∎ ∎

chenjian_math@163.com

L.P. Tang 33institutetext: National Center for Applied Mathematics in Chongqing, and School of Mathematical Sciences, Chongqing Normal University, Chongqing 401331, China

tanglipings@163.com

🖂X.M. Yang 44institutetext: National Center for Applied Mathematics in Chongqing, and School of Mathematical Sciences, Chongqing Normal University, Chongqing 401331, China

xmyang@cqnu.edu.cn

Barzilai-Borwein Proximal Gradient Methods for Multiobjective Composite Optimization Problems with Improved Linear Convergence

Abstract

When minimizing a multiobjective optimization problem (MOP) using multiobjective gradient descent methods, the imbalances among objective functions often decelerate the convergence. In response to this challenge, we propose two types of the Barzilai-Borwein proximal gradient method for multi-objective composite optimization problems (BBPGMO). We establish convergence rates for BBPGMO, demonstrating that it achieves rates of , , and for non-convex, convex, and strongly convex problems, respectively. Furthermore, we show that BBPGMO exhibits linear convergence for MOPs with several linear objective functions. Interestingly, the linear convergence rate of BBPGMO surpasses the existing convergence rates of first-order methods for MOPs, which indicates its enhanced performance and its ability to effectively address imbalances from theoretical perspective. Finally, we provide numerical examples to illustrate the efficiency of the proposed method and verify the theoretical results.

Keywords:

Multiobjective optimization Barzilai-Borwein’s rule Proximal gradient method Linear convergenceMSC:

90C29 90C301 Introduction

In the realm of multiobjective optimization, the primary goal is to simultaneously optimize multiple objective functions. Generally, finding a single solution that achieves the optima for all objectives at once is not feasible. As a result, the concept of optimality is defined by either Pareto optimality or efficiency. A solution is deemed Pareto optimal or efficient if no objective can be improved without sacrificing the others. As society and the economy progress, the applications of this type of problem have proliferated across a multitude of domains, such as engineering MA2004 , economics FW2014 ; TC2007 , management science E1984 , and machine learning SK2018 ; YL2021 , etc.

Solution strategies play a pivotal role in the realm of applications involving multiobjective optimization problems (MOPs). Over the past two decades, multiobjective gradient descent methods have gained escalating attention within the multiobjective optimization community. These methods generate descent directions by solving subproblems, eliminating the need for predefined parameters. Subsequently, line search techniques are employed along the descent direction to ensure sufficient improvement for all objectives. Attouch et al. AGG2015 pointed out an attractive property of this method in fields like game theory, economics, social science, and management: it improves each of the objective functions. As far as we know, the study of multiobjective gradient descent methods can be traced back to the pioneering work by Mukai M1980 . Later, Fliege and Svaiter FS2000 independently reinvented the steepest descent method for MOPs (SDMO). Their work elucidated that the multiobjective steepest descent direction reduces to the steepest descent direction when dealing with a single objective. This observation inspired researchers to extend ordinary numerical algorithms for solving MOPs (see, e.g., AP2021 ; BI2005 ; CL2016 ; FD2009 ; FV2016 ; GI2004 ; LP2018 ; MP2018 ; MP2019 ; P2014 ; QG2011 and references therein).

Although multiobjective gradient descent methods are derived from their single-objective counterparts, there exist certain theoretical gaps between the two types approaches. Recently, Zeng et al. ZDH2019 and Fliege et al. FVV2019 have studied the convergence rates of SDMO. They proved that SDMO converges at rates of , , and for nonconvex, convex, and strongly convex problems, respectively. Tanabe et al. TFY2023 obtained similar results for the proximal gradient method for MOPs (PGMO) TFY2019 . It is worth noting that when minimizing a -strongly convex and -smooth function using vanilla gradient method, the rate of convergence in terms of is . However, for MOPs, the linear convergence rate of SDMO is , where and . Consequently, imbalances among objective functions, arising from the substantially distinct curvature matrices of different objective functions, can lead to a small value of . Particularly, even though each of the objective functions are not ill-conditioned (a relative small ), the overall condition number can be tremendous. This observation explains why each objective is relatively easy to optimize individually but challenging when attempting to optimize them simultaneously. To the best of our knowledge, most of first-order methods for MOPs suffer slow convergence due to the imbalances among objectives. Naturally, questions arise: How to accelerate multiobjective first-order methods and bridge the theoretical gap between first-order methods for SOPs and MOPs?

To accelerate multiobjective first-order methods, Lucambio Pérez and Prudente LP2018 utilized previous information and propose nonlinear conjugate gradient methods for MOPs. EI Moudden and EI Mouatasim EE2021 approximated the Hessian using diagonal matrices and introduced diagonal steepest descent methods for MOPs. Very recently, motivated by Nesterov’s accelerated method N1983 , Tanabe et al. proposed an accelerated proximal gradient method for MOPs. Sonntag and Peitz SP2022 ; SP2023 investigated accelerated multiobjective gradient methods from continuous-time perspective. Although these methods achieved improved performance, the theoretical gap between first-order methods for SOPs and MOPs remains open. On the other hand, some studies GK2021 ; MF2019 ; MP2016 have pointed out that Armijo line search often generates a relative small stepsize in SDMO, which slows down convergence. Chen et al. CTY2023 elucidated that the small stepsize is mainly due to the imbalances among objectives. Regarding the multiobjective steepest descent direction, it holds that

where is the dual variable of direction-finding subproblem. The relation implies that each iteration produces a similar amount of descent for different objectives, which results in small stepsize due to the imbalances among objectives. To address this issue, Chen et al. CTY2023 proposed the Barzilai-Borwein descent method for MOPs (BBDMO), which dynamically tunes gradient magnitudes using Barzilai-Borwein’s rule BB1988 in the direction-finding subproblem. Along the Barzilai-Borwein descent direction, different objectives have distinct amount of descent. Specifically,

where is given by Barzilai-Borwein method. Theoretical results indicate that BBDMO can achieve a better stepsize, and numerical results demonstrate that it requires fewer iterations and function evaluations. Despite the excellent performance in practice, the theoretical guarantee of faster convergence of BBDMO remains unknown.

In this paper, we turn our attention towards the generic model of unconstrained multiobjective composite optimization problems, which is formulated as follows:

| (MCOP) |

where is a vector-valued function. Each component , , is defined by

where is continuously differentiable and is proper convex and lower semicontinuous but not necessarily differentiable. This type of problem finds wide applications in machine learning and statistics, and gradient descent methods tailored for it have received increasing attention (see, e.g., A2023 ; AFP2023 ; TFY2019 ; TFY2022 ). To this end, we propose two types of Barzilai-Borwein proximal gradient methods for MCOPs (BBPGMO). We analyze the convergence rates of BBPGMO and provide new theoretical results, paving the way for explaining its fast convergence behavior in practice. The main contributions of this paper can be summarized in the following points:

(i) To mitigate the imbalances among objective functions, we propose two types of Barzilai-Borwein proximal gradient methods for MCOPs. The first method employs Armijo line search, the Barzilai-Borwein’s rule is applied to every objective in direction-finding subproblem. It coincides with BBDMO when , . Additionally, we devise a new proximal gradient method for MCOPs without line search, where the smooth parameter is employed to tune the corresponding objective in the direction-finding subproblem. It is worth noting that the global smoothness parameters for a general MOP are unknown and tend to be conservative, we thus propose an adaptive method to estimate the local smoothness parameters, in which the initial values are obtained through the Barzilai-Borwein method.

(ii) With line search, we prove that every accumulation point generated by BBPGMO is a Pareto critical point. Moreover, We establish strong convergence of the sequence generated by BBPGMO under standard convexity assumption. In the strongly convex case, it is proved that the produced sequence converges linearly to a Pareto solution. We also provide the convergence rates of the adaptive Barzilai-Borwein proximal gradient method for MCOPs (ABBPGMO). Notably, in the case of strong convexity, the rate of convergence in terms of is . The improved linear convergence explains why the BBPGMO outperforms the PGMO from a theoretical perspective.

(iii) We establish the linear convergence of BBPGMO for MOPs with some linear objectives. This finding shows that BBPGMO can achieve fast convergence even when dealing with problems with linear objectives, which are known to impose significant imbalances in multiobjective optimization CTY2023 .

The paper is organized as follows. In section 2, we present some necessary notations and definitions that will be used later. In section 3, we propose two types of Barzilai-Borwein proximal gradient methods, and present some preliminary lemmas. The convergence rates of BBPGMO are analyzed in section 4. In section 5, we present an efficient approach to solve the subproblem using its dual. The numerical results are presented in section 6, which demonstrate that BBPGMO outperforms PGMO and verify the theoretical results. Finally, we draw some conclusions at the end of the paper.

2 Preliminaries

Throughout this paper, the -dimensional Euclidean space is equipped with the inner product and the induced norm . We denote by the Jacobian matrix of at , by the gradient of at . Moreover, we denote

the directional derivative of at in the direction . The Moreau envelope of is given by

The proximal operator of is denoted by

For simplicity, we denote , and

the -dimensional unit simplex. In case of misunderstand, we define the order in as

In the following, we introduce the concepts of optimality for (MCOP) in the Pareto sense.

Definition 1.

A vector is called Pareto solution to (MCOP), if there exists no such that and .

Definition 2.

A vector is called weakly Pareto solution to (MCOP), if there exists no such that .

Definition 3.

A vector is called Pareto critical point of (MCOP), if

From Definitions 1 and 2, it is evident that Pareto solutions are always weakly Pareto solutions. The following lemma shows the relationships among the three concepts of Pareto optimality.

Lemma 1 (Theorem 3.1 of FD2009 ).

The following statements hold.

Definition 4.

A differentiable function is -smooth if

holds for all . And f is -strongly convex if

holds for all .

-smoothness of implies the following quadratic upper bound:

On the other hand, -strong convexity yields the quadratic lower bound:

3 BBPGMO: Barzilai-Borwein proximal gradient method for MCOPs

3.1 Proximal gradient method for MCOPs

In this subsection, we recall two types of multiobjective proximal gradient methods for (MCOP). Defined the function by

The proximal gradient method updates iterates as follows:

where is a descent direction and is the stepsize. The descent direction is the unique optimal solution to the following subproblem with :

| (1) |

By Sion’s minimax theorem S1958 , there exists such that

and

| (2) |

To compute the stepsize , let be a predefined constant, the condition for accepting is given by:

| (3) |

Initially, set . If (3) is not satisfied, we update using the following rule:

The proximal gradient method for MCOPs with line search is described as follows.

Assume that is -smooth for , the stepsize can be fixed as . Denote , the proximal gradient method for MCOPs without line search is described as follows.

3.2 Barzilai-Borwein proximal gradient method for MCOPs

As described in (CTY2023, , Section 4), the relation (2) implies that each iteration yields a similar amount of descent for different objective functions (), which can result in slow convergence for imbalanced multiobjective optimization problems. To address this issue and achieve distinct amounts of descent for different objective functions, we introduce the Barzilai-Borwein proximal gradient direction as follows:

| (4) |

where is the minimizer of

| (5) |

and is set as follows:

| (6) |

for all , where is a sufficient large positive constant and is a sufficient small positive constant,

Proposition 1.

Proof.

Remark 1.

Since is objective-based, equation (8) indicates that, along with the Barzilai-Borwein proximal gradient direction, different objective functions have distinct amount of descent.

Next, we will present several properties of .

Lemma 2.

Let be defined as (4), then we have

| (10) |

Proof.

The assertion can be obtained by using the same arguments as in the proof of (TFY2019, , Lemma 4.1).

Lemma 3.

Let be defined as (4), then the following statements hold.

-

the following assertions are equivalent:

The point is non-critical;

;

is a descent direction.

-

if there exists a convergent subsequence such that , then is Pareto critical.

Proof.

Since , assertion (i) can be obtained by using the same arguments as in the proof of (TFY2019, , Lemma 3.2). Nexct, we prove assertion (ii). We use the definition of and the fact that to get

| (11) | ||||

where the second inequality follows by (TFY2020, , Theorem 4.2) and the fact that ( is a large positive constant), and the last inequality is given by (TFY2019, , Lemma 4.1). On the other hand, from and the continuity of for , we obtain

This together with (11) gives . Moreover, from the continuity of ((TFY2019, , Lemma 3.2)) and the fact that , we can deduce that . The desired result follows.

Remark 2.

The continuity of plays a key role in proving the global convergence of PGMO. For BBPGMO, the corresponding condition can be replaced by Lemma 3(ii).

3.2.1 Barzilai-Borwein proximal gradient method with line search

For each iteration , once the unique descent direction is obtained, the classical Armijo technique is employed for line search.

The following result demonstrates that the Armijo technique will accept a stepsize along with .

Lemma 4.

Assume that is not Pareto critical. Then there exists such that

holds for all .

Proof.

The proof is similar to (TFY2019, , Lemma 3.3), we omit it here.

The stepsize obtained by Algorithm 3 has a lower bound.

Lemma 5.

Assume is -smooth for , then the stepsize generated by Algorithm 3 satisfies , where .

Proof.

It is sufficient to prove , then backtracking is conducted, leading to the inequality:

| (12) |

for some . Since is -smooth for , we can derive the following inequalities:

where the second inequality follows from the convexity of . Combining this inequality with (12), we obtain

for some . Utilizing (10), we arrive at

| (13) |

for some , it holds that . This completes the proof.

The Barzilai-Borwein proximal gradient method for MCOPs with line search is described as follows.

3.2.2 Adaptive Barzilai-Borwein proximal gradient method

Under the assumption that is -smooth for , we also devise the following Barzilai-Borwein proximal gradient method for MCOPs without line search.

Remark 3.

It is worth noting that Algorithm 2 utilizes the maximal global smoothness parameter for all objectives, which may be too conservative for objectives with small global smoothness parameters. Instead, Algorithm 5 employs a separate global smoothness parameter for each objective. This strategy can help alleviate interference among the objectives.

However, in practice, the global smoothness parameter is often unknown and tends to be conservative. To address this issue, we propose an adaptive Barzilai-Borwein proximal gradient method to estimate the local smoothness parameters. The method is described as follows:

In Algorithm 6, lines 8-15 are responsible for estimating the local smoothness parameter for . The following proposition demonstrates that the procedure is well-defined.

Proposition 2.

If is -smooth for , then the repeat loop of Algorithm 6 terminates in a finite number of iterations, and .

Proof.

Note that is -smooth for , we have

The desired results follow directly from this inequality.

Remark 4 (Adaptivity to local smoothness).

The Barzilai-Borwein’s rule (line 3) plays an important role in estimating the initial smoothness parameters. One significant advantage of this approach, compared to simply setting , is that lines 8-15 can adapt to the local smoothness based on the iteration trajectory. As a result, the procedure can better adapt to the characteristics of the problem and improve real-world performance significantly.

3.3 Merit function

Before presenting the convergence results of BBPGMO, we introduce two types of merit functions for (MCOP) that quantify the gap between the current point and the optimal solution. The merit functions will be used in convergence rates analysis.

| (14) |

| (15) |

where , .

We can demonstrate that and serve as merit functions, satisfying the criteria of weak Pareto and critical point, respectively.

Proposition 3.

Proof.

Proposition 4.

Proof.

(i) Assertion (i) follows directly by the definition of .

(ii) The assertion can be obtained by using the same arguments as in the proof of (TFY2020, , Theorem 4.2).

(iii) From the definition of , we obtain . Next, we need to prove

A direct calculation gives

where and the last inequality is given by the assertion (ii). The desired result follows.

4 Convergence rates analysis

Relation (8) shows that, along the Barzilai-Borwein proximal gradient direction, different objectives can achieve distinct descent. Hence, BBPGMO has the ability to mitigate the imbalances among objectives. Naturally, a question arises that: Does BBPGMO exhibit improved convergence rates? The primary objective of this section is to analyze the convergence rates of BBPGMO, and provide a positive answer to this question.

In Algorithms 4-6, it can be observed that these algorithms terminate either with a Pareto critical point in a finite number of iterations or generates an infinite sequence of points. In the subsequent analysis, we will assume that these algorithms produce an infinite sequence of noncritical points.

4.1 Convergence rates analysis of BBPGMO with line search

First, we analyze the convergence rates of BBPGMO with line search.

4.1.1 Global convergence

Theorem 4.1.

Assume that is a bounded set. Let be the sequence generated by Algorithm 4. Then, the following statements hold.

-

has at least one accumulation point, and every accumulation point is a Pareto critical point.

-

If is -smooth for , then

Proof.

(i) From the boundedness of and the fact that is decreasing, there exists such that and . The assertion (i) can be obtained by using the same arguments as in the proof of (TFY2019, , Theorem 4.2).

(ii) By using (10) and the line search condition, we have

Taking the sum of the above inequality over , we obtain

Rearranging the terms and using the fact that , we have

The desired result follows.

4.1.2 Strong convergence

Before presenting the strong convergence of Algorithm 4, we recall the following result on non-negative sequences.

Lemma 6 (Lemma 2 of P1987 ).

Let and be non-negative sequences. Assume that and , then converges.

Theorem 4.2.

Assume that is a bounded set, is convex and -smooth for . Let be the sequence generated by Algorithm 4. Then, the following statements hold.

-

converges to some weak Pareto solution .

-

There exists a constant such that

Proof.

(i) From the convexity of for , we have

| (16) |

Applying Theorem 4.1(i), denote an accumulation point of . We use to get

| (17) |

Furthermore, utilizing (B2017, , Theorem 6.39 (iii)) and the expression (7), we can derive the inequality:

By rearranging the terms and utilizing the facts that is convex and -smooth for , we can obtain

where the last inequality is due to (16). By substituting , we have

Substituting the above inequality into (17), it follows that

where the second inequality follows by . Denote

We use (10) to get

where the second inequality is given by . Then, by applying Lemma 6, we can conclude that the sequence converges. This, together with the fact that is an accumulation point of , implies converges to . Moreover, the convexity of yields that is a weakly Pareto solution.

(ii) Dividing (16) by and using the -smoothness of , we can deduce the following result:

Recall that is the minimizer of (5) and is convex for all , we can derive the following inequalities:

Now, let’s select with and . From the convexity of , , we obtain

| (18) | ||||

By the definition of , we can deduce that . On the other hand, the monotonicity of the implies . Therefore, considering the boundedness of (denoted by as the diameter of ), we can conclude that

Substituting the bound into (18), we obtain

| (19) |

By the arbitrary of , we observe that the minimum on the right-hand side of (19) is attained at

Since converges to some weak Pareto solution, it follows by Proposition 3 (ii) that converges to (). Then there exists such that for all . Consquently, for ,

| (20) | ||||

On the other hand, we can utilize the Armijo line search condition and (10) to derive the following inequality:

Hence,

Substituting the preceding relation into (20), for all , we have

Rearranging and utilizing the fact that , we have

| (21) |

where , with . Rearranging and taking the minimum and supremum with respect to and on both sides, respectively, we obtain

namely,

Dividing the above inequality by and using (the monotonicity of ), for all , we have

Now, taking the sum of the preceding relation over , we obtain

It follows that

where . Without loss of generality, there exists such that

This completes the proof.

4.1.3 Linear convergence

Theorem 4.3.

Assume that is -smooth and strongly convex with modulus , for . Let be the sequence generated by Algorithm 4. Then, the following statements hold.

-

converges to some Pareto solution .

-

Proof.

(i) Since is strongly convex and is convex, the level set is bounded, and any weak Pareto solution is a Pareto solution. Therefore, assertion (i) is the consequence of Theorem 4.2(i).

(ii) Since is -strongly convex and -smooth, we can establish the following bounds:

This, together with the facts that is a sufficient small positive constant and is a sufficient large positive constant, leads to

| (22) |

Recall that the Armijo line search satisfies

A direct calculation gives

| (23) | ||||

where the last inequality is is a consequence of (13) and (22). Furthermore, due to the strong convexity of , we have

Taking the supremum and minimum with respect to and on both sides, respectively, we obtain

where the second inequality is due to Proposition 4(iii) and the fact that , the last inequality is given by . The above inequalities can be reformulated as

Together with (23), the preceding inequality yields

Then, for all , we have

Taking the supremum and minimum with respect to and on both sides, respectively, we obtain

This completes the proof.

Compared to the linear convergence of multiobjective proximal gradient method, the result in Theorem 4.3 is objective-independent but has a higher order coefficient. However, the conservative nature of the bound in Theorem 4.3 suggests that it can be improved in practice. In the following proposition, we present a better bound.

Proof.

The proof follows a similar approach as in Theorem 4.3, we omit it here.

4.2 Convergence rates analysis of ABBPGMO

In this subsection, we assume that is -smooth for . We also analyze the convergence rates of adaptive BBPGMO.

4.2.1 Global convergence

Theorem 4.4.

Assume that is a bounded set. Let be the sequence generated by Algorithm 6. Then, the following statements hold.

-

has at least one accumulation point, and every accumulation point is a Pareto critical point.

-

.

Proof.

Corollary 1.

Assume that is a bounded set. Let be the sequence generated by Algorithm 5. Then, the following statements hold.

-

has at least one accumulation point, and every accumulation point is a Pareto critical point.

-

.

4.2.2 Strong convergence

Before presenting the strong convergence, we establish a fundamental inequality.

Lemma 7.

Assume that is strongly convex with modulus . Then, there exists such that

| (24) | ||||

Proof.

We are now in the position to prove the strong convergence of Algorithm 6.

Theorem 4.5.

Assume that is a bounded set and is convex, . Let be the sequence generated by Algorithm 6. Then, the following statements hold.

-

converges to some weak Pareto solution .

-

where

Proof.

(i) From Theorem 4.4(i), there exists a Pareto critical point such that , and is an accumulation point of . Moreover, is a weak Pareto solution due to the convexity of . Applying fundamental inequality (24) and the convexity of , for all we have

| (25) |

Substituting into the above inequality, we obtain

Note that , it follows that

Therefore, the sequence converges. This, together with the fact that is an accumulation point of , implies that converges to .

(ii) Taking the sum of (25) over to , we obtain

for all . Since for all , it leads to

For all , together with the fact that , the preceding relation yields

Denote , we can deduce that and

Select , it holds that

By the definition of , we deduce that , which implies , the desired result follows.

Corollary 2.

Assume that is a bounded set and is convex, . Let be the sequence generated by Algorithm 5. Then, the following statements hold.

-

converges to some weak Pareto solution .

-

where

4.2.3 Linear convergence

Theorem 4.6.

Assume that is strongly convex with modulus , . Let be the sequence generated by Algorithm 6. Then, the following statements hold.

-

converges to some Pareto solution .

-

Proof.

(i) Since is strongly convex and is convex, then the level set is bounded and any weak Pareto solution is Pareto solution. Therefore, assertion (i) is a consequence of Theorem 4.5(i).

(ii) By substituting into inequality (24), we obtain

Applying , it follows that

| (26) |

where the last inequality holds due to the facts and .

Corollary 3.

Assume that is strongly convex with modulus , . Let be the sequence generated by Algorithm 5. Then, the following statements hold.

-

converges to some Pareto solution .

-

In the following, we give the relationships among the new multiobjective proximal gradient method, multiobjective proximal gradient method and proximal gradient method for SOPs.

Remark 6.

When , both the new multiobjective proximal gradient method and the multiobjective proximal gradient method collapse to the proximal gradient method for SOPs. Notably, when , the new multiobjective proximal gradient method is faster than the multiobjective proximal gradient method and has at least the same rate of convergence as the proximal gradient method for the with the smallest , . On the other hand, the new multiobjective proximal gradient method exhibits rapid linear convergence as long as all differentiable components are not ill-conditioned. However, the multiobjective proximal gradient method may converge slowly even if all differentiable components are not ill-conditioned.

Remark 7.

Based on Proposition 5 and Corollary 3, we observe that by setting and in Algorithm 4, the rates of linear convergence in terms of and are and , respectively. On the other hand, if we set as (6), we have . Intuitively, we believe that the rate of linear convergence for Algorithm 4 is not worse than , since .

4.3 Linear convergence with some linear objective functions

In view of the first inequality in (26), the rate of linear convergence in terms of is actually for Algorithm 5. On the other hand, Lemma 7 is valid for weakly convex function , i.e., . Consequently, Algorithm 5 exhibits linear convergence rate as long as . A similar statement holds for (new) PGMO without line search. However, such a statement holds under the restrictive condition , and there may exist counterexamples that show these algorithms do not converge linearly. Naturally, a question arises: Does ABBPGMO or PGMO without line search have a linear convergence rate without strong convexity assumption on some objective functions?

To the best of our knowledge, in SOPs, this question has been addressed through the study of error bound conditions, which have been extensively explored (see, e.g., LT1993 ; NNG2019 ; Z2020 and references therein). However, in the context of MOPs, this area has received little attention TFY2020 . In the following, we do not delve into the study of error bound conditions for MOPs. Instead, we focus on linear constrained MOP with linear objective functions, which is described as follows:

| (LCMOP) |

where is a vector-valued function; the component is linear for , and -strongly convex and -smooth for , respectively; with . This type of problem has wide applications in portfolio selection M1952 , and can be reformulated as (MCOP) with , where

When minimizing (LCMOP) using ABBPGMO, the subproblem (5) is reformulated as follows:

By KKT conditions, we obtain , where and is the -th and -th row of and , respectively. The vector is a solution of the following Lagrangian dual problem:

And complementary slackness condition gives that

| (27) |

Denote , this together with (27) and the fact that implies

Before presenting the linear convergence of ABBPGMO for (LCMOP), let’s first define the following multiobjective linear programming problem:

| (MLP) |

It is important to note that every weakly Pareto solution of (MLP) is also a weakly Pareto solution of (LCMOP).

Proposition 6.

Proof.

(i) Since is strongly convex for , the level set is bounded. Then assertion (i) is a consequence of Theorem 4.5(i).

(ii) We refer to Theorem 4.6(ii), which states:

| (28) |

Given that is not a weakly Pareto solution of (MLP), we deduce , where represents the gradient of the linear function . Furthermore, since , we can infer that is finite. Consequently, we can define . By direct calculation, we have

| (29) | ||||

where the second equality follows from the fact that for all , and the last inequality is given by the definition of . By simple calculation, we have

where the last inequality is due to -strong convexity of , and the fact that is a solution of dual problem. This together with (29) implies

Denoting , and utilizing the -smoothness of , we derive an upper bound of :

Therefore, we obtain

| (30) |

Substituting the above bound and into (28), we have the desired result.

As mentioned in CTY2023 , linear objectives can often introduce significant imbalances in MOPs, which decelerates the convergence of SDMO. In the context of BBDMO, Chen et al. provided two examples (CTY2023, , Examples 2,3) to illustrate why a small value of is sufficient to mitigate the influence of the linear objectives in direction-finding subproblems. In what follows, we attempt to confirm the statement from a theoretical perspective.

Remark 8.

From the proof of Proposition 6(ii), it is evident that by choosing a sufficiently small value of , the sum of dual variables of liner objectives tends to . This effectively mitigates the influence of the linear objectives in direction-finding subproblems. Furthermore, since is proportional to , the linear convergence rate can also be improved by selecting a sufficiently small value for . Overall, this analysis supports the idea that appropriately choosing a small is beneficial in dealing with the impact of linear objectives and improving the convergence rate of the algorithm.

Remark 9.

The assumption of Proposition 6(ii) seems restrictive. In practice, the Pareto set of (LCMOP) can be a -dimensional manifold, and the Pareto set of (MLP) can be a -dimensional sub-manifold within the -dimensional manifold. As a result, for a random initial point , the probability that is not a weakly Pareto solution of (MLP) can be . Additionally, when , meaning (MLP) has no inequality constraints, then the problem can either have no weakly Pareto solution, or every feasible point can be considered a weakly Pareto solution. In other words, ABBPGMO converges linearly for equality constrained (LCMOP).

Next, we analyze convergence rate of PGMO without line search for (LCMOP).

Proposition 7.

Proof.

(i) The proof follows a similar approach as in Proposition 6(i).

(ii) Setting in ABBPGMO, it coincides with PGMO without line search. Consequently, (28) collapses to:

| (31) |

Substituting into (29), it follows that

Rearranging the above inequality, we have

Since converges to a weakly Pareto point, it follows that . Then there exists such that . This implies that

where By substituting the above bound into (31), we obtain

Without loss of generality, there exists such that

From Proposition 7, PGMO without line search only achieves -linear convergence. The following example illustrates that at the early stage of the method, can equal to . In other words, we can not obtain -linear convergence of the method for (MCOP).

Example 1.

Consider the multiobjective optimization problem:

where , ( is a relative small positive constant), and By simple calculations, we have

and the Pareto set is . Given a feasible , at the early stage () of PGMO without line search, we have , and . At this stage, we have , which tends to for sufficient small .

5 Solving the subproblem via its dual

The efficiency of BBPGMO does not only depend on the outer iteration but also how to solve the subproblem efficiently. Motivated by (TFY2022, , Section 6), we obtain the descent direction by solving the subproblem via its dual, and the dual can be solved by Frank-Wolfe/conditional method efficiently. The subproblem (5) can be reformulated as:

By Sion’s minimax theorem, the above problem is equivalent to

On the other hand, we can deduce that

Hence, the dual problem of (5) can be stated as follows:

| (DP) | ||||

where

From Proposition 1, we have

| (32) |

where is a solution of (DP). Note that the dual problem is a convex problem with unit simplex constraint, which can be efficiently solved by Frank-Wolfe method. The following proposition introduces how to compute .

Proposition 8.

The function is continuously differentiable and

where

and

Proof.

We use (BS2000, , Theorem 4.13) to get

On the other hand, we have

The desired result follows by adding the above two equalities.

Proposition 8 highlights the importance of the cheap proximal operation for in solving the dual problem. Fortunately, the cheap proximal operation can be found in machine learning and statistics, where for .

6 Numerical results

In this section, we present numerical results to demonstrate the performance of BBPGMO for various problems. All numerical experiments were implemented in Python 3.7 and executed on a personal computer equipped with an Intel Core i7-11390H, 3.40 GHz processor, and 16 GB of RAM. For BBPGMO, we set and in equation (6)111For larger-scale and more complicated problems, smaller values for and larger values for should be selected.. In the line search procedure, we set and . To ensure that the algorithms terminate after a finite number of iterations, we use the stopping criterion for all tested algorithms. We also set the maximum number of iterations to 500.

6.1 Comparing with PGMOμ and PGMOL

As described in Remark 7, in the case of strong convexity, BBPGMO may outperform PGMOμ and PGMOL, where and for , respectively. In the following, we present comparative numerical results to validate this statement. We consider a series of quadratic problems defined as follows:

where is a diagonal matrix with diagonal elements randomly generated from the uniform distribution [1, 100]. Each component of is randomly generated from the uniform distribution [-10, 10]. Table 1 provides a problem illustration and the corresponding numerical results. The second column presents the dimension of the variables, while and represent the lower and upper bounds of the variables, respectively. For each problem, we perform 200 computations using the same initial points for different tested algorithms. The initial points are randomly selected within the specified lower and upper bounds. Box constraints are handled by augmented line search, which ensures that . The recorded averages from the 200 runs include the number of iterations, the number of function evaluations, and the CPU time.

| Problem | BBPGMO | PGMOμ | PGMOL | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| iter | feval | time | iter | feval | time | iter | feval | time | ||||||

| a | 2 | (-2,-2) | (2,2) | 3.12 | 3.50 | 2.11 | 12.12 | 27.68 | 4.30 | 7.33 | 7.33 | 2.73 | ||

| b | 10 | (-2,…,-2) | (2,…,2) | 18.95 | 26.22 | 25.23 | 128.68 | 738.29 | 158.91 | 101.09 | 101.09 | 25.55 | ||

| c | 50 | (-2,…,-2) | (2,…,2) | 18.74 | 25.29 | 48.20 | 83.32 | 432.25 | 133.44 | 60.48 | 60.48 | 53.44 | ||

| d | 100 | (-2,…,-2) | (2,…,2) | 26.73 | 39.51 | 88.90 | 76.79 | 420.34 | 328.28 | 79.08 | 79.08 | 92.11 | ||

| e | 100 | 100(-1,…,-1) | 100(1,…,1) | 54.98 | 87.47 | 112.66 | 222.40 | 1223.27 | 218.91 | 354.38 | 354.38 | 61.88 |

In Table 1, we provide the average number of iterations (iter), average number of function evaluations (feval), and average CPU time (time ()) for each test problem across the different algorithms. In terms of the average number of iterations and average number of function evaluations, the numerical results confirm that BBPGMO outperforms both PGMOμ and PGMOL.

6.2 Comparing with PGMO

In this subsection, we conduct a comparison between BBPGMO and PGMO for different problems. Each objective function in the tested problems consists of two components: for , and the details of are provided in Table 2. The second and third columns present the dimension of variables and objective functions, respectively. The lower and upper bounds of variables are denoted by and , respectively. For each problem, we perform 200 computations using the same initial points for different tested algorithms. The initial points are randomly selected within the specified lower and upper bounds. Box constraints are handled by augmented line search, which ensures that . The recorded averages from the 200 runs include the number of iterations, number of function evaluations, CPU time, and stepsize.

| Problem | Reference | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| BK1 | 2 | 2 | (-5,-5) | (10,10) | BK1 | |||||

| DD1 | 5 | 2 | (-20,…,-20) | (20,…,20) | DD1998 | |||||

| Deb | 2 | 2 | (0.1,0.1) | (1,1) | D1999 | |||||

| Far1 | 2 | 2 | (-1,-1) | (1,1) | BK1 | |||||

| FDS | 5 | 3 | (-2,…,-2) | (2,…,2) | FD2009 | |||||

| FF1 | 2 | 2 | (-1,-1) | (1,1) | BK1 | |||||

| Hil1 | 2 | 2 | (0,0) | (1,1) | Hil1 | |||||

| Imbalance1 | 2 | 2 | (-2,-2) | (2,2) | CTY2023 | |||||

| Imbalance2 | 2 | 2 | (-2,-2) | (2,2) | CTY2023 | |||||

| JOS1a | 50 | 2 | (-2,…,-2) | (2,…,2) | JO2001 | |||||

| JOS1b | 100 | 2 | (-2,…,-2) | (2,…,2) | JO2001 | |||||

| JOS1c | 100 | 2 | (-50,…,-50) | (50,…,50) | JO2001 | |||||

| JOS1d | 100 | 2 | (-100,…,-100) | (100,…,100) | JO2001 | |||||

| LE1 | 2 | 2 | (-5,-5) | (10,10) | BK1 | |||||

| PNR | 2 | 2 | (-2,-2) | (2,2) | PN2006 | |||||

| VU1 | 2 | 2 | (-3,-3) | (3,3) | BK1 | |||||

| WIT1 | 2 | 2 | (-2,-2) | (2,2) | W2012 | |||||

| WIT2 | 2 | 2 | (-2,-2) | (2,2) | W2012 | |||||

| WIT3 | 2 | 2 | (-2,-2) | (2,2) | W2012 | |||||

| WIT4 | 2 | 2 | (-2,-2) | (2,2) | W2012 | |||||

| WIT5 | 2 | 2 | (-2,-2) | (2,2) | W2012 | |||||

| WIT6 | 2 | 2 | (-2,-2) | (2,2) | W2012 |

| Problem | BBPGMO | PGMO | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| ite | feval | time () | stepsize | ite | feval | time () | stepsize | |||

| BK1 | 1.00 | 1.00 | 1.41 | 1.00 | 3.16 | 4.15 | 7.11 | 0.84 | ||

| DD1 | 4.54 | 4.91 | 34.30 | 0.98 | 41.20 | 70.54 | 153.36 | 0.73 | ||

| Deb | 6.96 | 10.93 | 33.20 | 0.68 | 27.97 | 255.00 | 94.92 | 0.12 | ||

| Far1 | 6.77 | 7.87 | 11.25 | 0.94 | 6.07 | 21.14 | 19.30 | 0.33 | ||

| FDS | 3.44 | 3.81 | 24.22 | 0.93 | 181.48 | 782.81 | 1206.17 | 0.25 | ||

| FF1 | 2.24 | 2.40 | 2.58 | 0.97 | 3.43 | 3.58 | 2.34 | 0.99 | ||

| Hil1 | 8.41 | 9.21 | 14.22 | 0.65 | 10.68 | 20.59 | 28.44 | 0.33 | ||

| Imbalance1 | 2.44 | 3.11 | 32.58 | 0.92 | 2.92 | 5.64 | 55.55 | 0.70 | ||

| Imbalance2 | 1.00 | 1.00 | 1.88 | 1.00 | 83.92 | 593.11 | 1465.16 | 0.03 | ||

| JOS1a | 1.00 | 1.00 | 1.80 | 1.00 | 151.08 | 198.97 | 25.23 | 0.97 | ||

| JOS1b | 1.00 | 1.00 | 2.81 | 1.00 | 265.82 | 289.11 | 43.59 | 0.99 | ||

| JOS1c | 1.00 | 1.00 | 1.72 | 1.00 | 385.68 | 387.23 | 33.91 | 1.00 | ||

| JOS1d | 1.00 | 1.00 | 1.56 | 1.00 | 406.49 | 409.25 | 41.72 | 1.00 | ||

| LE1 | 5.46 | 6.27 | 6.17 | 0.71 | 12.16 | 16.72 | 9.38 | 0.70 | ||

| PNR | 3.31 | 3.72 | 8.05 | 0.95 | 10.07 | 39.91 | 34.61 | 0.18 | ||

| VU1 | 2.08 | 2.15 | 2.66 | 0.98 | 12.90 | 12.97 | 2.03 | 0.99 | ||

| WIT1 | 2.95 | 3.26 | 7.27 | 0.96 | 27.64 | 145.06 | 115.55 | 0.12 | ||

| WIT2 | 3.16 | 3.37 | 9.06 | 0.97 | 48.10 | 286.32 | 178.05 | 0.06 | ||

| WIT3 | 3.94 | 4.26 | 16.64 | 0.97 | 18.61 | 79.91 | 77.42 | 0.15 | ||

| WIT4 | 4.01 | 4.17 | 16.09 | 0.98 | 6.51 | 19.26 | 25.08 | 0.30 | ||

| WIT5 | 3.21 | 3.46 | 12.19 | 0.98 | 5.13 | 12.38 | 22.11 | 0.41 | ||

| WIT6 | 1.00 | 1.00 | 3.67 | 1.00 | 1.87 | 2.87 | 6.72 | 0.73 | ||

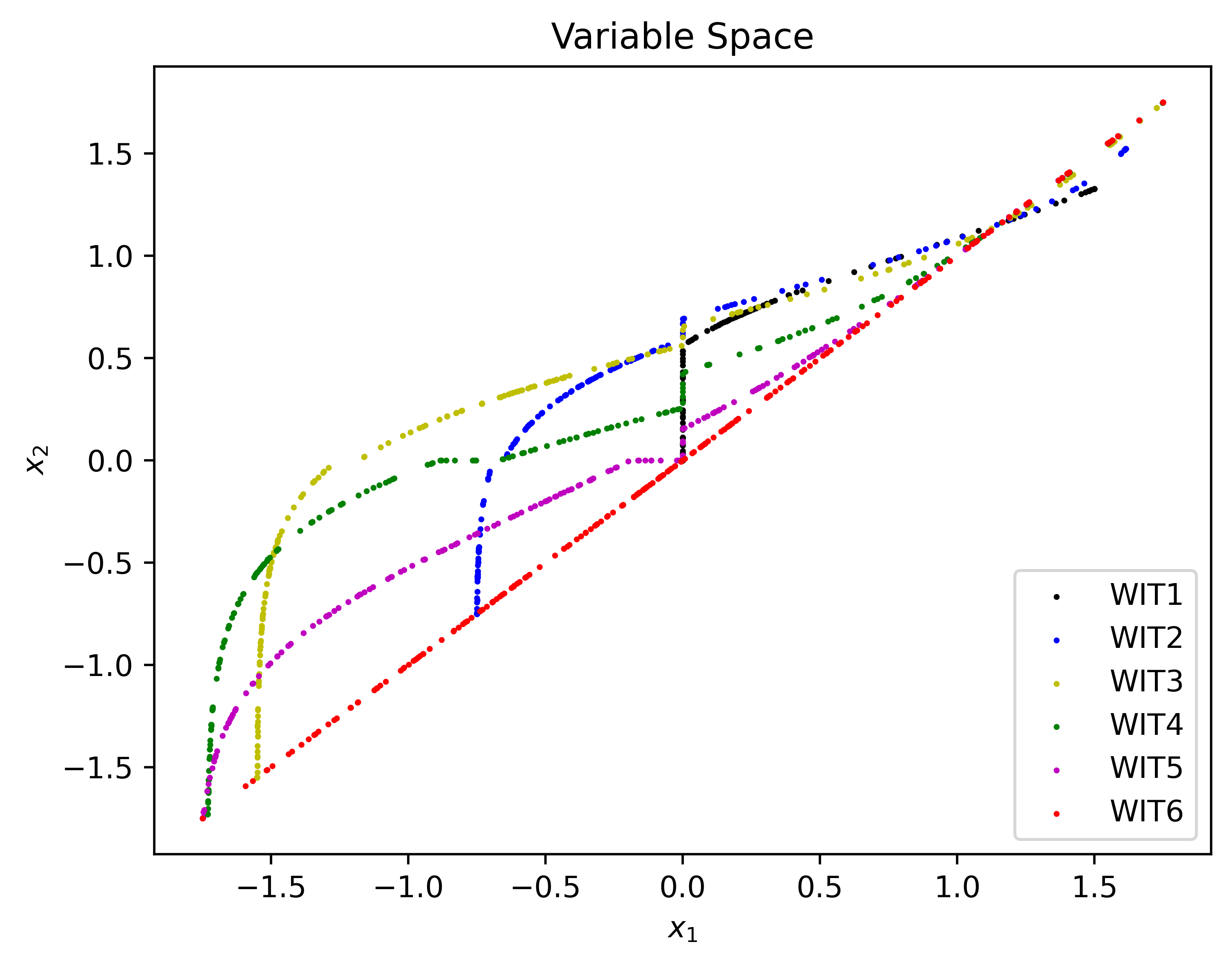

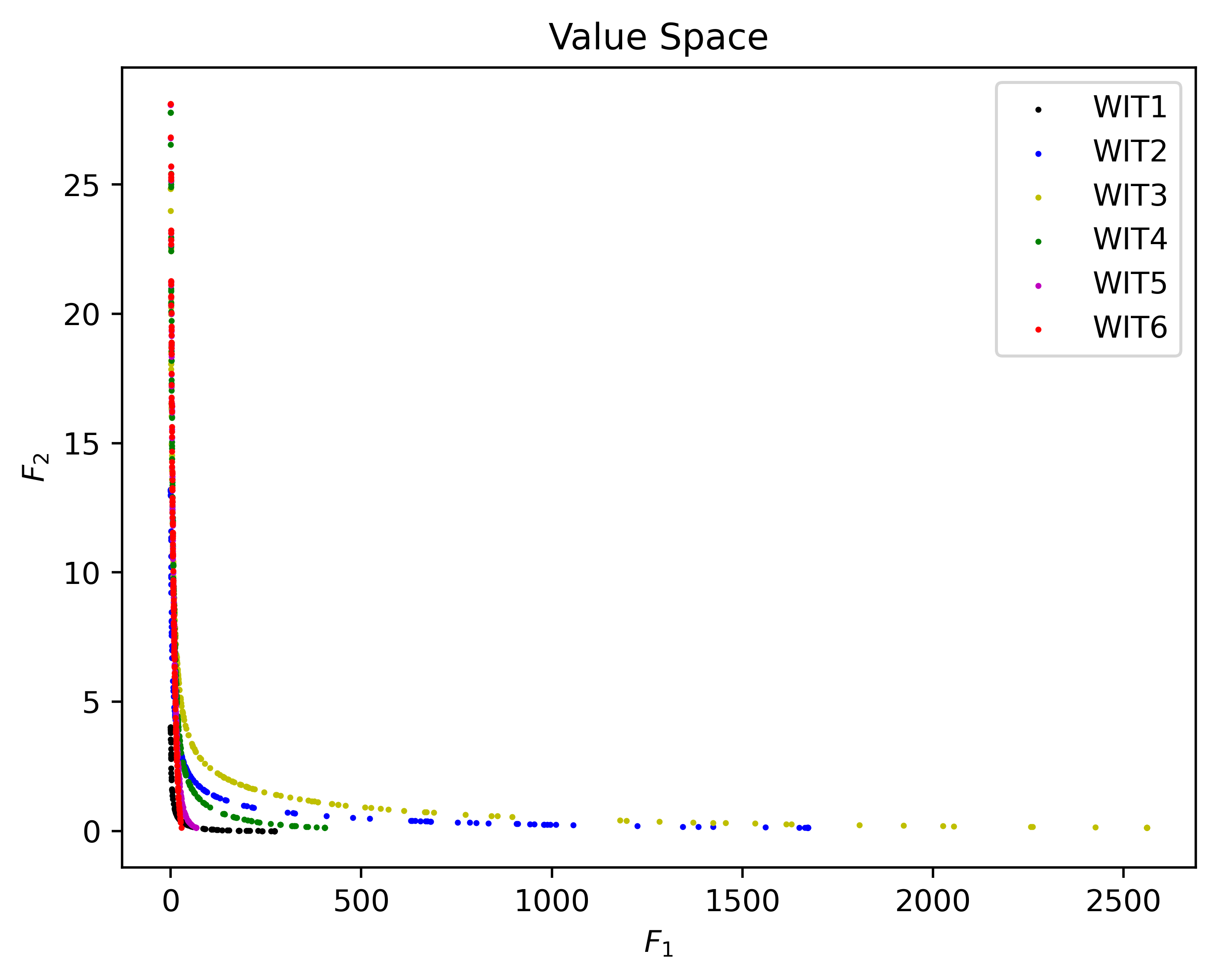

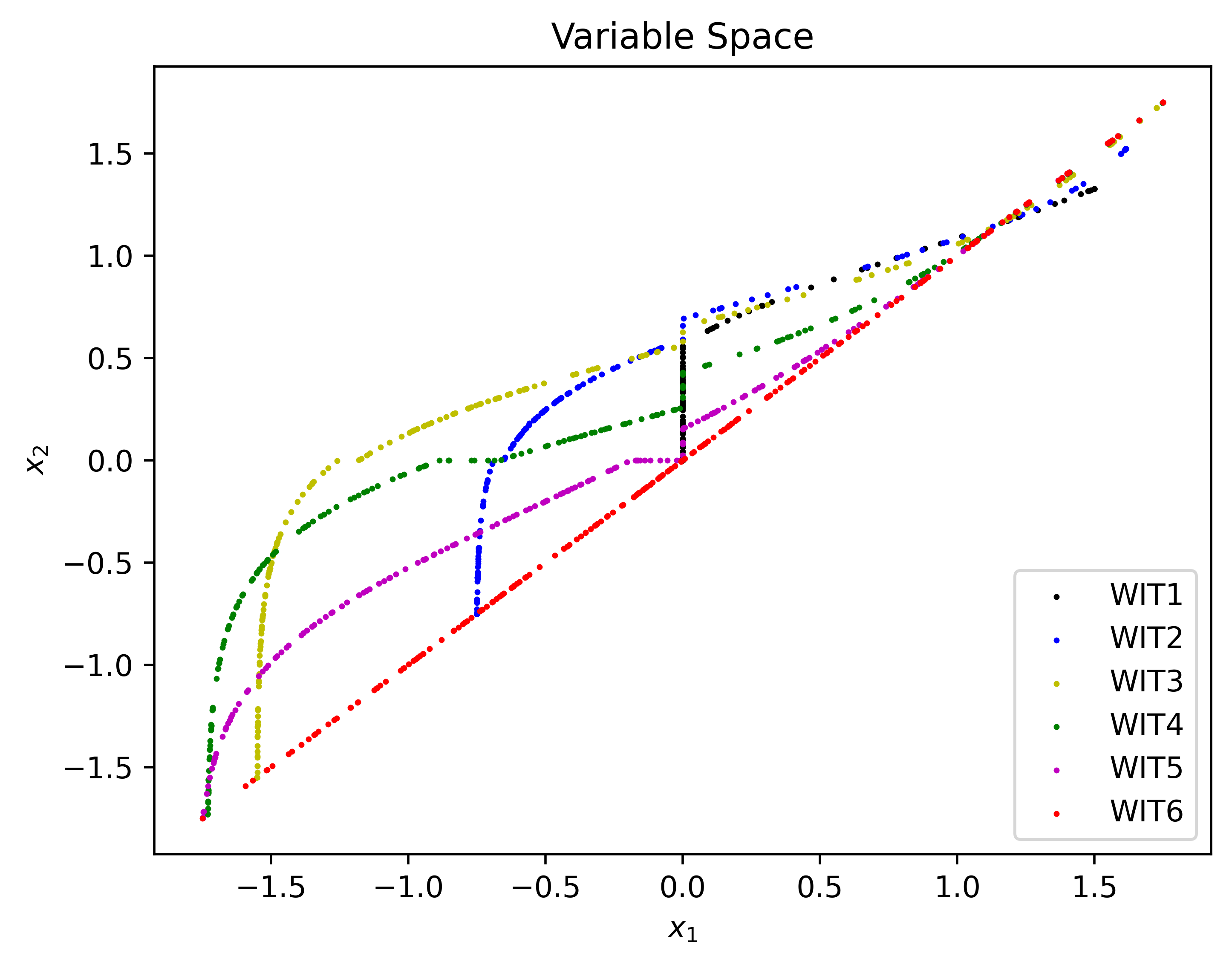

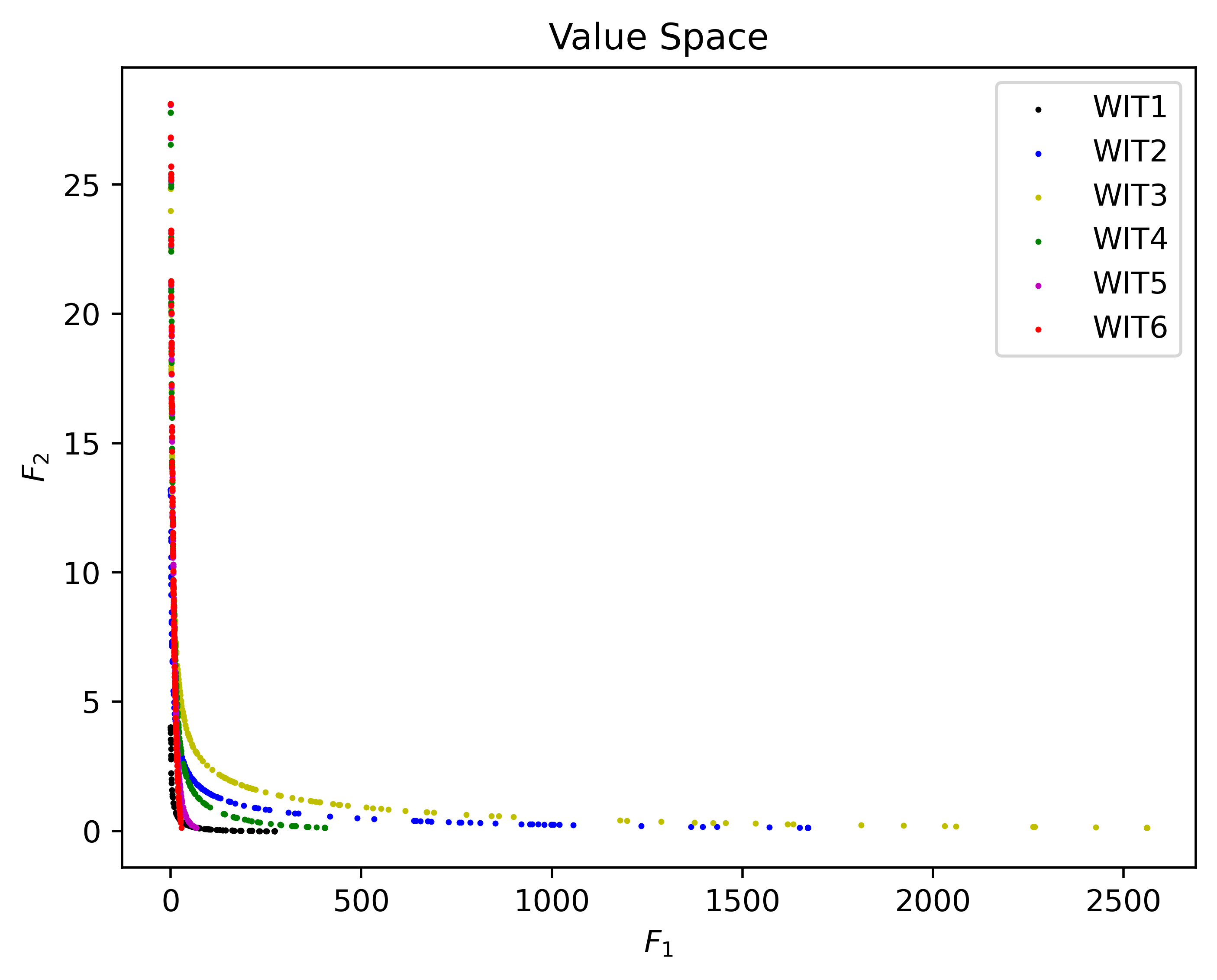

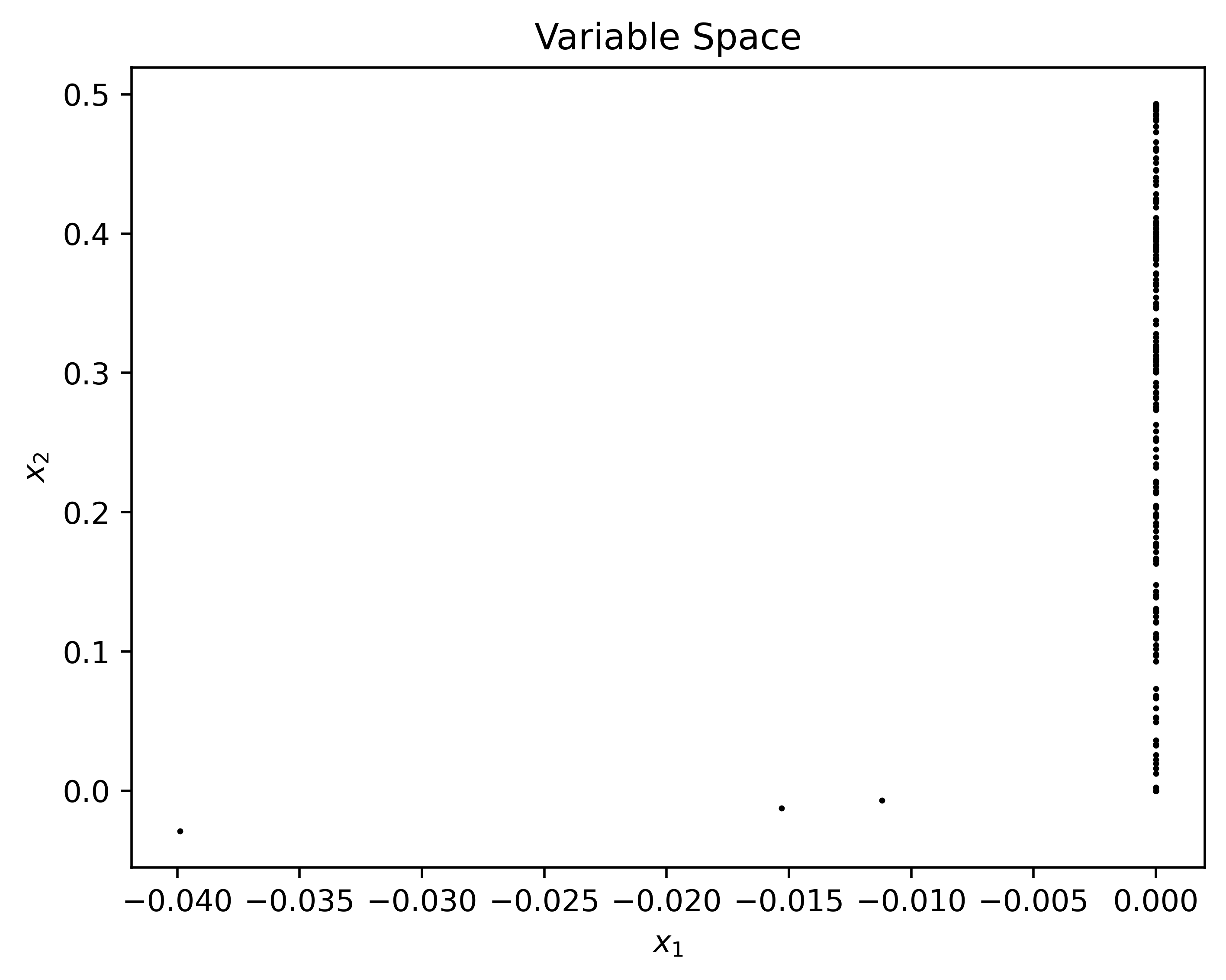

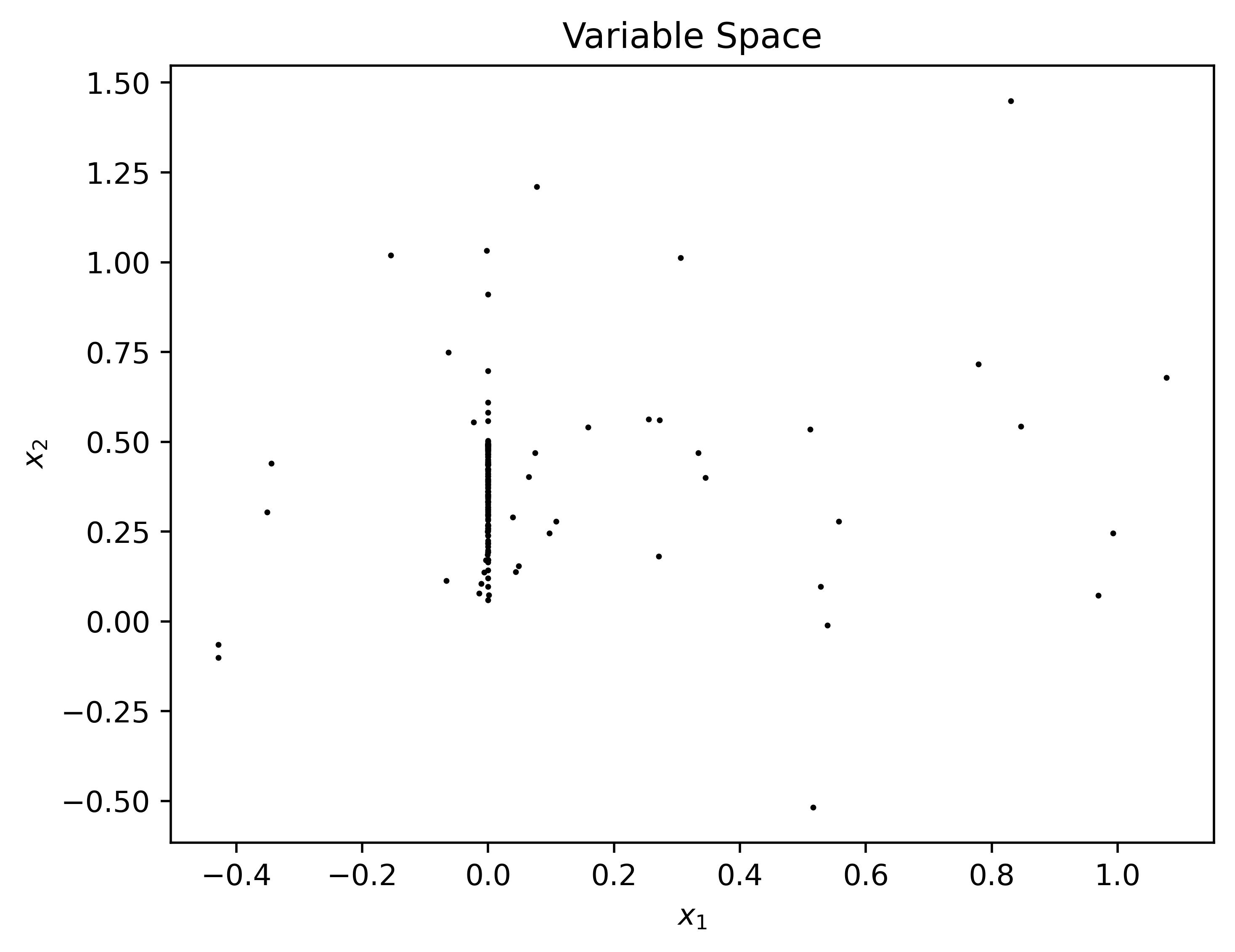

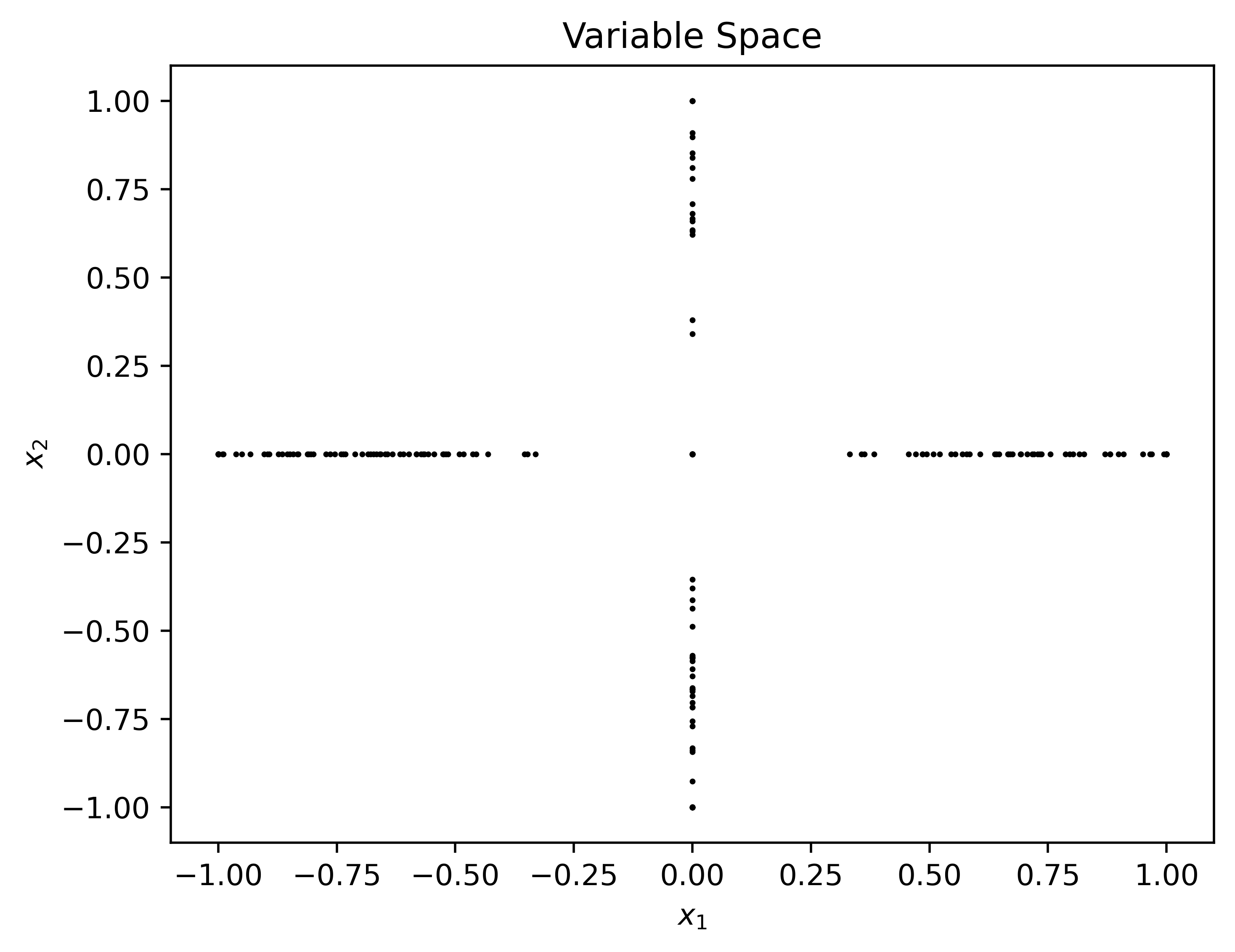

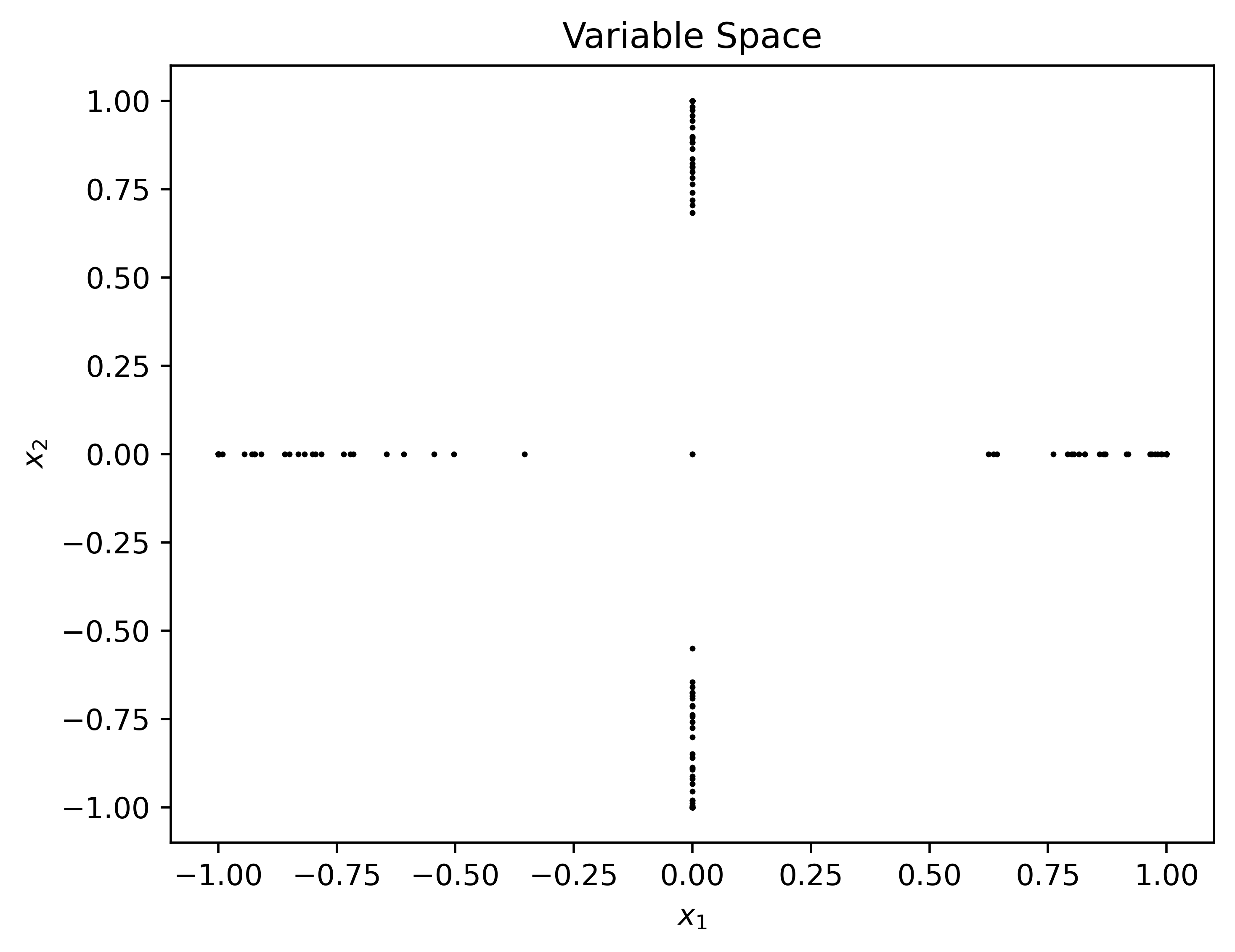

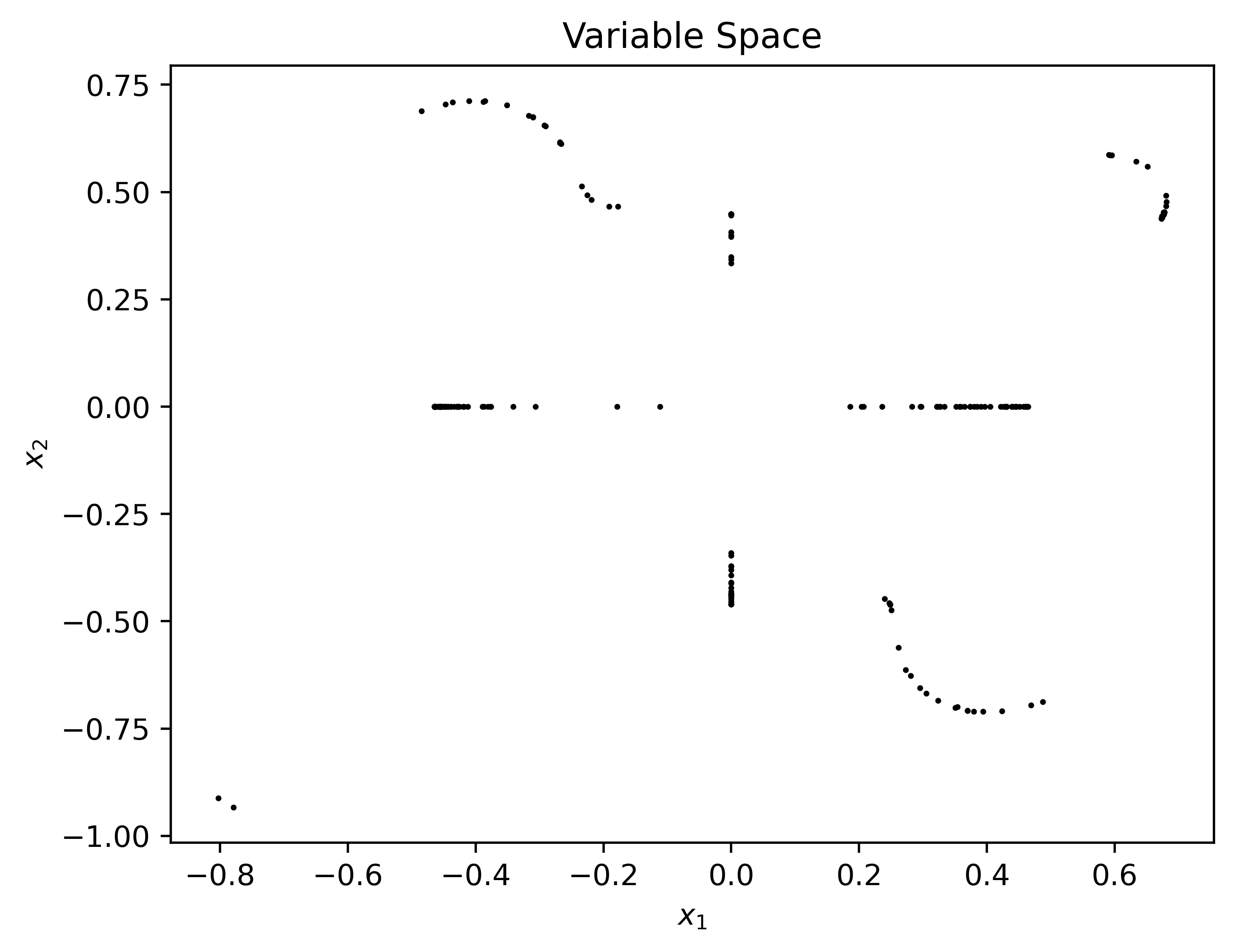

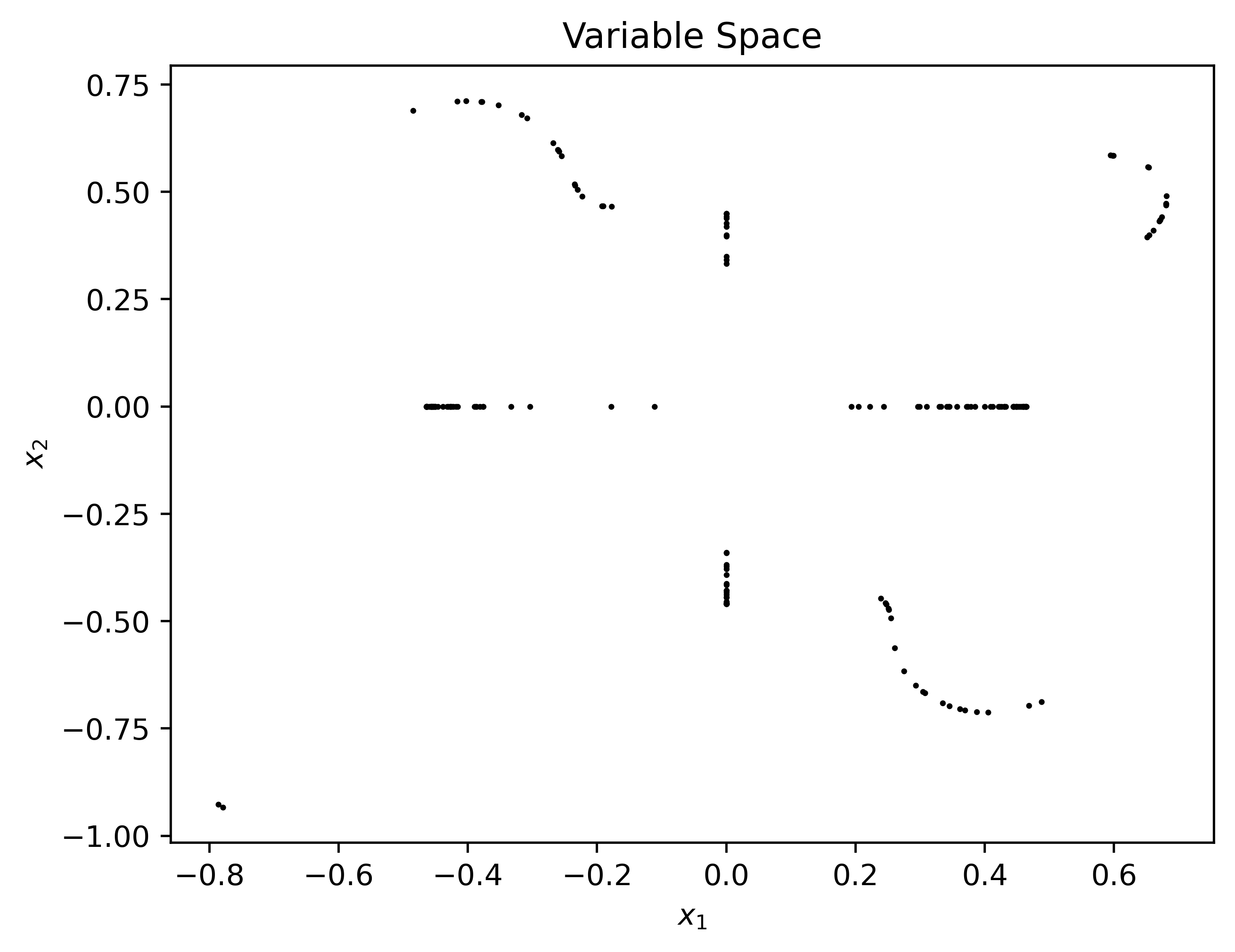

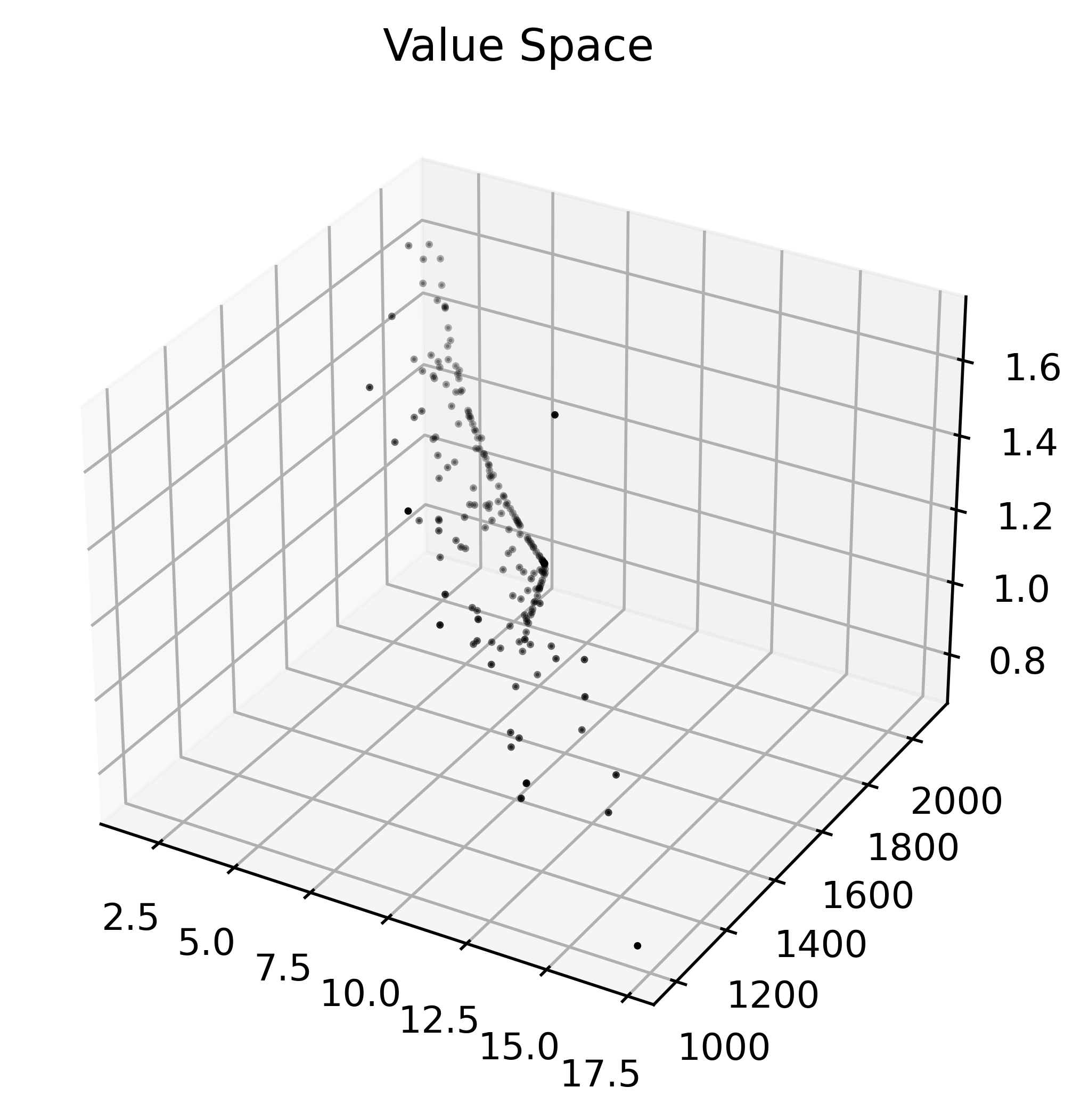

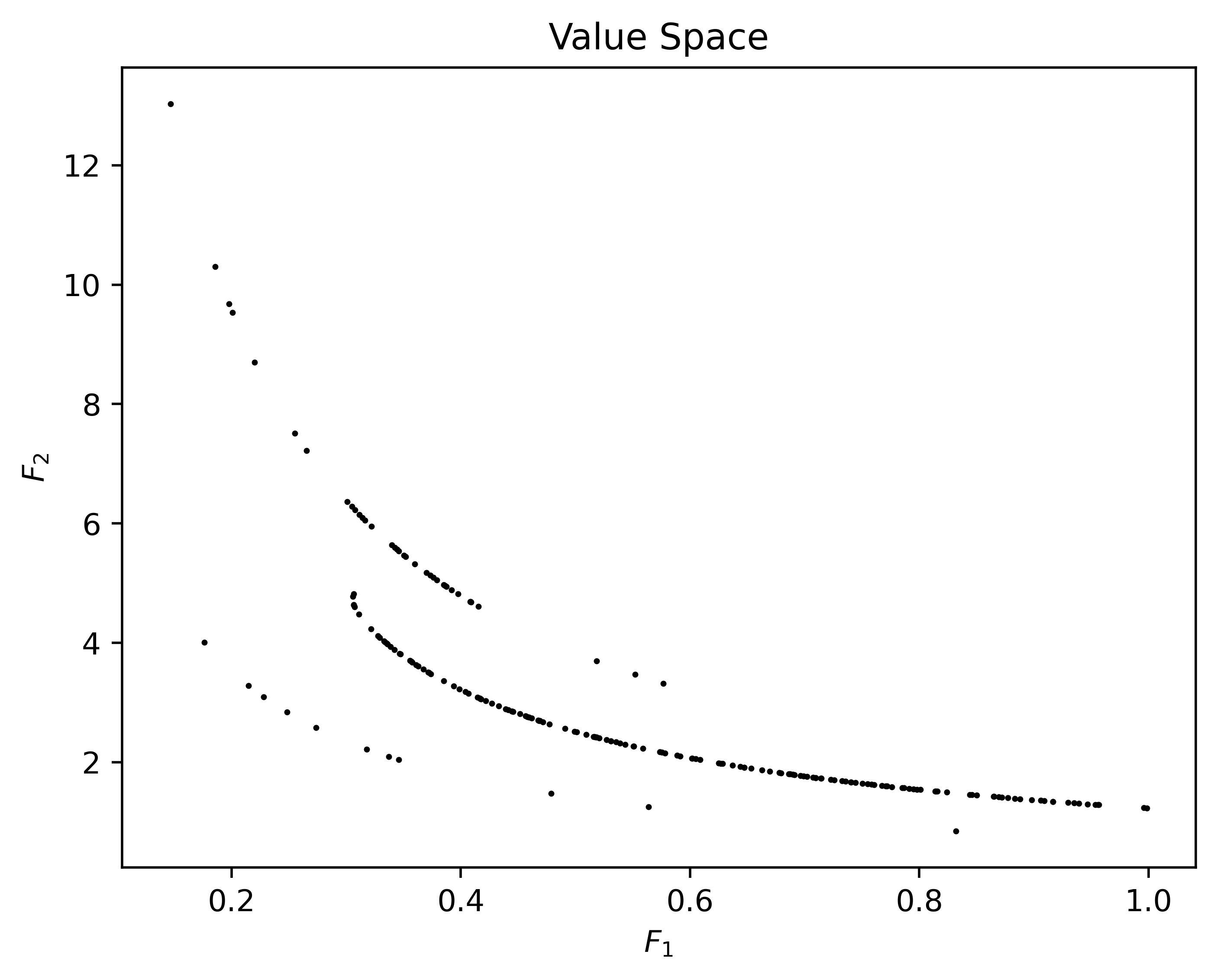

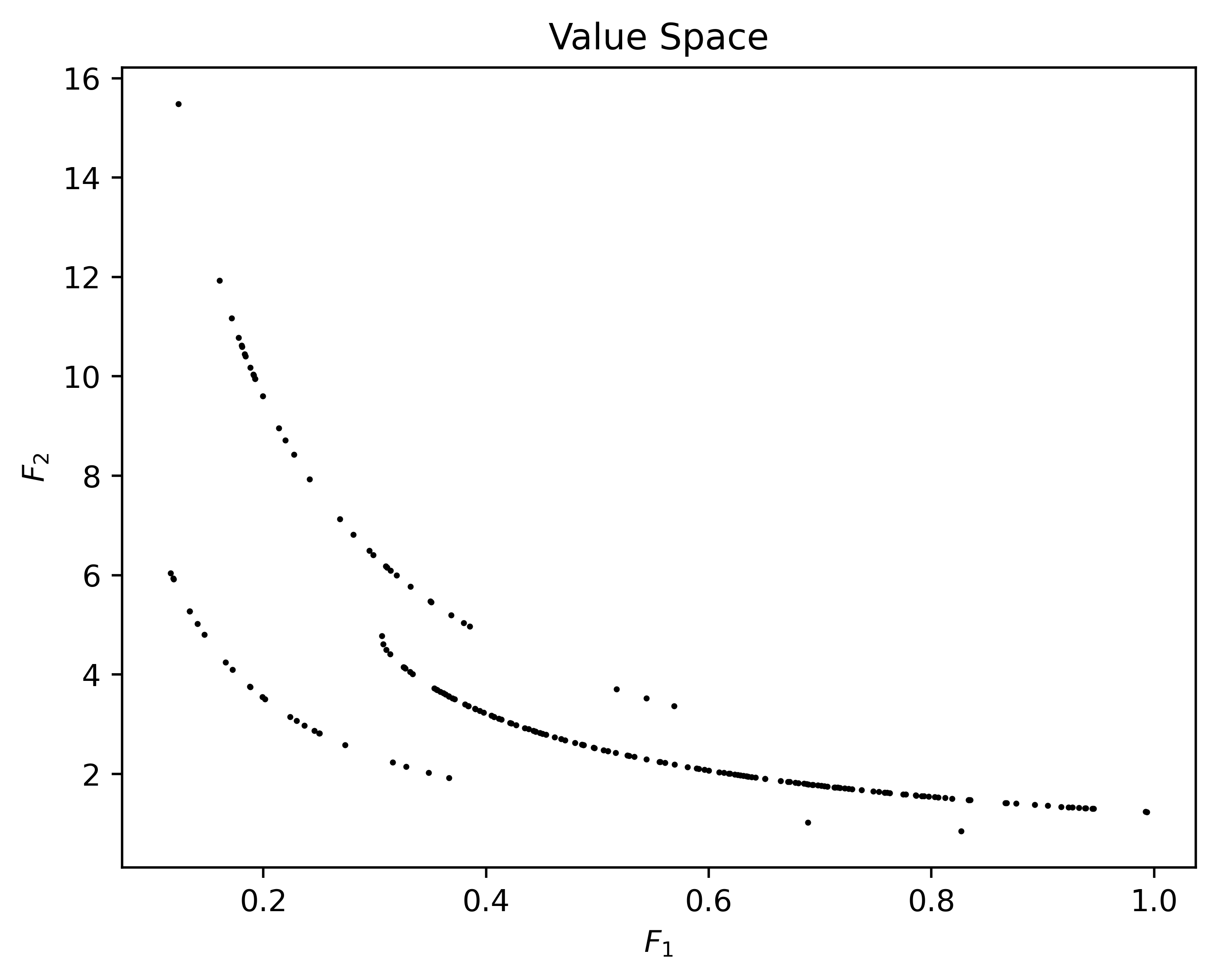

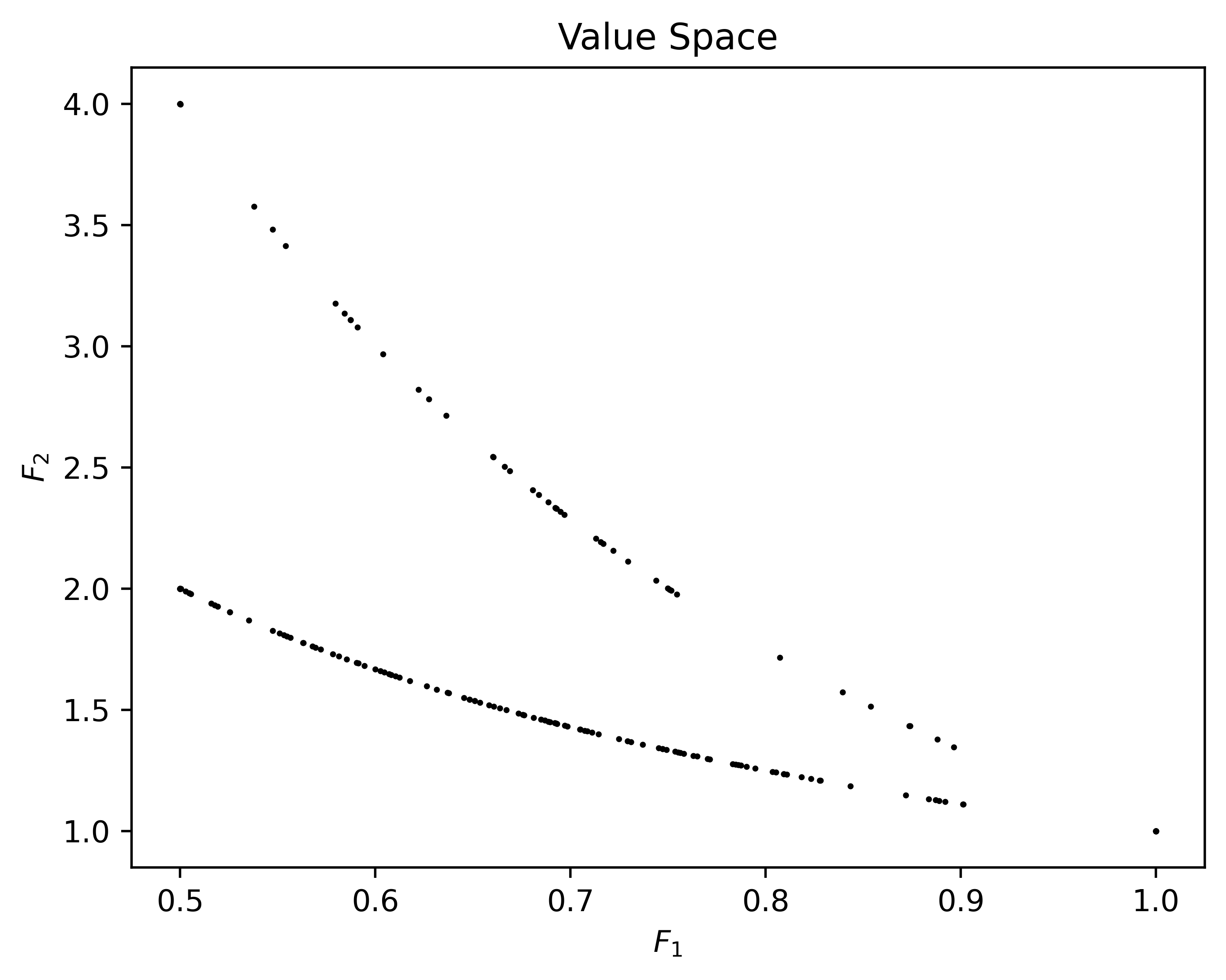

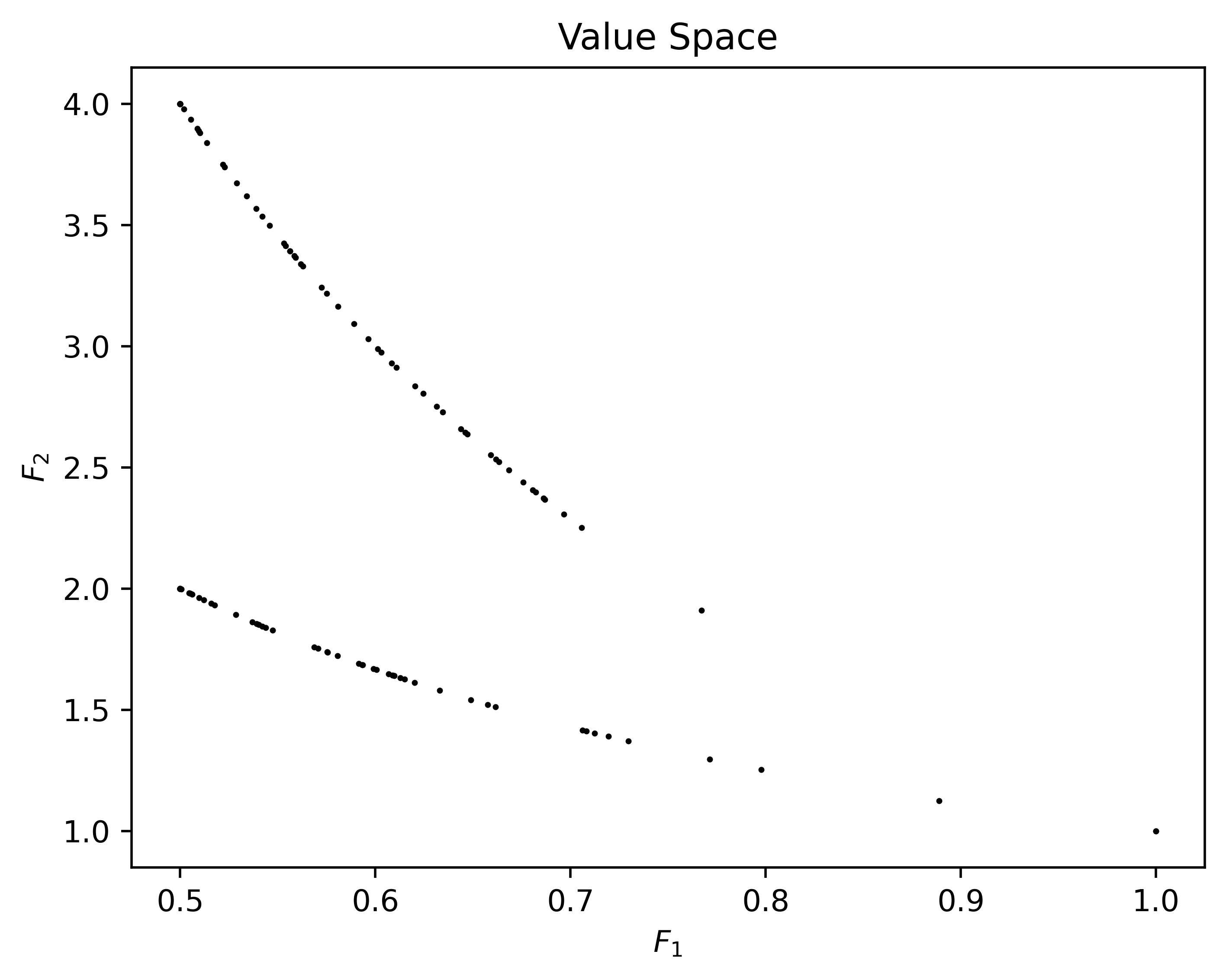

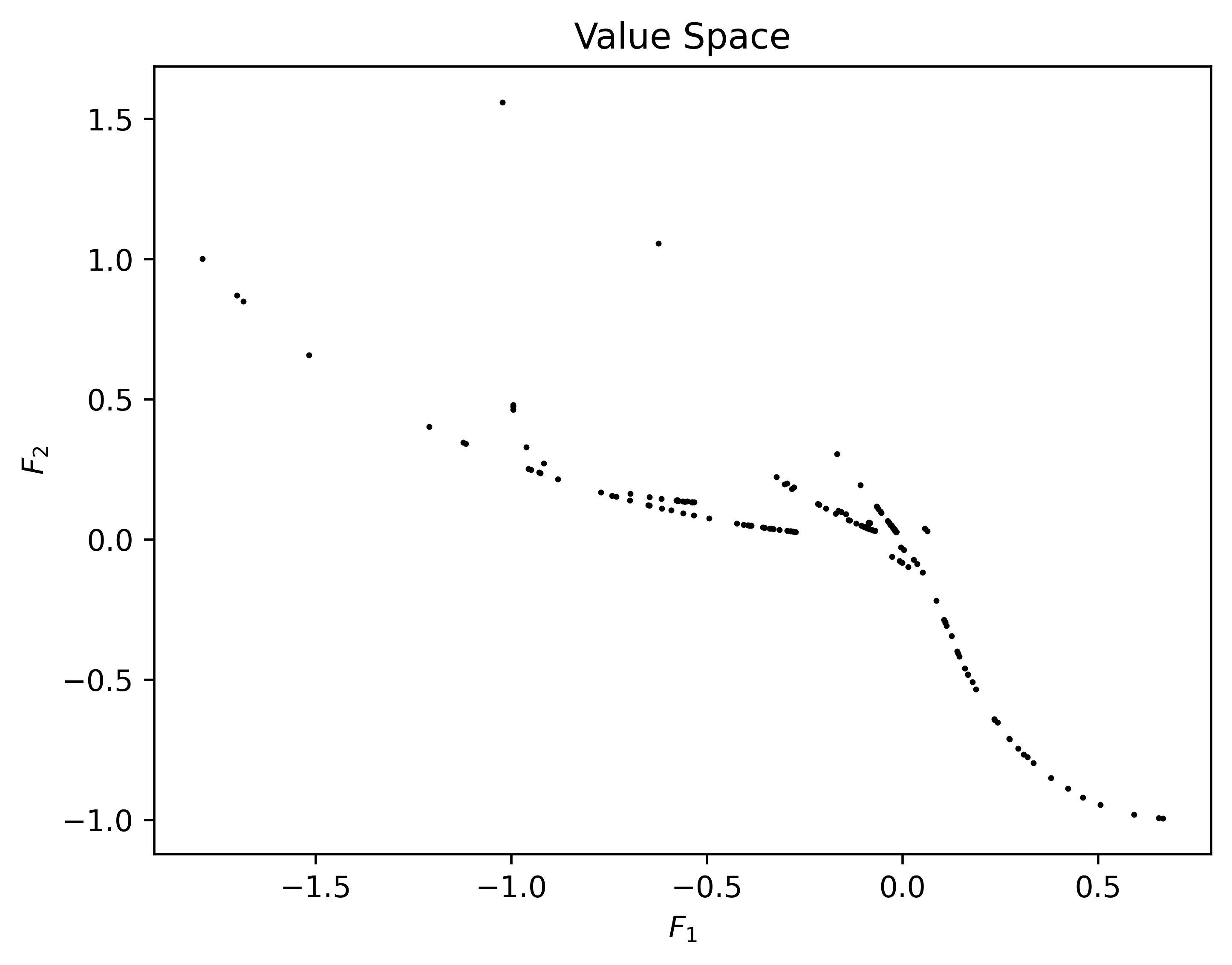

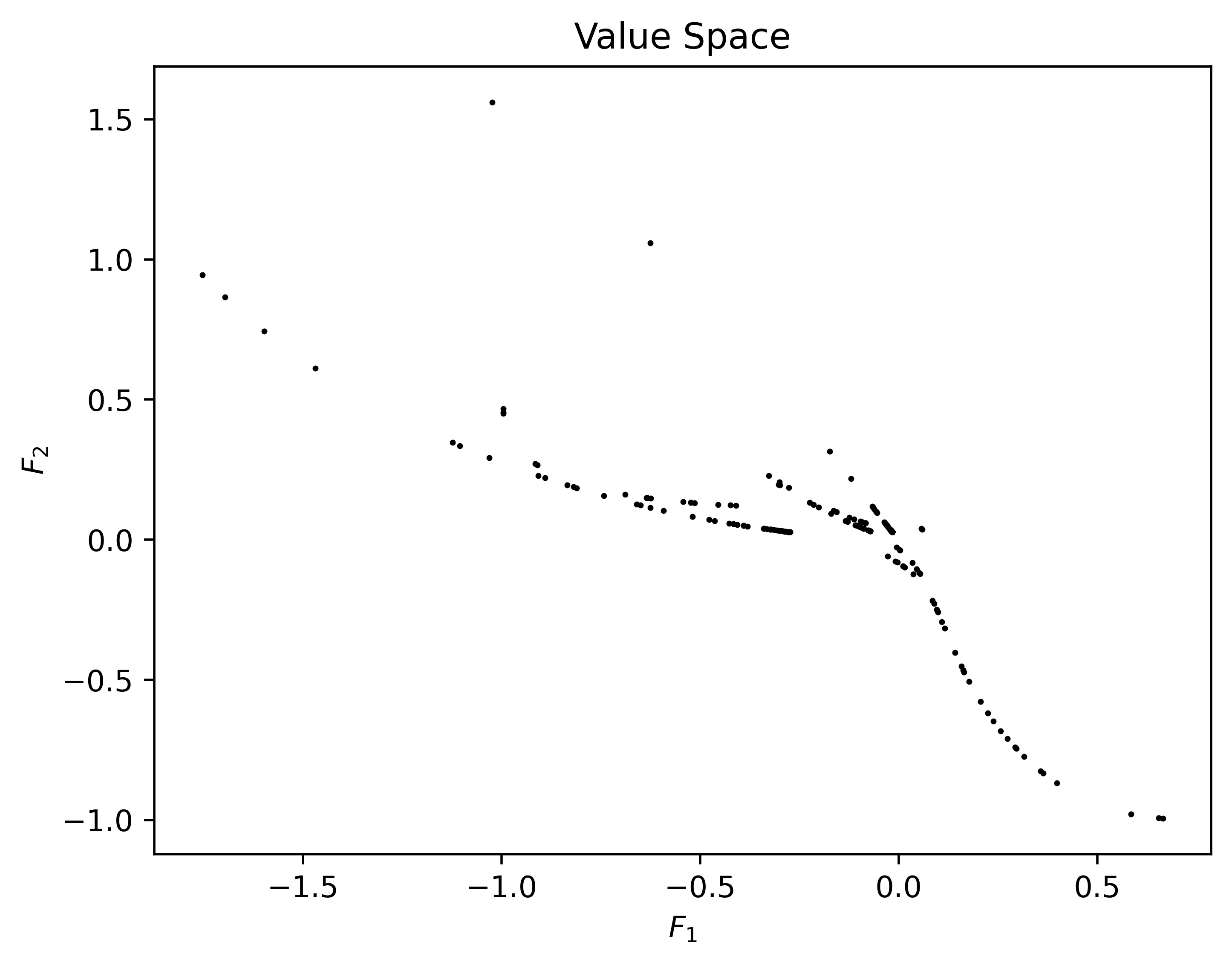

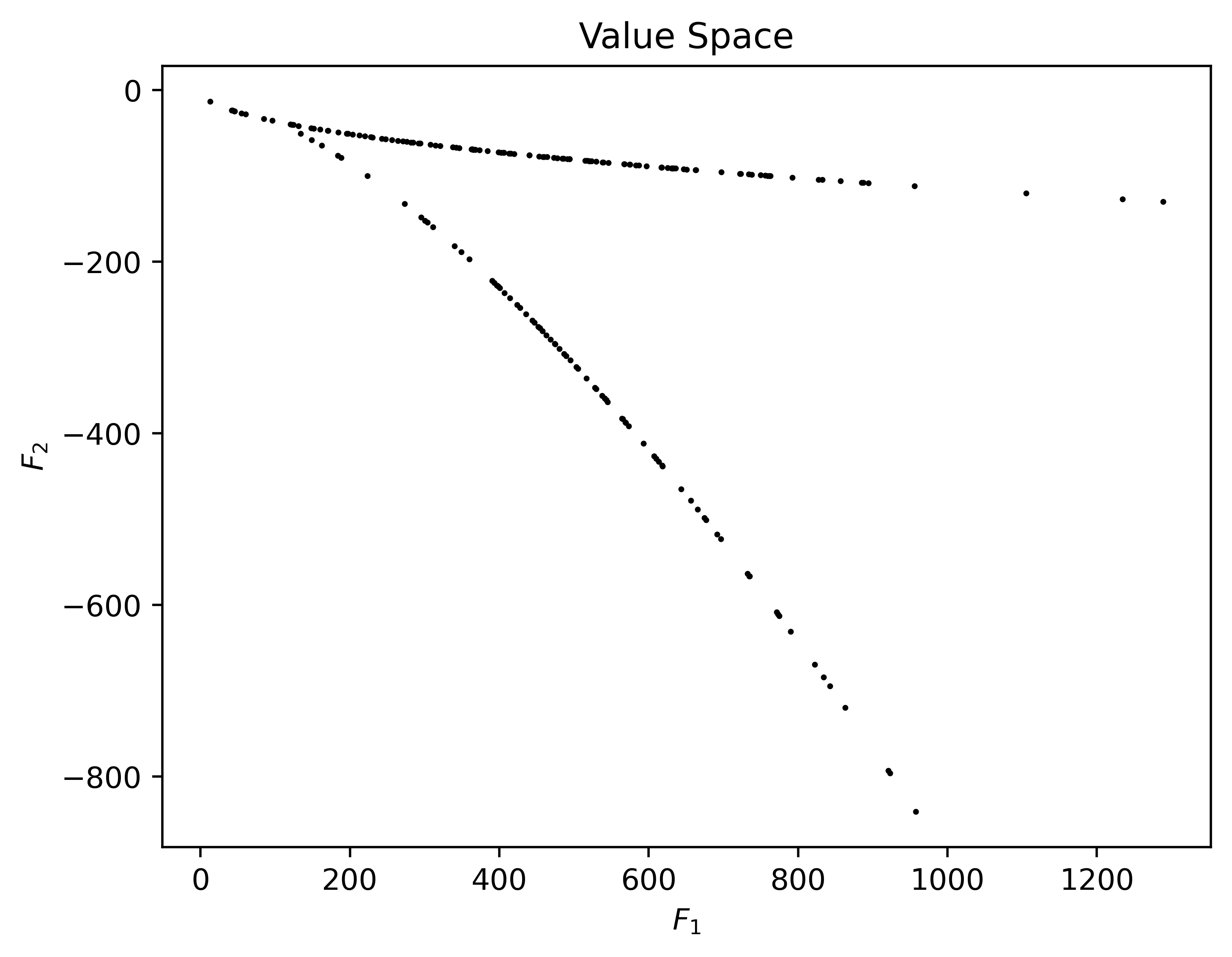

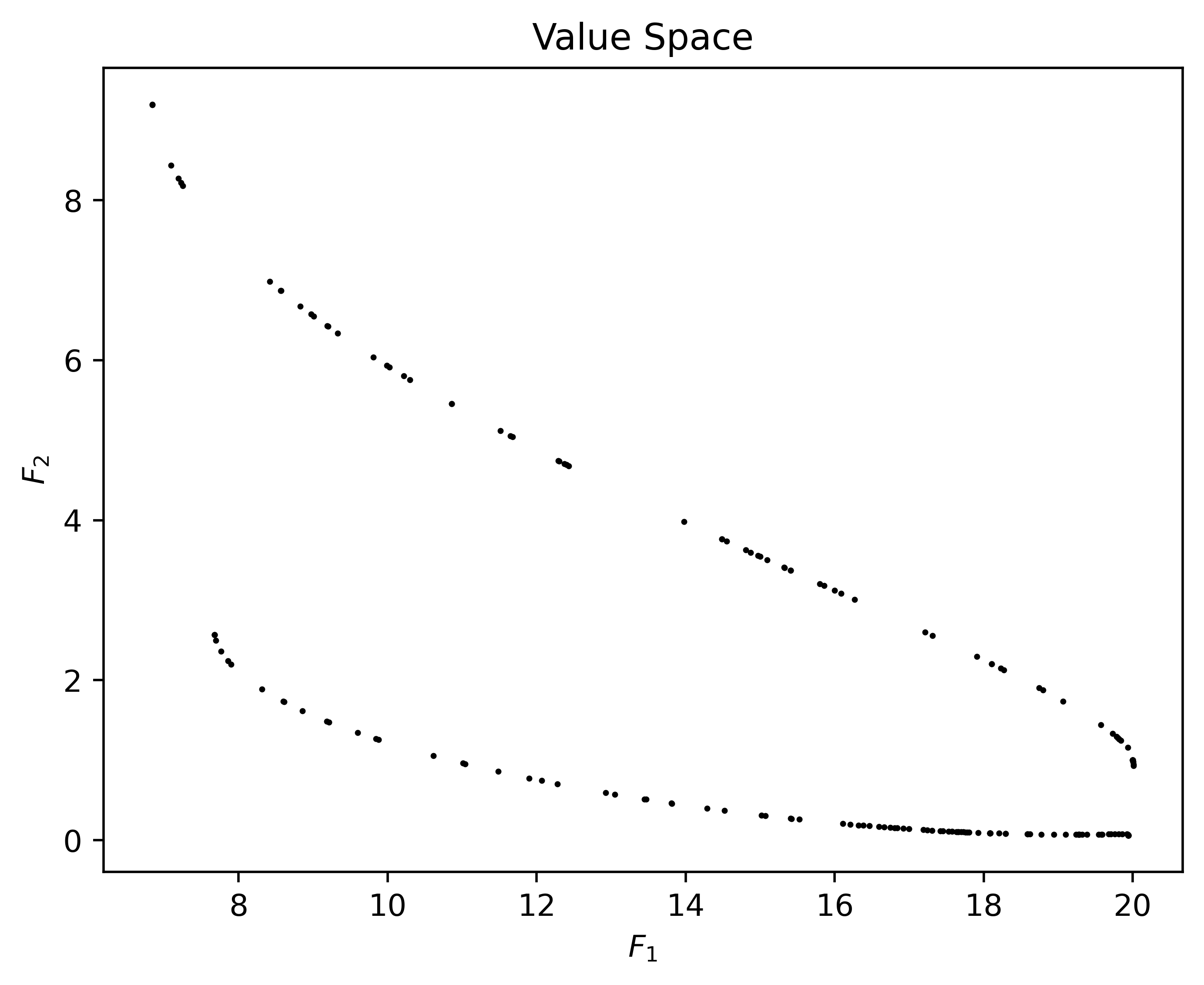

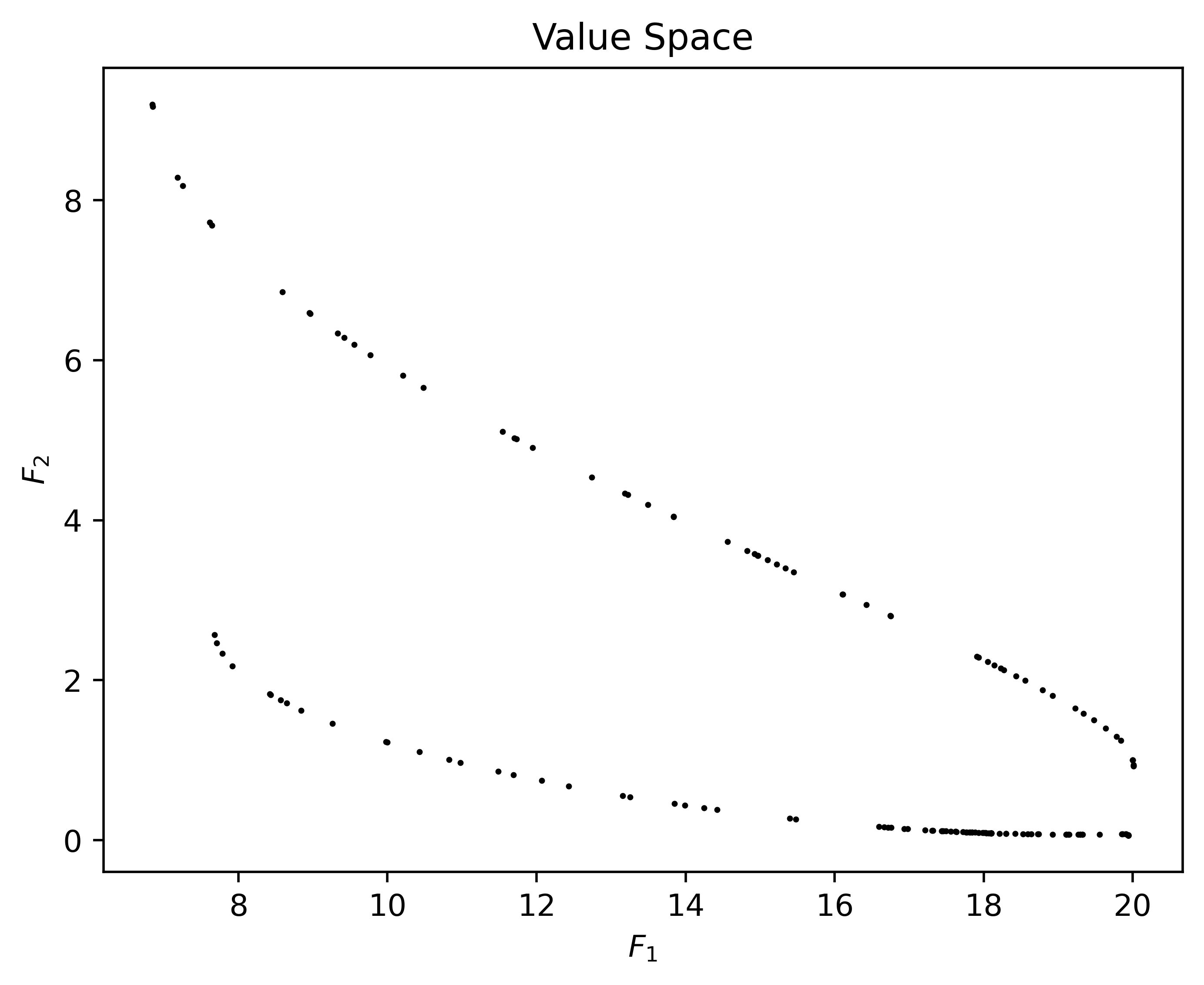

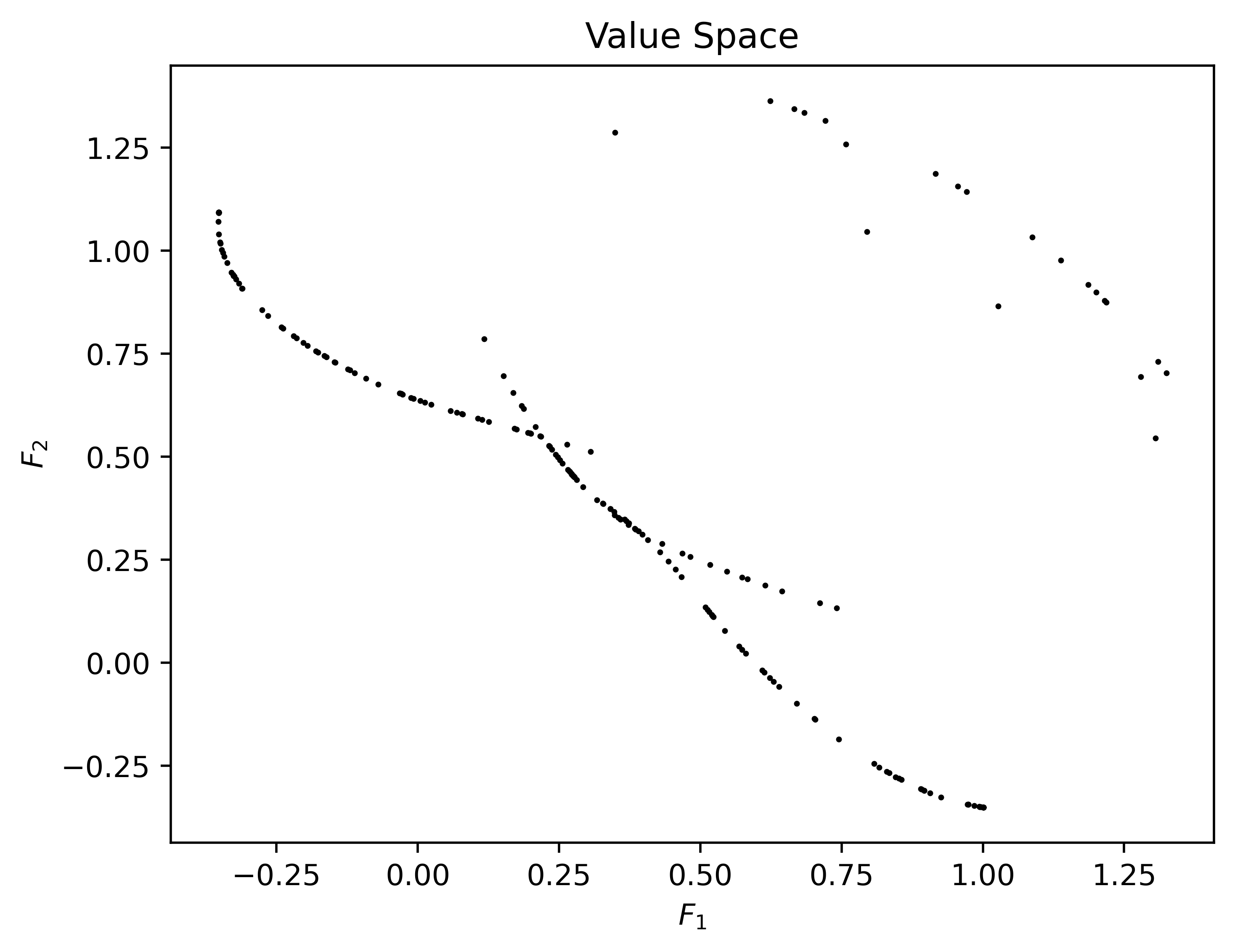

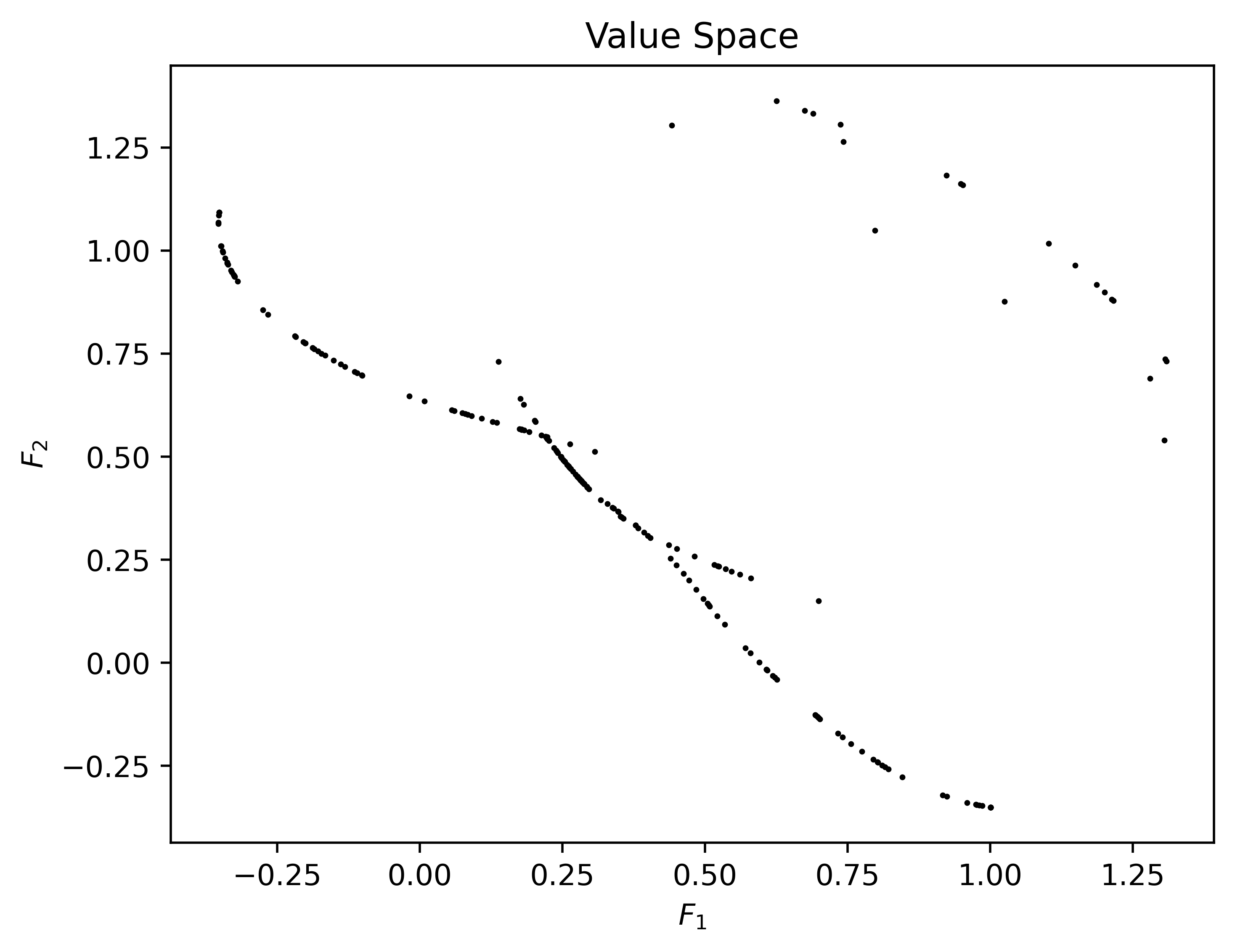

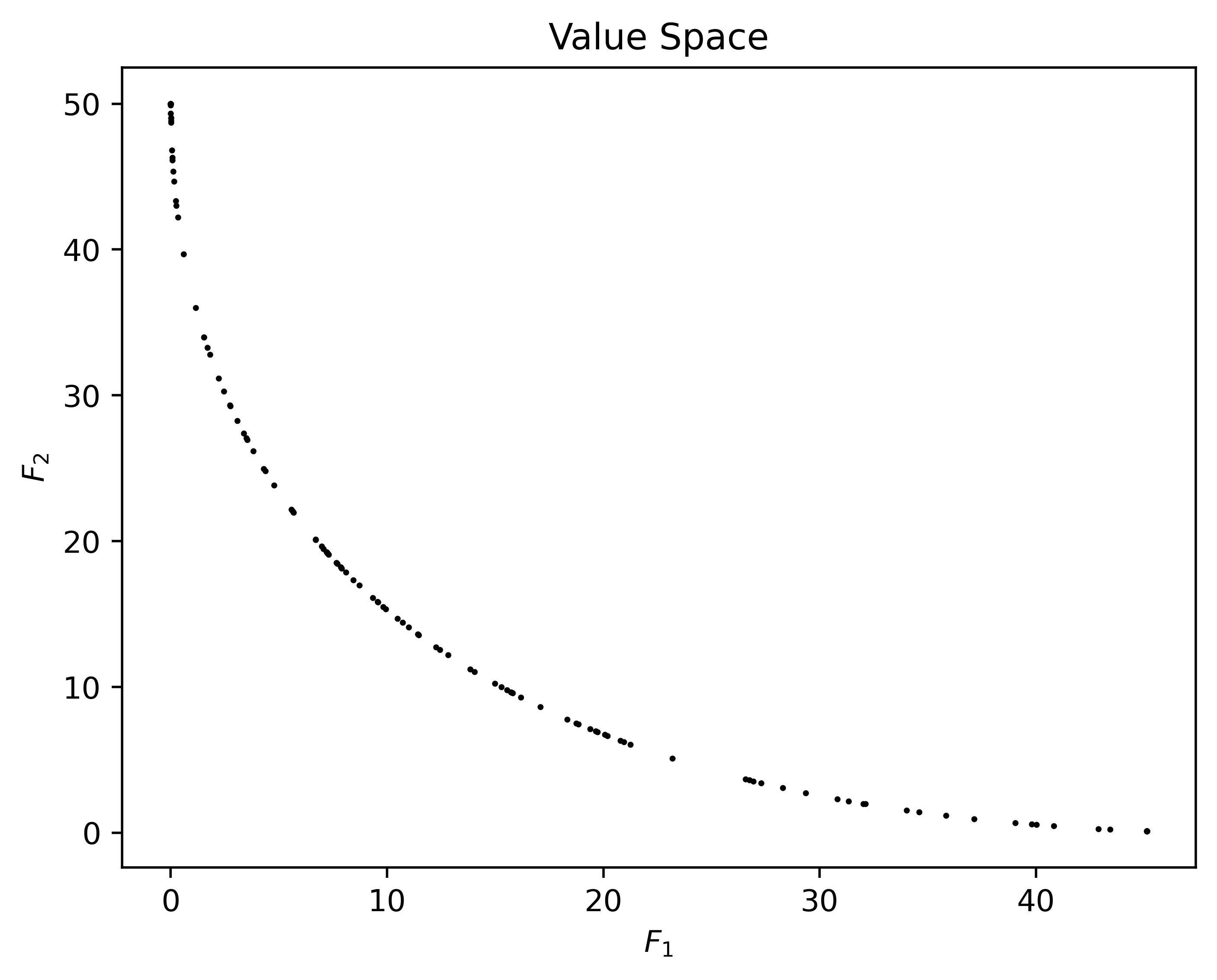

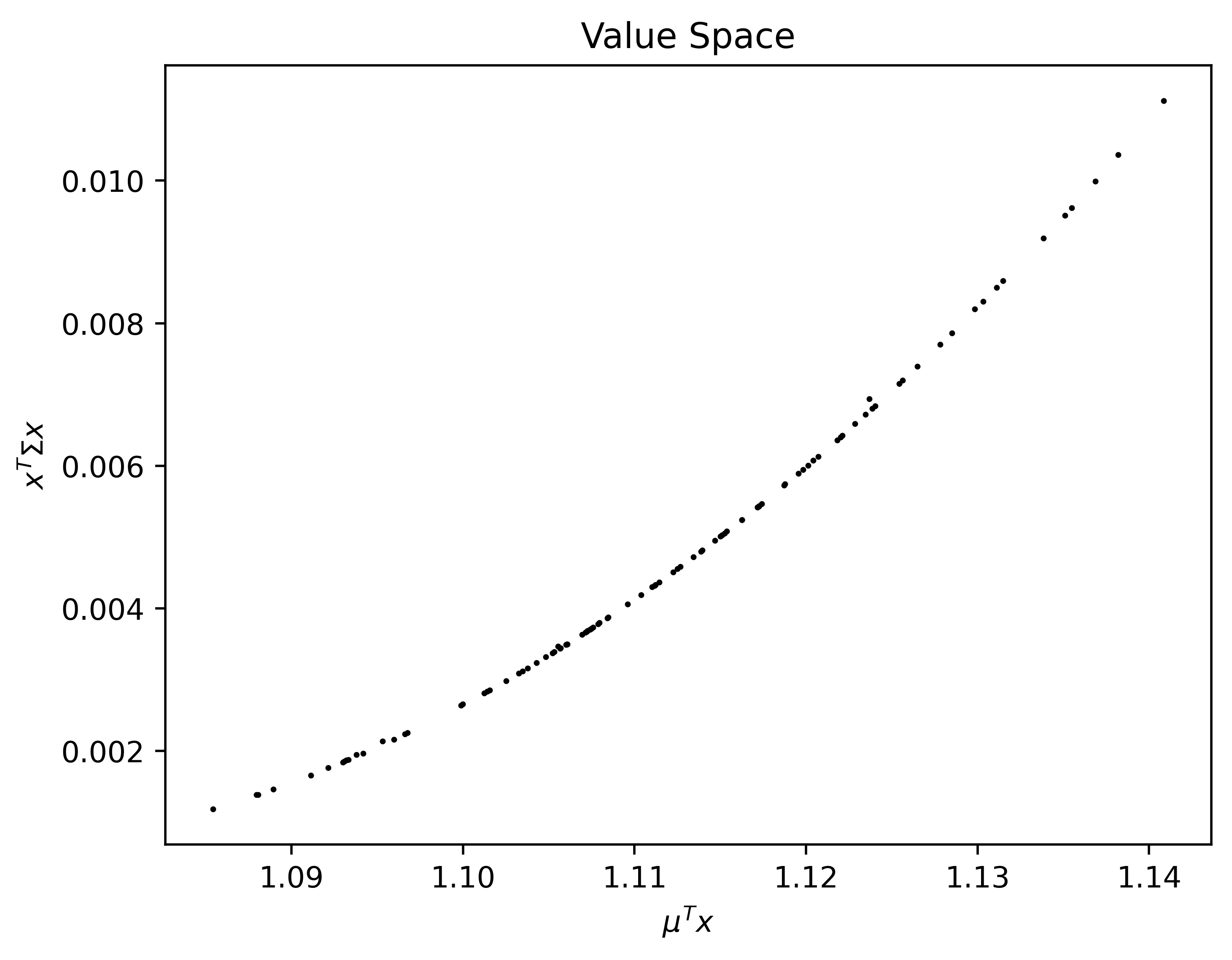

The obtained Pareto sets and Pareto fronts for some test problems are depicted in Figures 1-4. Notably, Figure 2 illustrates that the solutions for problems FDS, Deb, VU1, and Far1 exhibit sparsity, validating the sparsity of the objective functions. This sparsity property holds significant importance in various applications such as machine learning, image restoration, and signal processing.

Table 3 provides the average number of iterations (iter), average number of function evaluations (feval), average CPU time (time ()), and average stepsize (stepsize) for each tested algorithm across the different problems. The numerical results confirm that BBPGMO outperforms PGMO in terms of average iterations, average function evaluations, and average CPU time. The average stepsize of BBPGMO is robust and falls within the range of for different problems, whereas the stepsize for PGMO exhibits significant variation. Furthermore, PGMO exhibits poor performance on problems DD1, Deb, FDS, imbalance2, JOS1a-d, and WIT1-2, which feature imbalanced and high-dimensional objective functions. Based on the performance of BBPGMO on these problems, we conclude that it is well-suited for addressing such challenges.

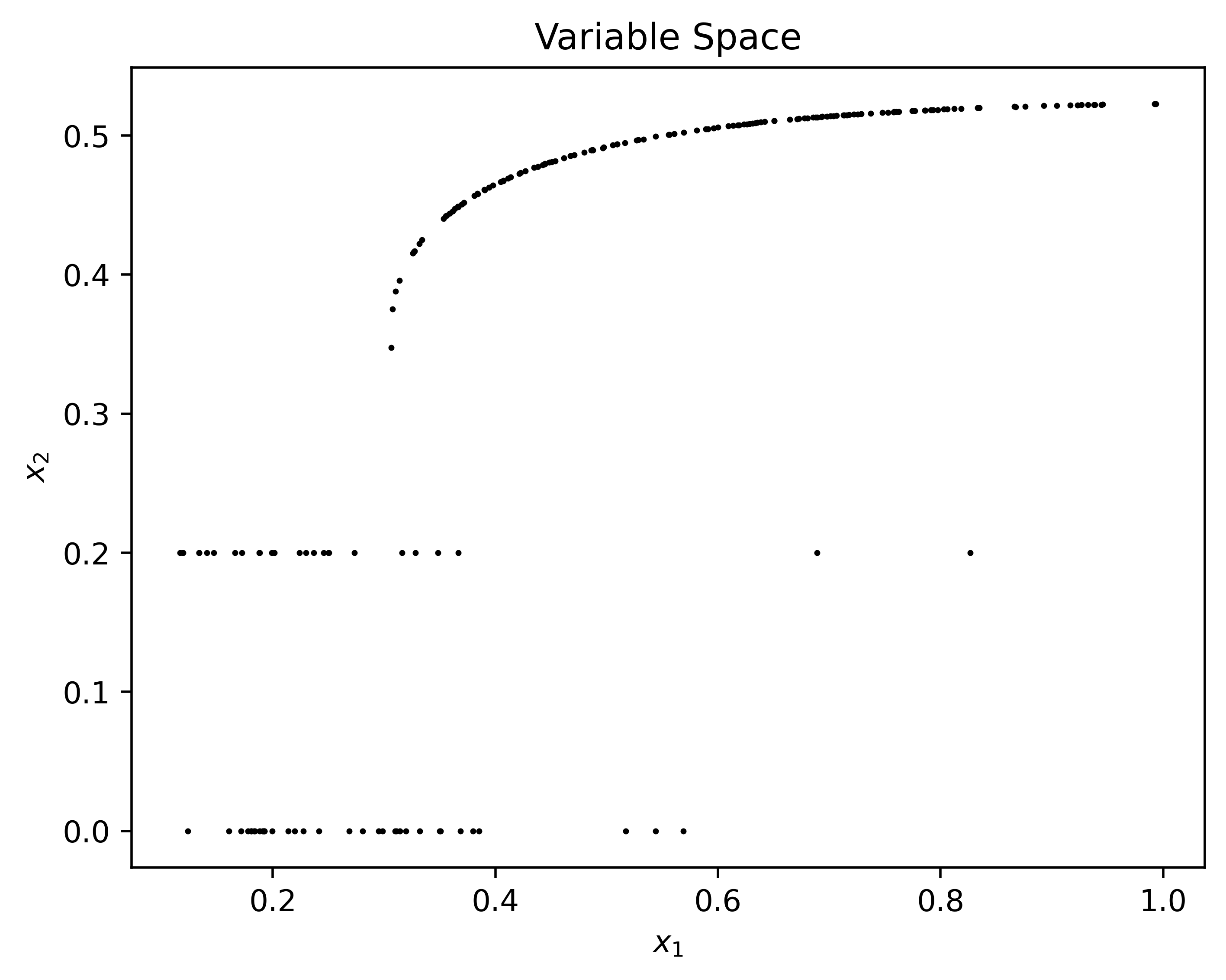

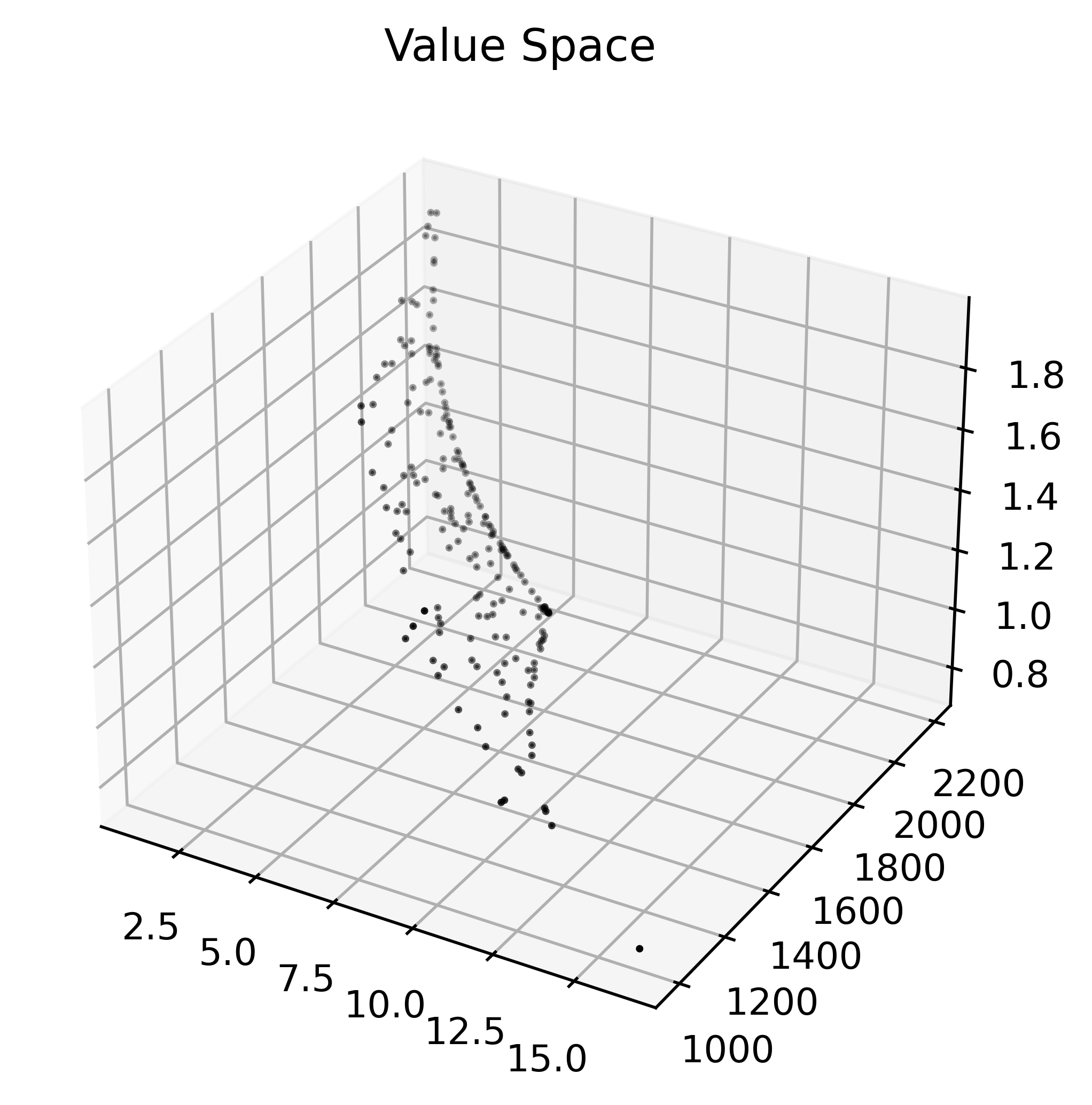

6.3 Application to Markowitz Portfolio Selection

In this subsection, we consider the Markowitz portfolio selection problem M1952 . Suppose there are securities, the expected returns and variance of returns are known. The - rule of Markowitz portfolio selection suggests investor selects one of efficient portfolios, which is a Pareto solution of the following bi-objective optimization problem:

As a specific example, the expected returns and variance of returns are estimated from real data on eight types of securities. The data can be found at

https://vanderbei.princeton.edu/ampl/nlmodels/markowitz/ and we use the data between the years and to estimate and which are given as follow:

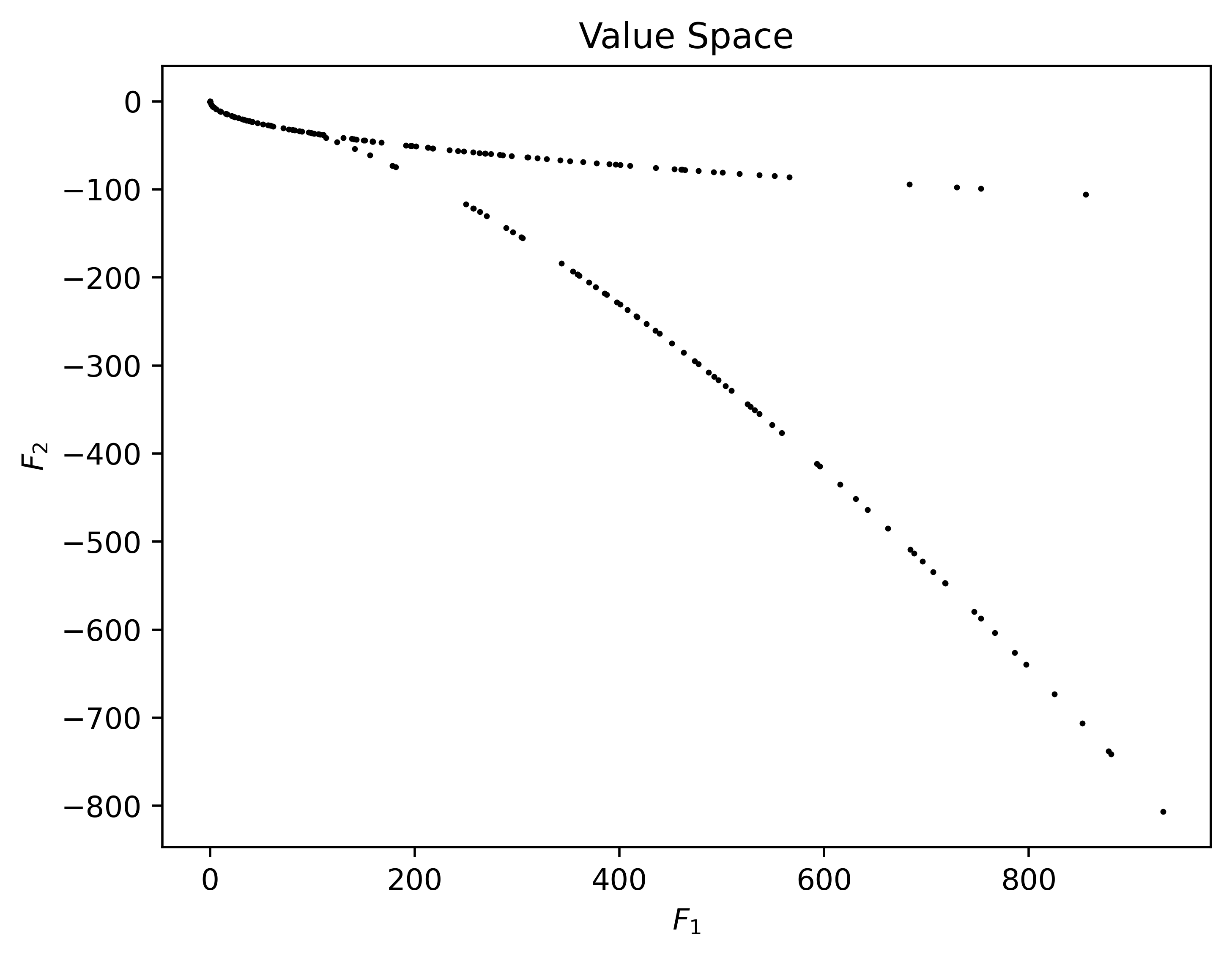

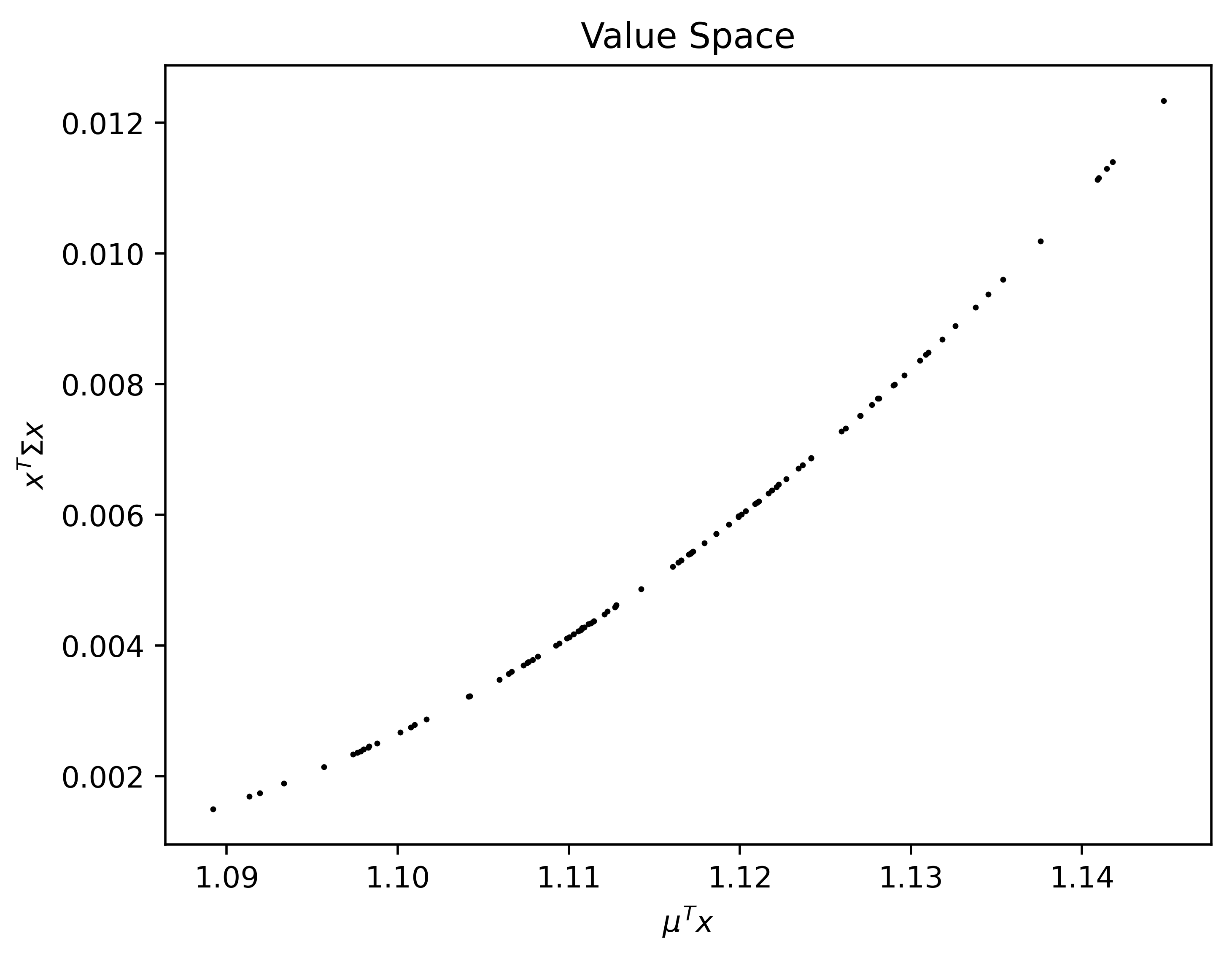

Figure 5 illustrates the obtained efficient combinations with 100 random start points in . The average number of iterations (iter), average number of function evaluations (feval), and average CPU time (time ()) are recorded in Table 4. The numerical results confirm that BBPGMO outperforms PGMO in Markowitz portfolio selection problem.

| iter | feval | time () | ||||

|---|---|---|---|---|---|---|

| BBPGMO | 7.19 | 9.36 | 349.53 | |||

| PGMO | 269.23 | 269.23 | 9454.38 |

7 Conclusions

In this paper, we proposed two types of proximal gradient methods for MCOPs and analyzed their convergence rates. Notably, in the case of strong convexity, the proposed method converges linearly at a rate of , whereas the linear convergence rate of PGMO is . The improved linear convergence confirms the BBPGMO’s superiority, and validates that the Barzilai-Borwein method can alleviate interference and imbalances among objectives. Interestingly, from the perspective of complexity, it also reveals that optimizing multiple objective functions simultaneously may be easier than optimizing the most difficult one (as long as for the worst ). Moreover, we obtained the linear convergence of BBPGMO for MOPs with some linear objectives. To the best of our knowledge, this is the first result demonstrating linear convergence of gradient descent methods for MOPs with some linear objectives. By setting , or , , all the theoretical results of BBPGMO are satisfied for corresponding gradient descent method and projected gradient method, respectively.

From a methodological perspective, it may be worth considering the following points:

-

•

From theoretical point of view, it is worth noting that BBPGMO can exhibit slow convergence when applied to ill-conditioned MOPs. Fortunately, the utilization of Barzilai-Borwein’s rule within multiobjective gradient descent methods does not impede the implementation of other acceleration strategies. Given the enhanced theoretical attributes associated with the Barzilai-Borwein methods, there exists an avenue of exploration into the applicability of conjugate gradient methods LP2018 , the Nesterov’s accelerated methods SP2022 ; SP2023 ; TFY2022 , and preconditioning methods GB2015 ; HL2015 ; W2015 based on the BBDMO or BBPGMO, respectively.

-

•

Recently, researchers have increasingly recognized multi-task learning as multiobjective optimization and have developed effective algorithms based on SDMO to train models (see, e.g., LZ2019 ; MR2020 ; SK2018 ). However, loss functions in machine learning often include an -regularized term to mitigate overfitting. On the other hand, as emphasized by Chen et al. CB2018 : “Task imbalances impede proper training because they manifest as imbalances between backpropagated gradients.” Fortunately, the BBPGMO is a first-order method capable of effectively handling imbalanced and high-dimensional multiobjective composite optimization problems. Theore, applying the BBPGMO to multi-task learning is a promising direction for future research.

References

- [1] M. A. T. Ansary. A newton-type proximal gradient method for nonlinear multi-objective optimization problems. Optimization Methods and Software, 38:570–590, 2023.

- [2] M. A. T. Ansary and G. Panda. A globally convergent SQCQP method for multiobjective optimization problems. SIAM Journal on Optimization, 31(1):91–113, 2021.

- [3] P. Assunção, O. Ferreira, and L. Prudente. A generalized conditional gradient method for multiobjective composite optimization problems. arXiv preprint arXiv:2302.12912, 2023.

- [4] H. Attouch, G. Garrigos, and X. Goudou. A dynamic gradient approach to pareto optimization with nonsmooth convex objective functions. Journal of Mathematical Analysis and Applications, 422(1):741–771, 2015.

- [5] J. Barzilai and J. M. Borwein. Two-point step size gradient methods. IMA Journal of Numerical Analysis, 8(1):141–148, 1988.

- [6] A. Beck. First-Order Methods in Optimization. Society for Industrial and Applied Mathematics, Philadelphia, PA, 2017.

- [7] J. F. Bonnans and A. Shapiro. Perturbation analysis of optimization problems. Springer New York, NY, USA, 2000.

- [8] H. Bonnel, A. N. Iusem, and B. F. Svaiter. Proximal methods in vector optimization. SIAM Journal on Optimization, 15(4):953–970, 2005.

- [9] G. A. Carrizo, P. A. Lotito, and M. C. Maciel. Trust region globalization strategy for the nonconvex unconstrained multiobjective optimization problem. Mathematical Programming, 159(1):339–369, 2016.

- [10] J. Chen, L. P. Tang, and X. M. Yang. A Barzilai-Borwein descent method for multiobjective optimization problems. European Journal of Operational Research, 311(1):196–209, 2023.

- [11] Z. Chen, V. Badrinarayanan, C.-Y. Lee, and A. Rabinovich. GradNorm: Gradient normalization for adaptive loss balancing in deep multitask networks. In J. Dy and A. Krause, editors, Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 794–803. PMLR, 10–15 Jul 2018.

- [12] I. Das and J. E. Dennis. Normal-boundary intersection: A new method for generating the pareto surface in nonlinear multicriteria optimization problems. SIAM Journal on Optimization, 8(3):631–657, 1998.

- [13] K. Deb. Multi-objective genetic algorithms: Problem difficulties and construction of test problems. Evolutionary Computation, 7(3):205–230, 1999.

- [14] M. El Moudden and A. El Mouatasim. Accelerated diagonal steepest descent method for unconstrained multiobjective optimization. Journal of Optimization Theory and Applications, 181(1):220–242, 2021.

- [15] G. Evans. Overview of techniques for solving multiobjective mathematical programs. Management Science, 30(11):1268–1282, 1984.

- [16] J. Fliege, L. M. Graa Drummond, and B. F. Svaiter. Newton’s method for multiobjective optimization. SIAM Journal on Optimization, 20(2):602–626, 2009.

- [17] J. Fliege and B. F. Svaiter. Steepest descent methods for multicriteria optimization. Mathematical Methods of Operations Research, 51(3):479–494, 2000.

- [18] J. Fliege and A. I. F. Vaz. A method for constrained multiobjective optimization based on SQP techniques. SIAM Journal on Optimization, 26(4):2091–2119, 2016.

- [19] J. Fliege, A. I. F. Vaz, and L. N. Vicente. Complexity of gradient descent for multiobjective optimization. Optimization Methods and Software, 34(5):949–959, 2019.

- [20] J. Fliege and R. Werner. Robust multiobjective optimization & applications in portfolio optimization. European Journal of Operational Research, 234(2):422–433, 2014.

- [21] N. Ghalavand, E. Khorram, and V. Morovati. An adaptive nonmonotone line search for multiobjective optimization problems. Computers & Operations Research, 136:105506, 2021.

- [22] P. Giselsson and S. Boyd. Metric selection in fast dual forward–backward splitting. Automatica, 62:1–10, 2015.

- [23] L. M. Graa Drummond and A. N. Iusem. A projected gradient method for vector optimization problems. Computational Optimization and Applications, 28(1):5–29, 2004.

- [24] C. Hillermeier. Generalized homotopy approach to multiobjective optimization. Journal of Optimization Theory and Applications, 110(3):557–583, 2001.

- [25] S. Huband, P. Hingston, L. Barone, and L. While. A review of multiobjective test problems and a scalable test problem toolkit. IEEE Transactions on Evolutionary Computation, 10(5):477–506, 2006.

- [26] Y. Jin, M. Olhofer, and B. Sendhoff. Dynamic weighted aggregation for evolutionary multi-objective optimization: Why does it work and how? In Proceedings of the Genetic and Evolutionary Computation Conference, pages 1042–1049, 2001.

- [27] X. Lin, H.-L. Zhen, Z. Li, Q.-F. Zhang, and S. Kwong. Pareto multi-task learning. In H. Wallach, H. Larochelle, A. Beygelzimer, F. Alché-Buc, E. Fox, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc., 2019.

- [28] L. R. Lucambio Pérez and L. F. Prudente. Nonlinear conjugate gradient methods for vector optimization. SIAM Journal on Optimization, 28(3):2690–2720, 2018.

- [29] Z. Q. Luo and P. Tseng. Error bounds and convergence analysis of feasible descent methods: A general approach. Annals of Operations Research, 46:157–178, 1993.

- [30] D. Mahapatra and V. Rajan. Multi-task learning with user preferences: Gradient descent with controlled ascent in pareto optimization. In H. D. III and A. Singh, editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 6597–6607. PMLR, 13–18 Jul 2020.

- [31] H. Markowitz. Portfolio selection. Journal of Finance, 7:77–91, 1952.

- [32] R. T. Marler and J. S. Arora. Survey of multi-objective optimization methods for engineering. Structural and Multidisciplinary Optimization, 26(6):369–395, 2004.

- [33] Q. Mercier, F. Poirion, and J. A. Désidéri. A stochastic multiple gradient descent algorithm. European Journal of Operational Research, 271(3):808–817, 2018.

- [34] K. Mita, E. H. Fukuda, and N. Yamashita. Nonmonotone line searches for unconstrained multiobjective optimization problems. Journal of Global Optimization, 75(1):63–90, 2019.

- [35] V. Morovati and L. Pourkarimi. Extension of zoutendijk method for solving constrained multiobjective optimization problems. European Journal of Operational Research, 273(1):44–57, 2019.

- [36] V. Morovati, L. Pourkarimi, and H. Basirzadeh. Barzilai and Borwein’s method for multiobjective optimization problems. Numerical Algorithms, 72(3):539–604, 2016.

- [37] H. Mukai. Algorithms for multicriterion optimization. IEEE Transactions on Automatic Control, 25(2):177–186, 1980.

- [38] I. Necoara, Y. Nesterov, and F. Glineur. Linear convergence of first order methods for non-strongly convex optimization. Mathematical Programming, 175:69–107, 2019.

- [39] Y. Nesterov. A method of solving a convex programming problem with convergence rate . In Soviet Mathematics Doklady, 1983.

- [40] B. T. Polyak. Introduction to Optimization. Optimization Software, Inc., New York, 1987.

- [41] Ž. Povalej. Quasi-Newton’s method for multiobjective optimization. Journal of Computational and Applied Mathematics, 255:765–777, 2014.

- [42] M. Preuss, B. Naujoks, and G. Rudolph. Pareto set and EMOA behavior for simple multimodal multiobjective functions”, booktitle=”parallel problem solving from nature - ppsn ix. pages 513–522, Berlin, Heidelberg, 2006. Springer Berlin Heidelberg.

- [43] S. Qu, M. Goh, and F. T. Chan. Quasi-Newton methods for solving multiobjective optimization. Operations Research Letters, 39(5):397–399, 2011.

- [44] H. Raguet and L. Landrieu. Preconditioning of a generalized forward-backward splitting and application to optimization on graphs. Siam Journal on Imaging Sciences, 8(4), 2015.

- [45] O. Sener and V. Koltun. Multi-task learning as multi-objective optimization. In S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018.

- [46] M. Sion. On general minimax theorems. Pacific Journal of Mathematics, 8(1):171–176, 1958.

- [47] K. Sonntag and S. Peitz. Fast multiobjective gradient methods with Nesterov acceleration via inertial gradient-like systems. arXiv preprint arXiv:2207.12707, 2022.

- [48] K. Sonntag and S. Peitz. Fast convergence of inertial multiobjective gradient-like systems with asymptotic vanishing damping. arXiv preprint arXiv:2307.00975, 2023.

- [49] H. Tanabe, E. H. Fukuda, and N. Yamashita. Proximal gradient methods for multiobjective optimization and their applications. Computational Optimization and Applications, 72:339–361, 2019.

- [50] H. Tanabe, E. H. Fukuda, and N. Yamashita. An accelerated proximal gradient method for multiobjective optimization. Computational Optimization and Applications, 2023.

- [51] H. Tanabe, E. H. Fukuda, and N. Yamashita. Convergence rates analysis of a multiobjective proximal gradient method. Optimization Letters, 17:333–350, 2023.

- [52] H. Tanabe, E. H. Fukuda, and N. Yamashita. New merit functions for multiobjective optimization and their properties. Optimization, 2023.

- [53] M. G. C. Tapia and C. A. C. Coello. Applications of multi-objective evolutionary algorithms in economics and finance: A survey. In 2007 IEEE Congress on Evolutionary Computation, pages 532–539, 2007.

- [54] A. J. Wathen. Preconditioning. Acta Numerica, 24:329–376, 2015.

- [55] K. Witting. Numerical algorithms for the treatment of parametric multiobjective optimization problems and applications. PhD thesis, Paderborn, Universität Paderborn, Diss., 2012, 2012.

- [56] F. YE, B. Lin, Z. Yue, P. Guo, Q. Xiao, and Y. Zhang. Multi-objective meta learning. In M. Ranzato, A. Beygelzimer, Y. Dauphin, P. Liang, and J. W. Vaughan, editors, Advances in Neural Information Processing Systems, volume 34, pages 21338–21351. Curran Associates, Inc., 2021.

- [57] L. Zeng, Y. H. Dai, and Y. K. Huang. Convergence rate of gradient descent method for multi-objective optimization. Journal of Computational Mathematics, 37(5):689–703, 2019.

- [58] H. Zhang. New analysis of linear convergence of gradient-type methods via unifying error bound conditions. Mathematical Programming, 180:371–416, 2020.