Online Game with Time-Varying Coupled Inequality Constraints

Abstract

In this paper, online game is studied, where at each time, a group of players aim at selfishly minimizing their own time-varying cost function simultaneously subject to time-varying coupled constraints and local feasible set constraints. Only local cost functions and local constraints are available to individual players, who can share limited information with their neighbors through a fixed and connected graph. In addition, players have no prior knowledge of future cost functions and future local constraint functions. In this setting, a novel decentralized online learning algorithm is devised based on mirror descent and a primal-dual strategy. The proposed algorithm can achieve sublinearly bounded regrets and constraint violation by appropriately choosing decaying stepsizes. Furthermore, it is shown that the generated sequence of play by the designed algorithm can converge to the variational GNE of a strongly monotone game, to which the online game converges. Additionally, a payoff-based case, i.e., in a bandit feedback setting, is also considered and a new payoff-based learning policy is devised to generate sublinear regrets and constraint violation. Finally, the obtained theoretical results are corroborated by numerical simulations.

Index Terms:

Decentralized online learning, generalized Nash equilibrium, online game, bandit feedback.I Introduction

Game theory has received growing attention recently owing to its wide applications in social networks [1], sensor networks [2], smart grid [3], and so on. In noncooperative games, the concept of Nash equilibrium (NE) plays a pivotal role by providing a rigorous mathematical characterization of the stable and desirable states, from which rational players have no incentive to deviate [4].

A challenge is to design decentralized algorithms for seeking NE in noncooperative games based on limited information available to each player. Generally, it is assumed that a coordinator exists to broadcast the data to players [5, 6, 7], that is, bidirectional communication with all the agents is required, which results in high communication loads and is impractical for many applications. Therefore, decentralized algorithms on computing NEs in noncooperative games without full action information, that is, in a partial decision information setting, have been getting more and more attention in recent years. To deal with such kind of scenarios, numerous results on the NE seeking problems have sprung up both in continuous-time [8, 9] and in discrete-time [10, 11, 12], where the algorithms were designed based on gradient descent and consensus schemes.

All the references mentioned above assumed that all players are rational, which, however, may not be practical particularly in uncertain, unpredictable or adversarial environments. Usually, the players only know they are involved in a repeated decision progress where a reward is returned after an action is made, while they have no knowledge on how the game generates the reward and they do not even know they are playing a game. In this regard, a player must adapt other players’ strategies in a dynamic manner by minimizing its (static or dynamic) regret, i.e., the cumulative payoff difference between a player’s actual policy and the best (fixed or time-varying) action in hindsight, which is commonly regarded as a concise and meaningful benchmark for quantifying the ability of an online algorithm for decision-making in the presence of uncertainties and unpredictabilities [13]. Along this line, mirror descent-based learning algorithms can achieve an order-optimal static regret bound, i.e., , when cost functions of players are convex [14].

It should be noted that the case where the game participated in by players remains unchanged throughout the learning process is most investigated. However, dynamic environments appear frequently in a multitude of practical applications, such as allocating radio resources and online auction, and then the games or the cost functions of players in games often vary with time due to exogenous variations. For example, in a repeated online auction where resources are auctioned off for several bidders, if the gain that each bidder gets for a unit of resource changes over time, then the bidders’ utilities are also time-varying. For this kind of online game, the authors in [15] studied the equilibrium tracking problem and analyzed convergence properties of mirror descent-based policies. Furthermore, a no-regret algorithm based on projection strategies and primal-dual methods was devised in [16] for online game with time-invariant nonlinear constraints.

It is well known that no-regret learning may not imply convergence to NEs even for the mixed-strategy learning in finite games. In fact, the empirical frequency of play generated by no-regret learning in finite games converges to the game’s set of coarse correlated equilibria, which may contain inadmissible strategies, such as the ones that assign positive weight only to dominated strategies[17]. The players’ learning policy may cycle even in two-player zero-sum games [18] and may also lead to an unpredictable and chaotic scenario. It has been proven in [19] that the sequence of play under no-regret learning for potential games converges, including the bandit feedback case. Therefore, it is not explicit to establish the relationship between the no-regret learning and convergence to NEs if no further assumptions or specialized techniques especially for online game with coupled constraints.

On the other hand, this issue becomes considerably intricate when at each round only the reward is revealed for an action profile, instead of the gradients of cost functions or the entire knowledge of cost functions. Bandit algorithms are suitable to solve this kind of problems, including optimization [20, 21] and NE seeking [22, 23]. As to repeated games, it is usually assumed that actions are synchronized across players and rewards are assumed to arrive instantaneously, and then the players need to infer gradient information from a single point observation at each round.

In this paper, we further investigate online game, where players selfishly and simultaneously minimize their own time-varying cost functions subject to local feasible set constraints and time-varying coupled nonlinear constraints. In the setup of full information feedback, i.e., both function values and gradient information are available, a decentralized online algorithm for the studied online game based on mirror descent and primal-dual schemes is devised, and is rigorously proved to ensure that the regrets and constraint violation grow sublinearly by appropriately choosing decaying stepsizes. Further analysis on the convergence of the generated sequence of play by the designed algorithm is provided. In addition, in view of the difficulty to compute the gradients of cost functions and constraint functions, a payoff-based online learning algorithm relying on one-point stochastic approximation is proposed, and the corresponding analysis is provided to show that the algorithm can achieve sublinear expected regrets and constraint violation. The main contributions of this paper are summarized as follows.

- 1)

-

2)

A challenging issue is to analyze the convergence of the generated sequence of strategies under no-regret learning even for static games. In this paper, strict analysis is provided to show that if the online game converges to a strongly monotone game, then the generated sequence of play by the designed algorithm can converge to the variational GNE of the game limit. Moreover, the convergence rate of the averaged strategy sequence is derived.

-

3)

A decentralized bandit online algorithm is further devised for the studied online game when only the values of local cost functions and nonlinear constraint functions are available after all the players’ decisions are made.

The rest of this paper is structured as follows. In Section II, some preliminaries and the problem formulation are introduced. Section III presents a decentralized learning algorithm for the studied online game in the setup of full information feedback, which is proved to be no-regret. The equilibrium convergence property of the designed algorithm is presented in Section IV. In Section V, a bandit feedback case is discussed. A numerical example is presented to show the effectiveness of the proposed algorithms in Section VI. Section VII makes a brief conclusion.

Notations. The symbols , , and represent the sets of real numbers, -dimensional real column vectors, and real matrices, respectively. Let be the set of -dimensional nonnegative vectors. The symbol (resp. ) represents an -dimensional vector, whose entries are 1 (resp. 0). For a vector or matrix , the transpose of is denoted by . The identity matrix of dimension is denoted by . For an integer , let . Let . denotes the Kronecker product of matrices and . For a vector , is the projection of onto . is the standard inner product of and . For two vectors , the symbol means that each entry of is nonpositive, while for two real symmetric matrices , and mean that is positive semi-definite and positive definite, respectively. Given two functions and , the notations and mean that there exists a positive constant such that and for all in the domain, respectively. A mapping , where , is -strongly monotone (), if for any , there holds . is the expectation operator.

II Preliminaries

II-A Graph Theory

Let be an undirected graph, where the vertex set is , the edge set is and the weighted adjacency matrix is . For any and , if and otherwise. In this paper, it is assumed that for all . is called a neighbor of if . Denote . A path from node to node is composed of a sequence of edges , . It is said that an undirected graph is connected if there exists a path from node to node for any two vertices . For communication graph , the following standard assumptions are imposed in this paper.

Assumption 1

The undirected graph is connected and the adjacency matrix satisfies that and .

II-B Problem Formulation

This paper studies online game with players, where is the set of players, represents the time-varying strategy set of players with being the shared convex constraint and being the private action set constraint of player , and is the time-varying cost function with being the private cost function of player . Here, and , . Denote by the joint action at time , where is the action of player at time , . Denote by the joint action at time of all the players except . For this time-varying game, it is impossible for every player to pre-compute a GNE of , satisfying

| (1) |

where . Thus, a new benchmark needs to be proposed to depict the performance of decentralized learning algorithms, such as regret, which is commonly regarded as a concise and meaningful benchmark for quantifying the ability of an online algorithm for decision-making in the presence of uncertainties and unpredictabilities [13]. In general, the (static) regret for player is defined as follows:

| (2) |

where is the learning time and

Intuitively, the regret captures the cumulative payoff difference between a player’s actual policy and the best action in hindsight.

Since the strategies of players should satisfy a coupled nonlinear constraint, a notion of regret associated with the constraint is also required. Specifically, for a decision sequence , the constraint violation measure is given as

| (3) |

It is said that an online algorithm is no-regret if all the regrets of players in (2) and the accumulation of constraint violations in (3) increase sublinearly, i.e., and .

In this paper, the objective is to devise no-regret algorithms for the studied online game and to discuss the equilibrium convergence properties of the designed algorithms.

To end this section, a blanket assumption on game is presented, which is also made in [25, 16]. For each player , let denote the th component of , i.e., .

Assumption 2

For each , the set is compact and convex. and are convex. and are uniformly bounded. Then there exists such that for any , ,

| (4) |

and exist and are uniformly bounded, that is, there exists such that for any , ,

| (5) |

where and . Moreover, the constraint set is assumed to be non-empty and Slater’s constraint qualification is satisfied.

II-C Bregman Divergence

For each player , the Bregman divergence of two points is defined as [26]

| (6) |

where is differentiable and -strongly convex for some constant , i.e., Thus, it can be easily derived that is -strongly convex for all with , i.e.,

| (7) |

and the generalized triangle inequality is satisfied, i.e.,

| (8) |

Bregman divergence is widely applied in machine learning and game theory, generalizing the standard Euclidean distance and the generalized Kullback-Leibler divergence. Specifically, when , Bregman divergence amounts to . If , then the Bregman divergence becomes the generalized Kullback-Leibler divergence . A mild assumption on Bregman divergence is given below.

Assumption 3

For any and , is Lipschitz with respect to the first variable , i.e., one can find a positive number such that for any ,

| (9) |

Assumption 3 can be satisfied when is Lipschitz on , which implies that for any , .

III Regret Minimization

At each time , player in the online game only receives the values of , , and , denoted as , , and , respectively. In the following, a decentralized online algorithm based on mirror descent and primal-dual methods will be devised for online game .

For each , define an augmented Lagrangian function at time as where is the Lagrange multiplier or the dual variable, is a stepsize, and is the regularization parameter. Inspired by the dynamic mirror descent for online optimization [27], a semi-decentralized primal-dual dynamic mirror descent can be designed as

| (10) | ||||

| (11) |

where and are time-varying stepsizes utilized in the primal and dual iterations. The main drawbacks of this algorithm are that each player should know the common Lagrange multiplier and the global nonlinear constraint function , which require a central coordinator to bidirectionally communicate with all the players. Motivated by the algorithm proposed in [28], by modifying (10) and (11), a decentralized online primal-dual dynamic mirror descent algorithm is designed as in Algorithm 1 for online game .

Each player maintains vector variables and at iteration .

Initialization: For any , initialize arbitrarily and .

Iteration: For , every player processes the following update:

| (12) | ||||

| (13) |

where , is the th element of , and , satisfying , are the stepsizes to be determined.

In what follows, some necessary lemmas are presented.

Lemma 1

Proof: See Appendix -A.

Proof: See Appendix -B.

Lemma 3

Proof: See Appendix -C.

It is now ready to give the sublinear bounds on the regrets and constraint violation for Algorithm 1.

Theorem 1

Proof: For the selected parameters and , it is easy to verify that . In addition, for any constant and positive integer , it holds that

| (23) |

Then,

| (24) |

Thus,

| (25) | ||||

| (26) |

Subsequently, one can obtain from Lemma 3 that

and

The result is thus proved.

Corollary 1

Proof: By the selection of and , one has that , and are in . Therefore, and .

Corollary 2

Proof: Let , then it is derived that and . The result is thus proved.

Remark 1

The regret bound in this paper is almost the same as the well-known order-optimal bound [14] when the constant is chosen small enough. In addition, the bound of the accumulated constraint violation is also sublinear with the bound . To our best knowledge, the obtained results here are the first ones for online game with time-varying coupled inequality constraints.

Remark 2

The feedback signal after choosing an action, such as the values and , is one of the most important ingredients in designing the learning scheme. In general, the exact gradients’ information is usually hard to grab because of stochastic factors and unknown structures of the payoff and constraint functions. Specifically, for an action profile , assume that the feedback signal is the noisy gradients, that is,

where and are random observation noises capturing all uncertainties and stochasticities. In this setting, the learning policy in Algorithm 1 is still applicable to generate a sequence of actions that ensures the sublinear bounds on the expected regrets and constraint violation by properly selecting stepsizes and under some mild conditions on the means and variances of noise variables and .

IV Tracking Nash Equilibria

Another important issue is whether the learning policy, Algorithm 1, ensures that the actions of players converge or track the GNEs for the studied online game. As pointed out in [15] that establishing a blanket casual link between no-regret play and convergence to NEs is impossible because of unilateral and coupled relationship among players, analyzing the equilibrium convergence properties of the designed learning algorithm is much more challenging and difficult especially under nonlinear coupled constraints. In this section, it is assumed that online game stabilizes to a -strongly monotone game , where with and with being convex and differentiable with respect to . Here, this stabilization is formally defined as

| (27) | |||

| (28) |

where and .

It should be noted that the convergence is defined in terms of the payoff gradients rather than the payoff functions mainly due to that a GNE is a solution to a variational inequality only involving the payoff gradients of players.

For the -strongly monotone game limit , one has for any ,

| (29) |

where is called the pseudo-gradient mapping of game . Note that the cost functions are convex and differentiable. Then it can be obtained from Theorem 3.9 in [29] that at any time , a solution to the following variational inequality:

| (30) |

is a GNE of , and this GNE is also called a variational GNE. In addition, the inequality (30) has a unique solution under the strong monotonicity of . Therefore, the existence and uniqueness of the variational GNE can be guaranteed under the convex payoff functions and strongly monotone pseudo-gradient mapping. It is noticed that finding all GNEs is very difficult even if the game is offline. Accordingly, we will focus on tracking the unique variational GNE as done in [30, 31] since the unique variational GNE enjoys good stability and has no price discrimination from the perspective of economics [32].

To proceed, a standard assumption is also needed.

Assumption 4

The constraint set is assumed to be non-empty and Slater’s constraint qualification is satisfied.

Under Assumption 4, the optimal dual variable to the Lagrangian function associated to game is bounded (cf. [33]), that is, there exists a positive constant such that

| (31) |

Now, it is ready to present the result on the convergence of the play sequence generated by Algorithm 1.

Theorem 2

Proof: See Appendix -D.

Corollary 3

Remark 3

In Theorem 2 and Corollary 3, only the convergence of the generated play sequence is acquired, while the convergence rate is difficult to establish. Instead, the convergence rate of the averaged strategy sequence is derived in what follows.

Theorem 3

Proof: See Appendix -E.

Remark 4

From Theorem 3, it can be seen that the convergence speed of the game sequence has an impact on the convergence rate of the generated averaged strategy . If are larger, then the convergence of to is faster. However, when and are large enough, that is, game converges to the strongly monotone game fast enough, or in other words, , then , which implies that the convergence rate of is independent of .

V Payoff-Based Learning

In this section, a payoff-based learning scheme, i.e., an online algorithm that only depends on payoff values after decisions are made, is devised, which is also called bandit feedback. First, the gradient estimator based on one-point bandit feedback is introduced. Then, by the analysis of the previous section, the convergence result for the payoff-based algorithm is presented.

The idea to estimate the payoff gradients relies on the so-called one-point stochastic approximation. Let be a function, where is a convex set. To estimate the gradient for some , it suffices to sample at , where is a constant and is a vector taking values uniformly at random from . Here, for each , is a vector with its th element being 1 and others 0. Then the estimate of is

Due to the constraint set , a problem that may arise is that the perturbation or the query point may not remain in the feasible set . To avoid this, one can first transfer to an interior of by a transformation of the form

where is an interior point of and is selected such that the ball centered at with radius is entirely contained in . With this transformation, it can ensure that the query point

is in the convex set since .

Based on the above introduced one-point gradient estimator, the process for estimating the payoff gradient of each player at time is given as follows:

-

1)

Each player chooses a point and selects a perturbation direction from uniformly at random. Subsequently, player adopts a strategy

(34) and then receives the corresponding reward or payoff value and the local constraint function value . Denote and .

-

2)

Each player makes an estimate of its payoff gradient and local constraint function gradient:

(35) (36) Denote .

Each player maintains vector variables and at iteration . Fix an interior point of , and choose such that . Let .

Initialization: For any , initialize arbitrarily and .

Iteration: For , every player performs the following update:

| (37) | ||||

| (38) | ||||

| (39) |

where , is the th element of , and , satisfying , are the stepsizes to be determined.

In Algorithm 2, each player chooses the sampling radius , and independently, only guaranteeing that and , which indeed can be ensured by , the particular selection of , and the decrease of . For example, if the convex set contains a ball , then can be selected as the original point and can be chosen as . is uniformly randomly chosen from . Let be the -algebra generated by and .

In what follows, by leveraging the analysis on establishing the regret bounds in Section III, we derive the corresponding result on Algorithm 2.

Theorem 4

Proof: See Appendix -F.

Corollary 4

Corollary 5

Proof: By letting , it is obtained that and . Then, the bound of is derived as . Making yields that . Via a simple computation, one has and .

Remark 5

In Algorithm 2, only payoff information and local constraint function values are used, which is usually easy to implement, but at the expense of a little bit worse bounds on the regrets and constraint violation compared with the full information case as shown in Corollary 2. Moreover, in the one-point bandit feedback case, the convergence in expectation of the play sequence generated by Algorithm 2 can be obtained similar to that in Section IV, whose details are omitted here.

VI A Numerical Example

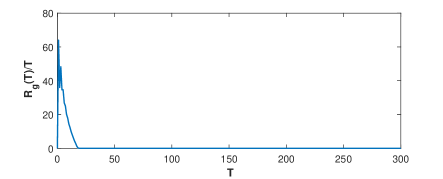

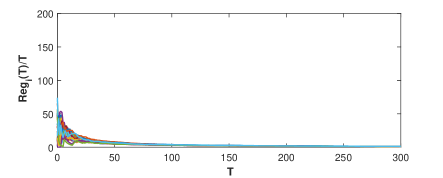

In this section, a time-varying Nash-Cournot game with production constraints and market capacity constraints is considered to illustrate the feasibility of the obtained algorithm. Similar to [16], we consider a Nash-Cournot game, in which there are firms communicating with each other via a connected graph . Denote by the quality produced by firm at time . In view of some uncertain and changeable factors such as marginal costs and demand for orders, the demand cost and the production cost may be time-varying. Assume that the production cost and the demand price of firm are and , respectively. Then, the overall cost function of firm is for and . In addition, the production quality constraint of firm is , while the market capacity constraint is modeled as a coupled inequality constraint , where is the local bound available to firm . In the offline and centralized setting, the GNE can be calculated as , where . In the online and decentralized setting, for Algorithm 1, set initial states randomly, , and choose and . , and are shown in Fig. 1 and Fig. 2, respectively. From these figures, one can see that the average regret and the average violation decay to zero as iteration goes on. That is, the regrets , , and the violation increase sublinearly, which are consistent with theoretical results in Section III.

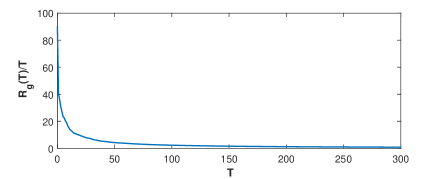

When players can only receive the rewards or payoff rather than the information on gradients of payoff and constraint functions after decisions are made, by the payoff-based learning algorithm (Algorithm 2), the simulations on and are shown in Fig. 3 and Fig. 4, respectively. Here, the interior point of is selected as , the radius is and the query radius is . From the simulations, one can see that the regrets and constraint violation increase sublinearly, which is consistent with theoretical results in Section V. Moreover, one also can see that the bounds of regrets and constraint violation are a little larger than those of the case of gradient accuracy feedback.

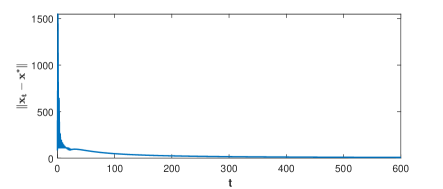

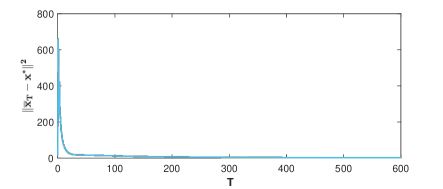

If the term is replaced by , then online game converges to a strongly monotone game with payoff function for and the coupled constraint . In this case, the errors and are shown in Fig. 5 and Fig. 6, respectively, where is the unique variational GNE of . These simulations demonstrate the theoretical results in Section IV.

VII Conclusion

In this paper, decentralized learning for online game with time-varying cost functions and time-varying general convex constraints was investigated. A novel decentralized online algorithm was devised based on the mirror descent and primal-dual strategy. It was rigorously proved that the proposed algorithm could achieve sublinearly bounded regrets and constraint violation by appropriately choosing decaying stepsizes. The convergence property of the no-regret learning was also analyzed. Furthermore, the one-point bandit feedback case was also studied. And all theoretical results have been validated by a numerical example.

Acknowledgment

The authors are grateful to Prof. Kaihong Lu for helpful discussion.

-A Proof of Lemma 1

It can be easily proved that (14) and (15) hold by mathematical induction [34]. Therefore, it suffices to prove (16) and (17). From the iteration (13), one has

| (46) |

where , . Denote and . Then

| (47) |

Under Assumption 1, one has , where . Consequently, taking norm on both sides of (47) yields

| (48) |

Note that

| (49) |

where the first inequality is derived based on for any two vectors with the same dimension, and the third inequality is obtained based on (4) in Assumption 2 and (15). Then,

Combined with , (16) is thus proved.

-B Proof of Lemma 2

For any , based on the optimality of in (12), one can obtain that for any ,

| (52) |

where for is used. Then, it can be derived from (52) that

| (53) |

where the equality is derived based on (8) and the last inequality is based on (7). Then, rearranging (53) yields

| (54) |

As to the first term on the right hand side of (54), we have

| (55) |

where the inequality is obtained by the Cauchy-Schwarz inequality and (5) in Assumption 2.

-C Proof of Lemma 3

On the other hand, by defined in Lemma 1, one obtains

| (60) |

Summing over gives that

| (61) |

where the inequality is derived based on .

-D Proof of Theorem 2

This theorem is proved by splitting two steps: first prove that converges to some finite value; and then prove that converges to by the mathematical induction method.

First, for any , let in (18) of Lemma 2. One has

| (68) |

that is,

| (69) |

Summing over yields

| (70) |

Note that

| (71) |

where the first inequality is obtained based on the -strong monotonicity of , the second inequality is derived by the fact that is a saddle point of the Lagrangian function , the convexity of and nonnegativity of , the third inequality is got following the KKT condition and (4) in Assumption 2, and the last inequality is deduced by (31).

In addition, by and , one has

| (72) |

where Lemma 1 and the notation have been used to derive the last inequality.

Similar to (60) and (61), one can derive that

Then combining with the conditions in (32), it can be verified that .

By defining an auxiliary variable , it holds

| (75) |

By Doob’s submartingale convergence theorem, it concludes that converges to some finite value and .

Then, it suffices to prove the convergence of by the mathematical induction method. Assume that does not converge to , then there is a subsequence of , , such that for some , . By (74), one has

| (76) |

Let , then . In view of and , it can be derived from (76) that

| (77) |

which contradicts the finite limit of . Therefore, the hypothesis does not hold and hence converges to .

-E Proof of Theorem 3

-F Proof of Theorem 4

The results in Lemma 1 still hold for Algorithm 2 by only replacing in (17) with . Then, based on the optimality of in (37), for any , one has

| (81) |

which implies

by taking , where (7) and (8) have been used to derive this inequality.

Taking expectation on both sides of the above inequality over yields that

| (82) |

where the fact that is independent of is applied.

For the first term on the right hand side of (82), one has

| (83) |

For the second term on the right hand side of (82), it can be obtained that

| (84) |

For the third term on the right hand side of (82), similar to (56), one can derive that

| (85) |

References

- [1] J. Ghaderi and R. Srikant, “Opinion dynamics in social networks with stubborn agents: Equilibrium and convergence rate,” Automatica, vol. 50, no. 12, pp. 3209–3215, 2014.

- [2] M. S. Stankovic, K. H. Johansson, and D. M. Stipanovic, “Distributed seeking of Nash equilibria with applications to mobile sensor networks,” IEEE Transactions on Automatic Control, vol. 57, no. 4, pp. 904–919, 2012.

- [3] W. Saad, Z. Han, H. V. Poor, and T. Başar, “Game-theoretic methods for the smart grid: An overview of microgrid systems, demand-side management, and smart grid communications,” IEEE Signal Processing Magazine, vol. 29, no. 5, pp. 86–105, 2012.

- [4] T. Başar and G. J. Olsder, Dynamic Noncooperative Game Theory. SIAM, 1999, vol. 23.

- [5] F. Facchinei and C. Kanzow, “Generalized Nash equilibrium problems,” Annals of Operations Research, vol. 175, no. 1, pp. 177–211, 2010.

- [6] C. K. Yu, M. Van Der Schaar, and A. H. Sayed, “Distributed learning for stochastic generalized Nash equilibrium problems,” IEEE Transactions on Signal Processing, vol. 65, no. 15, pp. 3893–3908, 2017.

- [7] J. S. Shamma and G. Arslan, “Dynamic fictitious play, dynamic gradient play, and distributed convergence to Nash equilibria,” IEEE Transactions on Automatic Control, vol. 50, no. 3, pp. 312–327, 2005.

- [8] C. De Persis and S. Grammatico, “Distributed averaging integral Nash equilibrium seeking on networks,” Automatica, vol. 110, p. 108548, 2019.

- [9] D. Gadjov and L. Pavel, “A passivity-based approach to Nash equilibrium seeking over networks,” IEEE Transactions on Automatic Control, vol. 64, no. 3, pp. 1077–1092, 2019.

- [10] J. Koshal, A. Nedić, and U. V. Shanbhag, “Distributed algorithms for aggregative games on graphs,” Operations Research, vol. 64, no. 3, pp. 680–704, 2016.

- [11] F. Salehisadaghiani, W. Shi, and L. Pavel, “Distributed Nash equilibrium seeking under partial-decision information via the alternating direction method of multipliers,” Automatica, vol. 103, pp. 27–35, 2019.

- [12] T. Tatarenko and A. Nedić, “Geometric convergence of distributed gradient play in games with unconstrained action sets,” IFAC-PapersOnLine, vol. 53, no. 2, pp. 3367–3372, 2020.

- [13] N. Cesa-Bianchi and G. Lugosi, Prediction, Learning, and Games. Cambridge University Press, 2006.

- [14] J. Abernethy, P. L. Bartlett, A. Rakhlin, and A. Tewari, “Optimal strategies and minimax lower bounds for online convex games,” in COLT’08: Proceedings of the 21st Annual Conference on Learning Theory, 2008.

- [15] B. Duvocelle, P. Mertikopoulos, M. Staudigl, and D. Vermeulen, “Multiagent online learning in time-varying games,” Mathematics of Operations Research, 2022.

- [16] K. Lu, H. Li, and L. Wang, “Online distributed algorithms for seeking generalized Nash equilibria in dynamic environments,” IEEE Transactions on Automatic Control, vol. 66, no. 5, pp. 2289–2296, 2021.

- [17] Y. Viossat and A. Zapechelnyuk, “No-regret dynamics and fictitious play,” Journal of Economic Theory, vol. 148, no. 2, pp. 825–842, 2013.

- [18] P. Mertikopoulos, C. Papadimitriou, and G. Piliouras, “Cycles in adversarial regularized learning,” in Proceedings of the Twenty-Ninth Annual ACM-SIAM Symposium on Discrete Algorithms. SIAM, 2018, pp. 2703–2717.

- [19] A. Heliou, J. Cohen, and P. Mertikopoulos, “Learning with bandit feedback in potential games,” Advances in Neural Information Processing Systems, vol. 30, 2017.

- [20] X. Cao and K. J. R. Liu, “Online convex optimization with time-varying constraints and bandit feedback,” IEEE Transactions on Automatic Control, vol. 64, no. 7, pp. 2665–2680, 2019.

- [21] X. Yi, X. Li, T. Yang, L. Xie, T. Chai, and K. H. Johansson, “Distributed bandit online convex optimization with time-varying coupled inequality constraints,” IEEE Transactions on Automatic Control, 2020, DOI: 10.1109/TAC.2020.3030883.

- [22] M. Bravo, D. Leslie, and P. Mertikopoulos, “Bandit learning in concave -person games,” in Proceedings of the 32nd International Conference on Neural Information Processing Systems (NeurIPS), 2018, pp. 5666–5676.

- [23] P. Mertikopoulos and Z. Zhou, “Learning in games with continuous action sets and unknown payoff functions,” Mathematical Programming, vol. 173, no. 1, pp. 465–507, 2019.

- [24] X. Li, L. Xie, and Y. Hong, “Distributed aggregative optimization over multi-agent networks,” IEEE Transactions on Automatic Control, vol. 67, no. 6, pp. 3165–3171, 2022.

- [25] F. Salehisadaghiani and L. Pavel, “Distributed Nash equilibrium seeking: A gossip-based algorithm,” Automatica, vol. 72, pp. 209–216, 2016.

- [26] L. M. Bregman, “The relaxation method of finding the common point of convex sets and its application to the solution of problems in convex programming,” USSR Computational Mathematics and Mathematical Physics, vol. 7, no. 3, pp. 200–217, 1967.

- [27] E. C. Hall and R. M. Willett, “Online convex optimization in dynamic environments,” IEEE Journal of Selected Topics in Signal Processing, vol. 9, no. 4, pp. 647–662, 2015.

- [28] M. J. Neely and H. Yu, “Online convex optimization with time-varying constraints,” arXiv preprint arXiv:1702.04783, 2017.

- [29] F. Facchinei and J.-S. Pang, “Nash equilibria: The variational approach,” Convex Optimization in Signal Processing and Communications, pp. 443–449, 2010.

- [30] S. Liang, P. Yi, and Y. Hong, “Distributed Nash equilibrium seeking for aggregative games with coupled constraints,” Automatica, vol. 85, pp. 179–185, 2017.

- [31] L. Pavel, “Distributed GNE seeking under partial-decision information over networks via a doubly-augmented operator splitting approach,” IEEE Transactions on Automatic Control, vol. 65, no. 4, pp. 1584–1597, 2020.

- [32] A. A. Kulkarni and U. V. Shanbhag, “On the variational equilibrium as a refinement of the generalized Nash equilibrium,” Automatica, vol. 48, no. 1, pp. 45–55, 2012.

- [33] A. Nedić and A. Ozdaglar, “Approximate primal solutions and rate analysis for dual subgradient methods,” SIAM Journal on Optimization, vol. 19, no. 4, pp. 1757–1780, 2009.

- [34] X. Yi, X. Li, L. Xie, and K. H. Johansson, “Distributed online convex optimization with time-varying coupled inequality constraints,” IEEE Transactions on Signal Processing, vol. 68, pp. 731–746, 2020.