Bootstrapping the Cross-Validation Estimate

Abstract

Cross-validation is a widely used technique for evaluating the performance of prediction models. It helps avoid the optimism bias in error estimates, which can be significant for models built using complex statistical learning algorithms. However, since the cross-validation estimate is a random value dependent on observed data, it is essential to accurately quantify the uncertainty associated with the estimate. This is especially important when comparing the performance of two models using cross-validation, as one must determine whether differences in error estimates are a result of chance fluctuations. Although various methods have been developed for making inferences on cross-validation estimates, they often have many limitations, such as stringent model assumptions This paper proposes a fast bootstrap method that quickly estimates the standard error of the cross-validation estimate and produces valid confidence intervals for a population parameter measuring average model performance. Our method overcomes the computational challenge inherent in bootstrapping the cross-validation estimate by estimating the variance component within a random effects model. It is just as flexible as the cross-validation procedure itself. To showcase the effectiveness of our approach, we employ comprehensive simulations and real data analysis across three diverse applications.

Keywords: random effects model, mean absolute prediction error, c-index, individualized treatment response score

1 Introduction

Predictive modeling has emerged as a prominent tool in biomedical research, encompassing diverse applications such as disease diagnosis, patient risk stratification, and personalized treatment recommendations, as seen in studies such as [25, 13, 24, 17]. A wide range of methods have been employed to create prediction models, from basic linear regression to sophisticated deep learning algorithms. Once the models have been developed, it’s crucial to assess their performance for a number of reasons. Firstly, the results from a model cannot be effectively utilized or interpreted without understanding its accuracy. For instance, a positive result from a model with a positive predictive value (PPV) of 20% will be treated differently from a positive result with a PPV of 1% by both physicians and patients. Secondly, with a wealth of prediction tools at hand, choosing the best model from a set of models can be a challenge, with multiple factors influencing the decision, including cost, interpretability, and, most importantly, the model’s future performance in a population. This performance can be measured in various ways, depending on the intended application of the model. If the model aims to predict clinical outcomes, its accuracy can be measured by a prediction accuracy metric, such as mean squared prediction error for continuous outcomes or a receiver operating characteristics (ROC) curve for classification. In other cases, the performance measure can be more complex. If the model is used to recommend treatment to individual patients, the model performance can be measured by the observed treatment benefit among patients who are recommended to receive a particular treatment according to the model. Lastly, even in the model construction step, evaluating the model performance is often needed for optimal tuning. For example, in applying neural networks, the network structure needs to be specified by the analyst to have best prediction performance.

Cross-validation is a commonly used technique to assess the performance of a predictive model and overcome the over-optimistic bias that results from using the same data for both training and evaluating the model [9, 12, 29, 21]. The approach involves using out-of-sample observations to evaluate model performance, thus avoiding optimism bias. The resulting cross-validation estimator is a random quantity, dependent on both the random splitting of data into training and testing sets, and the observed data itself. To reduce the randomness due to the splitting of data, one can repeat the training and testing process multiple times and average the prediction performance on the testing data. The randomness inherent in the observed data reflects the fact that if a new set of data were randomly sampled from the underlying population, the cross-validation results would be different from those based on the current observed data. In essence, the cross-validation estimator is a statistic, or a function of random data, despite its complex construction.

Realizing this fact, it is important to derive and estimate the distribution of this statistic so that we may (1) understand what population parameter the cross-validation procedure estimates and (2) attach an appropriate uncertainty measure to the cross-validation estimate [3, 20, 34]. For the simple case of large sample size and small number of parameters, the asymptotic distribution of the cross-validation estimator has been studied in depth [8, 27, 15, 19]. For example, when the model training and validation are based on the same loss function, the cross-validation estimator is asymptotically Gaussian [8]. A computationally efficient variance estimator for the cross-validated area under the ROC curve has also been proposed, if the parameters used in the classifier are estimated at the root rate [19]. More recently, Bayle et al. have established the asymptotic normality of general -fold cross-validated prediction error estimates and proposed a consistent variance estimator under a set of stability conditions [3]. The learning algorithm can be general and flexible, but the error estimate in the validation set needs to be in the form of sum of identically independent distributed random elements. The validity of their proposed variance estimate requires that the variation from model training is dominated by that in estimating the prediction error in the testing set. Along a similar line, Austern and Zhou (2020) have also studied the asymptotic distribution of fold cross-validation estimates allowing increases with the sample size [1]. The proposed variance estimator is very similar to that in [3]. Asymptotic normality of the cross-validation estimator has been established when the prediction model is trained on the same loss as is used for evaluation, the same case as in [8]. A nested cross-validation method has been introduced to automatically quantify the uncertainty of the cross-validation estimate and construct confidence intervals for the model performance [2]. The key is to use an additional loop of cross-validations to correct the finite-sample bias of the variance estimator proposed in [3, 1]. However, this method still requires specific forms for the performance measure of interest and may not be applicable in certain applications.

The majority of previous work on cross-validation assumes a simpler form for the performance measure, such as the average of a random variable, and requires that the prediction model is trained using the same loss function. However, there are applications of cross-validation not covered by these conventional approaches, as demonstrated in Example 3 of the paper. Additionally, the validity of the proposed confidence intervals relies on suitable stability conditions and large sample approximations. Although resampling methods are a well-known approach for estimating the variance of a statistic and can provide fairly accurate approximations even with small to moderate sample sizes, the main challenge with using them in this setting is the computational speed. This paper aims to characterize the underlying population parameter estimated by the cross-validation procedure and to propose a general, computationally efficient resampling method for constructing a confidence interval for this population parameter, removing as many restrictions as possible.

2 Method

In a very general setup, we use random vector to denote individual observations, and the observed data consist of independent identically distributed (i.i.d.) copies of , i.e., The output of the training procedure is a parameter estimate, which can be a finite dimensional vector or infinite dimensional functions, denoted by to emphasize its dependence on observed data and the fact that it is a random quantity. In evaluating the “performance” of in a new testing set consisting of i.i.d. observations a summary statistic is calculated as a function of testing data and which can be written as

It is possible to make inference and derive confidence interval on by treating or both and as random. In most applications, however, we only have a single dataset, and the cross-validation procedure is needed in order to objectively evaluate the model performance. Specifically, In cross-validation, we randomly divide the observed data into two non-overlapping parts denoted by and , and calculate In order to reduce the variability of random splits, the aforementioned step is oftentimes repeated many times and the average performance measure is obtained as the final cross-validation estimator of the model performance:

where represents the th split. The number of replications, , needs to be relatively large to reduce the Monte-Carlo variation due to random splits. It is often in the range of several hundreds in practice. Note that although we used to represent the model performance in consistent with notations used in the literature [2], the performance measure is not necessarily a prediction error. It can be other metric with a higher value indicating a good performance as discussed in the following sections.

2.1 Applications

Many cross-validation applications can fit into the very general framework described above. In this paper, we will focus on several typical examples.

2.1.1 Application 1

In the first example, we are interested in evaluating the performance of predicting continuous outcomes measured by mean absolute prediction error [27, 32]. The result can help us to determine, for example, whether a newly developed prediction algorithm significantly outperform an existing model. The prediction model can be constructed by fitting a standard linear regression model, i.e., calculating a regression coefficient vector by minimizing a loss function

based on a training dataset , where is the baseline covariate for the th patient and including an intercept. If nonlinear prediction models are considered, then one may construct the prediction model via a more flexible machine learning algorithm such as random forest or neural network. In all cases, the prediction error in a testing set is calculated as

where is the number of observations in the testing set. In cross-validation, we may repeatedly split an observed dataset into training and testing sets of given sizes, , and obtain the corresponding cross-validated mean absolute prediction error estimator, . In the end, the sample average of those resulting cross-validated mean absolute prediction error estimators becomes the final estimator measuring the predictive performance of the linear model. In this application, with and being the predictor and outcome of interest, respectively, , and the summary statistic measuring the prediction performance is:

2.1.2 Application 2

In the second example, we are interested in evaluating the performance of a prediction model in predicting binary outcomes by its c-index for new patients, which is the area under the ROC curve [11, 23]. The result can help us to determine, for example, whether c-index from a new prediction model is significantly higher than 0.5 or a desirable level. The prediction model can be constructed via fitting a logistic regression model, i.e., calculating a regression coefficient vector by maximizing the log-likelihood function

based on a training dataset . If the dimension of the predictor is high, a lasso-regularization can be employed in estimating . In any case, a concordance measure, the c-index in a testing set can be calculated as

where is the number of observations in the set In cross-validation, we may repeatedly split the observed dataset into training and testing sets, and obtain the corresponding cross-validated c-indexes . In the end, the sample average of those resulting cross-validated c-index estimator is our final estimator measuring the classification performance of the logistic regression. In this application, with and being the predictor and a binary outcome of interest, respectively, , and

Remark 1

In evaluating the performance of the logistic regression model for predicting binary outcomes, we may choose to use the entire ROC curve to measure the model performance. Since the construction of a stable ROC curve requires sufficient number of cases, i.e, observations with and controls, i.e., observations with one may want to construct the ROC curve with as many observations from testing set as possible. In particular, one can implement the -fold cross-validation, i.e., randomly splitting the observed dataset in to parts of approximately equal sizes: Let be the regression coefficient estimated based on observations not in the th part of the observed data. We may then construct the predicted risk score for patients in the th part as Cycling through we can obtain a predicted risk score for every patient as

where represents the particular division of the observed dataset into parts. The ROC curve can then be calculated as

where is the empirical survival function of depending on the particular division of . In cross-validation, we may repeatedly split the observed dataset into parts and obtain the corresponding cross-validated ROC curve , and the sample average of those resulting ROC curves becomes the final estimator of the ROC curve measuring the predictive performance of the logistic regression. In this example,

where is empirical survival function of Our proposed method will cover inference for estimator from fold cross-validation as well.

2.1.3 Application 3

In the third example, we are interested in developing a precision medicine strategy and evaluating its performance in a randomized control setting. Specifically, the precision medicine strategy here is a binary classification rule to recommend a treatment to a patient based on his or her baseline characteristics to maximize the treatment benefit for individual patient as well as in a patient population of interest. Before applying this recommendation to clinical practice, it is important to estimate the uncertainty of the treatment effect in the identified subgroup who would be recommended for the treatment, to make sure the anticipated stronger treatment effect is real. There are many different ways of constructing such a treatment recommendation classifier [5, 26]. For example, one may first construct a individualized treatment response (ITR) score by minimizing a loss function based on a training dataset

where is the response of interest with a higher value being desirable, is a binary treatment indicator and independent of the baseline covariate (i.e., the treatment is randomly assigned to patients in the training set), and Let the resulting minimizers of and be and , respectively [26, 33]. Note that we have the decomposition that

where is the potential outcome if the patient receives treatment and the observed outcome Therefore, minimizing the original loss function with respect to amounts to approximating the conditional average treatment effect (CATE),

via , a linear function of , because the solution minimizes a loss function, whose population limit is

The constructed ITR score is which can be used to guide the treatment recommendation for individual patient. There are other ways of constructing the ITR score approximating the CATE. Once an estimated ITR score is available, one may recommend treatment to patients whose and treatment to patients whose where is a constant reflecting the “cost” of the treatment. Here, we choose for simplicity. In the testing set, one may evaluate the performance of this recommendation system by estimating the average treatment effect among the subgroup of patients recommended to receive the treatment i.e, and among the subgroup of patients recommended to receive the treatment i.e., Specifically, we may consider the observed treatment effects

and

If takes a “large” positive value and takes a “large” negative value, (in other words, the treatment effect is indeed estimated to be greater among those who are recommended to receive the treatment based on the constructed ITR score), then we may conclude that is an effective treatment recommendation system. In cross-validation, we may repeatedly divide the observed data set into training and testing sets, and obtain the corresponding cross-validated treatment effect difference . In the end, the sample average of those resulting cross-validated treatment effect estimators is our final cross-validation estimator measuring the performance of the treatment recommendation system. In this application with , and being predictors, treatment assignment indicator, and a binary outcome, respectively, , and

or

2.2 The Estimand of Cross-validation

The first important question is what population parameter the cross-validation procedure estimates. As discussed in [2], there are several possibilities. The first obvious population parameter is

where is the training set of sample size and is a new independent testing set of sample size drawing from the same distribution as the training dataset, . This parameter depends on the training set and directly measures the performance of the prediction model obtained from observed data in a future population. The second population parameter of interest is

the average performance of prediction models trained based on “all possible” training sets of size sampled from the same distribution as the observed dataset, The subscript emphasizes the fact that this population parameter only depends on the sample size of the training set While is the relevant parameter of interest in most applications, where we want to know the future performance of the prediction model at hand, is a population parameter reflecting the expected performance of prediction models trained via a given procedure. The prediction performance of the model from the observed dataset can be better or worse than this expected average performance. It is known that the cross-validation targets on evaluating a training procedure rather than the particular prediction model obtained from the training procedure. Specifically, the cross-validation estimator actually estimates in the sense that

where is the sample size of the training set used in constructing the cross-validation estimate, i.e., the dataset is repeatedly divided into a training set of size and a testing set of size in cross-validation. Here, and are two mean zero random noises and oftentimes nearly independent. In many cases , when is not substantially smaller than If we ignore their differences, then can also be viewed as an approximately unbiased estimator for , because

whose mean is approximately zero. On the other hand, the variance of tends to be substantially larger than the variance of since and are often independent and the variance of is nontrivial relative to that of . This is analogous to the phenomenon that the sample mean of observed data is a natural estimator of the population mean. It also can be viewed as an unbiased “estimator” of the sample mean of a set of future observations, because the expectation of sample mean of future observations is the same as the population mean, which can be estimated by the sample mean of observed data. In this paper, we take as the population parameter of interest, because approximately is simply plus a random noise , which may be independent of the cross-validation estimate. In other words, we take the view that the cross-validation estimate evaluates the average performance of a training procedure rather than the performance of a particular prediction model. As the training sample size goes to infinity, we write When is sufficiently large,

In the following, we use a simple example to demonstrate the relationship of aforementioned quantities.

2.2.1 A Toy Example

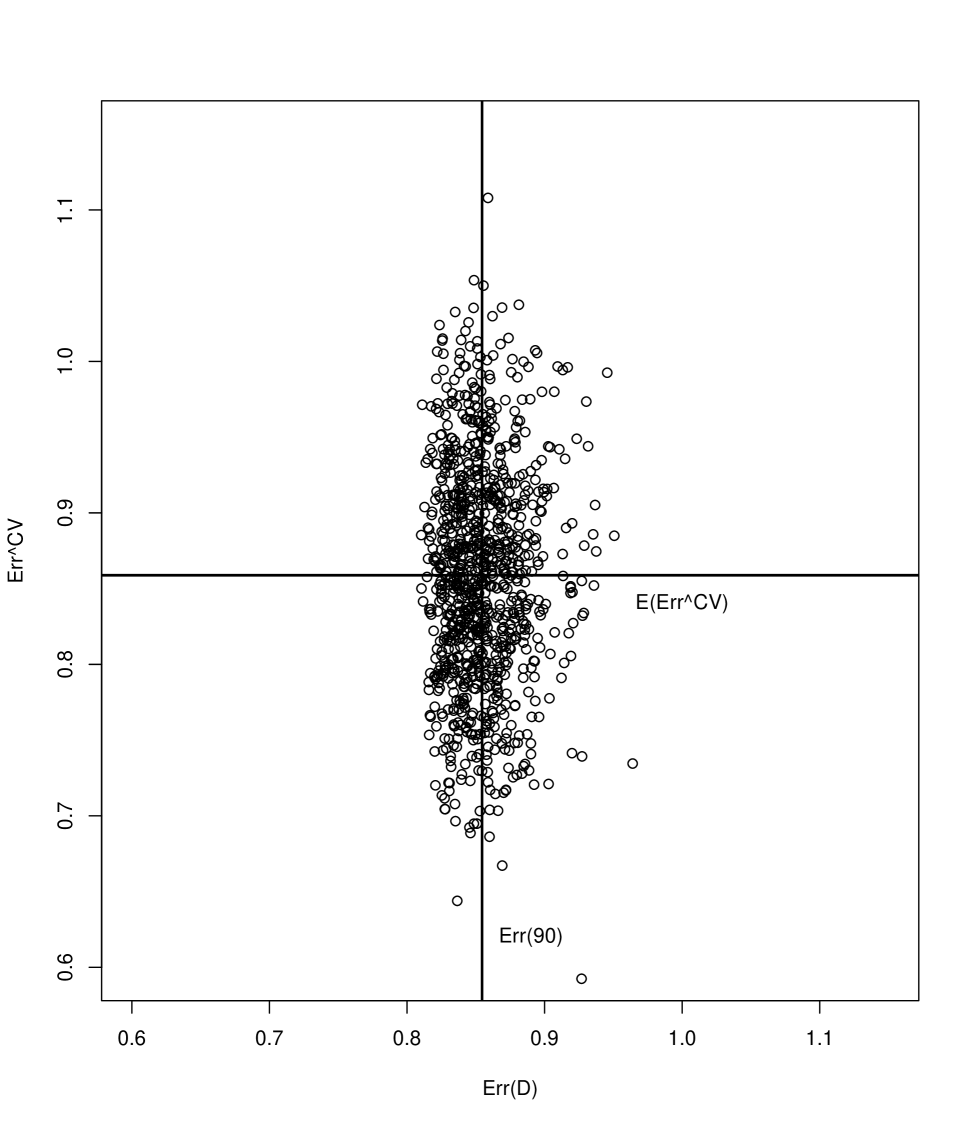

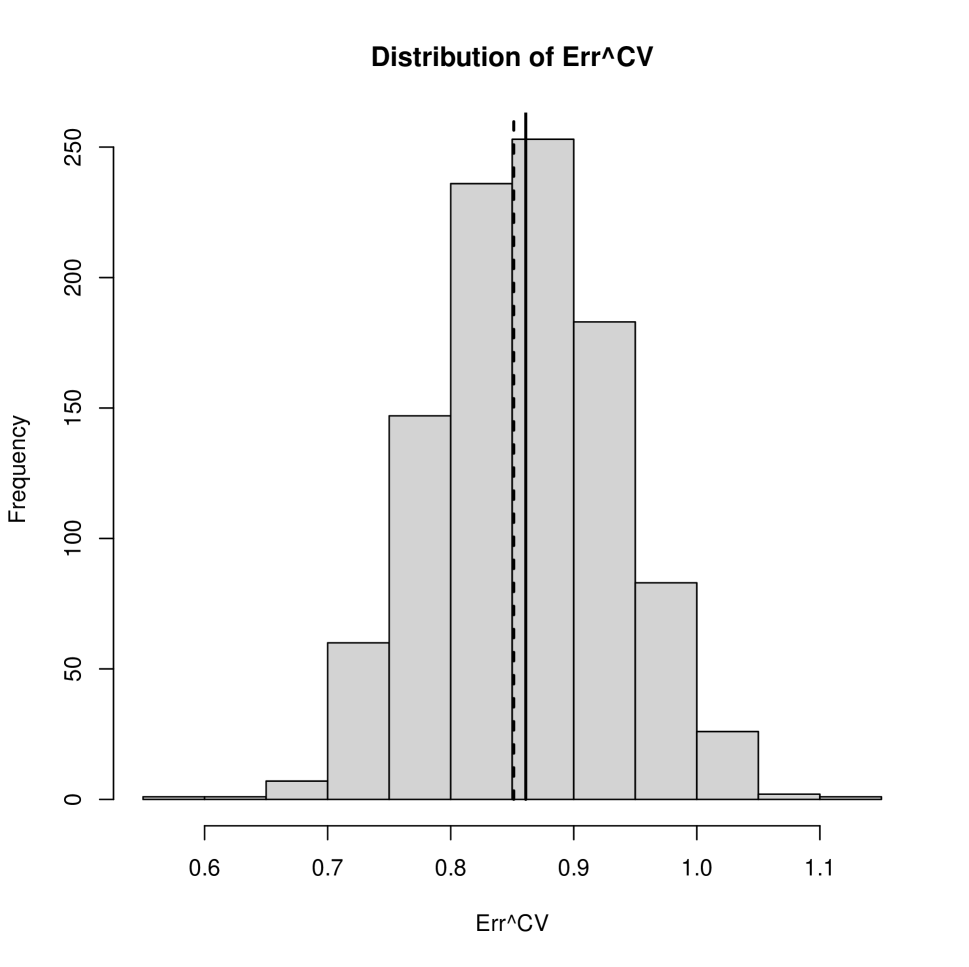

Consider the linear prediction model in section 2.1.1. Suppose that covariate , and the response where is 10 by 10 identity matrix, , and We were interested in constructing a prediction model via fitting a linear regression model and evaluating its performance in terms of the mean absolute prediction error. To this end, for each simulated dataset we estimated the regression coefficients of the linear model by ordinary least square method and denoted the estimators of and by and respectively. Then we calculated the true mean absolute prediction error as the expectation of where is a random variable. This expectation was , the prediction error of the model trained based on dataset in a future population. We also constructed the cross-validation estimate of the prediction error by repeatedly splitting into a training set of size and a testing set of size The resulting estimator for the estimation error was Repeating these steps, we obtained 1000 pairs of and from simulated datasets. The empirical average of 1000 s was an approximation to Figure 1(a) is the scatter plot of vs. based on 1000 simulated datasets. It was clear that and were almost independent but shared a similar center. Specifically, the empirical average of was 0.859, and the empirical average of was 0.851. Therefore, the cross-validated error estimator can be viewed as a sensible estimator for , and more precisely an unbiased estimator for , whose value was estimated as 0.861 using the same simulation described above. Note that and and are fairly close. The distribution of the cross-validated error estimators along with and are plotted in Figure 1(b), suggesting that the small difference between and is negligible relative to the variation of the cross-validation estimator itself. In addition, can also be thought as a “prediction” to since the latter was approximately plus an independent mean zero “measurement error”.

2.3 Statistical Inference on

In this section, we aim to construct a valid confidence interval for based on the cross-validated estimate. First, we define the cross-validated estimate with repeated training and testing splits as

where the expectation is with respect to random division of training and testing sets. One may anticipate that is a “smooth” functional with respect to the empirical distribution of observed data , because each individual observation’s contribution to the final estimator is “averaged” across different training and testing divisions. Therefore, we expect that is a root- regular estimator of , i.e.,

in distribution as , the sample size of , goes to infinity and Indeed, under the following regularity conditions, this weak convergence holds in general.

-

C1

has a first order expansion, i.e,

where is a consistent estimator for a population parameter based on and are independent mean zero random elements with a finite variance.

-

C2

The process is stochastic equal continuous at , i.e.,

as where is an appropriate norm measuring the distance between and [16]

-

C3

The random sequences

converges to a mean zero Gaussian distribution, where are independent mean zero random elements with a finite variance.

-

C4

There exists a linear functional indexed by such that

In the Appendix, we have provided an outline to show that

where After taking expectation with respect to the random training and testing division, i.e., indicators

and

converges weakly to a mean zero Gaussian random distribution with a variance of

For a finite sample , we expect that the difference between and may be negligible. Specifically, the distribution of

can be approximated by if the following condition holds

-

C5

where is based on training set of size and the expectation is with respect to

This assumption is in general true, since often converges to a smooth functional of as and the expectation of the limit can be approximated by with the approximation error bounded by which is in the order of following condition C1. Since is closer to than in finite sample setting, the Gaussian approximation for is likely to be more accurate. As a consequence, an asymptotical confidence interval for can be constructed as

where is a consistent estimator of the standard error However, in general it is difficult to obtain such a consistent variance estimator when complex procedures such as lasso regularized regression or random forest are used for constructing the prediction model as in three examples discussed above. An appealing solution is to use the nonparametric bootstrap to estimate [7, 10]. The rational is that, under the same set of assumptions,

where is the cross-validated estimator based on bootstrapped data , , is the number of observation in and is the product probability measure with respect to random data and the independent random weights Therefore, conditional on observed data

converges weakly to a mean zero Gaussian distribution with a variance of

Operationally, the following naive bootstrap procedure is expected to generate a consistent variance estimator of ,

small

The variance can be estimated by times the empirical variance of bootstrapped cross-validation estimates However, there are several concerns in this naive resampling procedure, which may result in poor performance in practice.

-

•

The bootstrap procedure samples observations with replacement and results in potential duplicates of the same observation in the bootstrapped dataset. Naively splitting the bootstrapped dataset into training and testing sets may result in overlap between them, which can induce nontrivial optimistic bias in evaluating the model performance. If we apply the naive bootstrap method to analyze the Toy Example described in section 2.2.1, then the empirical average of bootstrapped cross-validation estimates was downward biased in comparison with by 0.80 standard deviation of cross-validation estimates The practical influence of overlap on the variance estimation is less clear but can be potentially nontrivial.

-

•

The training set of size in the bootstrapped dataset contains substantially fewer than distinct observations, which reduces the “effective” sample size for training a prediction model and induces a downward bias in evaluating the average model performance. This downward bias may be smaller or greater than the optimism bias induced by the overlap between training and testing sets depending on specific applications, but is undesirable in general.

-

•

To obtain a cross-validated estimate for each bootstrap sample, one needs to perform the cross-validation multiple times to reduce the Monte-Carlo variation due to random training/testing divisions, i.e., needs to be sufficiently big such as In addition, the number of bootstraps also can not be too small. The conventional recommendation for estimating variance of a statistic using bootstrap is to set the number of bootstraps In such a case, one needs to train and evaluate the prediction model more than times and the corresponding computational burden can be prohibitive for complex training algorithm.

In this paper, we present a modified bootstrap procedure to overcome aforementioned difficulties.

First, in implementing cross-validation on a bootstrapped dataset, we view bootstrapped data as a weighted samples of the original data, i.e., observation is weighted by a random weight , which is the number of this observation selected in this bootstrap iteration. In cross-validation, we first split the original dataset into training and testing sets, and bootstrapped training and testing sets denoted by and , respectively, are then constructed by collecting all observations in and respectively, but with their respective bootstrap weights. Since and have no overlap, as well. Therefore, we don’t allow that the same observation used in both training and testing. One consequence is that the sample sizes of and are not fixed across different bootstrap samples. But their average sample sizes remain the same as those for and

Second, we note that the effective sample size of the training set based on the bootstrapped data can be substantially smaller than . Specifically, the number of distinct observations in is on average [9]. Therefore, it is desirable to increase the number of distinct observations of by allocating more observations to , which is used to generate in a bootstrapped dataset. Ideally, we may want to increase the sample size of such that the number of distinct observations used for training is close to in bootstrapped cross-validation, i.e., which requires to increase the sample size in from to On the other hand, the sample size of and thus would be reduced by using a larger training set in the bootstrapped cross-validation and such a large reduction in testing sample size may increase the variance of the resulting estimate. In summary, while we want to increase the sample size in the training set to reduce the bias of estimating the model performance in bootstrapped cross-validation due to the fact that fewer distinct observations are used to train the prediction model, we also want to limit the reduction in the number of testing samples so that the variance of the cross-validation estimate would not be greatly affected by this adjustment in training and testing sample sizes. A compromise is to find a adjusted sample size by minimizing the loss function

| (1) |

where the first and second terms control the closeness of the “effective” sample size in the bootstrapped training set to and the relative change in the sample size of the testing set after the adjustment, respectively. Here, controls the relative importance of theses two tasks in determining the final adjustment. In our limited experience, we have found that the performance of the resulting resampling procedure was not very sensitive to the selection of this penalty parameter within a wide range, and we recommended to set in practice.

More importantly, to alleviate the computational demand for the bootstrap procedure, we propose the following algorithm:

The rational is that the center of , is approximately the cross-validation estimate based on the bootstrapped dataset as the number of random training and testing division increasing to infinity. Under this framework, measures the between-bootstrap variance, which is the bootstrap variance estimator we aim to calculate, and measures the within-bootstrap variance, i.e., the variance due to random training and testing divisions. The empirical variance of based on a very big is approximately unbiased in approximating corresponding to the naive bootstrap procedure. However, this naive approach is very inefficient and there is no need to choose a very large for eliminating the Monte-Carlo variance in estimating cross-validation prediction error for every bootstrapped dataset. Alternatively, an accurate moment estimate for the variance component in the random effects model can be constructed with a moderate , say and a reasonably large say 400. This can substantially reduce the computational burden from 80,000 model training to 8,000 model training.

Remark 2

The total number of model training is A natural question is how to efficiently allocate the number of bootstraps and number of cross-validations per bootstrap given the total number of model training. The variance estimator, is a random statistic itself with a variance [4, 31], which can be approximated by

where

is an estimator for It is not difficult to show that fixing , the variance is minimized when

and

It suggests that the optimal number of cross-validation per bootstrap should be approximately constant, whose value may depend on the specific problem but doesn’t change with the budget for the total number of model training. Normally, can be substantially greater than and should be set to be close to their ratio. In the toy example, this ratio is approximately 20. On the other hand, we always can increase the number of bootstraps to improve the precision in approximating the bootstrap variance estimator.

Remark 3

The number of distinct observations used in training the bootstrapped prediction model is smaller than . Specifically, the number of distinct observations in bootstrapped training set is on average only Therefore, there is a tendency that the “effective total sample size” in bootstrap procedure is smaller than which may cause a upward bias in estimating the variance of using the bootstrap variance estimator To correct this bias, we can consider an adjusted variance estimator

where the factor is introduced to account for the reduced sample size in bootstrapped training set. Note that we do not recommend a similar adjustment of the sample size in the testing set, even though that the number of distinct observations in the testing set is also smaller than in bootstrap, because in general this reduction in the number of distinct observations doesn’t affect the variance estimation.

Sometimes, training the prediction model can be very expensive in terms of computation, and it may not be feasible to conduct even the accelerated bootstrap. For example, one may only can train the prediction model 50-100 times. In such a case, regardless of the selection of and , the Monte-Carlo error in estimating the bootstrap variance may not be ignorable. Consequentially,

may not follow a standard normal distribution. On the other hand, if we can empirically approximate this distribution, then one still can construct a 95% confidence interval for based on One analogy is that the confidence interval for the population mean of a normal distribution can be constructed using t-distribution rather than the normal distribution in small sample size setting. With a slight abuse of notations, let be the bootstrap variance estimator, if both and , i.e., the bootstrap variance estimator without any Monte Carlo error, and we have

| (2) |

The first term of the left hand side of (2) should be approximated well by a standard Gaussian distribution since the “ideal” bootstrap variance estimator is used. The second term is independent of the first term and reflects the Monte-Carlo variation of approximating via a small number of bootstrap and cross-validation iterations. To approximate the distribution of this ratio, we can bootstrap the variance estimator based on fitting the random effects model. This observation motivated the following additional steps presented in algorithm 3 after line (12-13) of algorithm 2, when very small and are used.

This resulting confidence interval is expected to be wider than that generated from the algorithm 2, since However, this is a necessary cost to pay for using a small number of bootstrap and cross validation iterations. Note that although two bootstraps have been used in the modified algorithm, the increase in computational burden is minimal. These two bootstrap steps are not nested and the second bootstrap only involves repeated estimation of the variance component of a simple random effects model, which can be completed relatively fast especially with small or moderate and The performance of this method depends on the normal approximation to the distribution of and the bootstrap approximation to the distribution of The second bootstrap is a calibration step for producing a confidence interval of with a coverage level comparable to that based on . If the latter yields a confidence interval which either too conservative or too liberal, then the new confidence interval based on additional bootstrap calibration would suffer the same limitation. Operationally, one may choose for example or A slightly bigger value for can prevent a negative or zero variance component estimator in fitting the random effects model.

3 Applications

3.1 Application 1

3.1.1 Theoretical Properties

In the first example, we are interested in estimating the mean absolute prediction error from a liner regression model via cross-validation. In this case, it is not difficult to verify conditions C1-C5 under reasonable assumptions. For example, under the condition that the matrix is non-singular, the least squared estimator of the regression coefficient in the linear regression model, converges to a deterministic limit as and

and thus C1 is satisfied. Second, the class of functions is Donsker, where is a compact set and This fact suggests that the empirical process

is stochastically continuous in where

As a consequence, condition C2 is satisfied. It is clear that is differentiable in in a small neighborhood of if the random variable has a differentiable density function, which suffices for condition C3. The central limit theorem implies that

converges weakly to a mean zero Gaussian distribution as under the assumption that is finite. Lastly, it is obvious that and C5 is also satisfied. Therefore, we expect that can be approximated by a mean zero Gaussian distribution whose variance can be consistently estimated by the proposed bootstrap method. Note that we don’t need to assume that the linear regression model is indeed correct for the relationship between and

3.1.2 Simulation Study

In numerical study, we first considered a simple setting, where followed a 10 dimensional standard multivariate Gaussian distribution and a continuous outcome was generated via the linear model

where and The regression coefficient was selected such that the proportion of the variation explained by the true regression model was 80%. We let the sample size and considered the cross-validation estimate for the mean absolute prediction error The true value of was obtained by averaging the empirical mean absolute prediction error of 5,000 estimated prediction models in an independent testing set consisting of 200,000 generated observations. Each prediction model was trained in a simulated training set of size Both training and testing sets were generated according to the linear regression model specified above. Next, we generated 1,000 independent datasets, of the size For each of dataset, we constructed the cross-validation estimator of . To this end, we divided the simulated dataset into training and testing sets times and calculated the resulting as the average of obtained mean absolute prediction errors in the testing set. We also implemented the fast bootstrap method to estimate the variance of the cross-validated estimates with bootstraps and relatively small number of cross-validations for each bootstrap, i.e., . Thus, constructing one confidence interval required model fitting. Based on 1,000 simulated datasets, we calculated the empirical mean and standard deviation of , and the empirical coverage level of 95% confidence intervals based on bootstrap variance estimator with and without the sample size adjustment. The results were reported in Table 1. Next, we examined the performance of bootstrap calibration in algorithm 3 for constructing 95% confidence intervals with a very small number of bootstraps. In particular, we set and the results are summarized in terms of empirical coverage probability of constructed confidence intervals with and without the bootstrap calibration. In this setting, the constructing a confidence interval requires only 500 model training, in contrast to 8,000 model training required by the proposed bootstrap procedure and 80,000 model training required by the regular bootstrap procedure. The results can be found in Table 2.

The empirical bias of in estimating is almost zero, relative to either the standard deviation of or the true value of The empirical coverage level of the 95% confidence interval based on bootstraps was fairly close to its nominal level as expected after the sample size adjustment. The confidence intervals were slightly conservative without the adjustment for the “effective” sample size. Ignoring the difference between and for we also examined the empirical coverage level of the constructed confidence interval with respect to which was the parameter of interest in [2]. The empirical coverage level was 92.5%. Therefore, in this case, the constructed confidence interval based on bootstrap method not only covered with sufficient probability as proposed, but also . In this setting, the standard deviation of , i.e., was 0.073, while the standard deviation of , i.e., was much smaller: 0.025. See Figure 1(a) for a graphic representation of this phenomena. Therefore, the coverage levels of constructed confidence intervals for and are similar. Lastly, one may construct the confidence interval for using the nested cross-validation method proposed in [2], since the estimator of mean absolute prediction error in the testing set was a simple average of random statistics. In the simulation, the empirical coverage level of 95% confidence intervals based on nested cross-validation was 91% for . It was interesting to note that its coverage level for was 91.8%, quite close to that for For confidence intervals constructed with a small number of bootstraps (, the empirical coverage level was substantially lower than that based on if no calibration for the confidence interval was made (Table 2). After the additional bootstrap calibration outlined in algorithm 3, however, the empirical coverage level became similar to or higher than that based on a large number of bootstraps. As a price of recovering the proper coverage level, the median width of calibrated confidence intervals increased 11-37% depending on the training size

In the second set of simulations, we let corresponding to a high dimensional case. In order to construct a prediction model in this case, we used the lasso regularization [28], i.e., minimizing the loss function

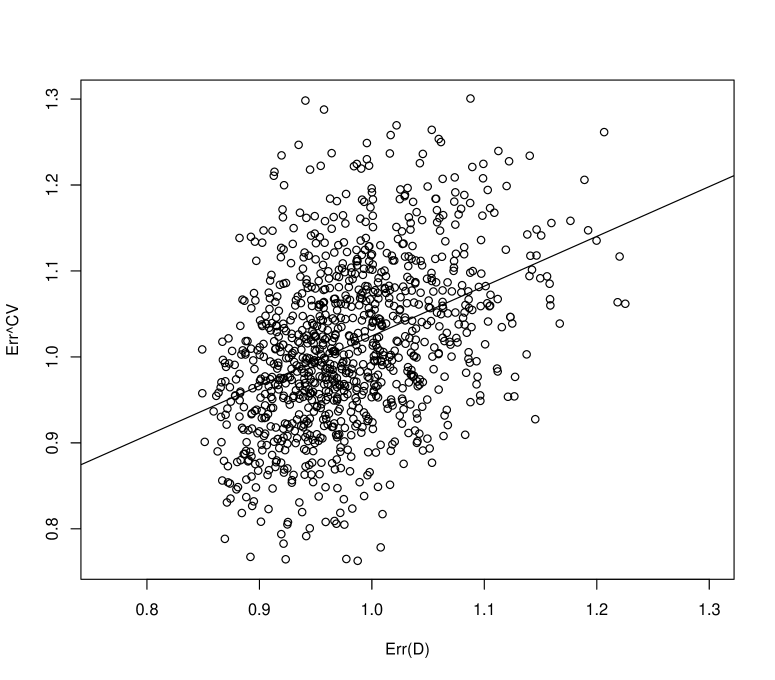

where the penalty parameter is fixed at 0.20 to save computational time. Letting the minimizer of the regularized loss be denoted by and , the outcome of a future patient with covariate was predicted by where For each of 1,000 simulated datasets, we computed , its variance estimator via proposed bootstrap method, and the true prediction error as in the low-dimensional case. We reported the true value of empirical mean and standard deviation of , and the empirical coverage level of the 95% confidence interval based on bootstrap variance estimate in Table 1. In addition, we examined the performance of the confidence intervals constructed via a small number of bootstraps, i.e., The corresponding results were summarized in Table 2. Similar to the low dimensional case, the empirical bias of in estimating was almost zero and the empirical coverage level of the 95% confidence interval was slightly higher than the nominal level of 95%. The over-coverage of confidence intervals based on was slightly smaller. The empirical coverage level of those confidence intervals was 98.8% with respect to Part of the reason of the high coverage level in this setting was the high correlation between and , which was 0.40 (Figure 2). In the low dimensional setting, this correlation was almost zero. Similar findings have been reported in [2] as well. Lastly, the empirical coverage level of 95% confidence intervals based on nested cross-validation was 93.9% for and 91.2% for where Without the bootstrap calibration, the empirical coverage level of confidence intervals constructed with a small number of bootstrap iterations was lower than those with After the bootstrap calibration, the empirical coverage level became similar to or higher than that based on a large number of bootstraps. The median width of calibrated confidence intervals increased 15-23% depending on the training size

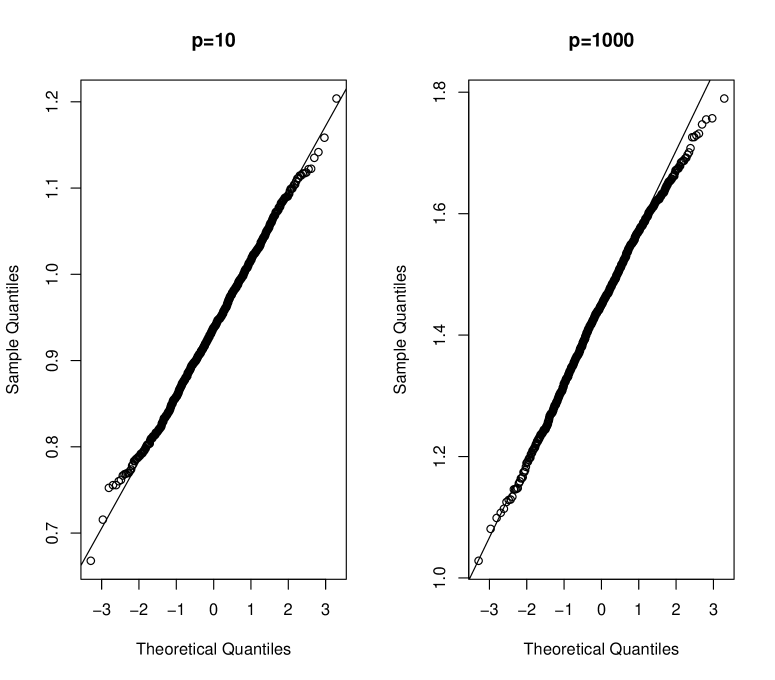

The lasso regularized estimator of the regression coefficient clearly does not follow a Gaussian distribution, and the theoretical justification for the Gaussian approximation of the cross-validated estimates provided for low dimensional setting is not applicable here. However, the empirical distribution of was quite “Gaussian” with its variance being approximated reasonably well by the proposed bootstrap method. This phenomena can be visualized by the QQ plot of with the smallest sample size of the training set, in Figure 3, where the role of lasso regularization was expected to be the biggest. It is clear that the Gaussian approximation holds well empirically for both low and high dimensional settings. One possible explanation was that the mean absolute prediction error is a smooth function of the testing data, and thus the cross-validation estimator is still a regular root estimator of . This observation suggests a broader application of the proposed method for constructing confidence intervals for

In summary, the proposed confidence interval has a reasonable coverage level but slightly conservative. Empirically, the interval can be viewed as confidence interval for both and when although the procedure was designed for the latter. In this case, the confidence interval based on nested cross-validation also had a proper coverage level for both and , even though the procedure was designed for the former. Furthermore, the bootstrap calibration can be used to maintain proper coverage level of confidence intervals constructed with a very small number of bootstraps at the cost of enlarging the resulting intervals.

| SD | Cov-adj | Cov | SD | Cov-adj | Cov | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 40 | 0.941 | 0.938 | 0.077 | 96.7% | 98.0% | 1.441 | 1.445 | 0.123 | 97.3% | 98.9% | |

| 45 | 0.920 | 0.918 | 0.076 | 96.9% | 98.1% | 1.334 | 1.341 | 0.126 | 97.0% | 98.9% | |

| 50 | 0.906 | 0.904 | 0.075 | 96.5% | 98.2% | 1.248 | 1.255 | 0.121 | 97.4% | 99.2% | |

| 55 | 0.894 | 0.892 | 0.074 | 96.4% | 98.1% | 1.179 | 1.187 | 0.115 | 97.6% | 99.4% | |

| 60 | 0.885 | 0.883 | 0.074 | 96.0% | 98.1% | 1.128 | 1.134 | 0.109 | 98.2% | 99.4% | |

| 65 | 0.877 | 0.875 | 0.074 | 95.5% | 98.2% | 1.087 | 1.093 | 0.103 | 98.6% | 99.3% | |

| 70 | 0.870 | 0.869 | 0.073 | 94.9% | 98.0% | 1.058 | 1.060 | 0.100 | 98.4% | 99.4% | |

| 75 | 0.865 | 0.864 | 0.073 | 94.6% | 97.9% | 1.031 | 1.034 | 0.097 | 98.5% | 99.5% | |

| 80 | 0.861 | 0.859 | 0.073 | 93.3% | 97.7% | 1.012 | 1.013 | 0.097 | 97.9% | 99.4% | |

| Confidence Intervals Based on | Confidence Intervals based on | ||||||

| Algorithm 2 | Algorithm 2 | Algorithm 3 | Algorithm 2 | Algorithm 2 | Algorithm 3 | ||

| 40 | 96.7% | 95.1% | 96.8% | 98.0% | 97.2% | 98.4% | |

| 45 | 96.9% | 95.2% | 96.9% | 98.1% | 97.4% | 98.7% | |

| 50 | 96.5% | 94.6% | 96.8% | 98.2% | 97.1% | 98.8% | |

| 55 | 96.4% | 94.4% | 96.7% | 98.1% | 97.2% | 98.9% | |

| 60 | 96.0% | 93.2% | 96.9% | 98.1% | 96.9% | 98.7% | |

| 65 | 95.5% | 93.1% | 96.7% | 98.2% | 96.7% | 98.9% | |

| 70 | 94.9% | 93.1% | 97.3% | 98.0% | 96.7% | 99.1% | |

| 75 | 94.6% | 91.6% | 97.7% | 97.9% | 95.9% | 98.8% | |

| 80 | 93.3% | 89.8% | 98.4% | 97.7% | 93.4% | 99.1% | |

| 40 | 97.3% | 95.9% | 98.6% | 98.9% | 97.5% | 99.3% | |

| 45 | 97.0% | 95.3% | 98.4% | 98.9% | 97.4% | 99.3% | |

| 50 | 97.4% | 95.6% | 98.5% | 99.2% | 98.0% | 99.4% | |

| 55 | 97.6% | 96.4% | 98.9% | 99.4% | 98.6% | 99.7% | |

| 60 | 98.2% | 97.2% | 99.2% | 99.4% | 98.6% | 99.7% | |

| 65 | 98.6% | 97.3% | 99.4% | 99.3% | 98.5% | 99.9% | |

| 70 | 98.4% | 97.5% | 99.5% | 99.4% | 98.7% | 99.8% | |

| 75 | 98.5% | 96.5% | 99.4% | 99.5% | 98.6% | 99.8% | |

| 80 | 97.9% | 96.1% | 99.4% | 99.4% | 98.4% | 99.7% | |

3.1.3 Real Data Examples

The example is from the UCI machine learning repository. The dataset contains per capita violent crime rate and 99 prediction features for their plausible connection to crime in 1,994 communities after dropping communities and features with missing data. The crimes rate was calculated as the number of violated crimes per 100,000 residents in the community of interest. The violent crimes included murder, rape, robbery, and assault. The crime rate ranged from 0 to 1.0 with a median of 0.15. The predictors in the analysis mainly involved the community of interest, such as the percent of the urban population, the median family income, and law enforcement, such as per capita number of police officers, and percent of officers assigned to drug units. The objective of the analysis was to use these 99 community features to predict the violent crime rate. For demonstration purpose, we considered a subset consisting of first 600 observations as the observed dataset. First, we constructed the prediction model by fitting a linear regression model with lasso regularization, where the penalty parameter was fixed at 0.005 for convenience. We applied our method for i.e., the proportion of the observations used for training varied from 10%, to 20%, 30%, , 90%. Based on 500 cross-validations, the cross-validation estimate of the mean absolute prediction error for different training sizes was 0.141, 0.121, 0.115, 0.113, 0.111, 0.110, 0.109, 0.109 and 0.108, respectively. The 95% confidence interval for was then constructed based on the proposed bootstrap method. The number of bootstraps was 500 and the number of cross validations per bootstrap was 20. The results are summarized in Table 3. We also constructed the confidence interval for using nested cross-validation. The resulting 95% confidence interval was [0.100, 0.116], which was fairly close to the bootstrap-based confidence interval for where the training size was the closest to

| MAPE1 | 95% CI | MAPE | 95% CI | MAPE | 95% CI | |||

| Lasso | Random Forest | Difference2 | ||||||

| 60 | 0.141 | [0.128, 0.154] | 0.121 | [0.110, 0.132] | 2.13 | [1.50, 2.76] | ||

| 120 | 0.121 | [0.109, 0.133] | 0.116 | [0.105, 0.126] | 0.58 | [0.08, 1.09] | ||

| 180 | 0.115 | [0.105, 0.126] | 0.113 | [0.103, 0.124] | 0.15 | [-0.34, 0.64] | ||

| 240 | 0.113 | [0.102, 0.123] | 0.112 | [0.101, 0.122] | 0.01 | [-0.46, 0.48] | ||

| 300 | 0.111 | [0.101, 0.121] | 0.111 | [0.101, 0.122] | -0.05 | [-0.51, 0.40] | ||

| 360 | 0.110 | [0.100, 0.120] | 0.110 | [0.100, 0.121] | -0.06 | [-0.52, 0.41] | ||

| 420 | 0.109 | [0.100, 0.119] | 0.109 | [0.099, 0.120] | -0.05 | [-0.52, 0.41] | ||

| 480 | 0.109 | [0.100, 0.118] | 0.109 | [0.098, 0.119] | -0.03 | [-0.50, 0.44] | ||

| 540 | 0.108 | [0.099, 0.117] | 0.108 | [0.098, 0.118] | 0.00 | [-0.48, 0.48] | ||

| mean absolute prediction error (MAPE). | ||||||||

| the difference in MAPE between the lasso regularized linear model and random forest. | ||||||||

We have also considered a different prediction model trained using random forest. The output the random forest algorithm was an ensemble of 200 regression trees constructed based on bootstrapped samples. Based on 500 cross-validations, the cross-validation estimator of the mean absolute prediction error for different training sizes was 0.121, 0.116, 0.113, 0.112, 0.111, 0.110, 0.109, 0.109, and 0.108, respectively, smaller than those from lasso regularized linear regression model in general. The 95% confidence intervals using the proposed bootstrap method were reported in Table 3. Furthermore, the confidence interval for based on nested cross-validation was [0.100, 0.115], which was also fairly close to the bootstrap-based confidence interval for as expected.

It appears that when sample size of the training data is small, the random forest generates more accurate predictions than the lasso-regularized linear model. When the sample size of the training set is greater than 200, however, the differences in prediction performance become very small. To account for the uncertainty, we also used the proposed bootstrap method to construct the 95% confidence interval for the difference in mean absolute prediction error between lasso regularized linear model and random forest. Indeed, when the 95% confidence interval for the difference in was [1.50, 2.76] suggesting a statistically significantly better prediction performance of the random forest. The superiority of random forest also holds for The results for other were reported in Table 3 showing no statistically significant difference between two prediction models.

3.2 Application 2

3.2.1 Theoretical Properties

In the second application, we are interested in estimating the c-index from a logistic regression model via cross-validation. In this case, it is not difficult to verify the conditions C1-C5 under conventional assumptions. For example, under the condition that there is no such that the hyperplane can perfectly separate observations with from those with and the matrix

is positive definite for all , the maximum likelihood estimator based on the logistic regression, converges to a deterministic limit in probability as and

and thus is satisfied [27]. Second, the class of functions is Donsker, where is a compact set in . This fact suggests that the U-process

is stochastically continuous, where

As a consequence, condition C2 is satisfied as and It is clear that is differentiable in in a small neighborhood of if has a differentiable density function, which suffices for condition C3. Next, the central limit theorem for U-statistics implies that

converges weakly to a mean zero Gaussian distribution as if Lastly, and C5 is satisfied. Therefore, we expect that can be approximated by a mean zero Gaussian distribution whose variance can be consistently estimated by the proposed bootstrap method. Note that we don’t need to assume that the logistic regression model is indeed correct for the conditional probability

3.2.2 Simulation Study

In the numerical study, we considered two settings corresponding to low and high dimensional covariates vector In the first setting, followed a 10 dimensional standard multivariate normal distribution and the binary outcome followed a Bernoulli distribution

where This regression coefficient was selected such that the mis-classification error of the optimal Bayesian classification rule was approximately 20%. We let the sample size and considered the cross-validation estimator for the c-index The true value of was obtained by averaging c-indexes of 5,000 logistic regression models trained in different training sets of size in an independent testing set consisting of 200,000 observations. We also constructed the cross-validation estimator of from 1,000 simulated datasets of size each. For each generated dataset, we divided the dataset into training and testing sets 400 times and calculated the resulting as the average of 400 c-indexes from testing sets. We first implemented the fast bootstrap method to estimate the variance of the cross-validated estimates with bootstraps and cross-validations per bootstrap. The 95% confidence interval for was constructed accordingly. Based on results from 1,000 datasets, we summarized the empirical average and standard deviation of for c-index and the empirical coverage level of 95% confidence intervals based on bootstrap variance estimates. The results were reported in Table 4. We also examined the performance of the bootstrap calibration in algorithm 2 for constructing 95% confidence intervals with a very small number of bootstraps. To this end, we set and the corresponding results were summarized in Table 5. The cross-validation estimator was almost unbiased in estimating with its empirical bias negligible in comparison with the standard deviation of The empirical coverage level of 95% confidence intervals with was fairly close to the nominal level. The coverage levels of the confidence intervals based on were approximately 90%, lower than 95%, for We also examined the empirical coverage level of confidence intervals based on with respect to for The coverage level was 89.5%, similar to that for When a small number of bootstraps was used, the coverage level of the confidence interval was markedly lower than those constructed via a large number of bootstraps. However, with the proposed bootstrap calibration, the coverage level became comparable to those using bootstraps. For example, when the empirical coverage level of confidence intervals based on was 94.2% for 90.5% for without calibration, but 98.2% for after calibration. The median width the calibrated confidence intervals increased depending on . In this particular setting, we have also examined the choice of as in other simulation studies but observed a nontrivial proportion of zero variance component estimator for large , suggesting insufficient number of bootstraps and cross-validation for differentiating intrinsic bootstrap variance from the Monte-Carlo variance due to cross-validation.

In the second set of numerical experiments, we have considered a high dimensional case where the dimension of , is set at 1000. To estimate , we have employed the lasso-regularized logistic regression analysis, where was the maximizer of

To save computational time, the penalty parameter was fixed at 0.10 in this simulation study. In this case, the lasso-regularized estimator was not a root “regular” estimator and its distribution could not be approximated well by a Gaussian. Therefore, the regularity condition C1 was not satisfied. However, the estimation of the c-index in the testing set was a very “smooth” step based on U-statistic and therefore, we still expected that the cross-validation estimator of the c-index to approximately follow a Gaussian distribution, whose variance could be estimated well by the proposed bootstrap method. Letting the maximizer of the regularized objective function be denoted by and , the c-index in the testing set is estimated by the concordance rate between and For each of 1,000 simulated datasets, we computed for c-index, its variance estimator via bootstrap, and the true prediction error We calculated and reported the true value of empirical mean and standard deviation of , and the empirical coverage level of 95% confidence intervals based on the proposed bootstrap variance estimator in Table 4. Similar to the low-dimensional case, Table 5 summarized the empirical coverage level of confidence intervals constructed only using a very small number of bootstraps. Similar to the low-dimensional case, the empirical bias of in estimating was almost zero and the empirical coverage level of the 95% confidence interval was very close to the nominal level of 95%. There was a moderate over-coverage of confidence intervals based on bootstrap variance estimates On the other hand, the empirical coverage level of those confidence intervals of with respect to was 96.1%. The empirical correlation coefficient between and was as high as 0.52 in this setting. When only a small number of bootstraps was used, the proposed bootstrap calibration recovered the coverage level to a comparable level of those using a large number of bootstraps. For example, when the empirical coverage level of the confidence interval based on was 93.9% for 91.9% for before the bootstrap calibration, and 94.3% for the bootstrap after calibration. The median width the calibrated confidence interval increased 10-14% depending on .

In summary, the proposed confidence intervals have a reasonable coverage. The interval can be viewed as confidence interval for both and when although the procedure was designed for the latter. In this case, the nested cross-validation is not directly applicable for c-index or ROC curve, since the parameter estimator in the test set doesn’t take a form of sum of independent, identically distributed random elements. Lastly, the bootstrap calibration can be used to effectively account for the variability of bootstrap variance estimator due to small number of bootstrap iterations in constructing confidence intervals for

| SD | COV-adj | COV | SD | COV-adj | COV | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 40 | 0.799 | 0.800 | 0.041 | 94.7% | 96.6% | 0.573 | 0.570 | 0.049 | 97.3% | 98.9% | |

| 45 | 0.810 | 0.812 | 0.041 | 94.6% | 96.4% | 0.588 | 0.585 | 0.059 | 96.2% | 98.6% | |

| 50 | 0.820 | 0.822 | 0.042 | 94.3% | 96.4% | 0.607 | 0.602 | 0.067 | 94.3% | 98.2% | |

| 55 | 0.827 | 0.829 | 0.042 | 93.8% | 96.0% | 0.623 | 0.618 | 0.075 | 92.7% | 97.9% | |

| 60 | 0.833 | 0.835 | 0.043 | 93.3% | 95.4% | 0.641 | 0.635 | 0.083 | 92.4% | 97.8% | |

| 65 | 0.838 | 0.839 | 0.043 | 92.9% | 95.3% | 0.659 | 0.652 | 0.089 | 91.7% | 97.5% | |

| 70 | 0.842 | 0.843 | 0.043 | 92.0% | 94.9% | 0.674 | 0.669 | 0.092 | 93.8% | 98.2% | |

| 75 | 0.845 | 0.847 | 0.043 | 91.0% | 94.3% | 0.691 | 0.685 | 0.098 | 93.9% | 98.4% | |

| 80 | 0.847 | 0.849 | 0.043 | 89.5% | 94.1% | 0.706 | 0.702 | 0.105 | 94.8% | 98.8% | |

| Confidence Intervals Based on | Confidence Intervals based on | ||||||

| Algorithm 2 | Algorithm 2 | Algorithm 3 | Algorithm 2 | Algorithm 2 | Algorithm 3 | ||

| 40 | 94.7% | 93.7% | 95.4% | 96.6% | 95.5% | 96.9% | |

| 45 | 94.6% | 93.0% | 94.9% | 96.8% | 95.1% | 97.2% | |

| 50 | 94.3% | 92.3% | 94.9% | 96.5% | 95.2% | 97.0% | |

| 55 | 94.2% | 91.6% | 94.3% | 96.0% | 95.0% | 96.5% | |

| 60 | 93.4% | 91.0% | 94.0% | 95.4% | 94.3% | 96.8% | |

| 65 | 93.1% | 90.8% | 94.5% | 95.4% | 94.2% | 96.4% | |

| 70 | 92.1% | 90.2% | 94.7% | 94.9% | 93.4% | 96.5% | |

| 75 | 91.1% | 89.2% | 95.7% | 94.3% | 93.0% | 97.7% | |

| 80 | 89.3% | 85.2% | 97.5% | 94.2% | 90.5% | 98.2% | |

| 40 | 97.3% | 95.3% | 98.7% | 98.9% | 97.4% | 99.3% | |

| 45 | 96.2% | 93.0% | 97.3% | 98.6% | 96.2% | 98.5% | |

| 50 | 94.3% | 92.2% | 95.4% | 98.2% | 95.7% | 98.2% | |

| 55 | 92.7% | 91.0% | 94.9% | 97.9% | 95.2% | 97.8% | |

| 60 | 92.4% | 91.5% | 94.5% | 97.8% | 95.0% | 97.2% | |

| 65 | 91.7% | 91.3% | 93.9% | 97.5% | 94.9% | 97.4% | |

| 70 | 93.8% | 91.9% | 94.2% | 98.2% | 95.6% | 97.5% | |

| 75 | 93.9% | 92.9% | 94.6% | 98.4% | 96.3% | 98.0% | |

| 80 | 94.8% | 92.8% | 96.7% | 98.8% | 96.0% | 99.0% | |

3.2.3 Real Data Examples

In the first example, we tested our proposed method on the MI dataset from UCI machine learning repository. The dataset contained 1700 patients and up to 111 predictors collected from the hospital admission up to 3 days after admission for each patient. We were interested in predicting all cause mortality. After removing features with more than 300 missing values, there were 100 prediction features available at the day 3 after admission including 91 features available at the admission. The observed data consisted of 652 patients with complete information on all 100 features. There were 72 binary, 21 ordinal, and 7 continuous features. Out of 652 patients, there were 62 deaths corresponding to a cumulative mortality of 9.5%. We considered training size which represented 30% to 90% of the total sample size. We considered four prediction models, all trained by fitting a lasso regularized logistic regression. Model 1 was based on 91 features collected at the time of admission; Model 2 was based on 100 features collected up to day 3 after hospital admission; Model 3 was based on 126 features collected at the time of admission after converting all ordinal features into multiple binary features; and Model 4 was based on 159 features collected up to day 3 after converting all ordinal features into multiple binary features. For simplicity, we fixed the lasso penalty parameter at 0.01 for fitting Model 1 and Model 3, and 0.0075 for fitting Model 2 and Model 4.

First, we estimated the cross-validated c-index, which was the AUC under the ROC curve based on 500 random cross-validations. We then constructed the 95% confidence interval based on standard error estimated via the proposed bootstrap method. The number of the bootstraps and the number of cross validations per bootstrap were set at 400 and 20, respectively. The results were reported in Table 6. Model 1 and Model 2 had similar predictive performance with a small gain in c-index by including 8 additional features collected after hospital admission. Likewise, Model 3 and Model 4 had similar predictive performance, which, however, was inferior to that of Models 1 and 2, suggesting that converting ordinal predictive features into multiple binary features may had a negative impact on the prediction performance of the regression model. On the one hand, converting ordinal features into binary features allowed more flexible model fitting. On the other hand, this practice increased the number of features and ignored the intrinsic order across different levels of an ordinal variable. Therefore, it was not a surprise that Models 3 and 4 were not as accurate as Models 1 and 2. We then formally compared the model performance by constructing the 95% confidence interval for the difference in c-index between Model 1 and Model 2; between Model 1 and Model 3; and between Model 2 and Model 4. The detailed comparison results for all training sizes were reported in Table 7. It was interesting to note that all confidence intervals include zero, suggesting that none of the observed differences in c-index between different models are statistically significant at the 0.05 level.

In the second example for binary outcome, we tested our proposal on the “red wine” data set studied in [6]. The data set contained measurements for 1,599 red wine samples and was also available in the UCI Repository. Each of the wine samples was evaluated by wine experts for its quality, which was summarized on a scale from 0 to 10, with 0 and 10 representing the poorest and highest quality, respectively. 11 features including fixed acidity, volatile acidity, citric acid, residual sugar, chlorides, free sulfur dioxide, total sulfur dioxide, density, pH, sulphates and alcohol were also measured for all wine samples. [6] compared different data mining methods aiming to predict the ordinal quality score using these eleven features. Here, we conducted a simpler analysis to identify wine samples with a quality score above 6. To this end, we coded a binary outcome , if the quality was and 0, otherwise. We selected an observed data set consisting of first 400 wines samples from the “red wine” data set. Although the sample size was not small relative to the number of predictive features, there were only 40 observations with in this subset. For the cross-validation, the training size We considered two prediction models: Model 1 was based on a regular logistic regression, and Model 2 was based on a random forest with 200 classification and regression trees. We estimated the c-index based on 500 random cross-validations for each training size based on the “observed” data set including wine samples. We then constructed 95% confidence interval for the c-index using the proposed bootstrap method with The results were reported in Table 8. It was clear that the random forest generated a substantially better prediction model than the logistic regression across all training sizes considered. The confidence intervals of the the difference in c-index were above zero when and 360, suggesting that the random forest was statistically significantly more accurate than the logistic regression model. It was also interesting to note that the performance of the random forest became better with increased training size, while the c-index of the logistic regression was relatively insensitive to This was anticipated considering the fact that the random forest fitted a much more complex model than the simple logistic regression and could make a better use of information provided by more training data for improving the prediction accuracy at local regions of the covariate space.

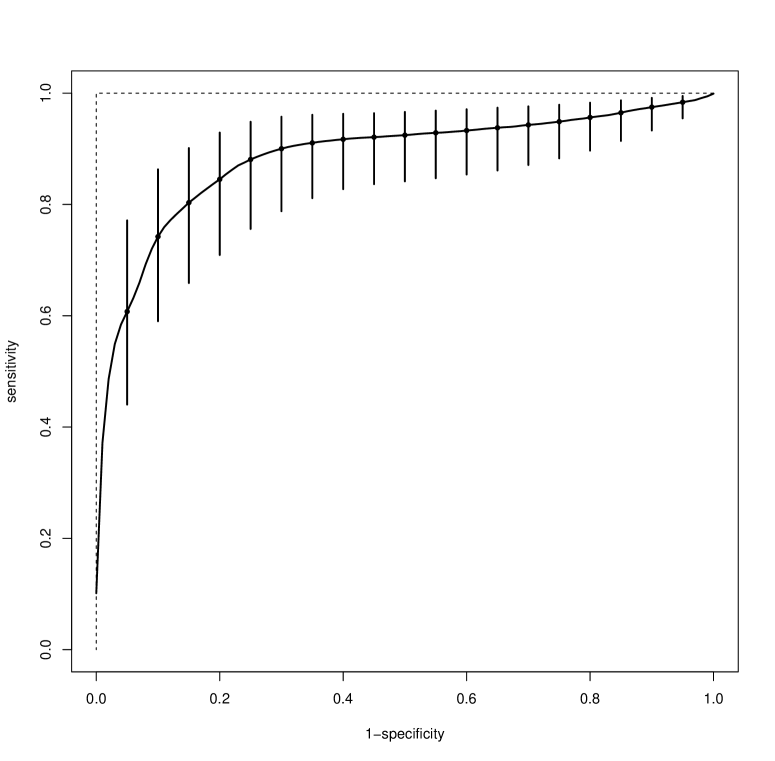

We then used the cross-validation to estimate the entire ROC curve based on the random forest with 200 regression and classification trees. Due to the small number of cases in the data set, we used the pre-validation method described in Remark 1 of section 2.1.2, i.e., constructing the ROC curve based on risk score for all samples estimated via a 10-fold cross-validation. To remove the Monte-Carlo variability in randomly dividing data into 10 parts, the final ROC curve was obtained by averaging over ROC curves from 500 10-fold cross-validations. We also plotted the ROC curve without cross-validation, which was clearly overly optimistic, since the AUC of the ROC curve was 1, representing a prefect prediction! The same bootstrap method could be used to estimate the point-wise confidence intervals of the ROC curve. Specifically, 500 bootstrapped data sets were generated and ROC curves from 20 12-fold cross-validations per bootstrapped data set were calculated. 12-fold instead of 10-fold cross-validation was employed to adjust for the reduced effective sample size in the training set. The bootstrap variance estimators for sensitivities corresponding to specificity level at were then obtained. The resulting confidence intervals representing the underlying predictive performance of the trained random forest were plotted in Figure 4, suggesting that the real sensitivity in external data would not reach 100% even for low specificity levels.

| AUC | 95% CI | AUC | 95% CI | ||

|---|---|---|---|---|---|

| 91 features at Day 0 | 100 features at Day 3 | ||||

| 196 | 0.711 | [0.645, 0.778] | 0.711 | [0.643, 0.779] | |

| 261 | 0.729 | [0.660, 0.798] | 0.731 | [0.659, 0.802] | |

| 326 | 0.743 | [0.672, 0.814] | 0.747 | [0.674, 0.820] | |

| 391 | 0.753 | [0.681, 0.825] | 0.760 | [0.687, 0.833] | |

| 456 | 0.759 | [0.688, 0.831] | 0.768 | [0.695, 0.841] | |

| 522 | 0.766 | [0.694, 0.837] | 0.777 | [0.705, 0.850] | |

| 587 | 0.771 | [0.702, 0.840] | 0.785 | [0.718, 0.852] | |

| 126 features at Day 0 | 159 features at Day 3 | ||||

| 196 | 0.676 | [0.596, 0.755] | 0.664 | [0.583, 0.745] | |

| 261 | 0.692 | [0.610, 0.773] | 0.678 | [0.594, 0.762] | |

| 326 | 0.700 | [0.616, 0.784] | 0.688 | [0.600, 0.776] | |

| 391 | 0.712 | [0.628, 0.796] | 0.702 | [0.614, 0.791] | |

| 456 | 0.716 | [0.631, 0.801] | 0.709 | [0.620, 0.798] | |

| 522 | 0.723 | [0.640, 0.806] | 0.718 | [0.630, 0.805] | |

| 587 | 0.729 | [0.644, 0.814] | 0.727 | [0.635, 0.819] | |

| AUC | 95% CI | AUC | 95% CI | AUC | 95% CI | |||

|---|---|---|---|---|---|---|---|---|

| Models 2 vs. 1 | Models 1 vs. 3 | Models 2 vs. 4 | ||||||

| 196 | -0.042 | [-2.361, 2.276] | 3.562 | [-1.400, 8.524] | 4.714 | [-0.647, 10.08] | ||

| 261 | 0.189 | [-2.469, 2.846] | 3.729 | [-1.571, 9.029] | 5.268 | [-0.564, 11.10] | ||

| 326 | 0.387 | [-2.432, 3.205] | 4.317 | [-1.300, 9.933] | 5.900 | [-0.293, 12.09] | ||

| 391 | 0.711 | [-2.076, 3.497] | 4.158 | [-1.468, 9.783] | 5.795 | [-0.621, 12.21] | ||

| 456 | 0.878 | [-1.963, 3.720] | 4.341 | [-1.560, 10.24] | 5.906 | [-0.690, 12.50] | ||

| 522 | 1.157 | [-1.810, 4.124] | 4.307 | [-1.699, 10.31] | 5.976 | [-0.731, 12.68] | ||

| 587 | 1.370 | [-1.508, 4.247] | 4.222 | [-1.998, 10.44] | 5.804 | [-1.338, 12.95] | ||

| AUC | 95% CI | AUC | 95% CI | AUC | 95% CI | |||

|---|---|---|---|---|---|---|---|---|

| Logistic Regression | Random Forest | Difference | ||||||

| 200 | 0.803 | [0.737, 0.869] | 0.855 | [0.780, 0.929] | -0.052 | [-0.112, 0.009] | ||

| 240 | 0.811 | [0.747, 0.875] | 0.866 | [0.791, 0.940] | -0.055 | [-0.114, 0.004] | ||

| 280 | 0.817 | [0.753, 0.880] | 0.874 | [0.797, 0.951] | -0.057 | [-0.118, 0.004] | ||

| 320 | 0.823 | [0.760, 0.881] | 0.885 | [0.812, 0.957] | -0.062 | [-0.119, -0.005] | ||

| 360 | 0.825 | [0.770, 0.879] | 0.897 | [0.837, 0.958] | -0.073 | [-0.129, -0.016] | ||

3.3 Application 3

3.3.1 Theoretical Properties

In the third application, we are interested in evaluating the performance of a precision medicine strategy. In this case, it is not difficult to verify conditions C1-C5 under suitable assumptions. For example, if the matrix is nonsingular, , and , i.e., the treatment assignment is randomized, then and converge to deterministic limits and respectively, as , and especially

where is an unique minimizer of the loss function

Thus condition C1 is satisfied. Second, the classes of functions , , , and are Donsker, where is a compact set in . This fact suggests that the stochastic processes

are all stochastically continuous in Therefore, the processes

and

are also stochastically continuous in , i.e., for As a consequence, condition C2 is satisfied. It is clear that and are differentiable in in a small neighborhood of if the random variable has a continuously differentiable bounded density function and is smooth in . This suffices for condition C3. Next, the central limit theorem and delta-method together imply that converges weakly to a mean zero Gaussian distribution as where Lastly, and C5 is satisfied. Therefore, the cross-validation estimator is a consistent estimator for and follows asymptotically a Gaussian distribution, whose variance can be estimated by the proposed bootstrap method.

3.3.2 Simulation Study

In the simulation study, the covariate was generated from a dimensional standard multivariate Gaussian distribution and the continuous outcome was generated via two linear regression models:

and

where , and The treatment assignment indicator was a random permutation of consisting of ones and zeros. The observed outcome The generated data

In the first set of simulations, we let and the sample size . We considered the cross-validation estimator for Due to symmetry, we only considered the case where was the average treatment effect among patients recommended to receive treatment denoted as the high value subgroup consisting of responders to the treatment . The true value of was computed by averaging the treatment effect among identified responders based on the estimated ITR scores from 5,000 generated training sets of size . The true treatment effect among responders was calculated with an independently generated testing set consisting of 200,000 patients. The true is 0.37, 0.39, 0.40, 0.42, 0.43, and 0.44 for 80, 90, 100, 110, 120, 130, and 140, respectively. The increasing trend in reflected the improved quality of the estimated ITR score based on a bigger training set. Note that in this setting, the average treatment effect among responders based on true individualized treatment effects was 0.56.

We constructed the cross-validation estimates of the from 1,000 datasets of size each. For each simulated data set , we divided the data set into a training set of size and a testing set of size . The ITR score was estimated based on the training set and responders in the testing set was identified as patients whose . The average treatment effect estimator among responders in the testing set was simply the average difference in between responders, who received the active treatment and responders, who received the control treatment This process was repeated 400 times and the resulting was the sample average of 400 average treatment effect estimators among identified responders in the testing set. In addition, we used the proposed bootstrap method to compute the standard error estimators and In computing them, we set the number of bootstraps to be 400 and the number of cross-validations per bootstrap to be The 95% confidence interval for was also constructed for each simulated data set We also examined the performance of constructed confidence intervals using only a very small number of bootstrap iterations by choosing

In the second set of simulations, we let In calculating the estimated regression coefficient in the ITR score we implemented the lasso regularized method. Specifically, we estimated by minimizing a regularized loss function

where and were appropriate penalty parameters. To save computational time, both penalty parameters were fixed at 0.10 in all simulations instead of being adaptively selected via cross-validation within the training set. The resulting minimizer of was denoted by and Similar to the low dimensional case, we simulated 1,000 datasets and for each generated dataset we calculated , the bootstrap standard error estimators and , and the corresponding 95% confidence intervals. Similar to the low dimensional case, we investigated the performance of the confidence intervals constructed using both a large number and a small number of bootstraps.

The simulation results including the true value of , the empirical average and standard deviation of cross-validation estimator , and the empirical coverage of 95% confidence intervals based on were summarized in Table 9. In addition, the empirical coverage levels of the constructed 95% confidence intervals based on were summarized in Table 10. For both low and high dimensional cases, the cross-validated estimator was almost unbiased in estimating , especially relative to the empirical standard deviation of . The empirical coverage level of 1000 constructed 95% confidence intervals for based on bootstrap variance estimator from a large number of bootstrap iterations was quite close to its nominal level. After sample size adjustment in variance estimation, the constructed confidence intervals based on slightly under-covered the true parameter with empirical coverage levels between 90% and 93%. When a small number of bootstrap iterations was used (), the proposed bootstrap calibration can be used to maintain the proper coverage level as Table 10 showed. As a price, the median width of calibrated confidence interval increased 14-28% depending on the training size and dimension . Note that the theoretical justification for the Gaussian approximation to the cross-validated estimator in high dimensional case was not provided as in the previous two examples. However, the empirical distribution of was quite “Gaussian” with its variance being approximated well by bootstrap method. This observation ensured the good performance of resulting 95% confidence intervals. In addition, the empirical coverage levels of the 95% confidence intervals of with respect to were 92.9% and 95.4% in low- and high- dimensional settings, respectively, where

In summary, proposed confidence intervals based on bootstrap standard error estimator have a good coverage level. The bootstrap calibration can effectively correct the under-coverage of the confidence intervals based on a very small number of bootstraps. The constructed confidence interval can be viewed as a confidence interval for both and when . In this case, due to the complexity of the evaluation procedure in the testing set, no existing method is readily available for studying the distribution of the cross-validation estimator for the average treatment effect among “responders”.

| SD | COV-adj | COV | SD | COV-adj | COV | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 80 | 0.369 | 0.377 | 0.196 | 92.7% | 95.1% | 0.079 | 0.082 | 0.190 | 92.7% | 95.9% | |