Distributed Consensus Algorithm for Decision-Making in Multi-agent Multi-armed Bandit

Abstract

We study a structured multi-agent multi-armed bandit (MAMAB) problem in a dynamic environment. A graph reflects the information-sharing structure among agents, and the arms’ reward distributions are piecewise-stationary with several unknown change points. The agents face the identical piecewise-stationary MAB problem. The goal is to develop a decision-making policy for the agents that minimizes the regret, which is the expected total loss of not playing the optimal arm at each time step. Our proposed solution, Restarted Bayesian Online Change Point Detection in Cooperative Upper Confidence Bound Algorithm (RBO-Coop-UCB), involves an efficient multi-agent UCB algorithm as its core enhanced with a Bayesian change point detector. We also develop a simple restart decision cooperation that improves decision-making. Theoretically, we establish that the expected group regret of RBO-Coop-UCB is upper bounded by , where is the number of agents, is the number of arms, and is the number of time steps. Numerical experiments on synthetic and real-world datasets demonstrate that our proposed method outperforms the state-of-the-art algorithms.

Index Terms:

Change point detection; Distributed learning; Multi-armed bandit; Multi-agent cooperationI Introduction

Multi-armed bandit (MAB) is a fundamental problem in online learning and sequential decision-making. In the classical setting, a single agent adaptively selects one among a finite set of arms (actions) based on past observations and receives a reward accordingly. The agent repeats this process over a finite time horizon to maximize its cumulative reward. The MAB framework has been applied in several areas such as computational advertisement [1], wireless communications [2] and online recommendation [3].

To date, most research on the MAB problem focuses on single-agent policies, neglecting the social components of the applications of the MAB framework; nevertheless, the ever-increasing importance of networked systems and large-scale information networks motivates the investigation of the MAB problem with multiple agents [4]. For example, the users targeted by a recommender system might be a part of a social network [5]. In that case, the network structure is a substantial source of information, which, if taken advantage of, significantly improves the performance of social learners through information-sharing. The core idea is to integrate a graph/network, where each node represents an agent, and the edges identity information-sharing or other relations among agents [6].

The state-of-the-art literature mainly concerns two variants of the MAB problem: (1) Stochastic bandits, where each arm yields a reward from an unknown, time-invariant distribution [7, 8]; and (2) Adversarial bandits, where the reward distribution of each arm may change adversarially at each time step [9]. However, some application scenarios do not fit in these two models. Specifically, in some applications, the arms’ reward distributions vary much less frequently which has difficulties in suiting an adversarial bandit model [10].

For example, in recommendation systems where each item represents an arm and users’ clicks are rewards, the users’ preferences towards items are unlikely to be time-invariant or change significantly at all time steps [11]. Other examples include investment options and dynamic pricing with feedback [12]. Consequently, we investigate an “intermediate setting” of a multi-agent system, namely the piecewise-stationary model. In such a model, the reward distribution of each arm is piecewise-constant and shifts at some unknown time steps called the change points.

I-A Related Work

The rising importance of networked systems, the development of online information-sharing networks, and emerging novel concepts such as the system of systems, motivate studying the multi-agent multi-armed bandit (MAMAB) problem as a framework to model distributed decision-making. And the MAMAB provides the required “learning-to-coordinate” framework in a distributed fashion [13].

Reference [14] investigates the multi-armed bandit problem with side observations from the network, where an external agent decides for the network’s users. The authors propose the -greedy-LP strategy, which explores the action for each user at a rate that is a function of its network position. Reference [15] studies the distributed MAMAB problem and proposes an online indexing policy based on distributed bipartite matching. The method ensures that the expected regret grows no faster than . However, the proposed policies in [14, 15] are agnostic of the network structure and do not consider the agents’ heterogeneity. In [16], the authors introduce the notion of sociability to model the likelihood probabilities that one agent observes its neighbors’ choices and rewards in the network graph. The proposed algorithm has as regret bound. Reference [17] assumes that each agent observes the instantaneous rewards and choices of all its neighbors only when exploring. Based on such an assumption, it proposes an algorithm with a regret-bound . In [16, 17, 18], the observation between agents are opportunistic and occasional, whereas, in the real-world applications like social networks, the observations are continuous. In [19], it is assumed that the communication among agents is only allowed by playing arms in a certain way. Two decentralized policies and are proposed for both single player MAB problem and multi-player MAB problem respectively, where stands for Exponentially spaced Exploration and Exploitation policy and TS stands for Thompson sampling. In [20], the problem setting includes several agents that synchronously play the same MAB game. They develop a gossip-based algorithm that guarantees expected regret bound. Reference [4] considers the same problem with and without collisions. The authors propose two algorithms and investigate the influence of communication graph structure on group performance. In [13], the stochastic MAMAB problem is studied. Different as previous research, [13] considers a dynamic scenario, where the players enter and leave at any time. Algorithms based on “Trekking approach” are proposed and sublinear regret is guaranteed with high probability in the dynamic scenario. Reference [21] investigates a decentralized MAMAB problem, where the arm’s reward distribution is the same for every agent while the information exchange is limited to be at most times, is the number of arms. A decentralized Thompson Sampling algorithm and a decentralized Bayes-UCB algorithm are proposed to solve the formulated MAMAB problem.

However, most previous research on MAMAB focuses on either the stochastic- or adversarial environment, while it largely neglects the piecewise-stationary setting. References [22, 23] introduce the piecewise-stationary MAB, where the reward distributions of arms remain stationary for some intervals (piecewise-stationary segments) but change abruptly at some potentially unknown time steps (change points). The piecewise-stationary environment is specifically beneficial for modeling the real environments[24], giving rise to several decision-making methods, especially for the single-agent MAB. The cutting-edge research on piecewise-stationary MAB includes two methods categories: passively adaptive and actively adaptive. The former makes decisions based on the most recent observations while unaware of the underlying distribution changes [23, 25, 26]. The latter incorporates a change point detector subroutine to monitor the reward distributions and restart the algorithm once a change point is detected [27, 28, 11]. Below, we discuss some examples of the two categories in single-agent MAB emphasizing adaptive methods due to their higher relevance to our research.

Algorithm Discounted UCB (D-UCB) [22, 12, 23] averages the past rewards with a discount factor, which results in as regret bound. In [23], the authors propose the sliding-window UCB (SW-UCB) method, which incorporates the past observations only within a fixed-length moving window for decision-making. The authors prove the regret bound . In [29], the authors propose a change-detection-based framework that actively detects the change points and restarts the MAB indices. They establish the regret bound for their proposed framework. The Monitored-UCB (M-UCB) algorithm [10] has a regret bound, which is slightly higher than CUMSUM-UCB; nonetheless, it is more robust as it requires little parameter specification. Reference [27] combines the bandit algorithm KL-UCB with a parameter-free change point detector, namely, the Bernoulli Generalized Likelihood Ratio Test (GLRT), to obtain a dynamic decision-making policy. The authors develop two variants, global restart, and local restart. They also prove the regret upper-bound for known number of change points . Similarly, [11] applies GLRT change point detector in solving a combinatorial semi-bandit problem in a piecewise-stationary environment, where the regret is upper bounded by .

I-B Our Contribution

Our main contributions are as follow:

-

•

We propose an efficient running consensus algorithm for piecewise-stationary MAMAB, called RBO-Coop-UCB. It addresses the multi-agent decision-making problem in changing environments by integrating a change point detector proposed in [30], namely, Restarted Bayesian online change point detector (RBOCPD) to a cooperative UCB algorithm.

-

•

To improve the decision-making performance via information-sharing, we incorporate an efficient cooperation framework in the proposed strategy RBO-Coop-UCB: 1) The agents share observations in neighborhoods to enhance the performance in arm selection. 2) We integrate a majority voting mechanism into the restart decision part. The cooperation framework is generic and easily integrable to solve piecewise-stationary bandit problems, especially in various actively adaptive MAB policies.

-

•

For any networked multi-agent systems, we establish the group regret bound . To the best of our knowledge, this is the first regret bound analysis for bandit policies with a RBOCPD.

-

•

By intensive experiments on both synthetic and real-world datasets, we show that our proposed policy, RBO-Coop-UCB, performs better than the state-of-the-art policies. We also integrate our proposed cooperative mechanism to different bandit policies and demonstrate performance improvement as a result of cooperation.

The paper is structured as follows. We formulate the problem in Section II. In Section III, we first explain the restarted Bayesian online change point detector, which utilized in the proposed algorithm. Then we develop an algorithmic solution to the formulated problem. In Section IV, we establish the theoretical guarantees, including the regret bound, for the proposed solution. In Section V, we evaluate our proposal via numerical analysis based on both synthetic- and real-world datasets. Section VI concludes the paper.

II Problem Formulation

We consider an -armed bandit with players (agents, hereafter) gathered in the set . The agents play the same piecewise-stationary MAB problems simultaneously for rounds. We use to denote the time-invariant action set. At time , the reward associated with arm is randomly sampled from distribution with mean . The rewards are independent across the agents and over time. The agents form a network modeled by an undirected graph where is the edge set. In , nodes and edges represent agents and the potential of communication, respectively. Two agents and are neighbors if . In addition to its own observation, each agent can observe its neighbors’ selected arms and sampling rewards.

At each time step, each agent pulls one arm and obtains a reward sampled from . We use to show the action of agent at time . Besides, is the sampling reward of arm at time . We assume that the reward distributions of arms are piecewise-stationary satifying the following Assumption 1.

Assumption 1 (Piecewise-stationary Bernoulli process [30]).

The environment is piecewise-stationary, meaning that it remains constant over specific periods and changes from one to another. Let denote the time horizon and the overall number of piecewise-stationary segments observed until time .

| (1) |

The reward distributions of arms are piecewise-stationary Bernoulli processes such that there exists an non-decreasing change points sequence verifying

The performance of each single agent is measured by its (dynamic) regret, the cumulative difference between the expected reward obtained by an oracle policy playing an optimal arm at time , and the expected reward obtained by action selected by agent

| (2) |

Reference [31] introduces the concept of dynamic regret. In contrast to a fixed benchmark in the static regret, dynamic regret compares with a sequence of changing comparators and therefore is more suitable for measuring the performance of online algorithms in piecewise-stationary environments [32]. In the multi-agent setting considered here, we study the network performance in terms of the regret experienced by the entire network; As such, the define the decision-making objective as to minimize the expected cumulative group regret,

| (3) |

III The RBO-Coop-UCB Algorithm

Notations. We use boldface uppercase letters to represent vectors and use calligraphic letters to represent sets. For example, denotes the sequence of observations from time step to and refers to the set containing the sampled rewards of arm by agent . The inner product is denoted by . refers to the big-O notation while refers to the small-o notation. denotes the indicator function. Table I gathers the most important notations.

The proposed algorithm, RBO-Coop-UCB, combines a network UCB algorithm (similar to [18, 4]) with a change detector running on each arm (based on Bayesian change point detection strategy [30]). Roughly-speaking, RBO-Coop-UCB involves three ideas:

(1) A unique cooperative UCB-based method that guides the network system towards the optimal arm in a piecewise-stationary environment;

(2) A change point detector introduced in Algorithm 1;

(3) A novel cooperation mechanism for change point detection to filter out the false alarms.

We summarize the proposed policy in Algorithm 2.

To the best of our knowledge, this is the first attempt to solve the MAMAB problem in a piecewise-stationary environment. Compare to the previous work [4, 16, 17, 18], our proposed algorithm is applicable to different multi-agent systems and non-stationary environment. In the following, we first introduce the restarted Bayesian online change point detection procedure (RBOCPD), which we utilize to develop our decision-making policy, RBO-Coop-UCB, which we then explain in detail.

| Notation | Meaning |

|---|---|

| : Sequence of observations from time up to time | |

| ; Empirical mean over | |

| ; Length of | |

| Current run-length | |

| Forecaster loss | |

| Forecaster weight | |

| Observation matrix, if and are neighbors | |

| Number of agents | |

| Number of arms | |

| Number of change points | |

| The real -th change point | |

| The -th detected change point | |

| Arm selected by agent at time | |

| Total number of times that agent observes from arm | |

| Estimated reward of arm by from agent | |

| Reward distribution of arm at | |

| Expected reward of arm at | |

| Sampling reward of arm at time | |

| Total reward that agent observes from arm | |

| Degrees of agent in |

III-A Restarted Bayesian Online Change Point Detector

Detecting changes in the underlying distribution of a sequence of observations [30] is a classic problem in statistics. The Bayesian online change point detection appeared first in [33, 34]. Since then, several authors have used it in different contexts [35, 36, 37, 38]. Nevertheless, the previous research seldom considers the theoretical analysis of its performance bounds, such as false alarm rate and detection delay. In [30], the authors develop a modification of Bayesian online change point detection and prove the non-asymptotic guarantees related to the false alarm rate and detection delay. Remark 5 in Appendix -A compares RBOCPD and other change point detectors in detail.

Let denote the number of time steps since the last change point, given the observed data , generated from the piecewise-stationary Bernoulli process described in Definition 1. The Bayesian strategy computes the posterior distribution over the current run-length , i.e., [33]. The following message-passing algorithm recursively infers the run-length distribution [30]

A simple example of the hazard function is a constant [30].

The RBOCPD algorithm assumes that each possible value of the run-length corresponds to a specific forecaster. The loss of forecaster at time related to underlying predictive distribution (UPM) then follows as

| (4) | ||||

where is the Laplace predictor [30], defined below.

Definition 1 (Laplace predictor).

The Laplace predictor takes as input a sequence and predicts the value of the next observation as

| (5) |

where corresponds to the uniform prior given to the process generating .

The weight of forecaster at time for starting time is the posterior , where

| (6) |

by using the hyperparameter (instead of the constant hazard function value ) and the initial weight . The initial weight is defined as

| (7) |

for some starting time , where is the cumulative loss incurred by the forecaster from time until time . Based on (III-A), the cumulative loss yields

| (8) |

Besides, RBOCPD includes a restart procedure to detect changes based on the forecaster weight. For any starting time ,

| (9) |

The intuition behind the criterion is the following: At each time with no change, the forecaster distribution concentrates around the forecaster launched at the starting time . Thus, if the distribution undergoes a change, a change becomes observable.

The restarted version of Bayesian Online Change Point Detector [30] can be formulated as follows.

III-B RBO-Coop-UCB Decision-Making Policy

The proposed algorithm is a Network UCB algorithm that allows for some restarts. Each agent runs the RBO-Coop-UCB in parallel to choose an arm to play. Also, each agent observes its neighbors’ choices and the corresponding rewards. To guarantee enough samples for change point detection, each arm will be selected several times in the exploration steps. Let and be some variables to denote the selected arm and received reward of agent at time , respectively, where is the i.i.d copy of . The total number of times that agent observes option ’s rewards yields

| (10) |

The empirical rewards of arm by agent at time is

| (11) |

where is the total reward observed by agent from option in trials. At every sampling time step, if the agent is in a forced exploration phase, it selects the arm using (17) to ensure a sufficient number of observations for each arm. Otherwise, it chooses the arm according to the sampling rule described in Definition 2.

Definition 2.

The sampling rule for agent at time is

| (12) |

with

| (13) | ||||

| (14) |

where is the latest change points detected by agent . is a constant and is an agent-based parameter where is the number of neighbors of agent . with a dimensional vector with all elements equal to , is the -th column of matrix . is the average degree of neighbors of agent . We assume that , , which indicates , .

Remark 1.

Different values of imply heterogeneous agents’ exploration. On the one hand, agents with more neighbors have more observations that reduce the uncertainties of their reward estimations and increase their exploitation potential. Less exploration then lowers the usefulness of the information they broadcast, thus decreasing its neighbors’ exploitation potential [18]. Therefore, to improve the group performance, we propose the heterogeneous explore-exploit strategies with sampling rule in Definition 2 that regulate exploitation potential across the network.

After agent receives the sampling reward and observes its neighbors’ sampling rewards, it combines the observed rewards into the observation collection to run the RBOCPD (Algorithm 1). In general, the set contains all the sampling rewards of arm observed by agent since the last change point . Each agent receives a binary restart signal afterward, where if there is a change point and zero otherwise. The agent calculates the restart signal using (9). The agents make final restart decisions using the cooperation mechanism described in Definition 3 based on its restart signal and observations.

Definition 3 (Cooperative restart mechanism).

Each agent makes the final restart decision using the majority voting outcome among neighbors: If more than half of its neighbors detect a change in one of the played arms, then the agent restarts its UCB indices as

| (15) |

However, different agents have distinct observations, so a simple majority voting mechanism at each time step might lead to miss-detection due to the agent’s asynchronous detection. Therefore, we propose an efficient cooperation mechanism for restart decision, where a restart memory time window records the previous restart of agents’ neighbors in a short period . The cooperation restart detection considers the majority voting of restart among neighbors in that period, i.e.,

| (16) |

Hence, the slower detector receives the restart information from the faster ones to prevent missing change points.

Remark 2.

The length of restart memory time window depends on the detection delay of RBOCPD, as shown in Theorem 5. Although each agent maintains a change point detector with its observations, which could be faster or slower, all detectors follow the same principle. We bound the detection delay in Theorem 5; Therefore, for every change point, the maximum detection time difference is bounded. As a result, selecting based on the delay to include all possible correct detections improves the regret bound.

| (17) |

| (18) |

IV Performance Analysis

In this section, we analyse the -step regret of our proposed algorithm RBO-Coop-UCB.

Assumption 2.

Define , where and . Then we assume that for all , , , .

Remark 3.

Assumption 2 is a standard assumption in non-stationary multi-armed bandit literature [10, 27, 11]. It guarantees that the length between two change points is sufficient to detect the distribution change with high probability. Besides, the detection delay is asymptotically order optimal. The asymptotic regime is reached when , and , when , we obtain that [30]

| (19) |

If we choose the hyperparameter in RBOCPD and plug it into the asymptotic expression of detection delay (19), we get

| (20) |

Lemma 1 (Regret bound of stationary RBO-Coop-UCB).

Consider a stationary environment, i.e., when , , and . Then the upper bound of the expected cumulative regret of RBOCPD-Coop-UCB for each agent follows as

where is the maximum gap between the mean rewards of arms, is the minimum gap between the mean rewards of arms, and is the false alarm rate under cooperation.

Proof:

See Appendix -B. ∎

Remark 4.

Lemma 1 shows that the regret of RBO-Coop-UCB incorporates several sources: false alarm, forced exploration, and the classic regret of the UCB algorithm.

Lemma 2 (False alarm probability in a stationary environment).

Consider the stationary scenario, i.e., , with confidence level . Define as the time of detecting the first change point of the -th base arm. Let , because RBO-Coop-UCB restarts the entire algorithm if a change point is detected on any of the base arms. The false alarm rate under cooperation is [30, 11]

| (21) |

Proof:

See Appendix -C. ∎

Lemma 3.

Define as the event when all the change points up to the -th one have been detected successfully by agent within a small delay. Formally, [27]:

| (22) |

and

| (23) |

Then, and , where is the detection time of the -th change point.

Proof:

See Appendix -D. ∎

Theorem 1.

Proof:

See Appendix -E. ∎

Corollary 1.

Let and . Then the regret of RBO-Coop-UCB have the following upper bound:

| (25) |

Proof:

See Appendix -F. ∎

V Experiments

In this section, we evaluate the performance of our proposed RBO-Coop-UCB algorithm in different non-stationary environments using synthetic datasets and real-world datasets. We compare RBO-Coop-UCB with five baselines from the cutting-edge literature and one variant of RBO-Coop-UCB. More precisely, we use DUCB [23] and SW-UCB (Sliding Window UCB) [23] as passively adaptive benchmarks for the piecewise-stationary multi-armed bandit, and M-UCB (Monitored-UCB) [10] and GLR-UCB [39, 27] as actively adaptive ones. For consistency, in addition to the non-cooperative setting (each agent runs the algorithm independently), we implement each of the above piecewise-stationary algorithms also in a cooperative setting (information-sharing). In addition, we compare with UCB [8] as a stochastic bandit policy and EXP3 [9] as an adversarial one. Finally, to validate the effectiveness of cooperation in change point detection, we implement GLR-Coop-UCB, which has a similar flow to RBO-Coop-UCB: It includes information-sharing and cooperative change point detection decision-making. The only difference between RBO-Coop-UCB and GLR-Coop-UCB is the implemented change point detector. The hyperparameter in our experiments are as follow.

-

•

UCB: None.

-

•

DUCB: Discount factor , here .

-

•

SW-UCB: Sliding window length , here .

-

•

M-UCB: , window size , , and .

-

•

GLR-UCB and GLR-Coop-UCB: , and .

-

•

RBO-UCB and RBO-Coop-UCB: , and .

Table II summarizes the performance of different change point detectors in all datasets. In the following section, we analyze the algorithms’ performance in details. All the experimental results are based on ten independent runs.

| Experiment | Algorithm |

Correct

Detection |

Delay (step) | False Alarm |

|---|---|---|---|---|

| Synthetic Dataset | RBO-Coop | 93/120 | 63.1 | 0.002% |

| RBO | 108/120 | 106.7 | 0.024% | |

| GLR-Coop | 60/120 | 98.8 | 0 | |

| GLR | 60/120 | 99.3 | 0.0003% | |

| Yahoo! Dataset | RBO-Coop | 314/400 | 234.8 | 0.001% |

| RBO | 358/400 | 257.2 | 0.004% | |

| GLR-Coop | 92/400 | 787.2 | 0.005% | |

| GLR | 77/400 | 730.3 | 0.006% | |

| Digital Market Dataset | RBO-Coop | 481/770 | 79.0 | 0.003% |

| RBO | 556/770 | 105.1 | 0.010% | |

| GLR-Coop | 178/770 | 242.2 | 0.009% | |

| GLR | 144/770 | 194.2 | 0.011% |

V-A Synthetic Dataset

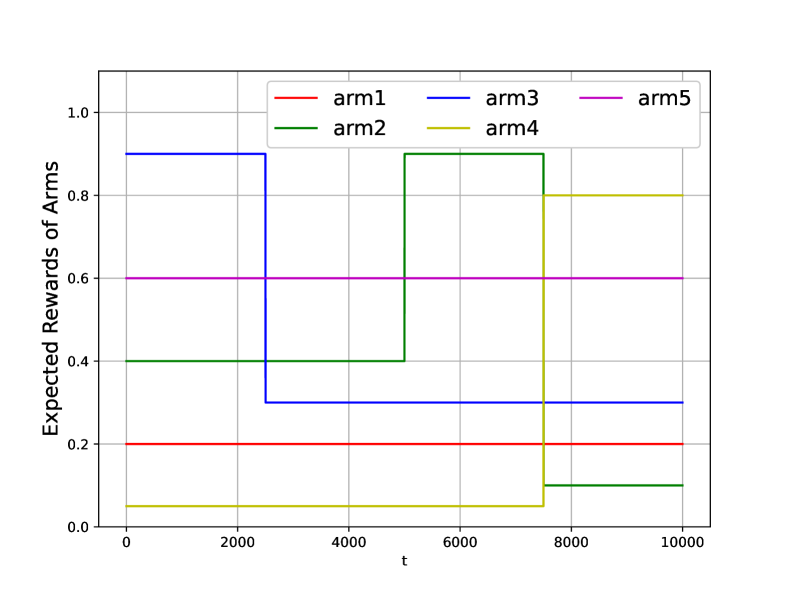

In this section, we consider the following MAMAB setting with synthetic dataset:

-

•

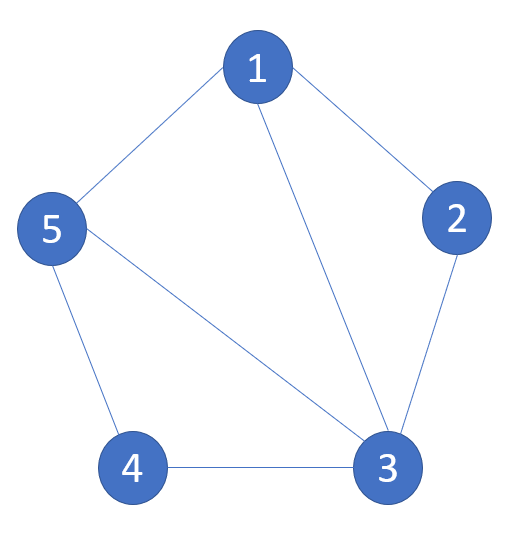

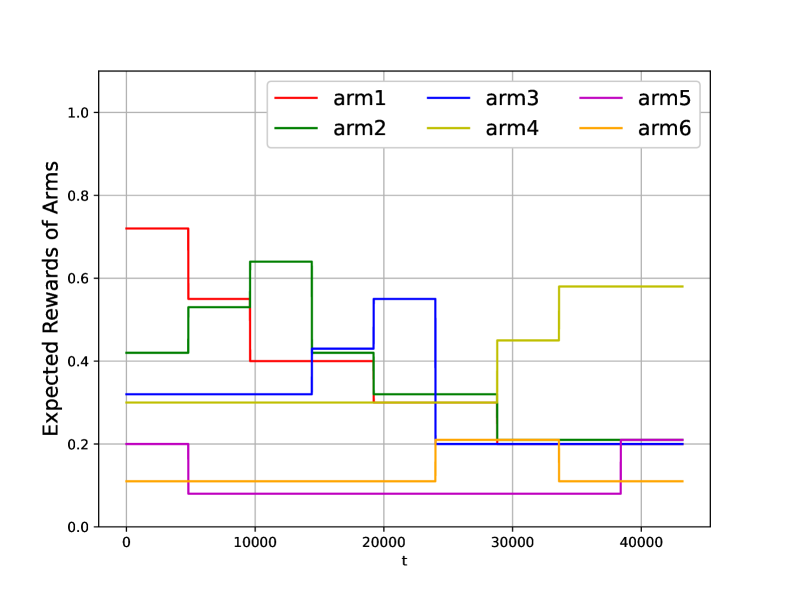

The network consists of agents and the agents face an identical MAB problem with arms.

-

•

There are piecewise-stationary Bernoulli segments, where only one base arm changes its distribution between two consecutive piecewise-stationary segments.

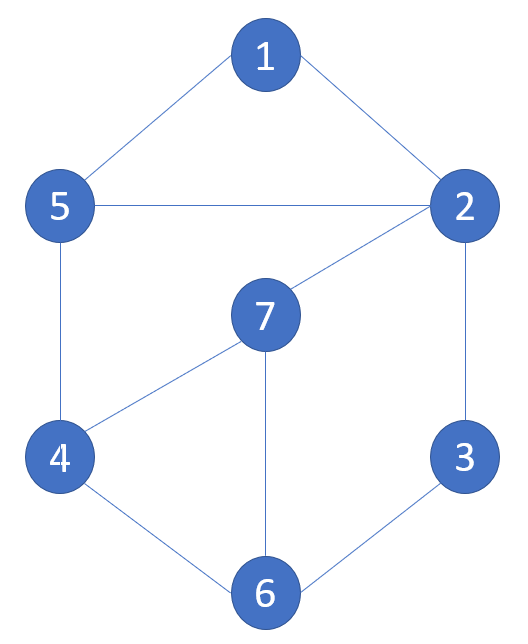

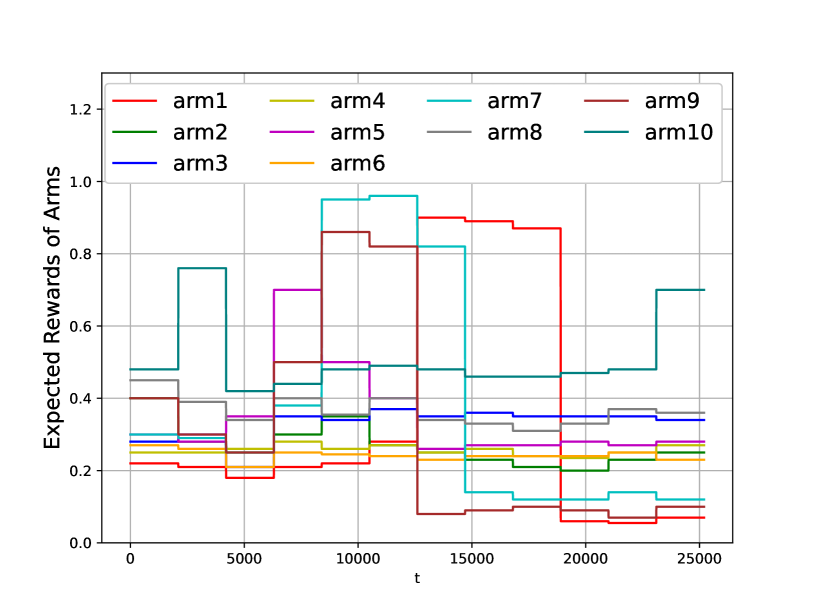

Figure 1(a) and Figure 1(b) respectively show the network and the arms’ reward distributions.

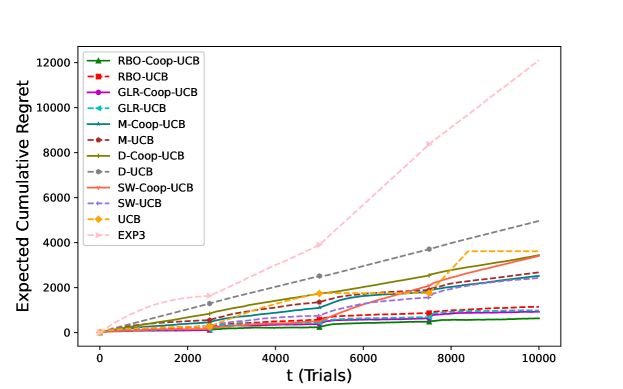

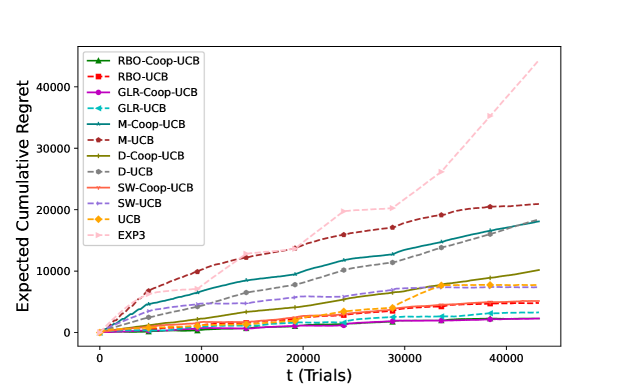

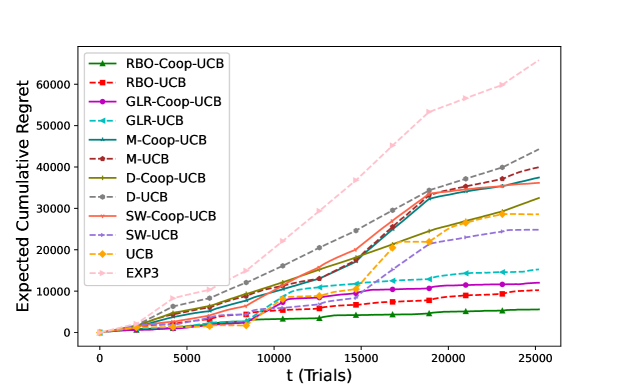

Figure 2 summarizes the average regret of all algorithms.

Based on Figure 2, RBO-Coop-UCB has the lowest regret among all piecewise-stationary algorithms. Compared with the algorithms with cooperation (such as RBO-Coop-UCB, GLR-Coop-UCB, and M-Coop-UCB, shown by solid lines), most algorithms without cooperation (such as RBO-UCB, GLR-UCB, and M-UCB, depicted by dashed lines) suffer from higher regrets. An exception is SW-UCB, whose regret is lower than that of SW-Coop-UCB. Our proposed cooperative framework is originally designed for actively adaptive algorithms (i.e., RBO-Coop-UCB, GLR-Coop-UCB, and M-Coop-UCB) and the cooperative restart decision-making does not exist in the passively adaptive algorithms (D-Coop-UCB, SW-Coop-UCB), that could be a reason for the higher regret in SW-Coop-UCB. In general, most algorithms have a lower regret than UCB and EXP3, which means that for optimal decision-making, it is essential to take into account the environment dynamics. Note that RBO-Coop-UCB performs better than GLR-Coop-UCB, whereas RBO-UCB has a higher regret than GLR-UCB. We investigate this effect in the following in detail.

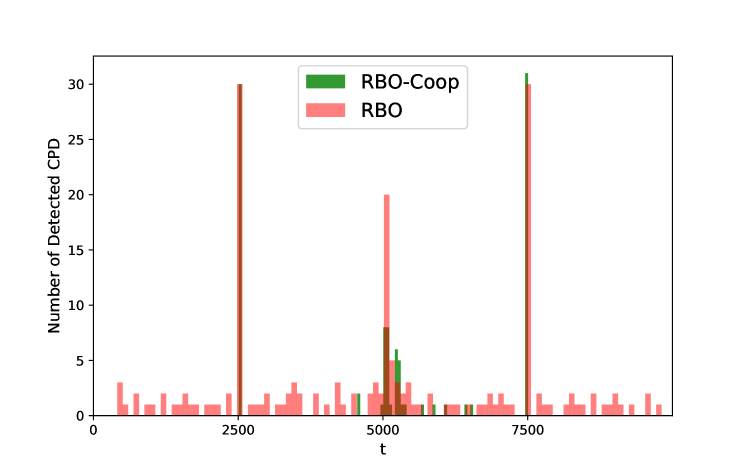

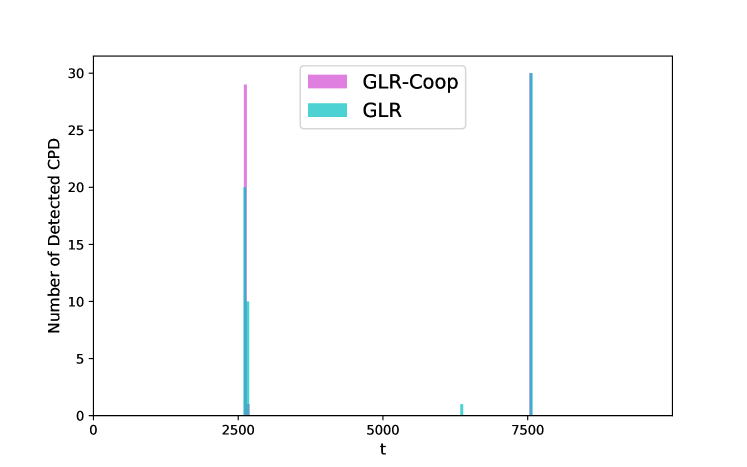

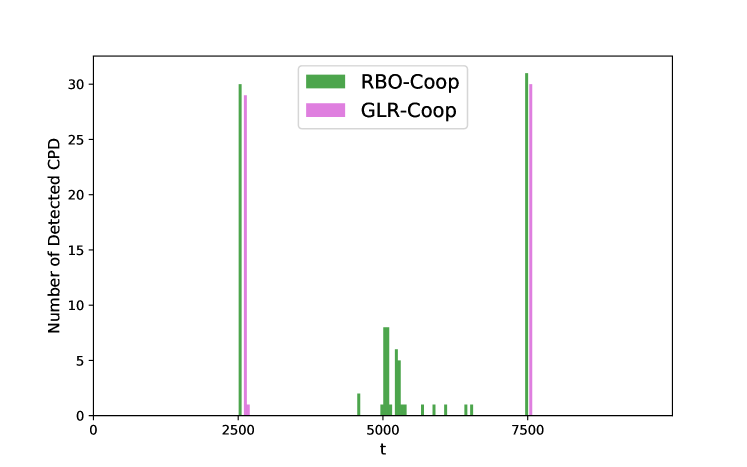

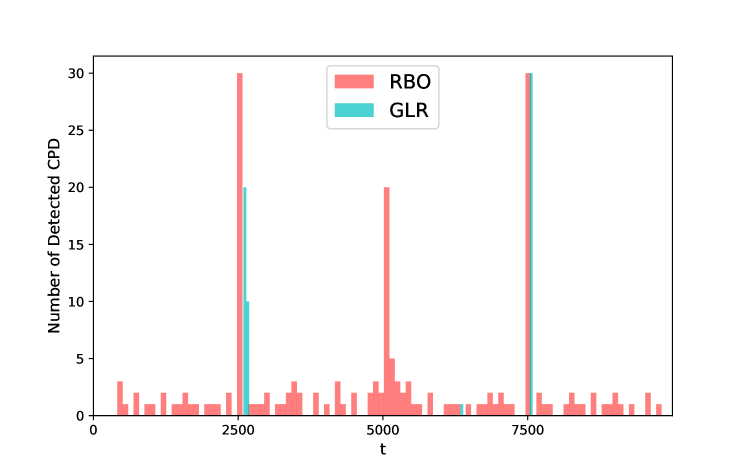

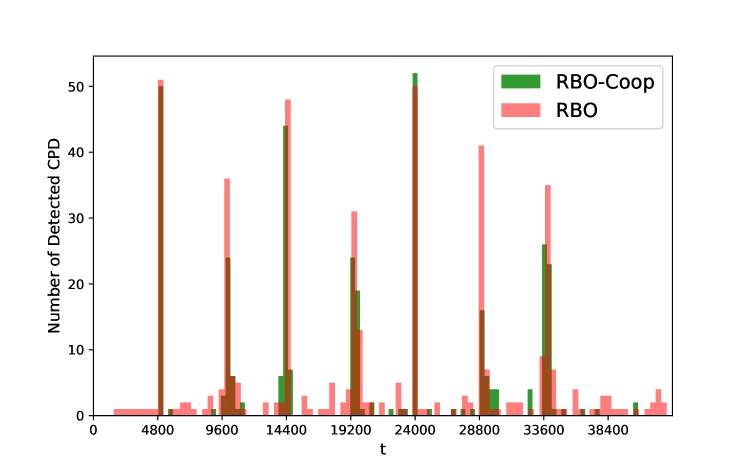

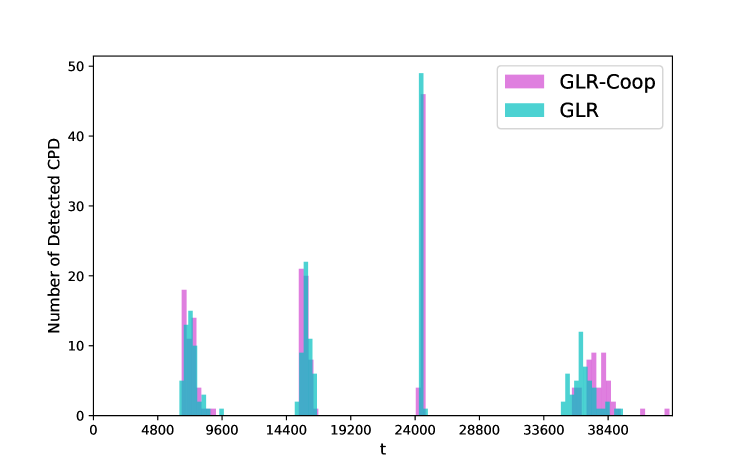

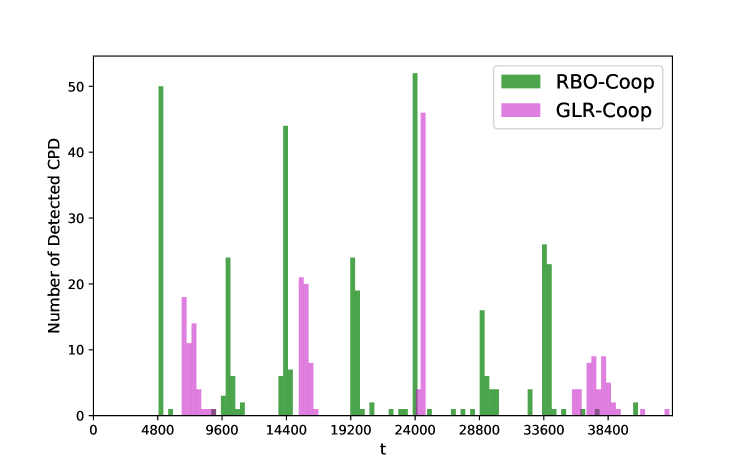

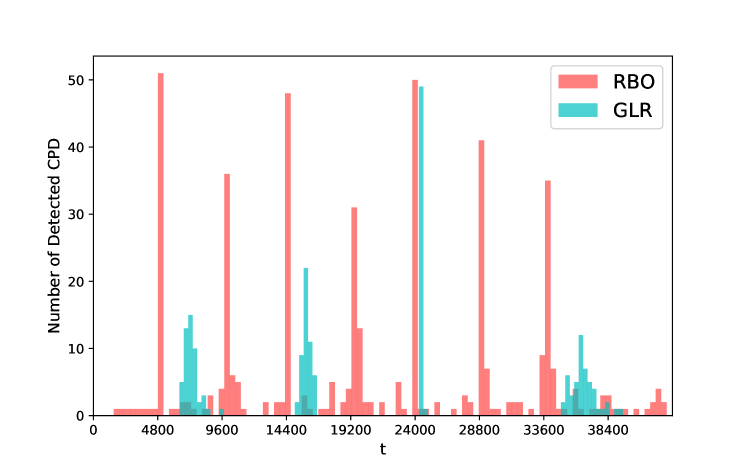

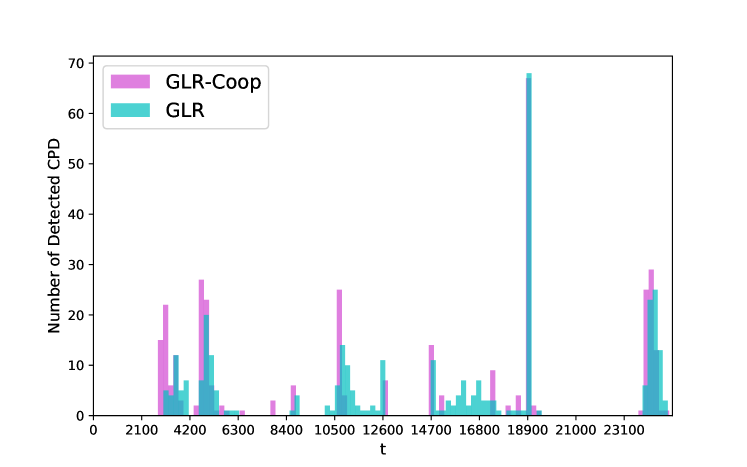

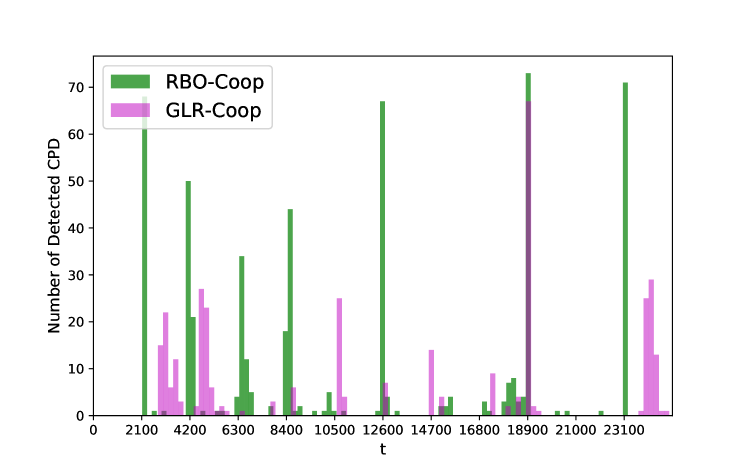

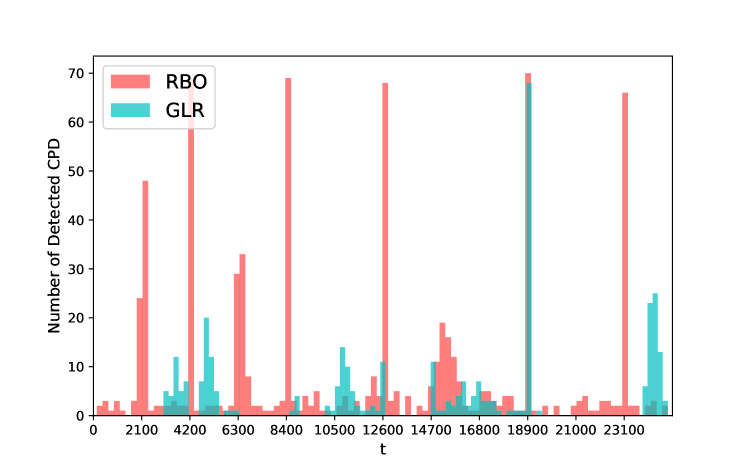

Figure 3 shows the histogram of time steps that different algorithms have identified as a change point. In Figure 3(a), there are three peaks (). Especially, for and , the times to be regarded as change point reaches almost 30 (three agents ten times). That means, with a high probability, RBO-Coop-UCB, and RBO-UCB detect the changes. Compared with RBO-Coop-UCB, RBO-UCB has more false alarms. Figure 3(b) demonstrates the change point detection of GLR-Coop-UCB and GLR-UCB. Compared with the algorithms with RBOCPD, those with GLRCPD benefit from fewer false alarms; however, they ignore the second change point . Figure 3(c) shows that RBO-Coop-UCB has a better performance than GLR-Coop-UCB in change point detection: It provides a higher correct detection rate for the first and third change points and has a smaller time step delay. Besides, RBO-Coop detects the GLR “undetectable" change point (second change point), which indicates its wider detectable range. In Figure 3(d), RBO has a higher correct detection rate than GLR; nevertheless, the false alarm rate of RBO is also very high, which is not negligible. The statistics shown in Table II also lead to the same conclusion. Frequent false alarm increases regret in RBO-UCB. In general, RBO-Coop and GLR-Coop have better detection than RBO and GLR, especially RBO-Coop, which proves the designed cooperation mechanism is effective and particularly suitable for the UCB algorithm incorporating RBOCPD. These are consistent with the conclusion drawn based on Figure 2.

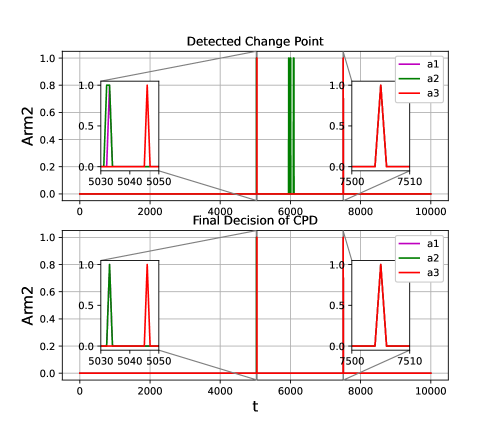

To clarify the cooperation mechanism in change point detection, we show the detection record and the final decisions in Figure 4. The figure illustrates the detection of each individual agent together with the final decision based on the neighborhood majority voting for arm 2. In that arm, the first change point occurs at . First, agent 2 detects that change, and then agent 1. Given the majority voting, agent 1 and 2 will restart their MAB policies after agent 1 detects the change. After several time steps, when agent 3 detects the change point, it has the restart history from its neighbor agent 2. Thus, it also restarts immediately at this time step. The same decision process follows by the second change at . Agent 2 suffers from several false alarms between the two points, which, however, the cooperation mechanism filters out. Thus, in the final decision, this period does not include any restart. In conclusion, the developed cooperation mechanism significantly reduces the false alarm rate and improves the chances of correct change detection.

V-B Real World Dataset

In this section, we evaluate our proposed algorithm based on two different real-world datasets: Yahoo dataset111Yahoo! Front Page Today Module User Click Log Dataset on https://webscope.sandbox.yahoo.com and digital marketing, which are same as the real-world dataset in [10]. To be more detailed, in Yahoo dataset we verify the effectiveness in piecewise-stationary Bernoulli distribution, which is also our original design while with the digital marketing dataset we verify a more general situation.

V-B1 Yahoo! Dataset

We evaluate our proposed algorithm based on a real-world dataset from Yahoo, which contains the user click log for news articles displayed on the Yahoo! Front Page [40]. To prepare the dataset, we follow the lines of [10]. Therein, the authors preprocess the Yahoo! dataset by manipulating it. They then demonstrate the arm distribution information in Figure 3 of that paper. To adapt to our multi-agent setting, we implement the experiment with agents. We enlarge the click rate of each arm by ten times [11].222This step is essential because in the original setting, the gap between RBOCPD and GLRCPD can be smaller than the minimum detectable value. Figure 5(a) and Figure 5(b) respectively show the network and the arms’ reward distributions.

Figure 6 shows the average regret of all algorithms while Figure 7 depicts the change point detection signals.

In Figure 6, RBO-Coop-UCB and GLR-Coop-UCB have the lowest regret, while GLR-UCB has a regret lower than RBO-UCB. The reason is explainable using Figure 7 and Table II. Algorithms with RBOCPD are more sensitive in detection; As such, they can detect change points faster. Besides, our proposed cooperation mechanism reduces false alarms while maintaining other performance indicators, such as correct detections and delays, at a comparable level. RBO-Coop detects more change points than GLR-Coop and guarantees fewer false alarms. In addition, according to the arms’ reward distributions, there are four change points in which the optimal arm remains fixed (); thus, a restart at these steps increases the regret. That observation explains the similar regret performance of RBO-Coop-UCB and GLR-Coop-UCB despite the former detecting more change points. Besides, according to Figure 6, the algorithms with cooperation (solid lines) always have lower regret than the algorithms without cooperation (dashed lines), which proves our designed cooperation mechanism enhances the performance.

V-B2 Digital Marketing Dataset

In [10], the authors preprocess the dataset. They show the corresponding arm reward distribution in Figure 5 of [10]. Unlike the Yahoo! dataset, where the arms distribution is piecewise-Bernoulli, here, we only assume that the distribution is bounded within . Similar to the previous experiment, we implement the dataset with a network with agents as shown in Figure 8(a). There are 12 piecewise-stationary segments as illustrated in Figure 8(b).

Figure 9 shows the average regret of different policies and Figure 10 demonstrates the performance of different change point detectors.

From Figure 9, RBO-Coop-UCB has the lowest regret. Figure 10(c) shows the detection performance. Accordingly, RBO-Coop performs better than GLR-Coop due to more sensitivity and lower delay.

According to the theoretical analysis in Remark 5, RBOCPD suffers a higher false alarm rate. In Experiment I, the regret of RBO-UCB is higher than GLR because of more frequent false alarms. In Experiment II, given a lower false alarm empirically according to Table II, the reason for higher regret of RBO-UCB than GLR-UCB is restarting all of the arms, even if the optimal one remains unchanged. As shown in Figure 10 and Table II, the false alarm of RBO in Experiment III is comparable to that of GLR, whereas its detection rate is much higher. Therefore, RBO has the second-best performance in this experiment. GLR does not perform at the expected level because it is not as robust as RBO when the gap in arms’ rewards between change points is small. Finally, except for SW-UCB, the other algorithms with cooperation have lower regret than the version without, which is the same as the results that appear in Figure 2.

VI Conclusion

We propose a decision-making policy for the multi-agent multi-armed bandit problem in a piecewise-stationary environment. The process involves the seminal UCB framework combined with an information-sharing mechanism and a change point detector based on the Bayesian strategy. We prove an upper bound for the group regret of our proposal. Numerical analysis shows the superior performance of our method compared to the state-of-art research. Future research directions include improving the UCB strategy by personalizing it for each agent. For example, it is beneficial to consider heterogeneous agents’ preferences. Besides, one might allow for different agent types and influence models and information-sharing under a directed graph model.

-A Performance Guarantees of RBOCPD

Lemma 4 (False alarm rate).

Assume that . Let . If is small enough such that [30]

then with probability higher than , no false alarm occurs in the interval :

| (26) |

Definition 4 (Relative gap ).

Let . The relative gap for the forecaster at time takes the following form (depending on the position of ) [30]:

Lemma 5 (Detection delay).

Let and . Also, is the change point gap. If is large enough such that [30]

| (27) |

Then the change point is detected (with a probability at least ) with a delay not exceeding such that

where

| (28) |

Definition 5 (Detectable change points).

A change point is -detectable (with probability ) with respect to the sequence for the delay function if [39]

| (29) |

where . That is, using only a fraction of the -many observations available between the previous change point and , the change can be detected at a time not exceeding the next change point.

Remark 5.

Compared to other change point detection methods used in MAB algorithms, RBOCPD has the same advantages as GLRCPD, such as few hyperparameters (in RBOCPD, only one hyperparameter ). Besides, it is robust to the lack of prior knowledge. Based on the theoretical analysis in Appendix E, F of [27] and our work, RBOCPD has lower computational complexity and higher robustness against small gap cases [30] while slightly higher false alarm rate than GLRCPD given the same hyperparameter (In GLRCPD the false alarm rate can be directly selected as hyperparameter while according to Lemma 4, in RBOCPD the false alarm rate ).

-B Proof of Lemma 1

First, we investigate the improvement in the false alarm as a result of cooperation in making the restart decision in each agent’s neighborhood, as the following Lemma 6 states.

Lemma 6 (False alarm rate under cooperation).

Define as the cooperative false alarm rate where each agent implements a change point detector. The false alarm rate in a information-sharing mechanism can be concluded as

| (30) |

where is the false alarm rate of every single agent, and is the number of neighbors of agent (degrees of node in graph ).

Proof.

For each agent, the false alarm rate is . Therefore, when cooperating, the probability that there are agents having false alarms at the same time is . Based on the information-sharing mechanism, the algorithm has a false alarm only when more than half of the neighbor agents report a false alarm. Therefore, considering all possible scenarios, the false alarm rate yields . Besides, a satisfies , , which implies that the cooperation in change point detectors reduces the false alarm rate. Different number of neighbors implies different value of and the higher is, the smaller is. ∎

Now we are in the position to prove Lemma 1.

The expected regret can be written as

| (31) |

where is the expected largest reward difference. Besides, and we have,

where refers to the regret of the forced exploration. Considering the worst situation, where all steps are not optimal, . Besides, [8]. Denote as the expected lowest reward difference, then for , , because , ,.

Fact 6 (Chernoff-Hoeffding bound).

Let be random variables with common range and such that . Let , then for all , and .

According to Fact 6, , and . Choose , . Therefore,

and the expected regret follows as

| (32) |

where . The first term is due to the false alarm probability in RBOCPD, the second term is because of the uniform exploration, and the last term is caused by UCB exploration.

-C Proof of Lemma 2

-D Proof of Lemma 3

Proof.

(a) is from Lemma 2.

According to Fact 7 and Definition 5, between change points and , each arm has been selected at least times. Given good event , we have . Besides, is detectable with probability based on Definition 5 within length because , where the first inequality results from the good event . Therefore, one can conclude that , which is equivalent to . That completes the proof.

∎

-E Proof of Theorem 1

The regret in the piecewise-stationary environment is a collection of regrets of good events and bad events. The regret of good events is because of UCB exploration, whereas that of bad events results from false alarms and long detection delays. The derivation of regret upper bound is similar to Lemma 1, as the regret of bad events can be bounded using the theoretical guarantee of the RBOCPD described in Appendix -A. Before proceeding to the detailed proof, we state the following fact:

Fact 7.

For every pair of instants between two restarts on arm , it holds .

Define the good event and good event . Recall the definition of the good event in (22). We note that is the intersection of the event sequence of and up to the -th change point. We decompose the expected cumulative regret with respect to the event . That yields

where , which is concluded from Lemma 1. By the law of total expectation,

| (33) |

Inequality (33) results from Lemma 3. Furthermore,

| (34) |

By combining the previous steps, we have

Similarly,

Furthermore, we have

| (35) |

Wrapping up previous steps, we arrive at

| (36) |

Recursively, we can bound by applying the same method as before. The regret upper bound then yields

| (37) |

where .

-F Proof of Corollary 1

Based on Theorem 1, the regret is upper bound by , let and ,

| (38) |

References

- [1] L. Tang, R. Rosales, A. Singh, and D. Agarwal, “Automatic ad format selection via contextual bandits,” in Proceedings of the 22nd ACM international conference on Information & Knowledge Management, 2013, pp. 1587–1594.

- [2] S. Maghsudi and S. Stańczak, “Joint channel selection and power control in infrastructureless wireless networks: A multiplayer multiarmed bandit framework,” IEEE Transactions on Vehicular Technology, vol. 64, no. 10, pp. 4565–4578, 2014.

- [3] S. Li, A. Karatzoglou, and C. Gentile, “Collaborative filtering bandits,” in Proceedings of the 39th International ACM SIGIR conference on Research and Development in Information Retrieval, 2016, pp. 539–548.

- [4] P. Landgren, V. Srivastava, and N. E. Leonard, “Distributed cooperative decision making in multi-agent multi-armed bandits,” Automatica, vol. 125, p. 109445, 2021.

- [5] N. Cesa-Bianchi, C. Gentile, and G. Zappella, “A gang of bandits,” Advances in neural information processing systems, vol. 26, 2013.

- [6] K. Yang, L. Toni, and X. Dong, “Laplacian-regularized graph bandits: Algorithms and theoretical analysis,” in International Conference on Artificial Intelligence and Statistics. PMLR, 2020, pp. 3133–3143.

- [7] T. L. Lai, H. Robbins et al., “Asymptotically efficient adaptive allocation rules,” Advances in applied mathematics, vol. 6, no. 1, pp. 4–22, 1985.

- [8] P. Auer, N. Cesa-Bianchi, and P. Fischer, “Finite-time analysis of the multiarmed bandit problem,” Machine learning, vol. 47, no. 2, pp. 235–256, 2002.

- [9] P. Auer, N. Cesa-Bianchi, Y. Freund, and R. E. Schapire, “The nonstochastic multiarmed bandit problem,” SIAM journal on computing, vol. 32, no. 1, pp. 48–77, 2002.

- [10] Y. Cao, W. Zheng, B. Kveton, and Y. Xie, “Nearly optimal adaptive procedure for piecewise-stationary bandit: a change-point detection approach,” AISTATS,(Okinawa, Japan), 2019.

- [11] H. Zhou, L. Wang, L. Varshney, and E.-P. Lim, “A near-optimal change-detection based algorithm for piecewise-stationary combinatorial semi-bandits,” in Proceedings of the AAAI Conference on Artificial Intelligence, vol. 34, no. 04, 2020, pp. 6933–6940.

- [12] J. Y. Yu and S. Mannor, “Piecewise-stationary bandit problems with side observations,” in Proceedings of the 26th annual international conference on machine learning, 2009, pp. 1177–1184.

- [13] M. K. Hanawal and S. J. Darak, “Multiplayer bandits: A trekking approach,” IEEE Transactions on Automatic Control, vol. 67, no. 5, pp. 2237–2252, 2021.

- [14] S. Buccapatnam, A. Eryilmaz, and N. B. Shroff, “Multi-armed bandits in the presence of side observations in social networks,” in 52nd IEEE Conference on Decision and Control. IEEE, 2013, pp. 7309–7314.

- [15] D. Kalathil, N. Nayyar, and R. Jain, “Decentralized learning for multiplayer multiarmed bandits,” IEEE Transactions on Information Theory, vol. 60, no. 4, pp. 2331–2345, 2014.

- [16] U. Madhushani and N. E. Leonard, “Heterogeneous stochastic interactions for multiple agents in a multi-armed bandit problem,” in 2019 18th European Control Conference (ECC). IEEE, 2019, pp. 3502–3507.

- [17] ——, “A dynamic observation strategy for multi-agent multi-armed bandit problem,” in 2020 European Control Conference (ECC). IEEE, 2020, pp. 1677–1682.

- [18] ——, “Heterogeneous explore-exploit strategies on multi-star networks,” in 2021 American Control Conference (ACC). IEEE, 2021, pp. 1192–1197.

- [19] N. Nayyar, D. Kalathil, and R. Jain, “On regret-optimal learning in decentralized multiplayer multiarmed bandits,” IEEE Transactions on Control of Network Systems, vol. 5, no. 1, pp. 597–606, 2016.

- [20] D. Martínez-Rubio, V. Kanade, and P. Rebeschini, “Decentralized cooperative stochastic bandits,” Advances in Neural Information Processing Systems, vol. 32, 2019.

- [21] A. Lalitha and A. Goldsmith, “Bayesian algorithms for decentralized stochastic bandits,” IEEE Journal on Selected Areas in Information Theory, vol. 2, no. 2, pp. 564–583, 2021.

- [22] L. Kocsis and C. Szepesvári, “Discounted UCB,” in 2nd PASCAL Challenges Workshop, vol. 2, 2006, pp. 51–134.

- [23] A. Garivier and E. Moulines, “On upper-confidence bound policies for switching bandit problems,” in International Conference on Algorithmic Learning Theory. Springer, 2011, pp. 174–188.

- [24] L. Wang, H. Zhou, B. Li, L. R. Varshney, and Z. Zhao, “Be aware of non-stationarity: Nearly optimal algorithms for piecewise-stationary cascading bandits,” arXiv preprint arXiv:1909.05886, 2019.

- [25] O. Besbes, Y. Gur, and A. Zeevi, “Stochastic multi-armed-bandit problem with non-stationary rewards,” Advances in neural information processing systems, vol. 27, pp. 199–207, 2014.

- [26] L. Wei and V. Srivatsva, “On abruptly-changing and slowly-varying multiarmed bandit problems,” in 2018 Annual American Control Conference (ACC). IEEE, 2018, pp. 6291–6296.

- [27] L. Besson and E. Kaufmann, “The generalized likelihood ratio test meets klUCB: an improved algorithm for piecewise non-stationary bandits,” Proceedings of Machine Learning Research vol XX, vol. 1, p. 35, 2019.

- [28] P. Auer, P. Gajane, and R. Ortner, “Adaptively tracking the best bandit arm with an unknown number of distribution changes,” in Conference on Learning Theory. PMLR, 2019, pp. 138–158.

- [29] F. Liu, J. Lee, and N. Shroff, “A change-detection based framework for piecewise-stationary multi-armed bandit problem,” in Proceedings of the AAAI Conference on Artificial Intelligence, vol. 32, no. 1, 2018.

- [30] R. Alami, O. Maillard, and R. Féraud, “Restarted Bayesian online change-point detector achieves optimal detection delay,” in International Conference on Machine Learning. PMLR, 2020, pp. 211–221.

- [31] M. Zinkevich, “Online convex programming and generalized infinitesimal gradient ascent,” in Proceedings of the 20th international conference on machine learning (icml-03), 2003, pp. 928–936.

- [32] P. Zhao, G. Wang, L. Zhang, and Z.-H. Zhou, “Bandit convex optimization in non-stationary environments,” The Journal of Machine Learning Research, vol. 22, no. 1, pp. 5562–5606, 2021.

- [33] R. P. Adams and D. J. MacKay, “Bayesian online changepoint detection,” stat, vol. 1050, p. 19, 2007.

- [34] P. Fearnhead and Z. Liu, “On-line inference for multiple changepoint problems,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), vol. 69, no. 4, pp. 589–605, 2007.

- [35] J. Mellor and J. Shapiro, “Thompson sampling in switching environments with Bayesian online change detection,” in Artificial Intelligence and Statistics. PMLR, 2013, pp. 442–450.

- [36] R. Alami, O. Maillard, and R. Féraud, “Memory bandits: a Bayesian approach for the switching bandit problem,” in NIPS 2017-31st Conference on Neural Information Processing Systems, 2017.

- [37] S. Maghsudi and M. van der Schaar, “A non-stationary bandit-learning approach to energy-efficient femto-caching with rateless-coded transmission,” IEEE Transactions on Wireless Communications, vol. 19, no. 7, pp. 5040–5056, 2020.

- [38] S. Maghsudi and D. Niyato, “On power-efficient planning in dynamic small cell networks,” IEEE Wireless Communications Letters, vol. 7, no. 3, pp. 304–307, 2018.

- [39] O.-A. Maillard, “Sequential change-point detection: Laplace concentration of scan statistics and non-asymptotic delay bounds,” in Algorithmic Learning Theory. PMLR, 2019, pp. 610–632.

- [40] L. Li, W. Chu, J. Langford, and X. Wang, “Unbiased offline evaluation of contextual-bandit-based news article recommendation algorithms,” in Proceedings of the fourth ACM international conference on Web search and data mining, 2011, pp. 297–306.