Provably Efficient Iterated CVaR Reinforcement Learning with Function Approximation and Human Feedback

Abstract

Risk-sensitive reinforcement learning (RL) aims to optimize policies that balance the expected reward and risk. In this paper, we present a novel risk-sensitive RL framework that employs an Iterated Conditional Value-at-Risk (CVaR) objective under both linear and general function approximations, enriched by human feedback. These new formulations provide a principled way to guarantee safety in each decision making step throughout the control process. Moreover, integrating human feedback into risk-sensitive RL framework bridges the gap between algorithmic decision-making and human participation, allowing us to also guarantee safety for human-in-the-loop systems. We propose provably sample-efficient algorithms for this Iterated CVaR RL and provide rigorous theoretical analysis. Furthermore, we establish a matching lower bound to corroborate the optimality of our algorithms in a linear context.

1 Introduction

Reinforcement learning (RL) [40, 47] is a general sequential decision-making framework for creating intelligent agents that interact with and learn from an unknown environment. RL has made ground-breaking achievements in many important application areas, e.g., games [33, 44], finance [23] and autonomous driving [43]. Despite the practical success, existing RL formulation focuses mostly on maximizing the expected cumulative reward in a Markov Decision Process (MDP) under unknown transition kernels. This risk-neutral criterion, however, is not suitable for real-world tasks that require tight risk control, such as automatic carrier control [25, 52], financial investment [51, 15] and clinical treatment planning [11]. To address this limitation, risk-sensitive RL has emerged as a promising research area, which aims to incorporate risk considerations into the RL framework.

A rich body of works have considered various risk measures into episodic MDPs with unknown transition kernels to tackle risk-sensitive tasks. Among different risk measures, the Conditional Value-at-Risk (CVaR) measure has received an increasing attention in RL, e.g., [8, 13, 39, 45, 5, 48]. CVaR is a popular coherent risk measure [39], which can be viewed as the expectation of the worst -percent of a random variable for a given risk level . It plays an important role to avoid catastrophic outcomes in financial risk controlling [15], safety-critical motion planning [20], and robust decision making [8]

However, existing CVaR-based RL works [5, 48, 13, 54] mainly focus on the tabular MDP, where the state and action spaces are finite, and the complexity bounds scale polynomially in the sizes of state and action spaces. As a result, the application of tabular MDPs can be limited, since in practical problems, the state and action spaces are often large or even infinite.

To extend the risk-sensitive RL theory and handle large state space, in this paper, we study Iterated CVaR RL with both linear and general function approximations in episodic MDPs (ICVaR-RL with linear and general function approximations). One key distinction of our work from existing function approximation results [26, 61, 14] is the Iterated CVaR objective. Iterated CVaR [10, 13] is an important variant of CVaR, which focuses on optimizing the worst -percent performance at each step, and allows the agent to tightly control the risk throughout the decision process. In this paper, we tackle the ICVaR-RL with function approximations by two novel sample-efficient algorithms, i.e., ICVaR-L (detailed in Section 4.1) and ICVaR-G (detailed in Section 4.2)

We further investigate ICVaR-RL with human feedback and present a provably efficient algorithm ICVaR-HF with general function approximation. Our exploration is motivated by the rapid development of Large Language Models (LLMs) such as ChatGPT. These models, as demonstrated in various studies [18, 37, 29, 19], operate in diverse conversational landscapes where precisely defining reward signals is challenging. This challenges the conventional RL paradigm, underscoring the crucial role of infusing human feedback [9, 46, 53, 37]. Furthermore, the risk control in intelligent systems such as ChatGPT is significant for preventing the generation of harmful or offensive content [64, 38]. This critical imperative underscores the need of approaches that are inherently risk-sensitive, especially in the intersection of large language models and RLHF. Our work infuses risk sensitivity into RLHF paradigms and formalizes the first risk-sensitive RLHF structure for further theoretical understanding of risk-sensitive RLHF.

However, the Iterated CVaR objective imposes significant technical challenges in the theoretical analysis of the function approximation and human feedback setting. (i) Since the Iterated CVaR measure is a quantile expectation on the distorted distribution, it destroys the linearity of the risk-neutral Bellman equation and makes it hard to estimate the true value function. Therefore, existing risk-neutral RL algorithms for function approximation fail in ICVaR-RL and new techniques are needed to handle this nonlinearity (See Section 4.1). (ii) In our function approximation setting, one cannot calculate the CVaR operator and estimate the transition by tranditional sample-mean technique efficiently, since the size of state space can be very large or even infinite. To address these difficulties, we develop novel CVaR approximation and parameter estimation methods in Section 4.1. (iii) The standard regret analysis For risk-neutral RL with human feedback is not suitable for our risk-sensitive setting. For example, since the preference-based human feedback is a comparison of the cumulative rewards of two trajectories, it is natural to apply this feedback to the risk-neutral RL (to maximize the cumulative rewards), while it can be non-trivial to apply this feedback to a risk-sensitive setting since the regret decomposition process for risk-neutral RLHF fails in analyzing the risk-sensitive goal. Moreover, previous online reward MLE algorithms focus on a finite reward function set [50], while we are dealing with an infinite reward function set.

In this paper, we present provable efficient algorithms for ICVaR-RL with function approximation and human feedback, and develop novel technical tools to address the challenges in Section 4 and 5. Our contribution can be summarized as follows.

-

•

We develop a provably efficient (both computationally and statistically) algorithm ICVaR-L for ICVaR-RL with linear function approximation, which achieves the regret upper bound , where is the risk level, is the dimension of state-action features, is the length of each episode, and is the number of episodes. Moreover, we construct a hard-to-learn instance for ICVaR-RL with linear function approximation, and establish an regret lower bound. This shows that algorithm ICVaR-L achieves a nearly minimax-optimal dependency on and , and the factor in our regret bound is unavoidable in general.

-

•

For ICVaR-RL with general function approximation, we propose algorithm ICVaR-G. We prove that ICVaR-G achieves a regret bound of based on a new elliptical potential lemma. Here is a dimensional parameter that depends on the eluder dimension and covering number of probability set (see Section 4.2 for the details).

-

•

We further extend ICVaR-RL to encompass Reinforcement Learning with Human Feedback (RLHF), incorporating general function approximation for both transition probabilities and reward modeling. We develop the first provably sample-efficient algorithm ICVaR-HF for risk-sensitive RLHF with novel discretization of infinite reward function set and regret decomposition method that achieves a regret bound of , where is a dimensional parameter for reward function set, and is the positive lower bound for the gradient of link function.

2 Related Works

Risk-sensitive RL with CVaR Measure

There are two types of CVaR measures, i.e., the static and dynamic (iterated) CVaR measures. [6, 8, 36, 56, 45] study the static CVaR measure, which considers the CVaR of cumulative reward in tabular MDPs with known transition kernels. [5, 48] investigate the static CVaR RL with unknown transition kernels. On the other hand, [13] propose Iterated CVaR RL (ICVaR-RL), an episodic risk-sensitive RL formulation with unknown transition kernels and the Iterated CVaR measure, and studies both regret minimization and best policy identification in tabular MDPs. In addition, [54] investigate a general iterated risk measure (including Iterated CVaR) in tabular MDPs. In contrast, we study Iterated CVaR RL with linear and general function approximations.

RL with Function Approximation

For risk-neutral RL, [55, 26, 22, 4, 61, 62, 60, 2] study linear function approximation in two types, i.e., linear MDPs and linear mixture MDPs. [22, 2] and [61] present nearly minimax optimal algorithms for Linear MDP and linear mixture MDP, respectively. [4, 49] study risk-neutral RL with general function approximation, which assumes that transition probabilities belong to a given function class. They establish sublinear regret bounds dependent on the eluder dimension of the given function class. [14] consider the first risk-sensitive RL with function approximation under the entropic risk measure, and [27] study RL with the iterated coherent risk measure with non-linear function approximation under a simulator assumption. Compared to [14] and [27], we investigate the function approximation for RL with Iterated CVaR measure without the simulator assumption.

RL with Human Feedback

[9] firstly propose the deep reinforcement learning models that are guided by human feedback. Then, there are many empirical works concentrating on the framework when the reward is parameterized as a neural network [37, 46, 53, 24, 29, 19]. Recently, [63, 58, 57] develop the theory of preference-based RLHF in the offline setting and present the Maximum Likelihood Estimation (MLE) for reward functions. [50] present the first online reward MLE algorithm in the risk-neutral RLHF for finite reward function set. Compared to their results, we formalize the first risk-sensitive RLHF problem, and present theoretical analysis for ICVaR-RL with general function approximation for infinite transition and reward function sets and comparison-based human feedback.

3 Preliminaries

3.1 Episodic Markov Decision Process (MDP)

We consider an episodic MDP parameterized by a tuple , where and represent the state space and action space respectively, is the number of episodes, and is the length of each episode. For step , is the transition kernel.

At the beginning of episode , an initial state is chosen by the environment. At each step , the agent observes the state , and chooses an action , where is a mapping from the state space to action space. For step , is the transition kernel which is unknown to the agent, and is the reward function which is deterministic and known to the agent.111This assumption is commonly considered in previous works [13, 14, 26, 61, 34]. Then, the MDP transitions to a next state that is drawn from the transition kernel . This episode will terminate at step , and the agent will advance to the next episode. This process is repeated episodes. The objective of the agent is to determine an optimal policy so as to maximize its performance (specified below).

3.2 Iterated CVaR RL

First, we give the definition of the Conditional Value-at-Risk (CVaR) operator which is firstly introduced in [3]. For a random variable with probability measure and given risk level :

| (1) |

which can be viewed as the expectation of the -worst-percent of the random variable . In this paper, we apply Iterated CVaR as the risk-sensitive criterion (similar to [13]).The MDPs with Iterated CVaR measure The Iterated CVaR MDP aims to maximize the objective which can be expressed as follows:

| (2) | ||||

where is the trajectory generated by policy and initial state . Maximizing this objective means finding the optimal policy to maximize the cumulative rewards obtained when transitioning to the worst -portion states at each step.

To evaluate the performance of RL algorithms, we adopt the regret minimization task. Consider the value function and Q-value function under the Iterated CVaR measure as the cumulative reward obtained when transitioning to the worst -portion states (i.e., with the lowest -portion values) at step

| (3) |

For simplicity, we use to denote the CVaR operator:

| (4) |

where . Let be the optimal policy which gives the optimal value function for any . Prior work [10] shows that always exists. In the regret minimization task, the agent aims to minimize the cumulative regret for all episodes, which is defined as

| (5) |

where is the policy taken by the agent in episode , and represents the sub-optimality of . Notice that when , the CVaR operator becomes the expectation operator, and Iterated CVaR RL degenerates to classic risk-neutral RL.

3.3 Linear and General Function Approximation

Assumption 1 (Linear function approximation [4, 14, 61]).

In the given episodic MDP , the transition kernel is a linear mixture of a feature basis , i.e., for any step , there exists a vector with such that

| (6) |

holds for any . Moreover, the agent has access to the feature basis .

In this paper, we assume that the given feature basis satisfying where for any bounded function and .222This assumption is also considered in [61, 62, 4, 14]. A episodic MDP with this type of linear function approximation is also called a linear mixture MDP.

In addition to the above linear mixture model, we also consider a general function approximation scenario, which is proposed by [4] and also considered in [14].

Assumption 2 (General function approximation).

In the given episodic MDP , the transition kernels where is a function class of transition kernels with the form . In addition, the agent has access to such function class .

Denote the bounded function set with form . With the given candidate set , we define a function class

| (7) |

where is a function with domain . For simplicity, we denote for function .

4 ICVaR-RL with Function Approximation

4.1 ICVaR-RL with Linear Function Approximation

In this section, we propose ICVaR-L (Algorithm 1), an optimistic value-iteration algorithm designed for ICVaR-RL with linear function approximation. ICVaR-L is inspired by the algorithm ICVaR-RM proposed in [13] for tabular MDPs, and incorporates two novel techniques: an -approximation of the CVaR operator and a new ridge regression with CVaR-adapted features for estimating the transition parameter .

Algorithm 1 presents the pseudo-code of ICVaR-L. ICVaR-L performs optimistic value iteration in Lines 3-9, where the key component is to calculate the optimistic Q-value function in Line 6 with an approximated CVaR operator and an exploration bonus term. Notice that directly calculating the CVaR operator is computationally inefficient. To maintain computational efficiency, we introduce a novel approximation of the CVaR operator:

| (8) |

where is an accuracy parameter, is a discrete -net of , i.e., . takes a supremum over the discrete finite set instead of a continuous interval , which can be computed efficiently. Notably, this approximation guarantees that the error between the approximated CVaR operator and the true CVaR operator is at most (shown in Lemma 1 in Appendix D.1).

We execute to play episode in Line 11, which is greedy with respect to the optimistic Q-value function. After that, we calculate the transition parameter estimator in Lines 12-14 by a new ridge regression:

| (9) |

Note that we consider as the regression features, which are different from used in previous risk-neutral linear mixture MDP works [61, 62]. The specific value of is determined in Line 12. Intuitively, the agent will explore the direction of the maximum norm of for every , such that every possible direction is eventually well explored.

Computation Efficiency

The efficient approximation technique and novel ridge regression enables us to effectively handle risk-sensitive RL problems with CVaR-type measures while maintaining computational efficiency. Moreover, the space complexity and computation complexity of ICVaR-L are and , respectively. Please refer to Appendix E for more detailed discussions.

We state the regret guarantee for Algorithm 1 as follows.

Comparison to Tabular ICVaR-RL

Theorem 1 states that ICVaR-L enjoys a regret bound

.

Intuitively, the exponential term of is due to the inherent hardness of the learning in risk MDPs, and the term expresses the complexity of the environment of MDPs.

In comparison to the regret bound for tabular ICVaR-RL in [13],

our result has the same order of dependence on and as the tabular setting, but does not depend on , which, in our setting, can be extremely large or even infinite.

The detailed proof of this theorem is given in Appendix D.

To bound the regret of Algorithm 1, we develop several novel analytical tools. (i) We present a novel lemma which shows that the error of approximating by is at most (Lemma 1 in Appendix D.1). By this lemma, we have a computationally efficient method to calculate an -approximation of the CVaR operator, which contributes to the computational efficiency of Algorithm 1. (ii) We establish a novel concentration argument in Lemma 2 in Appendix D.2, which exhibits that the transition parameter lies in an ellipsoid centered at the estimator . Then, we can bound the deviation between the transition parameter and the estimator for the CVaR operator . This result is formally present in Lemma 3 in Appendix D.2.

Moreover, we construct a hard-to-learn MDP instance for ICVaR-RL with linear function approximation, and establish a regret lower bound . The formal theorem (Theorem 4) and proof are detailed in Appendix F due to space limit. We can see that ICVaR-L achieves a nearly minimax optimal with respect to factors and , and the factor in our regret upper bound is unavoidable in general.

4.2 ICVaR-RL with General Function Approximation

In this section, we present our results for Iterated CVaR RL with general function approximation defined in Section 3.3. Specifically, we propose algorithm ICVaR-G (Algorithm 3). In each episode, ICVaR-G (i) estimates the confidence set of the transition kernels by constructing a set centered at the empirical mean with radius , and (ii) choose the policy with the highest possible ICVaR value in this confidence set of the transition kernels. The pseudo-code and detailed description of ICVaR-G presented in Appendix G due to space limit), and establish the following performance guarantee.

Theorem 2.

Suppose Assumption 2 holds and for some positive constant , we set the estimation radius . Then, with probability at least , the regret of ICVaR-G (Algorithm 3) satisfies

| (11) |

where is the eluder dimension of , and is the -covering number of function class under the norm .333For any , . By setting the dimensional parameter , we have .

The dominating term of the regret bound in Theorem 2 is , which enjoys the same order of , and as the result of ICVaR-L in Theorem 1. Moreover, in the case where Assumption 1 holds (i.e., linear function approximation), we have and . This means that we can recover the bound in Theorem 1. The main analytical novelty of Theorem 2 includes a novel elliptical potential lemma for a more fine-grained analysis of regret summation. We begin with bounding the deviation term , where is defined as

| (12) |

Intuitively, can be interpreted as the diameter of . Then, our new elliptical potential lemma (Lemma 9 in Appendix H.3) provides a more refined result by demonstrating in terms of . This result is tighter than existing result in previous works [42, 4, 14]. With the refined elliptical potential lemma, we can then perform a more fine-grained analysis of regret summation similar to the proof of Theorem 1. The detailed proof of Theorem 2 is deferred to Appendix H.

5 ICVaR-RL with Human Feedback

We further extend our results to investigate risk-sensitive RL in the human feedback (RLHF) setting. In this setting, the ground truth reward functions are unknown and the agent cannot observe numerical reward signals, but only receives comparison feedback. Specifically, the agent provides two trajectories to a human expert, and the expert judges which trajectory is better. Below we introduce the formal definition of comparison feedback, following previous risk-neutral RLHF works [50, 57, 58]. First, we assume that there is an underlying reward function which guides the feedback of human.

Assumption 3 (Underlying reward [9]).

There is a unknown underlying reward for some known infinite function set . Every reward consists of reward functions, i.e., , and satisfies that for every trajectory , we have . For a fixed trajectory , we define a regularized reward based on benchmark .

This underlying reward assumption is a common assumption for comparison feedback and widely used in [9, 63, 57, 58, 50]. Following [50], we assume that the human’s preference is drawn from a Bernoulli distribution parameterized by a general link function .

Assumption 4 (Comparison oracle [50]).

A comparison oracle takes in two trajectories and returns

where is a known link function, e.g., sigmoid function. Here is the human preference over . The output indicates , and indicates . Moreover, we assume that the link function satisfies the following properties:

-

•

Completeness: , and for any , we have .

-

•

Regularity: For any , we have for some constant .

Remark

The Bradley-Terry-Luce (BTL) model [7], a famous RLHF model, is exactly the case when the link function is chosen as the sigmoid function . The completeness assumption is based on the common knowledge that the consistency of the comparison between two trajectories should be upheld regardless of their given order. Thus, since , we have . The regularity assumption is common in the bandit literature [16, 30] and necessary for the existence of optimal policy [50].

Here we consider the general function approximation setting defined in Section 3.3. For given reward functions and possible transition kernel set , we define the optimistic value function recursively as follows.

| (13) |

Inspired by [49, 4, 14], we develop our risk-sensitive algorithm ICVaR-HF. As shown in Algorithm 2, in Line 1, we choose a benchmark trajectory by executing an arbitrary policy. In every episode, we select an estimated reward to maximize the optimistic value function in Line 4. We calculate the optimistic value and Q-value functions by value iteration, and determine the policy in Lines 5- 8. In Line 9, we execute the policy and generate the trajectory , and in Line 10, we feed trajectories to the comparison oracle. In Line 11, we adopt MLE to update the confidence reward function set , where we use the following log-likelihood function (which is also considered in [63, 57, 58, 50]):

| (14) |

In Lines 12- 15, we apply the transition estimation. to estimate the transition kernel in Line 13 by a novel distance function , and select a confidence set in Line 14, where belongs to with high probability (as detailed in Lemma 6 in Appendix H.2).

The construction of distance function is inspired by previous risk-neutral works [4, 14]. Recall the definition of function class in Eq. (7). Let be the domain of . We use the functions in to measure the difference between two probability kernels in . Specifically, for all , let maximize the diameter of by function :

| (15) |

Denote . Then, we can define the distance functions for . Equipped with this distance function, we can estimate by , where and for any . That is, is the one with the lowest gap to the sequence which contains the information of history trajectories. In addition, is the confidence set centered at with radius . The theoretical guarantee for ICVaR-HF is presented below.

Theorem 3.

For some positive constant , we set the estimation radius and for some constant . Denote Then with probability at least , the regret of Algorithm 2 satisfies

| (16) |

where the dimension parameters detailed in Theorem 2, and . Here is the eluder dimension of , and is the -bracketing number of under norm . 444The formal definition of bracketing number is detailed in Definition 4 in Appendix I.1, which is a common discretization for function class in MLE analysis [17, 32].

The full proof is presented in Appendix I. Notice that the regret bound for Algorithm 2 is sublinear to , making ICVaR-HF the first provably efficient algorithm for risk-sensitive RLHF. The first term of the regret is similar to the result in Theorem 2 for ICVaR-RL with general function approximation, which is the cost of learning the transition estimation. The second term is cost of learning the unknown reward functions, which requires our novel regret decomposition method to bridge the gap of the dislocation of the risk-sensitive value function and cumulative reward served for human feedback comparison oracle. Moreover, we apply the discretization method to to get the term (instead of the term in [50]), which remains finite even when is an infinite reward function set.

6 Conclusion and Future Works

In this paper, we investigate the risk-sensitive RL with an ICVaR objective, i.e., ICVaR-RL, with linear and general function approximations and human feedback. We propose two provably sample efficient algorithms, ICVaR-L and ICVaR-G for function approximation ICVaR-RL, by developing novel techniques including an efficient approximation of the CVaR operator, a new ridge regression with CVaR-adapted regression features, and a refined elliptical potential lemma. We also develop the first provably efficient risk-sensitive RLHF algorithm ICVaR-HF with general function approximation, and develop novel theoretical techniques for regret decomposition of risk-sensitive RLHF and the reward MLE for infinite reward set. This paper leaves several interesting directions for future works, e.g., further closing the gap between the upper and lower regret bound for ICVaR-RL with function approximation on and , and extending the risk-sensitive RLHF problem to more risk measures and more human feedback settings.

References

- [1] Yasin Abbasi-yadkori, Dávid Pál, and Csaba Szepesvári. Improved algorithms for linear stochastic bandits. Advances in Neural Information Processing Systems, 24, 2011.

- [2] Alekh Agarwal, Yujia Jin, and Tong Zhang. VOL: Towards optimal regret in model-free rl with nonlinear function approximation. arXiv preprint arXiv:2212.06069, 2022.

- [3] Philippe Artzner. Thinking coherently. Risk, 10:68–71, 1997.

- [4] Alex Ayoub, Zeyu Jia, Csaba Szepesvari, Mengdi Wang, and Lin Yang. Model-based reinforcement learning with value-targeted regression. In International Conference on Machine Learning, pages 463–474. PMLR, 2020.

- [5] Osbert Bastani, Jason Yecheng Ma, Estelle Shen, and Wanqiao Xu. Regret bounds for risk-sensitive reinforcement learning. Advances in Neural Information Processing Systems, 35:36259–36269, 2022.

- [6] Kang Boda, Jerzy A Filar, et al. Time consistent dynamic risk measures. Mathematical Methods of Operations Research, 63(1):169–186, 2006.

- [7] Ralph Allan Bradley and Milton E Terry. Rank analysis of incomplete block designs: I. the method of paired comparisons. Biometrika, 39(3/4):324–345, 1952.

- [8] Yinlam Chow, Aviv Tamar, Shie Mannor, and Marco Pavone. Risk-sensitive and robust decision-making: a cvar optimization approach. Advances in neural information processing systems, 28, 2015.

- [9] Paul F Christiano, Jan Leike, Tom Brown, Miljan Martic, Shane Legg, and Dario Amodei. Deep reinforcement learning from human preferences. Advances in neural information processing systems, 30, 2017.

- [10] Shanyun Chu and Yi Zhang. Markov decision processes with iterated coherent risk measures. International Journal of Control, 87(11):2286–2293, 2014.

- [11] Antonio Coronato, Muddasar Naeem, Giuseppe De Pietro, and Giovanni Paragliola. Reinforcement learning for intelligent healthcare applications: A survey. Artificial Intelligence in Medicine, 109:101964, 2020.

- [12] Pierre Devolder and Adrien Lebègue. Iterated var or cte measures: A false good idea? Scandinavian Actuarial Journal, 2017(4):287–318, 2017.

- [13] Yihan Du, Siwei Wang, and Longbo Huang. Provably efficient risk-sensitive reinforcement learning: Iterated CVar and worst path. In The Eleventh International Conference on Learning Representations, 2023.

- [14] Yingjie Fei, Zhuoran Yang, and Zhaoran Wang. Risk-sensitive reinforcement learning with function approximation: A debiasing approach. In International Conference on Machine Learning, pages 3198–3207. PMLR, 2021.

- [15] Carlo Filippi, Gianfranco Guastaroba, and Maria Grazia Speranza. Conditional value-at-risk beyond finance: a survey. International Transactions in Operational Research, 27(3):1277–1319, 2020.

- [16] Sarah Filippi, Olivier Cappe, Aurélien Garivier, and Csaba Szepesvári. Parametric bandits: The generalized linear case. Advances in neural information processing systems, 23, 2010.

- [17] Sara A Geer. Empirical Processes in M-estimation, volume 6. Cambridge university press, 2000.

- [18] Amelia Glaese, Nat McAleese, Maja Trebacz, John Aslanides, Vlad Firoiu, Timo Ewalds, Maribeth Rauh, Laura Weidinger, Martin Chadwick, Phoebe Thacker, Lucy Campbell-Gillingham, Jonathan Uesato, Po-Sen Huang, Ramona Comanescu, Fan Yang, Abigail See, Sumanth Dathathri, Rory Greig, Charlie Chen, Doug Fritz, Jaume Sanchez Elias, Richard Green, Soňa Mokrá, Nicholas Fernando, Boxi Wu, Rachel Foley, Susannah Young, Iason Gabriel, William Isaac, John Mellor, Demis Hassabis, Koray Kavukcuoglu, Lisa Anne Hendricks, and Geoffrey Irving. Improving alignment of dialogue agents via targeted human judgements, September 2022.

- [19] Caglar Gulcehre, Tom Le Paine, Srivatsan Srinivasan, Ksenia Konyushkova, Lotte Weerts, Abhishek Sharma, Aditya Siddhant, Alex Ahern, Miaosen Wang, Chenjie Gu, Wolfgang Macherey, Arnaud Doucet, Orhan Firat, and Nando de Freitas. Reinforced Self-Training (ReST) for Language Modeling, August 2023.

- [20] Astghik Hakobyan, Gyeong Chan Kim, and Insoon Yang. Risk-aware motion planning and control using cvar-constrained optimization. IEEE Robotics and Automation letters, 4(4):3924–3931, 2019.

- [21] Mary R Hardy and Julia L Wirch. The iterated cte: a dynamic risk measure. North American Actuarial Journal, 8(4):62–75, 2004.

- [22] Jiafan He, Heyang Zhao, Dongruo Zhou, and Quanquan Gu. Nearly minimax optimal reinforcement learning for linear markov decision processes. arXiv preprint arXiv:2212.06132, 2022.

- [23] John C Hull. Options futures and other derivatives. Pearson Education India, 2003.

- [24] Borja Ibarz, Jan Leike, Tobias Pohlen, Geoffrey Irving, Shane Legg, and Dario Amodei. Reward learning from human preferences and demonstrations in atari. Advances in neural information processing systems, 31, 2018.

- [25] David Isele, Alireza Nakhaei, and Kikuo Fujimura. Safe reinforcement learning on autonomous vehicles. In 2018 IEEE/RSJ International Conference on Intelligent Robots and Systems (IROS), pages 1–6. IEEE, 2018.

- [26] Chi Jin, Zhuoran Yang, Zhaoran Wang, and Michael I Jordan. Provably efficient reinforcement learning with linear function approximation. In Conference on Learning Theory, pages 2137–2143. PMLR, 2020.

- [27] Thanh Lam, Arun Verma, Bryan Kian Hsiang Low, and Patrick Jaillet. Risk-aware reinforcement learning with coherent risk measures and non-linear function approximation. In The Eleventh International Conference on Learning Representations, 2023.

- [28] Tor Lattimore and Csaba Szepesvári. Bandit algorithms. Cambridge University Press, 2020.

- [29] Harrison Lee, Samrat Phatale, Hassan Mansoor, Kellie Lu, Thomas Mesnard, Colton Bishop, Victor Carbune, and Abhinav Rastogi. RLAIF: Scaling Reinforcement Learning from Human Feedback with AI Feedback, September 2023.

- [30] Lihong Li, Yu Lu, and Dengyong Zhou. Provably optimal algorithms for generalized linear contextual bandits. In International Conference on Machine Learning, pages 2071–2080. PMLR, 2017.

- [31] Qinghua Liu, Alan Chung, Csaba Szepesvari, and Chi Jin. When Is Partially Observable Reinforcement Learning Not Scary? In Proceedings of Thirty Fifth Conference on Learning Theory, pages 5175–5220. PMLR, June 2022.

- [32] Qinghua Liu, Praneeth Netrapalli, Csaba Szepesvari, and Chi Jin. Optimistic MLE: A Generic Model-Based Algorithm for Partially Observable Sequential Decision Making. In Proceedings of the 55th Annual ACM Symposium on Theory of Computing, STOC 2023, pages 363–376, New York, NY, USA, June 2023. Association for Computing Machinery.

- [33] Volodymyr Mnih, Koray Kavukcuoglu, David Silver, Andrei A Rusu, Joel Veness, Marc G Bellemare, Alex Graves, Martin Riedmiller, Andreas K Fidjeland, Georg Ostrovski, et al. Human-level control through deep reinforcement learning. nature, 518(7540):529–533, 2015.

- [34] Aditya Modi, Nan Jiang, Ambuj Tewari, and Satinder Singh. Sample complexity of reinforcement learning using linearly combined model ensembles. In International Conference on Artificial Intelligence and Statistics, pages 2010–2020. PMLR, 2020.

- [35] Takayuki Osogami. Iterated risk measures for risk-sensitive markov decision processes with discounted cost. In Proceedings of the Twenty-Seventh Conference on Uncertainty in Artificial Intelligence, UAI’11, page 573–580, Arlington, Virginia, USA, 2011. AUAI Press.

- [36] Jonathan Theodor Ott. A Markov Decision Model for a Surveillance Application and Risk-Sensitive Markov Decision Processes. PhD thesis, 2010.

- [37] Long Ouyang, Jeffrey Wu, Xu Jiang, Diogo Almeida, Carroll Wainwright, Pamela Mishkin, Chong Zhang, Sandhini Agarwal, Katarina Slama, Alex Ray, et al. Training language models to follow instructions with human feedback. Advances in Neural Information Processing Systems, 35:27730–27744, 2022.

- [38] Yi Qi, Xingyu Zhao, and Xiaowei Huang. safety analysis in the era of large language models: a case study of stpa using chatgpt. arXiv preprint arXiv:2304.01246, 2023.

- [39] R Tyrrell Rockafellar, Stanislav Uryasev, et al. Optimization of conditional value-at-risk. Journal of risk, 2:21–42, 2000.

- [40] Stuart J Russell. Artificial intelligence a modern approach. Pearson Education, Inc., 2010.

- [41] Daniel Russo and Benjamin Van Roy. Eluder Dimension and the Sample Complexity of Optimistic Exploration. In Advances in Neural Information Processing Systems, volume 26. Curran Associates, Inc., 2013.

- [42] Daniel Russo and Benjamin Van Roy. Learning to optimize via posterior sampling. Mathematics of Operations Research, 39(4):1221–1243, 2014.

- [43] Ahmad EL Sallab, Mohammed Abdou, Etienne Perot, and Senthil Yogamani. Deep reinforcement learning framework for autonomous driving. arXiv preprint arXiv:1704.02532, 2017.

- [44] David Silver, Julian Schrittwieser, Karen Simonyan, Ioannis Antonoglou, Aja Huang, Arthur Guez, Thomas Hubert, Lucas Baker, Matthew Lai, Adrian Bolton, et al. Mastering the game of go without human knowledge. nature, 550(7676):354–359, 2017.

- [45] Silvestr Stanko and Karel Macek. Risk-averse distributional reinforcement learning: A cvar optimization approach. In IJCCI, pages 412–423, 2019.

- [46] Nisan Stiennon, Long Ouyang, Jeffrey Wu, Daniel Ziegler, Ryan Lowe, Chelsea Voss, Alec Radford, Dario Amodei, and Paul F Christiano. Learning to summarize with human feedback. In Advances in Neural Information Processing Systems, volume 33, pages 3008–3021. Curran Associates, Inc., 2020.

- [47] Richard S Sutton and Andrew G Barto. Reinforcement learning: An introduction. MIT press, 2018.

- [48] Kaiwen Wang, Nathan Kallus, and Wen Sun. Near-minimax-optimal risk-sensitive reinforcement learning with cvar. arXiv preprint arXiv:2302.03201, 2023.

- [49] Ruosong Wang, Russ R Salakhutdinov, and Lin Yang. Reinforcement learning with general value function approximation: Provably efficient approach via bounded eluder dimension. Advances in Neural Information Processing Systems, 33:6123–6135, 2020.

- [50] Yuanhao Wang, Qinghua Liu, and Chi Jin. Is RLHF More Difficult than Standard RL?, June 2023.

- [51] Zhicheng Wang, Biwei Huang, Shikui Tu, Kun Zhang, and Lei Xu. Deeptrader: a deep reinforcement learning approach for risk-return balanced portfolio management with market conditions embedding. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 35, pages 643–650, 2021.

- [52] Lu Wen, Jingliang Duan, Shengbo Eben Li, Shaobing Xu, and Huei Peng. Safe reinforcement learning for autonomous vehicles through parallel constrained policy optimization. In 2020 IEEE 23rd International Conference on Intelligent Transportation Systems (ITSC), pages 1–7. IEEE, 2020.

- [53] Jeff Wu, Long Ouyang, Daniel M. Ziegler, Nisan Stiennon, Ryan Lowe, Jan Leike, and Paul Christiano. Recursively Summarizing Books with Human Feedback, September 2021.

- [54] Wenhao Xu, Xuefeng Gao, and Xuedong He. Regret bounds for markov decision processes with recursive optimized certainty equivalents. arXiv preprint arXiv:2301.12601, 2023.

- [55] Lin Yang and Mengdi Wang. Reinforcement learning in feature space: Matrix bandit, kernels, and regret bound. In International Conference on Machine Learning, pages 10746–10756. PMLR, 2020.

- [56] Pengqian Yu, William B Haskell, and Huan Xu. Approximate value iteration for risk-aware markov decision processes. IEEE Transactions on Automatic Control, 63(9):3135–3142, 2018.

- [57] Wenhao Zhan, Masatoshi Uehara, Nathan Kallus, Jason D Lee, and Wen Sun. Provable offline reinforcement learning with human feedback. arXiv preprint arXiv:2305.14816, 2023.

- [58] Wenhao Zhan, Masatoshi Uehara, Wen Sun, and Jason D Lee. How to query human feedback efficiently in rl? arXiv preprint arXiv:2305.18505, 2023.

- [59] Zihan Zhang, Jiaqi Yang, Xiangyang Ji, and Simon S Du. Improved variance-aware confidence sets for linear bandits and linear mixture mdp. Advances in Neural Information Processing Systems, 34:4342–4355, 2021.

- [60] Heyang Zhao, Jiafan He, Dongruo Zhou, Tong Zhang, and Quanquan Gu. Variance-dependent regret bounds for linear bandits and reinforcement learning: Adaptivity and computational efficiency. arXiv preprint arXiv:2302.10371, 2023.

- [61] Dongruo Zhou, Quanquan Gu, and Csaba Szepesvari. Nearly minimax optimal reinforcement learning for linear mixture markov decision processes. In Conference on Learning Theory, pages 4532–4576. PMLR, 2021.

- [62] Dongruo Zhou, Jiafan He, and Quanquan Gu. Provably efficient reinforcement learning for discounted mdps with feature mapping. In International Conference on Machine Learning, pages 12793–12802. PMLR, 2021.

- [63] Banghua Zhu, Jiantao Jiao, and Michael I Jordan. Principled reinforcement learning with human feedback from pairwise or -wise comparisons. arXiv preprint arXiv:2301.11270, 2023.

- [64] Terry Yue Zhuo, Yujin Huang, Chunyang Chen, and Zhenchang Xing. Exploring ai ethics of chatgpt: A diagnostic analysis. arXiv preprint arXiv:2301.12867, 2023.

Appendix A Notations

In this appendix, we present the basic notations used in this paper.

For a positive integer , For a non-zero real number , the sign operator . For a -dimension vector and a positive definite matrix , be the norm of vectors in under a positive matrix . The operator . For two positive sequences , if there exists a positive constant such that for any , and if there exists satisfying for any . further suppresses the polylogarithmic factors in .

Measurable space and -algebra.

To discuss the performance of the algorithm on any MDP instance, we should establish the formal definition of the probability space considered in the problem. Since the stochasticity in the MDP is due to the transition, we define the probability space as and the probability measure as the gather of transition probabilities and the policy obtained from the algorithms. Thus, we work on the probability space , where is the product -algebra generated by the discrete -algebras underlying and . To analyze the random variable on step in episode , we inductively define as follows. First let for any . Then set for any and .

Appendix B The Objective of ICVaR-RL

The fourmulation investigated in this paper is iterated CVaR MDP, which is also studied by [21, 35, 10, 13]. The Iterated CVaR MDP aims to maximize the objective which can be expressed as follows:

| (17) | ||||

where for and is the initial state. Maximizing this objective means finding the optimal policy to maximize the cumulative rewards obtained when transitioning to the worst -portion states at each step. With this objective, we consider the regret minimization setting to evaluate the efficiency of our RL algorithms.

Application

Intuitively, the ICVaR-RL concerns the worst -portion situations at each step. This formulation is most suitable for safety-critical applications where there is a fatal failure probability that leads to catastrophic states at each decision stage. Our goal is to find a policy that guarantees safety even when disaster might happen at each transition. For example, consider the financial dynamic investment [12], where one needs design a risk-sensitive dynamic investment strategy. There is a small probability, at each time during execution, that the investor encouters a catastrophic states. In order to guarantee safety at each step, [12] studies iterated CVaR measure under a Black–Scholes–Merton market.

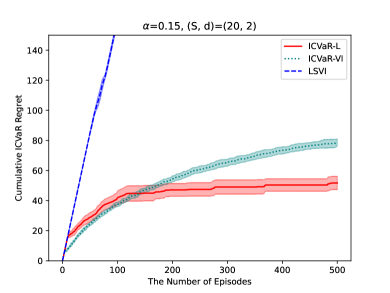

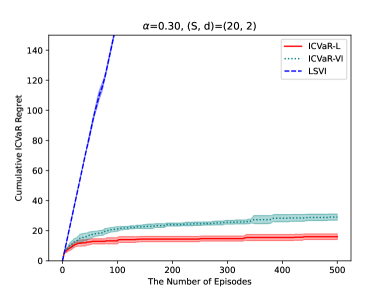

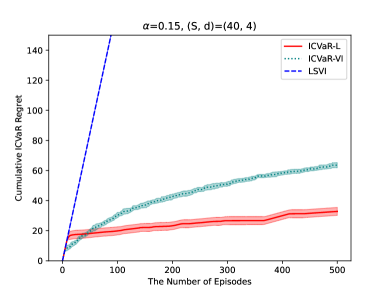

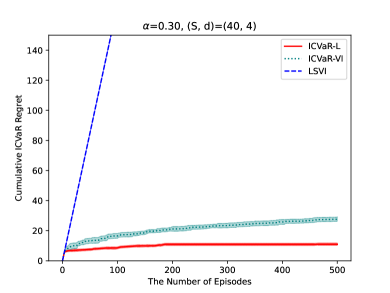

Appendix C Numerical Experiments For Algorithm 1

In this section, we evaluate the empirical performance of ICVaR-L (Algorithm 1). Since there is no other prior comparable efficient algorithms for ICVaR-RL with function approximation, we compare our algorithm with the ICVaR-VI algorithm [13] which is designed for ICVaR-RL in Tabular MDPs, and the LSVI algorithm [62] for risk-neutral RL in linear mixture MDPs. These two baselines are the closest comparable algorithms to ICVaR-L in ICVaR-RL with linear function approximation. The empirical performance is evaluated with respect to the cumulative regret defined in Eq. 5.

C.1 Experiment Environment

In our experiments, we consider a risk MDP with states space and action space . The agent will start at the initial state . In this state, the agent will not receive reward. Then with action , the agent will transfer to a conservative state , i.e. . Otherwise, the agent will transfer to an aggressive state with action , i.e., . With any action , the agent will receive no reward in state , in state , and in state .

The conservative state is associated with . The agent at will transfer into with equal probability by action . With sub-optimal action , the agent will not move in state , i.e. . In , the agent will receive reward and transfer back to with for any .

The aggressive state is associate with and disaster state . For any , we still have for any . However, the disaster state satisfies for any . With probability , the state and will transfer to , i.e. . Otherwise the agent will stay in .

In this MDP, the agent will receive a higher expected cumulative reward if it chooses at initial state to reach the aggressive state . However, it is not a risk-sensitive choice. This is because with small , the Iterated CVaR MDP prefer the conservative choice which gives stable return, where the aggressive choice may lead to a disaster state.

C.2 Numerical Results

We evaluate the cumulative ICVaR-type regret defined in Eq. 5 for algorithms ICVaR-L, ICVaR-VI [13] and LSVI[62], where ICVaR-L is our Algorithm 1 for ICVaR-RL with linear function approximation, ICVaR-VI is the algorithm for ICVaR-RL in tabular MDPs [13], and LSVI is the risk-neutral RL for MDP with linear function approximation [62].

In our experiment, we set , and . We explore MDPs with different sizes of state space and dimensions, denoted by . We set and to represent small and large MDPs, respectively, with as the feature dimension in Assumption 1. For each case, we conduct independent runs and report the average regret across runs with confidence intervals. The results are presented in Figures 1 and 2

As depicted in Figures 1 and 2, ICVaR-L consistently exhibits a sublinear regret with respect to the number of episodes, validating our theoretical result in Theorem 1. Notably, for each , the regret of ICVaR-L is significantly lower than those of other algorithms.

Comparing ICVaR-L with the tabular algorithm ICVaR-VI, our algorithm demonstrates faster learning of the optimal risk-sensitive policy, highlighting its efficiency in adopting linear function approximation. Furthermore, LSVI exhibits a nearly linear regret with the number of episodes, indicating its struggle to learn the optimal risk-sensitive policy.

These experimental evidences demonstrate the efficiency of ICVaR-L in risk-sensitive linear RL scenarios, providing empirical supports for its theoretical advancements.

Appendix D Proof of Theorem 1: Regret Upper Bound for Algorithm 1

In this section, we present the complete proof of Theorem 1.

First, we give an overview of the proof. In Appendix D.1, we bound the approximation error of CVaR operator from taking the supremum in finite set instead of interval in Eq. 8. We propose Lemma 1 which bounds the error of approximating by . In Appendix D.2, we establish the concentration argument with respect to our estimated parameter and the true parameter for step . Lemma 2 shows that with high probability, and Lemma 3 upper bounds the deviation term based on the concentration of . In Appendix D.3, Lemma 4 implies that our calculation of functions and is optimistic. Finally, we apply regret decomposition method and bound the regret of Algorithm 1 in Appendix D.4.

D.1 Error of CVaR Approximation

Below we show that the error of approximating the CVaR operator by the technique of taking supremum on the discrete set is small.

Lemma 1.

Assume the transition kernel is parameterized by transition parameter , i.e. for any . We denote

| (18) |

For a given constant and fixed a value function , we have

| (19) |

Proof.

First, we denote . Let . Then, we have by propterties of CVaR operator [39].

If , we have . It suffices to consider . Suppose for some positive integer .

By the property of CVaR operator, we have

| (20) |

Then, we assume , . Denote as . Noticing that , we have:

| (21) |

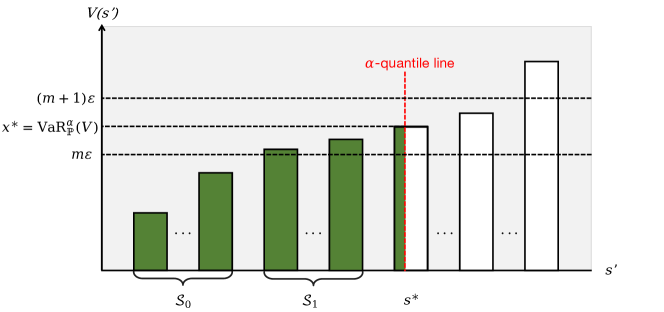

We give Figure 3 where we sort the successor states by in ascending order, and the red virtual line denotes the -quantile line. The black virtual line denotes the value of , and the sets of states , are marked on the figure.

Then, we have

| (24) | ||||

where the first inequality holds by triangle inequality, and the second inequality holds by the definition of , and the last one holds by the definition of .

Thus

| (25) | ||||

where equality holds since by definition. ∎

D.2 Concetration Argument

We show that our estimated parameter is a proper estimation of the true parameter for all episodes and steps . In fact, we can prove that falls in an ellipsoid centered at with high probability. In order to define the bonus term, we define a function that chooses the ideal based on given state-action pair by

| (26) |

Then, we denote as the maximum norm of for with a given state-action pair :

| (27) |

Lemma 2 (Concentration on ).

For , we have that with probability at least ,

| (28) |

holds for any and .

Proof.

First, we fixed an . Let and . We have is measurable, is measurable. And is a martingale difference sequence and -sub-Gaussian. We have

| (29) | ||||

Then, we can write

| (30) |

where first inequality is due to Eq. 29 and triangle inequality, and the second one comes from .

Combined with the concentration argument above, we can bound the deviation term of and with respect to the CVaR operator.

Lemma 3.

For , any and any , we have that with probability at least , the following holds:

| (32) |

D.3 Optimism

We use upper confidence bound-based value iteration as in [26, 61] to calculate the optimistic value and Q-value functions , , and construct the policy in a greedy manner. Then, we prove the optimism of below.

Lemma 4 (Optimism).

For , , and any , , with probability at least , we have

| (35) |

Proof.

We prove this argument by induction in . For , we have for any and . For , assume that with probability at least , for any and . Consider the case of . For any and , we have that with probability at least ,

| (36) | ||||

where the inequality comes from Lemma 1 and Lemma 3 which show that

| (37) |

and

| (38) |

Since for any and with probability at least . Then by union bound, we have holds for any and with probability at least . Take the supremum on the left and right side for , we have for any and with high probability. This implies the case of . By induction, we finish the proof. ∎

D.4 Regret Summation

In this section, we provide the proof of the main theorem. Here we follow the definitions in [13].

For a fixed risk level , value function , and a transition distribution , we denote the conditional probability of transitioning to from conditioning on transitioning to the -portion tail states as . is a distorted transition distribution of based on the lowest -portion values of , i.e.,

| (39) |

Moreover, let for real valued function .

Then, we consider the visitation probability of the trajectories. Let be the polices produced by ICVaR-L in the Let denote the probability of visiting at step of episode , i.e. the probability of visiting under the transition probability of the MDP with policy at step , starting with state initially. Similarly, we use to denote the conditional probability of visiting at step of episode conditioning on the distorted transition probability and policy at step .

Equipped with these notations, now we present our proof of the main theorem for ICVaR-RL with linear function approximation.

Proof of Theorem 1.

First we perform the regret decomposition. The following holds with probability at least :

| (40) | ||||

where the inequality holds by applying Lemma 3,1, and 20 to bound , and respectively. By recursively apply the same method of Eq. 40 to for , we have that with probability at least ,

| (41) | ||||

where we denote , then . The first inequality is exactly Eq. 40, the second inequality holds by recursively apply the same method of Eq.40 to for , and the last inequality holds by by Lemma 21. Then, we have that with probability at least ,

| (42) | ||||

We can bound term by similar approach in [13]. By Cauchy inequality, we have

| (43) | ||||

where the equality holds due to by definition. By Lemma 21, we have

| (44) | ||||

where denotes the distribution of pair playing the MDP with initial state and policy . Let , where is defined in Appendix A. We have is measurable. Set , we have , and is measurable. According to Lemma 19, we have the following holds with probability .

| (45) |

Notice that we can apply the elliptical potential lemma (Lemma 18) to the first term on the right hand side. Thus we can bound term in Eq. LABEL:Eq_999 with high probability. Combine the arguments above, we have that with probability at least ,

| (46) | ||||

where the first inequality is due to Eq. LABEL:Eq_999 and Eq. 43, the second inequality is due to Eq. 44, the third inequality holds by Eq. 45, and the last inequality holds by and elliptical potential lemma (Lemma 18). ∎

Appendix E Space and Computation Complexities of Algorithm 1

In this section, we discuss the space and computation complexities of Algorithm 1. We consider the setting of ICVaR-RL with linear function approximation, where the size of can be extremely large and even infinite. We will show that the space and computation complexities of Algorithm 1 are only polynomial in and . Noticing that is given by Theorem 1, we have is also polynomial in . We will include the size of into the complexities of Algorithm 1.

E.1 Space Complexity

Though in episode , we calculate the optimistic Q-value function for every -pair in Line 6 of Algorithm 1, we only need to calculate the Q-value and value functions for the observed states to produce the exploration policies in episode , and calculate the estimator for any in episode . Thus we need to store the covariance matrix , regression features for any and value . The total space complexity is .

E.2 Computation Complexity

By the above argument, we only need to calculate the optimistic value and Q-value functions for the observed states in episode . We show that the total complexity is by analyzing the specific steps of Algorithm 1 in two parts.

E.2.1 Calculation of the Optimistic Value and Q-Value Functions

We discuss the complexities of calculating optimistic value iteration steps (Lines 3-9) in this section.

First, we need to calculate for every action to produce the exploration policy at step in episode . In Line 6, calculating the approximated CVaR operator costs operations. Calculating costs operations since the number of non-zero elements of is at most . Computing the bonus term needs operations. Thus, calculating for any needs operations.

E.2.2 Calculation of the Parameter Estimators

Appendix F Regret Lower Bound for ICVaR-RL with Linear Function Approximation

In this section, we present the brief introduction to the idea of the lower bound instance and the complete proof of Theorem 4. The formal theorem for regret lower bound in ICVaR-RL with linear function approximation is presented below.

Theorem 4.

Let , , and an interger . Then, for any algorithm, there exists an instance of Iterated CVaR RL under Assumption 1, such that the expected regret is lower bounded as follows:

| (47) |

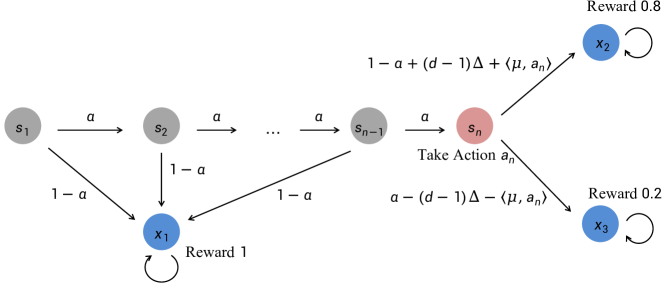

First we briefly explain the the key idea of constructing the hard instance. Consider the action space as and a parameter set , where is a small constant. The instance contains states with regular states and three absorbing states . Moreover, we uniformly choose a vector from . Set for any . Then, we can generate the transition probabilities and reward function shown in Figure 4 by properly define the feature mapping.

Intuitively, the structure of the instance in Firgure 4 is combined with a chain of regular states and a hard-to-learn bandit state (inspired by the construction for tabular MDP in [13]). With probability of , the agent can move from to for . Since we consider the worst--portion case under the Iterated CVaR criterion, the CVaR-type value function of only depends on the state for . At state , there is a linear-type hard-to-learn bandit (inspired by the construction for the lower bound instance of linear bandits [28]). By construction, the absorbing state is better than . Hence, the best policy at is . As a result, the agent needs to learn the positive and negative signs of every element of by reaching and pull the bandit.

Proof of Theorem 4.

We define the hard-to-learn instance (shown in Figure 4), which is inspired by the lower-bound instances constructed in [13, 61, 28]. For given integers , and risk level , consider the action space as and a parameter set , where is a constant to be determined. The instance contains states with regular states and three absorbing states . Moreover, we uniformly choose a from .

Then, we introduce the reward function of this instance. For any step , the reward function for any regular state with and action . The reward functions of absorbing states are , , and for any step and action .

For the transition kernels, set for any . For any and action , let and . Then the transition probabilities at regular state are and since we will only reach at step . For any action , let and . Then, we have and for any . For the absorbing states with , let and for . Thus for and any , .

In this instance, we have

| (48) |

| (49) |

Thus we have

| (50) |

where Then if Algorithm produces policy in episodes, we have

| (51) |

Since we uniformly choose from , we have

| (52) |

Denote be the conditional expectation on the fixed . For fixed , we denote which differs from at its -th coordinate.

Assume . By Pinsker’s inequality (Exercise 14.4 and Eq.12, 14 in [28]), we have the following lemma.

Lemma 5.

For fixed , we have

| (53) |

where denotes the joint distribution over all possible reward sequences of length under the MDP parameterized by .

Denote which differs from at its -th coordinate. Let be the probability to reach in each episode. By construction, we have . Denote as the Bernoulli distribution with parameter . Let . By definition of KL divergence, we have

| (54) |

Let where is a small constant such that . Then, we have

| (55) |

Combined with above equations, we can bound the expectation of the regret as:

| (56) | ||||

where the inequality holds by Lemma 5 and Eq. 55. Since , we have

| (57) |

∎

Appendix G Algorithm for ICVaR-RL with general function approximation: ICVaR-G

Overall, in each episode, the algorithm first calculates to estimate the transition kernel by a least square problem in Line 11 and selects a confidence set in Line 12, such that is likely to belong to with high probability (as detailed in Lemma 6 in Appendix H.2). Subsequently, the algorithm calculates the optimistic value functions in Line 5, 6 based on the selected set and chooses the exploration policy using a greedy approach in Line 7.

Appendix H Proof of Theorem 2: Regret Upper Bound for Algorithm 3

In this section, we present the full proof of Theorem 2 for ICVaR-RL with general function approximation under Assumption 2. The proof consists of two parts. In Appendix H.2, we establish the concentration argument which shows with high probability in Lemma 6. With the concentration argument, we can prove the optimism of and in Lemma 7, and further bound the deviation term for general setting in Lemma 8. In Appendix H.3, we present our novel elliptical potential lemma in Lemma 9, and prove Theorem 2 by regret decomposition and regret summation.

H.1 Definition of Eluder Dimension and Covering Number

To introduce the eluder dimension, we first define the concept of -independence.

Definition 1 (-dependence [41]).

For and function class whose elements are with domain , an element is -dependent on the set with respect to , if any pair of functions with satisfies . Otherwise, is -independent on if it does not satisfy the condition.

Definition 2 (Eluder dimension [41]).

For any , and a function class whose elements are in domain , the Eluder dimension is defined as the length of the longest possible sequence of elements in such that for some , every element is -independent of its predecessors.

Next we give the formal definition of the covering number. It is a widely used definition [4, 26, 14].

Definition 3 (Covering Number).

For the function set with norm and a given positive constatn , we can define the -net of as such that for any , we have satisfying . The -covering number is the minimum size of the -net of .

H.2 Concentration Argument

In this section, we apply the techniques firstly proposed by [41] and also used in [4, 14] to establish the concentration argument, which shows that is belong to our confidence set with high probability.

Lemma 6.

We have that for , with probability at least , holds for any and .

Proof.

Firstly we fix . By definition of and the delta distribution , we have

| (58) |

and . Let and . Then, we have that is measurable and is measurable. Note that is -sub-gaussian conditioning on , and .

Moreover, by definition of and function class , we have

| (59) |

Let . By Lemma 22, for any , with probability at least , for all , we have . Here

| (60) |

where is defined by Eq. 121 in Lemma 22, and is the covering number of with norm and covering radius . Since , we have .

Moreover, we have

| (61) | ||||

where the first inequality holds by for any , the second inequality holds by the triangle inequality, and the third equality is due to the definition of nor . Thus we have . Since

| (62) |

we have for any with probability at least .

Finally, by union bound, we have holds for any with probability at least . ∎

With the concentration property in Lemma 6, we can easily show the construction of and is optimistic in Algorithm 3.

Lemma 7 (Optimism).

If the event in Lemma 6 happens, we have

| (63) |

The following lemma upper bounds the deviation term by .

Lemma 8.

If the event in Lemma 6 happens,

| (65) |

Proof.

The left side holds trivially by the result of Lemma 6. We only need to prove the right side.

| (66) | ||||

where the first inequality holds by the property of supremum, and the second inequality holds by holds by under the event happens in Lemma 6, and the rest equalities are due to the definition of in Eq. 15 and in Eq. 12. ∎

H.3 Regret Summation

In this section, we firstly propose a refined elliptical potential lemma for ICVaR-RL with general function approximation. Then, we apply the similar methods in the proof of linear setting to get the regret upper bound.

Noticing that [42] presents a similar elliptical potential lemma (Lemma 5 in [42]) used in [4, 14] which shows that with respect to the term of . Inspired by this version of elliptical potential lemma, our Lemma 9 is a refined version which gives a sharper result.

Lemma 9 (Elliptical potential lemma for general function approximation).

We provide the elliptical potential lemma for general function approximation. We have

| (67) |

Proof.

Our proof is inspired by the proof framework of Lemma 5 in [42]. First we recall the definition of in the proof of Lemma 6, i.e, . For simplicity, let . Then for fixed , we know since for any probability kernel . Then, we can reorder the sequence such that . Then, we have

| (68) |

for some . Since the second term is less than trivially, we only consider the first term. Then, we fix and let and we have

| (69) |

By Lemma 23, we have

| (70) |

For simplicity, we denote . Since , we have , which implies . By Eq. 70, we have . Notice that this property holds for every fixed . Combined with , we have

| (71) | ||||

where the first inequality is due to Eq. 68, the second inequality holds by for any and , and the last inequality is due to the property of harmonic series. Sum over Eq. 71 for , we get the result. ∎

Combined by this refined elliptical potential lemma, we can prove the main theorem of ICVaR-RL with general function approximation.

Proof of Theorem 2.

This proof is similar to the proof of Theorem 1 with tiny adaption. Firstly, by standard regret decomposition method, we have that with probability at least , the event in Lemma 6 happens and

where the inequality holds by Lemma 8 and Lemma 20. Here is defined above in Eq.39. Next we use the techniques of the proof in Section D.4 to bound the regret. Specifically, we have

| (72) |

This implies that the regret of the algorithm satisfies

| (73) | ||||

with probability at least . Here is defined in Appendix D.4. By Cauchy inequality, we have

| (74) | ||||

where the equality holds due to by definition. By Lemma 21, we have

| (75) | ||||

where denotes the distribution of pair playing the MDP with initial state and policy . Since , by Lemma 19, we have

| (76) |

Apply Lemma 9 to , we can bound the regret with probability at least

| (77) | ||||

where , the first inequality holds by Eq. 75, 76, and the second inequality holds by Lemma 9. ∎

Appendix I Proof of Theorem 3: Regret Upper Bound for Algorithm 2

In this section, we present the proof of Theorem 3. First we give some notations used in this section. We denote presents the value function for MDP with transition kernels and reward function . Thus we define , the regret can be write as

| (78) |

Overall, we bound the reward estimation error in Appendix I.1 and apply the regret decomposition method to bound the regret summation in Appendix I.2.

I.1 Reward Estimation Error

Definition 4 (Bracketing number, [17, 32]).

Given a function set , let and be two functions belonging to . Suppose that . The interval denotes the set of all functions satisfying pointwisely. is referred to as an -bracket set if the norm according to a given norm . Then the minimum number of the -bracket sets needed to cover is defined as the bracketing number , where represents the chosen norm. And we denote is a member of the minimum -brackets covering as the -bracketing covering of .

In this section, we denote as the -bracketing of with norm and the bracketing number is . Then for every , there exists a such that and for every .

Then we present the reward concentration in the following lemma.

Lemma 10.

For and some constant , with probability at least , we have

| (79) |

Proof.

The proof of this lemma is inspired by Lemma D.1 in [50]. Notice that [50] only deal with the setting when is a finite set, and in our problem the reward function set might be infinite. We expand the proof to infinite situations inspired by [32, 31] which present the MLE analysis to transition probabilities and including the discretization techniques such as -bracketing number in partially observed MDPs (POMDPs).

First we denote as the distribution of trajectory when the agent starts with the initial state and executes the policy . And we use to represent the set of all possible trajectories. For every , we have

| (80) | ||||

where denotes the probability of generating trajectory by executing the policy . If we fix some , we have

| (81) | ||||

where the first equality comes from the orcale of human feedback defined in Assumption 4, the second equality comes from the definition of in Eq. 14, and the third and forth equalities are due to the completeness of link function in Assumption 4. Thus we have

| (82) |

Thus, by Markov’s inequality, we have

| (83) |

Taking a union bound for all and , for some constant , we have

| (84) |

Since we have for every , there exists , and for every , we have

| (85) |

Then we have

| (86) |

which implies

| (87) |

This inequality instantly gives the result. ∎

Lemma 11.

For and positive constant , we have for every holds with probability at least .

Proof.

Recall the definition of and log likelihood function . By lemma 10 conditional on event , we have the following holds for every

| (88) |

Then we have . ∎

Lemma 12.

For constant , we have the following inequality holds with probablity at least for every

| (89) |

where is the positive lower bound of the gradient of link function .

Proof.

The proof of this lemma is inspired by the proof of Proposition 14 in [31] which develops the analytic tools for transition probabilities’ MLE in POMDPs. In our works, we develop the techniques for reward MLE.

By Lemma 15 in [31] and the inquality , we have with probability at least , the following inequality holds for every .

| (90) |

By algebra, we have

| (91) |

Recall the regularity assumption of link function , we have . Thus we have

| (92) | ||||

Moreover, for every , there exists a such that for every . Thus we have

| (93) |

This implies the conclusion. ∎

Inspired by the study of the relation between eluder dimension and sample complexity in [41], we derive the following lemma which is similar to Proposition 3 in [41].

Lemma 13.

For all and , we have

| (94) |

Proof.

This proof is inspired by the proof of Proposition 3 in [41]. We denote . If for some fix , then we have . If is -dependent on a subsequence of , then we have

| (95) |

Therefore, if is -dependent on disjoint subsequences of , we have

| (96) |

Then we know that . Denote . We want to prove the following claim:

Claim

For any , there is some in sequence that is -dependent on at least disjoint subsequences of .

For an integer with , we will construct disjoint subsequences . First let . If is -dependent on , we have done. Otherwise select a subsequence such that is -independent with respect to . Then add into . Repeat this process for with until is -dependent on each subsequence or . If is -dependent on , then we get the result. If , then . Since every element in is -independent of its predecessors by construction, we have for every by the definition of eluder dimension. Thus for . Thus cannot be -independent with respect to any by the definition of eluder dimension. Then we have must be -dependent on each subsequence, which proves our claim.

Take as a subsequence consisting of elements satisfying . Then each is -dependent on disjoint subsequences of . By above argument, we know . Equip with the claim above, there exist a such that is -dependent on at least disjoint subsequences of . This shows that Then we have

| (97) |

which implies the result. ∎

Lemma 14.

For , the error of the reward estimation can be bounded as follows with probability at least .

| (98) |

Proof.

This proof is very similar to the proof of Lemma 9. Let and . Then we need to bound . First we can reorder the sequence such that . Then we have

| (99) |

where satisfying that . Fix some and denote , we have

| (100) |

By Lemma 13 we have

| (101) |

Since , we have . Moreover, with Eq. 101, we have

| (102) |

Since is chosen arbitrary, we have for every . By definition, for every . Therefore,

| (103) | ||||

∎

I.2 Regret Summation

Lemma 15.

With probability at least for given constant , we have for every and .

Lemma 16.

Given a positive constant . With probability at least , we have the following inequality holds for every .

| (106) | ||||

Combine with above lemmas, we are ready to prove Theorem 3.

Proof of Theorem 3.

By Lemma 15, we have with probability at least ,

| (109) | ||||

where the second equality is due to is fixed. Denote . Consider the regret decomposition for every episode , by Lemma 16, we have

| (110) | ||||

Bounding the first term is almost same as the proof of Theorem 2, which also gives an insight into bounding . Therefore, by Cauchy-Schwartz inequality, we have

| (111) | ||||

where denotes the distribution of pair playing the MDP with initial state and policy . Since , by Lemma 19, we have with probability at least ,

| (112) |

Apply Lemma 9, we have with probability at least ,

| (113) | ||||

Bounding the second term shares almost the same techniques as bounding . Thus we have with probability at least ,

| (114) | ||||

Notice that by Lemma 19, we have with probability at least ,

| (115) |

Since we have bounded the reward estimation error in Lemma 13, we can bound by

| (116) | ||||

where the inequality holds with probability at least

Appendix J Auxiliary Lemmas

In this section, we present several auxiliary lemmas used in this paper.

Lemma 17 (Hoeffding-type Self-normalized Bound, Theorem 2 in [1]).

Let be a filtration. Let be a real-valued stochastic process such that is -measurable and is conditionally -sub-Gaussian for some . Let be a -valued stochastic process such that is -measurable. Assume that is a positive definite matrix. For any , define

Then for any , with probability at least , for all ,

Lemma 18 (Elliptical Potential Lemma, Lemma 11 in [1]).

For , sequence , and , assume for all . If , we have that

| (118) |

Lemma 19 (Lemma 9 in [59]).

Let be a filtration. Let be a sequence of random variables such that almost surely, that is measurable. For every , we have

| (119) |

Lemma 20 (Lemma 11 in [13]).

For any , distribution , and functions such that for any .

Lemma 21 (Lemma 9 in [13]).

For any functions , , and such that .

| (120) |

where denotes the conditional probability of visiting at step of episode , conditioning on transitioning to the worst -portion successor states (i.e. with the lowest -portion values at each step .

Lemma 22 (Theorem 6 in [4]).

Let be a sequence of random elements, for some measurable set and . Let be a set of real-valued measurable function with domain . Let be a filtration such that for all , is measurable and such that there exists some function such that holds for all . Let . Let be the -covering number of at scale . For , define .

If the functions in are bounded by the positive constant . Assume that for each , is conditionally -sub-gaussian given . Then for any , with probability , for all , , where

| (121) |