Tight Distribution-Free Confidence Intervals for Local Quantile Regression

Abstract

It is well known that it is impossible to construct useful confidence intervals (CIs) about the mean or median of a response conditional on features without making strong assumptions about the joint distribution of and . This paper introduces a new framework for reasoning about problems of this kind by casting the conditional problem at different levels of resolution, ranging from coarse to fine localization. In each of these problems, we consider local quantiles defined as the marginal quantiles of when is resampled in such a way that samples near are up-weighted while the conditional distribution does not change. We then introduce the Weighted Quantile method, which asymptotically produces the uniformly most accurate confidence intervals for these local quantiles no matter the (unknown) underlying distribution. Another method, namely, the Quantile Rejection method, achieves finite sample validity under no assumption whatsoever. We conduct extensive numerical studies demonstrating that both of these methods are valid. In particular, we show that the Weighted Quantile procedure achieves nominal coverage as soon as the effective sample size is in the range of 10 to 20.

1 Introduction

1.1 Motivation

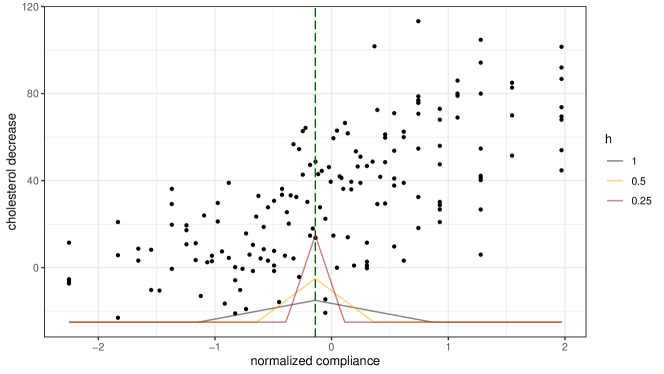

Consider the following real dataset from Efron and Feldman, (1991): 164 male doctors were treated with cholestryamine, a drug known to decrease cholesterol level. In addition to the cholesterol level, the compliance of each subject, defined as the proportion of the drug actually taken from the intended dose, is also available. Figure 1 shows a scatter plot of decrease in cholesterol versus compliance.

To understand the relationship between a set of predictors and an outcome , statisticians often report inferences about the conditional mean or the conditional median . Inference problems of these kinds are traditionally modeled by using a surface plus noise model . To provide inference based on the fitted model, we usually require assumptions such as smoothness of and some structure on the noise such as sub-Gaussianity. These assumptions can be problematic since they are empirically unverifiable as pointed out in Donoho, (1988). Moreover, it is unclear what we even mean by the conditional distribution of at exactly being since it is hard to understand if there actually exists a population of people having a level of compliance equal to 50% whatever the level of precision.

Keeping this in mind, we suggest a shift in emphasis from these classical objects of inference. Our main idea is instead to consider the distribution of when is near a point of interest: more specifically, we aim to determine the quantile of when is near .

Imagine a researcher comes up with a kernel and a bandwidth that models the weights and degree of nearness to the point . This yields a reweighted covariate distribution defined as

where is the original covariate distribution. If the kernel is non-increasing with respect to the distance from 0, gives more weight to samples with covariates close to and less weight to samples that are farther away from . We take our new object of inference to be

i.e., the median of the marginal distribution of where is localized to the space near .

Going back to the compliance example, say we are using a triangular kernel of bandwidth for reweighting. Then, our object of inference at compliance is the median of the decrease in cholesterol level for people who comply between and with more weight towards compliance; this value comes from a more interpretable population than one in which some people have a compliance exactly equal to . Additionally, by adjusting , we have the freedom to change the resolution at which we localize the covariate space. If we take the kernel bandwidth to be small, we are smoothing the outcome over a small neighborhood. Figure 1 plots the triangular kernel centered at (corresponding to -0.14 for normalized compliance) as the bandwidth varies.

By rethinking the object of inference, in a way that considers the resolution of the observation of the underlying covariate distribution, we are able to provide reliable inference without making any modeling assumptions. This is in stark contrast to classical nonparametric methods that impose unverifiable assumptions on the underlying distribution to offer confidence intervals for the conditional mean or quantile. Additionally, these methods often produce confidence intervals that depend on unknown constants. We provide a discussion on nonparametric methods in Section 1.4.

1.2 Problem statement

Consider i.i.d. data , where each is a random vector in , is a response variable of interest and is a -dimensional vector of covariates. Suppose has an unknown density . 111 can be the Radon-Nikodym derivative with respect to any arbitrary measure, but we will use the term “density” for simplicity. We are interested in the local distribution of the response variable at a point . Localization is done by reweighting the distribution of the covariates with some uniformly bounded kernel that is non-negative and obeys . Define the covariate-shifted distribution (depending on ) as

We are interested in making claims about the quantiles of with respect to the marginal distribution of , that is, the distribution of when .

In the interest of lightening the notation, the distributions defined above do not explicitly show the dependence on , and .222The covariate-shifted joint probability distribution function will be denoted as , and the marginal probability distribution function and the cumulative distribution function will be denoted as and , respectively.

Our new object of inference is

| (1) |

which is the -th quantile of the distribution . This parameter has an intuitive interpretation; as we shall see, it can also be reliably inferred without making any unverifiable assumptions on the underlying distribution.

1.3 Summary of key results

This paper builds distribution-free confidence intervals for that have length vanishing to 0 as the sample size goes to infinity. The first method we propose is the Weighted Quantile method (Algorithm 1) introduced in Section 2. This method achieves asymptotically valid coverage and provides an optimal confidence interval in the sense that it is asymptotically uniformly most accurrate unbiased. The second is the Quantile Rejection method (Algorithm 3). The method uses rejection sampling to achieve finite sample coverage.

In Section 4, we provide various numerical experiments, which empirically confirm that both of our proposed methods have valid coverage. In Section 5, we apply our proposed methods to the compliance example from Section 1.1 and a California housing dataset. Finally, we show in Section 6 that it is impossible to design shorter intervals.

The two methods proposed in the paper are implemented in https://github.com/Jayoon/resolution_paper. The R code for reproducing the experiments and analysis is also available in the same repository.

1.4 Past/related works

Distribution-free inference

Much interest has been devoted to constructing distribution-free prediction intervals for given exchangeable training data . Often, this is done using techniques known as conformal inference (Vovk et al.,, 2005). Conformal prediction intervals achieve distribution-free marginal coverage . Also, it is known to be impossible to construct a bounded prediction interval that satisfies a stronger notion of conditional coverage as shown in Vovk, (2012); Lei and Wasserman, (2014). Prediction intervals differ from confidence intervals in that they have to capture the inherent randomness of and so cannot have width converging to 0 even as the sample size goes to infinity. For non-exchangeable data, Tibshirani et al., (2019) provides a method for computing a valid prediction interval when the test set is a covariate-shifted distribution of the training set. While our paper also considers a covariate-shifted distribution as a target, the difference lies in that Tibshirani et al., (2019) constructs a prediction interval for , while our paper constructs a confidence interval for a fixed parameter.

Distribution-free confidence intervals that are finite-sample valid for parameters such as the mean , quantile , conditional mean , and conditional quantiles have been extensively studied. A classical result of Bahadur and Savage, (1956) shows that it is impossible to get a bounded confidence interval for the mean without restricting the distribution class. The basic idea is that if the distribution class is too large, there always exist two almost indistinguishable distributions that have an arbitrarily large mean difference. Fortunately, constructing finite-sample confidence interval for quantiles is possible since the probability of a quantile being between any observations can be bounded in terms of binomial probabilities (Noether,, 1972). However, it is impossible to construct a non-trivial distribution-free confidence interval for the conditional quantiles. Barber, (2020) showed that in a binary regression setting where with nonatomic joint distribution (meaning a distribution without point masses), the expected length of any confidence interval for the conditional label probability has a non-vanishing lower bound. Similarly, Medarametla and Candès, (2021) show that there does not exist any distribution-free confidence interval for the conditional median that has vanishing width as the sample size goes to infinity. Note that both results have assumed the distribution is nonatomic. When this assumption is removed, Lee and Barber, (2021) characterize a regime where non-trivial distribution-free inference for is possible in the case where the response variable is bounded. They introduce the concept of effective support size of and show that if it is smaller than the square of the sample size, one can construct a confidence interval of vanishing length.

Nonparametric statistics

In nonparametric inference, the goal is to make as few assumptions on the model as possible. This is usually done by assuming only that the regression function belongs to a restricted function class and the covariate distribution is continuous. The function class usually characterizes the smoothness of by positing the existence of a certain number of bounded derivatives. Examples of widely used function classes are Hölder classes and Besov classes (Tsybakov,, 2008). Such assumptions are crucial to make the estimators of have desirable properties such as consistency or optimality. Moreover, in order to obtain uniform confidence intervals over a function class for a linear functional of the regression function such as , assuming knowledge about the smoothness constant cannot be avoided (Low,, 1997; Armstrong and Kolesár,, 2018). The hardness of constructing nonparametric confidence intervals comes from the difficulty of measuring the bias of the regression function estimate. For instance, smoothing methods using kernels or local polynomials require a choice of a bandwidth , which corresponds to the amount of smoothing. Theoretically, based on the assumed smoothness, the bandwidth is chosen to set the rate of convergence of bias and variance to be the same. In practice, we can obtain a data-driven bandwidth by minimizing some criterion such as a generalized cross-validation error or use a plug-in bandwidth, which is obtained by replacing unknown components of the optimal bandwidth with estimates. For more literature on nonparametric inference, see for example, Wasserman, (2006); Giné and Nickl, (2021) and references therein.

Instead of choosing a single optimal smoothing parameter, Chaudhuri and Marron, (2000) consider a family of smooth curve estimates by varying the smoothing parameter or the bandwidth . This has some similarity to our work in the sense that they turn their attention to , which is a smoothed version of the regression function . However, their inference focuses only on identifying statistically significant local maximizers and minimizers of .

2 Weighted Quantile method

We now outline our first of two methods. First, we introduce the method in Section 2.1. Then we show that the proposed confidence interval is efficient in Section 2.2 We provide proofs for all the results from this section in Appendix A.

2.1 Method

Suppose we have i.i.d. samples from some distribution . Then, a natural estimate of the distribution function of is its empirical cumulative distribution function , which weighs each sample equally. In our setting, we are interested in estimating a shifted distribution given samples from . Noting that the likelihood ratio of the joint shifted distribution and the original distribution is proportional to , one possible way to estimate the distribution function of is to reweight each sample from proportional to the likelihood ratio. We denote the reweighted distribution as

| (2) |

where . Without loss of generality, assume that is strictly positive. (If , we only have samples outside the region of interest and, therefore, cannot do meaningful inference.)

Lemma 2.1.

Let be defined as (2). Then the following holds:

-

(a)

is right continuous and monotonically increasing in .

-

(b)

Suppose that is differentiable at . Then, for every sequence such that ,

as .

-

(c)

We have

Above, denotes expectation over samples from .

By taking appropriate quantiles of the reweighted distribution function as the endpoints, we can construct confidence intervals that have valid asymptotic coverage.

Let

| (3) |

where denotes the -th quantile of the distribution .

Proposition 2.2.

In Algorithm 1, we summarize the Weighted Quantile method with specific and that satisfies equation (4). We note that for the case of , the asymptotic variance of at simplifies to and we could use in Step 4 of Algorithm 1.

-

1.

Compute for .

-

2.

Set .

-

3.

Compute .

-

4.

Compute

-

5.

Compute and .

-

6.

Set .

Our next Theorem shows that this yields exact asymptotic coverage.

Theorem 2.3.

For all distributions on such that is differentiable at , the output of the Weighted Quantile Algorithm has asymptotic coverage,

On choosing the bandwidth

We recommend using the method only when the effective sample size is sufficiently large. If the effective sample size is too low, there are not sufficiently many samples near the point of interest to guarantee coverage. Numerical studies in Section 4 show that the method usually attains the desired coverage when for . For extreme quantiles, we would need more samples as is typically the case with any inference methods for extreme quantiles.

2.2 Optimality

The Weighted Quantile method guarantees asymptotic coverage of for any distribution that has a derivative at . We now study the efficiency of the confidence interval by showing that it is asymptotically uniformly most accurate unbiased.

First, we begin by reformulating the problem as an M-estimation task. Let be the pinball loss, defined as

Then, the -th quantile, , of a distribution can be written as

Therefore, the object of inference can be understood as a solution to the minimization problem

which is a locally weighted quantile. In fact, is an M-estimator.

A notion of semiparametric optimality is adequate in this setting since we have an infinite-dimensional model and are interested in estimating . Semiparametric efficiency bounds stem from an ingenious idea of Stein (Stein et al.,, 1956) and have been expanded by Koshevnik and Levit, (1976); Bickel et al., (1993) and many others. The idea is to consider one-dimensional parametric submodels containing , compute the local asymptotic minimax bound, and take the supremum over all possible submodels. More formally, let be a collection of smooth one-dimensional submodels where and is differentiable at . Then by taking the supremum over all possible submodels’ local asymptotic minimax bound, we obtain the semiparametric efficiency bound for as follows:

| (5) |

The denominator on the right-hand side is the Fisher information in the parametric submodel at . Any estimator that attains the lower bound is called semiparametrically efficient. We call the Efficient Influence Function (EIF) for estimating if an estimator is asymptotically linear with influence function , and attains the lower bound in (5). For more details on semiparametric models and asymptotic efficiency, see Chapter 25 of Van der Vaart, (2000) and references therein.

In order to compute the semiparametric efficiency bound for , we introduce some notation. Let for , and . Let be a collection of distributions such that for each there exists a unique minimizer of over , is finite and is finite and positive. Then, Proposition 2.4 shows that we can compute the semiparametric efficiency bound for in the form of a worst-case variance .

Proposition 2.4.

The semiparametric efficiency bound for relative to the paths in the model at the distribution is

In other words,

and the Efficient Influence Function of is .

We now show that is an efficient estimator for by providing an asymptotic expansion of the quantile obtained from the reweighted cumulative distribution in (2). Since the Weighted Quantile method defines the lower and upper bounds of the confidence interval in terms of the quantiles of , the expansion allows us to asymptotically analyze the interval.

Proposition 2.5.

Suppose is differentiable at with a positive derivative. Then, for any , satisfies

with .

Taking in Proposition 2.5, we obtain the following corollary:

Corollary 2.6.

is a semiparametrically efficient estimator of .

Testing procedures based on efficient estimators are asymptotically uniformly most powerful. For two-sided testing, the test is asymptotically uniformly most powerful unbiased, and inverting the test leads to an asymptotically uniformly most accurate unbiased (UMAU) confidence interval (Choi et al.,, 1996). -UMAU confidence interval for satisfies the following:

-

(i)

.

-

(ii)

for all .

-

(iii)

For any other confidence interval satisfying (i) and (ii), for all .

It turns out that the confidence interval from the Weighted Quantile method when is asymptotically uniformly most accurate unbiased.

Theorem 2.7.

Let be the output of Algorithm 1 with . Then the confidence interval is asymptotically uniformly most accurate unbiased.

3 Quantile Rejection method

Whereas the previous section provided an asymptotically valid method, in this section, we give a method valid in finite samples. This rests on distribution-free quantile inference and rejection sampling.

3.1 Distribution-free quantile inference

We begin by observing that distribution-free, finite-sample-valid, confidence intervals for any quantile of a distribution can be computed via order statistics (Noether,, 1972). To see this, suppose are i.i.d. samples from any (not necessarily continuous) and set to be the -th quantile of . Let and . Then, and where denotes the left limit of at . Note that stochastically dominates and stochastically dominates since and . We deduce that

and

where (resp. ) is the maximum (resp. minimum) index of the order statistics with the same value as . When all the ’s are distinct, and will simply be equal to . For ease of notation, define and and set

| (6) | ||||

Then, we have that the coverage of by is

| (7) |

Note that the two-sided interval asymptotically vanishes as long as and for all for some sufficiently small , or if jumps at .

We summarize the above procedure in Algorithm 2. The validity of the algorithm follows from the above argument.

-

1.

Compute the order statistics of , and set and .

-

2.

Compute (resp. ) to be the maximum (resp. minimum) index of the order statistics with the same value as for .

-

3.

Set and as in (6).

3.2 Rejection sampling strategy

Rejection sampling (Von Neumann,, 1951) is a method to obtain samples from a target distribution that is hard to sample from directly by using samples from a proposal distribution that can be sampled from more easily. Suppose the likelihood ratio of and is uniformly bounded by some constant , and that is computable. To perform rejection sampling, we begin by generating i.i.d. samples from . Then, for each sample from , we calculate . If this ratio is greater than a random sample from a uniform distribution between 0 and 1, we accept as a sample from .

In particular, we can apply rejection sampling in our setting to obtain i.i.d. samples from the shifted distribution given samples from . Since the likelihood ratio is uniformly bounded by

and is known, we can formulate Algorithm 3 as follows:

-

1.

Apply rejection sampling to the samples and obtain , which are i.i.d. samples from the target distribution .

-

2.

Apply distribution-free quantile inference on .

-

1.

Compute .

-

2.

Sample and include samples with indices obeying in .

-

3.

Take to be the -confidence interval with lower tail probability and upper tail probability using samples and Algorithm 2.

Theorem 3.1.

Proof.

The coverage statement (8) follows directly from the fact that the samples obtained from rejection sampling are i.i.d. draws from and the distribution-free quantile inference procedure has coverage guarantee as shown in (7).

The relationship implies that the interval is two-sided. The number of samples obtained from rejection sampling, that is , follows a binomial distribution , and hence goes to almost surely. Since the procedure provides a confidence interval with width converging to 0 as under the condition we assumed for , we have that the width of the algorithm converges to 0 as . ∎

Remarks

The distribution-free quantile inference procedure will usually provide coverage slightly greater than . We can make the coverage exact by adding another layer of randomness in the procedure as in Zieliński and Zieliński, (2005).

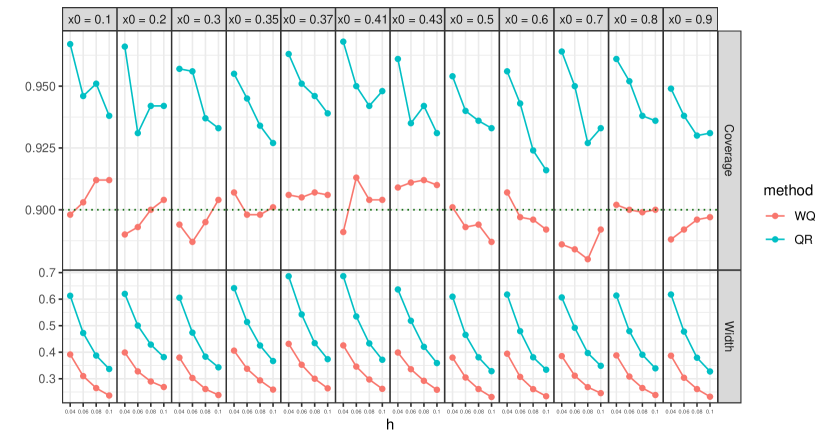

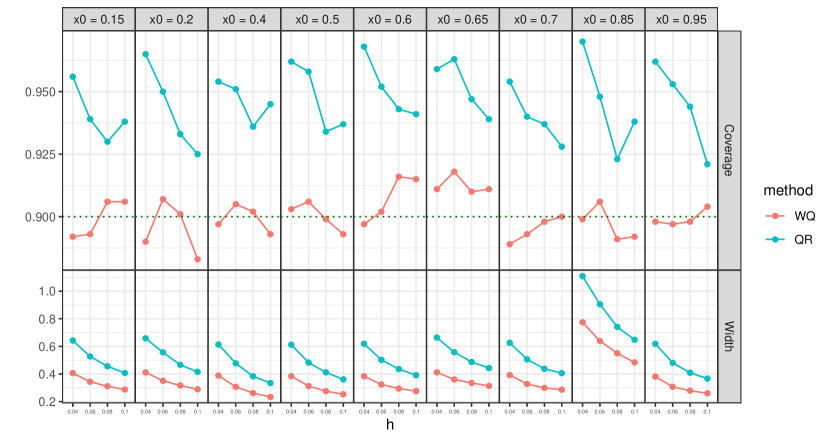

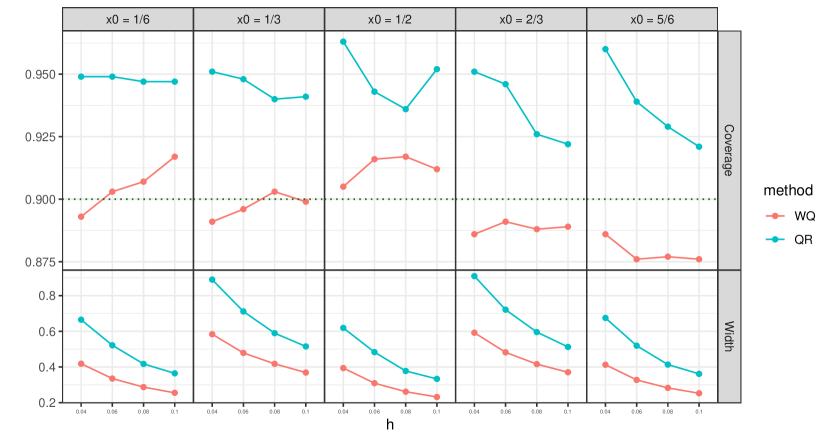

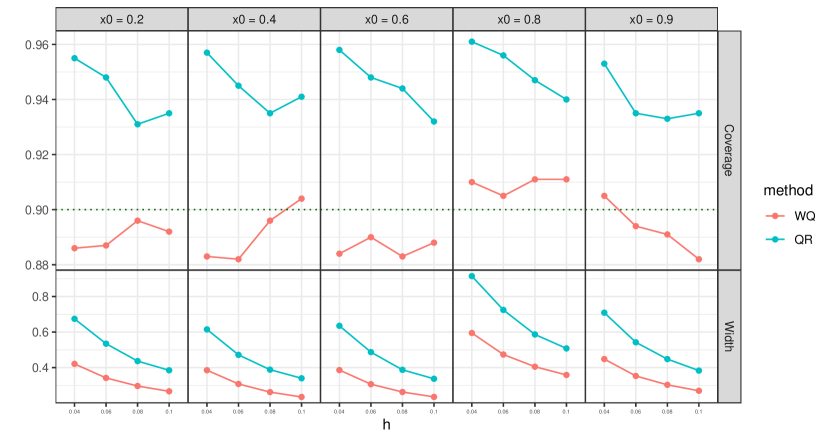

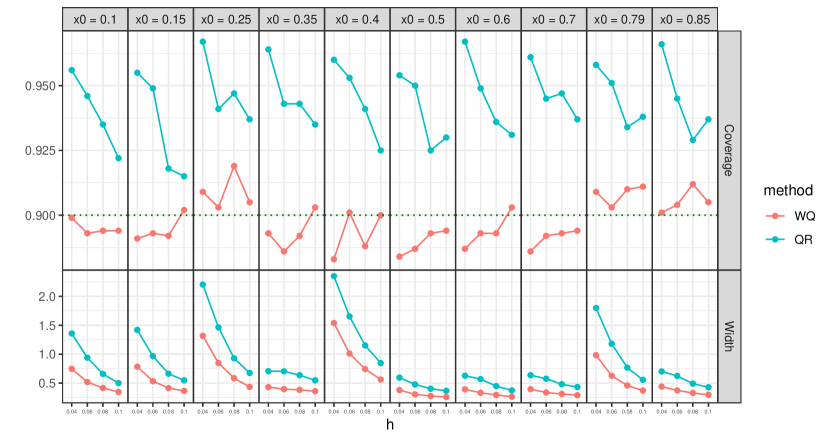

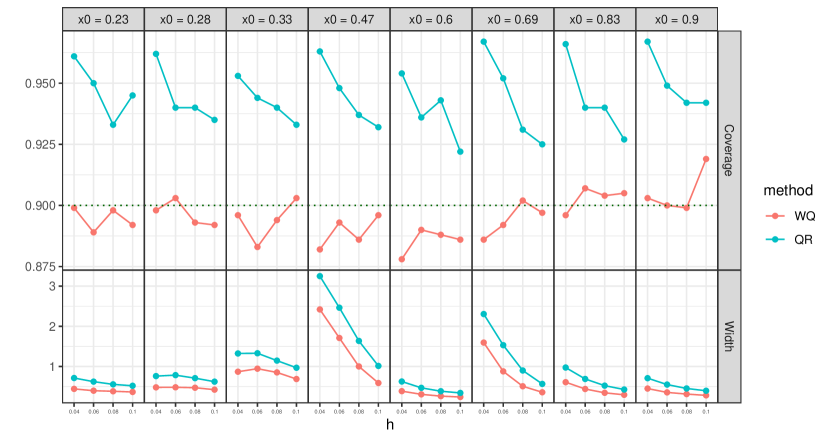

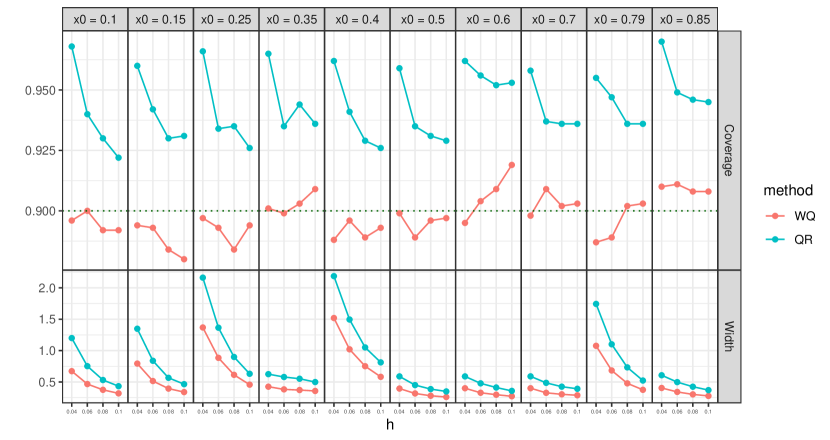

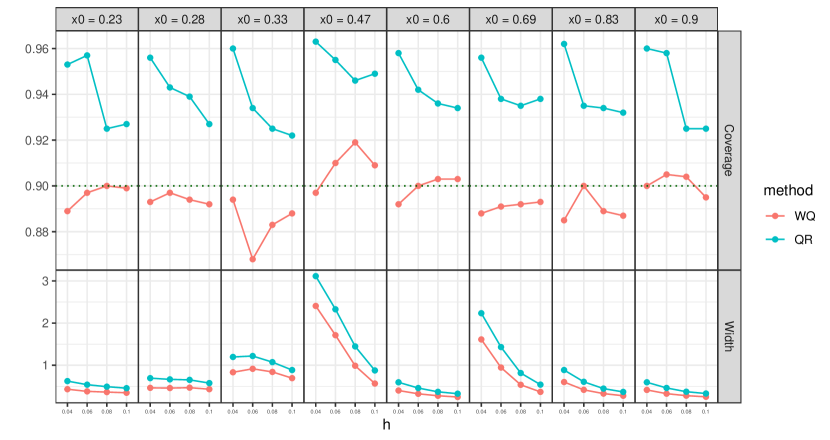

4 Numerical experiments

We examine the empirical coverage and width of the confidence intervals constructed by the Weighted Quantile and Quantile Rejection methods. We shall see that in some settings, the confidence intervals must necessarily be wide in order to be valid. Since we are posing a new inference problem, for comparing purposes, we were not able to find existing methods that achieve the same goal.

4.1 Setup

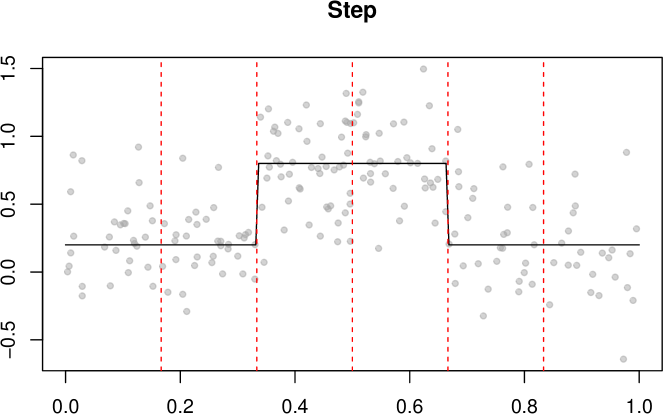

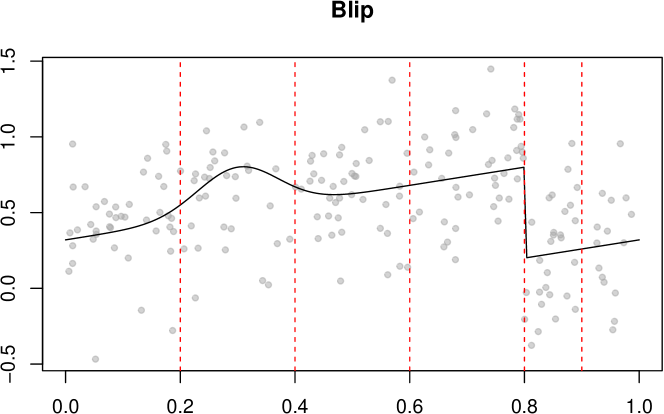

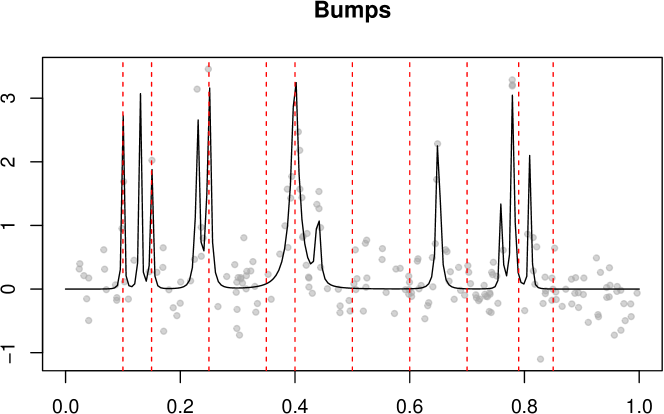

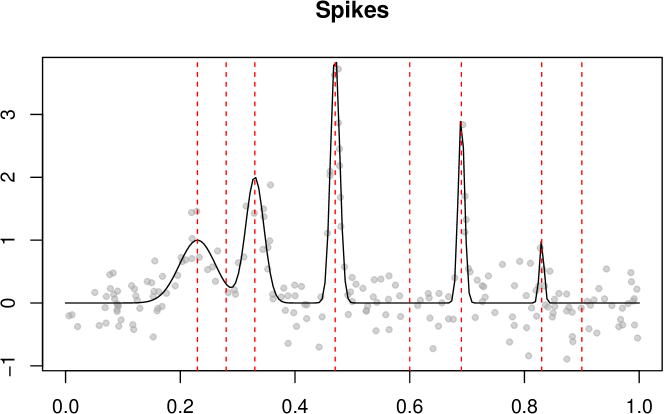

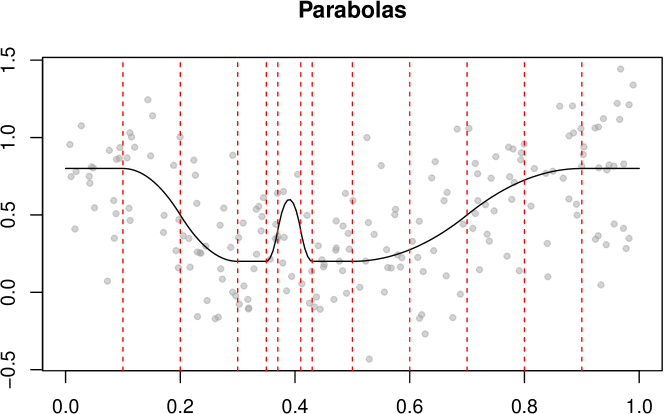

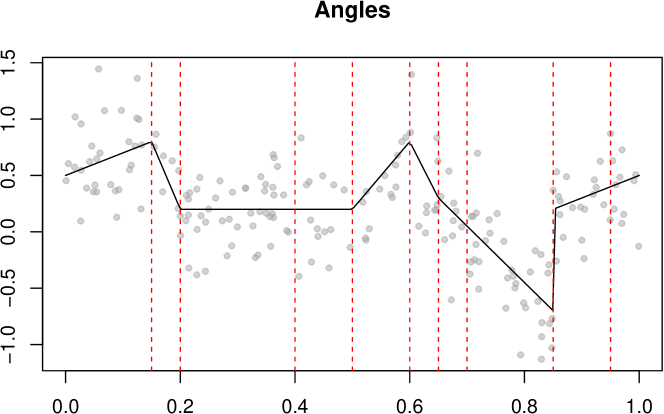

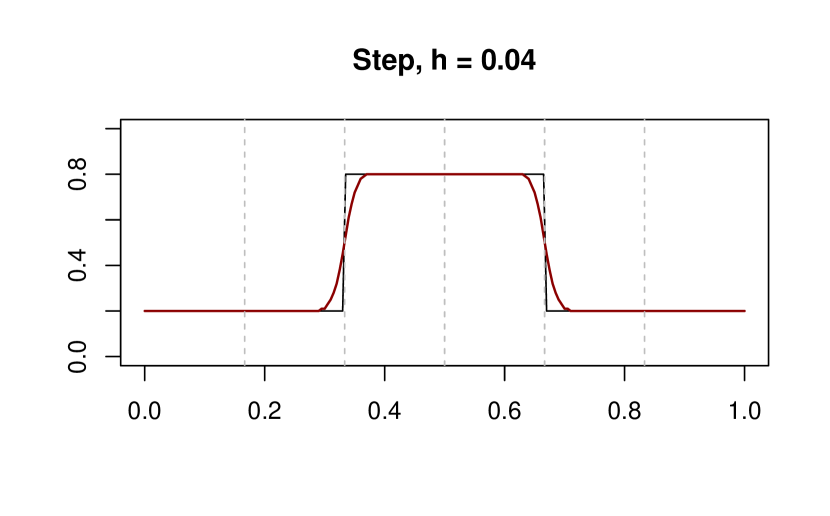

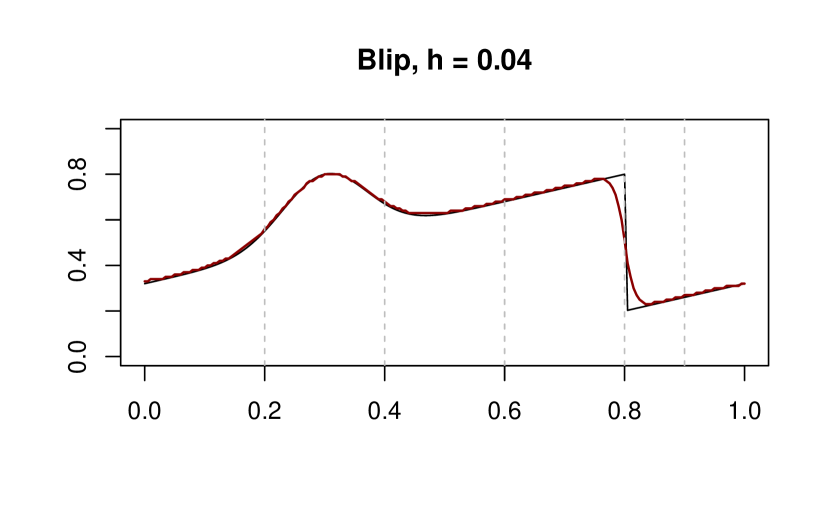

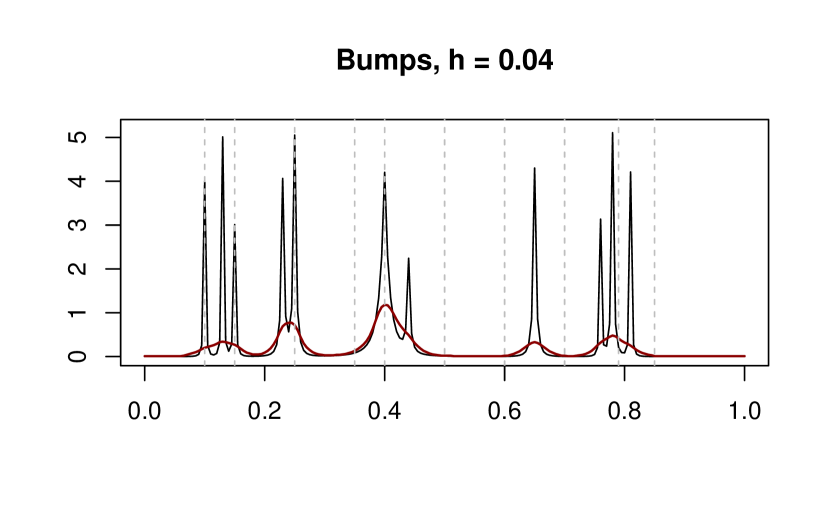

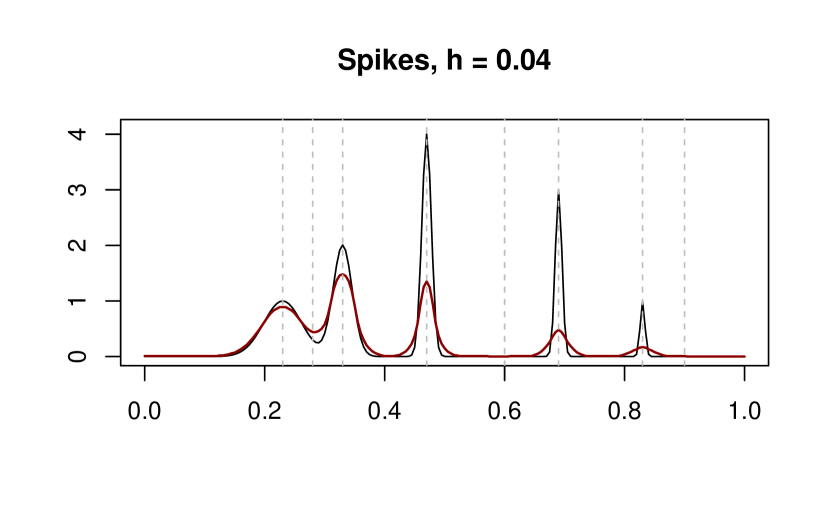

We generate i.i.d. samples with and . The regression functions are selected from a set commonly used in the nonparametric regression literature (Donoho and Johnstone,, 1994). Figure 2 illustrates these functions, and their formulas are provided in Appendix B.1.

The noise is drawn from one of the distributions specified below:

-

Sett1ng 1.

,

-

Sett2ng 2.

,

-

Sett3ng 3.

.

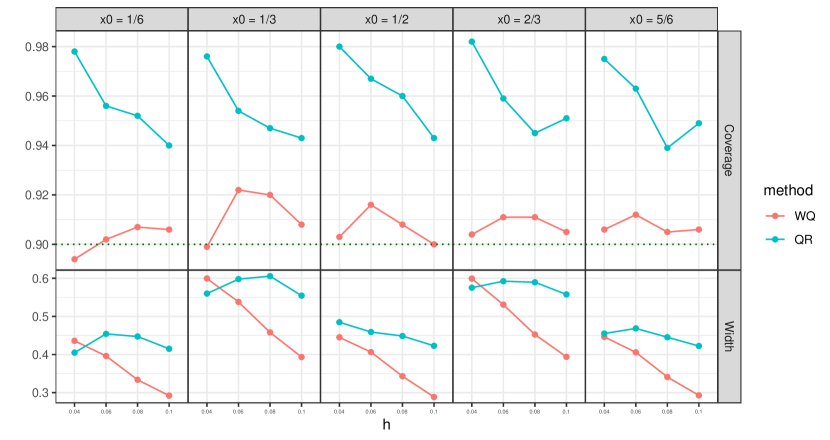

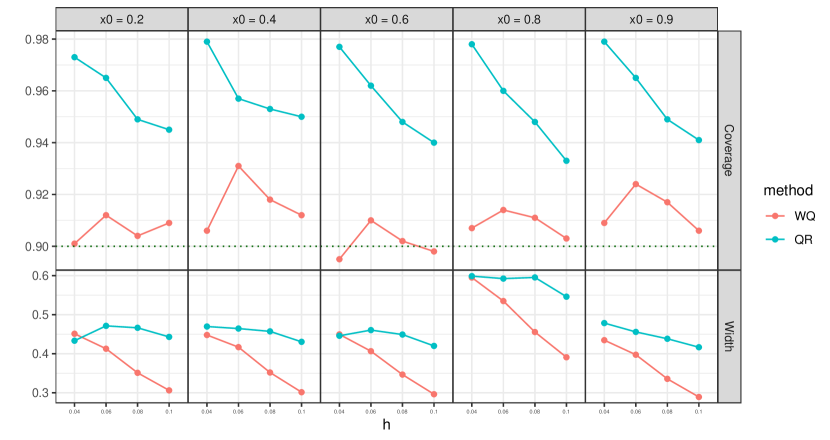

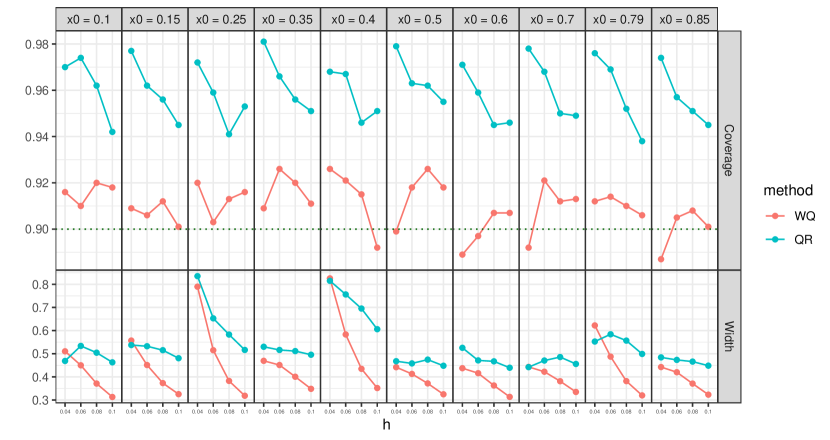

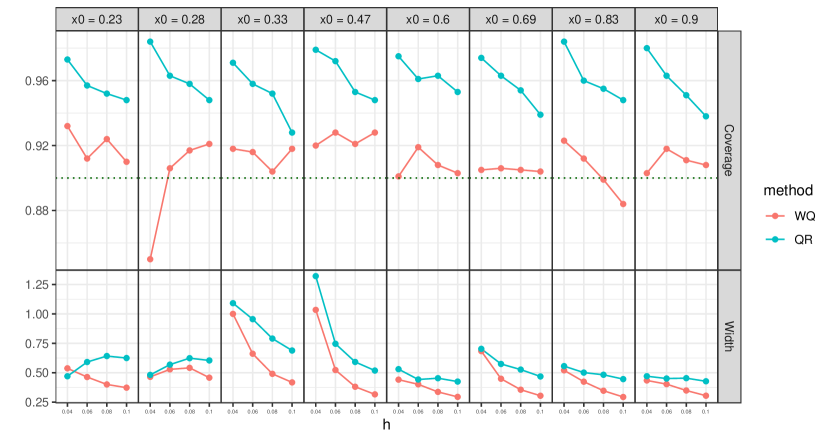

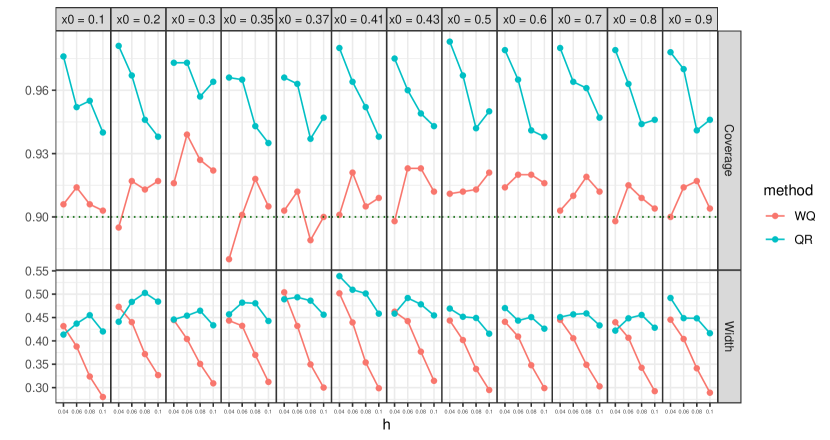

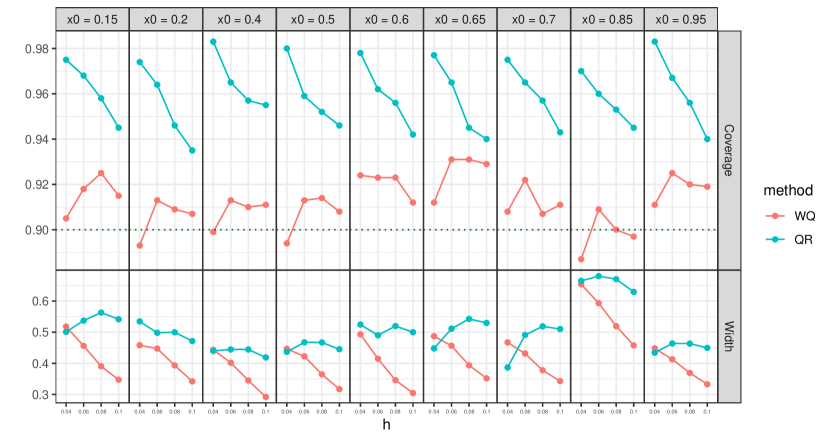

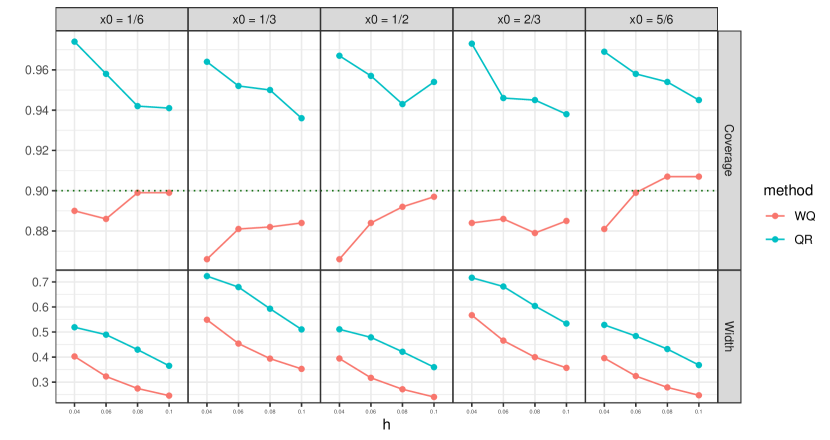

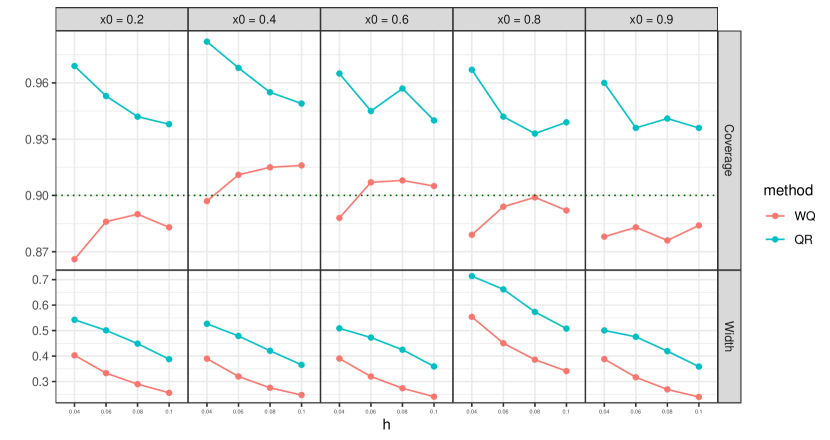

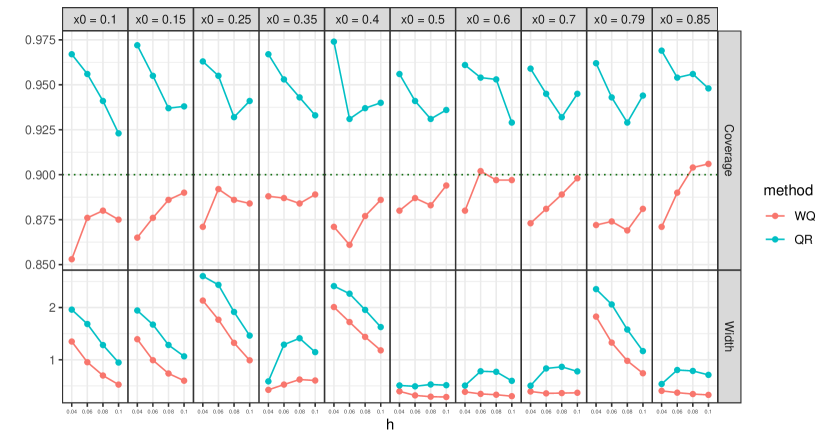

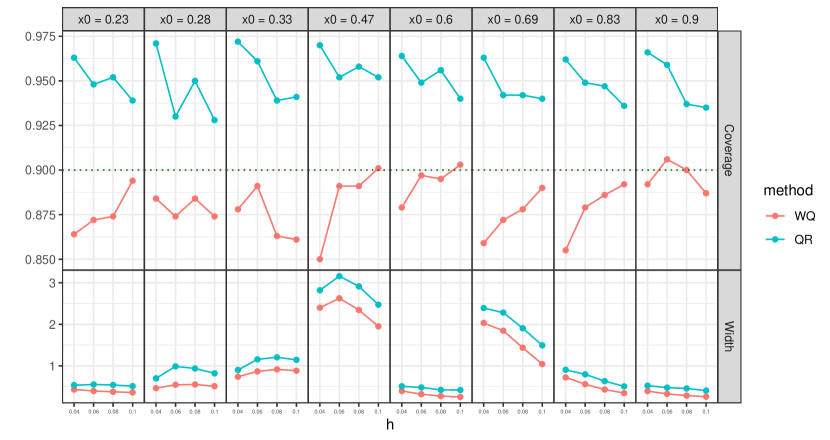

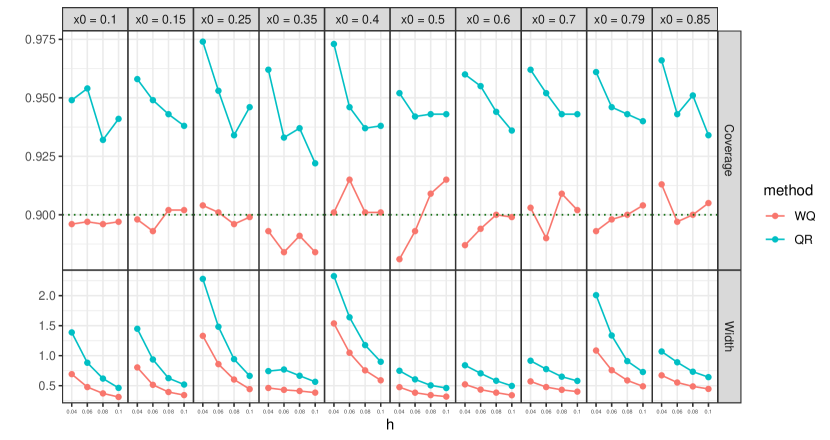

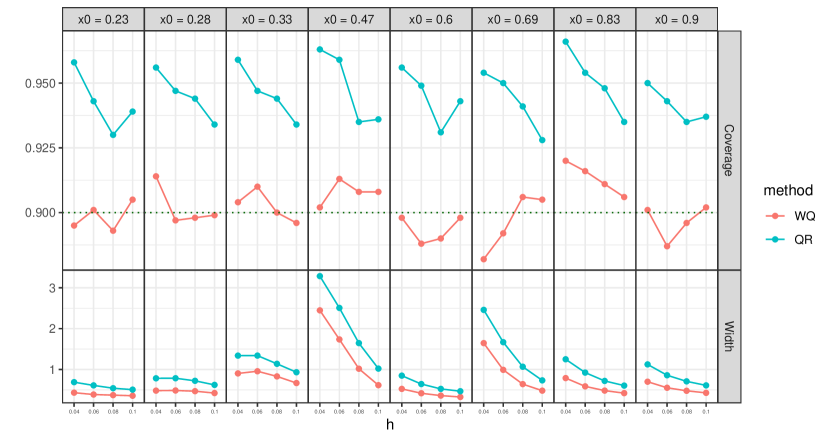

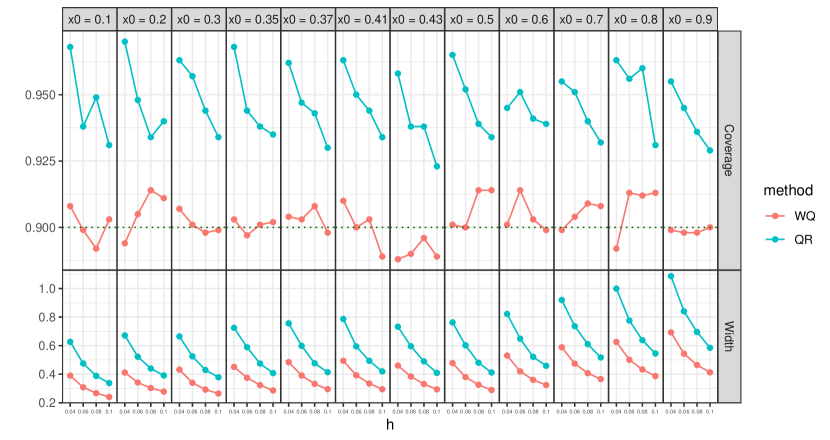

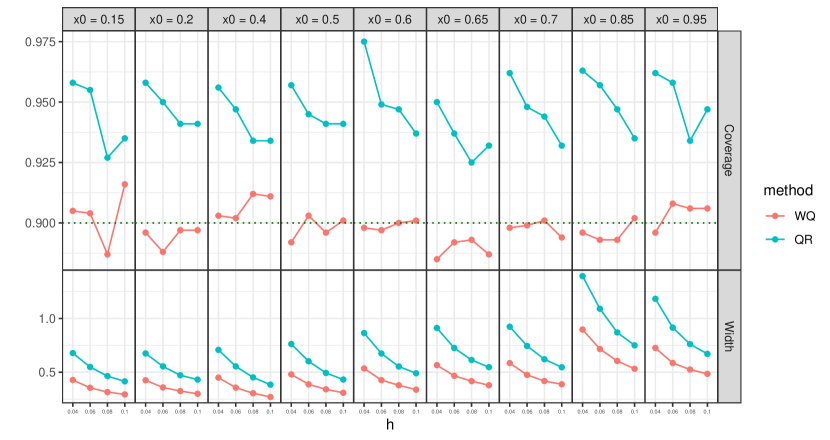

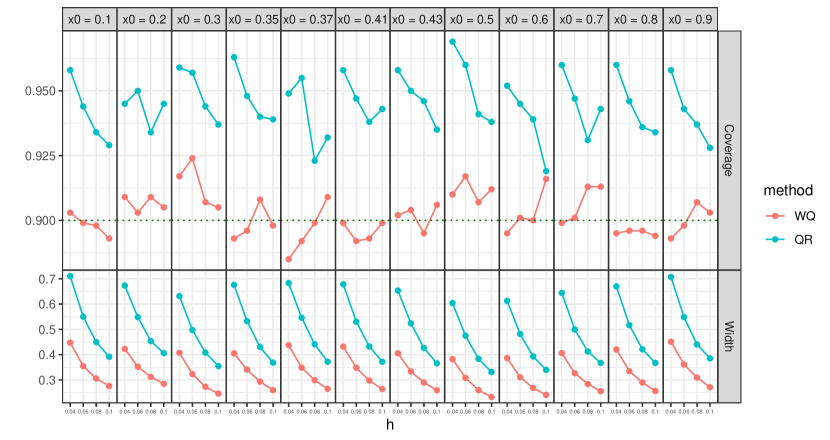

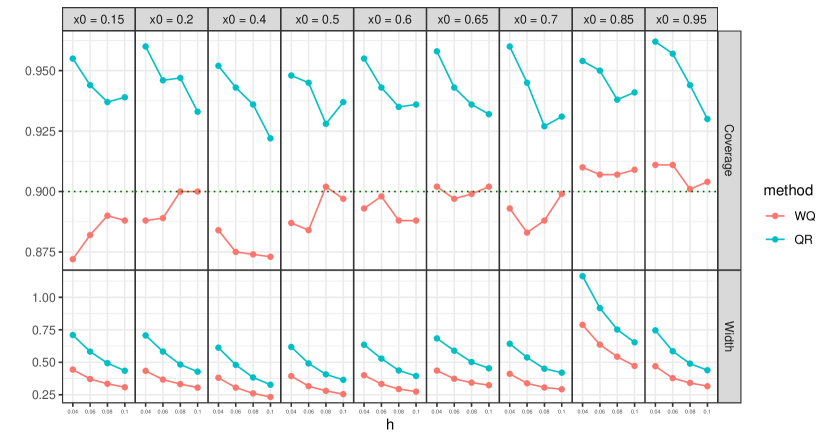

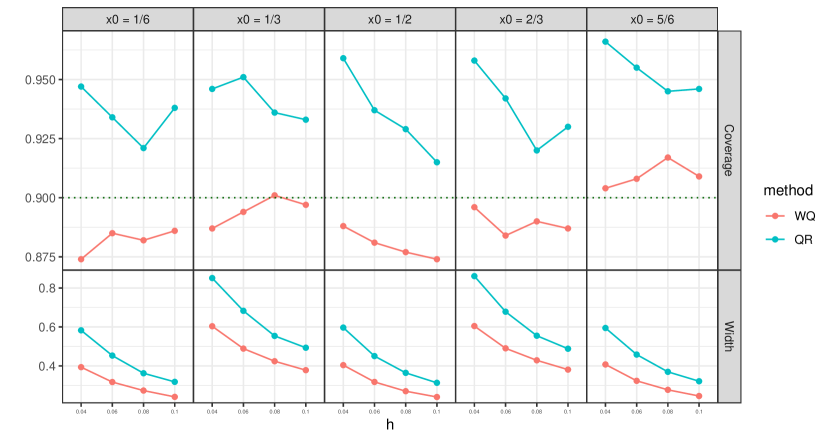

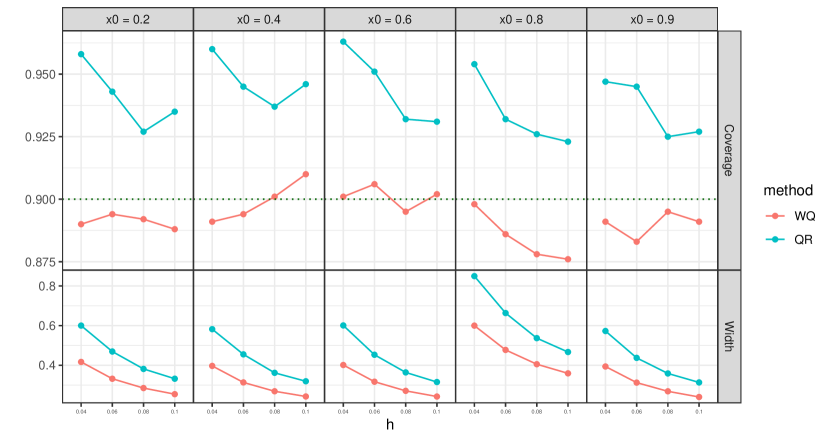

We show results for the homoscedastic case (Setting 1) in this section and present results for other settings in Appendix B.4.

The vertical dotted red lines in Figure 2 are local points where we will compute the confidence intervals. The points were chosen to include extreme points or points at which the regression function is rapidly changing.

Recall that our target depends on the kernel, bandwidth, and the quantile, which can be flexibly chosen by the user. We consider the following different settings for the target :

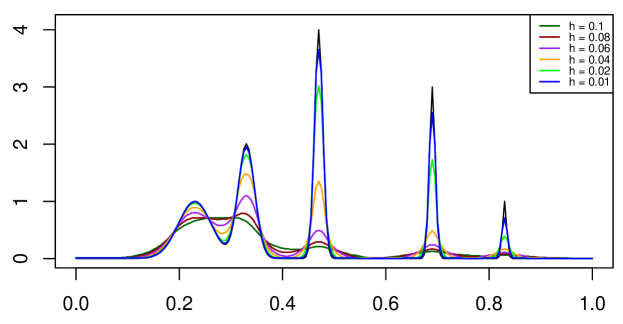

We show how the object of inference varies with when the signal is the spikes function in Figure 3 (smaller values of mean increased resolution).

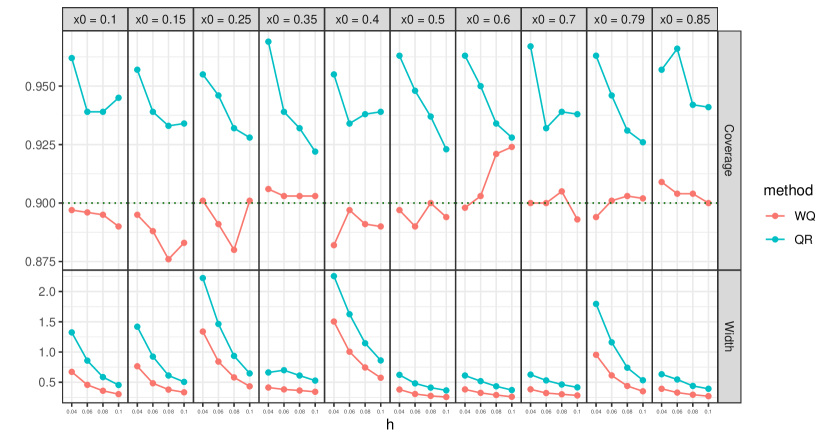

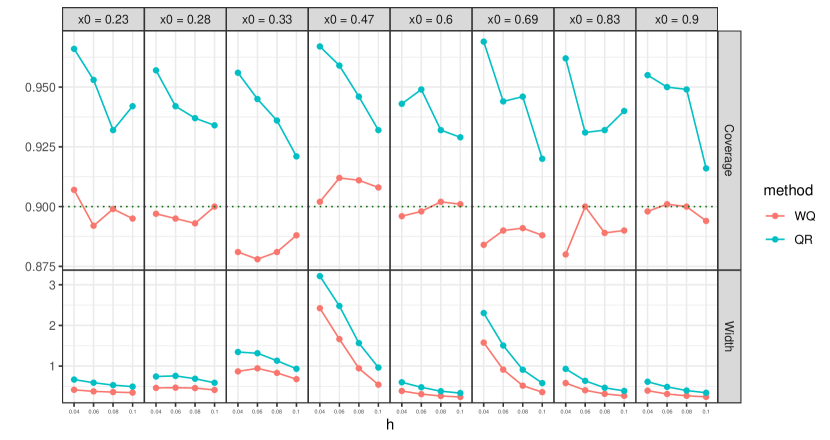

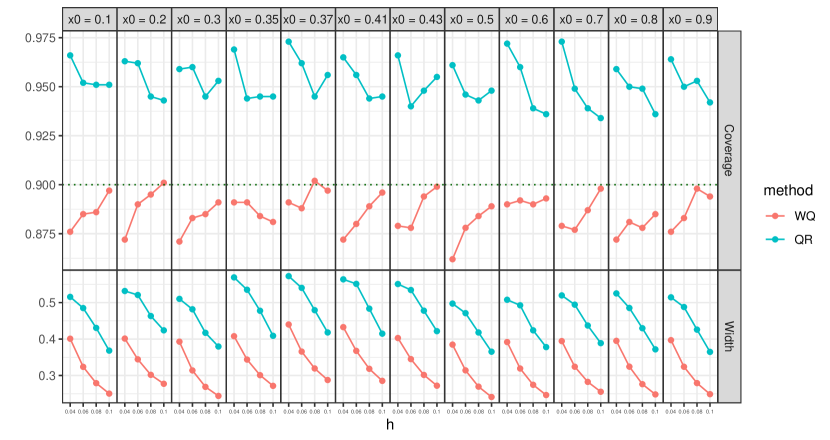

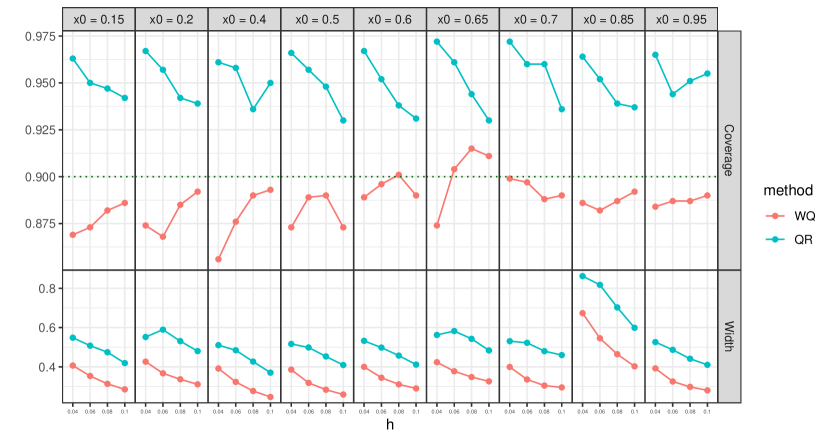

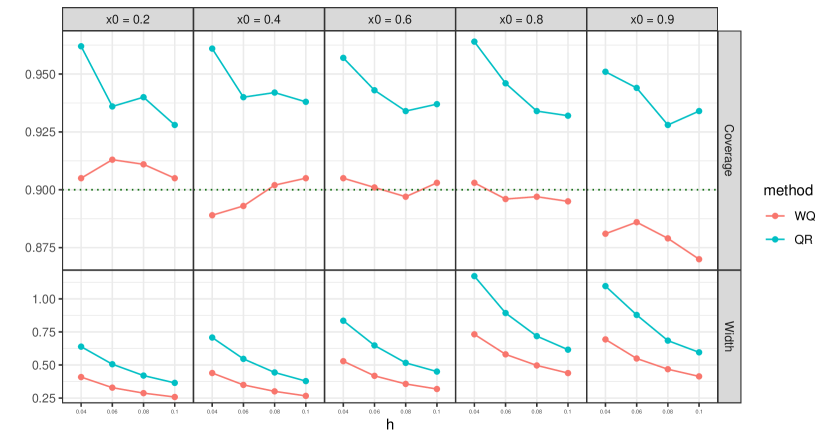

We apply the Weighted Quantile and Quantile Rejection methods with target coverage of and . For each configuration, we take the sample size to be and generate a total of datasets.

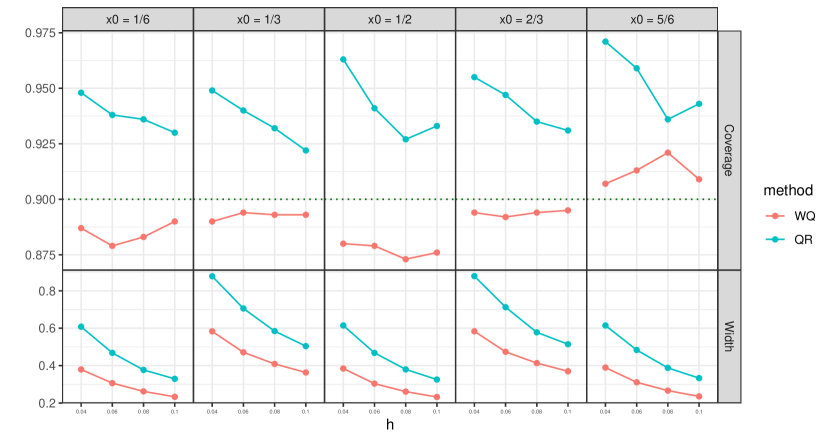

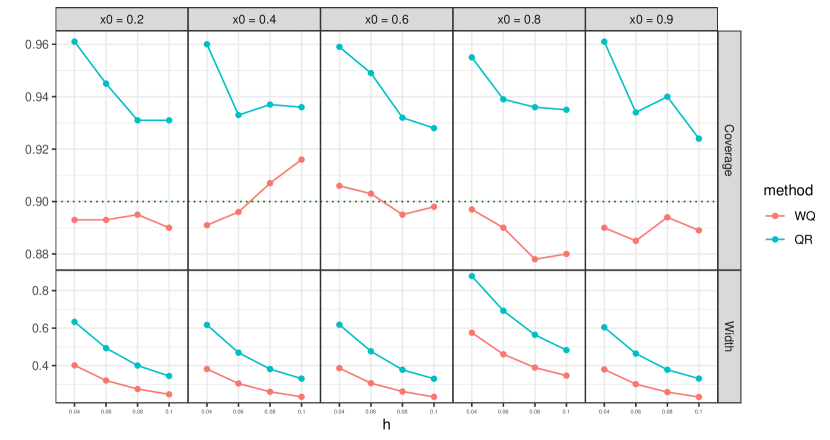

4.2 Coverage and width

Figures 4 - 5 show the average width and empirical coverage. Additional results for different signals are in Appendix B.2. We can see that both the Weighted Quantile method and Quantile Rejection method achieve 90% coverage, regardless of the underlying distribution. The Quantile Rejection method tends to overcover and has a wider average width than the Weighted Quantile method. This is because it operates on a reduced sample size. In addition, the Quantile Rejection method outputs unbounded confidence intervals when the local sample size is extremely small. For example, the confidence interval for the median when will be the real line if there are only 4 local samples. When computing the width, we take the average of the bounded confidence intervals’ width and indicate the percentage of infinite length CIs below each plot. While we have only an asymptotic guarantee for the Weighted Quantile method, the simulations show that it achieves the nominal coverage even at moderate sample sizes and points where rapid variations occur.

5 Real data examples

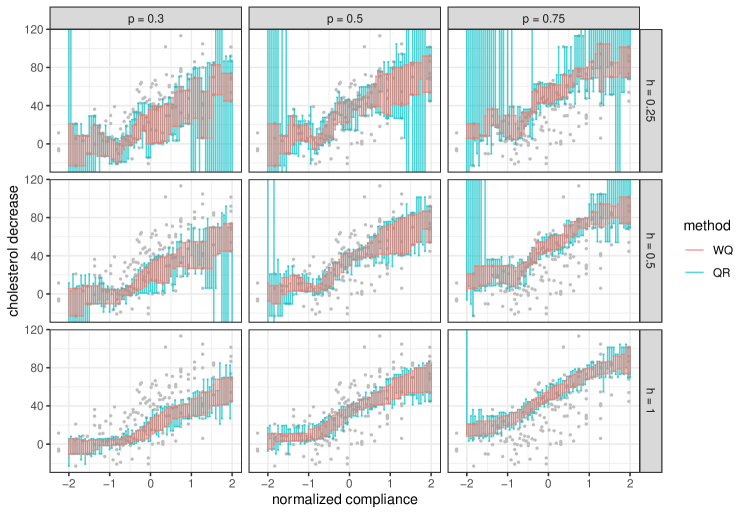

5.1 Compliance data

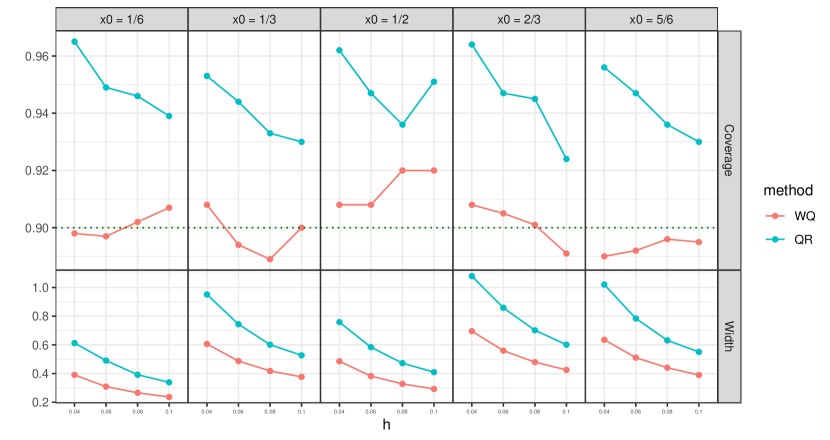

In this section, we go back to the compliance example (Efron and Feldman,, 1991) introduced in Section 1.1 and apply the Weighted Quantile and Quantile Rejection methods. We provide confidence intervals for the object of inference on a grid of ’s ranging from to and quantile values . The bandwidth is applied to the triangular kernel for . We plot the confidence intervals obtained by the two proposed methods.

We cannot verify the coverage of the confidence intervals since the true underlying distribution is unknown. However, we can say with confidence 90% that the median decrease in cholesterol level for people who comply between 45% and 55% (this corresponds to in normalized compliance) with more weights on people that comply near 50%, is in the range of 18.0 to 44.5 when we apply the Weighted Quantile method (18.0 to 47.25 for the Quantile Rejection method).

Moreover, we can observe that the confidence intervals get narrower as the bandwidth increases. This is natural since the effective sample size increases. We also see that the confidence intervals obtained from the Weighted Quantile method are narrower than those obtained from the Quantile Rejection method, as expected.

5.2 California housing data

We employ our proposed methods to obtain confidence intervals for the median housing prices of California districts, based on a modified version of the California Housing dataset. The dataset is based on the 1990 California census data and was originally obtained from the StatLib repository. The dataset contains information on the location of each census block group in California in terms of longitude and latitude along with housing characteristics such as average number of rooms and median age. We denote the variables as : median house value, : longitude, : latitude, : median housing age, and : average number of rooms.

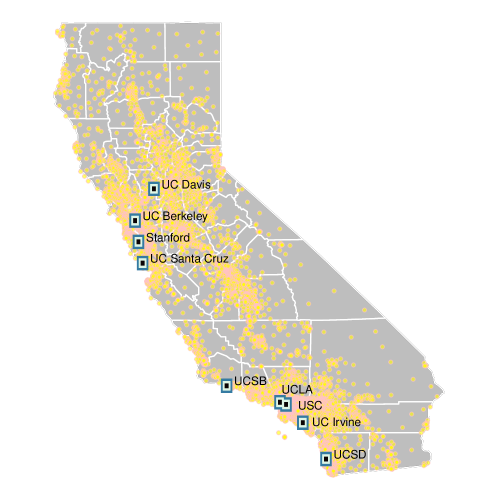

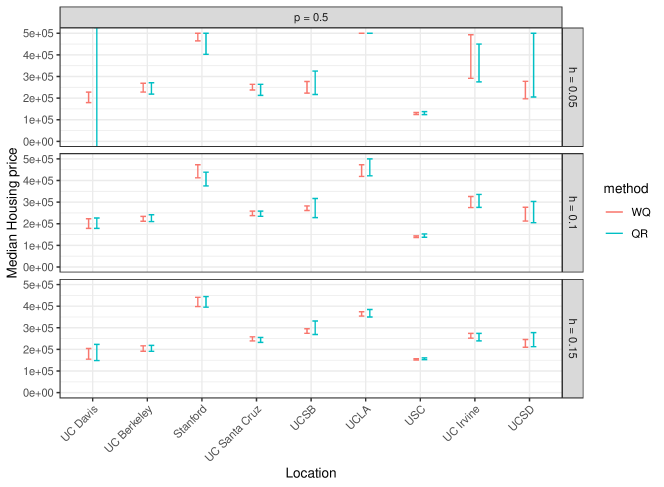

We begin by considering the local weighted quantile with longitude and latitude chosen from 9 universities in California as displayed in Figure 7. We use a triangular kernel and set the bandwidth to be for both longitude and latitude. The squares surrounding each region in Figure 7 show the local regions considered when we set to be 0.05, 0.1, and 0.15. The confidence intervals obtained from applying the Weighted Quantile and Quantile Rejection methods are plotted in Figure 8. We observe that the width of the confidence interval decreases when the bandwidth increases as effective sample size increases. Note that UCLA at has confidence interval of [500,001, 500,001]. This is because the housing price in this dataset is right-censored at $500,001 and a large proportion of the houses in this region has a value greater than k.

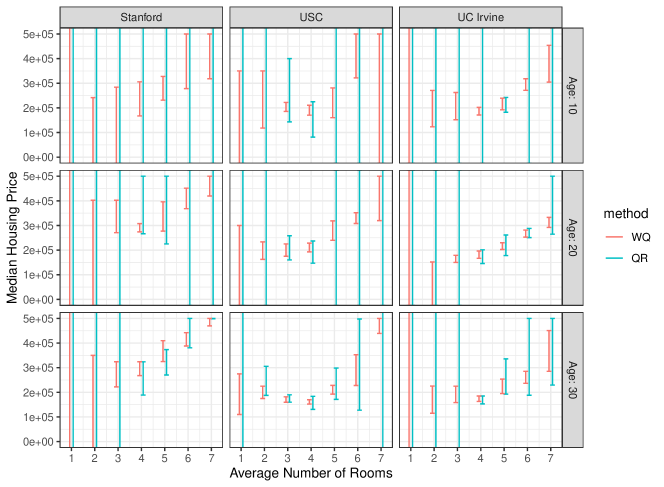

Next, we apply the method using two additional covariates: median age of houses and average number of rooms. For the median age of houses, we set the point of interest to be 10, 20, and 30 with , and for the average number of rooms, we set to be 1 to 7 with , both with the triangular kernel. For the longitude and latitude, we set to ensure sufficient samples in the region of interest. The confidence intervals obtained from applying the proposed methods in three locations (Stanford, USC, UC Irvine) are plotted in Figure 9. The confidence intervals are generally wider than those obtained using only two covariates. We observe a trend of increasing housing prices when the average number of rooms exceeds 4 in all locations. It is not evident from the confidence intervals that the age of housing has a drastic impact on house prices.

6 Indistinguishable distributions

Finally, we investigate the efficiency of the methods. We have shown in Section 2.2 that the Weighted Quantile method is unimprovable at least in a local asymptotic minimax (LAM) sense. We here demonstrate the existence of a distribution that is almost indistinguishable form the true distribution but has a significantly different value of . This implies that the confidence interval covering the target must be sufficiently wide to factor in the uncertainty.

We look at the setting where the underlying regression function is the Spikes signal with the target at and a triangular kernel with . The value of is 1.35, and in the simulation study, we have seen that with samples, the average width of the confidence interval for is 2.49.

The distribution function of the shifted distribution is

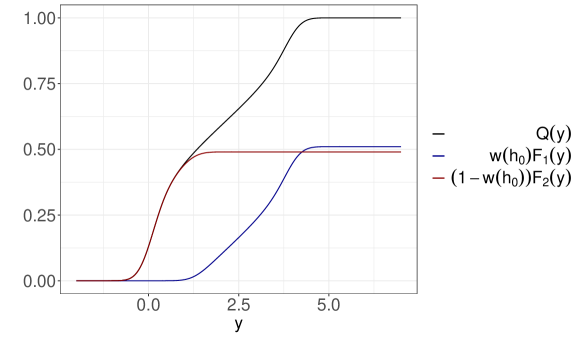

where is the density function of the Gaussian distribution with mean 0 and standard deviation , is the Spikes signal, and . Figure 10 shows the cdf of .

Our goal is to find a distribution that is very close to in the sense that it is almost indistinguishable with samples. Note that depends only on values of in the range . Therefore, we take to be equal to when . Now, we decompose into two parts according to whether or not. We view as a mixture of two distribution functions and :

where

Figure 10 shows the mixture components in the case where .

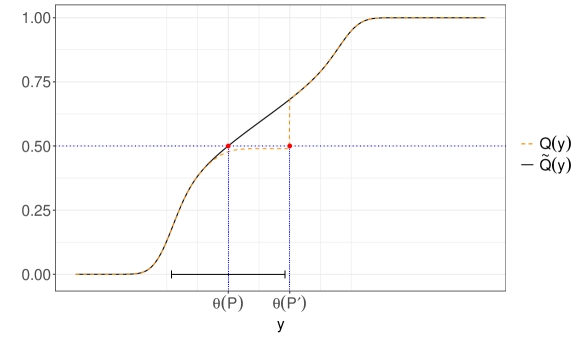

The idea is to modify the distribution of when . Thinking in terms of the mixture components, we find a distribution function so that and . can be any distribution since we are in a distribution-free setting. Say we want . Define by moving the mass of such that to so that . Figure 11 plots and and marks and .

Note that can be constructed from with and

In this case,

When , we have . This implies that and are nearly indistinguishable from 200 random samples. However, our value of differs by more than half the confidence interval width of which is 1.245. Therefore, we can see that our method is not conservative but actually reflects the necessary uncertainty since nothing is assumed about the underlying distribution.

7 Discussion

This paper challenges the traditional inference targets such as the conditional mean and quantile, by pointing out the ambiguity of the notion of conditional distribution of a response variable given a covariate being equal to some specific value. Instead, we propose a new object of inference that allows us to gain a localized understanding of the outcome, with the level of resolution being flexible and determined by the user’s needs. Our approach yields reliable and easily computable confidence intervals without hidden constants.

A finite-sample valid confidence interval for the univariate mean that is asymptotically efficient can be constructed when the distribution is supported on a compact set (Romano and Wolf,, 2000). We leave it as future work to investigate if the Quantile Rejection method which is finite-sample valid is also efficient. If not, it is of interest to see if this gap can be reduced or if it is theoretically impossible to obtain finite-sample validity without loss of efficiency.

Acknowledgments

J.J. would like to thank Sky Cao, Isaac Gibbs, Kevin Guo, Ying Jin and Chiara Sabatti for helpful discussions and feedback. J.J. was partly supported by ILJU Academy and Culture Foundation and a Ric Weiland Graduate Fellowship. E.C. was supported by the Office of Naval Research grant N00014-20-1-2157, the National Science Foundation grant DMS-2032014, the Simons Foundation under award 814641, and the ARO grant 2003514594.

Appendix A Deferred proofs

Lemma A.1 (Lehmann et al., (2005) Lemma 11.3.3).

Let be i.i.d. with mean 0 and finite variance . Let be a sequence of constants. If , then .

Lemma A.2 (Lemma in David and Nagaraja, (2004) Section 10.2).

Let , and be two sequences of random variables such that

-

1.

,

-

2.

for every and every ,

-

(a)

,

-

(b)

.

-

(a)

Then, .

Proof.

Proof in p.286 of David and Nagaraja, (2004). ∎

A.1 Proof of Lemma 2.1

-

(a)

Right continuity holds since are right continuous functions and ’s are non-negative with their sum being strictly positive. Monotonicity holds by the construction of .

-

(b)

Let be the estimator of that is not normalized by , but has weights that are exactly the likelihood ratio of and . We first show that

as . Note that is an unbiased estimator of since

Thus, and it suffices to show that to show that .We have that

So, we are left to show that for any ,

(9) Let and . Then,

for . We have that converges to 0 since and converges to 0 as by the differentiability of at and both and converges to .

We have shown (b) for rather than . Since , it suffices to show that

(10) We have

Moreover,

and since , we have

and obtain (10).

-

(c)

Applying the multivariate central limit theorem to the sum of ’s, we obtain

We can rewrite as

Then, for function which is differentiable at , we can apply the delta method and get

for . Since , we have

and , since .

A.2 Proof of Proposition 2.2

Note that using Slutsky’s theorem and (c) of Lemma 2.1, we have

as for . Similar calculations on the upper bound gives the desired result.

A.3 Proof of Theorem 2.3

It suffices to show that

as it will imply that the and in Step 5 of Algorithm 1 satisfies (4) by Slutsky’s theorem and continuous mapping theorem.

First, the denominator converges in probability to a positive value. By law of large numbers and continuous mapping theorem, as the kernel is uniformly bounded. For the numerator, if suffices to show that

Denote and . Then, we need to show that for . Say the kernel is uniformly bounded by some constant . For some , there exists such that

| (11) |

since is differentiable at . Note that

| (12) | ||||

| (13) |

For the second term in (13),

as by the consistency of from Proposition 2.5. Since is monotone increasing, if ,

Therefore, we can bound the first term (12) by

| (14) | ||||

| (15) |

Using the triangular inequality, (14) is bounded by

Now, note that

and so

which converges to 0 as since by the weak law of large numbers. Analogous to the above argument, (15) converges to 0. Therefore, we have .

A.4 Proof of Proposition 2.4

Semiparametric efficient bound for M-estimators can be computed using results from Newey, (1990). The Efficient Influence Function (EIF) for estimating is

for . So, the semiparametric efficiency bound for estimating is . Note that

and

Also,

and so

We proved the equality of the numerator. Now, note that

and hence

Therefore, we have .

A.5 Proof of Proposition 2.5

Let , , and . Then, , and it suffices to show that satisfies the conditions of Lemma A.2. First, we have that is by Lemma 2.1 (c). For , note that

where and . Using differentiability of at , we have that

where the last equality follows from . For any , there exists some such that for all . Then, for ,

| (16) |

Note that

by Lemma 2.1 (b) using the fact that . Using and (16), we get that as , and we have verified the first condition of (b) in Lemma A.2. The second condition of (b) can be proved similarly. Now, applying Lemma A.2, .

A.6 Proof of Corollary 2.6

A.7 Proof of Theorem 2.7

From Theorem 2 of Choi et al., (1996), we know that is an asymptotically uniformly most accurate unbiased confidence interval up to equivalence where is a consistent estimator of . In the proof of Theorem 2.3, we have shown that the quantiles and obey equation (4). In particular, the quantiles are away from . Thus, we can apply Proposition 2.5 to each quantile when and obtain

Hence, we can see that the confidence interval from the weighted quantile method is equivalent to and is asymptotically uniformly most accurate unbiased.

Appendix B Additional numerical studies

In this section, we provide additional details on the simulation studies and the deferred results for the simulation studies conducted in different settings.

B.1 Regression functions

-

1.

Step

-

2.

-

3.

Spikes

-

4.

Bumps

for

-

5.

Parabolas

where .

-

6.

Angles

Figure 12 shows as a function of for a triangular kernel for which .

B.2 Additional results from Setting 1

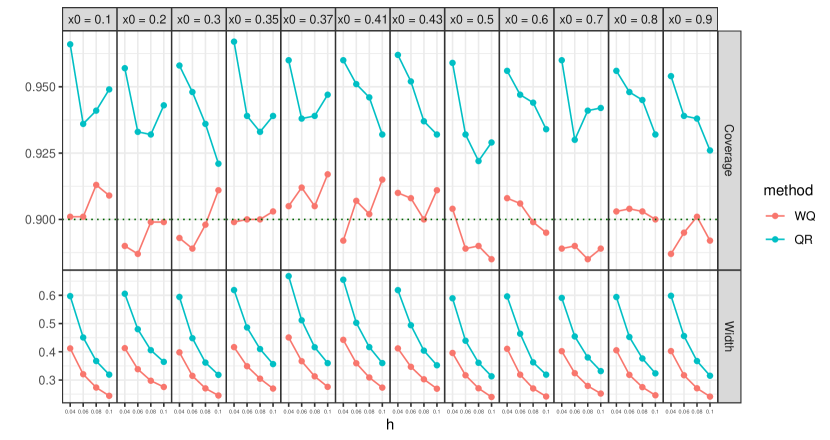

B.3 Different quantiles

In this section, we show the empirical width and coverage using the proposed method for when and with the triangular kernel.

B.3.1

B.3.2

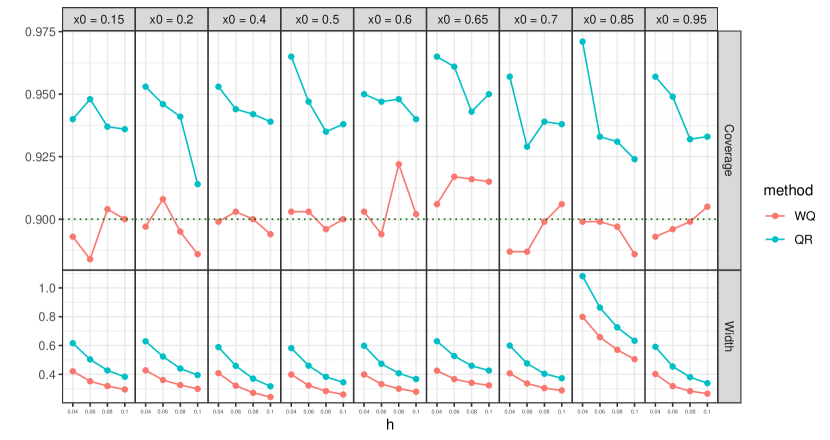

B.4 Heteroscedastic case

In this section, we show the empirical width and coverage using the proposed method for when the noise distribution is heteroscedastic with the triangular kernel.

B.4.1 Setting 2

We consider the setting where the noise distribution is .

B.4.2 Setting 3

We consider the setting where the noise distribution is .

B.5 Biweight kernel

In this section, we show the empirical width and coverage using the proposed method for with the biweight kernel.

References

- Armstrong and Kolesár, (2018) Armstrong, T. B. and Kolesár, M. (2018). Optimal inference in a class of regression models. Econometrica, 86(2):655–683.

- Bahadur and Savage, (1956) Bahadur, R. R. and Savage, L. J. (1956). The nonexistence of certain statistical procedures in nonparametric problems. The Annals of Mathematical Statistics, 27(4):1115–1122.

- Barber, (2020) Barber, R. F. (2020). Is distribution-free inference possible for binary regression? Electron. J. Statist., 14(2):3487–3524.

- Bickel et al., (1993) Bickel, P. J., Klaassen, C. A., Bickel, P. J., Ritov, Y., Klaassen, J., Wellner, J. A., and Ritov, Y. (1993). Efficient and adaptive estimation for semiparametric models, volume 4. Springer.

- Chaudhuri and Marron, (2000) Chaudhuri, P. and Marron, J. S. (2000). Scale space view of curve estimation. Annals of Statistics, pages 408–428.

- Choi et al., (1996) Choi, S., Hall, W. J., and Schick, A. (1996). Asymptotically uniformly most powerful tests in parametric and semiparametric models. The Annals of Statistics, 24(2):841–861.

- David and Nagaraja, (2004) David, H. A. and Nagaraja, H. N. (2004). Order statistics. John Wiley & Sons.

- Donoho, (1988) Donoho, D. L. (1988). One-Sided Inference about Functionals of a Density. The Annals of Statistics, 16(4):1390 – 1420.

- Donoho and Johnstone, (1994) Donoho, D. L. and Johnstone, J. M. (1994). Ideal spatial adaptation by wavelet shrinkage. biometrika, 81(3):425–455.

- Efron and Feldman, (1991) Efron, B. and Feldman, D. (1991). Compliance as an explanatory variable in clinical trials. Journal of the American Statistical Association, 86(413):9–17.

- Giné and Nickl, (2021) Giné, E. and Nickl, R. (2021). Mathematical foundations of infinite-dimensional statistical models. Cambridge university press.

- Koshevnik and Levit, (1976) Koshevnik, Y. A. and Levit, B. Y. (1976). On a non-parametric analogue of the information matrix. Teoriya Veroyatnostei i ee Primeneniya, 21(4):759–774.

- Lee and Barber, (2021) Lee, Y. and Barber, R. (2021). Distribution-free inference for regression: discrete, continuous, and in between. Advances in Neural Information Processing Systems, 34.

- Lehmann et al., (2005) Lehmann, E. L., Romano, J. P., and Casella, G. (2005). Testing statistical hypotheses, volume 3. Springer.

- Lei and Wasserman, (2014) Lei, J. and Wasserman, L. (2014). Distribution-free prediction bands for non-parametric regression. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):71–96.

- Low, (1997) Low, M. G. (1997). On nonparametric confidence intervals. Ann. Statist., 25(6):2547–2554.

- Medarametla and Candès, (2021) Medarametla, D. and Candès, E. (2021). Distribution-free conditional median inference.

- Newey, (1990) Newey, W. K. (1990). Semiparametric efficiency bounds. Journal of applied econometrics, 5(2):99–135.

- Noether, (1972) Noether, G. E. (1972). Distribution-free confidence intervals. The American Statistician, 26(1):39–41.

- Romano and Wolf, (2000) Romano, J. P. and Wolf, M. (2000). Finite sample nonparametric inference and large sample efficiency. Annals of Statistics, pages 756–778.

- Stein et al., (1956) Stein, C. et al. (1956). Efficient nonparametric testing and estimation. In Proceedings of the third Berkeley symposium on mathematical statistics and probability, volume 1, pages 187–195.

- Tibshirani et al., (2019) Tibshirani, R. J., Foygel Barber, R., Candes, E., and Ramdas, A. (2019). Conformal prediction under covariate shift. Advances in neural information processing systems, 32.

- Tsybakov, (2008) Tsybakov, A. B. (2008). Introduction to Nonparametric Estimation. Springer Publishing Company, Incorporated, 1st edition.

- Van der Vaart, (2000) Van der Vaart, A. W. (2000). Asymptotic statistics, volume 3. Cambridge university press.

- Von Neumann, (1951) Von Neumann, J. (1951). 13. various techniques used in connection with random digits. Appl. Math Ser, 12(36-38):3.

- Vovk, (2012) Vovk, V. (2012). Conditional validity of inductive conformal predictors. In Asian conference on machine learning, pages 475–490. PMLR.

- Vovk et al., (2005) Vovk, V., Gammerman, A., and Shafer, G. (2005). Algorithmic learning in a random world. Springer Science & Business Media.

- Vovk and Wang, (2020) Vovk, V. and Wang, R. (2020). Combining p-values via averaging. Biometrika, 107(4):791–808.

- Wasserman, (2006) Wasserman, L. (2006). All of nonparametric statistics. Springer Science & Business Media.

- Zieliński and Zieliński, (2005) Zieliński, R. and Zieliński, W. (2005). Best exact nonparametric confidence intervals for quantiles. Statistics, 39(1):67–71.