Improved Financial Forecasting via Quantum Machine Learning

Abstract

Quantum algorithms have the potential to enhance machine learning across a variety of domains and applications. In this work, we show how quantum machine learning can be used to improve financial forecasting. First, we use classical and quantum Determinantal Point Processes to enhance Random Forest models for churn prediction, improving precision by almost 6%. Second, we design quantum neural network architectures with orthogonal and compound layers for credit risk assessment, which match classical performance with significantly fewer parameters. Our results demonstrate that leveraging quantum ideas can effectively enhance the performance of machine learning, both today as quantum-inspired classical ML solutions, and even more in the future, with the advent of better quantum hardware.

1 Introduction

Quantum computing is a rapidly evolving field that promises to revolutionize various domains, and finance is no exception. There is a variety of computationally hard financial problems for which quantum algorithms can potentially offer advantages [24, 16, 39, 6], for example in combinatorial optimization [34, 42], convex optimization [30, 43], monte carlo simulations [15, 44, 21], and machine learning [41, 18, 1].

In this work, we explore the potential of quantum machine learning methods in improving the performance of forecasting in finance, specifically focusing on two use cases within the business of Itaú Unibanco, the largest bank in Latin America.

In the first use case, we aim to improve the performance of Random Forest methods for churn prediction. We introduce quantum algorithms for Determinantal Point Processes (DPP) sampling [29], and develop a method of DPP sampling to enhance Random Forest models. We evaluate our model on the churn dataset using classical DPP sampling algorithms and perform experiments on a scaled-down version of the dataset using quantum algorithms. Our results demonstrate that, in the classical setting, the proposed algorithms outperform the baseline Random Forest in precision, efficiency, and bottom line, and also offer a precise understanding of how quantum computing can impact this kind of problem in the future. The quantum algorithm run on an IBM quantum processor gives similar results as the classical DPP on small batch dimensions but falters as the dimensions grow bigger due to hardware noise.

In the second use case, we aim to explore the performance of neural network models for credit risk assessment by incorporating ideas from quantum compound neural networks [33]. We start by using quantum orthogonal neural networks [33], which add the property of orthogonality for the trained model weights to avoid redundancy in the learned features [3]. These orthogonal layers, which can be trained efficiently on a classical computer, are the simplest case of what we call compound neural networks, which explore an exponential space in a structured way. For our use case, we design compound neural network architectures that are appropriate for financial data. We evaluate their performance on a real-world dataset and show that the quantum compound neural network models both have far fewer parameters and achieve better accuracy and generalization than classical fully-connected neural networks.

This paper is organized as follows: In section 2, we focus on the churn prediction use case and present the DPP-based quantum machine learning methods. In section 3, we present quantum neural network models for risk assessment. Finally, in section 4, we conclude the paper and discuss potential future research directions.

2 DPP-enhanced Random Forest models for churn prediction

2.1 Use case

In this study, we focus on predicting customer churn in a banking setting. Churn, defined as a customer withdrawing more than a certain amount of money in a single month, is a significant concern for retail banks. Our objective is to predict which customers are most likely to churn in the next three months using customer data from the previous six months.

The primary dataset used in this study consists of 304,000 datapoints, with 153 features for each datapoint. Each datapoint represents a banking customer at a particular month in time, with the features representing various aspects of their activity over the previous six months. The target variable is a binary flag indicating whether or not the customer churned in at least one of the following three months. The data was anonymized and standardized before being split into training and test sets based on time period, with 130,000 datapoints being set aside as the test set and 174,000 datapoints used for training. The data was split in a way that did not produce any significant covariate shift between the train and test sets.

With the end goal of preventing churn, the model works by flagging customers with the highest risk of potential churn. For these flagged customers, the bank can deploy a representative to intervene and better understand their needs. However, resource limitations make it necessary to flag a relatively small number of customers with high confidence. The focus of this exploration was to reduce false positives in the flagged customers to increase the efficiency of bank interventions. In terms of the precision-recall trade-off, our model should be tuned to provide the highest possible precision for low recall values. Despite this simplification to a classification problem, the primary business KPI is the amount of withdrawal money correctly captured by the model, as discussed more in Sec. 2.4.3.

This use case already had a solution in production: a Random Forest classifier [7], whose performance was used as a benchmark. The model in production already captured a significant amount of churn, but there was clear room for improvement in the amount of withdrawals captured (see Fig. 4). Moreover, given the large number of customers in the dataset and the relative homogeneity of the population of interest, there existed an opportunity to employ techniques that explicitly try to explore diversity in the data.

2.2 Determinant sampling

We will now introduce the Determinantal Point Process (DPP), which lies at the core of the methodology behind our solution to the churn problem. DPPs are a class of probabilistic models that can be used to sample diverse subsets of items from a larger set. They were first formalized by Macchi in 1975 as a way to model fermions in quantum mechanics [38]. More recently, these models are showing increasing promise in the context of machine learning [32], where they can be used for a variety of tasks, such as building unbiased estimators for linear regression [13], performing monte carlo estimation [4], and promoting diversity in model outputs [17].

2.2.1 Definitions

A point process on a set is a probability measure over the subsets of . Sampling from a point process on will produce some subset with probability . A repulsive point process is a point process in which points that are more similar to each other are less likely to be selected together.

A determinantal point process is a particular case of a repulsive point process, in which the selection probability of a subset of items is given by a determinant. Given a real, symmetric matrix indexed by the elements of :

where denotes the submatrix indexed by the set and is the cardinality of . In other words, the marginal distribution is defined by the subdeterminants of K.

The above is the most general definition, but in machine learning, we typically focus on a slightly more restrictive class of DPPs called -ensembles. In -ensembles, the whole distribution, not just the marginals, is given by the subdeterminant of a real, symmetric matrix .

Just like , is indexed by the elements of . Because of some convenient properties of the determinant [32], we can explicitly write down the distribution of an -ensemble:

In machine learning literature, DPPs are typically defined over a set of points , with each item a row in the data matrix . If we preprocess such that its columns are orthonormal and choose to be the inner-product similarity matrix, i.e. , then the distribution becomes even simpler to write down. Instead of explicitly computing the matrix, we can write the distribution in terms of the data matrix itself, courtesy of the Cauchy-Binet formula,

| (1) |

Moreover, the distribution will almost surely produce samples with size , the rank of the orthogonalized data matrix . This kind of DPP is denoted -DPP. We will focus here on an application of sampling from a -DPP from a data matrix X.

2.2.2 Unbiased least-squares regression

One unique feature of the DPP compared to i.i.d sampling techniques is that it can lead to provably unbiased estimators for least-squares linear regression [11] [14]. Given an data matrix and a target vector , where , we wish to approximate the least squares solution . represents the best-fit parameters to a linear model to predict .

Surprisingly, if we sample points from DPP() and solve the reduced system of equations , we get an unbiased estimate of . Formally, if ,

This allows us to create an "ensemble" of unbiased linear regressors, each trained on a DPP sample. In some regard, this was the inspiration for trying an ensemble of decision trees trained on DPP samples, as detailed in Sec. 2.3.

2.2.3 Algorithms for sampling

There are several efficient algorithms for sampling from DPPs and computing their properties. The naive sampling method — calculating all subdeterminants and performing sampling — takes exponential time. The first major leap in making DPP sampling feasible on today’s computers was the "spectral method" [31, 25]. This algorithm performs an eigendecomposition of the kernel matrix before applying a projection-based iterative sampling approach. Thus, the first sample takes time, and subsequent samples take .

Monte Carlo methods have been proposed to approximate the DPP distribution [2, 35], though they are not exact, and are often still prohibitively slow with a runtime of per sample.

In a counter-intuitive result, [12] and [8] proposed methods that avoid performing the full DPP sampling procedure on large parts of the basis set. This approach resulted in a significant reduction in runtime, making DPPs more practical for mid-to-large-scale datasets. These techniques allow exact sampling of subsequent -DPP samples in , independent of the size of the full basis set . Many of these algorithms are implemented in the open-source DPPy library[20], which we used in the experiments in this paper.

Recent work has shown that quantum computers are in principle able to sample from DPPs in even lower complexity in some cases. We describe this quantum algorithm in Sec. 2.5. This and several other algorithms which arise from the techniques introduced in [29] are a budding area of research in the quantum computing space, and will hopefully inspire more applications like the one we describe in this paper. For example, in [28], DPPs and deterministic DPPs were used to improve the methods for the imputation of clinical data.

2.3 DPP-Random Forest Model

The Random Forest algorithm was introduced in 2001 by Leo Brieman [7] and has since become one of the most popular supervised machine learning algorithms. This model consists of an ensemble of decision trees, each trained on a subsample of rows and features from the dataset. Subsampling makes the model more robust to variance in the training data. In normal operation, this subsampling is done in a data-independent random manner.

In this paper, we propose an extension of the Random Forest, called the DPP-Random Forest (DPP-RF), which utilizes Determinantal Point Processes (DPPs) to subsample rows and features for individual decision trees. These data-dependent DPP samples better preserve the diversity of observations (customers, in our case) and features in comparison to uniform sampling.

2.3.1 DPP sampling methodology

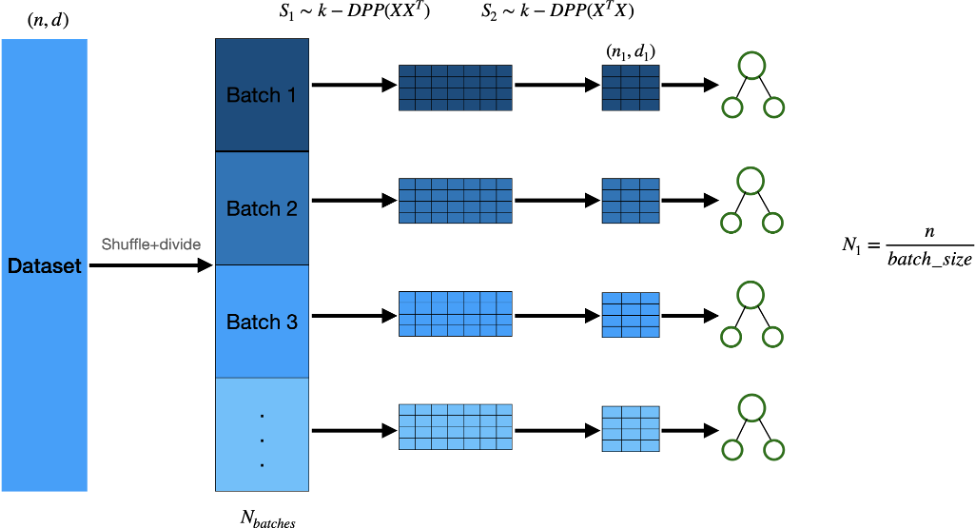

Sampling from a DPP on the entire dataset of 174,000 points is computationally infeasible — something that future full-scale quantum computers can potentially change. To be able to test these techiques today, a novel sampling procedure had to be developed, which is both efficient and preserves many of the benefits of DPPs. The procedure can be summarized as follows:

-

1.

Divide the training set into smaller batches;

-

2.

Sample -DPP data points from every batch;

-

3.

Sample -DPP features;

-

4.

Train a first group of decision trees on these small patches of data;

Figure 1: Steps 1 to 4 of the DPP-Random Forest algorithm. -

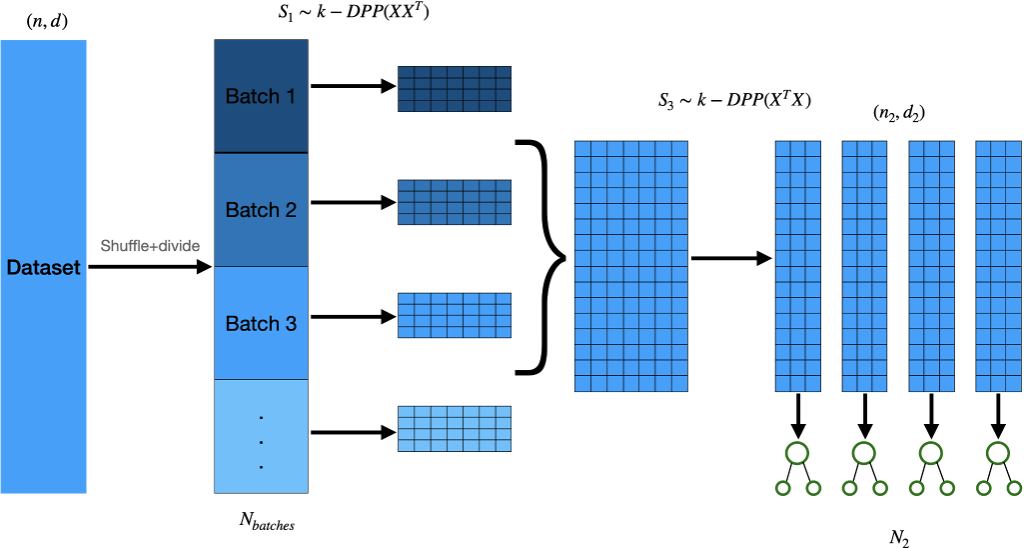

5.

Aggregate the patches of data resulting from step 2 to create a larger dataset ;

-

6.

Repeat for times: sample -DPP features to create a long matrix;

-

7.

Train a second group of decision trees on these new datasets;

Figure 2: Steps 5 to 7 of the DPP-Random Forest algorithm. -

8.

Combine and by aggregating them to make predictions (similar to the classical Random Forest algorithm).

2.4 Results

We focused on three key performance indicators (KPIs): the precision-recall curve, the training time and the bottom line. In addition, we benchmarked our proposed DPP-RF method by constructing models on public tabular classification tasks.

2.4.1 Precision-recall

To evaluate the performance of our proposed method, we optimized hyperparameters and measured the precision for a low fixed recall (6% in this case). As seen in Figure 3, our method showed an improvement in precision from for the benchmark model to with the new model. Our method also provided similar improvements in precision for the relevant range of small recall.

2.4.2 Training time

The DPP-RF model has a longer training time compared to the traditional random forest on a classical computer: it took 54 minutes to train the model with the best hyperparameters, compared to 311 seconds for the benchmark model. The models were trained on a computer with an Intel© Core™ i5-8350U CPU running at 1.70 GHz, 24 GB of RAM and Windows 10 version 21H2, compilation 19044.2604.

Indeed, the training time of a DPP-RF model depends heavily on the choice of values for its hyperparameters. Notably, the size of the batches from which we take DPP samples — termed "batch size" — can increase the runtime dramatically if set higher than 1000. In our hyperparameter search, we limited our search to hyperparameters which keep the runtime reasonable, although still relatively long.

The computational bottleneck in this algorithm is DPP sampling, which was done using the classic SVD-based approach [25]. We believe that improved classical sampling techniques [8] and future quantum techniques (Sec. 2.5) can reduce the runtime dramatically.

Within the bank, the churn model is retrained just once every few months, so the training time was not prohibitive. However, faster sampling algorithms still serve to increase the range of feasible hyperparameters (especially the batch size).

2.4.3 Bottom line — withdrawals captured

From a business perspective, the most direct indicator of the success of the model is the amount of assets under management (AUM) that can be salvaged via interventions. Thus, we evaluated the amount of money withdrawn every month by the 500 customers flagged by the model, i.e., the 500 customers which had the highest predicted probability of churning in one of the following 3 months. As seen in figures 4, 5 and 6, our model showed substantial overall improvements. The true financial impact of these predictions is dependent on the success of the interventions as well as the bank’s profit-per-dollar-AUM.

2.4.4 Summary of results

The proposed DPP Random Forest model provides significant improvements in precision and bottom line. The results are summarized in the following table.

| Metric | Benchmark model | Proposed model |

|---|---|---|

| Precision | 71.6% | 77.5% |

| % total withdrawals captured | 61.42% | 62.77% |

| % maximum possible withdrawals captured | 69.18% | 70.72% |

| Train time | 311s | 54 min |

2.4.5 Further Benchmarks

We further benchmarked our model on various classification datasets from OpenML. All except one (madelon) of these datasets were used in [22] and preprocessed accordingly. They were chosen to be representative of a wide variety of classification tasks. Each dataset was split into train, validation, and test sets. For each model, 400 sets of hyperparameters were randomly chosen and evaluated on the validation set. Both models used the same hyperparameter space, except for the addition of the batch_size parameter for the DPP-RF. The hyperparameters which gave the best results on the validation set were evaluated on the test set, and the results are reported below. Models were evaluated with the ROC-AUC metric111The area under the receiver operating characteristic curve (ROC-AUC) is a common metric for two-class classification tasks, and evaluates the ability of the model to produce a proper ranking of datapoints by likelihood of being class 1..

| Dataset | Random Forest | DPP Random Forest |

|---|---|---|

| madelon | 0.916 | 0.941 |

| credit-default | 0.856 | 0.856 |

| house-pricing | 0.948 | 0.939 |

| Jannis | 0.866 | 0.870 |

| eye movements | 0.704 | 0.710 |

| bank-marketing | 0.881 | 0.881 |

| wine | 0.901 | 0.906 |

| california | 0.962 | 0.963 |

2.5 Quantum algorithm for Determinantal Point Processes

2.5.1 Quantum circuits

Classical DPP sampling algorithms have improved significantly since their inception, but it still remains infeasible to sample from large datasets like ours. Recent work by Kerenidis and Prakash [29] has shown that a quantum computer can more natively perform DPP sampling, achieving a gate complexity of and a circuit depth of for an orthogonal matrix of size . The classical time complexity for sampling is [25]. Note that when is very large, then one can reduce the number of rows to before performing the sampling [8].

For a thorough review of the quantum methods and circuits, we refer the reader to [29]. The circuit is described in brief below.

Given an orthogonal matrix , the quantum DPP circuit applied on performs the following operation:

| (2) |

where is the submatrix obtained after sampling the rows of indexed by ; is the characteristic vector of (with 1’s in the positions indexed by the elements of S) and represents the quantum -DPP circuit, as detailed below.

Thus, the probability of sampling , i.e., of measuring , is: , where . This draws the link between the quantum determinantal sampling circuit and the classical -DPP model as seen in eq. 1.

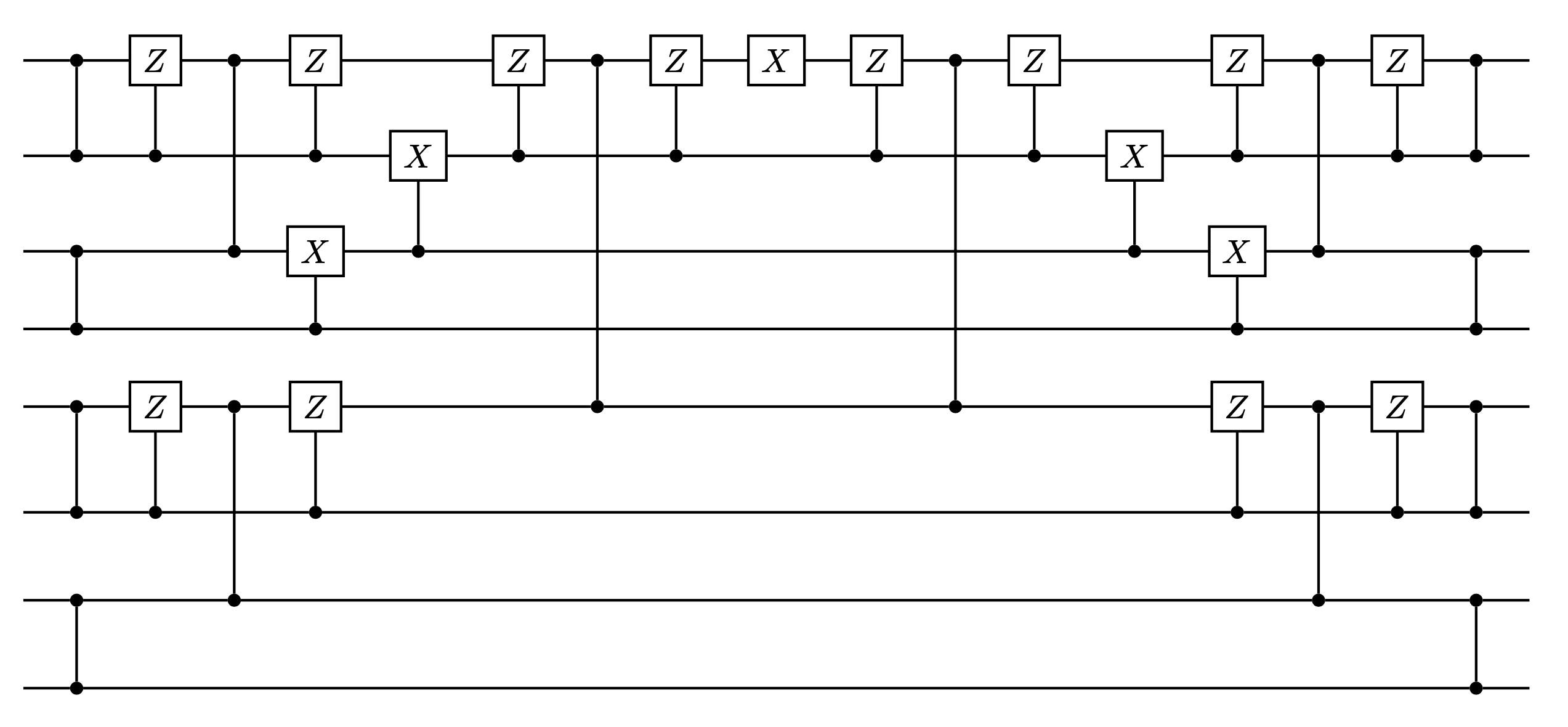

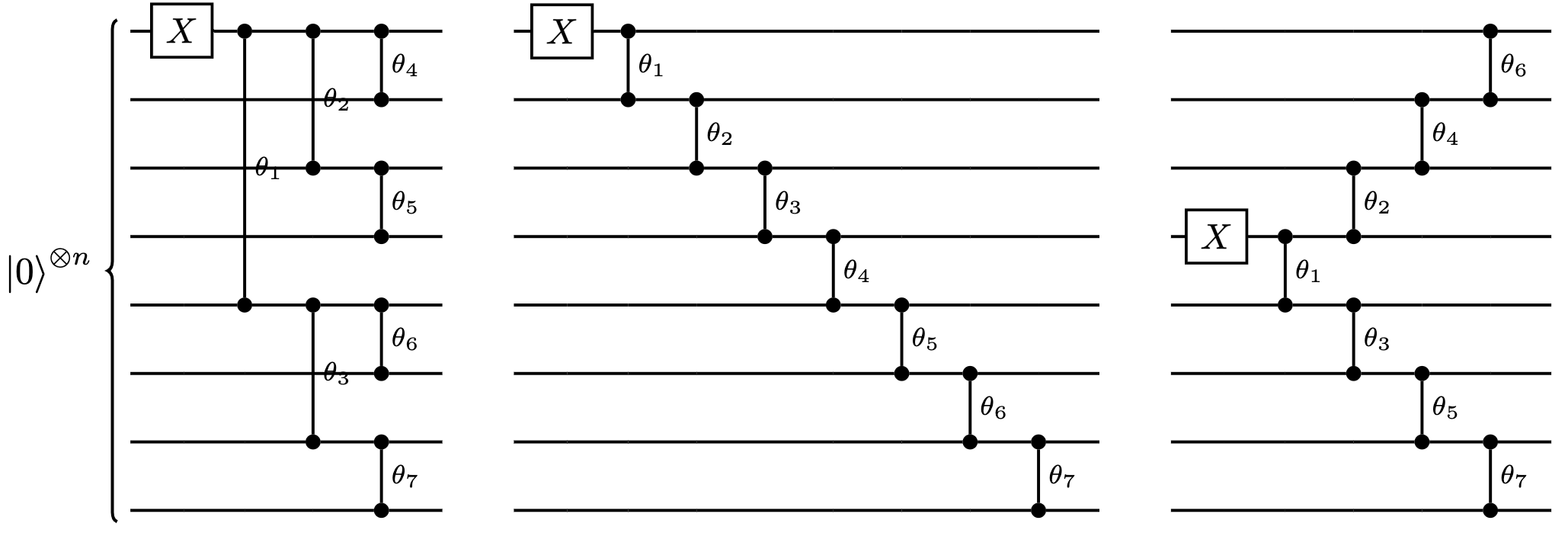

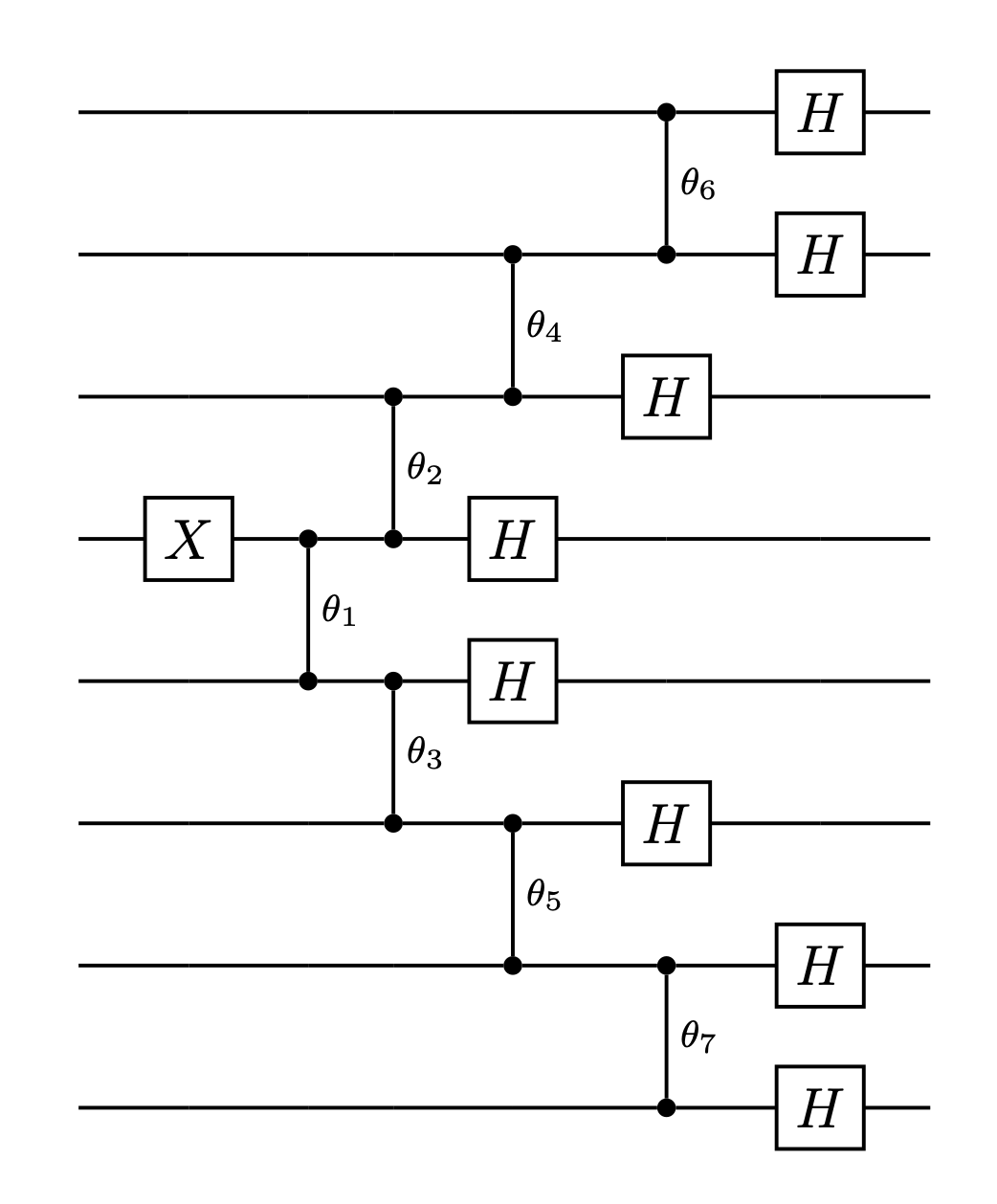

To construct the quantum -DPP circuit, we need to first introduce a circuit known as a Clifford loader, which performs the following operation:

| (3) |

The Clifford loader was shown to have a log-depth circuit in [29], and is shown for in fig 8, in which the gates represented by vertical lines are RBS gates — parameterized, hamming weight preserving two-qubit gates.

The full quantum -DPP circuit is a series of clifford loaders, one for each orthogonal column of :

| (4) |

An example of a -DPP circuit as a series of cliffords for is shown in fig. 8.

2.5.2 Hardware experiment results

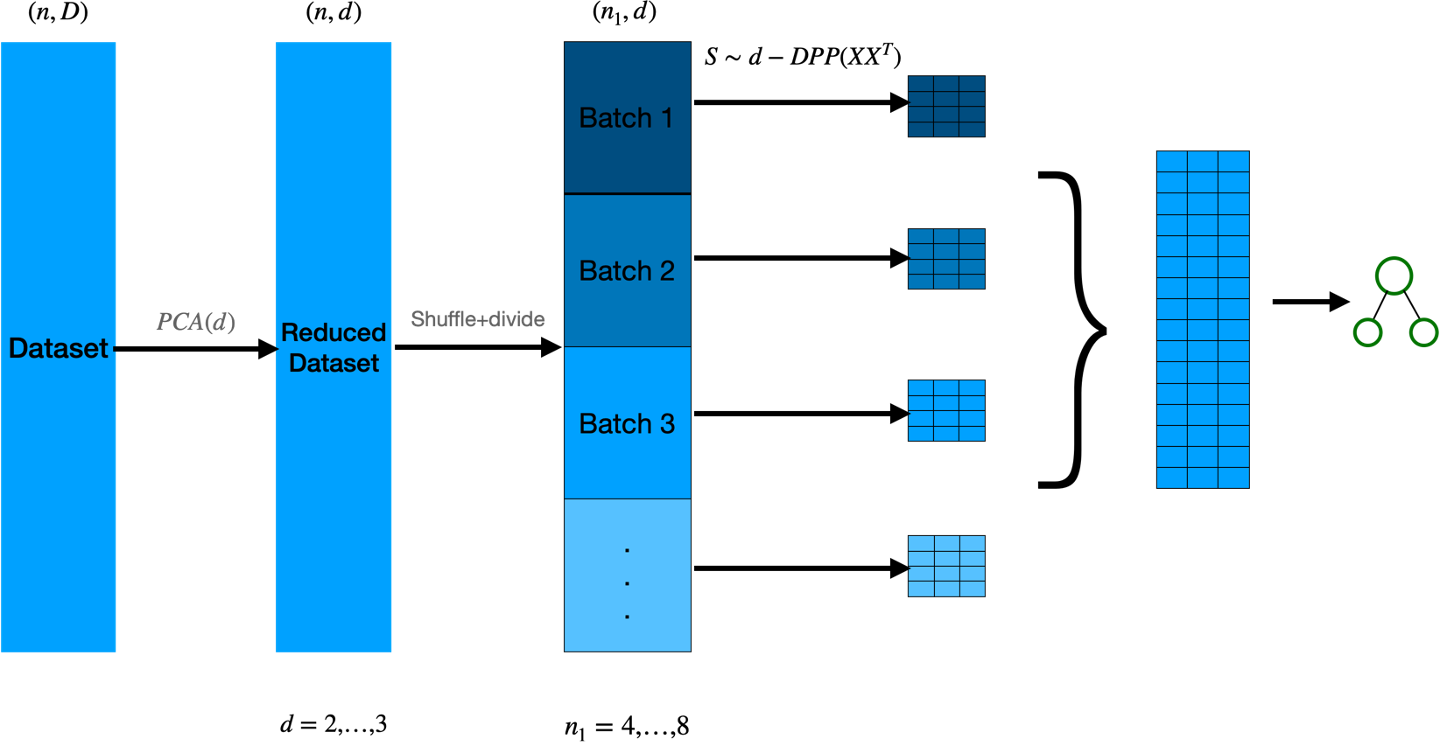

As a hardware experiment, we aimed to implement a simplified version of our algorithm on a quantum processor. We chose to use the "ibmq_guadelupe" 16-qubit chip, which is only capable of running small quantum DPP circuits for matrices of certain dimensions, such as . As a result, we had to reduce the size of our problem.

To accomplish this, we defined reduced train/test sets: a train set of 1000 points from 03/2019 and a test set of 10000 points from 04/2019. The quantum hardware-ready simplified algorithm is outlined in Figure 9. It includes the following steps:

-

1.

Applying PCA to reduce the number of columns from 153 to ;

-

2.

Dividing the dataset into batches of points;

-

3.

Sampling -DPP rows from each batch, resulting in small patches of data;

-

4.

Aggregating these patches to form a larger dataset, then training one decision tree on this dataset.

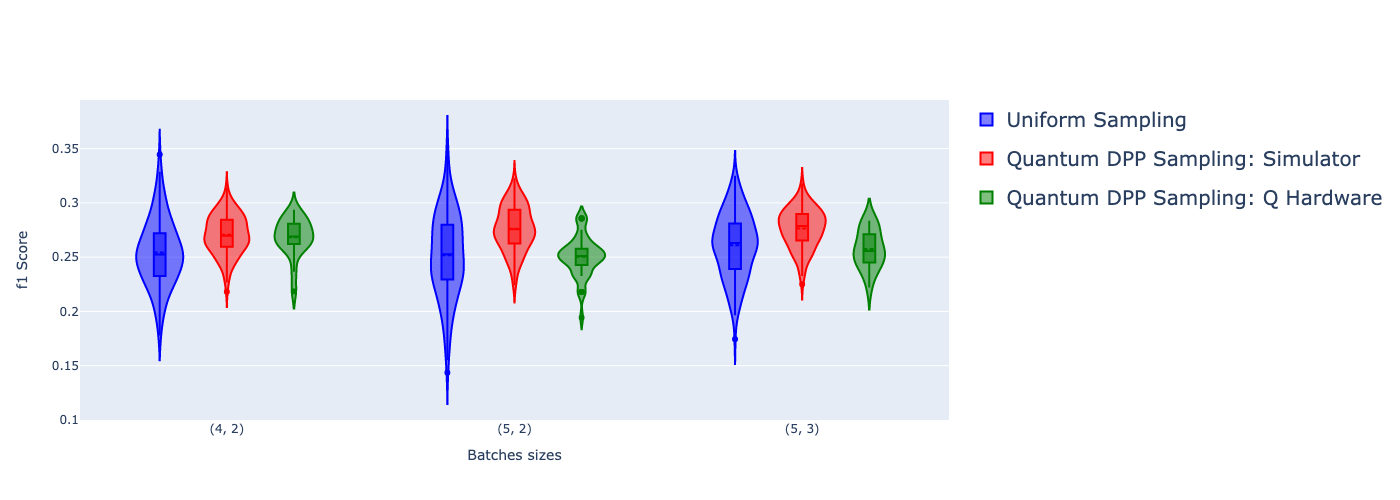

We repeated this process for a number of trees and estimated the F1222We chose the F1 score as the evaluation metric for two reasons. Firstly, a single decision tree, unlike the random forest, does not provide an estimate of the likelihood, which is required for the computation of ROC-AUC as we had used before. Secondly, we had an imbalanced dataset and thus needed a metric which balanced precision and recall. The F1 score is particularly effective when used in these scenarios. score for every tree. We then compared the results for different sampling methods: uniform sampling, quantum DPP sampling using a simulator, and quantum DPP sampling using a quantum processor.

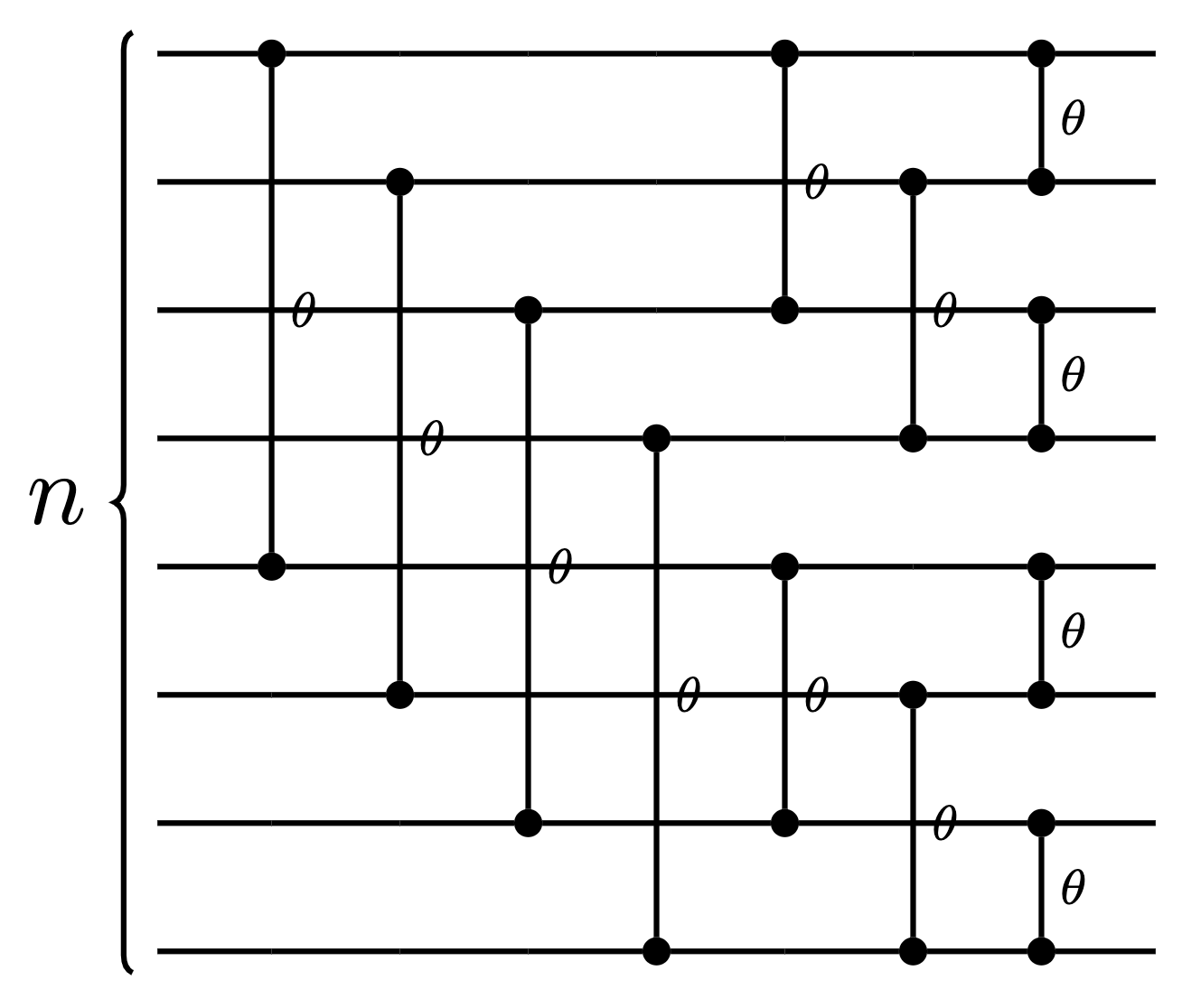

The IBM quantum computer only allows using RBS gates on adjacent qubits, so we cannot use the circuit described in section 2.5.1. Instead, we use two different Clifford loader architectures which only use adjacent-qubit connectivity, visualized in fig 11. The diagonal clifford loader is explained in [29], and the semi-diagonal loader is a modification that halves the circuit depth. As an error mitigation measure, we disregarded all results which did not have the expected hamming weight (). The results are shown in the violin plots in Figures 12 and 13.

The results indicate that for small matrix dimensions — up to (6,2) — the IBM quantum processor gives results similar to the ones achieved with the simulator. However, as the dimensions grow bigger, the samples from the quantum DPP circuits lead to worse classifier performance. This highlights the limitations of the available quantum hardware, which is prone to errors.

3 Quantum Neural Networks for credit risk assessment

3.1 Use case

In the second study, we focus on the problem of credit-default prediction associated with credit applications from Small and Medium Enterprises (SMEs). The Credit operation is one of the largest and most important operations in a retail banking institution. Throughout the credit journey (life-cycle) of a customer within the bank, several different models are used at different points of the journey and for different purposes, such as the determination of interest rates, offering of different products, etc.

The credit granting model is a particularly important one since it determines whether or not a credit relationship will be established. It is also particularly challenging in the case of SMEs, where the relationship with the bank often starts only when the SME submits an application for credit, so very little data is available. Given these challenges, we propose the use of quantum techniques aiming at improving the predictive performance of the credit granting model.

The credit granting decision may be seen as a binary classification problem, in which the objective is to predict if the SME will default on credit. More specifically, we are interested in calculating the so-called probability of default (PD), which is given by . The PD information is used internally for other pipelines primarily concerned with the determination of credit ratings for the SMEs (though in this study, we focus solely on the PD model), so the PD distribution is the main output of interest from the model. For this reason, we do not threshold the probability outputs from the model — thus, we use threshold-independent classification metrics to evaluate its predictive performance. Namely, the main Key Performance Indicator (KPI) that we use is the Gini score, constructed from the Area Under the Curve (AUC) of the ROC (Receiver Operating Characteristic) curve as . The Gini score is easily interpreted by the business team and allows for a holistic estimation of the model’s impact.

In this study, we chose to focus on the development of an "internal model" of credit default, which only uses features collected by Itaú, without considering any external information (from credit bureaus, for instance). The dataset used consists of observations, each one represented by 32 features: 31 numerical and 1 categorical. Each observation represents a given SME customer in a specified reference month, whose observed target indicates its default behaviour and whose features consist of internal information about the company. The data was anonymized, standardized, and split into training and test sets based on the time period: the training set consists of observations covering 12 months of data, while in the test set, we have observations covering the subsequent 8 months.

The dataset also contains a large number of missing values, which motivated the experimentation of different imputation techniques (such as simple imputer, iterative imputer, MICE [45]). The best results were achieved using the iterative imputer, so this was the pre-processing employed in all the results which will be presented.

3.2 Quantum Neural Networks with Orthogonal and Compound Layers

In recent years, variational/parameterized quantum circuits [5] have become very prominent as NISQ-friendly QML techniques. When applied to classification problems, they are commonly known as Variational Quantum Classifiers (VQC) [23]. The quantum circuits associated with VQCs may be schematically thought of as composed of three layers: the feature map , which encodes classical data into quantum states; the variational layer , which is the part of the circuit parameterized by a set of parameters which are learned in the training process; and finally, the measurement layer, which measures the quantum registers and produces classical information used in training and inference.

The feature map and variational layers can take different forms, called ansätze, consisting of many possible different quantum gates in different configurations. Such immense freedom raises an important question: how should one choose an architecture for a given problem, and can it be expected to yield a quantum advantage? This question is of major practical importance, and although benchmark results have been shown for very particular datasets [23, 37], there is little consensus on which ansätze are good choices for machine learning.

In our work, we use quantum neural networks with orthogonal and compound layers. Although these neural networks roughly match the general VQC construction, they produce well-defined linear algebraic operations, which not only makes them much more interpretable but gives us the ability to analyze their complexity and scalability. Because we understand the actions of these layers precisely, we are able to identify instances for which we can design efficient classical simulators, allowing us to classically train and test the models on real-scale datasets.

A standard feed-forward neural network layer modifies an input vector by first multiplying it by a weight matrix and then applying a non-linearity to the result. Feed-forward neural networks usually use many such layers and learn to predict a target variable by optimizing the weight matrices to minimize a loss function. Enforcing the orthogonality of these weight matrices, as proposed in [26], brings theoretical and practical benefits: it reduces the redundancy in the trained weights and can avoid the age-old problem of vanishing gradients. However, the overhead of typical projection-based methods to enforce orthogonality prevents mainstream adoption.

In [33], an improved method of constructing orthogonal neural networks using quantum ideas was developed. We shall describe it below in brief.

3.2.1 Data Loaders

In order to perform a machine learning task with a quantum computer, we need to first load classical data into the quantum circuit.

Unary data loading circuits

The first way we will load classical data is an example of amplitude encoding, which means that we load the (normalised) vector elements as the amplitudes of a quantum state. In [27], three different circuits to load a vector using gates are proposed. The circuits range in depth from to , with varying qubit connectivity (see Fig.14). They use the unary amplitude encoding, where a vector is loaded in the quantum state , where is the quantum state with all qubits in except the qubit in state (e.g., ). The circuit uses gates: a parameterized two-qubit hamming weight-preserving gate implementing the unitary given by Eq.5:

| (5) |

The parameters of the RBS gates are classically pre-computed to ensure they encode the correct vector .

-loading circuits

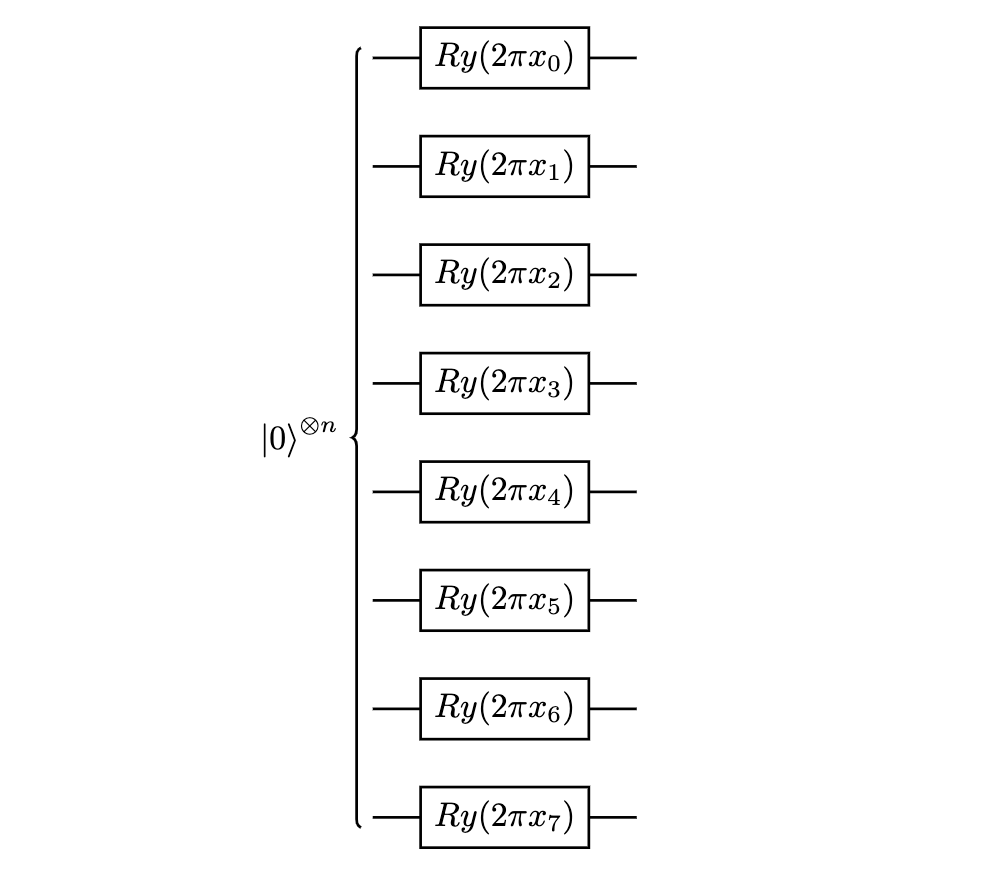

We will also use data loading procedures beyond the unary basis. In particular, for a normalised input vector , we use qubits, where on each of the qubits, we apply an rotation gate where the angle parameter on the qubit is , according to Eq. 6. Multiplication with allows us to cover the entire range of the and functions. This technique loads the data in the entire -dimensional Hilbert space encompassing all the hamming weights from to . This loading technique has constant depth independent of , and we refer to it as the RY loading, whose circuit for is illustrated in Fig. 17.

| (6) |

-loading circuits

Lastly, we define a different technique for loading the data in the entire -dimensional Hilbert space, which loads the vector in the unary basis and then applies a Hadamard gate on each qubit. This operation applies a Fourier transform on and gives us a state encompassing all the hamming weights from to at no additional cost to the circuit depth. We call this the -loading, whose circuit for is illustrated in Fig. 17.

| (7) |

3.2.2 Quantum Orthogonal and Compound Layers

Quantum orthogonal layers consist of a unary data loader plus a parametrised quantum circuit made of gates, while quantum compound layers consist of a general data loader plus a parametrised quantum circuit made of gates.

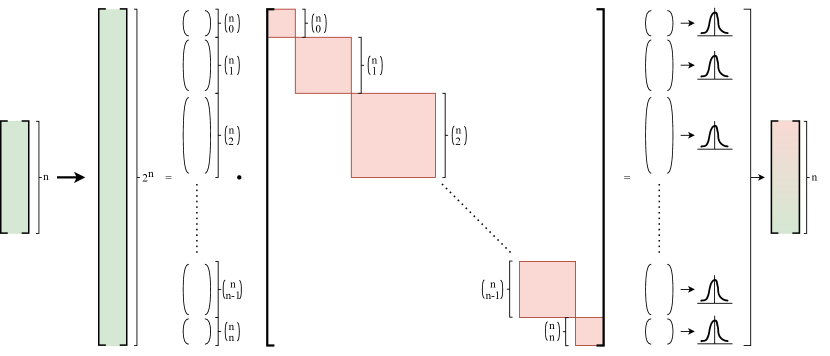

gates and circuits preserve the hamming weight of the input state: if we use a unary data loader, then the output of the layer will be another vector in unary amplitude encoding. Similarly, if the loaded quantum state is a superposition of only basis states of hamming weight , so is the output state. More generally, we can think of such hamming-weight preserving circuits with qubits as block-diagonal unitaries that act separately on subspaces, where the subspace is defined by all computational basis states with hamming weight equal to . The dimension of these subspaces is equal to . The first block of this unitary is an orthogonal matrix, such that when a vector is loaded in the unary basis, this circuit simply performs orthogonal matrix multiplication. In general, the -th block of this unitary applies a compound matrix of order k of the unary matrix. The dimension of this -th order compound matrix is . We refer to the layers that use bases beyond the unary as compound layers.

There exist many possibilities for building a parametrised quantum circuit made of gates which can be used in a quantum orthogonal or compound layer, each with different properties.

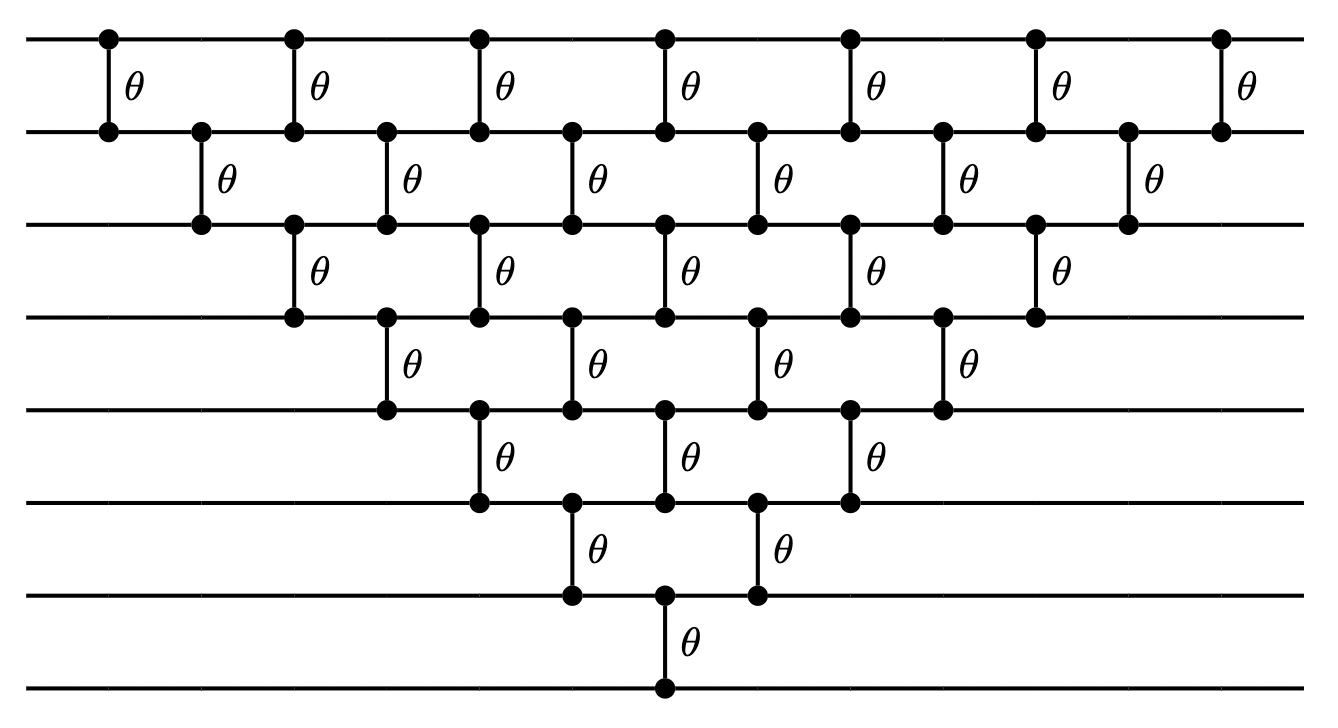

The Pyramid circuit (Fig.21), proposed in [33], is a parameterized quantum circuit composed of exactly gates. This circuit requires only adjacent qubit connectivity, which makes it suitable for most superconducting qubit hardware. In addition, when restricted to the unary basis, the pyramid circuit expresses exactly the Special Orthogonal Group, i.e. orthogonal matrices with the determinant equal to . To allow this circuit to express the entire orthogonal group, we can add a final gate on the last qubit. This allows us to express orthogonal matrices with a determinant as well. The pyramid circuit is, therefore, very general and covers all the possible orthogonal matrices of size .

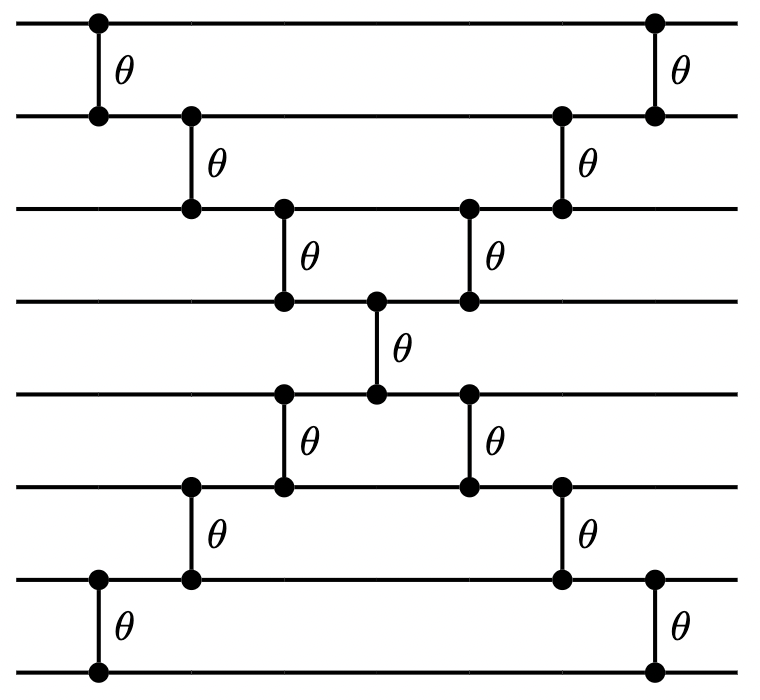

The circuit (Fig.21), introduced in [9], uses just gates and has nearest-neighbor connectivity. Due to reduced depth and gate complexity, it accumulates less hardware noise.

The Butterfly circuit (Fig.21) is inspired by the classical fast Fourier transform algorithm, and uses gates. It was also introduced in [9], and despite having reduced expressivity compared to the Pyramid circuit, it often performs just as well.

In [33], a method is proposed to train orthogonal layers for the unary basis by computing the gradient of each parameter using backpropagation. This backpropagation method for the pyramid circuit (which is the same for any circuit with gates) takes time , corresponding to the number of gates, and provides a polynomial improvement in runtime compared to the previously known orthogonal neural network training algorithms which relied on an SVD operation [26]. Since the runtime corresponds to the number of gates, it is lower for the butterfly and circuits. See Table 3 for full details on the comparison between the three types of circuits. For the compound layers, we need to consider the entire space and thus train an exponential size weight matrix, which takes exponential time on a classical computer. In principle, a compound layer can also be trained using the parameter shift rule for quantum circuits, which can be more efficient since the number of parameters is polynomial in the input size, though noise in current quantum hardware makes this impractical for the time being.

| Circuit | Hardware Connectivity | Depth | # Gates |

|---|---|---|---|

| Pyramid | Nearest-Neighbor | ||

| X | Nearest-Neighbor | ||

| Butterfly | All-to-all |

3.2.3 Expectation-per-subspace Compound Layer

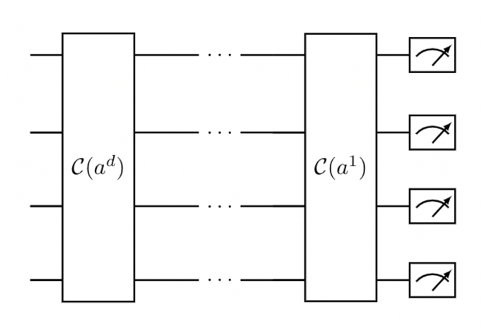

We describe here a compound layer that we call the Expectation-per-subspace compound layer. This layer involves loading the input vector using a non-unary basis which could be done either via the -loading or the -loading circuit as previously defined. Then, we apply a parameterized quantum circuit with RBS gates, e.g. a pyramid circuit, which performs the compound matrix operation on all the fixed hamming weight subspaces. More precisely, we can think of the operation as performing the matrix-vector multiplication of an matrix with an -dimensional vector for each hamming weight from to . Note that for and , the dimension is and hence the unitary acts as identity.

If we look at the output quantum state, it defines a distribution over a domain of size . Given the exponential size of the distribution, it is not advisable to try and train the entire distribution, since that would take exponential time. However, one can still try to use a loss function that contains some information about the distribution. For example, one can use the expectation of the distribution, which is what normally happens in variational quantum algorithms where one approximates this expectation by using a number of measurement outcomes. Given the fact that our unitary is block-diagonal, one can try to define a more complex loss function that contains more information about the distribution. In particular, one can split the domain of the distribution into subdomains, one for each subspace, and then train on all these expectations.

This is what we do in the Expectation-per-subspace compound layer, where for each from to , we take the outputs corresponding to the hamming weight strings and sort them. Now, for each , we assign values which are equally spaced between two bounds and (which are and , in our models) to the strings. We normalise the outputs using the -norm to correspond to a probability distribution over the values between and , and then we calculate the expectation value for that hamming weight. This gives us a set of values corresponding to each hamming weight. Since for hamming weight and the dimension of the subspace is 1 (the all zero and all one strings), we combine them and calculate the expectation for these two together and make the layer have outputs. The entire operation is illustrated in Fig. 22.

3.2.4 An Orthogonal Neural Network Architecture for Credit Risk Assessment

We first deploy a variant of Residual Neural Networks using orthogonal layers (which we call OrthoResNN). We use a three-layered network which takes a -dimensional vector as input and outputs a -dimensional vector denoting the probability of predicting and for the data point. Our first layer is a standard feed-forward layer of size followed by a activation. Then, we apply an orthogonal layer (semi-diagonal loader and circuit). Note that measurements provide the sampled distribution, which corresponds to the square of the probability amplitudes. Since this squaring is a type of non-linearity, we do not apply any additional non-linearity to it but add the bias directly. In the spirit of residual neural networks (ResNN), we make a skip connection by adding the input of the orthogonal layer to the output. Finally, we apply another standard feed-forward layer of size followed by a softmax layer to make it predict the probabilities. This architecture is illustrated in Fig. 23. Moreover, we also perform our simulations for the model without skip connections (which we call OrthoFNN). Such a model is a basic feed-forward neural network (FNN) of size where the layer is an orthogonal layer. The architecture is exactly the same as Fig. 23 without the skip connections.

3.2.5 A Compound Neural Network Architecture for Credit Risk Assessment

We also define a quantum neural network architecture that contains a quantum compound layer, using a non-unary basis for loading the data and exploring the entire -dimensional Hilbert space. Our first layer is a standard feed-forward layer of size followed by a activation. After this, we apply an Expectation-per-subspace compound layer using a non-unary data loading technique. We tried both the -loading and -loading techniques. After adding the biases, we apply a activation. Then, we apply another standard feed-forward layer of size to get the two outputs. We use softmax to convert the outputs to probabilities. Again, in the experiments, we try the same model architectures with and without the ResNN-like skip connection procedure, which we respectively call ExpResNN and ExpFNN. Fig. 24 illustrates the ExpResNN architecture for the -loading. The ExpFNN architecture is the same as Fig. 24 without the skip connection. The same models can use the -loading instead of the -loading.

3.3 Results

3.3.1 Classical Results

The neural network experiments were performed using the dataset described in Sec. 3.1, with the iterative imputation method to fill in the missing data. The training of the networks was performed using the JAX package by Google. We train our models for epochs. The learning rate reduces by half after every epochs and is initially set to . We performed simulation experiments for two types of model architectures: Feed-forward Neural Networks (FNN) and Residual Neural Networks (ResNN). Each of them has three types of layers: the standard fully-connected layer, the orthogonal layer and the expectation-per-subspace compound layer.

In our experimental setup, the fully connected layer (FNN) produced a test Gini score of , which we consider the classical benchmark. We performed the same experiment with an orthogonal layer using the semi-diagonal loader and the X circuit (OrthoFNN), which achieved a Gini score of as well. Finally, we tried the expectation-per-subspace compound layer with the Hadamard loader and X circuit (ExpFNN), which produced a Gini score of . While the performance of the OrthoFNN and ExpNN remained nearly the same as the FNN layer, these new layers learn the angles of RBS gates instead of elements of the weight matrix, dramatically reducing the number of parameters needed. The results are shown in Table 4.

| Model | Test Gini |

|---|---|

| FNN | 53.7% |

| OrthoFNN | 53.7% |

| ExpFNN | 53.7% |

We then performed our classical experiments using the more advanced residual neural networks. The model with a standard fully-connected layer (ResNN) gave us a test Gini score of , which we took as our benchmark. We then trained the orthogonal residual neural network model (OrthoResNN), which gave us a Gini score of . Finally, we tried the residual neural network with the expectation-per-subspace compound layer (ExpResNN) with -loading, which gave us a Gini score of . Both quantum neural networks proposed in this paper outperformed the standard fully-connected layer and used significantly fewer parameters. The results are shown in Table 5.

| Model | Test Gini |

|---|---|

| ResNN | 53.7% |

| OrthoResNN | 54.1% |

| ExpResNN | 53.9% |

3.3.2 Quantum Hardware Results

Using a classical computer, inference using an orthogonal layer takes time , while for a general compound layer, this time is exponential in . Using a quantum computer, inference with an orthogonal or compound layer uses a quantum circuit that has depth (Pyramid or X) or (Butterfly), and gates. Therefore, one may find a further advantage if the inference is performed on a quantum computer. This motivated us to test the inference step on currently available quantum hardware, which was done for the classically trained OrthoResNN and ExpFNN models.

The data loader and orthogonal/compound layer circuits employed in our model architectures are NISQ-friendly and particularly suitable for superconducting qubits, with low depth and nearest-neighbours qubit connectivity. Thus, we chose to use IBM’s 27-qubit machine ibm_hanoi (see Fig.25).

To perform inference on ibm_hanoi, we used the semi-diagonal data loader and X circuit to implement the OrthoResNN model; and the Hadamard loader and X circuit for the ExpFNN model — the same architectures described in Sec. 3.3.1. Both neural networks were trained classically, and the trained parameters were used to construct our quantum circuits for inference.

Given the large size of the test dataset ( data points), we decided to perform inference using the trained models on a small test subsample of test points, corresponding to the maximum number of circuits we could send in one job to the IBM machine. After testing different subsamples with the OrthoResNN model333We made sure to pick a representative subsample of observations, for which we would have neither a heavily under nor overestimated Gini score compared to the one for the full test set. By selecting 50 different subsamples of randomly chosen 300 observations and performing the classical inference, we found Gini scores between 45.9% and 64.3%, with an average of 54.44%. This further supports the fact that the subsample that we chose correctly yields the (approximate) expected value for this Gini score distribution, which then yields an unbiased subsample Gini score. The same procedure was performed for the ExpFNN experiment., we selected one for which we achieved a subsample test Gini score of 54.19% using a noiseless simulator (blue ROC curve in Figure 26). The same was done for the ExpFNN experiment, yielding a subsample test Gini of 53.90% with the noiseless simulator. These values were taken as the best possible Gini scores if the inference was performed on noiseless quantum hardware, which could then be compared with the values actually achieved with ibm_hanoi.

The circuits were then run on the quantum processor. Due to its limited Hilbert space of size , the OrthoResNN has a natural error-rejection procedure: any measurements outside of the unary basis can be disregarded as errors. As a result, the inference yielded a Gini score of , as shown in the orange ROC curve in Fig. 26. The achieved Gini was not too far from the noise-free simulation result (54.19%), but there was clearly room for improvement in order to close the 4 pp difference. We also attempted inference with the more complex ExpFNN, which yielded a Gini score of 40.20%, much farther from the noiseless simulation Gini of 53.90%. Since the ExpFNN uses the entire -dimensional Hilbert space, it is more prone to errors due to noise, as the error-rejection procedure used for the OrthoResNN cannot be employed.

Improving the Hardware Results with Error Mitigation Techniques

Error mitigation and error suppression techniques undoubtedly play a very important role in NISQ-era quantum computing. While these techniques alone may not be sufficient to fully overcome the imperfections of current quantum systems, they can push the practical limits of what can be achieved. As a next step, for the OrthoResNN model, we experimented with various error mitigation and suppression approaches, going beyond the simple hamming-weight postselection procedure, in an attempt to close the gap of 4 pp between the Gini score from the noisy simulation and the one from hardware execution.

The first approach that we tried was a correlated readout mitigator. This is a purely classical post-processing technique which demands the construction of a calibration circuit for each one of the possible states of the full qubits Hilbert space. The calibration circuits’ execution (simulated using ibm_hanoi’s backend information, in our case) yields a assignment matrix, which is used to understand how errors might occur during readout. One can see that this method rapidly becomes intractable as the number of qubits increases. In our case, for , the Gini score improved to 50.24%, a small improvement of only 0.05 pp.

Thus, in order to investigate the effect of more robust error suppression and mitigation techniques in our results, we moved on to a new round of hardware experiments, performing the inference by executing the exact same OrthoResNN circuits via the Qiskit Runtime [10] service using the Sampler primitive, which allows one to use circuit optimization as well as error suppression and mitigation techniques, as detailed below.

Firstly, we used circuit optimization at the point of circuit transpilation and compilation by setting the optimization_level parameter to the highest possible value, 3. This performs the following circuit optimization routines: Layout selection and routing (VF2 layout pass and SABRE layout search heuristics [36]; 1 qubit gate optimization (chains of single-qubit u1, u2, u3 gates are combined into a single gate); commutative cancellation (cancelling of redundant self-adjoint gates); 2 qubit KAK optimization (decomposition of 2-qubit unitaries into the minimal number of uses of 2-qubit basis gates).

Secondly, we used the Dynamical Decoupling error suppression technique [46, 19]. This technique works as a pulse schedule by inserting a DD pulse sequence into periods of time in which qubits are idle. The DD pulses effectively behave as an identity gate, thus not altering the logical action of the circuit, but having the effect of mitigating decoherence in the idle periods, reducing the impact of errors.

Thirdly, we used the M3 (Matrix-free Measurement Mitigation) error mitigation technique [40] by setting the Sampler resilience_level parameter to 1 (the only option available for the Sampler primitive). This provides mitigated quasi-probability distributions after the measurement. M3 works in a reduced subspace defined by the noisy input bitstrings supposed to be corrected, which is often much smaller than the full qubits Hilbert space. For this reason, this method is much more efficient than the matrix-based readout mitigator technique mentioned above. M3 provides a matrix-free preconditioned iterative solution method, which removes the need to construct the full reduced assignment matrix but rather computes individual matrix elements, which uses orders of magnitude less memory than direct factorization.

By employing these three techniques, we were able to achieve a Gini score of 53.68% for the OrthoResNN (Fig. 26). This is a 3.49 pp improvement from the initial 50.19% Gini of the unmitigated run, falling only 0.53 pp behind the ideal noiseless execution (54.21% Gini)! This remarkable result underscores the NISQ-friendliness of the orthogonal layer and highlights the importance of error suppression and mitigation techniques in the NISQ era.

It is important to note that circuit optimization, error suppression, and mitigation techniques typically result in some classical/quantum pre/post-processing overhead to the overall circuit runtime. Some of these techniques are based on heuristics and/or do not have efficient scaling at larger circuit sizes. It is important to balance the desired levels of optimization and resilience with the required time for the full execution, especially as the circuit sizes increase.

3.3.3 Further Benchmarks

We benchmarked the OrthoFNN architecture on different classification datasets from OpenML as we did for the Random Forests (Sec. 2.4.5). We trained fully connected neural networks (FNNs) using the same model parameters and hyperparameters. We first use a fully connected layer of output nodes followed by GeLU. Then, we extract the features using a fully connected layer, which is done using the Pyramid circuit in the case of the orthogonal FNN, followed by tanh. In the end, we use another fully connected layer with output nodes. For all the datasets and models, we use a batch size of and a learning rate of . Each is trained for epochs and evaluated with the ROC-AUC metric. The results are summarised in Table 6, in which one can see that the OrthoFNN model was superior in most of the tasks.

| Dataset | FNN | OrthoFNN |

|---|---|---|

| madelon | 0.624 | 0.636 |

| credit-default | 0.647 | 0.634 |

| house-pricing | 0.780 | 0.781 |

| Jannis | 0.791 | 0.797 |

| eye movements | 0.580 | 0.578 |

| bank-marketing | 0.847 | 0.850 |

| wine | 0.553 | 0.640 |

| california | 0.634 | 0.668 |

4 Conclusion

In this work, we have explored the potential of quantum machine learning methods in improving forecasting in finance, with a focus on two specific use cases within the Itaú business: churn prediction and credit risk assessment. Our results demonstrate that the proposed algorithms, which leverage quantum ideas, can effectively enhance the performance of Random Forest and neural networks models, achieving better accuracy and generalization.

In the present day, quantum hardware is not powerful enough to provide real improvements or conclusive large-scale benchmarks. Performance enhancements can be achieved today by turning these quantum ideas into classical ML solutions run on GPUs. However, with the advent of better quantum hardware, we expect these methods to run faster and produce even better results when run on quantum computers.

The general nature of the proposed methods makes them applicable to other use cases in finance and beyond, although they must be tuned to specific datasets and tasks. We hope this work inspires confidence that QML research holds promise both for today as well as for the coming era of scaled, fault-tolerant quantum hardware.

Disclaimer

This paper is a research collaboration between Itaú Unibanco and QC Ware. Any opinions, findings, conclusions or recommendations expressed in this material are those of the authors and do not necessarily reflect the views of Itaú Unibanco. This paper is not and does not constitute or intend to constitute investment advice or any investment service. It is not and should not be deemed to be an offer to purchase or sell or a solicitation of an offer to purchase or sell, or a recommendation to purchase or sell any securities or other financial instruments. Moreover, all data used in this study is compliant with the Brazilian General Data Protection Law.

References

- [1] Javier Alcazar, Vicente Leyton-Ortega, and Alejandro Perdomo-Ortiz. Classical versus quantum models in machine learning: insights from a finance application. Machine Learning: Science and Technology, 1(3):035003, 2020.

- [2] Nima Anari, Shayan Oveis Gharan, and Alireza Rezaei. Monte carlo markov chain algorithms for sampling strongly rayleigh distributions and determinantal point processes. In Vitaly Feldman, Alexander Rakhlin, and Ohad Shamir, editors, 29th Annual Conference on Learning Theory, volume 49 of Proceedings of Machine Learning Research, pages 103–115, Columbia University, New York, New York, USA, 23–26 Jun 2016. PMLR.

- [3] Martin Arjovsky, Amar Shah, and Yoshua Bengio. Unitary evolution recurrent neural networks. In International conference on machine learning, pages 1120–1128. PMLR, 2016.

- [4] Rémi Bardenet and Adrien Hardy. Monte carlo with determinantal point processes. The Annals of Applied Probability, 30(1):368–417, 2020.

- [5] Marcello Benedetti, Erika Lloyd, Stefan Sack, and Mattia Fiorentini. Parameterized quantum circuits as machine learning models. Quantum Science and Technology, 4(4):043001, November 2019.

- [6] Adam Bouland, Wim van Dam, Hamed Joorati, Iordanis Kerenidis, and Anupam Prakash. Prospects and challenges of quantum finance, 2020.

- [7] Leo Breiman. Random forests. Machine Learning, 45(1):5–32, Oct 2001.

- [8] Daniele Calandriello, Michal Derezinski, and Michal Valko. Sampling from a k-dpp without looking at all items. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 6889–6899. Curran Associates, Inc., 2020.

- [9] El Amine Cherrat, Iordanis Kerenidis, Natansh Mathur, Jonas Landman, Martin Strahm, and Yun Yvonna Li. Quantum vision transformers. arXiv preprint arXiv:2209.08167, 2022.

- [10] Qiskit contributors. Qiskit: An open-source framework for quantum computing. 2021.

- [11] M. Derezinski. Volume sampling for linear regression. UC Santa Cruz Electronic Theses and Dissertations, 36, 2018.

- [12] Michal Derezinski, Daniele Calandriello, and Michal Valko. Exact sampling of determinantal point processes with sublinear time preprocessing. In H. Wallach, H. Larochelle, A. Beygelzimer, F. d'Alché-Buc, E. Fox, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc., 2019.

- [13] Michał Derezinski and Michael W Mahoney. Determinantal point processes in randomized numerical linear algebra. Notices of the American Mathematical Society, 68(1):34–45, 2021.

- [14] Michat Dereziński, Manfred K. Warmuth, and Daniel Hsu. Leveraged volume sampling for linear regression. In Proceedings of the 32nd International Conference on Neural Information Processing Systems, NIPS’18, page 2510–2519, Red Hook, NY, USA, 2018. Curran Associates Inc.

- [15] João F. Doriguello, Alessandro Luongo, Jinge Bao, Patrick Rebentrost, and Miklos Santha. Quantum Algorithm for Stochastic Optimal Stopping Problems with Applications in Finance. In François Le Gall and Tomoyuki Morimae, editors, 17th Conference on the Theory of Quantum Computation, Communication and Cryptography (TQC 2022), volume 232 of Leibniz International Proceedings in Informatics (LIPIcs), pages 2:1–2:24, Dagstuhl, Germany, 2022. Schloss Dagstuhl – Leibniz-Zentrum für Informatik.

- [16] Daniel J. Egger, Claudio Gambella, Jakub Marecek, Scott McFaddin, Martin Mevissen, Rudy Raymond, Andrea Simonetto, Stefan Woerner, and Elena Yndurain. Quantum computing for finance: State-of-the-art and future prospects. IEEE Transactions on Quantum Engineering, 1:1–24, 2020.

- [17] Mohamed Elfeki, Camille Couprie, Morgane Riviere, and Mohamed Elhoseiny. Gdpp: Learning diverse generations using determinantal point processes. In International conference on machine learning, pages 1774–1783. PMLR, 2019.

- [18] Dimitrios Emmanoulopoulos and Sofija Dimoska. Quantum machine learning in finance: Time series forecasting. arXiv e-prints, pages arXiv–2202, 2022.

- [19] Nic Ezzell, Bibek Pokharel, Lina Tewala, Gregory Quiroz, and Daniel A. Lidar. Dynamical decoupling for superconducting qubits: a performance survey. 7 2022.

- [20] Guillaume Gautier, Guillermo Polito, Rémi Bardenet, and Michal Valko. Dppy: Dpp sampling with python. Journal of Machine Learning Research, 20(180):1–7, 2019.

- [21] Tudor Giurgica-Tiron, Iordanis Kerenidis, Farrokh Labib, Anupam Prakash, and William Zeng. Low depth algorithms for quantum amplitude estimation. Quantum, 6:745, June 2022.

- [22] Leo Grinsztajn, Edouard Oyallon, and Gael Varoquaux. Why do tree-based models still outperform deep learning on typical tabular data? In Thirty-sixth Conference on Neural Information Processing Systems Datasets and Benchmarks Track, 2022.

- [23] Vojtěch Havlíček, Antonio D Córcoles, Kristan Temme, Aram W Harrow, Abhinav Kandala, Jerry M Chow, and Jay M Gambetta. Supervised learning with quantum-enhanced feature spaces. Nature, 567:209–212, 2018.

- [24] Dylan Herman, Cody Googin, Xiaoyuan Liu, Alexey Galda, Ilya Safro, Yue Sun, Marco Pistoia, and Yuri Alexeev. A Survey of Quantum Computing for Finance. Papers 2201.02773, arXiv.org, January 2022.

- [25] J. Ben Hough, Manjunath Krishnapur, Yuval Peres, and Bálint Virág. Determinantal Processes and Independence. Probability Surveys, 3(none):206 – 229, 2006.

- [26] Kui Jia, Shuai Li, Yuxin Wen, Tongliang Liu, and Dacheng Tao. Orthogonal deep neural networks. IEEE transactions on pattern analysis and machine intelligence, 2019.

- [27] S Johri, S Debnath, A Mocherla, A Singh, A Prakash, J Kim, and I Kerenidis. Nearest centroid classification on a trapped ion quantum computer. npj Quantum Information (to appear), arXiv:2012.04145, 2021.

- [28] Skander Kazdaghli, Iordanis Kerenidis, Jens Kieckbusch, and Philip Teare. Improved clinical data imputation via classical and quantum determinantal point processes. arXiv preprint arXiv:2303.17893, 2023.

- [29] Iordanis Kerenidis and Anupam Prakash. Quantum machine learning with subspace states. arXiv preprint arXiv:2202.00054, 2022.

- [30] Iordanis Kerenidis, Anupam Prakash, and Dániel Szilágyi. Quantum algorithms for portfolio optimization. In Proceedings of the 1st ACM Conference on Advances in Financial Technologies, AFT ’19, page 147–155, New York, NY, USA, 2019. Association for Computing Machinery.

- [31] Alex Kulesza and Ben Taskar. K-dpps: Fixed-size determinantal point processes. In Proceedings of the 28th International Conference on International Conference on Machine Learning, ICML’11, page 1193–1200, Madison, WI, USA, 2011. Omnipress.

- [32] Alex Kulesza and Ben Taskar. Determinantal point processes for machine learning. Foundations and Trends® in Machine Learning, 5(2–3):123–286, 2012.

- [33] Jonas Landman, Natansh Mathur, Yun Yvonna Li, Martin Strahm, Skander Kazdaghli, Anupam Prakash, and Iordanis Kerenidis. Quantum Methods for Neural Networks and Application to Medical Image Classification. Quantum, 6:881, December 2022.

- [34] Lucas Leclerc, Luis Ortiz-Guitierrez, Sebastian Grijalva, Boris Albrecht, Julia R. K. Cline, Vincent E. Elfving, Adrien Signoles, Loïc Henriet, Gianni Del Bimbo, Usman Ayub Sheikh, Maitree Shah, Luc Andrea, Faysal Ishtiaq, Andoni Duarte, Samuel Mugel, Irene Caceres, Michel Kurek, Roman Orus, Achraf Seddik, Oumaima Hammammi, Hacene Isselnane, and Didier M’tamon. Financial risk management on a neutral atom quantum processor, 2022.

- [35] Chengtao Li, Suvrit Sra, and Stefanie Jegelka. Fast mixing markov chains for strongly rayleigh measures, dpps, and constrained sampling. In Daniel D. Lee, Masashi Sugiyama, Ulrike von Luxburg, Isabelle Guyon, and Roman Garnett, editors, Advances in Neural Information Processing Systems 29: Annual Conference on Neural Information Processing Systems 2016, December 5-10, 2016, Barcelona, Spain, pages 4188–4196, 2016.

- [36] Gushu Li, Yufei Ding, and Yuan Xie. Tackling the Qubit Mapping Problem for NISQ-Era Quantum Devices. arXiv e-prints, page arXiv:1809.02573, September 2018.

- [37] Yunchao Liu, Srinivasan Arunachalam, and Kristan Temme. A rigorous and robust quantum speed-up in supervised machine learning. Nature Physics, 17(9):1013–1017, July 2021.

- [38] Odile Macchi. The coincidence approach to stochastic point processes. Advances in Applied Probability, 7(1):83–122, 1975.

- [39] McKinsey & Company. Quantum computing: An emerging ecosystem and industry use cases, 2021. Accessed: February 16, 2023.

- [40] Paul D. Nation, Hwajung Kang, Neereja Sundaresan, and Jay M. Gambetta. Scalable mitigation of measurement errors on quantum computers. PRX Quantum, 2:040326, 2021.

- [41] Marco Pistoia, Syed Farhan Ahmad, Akshay Ajagekar, Alexander Buts, Shouvanik Chakrabarti, Dylan Herman, Shaohan Hu, Andrew Jena, Pierre Minssen, Pradeep Niroula, Arthur Rattew, Yue Sun, and Romina Yalovetzky. Quantum machine learning for finance, 2021.

- [42] Patrick Rebentrost and Seth Lloyd. Quantum computational finance: quantum algorithm for portfolio optimization. arXiv preprint arXiv:1811.03975, 2018.

- [43] Patrick Rebentrost, Alessandro Luongo, Samuel Bosch, and Seth Lloyd. Quantum computational finance: martingale asset pricing for incomplete markets, 2022.

- [44] Yohichi Suzuki, Shumpei Uno, Rudy Raymond, Tomoki Tanaka, Tamiya Onodera, and Naoki Yamamoto. Amplitude estimation without phase estimation. Quantum Information Processing, 19(2):75, Jan 2020.

- [45] Stef van Buuren and Karin Groothuis-Oudshoorn. mice: Multivariate imputation by chained equations in r. Journal of Statistical Software, 45(3):1–67, 2011.

- [46] Lorenza Viola and Seth Lloyd. Dynamical suppression of decoherence in two state quantum systems. Phys. Rev. A, 58:2733, 1998.