Front-door Adjustment Beyond Markov Equivalence with Limited Graph Knowledge

Abstract

Causal effect estimation from data typically requires assumptions about the cause-effect relations either explicitly in the form of a causal graph structure within the Pearlian framework, or implicitly in terms of (conditional) independence statements between counterfactual variables within the potential outcomes framework. When the treatment variable and the outcome variable are confounded, front-door adjustment is an important special case where, given the graph, causal effect of the treatment on the target can be estimated using post-treatment variables. However, the exact formula for front-door adjustment depends on the structure of the graph, which is difficult to learn in practice. In this work, we provide testable conditional independence statements to compute the causal effect using front-door-like adjustment without knowing the graph under limited structural side information. We show that our method is applicable in scenarios where knowing the Markov equivalence class is not sufficient for causal effect estimation. We demonstrate the effectiveness of our method on a class of random graphs as well as real causal fairness benchmarks.

1 Introduction

Causal effect estimation is at the center of numerous scientific, societal, and medical questions (Nabi et al., 2019; Castro et al., 2020). The operator of Pearl represents the effect of an experiment on a causal system. For example, the probability distribution of a target variable after setting a treatment to is represented by and is known as an interventional distribution. Learning this distribution for any realization 111Depending on the context, causal effect estimation sometimes refers to the estimating the difference of assigning vs. on the target variable , e.g., . This quantity is computable if we can identify for . is what causal effect estimation entails. This distribution is different from the conditional distribution as there may be unobserved confounders between treatment and outcome that cannot be controlled for.

A causal graph, often depicted as a directed acyclic graph, captures the cause-and-effect relationships between variables and explains the causal system under consideration. A semi-Markovian causal model represents a causal model that includes unobserved variables influencing multiple observed variables (Verma and Pearl, 1990; Acharya et al., 2018). In a semi-Markovian graph, directed edges between observed variables represent causal relationships, while bi-directed edges between observed variables represent unobserved common confounding (see Figure 1). Given any semi-Markovian graph, complete identification algorithms for causal effect estimation are known. For example, if is uniquely determined by the observational distribution and the causal graph, the algorithm by Shpitser and Pearl (2006) utilizes the graph to derive an estimand, i.e., the functional form mapping the observational distribution to the interventional distribution.

Certain special cases of estimands have found widespread use across several domains. One such special case is the back-door adjustment (Pearl, 1993) shown in Figure 1(left). The back-door adjustment utilizes the pre-treatment variable (that blocks back-door paths) to control for unobserved confounder as follows:

| (1) |

where the do-calculus rules of Pearl (1995) are used to convert interventional distributions into observational distributions by leveraging the graph structure. However, the back-door adjustment is often inapplicable, e.g., in the presence of an unobserved confounder between and . Surprisingly, in such scenarios, it is sometimes possible to find the causal effect using the front-door adjustment (Pearl, 1995) shown in Figure 1(right). Utilizing the front-door variable , the front-door adjustment estimates the causal effect from observational distributions using the following formula (which is also obtained through the do-calculus rules and the graph structure):

| (2) |

Recently, front-door adjustment has gained popularity in analyzing real-world data (Glynn and Kashin, 2017; Bellemare et al., 2019; Hünermund and Bareinboim, 2019) due to its ability to utilize post-treatment variables to estimate effects even in the presence of confounding between and . However, in general, front-door adjustment also relies on knowing the causal graph, which may not always be feasible, especially in domains with many variables.

An alternative approach uses observational data to infer a Markov equivalence class, which is a collection of causal graphs that encode the same conditional independence relations (Spirtes et al., 2000). A line of work (Perkovic et al., 2018; Jaber et al., 2019) provide identification algorithms for causal effect estimation from partial ancestral graphs (PAGs) (Zhang, 2008), a prominent representation of the Markov equivalence class, whenever every causal graph in the collection shares the same causal effect estimand. However, learning PAGs from data is challenging in practice due to the sequential nature of their learning algorithms, which can propagate errors between tests (Strobl et al., 2019a). Further, to the best of our knowledge, there is no existing algorithm that can incorporate side information, such as known post-treatment variables, into PAG structure learning.

In this work, we ask the following question: Can the causal effect be estimated with a testable criteria on observational data by utilizing some structural side information without knowing the graph?

Recent research has developed such testable criteria to enable back-door adjustment without knowing the full causal graph (Entner et al., 2013; Cheng et al., 2020; Gultchin et al., 2020; Shah et al., 2022). These approaches leverage structural side information, such as a known and observed parent of the treatment variable . However, no such results have been established for enabling front-door adjustment. We address this gap by focusing on the case of unobserved confounding between and , where back-door adjustment is inapplicable. Traditionally, this scenario has been addressed by leveraging the presence of an instrumental variable (Mogstad and Torgovitsky, 2018) or performing sensitivity analysis (Veitch and Zaveri, 2020), both of which provide only bounds in the non-parametric case. In contrast, we achieve identifiability by utilizing structural side information.

Contributions. We propose a method for estimating causal effects without requiring the knowledge of causal graph in the presence of unobserved confounding between treatment and outcome. Our approach utilizes front-door-like adjustments based on post-treatment variables and relies on conditional independence statements that can be directly tested from observational data. We require one structural side information which can be obtained from an expert and is less demanding than specifying the entire causal graph. We illustrate that our framework provides identifiability in random ensembles where existing PAG-based methods are not applicable. Further, we illustrate the practical application of our approach to causal fairness analysis by estimating the total effect of a sensitive attribute on an outcome variable using the German credit data with fewer structural assumptions.

1.1 Related Work

Effect estimation from causal graphs/Markov equivalence Class: The problem of estimating interventional distributions with the knowledge of the semi-Markovian model has been studied extensively in the literature, with important contributions such as Tian and Pearl (2002) and Shpitser and Pearl (2006). Perkovic et al. (2018) presented a complete and sound algorithm for identifying valid adjustments from PAGs. Going beyond valid adjustments, Jaber et al. (2019) proposed a complete and sound algorithm for identifying causal effect from PAGs. However, our method can recover the causal effect in scenarios where these algorithms are inapplicable.

Effect estimation via front-door adjustment with causal graph: Several recent works have contributed to a better understanding of the statistical properties of front-door estimation (Kuroki, 2000; Kuroki and Cai, 2012; Glynn and Kashin, 2018; Gupta et al., 2021), proposed robust generalizations (Hünermund and Bareinboim, 2019; Fulcher et al., 2020), and developed procedures to enumerate all possible front-door adjustment sets (Jeong et al., 2022; Wienöbst et al., 2022). However, all of these require knowing the underlying causal graph. In contrast, Bhattacharya and Nabi (2022) verified the front-door criterion without knowing the causal graph using Verma constraint-based methodology. However, this approach is only applicable to a small set of graphs. Our proposed approach relies on conditional independence and is applicable to a broad class of graphs.

2 Preliminaries and Problem Formulation

Notations.

For a sequence of realizations , we define . For a sequence of random variables , we define . Let denote the indicator function.

Semi-Markovian Model and Effect Estimation.

We consider a causal effect estimation task where represents the set of observed features, represents the observed treatment variable, and represents the observed outcome variable. We denote the set of all observed variables jointly by . Let denote the set of unobserved features that could be correlated with the observed variables.

We assume follows a semi-Markovian causal model (Tian and Pearl, 2002) as below.

Definition 1.

A semi-Markovian causal model (SMCM) is specified as follows:

-

1.

is a directed acyclic graph (DAG) over the set of vertices such that each element of the set has no parents.

-

2.

, let and denote the set of parent of in and , respectively.

-

3.

is the unobserved joint distribution over the unobserved features.

-

4.

The observational distribution is given by .

-

5.

The interventional distribution when the variables are set to a fixed value is given by

(3) -

6.

For any , if , then and have a bi-directed edge in .

In this work, we are interested in the causal effect of on , i.e., . We define this formally by marginalizing all variables except in the interventional distribution in (3).

Definition 2.

The causal effect of (when forced to a value ) on is given by:

| (4) |

Next, we define the notion of average treatment effect for a binary treatment .

Definition 3.

The average treatment effect (ATE) of a binary treatment on outcome is given by ATE = .

Next, we define when the causal effect (Definition 2) is said to be identifiable from the observational distribution and the causal graph.

Definition 4.

(Causal effect identifiability) Given an observational distribution and a causal graph , the causal effect is identifiable if it is identical for every semi-Markovian Causal model with same graph and same observational distribution .

In a causal graph , a path is an ordered sequence of distinct nodes where each node is connected to the next in the sequence by an edge. A path starting at node and ending at node in is blocked by a set if there exists such that (a) is not a collider or (b) is a collider and neither nor any of it’s descendant is in . Further, and are said to be d-separated by in if blocks every path between and in . Let denote that and are d-separated by in . Similarly, let denote that and are conditionally independent given . We assume causal faithfulness, i.e., any conditional independence implies a d-separation relation in the causal graph .

2.1 Adjustment using pre-treatment variables

It is common in causal effect estimation to consider pre-treatment variables, i.e., variables that occur before the treatment in the causal ordering, and identify sets of variables that are valid adjustments. Specifically, a set forms a valid adjustment if the causal effect can be written as . In other words, a valid adjustment averages an estimate of regressed on and with respect to the marginal distribution of . A popular criterion to find valid adjustments is to find a set that satisfies the back-door criterion (Pearl, 2009). Formally, a set satisfies the back-door criterion if (a) it blocks all back-door paths, i.e., paths between and that have an arrow pointing at and (b) no element of is a descendant of . While, in general, back-door sets can be found with the knowledge of the causal graph, recent works (see the survey Cheng et al. (2022)) have proposed testable criteria for identifying back-door sets with some causal side information, without requiring the entire graph.

2.2 Adjustment using post-treatment variables

While back-door adjustment is widely used, there are scenarios where no back-door set exists, e.g., when there is an unobserved confounder between and . If no back-door set can be found from the pre-treatment variables, Pearlian theory can be used to identify post-treatment variables, i.e., the variables that occur after the treatment in the causal ordering, to obtain a front-door adjustment.

Definition 5 (Front-door criterion).

A set satisfies the front-door criterion with respect to and if (a) intercepts all directed paths from to (b) all back-door paths between and are blocked, and (c) all back-door paths between and are blocked by .

If a set satisfies the front-door criterion, then the causal effect can be written as

| (5) |

Intuitively, front-door adjustment estimates the causal effect of on as a composition of two effects: the effect of on and the effect of on . However, one still needs the knowledge of the causal graph to find a set satisfying the front-door criterion.

Inspired by the progress in finding back-door sets without knowing the entire causal graph, we ask: Can testable conditions be derived to identify front-door-like sets using only partial structural information about post-treatment variables? To that end, we consider the following side information.

Assumption 1.

The outcome is a descendant of the treatment .

Assumption 2.

There is an unobserved confounder between the outcome and the treatment .

Assumption 3.

, the set of all children of the treatment , is observed and known.

Assumption 1 is a fundamental assumption in most causal inference works, as it forms the basis for estimating non-trivial causal effects. Without it, the causal effect would be zero. Assumption 2 rules out the existence of sets that satisfy the back-door criteria, necessitating a different way of estimating the causal effect. Assumption 3 captures our side information by requiring every children of the treatment to be known and observed. To contrast, the side information in data-driven works on back-door adjustment requires a parent of the treatment to be known and observed (Shah et al., 2022).

Our assumptions imply that intercepts all the directed paths from to . Given this, it is natural to ask whether satisfies the front-door criterion (Definition 5). We note that, in general, this is not true. We illustrate this via Figure 2 where we provide a causal graph satisfying our assumptions. However, is not a valid front-door set in as the back-door path between and via is not blocked by . Therefore, estimating the causal effect by assuming is a front-door set might not always give an unbiased estimate. In the next section, we leverage the given side information and provide testable conditions to identify front-door-like sets.

3 Front-door Adjustment Beyond Markov Equivalence

In this section, we provide our main results, an algorithm for ATE estimation, and discuss the relationship to PAG-based methods. Our main results use observational criteria for causal effect estimation under Assumptions 1 to 3 using post treatment variables.

3.1 Causal effect estimation using post-treatment variables

First, we state a conditional independence statement implying causal identifiability. Then, we provide additional conditional independence statements resulting in a unique formula for effect estimation.

Causal identifiability (Definition 4) implies that the causal effect is uniquely determined given an observational distribution and the corresponding causal graph . We now show that satisfying a conditional independence statement (which can be tested solely from observational data, without requiring the graph ) guarantees identifiability. We provide a proof in Appendix C.

Theorem 1 (Causal Identifiability).

While the above result leads to identifiability, it does not provide a formula to compute the causal effect. In fact, the conditional independence alone is insufficient to establish a unique formula, and different causal graphs lead to different formula. To illustrate this, we provide two SMCMs where Assumptions 1 to 3 and hold, i.e., causal effect is identifiable from observational data via Theorem 1, but the formula is different. First, consider the SMCM in Figure 3(left) with where causal effect is given by following formula (derived in Appendix C):

| (6) |

Next, consider the SMCM in Figure 3(right) with where the causal effect is given by the front-door adjustment formula in (5) as satisfies the front-door criterion. It remains to explicitly show that the formula in (6) is different from (5). To this end, we create a synthetic structural equation model (SEM) respecting the graph in Figure 3(left) and show that the formula in (5) gives a non-zero ATE error. In our SEM, the unobserved variable has a uniform distribution over . Each observed variable except is a sum of a linear combination of its parents with coefficients drawn from uniform distribution over and a zero-mean Gaussian noise. The treatment variable is binarized by applying a standard logistic model to a linear combination of its parents with coefficients drawn as before. The ATE error averaged over 50 runs with 50000 samples in each run is . See more experimental details in Appendix F.

Next, we provide two additional conditional independence statements that imply a unique formula for causal effect estimation. Our result is a generalized front-door with a formula identical to (5) as if were a traditional front-door set. We also offer an alternative formula by utilizing a specific partition of obtained from the conditional independence statements. We provide a proof in Appendix D.

3.2 Algorithm for ATE estimation

The ATE can be computed by taking the first moment version of 9 or 10. In Algorithm 1, we provide a systematic way to estimate the ATE using Theorem 2 by searching for a set such that (a) p-value of conditional independence in 7 passes a threshold and (b) there exists a decomposition such that p-values of conditional independencies in 8 pass the threshold . Then, for every such , the algorithm computes the ATE using the first moment version of 9, and averages. The algorithm produces another estimate by using 10 instead of 9.

3.3 Relation to PAG-based algorithms

Now, we exhibit how our approach can recover the causal effect in certain scenarios where PAG-based methods are not suitable. PAGs depict ancestral relationships (not necessarily direct) with directed edges and ambiguity in orientations (if they exist across members of the equivalence class) by circle marks. Figure 4(c) shows the PAG consistent with SMCM in Figure 4(a). While we formally define PAGs in Appendix A, we refer interested readers to Triantafillou and Tsamardinos (2015). The IDP algorithm of Jaber et al. (2019) is sound and complete for identifying causal effect from PAGs.

Consider SMCM in Figure 4(a) where our approach recovers the causal effect as Assumptions 1 to (3), (7), and (8) hold (where and can be tested from observational data). However, the IDP algorithm fails to recover the effect from the PAG. To see this, consider SMCM in Figure 4(b) which is Markov equivalent to SMCM in Figure 4(a), i.e., the PAG in Figure 4(c) is also consistent with SMCM in Figure 4(b). Intuitively, when the strength of the edge between and is very small but the strength of the edge between and is very high for both Figure 4(a) and Figure 4(b), causal effect in Figure 4(b) remains high while the causal effect in Figure 4(a) goes to zero. We note that Assumptions 1 and 3, and (7) do not hold for the SMCM in Figure 4(b).

Remark 1.

Obtaining a PAG typically requires a large number of conditional independence tests (Claassen et al., 2013) and erroneous tests can potentially alter the structure of the PAG non-locally. Moreover, incorporating arbitrary side information into a PAG in a systematic way is still an open problem. In contrast, our approach does not rely on constructing a graphical object such as a PAG.

4 Empirical Evaluation

We evaluate our approach empirically in 3 ways: we demonstrate the applicability of our method on a class of random graphs, we assess the effectiveness of our method in estimating the ATE using finite samples, and we showcase the potential of our method for causal fairness analysis.

4.1 Applicability to a class of random graphs

In this experiment, we create a class of random SMCMs, sample 100 SMCMs from this class, and check if 7 and 8 hold by checking for corresponding d-separations in the SMCMs.

Creation of random SMCMs.

Let denote the dimension of observed variables including , , and . Let denote a causal ordering of these variables. Our random ensemble depends on two parameters: which is the expected in-degree of variables and which controls the number of unobserved features. For , we add with probability 0.5 if and with probability if . We note that this procedure is such that the expected in-degree for is as desired. Next, for , we add with probability . Then, we choose as , any variable that is ancestor of but not its parent or grandparent as , and all children of as . Finally, we add if missing.

Results. We compare the success rate of two approaches: exhaustive search for satisfying 7 and 8 which is exponential in and search for a of size at-most 5 satisfying 7 and 8 which is polynomial in . We provide the number of successes of these approaches as a tuple in Table 1 for various , , and . We see that the two approaches have comparable performances. We also compare with the IDP algorithm by providing it the true PAG. However, it gives 0 successes across various , , and . We provide results for another random ensemble in Appendix F.

4.2 Estimating the ATE

In this experiment, we generate synthetic data using the 6 random SMCMs in Section 4.1 for , , and where our approach was successful indicating existence of such that the conditional independence statements in Theorem 2 hold. Then, we use Algorithm 1 to compute the error in estimating ATE and compare against a Baseline which uses the front-door adjustment in 5 with given the side information in Assumption 3. We provide the results for the same experiment for specific choices of SMCMs including the one in Figure 2 in Appendix F. We also provide the 6 random SMCMs in Appendix F. We use RCoT hypothesis test (Strobl et al., 2019b) for conditional independence testing from finite data.

Data generation. We use the following procedure to generate data from every SMCM. We generate unobserved variables independently from which denotes the uniform distribution over . For every observed variable , let denote the set of observed and unobserved parents of stacked as a column vector. Then, we generate as

| (11) |

where the coefficients with every entry sampled independently from . Also, to generate the true ATE, we intervene on the generation model in 11 by setting and .

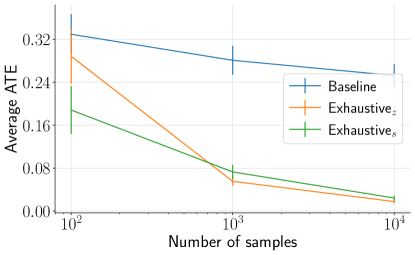

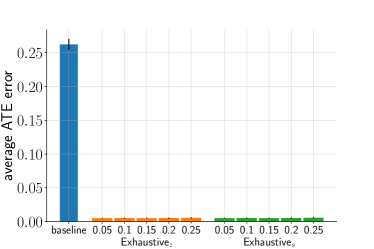

Results. For every SMCM, we generate samples of every observed variable in every run of the experiment. We average the ATE error over 10 such runs where the coefficients in 11 vary across runs. We report the average of these averages over the 6 SMCMs in Figure 5 for various . While the error rates of Baseline and Algorithm 1 are of the similar order for , Algorithm 1 gives much lower errors for and showing the efficacy of our method.

4.3 Experiments with real-world fairness benchmarks

Next, we describe how our results enable finding front-door-like adjustment sets in fairness problems. In a typical fairness problem, the goal is to ensure that the outcome variable does not unfairly depend on the sensitive/protected attribute, e.g., race or gender (which we define to be treatment variable , which would reflect undesirable biases. Often, the outcome is a descendant of the sensitive attribute (as per Assumption 1), and both outcome and sensitive attribute are confounded by unobserved variables (as per Assumption 2). Furthermore, there are be a multitude of measured post-sensitive-attribute variables that can affect the outcome. This stands in contrast to the usual settings for causal effect estimation, where pre-treatment variables are primarily utilized.

Fairness problems are typically evaluated using various fairness metrics, such as causal fairness metrics or observational metrics. Causal metrics require knowing the underlying causal graph, which can be a challenge in practice. Observational criteria can be decomposed into three types of effects (Zhang and Bareinboim, 2018; Plecko and Bareinboim, 2022): spurious effects, direct effects, and indirect effects (through descendants of sensitive attribute). In some scenarios, capturing the sum of direct and indirect effects is of interest, but even this requires knowing the causal graph.

Now, we demonstrate the application of our adjustment formulae in Theorem 2 to compute the sum of direct and indirect effects of the sensitive attribute on the outcome, while separating it from spurious effects. The sum of these effects is indeed the causal effect of sensitive attribute on the outcome. In other words, we consider the following fairness metric: . We assume that all the children of the sensitive attribute are known, which may be easier to justify compared to the typical assumption in causal fairness literature of knowing the entire causal graph.

German Credit Dataset.

The German Credit dataset (Hofmann, 1994) is used for credit risk analysis where the goal is to predict whether a loan applicant is a good or bad credit risk based on applicant’s 20 demographic and socio-economic attributes. The binary credit risk is the outcome and the applicant’s age (binarized by thresholding at (Kamiran and Calders, 2009)) is the sensitive attribute . Further, the categorical attributes are one-hot encoded.

We apply Algorithm 1 with and where we search for a set of size at most under the following two distinct assumptions on the set of all children of :

-

1.

When considering # of people financially dependent on the applicant, applicant’s savings, applicant’s job, Algorithm 1 results in purpose for which the credit was needed, indicator of whether the applicant was a foreign worker, installment plans from providers other than the credit-giving bank, , and .

-

2.

When considering # of people financially dependent on the applicant, applicant’s savings, Algorithm 1 results in purpose for which the credit was needed, applicant’s checking account status with the bank, installment plans from providers other than the credit-giving bank, , and .

Under the first assumption above, the causal effect using the adjustment formulae in (9) and (10) have same sign and are close in magnitude. However, under the second assumption, the effect flips sign. The results suggest that the second hypothesis regarding is incorrect, implying that applicant’s job may indeed be a direct child of applicant’s age, which aligns with intuition.

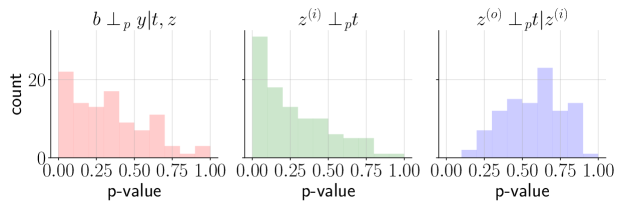

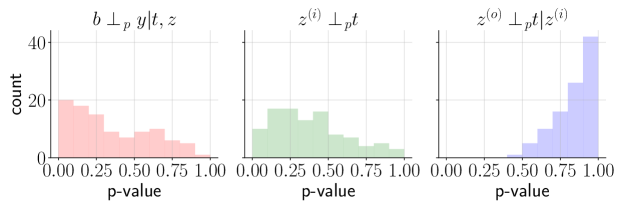

The dataset has only 1000 samples, which increases the possibility of detecting independencies in our criterion by chance, even with the size of constrained. To address this issue, we use 100 random bootstraps with a sample size equal to half of the training data and evaluate the p-value of our conditional independence criteria for all subsets returned by our algorithm. We select the subset with the highest median p-value (computed over the bootstraps) and use it in our adjustment formulae on a held out test set. To assess the conditional independencies associated with the selected , we plot a histogram of the corresponding p-values for all these bootstraps. If the conditional independencies hold, we expect the p-values to be spread out, which we observe in the histograms in Figure 6 for the first choice of . We report similar results for the second choice of in Appendix F.

Adult Dataset: We perform a similar analysis on the Adult dataset (Kohavi and Becker, 1996). With suitable choices of , Algorithm 1 was unable to find a suitable satisfying . This suggests that in this dataset, there may not be any non-child descendants of the sensitive attribute, which is required for our criterion to hold. More details can be found in Appendix F.

5 Conclusion and Discussion

In this work, we proposed sufficient conditions for causal effect estimation without requiring the knowledge of the entire causal graph using front-door-like adjustment given structural side information. We showed our approach can identify causal effect in graphs where known Markov equivalence classes do not allow identification.

Our approach relies primarily on two assumptions: Assumption 2 and Assumption 3. Assumption 2 plays a crucial role in Theorem 2 (see the discussion in Section D.3) as it requires the presence of an unobserved confounder between the treatment variable and the outcome variable. This assumption is necessary for the applicability of our approach. If Assumption 2 does not hold, it implies that there is a set that satisfies the back-door criterion, and existing methods for finding back-door adjustment sets (Entner et al., 2013; Cheng et al., 2020; Shah et al., 2022) can be utilized. However, it is important to note that in many real-world scenarios, the presence of unobserved variables that potentially confound the treatment and the outcome is common, and Assumption 2 holds in such cases. Assumption 3 is the requirement of knowing the entire set of children of the treatment variable within the causal graph. While this is strictly less demanding than specifying the entire causal graph, it may still present practical challenges in real-world scenarios. For instance, in large-scale observational studies or domains with numerous variables, exhaustively identifying all the children may be computationally demanding. Therefore, it is important to understand whether one can estimate the causal effect using front-door-like adjustment with even less side information, e.g., knowing only one child of the treatment variable or knowing any subset of children of the treatment variable. However, until then, one could seek input from domain experts. These experts possess valuable knowledge and insights about the specific domain under study, which can aid in identifying all the relevant variables that serve as children of the treatment.

Lastly, Algorithm 1 has an exponential time complexity due to its search over all possible subsets of observed variables (except ). While this is inherent in the general case, recent work by Shah et al. (2022) proposed a scalable approximation for conditional independence testing using continuous optimization by exploiting the principle of invariant risk minimization, specifically for back-door adjustment without the need for the causal graph. However, extending this approach to multiple conditional independence tests, as required in 7 and 8, remains an open challenge. Therefore, exploring the development of continuous optimization-based methods for scalability of front-door adjustment in the absence of the causal graph is an exciting direction for future work.

Acknolwedgements

Murat Kocaoglu acknowledges the support of NSF Grant CAREER 2239375.

References

- Acharya et al. (2018) J. Acharya, A. Bhattacharyya, C. Daskalakis, and S. Kandasamy. Learning and testing causal models with interventions. Advances in Neural Information Processing Systems, 31, 2018.

- Bellemare et al. (2019) M. F. Bellemare, J. R. Bloem, and N. Wexler. The paper of how: Estimating treatment effects using the front-door criterion. Technical report, Working paper, 2019.

- Bhattacharya and Nabi (2022) R. Bhattacharya and R. Nabi. On testability of the front-door model via verma constraints. In Uncertainty in Artificial Intelligence, pages 202–212. PMLR, 2022.

- Castro et al. (2020) D. C. Castro, I. Walker, and B. Glocker. Causality matters in medical imaging. Nature Communications, 11(1):1–10, 2020.

- Cheng et al. (2020) D. Cheng, J. Li, L. Liu, K. Yu, T. D. Lee, and J. Liu. Towards unique and unbiased causal effect estimation from data with hidden variables. arXiv preprint arXiv:2002.10091, 2020.

- Cheng et al. (2022) D. Cheng, J. Li, L. Liu, J. Liu, and T. D. Le. Data-driven causal effect estimation based on graphical causal modelling: A survey. arXiv preprint arXiv:2208.09590, 2022.

- Claassen et al. (2013) T. Claassen, J. M. Mooij, and T. Heskes. Learning sparse causal models is not np-hard. In Proceedings of the Twenty-Ninth Conference on Uncertainty in Artificial Intelligence, pages 172–181, 2013.

- Entner et al. (2013) D. Entner, P. Hoyer, and P. Spirtes. Data-driven covariate selection for nonparametric estimation of causal effects. In Artificial Intelligence and Statistics, pages 256–264. PMLR, 2013.

- Fulcher et al. (2020) I. R. Fulcher, I. Shpitser, S. Marealle, and E. J. Tchetgen Tchetgen. Robust inference on population indirect causal effects: the generalized front door criterion. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 82(1):199–214, 2020.

- Glynn and Kashin (2017) A. N. Glynn and K. Kashin. Front-door difference-in-differences estimators. American Journal of Political Science, 61(4):989–1002, 2017.

- Glynn and Kashin (2018) A. N. Glynn and K. Kashin. Front-door versus back-door adjustment with unmeasured confounding: Bias formulas for front-door and hybrid adjustments with application to a job training program. Journal of the American Statistical Association, 113(523):1040–1049, 2018.

- Gultchin et al. (2020) L. Gultchin, M. Kusner, V. Kanade, and R. Silva. Differentiable causal backdoor discovery. In International Conference on Artificial Intelligence and Statistics, pages 3970–3979. PMLR, 2020.

- Gupta et al. (2021) S. Gupta, Z. C. Lipton, and D. Childers. Estimating treatment effects with observed confounders and mediators. In Uncertainty in Artificial Intelligence, pages 982–991. PMLR, 2021.

- Hofmann (1994) H. Hofmann. Statlog (German Credit Data). UCI Machine Learning Repository, 1994.

- Hünermund and Bareinboim (2019) P. Hünermund and E. Bareinboim. Causal inference and data fusion in econometrics. arXiv preprint arXiv:1912.09104, 2019.

- Jaber et al. (2019) A. Jaber, J. Zhang, and E. Bareinboim. Causal identification under markov equivalence: Completeness results. In International Conference on Machine Learning, pages 2981–2989. PMLR, 2019.

- Jeong et al. (2022) H. Jeong, J. Tian, and E. Bareinboim. Finding and listing front-door adjustment sets. arXiv preprint arXiv:2210.05816, 2022.

- Kamiran and Calders (2009) F. Kamiran and T. Calders. Classifying without discriminating. In 2009 2nd international conference on computer, control and communication, pages 1–6. IEEE, 2009.

- Kohavi and Becker (1996) R. Kohavi and B. Becker. UCI machine learning repository, 1996. URL http://archive.ics.uci.edu/ml/datasets/adult.

- Kuroki (2000) M. Kuroki. Selection of post-treatment variables for estimating total effect from empirical research. Journal of the Japan Statistical Society, 30(2):115–128, 2000.

- Kuroki and Cai (2012) M. Kuroki and Z. Cai. Selection of identifiability criteria for total effects by using path diagrams. arXiv preprint arXiv:1207.4140, 2012.

- Mogstad and Torgovitsky (2018) M. Mogstad and A. Torgovitsky. Identification and extrapolation of causal effects with instrumental variables. Annual Review of Economics, 10:577–613, 2018.

- Nabi et al. (2019) R. Nabi, D. Malinsky, and I. Shpitser. Learning optimal fair policies. In International Conference on Machine Learning, pages 4674–4682. PMLR, 2019.

- Pearl (1993) J. Pearl. [bayesian analysis in expert systems]: Comment: graphical models, causality and intervention. Statistical Science, 8(3):266–269, 1993.

- Pearl (1995) J. Pearl. Causal diagrams for empirical research. Biometrika, 82(4):669–688, 1995.

- Pearl (2009) J. Pearl. Causality. Cambridge university press, 2009.

- Perkovic et al. (2018) E. Perkovic, J. Textor, M. Kalisch, and M. H. Maathuis. Complete graphical characterization and construction of adjustment sets in markov equivalence classes of ancestral graphs. The Journal of Machine Learning Research, 2018.

- Plecko and Bareinboim (2022) D. Plecko and E. Bareinboim. Causal fairness analysis. arXiv preprint arXiv:2207.11385, 2022.

- Shah et al. (2022) A. Shah, K. Shanmugam, and K. Ahuja. Finding valid adjustments under non-ignorability with minimal dag knowledge. In International Conference on Artificial Intelligence and Statistics, pages 5538–5562. PMLR, 2022.

- Shpitser and Pearl (2006) I. Shpitser and J. Pearl. Identification of joint interventional distributions in recursive semi-markovian causal models. In Proceedings of the National Conference on Artificial Intelligence, volume 21, page 1219. Menlo Park, CA; Cambridge, MA; London; AAAI Press; MIT Press; 1999, 2006.

- Spirtes et al. (2000) P. Spirtes, C. N. Glymour, and R. Scheines. Causation, prediction, and search. MIT press, 2000.

- Strobl et al. (2019a) E. V. Strobl, P. L. Spirtes, and S. Visweswaran. Estimating and controlling the false discovery rate of the pc algorithm using edge-specific p-values. ACM Transactions on Intelligent Systems and Technology (TIST), 10(5):1–37, 2019a.

- Strobl et al. (2019b) E. V. Strobl, K. Zhang, and S. Visweswaran. Approximate kernel-based conditional independence tests for fast non-parametric causal discovery. Journal of Causal Inference, 7(1), 2019b.

- Tian and Pearl (2002) J. Tian and J. Pearl. A general identification condition for causal effects. eScholarship, University of California, 2002.

- Triantafillou and Tsamardinos (2015) S. Triantafillou and I. Tsamardinos. Constraint-based causal discovery from multiple interventions over overlapping variable sets. The Journal of Machine Learning Research, 16(1):2147–2205, 2015.

- Veitch and Zaveri (2020) V. Veitch and A. Zaveri. Sense and sensitivity analysis: Simple post-hoc analysis of bias due to unobserved confounding. Advances in Neural Information Processing Systems, 33:10999–11009, 2020.

- Verma and Pearl (1990) T. Verma and J. Pearl. Causal networks: Semantics and expressiveness. In Machine intelligence and pattern recognition, volume 9, pages 69–76. Elsevier, 1990.

- Wienöbst et al. (2022) M. Wienöbst, B. van der Zander, and M. Liśkiewicz. Finding front-door adjustment sets in linear time. arXiv preprint arXiv:2211.16468, 2022.

- Zhang (2008) J. Zhang. On the completeness of orientation rules for causal discovery in the presence of latent confounders and selection bias. Artificial Intelligence, 172(16-17):1873–1896, 2008.

- Zhang and Bareinboim (2018) J. Zhang and E. Bareinboim. Fairness in decision-making—the causal explanation formula. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 32, 2018.

Appendix

Appendix A Preliminaries about ancestral graphs

In this section, we provide the definition of partial ancestral graphs (PAGs). PAGs are defined using maximal ancestral graphs (MAGs). Below, we define MAGs and PAGs based on their construction from directed acyclic graphs (DAGs).

A MAG can be obtained from a DAG as follows: if two observed nodes and cannot be d-separated conditioned on any subset of observed variables, then is added in the MAG if is an ancestor of in the DAG, is added in the MAG if is an ancestor of in the DAG, and is added in the MAG if and are not ancestrally related in the DAG. After the above three operations, if both and are present, we retain only the directed edge. In general, a MAG represents a collection of DAGs that share the same set of observed variables and exhibit the same independence and ancestral relations among these observed variables. It is possible for different MAGs to be Markov equivalent, meaning they represent the exact same independence model.

A PAG shares the same adjacencies as any MAG in the observational equivalence class of MAGs. An end of an edge in the PAG is marked with an arrow ( or ) if the edge appears with the same arrow in all MAGs in the equivalence class. An end of an edge in the PAG is marked with a circle () if the edge appears as an arrow ( or ) and a tail () in two different MAGs in the equivalence class.

Appendix B Rules of do-calculus

In this section, we provide the do-calculus rules of Pearl (1995) that are used to prove our main results in the following sections. We build upon the definition of semi-Markovian causal model from Section 2.

For any , let be the graph obtained by removing the edges going into in , and let be the graph obtained by removing the edges going out of in .

Theorem 3 (Rules of do-calculus, Pearl (1995)).

For any disjoint subsets , we have the following rules.

-

Rule 1

: if in .

-

Rule 2

: if in .

-

Rule 3

: if in ,

where is the set of nodes in that are not ancestors of any node in in . Pearl (1995) also gave an alternative criterion for Rule 3.

-

Rule 3a

: if in ,

where is the graph obtained from after adding a node and edges from to every node in .

Also, throughout our proofs, we use the following fact.

Fact 1.

Consider any obtained by removing any edge(s) from . For any sets of variables , if and are d-separated by in than and are d-separated by in .

Appendix C Causal Identifiability

In this section, we derive the causal effect for the SMCM in Figure 3(top), i.e., 6, as well as prove Theorem 1 one by one.

C.1 Proof of 6

First, using the law of total probability, we have

| (12) |

Now, we show that the two terms in RHS of 12 can be simplified as follows

| (13) | ||||

| (14) |

Proof of 13:

Proof of 14:

C.2 Proof of Theorem 1

Let denote the union of and the set of ancestors of , and let denote the subgraph of composed only of nodes in . First, we show that if holds for some , then there is no bi-directed path between to in .

Lemma 1.

Given this claim, Theorem 1 follows from Tian and Pearl (2002, Theorem 4). It remains to prove Lemma 1.

Proof of Lemma 1.

We prove this result by contradiction. First, from 1 and 3, and for some . Assume there exists a bi-directed path between and some in . Let denote the shortest of these paths. This path is of the form for some where for every . We have the following two cases depending on the value of .

-

(i)

: In this case, consider the path in of the form: in (such a path exists because of 2). The path is unblocked when and are conditioned on contradicting .

-

(ii)

: In this case, consider the path in of the form: (such a path exists because of 2). We have the following two scenarios depending on whether the path is unblocked or blocked when and are conditioned on. Suppose we condition on and .

-

(a)

The path is unblocked: In this case, by assumption, is contradicted.

-

(b)

The path is blocked: We create a set such that for any the following are true: for some , , there is no descendant path between and some , and there is no descendant path between and .

In this scenario, because is blocked. Let be that node which is closest to in the path . By the choice of , the path is unblocked (when and are conditioned on). Furthermore, by the definition of , (because for some ) and there exists a descendant path between and such that as well as for every . Therefore, the path is unblocked (when and are conditioned on).

Consider the path obtained after concatenating and at . This path is unblocked (when and are conditioned on) because: is unblocked, is unblocked, and there is no collider at in this path (because is a descendant path to ). However, this contradicts .

-

(a)

Appendix D A generalized front-door condition

In this section, we prove Theorem 2. We begin by stating a few d-separation statements used in this proof. See Appendix E for a proof.

Lemma 2.

Now, we proceed with the proof in two parts. In the first part, we prove 9, and in the second part, we prove 10.

D.1 Proof of 9

First, using the law of total probability, we have

| (32) |

Now, we show that the two terms in RHS of 32 can be simplified as follows

| (33) | ||||

| (34) |

Proof of 33:

We have

| (35) | ||||

| (36) | ||||

| (37) | ||||

| (38) |

where follows from Rule 1, 7, and 1, follows from Rule 2, 7, and 1, and follows from Rule 3a and Lemma 2(a), and follows from the law of total probability.

Proof of 34:

From the law of total probability, we have

| (43) |

Now, we simplify the first term in 43 as follows:

| (44) | |||

| (45) | |||

| (46) | |||

| (47) | |||

| (48) |

where and follow from the definition of conditional probability, follows from Rule 2, 8, and 1, and follows from Rule 2 and Lemma 2(c). Likewise, we simplify the second term in 43 as follows:

| (49) |

D.2 Proof of 10

First, using the law of total probability, we have

| (51) |

Now, we show that the first term in RHS of 51 can be simplified as follows

| (52) | |||

| (53) |

where . Using 49 and 53 in 51, completes the proof of 10 as follows:

| (54) | |||

| (55) | |||

| (56) |

where follows from the definition of conditional probability.

Proof of 53:

From the law of total probability, we have

| (57) | |||

| (58) |

Now, we simplify the first term in 58 as follows:

| (59) | |||

| (60) | |||

| (61) | |||

| (62) |

where follows from Rule 2, Lemma 2(e), and 1, follows from Rule 3a and Lemma 2(a), and follows from the law of total probability. We further simplify the first term in 62 as follows:

| (63) |

where follows from Rule 2 and Lemma 2(e). Using 63 and 42 in 62, we have

| (64) |

Now, we simplify the second term in 58 as follows:

| (65) |

D.3 Necessity of Assumption 2

In this section, we provide an example to signify the importance of Assumption 2 to Theorem 2. Consider the semi-Markovian causal model in Figure 7 where Assumptions 1 and 3 hold but Assumption 2 does not hold.

While satisfies 7 and 8 where , the causal effect is not equal to the formulae in 9 or 10. To see this, we note that the set is a back-door set in Figure 7 implying

| (66) |

Now, we simplify the right hand side of 66 to show explicitly that it is not equivalent to 9. From the law of total probability, we have

| (67) | ||||

| (68) |

where follows because and follows is independent of every other variable conditioned on . Plugging 68 in 66, we have

| (69) |

Lastly, using the law of total probability, 9 can be rewritten as

| (70) |

Therefore, the variables and could be such that 69 is different from 70. We note that similar steps can be used to show that 66 is not equivalent to 10. In conclusion, Assumption 2 is crucial for the formulae in 9 and 10 to hold.

Appendix E Proof of Lemma 2

First, we state the following d-separation criterion used to prove Lemma 2(b) and Lemma 2(d). See Section E.1 for a proof.

Now, we prove each part of Lemma 2 one-by-one.

Proof of Lemma 2(a)

In , all edges going into are removed. Under 3, this implies that all edges going out of are removed. Now, consider any path between and in . This path takes one of the following two forms: or . In either case, there is a collider at in . This collider is blocked when and are conditioned on because , , and does not have any descendants in . Therefore, in . Similarly, the collider is blocked when and are conditioned on because , , and does not have any descendants in . Therefore, in .

Proof of Lemma 2(b)

We prove this by contradiction. Assume there exists at least one unblocked path between and some in . Let denote any such unblocked path.

Proof of Lemma 2(c)

We prove this by contradiction. Assume there exists at least one unblocked path between and some in when is conditioned on. Let denote any such unblocked path.

Suppose, we uncondition on . From 8(i) and 1, we have in . Therefore, is blocked in when is unconditioned on. Now, we create a set consisting of all the nodes at which is blocked in when is unconditioned on. Define the set such that for any , the following are true: , contains a collider at in , and there exists an unblocked descendant path from to some in .

Now, we must have , since is blocked in when is unconditioned on. Let be that node which is closest to in the path , and let be an unblocked descendant path from to some in (there must be one from the definition of the set ). Consider the path obtained after concatenating and . By the definition of and the choice of , is unblocked in since is unblocked in , is unblocked in , and there is no collider at in . However, this contradicts in (which follows from Lemma 2(b)).

Proof of Lemma 2(d)

We prove this by contradiction. Assume there exists at least one unblocked path between and in when is conditioned on. Let denote the shortest of these unblocked path. By definition of , this path has to be of the form: for some . Now, we have the following three cases:

-

(i)

contains : In this case, because a path is a sequence of distinct nodes, has to be . By assumption, is unblocked when is conditioned on. Since there is a collider at in , there exists at least one unblocked descendant path from to when is conditioned on. Let denote the shortest of these paths from to some in . We note that this path also exists in and is of the form

Suppose we uncondition on . Consider the path between and of the form in . This path remains unblocked even when is unconditioned on as it does not have any colliders. This contradicts (which follows from 8).

-

(ii)

contains for some such that : In this case, the path has to be of the form . Therefore, there exists at least one collider on the path . Let be the collider on the path that is closest to . Consider the path . We note that this path also exists in and is of the form .

By assumption, is unblocked when is conditioned on. Since there is a collider at in , there exists at least one unblocked descendant path from to when is conditioned on. Let denote the shortest of these paths from to some in . We note that this path also exists in and is of the form .

Suppose we uncondition on . Consider the path between and in obtained after concatenating and . This path, of the form , remains unblocked even when is unconditioned on as it does not have any colliders. This contradicts (which follows from 8).

-

(ii)

does not contain for every : By assumption, is unblocked in when is conditioned on. Therefore, if does not contain the edge for any , there exists a path between to in that is unblocked when is conditioned on, and takes one of the following two forms: or . Then, it is easy to see that the path also remains unblocked in while is conditioned on. However, this contradicts in (which follows from Lemma 3).

Proof of Lemma 2(e)

We prove this by contradiction. Assume there exists at least one unblocked path between and some in when and are conditioned on. Let denote the shortest of these unblocked path. Therefore, no , such that , is on the path , i.e., . Further, takes one of the following two forms because all the edges going out of are removed in : or .

Suppose we condition on (while and are still conditioned on). From 7 and 1, we have in . Therefore, the path is blocked in when is conditioned on (while and are still conditioned on). Let be any node at which is blocked in when is conditioned on (while and are still conditioned on). We must have that and . Suppose we uncondition on (while and are still conditioned on). Then, the path is unblocked in .

We consider the following two scenarios depending on whether or not contains . In both scenarios, we show that there is an unblocked path between and in when we condition on (while and are still conditioned on).

-

(i)

contains : Consider the path which is unblocked in when and are conditioned on. Further, by the choice of , no is on the path . Therefore, the path in remains unblocked when we condition on (while and are still conditioned on).

-

(ii)

does not contain : Consider the path (by including the extra edge ) which takes one of the following two forms: or . Further, by the choice of , no () is on the path . Suppose we condition on (while and are still conditioned on). Then, the path in is unblocked because the collider at is unblocked when is conditioned on and the path in remains unblocked when is conditioned on (while and are still conditioned on).

Now, suppose we uncondition on (while and are still conditioned on). We have the following two scenarios depending on whether or not in remains unblocked. In both scenarios, we show that there is an unblocked path between and in when we uncondition on (while and are still conditioned on).

-

1.

If remains unblocked: In this case, in is an unblocked path between and when and are conditioned on, as desired.

-

2.

If does not remain unblocked: In this case, it is the unconditioning on (while and are still conditioned on) that blocks . Now, we create a set consisting of all the nodes at which is blocked in when is unconditioned on (while and are still conditioned on). Define the set such that for any , the following are true: , contains a collider at in , and there exists an unblocked descendant path from to in .

Now, we must have , since is blocked in when is unconditioned on (while and are still conditioned on). Let be that node which is closest to in the path , and let be an unblocked descendant path from to in (there must be one from the definition of the set ). Consider the path obtained after concatenating and . By the definition of and the choice of , is unblocked in when is unconditioned on (while and are still conditioned on) since is unblocked, is unblocked, and there is no collider at in . Therefore, we have an unblocked path between and in when and are conditioned on, as desired.

E.1 Proof of Lemma 3

First, we claim in . We assume this claim and proceed to prove the statement in the Lemma by contradiction. Assume there exists at least one unblocked path between and some in when is conditioned on. Let denote the shortest of these unblocked path. Therefore, no such that is not on the path , i.e., .

Suppose we condition on (while is still conditioned on). From the claim, is blocked in when is conditioned on (while is still conditioned on). Let be any node at which is blocked in when is conditioned on (while is still conditioned on). We must have that and . Then, the path is unblocked in when is unconditioned on (while is still conditioned on).

Further, no is on the path . As a result, the path remains unblocked when is conditioned on (while is still conditioned on). However, this contradicts in (which follows from 8 and 1).

Proof of Claim - in : It remains to prove the claim in . We prove this by contradiction. Assume there exists at least one unblocked path between and some in when is conditioned on. Let denote any such unblocked path. This path takes one of the following two forms: or because all edges going out of are removed in .

Suppose we condition on (while is still conditioned on). The path remains unblocked because (a path is a sequence of distinct nodes). Then, the path of the form or is unblocked because the additional conditioning on (while is still conditioned on) unblocks the collider at . However, this contradicts in (which follows from 7 and 1).

Appendix F Experimental Results

In this section, we provide additional experimental results. First, we provide more details regarding the numerical example in Section 3.1. Next, we demonstrate the applicability of our method on a class of graphs slightly different from the one in Section 4.1. Then, we provide the 6 random graphs from Section 4.2 as well as ATE estimation results on specific choices of SMCMs including the one in Figure 2. Finally, we provide histograms analogous to Figure 6 for the second choice of on German credit dataset as well as details about our analysis with Adult dataset.

F.1 Numerical example in Section 3.1

F.2 Applicability to a class of random graphs

As in Section 4.1, we create a class of random SMCMs, sample 100 SMCMs from this class, and check if 7 and 8 hold by checking for corresponding d-separations in the SMCMs. The class of random graphs considered here is analogous to the class of random graphs considered in Section 4.1 expect for the choice of . Here, we choose any variable that is ancestor of but not its parent as . This is in contrast to Section 4.1 where we choose any variable that is ancestor of but not its parent or grandparent as . We compare the success rate of the same two approaches: exhaustive search for satisfying 7 and 8 and search for a of size at-most 5 satisfying 7 and 8. We provide the number of successes of these approaches as a tuple in Table 2 for various , , and . As before, we see that the two approaches have comparable performances and the IDP algorithm gives 0 successes across various , , and even though it is supplied with the true PAG. Also, as expected the number of successes for this class of graphs is much lower than the class considered in Section 4.1.

F.3 ATE estimation

We also conduct ATE estimation experiments on four specific SMCMs. The first SMCM is the graph in Figure 2. The remaining graphs, named , are shown in Figure 8, and are obtained by adding additional edges and modifying . These SMCMs are designed in a way such that there exists satisfying the conditional independence statements in Theorem 2.

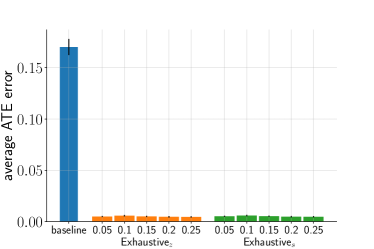

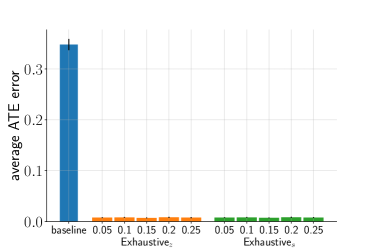

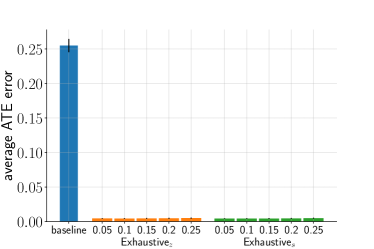

We follow a data generation procedure similar to the one in Section 4.2. In contrast, we show the performance of our approach for a fixed but different thresholds of p-value . We average the ATE error over 50 runs where in each run we set . As we see in Figure 9, both the ATE estimates returned by Algorithm 1 are far superior compared to the naive front-door adjustment using .

F.4 German Credit dataset

As in Section 4.3, we assess the conditional independence associated with the selected for the choice of # of people financially dependent on the applicant, applicant’s savings, Algorithm 1 results in purpose for which the credit was needed, applicant’s checking account status with the bank via 100 random bootstraps. We show the corresponding p-values for these bootstraps in a histogram in Figure 10 below. As expected, we observe the p-values to be spread out.

F.5 Adult dataset

The Adult dataset (Kohavi and Becker, 1996) is used for income analysis where the goal is to predict whether an individual’s income is more than $50,000 using 14 demographic and socio-economic features. The sensitive attribute is the individual’s sex, either male or female. Further, the categorical attributes are one-hot encoded. As with German Credit dataset, we apply Algorithm 1 with and where we search for a set of size at most under the following two assumptions on the set of all children of : (1) # individual’s relationship status (which includes wife/husband) and (2) # individual’s relationship status (which includes wife/husband), individual’s occupation. In either case, Algorithm 1 was unable to find a suitable satisfying . This suggests that in this dataset, there may not be any non-child descendants of the sensitive attribute, which is required for our criterion to hold.

F.6 Licenses

In this work, we used a workstation with an AMD Ryzen Threadripper 3990X 64-Core Processor (128 threads in total) with 256 GB RAM and 2x Nvidia RTX 3090 GPUs. However, our simulations only used the CPU resources of the workstation.

We mainly relied on the following Python repositories — (a) networkx (https://networkx.org), (b) causal-learn (https://causal-learn.readthedocs.io/en/latest/), (c) RCoT (Strobl et al., 2019b) and (d) ridgeCV, (https://github.com/scikit-learn/scikit-learn/tree/15a949460/sklearn/linear_model/_ridge.py). We did not modify any of the code under licenses; we only installed these repositories as packages.

In addition to these, we used two public datasets (a) German Credit dataset (https://archive.ics.uci.edu/ml/datasets/statlog+(german+credit+data)) and (b) Adult dataset (https://archive.ics.uci.edu/ml/datasets/adult). These datasets are commonly used benchmark datasets for causal fairness, which is why we chose them for our comparisons.