Data-Driven Online Model Selection With Regret Guarantees

Aldo Pacchiano Christoph Dann Claudio Gentile

Boston University Broad Institute of MIT and Harvard Google Research Google Research

Abstract

We consider model selection for sequential decision making in stochastic environments with bandit feedback, where a meta-learner has at its disposal a pool of base learners, and decides on the fly which action to take based on the policies recommended by each base learner. Model selection is performed by regret balancing but, unlike the recent literature on this subject, we do not assume any prior knowledge about the base learners like candidate regret guarantees; instead, we uncover these quantities in a data-driven manner. The meta-learner is therefore able to leverage the realized regret incurred by each base learner for the learning environment at hand (as opposed to the expected regret), and single out the best such regret. We design two model selection algorithms operating with this more ambitious notion of regret and, besides proving model selection guarantees via regret balancing, we experimentally demonstrate the compelling practical benefits of dealing with actual regrets instead of candidate regret bounds.

1 INTRODUCTION

In online model selection for sequential decision making, the learner has access to a set of base learners and the goal is to adapt during learning to the best base learner that is the most suitable for the current environment. The set of base learners typically comes from instantiating different modelling assumptions or hyper-parameter choices, e.g., complexity of the reward model or the -parameter in -greedy. Which choice, and therefore which base learner, works best is highly dependent on the problem instance at hand, so that good online model selection solutions are important for robust sequential decision making. This has motivated an extensive study of model selection questions (e.g., Agarwal et al., 2017; Abbasi-Yadkori et al., 2020; Ghosh et al., 2020; Chatterji et al., 2020; Bibaut et al., 2020; Foster et al., 2020; Lee et al., 2020; Wei et al., 2022, and others cited below) in bandit and reinforcement learning problems. While some of these works have developed custom solutions for specific model selection settings, for instance, selecting among a nested set of linear policy classes in contextual bandits (e.g. Foster et al., 2019), the relevant literature also provides several general purpose approaches that work in a wide range of settings. Among the most prominent ones are FTRL-based (follow-the-regularized-leader) algorithms, including EXP4 (Odalric and Munos, 2011), Corral (Agarwal et al., 2017; Pacchiano et al., 2020b) and Tsallis-INF (Arora et al., 2020), as well as algorithms based on regret balancing (Abbasi-Yadkori et al., 2020; Pacchiano et al., 2020a; Cutkosky et al., 2021; Pacchiano et al., 2022).

These methods usually come with theoretical guarantees of the following form: the expected regret (or high-probability regret) of the model selection algorithm is not much worse than the expected regret (or high probability regret) of the best base learner. Such results are reasonable and known to be unimprovable in the worst-case (Marinov and Zimmert, 2021). Yet, it is possible for model selection to achieve expected regret that is systematically smaller than that of any base learner. This may seem surprising at first, but it can be explained through an example when considering the large variability across individual runs of each base learner on the same environment.

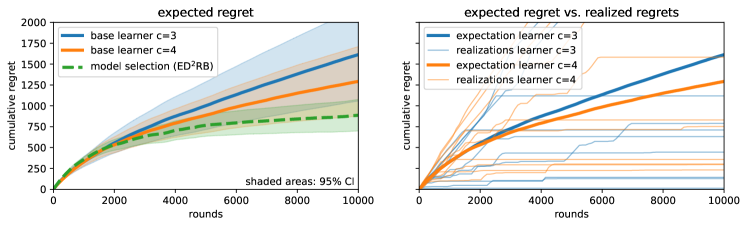

The situation is illustrated in Figure 1. On the left, we plot the cumulative expected regret of two base learners, along with the corresponding behavior of one of our model selection algorithms (ED2RB – see Section 3.2 below) run on top of them. On the right, we unpack the cumulative expected regret curve of one of the two base learners from the left plot, and display ten independent runs of this base learner on the same environment, together with the resulting expected regret curve (first 1000 rounds only). Since the model selection algorithm has access to two base learners simultaneously, it can leverage a good run of either of two, and thereby achieve a good run more likely than any base learner individually, leading to overall smaller expected regret.

Such high variability in performance across individual runs of a base learner is indeed fairly common in model selection, for instance when base learners correspond to different hyper-parameters that control the explore-exploit trade-off. For a hyper-parameter setting that explores too little for the given environment, the base learner becomes unreliable and either is lucky and converges quickly to the optimal solution or unlucky and gets stuck in a suboptimal one. This phenomenon is a key motivation for our work. Instead of model selection methods that merely compete with the expected regret of any base learner, we design model selection solutions that compete with the regret realizations of any base learner, and have (data-dependent) theoretical guarantees that validate this ability.

While the analysis of FTRL-based model selection algorithms naturally lends itself to work with expected regret (e.g. Agarwal et al., 2017), the existing guarantees for regret balancing work with realized regret of base learners (e.g. Pacchiano et al., 2020a; Cutkosky et al., 2021). Concretely, regret balancing requires each learner to be associated with a candidate regret bound, and the model selection algorithm competes with the regret bound of the best among the well-specified learner, those learners whose regret realization is below their candidate bound. Setting a-priori tight candidate regret bounds for base learners is a main limitation for existing regret balancing methods, as the resolution of these bounds is often the one provided by a (typically coarse) theoretical analysis. As suggested in earlier work, we can create several copies of each base learner with different candidate bounds, but we find this not to perform well in practice due to the high number of resulting base learners. Another point of criticism for existing regret balancing methods is that, up to deactivation of base learners, these methods do not adapt to observations, since their choice among active base learners is determined solely by the candidate regret bounds, which are set a-priori.

In this work, we address both limitations, and propose two new regret balancing algorithms for model selection with bandit feedback that do not require knowing candidate regret bounds. Instead, the algorithms determine the right regret bounds sequentially in a data-driven manner, allowing them to adapt to the regret realization of the best base learner. We prove this by deriving regret guarantees that share the same form with existing theoretial results, but replace expected regret rates or well-specified regret bounds with realized regret rates, which can be much sharper (as in the example in Figure 1). From an empirical standpoint, we illustrate the validity of our approach by carrying out an experimental comparison with competing approaches to model selection via base learner pooling, and find that our new algorithms systematically outperform the tested baselines.

2 SETUP AND NOTATION

We consider a general sequential decision making framework that covers many important problem classes such as multi-armed bandits, contextual bandits and tabular reinforcement learning as special cases. This framework or variations of it has been commonly used in model selection (e.g. Cutkosky et al., 2021; Wei et al., 2022; Pacchiano et al., 2022).

The learner operates with a policy class and a set of contexts over which is defined a probability distribution , unknown to the learner. In bandit settings, each policy is a mapping from contexts to , where is an action space and denotes the set of probability distributions over . However, the concrete form of , or is not relevant for our purposes. We only need that each policy is associated with a fixed expected reward mapping of the form , which is unknown to the learner. In each round of the sequential decision process, the learner first decides on a policy . The environment then draws a context as well as a reward observation such that . The learner receives before the next round starts.

We call the value of a policy and define the instantaneous regret of as

| (1) |

where is an optimal policy and its value. The total regret after rounds of an algorithm that chooses policies is . Note that is a random quantity since the policies selected by the algorithm depend on past observations, which are themselves random variables. Yet, we use in (1) a pseudo-regret notion that takes expectation over reward realizations and context draws. This is most convenient for our purposes but we can achieve guarantees without those expectations by paying an additive term, as is standard. We also use for the total value accumulated by the algorithm over the rounds.

Base learners.

The learner (henceforth called meta-learner) is in turn given access to base learners that the meta-learner can consult when determining the current policy to deploy. Specifically, in each round , the meta-learner chooses one base learner to follow and plays the policy suggested by this base learner. The policy that base learner recommends in round is denoted by and thus . We shall assume that each base learner has an internal state (and internal clock) that gets updated only on the rounds where that base learner is chosen. After being selected in round , base learner will receive from the meta-learner the observation . We use to denote the number of times base learner happens to be chosen up to round , and by the total value accumulated by base learner up to this point. It is sometimes more convenient to use a base learner’s internal clock instead of the total round index . To do so, we will use subscripts with parentheses to denote the internal time index of a specific base learner, while subscripts refer to global round indices. For example, given the sequence of realizatons , is the policy base learner wants to play when being chosen the -th time, i.e., . The total regret incurred by a meta-learner that picks base learners can then be decomposed into the sum of regrets incurred by each base learner:

2.1 Data-Driven Model Selection

Our goal is to perform model selection in this setting: We devise sequential decision making algorithms that have access to base learners as subroutines and are guaranteed to have regret that is comparable to the smallest realized regret, among all base learners in the pool, despite not knowing a-priori which base learner will happen to be best for the environment at hand ( and ), and the actual realizations .

In order to better quantify this notion of realized regret, the following definition will come handy.

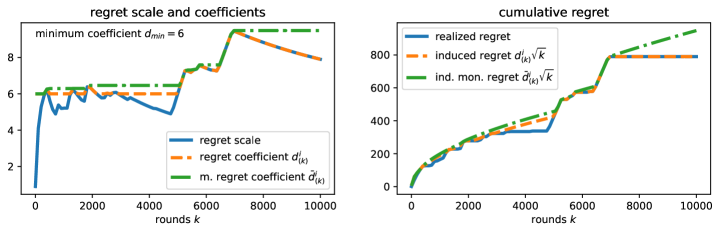

Definition 2.1 (regret scale and coefficients).

The regret scale of base learner after being played rounds is . For a positive constant , the regret coefficient of base learner after being played rounds is defined as

That is, is the smallest number such that the incurred regret is bounded as . Further we define the monotonic regret coefficient of base learner after being played rounds as .

We use a rate in this definition since that is the most commonly targeted regret rate in stochastic settings. Our results can be adapted, similarly to prior work (Pacchiano et al., 2020a) to other rates but the barrier for model selection (Pacchiano et al., 2020b) remains of course.

It is worth emphasizing that both and in the Definition 2.1 are random variables depending on , where . We illustrate them in Figure 2.

2.2 Running Examples

The above formalization encompasses a number of well-known online learning frameworks, including finite horizon Markov decision processes and contextual bandits, and model selection questions therein. We now introduce two examples but refer to earlier works on model selection for a more exhaustive list (e.g. Cutkosky et al., 2021; Wei et al., 2022; Pacchiano et al., 2022).

Tuning UCB exploration coefficient in multi-armed-bandits. As a simple illustrative example, we consider multi-armed bandits where the learner chooses in each round an action from a finite action set and receives a reward drawn from a distribution with mean and unknown but bounded variance . In this setting, we directly identify each policy with an action, i.e., and define the context as empty. The value of an action / policy is simply .

The variance strongly affects the amount of exploration necessary, thereby controlling the difficulty or “complexity” of the learning task. Since the explore-exploit of a learner is typically controlled through a hyper-parameter, it is beneficial to perform model selection among base learners with different trade-offs to adapt to the right complexity of the environment at hand. We use a simple UCB strategy as a base learner that chooses the next action as where and are the number of pulls of arm so far and the average reward observed. Here is the confidence scaling and we instantiate different base learners with different choices for . The goal is to adapt to the best confidence scaling , without knowing the true variance .111We choose this example for its simplicity. An alternative without model selection would be UCB with empirical Bernstein confidence bounds (Audibert et al., 2007). However, adaptation with model selection works just as well in more complex settings e.g. linear bandits and MDP, where empirical variance confidence bounds are not available or much more complicated.

Nested linear bandits. In the stochastic linear bandit model, the learner chooses an action from a large but finite action set , for some dimension and receives as reward + white noise, where is a fixed but unknown reward vector. This fits in our framework by considering policies of the form for a parameter , defining contexts as empty and the mean reward as , which is also the value .

We here consider the following model selection problem, that was also a motivating application in Cutkosky et al. (2021). The action set has some maximal dimension , and we have an increasing sequence of dimensions . Associated with each is a base learner that only considers policies of the form for and being the projection onto the first dimensions. That is, the -th base learner operates only on the first components of the unknown reward vector . If we stipulate that only the first dimensions of are non-zero ( being unknown to the learner) we are in fact competing in a regret sense against the base learner that operates with the policy class , the one at the “right” level of complexity for the underlying .

Nested stochastic linear contextual bandits. We also consider a contextual version of the previous setting (Lattimore and Szepesvári, 2020, Ch. 19) where where context are drawn i.i.d. and which a policy maps to some action . The expected reward is then for a known feature embedding , and an unknown vector . Just as above, we consider the nested version of this setting where and live in a large ambient dimension but only the first entries of are non-zero.

3 DATA-DRIVEN REGRET BALANCING

We introduce and analyze two data-driven regret balancing algorithms, which are both shown in Algorithm 1. Both algorithms maintain over time three main estimators for each base learner: (1) regret coefficients , meant to estimate the monotonic regret coefficients from Definition 2.1, (2) the average reward estimators , and (3) the balancing potentials , which are instrumental in the implementation of the exploration strategy based on regret balancing. At each round the meta-algorithm picks the base learner with the smallest balancing potential so far (ties broken arbitrarily). The algorithm plays the policy suggested by that base learner on the current context , receives the associated reward , and forwards back to that base learner only.

Where our two meta-learners differ is how they update the regret coefficient of the chosen learner and its potential . We now introduce each version and the regret guarantee we prove for it.

3.1 Balancing Through Doubling

Our first meta-algorithm (Doubling Data Driven Regret Balancing or D3RB) is shown on the left in Algorithm 1. Similar to existing regret balancing approaches (Pacchiano et al., 2020b, 2022), D3RB performs a misspecification test which checks whether the current estimate of the regret of base learner is compatible with the data collected so far. The test compared the average reward of the chosen learner against the highest average reward among all learners . If the difference is larger than the current regret coefficient permits (accounting for estimation errors by considering appropriate concentration terms), then the we know that is too small to accurately represent the regret of learner and we double it. This deviates from prior regret balancing approaches (Pacchiano et al., 2020b; Cutkosky et al., 2021) that simply eliminate a base learner if the misspecification test fails for a given candidate regret bound. Finally, D3RB sets the potential as so that the potential represents an upper-bound on the regret incurred by .

Our doubling approach for is algorithmically simple but creates main technical hurdles compared to existing elimination approaches since we have to show that the regret coefficients are adapted fast enough to be accurate and do not introduce undesirable scalings in our upper bounds. By overcoming these hurdles in our analysis, we show the following result quantifies the regret properties of D3RB in terms of the monotonic regret coefficients of the base learners at hand.

theoremmaindouble With probability at least , the regret of D3RB (Algorithm 1, left) with parameters and is bounded in all rounds as222 Here and throughout, hides log-factors.

where is the smallest monotonic regret coefficient among all learners (see Definition 2.1). We defer a discussion of this regret bound and comparison to existing results to Section 3.3.

3.2 Balancing Through Estimation

While D3RB retains the misspecification test of existing regret balancing approaches, our second algorithm, Estimating Data-Driven Regret Balancing or ED2RB, takes a more direct approach. It estimates the regret coefficient (see right in Algorithm 1) directly as the highest difference in average reward between and any other learner scaled by , the number of times has been played. Again, we include appropriate concentration terms to account for estimation errors as well as a lower bound of to ensure stability.

Since this direct estimation approach is more adaptive compared to the doubling approach, it requires a finer analysis to show that the changes in the estimator does not interfere with the balancing property of the algorithm. To ensure the necessary stability, we use a clipped version in ED2RB of the potential of D3RB. The function therein clips the real argument to the interval , and makes the potential non-decreasing and not increasing too quickly.

This more careful definition of the balancing potentials allows us to replace in the regret bound the monotonic regret coefficient with the sharper regret coefficient in the regret guarantee for ED2RB: {restatable}theoremmainestimate With probability at least , the regret of ED2RB (Algorithm 1, right) with parameters and is bounded in all rounds as

where is the smallest regret coefficient among all learners, and is the last time when base learner was played and .

3.3 Discussion, Comparison to the Literature

One way to interpret Theorem 3.1 is the following. If the meta-learner were given ahead of time the index of the base learner achieving the smallest monotonic regret coefficient , then the meta-learner would follow that base learner from beginning to end. The resulting regret bound for the meta-learner would be of the form . Then the price D3RB pays for aggregating the base learners is essentially a multiplicative factor of the form .

Up to the difference between and , the guarantees in Theorem 3.1 and Theorem 3.2 are identical. Further, since , the guarantee for ED2RB is never worse than that for D3RB. It can however be sharper, e.g., in environments with favorable gaps where we expect that a good base learner may achieve a regret instead of a rate and thus of that learner would decrease with time. The regret coefficient can benefit from this while cannot decrease with , and thus provide a worse guarantee.

Both D3RB and ED2RB rely on a user-specified parameter . In terms of regret coefficients, the regret bounds of the two algorithms have the general form . So, if we knew beforehand something about , we could set , and get a linear dependence on , otherwise we can always set as default (as we did in Theorem 3.1 and Theorem 3.2). Both our data-dependent guarantees recover existing data-independent results up to the precise dependency. Specifically, ignoring factors, our bounds scale at most as , while the previous literature on the subject (e.g., Cutkosky et al. (2021), Corollary 2) scales as . We recall that in the data-independent case, regret lower bounds are contained (in a somewhat implicit form) in Marinov and Zimmert (2021), where it is shown that one cannot hope in general to achieve better results in terms of and , like in particular a regret bound. Only a -like regret guarantee is generally possible.

These prior model selection results based on regret balancing require candidate regret bounds to be specified ahead of time. Hence, the corresponding algorithms cannot leverage the favorable cases that our data-dependent bounds automatically adapt to. In particular, in Cutkosky et al. (2021), the optimal parameter is the smallest candidate regret rate that is larger than the true rate of the optimal (well-specified) base learner. Instead, we do not assume the availability of such candidate regret rates, and our is the true regret rate of the optimal base learner. In short, Cutkosky et al. (2021)’s results are competitive with ours only when the above candidate regret rate happens to be very accurate for the best base learner, but this is a fairly strong assumption. Although theoretical regret bounds for base learners can often guide the guess for the regret rate, the values one obtains from those analyses are typically much larger than the true regret rate, as theoretical regret bounds are usually loose by large constants.

So, the goal here is to improve over more traditional data-independent bounds when data is benign or typical. Observe that in practice can also be decreasing with (as we will show multiple times in our experiments in Section 4). One such relevant case is when the individual base learner runs have large variances (recall Figure 1).

From a technical standpoint, we do indeed build on the existing technique for analyzing regret balancing by Pacchiano et al. (2020b); Cutkosky et al. (2021). Yet, their analysis heavily relies on fixed candidate regret bounds, and removing those introduces several technical challenges, like disentangling the balancing potentials from the estimated regret coefficients , and combine with clipping or the doubling estimator. This allows us to show the necessary invariance properties that unlocks our improved data-dependent guarantees. See Appendix C and D.

Departing from regret balancing techniques, model selection can also revolve around Follow-The-Regularized Leader-like schemes (e.g., (Agarwal et al., 2017; Pacchiano et al., 2020b; Arora et al., 2020)). However, even in those papers, is the expected regret scale, thus never sharper than our , and also not able to capture favorable realizations. As we shall see in Section 4, there is often a stark difference between the expected performance and the data-dependent performance, which confirms that the improvement in our bounds is important in practice.

4 EXPERIMENTS

We evaluate our algorithms on several synthetic benchmarks (environments, base-learners and model selection tasks), and compare their performance against existing meta-learners. For all details of the experimental setup and additional results, see Appendix E.

These experiments are mostly intended to validate the theory and as a companion to our theoretical results. In these experiments, we vary the parameters that we expect to be most important for model selection Varying the difficulty of the learning environment itself is something that should mostly be absorbed by base-learners, for example, by choosing base learners operating on more powerful function classes than we do here. Yet, it is important to observe that the meta-algorithms are fairly oblivious to the difficulty of the environment. All that matters here is the regret profile of the base learners. In our experiments, we therefore decided to explore the landscape of model selection by varying the nature of the model selection task itself (dimension, self model selection, and confidence scaling) while keeping the underlying environments fairly simple.

Environments and base-learners: As the first environment, we use a simple 5-armed multi-armed bandit problem (MAB) with standard Gaussian noise. We then use two linear bandit settings, as also described in Section 2.2: linear bandits with stochastic rewards, either with a stochastic context (CLB) or without (LB). As base learners, we use UCB for the MAB environment (see also Section 2.2) and Linear Thompson (LinTS) sampling (Abeille and Lazaric, 2017) for the LB and CLB setting.

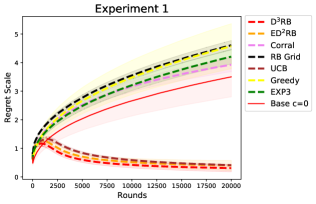

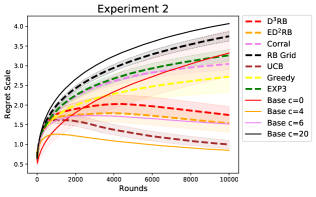

Model selection task: We consider 3 different model selection tasks. All the results are reported in Figure 3. In the first, conf (“confidence”), we vary the explore-exploit trade-off in the base learners. For UCB, different base learners correspond to different settings of , the confidence scaling that multiplies the exploration bonus. Analogously, for LinTS, we vary the scale of the parameter perturbation. For the second task dim (“dimension”), we vary the number of dimensions the base learner considers when choosing the action (see second and third example in Section 2.2, as well as Figure 3 for results). Finally, we also consider a “self” task, where all base learners are copies of the same algorithm.

| Env. | Learners | Task | D3RB | ED2RB | Corral | RB Grid | UCB | Greedy | EXP3 | |

| 1. | MAB | UCB | self | |||||||

| 2. | MAB | UCB | conf | |||||||

| 3. | LB | LinTS | conf | |||||||

| 4. | CLB | LinTS | conf | |||||||

| 5. | LB | LinTS | dim | |||||||

| 6. | CLB | LinTS | dim |

Meta-learners: We evaluate both our algorithms, D3RB and ED2RB, from Algorithm 1. We compare them against the Corral algorithm (Agarwal et al., 2017) with the stochastic wrapper from Pacchiano et al. (2020b), as a representative for FTRL-based meta-learners. We also evaluate Regret Balanncing from Pacchiano et al. (2020b); Cutkosky et al. (2021) with several copies of each base learner, each with a different candidate regret bound, selected on an exponential grid (RB Grid). We also include in our list of competitors three popular algorithms, the Greedy algorithm (always selecting the best base learner so far with no exploration), UCB (Auer et al., 2002a) and EXP3 (Auer et al., 2002b). These are legitimate choices as meta-algorithms, but either they do not come with theoretical guarantees in the model selection setting (UCB, Greedy) or enjoy worse guarantees (Pacchiano et al., 2020b).

Discussion. An overview of our results can be found in Table 1, where we report the cumulative regret of each algorithm at the end of each experiment. Figure 3 contains the entire learning curves (as regret scale = cumulative regret normalized by ). We observe that D3RB and ED2RB both outperform all other meta-learners on all but the second benchmark. UCB as a meta-learner performs surprisingly well in benchmarks on MABs but performs poorly on the others. Thus, our methods feature the smallest or close to the smallest cumulative regret among meta-learners on all benchmarks.

Comparing D3RB and ED2RB, we observe overall very similar performance, suggesting that ED2RB may be preferable due to its sharper theoretical guarantee. While the model selection tasks conf and dim are standard in the literature, we also included one experiment with the self task where we simply select among different instances of the same base learner. This task was motivated by our initial observation (see also Figure 1) that base learners have often a very high variability between runs and that model selection can capitalize on. Indeed, Figure 3 shows that our algorithms as well as UCB achieve much smaller overall regret than the base learner. This suggests that model selection can be an effective way to turn a notoriously unreliable algorithm like the base greedy base learner (UCB with is Greedy) into a robust learner.

5 CONCLUSIONS

We proposed two new algorithms for model selection based on the regret balancing principle but without the need to specify candidate regret bounds a-priori. This calls for more sophisticated regret balancing mechanics that makes our methods data-driven and as an important benefit allows them to capitalize on variability in a base learner’s performance. We demonstrate this empirically, showing that our methods perform well across several synthetic benchmarks, as well as theoretically. We prove that both our algorithms achieve regret that is not much worse than the realized regret of any base learner. This data-dependent guarantee recovers existing data-independent results but can be significantly tighter.

In this work, we focused on the fully stochastic setting, with contexts and rewards drawn i.i.d. We believe an extension of our results to arbitrary contexts is fairly easy by replacing the deterministic balancing with a randomized version. In contrast, covering the fully adversarial setting is likely possible by building on top of (Pacchiano et al., 2022) but requires substantial innovation.

References

- Abbasi-Yadkori et al. (2020) Y. Abbasi-Yadkori, A. Pacchiano, and M. Phan. Regret balancing for bandit and rl model selection. arXiv preprint arXiv:2006.05491, 2020.

- Abeille and Lazaric (2017) M. Abeille and A. Lazaric. Linear thompson sampling revisited. In Artificial Intelligence and Statistics, pages 176–184. PMLR, 2017.

- Agarwal et al. (2017) A. Agarwal, H. Luo, B. Neyshabur, and R. E. Schapire. Corralling a band of bandit algorithms. In Conference on Learning Theory, pages 12–38. PMLR, 2017.

- Arora et al. (2020) R. Arora, T. V. Marinov, and M. Mohri. Corralling stochastic bandit algorithms. arXiv preprint arXiv:2006.09255, 2020.

- Audibert et al. (2007) J.-Y. Audibert, R. Munos, and C. Szepesvari. Tuning bandit algorithms in stochastic environments. In Algorithmic Learning Theory: 18th International Conference, ALT 2007, Sendai, Japan, October 1-4, 2007. Proceedings 18, pages 150–165. Springer, 2007.

- Auer et al. (2002a) P. Auer, N. Cesa-Bianchi, and P. Fischer. Finite-time analysis of the multiarmed bandit problem. Mach. Learn., 47(2–3):235–256, 2002a.

- Auer et al. (2002b) P. Auer, N. Cesa-Bianchi, Y. Freund, and R. E. Schapire. The nonstochastic multiarmed bandit problem. SIAM Journal on Computing, 32(1):48–77, 2002b.

- Bibaut et al. (2020) A. F. Bibaut, A. Chambaz, and M. J. van der Laan. Rate-adaptive model selection over a collection of black-box contextual bandit algorithms. arXiv preprint arXiv:2006.03632, 2020.

- Chatterji et al. (2020) N. Chatterji, V. Muthukumar, and P. Bartlett. Osom: A simultaneously optimal algorithm for multi-armed and linear contextual bandits. In International Conference on Artificial Intelligence and Statistics, pages 1844–1854, 2020.

- Cutkosky et al. (2021) A. Cutkosky, C. Dann, A. Das, C. Gentile, A. Pacchiano, and M. Purohit. Dynamic balancing for model selection in bandits and rl. In Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pages 2276–2285. PMLR, 2021.

- Foster et al. (2020) D. Foster, C. Gentile, M. Mohri, and J. Zimmert. Adapting to misspecification in contextual bandits. In Advances in Neural Information Processing Systems, 2020.

- Foster et al. (2019) D. J. Foster, A. Krishnamurthy, and H. Luo. Model selection for contextual bandits. In Advances in Neural Information Processing Systems, pages 14741–14752, 2019.

- Ghosh et al. (2020) A. Ghosh, A. Sankararaman, and K. Ramchandran. Problem-complexity adaptive model selection for stochastic linear bandits. arXiv preprint arXiv:2006.02612, 2020.

- Howard et al. (2018) S. R. Howard, A. Ramdas, J. Mc Auliffe, and J. Sekhon. Uniform, nonparametric, non-asymptotic confidence sequences. arXiv preprint arXiv:1810.08240, 2018.

- Lattimore and Szepesvári (2020) T. Lattimore and C. Szepesvári. Bandit algorithms. Cambridge University Press, 2020.

- Lee et al. (2020) J. N. Lee, A. Pacchiano, V. Muthukumar, W. Kong, and E. Brunskill. Online model selection for reinforcement learning with function approximation. arXiv preprint arXiv:2011.09750, 2020.

- Marinov and Zimmert (2021) T. V. Marinov and J. Zimmert. The pareto frontier of model selection for general contextual bandits. Advances in Neural Information Processing Systems, 34:17956–17967, 2021.

- Odalric and Munos (2011) M. Odalric and R. Munos. Adaptive bandits: Towards the best history-dependent strategy. In Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics, pages 570–578. JMLR Workshop and Conference Proceedings, 2011.

- Pacchiano et al. (2020a) A. Pacchiano, C. Dann, C. Gentile, and P. Bartlett. Regret bound balancing and elimination for model selection in bandits and rl. arXiv preprint arXiv:2012.13045, 2020a.

- Pacchiano et al. (2020b) A. Pacchiano, M. Phan, Y. Abbasi-Yadkori, A. Rao, J. Zimmert, T. Lattimore, and C. Szepesvari. Model selection in contextual stochastic bandit problems. arXiv preprint arXiv:2003.01704, 2020b.

- Pacchiano et al. (2022) A. Pacchiano, C. Dann, and C. Gentile. Best of both worlds model selection. In Advances in Neural Information Processing Systems, volume 35, pages 1883–1895. Curran Associates, Inc., 2022.

- Wei et al. (2022) C.-Y. Wei, C. Dann, and J. Zimmert. A model selection approach for corruption robust reinforcement learning. In International Conference on Algorithmic Learning Theory, pages 1043–1096. PMLR, 2022.

Appendix

The appendix contains the extra material that was omitted from the main body of the paper.

Appendix A DETAILS ON FIGURE 1

We consider a -armed bandit problem with rewards drawn from a Gaussian distribution with standard deviation and mean for each arm respectively. We use a simple UCB strategy as a base learner that chooses the next action as where and are the number of pulls of arm so far and the average reward observed. The base learners use and or respectively.

Appendix B ANALYSIS COMMON TO BOTH ALGORITHMS

Definition B.1.

We define the event in which we analyze both algorithms as the event in which for all rounds and base learners the following inequalities hold

for the algorithm parameter and a universal constant .

Lemma B.2.

Event from Definition B.1 has probability at least .

Proof.

Consider a fixed and and write

Let be the sigma-field induced by all variables up to round before the reward is revealed, i.e., . Then, is a martingale-difference sequence w.r.t. . We will now apply a Hoeffding-style uniform concentration bound from Howard et al. (2018). Using the terminology and definition in this article, by case Hoeffding I in Table 4, the process is sub- with variance process . Thus by using the boundary choice in Equation (11) of Howard et al. (2018), we get

for all where with probability at least . Applying the same argument to gives that

holds with probability at least for all .

We now take a union bound over and rebind . Then picking the absolute constant sufficiently large gives the desired statement. ∎

Lemma B.3 (Balancing potential lemma).

For each , let be a nondecreasing potential function that does not increase too quickly, i.e.,

and that for all . Consider a sequence such that and , i.e., is always chosen as the smallest current potential. Then, for all

Proof.

Our proof works by induction over . At , we have for all and thus, by assumption, the statement holds. Assume now the statement holds for . Notice that since and are non-decreasing, we have for all

Further, for all that were not chosen in round , we even have for all . We now distinguish two cases:

Case .

Since the potential of all that attain the is unchanged, we have

and therefore .

Case .

Since attains both the maximum and the minimum, and hence all potentials are identical, we have

∎

Appendix C PROOFS FOR THE DOUBLING ALGORITHM (ALGORITHM 1, LEFT)

Lemma C.1.

In event , for each base learner all rounds , the regret multiplier satisfies

Proof.

Note that instead of showing this for all rounds , we can also show this equivalently for all number of plays of base learner . If the statement is violated for base learner , then there is a minimum number of plays at which this statement is violated. Note that by definition and by initialization , hence this cannot be .

Consider now the round where the learner was played the -th time, i.e., the first round at which the statement was violated. This means but still holds. Since can be at most , we have . We will now show that in this case, the misspecification test could not have triggered and therefore which is a contradiction. To show that the test cannot trigger, consider the LHS of the test condition and bound it from below as

| (Event ) | ||||

| () | ||||

| (definition of ) | ||||

| (definition of regret) | ||||

| (definition of ) | ||||

| (Event ) |

This holds for any and thus, the test does not trigger. ∎

Corollary C.1.

In event , for each base learner all rounds , the number of times the regret multiplier has doubled so far is bounded as follows:

Lemma C.2.

The potentials in Algorithm 1 (left) are balanced at all times up to a factor , that is, for all rounds and base learners .

Proof.

We will show that Lemma B.3 with holds when we apply the lemma to .

First for all and, thus, the initial condition holds. To show the remaining condition, it suffices to show that is non-decreasing in and cannot increase more than a factor of per round. If was not played in round , then and both conditions holds. If was played, i.e., , then

∎

Lemma C.3.

In event , the regret of all base learners is bounded in all rounds as

where is an arbitrary base learner with .

Proof.

Consider a fixed base learner and time horizon , and let be the last round where was played but the misspecification test did not trigger. If no such round exists, then set . By Corollary C.1, can be played at most times between and and thus

If , then the desired statement holds. Thus, it remains to bound the first term in the RHS above when . Since and the test did not trigger we have, for any base learner with ,

| (definition of regret) | ||||

| (definition of regret) | ||||

| (definition of regret rate) | ||||

We now use the balancing condition in Lemma C.2 to bound the first factor . This condition gives that . Since both and , we have and . Thus, we get

| (2) |

Plugging this back into the expression above, we have

To bound the last two terms, we use the fact that the misspecification test did not trigger in round . Therefore

| (event ) | ||||

| (test not triggered) |

Rearranging terms and plugging this expression in the bound above gives

| (Equation 2) | ||||

| (Equation 2) | ||||

| () | ||||

| (Lemma C.1) |

Finally, since and therefore and (and similarly for ), the statement follows. ∎

*

Proof.

By Lemma B.2, event from Definition B.1 has probability at least . In event , we can apply Lemma C.3 for each base learner. Summing up the bound from that lemma gives

Plugging in yields

as desired. ∎

Appendix D PROOFS FOR THE ESTIMATING ALGORITHM (ALGORITHM 1, RIGHT)

Lemma D.1.

In event , the regret rate estimate in Algorithm 1 (right) does not overestimate the current regret rate, that is, for all base learners and rounds , we have

Proof.

Note that the algorithm only updates when learner is chosen and only then changes. Further, the condition holds initially since . Hence, it is sufficient to show that this condition holds whenever is updated. The algorithm estimates as

If , then the result holds since by definition . In the other case, we have

| (event ) | ||||

| (definition of optimal value ) | ||||

| (regret definition) | ||||

| (definition of ) |

as claimed. ∎

Lemma D.2.

In event , the balancing potentials in Algorithm 1 (right) satisfy for all and where

Proof.

If , then , and . It is therefore sufficient to only check this condition for . By definition of the balancing potential, we have when

where the last inequality holds because of Lemma D.1. If , then and by definition, and the statement holds. Otherwise, we can assume that by induction. This gives

We notice that . Since each term inside the is non-decreasing in , is also non-decreasing in , and therefore , as anticipated. ∎

Lemma D.3.

In event , for all and , the number of times the balancing potential doubled until time in Algorithm 1 (right) is bounded by

Proof.

The balancing potential is non-decreasing in and . Further, by Lemma D.2, we have

Thus, the number of times can double is at most

∎

Lemma D.4.

The balancing potentials in Algorithm 1 (right) are balanced at all times up to a factor , that is, for all rounds and base learners .

Proof.

We will show that Lemma B.3 with holds when we apply the lemma to .

First for all and, thus, the initial condition holds. To show the remaining condition, it suffices to show that is non-decreasing in and cannot increase more than a factor of per round. This holds by the clipping in the definition of in the algorithm. ∎

Lemma D.5.

In event , the regret of all base learners is bounded in all rounds as

where is an arbitrary base learner with and is the last round where and .

Proof.

Consider fixed base learner and time horizon , and let be the last round where was played and did not double, i.e., . If no such round exists, then set . By Lemma D.3, can be played at most times between and and thus

If , then the desired statement holds. Thus, it remains to bound the first term above when . We can write the regret of base learner up to in terms of the regret of any learner with as follows:

| (definition of regret) | ||||

| (definition of regret) | ||||

| (definition of regret rate) | ||||

We now use the balancing condition in Lemma D.4 to bound the first factor . This condition gives that . Since and, thus, the balancing potential was not clipped from above, we have . Further, since we can apply Lemma D.2 to get . Thus, we get

| (3) |

Plugging this back into the expression above, we have

To bound the last two terms, we use the regret coefficient estimate:

| (event ) | ||||

| (definition of ) | ||||

| ( and ) | ||||

| (Equation 3) | ||||

| () | ||||

| (Lemma D.4) | ||||

| (Lemma D.2) |

Plugging this back into the expression above, we get the desired statement:

∎

*

Proof.

By Lemma B.2, event from Definition B.1 has probability at least . In event , we can apply Lemma D.5 for each base learner. Summing up the bound for all base learners with from that lemma gives

Here we have used that for all by the definition of . Plugging in gives

as claimed. ∎

Appendix E EXPERIMENTAL DETAILS

We used a 50 core machine to run our experiments. We made use of this computing infrastructure by parallelizing our experiment runs. The experiments take 12 hours to complete.

E.1 Meta-Learners

We now list the meta-learners used in our experiments.

Corral.

We used the Corral Algorithm as described in Agarwal et al. (2017) and Pacchiano et al. (2020b). Since we work with stochastic base algorithms we use the Stochastic Corral version of Pacchiano et al. (2020b) where the base algorithms are updated with the observed reward instead of the importance sampling version required by the original Corral algorithm of Agarwal et al. (2017). The pseudo-code is in Algorithm 2. In accordance with theoretical results we set . We test the performance of the Corral meta-algorithm with different settings of the initial learning rate . In the table and plots below we call them CorralLow, Corral and CorralHigh respectively. In Table 4 we compare their performance on different experiment benchmarks. We see Corral and CorralHigh achieve a better formance than CorralLow. The performance of Corral and CorralHigh is similar.

EXP3.

At the beginning of each time step the EXP3 meta-algorithm samples a base learner index from its base learner distribution . The meta-algorithm maintains importance weighted estimator of the cumulative rewards for each base learner for all . After receiving feedback from base learner the importance weighted estimators are updated as . The distribution where is a and are a learning rate and exploration parameters. In accordance with theoretical results (see for example (Lattimore and Szepesvári, 2020, Th. 11.1)) in our experiments we set the learning rate to and set the forced exploration parameter . We test the performance of the EXP3 meta-algorithm with different settings of the forced exploration parameter . In Table 4 we call them EXP3Low, EXP3 and EXP3High. All these different variants have a similar performance.

Greedy.

This is a pure exploitation meta-learner. After playing each base learner at least once, the Greedy meta-algorithm maintains the same cumulative reward statistics as D3RB and ED2RB. The base learner chosen at time is .

UCB.

We use the same UCB algorithm as described in Section 2.2. We set the scaling parameter .

D3RB and ED2RB.

These are the algorithms in Algorithm 1. We set therein and .

E.2 Base Learners

All base learners have essentially been described, except for the Linear Thompson Sampling Algorithm () algorithm, which was used in all our linear experiments.

In our implementation we use the algorithm described as in Abeille and Lazaric (2017). On round the Linear Thompson Sampling algorithm has played with observed responses . The rewards are assumed to be of the form for an unknown vector and a conditionally zero mean random variable . An empirical model of the unknown vector is produced by fitting a ridge regression least squares estimator for a user specified parameter . This can be written in closed form as where matrix where row equals . At time a sample model is computed where and is a confidence scaling parameter. This is one of the parameters that we vary in our experiments. If the action set at time equals (in the contextual setting changes every time-step while in the fixed action set linear bandits case it ) the action . In our experiments and is set to a scaled version of the vector . In the detailed experiment description below we specify the precise value of in each experiment.

E.3 Detailed Experiments Description

Figure 4 illustrates the overall structure of our experiments. Experiments through are those also reported in the main body of the paper. The below table contains a detailed description of each experiment, together with the associated evidence in the form of learning curves (regret scale vs. rounds). Finally, Table 2 contains the final (average) cumulative regret for each meta-learner on each experiment.

| Description | Figure |

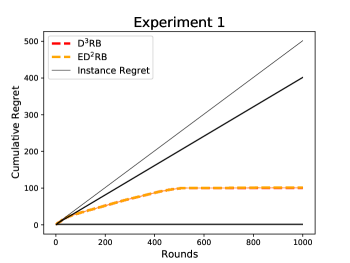

| Experiment 1. Self model selection for a armed Gaussian bandit problem with means and standard deviations equal to . The base learners are algorithms with a confidence scaling . This reduces them to instances of Greedy. It is well known that greedy algorithms do not satisfy a sublinear expected regret bound. These results show that combining multiple instances of Greedy via self model selection can turn them into algorithms with a sublinear regret guarantee. We initialize Greedy base learners. |

![[Uncaptioned image]](/html/2306.02869/assets/x10.png)

|

Experiment 2.Model selection for a armed Gaussian bandit problem with means and standard deviations equal to where we select among UCB base learners with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x11.png)

|

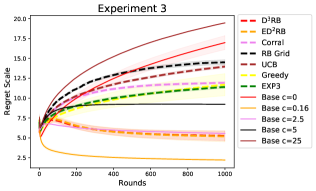

Experiment 3.Linear bandits model selection where we select among LinTS base learners with different confidence scalings. The action set is the dimensional unit sphere. The vector equals . The base learners are LinTS instances with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x12.png)

|

| Description | Figure |

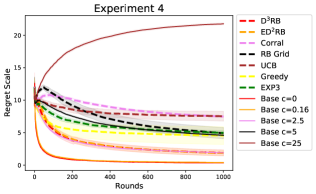

Experiment 4.Contextual linear bandits model selection where we select among LinTS base learners with different confidence scalings. The contexts are generated by producing i.i.d. uniformly distributed vectors from the unit sphere. The ambient space dimension is . The vector is . The base learners are LinTS instances with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x13.png)

|

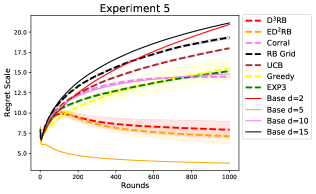

Experiment 5.Nested linear bandits model selection where we select among different LinTS base learners with different ambient dimensions. The action set is the unit sphere and the true ambient dimension equals . The vector is and the base learners are LinTS instances with dimensions , and confidence scaling . |

![[Uncaptioned image]](/html/2306.02869/assets/x14.png)

|

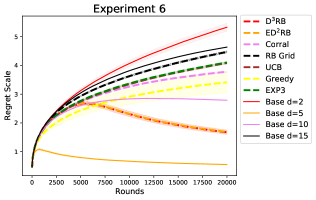

Experiment 6.Nested contextual linear bandits model selection where we select among different LinTS base learners with different ambient dimensions. The context set is generated by sampling i.i.d. vectors from the unit sphere. The true ambient dimension equals . The vector equals and the base learners are LinTS instances with dimensions and confidence scaling . |

![[Uncaptioned image]](/html/2306.02869/assets/x15.png)

|

| Description | Figure |

Experiment A.Selecting among different confidence scalings in a armed Bernoulli bandit problem with mean rewards . We select among UCB base learners with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x16.png)

|

Experiment B.Selecting among different confidence scalings in a armed bandit problem with reward distributions and where samples from are of the form where are two Bernoulli variables with means in . We test self-model selection among UCB base learners with confidence scalings . |

![[Uncaptioned image]](/html/2306.02869/assets/x17.png)

|

Experiment C.Linear bandit model selection where we select among LinTS base learners with different confidence scalings. The action set equals the dimensional hypercube (i.e., the arm set equals ). The vector equals . The base learners are LinTS instances with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x18.png)

|

| Description | Figure |

Experiment D.Linear bandit model selection where we select among LinTS base learners with different confidence scalings. The action set equals the dimensional hypercube (i.e., the arm set equals ). The vector equals . The base learners are LinTS instances with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x19.png)

|

Experiment E.Linear bandit model selection where we select among LinTS base learners with different confidence scalings. The action set equals the dimensional hypercube (i.e., the arm set equals ). The vector equals . The base learners are LinTS instances with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x20.png)

|

Experiment F.Linear bandit model selection where we select among LinTS base learners with different confidence scalings. The action set equals the dimensional unit sphere. The vector equals . The base learners are LinTS instances with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x21.png)

|

| Description | Figure |

Experiment G.Linear bandit model selection where we select among LinTS base learners with different confidence scalings. The action set equals the dimensional unit sphere. The vector equals . The base learners are LinTS instances with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x22.png)

|

Experiment H.Contextual linear bandit model selection where we select among LinTS base learners with different confidence scalings. The contexts are generated by producing i.i.d. uniformly distributed vectors from the unit sphere. The ambient space dimension equals . The vector equals . The base learners are LinTS instances with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x23.png)

|

Experiment I.Contextual linear bandit model selection where we select among LinTS base learners with different confidence scalings. The contexts are generated by producing i.i.d. uniformly distributed vectors from the unit sphere. The ambient space dimension equals . The vector is . The base learners are LinTS instances with confidence scalings in . |

![[Uncaptioned image]](/html/2306.02869/assets/x24.png)

|

| Description | Figure |

Experiment J.Nested linear bandit model selection where we select among different LinTS base learners with different ambient dimensions. The action set is the unit sphere and the true ambient dimension is . The vector is and the base learners are LinTS instances with dimensions , and confidence scaling . |

![[Uncaptioned image]](/html/2306.02869/assets/x25.png)

|

Experiment K.Nested linear bandit model selection where we select among different LinTS base learners with different ambient dimensions. The action set is the hypercube and the true ambient dimension is . The vector is and the base learners are LinTS instances with dimensions and confidence scaling . |

![[Uncaptioned image]](/html/2306.02869/assets/x26.png)

|

Experiment L.Nested linear bandit model selection where we select among different LinTS base learners with different ambient dimensions. The action set is the hypercube and the true ambient dimension is . The vector is and the base learners are LinTS instances with dimensions and confidence scaling . |

![[Uncaptioned image]](/html/2306.02869/assets/x27.png)

|

| Name | Env. | Learners | Task | Arms | D3RB | ED2RB | Corral | RB Grid | UCB | Greedy | EXP3 |

| 1. | MAB | UCB | self | Gaussian | |||||||

| B. | MAB | UCB | self | Bernoulli | |||||||

| 2. | MAB | UCB | conf | Gaussian | |||||||

| A. | MAB | UCB | conf | Bernoulli | |||||||

| 3. | LB | LinTS | conf | Sphere | |||||||

| F. | LB | LinTS | conf | Sphere | |||||||

| G. | LB | LinTS | conf | Sphere | |||||||

| C. | LB | LinTS | conf | Hypercube | |||||||

| D. | LB | LinTS | conf | Hypercube | |||||||

| E. | LB | LinTS | conf | Hypercube | |||||||

| 4. | CLB | LinTS | conf | Context. | |||||||

| H. | CLB | LinTS | conf | Context. | |||||||

| I. | CLB | LinTS | conf | Context. | |||||||

| 5. | LB | LinTS | dim | Sphere | |||||||

| J. | LB | LinTS | dim | Sphere | |||||||

| K. | LB | LinTS | dim | Hypercube | |||||||

| L. | LB | LinTS | dim | Hypercube | |||||||

| 6. | CLB | LinTS | dim | Context. |

| Name | Env. | Learners | Task | Arms | CorralLow | Corral | CorralHigh |

| 1. | MAB | UCB | self | Gaussian | |||

| B. | MAB | UCB | self | Bernoulli | |||

| 2. | MAB | UCB | conf | Gaussian | |||

| A. | MAB | UCB | conf | Bernoulli | |||

| 3. | LB | LinTS | conf | Sphere | |||

| F. | LB | LinTS | conf | Sphere | |||

| G. | LB | LinTS | conf | Sphere | |||

| C. | LB | LinTS | conf | Hypercube | |||

| D. | LB | LinTS | conf | Hypercube | |||

| E. | LB | LinTS | conf | Hypercube | |||

| 4. | CLB | LinTS | conf | Context. | |||

| H. | CLB | LinTS | conf | Context. | |||

| I. | CLB | LinTS | conf | Context. | |||

| 5. | LB | LinTS | dim | Sphere | |||

| J. | LB | LinTS | dim | Sphere | |||

| K. | LB | LinTS | dim | Hypercube | |||

| L. | LB | LinTS | dim | Hypercube | |||

| 6. | CLB | LinTS | dim | Context. |

| Name | Env. | Learners | Task | Arms | EXP3Low | EXP3 | EXP3High |

| 1. | MAB | UCB | self | Gaussian | |||

| B. | MAB | UCB | self | Bernoulli | |||

| 2. | MAB | UCB | conf | Gaussian | |||

| A. | MAB | UCB | conf | Bernoulli | |||

| 3. | LB | LinTS | conf | Sphere | |||

| F. | LB | LinTS | conf | Sphere | |||

| G. | LB | LinTS | conf | Sphere | |||

| C. | LB | LinTS | conf | Hypercube | |||

| D. | LB | LinTS | conf | Hypercube | |||

| E. | LB | LinTS | conf | Hypercube | |||

| 4. | CLB | LinTS | conf | Context. | |||

| H. | CLB | LinTS | conf | Context. | |||

| I. | CLB | LinTS | conf | Context. | |||

| 5. | LB | LinTS | dim | Sphere | |||

| J. | LB | LinTS | dim | Sphere | |||

| K. | LB | LinTS | dim | Hypercube | |||

| L. | LB | LinTS | dim | Hypercube | |||

| 6. | CLB | LinTS | dim | Context. |