monthyeardate\monthname[\THEMONTH] \THEYEAR

Semiparametric Efficiency Gains From Parametric Restrictions on Propensity Scores

Abstract

We explore how much knowing a parametric restriction on propensity scores improves semiparametric efficiency bounds in the potential outcome framework. For stratified propensity scores, considered as a parametric model, we derive explicit formulas for the efficiency gain from knowing how the covariate space is split. Based on these, we find that the efficiency gain decreases as the partition of the stratification becomes finer. For general parametric models, where it is hard to obtain explicit representations of efficiency bounds, we propose a novel framework that enables us to see whether knowing a parametric model is valuable in terms of efficiency even when it is very high-dimensional. In addition to the intuitive fact that knowing the parametric model does not help much if it is sufficiently flexible, we reveal that the efficiency gain can be nearly zero even though the parametric assumption significantly restricts the space of possible propensity scores.

1 Introduction

Let be a treatment indicator such that if an individual is treated, and and denote potential outcomes for and respectively. For each individual, we observe the treatment status the realized outcome and a covariate vector which takes values on some set We consider the average treatment effect on the treated, Suppose that the propensity score is where is the indicator function, and is a partition of the covariate space. In other words, it is constant in each region of the partition. As usual, we assume the conditional independence and the overlap condition.111See Assumption 2.2 for details. We consider three different situations: (K) is known, (P) is known to be constant on each region, but and are unknown, and (UK) is unknown. Note that (P) corresponds to situations where researchers put a parametric restriction on the propensity score. Let and be the semiparametric efficiency bounds of the ATT under (K), (P), and (UK), respectively. Clearly, the model under (P) is smaller than the model under (UK) because it is known that is piecewise constant. On the other hand, the model under (P) is larger than the model under (K) because and are not available. These observations imply This kind of comparison among the efficiency bounds of different models has received attention in causal inference since [12], who shows that holds generically. However, how much knowing the propensity score improves the efficiency is still unclear. In this paper, we address this question, allowing for multivalued treatments and causal parameters defined via general moment conditions.

One of the key contributions of this paper is to obtain explicit formulas of (the main components of) the efficiency gains and when the propensity score is known to be stratified, as in the example above. This class of propensity scores appears in many empirical studies as reviewed below, and importantly, it covers cases where the propensity score depends only on categorical covariates. The formulas provide insightful implications about the efficiency gains. First, once we know how the covariate space is split, we can match observations that lie in the same region of the partition, which enables the efficient estimation of the parameters of interest conditional on each region. This leads to the efficiency improvement as it removes heterogeneity within each subclass. If we know the values of the propensity score in each region in addition to how the space is split, we can efficiently aggregate the local estimates we obtain, which makes the other improvement Because such estimates are biased in general, it is important to aggregate them so that their biases cancel each other out. When the partition is coarse (i.e., the model is small), the gain from matching observations within the same region is dominant, and consequently, is close to As the partition becomes finer (i.e., the model becomes larger), the matching effect decreases, so that knowing the partition becomes less beneficial, and and become similar.

The idea that as the parametric model of the propensity score gets larger, its bound also gets larger should hold beyond the stratified propensity score. Unfortunately, it is hard to obtain explicit formulas of efficiency gains for other parametric models, because involves a complicated matrix inversion, which is solvable only when the propensity score is stratified. Instead of relying on such formulas, we introduce a new framework. We first define a growing sequence of parametric models of the propensity score, keeping the “structure” of the model fixed. We then consider efficiency bounds along the sequence. We are interested in whether the limit of the sequence of efficiency bounds is equal to the nonparametric bound If it is, it implies that knowing the parametric structure is nearly equivalent to knowing nothing in terms of efficiency, especially when the model is high-dimensional. Otherwise, it means that the parametric structure intrinsically narrows down the space of possible propensity scores. Theorem 5.1 shows that approaches if and only if the set of scores of the parametric model approximates two specific functions that are composed of propensity scores and the mean regression functions of moment functions. This result implies the intuitive fact that if a parametric model is sufficiently flexible, then assuming it is almost equivalent to assuming a nonparametric model. More importantly, it also tells us that as long as the condition of Theorem 5.1 is satisfied, it may hold that even though the parametric model is not much flexible and does not approximate all functions in the nonparametric model. In other words, there are restrictive parametric models under which propensity scores are almost ancillary for estimating parameters of interest.

Related Literature. In the binary treatment setup, the propensity score method is proposed by [20] and [21]. [12] computes asymptotic variance bounds for the average treatment effect (ATE) and the ATT and proposes efficient estimators of them by applying the theory of semiparametric estimation ([19] and [1]). [14] give another efficient estimator called the inverse probability weighted estimator, of which finite sample performances are investigated in [13]. For the quantile treatment effect (QTE), which is often of interest for measuring inequality, [10] obtains similar efficiency results. In the missing data literature, [5] derive the semiparametric efficiency bound for the parameter conditional on the treated subpopulation when the propensity score is correctly specified by a parametric model.

Theoretical studies on the estimation of treatment effects in a multivalued treatment setup are initiated by [17], who generalizes the framework of Rosenbaum and Rubin. For efficient estimation, [3] provides the efficient influence function and the semiparametric efficiency bound for parameters defined via general moment conditions, extending results given by [12] and [14] in the binary setup. While [3] focuses on multivalued treatment effects on the whole population, [9] considers the efficient estimation of the average treatment effect on the treated, and [18] investigates efficiency bounds for multivalued treatment effects on subpopulation in general, but those for parametric propensity scores are not covered.

In a large fraction of empirical studies, the propensity score is modeled by a parametric model. In observational studies, where the propensity score is not available to analysts, the propensity score is often specified by the logit or probit model. See, for example, [22] and [16]. Even in experimental studies, an experiment designer often stratifies participants for the sake of estimation efficiency as in, for example, [8], [2] and [15]. Propensity scores in stratified experiments can be thought of as being parameterized by assigning probabilities on each stratum.

[12] points out that knowing the propensity score affects the semiparametric efficiency bound of the ATT, while it is ancillary for the estimation of the ATE. [11] explains why this happens qualitatively, which is valid even in multivalued treatment cases. The argument by [5], who examine the semiparametric efficiency bound when the propensity score is correctly specified by a parametric model in the binary setup, reveals that knowing the parametric model where the true propensity score lives improves the efficiency, but the amount of the improvement is unclear because the efficiency bound has an analytically complicated representation. In Section 4, we avoid this issue by focusing on the stratified experiment setup, which is analytically tractable. It is also noteworthy that our results also include a direct answer to the conjecture raised in page 325 of [12]: does the knowledge about the propensity score matter in stratified experiments?

To the best of our knowledge, [18] is the only study that investigates the value of the knowledge of the propensity score in the multivalued treatment setup. The paper does so by considering how propensity scores are incorporated into the efficient influence function. Although [18] is the closest work to this paper, the paper models the “partial knowledge” of the propensity score differently than we do. [18] considers the cases where an analyst knows the propensity scores for some treatments but not for the others. On the other hand, we think of the “partial knowledge” as in which parametric model the propensity score lives. In this regard, [18] and the present paper complement each other.

The theory we propose in Section 5 may look similar to the notion of sieves ([4]) in that both consider a growing sequence of parametric models. However, they have completely distinct goals. Sieves are typically used when the target parameter is defined as the solution of an infinite-dimensional optimization problem, which is difficult to compute in general. The sieve method considers a growing sequence of lower dimensional spaces that approximates the original space. By solving the problem constrained on the approximating space, it provides flexible and robust estimators of the infinite-dimensional parameter. On the other hand, this paper addresses the following question: if the true parameter lives in a low-dimensional parameter space, but an analyst assumes a high-dimensional model, how much efficiency would he or she lose? Thus, we are interested in any increasing sequence of parametric models, including one that does not approximate the nonparametric model.

2 Setup and Identification

Suppose that there are a finite number of treatments and corresponding potential outcomes assuming no interference. Let be a -valued random variable that indicates which treatment is assigned. The observed outcome is, therefore, where In addition, a random covariate vector which is fully supported on a set is also available to the analyst. The dataset consists of of all participants. Let and be the distributions of and respectively, which are not available to the analyst.

We describe the parameter of interest following [3] and [18]. Let be a nonempty set of subpopulation. The target parameter is where is defined as a solution of

for a known possibly nonsmooth moment function where allowing for over-identification. In what follows, we omit the subscript of parameters that indicates the conditioning set if it does not cause a confusion, so that and will be just written as and respectively.

To identify the parameter, we impose the following assumption.

Assumption 2.1.

For each is the unique solution of

This framework unifies many interesting causal parameters. In the binary treatment case for example, the ATE corresponds to and Similarly, one can deal with the ATT by considering For the moment function leads to the QTE at th quantile. Also, suppose that there are three treatments: and that a policy maker is considering abolishing treatments and and transferring people who are assigned to them to treatment In this case, she would be interested in the average potential outcome of treatment for those with and

The (generalized) propensity score is assumed to be correctly specified by a -dimensional smooth parametric model That is, for some In abuse of notation, we also denote and For let and

Following the literature, we assume the ignorability.

Assumption 2.2.

- (Unconfoundedness)

-

for all

- (Overlap)

-

There exists such that almost surely for all

The first condition ensures that one can compare outcomes with different treatments conditioning on covariates. The second condition is sufficient for identifying the parameter and for the semiparametric efficiency bound to be finite. Under Assumption 2.2, the parameter of interest is identified as

where Note that since is constant, it is irrelevant to the identification.

The score function for the parametric model of the propensity score is defined as

Similarly, let Note that in general. Let For the regularity of this parametric propensity score, we assume the following condition.

Assumption 2.3.

exists and is invertible.222For a column vector define

This condition essentially requires that the Fisher information is invertible, which guarantees that the parameterization is not degenerate, i.e., no components of are redundant. A similar condition is assumed in Theorem 3 of [5].

As in [3], we impose the following assumption.

Assumption 2.4.

For each it holds that and

is column full-rank.333We denote the Euclidean norm by

This is another condition for the finiteness of the efficiency bound. Note that we implicitly assume that is differentiable in although the moment function itself may be non-smooth.

3 Semiparametric Efficiency Bounds

3.1 Derivation

In this section, we derive the efficient influence function and semiparametric efficiency bound for in the framework offered by [1] and [12].

Fix Define functions and as

With these functions in hand, let where

for

The three functions, and are key components of the efficient influence function of that is derived in Theorem 3.1 below. They correspond to the scores of the distribution of conditional on and the propensity score, and the marginal distribution of respectively.

Also, let

which is the matrix that has on its block diagonal. Note that is column full-rank under Assumption 2.4. The following theorem gives the efficient influence function and efficiency bound of

Theorem 3.1.

This result is a direct generalization of Theorem 3 of [5] to the multivalued treatment environment. Indeed, when the treatment variable is binary (), our result coincides with theirs. Recall that [18] considers the efficiency in the cases where the propensity score is partially known, i.e., is known for some but not for others. On the other hand, we model the “partial knowldge” of the propensity score by imposing a parametric assumption.

Efficiency bounds are usually used to see whether a given estimator is semiparametrically efficient, i.e., no regular estimator has a smaller asymptotic variance than it does. In addition to this, they can be used to construct efficient estimators. For example, [3] proposes an efficient estimator of treatment effects based on the moment condition induced by the efficient influence function. In general, estimators based on efficient influence functions are often called debiased machine learning (DML) estimators and shown to be efficient in many examples ([6], [7]). DML estimators achieve the efficiency by debiasing biases that arise from estimating nuisance parameters, such as propensity scores. Efficient influence functions are useful for constructing efficient estimators, especially when nuisance parameters are high-dimensional and difficult to estimate.

3.2 Examples

Example 1.

Consider The propensity score is assumed to be correctly specified by a parametric model The efficiency bound of is

where 444 denotes the variance operator. and

In particular, for the case of and we obtain the efficiency bound for the ATT,

| (1) | ||||

This gives a counterpart of Theorem 1 of [12] when there is a parametric restriction on the propensity score.

Example 2.

For consider Then, the moment condition implies that is the -quantile of conditional on For a parametric propensity score the efficiency bound of is

where is the density of the distribution of conditional on and

When and a similar calculation yields the efficiency bound for the quantile treatment effect on the treated,

This is an analog of equation (10) of [10] when the propensity score is parametrically specified.

3.3 Basic Comparison

We compare the efficiency bound for a parametric model derived in Theorem 3.1 with the bounds for the cases where the propensity score is known or unknown. In this subsection, we overview preliminary comparison results.

According to Corollary 1 of [18], the counterparts of when the propensity score is known or unknown are and where

| (2) |

and

| (3) |

Therefore, the efficiency bounds are

respectively.

In what follows throughout the paper, we assume the just-identification, i.e., Although we are interested in the relationship among and we can focus on the comparison among and as for two positive semidefinite matrices and it holds

| (4) |

Considering the complexity of the models, it is qualitatively obvious that

| (5) |

First, consider the case of It holds that because it holds since

We also have as These observations lead to a well-known result: the relationship (5) holds all with equality. In other words, knowing the propensity score does not improve the efficiency, as discovered by [12] and [18].

In what follows, we assume unless stated otherwise. The connection between and can be understood geometrically.

Proposition 3.1.

The function is the projection of that is, for each the unique solution of

is given by

4 Efficiency Gains in Stratified Experiments

In this section, we take a quantitative approach to investigate how much a parametric restriction on the propensity score improves the efficiency bound of parameters of interest in stratified experiments. When the propensity score is known to be stratified, the efficient influence function and the semiparametric efficiency bound turn out to have closed forms. After deriving analytic formulas, we discuss efficiency gains from knowing the restriction on the propensity score.

Let us first define the class of stratified propensity scores. To do so, fix a measurable (disjoint) partition of the space of covariate vectors. Consider the following class of propensity scores

for some constants We call this form of propensity score a -stratified propensity score with partition This class is parameterized by -parameters that live in

The probabilities for are specified as for Let be the true propensity score. We denote

The class of stratified propensity scores covers many important situations. For example, it includes cases where the propensity score is known to depend only on categorical covariates such as race, gender, month of birth, city of residence, and so on. Even when covariates are continuous, people often discretize them in practice, which also falls within the scope of the current setting.

As in Section 3.3, let and be the efficiency bounds of when the propensity score is known, known to be -stratified by partition and unknown, respectively. We are interested in the relationship among these bounds, but thanks to (4), we focus on the comparison among and We regard as the efficiency gain (value) from knowing that the propensity score is -stratified, and similarly, is the value of knowing the propensity score on each subclass. The stratification structure allows us to obtain analytical formulas of these quantities.

Theorem 4.1.

It holds that

and

Remark 4.1.

The formulas in Theorem 4.1 are explicit in the sense that the matrix inversion that appears in is resolved. This happens only for the stratified propensity score and cannot be extended to other parametric models. The reason is as follows. Recall that we are interested in the inverse of

In general, it is difficult to find an explicit formula for the inverse of the sum of matrices, like the one in the RHS, and this causes a problem in most parametric models. For the stratified propensity score, however, the sum can be nicely decomposed into diagonal matrices, and it turns out to be explicitly invertible using the Woodbury formula. This calculation exploits the property of stratified experiments that the parameter affects the propensity score only on the th cell See Appendix A.3 for more technical details.

As we have discussed the case of in Section 3.3, we focus on in what follows. Notice that a -stratified propensity score coincides with a constant propensity score, in which cases treatments are assigned completely at random. As the two formulas in Theorem 4.1 suggest, for it holds

An implication of this result is that the knowledge that the propensity score is constant over the whole covariate space strictly improves the efficiency (), but full information of the propensity score does not bring any additional value (). This observation generalizes [12] that finds a similar fact in binary treatment cases.

In the stratified experiment setup, the value of imposing a parametric restriction captures the in-class variance while the additional value of pinning down the propensity score embodies the between-class bias. Too see this, suppose first that we know that the true propensity score is -stratified by a given partition. In this case, data in each subclass can be thought of as sample from a random assignment. It holds that

that is, the moment for subpopulation in each subclass can be estimated based on all data points including observations to which the treatments in are not assigned. Since all information in each subclass is exploited in this way, the knowledge of the partition removes the in-class efficiency loss.666[11] provides a similar observation for binary average treatment effects on the treated.

Even if the functional form of the propensity score is known, there may be another source of efficiency loss that we call the between-class bias. To see this, notice that

This decomposition implies that the moment function of interest is an aggregation of local conditional expectations in each subclass with a weight depending on the propensity score. Therefore, one cannot reproduce the moment function efficiently without knowing the exact values of the propensity score, which leads to efficiency loss. There is no loss in the absence of knowledge of the propensity score only when is constant or The former case does not hold generically. The latter is consistent with the result from [12], who shows that knowing that the propensity score is constant is the same as knowing its value in terms of efficiency, but our result also indicates that is just a special case in that the between-bias is zero despite the fact that the exact value of the propensity score is unavailable.

At the end of this section, we consider the behavior of the efficiency gain from knowing the partition when it is infinitely fine. Intuitively, if cells of the partition are tiny, just knowing the partition is almost useless because the in-class variance of each cell is small. This observation is justified in the following proposition by considering a nested sequence of partitions.

Proposition 4.1.

Let be an increasing sequence of natural numbers. For each let be a partition of satisfying the following condition: for any and there uniquely exists such that and Then, it holds that

On the other hand, if the partition is known to be coarse, the efficiency is improved, as the following proposition claims.

Proposition 4.2.

In the same setup as Proposition 4.1, assume Then, it holds that if is not constant on any open ball in

The assumption of Proposition 4.2 describes the situation where it is known that there is a unignorable region where assignments are completely at random. In this case, the propensity score is restricted to the space of functions that are constant on the region, which leads to an efficiency gain.

5 Efficiency Gains from Large Parametric Models

5.1 General Theory

We have shown in Section 3 that imposing a parametric restriction on the propensity score weakly improves estimation efficiency, but as shown in Propositions 4.1 and 4.2, the amount of the efficiency gain varies depending on the parametric model assumed. In order to see what kinds of parametric restrictions are valuable in terms of efficiency, it is helpful to compute the reduction in the efficiency bound as in Section 4. Unfortunately, however, it is hard to find an explicit formula of this quantity in general because it involves a convoluted matrix inversion in In this section, we take a more conservative approach, instead of calculating it explicitly. Specifically, we investigate how the amount of the efficiency improvement changes as the parametric model becomes infinitely “large.” To formally study asymptotics for parametric models, we first define a countably infinite-dimensional model, which is thought of as the “structure” of the parametric model, and then restrict it to obtain a sequence of finite-dimensional parametric submodels in a way that they are nested. We consider efficiency bounds along this sequence and see whether their limit attains the bound for the unknown propensity score. If it does, then it implies that imposing the parametric model is almost the same as estimating the propensity score nonparametrically, especially when is large, so that the parametric restriction does not help significantly in terms of efficiency. If the nonparametric bound is not attained even asymptotically, on the other hand, it means that the parametric structure intrinsically restricts the space of possible propensity scores.

As we have seen in the previous section, when there is no efficiency gain from knowing the propensity score. Since the object of interest here is the difference we assume throughout this section. We also assume otherwise, the knowledge about the propensity score does not matter too.

To describe situations where the number of parameters grows with the “structure” of a parametric model fixed, we consider a nested family of parametric models that is induced by a large base model. Let be a countably infinite-dimensional parameter space where which defines a base model of the propensity score, Let be an increasing sequence. Assume that the true propensity score is of finite dimension, i.e., for some Define a -dimensional parametric submodel of as

That is, the submodel is parameterized by the first elements of which is denoted by It is obvious that these models are nested in the sense that

where is the set of all possible propensity scores.

Let be the semiparametric efficiency bound in Theorem 3.1 when the propensity score is assumed to lie in Then, is nondecreasing in in the sense of positive semidefinite matrix since is nondecreasing. It is also bounded above by which is the semiparametric efficiency bound for so that the sequence converges to some positive definite matrix denoted by 777For the proof, see Appendix A.6. It holds in general that

The score of the parametric model is

Also, define a matrix valued function

For and let

where Note that is a vector consisting of at most two functions. In particular, its entries indexed by have and the others have

Now, we introduce the following condition.

Condition F.

For any and it holds that

As we see in Appendix A.7, the two functions and which form appear in the efficient influence function of under the nonparametric model It is also shown that the function is the counterpart of under the parametric model Therefore, Condition F implies that the sequence of efficient influence functions of the increasing parametric models converges to that of the nonparametric model.

It is intuitive that the efficiency bound of the limit parametric model is equal to that of the nonparametric model if the parametric model is sufficiently “flexible.” Condition F can be thought of as a criterion of such flexibility and is shown to characterize when a parametric restriction on the propensity score does not improve the efficiency bound asymptotically.

Theorem 5.1.

Condition F holds if and only if

Theorem 5.1 tells us that knowledge of a parametric restriction on the propensity score that violates Condition F is beneficial in terms of efficiency because it improves the efficiency bound even asymptotically, i.e., It also implies that as long as Condition F is satisfied, it may hold that even though In other words, restricting the space of propensity scores does not necessarily improve estimation efficiency.

5.2 Application to Logistic Propensity Scores

In this subsections, we give two examples that satisfy or violate Condition F for logistic propensity scores.

Full-rank logistic propensity scores. Consider a parameter

Let be a dictionary of functions of covariate Let

The object of interest here is a full-rank logistic propensity score that is defined as

for and In this example, the base model is By restricting the space of we can obtain a nested sequence of finite-dimensional parametric models as follows:

Note that is -dimensional where Suppose that the true propensity score is of order i.e., with the true parameter and the corresponding The following result provides a necessary and sufficient condition for the bound for this parametric model to approach the nonparametric bound.

Proposition 5.1.

For a full-rank logistic propensity score, if and only if the linear span of contains

for all and

An implication of this proposition is that if the true propensity score is indeed full-rank logistic with that spans knowing this does not improve the efficiency bound when the parametric model has many parameters. In other words, such a parametric restriction provides no efficiency gain asymptotically. However, the condition of the statement does not require to span in which case, the parametric model of the propensity score is restrictive compared to the nonparametric one. Proposition 5.1 claims that knowing unignorable aspects of the propensity score does not necessarily improve the efficiency.

Note that Proposition 5.1 is a similar result to Proposition 4.1. Both propositions tell us that if the propensity score is known to lie in a large parametric model, estimating parameters of interest in the parametric model is as hard as doing so nonparametrically.

Degenerate logistic propensity scores. As an example that violates Condition F, we define a degenerate logistic propensity score as

for where Note that does not depend on This model is obtained by restricting the parameter space of the full-rank logistic propensity score by setting Under this model, the propensity scores for are all identical.

Proposition 5.2.

For a degenerated logistic propensity score, if (i) and (ii)

To understand the assumption of the proposition, recall that Without loss, we may assume Then, condition (ii) is automatically satisfied; otherwise Condition (i) requires to have at least one element other than In the case of this is satisfied, for example, when we are interested in treatment effects on those who are assigned to Notice that condition (i) is never satisfied for binary treatments, (unless ). Indeed, holds for such cases, if the dictionary spans See Appendix A.9 for further details.

Proposition 5.2 implies that under the obviously verifiable conditions, the space of degenerated logistic propensity scores is restrictive, and consequently, assuming this structure improves the estimation efficiency even asymptotically.

Appendix A Proofs

A.1 Proof of Theorem 3.1

Proof.

We trace the approach given by [1] and [12]. We consider a semiparametric model such that

where is a density on for each and is a density on Consider a regular parametric submodel

with the true value and the corresponding score is

where

Thus, the tangent space of at the true parameter is where

where is the distribution of conditional on and denotes the space of square integrable functions with mean zero.

The moment condition implies that for any matrix it holds

On the parametric submodel, it holds

Differentiating both sides in we obtain

For any regular parametric submodel with score , it holds that

for each Thus, we have

Substituting gives the efficient influence function

The efficiency bound is, therefore, ∎

A.2 Proof of Proposition 3.1

Proof.

The solution coincides with that of

By the standard formula of least squares, the objective is minimized at

where the second equality follows since

holds. ∎

A.3 Proof of Theorem 4.1

We first derive the efficient influence function by applying Theorem 3.1.

Theorem A.1.

For the -stratified propensity score with partition the efficient influence function is given by that in Theorem 3.1 with

where and

Proof of Theorem A.1.

Notice that

for and

where is the -dimensional th unit vector and is the -dimensional vector of ones. Then, we have

and therefore,

One can also verify

where and is the matrix consisting of ones. To find its inverse, we use the following lemma.

Lemma A.1.

Let and for Then,

where

Using this lemma, we have

Thus, we obtain

which completes the proof. ∎

Proof of Lemma A.1.

Since we have

by the Woodbury formula, where

Then, one can also verify

which completes the proof. ∎

Proof of Theorem 4.1.

Remark A.1.

As we show in Proposition 3.1, and are orthogonal. It is easy to verify it in this specific example as follows.

A.4 Proof of Proposition 4.1

Proof.

Notice that

For the first parenthesis, we have

and similarly, for the second parenthesis, it holds that

Therefore, it holds that ∎

A.5 Proof of Proposition 4.2

Proof.

There exists a sequence such that is nonincreasing and Thus, there is an open ball such that It holds that

because is not constant on ∎

A.6 Convergence of a bounded and nondecreasing sequence of positive semidefinite matrices

We show the following statement.

Lemma A.2.

Let be a nondecreasing sequence of positive semidefinite matrices that is bounded above by another positive semidefinite matrix. Then, exists.

Proof.

For each a real sequence is nondecreasing and bounded, so that its limit exists. The conclusion holds because the element of can be written as

which converges. ∎

A.7 Proof of Theorem 5.1

Let

Also, let and where

for

The fact that follows by setting

Let and Notice that is the projection of onto by Proposition 3.1.

We show the following theorem, which immediately implies Theorem 5.1.

Theorem A.2.

The following are equivalent:

-

(1)

Condition F holds;

-

(2)

in

-

(3)

in the sense of positive semidefinite matrix.

Proof.

Let for and Then, it holds that

Since the LHS converges to zero as by (2), we have

Let Since is the projection of onto it holds

For the second term, since

it holds that

Therefore, we have

By taking the infimum over in the RHS, Condition F implies that

It is sufficient to show where denotes the Frobenius norm. It holds that

For each we have by (2),

which implies (3).

Since is the projection of onto it holds that

By we have

which implies ∎

Proof of Theorem 5.1.

It follows from the equivalence between conditions (1) and (3). ∎

A.8 Proof of Proposition 5.1

A.9 Proof of Proposition 5.2

Proof.

Let

In a similar manner to the proof of Proposition 5.1, it can be shown that

and for

As the rank of this vector is at most one, it cannot approximate unless it contains only one function, which is not the case if and Hence, we have the conclusion. ∎

Remark A.2.

When the treatment is binary (i.e., ), contains only one function. Thus, if the dictionary is rich enough, can approximate which implies that Condition F holds and

Appendix B Applying Theorem 5.1 to Stratified Propensity Scores

In this section, we apply the theory developed in Section 5 to stratified propensity scores. In Section 4, we have defined them as

where are parameters for a fixed partition Since this parameterization depends on the partition and does not fit the framework in Section 5, we need to redefine stratified propensity scores.

First, we construct a tree-diagram-like index. Let which is an index set at level For each let be an index set at level that follows Again, for each let be an index set at level that follows and define similar index sets sequentially. Let be the set of possible indices with size For example, if then and Finally, let be the set of all possible indices.

Consider a family of measurable subsets of the covariate space such that

Notice that gives a partition of for each and that it is nested in the sense that if then for any there uniquely exists such that (The first numbers of such are exactly ) In particular, is a partition of at level

Example 3.

Figure 1 describes such partitions up to level for As in the figure, it holds that

Let and We (re)define a stratified propensity score parameterized by where and for each as

| (6) |

for and The base model here is The induced nested parametric models are

and

Let us see why this parameterization makes sense to define a stratified propensity score. If is satisfied, the propensity score (6) can be written as

| (7) |

where

| (8) |

which implies that is stratified in the sense of Section 4. Conversely, suppose a propensity score satisfies (7) with parameters satisfying Then, there uniquely exists such that it satisfies the relationship (8). For these parameters, (7) is written as (6). Therefore, the parameterization (6) successfully represents the stratified propensity score.

Remark B.1.

One might wonder why we do not use directly, which seems more straightforward than using ’s. Unfortunately, this causes an over-parameterization problem. That is, for a given stratified propensity score, there are multiple parameters that produce it. This is why we put parameters on rather than

By applying Theorem 5.1 to this setup, we have the following proposition.

Proposition B.1.

For a stratified propensity score, if spans

Proof.

The score of is

and

Therefore, for

If spans then Condition F is satisfied. Hence, the conclusion follows. ∎

For to span each must get finer as the level of the index gets deeper. This statement implies that if this holds, knowing how the covariate space is split is not beneficial in terms of efficiency.

The following gives an insightful sufficient condition for a parametric restriction to improve the efficiency even asymptotically.

Proposition B.2.

For all and suppose that is not constant on any open ball in For a stratified propensity score, if

Proof.

Let Then, there exists a sequence such that and Let Since it contains an open ball, so that is not constant on Hence, cannot approximate on ∎

The condition on the partition holds if, for example, there is a part where the partition does not become finer than a certain level, or formally, if there exist and a sequence such that This is exactly when one assumes that the true propensity score is constant on an unignorable region which consequently restricts the space of possible propensity scores by removing the possibility that it takes different values there.

Appendix C Numerical Studies

In this section, we evaluate efficiency gains from knowing the propensity score numerically. For a binary treatment, we consider semiparametric efficiency bounds of the ATT, for different specifications. The setup, which is partly inspired by [18], is as follows. A two-dimensional covariate vector is uniformly distributed on Potential outcomes are and where and are drawn from independently of other variables. The true propensity score is

We assume the propensity score is known to be stratified. We consider the following two partitions:

-

(1)

for

-

(2)

and for

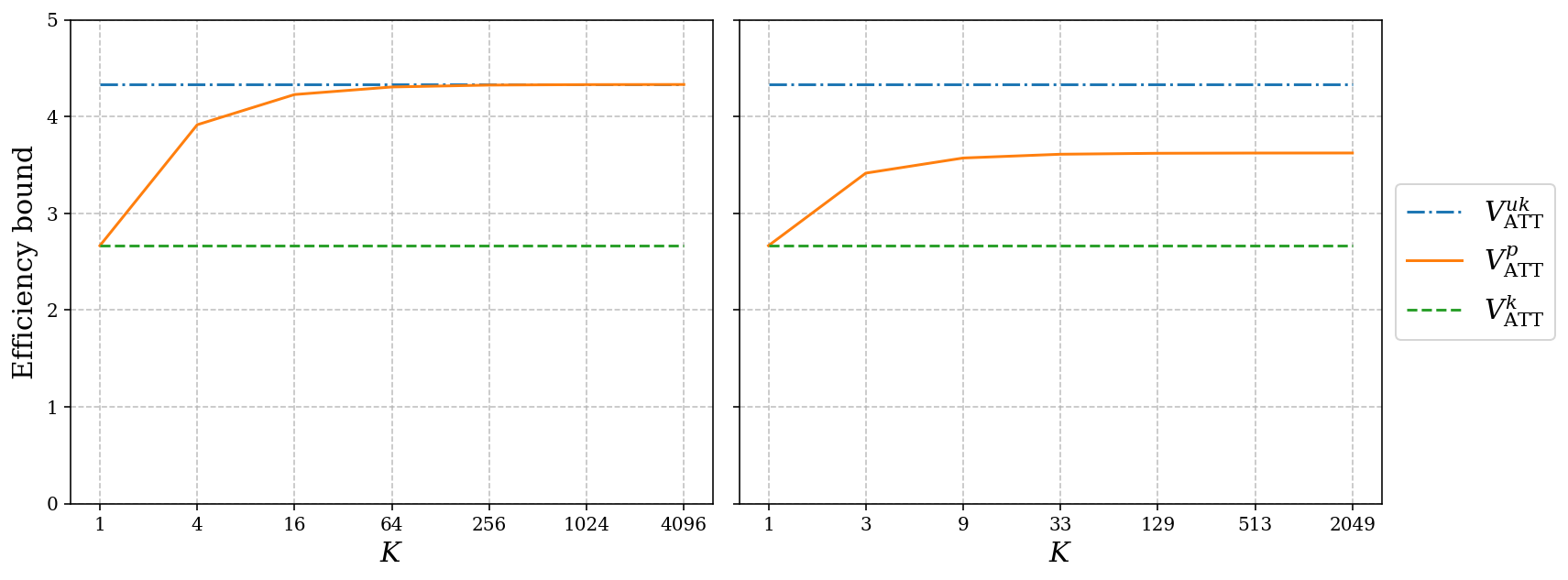

Partition (1) equally splits and each cell gets smaller as increases. By Proposition 4.1, we know that the efficiency gain from knowing the partition vanishes as goes to the infinity. In partition (2), on the other hand, the right half of remains coarse. By Proposition 4.2, the efficiency gain should stay positive even for large Note that the number of cells in partition (1) is while that of partition (2) is if and if From Theorem A.1 and the formula (1) of the efficiency bound of ATT, for a given partition we have and

Figure 2 reports the three efficiency bounds for different partitions. As the theory predicts, approaches zero as becomes large in the left panel while it remains positive in the right panel. In the left panel, we see that the value of knowing the partition drops drastically, as increase from to which implies that even relatively coarse partitions deteriorate the efficiency a lot. In the right panel, the efficiency gain for large can be interpreted as the value of knowing that the propensity score is constant on the right half of

References

- [1] PJ Bickel, CAJ Klaassen, Y Ritov and JA Wellner “Efficient and adaptive estimation for semiparametric models” Springer, 1993

- [2] Federico A Bugni, Ivan A Canay and Azeem M Shaikh “Inference under covariate-adaptive randomization with multiple treatments” In Quantitative Economics 10.4 Wiley Online Library, 2019, pp. 1747–1785

- [3] Matias D Cattaneo “Efficient semiparametric estimation of multi-valued treatment effects under ignorability” In Journal of Econometrics 155.2 Elsevier, 2010, pp. 138–154

- [4] Xiaohong Chen “Large sample sieve estimation of semi-nonparametric models” In Handbook of econometrics 6 Elsevier, 2007, pp. 5549–5632

- [5] Xiaohong Chen, Han Hong and Alessandro Tarozzi “Semiparametric efficiency in GMM models with auxiliary data” In The Annals of Statistics 36.2 Institute of Mathematical Statistics, 2008, pp. 808–843

- [6] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey and James Robins “Double/debiased machine learning for treatment and structural parameters.” In Econometrics Journal 21.1, 2018

- [7] Victor Chernozhukov, Juan Carlos Escanciano, Hidehiko Ichimura, Whitney K Newey and James M Robins “Locally robust semiparametric estimation” In Econometrica 90.4 Wiley Online Library, 2022, pp. 1501–1535

- [8] Alberto Chong, Isabelle Cohen, Erica Field, Eduardo Nakasone and Maximo Torero “Iron deficiency and schooling attainment in Peru” In American Economic Journal: Applied Economics 8.4 American Economic Association 2014 Broadway, Suite 305, Nashville, TN 37203-2425, 2016, pp. 222–255

- [9] Max H Farrell “Robust inference on average treatment effects with possibly more covariates than observations” In Journal of Econometrics 189.1 Elsevier, 2015, pp. 1–23

- [10] Sergio Firpo “Efficient semiparametric estimation of quantile treatment effects” In Econometrica 75.1 Wiley Online Library, 2007, pp. 259–276

- [11] Markus Frölich “A note on the role of the propensity score for estimating average treatment effects” In Econometric Reviews 23.2 Taylor & Francis, 2004, pp. 167–174

- [12] Jinyong Hahn “On the role of the propensity score in efficient semiparametric estimation of average treatment effects” In Econometrica JSTOR, 1998, pp. 315–331

- [13] Andrew Herren and P Richard Hahn “On true versus estimated propensity scores for treatment effect estimation with discrete controls” In arXiv preprint arXiv:2305.11163, 2023

- [14] Keisuke Hirano, Guido W Imbens and Geert Ridder “Efficient estimation of average treatment effects using the estimated propensity score” In Econometrica 71.4 Wiley Online Library, 2003, pp. 1161–1189

- [15] Han Hong, Michael P Leung and Jessie Li “Inference on finite-population treatment effects under limited overlap” In The Econometrics Journal 23.1 Oxford University Press, 2020, pp. 32–47

- [16] Kosuke Imai and David A Van Dyk “Causal inference with general treatment regimes: Generalizing the propensity score” In Journal of the American Statistical Association 99.467 Taylor & Francis, 2004, pp. 854–866

- [17] Guido W Imbens “The role of the propensity score in estimating dose-response functions” In Biometrika 87.3 Oxford University Press, 2000, pp. 706–710

- [18] Ying-Ying Lee “Efficient propensity score regression estimators of multivalued treatment effects for the treated” In Journal of Econometrics 204.2 Elsevier, 2018, pp. 207–222

- [19] Whitney K Newey “Semiparametric efficiency bounds” In Journal of applied econometrics 5.2 Wiley Online Library, 1990, pp. 99–135

- [20] Paul R Rosenbaum and Donald B Rubin “The central role of the propensity score in observational studies for causal effects” In Biometrika 70.1 Oxford University Press, 1983, pp. 41–55

- [21] Paul R Rosenbaum and Donald B Rubin “Reducing bias in observational studies using subclassification on the propensity score” In Journal of the American statistical Association 79.387 Taylor & Francis, 1984, pp. 516–524

- [22] Shu Yang, Guido W Imbens, Zhanglin Cui, Douglas E Faries and Zbigniew Kadziola “Propensity score matching and subclassification in observational studies with multi-level treatments” In Biometrics 72.4 Wiley Online Library, 2016, pp. 1055–1065