Decentralized Prediction Markets and Sports Books

Abstract

Prediction markets allow traders to bet on potential future outcomes. These markets exist for weather, political, sports, and economic forecasting. Within this work we consider a decentralized framework for prediction markets using automated market makers (AMMs). Specifically, we construct a liquidity-based AMM structure for prediction markets that, under reasonable axioms on the underlying utility function, satisfy meaningful financial properties on the cost of betting and the resulting pricing oracle. Importantly, we study how liquidity can be pooled or withdrawn from the AMM and the resulting implications to the market behavior. In considering this decentralized framework, we additionally propose financially meaningful fees that can be collected for trading to compensate the liquidity providers for their vital market function.

Keywords: Decentralized Finance, FinTech, Decentralized Exchange, Automated Market Makers, Prediction Market, Sports Book.

1 Introduction

Decentralized Finance (DeFi) is a novel paradigm utilizing blockchain for intermediating financial transactions. Without utilizing traditional financial intermediaries, DeFi companies provide services in several areas of finance including, but not limited to, lending and borrowing, insurance underwriting, and trading. Herein, we construct a novel formulation for prediction markets within this decentralized paradigm. These markets allow for traders to bet on external outcomes (e.g., sports scores or economic data). Specifically, we formulate these decentralized markets via automated market makers (AMMs). Historically, prediction market AMMs have been considered in a centralized paradigm. However, with the advent of blockchain, decentralized AMMs for digital assets have been created and grown in prominence. These prediction markets function wherein bettors transact against some liquidity pool which takes the other side of every trade. As we will formulate below, and as is commonly formulated for decentralized AMMs, the cost of betting in these markets is found by balancing the liquidity available for all possible outcomes according to mathematical formulas. In contrast to the centralized prediction markets, these decentralized AMMs permit any investor to pool resources into the AMM to assist in making the market; in exchange, these investors share in the profits of the AMM (via fees collected).

The organization of this paper is as follows. The motivation for studying decentralized prediction market AMMs is provided within Section 1.1. A review of the literature on prediction markets and AMMs is provided within Section 1.2. We conclude the introduction with an overview of the primary contributions of this work in Section 1.3. A summary and generalization of prior works on prediction markets is provided within Section 2. This discussion is followed by our proposed structure for a prediction market AMM in an axiomatic framework within Section 3.1. With that discussion, we formulate meaningful mathematical and financial properties for the cost function and pricing oracle in Section 3.2. For instance, we demonstrate that there natively exists bid and ask pricing oracles with a pricing probability measure on the underlying measurable space sandwiched between these prices. In Section 4, we study the problem of decentralized liquidity provision for these prediction markets. In particular, we discuss how to provide liquidity so as to decrease price slippage during trading. In Section 5, we present a discussion for how to explicitly collect fees on bets in this market. Notably, due to the general construction utilized herein, these fees are assessed in a non-trivial manner so as to retain the important financial properties of the AMM. Finally, in Section 6, we consider two numerical case studies. First, we provide an empirical study for the behavior of an AMM when applied to data on sports betting for the 2023 Super Bowl. Second, we apply a prediction market AMMs for the purposes of quoting financial options prices. We summarize and conclude in Section 7.

1.1 Motivation

DeFi has the opportunity to democratize finance insofar as it opens the positions of financial intermediaries to individual investors. Prior to the “crypto winter” in May 2022, the value of all DeFi projects reached a high of $180B.111https://tradingview.com/markets/cryptocurrencies/global-charts/ AMMs offer a prominent example of a successful DeFi application; these entities create spot markets between digital assets by holding liquidity pools in an equilibrium. As a decentralized market, these AMMs allow investors to pool their own assets into the market in exchange for a fraction of the fees being collected from trading with the pool.

Though AMMs are now regarded as a key component of DeFi, the idea of an automated market maker was first proposed for use in prediction markets (see the literature review in Section 1.2 below or [32, Section 1.1]). However, in the context of prediction markets, such AMMs have been written as centralized markets only. The goal of this paper is to revisit prediction market AMMs with an emphasis on how to decentralize behaviors. In doing so, we seek to unify the concepts of AMMs for spot markets and prediction markets. In particular, the decentralized paradigm requires careful consideration for how to accommodate changing liquidity at the AMM (to permit investors to pool or withdraw liquidity) between the opening of the market and prior to the revelation of the realized event.

More specifically, once we define the notion of the prediction market, we want to consider the properties of these AMMs, i.e., for the cost assessed to bettors and the quoted pricing measure. Though many of these properties have been studied previously in the centralized market setting (see the literature review in Section 1.2 below), all works the authors’ are aware of require a finite set of possible outcomes and without any explicit consideration for the impact of liquidity on market behavior. Herein, we generalize such markets to allow for bets to be placed on general probability spaces with the explicit dependence on liquidity. Furthermore, due to the possibility of investing into the AMM, it is important to quantify the fees charged to traders. As highlighted in, e.g., [8], naively defining transaction costs can lead to unforeseen consequences to the profits of the AMM. Therefore, to avoid obvious mis-pricing, we also investigate these issues within the setting of prediction markets; prior works avoid these issues due to the centralized nature of the market.

Lastly, by introducing the mathematical construction for decentralized prediction markets, we believe that new products can be introduced to allow for, e.g., decentralized sports books which operate at a fraction of the cost of centralized sports books. Therefore, throughout this work we keep an eye towards the practicality of implementation and costs for these operations.

1.2 Literature review

Prediction markets seek to elicit probabilities of events through the aggregation of investor beliefs. If an investor has a different belief of the likelihood of an event he or she can transact to capture that discrepancy which moves the quoted probabilities. These markets can be applied to weather forecasting (e.g., [27]) or economic forecasting (e.g., [28]). However, even in a finite state space, Bayesian updating of these probabilities can be analytically and computationally challenging (see, e.g., [6, 18, 19]). One approach taken in practice is to use a scoring rule; repeated games with the scoring rule will lead to a Nash equilibrium [23] and thus convergence to a common estimator for the market participants [26, 20].

In practice, financial [24], sports [22] and election prediction markets perform well. However, these markets can sometimes result in irrational prices, especially when market liquidity is low. Choosing the correct market structure, i.e., a scoring rule with appropriate properties such as the logarithmic scoring rule of [21] or a Bayesian framework of [14], can improve market performance. Hanson’s logarithmic scoring rule has been implemented in a dynamic prediction market and achieved good results [30]. It has been generalized, and characterized as utility functions, in [12]. Furthermore, that paper highlights an additional property for a market to have, i.e., bounded loss. [29] emphasizes other desirable properties for prediction markets, e.g., liquidity sensitivity. We also refer the reader to [34, 33] for a survey of literature on prediction markets.

These predictions market scoring rules form AMMs. More recently, AMMs have been used prominently as decentralized markets for digital assets. These decentralized AMMs were described in the early whitepapers of [36, 1]. Those whitepapers emphasize the key mathematical and algorithmic components of AMMs. One such idea that provides an algorithm for an AMM to decide on quantities to swap is the constant function, see e.g. [4, 25, 3, 13, 2, 9]. The structure for many decentralized AMMs was provided in [35, 5]. These constructions were generalized and given axiomatic foundations in [32, 8, 16].

1.3 Primary contributions

As the goal of this work is to construct decentralized prediction markets via AMMs, our primary contributions are threefold.

-

•

We generalize the classical prediction market AMM setting of [21] from a finite to a general probability space. In particular, we follow the approach of [12, 29] to study these AMMs as utility functions with an axiomatic construction. In doing so, we investigate the properties of the cost function and pricing oracle of these AMMs. For instance, we demonstrate that with our proposed structure, there is guaranteed to exist a pricing measure sandwiched between the bid and ask pricing oracles.

-

•

We formalize the decentralized liquidity provision for prediction market AMMs to demonstrate that these markets can be made in a decentralized framework. In particular, we provide details on how to add or withdraw liquidity after some bets have already been placed and the impacts that these variations in liquidity have on market behavior. Notably, this added liquidity is not deterministic but rather a bet itself.

-

•

We define a novel fee structure to retain the important financial properties on the cost function while allowing liquidity providers to collect a profit from their investments. As far as the authors are aware, no prior work on prediction markets have explicitly defined the fees to be collected.

2 Generalized Structure for Automated Market Makers

We wish to begin our study of automated market makers for prediction markets by recalling (a generalization of) Hanson’s market maker [21]. This construction follows the utility function framework of [11] but with explicit consideration for the liquidity available.

Definition 2.1.

Consider a probability space .222In this context, represents a physical measure that is not used throughout our analysis, except in examples. Let denote the space of uniformly bounded random variables and . An automated market maker [AMM] is a utility function that is nonincreasing in its first (random-valued) component and nondecreasing in its second (real-valued) component.

We can interpret an AMM as the utility of betting positions and liquidity . More specifically, denotes the payout that would need to be made by the market maker in the event that outcome is realized; denotes the capital held by the market maker that is available to be used for the eventual payouts when the predicted event is realized. Bets with negative payouts, e.g., from selling a bet to the AMM, can be accommodated by buying the complement and shifting the liquidity accordingly as will be made clear in (2.1) below.

Remark 1.

Herein we introduced the AMM and, therefore, the prediction market as a betting market on the real line (see, e.g., [17]). The more typical case for prediction markets incorporate finite probability spaces only. We will frequently utilize the finite probability space with for every and in the examples within this work.

The purpose of an automated market maker is to act as a liquidity provider so that individuals can place bets in the prediction market. To place a bet with a payout of , the bettor must make a payment of

| (2.1) |

with initial betting positions and liquidity .333Prior works on prediction market AMMs, e.g. [11], formulate the cost via integration of infinitely small transactions instead as they do not explicitly consider the available liquidity ; it can readily be shown that these formulations are equivalent. In doing so, prior works focus on proving there exists a bounded loss so that there is some minimal liquidity that guarantees AMM solvency. This is the minimal amount of added liquidity necessary to guarantees that the market maker has a nondecreasing utility. Explicitly, in this way, we separate the random part of the bet () from its direct impact on liquidity (). In fact, this formulation encodes that a trader provides her own liquidity needs for the constant part () of any bet. We wish to remark that the setting in which almost surely corresponds with purchasing bets whereas allows for the trader to sell a bet to the AMM (i.e., receive a guaranteed payment today in exchange for paying if a specific event occurs). Though we do not impose it here, it may be desirable for the AMM to impose a no-short selling constraint on the traders so that the AMM does not need to worry about counterparty risk in the future.

Remark 2.

The purchasing price for some bet can be viewed as a utility indifference price (see e.g. [10]). Specifically, assuming is strictly increasing in its second (liquidity) input and sufficiently continuous, we can rewrite as the unique solution to provided it exists (i.e., the AMM is liquid enough to trade the bet ). Herein, we choose to follow the optimization formulation of (2.1) as existence and uniqueness of the cost is trivial for all .

In addition to acting as a liquidity provider, the AMM can also provide pricing oracles which give the marginal cost of placing positive and negative bets respectively. More specifically, we define the ask and bid pricing oracles, respectively, as the cost of placing positive and negative marginal sized bets:

| (2.2) |

for any bet , betting position and liquidity . It is desirable that , and that there exists a probability measure such that the bid and ask prices sandwich an expectation with respect to .

Assuming that the cost function has sufficient mathematical regularity to guarantee its differentiability, the bid and ask spread disappears, and the (unique) price becomes

| (2.3) |

This also selects the unique measure , the expectation with respect to which must then be equal to , i.e., for any . As such, we can view as a pricing measure, providing a ‘quoted price’ for via . Notably, this quoted price differs from due to the price slippage inherent in the form of given in (2.1).

Example 2.2.

Within this example we want to study the classical structure of Hanson’s AMM [21] with logarithmic scoring rule. As provided in [11], this AMM can be formulated according to Definition 2.1 as a utility function for any bet sizes and liquidity as

for where, by convention, for any . By construction of this utility function, the cost of purchasing a bet with payout of is explicitly provided by:

Recall from Remark 2 that the cost can be viewed as a utility indifference price. Specifically writing , and assuming is strictly increasing, we can rewrite as the unique solution to .

As mentioned within Remark 1, these prediction markets are often considered for finite probability spaces only. Consider now the finite probability space as constructed within that remark. Hanson’s AMM is more commonly written as the integral of the marginal costs [7], i.e., for

As is made clear from the cost function , Hanson’s AMM prices bets independent to the liquidity available. However, in practice, it is important that the market maker has sufficient liquidity to cover any bets that need to be paid out, i.e., at any realized bets and liquidity . Formally, we want for any , and so that the liquidity after a bet is placed is always sufficient to cover the worst case payouts (and assuming such a property holds before is traded). By bounding the log-sum-exponential functions, it can be readily shown that . That is, sufficient liquidity exists if or, equivalently, the risk aversion is sufficiently large. Beginning from and initial liquidity , this gives an initial bound ; in fact, in this initial time point, this bound is necessary and sufficient for the AMM to have the requisite liquidity for any bet. Furthermore, this inital bounding condition is sufficient for the AMM to be liquid throughout its operation.444This can be demonstrated due to the path independence property as introduced in Theorem 3.4(4) below.

The generalized structure of AMMs presented here is broad so as to encompass even structures that may not have sufficient liquidity to cover all possible bets (i.e., if ). For instance, if for Hanson’s AMM presented in Example 2.2 over a finite probability space, then there exists some bet that creates a probability that the market maker will default on (a fraction of) its obligations; notably this occurs once an infinite number of events needs to be considered. Taking the inspiration from the form and following the structure of the utility functions in [11], for the remainder of this work, we will focus on a special structure for AMMs based on the remaining liquidity for all outcomes, i.e., such that for some continuous and nondecreasing utility function . As will be shown in the subsequent sections, these liquidity-based AMMs can readily guarantee sufficient liquidity will always exist (as well as other useful properties for a market); we refer the interested reader to [11] which discusses the maximum loss for such an AMM under the finite probability space . Additionally, by specifically accounting for liquidity in the structure of an AMM, we allow for changes and dynamics in liquidity to occur. In particular, we permit investors to pool liquidity into the AMM (even after betting has started) to collect a portion of the market proceeds; this notion of pooling liquidity is expanded upon in Section 4. This decentralization can lead to more responsive liquidity provision as investors flock to volatile markets (to collect fees, see Section 5). Due to monotonicity (and as will be formally proven below), this increased liquidity has the ancillary benefit of reducing the price impacts from trading which ex-ante drives down the volatility.

3 Liquidity-Based Automated Market Makers

As discussed above, within this section we wish to study those automated market makers of the form for some utility function .555In the subsequent sections we will explicitly provide the domain of . Within Section 3.1, we propose some basic axioms that any such liquidity-based automated market maker should satisfy. The implications of these axioms on bets are investigated within Section 3.2. To simplify notation, for the remainder of this work we will let denote the liquidity remaining for each outcome (contingent on that outcome being realized); we will demonstrate in Section 3.2 that we can always guarantee that under the desired axioms (provided that for the initial liquidity of the market maker).

3.1 Construction

As expressed in the introduction of this section, our first goal is to characterize the liquidity-based automated market makers as utility functions satisfying useful mathematical properties.666We will set for . The following definition encodes the minimal set of axioms that we utilize throughout this work.

Definition 3.1.

A utility function is a liquidity-based automated market maker [LBAMM] if:

-

1.

is upper semi-continuous with respect to the weak* topology;777For any in the domain of and any , there exists a neighborhood of in the weak* topology on such that for all in this neighborhood, .

-

2.

is strictly increasing;888For any , if a.s. and , then . and

-

3.

is quasiconcave.999For all and for all , .

Remark 3.

Let denote the liquidity remaining for each outcome. Then as described in (2.1) above, the cost under an LBAMM of purchasing a payoff of is defined such that

| (3.1) |

To simplify notation, where clear from context, we will drop the explicit dependence of on , i.e., we will denote .

Before continuing our study of the properties of LBAMMs, we wish to provide a simple example of one such AMM in a finite probability space. This construction is based on Uniswap V2 which is a popular AMM in decentralized finance [1]. As we will see, this construction provides a closed form representation for the cost of a bet in the 2 event setting. We note that this AMM was first discussed in [11] for prediction markets (in a finite probability space) before its use in decentralized finance.

Example 3.2.

Consider the finite probability space as in Remark 1 with for every with cardinality . Consider the logarithmic utility function if and otherwise. Then, for any , the cost for the bettor

satisfies a constant product rule

In particular, for the setting with only possible outcomes,

| (3.2) | ||||

| (3.3) |

for any and . We implement this utility function within Section 6.1 as an empirical case study.

We wish to note that the logarithmic utility of Example 3.2 in a general probability space does not, necessarily, satisfy all conditions of an LBAMM. In the following example, which concludes this discussion of the definition of LBAMMs, we introduce a modification which can be used to extend the logarithmic utility to general probability spaces.

Example 3.3.

Consider a general probability space . Let be a strictly increasing, concave, and weak* upper semi-continuous function with . (For example, one might choose the logarithmic utility function as seen in Example 3.2 or, more generally, set for some as taken in the Liquid StableSwap of [8].) Fix , and define such that for all :

where . It is straightforward to verify that this utility function satisfies all the required properties of an LBAMM as per Definition 3.1. Note that, under the finite probability space , if then . This utility function structure is implemented within Section 6.2 to construct a simple financial derivatives market.

3.2 Properties

Given the construction of an LBAMM in Definition 3.1, we can now consider the formal properties of the cost functions defined in (3.1).

Theorem 3.4.

Let be an LBAMM with remaining liquidity and associated payment function .

-

1.

No arbitrage: for with attainment if and only if for some .

-

2.

Liquidity-bounded loss: and for any .

-

3.

Convex, monotone and lower semi-continuous: is strictly increasing, convex and lower semi-continuous (in the weak* topology).

-

4.

Path independent: for . As a direct consequence for any and .

Proof.

-

1.

By construction of the cost function , it easily follows that . If for some , then trivially, . Now, let’s consider the case where (the case of follows similarly). If , then by the strict monotonicity of the utility function (and using the fact that from Property 2), we have . This contradicts Property 2, which is proved below.

-

2.

Note that the sequence a.s. as . Then, by Remark 3, we have as implied by the construction of . Consequently, which ensures that for all . Furthermore, given that for , the equality must be satisfied due to the property of continuity from above.

-

3.

-

(a)

Monotonicity: To prove the monotonicity of , let’s consider an arbitrary and . Assume . By the strict monotonicity of the utility function and Property (2), we arrive at a contradiction:

-

(b)

Convexity: To prove the convexity of we will consider its epigraph. That is,

(3.4) Since is a constant, the epigraph of is convex due to the quasiconcavity of the utility function .

-

(c)

Lower semi-continuity: As seen in (3.4), the epigraph of corresponds to the hypograph for . Therefore, by upper semi-continuity of , the function is lower semi-continuous.

-

(a)

- 4.

∎

Remark 4.

- 1.

- 2.

-

3.

As a direct consequence of Theorem 3.4(1) and (4), a clear no round-trip arbitrage argument follows. Specifically, for any and ,

That is, a guaranteed payoff of can only be obtained at a cost of . In particular, so that buying, and immediately selling, a bet results in no profits (or losses) for the trader. This can be viewed as a version of the prior notion that the LBAMM can never default as, if an arbitrage such as this existed, traders could exploit this design flaw in order to guarantee profits at the expense of the LBAMM, which in the extreme case can cause the LBAMM to default on payments.

Corollary 3.5.

Let be an LBAMM with remaining liquidity . The associated payment function is Lipschitz continuous in the bet size with Lipschitz constant .

Proof.

Let . By the monotonicity and translativity proven in Theorem 3.4:

By symmetry between and , Lipschitz continuity follows. ∎

Let be fixed. We now wish to consider the ask and bid pricing oracles, , associated with the liquidity-based AMMs. Specifically, as constructed for the general AMMs in Section 2, we define the ask and bid pricing oracles, respectively, as the cost of placing a positive and negative marginal sized bet. That is,

| (3.5) |

Theorem 3.6.

Let be an LBAMM with remaining liquidity . The associated pricing oracles , defined in (3.5), satisfy for all . Furthermore, there exists a measure such that for all .

Proof.

Since is convex by Theorem 3.4, it is straightforward to verify that are well-defined and is a coherent risk measure. By the dual representation of coherent risk measures (see, e.g., [15, Corollary 4.34]) , there exists a set of probability measures which are absolutely continuous with respect to , i.e., , such that . Moreover, by construction, . We thus conclude that for all and all . ∎

Remark 5.

From Theorem 3.6, we note that:

-

1.

Theorem 3.6 guarantees the existence of a pricing measure that sits within the bid-ask spread, i.e., for any . We regard any such measure as a pricing measure as it is consistent with the quoted (bid and ask) prices in the market. Furthermore, we wish to note that if for all (i.e., with ), we can guarantee the existence of an equivalent pricing measure .

-

2.

The pricing oracle is, in fact, the largest coherent risk measure that is dominated by the cost function . A similar statement can be given for the pricing oracle on the negative of a bet.

-

3.

If is differentiable at 0, then there is no bid-ask spread, and for every . This differentiability follows if is Fréchet differentiable; however, we note that the construction in Example 3.3 is not Fréchet differentiable if .

4 Decentralized liquidity pooling

Thus far within this work we have formally introduced the AMMs for prediction markets. Such structures as previously studied (in, e.g., [12, 31, 29]) are considered with fixed available liquidity with a central operator running the AMM. Herein we wish to explore aspects of a decentralized AMM for prediction markets. Specifically, we consider an AMM to be decentralized if the liquidity pool is comprised of investments by diverse individuals and entities; furthermore, these investors can both add or remove liquidity at any time prior to the realization of the random event , even after some bets have already been placed.

First, we wish to note that investing as a liquidity provider is “simple” prior to the opening of the market to trades. Specifically, if an investor provides of liquidity to the market, then they receive a payout at the conclusion of the market equal to a fraction (where is the total initial market liquidity) of . That is, liquidity provision is a bet with payoff dependent on the state of the market.

Second, if an investor wishes to either add or remove liquidity after the market has opened to trades then we take the idea that these are special kinds of bets that adjust dynamically with the state of the market. We will focus our discussion on the liquidity provision case as selling a liquidity position acts similarly. Key to the construction of this special trade is that providing liquidity to the market should reduce the cost of trading for any counterparty. As such, we follow the idea from, e.g., [8] that pooling must be taken so that the pricing oracles are unaffected. We will, however, consider this trade in a generic manner first and then propose the specific structure for the constancy of the pricing oracles.

Briefly, let be a position that the liquidity provider is willing to sell in exchange for a fraction of the liquidity remaining. In particular, the investor wishes to guarantee that this fraction of liquidity remaining is accurate after she places her own bet, i.e., for some . Solving for , we solve the inverse problem to determine the fraction of the liquidity that is being purchased, i.e., .

Proposition 4.1.

Fix the pool size and new liquidity provision . There exists a unique fraction of the pool size purchased such that

| (4.1) |

Similarly, there exists a unique fraction of the pool size sold at satisfying (4.1) for with .

Proof.

Let and assume that ; as the proof for with is similar, we omit it here. By (strong) continuity of (see Corollary 3.5), it immediately follows that is continuous on . We also have that and The existence of now follows. Using the fact that , and therefore is strictly increasing, and the fact that is also strictly increasing (see Theorem 3.4(3)), we get that is strictly increasing as well. Thus we get the desired uniqueness. ∎

Notably, the bet is made in such a way that it will always rebalance to maintain a payout of fraction of the remaining liquidity as new bets are made. Let be the effective liquidity after pooling the liquidity. When the next trade occurs, the liquidity provider (through, e.g., a smart contract) needs to simultaneously update their position. That is, when a new bet is made, the trader will be charged where is the new holdings for the liquidity provider, i.e., so that the liquidity provider maintains the fraction of remaining liquidity after the bet occurs.

Proposition 4.2.

Fix the pool size after a liquidity provision (or withdrawal) of was made. The cost of trading is provided by the mapping .

Proof.

The cost of trading with the liquidity provision that rebalances to stay in line with the market is given by where is the rebalancing required for the liquidity provider. That is, satisfies the equilibrium . Fixing , this implies . Therefore the result follows from translativity of the cost fuction (see Theorem 3.4(4))

∎

With this foundation for the interaction of the liquidity provision and trades, we now want to specify so that the pricing oracles are kept constant, i.e., and . Providing liquidity in this way pooling does not influence the pricing measure quoted by the market.

Corollary 4.3.

Fix and let the liquidity provided (or withdrawn) be given by . The fraction of the pool provided (or withdrawn) is given by and the pricing oracles are invariant to the liquidity provision () or withdrawal ().

Proof.

Recall is the unique root of as defined in (4.1). It trivially follows from that construction that is a root of . Furthermore, and as a direct consequence, the pricing oracles after the liquidity provision or withdrawal are provided by and similarly for . ∎

This swap is a fraction of the current pool for that same fraction of the final pool (along with any collected fees). If no trades occur, then the investor will get their initial investment back exactly.

Remark 6.

Note that before the first trade is made, the liquidity pool is for initial liquidity . Therefore, adding fixed liquidity adheres to the proportional rule of Corollary 4.3.

It remains to prove that providing liquidity reduces the costs for counterparties to buy or sell bets. This is proven in the following lemma by noting that under the proportional liquidity provision .

Lemma 4.4.

Fix the bet . The cost of purchasing this bet is nonincreasing in the liquidity provision , i.e., is nonincreasing.

Proof.

Remark 7.

Before concluding this section, we want to briefly discuss the provision of fixed liquidity, i.e., for some . Though tempting as it provides a fixed quantity of liquidity to the market, this provision will (generally) alter the pricing oracles. In modifying the pricing oracles, it can be that a bet becomes more expensive after the deposit of than before. This is counter to the notion of a liquidity provision; we further note that cryptocurrency AMM markets explicitly accept liquidity only so that the pricing oracles are kept invariant to the change in pool sizes [8].

5 Fee structure

Throughout this work we have considered the market making problem without any explicit fees that are being collected by the market maker. In this section we aim to define a manner in which the AMM can collect fees while retaining the meaningful properties of the no-fee setting as encoded in Section 3.2 above.

Conceptually, due to the translativity of the cost function , the AMM is indifferent to any almost sure bet. As such, we propose that fees are only collected on the (positive) random portion of the bet . That is, for the fixed fee level , the cost of purchasing in the pool is given by

| (5.1) |

In this way, the AMM collects in cash to be paid out to the liquidity providers. This surplus is collected by the AMM poolers in compensation for the liquidity they provide. The no-fee setting corresponds exactly to ; as will be discussed below, for a well-functioning market, we will want to cap the fees at (see Remark 11). We recall from the original setup in (2.1) that the cost function is only applied to the random part of a bet with the essential infimum being accounted for in the liquidity; as such this fee structure matches the logic applied to AMMs generally.

Remark 8.

The fee structure (5.1) corresponds with that of cryptocurrency AMMs as encoded in, e.g., [4, 25] in which the trader pays (a fixed fraction of) the assets they sell; herein the bettor is “selling” cash in exchange for the random payoff. We note that the notation utilized here differs as, traditionally for cryptocurrency AMMs, the inverse is considered as the primitive instead.

We further wish to note that collecting fees as a fraction of the purchased bet results in random fees rather than a deterministic amount. Due to this, we opt solely to investigate the assessment of fees on the cost rather than the size of the bet .

Remark 9.

By defining the fees on the (positive) random portion of the bet , we eliminate a possible violation of the law of one price. Specifically, the cost of buying is identical to the cost of buying the fixed payout of and selling . Neglecting counterparty risks, the payoff of these bets are functionally identical and, in assessing fees only on the random portion of a bet, so are their costs.

Proposition 5.1.

Let be an LBAMM with remaining liquidity and associated payment function . For any fixed bet , the mapping is strictly increasing in fee level. Furthermore, for any and .

Proof.

Herein, we assume that the collected fees are immediately distributed to the liquidity providers. As such, when a bet is placed, the pool still updates from to as in the no-fee setting. By collecting and disbursing fees in this manner, the impact on our discussion of liquidity pooling in Section 4 remains unaffected.

Corollary 5.2.

Let be an LBAMM with remaining liquidity and associated payment function . Fix the fee level and define as in (5.1). It then satisfies the following properties:

-

1.

No arbitrage: ;

-

2.

Increasing utility: for and with strict inequality becoming an equality if if or for some ;

-

3.

Convex and monotone: is convex and strictly increasing;101010We interpret with as the random portion and the constant portion of a bet. Notably so that this domain does not restrict the space of bets under consideration.

-

4.

(Lower semi-)Continuous: is lower semi-continuous in the weak* topology and Lipschitz continuous with Lipschitz constant 1; and

-

5.

Path independent: for such that . As a direct consequence, this path independence applies to splitting a trade for any and translativity for any and .

Proof.

Remark 10.

-

•

Note that the monotonicity of with fees is more delicate than in the no-fee setting. This is due to the way in which fees are collected on the random portion of the bet only. Therefore, the monotonicity of costs need to be assessed separately on the random portion (with ) and the constant shift . In fact, as observed by the upper bound on , it is possible that there exists some bet so that which would violate the naive attempt at monotonicity of . For instance, consider the LBAMM from Example 3.2 with ; if then . In fact, setting in that same example guarantees that is (strictly) decreasing as increases.

-

•

Though convexity of in Corollary 5.2 was only stated on the domain , this can readily be shown to be equivalent to convexity of .

-

•

Note that path independence is now only defined for trades with additive essential infima. The general case for path independence, which holds in the no-fee setting as encoded in Theorem 3.4(4), is not desirable when fees are assessed. This becomes clear when considering a round trip trade when is bought and then subsequently sold; path independence would imply such a trade nets for the liquidity providers which would violate the collection of any fees on the purchase or liquidation of the position.

We wish to conclude our discussion of fees by considering how these fees will be quoted to users through the bid and ask prices, i.e., the modifications to the pricing oracles. Specifically, we define the bid and ask prices, respectively, as (see (3.5))

for any . That is, buying a marginal unit of a bet with payoff will have a per unit cost of which is increasing in . Further, selling a marginal unit of that bet will recover which decreases as increases. As expected, for every and pool size . However, as encoded here, the fees may not apply equally on both sides of the market, i.e., often .

Remark 11.

Noting that a bettor will never elect to buy a bet costing more than its (essential) supremum nor sell to recover less than its (essential) infimum, the pricing oracles have the effective bounds of and for any and . In this way the ask price (including fees when ) is bounded from above by the essential supremum and the bid price is bounded from below by the essential infimum (i.e., and ). Implicitly to this construction, and necessary to be assumed in practice, the fees must therefore be bounded so that the bid and ask prices are ordered properly to follow financial logic.

6 Case Studies

Within this section, we wish to explore two case studies to explore the versatility and applicability of the AMMs constructed within this work. First, we will replicate a two outcome sports book with data collected for Super Bowl LVII. With this empirical case study, we explore the potential profits and losses accrued by the liquidity providers. In the other case study, we explore the use of an AMM for financial derivatives by simulating a system with a continuous probability space; in doing so, we prove the viability of our system to adjust the quoted distribution to investor actions.

6.1 Super Bowl LVII

Sports betting on the Super Bowl is big business, with $16 billion wagered in 2023 on Super Bowl LVII alone.111111https://www.espn.com/chalk/story/_/id/35607249/survey-record-504-million-adults-bet-16b-super-bowl One popular way to bet on a single game is with the money line. As opposed to the probabilities quoted within this work, the money line quotes the profits that would be gained from a winning bet of $100 (if the underdog) (i.e. if the money line is , then betting , will get in case the bid wins), or how much needs to be bet to win $100 (if the favorite) (i.e. if the money line is , betting will obtain in case the bid wins). Therefore, it is easy to reformulate the money line as probabilities. Specifically, if is the quoted money line for one team to win, then the ask probability is .

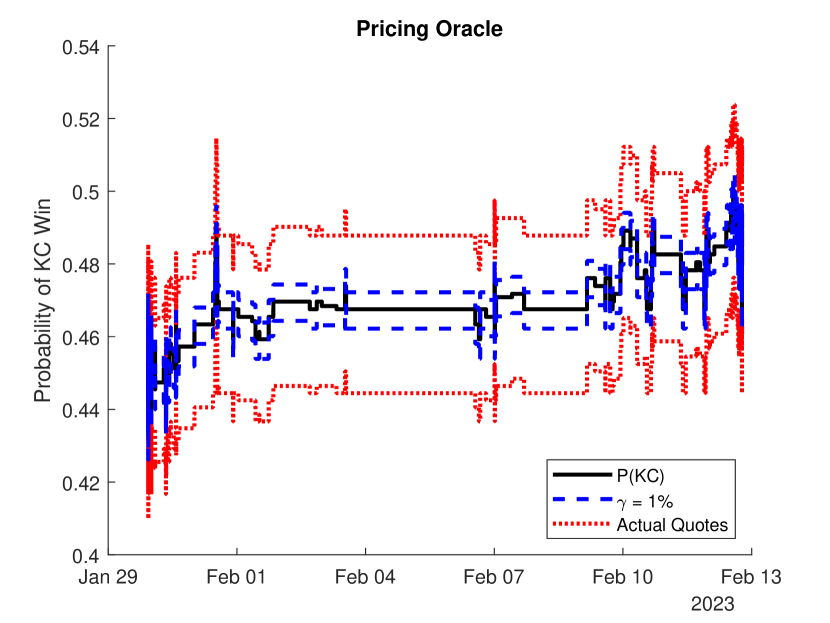

Consider the possible outcomes for Super Bowl LVII played between the Kansas City Chiefs (KC) and the Philadelphia Eagles (PHI), i.e., where we denote the events based on the eventual winner. In the 2 weeks leading off to the start of the game (i.e., once the two final teams are determined), bets are accepted at numerous sports books on this two-event sample space. For the purposes of this data, we collected money line data from Bookmaker.121212Made available from https://pregame.com/game-center/193165/odds-archive The time series of quoted (implied) bid and ask probabilities for KC are displayed within Figure 1(a). (Note that the bid and ask probabilities for PHI are such that and respectively.)

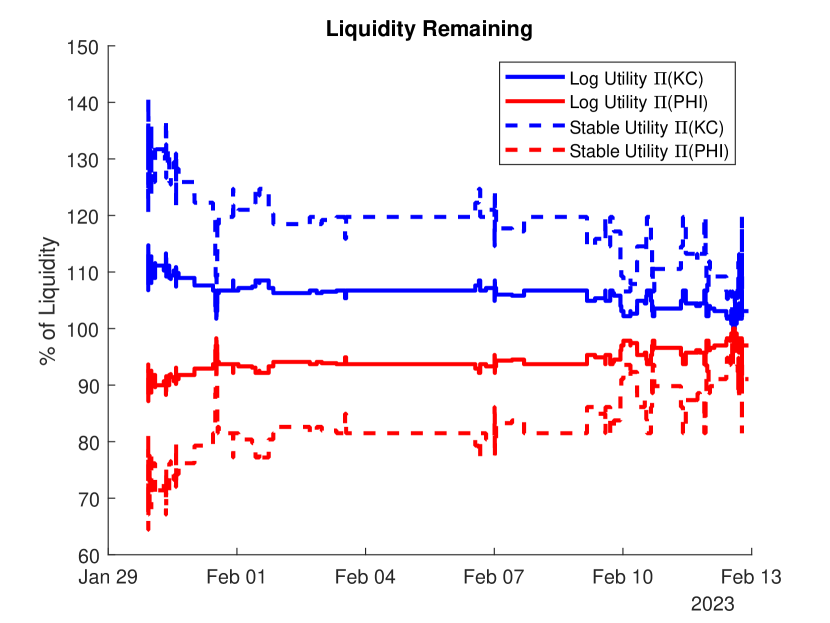

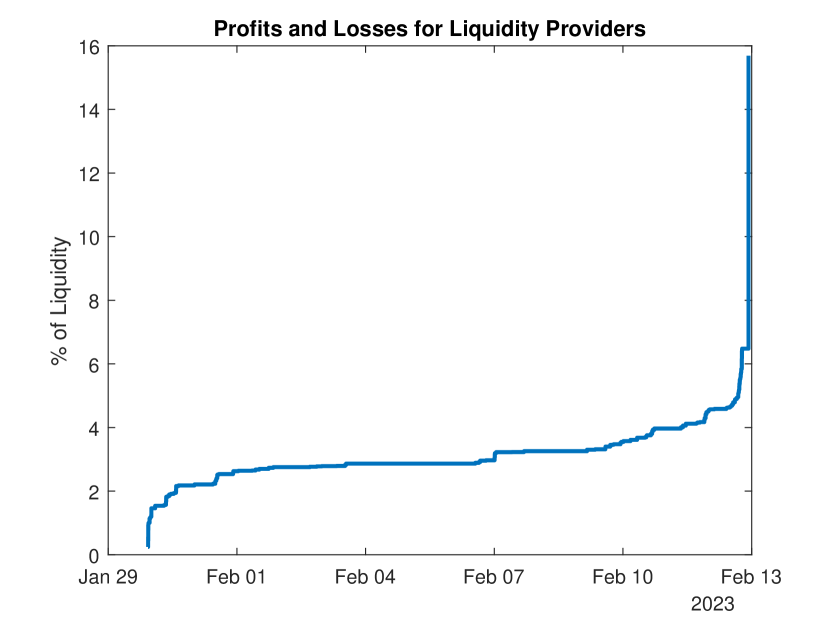

Using this bid-ask spread, we were able to determine the (implied) mid-price by normalizing the ask prices to sum to 1. This price oracle, as displayed in Figure 1(a), drives our backtesting system. Within this construction we consider 2 utility functions: (i) the expected logarithm utility function as discussed in Example 3.2 and (ii) the Liquid StableSwap utility function ( with ) introduced in [8]. With these LBAMMs, we deduce the trades necessary to exactly replicate this pricing oracle (without fees). Assuming liquidity was initially available to the AMM, the liquidity available at any time can be determined via

for the logarithmic utility and numerically for Liquid StableSwap. Notably, for both of these LBAMMs, the liquidity available scales linearly with the initial liquidity ; for this reason we quote all profits and losses as a percentage of the initial liquidity rather than as an absolute value. The liquidity remaining, as a percentage of the initial liquidity, is shown as a time series in Figure 1(d). By computing the liquidity remaining at all times, it is also possible to determine the bets that are actualized. In this way, we can determine profits gained from fees on trades over time as well as the gains or losses based on the final outcome of the event.

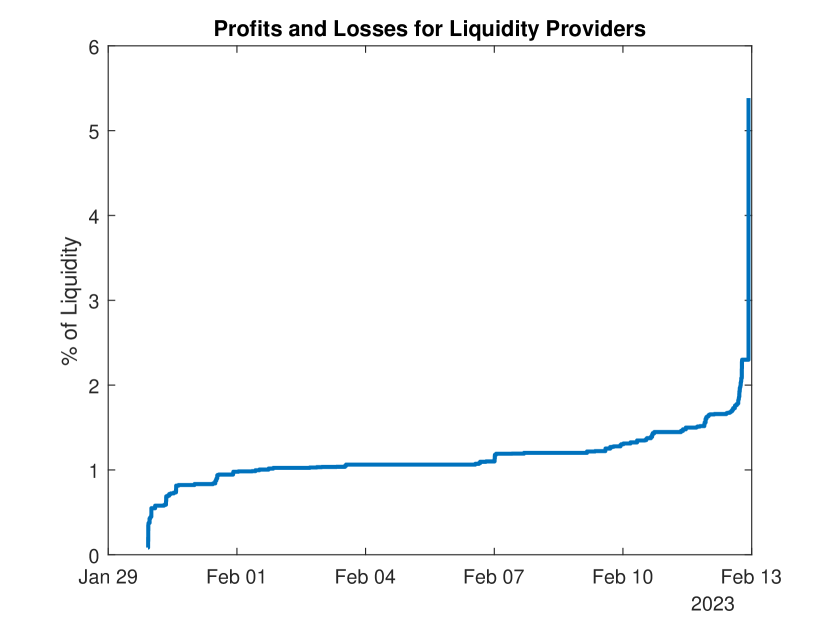

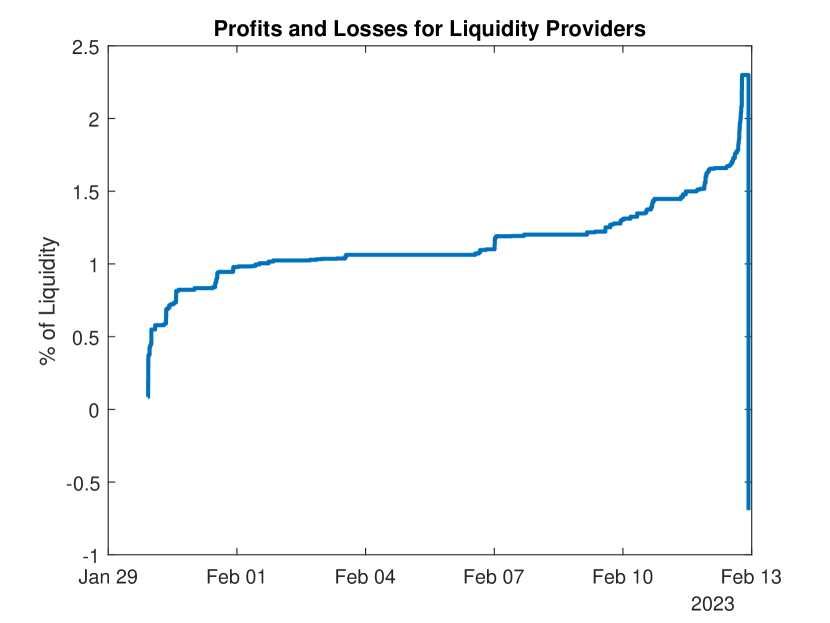

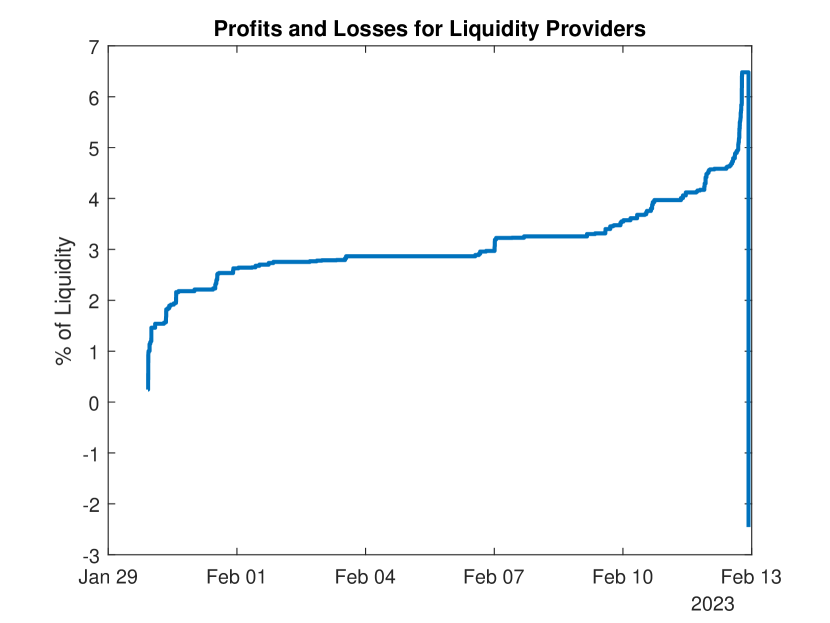

Consider, first, the logarithmic utility function. In Figure 1(b) we see how these profits accumulate until the game outcome () is realized with .131313Bookmaker adjusts the money line less frequently than our LBAMM would, thus the profits quoted herein are a lower bound to those that would be collected in practice due to the accumulation of many small trades which introduce additional volatility. The quoted bid-ask spread over time with this fee is shown in Figure 1(a). Notably, in Figure 1(b) and Figure 1(c), we see that the final profits for the liquidity providers can depend significantly on the realized outcome of the game with approximately return just prior to the start of the game. Due to the victory of KC, this would jump to nearly return; in the counterfactual scenario of a PHI win, the liquidity providers would, instead, be subject to a nearly loss. If the fees were increased to only (an increase of just 30bps), then a liquidity provider would break even when if PHI was realized and have over return from the KC victory.

In contrast, by selecting the Liquid StableSwap utility function, we are able to increase the fees collected from trading substantially. In Figure 1(e) we see how these profits accumulate until the game outcome () is realized with .141414As we fixed the prices based on the data, this bid-ask spread is identical to that found with the logarithmic utility function. From the fees alone, liquidity providers would experience almost a return prior to the start of the game. Due to the victory of KC, this would jump to nearly return; in the counterfactual scenario of a PHI win, the liquidity providers would, instead, be subject to a loss. With these greater potential losses, the fees would need to increase to (an increase of just 38bps) to guarantee a liquidity provider breaks even when PHI was realized (and over return from the KC victory).

6.2 Financial Derivatives

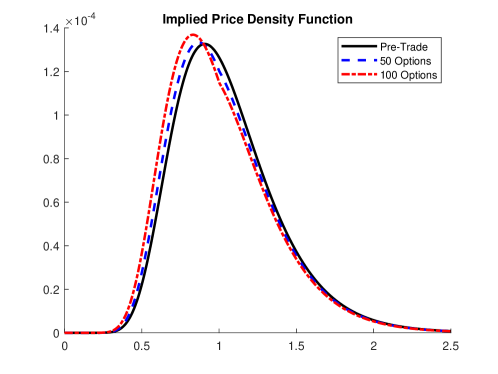

In this final case study, we explore the use of an LBAMM for pricing European options with a fixed expiry. Notably, for this construction, we want to consider a general probability space rather than the finite probability space considered in the prior case study. In doing so, we consider the LBAMM based on the scaled and shifted logarithmic utility function as is considered in Example 3.3 with chosen arbitrarily. This AMM is constructed with initial liquidity of distributed so as to create an initial lognormal distribution for the price at the maturity time.

In order to avoid this derivatives market from converging to a Dirac measure, we assume that market trading ends a fixed amount of time prior to expiry. Due to the liquidity-bounded loss for the LBAMM, this market is able to trade any measurable payoff structure . In Figure 2, the price density is plotted under three circumstances: (i) the initial lognormal distribution; (ii) after 50 put options with strike at $1 have been purchased (at an average cost of $0.1103 per contract); and (iii) after 100 put options with strike at $1 have been purchased (at an average cost of $0.1166). It can clearly be seen that these derivative purchases appropriately shift the mass of probability leftward and increase its peakedness. In addition, though subtle, there is a kink in the distribution at $1 to match up with the strike price used. Finally, we would like to point out that in the lognormal setup used for this case study, we can compare these per-contract costs to the Black-Scholes price of $0.0997. This price corresponds to the cost of a hedge under a risk-neutral measure. This should be compared to the price we obtained earlier, which represents the utility indifference price in a scenario where no hedging is allowed.

7 Conclusion

To summarize, in this manuscript, we have presented a general utility framework for a prediction market maker over general probability spaces. The novelty of this framework is that it considers the liquidity separately and in a decentralized way, which in turn allows for addition liquidity to be provided or withdrawn after the market opened and bets have already been received. We have also investigated the resulting properties of the pricing oracles. Additionally, we have proposed a novel way to charges fees on the random part of the bet that does not create an arbitrage.

Future research in decentralized prediction markets should address the problem of optimizing fees so as to maximize (risk-adjusted) profits gained by the liquiidty providers. Doing so will require dynamic models of betting so as to accurately study risks and returns. Additionally, in the proposed setup, we ignore the role of information on prediction markets; if an event becomes a certainty prior to the maturity of the bet, the liquidity providers would be arbitraged until no assets remain. To avoid such a fate, we recommend a dynamic fee schedule which can counteract the informational gains of bettors. Such a system, especially to optimize this fee schedule, would be of great import for practical implementations.

References

- [1] Hayden Adams, Noah Zinsmeister, and Dan Robinson. Uniswap v2 core. 2020.

- [2] Álvaro Cartea, Fayçal Drissi, and Marcello Monga. Decentralised finance and automated market making: Execution and speculation. Available at SSRN 4144743, 2022.

- [3] Guillermo Angeris, Akshay Agrawal, Alex Evans, Tarun Chitra, and Stephen Boyd. Constant function market makers: Multi-asset trades via convex optimization. arXiv preprint arXiv:2107.12484, 2021.

- [4] Guillermo Angeris and Tarun Chitra. Improved price oracles: Constant function market makers. In Proceedings of the 2nd ACM Conference on Advances in Financial Technologies, pages 80–91, 2020.

- [5] Guillermo Angeris, Alex Evans, and Tarun Chitra. When does the tail wag the dog? curvature and market making. arXiv preprint arXiv:2012.08040, 2020.

- [6] Robert J Aumann. Agreeing to disagree. In Readings in Formal Epistemology, pages 859–862. Springer, 2016.

- [7] Henry Berg and Todd A Proebsting. Hanson’s automated market maker. The Journal of Prediction Markets, 3(1):45–59, 2009.

- [8] Maxim Bichuch and Zachary Feinstein. Axioms for automated market makers: A mathematical framework in fintech and decentralized finance. arXiv preprint arXiv:2210.01227, 2022.

- [9] Agostino Capponi and Ruizhe Jia. The adoption of blockchain-based decentralized exchanges. arXiv preprint arXiv:2103.08842, 2021.

- [10] René Carmona. Indifference pricing: theory and applications. Princeton University Press, 2008.

- [11] Yiling Chen and David M Pennock. A utility framework for bounded-loss market makers. In 23rd Conference on Uncertainty in Artificial Intelligence, UAI 2007, pages 49–56, 2007.

- [12] Yiling Chen and David M Pennock. A utility framework for bounded-loss market makers. arXiv preprint arXiv:1206.5252, 2012.

- [13] Joseph Clark. The replicating portfolio of a constant product market. Available at SSRN 3550601, 2020.

- [14] Min Dai, Yanwei Jia, and Steven Kou. The wisdom of the crowd and prediction markets. Journal of Econometrics, 222(1):561–578, 2021.

- [15] H. Föllmer and A. Schied. Stochastic Finance: An Introduction in Discrete Time. De Gruyter Studies in Mathematics. De Gruyter, 2nd edition, 2008.

- [16] Rafael Frongillo, Maneesha Papireddygari, and Bo Waggoner. An axiomatic characterization of cfmms and equivalence to prediction markets. arXiv preprint arXiv:2302.00196, 2023.

- [17] Xi Gao, Yiling Chen, and David M Pennock. Betting on the real line. In International Workshop on Internet and Network Economics, pages 553–560. Springer, 2009.

- [18] John D Geanakoplos and Heraklis M Polemarchakis. We can’t disagree forever. Journal of Economic theory, 28(1):192–200, 1982.

- [19] Robin Hanson. Disagreement is unpredictable. Economics Letters, 77(3):365–369, 2002.

- [20] Robin Hanson. For bayesian wannabes, are disagreements not about information? Theory and Decision, 54(2):105–123, 2003.

- [21] Robin Hanson. Logarithmic market scoring rules for modular combinatorial information aggregation. The Journal of Prediction Markets, 1(1):3–15, 2007.

- [22] Donald B Hausch, Victor SY Lo, and William T Ziemba. Efficiency of racetrack betting markets, volume 2. World Scientific, 2008.

- [23] Ehud Kalai and Ehud Lehrer. Rational learning leads to nash equilibrium. Econometrica: Journal of the Econometric Society, pages 1019–1045, 1993.

- [24] Stephen F LeRoy. Market efficiency: Stock market behaviour in theory and practice, 1998.

- [25] Alex Lipton and Artur Sepp. Automated market-making for fiat currencies. arXiv preprint arXiv:2109.12196, 2021.

- [26] Dov Monderer and Dov Samet. Approximating common knowledge with common beliefs. Games and Economic Behavior, 1(2):170–190, 1989.

- [27] Allan H Murphy and Robert L Winkler. Probability forecasting in meteorology. Journal of the American Statistical Association, 79(387):489–500, 1984.

- [28] FM O’Carroll. Subjective probabilities and short-term economic forecasts: an empirical investigation. Journal of the Royal Statistical Society: Series C (Applied Statistics), 26(3):269–278, 1977.

- [29] Abraham Othman, David M Pennock, Daniel M Reeves, and Tuomas Sandholm. A practical liquidity-sensitive automated market maker. ACM Transactions on Economics and Computation (TEAC), 1(3):1–25, 2013.

- [30] Abraham Othman and Tuomas Sandholm. Automated market-making in the large: the gates hillman prediction market. In Proceedings of the 11th ACM conference on Electronic commerce, pages 367–376, 2010.

- [31] Abraham Othman and Tuomas Sandholm. Profit-charging market makers with bounded loss, vanishing bid/ask spreads, and unlimited market depth. In Proceedings of the 13th ACM Conference on Electronic Commerce, pages 790–807, 2012.

- [32] Jan Christoph Schlegel, Mateusz Kwaśnicki, and Akaki Mamageishvili. Axioms for constant function market makers. Available at SSRN, 2022.

- [33] George Tziralis and Ilias Tatsiopoulos. Prediction markets: An extended literature review. The journal of prediction markets, 1(1):75–91, 2007.

- [34] Justin Wolfers and Eric Zitzewitz. Prediction markets in theory and practice, 2006.

- [35] Jiahua Xu, Krzysztof Paruch, Simon Cousaert, and Yebo Feng. Sok: Decentralized exchanges (dex) with automated market maker (amm) protocols. arXiv preprint arXiv:2103.12732, 2021.

- [36] Yi Zhang, Xiaohong Chen, and Daejun Park. Formal specification of constant product () market maker model and implementation. 2018.