High-dimensional canonical correlation analysis

Abstract.

This paper studies high-dimensional canonical correlation analysis (CCA) with an emphasis on the vectors that define canonical variables. The paper shows that when two dimensions of data grow to infinity jointly and proportionally, the classical CCA procedure for estimating those vectors fails to deliver a consistent estimate. This provides the first result on the impossibility of identification of canonical variables in the CCA procedure when all dimensions are large. As a countermeasure, the paper derives the magnitude of the estimation error, which can be used in practice to assess the precision of CCA estimates. Applications of the results to cyclical vs. non-cyclical stocks and to a limestone grassland data set are provided.

1. Introduction

1.1. Background

Canonical correlation analysis (CCA) is a classical statistical analysis method used to find a common structure between two data sets. It was first introduced in Hotelling (1936) and remains in active use today. CCA can be viewed as a generalization of principal component analysis (PCA) from one set of variables to two: in PCA the goal is to find a signal (or factor) in a large matrix with a large amount of noise, while CCA searches for a common signal among two large matrices with a large amount of noise. We refer the reader to the textbooks Thompson (1984); Gittins (1985); Anderson (2003), and Muirhead (2009) for introductions to CCA.

There are numerous applications of CCA in the social and natural sciences. In genomics CCA is used to find commonalities between multiple assays coming from the same set of individuals (see, e.g., Witten and Tibshirani (2009) and references therein). In neuroscience it is used to match brain measurements with behavioral and medical scores (e.g., Wang et al. (2020); Zhuang et al. (2020)). Similarly, in ecology CCA is used to correlate characteristics of living species with those of their habitats (e.g., Gittins (1985) and Simon (1998, Chapter 23)). In econometrics CCA is used to select the number of factors driving the behaviour of various processes (see, e.g., Breitung and Pigorsch (2013); Andreou et al. (2019), and Choi et al. (2021)). Further, in time series econometrics CCA appears in cointegration analysis: a strong correlation between first differences (which are stationary) and lags (which are nonstationary) indicates the presence of cointegration (cf. Johansen (1988)).

Beyond the cases outlined above, there are numerous settings where CCA can provide a meaningful alternative approach and complement previous methods. For example, in sociology and applied economics CCA can provide a framework for analysis of the relationships between various measures of socioeconomic characteristics and investments, on one side, and labour market outcomes and associated skills, on the other side (cf. the production function in Cunha et al. (2010) and the results of Papageorge and Thom (2020)). In finance and financial econometrics an important question, which can be addressed via CCA, is whether different types of stocks are highly correlated and, thus, can be used to create portfolios for pairs trading (e.g., one could exploit a correlation between stocks from different industries or between traditional stocks and cryptocurrencies).

One may notice that most of the above examples ideally require working with very large (across all dimensions) data sets. However, the high-dimensional machinery for CCA (in contrast to that for PCA) is still very much underdeveloped. Thus, the development of new tools and theory suitable for high-dimensional settings remains vital. In this paper we aim to provide such techniques.

1.2. High-dimensional CCA setup.

Formally, if we have two random vectors and , then the first goal of CCA is to find deterministic vectors that maximize the correlation between and , where T is the matrix transposition. That is, we are trying to find highly correlated combinations of coordinates of and . The maximal correlation value is called the largest canonical correlation, and the corresponding and form the first pair of canonical variables. Other canonical correlations (there are of them) can be found iteratively. Equivalently111Although proving it is not straightforward, the equivalence of the two procedures is a known fact in linear algebra; we also explain it in Appendix A.2., all canonical correlations can be found as the eigenvalues of matrix or as the eigenvalues of the matrix . Multiplying the corresponding eigenvectors of the former and the latter matrices, respectively, by and , we obtain all the pairs of canonical variables. We call the setup with two random vectors a population formulation.

In contrast, in the sample formulation, two vectors are replaced by two matrices (e.g., we observe samples of and samples of ). Let those samples be ( matrix) and ( matrix). The finite sample analogues of the canonical correlations, the sample canonical correlations, are computed by maximizing the sample correlations between the -dimensional vectors and . Equivalently, their squares are eigenvalues of . The canonical correlation vectors are eigenvectors of the preceding product of matrices and another similar expression. The corresponding and are called sample canonical variables.

Assume that the columns of and are i.i.d. Then, when is large while and are fixed, the sample covariances of and as well as their cross-covariances are consistent estimators of their population counterparts. Therefore, is a consistent estimate of its population analogue , and we obtain consistent estimates of the squared correlation coefficients and corresponding vectors. The exact distribution of the sample canonical correlations and variables and their asymptotic behavior in the fixed and regime have attracted the attention of many researchers, with the seminal results going back to Hsu (1939, 1941) and Constantine (1963) and the latest corrections to the results on canonical variables being much more recent (see Anderson (1999)).

The properties of CCA when all three dimensions are large and comparable have not yet been properly analyzed. The remarkable seminal result in this direction is that of Wachter (1980), who studies the case when and are uncorrelated and columns and are independent samples of and , respectively. Wachter (1980)222See also Bouchaud et al. (2007) for an independent rediscovery of this result. shows that despite and being independent, the empirical distribution of the sample canonical correlations has a nontrivial limit as with , ; in particular, the majority of the correlations are bounded away from . The conceptual conclusion is that in the large setting the sample canonical correlations do not deliver consistent estimates of the population canonical correlations, which in this case all equal zero due to and being independent. These results have been extended very recently in Bao et al. (2019) and Yang (2022b) to the case when some (but finitely many as the dimensions grow) population correlations are allowed to be nonzero. Conceptually similar results are obtained: the sample squared canonical correlations are always larger and bounded away from their population counterparts. However, there is an explicit dependence between the sample and population canonical correlations, and therefore, knowing the former allows one to reconstruct the latter. Hence, it is possible to identify nontrivial population canonical correlations.

No progress has been achieved so far to tackle the challenging properties of the corresponding vectors of canonical variables in the regime in which are large and proportional to each other. In practice squared correlation coefficients can be used to test whether there is a common signal between two data sets (i.e., the largest coefficient is statistically larger than zero). However, vectors are required to be able to say something about the nature of this commonality: where it comes from, what it represents, etc. The asymptotic analysis of these vectors is the central topic of the present paper.

To address the problem of estimating CCA vectors, we first assume that and are Gaussian and independent across samples of and but allow to be correlated with . We start with and having exactly one nonzero canonical correlation and refer to it as the signal, while the remaining uncorrelated parts of and are viewed as the noise. We characterize (in terms of the parameters and the covariances between coordinates of and ) when we can detect a nonzero canonical correlation, i.e., when there is enough signal in the data compared to the pure noise case. Next, we develop formulas for sample and , which allow us to show that, for finite ratios , one cannot consistently estimate true values and . The estimated canonical variables and will always lie on cones around the true population canonical variables and . We provide explicit formulas for the width of these cones. They show that the cones shrink as we increase the ratios and that ultimately consistency is restored in the limit.

Next, we provide various generalizations from the i.i.d. Gaussian setting with one signal. First, motivated by the fact that often data are far from normal (especially in financial applications), we relax our assumptions to accommodate any distribution as long as its first four moments match the Gaussian moments. Second, we allow for correlated realizations. We do this separately333 Our generalizations do not allow a simultaneously correlated structure for the signal and the noise parts. Because of this restriction, we cannot yet tackle an important cointegration setting mentioned earlier. The no-signal (or no-cointegration) situation for this setting has been analyzed recently in Onatski and Wang (2018, 2019) and Bykhovskaya and Gorin (2022a, b), and while we hope that the methods in this article will eventually help advance understanding of the situation with finitely many signals (or finitely many cointegrating relations), we do not address this question here. for signal parts (i.e., the signal is not independent across ) and for the noise part (i.e., the noise is not independent across ). Finally, we extend the machinery to allow for multiple vectors and , i.e., multiple nonzero canonical correlations in the population setting. In other words, we allow the signal to be of any finite rank, and the vectors and are replaced by matrices.

1.3. Other related literature

CCA is closely connected to the literature on factors. First, as mentioned above, some methods for factor estimation rely on CCA. The idea is that the correlation between different sets of variables, which is captured by CCA, can be fundamentally related to the presence and properties of factors. For instance, one can distinguish between common and group-specific factors (see, e.g., Andreou et al. (2019) and Choi et al. (2021)).

Another point of view on the interconnection between factors and CCA comes from the interpretation of canonical variables as common explanatory factors between two data sets. The main difference is that factors operate with a single matrix/data set while canonical correlations require two matrices/data sets. The main approach for finding factors is via PCA and its modifications (cf. Bai and Ng (2008); Stock and Watson (2011); Fan et al. (2016) and references therein). There are many similarities in the spirit of the modeling and results between CCA and PCA. However, CCA as considered in our present paper is much more challenging and involved than PCA. This is perhaps an inherent feature of the CCA procedure, which involves matrix inversion, a much more complicated operation to carry out than simply calculating a product.444The reader is invited to compare the difficulty of the answers in our Theorem 3.4 with that of the parallel Theorems 2.9 and 2.10 in Benaych-Georges and Nadakuditi (2012) for the PCA setting.

In statistics and probability factors (signals in the data) are often modeled as a spiked random matrix.555This terminology goes back to Johnstone (2001). A spiked random matrix is a sum of a full-rank noise matrix and a small-rank signal matrix. Often this is embedded in the PCA setting: one observes a matrix , where is treated as a low-rank signal and is treated as noise, and tries to reconstruct from observing through its singular values and vectors. , , and here are rectangular matrices with both dimensions assumed to be large. In econometrics represents a product of factors and their loadings, while is composed of idiosyncratic errors.

For such a setting, Baik et al. (2005) and Baik and Silverstein (2006) discovered the phenomenon now known as the BBP phase transition: when the signal is small while the noise is given by a matrix with i.i.d. mean zero elements, one cannot detect the presence of the signal from singular values of , while for a large signal, the largest singular values of connect to those of through explicit formulas. The corresponding singular vectors can be used as an estimate of ; however, this estimate is inconsistent, in parallel to what we observe in the CCA setting (see Johnstone and Lu (2009); Paul (2007); Nadler (2008) and references therein for earlier work in the learning theory literature in physics). If we extend the parallel, consistency in the PCA setting can be partially restored if we allow one of the dimensions of the rectangular matrix of interest to be much larger than another. In the econometrics literature, the same transition appears in the framework of weakly influential factors (see Onatski (2012) and references therein); when factors become strong, estimation consistency is restored.

Even closer to our setting is that in Gavish et al. (2022), which deals with spiked –matrices (and also contains many other references). An –matrix, which comes from the –test, deals with the ratio of two large matrices. In the benchmark situation of no spikes (or no signal) there is a way to directly match an –matrix with random matrices appearing in CCA. However, this connection disappears as soon as signals in the data are present.

1.4. Outline of the paper.

The remainder of the paper is organised as follows. Section 2 discusses the basic setting of i.i.d. normal vectors. Various generalizations (to the cases with nonnormal errors, correlated observations, and multiple signals) are presented in Section 3. Section 4 provides two empirical illustrations of our results. Finally, Section 5 concludes. Proofs and additional data details are given in appendices.

2. Basic framework

2.1. Population setting

Let and be - and - dimensional random vectors with zero means and nondegenerate covariance matrices, where here and below denotes matrix transposition. Without loss of generality, we assume .

Assumption I.

The vectors and satisfy the following:

-

(1)

The vectors and are jointly Gaussian with zero means.

-

(2)

There exist nonzero deterministic vectors such that

-

(a)

For any , if and are uncorrelated, then and are also uncorrelated;

-

(b)

For any , if and are uncorrelated, then and are also uncorrelated.

-

(a)

The pair represents the signal in the data, while the remaining part is treated as the noise, which is uncorrelated with the signal. Ultimately, we are interested in the signal and would like to filter out the influence of the noise.

Example 2.1.

Assumption I is satisfied with if is a mean zero Gaussian vector such that, for each , the coordinate is uncorrelated with and with and, for each , the coordinate is uncorrelated with and with . In other words, the only possible nonzero correlations are between and , between and , , and between and , . These correlations can be arbitrary.

Any other example can be obtained from the preceding by a change of basis.

Definition 2.2.

Let , , and be the squared correlation coefficient:

The number and the vectors and of Assumption I can be read from the covariance structure of and , as the following lemma666In the setting of Example 2.1, the statement of Lemma 2.3 is straightforward. The general situation is reduced to this example by a change of basis. explains.

Lemma 2.3.

The number equals the single nonzero eigenvalue of the matrix and the single nonzero eigenvalue of the matrix . and are the corresponding eigenvectors of the former and the latter matrices, respectively.

2.2. Sample setting

Let be a matrix composed of independent samples of . The matrix represents observed data, which comes from the population setting 2.1. We are interested in finding the signal or vectors . In the sample setting they come from the squared sample canonical correlations and their corresponding vectors. The vectors for the largest correlation represent the sample analogues of and . The following definition is motivated as a sample version of Lemma 2.3.

Definition 2.4.

The squared sample canonical correlations are defined as eigenvalues of the matrix or as the largest777We recall that . eigenvalues of the matrix . We set to be the eigenvector of the former matrix, corresponding to its largest eigenvalue, and we set to be the eigenvector of the latter matrix, corresponding to its largest eigenvalue.

The sample canonical variables are defined as and . We also set and .

2.3. Results

In the sample setting of Section 2.2, we are going to assume that , , and . We define five constants depending on these parameters:

| (1) | ||||

| (2) | ||||

| (3) | ||||

| (4) |

Theorem 2.5.

Suppose that Assumption I holds, that the columns of the data matrix are i.i.d., and that the squared sample canonical correlations and variables are constructed as in Section 2.2. Let tend to infinity and depend on it in such a way that the ratios and converge888To match the notations of Bao et al. (2019), we should set and . Bao et al. (2019) contains an earlier proof of (5) by another method; the part in (6) and (7) is new. to and , respectively, and . Simultaneously, suppose that .

-

1.

If , then , and for the two largest squared sample canonical correlations , we have

(5) The squared sine of the angle between and defined as satisfies

(6) The squared sine of the angle between and satisfies

(7) -

2.

If instead , then

(8)

Remark 2.6.

While we do not prove it in this text, we expect (based on the related results in Benaych-Georges and Nadakuditi (2011, 2012) and Bloemendal et al. (2016)) that in the case with strict inequality the angles and tend to as , with distance to of order (see Figure 2 for an illustration). Intuitively, it suggests that there is no way to recover asymptotic information on or in this case999See additional discussion of what can be recovered for the cases analogous to in similar contexts in Onatski et al. (2013) and Johnstone and Onatski (2020)..

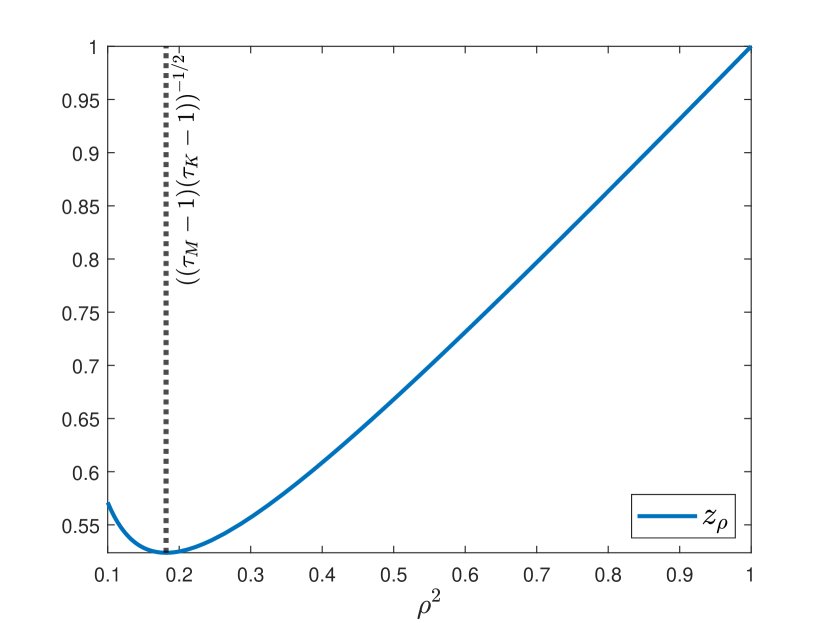

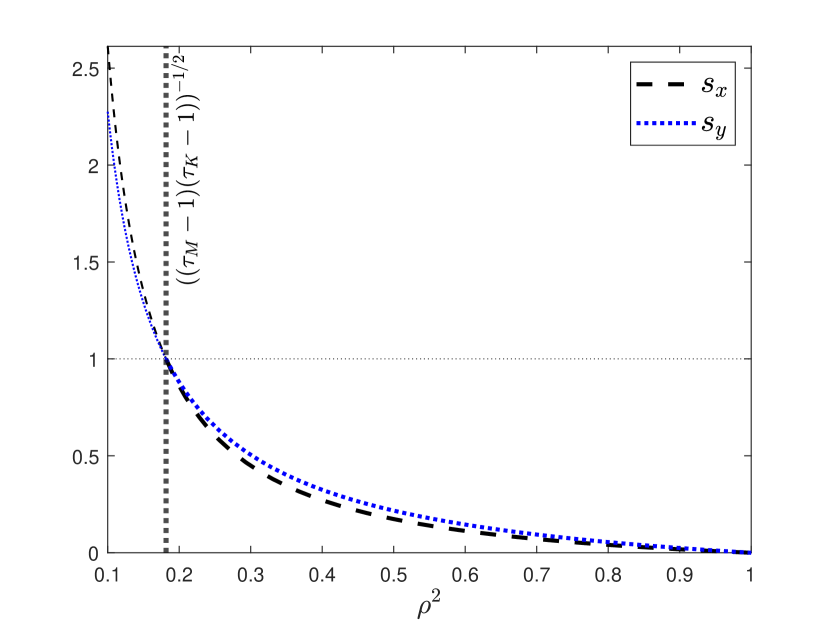

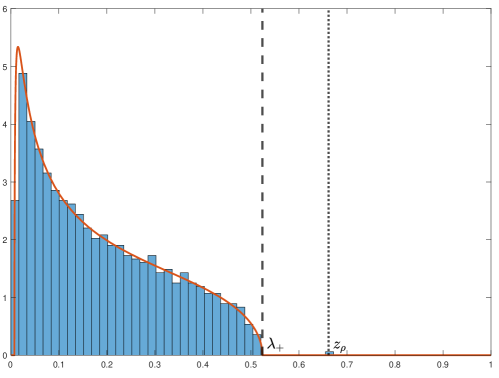

Figure 1 illustrates the dependence of on the squared correlation coefficient . Notice that as a function of has a minimum at the cutoff and is monotone increasing above the cutoff. The values of and are between and for above the same cutoff. These properties continue to hold for general values of .

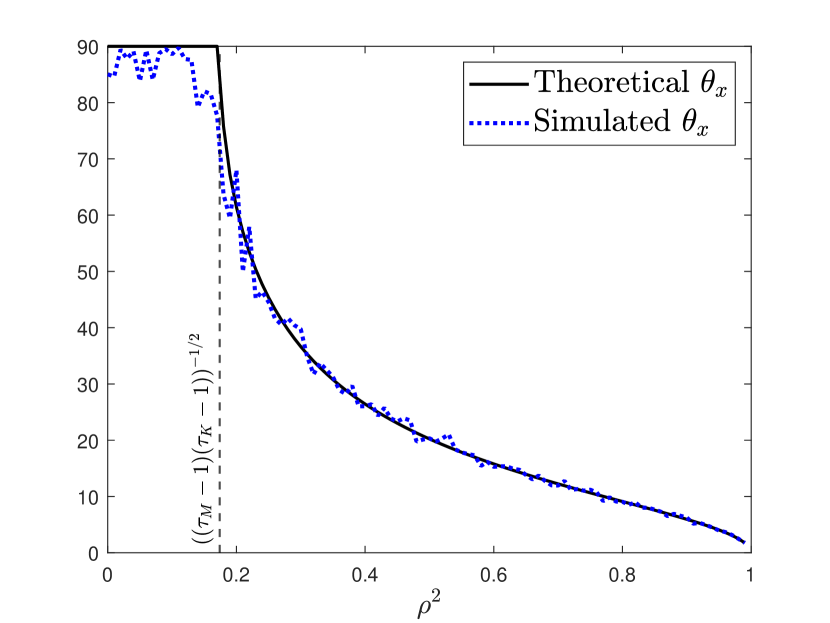

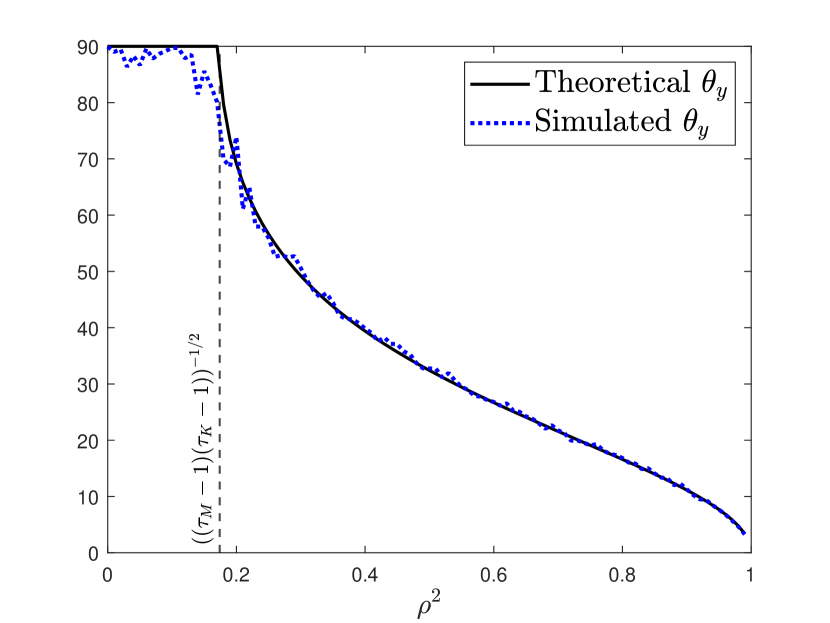

Figure 2 shows results from a single simulation (for each fixed value , we run one simulation) vs. theoretical predictions. As we can see, the simulated path is very close to the theoretical one, with largest discrepancy around the cutoff .

theoretical and simulated angles.

theoretical and simulated angles.

2.4. Implications of Theorem 2.5

There are several aspects of Theorem 2.5 worth emphasizing. First, in practice, when one is working with real data, the true value of is unknown, and the results of Theorem 2.5 should be applied in the following way.

Given that the model matches the data, by Wachter (1980) and Johnstone (2008), most of the squared canonical correlations should belong to the interval101010Wachter (1980) shows that the empirical distribution of the squared canonical correlations converges as to the Wachter distribution of density , see Appendix B.2.. If there is a gap between the largest canonical correlation and , as in Figure 3, then in line with Eq. (5), one can take as an approximation of . Treating as known and approximating , with , , Eq. (2) becomes a quadratic equation in . Solving it (using to choose the correct root out of the two), we obtain an estimate for , and further plugging into (3) and (4) and using (6) and (7), we obtain an estimate for the angle between and or between and . If several canonical correlations larger than are observed, then one needs to use an extension of Theorem 2.5 provided in Theorem 3.7: for each of these canonical correlations one can use exactly the same procedure as just outlined.

The second essential aspect of Theorem 2.5 is the choice of the angles (between and ) and (between and ) as the measure of the quality of approximations of and for and , respectively. In principle, one could have concentrated on the angle between and (or and ) instead. However, those angles depend on the choice of units of measurement: the angle changes if we multiply one of the coordinates of by a constant (equivalently, divide a component of or a row in by the same constant). Hence, asymptotic theory for these angles would require some normalization conditions on the coordinates of (and, in fact, correlations between different components of would also become important), but such natural normalizations are rare in real data because different coordinates of might be coming from very different sources or types of observations. By concentrating on and , we avoid this problem entirely, and in particular, the result in Theorem 2.5 does not depend on the covariance matrix of the vector (and similarly on the covariance matrix of the vector ), which can be arbitrary, as long as it satisfies Assumption I.

Finally, the angles , and the limiting value for the largest squared canonical correlation depend on , , and in a nontrivial fashion, leading to important features of the formulas (2), (3), and (4):

-

•

For any values of , with and , we always have and , (see Figure 1). In other words, the largest sample canonical correlation overestimates the true largest correlation , while the estimates for the canonical variables are never consistent but rather inclined by nonvanishing angles toward the desired true directions (see Figure 4).

-

•

If , with and , then the asymptotic value of the largest canonical correlation, , is again larger than . While we do not prove it in this text, we expect that the asymptotic values of and are close to in this situation, i.e., that the estimates for the canonical variables are almost orthogonal to the desired true directions (cf. the simulated curves in Figure 2).

-

•

If both and become large while is fixed, then the condition becomes trivially true, and . Therefore, , , and become consistent estimates of , and , respectively.

-

•

If becomes large while and remain fixed (this means that and are of the same magnitude but is much smaller), then remains larger than , and remains positive. However, tends to , which means that becomes a consistent estimate of .

3. General framework

In the previous section we presented our main theorem in the basic setting of i.i.d. Gaussian data with a single nonzero canonical correlation in the population. The results are the most transparent in this case, yet many important generalizations can be derived. In this section we state four such generalizations by

-

(1)

Relaxing Gaussianity Assumption I.(1);

-

(2)

Allowing for signals and that are correlated along dimension ;

-

(3)

Allowing for noise (orthogonal to and ) that is correlated along dimension at the expense of more complicated formulas governing the answers in an extension of Theorem 2.5; and

-

(4)

Allowing for multiple signals.

3.1. Non-Gaussian data

Definition 3.1.

We say that a mean zero random vector is fourth-moment Gaussian if there exists a jointly Gaussian mean zero vector such that the covariance matrix and the joint fourth moments of match those of .

Definition 3.1 is equivalent to requiring the fourth joint moments of to satisfy the Wick rule: for any , we should have

| (9) |

For , (9) reduces to a single condition . For , there are five conditions: , , , , and .

We now present a relaxation of Assumption I on the random vectors and .

Assumption II.

There exists a deterministic vector and a deterministic matrix of rank ; and a deterministic vector and a deterministic matrix of rank such that

-

(1)

The random variables and are jointly fourth-moment Gaussian with mean zero, as in Definition 3.1 with .

-

(2)

There exists a –dimensional vector where has coordinates and has coordinates , for which

-

•

All components are jointly independent with each other and with both and .

-

•

, , , and , , .

-

•

For constants and , and .

-

•

and .

-

•

Assumption II splits the vectors and into two components: the correlated signal part and the remaining noise part . The coordinates of the latter are independent but not necessarily identically distributed. Assumptions I and II coincide in the case of Gaussian and .

Theorem 3.2.

| Angles (in degrees) | ||

|---|---|---|

| Theoretical | Simulation | |

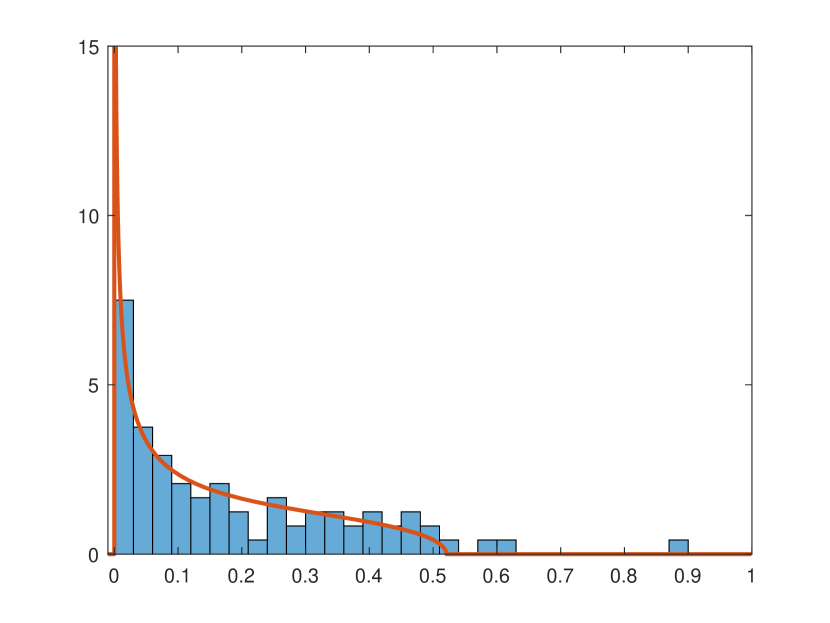

The implications of Theorem 3.2 are the same as those discussed in Section 2.4. Thus, practical implementations remain the same. One can possibly relax or come up with alternatives to our moment conditions in Assumption II (see Yang (2022b) for one possible approach). As shown in Figure 5, uniform errors , whose fourth moment does not coincide with the fourth moment of a Gaussian distribution, still lead to the same results111111Note, however, that in the regime with fixed and , Muirhead and Waternaux (1980) show that some of the asymptotic distributions are sensitive to the fourth moments. as in Theorem 3.2.

3.2. Correlated signal

For the next generalization we need to adjust the procedure of Section 2.2 and no longer assume that the data are obtained from i.i.d. samples of and vectors.

We still use Definition 2.4: we are given a matrix and matrix , and we compute their sample canonical correlations and corresponding variables. What changes is the probabilistic mechanism creating these matrices: while in Section 2 we started from vectors and and then considered i.i.d. samples of them, now we weaken the i.i.d. assumption and therefore have to introduce assumptions directly on the distributions of and rather than on and . Despite the more complicated probabilistic setting, the final interpretation remains the same: the signal part of the data comes from two deterministic vectors and , and we are trying to reconstruct them using and of Definition 2.4.

Hence, our assumptions are now phrased in terms of and matrices and , respectively.

Assumption III.

There exists a deterministic vector and a deterministic matrix of rank , and a deterministic vector and a deterministic matrix of rank , such that the matrix elements of the matrices and are i.i.d. random variables independent from and .

Note that there are no restrictions on and in Assumption III. In particular, they are allowed to have correlated or even deterministic coordinates. In the setting of Assumption III, we replace the squared correlation coefficient of Definition 2.4 with its sample version:

| (10) |

As before, we treat vectors and as the signal part of the data and the rest as the noise. Note that if and have i.i.d. Gaussian components, then Assumption III coincides with Assumption I.121212The statements of the second parts of Assumptions I and III differ only by a linear transformation of the noise part. In this situation differs from from Definition 2.4, but their difference tends to as by the law of large numbers.

Theorem 3.3.

Suppose that the squared sample canonical correlations and variables are constructed as in Definition 2.4 with data matrices and satisfying Assumption III. Let tend to infinity and depend on it in such a way that the ratios and converge to and , respectively, and . Simultaneously, suppose that . Then, the conclusions of Theorem 2.5 continue to hold.

The practical implementation of the procedure discussed at the beginning of Section 2.4 continues to hold in the setting of Theorem 3.3. Theorem 3.3 uses the Gaussianity of the noise part of the data, and . While it is plausible that this restriction can be relaxed, we do not address such a question in this paper.

3.3. Correlated noise

In the next extension we relax the assumption that the noise has independent coordinates. This complements the correlated signal of Section 3.2. The results for the correlated noise depend on the knowledge of the canonical correlations of the noise itself, and the formulas become much more complicated than in Theorems 2.5, 3.2, and 3.3. Nevertheless, one can still efficiently use them when working with the data. Our assumptions are again phrased in terms of and matrices and , respectively.

Assumption IV.

There exists a deterministic vector and a deterministic matrix of rank , and a deterministic vector and a deterministic matrix of rank , such that:

-

(1)

We set and and assume that is matrix with i.i.d. rows.131313As the proof of Theorem 3.4 reveals, it is also sufficient to require only that the rows are uncorrelated if we additionally assume that the joint distribution of all matrix elements is fourth-moment Gaussian. Each row is a mean zero fourth-moment Gaussian (as in Definition 3.1) two-dimensional vector with covariance matrix .

-

(2)

The matrices and are assumed to be independent with and .

In the setting of Assumption IV, we set . The matrices and in the assumption might depend on each other and might be deterministic. These are and matrices, respectively, and we denote through their sample squared canonical correlations, which are eigenvalues of the matrix .

Theorem 3.4.

Suppose that the squared sample canonical correlations are constructed as in Definition 2.4 with data matrices and satisfying Assumption IV. Let be one of the squared sample canonical correlations141414It does not have to be the largest one. and , be the corresponding canonical variables. Let tend to infinity and depend on it in such a way that and converge to and , respectively, and . In addition, fix , and let

| (11) |

Then, as , any canonical correlation that is at a distance of at least from all satisfies the following relation151515In these formulas is a remainder, which tends to as with fixed , and ., and any solving this relation (and a distance of at least away from ) is a canonical correlation:

| (12) |

Let us further denote

| (13) |

let be the squared cosine of the angle between and defined as , and let be the squared cosine of the angle between and . Then we have

| (14) |

| (15) |

The main application of Theorem 3.4 is for when we deal with the largest canonical correlation . If the observed and are at distance of at least apart (which is true, for instance, if ; see the inequalities in Lemma A.6 for a justification), then we can use the formulas (14)–(15) to assess the quality of the estimation of canonical variables.

The formulas in Theorem 3.4 depend on the unknown function . There are two ways to avoid this difficulty. First, by imposing additional assumptions on the noise, one can deduce exact asymptotic formulas for —this is how we deduce Theorems 2.5 and 3.2 from Theorem 3.4. In those theorems approximates the Stieltjes transform of the Wachter distribution, with the density shown by orange curves in Figures 3 and 5(a), as well as in Figures 6(a) and 7(a) appearing later.

Alternatively, one can reuse the observed squared canonical correlations through the following approximation statement, which is a direct corollary of Lemma A.6 from the appendix.

Lemma 3.5.

Take , and let and be and matrices, respectively. In addition, fix matrix and matrix . Let be the squared sample canonical correlations between and ; let be the squared sample canonical correlations between and . For each , we have

| (16) |

where the convergence is uniform over the choices of , , , , , and , and over complex bounded away from the segment .

Theorem 3.4 and Lemma 3.5 lead to the following practical algorithm: compute the sample squared canonical correlations between and , and check whether there is a significant gap between and the rest (cf. Figure 3). If so, then applying Lemma 3.5 with , we can use to approximate and then rely on (12), (14), and (15) to estimate , , and .

3.4. Multiple signals

The four theorems—2.5, 3.2, 3.3, and 3.4— assumed that there is a unique signal in the part of the data and a unique signal in the part of the data. All the theorems have extensions to the situation of several signals. In the extended statements exactly the same procedures are used for each signal.

We start from the basic setup of Section 2.2. The population setting of Assumption I says that there is exactly one nonzero canonical correlation161616In the population setting, squared canonical correlations can be computed as eigenvalues of the matrix . between and , and it corresponds to the canonical variables and . Instead, assume that there are nonzero canonical correlations:

Assumption V.

The vectors and satisfy the following:

-

(1)

The vectors and are jointly Gaussian with mean zero.

-

(2)

There exist nonzero deterministic vectors and nonzero deterministic vectors such that

-

(a)

for each .171717Any vectors , can be linearly transformed to satisfy this condition (cf. Lemma A.2).

-

(b)

Let denote the squared correlation coefficient between and , as in Definition 2.2. We assume that these numbers are all distinct.

-

(c)

For any , if is uncorrelated with all , , then and are also uncorrelated;

-

(d)

For any , if is uncorrelated with all , , then and are also uncorrelated.

-

(a)

Example 3.6.

Assumption I is satisfied with being the th coordinate vector in and being the th coordinate vector in , , if is a mean zero Gaussian vector such that the only possible nonzero correlations are between and for , between and for , and between and for . Additionally, assume that the squared correlation coefficients between and , , are all distinct.

Any other example can be obtained from the preceding by a change of basis.

As in Section 2.2, we let be a matrix composed of independent samples of . The squared sample canonical correlations are the eigenvalues of the matrix or largest eigenvalues of the matrix . Choosing one eigenvalue , we set to be the corresponding eigenvector of the former matrix, and we set to be the eigenvector of the latter matrix, corresponding to the same eigenvalue. The sample canonical variables are defined as and . We also set and , where is chosen so that is the -th largest elements of .

Theorem 3.7.

Suppose that Assumption V holds and the columns of the data matrix are i.i.d. Let and tend to infinity in such a way that the ratios and converge to and , respectively, and . Suppose also that , , with the numbers all being distinct. Then, for each , we have

- I.

-

II.

If the -th largest number from is at most , then

Finally,

Remark 3.8.

| Angles (in degrees) | ||

|---|---|---|

| Theoretical | Simulation | |

Figure 6 illustrates Theorem 3.7: there are three signals of different strength indicated by the three separate right-most eigenvalues. The corresponding angles increase when the strength of the signal goes down (smaller ), as can be seen from Table 6(b). Note also that the theoretical formulas are close to what one obtains in the simulations.

Theorem 3.7 helps one find the number of signals when it is unknown. The eigenvalues to the right of represent signals, and thus, one can visually deduce181818We expect that it should be possible to construct a formal test of the number of signals; in the setting of factors a parallel question has generated considerable interest and results (see, e.g., Bai and Ng (2002, 2007); Hallin and Liska (2007); Onatski (2009); Ahn and Horenstein (2013)). how many there are by looking at a histogram (e.g, one clearly sees three signals in Figure 6). In practice we do not know the values of a priori. Instead, we should look at the squared sample canonical correlations : if several of the largest ones are well separated from and from each other, then we can use Theorem 3.7, reconstruct the corresponding and deduce the values for the angles and .

The requirement that all are distinct is not simply a technical artifact. Indeed, if two canonical correlations coincide, then the corresponding canonical variables are no longer well defined because any linear combination of two eigenvectors with the same eigenvalue is again an eigenvector with the same eigenvalue.

Theorems 3.2, 3.3, and 3.4 have very similar extensions to the case of nontrivial canonical correlations. The extension of Theorem 3.2 is exactly the same: the data are allowed to be fourth-moment Gaussian rather than Gaussian. In the extension of Theorem 3.3 we have vectors , , , which represent “true” canonical variables (and therefore , are pairwise orthogonal except for the allowed correlation when , which should result in distinct correlation coefficients as we vary ). In the extension of Theorem 3.4, we have random vectors , , , with i.i.d. components, which represent the canonical variables in the population, and the corresponding canonical correlations should be all distinct. In each extension, the final statement is as in Theorem 3.7: the relations for each are exactly the same as for the situation, and we omit further details.

4. Empirical illustrations

In this section we provide an empirical implementation of our approach in two data sets. The first example provides insights into the behavior of the stock market and analyzes the relationship between cyclical and non-cyclical (defensive) stocks. The second example complements Bao et al. (2019) in analyzing a limestone grassland data set.

4.1. Cyclical vs. non-cyclical stocks

How to model and explain stock returns has always been an important question in finance and financial econometrics. There are many different approaches and techniques, including asset pricing models, volatility models, and dimension-reduction factor models. This section adds CCA to the list and shows how this method can be used to analyze stock returns. We rely on the fact that CCA requires two corpuses of data and concentrate on consumer cyclical and non-cyclical (consumer defensive) stocks. The former are known to follow the state of the economy, while the latter are not related to business cycles and are useful during economic slowdowns. Knowing their correlations can be helpful for portfolio allocation.

| Angle (in degrees) | Sine squared | ||||

|---|---|---|---|---|---|

| st signal | |||||

| nd signal | |||||

| rd signal |

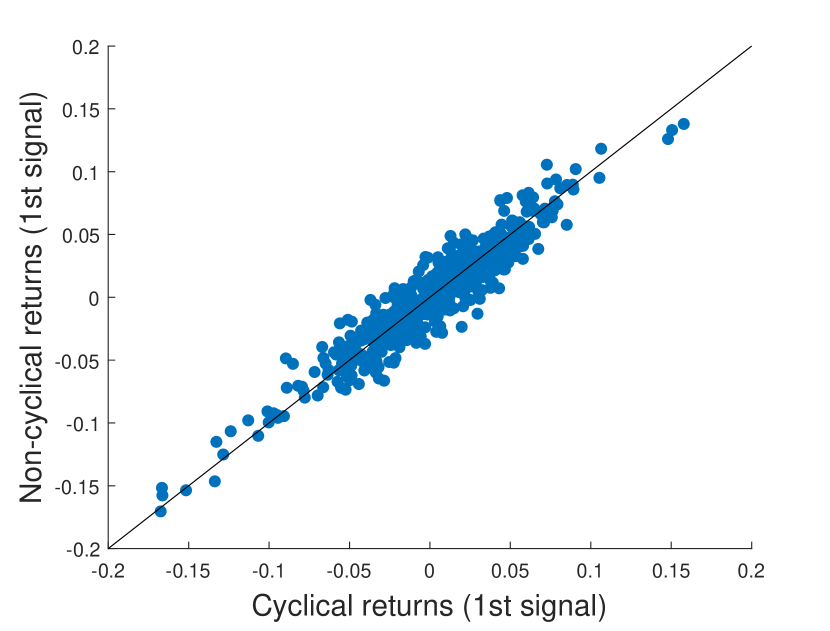

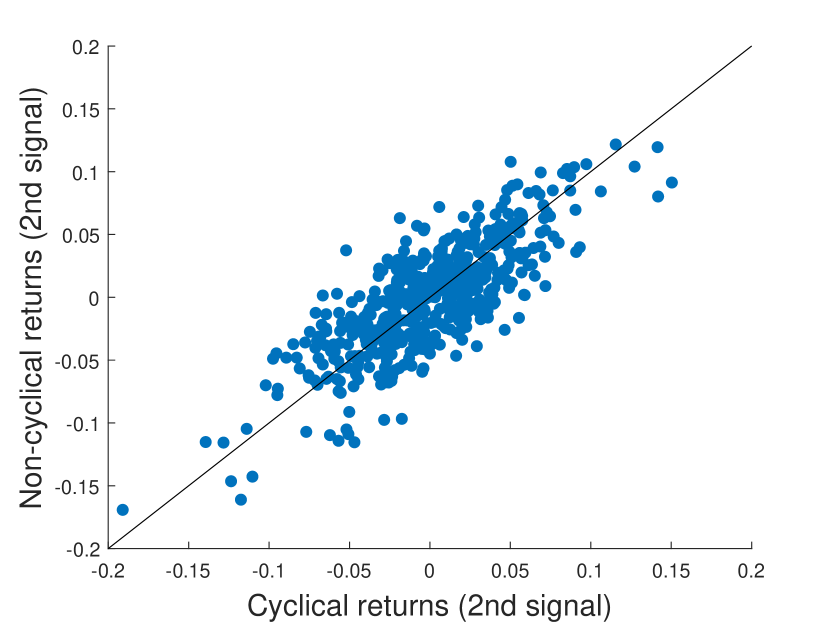

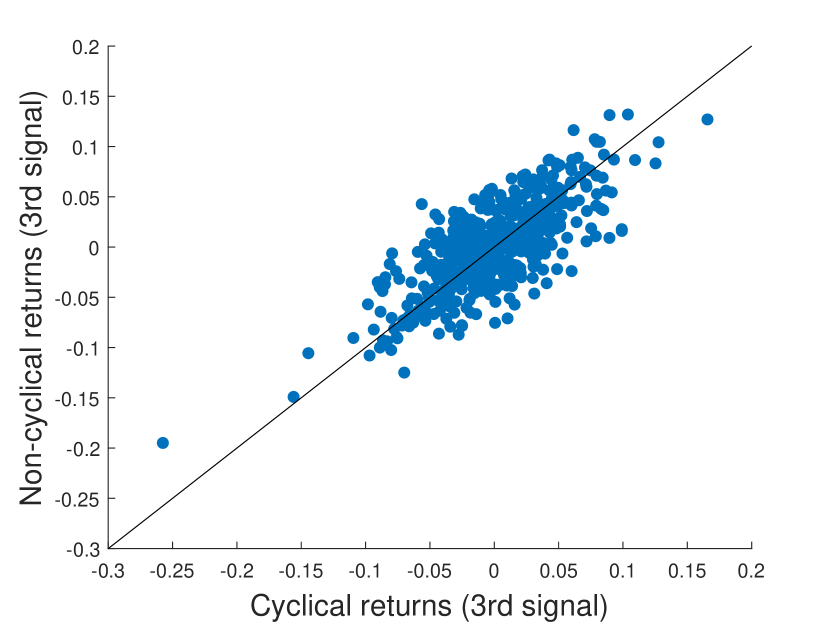

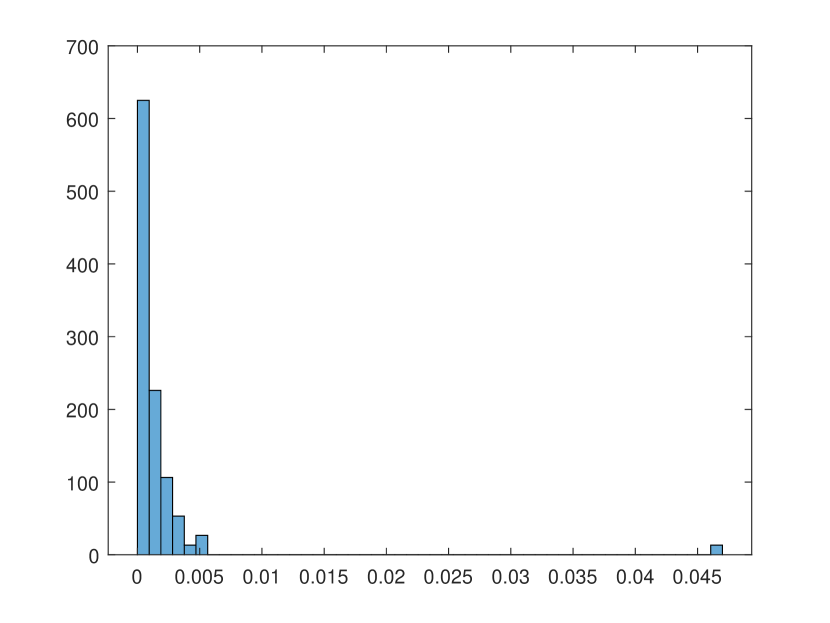

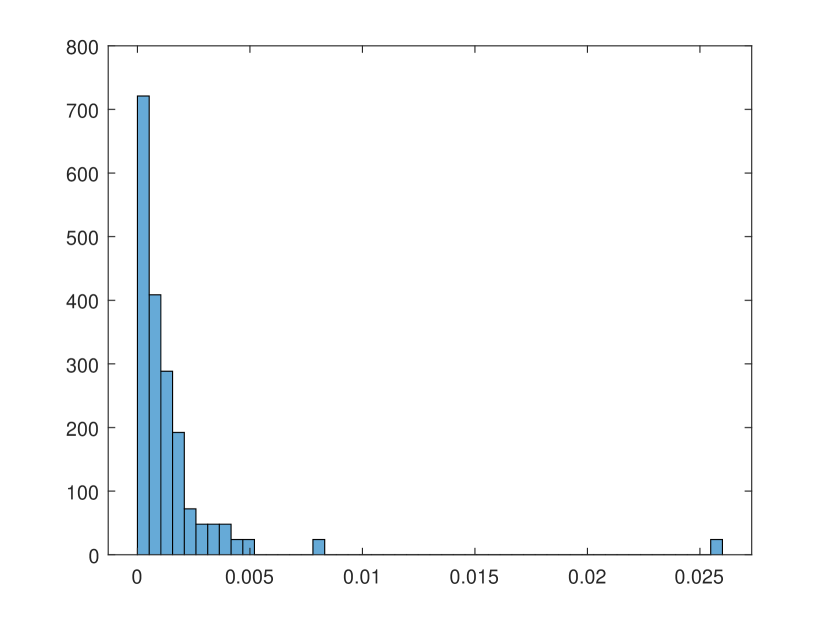

We use weekly returns (which are widely believed to be uncorrelated across time) for the largest cyclical and largest non-cyclical stocks over ten years (), which gives us observations across time. The time window is chosen to exclude the financial crisis and COVID-19 periods. The exact list of stocks is reported in Appendix C. Figure 7(a) shows the squared sample canonical correlations between the returns of the two groups of stocks. We can see that the overall shape of the histogram of the correlations matches the Wachter distribution (as discussed in Section 2.4, this indicates that the data matches our modelling assumptions and we can use the formulas of Theorem 3.7) and, at the same time, that the three largest correlations are clearly separated from the rest. The largest squared sample canonical correlation, which is close to , represents a very strong signal, which can be interpreted as an overall market movement. In favor of this interpretation is also the fact that the majority of the coordinates in the corresponding pair of eigenvectors191919We do not report the eigenvectors for the sake of space. are positive. For the cyclicals, the sum of squares of the positive coordinates is out of , and for the noncyclicals, it is out of . Two other correlations represent medium-strength signals. The presence of exactly three signals is interesting for several reasons. First, it is resonant of the three factors of Fama and French (1992). Second, it is in noticeable contrast to the results of a principal component analysis (PCA) applied to the same stock returns. PCA often shows few or even only one clearly distinct factor for a large group of stocks; see, e.g., Potters and Bouchaud (2020, 20.4.2 A One-Factor Model). For our two groups of stocks, PCA indicates the presence of at most two factors—fewer than what we detect with CCA. Figure 10 in Appendix C shows the PCA eigenvalues, i.e., eigenvalues of and , where and are the de-meaned cyclical and non-cyclical returns, respectively. We can see that the cyclicals have only one strong factor while the non-cyclicals have two. As with CCA, the largest eigenvalue in PCA is believed to be market related. In our stock returns data set, the largest factors are highly correlated across the two groups (the correlation is ) and with their CCA counterparts (the first pair of canonical variables). The two other CCA pairs of canonical variables are capturing additional information (cf. the size and value factors in Fama and French (1992)) not reflected by PCA. Based on the above, we observe that CCA picks up more information than PCA by extracting additional relevant factors.

The exact values of the CCA signals are reported in Table 7(b). The correlations and angles in Table 7(b) are calculated based on the results of Theorem 3.7. Since we have , the angles are the same for the cyclicals and non-cyclicals, and we report only one angle per signal. In line with the strength of the signals, the angle between the first estimated signal and the unobserved truth is the smallest, showing precise estimation. The two other signals are weaker, leading to larger angles, i.e., large estimation error. This observation is reinforced by Figure 8, which shows a scatter plot of the cyclical vs. non-cyclical canonical variables. The points in Figure 8(a) show the tightest fit to the -degree line, demonstrating a very strong correlation, while those in Figures 8(b) and 8(c) are more spread out. The tightness in Figures 8(b) and 8(c) is approximately the same, in line with the second- and third-largest eigenvalues being very close.

4.2. The limestone grassland community data

| Eigenvector | Angle | Sine | |

|---|---|---|---|

| (in degrees) | squared | ||

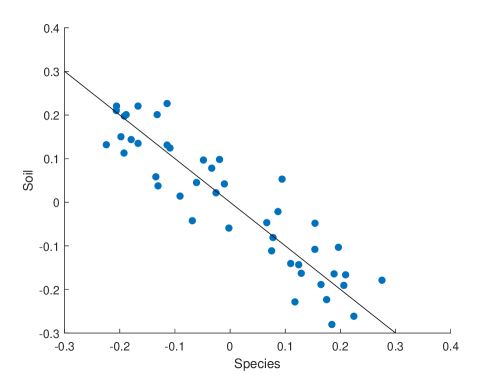

One of the classic data sets examined by CCA is the limestone grassland community data from Anglesey, North Wales (Gittins (1985)); for instance, these data were discussed recently in Bao et al. (2019). The goal of the CCA application in this case is to identify the relationship between several soil properties and the representation of plant species. There are species considered—Helictotrichon pubescens, Trifolium pratense, Poterium sanguisorba, Phleum bertolonii, Rhytidiadelphus squarrosus, Hieracium pilosella, Briza media, and Thymus drucei—and soil characteristics—depth (), extractable phosphate (), exchangeable potassium (), and cross-product terms between all three soil variables (). The number of random samples is .202020Although the dimensions seem small, Monte Carlo simulations (not shown) indicate that Theorem 2.5 gives a good approximation for these values: the theoretical and simulated angles are close to each other. To analyze the data, we first de-mean all the variables (the means are calculated across -space). After that we find that the six nonzero squared canonical correlations are , and we have , which indicates the presence of a rank signal. This signal has estimated strength or . As can be seen from Table 1, the estimation precision is quite high; i.e., angles and are small (the angles are obtained via Theorem 2.5). The estimated vectors and suggest that most of the correlation comes from the first coordinate of (Helictotrichon pubescens) and the third coordinate of (potassium). That is, more potassium in the soil is strongly correlated with the presence of Helictotrichon pubescens. Figure 9 shows a scatter plot of . As we can see, the data points lie close to the -degree line, which indicates a correlation close to .

5. Conclusion

High-dimensional econometrics and statistics have been playing an increasingly prominent role in the analysis of data in social sciences (see, e.g., Fan et al. (2011)). One popular methods for dealing with two large data sets is canonical correlation analysis (CCA). However, little is known about the performance of CCA in the high-dimensional setting where all dimensions of data are large and comparable. This paper provides one of the first results on the precision of CCA in high dimensions. To be more precise, we show that estimation of canonical vectors is inconsistent and compute the exact degree of inconsistency in terms of angles between the true and estimated canonical variables. Consistency can be restored as one of the dimensions becomes much larger than the others.

There are various directions for future research on high-dimensional CCA. The first important generalization is to allow for full correlation across in the data, i.e., for a setting where both the signal and the noise are dependent across the dimension. This extension will make the results useful for a typical time series setting, where the coordinate represents time. One would hope that for stationary time series results in line with Theorem 3.4 continue to hold. An interesting application would be to then use the procedure on the FRED-MD macro time series data set (McCracken and Ng (2016)) and look for canonical correlations between real and nominal variables. Generally, the traditional approach to searching for factors in the FRED-MD data is principal component analysis (PCA). However, this approach does not use any additional information on the type of each variable; i.e., real and nominal variables are mixed together. CCA applied to a subset of real variables vs. a subset of nominal variables can potentially provide another “common” factor.

Another noteworthy area of interest concerns deriving the asymptotic distribution of the angles and —this would require developing a version of a central limit theorem. An asymptotic distribution of the angles can be required for various procedures that use angles as an input (such as confidence interval construction, the delta method, and simulation of bootstrap standard errors).

Finally, a more refined analysis of what is happening near the identification boundary in the spirit of local to unit root limit theory is of theoretical interest. We expect that novel equations involving random functions should appear in the process of answering this question.

Appendix A The master equation

The proofs of all our theorems are based on the master equation — an exact equation satisfied by the canonical correlations and corresponding variables. For illustration purpose, we start by presenting the main ideas for developing such an equation in a simpler setting of principal component analysis (PCA) in Appendix A.1. We then proceed to the canonical correlation analysis (CCA) situation of our main interest in Appendix A.2. Appendix B analyzes these equations as the dimensions go to infinity jointly and proportionally.

A.1. PCA master equation

Suppose that we are given matrix , in which the rows are indexed by and . We treat the –th row as “signal” and the remaining rows as “noise”. Let denote the latter, i.e., it is the matrix formed by rows of . As for the former, we let denote the length of the zeroth row of (treated as a –dimensional vector) and let be the unit vector in the direction of this row.

We would like to connect the singular values and singular vectors of to the triplet: singular values and vectors of ; ; and . The goal is to view this connection through the lenses of reconstruction of and by the singular values and vectors of .

Because the singular values are invariant under orthogonal transformations in –dimensional space, the fact that “signal” is the th row of is not important: it could have been any other row or their linear combination. Rephrasing, we would like to understand how the singular value decomposition of distinguishes the signal vector from the background noise.212121A related, but slightly different setup is to take a noise matrix and rank signal matrix of the same size, set and aim to identify from singular values (and vectors) of . Applying orthogonal transformation, one can again assume that has only first nonzero row, however, this time the first row of is not pure signal, but is also contaminated by the noise coming from the first row of . Therefore, in this setup the noise has two effects: it contaminates by simple addition and then plays a role in computation of singular values. In contrast, in our setup we distinguish the two effects and only look into the second one (because the role of the first one is quite straightforward).

We let , , be the left singular vector (of dimensions), right singular vector (of dimensions), singular value triplets for , which means that

and , . We order the singular values so that .

Next, let be a left singular vector of . We represent it through coordinates in the orthonormal basis

| (20) |

of –dimensional space and normalize by .

Proposition A.1.

Suppose that is a left singular vector of in basis (20) and with a squared singular value . Then

| (21) |

Proof.

Each left singular vector of is an –dimensional column-vector of unit length, which is an eigenvector of ; equivalently, this is one of the critical points (on the space of unit vectors) for the quadratic form

with the eigenvector of largest eigenvalue corresponding to the maximum of this quadratic form. Then we have

We aim to find critical points of subject to the constraint . Thus, we introduce the Lagrange multiplier and find critical points of the function

Taking derivatives with respect to , we get:

| (22) |

The equations (22) are supplemented by the normalization condition . Note that equations (22) equivalently express the fact that is an eigenvector with eigenvalue for the matrix written in the orthonormal basis (20). From this interpretation we see that the values of , for which (22) has a solution, are precisely eigenvalues of , i.e., squared singular values of . On the other hand, (22) can be also solved directly. Indeed, the first set of equations leads to

| (23) |

Plugging the expressions for into the last equation of (22), we get

If , then so are all through (23), which contradicts the normalization. Hence, we can divide by , arriving at the final equation for :

| (24) |

which is equivalent to the first equation in (21).

Here is a brief qualitative analysis of the formulas (21). First, let us treat the first equation in (21) in the form (24) as an equation on , assuming that the values of , and , …, are known. Let us also assume, for simplicity, that all are distinct222222If , then an additional singular value appears.. After multiplying by , the equation (24) becomes a degree polynomial equation on ; hence, it has complex roots. For each , the difference between right-hand side and left-hand side of (24) continuously varies from to on segment; hence there is one root of the equation on each such segment. In addition, by the same sign change argument there is one more root on and one more root on . We are mostly interested in the latter two values of , because one can easily distinguish a separated largest/smallest singular value from others, while doing the same for singular values in the bulk of spectrum is challenging.

Next, let us treat the formulas (21) as a parameterization of and by the value of . When we work with data, we know : this is one of the squared singular values of the matrix . Therefore, it is reasonable to ask what information on (unknown to us) and it provides. There are two important regimes here:

-

(1)

If is large, then is also large, while approaches .

-

(2)

If is close to , then is also close to , while approaches .

On the other hand, for the intermediate values of and , the value of is typically quite far away from . The conclusion is that we can effectively distinguish the signal vector (the zeroth row of ), if its length is either very small or very large, as compared to the values of , which are singular values of the matrix formed by the remaining rows of . Recall that represents the noise part; it is, perhaps, strange to ask the noise to be large enough, and much more natural to assume that the noise is small enough. Hence, in practice, the situation of interest is when the length of the signal vector is large (rather than small) compared to the magnitude of the noise.

A.2. CCA master equation

We proceed to the canonical correlations analysis setting. Suppose that we are given two subspaces, and in –dimensional space and let . In addition, we have two vectors and , which we add to spaces and . Define

Our task is to reconstruct the vectors and inside the spaces and , respectively, by analyzing the canonical correlations between and .

We start by bringing the pair of subspaces and to the canonical form. The following definitions of canonical correlations and variables can already be found in Hotelling (1936), see bottom of page 330 there. We also refer to the textbook Anderson (2003, Chapter 12).

Lemma A.2.

Suppose that and let and be -dimensional and -dimensional subspaces of dimensional space, respectively. Then there exist two orthonormal bases: vectors span and vectors span – such that for all meaningful indices and :

| (26) |

where .

The numbers are called canonical correlation coefficients between subspaces and ; they are also cosines of the canonical angles between the subspaces. The vectors , , and , , are called canonical variables; they split into pairs and singletons , . In some of the following formulas we also use with under the convention:

| (27) |

There are two equivalent ways to find the canonical correlations and variables:

-

•

If we consider a function , in which varies over all unit vectors in and varies over all unit vectors in , then , , are critical points of and corresponding values of . In particular, is the maximum of , which is achieved at . The remaining vectors , are an arbitrary orthogonal basis in the part of orthogonal to all vectors of and .

-

•

For a subspace , let us denote through the orthogonal projector on . Then nonzero , are nonzero eigenvalues of and are corresponding eigenvectors. Simultaneously, nonzero are eigenvalues of . If we identify the spaces and with spans of rows of and matrices, then this is equivalent232323One can move from the right to the left in without changing the eigenvalues. We get the matrix , which is the same as and has the same eigenvalues as . to Definition 2.4.

Throughout the rest of this section we use the bases of Lemma A.2.

In exactly the same fashion we can also define the canonical correlation coefficients and corresponding variables for the spaces and . The next theorem connects them to , and the data of Lemma A.2

Take two vectors and , such that and is a pair of canonical variables for and . We normalize the vectors so that

| (28) |

The next theorem is a direct analogue of Proposition A.1 in the CCA setting.

Theorem A.3.

Remark A.4.

Comparing to the PCA setting, (29) is an analogue of the first equation in (21) and (30), (31) are analogues of the second equation in (21). A version of (32), (33) for the PCA would be the computation of the scalar product between and the right singular vector corresponding to the singular value , which we omitted there.

Proof of Theorem A.3.

We seek for a pair of vectors and , which represent critical points of the function

subject to the normalization constraints

| (36) |

In this way, , is a pair of canonical variables for and and the corresponding value of is a canonical correlation coefficient.

Introducing the Lagrange multipliers and corresponding to two normalizations (36), we are led to the Lagrangian function

| (37) |

We need to find critical points of this function. Differentiating with respect to and , we get a system of homogeneous linear equations on coordinates of and :

| (38) |

In the matrix form, the equations (38) can be rewritten as

| (39) |

where and are treated as column-vectors of sizes and , respectively, and are matrices of scalar products:

| (40) |

with , . Note that (39) implies eigenrelations

| (41) |

Comparing (41) with standard algorithms for finding canonical correlations as in Definition 2.4, we conclude that should necessary be one of the squared sample canonical correlations between spaces and . On the other hand, the equations (38) can be solved directly.242424On the technical level, this is the main difference of our approach from the previous attempts on this problem in the literature: solving (41) is difficult, because the left-hand sides involve matrix inversions. On the other hand, directly solving (38) by exploiting their block structure turns out to be much simpler. We first combine the second and the forth equation for and treat the result as a system of two linear equations on the variables :

| (42) |

We solve these equation by inverting the matrix in the left-hand side:

Multiplying by the right-hand side of (42), the solution is

| (43) |

In addition, for , we rewrite the last equation of (38) in a similar form:

| (44) |

which can be thought of as the second equation of (43) with . Next, we plug (43) and (44) back into the first and third equations of (38) and get:

| (45) |

| (46) |

where we adopted the agreement for . (45) and (46) is a system of two homogeneous linear equations on . If the system is non-degenerate, then the only solution is , which then leads through (43) and (44) to vanishing of all , , which contradicts the normalization condition (28). Hence, the system must be degenerate, which is equivalent to vanishing of the determinant of matrix of its coefficients. Noticing that the coefficient of in (45) and the coefficient of in (46) are two equivalent forms of the same expression, the condition becomes

| (47) |

Denoting , we arrive at the desired (29). Recalling the interpretation of explained after (41), (29) is the equation for the squared canonical correlation coefficients between subspaces and .

Once is identified from (29), we plug it back into (46) and find the relation

| (48) |

where is given by (35). Further, (43) transforms into

| (49) |

The normalization equation becomes the desired (31):

We further reconstruct by using (45) instead of (46) in the form:

where is given by (34). Then we transform (43) into

| (50) |

The normalization condition becomes the desired (30):

The formulas for the scalar products (32) and (33) follow by using (50) and (49), respectively. ∎

Lemmas A.5 and A.6 clarify the structure of (29) in Theorem A.3 treated as an equation on an unknown variable , assuming that all , , , and are given.

Lemma A.5.

The identity (29), treated as an equation on an unknown , is equivalent to a polynomial equation of degree , and, therefore, has roots.

Proof.

Let us study the behavior of (29) near . The left-hand side behaves as:

| (51) |

The right-hand side behaves as:

| (52) |

We notice the cancelation of the double pole in the difference of the left-hand side and right-hand side. Hence, the difference has only a simple pole. Therefore, if we multiply both sides of (29) by , we get a polynomial equation252525Note that there is no singularity at : all denominators with are matched with factors in numerators. of degree . ∎

Lemma A.6.

Let roots of (29) be denoted . Then

-

(1)

All are real numbers between and .

-

(2)

If we arrange in the decreasing order, then there exists another sequence of real numbers , such that two interlacing conditions hold:

(53) (54)

Proof.

It is tricky to see this property by directly analyzing the equation (29) and we proceed in another way262626We are grateful to G. Olshanski for a discussion leading to this argument. by using the identification of with squared canonical correlation coefficients between and , as claimed in Theorem A.3. It immediately follows that they are real numbers between and . Next, by definition, are squared canonical correlations between and . The numbers in (53), (54) also have a similar interpretation: they are squared canonical correlations between and .

In order to see interlacement, it is helpful to use the identification of canonical correlations with eigenvalues of products of projectors. are nonzero eigenvalues of , while are nonzero eigenvalues of . If we choose an orthonormal basis of , for which is spanned by the first basis vectors, then the former matrix (ignoring zero part) becomes a matrix, while the latter matrix is its principal submatrix. Hence, (53) are classical (see e.g., Bhatia (1997, Corollary III.1.5)) interlacing inequalities between eigenvalues of a symmetrix matrix and its submatrix. On the other hand, we can also identify with nonzero eigenvalues of . Then (54) is obtained by comparing this matrix (viewed as matrix in ) with its submatrix , whose nonzero eigenvalues are ; the interlacing condition looks slightly different because of the additional s among the eigenvalues: if we add the smallest coordinate , then one can think of (54) as being of the same form as (53). ∎

Appendix B Asymptotic approximations

The proofs of all theorems in Sections 2 and 3 are based on the asymptotic approximations of the formulas of Theorem A.3. We first prove Theorem 3.4, and then show that all other theorems in Sections 2 and 3 are its corollaries.

B.1. Proof of Theorem 3.4

Lemma B.1.

Proof.

Suppose that Assumption IV holds with some vectors , , some matrices , , and some date , . Our task is to transform the data to the form claimed in Lemma B.1. Let be matrix, whose first row is and the remaining rows are given by matrix . We claim that is invertible. Indeed, if is degenerate, while has rank , then there should be a way to express as a linear combination of rows of . Hence, is a linear combination of rows of . But then independence of and postulated in Assumption IV.(2) is impossible. Similarly, we define an invertible matrix to be matrix, whose first row is and remaining rows are given by .

We let and and rephrase everything in terms of and . Note that the canonical correlations and variables in Theorem 3.4 depend only on the linear subspaces (in –dimensional space) spanned by the rows of and , rather than on the matrices and themselves. Hence, due to invertibility of and , they are the same for the matrices and . Hence, , , and in Theorem 3.4 are unchanged. Simultaneously, , , , do not change since , , , , where , , , are from the statement of the lemma. Thus, all the ingredients in the formulas (11)-(15) remain the same. ∎

The next step is to get to rid of (unknown to us) , , , appearing in the formulas of Theorem A.3.

Lemma B.2.

Suppose that in –dimensional space we are given a pair of random vectors and a collection of vectors , and numbers , with such that

-

•

The matrix has fourth-moment Gaussian elements, in the sense of Definition 3.1, such that the rows are mean zero and uncorrelated with each other. The covariance matrix of each row is the same .

-

•

Either , , are deterministic, or independent with .

-

•

The scalar products for are , , .

Then as we have

| (55) | ||||||

| (56) | ||||||

| (57) | ||||||

| (58) | ||||||

| (59) |

where the sign means that the difference between right- and left-hand sides is (tends to in probability after dividing by ) uniformly in complex bounded away from all zeros of the denominators, . Similar asymptotic approximations hold if we replace all denominators with .

Proof.

We condition on , , throughout the proof and assume them to be deterministic.

Step 1. Let us show that the expectation of the left-hand side matches the right-hand side in all approximations. Take any two deterministic –dimensional vectors and . Using the uncorrelated mean assumption on the components of and , we have

Similarly,

Applying these expectation identities and using the scalar products table for and , we conclude that the expectations of the left sides of (55)-(59) are given by the right sides.

Step 2. Next, we show that the terms in the sums in (55)-(59) are uncorrelated. For that we take four –dimensional deterministic vectors , , , such that

Since the coordinates of are mean , uncorrelated, fourth-moment Gaussian, we have:

| (60) | ||||

where in transition from the second to the third line we used that all the joint moments of coordinates, in which some coordinate is repeated one time, vanish because of fourth-moment Gaussian assumption, and the sum in the third line vanishes by the same reason. In the same way, we get

| (61) |

And by a similar computation, we have

| (62) | ||||

Altogether, (60), (61), and (62) show that all the sums in (55)-(59) have uncorrelated terms.

Step 3. The statement of the lemma for a fixed follows by the weak law of large numbers for uncorrelated sum: the variance of each sum is upper bounded by a constant times .

In order to prove the uniformity in , let denote the difference of the left- and right-hand sides in one of the approximations (55)–(59). We fix and aim to prove that tends to in probability as uniformly over all at distance at least from . Choose and note that the magnitude of each term in the sums (55) is upper bounded by . Hence, there exists a constant , such that

| (63) |

Introduce a compact set given by

There exists a constant , depending only on , such that is –Lipshitz on :

Therefore, we can choose a finite collection of points , such that does not grow with and

| (64) |

The right-hand side of the last formula tends to as by the fixed convergence result. Hence, combining with (63) we deduce the desired uniformity in . ∎

Proof of Theorem 3.4.

Using Lemma B.1, we assume without loss of generality that and , which means that the signal vectors are the first rows of and , respectively. Further, by the same lemma we assume and , which means that the noise part is given by the remaining rows of , denoted as matrix and remaining rows of denoted as matrix . This is the setting of Theorem A.3 and we apply it.

We divide (29) by and note that by the law of large numbers

| (65) |

Hence, using Lemma B.2, we get an asymptotic approximation of (29):

The desired (12) is an equivalent form of the same equation with renamed variable .

Further, recalling that in Theorem 3.4 and Definition 2.4 becomes in Theorem A.3, while in Theorem 3.4 becomes , and noticing that was normalized in our procedure, while was not, we rewrite as

| (66) |

For the denominator in (66) we use (65). For the numerator we first use (32) to express it through . Using Lemma B.2 and notation (11), we get

| (67) |

In the last formula can be replaced with leading to another error. For , we use (30), Lemma B.2 and (65) getting:

Next, we analyze the asymptotics of from (34) using again Lemma B.2 and (65):

| (68) | ||||

This is precisely the function of (13). Hence, plugging and into (67) and recalling that , we get (14).

B.2. Proofs of Theorems 2.5 and 3.2.

Theorem 3.2 is a particular case of Theorem 3.4, and the proof of Theorem 3.2 consists of simplifications of the formulas (12)–(15) in the i.i.d. noise situation, which we do in this section.

Take two real parameters272727In order to match the notations of Bao et al. (2019), we should set there and . In order to match the notations of Bykhovskaya and Gorin (2022a, b), we should set there , . with and define the Wachter distribution through its density

| (69) |

where the support of the measure is defined via

| (70) |

One can check that for every with and that (69) is a probability measure. A direct computation also shows that:

Lemma B.3.

The modified Stieltjes transform of is:

| (71) |

where the branch of the square root is chosen so that for large positive the value of the square root is positive and for negative it is negative.

Theorem B.4.

For , let and be and random matrices, respectively, so that all their matrix elements are independent mean variance random variables with uniformly bounded th moments for some . Let be squared sample canonical correlation coefficients between and , as in Definition 2.4, and let be their empirical distribution:

Then as , so that and with , , we have

Proof.

Corollary B.5.

Proof.

Our next step is to analyze the behavior of the relation (12) in the i.i.d. noise setting and derive the formula (2).

Lemma B.6.

Proof.

The second factor in the numerator of (72) is

| (76) |

the third factor is

| (77) |

and the expression in denominator (which is being squared) is

| (78) |

After a long, but straightforward computation, based on (76), (77), (78), and (70) we transform the left-hand of (72) into

| (79) |

which matches (75) if we set .

Note that (79) is a monotonously increasing function of . Hence, for in this interval, it takes exactly once all values between the value at , which is

and the value at , which is

Therefore, for satisfying (73), there exists a unique , solving (72) and this is given by (75). Simultaneously, we have shown that for , (72) does not have solutions .

Remark B.7.

We further simplify the functions and of Theorem 3.4 in the i.i.d. noise case.

Lemma B.8.

Consider the limit versions of and explicitly given by:

| (80) |

If we plug given by (74), then these functions become the following functions of , respectively:

| (81) |

Proof.

Lemma B.9.

In the limit , so that and with , , in the independent noise case under Assumption II, we have

| (84) |

| (85) |

Proof.

In the previous two lemmas we investigated the asymptotic behavior of all ingredients of the formulas (14) and (15) expect for . Differentiating (71), we have

Using (74) and (82), we compute

Next, we start plugging all the computed ingredients into (14). An interesting cancelation happens: the squared factor in the first line282828We recall from the proof of Theorem A.3 that this factor is the ratio of and . of (14) simplifies to 1:

The two last lines of (14) transform into (84) after another compuation. The same simplification happens for the first line of (15):

Corollary B.10.

Now we have all the ingredients.

Proof of Theorem 3.2.

First, suppose that , then by Lemma B.6, and the solution to the equation (12) converges to as . By Theorem 3.4 and Corollary B.5 this implies that the largest canonical correlation converges to as .

Because (12) is approximation of the equation (29) of Theorem A.3 solved by each of the canonical correlations , and the limiting equation by Lemma B.6 has only one solution larger than , we conclude that . On the other hand, by the interlacing inequalities of Lemma A.6, , and the latter converges to by Theorem B.4, implying . We conclude that converges in probability to as . Hence, (5) is proven.

Proof of Theorem 2.5.

We would like to show that Assumption I implies Assumption II and, therefore, Theorem 3.2 implies Theorem 2.5.

The parts in Assumption II about being fourth-moment Gaussian and about the existence of the th moments are automatic in the Gaussian setting. It remains to choose the matrices and . Let us introduce a positive definite symmetric bilinear form on vectors in , given by

Essentially, is the covariance matrix of . Let be –dimensional subspace in consisting of vectors –orthogonal to :

Similarly, we let be the covariance matrix of and let be –dimensional subspace in consisting of vectors –orthogonal to . Note that the spaces and are linear spaces of the vectors mentioned in Assumption I.

Choose a –orthonormal basis in :

Also choose a –orthonormal basis in . Define to be matrix whose –th row is formed by the coordinates of , and define to be matrix whose –th row is formed by the coordinates of .

B.3. Proof of Theorem 3.3

The idea of the proof is to use rotational invariance of the Gaussian law to reduce Theorem 3.3 to Theorems 2.5 or 3.2.

We rely on the following basic property of Gaussian distributions.

Lemma B.11.

Let be random matrix, such that each column is a mean Gaussian vector (of an arbitrary covariance) and the columns are i.i.d.. In addition, let be orthogonal matrix which is independent from . Then:

-

(1)

has the same distribution as .

-

(2)

is independent from .

Proof.

Let us condition on the value of . The random vector formed by vectorizing is a linear transformation of the vectorization of ; hence, it is Gaussian. The orthogonality of implies that the covariance structure of the matrix elements of is the same as the one for . Since the laws of mean Gaussian vectors are uniquely determined by the covariances, we conclude that the distributions of and coincide conditionally on .

Because the law of is the same for any choice of , we also conclude the independence between and . ∎

Throughout the proof of Theorem 3.3 we condition on the vectors and in Assumption III and treat them as deterministic. Because the canonical correlations and corresponding angles between true and estimated canonical variables are unchanged when we rescale or , we can and will assume without loss of generality that they are normalized so that . Therefore, also

where is given in Eq. (10). The choice of the sign in the last formula is merely a question of the definition of , because (10) only fixes its square. Hence, we assume without loss of generality that the sign is .

We introduce an additional uniformly random orthogonal matrix , which is independent from the rest of the data in Theorem 3.3. Note that an orthogonal transformation in –dimensional space does not change the scalar products, lengths, and angles between vectors. Therefore, is we replace in Theorem 3.3 the matrices and with and , respectively, then the distributions of squared canonical correlations between and and corresponding angles between true and estimated canonical variables is unchanged. Hence, it is sufficient to establish the conclusion of Theorem 3.3 for data matrices and .

For the and of Assumption III, by Lemma B.11, and are matrices of i.i.d. Gaussian random variables and they are independent from and hence from the vectors and . Therefore, the noise part and matches the i.i.d. setting of Theorems 2.5 and 3.2.

Let us look at the signal part: the pair of the –dimensional vectors is obtained from the pair of vectors by applying uniformly random orthogonal rotation matrix. Denote . At this point, the only difference between the present setting and the one of Theorem 2.5 is whether and have i.i.d. Gaussian components or not. Recall that the only place where the i.i.d. Gaussian assumption on the signal vector was used on our path to Theorem 2.5 through Theorems A.3 and 3.4 is in Lemma B.2. Hence, to finish the proof of Theorem 3.3 we show the following generalization:

Lemma B.12.

Set , . Then the asymptotic approximations of Lemma B.2 remain true for .

Proof.

The random vectors and do not have i.i.d. components, however, we can construct them from vectors with i.i.d. components. For that, let us write , where is a vector orthogonal to . Our normalizations imply that the squared length of is . Observe that is a uniformly random pair of orthogonal vectors of length in –dimensional space. Here is an alternative way to construct such a pair: Take two independent vectors and with i.i.d. components, represented as matrices. Set

| (88) |

The invariance of the i.i.d. Gaussian vectors and under orthogonal transformations readily implies that has the same distribution as . Hence, we can also write

| (89) |

Note that all the random constants appearing in (88) have straightforward deterministic limits by the law of large numbers for i.i.d. random variables: as

Hence, we have the following chain of reductions: the conclusion of Lemma B.2 holds for with , , therefore, it also holds for with , , and therefore, it also holds for with , . ∎

B.4. Proof of Theorem 3.7

By the same argument as in Lemma B.1, we can assume without loss of generality that the signal vectors are represented by the first rows in and by the first rows in . The remaining rows in and rows in represent the noise.

Next, we apply Theorem 3.4 times: we start from and matrices and representing noise and then add the rows representing signal one by one. We claim that after the addition of signals, the squared canonical correlations appearing in (11) have the three following features as : fix arbitrary small ,

-

(1)

All but finitely many squared canonical correlations belong to the segment as and their empirical distribution converges to the Wachter law, as in Theorem B.4;

-

(2)

There might be several outliers in –neighborhoods of points corresponding to those , , which are larger than ;

-

(3)

There are no other squared canonical correlations outside beyond those described in above.