Robust covariance estimation with missing values and cell-wise contamination

Abstract

Large datasets are often affected by cell-wise outliers in the form of missing or erroneous data. However, discarding any samples containing outliers may result in a dataset that is too small to accurately estimate the covariance matrix. Moreover, the robust procedures designed to address this problem require the invertibility of the covariance operator and thus are not effective on high-dimensional data. In this paper, we propose an unbiased estimator for the covariance in the presence of missing values that does not require any imputation step and still achieves near minimax statistical accuracy with the operator norm. We also advocate for its use in combination with cell-wise outlier detection methods to tackle cell-wise contamination in a high-dimensional and low-rank setting, where state-of-the-art methods may suffer from numerical instability and long computation times. To complement our theoretical findings, we conducted an experimental study which demonstrates the superiority of our approach over the state of the art both in low and high dimension settings.

1 Introduction

Outliers are a common occurrence in datasets, and they can significantly affect the accuracy of data analysis. While research on outlier detection and treatment has been ongoing since the 1960s, much of it has focused on cases where entire samples are outliers (Huber’s contamination model) (huberRobustEstimationLocation1964, ; tukeyNintherTechniqueLowEffort1978, ; hubertMinimumCovarianceDeterminant2018, ). While sample-wise contamination is a common issue in many datasets, modern data analysis often involves combining data from multiple sources. For example, data may be collected from an array of sensors, each with an independent probability of failure, or financial data may come from multiple companies, where reporting errors from one source do not necessarily impact the validity of the information from the other sources. Discarding an entire sample as an outlier when only a few features are contaminated can result in the loss of valuable information, especially in high-dimensional datasets where samples are already scarce. It is important to identify and address the specific contaminated features, rather than simply treating the entire sample as an outlier. In fact, if each dimension of a sample has a contamination probability of , then the probability of that sample containing at least one outlier is given by , where is the dimensionality of the sample. In high dimension, this probability can quickly exceed , surpassing the breakdown point of many robust estimators designed for the Huber sample-wise contamination setting. Hence, it is crucial to develop robust methods that can handle cell-wise contaminations and still provide accurate results.

The issue of cell-wise contamination, where individual cells in a dataset may be contaminated, was first introduced in (alqallafPropagationOutliersMultivariate2009, ). However, the issue of missing data due to outliers was studied much earlier, dating back to the work of rubinInferenceMissingData1976 . Although missing values in a dataset are much easier to detect than outliers, they can lead to errors in estimating the location and scale of the underlying distribution (littleStatisticalAnalysisMissing2002, ) and can negatively affect the performance of supervised learning algorithms (josseConsistencySupervisedLearning2020, ). This motivated the development of the field of data imputation. Several robust estimation methods have been proposed to handle missing data, including Expectation Maximization (EM)-based algorithms (dempsterMaximumLikelihoodIncomplete1977, ), maximum likelihood estimation (jamshidianMLEstimationMean1999, ) and Multiple Imputation (littleStatisticalAnalysisMissing2002, ), among which we can find k-nearest neighbor imputation troyanskayaMissingValueEstimation2001 and iterative imputation buurenMiceMultivariateImputation2011 . Recently, sophisticated solutions based on deep learning, GANs yoonGAINMissingData2018 ; matteiMIWAEDeepGenerative2019 ; dongGenerativeAdversarialNetworks2021 , VAE maVAEMDeepGenerative2020 or Diffusion schemes zhengDiffusionModelsMissing2023 have been proposed to perform complex tasks like artificial data generation or image inpainting. The aforementioned references focus solely on minimising the entrywise error for imputed entries. Noticeably, our practical findings reveal that applying state-of-the-art imputation methods to complete the dataset, followed by covariance estimation on the completed dataset, does not yield satisfactory results when evaluating the covariance estimation error using the operator norm.

| Estimator | Computation time | Matrix | |

|---|---|---|---|

| p=50 | p=100 | inversion | |

| tailMV | no | ||

| DDCMV | no | ||

| DI | yes | ||

| TSGS | yes | ||

In comparison to data missingness or its sample-wise counterpart, the cell-wise contamination problem is less studied. The Detection Imputation (DI) algorithm of raymaekersHandlingCellwiseOutliers2020 is an EM type procedure combining a robust covariance estimation method with an outlier detection method to iteratively update the covariance estimation. Other methods include adapting methodology created for Huber contamination for the cell-wise problem, such as in danilovRobustEstimationMultivariate2012 or agostinelliRobustEstimationMultivariate2014 . In high dimensional statistics, however, most of these methods fail due to high computation time and numerical instability. Or they are simply not designed to work in this regime since they are based on the Mahalanobis distance, which requires an inversion of the estimated covariance matrix. This is a major issue since classical covariance matrix estimators have many eigenvalues close to zero or even exactly equal to zero in high-dimension. To the best of our knowledge, no theoretical result exists concerning the statistical accuracy of these methods in the cell-wise contamination setting contrarily to the extensive literature on Huber’s contamination abdallaCovarianceEstimationOptimal2023 .

Contributions. In this paper we address the problem of high-dimensional covariance estimation in the presence of missing observations and cell-wise contamination. To formalize this problem, we adopt and generalize the setting introduced in farcomeniRobustConstrainedClustering2014 . We propose and investigate two different strategies, the first based on filtering outliers and debiasing and the second based on filtering outliers followed by imputation and standard covariance estimation. We propose novel computationally efficient and numerically stable procedures that avoid matrix inversion, making them well-suited for high-dimensional data. We derive non-asymptotic estimation bounds of the covariance with the operator norm and minimax lower bounds, which clarify the impact of the missing value rate and outlier contamination rate. Our theoretical results also improve over louniciHighdimensionalCovarianceMatrix2014 in the MCAR and no contamination. Next, we conduct an experimental study on synthetic data, comparing our proposed methods to the state-of-the-art (SOTA) methods. Our results demonstrate that SOTA methods fail in the high-dimensional regime due to matrix inversions, while our proposed methods perform well in this regime, highlighting their effectiveness. Then we demonstrate the practical utility of our approach by applying it to real-life datasets, which highlights that the use of existing estimation methods significantly alters the spectral properties of the estimated covariance matrices. This implies that cell-wise contamination can significantly impact the results of dimension reduction techniques like PCA by completely altering the computed principal directions. Our experiments demonstrate that our methods are more robust to cell-wise contamination than SOTA methods and produce reliable estimates of the covariance.

2 Missing values and cell-wise contamination setting

Let be i.i.d. copies of a zero mean random vector admitting unknown covariance operator , where is the outer product. Denote by the th component of vector for any . All our results are non-asymptotic and cover a wide range of configurations for and including the high-dimensional setting . In this paper, we consider the following two realistic scenarios where the measurements are potentially corrupted.

Missing values.

We assume that each component is observed independently from the others with probability . Formally, we observe the random vector defined as follows:

| (1) |

where are independent realisations of a bernoulli random variable of parameter . This corresponds the Missing Completely at Random (MCAR) setting of rubinInferenceMissingData1976 . Our theory also covers the more general Missing at Random (MAR) setting in Theorem 2.

Cell-wise contamination.

Here we assume that some missing components can be replaced with probability by some independent noise variables, representing either a poisoning of the data or random mistakes in measurements. The observation vector then satisfies:

| (2) |

where are independent erroneous measurements and are i.i.d. bernoulli random variables with parameter . We also assume that all the variables , , , are mutually independent. In this scenario, a component is either perfectly observed with probability , replaced by a random noise with probability or missing with probability . Cell-wise contamination as introduced in alqallafPropagationOutliersMultivariate2009 corresponds to the case where , and thus .

In both of these settings, the task of estimating the mean of the random vectors is well-understood, as it reduces to the classical Huber setting for component-wise mean estimation. One could for instance apply the Tuker median on each component separately alqallafPropagationOutliersMultivariate2009 . However, the problem becomes more complex when we consider non-linear functions of the data, such as the covariance operator. Robust covariance estimators originally designed for the Huber setting may not be suitable when applied in the presence of missing values or cell-wise contaminations.

We study a simple estimator based on a correction of the classical covariance estimator on as introduced in louniciHighdimensionalCovarianceMatrix2014 for the missing values scenario. The procedure is based on the following observation, linking the covariance of the data with missing values and the true covariance:

| (3) |

Note that this formula assumes the knowledge of . In the missing values scenario, can be efficiently estimated by a simple count of the values exactly set to or equal to NaN (not a number). In the contamination setting (2), the operator satisfies, for :

In this setting, as one does not know the exact location and number of outliers we propose to estimate by the proportion of data remaining after the application of a filtering procedure.

Notations.

We denote by the Hadamard (or term by term) product of two matrices and by the outer product of vectors, i.e. . We denote by and the operator and Frobenius norms of a matrix respectively. We denote by the vector -norm.

3 Estimation of covariance matrices with missing values

We consider the scenario outlined in (1) where the matrix is of approximately low rank. To quantify this, we use the concept of effective rank, which provides a useful measure of the inherent complexity of a matrix. Specifically, the effective rank of is defined as follows

| (4) |

We note that . Furthermore, for approximately low rank matrices with rapidly decaying eigenvalues, we have . This section presents a novel analysis of the estimator defined in equation (3), which yields a non-asymptotic minimax optimal estimation bound in the operator norm. Our findings represent a substantial enhancement over the suboptimal guarantees reported in louniciHighdimensionalCovarianceMatrix2014 ; klochkovUniformHansonWrightType2019 . Similar results could be established for the Frobenius norm using more straightforward arguments, as those in buneaSampleCovarianceMatrix2015 or puchkinSharperDimensionfreeBounds2023 . We give priority to the operator norm since it aligns naturally with learning tasks such as PCA. See 15-AIHP705 ; Koltchinskii2017 ; 16-AOS1437 and the references cited therein.

We need the notion of Orlicz norms. For any , the -norms of a real-valued random variable are defined as: . A random vector is sub-Gaussian if and only if , .

Minimax lower-bound.

We now provide a minimax lower bound for the covariance estimation with missing values problem. Let the set of symmetric semi-positive matrices. Then, define the set of matrices of with effective rank at most .

Theorem 1.

Let be strictly positive integers such that . Let be i.i.d. random vectors in with covariance matrix . Let be an i.i.d. sequence of Bernoulli random variables with probability of success , independent from the . We observe i.i.d. vectors such that , , . Then there exists two absolute constants and such that:

| (5) |

where represents the infimum over all estimators of matrix based on .

Sketch of proof.

We first build a sufficiently large test set of hard-to-learn covariance operators exploiting entropy properties of the Grassmann manifold such that the distance between any two distinct covariance operator is at least of the order . Next, in order to control the Kullback-Leibler divergence of the observations with missing values, we exploit in particular interlacing properties of the eigenvalues of the perturbed covariance operators thompsonPrincipalSubmatricesNormal1966 . ∎

This lower bound result improves upon (louniciHighdimensionalCovarianceMatrix2014, , Theorem 2) as it relaxes the hypotheses on and . More specifically, the lower bound in louniciHighdimensionalCovarianceMatrix2014 requires while we only need the mild assumption . Our proof leverages the properties of the Grassmann manifold, which has been previously utilized in different settings such as sparse PCA without missing values or contamination vuMinimaxSparsePrincipal2013 and low-rank covariance estimation without missing values or contamination koltchinskiiEstimationLowRankCovariance2015 . However, tackling missing values in the Grassmann approach adds a technical challenge to these proofs as they modify the distribution of observations. Our proof requires several additional nontrivial arguments to control the distribution divergences, which is a crucial step in deriving the minimax lower bound.

Non-asymptotic upper-bound in the operator norm.

We provide an upper bound of the estimation error in operator norm. We write . Let be the classical covariance estimator of the covariance of . When the dataset contains missing values and corruptions, is a biased estimator of . Exploiting Equation (3), louniciHighdimensionalCovarianceMatrix2014 proposed the following unbiased estimator of the covariance matrix :

| (6) |

The following result is from (klochkovUniformHansonWrightType2019, , Theorem 4.2).

Lemma 1.

Let be i.i.d. sub-Gaussian random variables in , with covariance matrix , and let be i.i.d bernoulli random variables with probability of success . Then there exists an absolute constant such that, for , with probability at least :

| (7) |

This result uses a recent unbounded version of the non-commutative Bernstein inequality, thus yielding some improvement upon the previous best known bound of louniciHighdimensionalCovarianceMatrix2014 . Theorem 1 and Lemma 1 provide some important insights on the minimax rate of estimation in the missing values setting. In the high-dimensional regime and , we observe that the two bounds coincide up to a logarithmic factor in , hence clarifying the impact of missing data on the estimation rate via the parameter .

Heterogeneous missingness.

We can extend the correction to the more general case where each feature has a different missing value rate known as the Missing at Random (MAR) setting in rubinInferenceMissingData1976 . We denote by the probability to observe feature , and we set . As in the MCAR setting, the probabilities can be readily estimated by tallying the number of missing entries for each feature. Hence they will be assumed to be known for the sake of brevity. Let be the vector containing the inverse of the observing probabilities and . In this case, the corrected estimator becomes :

| (8) |

Let and be the largest and smallest probabilities to observe a feature.

Theorem 2.

(i) Let be i.i.d. sub-Gaussian random variables in , with covariance matrix . We consider the MAR setting described above. Then the estimator (8) satisfies, for any , with probability at least

| (9) |

(ii) Let be strictly positive integers such that . Let be i.i.d. random vectors in with covariance matrix . Then,

| (10) |

If then the rates for the MCAR and MAR settings match. The proof is a straightforward adaptation of the proof in the MCAR setting.

4 Optimal estimation of covariance matrices with cell-wise contamination

In this section, we consider the cell-wise contamination setting (2).We derive both an upper bound on the operator norm error of the estimator (6) and a minimax lower bound for this specific setting. Let us assume that the are sub-Gaussian r.v. Note also that is diagonal in the cell-wise contamination setting (2).

Minimax lower-bound.

The lower bound for missing values still applies to the contaminated case as missing values are a particular case of cell-wise contamination. But we want a more general lower bound that also covers the case of adversarial contaminations.

Theorem 3.

Let be strictly positive integers such that . Let be i.i.d. random vectors in with covariance matrix . Let be i.i.d. sequence of bernoulli random variables of probability of success , independent to the . We observe i.i.d. vectors satisfying (2) where are i.i.d. of arbitrary distribution . Then there exists two absolute constants and such that:

| (11) |

where represents the infimum over all estimators of matrix and is the maximum over all contamination .

The proof of this theorem adapts an argument developed to derive minimax lower bounds in the Huber contamination setting. See App. G.3 for the full proof.

Non-asymptotic upper-bound in the operator norm.

Note that the term in the cell-wise contamination setting is negligible when or . Using the DDC detection procedure of raymaekersHandlingCellwiseOutliers2020 , we can detect the contaminations and make smaller without decreasing too much. For simplicity, we assume from now on that the are i.i.d. with common variance . Hence . We further assume that the are sub-Gaussian since we observed in our experiments that filtering removed all the large-valued contaminated cells and only a few inconspicuous contaminated cells remained. Our procedure (6) satisfies the following result.

Theorem 4.

See App F.3 for the proof. As emphasized in koltchinskiiConcentrationInequalitiesMoment2017 , the effective rank provides a measure of the statistical complexity of the covariance learning problem in the absence of any contamination. However, when cell-wise contamination is present, the statistical complexity of the problem may increase from to . Fortunately, if the filtering process reduces the proportion of cell-wise contamination such that and . Then we can effectively mitigate the impact of cell-wise contamination. Indeed, we deduce from Theorem 4 that

| (12) |

where we considered for convenience the reasonable scenario where and . The combination of the upper bound (12) with the lower bound in Theorem (3) provides the first insights into the impact of cell-wise contamination on covariance estimation.

5 Experiments

In our experiments, MV refers either to the debiased MCAR covariance estimator (6) or to its MAR extension (8). The synthetic data generation is described in App. A. We also performed experiments on real life datasets described in App. B. All experiments were conducted on a 2020 MacBook Air with a M1 processor (8 cores, 3.4 GHz). 111Code available at https://github.com/klounici/COVARIANCE_contaminated_data

5.1 Missing Values

We compared our method to popular imputations methods: KNNImputer (KNNI), which imputes the missing values based on the k-nearest neighbours (troyanskayaMissingValueEstimation2001, ), and IterativeImputer (II), which is inspired by the R package MICE (buurenMiceMultivariateImputation2011, ), as coded in sklearn scikit-learn ; and two recent GANs-based imputation methods MIWAE (matteiMIWAEDeepGenerative2019, ) and GAIN (yoonGAINMissingData2018, ) as found in the package hyperimpute (Jarrett2022HyperImpute, ). The deep methods were tested using the same architectures, hyperparameters and early stopping rules as their respective papers.

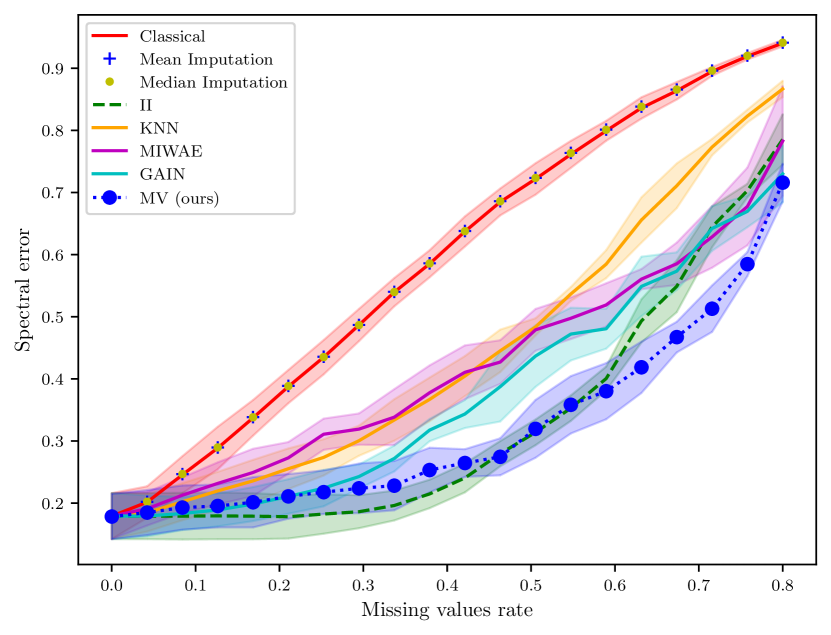

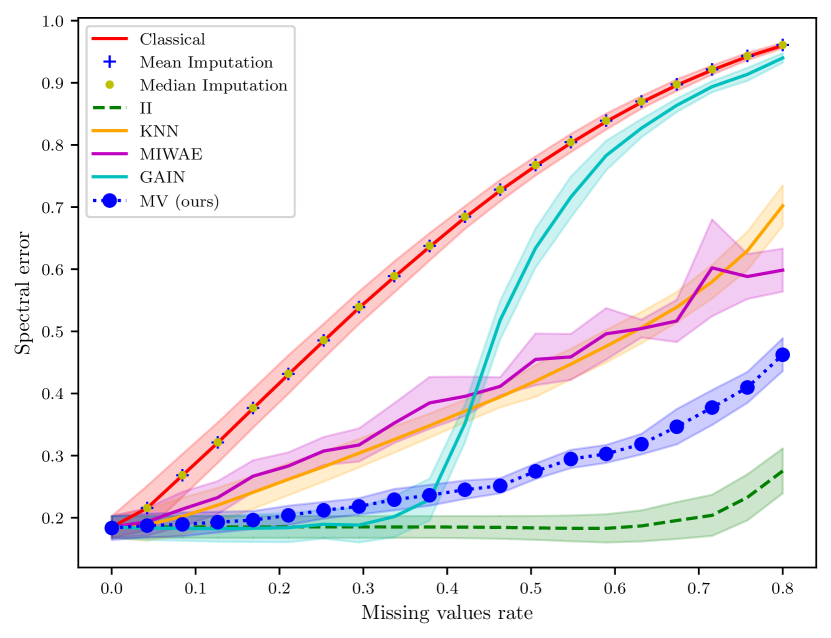

In Figures 3, 3 and Table 1, we compare our estimator MV defined in (6) to these imputation methods combined with the usual covariance estimator on synthetic data (see App. A for details of data generation) in terms of statistical accuracy and execution time. First, MV beats all other methods in low-dimensional scenarios and maintains a competitive edge with II in high-dimensional situations when the missing data rate remains below . Furthermore, it stands as the second-best choice when dealing with missing data rates exceeding . Next, MV has by far the smallest execution time down several orders of magnitude while the execution time of II increases very quickly with the dimension and can become impractical (see Figure 9 for a dataset too large for II). Overall, the procedures MV and II perform better than MIWAE and GAIN in this experiment. Our understanding is that MIWAE and GAIN use training metrics designed to minimize the entrywise error of imputation. We suspect this may be why their performances for the estimation of covariance with operator norm are not on par with other minimax methods. An interesting direction would be to investigate whether training MIWAE and GAIN with different metrics may improve the operator norm performance.

We refer to App. E for more experiments in the MAR setting of (matteiMIWAEDeepGenerative2019, , Annex 3) which led to similar conclusions. These results confirm that imputation of missing values is not mandatory for accurate estimation of the covariance operator. Another viable option is to apply a debiasing correction to the empirical covariance computed on the original data containing missing values. The advantage of this approach is its low computational cost even in high-dimension.

| method | |||

|---|---|---|---|

| MV (ours) | |||

| KNNImputer (KNN) | |||

| IterativeImputer (II) | |||

| Gain | |||

| MIWAE |

5.2 Cell-wise contamination

Methods tested.

Our baselines are the empirical covariance estimator applied without care for contamination and an oracle which knows the position of every outlier, deletes them and then computes the MV bias correction procedure (6). In view of Theorems 1 and 1, this oracle procedure is the best possible in the setting of cell-wise contamination. Hence, we have a practical framework to assess the performance of any procedure designed to handle cell-wise contamination.

The SOTA methods in the cell-wise contamination setting are the DI (Detection-Inputation) method raymaekersHandlingCellwiseOutliers2020 and the TSGS method (Two Step Generalised S-estimator) agostinelliRobustEstimationMultivariate2014 . Both these methods were designed to work in the standard setting but cannot handle the high-dimensional setting as we already mentioned. Nevertheless, we included comparisons of our methods to them in the standard setting . The code for DI and TSGS are from the R packages cellwise and GSE respectively.

We combine the DDC detection procedure rousseeuwDetectingDeviatingData2018 to first detect and remove outliers with several estimators developed to handle missing values. Our main estimators are DDCMV (short for Detecting Deviating Cells Missing Values), which uses first DDC and then computes the debiaised covariance estimator (6) on the filtered data, and tailMV, which detects outliers through thresholding and then uses again (6). But we also proposed to combine the DDC procedure with imputation methods KNNI, II, GAIN and MIWAE and finally compute the standard covariance estimator on the completed data. Hence we define four additional novel robust procedures which we call DDCKNN, DDCII, DDCGAIN and DDCMIWAE. To the best of our knowledge, neither the first approach combining filtering with debiasing nor the second alternative approach combining filtering with missing values imputation have never been tested to deal with cell-wise contamination. A detailed description of each method is provided in App. C.

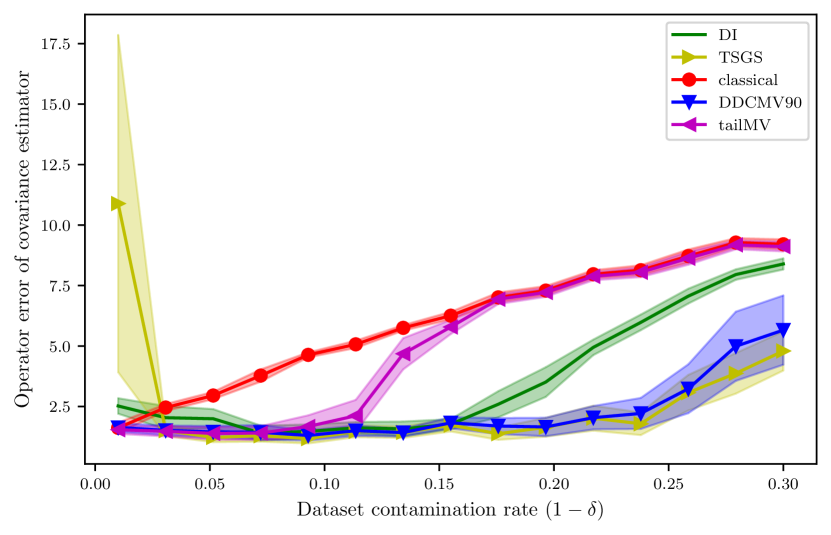

Outlier detection and estimation error under cell-wise contamination on synthetic data.

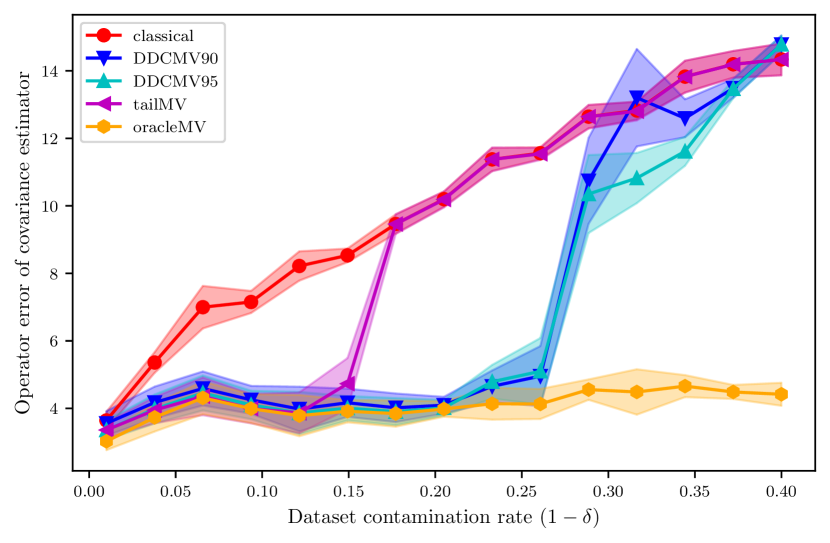

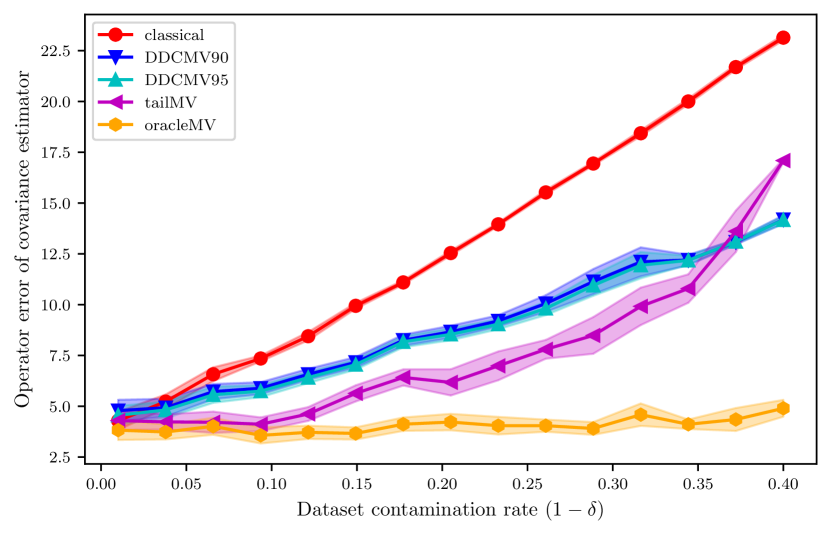

We showed that the error of a covariance estimator under cell-wise contamination depends on the proportion of remaining outliers after a filtration. In Table 2 we investigate the filtering power of the Tail Cut and DDC methods in presence of Dirac contamination. We consider the cell-wise contamination setting (2) in the most difficult case which means that an entry is either correctly observed or replaced by an outlier (in other words, the dataset does not contain any missing value). For each values of in a grid, the quantities and are the proportions of true entries and remaining contaminations after filtering averaged over repetitions. The DDC based methods are particularly efficient since the proportion of Dirac contamination drops from to virtually for any . In Figures 1 and 5, we see that the performance of our method is virtually the same as the oracle OracleMV as long as the filtering procedure correctly eliminates the Dirac contaminations. As soon as the filtering procedure fails, the statistical accuracy brutally collapses and our DDC based estimators no longer do better than the usual empirical covariance. In Table 8 and Figure 5, we repeated the same experiment but with a centered Gaussian contamination. Contrarily to the Dirac contamination scenario, we see in Figure 5 that the statistical accuracy of our DDC based methods slowly degrades as the contamination rate increases but their performance remains significantly better than that of the usual empirical covariance.

| Contamination | Tail cut | DDC | DDC | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| rate () | std | std | std | std | std | std | ||||||

| 0.1 | 99.6 | 0.023 | 0.000 | 0.000 | 99.1 | 0.029 | 0.000 | 0.000 | 94.8 | 0.054 | 0.00 | 0.00 |

| 1 | 98.8 | 0.027 | 0.000 | 0.000 | 98.2 | 0.037 | 0.000 | 0.00 | 94.3 | 0.102 | 0.00 | 0.00 |

| 5 | 94.9 | 0.013 | 0.000 | 0.000 | 94.6 | 0.018 | 0.000 | 0.000 | 91.8 | 0.060 | 0.00 | 0.000 |

| 10 | 90.0 | 0.004 | 0.000 | 0.000 | 89.9 | 0.016 | 0.00 | 0.000 | 88.2 | 0.109 | 0.000 | 0.000 |

| 20 | 80.0 | 0.000 | 20.0 | 0.000 | 80.0 | 0.003 | 0.017 | 0.035 | 79.4 | 0.035 | 0.009 | 0.022 |

| 30 | 70.0 | 0.000 | 30.0 | 0.000 | 70.0 | 0.001 | 3.48 | 2.19 | 69.9 | 0.015 | 2.930 | 2.31 |

5.3 The effect of cell-wise contamination on real-life datasets

We tested the methods on datasets from sklearn and Woolridge’s book on econometrics wooldridgeIntroductoryEconometricsModern2016 . These are low dimensional datasets (less than features) representing various medical, social and economic phenomena. We also included high-dimensional datasets. See App. B for the list of the datasets.

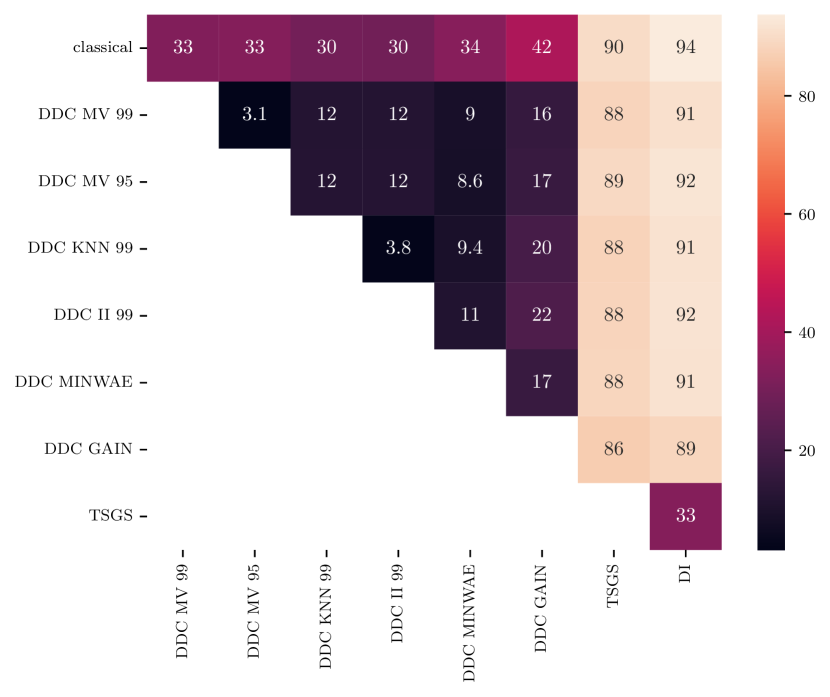

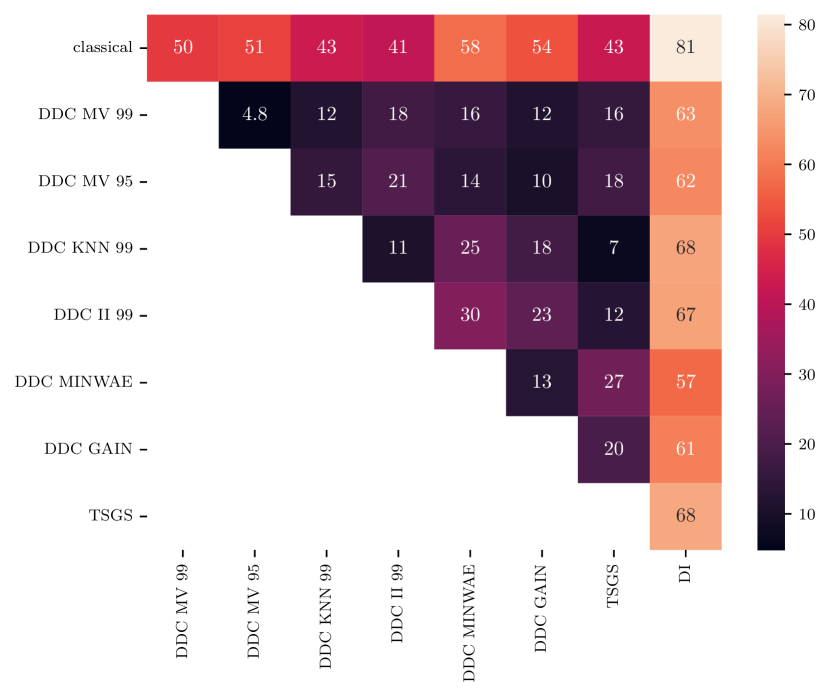

One interesting observation is that the instability of Mahalanobis distance-based algorithms is not limited to high-dimensional datasets. Even datasets with a relatively small number of features can exhibit instability. This can be seen in the performance of DI on the Attend dataset, as depicted in Figure 7, where it fails to provide accurate results. Similarly, both TSGS and DI fail to perform well on the CEOSAL2 dataset, as shown in Figure 7, despite both datasets having fewer than features.

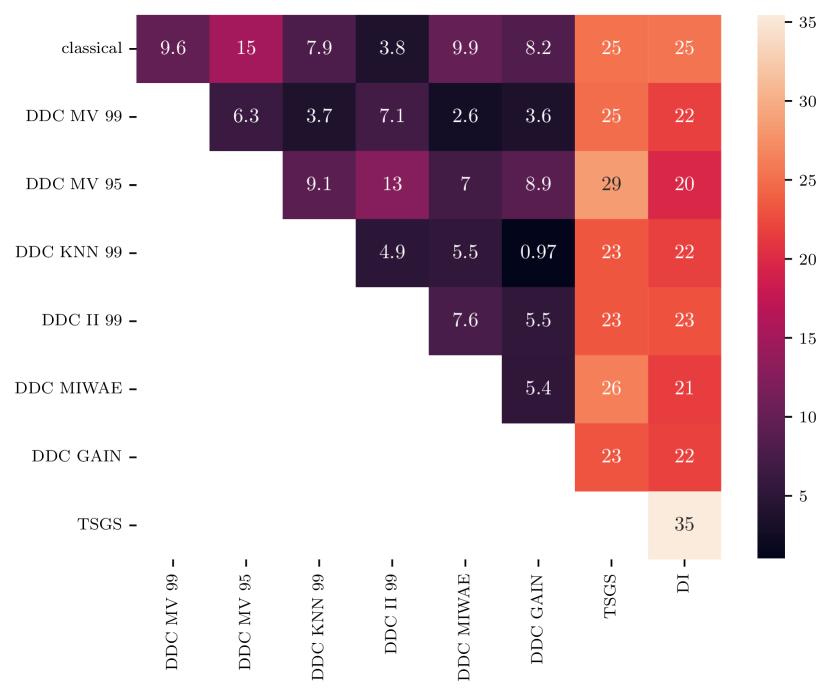

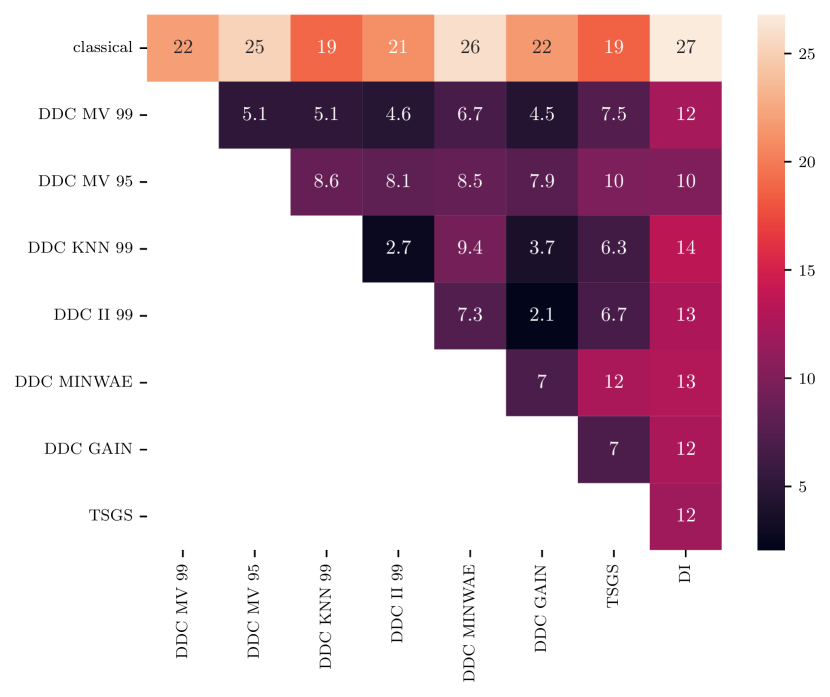

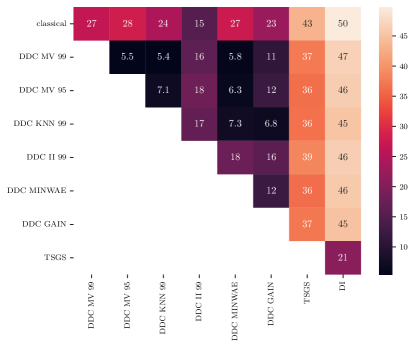

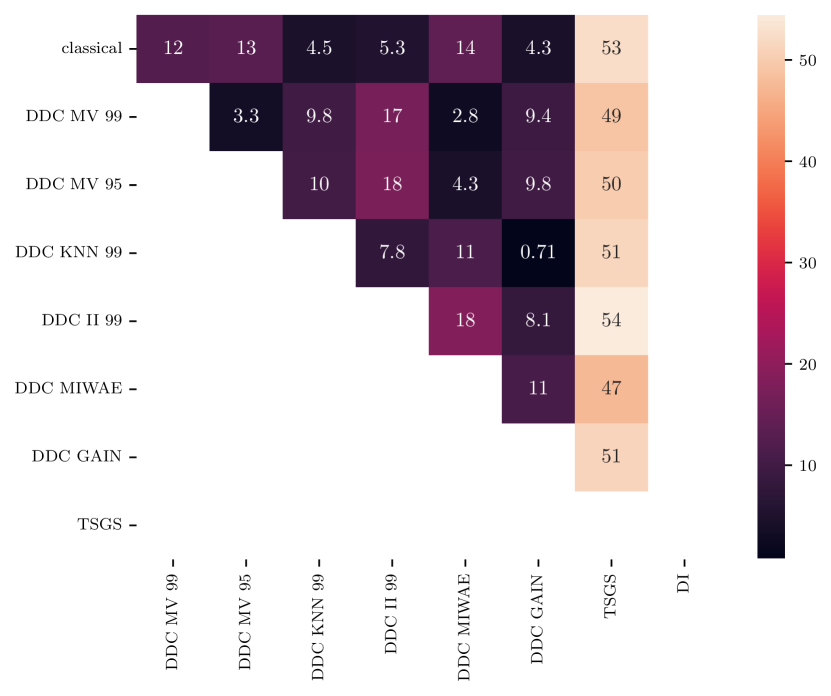

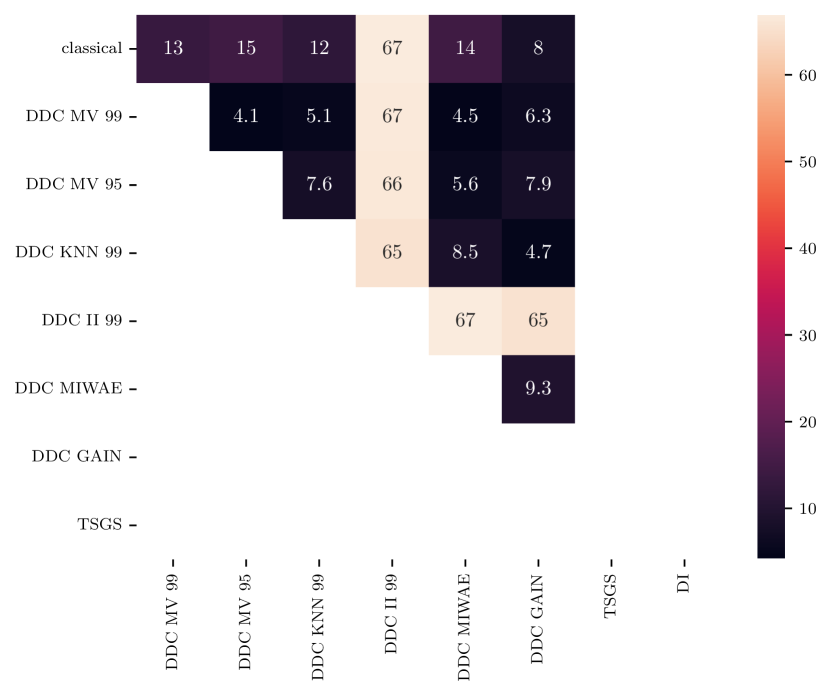

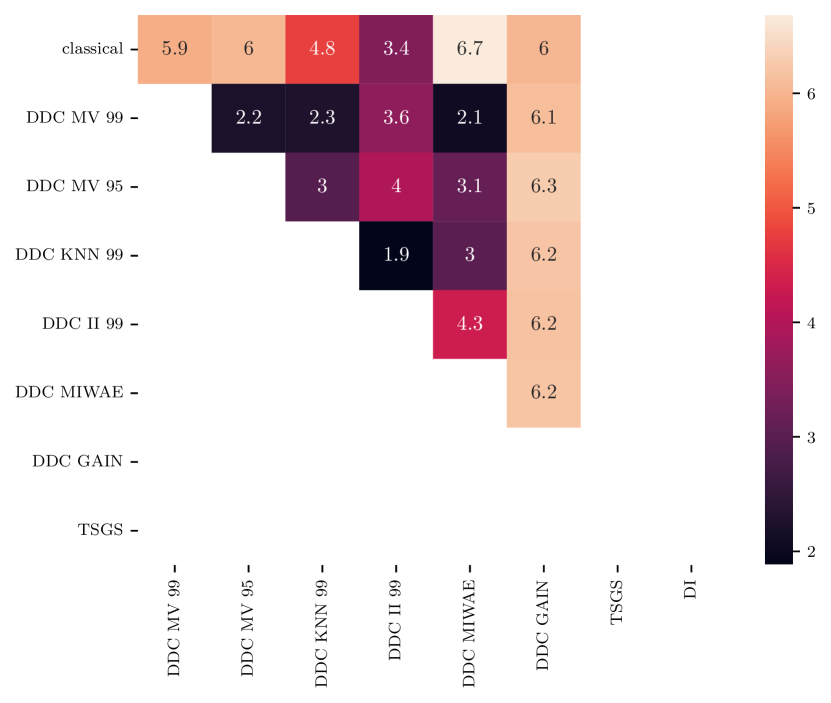

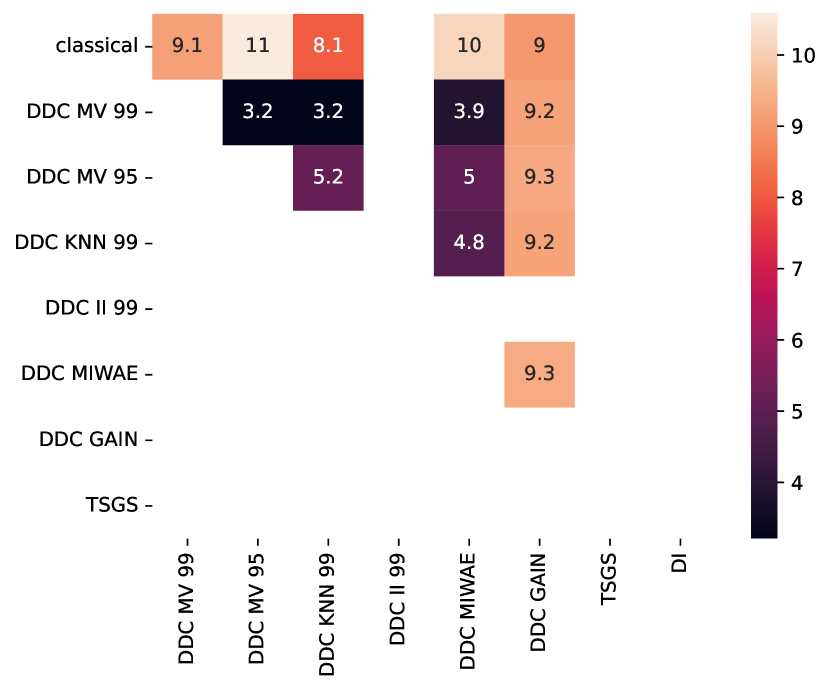

On the Abalone dataset, once we have removed 4 obvious outliers (which are detected by both DDC and the tail procedure), all estimators reached a consensus with the non-robust classical estimator, meaning that this dataset provides a ground truth against which we can evaluate and compare the performance of robust procedures in our study. To this end, we artificially contaminate of the cells at random in the dataset with a Dirac contamination and compare the spectral error of the different robust estimators. As expected, TSGS and all our new procedures succeed at correcting the error, however DI becomes unstable (see Table 3). DDC MIWAE is close to SOTA TSGS for cellwise contamination and DDC II performs better. We also performed experiments on two high-dimensional datasets, where our methods return stable estimates of the covariance (DDCMV99 and DDCMV95 are within of each other) and farther away from the classical estimator (See Figures 9 and 9 ). Note also that DDCII’s computation time explodes and even returns out-of-memory errors due to the high computation cost of II that we already highlighted in Table 1.

| relative | Classical | DDCMV99 | DDCMV95 | DDC II | DDC KNN | DDC | DDC | TSGS | DI |

|---|---|---|---|---|---|---|---|---|---|

| error to | estimator | MIWAE | GAIN | ||||||

| Truth | 12.8 | 4.12 | 6.81 | 1.70 | 2.06 | 3.46 | 5.06 | 3.06 | 8.85 |

| std | 0.45 | 0.29 | 0.26 | 0.10 | 0.092 | 0.18 | 0.35 | 0.21 | 1.48 |

| Classical | - | 13.1 | 14.3 | 13.0 | 13.0 | 12.9 | 13.1 | 13.4 | 14.9 |

| DDCMV99 | - | - | 2.99 | 2.52 | 2.22 | 1.87 | 2.66 | 5.44 | 8.79 |

| DDCMV95 | - | - | - | 5.27 | 5.03 | 4.04 | 3.71 | 8.28 | 9.99 |

| DDC II | - | - | - | - | 0.465 | 1.88 | 3.49 | 3.27 | 8.28 |

| DDC KNN | - | - | - | - | - | 1.58 | 3.19 | 3.46 | 8.15 |

| DDC MIWAE | - | - | - | - | - | - | 1.70 | 4.50 | 7.22 |

| DDC GAIN | - | - | - | - | - | - | - | 5.97 | 6.71 |

| TSGS | - | - | - | - | - | - | - | - | 6.94 |

6 Conclusion and future work

In this paper, we have extended theoretical guarantees on the spectral error of our covariance estimators robust to missing data to the missing at random setting. We have also derived the first theoretical guarantees in the cell-wise contamination setting. We highlighted in our numerical experimental study that in the missing value setting, our debiased estimator designed to tackle missing values without imputation offers statistical accuracy similar to the SOTA IterativeImputer for a dramatic computational gain. We also found that SOTA algorithms in the cell-wise contamination setting often fail in the standard setting for dataset with fast decreasing eigenvalues (resulting in approximately low rank covariance), a setting which is commonly encountered in many real life applications. This is due to the fact that these methods use matrix inversion which is unstable to small eigenvalues in the covariance structure and can even fail to return any estimate. In contrast, we showed that our strategy combining filtering with estimation procedures designed to tackle missing values produce far more stable and reliable results. In future work, we plan to improve our theoretical upper and lower bounds in the cell-wise contamination setting to fully clarify the impact of this type of contamination in covariance estimation.

Acknowledgements.

This paper is based upon work partially supported by the Chaire Business Analytic for Future Banking and EU Project ELIAS under grant agreement No. 101120237.

References

- [1] Pedro Abdalla and Nikita Zhivotovskiy. Covariance Estimation: Optimal Dimension-free Guarantees for Adversarial Corruption and Heavy Tails, July 2023.

- [2] Claudio Agostinelli, Andy Leung, Victor J. Yohai, and Ruben H. Zamar. Robust estimation of multivariate location and scatter in the presence of cellwise and casewise contamination, June 2014.

- [3] Fatemah Alqallaf, Stefan Van Aelst, Victor J. Yohai, and Ruben H. Zamar. Propagation of outliers in multivariate data. The Annals of Statistics, 37(1):311–331, February 2009.

- [4] Florentina Bunea and Luo Xiao. On the sample covariance matrix estimator of reduced effective rank population matrices, with applications to fPCA. Bernoulli, 21(2), May 2015.

- [5] Mengjie Chen, Chao Gao, and Zhao Ren. Robust Covariance and Scatter Matrix Estimation under Huber’s Contamination Model. arXiv:1506.00691 [math, stat], June 2017.

- [6] Mike Danilov, Victor Yohai, and Ruben Zamar. Robust Estimation of Multivariate Location and Scatter in the Presence of Missing Data. JASA. Journal of the American Statistical Association, 107, September 2012.

- [7] A. P. Dempster, N. M. Laird, and D. B. Rubin. Maximum Likelihood from Incomplete Data via the EM Algorithm. Journal of the Royal Statistical Society. Series B (Methodological), 39(1):1–38, 1977.

- [8] Sheela Devadas, Peter J Haine, and Keaton Stubis. The Schur-Horn Theorem. 2015.

- [9] Weinan Dong, Daniel Yee Tak Fong, Jin-sun Yoon, Eric Yuk Fai Wan, Laura Elizabeth Bedford, Eric Ho Man Tang, and Cindy Lo Kuen Lam. Generative adversarial networks for imputing missing data for big data clinical research. BMC Medical Research Methodology, 21(1):78, April 2021.

- [10] Alessio Farcomeni. Robust Constrained Clustering in Presence of Entry-Wise Outliers. Technometrics, 56, February 2014.

- [11] Peter J. Huber. Robust Estimation of a Location Parameter. The Annals of Mathematical Statistics, 35(1):73–101, 1964.

- [12] Peter J. Huber and Elvezio M. Ronchetti. Robust Statistics, 2nd Edition | Wiley. Wiley Series in Probability and Statistics. John Wiley and Sons, Inc., 2009.

- [13] Mia Hubert, Michiel Debruyne, and Peter J. Rousseeuw. Minimum Covariance Determinant and Extensions. WIREs Computational Statistics, 10(3), May 2018.

- [14] Mortaza Jamshidian and Peter M. Bentler. ML Estimation of Mean and Covariance Structures with Missing Data Using Complete Data Routines. Journal of Educational and Behavioral Statistics, 24(1):21–41, 1999.

- [15] Daniel Jarrett, Bogdan Cebere, Tennison Liu, Alicia Curth, and Mihaela van der Schaar. Hyperimpute: Generalized iterative imputation with automatic model selection. 2022.

- [16] Charles R. Johnson. Matrix theory and applications (charles r. johnson, ed.). Proceedings of symposia in applied mathematics, 40, 1989.

- [17] Julie Josse, Nicolas Prost, Erwan Scornet, and Gaël Varoquaux. On the consistency of supervised learning with missing values. arXiv:1902.06931 [cs, math, stat], July 2020.

- [18] Yegor Klochkov and Nikita Zhivotovskiy. Uniform Hanson-Wright type concentration inequalities for unbounded entries via the entropy method, August 2019.

- [19] Vladimir Koltchinskii and Karim Lounici. Asymptotics and concentration bounds for bilinear forms of spectral projectors of sample covariance. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 52(4):1976 – 2013, 2016.

- [20] Vladimir Koltchinskii and Karim Lounici. Concentration inequalities and moment bounds for sample covariance operators. Bernoulli, 23(1):110–133, February 2017.

- [21] Vladimir Koltchinskii and Karim Lounici. New asymptotic results in principal component analysis. Sankhya A, 79(2):254–297, Aug 2017.

- [22] Vladimir Koltchinskii and Karim Lounici. Normal approximation and concentration of spectral projectors of sample covariance. The Annals of Statistics, 45(1):121 – 157, 2017.

- [23] Vladimir Koltchinskii, Karim Lounici, and Alexander B. Tsybakov. Estimation of Low-Rank Covariance Function, April 2015.

- [24] Andy Leung, Hongyang Zhang, and Ruben H. Zamar. Robust regression estimation and inference in the presence of cellwise and casewise contamination. Computational Statistics & Data Analysis, 99:1–11, July 2016.

- [25] Roderick Little and Donald Rubin. Statistical Analysis with Missing Data, Second Edition. Wiley Series in Probability and Mathematical Statistics. Probability and Mathematical Statistics. Wiley edition, 2002.

- [26] Karim Lounici. High-dimensional covariance matrix estimation with missing observations. Bernoulli, 20(3):1029–1058, August 2014.

- [27] Chao Ma, Sebastian Tschiatschek, José Miguel Hernández-Lobato, Richard Turner, and Cheng Zhang. VAEM: A Deep Generative Model for Heterogeneous Mixed Type Data, June 2020.

- [28] Pierre-Alexandre Mattei and Jes Frellsen. MIWAE: Deep Generative Modelling and Imputation of Incomplete Data Sets. In Kamalika Chaudhuri and Ruslan Salakhutdinov, editors, Proceedings of the 36th International Conference on Machine Learning, ICML 2019, 9-15 June 2019, Long Beach, California, USA, volume 97 of Proceedings of Machine Learning Research, pages 4413–4423. PMLR, 2019.

- [29] Alain Pajor. Metric Entropy of the Grassmann Manifold. Complex Geometry Analysis, 34:181–188, 1998.

- [30] F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay. Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- [31] Nikita Puchkin, Fedor Noskov, and Vladimir Spokoiny. Sharper dimension-free bounds on the Frobenius distance between sample covariance and its expectation, August 2023.

- [32] Jakob Raymaekers and Peter J. Rousseeuw. Handling cellwise outliers by sparse regression and robust covariance. arXiv:1912.12446 [stat], December 2020.

- [33] Jakob Raymaekers and Peter J. Rousseeuw. Fast robust correlation for high-dimensional data. Technometrics, 63(2):184–198, April 2021.

- [34] Peter J. Rousseeuw and Wannes Van den Bossche. Detecting deviating data cells. Technometrics, 60(2):135–145, April 2018.

- [35] Donald B. Rubin. Inference and Missing Data. Biometrika, 63(3):581–592, 1976.

- [36] Eckhard Schlemm. The kearns–saul inequality for bernoulli and poisson-binomial distributions. Journal of theoretical probability, 29:48–62, 2016.

- [37] R. C. Thompson. Principal submatrices of normal and Hermitian matrices. Illinois Journal of Mathematics, 10(2):296–308, June 1966.

- [38] Joel A. Tropp. An introduction to matrix concentration inequalities. Foundations and Trends® in Machine Learning, 8(1-2):1–230, 2015.

- [39] Olga Troyanskaya, Michael Cantor, Gavin Sherlock, Pat Brown, Trevor Hastie, Robert Tibshirani, David Botstein, and Russ B. Altman. Missing value estimation methods for DNA microarrays. Bioinformatics, 17(6):520–525, June 2001.

- [40] Alexandre B. Tsybakov. Nonparametric estimators. In Alexandre B. Tsybakov, editor, Introduction to Nonparametric Estimation, Springer Series in Statistics, pages 1–76. Springer, New York, NY, 2009.

- [41] John W. Tukey. The Ninther, a Technique for Low-Effort Robust (Resistant) Location in Large Samples. In H. A. David, editor, Contributions to Survey Sampling and Applied Statistics, pages 251–257. Academic Press, January 1978.

- [42] Stef van Buuren and Karin Groothuis-Oudshoorn. Mice: Multivariate Imputation by Chained Equations in R. Journal of Statistical Software, 45:1–67, December 2011.

- [43] Roman Vershynin. Introduction to the non-asymptotic analysis of random matrices, November 2011.

- [44] Roman Vershynin. High-Dimensional Probability: An Introduction with Applications in Data Science. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 2018.

- [45] Vincent Q. Vu and Jing Lei. Minimax sparse principal subspace estimation in high dimensions. The Annals of Statistics, 41(6):2905–2947, December 2013.

- [46] Jeffrey M. Wooldridge. Introductory econometrics : a modern approach / Jeffrey M. Wooldridge,… Cengage learning, 2016.

- [47] Jinsung Yoon, James Jordon, and Mihaela van der Schaar. GAIN: Missing Data Imputation using Generative Adversarial Nets, June 2018.

- [48] Shuhan Zheng and Nontawat Charoenphakdee. Diffusion models for missing value imputation in tabular data, March 2023.

Appendix A presents the synthetic data generation procedure used throughout our experiments. Appendix B and in particular Table 5 list the real life datasets presented in the paper. The cell-wise contamination correction methods are shown in Appendix C, with the DDC algorithm of [34] further detailed in Appendix D for convenience. The upper bound proofs can be found in Appendix F and the lower bound proofs in Appendix G, so that similar proof techniques can be grouped together for clarity. Additional technical elements of these proofs are collected in Appendix H when we felt that they impacted the latter’s readability. Finally, we show the full results of our experiments in Appendix I.

| Symbol | Description | Symbol | Description |

|---|---|---|---|

| The random variable of interest | Unbiased estimator of the covariance of | ||

| The observed contaminated random variable | Empirical covariance of | ||

| Dimension of the random variable | Noise covariance matrix | ||

| Number of samples | Vector norm (Euclidean norm) | ||

| Probability that a cell be observed correctly | Operator norm of | ||

| Bernoulli random variable of probability | Frobenius norm of | ||

| Probability that an unobserved cell be contaminated | -Orlicz norm of | ||

| Bernoulli random variable of probability | Hadamard or term by term product of matrices | ||

| True covariance matrix of | Outer product of vectors | ||

| True covariance matrix of | Indicator function | ||

| Effective rank of | Domination with regard to an absolute constant |

Appendix A Synthetic data generation

We generate synthetic datasets of realisations of a multivariate centered normal distribution. Its covariance matrix is defined as follows. We first set the eigenvalues as for , where is the requested effective rank of the matrix. This approximation guaranties that the true effective rank is below for . Then, using the ortho-group tool from scipy.stats, we create a random orthonormal matrix and set , which is symmetric and of low effective rank at most . Finally, we divide by its largest diagonal term so that the variances of the marginals be closer to .

We contaminate our synthetic datasets using a binary mask obtained by computing the realisation of i.i.d. bernoulli random variables. We fill the resulting missing data with either samples of a isotropic gaussian of covariance , where is the strength of the contamination (which we call the Gaussian contamination) or a array of value (which we call the Dirac contamination). Let be a random vector following one of those two contaminations, the data we feed all algorithms is then .

Appendix B Real life data set

For our real data experiments, we removed any categorical variable from the datasets since this work focuses on covariance estimation.We also applied a log transform to skewed variables to ensure that they are sub-Gaussian. The list of datasets can be found in Table 5. Finally, the Abalone dataset contains four obvious outliers that we removed in our experiments (although they were easily detected by both DDC and the thresholding procedure) in order to obtain a perfect dataset (no missing values, no contaminations) allowing us to compute the ground truth covariance. We have then injected missing values and cell-wise contaminations in this dataset and compared our robust procedures to the ground truth. We also note that the three UCI datasets were downloaded from sklearn.

| Name | Source | Description | |||

|---|---|---|---|---|---|

| Abalone | UCI | 7 | 4173 | 1.0 | Caracteristics of abalone specimens |

| Breast Cancer | UCI | 13 | 178 | 2.3 | Data on cell nuclei |

| Wine | UCI | 30 | 69 | 2.8 | Chemical data on wine varieties |

| Cameras | R | 11 | 1038 | 2.7 | Camera caracteristics over different models |

| Attend | [46] | 8 | 680 | 2.0 | Class attendance |

| Barium | [46] | 11 | 131 | 2.4 | Barium exports |

| CEOSAL2 | [46] | 13 | 177 | 2.5 | Firm accountancy data |

| INTDEF | [46] | 12 | 49 | 2.2 | USA deficit |

| SP 500 | yfinance | 496 | 502 | 2.7 | Returns of SP 500 companies in 2021/2022 |

| NASDAQ | yfinance | 1442 | 502 | 4.0 | Returns of NASDAQ companies in 2021/2022 |

Appendix C Methods compared in the cell-wise contamination setting

C.1 Baseline methods

Classical

denotes the empirical covariance estimator applied without care for contamination. We expect all other methods to perform better than it.

oracleMV

is an oracle that knows which cells are contaminated. This method shows the performance of our corrected estimator in the case of a perfect outlier detection algorithm, hence providing an idea of the optimal precision attainable with regard to the available information.

C.2 Our methods

tailMV

or tail Missing Values, is an estimator built by deleting extreme values in the dataset. It is actually one of the intermediary steps of DDC and we wanted to test how efficient it was on its own. We use the robust Huber estimator of the python package Statsmodel.robust [12] to compute the standard deviation of each marginal and eliminate any cell with value above times these estimates.

DDCMV

short for Detecting Deviating Cells Missing Values, is an estimator built using the DDC detection procedure of [32], where detected outliers are removed and considered as missing values. A detailed description of DDC is provided in appendix D. We then apply our corrected covariance estimator. We will add to the name of the method the quantile at which we consider a data as an outlier (DDCMV99 uses the 99-percentile of for instance). When nothing is mentioned, assume that DDCMV99 is used. In our experiments, we use the R implementation found in the package cellWise, whose results are then sent to a python script for formatting.

DDCKNN

detects outliers with the DDC procedure, removes them and imputes the missing values using the k-nearest neighbour procedure of [39] as implemented in sklearn under the name KNNImputer.

DDCII

also detects and removes outliers with the DDC procedure, then imputes the missing values using sklearn’s Iterative Imputer class.

DDCGAIN

is the combination of the DDC algorithm for outlier detection followed by the GAIN deep imputation method of [47].

DDCMIWAE

is the combination of the DDC algorithm for outlier detection followed by the MIWAE deep imputation method of [28].

C.3 SOTA methods for cell-wise contamination

DI

or Detection Imputation [33] Is an iterative algorithm made of two alternating steps inspired by the Expectation Maximisation (EM) algorithm. The first detects outliers with regard to a previously estimated covariance matrix, then the second computes a new covariance matrix having removed the previously detected outliers using the M step of EM, but with bias correction. This new matrix is then the basis for the next detection step and so on. The authors found their algorithm to have a complexity, with the number of iterations, and make the assumption that the covariance matrix is of full rank to perform matrix inversion, both facts that make it difficult to use in high dimensions.

TSGS

or Two Steps Generalised S-estimator [2] and [24] is also based on a two step process of detection then correction. Detection is based on the same DDC procedure while the estimation phase is based on the Generalised S-estimator of [6]. S-estimators are based on the Mahalonobis distance and thus require the true covariance matrix to be invertible. This may lead to numerically instability in our approximately low rank setting. However, if the matrix is of full rank, the generalised version of these estimators are proven to be consistent in the Missing Completely At Random setting.

Appendix D The Detecting Deviating Cells algorithm

This section is entirely based on [34], whose algorithm we describe here for convenience. DDC (Detecting Deviating Cells) is a 7 steps algorithm. In the following, let be our dataset of samples from data with dimension .

Step 1: standardisation

We start by assuming that the follow a normal distribution and we set

with being the empirical mean of marginal , and its standard deviation.

Step 2: cutoff

DDC sets to NA all values of if

with the centile of a distribution, where by default.

Step 3: bivariate relationship

The algorithm then computes the correlation between each couple of marginals. If ; set . Otherwise,

with the robust slope in the linear regression of using .

Step 4: comparison

Then DDC tries to predict the expected values of each according to a weighted mean of the values of the other marginals, using the previously computed correlations as weights.

with the weighted mean using as weights.

Step 5: deshrinkage

DDC adjusts the mean to account for shrinkage.

Step 6: residual computation

Then, one can take the residuals:

Step 7: destandardisation

Finally, DDC returns the data to its actual location and scale. The residuals can then be tested using a law to determine whether or not they are outliers.

Appendix E Missing at Random experiment

To assess our estimator (8) in the heterogeneous missingness setting, we replicated the MAR experiment of [28, Annex 3]. In this experiment, the data is missing with a different probability for each feature. These probabilities are fixed prior to the experiment and depend on the data, although the bernoulli random variables are still independent to the data. Just as in [28], the probability that an is observed depends on the first 15 samples and:

| (13) |

We compared our debiasing estimator (8) to the traditional KNNimputer, IterativeImputer and the recent imputation methods GAIN and MIWAE which are expected to perform better in this setting. On the Abalone dataset (Table 7), MV is the most accurate for the operator norm and MIWAE and GAIN are far behind and performs worse than IterativeImputer or KNNimputer. The Breast Cancer data was used both in [28, 47]. We used the colab code provided by [28] to implement MIWAE method. For GAIN we use the defaults parameters as in the HyperImpute library. We see in Table 7 that GAIN is the second best method behind MV and is better than IterativeImputer. We also note that, in all our experiments, the computation times were far longer for GAIN and MIWAE than for our debiasing scheme MV.

| Method | mean error | std |

|---|---|---|

| classical | ||

| MV | ||

| II | ||

| KNN | ||

| GAIN | ||

| MIWAE |

| Method | mean error | std |

|---|---|---|

| classical | ||

| MV | ||

| II | ||

| KNN | ||

| GAIN | ||

| MIWAE |

Appendix F Proofs of upper bounds

F.1 Tools and definitions

F.1.1 Basic properties of random vectors

We recall the definition and some basic properties of sub-exponential random vectors.

Definition 1.

For any , the -norms of a real-valued zero mean random variable are defined as:

We say that a random variable with values in is sub-exponential if for some . If , we say that is sub-Gaussian.

Lemma 2 (Lemma 5.14 in [43]).

If a real-valued random variable is sub-Gaussian, then is sub-exponential. Indeed, we have:

.

Definition 2.

The -norms of a random vector are defined as:

We will use the following definition of sub-Gaussian vectors that can be found in [20].

Definition 3.

A random vector is sub-Gaussian if and only if , .

We recall a version of Bernstein’s inequality (see corollary 5.17 in [43]):

Proposition 1.

Let be independent sub-exponential zero mean real-valued random variables. Set . Then, for , with probability at least :

| (14) |

where is an absolute constant.

F.2 Proofs of upper bounds in the setting of heterogeneous missingness

We denote by the matrix obtained by putting to the diagonal entries of matrix .

Following [26], we first note that

| (15) |

Hence, in view of [16, Theorem 3.1.d, page 95], we have that

| (16) |

We now extend several arguments in [26, 18] developed in the MCAR setting (same observation rate for all the features) to the heterogeneous missingness setting where each feature has possibly a different observation rate from the others features.

Lemma 3.

Let be a random vector admitting covariance . Define for all , where the are independent Bernoulli random variables with and . We have

and

Proof.

Let us first look at . We define . We also denote by the conditional expectation with respect to given . We compute the following representation:

Let us name the following matrices:

-

•

-

•

-

•

-

•

We note first that since is positive semi-definite. Here this inequality is to be understood in the matrix sense (Let and be symmetric matrices. We say that if for any , ).

Notice also that . Finally, we have that . Hence:

| (17) |

Let us now compute the expectations according to . Following [26], we find that:

| (18) |

By elementary computations

Hence and

| (19) |

Next, we tackle the diagonal matrix. By the equivalence of the moment of sub-Gaussian distributions we have that . Thus we get that:

Finally, let us compute . For any such that , we have by Cauchy-Schwartz

Looking at the first expectation:

Exploiting the sub-Gaussianity of , it was proved in [26] that

We study now the term . Again by sub-Gaussianity of , we have equivalence of the moments. That is for any unit vector

Combining the last four displays, we obtain that

| (20) |

The second inequality of the lemma follows from a similar and actually simpler argument. We have

where we have used again the sub-Gaussianity of the random vector and the fact that for any . ∎

Lemma 4.

Under the same assumptions as the previous lemma, for any such that ,

and

Proof.

Let us consider two vectors and of . First, let us demonstrate the first assertion. By using :

Looking at the first term, we use the decoupling principle of [44, Theorem 6.1.1] to create an independent copy of with same law such that:

Here all the terms except and are equal to zero. We have that for all , thus:

The second term can be bounded using and Cauchy-Schwarz:

The rest of the proof follows the same arguments to those in the proof of [18, Lemma 4.4].

Regarding the second assertion, it is immediate to see that:

∎

F.3 Proof of the upper bounds in the contaminated case

Proof of Theorem 4.

First, observe that:

| (21) |

Thus we need to control the error on the observed covariance matrix. Here the error can decomposed as follows:

| (22) |

where the three empirical matrices are

-

1.

, the empirical covariance matrix of the and ;

-

2.

, the empirical covariance of the is such that ;

-

3.

is the empirical covariance between the and the and has a null diagonal and also a null expectation.

Using [18], we get that there exists an absolute constant such that, with probability at least ,

| (23) |

To tackle the second term, we will use a standard argument for isotropic sub-Gaussian random vectors (see for instance the proof of Theorem 5.39 in [43]) combining a vector Bernstein inequality [43, Corollary 5.17] with an union bound. Hence we obtain with probability at least

| (24) |

Set and . We note that for any . Using the properties of the Orlicz norm, we easily get that . Next, by triangular inequality, we note that . Theorem 1.1 in [36] guarantees that for any . Since as , we obtain that .

Hence the previous display becomes

| (25) |

Now we need to control the norm of

To this end, we apply again the noncommutative Bernstein inequality of [18, Proposition 4.1]. Note that this result was stated for Hermitian matrices, but the result can be easily extended to arbitrary matrices by applying the self-adjoint dilation trick (See for instance [38] for more details).

In what follows, for any , we set

For the sake of simplicity, we will write without any index to designate any of the ’s. Notice that is symmetric by construction but has no diagonal term.

Lemma 5.

Under the assumptions of Theorem 4, we have

Proof.

We first compute the matrix product . For any

| (26) |

Let us call and the two terms inside the first factor and and the two terms in the second factor. Observe that most terms simplify when taking the expectation:

-

•

times : is always zero. Indeed, if then by independence of and ; otherwise .

-

•

times : only remains if or .

-

•

times : is zero if by independence of and , otherwise the whole sum remains.

-

•

with : is always zero if by independence of and and if then .

We can thus rewrite:

By computing the expectations using the independence of our variables, we get:

Thus, for the matrix such that:

We can write the expectation as

| (27) |

With our i.i.d. assumptions on the ’s contaminations, we can simplify the previous expression of

Denote by the matrix with all its entries equal to . Then we have the following equivalent representation for

| (28) |

We deduce from the previous display and (27) that

Lemma 6.

We can bound the psi-1 norm of the maximum of the as follows:

| (29) |

Proof.

Indeed, as recalled in [18, Remark 4.1],

By definition of the spectral norm:

| (30) |

Then, we can see that is sub-exponential

| (31) |

Since is sub-Gaussian, we get

| (32) |

Similarly, we get that:

| (33) |

Which in turn gives us that

| (34) |

∎

Appendix G Proof of lower bounds

The first two subsections deal with the lower bound of theorem 1, the third extends it to the contaminated case.

G.1 Hypothesis construction in the Grassmannian manifold

Let be a matrix with orthonormal rows. Each matrix describes a subspace of , where and is its projector in . The set of all is the Grassmannian manifold , which is the set of all -dimensional subspaces of . The Grassmannian manifold is a smooth manifold of dimension , where one can define a metric for all subspaces :

| (36) |

where and are the projectors to the subspaces and respectively and and are the matrix with orthonormal rows associated with and respectively. In the remainder of the proof, we will identify the projectors to the subspaces. A result on the entropy of Grassmanian manifolds [29] shows that:

Proposition 2.

For all , there exists a family of orthonormal projectors such that:

| (37) |

and, ,

| (38) |

for some small enough absolute constant , where is the cardinal of set .

Without loss of generality, we assume that the block matrix belongs to the set . Indeed, the Frobenius norm is invariant through a change of basis.

Let us then build such a set of hypotheses. Let where is an absolute constant We set and where was introduced above. Let us define the family of symmetric matrices , as follows : , where is the identity matrix. These covariance matrices belongs to the class of spiked covariance matrices.

Then, we can see that, for , by setting :

| (39) |

G.2 KL-divergence of hypotheses

Now that we have our candidate covariances , let us define the associated distributions. For , let be i.i.d. random variables following a gaussian law. Let be each vectors of i.i.d bernoulli random variables of probability of success , and let be random variables such that, , with the Hadamard or term-by-term product. Let us also define as the distribution of and the conditional distribution of the knowing . Finally, let be the expectation given the distribution associated with the -th projector and the expectation over .

For , let us compute the Kullback-Leibler divergence from to .

| (40) |

Since , , for all and for each realisation , , thus .

Define the set of indices kept by vector and . Then, define the mapping such that , such that is a dimensional vector containing the components of whose index are in . Let the right inverse of .

Note that , , with the projector to the subspace of orthogonal to the one described by . Let us define . Then, observe that is invertible, with inverse since and are diagonal matrices. We thus get, for :

| (41) |

First, using a result of linear algebra described in section H.2, we show that:

| (42) |

In the high-dimensional regime , we obtain

| (43) |

Next, let us focus on bounding . Remember that is diagonal. Using the fact that , we get:

| (44) |

Finally, using the fact demonstrated in appendix H.4 and the upper bound of proposition 2, we get that:

| (45) |

Thus, since , and since we assumed that :

| (46) |

for . According to theorem 2.5 of [40], the previous display combined with (39) gives

| (47) |

where and are two absolute constants. This fact, in turn, implies the lower bound of theorem 1, since, for all matrices of our hypothesis set:

| (48) |

Indeed, otherwise, we would get

| (49) |

which contradicts equation 39.

The heterogeneous result follows immediately by replacing with $̱\delta$.

G.3 Lower bound in the contaminated case

The bound of theorem 3 is made of two terms. The left term is the missing values lower bound, since missingness is a particular case of contamination. The second term is a result from the Huber contamination analysis of [5], which we develop here.

The proof is based on Le Cam’s two point argument (see e.g. chapter 2.3 of [40]). Let and where is the matrix with zeros except in the entry, which is equal to . Then, let and . We will now build two contaminations and such that they render and undistinguishable under cell-wise contamination of parameter and . Notice for now that:

| (50) |

and by Pinsker’s inequality [40, Lemma 2.5]:

| (51) |

and fix such that .

We will create our and such that they both have independent components. Since and are isotropic Gaussians and the contamination is completely at random, we can decompose the contaminated distributions and as follows:

and

Notice that taken separately, the components can be considered to be univariate Gaussian distributions under a Huber contamination. We can now try to build and so that and are equal in distribution. Let us first set for , since the components of and are equal in distribution for the contamination we choose here doesn’t matter much.

The rest of the proof is heavily inspired by [5, Appendix E]. Set the following densities:

Then, define the following contaminations and :

and

which are probability measures.

Proof.

First, notice that:

since their difference is 0 and both are positive. Notice also that:

Then we have that:

and

And the same goes for . ∎

We will now show that the contaminated measures:

are in fact the same.

Proof.

A simple computation gives that:

∎

Finally, notice that the contamination isn’t exactly the one we are interested in. However, we can prove by adapting the proof of [5, Lemma 7.2] that:

Proof.

Let and the contamination leading to . Then, by setting we have:

Which proves the inclusion. ∎

Appendix H Proofs of technical results

H.1 Proof of the correction formula (3)

Let be a zero mean random vector of admitting covariance matrix . Let be a zero mean random vector, independent from , with diagonal covariance matrix . Let and sequences of Bernoulli random variables of probability respectively and , independent from both and and such that . Then, let . We have that:

| (52) |

This means that we have, by independence of the and the , and by independence of the with each other:

| (53) |

Thus:

| (54) |

Which in turn means that:

| (55) |

This gives the general correction formula with independent contamination. For the missing values correction, simply set the zero matrix.

H.2 Bounds on the determinant of in equation 43

Theorem 13 of [37] states that, for any matrix of size with eigenvalues , each with multiplicity such that , then any principal submatrix , that is, a matrix created by removing line and column from , has eigenvalues with multiplicity . The remaining eigenvalues have values between and .

In our case, the matrix has only two eigenvalues: and , with multiplicity and respectively. One will easily find by recurrence on the number of deleted dimensions, which is with , that:

| (56) |

where , .

This means, in particular, that:

| (57) |

Now, let us demonstrate the statement in equation 43. We have and having the same eigenvalues and with multiplicity respectively and . Let be the number of remaining components after applying the boolean filter (thus there are deleted components). Since is diagonal, we know that will also have eigenvalues and , with multiplicity and respectively, where and where is the binomial distribution.

Then, using the lower bound we just demonstrated, we get that:

| (58) |

In particular, we know that , so and

| (59) |

H.3 Behaviour of the with regard to matrix multiplication

We know that . Furthermore, , where is the diagonal matrix where the th diagonal term is if only if , and otherwise.

Finally, notice that in the general case, , except when either or is diagonal. Indeed, for :

| (60) |

Which, if is diagonal, simply gives:

| (61) |

H.4 Proof of the upper bound of the frobenius norm with missing values

Let be any matrix, then, using the fact that the are boolean vectors:

| (62) |

Appendix I Tables

| Contamination | Tail cut | DDC | DDC | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| rate | std | std | std | std | std | std | ||||||

| 0.1 | 99.6 | 0.025 | 0.034 | 0.003 | 99.0 | 0.033 | 0.055 | 0.003 | 94.8 | 0.091 | 0.053 | 0.003 |

| 1 | 98.8 | 0.025 | 0.372 | 0.022 | 98.2 | 0.040 | 0.597 | 0.015 | 94.1 | 0.058 | 0.565 | 0.016 |

| 5 | 94.9 | 0.011 | 1.87 | 0.157 | 94.5 | 0.035 | 3.01 | 0.055 | 91.1 | 0.090 | 2.84 | 0.046 |

| 10 | 89.9 | 0.008 | 3.99 | 0.277 | 89.6 | 0.017 | 6.19 | 0.093 | 87.1 | 0.052 | 5.80 | 0.064 |

| 20 | 80.0 | 0.003 | 9.69 | 0.239 | 79.7 | 0.028 | 13.8 | 0.113 | 78.4 | 0.072 | 12.6 | 0.104 |

| 30 | 70.0 | 0.000 | 17.1 | 0.705 | 70.0 | 0.001 | 22.1 | 0.387 | 69.6 | 0.038 | 19.7 | 0.275 |

| Contamination | Tail cut | DDC | DDC | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| rate | std | std | std | std | std | std | ||||||

| 0.1 | 69.5 | 0.001 | 0.000 | 0.000 | 98.0 | 0.010 | 0.000 | 0.000 | 93.2 | 0.020 | 0.000 | 0.000 |

| 1 | 68.9 | 0.005 | 0.000 | 0.000 | 97.2 | 0.023 | 0.000 | 0.000 | 92.6 | 0.039 | 0.000 | 0.000 |

| 5 | 66.2 | 0.034 | 0.000 | 0.000 | 93.6 | 0.043 | 0.000 | 0.000 | 89.8 | 0.083 | 0.000 | 0.000 |

| 10 | 62.8 | 0.016 | 0.000 | 0.000 | 89.0 | 0.034 | 0.000 | 0.000 | 86.0 | 0.045 | 0.000 | 0.000 |

| 20 | 56.0 | 0.002 | 6.00 | 0.000 | 79.9 | 0.070 | 0.138 | 0.163 | 79.6 | 0.355 | 0.001 | 0.003 |

| 30 | 49.0 | 0.000 | 9.00 | 0.000 | 70.0 | 0.000 | 29.5 | 0.036 | 70.0 | 0.000 | 24.2 | 0.127 |

| Contamination | Tail cut | DDC | DDC | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| rate | std | std | std | std | std | std | ||||||

| 0.1 | 69.5 | 0.001 | 0.016 | 0.010 | 98.0 | 0.013 | 0.059 | 0.009 | 93.2 | 0.019 | 0.056 | 0.009 |

| 1 | 68.9 | 0.004 | 0.162 | 0.029 | 97.7 | 0.044 | 0.570 | 0.040 | 92.6 | 0.075 | 0.545 | 0.042 |

| 5 | 66.2 | 0.028 | 0.852 | 0.055 | 93.5 | 0.058 | 2.86 | 0.045 | 89.8 | 0.119 | 2.73 | 0.050 |

| 10 | 62.8 | 0.012 | 1.80 | 0.072 | 88.8 | 0.047 | 5.84 | 0.089 | 85.9 | 0.111 | 5.56 | 0.100 |

| 20 | 55.9 | 0.008 | 3.95 | 0.088 | 79.6 | 0.044 | 12.5 | 0.098 | 77.7 | 0.123 | 11.6 | 0.103 |

| 30 | 49.0 | 0.003 | 6.62 | 0.093 | 68.0 | 0.553 | 21.3 | 0.892 | 66.8 | 0.746 | 19.5 | 0.662 |