Decentralized Decision-Making in Retail Chains:

Evidence from Inventory Management††thanks: We are grateful for the valuable comments received from Heski Bar-Isaac, Loren Brandt, Avi Goldfarb, Jiaying Gu, George Hall, Jordi Mondria, Bob Miller, John Rust, Steven Stern, Junichi Suzuki, and Kosuke Uetake, as well as from seminar participants at Cambridge, Stony Brook, Toronto, UBC-Sauder, EARIE conference, IIOC conference, CEA conference, and the Georgetown conference honoring John Rust. The data used in this paper was obtained through a request made under the Canadian Access to Information Act. We sincerely appreciate the generous assistance provided by LCBO personnel.

Abstract

This paper investigates the impact of decentralizing inventory decision-making in multi-establishment firms using data from a large retail chain. Analyzing two years of daily data, we find significant heterogeneity among the inventory decisions made by 634 store managers. By estimating a dynamic structural model, we reveal substantial heterogeneity in managers’ perceived costs. Moreover, we observe a correlation between the variance of these perceptions and managers’ education and experience. Counterfactual experiments show that centralized inventory management reduces costs by eliminating the impact of managers’ skill heterogeneity. However, these benefits are offset by the negative impact of delayed demand information.

Keywords: Inventory management; Dynamic structural model; Decentralization; Information processing in organizations; Retail chains; Managerial skills; Store managers.

JEL codes: D22, D25, D84, L22, L81.

1 Introduction

Multi-establishment firms can adopt various decision-making structures ranging from centralized decisions at the headquarters to a more decentralized approach where decision authority is delegated to individual establishments. Determining the optimal decision-making process for a firm involves weighing different trade-offs. A decentralized decision-making structure empowers local managers to leverage valuable information specific to their respective stores. This information, which may be difficult or time-consuming to communicate to headquarters, can be utilized effectively at the local level. However, decentralization also entails granting autonomy to heterogeneous managers who possess varied skills. This heterogeneity can lead to suboptimal outcomes for the overall firm. When determining the degree of decentralization in their decision-making structure, multi-establishment firms must evaluate this trade-off. They need to consider the benefits of local knowledge and timely decision-making against the potential challenges posed by managerial heterogeneity.

In this study, we investigate the inventory management decisions made by store managers at the Liquor Control Board of Ontario (LCBO) and examine the impact on the firm’s performance of delegating these decisions to the store level. The LCBO is a provincial government enterprise responsible for alcohol sales throughout Ontario. As a decentralized retail chain, each store has a degree of autonomy in its decision-making process. Specifically, store managers have discretion in two key areas of inventory management: assortment decisions (i.e., determining which products to offer) and replenishment decisions (i.e., when and how much to order for each product). Replenishment decisions involve forming expectations about future demand to determine the optimal order quantity and timing. To conduct our analysis, we utilize a comprehensive dataset obtained from the LCBO, encompassing daily information on inventories, orders, sales, stockouts, and prices for every store and product (SKU) from October 2011 to October 2013 (677 working days).333These data were obtained under the Access to Information Act, with assistance from the LCBO personnel. Additionally, we supplement our main dataset with information from LCBO reports and gather data on store managers’ education and experience from professional networking platforms such as LinkedIn.

The LCBO data and framework provide a unique setting to study inventory management due to the simple pricing mechanism employed, where prices are set as a fixed markup over wholesale cost. This feature of the market allows us to focus specifically on the inventory setting problem without the need to incorporate a model where equilibrium prices are explicitly determined by inventory decisions. By abstracting from the complex relationship between prices and inventory decisions, we can concentrate our analysis on understanding the factors influencing inventory management within the LCBO retail chain.

By employing descriptive evidence and the estimation of reduced-form models of inventory decision rules, we first show substantial heterogeneity across store managers’ replenishment decisions. Observable store characteristics – such as demand level, size, category, and geographic location – explain less than half of the differences across store managers in their inventory decision rules.

To gain a deeper understanding of the factors contributing to this heterogeneity, we propose and estimate a dynamic structural model of inventory management. The model allows for differences across stores in demand, storage costs, stockout costs, and ordering costs. Leveraging the high-frequency nature of the daily data, we obtain precise estimates of holding cost, stockout cost, and ordering costs at both the individual product (SKU) and store levels. Our findings reveal significant heterogeneity across stores in all the revealed-preference cost parameters. Remarkably, observable store characteristics only account for less than of this heterogeneity. Furthermore, we uncover a correlation between the remaining heterogeneity and managers’ education and experience, suggesting that manager characteristics contribute to this residual variation. We interpret this unexplained heterogeneity as the result of local managers’ idiosyncratic perceptions regarding store-level costs.

Using the estimated structural model, we quantify the impact of store manager heterogeneity on inventory outcomes. Overall, eliminating the idiosyncratic heterogeneity in cost parameters produces significant effects on inventory management. Specifically, we observe a -day increase in the waiting time between orders, a decrease in the average order amount equivalent to days of average sales, and a reduction in the inventory-to-sales ratio. However, the frequency of stockouts remains largely unaffected. These findings indicate that if the idiosyncratic component of costs represents a biased perception by store managers, it has a substantial negative impact on the firm’s profitability. This is due to increased storage and ordering costs while having little effect on stockouts and revenue generation.

Finally, we conduct an evaluation of the effects associated with centralizing the decision-making of inventory management at the LCBO headquarters. To simulate this counterfactual experiment, we take into account information provided by company reports, which indicate that store-level sales information is processed by the headquarters with a one-week delay. The main trade-off examined in this experiment revolves around the fact that a centralized inventory management system eliminates the influence of store managers’ heterogeneous skills and biased perceptions of costs. However, it also relinquishes the advantages derived from store managers’ just-in-time information about demand and inventories. Our findings reveal that implementing a centralized inventory management system would result in a substantial reduction in ordering and storage costs, with an average cost decrease of and a reduction for the median store. Despite the significant cost reduction, this benefit is nearly completely offset by the negative impact on profits due to the delayed information about demand. Consequently, the net effect on profits is modest, with a mere increase in annual profit for LCBO, equivalent to million. We further explore the implications of this trade-off for designing a more efficient inventory system that incorporates elements of both centralized and decentralized approaches.

This paper contributes to the growing empirical literature exploring the trade-offs between centralization and decentralization of decision-making in multi-division firms. Notably, DellaVigna and Gentzkow (2019) observe that most retail chains in the US employ uniform pricing across their stores, despite substantial differences in demand elasticities and potential gains from third-degree price discrimination. The authors discuss possible explanations for this phenomenon. In a study of a major international airline company, Hortaçsu et al. (2021) analyze a pricing system that combines decision rights across different organizational teams. They find that despite employing advanced techniques, the pricing system fails to internalize consumer substitution effects, exhibits persistent biases in demand forecasting, and does not adapt to changes in opportunity costs. These inefficiencies are primarily attributed to limited coordination between teams. Examining decentralization decisions from a diverse set of firms across 11 OECD countries, Aghion et al. (2021) show that firms that delegate decision power from central headquarters to plant managers exhibited better performance during the Great Recession compared to similar firms with more centralized structures. The empirical evidence presented in their study supports the interpretation that the value of local information increases during turbulent economic times. Our paper contributes to this literature by being, to the best of our knowledge, the first empirical study to examine the trade-offs related to the (de)centralization of inventory management within retail chains, and specifically the role of store managers’ heterogeneous skills.

This paper also contributes to the empirical literature on dynamic structural models of inventory behavior. Previous contributions in this area include works by Aguirregabiria (1999), Hall and Rust (2000), Kryvtsov and Midrigan (2013), and Bray et al. (2019) in the context of firm inventories, as well as Eberly (1994), Attanasio (2000), and Adda and Cooper (2000) in the domain of household purchases of durable products. We contribute to this literature by using high-frequency (daily) data at the granular store and product level to estimate cost parameters using a dynamic structural model.

Finally, our paper contributes to the literature on structural models with boundedly rational firms. Most of this literature studies firms’ entry/exit decisions (Goldfarb and Xiao, 2011; and Aguirregabiria and Magesan, 2020), pricing decisions (Huang et al., 2022; Ellison et al., 2018), and bidding behavior in auctions (Hortaçsu and Puller, 2008; Doraszelski et al., 2018; Hortaçsu et al., 2019). To the best of our knowledge, our paper represents the first investigation into bounded rationality in firms’ inventory decisions. This research also contributes to the existing literature by combining revealed-preference estimates of managers’ perceived costs with a decomposition of these costs into the objective component explained by store characteristics and the subjective component associated with managers’ education and experience.

The rest of the paper is organized as follows. Section 2 describes the institutional background of the LCBO and presents the dataset and descriptive evidence. Section 3 presents evidence of managers following decision rules and illustrates the heterogeneity in these thresholds across store managers. Section 4 presents the structural model and its estimation. The counterfactual experiments to evaluate the effects of decentralization are described in section 5. We summarize and conclude in Section 6.

2 Firm and data

2.1 LCBO retail chain

History. LCBO was founded in 1927 as part of the passage of the Ontario Liquor Licence Act.444The information in this section originates from various archived documents from the LCBO. General information about the company and its organization is based on the company’s annual reports Liquor Control Board of Ontario (2012) and Liquor Control Board of Ontario (2013), and the collective agreement between the LCBO and OPSEU. Information regarding headquarters’ order recommendations (Suggested Order Quantities, SOQs) originates from the report Liquor Control Board of Ontario (2016). Additional information regarding the role of store managers originates from an interview we conducted with an LCBO store manager from a downtown Toronto store. This act established that LCBO was a crown corporation of the provincial government of Ontario. Today, the wine retail industry in Ontario is a triopoly - consisting of 634 LCBO stores, 164 Wine Rack stores, and 100 Wine Shop stores. Despite its government ownership, LCBO is a profit maximizing company. As described in its governing act, part of its mandate is "generating maximum profits to fund government programs and priorities".555See https://www.lcbo.com/content/lcbo/en/corporate-pages/about/aboutourbusiness.html.

Store managers. According to the LCBO, store managers are responsible for managing their "store, sales and employees to reflect [their] customers’ needs and business goals", with a particular focus on the inventory management of their store. Managers must oversee their store’s overall inventory level to ensure that daily demand is met. For incentive purposes, part of the store managers’ remuneration depends on the overall sales performance of their store. The managers’ pay is therefore closely tied to their stores’ profits. In order to satisfy daily demand, managers periodically restock their shelves by ordering products from the nearest distribution center. The order is then delivered by trucks according to a pre-determined route and schedule. In addition to the ordering decisions, managers are also responsible for their store’s product assortment, as they must decide which products to offer at their store in order to cater to local demand. Inventory management at LCBO, therefore, entails a dual responsibility for store managers: providing products that are in high demand and keeping these products stocked on the shelves.

Classification of stores. The LCBO classifies its stores into six categories, AAA, AA, A, B, C, and D, ranging from the highest to the lowest. These classifications primarily reflect variations in store size and product assortment. However, there are also differences in the consumer shopping experience across these classifications, with the AAA and AA stores being considered flagship stores.

Headquarters. Headquarters are in charge of the assignment of store managers across the different stores. Assignments are occasionally shuffled due to managers being promoted (demoted) to higher- (lower-) classified stores, with seniority being a main factor in the promotion decision. Another responsibility of headquarters is to assist store managers in their inventory decisions. Headquarters use forecasting techniques to provide recommendations to managers regarding how much to order for each product at their store. In the company’s internal jargon, these recommendations are referred to as Suggested Order Quantities (SOQs). For each store and product, headquarters generate order recommendations based on the previous week’s sales and inventory information.666More specifically, order recommendations are a function of the Average Rate of Sale (ARS) of the product from the previous week, and of seasonal brand factors. Importantly, this entails that headquarters process store-level information with a weekly delay. Headquarters do not use just-in-time daily information that store managers may be using in their replenishment decisions. This informational friction may play a role in the optimal allocation of decision rights.

Pricing. LCBO and its competitors are subject to substantial pricing restrictions. Prices must be the same across all stores in all markets for a given store-keeping unit (SKU). There is no price variation across the LCBO and its competitors. Retail prices are determined on a fixed markup over the wholesale price set by wine distributors. Furthermore, the percentage markup applies to all the SKUs within broadly defined categories.777See Aguirregabiria et al. (2016) for further details about markups at LCBO.

No franchising system. The LCBO operates its stores without adopting a franchising system. Instead, all store managers are employees of the LCBO. As a result, store managers are not required to pay any franchise fees, fees per order, or any other types of fees to the firm. The absence of a franchising system ensures that the store managers operate within the organizational structure of the LCBO as employees, without the additional financial obligations associated with a franchising arrangement.

Union. Most employees at the LCBO are unionized under the Ontario Public Service Employees Union (OPSEU). As of 2022, the OPSEU "represents more than 8,000 workers at the Liquor Control Board of Ontario", with their main goal being to "establish and continue harmonious relations between the [LCBO] and the employees". Members of the union include store managers, retail workers, warehouse workers, and corporate workers.

2.2 Data from LCBO

Our analysis combines three data sources: the main dataset provided by the LCBO; data on store managers’ experience and education collected from the social media platform LinkedIn; and consumers’ socioeconomic characteristics from the 2011 Census of Population.

We use a comprehensive and rich dataset obtained from the LCBO, encompassing daily information on inventories, sales, deliveries, and prices of every product sold at each LCBO store. The dataset covers a period of two years, specifically from October 2011 to October 2013, spanning a total of 677 days. With a total of 634 stores operating across Ontario and an extensive product range consisting of over 20,000 different items, our dataset comprises approximately 720 million observations. Moreover, the dataset includes additional valuable information, such as product characteristics, store characteristics (including location, size, and store category), and the store manager’s name.

Table 1 presents summary statistics. The average store has an assortment of items. Weekly sales per store amount to units, translating to an average of units sold per item. The average weekly revenue per store is , resulting in in revenue per item per week and in revenue per unit sold. Regarding deliveries, stores receive shipments at approximately days per week, with total weekly deliveries containing an average of units. Stockout events occur, on average, times per week across all stores.

Notably, these figures exhibit significant variation across different store types. Larger stores, as expected, generate higher weekly revenues. For instance, AAA and AA stores generate average weekly revenues of and , respectively, while C and D stores generate average weekly revenues of and , respectively. Stockout events appear to be more prevalent in larger stores compared to smaller ones. The average AAA store experiences stockout events per week, whereas the average D store encounters stockout events per week. Additionally, larger stores tend to place orders more frequently and in larger quantities. On average, AAA and AA stores receive orders and days per week, totaling and units, respectively. In contrast, C and D stores receive orders and days per week, amounting to and units, respectively.

The bottom panel in Table 1 presents inventory-to-(daily)sales ratios and ordering frequencies. These statistics are closely related to the decision rules that we analyze in Section 3. At the store-product level, the inventory-to-sales ratio before and after an order corresponds to the thresholds s and S, respectively. On average, stores maintain enough inventory to meet product demand for approximately days, initiate an order when there is sufficient inventory for about days, and the ordered quantity covers sales for around days. In terms of ordering frequency, the average store and product place an order approximately once every two weeks, equivalent to a frequency of .

Average inventory-to-sales ratios tend to decrease with store size/type, although this difference is influenced by the composition effect arising from varying product assortments across store types. For the remainder of the paper, to account for this composition effect and reduce the computational burden of estimating our model across numerous products, we focus on a working sample consisting of a few products carried by all stores. This approach allows us to manage the complexity associated with different product assortments while maintaining the robustness of our analysis.

| Type of store | |||||||

| All | AAA | AA | A | B | C | D | |

| Mean | Mean | Mean | Mean | Mean | Mean | Mean | |

| (st.dev) | (st.dev) | (st.dev) | (st.dev) | (st.dev) | (st.dev) | (st.dev) | |

| Number of Observations | |||||||

| Number of Stores | 634 | 5 | 25 | 148 | 157 | 164 | 135 |

| Number of Unique Products | 22,327 | 18,200 | 18,879 | 20,860 | 17,769 | 13,527 | 9,198 |

| Number of Days | 677 | 676 | 676 | 676 | 677 | 676 | 675 |

| Sales & Stockouts Per Store | |||||||

| Revenue per week ($) | 162,249 | 874,367 | 518,067 | 320,263 | 162,588 | 59,327 | 23,912 |

| (158,268) | (255,172) | (111,241) | (75,387) | (47,385) | (21,159) | (10,503) | |

| Units sold per week | 12,908 | 57,160 | 38,369 | 25,665 | 14,068 | 4,522 | 1,730 |

| (11,885) | (8,992) | (5,399) | (5,405) | (4,554) | (1,820) | (819) | |

| Stockout events per week | 414 | 1,202 | 912 | 699 | 371 | 273 | 204 |

| (326) | (429) | (279) | (306) | (152) | (252) | (200) | |

| Inventories Per Store | |||||||

| Number of products | 2,028 | 6,477 | 4,852 | 3,555 | 2,102 | 1,098 | 742 |

| (1,416) | (1,018) | (745) | (937) | (706) | (291) | (190) | |

| Delivery days per week | 5.37 | 6.30 | 6.27 | 6.23 | 6.06 | 5.09 | 3.83 |

| (1.08) | (0.01) | (0.05) | (0.11) | (0.31) | (0.66) | (0.88) | |

| Delivery units per week | 12,257 | 51,339 | 35,710 | 24,350 | 13,476 | 4,395 | 1,660 |

| (11,108) | (6,872) | (4,848) | (5,063) | (4,478) | (1,792) | (814) | |

| Inventory Ratios Per Store | |||||||

| Inventory to (daily) sales ratio | 23.31 | 15.67 | 15.74 | 16.89 | 18.97 | 25.21 | 34.23 |

| (9.86) | (2.16) | (2.74) | (3.32) | (5.24) | (7.20) | (11.85) | |

| Inventory to sales ratio after order | 18.48 | 8.78 | 10.34 | 12.18 | 15.13 | 21.65 | 26.87 |

| (9.16) | (0.62) | (1.55) | (2.76) | (4.40) | (7.38) | (11.72) | |

| Inventory to sales ratio before order | 8.62 | 5.31 | 6.83 | 7.82 | 8.88 | 9.23 | 8.92 |

| (3.59) | (0.60) | (1.40) | (2.39) | (2.97) | (3.66) | (4.99) | |

| Ordering frequency | 0.07 | 0.10 | 0.10 | 0.09 | 0.08 | 0.06 | 0.04 |

| (0.02) | (0.01) | (0.01) | (0.01) | (0.02) | (0.01) | (0.02) | |

2.3 Working sample

In our econometric models, estimated in Sections 3 and 4, the parameters are unrestricted at the store-product level. Considering that our dataset comprises nearly 2 million store-product pairs, estimating these models for every store-product combination would be exceedingly time-consuming. To save time while maintaining the integrity of our analysis, we have employed a different approach. Specifically, we estimate the econometric models for every store in our dataset but limited the analysis to a selected subset of 5 products.

We employ two criteria to determine the product basket for our analysis. Firstly, we select products that exhibit high sales across all LCBO stores, ensuring that their inventory decisions significantly impact the firm’s overall profitability. Secondly, we include products from each broad category to account for product-level heterogeneity. These categories encompass white wine, red wine, vodka, whisky, and rum. Table 2 provides an overview of the five selected products that satisfy these criteria. By focusing on this subset, we capture a diverse range of products that are representative of the different categories while also being impactful in terms of their sales performance.

| SKU | SKU | SKU | SKU | SKU | |

|---|---|---|---|---|---|

| #67 | #117 | #340380 | #550715 | #624544 | |

| Product Information | |||||

| Name | Smirnoff | Bacardi Superior | Two Oceans | Forty Creek | Yellow Tail |

| Vodka | White Rum | Sauvignon Blanc | Barrel Select Whisky | Shiraz | |

| Category | Vodka | Rum | White Whine | Whisky | Red Wine |

| Average Retail Price ($) | 25.28 | 24.93 | 9.98 | 25.86 | 11.83 |

Table 3 provides summary statistics for our working sample. On average, the stores in our working sample sell units per week, equivalent to units per SKU. The average weekly revenue per store is , resulting in in revenue per SKU per week and in revenue per unit sold. Regarding deliveries, stores in our working sample receive shipments approximately 2 days per week, with each delivery containing an average of units. The average number of stockout events per week per store is .

Similar to Table 1, these numbers exhibit significant variation across different store types. Larger stores generate higher average weekly revenues compared to smaller ones. For instance, the average AAA and AA stores generate weekly revenues of and , respectively, while the smaller C and D stores generate average weekly revenues of and , respectively. Contrary to the full sample, stockout events appear to occur more frequently in smaller stores than in larger ones within our working sample. The average D store experiences stockout events per week, while the average AAA store encounters stockout events per week. Delivery patterns in our working sample follow a similar trend to Table 1, with larger stores placing larger and more frequent orders. The average AAA store receives deliveries 4 days per week, totaling 272 units per week, whereas the average D store only receives deliveries 0.6 days per week, amounting to 15 units per week.

| Type of store | |||||||

| All | AAA | AA | A | B | C | D | |

| Mean | Mean | Mean | Mean | Mean | Mean | Mean | |

| (st.dev) | (st.dev) | (st.dev) | (st.dev) | (st.dev) | (st.dev) | (st.dev) | |

| Number of Observations | |||||||

| Number of Stores | 634 | 5 | 25 | 148 | 157 | 164 | 135 |

| Number of Unique Products | 5 | 5 | 5 | 5 | 5 | 5 | 5 |

| Number of Days | 677 | 676 | 676 | 676 | 677 | 676 | 675 |

| Sales & Stockouts Per Store | |||||||

| Revenue per week ($) | 1,687 | 5,197 | 4,511 | 3,192 | 1,801 | 821 | 302 |

| (1,402) | (1,487) | (1,415) | (835) | (660) | (443) | (200) | |

| Units sold per week | 91 | 274 | 252 | 173 | 98 | 43 | 15 |

| (75) | (51) | (65) | (39) | (33) | (22) | (10) | |

| Stockouts events per week | 0.37 | 0.14 | 0.13 | 0.21 | 0.28 | 0.49 | 0.56 |

| (0.39) | (0.07) | (0.11) | (0.15) | (0.23) | (0.35) | (0.60) | |

| Inventories Per Store | |||||||

| Number of products Offered | 4.85 | 5 | 5 | 5 | 5 | 4.90 | 4.42 |

| (0.51) | (0) | (0) | (0) | (0) | (0.34) | (0.92) | |

| Delivery days per week | 1.94 | 4.04 | 3.79 | 3.20 | 2.28 | 1.20 | 0.62 |

| (1.15) | (0.29) | (0.24) | (0.49) | (0.56) | (0.51) | (0.35) | |

| Delivery units per week | 88 | 272 | 243 | 167 | 95 | 42 | 15 |

| (73) | (55) | (68) | (38) | (33) | (21) | (9) | |

| Inventory Ratios Per Store | |||||||

| Inventory to sales ratio | 20.97 | 28.27 | 25.18 | 24.93 | 24.07 | 18.80 | 14.59 |

| (7.03) | (8.06) | (7.18) | (6.44) | (6.91) | (4.84) | (3.46) | |

| Inventory to sales ratio after order | 20.80 | 21.02 | 18.85 | 20.09 | 22.48 | 21.46 | 19.17 |

| (4.94) | (10.69) | (4.11) | (4.46) | (6.18) | (4.07) | (3.81) | |

| Inventory to sales ratio before order | 13.06 | 17.48 | 15.77 | 16.61 | 16.25 | 10.90 | 7.43 |

| (5.33) | (7.10) | (3.42) | (3.83) | (4.72) | (3.44) | (2.95) | |

| Ordering frequency | 0.15 | 0.31 | 0.30 | 0.25 | 0.17 | 0.09 | 0.05 |

| (0.09) | (0.06) | (0.06) | (0.06) | (0.05) | (0.04) | (0.03) | |

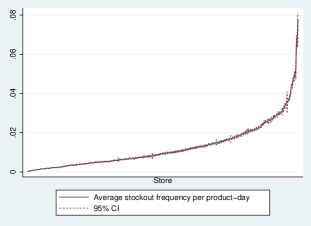

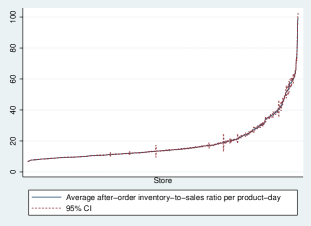

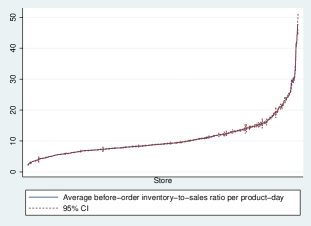

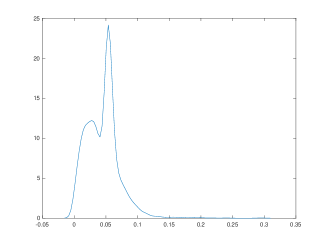

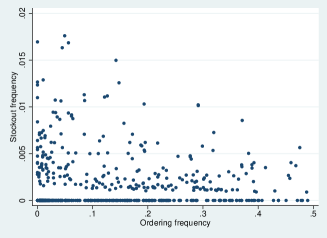

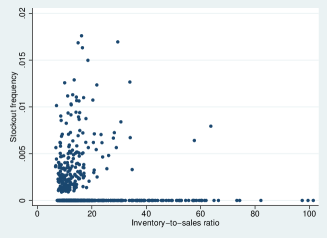

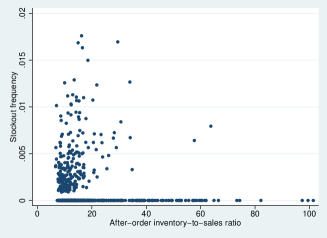

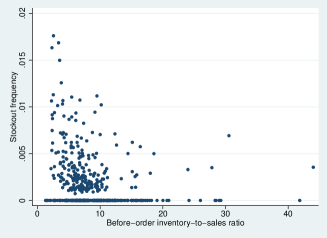

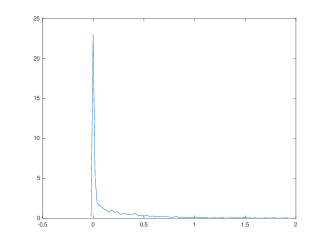

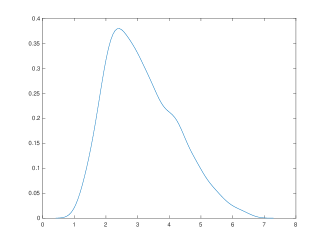

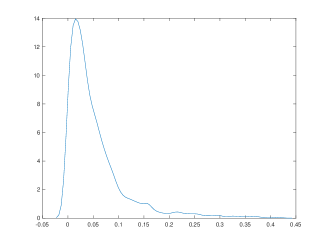

Figure 1 shows strong heterogeneity across stores in several measures related to inventory management of the five products in our working sample. The figures in panels (a) to (f) are inverse cumulative distributions over stores, together with their confidence bands.888For every store, the confidence interval is based on the construction of store-product-specific rates. The confidence interval is determined by percentiles and in this distribution.

Panel (a) presents the distribution of the stockout rate. For store , we have:

| (1) |

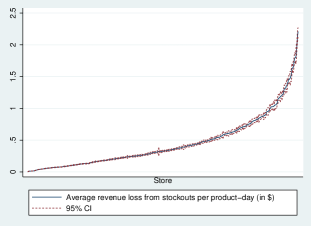

The figure shows a large spread of stockout rates: the and percentiles are and , respectively. Panel (b) shows substantial heterogeneity across stores in the revenue-loss per-product-day generated by stockouts. Indexing products by , and using to represent the number of products, the revenue-loss for store is:

| (2) |

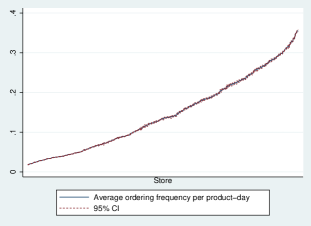

The and percentiles are and per product-day, respectively. Aggregated at the annual level and over all the products offered in a store, they imply an average annual revenue-loss of approximately at the percentile and at the percentile. Panel (c) presents the ordering frequency of stores in our sample calculated as:

| (3) |

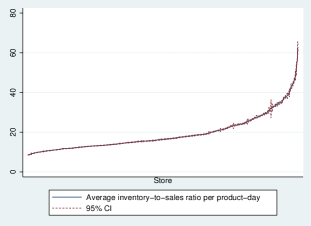

This ordering rate varies significantly across stores, with the percentile being and the being . Panels (d) to (f) present the empirical distributions for the inventory-to-sales ratio, for this ratio just before an order (a measure of the lower threshold s), and for this ratio just after an order (a measure of the upper threshold S). Indexing days by :

| (4) |

The distribution of the inventory-to-sales ratio shows that stores at the and percentiles hold inventory for days and days of average sales, respectively. For the upper threshold S (in Panel (e)), the values of these percentiles are and days, and for the lower threshold s (in Panel (f)) they are and days.

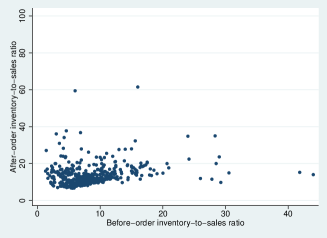

Given these substantial differences in inventory outcomes across stores, it is interesting to explore how they vary together. We present these correlations in Appendix A.1 (Figure 10). The strongest correlation appears for the positive relationship between our measures of the thresholds S and s. This correlation can be explained by store heterogeneity in storage costs: a higher storage cost implies lower values of both and . We confirm this conjecture in the estimation of the structural model in Section 4.

After Order

Before Order

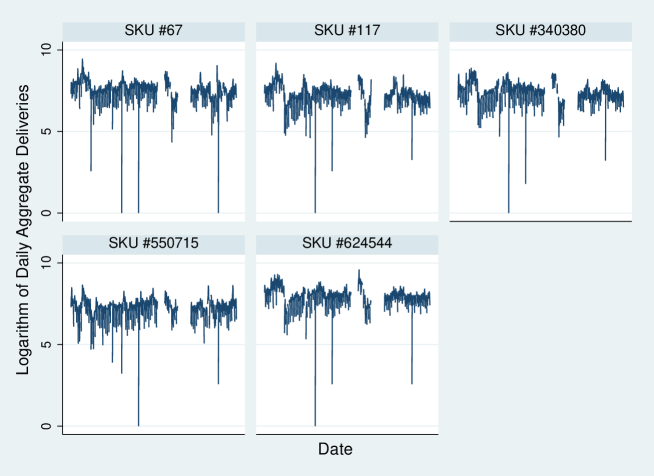

To investigate the possibility of stockouts at the warehouse level and their potential impact on store-level stockouts, we also analyze aggregate daily deliveries from the warehouse to all 634 stores. Given that the products in our working sample are popular items, we interpret a zero value in aggregate daily deliveries as a stockout event at the warehouse. The results of our analysis, presented in Section A.4 in the Appendix, reveal that warehouse stockouts are negligible for our working sample. For each product within the working sample, warehouse stockout events occur on no more than 3 out of the 677 days in the sample, which accounts for less than of the observed period. These findings suggest that stockouts observed at the store level are primarily driven by factors other than warehouse-level stockouts.

2.4 Data on store managers’ education and experience

In addition to the main dataset, we enhance our analysis by incorporating information on store managers’ human capital. Leveraging the professional social networking platform LinkedIn, we gather data on the education and experience of store managers from their public profiles. Out of the 634 store managers in our dataset, 600 are identifiable by name in the LCBO’s records.999During our sample period, some stores are overseen by interim managers who are not identified by name in our main dataset. Within this subset, we were able to locate public LinkedIn profiles for 143 managers, allowing us to retrieve valuable information about their educational background and work experience.

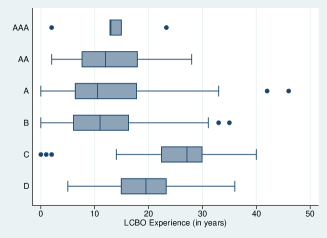

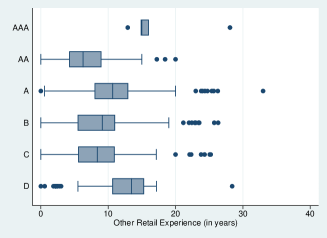

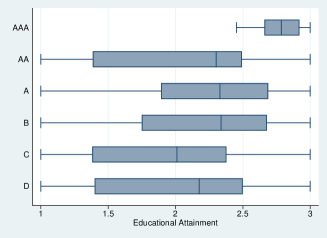

Table 4 presents summary statistics for the variables related to store managers’ educational background and work experience. Notably, we observe a pattern in which managers with greater experience and higher educational attainment tend to be assigned to higher-classified stores. This finding suggests a positive correlation between manager characteristics and store classification, indicating that the LCBO may allocate more experienced and highly educated managers to stores of higher importance or larger scale. In Appendix A.2, we provide more detailed information on the positive relationship between manager characteristics and the classification of stores within the LCBO retail chain.

| Type of store | |||||||

| Statistic | All | AAA | AA | A | B | C | D |

| # of stores | 634 | 5 | 25 | 148 | 157 | 163 | 125 |

| (%) | (100.0) | (0.8) | (4.0) | (23.3) | (24.7) | (25.9) | (21.3) |

| # managers with observed education | 86 | 1 | 8 | 30 | 32 | 5 | 10 |

| (%) | (100.0) | (1.2) | (9.3) | (34.9) | (37.2) | (5.8) | (11.6) |

| # managers with observed LCBO exper. | 136 | 3 | 9 | 48 | 44 | 20 | 12 |

| (%) | (100.0) | (2.2) | (6.6) | (35.3) | (32.4) | (14.7) | (8.8) |

| # managers with observed industry exper. | 72 | 1 | 7 | 30 | 26 | 5 | 3 |

| (%) | (100.0) | (1.4) | (9.7) | (41.7) | (36.1) | (6.9) | (4.2) |

| Dummy highest degree = high school (Mean) | 0.093 | 0.000 | 0.000 | 0.067 | 0.094 | 0.200 | 0.200 |

| Dummy highest degree = college (Mean) | 0.395 | 0.000 | 0.625 | 0.333 | 0.375 | 0.600 | 0.400 |

| Dummy highest degree = university (Mean) | 0.512 | 1.000 | 0.375 | 0.600 | 0.531 | 0.200 | 0.400 |

| Years LCBO exper. (Mean) | 13.7 | 10.0 | 12.3 | 12.2 | 9.7 | 24.7 | 17.8 |

| Years industry (non-LCBO) exper. (Mean) | 9.8 | 15.0 | 8.0 | 11.2 | 9.8 | 5.8 | 5.3 |

3 (S,s) decision rules

3.1 Model

In this section, we study store managers’ inventory behavior through the eyes of decision rules. In its simplest form, this decision rule involves time-invariant threshold values. When assuming lump-sum (fixed) ordering costs, quasi-K-concavity of the profit function with respect to orders, and time-invariant expected demand, the profit-maximizing inventory decision rule follows a structure (Arrow et al., 1951; Scarf, 1959; Denardo, 1981). The rule is characterized by two threshold values: a lower threshold denoted as , which represents the stock level that triggers a new order (known as the "safety stock level"), and an upper threshold denoted as , which indicates the stock level to be achieved when an order is placed. Thus, if represents the stock level at the beginning of day , and represents the orders placed on day , the rule can be defined as follows:

| (5) |

Hadley and Whitin (1963) and Blinder (1981) provide comparative statics for the thresholds as functions of the structural parameters in the firm’s profit function. They provide the following results:

| (6) |

where represents expected demand, is the inventory holding cost per period and per unit, is the fixed (lump-sum) ordering cost, is the unit ordering cost, and is the stockout cost per period. These ’s are the parameters in the structural model that we estimate in Section 4. We investigate the predictions of equation (6) in Section 5.

The optimality of the decision rule extends to models with state variables that evolve over time according to exogenous Markov processes. Let denote the vector of these exogenous state variables, which can include factors influencing demand, unit ordering costs, wholesale prices, and the product’s retail price (when taken as given by the store manager), as is the case in our problem. The optimal decision rule in this context follows a structure, where the thresholds and are time-invariant functions of these state variables: and .

In this section, our empirical approach is inspired by the work of Eberly (1994), Attanasio (2000), and Adda and Cooper (2000). These studies utilize household-level data on durable product purchases, specifically automobiles, to estimate decision rules. In these decision rules, the thresholds are functions of household characteristics, prices, and aggregate economic conditions. This approach can be seen as a "semi-structural approach," where the use of rules is motivated by a dynamic programming model of optimal behavior. However, the specification of the thresholds as functions of state variables does not explicitly incorporate the structural parameters of the model.

In Section 4, we present a full structural approach that explicitly incorporates the structural parameters of the model. Furthermore, in Section 5, we utilize the estimated structural model to conduct counterfactual policy experiments, which address the questions that motivated this paper. However, before delving into the full structural analysis, we find it valuable to explore the data using a more flexible empirical framework that remains consistent with the underlying structural model. We investigate heterogeneity between store managers’ inventory decisions by estimating rules at the store-product level. These decision rules are consistent with our structural model but they are more flexible. This allows us to gain insights and assess the suitability of the decision rules in capturing the inventory behavior of store managers within the LCBO retail chain.

Given that our dataset contains 677 daily observations for every store and product, and that the ordering frequency in the data is high enough to include many orders per store-product, we can estimate the parameters in the decision rules at the store-product level. In this section, we omit store and product sub-indexes in variables and parameters, but it should be understood that these sub-indexes are implicitly present.

We consider the following specification for the thresholds:101010We attempted to incorporate demand volatility, represented by , as an explanatory variable in the decision rule. However, we encountered high collinearity between the time series of (expected demand) and , making it challenging to estimate their separate effects on the thresholds. It is worth noting that according to the Negative Binomial distribution, . Consequently, we can interpret the effect of on the thresholds as the combined impact of both expected demand and volatility.

| (7) |

where is the product’s retail price, is the expected demand, and and represent state variables which are known to the store manager but are unobservable to us as researchers.111111For instance, and may include shocks in fixed and variable ordering costs, or measurement error in our estimate of expected demand. The vector of exogenous state variables is . The ’s are reduced form parameters which are constant over time but vary freely across stores and products and are functions of the structural parameters that we present in our structural model in Section 4.

Our measure of expected demand is based on an LCBO report regarding the information that headquarters use to construct order recommendations for each store (Liquor Control Board of Ontario, 2016). Relying on this report, we assume that store managers obtain predictions of demand for each product at their store using information on the product’s retail price (), the average daily sales of the product over the last seven days, (that we represent as ), and seasonal dummies.

Since the observed quantity sold has discrete support , we consider that demand has a Negative Binomial distribution where the logarithm of expected demand at period has the following form:

| (8) |

where is the quantity sold of the store-product at day , is a vector of parameters that are constant over time but vary freely across store-products, and is a vector of monomial basis in variables and .

We denote equation (8) as the sales forecasting function. It deserves some explanation. First, it is important to note that this is not a demand function. For this inventory decision problem, managers do not need to know the demand function but only the best possible predictor of future sales given the information they have. Second, this specification ignores substitution effects between products within the same category or across categories. Ignoring substitution effects in demand is fully consistent with LCBO’s report and with the firm’s price setting, which completely ignores these substitution effects (see Aguirregabiria et al., 2016).121212Recent papers show that the pricing decisions of important multi-product firms do not internalize substitution or cannibalization effects between the firm’s own products. See, for instance, Hortaçsu et al. (2021)’s study of the pricing system of a large international airline company, DellaVigna and Gentzkow (2019) and Hitsch et al. (2021) on uniform pricing at US retail chains, Cho and Rust (2010) on pricing of car rentals, or Miravete et al. (2020) for liquor stores in Pennsylvania. In the Appendix (Section A.3), we present a summary of the estimation results of the sales forecasting function for every store and every product in our working sample.

The model in equations (5) and (7) implies that the decision of placing an order () or not () has the structure of a linear-in-parameters binary choice model.

| (9) |

where is the indicator function; is the standardized version of , as is the standard deviation of ; and there is the following relationship between and parameters: ; ; ; and . These expressions show that, given the parameters , we can identify the parameters and . We assume that has a Normal distribution, such that equation (9) is a Probit model, and we estimate the parameters by maximum likelihood.

Our model also implies that in days with positive orders () the logarithm of the total quantity offered, , is equal to the logarithm of the upper-threshold, , and this implies the following linear-in-parameters (censored) regression model:

| (10) |

Equation (10) includes the selection condition . That is, the upper-threshold is observed only when an order is placed. This selection issue implies that OLS estimation of equation (10) yields inconsistent estimates of the parameters and the threshold itself. However, the model implies an exclusion restriction that provides identification of the parameters in equation (10). The inventory level affects the binary decision of placing an order or not (as shown in equation (9)), but conditional on placing an order, it does not affect the value of the upper-threshold in the right-hand-side of regression equation (10). Therefore, using (9) as the selection equation, we can identify the parameters in (10) using a Heckman two-step approach.131313This exclusion restriction in models have been pointed out by Bertola et al. (2005).

Part of the variation in parameter estimates across stores and products is attributable to estimation error rather than genuine heterogeneity. For any given parameter , where and represent store and product indices respectively, let denote its consistent and asymptotically normal estimate, with an asymptotic variance of . Using this asymptotic distribution, we can establish a relationship between the variances of and across stores and products: , where represents the mean of asymptotic variances across stores and products. Since , this equation demonstrates that overestimates the true dispersion . To mitigate this excess dispersion or spurious heterogeneity arising from estimation error, we employ a shrinkage estimator. The details of this estimator are described in section A.8 in the Appendix.

3.2 Estimation of (S,s) thresholds

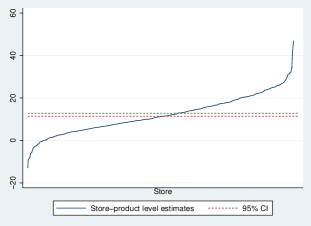

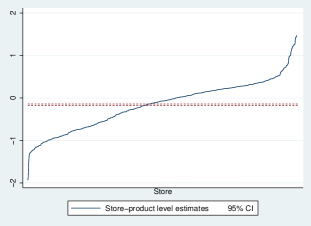

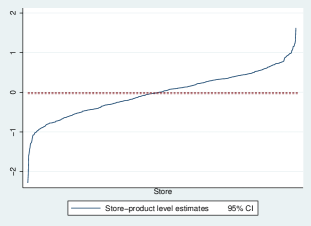

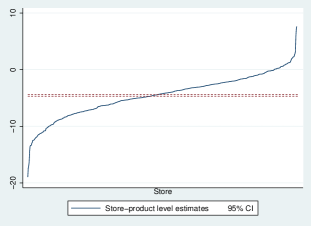

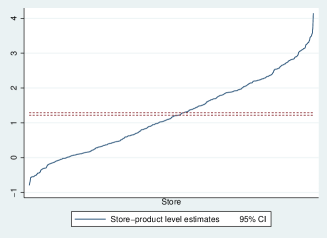

Figure 2 presents the average estimates of parameters , , , and in the lower threshold for each store, where the average is obtained over the five products in the working sample. We sort stores from the lowest to the largest average estimate such that this curve is the inverse CDF of the average estimate. The red-dashed band around the median of this distribution is the confidence band under the null hypothesis of homogeneity across stores.141414The reported confidence interval incorporates the Bonferroni correction for multiple testing. In this context, the implicit null hypothesis is that every store does not differ significantly from the average store. By applying the Bonferroni correction, we account for the increased probability of observing a significant difference by chance when conducting multiple tests. The signs of the parameter estimates are for the most part consistent with the predictions of the model. These distributions show that the parameter estimates vary significantly across stores. For , , and , we have that 95%, 95%, 98%, and 95% of stores, respectively, lie outside of the Bonferroni confidence interval.

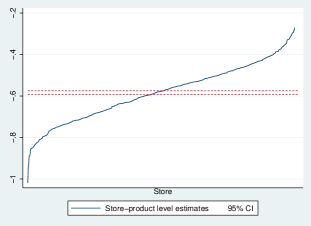

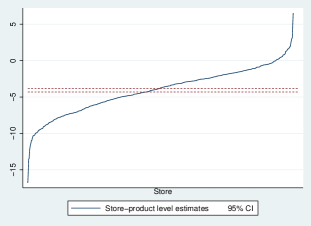

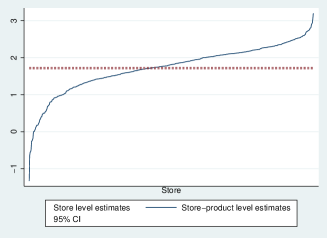

Figure 3 presents the inverse CDF of the store-specific average of the parameters , , and in the upper threshold, as well as the Bonferroni confidence interval under the null hypothesis of homogeneity. As expected, we have strong evidence of heterogeneity in our estimates. For , , and , approximately 96%, 97%, and 97% of stores lie outside of the confidence bands, respectively.

Given that we have estimates at the store-product level, we can also explore the heterogeneity in these estimates within stores. Table 5 presents a decomposition of the variance of parameter estimates into within-store (between products) and between-store variance. The parameters associated with expected demand and the lower threshold inventory parameter show a between-store variance that is at least as large as the within-store variance. For the constant parameters and the price parameters, the variance is larger across products.

| Variance | |||||||

|---|---|---|---|---|---|---|---|

| Between-store Variance | 69.41 | 0.02 | 0.28 | 8.54 | 110.18 | 0.27 | 12.01 |

| Within-store Variance | 81.01 | 0.02 | 0.07 | 9.78 | 183.81 | 0.11 | 19.35 |

The parameter estimates imply values for the thresholds. In section A.5 in the Appendix, we investigate heterogeneity across stores in the estimated thresholds. We find strong between-store heterogeneity, especially in the lower threshold .

4 Structural model

We propose and estimate a dynamic structural model of inventory management. A price-taking store sells a product and faces uncertain demand. The store manager orders the product from the retail chain’s warehouse, and any unsold product rolls over to the next period’s inventory. The store-level profit function incorporates four store-specific costs associated with inventory management: per-unit inventory holding cost (), stockout cost (), fixed ordering cost (), and per-unit ordering cost ().

4.1 Non-separability of inventory decisions across products

At LCBO, store managers are responsible for making inventory decisions for thousands of products. These decisions are not independent of each other due to various factors. Firstly, when a product experiences a stockout, consumers may opt to substitute it with a similar available product. As a result, the cost of a stockout for the store is influenced by the availability of substitute products. Secondly, storage costs are affected by the total volume of items and units in the store, which means the inventory management of one product can impact the storage costs of other products. Lastly, the store’s ordering cost is dependent on the cost of filling a truck with units of multiple products and transporting them from the warehouse to the store. The decision to order a truck and the cost associated with it are not separable across products.

We can think of a model that fully accounts for the inter-dependence inventory decisions across products. In this model, a store manager maximizes the aggregate profit from all the products taking into account the substitutability of similar products under stockouts and subject to two overall store-level constraints: the total storage capacity of the store and the capacity of the delivery truck. Our store-product level model aligns with this multiple-product inventory management framework.

By using duality theory, we can show that the marginal conditions for optimality in the multiple-product model are equivalent to those in our single-product model, under appropriate interpretations of our store-product level structural parameters. The inventory holding cost parameter represents the shadow price or Lagrange multiplier associated with the storage capacity constraint at store . Similarly, the fixed and unit ordering costs, and respectively, reflect the shadow prices of the truck’s capacity constraint at the extensive and intensive margins. Lastly, the stockout cost parameter accounts for the impact of consumer substitution within the store when a stockout occurs for product at store .

In estimating our model, our approach is valid as long as these Lagrange multipliers do not exhibit significant variation over time. For our counterfactual experiments, we assume that these Lagrange multipliers remain constant in the counterfactual scenario.

To summarize, our approach does not assume the separability of inventory management across products, as this would be an unrealistic assumption. Instead, we employ certain assumptions and shortcuts to address the complexities of the joint inventory management problem, while still maintaining a realistic framework that is consistent with the interdependencies among products.

4.2 Sequence of events and profit

For notational simplicity, we omit store and product indexes. Time is indexed by . One period is one day. Every day, the sequence of events is the following.

Step (i). The day begins with the store manager observing current stock (), the retail price set by headquarters (), and her expectation about the mean and variance of the distribution of log-demand: and , respectively. Given this information, the store manager orders units of inventory from the distribution center. There is time-to-build in this ordering decision. More specifically, it takes one day for an order to be delivered to the store and become available to consumers.151515Based on the interviews we conducted with store managers, the most common delivery lag reported is one day. Delivery lags exceeding three days were described as extremely rare. The ordered amount is a discrete variable with support set .

Step (ii). Demand is realized. Demand has a Negative Binomial distribution with log-expected demand and variance:

| (11) |

where , , , and are parameters; is a vector of seasonal dummies (i.e., weekend dummy and main holidays dummy); is the average daily sales of the product in the store during the last seven days; and denotes the over-dispersion parameter in the Negative Binomial. We use to represent the distribution of conditional on . Importantly, the stochastic demand shock is unknown to the store manager at the beginning of the day when she makes her ordering decision.

Step (iii). The store sells units of inventory, which is the minimum of supply and demand:

| (12) |

The store generates flow profits . The profit function has the following form:

| (13) |

where is the wholesale price, and , , , , and are store-product-specific structural parameters. When , the term captures the situation where the cost of a stockout can be smaller than the revenue loss from excess demand because some consumers substitute the product within the store. On the other hand, if , this term can represent an additional reputational cost of stockouts that goes beyond the lost revenue (see Anderson et al., 2006). The term represents the storage cost associated with holding units of inventory at the store. Parameter denotes the per-unit cost incurred by the store manager when placing an order, and represents the fixed ordering cost, including the transportation cost from the warehouse to the store. The variable corresponds to a stochastic shock with a mean of zero that affects ordering costs. More specifically, variables , , …, are i.i.d. with a Extreme Value type 1 distribution. Parameter represents the standard deviation of the shocks in ordering costs.

These parameters are the store manager’s perceived costs. For instance, the fixed ordering cost and the per-unit holding cost can be interpreted as the manager’s perception of the shadow prices (or Lagrange multipliers) associated to the capacity constraints of a delivery truck and of the store, respectively.

Price-cost margins. LCBO’s retail prices are a constant markup over their respective wholesale prices. There are different markups for Ontario products ( markup) and non-Ontario products ( markup) (see Aguirregabiria et al., 2016). A constant markup, say , implies that the price-cost margin is proportional to the retail price: , where represents the Lerner index that by definition is equal to . The Lerner index is equal to for Ontario products and to for non-Ontario products.

Step (iv). Orders placed at the beginning of day , , arrive to the store at the end of the same day or at the beginning of . Inventory is updated according to the following transition rule:

| (14) |

Finally, next period price is realized according to a first order Markov process with transition distribution function .

4.3 Dynamic decision problem

A store manager chooses the order quantity to maximize her store’s expected and discounted stream of current and future profits. This is a dynamic programming problem with state variables and and value function . This value function is the unique solution of the following Bellman equation:

| (15) |

where is the store’s one-day discount factor; is the expected profit function up to the shock; and is the expectation over the i.i.d. distribution of , and over the distribution of conditional on . The latter distribution consists of the transition probability and the distribution of demand conditional on which together with equations (12) and (14) determines the distribution of . The solution of this dynamic programming problem implies a time-invariant optimal decision rule: . This optimal decision rule is defined as the arg max of the expression within brackets in the right-hand-side of equation (15).

For the solution and estimation of this model, we follow Rust (1987, 1994) and use the integrated value function and the corresponding integrated Bellman equation. Given the Extreme Value distribution of the variables, the integrated Bellman equation has the following form:

| (16) |

The expected profit function is linear in the parameters. That is,

| (17) |

where is the vector of structural parameters , , , , , and is the following vector of functions of the state variables:

| (18) |

where the expectation is taken over the distribution of demand conditional on .

We consider a discrete space for the state variables .161616In the estimation, we discretize the state space using a k-means algorithm. Let be the support set of . We can represent the value function as a vector in the Euclidean space , and the transition probability functions of for a given value of as an matrix . Taking this into account, as well as the linear-in-parameters structure of the expected profit , the integrated Bellman equation in vector form is:

| (19) |

where is a matrix that in row contains vector for .

The Conditional Choice Probability (CCP) function, , is an integrated version of the decision rule . For any and , the CCP is defined as , where is the CDF of . For the Extreme Value type 1 distribution, the CCP function has the Logit form:

| (20) |

Following Aguirregabiria and Mira (2002), we can represent the vector of CCPs, , as the solution of a fixed-point mapping in the probability space: . Mapping is denoted the policy iteration mapping, and it is the composition of two mappings: . Mapping is the policy improvement. It takes as given a vector of values and obtains the optimal CCPs as "best responses" to these values. Mapping is the valuation mapping. It takes as given a vector of CCPs and obtains the corresponding vector of values if the agent behaves according to these CCPs.171717See Puterman (2014) for a description of these three mappings in the context of a general dynamic programming problem. In our Logit model, the policy improvement mapping has the following vector form, for any :

| (21) |

The valuation mapping has the following form:

| (22) |

where is Euler’s constant, and is the element-by-element vector product.

4.4 Parameter estimates

For every LCBO store and product in our working sample, we estimate the store-product specific parameters in vector using a Two-Step Pseudo Likelihood (2PML) estimator (Aguirregabiria and Mira (2002)). Given a dataset and arbitrary vectors of CCPs and structural parameters , define the pseudo (log) likelihood function:

| (23) |

where is the policy iteration mapping defined by the composition of equations (21) and (22). Note that the likelihood function is a function of the store’s one-day discount factor . In the estimation, we fix the value181818We could eventually relax this assumption and treat as a parameter to be estimated, and allow it to vary across store managers in order to potentially capture different degrees of myopia or impatience. of this discount factor equal to . In the first step of the 2PML method, we obtain a reduced form estimation of the vector of CCPs using a Kernel method. In the second step, the 2PML estimator is the vector that maximizes the pseudo-likelihood function when . That is:

| (24) |

Aguirregabiria and Mira (2002) show that this estimator is consistent and asymptotically normal with the same asymptotic variance as the full maximum likelihood estimator. In section A.6 in the Appendix, we provide further details on the implementation of this estimator.

In a similar vein to the estimation of thresholds in section 3, a portion of the variation in parameter estimates can be attributed to estimation error rather than genuine heterogeneity. To address this issue and mitigate the excessive dispersion or spurious heterogeneity resulting from estimation error, we employ a shrinkage estimator. The details of this estimator can be found in section A.8 in the Appendix.

Table 6 presents the medians from the empirical distributions (across stores and products) of our estimates of the four structural parameters, measured in dollar amounts.191919More specifically, we first obtain the two-step PML estimate of the vector , , , , , and then we divide elements 2 to 5 of this vector by the first element to obtain estimates of costs in dollar amount. We use the delta method to obtain standard errors. The median values of the estimates are for the per-unit inventory holding cost, for the stockout cost, for the fixed ordering cost, and for the per-unit ordering cost. To have an idea of the importance of these dollar amounts, in Section 4.5 below we provide measures of the implied magnitude of each cost relative to revenue. These magnitudes are consistent with other cost estimates in the inventory management literature (see Aguirregabiria [1999], Bray et al. [2019]). Median standard errors and t-statistics in Table 6 show that the inventory holding cost and the fixed ordering cost are very precisely estimated (median t-ratios of and , respectively), while a substantial fraction of the estimates of the stockout cost are quite imprecise (median t-ratio of ).

| Median | Std. Dev. | Median | Median | |

| Estimate | Estimate | S.e. | t-stat. | |

| : Per-unit Inventory Holding Cost | 0.0029 | 5.3259 | ||

| : Stockout Cost | 0.3094 | 0.2672 | ||

| : Fixed Ordering Cost | 1.0847 | 12.6557 | ||

| : Per-Unit Ordering Cost | 0.0607 | 1.4763 | ||

| # of observed store-product pairs | 3,076 | |||

| # of store-product pairs with structural estimates | 2,589 |

4.5 Relative contribution of the different costs

In this section we assess the magnitude of the different inventory management costs relative to store revenues. The purpose of this exercise is twofold. First, we want to evaluate whether our parameter estimates imply realistic magnitudes for the realization of these costs. And second, it is relevant to measure to what extent the heterogeneity in cost parameters that we have presented above generates heterogeneity in profits across stores. Conditional on their perception of cost parameters, store managers’ optimal behavior should compensate – at least partly – for the differences in cost parameters such that heterogeneity in realized costs should be smaller. We want to measure the extent of this compensating effect.

For each component of the inventory management cost, and for every store-product, we calculate the ratio between the realized value of the cost during our sample period and the realized value of revenue during the same period. More specifically, we calculate the following ratios for every store-product: inventory holding cost to revenue; stockout cost to revenue; fixed ordering cost to revenue; variable ordering cost to revenue; and total inventory management cost to revenue. We have an empirical distribution over store-products for each of these ratios.

Table 7 presents the median and the standard deviation in these distributions. To evaluate the magnitude of these ratios, it is useful taking into account that – according to the LCBO’s annual reports – the total expenses to sales ratio of the retail chain is consistently around each year.202020Of course, these expenses do not include the cost of merchandise. According to our estimate, the total inventory cost-to-revenue ratio for the median store is approximately . This would imply that the retail chain’s cost of managing the inventories of their stores would represent around of total costs, which entails that non-inventory related costs would account for approximately of total costs (e.g. labor costs, fixed capital costs, delivery costs). This seems to be of the right order of magnitude. Table 7 shows that the fixed ordering cost is the largest realized cost for store managers at LCBO, followed by storage costs. Realized stockout costs are negligible. This is due to a combination of a small parameter that captures the stockout cost, and infrequent stockouts in our working sample.

| Median | St. Dev. | |

|---|---|---|

| Inventory Holding Cost to Revenue Ratio (%) | 0.2863 | 0.2182 |

| Stockout Cost to Revenue Ratio (%) | 0.0005 | 0.0197 |

| Fixed Ordering Cost to Revenue Ratio (%) | 0.8731 | 0.7728 |

| Variable Ordering Cost to Revenue Ratio (%) | 0.2045 | 0.1895 |

| Total Inventory Cost to Revenue Ratio (%) | 1.3749 | 0.9235 |

In section A.9 in the Appendix, we present the empirical distribution across stores and products of each of the four cost-to-revenue ratios. We also show the extent to which managers’ inventory decisions compensate for the heterogeneity in the structural parameters.

4.6 Heterogeneity in cost parameters

Below, we investigate two potential sources for the large heterogeneity in our cost parameters: (i) differences across stores, such as store type according to LCBO’s classification of stores, physical area, total product assortment, distance to the warehouse, and consumer socioeconomic characteristics; and (ii) differences across local managers. Our goal in this section is to separate the heterogeneity attributable to store characteristics, and the heterogeneity stemming from the managers themselves. We proceed using a sequential approach. First, we regress our parameter estimates on a set of store characteristics. Then, we take the residual components from the first step and regress them on manager characteristics.

| () | () | () | () | |

| Est. | Est. | Est. | Est. | |

| (s.e.) | (s.e.) | (s.e.) | (s.e.) | |

| Store Class | ||||

| AA | 0.000554 | -0.0216 | -0.164 | 0.00302 |

| (0.000411) | (0.0194) | (0.185) | (0.00587) | |

| A | 0.000511 | -0.0204 | -0.203 | 0.00816 |

| (0.000397) | (0.0181) | (0.178) | (0.00572) | |

| B | -0.000415 | -0.0237 | 0.108 | 0.00761 |

| (0.000434) | (0.0204) | (0.190) | (0.00590) | |

| C | -0.00209∗∗∗ | -0.0531∗∗ | 0.785∗∗∗ | 0.00477 |

| (0.000520) | (0.0243) | (0.221) | (0.00657) | |

| D | -0.00334∗∗∗ | -0.0379 | 1.223∗∗∗ | 0.00479 |

| (0.000564) | (0.0262) | (0.244) | (0.00693) | |

| ln(Product Assortment Size) | 0.000336 | -0.00932 | -0.364∗∗∗ | 0.00388∗ |

| (0.000205) | (0.00973) | (0.0775) | (0.00201) | |

| ln(Population in City) | -0.0000801∗∗ | -0.00136 | 0.00948 | 0.000413 |

| (0.0000381) | (0.00220) | (0.0186) | (0.000483) | |

| ln(Median Income in City) | 0.000362 | 0.0493∗ | -0.0577 | 0.00795 |

| (0.000520) | (0.0255) | (0.212) | (0.00646) | |

| Location dummies (25 regions, 4 districts) | YES | YES | YES | YES |

| Product dummies (5 products) | YES | YES | YES | YES |

| R-squared | 0.3954 | 0.1345 | 0.5265 | 0.0598 |

| Observations | 2,589 | 2,589 | 2,589 | 2,589 |

| (1) Location dummies based on LCBO’s own division of Ontario into 25 regional markets and 4 districts. | ||||

| (2) Robust standard errors clustered at the store level in parentheses | ||||

| (3) * means p-value<0.10, ** means p-value<0.05, *** means p-value<0.01 | ||||

First step: store characteristics. Table 8 presents estimation results from the first-step regressions of each estimated cost parameter against store and location characteristics: LCBO’s store type dummies (6 types); LCBO’s regional market dummies (25 regions); logarithm of the number of unique products offered by the store; logarithm of population in the store’s city; and logarithm of median income level in the store’s city. As we have cost estimates at the store-product level, we also include product fixed effects.212121Note that the store location dummies capture various factors, including the effect of the distance between the store and the warehouse.

These store and location characteristics can explain an important part of the variation across stores in inventory holding costs and fixed ordering costs: the R-squared coefficients for these regressions are , and , respectively. Fixed ordering costs decline significantly with the number of products in the store, which is consistent with economies of scope in ordering multiple products. Inventory holding costs increase with assortment size and are significantly higher for stores relative to stores. In contrast, only of the variation in unit ordering costs and of the variation in stockout costs can be explained by these store and location characteristics. These results are robust to other specifications of the regression equation based on transformations of explanatory or/and dependent variables.

Second step: manager characteristics. Table 9 presents the estimation results from the second-step regressions of cost parameters on manager characteristics (educational attainment, years of experience at the LCBO, and other industry experience), after controlling for the variation explained by store characteristics. The overall finding is that managers’ education and experience have non-significant effects in these regressions. There are two main reasons that can explain these negligible effects.

First, there is a substantial correlation between store characteristics and managers’ skills. More skilled managers tend to be allocated to higher-class stores (positive assortative matching). Therefore, in the first-step regression, where store characteristics are included, these characteristics are also capturing the effect of managers’ skills. As a result, the direct effect of managers’ skills in the second-step regressions becomes less apparent.

Second, the insignificant effect of managers’ skills on the estimated cost parameters aligns with the interpretation that the residual component of these parameters is associated with biased perceptions. More skilled managers may have a better measure of these costs, while less skilled managers may have noisier estimates. However, this does not imply a larger or smaller effect of managers’ skills on the mean value of cost parameters. Instead, the effect would appear in the variance of the cost parameters, indicating differences in the precision of their estimates. Indeed, when we regress the variance of the cost parameters on managers’ skills, we find evidence supporting this interpretation.

| () | () | () | () | |

| Est. | Est. | Est. | Est. | |

| (s.e.) | (s.e.) | (s.e.) | (s.e.) | |

| Educational Attainment | ||||

| High School | -0.0000165 | 0.000752 | -0.0000456 | 0.000420 |

| (0.000237) | (0.0122) | (0.0769) | (0.00271) | |

| University | -0.0000801 | 0.00474 | 0.0194 | -0.000213 |

| (0.000170) | (0.00794) | (0.0577) | (0.00183) | |

| LCBO Experience | -0.000204 | 0.00228 | -0.0000967 | |

| (0.00000627) | (0.000270) | (0.00223) | (0.0000669) | |

| Other Experience | 0.0000156 | 0.000576 | 0.00471 | -0.0000587 |

| (0.0000125) | (0.000475) | (0.00437) | (0.000115) | |

| R-squared | 0.0095 | 0.0051 | 0.0058 | 0.0038 |

| Observations | 2,589 | 2,589 | 2,589 | 2,589 |

| (1) Robust standard errors clustered at the store level in parentheses | ||||

| (2) * means p-value<0.10, ** means p-value<0.05, *** means p-value<0.01 | ||||

| (3) We use multiple imputation to account for missing values of our explanatory variables | ||||

In Section A.10 of the Appendix, we also examine how the variance of the cost parameters depends on store characteristics. We find that the dispersion of the (second-step) manager component of costs is larger on average for lower-class stores. Since managers in these stores generally have lower levels of human capital (i.e. education and experience), we interpret the second-step manager component as a biased perception of the true cost from the point of view of store managers. That is, the (first-step) store component of the costs will be interpreted as the true cost, and the manager component will be interpreted as deviations from this true cost. In order to illustrate the interpretation of the residual component as manager bias, we present in Section A.10 of the Appendix two granular examples in which pairs of stores – located in close proximity to each other – are similar in size, sales, store classification, but have very different levels of manager experience and estimates of the cost parameters.

We explore the interpretations of our cost parameters, and their impact on store-level inventory outcomes, in the subsequent counterfactual experiments of Section 5.

5 Counterfactual experiments

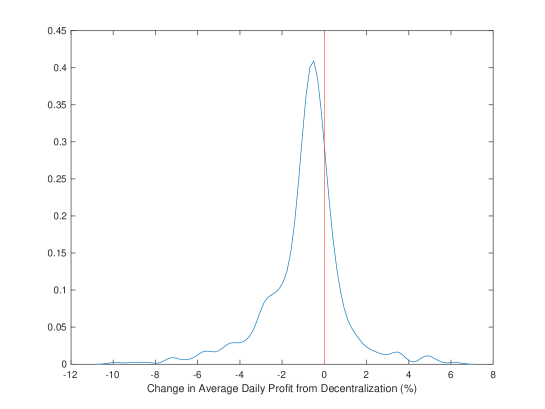

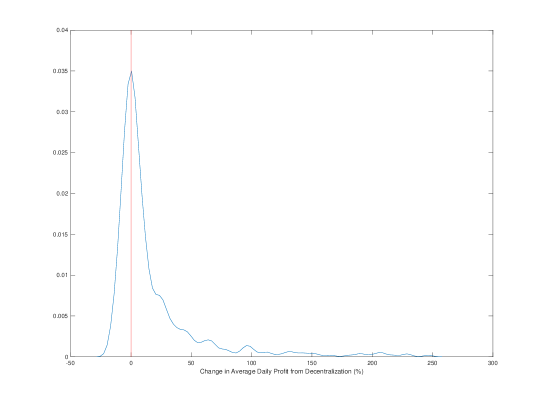

This section presents two sets of counterfactual experiments based on the model that we have estimated in the previous section. First, we study the contribution to inventory management outcomes from the heterogeneity in store managers’ perceptions of costs. Second, we evaluate the effects of a counterfactual centralization of inventory management decisions at LCBO headquarters. We present this counterfactual experiment under different scenarios on the information that headquarters has about demand and costs at the store level.

5.1 Removing store managers’ idiosyncratic effects

Let be the vector of estimates of cost parameters for product and store . Based on the regressions in Tables 8 and 9, we decompose this vector into two additive and orthogonal components: the part explained by store and location characteristics, that we represent as ; and the part explained by local managers, . Below, we construct a counterfactual scenario that removes the idiosyncratic component from the inventory decision problem for store and product . For every store-product in our working sample, we implement a separate counterfactual experiment for each of the four cost parameters, and one experiment that shuts down together the manager component of the four cost parameters. This implies a total number of experiments.

We implement each of these experiments by solving the dynamic programming problem and obtaining the corresponding CCPs under the counterfactual values of the structural parameters. We use this vector of CCPs to calculate the corresponding ergodic distribution of the state variables for the store-product.222222Note that this ergodic distribution incorporates the seasonal effects in the demand part of the model, as seasonal dummies are a component of the vector of state variables of the model. Finally, we use the vector of CCPs and the ergodic distribution to calculate mean values of relevant outcome variables related to inventory management. We compare these average outcomes with their corresponding values under the factual values of structural parameters. In terms of outcome variables, we look at the same descriptive statistics as those reported in Table 1 and Figure 1: stockout frequency, ordering frequency, inventory to sales ratio, inventory to sales ratio after an order (i.e. S threshold), and inventory to sales ratio before an order (i.e. s threshold).

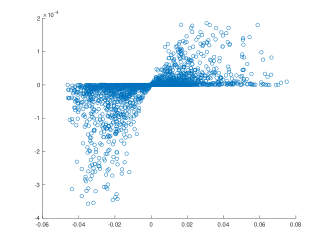

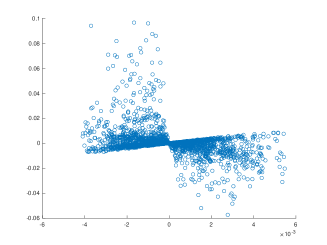

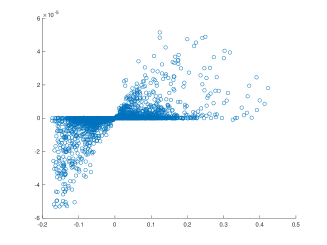

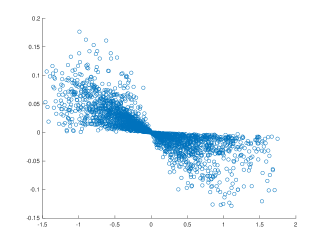

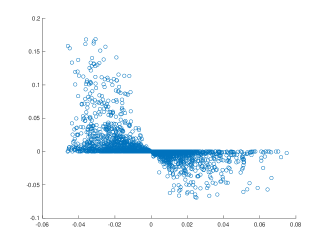

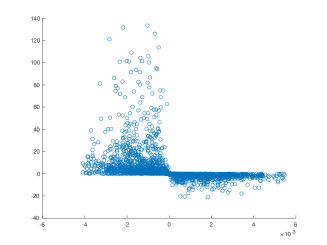

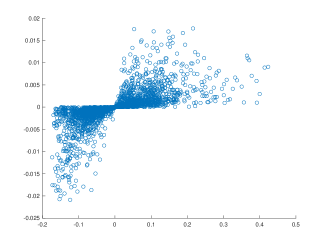

Figures 5 (for stockout frequency), 6 (for ordering frequency), and 7 (for inventory-to-sales ratio) summarize the results from these experiments. In each figure, the horizontal axis measures the value of the corresponding parameter , and the vertical axis measures the difference in the mean value of the outcome variable between the factual and the counterfactual scenario. For instance, in Figure 5(a), the horizontal axis represents , and the vertical axis measures , where is stockout frequency.

Note that the counterfactual experiment of shutting down to zero is equivalent to a change in parameter from the counterfactual value to the factual value . Therefore, we can see the cloud of points in, say, Figure 5(a) as the results of many comparative statics exercises, all of them consisting in changes in the value of parameter . In these figures, there are multiple curves relating a change in with a change in the outcome variable because store-products have different values of the other structural parameters. However, each of these figures shows a monotonic relationship between a change in a cost parameter and the corresponding change in an outcome variable.

Stockout Frequency on y-axis, on x-axis

We compare the relationship between parameters and outcomes implied by these figures with the theoretical predictions from the model as depicted in equation (6). More specifically, note that is negatively related to the ordering frequency (the larger the , the smaller the ordering frequency); is negatively related to the stockout rate (the larger the , the smaller the stockout rate); and the levels of both and are positively related to the inventory to sales ratio (the larger the and , the larger the ratio). The pattern in our figures is fully consistent with Blinder’s theoretical predictions for this class of models.

Figure 5 depicts the relationship between cost parameters and the stockout frequency. According to Blinder’s formula, the lower threshold depends negatively on and , and positively on , while the effect of is ambiguous. Panels (a) to (d) in Figure 5 confirm the signs of these effects on the stockout frequency.

Ordering Frequency on y-axis, on x-axis

In Figure 6, we present the relationship between cost parameters and the ordering frequency. Blinder’s formula says that depends negatively on and positively on . Panels (a) and (c) confirm the sign of these effects on the ordering frequency. According to Blinder, the sign of the effects of and on ordering frequency is ambiguous because they affect the two thresholds and in the same direction. In Panel (b), we find a positive relationship between the stockout cost and ordering frequency. Panel (d) shows that the frequency of placing an order falls when the unit ordering cost increases.

Inventory to Sales Ratio on y-axis, on x-axis

Figure 7 illustrates the relationship between cost parameters and the inventory-to-sales ratio. Blinder’s formula establishes that the two thresholds and depend negatively on and positively . Panels (a) and (b) confirm these signs for the inventory-to-sales ratio. However, according to Blinder’s formula, the sign of the effects of and on the inventory-to-sales ratio is ambiguous. Panels (c) and (d) show negative effects of and on the inventory-to-sales ratio.

| Parameters Shut Down | ||||||

|---|---|---|---|---|---|---|

| None | All | |||||

| Store-product level inventory outcomes | Mean | Mean | Mean | Mean | Mean | Mean |

| (st.dev) | (st.dev) | (st.dev) | (st.dev) | (st.dev) | (st.dev) | |

| Stockout Frequency | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| (0.0004) | (0.0003) | (0.0004) | (0.0004) | (0.0004) | (0.0003) | |

| Ordering Frequency | 0.1776 | 0.1770 | 0.1776 | 0.1714 | 0.1729 | 0.1618 |

| (0.1329) | (0.1353) | (0.1329) | (0.1260) | (0.1313) | (0.1240) | |

| Inventory to Sales Ratio | 26.8373 | 23.3465 | 26.8376 | 27.8804 | 25.7753 | 22.1358 |

| (21.1587) | (13.3625) | (21.1589) | (25.1945) | (19.1622) | (11.8119) | |

| Inventory to Sales Ratio After Order | 31.6917 | 26.7060 | 31.6920 | 33.7313 | 29.6416 | 24.2525 |

| (29.7575) | (17.9471) | (29.7576) | (36.5440) | (25.5906) | (13.9094) | |

| Inventory to Sales Ratio Before Order | 22.6063 | 18.3920 | 22.6066 | 24.6034 | 20.9836 | 16.6467 |

| (22.0222) | (12.2635) | (22.0224) | (28.0980) | (18.7917) | (8.7038) | |

| Change in Total Inventory Cost (%) | – | -4.1913 | 0.0005 | 1.5256 | -4.5866 | -12.0838 |

| (11.7293) | (0.0048) | (24.1220) | (11.4978) | (17.5204) | ||