Intertwining the Busemann process of the directed polymer model

Abstract.

We study the Busemann process of the planar directed polymer model with i.i.d. weights on the vertices of the planar square lattice, both the general case and the solvable inverse-gamma case. We demonstrate that the Busemann process intertwines with an evolution obeying a version of the geometric Robinson–Schensted–Knuth correspondence. In the inverse-gamma case this relationship enables an explicit description of the distribution of the Busemann process: the Busemann function on a nearest-neighbor edge has independent increments in the direction variable, and its distribution comes from an inhomogeneous planar Poisson process. Various corollaries follow, including that each nearest-neighbor Busemann function has the same countably infinite dense set of discontinuities in the direction variable. This contrasts with the known zero-temperature last-passage percolation cases, where the analogous sets are nowhere dense but have a dense union. The distribution of the asymptotic competition interface direction of the inverse-gamma polymer is discrete and supported on the Busemann discontinuities. Further implications follow for the eternal solutions and the failure of the one force–one solution principle for the discrete stochastic heat equation solved by the polymer partition function.

Key words and phrases:

Busemann function, cocycle, directed polymer, geometric RSK, Gibbs measure, intertwining, inverse-gamma, log-gamma, one force–one solution, stochastic heat equation1991 Mathematics Subject Classification:

60K35, 65K371. Introduction

1.1. Motivation and objective of this paper

The investigation of Busemann functions and semi-infinite geodesics in first- and last-passage percolation has been in progress for three decades, since the seminal work of Newman [45] and Hoffman [31, 32]. More recent is the study of the analogous Busemann functions and semi-infinite polymer measures in positive-temperature polymer models. On the planar square lattice this work began with [27] on the inverse-gamma polymer model. In [24] Busemann functions were studied as extrema of variational formulas for shape functions and limiting free energy densities. On the dynamical systems side, [6] utilized Busemann functions and polymer measures to define attractive eternal solutions to a randomly forced Burgers equation in semi-discrete space-time. General theory of the full Busemann process and polymer measures of nearest-neighbor directed polymers on the planar lattice, for general i.i.d. weights, was developed in [38, 39].

The present paper continues the line of work of [27, 38, 39] to advance both the general theory of the Busemann process in directed lattice polymers and the results specific to the inverse-gamma case.

Next we introduce informally the notions of Busemann function and Busemann process, give a brief account of the present state of the subject, and then turn to the main novel aspects of this paper. Rigorous definitions and statements begin in Section 2. The literature is vast. To keep this introduction to a reasonable length we refer the reader to the papers cited above for further coverage of the history. Section 1.8 below summarizes the organization of the paper.

1.2. Busemann functions and Busemann process

Given a random field with a metric-like interpretation and a planar direction vector , an individual Busemann function is a limit of the type

| (1.1) |

where is a sequence of vertices with asymptotic direction . In a first- or last-passage growth model, is the passage time between and . In a polymer model or a model of random paths in a random potential, is the free energy (logarithm of the partition function) of paths between and . Several different approaches exist now for proving such a limit almost surely for a given direction .

The (global, or full) Busemann process is a stochastic process that combines the individual Busemann functions into a single random object. Since there are uncountably many directions , the limits (1.1) alone do not define this object. But once a global process is constructed, it turns out that the distributional and regularity properties of the function capture useful information about the field .

1.3. Busemann process state of the art

The global Busemann process can be constructed in fairly broad generality in planar growth and polymer models, with an argument that combines weak convergence and monotonicity. In this approach the limits (1.1) are not taken as the starting point, but instead proved after has been constructed, and then typically under some regularity assumptions on the shape function. In the planar corner growth model (CGM), equivalently, in planar directed nearest-neighbor last-passage percolation (LPP) this was done in [26], by appeal to weak convergence results from queueing theory. A more general construction for both LPP and the directed nearest-neighbor polymer model was undertaken in [38], based on the weak convergence argument of [20]. Recent extensions of this theory to higher dimensions and ergodic weights appear in [29, 35].

The general construction gives little insight into the distribution or the regularity of the Busemann process. Explicit properties of the joint distribution of the Busemann process have been established in solvable LPP models: in the exponential CGM [21], in Brownian LPP [53], and in the directed landscape [12]. The results of [40] on the geometry of geodesics illustrate the gap between what can presently be achieved in general LPP and in the solvable exponential case. In positive temperature the Busemann project is in progress for the Kardar–Parisi–Zhang (KPZ) equation, with the construction of the Busemann process and applications to ergodicity and synchronization in [41], and its distributional properties forthcoming [30]. The first lattice polymer case of the Busemann distribution is developed in the present paper.

In LPP models the Busemann process serves as an analytic device for studying infinite geodesics. A common suite of results has emerged across several models:

-

(a)

On an event of probability one, there is a Busemann process defined simultaneously across all directions.

-

(b)

The Busemann function in a particular direction encodes a family of coalescing semi-infinite geodesics. Discontinuities of the Busemann process correspond to the existence of multiple coalescing families with the same asymptotic direction.

-

(c)

When the joint distribution of the Busemann process can be described, it has revealed that the set of discontinuities is a countable dense subset of directions.

In addition to revealing geometric properties of semi-infinite geodesics, the explicit Busemann process is useful for estimates. Examples include matching upper and lower bounds on coalescence [51] and nonexistence of bi-infinite geodesics [7]. Before the full development of the Busemann process, certain explicit stationary LPP and polymer models were discovered and utilized to establish KPZ fluctuation exponents. The seminal work [13] came in Poissonian LPP, followed by [8] in the exponential CGM. In positive temperature [50] introduced the inverse-gamma polymer.

In positive-temperature polymer models, analogues of objectives (a) and (b) above were accomplished in [38] for general i.i.d. weights. Our paper sharpens their general results on the regularity of and then focuses on objective (c), the joint distribution of the Busemann process across multiple directions, and several corollaries. The next sections 1.4–1.7 provide an overview of the contents of this paper.

1.4. Characterization of the Busemann process of the directed polymer model

Our main results for the Busemann process are the following.

- (i)

- (ii)

-

(iii)

Under general weights, the joint distribution of the Busemann process on a lattice level is identified as the invariant distribution of a certain Markov process. This distribution is shift-ergodic and unique subject to a condition on asymptotic slopes (Theorem 3.3). The Markovian evolution intertwines with another Markov process that obeys a version of geometric RSK (discussed below in Section 1.6).

Items (i) and (ii) deviate from what is true in zero-temperature LPP. In that setting, each individual Busemann function is constant on random open intervals whose union is a dense set of directions [40, Lem. 3.3]. The full set of discontinuities does not in general appear on each edge but can be seen along any bi-infinite down-right path [40, Lem. 3.6]. In the exponential case, the discontinuities of an individual Busemann function can accumulate only at the extreme directions and , while globally (across all ) the discontinuities are dense [21].

Item (iii) generalizes the invariance, ergodicity, and uniqueness results from [39], which considered the Busemann function for a single direction. The intertwining feature we develop is actually trivial in that setting. That is, the two Markov processes mentioned in item (iii) evolve differently only when multiple direction parameters are treated simultaneously.

The special case of the joint distribution of two inverse-gamma Busemann functions from this work has already been in circulation, prior to the publication of this paper. In earlier collaborative work of the third author, this bivariate case was applied in [11] to prove nonexistence of bi-infinite polymer Gibbs measures and in [48] to derive coalescence estimates for polymers.

1.5. Competition interface

In zero-temperature models such as LPP, geodesics emanating from a common point of origin spread on the lattice in a tree-like fashion and divide the lattice into disjoint clusters, depending on the initial choices made by the paths. The boundaries of these clusters are called competition interfaces, a notion introduced in [23] and further studied by [14, 22] in conjunction with its coupling to a second-class particle in TASEP. These interfaces convey essential geometric information and turn out to be intimately linked to the Busemann process [25, 21, 40, 52].

At positive temperature, geodesics are replaced by polymer measures, and so the random environment does not by itself generate a tree-forming family of paths. Instead, one must sample from a natural coupling of the quenched polymer measures, thereby adding an additional layer of randomness. This type of coupling appeared in [27], and the resulting competition interface was shown in [38] to have a random asymptotic direction whose distribution is determined by a nearest-neighbor Busemann function.

In Section 3.3, we extend this theme by realizing—in a single coupling—an interface direction from every point on the lattice (Theorem 3.6). Whereas the coupling from [27, 38] is of finite-volume polymer measures, ours is of semi-infinite polymer measures associated to the global Busemann process. Consequently, the results discussed in item (i) of Section 1.4 allow us to relate the interface directions to discontinuities of the Busemann process (Theorem 3.9). This is similar in spirit to the LPP result [40, Thm. 3.7], but in our case the additional randomness poses a new challenge to establishing the desired relation. Moreover, the substantially different topology of the discontinuity set in the positive-temperature setting changes how competition interfaces witness this set.

1.6. Polymers, geometric RSK, and intertwining

The classical Robinson–Schensted–Knuth (RSK) correspondence from combinatorics—in its various incarnations—has played a major role in the integrable work on last-passage growth models in the KPZ (Kardar–Parisi–Zhang) class. The geometric version of the RSK mapping (gRSK), introduced by Kirillov111Kirillov called his construction tropical RSK. To be consistent with the modern notion of tropical mathematics, [18] renamed the algorithm geometric RSK. [44] and investigated by Noumi and Yamada [46], serves the analogous function in positive-temperature directed polymer models. The polymer connection of gRSK was initially developed in [18, 47]. For recent work and references on the polymer-gRSK connection, see [17].

Intertwinings of mappings and Markov kernels is a central feature in this work. In [18], the application of gRSK to the inverse-gamma polymer and an intertwining argument led to a closed-form expression for the distribution of the polymer partition function. Subsequently [9] used this formula to establish the Tracy–Widom limit of the free energy.

In our paper two Markovian dynamics on the lattice are intertwined by an explicit mapping. The first one, called the sequential process, is defined by a transformation whose key ingredient is geometric row insertion. For this we formulate a gRSK algorithm that produces polymer partition functions on a bi-infinite strip with a boundary condition (Section 7.2). The second, called the parallel process, is the dynamics obeyed by the Busemann process as it evolves from one lattice level to the next. The intertwining structure is valid for general weights (Theorem 6.14).

Under inverse-gamma weights the sequential transformation has readily accessible product-form invariant probability measures (Theorem 8.2). Through the intertwining map these measures push forward into invariant measures of the parallel transformation. A uniqueness theorem for the latter identifies these probability measures as joint distributions of Busemann functions (Theorem 6.23).

1.7. Failure of one force–one solution

In the study of stochastically forced conservation laws, a principal example of which is the stochastic Burgers equation (SBE), the one force–one solution principle (1F1S) is the statement that for a given realization of the driving noise and a given value of the conserved quantity, there is a unique eternal solution that is measurable with respect to the history of the noise. Attractivity of the eternal solution is also at times included in 1F1S, and stochastic synchronization is an alternative term in this context. A connection with polymer models comes from viewing the polymer free energy as a solution of a stochastically forced viscous Hamilton–Jacobi equation. In the physics literature this connection goes back to [33, 34], while on the mathematical side an early paper was [43].

In 1F1S results there is a demarcation that is analogous to the distinction between a single Busemann function and the global Busemann process , described above in Section 1.2:

-

(i)

In much of the literature, the 1F1S principle is investigated for a fixed value of the conserved quantity and is shown to hold on a full-probability event depending on . Significant examples include [4] for an inviscid Burgers equation in a Poisson random field and [6] for a viscous Burgers equation in semi-discrete space-time.

-

(ii)

Alternatively, one can fix the realization of the noise and consider the entire uncountable space of values of the conserved quantity. This approach, called quenched 1F1S, was recently initiated in [41] for the KPZ equation.

In Section 5 we observe that the exponential of the Busemann process gives eternal solutions to a discrete difference equation, simultaneously for all values of the conserved quantity on a single event of full probability (Theorem 5.2). This equation is a discrete analogue of the stochastic heat equation, which, as is well known, is linked to the KPZ equation and SBE through the Hopf–Cole transform. In the inverse-gamma case our results on the Busemann process imply that, with probability one, there is a countable dense set of values of the conserved quantity at which there are at least two eternal solutions (Theorem 5.3). This is the first example of failure of 1F1S in a positive temperature lattice model. This failure of 1F1S at the discontinuities of the Busemann process was anticipated in the unpublished manuscript [37]. The analogous result for the KPZ equation is in progress [30].

1.8. Organization of the paper

The directed polymer model together with known results we use is introduced in Section 2. Our main results for the general polymer appear in Section 3 and for the inverse-gamma polymer in Section 4. Eternal solutions to a discrete stochastic heat equation and the failure of 1F1S in the inverse-gamma model are touched upon in Section 5.

Proofs begin in Section 6. Sections 6.1–6.4 develop the dynamics of the Busemann process, the intertwining argument, and the Markovian characterization of the joint distribution of Busemann functions. Section 6.5 proves Theorem 3.2 on the discontinuities of the mapping .

Section 7 is an interlude that puts the technical development of Section 6 in the context of the geometric RSK mapping.

Section 8 picks up the development of proofs again. This section focuses on the inverse-gamma model, except its Section 8.2 that develops an alternative approach to the intertwining mapping through triangular arrays of infinite sequences. The results of Section 8.2 are valid for general weights, but our application is presently only for inverse-gamma weights. In particular, this array construction yields the independent-increments property of the nearest-neighbor Busemann function.

The appendices contain various generalities and technical points.

1.9. Notation and conventions

We collect here items for quick reference. Some are reintroduced in appropriate places in the body of the text.

Our convention for infinite paths is that they proceed south and west, or, down-left, but direction vectors are members of and so point north and east. As an instance of this convention, will denote a limit such as (1.1) when .

Intervals of integers are written as . Subsets of reals and integers are indicated by subscripts, as in and . Spaces of bi-infinite sequences of restricted values are denoted by . On and the origin is and the standard basis vectors are and . In different contexts an integer variable is used to represent evolution in the vertical direction and along anti-diagonal levels .

Inequalities between vectors and sequences and are coordinatewise: means for all , and the strict version means that for all . For points and on the plane or the lattice , the strict southeast ordering means that and . Its weak version means that or .

A vector or sequence with a range of indices is marked with a colon, for example . The left tail logarithmic Cesàro average of a positive sequence is denoted by .

The standard gamma and beta functions are and . The digamma function is and the trigamma .

The end of a numbered remark and definition is marked with .

1.10. Acknowledgements

The authors thank C. Janjigian for useful comments on the manuscript.

2. Directed polymer model: definitions and prior results

Polymer models take as input a random environment and produce as output a family of measures on paths. We focus on the standard (1+1)-dimensional discrete model, in which the random environment consists of i.i.d. random variables indexed by the vertices of and the paths are up-right nearest-neighbor trajectories on .

2.1. Random environment and recovering cocycles

Let be a Polish probability space equipped with a group of continuous222The authors of [38] communicated to us that this assumption of continuity is needed for their construction, which we cite below as Theorem D. bijections (called translations) that map , are measure-preserving ( for all ), and satisfy . We then assume

| (2.1) | ||||

It is common to write with as the random environment and as an inverse temperature parameter. Our positivity condition comes from having already applied the exponential.

To prepare for our discussion of Busemann functions, let us introduce the broader notion of a cocycle. A cocycle on is a function such that

| (2.2a) | ||||

| One consequence of this definition is that a cocycle is uniquely determined by its restriction to nearest-neighbor edges, i.e. the values of and for . The cocycles of interest to us are those satisfying a second property: given a specific realization of the weights , a cocycle is said to recover these weights if | ||||

| (2.2b) | ||||

Given the weights, it is generally unclear how many—or even if—recovering cocycles exist. The next few sections will describe how, in the setting of (LABEL:ranenv), one can furnish a one-parameter family of recovering cocycles known as the Busemann process.

2.2. Path spaces, finite polymer measures, and the limit shape

A (directed) path on is a sequence of vertices such that for each . The lattice divides into anti-diagonal levels,

| (2.3) | ||||

We typically index paths so that . For and , we denote the set of paths between and by

This set is nonempty if and only if , by which we mean that both and hold. The projection random variables on any path space are denoted by or whenever the indices make sense (we will always use ).

Given a collection of weights , we consider the following probability measure on (whenever ):

| (2.4) |

That is, the likelihood under of sampling a particular path is proportional to the product of the weights witnessed along said path, and serves as the normalizing constant (also known as the partition function) ensuring that has total mass :

| (2.5) |

Since all paths terminating at must pass through either or , (2.5) can also be thought of as a recursion:

| (2.6) | ||||

The marginals of under can be obtained by multiplying partition functions: for any sequence , we have

| (2.7) | ||||

In the directed polymer literature, usually one is interested in fixing the starting point at and studying the properties of as the terminal point is pushed to infinity along a particular direction in the northeast quadrant. Here we take the opposite (but entirely analogous) perspective of fixing the terminal location at and pulling the starting point to negative infinity along some direction in the southwest quadrant.333When time proceeds in the up-right diagonal direction, under this convention the Busemann process is related to the environment from the past rather than the future; see (2.25). This is consistent with the language of SHE and 1F1S in Section 5. This results in a law of large numbers known as a shape theorem, made precise below.

Theorem A.

[38, Sec. 2.3] Assume (LABEL:ranenv). Then there exists a nonrandom function such that

This function is concave, continuous, and positively homogeneous in the sense that

| (2.8) | ||||

The concavity of the shape function is due to superadditivity of free energy, which can be seen from the fact that the left-hand side of (2.7) is at most :

In general, further regularity of beyond Theorem A is unknown, although it is believed that is differentiable in great generality. Here, as in FPP and LPP, curvature and differentiability of the limit shape is a central and long-standing open problem [3].

2.3. Infinite polymer measures

Following Theorem A, it is natural to ask if the polymer measures (2.4) themselves have a limit, and to what extent this limit depends on the chosen direction . Supposing we fix a root vertex , the limit should be a measure on the following space of semi-infinite backward paths:

This space is equipped with the usual cylindrical -algebra. If a limiting measure is to be identified, in a Gibbsian spirit we desire that its finite-dimensional conditional distributions agree with those of the pre-limiting measures from (2.4). So we say that a probability measure on is a semi-infinite polymer measure rooted at if, whenever (so that is nonempty), we have the following equality of measures:

| (2.9a) | ||||

| In words, conditioning the measure to pass through induces a marginal distribution (on the portion of the path between and ) that is exactly the measure from (2.4). To ensure the left-hand side of (2.9a) makes sense, we require the non-degeneracy condition | ||||

| (2.9b) | ||||

The other natural requirement is that limiting measures rooted at different vertices are consistent with one another. So let be a family of measures such that is a semi-infinite polymer measures rooted at for each . This family is consistent if, whenever , we have

| (2.9c) |

That is, conditioning the measure to pass through induces a marginal distribution (on the portion of the path between and ) that is exactly .

We then have the following (deterministic) relation between consistent families of semi-infinite polymer measures and recovering cocycles.

Theorem B.

Because polymer measures are equipped with the structure of partition functions (2.5), this result suggests a fundamental entry point to characterizing recovering cocyles. Observe that for any , we have

| (2.11) | ||||

Notice that the ratio occupies the same role in (2.11) as in (2.10). In the spirit of Theorem A, one hopes that if is sent to and given some limiting direction, then this ratio will converge, presumably to for some recovering cocycle . The cocycles realized in this way are called Busemann functions, and through Theorem B they encode limits of the measure from (2.4) as is pulled to negative infinity in southwest quadrant.

2.4. Busemann process

We now make rigorous the discussion that punctuated Section 2.3. First we must state some definitions to capture the role played by limit directions. To simplify matters, note that because of homogeneity (2.8), the shape function is completely determined by its restriction to the one-dimensional line segment between and . We will denote this line segment by ( when excluding the endpoints), where we think of as the minimal element according to southeast ordering. We formalize this order by writing when the two directions satisfy , and when .

Next, since is concave we can define “one-sided” derivatives: let and be the vectors in defined by

The set of directions of differentiability is

There may be linear segments of on either side of a given , which are recorded by the following two closed subintervals:

| (2.12) | ||||

The endpoints of these intervals will be denoted by

| (2.13) | ||||

where the infimum and supremum are taken with respect to the southeast order on . Since is known to have no linear segment containing or (see [38, Lem. B.1]), we always have . Finally, for convenience we will write

We say that is strictly concave at if this interval is degenerate, i.e. .

Given , let us say that a sequence of is -directed as if the set of limit points of is contained in .

Theorem C.

[38, Thm. 3.8] Assume (LABEL:ranenv), and suppose is such that . Then there is a full-probability event on which the following holds. For each , the following limit exists and is the same for every -directed sequence :

| (2.14) | ||||

Furthermore, if also satisfies , and has , then on we have the following inequalities for all :

| (2.15) | ||||

Because of the telescoping identity

the function in (2.14) satisfies the cocycle condition (2.2a). It also satisfies the recovery condition (2.2b), since (2.6) leads to

So Theorem C produces a recovering cocycle for each direction . Crucially, though, the full-probability event in Theorem C depends on . So in order to realize a cocycle simultaneously for all uncountably many values of , (2.14) is not sufficient. Hence the importance of (2.15), which allows one to

-

1.

First realize the nearest-neighbor Busemann functions for a countable dense collection of direction parameters .

-

2.

Next extend to all by taking monotone limits.

-

3.

Finally, extend additively to all of according to (2.2a).

Since left limits and right limits may not agree, this construction results in two Busemann processes: a left-continuous version and a right-continuous version .

Theorem D.

[38, Thm. 4.7, Lem. 4.13, Thm. 4.14] Assume (LABEL:ranenv). Then there exists a family of random variables

and a full-probability event with the following properties:

-

•

Each is a covariant cocycle on , the cocycle part meaning that

(2.16) and the covariant part meaning that

(2.17) -

•

Almost surely each recovers the vertex weights: on the event ,

(2.18) -

•

When restricted to nearest-neighbor pairs, the Busemann functions exhibit the following monotonicity: if , then for every we have

(2.19a) (2.19b) -

•

For fixed and , the maps and are the left- and right-continuous versions of each other. That is, under the southeast ordering of , we have these monotone limits:

(2.20) Towards the endpoints of , for and both signs , we have these monotone limits on the event :

(2.21) -

•

The Busemann process is constant on linear segments of the limit shape:

(2.22) -

•

Extended Busemann limits: on the event , for any -directed sequence ,

(2.23a) (2.23b) -

•

For every , , and , the random variable belongs to and has expected value

(2.24) -

•

For any set , let . Then we have independence of the following two collections of random variables:

(2.25)

Remark 2.1 (Construction of the Busemann process and a regularity assumption).

The discussion before Theorem D overlooked one important detail: to invoke Theorem C requires certain assumptions about the direction . The condition that belongs to is not a major impediment since the shape function is concave and thus differentiable at a dense set of points. But the additional assumption that and belong to is a serious limitation if has linear segments whose endpoints are not points of differentiability. Thus it is common in the literature to assume that if has any linear segments, then it is differentiable at the endpoints of those segments. Equivalently,

| (2.26) | ||||

Making this assumption means every automatically satisfies the second condition and thus can be used in Theorem C. This in turn would mean the Busemann process is a measurable function of the weights .

Nevertheless, Theorem D was proved in [38] without (2.26) by an adaptation of the strategy from [20]. The shortcoming is that the resulting Busemann process is constructed as a weak limit and is not a function of the original weights . Moreover, one needs to expand the original probability space in order to accommodate this weak limit, meaning Theorem D would be more properly stated as “There exists some probability space such that (LABEL:ranenv) holds and…” We regard the expansion of the probability space as given and will not make any further distinctions.

Our main results avoid making the assumption (2.26). One consequence of this is that we do not know if the Busemann process is ergodic under translations, which makes certain arguments more challenging. Fortunately, we are able to show (and at one point need to use) that horizontal Busemann increments are ergodic under the translation (Theorem 3.3). This extends [39, Thm. 3.5] to joint distributions involving multiple direction parameters.

Remark 2.2 (Discontinuities and null events).

A combination of the monotonicity (2.19) and the mean identity (2.24) implies that for each , on a full-probability event that depends on . In particular, when desirable, any full-probability event can be assumed to satisfy for all in any fixed countable set of directions of differentiability. The construction of the Busemann process described above Theorem D relies implicitly on this property. Another consequence of this feature is that any statement about the distribution of countably many functions with can drop the signs .

Random directions of discontinuity can still arise among the uncountably many differentiability directions. One of the main points of our paper is to describe properties of these directions. In Corollary 4.4 we determine that this set of discontinuities is dense in the inverse-gamma case, thereby providing the first existence result for discontinuities in a positive-temperature lattice model. We cannot prove this existence in general, but we do present some new properties of the discontinuity set in Section 3.1.

The bounds in (2.23) leave open the possibility that in a jump direction the Busemann functions cannot be realized as limits. To close this possibility, Proposition A.2 in Appendix A.2 shows that the extreme inequalities in (2.23) are in fact equalities for suitable sequences . This statement holds simultaneously in all directions with probability one, under the assumption (2.26).

Remark 2.3 (Monotonicity).

As stated, (2.19) is a sure event. But on the almost sure event from Theorem D, the recovery property (2.18) allows an upgrade to a more complete statement:

| (2.27a) | ||||

| (2.27b) | ||||

Furthermore, two special cases of (2.24) are and . The inner products on the right-hand sides must obey the same monotonicity as (2.27): for ,

| (2.28a) | ||||

| (2.28b) | ||||

These inequalities are useful to have recorded when working with rather than the Busemann functions directly.

3. Main results under general i.i.d. weights

3.1. Busemann process indexed by directions

Our first result is about the monotonicity of nearest-neighbor Busemann functions and will be proved at the end of Section 6.4. Combined with (2.22), it reveals that is constant on linear segments of and strictly monotone otherwise.

Theorem 3.1.

Assume (LABEL:ranenv). Then there exists a full-probability event on which the following holds. For each pair of directions in that do not lie on the same closed linear segment of , we have the strict inequalities

| (3.1) | ||||

Next we consider discontinuities of the Busemann process. Define the -dependent set of exceptional directions where the Busemann process experiences a jump:

For any sequences of vertices such that for each , the cocycle property (2.16) gives . Each nearest-neighbor increment is a monotone function of by (2.19) and thus has at most countably many discontinuities. Hence is at most countable. Under a differentiability assumption on the shape function , [38, Thm. 3.10(c)] implies that is either empty or infinite. Membership has implications for the existence and uniqueness of -directed polymer Gibbs measures. The reader can find such results proved under the regularity assumption (2.26) in [38, Thm. 3.10]. In Remark 4.5 we state these consequences in the inverse-gamma case.

The following theorem is proved in Section 6.5. Part (a) is the main novelty, as part (b) is morally contained in [38, Thm. 3.2].

Theorem 3.2.

Assume (LABEL:ranenv). Then there exists a full-probability event on which the following statements hold.

-

(a)

The set of discontinuities of the function is the same for all nearest-neighbor edges. That is, for each ,

-

(b)

For each , contains the set of directions at which the shape function is not differentiable.

3.2. Joint distribution of the Busemann process

This section gives a preliminary characterization of the joint distribution of the Busemann process, without full technical details. The complete description requires additional developments and appears in Section 6.

The cocycle property (2.16) and the recovery property (2.18) together imply that, once the weights are given, the Busemann function is completely determined by its values on horizontal nearest-neighbor edges. Hence it is sufficient to describe the joint distribution on horizontal levels. Since the Busemann process is stationary under each lattice translation, every level has the same distribution.

On each lattice level , define the sequence of exponentiated horizontal nearest-neighbor Busemann increments

| (3.2a) | |||

| Fix directions in and signs . Condense the notation of the -tuple of sequences as | |||

| (3.2b) | |||

The values at level can be calculated from the level- values and the level- weights by a deterministic mapping that we encode as

| (3.3) |

This mapping , called the parallel transformation, depends on a given sequence of weights and acts on -tuples of sequences. It is defined in equation (6.22) in Section 6.2. Since is independent of , it follows that the process is an -valued stationary Markov chain.

In the next statement, translation on the sequence space is the operation that acts on an element by shifting the -index: . Recall the mean (2.24).

Theorem 3.3.

Assume (LABEL:ranenv). Let . The property

| (3.4) | ||||

determines uniquely a probability distribution on the sequence space that is stationary for the Markov chain (3.3) and invariant and ergodic under the translation of the -index. In particular, for each , the -tuple of sequences defined in (3.2) has distribution .

A precise version of this theorem is stated and proved as Theorem 6.23 in Section 6.4. Since this theorem concerns a fixed finite set of directions, the sign makes a difference only if . When are directions of differentiability, the signs can be dropped from the statement. This was explained in Remark 2.2.

Remark 3.4 (State space for the entire Busemann process on a lattice level).

We have considered the joint distribution of finitely many exponentiated Busemann functions at height of the lattice, as captured by the -tuple of sequences in (3.2b). If desired, one can consider the Markovian evolution of the full -indexed process where each -indexed component is the sequence with coordinates . The state space of could be realized as follows. Let be a given nonincreasing cadlag function, and define the space

Above denotes the space of cadlag functions with the standard Skorokhod topology, with southeast ordering on the parameter domain , and is the left tail logarithmic Cesàro average of the sequence , defined in (6.1). A state space of this type was introduced for the KPZ fixed point in [12].

Remark 3.5 (Vertical increments).

Theorem 3.3 considers only horizontal Busemann increments, but the vertical increments could be treated similarly thanks to reflection symmetry of the i.i.d. weights . Once indices and exchange roles and is replaced with in (3.4), the analogous result holds. Granting such a result, it follows that the process discussed in Remark 3.4 has the same distribution as , where is defined in (6.71), and is the reflection of across the direction. This fact, although very intuitive, is not immediately apparent from Theorem D.

3.3. Competition interface directions

To give context to our results, we begin by defining the competition interface from [27, 38]. Recall the point-to-point polymer measure from (2.4), defined for each pair in . One can see from (2.7) that is an up-right Markov chain starting at and ending at , with transition probabilities

Given a realization of the weights , these walks can be coupled together using an auxiliary set of random variables as follows.

For , let be a probability measure under which the values of the weights have been fixed:

| (3.5) | ||||

Assume there is a family of random variables that are i.i.d. uniform on under . Now recall the set from (2.3), consisting of with . For each pair with and , define the path starting at and proceeding up or right according to the following rule. If and is equal to , then set

| (3.6) | ||||

In this way, has the law of under . Furthermore, if , then since the right-hand side of (3.6) does not depend on . So by planarity, the sets and are disjoint, and there exists a down-left path separating these two clusters; see Figure 3.1 for an example when . This path is called the competition interface and was shown in [38, Thm. 3.12] to have a random asymptotic direction , under assumption (2.26). That is, for -almost every , there is a quenched law of large numbers

with the limit distribution

| (3.7) |

The appearance of the Busemann function in (3.7) suggests a connection to semi-infinite polymer measures, and that is what our paper addresses.

Consider now the family of Gibbs measures associated to the Busemann function as in Theorem B. In other words, is the quenched distribution of semi-infinite southwest polymer paths rooted at . Each is a down-left Markov chain with transition probability

| (3.8) |

Note that these transition probabilities inherit the monotonicity of the Busemann process: if either or , then (2.19a) implies

| (3.9) | ||||

We now proceed to couple all the distributions .

For each , let be as in (3.5) with the additional guarantee of fixing the values of the Busemann process:444When (2.26) is assumed, (3.10) is implied by (3.5) because then the Busemann process is a function of the weights (see Remark 2.1).

| (3.10) | ||||

This means the transition probability in (3.8) is deterministic under . For each direction , sign , root vertex , and tiebreaker , define the random path inductively as follows. Fix the root location . For , if is equal to , then set

| (3.11) |

Under , the path has distribution because its transition probability from to is clearly . The tiebreaker is included because takes uncountably many values. Indeed, for any fixed , we have and so the walks and agree -almost surely. But considering all values of simultaneously leaves open the possibility that and separate at some lattice vertex.

Notice that the protocol (3.11) does not depend on . That is, for given and , any two walks and that meet at some will thereupon remain together forever. Therefore, it suffices to understand the behavior of at , which is the content of the following theorem.

Theorem 3.6.

Assume (LABEL:ranenv). For -almost every , the following holds. Under there exist independent -valued random directions with the following properties.

-

(a)

The marginal distribution is, for ,

(3.12) -

(b)

Let . Then -almost surely the walks (3.11) behave as follows at .

-

(b.i)

Suppose . Then for both signs and tiebreakers , and .

-

(b.ii)

Suppose . Then the tiebreaker separates the walks but the distinction has no effect: for both , and .

-

(b.iii)

Suppose . Then the distinction separates the walks but the tiebreaker has no effect: for both , and .

-

(b.i)

Remark 3.7.

(Relation to competition interface) There is an obvious duality between the constructions of and . The former separates finite up-right paths ending at , while the latter separates semi-infinite down-left paths starting at . Comparison of (3.7) and (3.12) shows that the two directions have the same quenched distribution. One compelling aspect of our construction is that is an independent family under , whereas is not. This allows us in Theorem 3.9 below to relate the interface directions to discontinuities of the Busemann process. Another advantage is that Theorem 3.6 does not require the regularity assumption (2.26). A disadvantage is that there is no canonical way to identify an interface with asymptotic direction , since two paths and can separate and rejoin several times.

While our presentation has coupled and through the same auxiliary randomness in (3.6) and (3.11), this is purely for simplicity, and there may be a more natural coupling offering additional insights. The connections between , , the geometry of polymer paths, and the regularity of the Busemann process are largely left open, elucidated below in Remark 3.11. In Section 4.4 we resolve some of these questions in the inverse-gamma case.

Remark 3.8.

(Comparison with zero temperature, part 1) In LPP there is no need for the auxiliary randomness supplied by , since in that setting the fundamental objects are geodesic paths rather than path measures. The finite paths in (3.6) are analogous to finite geodesics, while the semi-infinite paths in (3.11) are analogous to semi-geodesics defined by Busemann functions (see [40, eq. (2.12)]). Those two families of geodesics share the same interface and so there is no distinction between and at zero temperature. That interface is defined so as to separate geodesics passing through from those passing through , just as in Figure 3.1.

We record further properties of our interface directions in the next theorem.

Theorem 3.9.

Assume (LABEL:ranenv). The following holds -almost surely, for -almost every .

-

(a)

Any direction appears at most once among .

The next three statements additionally require regularity assumption (2.26).

-

(a)

Suppose satisfies one of these two conditions:

-

•

for some ; or

-

•

do not lie on the same closed linear segment of .

Then for each and any tiebreakers , the walks and eventually separate permanently. That is, there exists such that for all .

-

•

-

(b)

Each discontinuity direction appears infinitely many times among .

-

(c)

The set is dense in in the complement of the linear segments of .

The proof of parts (a)–(c) given below utilizes the extremality of the polymer Gibbs measures , which presently has been proved only under assumption (2.26) [38].

Remark 3.10.

(Comparison with zero temperature, part 2) In LPP with continuous weights, the almost-sure uniqueness of finite geodesics implies that once semi-infinite geodesics separate, they cannot meet again. Part (a) in Theorem 3.9 is the analogous result here. It is not possible to eliminate all reunions since the uniform variables guiding the polymer walks are chosen independently, which allows any two walks and to meet with positive -probability even after separating.

Parts (a) and (b) are similar to the statement in LPP that the set lies in the union of the supports of the Lebesgue–Stieltjes measures of the Busemann functions [40, Thm. 3.7(a)]. In the exactly solvable exponential case, the maps are step functions by [21, Thm. 3.4], and is exactly the union of their jumps [40, Thm. 3.7(b)]. We prove analogous statements for the inverse-gamma polymer model in Theorems 4.3 and 4.6.

Remark 3.11 (Open questions).

-

(I)

The fundamental open question is whether the Busemann functions are continuous or not. By parts (a) and (b) of Theorem 3.9, this would be reflected in the distribution of and . Does the set consist of only discontinuities of the Busemann functions? If so, then the existence and denseness of these discontinuities would follow from Theorem 3.9(c).

-

(II)

Do the rich connections between the regularity of the Busemann process and the geometric properties of semi-infinite geodesics in LPP found in [40, Sec. 3.1] appear in some form for positive-temperature polymers? For example, it follows from the coalescence theorem in [38, App. A.2] that for each pair there exists a dense open subset with the following property. For each open subinterval of , there exists a pair of finite down-right paths that emanate from and and meet at a point , and for each direction , sign and tiebreaker , the walks and follow these paths to their coalescence point. Are the coalescence points related to singularities of the Busemann functions or to the directions or ?

In Section 4.4 we answer part (I) in the affirmative for the inverse-gamma polymer. The questions in part (II) are left for the future even in the exactly solvable case.

The remainder of this section proves Theorems 3.6 and 3.9, by appeal to Theorems 3.1 and 3.2. The proposition below establishes the existence and uniqueness of the directions that dictate where walks split. We choose to define our objects in sufficient generality to account for zero-probability events, since that has turned out to be necessary for a full understanding in the zero-temperature case. Hence below we first define two values and then show that they agree -almost surely for -almost every .

For use below, note that the limits in (2.21) give the degenerate transition kernels

| (3.13) | ||||

Proposition 3.12.

For -almost every , the following is true. For any realization of and at each vertex , there exist unique in such that the following implications are true. For any and signs ,

| (3.14a) | ||||

| and | (3.14b) | |||

Furthermore, we have these inequalities:

| (3.15) |

Disagreement happens if and only if is a maximal linear segment of and for some (and hence any) .

Proof.

Existence. Set

| (3.16) | ||||

Since and are the left- and right-continuous versions of the same nondecreasing function, these definitions are independent of the signs . It follows from (3.13) that for , the infimum and the supremum are over nonempty sets and each lies in the open segment . Suppose . Then , which implies . Thus . The definitions (3.16) imply the properties in (3.14). Thus we have found at least one pair that satisfies (3.14).

Uniqueness. Suppose . Then for either ,

The first inequality shows that cannot be replaced by without violating (3.14b). The second inequality shows that cannot be replaced by without violating (3.14a). A similar argument establishes the uniqueness of .

Properties. The extreme inequalities of (3.15) follow from (3.9) since . The inner inequalities of (3.15) follow from letting and in the definitions in (3.16), because is continuous from the left and from the right.

Suppose is a maximal linear segment of and for some . Then for each , by the strict inequality of Theorem 3.1, we have . Hence by definition (3.16). Similarly .

Conversely, suppose . This implies because of (3.9). Then the middle inequalities of (3.15) force . Again by the strict inequality of Theorem 3.1, must be a linear segment for . Moreover, it must be a maximal linear segment because Busemann functions are constant on linear segments by (2.22), yet , were chosen in (3.16) to be extremal. ∎

Proof of Theorem 3.6.

First we argue that so that we can define

| (3.17) | ||||

By Proposition 3.12, we need to rule out the possibility that for some in an open linear segment of the shape function . Indeed, there are at most countably many such segments and, by (2.22), is constant on each such segment. So needs to avoid only countably many values (depending on ), which occurs -almost surely.

Given , for each the variable is a function of , a fact which is immediate from (3.16) and (3.17). Hence the random variables are independent under . To obtain the marginal distribution claimed in (3.12), we establish inequalities in both directions. Utilize (3.14b) and the right-hand side of (3.15) to write

Since is uniform on , this says

The second inequality is one direction of (3.12). To obtain the other direction, we employ the first inequality:

The marginal distribution claimed in part (a) has been verified.

The final observation we need is that

| (3.18) |

which is true because is at most countable and fixed by . In light of (3.17) and (3.18), we infer from (3.15) that -almost surely one of these two cases happens at every :

| (3.19a) | ||||

| or | (3.19b) | |||

The claims (b)(b.i)–(b)(b.iii) follow readily from the above dichotomy (3.19) and definition (3.11). ∎

Proof of Theorem 3.9.

Part (a) follows from the fact that under the variables are independent and, by (3.12) and Theorem 3.2, each has the same set of atoms.

Part (a). We claim that there exists an event of full -probability such that for all ,

| (3.20) |

Indeed, by [38, Rmk. 5.9], under assumption (2.26) there exists of full -probability such that for each , , , and , the path measure from (3.8) is extreme among the semi-infinite Gibbs measures rooted at . By [38, Thm. 3.10(d) and Thm. 5.7], this extremality implies that for all ,

Since has distribution under , it follows that for either tiebreaker ,

| (3.21) | ||||

This does not immediately imply (3.20) since the event on the left-hand side of (3.21) is -dependent, but we will extend it as follows.

Let be a countable dense subset of that contains the discontinuity set . For , the following occurs with full -probability by (3.21):

| (3.22) | ||||

and also

| (3.23) | ||||

Consider any . We necessarily have , and so . Pick so that . By the monotonicity (3.9) and the decision rule (3.11), we have

| (3.24) | ||||

This ordering and standard monotonicity of partition function ratios (e.g. [11, Lem. A.2]) give

| (3.25) | ||||

Since (3.22) applies to the leftmost and rightmost ratios above, the subsequential limits of the middle ratio are caught between and . As we let and , these converge to thanks to (2.20). We have thus argued that (3.22) is sufficient to establish the claim (3.20). It should be noted that our use of (3.25) is permitted because (3.23) implies and are -directed and -directed, respectively. By the curvature result [38, Lem. B.1], the closed intervals and do not contain or , and so for all sufficiently negative . The ordering (3.24) then forces as well.

To complete the proof of part (a), observe that if for infinitely many , then along this subsequence the limits in (3.20) give for all . Under the assumptions on the pair , this violates either Theorem 3.1 or 3.2.

Part (b). By part (a), for each , from any initial vertex the walks separate. By Theorem 3.6(b)(b.i) and (b)(b.iii), this can happen only if for infinitely many .

4. Main results under inverse-gamma weights

4.1. Inverse-gamma basics

The Gamma function is . The digamma and the trigamma functions are, respectively, and . A positive random variable has the gamma distribution with parameter , abbreviated Ga, if has density function for . has the inverse-gamma distribution with parameter , Ga, if its reciprocal satisfies Ga. Then has density function for and satisfies the identities and . is stochastically decreasing in the parameter (Lemma C.1 in Appendix C). The beta variable Be has density for .

Fix and assume that

| the weights are i.i.d. random variables | (4.1) | |||

| with marginal distribution Ga. |

The limiting free energy or shape function is explicitly described as follows (see (2.15) and (2.16) of [50]). On the axes for . In the interior, for each there is a unique real such that

| (4.2) | ||||

The minimizer in (4.2) is the solution of the equation

| (4.3) |

The shape function is continuous on , and differentiable and strictly concave throughout . In particular, assumption (2.26) is satisfied.

The correspondence (4.3) gives the following bijective mapping between direction vectors and parameters :

| (4.4) |

The function is strictly positive and strictly decreasing on , with limits and . Thus the bijection from onto is strictly decreasing in the southeast ordering on . In particular, the boundary values are and .

4.2. Global Busemann process

As observed in Section 3.2, the entire Busemann process can be characterized by the joint distribution of horizontal nearest-neighbor increments on a single lattice level. Similarly to Section 3.2, we give here a quick preliminary description of this distribution. Full details rely on the development of Section 6 and are presented in Section 8.

We introduce notation for products of inverse gamma distributions. Let be an -tuple of positive reals. Let denote an -tuple of positive bi-infinite random sequences . Then define the probability measure on as follows:

| has distribution if all the coordinates are mutually | (4.5) | |||

| independent with marginal distributions Ga. |

To paraphrase (4.5), under each is a sequence of i.i.d. inverse-gamma variables with parameter and the sequences are mutually independent.

Denote the sequence of level- weights by . Recall the notation (3.2) for sequences of exponentiated horizontal nearest-neighbor Busemann increments: . Fix directions in and signs . There exists a sequence space that supports the product measure and a Borel mapping such that the following theorem holds.

Theorem 4.1.

Assume (4.1). At each level , the joint distribution of the -tuple of sequences satisfies

The theorem states that on a single horizontal level the joint distribution of the original weights and the Busemann functions is a deterministic push-forward of the distribution of independent inverse gamma variables with the same marginal distributions. Since is differentiable, the signs are irrelevant (recall Remark 2.2) and included only for completeness. For this reason the parametrization of the measures ignores the signs.

The space and the mapping are defined in equations (6.27) and (6.30). The precise version of Theorem 4.1 is proved as Theorem 8.4 in Section 8.1. The mapping preserves the distributions of individual sequence-valued components:

| (4.6) |

If instead of horizontal increments on a horizontal line, we considered vertical increments on a vertical line, the statement would be this:

| (4.7) |

These marginal properties (4.6) and (4.7) of the Busemann functions were derived earlier in [27]. They follow from Lemma 8.1 in Section 8.1.

Remark 4.2 (The order relations in Theorem 4.1).

The assumption , strict concavity of , and Theorem 3.1 combine to imply the almost sure strict coordinatewise inequalities

| (4.8) |

This same conclusion follows also from a property of the mapping given in Lemma 6.6 in in Section 6.2. In general, the product measure is supported on iff . Thus to apply the mapping , it was necessary to put the components in order by ordering the parameters as in . This ordering of parameters is consistent with (4.8) and, through the monotonicity of (4.4), consistent with .

4.3. Busemann process across an edge

We fix a horizontal edge and describe the Busemann process on this edge. To have a process indexed by reals, we switch from to the parameter . Then is an increasing cadlag process which has been extended to the parameter value by setting . This process is continuous at by (2.21). The minus superscript in is just for the path regularity. In statements about finite-dimensional distributions we drop it.

Let be the inhomogeneous Poisson point process on with intensity measure with density function

We use to denote both the random discrete set of locations and the resulting Poisson random measure. The Laplace functional of is given by

| (4.9) |

for nonnegative Borel functions .

Define the nondecreasing cadlag process so that the initial value Ga-1() is independent of and

| (4.10) |

Theorem 4.3.

Assume i.i.d. inverse-gamma weights (4.1). For each , the nondecreasing cadlag processes and are equal in distribution.

See Figure 4.1 for an example sample path. Theorem 4.3 is proved by establishing that has independent increments as does , and by showing that their increments have identical distributions. Independent increments means that for , the random variables are independent. From the proof we see that for , the distribution of an increment satisfies

which is consistent with the expectation that already followed from (4.6):

We state a corollary about the jumps of the inverse-gamma Busemann process. Let be the point process on of downward jumps of size of the Busemann function :

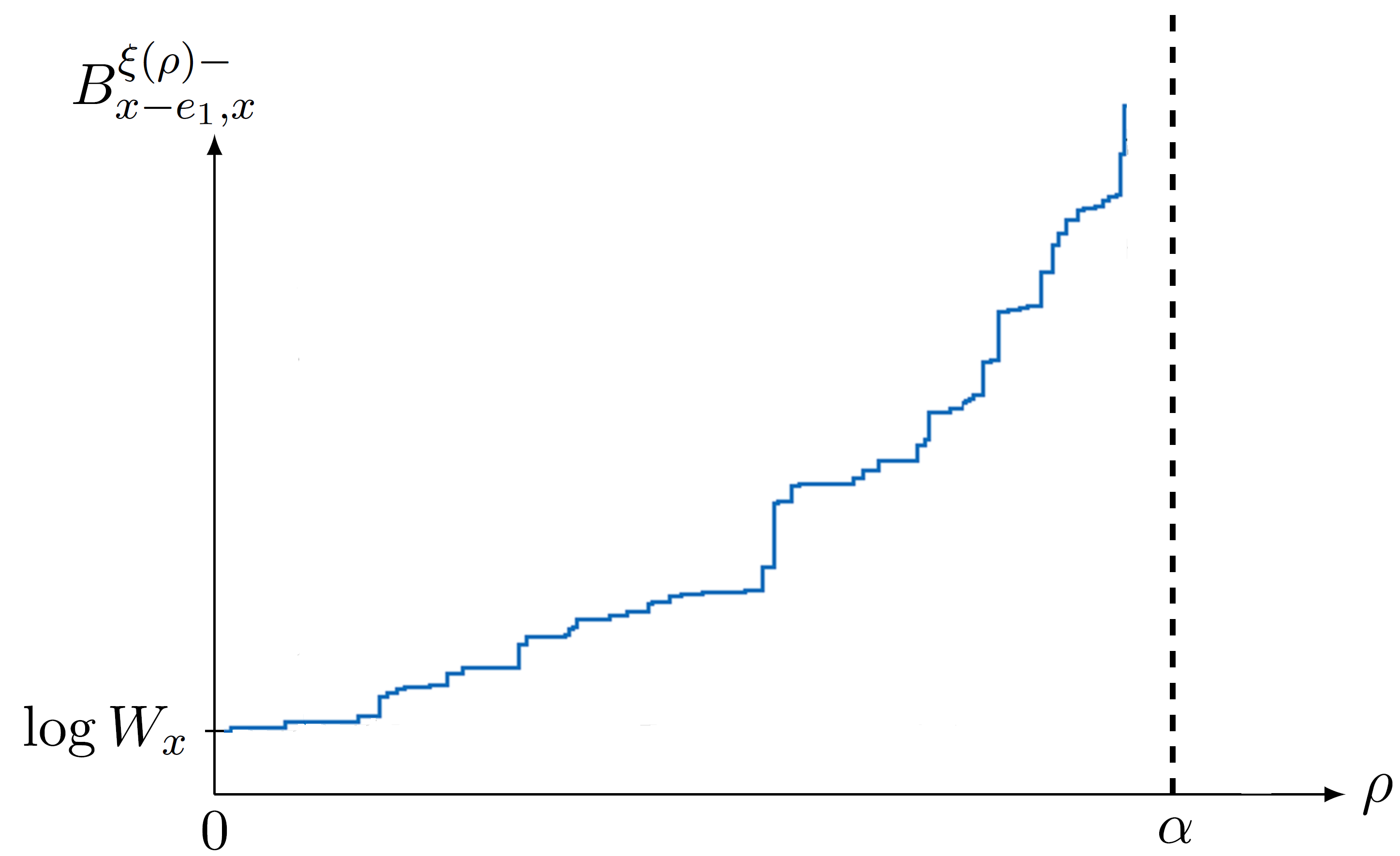

For distributional statements about the choice of is immaterial. We observe below that large jumps accumulate only at , while small jumps are dense everywhere. This is consistent with the continuity (2.21) of at the right endpoint .

Corollary 4.4.

-

(a)

Let . is a Poisson process on with intensity measure

(4.11) In particular, is a finite Poisson variable for each and so almost surely there is a last jump of size before . By contrast, with probability one, for each .

-

(b)

With probability one, the set of jump directions is dense in .

We prove the corollary at the end of this section after some further remarks.

Remark 4.5 (Inverse-gamma polymer Gibbs measures).

We combine results from [38] with our results to state facts about the polymer Gibbs measures of the inverse-gamma polymer model.

For each there is a -dependent full-probability event on which there is a unique -directed polymer Gibbs measure rooted at each . This comes from combining [38, Thm. 3.7] with the strict concavity and differentiability of the inverse-gamma shape function.

There exists a full-probability event on which the following holds for each : For each there is a unique -directed polymer Gibbs measure rooted at . For each , there are at least two -directed extreme polymer Gibbs measure rooted at . These statements come from [38, Thm. 3.10(e)–(f)] and the strict concavity of the inverse-gamma shape function.

An important open problem is the number of extreme Gibbs measures at directions , rooted at a particular . This problem, including its zero-temperature analogue, has been solved in one context only, namely in the exponential corner growth model. The statement there is that in directions of discontinuity of the Busemann process, there are exactly two semi-infinite geodesics from each initial vertex [19, 40]. Based on this, the natural conjecture is that, rooted at each , there are exactly two extreme polymer Gibbs measures in directions .

Proof of Corollary 4.4.

For both processes and , on any compact interval the finite ordered sequence of jumps of size can be captured with measurable functions of the path. Thus the processes of such jumps have the same distribution for both and . For the Poisson description of these jumps is clear from (4.10). Hence the same description works for . To get the first statement of part (a), map this Poisson process back to via the bijection (4.4).

4.4. Competition interface under inverse-gamma weights

Theorem 4.6.

Assume i.i.d. inverse-gamma weights (4.1). Then the following hold almost surely: and for each , .

The proof of the theorem comes after this lemma.

Lemma 4.7.

Assume i.i.d. inverse-gamma weights (4.1). Then -almost surely

| (4.12) |

Proof.

The upper bound comes because is nondecreasing in the southeast ordering:

For the opposite bound, to use the explicit construction (4.10) of the cadlag process we switch to the nondecreasing cadlag process indexed by the real variable . Below the left limit of this process is

where is equivalent to because the bijection (4.4) is strictly decreasing. We have

The equality in distribution above is justified by Theorem 4.3. A special case of the cadlag Itô formula for a function of a process of bounded variation gives

(Corollary 6.3(b) in the lecture notes [49].) Apply this to . The construction (4.10) implies that the integral and the sum of the last terms cancel each other for , and we are left with

Letting sends to zero and justifies equality () above. ∎

5. Discrete stochastic heat equation

This section records implications of our results for a lattice version of the stochastic heat equation (SHE). To place this section in context, we discuss briefly the standard SHE and the related KPZ and stochastic Burgers equations.

5.1. Polymers, SHE, KPZ and SBE

In continuous time and space, the SHE with multiplicative space-time white noise is the stochastic partial differential equation

| (5.1) | ||||

With point mass initial condition , (5.1) is formally solved by the rescaled partition function of the continuum directed random polymer (CDRP) [1]:

where the expectation is over Brownian bridges from to , is the Wick exponential, and is the heat kernel.

Switching to the free energy ( is also called the Hopf–Cole transform) takes us formally from SHE to to the Kardar–Parisi–Zhang (KPZ) equation

| (5.2) | ||||

Originally proposed in [42] as a model for the height profile of a growing interface, (5.2) is the universal scaling limit of various 1+1 dimensional stochastic models under the so-called intermediate disorder scaling and is itself a member of the KPZ universality class; see [16] for a survey.

Upon formally taking a spatial derivative we arrive at the (viscous) stochastic Burgers equation (SBE)

| (5.3) | ||||

The one force–one solution principle (1F1S) is concerned with the existence and uniqueness of eternal solutions to (5.3) and its inviscid counterpart. This program was initiated by Ya. Sinai [54].

5.2. Polymers and discrete SHE

The directed polymer model of our paper is associated with a particular discretization of (5.1) on the planar integer lattice . Given an assignment of strictly positive weights, consider solutions of the equation

| (5.4) | ||||

Remark 5.1.

Equation (5.4) is a natural discrete counterpart of (5.1) because both are equations for polymer partition functions. We can also render (5.4) formally similar to (5.1) by choosing suitable variables. Let the forward diagonal represent the time direction and the positive spatial direction. Suppose first that . Then several applications of (5.4) yield

| (5.5) | ||||

This is a finite difference version of the heat equation . Next, let for i.i.d. mean zero random variables . Then the right-hand side of (5.5) acquires an additional term which is a linear combination of the -terms on the right with mean-zero random coefficients. This is a discrete, though somewhat complicated, version of the multiplicative noise term in (5.1).

With partition functions defined as in (2.5), equation (5.4) extends across multiple levels:

| (5.6) |

Equation (5.6) prescribes how to calculate, from an initial condition , the unique solution on all later levels , . Instead of an initial value problem, we consider eternal solutions. An eternal solution is a function such that (5.4) (equivalently, (5.6)) holds at every . Strictly positive eternal solutions of (5.6), up to constant multiples, are in bijective correspondence with recovering cocycles and with consistent families of rooted polymer Gibbs measures. These elementary results are developed in Appendix B.

Existence and uniqueness questions of eternal solutions are typically posed under given weights and for a given value of a conserved quantity. Equation (5.4) has a natural conserved quantity in the asymptotic logarithmic slope. If the weights satisfy

then the quantity

| (5.7) |

is preserved by the evolution (5.4). That is, if the limit (5.7) holds at level , it continues to hold at all subsequent levels.

The Busemann process gives the following theorem on the almost sure existence of eternal solutions under i.i.d. random weights.

Theorem 5.2.

Assume (LABEL:ranenv). There exists a full-probability event such that for each , , , and , the function defined by

satisfies the following properties.

Further properties of the eternal solutions can of course be inferred from the properties of the Busemann functions. Some comments on the theorem follow. Part (i) is straightforward and follows from Lemma B.1 in Appendix B. Part (ii) is a restatement of Theorem A.1 in Appendix A.1. This part identifies the conserved quantity in (5.7) for the solution as .

The eternal solutions of the conservation law required by 1F1S must depend only on the past of the weights. In our setting this is the past measurability of the ratios in part (iii). This is the natural statement, for if we imitate the connection from SHE to SBE, then the differences are the discrete counterpart of the solution to SBE (5.3). The solution itself is determined by the past weights only up to a multiplicative constant. Part (iii) is a consequence of the construction of the Busemann process described below Theorem C. This construction realizes the Busemann function from countably many limits of the form (2.14), and each of these limits is determined only by weights in the past. But this strategy requires assumption (2.26) (see Remark 2.1), hence this assumption’s appearance in part (iii).

Theorem 5.2 opens the possibility of failure of 1F1S. In the inverse-gamma case we have a theorem.

Theorem 5.3.

Assume i.i.d. inverse-gamma weights (4.1). Then there exists a full-probability event with the following property. For each there exists a countably infinite dense set such that for each and each base point , and are two distinct eternal solutions with the same conserved quantity .

Theorem 3.1 implies that all the nearest-neighbor ratios differ for and . Theorem 5.3 follows from the characterization of the discontinuity set in Corollary 4.4 and the differentiability of the inverse-gamma polymer shape function on . We cannot state the theorem for general weights because we do not presently know whether in general the Busemann process has discontinuities among directions of differentiability.

This is the end of the discussion of the main results and we turn to develop proofs.

6. Proofs in the general environment

This section develops the characterization of the joint distribution of finitely many Busemann functions on a lattice level. The approach is to identify this measure as the unique stationary distribution of a Markov chain. This Markov chain (the parallel process) intertwines with another Markov chain (the sequential process) which utilizes geometric row insertion. This section culminates in the proofs of three main results:

- •

- •

- •

The gRSK connection is explained in Section 7 and the outcome of this section applied to the inverse-gamma polymer in Section 8.1.

6.1. Update map

As for the corner growth model in [21], to capture the Busemann process it is advantageous to formulate the directed polymer model on a half-plane. In this section we define and investigate the update map that constructs ratios of partition functions from one lattice level to the next. Similar mechanics were developed in [39, Sec. 4] to study the ergodicity and uniqueness of the distribution of a recovering cocycle.

Our basic state space is the space of bi-infinite sequences of strictly positive real numbers for which a finite left tail logarithmic Cesàro limit exists:

| (6.1) | ||||

Let denote the space of such sequences. Then define the space

| (6.2) | ||||

On we define the update map together with two related maps and that are central to our analysis. Given input , let us locally denote the outputs of these three maps by

| (6.3) |

First define by setting

| (6.4) | ||||

Note that the right-hand side is finite if and only if

Consequently, it suffices to have for to be well-defined. Then define the transformations and in (6.3) by

| (6.5) | ||||

By reindexing the sum and then the product, we obtain

| (6.6) | ||||

Since all quantities are positive, it is clear that maps into .

The remainder of this section proves several technical lemmas about these mappings for later use. The reader may proceed to Section 6.2 and return to these lemmas when needed. The first lemma checks that and map into and preserve the Cesàro means. Lemma 6.2 shows that is injective, unlike the analogue defined in [21, eq. (2-22)].

Lemma 6.1.

For , the sequences and defined in (6.5) satisfy

| (6.7) | ||||

Proof.

The definition of in (6.5) gives . Similarly, dividing both sides of (6.6) by gives . From these two equalities of ratios,

Therefore, both statements in (6.7) are implied by

| (6.8) | ||||

The remainder of the proof establishes this limit.

Since exists and is finite, we necessarily have as . It thus suffices to show that . To this end, for we use (6.4) to write

| (6.9) | ||||

Now, given any , let us identify sufficiently negative that

Applying this estimate inside all the exponentials of (6.9), we obtain the following for all and :

| (6.10) | ||||

Upon observing that for any positive constant we have

we conclude from (6.10) that

Since is arbitrary, (6.8) follows and the proof is completed. ∎

Next we show the injectivity of the update map.

Lemma 6.2.

The map is injective on and has a continuous inverse mapping defined on its image.

Proof.

First we realize the following identity by inserting the recursion (6.6) into the definition of from (6.5):

| (6.11) | ||||

Solving for results in

| (6.12) | ||||

Now insert the expression from (6.5) into the right-hand side, and then rewrite using (6.12):

| (6.13) | ||||

We note that (6.11) implies for all , so the final expression in (6.13) is well-defined. Indeed, (6.13) shows that is uniquely determined by and , meaning is injective for any fixed . Continuity of the inverse map is evident from the formula (6.13), since the image of is a subset of . ∎

The next lemma shows that under a non-explosion condition, the recursions (6.6) and (6.11) uniquely identify the outputs.

Lemma 6.3.

Let . Let satisfy the recursion

| (6.14) |

Assume for some subsequence . Then .

Furthermore, suppose satisfies

| (6.15) |

Then .

Proof.

The assumption guarantees that and are well-defined. Iterating the assumed recursion (6.14) for gives, for ,

By the assumptions, along a subsequence the first term on the last line is eventually for some . Passing to the limit along this subsequence shows that matches the formula (6.4) for . Now (6.15) agrees with (6.11) for . ∎

The next lemma concerns monotonicity. The inequalities are understood coordinatewise: means that for every and, similarly, means for every .

Lemma 6.4.

Let be any element of .

-

(a)

We have .

-

(b)

If , then

(6.16) If we further know that , then

(6.17)

Proof.

The last lemma shows that when additional control is available, the update map itself possesses continuity in the product topology.

Lemma 6.5.

Let and let be a sequence of elements of such that coordinatewise as . Assume there is a pair such that and . Define the outputs and . Then coordinatewise.

Proof.

Let and . We verify that

| (6.18) |

By the recursive formula (6.6), it suffices to show that (6.18) holds for arbitrarily large negative . From (6.9) write

| (6.19) |

For each and we have

and the latter terms are summable by the assumption . Thus the right-hand side of (6.19) converges to the same expression without the -superscripts and (6.18) has been verified. From (6.5) follows then that . ∎

6.2. Intertwined dynamics on sequences: fixed weight sequence

For any positive integer and real number , define the space

| (6.20) | ||||

To condense notation, we write Fix a weight sequence with

| (6.21) | ||||

We define two mappings, the parallel transformation and the sequential transformation.

(A) The parallel transformation is the simultaneous application of the update map to several sequences with the same weight sequence :

| (6.22) | ||||

This is the transformation we ultimately care about, as it is the one obeyed by Busemann functions. By Lemma 6.1, the Cesàro limits of the input sequences are all preserved:

| (6.23) | ||||

(B) The sequential transformation again applies the update map to each input sequence , but with weights that are themselves updated between each application. It is defined by

| (6.24a) | ||||

| where (recall the map from (6.3) and (6.5)) | ||||

| (6.24b) | ||||

Lemma 6.1 guarantees , hence all the operations in (6.24) are well-defined and again preserve Cesàro limits:

| (6.25) | ||||

The definition (6.24) has also a recursive formulation:

| (6.26) | ||||

Next we construct a mapping that intertwines and . Whereas the domain of the parallel and sequential transformations imposes no relationship between , the intertwining map works on the following “ordered” spaces that generalize (6.2):

| (6.27) | ||||

With this definition, we can proceed with the construction. To begin, Lemma 6.1 allows us to apply the update map iteratively, as follows. We first define to be the identity map,

Next we take to be the map itself, as in (6.3). That is,

| (6.28) | ||||

And for , we define through a recursive equation which generalizes (6.28):

| (6.29) |

By Lemma 6.1 the Cesàro means are again preserved: . Furthermore, we have this strict monotonicity:

Lemma 6.6.

For any , the following inequality holds:

Proof.

Finally, define the map by

| (6.30) | ||||

By the observations above, preserves the Cesàro means of the component sequences. By Lemma 6.6, map produces a coordinatewise strictly ordered -tuple of sequences.

Remark 6.7.

The right-hand side of (6.29) makes sense if is well-defined and , in which case Lemma 6.1 gives

By the same reasoning, makes sense if is well-defined and , in which case

Continuing this logic until we reach

we conclude that is well-defined whenever

| (6.31) | ||||

and in this case we have

| (6.32) | ||||

In particular, the condition is stronger than needed for (6.29) all by itself. But for the right-hand side of (6.30) to make sense, we require (6.31) for each . Taken together, these conditions amount to exactly ; this is why the domain of is .

Below is the set of nonzero reals and the space of sequences of nonzero reals.

Lemma 6.8.

Fix .

-

(a)

There exists a Borel set and a continuous mapping such that and is the identity on .

-

(b)

Let with . Then the maps and are injective on .

Proof.

Part (a). Our starting point is the inverse of the update map deduced in Lemma 6.2. Let

and following (6.13) define the image of the mapping by

is a continuous mapping on the (obviously nonempty) Borel set . Observe also that, given , is a well-defined element of iff .

Extend to a sequence of mappings for as follows. Let be the identity mapping on . Then let

For define inductively first

and then by

| (6.33) |

One sees inductively that each is Borel and continuous. Furthermore, we have this converse:

| given , is a well-defined element of only if . | (6.34) |

This is clear for , it was observed above for , and it follows for again by induction. If is an element of then so is . By induction, this implies . This in turn requires that for , which forces . These conditions constitute .

Next we show that

| (6.35) |

This also verifies that each is nonempty. By Lemma 6.4(a), and from the proof of Lemma 6.2,

| (6.36) | ||||

Next, inductively by Lemma 6.4, for each and . That is, for we have and

| (6.37) | ||||