NFT.mine: An xDeepFM-based Recommender System for Non-fungible Token (NFT) Buyers

Abstract.

Non-fungible token (NFT) is a tradable unit of data stored on the blockchain which can be associated with some digital asset as a certification of ownership. The past several years have witnessed the exponential growth of the NFT market. In 2021, the NFT market reached its peak with more than $40 billion trades. Despite the booming NFT market, most NFT-related studies focus on its technical aspect, such as standards, protocols, and security, while our study aims at developing a pioneering recommender system for NFT buyers. In this paper, we introduce an extreme deep factorization machine (xDeepFM)-based recommender system, NFT.mine111Source code available at https://github.com/wallerli/NFT.mine, which achieves real-time data collection, data cleaning, feature extraction, training, and inference. We used data from OpenSea, the most influential NFT trading platform, to testify the performance of NFT.mine. As a result, experiments showed that compared to traditional models such as logistic regression, naive Bayes, random forest, etc., NFT.mine outperforms them with higher AUC and lower cross entropy loss and outputs personalized recommendations for NFT buyers.

1. Introduction

1.1. Overview of Non-fungible Token (NFT)

Non-fungible token (NFT) is a unit of data stored on the blockchain (Wilson et al., 2021), which can be used as a certification of ownership associated with some digital asset because of its cryptographic characteristics, including uniqueness, indivisibility, transferability, and encipherment protection (Wang et al., 2021).

Blockchain is the core technology of NFT, which can be regarded as one kind of distributed database system where transaction information is stored with encoding and each transaction can be validated by all blockchain users (Nofer et al., 2017).

Compared to other blockchain-based cryptocurrencies such as Bitcoin (BTC), Dogecoin (DOGE), Ethereum (ETH), etc. (Hayes, 2022), NFT is the most ideal choice to identify the uniqueness of digital commodities, since classical cryptocurrencies are not distinguishable (Nakamoto, 2008). For example, two BTCs can be completely identical and exchangeable. In contrast, the intrinsic non-fungible attribute of NFT enables its owner to prove the ownership in a transparent form, as every historical transaction is retrievable (Wood et al., 2014).

Besides blockchain, smart contract and encoding are also crucial technologies for NFT. The idea of smart contract was first introduced for efficient digital negotiations and was widely implemented in Ethereum systems (Szabo, 1996). It provides a standard decentralized method for digital currency exchange. Based on consistently shared parameters and instructions across the distributed nodes, smart contract makes transactions transparent across multi-parties, which forms the foundation of NFT trading (Evans, 2019).

Encoding is widely used to realize blockchains and smart contracts. By converting transaction information into compressed and encrypted data, transaction history can only be decoded and validated by owners with private keys (e.g. hex-value keys) (Wood et al., 2014).

NFT has a lot of advantages because of its decentralized architecture, (Wang et al., 2021) and these advantages make NFT an emerging and promising technology for many real-world applications. For example, traditional online ticketing usually needs the help of a trusted third party, such as TicketMaster (Zynda, 2004), while NFT-based ticketing is an efficient and safe solution for online ticketing without any trusted third party (Wang et al., 2021). Metaverse is a new concept developed recently, where people are connected in a virtual world that operates like the real society (Mystakidis, 2022). In metaverse, NFT is a tool for transactions, some well-known NFT-empowered metaverses are Sandbox 222https://sandboxvr.com/ and Decentraland 333https://decentraland.org/. In addition to online ticketing and metaverse, NFT is also widely used for digital assets trading on online platforms, such as OpenSea 444https://opensea.io/, which we will mention later.

1.2. The NFT Market

In 2021, the NFT market reached a historical record-break high, as nearly $41 billion worth of cryptocurrency trades were made (Versprille, 2022). Looking back on the development of NFT, the first noticeable and popular NFT-based trading example is CryptoKitties, a game that allows its players to buy, breed, and sell virtual pets on Ethereum (Wong, 2017). However, for nearly 2 years since CryptoKitties, the NFT market didn’t see much expansion. It was not until July 2020, an artist called Beeple auctioned an NFT of his creation at Christie’s for more than $69 million (Riegelhaupt, 2021), the NFT market experienced an explosive growth.

The items traded on the NFT market are called collections, which can be clustered into 6 categories: art, collectible, games, metaverse, other, and utility (Nadini et al., 2021). Based on these 6 categories, Nadini et al. (Nadini et al., 2021) analyzed each category’s share of volume and transactions with respect to time, distribution of NFT prices across different categories, and frequencies of individual assets exchanges. As a result, the NFT market is continuously growing, pricing of NFT is complicated as NFT prices fluctuate a lot, and NFT buyers form clear clusters. Therefore, a recommender system for NFT buyers is essential and profitable, because it can help buyers to locate the most attractive NFTs for them at reasonable prices.

1.3. Recommender System

A recommender system is a subclass of information filtering system (Ricci et al., 2011) that receives user information such as ratings, preferences, search results, and generates personalized recommendations to a collection of users for commodities that might attract their eyes (Melville and Sindhwani, 2010). Collaborative filtering, content-based recommendation, hybrid recommendation are three most commonly used models for a recommender system (Adomavicius and Tuzhilin, 2005).

In recent years, deep learning played an important role in recommender systems, and it was proved to be a feasible choice to improve recommendation performance (Zhang et al., 2019). In this study, we introduce NFT.mine that uses deep learning for NFT recommendation. NFT.mine receives trading records collected in real-time from OpenSea platform, interprets NFT features by xDeepFM-based architect, and outputs personalized recommendations for each NFT buyer in the market.

2. Related Work

In this section, we introduce some previous studies on NFT and recommender systems that provide us with incisive insights into this study.

Many studies focus on the methodologies for NFT market analysis. One example is mentioned above in Section 1.2, which is Nadini et al.’s (Nadini et al., 2021) study based on NFT categorization and market analysis as a function of time. Similar to Nadini et al.’s study, Wang et al. (Wang et al., 2021) used primary-sales and secondary-sales data to investigate the NFT market’s activity. Other studies combine the analysis of the NFT market with cryptocurrencies. For example, Michael Dowling (Dowling, 2021) defined a spillover index and found the influence of volatility transmission effect between cryptocurrencies and NFT trading is not significant, while his wavelet coherence analysis suggests a correlation between cryptocurrencies and NFTs. Lennart Ante (Ante, 2021) proposed a vector autoregressive (VAR) framework to understand the interrelationships between NFT sales, NFT users, and pricings of cryptocurrencies; as a result, Ante concluded that the NFT market is dependent on the cryptocurrency market.

NFT pricing and sales prediction is another heated topic. For example, Michael Dowling (Dowling, 2022) collected 4,936 secondary market trades data in Decentraland (a blockchain virtual world) and used automatic variance ratio (AVR) test, automatic portmanteau (AP) test, and Domínguez and Lobato (DL) (Dominguez and Lobato, 2003) consistent test to price NFTs. Nadini et al. (Nadini et al., 2021) constructed a linear regression model to estimate the primary-sales and secondary-sales of NFTs. Besides the simplest linear regression model, other more complicated models can also be used to price NFTs. An example is Schnoering and Inzirillo (Schnoering and Inzirillo, 2022), they built a multiplicative pricing model based on the scale price, assets traits, scarcity of assets, and global state of the NFT market. As a result, the multiplicative pricing model can be applied for diagnostic tests, dynamics analysis, and performance evaluation of the NFT market.

Based on studies about NFT market analysis and NFT pricing and sales prediction, we summarized methodologies for data preprocessing and exploratory data analysis (EDA) and implemented these methodologies in our study. The data preprocessing and EDA parts will be introduced in detail in Section 3.

Studies that focus particularly on recommender systems for NFT buyers are rare, but studies that investigate recommender systems with deep learning techniques can provide us with some incisive information. Zhang et al. (Zhang et al., 2019) summarized two deep learning-based recommendation categories, recommendation with neural building blocks and recommendation with deep hybrid models. For the first category, different neural networks are used for different purposes. For example, MLP learns feature extraction well, which was utilized by Covington et al. (Covington et al., 2016) for YouTube recommendation and Alashkar et al. (Alashkar et al., 2017) for makeup recommendation. For the second category, different deep learning techniques are combined together to build more powerful recommender systems. For example, our proposed recommender system, NFT.mine, is based on extreme deep factorization machine (xDeepFM) proposed by Lian et al. (Lian et al., 2018).

3. Dataset Preparation

3.1. Dataset Collection

We conducted comprehensive research on the NFT market and concluded that the most popular NFT trading platform that is open to data collection is OpenSea. OpenSea API is open for developers and allows developers to get asset, event, account, and collection information.

Based on OpenSea API, we developed a real-time Python scraper that retrieves each NFT transaction event at each timestamp, then saved the collected data as a JSON file for data cleaning and EDA.

| Feature | Meaning | # of Unique Values | Most Frequent Value |

|---|---|---|---|

| asset_id | Asset ID | 309,383 | 381803879 (550 times) |

| num_sales | Number of sales associated with the asset | 23 | 1 (175,180 times) |

| asset_image_url | Asset image URL | 232,517 | https://lh3.googleusercontent.com/… (3,984 times) |

| asset_name | Asset name | 255,065 | Life (4,233 times) |

| asset_address | Asset contract address | 4,595 | 0x582048c4077a34e7c3799962f1f8c… (8,633 times) |

| collection_slug | Collection category | 4,669 | galverse (8,633 times) |

| created_date | Timestamp of the transaction | 368,693 | 2022-04-16T02:32:03.169797 (2 times) |

| event_type | Status of the transaction | 2 | successful (363,070 times) |

The dataset used in this paper contains 396,707 NFT transaction records from OpenSea database with 185 features from 12 April 2022 to 17 April 2022.

Table 1 lists some important features of the OpenSea dataset, which includes feature meaning, number of unique values, and the most frequent value of each feature.

3.2. Data Cleaning

After data collection, we did data cleaning. successful and bid_withdrawn are two event types (event_type) from which we could get sufficient features. successful means a transaction was completed successfully, bid_withdrawn means the NFT buyer withdrew his/her bid and the transaction was canceled. We set the label of both event types to 1 as the buyer shows transaction interest. We then generated all combinations of user and NFT asset pairs and sampled data associated with label 0, which means a NFT buyer shows no interest in buying a particular NFT.

Besides target variable selection, we did date-time alignment, empty rate calculation, and obtained each feature’s most popular values. We conducted date-time alignment to make sure all transaction timestamps fall between 2022-04-12 15:00 to 2022-04-17 21:00. Afterwards, we removed columns that have a large proportion of empty entries by calculating the empty rate () of each column. We set a threshold of 0.25 and removed features with an empty rate larger than 0.25 from the set of training features. After this step, we obtained the number of unique values of each feature and the most frequent values to have a general idea of the training features.

3.3. Exploratory Data Analysis (EDA)

3.3.1. Univariate Analysis

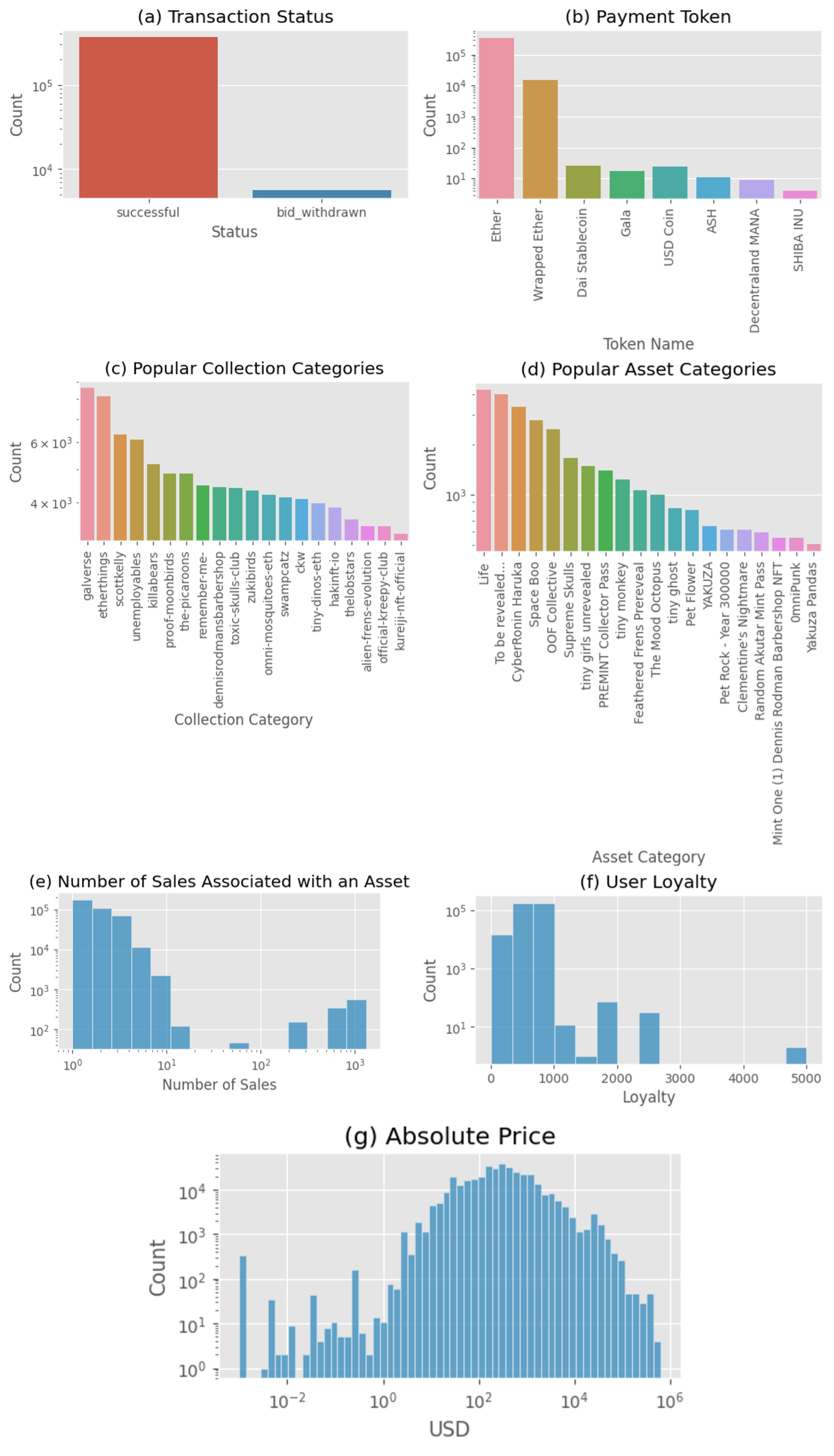

Exploratory data analysis (EDA) in this study contains four parts. For the first part, univariate analysis, we focused on features such as transaction status, payment token, user loyalty, number of sales associated with an asset, etc., to find out patterns in the OpenSea dataset.

As a result, we found that most transactions are labeled successful (Fig.2.a) and the top two payment tokens are Ether and Wrapped Ether (Fig.2.b); the most popular collection categories are galverse, etherthings, scottkelly, etc. (Fig.2.c) and the most popular asset categories are Life, To be revealed, CyberRonin Haruka, etc. (Fig.2.d); for each transaction, the number of sales associated with the asset is around 1 to 10 (Fig.2.e) and the user loyalty falls between 0 to 1,000 (Fig.2.f); in addition, we visualized the distribution of absolute NFT prices in USD (Fig.2.g) and found that the majority of sales are at a price from 10 USD to 10,000 USD.

3.3.2. Correlation Analysis

We conducted pairwise correlation analysis for feature selection.

As a result, we picked 22 features and found that asset_loyalty highly correlates with collection_loyalty and abosolute_price and total_price also have a strong positive correlation (Fig.3). These highly correlated features bring no additional information, so we dropped some redundant features to reduce the model complexity.

3.3.3. Bivariate Analysis

We visualized the relationships between price and transaction status (Fig4.a) and price and payment type (Fig4.b). From the box plots, we can tell that bid_withdrawn transactions correspond to a higher mean price than successful ones, while different payment types correspond to different mean prices.

3.3.4. Multivariate analysis

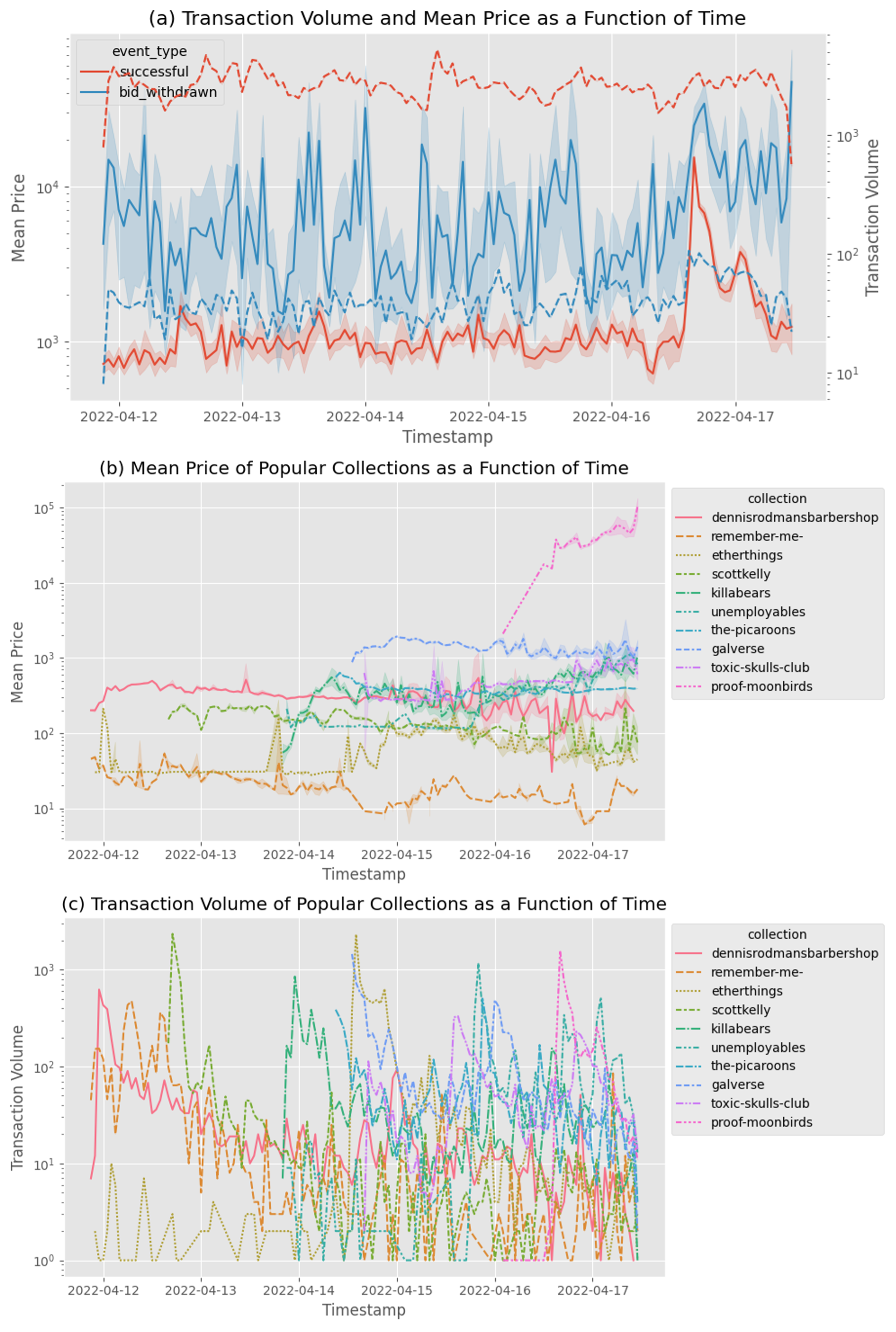

We also conducted multivariate analysis and plotted the market trend as a function of time (Fig.5).

4. Approach

This section introduces our proposed xDeepFM-based recommender system, NFT.mine. We first compare the performance of NFT.mine with other baseline models by various metrics. Then we explain the architecture and functionalities of NFT.mine. Because xDeepFM is capable of interpreting deep factorization of the data features, we can use it to develop the first-ever high-performing recommender system for NFT buyers, which is a pioneering work in this area.

4.1. Baseline Models

4.1.1. Logistic Regression (LR)

LR predicts the probability of an event by sigmoid function with a linear combination of inputs (Wright, 1995). We implemented LR using LogisticRegression from sklearn library.

4.1.2. Naive Bayes (NB)

NB assumes independence between input features and can be used for probability estimation (Lowd and Domingos, 2005). We implemented NB using GaussianNB from sklearn library.

4.1.3. Random Forest (RF)

RF is an ensemble learning method for classification (Belgiu and Drăguţ, 2016). We implemented RF using RandomForestClassifier from sklearn library.

4.2. Evaluation Metrics

4.2.1. Area under the ROC Curve (AUC)

AUC measures the area underneath the ROC curve, ranging from 0 to 1, higher AUC value represents better performance.

4.2.2. Cross Entropy Loss (Logloss)

Logloss measures the difference between predicted labels and true labels, lower Logloss value represents better performance.

4.3. NFT.mine

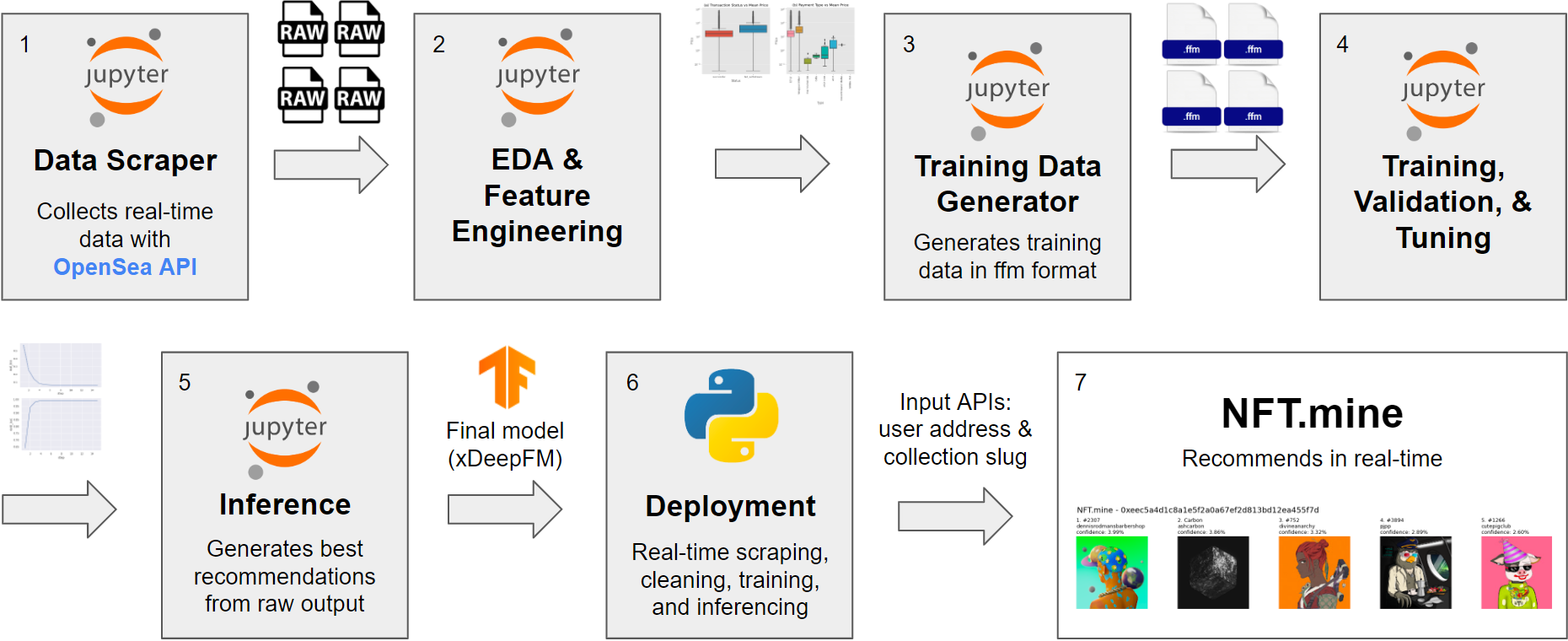

NFT.mine is an end-to-end recommender system, including real-time data collection, data analysis, feature selection, model training, and model inference (Fig.6). There are five modules in NFT.mine, including Python scrapper, EDA module, dataset module, server module, and xDeepFM model.

We built NFT.mine based on (rec, [n.d.]). We integrated significant modifications, including metric collection, hyperparameter tuning, and performance validation to the xDeepFM recommender, which is composed of an embedding layer, a compressed interaction network (CIN), a deep neural network (DNN), and a linear network.

The input features are in FFM format, including the buyer’s address, total amount, collection slug, etc. After the training stage, the trained model is stored on cloud where the server loads from.

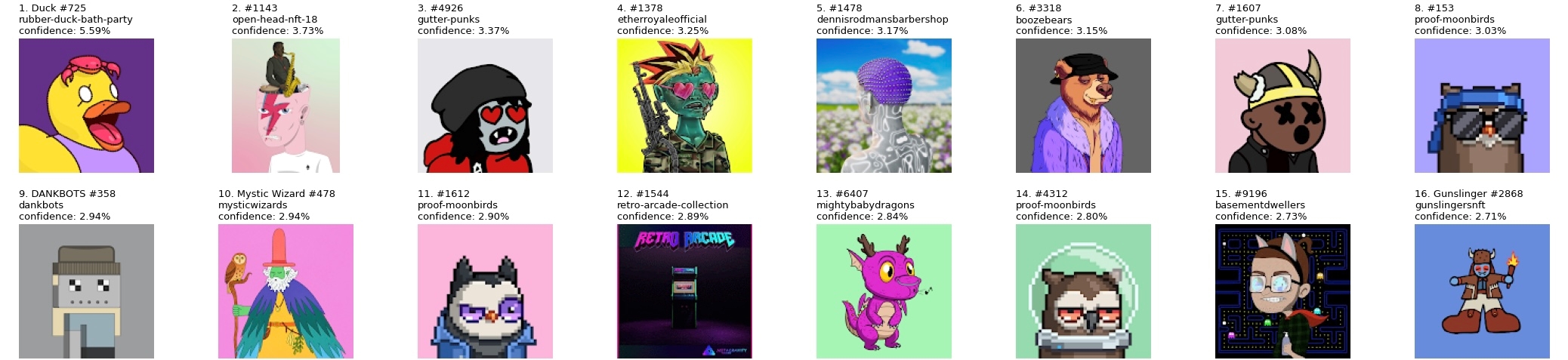

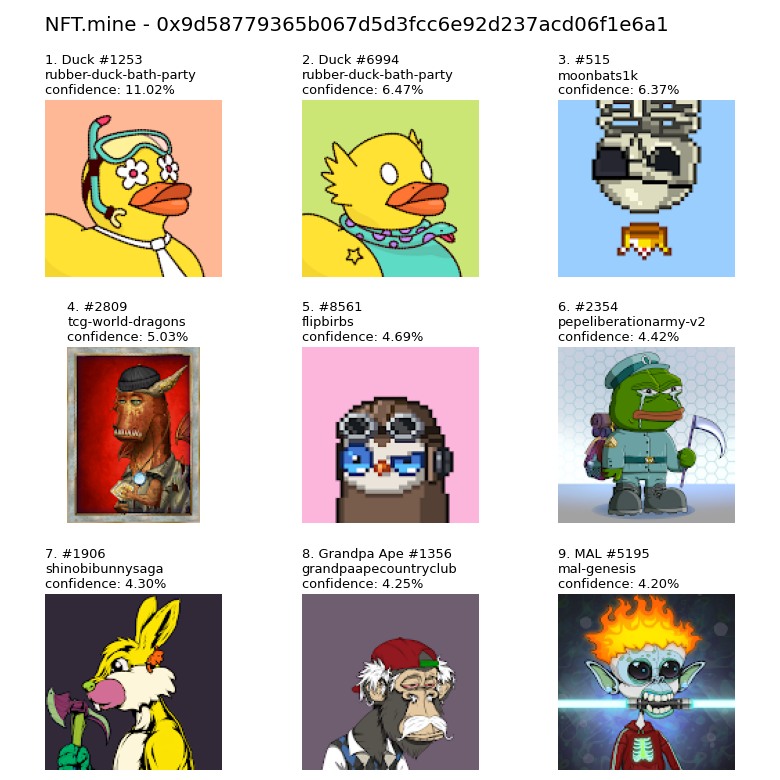

The server module receives user information as its input and outputs the recommended NFTs. The recommended NFTs are inferred based on the trained model. NFT.mine pairs users to NFTs and inputs these pairs into xDeepFM to obtain a series of probabilities. The NFTs are sorted by probabilities and NFT.mine returns the top-K recommended NFTs (Fig.7).

If a user only wants to get the recommended NFTs from a certain collection, he/she could specify the collection and the results only include NFTs from that collection (Fig.8).

5. Evaluation

In this section, we introduce how to build NFT.mine as an end-to-end recommender system, including environment setup, dataset preparation, training and inference setup, and recommendation performance.

5.1. Experiment Setup

We used utilities provided by Microsoft, which support several common tasks for a recommender system, including loading datasets in different formats for different algorithms, splitting training and test datasets, and evaluating model outputs. We used TensorFlow 2.8.0 version for experiments.

5.1.1. Asset-based and Collection-based Datasets

For dataset preparation, we used two different methods to split raw data into an asset-based dataset and a collection-based dataset. For asset-based dataset, we grouped data by asset_name, so each line represents one kind of NFT asset. For collection-based dataset, we grouped data by collection_slug, so each line represents one kind of NFT collection.

Because xDeepFM receives input data in FFM format: ¡label¿ ¡field_id¿:¡feature_id¿:¡feature_value¿, before feeding data into NFT.mine, we first converted raw data into FFM format by an open-source libffm tool.

5.1.2. Training and Inference

After dataset preparation and format conversion, we split both asset-based and collection-based datasets into training (90%), validation (10%), and test (10%) sets. Then we ran NFT.mine on these datasets. In addition, We implemented baseline models, including linear regression, decision tree, and random forest using sklearn and ran baseline models on the raw dataset.

5.2. Experiment Results

| Model | AUC | Logloss |

|---|---|---|

| NB | 0.9360 | 0.1908 |

| RF | 0.9429 | 0.4747 |

| LR | 0.9708 | 0.3275 |

| xDeepFM | 0.9943 | 0.0532 |

Table 2 shows AUC and Logloss for baseline models versus xDeepFM. Among all baseline models, the best AUC is 97% and Logloss is 0.19. For xDeepFM, AUC reaches 99% and Logloss drops to 0.053. During the experiments, the training loss dropped to almost 0 after epoch 10, evaluation loss dropped to almost 0 after epoch 6, and AUC climbed up to around 1 after epoch 4.

Based on the experiment results, we succeeded in improving our recommender’s accuracy by 5% more compared with traditional approaches.

6. Conclusion

NFT.mine is a pioneering work in NFT recommendation. We built an end-to-end NFT recommender system, which pulls the latest data from OpenSea, performs exploratory data analysis, executes model training and inference, and outputs personalized NFT recommendations. NFT.mine achieves an AUC of 99.4% and Logloss of 0.05.

References

- (1)

- rec ([n.d.]) [n.d.]. Microsoft Recommenders. https://github.com/microsoft/recommenders.

- Adomavicius and Tuzhilin (2005) Gediminas Adomavicius and Alexander Tuzhilin. 2005. Toward the next generation of recommender systems: A survey of the state-of-the-art and possible extensions. IEEE transactions on knowledge and data engineering 17, 6 (2005), 734–749.

- Alashkar et al. (2017) Taleb Alashkar, Songyao Jiang, Shuyang Wang, and Yun Fu. 2017. Examples-rules guided deep neural network for makeup recommendation. In Proceedings of the AAAI conference on artificial intelligence, Vol. 31.

- Ante (2021) Lennart Ante. 2021. The non-fungible token (NFT) market and its relationship with Bitcoin and Ethereum. Available at SSRN 3861106 (2021).

- Belgiu and Drăguţ (2016) Mariana Belgiu and Lucian Drăguţ. 2016. Random forest in remote sensing: A review of applications and future directions. ISPRS journal of photogrammetry and remote sensing 114 (2016), 24–31.

- Covington et al. (2016) Paul Covington, Jay Adams, and Emre Sargin. 2016. Deep neural networks for youtube recommendations. In Proceedings of the 10th ACM conference on recommender systems. 191–198.

- Dominguez and Lobato (2003) Manuel A Dominguez and Ignacio N Lobato. 2003. Testing the martingale difference hypothesis. Econometric Reviews 22, 4 (2003), 351–377.

- Dowling (2021) Michael Dowling. 2021. Is non-fungible token pricing driven by cryptocurrencies? Finance Research Letters (2021), 102097.

- Dowling (2022) Michael Dowling. 2022. Fertile LAND: Pricing non-fungible tokens. Finance Research Letters 44 (2022), 102096.

- Evans (2019) Tonya M Evans. 2019. Cryptokitties, cryptography, and copyright. AIPLA QJ 47 (2019), 219.

- Hayes (2022) Adam Hayes. 2022. 10 Important Cryptocurrencies Other Than Bitcoin. (March 2022). https://www.investopedia.com/tech/most-important-cryptocurrencies-other-than-bitcoin/

- Lian et al. (2018) Jianxun Lian, Xiaohuan Zhou, Fuzheng Zhang, Zhongxia Chen, Xing Xie, and Guangzhong Sun. 2018. xdeepfm: Combining explicit and implicit feature interactions for recommender systems. In Proceedings of the 24th ACM SIGKDD international conference on knowledge discovery & data mining. 1754–1763.

- Lowd and Domingos (2005) Daniel Lowd and Pedro Domingos. 2005. Naive Bayes models for probability estimation. In Proceedings of the 22nd international conference on Machine learning. 529–536.

- Melville and Sindhwani (2010) Prem Melville and Vikas Sindhwani. 2010. Recommender systems. Encyclopedia of machine learning 1 (2010), 829–838.

- Mystakidis (2022) Stylianos Mystakidis. 2022. Metaverse. Encyclopedia 2, 1 (2022), 486–497.

- Nadini et al. (2021) Matthieu Nadini, Laura Alessandretti, Flavio Di Giacinto, Mauro Martino, Luca Maria Aiello, and Andrea Baronchelli. 2021. Mapping the NFT revolution: market trends, trade networks, and visual features. Scientific reports 11, 1 (2021), 1–11.

- Nakamoto (2008) Satoshi Nakamoto. 2008. Bitcoin: A peer-to-peer electronic cash system. Decentralized Business Review (2008), 21260.

- Nofer et al. (2017) Michael Nofer, Peter Gomber, Oliver Hinz, and Dirk Schiereck. 2017. Blockchain. Business & Information Systems Engineering 59, 3 (2017), 183–187.

- Ricci et al. (2011) Francesco Ricci, Lior Rokach, and Bracha Shapira. 2011. Introduction to recommender systems handbook. In Recommender systems handbook. Springer, 1–35.

- Riegelhaupt (2021) Rebecca Riegelhaupt. 2021. Beeple’s Purely Digital NFT-Based Work of Art Achieves $69.3 M at Christie’s. (11 March 2021). https://www.christies.com/about-us/press-archive/details?PressReleaseID=9970&lid=1

- Schnoering and Inzirillo (2022) Hugo Schnoering and Hugo Inzirillo. 2022. Constructing a NFT Price Index and Applications. arXiv preprint arXiv:2202.08966 (2022).

- Szabo (1996) Nick Szabo. 1996. Smart contracts: building blocks for digital markets. EXTROPY: The Journal of Transhumanist Thought,(16) 18, 2 (1996), 28.

- Versprille (2022) Allyson Versprille. 2022. NFT Market Surpassed $40 Billion in 2021. (6 January 2022). https://www.bloomberg.com/news/articles/2022-01-06/nft-market-surpassed-40-billion-in-2021-new-estimate-shows

- Wang et al. (2021) Qin Wang, Rujia Li, Qi Wang, and Shiping Chen. 2021. Non-fungible token (NFT): Overview, evaluation, opportunities and challenges. arXiv preprint arXiv:2105.07447 (2021).

- Wilson et al. (2021) Kathleen Bridget Wilson, Adam Karg, and Hadi Ghaderi. 2021. Prospecting non-fungible tokens in the digital economy: Stakeholders and ecosystem, risk and opportunity. Business Horizons (2021).

- Wong (2017) Joon Ian Wong. 2017. The ethereum network is getting jammed up because people are rushing to buy cartoon cats on its blockchain. (4 December 2017). https://qz.com/1145833/cryptokitties-is-causing-ethereum-network-congestion/

- Wood et al. (2014) Gavin Wood et al. 2014. Ethereum: A secure decentralised generalised transaction ledger. Ethereum project yellow paper 151, 2014 (2014), 1–32.

- Wright (1995) Raymond E Wright. 1995. Logistic regression. (1995).

- Zhang et al. (2019) Shuai Zhang, Lina Yao, Aixin Sun, and Yi Tay. 2019. Deep learning based recommender system: A survey and new perspectives. ACM Computing Surveys (CSUR) 52, 1 (2019), 1–38.

- Zynda (2004) Tarra Zynda. 2004. Ticketmaster Corp. v. Tickets. com, Inc.-Preserving Minimum Requirements of Contract on the Internet. Berkeley Tech. LJ 19 (2004), 495.