Maximally Machine-Learnable Portfolios

First Draft: December 5, 2022

This Draft: April 24, 2023 )

Abstract

When it comes to stock returns, any form of predictability can bolster risk-adjusted profitability. We develop a collaborative machine learning algorithm that optimizes portfolio weights so that the resulting synthetic security is maximally predictable. Precisely, we introduce MACE, a multivariate extension of Alternating Conditional Expectations that achieves the aforementioned goal by wielding a Random Forest on one side of the equation, and a constrained Ridge Regression on the other. There are two key improvements with respect to Lo and MacKinlay’s original maximally predictable portfolio approach. First, it accommodates for any (nonlinear) forecasting algorithm and predictor set. Second, it handles large portfolios. We conduct exercises at the daily and monthly frequency and report significant increases in predictability and profitability using very little conditioning information. Interestingly, predictability is found in bad as well as good times, and MACE successfully navigates the debacle of 2022.

1 Introduction

A natural trading strategy is to buy (sell) assets whose price one expects to appreciate (depreciate) with higher certainty. That is, out of a basket of securities, it may be preferable to focus active trading efforts on the most predictable assets given one’s information set. It is well known that marginal predictive accuracy improvements can translate into substantial profits without equally substantial risks for investors. But such desirable assets are in very short supply, if they can be identified at all. Consequently, a natural question is whether we can reach to the ideal by constructing more predictable synthetic securities as linear combinations of (mostly) unpredictable existing ones. This paper devises a data mining technique that drills out those – Maximally Machine-Learnable Portfolios (MMLP) – by directly optimizing portfolio weights so to maximize forecasting accuracy, and thereby risk-adjusted returns.

The origins of such ideas lie within loMacKinlay1997’s maximally predictable portfolios (MPP), where a set of weights are chosen so to maximize the of with a tightly specified linear regression based on a few factors. In this convenient sparse (both in returns and predictors) linear framework, obtaining the MPP reduces to solving an eigenvalue problem (akin to canonical correlation analysis) subject to a constraint.111In practice, solving the non-convex fractional programming optimization problem this quickly becomes a daunting task – particularly when considering many assets, factors, and constraints on the portfolio’s composition (GotohFujisawa2014). For this reason, many alternative numerical methods have been proposed to solve more successfully the MPP problem (Yamamotoetal2007; Konnoetal2010; Konnoetal2010b; TakayaetKonno2010; GotohFujisawa2014). Recent applications include harris2022 and BaoetAl2022. Fundamental limitations are apparent. First, the predictive function is of rather limited sophistication. Namely, it is linear, low-dimensional, and most often unregularized. This limits the obtained MPPs to lie within a narrow space of maximally linearly-predictable portfolios. Clearly, additional patterns of predictability are likely to be found when allowing for complex nonlinear relationships while keeping an eye on the characteristically hostile signal-to-noise ratio (SNR) of asset pricing applications. Second, the portfolio side of the equation is similarly unregularized, opening two evenly unpleasant routes. One can either limit the number of assets to be included and severely bound the space of MPP candidates, or run into the well-documented estimation problems of (large) covariance matrices (ledoit2004honey). MMLPs are designed to avoid all of the above by including a powerful nonlinear nonparametric function approximator on the right hand side, and regularization schemes for both the learnable portfolio weights and the corresponding predictive function. Those qualities, flexible nonlinearities and thoughtful regularization, have both been instrumental to the ML renaissance in empirical asset pricing (gu2020empirical; ChenPelgerZhu2021; Nagel2021), and will be so again crossing the bridge from MPP to MMLP.

MACE. We introduce MACE, which stands for Multivariate Alternating Conditional Expectations, and is a multifaceted generalization of BreimanFriedman1985’s ACE algorithm. The latter was originally designed for nonlinearly transforming a univariate regression target to maximize association. As the name suggests, ACE achieves its aim by alternating the estimation of two functions (one for the right-hand side (RHS), and another for the left-hand side (LHS)) taking the other as fixed at each iteration, very much in the spirit of EM algorithms. Adapting ACE to the MMLP problem, MACE modifies it in two key aspects. First, the LHS is multivariate (an extension) and linear (a restriction). Second, it replaces ACE’s rudimentary additive polynomial models by a Ridge Regression (RR) on the portfolio side and a Random Forest (RF) on the prediction side. RR provides a linear and regularized fit for the LHS, avoiding overfitting and non-plausible allocations. RF is a powerful off-the-shelf predictive algorithm that (i) handles high-dimensional data, (ii) can approximate a wide range of unspecified nonlinearities, (iii) requires little tuning, (iv) very rarely overfits. Then comes a panoply of algorithmic details that make the cohabitation of aforementioned elements possible: a learning rate, block out-of-bag sampling, decreasingly random optimization, and bagging strategies rather than predictions. Those are all extensively discussed in the paper.

We also examine the link between MACE and traditional mean-variance portfolio optimization. In short, it minimizes the portfolio variance that is orthogonal to the information set. Given the low level of predictability that is characteristic for this application, the unconditional and conditional solutions are not miles apart in terms of resulting variance. This simple observation provides an explanation for the good variance properties of the algorithm as well as previous observations for MPPs (BaoetAl2022; harris2022). It also explains why, as we will see, that taking the MACE portfolio as fixed and not trading it according to RF also delivers competitive results.

Regarding portfolio construction, the majority of the literature relies on a two-step procedure, prediction coming first and portfolio construction, following various fixed rules, coming next. MACE, in contrast, fits into a more recent stream of studies that optimizes portfolio weights directly – explicitly or implicitly encompassing the prediction step. For instance, CongEtAl2021 do so with a reinforcement learning algorithm targeting Sharpe Ratios fueled with a large database à la gu2020empirical, and FiroozyeEtAll2022 deploy linearity to rewrite their simultaneous mean-variance/prediction problem with vector autoregressive predictions as canonical regression analysis. MACE’s advantages with respect to those alternatives are hereby visible. It is nonlinear and nonparametric, yet remains simple, transparent and rather traditional in its trading decisions, and works with or without terabytes of data. Statistically, it is a kind of semi-parametric canonical correlation analysis (michaeli2016nonparametric) supplied with various desirable features for financial forecasting. Economically, it is a conceptually simple extension of the mean-variance principle.

Statistical Arbitrage at the Daily Frequency. We consider two applications. The first is creating portfolios of the 20, 50, and 100 most capitalized firms on the NASDAQ for trading at the daily frequency. We evaluate those from January 2017 to December 2022, an era for which gains of ML-based statistical arbitrage are expected to be low, if they exist at all (krauss2017deep). The information set is lagged returns of the portfolio itself. Thus, in this setup MACE is looking for maximally nonlinearly mean-reverting portfolios. And indeed it does find some, scoring enviable returns and risk-reward ratios. Nonlinearities prove instrumental to such results as the degree of mean-reversion (when approximated linearly) is shown to be highly state-dependent. Out-of-sample testifies to that, ranging from a moderate 0.5-0.9% in calmer periods, to 12% during the first wave of Covid-19, and a staggering 20% when zooming in on March 2020. MACE is shown to heavily rely on day-to-day oscillations to achieve swift returns in tumultuous months – a behavior learned in part from the financial crisis. Most importantly, it also outperforms benchmarks outside of high volatility episodes, both in bull and bear markets. In particular, all MACEs deliver positive returns in 2022, ranging from 5% to 23%. This and other features lead MACE, sometimes with only 20 highly liquid stocks, to nearly double the market’s Sharpe Ratio.

This application expands on various strands of the statistical arbitrage literature, where many tactics (ranging from heuristics to cointegration tests) have been proposed to identify mean-reverting portfolios or pairs with predictable spreads (see krauss2017 for an extensive survey). Typically, the candidate securities are fixed ex-ante rather than “discovered”, and mean reversion is linear. Nonetheless, when a good discovery is made – like that of MedhatSchmeling2022 exploiting very different time series behaviors for low- vs. high-turnover stocks – gains can be huge. Our approach mines for such discoveries. Hence, more closely related are the works of Aspremont2011, CuturiAspremont2013, and FogarasiLevendovszky2013 who also focus on constructing maximally mean reverting portfolios. Linearity is inherent, and allows for such problems to be reformulated as extensions of canonical correlation analysis with a varying degree of elaboration. An important focus of the literature, as it is the case for MPPs, has been on improving computations and placing reasonable constraints (like sparsity) on the allocation (ZhaoPalomar2016; ZhaoPalomar2018; GriveauCalderhead2021). Nonetheless, linearity remains pervasive, with some directly targeting linear autocorrelation statistics (ZhaoPalomar2016), and others embedding directly linear forecasting models, like Vector Autoregressions, within the optimization framework (GriveauCalderhead2021; FiroozyeEtAll2022). Therefore, MACE, through its use of RF, evidently widens the space of exploitable time series dependence for statistical arbitrage. Additionally, the portfolio side of the equation is not constrained computationally nor statistically from including a myriad of stocks and a long daily sample, a case of interest from a conceptual standpoint (testing market efficiency) and eventually practical in an era of shrinking transaction costs.

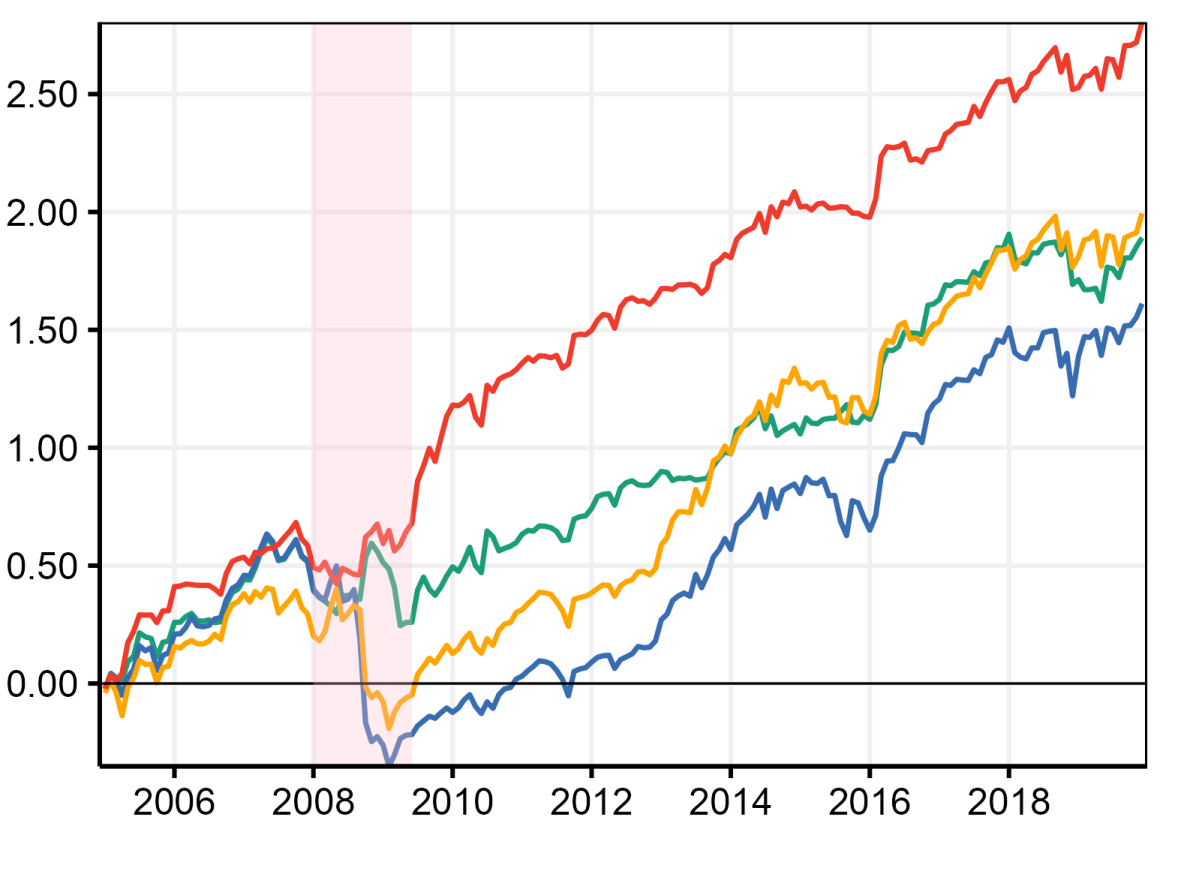

Monthly Trading Based on Macroeconomic Indicators. The second application is at the monthly frequency and utilizes the canonical WelchGoyal2008 data set to construct an MMLP with a subset of large-cap individual stock returns from CRSP. Thus, it uses no firm characteristics and is rather looking for aggregate predictability based on trivially available macroeconomic indicators. All RFs (MACE or not) struggle to deliver positive ’s from the late 1980s up to the mid-2000s. However, MACE hits an of above 4% in the last 15 years of our sample ending in 2019 – an era for which predictability and associated economic gains (ML-based or not) are often reported to have waned (chordia2014have; han2018firm; gu2020empirical; CongEtAl2021). This is achieved in part during the financial crisis and the years thereafter, where MACE limits losses considerably, and catches up with the pre-crisis trend as early as mid-2009. Other non-MACE portfolios using RF as the predictive function also manage to somehow mitigate losses during the meltdown, but then fail to find and leverage predictability when exiting the Great Recession. Moreover, during the slowdown of 2018, only MACE continues with mostly unabated upward-trending returns. We find, using interpretable ML tools, that this success is attributable to MACE uncovering a portfolio with a subtle response to elevated volatility, in the form of a nonlinearly time-varying risk premium.

Our approach thus differs from gu2020empirical and the vast body of (monthly) studies who use a pooled panel approach with nearly 2 million observations of stock returns from roughly 30,000 U.S.-listed companies, with a corresponding feature set of over 100 company characteristics and macro-predictors. This is also the backbone of CongEtAl2021’s reinforcement learning approach. A similar pooled panel with many cross-sectional and time series characteristics is also found for exchange rates in filippou2022out and for cryptocurrencies in FilippouRapachThimsen2021. Given that MACE does not predict each stock separately, and rather focuses on forecasting a single synthetic index with easily available time series, it can be described, at least in relative terms, as a very low-maintenance strategy. Moreover, by construction, it cannot rely on cross-sectional anomalies that have already dissipated, or focus on illiquid, once non-adequately priced stocks. Obviously, MACE is not exempt either from risking an eventual depletion of its sources of predictability. Nonetheless, those concerns are alleviated by the multi-solution nature of the algorithm and the opaque prediction function. Indeed, MACE’s market timing comes from a (mostly) black box prediction function that cannot be easily deduced by other market participants, and most importantly, if a certain linear combination has been overharvested, MACE can dig out others.

2 MACE

The sophistication of MMLPs, particularly the use of nonlinear tree ensembles-based predictions, necessitates the design of a vastly different framework for optimization than what prevailed for MPPs.

2.1 The Algorithm

MACE is, for the most part, a conceptually trivial extension of ACE. Its successful empirical development, however, requires a fair amount of subtle machine learning craftsmanship. BreimanFriedman1985’s ACE applied to a generic -step ahead forecasting problem of a single target reads as

| (1) |

where and are unknown functions, is the prediction error, is the matrix of available predictors at time (which may include lags or various indicators). Thus, the sole deviation from the textbook predictive regression setup is the introduction of . ACE’s goal is to find the optimal transformation of , in the sense that it is maximally predictable by the output of . BreimanFriedman1985 show that and can be obtained from running an iterative algorithm that alternates between obtaining the conditional expectation of given for a fixed and the conditional expectation of given for a fixed . Following the original incarnation, and typically consist of backfitted polynomial functions, which used to be a popular nonparametric ML approach – before being outshadowed by the advent of tree ensembles in the 1990s and the resurrection of neural networks in the mid-2000s. Nonetheless, the polynomial approach still remains the predictive function in recent ACE applications (gopinathan2019stock; rao2022nonstationary).

This paper extends ACE in three ways so that it can uncover a modern brand of maximally predictable portfolios: (i) is replaced by and by , (ii) we impose a series of constraints on so that its output is a portfolio, and (iii) is a high-performing off-the-shelf modern ML tool. All three are vital to the current application, to a varying degree of obviousness. (i) puts the M in MACE by making it a multivariate problem and therefore allowing for ’s input to be, for instance, a panel of stock returns. From this, (1) becomes the general MACE problem

| (2) |

which lies within the broad class of nonparametric canonical correlation problems (michaeli2016nonparametric). This is also contained within the class of models for which makur2015efficient develop theoretical guarantees for generic ACE-type algorithms. Now, (ii) restricts ’s original nonparametric ambitions to that of learning a linear combination of ’s (with positive weights summing to 1) so is a portfolio return series — as opposed to being literally anything, which could nevertheless be of interest in other financial applications. The minimization problem that ensues is

| (3) |

where is hereafter also assumed to be a panel of stock returns . The addition of provides regularization with intensity (an hyperparameter) that will guard against overfitting and non-realistic allocations (carrasco2011optimal). The non-negativity constraint may or may not be activated. For instance, it will be turned off in our daily application. Its activation implies additional shrinkage beyond that of the norm by inducing some sparsity (some weights will be constrained to 0). Lastly, (iii) is what will provide MACE with forecasting power. is chosen to be a Random Forest (RF) for various reasons, some more subtle than others (see section 2.4). Surely, what we want first and foremost, is to be a solid off-the-shelf predictive model handling nonlinearities and high-dimensional data while keeping overfitting in check without extensive hyperparameter tuning (MSoRF). Clearly, RF checks the first two boxes, along with Boosted Trees and (Deep) Neural Networks (ESL). The last requirement is met by RF, but not nearly as much by the other two well-known families of ML algorithms. As will become apparent in section 2.4, due to the iterative nature of the MACE (and, in general, the idea of having a function on each side of the equation), RF’s easily obtainable out-of-bag predictions, that are resilient to overfitting, will be a key ingredient in our routine.

Initialization. Algorithm 1 is divided into two key steps, which are, intuitively, the updating of the right hand and left-hand side parameters, respectively. We initialize as a plausible portfolio. When is activated, such a portfolio is the equally-weighted one (as used in section 4.1). When it is not (as in section 3.1), one can use the solution to the classic (and static) global minimum variance portfolio problem, which is an equally intuitive initialization point, especially given the forthcoming discussion in section 2.2. Regarding , it is set to 0 and for line 4 in iteration . This simply means MACE is initiated at the equally-weighted portfolio (or else) and its corresponding RF conditional mean.

Given the inherent non-convexity of the objective and the plethora of possible solutions, initialization can matter. This is especially true in extremely low SNR environments and when regressors are generated endogenously – like in our daily returns prediction application. Our approach to the multiplicity-of-solutions problem is in the spirit of deep learning rather than classical econometrics. Indeed, a fair amount of ink has been spent on devising efficient algorithms to uncover the global optimum within a very restricted class of MPP problems, in part because the attained both in-sample and out-of-sample was regarded as a metric of market inefficiency. We deviate from the statistical philosophy of going at lengths to obtain “true parameters” and rather look for “useful parameters", that is, any solution that can generate value for wealth management strategists. Of course, the two objectives are surely not mutually exclusive, but they entail a different focus. Thus, in our applications, we do not especially care for being unique nor the truest solution to anything, but rather aim at building a portfolio and a predictive function that generalizes well— that is, it maximizes and . In that spirit, devising mechanisms to maximize remain essential, but they are coupled with equally relevant algorithmic elements to insure such feats can be reproduced out-of-sample. Limiting overfitting in both and is a necessary condition to successfully trade such a portfolio. Thus, in the coming paragraphs, we explain the nuts and bolts of MACE, and how it spreads the ML gospel of the bias and variance trade-off to the MMLP problem.

The Random Forest Step and Block Out-of-Bag Subsampling. In many ways, MACE is a traditional EM algorithm, where we optimize certain parameters while keeping others fixed, reverse roles in the following step, and alternate until some stopping criterion is met. Accordingly, the first step predicts a fixed portfolio using RF. Then, predictions are updated as a convex combination of (current predictions) and the previous iteration’s predictions , where the speed of adjustment is determined by the learning rate .

When constructing , it is imperative that one does not use RF’s fitted values, which are inevitably prone to immense overfitting. Indeed, RF’s fit always delivers close to 1 (for any standard tuning parameters combinations) even though the true is nowhere near that (see MSoRF for an explanation and a barrage of examples with classic datasets). This does not prevent RF from delivering stellar ’s – the traditional object of interest – and it is why the differential has mostly stayed under the radar of the ML community. Whenever RF’s in-sample predictions are required, one shall use the so-called out-of-bag (OOB) predictions, which are, by construction, immune to overfitting in a cross-sectional context – in the sense that their predictive accuracy will be exactly aligned with what one should expect out-of-sample (breiman2001; ESL). In other words, such predictions include the conditional mean, whatever its quality may be, and little to none true error term (MSoRF). This is particularly crucial in MACE given that such predictions are to be fitted by another ML algorithm in a subsequent step. In a manner, this approximates the ideal “cross-fitting” solution where, in our context, the Ridge Regression step would be conducted on one half of the sample, and the RF step on the remaining half. The latter (rather demanding) scheme is the backbone of so-called honest causal forest (athey2019grf) in heterogeneous treatment effect estimation. In fact, it can be shown that OOB sampling and variants provide a convenient approximation when sample sizes are limited or other practical aspects render plain splitting nonoperational (chen2022debiased).

The only thing standing in the way of such properties to be applied to our problem is the time series nature of our data. Indeed, time series dependence in the left-hand side (LHS) or right-hand side (RHS) variables, which creates major complications for classical bootstrap inference, generates similar hurdles for the validity of out-of-bag predictions. While that in is negligible for , it is certainly not so when considering , the average return between and (in effect, a sliding moving average). This is even more prevalent in the case of where predictors, while being stationary, may be quite persistent. This persistence will break the non-overfitting properties of OOB predictions – with an immediate consequence that includes overfitted elements of , and thus failing to approximate the LHS and RHS being trained on “truly” separate data sets. All this is obviously related to how time series dependence biases downward bootstrapped standard errors used in small sample frequentist inference (kreiss2012bootstrap), and the solution to the aforementioned problem – block bootstrapping or subsampling – is backed out from the wide literature on the subject (hyndman2018forecasting). Thus, to obtain a which is plausibly exempt from overfitting, we will use block out-of-bag in-sample predictions. Such techniques have been used to reliably extract more “structural” quantities like various macroeconomic latent states in MRF and HNN.

The Ridge Step. The Ridge step takes RF predictions as given and optimizes so that matches as closely as possible the predictions, in essence, collaborating with so as to maximize association. The Ridge Regression apparatus comes with trivially implementable, yet healthy and necessary sources of regularization (carrasco2011optimal). First, there is penalizing extreme allocations and shrinking to the equally-weighted portfolio – as opposed to 0 in a typical Ridge Regression. This is due to the unconditional variance of the portfolio being fixed to 1 (line 6) for identification purposes during estimation.222Indeed, it is easy to see in (2) why this is necessary : replacing by and by (where is an arbitrary scalar) gives rise to the same likelihood. Naturally, this cannot occur when is the identity function, as in typical regression problems, but is inevitable within ACE and its descendants. Thus, everything being shrunk to the same value is what remains of the original ridge “prior” that every coefficient is shrunk to (the same value of) 0. Given that the resulting portfolio will eventually be rescaled to satisfy the capital budget constraint (), is the value towards which the shrinkage is effectively pointing at.

Another source of regularization in the Ridge step is obviously the long-only constraint . It embeds the prior knowledge that we “unconditionally” expect the market to follow an upward trajectory, and that MACE should preferably focus on portfolios of which it will most often hold a long position. Additionally, for our monthly rebalancing application, limiting the occurrences of overall short positions is desirable from a risk management perspective. This frequently imposed constraint in mean-variance optimization problems also plays here the additional role of limiting the Ridge’s step expressivity by chopping out a wide space of potential ’s. As in anything, good regularization balances bias and variance wisely by imposing constraints that will contort our likelihood the least. Accordingly, the implicit prior motivating for one-month ahead forecasts may not always be as well motivated for much shorter horizons – and indeed, we will relax that restriction in the daily application.

Learning Rate. Among the few more subtle technical extensions to ACE, we use out-of-bag block-subsampled predictions and introduce a learning rate – whose combined action is mostly to curb overfitting and facilitate optimization. Their importance in practice is paramount since we are dealing with a high-dimensional Ridge Regression on one side and a RF on the other, with both having the ability of overfitting the training data, even if the other side of the aisle remains static. Directly inspired from Boosting and Neural Networks, the use of a learning rate curbs this problem and avoids zigzagging optimization paths. There is an obvious trade-off between and , with a lower necessitating a larger . In our experience, anything above 0.2 can quickly lead to unstable computations, learning rates above 0.1 will often lead to overfitted solutions (when the SNR is very low), and the optimization of larger portfolios may get suck with too small of a learning rate (like anything below 0.01). What lies within the 0.01-0.1 range usually provides interchangeable results and the symptoms of an impotent learning rate can easily be diagnosed from looking at the path of the in-sample loss.

2.2 Relationship to Mean-Variance Portfolio Optimization

MACE constructs a portfolio to be actively traded. Nonetheless, as we will see later, the raw MMLP portfolio often has nice properties when combined with much more passive trading (e.g., using a prevailing mean instead of RF). Notably, it has fine variance properties, even though variance is not explicitly minimized. Or is it? Furthermore, its predecessor, maximally predictable portfolios, have been noted to have good variance properties without necessarily aiming for it (BaoetAl2022; harris2022). In the brief discussion below, we show that this is no coincidence.

First, note that, in the absence of any predictability, i.e., in the true DGP, the conditional mean is the unconditional mean (, then (3) becomes

where is the portfolio return -steps ahead. In population, this problem is

which is a regularized mean-variance optimization problem (as in, e.g., carrasco2011optimal) without the minimum return constraint. This constraint, where is a minimal (unconditionally) expected return, bears a different meaning within the MMLP framework simply because the designed portfolio is meant for active trading, not to buy and hold. Nonetheless, as will be discussed in section 3.3, it is possible to bring some of it back in the form of healthy regularization for the MACE allocation by applying an analogous constraint on the mean of the conditional mean. This will in most circumstances, non-trivially improve out-of-sample economic performance.

According to previous observations, what MACE is doing in population, when is a non-trivial function and the “true” is larger than 0, is solving

Thus, minimizing the error term in (3) is equivalent to minimizing the residual variance of the portfolio, that is, the share of variance unexplained by the conditioning information. Given that true are never too far from 0 in predictive financial time series regressions, it is not surprising that MMLPs (or MPPs) have desirable unconditional variance properties. Equivalently, the above can be rewritten as

| (4) |

where the apparition of the term highlights an opportunity. From an economic utility maximization perspective, MACE’s objective function postulates that it is not volatile returns (before active trading) per se that brings disutility, but prediction errors. In a world with small predictive margins, those two distinct objectives are in most contexts approximately equivalent. Nonetheless, this suggests that MACE is eager to handle more unconditional variance in the buy-and-hold return if some of it is predictable – and will be compensated by proactive trading based on informative signals. Hence, from the formulation in (4), there is an imminent tension for in the MACE problem because of its dual mandate, i.e., minimizing and maximizing . Those may push in the same direction, or they may not – depending on what lies in and the shape of . The benefits of all forms of regularization on risk-reward ratios also become obvious from (4). An overconfident MACE allocation will inflate in-sample. If it fails to replicate predictive gains out-of-sample, it is likely left with a portfolio with higher unconditional variance that the global minimum variance solution, but no meaningful predictability to tame it.

2.3 MACE vs. Predicting Single Stocks Returns Separately

When it comes to time series predictions of stock returns, a popular ML approach is to conduct a pooled (nonlinear nonparametric) regression for a panel of stocks and their corresponding characteristics. gu2020empirical is the prime example, and they translate their predictions into returns via a long-short portfolio strategy. Alternatively, one can model each stock return separately with its own time series regression, but this has important limitations. In contrast to the above, MACE forecasts a single series, the portfolio’s return. From the linearity of the portfolio, we have that where is a vector of conditional expectations for each stock. Thus, one can legitimately wonder why not simplifying the algorithm considerably by (i) getting expectations from pooled or individual predictive regressions and then (ii) running the global minimum variance problem on residuals from such regressions. Precisely, solving

after obtaining externally. There are quite a few reasons not to consider such a route, some conceptual and others, practical. All of them are worth mentioning here because they highlight some of MACE’s advantage that may so far have gone unnoticed.

is arguably much harder to learn than typical candidates from aggregate data, simply by the virtue of the latter being a portfolio. Single stock returns contain a lot of variation that cannot be captured by macroeconomic predictors, and with a small fraction of it being explainable by micro-level firm characteristics, often for low-capitalization stocks. What remains is a large amount of noise weakening the potential through an unappealing SNR and increased estimation error. This crucially matters because (i) the extremely low SNR for separate stock returns is a serious impediment to any algorithm attempting to learn and (ii) the chosen individual model will often be one that puts a higher weight on minimizing estimation variance rather than entertaining ambitions to tackle bias2. Thus, it can easily turn out that the selected/cross-validated is the null function (or close to it) whereas the true DGP does, in fact, have an yielding a positive . In other words, choosing and optimizing ML (or any) models to predict separately might be at odds with the final objective of getting a fine estimate of . And because of that, a positive remains unattainable without exceedingly large samples.

One way out is the pooled (or global) regression approach with firm-level characteristics, where ’s potency is revived through much more data and information on cross-sectional variation. Another route is to predict directly what one will end up trading, that is, the portfolio return. By the joint optimization of and , provides a more easily-forecastable target. Hence, the previously undetected becomes an attainable target because collaborates in making win at the bias-variance trade-off. This is convenient since getting a vector worthy of use is not necessarily an easy task, requiring large amounts of micro-level data not always easily accessible in real time, and a fair amount of computing resources. In comparison, MACE finds profitable predictability in a convenient low-maintenance setting.

Given the attention they get, predicting indexes such as the S&P 500 rarely deliver sizable s at short horizons. But there are numerous ways into which stocks can be assembled, and some of those blends may be more promising than others from a predictive viewpoint. Linking it back to the econometric literature on the benefits and costs of aggregation (forecasting aggregates vs. aggregating components’ forecasts), MACE can be seen as finding the optimal aggregation that keeps variance low (by aggregating) and yet keeps bias2 similarly low by creating an aggregate with limited aggregation bias from neglecting heterogeneity (lutkepohl2011forecasting).

2.4 Why Random Forest?

A natural question to ask is: why Random Forest? In principle, RF could be replaced by any ML algorithm. In practice, not quite so, and for many reasons. First, RF is the only algorithm which provides internally out-of-bag predictions. Obviously, nothing prevents a very patient researcher to bootstrap-aggregate Boosting and Neural Networks at every iteration and incur a substantial computational burden. This is especially true of applications with many observations and regressors. Putting things in perspective, to obtain rightful ’s from Boosting and NN, it would take approximately 500 times (a reasonable number of bootstraps) longer than RF, assuming that the three algorithms have a roughly similar computational time (which is quite generous to Boosting and NN in this application). Alternatively, one can ditch any call on to OOB predictions, and extremely carefully tune hyperparameters. Given the impracticability of such an approach (for anything more complicated than Ridge, Lasso, and derivatives) and known results about the virtues of cross-fitting and analogous methods (chernozhukov2018double), it appears that justifying the costs of going for such an alternative route would require glowing expected benefits.

There aren’t. Boosting, which, is often seen as marginally superior to RF in tabular data tasks, often does so by providing mostly small improvements in high SNR environments – a far cry from our financial application. In fact, with RF being less capricious tuning-wise, it has been reported in many low SNR applications to be equally if not more competitive than Boosting (see gu2020empirical and krauss2017deep for returns, and GCLSS2018 and MDTM for macroeconomic forecasting). Additionally, extensive tuning is often required for Boosting to have an edge on RF, which is highly impractical within an iterative procedure.

Deep Neural Networks, which incredible merits in non-tabular data tasks are indisputable (deeplearning), are known to still take the backseat to tree-based methods when it comes to tabular data (grinsztajn2022tree). Moreover, it has been the subject of considerable discussion that basic feature-engineering (like creating lags) combined with tree-based methods may outperform NNs with architectures tailored for time series data (elsayed2021we). Of course, none of this rejects the possibility that letting be constructed from some sophisticated deep recurrent network of any breed (like those in babiak2020deep) could further improve results. Rather, what it suggests is that this paper’s results will not be severely handicapped by leaving the aforementioned extensions for future research.

A last deep learning-based alternative is to consider a neural network with two hemispheres as in HNN – one linear for the LHS and one for the RHS – with a loss function being the squared distance between their respective outputs, reminiscent of developments in andrew2013deep and michaeli2016nonparametric. This ditches the need for alternating anything and can be optimized directly through gradient descent. There are quite a few complications, however. The first, quite subtle in nature, is that modern neural networks, very large and deep, vastly overfit the data in-sample, yet produce stellar out-of-sample performance for many tasks. This phenomenon has many names – double descent and benign overfitting among them – and now has a theoretical literature of its own (belkin2019reconciling; hastie2019surprises; bartlett2020benign). The problem this poses for building a MMLP is that, if the most promising neural network attains a fitting what is almost pure noise, there is neither room nor need in-sample to have the LHS collaborate in increasing the fit. Given that our application has a SNR which is a far cry from 1 and those of other typical successful deep learning applications, it is a severe complication. Nevertheless, using (often unstable) small networks, carefully crafting their design, and considering an extensive hyperparameters search – all this to avoid the slightest bit of overfitting in – could maybe make the derivation of MMLPs from such an approach less ill-fated. In the concluding remarks, we provide additional thoughts and suggestions on how this could perhaps be done in future research.

2.5 Setting Hyperparameters

Given that MACE incorporates two ML algorithms, it inevitably has quite a few hyperparameters (HP), which, for convenience, are summarized in Table 1. Fortunately, RF is well known to be very robust to tuning parameters choices (with default values often very hard to beat, see MSoRF and references therein), and ridge is sparsely hyperparametrized. We opt for setting tuning parameters to fixed values, with their calibration being motivated by domain knowledge and observations of the (block) out-of-bag error metric ().

Given the nature of the MMLP problem – the prediction of a non-fixed target – considering a validation set as is often seen in ML forecasting studies in economics and finance (gu2020empirical; GCLSS2018) is an avenue with strong headwinds and likely limited benefits. This is due to the multiplicity of solutions where identical HPs, when re-estimating the model with more data (e.g., reincorporating the validation data), can lead to different solutions. This is not unique to MACE in the ML realm, as this is a commonly known feature of modern neural networks. Also, there is an imminent tension between maximizing the reliability of the validation set and minimizing the likelihood of moving to a different optimum than what we optimized the hyperparameters for. The former calls for a longer validation set and the latter for a shorter one. In the light of all that, it appears more reasonable to rely on common sense whenever possible, and on the blocked , which is a proper CV metric for time series (bergmeir2018note), whenever data-driven guidance is needed.

| Monthly Data | Daily Data () | Daily Data () | ||||

| 0.1 | 0.01 | 0.05 | ||||

| 100 | 250 | 500 | ||||

| stopping.rule | early stopping | early stopping | ||||

| mtry | ||||||

| minimal.node.size | 20 | 200 | 200 | |||

| block.size | 24 months | 2 months | 2 months | |||

| subsampling.rate | 80% | 80% | 80% | |||

| number.of.trees | 500 | 1500 | 1500 | |||

We first concentrate on those HPs pertaining to MACE’s iterative optimization itself. The learning rate is set at 0.1 for monthly data, which always delivers a stable solution and never gets stuck. For daily data, more care is needed given that is not fixed. The smallest learning rate always appears desirable – as often observed for Boosting (ESL) – but we have noticed that too small of a coupled with large portfolios may lead to the algorithm not optimizing at all in-sample (analogous to exaggeratedly tiny learning rates for deep learning). Thus, it is set to 0.01 for , but 0.01 being not large enough for in-sample loss to start decreasing, we increase it to 0.05.

Closely related are the choice of , the maximal number of iterations, and the stopping method. For monthly frequency, we find that is well enough for MACE to converge and that performance never seems to deteriorate substantially with , even after some plateau is achieved. Thus, the stopping criterion is simply . Things are not so easy with the daily application where regressors are created endogenously. First, we set since is considerably smaller. Since optimization is much more demanding in this environment, it is not impossible for the OOB error to start increasing beyond a certain – i.e., suggesting the LHS is starting to overfit. Hence, we set , which can be seen as some form of internal early stopping, a key player in the regularization arsenal of modern deep neural networks (deeplearning). Early stopping is typically implemented using a validation set, but here, for aforementioned reasons, it is more preferable to use RF’s internal error metric.

The next four hyperparameters in Table 1 are those of RF. For monthly data, mtry is set to the default value of , one that is typically hard to beat, except in extremely low SNR environments (ESL; olson2018making). At the daily frequency, we noticed that could never deliver for any . Given that the daily application has a much lower SNR and a sparser (hence, less potential for diversification in RF (MSoRF)), it is not entirely surprising that might be too large and lead to early overfitting. Thus, we set which kills two birds with one stone by decreasing computing time sharply.

In a similar spirit, minimal.node.size is set to a very high value of 200 in the daily application (nonetheless of the training sample size), which greatly helps in easing the daily application’s computational burden all the while helping improving performance as measured by the OOB. Default values for minimal.node.size usually go up to 10. However, when faced with a low SNR, deep trees are either redundant or harmful, because additional splits allowed by vs. are typically fitting the noise and cancel out through bagging in the out-of-sample projection (MSoRF). Limiting the expressivity of RF is not without precedent for predicting returns, as gu2020empirical report using trees of very limited depth. For the monthly frequency application, we set it to , a moderately high value that eases computations without any apparent effect on (vs. default values).

The next two tuning parameters of RF are subsampling.rate and block.size. We set for all applications, which is standard. block.size, on the other hand, needs to be chosen slightly more carefully to balance two goals. As already hinted at above, too low of a block size will lead to including fitted noise, to be subsequently fed into the Ridge Regression. An overkill block size will seriously handicap bagging by limiting the number of different block combinations used to construct the trees in the ensemble, ultimately weakening RF (on the variance side) by decreasing the diversity of trees. Thus, we set block.size to be a window size within which any form of meaningful dependence between the first and the last observations will have faded away, for both and . For the monthly application, we set it to two years, which very well cover the dependence in and the stationarized WelchGoyal2008 predictors in . In the daily application, since and are daily returns with minimal time series dependence, two business months appears more than sufficient to maintain the interchangeability of the blocks, and leaving plenty of room for bagging to fulfill its task.

A last hyperparameter for RF is the number of trees. It is not a tuning parameter per se because there is no statistical trade-off for its choice: the larger the better, with the only constraint being computational burden (ESL). Given that RF predictions usually stabilize (by the law of large numbers for an average) well before 500 trees, 500 is usual the default setting for number.of.trees in many RF implementations and is what is used for the monthly application. Yet, there is a subtle twist, that leads us to increase number.of.trees up to 1500 for the daily application. We are generating regressors endogenously – in essence using lags of a continuously updated target –rather than taking to be fixed observed predictors. In doing so, we may incur attenuation bias in RF attributable to the generated regressor problem. More precisely, “measurement error” can impair RF’s ability to detect nonlinear time-series dependence because, being out-of-bag predictions, there are an average of trees, which falls to 100 with . Bumping number.of.trees to 1500 makes it an average of 300 single tree predictions for , which is enough to curb measurement error problems without exploding computational costs.

Finally, we must set a value for in the Ridge Regression step. While it could be tempting to cross-validate internally at each step, the optimally chosen at each may be well off from that of the final , and lead optimization in a poor direction. For instance, in early steps, cross-validation can easily choose a that shrinks the portfolio excessively, because, at that early stage , there is, indeed, very little or no predictability being detected. Moreover, on top of withstanding the additional computational demand, changing may lead to certain steps not improving the loss, thereby impairing the EM-style algorithm’s ability to minimize the overall loss. Therefore, for the monthly application, we set such that it attains an in-sample of 0.05, which is a high yet not unreachable mark. In the daily application, facing the inevitability that is unlikely to stand above 1%, is chosen at each step so to target .

3 Application I: Daily Stock Returns Prediction

We begin our exploration of MACE by constructing maximally ML-predictable portfolios at the daily frequency. The high frequency brings both opportunities and difficulties. Among the former is the availability of more data points, and a lessened need to rely on data going way back to the late 1950s, as is typically the case in monthly exercises. In terms of the latter, an even more hostile signal-to-noise ratio comes to mind, as well as the scarcity of freely available predictors at such frequency.

Here, comprises individual stock returns for firms listed on the NASDAQ. We keep of them with highest market capitalization on January 3 2017, which is the date of the beginning of our test sample. Hence, there is no look ahead bias for the test sample and the stocks are as liquid as it gets. For computational reasons, we do not re-estimate models and consider a fixed train-test split of the data, as done in, e.g., ChenPelgerZhu2021 and fallahgoul2020asset. The training set is thus 2000/03/02–2016/30/12 and the test set 2017/03/01–2022/07/12. Thus, the test set includes a fair level of variety in terms of “financial regimes”. In chronological order, we have: a relatively quiet period, a crisis period with extremely high volatility, an unprecedentedly bullish bull market, and a long-lasting bear market.

As mentioned above, gathering many exogenous predictors available in real-time for is not easy and often not cost-free. In this application, we will see whether MACE can generate predictability with nothing more than time-series properties of the portfolio. Creating portfolios or stock combinations that have exploitable persistence properties (for mean reversion- or momentum-based trading strategies) has been studied, for instance, in Aspremont2011. Nonetheless, the near universe of following studies, by the limitations of relying on variants of canonical correlation analysis, are bounded to consider only linear autoregressive properties. Needless to say, if there is any remaining form of mean reversion that has not been drilled out yet, it will need to be complex in or – or both. Thus, being a RF able to estimate any form of nonlinear nonparametric dependence may help in finding mean reversion patterns that remained undetected to the naked eye or simpler algorithms.

Beyond its coverage of heterogeneous financial conditions, the test set is interesting in its own right simply by the virtue of being recent. krauss2017deep finds substantial gains from a simple daily long-short strategy using signals from predicting single stocks separately via tree-based techniques (among others) with lag returns as predictors (as we use). However, and now a recurring theme, the improvements are circumspect to the pre-2010 era, which, as the authors note, is likely due to the widespread dissemination in the 2010s of the very techniques they use. Thus, an interesting question is whether MACE (and other less obvious uses of ML) will find exploitable nonlinear mean reversion in a period where simpler methods could not. In a similar spirit, localized episodes of predictability, reasonably frequent before 2000, are found to be a much rarer event afterwards (FarmerEtAl2022). A related question is whether MACE, through ML-based nonlinearities in , can capture and exploit those in real time rather than only observing them ex-post.

It is natural to wonder whether MACE-based predictability will outlive its test set, that is, after the profitable pattern is openly communicated to other market participants. MACE’s design partly protects against early depletion by (i) forecasting a synthetic security (rather than highly scrutinized stocks or portfolios) and (ii), doing so with a mostly opaque model. Additionally, as discussed in section 2, MACE can generate plenty of solutions, with most of them achieving the predictability goal in different ways. Hence, in principle, there should be no shortage of possibilities for enlarging the set of nonlinearly mean-reverting synthetic securities, especially keeping in mind that our application deliberately focuses on creating them from a narrow set of well-known stocks.

Nonlinear Mean Reversion Machine. In what follows, we describe the remaining building blocks necessary to go from plain MACE to a version specialized for daily data. Throwing many lags of many stocks at the daily frequency directly in will be at the nexus of computational and statistical inefficiency. A more manageable and promising route is the parsimonious problem

| (5) |

where features – lags of the portfolio returns – are created endogenously given the portfolio weights.333Note that for a linear , this optimization problem could be solved by nonlinear least squares or some sort of generalized eigenvalue problem as studied in Aspremont2011 and others. There are two substantial modifications to Algorithm 1. The first is that we drop the constraint. Keeping such a constraint in place – as in the monthly application of section 4.1 – would push MACE to find portfolios for which it will most often go long with, and avoid relying extensively on short-selling to turn a profit. Such a restriction comes with the prior that, at the lowest frequencies, the market is always expected to go upward and that a successful strategy should not immensely deviate from this evident fact about the unconditional mean. At the daily frequency, however, the importance of the low-frequency component justifying a long position for the long-run is much tinier– and we want the configuration of the daily MACE to absorb this knowledge. More importantly, appears unnecessary given that the portfolio will be bought or sold plausibly every day, and single-stock short positions will be short-lived by construction. The relaxation of this constraint now allows MACE to simultaneously hold short and long positions over single assets, even though we may go long or short with the overall portfolio.

The second modification is, obviously, the inclusion of an additional step before the RF step that creates lags of the portfolio as it is constituted at iteration . Given the SNR faced in this application, cleverly designed regularization is key. For that sake, we apply the MARX (Moving Average Rotation of ) transformation of such lags (MDTM) and stack those in . As argued in MDTM, the transformation implies more approximate implicit regularization at high frequencies than raw lags themselves. Precisely, in a linear model with an or norm on coefficients, this switches the model from shrinking each coefficient towards zero to being shrunk to one another successively. For more complex ML methods where the implicit regularization (almost always entailing the prior that each feature should contribute, but marginally) cannot easily be altered by changing the penalty (like RF or Neural Networks), MARX is a trivial additional step that can help bolster predictability by embedding a more appropriate prior in the model. Its implementation is simply a one-sided moving average of the lagged portfolio return (of increasing length, up to a month) instead of raw lags — which, in the current application, is analogous to a basket of momentum indicators. 444Note that in a linear model with no regularization, by the virtue of MARX being a rotation of , it does not alter the span of predictors and yield identical fitted values. However, this is not true of regularized and/or nonparametric methods, which is our prediction tool in this paper.

We benchmark MACE for each against a set of relevant and informative competitors: equal weights and the minimum variance portfolio. The latter correspond to the initialization values of MACE. We also include the S&P 500. Those are all predicted with a prevailing mean and RF. Going forward we denote the prevailing mean models as EW (PM), MinVar (PM), S&P 500 (PM) and the RF models EW (RF), MinVar (RF), and S&P 500 (RF) respectively. RF models are also procured with MARX-transformed features. Finally, we complement those with MACE (PM), which is a portfolio constructed with Algorithm 1 but where RF predictions are substituted out-of-sample by MACE’s portfolio prevailing mean. This serves the purpose of evaluating MACE’s raw portfolio return (since, in effect, it comes from a well-defined mean-variance problem as per section 2.2’s discussion) and quantifying how much of MACE’s success comes form leveraging predictability.

Trading. Relative weights are fixed, but absolute weights (i.e., the overall position on the synthetic asset or portfolio) are changing in every period. To transform predictions into trading positions for economic evaluation metrics, we solve the prototypical mean-variance problem for a single return

| (6) |

as is laid out in FilippouRapachThimsen2021 and many others. The risk aversion parameter is set to 5 and is constrained to lie between -1 for 2 for reasonable allocations.

Evaluation Metrics. The evaluation metrics are the out-of-sample , average annualized return (), and the annualized Sharpe Ratio () – where returns are collected from the trading exercise as described in Equation (6). Following campbell2008predicting and the ensuing literature, the out-of-sample of model for forecasting portfolio return is defined as where PM stands for the prevailing mean and . PM is specified to be the historical mean of the training sample. Given the inherent unpredictability of financial markets, this not-so naive benchmark is in fact one that is notoriously difficult to beat.

To bring further enlightenment, we also report for key subsamples in Table 2. Namely, we report , which is the for the onset of the first wave of Covid-19, defined as February, March, and April 2020. Those 3 months were characterized by a level of volatility unseen since the financial crisis, and consists of the only recession in our test set. It is well documented that predictability is more likely to be found during bad economic times (see LiZakamulin2020 and the many references therein). Thus, we wish to investigate whether (i) MACE follows that rule and (ii) if it can find predictability outside of the recessionary episode. Accordingly, is the excluding those three months. In a similar spirit to , we include (the from the first business day of 2022 until the end of our sample in December 2022) and , which is the corresponding annualized return for the same era. This allows to shed light on (i) whether there was any meaningful predictability to be found in the long-lasting bear market of 2022 and (ii) whether active daily trading with MACE or other RF-based strategies can avoid the sharp losses of the US stock market in 2022.

We complement this extended set of metrics with keating2002universal’s Omega Ratio (), an increasingly popular measure of the risk-reward ratio that leverages all the moments of the distribution of returns (whereas only exploits the first two). This measure is particularly useful in situations where the distribution of returns is skewed, as only negative deviations from a certain threshold – e.g. the mean return of a benchmark, or an investor’s desired average return – contribute to the risk component. First, we do find positive skewness in MACE-based returns. Second, and in a more striking fashion, RF-based returns, when predictability is non-negligible, are found to be much more leptokurtic (i.e., Laplacian-looking) than those of other strategies, even when excluding CovidW1. This is not unheard of for ML-based strategies (ChenEtAl2021). Thus, to compare apples with apples without the inherent assumption of normality in and to avoid penalizing similarly both large positive and negative returns, we include in Table 2 as a supplementary risk-reward ratio.555The expected benchmark model return in used as a cutoff is the mean return of the S&P 500 in the training set (balder2017risk). Doubling it does not alter rankings.

3.1 Results

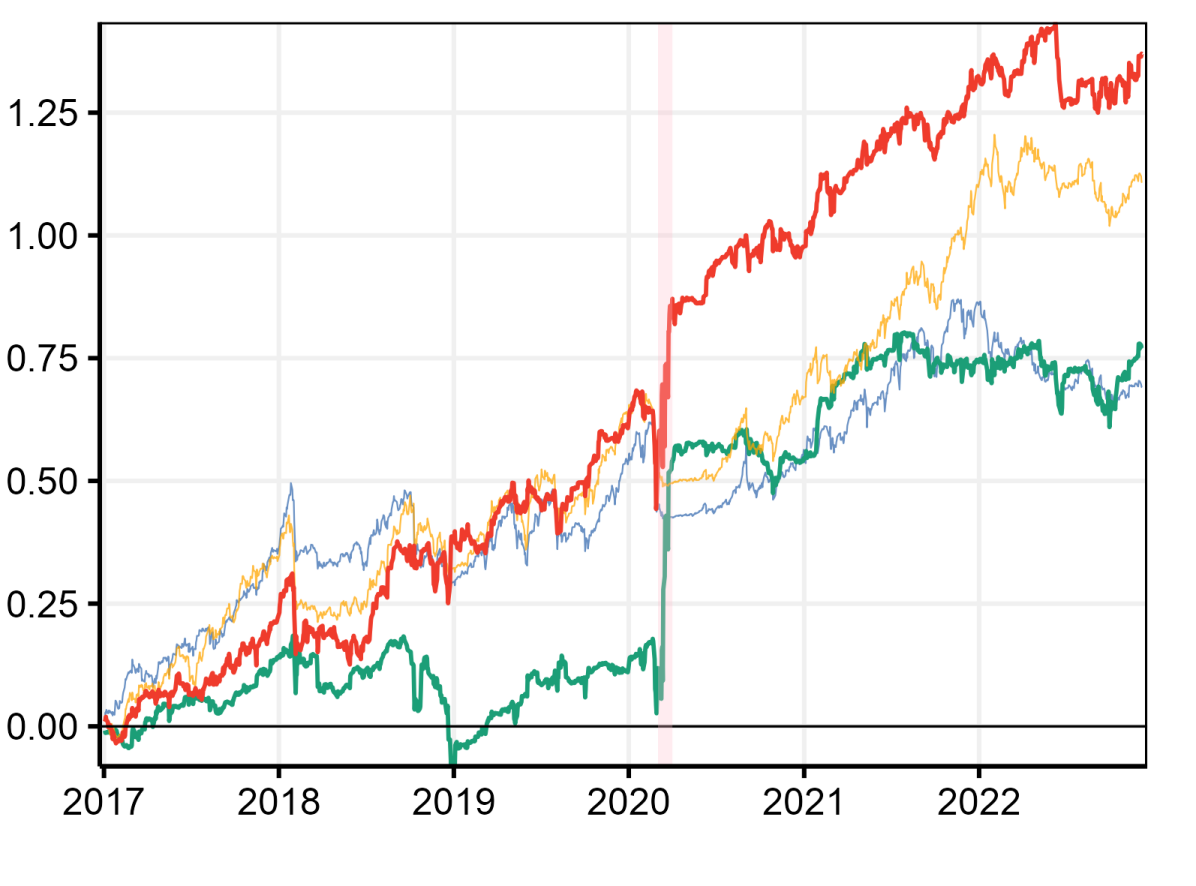

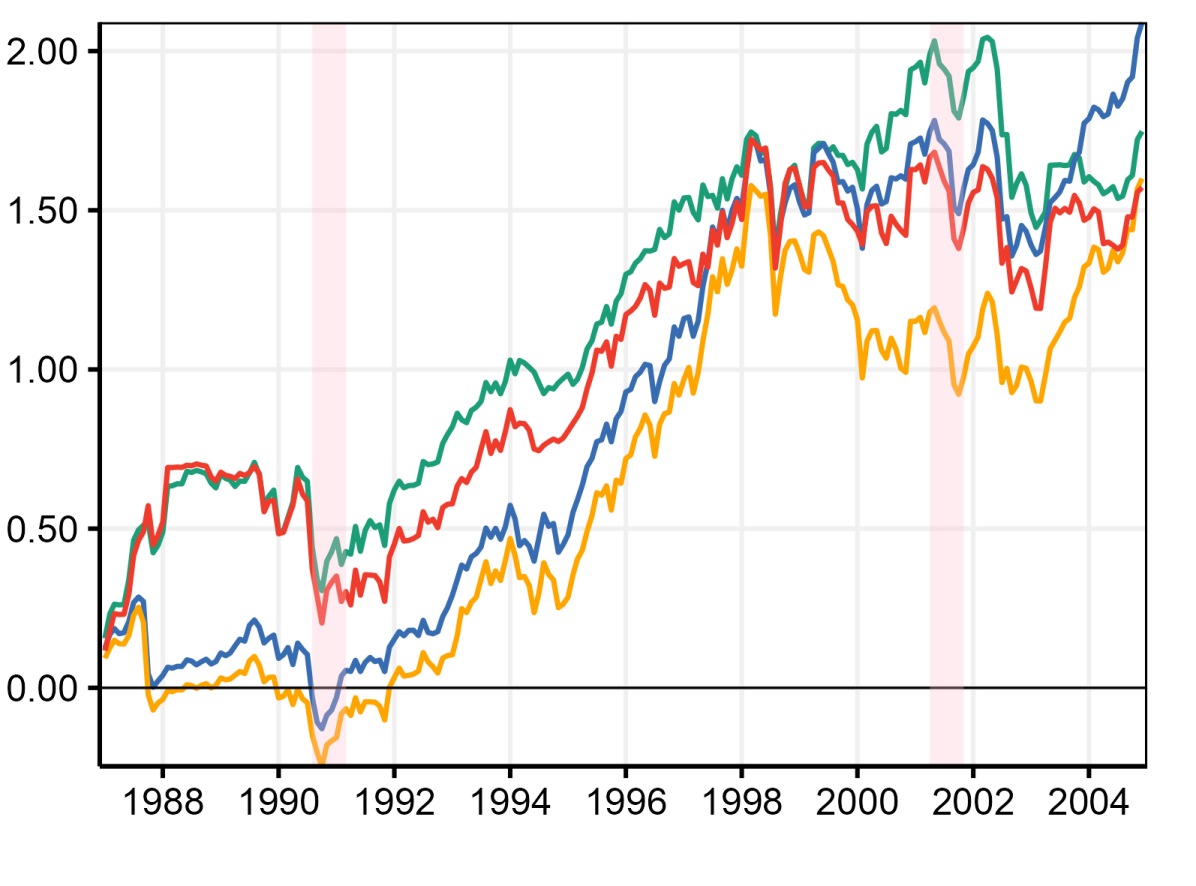

We report relevant summary statistics for our daily exercise in Table 2. Log cumulative return plots for the small () and large () portfolios are shown in Figure 1 and Comparison of MACE to Random Alternatives plots are available in Figure ‣ 3.1. To alleviate notation, MACE (, PM) will be written as MACE100 (PM) and other accordingly. Additionally, MACE using RF for prediction is simply denoted MACE.

| \rowcolorgray!15 | \cellcolorgray!15 | ||||||||||||||||

| MACE | 3.42 | 7.86 | 0.56 | -0.55 | 23.10 | 0.99 | 5.03 | 1.18 | |||||||||

| MACE (PM) | 0.01 | -0.05 | 0.04 | -0.12 | 18.71 | 1.04 | 0.75 | 1.13 | |||||||||

| EW (RF) | -4.71 | -9.39 | -1.21 | 0.33 | 9.15 | 0.34 | 36.43 | 1.02 | |||||||||

| EW (PM) | -0.04 | -0.06 | -0.03 | -0.10 | 14.28 | 0.78 | -10.23 | 1.08 | |||||||||

| MinVar (RF) | -1.57 | -2.69 | -0.80 | -0.61 | 7.55 | 0.42 | 2.94 | 1.01 | |||||||||

| MinVar (PM) | -0.01 | -0.04 | 0.02 | -0.13 | 18.13 | 1.00 | -3.32 | 1.12 | |||||||||

| \rowcolorgray!15 | \cellcolorgray!15 | ||||||||||||||||

| MACE | 0.89 | 3.88 | -1.07 | -0.14 | 20.42 | 0.91 | 18.41 | 1.14 | |||||||||

| MACE (PM) | -0.04 | -0.04 | -0.04 | -0.03 | 14.52 | 0.78 | 4.66 | 1.08 | |||||||||

| EW (RF) | -1.01 | -0.95 | -1.06 | -0.87 | 9.82 | 0.37 | 4.55 | 1.03 | |||||||||

| EW (PM) | -0.05 | -0.05 | -0.05 | -0.06 | 13.23 | 0.73 | -8.30 | 1.07 | |||||||||

| MinVar (RF) | 0.75 | 1.94 | -0.01 | -0.25 | 17.32 | 0.96 | 3.48 | 1.11 | |||||||||

| MinVar (PM) | -0.04 | -0.04 | -0.03 | -0.02 | 14.39 | 0.83 | 7.19 | 1.08 | |||||||||

| \rowcolorgray!15 | \cellcolorgray!15 | ||||||||||||||||

| MACE | 4.05 | 12.20 | 0.86 | 0.23 | 41.36 | 1.59 | 23.93 | 1.33 | |||||||||

| MACE (PM) | -0.02 | 0.01 | -0.03 | -0.22 | 15.20 | 0.91 | -16.81 | 1.09 | |||||||||

| EW (RF) | 0.00 | 1.17 | -0.99 | -0.94 | 9.88 | 0.38 | -10.48 | 1.03 | |||||||||

| EW (PM) | -0.05 | -0.04 | -0.06 | -0.03 | 12.62 | 0.69 | -10.26 | 1.06 | |||||||||

| MinVar (RF) | 0.96 | 2.06 | 0.25 | -0.16 | 18.87 | 0.99 | -7.01 | 1.12 | |||||||||

| MinVar (PM) | -0.02 | -0.05 | 0.00 | 0.06 | 10.18 | 0.58 | -6.39 | 1.04 | |||||||||

| S&P 500 (RF) | 2.88 | 7.41 | -0.14 | 0.09 | 13.29 | 0.64 | 2.80 | 1.09 | |||||||||

| S&P 500 (PM) | -0.01 | -0.06 | 0.03 | -0.32 | 11.65 | 0.69 | -17.98 | 1.06 |

-

Notes: The first column-wise panel consists of out-of-sample ’s for different test (sub-)samples. The second are economic metrics, where := Annualized Returns, := Sharpe Ratio, := Annualized Returns for 2022, := Omega Ratio. All statistics but and are in percentage points. Returns and risk-reward ratios are based on trading each portfolio using a simple mean-variance scheme with risk aversion parameter . PM means the prediction is based on the respective prevailing mean with a lookback period of ten years, while RF means using that of a Random Forest. The 4 row-wise panels are for portfolios of stocks and the S&P 500 index. Numbers in bold are the best statistic within portfolios of the same size. Numbers in green are the best statistic of the whole column (that is, across all portfolio sizes and including S&P 500).

Statistical Results. For all three MACE specifications, we find strong evidence of predictability through time-series dependence at the daily frequency. Out-of-sample ’s are abnormally high and distance most of the competitors for all subsamples but 2022. In the latter case, only MACE100 achieves a positive that narrowly beats that of S&P 500 (RF). The bulk of predictability is indeed found during the first wave of the Covid-19 pandemic, with local for the three MACEs ranging from 3.88% to a stunning 12.20%. While MACE hits the two highest marks for the era, unusually high ’s (taking FarmerEtAl2022’s local predictability results as a reasonable yardstick) are not its exclusivity. S&P 500 (RF) also delivers a large during the era (7.4%), and EW100 (RF) and MinVar100 (RF) are getting 1.17% and 2.06%, respectively.

What is more exclusive, however, is predictability outside of the turbulent spring of 2020. MACE20 and MACE100 achieve it both with 0.56% and 0.86%, which are sizable at the daily frequency, especially in good times (LiZakamulin2020; FarmerEtAl2022). All other RF-based models fail to deliver , all situated in the vicinity of -1% , except for MinVar100 (RF) at 0.25%, the closest competitor to MACE on this metric. Obviously, negative ’s at such a frequency and with so little conditioning information are what one would expect. 666In a recent evaluation from an out-of-sample period overlapping with ours, haase2022predictability get nearly all negative for 20 models using vast conditioning information for prediction at the weekly frequency. Nonetheless, two MACEs out of three outperform this predicament. And it holds up in 2022. We see that MACE100 has a marginal outperformance during the bear market at 0.23%. For other models, negative are again the norm rather than the exception, with notable deviations by S&P 500 (RF) at 0.09% and EW20 (RF) at 0.33%. However, in the latter case, it delivers the worst of any model for the other three subsamples. In fact, MACE100 is the only model with four positive out of four.

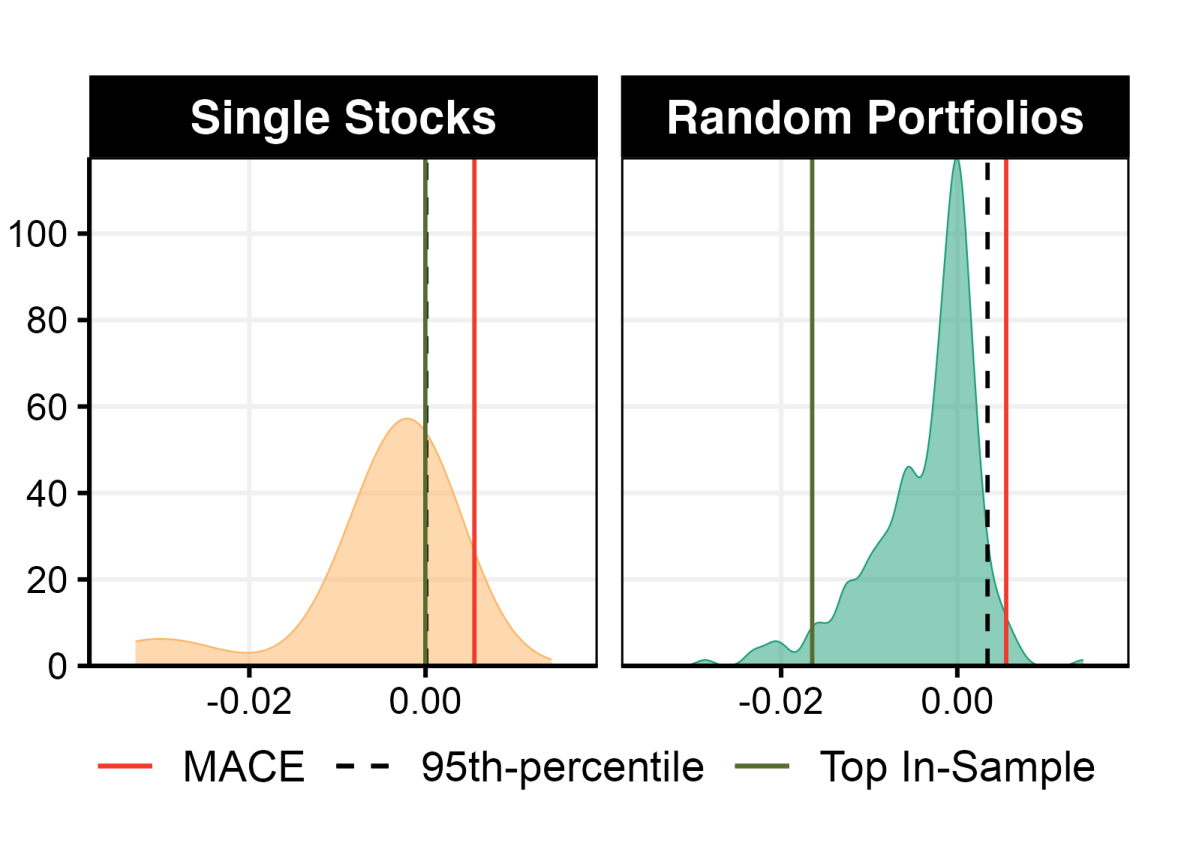

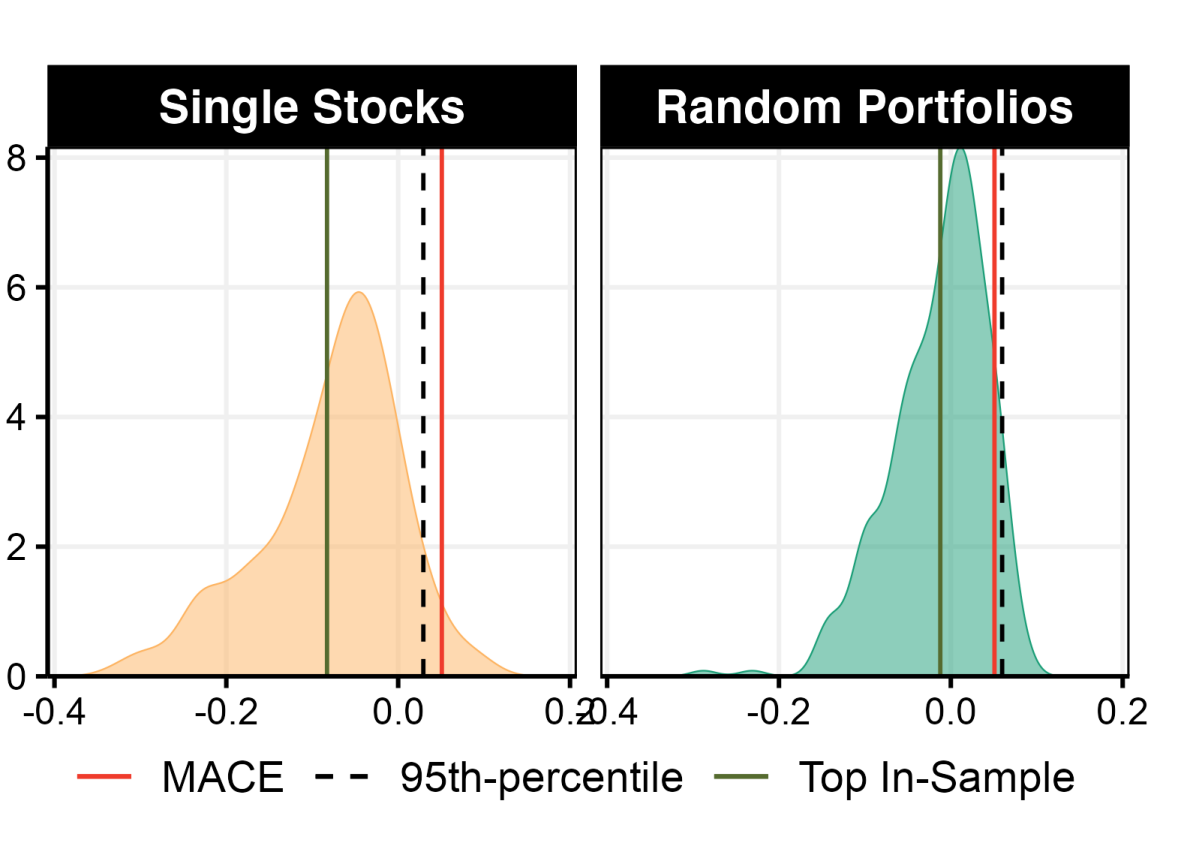

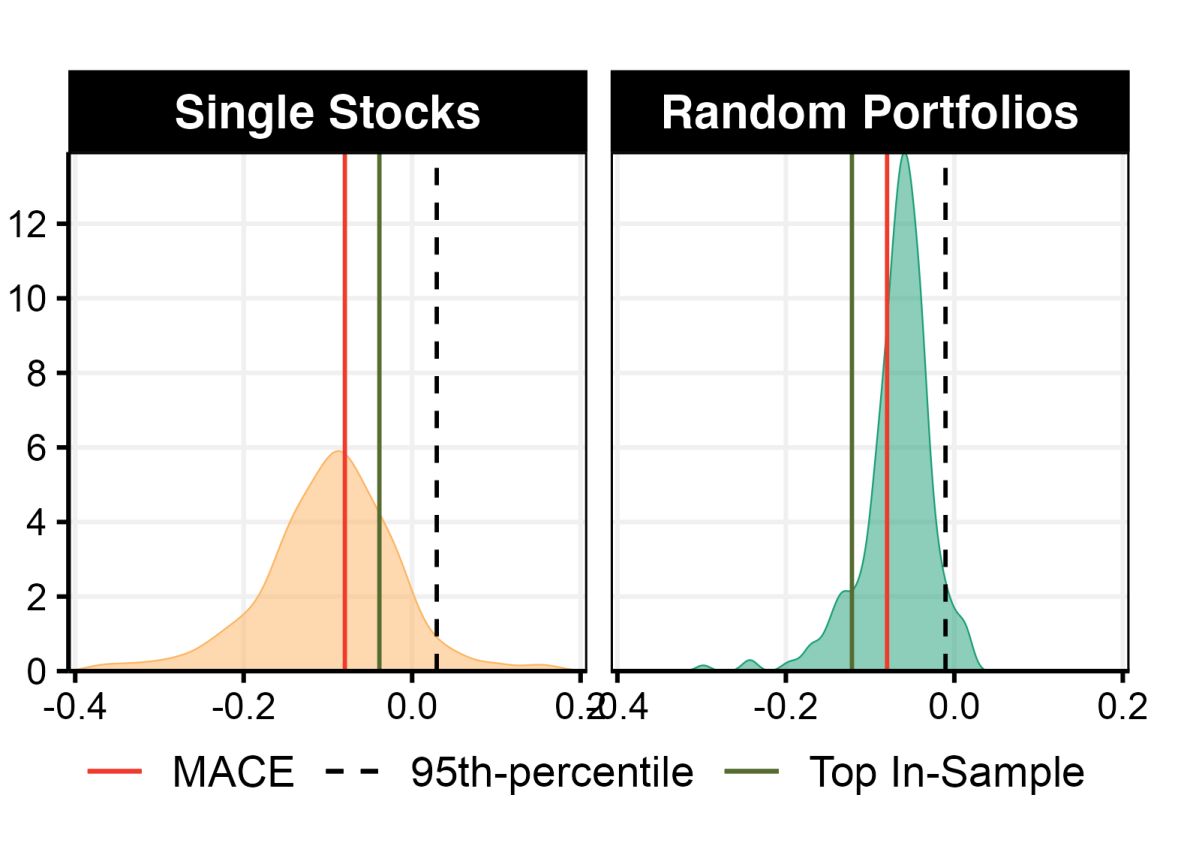

It is interesting to get a sense where MACE’s out-of-sample ’s stand with respect to random alternatives, like single stocks (in effect corner solutions of the MACE) and random portfolios. Especially, in the latter case, it can be seen as an implicit out-of-sample statistical test for the procedure itself. It aims at answering: if we were to draw random stock combinations and predicting them with RF rather than running MACE, how many of those would fare better out-of-sample? The location and shape of the distribution will also be informative about how much room MACE had to find a MLPP. We draw 150 such random portfolios with imposed, and 150 without.

Figure ‣ 3.1 reports such results for and (forming two complementary samples). First, we observe how the prospects of predictability change from CovidW1 to , with the random portfolios distributions showing negative means and clear negative skewness without CovidW1 data for both and . ’s for random portfolios see a sharp decrease in negative skewness for both portfolio size. In fact, for , skewness visibly becomes mildly positive. Additionally, we can see a shift in location, with random portfolios’ mean being approximately 0 and that of being mildly positive. A similar pattern is observed for single stocks, but is inevitably rougher given and single stocks having higher variance than linear combinations of them.

-

Notes: This plot shows distributions of OOS-’s, for different portfolio sizes and subsamples. The "Single Stocks" panel reports the distribution of the ’s obtained from predicting each stock in the panel separately with RF. The "Random Portfolios" panel shows the distribution of 300 obtained from predicting randomly drawn portfolios with RF. Top In-Sample denotes the OOS- of the single stock, random portfolio respectively, that achieved the highest during training. 95-percentile denotes marks the 95 percentile of the corresponding distribution shown in the graphs.

Those distributions, in themselves, highlight some things we already know, like the immense difficulty of finding predictability outside of “bad” economic times: almost 95% of random portfolios have a , yet ’s greater than 0 constitute approximately 50% of the . Obviously, MACE’s objective is not only to beat those odds by systematically landing on the “good” side of the distribution, but also to strive for the rightmost part of it. And it is what we see in all four cases of Figure ‣ 3.1. Indeed, the red line is to the right of the dashed line, meaning we can reject the null (at 5% confidence level, against a one-sided alternative) that MACE is randomly drawn portfolio. Also, the red line is always to the right of the best in-sample single stock or random combination.

Economic Results. From Table 2, we see that MACE generates the highest return for all portfolio class sizes, with MACE100 leading the march with a massive 41.36% annualized return over 2016-2022. MACE20 and MACE50 deliver more “reasonable” returns of 23.1% and 20.42%, which are nonetheless meaningfully higher than alternatives. Closest contenders include MACE (PM) itself and sometimes MinVar (PM or RF, depending on ). Hence, only MACE appears to consistently deliver the highest return. Obviously, that could all be at the expense of significantly more risk.

Indeed, we see that the variance of MACE’s returns often appears to be higher than that of alternatives since its is narrowly behind that of alternatives for (0.99 vs. 1.04) and (0.91 vs 0.96). Note, however, that MACE is consistently among top contenders whereas, e.g. , MinVar (RF), delivers the leading 0.96 for and the second-to-last 0.42 for . For , MACE gets a dominating annualized of 1.59, suggesting most of the 41.36% return it gets is not due to unshackled variance. The closest alternative among all ’s is for MACE (PM, ).

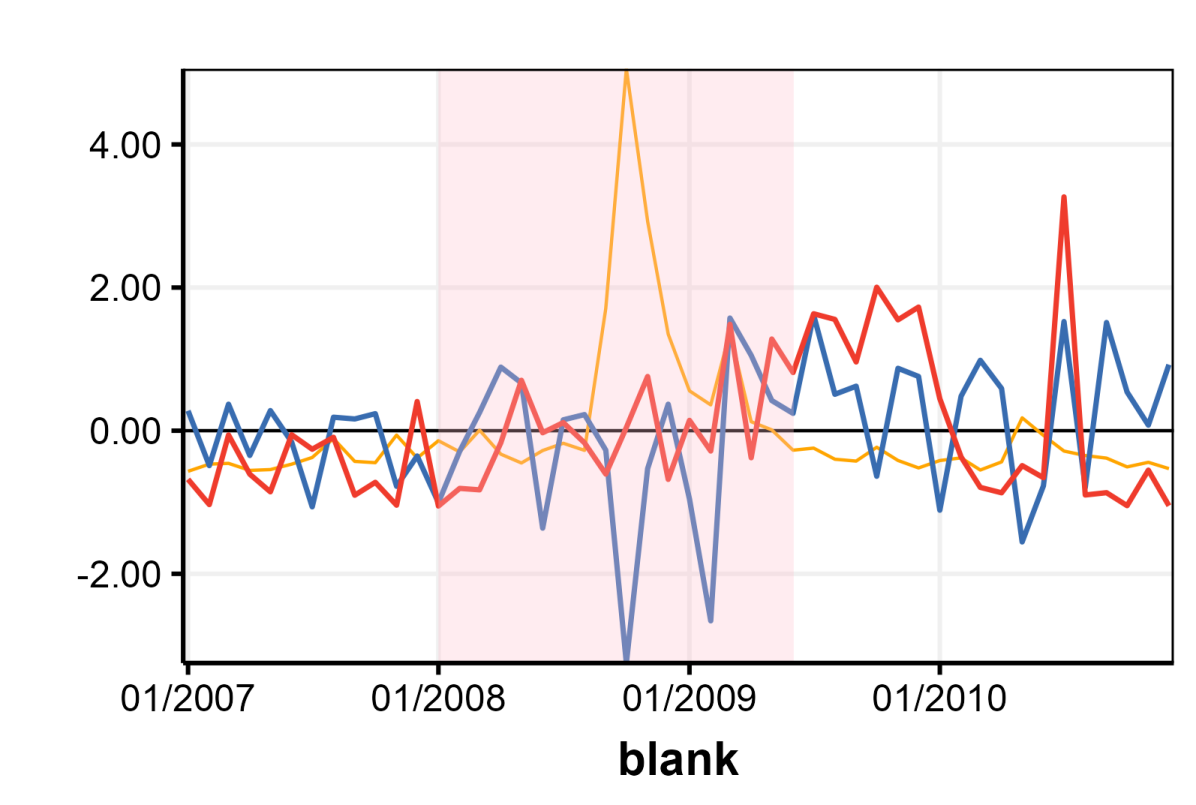

Figure 1 is telling about how that came about. First, there are the eye-grabbing flash gains during the onset of the Pandemic. These are unpacked in their own section 3.2. Given that major crisis only appear to occur on semi-decadal frequency, it is natural to wonder whether MACE100’s would still be as startling without its miracle run in March 2020. By peaking at Figure 1(b), it seems so: translating downward the red line by 0.6 from 2020 onward still make it land comfortably above competitors in terms of final cumulative returns. Moreover, those are increasing in a nearly linear fashion starting from 2018. The excluding the highly profitable month is 1.32, which confirms visual observations. Looking at MACE100 (PM)’s cumulative returns is also revealing for MACE100’s overall performance. The latter is magnified during the early stages of the Pandemic because the former (i.e., the raw portfolio itself) suffers minimal losses. However, we see that MACE100 (PM) proves inferior to its RF-based counterpart by delivering approximately 0 returns in 2018, 2020 as well as 2021, and losses in 2022.

The column also helps in understanding overall returns. The variance among results for this metric is vast. Some strategies suffered important losses, yielding returns that are quite correlated with the overall bear market. Others turned into a massive profit. All three MACEs do fine, with MACE100 delivering almost 24%, with apparently (Figure 1) higher variance than previous years, however. MACE20 is lowest among the three, with 5.03% and facing a major setback midyear by losing 10% in a bit more than a week. We will see in section 3.3 that such setbacks can be smoothed out, most notably, by “bagging strategies”. While MACE20 and MACE arguably get a headstart for 2022 with raw portfolios (PM) delivering marginally positive returns, that of MACE100 (PM) is a dramatic -16.81%. In all three cases, it is the effect of active trading using RF predictions that avoids the failure of many strategies in 2022. It is also true, to a lesser extent, for S&P 500 (RF) which turns in 2.80% while the PM version suffers major losses. In fact, there are quite a few RF-based strategies that are profitable in 2022, however, unlike MACEs, those are not accompanied with enviable returns in less turbulent years.

The large positive jumps in returns that many RF-based methods experience may be seen unfavorably by . From our inspections, many RF-based strategies generate returns that are always more leptukurtic – almost Laplacian-looking – than strategies based on the prevailing mean. For instance, excluding CovidW1, MACE100 has a kurtosis of 5.96 vs 2.43 for MACE100 (PM), and S&P 500 (RF) has 9.52 vs 6.87 for its prevailing mean version. Again with the aforementioned exclusion zone, we also notice that MACE100 returns have positive skewness (0.2), which is highly preferable, whereas all other strategies have negative skewness. The other two RF-based MACE’s do not have positive skewness, but it is always the least negative among its portfolio size group. Including CovidW1 only magnifies (substantially) the extent of such findings. Thus, a performance measure that appreciates such subtleties about return distribution, going beyond mean and variance, may give a different assessment of portfolios predicted by RF. This is indeed what we find. MACE (non-PM) portfolios always deliver the highest within -wise groups. Notable changes in ranking with respect to are MACE20 going from (narrowly) third to clearly first within its group, MACE50 moving from second to first with the group, and S&P 500 (RF) beating S&P 500 (PM).

Among other stylized facts, we observe that, in line with theoretical observations in section 2.2 – equation 4 in particular – the variance of MACE portfolio return before trading is higher than all other portfolios. For instance, MACE100 unconditional standard deviation is 1.54 out-of-sample excluding CovidW1 and 1.44 in-sample, whereas the MinVar portfolio (effectively MACE100 at ) has 0.56 and 0.69. Thus, in its quest for higher predictability and returns, MACE creates a synthetic asset which unconditional volatility is higher and which is tamed through more accurate predictions. We see that this higher volatility is no out-of-sample “surprise” as the training and test nearly coincides on this metric. This is not true for MinVar. Those observations highlight both opportunities and perils for the MACE. The opportunities have already been documented widely. The peril is that of overfitting: letting MACE overfit will lead to higher unconditional variance out-of-sample than what can be inferred from the in-sample performance. From a risk-reward perspective, this could be a lose-lose situation. Clearly, the MACEs studied here are doing fine in that regard, but one should always bear in mind the dual costs of overfitting in the MMLP problem.

In Appendix A.1, we report how and MACE20 and MACE100 performances are affected from introducing various levels of transaction costs (TC). MACE20 is mostly unaffected under reasonable TC levels, loosing about 1% in returns for any 0.5 percentage points increase in TCs. However, given the highly-liquid nature of the considered stocks, a more realistic ballpark is 0.1% as recommended by DeNardEngleKelly2023 for trading Volatility Lab’s 177 sustainable funds. MACE100 inevitably takes larger hits (at worst -10% returns with 1% TCs). Nonetheless, even in such strenuous conditions, it remain by far the dominant strategy as per all performance metrics. Smaller TCs keep MACE100’s annualized return still above 35% and risk-reward in a enviable place.

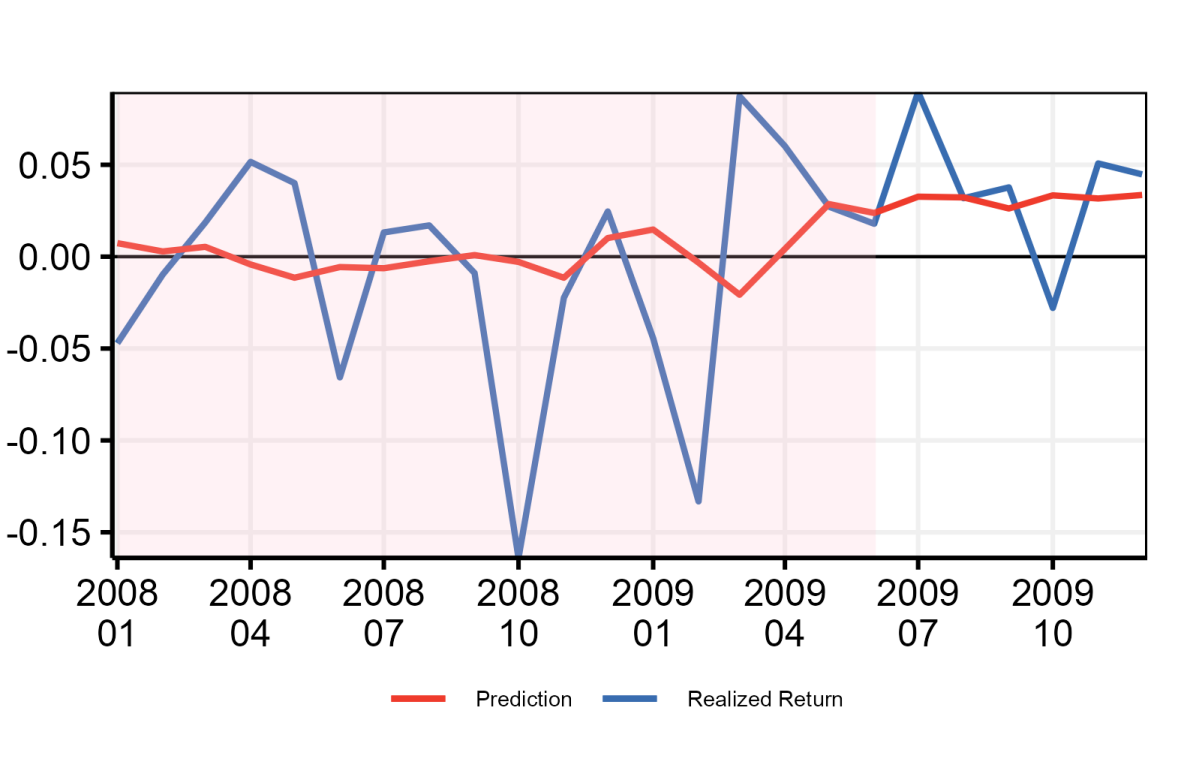

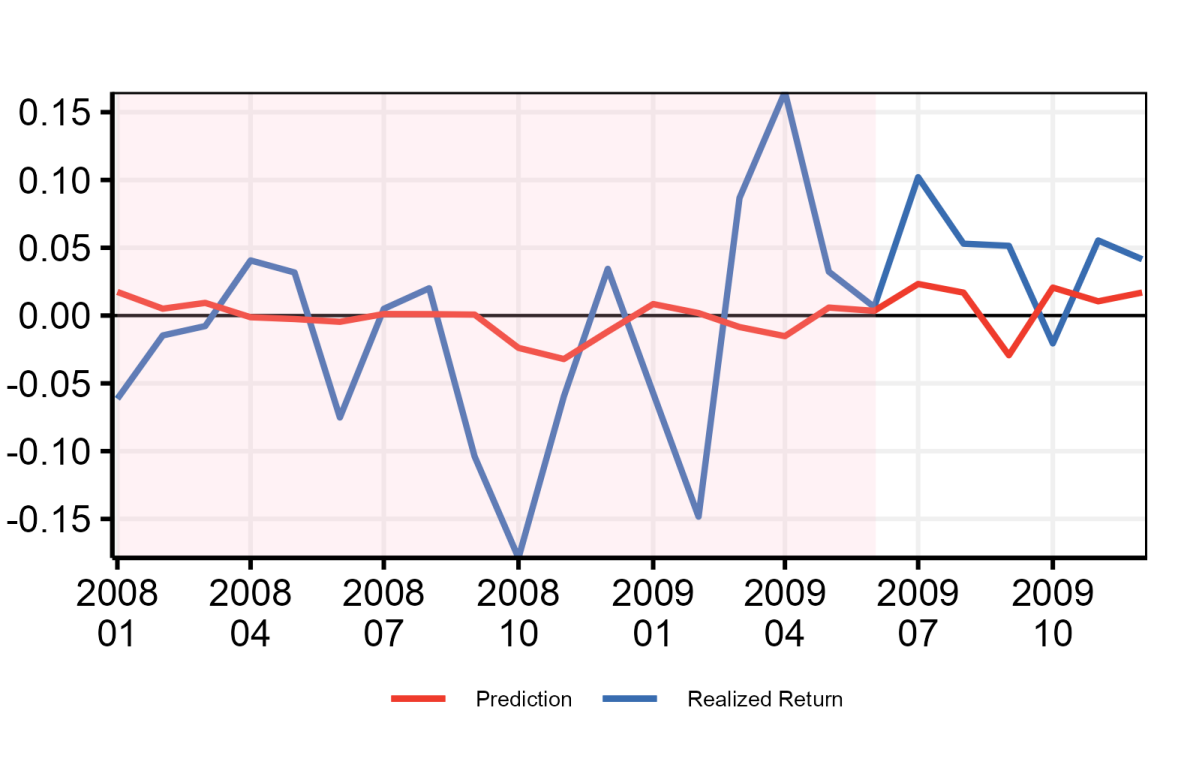

3.2 Understanding March 2020

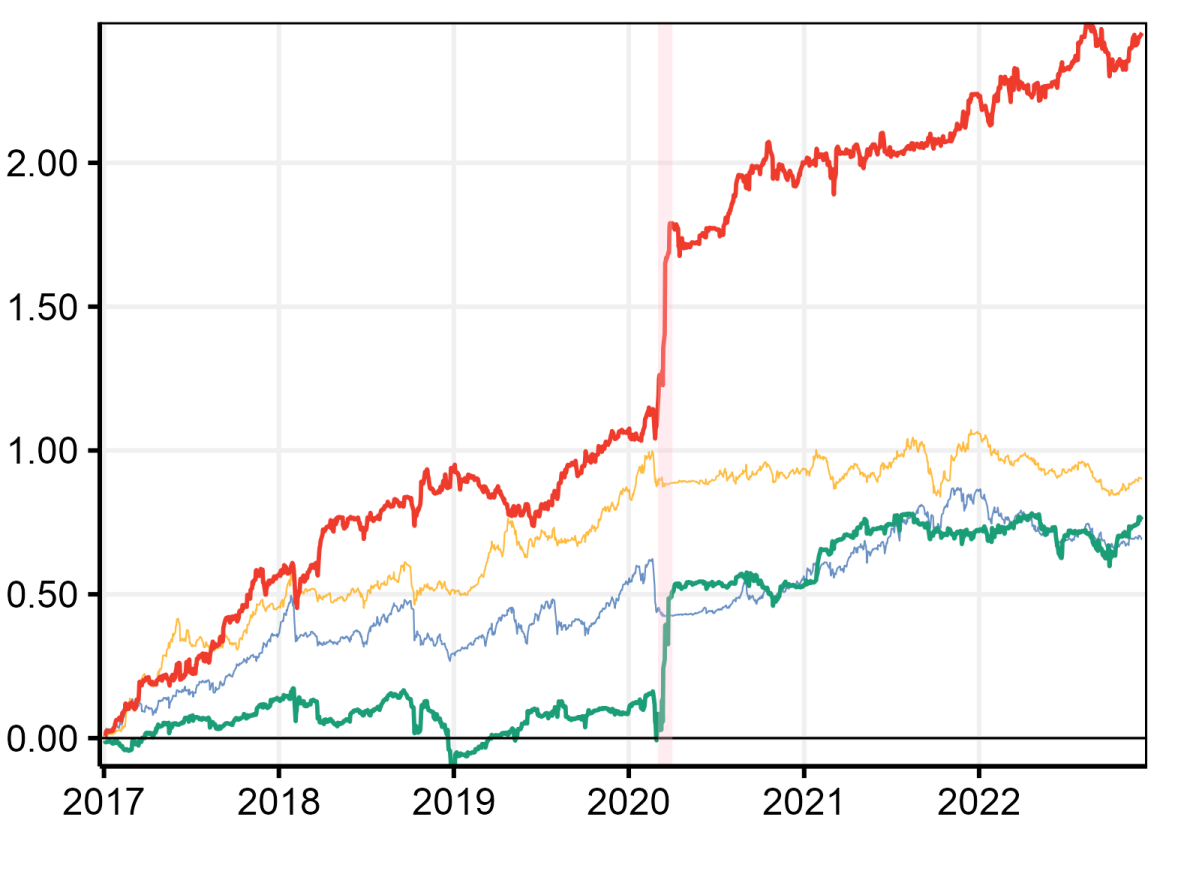

It is quite a sight in Figure 1 that MACEs generate massive gains during the short-lived Pandemic recession. These can obviously be linked back to the abnormally high ’s observed for that era.777Increased predictability in the early Covid era has also been noted in in-sample analyses such as LalwaniMeshram2020 who found that the stock returns in certain industries are statistically significantly more predictable during 2020Q1 than a few months prior. A similar result is found for S&P 500 (RF). However, S&P 500 (RF) is brought down by a dismal performance for the three years preceding 2020. A similar pattern holds for EW (RF) (unreported), where returns are dismal for the entirety of the test set. This highlights that RF-based models can most definitely fail to outperform basic strategies and that the MACE “treatment effect” is paramount in giving them consistently the upper hand.

MACEs’ and S&P 500 (RF)’s winning streak (both for and ) spans approximately 21 business days starting from early March 2020. Its intensity is greater for MACE100 and S&P 500 (RF) where wealth is approximately tripled in one month. Indeed, zooming in on these precise days, MACE100 hits a local of 20% and its sign prediction accuracy is 78 %. Needless to say, losing money only once every five days, thus compounding returns most days of the week in a time of high volatility, is what generates the rocket increase in profits during March 2020.

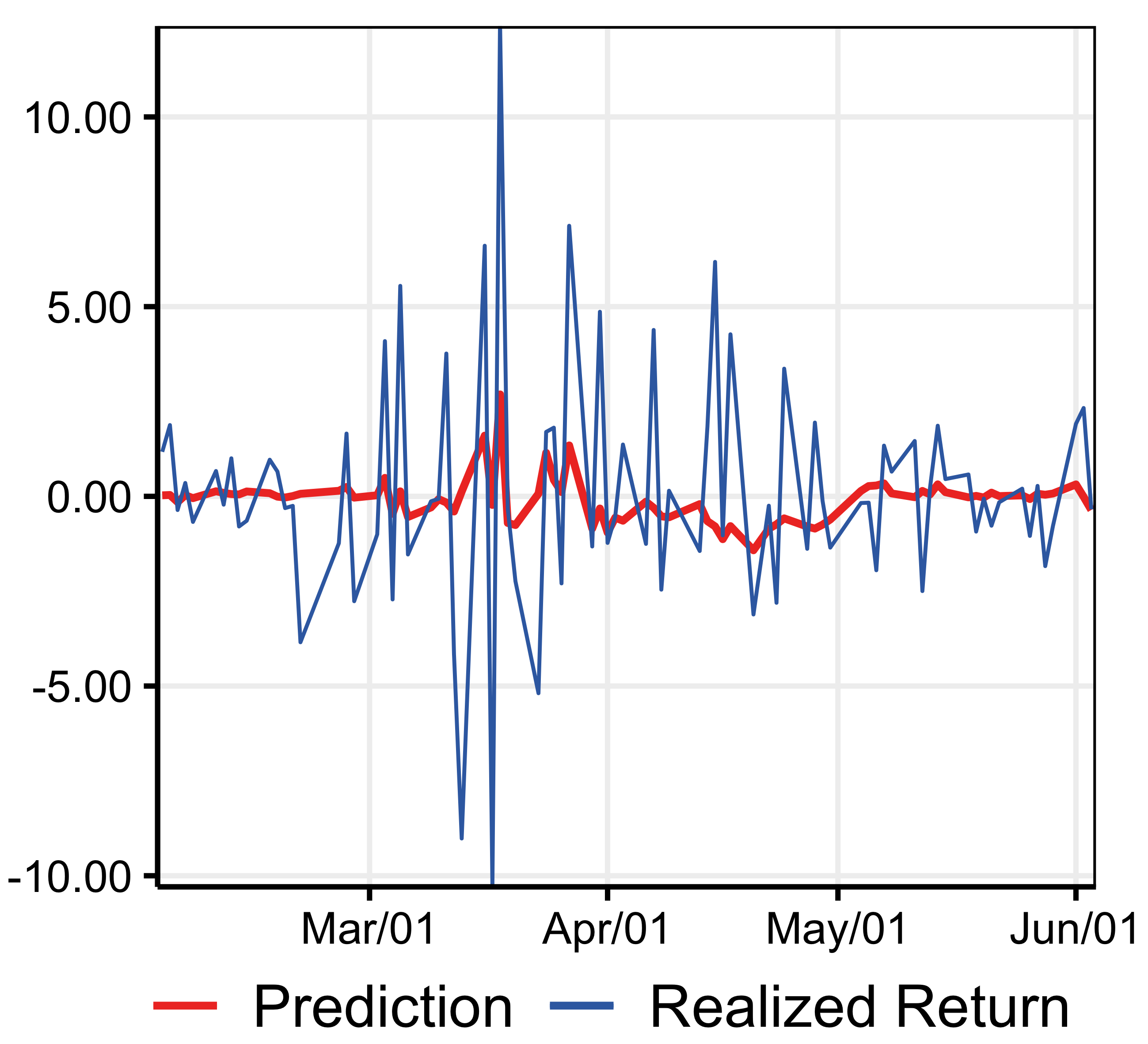

Predictability patterns are clearly visible in Figure 2, where the RF embedded in MACE predicts many of the bounce backs and the overall zigzagging nature of the market in times of crisis. To the naked eye, it looks like RF, in part, uses strong negative autocorrelation from one day to the next–thus, fast-paced mean reversion. Table 3 verifies such intuition with a first order approximation to nonlinear day-to-day dynamics. We find that the AR(1) coefficient for both MACE100 and S&P 500 are strongly negative and highly statistically significant (-stats above 4) during the first four months of the Pandemic. RF predictions provide significant economic value in this period because they precisely capture just that—those are strongly negatively correlated with yesterday’s return.

With for the two targets in vicinity of -0.6, it is natural to ask where RF may have learned that. It is equally natural to conjecture it did so during the last major financial crisis. The third panel of Table 3 verifies that. We see, albeit in a marginally more subtle way, that (i) returns are significantly negatively autocorrelated on a daily basis and (ii) RF predictions leverage the phenomenon to a non-trivial extent.

While some statistically significant mean-reversion remains in MACE100 outside of the pandemic, it is smaller by orders of magnitude. For the S&P 500, it is completely gone, one would expect. Thus, given the wide heterogeneity, a successful model must detect ex-ante whether we are in a state of strong daily mean reversion or one where there is little to none at all. It is an aspect in which the nonlinear nature of RF becomes key. This state-dependence is obviously only one of the many time series nonlinearities that tree ensembles can capture (MRF). Finally, it is worth remembering that, even within those two hypothetical states, the linear approximation in Table 3 only captures a fraction of RF nonlinear predictive dynamics. This is particularly true for where RF’s prediction correlates very little with the first lag. Even during CovidW1, it is worth noting that the first lag explains less than 40% of the variance of RF predictions.

| \rowcolorwhite | CovidW1 | 2008 | ||||

|---|---|---|---|---|---|---|

| MACE100 | S&P 500 (RF) | MACE100 | S&P 500 (RF) | MACE100 | S&P 500 (RF) | |

| Coefficient | -0.451 | -0.402 | -0.074 | -0.036 | -0.104 | -0.156 |

| Standard Error | 0.097 | 0.100 | 0.027 | 0.027 | 0.063 | 0.062 |

| -0.616 | -0.577 | 0.102 | 0.014 | -0.243 | -0.173 | |

-

Notes: This table reports the AR(1) coefficient and its standard error for two different return series on two non-overlapping subsamples of the test set spanning from 2016 to 2022 as well as 2008 from the training sample. is the correlation between Random Forest’s prediction of the portfolio’s return and the realized return on the previous business day.

3.3 Bagging Strategies and Other Algorithmic Refinements

In a real-life implementation of a daily trading strategy, one may be more than willing to exchange transaction costs for computational costs. This is particularly true for MACE-based strategies, where all the computational burden is incurred while finding , which remains fixed ever after, limiting daily computing costs to that of making one prediction with a Random Forest.

In this subsection, we activate two algorithmic refinements that help in improving the results in terms of annualized returns and Sharpe Ratios. First, we introduce a modification to the Ridge Regression step that brings back part of the unconditionally expected return constraint that is usually part of classical mean-variance portfolio optimization. In our setup, it will have a second nature as unconditional return regularization. Second, we introduce “bagging of strategies” as a reasonably intuitive way to (i) tame the variance of returns and (ii) decrease the dependence of the solution on initialization values. This latter refinement, basically ensembling strategies, multiplies the computational cost by the size of the ensemble ().