Optimizing Investment Strategies with Lazy Factor and Probability Weighting: A Price Portfolio Forecasting and Mean-Variance Model with Transaction Costs Approach

††thanks: *Corresponding author

Abstract

Market traders often engage in the frequent transaction of volatile assets to optimize their total return. In this study, we introduce a novel investment strategy model, anchored on the ’lazy factor.’ Our approach bifurcates into a Price Portfolio Forecasting Model and a Mean-Variance Model with Transaction Costs, utilizing probability weights as the coefficients of laziness factors. The Price Portfolio Forecasting Model, leveraging the EXPMA Mean Method, plots the long-term price trend line and forecasts future price movements, incorporating the tangent slope and rate of change. For short-term investments, we apply the ARIMA Model to predict ensuing prices. The Mean-Variance Model with Transaction Costs employs the Monte Carlo Method to formulate the feasible region. To strike an optimal balance between risk and return, equal probability weights are incorporated as coefficients of the laziness factor. To assess the efficacy of this combined strategy, we executed extensive experiments on a specified dataset. Our findings underscore the model’s adaptability and generalizability, indicating its potential to transform investment strategies.

Index Terms:

EXPMA, ARIMA, Quantitative investment, Markowitz Mean-Variance Model, Laziness FactorI Introduction

In recent years, there has been a notable transition in the investment sector, moving from primarily qualitative decision-making to a more data-centric, quantitative approach, driven by advancements in computer technology [1]. This paradigm shift, known as ”Quantitative Investment,” is fundamentally reshaping investment practices.

Quantitative investment capitalizes on comprehensive data analysis and complex modeling to identify promising investment opportunities and devise efficient strategies [2]. This systematic method effectively mitigates emotional reactions to temporary market volatilities, fostering long-term investor commitment. By harnessing positive market trends, it generates long-term returns and promotes market stability. The growing acceptance of this approach [3] signals a promising future for quantitative investment in the financial sector. Alongside its expansion, there arises a need for more refined and sophisticated quantitative models to meet the dynamic market demands [4]. This ongoing requirement underscores the investment market’s dynamism and the relentless search for innovative solutions [5] to optimize investment strategies and results.

Despite their noted benefits, current quantitative investment methods often exhibit limitations in adaptability and generalizability [6, 7]. These approaches primarily rely on complex models to predict market trends, often overlooking inherent market variability [8]. Moreover, such strategies usually adhere strictly to either long-term or short-term forecasting, neglecting the potential for synergistic insights offered by an integrated perspective [9].

In response, this study introduces a new investment strategy model, designed for market traders frequently involved in volatile asset transactions to optimize their total return. Our proposed model, anchored on the ’lazy factor’, consists of two main components: a Price Portfolio Forecasting Model and a Mean-Variance Model with Transaction Costs. The model utilizes probability weights as the laziness factor’s coefficients.

The Price Portfolio Forecasting Model leverages the EXPMA Mean Method to establish the long-term price trend line, and forecasts price movements based on the tangent slope and rate of change. For short-term investments, we employ the ARIMA model to predict upcoming price trends. Simultaneously, the Mean-Variance Model, incorporating Transaction Costs, uses the Monte Carlo Method to define the feasible region. The model balances risk and return optimally by integrating equal probability weights as the laziness factor’s coefficients.

II Related Work

In this section, we provide a comprehensive overview of the current literature related to price-based portfolio investment strategies, encompassing both technical analysis and trading strategies.

II-A Investment methods

Portfolio investment strategies use historical price or volume data to predict future trends by analyzing the embedded quantitative relationships [10]. Traditional financial time series models, such as ARIMA [11, 12, 13], gray forecasting models [14], and Markov chain Monte Carlo methods [15], have shown excellent performance for short-term forecasting.

As machine learning continues to evolve, it offers investors the capability to decipher concealed patterns in asset prices, correlations, and volatilities. This enables the formation of portfolios optimized for risk-adjusted returns [16]. Buczynski et al. [17] deliver a comprehensive review of numerous academic studies, providing an investment management viewpoint. Zhang [18] advocates for the use of machine learning algorithms in stock selection, highlighting their effectiveness in formulating investment strategies. In a parallel vein, Yi [4] presents a multifactor investment methodology underpinned by pivotal elements of corporate finance and valuation, further streamlining portfolio selection through a machine learning-based classification system.

II-B Trading strategies

Trading strategies aim to guide investors in wisely allocating their capital, managing risk-reward balance, and achieving wealth accumulation. The development of capital markets and the rapid growth of investment products led to the introduction of portfolio investment strategies [19].

Markowitz and Todd [20] first proposed the theory of portfolio selection. The mean-variance analysis, a key portfolio methodology, is continually optimized and adapted. However, actual results often diverge from predictions. Jobson and Korkie [21] suggested that complex investment strategies may not perform as well as simpler ones due to estimation errors. Additionally, equal-weighted investment strategies are also gaining popularity.

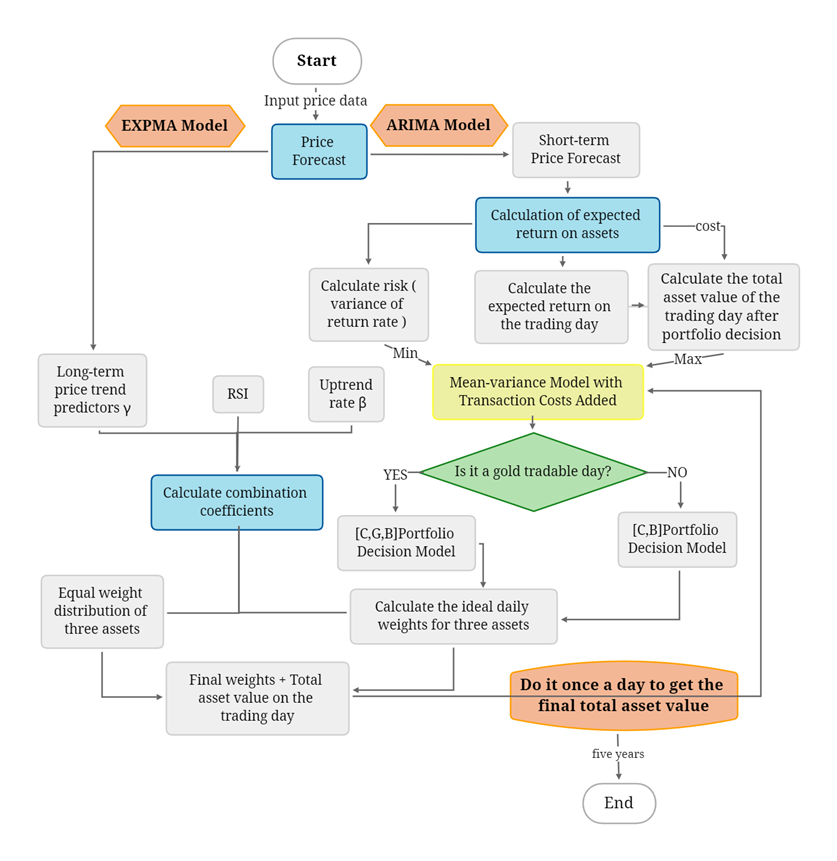

III Our Approach

This section details our proposed Price Portfolio-Forecasting Model, designed to predict future price trends for optimal portfolio strategizing. By integrating technical analysis and trading-based strategies, we have developed a comprehensive model. This leverages the Exponential Moving Average (EXPMA) Mean Method for long-term price trend analysis and employs the AutoRegressive Integrated Moving Average (ARIMA) model for short-term price predictions.

III-A Price Portfolio-Forecasting Model

The insights derived from previous research have served as an inspiration for our approach. As a case study, we consider a specific day and engage in information extraction from the historical prices of gold and Bitcoin. The goal is to anticipate future price trends, which then serves as a determinant in devising an optimal portfolio strategy.

III-A1 Model for Long-Term Forecasting based on EXOMA Averages

Drawing parallels with the stock market, we initially employ the Moving Average (MA) and Simple Moving Average (SMA) methods to compute the 5-day, 20-day, and 60-day averages of historical prices. These averages over distinct time intervals are then connected to shape short-term, medium-term, and long-term trend lines, respectively. The calculation formula is expressed as follows:

| (1) |

Here, with representing gold and denoting bitcoin.

We improve the model by using exponential and smoothing coefficients to obtain the EXPMA model considering the lag of the mean in tracking the price makes it does not reflect the trend change in time. The calculation formula is as follows.

| (2) | ||||

III-A2 Short-Term Forecasting based on ARIMA Series

From the previous analysis, the results of short-term forecasting are closer to the real price. Thus, the ARIMA (autoregressive moving average) model is considered to forecast the short-term prices to obtain the possible prices for the next day and provide the expected return value for the investment strategy of that day.

In the ARIMA model, we use the observed values of the past price series of gold to derive future prices. The future prices are expressed as linear functions of the current and lagged periods of the lagged and stochastic disturbance terms. The general form of the model is as follows:

| (3) |

The expansion of the time interval will increase the error of the price forecast. We keep adjusting the length of the interval to find the optimal value in the process of forecasting. Eventually, we found that the traditional forecasting model generally considers the amount of data within 100 for data with large price changes such as gold and bitcoin combined with the information. Too much data, on the contrary, can lead to prediction results deviating from expectations.

III-B Integration of Transaction Costs into the Price Portfolio-Forecasting Model using the Mean-Variance Model

III-B1 Gold trading days

Markowitz treats return as a random variable, takes the mean of asset return as the expected return [22], and defines risk as the coefficient of fluctuation size of return - variance, which is actually the degree of penalty for deviation of asset return from the expected return. With expected return maximization and risk minimization as the objective function, the problem is treated as a multi-objective planning problem [23].

Since the daily [cash, gold, bitcoin] portfolio needs to be obtained, cash is also considered as an asset in this paper, so the model includes three risky assets: cash, gold, and bitcoin, but the complexity of the model is not increased too much due to the special nature of cash.

The rates of return for the three risky assets are represented by , and for cash, it is understood due to its unique nature. For the firm, the rate of return is defined as the ratio of net profit to the average capital employed. In this study, we estimate the rate of return based on the current asset prices and make a short-term forecast for tomorrow’s prices.

| (4) |

The weights of cash, gold and bitcoin obtained under the investment strategy of date t (i.e., the proportion of actual holdings) are , and , .

Then the expected return rate is the portfolio under this strategy is the weighted average of the expected returns of gold and bitcoin, denoted as .

The risk of the portfolio is expressed as:

| (5) |

The notation signifies that represents the covariance of the returns of gold and bitcoin (and vice versa), which is the product of the correlation coefficient of their returns, , and the standard deviations of their individual returns, and . This is mathematically represented as . The portfolio risk escalates progressively as the correlation coefficient varies between -1 and 1. Unless the correlation coefficient equals 1, the risk of a binary portfolio, , consistently remains below the weighted average of the separate investment risks. This demonstrates that investment in a portfolio can mitigate investment risk.

Assuming that the initial assets are , the total value of assets after the investment strategy at date t:

| (6) |

The term represents the gold holdings on the day before trading day t, and represents gold holdings after the investment decision on trading day t. The absolute difference between the two symbolizes the trading volume of gold on day t. A similar interpretation applies to bitcoin. (The ultimate goal is to obtain the decision after W on 2021.2.2.)

The investor aims for the highest possible return rate and the lowest possible uncertainty risk [24]. The ideal objective is to balance these two conflicting goals. The conventional Markowitz mean-variance model pursues maximum expected return and minimum risk. Considering transaction costs that accompany every gold or bitcoin purchase or sale, this paper proposes the maximum total asset value on transaction day t as the objective function.

| (7) |

| (8) |

| (9) |

III-B2 Non-Trading Days for Gold (Weekends and Holidays)

On non-trading days for gold, the gold holdings and closing prices are carried over from the previous trading day. The model then treats only cash and bitcoin as risky assets, with the total asset value equating to the previous day’s total value of cash and bitcoin. We adapt our model for these two risky assets, which can be calculated similarly.

III-C Portfolio Investment Strategy Considering the Laziness Factor

The mean-variance approach used practically, necessitates precise estimates of individual asset returns’ mean and variance. Estimation errors can cause the mean-variance efficient portfolio to diverge from the true efficient portfolio. The equal-weight investment strategy, on the other hand, eliminates estimation errors by assigning equal weights to portfolio assets without requiring parameter estimation or optimization techniques. Additionally, this strategy is unaffected by external or personal investor factors [25].

Hence, we propose a blend of the equal-weight strategy and a mean-variance model incorporating transaction costs. This includes a quadratic combination of gold and bitcoin weights for different risk levels, thereby considering the laziness factor. The approach aims to stabilize weights and reduce local optimal solution responsiveness.

-

•

Equal weights

Cash, gold, and bitcoin within the portfolio are given equal weights: . These weights are irrespective of asset return distribution characteristics.

-

•

The laziness factors

The laziness factors, and , are considered. Here, and denote the portfolio coefficients of the equal-weighted strategy and the mean-variance model considering transaction costs, respectively. Hence, , with constraints .

-

•

Weighting Coefficients Determination

The weights , derived from the model, function as ideal weights. These are combined with equal weights to temper potential discrepancies and significant fluctuations. Combination coefficients are computed considering the Relative Strength Index (RSI), rate of change (), and mid to long-term trend indicators (slope of moving average ).

The RSI, calculated as the average closing gain over the sum of average closing gain and loss, times 100%, indicates trading tendencies and trend momentum, assisting short-term investments.

denotes the ratio of the price increase and decrease days for cash, gold, and bitcoin in the fortnight before the trading day, illustrating asset price uncertainty.

| Impact Indicators | Results | ||

|---|---|---|---|

| RSI |

|

||

|

|||

|

The influence of all the above three indicators on the ideal weight is to make it higher, so this paper considers expressing the combination coefficient as:

| (10) |

The combination coefficients were calculated based on the five years of data given in the title and the mean value was processed to obtain: .

III-D Calculating the total asset value

Starting from 11/9/2016, since there is no historical data in the initial period to refer to help make decisions, this paper treats the previous month as an empty period to accumulate historical data and make portfolio decisions starting from 11/10/2016.

After the above steps, we obtain the portfolio weights for the adjusted trading day t. Therefore, after the daily portfolio decision is completed, the total asset value for the day is: . And , which .

IV Experiments

IV-A Data Description

This study utilizes a portfolio consisting of gold and Bitcoin trades, incorporating historical gold and Bitcoin price data: London Bullion Market Association’s daily gold prices (9/11/2016 - 9/10/2021) and NASDAQ’s Bitcoin daily prices (9/11/2016 - 9/10/2021).

IV-B Performance Evaluation

IV-B1 Long-Term Forecasting Performance

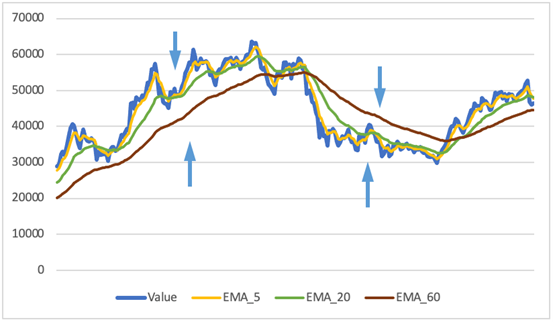

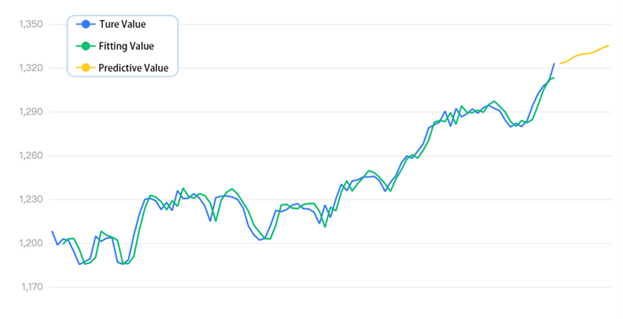

The 2021 Bitcoin price trend serves as an example, with results illustrated in the subsequent chart.

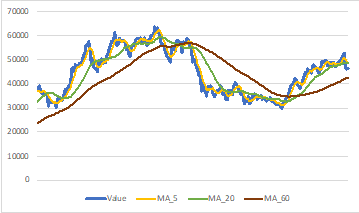

(a) MA (b) EMA

Fig 3 shows that the EMA trend line is more accurate than MA in predicting price trends. Short-term price trends help predict next-day prices, while long-term trends provide insight into overall price movements over extended periods. The chart also identifies instances, marked by blue arrows, where short-term trends contradict long-term ones.

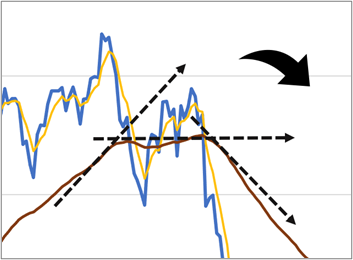

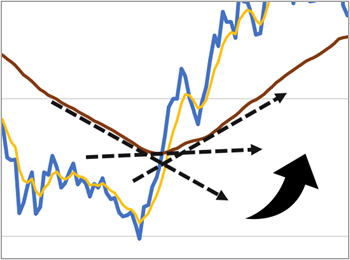

As illustrated in Figure 2, two inflection points on the long-term trend line are significant. The change in slope K at these points indicates a sudden alteration in the asset price trend. Specifically, a convex point presages a future decrease in price, while a concave point forecasts a future increase [26]. This transition is quantified by the rate of change in slope K’ between consecutive tangent lines.

Informed by these findings, we suggest the following strategy: The anticipation of a price rise materializes when short-term moving averages intersect and surpass the long-term averages. Conversely, a prediction of a price fall emerges when short-term moving averages intersect and fall beneath the long-term averages.

Smoothness Test

For the ARIMA model to predict time series data effectively, stability is crucial to capture the regularity [27]. Given the volatility of gold prices, the ADF test is initially applied to check the unit root of the original series. The original non-stationary time series is then converted into a stationary one through differential transformation. The smoothness test results are presented in the ensuing table.

| Difference Order | t | P | AIC | Threshold Value | ||

|---|---|---|---|---|---|---|

| 1% | 5% | 10% | ||||

| 0 | 0.321 | 0.978 | 530.564 | -3.507 | -2.895 | -2.585 |

| 1 | -5.988 | 0.000*** | 522.718 | -3.507 | -2.895 | -2.585 |

| 2 | -7.477 | 0.000*** | 528.297 | -3.51 | -2.896 | -2.585 |

As can be seen from the above table, at a difference score of 0, the significance P-value is 0.978, indicating that the original gold price series is not smooth. At a difference score of 1, the significance P-value is 0.000***, which presents significance at the level, and the differenced price series to reach a smooth state. The smoothing results are as follows.

(a) Original (b) Smoothed

ARIMA Model

The development of the ARIMA model commences with the establishment of the model order, leveraging autocorrelation coefficients, partial autocorrelation coefficients, and other parameters. An optimal model is identified in accordance with the Akaike information criterion for fixed-order selection.

The subsequent stages encompass parameter estimation and validation, including the significance of parameters, the robustness of the model, and an examination of whether the residual series constitutes a white noise series [28]. If the model does not pass the test, the selection of a new model becomes necessary. The process culminates with the presentation of correlation results.

| Item | Symbol | Value |

|---|---|---|

| Number of Samples | Df Residuals | 87 |

| N | 93 | |

| Q Statistics | Q6(p) | 0.039(0.844) |

| Q12(p) | 6.124(0.409) | |

| Q18(p) | 8.165(0.772) | |

| Q24(p) | 13.321(0.772) | |

| Q30(p) | 27.206(0.295) | |

| Information | AIC | 619.465 |

| Fitting Optimization | R^2 | 0.964 |

From the above table, Q6 does not show significance at the level, and the gold price residual series is a white noise series. Meanwhile, the goodness-of-fit R-squared of the model is 0.964, which is a good fit.

Future Price Forecast

The final results of the model solution are as follows.

| (11) |

The predicted price of gold for the next day is 1322.966 and the actual price is 1318.7, with an error rate of about 0.32, which shows the high prediction accuracy.

IV-B2 Portfolio-Investment Strategy Model with Laziness Factor

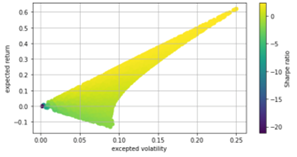

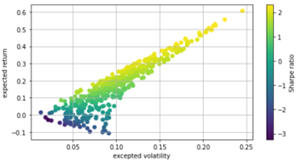

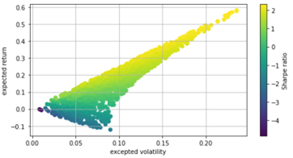

We define a feasible set for three risky assets using the complete range of weight ratios, based on two months of data. The Monte Carlo method generates data sets at 500, 1000, and 10,000 intervals. Results, including the risk and expected return, are visualized in Figure 5. The minimum risk is at the apex of the left convex curve.

Figure 5 also displays cumulative returns for cash, gold, and bitcoin. Notably, bitcoin shows a consistent upward trend, outperforming in later stages, reflecting its increasing dollar value over the last five years.

Within the feasible set, two key portfolio characteristics can be discerned: 1) the portfolio that provides the maximum expected return for a specific level of risk; 2) the portfolio that maintains the least risk for a given expected return. These portfolios represent optimal points, and together they establish a curve referred to as the minimum variance frontier or the efficient frontier for risky assets.

Further analysis allows for the identification of the portfolio weight on the efficient frontier where the Sharpe ratio reaches its maximum. This point represents the tangency between the capital allocation line (CAL) and the efficient frontier, known in the field as the Capital Market Line (CML).

| Date | C | G | B | Total Return | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2016/9/11 | 1000 | 0 | 0 | 1000 | |||||||||||||||

|

|

|

|

|

|||||||||||||||

| 2018/9/7 | 1808.8 | 0.74323 | 0.60436 | 6618.17 | |||||||||||||||

| 2018/9/8 | 1813.2 | 0.73423 | 0.61716 | 6622.37 | |||||||||||||||

| 2018/9/9 | 1817.6 | 0.73423 | 0.6283 | 6647.67 | |||||||||||||||

|

|

|

|

|

|||||||||||||||

| 2021/9/7 | 25748 | 2.1982 | 2.0051 | 135339.5 | |||||||||||||||

| 2021/9/8 | 25811 | 2.2248 | 2.2666 | 135884.5 | |||||||||||||||

| 2021/9/9 | 25873 | 2.2274 | 2.3081 | 136216.1 |

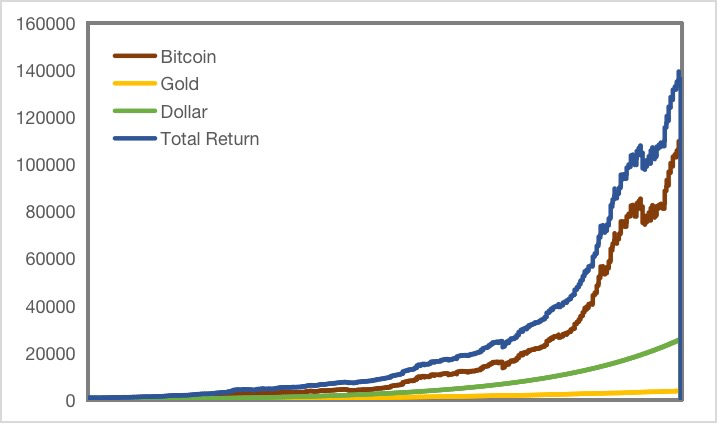

Finally, the initial $1000 is calculated in a loop to get the final total value of $136216.1 on 10/9/2021. It shows that our model achieves a remarkable annualized rate of return of 27.04, which demonstrate the strong profitability.

As can see from the trend in Fig 8, Bitcoin has the largest impact on total returns, with gold only accounting for a small percentage.

IV-C Experimental Evaluation of Portfolio Investment Strategy Model

IV-C1 Intra-Model Test

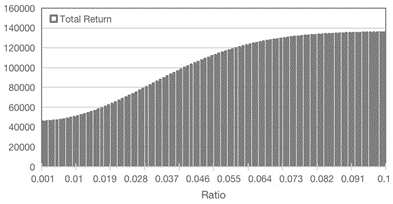

The Markowitz mean-variance model brings substantial benefits, particularly diversification, a principle advocated by Nobel laureate economist James Tobin: ”Don’t put your eggs in one basket”. This principle allows investors to reduce risk without sacrificing expected returns by combining different assets [29]. A backtest conducted on trades using this model yielded a profitability rate of 135.2161% and a maximum retracement rate of 2.5044%. When combined with real market data, it shows enhanced returns and diminished risk, thus illustrating the efficacy of our developed portfolio optimization model. To temper the sensitivity of the ideal weight results to the local optimal solution, we included a laziness factor, combining equal probability weights (i.e., 1/3) with the ideal weights through a quadratic combination. Adjusting the combination coefficients before equal weights allows us to ascertain the final asset value as these coefficients change, with the results shown in Fig 9.

The total value of the final assets obtained when tends to be optimal. It can be seen that the portfolio factors we have selected can achieve the optimal portfolio strategy.

IV-C2 Out-of-Model Tests

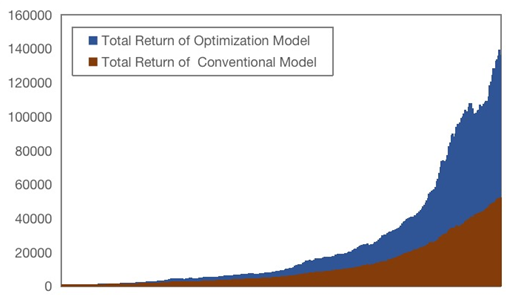

A control group is set up: no laziness factor is added, i.e. no quadratic combination of equal probability weights 1/3 with the ideal weights is added to stabilize the weights, and only the ideal weights derived from the mean-variance model with transaction costs are used for portfolio decisions.

The daily portfolio strategy and the total asset value for each day over the five years are derived and the results are compared with those of the optimization model. The results are shown in Fig 10.

As can be seen from the results, the daily total asset value of our built model is generally higher than the results without the laziness factor, and the final 9/10/19 total value is higher than the results without the laziness factor by approximately 160.81. Thus, it can be shown that the optimization model we have built provides the best portfolio strategy.

V Conclution

In this paper, we propose a dual-model portfolio investment strategy that amalgamates long-term (EXPMA-based) and short-term (ARIMA-based) price forecasting with an optimized mean-variance approach, underscored by a laziness factor. Back-testing of trades showcases the model’s superior performance and stability. Future work envisages integrating machine learning for price forecasting and personal trader factors to augment the model’s practicality.

References

- [1] Y. Pan and L. Zhang, “Roles of artificial intelligence in construction engineering and management: A critical review and future trends,” Automation in Construction, vol. 122, p. 103517, 2021.

- [2] A. Ashta and H. Herrmann, “Artificial intelligence and fintech: An overview of opportunities and risks for banking, investments, and microfinance,” Strategic Change, vol. 30, no. 3, pp. 211–222, 2021.

- [3] C. Xiao, W. Xia, and J. Jiang, “Stock price forecast based on combined model of ari-ma-ls-svm,” Neural Computing and Applications, vol. 32, pp. 5379–5388, 2020.

- [4] K. Yi, “The multifactor quantitative investment model based on association rule mining and machine learning,” Wireless Communications and Mobile Computing, vol. 2022, 2022.

- [5] J. Alberg and Z. C. Lipton, “Improving factor-based quantitative investing by forecasting company fundamentals,” arXiv preprint arXiv:1711.04837, 2017.

- [6] L. Leung, “Validity, reliability, and generalizability in qualitative research,” Journal of family medicine and primary care, vol. 4, no. 3, p. 324, 2015.

- [7] A. Queirós, D. Faria, and F. Almeida, “Strengths and limitations of qualitative and quantitative research methods,” European journal of education studies, 2017.

- [8] F. Petropoulos, D. Apiletti, V. Assimakopoulos, M. Z. Babai, D. K. Barrow, S. B. Taieb, C. Bergmeir, R. J. Bessa, J. Bijak, J. E. Boylan et al., “Forecasting: theory and practice,” International Journal of Forecasting, 2022.

- [9] V.-D. Ta, C.-M. Liu, and D. A. Tadesse, “Portfolio optimization-based stock prediction using long-short term memory network in quantitative trading,” Applied Sciences, vol. 10, no. 2, p. 437, 2020.

- [10] S. J. Binoy and J. Jos, “Financial market forecasting using macro-economic variables and rnn,” in 2022 2nd International Conference on Advance Computing and Innovative Technologies in Engineering (ICACITE). IEEE, 2022, pp. 1366–1371.

- [11] J. Zhang, Y. Huang, C. Huang, W. Huang et al., “Research on arima based quantitative investment model,” Academic Journal of Business & Management, vol. 4, no. 17, 2022.

- [12] Y. Sun, T. Dong, and B. Shan, “Research on stock quantitative investment strategy based on arima-garch-mlp model,” in 2022 IEEE Conference on Telecommunications, Optics and Computer Science (TOCS). IEEE, 2022, pp. 984–990.

- [13] N. Han, S. Zhang, H. Wang, Z. Chen, X. Hou, and Z. Sun, “Quantitative investment decision model based on arima and iterative neural network,” in 2022 IEEE Conference on Telecommunications, Optics and Computer Science (TOCS). IEEE, 2022, pp. 1076–1081.

- [14] N. Norouzi and M. Fani, “Black gold falls, black plague arise-an opec crude oil price forecast using a gray prediction model,” Upstream Oil and Gas Technology, vol. 5, p. 100015, 2020.

- [15] O. V. De la Torre-Torres, D. Aguilasocho-Montoya, J. Álvarez-García, and B. Simonetti, “Using markov-switching models with markov chain monte carlo inference methods in agricultural commodities trading,” Soft Computing, vol. 24, pp. 13 823–13 836, 2020.

- [16] J. Li, X. Wang, S. Ahmad, X. Huang, and Y. A. Khan, “Optimization of investment strategies through machine learning,” Heliyon, 2023.

- [17] W. Buczynski, F. Cuzzolin, and B. Sahakian, “A review of machine learning experiments in equity investment decision-making: why most published research findings do not live up to their promise in real life,” International Journal of Data Science and Analytics, vol. 11, pp. 221–242, 2021.

- [18] K. Zhang, “Research on quantitative investment based on machine learning,” in 2020 2nd International Conference on Economic Management and Cultural Industry (ICEMCI 2020). Atlantis Press, 2020, pp. 245–249.

- [19] R. Cesari and M. Marzo, “Trading strategies, portfolio monitoring and rebalancing,” Portfolio Theory and Management, OUP, New York, pp. 383–401, 2013.

- [20] H. M. Markowitz and G. P. Todd, Mean-variance analysis in portfolio choice and capital markets. John Wiley & Sons, 2000, vol. 66.

- [21] J. D. Jobson and B. Korkie, “Estimation for markowitz efficient portfolios,” Journal of the American Statistical Association, vol. 75, no. 371, pp. 544–554, 1980.

- [22] J. Lin, “Improved markowitz portfolio investment model based on arima model and bp neural network,” in 2022 IEEE 2nd International Conference on Data Science and Computer Application (ICDSCA). IEEE, 2022, pp. 504–507.

- [23] P. Xidonas, G. Mavrotas, C. Hassapis, and C. Zopounidis, “Robust multiobjective portfolio optimization: A minimax regret approach,” European Journal of Operational Research, vol. 262, no. 1, pp. 299–305, 2017.

- [24] P. Y. Cheng, “Risk willingness and perceived utilities to explain risky investment choices: a behavioral model,” Journal of Behavioral Finance, vol. 20, no. 3, pp. 255–266, 2019.

- [25] P. J. Haensly, “Risk decomposition, estimation error, and naïve diversification,” The North American Journal of Economics and Finance, vol. 52, p. 101146, 2020.

- [26] G. J. Warren, “Choosing and using utility functions in forming portfolios,” Financial Analysts Journal, vol. 75, no. 3, pp. 39–69, 2019.

- [27] S. Du, Y. Sun, Y. Hu, and Z. Lu, “Implementation of markowitz mean-variance model based on matrix-valued factor algorithm,” in 2019 IEEE 5th Intl Conference on Big Data Security on Cloud (BigDataSecurity), IEEE Intl Conference on High Performance and Smart Computing,(HPSC) and IEEE Intl Conference on Intelligent Data and Security (IDS). IEEE, 2019, pp. 85–89.

- [28] A. A. Ariyo, A. O. Adewumi, and C. K. Ayo, “Stock price prediction using the arima model,” in 2014 UKSim-AMSS 16th international conference on computer modelling and simulation. IEEE, 2014, pp. 106–112.

- [29] W. Lefebvre, G. Loeper, and H. Pham, “Mean-variance portfolio selection with tracking error penalization,” Mathematics, vol. 8, no. 11, p. 1915, 2020.