Two-step inertial Bregman alternating structure-adapted proximal gradient descent algorithm for nonconvex and nonsmooth problems††thanks: Supported by Scientific Research Project of Tianjin Municipal Education Commission (2022ZD007).

Abstract. In this paper, we propose accelerated alternating structure-adapted proximal gradient descent method for a class of nonconvex and nonsmooth nonseparable problems. The proposed algorithm is a monotone method which combines two-step inertial extrapolation and Bregman distance. Under some assumptions, we prove that every cluster point of the sequence generated by the proposed algorithm is a critical point. Furthermore, with the help of Kurdyka–Łojasiewicz property, we establish the convergence of the whole sequence generated by proposed algorithm. In order to make the algorithm more effective and flexible, we also use some strategies to update the extrapolation parameter and solve the problems with unknown Lipschitz constant. Moreover, we report some preliminary numerical results on involving nonconvex quadratic programming and sparse logistic regression to show the feasibility and effectiveness of the proposed methods.

Key words: Accelerated methods; Nonconvex and nonsmooth nonseparable optimization; Extrapolation; Bregman distance; Kurdyka–Łojasiewicz property.

1 Introduction

In this paper, we will consider to solve the following nonconvex and nonsmooth nonseparable optimization problem:

| (1.1) |

where , are continuously differentiable, is a proper, lower semicontinuous function. Note that here and throughout the paper, no convexity is assumed on the objective function. Problem (1.1) is used in many application scenarios, such as signal recovery [1, 2, 3], nonnegative matrix facorization [4, 5], quadratic fractional programming [6, 7], compressed sensing [8, 9], sparse logistic regression [7] and so on.

The natural method to solve problem (1.1) is the alternating minimization (AM) method (also called block coordinate descent (BCD) method), which, from a given initial point , generates the iterative sequence via the scheme:

| (1.2) |

If is convex and continuously differentiable, and it is strict convex of one argument while the other is fixed, then the sequence converges to a critical point [10, 11].

To relax the requirements of AM method and remove the strict convexity assumption, Auslender [12] introduced proximal terms to (1.2) for convex function :

| (1.3) |

where and are positive sequences. The above proximal point method, which is called proximal alternating minimization (PAM) algorithm, was further extended to nonconvex nonsmooth functions. Such as, in [13], Attouch et al. applied (1.3) to solve nonconvex problem (1.1) and proved the sequence generated by the proximal alternating minimization algorithm (1.3) converges to a critical point. More convergence analysis of the proximal point method can be found in [14, 15].

Because the proximal alternating minimization algorithm requires an exact solution at each iteration step, the subproblems are very expensive if the minimizers of subproblems are not given in a closed form. The linearization technique is one of the effective methods to overcome the absence of an analytic solution to the subproblem. Bolte et al. [16] proposed the following proximal alternating linearized minimization (PALM) algorithm under the condition that the coupling term is continuously differentiable:

| (1.4) |

The step size and are limited to

where “Lip” denotes the Lipschitz constant of the function in parentheses. In this way, the solution of some subproblems may be expressed by a closed-form or can be easily calculated. The global convergence result was established if satisfied the Kurdyka–Łojasiewicz property.

When and are continuously differentiable, a natural idea is to linearize and . Nikolova et al. [17] proposed the corresponding algorithm, called alternating structure-adapted proximal gradient descent (ASAP) algorithm with the following scheme:

| (1.5) |

where . With the help of Kurdyka–Łojasiewicz property they establish the convergence of the whole sequence generated by (1.5).

The inertial extrapolation technique has been widely used to accelerate the iterative algorithms for convex and nonconvex optimizations, since the cost of each iteration stays basically unchanged [18, 19]. The inertial scheme, starting from the so-called heavy ball method of Polyak [20], was recently proved to be very efficient in accelerating numerical methods, especially the first-order methods. Alvarez et al. [21] applied the inertial strategy to the proximal point method and proved that it could improve the rate of convergence. The main feature of the idea is that the new iteration use the previous two or more iterations.

Based on (1.4), Pock and Sabach [22] proposed the following inertial proximal alternating linearized minimization (iPALM) algorithm:

| (1.6) |

where . They proved that the generated sequence globally converges to critical point of the objective function under the condition of the Kurdyka–Łojasiewicz property. When , iPALM reduces to PALM. Then Cai et al. [23] presented a Gauss–Seidel type inertial proximal alternating linearized minimization (GiPALM) algorithm for solving problem (1.1):

| (1.7) |

By using inertial extrapolation technique, Xu et al. [7] proposed the following accelerated alternating structure-adapted proximal gradient descent (aASAP) algorithm:

| (1.8) |

Compared with the traditional extrapolation algorithm, the main difference is to ensure that the algorithm is a monotone method in terms of objective function value, while general extrapolation algorithms may be nonmonotonic.

Bregman distance is a useful substitute for a distance, obtained from the various choices of functions. The applications of Bregman distance instead of the norm gives us alternative ways for more flexibility in the selection of regularization. Choosing appropriate Bregeman distances can obtain colsed form of solution for solving some subproblem. Bregman distance regularization is also an effective way to improve the numerical results of the algorithm. In [24], the authors constructed the following two-step inertial Bregman alternating minimization algorithm using the information of the previous three iterates:

| (1.9) |

where denotes the Bregman distance with respect to , respectively. The convergence is obtained provided an appropriate regularization of the objective function satisfies the Kurdyka–Łojasiewicz inequality. Based on alternating minimization algorithm, Zhao et al. [25] proposed the following inertial alternating minimization with Bregman distance (BIAM) algorithm:

| (1.10) |

Suppose that the benefit function satisfies the Kurdyka–Łojasiewicz property and the parameters are selected appropriately, they proved the convergence of BIAM algorithm.

In this paper, based on the alternating structure-adapted proximal gradient methods, we combine inertial extrapolation technique and Bregman distance to construct two-step inertial Bregman alternating structure-adapted proximal gradient descent algorithm. And in order to make the proposed algorithm more effective and flexible, we also use some strategies to update the extrapolation parameter and solve the problems with unknown Lipschitz constant. Under some assumptions about the penalty parameter and objective function, the convergence of the proposed algorithm is obtained based on the Kurdyka–Łojasiewicz property. Moreover, we report some preliminary numerical results on involving quadratic programming and logistic regression problem to show the feasibility and effectiveness of the proposed method.

The article is organized as follows. In Section 2, we recall some concepts and important lemmas which will be used in the proof of main results. In Section 3, we present the Two-step inertial Bregman alternating structure-adapted proximal gradient algorithm and show its convergence. Finally, in Section 4, the preliminary numerical examples on nonconvex quadratic programming and sparse logistic regression problem are provided to illustrate the behavior of the proposed algorithm.

2 Preliminaries

Consider the Euclidean vector space of dimension , the standard inner product and the induced norm on are denoted by and , respectively. We use to stand for the limit set of .

The domain of are defined by dom. We say that is proper if dom, and is called lower semicontinuous at if for every sequence converging to . If is lower semicontinuous in its domain, we say is a lower semicontinuous function. If dom is closed and is lower semicontinuous over dom , then is a closed function. Further we recall some generalized subdifferential notions and the basic properties which are needed in this paper.

2.1 Subdifferentials

Definition 2.1.

(Subdifferentials) Let be a proper and lower semicontinuous function.

(i)For dom, the Fréchet subdifferential of at , written , is the set of vectors which satisfy

(ii)If dom, then . The limiting-subdifferential [26], or simply the subdifferential for short, of at dom, written , is defined as follows:

Remark 2.1.

(a) The above definition implies that for each , where the first set is convex and closed while the second one is closed (see[27]).

(b) (Closedness of ) Let and be sequences in such that for all . If and as , then .

(c) If be a proper and lower semicontinuous and is a continuously differentiable function, then for all .

In what follows, we will consider the problem of finding a critical point dom.

Lemma 2.1.

(Fermat’s rule[28]) Let be a proper lower semicontinuous function. If has a local minimum at , then .

We call is a critical point of if . The set of all critical points of denoted by crit.

Lemma 2.2.

(Descent lemma[29]) Let be a continuously differentiable function with gradient assumed -Lipschitz continuous. Then

| (2.1) |

2.2 The Kurdyka–Łojasiewicz property

In this section, we recall the KŁ property, which plays a central role in the convergence analysis.

Definition 2.2.

(Kurdyka–Łojasiewicz property [13]) Let be a proper and lower semicontinuous function.

(i)The function is said to have the Kurdyka–Łojasiewicz (KŁ) property at dom if there exist , a neighborhood of and a continuous concave function such that , is on , for all it is and for all in the Kurdyka–Łojasiewicz inequality holds,

(ii)Proper lower semicontinuous functions which satisfy the Kurdyka–Łojasiewicz inequality at each point of its domain are called KŁ functions.

Lemma 2.3.

(Uniformized KŁ property[28]) Let be a compact set and let be a proper and lower semicontinuous function. Assume that is constant on and satisfies the KŁ property at each point of . Then, there exist and such that for all and for all , one has

2.3 Bregman distance

Definition 2.3.

A function is said convex if dom is a convex set and if, for all , dom, ,

is said -strongly convex with if is convex, i.e.,

for all , dom and .

Suppose that the function is differentiable. Then is convex if and only if dom is a convex set and

holds for all , dom. Moreover, is -strongly convex with if and only if

for all , dom.

Definition 2.4.

Let be a convex and Gâteaux differentiable function. The function dom intdom, defined by

is called the Bregman distance with respect to .

From the above definition, it follows that

| (2.2) |

if is -strongly convex.

3 Algorithm and convergence analysis

Assumption 3.1.

(i) is lower bounded.

(ii) and are continuously differentiable and their gradients and are Lipschitz continuous with constants , respectively.

(iii) is a proper, lower semicontinuous.

(iv) is -strongly convex differentiable function, , . And the gradient is -Lipschitz continuous, i.e.,

| (3.1) | ||||

3.1 The proposed algorithm

| (3.2) |

| (3.3) |

| (3.4) |

| (3.5) |

Remark 3.1.

Remark 3.2.

Compared with the traditional extrapolation algorithm, the main difference is step 3 which ensures the algorithm is a monotone method in terms of objective function value, while general extrapolation algorithms may be nonmonotonic.

For extrapolation parameters and , there are at least two ways to choose them, either as costant or by dynamic update. For example, in [31, 32] it was defined as

| (3.7) |

where . In order to make Algorithm 1 more effective, we present an adaptive method to update the extrapolation parameter , , which is given in Algorithm 2.

| (3.8) |

| (3.9) |

| (3.10) | ||||

| (3.11) | ||||

Remark 3.3.

Remark 3.4.

A possible drawback of Algorithm 1 and Algorithm 2 is that the Lipschitz constants , are not always known or computable. However, the Lipschitz constant determines the strong convexity modulus range of and . Especially, if , the Lipschitz constant , determines the range of stepsize in (3.6). Even if the Lipschitz constant is known, it is always large in general, which makes the strong convexity modulus , very small. Therefore, in order to improve the efficiency of the algorithm, a method for estimating a proper local Lipschitz constant will be given below.

A backtracking method is proposed to evaluate the local Lipschitz constant. We adopt Barzilai-Borwein (BB) method [33] with lower bound to initialize the stepsize at each iteration. The procedure of computing the stepsize of the -subproblem is shown in the following box.

Backtracking with BB method with lower bound

Compute the BB stepsize: set ,

Backtracking: set .

Repeat compute:

until

(3.12)

Remark 3.5.

The stepsize of -subproblem can be obtained similarly. The process of enlarging is actually approaching the local Lipschitz constant of . Since is gradient Lipschitz continuous, the backtracking process can be terminated in finite steps for achieving a suitable .

3.2 Convergence analysis

In this section, we will prove the convergence of Algorithm 1. Note that the bound of and is no more than and in Algorithm 2, respectively. So the convergence properties of Algorithm 1 are also applicable for Algorithm 2.

Under Assumption 3.1, some convergence results will be proved (see Lemma 3.1). We will also consider the following additional assumptions to establish stronger convergence results.

Assumption 3.2.

(i) is coercive and the domain of is closed.

(ii) The subdifferential of obeys:

(iii) has the following form

where is continuous on its domain; is a continuous function on dom such that for any , the partial function is continuously differentiable about . Besides, for each bounded subset , there exists , such that for any , , it holds that

Remark 3.6.

(i) Assumption 3.2(i) ensure that the sequences generated by our proposed algorithms is bounded which plays an important role in the proof of convergence.

Lemma 3.1.

Suppose that Assumption 3.1 hold. Let and are sequences generated by Algorithm 1. The following assertions hold.

(i) The sequences , are monotonically nonincreasing and have the same limiting point, i.e.

In particular,

| (3.13) | ||||

where

(ii) and hence

Proof.

(i) From Lemma 2.2, we have

| (3.14) |

According to -subproblem in the iterative scheme (3.2), we obtain

which implies that

| (3.15) |

By (2.2), it follows from (3.14) and (3.15) that

| (3.16) | ||||

Similarly, for -subproblem, we can get

| (3.17) |

Adding (3.16) and (3.17), we have

| (3.18) | ||||

which can be abbreviated as

| (3.19) |

By the choice of (3.4) and (3.5) for in Algorithm 1, we get

| (3.20) | ||||

Hence and are nonincreasing sequences, and

| (3.21) |

holds. Furthermore, is lower bounded according to Assumption 3.1, therefore the sequence is convergent. Let . Taking limit on (3.21), and using the squeeze theorem, we get .

Lemma 3.2.

Proof.

From the iterative scheme (3.2), we know

By Fermat’s rule, satisfies

which implies that

| (3.28) |

Similarly, by -subproblem in iterative scheme (3.2), we have

which implies that

| (3.29) |

From Assumption 3.2 (iii), we know that

According to (3.28), we have

| (3.30) |

It follows from (3.25) that

| (3.31) |

Hence,

Now we begin to estimate the norms of and . Under Assumption 3.2 (i) that is coercive, we deduce that is a bounded set. Then from Assumption 3.2 (iii) and (3.1), we have

and hence

The above inequality holds from the fact that

Set . Then

So the conclusion holds. ∎

Below, we would summarize some properties about cluster points and prove every cluster point of a sequence generated by Algorithm 1 is the critical point of . For simplicity, we introduce the following notations. Let

So

Let be the sequence generated by Algorithm 1 with initial point . Under Assumption 3.2 (i) that is coercive, we deduce that is a bounded set, and it has at least one cluster point. The set of all cluster points is denoted by , i.e.,

Lemma 3.3.

Suppose Assumption 3.1 and Assumption 3.2 hold, let be a sequence generated by Algorithm 1 with initial point . Then the following results hold.

(i) is a nonempty compact set, and is finite and constant on ,

(ii) ,

(iii) .

Proof.

(i) The fact is bounded yields is nonempty. In addition, can be reformulated as an intersection of compact sets

which illustrates that is a compact set.

For any , there exists a subsequence such that

Since is continuous, we have

According to Lemma 3.1, we know that converges to globally. Hence

| (3.32) |

which means is a constant on .

(ii) Take , then such that . From (3.24), we have

hence,

By (3.27), we get

So

Based on the result , and the closedness property of , we conclude that , which means is a critical point of , and .

(iii) We prove the assertion by contradiction. Assume that . Then, there exists a subsequence and a constant such that

| (3.33) |

On the other hand, is bounded and has a subsequence converging to a point in . Thus,

which is a contradiction to (3.33). ∎

Now, we can prove the main convergence results of proposed algorithms under KŁ property.

Theorem 3.1.

Suppose Assumptions 3.1 and 3.2 hold and is a sequence generated by Algorithm 1 with initial point . Assume that is a KŁ function. Then the following results hold.

(i) ,

(ii) The sequence converges to a critical point of .

Proof.

In the process of our proof, we always assume . Otherwise, there exists an integer such that . The sufficient decrease condition (Lemma 3.1) implies . It follows that for any and the assertions holds trivially.

(i) Since is a nonincreasing sequence and from (3.32), for any , there exists a positive integer such that

which means

On the other hand, . Therefore for any , there exists a positive integer , such that

Let . Then for all , we have

Note that is a constant on the compact set . According to Lemma 2.3, there exists a concave function such that

| (3.34) |

From Lemma 3.2, we obtain that

| (3.35) |

Substituting (3.35) into (3.34), we get

From the concavity of , we have

It follows that

| (3.36) |

The last inequality is from Lemma 3.1.

For convenience, we define . It is obvious that is nonincreasing of . Let and . Then (3.36) can be simplified as

i.e.,

Using the fact that for , we infer

| (3.37) |

Summing up (3.37) for yields

Eliminating the same terms of the inequality, we have

Let , we get

| (3.38) |

Note that , and investigating the iterative point in Algorithm 1. If is generated by (3.4), then

| (3.39) |

If is generated by (3.5), then

No matter how is generated, we always have

| (3.40) |

Summing up (3.40) for we get

| (3.41) |

Note that . Let , then , and it holds that

| (3.42) |

and

| (3.43) |

Combining (3.41), (3.42) and (3.43), we have

| (3.44) |

The last inequality holds from (3.38). Taking the limit as , and using the fact , we obtain

This shows that

| (3.45) |

Since KŁ property is also a very useful tool to establish the convergence rate of many first-order methods. Based on KŁ inequality, Attouch and Bolte [34] first established convergence rate results which are related to the desingularizing function for proximal algorithms. Similar to the derivation process of [34], we can obtain convergence rate results as following.

Theorem 3.2.

(Convergence rate) Let Assumption 3.1 and 3.2 hold and let be a sequence generated by Algorithm 1 with as initial point. Assume also that is a KŁ function and the desingularizing function has the form of with , . Let , . The following assertions hold.

(i) If , the Algorithm 1 terminates in finite steps.

(ii) If , then there exist and such that

(iii) If , then there exist and such that

4 Numerical experiments

In this subsection, we provide some numerical experiments which we carried out in order to illustrate the numerical results of Algorithm 1 and 2 with different Bregman distances.

The following list are various functions with its Bregman distances:

(i) Define the function with domain

and range ran. Then

and the Bregman distance (the Itakura-Saito distance) with respect to is

(ii) Define the function with domain and range ran. Then and the Bregman distance (the squared Euclidean distance) with respect to is

It is clear that is -strongly convex ().

4.1 Nonconvex quadratic programming

We consider the following quadratic programming problem

| (4.1) | ||||

where is a symmetric matrix but not necessarily positive semidefinite, is a vector and is a ball. By introducing an auxiliary variable , (4.1) can be reformulated as

| (4.2) | ||||

where is the indictor function with respect to ball , defined by

We use penalty method to handle the constraint. The problem can be transformed into

| (4.3) |

where be a penalty parameter. When is large enough, the solution of (4.3) is an approximate solution of problem (4.2).

Let

Obviously, and are smooth functions, and the Lipschitz constant of , i.e. , is the maximal singular value of . Note that when is not positive semidefinite, is a nonconvex function. We can solve (4.3) by Algorithm 1 and Algorithm 2. Let , we can elaborate the -subproblem and -subproblem of our algorithms respectively as follows.

The -subproblem corresponds to the following optimization problem

The -subproblem corresponds to the following optimization problem

which has an explicit expression

In numerical experiments, we set , where is a matrix generated by i.i.d. standard Gaussian entries. The vector is also generated by i.i.d. standard Gaussian entries. We take and the radius of the ball is . Since , any positive number can be the Lipschitz constant of . We set . We selected the starting point randomly, and use

as the stopping criteria. In the numerical results, “Iter.” denotes the number of iterations. “Time” denotes the CPU time. “Extrapolation” records the number of taking extrapolation step, i.e., the number of adopting (3.4).

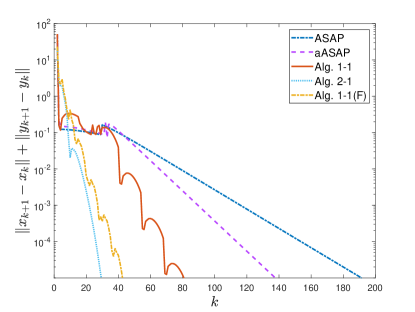

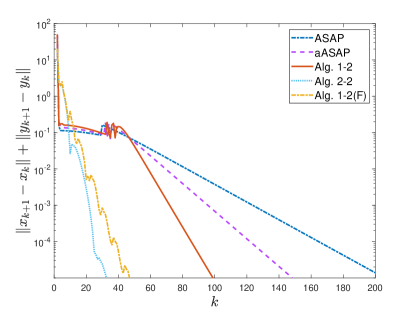

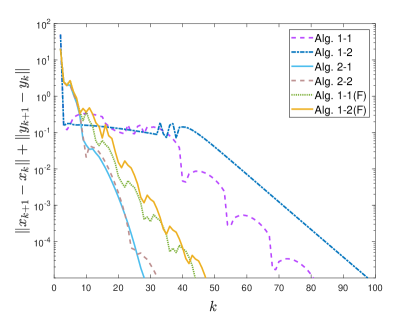

In order to show the effectiveness of the proposed algorithms, we compare Algorithm 1, Algorithm 2 with ASAP [17] and aASAP [7] for different Bregman distance. Note that when , Algorithm 1 and Algorithm 2 correspond to ASAP. For aASAP, we take . For Algorithm 1, we set . And we also take extrapolation parameter dynamically updating with . Even if the theoretical bound of extrapolation parameter with dynamically updating dost not permit to go beyond , for the convergence is also obtained for this case with a better performance. For Algorithm 2, we set as the initial extrapolation parameter and . We use “Alg. 1-i” and “Alg. 2-i” to denote Algorithm 1 and Algorithm 2 with , respectively, where extrapolation parameter . We use “Alg. 1-i(F)” and “Alg. 2-i(F)” to denote Algorithm 1 and Algorithm 2 with , respectively, where extrapolation parameter .

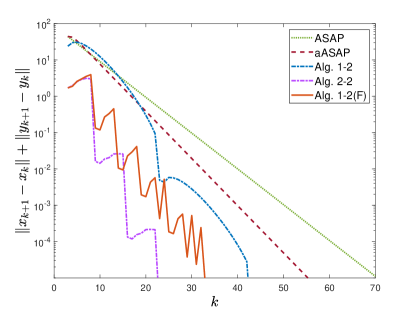

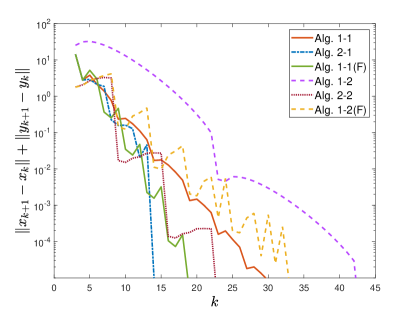

In Table 1, we list the iterations, CPU time and extrapolation step of the above algorithm for different Bregman distance. In Figure 1, (a) and (b) reports the result of different extrapolation parameter, respectively, (c) reports the result of different Bregman distance. It can be seen that the Itakura-Saito distance have computational advantage than the squared Euclidean distance for Algorithm 1 and Algorithm 2 in terms of number of iteration and CPU time. Compared with one-step extrapolation and original algorithm, two-step extrapolation performs much better. It shows that Algorithm 2 with adaptive extrapolation parameters performs the best among all algorithms.

| Itakura-Saito distance | squared Euclidean distance | |||||||

| Algorithm | Iter. | Time(s) | Extrapolation | Algorithm | Iter. | Time(s) | Extrapolation | |

| ASAP | 192 | 0.5906 | 191 | ASAP | 202 | 0.6456 | 201 | |

| aASAP | 138 | 0.4127 | 137 | aASAP | 147 | 0.4590 | 146 | |

| Alg. 1-1 | 81 | 0.3169 | 72 | Alg. 1-2 | 98 | 0.2725 | 96 | |

| Alg. 2-1 | 28 | 0.0156 | 26 | Alg. 2-2 | 33 | 0.0469 | 28 | |

| Alg. 1-1(F) | 44 | 0.0898 | 31 | Alg. 1-2(F) | 48 | 0.1013 | 34 | |

4.2 Sparse logistic regression

In this subsection, we apply our algorithms to solve the sparse logistic regression problem. It is an attractive extension to logistic regression as it can reduce overfitting and perform feature selection simultaneously. We consider the Capped- regularized logistic regression problem [37], defined as

| (4.4) |

where , ,

By the similar method as the former example, we transform (4.4) to

| (4.5) | ||||

which can be described as

| (4.6) |

Let

| (4.7) | ||||

It is easy to verify that all the functions satisfy the assumptions. However, when is large, is difficult to compute, we cannot determine the strong convexity modulus range of the Bregman function. So we need to use backtracking strategy to solve the problem. Let , we can elaborate the -subproblem and -subproblem of our algorithms respectively as follows.

The -subproblem in (4.6) corresponds to the following optimization problem

The -subproblem in (4.6) corresponds to

For convenience, we set

| (4.8) |

where , Then has a separable structure. It can be decomposed into one-dimensional subproblems. Let be the -th component of . Then each component of can be calculated from

| (4.9) |

where denotes the -th component of . Then (4.9) can be described as follows

Furthermore,

Set . Then can be expressed by

In the experiment, we take and the parameters of the problem are set as , which is the same as [38]. The backtracking parameters of the algorithm are set as . We selected the starting point for all algorithms randomly and use

as the stopping criteria. In the numerical results, “Iter.” denotes the number of iterations. “Time” denotes the CPU time. “Extrapolation” records the number of taking extrapolation step.

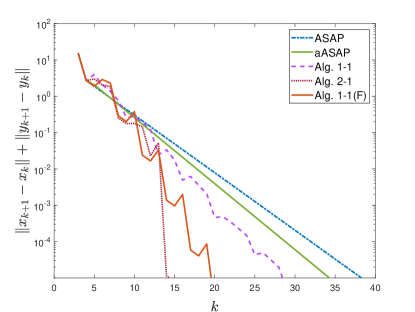

In order to show the effectiveness of the proposed algorithms, we compare our algorithms with ASAP [17] and aASAP [7]. The extrapolation parameter of aASAP is . In Algorithm 1, we set . And we also take extrapolation parameter dynamically updating with . For Algorithm 2, we set as the initial extrapolation parameter and . We also use “Alg. 1-i” and “Alg. 2-i” to denote Algorithm 1 and Algorithm 2 with , respectively, where extrapolation parameter . We use “Alg. 1-i(F)” and “Alg. 2-i(F)” to denote Algorithm 1 and Algorithm 2 with , respectively, where extrapolation parameter .

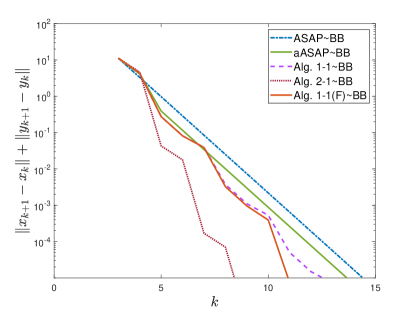

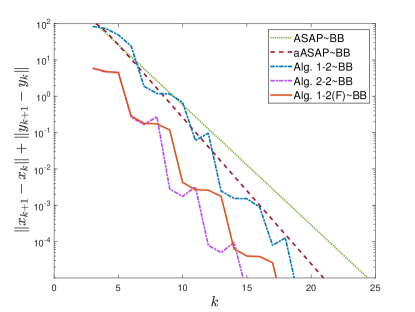

Figure 2 shows the performance of different algorithms. We also list the iteration number, the CPU time, and the extrapolation number on the test set of each algorithm in Table 2. Figure 2 (a) and (b) reports the result of different extrapolation parameter, respectively. It shows that Algorithm 2 with adaptive extrapolation parameters performs the best among all algorithms. Figure 2 (c) reports the result of different Bregman distance. It shows that the Itakura-Saito distance have computational advantage than the squared Euclidean distance.

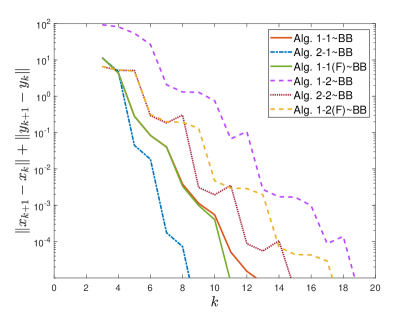

We also use BB rule improves the computational efficiency of each algorithm. The symbol in Table 3 and Figure 3 “BB” means that the algorithm adopts the BB rule with lower bound of in backtracking process. It shows that using BB rule to initialize the stepsize can improve the efficiency of all algorithms.

| Itakura-Saito distance | squared Euclidean distance | |||||||

| Algorithm | Iter. | Time(s) | Extrapolation | Algorithm | Iter. | Time(s) | Extrapolation | |

| ASAP | 39 | 9.3456 | 38 | ASAP | 71 | 18.3569 | 70 | |

| aASAP | 35 | 8.3227 | 34 | aASAP | 56 | 14.0903 | 55 | |

| Alg. 1-1 | 29 | 6.9867 | 21 | Alg. 1-2 | 43 | 11.0023 | 39 | |

| Alg. 2-1 | 15 | 3.4024 | 7 | Alg. 2-2 | 23 | 6.1576 | 16 | |

| Alg. 1-1(F) | 19 | 5.5435 | 8 | Alg. 1-2(F) | 33 | 7.9012 | 20 | |

| Itakura-Saito distance | squared Euclidean distance | |||||||

| Algorithm | Iter. | Time(s) | Extra. | Algorithm | Iter. | Time(s) | Extra. | |

| ASAPBB | 15 | 4.3476 | 14 | ASAPBB | 25 | 6.4702 | 24 | |

| aASAPBB | 14 | 4.0324 | 13 | aASAPBB | 21 | 6.0604 | 20 | |

| Alg. 1-1BB | 13 | 3.9198 | 7 | Alg. 1-2BB | 19 | 5.3523 | 10 | |

| Alg. 2-1BB | 9 | 2.9745 | 5 | Alg. 2-2BB | 15 | 4.1270 | 8 | |

| Alg. 1-1(F)BB | 11 | 3.5435 | 6 | Alg. 1-2(F)BB | 17 | 4.9352 | 9 | |

5 Conclusion

In this paper, we introduce a two-step inertial Bregman alternating structure-adapted proximal gradient descent algorithm for solve nonconvex and nonsmooth nonseparable optimization problem. Under some assumptions, we proved that our algorithm is a descent method in sense of objective function values, and every cluster point is a critical point of the objective function. The convergence of proposed algorithms are proved if the objective function satisfies the Kurdyka–Łojasiewicz property. Furthermore, if the desingularizing function has the special form, we also established the linear and sub-linear convergence rates of the function value sequence generated by the algorithm. In addition, we also proposed a backtracking strategy with BB method to make our algorithms more flexible when the Lipschitz constant is unknown or difficult to compute. In numerical experiments, we apply different Bregman distance to solve nonconvex quadratic programming and sparse logistic regression problem. Numerical results are reported to show the effectiveness of the proposed algorithm.

References

- [1] Nikolova M., Ng M.K., Zhang S.Q., Ching W.K., Efficient reconstruction of piecewise constant images using nonsmooth nonconvex minimization, SIAM J. Imaging Sci., 2008, 1(1), 2-25.

- [2] Gu S.H., Zhang L., Zuo W.M., Feng X.C., Weighted nuclear norm minimization with application to image denoising, In: Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition (CVPR), 2014, 2862-2869.

- [3] Bian W., Chen X.J., Linearly constrained non-Lipschitz optimization for image restoration, SIAM J. Imaging Sci., 2015, 8(4), 2294-2322.

- [4] Paatero, P., Tapper, U., Positive matrix factorization: a nonnegative factor model with optimal utilization of error estimates of data values, Environmetrics 5, 1994, 111-126.

- [5] Lee, D.D., Seung, H.S., Learning the parts of objects by nonnegative matrix factorization, Nature 401, 1999, 788-791.

- [6] Bot R.I., Csetnek E.R., Vuong P.T., The forward-backward-forward method from continuous and discrete perspective for pseudo-monotone variational inequalities in hilbert spaces, Eur. J. Oper. Res., 2020, 49-60.

- [7] Xu L.L., Xin Y., Vuong P.T., Some accelerated alternating proximal gradient algorithms for a class of nonconvex nonsmooth problems, J. Glob. Optim., 2022, https://doi.org/10.1007/s10898-022-01214-3.

- [8] Attouch H., Bolte J., Svaiter B.F., Convergence of descent methods for semi-algebraic and tame problems: proximal algorithms, forward-backward splitting, and regularized Guass-Seidel methods, Math. Program., 2013, 137, 91-129.

- [9] Donoho D.L., Compressed sensing, IEEE Trans. Inform. Theory, 2006, 4, 1289-1306.

- [10] Bertsekas D.P., Nonlinear programming, J. Oper. Res. Soc., 1977, 48, 334-334.

- [11] Beck A., Tetruashvili L., On the convergence of block coordinate descent type methods, SIAM J. Optim., 2013, 23, 2037-2060.

- [12] Auslender A., Asymptotic properties of the Fenchel dual functional and applications to decomposition problems, J. Optim. Theory Appl., 1992, 73(3), 427-449.

- [13] Attouch H., Bolte J., Redont P., Soubeyran A., Proximal alternating minimization and projection methods for nonconvex problems: an approach based on the Kurdyka–Łojasiewicz inequality, Math. Oper. Res., 2010, 35, 438-457.

- [14] Attouch, H., Redont, P., Soubeyran, A., A new class of alternating proximal minimization algorithms with costs-to-move, SIAM J. Optim. 2007, 18, 1061-1081.

- [15] Xu, Y., Yin, W., A block coordinate descent method for regularized multiconvex optimization with applications to nonnegative tensor factorization and completion, SIAM J. Imaging Sci, 2013, 6, 1758-1789.

- [16] Bolte J., Sabach S., Teboulle M., Proximal alternating linearized minimization for nonconvex and nonsmooth problems, Math. Program., 2014, 146, 459-494.

- [17] Nikolova M., Tan P., Alternating structure-adapted proximal gradient descent for nonconvex block-regularised problems, SIAM J. Optim., 2019, 29(3), 2053-2078.

- [18] Ochs P., Chen Y., Brox T., and Pock T., iPiano: Inertial proximal algorithm for nonconvex optimization, SIAM J. Imaging Sci., 2014, 7(2), 1388-1419.

- [19] Boţ R.I., Csetnek E.R., An inertial Tseng’s type proximal algorithm for nonsmooth and nonconvex optimization problems, J. Optim. Theory Appl., 2016, 171(2), 600-616.

- [20] Polyak B.T., Some methods of speeding up the convergence of iteration methods, USSR Comput. Math. Math. Phys., 1964, 4, 1-17.

- [21] Alvarez, F., Attouch, H., An inertial proximal method for maximal monotone operators via discretization of a nonlinear oscillator with damping. Set-Valued Anal. 2001, 9(1), 3-11.

- [22] Pock T., Sabach S., Inertial proximal alternating linearized minimization (iPALM) for nonconvex and nonsmooth problems, SIAM J. Imaging Sci., 2017, 9, 1756-1787.

- [23] Gao X., Cai X.J., Han D.R., A Gauss-Seidel type inertial proximal alternating linearized minimization for a class of nonconvex optimization problems, J. Glob. Optim., 2020, 76, 863-887.

- [24] Zhao J., Dong Q.L., Michael Th.R., Wang F.H., Two-step inertial Bregman alternating minimization algorithm for nonconvex and nonsmooth problems, J. Glob. Optim., 2022, 84, 941-966.

- [25] Chao M.T., Nong F.F., Zhao M.Y., An inertial alternating minimization with Bregman distance for a class of nonconvex and nonsmooth problems, J. Appl. Math. Comput., 2023, 69, 1559-1581.

- [26] Mordukhovich B., Variational Analysis and Generalized Differentiation, I: Basic Theory. Grundlehren der Mathematischen Wissenschaften, Vol. 330. Springer-Verlag, Berlin, 2006.

- [27] Rockafellar R.T., Wets R., Variational analysis, Grundlehren der Mathematischen Wissenschaften, Vol. 317. Springer, Berlin, 1998.

- [28] Rockafellar, R.T., Wets, J.B.: Variational Analysis. Springer, New York, 1998.

- [29] Bertsekas D.P., Tsitsiklis J.N., Parallel and Distributed Computation: Numerical Methods, Prentice hall, Englewood Cliffs, NJ, 1989.

- [30] Wang F., Cao W., Xu Z., Convergence of multi-block Bregman ADMM for nonconvex composite problems, Sci. China Inf. Sci., 2018, 61, 122101.

- [31] Li, H., Lin, Z., Accelerated proximal gradient methods for nonconvex programming, In: Advances in Neural Information Processing Systems, pp,2015, 379-387.

- [32] Li, Q., Zhou, Y., Liang, Y., Varshney, P.K., Convergence analysis of proximal gradient with momentum for nonconvex optimization. In: Proceedings of the 34th International Conference on Machine Learning, 2017,2111-2119.

- [33] Barzilai, J., Borwein, J.M., Two-point step size gradient methods, IMA J. Numer. Anal. 1998, 8, 141-148.

- [34] Attouch, H., Bolte, J.: On the convergence of the proximal algorithm for nonsmooth functions involving analytic features. Math. Program. Ser. B, 2009, 116, 5-16.

- [35] Li, H., Lin, Z.: Accelerated proximal gradient methods for nonconvex programming. In: Advances in Neural Information Processing Systems, pp., 2015, 379-387.

- [36] Li, Q., Zhou, Y., Liang, Y., Varshney, P.K., Convergence analysis of proximal gradient with momentum for nonconvex optimization. In: Proceedings of the 34th International Conference on Machine Learning, 2017, 2111-2119.

- [37] Zhang, T., Analysis of multi-stage convex relaxation for sparse regularization, J. Mach. Learn. Res. 2010, 11, 1081-1107.

- [38] Gong, P., Zhang, C., Lu, Z., Huang, J., Ye, J., A general iterative shrinkage and thresholding algorithm for nonconvex regularized optimization problems. In: International Conference on Leadership and Management, 2013, 37-45.