Ranking and Selection in Large-Scale Inference of Heteroscedastic Units

Abstract

The allocation of limited resources to a large number of potential candidates presents a pervasive challenge. In the context of ranking and selecting top candidates from heteroscedastic units, conventional methods often result in over-representations of subpopulations, and this issue is further exacerbated in large-scale settings where thousands of candidates are considered simultaneously. To address this challenge, we propose a new multiple comparison framework that incorporates a modified power notion to prioritize the selection of important effects and employs a novel ranking metric to assess the relative importance of units. We develop both oracle and data-driven algorithms, and demonstrate their effectiveness in controlling the error rates and achieving optimality. We evaluate the numerical performance of our proposed method using simulated and real data. The results show that our framework enables a more balanced selection of effects that are both statistically significant and practically important, and results in an objective and relevant ranking scheme that is well-suited to practical scenarios.

Key words and phrases: Compound decision theory; Composite null hypotheses; Deconvolution estimates; Empirical Bayes; False discovery rate; Weighted multiple testing.

1 Introduction

Allocating limited resources among numerous potential candidates is a common problem faced by both individuals and organizations. This dilemma is encountered by NBA basketball recruiters as they search for promising talents, public policy makers as they fund educational programs, and internet users on platforms such as Yelp as they decide which restaurants to visit. Such decision-making scenarios give rise to the ranking and selection problem, a fundamental statistical issue that requires the comparison of multiple unknown parameters.

Ranking and selection has been a classical topic in multiple comparisons (Mosteller, 1948; Paulson, 1949; Bechhofer, 1954; Gupta, 1965; Panchapakesan, 1971; Goel and Rubin, 1977), and its integration into other branches of statistics, operations research, and computing has made it a critical and constantly evolving area of study (Chen et al., 2000; Boyd et al., 2012; Luo et al., 2015; Ni et al., 2017; Kamiński and Szufel, 2018; Zhong et al., 2022). The decision process has two critical components: first, establishing a meaningful criterion for ordering a pool of potential candidates, and second, selecting a subset of “most meritorious” candidates with a certain level of confidence. Properly accounting for the heteroscedasticity across data from diverse study units is essential for producing effective, sensible, and fair decisions in the ranking and selection process. In what follows, we first provide an overview of conventional practices and identify relevant issues, followed by an exposition of our new framework for addressing the challenge of heteroscedasticity. Finally, we discuss related works and highlight the contributions of our approach.

1.1 Conventional practices and issues

Ranking is essential in multiple comparisons to evaluate and identify top-performers from a pool of potential candidates. While the importance of each candidate is linked to the magnitude of its associated parameter, the decision-making process also takes into account the associated uncertainties in order to ensure that the top candidates indeed belong to the “most meritorious” group. The two perspectives, namely the parameter magnitude and the confidence level in the assertions being made, are reflected by the estimated effect size and its associated statistical significance, respectively. In homoscedastic models, these two perspectives yield the same ranking. However, in cases where the data are heteroscedastic across the study units, the rankings based on these two perspectives may disagree. As demonstrated shortly, the issue is further exacerbated in large-scale settings where thousands of candidates are being considered at once. Developing a sensible ranking and selection criterion that partially mitigates the conflict between the two perspectives poses a critical challenge in large-scale multiple comparison problems.

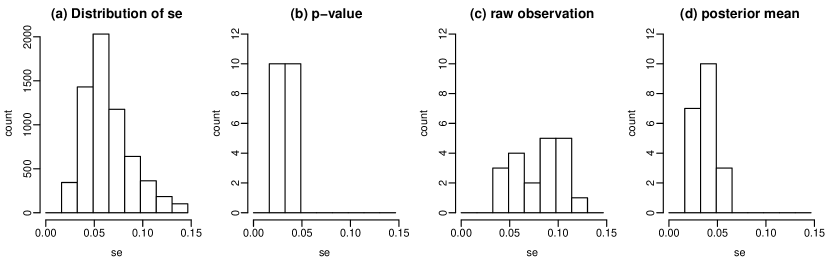

To demonstrate the inadequacy of conventional practices, we analyze the 2005 Annual Yearly Performance (AYP) data to identify K-12 schools with significant gaps in passing rates between socioeconomically advantaged (SEA) and disadvantaged (SED) students. The raw observations are the empirical differences in passing rates between the two groups, with the standard errors (SEs) being linked to the number of students in the schools. More details of the study are provided in Section 6.1. We consider three selection strategies, which are respectively based on statistical significance (-value), observed gap in passing rates (raw observation), and posterior mean (computed using Tweedie’s formula). The results of our exploratory analysis are presented in Figure 1. Panel (a) shows the distribution of the SE. Panels (b), (c) and (d) show the distribution of 20 selected schools according to -value, observed gap and posterior mean, respectively. Figure 1 reveals that selecting schools based on -values and posterior means tends to result in an over-representation of schools with low SEs, while selecting based on raw observations may lead to an over-representation of those with high SEs. The design of this analysis draws on earlier works, including Sun and McLain (2012) and Henderson and Newton (2016), which have identified and provided initial insights into some perplexing phenomena that arise under heteroscedastic models. For example, Sun and McLain (2012) found that the largest 1% of K-12 schools are over-represented among the worst performing ten schools when the selection is based on p-values.

Although all three selection criteria have their advantages in capturing either the effect sizes or accounting for associated uncertainties, the over-representation of subgroups with high/low SEs is undesirable and runs counter to practical wisdom. We aim to develop a new ranking and selection framework that resides between the three polarized selection criteria, striking a balance between their respective advantages and disadvantages. The AYP data will be revisited under our new framework in Section 6.1.

1.2 False discovery rate analysis under heteroscedasticity

We begin by examining the use of the false discovery rate (FDR) framework (Benjamini and Hochberg, 1995; Storey, 2002; Genovese and Wasserman, 2004) in the context of selecting important candidates. Most FDR methods operate in two steps: ranking and thresholding, where the building block of operation is the -value (Benjamini and Hochberg, 1995) or the local false discovery rate (lfdr; Efron et al., 2001; Sun and Cai, 2007). Both the -value and lfdr tend to prioritize the stability of data over effect sizes, which leads to the over-selection of schools with low SEs in the AYP analysis. To comprehend the limitations of the conventional formulation, we can refer to the theory in Sun and Cai (2007), which shows that thresholding lfdr is optimal in the sense that it maximizes the average power subject to the constraint on the FDR. This perspective reveals two major issues that contribute to the difficulties of utilizing the FDR framework in heteroscedastic models.

The first issue is that the concept of average power, which is defined as the expected proportion of non-nulls that are correctly rejected, overlooks the severity of missed signals. This gives rise to a significant limitation that is particularly concerning in situations with substantial heteroscedasticity across units. Specifically, the identification of a large signal should be rewarded more than that of a small signal, even if both study units have the same level of statistical significance. However, this principle is not fulfilled by the conventional FDR formulation. To correct the inherent bias in conventional FDR analyses, it is desirable to modify the power concept such that selection of larger effects is prioritized with a higher reward.

The second issue pertains to the conventional multiple testing framework, which employs a thresholding procedure that is contingent on a fixed ordering determined by a predefined significance index, such as the -value or lfdr. However, our optimality theory on prioritized selection reveals that the existence of such an ordering is not guaranteed. The absence of a universally optimal ordering poses a significant challenge in developing an objective ranking, as the rankings can be inconsistent across users who may judiciously select different confidence or reference levels.

1.3 A preview of the proposed method

Our proposal presents a new multiple comparison framework that addresses the two aforementioned issues by incorporating a modified power notion to prioritize the selection of important effects and employing a novel ranking index to assess the relative importance of units.

We first study the prioritized selection problem by utilizing a constrained optimization formulation. The goal is to control a user-specified FDR while maximizing a modified power concept that assigns higher rewards to selections of larger effects. The solution leads to a selection method that carefully weighs the candidate’s effect size against its significance. The new formulation reduces the bias inherent in commonly used significance indices that favor stability, ensuring that the effect size is more fairly represented in the selection process.

We then turn to the ranking issue by introducing a novel concept called the “r-value,” which provides a measure of the relative importance of study units in a list. The importance of different units is captured by how early they are selected according to a varying target. The earlier a unit is selected, the more important it is considered to be relative to the other units – thus an objective ranking of study units is generated.

1.4 Our contributions

In scenarios where study units display substantial heteroscedasticity, the proposed ranking and selection procedure offers a valuable alternative to conventional FDR analyses. Our method enables a more balanced selection of effects that are both statistically significant and practically important, resulting in a ranking that is objective and relevant for practical scenarios. To tackle the complexity that arises from our revised notion of power, we have devised an oracle procedure and developed a theory to establish its optimality. The new theory offers a significant advance in contrast to the weighted FDR theory in Basu et al. (2018). Furthermore, we have developed a computational shortcut of the oracle procedure, and rigorously established the asymptotic properties of the corresponding data-driven algorithm. Our work presents a unified framework that explicitly incorporates considerations of effect size, statistical significance, error control, theoretical guarantees, and computational efficiency for analyzing heteroscedastic data.

Previous studies have made progress in addressing some, but not all, of our challenges. Sun and McLain (2012) proposed a decision-theoretic framework that incorporates information about effect sizes, but their approach relies on standardization and does not resolve the issue of over-representation of small variances. Henderson and Newton (2016) put forth the maximal agreement method to avoid over-representation. However, their formulation differs significantly from ours in two aspects: firstly, the question of error rate control is left unaddressed, and secondly, the joint consideration of effect size and significance is absent. Gu and Koenker (2023) devised a robust set of ranking and selection methods within a compound decision-theoretic framework. Notably, they extended the maximal agreement method to include false discovery control. However, the challenge of balancing statistical significance and effect size has not been fully resolved. Finally, Fu et al. (2022) demonstrated that standardization can distort structural information about the alternative distribution, but their analysis had focused on the conventional FDR framework.

1.5 Organization

The paper is structured as follows. Section 2 presents the problem formulation and an oracle procedure for prioritized selection. In Section 3, we develop a data-driven procedure and establish its theoretical guarantees. Section 4 introduces the r-value and discusses its agreeability property. Sections 5 and 6 present results to illustrate the numerical performance of our proposed ranking and selection methods by using both simulated and real data.

2 Prioritized Selection with FDR Control

This section first introduces the model, notation and problem formulation, then proposes an oracle procedure for prioritized selection of important effects.

2.1 Problem formulation

Suppose , are independent observations from a random mixture model with possibly heteroscedastic errors:

| (2.1) |

where and come from unspecified distributions with bounded supports:

| (2.2) |

To focus on the central idea, we assume that are known, a common practice pursued, for example, in Efron (2011), Xie et al. (2012), and Weinstein et al. (2018). The issue of estimating unknown and heterogeneous has been considered in Gu and Koenker (2017a), Gu and Koenker (2017b), Banerjee et al. (2020), Kwon and Zhao (2023).

Let be a user-specified indifference region. Without loss of generality, suppose one wishes to test whether the effect size surpasses a given threshold , hence . Upon observing , the null and alternative hypotheses are

| (2.3) |

Denote the true state of the th item, and the decision we make about that item, where if the th item is selected (or claimed as an important case) and otherwise. Let .

In large-scale selection problems, a practical and effective goal is to control the false discovery rate (Benjamini and Hochberg, 1995)

where . A closely related quantity is the marginal false discovery rate

Under certain first- and second-order conditions, the mFDR asymptotically equals the FDR (Genovese and Wasserman, 2002; Cai et al., 2019). For theoretical convenience we adopt mFDR in our discussion.

In conventional FDR analysis, the goal is to find a decision rule that controls the error rate at pre-specified level with the largest power. A widely used metric for evaluating the power of a multiple testing procedure is the expected number of true positives

| (2.4) |

To prioritize the selection of large effects, we propose to modify the power concept as

| (2.5) |

The traditional power concept (2.4) has undergone two modifications, initially replacing the indicator with the actual difference , followed by substituting the unbiased estimate in place of , resulting in the revised power concept (2.5). The first modification allows for the revised power metric to precisely capture the impact of signal magnitude, while the subsequent alteration is crucial for avoiding technical intricacies, as the unknown poses a significant difficulty in constructing the oracle rule in Section 2.2.

The above considerations give rise to the following constrained optimization problem, in which we aim to develop a selection rule to

| (2.6) |

Remark 1.

Our formulation can be extended by replacing with a more general function . If one only cares about detecting the true state of nature and ignores the severity of missed signals, then we can take . The other possible choice for is , which ensures that the weight is always positive. Moreover, the choice of simplifies subsequent analyses. However, our preference lies with over , as the former penalizes the identification of small effects. This preference is in line with the objective of our formulation, which aims to allocate a more balanced representation to the effect size during the selection process. In Section 2.2, we will demonstrate the critical role of the sign of in the analysis. In contrast to the weighted FDR problem discussed in Basu et al. (2018), where the weights are assumed to be non-negative and independent of , the “weights” in our formulation are allowed to be negative and depend on . The difference poses new challenges in developing both oracle and data-driven procedures. We discuss related issues in subsequent sections.

2.2 Oracle selection procedure

This section considers an ideal scenario where an oracle knows and in (2.2). The oracle rule weighs the tradeoffs between -investing and -investing processes, two concepts that we shall elaborate on shortly, and assesses their impacts on the modified power and FDR capacity, respectively. In what follows, we present a heuristic argument to explain how we arrive at the oracle rule, and rigorously prove its optimality in Theorem 1.

The process of -investing (Foster and Stine, 2008; Gang et al., 2023), which is used to evaluate the gains and losses in making a discovery, relies on the conditional local false discovery rate (Clfdr, Cai and Sun (2009); Efron (2012); Sun and McLain (2012)). The Clfdr is defined as

| (2.7) |

where and . The ordered values of Clfdr are denoted . As shown by Sun and Cai (2007), the following step-wise algorithm, which uses the Clfdr as a basic operation unit, is asymptotically optimal in the sense that it maximizes the ETP subject to the constraint .

| (2.8) |

The Clfdr algorithm (2.8) can be interpreted as a varying-capacity knapsack process (Basu et al., 2018; Gang et al., 2023). Specifically, (2.8) can be viewed as an iterative decision process where the initial -wealth is invested by rejecting hypotheses sequentially. The process adheres to the following constraint:

| (2.9) |

where is the collection of rejected hypotheses at step , and may be viewed as the capacity of the knapsack at step , with the default choice . Under this view, the -investing process corresponds to a knapsack problem whose capacity may either expand or shrink over time. If with () is rejected, then increases (decreases) by .

The -investing process, on the other hand, is relatively straightforward. When a hypothesis with () is rejected, the return on investment increases (decreases) empirically by .

Jointly considering the gains and losses in the -investing and -investing processes, we divide the hypotheses into four groups:

-

0.

and ;

-

1.

and ;

-

2.

and ;

-

3.

and .

Our problem formulation suggests that units in group 0 should always be selected, as their selection results in an increase in both -wealth and power. Conversely, units in group 3 should never be selected, as their selection leads to decreases in both -wealth and power. The tradeoffs involved in selecting units from groups 1 and 2 are nuanced. In the case of group 1, selecting units comes at the cost of sacrificing capacity, but also results in increased power. We hypothesize that the optimal strategy involves selecting units with a high value-to-cost ratio, defined as

| (2.10) |

By contrast, selecting units from group 2 involves trading power for increased capacity. Consequently, the statistic can be viewed as a cost-to-value ratio. Therefore, it is desirable to select units with low values of from group 2. For theoretical convenience, we consider a bounded, continuous and monotone transformation of . Let . An example of such a transformation could be the hyperbolic tangent function . We hypothesize that the optimal decision rule can be expressed in the following form:

| (2.11) |

where and are thresholds to be determined. Define

We consider a class of decision rules of the form (2.11), and denotes its mFDR and modified power by and respectively. Note that and are both continuous and bounded functions of . Moreover, both are constant outside of the rectangle . Hence, without loss of generality, we restrict and to the compact set . Define

| (2.12) |

We state our first main result:

Theorem 1.

The oracle procedure proposed above controls mFDR at level and is optimal in the sense that for any decision rule that controls mFDR at level , we always have .

2.3 Incorporating effect size: an illustrative example

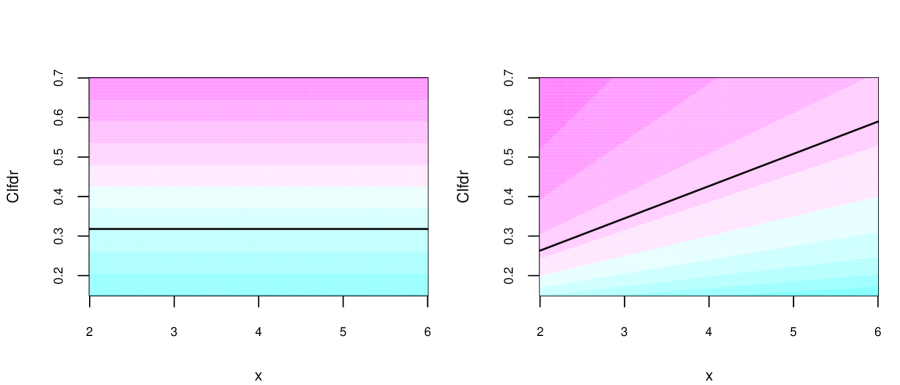

This section provides a toy example to contrast two oracle rules designed to maximize the conventional power (2.4) and modified power (2.5), respectively. The fundamental operational units for the two oracle rules are Clfdr and , defined by (2.7) and (2.10), respectively.

Suppose we are interested in testing , based on data generated from the following model:

The oracle rule that maximizes the ETP in equation (2.4) is defined as , where and is determined by the desired FDR level . For the oracle rule maximizing (2.5), Group 2 is empty, and the oracle rule for units in Group 1 is . Assuming known distributional information, we can determine and through numerical approximations such that the FDR levels of both oracle rules are exactly controlled at .

Figure 2 displays the rejection regions of the oracle rules and , depicted by the corresponding black lines. The left panel of Figure 2 shows the heat map for Clfdr values, with the x-axis representing raw observations and the y-axis representing Clfdr values. On the right panel, we present the heat map for values, with the x-axis and y-axis representing and Clfdr values, respectively. We observe that, in contrast to the patterns in the left panel, where the rejection region only depends on Clfdr values, our new oracle rule yields a rejection region, shown on the right panel, where the Clfdr threshold for the oracle increases as increases. It is clear that our oracle rule with prioritized selection depends on both statistical significance and effect size, and exhibits a preference for selecting units with larger compared to the oracle rule that aims to maximize conventional power.

3 Data-driven procedure

This section presents the development of our data-driven procedure, including a non-parametric deconvoluting method (Section 3.1), a computational shortcut (Section 3.2), and a theoretical analysis (Section 3.3).

3.1 Nonparametric deconvolution

We propose a non-parametric -modeling approach to estimating , which plays a critical role in computing the value of . Although prior research by Efron (2016), Gu and Koenker (2017b) and Gu and Koenker (2023) has tackled this issue, the theoretical properties of these methods remain largely unknown. Our new -modeling method, which is based on the density matching idea, offers a fast and stable algorithm that performs comparably to competing methods, while having a form that greatly simplifies the theoretical analysis of the data-driven procedure.

Assume , . The -modeling approach (Jiang and Zhang, 2009; Koenker and Mizera, 2014) involves approximating using a mixture of point masses. We form a grid of size evenly spaced between and :

where and . Then can be approximated by , where is the Dirac delta function centered at . The task at hand then boils down to determining the optimal weights , which can be efficiently solved through a direct optimization approach.

We outline a “density matching” approach for formulating the optimization objective function. Specifically, two different techniques are employed to derive the density estimate, namely, , which is constructed based on a given , and , which is constructed using a weighted bivariate kernel estimator. The objective function is designed to ensure a high degree of similarity between the two density estimators.

First, upon obtaining , a natural estimate for is readily provided by

On the other hand, can be estimated by employing a weighted bivariate kernel estimator:

where is a pair of bandwidths, determines the contribution of based on , is a bandwidth that varies across , and is a Gaussian kernel. The motivation behind this approach is to leverage the smooth variation of with respect to . The variable bandwidth is utilized to account for the heteroscedasticity inherent in the data, resulting in data points with higher variation being associated with flatter kernels.

To minimize the discrepancy between and , we aim to find that solves the following convex optimization problem:

| (3.13) |

Denote the optimizer of (3.13), then and can be computed as

Finally, can be estimated correspondingly using a plug-in method.

3.2 A computational shortcut and the step-wise algorithm

The oracle rule necessitates a search over a two-dimensional space, denoted by , for identifying the optimal cutoffs defined in (2.12). This task can be computationally demanding. To overcome this challenge, we propose in this section a computational shortcut that leads to a considerable improvement in computational efficiency.

To maximize for a given , our strategy must reject as many hypotheses as possible from group 1. This involves the selection of the smallest that satisfies the mFDR constraint. Consequently, the optimal solution must be located on the one-dimensional curve

where . The problem boils down to determining the optimal on such that can be maximized. The following proposition establishes that if starts to decrease along the curve in the direction of increasing , then it will continue to decrease in the direction of increasing .

Proposition 1.

Consider three decision rules , , of the form described in (2.11) with all on . If and , then we must have .

Proposition 1 inspires us to adopt the following strategy: searching along the curve in the direction of increasing and stopping when begins to decrease. More precisely, we first select as many units as possible from group 1 and record the resulting (Step 3). Next, we select a single hypothesis from group 2 (Step 4), which decreases the but increases the FDR capacity. We then return to Step 3 and select as many units as possible from group 1 using the additional FDR capacity, and record the new . We compare the new with the previous . If the increases after the iteration, we repeat the aforementioned process (e.g. continue to Step 4 and return to Step 3), otherwise we stop the procedure and output the thresholds. The operation of the step-wise data-driven procedure is detailed in Algorithm 1.

3.3 Theoretical properties of the data-driven procedure

In Section 2.2, we have demonstrated that the oracle rule is both valid and optimal in the sense that it satisfies the FDR constraint and has the largest ETP* among all valid FDR rules. In this subsection, we aim to establish that the data-driven procedure , defined in Algorithm 1, asymptotically approaches the performance of the oracle rule , and therefore is asymptotically valid and optimal. Before we proceed with our theoretical analysis, we state the following regularity conditions.

-

(A1) and for some , , .

-

(A2) The bandwidths satisfy , where and are small positive constants such that .

-

(A3) The grid size satisfies .

Remark 2.

Assumption (A1) is a reasonable requirement for the boundedness of and in most practical scenarios. Similarly, Assumption (A2) is fulfilled by commonly utilized bandwidth choices in Wand and Jones (1994). Proper selections of grid size by users can satisfy Assumption (A3), which can be relaxed to as . While a larger does not compromise the quality of the deconvolution estimate in theory, it may increase computational times. In Section C, we show that the grid size does not need to be of order greater than . The performance of the estimator is contingent on the rate of convergence of . With appropriate selections of and , the fastest rate of convergence for is . A sufficient grid size is one that allows to approximate at a rate of in integrated mean squared error.

We first state a crucial proposition that establishes the theoretical properties of the proposed density estimator .

Proposition 2.

Suppose condition (A1), (A2), and (A3) hold, then when .

Now we present our theory on the asymptotic validity and optimality of the data-driven prioritized selection procedure.

Theorem 2.

Under Conditions (A1), (A2) and (A3), the data-driven procedure described in Algorithm 1 controls mFDR at level and as .

4 The R-Value in Multiple Comparisons

In this section, we investigate the integration of ranking and selection in a unified multiple comparison framework. Our proposed approach involves generating a ranking based on a suitable selection rule, and utilizing a novel ranking metric called the r-value. This metric reflects the relative order in which different units are selected, thereby providing a practical criterion for assessing the relative importance of the units within a list.

We present two r-value notions. The first, presented in Section 4.1, discusses the situation where the reference level is fixed and the r-values are generated by varying the confidence level . The second, presented in Section 4.2, discusses the situation where the confidence level is fixed and the r-values are generated by varying the reference level . Important properties of the r-values are investigated in Section 4.4.

4.1 R-values generated by varying the confidence level

The conventional multiple testing framework relies on a thresholding procedure that assumes the presence of a significance index, such as the -value or local false discovery rate, which provides a consistent ranking of study units that remains invariant across all FDR levels. However, in the case of a heteroscedastic setup, such a ranking cannot be provided. For instance, in the oracle rule (2.11), study units may be selected into the rejection set in different orders at varying FDR levels since the optimal statistic depends on . As a result, the ranking would be inconsistent across different users who may select different FDR levels in their analysis. Furthermore, there is no natural order for the subjects in group 0, as all units in the whole group are selected simultaneously.

Next we propose the pivotal notion of r-value, which has the ability to convert any selection procedure that controls the error probability into a meaningful and coherent ranking metric.

Definition 1.

Let denote the set of units selected by a pre-defined selection procedure that controls the error rate at level . The r-value of a unit linked with is defined as

| (4.14) |

Remark 3.

When combined with the novel prioritized selection procedure that solves (2.6), the r-value corresponds to the minimum FDR level at which a study unit can be selected. This ranking metric addresses the inconsistency issue that may arise from the subjective specification of values, offering an objective and consistent means of ranking across different users.

4.2 R-values generated by varying the reference level

The specification of in practical scenarios hinges on prior domain expertise, which may be subjective and vary among users. Since the oracle statistic (2.10) and the corresponding data-driven quantity are contingent on , divergent selections of among analysts may yield inconsistent rankings. Assuming a consensus on the choice of the confidence parameter (e.g., 0.05), it is possible to generate r-values by varying the reference level . Suppose we vary from to , then the earlier a unit is selected, the more important it is considered to be relative to the other units – thus an objective ranking of study units is generated.

Definition 2.

Let denote the set of units selected by a pre-defined selection procedure that aims to select units with effect size larger than . The r-value of a unit associated with is defined as follows:

provided that no ties exist between ’s.

Here, is the standardized rank taking values in , which is suitable in situations where only the relative position of the study units is relevant. The non-standardized r-value of a particular unit corresponds to the largest predetermined reference value at which unit can be selected with confidence.

4.3 Which r-value to use

By integrating our r-value with the prioritized selection framework (2.6), we have developed a solution that is both intuitive and logically coherent for the challenging problem of ranking and selection under heteroscedastic setups. Both definitions of the r-value have their own advantages and drawbacks. To generate the r-value in this context, one can vary either or , depending on whether a consensus has been reached on the confidence level or reference level.

It is worth noting that Definition 2 of the r-value appears to align more closely with the primary objective of the two applications presented in Section 6, which is to identify schools/funds where there exists a substantial gap between two groups, with a predetermined level of confidence. By adopting Definition 2, we are able to circumvent the challenge of establishing a suitable gap threshold, which can be subjective in practice due to, say, the variability in passing rates between schools and the absence of a clear benchmark difference. Rather than focusing on the specific threshold value, our approach aims to detect substantial effect gaps with confidence, which better aligns with the practical needs of the analysis.

4.4 Agreeability of ranking

The proposed framework of “select and then rank” offers an appealing alternative to the conventional approach of “rank and then select,” which is impractical in the presence of heteroscedastic data. For example, Definition 1 first tackles the selection issue through constrained optimization, resulting in an objective solution for any given . Next, the ranking issue is handled using the r-value, which is determined by sequentially adjusting the selection level without any user input. Consequently, the needs for a universally applicable test statistic and a potentially subjective choice of can be eliminated, thus preventing the issue of inconsistent rankings.

To demonstrate the appropriateness of the ranking generated by r-values, we introduce the concept of agreeability. As previously mentioned, the ranking in heteroscedastic scenarios must consider two factors: effect size (captured by ) and statistical significance (captured by Clfdr or its estimate ). The following theorem asserts that if unit dominates unit in terms of both effect size and statistical significance, then the use of the r-value ensures that unit will be ranked higher than unit .

Theorem 3.

Let and be the r-values produced by the oracle procedure (2.12) and the data-driven procedure (Algorithm 1), respectively, for . Then both the oracle and data-driven procedures are agreeable in the sense that if and (or ), then (or ). This assertion holds true for both Definition 1 and Definition 2 with .

Remark 4.

Agreeability can be seen as a less stringent version of the nestedness notion. Gu and Koenker (2023) explored the notion of nestedness in ranking and selection, while Henderson and Newton (2016) suggested some potential issues regarding the nestedness requirement in the presence of heteroscedasticity. In Section E of the Supplementary Material, we precisely define the nestedness property and present counterexamples to demonstrate why nested selection may be infeasible under heteroscedastic setups.

5 Numeric experiments

We begin by presenting the implementation details of the data-driven procedure in Section 5.1. To demonstrate the effectiveness of the modified power function, Section 5.2 provides a comparative analysis of the ETP* and ETP across several settings. In Section 5.3, we investigate the performance of the prioritized selection procedure and compare it with competing methods in a scenario where both and are continuous. In Section 5.4, we present additional results for the case where both and are discrete, and where is correlated with .

5.1 Some implementation details

The nonparametric deconvolution method discussed in Section 3.1 requires the estimation of , , which involves specifying the tuning parameters . In our analysis, we have employed the rule of thumb in Silverman (1986), which suggests and , where and are the standard deviation and interquartile range of the input vector, respectively. In all our simulation studies, we have chosen a grid size of 50.

To ensure numerical stability, we suggest selecting the support of the grid to be , where represents the empirical quantile function of . We solve the convex optimization problem (3.13) using the CVXR package in R (cvxr).

5.2 A comparative analysis of ETP* and ETP

In this section, we conduct numerical studies to demonstrate that maximizing ETP and ETP* are two distinct objectives. We generate observations that follow the hierarchical model described below.

We aim to test the hypotheses versus , for , where . We compare the performance of the following three methods:

We repeat the experiment on 100 datasets, and set the nominal FDR level to , and report the results based on the average of the 100 replications. The data-driven method requires the independence between and . To ensure the validity of the data-driven approach, we first partition the data into two groups based on whether or . We then estimate separately for each of the two groups.

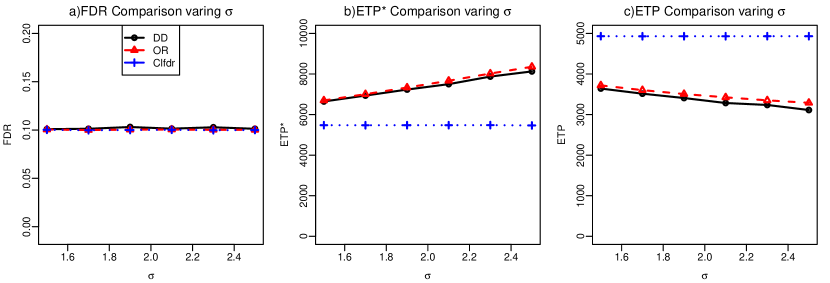

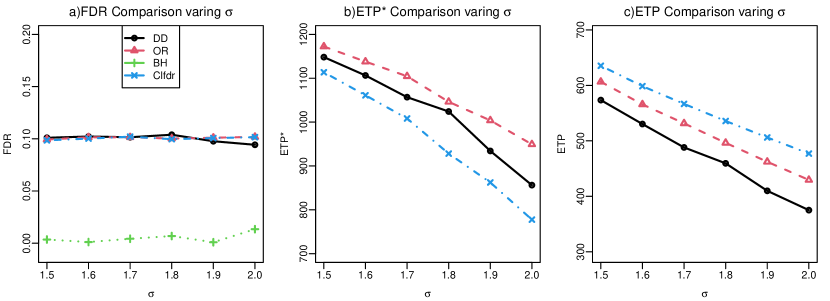

We calculate the FDR as the average of the FDPs over 100 replications. The FDP is defined as . Similarly, we compute the ETP and ETP* as the averages of and , respectively, over 100 replications. The value of varies from 1.5 to 2.5 across different settings. We present the results in Fig 3.

The results indicate that all three methods effectively control the FDR at the nominal level. However, there are significant differences in their power performance. In particular, the ETP* values of the OR and DD methods are substantially higher than that of Clfdr, while Clfdr exhibits a significantly higher ETP than OR and DD. This observation aligns with the fact that the Clfdr method is designed to optimize traditional power, whereas OR and DD are developed with the objective of optimizing modified power.

5.3 Comparison for independent and

Next, we consider the following setting:

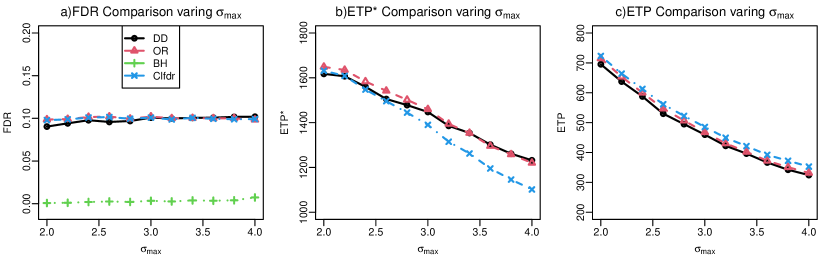

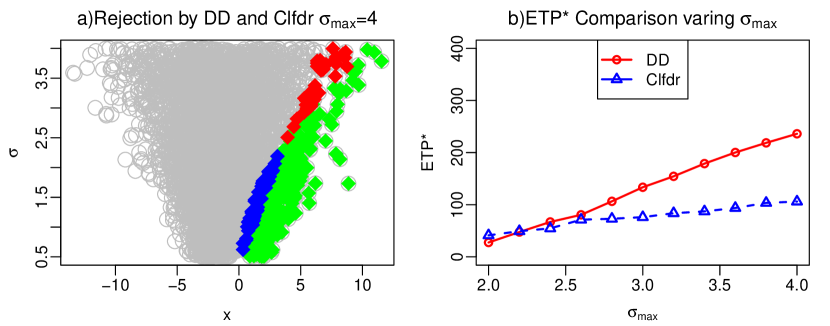

We aim to test the hypotheses versus , with . In addition to the three methods compared in Section 5.2, we also incorporate the widely used Benjamini-Hochberg procedure (BH) procedure in the comparison. The p-values are computed as , where is the cumulative distribution function of a standard normal variable. The nominal FDR level is set to , while varies from 2 to 4 for different settings. The results are obtained by averaging the results in 100 replications and are presented in Fig 5.

We can observe two important patterns. Firstly, BH appears to be excessively conservative, suggesting that -value based methods may not be well-suited for testing composite hypotheses. Secondly, DD, OR, and Clfdr exhibit comparable levels of FDR but display noticeable differences in their ETP* and ETP values.

A more detailed comparison of the hypotheses rejected by DD and Clfdr underscores the marked differences between these two methods. In Fig 5 (a), we look at one particular run with . The gray dots are hypotheses not rejected by either DD or Clfdr, green dots are hypotheses rejected by both DD and Clfdr, red dots are hypotheses rejected by DD but not Clfdr, and blue dots are hypotheses rejected by Clfdr but not DD.

Upon close examination, it is evident that DD is more likely to reject hypotheses with higher values when compared to Clfdr. If we exclude the hypotheses that are rejected by both DD and Clfdr and assess the ETP* for the remaining hypotheses, a distinct contrast emerges, as depicted in Figure 5 (b). For the hypotheses that are rejected by only one method, DD has a superior ETP* in comparison to Clfdr. Additionally, the difference in ETP* becomes more pronounced as the degree of heteroscedasticity increases.

5.4 Comparison for correlated and

In this section, we present simulation results in a more complex scenario where and are correlated. Let be an indicator function that takes the value of at and elsewhere. The model first generates from two groups and then generates in a manner that is dependent on , as described below:

The hypotheses to be tested in our study are vs , where . The value of varies between 1.5 to 2 for different settings. It is important to note that in our design, is sampled from a mixture distribution, where a vast majority of values are generated from , corresponding to small effects. However, there is a small fraction of values that correspond to large effects. Furthermore, the effect sizes tend to increase as the variance becomes larger.

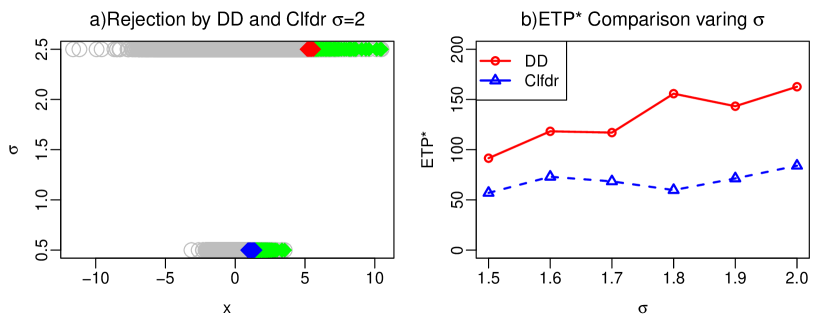

We perform simulation experiments on 100 datasets and apply DD, OR, Clfdr, and BH to select important units at FDR level . The accuracy of the deconvolution estimation method relies on the independence between and . Therefore, we initially partitioned the data into two groups based on whether or , and estimated separately for each group. A summary of results for different values of is presented in Figure 6.

Our analysis reveals several patterns. Firstly, all methods maintain FDR control at the nominal level. Secondly, BH is excessively conservative, resulting in ETP* and ETP values that are significantly lower than the other three methods. Therefore, we exclude BH from the ETP* and ETP plots. Thirdly, DD and OR outperform Clfdr in terms of the ETP* criterion, whereas Clfdr outperforms DD and OR regarding the ETP criterion. To make a further comparison between Clfdr and DD, we present a scatter plot of rejected hypotheses when in Figure 7. In Figure 7 (a), the hypotheses rejected by DD but not Clfdr all have . This implies that DD is more sensitive to larger variances than Clfdr. In Figure 7 (b), we observe that DD has a significantly higher ETP* on hypotheses where Clfdr and DD disagree.

6 Real Data Applications

In this section, we analyze the test performance data of K-12 schools from the 2005 Annual Yearly Performance (AYP) study (Section 6.1) and mutual fund data obtained from the Center for Research in Security Prices (CRSP) (Section 6.2).

6.1 AYP data

The unprocessed data sets for the AYP study are available at https://www.cde.ca.gov/re/pr/api-datarecordlayouts.asp. We begin by defining and as the passing rates of students from socially-economically advantaged backgrounds (SEA) and socially-economically disadvantaged backgrounds (SED), respectively Our objective is to identify significant differences in the passing rates for each school , where and . The standard error of is calculated as

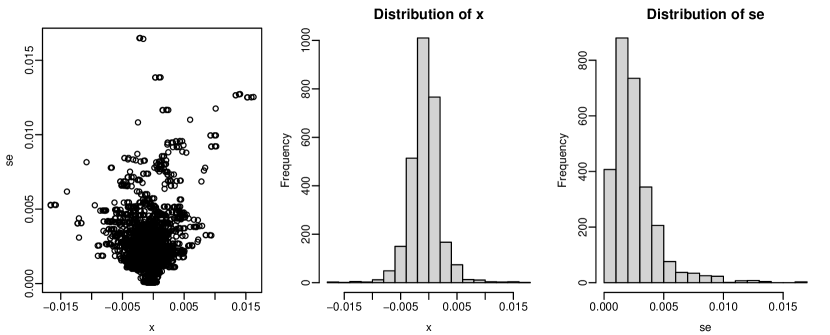

where and are the number of SEA and SED students tested, respectively. To ensure numerical stability, we remove observations that have a standard error below the percentile or above the percentile. Figure 8 presents the scatter plot and histograms of the observed data.

We aim to test the following hypotheses: vs , with being the cutoff of the indifference region and FDR level set at . We calculate the z-values as , and the p-values as , where is the standard normal cumulative distribution function.

Our primary focus is to compare our approach against analyses that solely rely on statistical significance indices (Clfdr and BH). In this context, the Clfdr method refers to the data-driven HART procedure (Fu et al., 2022). We summarize the results in Table 1, which reports the total number of rejections (a proxy for traditional power) and weighted number of rejections based on Equation (2.6) (a proxy for modified power).

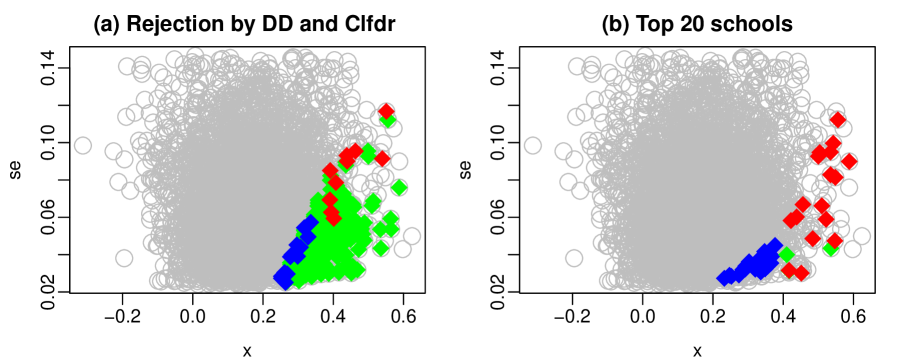

We can see that DD and Clfdr outperform BH in terms of both the traditional and modified powers. Although DD and Clfdr exhibit similar performances, the hypotheses rejected by the two methods exhibit different patterns. Figure 9 (a) displays a scatter plot of hypotheses rejected by Clfdr and DD. The gray circles represent hypotheses that were not rejected by either method, the green dots represent hypotheses rejected by both Clfdr and DD, the red dots represent hypotheses rejected by DD but not Clfdr, and the blue dots represent hypotheses rejected by Clfdr but not DD. It is clear that DD displays a predilection for rejecting hypotheses with larger effect sizes, while Clfdr has a preference for rejecting hypotheses with low standard error. Figure 9 (b) presents the top 20 schools ranked according to both p-values (indicated by blue dots) and r-values (represented by red dots). Notably, the r-value demonstrates a distinct inclination towards schools with larger effect sizes as compared to the p-value.

| DD | Clfdr | BH | |

|---|---|---|---|

| Number of hypotheses rejected | |||

| Modified Power |

6.2 CRSP data

In this section, we analyze mutual fund data obtained from CRSP accessed via the Wharton WRDS database at the University of Pennsylvania. The goal is to compare our ranking and selection method against Clfdr and BH that are solely based on significance indices.

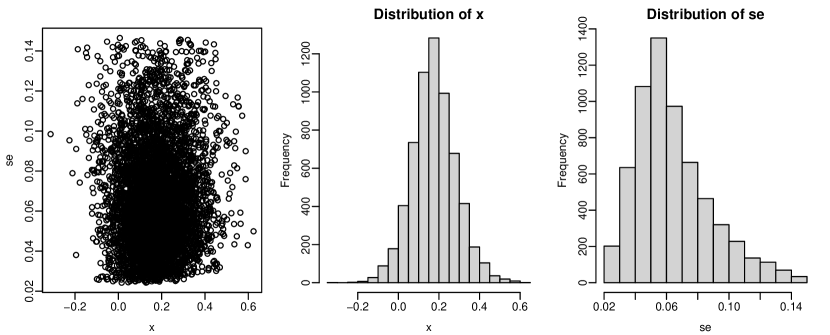

We analyze the estimated returns of mutual funds, which are denoted as , over an average of 31 months of performance from the end of April 2006 to the end of October 2008. These estimated returns are obtained from the intercept term of Carhart’s four-factor model (Carhart, 1997). The standard error of the returns, denoted as , is computed as the estimated standard error of the intercept term in the model. The dataset comprises pairs of observations (, ). To ensure numerical stability, we exclude observations with standard errors below the 0.1% and above the 99.9% percentiles. Figure 10 visually depicts the distribution of the data.

Our objective is to identify mutual funds that exhibit positive returns. Therefore, we consider the following hypotheses: vs , with . We set the target FDR level at . The z-values and corresponding p-values are obtained as before.

The results, presented in Table 2, reveal that Clfdr rejects more hypotheses than DD. However, Clfdr exhibits negative modified power, indicating its tendency to select portfolios with negative returns. This phenomenon occurs because Clfdr does not consider the value of the returns, leading it to select hypotheses with estimated returns () slightly lower than the null hypothesis (), which corresponds to negative true returns. Clfdr selects such units because they do not increase the overall FDR above the target level. In practice, this type of “over-selection” is often undesirable, as demonstrated in this example.

| DD | Clfdr | BH | |

|---|---|---|---|

| Number of hypotheses rejected | |||

| Modified Power |

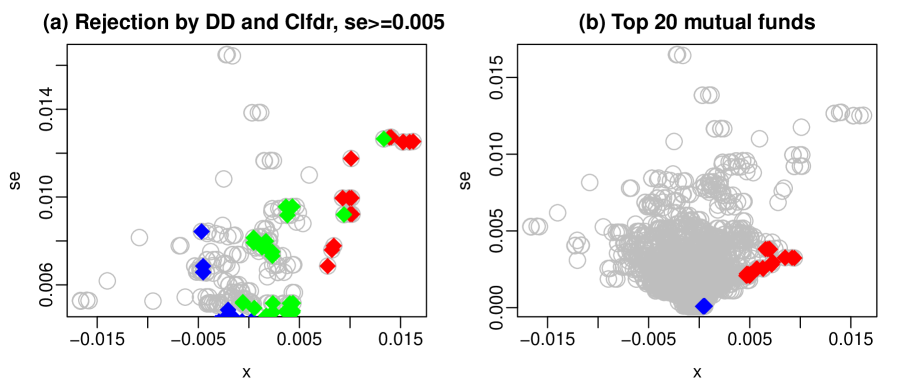

We proceed by examining the units selected by DD but not Clfdr, and vice versa. To provide a more informative comparison, we focus on hypotheses with . The results are presented in Figure 11 (a). We observe that the units selected by DD and Clfdr with differ significantly. DD selects units with both high estimated returns () and high SEs, indicating its tendency to trade high variability for potentially high returns. Figure 11 (b) displays the top 20 mutual funds ranked according to p-values (blue dots) and r-values(red dots). The results indicate that the r-value places higher priority on selecting funds with higher returns, whereas the p-value favors the selection of funds with smaller SEs.

References

- Banerjee et al. (2020) Banerjee, T., L. J. Fu, G. M. James, and W. Sun (2020). Nonparametric empirical bayes estimation on heterogeneous data. arXiv preprint arXiv:2002.12586.

- Basu et al. (2018) Basu, P., T. T. Cai, K. Das, and W. Sun (2018). Weighted false discovery rate control in large-scale multiple testing. Journal of the American Statistical Association 113(523), 1172–1183. PMID: 31011234.

- Bechhofer (1954) Bechhofer, R. E. (1954). A Single-Sample Multiple Decision Procedure for Ranking Means of Normal Populations with known Variances. The Annals of Mathematical Statistics 25(1), 16 – 39.

- Benjamini and Hochberg (1995) Benjamini, Y. and Y. Hochberg (1995). Controlling the false discovery rate: a practical and powerful approach to multiple testing. Journal of the royal statistical society series b-methodological 57(1), 289–300.

- Benjamini and Hochberg (2000) Benjamini, Y. and Y. Hochberg (2000). On the adaptive control of the false discovery rate in multiple testing with independent statistics. Journal of educational and Behavioral Statistics 25(1), 60–83.

- Boyd et al. (2012) Boyd, S., C. Cortes, M. Mohri, and A. Radovanovic (2012). Accuracy at the top. In F. Pereira, C. Burges, L. Bottou, and K. Weinberger (Eds.), Advances in Neural Information Processing Systems, Volume 25. Curran Associates, Inc.

- Cai and Sun (2009) Cai, T. T. and W. Sun (2009). Simultaneous testing of grouped hypotheses: Finding needles in multiple haystacks. Journal of the American Statistical Association 104(488), 1467–1481.

- Cai et al. (2019) Cai, T. T., W. Sun, and W. Wang (2019). Covariate-assisted ranking and screening for large-scale two-sample inference. Journal of The Royal Statistical Society Series B-statistical Methodology 81, 187–234.

- Carhart (1997) Carhart, M. M. (1997). On persistence in mutual fund performance. The Journal of Finance 52(1), 57–82.

- Chen et al. (2000) Chen, C.-H., J. Lin, E. Yücesan, and S. E. Chick (2000, jul). Simulation budget allocation for further enhancing the efficiency of ordinal optimization. Discrete Event Dynamic Systems 10(3), 251–270.

- Efron (2011) Efron, B. (2011). Tweedie’s formula and selection bias. Journal of the American Statistical Association 106(496), 1602–1614.

- Efron (2012) Efron, B. (2012). Large-scale inference: empirical Bayes methods for estimation, testing, and prediction, Volume 1. Cambridge University Press.

- Efron (2016) Efron, B. (2016). Empirical bayes deconvolution estimates. Biometrika 103(1), 1–20.

- Efron et al. (2001) Efron, B., R. Tibshirani, J. D. Storey, and V. Tusher (2001). Empirical bayes analysis of a microarray experiment. Journal of the American statistical association 96(456), 1151–1160.

- Foster and Stine (2008) Foster, D. P. and R. A. Stine (2008). -investing: a procedure for sequential control of expected false discoveries. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 70(2), 429–444.

- Fu et al. (2022) Fu, L., B. Gang, G. M. James, and W. Sun (2022). Heteroscedasticity-adjusted ranking and thresholding for large-scale multiple testing. Journal of the American Statistical Association 117(538), 1028–1040.

- Gang et al. (2023) Gang, B., W. Sun, and W. Wang (2023). Structure–adaptive sequential testing for online false discovery rate control. Journal of the American Statistical Association 118(541), 732–745.

- Genovese and Wasserman (2002) Genovese, C. and L. Wasserman (2002). Operating characteristics and extensions of the false discovery rate procedure. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 64(3), 499–517.

- Genovese and Wasserman (2004) Genovese, C. and L. Wasserman (2004, 06). A stochastic process approach to false discovery control. Ann. Statist. 32(3), 1035–1061.

- Goel and Rubin (1977) Goel, P. K. and H. Rubin (1977). On selecting a subset containing the best population-a bayesian approach. The Annals of Statistics 5(5), 969–983.

- Gu and Koenker (2017a) Gu, J. and R. Koenker (2017a). Empirical bayesball remixed: Empirical bayes methods for longitudinal data. Journal of Applied Econometrics 32(3), 575–599.

- Gu and Koenker (2017b) Gu, J. and R. Koenker (2017b). Unobserved heterogeneity in income dynamics: An empirical bayes perspective. Journal of Business & Economic Statistics 35(1), 1–16.

- Gu and Koenker (2023) Gu, J. and R. Koenker (2023). Invidious comparisons: Ranking and selection as compound decisions. Econometrica 91(1), 1–41.

- Gupta (1965) Gupta, S. S. (1965). On some multiple decision (selection and ranking) rules. Technometrics 7(2), 225–245.

- Henderson and Newton (2016) Henderson, N. C. and M. A. Newton (2016). Making the cut: improved ranking and selection for large-scale inference. Journal of the Royal Statistical Society. Series B, Statistical methodology 78(4), 781.

- Jiang and Zhang (2009) Jiang, W. and C.-H. Zhang (2009). General maximum likelihood empirical bayes estimation of normal means. The Annals of Statistics 37(4), 1647–1684.

- Kamiński and Szufel (2018) Kamiński, B. and P. Szufel (2018). On parallel policies for ranking and selection problems. Journal of Applied Statistics 45(9), 1690–1713.

- Koenker and Mizera (2014) Koenker, R. and I. Mizera (2014). Convex optimization, shape constraints, compound decisions, and empirical bayes rules. Journal of the American Statistical Association 109(506), 674–685.

- Kwon and Zhao (2023) Kwon, Y. and Z. Zhao (2023). On f-modelling-based empirical bayes estimation of variances. Biometrika 110(1), 69–81.

- Luo et al. (2015) Luo, J., L. J. Hong, B. L. Nelson, and Y. Wu (2015). Fully sequential procedures for large-scale ranking-and-selection problems in parallel computing environments. Operations Research 63(5), 1177–1194.

- Mosteller (1948) Mosteller, F. (1948). A -Sample Slippage Test for an Extreme Population. The Annals of Mathematical Statistics 19(1), 58 – 65.

- Ni et al. (2017) Ni, E. C., D. F. Ciocan, S. G. Henderson, and S. R. Hunter (2017). Efficient ranking and selection in parallel computing environments. Operations Research 65(3), 821–836.

- Panchapakesan (1971) Panchapakesan, S. (1971). On a subset selection procedure for the most probable event in a multinomial distribution**this research was supported in part by the office of naval research contract n00014-67-a-0226-00014 and the aerospace research laboratories contract af33 (615)67c1244 at purdue university. reproduction in whole or in part is permitted for any purposes of the united states government. In S. S. Gupta and J. Yackel (Eds.), Statistical Decision Theory and Related Topics, pp. 275–298. Academic Press.

- Paulson (1949) Paulson, E. (1949). A Multiple Decision Procedure for Certain Problems in the Analysis of Variance. The Annals of Mathematical Statistics 20(1), 95 – 98.

- Silverman (1986) Silverman, B. W. (1986). Density estimation for statistics and data analysis, Volume 26. CRC press.

- Storey (2002) Storey, J. D. (2002). A direct approach to false discovery rates. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 64(3), 479–498.

- Sun and Cai (2007) Sun, W. and T. T. Cai (2007). Oracle and adaptive compound decision rules for false discovery rate control. Journal of the American Statistical Association 102(479), 901–912.

- Sun and McLain (2012) Sun, W. and A. C. McLain (2012). Multiple testing of composite null hypotheses in heteroscedastic models. Journal of the American Statistical Association 107(498), 673–687.

- Wand and Jones (1994) Wand, M. P. and M. C. Jones (1994). Kernel Smoothing, Volume 60 of Chapman and Hall CRC Monographs on Statistics and Applied Probability. Chapman and Hall CRC.

- Weinstein et al. (2018) Weinstein, A., Z. Ma, L. D. Brown, and C.-H. Zhang (2018). Group-linear empirical bayes estimates for a heteroscedastic normal mean. Journal of the American Statistical Association 0(0), 1–13.

- Xie et al. (2012) Xie, X., S. Kou, and L. D. Brown (2012). Sure estimates for a heteroscedastic hierarchical model. Journal of the American Statistical Association 107(500), 1465–1479.

- Zhong et al. (2022) Zhong, Y., S. Liu, J. Luo, and L. J. Hong (2022). Speeding up paulson’s procedure for large-scale problems using parallel computing. INFORMS Journal on Computing 34(1), 586–606.

Online Supplementary Material for “Ranking and Selection in Large-Scale Inference of Heteroscedastic Units”

This Online Supplement contains the proofs of main theorems and propositions (A), proofs of technical lemmas (B), a discussion on the grid size (C), a discussion on special cases of the r-value notion (D), and a discussion on the “nestedness” property (E).

Appendix A Proof of main Theorems and Propositions

A.1 Proof of Theorem 1

Observe that solving the constrained optimization problem (2.6) is equivalent to solving the subsequent problem:

We divide the discussion into the following scenarios.

1. Decisions for units in group 0.

Let be a decision rule satisfying . Denote by the set of hypotheses rejected by . Suppose that the null hypothesis from group 0 is not rejected by . Consider another decision rule with . It is clear that

| and |

Hence, the optimal procedure must reject all hypotheses from group 0.

2. Decisions for units in group 3.

Next, suppose rejects the null hypothesis from group 3. Consider a new decision rule with . It is clear that

| and . |

Hence, the optimal procedure does not reject any hypothesis from group 3.

3. Decisions for units in group 1 and group 2.

Let , and . Then and respectively correspond to the decisions for units in group 1 and group 2.

Remark 5.

We pause momentarily to offer clarification on the key concepts that will be presented in the remainder of the proof. It is important to note that the -investing and -investing processes are interdependent, which means that the optimal cutoff in group 1 is contingent on the cutoff chosen in group 2. As a result, the derivation of the optimal decision rule can be challenging. However, an important observation is that if any decision procedure deviates from the oracle rule for group 1, it can be uniformly enhanced by ranking hypotheses in group 1 based on the ordering of in descending order and then selecting a suitable threshold. This argument applies similarly in the opposite direction for selection of units in group 2. Therefore, although the process of determining the optimal pairs of may be complex, the format of the optimal decision rule can be determined.

Subsequently, we will demonstrate separately that both and , when holding the part fixed, correspond to optimal rejection sets that cannot be further improved.

Suppose satisfies and . The oracle rule on group 1 can be expressed as

| (A.15) |

Let and . For , we have and hence . Similarly for , we have and . Thus,

| (A.16) |

Given , is chosen as small as possible such that or until the entire group 1 is rejected. Such exists because is a continuous and monotone function of when ignoring the decisions in the other group. The argument follows from that in (Cai et al., 2019). In particular, this implies

| (A.17) |

Recall the definition of the power function

By employing a similar line of reasoning as described above, it can be shown that the optimal procedure involves ranking hypotheses in group 2 in ascending order of and selecting an appropriate threshold.

Finally, we combine the claims from the four groups, and claim that the oracle rule is optimal in the sense of (2.6).

A.2 Proof of Proposition 1

It is worth noting that if and are points on and , then we must have . Additionally, if , then we must have .

Suppose , the we can find another point such that , and . Similarly, suppose , the we can find another point such that , and

Thus, if we can show the claim holds under the assumption that , then the desired result follows.

We introduce some notations:

-

•

.

-

•

.

-

•

is the vector restricted to group .

-

•

is the vector restricted to the non-zero entries in .

-

•

a vector of ’s.

-

•

-

•

if is a vector and is a number, then .

By our ranking strategy for the units in group 1 and group 2 in the oracle rule, we have

| (A.18) | |||||

| (A.19) |

Next, note that implies

which can be re-written as

| (A.20) | ||||

Similarly the condition implies that

Hence we have

Now we can see that

which implies that and the desired result follows.

A.3 Proof of Proposition 2

We first state a useful lemma:

Lemma 1.

Suppose , for . Let be the empirical density function . Let and . Then for every , as .

Lemma 1 implies it is possible to find a set and such that for all , . Consider the following set of functions

We can make the grid fine enough so that for any and , there exists such that . Hence

If we let , then for . It follows that there exists

such that .

Using standard arguments in density estimation theory (e.g. Wand and Jones (1994)), we have

By assumption (A2) . It follows that

By definition of the minimization problem, we have . Thus, and , where and . Here is taken with respect to and , is taken with respect to the data that are used to construct .

Note that is continuous, then there exists such that as . Let and . Since

it follows that . Thus and are bounded below by a positive number for large except for an event that has a low probability. Similar arguments can be applied to the upper bound of and , as well as to the upper and lower bounds for and . Therefore, we conclude that , , and . are all bounded in the interval , for large except for an event, say that has low probability. Let and . We have

Since is bounded by 1, we have

Thus, Let . Then we have

and the desired result follows.

A.4 Proof of Theorem 2

We begin with a summary of notation used throughout the proof:

-

•

.

-

•

.

-

•

.

-

•

.

-

•

.

-

•

-

•

We first show . Note that by the WLLN, so that we only need to establish . We state a lemma that will be useful for the proof:

Lemma 2.

Let and then .

By Lemma 2 and Cauchy-Schwartz inequality, we have

Let . It follows that

By Lemma 2, , applying Chebyshev’s inequality, we obtain

Next we show uniformly. Since for all on the rectangle , given any the Lebesgue measure of the set

approaches 0. Suppose there exists such that for any there is and with , since is smooth, there exists a square centered at with side length such that

Consider the triangle with vertices at , call this triangle . It is clear that by definition of we have

Since and . It follows that . Note that only depends on , hence the area of does not go to 0 as , a contradiction. Similarly, there is no and such that for any , there exists with

This implies uniformly. Use similar arguments, we can also show uniformly. Define

It is clear that the data-driven algorithm only searches among the points on . By uniform convergence, given any , we can find such that for all for all . This shows .

Next we show is asymptotically optimal. By uniform continuity of , given any , there exists such that for all . With probability goes to 1, there exists a point . By uniform convergence of to , we can choose big enough so that , thus

Again by uniform convergence we have for all big enough. By definition , thus

It follows that , proving the desired result.

A.5 Proof of Theorem 3

Since the two definitions of r-value share the same selection procedure, it suffices

to show that if and then the rejection of hypothesis implies the rejection of hypothesis .

We break the proof into several cases:

case 1: If hypothesis belongs to group 0, then by definition hypothesis also belongs to group 0, hence it is also rejected.

case 2: If hypothesis belongs to group 1, then hypothesis is either in group 0 or in group 1 with . By definition of the oracle procedure, hypothesis is rejected.

case 3: If hypothesis belongs to group 2, then hypothesis is either in group 0 or in group 2 with . By definition of the oracle procedure, hypothesis is rejected.

The proof for the data-driven procedure with Clfdr substituted by and replaced by can be derived using the same argument.

Appendix B Proof of Lemmas

B.1 Proof of Lemma 1

We use the bias-variance decomposition:

Write as a mixture of point mass where . By definition,

. Also since is bounded, it follows that . Therefore

B.2 Proof of Lemma 2

We state a fact that will be helpful:

Lemma 3.

.

Lemma 3 is proved in section B.3. By definition of and we have the following:

Denote the three sums on the RHS as , , and respectively. By Proposition 2, . To show we only need to show . We say or is from group if is from group . can only happen when at least one of the following holds:

-

1.

and are not from the same group.

-

2.

and both from group 1 but and .

-

3.

and both from group 1 but and .

-

4.

and both from group 2 but and .

-

5.

and both from group 2 but and .

Since The probability that and are not from the same group is bounded by

| (B.21) |

Note that

The first term on the right hand is vanishingly small as because is a continuous random variable. The second term converges to by Proposition 2. We conclude that

Use similar argument, the remaining terms in (B.21) are , the probability of the first situation occurs is .

For situation 2, we have

The first term on the right hand is vanishingly small as because is a continuous random variable. The second term converges to by Lemma 3. we conclude that

In a similar fashion, we can show that situation 3-5 are all . The lemma follows.

B.3 Proof of Lemma 3

Let . Then as . Let and . Since . We have . Thus and are bounded below by a positive number for large except for an event that has a low probability. Note that

It follows that on . Note that

And since has bounded support and the noise is Gaussian, it follows that

Hence . Since and are continuous function of and respectively and is bounded it follows that and .

Appendix C Grid Size

In the proof of Proposition 2, we have used the fact that

The optimal rate of is and is achieved when . Since has bounded support, for any we can always find such that . Let , then

| (C.22) |

We want the above to be of order uniformly for any . If has order greater than then it is clear that the RHS of (C.22) is . When has order less than , since we focus on By Taylor’s expansion, we have

It is clear that if then the above is , it follows that the a grid size of is sufficient.

Appendix D R-value, -value and -value

This section presents two examples that illustrate how to transform a selection procedure into an informative ranking metric using Definition 1 for the r-value.

Example 1.

Suppose that our objective is to identify significant cases among multiple candidate units while controlling the per-comparison error rate (PCER). To achieve this, we can employ a simple selection rule, denoted by , , where represents either a t-statistic or a -statistic. By sequentially varying the PCER level from 0 to 1, the study units can be selected in an ordered order. If we consider a scenario where the global null hypothesis is valid, and hypotheses are selected at a PCER level of , then the minimum required for a case to be chosen is equivalent to the familiar -value. The -value can subsequently be used as a ranking variable to signify a unit’s position in the list.

Example 2.

In the second example, let us consider the application of the adaptive -value procedure (Benjamini and Hochberg, 2000) to select units while controlling the positive false discovery rate (pFDR) at a given level of . By gradually increasing , an informative ranking of the units can be obtained. The minimum pFDR level required for a unit to be selected is known as the -value (Storey, 2002), which can be employed as a ranking variable to indicate the unit’s relative position in the list. The earlier a unit is selected, the more crucial it is deemed to be in comparison to the remaining units.

The r-value is a versatile concept that can be applied to a broad range of selection procedures, as illustrated by the two examples presented above. Specifically, we have shown that the -value and -value can be regarded as particular cases of the r-value, which can be obtained by varying the confidence level .

Finally, our r-value, which is based on varying , draws inspiration from and is closely linked to the r-value presented in Henderson and Newton (2016). Nonetheless, the two definitions diverge significantly with regards to the optimization criterion and the intended goal of analysis.

Appendix E The Nestedness Property in Sequential Selection

The topic of nested selection has been previously addressed in Gu and Koenker (2023) and Henderson and Newton (2016). In an ideal scenario, if we relax the constraint by reducing or increasing , we would expect that hypotheses rejected under the stricter condition would remain rejected under the relaxed constraint. However, the oracle procedure outlined in Section 2.2 may not satisfy the nestedness property defined in Definitions 3 or 4.

Section 4 introduced two notions of r-value, leading to the definition of two types of nestedness that will be discussed in the next two subsections respectively.

E.1 Nestedness induced by varying

Definition 3.

Consider and as defined in Definition 1. A testing procedure is nested if the rejection regions and satisfy the inclusion property for all .

To illustrate why the oracle selection procedure is not nested according to Definition 3, consider the following example. Recall that . Suppose we have , with being slightly larger than . Additionally, assume that and are both relatively large, while and are relatively small for . It is worth noting that there are more than hypotheses in total, but we are focusing on these particular hypotheses for the sake of clarity and simlicity.

It is possible to select a value of such that is rejected, while are not. However, if we slightly increase the target FDR level to , then will exceed (assuming for ). Consequently, it is possible for hypothesis 1 to be rejected at FDR level , but not at level , violating the nestedness property.

E.2 Nestedness induced by varying

Definition 4.

Consider and as defined in Definition 2. A testing procedure is nested if for all we have .

To further illustrate this point, consider the following example, where the observations are generated from the following model:

Consider the scenario in which we have two data points, and . We fix and set . Numerical calculations reveal that both and belong to group 1, with . Consequently, it is possible that is rejected while is not. However, if we lower to 5.9, still belongs to group 1, but now belongs to group 0. As a result, is rejected, but may not be. Therefore, the oracle selection procedure is not nested, as per Definition 4.

E.3 Conclusion

In summary, agreeability appears to be a more appropriate criterion for ranking procedures in the presence of heteroscedasticity. Our analysis has demonstrated that the r-values derived from Definitions 1 and 2 both meet the requirement of agreeability, which in turn results in ranking rules that are meaningful and valid.