Exact Parameter Identification in PET Pharmacokinetic Modeling Using the Irreversible Two Tissue Compartment Model ††thanks: This work was partly funded by the NIH grants P41-EB017183 and R01-EB031199-02.

Abstract

This work is concerned with the identifiability of metabolic parameters from multi-region measurement data in quantitative PET imaging. It shows that, for the frequently used two-tissue compartment model and under reasonable assumptions, it is possible to uniquely identify metabolic tissue parameters from standard PET measurements, without the need of additional concentration measurements from blood samples. This result, which holds in the idealized, noiseless scenario, indicates that costly concentration measurements from blood samples in quantitative PET imaging can be avoided in principle. The connection to noisy measurement data is made via a consistency result, showing that exact reconstruction is maintained in the vanishing noise limit. Numerical experiments with a regularization approach are further carried out to support these analytic results in an application example.

Keywords: Quantitative PET imaging, two-tissue compartment model, exact reconstruction, Tikhonov regularization, iteratively regularized Gauss Newton method

MSC Codes: 65L09, 94A12, 92C55, 34C60

1 Introduction

Positron emission tomography (PET) is a non-invasive clinical technique that images the four dimensional spatio temporal distribution of a radio tracer in-vivo. In quantitative dynamic PET imaging, after tracer injection, several 3D PET images at different time points are acquired and reconstructed. The injected tracer is supplied to the tissues via the arteries and capillaries. As a response to this “arterial tracer input”, the tracer is exchanged with tissues. This exchange can include reversible and/or irreversible binding and eventually metabolization of the tracer.

Using the right tracer, the time series of reconstructed PET images reflecting the tissue response, a measurement of the arterial tracer input, and a dedicated pharmacokinetic model, it is possible to generate images reflecting certain physiological parameters. Depending on the tracer, these parametric images can reflect e.g. blood flow, blood volume, glucose metabolism or neuro receptor dynamics.

Pharmacokinetic modeling in PET is commonly performed using compartment models, where the compartments usually reflect tissue subspaces. Example for such subspaces are the extra cellular spaces where the tracer is free or bound.111Note that the exact interpretation of the biological meaning of the compartments is highly non-trivial. The dynamics between the arterial blood and tissue compartments is typically described using ordinary-differential-equation (ODE) models. For PET tracers with irreversible binding, such as [18F]Fluorodeoxyglucose (FDG) [14] or [11C]Clorgyline [10], the irreversible two tissue compartment model can be used to describe the tracer dynamics, see Figure 1 for a scheme of this model.

The identification of the kinetic parameters describing the tissue response to the arterial tracer supply in a given region is commonly done using the following input data:

-

1.

The tracer concentration in tissue . This quantity, which is equal to the sum of all the tracer concentrations in all extra-vascular compartments, can be directly obtained from the time series of reconstruction PET images - either on a region-of-interest (ROI) or at voxel level.

-

2.

The arterial “input function” or plasma concentration of the non-metabolized tracer describing the concentration of tracer in the arterial blood plasma that is supplied to tissue and available for exchange (and metabolism). A direct measurement of is complicated. Typically, it is based on an external measurement of a time series of arterial blood samples taken from a patient, e.g. using a well counter. Unfortunately, the total arterial blood tracer concentration obtained from the well counter measurements usually overestimates since the measured activity of the blood samples also includes activity from radioactive molecules that are not available for exchange with tissue because of (i) parts of the radio tracer being bound to plasma proteins and (ii) activity originating from metabolized tracer molecules that were transfered back from tissue into blood. Measuring the contributions of the latter two effects, summarized in the parent plasma fraction , requires further advanced chemical processing and analysis of the blood samples and is thus time consuming and expensive.

To avoid the necessity of arterial blood sampling, which itself is a very challenging process in clinical routine, many attempts have been made to derive the arterial input function directly from the reconstructed PET images (also called “image-based arterial input function”) by analyzing the tracer concentration in regions of interest of the PET images containing arterial blood, such as the left ventricle, the aorta, or the carotic arteries. Note, however, that by using any image-based approach for the estimation of the arterial input function, the contributions of tracer bound to plasma proteins and metabolized tracers cannot be determined. In other words, any image-based approach can only estimate instead of since no measurement of the parent plasma fraction is available.

Motivated by the problem, we consider the question whether the identification of kinetic parameters using data from multiple anatomical regions of interest and the irreversible two tissue compartment model is possible without having access to the common parent plasma fraction and/or the common total arterial blood tracer concentration .

In existing literature on modeling approaches for quantitative PET, see for instance [17] and [16] for a review, this question has been addressed from a computational perspective. The work [17], for instance, accounts for a low number of measurements of the arterial concentration of non-metabolized PET tracer by using a non-linear mixed effect model for the parent plasma fraction, i.e., the parameters defining the parent plasma fraction are modeled as being partially patient-specific and partially the same for a population sample. Moreover, the general idea of jointly modeling the tissue response in different anatomical regions to obtain unknown common parameters or to reduce the variance in the estimated region-dependent parameters has been proposed in [13, 7, 15, 3].

Despite these and many more computational approaches for parameter identification in pharmacokinetic modeling using the irreversible two tissue compartment model, a mathematical analysis about the necessity of measurements of and/or for successful parameter identification, even in an idealized, noiseless scenario, does not exist. In addition to that, even in the presence of an arbitrary number of such measurements, it is not clear from an analytical perspective if the tissue parameters in specific ODE-based compartment models can be recovered uniquely.

The aim to this work is to answer these questions. Using a polyexponential parametrization of the arterial plasma concentration, which is frequently used in practice, we prove the following: Let be the kinetic parameters of different anatomical regions of the irreversible two tissue compartment model, let be the number of time-points where PET measurements of the tissue tracer concentration are available, and let be the degree of the polyexponential parametrization. Then, if , and under some non-restrictive technical conditions as stated in Theorem 14, the parameters for can be identified uniquely already from the available measurements of the tracer concentration in the different tissues without the need for and . Further, the can also be identified already from these measurements up to a constant that is the same for all regions . In addition, the parameters can be identified exactly if a sufficient number of measurements of the total arterial tracer concentration is available, without the need for .

Besides these unique identifiability results that consider the idealized case of a noise-free measurement, we also present analytical results for a standard Tikhonov regularization approach that addresses the situation of noisy measurements. Using classical results from regularization theory, we show that the Tikhonov regularization approach is stable w.r.t. perturbations of the data and, in the vanishing noise limit, allows to approximate the ground-truth tissue parameters. Numerical experiments further illustrate our analytic results also in an application example.

Scope of the paper. In Section 2, we introduce the irreversible two tissue compartment model and provide basic results on explicit solutions both in the general case and in case the arterial concentration is parametrized via polyexponential functions. In Section 3 we present and prove our main results on unique identifiability of parameters. In Section 4 we introduce a Tikhonov regularization approach and show stability and consistency results, and in Sections 5 and 6 we provide a numerical algorithm and numerical experiments for an application example.

2 The irreversible two tissue compartment model

The irreversible two tissue compartment model describes the interdependence of the concentration of a radio tracer in the arterial blood plasma and in the extra-vascular compartment, where the latter is further decomposed in a free and a bound compartment. Note that in the irreversible model, once the radio tracer has reached the bound compartment, it is trapped. A visualization of the model is provided in Figure 1.

We denote by the arterial plasma concentration of the non-metabolized PET tracer. Further, for any anatomical region , we denote by and the free and the bound compartment of the tracer in region , respectively, and by we denote the sum of the two compartments in region . Using the irreversible two tissue compartment model, the interaction of these quantities is described by the following system of ordinary differential equations (ODEs):

| (S) |

Here, the parameters , and are the tracer kinetic parameters that define the interaction of the different compartments in region .

Our goal is to identify the parameters , and for each . For this, we can use measurements of the at different time-points obtained from reconstructed PET images at different time points after tracer injection. Further, the parameter identification typically relies on additional measurements related to . Here, the standard procedure is to take arterial blood samples and to measure the total activity concentration of the arterial blood samples, given as . The relation of the total concentration to the arterial plasma concentration of non-metabolized tracer is described via an unknown parent plasma fraction function with as

As described above, to obtain and thus , a time-consuming and costly plasma separation and metabolite analysis of the blood samples has to be performed.

In order to realize the parameter identification for the ODE model (S) in practice, the involved functionals need to be discretized, e.g., via a suitable parametrization. For the arterial concentration , it is standard to use a parametrization via polyexponential functions as defined in the following.

Definition 1 (Polyexponential functions).

We call a function polyexponential of degree if there exist for where the are pairwise distinct and for all such that

We write and call the zero-function polyexponential of degree zero. By we denote the set of polyexponential functions of degree less or equal to , and by the set of polyexponential functions (of any degree).

Remark 2.

It obviously holds that is a vector space, and even a subalgebra of . It is also worth noting that, as direct consequence of the Stone-Weierstrass Theorem, polyexponential functions are dense in the set of continuous functions on compact domains. Thus, they are a reasonable approximation class also from the analytic perspective.

Modeling as polyexponential function already defines a parametrization of the resulting solutions of the ODE system (S). As we will see in Lemma 5 below, the following notion of generalized polyexponential functions is the appropriate notion to describe such solutions.

Definition 3 (Generalized Polyexponential class).

We call a function generalized polyexponential if it is of the form

where the are polynomials of degree , respectively, and the are pairwise distinct constants. We denote the class of such generalized polyexponential functions with polynomials of degree at most by

We define the degree of by

In case we write for the resulting polyexponential class.

The next two results, which follow from standard ODE theory, provide explicitly the solutions of the ODE system (S), once in the general case and once in case is modeled as polyexponential function.

Lemma 4.

Let be continuous, and let the parameters , and be fixed for such that . Then, for each , the ODE system (S) admits a unique solution that is defined on all of , and such that is given as

| (1) |

Proof.

Fix . From the equation for in (S) it immediately follows that

| (2) |

This in turn implies that

and, consequently, that

as claimed. ∎

Lemma 5.

Proof.

This follows immediately by inserting the representation of in (1). ∎

Remark 6 (Sign of exponents ).

Note that for the ground truth arterial concentration , we will always have (in particular ) for all , since otherwise this would imply the unphysiological situation that for .

3 Unique identifiability

In view of Lemma 5 from the previous section, it is clear that the question of unique identifiability of the parameters , and from measurements of at time points is related to the question of uniqueness of interpolations with generalized polyexponential functions. A first, existing result in that direction is as follows.

Lemma 7 (Roots of generalized polyexponential functions).

Let be polynomials of degree such that at least one of them is not identically zero, and let the constants be pairwise distinct. Then the function

admits at most real roots.

Proof.

See [12, Exercise 75 (p. 48)]. ∎

As a consequence of the previous proposition, we now obtain the following unique interpolation result for generalized polyexponential functions.

Lemma 8 (Unique interpolation).

Let be such that

Then, for any choice of tuples , , with , there exists at most one generalized polyexponential function such that

| (4) |

for , i.e., in case

are two generalized polyexponential functions with fulfilling the interpolation condition (4), then, up to re-indexing,

for all and for all where .

Proof.

Let both fulfill the interpolation condition (4), and, w.l.o.g., assume that and for all . Then, and for . Lemma 7 then implies that all polynomials appearing in in a representation as in Definition 3 are identically zero. This implies that the and coincide up to re-indexing and, likewise, that the corresponding coefficient and where the corresponding polynomials are non-zero coincide as well. ∎

Based on this result, we now address the question of uniquely identifying the parameters of the ODE system (S) from time-discrete measurements with and measurements . For this, we first introduce the following notation.

Definition 9 (Parameter configuration).

We call the parameters , , together with the functions and

a configuration of the irreversible two tissue compartment model if for , the , are pairwise distinct, and, for , with the solution of the ODE system (S) with arterial concentration and parameters .

Central for our unique identifiability result will be the following technical assumption on a parameter configuration .

| (A) |

As the following lemma shows, this assumption holds in case our measurement setup comprises sufficiently many regions where the parameters and are pairwise distinct. This is reasonable to assume in practice, and also it is a condition which is to be expected: Our unique identifiability result will require a sufficient amount of different regions, and different regions with the same tissue parameter do not provide any additional information on the dynamics of the ODE model.

Lemma 10.

Assume that there are at least regions , with , where each the and the are pairwise distinct for . Then Assumption (A) holds.

Proof.

For , note that

is a polynomial in of degree at most . Hence it can admit at most distinct roots. Now since there are at least regions where each the and the are pairwise distinct, for at least four of them, say , cannot be a root of the above polynomial. Further, for those four regions, since the are pairwise distinct, for any given , at most one can be such that . As a consequence, the remaining three are such that the conditions of Assumption (A) hold. ∎

Based on Assumption (A), we now obtain the following proposition, which is the technical basis for our subsequent results on unique identifiability.

Proposition 11.

Let be a configuration of the irreversible two tissue compartment model with for , , , for all and such that Assumption (A) holds. Let further be distinct points such that

Then, with any other configuration of the irreversible two tissue compartment model such that , and for all , it follows from for that

for all , that there exists a constant such that

for all , that and that (up to re-indexing)

Proof.

Take and

to be two configurations as stated in the proposition, such that in particular

| (5) |

for .

Now since for all , we obtain the following representation of :

| (6) |

In particular, for any region , the coefficients of for in this representation are given as either

in case or

otherwise. The latter can only be zero if , which can happen for at most one by the being pairwise distinct. Since by assumption, this implies in particular that is a non-zero function for any . As a consequence of (5), the condition and the unique interpolation result of Lemma 8, this implies that is a non-zero function, such that in particular for all . Together with the assumption that for all , we also obtain that for all , since otherwise would have a non-zero coefficient of . As a consequence, also admits a representation as in (6).

Uniqueness of the exponents . As first step, we now aim to show that (in particular for all ) and that (up to re-indexing) for all .

We start with a region . In this region, as argued above, the coefficients of the for can be zero for at most one . Since further at most one can be such that , the unique interpolation result of Lemma 8 applied to and yields that and that (up to re-indexing) for all .

Now as a consequence of Assumption A, we can pick a region with where . Since already it further must hold that . This means that the coefficients of both and in the representation of as in (3) are non-zero. Again by the being pairwise distinct, this implies that and that (up to re-indexing) either or .

Case I. Assume that . If also (and ) we are done with this step, so assume the contrary.

Now as a consequence of Assumption A, we can pick and to be regions where and either or the coefficient of in the representation of is non-zero. The fact that , together with by assumption, further yields that for all .

Now we argue that in each region with , it must hold that either or . To this aim, we make another case distinction for a fixed .

Case I.A Assume that there exists with . From the fact that this can happen at most for one and that , it follows that the coefficient of is non-zero. Consequently, it follows from the unique interpolation result that as claimed.

Case I.B Assume that for all . This means that for all . But since the coefficient of is non-zero, by the unique interpolation result it must hence hold that either or as claimed. This concludes Case I.B.

Now given that either or for all , one of the two cases must happen at least twice. By uniqueness of the for , only can happen twice. On the other hand, since for all , this yields that at least two coincide, which is a contradiction. Hence Case I is complete.

Case II. Assume that . In this case, interchanging the role of and , we can argue that exactly as in Case I.

Uniqueness of at least three of the exponents . Let be any region such that either for some (such that the coefficient of in the representation of is non-zero) or the coefficient of in the representation of is non-zero, and note that, according to Assumption A, at least three such regions exist.

Case I. Assume that there exists such that . This implies that the coefficient of is non-zero and, consequently, already that by uniqueness of exponents.

Case II. Assume that for all . Now since then the coefficient of is non-zero by assumption, must match some exponent in the representation of . It cannot match any of the since for all , hence again follows.

Uniqueness of at least three of the exponents . First note that for any where , from the unique interpolation result, it follows that

| (7) |

for all . Indeed, in case , it follows from the coefficients of in and being equal that

which implies that and, using that and , further yields as claimed.

In the other case, the equality (7) follows directly from the coefficients of in and being equal.

Now let be any region where , and for which we want to show that and . Again we consider several cases.

Case I. Assume that there exists such that . In this case, it follows from (7) that also (note that and since ), hence and, consequently, holds.

Case II. Assume that for all . In this case, using Assumption A and the previous step, we can select to be a second region where again and such that the . We have two cases.

Case II.A Assume that there exists such that . As in Case I above, this implies that . Further, choosing two indices such that are pairwise distinct, it follows that and by the being different. Using (7) and this implies

Using that the cannot be zero, these two equations imply

Combining this with the equations (7) for and we obtain

Reformulating this equation and using that this implies that and, consequently, holds.

Case II.B Assume that for all . Defining , we then obtain from (7) for pairwise distinct that

for . From this, we conclude that

| (8) |

for with .

Multiplying (8) with the denominator and further dividing by we obtain

for with . Subtracting the above equation for from the same equation for and dividing by we obtain

| (9) |

Similarly, subtracting the above equation for from the same equation for and dividing by we obtain

| (10) |

Combining the last two equations and using that we obtain

i.e., and for . Inserting this into (9) we obtain

which, together with , yields and hence in particular as desired. Together with this yields that also .

Uniqueness of the remaining and of the up to a constant factor. Take to be a region where (we know already that such a region exists). It then follows from (7) that

| (11) |

for . Thus, with , we have that for all . We now aim to show that, for all , , and .

Consider fixed. To simplify notation, we drop here the index , e.g., we write , and and similar for .

In case for some , we know already from the previous step that and , such that, from equating coefficients in the representations of and , we get

such that also as desired.

In the other case that for all , we get from equating coefficients in the representations of and , using , that

| (12) |

for , where the are pairwise distinct by the being pairwise distinct. Now we show that, from (12), it follows that , and . For this, we again need to distinguish several cases.

Case I. for at least one . This implies that also and hence that . Considering with it follows from the being pairwise distinct that for , which implies that also for and, consequently, that

| (13) |

for . Now if , one may derive by rearranging the terms in (13) for . Hence, by inserting the obtained equalities and in (12) we further deduce . If, on the other hand we can plug in the definition of and obtain

which yields and hence a contradiction.

Case II. for all . In this case we can reformulate (12) to obtain

| (14) |

for all . In particular, this yields

Now if , this implies and hence a contradiction. Thus, using that we we can reformulate the previous equation to obtain

| (15) |

Now, in equation (12) for , replacing by the equality (14) for and plugging in the expression (15) for we obtain, after some reformulations,

| (16) |

Using the definition of the in (12) we derive that the factor after in (16) corresponds to the term

which is nonzero by the being pairwise distinct. Thus, again plugging in the definition of the in (12) and rearranging the terms in (16) yields after some computations and, consequently, also and by the previous considerations.

As a consequence, the remaining considered in this final part of the proof are uniquely determined as and ∎

The previous result shows that, already under knowledge of for and sufficiently many distinct time-points , the coefficients and the coefficients can be determined uniquely and uniquely up to a constant, respectively. Considering the ODE system (S), it is clear that this result cannot be improved in the sense that the constant factor of cannot be determined without any knowledge of (since one can always divide all by a constant and multiply by the same constant).

In case one aims to determine all parameters of a given configuration uniquely, some additional measurements related to are necessary. It is easy to see that a single, non-zero measurement of , for instance, would suffice. Indeed, given the value of a ground truth at some time-point , the equality together with the result from Proposition 11 immediately imply that such that all parameters are uniquely defined.

In current practice, indeed measurements of are obtained via an expensive blood-sample analysis, and used for parameter identification, see for instance [17]. As discussed in the introduction, however, in contrast to obtaining measurements of , it is much simpler to obtain measurements of the total concentration , where with the unknown parent plasma fraction .

As the following result shows, measurements of only are indeed sufficient to uniquely identify all remaining parameters, provided that one has sufficiently many measurements in relation to a parametrization of . To formulate this, we need a notion of parametrization of the parent plasma fractions.

Definition 12 (Parametrized function class for parent plasma fractions).

For any , we say that a set of functions is a degree- parametrized set if for any and it holds that attaining zero at distinct points implies that and .

Simple examples of degree- parametrized sets of functions are polynomials of degree that satisfy for some given with or polyexponential functions of degree (if is even) that satisfy for some given with . The latter is a frequently used type of parametrization for parent plasma functions (where is required), see for instance [17].

Proposition 13.

Proof.

Proposition 11 already implies that . Using that, by assumption,

we obtain for . Since are parent plasma fractions contained in the same degree- parametrized set, this implies that and as claimed. ∎

The following theorem now summarizes results of the previous two propositions in view of practical applications.

Theorem 14.

Let

be a ground-truth

configuration of the irreversible two tissue compartment model such that

-

1.

, and for all ,

-

2.

There are at least regions where each the and the are pairwise distinct for .

Let further be be the ground truth total concentration.

Then, for any other parameter configuration such that the conditions 1) and 2) above also hold, it follows from

with and the pairwise distinct, that, for some constant ,

that , and that (up to re-indexing)

If further is a ground-truth parent

plasma fraction in a degree-

parametrized set of functions and is a parent plasma fraction in the same

degree- parametrized set of functions such that

with the pairwise distinct and given, then and

Proof.

This is an immediate consequence of Lemma 10 and Proposition 11: Indeed, Lemma 10 ensures that the assumptions of Proposition 11 are satisfied provided that 1.) and 2.) hold. In case the result immediately follows from Propositions 11 and 13. In case it follows from interchanging the roles of the two configurations and again applying Propositions 11 and 13. ∎

Remark 15 (Interpretation for practical application).

Besides putting some basis assumptions on the ground truth-configuration and requiring positivity of the metabolic parameters, the previous theorem can be read as follows: If one obtains a configuration that matches the measured data, it can be guaranteed to coincide with ground-truth configuration if at least of the found terms and are pairwise distinct.

Remark 16 (Generalization for nontrivial fractional blood volume).

Following standard approaches in quantitative PET modeling, we assume here that the PET images provide exactly the tissue concentration . A more realistic model would be that the voxel measurements provide a convex combination of the tissue and blood tracer concentration given by , where fbv with describes the fractional blood volume. In case the parameter fbv is known and is available at the same time points as the PET image measurements, our results cover also this setting. The general case, where both fbv and are unavailable, can be addressed by similar techniques as in the proof of Proposition 11. Here, the idea would be to employ a polyexponential parametrization also for , and assuming enough measurements of to be available in order to apply the unique interpolation result of Lemma 8. One would further have to ensure positivity of , the intial condition and conditions on the attenuation such as monotonicity and limiting conditions with respect to time approaching zero and infinity, respectively. These requirements imply corresponding conditions on the parameters of and .

4 A Tikhonov approach for parameter identification with noisy data

In the previous section we have established that, under appropriate conditions, the parameters of the irreversible two tissue compartment model in regions can be obtained uniquely from measurements , and measurements for . While this result shows that parameter identification is possible in principle, it considers the idealized scenario of exact measurements. In this section, we consider the situation of noisy measurements, for which we develop a Tikhonov approach for stable parameter identification. As main analytic results of this section, we show i) a stability result, i.e., that the proposed Tikhonov approach is stable with respect to (noise) variations in the measurements (see Theorem 18) and ii) a consistency result, i.e., that in the limit of vanishing noise, solutions of the Tikhonov approach converge to the ground truth parameters (see Theorem 20).

As first step, we define a forward model that maps the unknown parameters to the available measurement data. To this aim, we define the arterial concentration as mapping

Further, we define a parametrized parent plasma fraction as mapping

| (17) | ||||

where is some (finite dimensional) parameter space and is a degree- parametrized set of functions.

Remark 17 (Parent plasma fraction example).

A classical model for the parent plasma fraction (see [16] for different models), that we will also use in our numerical experiments below, is the biexponential model

Here and the degree of is .

In addition to the parameters of the functions modeling the arterial concentration and the parent plasma fraction, the forward model also includes the parameters for compartments. With this, the unknown parameters are summarized by and we denote by the resulting parameter space with norm

where denotes the Euclidean norm. Given measurement points for and for the total concentration , those parameters are mapped forward to a measurement space , again equipped with the Euclidean norm via the function

| (18) | ||||

where, for

| (19) |

and

| (20) |

Here denotes the solution of the irreversible two tissue compartment ODE model (S) with parameters and arterial concentration . Note that depends on the data that must be obtained from blood samples or PET measurements, which we assume to be given throughout this section. A further adaption of the model to include also as possibly noise measurement is possible with the same techniques as below, but will be omitted for the sake of simplicity.

Now denoting by for measurements corresponding to the ground-truth parameters, our goal is to find parameters such that

Accounting for the fact that the given parameters are perturbed by measurement noise, i.e., we are actually given with

we address the parameter identification problem via a minimization problem of the form

| (21) |

Here is a -dimensional vector of zeros, summarizes the available measurements for , i.e.,

and is an initial guess on the ground truth parameters. The above approach corresponds to Nonlinear Tikhonov-Regularisation, for which stability and consistency results can be ensured as follows.

Theorem 18 (Well-posedness and stability).

Let the parent plasma fractions be such that the mapping is continuous for any . Then, for any given datum , the minimization problem (21) admits a solution. Moreover, solutions are stable in the sense that, if is a sequence of data converging to some datum , then, any sequence of solutions of (21) with data admits a convergent subsequence, and the limit of any convergent subsequence is a solution of (21) with data .

Proof.

Since and are finite dimensional and is obviously closed, this follows from classical results in regularization theory, see for instance [4, Theorem 10.2] provided that is continuous.

We start with continuity of as in (19), the first component of . For this, it suffices to show that the mapping from the the parameter to , with fixed, is continuous, which, in turn, follows from the representation of as in (1) if, for any and any sequence converging to it holds that

| (22) |

By Hölder’s inequality, the latter follows from in , which, in turn, follows via the Lebesgue dominated convergence theorem from point-wise convergence of and the fact that on can easily be bounded by a constant independent of .

Regarding as in (20), the second component of , continuity immediately follows from continuity of and for any fixed, where the latter holds by assumption. ∎

Remark 19 (Continuity of ).

Note that the assumption of continuity of is only necessary since we allow for arbitrarily parametrized parent plasma fractions; it holds in particular for the biexponential model of Remark 17 and will typically hold for any reasonable parametrization.

At last in this section we now establish a consistency result.

Theorem 20 (Consistency).

Let be a ground-truth configuration of the irreversible two tissue compartment model satisfying the assumptions of Theorem 14, and let be a ground-truth parent plasma fraction.

With the corresponding parameters and the corresponding measurement data, let be any sequence of noisy data such that with , .

Then, any sequence of solutions of (21) with data and such that and as admits a convergent subsequence. Any limit of such a subsequence, such that the corresponding parameter configuration satisfies the assumptions of Theorem 14, coincides with . Further, if any limit of a convergent subsequence corresponds to a parameter configuration satisfying the assumptions of Theorem 14, then the entire sequence converges to .

Remark 21 (Interpretation of the consistency result).

When choosing and , and given the definition of as in (18), the above consistency result together with the unique reconstructability result of Theorem 14 can be interpreted as follows: Whenever the parameters corresponding to a limit of are such that at least of the parameters and are pairwise distinct, then one can ensure that .

Remark 22 (Multi-parameter regularization).

The setting of (21) and the subsequent results on well-posedness and consistency can be generalized to incorporating different regularization parameters for the different norms and data terms, see for instance [6], which is reasonable given the fact that the parameters might live on different scales, and given the fact that the noise level of different measurements over time might be different.

Remark 23 (Model Variations).

Currently, in the setting of (21), the parameters are bounded away from zero by . For the , we currently do not pose any constraints even though, as mentioned in Remark 6, only the choice is reasonable from a physiological perspective. Likewise, as parametrized in (4), does not necessarily satisfy . These two conditions, however, can be easily incorporated in the model via the additional constraint for some and via setting , respectively.

5 Numerical solution algorithm

In this section, we provide proof-of-concept numerical experiments that illustrate the analytic unique identifiability results of Sections 3 and 4 also numerically.

5.1 Experimental setup

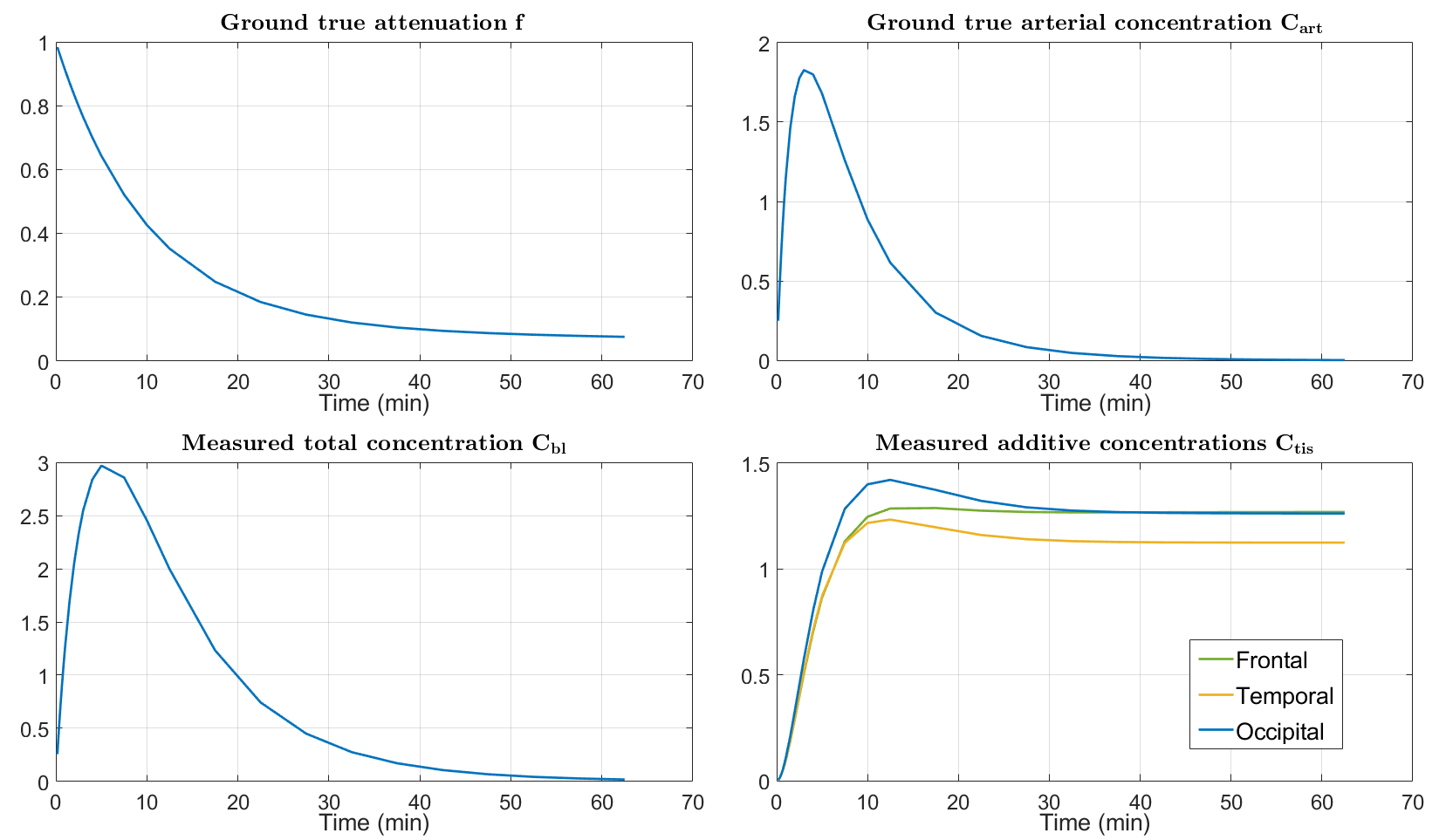

We consider the following experimental setup: As ground truth data, we consider different anatomical regions, where, based on the realistic values provided in [8, Table 1], the parameters are chosen as

| (23) |

Here, region 1 corresponds to the frontal cortex, region 2 to the temporal cortex and region 3 to the occipital cortex in the human brain. We model the true arterial concentration by the triexponential function given by

and the parent plasma fraction for the biexponential model by

for where . See Figure 2 for the visualisation of the parent plasma fraction, the arterial concentration and the measured total and additive concentrations.

We assume that we conduct a PET examination for time frames where, equidistantly distributed, six take place in the first minutes, four in the following two minutes, two in the next two minutes, three in the next minutes and finally ten in the remaining minutes. Regarding , we assume that measurements are available at the same timepoints at which measurements of are available, i.e., . This reflects the situation that an estimate of the total arterial tracer concentration is obtained from the PET images (rather than blood sampling), a technique that for which many recent works exist [18]. In view of Propositions 11 and 13, the above experimental setting satisfies the assumptions such that unique identifiability from noiseless data can be guaranteed.

We summarize the unknown parameters of this setting by

where denotes the ground-truth parameters as specified above. For a given number of measurements , the data is summarized in vectorized form via

where, abusing notation, is a vectorized version of the forward model of (18).

For the subsequent numerical experiments, we will also consider noisy versions of the data, denoted by with being the noise level. Those are defined by adding Gaussian noise with zero mean and variance to each of the first entries of (note that no noise is added to the zero-entries), i.e., with for , such that

where denotes the expectation.

As we are dealing with locally convergent methods, it will also be important to choose a reasonable initial guess for the algorithm. In order to test the performance of the algorithm in dependence on how close the initial guess is to the true solution, we employ the following steps to obtain perturbed initial guesses. Given a level of perturbation , we define

| (24) |

where , i.e., is uniformly distributed on and , i.e., is Gaussian distributed with mean and variance . This results in a expected squared deviation of from as by

| (25) |

where and for are independent random variables.

5.2 Algorithmic implementation

In order to numerically solve the non-linear parameter identification, we employ the iteratively regularized Gauss-Newton method of [1], see also [4, Section 11.2]. This is a standard method for solving non-linear inverse problems. It is related to the Tikhonov approach discussed in Section 4 in the sense that similar results on stability and convergence/consistency (under appropriate source conditions) can be obtained, see for instance [2, 5], but different to the Tikhonov approach, regularization is achieved by early stopping of the algorithm rather than adding an additional penalty term to the data-fidelity term. Early stopping has the advantage that, using an estimate of the noise level of the data, the discrepancy principle [4, Section 4.3] can be used to determine the appropriate amount of regularization, without requiring multiple solutions of a minimization problem as would be the case with the Tikhonov approach.

Given an initial guess and a sequence of regularization parameters such that

| (26) |

where is some constant, the iteration steps of the iteratively regularized Gauss-Newton method for are given as

| (27) |

where denotes the Jacobian Matrix of at and its transpose.

Those iteration steps are repeated until the discrepancy principle is satisfied, that is, until holds for the first time, where is an estimate of and with is a parameter. The iterate is then returned as the approximate solution of .

Remark 24 (Guaranteed convergence).

Since the parameter identification problem addressed here is highly non-linear, global convergence guarantees for any numerical solution algorithm are out of reach. For the iteratively regularized Gauss-Newton method together with the discrepancy principle, as considered here, at least local convergence guarantees can be obtained as long as a particular source condition, i.e., a regularity condition on the ground truth solution holds, see [5] for details.

In a practical application, the iteration (27) is combined with a projection on , which is a closed, convex set for which the projection is explicit (we denote the projection map by ), see [9, Theorem 4] for corresponding results on convergence of such a projected method. Together with this, we arrive at the algorithm for solving as provided in Algorithm 1, where we set for defining .

For the regularization parameters we choose the ansatz

| (28) |

for where and are fixed parameters. Besides fulfilling the decay conditions of (26), this choice is motivated by the goal of penalizing deviations from the initial guess rather strongly at early iterations ( large), and avoiding an exploding condition number of the matrix , that needs to be inverted at each iteration, during later iterations ( rather small).

For the realization of the forward operator and the adjoint of its Fréchet-Differential the main idea is to vectorise the computations and omit expensive for-loops. For that, one may exploit that the entries of and , which mostly consist of integral type entities, may be computed analytically. The elementary components are of the form , , and . The latter may be computed by hand applying integration by parts. The corresponding terms, which depend on a combination of time evaluations, region and polyexponential parameters of , are saved in three-dimensional tensors which are overloaded throughout a respective iteration to finally build up the adjoint operator of the Fréchet-Differential. For the implementation of the IRGNM we will use the computational software Matlab (see [11]).

6 Experimental results

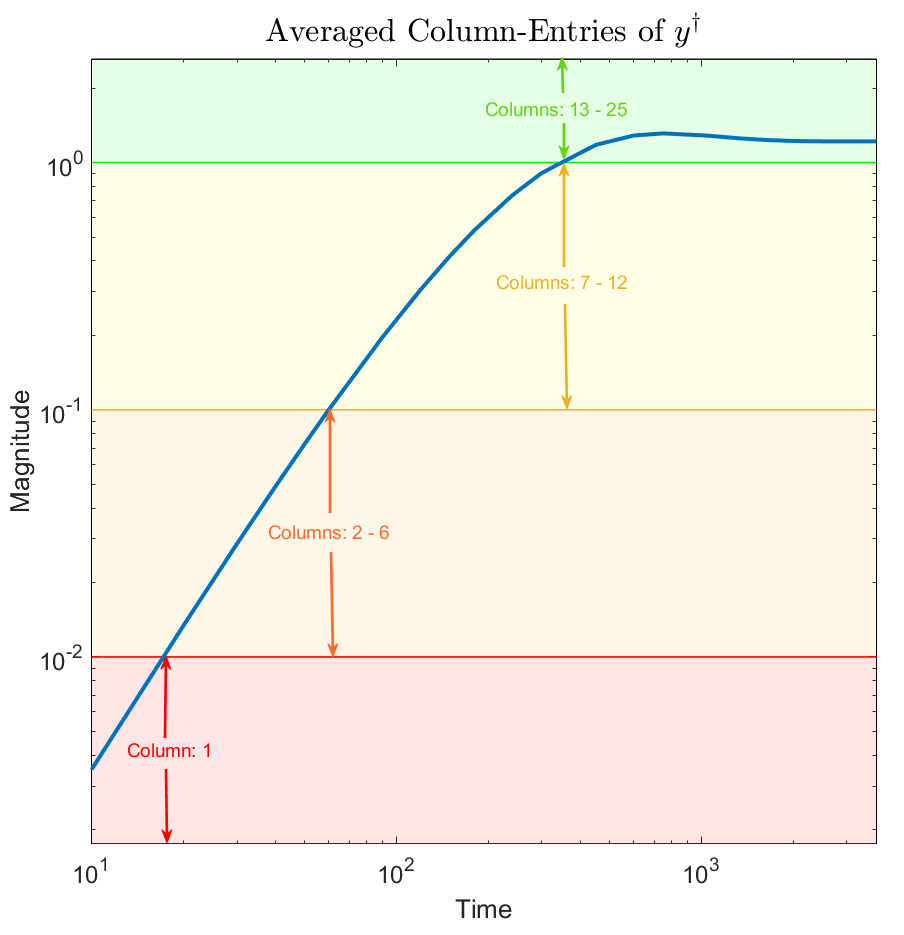

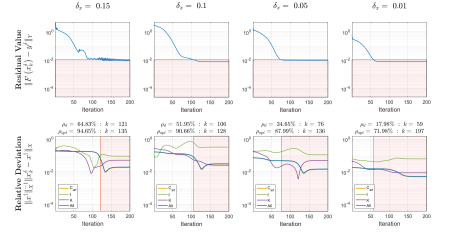

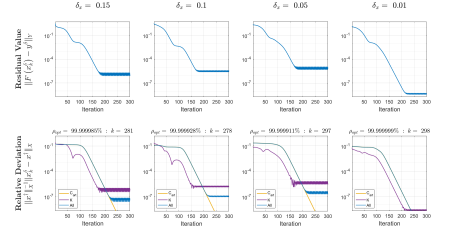

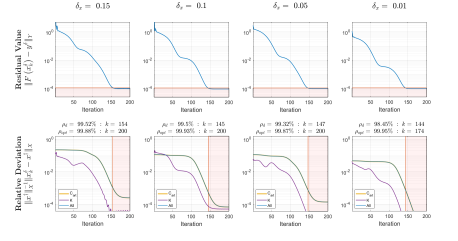

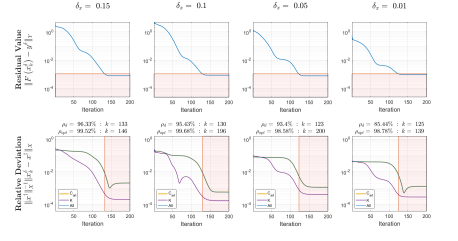

In order to evaluate the identifiability of the parameters from noisy data , we consider both the situation of noiseless data ( and different noise levels . For the latter, it is important to note that, relative to the magnitude of the data, the noise level is already rather high. Indeed, as can be observed in Figure 3, which depicts the average magnitudes of different regions in the data, about of the measurements have a magnitude below . For those values, adding Gaussian noise with standard deviation , for instance, results in noisy data whose standard deviation is already between and of the magnitude of the data itself.

For defining the initialization of the algorithm, we test with perturbations of the ground truth as defined in (24) for . Recall that those are relative perturbations such that the square root of the expected squared deviation from the ground truth is between for and for .

To quantify the improvement compared to the initialization that is obtained by the algorithm, in addition to plotting the residual value and the relative error over iterations, we provide the following two values:

provides the best possible improvement (in percent, relative to the initialization) that was obtained during all iterations, and

provides the improvement that was obtained at iteration where the algorithm was stopped by the discrepancy principle, i.e., the first iteration where was fulfilled.

Experiments where carried out for each combination of and as above. In order to obtain representative results, each experiment was carried out 100 times. Those experiments where the algorithm diverged (i.e., no improvement compared to the initialization was achieved) were dropped (see Table 1 for the number of dropped experiments for each parameter combination) and, among the remaining ones, the one whose performance was closest do the median performance of all repetitions was selected for the figures below.

| 0/0 | 0/0 | 0/0 | 0/0 | |

| 77/36 | 65/17 | 30/2 | 4/0 | |

| 58/21 | 40/8 | 18/1 | 2/0 | |

| 32/14 | 29/4 | 13/1 | 2/0 |

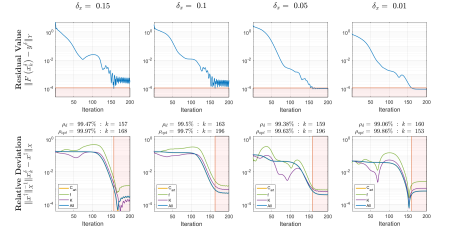

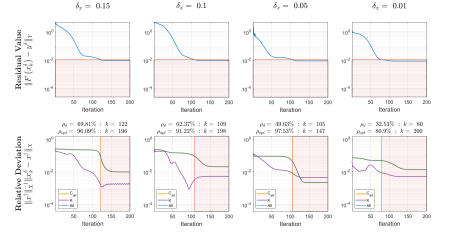

Figures 4 to 7 show the result obtained for different choices of . In those figures, the top and bottom rows depict the evaluation of the residual value and the relative error over iterations, respectively, both with a logarithmic scale for the vertical axis. The different columns show results for the different choices of . The values of and (the latter only for ), together with the respective iterations, are provided at the top of plots of the second row. Note that, while the algorithm was always run until a fixed, maximal number of iterations (300 for and for ) for obtaining the figures, in practice the iterations would be stopped by the discrepancy principle for . For , the red lines always indicate the levels of the residual value (top row) and iteration number (bottom row) where the algorithm would have stopped according to the discrepancy principle.

In Figure 4, which considers the noiseless case, one can observe that the ground truth parameters are approximated very well for all levels of . This confirms our analytic unique identifiability result also in practice.

Considering Figures 5 to 7, one can observe that, in the low noise regime, a good approximation of the ground truth is still possible across different values of . For higher noise, a good initialization (i.e., a small value of ) is of increasing importance and, in some cases, in particular for and the parameters of the parent plasma fraction , the ground truth can not be recovered reasonably well.

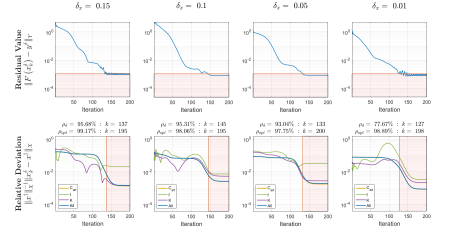

In a second set of experiments, we consider the situation that not only , but also measurements of the values of are available at the time-points . While it is possible in practice to obtain those values via blood sample analysis, this procedure is time consuming and expensive, such that it is a relevant question to what extent such samples improve the identifiability of the tissue parameters.

Again, for each combination of and , each experiment was carried out 100 times, the number of divergent experiments is shown in Table 1 and the Figures show the experiment whose performance was closest to the median performance of the non-divergent experiments.

Results are shown in Figures 8 to 11, where the quantities shown in and above the plots are the same as in Figures 4 to 7. It can be observed that the performance with known is improved compared to the situation where only is known, across all choices of and . While for , both versions yield acceptable results, for knowledge of enables a good approximation of the ground truth parameters in situations where this was not possible with knowing only . This indicates that, as one would expect, the problem of also identifying from measurements is significantly more difficult and there is a benefit (at least for this solution methods) in measuring via blood samples.

7 Conclusions

In this work, we have shown that most tissue parameters of the irreversible two-tissue compartment model in quantitative PET imaging can, in principle, be recovered from standard PET measurements only. Furthermore, a full recovery of all parameters is possible provided that sufficiently many measurements of the total arterial concentration are available. This is important, since it shows that parameter recovery is possible via using only quantities that are easily obtainable in practice, either directly from the acquired PET images or with a relatively simple analysis of blood samples. While these results consider the idealized scenario of noiseless measurements, we have further shown that standard Tikhonov regularization applied to this setting yields a stable solution method that is capable of exact parameter identification in the vanishing noise limit.

These findings open the door to a comprehensive numerical investigation of parameter identification based on only PET measurements and estimates of the total arterial tracer concentration, using real measurement data and advanced numerical algorithms. While the numerical results in this paper provide a first indication that it can be possible to transfer our analytical results to concrete applications, we expect that a comprehensive effort is necessary to obtain a practically usable numerical framework for parameter identification. This will be the next step of our research in that direction.

References

- [1] A. B. Bakushinskii, The problem of the convergence of the iteratively regularized gauss-newton method, Computational Mathematics and Mathematical Physics, 32 (1992), p. 1353–1359.

- [2] B. Blaschke, A. Neubauer, and O. Scherzer, On convergence rates for the iteratively regularized gauss-newton method, IMA Journal of Numerical Analysis, 17 (1994), pp. 421–436.

- [3] Y. Chen, J. Goldsmith, and R. T. Ogden, Nonlinear Mixed-Effects Models for PET Data, IEEE Transactions on Biomedical Engineering, 66 (2019), pp. 881–891.

- [4] H. W. Engl, M. Hanke, and A. Neubauer, Regularization of Inverse Problems, Springer Science & Business Media, Berlin Heidelberg, 2000.

- [5] T. Hohage, Logarithmic convergence rates of the iteratively regularized gauss - newton method for an inverse potential and an inverse scattering problem, Inverse Problems, 13 (1997), pp. 1279–1299.

- [6] M. Holler, R. Huber, and F. Knoll, Coupled regularization with multiple data discrepancies, Inverse Problems, 34 (2018), p. 084003.

- [7] R. Huesman and P. Coxson, Consolidation of common parameters from multiple fits in dynamic PET data analysis, IEEE Transactions on Medical Imaging, 16 (1997).

- [8] W. J. Jagust, J. P. Seab, R. H. Huesman, P. E. Valk, C. A. Mathis, B. R. Reed, P. G. Coxson, and T. F. Budinger, Diminished glucose transport in alzheimer’s disease: Dynamic pet studies, Journal of Cerebral Blood Flow and Metabolism, 11 (1991), pp. 323–330.

- [9] B. Kaltenbacher and A. Neubauer, Convergence of projected iterative regularization methods for nonlinear problems with smooth solutions, Inverse Problems, 22 (2006), pp. 1105–1119.

- [10] J. Logan, J. S. Fowler, Y.-S. Ding, D. Franceschi, G.-J. Wang, N. D. Volkow, C. Felder, and D. Alexoff, Strategy for the formation of parametric images under conditions of low injected radioactivity applied to PET studies with the irreversible monoamine oxidase a tracers [11c]clorgyline and deuterium-substituted [11c]clorgyline, Journal of Cerebral Blood Flow & Metabolism, 22, pp. 1367–1376.

- [11] MATLAB, 9.8.0.1721703 (R2020a) Update 7, The MathWorks Inc., Natick, Massachusetts, 2020.

- [12] G. Polya and G. Szegö, Aufgaben und Lehrsätze aus der Analysis - Zweiter Band: Funktionentheorie · Nullstellen Polynome · Determinanten Zahlentheorie, Springer-Verlag, Berlin Heidelberg New York, 2013.

- [13] R. R. Raylman, G. D. Hutchins, R. S. B. Beanlands, and M. Schwaiger, Modeling of Carbon-11-Acetate Kinetics by Simultaneously Fitting Data from Multiple ROIs Coupled by Common Parameters, Journal of Nuclear Medicine, 35 (1994), pp. 1286–1291.

- [14] L. Sokoloff, Mapping cerebral functional activity with radioactive deoxyglucose, Trends in Neurosciences, 1, pp. 75–79. Publisher: Elsevier.

- [15] R. Todd Ogden, F. Zanderigo, and R. V. Parsey, Estimation of in vivo nonspecific binding in positron emission tomography studies without requiring a reference region, NeuroImage, 108 (2015), pp. 234–242.

- [16] M. Tonietto, G. Rizzo, M. Veronese, M. Fujita, S. Zoghbi, P. Zanotti-Fregonara, and A. Bertoldo, Plasma radiometabolite correction in dynamic pet studies: Insights on the available modeling approaches, Journal of Cerebral Blood Flow & Metabolism, 36 (2015), pp. 326–339.

- [17] M. Veronese, R. N. Gunn, S. Zamuner, and A. Bertoldo, A non-linear mixed effect modelling approach for metabolite correction of the arterial input function in pet studies, NeuroImage, 66 (2013), pp. 611–622.

- [18] P. Zanotti-Fregonara, K. Chen, J.-S. Liow, M. Fujita, and R. B. Innis, Image-derived input function for brain PET studies: Many challenges and few opportunities, Journal of Cerebral Blood Flow & Metabolism, 31, pp. 1986–1998.