Supportive Fintech for Individuals with Bipolar Disorder: Financial Data Sharing Preferences to Support Longitudinal Care Management

Abstract.

Financial stability is a key challenge for individuals living with bipolardisorder (BD). Symptomatic periods in BD are associated with poor financial decision-making, contributing to a negative cycle of worsening symptoms and an increased risk of bankruptcy. There has been an increased focus on designing supportive financial technologies (fintech) to address varying and intermittent needs across different stages of BD. However, little is known about this population’s expectations and privacy preferences related to financial data sharing for longitudinal care management. To address this knowledge gap, we have deployed a factorial vignette survey using the Contextual Integrity framework. Our data from individuals with BD (N=480) shows that they are open to share financial data for long term care management. We have also identified significant differences in sharing preferences across age, gender, and diagnostic subtype. We discuss the implications of these findings in designing equitable fintech to support this marginalized community.

1. Introduction

Bipolar disorder (BD) is a serious mental illness characterized by periods of mania and depression. A chronic illness with no known cure, BD requires life-long management of symptoms varying in intensity through time. BD ranks as the sixth leading cause of disability globally (Murray, 1996) and carries significant macroeconomic impacts. A 2015 analysis estimated its total costs in the US economy to be $202.1 billion, amounting to $81,559 per individual (Cloutier et al., 2018; Bessonova et al., 2020). While BD has been associated with an increased capacity for creativity (Greenwood, 2020), its disruptive impacts are often significant and long-lasting.

Financial difficulties are so frequently associated with symptomatic periods of BD that the American Psychiatric Association includes anomalous spending or otherwise risky financial behaviors among its diagnostic criteria (American Psychiatric Association, 2013). A recent population-scale study found that individuals with BD type I were 50% more likely to declare bankruptcy than the healthy comparison group (Nau et al., 2023). Money-related factors like these have been shown to contribute to a worsening of mental health symptoms, including lower self-esteem and debt-related anxiety (Richardson et al., 2021).

We believe these challenges pose an unmet call to design data-driven tools to support financial stability throughout the course of illness. Prior work has demonstrated that financial technologies can be appropriately situated within the lives of individuals with mental illness (Barros Pena et al., 2021a; Blair et al., 2022), including in ways that support third-party collaboration (Barros Pena et al., 2021b). Open banking technologies now afford researchers the access to financial data granularity necessary to create systems that can deliver timely, personalized support for these highly individualized needs.

However, we do not yet know if individuals with BD are comfortable sharing their financial data to support longitudinal care management. To this end, we deployed a large-scale international survey (n=480) to explore the financial data sharing preferences of individuals with BD. We used a factorial vignette design to understand sharing preferences across different contexts: how much financial information is shared, with whom it is shared, and for what purposes. To complement these insights, we also asked participants about their current financial management strategies and how their care partners have helped them manage spending behaviors. In this work we present both quantitative and qualitative findings to highlight the complex needs and attitudes toward financial data sharing that exist within this population.

Overall, participants were most comfortable using financial data for self-management (i.e., sharing data with only themselves), followed by sharing with clinicians, and then family. However, there were some demographic differences in these sharing preferences. In particular, those who were married or had children were more likely to be comfortable sharing financial data with families. Conversely, women were considerably less likely to share financial data with family. Despite, these responses to vignette scenarios, open-ended responses showed that the majority of participants involved their care partners in managing their finances, to varying degrees, from having full control of their bank accounts to offering occasional financial advice.

Based on these insights, we establish that individuals with BD are interested in using financial data for long-term BD management. However, there are complex privacy needs and risks that must be considered when designing support systems built on financial data sources. We also discuss design recommendations for using financial data to support long-term BD management. More specifically, financial data sources show promise to support BD self-management, improve financial decision-making and literacy, assist with care partner collaboration, and integrate into existing clinical practices.

2. Related Work

2.1. Money Issues and Mental Health

The interrelationship between money and mental illness is complex and limited by scarce longitudinal assessment methods. A review of existing literature reveals multiple theories to frame these relationships. For example, the social drift hypothesis identifies mental health problems as a causal influence of financial difficulties, while the social causation hypothesis states that negative financial circumstances create the conditions for mental health issues to develop (Ljungqvist et al., 2016). Despite this theoretical disagreement, strong correlations have been demonstrated between financial issues (debt, specifically) and mental illness. In a nationally representative sample of England, Scotland, and Wales, debt was three times more common in individuals with common psychiatric disorders and four times more common for those individuals living with psychosis (Jenkins et al., 2008). However, relying on patient self-report to account for debt remains challenging for many studies. Feelings of shame or guilt may lead a patient to underreport debt and other borrowing behaviors, while more severe conditions like psychosis may result in a patient’s diminished capacity to understand financial issues altogether (Jenkins et al., 2008).

Several authors have identified the need to overcome these limitations in part to more adequately understand how and when to intervene. For example, Richardson et al. addressed the need for “longitudinal studies to determine causality and establish potential mechanisms and mediators of the relationship” (Richardson et al., 2013) between unsecured debt and mental health. Others have called for “standardized measures of financial hardship which adequately measure the nature and severity of stressor causes” (Frankham et al., 2020).

2.2. Bipolar Disorder and Money

As noted earlier, the American Psychiatric Association considers risky or impulsive financial behavior a diagnostic criteria of this illness. While the exact manifestations of these behaviors are highly individuated, prior work has shown that common patterns of impulsivity in spending exist during symptomatic periods for patients with BD. Richardson, et al. noted a “vicious cycle” where impulsive spending caused anxious states which led to additional impulsive spending. More recent work explored the temporal relationships between impulsive spending and other financial difficulties for patients with bipolar disorder: A number of psychological variables (dysfunctional assumptions surrounding one’s capacity for achievement, for example) remained correlated with financial variables throughout time (Richardson et al., 2021). This study was the first to empirically show a potential link between characteristic dysfunctional assumptions of BD (here, grandiosity) and impulsive spending.

In addition to the influence of these psychological variables, research has shown that impulsive spending can be attributed to a lack of mindful awareness during episodic states (Richardson et al., 2013). Some patients intentionally develop compensatory strategies to manage their capacity for attention and self-awareness by deliberately attempting to slow their cognition (Cheema et al., 2015). Murnane, et al. reported similarly deliberate attempts at self-regulation, documenting that patients reflected on longitudinally-collected personal informatics data to compare their current state to a documented baseline (Murnane et al., 2018). These examples signal a willingness of patients to employ various techniques to maintain vigilance over symptomatic relapse.

2.3. The Shared Costs of Crisis in Bipolar Disorder

There is good reason for patients to expend this energy on monitoring and self-regulation. A relapse can dramatically reconfigure entire families in a brief period of time. As described by Reinares, et al., “the illness not only affects the patient but also their relatives, who suffer the consequences of the episodes and usually become the main caregivers. Every new relapse is a stressful event that generates painful emotions, disrupts the patient’s life and familial equilibrium leading to changes in the roles of each member, and requires the development and adjustment of coping strategies” (Reinares et al., 2016).

Some patients willingly anticipate and plan for these relapses in order to minimize their impacts. The non-trivial role of early-warning signs detected by these acts of vigilance have been documented in recent personal informatics literature and may involve the attention and discretion of family members. Some families have constructed and employed “emergency plans” based on symptom severity with the help of their therapists (Murnane et al., 2018). To quote one such participant’s deliberate instructions, “If I start pacing a lot, if I want some money, if I start drinking again. That’s stage one. Stage two - I’m just not paying attention to you, still pacing, and I’m giddy - that’s when you need to take me to the hospital.” It is revealing that this participant specifically mentioned the role that money plays in their plans. This “staged” approach to planning is also referenced in financial capacity literature, with a call for “spontaneous delegation” of specific financial tasks to caregivers only during periods of diminished capacity (Dunphy et al., 2014).

2.4. On Financial Peer Support

Prior work on financial intervention design has shown that goal-oriented interventions are among the most effective and engaging (Jiménez-Solomon et al., 2016), and that the inclusion of self-prescribed goals or parameters in algorithmic interventions are among the most strongly called for in existing literature (Farr et al., 2019). Kameswaran, et al. explored the nature of financial collaboration work between family and friends and individuals with vision impairments, noting the importance of obtaining the “right help at the right time” (Kameswaran and Muralidhar, 2019), adding that participants did not report collaboration as “impinging on their sense of independence, likely because of the lack of other ways to work around the challenge of inaccessible [financial] notes, which made seeking help a necessity.” In fact, third-party financial control may be desired by some individuals with serious mental illness (Harper et al., 2018). The social nature of financial health is further clarified by Snow, et al. who note the “importance of social connections in overall financial wellbeing and identifies people’s capacity to live well and share, regardless of their financial circumstances” (Snow et al., 2017).

2.5. Care Partner Responsibilities

As referenced in prior sections, Reinares, et al. identify “financial hardships” as an objective burden to caregivers of individuals with BD (Reinares et al., 2014), and Targum, et al. found that financial difficulties were among the most troubling consequences of this illness for both patients and their spouses (Targum, 1981). Writing in the context of psychotic disorders, Labrum, et al. warn against the supportive actions of family possibly resulting in the infringement of a patient’s autonomy, stating that mental health professionals should assess a financial intervention’s “impact on persons with psychotic disorders, their family members, and the quality of [these] relationships” (Labrum, 2018). The potential impact on caregivers is addressed more directly by Brown, et al.: “Trusted others who are concerned for the individual […] often experience decline in mental wellbeing that can present itself as a similar kind of suffering” (Brown and Choi, 2017), noting the need for reciprocal support as an antidote to this decline.

2.6. The Opportunities of Open Banking Technologies

2.6.1. The Moneywork Framing

The Moneywork literature explores the social nature of financial behaviors occurring throughout the process of a transaction (Perry and Ferreira, 2018). As noted earlier in this review, this framing has been extended to the study of supportive behaviors for individuals with disabilities (Kameswaran and Muralidhar, 2019). The authors noted that participants’ perceived necessity for aid fostered trust between these individuals and their collaborators. The authors went on to cite the role of “articulation work”, or of supportive, pre-transactional activities, to make cash available for individuals with vision impairments to conduct their business endeavors.

2.6.2. Financial Intervention Design

Prior work by Farr, et al. articulates (1) the pressing need for banking institutions to offer supportive features for individuals with mental illness, and (2) that many individuals with mental illnesses require support some of the time. The authors define third-party supportive behaviors by drawing an important distinction between monitoring behaviors, such as view-only access to financial statements, and controlling behaviors, such as payee relationships or self-imposed spending limits. Several supportive features are recommended for institutions sympathetic to these issues: Institutions might consider adding frictions to spending such as self-imposed limits to debit card usage, or the ability to set a “cooling off” period for transactions of a certain dollar amount or made during specified hours. It is worth noting the concept of frictional “microboundaries” exists elsewhere in HCI literature as a means of encouraging “mindful reflection” (Cox et al., 2016) in order to slow down the actions of a user, which the authors suggest may prompt individuals to engage in more intentional actions.

2.6.3. Financial Collaboration in Mental Health

In a sense, extending “articulation work” towards mutual collaboration around harm-reducing financial management activities in the context of this illness is the work of this proposal. This is not completely without precedent. Barros Pena, et al. extended moneywork to third-party access in mental health contexts (Barros Pena et al., 2021b). The authors used the UK Open Banking API to create and deploy a third-party financial access tool, recruiting 14 individuals who self-identified as living with a mental health condition. These individuals each chose a “trusted ally who received notifications when certain transactions took place” in their bank accounts. The notable contributions of this work point “beyond discourses of protection and control in order to enable meaningful financial collaboration.” They note that “moneywork, as conceptualized in HCI literature, can thus provide a useful framework for the study of the added labour taking place within the cycle of mental illness and financial hardship.”

Despite what this body of research tells us of the cyclical relationship between money and mental health, the increased support needed for long-term BD management, and the new opportunities financial technologies can provide—little is known from the perspectives of individuals with BD. While financial data may provide additional insight on key symptomatic behaviors of BD and help inform interventions, it is unclear how comfortable individuals with BD may be with using financial data for these purposes. Moreover, individuals with BD may have different attitudes toward sharing financial information with others. Our work addresses these important research gaps towards developing supportive fintech that is sensitive to the unique needs of those with BD.

To guide this exploratory study, we asked the following research questions:

-

(1)

How do individuals with BD feel about using their financial data for self-management of BD?

-

(2)

How do individuals with BD feel about sharing financial data with others?

-

(3)

How do their data sharing attitudes change regarding the a) recipient, b) context of use, and c) data type?

-

(4)

How do individuals with BD currently involve care partners in their financial management strategies?

3. Methods

This study focuses on identifying privacy norms, preferences, and expectations related to financial data sharing for longitudinal care management in BD. Toward this goal, we designed and deployed an online survey to collect data from individuals with BD. In the following sections, we describe the survey design, data collection process, and analysis steps.

3.1. Survey Design

We used the Contextual Integrity (CI) framework (Nissenbaum, 2004) for the survey. Recent studies have successfully used the CI framework to assess privacy norms and concerns regarding health data sharing (Silber et al., 2021; Utz et al., 2021). The CI framework theorizes that privacy norms surrounding information transfers are determined by both i) appropriateness of information sharing in a given context; and ii) recipients of shared information. Following the CI framework, the survey used a factorial vignette design (Finch, 1987). Survey participants are asked to provide privacy rating of hypothetical scenarios. Each scenario can include multiple factors representing individual elements of the CI framework (e.g., data types, context of uses, and data recipients). The factorial vignette approach systematically varies these factors to assess which contextual factors might impact privacy norms and data sharing preferences. Furthermore, it allows determining relative importance of these factors across different subgroups. Prior work has used factorial vignette design to understand contextual privacy (Silber et al., 2021; Utz et al., 2021).

3.1.1. Vignettes

To design the vignettes, we iteratively selected contextual factors and their associated values. We used prior work to identify potentially relevant factors including type of financial account, granularity of collected financial data, duration of data storage, and primary and secondary contexts of use. We then selected down most important factors through discussion among authors.

These selected factors included: (1) actors — recipients of information; (2) contexts of data use; and (3) data granularity. We also identified relevant levels for each of this factors. The survey used 3 factors each containing 3 levels resulting in a total of 27 vignettes. Table LABEL:tbl-factors lists these factors and their respective levels. Each hypothetical vignette was then created using the following template: “An app accesses [Granularity] so it can [Context]. This app will share these insights with [Recipient].” We chose a full-factorial design for the survey with each participant rating all vignettes. For each vignette, participants rated their level of comfort when sharing financial data on a scale of 0–10, where 0 is “extremely uncomfortable” and 10 is “very comfortable”.

| Factor | Level |

|---|---|

| Actor (Recipient) | You |

| Family | |

| Clinician | |

| Context of use | To predict relapse |

| To compare mood logs with spending behavior | |

| To identify distinct changes in spending | |

| Granularity (Data type) | All purchase details |

| Purchase timing and category | |

| Purchase timing and amount |

3.2. Questionnaire Survey

The following details our survey questions in the order they were asked of participants.

Demographics

First, we described the purpose of our study, defined eligibility criteria, and prompted participants for their consent to proceed. We prompted participants for their age, gender, ethnic background, marital status, and education levels. Then, we prompted for their country of residence.

Financial Environments

We asked about their employment status and information related to their annual individual income excluding welfare or benefits, whether they had access to a financial institution, how often they check their account balances, and what methods they use to review their spending behaviors. We prompted individuals to self-report their debt in their local currency. However, due to high levels of missing data, we did not include this section in our analysis. Additionally, participants rated their agreement towards a series of statements regarding financial hardship, worry, and anxiety. We also prompted for the perceived frequency, volume, and category of their online transactions when using a credit/debit card, amount and nature of purchases they made with cash, and their usage patterns of money-related digital technologies.

BD related Spending Behaviors

Following this, we prompted users to consider whether their spending changes during manic or depressive episodes, in what specific ways and about their specific goals for these types of spending. We also asked participants whether they have ever (1) considered bankruptcy or (2) had ever declared bankruptcy due to large purchases or impulsive spending occurring during a manic episode.

Financial Management Strategies

To better understand their current practices of self-management and collaborative management of impulsive financial behaviors, we asked individuals whether they actively attempt to reduce or prevent impulsive spending, what strategies they make use of towards those goals, if/how they have involved family or friends to help prevent impulsive spending, and whether they would be willing to rely on technology or their creditors to help impede overspending.

Vignettes

As described in Section 3.1.1, we then concluded the survey by presenting participants with a total of 27 hypothetical scenarios to determine their level of financial data sharing preferences across three dimensions of the CI framework—actor (recipient), context of use, and granularity (data type).

3.3. Deployment

We deployed the survey in the United States, Ireland, and the United Kingdom between July 2022 to May 2023. We focused on these countries due to institutional access available to authors. Furthermore, we wanted to explore potential differences in privacy norms and expectations across different geographical regions. We shared the survey through social media and distribution channels of several international organizations including the Depression and Bipolar Support Alliance (DBSA) and Bipolar UK. The survey collected data from individuals with self-reported bipolar diagnosis, which is consistent with prior work on this population (Matthews et al., 2017b; Hindley et al., 2019).

3.4. Ethics

The study was approved by Institutional Review Board and Ethics committee at [redacted]. Furthermore, we followed relevant data protection guidelines including the General Data Protection Regulation (GDPR) from European Union.

3.5. Data Analysis

To better understand the complexity of financial data sharing preferences, we took a mixed methods approach to analysis. We conducted statistical analyses on participant vignette responses to determine attitudes toward the hypothetical financial data sharing scenarios. We used a qualitative, thematic analysis to understand the current ways participants actively engaged with their care partners to manage their financial decisions.

3.5.1. Statistical Analysis

We used R for the data analysis. The vignette survey data has a hierarchical structure given each respondent answered all vignettes. We used multilevel modeling (lme4) to account for the nested data structure. The resulting raw Qualtrics dataset was preprocessed to maintain a “long” format compatible with the requirements of lme4. Our response variable (y in the formula given in supplementary material) is the numerical rating for each vignette permutation.

Model Selection

We followed best practice guidance (Zuur et al., 2009; Meteyard and Davies, 2020; Baguley et al., 2022) during model creation, selection, and validation. Specifically, we modeled unconditional means using maximum likelihood (ML) in order to assess the variance of random effects, initially chosen based on sampling unit (e.g., participant and vignette item). We defined a maximal model to include closed-ended factors for analysis and set random intercepts per respondent. We used buildmer (Voeten, 2019) to perform backwards variable selection. Model selection was performed by iteratively removing non-significant factors based on the Bayes information criterion (BIC) of the resulting models. BIC has been shown to choose models that are more parsimonious than alternative methods (Neath and Cavanaugh, 2012) during model selection, making it an appropriate choice for our exploratory analysis. Visual inspection of residual plots did not show obvious deviations from homoscedasticity or normality. The final maximal model formula can be found in our supplementary materials.

Estimated Marginal Means

We performed unplanned post-hoc tests to explore differences between factor levels. To this end, we used emmeans (Lenth, 2023) to compute estimated marginal means at all factor levels. In emmeans, estimated marginal means are computed by holding all numeric covariates at their means, then averaging across a balanced grid of categorical predictors (Heiss, 2022). To further understand differences between factor levels, we used the contrast() function in emmeans to calculate differences between marginal means. We report these estimated marginal means (EMM) and their comparisons in the sections that follow.

3.5.2. Thematic Analysis

For the open-ended questions in this survey, we used a bottom-up thematic analysis and open coding to attach relevant labels to survey responses (Braun and Clarke, 2019). To understand the role of care partners and the collaborative strategies respondents currently use, we reviewed responses to the following questions:

-

•

What strategies have you used to reduce or prevent spending?

-

•

How have family or friends helped you prevent spending?

-

•

What other techniques have you used to reduce the risk of impulsive spending?

First, we applied this process to responses for each individual survey question and then expanded to address persistent themes across all questions asked. Through further iterations, we collapsed these initial labels into categories until they solidified across all survey questions and responses. The resultant themes reached Glaser and Strauss’ data saturation standards for qualitative studies using Grounded Theory (Glaser and Strauss, 2017). In other words, these themes remained persistent with no additional findings or variation throughout the full data set.

3.5.3. Positionality Statement

The first and second author lead the development the survey questionnaire and analysis protocols, with the insight of other authors throughout each stage. The first author conducted the quantitative analysis of the factorial vignettes, while the second author lead the qualitative thematic analysis, based on their prior experience and expertise. Both analyses were reviewed by the research team. Two authors have lived experience with bipolar disorder, which afforded unique perspectives into the development of the survey and the insights provided by participants. Authors 1, 2, 4, and 7 all have experience designing and developing technologies within health contexts and for underrepresented or stigmatized populations. Three clinicians with significant experience with bipolar disorder research and clinical practice were involved this the development of the survey and interpreting the subsequent results (authors 3, 5, and 6). By establishing high levels of agreement among an interdisciplinary research team, we aim to ensure the robustness and replicability of our work.

4. Results

This section describes the outcomes of our quantitative and qualitative analysis. We first describe the participant demography. Next, we report the norms and preferences in sharing financial data. We also identify how different contextual and demography factors impact sharing preferences. Finally, we describe findings from our thematic analysis of open-ended survey questions involving strategies for self-management and collaborative decision-making.

4.1. Demography

The survey population included individuals with different diagnostic subtypes of BD. We collected data from individuals with BD type I (38%), bipolar disorder type II (40%), BD not otherwise specified (14%), and cyclothymia (6.5%). 6.5% of respondents did not know their diagnostic subtype. Majority of the participants (96%) had access to bank accounts (i.e., “banked individuals”). 21% of participants reported having declared bankruptcy due to impulsive spending during manic episodes, while 37% reported having considered declaring bankruptcy for the same reason. This is consistent with prior work on higher likelihood of experiencing bankruptcy in BD (Nau et al., 2023).

The survey respondents were most likely to have completed a 4-year university degree (38%) and to live in an urban environment (48%). Most individuals reported being single and having never married (31%), while 29% reported being married with children and 13% were married without children. The survey population included 64% individuals who identified as female, 32% as male, 3.1% as non-binary, and 0.3% preferred to not describe their gender. The majority of the survey respondents were white (88%) and 16% describe their ethnic background as Hispanic in origin. Respondents were from the United States (42%), the United Kingdom (39%), or Ireland (11%), while 8% did not identify their country of origin. Neither ethnicity nor country were found to be significant in our full model. We have provided detailed demographic information as a supplementary document.

4.2. Privacy Norms for Sharing Financial Data to Support Longitudinal BD management

Overall, participants were willing to share financial data to support longitudinal BD management. The mean rating for all vignettes was 6.1 (SD=3.12) in a 0—10 scale (0 = ‘extremely uncomfortable’, 10 = ‘very comfortable’). Figure 1 shows overall distribution of privacy ratings across different recipients and data granularity. Participants were most comfortable to share data with themselves as expected. Data sharing scenarios with family members and clinicians received high average ratings as well indicating overall acceptance by our participants. We have included descriptive statistics for all vignettes in supplementary materials.

A faceted categorical box plot showing comfort ratings on the Y axis and data granularity categories on the X axis. The plot is faceted by data recipient (actor). For each facet, comfort ratings are shown on a scale of 0–10 for three data granularities. Participants were most comfortable sharing for self-review across all data granularities.

4.2.1. Factors Impacting Financial Data Sharing Preferences

Following the CI framework, we explored relative importance and impacts of contextual factors in financial data sharing preferences.

Actors

Among the contextual factors, we have found actors (data recipients) to be consistently significant in determining data sharing preferences. Participants were most comfortable sharing financial data with themselves (EMM=7.44, SE=0.12). They were relatively less comfortable sharing financial data and insights with clinicians (EMM=5.44, SE=0.12) and their families (EMM=4.94, SE=0.12). Tukey pairwise comparisons showed that sharing for one’s own review predicted higher levels of comfort when compared to sharing with clinicians (estimate=2.0, SE=0.06, p=.00) and sharing with family members (estimate=2.5, SE=0.06, p=.00). This implies that individuals with BD are most comfortable sharing financial data for their own review in self-management activities.

Contexts of Use

Context of use was not a significant factor in our data set. Estimated marginal means were similar across different contexts of use scenarios — comparing mood logs to spending habits (EMM=5.96, SE=0.12), identifying distinct changes in spending (EMM=5.96, SE=.0.12), and predicting relapse (EMM=5.89, SE=0.12). No significant pairwise differences were shown in these factor levels. In other words, participants were not concerned about how financial data might be used when it comes to supporting longitudinal BD management.

Financial Data Granularity

However, granularity of financial data was an important factor in sharing preferences. Individuals were most comfortable sharing the amount and timing of transactions (EMM=6.01, SE=0.12) and slightly less comfortable sharing category and timing (EMM=5.96, SE=0.12) or all transaction details (EMM=5.84, SE=0.12). Contrast analysis for these factor levels shows a significant negative effect when sharing all transaction details (estimate=-0.97, SE=0.03, p=.01). This suggests that participants are less comfortable sharing all available transaction details. A Tukey pairwise comparison showed a significant difference between sharing all transaction details and sharing the amount and timing of transactions (estimate=-0.171, SE=0.57, p=.00). These results suggest that financial data granularity can impact sharing preferences with our participants being more comfortable sharing only the amount and timing of transactions.

4.2.2. Differences in Sharing Preferences Across Subgroups

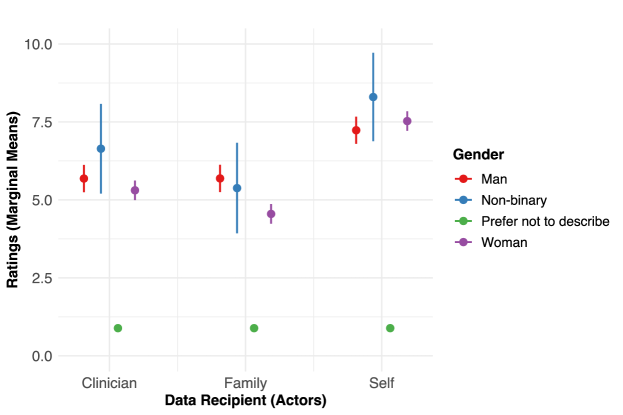

An interaction plot showing estimated marginal means of participant comfort ratings by self-identified gender. Data Recipients (Actors) are on the X axis. Estimated marginal means of comfort ratings are on the Y axis. A legend lists ”Man”, ”Woman”, ”Refer not to describe”, and ”Non-binary”. Each legend item is displayed for each data recipient category.

We also explored how demography differences might impact financial data sharing preferences. In our dataset, young adults (aged 18–24) were most comfortable sharing financial data with themselves (EMM=8.73, SE=0.40) and their clinicians (EMM=6.29, SE=0.40). However, they were less comfortable in sharing data with their family members (EMM=4.26, SE=0.40). Individuals in mid-life (aged 35–44) similarly reported higher levels of comfort reported in sharing data with themselves (EMM=7.76, SE=0.24) and their clinicians (EMM=5.86, SE=0.25). However, they were also more comfortable in sharing with family members (EMM=5.66, SE=0.25) compared with young adults. We conducted a contrast analysis of estimated marginal means, which further confirms the willingness to share with family members of this group to be significant (estimate=0.66, SE=0.42, p=.03). Moreover, participants were more comfortable sharing with family when they were married with children (EMM=5.76, SE=0.23) or living with a partner (EMM=5.50, SE=0.38). However, only the effect of being married with children was significant in a contrast analysis (estimate=0.96, SE=0.32, p=.03). No other marital statuses were found to be significant factors in our analysis.

We found gender differences in willingness to share financial data as well. Overall, women were comfortable sharing financial data with themselves (EMM=7.59, SE=0.15). However, they reported to be considerably less willing to share financial data with family members (EMM=4.61, SE=0.15). A Tukey pairwise comparison further revealed women were significantly less comfortable sharing with their family members than men (estimate=-1.14, SE=0.27, p=.00). These differences are visualized in Figure 2. Such gender differences in financial data sharing preferences has potentially important implications for designing supportive fintech for this population.

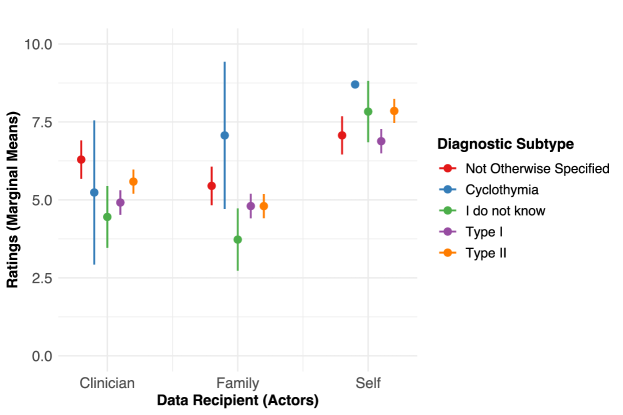

We also analyzed sharing preferences across BD subtypes. Individuals with BD type II were comfortable sharing financial data with themselves (EMM=7.93, SE=0.19) and with clinicians (EMM=5.66, SE=0.19). However, they were less comfortable sharing with their family members (EMM=4.87, SE=0.19). On the other hand, individuals with BD type I were in general less willing to share financial data compared with other diagnostic subtypes including with themselves (EMM=6.96, SE=0.20), with family (EMM=4.88, SE=0.20), and with clinicians (EMM=4.99, SE=0.20). There was a significant difference across BD type I and type II in willingness to share data with themselves (estimate=-0.97, SE=0.27, p=.00). This finding is consistent with prior work on the differences between BD diagnostic types. Bipolar disorder type I is associated with tendencies towards paranoia (Látalová, 2009), which can potentially influence their sharing preferences and privacy expectations for financial data. Figure 3 visualizes group differences between diagnostic subtypes across data recipients.

An interaction plot showing estimated marginal means of participant comfort ratings by diagnostic subtype. Data Recipients (Actors) are on the X axis. Estimated marginal means of comfort ratings are on the Y axis. A legend titled ”Diagnostic Subtype” shows 5 items: ”Not Otherwise Specified”, ”Cyclothymia”, ”I do not know”, ”Type I”, and ”Type 2”. Each legend item is displayed for each data recipient category.

4.2.3. Data Sharing Preferences and Willingness to Accept External Support for Financial Stability

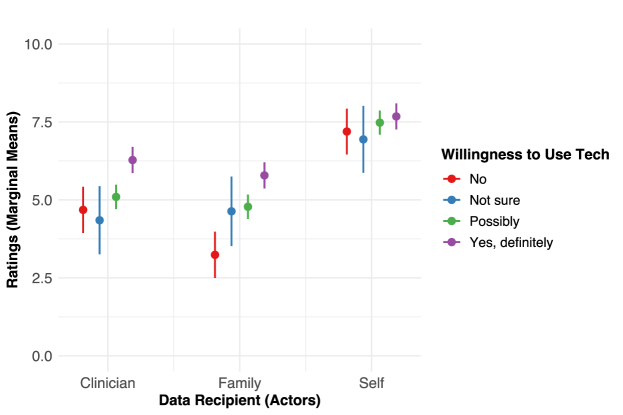

An interaction plot showing estimated marginal means of participant comfort ratings by willingness to use technology to impede overspending. Data Recipients (Actors) are on the X axis. Estimated marginal means of comfort ratings are on the Y axis. A legend titled ”Willingness to Use Tech” shows 4 items: ”No”, ”Not sure”, ”Possibly”, ”Yes, definitely”. Each legend item is displayed for each data recipient category.

We investigated how willingness to use external support for financial stability might relate to data sharing preferences for individuals with BD. In our data set, participants willing to rely on technology or their creditors to prevent overspending were among the most comfortable sharing financial data. Participants who responded “Yes, definitely” to being willing to rely on technology to prevent overspending were highly comfortable sharing data with themselves (EMM=7.73, SE=0.21), with family (EMM=5.86, SE=0.21), and with clinicians (EMM=6.33, SE=0.21). Willingness to rely on creditors to help prevent overspending also reflected a similar pattern of high acceptance of sharing financial data with themselves (EMM=7.76, SE=0.23), with family (EMM=6.27, SE=0.23), and with clinicians (EMM=6.69, SE=0.23).

These differences were significant in both cases. Those who responded “Yes, definitely” to technological help with overspending were more likely to share with family (estimate=1.50, SE=0.22, p=.00) and with clinicians (estimate=1.53, SE=0.22, p=.00). Those who responded “Yes, definitely” to help from creditors with overspending were more likely to share with family (estimate=1.18, SE=0.24, p=.00) and to share with clinicians (estimate=1.18, SE=0.24, p=.00). No significant differences were found when sharing with oneself.

Participants who were unwilling to adopt these external support were significantly less comfortable in sharing financial data. Individuals unwilling to use technology to impede overspending were significantly less likely to be comfortable sharing with family (estimate=-1.37, SE=0.33, p=.00) and less comfortable sharing with clinicians. Although this difference was not significant (estimate=-0.42, SE=0.32, p=.26), we identify significant differences between response groups as described below. Participants unwilling to allow creditors to impede overspending were also less comfortable sharing with family (estimate=-0.84, SE=0.25, p=.00) and with clinicians (estimate=-0.50, SE=0.25, p=.06).

The differences in these groups (i.e., between “No” and “Yes, definitely”) were significant. With respect to willingness to rely on technology, a Tukey pairwise comparison between these response groups resulted in significant differences in family sharing (estimate=-0.25, SE=0.43, p=.00) and when sharing with clinicians (estimate=-1.60, SE=0.43, p=.00). With respect to willingness to rely on creditors, a Tukey pairwise comparison showed similar patterns. Differences between these two response groups were significantly lower in family sharing (estimate=-2.32, SE=0.36, p=.00) and in clinician sharing (estimate=-2.03, SE=0.36, p=.00). Figure 4 shows the differences in sharing preferences across these subgroups.

4.3. Collaborative Interactions and Strategies to Sustain Financial Stability

We conducted a thematic analysis of open-ended survey responses to better understand the current practices and challenges in collaborative financial management for individuals with BD. The majority of respondents reported involving their family or friends to help manage their spending decisions and overall finances. Specifically, half of the survey respondents reported actively involving others to help prevent impulsive spending. Participants engaged in a broad spectrum of collaborative interactions to support their financial wellbeing, ranging from disclosing financial information to relinquishing complete control to their care partners.

4.3.1. Levels of Financial Collaboration

Care partners were sometimes provided direct financial assistance to sustain longitudinal financial stability for individuals with BD. Specifically, family members might pay off debts or loan money to improve their financial situation. Such assistance might also include longitudinal monitoring and management over time by care partners. For example, P34 noted: “my mom helped me pay off a lot of credit card debt. After that she stayed on my account so she could semi monitor and make sure I don’t get into so much debt again.”

Participants also mentioned handing over some level of control in financial decisions to care partners. Many individuals had a spouse or a parent fully managing their individual or household finances on a long-term basis. One participant commented: “my husband takes care of the finances now. I do not have access to money” (P460). Others called on friends or family to take over their finances during the onset of symptomatic episodes. For example, P233 noted: “When I’m manic, I’ll transfer some of my money to a family member so I don’t have immediate access to it, preventing impulsive spending.” Some participants also took collaborative steps to prevent overspending for specific events. As P413 commented, they “have had friends been in charge of [their] wallet on nights out.”

Some participants maintain financial control, while allowing care partners to monitor their behaviors. Additionally, a care partner may have the password to their online banking account or a copy of their credit card statement but not the permissions to make or stop any transactions. This type of strategy was exemplified by P87 who had family members “watch out for any overly generous or excessive spending” or P442 who regularly“sent credit card statements to [her] husband.”

Some care partners took on the role of financial advisor. In this case, respondents might not give direct access to banking information, but shared details about their finances during regularly scheduled money talks or while asking for occasional advice. During these money talks, respondents and their care partners might check in about budgeting goals and overall progress. Respondents also sought out advice or approval prior to making specific financial decisions, such as especially large purchases. For example, P375 commented: “I find it helps if I talk to my spouse or other family/friends sometimes when I am considering a large purchase. It makes me pause and be more realistic.”

Care partners also devised specific strategies to ensure longitudinal financial stability of individuals with BD. P305 commented that “friends accompany me at home to make delicious food and other distractions.” Care partners might be able to identify early warning signs and spending triggers of individuals, which can lead to proactive collaborative interactions to maintain financial wellbeing of individuals with BD. As P472 noted: “My friends help me find alternatives when I’m really wanting an expensive new project.”

4.3.2. Financial Collaboration Strategies in Practice

Symptom severity and need for support change considerably across different stages in BD. Our dataset reflects the varying and intermittent needs of individuals with BD when it comes to financial collaboration. Many respondents did not rely on one collaboration strategy but switched between them over time or used them in tandem with each other as a safety net. This scaling up or down in care partner involvement would depend on their current need (e.g., symptom severity) and past success using these strategies. This scaling up process is exemplified by P99, “[My] partner has access to view [my] account. [He] has [the] ability to prevent access to [my] main account if needed.” This was especially the case for direct financial assistance. For example, some care partners would first provide financial assistance towards a respondent’s debt and then engage in monitoring behaviors to help them avoid having to do so again in the future. For instance, P351 commented:“My parents paid off a credit card and then took the card for a time so I wasn’t tempted to spend anything on it.”

4.3.3. Challenges for Financial Collaboration

Despite regularly using these strategies, responses show that these efforts are not always successful in practice. Participants reported that they would find ways to circumvent spending restrictions and collaborative management steps. For example P73 noted: “my husband manages our finances, but I still find ways around it.” Furthermore, collaborative strategies between some individuals with BD and their care partners were not consistently effective as noted by P106 “my husband double checks my bank account, tells me to stop spending. Sometimes I listen.”

For some, these financial management efforts can negatively impact interpersonal relationships. Some responses noted how closely their care partners watch their spending and their overall behaviors. Some participants also mentioned the level of judgment they felt from others stemming from such surveillance. For example, P350 commented “my spouse yells at me which does not help at all as it adds to my guilt”. Some participants mentioned constant surveillance of their spending behaviors by care partners (P35: “they’re always looking over my shoulder”). P451 also noted “my husband keeps a check on my spending—watching packages arrive, watching our vacations, watching my time on computer [and] phone.”

Some participants highlighted potential concerns regarding surveillance and losing control over their financial decision-making. For example, P187 commented: “I didn’t have a bank account so then [my] partner was meant to manage finances etc. Bad idea for all sorts of reasons [by the way].” Prior work has identified how surveillance can enable financial abuse (Bellini, 2023). These factors might explain our earlier findings regarding gender differences in sharing preferences — specifically, why women in general might feel less comfortable sharing financial data with their family members.

Participants also noted the lack of care partner expertise and understanding to adequately support their needs over different stages of BD. In some cases, friends or family simply did not see the need for extra support. P450 noted her failed attempt at asking for help: “I asked a friend to hold my debit card for me so that I could not use it without getting it from her, but she found it funny and told me to shop for myself and enjoy whatever I bought. It didn’t make sense to her.” Others had care partners who believed that managing their spending was something they should be able to do on their own. For example, P169 noted the lack of support from their partner: “I have asked my partner to take over my finances but he won’t because he thinks it’s a form of codependency”. Due to the lack of expertise and education, care partners may not understand the mechanisms driving these behaviors and the type of support needed to accomplish their goals. The resultant lack of support and understanding might cause further guilt and shame for individuals seeking out help.

4.3.4. Motivation for Financial Collaboration

The survey data also provides insights on why individuals with BD may be highly motivated to engage in collaborative financial interaction, despite the challenges it can present. To start, individuals may be in a situation where they need direct financial assistance to gain better footing before they can begin actively working toward financial stability. Specifically, individuals with BD might need such support following an episodic period, which can lead to high level of debt or even risk of bankruptcy (Nau et al., 2023). By paying off debts or loaning money, care partners provide individuals with a clean(er) slate and allow them to move toward better financial stability. Similarly, collaborative management steps including periodic monitoring can help towards longitudinal financial stability. As P124 commented:“My husband has taken my card, blocked PayPal, and then helped me set up a budget.” Participants also noted how collaborative interactions can lead to better informed decision-making over time. Individuals may be especially motivated to involve others when making large purchases or important financial commitments. For example, P63 commented: “If I’m getting too silly, mum will come shopping [with me] and be the voice [of] reason for me.”

Lastly, individuals may see their care partners as a source of new information and an opportunity to learn new financial skills, such as budgeting strategies or spending priorities. P112 noted how their care partners“help me ring-fence money so that I can’t easily spend [it] and will give honest input on big purchases.” Friends or family members may also share their own experiences and best practices, providing a blueprint for individuals who want to establish new financial behaviors and long-term goals.

5. Discussion

Our survey suggests that there is a high level of acceptance of using financial data for BD management. However, some demographic groups may be more hesitant to share their financial data with others. Despite this, the majority of respondents also reported actively involving friends and family in their financial management strategies. Following these findings, we discuss the unique privacy needs of individuals with BD. We also suggest potential directions for designing supportive financial technologies for this population including self-management, financial collaboration, clinical care, and financial literacy resources to support long-term stability. We also identify challenges and needs for risk mitigation in financial technologies aiming to support individuals with BD.

5.1. Privacy Norms and Sharing Preferences are Nuanced and Context Dependent

BD can lead to complex and highly individualized symptoms and behavioral outcomes. The resultant privacy needs and sharing preferences for financial data are varied and context dependent. Attitudes toward financial data sharing may change over time and context, may go against support needs, and be affected by perceived risks of financial abuse and exploitation. In the following sections, we discuss factors and contexts that might impact privacy norms and sharing preferences for financial data.

5.1.1. Changing Needs Over Time

Privacy norms are not static. Rather, they change over time and situational contexts. For individuals with BD, data sharing preferences may change over time in relation to their illness state, life stages, financial standing, and availability of support networks. Supportive fintech for this population must accommodate temporal and intermittent privacy norms occurring throughout the stages of illness. The role of temporal variation is significant for those living with BD (Moskalewicz and Schwartz, 2020). Prior work has documented how these states might be accommodated in the design of interfaces and clinical workflows (Hoefer et al., 2021; Matthews et al., 2017a). As such, it is important to consider how fintech can support inevitable changes in needs and preferences related to financial data sharing, disclosure, and collaboration over time.

5.1.2. Individuals who need help the most may be among the most reluctant to seek it out

Our findings also indicate how sharing preferences can lead to paradoxical outcomes. Specifically, individuals with BD type I were considerably less willing to share financial data to support longitudinal management. This is consistent with prior findings — BD type I is associated with paranoia (Látalová, 2009). However, this lack of willingness to engage in collaborative, supportive interactions might lead to financial instability and poor decision-making over time. Indeed, individuals living with BD type I are 50% more likely to declare bankruptcy. Reluctance to share data might also depend on the degree of financial difficulties faced by individuals. Considering the stigmatizing nature of financial hardship and debt, the resultant feelings of shame, guilt, or fear of judgment may make individuals less likely to share this information with others, even though they may stand to benefit most from additional care partner support. On the other hand, those with BD type II were more willing to share financial data to support longitudinal management. Tondo et al. (Tondo et al., 2022) reported that individuals with BD type 2 were more often employed, married, had children, and a reported a higher SES rating than other diagnostic types.

These findings indicate the need for highly personalized supportive systems that can adapt to individuals’ preferences and address access barriers. For example, a series of brief, highly targeted scenarios incorporating contextual privacy factors could later inform tailored guidance. Incorporating the framework of contextual privacy into an onboarding process could result in personalized recommendations related to data sharing preferences (i.e., what data types are collected, what they can be used for) and potential approaches to collaboration. In this way, a system could “meet users where they are at” in terms of privacy expectations and disclosure preferences.

5.1.3. Risk for Exploitation

While individuals with BD are open to engage in collaborative financial management, it is important to acknowledge the risk for exploitation when relinquishing financial control and access over to other people. Prior work has documented how technology can and has been used as a tool for financial abuse within the general population(Bellini, 2023). We note that several collaborative management practices reported by our participants—though not inherently malicious—share some similarities with Bellini’s taxonomy of how abusers might use technology to attack survivors’ finances(Bellini, 2023). While this prior work highlights the common motivations of restricting access, monitoring activities, and “sabotaging” independence as a means of control, our findings show that similar approaches are often taken by care partners to provide support or actions actively requested by individuals with BD to help prevent impulsive spending and future debt.

The context of BD may increase an individual’s need to have other people involved in their financial decisions. It may also increase their potential risk for exploitation or financial abuse. This may help explain some of the demographic differences in our survey—in particular, that women may perceive themselves an elevated risk of financial exploitation or abuse (Sharp-Jeffs et al., 2015). These risks may then be compounded by existing BD-related discrimination and mistreatment (Farrelly et al., 2014), leading some individuals to prefer limiting access to their financial information to avoid potential negative outcomes.

Exploitation risks identified in other populations can provide useful insights for system designers aiming to support financial collaboration for individuals with BD. Specifically, the elderly and individuals with dementia often need collaborative support to manage their finances. However, recent studies have identified risks as well as serious concerns of financial abuse and exploitation for this population (Gabler et al., 2017; Zhang et al., 2023). Future research should aim to address related concerns in BD and take steps to mitigate these risks when supporting collaborative financial interactions.

5.2. Supporting Longitudinal Financial Management for Individuals with BD

5.2.1. Self-Management of BD

Respondents were highly comfortable having their financial data accessible for their own personal use. Therefore, intervention systems informed by financial data patterns can provide additional insights and new opportunities for BD self-management. By combining BD-related data sources with financial data, users can explore the complex relationships between mood and finances, understand the ways in which these behaviors may be interrelated, and identify unique behavioral triggers they may experience. Providing the ability to view financial and BD-related data in tandem can help users take a more holistic approach to their wellbeing and long-term stability goals.

More specifically, users can gain a better understanding of how life stressors may manifest as financial behaviors, such as impulsive spending sprees or falling behind on bill payments. Through continued use, financial data and noted behavioral patterns can act as indicators of BD status and lower some of the user burdens to manually track relevant behaviors. For instance, if a system senses problematic behavioral patterns in financial data indicative of previous mood episodes, users could be alerted to the risk of potential relapse onset. This preemptive warning would allow individuals to make arrangements, notify care partners, and follow up with their clinicians to better prepare for illness management. In other words, integrating financial data can give individuals a more complete picture of their illness trajectory and more time to adequately prepare for changes in symptoms. Having more time and information prior to onset is crucial for minimizing the impact of mood episodes and effective self-management in BD (Blair et al., 2023).

5.2.2. Improving Financial Decision-Making and Literacy

Future intervention design should support developing new skills and habits to sustain financial stability. It can be particularly useful to address financial anxiety, which can often lead to counter-productive outcomes including avoidance behaviors. We believe it will be highly beneficial to design personalized interventions focusing on financial wellbeing and stability for individuals with BD. Such interventions can leverage existing clinical practices, including cognitive financial behavioral therapy (CFBT) (Nabeshima and Klontz, 2015) and dialectical behavior therapy (DBT) (Richardson et al., 2021; Van Dijk et al., 2013), and mindfulness activities. These interventions can be particularly effective in addressing guilt and shame associated with financial loss and instability following illness episodes in BD.

Future fintech systems can also provide users with opportunities to improve overall financial literacy. Data-driven and personalized financial literacy tools could help users set more appropriate and manageable goals, establish new money management routines, and address financial anxieties. In our survey, some individuals noted that they seek financial knowledge from their support networks. However, there is an opportunity to create personalized support system that can generate resources tailored to address individual financial habits and needs. Collaborative financial literacy might also lead to better interactions and understanding between individuals with BD and their care partners.

5.2.3. Enabling Collaborative Financial Interactions and Support

Collaborate financial management can be challenging. It can lead to tensions and fraught relationships, even risks of domestic violence (Labrum and Solomon, 2016). Future fintech design should specifically aim to ease these conflicts. Such design can prioritize positive communication skills, focus on attainable goal setting, work to reduce feelings of financial shame and guilt, and help care partners gain a stronger understanding of the needs and experiences of those with BD.

Given the challenges present for financial collaborative management, these systems should also provide additional guidance to users as they select who should be involved in their financial management plans and in what capacity. In the context of BD, this could be a difficult process, especially for those who have limited or strained social networks(Blair et al., 2023). Additionally, this decision may involve balancing the feelings of family obligation against choosing individuals that they are most comfortable with. Given these unique privacy characteristics, future design should aim to meet users where they are regarding privacy and disclosure with others from the start of system use. Similar vignette based approaches can be used during system onboarding to tailor sharing recommendations to their unique preferences and allow users to dictate what financial information is shared, with whom, and under what circumstances. As these privacy preferences may change over time, a system should also provide options to include care partners or clinicians in later stages of use. Similarly, users should be able to disclose more or less information to others and reassign care partner roles and permissions as their needs and comfort-levels change.

5.2.4. Integration with Existing Clinical Practices

Financial behavioral data could also be used within clinical settings for more comprehensive BD care plans. To start, patients and clinicians can target “financial stability” as a specific treatment goal and measure progress through individualized financial behaviors. This is especially important for long-term stability considering the cyclical effects between mood and financial difficulties (Richardson et al., 2013). By addressing financial challenges and money-related stress, patients may more easily achieve other mood-related goals in their overall care plan.

Moreover, clinicians can also incorporate financial data alongside existing, validated clinical measures for effective decision-making. While some participants were open to sharing financial information with clinicians, it will be critical to ensure transparency for effective integration with existing clinical practices. Specifically, the type and granularity of data shared with clinicians should be determined based on individuals’ comfort level, their unique needs, and the specific behavior change goals they wish to target. For example, if impulsive spending bursts are highly characteristic of an individual’s mood status, they may share transaction timing data with their clinicians rather than all of their purchasing details. This could help individuals and clinicians set and monitor goals targeting impulsive spending while preserving privacy. Conversely, individuals could share all purchase details within their financial data if their main financial goal is to gain a better understanding of the relationship between their mood and spending, as well as uncover potential behavioral triggers that can affect long-term BD management more broadly. Overall, we believe current clinical practices and decision-making will significantly benefit by integrating financial behavior data.

5.2.5. Preventing Financial Abuse

It is crucial that future work explores the delicate balance between supportive control of finances and exploitation to better protect users with BD. Future design should be mindful of these risks, minimally restrictive in relation to symptomatic need, and include adequate safeguards against potential misuse of these financial technologies. Given the similar financial exploitation risks well-documented for the elderly (Zhang et al., 2023) or individuals with dementia (Gabler et al., 2017), future design should leverage insights on financial abuse and exploitation within these populations. Additionally, clinicians working with patients on financial management goals could employ screening measures to assess potential risk for financial exploitation within their support networks (Greene, 2022). Moving forward, it is important to focus on developing features that support healthy “financial collaboration” rather than creating system structures that inadvertently enable or promote malicious “financial control” of already marginalized users.

5.3. Limitations

Our study has several limitations. First, given the dearth of literature surrounding this topic, our quantitative analysis was exploratory in nature. Given these initial insights, future research can take a hypothesis-driven approach to investigate the specific factors that impact willingness to adopt supportive financial technologies and share this data with care partners. Despite the large sample of individuals with BD used in this study, respondents leaned heavily white and female regarding ethnicity and gender. While the insights gathered through this work may not speak universally for all individuals with BD, population-level diagnosis rates show that individuals with BD are more likely to be demographically white and female (Shippee et al., 2011). We distributed this survey internationally, however our sample was limited to higher income countries in North America and Europe. Therefore our findings may not reflect the attitudes, needs, or experiences of those in lower and middle income countries. Additionally, this sample may not take into account other cultural norms and familial customs that may play a role in how individuals may involve care partners in their financial decisions or their attitudes toward sharing financial information with others. Lastly, 96% of our respondents reported having access to a bank account. Therefore, our findings may not represent “unbanked” individuals—those who fall through the cracks of the formal economy or choose not to use traditional banking institutions. However, prior research has demonstrated how digital finance systems can still help support traditionally unbanked individuals (Ibtasam et al., 2017). Further research is needed to understand their unique attitudes toward using financial data to support BD care and their sharing preferences.

5.4. Conclusion

This paper focuses on understanding financial data sharing preferences to support longitudinal management of bipolar disorder. Our data shows that individuals with bipolar disorder were willing to share financial data for personalized support and insights. However, we also identified significant demographic differences in sharing preferences across gender, age, and marital status. Specifically, women, younger adults, and those with more severe subtypes of BD may be reluctant to share financial data with others. Based on these insights, we discussed the unique privacy needs that should inform the future development of fintech systems to support higher-risk user groups. Finally, we have provided design suggestions for how financial behavioral data can be integrated into BD self-management and clinical practices, inform financial decisions and literacy resources, and improve collaboration with care partners. We consider this work a crucial step forward to develop personalized, privacy-aware systems to support financial stability and long-term BD care.

References

- (1)

- American Psychiatric Association (2013) American Psychiatric Association. 2013. Diagnostic and Statistical Manual of Mental Disorders (fifth edition ed.). American Psychiatric Association. https://doi.org/10.1176/appi.books.9780890425596

- Baguley et al. (2022) Thom Baguley, Grace Dunham, and Oonagh Steer. 2022. Statistical Modelling of Vignette Data in Psychology. British Journal of Psychology 113, 4 (Nov. 2022), 1143–1163. https://doi.org/10.1111/bjop.12577

- Barros Pena et al. (2021a) Belén Barros Pena, Bailey Kursar, Rachel E Clarke, Katie Alpin, Merlyn Holkar, and John Vines. 2021a. Financial Technologies in the Cycle of Poor Mental Health and Financial Hardship: Towards Financial Citizenship. In Proceedings of the 2021 CHI Conference on Human Factors in Computing Systems. Association for Computing Machinery, New York, NY, USA, 1–16.

- Barros Pena et al. (2021b) Belén Barros Pena, Bailey Kursar, Rachel E. Clarke, Katie Alpin, Merlyn Holkar, and John Vines. 2021b. ”Pick Someone Who Can Kick Your Ass” - Moneywork in Financial Third Party Access. Proceedings of the ACM on Human-Computer Interaction 4, CSCW3 (Jan. 2021), 218:1–218:28. https://doi.org/10.1145/3432917

- Bellini (2023) Rosanna Bellini. 2023. Paying the Price: When Intimate Partners Use Technology for Financial Harm. In Proceedings of the 2023 CHI Conference on Human Factors in Computing Systems. ACM, Hamburg Germany, 1–17. https://doi.org/10.1145/3544548.3581101

- Bessonova et al. (2020) Leona Bessonova, Kristine Ogden, Michael J Doane, Amy K O’Sullivan, and Mauricio Tohen. 2020. The Economic Burden of Bipolar Disorder in the United States: A Systematic Literature Review. ClinicoEconomics and Outcomes Research 12 (Dec. 2020), 481–497. https://doi.org/10.2147/CEOR.S259338

- Blair et al. (2022) Johnna Blair, Jeff Brozena, Mark Matthews, Thomas Richardson, and Saeed Abdullah. 2022. Financial Technologies (FinTech) for Mental Health: The Potential of Objective Financial Data to Better Understand the Relationships between Financial Behavior and Mental Health. Frontiers in Psychiatry 13 (2022).

- Blair et al. (2023) Johnna Blair, Dahlia Mukherjee, Erika FH Saunders, and Saeed Abdullah. 2023. Knowing How Long a Storm Might Last Makes it Easier to Weather: Exploring Needs and Attitudes Toward a Data-driven and Preemptive Intervention System for Bipolar Disorder. In Proceedings of the 2023 CHI Conference on Human Factors in Computing Systems. 1–12.

- Braun and Clarke (2019) Virginia Braun and Victoria Clarke. 2019. Reflecting on Reflexive Thematic Analysis. Qualitative research in sport, exercise and health 11, 4 (2019), 589–597.

- Brown and Choi (2017) Alice V. Brown and Jaz Hee-jeong Choi. 2017. Towards Care-based Design: Trusted Others in Nurturing Posttraumatic Growth Outside of Therapy. In Proceedings of the 8th International Conference on Communities and Technologies. ACM, Troyes France, 56–63. https://doi.org/10.1145/3083671.3083703

- Cheema et al. (2015) Marvi K. Cheema, Glenda M. MacQueen, and Stefanie Hassel. 2015. Assessing Personal Financial Management in Patients with Bipolar Disorder and Its Relation to Impulsivity and Response Inhibition. Cognitive Neuropsychiatry 20, 5 (Sept. 2015), 424–437. https://doi.org/10.1080/13546805.2015.1076722

- Cloutier et al. (2018) Martin Cloutier, Mallik Greene, Annie Guerin, Maelys Touya, and Eric Wu. 2018. The Economic Burden of Bipolar I Disorder in the United States in 2015. Journal of Affective Disorders 226 (Jan. 2018), 45–51. https://doi.org/10.1016/j.jad.2017.09.011

- Cox et al. (2016) Anna L. Cox, Sandy J.J. Gould, Marta E. Cecchinato, Ioanna Iacovides, and Ian Renfree. 2016. Design Frictions for Mindful Interactions: The Case for Microboundaries. In Proceedings of the 2016 CHI Conference Extended Abstracts on Human Factors in Computing Systems (CHI EA ’16). Association for Computing Machinery, New York, NY, USA, 1389–1397. https://doi.org/10.1145/2851581.2892410

- Dunphy et al. (2014) P. Dunphy, A. Monk, J. Vines, M. Blythe, and P. Olivier. 2014. Designing for Spontaneous and Secure Delegation in Digital Payments. Interacting with Computers 26, 5 (Sept. 2014), 417–432. https://doi.org/10.1093/iwc/iwt038

- Farr et al. (2019) B Farr, B Cash, and A Harper. 2019. Why Financial Institutions Need to Offer Supportive Banking Features. Unpublished. The Ludwig Center for Community and Economic Development at Yale Law School.

- Farrelly et al. (2014) Simone Farrelly, Sarah Clement, Jheanell Gabbidon, Debra Jeffery, Lisa Dockery, Francesca Lassman, Elaine Brohan, R Claire Henderson, Paul Williams, Louise M Howard, et al. 2014. Anticipated and experienced discrimination amongst people with schizophrenia, bipolar disorder and major depressive disorder: a cross sectional study. BMC psychiatry 14, 1 (2014), 1–8.

- Finch (1987) Janet Finch. 1987. The Vignette Technique in Survey Research. Sociology 21, 1 (Feb. 1987), 105–114. https://doi.org/10.1177/0038038587021001008

- Frankham et al. (2020) Charlotte Frankham, Thomas Richardson, and Nick Maguire. 2020. Psychological Factors Associated with Financial Hardship and Mental Health: A Systematic Review. Clinical Psychology Review 77 (April 2020), 101832. https://doi.org/10.1016/j.cpr.2020.101832

- Gabler et al. (2017) Nicole Gabler, Christina Harrison, Dianey Leal, Elizabeth McCrory, Jyotsna Rege, Sarayu Sankar, and Sydney Thomas. 2017. Examining the Prevalence of Financial Exploitation of Individuals Suffering from Alzheimer’s and Dementia Related Diseases in Texas. Technical Report.

- Glaser and Strauss (2017) Barney G Glaser and Anselm L Strauss. 2017. The Discovery of Grounded Theory: Strategies for Qualitative Research. Routledge.

- Greene (2022) Aaron J Greene. 2022. Elder financial abuse and electronic financial instruments: present and future considerations for financial capacity assessments. The American Journal of Geriatric Psychiatry 30, 1 (2022), 90–106.

- Greenwood (2020) Tiffany A. Greenwood. 2020. Creativity and Bipolar Disorder: A Shared Genetic Vulnerability. Annual Review of Clinical Psychology 16, 1 (2020), 239–264. https://doi.org/10.1146/annurev-clinpsy-050718-095449

- Harper et al. (2018) Annie Harper, Martha Staeheli, Dawn Edwards, Yolanda Herring, and Michaella Baker. 2018. Disabled, Poor, and Poorly Served: Access to and Use of Financial Services by People with Serious Mental Illness. Social Service Review 92, 2 (June 2018), 202–240. https://doi.org/10.1086/697904

- Heiss (2022) Andrew Heiss. 2022. Marginalia: A Guide to Figuring out What the Heck Marginal Effects, Marginal Slopes, Average Marginal Effects, Marginal Effects at the Mean, and All These Other Marginal Things Are. https://www.andrewheiss.com/blog/2022/05/20/marginalia. https://doi.org/10.59350/40xaj-4e562

- Hindley et al. (2019) Guy Hindley, Lucy A. Stephenson, Alex Ruck Keene, Larry Rifkin, Tania Gergel, and Gareth Owen. 2019. “Why Have I Not Been Told about This?”: A Survey of Experiences of and Attitudes to Advance Decision-Making amongst People with Bipolar. Wellcome Open Research 4 (April 2019), 16. https://doi.org/10.12688/wellcomeopenres.14989.2

- Hoefer et al. (2021) Michael Jeffrey Daniel Hoefer, Lucy Van Kleunen, Cassandra Goodby, Lanea Blyss Blackburn, Priyanka Panati, and Stephen Voida. 2021. The Multiplicative Patient and the Clinical Workflow: Clinician Perspectives on Social Interfaces for Self-Tracking and Managing Bipolar Disorder. In Designing Interactive Systems Conference 2021. Association for Computing Machinery, New York, NY, USA, 907–925.

- Ibtasam et al. (2017) Samia Ibtasam, Hamid Mehmood, Lubna Razaq, Jennifer Webster, Sarah Yu, and Richard Anderson. 2017. An exploration of smartphone based mobile money applications in Pakistan. In Proceedings of the Ninth International Conference on Information and Communication Technologies and Development. 1–11.

- Jenkins et al. (2008) Rachel Jenkins, Dinesh Bhugra, Paul Bebbington, Traolach S. Brugha, Michael Farrell, Jeremy W. Coid, Tom Fryers, Scott Weich, Nicola Singleton, Nicola Singleton, Howard Meltzer, Howard Meltzer, and Howard Meltzer. 2008. Debt, Income and Mental Disorder in the General Population. Psychological Medicine (2008). https://doi.org/10.1017/s0033291707002516

- Jiménez-Solomon et al. (2016) Oscar G. Jiménez-Solomon, Pablo Méndez-Bustos, Margaret Swarbrick, Samantha Díaz, Sissy Silva, Maura Kelley, Steve Duke, and Roberto Lewis-Fernández. 2016. Peer-Supported Economic Empowerment: A Financial Wellness Intervention Framework for People with Psychiatric Disabilities. Psychiatric Rehabilitation Journal 39, 3 (Sept. 2016), 222–233. https://doi.org/10.1037/prj0000210

- Kameswaran and Muralidhar (2019) Vaishnav Kameswaran and Srihari Hulikal Muralidhar. 2019. Cash, Digital Payments and Accessibility: A Case Study from Metropolitan India. Proc. ACM Hum. Comput. Interact. (2019). https://doi.org/10.1145/3359199

- Labrum (2018) Travis Labrum. 2018. Characteristics Associated with Family Money Management for Persons with Psychiatric Disorders. Journal of Mental Health 27, 6 (Dec. 2018), 504–510. https://doi.org/10.1080/09638237.2018.1466032

- Labrum and Solomon (2016) Travis Labrum and Phyllis L Solomon. 2016. Factors associated with family violence by persons with psychiatric disorders. Psychiatry research 244 (2016), 171–178.

- Látalová (2009) K. Látalová. 2009. Bipolar Disorder and Aggression. International Journal of Clinical Practice 63, 6 (2009), 889–899. https://doi.org/10.1111/j.1742-1241.2009.02001.x

- Lenth (2023) Russell V. Lenth. 2023. Emmeans: Estimated Marginal Means, Aka Least-Squares Means.

- Ljungqvist et al. (2016) Ingemar Ljungqvist, Alain Topor, Henrik Forssell, Idor Svensson, and Larry Davidson. 2016. Money and Mental Illness: A Study of the Relationship between Poverty and Serious Psychological Problems. Community Mental Health Journal (2016). https://doi.org/10.1007/s10597-015-9950-9

- Matthews et al. (2017a) Mark Matthews, Elizabeth Murnane, and Jaime Snyder. 2017a. Quantifying the Changeable Self: The Role of Self-Tracking in Coming to Terms With and Managing Bipolar Disorder. Human–Computer Interaction 32, 5-6 (Nov. 2017), 413–446. https://doi.org/10.1080/07370024.2017.1294983