2.

This proof is analogous to that of Proposition 4.1. Most of the details have been skipped for brevity. Choose .

Step 1: Regularity of and decomposition into integral form. As , by the Fundamental Theorem of Calculus we have for any with and . Now we may write as

Observe

Therefore

Step 2: Comparison between the delayed loss and the instantaneous loss. As in Proposition 4.1, we have

Note as for all , we see that the second term above is bounded above by . Therefore,

| (A.14) |

where

Step 3: Bounds on . As in Proposition 4.1, the presence of in makes the function to general to do any analysis, hence we shall construct polynomial bounds on . Then we may be able to apply generalised versions of Gronwall’s Lemma. Recall , therefore

Case 1:

Case 2:

As the support of is in

Step 4: Gronwall type argument. Now that we have sufficiently simplified , we may put Eq. A.14 into a form where we may apply Gronwall’s inequality. By step 4 case 1 and (A.14), we have for

By step 4 case 2 and (A.14), we have for

where the second term in the last line is the higher order terms from employing Taylor’s Theorem. By applying the Monotone Convergence Theorem, we have swapped integrals and sums. We shall now turn our attention onto the expression

We shall proceed in two cases.

Case 1:

where the first inequality follows from the fact that as and for .

Case 2:

We observe that

and

where the upper bound in the last inequality follows from the fact that . Therefore we have shown Therefore, we have shown that

for all . As and are bounded by , so independent of being greater or less than we have

for any . Lastly by Proposition A.10 using and , then as and

This completes the proof. ∎

Appendix B Further numerical analysis

In Section 4.2, we considered 6 examples to compare the theoretical rate of convergence with that obtained in practice. The parameters used for each simulation are given in Table 1.

| Simulation | CC1111Continuous case 1 | CC2222Continuous case 2 | DC1333Discontinuous case 1 | DC2444Discontinuous case 2 | CNC1555Common noise case 1: with increasing path | CNC 2666Common noise case 2: with decreasing path |

| Initial Condition | ||||||

With the chosen parameters, we generated the convergence graphs in Fig. 1(b), Fig. 2(c) and Fig. 3(c) from , where , with and as positive constants, and is the corresponding difference between the smoothed and limiting loss functions. Assuming a power law relationship between the error and the parameter ,

where and are constants, we performed a linear regression on versus , which determined the line of best fit shown in the plots. The slope, shown in Table 2, represents our best estimate for the rate of convergence for each specific setting.

| Setting | CC1 | CC2 | DC1 | DC2 | CNC1 | CNC2 |

|---|---|---|---|---|---|---|

| Rate |

To assess if the estimated slope corresponds to an asymptotic value, we also conducted an alternative analysis of the rate of convergence. By computing the ratio between two consecutive errors, we observe

and taking logarithms with base , we may deduce

By using the relationship that for any , we obtain approximate expressions for as follows:

| (B.1) |

where represents the logarithm with respect to any base.

| Simulation | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| CC1 | |||||||||

| CC2 | |||||||||

| DC1 | |||||||||

| DC2 | |||||||||

| CNC1 | |||||||||

| CNC2 | |||||||||

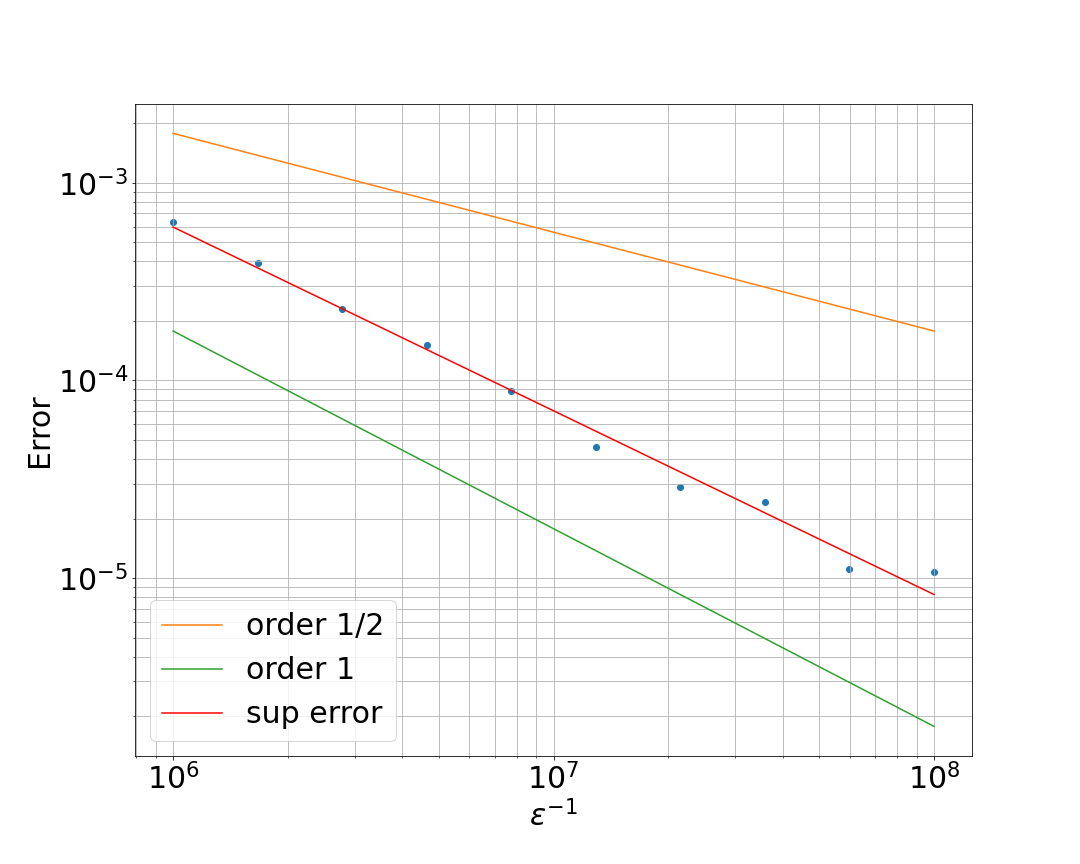

From Table 3, it is evident that in the cases of CC1 and CC2, the rate of convergence approaches asymptotically. However, for all other scenarios, there appears to be no distinct pattern or clear convergence of the gradients. Nevertheless, the gradients generally lie between and .

Furthermore, we investigated the sensitivity of the convergence rate analysis to the choice of . It is clear that for meaningful approximations to the smoothed system it is needed that is sufficiently small compared to , which necessitates extremely small time steps and makes the simulation of the particle systems computationally costly. To assess whether is sufficiently small, we generated in Fig. 4(c) and Table 4 rate of convergence plots with different values of . For each , we selected several values of that were uniformly spaced (after taking logarithms) within the interval . The findings indicate that the estimated rate of convergence remains consistent with respect to variations in .

| Simulation | ||||||||

|---|---|---|---|---|---|---|---|---|

| CC1 | ||||||||

| CC2 | ||||||||

| DC1 | ||||||||

| DC2 | ||||||||

| CNC1 | ||||||||

| CNC2 | ||||||||

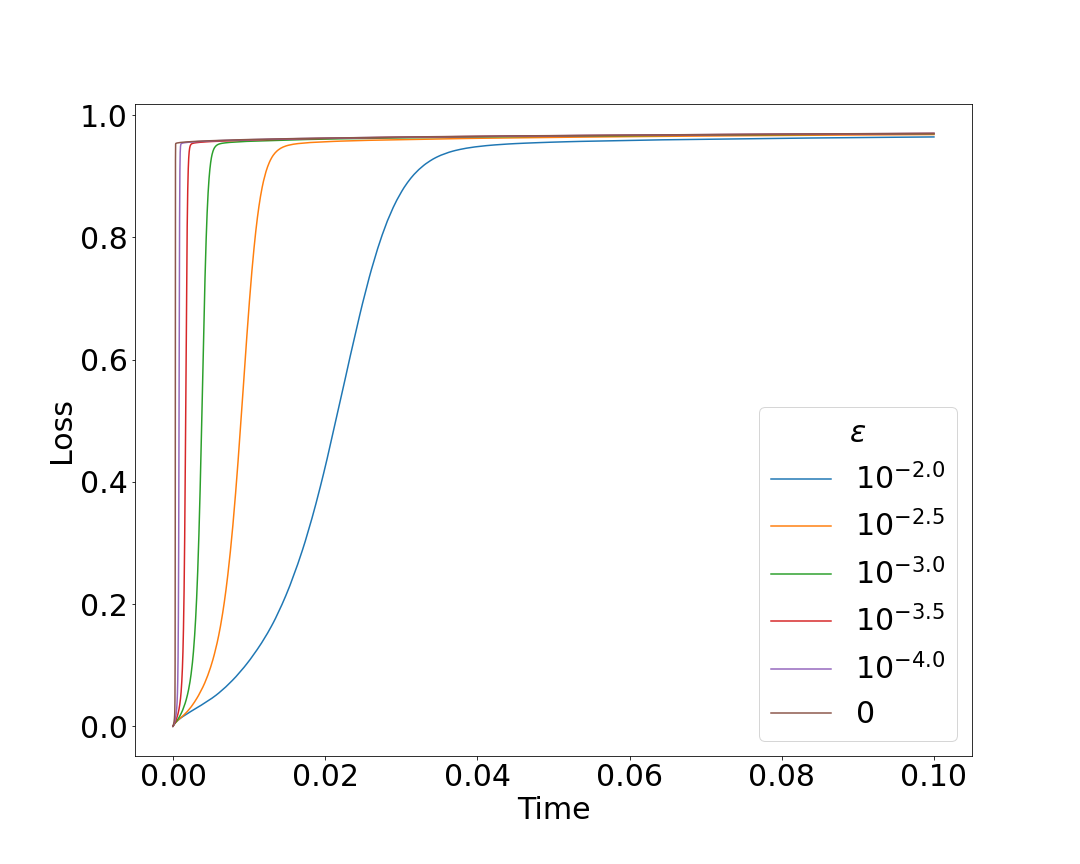

Finally, we investigated a scenario where the initial condition is Hölder continuous near the boundary without any observed jump discontinuity in the simulations, specifically, with . By [10, Theorem 1.1], the limiting loss function is -Hölder continuous at . The rate of convergence appears to be between and in this setting.

| Gradient |

|---|

References

- [1] Florin Avram and Murad S. Taqqu “Probability bounds for M-Skorohod oscillations” In Stochastic Processes and their Applications 33.1, 1989, pp. 63–72

- [2] Patrick Billingsley “Convergence of Probability Measures” John Wiley & Sons, 2013