[1,1]\fnmRasoul \surAmirzadeh

These authors contributed equally to this work.

These authors contributed equally to this work.

These authors contributed equally to this work.

1]\orgdivSchool of Information Technology, \orgnameDeakin University, \orgaddress\street Waurn Ponds Campus, \cityGeelong, \postcode3216, \stateVictoria, \countryAustralia

2]\orgdivBusiness School, \orgname Deakin University, \orgaddress\streetBurwood, \cityMelbourne, \postcode3125, \stateVictoria, \countryAustralia

Causal Feature Engineering of Price Directions of Cryptocurrencies using Dynamic Bayesian Networks

Abstract

Cryptocurrencies have gained popularity across various sectors, especially in finance and investment. The popularity is partly due to their unique specifications originating from blockchain-related characteristics such as privacy, decentralisation, and untraceability. Despite their growing popularity, cryptocurrencies remain a high-risk investment due to their price volatility and uncertainty. The inherent volatility in cryptocurrency prices, coupled with internal cryptocurrency-related factors and external influential global economic factors makes predicting their prices and price movement directions challenging. Nevertheless, the knowledge obtained from predicting the direction of cryptocurrency prices can provide valuable guidance for investors in making informed investment decisions. To address this issue, this paper proposes a dynamic Bayesian network (DBN) approach, which can model complex systems in multivariate settings, to predict the price movement direction of five popular altcoins (cryptocurrencies other than Bitcoin) in the next trading day. The efficacy of the proposed model in predicting cryptocurrency price directions is evaluated from two perspectives. Firstly, our proposed approach is compared to two baseline models, namely an auto-regressive integrated moving average and support vector regression. Secondly, from a feature engineering point of view, the impact of twenty-three different features, grouped into four categories, on the DBN’s prediction performance is investigated. The experimental results demonstrate that the DBN significantly outperforms the baseline models. In addition, among the groups of features, technical indicators are found to be the most effective predictors of cryptocurrency price directions.

keywords:

Cryptocurrencies, Altcoins, Dynamic Bayesian networks, Price direction prediction, Causal feature engineering1 Introduction

The cryptocurrency market has emerged as an important player in global financial markets despite its relatively short lifespan Gajardo et al. (2018); Maasoumi and Wu (2021). Since the inception of cryptocurrencies in 2012,111Initiated by “Bitcoin: A Peer-to-Peer Electronic Cash System” paper published by a scholar named Nakamoto Satoshi Nakamoto and Bitcoin (2008). cryptocurrency market capitalisation has substantially soared. For instance, the total market capitalisation of cryptocurrencies witnessed an increase from 17 billion dollars at the beginning of 2017 to 1.1 trillion dollars at the beginning of 2023. This exponential growth has made cryptocurrencies a potential investment opportunity and attracted a considerable number of new investors to this market.

Despite the attractiveness of the cryptocurrency market, there are several challenges concerning the profitability of cryptocurrency trading. In addition to common challenges that affect investment decisions in traditional financial assets, such as accurate price prediction and being influenced by global economic and non-economic factors, cryptocurrencies face distinct challenges due to their unique ecosystem. The challenges that contribute to the volatility of their prices include mining difficulty, the security of wallets and cryptocurrency exchanges, blockchain-related energy consumption, and the lack of international acceptance and legislation (Sabry et al., 2020). Besides, the cryptocurrency market is characterised by high volatility, no closed trading periods, and being impacted by public sentiment that distinguishes it from other financial markets (Valencia et al., 2019). Hence, the interplay between these unique characteristics of cryptocurrencies and challenges in the financial markets adds further complexity to predicting cryptocurrency market behaviour.

Although knowledge about the future price movement directions of financial assets is useful for investors, predicting those movements is a complex task in financial time series analysis (Ismail et al., 2020). This challenge is primarily due to the inherently complex, nonlinear, and noisy attributes of financial data (Wang et al., 2021). In addition, there are numerous factors affecting the variability in the financial data that necessitate feature engineering beyond associations derived from correlations. Furthermore, in a multivariate time series representation of several financial entities, the fluctuation in one variable can drastically affect the values of other variables, which makes the task of prediction even harder (Quesada et al., 2022). Nevertheless, predicting price direction is useful for short-term investors to reduce cryptocurrency market potential risks by taking necessary steps when their investment value may increase or decrease due to market conditions (Ismail et al., 2020). Additionally, predicting the direction of prices can generate ‘buy’ and ‘sell’ signals, which can be used by algorithmic traders to develop automated trading activities (Qiao and Beling, 2016). Therefore, by reducing the quantitative price value prediction problem to a narrower version in terms of classifying price movement direction, it becomes possible to determine trend changes qualitatively for a given window of time (Wang et al., 2015). Adopting this approach can potentially result in a useful technique for predicting cryptocurrency market directions and is an essential step toward designing reliable procedures for predicting the actual quantitative prices of financial assets (Quesada et al., 2022).

Although Bitcoin has long been considered the most widespread and valuable cryptocurrency, studies, such as Akyildirim et al. (2021) and Ji et al. (2019), suggest that Bitcoin is losing its dominance to altcoins. In fact, statistics indicate altcoins are growing significantly in popularity. For example, the total market capitalisation of altcoins has increased from around 9% in January 2017 to 60% in January 2023 based on data obtained from www.coinmarketcap.com. Additionally, the number of different cryptocurrencies has soared recently, with over 20,000 altcoins now available on the market, compared to just 50 at the end of 2013. These trends emphasise the need for more studies to analyse altcoins further in the cryptocurrency domain. While Bitcoin remains the major player in the cryptocurrency market, it is essential to explore the features and characteristics of altcoins to comprehend their potential impact on the market and inform investment decisions.

Artificial intelligence methods including machine learning (ML) algorithms have proven to be effective in prediction across various fields, including finance. As a result, financial technology (Fintech)222The term ‘Fintech’ refers to individuals or companies that bring innovation and disruption to the financial industry by merging technological and financial capabilities (Altan et al., ). companies are increasingly utilising ML techniques, such as long short-term memory (Swathi et al., 2022) and artificial neural networks (Liu and Ma, 2022), to address the challenge of price prediction in the cryptocurrency market. However, as surveyed in Amirzadeh et al. (2022), finding an appropriate ML technique to address the challenges of predictions with high accuracy and effective feature engineering is not straightforward. In particular, the accuracy of prediction is highly sensitive to the choice of the model and corresponding hyper-parameters (Cummings and Li, 2021).

Dynamic Bayesian networks (DBNs) is a widely used ML method for learning dependencies between random variables in time-series data (Grzegorczyk and Husmeier, 2019). They are versatile tools for modelling complex systems that change over time and can be used to gain knowledge about the causal relationships between variables. DBNs are useful for applications such as prognosis, fault detection, reliability analysis, risk assessment, and safety evaluation Türkali (2020). In particular, DBNs are already used for prediction (Sabourin et al., 2011), smoothing and filtering (Xiao et al., 2017), and are frequently utilised in fields such as robotics (Premebida et al., 2017), speech recognition (Nefian et al., 2002), and finance (Tan et al., 2011).

Since our research aims at predicting the price directions of cryptocurrencies along with causal feature engineering, we choose DBNs as a suitable model for accomplishing this task due to their computational and inferential attributes. First, in the context of financial multivariate time series, it is essential to consider the effect of fluctuations in one variable on the entire system, as changes in one component can generate linear or nonlinear changes in others. A DBN model can effectively address this challenge (Quesada et al., 2022). Furthermore, in the presence of numerous factors affecting the fluctuations of financial time series data, they are able to learn the most influential set of features from data (Zhang et al., 2016). DBNs also provide an approach for performing a probabilistic inference of the status of partially observable or unobservable components (Zhao et al., 2021). Compared to some ML models used for classification, which are limited to predicting only the direction of market movement without accounting for the magnitude or duration of price movement directions (Valencia et al., 2019), DBNs offer the advantage of providing a probabilistic inference for both upward and downward price movements, providing an estimation of the likelihood or probability of such movements. Despite all these important attributes of DBNs, they are rarely used in analysing and predicting cryptocurrency prices.

In response to the challenges in predicting price directions in financial assets, in this work, we use DBNs to predict the price movement directions of altcoins. The study investigates the effectiveness of DBNs in predicting the daily price directions of five popular altcoins, which are chosen for two reasons including (mainly) market capitalisation and data availability. The performance of the DBN model is compared with two frequently used baseline models, namely autoregressive integrated moving average (ARIMA) and support vector regression (SVR) models. Moreover, the research explores a hypothesis of whether increasing the number of features fed into the DBN leads to a monotonic improvement in precision accuracy. To test this hypothesis, we examine the influence of combining different feature categories with basic price information on the performance of DBNs in predicting market directions. Overall, this research provides insights into the efficacy of DBNs and feature engineering in cryptocurrency market prediction. The contributions of our research are:

-

•

Investigate daily price directions for five popular altcoins: Binance Coin, Ethereum, Litecoin, Ripple, and Tether.

-

•

Explore the causal influence of four groups of features, including basic price information, social media, macro-financial data, and technical indicators, on the altcoin price prediction.

-

•

Proposes DBNs as a suitable modelling technique for investigating causal influences in cryptocurrency markets. Specifically, by predicting the direction of price movement, DBNs can generate probabilistic ‘buy’ and ‘sell’ signals, which can be helpful for investors in making investment decisions.

The remainder of this paper is structured as follows. In Section 2, a literature review is provided on the studies related to predicting cryptocurrency prices. Section 3 introduces DBNs. Section 4 outlines the selection of features. Section 5 provides information on experimental design and data analysis procedures. The findings of our study are discussed in Section 6. Finally, Section 7 provides concluding remarks on the study and suggests directions for future research.

2 Related work

In this section, we review a set of recent academic publications concerning using ML models in predicting price movement directions. We first briefly consider the feature engineering side of devising ML models including incorporating technical indicators, social media data, and their impact on the accuracy of the models. We then survey the applications of BNs in predicting upward and downward trends in financial markets.

Technical indicators are commonly used features in ML studies for predicting various financial markets, as seen in Borovkova and Tsiamas (2019) and Choudhry and Garg (2008). However, they have received less attention as input features in the cryptocurrency literature. For instance, a tree-based classification model is built by Huang et al. (2019) to assess whether Bitcoin returns are predictable. They create 124 indicators based on five categories of them using Python’s TA-Lib library, which include overlap study, momentum, cycle, volatility, and pattern recognition indicators. According to their results, the model has predictive power for narrow intraday ranges of Bitcoin and outperforms the buy-and-hold strategy. The study also concludes that technical analysis is useful in the Bitcoin market, despite the fact that non-fundamental factors are the primary drivers of its value. Also, a study by Alonso-Monsalve et al. (2020) predicts trends of six popular cryptocurrencies (Bitcoin, Dash, Ethereum, Litecoin, Monero, and Ripple) using eighteen technical indicators derived from one-year data. They classify one-minute trends into three categories (increase, neutral, or decrease) using four different neural network architectures, including convolutional neural networks and multilayer perceptrons. Their results suggest that all cryptocurrencies are predictable to a certain extent by using technical indicators. However, the study focuses on short-term trend prediction, which is subject to the limitations such as response times and liquidity issues. Moreover, their proposed hybrid network outperforms other models, and their performances are better at predicting Bitcoin, Ethereum, and Litecoin. In another study, Akyildirim et al. (2021) test the predictability of twelve cryptocurrencies using four ML algorithms, including support vector machine (SVM) and logistic regression. For their investigations, they use past price information and eight technical indicators, including the five-day relative strength index (RSI) and simple moving average (SMA) as features for their models. The results show that all four algorithms have an average classification accuracy consistently above the 50% threshold for all cryptocurrencies.

The influence of popular social platforms, such as Twitter, on cryptocurrency price movements, has received substantial attention (Ye et al., 2022; Zou and Herremans, 2022) in the literature. In a work by Abraham et al. (2018), the authors predict changes in Bitcoin and Ethereum prices using Twitter and Google Trends data. According to their study, the volume of tweets is a predictor of price direction rather than sentiment. Moreover, they employ a sentiment analysis tool in the study and observe that the sentiment of tweets tends to remain positive, regardless of price changes in their investigation. In another study, Valencia et al. (2019) use multilayer perceptron, SVM, and random forest to predict the price movement of four cryptocurrencies (Bitcoin, Ethereum, Ripple, and Litecoin) by incorporating Twitter data and raw price data as two feature groups. The Twitter data used in the study include the sentiment of daily tweets, which are grouped into four categories of positive, negative, neutral, and compound sentiments. The models’ performances are compared based on independent feature groups and their combinations. The results suggest that Twitter data alone has the potential to predict specific cryptocurrencies where the best results are obtained for Bitcoin. However, there is not a universally accepted criterion for evaluating the model performance in predicting different cryptocurrencies. For example, different models show superiority on different coins based on accuracy and precision performance criteria.

Despite the considerable capacity of DBNs in modelling complex stochastic situations and detecting features with causal relationships, it has rarely been used in analysing the cryptocurrency market. However, a number of studies investigating Bayesian networks (BNs) and DBNs are presented here as examples. For instance, Wang et al. (2015) apply DBNs to predict the stock market trend in both the US and China markets by incorporating nine macroeconomic factors into their DBNs. The study results show that the proposed method effectively captures changes in market trends that preceded actual turning points of stocks by a lead margin of a few months. However, the models do not determine the direction of the trend changes. As another example, Jangmin et al. (2004) implement a variant of DBNs to model the dynamics of trends of prices of twenty companies in the Korean stock market. The results show that the proposed model can not outperform the buy-and-hold strategy as the first baseline model, since the test period of the dataset was in its bull market, and the buy-and-hold strategy naturally wins. However, the model outperforms the triple exponential average indicator, as the second baseline model, in terms of cumulative profit. In another DBNs-related study, Wang et al. (2017) investigate the potential of DBNs in predicting stock prices and generating profits in the stock market. They model the stock prices of NASDAQ and the Stock Exchange of Thailand using five years of historical intraday closing-price data. The profit generated by their model is compared with several benchmarks, including the buy-and-hold strategy, and it statistically outperforms the benchmark strategies.

Regarding studies about predicting price movement direction, to detect the upward and downward movement of stock indices, Zuo and Kita (2012) utilised BNs for the task. The accuracy and total profit of the BN are compared with psychological line and trend estimation algorithms. The psychological line in the study uses a predefined formula to analyse the prices of previous days and provide insights on whether the price will increase or decrease on the next day. The proposed model demonstrates an accuracy rate of around 60%, which is approximately 10% higher than the other investment strategies investigated in the study. BNs also generate much greater profit than baseline models. In addition, Malagrino et al. (2018) use BNs to investigate the impact of foreign markets on Brazil’s main stock exchange index (iBOVESPA). Two different BN topologies are designed using 24- and 48-hour timeframes, with each BN predicting the index’s next-day closing direction (up or down). The study evaluates the performance of each BN using sets of one, two, and three different indices from three continents. The results reveal that the 24-hour BNs achieve a mean accuracy rate of approximately 71%, which is better than the 68% accuracy rate achieved by its 48-hour counterpart model. Additionally, the study found that the BN models’ performance improves when fewer indices are included in the BNs.

3 Dynamic Bayesian networks

BNs are a powerful tool for modelling complex systems and can be used to extract the underlying causal relationships between variables (Heckerman, 2008). They are a type of probabilistic graphical model (PGM) used to represent stochastic relationships between random variables through directed acyclic graphs (DAGs) (Alameddine et al., 2011). They are based on the Bayesian theory of conditional probability and can be used for reasoning, prediction, and decision-making in a wide range of fields from environmental management (Death et al., 2015), maritime accidents (Kuzmanić Skelin et al., 2021) to wind energy industry (Adedipe et al., 2020) and credit assessment (Masmoudi et al., 2019). In a BN, nodes represent variables, and directed edges represent the conditional dependencies between variables. Each node in the network is associated with a probability distribution that describes the probabilities of possible values of that variable given the probabilities of values of its parent variables. These joint probability distributions over the nodes are represented by conditional probability tables (CPTs) for each node (Rohmer, 2020). BNs can be utilised to perform inference, which involves using the network structure of the variables in the system to make predictions or draw conclusions about the state of the system given some evidence or observations. In particular, the capacity of a visual representation of dependencies in a system using DAGs makes BNs a versatile tool for communicating some properties of the system. They can handle missing data and hidden variables, and on top of that training of BNs inherently allow for avoiding overfitting (Heckerman, 2008), which is a common problem in ML modelling.

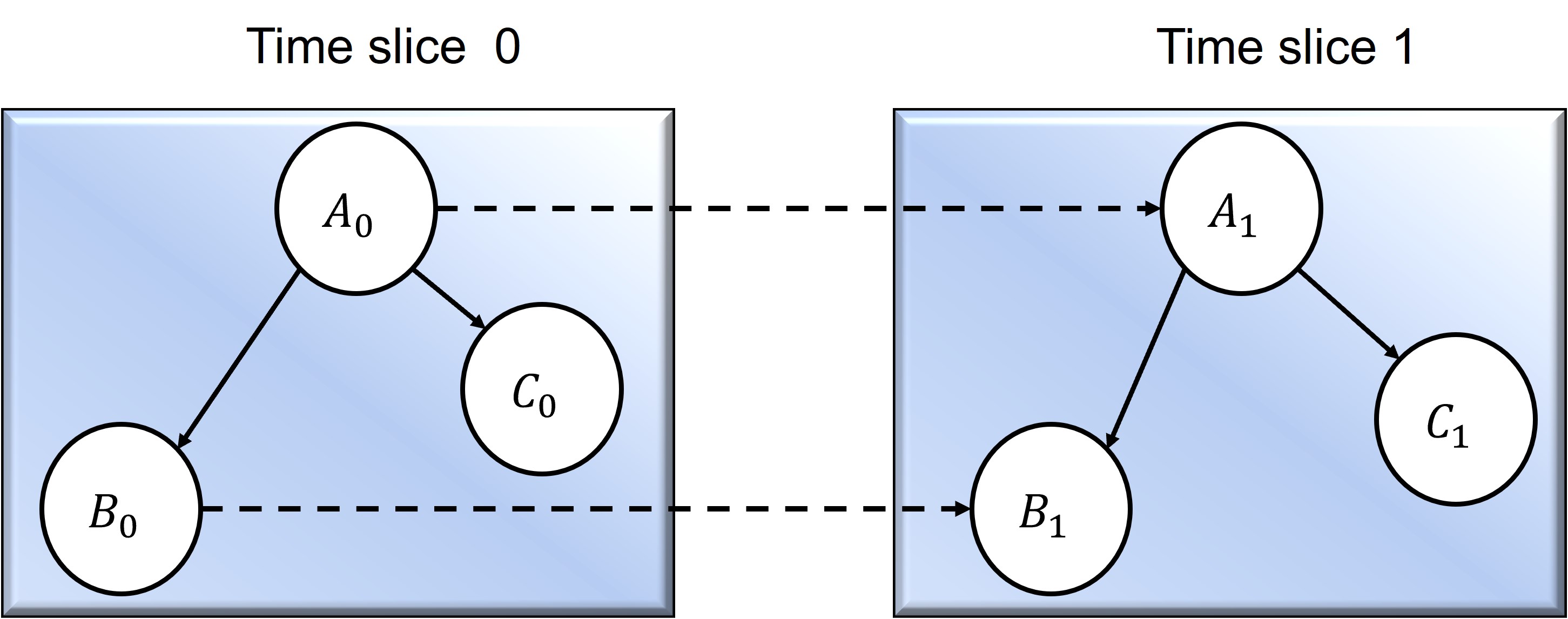

DBNs are a type of BNs that can be used to model systems that change over time. Unlike static BNs, which only model dependencies between random variables at a single point in time, DBNs represent the temporal evolution of a system by establishing time-dependent dependencies between variables. In a DBN, each node represents a random variable at a specific point in time, and directed edges model the conditional dependencies between variables at the same or different time intervals (Shiguihara et al., 2021). A DBN is composed of two parts: time slices and inter-slice arcs. A time slice represents the states of the system at a given time and is essentially an identical BN at each time step. Within a time slice, the relationships between variables are represented by intra-slice arcs. The second component of a DBN is inter-slice arcs, also known as temporal arcs. These arcs represent the relationships between variables within a time slice or between certain variables across time slices. These components are illustrated in Figure 1(a). In addition, a basic assumption in constructing DBN is that the system follows a first-order Markov process, in which the state of the system at time only depends on its state at the previous time slice . In other words, future temporal nodes at time are only connected to corresponding nodes at the previous time slice (Portinale et al., 2010; Gao et al., 2014; Wu et al., 2015).

The process of building a DBN is iterative. Each time slice requires the same structural form as the previous or next slice, and time slices reflect the change in probabilities of the variables (Zhang et al., 2023). In particular, converting a static BN to a DBN involves three main steps. The first step is to modify the BN structure to incorporate the dynamics of the process. Next, one needs to introduce a time parameter in the definition of the states of all nodes to describe the temporal relationship. Finally, the static BN is repeated for time steps and the belief in the system is updated for the given time step (Voronenko et al., 2020; Amin et al., 2019).

From a mathematical perspective, a DBN is a pair (,), where is a BN model that defines the prior network, and is a two-time slice temporal BN (2TBN) which defines the relationship between two consecutive time slices through a transition probability table (Zhang et al., 2023; Wu et al., 2016). The joint probability distribution of a DBN can be demonstrated as

where is the node at time step , and represents the parent nodes of in the corresponding DAG. Furthermore, the conditional probability indicates that the transition probabilities are a product of the CPTs in the 2TBN, where is the full-time horizon ( in this study), and in the number of nodes in . Once the probabilities on nodes in a DBN are determined through the joint probability distribution calculation, different forms of reasoning and inferencing such as prediction, diagnosis, or decision-making can be performed.

4 The conceptual framework of data features and the proposed model

This section outlines the framework for the development of a prediction model for price movement directions. It briefly discusses the rationale for selecting particular features for this study. Then, a detailed explanation of the process of developing a DBN based on these features is provided.

4.1 Conceptual model of data features

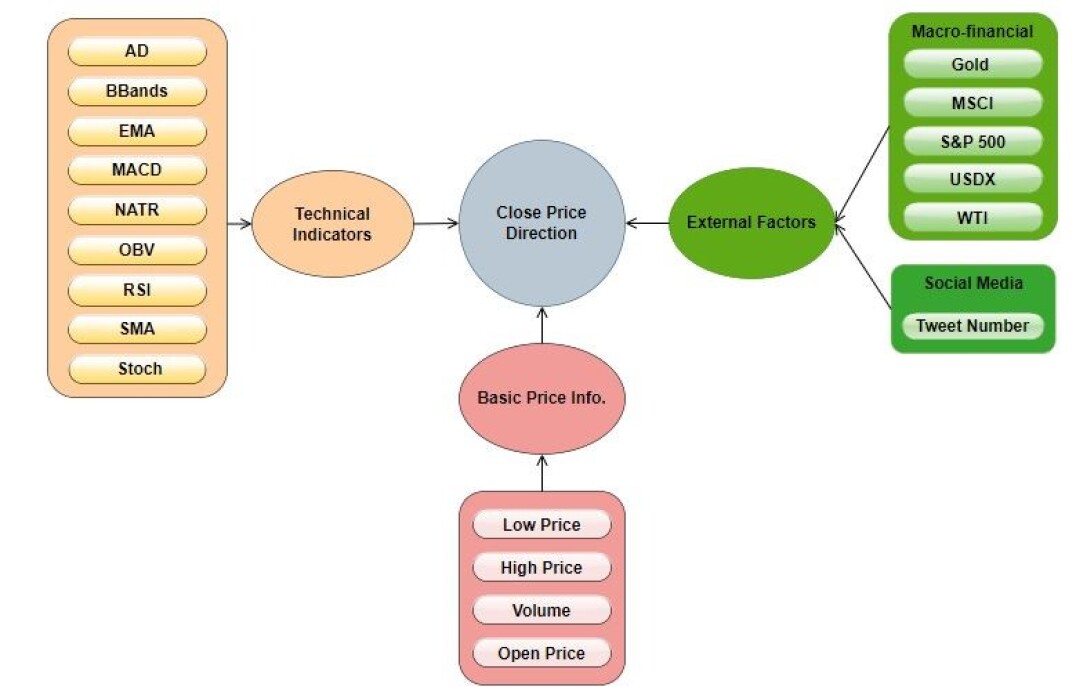

For the purpose of predicting price directions of altcoins, three distinct categories of features are investigated to analyse their impact on the prediction accuracy of our proposed model. Figure 2 presents the conceptual framework of our proposed cryptocurrency price prediction model that explains the structure of the selected groups of features, which we demonstrate here.

The first group of features incorporates basic price data, including daily open, high, low, and close prices, along with trading volume (OHLCV). This group of features provides a comprehensive overview of a financial asset’s status on a given day (Motard, 2022).

Apart from the raw price and volume data, price movements can be predicted using technical indicators (Alonso-Monsalve et al., 2020). Technical indicators are derived from price data using mathematical formulas and are widely utilised to identify trends and buy and sell signals in financial markets (Manujakshi et al., 2022). By including technical indicators in our study, additional insights into the prediction of potential directions of price movements can be gained and, consequently, enhance the accuracy of the proposed model. However, considering the complexity of financial data, relying on a single technical indicator may not yield reliable trading strategies. Therefore, we use a combination of various types of technical indicators in our proposed model, including accumulation/distribution (AD), Bollinger bands (BBands), exponential moving average (EMA), on-balance volume (OBV), moving average convergence/divergence (MACD), normalised average true range (NATR), relative strength indicator (RSI), simple moving average (SMA), and stochastic oscillator (Stoch). These technical indicators provide valuable insights into various aspects of a financial market, such as the strength of upward and downward trends, potential trend reversal signals, as well as price volatility. Further references on details and applications of these technical indicators can be found in (Alonso-Monsalve et al., 2020; Srivastava et al., 2021).

Additionally, cryptocurrency prices can be affected by external factors that are not directly related to the cryptocurrency price data. External factors contain adoption and attractiveness along with macro-financial drivers (Ciaian et al., 2016; Poyser, 2019). The adoption and attractiveness, rooted in behavioural finance,333Behavioural finance is a relatively new school of thought in the finance domain that describes the psychological reasons behind the decision-making of investors (Königstorfer and Thalmann, 2020). is described as the investment attractiveness of the cryptocurrency market and intentions of investors to utilise this new financial product (Ricciardi and Simon, 2000). In the context of cryptocurrency adoption and attractiveness, sentiment analysis of posts on Twitter is popular social media data for determining public opinion about the market (Chursook et al., 2022). Therefore, we include the daily tweet numbers associated with each altcoin in the study. Regarding macro-financial factors, several traditional financial assets and indices from diverse economic classes, such as currencies, commodities, and stock indices, are frequently selected in cryptocurrency and financial literature (Corbet et al., 2018; Charfeddine et al., 2020; Ji et al., 2018). Hence, gold, the US dollar index (USDX), Standard & Poor’s 500 Index (S&P 500), MSCI, and West Texas Intermediate (WTI) are selected as macro-financial factors in this study. A short summary of these features is provided in Table 1.

| Type | Feature | Description | Time window |

|---|---|---|---|

| Macro-financial | Gold | The gold spot market price in US dollars | Daily |

| MSCI | A market capitalisation-weighted index comprising 1,546 companies from around the world | Daily | |

| S&P500 | A market capitalisation-weighted index of the 500 leading publicly traded companies in the US | Daily | |

| USDX | The value of the US dollar relative to a basket of six foreign currencies | Daily | |

| WTI | A popular oil price benchmark | Daily | |

| OHLVC | Close price |

The price at which a cryptocurrency is last

traded in a trading interval |

Daily |

| Low price | It is a cryptocurrency’s lowest trading price in a trading interval | Daily | |

| High price | A cryptocurrency’s highest trading price in a trading interval | Daily | |

| Open price | The price at which a cryptocurrency is first traded in a trading interval | Daily | |

| Volume | The total number of cryptocurrencies traded in a trading interval | Daily | |

| Social media | Tweet number | The number of daily tweets associated with a cryptocurrency | Daily |

| Technical indicators | AD | It uses volume and price to calculate the money flow into or out of a security and determines the accumulation or distribution of funds by traders. | Last Period |

| BBands | It consists of a band of three lines, usually SMA in the middle, and the upper and lower bands are positioned two standard deviations away from the SMA. | 5 days | |

| EMA | It uses moving averages; however, it applies more weight to recent data points to reduce the data lag. | 10 days | |

| MACD | MACD measures two EMAs (typically EMA for 12 and 26 days). |

Fast period=12

slow period=26 signal period=9 |

|

| NATR | It is a metric to measure volatility. | 14 day | |

| OBV | OBV is a cumulative indicator that measures the buying and selling pressure. | Last period | |

| RSI | It indicates overbought and oversold conditions by comparing the magnitude of gains and losses in stocks. | 14 days | |

| SMA | The SMA average data points for a given period. | 10 days | |

| Stoch | It is a range-bound momentum indicator that potentially determines overbought and oversold situations. | 14 days |

4.2 Developing a DBN model for price prediction

In this study, we employ DBNs to enhance the prediction of altcoin price movement direction. Initially, we use static BNs to uncover the structure of causal relationships within the training data, enabling us to capture the connections between price features and generate probability distributions for the states of the system. However, to accommodate the cryptocurrency market’s dynamic nature and its time series data, we convert the static BNs into DBNs. Our proposed DBNs incorporate a time step of the last five days, allowing the model to incorporate price data from the preceding five days to predict today’s price direction. By considering this historical information, we aim to improve the accuracy of our predictions and account for the evolving market conditions.

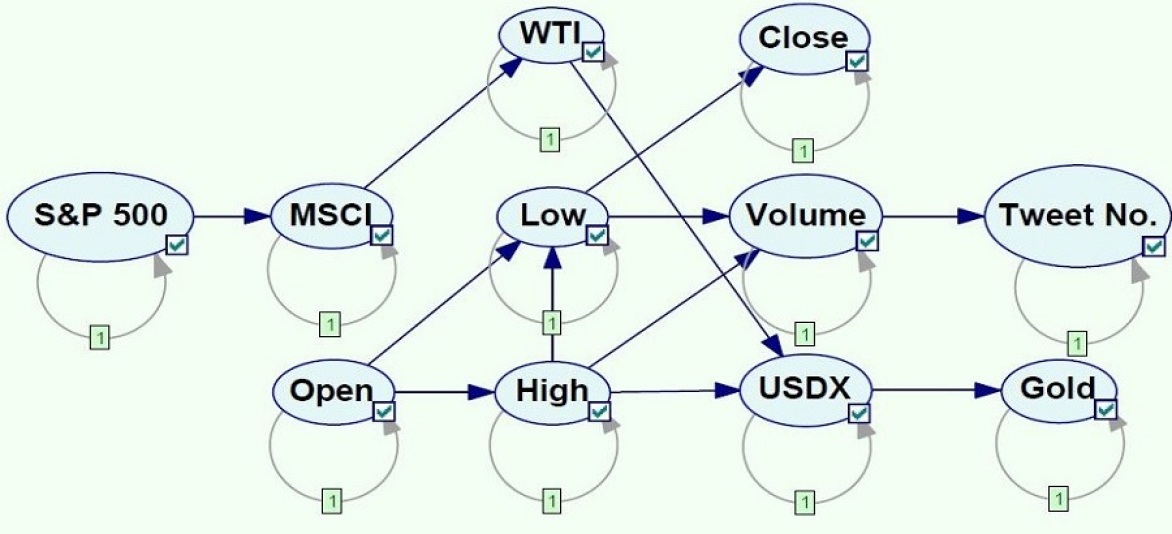

The architecture of our proposed DBN is shown in Figure 3. To simplify the visual representation of the model, the names of the selected feature groups are abbreviated. Accordingly, TI represents technical indicators, Price is the OHLV features, SM represents social media, which is the tweet number in this study, and finally, FA stands for financial assets. For the purposes of this study, it is assumed that each feature group is independent of one another. It means that there is no inter-slice arc between two consecutive time frames. However, features may be connected within a time frame based on the causal structure in the data learned using static BNs.

5 Experimental design

The study aims to predict the daily price direction of five altcoins using DBNs. Additionally, it explores the impact of various combinations of feature groups on the model’s price prediction performance. To achieve this goal, four distinct feature groups are created as follows:

-

•

The first combination includes only the OHLCV data.

-

•

The second combination incorporates OHLCV with external price factors containing Twitter data and traditional financial assets.

-

•

The third combination uses OHLCV data along with nine technical indicators.

-

•

The fourth combination includes all features.

It is important to note that traditional financial asset data is generally unavailable on weekends, unlike cryptocurrencies and Twitter data. Therefore, weekday data points from these three sources are aligned to create a unified database for each altcoin, enabling numerical analysis. Table 2 outlines the different combinations of features with each combination assigned a unique number, ranging from 1 (with the fewest number of features) to 4 (with the largest number of features). After creating the four groups of features, they were preprocessed using the min-max normalisation method to balance the input data ranges. Min-max normalisation has been reported to deliver satisfactory performance in supervised and unsupervised learning tasks Wijaya et al. (2021).

| Combination No. | Groups of features | No. of features |

|---|---|---|

| 1 | OHLCV | 5 |

| 2 | OHLCV and external factors | 11 |

| 3 | OHLCV and technical indicators | 15 |

| 4 | OHLCV, external factors, and technical indicators | 23 |

Since the price data are continuous, and we predict future price directions, which are categorical variables, it is necessary to categorise the data prices into several market states. An appropriate choice of market states is dependent on the model choice or data, and it can impact the model’s performance. For instance, there are studies that use three states for market trends, including downward, steady, and upward, while others may consider two additional trend states of strong downward and strong upward. Based on the results presented in Amirzadeh et al. (2023), the two states of ‘Downward’ and ‘Upward’ provide the best model performance for BNs applied on cryptocurrencies. Consequently, the data is labelled into these two states for market data. Specifically, each data record was labelled as ‘Downward’ if today’s record value was lower than the previous day’s and ‘Upward’ otherwise. Equation 1 outlines the labelling approach for the data records.

| (1) |

where means the data record of the next day, and is the data record of the current date. Furthermore, the labelled data was split into training and testing sets, with 67% of the data allocated for training and 33% for testing. This split ratio is widely adopted for data mapping and independent accuracy assessment Lyons et al. (2018).

To implement the DBNs, we utilised the GeNIe software package through the PySMILE wrapper. PySMILE is a Python-based package that allows for Bayesian inference and modification of the Bayesian network using Python (BayesFusion, 2017). Therefore, we fed the training set of each feature group into our implemented PySMILE code to learn the structure and parameters of the corresponding DBNs. Once the DBNs were constructed from the training set, a five-day moving window was generated from the test set and fed as inputs to the DBNs to predict price directions. Specifically, the last five-day data were used as inputs to the DBNs to predict the closing price on the fifth day.

We compare the prediction accuracy of our proposed DBNs models against two baseline models, namely autoregressive integrated moving average (ARIMA) and support vector machine (SVR). ARIMA and SVR are well-known and frequently used models for accurately predicting time series in various nonlinear systems, including economic and financial systems (Fawzy et al., 2020; Lee et al., 2019). We employed GridSearchCV (Alhakeem et al., 2022) to tune the hyperparameters of the SVR model and grid search logic (Chivukula and Lakshmi, 2020) to adjust the parameters of the ARIMA model to obtain the best predictions. Moreover, since the outputs of these models are continuous values, we labelled the price prediction as upward or downward based on Equation1.

To evaluate the performance of the models, we compare the predictions generated by DBNs, ARIMA, and SVR models to the actual price directions using the precision metric. In order to ensure a consistent and standardised analysis of the numerical findings, we decide to utilise a single metric, precision, despite the practice of employing multiple metrics in certain publications. The precision metric measures the number of true positives when the model correctly predicts the positive records relative to the total number of positive predictions (Quiroz and Alférez, 2020). Mathematically, the precision metric is defined as follows.

where TP is the number of true positives, and FP is the number of false positives.

5.1 Data

For the investigation of altcoins in this research, Binance Coin, Ethereum, Litecoin, Ripple, and Tether are selected based on several criteria. Firstly, they have consistently ranked among the top ten cryptocurrencies in terms of market capitalisation for several years, regardless of their popularity. Collectively, their market capitalisation represents over 30% of the cryptocurrency market at the beginning of 2023, which is a significant proportion of the cryptocurrency market. Additionally, using altcoins with an extended data period allows for a robust analysis of the unpaired correlations between these cryptocurrencies and traditional financial assets with a decades-long history of data. Therefore, one of the criteria for selecting altcoins is a minimum trading period of at least 1,100 daily data records, equivalent to around four years. It also allows for statistically significant analysis supported by the historical price data of these altcoins.

To obtain the daily price data for both altcoins and traditional financial assets, we use the Yahoo Finance website (https://finance.yahoo.com/). This data is collected using the yfinance Python package. Additionally, we extract the daily tweet count associated with each altcoin from www.bitinfocharts.com. The analysis of the impact of the social media data on Tether is excluded because this coin’s daily tweet data is unavailable. Descriptive statistics of close price data of altcoins and traditional financial assets are presented in Table 3. The differences in averages in column one are the main driver to scale the data as explained in the previous section.

| Mean | Std. Dev. | Min. | Median | Max. | Obs. | |

|---|---|---|---|---|---|---|

| Binance coin | 151.56 | 187.21 | 4.53 | 27.22 | 675.69 | 1171 |

| Ethereum | 1150.13 | 1225.25 | 884.31 | 474.21 | 4812.09 | 1206 |

| Litecoin | 101.55 | 64.61 | 75.172 | 23.47 | 377.39 | 1206 |

| Ripple | 0.52 | 0.33 | 0.14 | 0.38 | 2.456 | 1184 |

| Tether | 1.01 | 0.01 | 0.97 | 1.02 | 1.09 | 1232 |

| Gold | 16.79 | 4.5 | 8.8 | 16.09 | 28.17 | 1464 |

| MSCI | 2360.99 | 410.09 | 1596 | 2197.15 | 3242.3 | 1464 |

| S&P 500 | 3265.73 | 718.52 | 2237.4 | 2985.61 | 4796.56 | 1464 |

| USDX | 96.36 | 4.61 | 88.59 | 96.13 | 114.11 | 1464 |

| WTI | 61.91 | 19.02 | -37.63 | 58.82 | 123.7 | 1464 |

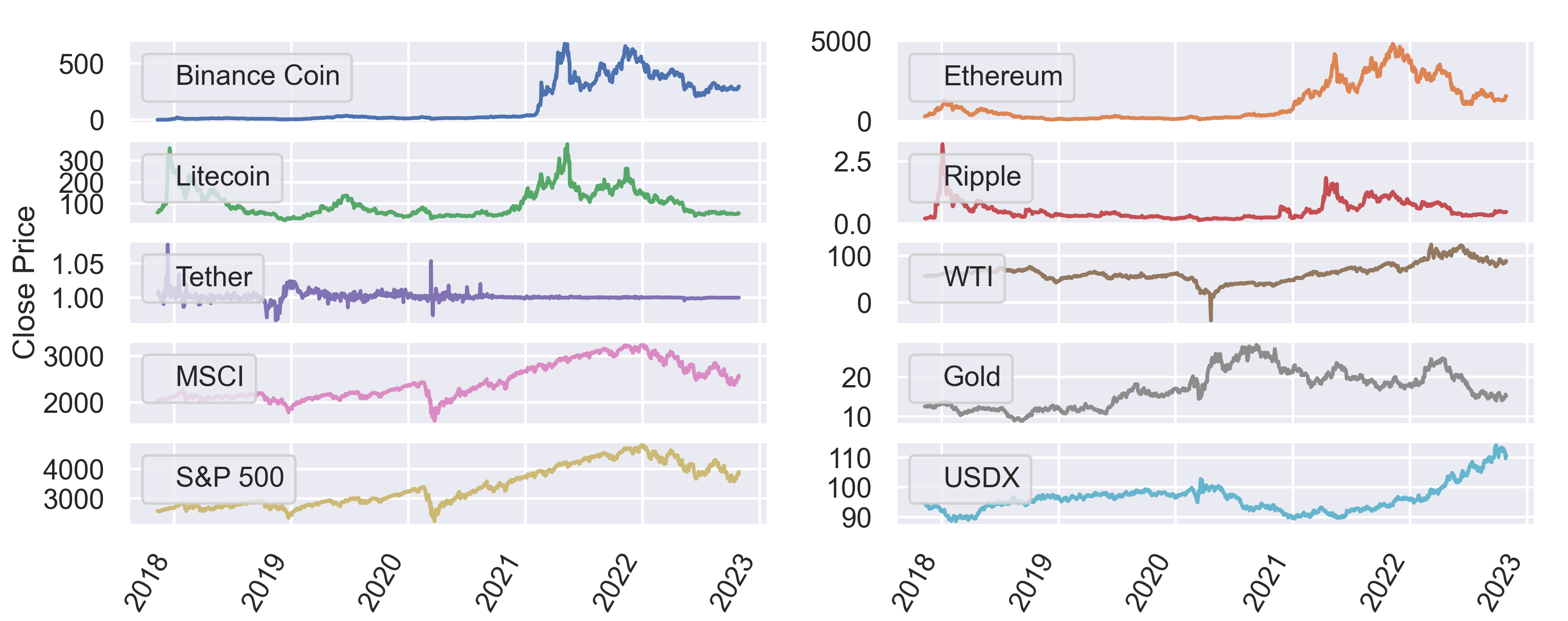

Furthermore, Figure 4 shows the close prices of altcoins and traditional financial assets from January 2018 to October 2023. The plots show that all traditional financial assets experienced growth during this period. However, the close price plots of Binance Coin and Ethereum demonstrate a relatively steady beginning, while Litecoin and Ripple experienced a considerably unstable period before a period of stability. Also, in 2021, all coins experienced high variation in their close prices except for Tether due to its functionality as a stablecoin. For instance, Ethereum’s close price variances were 44931.208 and 920876.95 before 2021 and after 2021, respectively. As a result, a high level of prediction error can be expected due to the increasing variances in data.

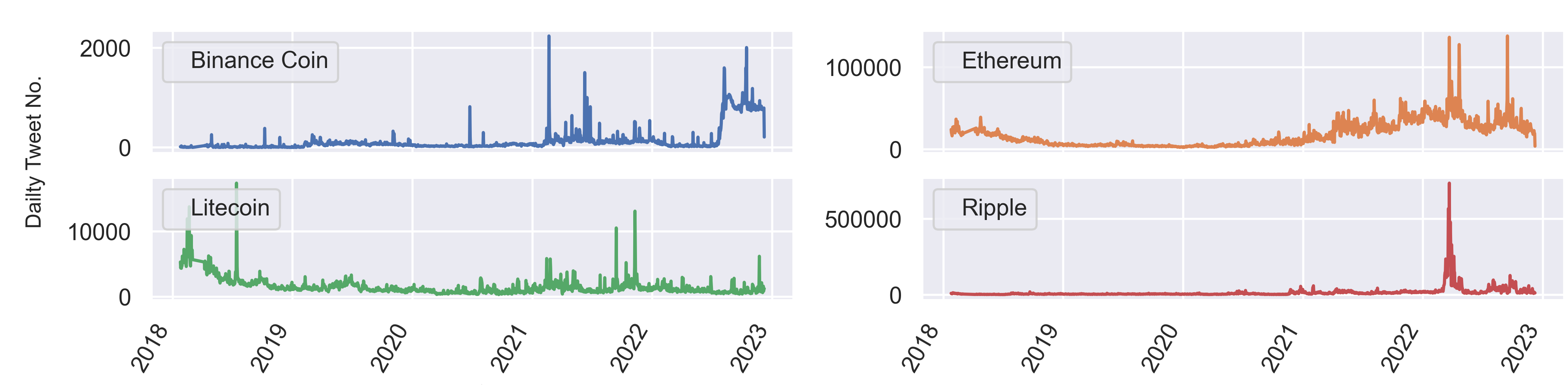

Table 4 provides summary statistics for the daily tweet numbers associated with each altcoin in this study between January 2018 and October 2022, and Figure 5 visually represents the statistics visually. As previously mentioned, daily tweet data associated with Tether is not available on www.bitinfocharts.com, and hence Tether is not present in Table 4 and Figure 5. As seen in Figure 5, despite several spikes, the trends of tweet numbers are relatively consistent compared to the price data in Figure 4. Moreover, the level of variances is higher during 2021 in comparison to other periods in the study. For example, the tweet number of Ethereum exhibited variances of 36959083.64 and 219624498.05 before and after 2021, respectively.

| Mean | Std. Dev. | Min. | Median | Max. | |

|---|---|---|---|---|---|

| Binance coin | 120.05 | 215.83 | 1 | 55 | 1601 |

| Ethereum | 17912.37 | 15881.35 | 2418 | 12058 | 138220 |

| Litecoin | 1544.24 | 1301.59 | 360 | 1172 | 13778 |

| Ripple | 17233.21 | 39085.54 | 2362 | 7498 | 735252 |

6 Results and discussions

We evaluate the effectiveness of our proposed DBN in predicting cryptocurrency price movements using precision as our evaluation metric. To assess our models’ efficacy, we compare their prediction results against those of baseline models, namely ARIMA and SVR. Furthermore, we investigate the impact of feature engineering on improving our DBNs’ performance. The experiments are conducted on a Windows 10 Enterprise operating system, running an Intel i7-Core(TM) CPU @ 1.90GHz, 2.11 GHz processor, and 16.0 GB of RAM. We implement SVR and ARIMA using two Python libraries, namely sklearn, and statsmodels.

Table 5 presents a summary of the performance results for the proposed DBNs as well as for ARIMA and SVR models, in predicting the close price of a coin for the next day. The table considers different feature combinations, and the ‘Feature group No.’ is defined in Table 2. ARIMA and SVR models use only the close price time series data of altcoins. The best-performing DBN for each group of features is reported in the ‘Best-performing DBN’ column. Additionally, the ‘Average for feature group’ row presents the average precision of each feature group for all altcoins.

| Model | DBN | ARIMA | SVR | ||||

|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | Best-performing DBN | Close price | Close price | |

| Binance Coin | 59.27 | 71.02 | 73.63 | 69.98 | DBN with (3) | 61.81 | 57.92 |

| Ethereum | 73.86 | 68.02 | 71.83 | 71.83 | DBN with (1) | 63.27 | 59.54 |

| Litecoin | 64.21 | 70.56 | 70.56 | 70.56 | DBN with (2) | 69.35 | 51.51 |

| Ripple | 72.87 | 66.67 | 77 | 72.87 | DBN with (3) | 48.64 | 46.35 |

| Tether | 57.57 | 57.57 | 55.09 | 50.12 | DBN with (1) | 39.81 | 41.54 |

| Average for feature group | 66.17 | 66.79 | 67.80 | 67.07 | 56.58 | 51.37 | |

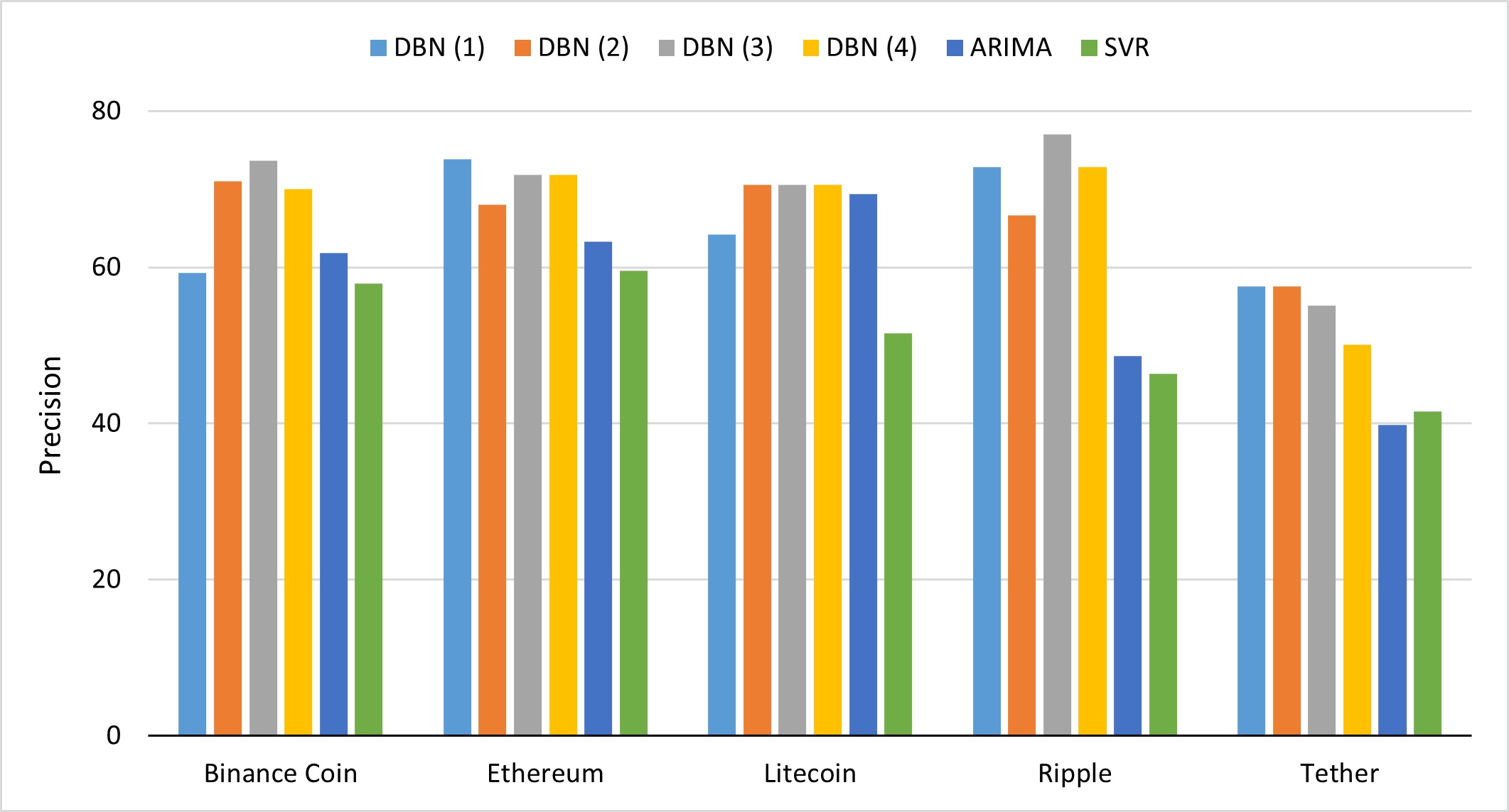

Table 5 summarises the effect of feature engineering on the performance of the DBNs used in this study. Columns (2) to (5) correspond to the different feature sets used for training the DBNs. Column (2) uses only OHLCV data, column (3) combines OHLCVs with external factors, column (4) uses OHLCVs and technical indicators, and column (5) uses all available features for training DBNs as defined in Table 2. As shown in Table 5 and Figure 6, there is no single DBN model that performs best for all the coins considered in the study. This result is consistent with other studies such as Valencia et al. (2019), indicating that different cryptocurrencies have varying specifications, and no one model can perform equally well on all of them. As one observation, the best performance for Ethereum and Tether are obtained using only OHLCV data, whereas the DBN with the full set of features never outperforms the other DBNs. Similar results are observed for Binance Coin and Ripple, where DBN (4) does not exhibit superior performance compared to other DBN models. This highlights the need for training a separate model for each coin and identifying the most influential set of features. In addition, to compare the different versions of DBNs, the last row of Table 5 provides the average precision of each model over all the altcoins in the study. Among the four different settings, the DBN with OHLCVs and technical indicators has a slightly higher average precision. Each of these two feature sets is also selected twice as the best-performing model, namely for Binance coin and Ripple.

In this study, the best-performing models for each altcoin were among the DBNs, and ARIMA and SVR never outperformed the best-performing DBN, despite their reputation in predicting time series data. However, as expected, there is no consensus on the best-performing model across all the altcoins. For Binance coin and Ripple, the best-performing model was a DBN trained with OHLCVs and technical indicators, while for Ethereum and Tether, the best-performing model was a DBN trained with only OHLCVs. It is worth noting that the performance difference between a DBN trained with only OHLCVs and the best-performing DBN was not significantly large for all the altcoins in the study. This can be attributed to the fact that technical indicators are derived from the OHLCV data using mathematical functions, and therefore, there is a considerable level of correlation between them.

According to the performance results presented in Table 5, the best-performing DBN consistently outperforms both ARIMA and SVR models. In fact, all versions of DBNs perform better than ARIMA and SVR except for a few minor cases. Only for Binance coin and Litecoin with DBN(1), the performance of ARIMA is slightly better than that version of DBN. Furthermore, the precision of ARIMA is generally better than SVR, except for Tether. As shown in Table 5, the precision results for Tether indicate that predicting this altcoin is more challenging than others, with a maximum precision of only . This conclusion is consistent with the plot of Tether in Figure 4, which shows that the coin has exhibited a steady and low-volatile behavior since 2021, making it difficult to learn about recent changes in the coin based on past movements. Moreover, among all the coins in this study, Ripple is the most predictable coin with a maximum precision rate of . This observation is in line with the close price plot of Ripple in Figure 4, where the coin exhibits similar volatility throughout the study period.

One of the aims of this research is to investigate the impact of different combinations of features on the performance of DBNs. It is observed that, on average, the combination of OHLCV and technical indicators yields the best results for all altcoins, with an average precision of . Conversely, DBNs built solely on OHLCV achieve the lowest performance, with an average precision of . However, it should be noted that adding more features to the DBN models does not always result in further improvement in precision and sometimes even decreases the performance. For example, the DBN model constructed with all features (Group No. 4) for Binance Coin has slightly lower performance () than the DBN model that only contains OHLCV and technical indicators (Group No. 3) with precision. This suggests that including external factors alongside other groups of features may negatively affect the precision of the DBN model for Binance Coin.

The influence of technical indicators on DBN performance varies among altcoins. For Binance Coin, Litecoin, and Ripple, introducing technical indicators to the basic DBN model (Group No. 1) significantly improves the model’s performance, while for Ethereum and Tether, it leads to a slight decrease in precision. In particular, using only Group No. 1 is sufficient for predicting Ethereum and Tether, as this group has the highest performance rate. It is worth noting that DBNs combining OHLCV and technical indicators (Group No. 3) consistently outperform those incorporating all features (Group No. 4).

The influence of external factors on the prediction performance of DBN models has mixed results. While introducing external factors (Group No. 2), which contains only tweet numbers and traditional financial assets, to the DBN model constructed by OHLCV improves the performances for predicting Binance Coin and Litecoin, it reduces the precision of the model outputs for Ethereum and Ripple. In the case of Tether, the performance of the DBN model remains unchanged between Group No. 1 and Group No. 2. Considering its DBN structure, these external factors do not influence the close price as they are isolated in the DBN model, and no arc connects them to OHLCV. Additionally, it should be noted that incorporating external factors along with OHLCV and technical indicators to construct all features does not consistently result in improved model precision. For example, in the case of Ripple, the DBN model constructed with all features (Group No. 4) has a lower performance than the DBN model constructed by combining OHLCV and technical indicators (Group No. 3). This indicates that not all external factors may have a significant impact on the prediction accuracy of the model. Hence, selecting the most relevant features is crucial for improving the precision of the DBN models. To facilitate a more comprehensive comparison of the discussed models, a visual representation of the results is presented in Figure 6.

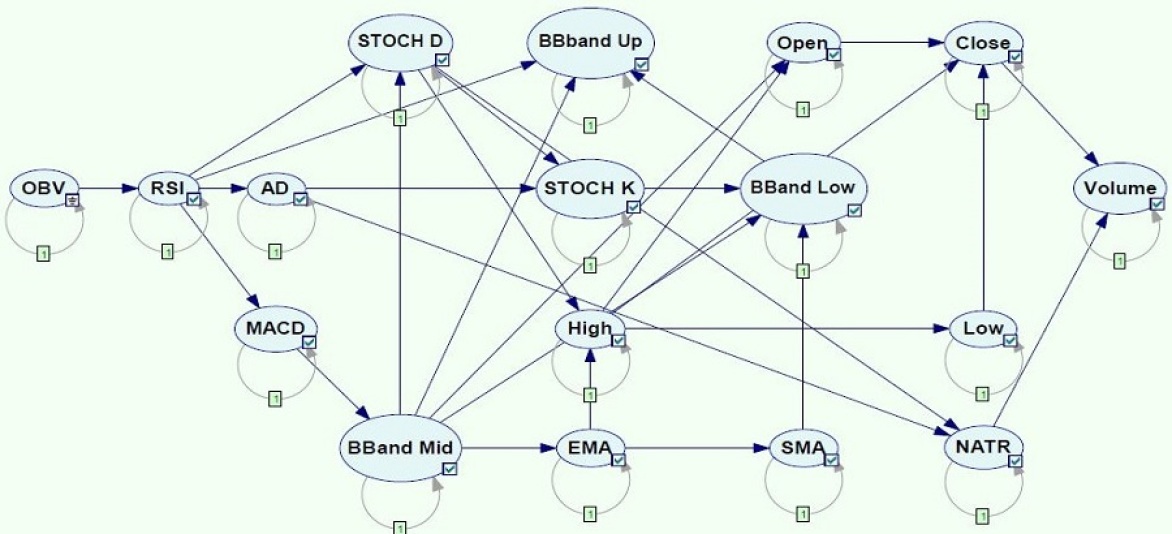

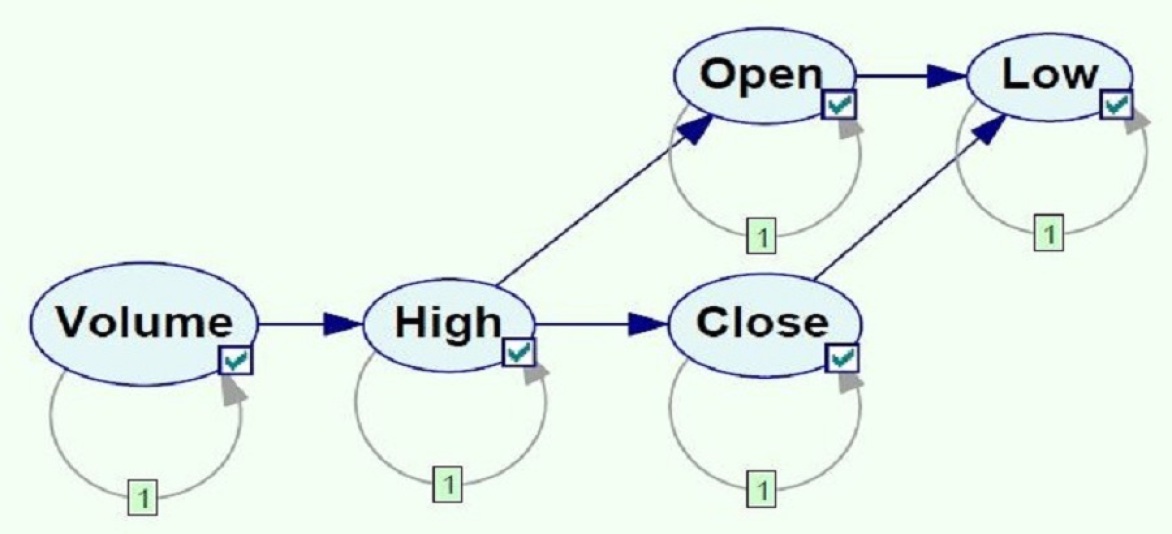

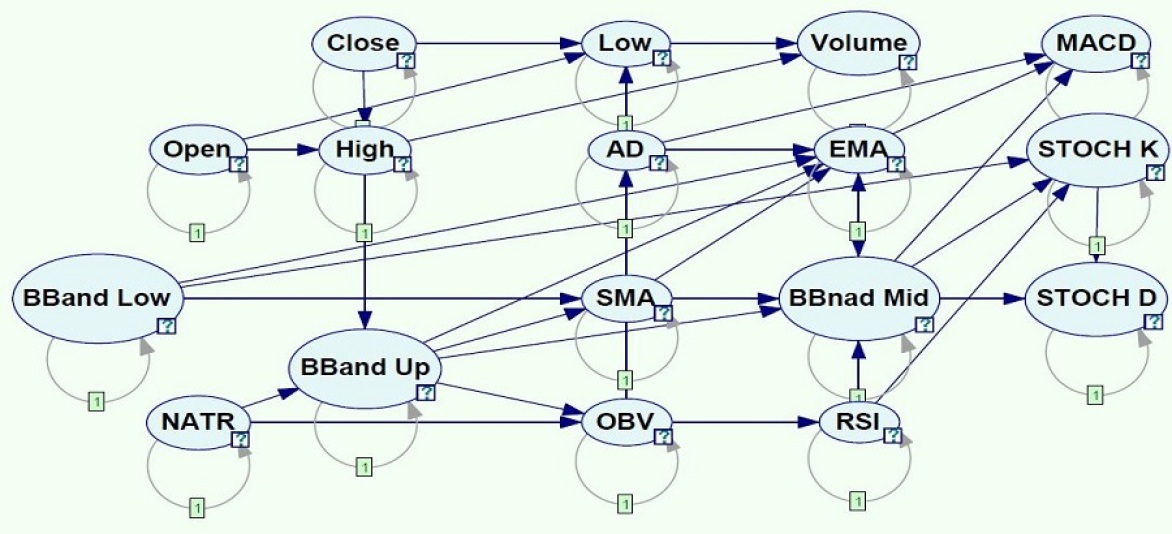

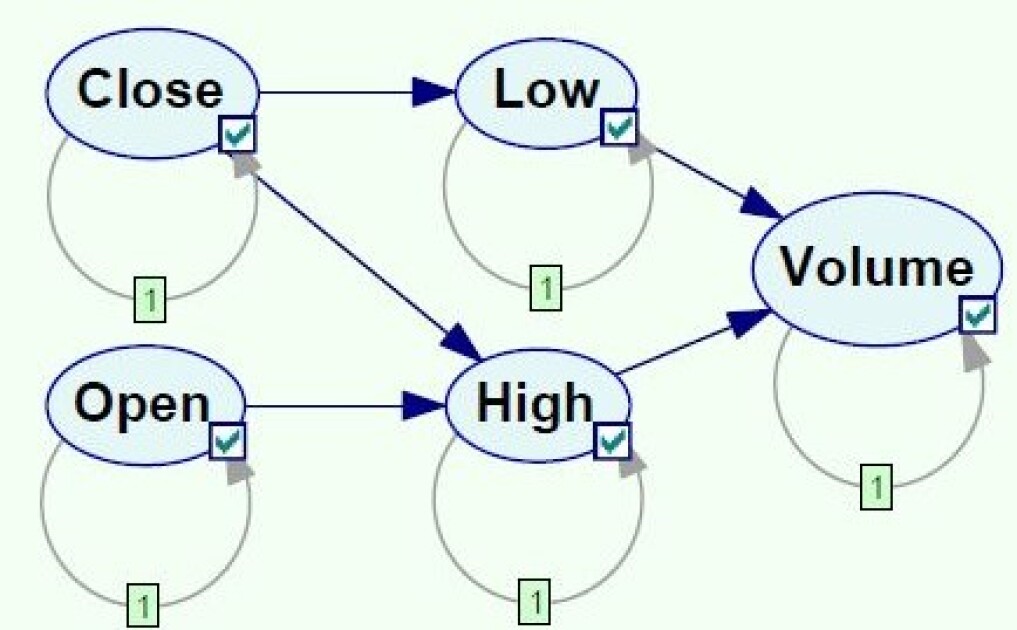

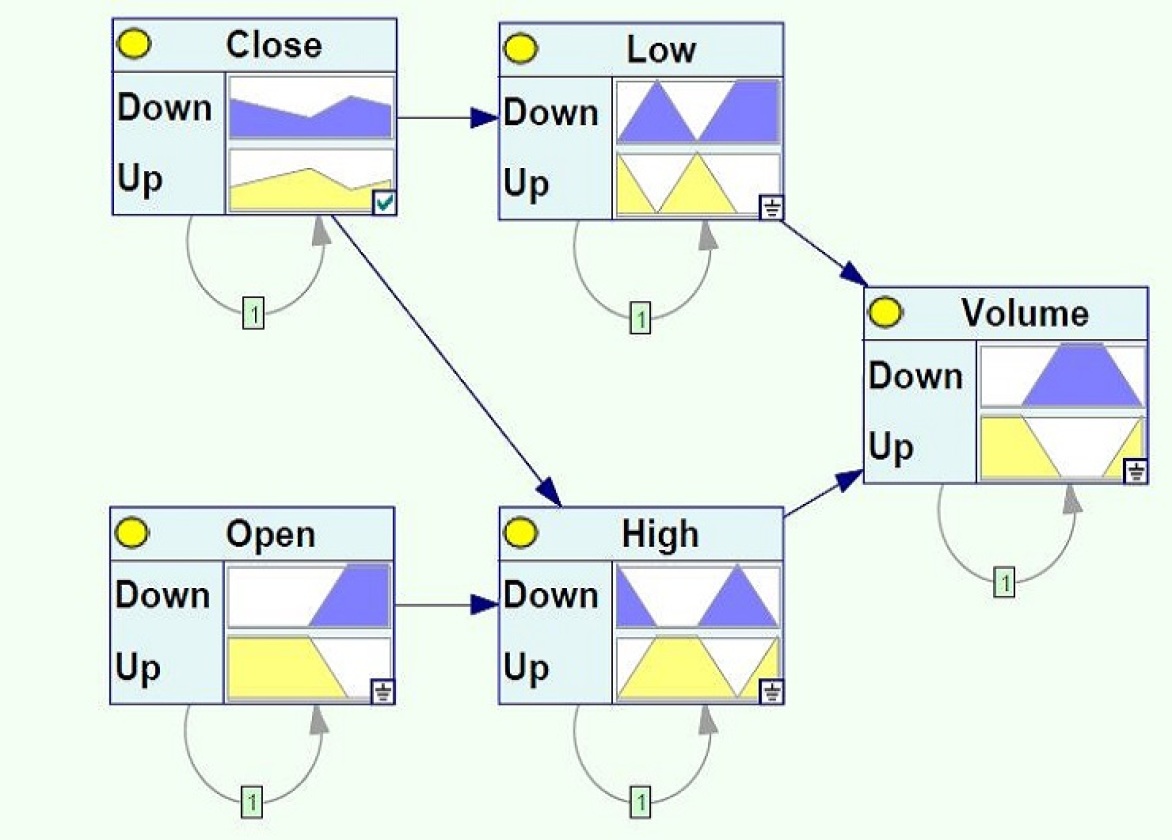

Figure 7 displays the best-performing DBNs based on the highest precision as the performance metric associated with each altcoin in Table 5. Binance Coin and Ripple achieve their best performance with DBN(3) (Sub-figures 7(a) and 7(d)), while Ethereum and Tether perform best with DBN(1) (Sub-figures 7(b) and 7(e)). Litecoin, on the other hand, stands out as the only coin with its best performance in DBN(2)(Sub-figure 7(c)).

Studying the structure of these DBNs in Figure 7 provides valuable insights for investors aiming to improve their predictions by identifying the key factors strongly associated with the close price of altcoins. The ability to analyse the structure and observe the interactions between nodes in a DBN distinguishes this method as an important tool from an explainability perspective in comparison to other deep learning techniques in AI. Notably, it is observed that all nodes within each DBN are interconnected, without any isolated nodes. This observation highlights the inherent interdependencies among these entities and their mutual influence on each other, specifically for the selected combination of feature categories. Moreover, the structure of DBNs varies across different altcoins, even within the same group of features, underscoring the unique characteristics of each altcoin. For instance, when examining Sub-figures 7(b) and 7(e), the causal relationships between the components of OHLCV features for Ethereum and Litecoin exhibit different dynamics. This distinction further emphasises the individual nature of each altcoin and the specific factors that influence their price movements.

The DBNs depicted in Figure 7 offer valuable insights into their structure, node interactions, and the factors influencing the target nodes. By exploring different angles, we can uncover unique characteristics associated with each DBN, aligning with the findings discussed in Section 1 of this paper on the characteristics of altcoins. For instance, in Subplot 7(a), the DBN representing Binance Coin, the root node OBV exhibits the highest influence, evidenced by its numerous descendants. Additionally, RSI and BBand mid nodes display significant interactivity, possessing the highest number of edges connecting them to other nodes. Contrastingly, Subplot 7(b), which showcases the best-performing DBN for Ethereum, reveals the Volume node as the root node with the most descendants. Among the other nodes, High exhibits the highest level of interactivity. Furthermore, regardless of the set of feature categories employed, the best-performing DBNs for Ethereum (Subplot 7(b)) and Tether (Subplot 7(e)) exhibit distinctly different structures in terms of node interactions. This emphasises the unique relationships between the nodes within each DBN and underscores the influence of specific factors on the price dynamics of Ethereum and Tether. The same argument is valid for Binance coin (Subplot 7(a)) and Ripple (Subplot 7(d)) as they share the same category of features with completely different dynamics among their respective nodes.

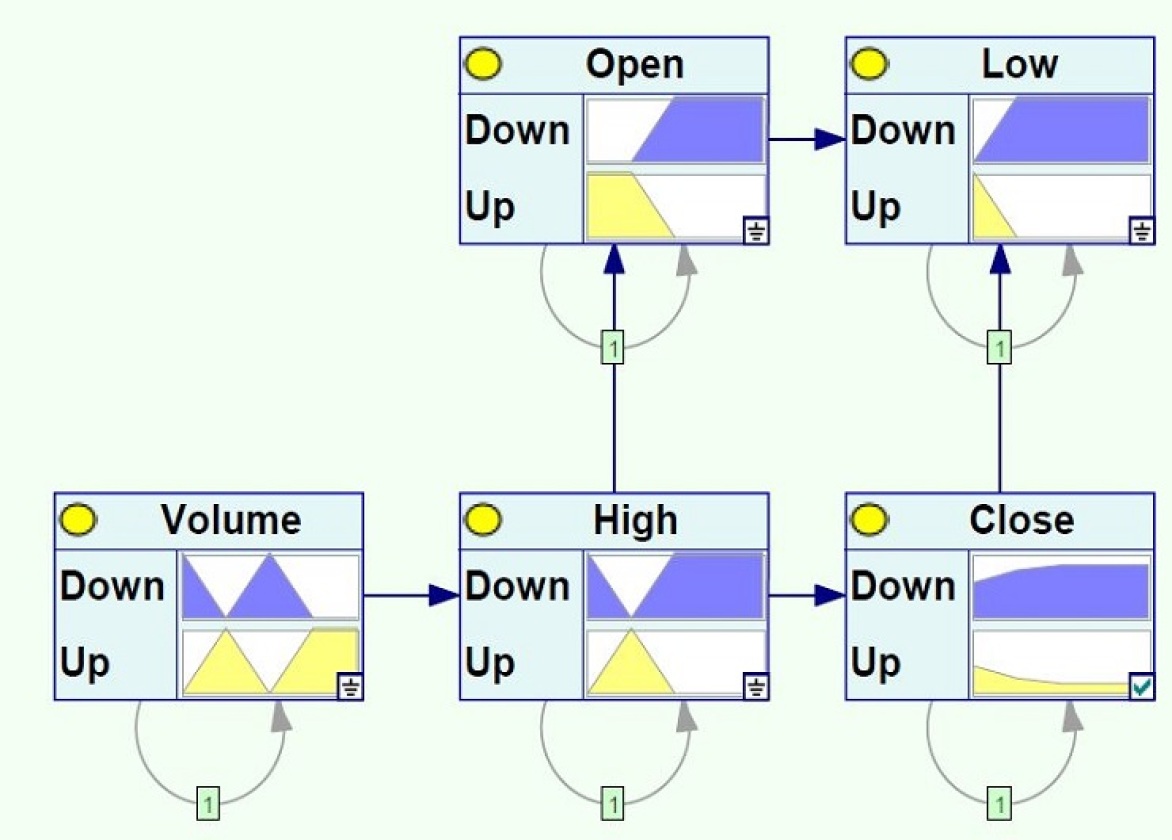

The best-performing DBNs for Ethereum and Tether, as shown in Table 5, utilise OHLCV data as their feature group. Additionally, these networks, illustrated in Subplots 7(b) and 7(e), respectively, exhibit the smallest number of nodes compared to the other networks. This characteristic makes them suitable for further visual examination of the interactions between their nodes. To analyse potential scenarios, we fix the states of the nodes, excluding the close node, and observe the corresponding changes in probabilities for the target node. Summarising the scenario presented in Table 6, Subplots 8(a) and 8(b) illustrate the changes in the close price. Our objective is to predict the direction of movement in the close price for the next day. In both cryptocurrencies, the probabilities of the close nodes changing to the down state, shown in purple, dominate. Therefore, the predictions of the DBNs indicate a downward movement for both coins. Notably, the probability of the close state being down is higher for Ethereum compared to Tether.

| Crytptocurrency | Feature | Five day movement scenario | ||||

|---|---|---|---|---|---|---|

| Ethereum | Open | Up | Up | Down | Down | Down |

| High | Down | Up | Down | Down | Down | |

| Low | Up | Down | Down | Down | Down | |

| Volume | Down | Up | Down | Up | Up | |

| Tether | Open | Up | Up | Up | Down | Down |

| High | Down | Up | Up | Down | Up | |

| Low | Up | Down | Up | Down | Down | |

| Volume | Up | Up | Down | Down | Up | |

7 Conclusions and future directions

The aim of this research is to explore the efficacy of DBNs in predicting the future price movement directions of five popular altcoins. The findings of this study have the potential to create a reliable decision-support system that can be used to enhance the accuracy of investment decisions and optimise trading strategies. The study demonstrates that DBNs outperform the two baseline models, ARIMA and SVR, for all altcoins in this study. Since different coins are affected differently by the nature of market dynamics, there are inconsistencies in DBN performance across the altcoins. In particular, the results show that DBNs exhibit higher prediction accuracy for Ripple and Ethereum, while it is lower for Tether.

Our study also investigates the impact of feature selection on model performance. Incorporating different combinations of four groups of Twenty-three features, our findings indicate that feature combinations yield mixed results for each altcoin. While the combination of basic price information and technical indicators generally produces the most accurate predictions, basic price information achieves the lowest prediction score among the group of features. The results highlight the importance of carefully selecting and incorporating relevant features to optimise the performance of ML models in predicting altcoin prices.

Currently, there is limited knowledge and experience of the potential capacity of DBNs in predicting cryptocurrency prices, and further research is required to understand the effectiveness of this approach in proposing profitable trade strategies. One potential research direction is to combine expert elicitation with learning DBNs. Incorporating expert opinions alongside data-driven approaches may reduce expert opinion’s inherent subjectivity and dependence on large-scale data. It could eventually lead to more accurate predictions of cryptocurrency price movements using DBNs. While our research focuses on external factors as a group of features for cryptocurrency price direction prediction, there could be a promising research direction for incorporating internal factors of the cryptocurrency market, such as blockchain information, to improve the accuracy of predictions of DBNs.

There are several factors to consider when designing an ML prediction model, and the choice of data frequency is important because it can significantly impact the performance of ML models. In this study, we use intraday price data for our predictions. However, using higher frequency data, such as four hours or one hour, could potentially lead to different results for DBNs’ precision. In particular, altcoins can behave differently in different time frames, especially in bear or bull market conditions. As a result, another potential research direction is to explore different data frequencies along with market conditions and their impacts on the performance of DBNs in price prediction.

References

- \bibcommenthead

- Gajardo et al. (2018) Gajardo, G., Kristjanpoller, W.D., Minutolo, M.: Does bitcoin exhibit the same asymmetric multifractal cross-correlations with crude oil, gold and djia as the euro, great british pound and yen? Chaos, Solitons & Fractals 109, 195–205 (2018)

- Maasoumi and Wu (2021) Maasoumi, E., Wu, X.: Contrasting cryptocurrencies with other assets: Full distributions and the covid impact. Journal of Risk and Financial Management 14(9), 440 (2021)

- Nakamoto and Bitcoin (2008) Nakamoto, S., Bitcoin, A.: A peer-to-peer electronic cash system. Bitcoin.–URL: https://bitcoin. org/bitcoin. pdf 4(2) (2008)

- Sabry et al. (2020) Sabry, F., Labda, W., Erbad, A., Malluhi, Q.: Cryptocurrencies and artificial intelligence: Challenges and opportunities. IEEE Access 8, 175840–175858 (2020)

- Valencia et al. (2019) Valencia, F., Gómez-Espinosa, A., Valdés-Aguirre, B.: Price movement prediction of cryptocurrencies using sentiment analysis and machine learning. Entropy 21(6), 589 (2019)

- Ismail et al. (2020) Ismail, M.S., Noorani, M.S.M., Ismail, M., Razak, F.A., Alias, M.A.: Predicting next day direction of stock price movement using machine learning methods with persistent homology: Evidence from kuala lumpur stock exchange. Applied Soft Computing 93, 106422 (2020)

- Wang et al. (2021) Wang, X., Yang, K., Liu, T.: Stock price prediction based on morphological similarity clustering and hierarchical temporal memory. IEEE Access 9, 67241–67248 (2021)

- Quesada et al. (2022) Quesada, D., Bielza, C., Fontán, P., Larrañaga, P.: Piecewise forecasting of nonlinear time series with model tree dynamic bayesian networks. International Journal of Intelligent Systems 37(11), 9108–9137 (2022)

- Qiao and Beling (2016) Qiao, Q., Beling, P.A.: Decision analytics and machine learning in economic and financial systems. Springer (2016)

- Wang et al. (2015) Wang, L., Wang, Z., Zhao, S., Tan, S.: Stock market trend prediction using dynamical bayesian factor graph. Expert Systems with Applications 42(15-16), 6267–6275 (2015)

- Akyildirim et al. (2021) Akyildirim, E., Aysan, A.F., Cepni, O., Darendeli, S.P.C.: Do investor sentiments drive cryptocurrency prices? Economics Letters 206, 109980 (2021)

- Ji et al. (2019) Ji, Q., Bouri, E., Lau, C.K.M., Roubaud, D.: Dynamic connectedness and integration in cryptocurrency markets. International Review of Financial Analysis 63, 257–272 (2019)

- (13) Altan, İ.M., Hatipoğlu, C., Gujrati, R.: Future of finance: Fintech. FUTURE 20(2), 511–523

- Swathi et al. (2022) Swathi, T., Kasiviswanath, N., Rao, A.A.: An optimal deep learning-based lstm for stock price prediction using twitter sentiment analysis. Applied Intelligence 52(12), 13675–13688 (2022)

- Liu and Ma (2022) Liu, G., Ma, W.: A quantum artificial neural network for stock closing price prediction. Information Sciences 598, 75–85 (2022)

- Amirzadeh et al. (2022) Amirzadeh, R., Nazari, A., Thiruvady, D.: Applying artificial intelligence in cryptocurrency markets: A survey. Algorithms 15(11), 428 (2022)

- Cummings and Li (2021) Cummings, M.L., Li, S.: Subjectivity in the creation of machine learning models. ACM Journal of Data and Information Quality 13(2), 1–19 (2021)

- Grzegorczyk and Husmeier (2019) Grzegorczyk, M., Husmeier, D.: Modelling non-homogeneous dynamic bayesian networks with piecewise linear regression models. Handbook of Statistical Genomics: Two Volume Set, 899–28 (2019)

- Türkali (2020) Türkali, B.: Evaluation of alternative maintenance strategies on a complex system in thermal power systems. Master’s thesis, Işık Üniversitesi (2020)

- Sabourin et al. (2011) Sabourin, J., Mott, B.W., Lester, J.C.: Modeling learner affect with theoretically grounded dynamic bayesian networks. In: ACII (1), pp. 286–295 (2011)

- Xiao et al. (2017) Xiao, Q., Chaoqin, C., Li, Z.: Time series prediction using dynamic bayesian network. Optik 135, 98–103 (2017)

- Premebida et al. (2017) Premebida, C., Faria, D.R., Nunes, U.: Dynamic bayesian network for semantic place classification in mobile robotics. Autonomous Robots 41(5), 1161–1172 (2017)

- Nefian et al. (2002) Nefian, A.V., Liang, L., Pi, X., Liu, X., Murphy, K.: Dynamic bayesian networks for audio-visual speech recognition. EURASIP Journal on Advances in Signal Processing 2002, 1–15 (2002)

- Tan et al. (2011) Tan, Z., Quek, C., Cheng, P.Y.: Stock trading with cycles: A financial application of anfis and reinforcement learning. Expert Systems with Applications 38(5), 4741–4755 (2011)

- Zhang et al. (2016) Zhang, C., Lim, P., Qin, A.K., Tan, K.C.: Multiobjective deep belief networks ensemble for remaining useful life estimation in prognostics. IEEE transactions on neural networks and learning systems 28(10), 2306–2318 (2016)

- Zhao et al. (2021) Zhao, Y., Tong, J., Zhang, L.: Rapid source term prediction in nuclear power plant accidents based on dynamic bayesian networks and probabilistic risk assessment. Annals of Nuclear Energy 158, 108217 (2021)

- Borovkova and Tsiamas (2019) Borovkova, S., Tsiamas, I.: An ensemble of lstm neural networks for high-frequency stock market classification. Journal of Forecasting 38(6), 600–619 (2019)

- Choudhry and Garg (2008) Choudhry, R., Garg, K.: A hybrid machine learning system for stock market forecasting. International Journal of Computer and Information Engineering 2(3), 689–692 (2008)

- Huang et al. (2019) Huang, J.-Z., Huang, W., Ni, J.: Predicting bitcoin returns using high-dimensional technical indicators. The Journal of Finance and Data Science 5(3), 140–155 (2019)

- Alonso-Monsalve et al. (2020) Alonso-Monsalve, S., Suárez-Cetrulo, A.L., Cervantes, A., Quintana, D.: Convolution on neural networks for high-frequency trend prediction of cryptocurrency exchange rates using technical indicators. Expert Systems with Applications 149, 113250 (2020)

- Akyildirim et al. (2021) Akyildirim, E., Goncu, A., Sensoy, A.: Prediction of cryptocurrency returns using machine learning. Annals of Operations Research 297(1), 3–36 (2021)

- Ye et al. (2022) Ye, Z., Wu, Y., Chen, H., Pan, Y., Jiang, Q.: A stacking ensemble deep learning model for bitcoin price prediction using twitter comments on bitcoin. Mathematics 10(8), 1307 (2022)

- Zou and Herremans (2022) Zou, Y., Herremans, D.: A multimodal model with twitter finbert embeddings for extreme price movement prediction of bitcoin. arXiv preprint arXiv:2206.00648 (2022)

- Abraham et al. (2018) Abraham, J., Higdon, D., Nelson, J., Ibarra, J.: Cryptocurrency price prediction using tweet volumes and sentiment analysis. SMU Data Science Review 1(3), 1 (2018)

- Jangmin et al. (2004) Jangmin, O., Lee, J.W., Park, S.-B., Zhang, B.-T.: Stock trading by modelling price trend with dynamic bayesian networks. In: International Conference on Intelligent Data Engineering and Automated Learning, pp. 794–799 (2004). Springer

- Wang et al. (2017) Wang, H., Chatpatanasiri, R., Sattayatham, P.: Stock trading using pe ratio: a dynamic bayesian network modeling on behavioral finance and fundamental investment. arXiv preprint arXiv:1706.02985 (2017)

- Zuo and Kita (2012) Zuo, Y., Kita, E.: Up/down analysis of stock index by using bayesian network. Engineering Management Research 1(2), 46 (2012)

- Malagrino et al. (2018) Malagrino, L.S., Roman, N.T., Monteiro, A.M.: Forecasting stock market index daily direction: A bayesian network approach. Expert Systems with Applications 105, 11–22 (2018)

- Heckerman (2008) Heckerman, D.: A tutorial on learning with bayesian networks. Innovations in Bayesian networks, 33–82 (2008)

- Alameddine et al. (2011) Alameddine, I., Cha, Y., Reckhow, K.H.: An evaluation of automated structure learning with bayesian networks: An application to estuarine chlorophyll dynamics. Environmental Modelling & Software 26(2), 163–172 (2011)

- Death et al. (2015) Death, R.G., Death, F., Stubbington, R., Joy, M.K., Belt, M.: How good are bayesian belief networks for environmental management? a test with data from an agricultural river catchment. Freshwater biology 60(11), 2297–2309 (2015)

- Kuzmanić Skelin et al. (2021) Kuzmanić Skelin, A., Vojković, L., Mohović, D., Zec, D.: Weight of evidence approach to maritime accident risk assessment based on bayesian network classifier. Transactions on Maritime Science 10(02), 330–347 (2021)

- Adedipe et al. (2020) Adedipe, T., Shafiee, M., Zio, E.: Bayesian network modelling for the wind energy industry: An overview. Reliability Engineering & System Safety 202, 107053 (2020)

- Masmoudi et al. (2019) Masmoudi, K., Abid, L., Masmoudi, A.: Credit risk modeling using bayesian network with a latent variable. Expert Systems with Applications 127, 157–166 (2019)

- Rohmer (2020) Rohmer, J.: Uncertainties in conditional probability tables of discrete bayesian belief networks: A comprehensive review. Engineering Applications of Artificial Intelligence 88, 103384 (2020)

- Shiguihara et al. (2021) Shiguihara, P., Lopes, A.D.A., Mauricio, D.: Dynamic bayesian network modeling, learning, and inference: A survey. IEEE Access 9, 117639–117648 (2021)

- Portinale et al. (2010) Portinale, L., Raiteri, D.C., Montani, S.: Supporting reliability engineers in exploiting the power of dynamic bayesian networks. International journal of approximate reasoning 51(2), 179–195 (2010)

- Gao et al. (2014) Gao, X.-G., Mei, J.-F., Chen, H.-Y., Chen, D.-Q.: Approximate inference for dynamic bayesian networks: sliding window approach. Applied intelligence 40(4), 575–591 (2014)

- Wu et al. (2015) Wu, X., Liu, H., Zhang, L., Skibniewski, M.J., Deng, Q., Teng, J.: A dynamic bayesian network based approach to safety decision support in tunnel construction. Reliability Engineering & System Safety 134, 157–168 (2015)

- Zhang et al. (2023) Zhang, B., Bai, L., Zhang, K., Kang, S., Zhou, X.: Dynamic assessment of project portfolio risks from the life cycle perspective. Computers & Industrial Engineering 176, 108922 (2023)

- Voronenko et al. (2020) Voronenko, M., Nikytenko, D., Krejci, J., Krugla, N., Naumov, O., Savina, N., Topalova, E., Filippova, V., Lytvynenko, V.: Dynamic bayesian networks application for economy competitiveness situational modelling. In: Conference on Computer Science and Information Technologies, pp. 210–224 (2020). Springer

- Amin et al. (2019) Amin, M.T., Khan, F., Imtiaz, S.: Fault detection and pathway analysis using a dynamic bayesian network. Chemical Engineering Science 195, 777–790 (2019)

- Wu et al. (2016) Wu, S., Zhang, L., Zheng, W., Liu, Y., Lundteigen, M.A.: A dbn-based risk assessment model for prediction and diagnosis of offshore drilling incidents. Journal of Natural Gas Science and Engineering 34, 139–158 (2016)

- Motard (2022) Motard, P.: Hierarchical reinforcement learning for algorithmic trading (2022)

- Manujakshi et al. (2022) Manujakshi, B., Kabadi, M.G., Naik, N.: A hybrid stock price prediction model based on pre and deep neural network. Data 7(5), 51 (2022)

- Srivastava et al. (2021) Srivastava, P.R., Zhang, Z.J., Eachempati, P.: Deep neural network and time series approach for finance systems: predicting the movement of the indian stock market. Journal of Organizational and End User Computing (JOEUC) 33(5), 204–226 (2021)

- Ciaian et al. (2016) Ciaian, P., Rajcaniova, M., Kancs, d.: The economics of bitcoin price formation. Applied Economics 48(19), 1799–1815 (2016)

- Poyser (2019) Poyser, O.: Exploring the dynamics of bitcoin’s price: a bayesian structural time series approach. Eurasian Economic Review 9(1), 29–60 (2019)

- Königstorfer and Thalmann (2020) Königstorfer, F., Thalmann, S.: Applications of artificial intelligence in commercial banks–a research agenda for behavioral finance. Journal of behavioral and experimental finance 27, 100352 (2020)

- Ricciardi and Simon (2000) Ricciardi, V., Simon, H.K.: What is behavioral finance? Business, Education & Technology Journal 2(2), 1–9 (2000)

- Chursook et al. (2022) Chursook, A., Dawod, A.Y., Chanaim, S., Naktnasukanjn, N., Chakpitak, N.: Twitter sentiment analysis and expert ratings of initial coin offering fundraising: Evidence from australia and singapore markets. TEM Journal 11(1), 44 (2022)

- Corbet et al. (2018) Corbet, S., Meegan, A., Larkin, C., Lucey, B., Yarovaya, L.: Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters 165, 28–34 (2018)

- Charfeddine et al. (2020) Charfeddine, L., Benlagha, N., Maouchi, Y.: Investigating the dynamic relationship between cryptocurrencies and conventional assets: Implications for financial investors. Economic Modelling 85, 198–217 (2020)

- Ji et al. (2018) Ji, Q., Bouri, E., Gupta, R., Roubaud, D.: Network causality structures among bitcoin and other financial assets: A directed acyclic graph approach. The Quarterly Review of Economics and Finance 70, 203–213 (2018)

- Wijaya et al. (2021) Wijaya, D.R., Sarno, R., Zulaika, E.: Dwtlstm for electronic nose signal processing in beef quality monitoring. Sensors and Actuators B: Chemical 326, 128931 (2021)

- Amirzadeh et al. (2023) Amirzadeh, R., Nazari, A., Thiruvady, D., Ee, M.S.: Modelling Determinants of Cryptocurrency Prices: A Bayesian Network Approach (2023)

- Lyons et al. (2018) Lyons, M.B., Keith, D.A., Phinn, S.R., Mason, T.J., Elith, J.: A comparison of resampling methods for remote sensing classification and accuracy assessment. Remote Sensing of Environment 208, 145–153 (2018)

- BayesFusion (2017) BayesFusion, L.: Genie modeler. User Manual. Available online: https://support. bayesfusion. com/docs/(accessed on 21 October 2019) 16, 30–32 (2017)

- Fawzy et al. (2020) Fawzy, H., Rady, E.H.A., Abdel Fattah, A.M.: Comparison between support vector machines and k-nearest neighbor for time series forecasting. J. Math. Comput. Sci. 10(6), 2342–2359 (2020)

- Lee et al. (2019) Lee, K., Lim, J., Yoon, D., Jung, H.: Prediction of shale-gas production at duvernay formation using deep-learning algorithm. SPE Journal 24(06), 2423–2437 (2019)

- Alhakeem et al. (2022) Alhakeem, Z.M., Jebur, Y.M., Henedy, S.N., Imran, H., Bernardo, L.F., Hussein, H.M.: Prediction of ecofriendly concrete compressive strength using gradient boosting regression tree combined with gridsearchcv hyperparameter-optimization techniques. Materials 15(21), 7432 (2022)

- Chivukula and Lakshmi (2020) Chivukula, R., Lakshmi, T.J.: Cryptocurrency price prediction: A machine learning approach. Sensors & Transducers 244(5), 44–47 (2020)

- Quiroz and Alférez (2020) Quiroz, I.A., Alférez, G.H.: Image recognition of legacy blueberries in a chilean smart farm through deep learning. Computers and Electronics in Agriculture 168, 105044 (2020)