Nonparametric Estimation of Large Spot Volatility Matrices for High-Frequency Financial Data

Abstract

In this paper, we consider estimating spot/instantaneous volatility matrices of high-frequency data collected for a large number of assets. We first combine classic nonparametric kernel-based smoothing with a generalised shrinkage technique in the matrix estimation for noise-free data under a uniform sparsity assumption, a natural extension of the approximate sparsity commonly used in the literature. The uniform consistency property is derived for the proposed spot volatility matrix estimator with convergence rates comparable to the optimal minimax one. For the high-frequency data contaminated by microstructure noise, we introduce a localised pre-averaging estimation method that reduces the effective magnitude of the noise. We then use the estimation tool developed in the noise-free scenario, and derive the uniform convergence rates for the developed spot volatility matrix estimator. We further combine the kernel smoothing with the shrinkage technique to estimate the time-varying volatility matrix of the high-dimensional noise vector. In addition, we consider large spot volatility matrix estimation in time-varying factor models with observable risk factors and derive the uniform convergence property. We provide numerical studies including simulation and empirical application to examine the performance of the proposed estimation methods in finite samples.

Keywords: Brownian semi-martingale, Factor model, Kernel smoothing, Microstructure noise, Sparsity, Spot volatility matrix, Uniform consistency.

1 Introduction

Modelling high-frequency financial data is one of the most important topics in financial economics and has received increasing attention in recent decades. Continuous-time econometric models such as the Itô semimartingale are often employed in the high-frequency data analysis. One of the main components in these models is the volatility function or matrix. In the low-dimensional setting (with a single or a small number of assets), the realised volatility is often used to estimate the integrated volatility over a fixed time period (e.g., Andersen and Bollerslev, 1998; Barndorff-Nielsen and Shephard, 2002, 2004; Andersen et al., 2003). In practice, it is not uncommon that the high-frequency financial data are contaminated by the market microstructure noise, which leads to biased realised volatility if the noise is ignored. Hence, various modification techniques such as the two-scale, pre-averaging and realised kernel have been introduced to account for the microstructure noise and produce consistent volatility estimation (e.g., Zhang, Mykland and Aït-Sahalia, 2005; Barndorff-Nielsen et al., 2008; Kalnina and Linton, 2008; Jacod et al., 2009; Podolskij and Vetter, 2009; Christensen, Kinnebrock and Podolskij, 2010; Park, Hong and Linton, 2016). Shephard (2005), Andersen, Bollerslev and Diebold (2010) and Aït-Sahalia and Jacod (2014) provide comprehensive reviews for estimating volatility with high-frequency financial data under various settings.

In practical applications, financial economists often have to deal with the situation that there are a large amount of high-frequency financial data collected for a large number of assets. A key issue is to estimate the large volatility structure for these assets, which has applications in various areas such as the optimal portfolio choice and risk management. Partly motivated by developments in large covariance matrix estimation for low-frequency data in the statistical literature, Wang and Zou (2010), Tao, Wang and Zhou (2013) and Kim, Wang and Zou (2016) estimate the large volatility matrix under an approximate sparsity assumption (Bickel and Levina, 2008); Zheng and Li (2011) and Xia and Zheng (2018) study large volatility matrix estimation using the large-dimensional random matrix theory (Bai and Silverstein, 2010); and Lam and Feng (2018) propose a nonparametric eigenvalue-regularised integrated covariance matrix for high-dimensional asset returns. Given that there often exists co-movement between a large number of assets and the co-movement is driven by some risk factors which can be either observable or latent, Fan, Furger and Xiu (2016), Aït-Sahalia and Xiu (2017), Dai, Lu and Xiu (2019) extend the methodologies developed by Fan, Liao and Mincheva (2011, 2013) to estimate the large volatility matrix by imposing a continuous-time factor model structure on the high-dimensional and high-frequency financial data, and Aït-Sahalia and Xiu (2019) study the principal component analysis of high-frequency data and derive the asymptotic distribution for the realised eigenvalues, eigenvectors and principal components.

The estimation methodologies in the aforementioned literature often rely on the realised volatility (or covariance) matrices, measuring the integrated volatility structure over a fixed time interval. In practice, it is often interesting to further explore the actual spot/instantaneous volatility structure and its dynamic change over a certain time interval, which is a particularly important measurement for the financial assets when the market is in a volatile period (say, the global financial crisis or COVID-19 outbreak). For a single financial asset, Fan and Wang (2008) and Kristensen (2010) introduce a kernel-based nonparametric method to estimate the spot volatility function and establish its asymptotic properties including the point-wise and global asymptotic distribution theory and uniform consistency. For the noise-contaminated high-frequency data, Zu and Boswijk (2014) combine the two-scale realised volatility with the kernel-weighted technique to estimate the spot volatility, whereas Kanaya and Kristensen (2016) propose a kernel-weighted pre-averaging spot volatility estimation method. Other nonparametric spot volatility estimation methods can be found in Fan, Fan and Lv (2007) and Figueroa-López and Li (2020). It seems straightforward to extend this local nonparametric method to estimate the spot volatility matrix for a small number of assets. However, a further extension to the setting with vast financial assets is non-trivial. There is virtually no work on estimating the large spot volatility matrix except Kong (2018), which considers estimating large spot volatility matrices and their integrated versions under the continuous-time factor model structure for noise-free high-frequency data.

The main methodological and theoretical contributions of this paper are summarised as follows.

-

•

Large spot volatility matrix estimation with noise-free high-frequency data. We use the nonparametric kernel-based smoothing method to estimate the volatility and co-volatility functions as in Fan and Wang (2008) and Kristensen (2010), and then apply a generalised shrinkage to off-diagonal estimated entries. With small off-diagonal entries forced to be zeros, the resulting large spot volatility matrix estimate would be non-degenerate with stable performance in finite samples. We derive the consistency property for the proposed spot volatility matrix estimator uniformly over the entire time interval under a uniform sparsity assumption, which is also adopted by Chen, Xu and Wu (2013), Chen and Leng (2016) and Chen, Li and Linton (2019) in the low-frequency data setting. In particular, the derived uniform convergence rates are comparable to the optimal minimax rate in large covariance matrix estimation (e.g., Cai and Zhou, 2012). The number of assets is allowed to be ultra large in the sense that it can grow at an exponential rate of with being the sampling frequency.

-

•

Large spot volatility matrix estimation with noise-contaminated high-frequency data and time-varying noise volatility matrix estimation. When the high-frequency data are contaminated by the microstructure noise, we extend Kanaya and Kristensen (2016)’s localised pre-averaging estimation method to the high-dimensional data setting. Specifically, we first pre-average the log price data via a kernel filter and then apply the same estimation method to the kernel fitted high-frequency data (at pseudo-sampling time points) as in the noise-free scenario. The microstructure noise vector is assumed to be heteroskedastic with the time-varying covariance matrix satisfying the uniform sparsity assumption. We show that the existence of microstructure noises slows down the uniform convergence rates, see Theorem 2. Furthermore, we combine the kernel smoothing with generalised shrinkage to estimate the time-varying noise volatility matrix and derive its uniform convergence property. To the best of our knowledge, there is virtually no work on large time-varying noise volatility matrix estimation for high-frequency data.

-

•

Large spot volatility matrix estimation with risk factors. Since the uniform sparsity assumption is often too restrictive, we relax this restriction in Section 4 and consider large spot volatility matrix estimation in the time-varying factor model at high frequency, i.e., a large number of asset prices are driven by a small number of observable common factors. By imposing the sparsity restriction on the spot idiosyncratic volatility matrix, we obtain the so-called “low-rank plus sparse” spot volatility structure. A similar structure (with constant betas) is adopted by Fan, Furger and Xiu (2016) and Dai, Lu and Xiu (2019) in estimation of large integrated volatility matrices. We use the kernel smoothing method to estimate the spot volatility and covariance of the observed asset prices and factors as well as the time-varying betas, and apply the shrinkage technique to the estimated spot idiosyncratic volatility matrix. We derive the uniform convergence property of the developed matrix estimates, partly extending the point-wise convergence property in Kong (2018). The developed methodology and theory can be further modified to tackle the noise-contaminated high-frequency data.

We argue that all three of the scenarios we consider above may be practically relevant. Microstructure noise is considered important in the very highest frequency of data, whereas researchers working with five minute data, say, often ignore the noise. For the lower frequency of data there is a lot comovement in returns and the factor model is designed to capture that comovement, whereas at the ultra high frequency, comovement is less of an issue; indeed, under the so-called Epps effect this comovement shrinks to zero with sampling frequency.

The rest of the paper is organised as follows. In Section 2, we estimate the large spot volatility matrix in the noise-free high-frequency data setting and give the uniform consistency property. In Section 3, we extend the methodology and theory to the noise-contaminated data setting and further estimate the time-varying noise volatility matrix. Section 4 considers the large spot volatility matrix with systematic factors. Section 5 reports the simulation studies and Section 6 provides an empirical application. Section 7 concludes the paper. Proofs of the main theoretical results are available in Appendix A. The supplementary document contains proofs of some technical lemmas and propositions and discussions on the spot precision matrix estimation and the asynchronicity issue. Throughout the paper, we let be the Euclidean norm of a vector; and for a matrix , we let and be the matrix spectral norm and Frobenius norm, , , and .

2 Estimation with noise-free data

Suppose that is a -variate Brownian semi-martingale solving the following stochastic differential equation:

| (2.1) |

where is a -dimensional standard Brownian motion, is a -dimensional drift vector, and is a matrix. The spot volatility matrix of is defined as

| (2.2) |

Our main interest lies in estimating when the size is large. As in Chen, Xu and Wu (2013) and Chen and Leng (2016), we assume that the true spot volatility matrix satisfies the following uniform sparsity condition: , where

| (2.3) |

where , is larger than a positive constant, is a fixed positive number and is a positive random variable satisfying . This is a natural extension of the approximate sparsity assumption (e.g., Bickel and Levina, 2008). Section 4 below will relax this assumption and consider estimating large spot volatility matrices with systematic factors. The asset prices are assumed to be collected over a fixed time interval at , where is the sampling frequency and with denoting the floor function. In the main text, we focus on the case of equidistant time points in the high-frequency data collection. The asynchronicity issue will be discussed in Appendix C.2 of the supplement.

For each , we estimate the spot co-volatility by

| (2.4) |

with

where , , is a kernel function, is a bandwidth shrinking to zero and . The use of rather than in the estimation (2.4) is to correct a constant bias when is close to the boundary points and . A naive method of estimating the spot volatility matrix is to directly use to form an estimated matrix. However, this estimate often performs poorly in practice when the number of assets is very large (say, ). To address this issue, a commonly-used technique is to apply a shrinkage function to when , forcing very small estimated off-diagonal entries to be zeros. Let denote a shrinkage function satisfying the following three conditions: (i) for ; (ii) if ; and (iii) , where is a user-specified tuning parameter. With the shrinkage function, we construct the following nonparametric estimator of :

| (2.5) |

where is a tuning parameter which is allowed to change over and denotes the indicator function. Section 5 discusses the choice of , ensuring that is positive definite in finite samples. Our estimation method of the spot volatility matrix can be seen as a natural extension of the kernel-based large sparse covariance matrix estimation (e.g., Chen, Xu and Wu, 2013; Chen and Leng, 2016; Chen, Li and Linton, 2019) from the low-frequency data setting to the high-frequency one. We next give some technical assumptions which are needed to derive the uniform convergence property of .

Assumption 1.

(i) and are adapted locally bounded processes with continuous sample path.

(ii) With probability one,

where . For the spot covariance process , there exist and , a positive random function slowly varying at and continuous with respect to , such that

| (2.6) |

Assumption 2.

(i) The kernel is a bounded and Lipschitz continuous function with a compact support . In addition, .

(ii) The bandwidth satisfies that and .

(iii) Let the time-varying tuning parameter in the generalised shrinkage be chosen as

where is defined in (2.6) and is a positive function satisfying that

Remark 1.

Assumption 1 imposes some mild restrictions on the drift and volatility processes. By a typical localisation procedure as in Section 4.4.1 of Jacod and Protter (2012), the local boundedness condition in Assumption 1(i) can be strengthened to the bounded condition over the entire time interval, i.e., with probability one,

which are the same as Assumption A2 in Tao, Wang and Zhou (2013) and Assumptions (A.ii) and (A.iii) in Cai et al (2020). It may be possible to relax the uniform boundedness restriction (when is allowed to diverge) at the cost of more lengthy proofs (e.g., Kanaya and Kristensen, 2016). Assumption 1(ii) gives the smoothness condition on the spot covariance process, crucial to derive the uniform asymptotic order for the kernel estimation bias. When the spot covariance is driven by continuous semimartingales, (2.6) holds with (e.g., Ch. V, Exercise 1.20 in Revuz and Yor, 1999). Assumption 2(i) contains some commonly-used conditions for the kernel function. Assumption 2(ii)(iii) imposes some mild conditions on the bandwidth and time-varying shrinkage parameter. In particular, when diverges at a polynomial rate of , Assumption 2(ii) reduces to the conventional bandwidth restriction. Assumption 2(iii) is comparable to that assumed by Chen and Leng (2016) and Chen, Li and Linton (2019). It is worthwhile to point out that the developed methodology and theory still hold when the time-varying tuning parameter in Assumption 2(iii) is allowed to vary over entries in the spot volatility matrix estimation, which is expected to perform well in finite samples. For example, we set in the numerical studies and shrink the -entry to zero if .

The following theorem gives the uniform convergence property (in the matrix spectral norm) for the spot volatility matrix estimator under the uniform sparsity assumption.

Theorem 1.

Remark 2.

(i) The first term of is , which is the bias rate due to application of the local smoothing technique. It is slower than the conventional -rate since we do not assume existence of smooth derivatives of (with respect to ). The second term of is square root of , a typical uniform asymptotic rate for the kernel estimation variance component. The uniform convergence rate in (2.7) is also similar to those obtained by Chen and Leng (2016) and Chen, Li and Linton (2019) in the low-frequency data setting (disregarding the bias order). Note that the dimension affects the uniform convergence rate via and and the estimation consistency may be achieved in the ultra-high dimensional setting when diverges at an exponential rate of . Treating as the “effective” sample size in the local estimation procedure and disregarding the bias rate , the rate in (2.7) is comparable to the optimal minimax rate in large covariance matrix estimation (e.g., Cai and Zhou, 2012).

(ii) If we further assume that is deterministic with continuous second-order derivative with respect to , and is symmetric, we may improve the kernel estimation bias order. In fact, following the proof of Theorem 1, we may show that

| (2.8) |

where . The above uniform consistency property only holds over the trimmed time interval due to the kernel boundary effect. In practice, however, it is often important to investigate the spot volatility structure near the boundary points. For example, when we consider one trading day as a time interval, it is particularly interesting to estimate the spot volatility matrix near the opening and closing times which are peak times in stock market trading. To address this issue, we may replace in (2.4) by a boundary kernel weight defined by

where is a boundary kernel satisfying (a key condition to improve the bias order near the boundary points). Examples of boundary kernels can be found in Fan and Gijbels (1996) and Li and Racine (2007). With this adjustment in the kernel estimation, we can extend the uniform consistency result (2.8) to the entire interval .

3 Estimation with contaminated high-frequency data

In practice, it is not uncommon that high-frequency financial data are contaminated by the market microstructure noise. The kernel estimation method proposed in Section 2 would be biased if the noise is ignored in the estimation procedure. Consider the following additive noise structure:

| (3.1) |

where , , is a vector of observed asset prices at time , and is a -dimensional vector of noises with nonlinear heteroskedasticity, is a matrix of deterministic functions, and independently follows a -variate identical distribution. The noise structure defined in (3.1) is similar to the setting considered in Kalnina and Linton (2008) which also contains a nonlinear mean function and allows the existence of endogeneity for a single asset. Throughout this section, we assume that is independent of the Brownian semimartingale .

3.1 Estimation of the spot volatility matrix

To account for the microstructure noise and produce consistent volatility matrix estimation, we apply the pre-averaging technique as the realised kernel estimate (Barndorff-Nielsen et al., 2008) can be seen as a member of the pre-averaging estimation class whereas the two-scale estimate (Zhang, Mykland and Aït-Sahalia, 2005) can be re-written as the realised kernel estimate with the Bartlett-type kernel (up to the first-order approximation). The pre-averaging method has been studied by Jacod et al. (2009), Podolskij and Vetter (2009) and Christensen, Kinnebrock and Podolskij (2010) in estimating the integrated volatility for a single asset and is further extended by Kim, Wang and Zou (2016) and Dai, Lu and Xiu (2019) to the large high-frequency data setting. Kanaya and Kristensen (2016) use a localised pre-averaging technique to estimate the spot volatility function for a single asset and derive the uniform convergence rate for the developed estimate. A similar technique is also used by Xiao and Linton (2002) to improve convergence of the nonparametric spectral density estimator for time series with general autocorrelation for low-frequency data.

We first pre-average the observed high-frequency data via a kernel filter, i.e.,

| (3.2) |

with , where , is a kernel function and is a bandwidth. Let , where is the -th component of and are the pseudo-sampling time points in the fixed interval with equal distance . Replacing by in (2.4), we estimate the spot co-volatility by

| (3.3) |

where

Furthermore, to obtain a stable spot volatility matrix estimate in finite samples when the dimension is large, as in (2.5), we apply shrinkage to , , and subsequently construct

| (3.4) |

where is another time-varying shrinkage parameter. We next give some conditions needed to derive the uniform consistency property of .

Assumption 3.

(i) Let be an independent and identically distributed (i.i.d.) sequence of p-dimensional random vectors. Assume that and

for any -dimensional vector satisfying .

(ii) The deterministic functions are bounded uniformly over , and satisfy that

Assumption 4.

(i) The kernel function is Lipschitz continuous and has a compact support . In addition, .

(ii) The bandwidth and the dimension satisfy that

where and .

(iii) Let and the time-varying tuning parameter be chosen as , where is defined as in Assumption 2(iii) and is defined as with replacing .

Remark 3.

We allow nonlinear heteroskedasticity on the microstructure noise. The i.i.d. restriction on may be weakened to some weak dependence conditions (e.g., Kim, Wang and Zou, 2016; Dai, Lu and Xiu, 2019) at the cost of more lengthy proofs. The moment condition in Assumption 3(i) is weaker than the sub-Gaussian condition (e.g., Bickel and Levina, 2008; Tao, Wang and Zhou, 2013) which is commonly used in large covariance matrix estimation when the dimension is ultra large. The boundedness condition on in Assumption 3(ii) is similar to the local boundedness restriction in Assumption 1(i). Assumption 4(ii) imposes some mild restrictions on and , which imply that there is a trade-off between them. When is larger, diverges at a faster exponential rate of but the bandwidth condition becomes more restrictive. If is divergent at a polynomial rate of , we may let be sufficiently close to zero, and then the bandwidth condition reduces to the conventional one as in Assumption 2(ii). The condition in Assumption 4(iii) is crucial to show that the error of the kernel filter tends to zero asymptotically, whereas the form of the time-varying shrinkage parameter is relevant to the uniform convergence rate of (see Proposition A.2).

Theorem 2.

Remark 4.

The uniform convergence rate in (3.5) relies on , and . With the high-frequency data collected at pseudo time points with sampling frequency , the rate is comparable to for the noise-free kernel estimator in Section 2. The rate is due to the error of the kernel filter in the first step of the local pre-averaging estimation procedure. In particular, when , is bounded, and with , the uniform convergence rate in (3.5) becomes . Furthermore, if , the rate is simplified to , comparable to those derived by Zu and Boswijk (2014) and Kanaya and Kristensen (2016) in the univariate high-frequency data setting.

3.2 Estimation of the time-varying noise volatility matrix

It is often interesting to further explore the volatility structure of microstructure noise. Chang et al. (2021) estimate the constant covariance matrix for high-dimensional noise and derive the optimal convergence rates for the developed estimate. In the present paper, we consider the time-varying noise covariance matrix defined by

| (3.6) |

It is sensible to assume that satisfies the uniform sparsity condition as in (2.3). For each , we estimate by the kernel smoothing method:

| (3.7) |

where is a bandwidth, and is defined similarly to in (2.4) but with replacing . As in (2.5) and (3.4), we again apply shrinkage to , , and construct

| (3.8) |

where is a time-varying shrinkage parameter. To derive the uniform consistency property of , we need to impose stronger moment condition on and smoothness restriction on .

Assumption 5.

(i) For any -dimensional vector satisfying , , .

(ii) The time-varying function satisfies that

where is a positive constant and .

Remark 5.

Assumption 5(i) strengthens the moment condition in Assumption 3(i) and is equivalent to the sub-Gaussian condition, see Assumption A1 in Tao, Wang and Zhou (2013). The smoothness condition in Assumption 5(ii) is similar to (2.6), crucial to derive the asymptotic order of the kernel estimation bias. The restrictions on and in Assumption 5(iii) are similar to those in Assumption 4(ii), allowing to be divergent to infinity at an exponential rate of .

In the following theorem, we state the uniform consistency result for with convergence rate comparable to that in Theorem 1.

Theorem 3.

Remark 6.

If the bandwidth parameter in (3.7) is the same as in (2.4), we may find that the uniform convergence rate would be the same as that in Theorem 1. Treating as the “effective” sample size and disregarding the bias order, we may show that the uniform convergence rate in (3.9) is comparable to the optimal minimax rate derived by Chang et al. (2021) for the constant noise covariance matrix estimation. Meanwhile, the kernel estimation bias order may be improved by strengthening the smoothness condition on and adopting the boundary kernel weight as suggested in Remark 2(ii).

4 Estimation with observed factors

The large spot volatility matrix estimation with the shrinkage technique developed in Sections 2 and 3 heavily relies on the uniform sparsity assumption (2.3). However, the latter may be too restrictive in practice since the price processes of a large number of assets are often driven by some common factors such as the market factors, resulting in strong correlation among assets and failure of the sparsity condition. To address this problem, we next consider the nonparametric time-varying regression at high frequency:

| (4.1) |

where is a matrix of time-varying betas (or factor loadings), and are -variate and -variate continuous semi-martingales defined by

| (4.2) |

respectively, and are drift vectors, , , and are -dimensional and -dimensional standard Brownian motions. For the time being, we assume that and are observable and noise free but is latent. Extension of the methodology and theory to the noise-contaminated high-frequency data will be considered later in this section.

Estimation of the constant betas via the ratio of realised covariance to realised variance is proposed by Barndorff-Nielsen and Shephard (2004), and extension to time-varying beta estimation has been studied by Mykland and Zhang (2006), Reiß, Todorov and Tauchen (2015) and Aït-Sahalia, Kalnina and Xiu (2020), some of which allow jumps in the semi-martingale processes. The main interest of this section lies in estimating the large spot volatility structure of . Letting and , and assuming orthogonality between and , see Assumption 6(iii) below, it follows from (4.1) that

| (4.3) |

As in Fan, Liao and Mincheva (2011, 2013), we impose the uniform sparsity restriction on instead of , i.e., . This is a reasonable assumption in practical applications as the asset prices, after removing the influence of systematic factors, are expected to be weakly correlated. Fan, Furger and Xiu (2016) and Dai, Lu and Xiu (2019) use a similar framework with constant betas to estimate large integrated volatility matrices.

Suppose that we observe and at regular points: , , as in Sections 2 and 3. Let be the spot covariance between and . We may use the kernel smoothing method as in (2.4) to estimate , and , i.e.,

| (4.4) | |||

| (4.5) | |||

| (4.6) |

where , , and is defined as in (2.4). Consequently, the time-varying betas and the spot idiosyncratic volatility matrix are estimated by

| (4.7) |

and

| (4.8) |

With the uniform sparsity condition, it is sensible to further apply shrinkage to , i.e.,

| (4.9) |

where is a time-varying shrinkage parameter. We finally estimate as

| (4.10) |

We need the following assumption to derive the uniform convergence property for and .

Assumption 6.

(ii) Let , and satisfy the boundedness and smoothing conditions as in Assumption 1.

(iii) For any and , for any , where is the -th element of , is the -th element of , and denotes the quadratic covariation.

(iv) The time-varying beta function satisfies that

where is the same as that in Assumption 1(ii). In addition, there exists a positive definite matrix (with uniformly bounded eigenvalues) such that

| (4.11) |

Remark 7.

The uniform boundedness and smoothness conditions imposed on the drift and spot volatility functions of and in Assumption 6(i)(ii) are the same as those in Assumption 1. This is crucial to ensure that the uniform convergence rates of , and (in the max norm) derived in Proposition A.4 are the same as that in Proposition A.1. The orthogonality condition in Assumption 6(iii) is commonly used to consistently estimate the time-varying factor model (e.g., Fan, Furger and Xiu, 2016; Dai, Lu and Xiu, 2019). Assumption 6(iv) is a rather mild restriction on time-varying betas and may be strengthened to improve the estimation bias order, see the discussion in Remark 2(ii). The condition (4.11) indicates that all the factors are pervasive.

We next present the convergence property of and defined in (4.9) and (4.10), respectively. Due to the nonparametric factor regression model structure (4.1), the largest eigenvalues of are spiked, diverging at a rate of . Hence, cannot be consistently estimated in the absolute term. To address this problem, as in Fan, Liao and Mincheva (2011, 2013), we measure the spiked volatility matrix estimate in the following relative error:

where the normalisation factor is used to guarantee that .

Theorem 4.

Remark 8.

Although is latent in model (4.1), the uniform convergence rate for in (4.12) is the same as that in Theorem 1 when is observable. Treating as the effective sample size in kernel estimation and disregarding the bias order in , the uniform convergence rate for in (4.13) is comparable to the convergence rates derived by Fan, Liao and Mincheva (2011) in low frequency and Fan, Furger and Xiu (2016) in high frequency. To guarantee uniform consistency in the relative matrix estimation error, we have to further assume that , limiting the divergence rate of the asset number, i.e., can only diverge at a polynomial rate of .

We next modify the above methodology and theory to accommodate microstructure noise in the asset prices and factors. Assume that

| (4.14) |

where and are matrices of deterministic functions similar to , and and are i.i.d. sequences of random vectors similar to . Since both and are latent, we need to first adopt the kernel pre-averaging technique proposed in Section 3.1 to obtain the approximation of and , and then apply the kernel smoothing and generalised shrinkage as in (4.4)–(4.10). This results in a three-stage estimation procedure which we describe as follows.

- 1.

- 2.

-

3.

Apply the generalised shrinkage to , i.e.,

where is the shrinkage parameter, and then estimate by

As shown in Theorem 2, the existence of microstructure noises slows down the uniform convergence rates. Following the proof of Lemma B.1 in Appendix B, we may show that

where denotes the -norm of a vector, and is defined in Assumption 4(iii). Modifying Proposition A.4 and the proof of Theorem 4 in Appendix A, we can prove that (4.12) and (4.13) hold but with replaced by defined in Assumption 4(iii), i.e.,

5 Monte-Carlo Study

In this section, we report the Monte-Carlo simulation studies to assess the numerical performance of the proposed large spot volatility matrix and time-varying noise volatility matrix estimation methods under the sparsity condition and the factor-based spot volatility matrix estimation. Here we only consider the synchronous high-frequency data. Additional simulation results for asynchronous high-frequency data are provided in the supplement.

5.1 Simulation for sparse volatility matrix estimation

5.1.1. Simulation setup

We generate the noise-contaminated high-frequency data according to model (3.1), where is taken as the Cholesky decomposition of the noise covariance matrix , is an independent -dimensional random vector of cross-sectionally independent standard normal random variables, the latent return process of assets is generated from the following drift-free model:

| (5.1) |

is a standard -dimensional Brownian motion, and is chosen as the Cholesky decomposition of the spot covariance matrix . In the simulation, we consider the volatility matrix estimation over the time interval of a full trading day, and set the sampling interval to be seconds, i.e., , to generate synchronous data. We consider three structures in and : “banding”, “block-diagonal”, and “exponentially decaying”. Following Wang and Zou (2010), we generate the diagonal elements of from the following geometric Ornstein-Uhlenbeck model (e.g., Barndorff-Nielsen and Shephard, 2002):

where is a standard -dimensional Brownian motion independent of , and is a random number generated uniformly between and , reflecting the leverage effects. The diagonal elements of are defined as daily cyclical deterministic functions of time:

where and reflect the observation by Kalnina and Linton (2008) that the noise level is high at both the opening and the closing times of a trading day and is low in the middle of the day, and the scalar controls the noise ratio for each asset which is chosen to match the highest noise ratio considered by Wang and Zou (2010). As in Barndorff-Nielsen and Shephard (2002, 2004), we define a continuous-time stochastic process by

where is a standard univariate Brownian motion independent of and . Let

where and . We will use and to define the off-diagonal elements in and , respectively, which are specified as follows.

-

•

Banding structure for and : The off-diagonal elements are defined by

and

for .

-

•

Block-diagonal structure for and : The off-diagonal elements are defined by

for , where is a collection of row and column indices located within our randomly generated diagonal blocks 111As in Dai, Lu and Xiu (2019), to generate blocks with random sizes, we fix the largest block size at when and randomly generate the sizes of the remaining blocks from a random integer uniformly picked between and . When , the largest size is , and the random integer is uniformly picked between and . Block sizes are randomly generated but fixed across all Monte Carlo repetitions..

-

•

Exponentially decaying structure for and : The off-diagonal elements are defined by

(5.2)

It is clear that the sparsity condition is not satisfied when the off-diagonal elements of and are exponentially decaying as in (5.2). The number of assets is set as and and the replication number is

5.1.2. Volatility matrix estimation

In the simulation studies, we consider the following volatility matrix estimates.

-

•

Noise-free spot volatility matrix estimate . This infeasible estimate serves as a benchmark in comparing the numerical performance of various estimation methods. As in Section 2, we apply the kernel smoothing method to estimate by directly using the latent return process , where the bandwidth is determined by the leave-one-out cross validation. We apply four shrinkage methods to for : hard thresholding (Hard), soft thresholding (Soft), adaptive LASSO (AL) and smoothly clipped absolute deviation (SCAD). For comparison, we also compute the naive estimate without applying any regularisation technique.

-

•

Noise-contaminated spot volatility matrix estimate . We combine the kernel smoothing with pre-averaging in Section 3.1 to estimate by using the noise-contaminated process . As in the noise-free estimation, we apply four shrinkage methods to for and also compute the naive estimate without applying the shrinkage.

-

•

Time-varying noise volatility matrix estimate . We combine the kernel smoothing with four shrinkage techniques in the estimation as in Section 3.2 and also the naive estimate without shrinkage.

The choice of tuning parameter in shrinkage is similar to that in Dai, Lu and Xiu (2019). For example, in the noise-free spot volatility estimate, we set the tuning parameter as where is chosen as the minimum value among the grid of values on such that the shrinkage estimate of the spot volatility matrix is positive definite. To evaluate the estimation performance of , we consider equidistant time points on and compute the following Mean Frobenius Loss (MFL) and Mean Spectral Loss (MSL) over repetitions:

| MFL | ||||

| MSL |

where , are the equidistant time points on the interval , and and are respectively the estimated and true spot volatility matrices at for the -th repetition. The “MFL” and “MSL” can be similarly defined for and .

5.1.3. Simulation results

Table 1 reports the simulation results when the dimension is . The three panels in the table (from top to bottom) report the results where the true volatility matrix structures are banding, block-diagonal, and exponentially decaying, respectively. In each panel, the MFL results are reported on the left, whereas the MSL results are on the right. The first two rows of each panel contain the MFL and MSL results for the spot volatility matrix estimation whereas the third row contains the results for the time-varying noise volatility matrix estimation.

For the noise-free estimate , when the volatility matrix structure is banding, the performance of the four shrinkage estimators are substantially better than that of the naive estimate (without any shrinkage). In particular, the results of the soft thresholding, adaptive LASSO and SCAD are very similar and their MFL and MSL values are approximately one third of those of the naive estimator. Meanwhile, the performance of the hard thresholding is less accurate (despite the much stronger level of shrinking used), but is still much better than the naive estimate. These results show that the shrinkage technique is an effective tool in estimating the sparse volatility matrix. Similar results are obtained for the noise-contaminated estimate . Unsurprisingly, due to the microstructure noise, the MFL and MSL values of the local pre-averaging estimates are noticeably higher than the corresponding values of the noise-free estimates. We next turn the attention to the time-varying noise volatility matrix estimate . As in the spot volatility matrix estimation, the naive method again produces the highest MFL and MSL values. The performance of the four shrinkage estimators are similar with the adaptive LASSO and SCAD being slightly better than the hard and soft thresholding. The simulation results for the block-diagonal and exponentially decaying covariance matrix settings, reported in the middle and bottom panels of Table 1, are fairly close to those for the banding setting. Overall, the results in Table 1 show that the shrinkage methods perform well not only in the sparse covariance matrix settings but also in the non-sparse one (i.e., the exponentially decaying setting).

Table 1: Estimation results for the spot volatility and time-varying noise covariance matrices when “Banding” Naive Hard Soft AL SCAD Naive Hard Soft AL SCAD MFL 14.396 11.407 5.490 4.038 4.830 MSL 3.963 1.799 1.073 0.867 0.987 MFL 18.497 12.899 12.196 12.064 12.177 MSL 4.796 2.347 2.260 2.255 2.262 MFL 11.714 4.226 4.740 3.237 3.960 MSL 3.281 0.682 1.039 0.571 0.753 “Block-diagonal” Naive Hard Soft AL SCAD Naive Hard Soft AL SCAD MFL 14.398 11.277 5.818 4.786 5.424 MSL 4.000 2.293 1.310 1.233 1.386 MFL 18.475 12.811 12.192 12.059 12.158 MSL 4.915 2.777 2.663 2.669 2.662 MFL 11.713 4.076 4.875 3.240 3.964 MSL 3.274 0.741 1.098 0.606 0.816 “Exponentially decaying” Naive Hard Soft AL SCAD Naive Hard Soft AL SCAD MFL 14.402 12.033 6.091 5.287 5.976 MSL 4.078 2.456 1.410 1.348 1.510 MFL 18.738 13.464 12.748 12.655 12.739 MSL 4.977 2.934 2.810 2.819 2.815 MFL 11.715 4.330 4.860 3.355 4.077 MSL 3.297 0.774 1.085 0.626 0.833

The selected bandwidths are for , and for , and for , where , , and .

The simulation results when the dimension is are reported in Table 2. Overall the results are very similar to those in Table 1, so we omit the detailed discussion and comparison to save the space.

Table 2: Estimation results for the spot volatility and time-varying noise covariance matrices when “Banding” Naive Hard Soft AL SCAD Naive Hard Soft AL SCAD MFL 21.971 4.067 5.167 4.916 3.954 MSL 3.907 0.621 0.715 0.698 0.568 MFL 28.479 19.193 18.617 17.930 18.466 MSL 4.767 2.339 2.281 2.228 2.281 MFL 18.269 4.045 4.826 5.532 4.547 MSL 3.307 0.461 0.540 0.675 0.519 “Block-diagonal” Naive Hard Soft AL SCAD Naive Hard Soft AL SCAD MFL 21.973 5.703 6.429 5.928 5.480 MSL 3.999 0.855 1.134 0.895 0.886 MFL 28.682 19.685 19.155 18.539 19.029 MSL 4.917 2.854 2.782 2.736 2.798 MFL 18.271 4.208 4.935 5.686 4.684 MSL 3.312 0.522 0.603 0.751 0.572 “Exponentially decaying” Naive Hard Soft AL SCAD Naive Hard Soft AL SCAD MFL 21.973 6.069 6.697 6.120 5.739 MSL 4.035 0.894 1.173 0.927 0.921 MFL 28.867 20.195 19.561 18.950 19.454 MSL 4.938 2.914 2.836 2.788 2.850 MFL 18.275 4.335 5.001 5.763 4.745 MSL 3.322 0.533 0.610 0.757 0.578

The selected bandwidths are for , , for and for , where , , and .

5.2 Simulation for factor-based spot volatility matrix estimation

5.2.1. Simulation setup

We generate via (4.1), where the -dimensional idiosyncratic returns follow the dynamics of defined in (5.1). In this simulation, we only consider . As in Aït-Sahalia, Kalnina and Xiu (2020), we adopt a three-factor model, where the factors are generated by

The factor volatilities are driven by

where , allowing for potential leverage effects in the factor dynamics. Both and are standard univariate Brownian motions. In the simulation, we set , , , , and .

We consider the following three cases for generating the time-varying beta processes: , .

-

•

Constant betas. The factor loadings are constants over time, i.e., , and . For each , we set and .

-

•

Deterministic time-varying betas. Consider the following deterministic function:

where , is a pair of two random numbers from whereas and are pairs of random numbers from .

-

•

Stochastic time-varying betas. As in Aït-Sahalia, Kalnina and Xiu (2020), we consider the following diffusion process:

where are standard Brownian motions independently over and , , , and .

5.2.2. Simulation Results

The spot idiosyncratic volatility matrix is estimated via (4.9). For ease of comparison, we use exactly the same bandwidth as in our first experiment. The results for the noise-free and noise-contaminated spot idiosyncratic volatility matrix estimates and measured by MFL and MSL are reported in Table 3, which reveal some desirable observations. Firstly, we note that our estimation results in terms of MFL and MSL are almost identical across different types of dynamics of factor loadings, indicating that the developed estimation procedure is robust in finite samples to different assumption of the factor loading dynamics as long as they satisfy our smooth restriction, see Assumption 6(iv). Secondly, the MFL and MSL values are similar to those reported in Table 2 which were obtained based on data generating model without common factors. This means that the proposed nonparametric time-varying high frequency regression can effectively remove common factors, resulting in accurate estimation of the spot idiosyncratic volatility matrix.

The factor-based spot volatility matrix of is estimated via (4.10). As discussed in Section 4, we measure the accuracy of the spiked volatility matrix estimate by the relative error defined above Theorem 4, i.e., consider the following Mean Relative Loss (MRL):

The relevant results are reported in Table 4, where and denote the noise-free and noise-contaminated factor-based spot volatility matrix estimates, respectively. We can see that the performance of the shrinkage estimates is substantially better than that of the naive estimate. Unsurprisingly, due to the presence of microstructure noise, the MRL results of are much higher than those of . As in Table 3, our proposed estimation is robust to different factor loading dynamics.

Table 3: Estimation results for the spot idiosyncratic volatility matrices

| “Banding” | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Dynamics | Frobenius Norm | Spectral Norm | |||||||||||

| Naive | Hard | Soft | AL | SCAD | Naive | Hard | Soft | AL | SCAD | ||||

| Constant | MFL | 21.9037 | 4.2461 | 5.2485 | 4.9880 | 3.9910 | MSL | 3.8887 | 0.6359 | 0.7291 | 0.7154 | 0.5720 | |

| MFL | 30.6646 | 19.3752 | 18.3036 | 17.7552 | 18.1388 | MSL | 11.1910 | 2.3576 | 2.2653 | 2.2160 | 2.2554 | ||

| Deterministic | MFL | 21.9127 | 4.1916 | 5.2503 | 4.9898 | 3.9842 | MSL | 3.8901 | 0.6313 | 0.7288 | 0.7144 | 0.5712 | |

| MFL | 30.5672 | 19.3633 | 18.2947 | 17.7267 | 18.1284 | MSL | 10.9662 | 2.3571 | 2.2636 | 2.2128 | 2.2536 | ||

| Stochastic | MFL | 21.9099 | 4.2123 | 5.2498 | 4.9893 | 3.9872 | MSL | 3.8896 | 0.6331 | 0.7289 | 0.7149 | 0.5717 | |

| MFL | 30.7323 | 19.3896 | 18.3164 | 17.7839 | 18.1538 | MSL | 11.3262 | 2.3603 | 2.2708 | 2.2203 | 2.2602 | ||

| “Block-diagonal” | |||||||||||||

| Dynamics | Frobenius Norm | Spectral Norm | |||||||||||

| Naive | Hard | Soft | AL | SCAD | Naive | Hard | Soft | AL | SCAD | ||||

| Constant | MFL | 21.9047 | 5.6802 | 6.4718 | 5.9421 | 5.4710 | MSL | 3.9741 | 0.8722 | 1.1481 | 0.9106 | 0.9014 | |

| MFL | 30.7266 | 19.8195 | 18.8114 | 18.3162 | 18.6638 | MSL | 10.9751 | 2.8701 | 2.7656 | 2.7097 | 2.7551 | ||

| Deterministic | MFL | 21.9137 | 5.6821 | 6.4738 | 5.9436 | 5.4729 | MSL | 3.9754 | 0.8718 | 1.1479 | 0.9103 | 0.9012 | |

| MFL | 30.6284 | 19.8161 | 18.8043 | 18.2953 | 18.6547 | MSL | 10.7452 | 2.8706 | 2.7663 | 2.7092 | 2.7559 | ||

| Stochastic | MFL | 21.9108 | 5.6811 | 6.4732 | 5.9433 | 5.4722 | MSL | 3.9751 | 0.8721 | 1.1480 | 0.9104 | 0.9013 | |

| MFL | 30.7955 | 19.8314 | 18.8237 | 18.3434 | 18.6767 | MSL | 11.1149 | 2.8719 | 2.7691 | 2.7142 | 2.7584 | ||

| “Exponentially decaying” | |||||||||||||

| Dynamics | Frobenius Norm | Spectral Norm | |||||||||||

| Naive | Hard | Soft | AL | SCAD | Naive | Hard | Soft | AL | SCAD | ||||

| Constant | MFL | 21.9057 | 6.0626 | 6.7715 | 6.1573 | 5.7617 | MSL | 4.0142 | 0.9106 | 1.1898 | 0.9453 | 0.9388 | |

| MFL | 30.8728 | 20.3802 | 19.2709 | 18.7715 | 19.1262 | MSL | 10.8858 | 2.9381 | 2.8260 | 2.7707 | 2.8154 | ||

| Deterministic | MFL | 21.9147 | 6.0709 | 6.7737 | 6.1589 | 5.7637 | MSL | 4.0156 | 0.9112 | 1.1896 | 0.9450 | 0.9387 | |

| MFL | 30.7746 | 20.3564 | 19.2632 | 18.7460 | 19.1173 | MSL | 10.6538 | 2.9354 | 2.8247 | 2.7673 | 2.8140 | ||

| Stochastic | MFL | 21.9118 | 6.0636 | 6.7730 | 6.1585 | 5.7630 | MSL | 4.0151 | 0.9106 | 1.1897 | 0.9451 | 0.9388 | |

| MFL | 30.9430 | 20.3820 | 19.2839 | 18.8017 | 19.1405 | MSL | 11.0295 | 2.9381 | 2.8291 | 2.7745 | 2.8173 | ||

Table 4: Mean relative loss for the factor-based spot volatility matrix estimation

| “Banding” | ||||||

|---|---|---|---|---|---|---|

| Dynamics | Naive | Hard | Soft | AL | SCAD | |

| Constant | 1.1192 | 0.5417 | 0.7802 | 0.7762 | 0.4391 | |

| 2.2280 | 1.7243 | 1.4939 | 1.4478 | 1.4654 | ||

| Deterministic | 1.1207 | 0.5257 | 0.7823 | 0.7775 | 0.4371 | |

| 2.2287 | 1.7182 | 1.4882 | 1.4385 | 1.4586 | ||

| Stochastic | 1.1208 | 0.5389 | 0.7829 | 0.7780 | 0.4406 | |

| 2.2273 | 1.7279 | 1.4986 | 1.4544 | 1.4719 | ||

| “Block-diagonal” | ||||||

| Dynamics | Naive | Hard | Soft | AL | SCAD | |

| Constant | 1.1192 | 0.3842 | 0.3650 | 0.3962 | 0.3249 | |

| 1.7146 | 0.8421 | 0.7938 | 0.7176 | 0.7514 | ||

| Deterministic | 1.1201 | 0.3840 | 0.3651 | 0.3958 | 0.3241 | |

| 1.7152 | 0.8410 | 0.7911 | 0.7155 | 0.7486 | ||

| Stochastic | 1.1202 | 0.3868 | 0.3678 | 0.3983 | 0.3272 | |

| 1.7146 | 0.8435 | 0.7949 | 0.7188 | 0.7528 | ||

| “Exponentially decaying” | ||||||

| Dynamics | Naive | Hard | Soft | AL | SCAD | |

| Constant | 1.1192 | 0.4086 | 0.3726 | 0.4055 | 0.3347 | |

| 1.7338 | 0.8636 | 0.8047 | 0.7272 | 0.7619 | ||

| Deterministic | 1.1201 | 0.4079 | 0.3727 | 0.4051 | 0.3339 | |

| 1.7344 | 0.8614 | 0.8016 | 0.7249 | 0.7589 | ||

| Stochastic | 1.1203 | 0.4111 | 0.3754 | 0.4075 | 0.3370 | |

| 1.7338 | 0.8645 | 0.8058 | 0.7283 | 0.7631 | ||

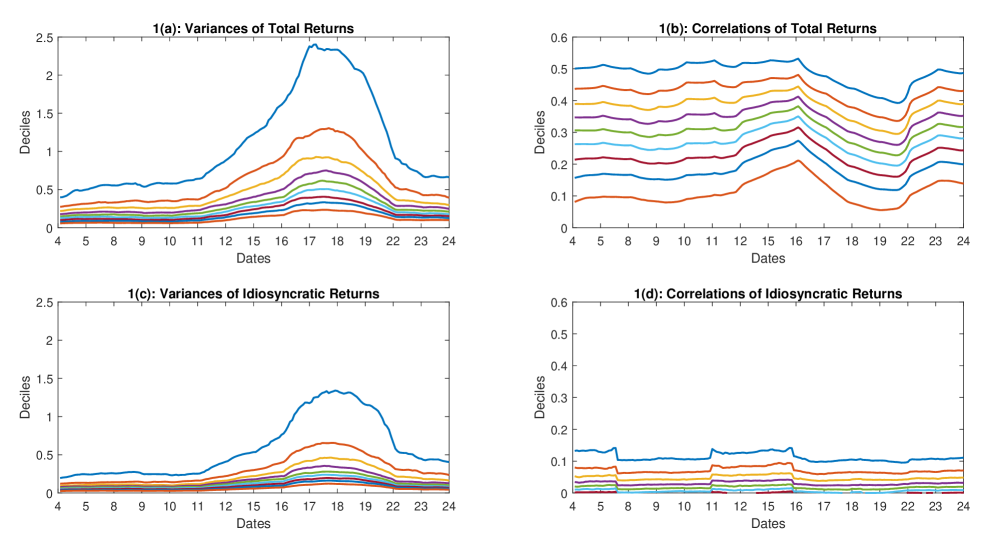

6 Empirical Study

We apply the proposed methods to the intraday returns of the S&P 500 component stocks to demonstrate the effectiveness of our nonparametric spot volatility matrix estimation in revealing time-varying patterns. We consider the 5-minute returns of the S&P 500 stocks collected in September 2008. On September 15 Lehman Brothers filed for bankruptcy, causing shockwaves throughout the global financial system. Hence, it is interesting to examine how the spot volatility structure of the returns evolved during this one-month period. In addition, to demonstrate the effectiveness of our model with observed risk factors in explaining the systemic component of the dependence structure, we also collect the 5-minute returns of twelve factors. The first three factors are constructed in Aït-Sahalia, Kalnina and Xiu (2020) as our proxy for the market (MKT), small-minus-big market capitalisation (SMB), and high-minus-low price-earning ratio (HML). The other nine factors are the widely available sector SDPR ETFs, which are intended to tract the following nine largest S&P sectors: Energy (XLE), Materials (XLB), Industrials (XLI), Consumer Discretionary (XLY), Consumer Staples (XLP), Health Care (XLV), Financial (XLF), Information Technology (XLK), Utilities (XLU). We sort our stocks according to their GICS (Global Industry Classification Standard) codes, so that they are grouped by sectors in the above order. Consequently, the correlation (sub)matrix for stocks within each sector corresponds to a block on the diagonal of the full correlation matrix (e.g., Fan, Furger and Xiu, 2016).

We only use stocks that are included in the S&P 500 index and whose GICS codes are unchanged in September 2008. We also exclude stocks that do not belong to any of the above nine sectors. This leaves us with a total of stocks. All the returns are synchronised via the previous-tick subsampling technique (Zhang, 2011), and overnight returns are removed because of potential dividends and stock splits. Consequently, we have time series observations for each of the stocks. For the 5-minute returns, we may assume that the potential impact of microstructure noises are negligible. The smoothing parameter in our kernel estimation is chosen as (equivalent to 2 trading days)222We experimented three bandwidth choices, namely, 1 day, 2 days and 3 days. We found that () produced clearly undersmoothed (oversmoothed) time series of estimated deciles of the cross sectional distribution of the variances and pairwise correlations of our returns, whereas seems to be most reasonable. Our qualitative conclusion is unaffected by the choices of within the range of 1 to 3 days..

We start with estimating the spot volatility matrices of the total returns (i.e., the observed returns) without incorporating the observed factors or applying any shrinkage. To visualise the potential time variation of the estimated spot matrices, as in Bibinger et al. (2019), we plot the time series of deciles of the distribution of the estimated spot variances and the pairwise correlations333The nine decile levels we use in this study are the 10th, 20th,…, and 90th percentiles.. The patterns of the spot variances and correlations in Figure 1(a) and (b) reveal some clear evidence of time variation in our sampling period. We note that the distributions of the variances are relatively narrow and stay low on the first few days of the month. However, close to Lehman Brothers’ announcement on the 15th, they start to rise and get wider quite rapidly and reach the peak around the 17th and the 18th. The spot variances at the peak are much higher than those on the earlier days of the month. The distributions return to the earlier level in the following week. In contrast, the distributions of pairwise spot correlations also start to shift up around the same time, but quickly reach the peak on the 16th (only one day after the bankruptcy news), and then dip to a relatively low point around the 19th before returning to the earlier level. Such time-varying features in the dynamics covariance structure are quite interesting and sensible, reflecting the impact of market news. Hence, our proposed spot volatility matrix estimation methodology provides a useful tool for revealing such dynamics.

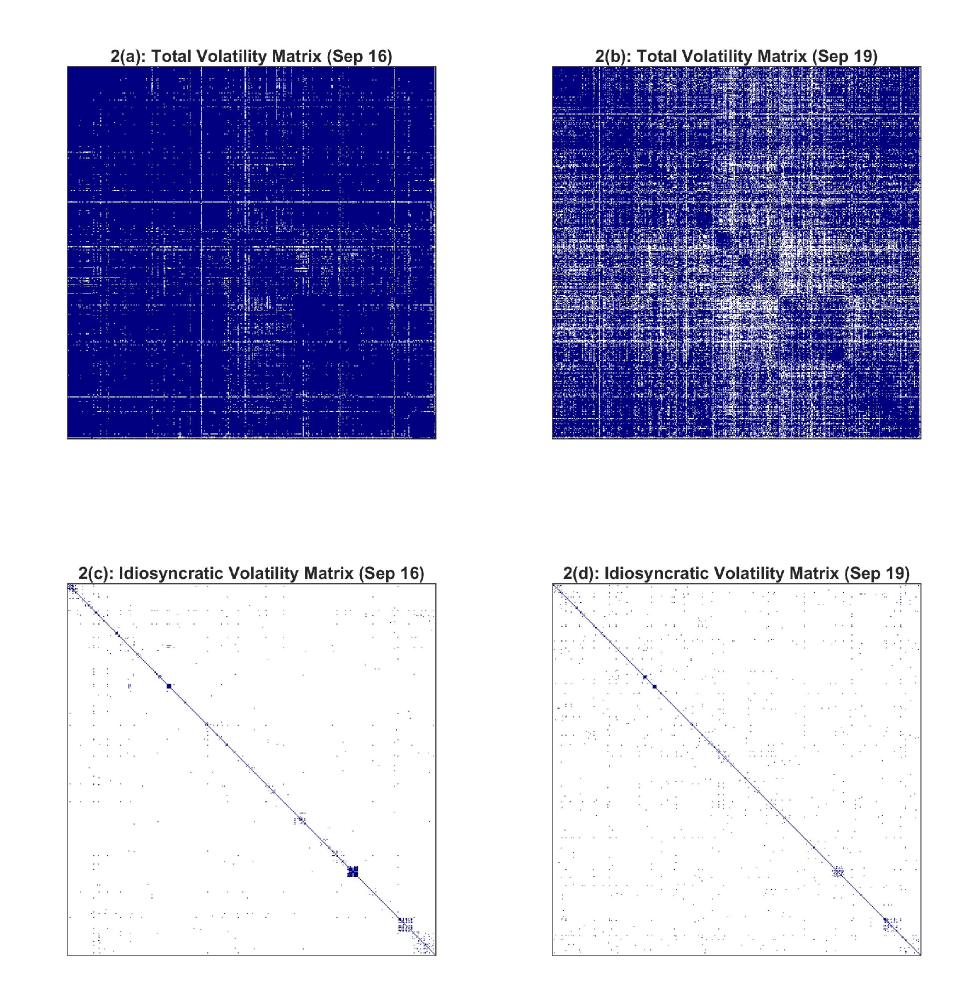

To examine whether it is appropriate to directly apply shrinkage techniques to the spot volatility matrices of the total returns, following Fan, Furger and Xiu (2016) we plot in Figure 2(a) and (b) their sparsity patterns on the 16th and the 19th of September 444Recall that as in Dai, Lu and Xiu (2019) our tuning parameter used for each pairwise spot covariance in our shrinkage method is proportional to the product of the spot standard deviations of the returns of that pair of assets. Therefore, the sparsity pattern is effectively determined by the spot correlation matrix.. The deep blue dots correspond to the locations of pairwise correlations that are at least , whereas the white dots correspond to those smaller than . Note that the covariance structure of the total returns is very dense on these two days. Therefore, it is not appropriate to directly apply the shrinkage technique as in Sections 2 and 3. Meanwhile, although both are quite dense, we can still clearly see their differences. Consistent with our observation from the decile plots of the correlations, we can see that the plot for the 16th is almost completely covered by blue dots, but the plot for the 19th in contrast has significantly more areas covered in white.

We next incorporate the twelve observed factors in the large spot volatility matrix estimation as suggested in Section 4. In particular, we are interested on estimating the spot idiosyncratic volatility matrix, which is expected to satisfy the sparsity restriction. To save space, we choose to only report results using the SCAD shrinkage due to its satisfactory performance in our simulations. In Figure 1(c) and (d), we plot the deciles of the estimated spot idiosyncratic variances and correlations over trading days. In Figure 1(c), we observe a significant upward shift of the distribution of the spot variances of the idiosyncratic returns around the time of Lehman Brothers’ bankruptcy, indicating that the observed factors may not fully capture the time variation of the spot variances. In contrast, the deciles of the spot correlations in Figure 1(d) seem to be quite flat throughout the entire month, suggesting that the systematic factors may explain the time variation in the distribution of the pairwise correlations better than that of the variances.

We finally plot the sparsity patterns of the two estimated spot idiosyncratic volatility matrices on 16 and 19 September in Figure 2(c) and (d), respectively. Unlike Figure 2(a) and (b), we note that the estimated spot idiosyncratic volatility matrices are highly sparse on the two days. This is consistent with our observation from Figure 1(d), confirming that the observed factors can effectively account for the time variation in the spot covariance structure of the returns. Meanwhile, we also note that the two idiosyncratic volatility matrices are clearly not diagonal and still carry some visible time variation. Lastly, it is worth mentioning that the estimated spot idiosyncratic volatility matrices do not exhibit significant correlations within the blocks along the diagonal lines, except for some very limited actions in the lower right corner of the two matrices (the lower right corner corresponds to the XLU sector according to our sorting).

7 Conclusion

We developed nonparametric estimation methods for large spot volatility matrices under the uniform sparsity assumption. We allowed for microstructure noise and observed common risk factors and employed kernel smoothing and generalised shrinkage. In each scenario we obtained the uniform convergence rates for the large estimated covariance matrices and these reflect the smoothness and sparsity assumptions we made. The simulation results show that the proposed estimation methods work well in finite samples for both the noise-free and noise-contaminated data. The empirical study demonstrated the effectiveness on S&P 500 stocks five minute data. Several issues can be further explored. For example, it is worthwhile to further study the spot precision matrix estimation which is briefly discussed in Appendix C.1 of the supplement and explore its application to optimal portfolio choice.

Acknowledgements

The authors would like to thank a Co-Editor and two reviewers for the constructive comments, which helped to improve the article. The first author’s research was partly supported by the BA Talent Development Award (No. TDA21210027). The second author’s research was partly supported by the BA/Leverhulme Small Research Grant funded by the Leverhulme Trust (No. SRG1920/ 100603).

References

- (1)

- Aït-Sahalia and Jacod (2014) Aït-Sahalia, Y. & J. Jacod (2014) High-Frequency Financial Econometrics. Princeton University Press.

- (3)

- Aït-Sahalia, Kalnina and Xiu (2020) Aït-Sahalia, Y., I. Kalnina, & D. Xiu (2020) High-frequency factor models and regressions. Journal of Econometrics 216, 86–105.

- (5)

- Aït-Sahalia and Xiu (2017) Aït-Sahalia, Y. & D. Xiu (2017) Using principal component analysis to estimate a high dimensional factor model with high-frequency data. Journal of Econometrics 201, 384–399.

- (7)

- Aït-Sahalia and Xiu (2019) Aït-Sahalia, Y. & D. Xiu (2019) Principal component analysis of high-frequency data. Journal of the American Statistical Association 114, 287–303.

- (9)

- Andersen and Bollerslev (1998) Andersen, T. G. & T. Bollerslev (1998) Answering the skeptics: yes, standard volatility models do provide accurate forecasts. International Economic Review 39, 885–905.

- (11)

- Andersen, Bollerslev and Diebold (2010) Andersen, T. G., T. Bollerslev, & F. X. Diebold (2010) Parametric and nonparametric volatility measurement. In Handbook of Financial Econometrics: Tools and Techniques (Y. Aït-Sahalia and L. P. Hansen, eds.), 67–137.

- (13)

- Andersen et al. (2003) Andersen, T. G., T. Bollerslev, F. X. Diebold, & P. Labys (2003) Modeling and forecasting realized volatility. Econometrica 71, 579–625.

- (15)

- Bai and Silverstein (2010) Bai, Z. & J. W. Silverstein (2010) Spectral Analysis of Large Dimensional Random Matrices. Springer Series in Statistics, Springer.

- (17)

- Barndorff-Nielsen and Shephard (2002) Barndorff-Nielsen, O. E. & N. Shephard (2002) Econometric analysis of realized volatility and its use in estimating stochastic volatility models. Journal of the Royal Statistical Society Series B 64, 253–280.

- (19)

- Barndorff-Nielsen and Shephard (2004) Barndorff-Nielsen, O. E. & N. Shephard (2004) Econometric analysis of realized covariation: High frequency based covariance, regression and correlation in financial economics. Econometrica 72, 885–925.

- (21)

- Barndorff-Nielsen et al. (2008) Barndorff-Nielsen, O. E., P. R. Hansen, A. Lunde, & N. Shephard (2008) Designing realised kernels to measure the ex-post variation of equity prices in the presence of noise. Econometrica 76, 1481–1536.

- (23)

- Bibinger et al. (2019) Bibinger, M., N. Hautsch, P. Malec, & M. Reiss (2019) Estimating the spot covariation of asset prices - statistical theory and empirical evidence. Journal of Business and Economic Statistics 37(3), 419–435.

- (25)

- Bickel and Levina (2008) Bickel, P. & E. Levina (2008) Covariance regularization by thresholding. Annals of Statistics 36, 2577–2604.

- (27)

- Cai et al (2020) Cai, T. T., J. Hu, Y. Li, & X. Zheng (2020) High-dimensional minimum variance portfolio estimation based on high-frequency data. Journal of Econometrics 214, 482–494.

- (29)

- Cai and Zhou (2012) Cai, T. T. & H. H. Zhou (2012) Optimal rates of convergence for sparse covariance matrix estimation. Annals of Statistics 40, 2389–2420.

- (31)

- Chang et al. (2021) Chang, J., Q. Hu, C. Liu, & C. Tang (2021) Optimal covariance matrix estimation for high-dimensional noise in high-frequency data. Working paper available at https://arxiv.org/abs/1812.08217.

- (33)

- Chen, Li and Linton (2019) Chen, J., D. Li, & O. Linton (2019) A new semiparametric estimation approach of large dynamic covariance matrices with multiple conditioning variables. Journal of Econometrics 212, 155–176.

- (35)

- Chen, Mykland and Zhang (2020) Chen, D., P. A. Mykland, & L. Zhang (2020) The five trolls under the bridge: principal component analysis with asynchronous and noisy high frequency data. Journal of the American Statistical Association 115, 1960–1977.

- (37)

- Chen, Xu and Wu (2013) Chen, X., M. Xu, & W. Wu (2013) Covariance and precision matrix estimation for high-dimensional time series. Annals of Statistics 41, 2994–3021.

- (39)

- Chen and Leng (2016) Chen, Z.& C. Leng (2016) Dynamic covariance models. Journal of the American Statistical Association 111, 1196–1207.

- (41)

- Christensen, Kinnebrock and Podolskij (2010) Christensen, K., S. Kinnebrock, & M. Podolskij (2010) Pre-averaging estimators of the ex-post covariance matrix in noisy diffusion models with non-synchronous data. Journal of Econometrics 159, 116–133.

- (43)

- Dai, Lu and Xiu (2019) Dai, C., K. Lu, & D. Xiu (2019) Knowing factors or factor loadings, or neither? Evaluating estimators for large covariance matrices with noisy and asynchronous data. Journal of Econometrics 208, 43–79.

- (45)

- Epps (1979) Epps, T. W. (1979) Comovements in stock prices in the very short run. Journal of the American Statistical Association 74, 291–298.

- (47)

- Fan, Fan and Lv (2007) Fan, J., Y. Fan, & J. Lv (2007) Aggregation of nonparametric estimators for volatility matrix. Journal of Financial Econometrics 5, 321–357.

- (49)

- Fan, Furger and Xiu (2016) Fan, J., A. Furger, & D. Xiu (2016) Incorporating global industrial classification standard into portfolio allocation: A simple factor-based large covariance matrix estimator with high frequency data. Journal of Business and Economic Statistics 34, 489–503.

- (51)

- Fan and Gijbels (1996) Fan, J. & I. Gijbels (1996) Local Polynomial Modelling and Its Applications. Chapman and Hall, London.

- (53)

- Fan, Liao and Mincheva (2011) Fan, J., Y. Liao, & M. Mincheva (2011) High-dimensional covariance matrix estimation in approximate factor models. Annals of Statistics 39, 3320–3356.

- (55)

- Fan, Liao and Mincheva (2013) Fan, J., Y. Liao, & M. Mincheva (2013) Large covariance estimation by thresholding principal orthogonal complements (with discussion). Journal of the Royal Statistical Society, Series B 75, 603–680.

- (57)

- Fan and Wang (2008) Fan, J. & Y. Wang (2008) Spot volatility estimation for high-frequency data. Statistics and Its Interface 1, 279–288.

- (59)

- Figueroa-López and Li (2020) Figueroa-López, J. E. & C. Li (2020) Optimal kernel estimation of spot volatility of stochastic differential equations. Stochastic Processes and Their Applications 130, 4693–4720.

- (61)

- Hayashi and Yoshida (2005) Hayashi, T. & N. Yoshida (2005) On covariance estimation of non-synchronously observed diffusion processes. Bernoulli 11, 359–379.

- (63)

- Jacod et al. (2009) Jacod, J., Y. Li, P. A. Mykland, M. Podolskij, & M. Vetter (2009) Microstructure noise in the continuous case: the pre-averaging approach. Stochastic Processes and Their Applications 119, 2249–2276.

- (65)

- Jacod and Protter (2012) Jacod, J. & P. Protter (2012) Discretization of Processes. Springer.

- (67)

- Kalnina and Linton (2008) Kalnina, I. & O. Linton (2008) Estimating quadratic variation consistently in the presence of endogenous and diurnal measurement error. Journal of Econometrics 147, 47–59.

- (69)

- Kanaya and Kristensen (2016) Kanaya, S. & D. Kristensen (2016) Estimation of stochastic volatility models by nonparametric filtering. Econometric Theory 32, 861–916.

- (71)

- Kim, Wang and Zou (2016) Kim, D., Y. Wang, & J. Zou (2016) Asymptotic theory for large volatility matrix estimation based on high-frequency financial data. Stochastic Processes and Their Applications 126, 3527–3577.

- (73)

- Kong (2018) Kong, X. (2018) On the systematic and idiosyncratic volatility with large panel high-frequency data. Annals of Statistics 46, 1077–1108.

- (75)

- Kristensen (2010) Kristensen, D. (2010) Nonparametric filtering of the realized spot volatility: a kernel-based approach. Econometric Theory 26, 60–93.

- (77)

- Lam and Feng (2018) Lam, C. & P. Feng (2018) A nonparametric eigenvalue-regularized integrated covariance matrix estimator for asset return data. Journal of Econometrics 206, 226–257.

- (79)

- Li and Racine (2007) Li, Q. & J. Racine (2007) Nonparametric Econometrics. Princeton University Press, Princeton.

- (81)

- Mykland and Zhang (2006) Mykland, P. A. & L. Zhang (2006) ANOVA for diffusions and Itô processes. Annals of Statistics 34, 1931–1963.

- (83)

- Park, Hong and Linton (2016) Park, S., S. Y. Hong, & O. Linton (2016) Estimating the quadratic covariation matrix for asynchronously observed high frequency stock returns corrupted by additive measurement error. Journal of Econometrics 191, 325-347.

- (85)

- Podolskij and Vetter (2009) Podolskij, M. & M. Vetter (2009) Estimation of volatility functionals in the simultaneous presence of microstructure noise and jumps. Bernoulli 15, 634–658.

- (87)

- Reiß, Todorov and Tauchen (2015) Reiß, M., V. Todorov, & G. Tauchen (2015) Nonparametric test for a constant beta between Itô semi-martingales based on high-frequency data. Stochastic Processes and Their Applications 125, 2955–2988.

- (89)

- Revuz and Yor (1999) Revuz, D. & M. Yor (1999) Continuous Martingales and Brownian Motion. Grundlehren der mathematischen Wissenschaften 293, Springer.

- (91)

- Shephard (2005) Shephard, N. (2005) Stochastic Volatility: Selected Readings. Oxford University Press.

- (93)

- Tao, Wang and Zhou (2013) Tao, M., Y. Wang, & H. H. Zhou (2013) Optimal sparse volatility matrix estimation for high-dimensional Itô processes with measurement errors. Annals of Statistics 41, 1816–1864.

- (95)

- Wang and Zou (2010) Wang, Y. & J. Zou (2010) Vast volatility matrix estimation for high-frequency financial data. Annals of Statistics 38, 943–978.

- (97)

- Xia and Zheng (2018) Xia, N. & X. Zheng (2018) On the inference about the spectral distribution of high-dimensional covariance matrix based on high-frequency noisy observations. Annals of Statistics 46, 500–525.

- (99)

- Xiao and Linton (2002) Xiao, Z. & O. Linton (2002) A nonparametric prewhitened covariance estimator. Journal of Time Series Analysis 23, 215–250.

- (101)

- Zhang (2011) Zhang, L. (2011) Estimating covariation: Epps effect, microstructure noise. Journal of Econometrics 160, 33–47.

- (103)

- Zhang, Mykland and Aït-Sahalia (2005) Zhang, L., P. A. Mykland, & Y. Aït-Sahalia (2005) A tale of two time scales: Determining integrated volatility with noisy high-frequency data. Journal of the American Statistical Association 100, 1394–1411.

- (105)

- Zheng and Li (2011) Zheng, X. & Y. Li (2011) On the estimation of integrated covariance matrices of high dimensional diffusion processes. Annals of Statistics 39, 3121–3151.

- (107)

- Zu and Boswijk (2014) Zu, Y. & H. P. Boswijk (2014) Estimating spot volatility with high-frequency financial data. Journal of Econometrics 181, 117–135.

- (109)

Appendix A: Proofs of the main results

In this appendix, we give the proofs of the main theorems. We start with four propositions whose proofs are available in Appendix B of the supplement.

Proposition A.2.

Proposition A.3.

Proposition A.4.

Proof of Theorem 1. By the definition of and the property of , we readily have that

| (A.4) | |||||

Define the event

where is a positive constant. For any small , by (A.1), we may find a sufficiently large constant such that

| (A.5) |

By property (iii) of the shrinkage function and (A.5), we have

and

conditional on the event . By the reverse triangle inequality and Proposition A.1,

on . Letting in Assumption 2(iii), as , we have

| (A.6) | |||||

on the event , where is defined in Assumption 2(iii). Note that the events and jointly imply that . Then, we may show that

| (A.7) | |||||

By Proposition A.1, we readily have that

| (A.8) |

By (A.6)–(A.8), and letting in (A.5), we complete the proof of Theorem 1.

Proof of Theorem 2. The proof is similar to the proof of Theorem 1 with Proposition A.2 replacing Proposition A.1. Details are omitted to save the space.

Proof of Theorem 3. The proof is similar to the proof of Theorem 1 with Proposition A.3 replacing Proposition A.1. Details are omitted to save the space.

Proof of Theorem 4. By Proposition A.4 and the definition of in (4.8), we may show that

| (A.9) |

With (A.9), following the proof of Theorem 1, we complete the proof of (4.12).

We next turn to the proof of (4.13). Note that

For any matrix , since all the eigenvalues of are strictly larger than a positive constant,

| (A.10) |

where is a generic constant whose value may change from line to line. By (4.12) and (A.10), we prove

| (A.11) |

By the definition of in (4.7) and Proposition A.4, we readily have that

| (A.12) |

Write and . Note that

By (A.10), (A.12) and Proposition A.4, we have

| (A.13) | |||||

Similarly, we can show that

| (A.14) |

By (4.3), Assumption 6(iv) and Sherman-Morrison-Woodbury formula, we may show that

| (A.15) |

Using (A.12), (A.15) and Proposition A.4, we have

| (A.16) | |||||

and

| (A.17) |

Similar to the proof of (A.16), we also have

| (A.18) |

and

| (A.19) |

By (A.15) and Proposition A.4, we may show that

| (A.20) | |||||

With (A.13), (A.14) and (A.16)–(A.20), we have

| (A.21) |

By virtue of (A.11) and (A.21), we complete the proof of (4.13).

Supplement to “Nonparametric Estimation of Large Spot Volatility Matrices for High-Frequency Financial Data”

In this supplement, we provide the detailed proofs of the propositions stated in Appendix A, discuss the spot precision matrix estimation, address the asynchronicity issue and report additional simulation results.

Appendix B: Proofs of technical results

As discussed in Remark 1, the local boundedness condition in Assumption 1(i) can be strengthened to the following uniform boundedness condition:

| (B.1) |

with probability one. Throughout this appendix, we let denote a generic positive constant whose value may change from line to line.

Proof of Proposition A.1. Throughout this proof, we let . By (2.1), we have

This leads to the following decomposition:

We next show that

| (B.3) |

Let , and be adapted to the underlying filtration . Note that

Hence, to show (B.3), it is sufficient to prove that

| (B.4) |

and

| (B.5) |

where is defined in Assumption 1(ii).

We next only prove (B.4) as the proof of (B.5) is analogous. Consider covering the interval by some disjoint intervals with centre and length , . Observe that

| (B.6) | |||||

As the kernel function has the compact support , we have, for any ,

where and . Letting be a standard normal random variable, by Lemma 1 in Fan, Li and Yu (2012), we have

| (B.7) |

Following the argument in the proof of Lemma 3 in Fan, Li and Yu (2012) and using (B.7), for ,

where satisfies that and is defined in (B.1). Consequently, we have

| (B.8) | |||||

where . By (B.8), using the Markov inequality and choosing , we can prove that

where is positive and becomes sufficiently large if we choose to be large enough. Then, by the Bonferroni inequality, we have

where the convergence is due to the fact as is divergent at a polynomial rate of and is sufficiently large, which implies that

| (B.9) |

By the smoothness condition on the kernel function in Assumption 2(i), we have

Similar to the proof of (B.9), we may show that

as is fixed and is uniformly bounded by . Hence, by the choice of , we have

| (B.10) |

Analogously, we also have

| (B.11) |

By (B.2), (B.3) and the Cauchy-Schwarz inequality, we have

indicating that

| (B.12) |

and similarly,

| (B.13) |

With (B.2), (B.3), (B.12) and (B.13), we prove that

| (B.14) |

Since is strictly larger than a positive constant uniformly over , by (B.14), we readily have that

| (B.15) |

On the other hand, by (2.6) in Assumption 1(ii), we may show that

| (B.16) |

Then we complete the proof of (A.1) by virtue of (B.15) and (B.16).

We next turn to the proof of Proposition A.2, in which a crucial step is to derive a uniform consistency for . The latter is stated in Lemma B.1 below.

Lemma B.1.

Suppose that Assumptions 1(i), 3 and 4(i)(ii) are satisfied. Then we have

| (B.17) |

Let , , and . We first consider . Define

| (B.19) |

where is defined in Assumption 4(ii). Note that

as . By the noise moment condition in Assumption 3(i) and the uniform boundedness condition on in Assumption 3(ii), we have

where is arbitrarily large. Then, by Assumptions 3(i), 4(ii) and the Bonferroni and Markov inequalities, we have, for any ,

for , where is defined in Assumption 3(i). Hence, we have

| (B.20) |

On the other hand, by Assumptions 3 and 4(i)(ii) as well as the Bernstein inequality for the independent sequence (e.g., Proposition 2.14 in Wainwright, 2019), we may show that

where diverges to infinity at a polynomial rate of , is positive and could be sufficiently large by letting be large enough. Therefore, we have

| (B.21) |

By (B.20) and (B.21), and noting that is strictly larger than a positive constant uniformly over , we readily have that

| (B.22) |

Write

note that

By (B.1) and Assumption 4(i), we have

| (B.23) |

By the Bonferroni inequality, we may show that, for any

| (B.24) | |||||

By the conditional Jensen inequality, we may verify that both and are sub-martingales, where . Using the moment generating function for the folded normal random variable and (B.1), we have

where is defined in (B.1). Combining the above arguments and using Doob’s inequality for sub-martingales, we may show that

| (B.25) | |||||

Then, choosing , by (B.24) and(B.25), we have

for any , which indicates that

| (B.26) |

By (B.23) and (B.26), we readily have that

| (B.27) |

For , we note that

By Assumption 4(i), we have

| (B.28) |

On the other hand, by (B.1),

Following the proof of (B.26), we may show that

indicating that

| (B.29) |

By virtue of (B.28) and (B.29), we prove that

| (B.30) |

Finally, for , we write it as

By Assumptions 1(i) and 4(i), we readily have that

| (B.31) |

Following the proof of (B.26), we may show that

and

when is sufficiently large. Consequently, we have

| (B.32) |

| (B.33) |

The proof of (B.17) in Lemma B.1 is completed with (B.22), (B.27), (B.30) and (B.33).

Proof of Proposition A.2. By (3.3), we have

where

By Proposition A.1, we have

| (B.34) |

By Lemma B.1 and Assumption 2(i), we have

| (B.35) |

By Proposition A.1, (B.35) and the Cauchy-Schwarz inequality, we have

| (B.36) |

The proof of (A.2) in Proposition A.2 is completed by virtue of (B.34)–(B.36).

Proof of Proposition A.3. By (3.1) and (3.7), we write

By Proposition A.1, we have

| (B.37) |

To complete the proof of (A.3), it is sufficient to show

| (B.38) |

In fact, combining (B.37) and (B.38), and using the Cauchy-Schwarz inequality, we

| (B.39) |

It remains to prove (B.38). We aim to show that

| (B.40) | |||

| (B.41) | |||

| (B.42) |

where . To save the space, we only provide the detailed proof of (B.40) as the proofs of (B.41) and (B.42) are similar (with minor modifications).

Note that

| (B.43) | |||||

Let ,

where is defined in Assumption 5(iii). Observe that

| (B.44) |

By Assumptions 3(ii) and 5(i), we have with being arbitrarily large. Then, by Assumption 5(i)(ii) and the Markov inequality, we have that, for any ,

| (B.45) | |||||

for , where , is defined in Assumption 3(ii) and is defined in Assumption 5(i).

Cover the closed interval by some disjoint intervals , , with the center and length . By the Lipschitz continuity of in Assumption 2(i), we have

| (B.46) | |||||

On the other hand, by the Bernstein inequality, we may show that