The cost of misspecifying price impact

Abstract.

Portfolio managers’ orders trade off return and trading cost predictions. Return predictions rely on alpha models, whereas price impact models quantify trading costs. This paper studies what happens when trades are based on an incorrect price impact model, so that the portfolio either over- or under-trades its alpha signal. We derive tractable formulas for these misspecification costs and illustrate them on proprietary trading data. The misspecification costs are naturally asymmetric: underestimating impact concavity or impact decay shrinks profits, but overestimating concavity or impact decay can even turn profits into losses.

1. Introduction

Price impact refers to price movements induced purely by trading flows, independently of their information content. For large investors, such adverse price moves caused by their own trades are the main source of transaction costs.111In this regime, other sources of costs such as proportional bid-ask spreads are of secondary concern and hence will be disregarded in the following; the interested reader is referred to Martin and Schöneborn (2011) for a detailed discussion of the role of such linear costs for the design of trading strategies that operate on a smaller scale. Price impact models are thus essential tools in algorithmic trading, allowing investment teams to estimate the effect of their trades on asset prices and thereby design, size and deploy systematic strategies. For instance, (capacity constrained) statistical arbitrage portfolios seek to achieve the best trade-off between price predictions and trading costs.222If transaction costs do no constrain the size of the portfolio tightly enough, it may also be risk constrained, cf., e.g., Gârleanu and Pedersen (2013) and the references therein.

The price forecast is commonly called an alpha signal. Turning the latter into optimal trades in turn requires an appropriate price impact model. Many empirical studies find a concave nonlinear relationship between order size and the price impact of sizeable trades, see, e.g., Bouchaud, Bonart, Donier, and Gould (2018); Webster (2023) and the references therein for an overview. More specifically, two essential parameters emerge when determining the evolution of price impact: concavity and impact decay.

Concavity describes how the marginal build-up of price impact slows beyond a certain order size: larger orders are cheaper than a linear model suggests. Impact decay describes how long trade-induced price moves linger in the market and affects how quickly portfolios can turn over.

This paper quantifies how incorrect calibration of these price impact parameters leads to significant misspecification costs for traders and portfolio managers. This allows to go beyond purely statistical parameter estimates by establishing P&L-driven error bounds for price impact parameters, which are crucial to any team estimating the actual trading capacity of their alpha signals.

To carry out this analysis, we derive closed-form expressions for misspecification costs in a nonlinear but nevertheless tractable price impact model introduced by Alfonsi, Fruth, and Schied (2010). This model was originally proposed and studied for optimal execution problems, but in fact admits explicit formulas for optimal trades with general alpha signals.

These in turn allow one to quantify how wrong model parameters can be before turning a profitable trading strategy for a given alpha signal into an unprofitable one. For example, linear price impact models as in Obizhaeva and Wang (2013) overestimate the transaction costs of large trades and thereby imply overly conservative trading strategies. However, they rarely turn a winning strategy into a losing one. Conversely, even relatively small overestimates of impact concavity can lead to overly aggressive trading that leads to losses despite an accurate alpha signal. Similarly, underestimating impact decay leads to conservative strategies that trade slower than optimal, which sacrifices some trading opportunities but does not lead to dramatic losses. In contrast, overly aggressive trades based on overestimates of impact decay can quickly turn a portfolio’s P&L negative.

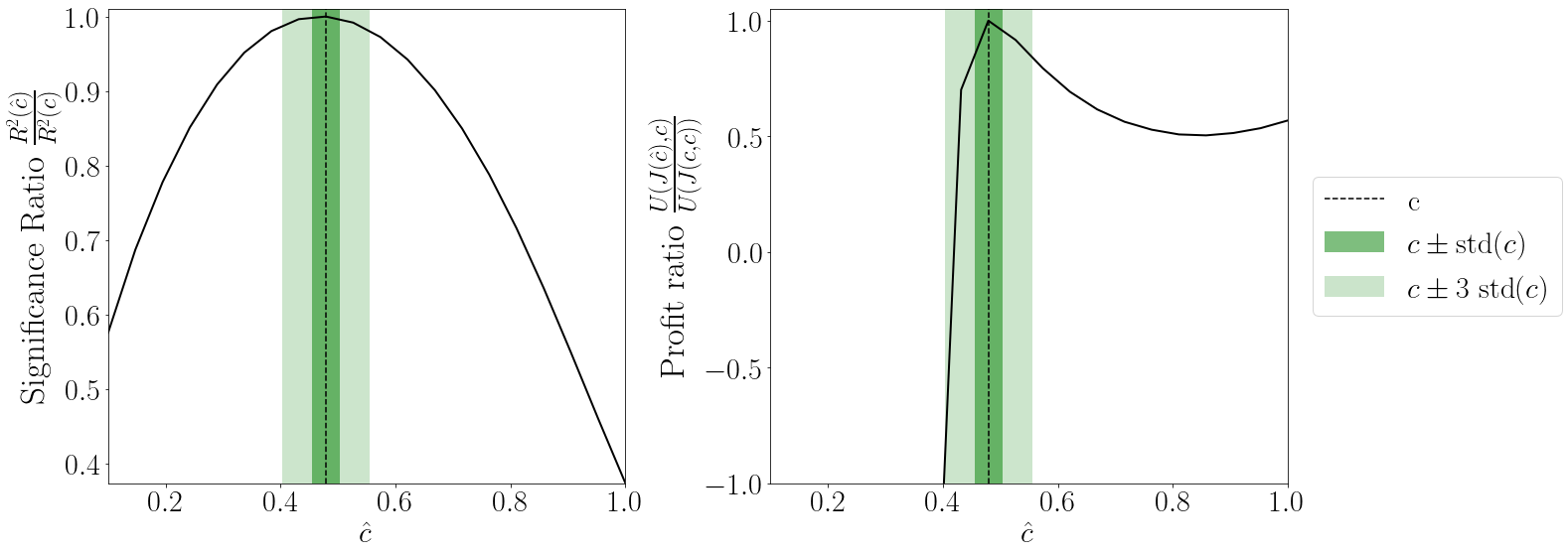

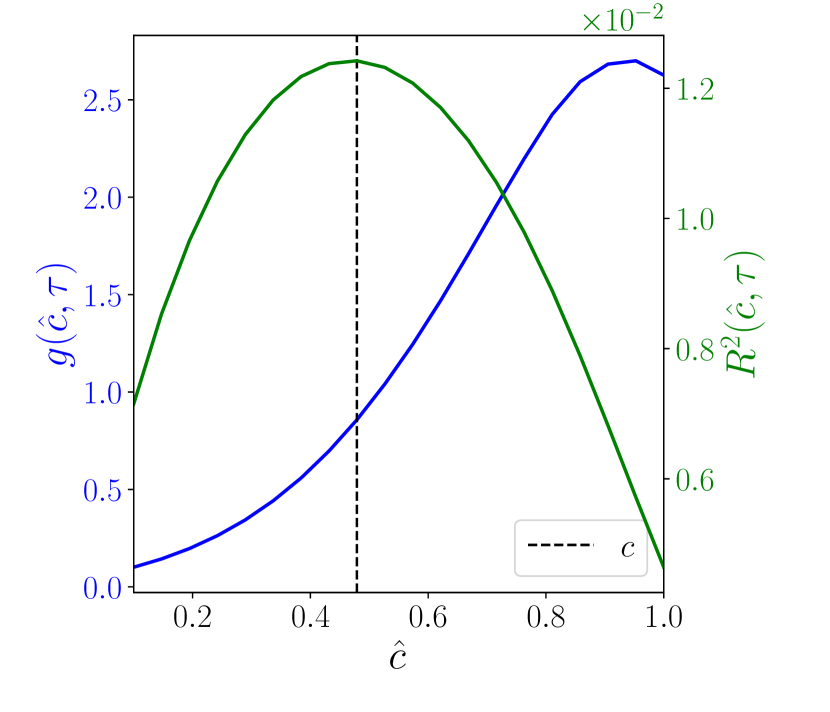

These fundamental asymmetries are illustrated in Figure 1, which contrasts the symmetric shape of the statistical model fit with the highly asymmetric nature of the corresponding P&Ls.

The remainder of the paper is organized in three parts:

-

•

Optimal Trading Strategy: Section 2 derives closed-form formulas for trading general alpha signals with non-linear price impact. These can be implemented into automated trading algorithms or used in Transaction Cost Analysis (TCA).

-

•

Empirical Estimation: Section 3 estimates the impact decay and concavity parameters of the non-linear price impact model using proprietary trading data.

- •

Both optimal trading and parameter estimation in models with nonlinear price impact are studied in greater detail in the technical companion paper of the present study (Hey, Mastromatteo, Muhle-Karbe, and Webster, 2023), to which we also refer for the derivations of the results presented here.

2. Optimal Trading Strategy

This section takes a price impact model as given and focuses on deriving the trading strategy that maximizes an alpha signal’s value net of price impact costs. We write for a portfolio’s position at time . Therefore, represents the trade at time . Let be an Itô process describing the midprice in the absence of trading, also called the “unperturbed” or “fundamental” price. The observed midprice at time is

where is the impact caused by the trades up to time .

2.1. The AFS model

We focus on the price impact model introduced by Alfonsi et al. (2010) (henceforth AFS) and studied further by Gatheral et al. (2012), which captures the nonlinear nature of price impact but nevertheless remains remarkably tractable.

In the AFS model, price impact is a nonlinear function of a moving average of current and past order flow:333To simplify the exposition, this paper focuses on price impact functions of power form and leaves the general treatment of the AFS model to the technical companion paper (Hey et al., 2023). One can also incorporate time-dependent and even stochastic liquidity by modelling as processes instead of constants. Such a model still leads to closed-form formulas, reported in the companion paper.

| (2.1) |

where is the exponentially weighted moving average

| (2.2) |

Here, describes the magnitude of price impact, measures its concavity, and describes the time scale over which impact decays.444Note that this specification implies that impact relaxes all the way to zero over long time horizons, i.e., trades have no permanent impact. But see Gabaix and Koijen (2021); Bouchaud (2022) for a detailed discussion of this point.

For , price impact is linear and one recovers the model of Obizhaeva and Wang (2013). corresponds to the “square-root law” practitioners commonly use in Transaction Cost Analysis (TCA).

2.2. The optimization problem

Given a model for the unperturbed price , a trading strategy and an impact model , a portfolio’s P&L has the dynamics555This representation holds exactly if the trading strategy is smooth. If the trading strategy includes larger transactions such as bulk trades or diffusive purchases and salers, then there are some additional correction terms detailed in the technical companion paper.

For many statistical arbitrage strategies, price impact rather than risk is the main capacity constraint. In this regime, one maximizes the expected P&L, given future return predictions. Such predictions take the form of an alpha signal:

In addition to the level of the current alpha prediction, another crucial statistic in this context is its decay, captured by its drift rate . For smooth alphas, this is simply the derivative .

For a given alpha signal, a risk-neutral statistical arbitrage portfolio maximizes

| (2.3) |

That is, each trade captures the expected alpha but pays price impact since – as noted above – the latter does eventually disappear.

2.3. Solving the problem in impact space

Maybe surprisingly, the statistical arbitrage problem (2.3) has a straightforward, closed-form solution for arbitrary alpha signals, even for non-linear price impact described by the AFS model. The result hinges on a simple observation, proven in the companion paper using a technique introduced by Fruth, Schöneborn, and Urusov (2013, 2019). The key insight is that, for any choice of position or, equivalently, the corresponding impact variable (respectively ), one has

Whence, by switching the control variables from positions to the corresponding impact (“passing to impact space”), the complex control problem (2.3) becomes a simple pointwise maximization. The optimal impact in turn is666The companion paper extends this result to general non-linear price impact functions as well as stochastic liquidity.

| (2.4) |

The corresponding optimal positions can be recovered via

| (2.5) |

Whence, even though the optimal trading strategy can become rather complex, switching to impact space allows one to retain a straightforward linear relationship between the optimal policy as well as the current alpha signal and its decay. Up to a bulk trade at the terminal time that exhausts all remaining alpha, it is optimal to keep impact equal to a constant fraction of the alpha signal, adjusted for alpha decay relative to impact decay. The intuition for this adjustment is that one has to trade more aggressively and accept higher impact costs for signals that decay quickly compared to impact, as already highlighted by Gârleanu and Pedersen (2013) for linear impact models:

“The alpha decay is important because it determines how long time the investor can enjoy high expected returns and, therefore, affects the trade-off between returns and transactions costs.”

The fraction of the adjusted alpha that is optimally paid in impact depends on the concavity parameter of the price impact function. For linear price impact (), the optimal impact is one half of the adjusted alpha, compare, e.g., (Isichenko, 2021, p. 193). For strictly concave price impact functions, this ratio increases and reaches two thirds for compatible with square-root impact. As a result, linear models prescribe to trade less aggressively than is optimal in their strictly concave counterparts. The impact scale does not appear in the formula for the optimal impact – it only determines how the corresponding optimal trades need to be chosen to attain the optimal impact state.

2.4. Implications for Trading

In trading applications, it is common to normalize the scaling factor as

| (2.6) |

where is the average daily volume (ADV); compare, e.g., Almgren et al. (2005). This normalization expresses the quantities of interest in trader-friendly units: return predictions compare to the volatility of price changes and trading volumes are expressed as fractions of the average daily volume . With this normalization, the price impact coefficient also becomes comparable across different contracts; our notation highlights that this estimate will depend on the corresponding impact concavity and decay time scale .

Long-term alpha signal

We first illustrate the application of the general optimal trading result (2.4) for the simplest case where is constant. This means that the signal predicts a return that happens in the distant future, e.g., an event at the end of the month when focusing on today’s trading. For square-root impact (), Equation (2.4) then simplifies to

| (2.7) |

That is, the optimal trading strategy (for sizeable orders) pays two thirds of the constant alpha in impact. The corresponding optimal order size is

| (2.8) |

Conversely, one implies a constant alpha from a long-term order of size via the formula

| (2.9) |

The order size formula 2.8 helps portfolio managers size trades considering price impact’s square-root law. Then, traders use the implied alpha formula 2.9 to agree on a baseline alpha with the portfolio team. After establishing a baseline alpha, the trading team can linearly add their own short-term signals into the trading strategy.

Mean-reverting alpha signal:

Another standard specification assumes that the alpha signal is an Ornstein-Uhlenbeck process with relaxation time :

Then, , i.e., the alpha decays exponentially in the absence of new information. In this model, a statistical arbitrage portfolio continuously updates its signals based on a steady information stream. The optimal impact in this context is

| (2.10) |

Whence, mean-reverting alphas should always be traded more aggressively than constant ones, and the size of this adjustment depends on the relative magnitudes of impact decay and alpha decay .

With decaying alpha, the portfolio’s turnover increases compared to a constant alpha scenario, as the mean-reverting alpha case leads to higher impact states. For instance, with square-root impact, the corresponding portfolio (2.5) trades faster over by a factor due to the alpha’s decay .

2.5. Implications for Transaction Cost Analysis (TCA)

Practitioners can directly use Equation (2.4) for TCA. Indeed, this optimality condition massively simplifies trade monitoring for statistical arbitrage portfolios. For instance, instead of scrutinizing each trade, portfolio managers can compare overall transaction costs with alpha signal characteristics. Verifying best execution then boils down to checking that alpha, impact, and alpha decay remain within reasonable bounds from the linear formula in Equation (2.4).

Let us illustrate with some examples how portfolio managers and traders can deploy this analysis for specific portfolios. Suppose the price impact model is of square root form () and first consider sizeable orders with constant long-term alpha. Then, in view of (2.7), one simply compares an order’s transaction costs to the alpha that triggered it.

For mean-reverting alphas the optimality equation (2.10) implies that one compares alpha capture to transaction costs considering the alpha’s decay rate and the impact model’s timescale . The quicker the alpha’s decay, the more impact the strategy has to create by trading faster in order to maximize profits.

The benefit to this impact-first approach to TCA is that, unlike in Section 2.4, one does not need to share order or portfolio data to verify a trading algorithm’s behavior: the entire analysis is done comparing alpha, impact, and alpha decay at the aggregate level.777(Webster, 2023, Chapter 3) details this TCA method for linear price impact models.

3. Empirical Estimation

3.1. Description of the data

The empirical analysis uses proprietary Capital Fund Management (CFM) trading data comprised of roughly meta-orders of future contracts traded over 2012-2022. The time at the start and the end of each meta-order is indicated, as well as the mid-price and the number of child-orders. All meta-orders were executed through at least three child-orders and accounted for a fraction between 0.01% and 10% of ADV; the average order size was of the order of 0.1%. No meta-order was traded longer than one day and the average execution time is 2.5h.

3.2. Fitting methodology

Price returns are fitted against the increments of a power-law price impact function of the form (2.1). Since i) no meta-order in the sample lasts more than one trading day, and ii) each of them is executed with a profile close to a TWAP, the volume impact is computed under the assumption that trades are executed uniformly during the execution time of each meta-order, i.e., . Note that the alpha signals driving the decision are typically realized over a time window much larger than one day, implying that it is appropriate to attribute to impact, rather than alpha, the average price variation occurring during the execution of meta-orders in the sample.

Given the three parameters of the AFS model are calibrated:

-

(i)

The concavity coefficient ;

-

(ii)

The impact decay timescale ;

-

(iii)

The scaling factor , normalized as in (2.6).

3.3. Estimating impact concavity

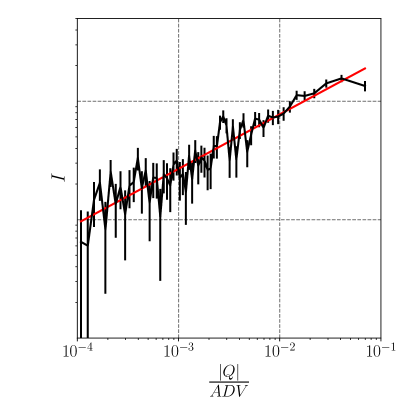

As an initial visualization of price impact concavity, Figure 2 plots the average return against order size without impact decay. The log-log plot is linear, indicating a power-law relationship in the tails. The slope of the log-log fit measures the exponent of the power law for sizable orders. Here, this analysis leads to an estimate of , consistent with the commonly observed square-root law (see e.g. Bouchaud et al. (2018)). The bootstrap confidence interval from Figure 1 in the introduction is computed with the standard deviation of this parameter estimate, .

The estimation of the price impact parameters with impact decay is more subtle. To this end, we consider a grid of impact decays and concavity parameters . For each pair, we then first compute the volume impact corresponding to the impact timescale according to (2.2); then the price impact is computed for the corresponding concavity parameter . With the impact variable at hand, we then run a linear regression of price changes against impact to determine the pre-factor of the price impact model.

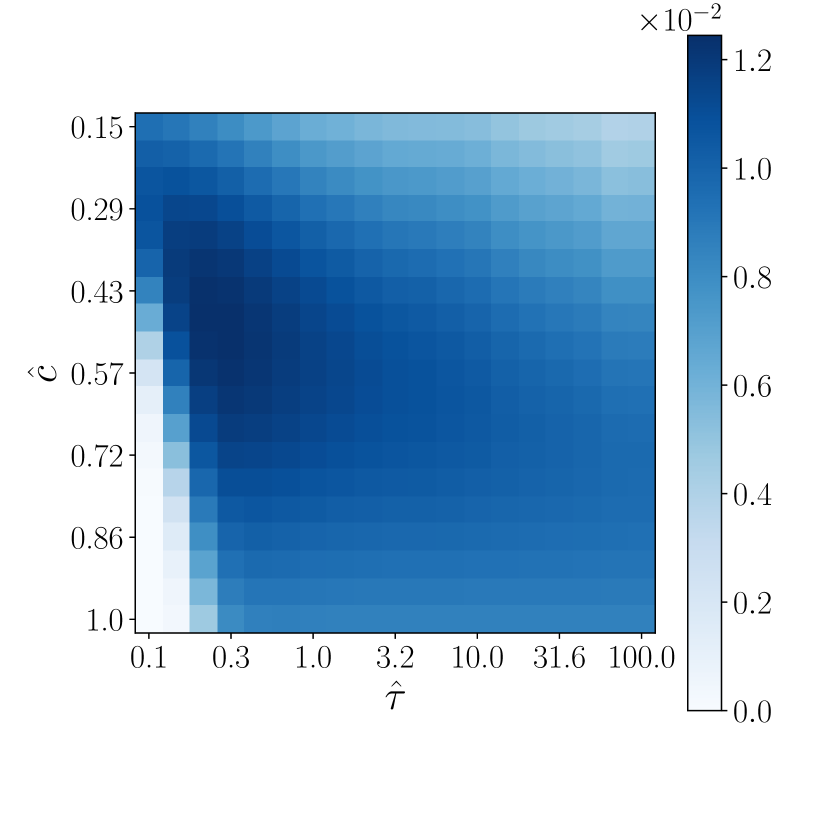

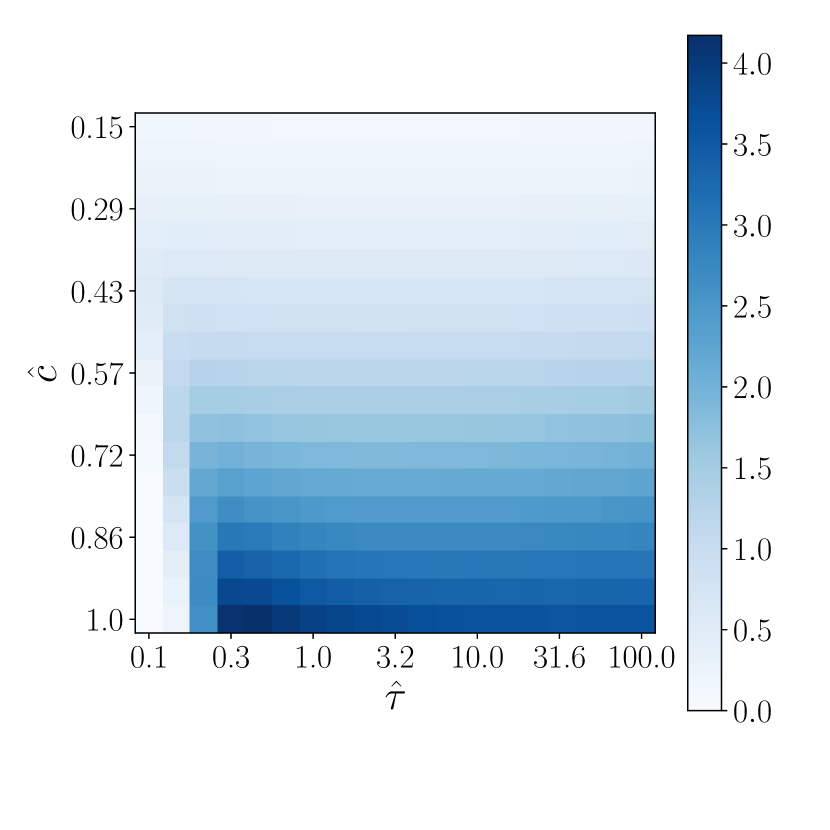

Figure 3 shows the model’s statistical sensitivity and pre-factor across a broad range of concavity and decay parameters. The heatmap of in Subfigure 3(a) shows an ellipsoid around the point estimated parameters . Figure 3(c) plots the statistical sensitivity of the model to the concavity parameter together with the pre-factor. Here, the point estimate of the decay parameter days remains fixed, i.e., and are displayed.

As the concavity parameter varies, the model’s peaks at and decreases markedly around this point estimate.888The magnitude of the model’s is consistent with results published in papers using the public trading tape. Indeed, when one runs the price impact model on the full trading tape, the varies between 10% and 20%. However, in this study, only CFM’s metaorders are used. Therefore, the drops in line with the fraction of the public tape CFM’s orders represent. The pre-factor increases with increasing concavity parameter. This increase is because the brunt of the data consists of smaller orders, leading to the linear model under-estimating impact compared to a concave model.

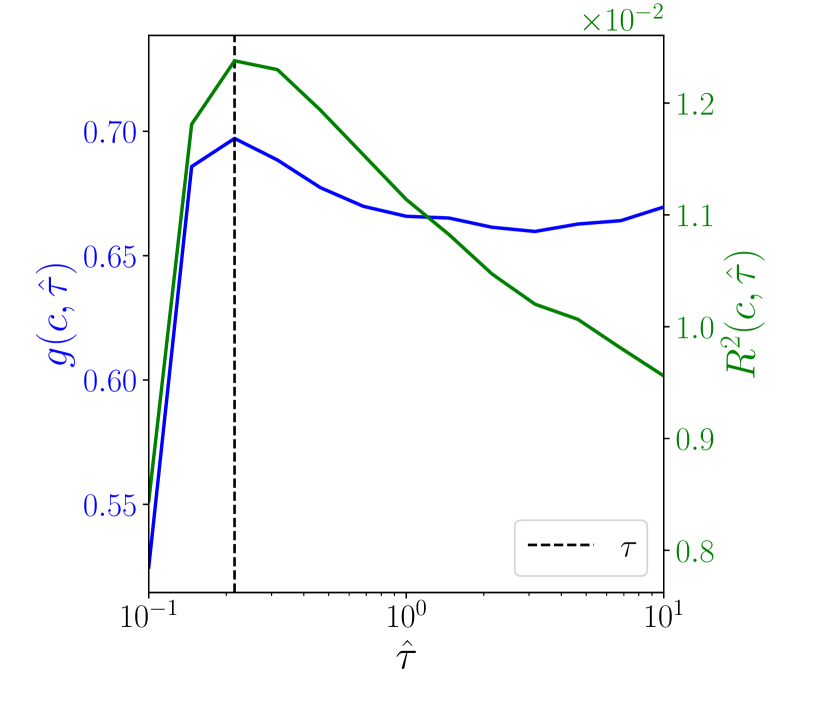

3.4. Estimating impact decay

To investigate the statistical sensitivity with respect to the impact decay, the concavity parameter is fixed at the point estimate and the impact decay varies. Figure 3(d) displays and . There is a peak at days, indicated that one measures the short-time scale of impact decay. The model’s pre-factor remains relatively constant for timescales larger than 0.1 days.

The primary take-away is that the statistical loss is significantly more sensitive to impact concavity than decay. For example, misspecifying instead of the point estimate reduces by 50%. Conversely, getting wrong by a factor of ten reduces by less than 2%.999This is not a new observation: studies across many datasets and asset classes agree on price impact’s concavity and general order of magnitude but disagree on decay. The reason is that different orders decay at different timescales, which are better captured by a multi-exponential or power law decay kernel. With linear price impact, there are some results for such decay kernels, cf. Bouchaud et al. (2004); Gatheral et al. (2012); Abi Jaber and Neuman (2022) and the references therein. Extending this analysis to models with nonlinear impact and impact decay is an important direction for future research

These empirical results do not imply that calibrating impact decay correctly is unimportant. Indeed, a central result in Section 4 is that a portfolio’s P&L can be highly sensitive to , even if statistically, is not as sensitive to .

4. Sensitivity Analysis

We now combine the theoretical and empirical results from the previous sections to quantify the performance losses caused by trading based on a misspecified model.

4.1. Quantifying misspecification costs

Recall that, for given estimates of impact concavity and decay, the corresponding fitted pre-factor is

Therefore, assuming are the correct model parameters, a portfolio trading an alpha signal with decay will implement

We call or, equivalently, , the misspecified policy. This is the optimal policy when the impact parameters correctly describe price impact, but not if these parameters differ from the price impact parameters of the actual data generating model. To ease notation, we omit the corresponding variables when one of the parameters is held fixed at its actual value, e.g., we use the shorthand .

The P&L of the misspecified policy under the actual price impact model with parameters , is

This general formula is straightforward to implement numerically in a back test. For instance, statistical arbitrage teams can plug in historical alpha signals to measure the expected P&L of trading based on when the actual parameters are .

To illustrate the misspecification formula’s implications, Sections 4.2 and 4.3 cover two common cases. By specifying concrete parametric alpha signals, the cost of misspecifying concavity or decay can be quantified in closed-form, which reveals the dependence on characteristics of the corresponding alpha signals without relying on a back test.

4.2. Misspecification cost of impact concavity

We first consider the simplest case of a constant alpha signal: , so that . For example, this assumption is reasonable when trading intraday based on a signal that predicts a return past today’s close, such as an event taking place the next day or week.

As impact decay only plays a minor role in this context,101010Indeed, for constant alpha, the P&L of the believed strategy only depends on the impact decay parameter through the estimate of the magnitude of price impact . As this dependence is rather weak, impact decay only plays a minor role in the absence of alpha decay. we assume for simplicity that it is correctly specified () and focus on the misspecification cost of the concavity parameter . In words:

How much P&L does the portfolio lose if it trades with the wrong price impact concavity?

For example, one canonical case is when and : then, one estimates the cost of implementing a linear price impact model when actual impact follows a square-root law.

The expected P&L for the misspecified policy is

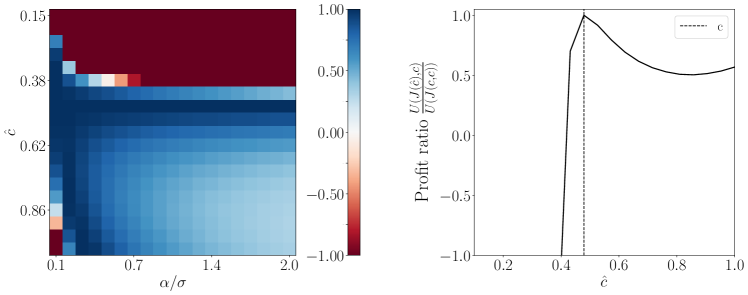

The natural comparison for this is the expected P&L of the optimal policy for the actual concavity parameter :

In this setting, the primary alpha characteristic is the signal’s Sharpe ratio, . A core result from Figure 4 is that misspecification costs are more sensitive to as a signal’s Sharpe ratio increases. Therefore, the stronger a team’s alpha signal, the more important it becomes to correctly estimate the price impact model’s concavity accurately.

In addition to quantifying the empirical sensitivity of P&L to misspecifications of the concavity parameter , the closed-form formulas also allow one to compute how wrong a parameter can become before turning profitable strategies unprofitable. Indeed, for each true parameter , there exists a critical value such that, for any choice , the expected P&L becomes a decreasing function of the alpha signal. Naturally, statistical arbitrage portfolios crucially need to avoid this critical regime where adding more predictive power leads to worse outcomes. Figure 4 illustrates the sharpness of the phase transition between profitable and non-profitable misspecified trading strategies. Because misspecification costs become more sensitive with higher alpha Sharpe ratios, the critical value becomes tighter as the Sharpe increases. Again, this highlights the importance of correctly estimating price impact’s concavity when trading high Sharpe ratio signals.

A crucial insight is that this misspecification risk is asymmetric: even for large over-estimates , the expected P&L typically remains positive (except for very small Sharpe ratios). The intuition is that overestimating the concavity parameter leads the portfolio to submit smaller trades. While this is suboptimal and sacrifices some profit opportunities, it will only lead to shrinking profits but not losses. Conversely, underestimates below the critical value can lead to significant losses, as the corresponding trading strategy submits outsized trades leading to excessive trading costs.

While these results are derived in a concrete model with a convenient closed-form solution, we expect them to remain true qualitatively across a much wider range of models. This leads to a practical takeaway when fitting price impact models: when considering confidence intervals for a price impact model’s concavity, the robust solution is to deploy a more conservative estimate from the upper part of the confidence interval, i.e., use a impact model that is somewhat less concave than the point estimate.

4.3. Misspecification cost of impact decay

We now turn to misspecification of the impact decay parameter , while keeping the concavity parameter fixed to its correct value. As impact decay predominantly interacts with the alpha decay, we study this for a mean-reverting alpha with . To obtain crisp results, we focus on the steady-state limit of the P&L. Unlike the model’s statistical , it turns out that the expected P&L is surprisingly sensitive to misspecifications in .

For the misspecified policy, we have

The optimal value derived from the policy for the actual impact decay is

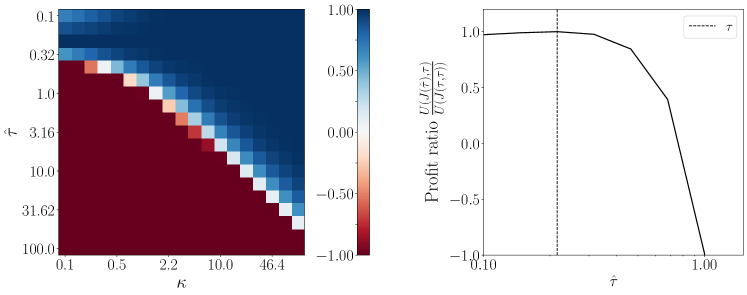

In this setting, the key alpha characteristic is its decay . More specifically, the ratio of performances for the misspecified and optimal policies mostly depends on the estimated and true impact decays through their ratios relative to alpha decay, and . Indeed, as depicted in Figure 3(d), is a good approximation for a wide range of decay parameters; with this, the ratio of performance simplifies to

The profit ratio between misspecified and optimal policy is displayed in Figure 5. There is a sharp boundary between the profitable and unprofitable regions that depends linearly on the ratios and . This boundary appears then curved in log-log scale on the left panel in Figure 5 separating the positive and negative profit regions. A wrong estimation of impact decay for a long-lasting alpha signal (small ) is less costly than for a fast decaying one.

Like for impact concavity, the costs of misspecifying impact decay are highly asymmetric. Indeed, overestimating impact decay quickly turns profitable alpha signals unprofitable, as illustrated in the right panel of Figure 5 for a moderate alpha decay time scale of 1 day. The intuition is that overestimated lead to larger than optimal impacts, i.e., overly aggressive trading just like underestimates of the concavity parameter.

5. Conclusion

In this paper, we investigate the effect that the misspecification of the price impact model has on the performance of a trader. This leads to three broad takeaways:

-

(i)

For the AFS model, the closed-form formula

relates the optimal impact state to a trader’s alpha level , alpha decay , impact concavity , and impact decay .

- (ii)

-

(iii)

The P&L cost of getting an impact parameter wrong can be evaluated using the AFS model’s tractable misspecification cost formula. This P&L-driven approach complements a statistical approach and shows that the opportunity costs of getting model parameters wrong are asymmetric:

-

•

It is better to over- than under-estimate . An excessively concave price impact model can lead to losses.

-

•

It is better to under- than over-estimate . A price impact model with excessively fast impact decay can lead to losses.

In both cases, overly aggressive trading has a substantially bigger effect than an overly cautious approach. While we illustrate this with the closed-form solutions for the AFS model, these insights are expected to remain qualitatively true for many models. Therefore, a general approach when considering confidence intervals for price impact model parameters is to deploy parameters within the error band that lead to more conservative trades.

-

•

Our results thereby support the relevance of a robust approach to optimal trading problems in the presence of trading costs, and supports the idea of jointly tackling parameter estimation and alpha exploitation.

References

- Abi Jaber and Neuman (2022) E. Abi Jaber and E. Neuman. Optimal liquidation with signals: the general propagator case. Preprint, 2022.

- Alfonsi et al. (2010) A. Alfonsi, A. Fruth, and A. Schied. Optimal execution strategies in limit order books with general shape functions. Quantitative Finance, 10(2):143–157, 2010.

- Almgren et al. (2005) R.F. Almgren, C. Thum, E. Hauptmann, and H. Li. Direct estimation of equity market impact. Risk, July, 2005.

- Bouchaud (2022) J.-P. Bouchaud. The inelastic market hypothesis: a microstructural interpretation. Quantitative Finance, 22(10):1785–1795, 2022.

- Bouchaud et al. (2018) J.-P. Bouchaud, J. Bonart, J. Donier, and M. Gould. Trades, Quotes and Prices. Cambridge University Press, Cambridge, UK, 2018.

- Bouchaud et al. (2004) J.P. Bouchaud, Y. Gefen, M. Potters, and M. Wyart. Fluctuations and response in financial markets: The subtle nature of random price changes. Quantitative Finance, 4(2):176–190, 2004.

- Fruth et al. (2013) A. Fruth, T. Schöneborn, and M. Urusov. Optimal trade execution and price manipulation in order books with time-varying liquidity. Mathematical Finance, 24(4):651–695, 2013.

- Fruth et al. (2019) A. Fruth, T. Schöneborn, and M. Urusov. Optimal trade execution and price manipulation in order books with stochastic liquidity. Mathematical Finance, 29(2):507–541, 2019.

- Gabaix and Koijen (2021) X. Gabaix and R. Koijen. In search of the origins of financial fluctuations: The inelastic markets hypothesis. Preprint, 2021.

- Gârleanu and Pedersen (2013) N. Gârleanu and L. H. Pedersen. Dynamic trading with predictable returns and transaction costs. Journal of Finance, 68(6):2309–2340, 2013.

- Gatheral et al. (2012) J. Gatheral, A. Schied, and A. Slynko. Transient linear price impact and Fredholm integral equations. Mathematical Finance, 22(3):445–474, 2012.

- Hey et al. (2023) N. Hey, I. Mastromatteo, J. Muhle-Karbe, and K. Webster. Optimal trading strategies for concave price impact. In preparation, 2023.

- Isichenko (2021) M. Isichenko. Quantitative portfolio management: The art and science of statistical arbitrage. John Wiley & Sons, Hoboken, NJ, 2021.

- Martin and Schöneborn (2011) R. Martin and T. Schöneborn. Mean reversion pays, but costs. Risk, February:96–101, 2011.

- Obizhaeva and Wang (2013) A. Obizhaeva and J. Wang. Optimal trading strategy and supply/demand dynamics. Journal of Financial Markets, 16(1):1–32, 2013.

- Webster (2023) K. Webster. Handbook of Price Impact Modeling. CRC Press, Boca Raton, FL, 2023.