Markov Decision Processes with Time-Varying Geometric Discounting

Abstract

Canonical models of Markov decision processes (MDPs) usually consider geometric discounting based on a constant discount factor. While this standard modeling approach has led to many elegant results, some recent studies indicate the necessity of modeling time-varying discounting in certain applications. This paper studies a model of infinite-horizon MDPs with time-varying discount factors. We take a game-theoretic perspective—whereby each time step is treated as an independent decision maker with their own (fixed) discount factor—and we study the subgame perfect equilibrium (SPE) of the resulting game as well as the related algorithmic problems. We present a constructive proof of the existence of an SPE and demonstrate the EXPTIME-hardness of computing an SPE. We also turn to the approximate notion of -SPE and show that an -SPE exists under milder assumptions. An algorithm is presented to compute an -SPE, of which an upper bound of the time complexity, as a function of the convergence property of the time-varying discount factor, is provided.

1 Introduction

Ever since Samuelson’s foundational work introduced the discounted utility theory (Samuelson 1937), discounted utility models have played a central role in sequential decision making. Building on earlier work that recognized the influence of time on individuals’ valuations of goods (e.g., see (Rae 1905; Jevons 1879; von Böhm-Bawerk 1922; Fisher 1930) and the discussion in (Loewe 2006)), Samuelson proposed a utility model in which a decision maker attempts to optimize the discounted sum of their utilities with a constant discount factor applied in every time step; this is known as geometric or exponential discounting.

Geometric discounting leads to many elegant and well-known results. In the context of Markov decision processes (MDPs) (Puterman 1994), it results in the decision maker’s preferences over the policies being invariant over time. Moreover, it is key to the existence and polynomial-time computability of an optimal policy. These results have contributed greatly to the popularity and wide applicability of the MDPs. Nevertheless, in many applications, in particular those pertaining to human decision making under uncertainty, time-varying discount factors are essential for capturing long-run utilities. For example, it is shown in laboratory settings that human decision makers often exhibit time-inconsistent behavior: people prefer $50 in three years plus three weeks to $20 in three years, yet prefer $20 now over $50 in three weeks (Green et al. 1994a). Such behaviors are better explained through time-varying discount factors. Unfortunately, many of the aforementioned results break with time-varying discounting. As Strotz (1955) showed, geometric discounting with a constant discounting factor is the only discount function that satisfies dynamic- or time-consistency.

In this paper, we study a model of infinite-horizon MDPs with time-varying geometric discounting. Our model seizes the idea of geometric discounting, but generalizes the discount factor to a function of time. In each time step, the function produces a discount factor, and the agent’s incentive is defined by the geometrically discounted sum of its future rewards with respect to this discount factor. Hence, the agent aims at optimizing a different objective in each time step. This changing incentive gives rise to a game-theoretic approach, proposed and studied in a series of works in the literature (Strotz 1955; Pollak 1968; Peleg and Yaari 1973; Lattimore and Hutter 2014; Jaśkiewicz and Nowak 2021; Lesmana and Pun 2021). Via this approach, the behavior of the sole agent in the process is interpreted as playing against its future selves in a sequential game. Analyzing the subgame perfect equilibrium (SPE) is therefore a naturally associated task, which we aim to address in this paper.

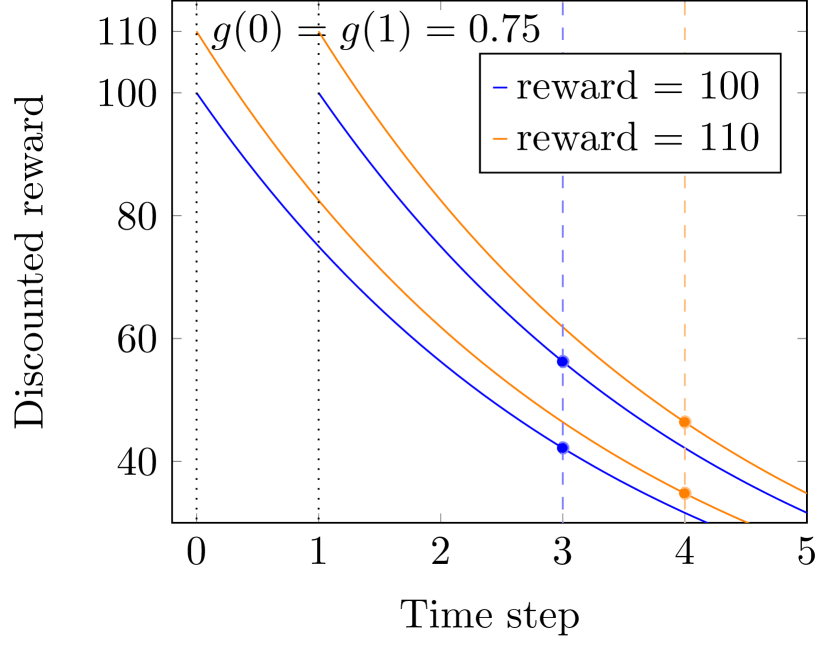

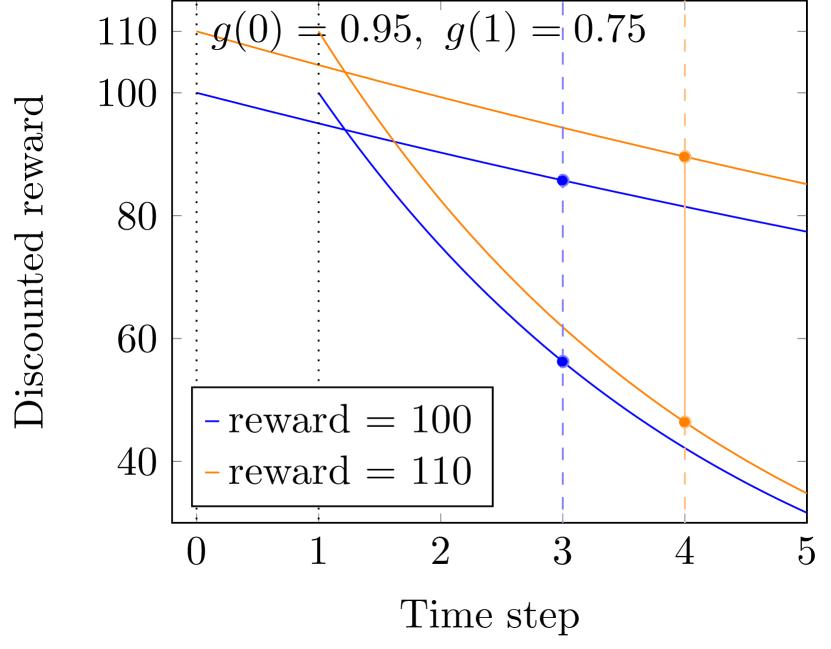

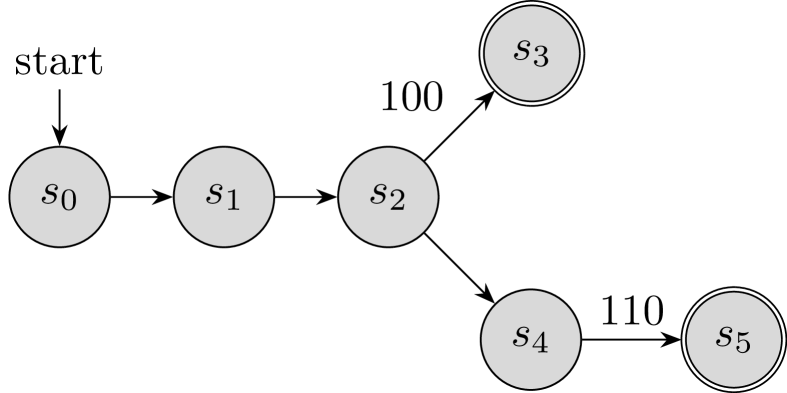

More concretely, Figure 1 presents an example that compares the behavior of this model to the standard model of geometric discounting, illustrating how time-varying geometric discounting can lead to time-inconsistency. In the example, the agent has to decide between getting a reward of at time step 3 (option A) and getting a slightly increased reward of one time step later (option B). This decision problem is captured by the MDP in Figure 1(c). Under the standard geometric discounting, the preference order of these two outcomes does not change over time: as illustrated in Figure 1(a), an agent that discounts its future with a constant factor would always prefer option A, no matter at time step 0 or 1. This is not anymore the case with time-varying discounting. An agent who applies a discount factor of is more farsighted and prefers the higher but delayed reward (i.e. option B). But if the agent becomes more myopic one time step later on by applying a reduced discount factor of , the preference order would change, and the agent would no longer want to stick to its initial plan. This situation is illustrated in Figure 1(b).

Time-inconsistent behavior may result from different forms of discounting. It may arise from a consistent way of planning but an inconsistent treatment of future time steps. In hyperbolic discounting, for example, the agent assigns a fixed sequence of varying discount factors to future time steps relative to the current step. In other words, the agent plans with consistency (using the same sequence over time) but treats the future inconsistently (discounting different time steps differently). In contrast, in our model, the agent discounts the future using a constant factor, but this factor might change over time. Human beings, for example, may start with very low discount factors when they are young, but increasingly think more about the future as they grow older. Conceivably, a young person, probably through observing this in elder people, knows that their way of discounting will change when they go into middle age. But still, they cannot do anything about their urge for immediate rewards. Likewise, the agent in our model knows how its rate changes in the future and tries to find a compromise between all the different preferences. This motivates the use of the SPE as our solution concept.

Contributions

Besides introducing a model of MDP with time-varying discounting, we make the following technical contributions.

-

•

We present a constructive proof for the existence of an SPE. Our proof differs from another non-constructive approach in the literature (Lattimore and Hutter 2014) which uses the compactness of the underlying space to argue about convergence.

-

•

From our constructive proof, an algorithm for computing an SPE can be readily extracted. Meanwhile, we demonstrate that the problem of computing an SPE is EXPTIME-hard even in restricted settings.

-

•

In order to circumvent some of the assumptions needed to construct an exact SPE, we turn to the relaxed notion of -SPE. We show that an -SPE exists under strictly milder assumptions and present an algorithm to compute an -SPE. Using a continuity argument of the value functions, we also derive an upper bound on the time complexity of the algorithm, as a function of the convergence property of the time-varying discount factors.

Related Work

A large body of experimental evidence suggests that human behavior is not characterized by geometric discounting with a constant discount factor. Empirical findings that do not support the hypothesis that discounting is consistent over time have been reported (Thaler 1981; Benzion et al. 1989; Redelmeier and Heller 1993; Green et al. 1994a; Kirby and Herrnstein 1995; Millar and Navarick 1984), implying dynamic inconsistency of human preferences. Prior work has also proposed and studied different forms of discounting, such as hyperbolic (Herrnstein 1961; Ainslie 1992; Loewenstein and Prelec 1992) or quasi-hyperbolic discounting (Phelps and Pollak 1968; Laibson 1997), which are considered to be more aligned with human behavior (Ainslie 1975; Green et al. 1994b; Kirby 1997). Interpretations of discounting functions as uncertainty over hazard rates were also proposed (Sozou 1998; Dasgupta and Maskin 2005).

Focusing on sequential decision making under uncertainty, this paper closely relates to the line of work that studies non-geometric discount factors and dynamic inconsistency in Markov decision processes and stochastic games (Shapley 1953; Alj and Haurie 1983; Puterman 1994; Nowak 2010; Jaśkiewicz and Nowak 2021; Lesmana and Pun 2021). Some recent works studied dynamic inconsistency using a game-theoretic framework akin to the ones by Strotz (1955); Pollak (1968); Peleg and Yaari (1973), where their focus is on the existence of an equilibrium in randomized stationary Markov perfect strategies (Jaśkiewicz and Nowak 2021), or an SPE in a finite horizon setting (Lesmana and Pun 2021). Arguably, the closest work to ours is the work of Lattimore and Hutter (2014), which considers “age-dependent” (time-varying) geometric discounting functions. The characterization results therein prove the existence of an SPE in the resulting game. Our results are complementary: we provide a constructive proof of the existence result and additionally study the computational complexity of the problem setting.

MDP-based settings similar to ours have also been considered in reinforcement learning (Sutton 1995; Sutton et al. 2011; White 2017; Pitis 2019; Fedus et al. 2019). Increasing the efficacy of learning by using multiple discount factors has been explored previously (Burda et al. 2018; Romoff et al. 2019). It is also worth mentioning settings that use a weighted reward criterion (e.g., Filar and Vrieze (2012)), where the objective can be expressed as the weighted sum of two value functions with different discount factors.

2 The Model

We consider an infinite horizon MDP , where is a finite state space of the environment, with , and is a union of finite action spaces, with each being the set of actions available in state . Moreover, is a reward function, such that when action is taken in state , a reward will be generated, and the state of the environment transitions according to the transition function , with probability to another state . Finally, is a starting state, and is a discount factor that is applied for defining the cumulative reward of a policy , i.e., the discounted sum of rewards obtained over an infinite horizon:

| (1) |

where the expectation is over the trajectory generated by starting from and following subsequently.

Two types of policies will be of interest in this paper: static policies and dynamic policies. A static policy assigns a (deterministic) action to each state, so that using policy , an agent performs action whenever the environment is in state , irrespective of the time step. In contrast, a dynamic policy is time-dependent and is defined as a sequence of static policies. At each time step , the static policy is employed to determine the action to take. Hence, dynamic policies are a generalization of static policies.111More generally, a static policy can also choose randomized actions, i.e., . Nevertheless, it is without loss of generality to consider only deterministic policies with respect to all the results in our paper. Hence, unless otherwise clarified, all static policies considered are deterministic ones, whereas we do allow the agent to use randomized static policies.

One may also consider policies that depend on the history (i.e., the trajectory of states and actions generated so far), but as it shall be clear this is unnecessary for the problems studied in this paper: the underlying process is Markovian and the agent always observes the state of the environment. Moreover, it is well-known that when the discount factor is a constant, to maximize the cumulative reward defined in (1) it suffices to consider static policies. Though this does not hold when the optimization horizon is finite (Shirmohammadi et al. 2019) or, as we will study in this paper, when varies with time.

Constant Discount Factor and Optimality

When a constant discount factor is applied, the optimality of a static policy with respect to (1) can be characterized using the value function defined as

| (2) |

for all , where

| (3) |

is called the Q-function. The value of corresponds to the expected sum of rewards when starting in state and following policy . A static policy is optimal if for every state and every action , it holds that

| (4) |

We denote by the set of all static policies, and by the set of all optimal policies with respect to a constant . It is well known that for all , and one can compute a policy in in polynomial time (Rincón-Zapatero and Rodríguez-Palmero 2003).

It will also be useful to introduce the notion of equivalent policies. Two policies are deemed equivalent if their value functions are identical for all states and discount factors.

[Equivalent policies] Two static policies are equivalent if for all and all it holds that . We write if and are equivalent.

Time-Varying Discounting—Game-Theoretic View

We generalize the above definition to MDPs with time-varying discounting (hereafter, MDPs for simplicity) by replacing the constant factor by a discount function , such that is the discount factor the agent applies at time step . We will only consider discount functions that converge to a value in when in this paper.

Time-varying discounting changes the agent’s incentive over time and as a result the agent behaves as if they are different agents. Hence, we apply a game-theoretic view and view the MDP as a sequential game played by countably many players. Every player is associated with a time step and decides on a static policy to use at that particular time step. Moreover, player represents the agent’s incentive at time step and cares about the subsequent cumulative reward with respect to the (constant) discount factor , i.e.,

| (5) |

when the environment is in state before player is to take an action, and the other players subsequently act according to given by the dynamic policy . In other words, each player has the same geometric-discounting-style vision as that defined in (1). The function can be viewed as the utility function of player conditioned on , and as the players’ strategy profile. The discount factor stays constant for this particular player, but it might be different for different players. We will analyze the subgame-perfect equilibrium (SPE) of the resulting game, which is the standard solution concept for sequential games (Osborne et al. 2004).

[SPE] A dynamic policy is an SPE if for all and it holds that: if for all .

In other words, in an SPE, from any time step onward, the players’ policies form a Nash equilibrium of the subsequent subgame, no matter what is. Note that the above definition takes the same form as a Nash equilibrium of the players’ policies because every player only plays at time step throughout the game.

We can use value functions to characterize an SPE: a dynamic policy is an SPE if it holds that

| (6) |

for all and , where for any we define

| (7) | ||||

| (8) |

Namely, each player has a value function and a Q-function for each time step , defined with respect to their own discount factor . We can make two observations below: the first observation follows by definition (i.e., (5)), and the second holds as the dynamic policy essentially degenerates to a static one in the stated situation.

for all .

Let be a dynamic policy and be a static policy. If for all , then for all and all .

We analyze the problem of computing an SPE. Since a solution to this problem is a dynamic policy over an infinite horizon, it is not immediately clear whether a solution admits any concise representation. We therefore consider only the first step () and the following decision problem: For a given action , is there an SPE such that ? (More formally, see the definition below.) We refer to this problem as SPE-Start.

[SPE-Start] An instance of SPE-Start is given by a tuple , consisting of an MDP (with a time-varying discount function ) and an action . It is a yes-instance if there exists an SPE such that ; and a no-instance, otherwise.

It is straightforward that when is a constant function, an SPE corresponds to an optimal policy for the MDP. Yet, it appears that SPE-Start is computationally more demanding than computing an optimal policy in a constant-discounting MDP: as we will show in the paper, SPE-Start is EXPTIME-hard, whereas the latter is well-known to be solvable in polynomial time.

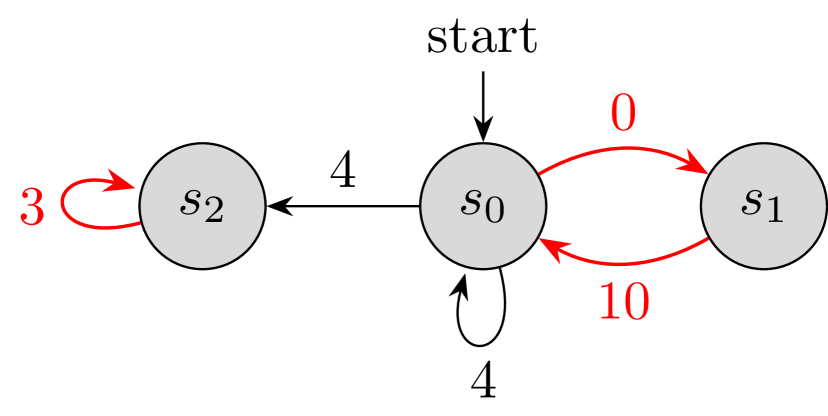

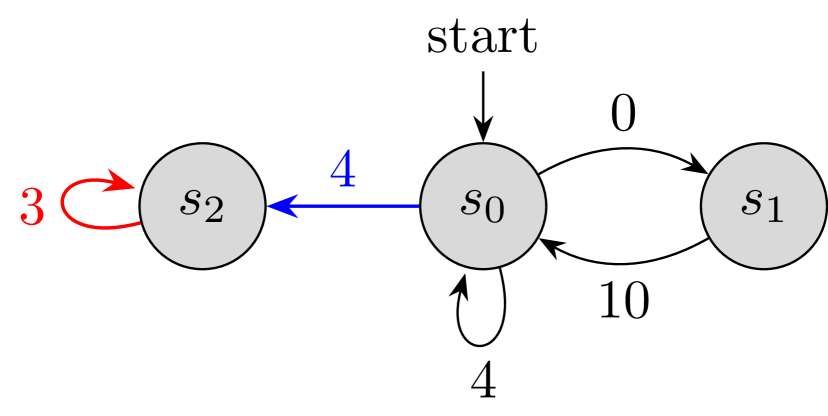

An Illustrating Example

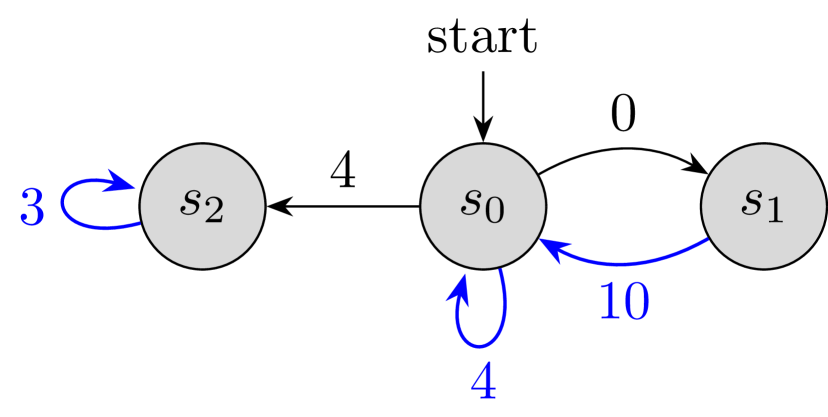

We conclude our description of the model with an illustrating example. Consider the MDP given in Figure 2, and two different discount factors, and . Let be the starting state. As we are solely considering deterministic state transitions in this example, we will identify actions starting in a certain state with the state it changes to, e.g. denotes the action that causes a transition from to .

As shown in Figure 2(a) and Figure 2(b), the optimal static policy of an agent who applies a constant discount factor in the classical setting, is given by , and . For , the optimal static policy differs from only in state , namely .

We want to compute an SPE for the setting where the first player discounts with and all subsequent players discount with . Since the discount factor is constant from time step 1 onward, we can fix the policies of players to to derive an SPE. Player knows all future players’ policies and can influence future rewards merely by choosing the current action. Starting in , the action given by policy would be the one that transitions to itself. As player 0 is fairly short-sighted, knowing that player 1 will choose an action leading to reward in the subsequent time step, it prefers taking an immediate reward of 4 and transitioning into state to stay there forever and keep receiving rewards of 3. Hence, an SPE is given by , where ; see Figure 2(c).

3 Existence of an SPE

We investigate the existence of an SPE. Indeed, the following result has already answered this question in affirmative.

Theorem 3.1 (Lattimore and Hutter 2014).

An (exact) SPE always exists.

The result applies even without our assumption on the convergence of the discount function but it is obtained via a non-constructive approach: by reasoning about a sequence of policies that are optimal for the truncated versions of the problem, each with a longer horizon than their predecessors. Hence, the proof does not yield any algorithm or procedure for obtaining an SPE. We next provide a constructive proof. The proof also forms the basis for deriving a complexity upper bound of SPE-Start as we will demonstrate later.

We will in particular show that there exists an SPE that is eventually constant, i.e., there exists a time step after which all the subsequent players use the same static policy. A mild assumption is needed for our proof: converges to a value outside of a set of degenerate points defined below.

[Degenerate point] A discount factor is called a degenerate point if contains more than one non-equivalent policy (see Section 2), i.e., , where is the set of equivalence classes on under the equivalence relation defined in Section 2, i.e., an element contains all policies equivalent to .

In what follows, let

be the set of degenerate points in . The assumption above ensures that the players will eventually adopt the same behavior after some time step , as if the subsequent process is a constant-discounting MDP. From that point on, the dynamic policy can be represented as a static one and we can use backward induction to derive policies for players in the previous time steps. More formally, the main result of this section is formulated as follows.

Theorem 3.2.

Suppose that exists and . Then there exists an SPE that is eventually constant, i.e., there exists a number such that for all .

Proof of Theorem 3.2

The key to the proof is to argue that is eventually constant after a certain time step . With this property, we can pick an arbitrary and assign it to all the players . This forms an SPE for the subgame starting at , and according to Observation 2, we can use as a basis and use backward induction to construct as the optimal policies of players with respect to , respectively. The approach is summarized in Algorithm 1.

Now to show that is eventually constant, we argue that the set of degenerate points is finite (Algorithm 1). Since , there must be a neighbourhood of in which does not intersect . After a certain time step, the tail of will be contained inside this neighbourhood, so Algorithm 1 then implies that becomes constant after a finite number of time steps.

[] is a finite set.

Proof.

Define

| (9) |

By definition, for any , there exist such that , which means that for all . Hence, is bounded from above by the number of s such that for some and some that are not equivalent. By Algorithm 1, , where both and are polynomial functions of with finite degrees. Hence, the number of zeros of is finite. ∎

[] Let be two policies and . The function can be written as

| (10) |

where and are polynomials of with finite degrees. This and subsequent omitted proofs can be found in the appendix.

[] For any interval such that , we have for any .

Proof.

Without loss of generality, suppose that and, for the sake of contradiction, . The fact that directly implies that as both sets contain only equivalent policies. Pick arbitrary and . We have and . As is a continuous function, there exists a such that , which implies and hence . This contradicts the assumption that . ∎

4 Complexity of SPE-Start

Consider using Algorithm 1 to construct an SPE. It requires specifying in the input which we have not yet described how to obtain. Indeed, this replies on the specific format of . In addition to the computational cost of obtaining , Algorithm 1 includes iterations, so the overall time complexity also depends on the magnitude of . The latter cost prevents the algorithm from being efficient if is exponential in the size of the problem, so the question is whether there are better algorithms that solve SPE-Start without going through all the iterations. It turns out that this is in general not possible: as we will show next, even for discount functions that admit efficient computation of , computing an SPE can be EXPTIME-hard.

EXPTIME-Hardness

We show that SPE-Start is EXPTIME-hard even when is a down-step function defined as follows:

| (11) |

where and is encoded in binary. Arguably this is one of the simplest forms of time-varying discounting, and can be encoded as .

Note that (11) does not define a finite horizon MDP. Instead, it defines a game where eventually all the players from time step onward exhibit a discount factor of 0. We will show that SPE-Start is EXPTIME-hard even when the discount function is restricted to this simple form. The proof uses a reduction from the following problem, termed ValIt (value iteration), which is known to be EXPTIME-complete (Shirmohammadi et al. 2019).

[ValIt] An instance of ValIt, given by , consists of an MDP with constant discount factor , an action , and finite time horizon encoded in binary. It is a yes-instance if there exists a dynamic policy such that and for all and , where

| (12) | ||||

| (13) |

and . Otherwise, it is a no-instance.

The functions in the above definition are akin to the value functions defined in (4) but with a time-dependency. Using ValIt, we prove the following result.

Theorem 4.1.

SPE-Start is EXPTIME-hard even when the discount function is a down-step function.

Proof sketch.

We reduce ValIt to SPE-Start. The main idea of the reduction is to construct an SPE-Start instance where all players will stick to the same static policies regardless of policies chosen by the preceding players. Figure 3 illustrates the MDP in the SPE-Start instance. A chain consisting of two states and is appended to every state in the ValIt instance. The high reward at ensures that is the dominant action for player , who has and only cares about the immediate reward; whereas the high penalty at ensures that is a dominated action for all players , who have . Hence, for every player in the SPE-Start instance, the process is equivalent to an MDP with time horizon . The procedure to derive in an SPE using backward induction is the same as computing the value functions of the ValIt instance. Every SPE is then associated to an optimal policy of ValIt. ∎

We remark that the binary encoding of plays a crucial role in the EXPTIME-hardness of SPE-Start. Indeed, if is encoded in unary or is a constant, the hardness will disappear. In general, an efficient algorithm for computing an SPE is possible but requires the assumption of converging fast enough to an interval between two consecutive numbers in . To ease part of the intricacies introduced by the requirement, a practical approach which we will present next is by considering the approximate notion of the SPE, the -SPE.

Remark

The down-step function we defined in (11) may appear to only be representative of decreasing functions. However, the EXPTIME-hardness remains if we consider simple increasing functions such that if , if , and ; our proof can be easily extended to such functions.

5 Approximate SPEs

The -SPE, defined below, assumes that the players are reluctant to deviate as long as the potential improvement is smaller than some .

[-SPE] A dynamic policy forms an -SPE if for all it holds that for all : for all such that for all .

The notion allows us to relax the assumption that converges to a point outside of and allows us to derive an upper bound of the computational complexity, too. Indeed, the existence of an -SPE, in particular an eventually constant one, does not require this assumption. Instead, we use the following continuity argument.

[] Suppose that all rewards are bounded by . Then for any discount factors and static policy , we have the following bound for all :

Theorem 5.1.

Suppose exists and . For any , there exists an -SPE that is eventually constant, i.e., there exists a such that for all .

Computing an -SPE

The slackness introduced by -SPE appears to suggest that it suffices to consider a finite time horizon: a player can cut off the time horizon up to a certain (finite) future time step, beyond which the sum of the discounted rewards is sufficiently small to be ignored. This is nevertheless not the case. Even if the horizon is cut off, there are still infinitely many players in the game and each player’s payoff is influenced by the subsequent players before the cutting off point. Hence, cutting off the time horizon does not reduce our consideration to a finite number of time steps.

To compute an -SPE, we use the continuity argument in Section 5. If we can pin down a time step after which the tail of is contained in a sufficiently small interval, we can use to compute an SPE for the subgame as if is constant after . This approximates an actual SPE provided that the tail of is sufficiently small. Hence, the time complexity depends on the rate at which converges. In accordance with our existence proof, let be such that

To derive a general result, we also assume that there is an oracle that, for any given , computes a time step such that for all . More specifically, we introduce the following notion called -convergence for the discount function.

[-convergence] Let and . A class of discount functions is -convergent if there is an oracle such that: for any and any with bit-size , computes an integer in time such that for all , and , where denotes the bit-size of the representation of .

For example, the class of down-step functions, defined in (11) and encoded as (in binary), is -convergent with and . Our next lemma provides a lower bound on the distance between any two points in the set .

Theorem 5.2.

Suppose that is -convergent and for a known constant . Then an -SPE can be computed in time

where .

Proof.

We use Algorithm 2 to compute an -SPE. To see that it correctly computes an -SPE, it suffices to argue that form an -SPE for the subgame after .

Indeed, for any player , we have . Hence, according to Section 5, we have for any static policy and . Let . We have

where as in Algorithm 2. Moreover, since the optimal static policy is at least as good as any dynamic policy for player . This means that for any strategy profile resulting from a deviation of player ,

Hence, Algorithm 2 generates an -SPE.

To see the time complexity of the algorithm, note that it takes time to run . In addition to that, the time it takes to run Algorithm 1 is bounded by . ∎

We remark that Theorem 5.2 only requires the mild assumption of a known constant gap between and the limit point of . If is unknown or the gap cannot be bounded by a constant, an -SPE can be computed via a more sophisticated algorithm with a higher time complexity. We provide this algorithm in the full version of this paper for theoretical interest.

Via Theorem 5.2, an exponential upper bound of the complexity of computing an -SPE can be derived when is the down-step function defined in (11) (for which ). This does not require any assumption on the convergence of with respect to . Better bounds can be derived if converges faster, e.g., or even , or when is not a variable of the model.

6 Conclusion

We study a model of infinite-horizon MDPs with time-varying discounting. Our model seizes the idea of geometric discounting, but with time-varying discount factors, and it allows for a game-theoretic interpretation. We study the SPE of the underlying game. Results on the existence and computation of an exact or an -SPE are presented. Future work may consider other types of discount functions, such as those described by Lattimore and Hutter (2014).

Acknowledgements

The authors would like to thank the anonymous reviewers for their insightful comments. This project was supported by DFG project 389792660 TRR 248–CPEC. Part of the work was done when Jiarui Gan was a postdoc at MPI-SWS, when he was supported by the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement No. 945719). Part of the work was done when Annika Hennes was an intern at MPI-SWS. Further, she was partially funded by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) – project number 456558332. Goran Radanovic’s research was, in part, funded by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) – project number 467367360.

References

- Ainslie [1975] George Ainslie. Specious reward: a behavioral theory of impulsiveness and impulse control. Psychological bulletin, 82(4):463, 1975.

- Ainslie [1992] George Ainslie. Picoeconomics: The strategic interaction of successive motivational states within the person. Cambridge University Press, 1992.

- Alj and Haurie [1983] Abderrahmane Alj and Alain Haurie. Dynamic equilibria in multigeneration stochastic games. IEEE Transactions on Automatic Control, 28(2):193–203, 1983.

- Benzion et al. [1989] Uri Benzion, Amnon Rapoport, and Joseph Yagil. Discount rates inferred from decisions: An experimental study. Management science, 35(3):270–284, 1989.

- Burda et al. [2018] Yuri Burda, Harrison Edwards, Amos Storkey, and Oleg Klimov. Exploration by random network distillation. In International Conference on Learning Representations, 2018.

- Dasgupta and Maskin [2005] Partha Dasgupta and Eric Maskin. Uncertainty and hyperbolic discounting. American Economic Review, 95(4):1290–1299, 2005.

- Fedus et al. [2019] William Fedus, Carles Gelada, Yoshua Bengio, Marc G Bellemare, and Hugo Larochelle. Hyperbolic discounting and learning over multiple horizons. arXiv preprint arXiv:1902.06865, 2019.

- Filar and Vrieze [2012] Jerzy Filar and Koos Vrieze. Competitive Markov decision processes. Springer Science & Business Media, 2012.

- Fisher [1930] Irving Fisher. Theory of interest: as determined by impatience to spend income and opportunity to invest it. Augustusm Kelly Publishers, Clifton, 1930.

- Green et al. [1994a] Leonard Green, Nathanael Fristoe, and Joel Myerson. Temporal discounting and preference reversals in choice between delayed outcomes. Psychonomic Bulletin & Review, 1(3):383–389, 1994a.

- Green et al. [1994b] Leonard Green, Astrid F Fry, and Joel Myerson. Discounting of delayed rewards: A life-span comparison. Psychological science, 5(1):33–36, 1994b.

- Hamilton [1853] William Rowan Hamilton. Lectures on Quaternions. Hodges and Smith, 1853.

- Herrnstein [1961] Richard J Herrnstein. Relative and absolute strength of response as a function of frequency of reinforcement. Journal of the experimental analysis of behavior, 4(3):267, 1961.

- Jaśkiewicz and Nowak [2021] Anna Jaśkiewicz and Andrzej S Nowak. Markov decision processes with quasi-hyperbolic discounting. Finance and Stochastics, 25(2):189–229, 2021.

- Jevons [1879] William Stanley Jevons. The theory of political economy. Macmillan and Company, 1879.

- Kirby [1997] Kris N Kirby. Bidding on the future: Evidence against normative discounting of delayed rewards. Journal of Experimental Psychology: General, 126(1):54, 1997.

- Kirby and Herrnstein [1995] Kris N Kirby and Richard J Herrnstein. Preference reversals due to myopic discounting of delayed reward. Psychological science, 6(2):83–89, 1995.

- Laibson [1997] David Laibson. Golden eggs and hyperbolic discounting. The Quarterly Journal of Economics, 112(2):443–478, 1997.

- Lattimore and Hutter [2014] Tor Lattimore and Marcus Hutter. General time consistent discounting. Theoretical Computer Science, 519:140–154, 2014.

- Lesmana and Pun [2021] Nixie S Lesmana and Chi Seng Pun. A subgame perfect equilibrium reinforcement learning approach to time-inconsistent problems. Available at SSRN 3951936, 2021.

- Loewe [2006] Germán Loewe. The development of a theory of rational intertemporal choice. Papers: revista de sociologia, pages 195–221, 2006.

- Loewenstein and Prelec [1992] George Loewenstein and Drazen Prelec. Anomalies in intertemporal choice: Evidence and an interpretation. The Quarterly Journal of Economics, 107(2):573–597, 1992.

- Mignotte [1982] Maurice Mignotte. Some useful bounds. In Computer algebra, pages 259–263. Springer, 1982.

- Millar and Navarick [1984] Andrew Millar and Douglas J Navarick. Self-control and choice in humans: Effects of video game playing as a positive reinforcer. Learning and Motivation, 15(2):203–218, 1984.

- Nowak [2010] AS Nowak. On a noncooperative stochastic game played by internally cooperating generations. Journal of optimization theory and applications, 144(1):88–106, 2010.

- Osborne et al. [2004] Martin J Osborne et al. An introduction to game theory, volume 3. Oxford University Press New York, 2004.

- Peleg and Yaari [1973] Bezalel Peleg and Menahem E Yaari. On the existence of a consistent course of action when tastes are changing. The Review of Economic Studies, 40(3):391–401, 1973.

- Phelps and Pollak [1968] Edmund S Phelps and Robert A Pollak. On second-best national saving and game-equilibrium growth. The Review of Economic Studies, 35(2):185–199, 1968.

- Pitis [2019] Silviu Pitis. Rethinking the discount factor in reinforcement learning: A decision theoretic approach. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 7949–7956, 2019.

- Pollak [1968] Robert A Pollak. Consistent planning. The Review of Economic Studies, 35(2):201–208, 1968.

- Puterman [1994] Martin L. Puterman. Markov Decision Processes: Discrete Stochastic Dynamic Programming. John Wiley & Sons, Inc., 1994.

- Rae [1905] John Rae. The sociological theory of capital: being a complete reprint of the new principles of political economy, 1834. Macmillan, 1905.

- Redelmeier and Heller [1993] Donald A Redelmeier and Daniel N Heller. Time preference in medical decision making and cost-effectiveness analysis. Medical Decision Making, 13(3):212–217, 1993.

- Rincón-Zapatero and Rodríguez-Palmero [2003] Juan Pablo Rincón-Zapatero and Carlos Rodríguez-Palmero. Existence and uniqueness of solutions to the Bellman equation in the unbounded case. Econometrica, 71(5):1519–1555, 2003.

- Romoff et al. [2019] Joshua Romoff, Peter Henderson, Ahmed Touati, Emma Brunskill, Joelle Pineau, and Yann Ollivier. Separating value functions across time-scales. In International Conference on Machine Learning, pages 5468–5477. PMLR, 2019.

- Samuelson [1937] Paul A Samuelson. A note on measurement of utility. The Review of Economic Studies, 4(2):155–161, 1937.

- Shapley [1953] Lloyd S Shapley. Stochastic games. Proceedings of the National Academy of Sciences, 39(10):1095–1100, 1953.

- Shirmohammadi et al. [2019] Mahsa Shirmohammadi, Nikhil Balaji, Stefan Kiefer, Petr Novotny, and Guillermo A Pérez. On the complexity of value iteration. In 46th International Colloquium on Automata, Languages, and Programming, ICALP 2019, July 9-12, 2019, Patras, Greece, 2019.

- Sozou [1998] Peter D Sozou. On hyperbolic discounting and uncertain hazard rates. Proceedings of the Royal Society of London. Series B: Biological Sciences, 265(1409):2015–2020, 1998.

- Strotz [1955] Robert Henry Strotz. Myopia and inconsistency in dynamic utility maximization. The review of economic studies, 23(3):165–180, 1955.

- Sutton [1995] Richard S Sutton. TD models: Modeling the world at a mixture of time scales. In Machine Learning Proceedings 1995, pages 531–539. Elsevier, 1995.

- Sutton et al. [2011] Richard S Sutton, Joseph Modayil, Michael Delp, Thomas Degris, Patrick M Pilarski, Adam White, and Doina Precup. Horde: A scalable real-time architecture for learning knowledge from unsupervised sensorimotor interaction. In The 10th International Conference on Autonomous Agents and Multiagent Systems-Volume 2, pages 761–768, 2011.

- Thaler [1981] Richard Thaler. Some empirical evidence on dynamic inconsistency. Economics letters, 8(3):201–207, 1981.

- von Böhm-Bawerk [1922] Eugen von Böhm-Bawerk. Capital and interest: A critical history of economical theory. Brentano, 1922.

- White [2017] Martha White. Unifying task specification in reinforcement learning. In International Conference on Machine Learning, pages 3742–3750. PMLR, 2017.

Appendix A Existence of an SPE

See 1

Proof.

Fix a deterministic policy and a state . For each state and each , let be the number of steps between the -th and the -th times the state is in , when one starts from and takes actions according to policy ; hence, is a random variable. These variables are independent and identical for . This way, we can write the cumulative reward as

| (14) |

where

| (15) |

with

As shown above, we let the last term be . Since are i.i.d., we then have

which means that

Substituting the above into (15) gives

| (16) |

It remains to do some analysis on and . Let denote the probability that we reach state in steps when we start from state and take actions according to , i.e.,

Let be a (row) vector, where each element is the probability of the state transitioning from to after action is taken. Similarly, let be a (column) vector and be a matrix. We can now write

Moreover, for , we have , and hence

Letting then gives

which is equivalent to

Indeed, since all entries in are at most 1 and , we have . This implies that the Neumann series converges to , which shows that the inverse of exists. The Cayley-Hamilton theorem [Hamilton, 1853] implies that the entries of are rational functions where the numerator and denominator are polynomials in of degree at most the size of , i.e., .

To sum up, we have

| (17) |

which is a function of the form

| (18) |

where and are polynomial functions of with finite degrees. A similar reasoning can be applied to , if we consider . We have

which is again a rational function with finite degrees. Hence, for all the functions and hence also their sum are rational functions of the form shown in (10). It follows that for any choice of , the function , according to its definition in (9), is also of the same form. ∎

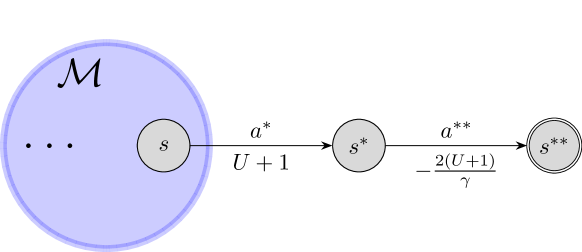

Appendix B EXPTIME-Hardness of SPE-Start

See 4.1

Proof.

We reduce an arbitrary instance of ValIt to the following instance of SPE-Start. Since ValIt is EXPTIME-complete [Shirmohammadi et al., 2019], the result follows.

Let be an MDP with , , i.e., we add two additional states and two additional actions. As illustrated in Figure 3, taking action in any state results in a deterministic state transition to . Moreover, in the only action available is , which takes the state to the terminal state with probability one. The transition dynamics remain the same with respect to all other state-action pairs . The reward function fulfils , such that

where . Finally, we let the discount function be a down-step function as defined in (11), where and are taken directly from the ValIt instance.

We will next argue that an optimal policy for the ValIt instance is equivalent to an SPE of the game defined by and . Specifically, we can map every ValIt solution to an SPE-Start solution in a way such that for all and . We argue that is an optimal policy for the ValIt instance if and only if is an SPE. Notably, we have , so the equivalence implies that an answer to the SPE-Start instance also answers ValIt and hence, ValIt is reduced to SPE-Start.

To prove the above statement, we first note that in an SPE, players will never choose action . Indeed, suppose player is the first one who takes action , then the process will terminate in two steps at , and the sum of discounted rewards for player (for whom we have ) in the subsequent two steps will be

where since this player is the first one to take action . In contrast, if this player switches to any action , the environment will remain in a state for at least one more step, whereby the subsequent sum of discounted rewards is at least

| (19) |

where , is the number of time steps where the state remains in , and . We have

so player obtains a strictly higher utility than when playing . Hence, the state of the environment will remain in when it is for player to play an action. Since , player will surely play action , whereby it obtains an immediate reward of , which is strictly larger than what can be obtained by taking any other actions according to the definition of . Hence, the game will proceed in exactly the same way after time step , irrespective of the actions performed by players . From the perspective of each player , their actions only change the game up to time step , so is a constant independent of , , and . This means that an SPE in this particular game, which can be characterized by (6)–(8) with constant , is effectively equivalent to an optimal policy defined through (12) and (13) (Note that (12) and (13) define the same optimal policies if we start by letting be any arbitrary constant). ∎

Appendix C Computation of SPEs and -SPEs

See 5

Proof.

Without loss of generality, we can assume . We will write . Note that this implies . Since , it suffices to bound for every . We have

Now consider the first term in the summation:

| (20) |

We now use the following inequality. For any , we have

The last inequality uses for and . Now we have the following bound on the first term in Equation 20.

Substituting the above bound in Equation 20 and using , we get the following bound:

We can establish a similar bound on

We can now bound as follows.

Summing the above bound over the states we get the desired bound. ∎

See 5.1

Proof.

First, we have already proven that in the case , there exists an exact SPE. Hence, in what follows, we assume that .

Now instead of finding a time step such that in the subsequent time steps will surely lie between two neighbouring points in , we find a such that for all , where we let be a number such that

and

By the convergence assumption and the fact that by definition, there indeed exists such a number . It then holds for all that

| (21) |

Hence,

| (22) |

According to Section 5, this means that

for any policy . In particular, let and be the optimal policies with respect to constant discount factors and , respectively. Applying the above inequality to these two policies gives

Hence, is a near-optimal policy for all players . We can then construct an -SPE by first letting for all , and then use Algorithm 1 to construct the preceding part of through backward induction. ∎

When Limit Point of Not Bounded Away From

We first prove the following lemma, which provides a lower bound for distances between points in . Intuitively, we can use this bound to locate a time step such that the tail of falls in between the largest point in and . Hence, the optimal policy with respect to is eventually constant and we can construct an exact SPE for the subgame after and use backward induction to construct policies for time steps before .

[] For any such that , we have

| (23) |

where and are large enough.

Proof.

Recall the expression for stated in (16):

Moreover, according to (17), we have . Using Cramer’s rule we can write the matrix as an matrix with entries where is the -th cofactor of the matrix . This implies that each entry of the matrix is a rational polynomial. Moreover, as the determinant of an matrix is the sum over all permutations of matrix elements, and each entry of the matrix is bounded between , both the numerator and the denominator of such an entry have degree at most and coefficient bounded between .

Additionally, each entry of can be represented by at most bits. Since multiplication (resp. addition) of two fractions of sizes and can be represented using (resp. ) bits, each coefficient of the above polynomials can be represented using at most bits. Therefore, we conclude that each entry of is a rational polynomial where both the numerator and the denominator have degree at most , maximum coefficient at most and maximum size of each coefficient is at most .

Now the polynomial is constructed through vector-matrix multiplication and vector-vector inner product. So the final result is a rational polynomial where the denominator polynomial from remains unchanged. Moreover, the numerator polynomial now has degree at most . Since and , the maximum value of a coefficient of the numerator polynomial does not increase. Finally, the polynomial can also be written as . Each entry in the summation is a multiplication between a coefficient of size at most and another coefficient of size at most . Therefore, the maximum size of any coefficient in the denominator is at most as long as we have .

By a similar argument as above, can be represented as a rational polynomial where both the numerator and the denominator have degree at most , maximum coefficient at most , and maximum size of each coefficient at most . It is also easy to see that the polynomial is similar. Now is constructed by multiplying two such rational polynomials, and the degree of both the denominator and the numerator polynomial is at most . Each coefficient of the new polynomial is the result of adding at most pairwise products. Therefore, the maximum value of any coefficient is at most as long as . And the maximum size of any coefficient is at most .

Now recall that we are interested in zeros of the following function (i.e., see (9) and (14)):

Since the polynomial is constructed by adding/subtracting rational polynomials, we will apply the following argument times. Suppose we add two rational polynomials of degree at most , maximum value of any coefficient at most , and maximum size of any coefficient at most . Then the resulting rational polynomial will have degree at most , maximum value of any coefficient at most , and maximum size of any coefficient at most . Repeating this process times, we get a polynomial with degree at most , maximum value of any coefficient at most . In order to determine the maximum value of any coefficient, let (resp ) be the degree (resp. maximum value) after the -th iteration. Then we have . Substituting , and , we get

| (24) |

By a similar argument, we can show that the maximum size of any coefficient is at most . Substituting , , , and , we get that is a rational polynomial where both the denominator and the numerator polynomial have the following guarantee – each polynomial has degree at most , maximum value of any coefficient at most , and maximum size of any coefficient at most . For simplicity, for large enough , these numbers are bounded by , , and , respectively.

In order to bound the gap between zeros of for all and all non-equivalent , we need to further consider the function

Since there are at most many policies in , the bounds we derived further blow up to , , and , respectively.

We now apply the following result from Mignotte [1982]. Given a degree polynomial with integer coefficients and maximum coefficient , its roots are separated by at least

where . We wish to find the zeros of the numerator polynomial of . However, the coefficients need not be integers. So we multiply each coefficient by , the least common multiple of the denominators of all the coefficients of the numerator polynomial. Since each coefficient has size at most , its denominator can be at most . Moreover, the degree of is at most . This gives us the following bound on the least common multiple .

| (25) |

Let us write to denote the polynomial multiplied by . Then the degree of is at most (say ) and maximum value of any coefficient is at most (say ). Now we can apply Mignotte’s result [Mignotte, 1982] to get the following bound:

This completes the proof. ∎

Now we prove a more general result than Theorem 5.2, where does not need to converge to a point sufficiently far away from 1. The method used for this is outlined in Algorithm 3.

Theorem C.1.

Suppose that is -convergent. An -SPE can be computed in time , where , , and .

Proof.

As illustrated in Algorithm 3, we first check whether or not converges to a point sufficiently far away from . We run the oracle on input , and suppose the output is ; hence,

for all .

Case 1.

If , then we know that for all ,

Hence, according to Appendix C, must lie between the largest element in and , and as a result for all . We can pick an arbitrary , and let for all in the SPE to be constructed.

Case 2.

If , it follows that

| (26) |

for all . Let

| (27) |

where is the bound of the rewards in the MDP. We run on input to determine a time step , which gives

According to (26) and (27), this also means that

and moreover

if we assume without loss of generality that . It then follows by (21), (22), and Section 5 that any is a near-optimal policy for player , with error at most to the optimum.

Therefore, in both cases, we let for all in the SPE to be constructed, and use Algorithm 1 to construct the remaining preceding part of . The whole process is outlined in Algorithm 3. The run time of the algorithm follows immediately. Specifically, it takes time to run , where the input used is either or (as specified in (27)), the size of the binary representation of which is . In addition to that, the time it takes to run Algorithm 1 is bounded by . ∎