Time Series Continuous Modeling for Imputation and Forecasting with Implicit Neural Representations

Abstract

We introduce a novel modeling approach for time series imputation and forecasting, tailored to address the challenges often encountered in real-world data, such as irregular samples, missing data, or unaligned measurements from multiple sensors. Our method relies on a continuous-time-dependent model of the series’ evolution dynamics. It leverages adaptations of conditional, implicit neural representations for sequential data. A modulation mechanism, driven by a meta-learning algorithm, allows adaptation to unseen samples and extrapolation beyond observed time-windows for long-term predictions. The model provides a highly flexible and unified framework for imputation and forecasting tasks across a wide range of challenging scenarios. It achieves state-of-the-art performance on classical benchmarks and outperforms alternative time-continuous models.

1 Introduction

Time series analysis and modeling are ubiquitous in a wide range of fields, including industry, medicine, and climate science. The variety, heterogeneity and increasing number of deployed sensors, raise new challenges when dealing with real-world problems for which current methods often fail. For example, data are frequently irregularly sampled, contain missing values, or are unaligned when collected from distributed sensors (Schulz and Stattegger, 1997; Clark and Bjørnstad, 2004). Recent advancements in deep learning have significantly improved state-of-the-art performance in both data imputation (Cao et al., 2018; Du et al., 2023) and forecasting tasks (Zeng et al., 2022; Nie et al., 2022). Many state-of-the-art models, such as transformers, have been primarily designed for dense and regular grids (Wu et al., 2021; Nie et al., 2022; Du et al., 2023). They struggle to handle irregular data and often suffer from significant performance degradation (Chen et al., 2001; Kim et al., 2019).

Our objective is to explore alternatives to SOTA transformers able to handle, in a unified framework, imputation and forecasting tasks for irregularly, arbitrarily sampled, and unaligned time series sources. Time-dependent continuous models (Rasmussen and Williams, 2006; Garnelo et al., 2018; Rubanova et al., 2019) offer such an alternative. However, until now, their performance has lagged significantly behind that of models designed for regular discrete grids. A few years ago, implicit neural representations (INRs) emerged as a powerful tool for representing images as continuous functions of spatial coordinates (Sitzmann et al., 2020; Tancik et al., 2020) with recent new applications such as image generation (Dupont et al., 2022) or even modeling dynamical systems (Yin et al., 2023).

In this work, we leverage the potential of conditional INR models within a meta-learning approach to introduce TimeFlow: a unified framework designed for modeling continuous time series and addressing imputation and forecasting tasks with irregular and unaligned observations. Our key contributions are the following:

-

•

We propose a novel framework that excels in modeling time series as continuous functions of time, accepting arbitrary time step inputs, thus enabling the handling of irregular and unaligned time series for both imputation and forecasting tasks. This is one of the very first attempts to adapt INRs that enables efficient handling of both imputation and forecasting tasks within a unified framework. The methodology which leverages the synergy between the model components, evidenced in the context of this application, is a pioneering contribution to the field.

-

•

We conducted an extensive comparison with state-of-the-art continuous and discrete models. It demonstrates that our approach outperforms continuous and discrete SOTA deep learning approaches for imputation. As for long-term forecasting, it outperforms existing continuous models both on regular and irregular samples. It is on par with SOTA discrete models on regularly sampled time series while allowing for a much greater flexibility for irregular samplings, allowing to cope with situations where discrete models fail. Furthermore, we prove that our method effortlessly handles previously unseen time series and new time windows, making it well-suited for real-world applications.

2 Related work

Discrete methods for time series imputation and forecasting.

Recently, Deep Learning (DL) methods have been widely used for both time series imputation and forecasting. For imputation, BRITS (Cao et al., 2018) uses a bidirectional recurrent neural network (RNN). Alternative frameworks were later explored, e.g., GAN-based (Luo et al., 2018; 2019; Liu et al., 2019), VAE-based (Fortuin et al., 2020), diffusion-based (Tashiro et al., 2021), matrix factorization-based (TIDER, Liu et al., 2023) and transformer-based (SAITS, Du et al., 2023) approaches. These methods cannot handle irregular time series. In situations involving multiple sensors, such as those placed at different locations, incorporating new sensors necessitates retraining the entire model, thereby limiting their usability. For forecasting, most recent DL SOTA models are based on transformers. Initial approaches apply plain transformers directly to the series, each token being a series element (Zhou et al., 2021; Liu et al., 2022; Wu et al., 2021; Zhou et al., 2022). These transformers may underperform linear models as shown in (Zeng et al., 2022). PatchTST (Nie et al., 2022) significantly improved transformers SOTA performance by considering sub-series as tokens of the series. However, all these models cannot handle properly irregularly sampled look-back windows.

Continuous methods for time series.

Gaussian Processes (Rasmussen and Williams, 2006) have been a popular family of methods for modeling time series as continuous functions. They require choosing an appropriate kernel (Corani et al., 2021) and may suffer limitations in large dimensions settings. Neural Processes (NPs) (Garnelo et al., 2018; Kim et al., 2019) parameterize Gaussian processes through an encoder-decoder architecture leading to more computationally efficient implementations. NPs have been used to model simple signals for imputation and forecasting tasks, but struggle with more complex signals. Bilos et al. (2023) parameterizes a Gaussian Process through a diffusion model, but the model has difficulty adapting to a large number of timestamps. Other approaches such as Brouwer et al. (2019) and Rubanova et al. (2019) model time series continuously with latent ordinary differential equations. mTAN (Shukla and Marlin, 2021) a transformer model uses an attention mechanism to impute irregular time series. While these approaches have shown significant progress in continuous modeling for time series, they are less efficient than the aforementioned discrete models for regular time series and lack extrapolation capability when dealing with complex dynamics.

Implicit neural representations.

The recent development of implicit neural representations (INRs) has led to impressive results in computer vision (Sitzmann et al., 2020; Tancik et al., 2020; Fathony et al., 2021; Mildenhall et al., 2021). INRs can represent data as a continuous function, which can be queried at any coordinate. While they have been applied in other fields such as physics (Yin et al., 2023) and meteorology (Huang and Hoefler, 2023), there has been limited research on INRs for time series analysis. Prior works (Fons et al., 2022; Jeong and Shin, 2022) focused on time series generation for data augmentation and on time series encoding for reconstruction but are limited by their fixed grid input requirement. DeepTime (Woo et al., 2022) is the closest work to our contribution. DeepTime learns a set of basis INR functions from a training set of multiple time series and combines them using a Ridge regressor. This regressor allows it to adapt to new time series. It has been designed for forecasting only. The original version cannot handle imputation properly and was adapted to do so for our comparisons. In our experiments, we will demonstrate that TimeFlow significantly outperforms DeepTime in imputation and also in forecasting tasks when dealing with missing values in the look-back window. TimeFlow also shows a slight advantage over DeepTime in forecasting regularly sampled series.

3 The TimeFlow framework

3.1 Problem setting

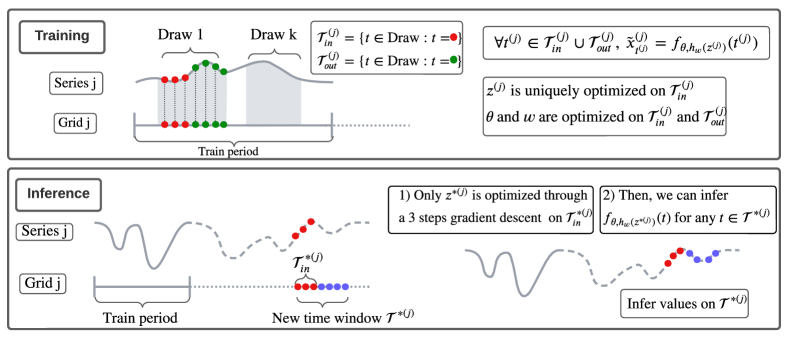

We aim to develop a unified framework for time series imputation and forecasting that reduces dependency on a fixed sampling scheme for time series. We introduce the following notations for both tasks. During training, in the imputation setting, we have access to time series in an observation set denoted as , which is a subset of the complete time series observation set . In the forecasting setting, we observe time series within a limited past time grid, referred to as the ’look-back window’ and denoted as (a subset of ), as well as a future grid, the ’horizon’, denoted as (also a subset of ). At test time, in both cases, and given an observed subset included in a possibly new temporal window , our objective is to infer the time series values within .

3.2 Key components

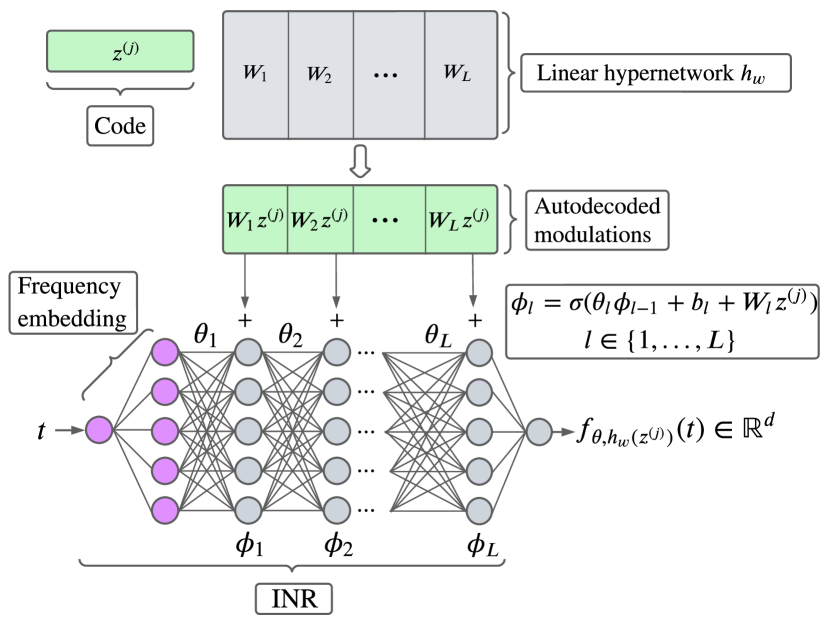

Our framework is articulated around three key components. (i) INR-based time-continuous functions: a time series is represented by a time-continuous function that can be queried at any time . For that, we employ implicit neural representations (INRs), which are neural networks capable of learning a parameterized continuous function from discrete data by minimizing the reconstruction loss between observed data and network’s outputs. (ii) Conditional INRs with modulations: An INR can represent only one function, whether it’s an image or a time series. To effectively represent a collection of time series using INRs, we improve their encoding by incorporating per-sample modulations, which we denote as . These modulations condition the parameters of the INRs. We use the notation to refer to the conditioned INR with the modulations . (iii) Optimization-based encoding: the conditioning modulation parameters are calculated as a function of codes that represent the individual sample series. We acquire these codes through a meta-learning optimization process using an auto-decoding strategy. Notably, auto-decoding has been found to be more efficient for this purpose than set encoders (Kim et al., 2019). In the following sections, we will elaborate on each component of our method. Given that the choices made for each component and the methodology developed to enhance their synergy are essential aspects, we provide a discussion of the various choices involved in Section 3.4.

INR-based time-continuous functions.

We implement our INR with Fourier features and a feed-forward network (FFN) with ReLU activations, i.e. for a time coordinate , the output of the INR is given by . The Fourier Features are a frequency embedding of the time coordinates used to capture high-frequencies (Tancik et al., 2020; Mildenhall et al., 2021). In our case, we chose , with the number of fixed frequencies. For an INR with layers, the output is computed as follows: (i) we get the frequency embedding , (ii) we update the hidden states according to for , (iii) we project onto the output space .

Conditional INRs with modulations.

As indicated, sample conditioning of the INR is performed through modulations of its parameters. In order to adapt rapidly the model to new samples, the conditioning should rely only on a small number of the INR parameters. This is achieved by modifying only the biases of the INR through the introduction of an additional bias term for each layer , also known as shift modulation. To further limit the versatility of the conditioning, we generate the instance modulations from compact codes through a linear hypernetwork with parameters , i.e., . Consequently, the approximation of a time series , denoted globally as , will depend on shared parameters and that are common among all the INRs involved in modeling the series family and on the code specific to series . The output of the -th layer of the modulated INR is given by , where , and are the parameters of the hypernetwork . This design enables gathering information across samples into the common parameters of the INR and hypernetwork, while the codes contain only specific information about their respective time-series samples. The architecture is illustrated in Figure 1.

Optimization-based encoding.

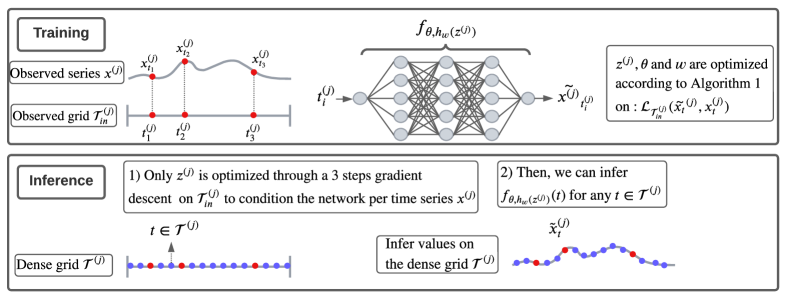

We condition the INR using the data from , and learn the shared INR and hypernetwork parameters and using for both imputation and forecasting, and for forecasting only. We achieve the conditioning on by optimizing the codes through gradient descent. The joint optimization of the codes and common parameters is challenging. In TimeFlow, it is achieved through a meta-learning approach, adapted from Dupont et al. (2022) and Zintgraf et al. (2019). The objective is to learn shared parameters so that the code can be adapted in just a few gradient steps for a new series . For training, we perform parameter optimization at two levels: the inner-loop and the outer-loop. The inner-loop adapts the code to condition the network on the set , while the outer-loop updates the common parameters using and also for forecasting. We present our training optimization in Algorithm 1. At each training epoch and for each batch of data composed of time series sampled from the training set, we first update individually the codes in the inner loop, before updating the common parameters in the outer loop using a loss over the whole batch. We introduce a parameter to weight the importance of the loss over w.r.t. the loss over for the outer-loop. In practice, when exists, i.e. for forecasting, we set and otherwise. We use an MSE loss over the observations grid . We denote and the learning rates of the inner- and outer-loop. Using steps for training and testing is sufficient for our experiments thanks to the use of second-order meta-learning as explained in Section 3.4.

3.3 TimeFlow inference

During the inference process, we aim to infer the time series value for each timestamp in the dense grid based on the partial observation grid . We can encounter two scenarios: (i) One where we observe the same time window as during training () as in the imputation setting in Section 4.1. (ii) One, where we are dealing with a newly observed time window (), as in the forecasting setting in Section 4.2. At inference, the parameters and are kept fixed to their final training values. We optimize the individual parameters based on the newly observed grid using the inner-steps of the meta-learning algorithm as described in Algorithm 2. We are then in position to query for any given timestamp .

3.4 Discussion on implementation choices

As indicated before, adapting the components and enhancing their synergy for the tasks of imputation and forecasting is not trivial and require careful choices. We conducted several ablation studies to provide a comprehensive examination of key implementation choices of our framework. Our findings indicate that: • An FFN with Fourier Features outperformed other popular INRs for the tasks considered in this study (Section A.2.1). • TimeFlow with a set encoder for learning the compact conditioning codes in place of the auto-decoding strategy used here, proved much less effective on complex datasets (Section A.2.4, Table 8). • Replacing the 2nd-order optimization for a 1st-order one, such as REPTILE, led to unstable training (Section A.2.4, Table 7). • Complexifying the modulation by introducing scaling parameters in addition to shift parameters did not provide performance gains (Section A.2.5). • Using 3 inner steps for training and inference struck a favorable balance between reconstruction capabilities and computational efficiency (Section A.2.3). • A latent code dimension of 128 was optimal for our tasks (Section A.2.2).

4 Experiments

We conducted a comprehensive evaluation of our TimeFlow framework across three different tasks, comparing its performance to state-of-the-art continuous and discrete baseline methods. In Section 4.1, we assess TimeFlow’s capabilities to impute sparsely observed time series under various sampling rates. Section 4.2 focuses on long-term forecasting, where we evaluate TimeFlow over standard long-term forecasting horizons. In Section 4.3, we tackle a challenging task forecasting with incomplete look-back windows, thus combining the challenges of imputation and forecasting. This demonstrates TimeFlow’s versatility and performance.

Datasets.

Our approach is well-suited for handling a large number of homogeneous phenomena measured over time. We tested our framework on three extensive multivariate datasets where a single phenomenon is measured at multiple locations over time. They are commonly used in time series imputation and long-term forecasting literature. The Electricity dataset comprises hourly electricity load curves of 321 customers in Portugal, spanning the years 2012 to 2014. The Traffic dataset is composed of hourly road occupancy rates from 862 locations in San Francisco during 2015 and 2016. Lastly, the Solar dataset contains measurements of solar power production from 137 photovoltaic plants in Alabama, recorded at 10-minute intervals in 2006. Additionally, we have created an hourly version, SolarH, for the sake of consistency in the forecasting section. These datasets exhibit diversity in various characteristics: • They exhibit diverse temporal frequencies, including daily and weekly seasonality observed in the Traffic and Electricity datasets, while the Solar dataset possesses only daily frequency. • There is individual variability across data samples and more pronounced trends in the Electricity dataset compared to the Traffic and Solar datasets.

4.1 Imputation

We consider the classical imputation setting where time series are partially observed over a given time window. Using our approach, we can predict for each time series the value at any timestamp in that time window based on partial observations.

Setting.

For a time series , we denote the set of observed points as and the ground truth set of points as . The observed time grids may be irregularly spaced and may differ across the different time series (). The model is trained for each following Algorithm 1. Then, we aim to infer for any unobserved the missing value conditioned on according to Algorithm 2. For this imputation task, the TimeFlow training and inference procedures are detailed in Section 3 and illustrated in Figure 2. For comparison with the SOTA imputation baselines, we assume that the ground truth time grid is the same for each sample. The subsampling rate is define as the rate of observed values.

Baselines.

We compare TimeFlow with various baselines, including discrete imputation methods, such as CSDI (Tashiro et al., 2021), SAITS (Du et al., 2023), BRITS (Cao et al., 2018), and TIDER (Liu et al., 2023), and continuous ones, such as Neural Process (NP, Garnelo et al., 2018), mTAN (Shukla and Marlin, 2021), and DeepTime with slight adjustments (Woo et al., 2022) (details cf. Section C.3). For each dataset, we divide the series into five independent periods (each time window consists of 2000 timestamps for Electricity and Traffic, and 10,000 timestamps for Solar), perform imputation on each time window and average the performance to obtain robust results. We evaluate the quality of the models for different subsampling rates, ranging from the easiest to the most difficult .

| Continuous methods | Discrete methods | ||||||||

| TimeFlow | DeepTime | mTAN | Neural Process | CSDI | SAITS | BRITS | TIDER | ||

| 0.05 | 0.324 0.013 | 0.379 0.037 | 0.575 0.039 | 0.357 0.015 | 0.462 0.021 | 0.384 0.019 | 0.329 0.015 | 0.427 0.010 | |

| 0.10 | 0.250 0.010 | 0.333 0.034 | 0.412 0.047 | 0.417 0.057 | 0.398 0.072 | 0.308 0.011 | 0.287 0.015 | 0.399 0.009 | |

| Electricity | 0.20 | 0.225 0.008 | 0.244 0.013 | 0.342 0.014 | 0.320 0.017 | 0.341 0.068 | 0.261 0.008 | 0.245 0.011 | 0.391 0.010 |

| 0.30 | 0.212 0.007 | 0.240 0.014 | 0.335 0.015 | 0.300 0.022 | 0.277 0.059 | 0.236 0.008 | 0.221 0.008 | 0.384 0.009 | |

| 0.50 | 0.194 0.007 | 0.227 0.012 | 0.340 0.022 | 0.297 0.016 | 0.168 0.003 | 0.209 0.008 | 0.193 0.008 | 0.386 0.009 | |

| 0.05 | 0.095 0.015 | 0.190 0.020 | 0.241 0.102 | 0.115 0.015 | 0.374 0.033 | 0.142 0.016 | 0.165 0.014 | 0.291 0.009 | |

| 0.10 | 0.083 0.015 | 0.159 0.013 | 0.251 0.081 | 0.114 0.014 | 0.375 0.038 | 0.124 0.018 | 0.132 0.015 | 0.276 0.010 | |

| Solar | 0.20 | 0.072 0.015 | 0.149 0.020 | 0.314 0.035 | 0.109 0.016 | 0.217 0.023 | 0.108 0.014 | 0.109 0.012 | 0.270 0.010 |

| 0.30 | 0.061 0.012 | 0.135 0.014 | 0.338 0.05 | 0.108 0.016 | 0.156 0.002 | 0.100 0.015 | 0.098 0.012 | 0.266 0.010 | |

| 0.50 | 0.054 0.013 | 0.098 0.013 | 0.315 0.080 | 0.107 0.015 | 0.079 0.011 | 0.094 0.013 | 0.088 0.013 | 0.262 0.009 | |

| 0.05 | 0.283 0.016 | 0.246 0.010 | 0.406 0.074 | 0.318 0.014 | 0.337 0.045 | 0.293 0.007 | 0.261 0.010 | 0.363 0.007 | |

| 0.10 | 0.211 0.012 | 0.214 0.007 | 0.319 0.025 | 0.288 0.018 | 0.288 0.017 | 0.237 0.006 | 0.245 0.009 | 0.362 0.006 | |

| Traffic | 0.20 | 0.168 0.006 | 0.216 0.006 | 0.270 0.012 | 0.271 0.011 | 0.269 0.017 | 0.197 0.005 | 0.224 0.008 | 0.361 0.006 |

| 0.30 | 0.151 0.007 | 0.172 0.008 | 0.251 0.006 | 0.259 0.012 | 0.240 0.037 | 0.180 0.006 | 0.197 0.007 | 0.355 0.006 | |

| 0.50 | 0.139 0.007 | 0.171 0.005 | 0.278 0.040 | 0.240 0.021 | 0.144 0.022 | 0.160 0.008 | 0.161 0.060 | 0.354 0.007 | |

| TimeFlow improvement | / | 20.5 | 49.1 | 30.5 | 38.9 | 16.9 | 14.7 | 50.9 | |

Results.

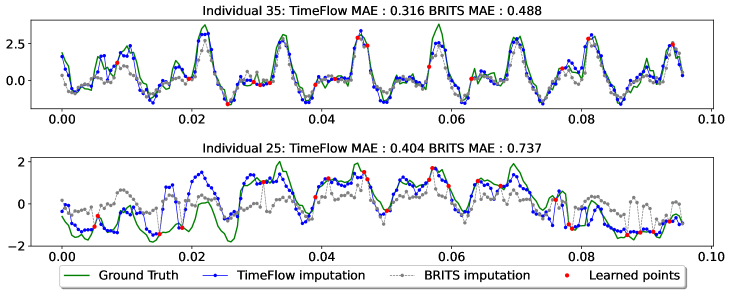

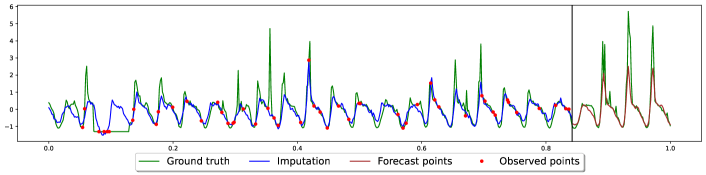

We show in Table 1 that TimeFlow outperforms both discrete and continuous models across almost all s for the given datasets. The relative improvements of TimeFlow over baselines are significant, ranging from 15% to 50%. Especially for the lowest sampling rate , TimeFlow outperforms all discrete baselines, demonstrating the advantages of continuous modeling. Additionally, it achieves lower imputation errors compared to continuous models in all but one cases. Qualitatively, we see on example series in Figure 3 that our model shows significant imputation capabilities, with on a subsampling rate at on the Electricity dataset. It captures well different frequencies and amplitudes in a challenging case (sample 35), although it underestimates the amplitude of some peaks. In a more challenging scenario (sample 25), where the series exhibit additional trend changes and frequency variations within the data, TimeFlow correctly imputes most timestamps, outperforming BRITS, which is the best-performing method for the Electricity dataset.

Imputation on previously unseen time series.

In more practical scenarios, such as cases involving the installation of new sensors, we often encounter new time series originating from the same underlying phenomenon. In such instances, it becomes crucial to make inferences for these previously unseen time series. Thanks to efficient adaptation in latent space, our model can easily be applied to these new time series (as shown in Section C.2, Table 12), contrasting with SOTA methods like SAITS and BRITS, which require full model retraining on the whole set of time series.

4.2 Forecasting

In this section, we are interested in the conventional long-term forecasting scenario. It consists in predicting the phenomenon in a specific future period, the horizon, based on the history of a limited past period, the look-back window. The forecaster is trained on a set of observed time series for a given time window (train period) and tested on new time windows.

Setting

For a given time series , denotes the look-back window and the horizon of points. During training, at each epoch, we train following Algorithm 1 with randomly drawn pairs of look-back window and horizon within the observed train period. Then, for a new time window , given a look-back window we forecast future values any , the horizon interval, following Algorithm 2. We illustrate the training and inference of TimeFlow for the forecasting task in Figure 4.

Baselines.

To evaluate the quality of our model in long-term forecasting, we compare it to the discrete baselines PatchTST (Nie et al., 2022), DLinear (Zeng et al., 2022), AutoFormer (Wu et al., 2021), and Informer (Zhou et al., 2021). We also include continuous baselines DeepTime and Neural Process (NP). In Table 2, we present the forecasting results for standard horizons in long-term forecasting: . The look-back window length is fixed to 512.

| Continuous methods | Discrete methods | |||||||

| TimeFlow | DeepTime | Neural Process | Patch-TST | DLinear | AutoFormer | Informer | ||

| Electricity | 96 | 0.228 0.028 | 0.244 0.026 | 0.392 0.045 | 0.221 0.023 | 0.241 0.030 | 0.546 0.277 | 0.603 0.255 |

| 192 | 0.238 0.020 | 0.252 0.019 | 0.401 0.046 | 0.229 0.020 | 0.252 0.025 | 0.500 0.190 | 0.690 0.291 | |

| 336 | 0.270 0.031 | 0.284 0.034 | 0.434 0.076 | 0.251 0.027 | 0.288 0.038 | 0.523 0.188 | 0.736 0.271 | |

| 720 | 0.316 0.055 | 0.359 0.051 | 0.607 0.150 | 0.297 0.039 | 0.365 0.059 | 0.631 0.237 | 0.746 0.265 | |

| SolarH | 96 | 0.190 0.013 | 0.190 0.020 | 0.221 0.048 | 0.262 0.070 | 0.208 0.014 | 0.245 0.045 | 0.248 0.022 |

| 192 | 0.202 0.020 | 0.204 0.028 | 0.244 0.048 | 0.253 0.051 | 0.217 0.022 | 0.333 0.107 | 0.270 0.031 | |

| 336 | 0.209 0.017 | 0.199 0.026 | 0.240 0.006 | 0.259 0.071 | 0.217 0.026 | 0.334 0.079 | 0.328 0.048 | |

| 720 | 0.218 0.041 | 0.229 0.024 | 0.403 0.147 | 0.267 0.064 | 0.249 0.034 | 0.351 0.055 | 0.337 0.037 | |

| Traffic | 96 | 0.217 0.032 | 0.228 0.032 | 0.283 0.027 | 0.203 0.037 | 0.228 0.033 | 0.319 0.059 | 0.372 0.078 |

| 192 | 0.212 0.028 | 0.220 0.022 | 0.292 0.024 | 0.197 0.030 | 0.221 0.023 | 0.368 0.057 | 0.511 0.247 | |

| 336 | 0.238 0.034 | 0.245 0.038 | 0.305 0.039 | 0.222 0.039 | 0.250 0.040 | 0.434 0.061 | 0.561 0.263 | |

| 720 | 0.279 0.050 | 0.290 0.052 | 0.339 0.038 | 0.269 0.057 | 0.300 0.057 | 0.462 0.062 | 0.638 0.067 | |

| TimeFlow improvement | / | 4.30 | 32.2 | -2.14 | 14.31 | 47.57 | 54.83 | |

Results.

The results in Table 2 show that our approach ranks in the top two across all datasets and horizons and is the overall best continuous method. TimeFlow’s performance is comparable to the current SOTA model PatchTST, with only 2% relative difference. Moreover, TimeFlow shows consistent results across the three datasets, whereas the other best discrete and continuous baselines, i.e. PatchTST and DeepTime, performance drops for some datasets. We also note that, despite the great performance of the SOTA PatchTST, other transformer-based baselines (discrete methods in Table 2) perform poorly. We provide a detailed insight on these results in Section D.1. Overall, although this evaluation setting favors discrete methods because the time series are observed at evenly distributed time steps, TimeFlow consistently performs as well as PatchTST and outperforms all the other methods, whether discrete or continuous. It is the first time that a continuous model has achieved the same level of performance as discrete methods within their specific setting.

Forecasting on previously unseen time series.

TimeFlow considers that the series observed at different locations are independent, similar to PatchTST, NP, and DeepTime. This allows it to generalize to previously unseen time series from the same phenomenon. Note that this is not the case for most discrete methods. We show in Section D.4, Table 17 that TimeFlow is able to generalize to previously unseen time series with no significant performance drop.

4.3 Challenging task: Forecast while imputing incomplete look-back windows

In real-world scenarios, it is common to encounter missing or irregularly sampled series when making predictions on new time windows (Cinar et al., 2018; Tang et al., 2020). Continuous methods can handle these cases, as they are designed to accommodate irregular sampling within the look-back window. In this section, we formulate a task to simulate these real-world scenarios. It’s worth noting that this task is often encountered in practice but is rarely considered in the DL literature.

Setting and baselines.

This scenario is similar to the forecast setting in Section 4.2 and illustrated in Figure 4. The difference is that during inference, the look-back window is subsampled at a rate smaller than the one used for the training phase. This simulates a situation with missing observations in the look back window. Consequently, two distinct tasks emerge during the inference phase: imputing missing points within the sparsely observed look-back window, and forecasting over the horizon with this degraded context. In Table 3, we compare to the two other continuous baselines, DeepTime and NP on Electricity and Traffic for different s and horizons.

| TimeFlow | DeepTime | Neural Process | ||||||

| Imputation error | Forecast error | Imputation error | Forecast error | Imputation error | Forecast error | |||

| Electricity | 96 | 0.5 | 0.151 0.003 | 0.239 0.013 | 0.209 0.004 | 0.270 0.019 | 0.460 0.048 | 0.486 0.078 |

| 0.2 | 0.208 0.006 | 0.260 0.015 | 0.249 0.006 | 0.296 0.023 | 0.644 0.079 | 0.650 0.095 | ||

| 0.1 | 0.272 0.006 | 0.295 0.016 | 0.284 0.007 | 0.324 0.026 | 0.740 0.083 | 0.737 0.106 | ||

| 192 | 0.5 | 0.149 0.004 | 0.235 0.011 | 0.204 0.004 | 0.265 0.018 | 0.461 0.045 | 0.498 0.070 | |

| 0.2 | 0.209 0.006 | 0.257 0.013 | 0.244 0.007 | 0.290 0.023 | 0.601 0.075 | 0.626 0.101 | ||

| 0.1 | 0.274 0.010 | 0.289 0.016 | 0.282 0.007 | 0.315 0.025 | 0.461 0.045 | 0.724 0.090 | ||

| Traffic | 96 | 0.5 | 0.180 0.016 | 0.219 0.026 | 0.272 0.028 | 0.243 0.030 | 0.436 0.025 | 0.444 0.047 |

| 0.2 | 0.239 0.019 | 0.243 0.027 | 0.335 0.026 | 0.293 0.027 | 0.596 0.049 | 0.597 0.075 | ||

| 0.1 | 0.312 0.020 | 0.290 0.027 | 0.385 0.025 | 0.344 0.027 | 0.734 0.102 | 0.731 0.132 | ||

| 192 | 0.5 | 0.176 0.014 | 0.217 0.017 | 0.241 0.027 | 0.234 0.021 | 0.477 0.042 | 0.476 0.043 | |

| 0.2 | 0.233 0.017 | 0.236 0.021 | 0.286 0.027 | 0.276 0.020 | 0.685 0.109 | 0.678 0.108 | ||

| 0.1 | 0.304 0.019 | 0.277 0.021 | 0.331 0.025 | 0.324 0.021 | 0.888 0.178 | 0.877 0.174 | ||

| TimeFlow improvement | / | / | 22.7 | 12.0 | 62.3 | 59.4 | ||

Results.

In Table 3, the results show that TimeFlow consistently outperforms other methods in imputation and forecasting for every scenarios. When comparing with the complete look-back windows observations scenario from Table 2, one observes that at a 0.5 sampling rate, TimeFlow presents only a slight reduction in performance, whereas other baseline methods experience more significant drops. For instance, when we compare forecast results between a complete window and a subsampled window for Electricity with a forecasting horizon of , TimeFlow’s error increases by a mere 4.6% (from 0.228 to 0.239). In contrast, DeepTime’s error grows by over 10% (from 0.244 to 0.270), and NP experiences a rise of around 25% (from 0.392 to 0.486).

For lower sampling rates, TimeFlow still delivers correct predictions. Qualitatively, we see on the series example in Figure 5 that despite observing only 10% of the look-back window, the model can correctly infer both the complete look-back window and the horizon. Both quantitative and qualitative results show the robustness and efficiency of TimeFlow on this particularly challenging setting.

5 Conclusion

We have introduced a unified framework for continuous time series modeling leveraging conditional INR and meta-learning. Our experiments have demonstrated superior performance compared to other continuous methods, and better or comparable results to SOTA discrete methods. One of the standout features of our framework is its inherent continuity and the ability to modulate the INR parameters. This unique flexibility lets TimeFlow effectively tackle a wide array of challenges, including forecasting in the presence of missing values, accommodating irregular time steps, and extending the trained model’s applicability to previously unseen time series and new time windows. Our empirical results have shown TimeFlow’s effectiveness in handling homogeneous multivariate time series. As a logical next step, extending TimeFlow’s capabilities to address heterogeneous multivariate phenomena represents a promising direction for future research.

References

- Bilos et al. [2023] M. Bilos, K. Rasul, A. Schneider, Y. Nevmyvaka, and S. Günnemann. Modeling temporal data as continuous functions with stochastic process diffusion. In A. Krause, E. Brunskill, K. Cho, B. Engelhardt, S. Sabato, and J. Scarlett, editors, International Conference on Machine Learning, ICML, volume 202 of Proceedings of Machine Learning Research, pages 2452–2470. PMLR, 2023.

- Brouwer et al. [2019] E. D. Brouwer, J. Simm, A. Arany, and Y. Moreau. Gru-ode-bayes: continuous modeling of sporadically-observed time series. In Proceedings of the 33rd International Conference on Neural Information Processing Systems, pages 7379–7390, 2019.

- Cao et al. [2018] W. Cao, D. Wang, J. Li, H. Zhou, Y. Li, and L. Li. Brits: bidirectional recurrent imputation for time series. In Proceedings of the 32nd International Conference on Neural Information Processing Systems, pages 6776–6786, 2018.

- Chen et al. [2001] H. Chen, S. Grant-Muller, L. Mussone, and F. Montgomery. A study of hybrid neural network approaches and the effects of missing data on traffic forecasting. Neural Computing & Applications, 10:277–286, 2001.

- Cinar et al. [2018] Y. G. Cinar, H. Mirisaee, P. Goswami, É. Gaussier, and A. Aït-Bachir. Period-aware content attention rnns for time series forecasting with missing values. Neurocomputing, 312:177–186, 2018.

- Clark and Bjørnstad [2004] J. S. Clark and O. N. Bjørnstad. Population time series: process variability, observation errors, missing values, lags, and hidden states. Ecology, 85(11):3140–3150, 2004.

- Corani et al. [2021] G. Corani, A. Benavoli, and M. Zaffalon. Time series forecasting with gaussian processes needs priors. In Machine Learning and Knowledge Discovery in Databases. Applied Data Science Track: European Conference, ECML PKDD 2021, Bilbao, Spain, September 13–17, 2021, Proceedings, Part IV 21, pages 103–117. Springer, 2021.

- Du et al. [2023] W. Du, D. Côté, and Y. Liu. Saits: Self-attention-based imputation for time series. Expert Systems with Applications, 219:119619, 2023.

- Dupont et al. [2022] E. Dupont, H. Kim, S. M. A. Eslami, D. J. Rezende, and D. Rosenbaum. From data to functa: Your data point is a function and you can treat it like one. In International Conference on Machine Learning, ICML 2022, 17-23 July 2022, Baltimore, Maryland, USA, volume 162 of Proceedings of Machine Learning Research, pages 5694–5725. PMLR, 2022.

- Fathony et al. [2021] R. Fathony, A. K. Sahu, D. Willmott, and J. Z. Kolter. Multiplicative filter networks. In International Conference on Learning Representations, 2021.

- Finn et al. [2017] C. Finn, P. Abbeel, and S. Levine. Model-agnostic meta-learning for fast adaptation of deep networks. In International conference on machine learning, pages 1126–1135. PMLR, 2017.

- Fons et al. [2022] E. Fons, A. Sztrajman, Y. El-Laham, A. Iosifidis, and S. Vyetrenko. Hypertime: Implicit neural representation for time series. CoRR, abs/2208.05836, 2022.

- Fortuin et al. [2020] V. Fortuin, D. Baranchuk, G. Rätsch, and S. Mandt. Gp-vae: Deep probabilistic time series imputation. In International conference on artificial intelligence and statistics, pages 1651–1661. PMLR, 2020.

- Garnelo et al. [2018] M. Garnelo, D. Rosenbaum, C. Maddison, T. Ramalho, D. Saxton, M. Shanahan, Y. W. Teh, D. J. Rezende, and S. M. A. Eslami. Conditional neural processes. In Proceedings of the 35th International Conference on Machine Learning, ICML, volume 80, pages 1690–1699. PMLR, 2018.

- Huang and Hoefler [2023] L. Huang and T. Hoefler. Compressing multidimensional weather and climate data into neural networks. In International Conference on Learning Representations, ICLR, 2023.

- Jeong and Shin [2022] K. Jeong and Y. Shin. Time-series anomaly detection with implicit neural representation. CoRR, abs/2201.11950, 2022.

- Kim et al. [2019] T. Kim, W. Ko, and J. Kim. Analysis and impact evaluation of missing data imputation in day-ahead pv generation forecasting. Applied Sciences, 9(1):204, 2019.

- Liu et al. [2022] S. Liu, H. Yu, C. Liao, J. Li, W. Lin, A. X. Liu, and S. Dustdar. Pyraformer: Low-complexity pyramidal attention for long-range time series modeling and forecasting. In The Tenth International Conference on Learning Representations, ICLR 2022, Virtual Event, April 25-29, 2022, 2022.

- Liu et al. [2023] S. Liu, X. Li, G. Cong, Y. Chen, and Y. Jiang. Multivariate time-series imputation with disentangled temporal representations. In The Eleventh International Conference on Learning Representations, ICLR, 2023.

- Liu et al. [2019] Y. Liu, R. Yu, S. Zheng, E. Zhan, and Y. Yue. Naomi: Non-autoregressive multiresolution sequence imputation. Advances in neural information processing systems, 32, 2019.

- Luo et al. [2018] Y. Luo, X. Cai, Y. Zhang, J. Xu, et al. Multivariate time series imputation with generative adversarial networks. Advances in neural information processing systems, 31, 2018.

- Luo et al. [2019] Y. Luo, Y. Zhang, X. Cai, and X. Yuan. E2gan: End-to-end generative adversarial network for multivariate time series imputation. In Proceedings of the 28th international joint conference on artificial intelligence, pages 3094–3100. AAAI Press, 2019.

- Mildenhall et al. [2021] B. Mildenhall, P. P. Srinivasan, M. Tancik, J. T. Barron, R. Ramamoorthi, and R. Ng. Nerf: Representing scenes as neural radiance fields for view synthesis. Communications of the ACM, 65(1):99–106, 2021.

- Nichol et al. [2018] A. Nichol, J. Achiam, and J. Schulman. On first-order meta-learning algorithms. arXiv preprint arXiv:1803.02999, 2018.

- Nie et al. [2022] Y. Nie, N. H. Nguyen, P. Sinthong, and J. Kalagnanam. A time series is worth 64 words: Long-term forecasting with transformers. CoRR, abs/2211.14730, 2022.

- Rasmussen and Williams [2006] C. E. Rasmussen and C. K. I. Williams. Gaussian processes for machine learning. Adaptive computation and machine learning. MIT Press, 2006.

- Rubanova et al. [2019] Y. Rubanova, R. T. Q. Chen, and D. Duvenaud. Latent odes for irregularly-sampled time series. CoRR, abs/1907.03907, 2019.

- Schulz and Stattegger [1997] M. Schulz and K. Stattegger. Spectrum: Spectral analysis of unevenly spaced paleoclimatic time series. Computers & Geosciences, 23(9):929–945, 1997.

- Shukla and Marlin [2021] S. N. Shukla and B. M. Marlin. Multi-time attention networks for irregularly sampled time series. In 9th International Conference on Learning Representations, ICLR 2021, Virtual Event, Austria, May 3-7, 2021, 2021.

- Sitzmann et al. [2020] V. Sitzmann, J. N. P. Martel, A. W. Bergman, D. B. Lindell, and G. Wetzstein. Implicit neural representations with periodic activation functions. In Advances in Neural Information Processing Systems 33: Annual Conference on Neural Information Processing Systems 2020, NeurIPS 2020, December 6-12, 2020, virtual, 2020.

- Tancik et al. [2020] M. Tancik, P. Srinivasan, B. Mildenhall, S. Fridovich-Keil, N. Raghavan, U. Singhal, R. Ramamoorthi, J. Barron, and R. Ng. Fourier features let networks learn high frequency functions in low dimensional domains. Advances in Neural Information Processing Systems, 33:7537–7547, 2020.

- Tang et al. [2020] X. Tang, H. Yao, Y. Sun, C. C. Aggarwal, P. Mitra, and S. Wang. Joint modeling of local and global temporal dynamics for multivariate time series forecasting with missing values. In The Thirty-Fourth AAAI Conference on Artificial Intelligence, AAAI 2020, The Thirty-Second Innovative Applications of Artificial Intelligence Conference, IAAI 2020, The Tenth AAAI Symposium on Educational Advances in Artificial Intelligence, EAAI, pages 5956–5963. AAAI Press, 2020.

- Tashiro et al. [2021] Y. Tashiro, J. Song, Y. Song, and S. Ermon. Csdi: Conditional score-based diffusion models for probabilistic time series imputation. Advances in Neural Information Processing Systems, 34:24804–24816, 2021.

- Woo et al. [2022] G. Woo, C. Liu, D. Sahoo, A. Kumar, and S. C. H. Hoi. Deeptime: Deep time-index meta-learning for non-stationary time-series forecasting. CoRR, abs/2207.06046, 2022.

- Wu et al. [2021] H. Wu, J. Xu, J. Wang, and M. Long. Autoformer: Decomposition transformers with auto-correlation for long-term series forecasting. In M. Ranzato, A. Beygelzimer, Y. N. Dauphin, P. Liang, and J. W. Vaughan, editors, Advances in Neural Information Processing Systems 34: Annual Conference on Neural Information Processing Systems 2021, NeurIPS 2021, December 6-14, 2021, virtual, pages 22419–22430, 2021.

- Yin et al. [2023] Y. Yin, M. Kirchmeyer, J.-Y. Franceschi, A. Rakotomamonjy, and P. Gallinari. Continuous pde dynamics forecasting with implicit neural representations. In International Conference on Learning Representations, ICLR, 2023.

- Zeng et al. [2022] A. Zeng, M. Chen, L. Zhang, and Q. Xu. Are transformers effective for time series forecasting? CoRR, abs/2205.13504, 2022.

- Zhou et al. [2021] H. Zhou, S. Zhang, J. Peng, S. Zhang, J. Li, H. Xiong, and W. Zhang. Informer: Beyond efficient transformer for long sequence time-series forecasting. In Proceedings of the AAAI conference on artificial intelligence, pages 11106–11115, 2021.

- Zhou et al. [2022] T. Zhou, Z. Ma, Q. Wen, X. Wang, L. Sun, and R. Jin. Fedformer: Frequency enhanced decomposed transformer for long-term series forecasting. In K. Chaudhuri, S. Jegelka, L. Song, C. Szepesvári, G. Niu, and S. Sabato, editors, International Conference on Machine Learning, ICML 2022, 17-23 July 2022, Baltimore, Maryland, USA, volume 162 of Proceedings of Machine Learning Research, pages 27268–27286. PMLR, 2022.

- Zintgraf et al. [2019] L. Zintgraf, K. Shiarli, V. Kurin, K. Hofmann, and S. Whiteson. Fast context adaptation via meta-learning. In International Conference on Machine Learning, pages 7693–7702. PMLR, 2019.

Appendix A Architecture details and ablation studies

A.1 Architecture details

For all imputation and forecasting experiments we choose the following hyperparameters :

-

•

dimension: 128

-

•

Number of layers: 5

-

•

Hidden layers dimension: 256

-

•

-

•

code learning rate ( in Algorithm 1):

-

•

Hypernetwork and INR learning rate:

-

•

Number of steps in inner loop:

-

•

Number of epochs:

-

•

Batch size: 64

It is worth noting that the hyperparameters mentioned above remain consistent across all experiments conducted in the paper. We chose to maintain a fixed set of hyperparameters for our model, while other imputation and forecasting approaches commonly fine-tune hyperparameters based on a validation dataset. The obtained results exhibit high robustness across various settings, suggesting that the selected hyperparameters are already effective in achieving reliable outcomes.

A.2 Ablation studies

A.2.1 Fourier features vs SIREN on imputation task

Baseline

The SIREN network differs from the Fourier features network because it does not explicitly incorporate frequencies as input. Instead, it is a multi-layer perceptron network that utilizes sine activation functions. An adjustable parameter, denoted , is multiplied with the input matrices of the preceding layers to capture a broader range of frequencies. For this comparison, we adopt the same hyperparameters described in Section A.1, selecting to align with Sitzmann et al. [2020]. Furthermore, we set the learning rate of both the hypernetwork and the INR to to enhance training stability. In Table 4, we compare the imputation results obtained by the Fourier features network and the SIREN network, specifically focusing on the first time window from the Electricity, Traffic and Solar datasets.

| TimeFlow | TimeFlow w SIREN | ||

| Electricity | 0.05 | 0.323 | 0.466 |

| 0.10 | 0.252 | 0.350 | |

| 0.20 | 0.224 | 0.242 | |

| 0.30 | 0.211 | 0.222 | |

| 0.50 | 0.194 | 0.209 | |

| Solar | 0.05 | 0.105 | 0.114 |

| 0.10 | 0.083 | 0.094 | |

| 0.20 | 0.065 | 0.079 | |

| 0.30 | 0.061 | 0.072 | |

| 0.50 | 0.056 | 0.066 | |

| Traffic | 0.05 | 0.292 | 0.333 |

| 0.10 | 0.220 | 0.252 | |

| 0.20 | 0.168 | 0.191 | |

| 0.30 | 0.152 | 0.163 | |

| 0.50 | 0.141 | 0.154 |

Results

According to the results presented in Table 4, the Fourier features network outperforms the SIREN network in the imputation task on these datasets. Notably, the performance gap between the two network architectures are more pronounced at low sampling rates. This disparity can be attributed to the SIREN network’s difficulty in accurately capturing high frequencies when the time series is sparsely observed. We hypothesize that the MLP with ReLU activations correctly learns the different frequencies of time series with multi-temporal patterns by switching on or off the Fourier embedding frequencies.

A.2.2 Influence of the latent code dimension

The dimension of the latent code is a crucial parameter in our architecture. If it is too small, it underfits the timeseries. Consequently, this adversely affects the performance of both the imputation and forecasting tasks. On the other hand, if the dimension of is too large, it can lead to overfitting, hindering the model’s ability to generalize to new data points.

Baselines

To investigate the impact of dimensionality on the performance of TimeFlow, we conducted experiments on the Electricity dataset, specifically focusing on the imputation task. We varied the sizes of within . The other hyperparameters are set as presented in Section A.1. The obtained results for each dimension are summarized in Table 5.

| Electricity | 0.05 | 0.370 | 0.364 | 0.323 | 0.354 |

| 0.10 | 0.302 | 0.301 | 0.252 | 0.283 | |

| 0.20 | 0.269 | 0.265 | 0.224 | 0.247 | |

| 0.30 | 0.242 | 0.245 | 0.211 | 0.238 | |

| 0.50 | 0.224 | 0.240 | 0.194 | 0.217 |

Results

The results presented in Table 5 highlight the importance of the -dimension, as it significantly impacts the results. We found that a dimension of 128 was a suitable compromise for all our experiments.

A.2.3 Influence of the number of gradient steps

As can be seen in Table 6, using three gradient steps at inference yield an inference of less than 0.2 seconds. The latter can still be reduced by doing only one step at the cost of an increase in the forecasting error. As observed in Table 6, increasing the number of gradient steps above 3 steps during inference does not improve forecasting performance.

| Gradient descent steps | 1 | 3 | 10 | 50 | 500 | 5000 |

| Inference time (s) | 0.109 0.003 | 0.176 0.009 | 0.427 0.031 | 3.547 0.135 | 17.722 0.536 | 189.487 8.060 |

| MAE | 0.351 0.038 | 0.303 0.041 | 0.300 0.040 | 0.299 0.039 | 0.302 0.038 | 0.308 0.037 |

A.2.4 TimeFlow variants with other meta-learning techniques

Baselines

Before converging to the current architecture and optimization of TimeFlow, we explored different options to condition the INR with the observations. The first one was inspired by the neural process architecture, which uses a set encoder to transform a set of observations into a latent code by applying a pooling layer after a feed forward network. We observed that this encoder in combination with the modulated fourier features network was able to achieve relatively good results on the forecasting task but suffered of underfitting on more complex datasets such as Electricity.

This led us to consider auto-decoding methods instead, i.e. encoder-less architectures for conditioning the weights of the coordinate-based network. We trained TimeFlow with the REPTILE algorithm [Nichol et al., 2018], which is a first-order meta-learning technique that adapts the code in a few steps of gradient descent. In contrast with a second-order method, we observed that REPTILE was less costly to train but struggled to escape sub optimal minima, which led to unstable training and underfitting.

From an implementation point of view, the only difference between second order and first order, is that in the latter the code is detached from the computation graph before taking the outer-loop parameter update. When the code is not detached, it remains a function of the common parameters , which means that the computation graph for the outer-loop also includes the inner-loop updates to the codes. Therefore the outer-loop gradient update involves a gradient through a gradient and requires an additional backward pass through the INR to compute the Hessian. Please refer to Finn et al. [2017] for more technical details.

| TimeFlow | TimeFlow w REPTILE | ||

| 0.05 | 0.324 0.013 | 0.363 0.062 | |

| 0.10 | 0.250 0.010 | 0.343 0.036 | |

| Electricity | 0.20 | 0.225 0.008 | 0.312 0.043 |

| 0.30 | 0.212 0.007 | 0.308 0.035 | |

| 0.50 | 0.194 0.007 | 0.305 0.046 | |

| 0.05 | 0.095 0.015 | 0.125 0.025 | |

| 0.10 | 0.083 0.015 | 0.123 0.032 | |

| Solar | 0.20 | 0.072 0.015 | 0.108 0.021 |

| 0.30 | 0.061 0.012 | 0.105 0.027 | |

| 0.50 | 0.054 0.013 | 0.102 0.021 | |

| 0.05 | 0.283 0.016 | 0.304 0.026 | |

| 0.10 | 0.211 0.012 | 0.264 0.009 | |

| Traffic | 0.20 | 0.168 0.006 | 0.242 0.019 |

| 0.30 | 0.151 0.007 | 0.218 0.020 | |

| 0.50 | 0.139 0.007 | 0.216 0.017 |

Results

In Table 7, we show the performance of first-order TimeFlow on the imputation task. In low sampling regimes the difference with TimeFlow is less perceptive, but its performance plateaus when the number of points increases. This is not surprising. Indeed, as though the task is actually simpler when increases, the optimization is made more difficult with the increased number of observations. We provide the performance of TimeFlow with a set encoder on the Forecasting task in Table 8. We observed that this version failed to generalize well for complex datasets.

| TimeFlow | TimeFlow w set encoder | ||

| 96 | 0.228 0.026 | 0.362 0.032 | |

| 192 | 0.238 0.020 | 0.360 0.028 | |

| Electricity | 336 | 0.270 0.031 | 0.382 0.038 |

| 720 | 0.316 0.055 | 0.431 0.059 | |

| 96 | 0.190 0.013 | 0.251 0.071 | |

| 192 | 0.202 0.020 | 0.239 0.058 | |

| SolarH | 336 | 0.209 0.017 | 0.235 0.040 |

| 720 | 0.218 0.048 | 0.231 0.032 | |

| 96 | 0.217 0.036 | 0.276 0.031 | |

| 192 | 0.212 0.028 | 0.281 0.034 | |

| Traffic | 336 | 0.238 0.034 | 0.297 0.042 |

| 720 | 0.279 0.050 | 0.333 0.048 |

A.2.5 Influence of the modulation

In TimeFlow, we apply shift modulations to the parameters of the INR, i.e. for each layer we only modify the biases of the network with an extra bias term . We generate these bias terms with a linear hypernetwork that maps the code to the modulations. The output of the -th layer of the modulated INR is thus given by , where and are parameters of the hypernetwork. However, another common modulation is the combination of the scale and shift modulation, which leads to the output of the -th layer of the modulated INR being given by , where , and and are parameters of the hypernetwork and is the Hadamard product.

In Table 9, we conduct additional experiments on the Electricity dataset in the forecasting setting with different time horizons. In these experiments, we compare two scenarios: one where the INR is modulated only by a shift factor and the other where the INR is modulated by both a shift and a scale factor. We kept the architecture and hyperparameters consistent with those described in Section A.1. The experiments shown in Table 9 indicate that the INR is longer to train with shift and scale modulations due to the increased number of parameters involved. Furthermore, we observe that the shift and scale modulated INR performed similarly or even worse than the INR with only shift modulation. These two drawbacks, namely an increased computational time and similar or worse performances, motivate modulating the INR only by a shift factor.

| 96 | 192 | 336 | 720 | |||||||||||||

|

|

|

|

|

|

|

|

|||||||||

|

0.233 0.014 | 2h30 | 0.245 0.016 | 2h31 | 0.264 0.020 | 2h33 | 0.303 0.041 | 2h46 | ||||||||

|

0.257 0.019 | 3h29 | 0.263 0.014 | 3h32 | 0.268 0.025 | 3h45 | 0.308 0.037 | 4h14 | ||||||||

A.2.6 Discussion on other hyperparameters

While the dimension of is indeed a crucial hyperparameter, it is important to note that other hyperparameters also play a significant role in the performance of the INR. For example, the number of layers in the FFN directly affects the ability of the model to fit the time series. In our experiments, we have observed that using five or more layers yields good performance, and including additional layers can lead to slight improvements in the generalization settings.

Similarly, the number of frequencies used in the frequency embedding is another important hyperparameter. Using too few frequencies can limit the network’s ability to capture patterns, while using too many frequencies can hinder its ability to generalize accurately.

The choice of learning rate is critical for achieving stable convergence during training. Therefore, in practice, we use a low learning rate combined with a cosine annealing scheduler to ensure stable and effective training.

Appendix B Datasets and normalization

For the complete datasets, Electricity dataset is available here, Traffic dataset here and Solar data set here.

Datasets information

Table 10 provides a concise overview of the main information about the datasets used for forecasting and imputation tasks.

| Dataset name | Number of samples | Number of time steps | Sampling frequency | Location | Years |

| Electricity | 321 | 26 304 | hourly | Portugal | |

| Traffic | 862 | 17 544 | hourly | San Francisco bay | |

| Solar | 137 | 52 560 | 10 minutes | Alabama | |

| SolarH | 137 | 8 760 | hourly | Alabama |

z-normalization

To preprocess each dataset, we apply the widely used z-normalization technique per-sample on the entire series:

Appendix C Imputation experiments

C.1 Models complexity

We can see in Table 11 that our method has fewer parameters than SOTA imputation methods, 10 times less than BRITS and 20 times less than SAITS. It is mainly due to their modelisation of interaction between samples. SAITS, which is based on transformers has the highest number of parameters when mTAN has the lowest number of parameters.

| TimeFlow | DeepTime | NeuralProcess | mTAN | SAITS | BRITS | TIDER | |

| Number of parameters | 602k | 1315k | 248k | 113k | 11 137k | 6 220k | 1 034k |

C.2 Imputation for previously unseen time series

Setting

In this section we analyze in details the imputations results for previously unseen time series described in Section 4.1. Specifically, TimeFlow is trained on a given set of time series within a defined time window and then used for inference on new time series. We train TimeFlow on 50 % of the samples and consider the remaining 50 % as the new time series.

We compare in Table 12 observed grid fit scores and missing grid inference scores for time series known at training and time series unknown at training.

| Known time series | New time series | ||||

| Fit | Inference | Fit | Inference | ||

| Electricity | 0.05 | 0.060 0.010 | 0.402 0.021 | 0.142 0.083 | 0.413 0.026 |

| 0.10 | 0.046 0.006 | 0.302 0.010 | 0.144 0.098 | 0.309 0.016 | |

| 0.20 | 0.067 0.015 | 0.285 0.014 | 0.154 0.089 | 0.291 0.022 | |

| 0.30 | 0.093 0.022 | 0.266 0.010 | 0.163 0.073 | 0.271 0.017 | |

| 0.50 | 0.108 0.012 | 0.236 0.010 | 0.167 0.061 | 0.245 0.017 | |

| Solar | 0.05 | 0.014 0.002 | 0.104 0.015 | 0.050 0.037 | 0.109 0.016 |

| 0.10 | 0.017 0.002 | 0.092 0.015 | 0.052 0.036 | 0.099 0.017 | |

| 0.20 | 0.028 0.008 | 0.078 0.014 | 0.058 0.031 | 0.089 0.017 | |

| 0.30 | 0.038 0.009 | 0.072 0.013 | 0.063 0.028 | 0.084 0.018 | |

| 0.50 | 0.045 0.011 | 0.066 0.013 | 0.067 0.025 | 0.080 0.019 | |

| Traffic | 0.05 | 0.044 0.003 | 0.291 0.013 | 094 0.051 | 0.291 0.012 |

| 0.10 | 0.033 0.001 | 0.209 0.010 | 0.093 0.060 | 0.216 0.012 | |

| 0.20 | 0.037 0.006 | 0.175 0.008 | 0.095 0.058 | 0.186 0.013 | |

| 0.30 | 0.048 0.005 | 0.164 0.006 | 0.098 0.051 | 0.175 0.013 | |

| 0.50 | 0.068 0.004 | 0.159 0.007 | 0.110 0.042 | 0.169 0.012 | |

Results

The results presented in Table 12 indicate that the inference MAE for missing grids shows consistency between known and new samples, regardless of the data or sampling rate. However, it is worth noting that there is a slight drop in performance compared to the results in table Table 1. This decrease is because in Table 12, the shared architecture is trained on only half the samples, affecting its overall performance.

C.3 Details on DeepTime adaptation for imputation

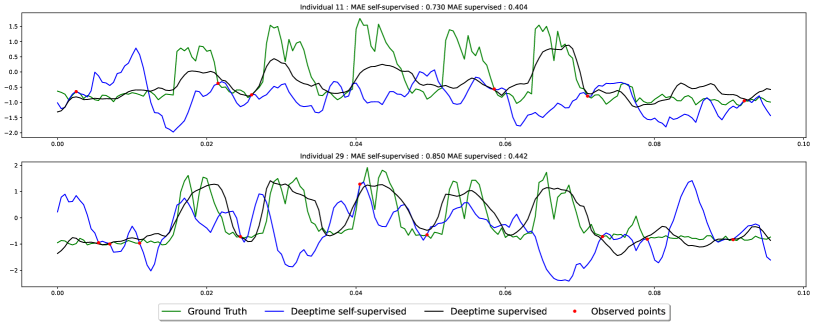

As DeepTime was proposed to address the forecasting task with a deeptime-index model, the authors did not tackle the task of imputation and left it out for future work. Given the success of this method and the motivation of our work, we wanted to explore its capabilities to impute time series with several subsampling rates. Following our current framework, we first tried to train the model in a self-supervised way, i.e. trying to reconstruct observations after the INR has been conditioned with the Ridge Regressor on the same set of observations, but discovered failure cases for . To be faithful to the original supervised training of DeepTime, we therefore randomly mask out 50% of the observations that we use as context for the Ridge Regressor and try to infer the other 50% (the targets) to train the INR.

We provide a qualitative comparison of the model’s performance with these two different training procedures in Figure 6. We can notice that the model that results from the self-supervised training perfectly fits the observations but completely misses the important patterns of the series. On the other hand, when DeepTime is trained to infer target values based on observations, it is able to capture the general trends. We think that in the small subsampling regime (), the Ridge Regressor easily fits very well all the observations which hinders the training of the INR’s basis.

Appendix D Forecasting experiments

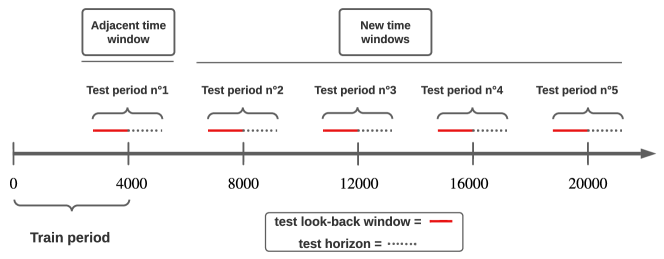

D.1 Distinction between adjacent time windows and new time windows during inference

In Section 4.2, we presented the forecasting results for periods outside the training period. These periods can be classified into two types: adjacent to or disjoint from the training period. Figure 7 illustrates these distinct test periods for the Electricity dataset. The same principle applies to the Traffic and SolarH datasets, with one notable difference: the number of test periods is smaller in these datasets compared to Electricity dataset due to the fewer time steps available.

In Table 2, we presented the results indistinctly for the two types of test periods: adjacent to and disjoint from the training window. Here, we aim to differentiate the results for these two types of window and emphasize their significant impact on Informer and AutoFormer results. Specifically, Table 13 showcases the results for the test periods adjacent to the training window. In contrast, Table 14 displays the results for the test periods disjointed from the training window

Results

TimeFlow, PatchTST, DLinear and DeepTime maintain consistent forecasting results whether tested on the period adjacent to the training period or on a disjoint period. However, AutoFormer and Informer show a significant drop in performance when tested on new disjoint periods.

| Continuous methods | Discrete methods | |||||||

| TimeFlow | DeepTime | Neural Process | Patch-TST | DLinear | AutoFormer | Informer | ||

| Electricity | 96 | 0.218 0.017 | 0.240 0.027 | 0.392 0.045 | 0.214 0.020 | 0.236 0.035 | 0.310 0.031 | 0.293 0.0184 |

| 192 | 0.238 0.012 | 0.251 0.023 | 0.401 0.046 | 0.225 0.017 | 0.248 0.032 | 0.322 0.046 | 0.336 0.032 | |

| 336 | 0.265 0.036 | 0.290 0.034 | 0.434 0.075 | 0.242 0.024 | 0.284 0.043 | 0.330 0.019 | 0.405 0.044 | |

| 720 | 0.318 0.073 | 0.356 0.060 | 0.605 0.149 | 0.291 0.040 | 0.370 0.086 | 0.456 0.052 | 0.489 0.072 | |

| SolarH | 96 | 0.172 0.017 | 0.197 0.002 | 0.221 0.048 | 0.232 0.008 | 0.204 0.002 | 0.261 0.053 | 0.273 0.023 |

| 192 | 0.198 0.010 | 0.202 0.014 | 0.244 0.048 | 0.231 0.027 | 0.211 0.012 | 0.312 0.085 | 0.256 0.026 | |

| 336 | 0.207 0.019 | 0.200 0.012 | 0.241 0.005 | 0.254 0.048 | 0.212 0.019 | 0.341 0.107 | 0.287 0.006 | |

| 720 | 0.215 0.016 | 0.240 0.011 | 0.403 0.147 | 0.271 0.036 | 0.246 0.015 | 0.368 0.006 | 0.341 0.049 | |

| Traffic | 96 | 0.216 0.033 | 0.229 0.032 | 0.283 0.028 | 0.201 0.031 | 0.225 0.034 | 0.299 0.080 | 0.324 0.113 |

| 192 | 0.208 0.021 | 0.220 0.020 | 0.292 0.023 | 0.195 0.024 | 0.215 0.022 | 0.320 0.036 | 0.321 0.052 | |

| 336 | 0.237 0.040 | 0.247 0.033 | 0.305 0.039 | 0.220 0.036 | 0.244 0.035 | 0.450 0.127 | 0.394 0.066 | |

| 720 | 0.266 0.048 | 0.290 0.045 | 0.339 0.037 | 0.268 0.050 | 0.290 0.047 | 0.630 0.043 | 0.441 0.055 | |

| Continuous methods | Discrete methods | |||||||

| TimeFlow | DeepTime | Neural Process | Patch-TST | DLinear | AutoFormer | Informer | ||

| Electricity | 96 | 0.230 0.012 | 0.245 0.026 | 0.392 0.045 | 0.222 0.023 | 0.240 0.025 | 0.606 0.281 | 0.605 0.227 |

| 192 | 0.246 0.025 | 0.252 0.018 | 0.401 0.046 | 0.231 0.020 | 0.257 0.027 | 0.545 0.186 | 0.776 0.257 | |

| 336 | 0.271 0.029 | 0.285 0.034 | 0.434 0.076 | 0.253 0.027 | 0.298 0.051 | 0.571 0.181 | 0.823 0.241 | |

| 720 | 0.316 0.051 | 0.359 0.048 | 0.607 0.15 | 0.299 0.038 | 0.373 0.075 | 0.674 0.245 | 0.811 0.257 | |

| SolarH | 96 | 0.208 0.005 | 0.206 0.026 | 0.221 0.048 | 0.293 0.089 | 0.212 0.019 | 0.228 0.027 | 0.234 0.011 |

| 192 | 0.206 0.012 | 0.207 0.037 | 0.244 0.048 | 0.274 0.060 | 0.223 0.029 | 0.356 0.122 | 0.280 0.033 | |

| 336 | 0.211 0.005 | 0.199 0.035 | 0.240 0.006 | 0.264 0.088 | 0.223 0.032 | 0.327 0.029 | 0.366 0.039 | |

| 720 | 0.222 0.020 | 0.217 0.028 | 0.403 0.147 | 0.262 0.083 | 0.251 0.047 | 0.335 0.075 | 0.333 0.012 | |

| Traffic | 96 | 0.218 0.042 | 0.229 0.032 | 0.283, 0.0275 | 0.204 0.039 | 0.229 0.032 | 0.326 0.049 | 0.388 0.055 |

| 192 | 0.213 0.028 | 0.220 0.023 | 0.292, 0.0236 | 0.198 0.031 | 0.223 0.023 | 0.575 0.254 | 0.381 0.049 | |

| 336 | 0.239 0.035 | 0.244 0.040 | 0.305, 0.0392 | 0.223 0.040 | 0.252 0.042 | 0.598 0.286 | 0.448 0.055 | |

| 720 | 0.280 0.047 | 0.290 0.055 | 0.339, 0.0375 | 0.270 0.059 | 0.304 0.061 | 0.641 0.072 | 0.468 0.064 | |

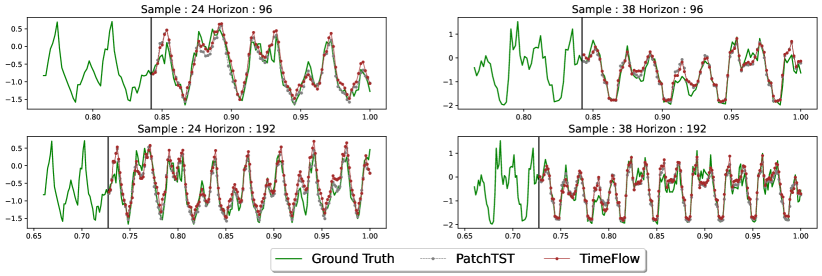

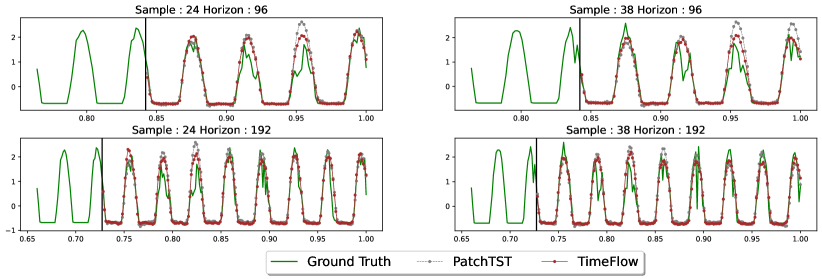

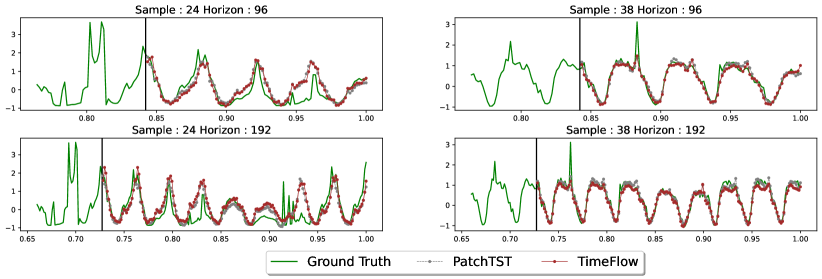

D.2 Plots comparison: TimeFlow vs PatchTST

Table 2 demonstrates the similar forecasting performance of TimeFlow and PatchTST across all horizons. To visually represent their predictions, the figures below showcase the forecasted outcomes of these methods for two samples (24 and 38) and two horizons (96 and 192) on the Electricity, SolarH, and Traffic datasets.

Results

The visual analysis of the figures above reveals that the predictions of TimeFlow and PatchTST are remarkably similar. For instance, when examining sample 24 and horizon 192 of the Traffic dataset, both forecasters exhibit similar error patterns. The only noticeable distinction emerges in the SolarH dataset, where PatchTST tends to overestimate certain peaks.

D.3 Models complexity

In this section, we present the parameter counts and the inference time for the main forecasting baselines. Except for TimeFlow and DeepTime, the number of parameters varies with the number of samples, the look-back window, and the horizon. Thus, we report the number of parameters for two specific configurations, including a fixed dataset, a fixed look-back window, and a fixed horizon. In Table 15, we see that for PatchTST and DLinear, the larger the horizon, the more the number of parameters increases. In Table 16, it is shown that all methods’ computational time increases with the horizon, which is expected. Moreover, TimeFlow is slower than the baselines that use forward computations only. Still, on the Electricity dataset, for example, the method can infer for 321 samples a horizon of 720 values with a look-back window of 512 timestamps in less than 0.2s, which does not look prohibitive for many real-world usages. This is mainly due to the small number of gradient steps at inference.

| TimeFlow | DeepTime | Neural Process | Patch-TST | DLinear | |

| 96 | 602k | 1 315k | 480k | 1 194k | 98k |

| 720 | 602k | 1 315k | 480k | 6 306k | 739k |

| TimeFlow | Patch-TST | DLinear | DeepTime | AutoFormer | Informer | |

| 96 | 0.147 0.007 | 0.016 0.002 | 0.007 0.003 | 0.006 0.002 | 0.027 0.001 | 0.0191 0.002 |

| 720 | 0.176 0.009 | 0.020 0.001 | 0.009 0.001 | 0.010 0.002 | 0.034 0.001 | 0.0251 0.002 |

D.4 Forecasting for previsouly unseen time series

Setting and baseline.

As mentioned in Section 4.2, most forecasters explicitly model the dependencies between samples, which limits their ability to generalize to new time series without retraining the entire model. However, TimeFlow, PatchTST, and DeepTime have the advantage of being reusable for new samples. In Table 17, we present the results of TimeFlow and PatchTST for new periods, considering both known samples and new samples. We train TimeFlow and PatchTST on 50 % of the samples and consider the remaining 50 % as the new time series.

| H | Known time series | New time series | |||

| TimeFlow MAE error | PatchTST MAE error | TimeFlow MAE error | PatchTST MAE error | ||

| Electricity | 96 | 0.228 0.023 | 0.211 0.007 | 0.241 0.023 | 0.224 0.020 |

| 192 | 0.244 0.022 | 0.225 0.014 | 0.254 0.024 | 0.238 0.024 | |

| 336 | 0.269 0.036 | 0.267 0.019 | 0.277 0.033 | 0.285 0.005 | |

| 720 | 0.331 0.058 | 0.310 0.026 | 0.333 0.059 | 0.331 0.045 | |

| Traffic | 96 | 0.226 0.035 | 0.208 0.036 | 0.222 0.031 | 0.203 0.037 |

| 192 | 0.217 0.028 | 0.202 0.029 | 0.215 0.026 | 0.199 0.030 | |

| 336 | 0.242 0.036 | 0.228 0.041 | 0.240 0.031 | 0.224 0.036 | |

| 720 | 0.283 0.053 | 0.275 0.059 | 0.283 0.049 | 0.272 0.055 | |

| SolarH | 96 | 0.237 0.077 | 0.256 0.055 | 0.236 0.081 | 0.256 0.062 |

| 192 | 0.238 0.051 | 0.251 0.239 | 0.239 0.058 | 0.250 0.050 | |

| 336 | 0.220 0.027 | 0.255 0.663 | 0.220 0.034 | 0.255 0.066 | |

| 720 | 0.240 0.039 | 0.267 0.062 | 0.240 0.042 | 0.267 0.063 | |

Results

Table 17 demonstrates the good adaptability of both methods to new samples, as the difference in MAE between known and new samples is marginal.

D.5 Influence of the look-back window for forecasting

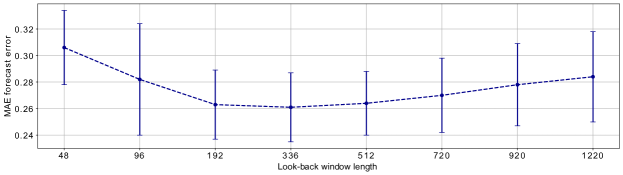

In Figure 11, it is shown that both excessively short and overly long look-back windows can harm TimeFlow forecasting performance. More precisely, the performances increases with the look-back window size up to a certain size, where the performances then drop slowly.

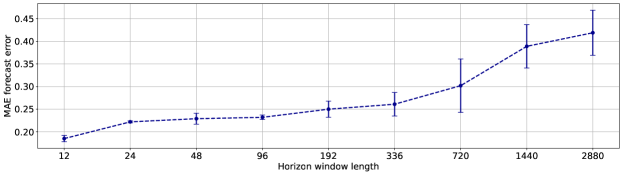

D.6 Influence of the horizon length for forecasting

In Figure 12, it is shown that the performances decrease with the length of the horizon. This is to be expected, since the longer the horizon, the harder the task.