A controller-stopper-game with hidden controller type

Abstract: We consider a continuous time stochastic dynamic game between a stopper (Player , the owner of an asset yielding an income) and a controller (Player , the manager of the asset), where the manager is either effective or non-effective. An effective manager can choose to exert low or high effort which corresponds to a high or a low positive drift for the accumulated income of the owner with random noise in terms of Brownian motion; where high effort comes at a cost for the manager. The manager earns a salary until the game is stopped by the owner, after which also no income is earned. A non-effective manager cannot act but still receives a salary. For this game we study (Nash) equilibria using stochastic filtering methods; in particular, in equilibrium the manager controls the learning rate (regarding the manager type) of the owner. First, we consider a strong formulation of the game which requires restrictive assumptions for the admissible controls, and find an equilibrium of (double) threshold type. Second, we consider a weak formulation, where a general set of admissible controls is considered. We show that the threshold equilibrium of the strong formulation is also an equilibrium in the weak formulation.

1 Introduction

We consider a continuous time two player stochastic game between a stopper (Player 1) and a controller (Player 2). The controlled process is given by

| (1) |

where is a process chosen by the controller, is a Brownian motion, is an independent Bernoulli random variable with indicating whether the controller is effective (or active) or not, and is a constant. On the other, based on the observations of , the stopper selects a stopping time at which the game ends.

For a given stopping-control strategy pair the reward of the stopper is

| (2) |

and the reward of the controller is

| (3) |

where is a constant (discount rate).

The control process values are restricted to take one of two constants at each time , where we assume that . The model is further specified in Sections 2 and 3 where we also define notions of (Nash) equilibria corresponding to both players wishing to maximize their respective rewards.

The interpretation is that is the accumulated income of Player who wants to maximize the discounted accumulated income by selecting a time at which the game ends. This income has a positive drift if and a negative drift if ; however, the outcome of cannot be observed by Player who must make the stopping decision based only on observations of . The stopping decision will in equilibrium, as we will show, be made based on the probability that Player assigns to the event , which is dynamically updated based on the observations of .

On the other hand, an active Player , i.e., in case , can affect the drift of the income by dynamically selecting the effort level, i.e., , and thereby, as we shall see, affect the probability that Player assigns to the event . The accumulated income of an active Player is based on the constant income rate minus the cost rate which is zero when effort is low and positive otherwise; cf. (3). Moreover, an active Player wants to dynamically select the effort level in order to maximize the discounted accumulated income of Player until Player ends the game. Player must therefore consider the trade-off between exerting a large effort, which is costly, and a small effort, which implies no cost but decreases the probability that Player assigns to compared to the large effort. An inactive Player cannot act at all.

In line with the interpretation above, our ansatz to this problem is to use stochastic filtering methods to search for an equilibrium which depends on the conditional probability of the event based on the observations of , which corresponds to Player 1’s continuously updated belief about Player 2 being active. Indeed, we find such an equilibrium of (double) threshold type meaning that we find two thresholds such that an equilibrium is that Player exerts the smaller effort when the conditional probability of is above and the larger effort when the conditional probability is below , and Player stops the game whenever the conditional probability of falls below ; see Remark 6 for details.

We study this game in an increasing order of generality regarding the set of admissible control strategies. First using a strong formulation and second using a weak formulation of the game. The same threshold equilibrium is obtained in both formulations.

-

•

Strong formulation: In the strong formulation we admit control strategies only of Markovian type in the sense that , where (a deterministic function) and is defined as a process which in equilibrium coincides with the conditional probability that the stopper assigns to . The process is here the strong solution to a particular stochastic differential equation; see the beginning of Section 2 for details. In this formulation the main results are: (i) we provide a verification theorem for a double threshold equilibrium, and (ii) we prove that a double threshold equilibrium exists under certain parameter restrictions.

-

•

Weak formulation: In the weak formulation, admissible control strategies correspond to a general set of stochastic processes adapted to a filtration generated by taking values in . Here, however, we start by defining as a Brownian motion and we achieve a controlled process analogous to the one in (1) by means of a measure change, with which we define the reward functions and a corresponding equilibrium; see Section 3 for details. The main result is that the double threshold equilibrium found in the strong formulation is also an equilibrium in the weak formulation, i.e., when allowing a larger set of admissible control strategies.

In Section 1.1 we survey related previous literature and clarify the contribution of the present paper. In Section 1.2 we present stochastic filtering arguments which are relevant to the subsequent sections. The strong formulation of our game is studied in Section 2. In particular, the beginning of Section 2 specifies the strong formulation further, Section 2.1 contains a heuristic derivation of an equilibrium candidate, Section 2.2 reports the verification result, and Section 2.3 reports the equilibrium existence result. The weak formulation is studied in Section 3.

1.1 Previous literature and contribution

The problem studied in the present paper belongs to a new class of dynamic stochastic control and stopping games with the key feature being that the player’s may be ghosts (cf. [7]) in the sense that a player does not necessarily exist, or equivalently is not activity, or not effective. This ghost feature was first studied in [7], where a two-player stopping game is studied and the term ghost was introduced. In [10], a controller-stopper-game where the stopper faces unknown competition in the form of a ghost controller is studied, in the context of a fraud detection application. In [11], a de Finetti controller-stopper-game (of resource extraction) where the controller faces unknown competition in the form of a stopper ghost with the option to extract all the remaining resources instantaneously is studied.

From a game theoretic interpretation our main contribution is that our game is a non-zero-sum game where the player objectives agree in the sense that both players would benefit if the hidden controller were revealed (in the case of an active Player ). In this sense, both players are not exactly competing against each other, but rather aiming on finding an agreement that would benefit both. Typically, such situations are complicated since it makes existence of (non-trivial) Nash equilibria sensitive to the specific player payoffs. This stands in contrast to previously studied games of these type, see e.g., [10] where the profit of one player is an immediate loss for the other, which results in opposite player objectives in the sense that the controller aims at staying hidden, which is the opposite to our situation.

From a technical view-point, our main contribution is twofold. First, we constrain the control process to take values in a finite set, i.e., . This means that we can interpret the problem of the controller as an optimal switching problem without a cost for switching, implying that switching (between the two control values ) may occur infinitely often, which stands in contrast to the usual formulation of optimal switching problems; see e.g., [25] and the references therein. Second, we consider a weak formulation for these types of games, based on defining the state process as a Brownian motion, and the reward functions in terms of measure changes. Then we show that the Nash equilibrium in Markovian strategies (i.e., in the strong formulation), is also a Nash equilibrium in the weak formulation.

This weak approach is inspired by [9], which formulates a weak approach in the study of a sequential estimation problem, where the optimizer can choose a bounded control representing the rate at which the information is received and a stopping time at which the experiment ends, in particular, [9] considers an optimization problem and not a game. Weak solution approaches to dynamic stochastic games have previously been considered in a variety of recent papers; see e.g., [26], and [27] which contain surveys of the related literature.

In a broader context, the problem studied in the present paper can be regarded as a controller-stopper-game under incomplete information. Controller-stopper-games were first studied for zero-sum games. In [19] a zero-sum game between a controller and a stopper is studied for a one-dimensional diffusion, whereas [1] considers the game in a multidimensional setting. In [24] a zero-sum game between a stopper and a controller choosing a probability measure is studied. Singular controls for zero-sum controller-stopper-games were studied in [16] for a one-dimensional diffusion and in [3, 4] for the multidimensional setting. In [17] zero-sum controller-stopper-games with singular control are studied for a spectrally one-sided Lévy process. A zero-sum game between a stopper and a player controlling the jumps of the state process is studied in [2].

Stochastic games under asymmetric information were first considered in [5], which considers a zero-sum stochastic differential game between two controllers. In [6] path-wise non-adaptive controls are studied for a zero-sum game between two controllers. An asymmetric information Dynkin game with a random expiry time observed by one of the players is studied in [20]. In [15] a two-player zero-sum game under asymmetric information is considered where only one player can observe the underlying Brownian motion, while the second the player only observes the strategy chosen by the first player. A zero-sum game where both players observe different processes is studied in [14]. Non-Markovian zero-sum games under partial information are also considered; see e.g., [8].

For a background regarding the interpretation of our game as a dynamic signaling game between an owner (Player 1, the stopper) and a manager (Player 2, the controller) see [12] and the references therein.

1.2 The underlying stochastic filtering theory arguments

The present section contains a brief account of the stochastic filtering arguments that underlie the analysis of the present paper. The section is included as an informal and heuristic precursor for content of the subsequent sections. A formal result in the direction of this section is Proposition 5.

Let us first consider the perspective of the stopper. Assuming that the controller uses a control strategy we obtain—using standard filtering theory; see e.g., [21, Chapter 8.1]—that the innovations process defined by

is a Brownian motion with respect to , where is defined as the smallest right-continuous filtration to which is adapted.

Relying again on basic filtering theory, and arguments similar to those in [10, Section 2.1], we find that if the strategy is -adapted—we shall later see that an equilibrium with this property can indeed be found—then the conditional probability (process) that the stopper assigns to the controller being active, i.e., is given by the stochastic differential equation (SDE)

| (4) |

Note that the observations above rely implicitly on the assumption that the control strategy is fixed in the sense that the stopper knows which process () that the controller uses. However, in order to verify that a candidate equilibrium strategy is indeed an equilibrium strategy (cf. Definition 2 below) we must be able to analyze what happens to an equilibrium stopping strategy—which as we shall see will be determined as a threshold time in terms of the conditional probability process—when the controller deviates from the candidate equilibrium strategy.

To this end observe that if we consider an -adapted candidate equilibrium strategy and an arbitrary admissible deviation (control) strategy , and now define a process to be given by

| (5) |

then depends, of course, on the equilibrium candidate as well as the deviation strategy . However, using the observations above it is also directly verified that in the special case of no deviation (i.e., with ). In other words, defined as in (5) coincides with the conditional probability process in the case of no deviation, but it also tells us how the controller affects in the case of deviation, and we may therefore, as we will see, use this definition of to find an equilibrium.

2 Strong formulation

Let be a probability space supporting the standard one-dimensional Brownian motion and the independent Bernoulli random variable , where we recall that .

Observe that if both the candidate equilibrium strategy and the deviation strategy in (5) are of Markov control type, specifically in the sense that and where , then in (5) will be given by the SDE

| (6) |

(Depending on the context we will, to ease notation, sometimes write and sometimes write .)

In the present section we will restrict the set of admissible control strategies to be of Markov control type. Recall that Section 3 contains a weak formulation of our game where we relax the notion of admissible strategies to be a set of general stochastic processes (taking values in ). By restricting to Markov controls we ensure that is obtained as the strong solution to (6); see Proposition 20 in Appendix A. Furthermore, using the definition of in (1) as well as (6) we note that the dynamics of can be written as

| (7) |

and that is -adapted. Formally, we restrict the set of admissible control strategies to be of Markov control type by identifying an admissible control strategy with a deterministic function according to , where is given by (6), and where satisfies the conditions of Definition 1 (which also defines the set of admissible stopping strategies).

Definition 1 (Admissibility in the strong formulation).

-

•

A Markov control (deterministic function) is said to be an admissible control strategy if it is RCLL (right-continuous with left hand limits). The set of admissible control strategies is denoted by .

-

•

A stopping time is said to be an admissible stopping strategy if it is adapted to . The set of admissible stopping strategies is denoted by .

To clarify, a control process is obtained by

where , with , is given by (6); i.e., a control process depends generally on a pair of admissible strategies which represents the candidate equilibrium strategy and the deviation strategy , respectively.

In line with Section 1, both players want to maximize their respective rewards and we define our Nash equilibrium accordingly.

Definition 2 (Nash equilibrium).

Remark 3.

In line with the usual interpretation of a Nash equilibrium we note that the first condition in (8) implies that deviating from the equilibrium is sub-optimal for the stopper, and that the second condition implies the same for the controller. Note also that the appearance of the equilibrium control in the right hand side of the second condition in (8) is due to the role that it plays for the determination of also when the controller deviates from the equilibrium, cf. (6).

Remark 4.

A connection between our equilibrium definition and a fixed-point in a suitable best response mapping can be established. In fact we will use this connection when proving the equilibrium existence result Theorem 10. Let be any given admissible strategy pair. Then we may, in line our equilibrium definition, define the (point-to-set) best response mapping of the stopper as

while the (point-to-set) best response mapping of the controller is given by

It is then immediately clear that our equilibrium definition corresponds to a fixed-point in the best response mapping

In the following result we conclude this section by establishing that does indeed correspond to the conditional probability of an active controller, i.e., , in case the controller does not deviate from an equilibrium (candidate).

Proposition 5.

Proof.

This proof is similar to that of [10, Proposition 11]. Define . Then , since is -adapted. Relying on standard filtering theory (see e.g., [21, Chapter 8.1] and arguments similar to those in the proof of [10, Proposition 11]), it can now be seen, for , that

where

is a Brownian motion with respect to . Hence, by the definition of in (1) it is directly seen that satisfies the SDE

Recalling the definition of in (6), we observe that and are both strong solutions to the same SDE in case . The results follow. ∎

2.1 Searching for a threshold equilibrium

The aim of the present section is to search for an equilibrium of threshold type in the sense that the equilibrium strategy pair satisfies where

| (10) | ||||

| (11) |

with .

Remark 6.

The (double) threshold strategy pair defined by (10)–(11) corresponds to (i) stopping the first time that —whose dynamics is in this case given by (6) with —falls below , and (ii) the controller using the control process , which is equal to the small controller rate when and the large controller rate when .

We remark that the content of this section is mainly of motivational value and that a corresponding formal result is the verification theorem reported in Section 2.2, below.

2.1.1 The perspective of the controller

Given a candidate equilibrium strategy and supposing that the stopper uses a candidate equilibrium threshold strategy of the kind (10) where , the controller faces the optimal control problem

| (12) |

where we recall that is given by (6); however, due to the conditioning on in the controller reward (see (3)) we may here set in (6).

Indeed writing and relying on (3) with the underlying process in the representation (6) with , we expect, using the usual dynamic programming arguments, that the optimal value satisfies

for all and , while equality should hold in case , i.e.,

We will from now on ease the presentation by sometimes writing e.g., instead of . By subtracting one of the two equations above from the other we obtain

which is equivalent to

| (13) |

We conclude that if is an equilibrium then must satisfy (13) for and all .

We now first consider the case with the deviation (if , then (13) trivially holds). In this case (13) becomes

which is equivalent to

| (14) |

Supposing that is decreasing (this is under additional assumptions on the model parameters verified in Proposition 27, below) we see, for any given equilibrium strategy , that if we can find a value for that gives equality in (14), then it is a lower threshold for the set of points where is possible; i.e., for any smaller than this threshold we must have . The interpretation is that if the stopper assigns a small probability to an active controller then the controller will control with the large rate .

We now consider the case and obtain, similarly to the above, the condition

which in turns gives the condition

| (15) |

Similarly to the analysis of (A) above, this gives us an upper threshold for where is possible; i.e., for any exceeding this threshold we need .

In order for (14) and (15) to be feasible conditions we need that minus is non-negative, which is is directly verified. Hence, with the observations above as a motivation we will search for an equilibrium strategy of the threshold type (11), where the threshold switching point is a such that

| (16) |

Note that (16) indicates that there may be multiple Nash equilibria, since every satisfying (16) results in an equilibrium candidate strategy for the controller. As our equilibrium controller candidate we will, however, consider a switching point that corresponds to equality in the right hand side inequality in (16). More precisely, we will search for an equilibrium controller strategy given by (11), with satisfying

| (17) |

Let us lastly note that if the players use a threshold strategy pair , defined as in (10)–(11), with , then it can be shown that the corresponding value for the controller, i.e.,

where is given by (6) with , coincides with defined as the solution to

| (18) | ||||

Indeed we will in the subsequent analysis show that we may choose a stopper-controller threshold pair which is an equilibrium with a controller value given by (18), under certain parameter assumptions; see Theorems 8 and 10.

Remark 7.

Note that (18) is a boundary value problem on , whose solution has been extended to be equal to zero on . The boundary conditions of (18) follow immediately from the boundary cases and , which result in immediate stopping (corresponding to no income for the controller) and never stopping (corresponding to the income rate earned forever), respectively.

2.1.2 The perspective of the stopper

If the players use a threshold strategy pair , defined as in (10)–(11), with , then the corresponding value for the stopper is

where is given by (6) with . However, since we may equivalently consider the dynamics of in the representation (9); cf. Proposition 5.

Relying again on Proposition 5 we may moreover use that and iterated expectation to replace in the stopper reward with ; in other words we have the representation

where is given by (9). Based on this it can be shown that the stopper reward coincides with defined as the solution to

| (19) | ||||

Note that (19) is also a boundary value problem on whose solution has been extended to be equal to zero on . The boundary conditions of (19) can be interpreted using arguments similar to those in Remark 7.

2.2 A threshold equilibrium verification theorem

Here we present our first main result, which is a verification theorem based on the equilibrium conditions that were informally derived in Section 2.1.

Theorem 8 (Verification).

Let satisfy . Let and be solutions to the boundary value problems (18) and (19). Suppose that

| (I) | ||||

| (II) | ||||

| (III) | ||||

| (IV) |

Then the stopper-controller strategy pair corresponding to

| (20) |

is a Nash equilibrium (Definition 8). Moreover, and correspond to the equilibrium values for the stopper and the controller respectively, i.e.,

Remark 9.

Proof.

(of Theorem 8.) For ease of exposition we write in this proof and .

Optimality of . Note that (I) and (II), together with the boundary condition , imply that . Thus, using the ODE in (19), we obtain

| (21) |

Let be fixed number. Relying on Proposition 5 which implies that solves (9), as well as (II) and Itô’s formula we obtain for an arbitrary stopping time that

where the Itô integral is a martingale since the integrand is bounded. Now use (19) and (21) to see that

| (22) |

Using the above together with Proposition 5 and iterated expectation, and (I), we find that

By sending and relying on dominated convergence we thus obtain

Using similar arguments as above with we find, by observing that we have equality in (22) for , that

(Note that the equality above is trivial when , since for ).

Using that is bounded together with we find using dominated convergence that the first expectation above converges to zero as . Hence, using dominated convergence again, we find that

We conclude that

Optimality of . The controller reward (3) is conditioned on . Hence, in order to find the optimal strategy for the controller, we consider the process defined by (6) with ; in particular, if the controller selects an admissible control , then is given by

We now define the process given by

Consider now an arbitrary admissible control strategy . Using Itô’s formula we obtain for that

Hence, is an Itô process with a drift coefficient given, for , by

Note that it also holds, for , that

Multiplying the equation above by and subtracting the resulting left hand side (which is zero) from the drift coefficient of yields that the drift coefficient of can, for , be written as

With arguments similar to those in Section 2.1.1 we find that conditions (III) and (IV) imply that the expression above is non-positive (compare the above expression with (13)), i.e., the drift of is non-positive (regardless of the choice of ).

We conclude that is a bounded process with non-positive drift. Using optional sampling we find

for any . Using dominated convergence and a.s. we find

Repeating the same arguments with we obtain that the drift of vanishes and that

We conclude that

∎

2.3 Equilibrium existence

The main result of this section is Theorem 10 which reports conditions on the primitives of the model that guarantee the existence of a threshold equilibrium. The proof of this result, which is reported in Section 2.4, relies on the Poincaré-Miranda theorem and is in this sense a fixed-point type proof. In particular, the Poincaré-Miranda theorem follows from the Brouwer fixed-point theorem; cf. e.g., [22].

The following notation will be used throughout this section

| (23) |

In particular, we will use these to express solutions to the ODEs in (18) and (19).

Theorem 10 (Equilibrium existence).

Suppose the model parameters and are such that

| (24) |

and

| (25) |

Then there exists constants such that the strategy pair given by (20) is a Nash equilibrium.

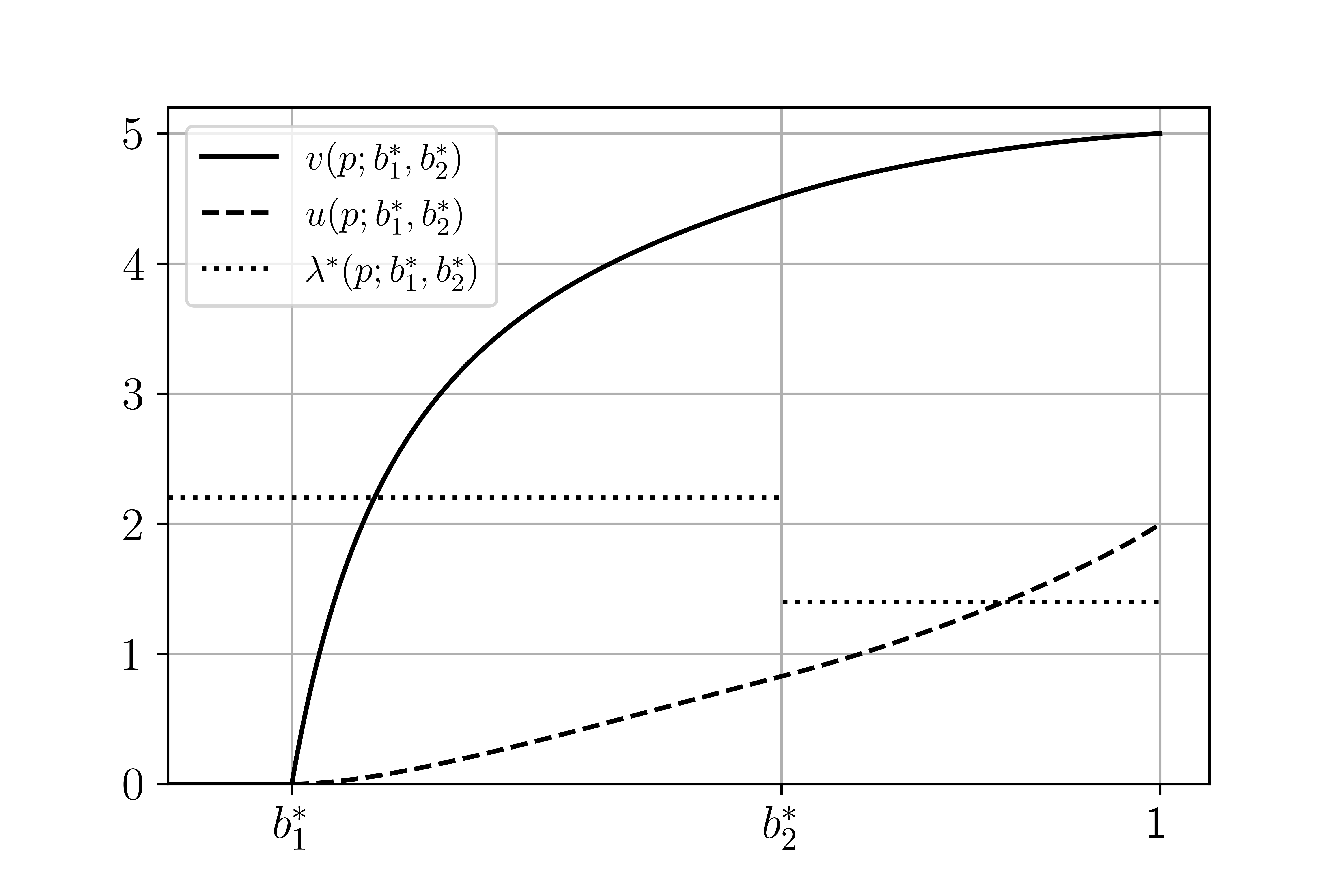

Figure 1 contains a numerical example.

Remark 11.

(i) The conditions (24)–(25) of Theorem 10 can be directly examined for any given parameter specification. (ii) If we set , then we can write these conditions as

and

Using this observation it is easily verified that there exists, for fixed and , a constant such that these conditions are satisfied for each . In other words, the conditions of Theorem 10 hold, i.e., an equilibrium exists, whenever and are sufficiently close to each other.

2.4 The proof of Theorem 10

The proof of Theorem 10 is found in Section 2.4.3. It relies on the content of Sections 2.4.1–2.4.2.

2.4.1 Observations regarding Equation (18)

Let be arbitrary constants. It can be verified that the solution to (18) is

| (26) |

where the constants can be determined by the boundary and smoothness conditions in (18). (Recall that are defined in (23).) However, instead of directly determining to attain these conditions we will determine these constants in order to attain only the boundary conditions and the continuity in (18) as well as the condition

| (27) |

(The interpretation of (27) is that condition (IV) in Theorem 10 holds from the right.) After this we will show that can be chosen so that (27) also holds from the left (i.e., so that satisfies all conditions of (18) as well as (IV)); see Lemma 12 below.

First use that implies that . Note also that (27) implies that

Using these constants we obtain from (26) that

| (28) |

Using the condition we obtain

and hence, using also continuity , we obtain

We need the following technical result in the proof of Theorem 10 (in Section 2.4.3). The proof can be found in Appendix B.

2.4.2 Observations regarding Equation (19)

Let be arbitrary constants. It can be verified that the solution to (19) is

| (32) |

where the constants are determined by the boundary and smoothness conditions in (19). The boundary condition gives us , while gives us

| (33) |

Finally, the remaining two conditions give us

and

| (34) |

We will make use of the following technical result in the proof of Theorem 10. The proof can be found in Appendix B.

2.4.3 The proof

Proof.

(Of Theorem 10.) The idea of the proof is to establish existence of a threshold strategy pair satisfying the conditions of Theorem 8. The proof consists of several parts. Here we establish existence of a pair with and corresponding functions and such that (18) and (19), as well as (II) and (IV) hold. The remaining conditions are established in Appendix C. In particular, (I) follows from Proposition 29 and (III) follows from Proposition 27.

Consider a pair with and let and be given by (26) and (32) with the constants determined as in Sections 2.4.1 and 2.4.2. Then all we have left to do to is to show that the pair can be chosen so that

| (35) | ||||

| (36) |

To this end we introduce the notation

for an arbitrary threshold strategy pair .

Using Lemma 13, it is easy to see that there exist constants such that: (i) for all , and for all , and (ii) is continuous on the set .

Fix two such values and (arbitrarily). We can now find a continuous extension of on the whole rectangle by

We conclude that is continuous on with the properties that for all and for all .

Using Equation (29) and (30) we find a continuous extension of on the whole rectangle by

| (37) |

Based on Lemma 12 (in particular the left hand side inequality of (31)) we may now conclude that: , for any and , for any .

3 Weak formulation

The purpose of this section is to consider a more general class of admissible control strategies compared to that of the strong formulation in Section 2. To this end we consider here a weak formulation of our game based measure changes and Girsanov’s theorem. We remark that this formulation is closely related to [9], where a similar weak solution approach is used for an optimal control problem with discretionary stopping. The main finding of the present section is that the double threshold equilibrium of Theorem 8 is a Nash equilibrium also in the weak formulation.

Let be a probability space supporting a one-dimensional Brownian motion and a Bernoulli random variable with . Denote by the smallest right continuous filtration to which is adapted. Define the terminal filtration according to . Define and analogously.

Definition 14 (Admissibility in the weak formulation).

-

•

A process is said to be an admissible control process if it has RCLL paths, is adapted to , and takes values in . The set of admissible control processes is denoted by .

-

•

A stopping time is said to be an admissible stopping strategy if it is adapted to . The set of admissible stopping strategies is denoted by .

Remark 15.

The set of admissible stopping strategies in the weak formulation is analogous to set of admissible stopping strategies in the strong formulation. The main difference is instead that we define as a Brownian motion in the weak formulation, whereas is given by (1) in the strong formulation.

Now for any given control process we define the process according to

| (39) |

By Girsanov’s theorem ([18, Chapter 3.5]) there exists a measure on , given by

| (40) |

such that is a Brownian motion on for each fixed . Moreover, we note that ) is a martingale by Novikov’s condition. Thus, the theory of the Föllmer measure gives us the existence of a measure on , which satisfies for every and ; see [9, Section 2], and also [13] and [18, p.192].

This allows us to give definitions of the reward functions based on measure changes.

Definition 16.

Given a strategy pair we define the payoff of the stopper as

| (41) |

and the payoff of the controller as

| (42) |

Remark 17.

Let us motivate Definition 16 further. In the strong formulation (Section 2) we consider a fixed probability measure and define the controlled process in terms of a control process and a given Brownian motion ; cf. (1). In the present weak formulation we instead define as a Brownian motion, and let the control process imply a measure change , such that defined by (39) is a Brownian motion under this measure. By comparing the resulting weak formulation equation for (i.e., (39)) and the equation for in the strong formulation (in (1)) the connection between the formulations becomes clear.

The Nash equilibrium is now defined in the usual way:

Definition 18.

A pair of admissible strategies is a said to be a Nash equilibrium if

| (43) |

for any pair of deviation strategies .

In line with the strong formulation solution approach (cf. (10) and (11)) we define a double threshold strategy pair , where , by

| (44) | |||

| (45) |

where is (in analogy with (7)) given by the SDE

| (46) |

(Recalling that is a Brownian motion we find that (46) has a strong solution using analogues arguments as in the strong solution formulation; cf. Proposition 20).

The main result of the present section is that the double threshold equilibrium investigated in the strong formulation is also an equilibrium in the weak formulation. Note that this implies that equilibrium existence in the weak formulation is guaranteed by the same parameter conditions as in Theorem 10.

Theorem 19.

Proof.

In this proof we write . For any admissible deviation strategy it follows from (39) and (46) that has the representation

| (47) |

where we recall that is a Brownian motion under the measure . We remark that depends in this sense on both and when the controller deviates from the equilibrium.

Note that the representation of in (47) is analogous to (6) in the strong formulation. Moreover, it is directly seen that the value functions are the same for both formulations in the case of no deviation, i.e.,

Hence, and , with and as in Theorem 8. Using this it is directly checked that the proof of Theorem 8 can be adjusted so that it shows that corresponds to an equilibrium also in the present weak formulation. Indeed, this requires only minor adjustments including that is here given by (47), and that the deviation strategies are allowed to be processes in . Particularly, note that Proposition 5 holds also in this case. ∎

Acknowledgment The authors are grateful to Erik Ekström at Uppsala University for discussions regarding games of the kind studied in the present paper, and suggestions that lead to improvements of this manuscript.

Appendix A Properties of in the strong formulation

Proposition 20.

The SDE (6) has a strong solution for any admissible pair of Markov strategies .

Proof.

Consider the interval , for a small arbitrary constant . Then the diffusion coefficient is uniformly bounded away from zero in . Thus we obtain for both cases and that: (i) a weak solution to (6) exists (cf. e.g., [18, Ch. 5]), and (ii) a solution to (6) is pathwise unique in (see [23]). By Lemma 21, we obtain that cannot reach or in finite time. Hence, (6) admits a strong solution by [18, Corollary 3.23]. ∎

Lemma 21.

For any pair it holds for given by (6) that

| (48) | ||||

| (49) |

Proof.

In order to prove (48), it is suffices to show that

where solves the SDE

| (50) |

with ; indeed, it follows by comparison (see [28, Chapter IX.3]) that a.s. (The existence of a strong solution to (50) is given by arguments similar to those in the proof of Proposition 20.)

Since is RCLL in (and is piece-wise constant), there exists a such that for . With some calculations we now obtain that the scale function of (50), is for given by

where , and density of the speed measure for is given by

Using that is increasing for we have

Hence, follows from Feller’s test for explosion, and (48) follows.

For reasons similar to the proof of the previous statement it is sufficient to prove that where

| (51) |

We fix a such that for . For (51) and , we have

where , and for , we have

Hence, for some positive constants , we have

Hence, follows by Feller’s test for explosion, and (49) follows.

∎

Appendix B Proofs of Lemmas 12 and 13

Proof.

(of Lemma 12.) Observe that

First we consider the limit . For the first part we have that

as , since . We consider the remaining term. We obtain

For we obtain using , that

as . For we have

as . Adding the limits gives us (29), and using (24) we thus obtain the first part of (31).

For the second limit we find

| (52) | ||||

We note that and further investigate the limit by considering the denominator and numerator of separately. For the denominator of we have that

as ; to see this use e.g., that is decreasing for . For the numerator of we use (24) to find

It follows that and by (52) we obtain (30) (from which the second part of (31) follows). Hence, statement (i) has been proved.

We need the following technical result in the proof of Lemma 13.

Lemma 22.

Let be given by (34), then we have

-

(a)

for ,

-

(b)

for .

Proof.

Let us prove (a) by showing that showing that is strictly decreasing in (recall that ); the result then follows by taking in . It holds that the denominator of is positive and strictly increasing in . To see this use e.g., that and that is strictly decreasing for , which implies that

Additionally, and implies that the numerator is positive and decreasing in . We conclude that is strictly decreasing on .

In order to prove (b) we write

where denotes the denominator of . Note that implies that the second expression is non-positive. Thus, by similar arguments to (a) the result follows by taking in the first and in the second expression. ∎

Appendix C Results for the proof of Theorem 10

Throughout this section we consider the setting of the proof of Theorem 10. Particularly, we here consider a pair such that (II) and (IV) hold. We also rely on condition (25).

Lemma 23.

It holds that for .

Proof.

Let us first prove by contradiction. Assume there exists a such that . Then and implies that there exists with such that attains a local maximum at . Using the ODE in (18) we find , which is a contradiction.

Lemma 24.

It holds that (a) , and (b) .

Proof.

We will only prove the first statement, since the second statement follows using analogues arguments. Suppose that . We will show that this implies that has a local minimum below zero, i.e., there exists a point such that and . This contradicts the ODE in (18) since (by (25)). We have three cases:

-

•

If , then and continuity immediately imply that has a local minimum below zero.

-

•

If , then the ODE in (18) implies that . Analogously to the first case this implies that has a local minimum below zero.

-

•

If , then we find using the ODE that for . Using also and the ODE we conclude that and . With this implies that has a local minimum below zero.

∎

Lemma 25.

It holds that for .

Proof.

We show that for by contradiction. The remaining case can be proved using analogues methods. To this end, assume that is the smallest point such that . We consider three cases:

- •

-

•

If , then is a local minimum and Lemma 24(a) implies that cannot be the first point with .

-

•

Consider the case . Then since and , we see that there must exist a second such that and is a local minimum. Let be the first such a point. Then it is easy to see, that and . However, using , and the ODE we find the contradiction

∎

Lemma 26.

Let . Then

-

(a)

for any satisfying ,

-

(b)

,

-

(c)

for any satisfying .

Proof.

Let us prove the statement in (a). With the help of the ODE, we observe that

Proposition 27.

It holds that is strictly decreasing for .

Proof.

By Lemma 26(a), the statement holds for , since (Lemma 23) and on . We prove for by contradiction. Note that , by and Lemma 26(a). For this purpose, let be a point such that , which is then a local minimum (by Lemma 26(c)). Hence, we obtain for (cf. Lemma 26(c)). This is a contradiction to Lemma 26(b). ∎

Lemma 28.

It holds that .

Proof.

We prove the statement by contradiction. To this end assume . Then we can use the calculations in the proof of Lemma 13 to arrive at (53), which with (II) gives us

| (55) |

Related to the numerator we introduce the function

It is easily verified that is increasing and that (use e.g., (25)). This is a contradiction to and the statement follows. ∎

Proposition 29.

It holds that for .

Proof.

We prove that for by contradiction. By definition, for . Lemma 28 establishes . Thus the ODE (19) and imply that is strictly increasing and convex on

which is non-empty. Suppose, in order to obtain a contradiction, that is the smallest point such that . It can then be verified that .

Let us consider the case . Recall that (53) holds for any . Hence, using instead of in (53) and the same reasoning that lead to (55) gives

Note that that we have , since both functions and satisfy the ODE in (19) on with the same boundary conditions, in particular (by (19)) and (by the contradiction assumption). Hence, using and arguments analogous to those after (55) we find that . However, is a contradiction to the definition of being the smallest point in where .

Let us consider the case . Then the contradiction is obtained in a similar way. More precisely, using the ODE (cf. (32)) with the boundary conditions and , we obtain

where

Using also , (25), and arguments analogous to those after (55), we find with some work that

∎

References

- [1] E. Bayraktar and Y.-J. Huang. On the multidimensional controller-and-stopper games. SIAM Journal on Control and Optimization, 51(2):1263–1297, 2013.

- [2] E. Bayraktar and J. Li. On the controller-stopper problems with controlled jumps. Applied Mathematics & Optimization, 80(1):195–222, 2019.

- [3] A. Bovo, T. De Angelis, and E. Issoglio. Variational inequalities on unbounded domains for zero-sum singular-controller vs. stopper games. arXiv preprint arXiv:2203.06247, 2022.

- [4] A. Bovo, T. De Angelis, and J. Palczewski. Zero-sum stopper vs. singular-controller games with constrained control directions. arXiv preprint arXiv:2306.05113, 2023.

- [5] P. Cardaliaguet and C. Rainer. Stochastic differential games with asymmetric information. Applied Mathematics and Optimization, 59:1–36, 2009.

- [6] P. Cardaliaguet and C. Rainer. Pathwise strategies for stochastic differential games with an erratum to “stochastic differential games with asymmetric information”. Applied Mathematics & Optimization, 68:75–84, 2013.

- [7] T. De Angelis and E. Ekström. Playing with ghosts in a Dynkin game. Stochastic Processes and their Applications, 130(10):6133–6156, 2020.

- [8] T. De Angelis, N. Merkulov, and J. Palczewski. On the value of non-Markovian Dynkin games with partial and asymmetric information. The Annals of Applied Probability, 32(3):1774–1813, 2022.

- [9] E. Ekström and I. Karatzas. A sequential estimation problem with control and discretionary stopping. Probability, Uncertainty and Quantitative Risk, 7(3):151–168, 2022.

- [10] E. Ekström, K. Lindensjö, and M. Olofsson. How to detect a salami slicer: A stochastic controller-and-stopper game with unknown competition. SIAM Journal on Control and Optimization, 60(1):545–574, 2022.

- [11] E. Ekström, A. Milazzo, and M. Olofsson. The de Finetti problem with unknown competition. arXiv preprint arXiv:2204.07016, 2022.

- [12] E. Ekström and T. Tolonen. Hiring and firing – a signaling game. http://www2.math.uu.se/ ekstrom/hiringfiring.pdf (2023-06-09), 2023.

- [13] H. Föllmer. The exit measure of a supermartingale. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 21:154–166, 1972.

- [14] F. Gensbittel and C. Grün. Zero-sum stopping games with asymmetric information. Mathematics of Operations Research, 44(1):277–302, 2019.

- [15] F. Gensbittel and C. Rainer. A two-player zero-sum game where only one player observes a Brownian motion. Dynamic Games and Applications, 8:280–314, 2018.

- [16] D. Hernandez-Hernandez, R. S. Simon, and M. Zervos. A zero-sum game between a singular stochastic controller and a discretionary stopper. The Annals of Applied Probability, 25(1):46–80, 2015.

- [17] D. Hernández-Hernández and K. Yamazaki. Games of singular control and stopping driven by spectrally one-sided Lévy processes. Stochastic Processes and their Applications, 125(1):1–38, 2015.

- [18] I. Karatzas and S. E. Shreve. Brownian Motion and Stochastic Calculus (Graduate Texts in Mathematics), 2nd edition. Springer, 1991.

- [19] I. Karatzas and W. D. Sudderth. The controller-and-stopper game for a linear diffusion. The Annals of Probability, 29(3):1111–1127, 2001.

- [20] J. Lempa and P. Matomäki. A Dynkin game with asymmetric information. Stochastics An International Journal of Probability and Stochastic Processes, 85(5):763–788, 2013.

- [21] R. S. Liptser and A. N. Shiryaev. Statistics of random processes: I. General theory, volume 1. Springer Science & Business Media, 2001.

- [22] J. Mawhin. Simple proofs of the Hadamard and Poincaré–Miranda theorems using the Brouwer fixed point theorem. The American Mathematical Monthly, 126(3):260–263, 2019.

- [23] S. Nakao. On the pathwise uniqueness of solutions of one-dimensional stochastic differential equations. Osaka Journal of Mathematics, 9(3):513 – 518, 1972.

- [24] M. Nutz and J. Zhang. Optimal stopping under adverse nonlinear expectation and related games. 2015.

- [25] M. Olofsson, T. Önskog, and N. L. Lundström. Management strategies for run-of-river hydropower plants: an optimal switching approach. Optimization and Engineering, pages 1–25, 2021.

- [26] T. Pham and J. Zhang. Two person zero-sum game in weak formulation and path dependent Bellman–Isaacs equation. SIAM Journal on Control and Optimization, 52(4):2090–2121, 2014.

- [27] D. Possamaï, N. Touzi, and J. Zhang. Zero-sum path-dependent stochastic differential games in weak formulation. The Annals of Applied Probability, 30(3):1415–1457, 2020.

- [28] D. Revuz and M. Yor. Continuous martingales and Brownian motion, volume 293. Springer Science & Business Media, 2013.