Decomposing cryptocurrency high frequency price dynamics into recurring and noisy components

Abstract

This paper investigates the temporal patterns of activity in the cryptocurrency market with a focus on Bitcoin, Ethereum, Dogecoin, and WINkLink from January 2020 to December 2022. Market activity measures - logarithmic returns, volume, and transaction number, sampled every 10 seconds, were divided into intraday and intraweek periods and then further decomposed into recurring and noise components via correlation matrix formalism. The key findings include the distinctive market behavior from traditional stock markets due to the nonexistence of trade opening and closing. This was manifest in three enhanced-activity phases aligning with Asian, European, and U.S. trading sessions. An intriguing pattern of activity surge in 15-minute intervals, particularly at full hours, was also noticed, implying the potential role of algorithmic trading. Most notably, recurring bursts of activity in bitcoin and ether were identified to coincide with the release times of significant U.S. macroeconomic reports such as Nonfarm payrolls, Consumer Price Index data, and Federal Reserve statements. The most correlated daily patterns of activity occurred in 2022, possibly reflecting the documented correlations with U.S. stock indices in the same period. Factors that are external to the inner market dynamics are found to be responsible for the repeatable components of the market dynamics, while the internal factors appear to be substantially random, which manifests itself in a good agreement between the empirical eigenvalue distributions in their bulk and the random matrix theory predictions expressed by the Marchenko-Pastur distribution. The findings reported support the growing integration of cryptocurrencies into the global financial markets.

Financial markets belong to the most complex dynamical structures associated with human activity. Their dynamics are affected by both the exogenous factors that operate on time scales largely independent of the internal market dynamics and the endogenous factors being inherent to a given market. Among the modern financial markets, the cryptocurrency market deserves special attention as it constitutes a symbol of our times and, like no other market, it operates continuously without interruptions, which allows it to react instantly to any news from the world. Based on the formalism paralleling the principal component analysis but applied to the correlation matrices connecting the consecutive trading intervals of equal length, the dynamics of price changes of several most traded cryptocurrencies is decomposed into sectors of exogenous and endogenous character. The former reflects selectively market susceptibility to the external news while the latter is largely consistent with the predictions of random matrix theory. This fact can be interpreted as an indication of the efficiency that the cryptocurrency trading dynamics has already attained.

I Introduction

It is well known that financial markets have recurring patterns in their activity Gerety and Mulherin (1991); Andersen and Bollerslev (1998); Bollerslev, Cai, and Song (2000). There are bursts in daily volatility related to various cyclical macroeconomic reports such as NFP (Nonfarm Payrolls), CPI (Consumer Price Index), ISM (Institute for Supply Management), PMI (Purchasing Managers Index), etc. Andersen et al. (2003); Evans and Speight (2010); Evans (2011); Harju and Hussain (2011), central banks’ monetary policy announcements Hussain (2011); Kenourgios, Papadamou, and Dimitriou (2015); Gębarowski et al. (2019), and even politician tweets Gjerstad et al. (2021). There is also a well-known fact that the stock market volatility shows a U-shape activity pattern related to the opening and the closing of a session Andersen, Bollerslev, and Cai (2000); Gubiec and Wiliński (2015); Andersen, Thyrsgaard, and Todorov (2019). An analogous intraweek effect has also been evidenced in previous research Berument and Kiymaz (2001). Conversely, in the foreign exchange market (Forex), which operates 24 hours a day and five days a week, periods of amplified activity can be attributed to the geographically diverse market participants Dacorogna et al. (1993). For example, a notable surge in activity is observed during the transitional period between the Asia/European and European/U.S. trading sessions Zhang (2018). On the other hand, certain markets exhibit their unique patterns like, for instance, the oil market experiencing activity increase at 16:30 UTC, which coincides with the weekly release of the U.S. Energy Information Administration Petroleum Status Report on the U.S. crude oil inventories Bu (2014). Despite these market-specific patterns, it is essential to recognize the interconnected nature of today’s financial markets due to the instantaneous dissemination of information Alves et al. (2020). For example, alterations in interest rates, primarily affecting Forex, reverberate promptly across various markets, particularly the stock market, demonstrating the profound global financial interdependence.

Since the introduction of Bitcoin in 2009, the cryptocurrency market has undergone exponential expansion, evolving from transactions primarily conducted on the internet fora to a significant market valued at over 1 trillion USD as of June 2023 CoinMarketCap , where transactions occur 24/7 on more than 600 platforms CoinMarketCap . Despite its persistent volatility, recurrent speculation bubbles and subsequent market crashes Gerlach, Demos, and Sornette (2019); Bellon and Figuerola-Ferretti (2022); Bazán-Palomino (2022); Wang et al. (2022), security breaches Charoenwong and Bernardi (2021), and spectacular collapses Fu et al. (2022); Briola et al. (2023); Vidal-Tomás, Briola, and Aste (2023), the trading characteristics of this market have been found to align considerably with those observed in the mature financial markets Bariviera, Zunino, and Rosso (2018); Drożdż et al. (2018); Sigaki, Perc, and Ribeiro (2019); Wątorek et al. (2021); Kwapień et al. (2022); Garcin (2023); Pessa, Perc, and Ribeiro (2023). Intriguingly, the correlation between the most frequently traded cryptocurrencies, specifically bitcoin and ether, and the stock indices and other financial assets has increased significantly, which suggests an emerging interconnectedness within the global financial ecosystem Manavi et al. (2020); Balcilar, Ozdemir, and Agan (2022); Wang, Liu, and Wu (2022); Wątorek, Kwapień, and Drożdż (2023); Drożdż, Kwapień, and Wątorek (2023).

While several trading characteristics of the cryptocurrency market echo those of the regular financial markets, key differentiating aspects exist. First, the cryptocurrency market operates continuously without defined opening and closing times. Furthermore, independent exchange rates across different platforms provide opportunities for arbitrage Makarov and Schoar (2020). Additionally, cryptocurrency prices are unusually susceptible to all sorts of rumors, like tweets Ante (2023), and manipulations in the form of the pump-and-dump schemes Li, Shin, and Wang (2021); Dhawan and Putnins (2022) and wash trading Cong et al. (2022). It is worth noting that despite a large universe of more than 10,000 cryptocurrencies, the market is largely dominated by bitcoin and ether. As of June 2023, these two assets represent approximately 70% of the market’s total capitalization, of which bitcoin accounts for around 50% and ether accounts for around 20% CoinMarketCap .

Even with a relatively nascent status of the cryptocurrency market, some research investigating its intraday and intraweek trading patterns has already been conducted. A time-of-day, day-of-week, and month-of-year periodicity in the bitcoin volatility and liquidity have been reported Baur et al. (2019) as well as a marked decrease in trading activity during weekends Baur et al. (2019); Kwapień et al. (2022). Moreover, atypical trade intensity and bitcoin volatility on Thursdays and Fridays have been identified Catania and Sandholdt (2019). Linkages between the amplified bitcoin trading activity and the trading hours of the major global stock markets have also been observed Dyhrberg, Foley, and Svec (2018); Eross et al. (2019); Wang, Liu, and Hsu (2020). Some influence of macroeconomic news on the intraday seasonal volatility for bitcoin and ether in the Gemini exchange before 2020 has also been found Omrane, Houidi, and Savaser (2023). Periodicity differences between the bitcoin and ether volatility and their liquidity across centralized (e.g., Binance and Coinbase) and decentralized (e.g., Uniswap) exchanges have been reported Hansen, Kim, and Kimbrough (2022). In the centralized exchanges, the patterns observed in high-frequency data were attributed to algorithmic trading Hansen, Kim, and Kimbrough (2022). However, earlier studies showed no effect of algorithmic trading on the intraday patterns of cryptocurrencies Petukhina, Reule, and Härdle (2021). Some studies have explored the microstructure characteristics of the bitcoin spot and futures markets Aleti and Mizrach (2021) and identified a higher degree of the microstructure noise in the cryptocurrency market in comparison to stock markets Dimpfl and Peter (2021).

Given the above observations, one may ask whether there exist recurrent patterns in the cryptocurrency market volatility and trading activity that parallel those observed in the traditional financial markets or they are fundamentally dissimilar. The present contribution addresses this question by employing the correlation matrix formalism and signal decomposition into principal components to isolate recurring activity patterns from noise, based on recent high-frequency price changes, volume, and the number of transactions. This approach has previously been proven successful in revealing patterns in the German stock index DAX Drożdż et al. (2001) and the brain sensory response Kwapień, Drożdż, and Ioannides (2000), as well as in capturing collectivity in the stock Drożdż et al. (2000); James and Menzies (2021); James, Menzies, and Gottwald (2022) and cryptocurrency Chaudhari and Crane (2020); Drożdż et al. (2020); James and Menzies (2022); Nguyen et al. (2022); Gavin and Crane (2023); James and Menzies (2023) markets together with its temporal changes in the cryptocurrency market Kwapień, Wątorek, and Drożdż (2021); James (2022).

II Data and methods

II.1 Data description and properties

The data set considered in this study encompasses four cryptocurrencies: Bitcoin (BTC), Ether (ETH), Dogecoin (DOGE), and WINkLink (WIN) and three observables: logarithmic price changes, transaction volume, and the number of transactions in time unit. Time series spanning 3 years (Jan 1, 2020 to Dec 31, 2022) have been downloaded from the Binance exchange Binance , which offers price quotations recorded with 10-second frequency. All prices are denominated in tether (USDT), the most frequently traded stablecoin on Binance.

BTC and ETH are the two highest capitalized and most liquid cryptocurrencies with the average inter-transaction time in the considered period being and Drożdż, Kwapień, and Wątorek (2023)). The price changes of these cryptocurrencies are strongly correlated with each other Wątorek, Kwapień, and Drożdż (2022) and, as it has recently been documented Drożdż, Kwapień, and Wątorek (2023), with the U.S. stock indices. DOGE is the most influential one among the meme coins; its spectacular price movements attracted media attention due to the impact of Elon Musk’s tweets Nani (2022). Despite its smaller capitalization compared to BTC and ETH, DOGE maintains substantial liquidity on the Binance exchange ( Drożdż, Kwapień, and Wątorek (2023)). WIN, a smart contract oracle and competitor to Chainlink, boasts significantly smaller capitalization, ranking beyond the top 100 cryptocurrencies CoinMarketCap . However, its inclusion here is justified by its distinct characteristics: absence of a correlation with the U.S. stock indices Drożdż, Kwapień, and Wątorek (2023). At the same time, its average inter-transaction time ( Drożdż, Kwapień, and Wątorek (2023)) is sufficient to carry out the analysis from a statistical perspective.

The logarithmic returns, derived from the price changes , were calculated as , where s. Subsequently, in conjunction with transaction volumes and the number of transactions , the return time series were segmented into day-long and week-long intervals. The former, ranging from 00:00:00 to 23:59:50, comprised data points across days. The latter, ranging from Sunday 00:00:00 to Saturday 23:59:50, comprised data points across weeks. The in-segment time series , , represent daily trading ( and ) and , , represent weekly trading ( and ).

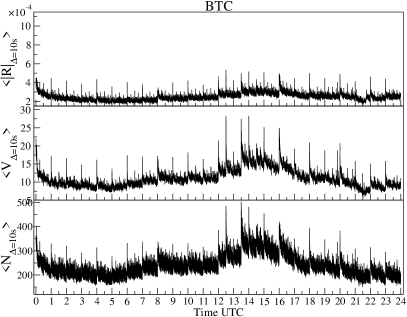

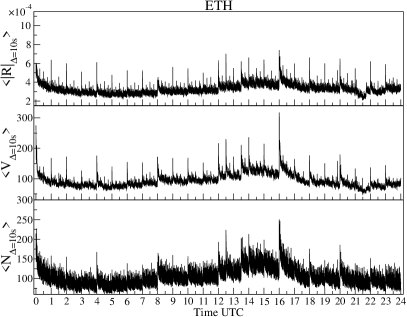

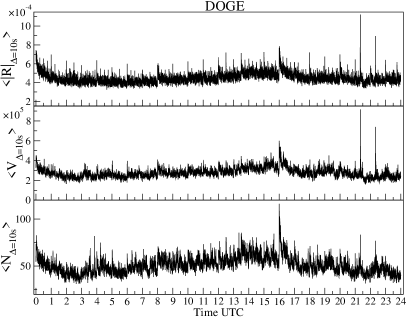

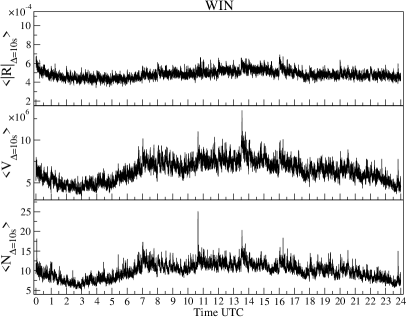

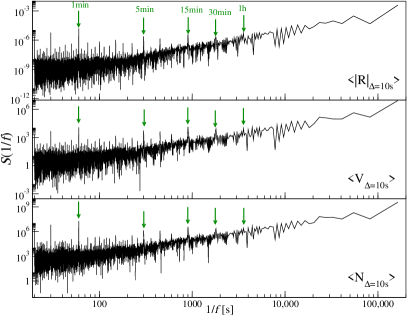

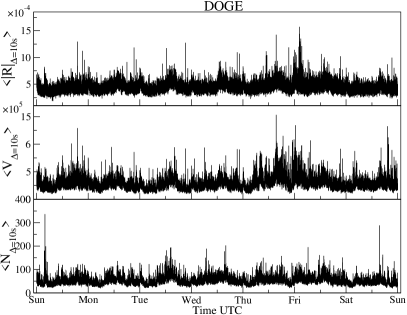

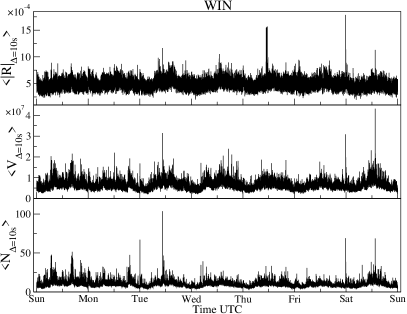

Initial patterns of the trading activity can be inferred from the average values of , , and calculated across the trading days, as illustrated in Fig. 1. Predominantly, liquidity disparities assessed through the number of transactions and volatility become apparent. As expected, BTC that is the highest capitalized and most recognizable cryptocurrency registers the most transactions per 10-second interval. Comparable transaction numbers are observed for ETH, particularly when accounting for its higher volume (in ETH units) and lower price. Conversely, DOGE exhibits on average half as many transactions per 10-second interval as ether. In the case of WIN a value of oscillates around 10.

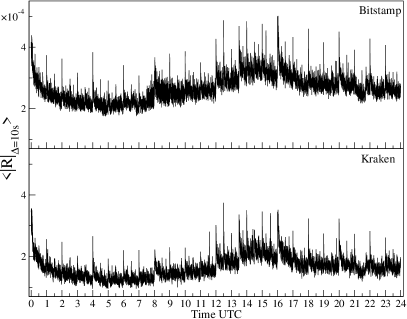

A strong pattern is visible in Fig. 1 in a form of the periodic spikes every full hour with minor peaks occurring every half an hour and quarter an hour for BTC and ETH. This pattern consists of increased volatility, volume, and the number of transactions. The related variations are also visible in the frequency domain, as illustrated in Fig.2. A similar pattern is also present for DOGE, albeit the hourly increase of volume and the number of transactions is less pronounced here. In contrast, such a pattern is absent in the least liquid of the considered cryptocurrencies, WIN. A potential explanation for the observed periodic patterns can be algorithmic trading, the effects of which have already been documented in stock markets as the periodic activity patterns corresponding to minutes Muravyev and Picard (2022) and hours Broussard and Nikiforov (2014). Interestingly, the comparable full-hour patterns have recently been reported for cryptocurrencies Hansen, Kim, and Kimbrough (2022). The same phenomenon of the amplified volatility at every full quarter, every half an hour, and every full hour can be observed during the same period (2020-2022) on the Kraken and Bitstamp exchanges as it is demonstrated in Fig. 3.

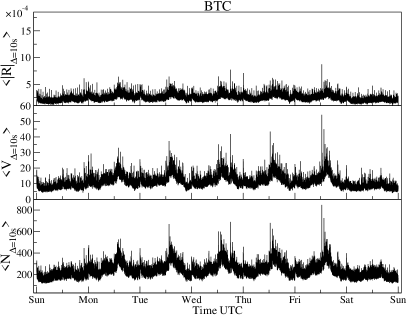

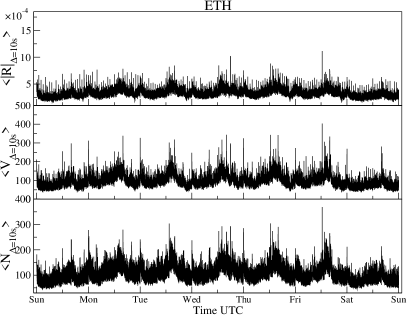

Different fluctuation patterns are associated with the trading activity of individual users on Binance, which is currently the largest cryptocurrency exchange in terms of the traded volume value CoinMarketCap . The Binance users are globally distributed, with the largest groups of users, each around 5%, residing in Turkey, Russia, Argentina, Vietnam, and Ukraine, while the remaining 75% are located in other countries Similarweb . Consequently, the peak volatility, volume, and transaction numbers are observed between 12:00 and 16:00 UTC, a timeframe coinciding with the overlap of the European and American trading sessions. Following this period, there is a significant decrease in market activity, reaching a day low after 21:00 UTC with the closure of the U.S. trading session. Another surge in the market activity aligns with the onset of the Asian trading session at 00:00 UTC, followed by a subsequent decline until the opening of the European session at 06:00 UTC. This pattern is particularly evident for the most liquid cryptocurrencies, BTC and ETH. However, this pattern is slightly perturbed for DOGE and apart from the peaks at 00:00 and 16:00 UTC, two additional peaks are noted at 21:20 and 22:20 UTC, which correspond to the highest volatility and volume periods. The least liquid one of the considered cryptocurrencies, WIN, exhibits near-constant volatility over a 24-hour period. The diurnal volume and transaction number patterns align with those observed for the most liquid cryptocurrencies.

Distinct weekly patterns are also discernible in the cryptocurrency market where trading is daily, as it is demonstrated in Fig. 4. For BTC and ETH, conspicuous surges of activity are seen during weekdays at midday, coinciding with the overlap of the European and American trading sessions. The largest values of , volume , and the transaction number manifest themselves on Fridays. The market dynamics on Thursdays, Wednesdays, and Tuesdays exhibit similar trends. Unlike this, a slight attenuation of trading activity is observed on Mondays. During weekends, when the traditional financial markets are closed, the cryptocurrency market exhibits significantly calmer trading. No such regular weekly pattern can be observed for the less liquid DOGE and WIN.

II.2 Correlation matrix and random matrix limit

After the exploration of the cryptocurrency market dynamics via the comparison of the average intraday and intraweek values, the correlation matrix formalism will be used now to calculate the intraday correlations in market activity. The most recurrent dynamical structures will be captured through the eigenvalues decomposition. Correlation matrix is defined as , where is a data matrix of size and denotes matrix transpose. In this general notation, stands for , , or , whereas P is day or week. After diagonalization of the correlation matrix

| (1) |

its eigenvalues are derived alongside the corresponding eigenvectors , where . Here, applies to intraday dynamics and applies to intraweek dynamics.

The derived empirical eigenvalue distribution can be tested against the Marchenko-Pastur distribution corresponding to the Wishart ensemble of random matrices Mehta (2004) that represent the universal properties of uncorrelated i.i.d. random variables with the Gaussian distribution Wishart (1928). The probability density function defining an eigenvalue distribution of has the analytical form

| (2) |

| (3) |

where and . This relationship is strictly valid in the infinite limit Marčenko and Pastur (1967) but a comparison of the empirical eigenvalue distribution with the Marchenko-Pastur distribution helps distinguish whether any correlated structures exist in the data. In the present case one may look for repeatable intraday or intraweek structures.

III Intraday patterns

III.1 Correlation characteristics

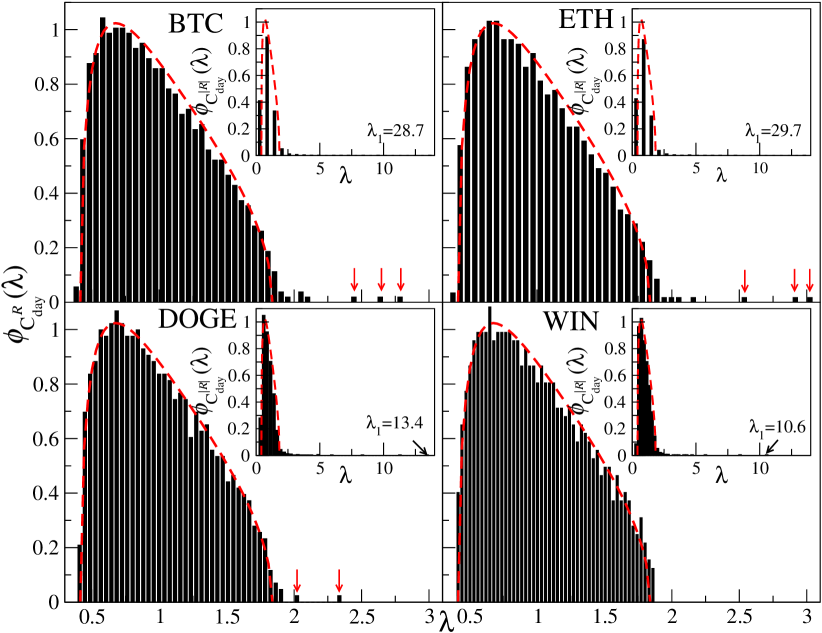

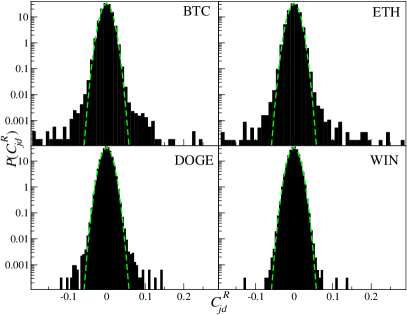

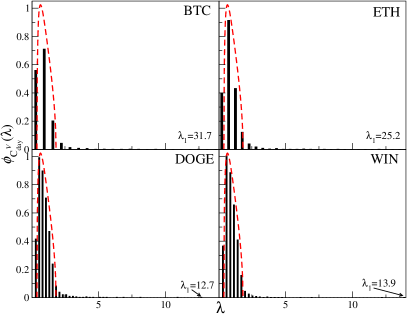

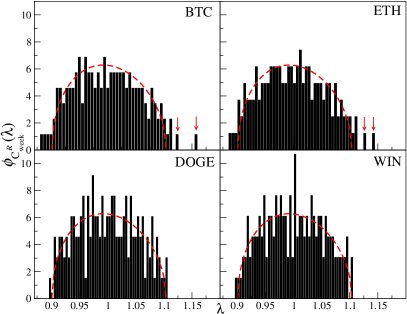

In this section, the properties of correlation matrices , and are explored. The eigenvalue distributions are juxtaposed with the theoretical Marchenko-Pastur distribution for random matrices to assess the presence of intraday structures that are genuinely recurring. As depicted in Fig.5, the majority of the empirical eigenvalues for reside within the Marchenko-Pastur (M-P region). Specifically, all eigenvalues fall within this region in the case of WIN. This indicates that there is no correlation among the intraday returns for this cryptocurrency, which implies no recurring intraday structure is detectable. The random nature of the correlations is further validated by the nearly Gaussian form of the off-diagonal element distribution for WIN, as shown in Fig.6 (although even in this case the Gaussianity of the distribution is still rejected by Kolmogorov-Smirnov and Jarque-Bera tests). This suggests that the cross-correlations are essentially random. A situation is different for the most liquid cryptocurrencies: BTC and ETH. Here, a handful of the eigenvalues are found outside the random region, signifying the existence of distinct, time-specific, recurrent structures in the intraday trading. The off-diagonal element distributions for BTC and ETH, illustrated in Fig. 6, deviate distinctly from the Gaussian distribution. Contrary to the situation with WIN, here the p.d.f. tails are heavier. DOGE presents a scenario intermediate to the previous ones with only two eigenvalues situated clearly outside the M-P region. This hints at the existence of some repetitive patterns, albeit less pronounced than in the case of BTC and ETH.

It is noteworthy that for all the considered cryptocurrencies, the eigenvalue bulk for aligns well with the bounds defined by the Marchenko-Pastur distribution for random matrices. This observation underscores the lack of shared information among the respective log-returns in different trading days. Conversely, multiple eigenvalues are situated outside the M-P region in the case of volatility (see the insets in Fig.5), which indicates recurrence in . This is a manifestation of the well-documented stylized facts demonstrating that there is no autocorrelation in log-returns and a long (which decays as a power law) memory in volatility Gopikrishnan et al. (1999); Ausloos (2000); Cont (2001); Jiang et al. (2019); Klamut et al. (2020); Klamut and Gubiec (2021).

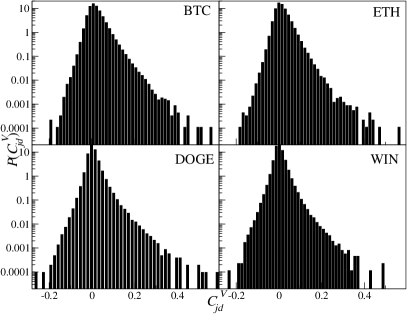

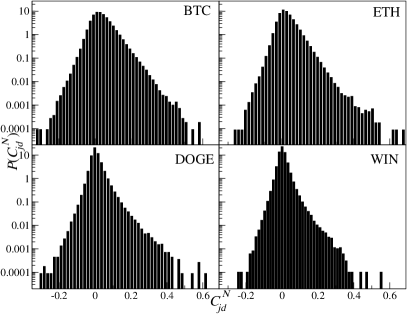

The correlations between and have different properties. They display a higher level of collectivity compared to . A significant number of eigenvalues deviate notably from the random region (as shown in Fig. 7) and the off-diagonal element distributions (as shown in Fig.8) also deviate substantially from the Gaussian distribution. Such effects are known to induce the eigenvalues standing outside the random matrix theory regime Drożdż et al. (2002). The global collective behavior epitomized by the largest eigenvalue is more pronounced in the case of BTC and ETH. These observations suggest that the intraday structures for volatility and the transaction number recur more frequently than those for log-returns . Furthermore, these findings corroborate the existence of repeatable patterns of correlated Binance user activity already seen in the average volume and transaction number in Fig. 1.

Another noteworthy observation is related to the congruence between the eigenvalue distributions and for volatility and volume . It suggests that the cross-correlations between the intraday absolute price fluctuations and the intraday volume are similar, implying that both quantities share the intraday patterns. This correspondence between volume and volatility can be interpreted as a manifestation of a linear form of the price impact function Bouchaud (2010). This particular relationship form has been subject of recent research focusing on the properties of the cryptocurrency market Drożdż, Kwapień, and Wątorek (2023).

III.2 Superposed time series

From an investor perspective, the most compelling facet of the market dynamics pertains to the timing of the recurrent patterns of the amplified market activity. To identify such intervals, the superposed time series are constructed in a form of eigensignals Drożdż et al. (2000):

| (4) |

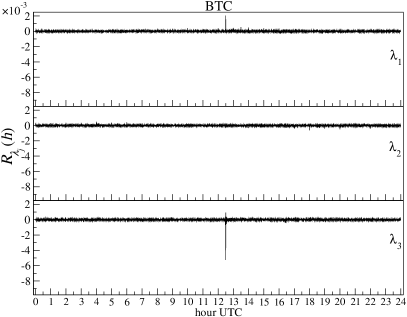

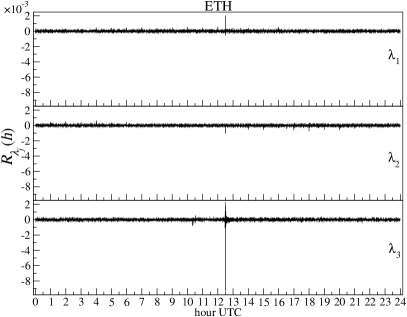

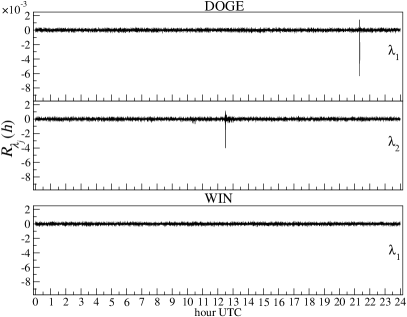

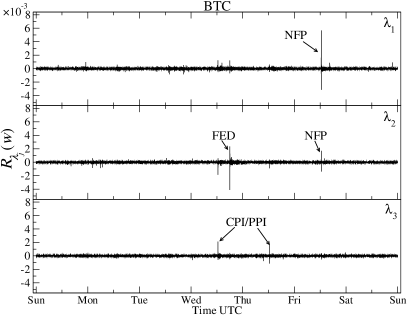

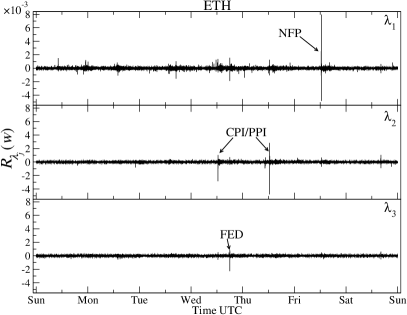

As illustrated in Fig 5, there are three eigenvalues notably outside the random region for the log-returns of BTC and ETH. Two such eigenvalues are present for DOGE, whereas none exists for WIN. These eigenvalues represent non-random intraday correlations and, hence, the corresponding eigenvectors might contain valuable insights into the recurrent structures of market dynamics. Consequently, the superposed time series for in the case of BTC and ETH and for DOGE are presented in Fig.9. Although all eigenvalues for WIN are located in the M-P region, the superposed time series for are also presented for comparison. The superposed log-returns for the least liquid cryptocurrency WIN merely represents noise (as anticipated). On the other hand, the most collective signal associated with portrays the most profound synchronicity of BTC and ETH, which occurs around 12:30 UTC. At this time, the numerous U.S. economic data are published. This timing also coincides with the peak synchronous activity reported for the DAX stock indexDrożdż et al. (2001). The second eigenvalue reflects the periodic market activity corresponding to full hours, potentially instigated by algorithmic trading. However, this pattern is significantly weaker than the one linked to . The third eigensignal also pinpoints the timeframe around 12:30 UTC. In contrast to , it points out to the occurrence of negative log-returns during that period.

Different patterns are observable in a signal corresponding to the most collective eigenvector for DOGE. In this case, the most frequent patterns in log-returns occur at 21:20 UTC. Notwithstanding, the same timeframe as in the case of for BTC and ETH, i.e., around 12:30 UTC, is indicated by . One plausible explanation for the disparate recurring patterns observed in DOGE could be the influence of Elon Musk’s tweets and the subsequent volatility spikes following their dissemination, as it was discussed in Shahzad, Anas, and Bouri (2022).

In the superposed log-return time series , the peak synchronous activity was observed to occur at 12:30 UTC for BTC and ETH. This raises a question which events occur on the most correlated days during that time. To address it, the off-diagonal elements of the correlation matrix for BTC are arranged in descending order. These elements, along with the timing of the pattern and the releases of macroeconomic news, are presented in Tab. 1. Consistent with the superposed time series evolution associated with the most collective eigenvector , the increased activity for nearly all strongly correlated days was found to happen at 12:30 UTC. Several U.S. macroeconomic news are released at this time on varying weekdays. The most recurrent events are the NFP - Nonfarm Payrolls report on unemployment (Friday 12:30) and the reports related to inflation: CPI - Consumer Price Index, PPI - Producer Price Index, PCE - Personal Consumption Expenditures, together with PI - Personal Income (Tue-Fri 12:30). The only exceptions are the two days featuring the publication of the statement post Federal Reserve meetings on Wednesday at 18:00. No day exhibiting a strong correlation has been found on weekends, which constitute periods devoid of any macroeconomic announcement in the U.S., and also on Monday, which is generally a quiet day for economic news. This suggests a degree of correlation between patterns in the BTC market activity and the news related to the U.S. economy. Interestingly, while the recurring patterns on the most strongly correlated days occurred at the consistent time of 12:30, these patterns emerged on different weekdays. Hence, a further investigation of the intraweek patterns of market dynamics would be appropriate.

| Date | time | day | event | Date | time | day | event | |

| 07.10.2022 | 12:30 | FRI | NFP | 0.25 | 28.10.2022 | 12:30 | FRI | PCE+PI |

| 21.09.2022 | 18:00 | WED | FED | 0.23 | 03.11.2021 | 18:00 | WED | FED |

| 07.10.2022 | 12:30 | FRI | NFP | 0.23 | 12.10.2022 | 12:30 | WED | PPI |

| 12.10.2022 | 12:30 | WED | PPI | 0.18 | 28.10.2022 | 12:30 | FRI | PCE+PI |

| 07.10.2022 | 12:30 | FRI | NFP | 0.17 | 04.11.2022 | 12:30 | FRI | NFP |

| 13.09.2022 | 12:30 | TUE | CPI | 0.14 | 13.07.2022 | 12:30 | WED | CPI |

| 15.11.2022 | 12:30 | TUE | PPI | 0.13 | 13.12.2022 | 12:30 | TUE | CPI |

| 10.11.2022 | 12:30 | THU | CPI | 0.12 | 13.12.2022 | 12:30 | TUE | CPI |

| 10.06.2022 | 12:30 | FRI | NFP | 0.12 | 07.10.2022 | 12:30 | FRI | NFP |

| 12.10.2022 | 12:30 | WED | PPI | 0.12 | 04.11.2022 | 12:30 | FRI | NFP |

| 10.06.2022 | 12:30 | FRI | NFP | 0.12 | 13.09.2022 | 12:30 | TUE | CPI |

| 13.07.2022 | 12:30 | WED | CPI | 0.12 | 30.09.2022 | 12:30 | FRI | PCE |

| 10.06.2022 | 12:30 | FRI | NFP | 0.12 | 13.07.2022 | 12:30 | WED | CPI |

| 10.06.2022 | 12:30 | FRI | NFP | 0.11 | 13.10.2022 | 12:30 | THU | CPI |

| 13.10.2022 | 12:30 | THU | CPI | 0.11 | 13.09.2022 | 12:30 | TUE | CPI |

| 12.10.2022 | 12:30 | WED | PPI | 0.11 | 13.10.2022 | 12:30 | THU | CPI |

| 28.10.2022 | 12:30 | FRI | PCE+PI | 0.10 | 04.11.2022 | 12:30 | FRI | NFP |

| 07.10.2022 | 12:30 | FRI | NFP | 0.10 | 05.08.2022 | 12:30 | FRI | NFP |

IV Intraweek patterns

In the preceding section, the existence of recurring structures within the intraday dynamics of the cryptocurrency market at specific temporal intervals was identified. It can be read from Table 1 that formation of these patterns is typically influenced by particular weekdays and the U.S. economic news releases. However, when analyzing it from a daily decomposition perspective, it is not feasible to distinguish the days exhibiting the strongest synchronous activity. In order to quantify this, the intraweek dynamics needs to be investigated as well by constructing the correlation matrix and the corresponding superposed time series:

| (5) |

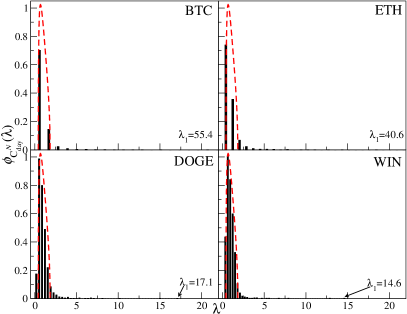

The eigenvalue distribution is presented in Fig. 10 to expose the patterns inherent to the intraweek market activity. Upon comparing it with the eigenvalue distribution for the intraday correlation matrix (Fig. 5), a lower number of eigenvalues is observed outside the M-P region. This result indicates that the collective behaviour is weaker here. It has been expected, however, given that the recurrent patterns are spread over an extended span of days. In the case of DOGE and WIN, all eigenvalues are contained within the M-P region, thereby confirming the absence of any recurrent intraweek structure. In contrast, three eigenvalues are detected outside the M-P distribution for BTC and ETH, leading to the possible computation of the superposed time series for .

With the reference to the intraday dynamics portrayed in Figure 9, it is discernible that the most recurrent structures emerge at 12:30 UTC. The intraweek decomposition, as shown in Figure 11, enables the identification of the specific days on which the amplified activity patterns appear. The superposed time series associated with the largest eigenvalue suggests that the most pronounced synchronous activity happens on Fridays at 12:30 UTC, which correlates with the Nonfarm Payroll (NFP) report (see Table 1). The second pattern associated with in the case of ETH and in the case of BTC is observed at 12:30 on Wednesdays and Thursdays when Consumer Price Index (CPI) and Producer Price Index (PPI) inflation reports are released. An additional pattern of the increased activity, corresponding to for BTC and for ETH, overlooked by the intraday decomposition, is manifest on Wednesdays at 18:00 UTC. This remains in agreement with the timing of the Federal Reserve statement releases.

The above findings indicate that the recurrent periods of the increased market activity coincide with the publication of the U.S. economic data. Their frequency can be a pivotal factor that influences the structure repeatability. Collectivity of the pattern related to the NFP reports is the strongest and attributable to its consistent monthly release schedule (Fridays at 12:30 UTC). In contrast, while the CPI and PPI reports are also published monthly, their release dates vary among the weekdays, excluding Mondays. The Federal Reserve meeting statements, associated here with and , are disclosed approximately every 2.5 months, consistently on Wednesdays at 18:00 UTC.

IV.1 Correlations in individual years

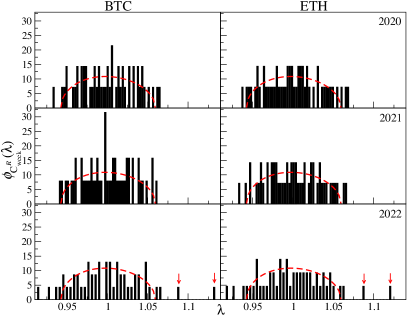

An interesting issue that emerges is related to the temporal uniformity of the identified activity patterns. The most important cross-correlated days were predominantly witnessed in 2022 (Table 1). To ensure divergence of the patterns across each year, the intraweek log-returns were sequentially decomposed for each year individually. Figure 12 reveals that only in 2022 there were two eigenvalues that lay outside the random-matrix region. This means that during 2020 and 2021 the market volatility did not exhibit any recurrent intraweek pattern and that such patterns manifested themselves exclusively in the year 2022. Such disparate results could potentially be attributed to the significant correlations that emerged between the primary cryptocurrencies, in particular BTC and ETH, and the U.S. stock indices Wątorek, Kwapień, and Drożdż (2023); Drożdż, Kwapień, and Wątorek (2023). Contrarily, WIN was identified as the most frequently traded cryptocurrency from the cohort of cryptocurrencies that were uncorrelated with the U.S. stock indices Drożdż, Kwapień, and Wątorek (2023). It might elucidate the fact that all eigenvalues of the correlation matrix related to this cryptocurrency were found within the M-P region, which indicates the prevalence of the noisy intraday fluctuations and, thereby, the absence of any easily discernible repeatable patterns of the market dynamics. Furthermore, in the case of DOGE, the correlations with the U.S. indices were notably lower if compared to BTC and ETH Wątorek, Kwapień, and Drożdż (2023). This observation may explain the relatively reduced occurrence of repetitive patterns in the DOGE dynamics.

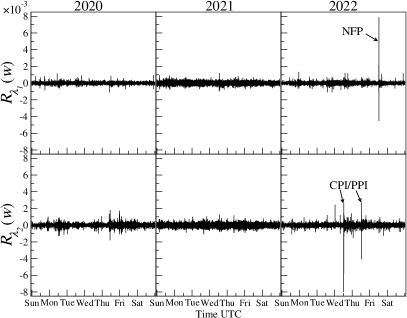

In line with the expectations derived from the number of eigenvalues situated outside the random matrix region for BTC in Fig. 12, the superposed time series , computed separately for each year from 2020 to 2022 display the absence of any recurrent pattern in 2020 and 2021 (Figure 13); they emerge only in 2022. The most pronounced collective effect associated with is observed on Fridays at 12:30, a phenomenon that was previously attributed to the monthly releases of the NFP report. The patterns corresponding to occur on Thursdays and Wednesdays at 12:30 UTC, which coincides with the inflation report releases. This is in agreement with the recent research findings that indicate a synchronized movement of BTC and ETH against the U.S. indices following the CPI announcements in 2022 Wątorek, Kwapień, and Drożdż (2023). The inflation metrics were subject to an intense scrutiny in 2022, which induced substantial volatility across all financial markets James, Menzies, and Chin (2022). While Bitcoin was fundamentally designed to serve as a safeguard against the policy of central banks and inflation owing to its a predetermined supply Choi and Shin (2022), its observed response to the inflation data, akin to the stock indices, may suggest a deviation from such an assigned role. This can be interpreted as yet another indication that BTC has transformed into a volatile financial asset, which exhibits correlations with the other volatile assets.

V Summary

By applying the correlation matrix formalism to decompose the cryptocurrency price dynamics into intraday and intraweek time series, this study demonstrates the efficacy of this formalism as a tool for identifying periods of increased market activity that are repeatable across different days or weeks. A comparison of the empirical eigenvalue distribution with the theoretical prediction for uncorrelated Gaussian time series expressed by the Marchenko-Pastur distribution allowed one here to discern the correlations pertaining to the synchronous behaviour of the cryptocurrency market from the overall noise. The price fluctuations (returns) of the most liquid cryptocurrencies – BTC and ETH – were identified to exhibit specific intraday and intraweek patterns. One such pattern involves the amplified market activity precisely at full hours and a couple of more subtle patterns involve similar effects at full quarters and half-hours. This is a cross-platform effect that cannot be confined to a unique trading platform. The algorithmic trading, a phenomenon well-recognized in the stock markets, offers a plausible explanation of this effect. It is worthwhile to note that, while the external factors considered here are responsible for the repeatable components of the market dynamics, the internal factors appear to be substantially random and unique as a good agreement between the empirical eigenvalue distributions in their bulk and the random matrix theory predictions expressed by the Marchenko-Pastur distribution.

Of a particular interest are the recurring patterns linked to the macroeconomic news releases. These moments are coupled with the increased activity of the market, which became evident predominantly in 2022. In the case of BTC and ETH, it could potentially be attributed to the emergence of the significant cross-correlation between the most liquid cryptocurrencies and the U.S. stock indices, in particular around the CPI report releases. It remains an open question whether these repeatable patterns observed in the cryptocurrency market are transmitted there through the cross-correlation with the U.S. indices, for which the amplified volatility is expected and well-documented, or they rather reflect an intrinsic reaction of the cryptocurrency market to such data. However, irrespective of the answer, which may form a basis for future research, the revealed dependence substantiates further that the cryptocurrency market has evolved into a valid and interrelated component of the global financial markets.

As a final remark, it needs to be emphasized that this methodology is largely universal and is expected to result in a similar decomposition of the dynamics for any market of reasonable liquidity.

Data Availability Statement

The data are freely available on Binance exchange Binance .

References

- Gerety and Mulherin (1991) M. S. Gerety and J. H. Mulherin, “Patterns in intraday stock market volatility, past and present,” Financial Analysts Journal 47, 71–79 (1991).

- Andersen and Bollerslev (1998) T. G. Andersen and T. Bollerslev, “Deutsche mark–dollar volatility: Intraday activity patterns, macroeconomic announcements, and longer run dependencies,” The Journal of Finance 53, 219–265 (1998).

- Bollerslev, Cai, and Song (2000) T. Bollerslev, J. Cai, and F. M. Song, “Intraday periodicity, long memory volatility, and macroeconomic announcement effects in the us treasury bond market,” Journal of Empirical Finance 7, 37–55 (2000).

- Andersen et al. (2003) T. G. Andersen, T. Bollerslev, F. X. Diebold, and C. Vega, “Micro effects of macro announcements: Real-time price discovery in foreign exchange,” American Economic Review 93, 38–62 (2003).

- Evans and Speight (2010) K. Evans and A. Speight, “International macroeconomic announcements and intraday euro exchange rate volatility,” Journal of the Japanese and International Economies 24, 552–568 (2010).

- Evans (2011) K. P. Evans, “Intraday jumps and us macroeconomic news announcements,” Journal of Banking & Finance 35, 2511–2527 (2011).

- Harju and Hussain (2011) K. Harju and S. M. Hussain, “Intraday seasonalities and macroeconomic news announcements,” European Financial Management 17, 367–390 (2011).

- Hussain (2011) S. M. Hussain, “Simultaneous monetary policy announcements and international stock markets response: An intraday analysis,” Journal of Banking & Finance 35, 752–764 (2011).

- Kenourgios, Papadamou, and Dimitriou (2015) D. Kenourgios, S. Papadamou, and D. Dimitriou, “Intraday exchange rate volatility transmissions across QE announcements,” Finance Research Letters 14, 128–134 (2015).

- Gębarowski et al. (2019) R. Gębarowski, P. Oświęcimka, M. Wątorek, and S. Drożdż, “Detecting correlations and triangular arbitrage opportunities in the Forex by means of multifractal detrended cross-correlations analysis,” Nonlinear Dynamics 98, 2349–2364 (2019).

- Gjerstad et al. (2021) P. Gjerstad, P. F. Meyn, P. Molnár, and T. D. Næss, “Do President Trump’s tweets affect financial markets?” Decision Support Systems 147, 113577 (2021).

- Andersen, Bollerslev, and Cai (2000) T. G. Andersen, T. Bollerslev, and J. Cai, “Intraday and interday volatility in the Japanese stock market,” Journal of International Financial Markets, Institutions and Money 10, 107–130 (2000).

- Gubiec and Wiliński (2015) T. Gubiec and M. Wiliński, “Intra-day variability of the stock market activity versus stationarity of the financial time series,” Physica A 432, 216–221 (2015).

- Andersen, Thyrsgaard, and Todorov (2019) T. G. Andersen, M. Thyrsgaard, and V. Todorov, “Time-varying periodicity in intraday volatility,” Journal of the American Statistical Association 114, 1695–1707 (2019).

- Berument and Kiymaz (2001) H. Berument and H. Kiymaz, “The day of the week effect on stock market volatility,” Journal of Economics and Finance 25, 181–193 (2001).

- Dacorogna et al. (1993) M. M. Dacorogna, U. A. Müller, R. J. Nagler, R. B. Olsen, and O. V. Pictet, “A geographical model for the daily and weekly seasonal volatility in the foreign exchange market,” Journal of International Money and Finance 12, 413–438 (1993).

- Zhang (2018) H. Zhang, “Intraday patterns in foreign exchange returns and realized volatility,” Finance Research Letters 27, 99–104 (2018).

- Bu (2014) H. Bu, “Effect of inventory announcements on crude oil price volatility,” Energy Economics 46, 485–494 (2014).

- Alves et al. (2020) L. G. Alves, H. Y. Sigaki, M. Perc, and H. V. Ribeiro, “Collective dynamics of stock market efficiency,” Scientific Reports 10, 21992 (2020).

- (20) CoinMarketCap, “CoinMarketCap,” https://coinmarketcap.com.

- Gerlach, Demos, and Sornette (2019) J.-C. Gerlach, G. Demos, and D. Sornette, “Dissection of Bitcoin’s multiscale bubble history from January 2012 to February 2018,” Royal Society Open Science 6, 180643 (2019).

- Bellon and Figuerola-Ferretti (2022) C. Bellon and I. Figuerola-Ferretti, “Bubbles in Ethereum,” Finance Research Letters 46, 102387 (2022).

- Bazán-Palomino (2022) W. Bazán-Palomino, “Interdependence, contagion and speculative bubbles in cryptocurrency markets,” Finance Research Letters 49, 103132 (2022).

- Wang et al. (2022) Y. Wang, F. Horky, L. J. Baals, B. M. Lucey, and S. A. Vigne, “Bubbles all the way down? Detecting and date-stamping bubble behaviours in NFT and DeFi markets,” Journal of Chinese Economic and Business Studies 20, 415–436 (2022).

- Charoenwong and Bernardi (2021) B. Charoenwong and M. Bernardi, “A decade of cryptocurrency ‘hacks’: 2011–2021,” Available at SSRN 3944435 (2021).

- Fu et al. (2022) S. Fu, Q. Wang, J. Yu, and S. Chen, “FTX collapse: A Ponzi story,” (2022), arXiv:2212.09436 [cs.CR] .

- Briola et al. (2023) A. Briola, D. Vidal-Tomas, Y. Wang, and T. Aste, “Anatomy of a stablecoin’s failure: The Terra-Luna case,” Finance Research Letters 51, 103358 (2023).

- Vidal-Tomás, Briola, and Aste (2023) D. Vidal-Tomás, A. Briola, and T. Aste, “FTX’s downfall and Binance’s consolidation: The fragility of centralised digital finance,” Physica A 625, 129044 (2023).

- Bariviera, Zunino, and Rosso (2018) A. F. Bariviera, L. Zunino, and O. A. Rosso, “An analysis of high-frequency cryptocurrencies prices dynamics using permutation-information-theory quantifiers,” Chaos 28, 075511 (2018).

- Drożdż et al. (2018) S. Drożdż, R. Gębarowski, L. Minati, P. Oświęcimka, and M. Wątorek, “Bitcoin market route to maturity? Evidence from return fluctuations, temporal correlations and multiscaling effects,” Chaos 28, 071101 (2018).

- Sigaki, Perc, and Ribeiro (2019) H. Y. Sigaki, M. Perc, and H. V. Ribeiro, “Clustering patterns in efficiency and the coming-of-age of the cryptocurrency market,” Scientific Reports 9, 1440 (2019).

- Wątorek et al. (2021) M. Wątorek, S. Drożdż, J. Kwapień, L. Minati, P. Oświęcimka, and M. Stanuszek, “Multiscale characteristics of the emerging global cryptocurrency market,” Physics Reports 901, 1–82 (2021).

- Kwapień et al. (2022) J. Kwapień, M. Wątorek, M. Bezbradica, M. Crane, T. Tan Mai, and S. Drożdż, “Analysis of inter-transaction time fluctuations in the cryptocurrency market,” Chaos 32, 083142 (2022).

- Garcin (2023) M. Garcin, “Complexity measure, kernel density estimation, bandwidth selection, and the efficient market hypothesis,” (2023), arXiv:2305.13123 [q-fin.ST] .

- Pessa, Perc, and Ribeiro (2023) A. A. Pessa, M. Perc, and H. V. Ribeiro, “Age and market capitalization drive large price variations of cryptocurrencies,” Scientific Reports 13, 3351 (2023).

- Manavi et al. (2020) S. A. Manavi, G. Jafari, S. Rouhani, and M. Ausloos, “Demythifying the belief in cryptocurrencies decentralized aspects. A study of cryptocurrencies time cross-correlations with common currencies, commodities and financial indices,” Physica A 556, 124759 (2020).

- Balcilar, Ozdemir, and Agan (2022) M. Balcilar, H. Ozdemir, and B. Agan, “Effects of COVID-19 on cryptocurrency and emerging market connectedness: Empirical evidence from quantile, frequency, and lasso networks,” Physica A 604, 127885 (2022).

- Wang, Liu, and Wu (2022) P. Wang, X. Liu, and S. Wu, “Dynamic linkage between Bitcoin and traditional financial assets: A comparative analysis of different time frequencies,” Entropy 24 (2022).

- Wątorek, Kwapień, and Drożdż (2023) M. Wątorek, J. Kwapień, and S. Drożdż, “Cryptocurrencies are becoming part of the world global financial market,” Entropy 25, 377 (2023).

- Drożdż, Kwapień, and Wątorek (2023) S. Drożdż, J. Kwapień, and M. Wątorek, “What is mature and what is still emerging in the cryptocurrency market?” Entropy 25 (2023).

- Makarov and Schoar (2020) I. Makarov and A. Schoar, “Trading and arbitrage in cryptocurrency markets,” Journal of Financial Economics 135, 293–319 (2020).

- Ante (2023) L. Ante, “How Elon Musk’s Twitter activity moves cryptocurrency markets,” Technological Forecasting and Social Change 186, 122112 (2023).

- Li, Shin, and Wang (2021) T. Li, D. Shin, and B. Wang, “Cryptocurrency pump-and-dump schemes,” (2021), SSRN:3267041 .

- Dhawan and Putnins (2022) A. Dhawan and T. J. Putnins, “A new wolf in town? pump-and-dump manipulation in cryptocurrency markets,” Review of Finance 27, 935–975 (2022).

- Cong et al. (2022) L. W. Cong, X. Li, K. Tang, and Y. Yang, “Crypto wash trading,” Tech. Rep. (National Bureau of Economic Research, 2022).

- Baur et al. (2019) D. G. Baur, D. Cahill, K. Godfrey, and Z. (Frank) Liu, “Bitcoin time-of-day, day-of-week and month-of-year effects in returns and trading volume,” Finance Research Letters 31, 78–92 (2019).

- Catania and Sandholdt (2019) L. Catania and M. Sandholdt, “Bitcoin at high frequency,” Journal of Risk and Financial Management 12 (2019).

- Dyhrberg, Foley, and Svec (2018) A. H. Dyhrberg, S. Foley, and J. Svec, “How investible is Bitcoin? Analyzing the liquidity and transaction costs of Bitcoin markets,” Economics Letters 171, 140–143 (2018).

- Eross et al. (2019) A. Eross, F. McGroarty, A. Urquhart, and S. Wolfe, “The intraday dynamics of bitcoin,” Research in International Business and Finance 49, 71–81 (2019).

- Wang, Liu, and Hsu (2020) J.-N. Wang, H.-C. Liu, and Y.-T. Hsu, “Time-of-day periodicities of trading volume and volatility in Bitcoin exchange: Does the stock market matter?” Finance Research Letters 34, 101243 (2020).

- Omrane, Houidi, and Savaser (2023) W. B. Omrane, F. Houidi, and T. Savaser, “Macroeconomic news and intraday seasonal volatility in the cryptocurrency markets,” Applied Economics 0, 1–17 (2023).

- Hansen, Kim, and Kimbrough (2022) P. R. Hansen, C. Kim, and W. Kimbrough, “Periodicity in cryptocurrency volatility and liquidity,” Journal of Financial Econometrics (2022).

- Petukhina, Reule, and Härdle (2021) A. A. Petukhina, R. C. G. Reule, and W. K. Härdle, “Rise of the machines? Intraday high-frequency trading patterns of cryptocurrencies,” The European Journal of Finance 27, 8–30 (2021).

- Aleti and Mizrach (2021) S. Aleti and B. Mizrach, “Bitcoin spot and futures market microstructure,” Journal of Futures Markets 41, 194–225 (2021).

- Dimpfl and Peter (2021) T. Dimpfl and F. J. Peter, “Nothing but noise? Price discovery across cryptocurrency exchanges,” Journal of Financial Markets 54, 100584 (2021).

- Drożdż et al. (2001) S. Drożdż, J. Kwapień, F. Grümmer, F. Ruf, and J. Speth, “Quantifying the dynamics of financial correlations,” Physica A 299, 144–153 (2001).

- Kwapień, Drożdż, and Ioannides (2000) J. Kwapień, S. Drożdż, and A. A. Ioannides, “Temporal correlations versus noise in the correlation matrix formalism: An example of the brain auditory response,” Physical Review E 62, 5557–5564 (2000).

- Drożdż et al. (2000) S. Drożdż, F. Gümmer, A. Z. Górski, F. Ruf, and J. Speth, “Dynamics of competition between collectivity and noise in the stock market,” Physica A 287, 440–449 (2000).

- James and Menzies (2021) N. James and M. Menzies, “Efficiency of communities and financial markets during the 2020 pandemic,” Chaos 31, 083116 (2021).

- James, Menzies, and Gottwald (2022) N. James, M. Menzies, and G. A. Gottwald, “On financial market correlation structures and diversification benefits across and within equity sectors,” Physica A 604, 127682 (2022).

- Chaudhari and Crane (2020) H. Chaudhari and M. Crane, “Cross-correlation dynamics and community structures of cryptocurrencies,” Journal of Computational Science 44, 101130 (2020).

- Drożdż et al. (2020) S. Drożdż, L. Minati, P. Oświęcimka, M. Stanuszek, and M. Wątorek, “Competition of noise and collectivity in global cryptocurrency trading: Route to a self-contained market,” Chaos 30, 023122 (2020).

- James and Menzies (2022) N. James and M. Menzies, “Collective correlations, dynamics, and behavioural inconsistencies of the cryptocurrency market over time,” Nonlinear Dynamics 107, 4001–4017 (2022).

- Nguyen et al. (2022) A. P. N. Nguyen, T. T. Mai, M. Bezbradica, and M. Crane, “The cryptocurrency market in transition before and after COVID-19: An opportunity for investors?” Entropy 24 (2022).

- Gavin and Crane (2023) J. Gavin and M. Crane, “Community detection in cryptocurrencies with potential applications to portfolio diversification,” in FinTech Research and Applications: Challenges and Opportunities (World Scientific, 2023) pp. 177–202.

- James and Menzies (2023) N. James and M. Menzies, “Collective dynamics, diversification and optimal portfolio construction for cryptocurrencies,” Entropy 25 (2023).

- Kwapień, Wątorek, and Drożdż (2021) J. Kwapień, M. Wątorek, and S. Drożdż, “Cryptocurrency market consolidation in 2020-2021,” Entropy 23 (2021).

- James (2022) N. James, “Evolutionary correlation, regime switching, spectral dynamics and optimal trading strategies for cryptocurrencies and equities,” Physica D 434, 133262 (2022).

- (69) Binance, “Binance,” https://www.binance.com/.

- Wątorek, Kwapień, and Drożdż (2022) M. Wątorek, J. Kwapień, and S. Drożdż, “Multifractal cross-correlations of bitcoin and ether trading characteristics in the post-COVID-19 time,” Future Internet 14 (2022).

- Nani (2022) A. Nani, “The doge worth 88 billion dollars: A case study of Dogecoin,” Convergence 28, 1719–1736 (2022).

- Muravyev and Picard (2022) D. Muravyev and J. Picard, “Does trade clustering reduce trading costs? evidence from periodicity in algorithmic trading,” Financial Management 51, 1201–1229 (2022).

- Broussard and Nikiforov (2014) J. P. Broussard and A. Nikiforov, “Intraday periodicity in algorithmic trading,” Journal of International Financial Markets, Institutions and Money 30, 196–204 (2014).

- (74) Similarweb, “Similarweb,” https://www.similarweb.com/website/binance.com/.

- Mehta (2004) M. L. Mehta, Random Matrices (Elsevier, 2004).

- Wishart (1928) J. Wishart, “The generalised product moment distribution in samples from a normal multivariate population,” Biometrika 20A, 32–52 (1928).

- Marčenko and Pastur (1967) V. A. Marčenko and L. A. Pastur, “Distribution of eigenvalues for some sets of random matrices,” Mathematics of the USSR-Sbornik 1, 457–483 (1967).

- Gopikrishnan et al. (1999) P. Gopikrishnan, V. Plerou, L. A. Nunes Amaral, M. Meyer, and H. E. Stanley, “Scaling of the distribution of fluctuations of financial market indices,” Physical Review E 60, 5305–5316 (1999).

- Ausloos (2000) M. Ausloos, “Statistical physics in foreign exchange currency and stock markets,” Physica A 285, 48–65 (2000).

- Cont (2001) R. Cont, “Empirical properties of asset returns: stylized facts and statistical issues,” Quantitative Finance 1, 223–236 (2001).

- Jiang et al. (2019) Z.-Q. Jiang, W.-J. Xie, W.-X. Zhou, and D. Sornette, “Multifractal analysis of financial markets: a review,” Reports on Progress in Physics 82, 125901 (2019).

- Klamut et al. (2020) J. Klamut, R. Kutner, T. Gubiec, and Z. R. Struzik, “Multibranch multifractality and the phase transitions in time series of mean interevent times,” Physical Review E 101, 063303 (2020).

- Klamut and Gubiec (2021) J. Klamut and T. Gubiec, “Continuous time random walk with correlated waiting times. the crucial role of inter-trade times in volatility clustering,” Entropy 23 (2021).

- Drożdż et al. (2002) S. Drożdż, J. Kwapień, J. Speth, and M. Wójcik, “Identifying complexity by means of matrices,” Physica A 314, 355–361 (2002).

- Bouchaud (2010) J.-P. Bouchaud, “Price impact,” in Encyclopedia of Quantitative Finance (Cambridge University Press, 2010) pp. 1–6.

- Shahzad, Anas, and Bouri (2022) S. J. H. Shahzad, M. Anas, and E. Bouri, “Price explosiveness in cryptocurrencies and Elon Musk’s tweets,” Finance Research Letters 47, 102695 (2022).

- James, Menzies, and Chin (2022) N. James, M. Menzies, and K. Chin, “Economic state classification and portfolio optimisation with application to stagflationary environments,” Chaos, Solitons & Fractals 164, 112664 (2022).

- Choi and Shin (2022) S. Choi and J. Shin, “Bitcoin: An inflation hedge but not a safe haven,” Finance Research Letters 46, 102379 (2022).