Semiparametric posterior corrections

Abstract

We present a new approach to semiparametric inference using corrected posterior distributions. The method allows us to leverage the adaptivity, regularization and predictive power of nonparametric Bayesian procedures to estimate low-dimensional functionals of interest without being restricted by the holistic Bayesian formalism. Starting from a conventional nonparametric posterior, we target the functional of interest by transforming the entire distribution with a Bayesian bootstrap correction. We provide conditions for the resulting one-step posterior to possess calibrated frequentist properties and specialize the results for several canonical examples: the integrated squared density, the mean of a missing-at-random outcome, and the average causal treatment effect on the treated. The procedure is computationally attractive, requiring only a simple, efficient post-processing step that can be attached onto any arbitrary posterior sampling algorithm. Using the ACIC 2016 causal data analysis competition, we illustrate that our approach can outperform the existing state-of-the-art through the propagation of Bayesian uncertainty.

1 Introduction

Functional estimation is emerging as a major paradigm in modern statistics (van der Laan and Rose, 2011; Buja et al., 2019a, b; Vansteelandt and Dukes, 2022). The definition of the estimand—the target of inference—is placed at the forefront of the statistical analysis, requiring the user to carefully articulate their scientific objectives. This helps to avoid the common pitfall in which the choice of estimand is informed by the choice of statistical model, rather than the other way round. Causal inference, in particular, has a natural affinity with functional estimation through the nonparametric identification of causal effects (Pearl, 2009; Hernán and Robins, 2020).

An important advantage of the functional approach is that we are free to estimate low-dimensional functionals without being restricted to low-dimensional models. Nonparametric methods provide greater flexibility in capturing complex relationships between variables, mitigating the risks of model misspecification bias. In particular, it is becoming increasingly popular to leverage highly flexible black-box algorithms (e.g. random forests, gradient boosting, deep learning) to estimate nuisance parameters (van der Laan and Rubin, 2006; Chernozhukov et al., 2018; Vansteelandt and Dukes, 2022).

Using infinite-dimensional models to estimate low-dimensional estimands is often referred to as semiparametric inference. By exploiting the smoothness (or differentiability) of the target functional, it may be possible to obtain estimators with parametric properties like -consistency and asymptotic normality, even if the nuisance parameter estimators converge at a slower rate (Murphy and van der Vaart, 2000; van der Laan and Rose, 2011; Kennedy, 2022; Hines et al., 2022). Some authors have suggested that semiparametric methods can bridge the “two cultures” of statistical modelling (Breiman, 2001) by combining the interpretability and efficiency of parametric inference with the robustness of black-box algorithms (Ogburn and Shpitser, 2021; Kennedy et al., 2021; Vansteelandt, 2021).

Nonparametric Bayesian approaches such as Bayesian additive regression trees (Chipman et al., 2007) have performed especially well in empirical studies for both prediction and inferring low-dimensional estimands such as causal effects (Hill, 2011; Dorie et al., 2019; Hahn et al., 2020). For parametric Bayesian models, the influence of the prior disappears asymptotically to first-order thanks to the renowned Bernstein-von Mises theorem (Le Cam, 1986; van der Vaart, 1998). For infinite-dimensional models however, the impact of the prior may remain significant in the asymptotic regime, and the prior specification cannot be completely justified by subjective beliefs (Diaconis and Freedman, 1986; Rousseau, 2016). This has led to a rich literature on the frequentist properties of Bayesian nonparametric methods, with a strong emphasis on posterior contraction rates (e.g. Ghosal and van der Vaart, 2017). In particular, many Bayesian approaches have been shown to enjoy excellent properties in terms of adaptive posterior contraction rates due to the flexibility enabled by hierarchical prior modelling (e.g. Rousseau, 2016; Ghosal and van der Vaart, 2017).

Bayesian approaches naturally deal with nuisance parameters by integrating them out, which allows for coherent inference on possibly multiple parameters of interest, whether they are estimated simultaneously or sequentially (e.g. Berger et al., 1999). Unfortunately, good adaptive contraction rates do not necessarily translate to good behaviour for marginal posterior distributions of specific functionals, even to first-order. Although there has been a growing literature on the existence of Bernstein-von Mises theorems in the semiparametric setting (Castillo, 2012; Rivoirard and Rousseau, 2012; Castillo and Nickl, 2014; Castillo and Rousseau, 2015), the results have been only partially positive, and it is now recognized that a given prior will perform well for some functionals of interest but not for others. This is perhaps unsurprising given that Bayesian inference is a “plug-in” approach, and similar phenomena have been observed for semiparametric plug-in estimators in the frequentist literature (Bickel and Ritov, 2003; van der Laan and Rubin, 2006; Robins et al., 2017). The reason is that flexible nonparametric methods must employ regularization to achieve good performance, and the “regularization bias” can bleed into the corresponding plug-in estimator, precluding fast convergence rates (van der Laan and Rubin, 2006; van der Vaart, 2014; Chernozhukov et al., 2018).

For some particular examples, it has been demonstrated that the asymptotic posterior bias for a nonparametric Bayesian model can be controlled by tailoring the prior specification to the estimand (Castillo and Rousseau, 2015; Ray and van der Vaart, 2020). This is undesirable from a practical perspective however, as it will require careful tuning (or even rewriting) of any existing software for posterior computation. Moreover, a different modification will be required for each estimand of interest. In any case, studying the existence of a Bernstein-von Mises theorem remains a formidable open question for many popular families of priors, such as nonparametric mixtures. For the implementations of nonparametric Bayesian procedures that are widely applied in practice, the existing empirical evidence suggests that the lack of a semiparametric Bernstein-von Mises theorem represents the rule, rather than the exception (Dorie et al., 2019; Ray and Szabó, 2019; Hahn et al., 2020).

To address these issues, we introduce a simple post-processing procedure that starts from a given posterior distribution on the whole data-generating distribution and then corrects the marginal posterior for each functional of interest. This operates by adding a stochastic term based on the efficient influence function of the functional (Pfanzagl, 1982; van der Vaart, 1991, 1998) and the Bayesian bootstrap (Rubin, 1981), which plays a crucial role for correcting not only the bias of the posterior but also its shape. The original user-specified Bayesian model can be left untouched, acting as a central hub from which we can target each estimand of interest individually.

We provide general conditions for these new one-step posteriors to satisfy a Bernstein-von Mises theorem, which ensures that central credible regions achieve approximately nominal coverage with the semiparametric efficient size. Unlike the semiparametric Bernstein-von Mises theorems derived for standard nonparametric posteriors (e.g. Castillo, 2012; Castillo and Rousseau, 2015), our conditions do not depend delicately on the likelihood and prior. Instead, we require only contraction rates and complexity bounds on the posterior with empirical process theory, leading to a Bayesian counterpart to the classical theory of influence-function-based estimation (Pfanzagl, 1982; van der Laan and Robins, 2003; van der Laan and Rose, 2011; Hines et al., 2022; Kennedy, 2022). In particular, the one-step posterior could be interpreted as a natural analogue of the one-step estimator (Pfanzagl, 1982; Newey et al., 1998) for correcting an entire posterior distribution rather than just a point estimator.

Our methodology, which we introduce in Section 2, is computationally efficient and attaches onto any existing posterior sampling implementation without modification of the original algorithm. The procedure takes each posterior sample and adds a randomized correction term, which only requires drawing an independent set of uniform Dirichlet weights of lengths equal to the sample size. A single set of posterior samples can be retained for simultaneous inference of multiple functionals of interest.

We apply our approach to the classic example of estimating the integrated squared density in Section 3. This was previously studied in a Bayesian setting by Castillo and Rousseau (2015) but only for random histogram priors on the interval . We verify the conditions for the more complex class of Dirichlet process Gaussian location mixtures (Shen et al., 2013). To the best our knowledge, this is the first Bernstein-von Mises theorem associated with priors based on nonparametric mixture models.

In Section 4, we study the estimation of the mean of an outcome that is missing-at-random. This is a problem that has received much attention due to its connections with estimating the average treatment effect in causal inference (Kang and Schafer, 2007; Robins et al., 2017). The conditions for the Bernstein-von Mises theorem are expressed here in terms of the propensity score and outcome regression models, showing that the one-step posterior possesses a doubly robust property, i.e. it depends on the combined contraction rates of both parameters. For this specific example in the binary outcome setting, Ray and van der Vaart (2020) proposed a correction approach that has similar motivations and asymptotic considerations to ours, but it requires a modification to the prior that can be relatively complicated to implement. Working within their set-up, we study the behaviour of the one-step posterior and provide a comparison of theoretical assumptions.

The last example is the average treatment effect on the treated (Rubin, 1977; Heckman and Robb, 1985), which has not been studied before from a large-sample Bayesian perspective. Due to its complex structure, this estimand poses some theoretical challenges. In Section 5, we introduce a slight modification of the correction algorithm, taking inspiration from estimating equation methodology. The resulting corrected posterior also satisfies a doubly robust property. Extensions of this approach to sample conditional treatment effects can be found in Section D.

We evaluate our methodology empirically in Section 6. The first simulation study validates the approach of Section 3, exhibiting the improved performance of the one-step posterior relative to the uncorrected posterior, which is heavily biased and exhibits substantial undercoverage. This is followed by a large-scale comparison with state-of-the-art causal algorithms using the ACIC 2016 data anaylsis competition (Dorie et al., 2019). Our method—applied to Bayesian additive regression trees (Chipman et al., 2007)—is the best performer in terms of both point and interval estimation. In fact, no other method was able to obtain nominal coverage across all of the data-generating mechanisms. We suggest that this superior performance could be attributed to the propagation of Bayesian uncertainty through the posterior correction to regularize the estimation, which cannot be exploited by the classical semiparametric approaches. Thus, we argue that the one-step posterior correction should appeal not only to Bayesians, but also to classically-minded users interested in leveraging the power of Bayesian algorithms while obtaining frequentist-calibrated inference.

2 Methodology

2.1 Set-up and background

Suppose that we observe independent and identically distributed data from a distribution known to belong to a set of probability measures on a Polish sample space . We will use the shorthand notation for . In particular, , where is the empirical measure, and we let denote the empirical process. For , let be the Hilbert space consisting of all measurable functions with equipped with the inner product and norm .

In a Bayesian analysis, we equip with a -field such that is a standard Borel space, and we specify a prior probability distribution on . Let denote a version of the posterior distribution given . The target estimand is , where is a measurable functional. For notational clarity, we have chosen the range space to be one-dimensional; generalizing our results to higher dimensions is straightforward (e.g. by applying the Cramèr-Wold device: see p. 16 of van der Vaart (1998)). This set-up includes “separated” semiparametric problems in which we have and , where , for some and is a possibly infinite-dimensional nuisance parameter.

An important special case is —the set of all probability measures on —equipped with its Borel -field for the weak topology (Ghosh and Ramamoorthi, 2003). Dirichlet processes (Ferguson, 1973) form the canonical family of prior distributions on . If for a finite positive measure on , then is a version of the posterior given . The process is known as the Bayesian bootstrap (Rubin, 1981), which can be interpreted as the noninformative limiting posterior for any sequence of Dirichlet process models in which the prior information goes to zero. The Bayesian bootstrap plays a central role in our methodology; we denote it by .

It is now necessary to introduce some concepts from semiparametric theory. We refer the reader to Section A for a detailed overview of the following definitions. The functional is required to be differentiable at all in the sense of van der Vaart (1991). The efficient influence function of at is a measurable function satisfying and . A sequence of regular estimators is said to be asymptotically efficient at if

| (1) |

The resulting limiting distribution is optimal in terms of both the convolution theorem (e.g. Theorem 25.20 of van der Vaart, 1998) and the local asymptotic minimax theorem (van der Vaart, 1992).

For smooth parametric models, it is well-known that—under mild regularity conditions—the marginal posterior of the parameter converges to a normal distribution centred at an efficient estimator (e.g. the maximum likelihood estimator) with covariance equal to the inverse Fisher information divided by the sample size. This is the (efficient) Bernstein-von Mises (BvM) theorem (Chapter 10 of van der Vaart (1998)). Consequently, the frequentist coverage of many credible regions—such as balls around the posterior mean, equal tails intervals, highest posterior density regions etc.—will be asymptotically equal to its nominal level, and their sizes will be asymptotically optimal.

A semiparametric BvM theorem describes the marginal posterior of the target functional on an infinite-dimensional model. Similar to the parametric case, we would like the marginal posterior to converge to a normal distribution centred at an efficient estimator with the efficient asymptotic variance. In this article, we study weak convergence of the posterior distributions, which we control using the bounded Lipschitz distance as in Castillo and Rousseau (2015) (see also Section B).

Definition 1.

Let denote the posterior law of , where is any sequence of estimators satisfying (1). The posterior satisfies the semiparametric Bernstein-von Mises theorem if

More informally, we can say that the posterior law of “converges weakly to in probability”.

In the non-Bayesian setting, efficient estimators have been obtained by one-step estimation (Pfanzagl, 1982; Newey et al., 1998), which operates by performing bias corrections that specifically target the estimand. Suppose we have an initial estimate of the data distribution, which induces a plug-in estimate . Since the efficient influence function acts as a first-order distributional derivative of the functional (Robins et al., 2017; Fisher and Kennedy, 2021; Kennedy, 2022), we might expect the “second-order remainder”

to have some form of quadratic dependence on the estimation error of . This suggests that would be an improvement over the plug-in estimator, but the true data distribution is of course unknown. Replacing with the empirical measure leads to

which is called the one-step estimator. We review sufficient conditions for the one-step estimator to be asymptotically efficient in Section A.2; as we will discuss in Section 2.3, the assumptions for our approach share key conceptual similarities.

Example 1 (The mean of an outcome that is missing-at-random).

Suppose the data takes the form , where is a vector of covariates, is a binary missingness indicator, and is the outcome variable of interest that is unobserved when . The target estimand is the outcome mean , which is identified by

under the ignorability (or missing-at-random) (Rubin, 1976) assumption , and the positivity (or overlap) assumption:

with -probability 1. In practical terms, the missingness is deemed to be uninformative with respect to the outcome after adjusting for a set of measured covariates. This example is closely related to estimating the average causal effect of a binary treatment in causal inference (see Section D or Morgan and Winship (2007)).

The data distribution is naturally parameterized in terms of the “propensity score” , the conditional outcome density , and the marginal covariate distribution . Let denote the “outcome regression function”, such that the target estimand can be written as

Thus, a plug-in estimator of takes the form

for estimates and of and respectively.

The efficient influence function of is

which was first derived in Robins and Rotnitzky (1992). As a result, the one-step estimator can be easily constructed as

where we have avoided the need to estimate but now require an estimate of the propensity score. In Section 4, we will study this example in the Bayesian setting.

2.2 The one-step posterior correction

If is well-defined for discrete distributions, its marginal posterior under a Dirichlet process prior on generally satisfies the semiparametric BvM theorem (see, for example, Theorem 12.2 of Ghosal and van der Vaart (2017) and the subsequent discussion). However, the functionals in semiparametric problems are usually defined with respect to restrictions on the data-generating distribution that require some smoothness, in which case Dirichlet processes are inappropriate. For instance, we might require to be dominated by the Lebesgue measure (e.g. Section 3), or we might impose positivity conditions as described in Example 1 (see also: Sections 4 and 5).

As discussed in the introduction, nonparametric smoothing in our prior may introduce a non-negligible bias in the posterior on a low-dimensional functional that precludes a BvM theorem. In some settings, it has been shown that this bias can be avoided by undersmoothing (Castillo, 2012; Castillo and Rousseau, 2015; Ray and van der Vaart, 2020); that is, we must ensure that the true parameters are at least as regular as the prior, e.g. support on sufficiently smooth Hölder and Sobolev spaces (Appendix C of Ghosal and van der Vaart, 2017). This is impractical, however, because the true regularities are unknown and the recovery of the nuisance parameters is degraded by overfitting, which can be detrimental to finite-sample performance. Moreover, undersmoothing may require non-trivial modifications to existing implementations of Bayesian computation methods.

Instead of tuning the prior, we propose an approach that adjusts the posterior directly. Our starting point is an ordinary Bayesian model that is—as usual—optimized to recover the whole data-generating distribution rather than any particular functional. This means that the prior can be specified according to conventional guidelines, and the posterior can be computed with standard methods. As discussed later, our approach will also allow us to circumvent some of the limitations of likelihood-based methods.

Definition 2.

The one-step posterior of the functional given is the pushforward measure of

on the product measure

The structure of the corrected parameter takes inspiration from the one-step estimator described in the previous subsection. Informally speaking, the initial estimate has been replaced by the parameter drawn from the initial posterior, and the empirical measure has been replaced by the Bayesian bootstrap parameter . In our case, we are correcting an entire probability distribution rather than just a point estimator.

We can sample from the one-step posterior via the simple hierarchical scheme in Algorithm 1. First, the user draws samples of from their initial posterior (e.g. via Markov chain Monte Carlo). Each posterior sample is then paired with an independent vector of uniform Dirichlet weights of length ; this arises from the representation

of the Bayesian bootstrap (e.g. Section 4.7 of Ghosal and van der Vaart, 2017), where . Finally, the draw of the estimand is summed with the weighted average of the efficient influence function at .

Algorithm 1 is attractive for several reasons. First, the same set of posterior samples of can be retained to use for different functionals. Second, there is no need to modify any existing implementation for sampling from ; the user can just take the output from the initial implementation and add the random correction terms. This extra step is extremely efficient as it only requires drawing independent sets of Dirichlet weights and averaging the efficient influence functions. Moreover, steps 3-6 in Algorithm 1 can be easily parallelized to save further time.

To provide some geometric intuition for our method, we adapt the ideas from Fisher and Kennedy (2021). Consider the following mixture distributions constructed from an arbitrary (representing a draw from our initial posterior) and the true distribution :

for . Within our model space , we could interpret as a line segment linking and (these line segments are not guaranteed to lie within the model in general, but we will overlook this for the purpose of exposition). This induces a path in the parameter space that reaches the true parameter value at . Starting at , we might hope to get closer to the truth by constructing a good approximation to this path.

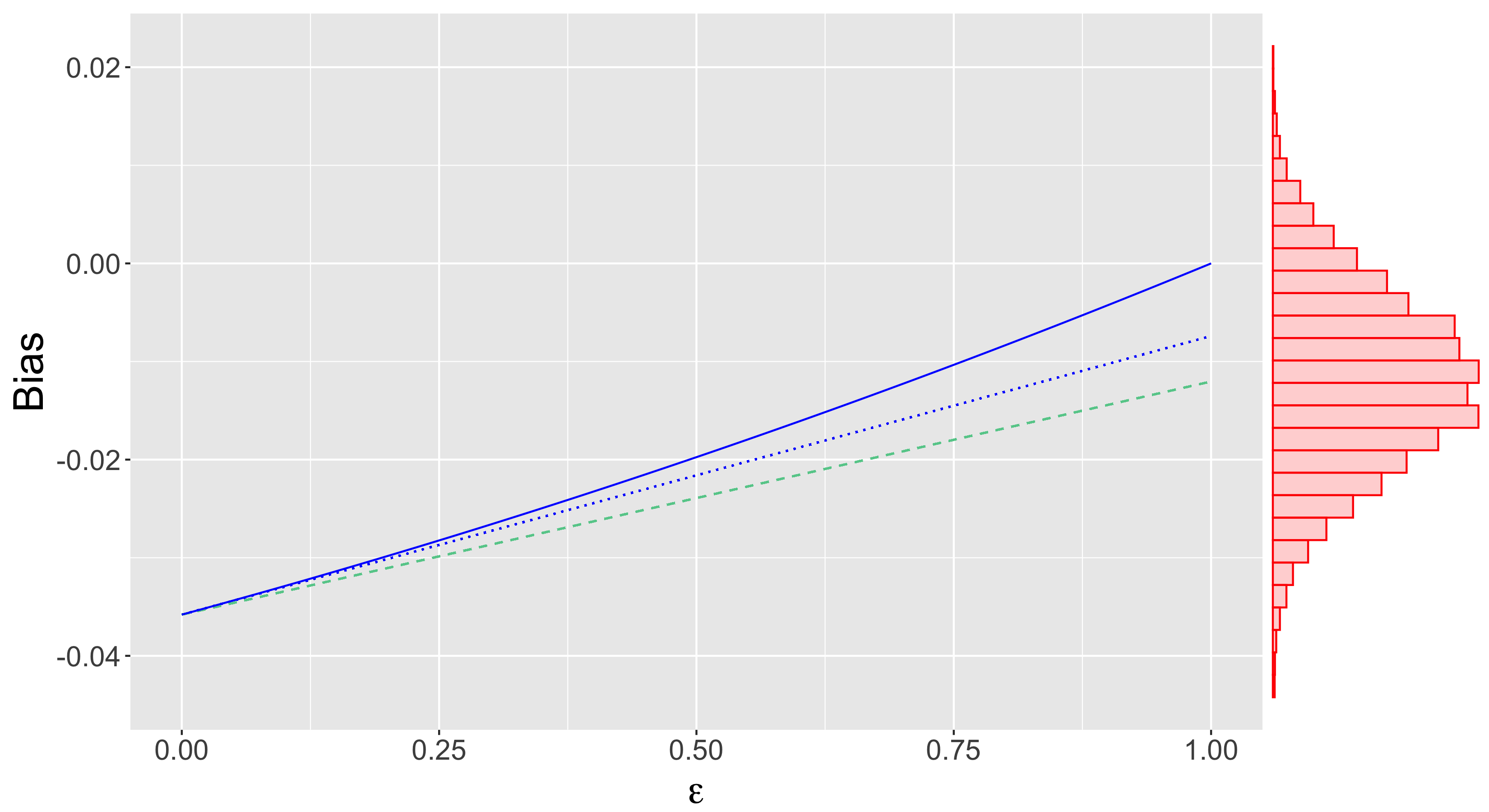

This idea is illustrated visually in Figure 1. The blue solid curve is equal to , and its tangent at —given by the blue dotted line—has slope . The one-step estimator—taking as the “initial estimate” of —estimates the slope with , and the resulting projection onto is shown by the green dashed line. With our posterior correction, the Bayesian bootstrap term gives us a distribution on the slope rather than just a point estimate. As a result, we also get a distribution on the intercept at after projecting along the tangent from , which is shown by the red histogram on the right. This intercept is the one-step corrected parameter; the histogram represents the uncertainty in conditional on the “posterior draw” . For the one-step posterior, this uncertainty is combined with the posterior uncertainty for , which we recall to be conditionally independent of given the data.

The reader may wonder why the empirical measure is insufficient for our posterior correction. We can illustrate the reason by considering linear functionals, which form the simplest class of examples. Let , where is a known bounded function. The efficient influence function is (e.g Castillo and Rousseau, 2015), such that

In words, the one-step corrected parameter is simply the Bayesian bootstrap expectation of , which we already know to satisfy the semiparametric Bernstein-von Mises theorem. If is replaced by in the correction, then the parameter reduces to the one-step estimator , which has zero posterior uncertainty. Thus, the Bayesian bootstrap correction term serves not only to debias the initial posterior but also to obtain the (asymptotically) correct posterior shape. This statement is established in generality in Section 2.3.

To summarize, the one-step posterior combines the uncertainty from two unknown quantities. First, we have the uncertainty in the functional , which arises from our initial posterior. Given a “starting point” , we also have uncertainty in , which is the slope of the tangent to the curve connecting to the truth . This latter source of uncertainty is modelled by replacing the unknown with the Bayesian bootstrap parameter .

2.3 Theory

In this subsection, we provide conditions for the one-step posterior to satisfy the semiparametric Bernstein-von Mises theorem; that is,

where denotes the posterior law of and is any sequence of estimators satisfying (1). As discussed in Section 2.1, this justifies the use of central credible sets as confidence regions.

Assumption 1.

There exists a sequence of measurable subsets of satisfying with

-

(a)

(No second-order bias)

-

(b)

(-convergence)

-

(c)

(Donsker class) The sets are eventually contained in a fixed -Donsker class (van der Vaart and Wellner, 1996).

We also provide an alternative to Assumption 1(c) below: 1(c∗)(i) weakens the Donsker condition at the cost of adding 1(c∗)(ii), which requires envelope function moment bounds. This alternative is also more appropriate if the sieve is not nested (i.e. we do not have ), which would likely preclude the possibility of finding a fixed Donsker class that satisfies Assumption 1(c).

Assumption 1.

-

(c∗)

-

(i)

(Convergence of under the empirical process)

This statement is interpreted in terms of outer probability (van der Vaart and Wellner, 1996) if the supremum is not measurable.

-

(ii)

(Bounding of envelope functions) The sets have envelope functions (i.e. for all and all ) satisfying

-

(i)

Theorem 2.

The structure of Assumption 1 mirrors the standard assumptions for one-step estimators to attain asymptotic efficiency (see Section A.2). To satisfy Assumptions 1(a) and 1(b), the sets are typically included in shrinking neighbourhoods of . In light of the earlier discussion about the quadratic nature of , this term can be neglected when these neighbourhoods shrink quickly enough. The empirical process conditions in Assumptions 1(c) and (c*) restrict the complexity of the posterior so that we can obtain uniform convergence results.

To provide some context for Assumption 1, we compare with the conditions for Theorem 2.1 in Castillo and Rousseau (2015), which is a semiparametric BvM result for functionals. As one might expect, the second-order remainder must be negligible in both cases (Assumption 1(a)) so that the functional is well-approximated by its linear expansion. Assumptions 1(b), (c) and (c*) are not explicitly required by Castillo and Rousseau (2015), but similar conditions are generally used to establish the asymptotically normal expansion of the likelihood (see (4.10) of Castillo and Rousseau (2015), Theorem 1 of Ray and van der Vaart (2020) and p. 373-374 of Ghosal and van der Vaart (2017)). Analogous conditions can also be found in the classical setting for semiparametric likelihood methods (Murphy and van der Vaart, 2000; Cheng and Kosorok, 2008a).

Crucially, our result avoids the restrictive “change-of-measure” condition in (2.14) of Castillo and Rousseau (2015) (see also (3.6) in Ray and van der Vaart (2020)). This depends delicately on the interplay between the model and the prior, which can fail if the prior is oversmooth or adaptive. From a technical viewpoint, the condition is also challenging to verify for complex priors.

As we will see with the examples, the efficient influence function often admits a natural representation of the form

where is a measurable function. Theorem 2 still holds if and are replaced by and respectively in Assumptions 1(b), (c) and (c*).

For our theoretical analysis, the conditional independence of and given is crucial. This is because we wish to utilize the desirable asymptotic properties of the Bayesian bootstrap, and these properties must continue to hold even if we condition on . Our method can be extended to work with proper Dirichlet process posteriors but this would necessitate additional assumptions on the prior base measure, so we will not pursue this further.

3 The integrated squared density

Suppose that we observe independent and identically distributed data from a distribution on that is absolutely continuous with respect to Lebesgue measure with a square-integrable density. We make slight changes in the notation by identifying distributions with their Lebesgue densities, e.g. is now identified by the true density . Consider the problem of estimating . There is a large literature on the estimation of (e.g. Bickel and Ritov, 1988; Birgé and Massart, 1995; Laurent, 1996; Newey et al., 1998; Giné and Nickl, 2008) and more generally, on power integrals for integers . The integrated squared density plays an important role in nonparametric rank statistics (p.266-267 of Prakasa Rao, 1983).

In Castillo and Rousseau (2015), the authors obtained a BvM theorem for this functional with random histogram priors, which are much simpler than common priors used in density estimation such as infinite mixture models. Under regularity assumptions on the true density , we prove in this section that the one-step posterior distribution satisfies the semiparametric BvM theorem for Dirichlet process Gaussian location mixtures. The prior on is defined by

| (2) |

where is the Gaussian density centred at with standard deviation , and is a distribution on with density that is positive and continuous and satisfies for some . For instance, we can choose to be a Gaussian distribution. As in Kruijer et al. (2010); Shen et al. (2013); Scricciolo (2014), we consider an inverse Gamma prior on : .

The efficient influence function for is (Bickel and Ritov, 1988), so the one-step corrected parameter is

It is straightforward to derive the second-order bias:

where denotes the -norm with respect to Lebesgue measure. We highlight the quadratic nature of this term; accordingly, we require the contraction rate for to be faster than .

We consider the following smoothness assumption on introduced by Shen et al. (2013).

Definition 3.

A density belongs to the class of locally -Hölder functions with polynomial function and if has derivatives with

Theorem 3.

Suppose that the true density belongs to a class for . Assume further that there exists such that for all

and is monotone non-increasing (resp. non-decreasing) for large enough (resp. large enough) and there exist such that

If we specify a Dirichlet process Gaussian location mixture prior for as defined above, then the one-step posterior distribution of the integrated squared density satisfies the semiparametric BvM theorem.

From Shen et al. (2013), under the above conditions the posterior distribution concentrates in Hellinger or distance at the rate for some , which is minimax adaptive up to a term for all (Maugis-Rabusseau and Michel, 2013). The condition is used to verify part (c*) of Assumption 7. It can be weakened to by considering the truncated prior: for some arbitrarily large but fixed constant .

Note that there are different definitions of the class in the literature, and all these variants can be used in Theorem 3. As in Donnet et al. (2018), this condition can be replaced by assuming the existence of a finite mixture of Gaussian densities with variance with at most support points such that the Kullback-Leibler divergence between and is of order .

4 The mean of an outcome that is missing-at-random

4.1 General methodology

In this section, we revisit the missing data example in Example 1. Recall that the data takes the form , where is a vector of covariates, is a binary missingness indicator, is the outcome variable of interest that is unobserved when , and the target estimand is

The density for a single observation can be written as

which factorizes over the parameters. Consequently, if the three parameters are given independent priors, they will remain independent given in the posterior. An important implication is that the model for will not feature in the marginal posterior of since the functional is only defined by the other two parameters. This well-known phenomenon is discussed in Robins and Ritov (1997); Robins et al. (2015) and Ray and van der Vaart (2020).

As stated earlier, the efficient influence function of is

so that the one-step corrected parameter

depends on only through and .

In the following, we state assumptions for the one-step posterior to satisfy the semiparametric BvM theorem, specializing the conditions in Assumption 1. Let and respectively denote the true values of and associated with .

Assumption 2.

There exists a sequence of measurable subsets of satisfying such that

-

(a)

(-convergence of and ) There exist numbers such that

and .

-

(b)

(Uniform bounding) For all sufficiently large , there exist fixed constants such that for all ,

-

(c)

(Donsker class) The sequences of sets and are both eventually contained in fixed -Donsker classes.

Theorem 4.

Under Assumption 2, the one-step posterior for the outcome mean satisfies the semiparametric BvM theorem.

Assumption 2(a) states that and must both converge uniformly on to their respective truths in , and their combined rate of convergence must be faster than . To connect this to Assumption 1(a), we note that the second-order bias takes the form

| (3) |

where the upper bound is due to Cauchy-Schwarz. Thus, Assumption 2(a) immediately implies Assumption 1(a).

The cross-term structure of the second-order bias enables the rate of convergence of one parameter to compensate for the other; this is a property known as “rate double robustness” (Rotnitzky et al., 2021). For example, if were to be modelled parametrically, then the posterior for would be permitted to contract around arbitrarily slowly. Alternatively, and could both be modelled using flexible nonparametric methods, and the condition would be satisfied provided that both their posteriors contract faster than . As mentioned earlier, the ordinary marginal posterior of under independent priors will not depend on the model for , so it cannot possess this double robust property (Robins et al., 2000, 2015).

The uniform bounds in Assumption 2(b) help to ensure that the -convergence of (i.e. Assumption 1(b)) follows from Assumption 2(a). The assumption that the propensity score is bounded away from zero is commonly referred to as “positivity” and is routine for any estimation approach that involves inverse probability weighting. As discussed in Section 4.2 of Kennedy (2022) in a classical setting, the boundedness of can be relaxed to bounded moment conditions by using Hölder’s inequality.

4.2 Comparison with prior augmentations in the least favourable direction

This example was studied by Ray and van der Vaart (2020) under the constraint that the outcome variables are binary. With similar motivations to our correction method, Ray and van der Vaart (2020) proposed constructing a preliminary estimator of the propensity score based on a separate dataset that is independent of and modelling the outcome regression function by

| (4) |

where is the expit function, and are parameters.

The prior on should be specified such that the resulting prior on captures the user’s a priori beliefs on . In contrast, the augmentation term plays a technical role, with the goal of satisfying the change-of-measure condition for the semiparametric BvM theorem as discussed in Section 2.2. The fluctuation parameter follows a prior independently of , where the variance is allowed to vary with . For the marginal covariate distribution, Ray and van der Vaart (2020) specified a Dirichlet process prior independent of . We will assume throughout that and satisfy the following assumption.

Assumption 3.

The true propensity score satisfies for some , and the preliminary estimators satisfy and

where .

Theorem 5 (Theorem 2 of Ray and van der Vaart (2020)).

Assume that there exist measurable sets of functions satisfying, for every and some numbers ,

| (5) | ||||

| (6) | ||||

| (7) | ||||

| (8) |

Under Assumption 3, if and , then the marginal posterior of satisfies the semiparametric Bernstein-von Mises theorem.

The critical aspect of the above result is that it avoids the change-of-measure condition in equation (3.6) of Theorem 1 of Ray and van der Vaart (2020) for establishing the semiparametric BvM theorem without the prior augmentation. We now compare this approach with the one-step posterior in this set-up. As discussed by Ray and van der Vaart (2020), the preliminary estimator could be interpreted as a degenerate prior on . This interpretation immediately suggests a corresponding one-step posterior by defining

| (9) |

To facilitate comparisons with the method of Ray and van der Vaart (2020), we will continue to describe the assumptions in terms of the parameter , where we have in this case.

Theorem 6.

Assume that there exist measurable sets of functions satisfying, for some numbers ,

| (10) | ||||

| (11) | ||||

| (12) |

Under Assumption 3, if , then the one-step posterior satisfies the semiparametric Bernstein-von Mises theorem.

A direct comparison of the assumptions for Theorems 5 and 6 is complicated slightly by the different specifications for the outcome regression function, which means that the sets and may not match. Nevertheless, we should keep in mind that the augmentation in (4) is motivated purely by improving the inference for rather than the recovery of . It is likely, therefore, that a prior on that satisfies the assumptions (5) - (8) (in combination with some sequence of priors for ) will also satisfy the assumptions (10) - (12) for the unaugmented regression model. (In any case, it will be simpler to check (10) - (12) due to the absence of the augmentation term.) We verify this claim below for a Gaussian process prior studied by Ray and van der Vaart (2020).

Following the set-up in Ray and van der Vaart (2020), we take the covariate space to be . The Riemann-Liouville process released at zero of regularity is defined by

| (13) |

where is the smallest integer that is strictly larger than , the are i.i.d. variables, and is an independent Brownian motion (see Chapter 11 of Ghosal and van der Vaart (2017)). We use this to define our prior for . For covariate spaces equal to for integer , the subsequent corollary can be easily extended to the Gaussian series priors considered by Ray and van der Vaart (2020).

Corollary 7.

Suppose that , for , where is the Hölder space of order on (see Chapter 4 of Giné and Nickl (2016)). Suppose further that we specify our one-step posterior using (9) and the Riemann-Liouville prior for defined by (13). Under Assumption 3, if and for

then the one-step posterior satisfies the semiparametric Bernstein-von Mises theorem.

The corresponding result for the prior augmentation method in Corollary 2 of Ray and van der Vaart (2020) requires the following additional condition:

For finite-sample inference, the need to tune is a substantial practical drawback of the prior augmentation approach relative to the one-step posterior. This is because the prior for will likely have a significant impact on the posterior for the target estimand, yet the augmentation term only plays a technical role, so there will be no subjective or substantive guidance to select .

From a computational perspective, the prior augmentation is also more difficult to implement than the one-step posterior correction—it is generally the case that existing software for posterior sampling will have to be rewritten in order to accommodate the new linear term. Furthermore, as Ray and van der Vaart (2020) wrote in their discussion, the augmented prior “will not perform better for any other functional”. Therefore, if multiple functionals are of interest, the user would have the time-consuming task of implementing distinct models for each functional. As we have mentioned previously, our approach handles this situation very efficiently because we can retain a single set of posterior samples from the initial model, with which we can compute all requisite corrected posteriors.

We recall that the theory provided by Ray and van der Vaart (2020) for this prior augmentation relies on an independent, auxiliary dataset to construct the propensity score estimate . A similar prior augmentation was studied by Ray and Szabó (2019) for continuous outcomes, and they evaluated the performance of their method empirically when is trained on the same data as the posterior. Using a point estimate in this fashion is similar to classical correction approaches like targeted maximum likelihood estimation (van der Laan and Rubin, 2006; van der Laan and Rose, 2011). As we will discuss further in Section 6.2, we have found that it is beneficial to instead incorporate the Bayesian uncertainty in the nuisance parameters (in this case the propensity score) by propagating the variation from the initial posterior to the one-step posterior.

5 The average treatment effect on the treated

Consider the problem of inferring the causal effect of a binary treatment on an outcome using observational data. Our data takes the form , where is a vector of pre-treatment covariates. Causal frameworks often posit the existence of counterfactual variables and define causal effects as contrasts between functionals of counterfactual distributions (e.g. Pearl, 2009; Hernán and Robins, 2020). In this case, we can define the pair of variables to be the potential outcomes associated with treatment values (“treated”) and (“controls”) respectively. Under the consistency assumption (Hernán and Robins, 2020)

we observe exactly one of for each unit in the dataset.

Our target estimand is the average treatment effect on the treated (ATT) (Rubin, 1977; Heckman and Robb, 1985)

which quantifies the average causal effect of withholding treatment on the population currently being treated. This can also be formulated without counterfactuals (e.g. Geneletti and Dawid, 2011; Dawid, 2021; Yiu et al., 2022).

An attractive aspect of the ATT is that it is identified under assumptions that are strictly weaker than those commonly specified for the more well-known average treatment effect . More specifically, the identification formula

| (14) |

can be obtained under the assumptions of unconfoundedness for controls

and weak overlap:

with -probability 1 (Imbens, 2004). Under violations of consistency or unconfoundedness for controls, our results still apply for estimation of the functional defined by (14) provided that weak overlap holds.

Similar to Section 4, it is natural to parameterize in terms of the propensity score , the conditional outcome density , and the marginal covariate density . For a single observation , the density

factorizes into the three parameters, so it is particularly convenient and intuitive to specify independent priors.

The functional in (14) has efficient influence function

| (15) |

where is the outcome regression function for the controls (Chapter 8 of van der Laan and Rose, 2011). We highlight the presence of the marginal probability of treatment assignment , which we can write as with respect to the natural parameterization in terms of and the marginal covariate distribution .

The behaviour of a posterior on will depend on the interplay between the models for and . In the construction of our one-step posterior, we have found it to be beneficial theoretically to replace with , which is partially due to the fact that the posterior for is guaranteed to contract to at the rate of without requiring additional assumptions on and . With a slight abuse of notation and terminology, we define the one-step corrected parameter to be

| (16) |

We clarify that the in the denominator of the expression is the same as the one that appears outside of the large square brackets. From a computational perspective, this means that the user does not need to draw an additional set of uniform Dirichlet weights for each posterior sample of . Moreover, (16) only depends on through and , so the user can undertake an initial posterior analysis that is conditional on the covariates and avoid computing the posterior for .

This example helps to illustrate that our framework offers the flexibility to attain more attractive theoretical properties by making modifications to the correction. Similar modifications are used for classical one-step estimation (e.g. Rotnitzky et al., 2021) with the empirical measure and the Bayesian bootstrap once again playing analogous roles. The corrected parameter defined in (16) also admits an alternative motivation by using the efficient influence function in (15) to define a Bayesian-bootstrap-weighted estimating equation

which is solved by . The relationship between one-step and estimating equation estimators is discussed in Hines et al. (2022) from a classical perspective.

Assumption 4.

Let and denote the true parameters associated with . There exists a sequence of measurable subsets of satisfying such that

-

(a)

(-convergence of and ) There exist numbers such that

and .

-

(b)

(Uniform bounding) For all sufficiently large , there exist fixed constants such that for all ,

-

(c)

(Donsker class) The sequences of sets and are both eventually contained in fixed -Donsker classes.

Theorem 8.

Assumption 4 has a similar form to Assumption 2 for the example in Section 4. In particular, the second-order bias in this case possesses a cross-term structure in terms of and , which induces the rate double robustness property in Assumption 4(a).

Given the conspicuous absence of from the definitions and assumptions, it is natural to ask whether one should model the parameters and with independent priors, such that the model for drops out of the analysis for , and the posterior for is derived solely from the data on the controls. In the heterogeneous causal effects literature, this separation of the regression model into the two treatment arms is called the T-learner approach (“two” learners; Künzel et al. (2019)).

In general, we would recommend against doing this and instead advocate for specifying a single regression model that treats as just another covariate, which is called the S-learner approach (“single” learner; Künzel et al. (2019)). Provided that Assumption 4 is satisfied, there is no difference in terms of asymptotic performance, but we would expect to obtain finite-sample efficiency gains from the pooling of information across the entire dataset.

An advantage of using the T-learner approach, however, would be to prevent potential model misspecification for from contaminating the posterior for , thereby reducing the risk of violating Assumption 4(a). There could also be a finite sample impact if and are very different (e.g. is much smoother than due to high heterogeneity in the conditional treatment effect given ), because prior regularization may shrink a joint posterior for towards a compromise that is detrimental to precision for . Ultimately, we would encourage the user to think carefully about their modelling specifications, both in terms of incorporating substantive knowledge and the implications concerning the theory we have provided.

6 Simulation studies

6.1 Estimating the integrated squared density under a Laplace distribution

Suppose that the data are generated i.i.d. from a distribution, which has density

The Laplace distribution was chosen because it is non-differentiable at , and we would expect this to induce oversmoothing in the Dirichlet process Gaussian mixture model from Section 3. We specified our (initial) Bayesian model according to (2) with the standard normal distribution for the base measure and the prior parameter values .

Our goal is to estimate the integrated squared density as described in Section 3. To evaluate the performance of the one-step posterior correction, we ran 1000 independent Monte Carlo trials for each of the two sample sizes and . For both the uncorrected and corrected posteriors, point estimation was evaluated using the posterior mean, and intervals were constructed using the 95% central credible region.

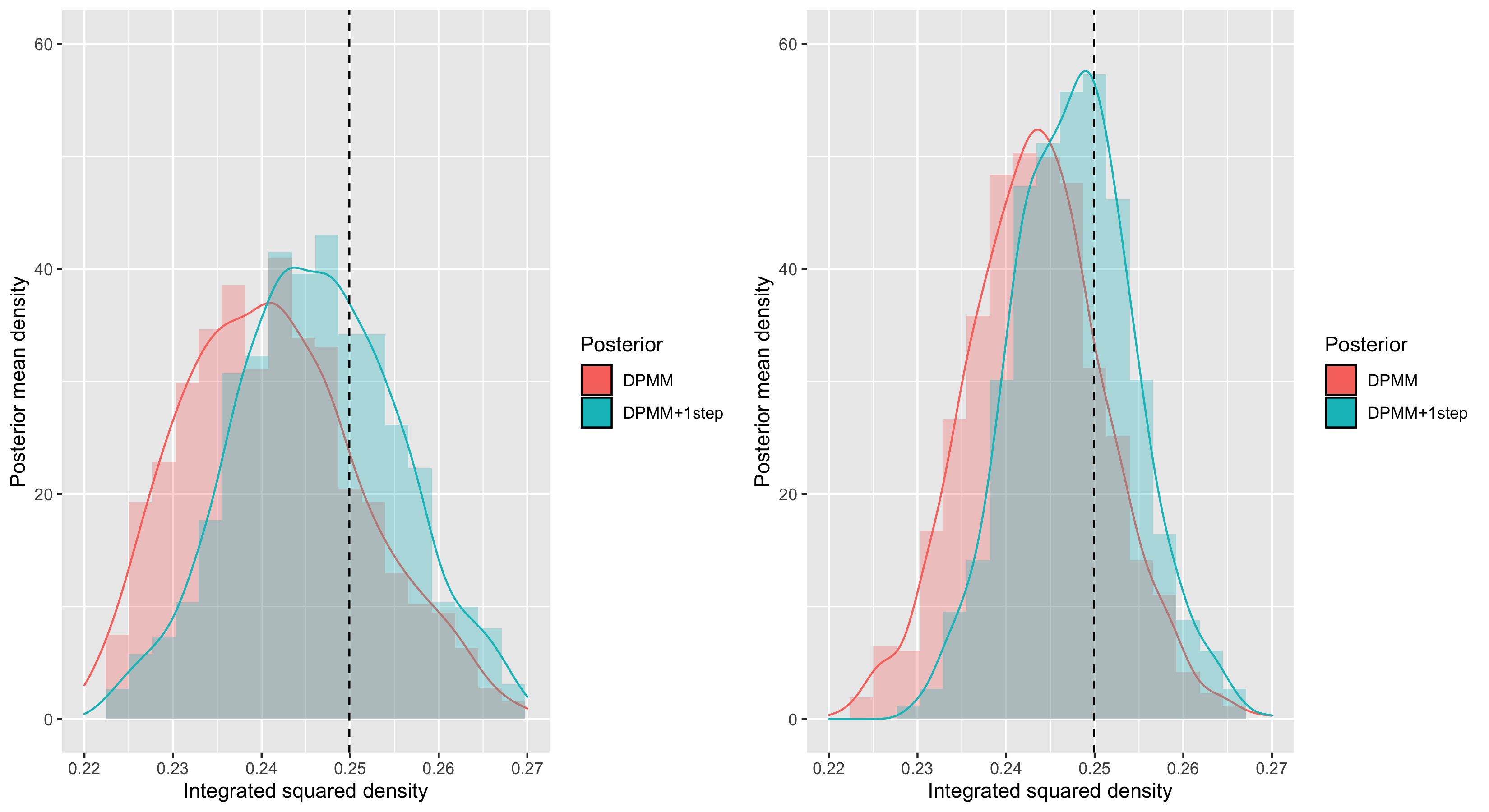

The numerical results can be found in Table 1. First, we can see that the one-step posterior improved on the initial posterior across all point estimation metrics. This was achieved through substantial bias reduction, which is illustrated visually by the histogram/density plots of the posterior mean in Figure 2.

The improvements in coverage are even more striking. For the larger sample size of , the one-step posterior was able to attain nominal coverage despite the fact that the initial posterior only achieved 67.4%. The poor performance of the initial posterior can be partially attributed to the aforementioned bias, which is of a similar order of magnitude to the average interval length. However, it also appears that the interval lengths are too short. This could have been caused by an overcurved likelihood or residual prior regularization, or both. In any case, it seems unlikely that the initial posterior satisfies the semiparametric BvM theorem for this Laplace example.

| Sample size | Method | Bias | MAE | RMSE | Cov | Int. len. |

|---|---|---|---|---|---|---|

| DPMM | -0.0098 | 0.0108 | 0.0185 | 64.9% | 0.0290 | |

| DPMM+1step | -0.0040 | 0.0072 | 0.0151 | 93.7% | 0.0434 | |

| DPMM | -0.0068 | 0.0073 | 0.0138 | 67.4% | 0.0210 | |

| DPMM+1step | -0.0025 | 0.0048 | 0.0116 | 95.8% | 0.0324 |

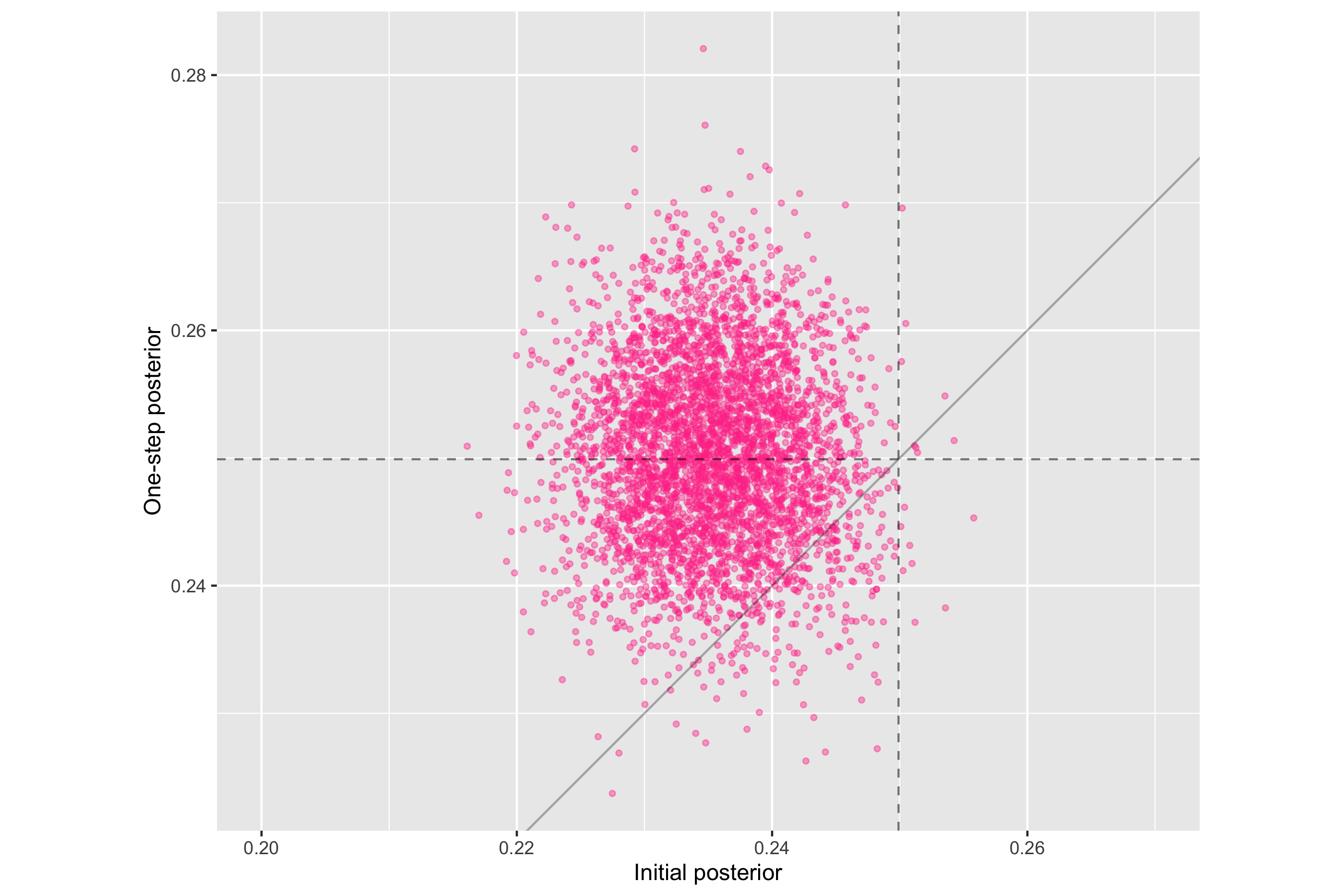

For further context, we have included a “before and after” scatter plot in Figure 3 that compares the samples from both posteriors for a single iteration of the experiment (). This plot illustrates that, despite the randomness of the correction terms, the draws from the initial posterior tend to be pulled in the direction of the true functional value.

6.2 The ACIC 2016 competition

The causal data analysis competition “Is Your SATT Where It’s At?” was held at the 2016 Atlantic Causal Inference Conference with the goal of providing a comprehensive, objective comparison of the available methods for estimating causal effects. A total of 24 submissions were compared in the “black box” section of the competition, which assessed the automated performance of the methods across 77 different simulation settings. Detailed descriptions of the competition design, motivations and findings can be found in Dorie et al. (2019).

Each dataset had a sample size of with the same data structure as Section 5; that is, for . The set of covariates was fixed across datasets—they were taken from a real study that examined the impact of birth weight on a child’s IQ and contained a mixture of categorical, binary, continuous and count variables (58 variables in total). Conditional on the covariates, the potential outcomes and treatment assignments were generated i.i.d. according to the configuration of simulation parameters, which included the degree of nonlinearity of the regression functions, the treated percentage, and the treatment effect heterogeneity. One hundred independent datasets were generated from each of the 77 settings, resulting in a total of 7700 datasets.

The target estimand is the sample average treatment effect on the treated (SATT)

| (17) |

which quantifies the average treatment effect among those treated in the dataset. But the SATT cannot be directly inferred in a semiparametric framework because we never observe when . An obvious alternative is to use the estimates for the (population) ATT as described in Section 5, but this would likely produce substantially conservative intervals for the SATT (Imbens, 2004). As a partial remedy, we will also consider estimates derived from the one-step posterior targeting a new estimand that we call the average covariate-conditional treatment effect on the treated (ACTT)

which replaces the unknown population covariate distribution in the ATT identification formula (14) with the empirical covariate distribution

We refer the reader to Section D for further information about the ACTT, including details on implementing the one-step posterior correction.

For our initial posterior, we modelled both the conditional outcome distribution and propensity score with Bayesian additive regression trees (BART) (Chipman et al., 2010). As discussed at the end of Section 5, we fitted the outcome regression model on both treatment arms together to pool information. In accordance with the “black box” nature of the competition, we used only the default hyperparameters in the R BART package implementations with no cross-validation (the propensity score model used the pbart procedure, which specifies a probit link). For each dataset, we obtained 4000 posterior samples aggregated from 4 independent chains after discarding 2000 burn-in samples. The posterior mean and the central 95% credible interval were used for point and interval estimation respectively.

We highlight two top performers from the competition (descriptions of the remaining submissions can be found on p. 62 of Dorie et al. (2019)). The “BART on Pscore” method (Hahn et al., 2020) fitted a BART outcome regression model that included an estimate of the propensity score (from a cross-validated probit BART model) as a splitting variable. A posterior for was then derived by replacing with in (17) (Hill, 2011). The argument put forth by Hahn et al. (2020) was that their augmentation helps to mitigate regularization bias when estimating the outcome regression function because the propensity score is likely to be correlated with in practice, e.g. a physician may assign treatment more readily to patients with worse risk factors. Accordingly, the propensity score should be an informative transformation of the covariates for predicting the outcome, which makes it easier for the BART model to approximate the truth with finite samples.

The “BART+TMLE” method employed a correction procedure similar to that of the one-step estimator. Targeted maximum likelihood estimation (TMLE) (van der Laan and Rubin, 2006; van der Laan and Rose, 2011) makes adjustments in the model space rather than the parameter space; an initial estimate is mapped to a targeted estimate such that for the population ATT. Consequently, the TMLE plug-in is approximately equal to its own one-step estimator and its variance can be estimated by provided that satisfies the requisite conditions for asymptotic efficiency (see Section A.2). In this case, the initial estimates of the outcome regression function and the propensity score were both derived from BART.

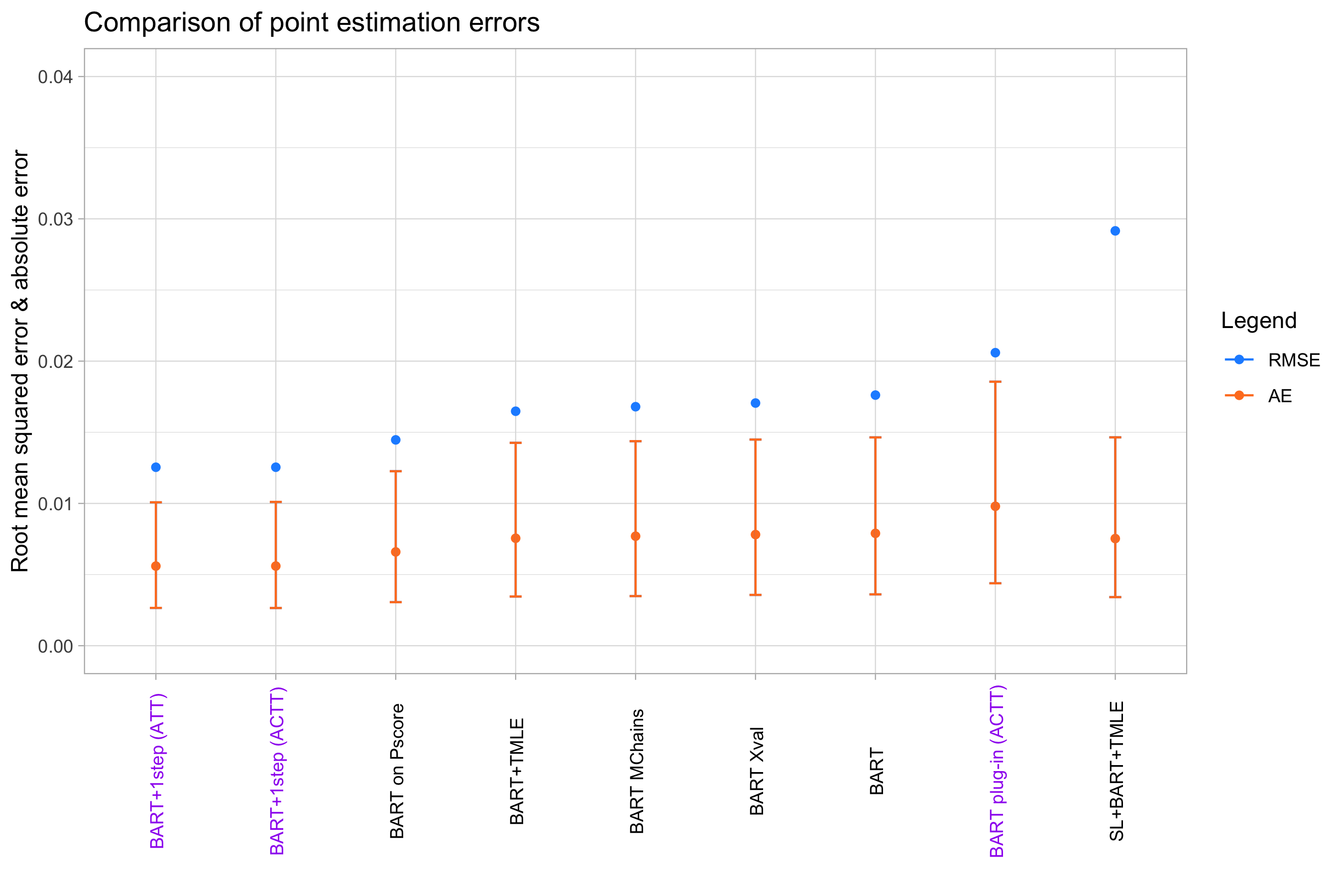

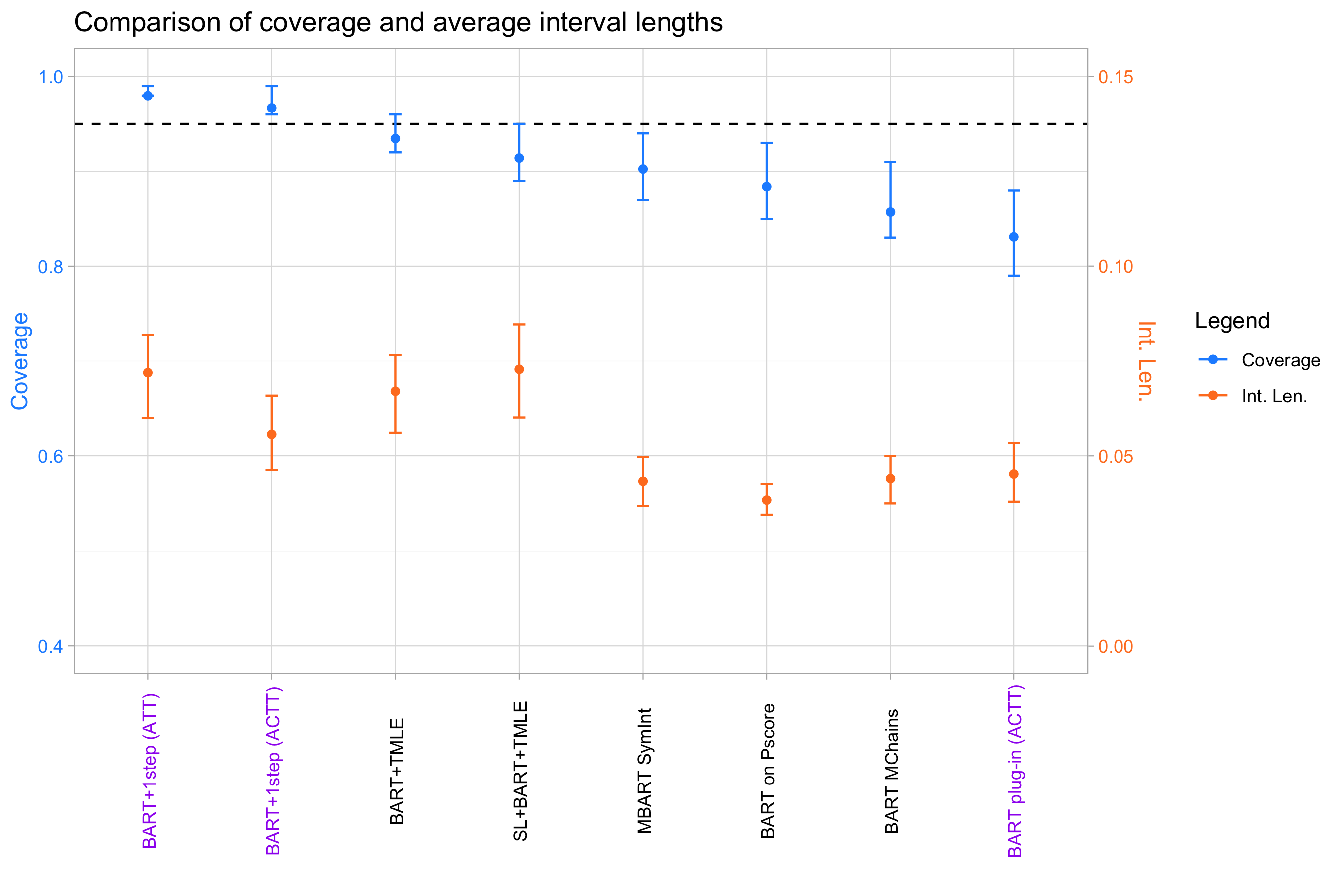

Figure 4 compares the standardized point estimation errors across all settings. The top performer from the competition submissions was “BART on Pscore”. In particular, it improved on “BART MChains”, which was the same procedure aside from the propensity score augmentation (“MChains” stands for multiple chains). We emphasize again, however, that the “BART on Pscore” augmentation does not target any particular low-dimensional functional, and the Bayesian update will instead use the estimated propensity score to help find a favourable bias-variance trade-off for the whole outcome regression function. In contrast, our one-step posteriors used the propensity score model to debias specifically in the direction of the ATT, which is perhaps why they were able to present further improvements in reducing the point estimation errors. However, as Hahn et al. (2020) pointed out, there is the option of combining “BART on Pscore” with a targeted approach like TMLE, and by extension, we can also combine it with the one-step posterior correction to reap the benefits of both approaches. For additional context, we have included the results for the BART ACTT posterior without the one-step correction (“BART plug-in (ACTT)”) and it is clear that the one-step ACTT posterior performs substantially better.

The results for interval estimation can be found in Figure 5. None of the competition submissions were able to attain the nominal coverage level of 95% across all 7700 datasets, with “BART+TMLE” coming the closest. We recall that the intervals for “BART+TMLE” were constructed for the population ATT rather than the SATT, so we would expect them to be conservative. As the direct comparator, the one-step ATT posterior was able to attain a conservative level of coverage, albeit with slightly wider intervals. As expected, the one-step ACTT posterior had shorter interval lengths than both methods, but it was still able to attain nominal coverage. Taking both coverage and interval lengths into account, the one-step ACTT posterior was the clear winner in this category. As before, we have included the results for the uncorrected ACTT posterior, which performed slightly worse than the other plug-in BART methods like “BART on Pscore” and “BART MChains”.

Earlier, we described how the variance of the TMLE estimator could be estimated by , which is the sample variance of the estimated efficient influence function divided by the sample size. Other influence-function-based methods like one-step estimation take the same approach but with replaced by the original estimate (Hines et al., 2022; Kennedy, 2022). This variance estimate is based on a first-order asymptotic approximation that assumes the second-order remainder terms to be negligible; in other words, the estimation uncertainty of (or ) is effectively treated as being zero. Perhaps unsurprisingly, the intervals derived from these variance estimates tend to undercover in practice (Gruber and van der Laan, 2019).

We can derive some further insight by formulating this in our one-step posterior correction framework. The classical one-step approach roughly corresponds to specifying a point-mass initial posterior on : , where the normal approximation used for constructing intervals is replaced by “Bayesian bootstrapping” the sampling distribution quantiles of akin to the percentile bootstrap (Efron and Hastie, 2016). In the context of using a Bayesian procedure like BART, this makes little sense. Instead, our one-step posterior propagates the uncertainty from the whole BART posterior, which has the effect of extracting more information from the BART model. For example, is the posterior tightly concentrated around its mean or is it widely spread out? This gives an indication regarding the amount of information that is contained in the data, which serves to regularize our one-step posterior for better inference.

In conclusion, the one-step posterior is a much more natural and effective way to leverage Bayesian procedures for semiparametric inference than classical approaches like one-step estimation and TMLE. We expect there to be the potential for further performance gains for one-step BART posteriors if the user employs cross-validation to select hyperparameters or augments the outcome regression model with an estimated propensity score augmentation like “BART on Pscore”.

7 Discussion

The holistic nature of Bayesian inference—automatic uncertainty quantification, marginalizing nuisance parameters, inference for all estimands in one stroke—is often cited as one of its key strengths. This wisdom is subverted in the semiparametric setting. A Bayesian user has the unenviable choice of either tailoring their model towards a particular estimand at the expense of all others or run the risk of obtaining biased, uncalibrated inference. Our one-step posterior correction allows us to circumvent this problem by targeting estimands after the initial model has been fitted.

The empirical evaluations provided suggest that our methodology can in fact outperform classical correction methods when using Bayesian algorithms. We have argued informally that this was achieved by drawing out more information from the initial posterior for regularization. It might be possible to offer more formal arguments by exploring higher-order properties of the one-step posterior; there are some precedents for this type of theory for semiparametric Bayes-like methods (Cheng and Kosorok, 2008a, b).

A potential obstacle for our approach is the requirement that the efficient influence function can be computed across the whole model. This could be particularly challenging for separated semiparametric models, because the efficient influence function is defined in terms of orthogonal projections (van der Vaart, 1998) and may not admit a tractable expression. However, with recent developments in numerical procedures for approximating efficient influence functions (Carone et al., 2019; Jordan et al., 2022), we anticipate that it will be possible to fully automate the one-step posterior correction in future work.

In this article, we have restricted our attention to conventional Bayesian models for deriving our initial posterior distribution. It is in fact possible to use other types of posteriors as long as they satisfy the requisite theoretical conditions, e.g. generalized posteriors (Bissiri et al., 2016), martingale posteriors (Fong et al., 2021), and posteriors arising from approximate computational algorithms like variational Bayes (Jordan et al., 1999). These frameworks still abide by the plug-in principle and may therefore have the potential to benefit from our methodology.

8 Acknowledgments

The authors thank Edward Kennedy and Kolyan Ray for their helpful input. AY receives funding from Novo Nordisk. CH is supported by The Alan Turing Institute, the Li Ka Shing Foundation, the Medical Research Council, the EPSRC through the Bayes4Health grant EP/R018561/1, AI for Science and Government UKRI, and the U.K. Engineering and Physical Sciences Research Council. JR has received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement No 834175).

References

- Berger et al. [1999] J. O. Berger, B. Liseo, and R. L. Wolpert. Integrated likelihood methods for eliminating nuisance parameters. Statistical Science, 14(1):1 – 28, 1999. doi: 10.1214/ss/1009211804. URL https://doi.org/10.1214/ss/1009211804.

- Bickel and Ritov [1988] P. Bickel and Y. Ritov. Estimating integrated squared density derivatives: sharp best order of convergence estimates. Sankhya, 50:381–393, 1988.

- Bickel and Ritov [2003] P. Bickel and Y. Ritov. Nonparametric estimators which can be “plugged-in”. Annals of Statistics, 31:1033–1053, 2003.

- Birgé and Massart [1995] L. Birgé and P. Massart. Estimation of integral functionals of a density. Annals of Statistics, 23:11–29, 1995.

- Bissiri et al. [2016] P. Bissiri, C. Holmes, and S. Walker. A general framework for updating belief distributions. Journal of the Royal Statistical Society, Series B, 78:1103–1130, 2016.

- Breiman [2001] L. Breiman. Random forests. Machine Learning, 45:5–32, 2001.

- Buja et al. [2019a] A. Buja et al. Models as approximations I: consequences illustrated with linear regression. Statistical Science, 34:523–544, 2019a.

- Buja et al. [2019b] A. Buja et al. Models as approximations II: a model-free theory of parametric regression. Statistical Science, 34:545–565, 2019b.

- Carone et al. [2019] M. Carone, A. Luedtke, and M. van der Laan. Toward computerized efficient estimation in infinite-dimensional models. Journal of the American Statistical Association, 114:1174–1190, 2019.

- Castillo [2008] I. Castillo. Lower bounds for posterior rates with Gaussian process priors. Electronic Journal of Statistics, 2:1281–1299, 2008.

- Castillo [2012] I. Castillo. A semiparametric Bernstein-von Mises theorem for Gaussian process priors. Probability Theory and Related Fields, 152:53–99, 2012.

- Castillo and Nickl [2014] I. Castillo and R. Nickl. On the Bernstein–von Mises phenomenon for nonparametric Bayes procedures. The Annals of Statistics, 42(5):1941 – 1969, 2014. doi: 10.1214/14-AOS1246. URL https://doi.org/10.1214/14-AOS1246.

- Castillo and Rousseau [2015] I. Castillo and J. Rousseau. A Bernstein-von Mises theorem for smooth functionals in semiparametric models. Annals of Statistics, 43:2353–2383, 2015.

- Cheng and Kosorok [2008a] G. Cheng and M. Kosorok. Higher order semiparametric frequentist inference with the profile sampler. Annals of Statistics, 36:1786–1818, 2008a.

- Cheng and Kosorok [2008b] G. Cheng and M. Kosorok. General frequentist properties of the posterior profile distribution. Annals of Statistics, 36:1819–1853, 2008b.

- Chernozhukov et al. [2018] V. Chernozhukov, D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21:C1–C68, 2018.

- Chipman et al. [2007] H. Chipman, E. Geroge, and R. McCulloch. Bayesian ensemble learning. Neural Information Processing Systems, 19:265–272, 2007.

- Chipman et al. [2010] H. Chipman, E. Geroge, and R. McCulloch. BART: Bayesian Additive Regression Trees. Annals of Applied Statistics, 4:266–298, 2010.

- Dawid [2021] A. Dawid. Decision-theoretic foundations for statistical causality. Journal of Causal Inference, 9:39–77, 2021.

- Diaconis and Freedman [1986] P. Diaconis and D. Freedman. On the Consistency of Bayes Estimates. The Annals of Statistics, 14(1):1 – 26, 1986. doi: 10.1214/aos/1176349830. URL https://doi.org/10.1214/aos/1176349830.

- Donnet et al. [2018] S. Donnet, V. Rivoirard, J. Rousseau, and C. Scricciolo. Posterior concentration rates for empirical Bayes procedures with applications to Dirichlet process mixtures. Bernoulli, 24(1):231 – 256, 2018. doi: 10.3150/16-BEJ872.

- Dorie et al. [2019] V. Dorie, J. Hill, U. Shalit, M. Scott, and D. Cervone. Automated versus do-it-yourself methods for causal inference: lessons learned from a data analysis competition. Statistical Science, 34:43–68, 2019.

- Dudley [2002] R. Dudley. Real Analysis and Probability. Cambridge University Press, Cambridge, 2002.

- Efron and Hastie [2016] B. Efron and T. Hastie. Computer Age Statistical Inference. Cambridge University Press, Cambridge, 2016.

- Ferguson [1973] T. Ferguson. A Bayesian analysis of some nonparametric problems. Annals of Statistics, 2:209–230, 1973.

- Fisher and Kennedy [2021] A. Fisher and E. Kennedy. Visually communicating and teaching intuition for influence functions. The American Statistician, 70:162–172, 2021.

- Fong et al. [2021] E. Fong, C. Holmes, and S. G. Walker. Martingale posterior distributions. arXiv preprint arXiv:2103.15671, 2021.

- Geneletti and Dawid [2011] S. Geneletti and A. Dawid. Defining and identifying the effect of treatment on the treated. In P. Illari, F. Russo, and J. Williamson, editors, Causality in the sciences, pages 728–749. Oxford University Press, 2011.

- Ghosal and van der Vaart [2017] S. Ghosal and A. van der Vaart. Fundamentals of Nonparametric Bayesian Inference. Cambridge University Press, Cambridge, 2017.

- Ghosh and Ramamoorthi [2003] J. Ghosh and R. Ramamoorthi. Bayesian Nonparametrics. Springer, New York, 2003.

- Giné and Nickl [2008] E. Giné and R. Nickl. A simple adaptive estimator of the integrated square of a density. Bernoulli, 14:47–61, 2008.

- Giné and Nickl [2016] E. Giné and R. Nickl. Mathematical foundations of infinite-dimensional statistical models. Cambridge University Press, Cambridge, 2016.

- Goldstein and Messer [1992] L. Goldstein and K. Messer. Optimal plug-in estimators for nonparametric functional estimation. Annals of Statistics, 20:1306–1328, 1992.

- Gruber and van der Laan [2019] S. Gruber and M. van der Laan. Comment on “Automated versus do-it-yourself methods for causal inference: lessons learned from a data analysis competition”. Statistical Science, 34:82–85, 2019.

- Hahn et al. [2020] P. Hahn, J. Murray, and C. Carvalho. Bayesian regression tree models for causal inference: regularization, confounding, and heterogeneous effects. Bayesian Analysis, 15:965–1056, 2020.

- Heckman and Robb [1985] J. Heckman and R. Robb. Alternative methods for evaluating the impact of interventions: An overview. Journal of Econometrics, 30:239–267, 1985.

- Hernán and Robins [2020] M. A. Hernán and J. Robins. Causal inference: What if. 2020.

- Hill [2011] J. Hill. Bayesian nonparametric modeling for causal inference. Journal of Computational and Graphical Statistics, 20:217–240, 2011.

- Hines et al. [2022] O. Hines, O. Dukes, K. Diaz-Ordaz, and S. Vansteelandt. Demystifying statistical learning based on efficient influence functions. The American Statistician, 76:292–304, 2022.

- Imbens [2004] G. Imbens. Nonparametric estimation of average treatment effects under exogeneity: a review. Review of Economics and Statistics, 86:4–29, 2004.

- Jordan et al. [1999] M. Jordan, Z. Ghahramani, Z. Jaakkola, and L. Saul. An introduction to variational methods for graphical models. Machine Learning, 37:183–233, 1999.

- Jordan et al. [2022] M. Jordan, Y. Wang, and A. Zhou. Empirical Gateaux derivative for causal inference. Neural Information Processing Systems, 35, 2022.

- Kang and Schafer [2007] J. Kang and J. Schafer. Demystifying double robustness: a comparison of alternative strategies for estimating a population mean from incomplete data (with discussion). Statistical Science, 22:523–39, 2007.

- Kennedy [2022] E. Kennedy. Semiparametric doubly robust targeted double machine learning: A review. arXiv, page 2203.06469, 2022.

- Kennedy et al. [2021] E. Kennedy, M. Bonvini, and A. Mishler. Comment on “Statistical Modeling: The Two Cultures” by Leo Breiman. Observational Studies, 7:145–156, 2021.

- Kruijer et al. [2010] W. Kruijer, J. Rousseau, and A. van der Vaart. Adaptive Bayesian density estimation with location-scale mixtures. Electronic Journal of Statistics, 4:1225–1257, 2010.

- Künzel et al. [2019] S. Künzel, J. Sekhon, P. Bickel, and B. Yu. Metalearners for estimating heterogeneous treatment effects using machine learning. Proceedings of the National Academy of Sciences, 116:4156–4165, 2019.

- Laurent [1996] B. Laurent. Efficient estimation of integral functionals of a density. Annals of Statistics, 24:659–681, 1996.

- Le Cam [1986] L. Le Cam. Asymptotic Methods in Statistical Decision Theory. Springer-Verlag, New York, 1986.

- Maugis-Rabusseau and Michel [2013] C. Maugis-Rabusseau and B. Michel. Adaptive density estimation using finite gaussian mixtures. ESAIM : P&S, 17:698–724, 2013. doi: 10.1051/ps/2012018.

- Morgan and Winship [2007] S. Morgan and C. Winship. Counterfactuals and Causal Inference: Methods and Principles for Social Research. Cambridge University Press, Cambridge, 2007.

- Murphy and van der Vaart [2000] S. Murphy and A. van der Vaart. On Profile Likelihood. Journal of the American Statistical Association, 95:449–465, 2000.

- Newey et al. [1998] W. Newey, F. Hsieh, and J. Robins. Undersmoothing and bias corrected functional estimation. MIT. Working Paper, 1998.

- Ogburn and Shpitser [2021] E. Ogburn and I. Shpitser. Causal Modelling: the Two Cultures. Observational Studies, 7:179–183, 2021.

- Pearl [2009] J. Pearl. Causal inference in statistics: An overview. Statistics surveys, 3:96–146, 2009.

- Pfanzagl [1982] J. Pfanzagl. Contributions to a General Asymptotic Statistical Theory. Springer, New York, 1982.

- Prakasa Rao [1983] B. Prakasa Rao. Nonparametric Functional Estimation. Academic Press, New York, 1983.

- Ray and Szabó [2019] K. Ray and B. Szabó. Debiased Bayesian inference for average treatment effects. Advances in Neural Information Processing Systems, 33, 2019.

- Ray and van der Vaart [2020] K. Ray and A. van der Vaart. Semiparametric Bayesian causal inference. Annals of Statistics, 48:2999–3020, 2020.

- Ray and van der Vaart [2021] K. Ray and A. van der Vaart. On the Bernstein-von Mises theorem for the Dirichlet process. Electronic Journal of Statistics, 15:2224–2246, 2021.

- Rivoirard and Rousseau [2012] V. Rivoirard and J. Rousseau. Bernstein-von Mises theorem for linear functionals of the density. Annals of Statistics, 40:1489–1523, 2012.

- Robins and Ritov [1997] J. Robins and Y. Ritov. Toward a curse of dimensionality appropriate (CODA) asymptotic theory for semi-parametric models. Statistics in Medicine, 16:285–319, 1997.

- Robins and Rotnitzky [1992] J. Robins and A. Rotnitzky. Recovery of information and adjustment for dependent censoring using surrogate markers. AIDS Epidemiology-Methodological Issues, pages 297–331, 1992.

- Robins et al. [2000] J. Robins, A. Rotnitzky, and M. van der Laan. Comment: On profile likelihood. Journal of the American Statistical Association, 95:477–482, 2000.

- Robins et al. [2015] J. Robins, M. Hernán, and L. Wasserman. Discussion of: On Bayesian estimation of marginal structural models. Biometrics, 71:296–299, 2015.

- Robins et al. [2017] J. Robins, L. Li, E. Tchetgen Tchetgen, and A. van der Vaart. Minimax estimation of a functional on a structured high-dimensional model. Annals of Statistics, 45:1951–1987, 2017.

- Rotnitzky et al. [2021] A. Rotnitzky, E. Smucler, and J. Robins. Characterization of parameters with a mixed bias property. Biometrika, 108:231–238, 2021.

- Rousseau [2016] J. Rousseau. On the frequentist properties of Bayesian nonparametric methods. Annual Review of Statistics and Its Application, 3:211–231, 2016.

- Rubin [1976] D. Rubin. Inference and missing data. Biometrika, 63:581–592, 1976.

- Rubin [1977] D. Rubin. Assignment to treatment group on the basis of a covariate. Journal of Educational Behavioral Statistics, 2:1–26, 1977.

- Rubin [1981] D. Rubin. The Bayesian bootstrap. Annals of Statistics, 9:130–134, 1981.

- Scricciolo [2014] C. Scricciolo. Adaptive Bayesian Density Estimation in -metrics with Pitman-Yor or Normalized Inverse-Gaussian Process Kernel Mixtures. Bayesian Analysis, 9:475–520, 2014.

- Shen et al. [2013] W. Shen, S. Tokdar, and S. Ghosal. Adaptive Bayesian multivariate density estimation with Dirichlet mixtures. Biometrika, 100:623–640, 2013.

- van der Laan and Robins [2003] M. van der Laan and J. Robins. Unified Methods for Censored Longitudinal Data and Causality. Springer-Verlag, New York, 2003.

- van der Laan and Rose [2011] M. van der Laan and S. Rose. Targeted Learning. Springer-Verlag, New York, 2011.

- van der Laan and Rubin [2006] M. van der Laan and D. Rubin. Targeted maximum likelihood learning. International Journal of Biostatistics, 2, 2006.

- van der Vaart [1991] A. van der Vaart. On differentiable functionals. Annals of Statistics, 19:178–204, 1991.

- van der Vaart [1992] A. van der Vaart. Asymptotic linearity of minimax estimators. Statistica Neerlandica, 2–3:179–194, 1992.

- van der Vaart [1998] A. van der Vaart. Asymptotic Statistics. Cambridge University Press, Cambridge, 1998.

- van der Vaart [2002] A. van der Vaart. Semiparametric statistics. In P. Bernard, editor, Lectures on Probability Theory and Statistics, pages 331–457. Springer Verlag, Berlin, 2002.

- van der Vaart [2014] A. van der Vaart. Higher order tangent spaces and influence functions. Statistical Science, 29:679–686, 2014.

- van der Vaart and Wellner [1996] A. van der Vaart and J. Wellner. Weak Convergence and Empirical Processes. Springer, New York, 1996.

- Vansteelandt [2021] S. Vansteelandt. Statistical modelling in the age of data science. Observational Studies, 7:217–228, 2021.

- Vansteelandt and Dukes [2022] S. Vansteelandt and O. Dukes. Assumption-lean Inference for Generalised Linear Model Parameters (with discussion). Journal of the Royal Statistical Society, Series B, 84:657–685, 2022.

- Yiu et al. [2022] A. Yiu, E. Fong, S. Walker, and C. Holmes. Causal predictive inference and target trial emulation. arXiv, page 2207.12479, 2022.

Appendix A An overview of semiparametric theory

A.1 Differentiable functionals and asymptotic efficiency

Semiparametric efficiency theory is concerned with estimators that are insensitive to small local changes in the data-generating distribution in any direction. The notion of “direction” is formalized by considering “smooth”, one-dimensional paths contained in the model that pass through a distribution , and the set of permitted directions is called the tangent space of the model at . The precise notion of “smoothness” is defined as follows.

Definition 4.

A parametric submodel with is differentiable in quadratic mean with score function if

| (18) |

In words, a parametric submodel is a one-dimensional model parameterized by that is contained in and passes through at with score function , which parameterizes the direction in which the submodel approaches as . The resulting high-level interpretation of the tangent space is the set of directions in which we can move an infinitesimal distance away from and still remain in the model .

The definition of the score function is closely related to the more familiar notion of

| (19) |

although neither definition is strictly stronger than the other. The quadratic mean version is more appropriate because it exactly ensures a type of local asymptotic normality (see Lemma 1.9 in van der Vaart [2002]). Despite that, explicit constructions of parametric submodels will usually make use of (19) instead (see the examples in Lecture 1 of van der Vaart [2002]).

A fundamental requirement for semiparametric efficiency theory is (pathwise) differentiability of the target functional.

Definition 5.

A functional (pathwise) differentiable at with respect to if:

-

(a)

the mapping is differentiable, and

-

(b)

there exists a fixed, measurable function such that

(20) for every and any parametric submodel with score function . We call a gradient of at .

The definition of pathwise differentiability above can be motivated as follows. Suppose we try to form a distributional Taylor expansion

| (21) |