Abstract

The variance gamma model is a widely popular model for option pricing in both academia and industry. In this paper, we provide a new perspective for pricing European style options for the variance gamma model by deriving closed-form formulas combining the randomization method and fractional derivatives. We also compare our results with various existing results in the literature by numerical examples.

Option Pricing for the Variance Gamma Model: A New Perspective

Yuanda Chen 111Department of Mathematics, Florida State University, 1017 Academic Way, Tallahassee, FL-32306, United States of America; ychen@math.fsu.edu, Zailei Cheng 222Department of Mathematics, Florida State University, 1017 Academic Way, Tallahassee, FL-32306, United States of America; zc12b@my.fsu.edu, Haixu Wang 333Department of Mathematics, Florida State University, 1017 Academic Way, Tallahassee, FL-32306, United States of America; hwang@math.fsu.edu

1 Introduction

The variance gamma process is a pure jump Lévy process that is widely used in option pricing. The process is obtained by evaluating arithmetic Brownian motion with drift at a random time given by a gamma process with unit mean rate and certain variance rate444See Section 2.1 for definitions.. The variance gamma process was first introduced by Madan and Seneta [25] as a candidate for modeling the underlying stock market returns, as an alternative to the classical Black-Scholes model. This alternative was sought primarily to obtain a process consistent with the observation that the local movement of log stock prices is heavy-tailed relative to the normal distribution, while the movement over large time intervals approaches normalities. The variance gamma process was first considered in the context of option pricing in Madan and Milne (1991) [24], where it was used to price European options. By comparing with the Black-Scholes model, they found that the variance gamma option values are higher, in particular, for out-of-the-money options with large maturity on stocks with high means, low variances and high kurtosis. As the variance gamma process is obtained by evaluating Brownian motion with drift at a random time governed by a gamma process, the additional parameters, i.e. the drift of the Brownian motion, and the volatility of the time change, provide control over the skewness and kurtosis of the return distribution. Madan et al. [23] estimated the statistical and risk-neutral densities using the S&P 500 data, and they observed that the statistical density is symmetric with some kurtosis, while the risk neutral density is negatively skewed with a larger kurtosis. The additional parameters also correct for pricing biases of the Black-Scholes model.

To obtain prices of European options under a variance gamma model, Madan and Milne (1991) [24] derived the option price as a weighted average of Black-Scholes formula with the maturity averaged with respect to a gamma density. Madan et al. (1998) [23] built on the formula in [24] and after applying a series of change of variables, they derived an alternative analytical formula for the option price using some special functions. Carr and Madan (1998) [6] proposed to use the fast Fourier transform method, and as a special case, the variance gamma model was studied. Fu (2000) [15] surveyed Monte Carlo methods for the variance gamma model, and discussed three methods for sequential simulation of the variance gamma process, two bridge sampling methods, variance reduction via importance sampling, and estimation of the Greeks. Cont and Voltchkova (2005) [11] described a finite difference scheme for solving the partial integro-differential equation arising from pricing European options under a variance gamma model. For pricing American options and path-dependent options under variance gamma models, we refer the readers to [16, 1, 18] and references therein for further details.

In this paper, we provide a new alternative analytical formula for pricing European style options for the variance gamma model, see Theorem 4. The closed-form formula is derived by combining the Carr’s randomization method [5] and fractional derivatives. The variance gamma model can be viewed as the Black-Scholes model with a random maturity which follows a gamma distribution. Carr’s randomization method was originally applied to compute the (American) option price for Black-Scholes model by approximating a finite maturity by a sequence of Erlang distributed random maturities. Carr [5] first derived the formula for the exponential distributed maturity, and by noting that the Erlang density is a derivative of integer orders of the exponential density, the formulas for the Erlang distributed random maturities were then derived. Since the variance gamma model can be viewed as the Black-Scholes model with maturity randomized by a gamma distribution, Carr’s randomization method provides explicit formula for a subclass of the variance gamma model, that is when the maturity is Erlang distributed555The Erlang distribution is a subclass of the gamma distribution.. We apply Carr’s randomization method to price European options for the variance gamma model, and the formula is exact when the random maturity is Erlang distributed. To fill in the gap between the Erlang maturity and the more general gamma maturity, we use the tools from the fractional calculus. This methodology is intuitive since the Erlang density can be obtained by taking derivatives of integer orders from the exponential density, and for the more general gamma density, fractional derivatives are the natural tools. We will introduce a non-conventional fractional derivative that is tailored to the particular application in our context to do the work.

Fractional derivatives and fractional calculus have been used in the literature on option pricing. For example, Cartea and del-Castillo-Negrete [9] showed that European-style option prices under particular Lévy processes (including the CGMY model) are governed by a fractional partial differential equation (FPDE) with two spatial fractional derivatives capturing the non-locality induced by pure jumps in the underlying price. See also [4, 8, 10, 14, 17, 26] and the references therein for applications of fractional calculus in option pricing. In these studies, the fractional derivative is typically taken with respect to either space (log stock price) or time (time to maturity). Our work differs from these studies in that there is no FPDE involved and the fractional derivative is taken with respect to the Laplace exponent of the Laplace transform of the option price.

We also compare our results with various existing methods in the literature by numerical examples. More precisely, we compare our results with the option pricing formula in Madan et al. [23] (MCC) and the fast Fourier transform method in Carr and Madan [6] (FFT). The runtime of our method is comparable with both MCC and FFT methods. When the maturity is Erlang distributed, our method is consistently faster across different regimes. Finally, in the short-maturity regimes, our method beats both MCC and FFT methods.

1.1 Organization of the paper

The rest of the paper is organized as follows. Section 2 reviews the definitions of variance gamma processes and fractional derivatives. Section 3 presents our main results on alternative closed-form formulas for European options under a variance gamma model. Section 4 discusses numerical experiments based on our new formulas and compare its efficiency with exsiting methods. Auxiliary technical proofs are collected in the appendix.

2 Preliminaries

2.1 A review of variance gamma processes

This section reviews the definition of variance gamma processes. See e.g. [23] for details.

Let us consider a Brownian motion with drift model which has an infinitesimal generator given by:

| (2.1) |

for any in the domain of the infinitesimal generator. The variance gamma process is obtained by evaluating the process at a random time change given by a gamma process with mean rate one, variance rate , and Note the gamma process is a Lévy process with independent gamma increments over non-lapping time intervals. The density of the increment on the time interval is given by the gamma density function with shape parameter and rate parameter , i.e., the density is

| (2.2) |

The variance gamma process is then defined by

| (2.3) |

where is a Gamma random variable with shape parameter and rate parameter Hence and In the variance gamma model, the stock price is defined as the exponential of the variance gamma process, that is,

| (2.4) |

2.2 Fractional Derivatives

In this section, we introduce the definition of fractional derivatives and their properties that we will work with in the paper.

Let us define the -th order fractional derivative as666In the literature, there are many ways to define fractional derivatives. For example, a more common definition is given by , which is known as the Riemann-Liouville Fractional Derivative, see e.g. [27]. This definition can be applied to compute the fractional derivative of , where , so that , but it can not be applied to that we want, where , in the sense that does not exist.

| (2.5) |

where provided that exists and is finite. When is a non-negative integer, it coincides with the ordinary derivatives of order . For , where is a non-negative integer, can be equivantly operated by first applying the ordinary derivatives and then applying the fractional derivative .

We now present two results on properties of fractional deratives. Lemma 1 will be useful in our theoretical analysis, while Lemma 2 will be useful for efficient numerical computations of option prices under the Variance Gamma model.

Lemma 1.

For any and , .

Lemma 2.

Let . Assume that is twice differentiable, and for every , . Then, we have

| (2.6) |

The proofs of these two lemmas are given in the appendix.

3 Option Pricing for the Variance Gamma Model

In this section, we present a new method based on combining Carr’s randomization and fractional derivatives for pricing vanila European options with the Variance Gamma process as the underlying proecess.

Without loss of generality, we assume that there is zero interest rate and no dividend yield. We are interested in computing the European put option price:

| (3.1) |

where is the strick price, is the maturity and is the stock price process introduced in Section 2.1. The European call option price can be computed via the put-call parity.

Recall that is a Brownian motion with drift and volatility , and its infinitesimal generator is given in (2.1). Define

| (3.2) |

It is clear that satisfies the equation:

| (3.3) |

with the initial condition . Taking the Laplace transform with respect to the time variable , we get

| (3.4) |

satisfies the equation:

| (3.5) |

By using dominated convergence theorem, one can show that

| (3.6) |

In addition, for all , , uniformly in . Thus, is infinitely differentiable w.r.t. and we find that the -th derivative of with respect to (w.r.t.) is given by

| (3.7) |

We first present a result which gives analytical expressions of for all . The main idea of the proof is to use the approach in Carr [5] and the PDE in (3.5) to iteratively solve the equation:

| (3.8) |

given , . The proof is lengthy so we leave the details to the appendix.

Proposition 3.

We have

| (3.9) |

In addition, for integer the -th derivative of w.r.t. is given by

where the coefficients can be determined recursively as

| (3.10) |

and for ,

with , and finally

| (3.11) | ||||

and

| (3.12) | ||||

where are given by:

| (3.13) |

With this proposition, we are now able to use fractional derivatives to give an explicit expression of European put option prices under the Variance Gamma model. The main result of this paper is given as follows.

Remark 5.

The Variance Gamma model can be viewed as the Black-Scholes model with random maturity that follows a gamma distribution. When is an integer, the random maturity has an Erlang distribution, and in Theorem 4, which has an exact expression given in Proposition 3. When is a fraction, the fractional derivative in Theorem 4 can be computed using Lemma 2

Proof of Theorem 4.

Recall that and we want to compute:

| (3.15) |

By definition

| (3.16) |

Let us assume that otherwise one can first differentiate with respect to integer times and then apply the fractional derivative.

It is easy to see that

| (3.17) |

Hence, we have

and the above formula works for .

More generally, if for some , then we have

The proof is therefore complete. ∎

4 Numerical Experiments

In this section, we numerically implement the put option price formula we obtained in Theorem 4, and compare our results with some existing methods in the literature, including the alternative closed-form formula in Madan et al. [23], the Fast Fourier Transform method in Carr and Madan [6].

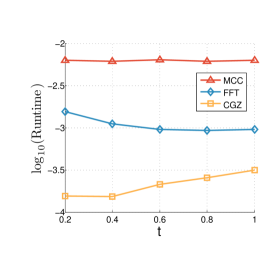

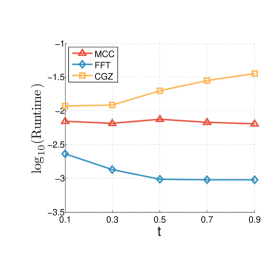

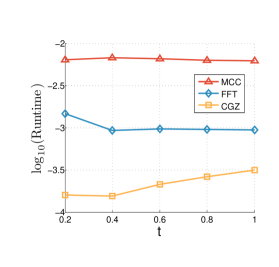

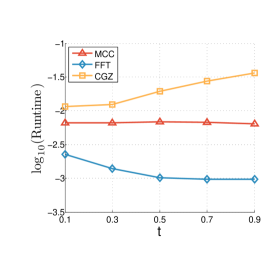

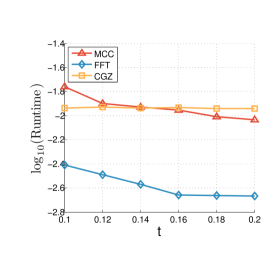

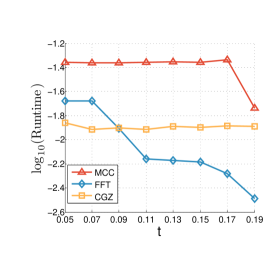

We compare the numerical results (CGZ) with the Carr and Madan [6] Fast Fourier Transform method (FFT) and the closed-form formula in Madan et al. [23] (MCC), and summarize the comparision results in Table 1, Table 2, Table 3 and Table 4, and Figure 1 and Figure 2.

In Table 1, Table 2 and Figure 1, we fix the model parameters to be , , and . This is the in-the-money case for the put option. The three methods give precisely the same price for the put options, and their price difference is negligible. In terms of runtime, the three methods are comparable. The FFT method beats MCC all the time. Our method (CGZ) has a clear advantage when is an integer, and when it is not an integer, our results still show very decent numerical performance.

In Table 3, Table 4, and Figure 2, we fix the model parameters to be , , and . This is the out-of-the-money case for the put option. We obtain similar phenomena as in the in-the-money case in Table 1, Table 2 and Figure 1.

| Put Price | Runtime | |||

|---|---|---|---|---|

| MCC | FFT | CGZ | ||

| 0.2 | 2.0107 | 0.0063 | 0.0016 | 0.0002 |

| 0.4 | 2.0339 | 0.0061 | 0.0011 | 0.0002 |

| 0.6 | 2.0662 | 0.0064 | 0.0010 | 0.0002 |

| 0.8 | 2.1038 | 0.0061 | 0.0009 | 0.0003 |

| 1.0 | 2.1441 | 0.0063 | 0.0010 | 0.0003 |

| Put Price | Runtime | |||

|---|---|---|---|---|

| MCC | FFT | CGZ | ||

| 0.1 | 2.0037 | 0.0070 | 0.0023 | 0.0117 |

| 0.3 | 2.0209 | 0.0065 | 0.0014 | 0.0122 |

| 0.5 | 2.0492 | 0.0074 | 0.0010 | 0.0196 |

| 0.7 | 2.0845 | 0.0068 | 0.0010 | 0.0281 |

| 0.9 | 2.1237 | 0.0064 | 0.0009 | 0.0355 |

| Put Price | Runtime | |||

|---|---|---|---|---|

| MCC | FFT | CGZ | ||

| 0.2 | 0.0163 | 0.0064 | 0.0015 | 0.0002 |

| 0.4 | 0.0489 | 0.0067 | 0.0009 | 0.0002 |

| 0.6 | 0.0919 | 0.0065 | 0.0010 | 0.0002 |

| 0.8 | 0.1401 | 0.0063 | 0.0010 | 0.0003 |

| 1.0 | 0.1903 | 0.0062 | 0.0009 | 0.0003 |

| Put Price | Runtime | |||

|---|---|---|---|---|

| MCC | FFT | CGZ | ||

| 0.1 | 0.0058 | 0.0066 | 0.0022 | 0.0116 |

| 0.3 | 0.0309 | 0.0067 | 0.0014 | 0.0124 |

| 0.5 | 0.0695 | 0.0068 | 0.0010 | 0.0195 |

| 0.7 | 0.1156 | 0.0068 | 0.0010 | 0.0276 |

| 0.9 | 0.1650 | 0.0064 | 0.0010 | 0.0361 |

| Put Price | Runtime | |||

|---|---|---|---|---|

| MCC | FFT | CGZ | ||

| 0.1000 | 0.0020 | 0.0173 | 0.0039 | 0.0115 |

| 0.1200 | 0.0027 | 0.0126 | 0.0032 | 0.0117 |

| 0.1400 | 0.0034 | 0.0117 | 0.0027 | 0.0116 |

| 0.1600 | 0.0043 | 0.0111 | 0.0022 | 0.0117 |

| 0.1800 | 0.0052 | 0.0098 | 0.0022 | 0.0114 |

| 0.2000 | 0.0063 | 0.0092 | 0.0022 | 0.0114 |

| Put Price | Runtime | |||

|---|---|---|---|---|

| MCC | FFT | CGZ | ||

| 0.0500 | 0.0026 | 0.0437 | 0.0210 | 0.0138 |

| 0.0700 | 0.0038 | 0.0435 | 0.0209 | 0.0122 |

| 0.0900 | 0.0051 | 0.0434 | 0.0124 | 0.0126 |

| 0.1100 | 0.0065 | 0.0438 | 0.0069 | 0.0122 |

| 0.1300 | 0.0081 | 0.0442 | 0.0067 | 0.0129 |

| 0.1500 | 0.0097 | 0.0439 | 0.0065 | 0.0127 |

| 0.1700 | 0.0115 | 0.0460 | 0.0052 | 0.0130 |

| 0.1900 | 0.0134* | 0.0183 | 0.0032 | 0.0129 |

5 Appendix: Proofs

Proof of Lemma 1.

Let . Then by the definition of fractional derivatives we can compute that for ,

Hence the proof is complete. ∎

Proof of Lemma 2.

From the definition of the fractional derivative, we have

By changing variable , we get and since is between and , we have is between and , and as a result, we get:

| (5.1) |

The proof is therefore complete. ∎

Proof of Proposition 3.

We first compute . For , we have

| (5.2) |

and for , we have

| (5.3) |

We can solve this equation and get:

| (5.4) |

for , and

| (5.5) |

for , where are the solutions of the equation:

| (5.6) |

and

| (5.7) |

Note that

| (5.8) |

is convex in and and , which implies that has exactly two solutions, one positive and the other one negative. Hence we have two solutions .

Next, let us show that . This comes from the boundary condition for as and .

Hence, we conclude that

| (5.9) |

We can then use being at to determine the coefficients :

Under the risk neutral measure with zero interest rate and zero dividend yield, the process is a martingale, and as a result,

| (5.10) |

and thus . We can then compute that

| (5.11) |

We next proceed to compute the first order derivative with respect to . Recall that

| (5.12) |

This implies that

| (5.13) |

For , we can compute that

if we choose

| (5.14) |

Similarly, we should choose

| (5.15) |

Finally, and are chosen so that is in at , which yields that

In general, for any ,

| (5.16) |

It follows that

For , we have

with the understanding that for .

It follows that, for ,

This implies that

| (5.17) |

and for ,

with .

References

- [1] Almendral, A. and Oosterlee, C. W. (2007). On American options under the Variance Gamma process. Applied Mathematical Finance. 14, 131-152.

- [2] Bouchard, B., El Karoui, N. and Touzi, N., (2005). Maturity randomization for stochastic control problems. The Annals of Applied Probability, 15(4), pp.2575-2605.

- [3] Boyarchenko, M., (2008). Carr’s randomization for finite-lived barrier options: Proof of convergence.

- [4] Boyarchenko, S. I., and S. Z. Levendorskii. (2002). Non-Gaussian Merton-Black-Scholes Theory. World Scientific.

- [5] Carr, P., (1998). Randomization and the American put. Review of Financial Studies, 11, 597-626.

- [6] Carr, P. and D. Madan. (1999). Option valuation using the fast Fourier transform. Journal of Computational Finance. 2, 61-73.

- [7] Carr, P. and Madan, D. (2009). Saddlepoint methods for option pricing. The Journal of Computational Finance, 13(1), p.49.

- [8] Cartea, Á. (2013). Derivatives pricing with marked point processes using tick-by-tick data. Quantitative Finance. 13, 111-123.

- [9] Cartea, Á. and del-Castillo-Negrete, D. (2007). Fractional diffusion models of option prices in markets with jumps. Physica A. 374, 749-763.

- [10] Chen, W., Xu, X. and S.P. Zhu. (2014). Analytically pricing European-style options under the modified Black-Scholes equation with a spatial-fractional derivative. Quarterly of Applied Mathematics. 72, 597-611.

- [11] Cont, R. and Voltchkova, E. (2005). A finite difference scheme for option pricing in jump diffusion and exponential Lévy models. SIAM Journal of Numerical Analysis. 43, 1596-1626.

- [12] Crocce, F., Häppölä, J., Kiessling, J. and Tempone, R. (2015). Error analysis in Fourier methods for option pricing. arXiv:1503.00019.

- [13] Faguet, D. and Carr, P., (1994). Fast accurate valuation of American options.

- [14] Fallahgoul, H., Focardi, S. and Fabozzi, F., (2016). Fractional Calculus and Fractional Processes with Applications to Financial Economics: Theory and Application. Academic Press.

- [15] Fu, M. C. (2000). Variance-Gamma and Monte Carlo. Advances in Mathematical Finance. pp. 21-34.

- [16] Hirsa, A. and D. Madan. (2001). Pricing American options under Variance Gamma. Journal of Computational Finance.

- [17] Itkin, A. and P. Carr. (2012). Using pseudo-parabolic and fractional equations for option pricing in jump diffusion models. Computational Economics. 40, 63-104.

- [18] Kaishev, V.K. and Dimitrova, D.S. (2009). Dirichlet bridge sampling for the variance gamma process: pricing path-dependent options. Management Science. 55, 483-496.

- [19] Kimura, T., (2010). Alternative randomization for valuing American options. Asia-Pacific Journal of Operations Research. 27, 167-187.

- [20] Lee, R.W., (2004). Option pricing by transform methods: extensions, unification and error control. Journal of Computational Finance. 7, 51-86.

- [21] Leippold, M. and Vasiljevic, N., (2017). Pricing and disentanglement of American puts in the hyper-exponential jump-diffusion model. Forthcoming at Journal of Banking and Finance.

- [22] Levendorskii, S., (2011). Convergence of price and sensitivities in Carr’s randomization approximation globally and near barrier. SIAM Journal on Financial Mathematics. 2, 79-111.

- [23] Madan, D. B., Carr, P. P. and E. C. Chang. (1998). The variance gamma process and option pricing. European Finance Review. 2, 79-105.

- [24] Madan, D. B. and F. Milne. (1991). Option pricing with VG martingale components. Mathematical Finance. 1, 39-55.

- [25] Madan, D. B. and E. Seneta. (1990). The V.G. model for share market returns. Journal of Business. 63, 511-524.

- [26] Marom, O. and E. Momoniat, E. (2009). A comparison of numerical solutions of fractional diffusion models in finance. Nonlinear Analysis: Real World Applications. 10, 3435-3442.

- [27] Miller, K.S. and B. Ross. An Introduction to the Fractional Calculus and Fractional Differential Equations. John Wiley & Sons, New York, NY, USA, 1993.

- [28] Whitley, A. (2009). Pricing of European, Bermudan and American Options under the Exponential Variance Gamma Process. MSc Thesis. University of Oxford.