Im and Grigas

Stochastic First-Order Algorithms for Constrained DRO

Stochastic First-Order Algorithms for Constrained Distributionally Robust Optimization

Hyungki Im \AFFDepartment of Industrial Engineering and Operations Research, University of California, Berkeley, Berkeley, CA 94720, \EMAILhyungki.im@berkeley.edu \AUTHORPaul Grigas \AFFDepartment of Industrial Engineering and Operations Research, University of California, Berkeley, Berkeley, CA 94720, \EMAILpgrigas@berkeley.edu

We consider distributionally robust optimization (DRO) problems, reformulated as distributionally robust feasibility (DRF) problems, with multiple expectation constraints. We propose a generic stochastic first-order meta-algorithm, where the decision variables and uncertain distribution parameters are each updated separately by applying stochastic first-order methods. We then specialize our results to the case of using two specific versions of stochastic mirror descent (SMD): (i) a novel approximate version of SMD to update the decision variables, and (ii) the bandit mirror descent method to update the distribution parameters in the case of -divergence sets. For this specialization, we demonstrate that the total number of iterations is independent of the dimensions of the decision variables and distribution parameters. Moreover, the cost per iteration to update both sets of variables is nearly independent of the dimension of the distribution parameters, allowing for high dimensional ambiguity sets. Furthermore, we show that the total number of iterations of our algorithm has a logarithmic dependence on the number of constraints. Experiments on logistic regression with fairness constraints, personalized parameter selection in a social network, and the multi-item newsvendor problem verify the theoretical results and show the usefulness of the algorithm, in particular when the dimension of the distribution parameters is large.

distributionally robust optimization, stochastic first-order methods, saddle point problems

1 Introduction

Recent increases in computational power, data availability, and improved modeling techniques have necessitated solving more and more real-world optimization problems under uncertainty. Models that perform robustly against changes in an uncertain environment are particularly appealing in both theory and practice. Distributionally robust optimization (DRO) (Wiesemann et al. 2014), a popular paradigm that is robust against distribution shift, has gained great interest in both the operations research (Bertsimas et al. 2018, Taskesen et al. 2021) and machine learning (Staib and Jegelka 2019, Duchi and Namkoong 2021) communities. DRO is a framework that seeks a robust solution that minimizes the worst-case expectation of the objective function in an ambiguity set of distributions . Most of the existing work considers problems with a single distributionally robust objective or constraint, and DRO with multiple expectation constraints has not been studied as extensively.

There are important problems that are formulated with multiple expectation constraints, including supervised learning problems with fairness constraints (Zafar et al. 2017, Taskesen et al. 2020, Akhtar et al. 2021), the Neyman-Pearson classification model (Tong et al. 2016). For example, fairness in machine learning has been widely studied recently, since, without such constraints or other mechanisms, it has been observed that machine learning models can learn historical biases toward sensitive information such as gender and race (Raghavan et al. 2020). Of course, this can be problematic if such models are used in important decision-making contexts, such as hiring decisions. At the same time, DRO has gained interest in the operations research and machine learning communities as a way to mitigate the risks of overfitting and distribution shift, and to generally increase model reliability (Shafieezadeh Abadeh et al. 2015, Mohajerin Esfahani and Kuhn 2018, Gotoh et al. 2021).

This paper considers a distributionally robust feasibility (DRF) problem with multiple expectation constraints. Namely, the task is to find such that

| (1) |

for all . The domain of the decision variable is a closed and convex set, and the set is a convex and compact ambiguity set for the -th constraint. Although we consider feasibility problems, our methodology can solve a corresponding class of distributionally robust optimization problems by using binary search on the optimal value and repeatedly solving a small number of instances of (1). In the model (1), the random variable follows the distribution , which is only known to live in the ambiguity set of distributions . Due to this ambiguity, the robust optimization methodology looks for a solution that satisfies the constraint for all possible distributions . Therefore, there is a trade-off between the robustness of the model and the final quality of the solution when the corresponding decision is implemented. As several authors have pointed out (see the discussion in Section 1.1), a careful choice of the ambiguity set , depending on the application context, can help balance this trade-off and enhance the effectiveness of model (1).

We define as the range of possible values of and assume that is a finite set of size . As a result, , where denotes a standard unit simplex, and . Throughout this paper, we assume that is a -Lipschitz convex function of , for all and . Then, (1) becomes a convex feasibility problem, albeit with a special structure. Under the assumption that is a finite set, we can reformulate DRF to a robust feasibility problem (RF), which is the corresponding feasibility problem for robust optimization (RO). We discuss in detail this connection between DRF and RF in Section 2.1. Based on this connection, algorithms for RF are clearly also applicable to solve the DRF problem we consider. Recently, Ho-Nguyen and Kılınç-Karzan (2018) presented an algorithm based on first-order methods. Although their algorithm has cheap per-iteration costs and is scalable to the dimension of the decision variables, it lacks scalability to the dimension of the distribution parameters . Since the dimension of the distribution parameters is sometimes set to the number of data samples in DRF, the lack of scalability in makes the application of these algorithms to solve large-scale problems challenging. In particular, the use of online first-order methods (FOMs) that use full gradient information is a crucial roadblock to the scalability of the algorithm of Ho-Nguyen and Kılınç-Karzan (2018).

In this paper, we propose an online stochastic first-order meta-algorithm that is scalable to both the dimensions of and . This meta-algorithm can be viewed as an extension of Ho-Nguyen and Kılınç-Karzan (2018) to a stochastic FOM version. However, the use of usual stochastic FOMs, such as stochastic gradient descent (SGD) or stochastic mirror descent (SMD), turns out to be costly, as the complexity of obtaining a stochastic gradient for (1) is linear in . In particular, as discussed in Section 2, we first need to obtain the index of the maximally violated constraint in (1) in order to obtain an appropriate stochastic gradient for (1). In general, the complexity of obtaining is , which we discuss in Section 3.1. To overcome this challenge, we propose a novel variant of SMD called -SMD. The -SMD method uses a stochastic -subgradient as its descent direction, and the complexity of obtaining the stochastic -subgradient is much cheaper in this setting than other stochastic FOMs such as SGD and SMD. Furthermore, we present a customized version of the meta-algorithm that uses -SMD as a stochastic FOM to update when the ambiguity set is the -divergence set. Our contributions can be summarized as follows:

-

1.

We propose a stochastic first-order meta-algorithm for the DRF problem. Our meta-algorithm allows using arbitrary and possibly distinct “basic” stochastic FOMs to update the and variables, respectively. We show that our meta-algorithm for the DRF problem inherits high-probability convergence results from the basic stochastic FOMs. Also, we argue that high-probability convergence is a key ingredient that makes the meta-algorithm scalable to the number of constraints.

-

2.

We propose an online stochastic FOM called -stochastic mirror descent (-SMD), which we apply as the basic stochastic FOM to update the decision variables in our meta-algorithm. We show that the per-iteration cost of -SMD is independent of the dimension of the distribution parameters. Furthermore, we introduce an efficient feasibility testing algorithm that uses stochastic approximation and takes advantage of the information obtained while running -SMD. We show that it is possible to determine the -feasibility of a given solution independently of the dimensions of both the decision variable and the distribution parameters.

-

3.

We propose using the Bandit Mirror Descent (BMD) method of Namkoong and Duchi (2016) to update the variables when the ambiguity set is a -divergence set. BMD has a low cost per iteration to update the variables . We extend the convergence analysis of BMD to a high-probability convergence guarantee and use this to show that the total iteration complexity of the customized meta-algorithm is almost independent of the dimension of the decision variables and distribution parameters.

-

4.

We examine the performance of our meta-algorithm using -SMD and BMD in extensive numerical experiments on large instances for three problem classes: logistic regression with fairness constraints, personalized parameter selection for a large-scale social network, and the multi-item newsvendor problem with a conditional value at risk (CVaR) constraint. We demonstrate performance improvements over the deterministic approach of Ho-Nguyen and Kılınç-Karzan (2018), the state-of-the-art method for large-scale RF problems, when is large.

1.1 Related Work

We review related works concerning DRO, RO, and associated algorithmic solution approaches. In DRO, the ambiguity set , the set of possible distributions of uncertain parameters, is a crucial design choice for the performance of the DRO model. Ideally, we want to choose an ambiguity set that balances accurate modeling (e.g., it encompasses the true distribution, if it exists), computational tractability, and an appropriate tuning of the level of conservativeness. Popular approaches include usßing moment-based constraints (Delage and Ye 2010, Hanasusanto et al. 2015, Chen et al. 2019) or constraints based on divergence/distance functions (Duchi et al. 2021, Blanchet et al. 2019, 2022) to define the ambiguity set. In particular, there has been an extensive body of literature focusing on studying DRO models with ambiguity sets defined by -divergences (Hu and Hong 2013, Namkoong and Duchi 2016, Duchi and Namkoong 2021) and the Wasserstein distance (Kuhn et al. 2019, Gao et al. 2022, Gao 2022), largely due to their computational tractability and statistical properties. Duchi and Namkoong (2021), among others, studied DRO with -divergence constraints, demonstrating finite sample minimax upper and lower bounds while also showcasing its distributional robustness. Additionally, other divergence options, such as maximum mean discrepancy (MMD) (Staib and Jegelka 2019, Zhu et al. 2020), have also been explored. Staib and Jegelka (2019) studied DRO with MMD distance, demonstrating that MMD DRO is approximately equivalent to regularization by the Hilbert norm and established connections with kernel ridge regression.

Alternatively, rather than defining the ambiguity set as a constraint, it is frequently incorporated into the objective function as a penalization (Levy et al. 2020, Gotoh et al. 2021, Jin et al. 2021, Qi et al. 2021). Gotoh et al. (2021) investigated the out-of-sample performance of DRO solutions with -divergence and demonstrated that calibrating the robust parameter, which determines the size of the ambiguity set, results in a greater variance reduction in out-of-sample loss with a minor trade-off in out-of-sample mean.

There has been some progress in developing scalable algorithms for DRO under various ambiguity sets and settings. Namkoong and Duchi (2016) proposed a primal dual algorithm to solve DRO with a -divergence ambiguity set. Also, due to the high cost of obtaining unbiased gradient estimators for the DRO objective, several works have focused on using biased estimators to solve DRO problems. Levy et al. (2020) propose a primal algorithm that utilizes a mini-batch gradient estimator for DRO with a -divergence set and CVaR-divergence set. Furthermore, they proposed an algorithm that uses a Multi-Level Monte Carlo (MLMC) estimator, in which the base sample size is proportional to , where represents the tolerance rate in their settings. Wang et al. (2021) recently introduced DRO with the Sinkhorn distance, which is a variant of the Wasserstein distance based on entropic regularization. They provide a dual reformulation of their problem and an efficient first-order algorithm utilizing biased gradients. Our approach also uses a biased estimator for updating , but it is important to note that the bias in our estimator stems from the presence of multiple constraints, whereas the bias in the aforementioned approaches results from the approximation error associated with the worst-case distribution for a given .

As DRO has its roots in the robust optimization literature (Ben-Tal et al. 2013), a strong connection can be established between DRO and RO, allowing for the exchange of ideas between the two sub-fields. A traditional approach to solving robust convex optimization is to change the problem into an equivalent robust convex counterpart, which can be solved by state-of-the-art convex solvers (Ben-Tal et al. 2009, Bertsimas et al. 2011, Ben-Tal et al. 2015a). However, the robust counterpart approach is often not scalable to the dimension of the decision variables. To remedy this scalability problem, Ben-Tal et al. (2015b) propose an algorithm that alternatively updates the decision variables () and the uncertain parameters () using two oracles: a feasibility oracle and a pessimization oracle. Although their algorithm handles the scalability of the dimension of , it still relies on the two oracles, which might be costly. Ho-Nguyen and Kılınç-Karzan (2018) introduced an algorithm that uses first-order methods. Their algorithm has much cheaper iterations than the cost of the feasibility and pessimization oracles, is more scalable to the dimension of the decision variable , and maintains the same convergence rates. In particular, Ho-Nguyen and Kılınç-Karzan (2018) bound the duality gap of their robust feasibility problem (in particular, its saddle point reformulation) by the sum of two weighted regret terms, and they update each weighted regret by using online convex optimization (OCO) methods (Shalev-Shwartz et al. 2011, Hazan et al. 2016). However, the use of deterministic gradients in their context makes it challenging for their algorithm to scale with respect to the dimension of the distribution parameters.

1.2 Notation

For any , define . Superscripts are used to represent items corresponding to the -th constraint. We use to denote the th element of the vector and use to denote the -dimensional vector of all ones. For a finite-dimensional real vector space , denotes its dual space, and represents the primal norm and associated dual norm respectively.

2 Stochastic First-Order Meta-Algorithm for DRF

In this section, we present a stochastic first-order meta-algorithm for the distributionally robust feasibility (DRF) problem. We begin by reformulating (1) to a convex-non-concave saddle point (SP) problem. All omitted proofs are included in the Appendix.

2.1 Convex-Non-Concave Saddle Point Problem

We begin by introducing the formal setting of our problem. We assume that the random variable has finite support represented by for all and assume that there exists such that , for all , , and for each constraint . Also, we assume the random variables for all are mutually independent. This assumption is without loss of generality and our results can be extended to dependent random variables ; we include a detailed discussion of the dependent case in the Appendix 6.1. We define , which is the Cartesian product of sets for all . Define by , for all . Furthermore, we define a vector-valued function by . Under our notation, we have . Then, we can write the DRF problem formally as:

Let us define a function as . Note that is a convex function of but not necessarily a concave function of . After changing the order of the maximum and supremum above, the standard relaxation to an -approximate feasibility problem is:

| (2) |

We call as a distributionally robust -feasibility certificate if it satisfies the feasibility condition of (2). Similarly, a realization of a distribution parameter is called a distributionally robust infeasibility certificate if satisfies for all . As is a convex-non-concave function, (2) can be considered as a convex-non-concave saddle point problem (convex-non-concave SP). We define the SP gap , which measures the accuracy of the given solution ) to (2), by

| (3) |

Theorem 2.1 (Theorem 3.1 of Ho-Nguyen and Kılınç-Karzan (2018))

Let be a convex function of but not necessarily a concave function of and be given. Suppose that we have and such that Then if , we have . Moreover, if and , we have .

Theorem 2.1 implies that it is sufficient to obtain a solution ) that satisfies , for example, to solve (2). Our meta-algorithm will obtain such a solution ) by iteratively generating and according to separate “basic” stochastic FOMs, and then taking convex combinations of the generated points . We define and , given a vector of convex combination weights .

To give an upper bound of , we define new error terms for given :

Then we have

As a result, it is sufficient to solve the -feasibility problem by obtaining that satisfies

| (4) |

Remark 2.2 (Weighted Regret)

The two terms and can be interpreted as weighted regret terms and we can use results from online convex optimization (OCO) to bound these terms respectively. In particular, let us first consider . Suppose and a sequence such that , for all , are given and let us define a function as . As is a convex function of , is also a convex function of . Then, we have

We see that can be interpreted as a weighted regret of a sequence of convex functions .

For , let us assume a sequence such that , for all , is given. Define a function as , for all . Since is a linear function of , is a concave function of . Then, for each , we have

Therefore, can be interpreted as a weighted regret of a sequence of convex functions , for all . \Halmos

2.2 Stochastic First-Order Meta-Algorithm for DRF

We are now ready to introduce our stochastic first-order meta-algorithm for the DRF problem. Similar to the work of Ho-Nguyen and Kılınç-Karzan (2018) in the deterministic case, we update the decision variables and the dimension parameters separately according to specific stochastic FOMs. Let us denote as the stochastic FOM used to update and denote as the stochastic FOM used to update , for each . We use to update based on and to update based on for all . We represent these updates as

| (5) | ||||

[High-Probability Convergence up to Precision ] For given sequences and , and given , algorithms and satisfy high-probability convergence up to precision if there exists an increasing and sublinear function and decreasing functions and such that

for all .

In Assumption 2.2, both and are expected to converge to zero, and is related to the desired level of tolerance. In particular, the additional error term appears in the -SMD algorithm introduced in Section 3.1, and it arises from the utilization of biased gradients within -SMD. However, is typically set to 0 in other stochastic FOMs with unbiased gradients. Some exemplary algorithms that satisfy the assumption of high probability convergence are stochastic gradient descent (SGD) and stochastic mirror descent (SMD). Both methods have high-probability convergence results with , , and . Under Assumption 2.2, we can set large enough so that and are sufficiently small with high probability and, correspondingly, by Theorem 2.1 and (4), we can solve (2) with high probability. Although it is plausible to set sufficiently large according to our theoretical results, it is usually more efficient to use the SP gap to terminate early in situations where the SP gap can be cheaply calculated periodically. Indeed, we can terminate early as soon as we find and that satisfy , where the SP gap is defined in (3). We can often calculate the SP gap in a reasonable time since is a piecewise linear function of and the complexity of calculating is often . We present the details of the SP gap calculation in Appendix 6.2.

In addition, we use the feasibility testing algorithm, denoted , which yields the values of and if they constitute an -feasible solution for the DRF problem; otherwise, it indicates infeasibility. Clearly, there are several algorithmic options available for . According to Theorem 2.1, given a pair satisfying condition , we can select as an algorithm that produces an -feasible solution in cases where ; otherwise, it returns infeasibility. Algorithm 1 represents this exact feasibility testing algorithm. However, this can be improved in terms of computational efficiency with specific choices of and . We discuss this further in Section 3.2.

Algorithm 2 represents the stochastic first-order meta-algorithm for the DRF problem, which includes the optional early termination criterion and uses for the feasibility testing algorithm at the very end (if we do not stop early). If we do allow the option of early termination, then the SP gap is calculated periodically at every -th iteration.

The following theorem shows the convergence guarantee of Algorithm 2.

Theorem 2.3

3 -Stochastic and Bandit Mirror Descent for DRF

In this section, we introduce two specific basic stochastic FOMs to improve the scalability and applicability of Algorithm 2. Namely, we introduce a new algorithm, -Stochastic Mirror Descent (-SMD), to update the variables (Section 3.1). -SMD not only improves the per-iteration cost associated with updating , but also offers a more efficient approach to design the feasibility test (Section 3.2). We also introduce Bandit Mirror Descent (BMD) (Namkoong and Duchi 2016) to update the variables (Section 3.3), and we develop a new high probability convergence guarantee for this method, which is needed in our setting to apply Theroem 2.3.

3.1 -Stochastic Mirror Descent

As mentioned earlier, can be interpreted as a weighted regret for , suggesting the use of online convex optimization methods to perform the updates. Note that these methods typically use unbiased stochastic gradients. However, we point out that using an online unbiased stochastic FOM for could cause a substantial computational burden when and are large. Note that in (5), the update of and does not occur simultaneously. As a result, we consider a sequence as given when we discuss the update of and vice versa. As we only discuss the update of in this section, we simplify our notation as follows throughout this section: we define as and as .

The main inefficiency of using an unbiased stochastic FOM comes from the structure of the function . In order to obtain an unbiased estimator of at and associated first-order information, we need to calculate an index . However, as , for all , the complexity of obtaining is , where is the average cost to compute , for all , and . Thus, calculating dominates the other steps of the stochastic FOMs and causes Algorithm 2 to lose scalability in .

To overcome this issue, we use an approximate maximizing index instead of an exact maximizing index . Algorithm 3 describes a procedure for obtaining this . We use samples of indices from distribution to obtain , which approximates for all . We call the “per-iteration sample size” to distinguish it from a batch size for stochastic gradients in a stochastic FOM.

Lemma 3.3 below shows that if the sample size is large enough to satisfy the condition in Definition 3.2, then is a good approximation of in the sense that the approximate subgradient set is close to the actual subgradient set . To explain this formally, we introduce the concept of -subgradients (see, e.g., Borwein (1982), Kiwiel (2004) and Bonettini et al. (2016) for more details).

Definition 3.1 (-subgradient)

For any given convex function and , where is a convex set, a vector is called an -subgradient of at if

We denote the set of all -subgradients of at by . \Halmos

Definition 3.2 (Approximation Condition)

For given , the per-iteration sample size satisfies the approximation condition, with parameters and , if it holds that

| (7) |

with probability at least . \Halmos

Notice that both and are fixed, user-specified, parameters that are independent of any other parameters in our context. We now introduce the key lemma for -SMD.

Lemma 3.3

For given , suppose that the per-iteration sample size satisfies the approximation condition with parameters . Let be defined as and be given. Then for any , is an -subgradient of , i.e., , with probability at least .

Remark 3.4 (Value of Per-iteration Sample Size K)

As is an unbiased estimator of , it is possible to choose that satisfies the approximation condition for small by the law of large numbers. However, being large is not desirable since the complexity of obtaining is . Intuitively, choosing on the order of is overly conservative to satisfy the approximation condition. In fact, we can satisfy this condition with since, in Appendix 6.4, we show that is almost independent of when is large. For example, using Bennet’s inequality (Wainwright 2019), we can choose to satisfy the approximation condition for any and . This value is independent of and much smaller than if is large. \Halmos

Our main basic stochastic FOM to update , -SMD, is a variant of SMD. So, we assume that the set follows the following mirror descent setup (Juditsky et al. 2011). {assumption}[Mirror Descent Setup] Let be a given differentiable and 1-strongly convex function and be the Euclidean space containing . We define the Bregman distance as and the -diameter . Then for any given , and , it is easy-to-compute .

We introduce our main online stochastic FOM for updating the variables, which we call -SMD, in Algorithm 4. The main difference from unbiased stochastic FOMs such as SGD or SMD is that -SMD uses a biased subgradient (which approximates an unbiased subgradient) of the objective. A desirable property of SMD is its high-probability convergence guarantee (Nemirovski et al. 2009). We now present such a high-probability convergence result for -SMD. In addition to the notation defined in Assumption 3.4, which will be used in Theorem 3.5, recall that denotes the uniform Lipschitz constant of functions for all and .

Theorem 3.5

Let be defined as for and be given. Given a sequence such that for all , let be the sequence generated by Algorithm 4 with diminishing step size , where the constant is defined as . Moreover, let be the sequence derived by normalizing . Given that the per-iteration sample size sequence satisfies Equation (7) in the approximation condition (Definition 3.2), for any , we have

| (8) |

Otherwise, if Equation (7) holds with probability at least , we have

| (9) |

Note that we choose the constant of the diminishing step-size in the above theorem to minimize the upper bound of in the statement of the Theorem. Also, the added term in equation (9) reflects the probability of satisfying equation (7) under the approximation condition. In Equation (8), we observe that -SMD satisfies Assumption 2.2 with , , and . Theorem 3.5 tells us that, relative to SMD, -SMD achieves a low cost per iteration of at the cost of an increase in tolerance error by . Furthermore, we can see that the upper bound of does not depend directly on the dimensions and , and often has a very low dependence on these parameters. For example, when , and is the entropy function, we have which indicates the low dependence of the upper bound of on . We emphasize that -SMD is independent of the choice of the convex ambiguity set. In addition to the reduced per iteration cost offered by -SMD, the information of for all , which we obtain from Algorithm 3, can be reused to develop an efficient feasibility testing algorithm, which is elaborated on in Section 3.2.

Remark 3.6 (Practical Performance with Diminishing Step Size)

The upper bound of in Theorem 3.5 contains a logarithmic term that can be removed if we use a constant step size. However, in practice, using a diminishing step size typically leads to a higher-quality solution with fewer iterations compared to a constant step size. As a result, to optimize the advantages of early termination, we choose the diminishing step size, despite its theoretical limitations. \Halmos

3.2 Efficient Feasibility Test

In Algorithm 1, we determine the -feasibility or infeasiblity of a given solution , satisfying , by comparing with . Given that , which can satisfied by taking sufficiently large in Algorithm 2, the complexity of Algorithm 1 is dominated by computing , which is . Since may be very large in settings with high dimensional distribution parameter vectors, the linear dependence of this complexity on is problematic. To confront this challenge, we introduce an efficient feasibility test. This test, when used in conjunction with -SMD as the updating algorithm for , streamlines the feasibility testing process and completely removes the linear dependence on . By cleverly reusing the information that was obtained during the application of -SMD, the new efficient feasibility test has computational complexity , where represents a new value for the total number of iterations in Algorithm 2. Importantly, we show that is within a constant factor of the value of required when we instead use the exact feasibility test Algorithm 1. As we will show in Section 3.4, and are both independent of .

Towards the goal of developing the efficient feasibility test, we introduce a result below that provides an alternative way of producing a certificate of the DRF problem.

Proposition 3.7

(Extension of Corollary 3.2 of Ho-Nguyen and Kılınç-Karzan (2018)) Let be a sequence with , for all and and be given. Suppose that there exists satisfying , , and , with probability at least . Let and . With probability at least , if , then is an -feasible certificate, and if , then problem (2) is infeasible.

Following Proposition 3.7, if we choose that satisfies

| (10) |

and set as and set , then we can set and produce a certificate for problem (2) by comparing with . Unfortunately, the complexity of computing is , which actually exceeds the complexity of determining , , as required by Algorithm 1. Nevertheless, using a stochastic approximation of , which we obtain almost for free by reusing the information of , allows us to develop the efficient feasibility test. Indeed, notice that is the approximate value of that satisfies (7). In this case, we assume and adjust the total number of iterations to satisfy

| (11) |

For clarity, we simplify our notation and denote and to simply express as . We approximate with , which we define as , for all and further define as .

Lemma 3.8

Let be given and and be a sequence that is generated by Algorithm 2 with -SMD as . If the per-iteration sample size satisfies the approximation condition with parameters and , then we have

| (12) |

with probability at least .

Lemma 3.8 suggests that is sufficiently close to to serve as a substitute for . Additionally, the complexity of calculating is , as it reuses the values of that were previously calculated. Because we use instead of , we need a different guideline to determine -feasibility other than comparing and . Instead, we compare with , and Algorithm 5 presents the efficient feasibility testing algorithm using this stochastic approximation. Notice that Algorithm 5 can be used after a sufficient number of iterations that satisfies (11). The following theorem implies that after iterations, Algorithm 5 gives us a correct solution to (2) with high probability.

Theorem 3.9

Let be given, and be a sequence generated by Algorithm 2 with -SMD as and the per-iteration sample size satisfies the approximation condition with parameter and . Suppose satisfies (11), and let . Then, Algorithm 5 returns either an -feasible solution or an infeasibility certificate of the DRF problem (2), with probability at least .

The remaining task is to contrast , which represents the total number of iterations required when using to determine the -feasibility of the problem, with , which is the total number of iterations when using Algorithm 1 for the same purpose. Notice that needs to satisfy (11), while needs to satisfy

| (13) |

In fact, considering , the relationship between and is . In particular, for all , we have that and will be within a constant factor of each other. In fact, if , then , although they are still within a constant factor of each other. In any case, we see that using the efficient feasibility test Algorithm 5 reduces the complexity of the subroutine of Algorithm 2, and sometimes requires less itearations in total. This reduction is highly beneficial when early termination (SP gap termination) in Algorithm 2 is unattainable and we ultimately need to rely on to solve the problem.

3.3 Bandit Mirror Descent

Let us now introduce Bandit Mirror Descent (BMD) (Namkoong and Duchi 2016), which provides an efficient update scheme for the variables in the case where the ambiguity set are constructed from -divergence sets. The -divergence set is defined as with parameter , where represents the -divergence between distributions and . In particular, if the distributions and have finite support, we have . We consider with parameters to be our ambiguity set, which is a slight variation of the set . This modification of the ambiguity set is related to BMD as we discuss later in this section. Notice that is bounded below with parameter and no longer needs to satisfy . Instead, we include a normalization step when obtaining a stochastic gradients of at or .

BMD is a variant of SMD, so it follows the mirror descent setup specified in Assumption 3.4 with and -diameter . The derivation for can be found in Appendix 7.3. Algorithm 6 shows the Bandit Mirror Descent under -divergence set. The main reason for the choice of instead of is because under , the individual probabilities could be small, causing the gradient estimator to have an excess variance. Namkoong and Duchi (2016) showed that the convergence of the algorithm still holds even if we use instead of . We further extend their convergence result to a high-probability convergence result. Before presenting the upcoming proposition, let us recall the definition of . is a constant that uniformly bounds for all and for . With this in mind, we present the following proposition.

Proposition 3.10

Let and for . Given a sequence where for all , let be the sequence generated from Algorithm 6 using a diminishing step-size , where the constant is defined as

| (14) |

and be the normalization of . For any , we have

Note that the upper bound of does not directly depend on , and satisfies Assumption 2.2 with . Also, following the work of Namkoong and Duchi (2016), we propose an efficient way of updating the variables in BMD in Appendix 8. In particular, we show that the complexity of the update of the variables at each iteration of BMD is . These results show the scalability of BMD to update variables.

3.4 Meta-Algorithm under -divergence set

Now we are ready to consider Algorithm 2, in the special case where we use Algorithm 4 to update the variables and use Algorithm 6 to update the variables. The following result shows its convergence and follows by combining Theorem 3.5 and Proposition 3.10 together.

Theorem 3.11

Let and for , and be given. Suppose that satisfies the approximation condition (Definition 3.2) with and . Consider the sequence generated by Algorithm 2, where the variables are generated using -SMD with a diminishing step-size of with , and the variables are generated using BMD with a diminishing step-size of with as specified in (14). Let be the normalization of , which is also the normalization of . For any , let

| (15) |

then we have

Remark 3.12 (Scalability of Algorithm 2 under -divergence set)

The total number of iterations of the version of Algorithm 2 considered in Theorem 3.11 must satisfy Equation (13), where and are as defined in (15). Notably, both and do not have direct dependence on the dimensions and . Therefore, the total number of iterations will also not depend directly on the dimensions. In Section 3.2, we show that this independence further extends to , the total iterations of Algorithm 2 when using efficient feasibility testing. Therefore, both and do not have direct dependence on the dimensions and . Moreover, as we discussed in (6), it is adequate to let . This, in turn, makes and scale logarithmically with the number of constraints . Lastly, as outlined in Section 3.1 and Appendix 8, the complexity of updating and is almost independent of . Overall, these results imply that our algorithm is scalable to and under the -divergence set. \Halmos

4 Experiments

In this section, we conduct numerical experiments to compare the performance of our stochastic online first-order meta-algorithm (SOFO-based approach) with the deterministic online first-order framework (OFO-based approach) of Ho-Nguyen and Kılınç-Karzan (2018). Note that we do not compare our approach with other algorithms, such as the pessimization oracle-based algorithm proposed by Mutapcic and Boyd (2009) and the dual-subgradient meta-algorithm proposed by Ben-Tal et al. (2015b), because these algorithms tend to struggle with the large-dimensional problem sizes considered in our study. Additionally, Ho-Nguyen and Kılınç-Karzan (2018) have already demonstrated the superior performance of their OFO-based approach as compared to these algorithms, especially as the dimensions get larger. As we consider problem sizes comparable to and even larger than Ho-Nguyen and Kılınç-Karzan (2018) (especially larger with regard to the dimenson of the distribution/uncertain parameters), we opt to only compare with the OFO-based approach of Ho-Nguyen and Kılınç-Karzan (2018).

4.1 Logistic Regression with Fairness Constraints

We first consider logistic regression with fairness constraints that reduce the correlation between the predicted labels of the classifier and sensitive attributes such as race or gender. In particular, we consider the following formulation adopted from Zafar et al. (2017).

In this formulation, denotes the feature vector for -th sample and denotes the corresponding response. The function is the standard sigmoid function and is a sensitive attribute with sample mean . As shown in Zafar et al. (2017), approximates the covariance between the sensitive attribute and the decision boundary of the classifier. We want to be small so that the classifier is uncorrelated to the sensitive attribute, and is often chosen to satisfy certain fairness criteria.

We use the adult income dataset (Asuncion and Newman 2007), which contains 45,000 examples with 14 features, including age, gender, and marital status. Our goal is to classify whether the income level is greater than $5K, and we consider gender as a sensitive attribute. In addition to the provided features, we add new features generated by considering all polynomial combinations of continuous variables with degrees less than equal to either 3 or 4. This results in the dimension of the features, and correspondingly , being either or , respectively. For simplicity of comparison, instead of solving the optimization problem, we solve the corresponding feasibility problem with the right-hand side of the objective function constraint set to ; as the optimization problem can be reduced to several feasibility problems, the results will be similar. We present the detailed parameter setting in Appendix 9.2.1. We simulate 20 times for each experiment and setting of parametrs that we vary. The experiments are performed on a Linux machine with a 2.3-GHz processor and 64GB memory using Python v3.7. While computing the SP gap, if a closed-form solution is not available, we used CVXPY v1.1.7 (Diamond and Boyd 2016) and Mosek v10.0.34 (ApS 2019) with standard parameter settings.

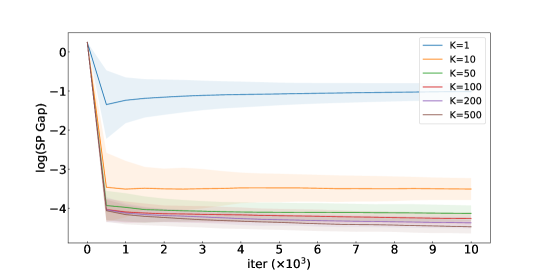

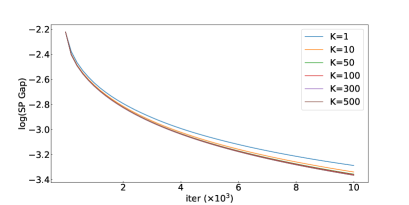

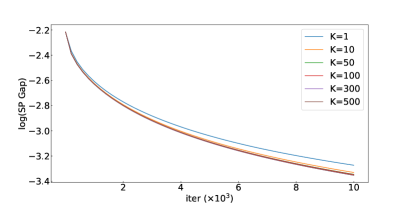

To find an appropriate practical per-iteration samples size , we tested different values and report the results in Table 1. Specifically, Table 1 shows the average percentage of iterations that satisfy either or out of the first 10,000 iterations (when ). We can see that even has around 38% accuracy, as we only have three constraints. Furthermore, the accuracy increases as increases. Figure 1 compares the convergence rate of the SOFO-based approach across different values of when . As our theory suggests, determines the convergence rate and also the precision of the solution that we can obtain. For the following experiments, we choose , which was large enough for SOFO to achieve the desired solution for our setting of ().

| 1 | 10 | 50 | 100 | 200 | 500 | |

|---|---|---|---|---|---|---|

| 174 | 38.4 | 43.4 | 49.5 | 53.2 | 56.4 | 60.3 |

| 300 | 38.4 | 43.5 | 49.7 | 53.2 | 56.5 | 60.4 |

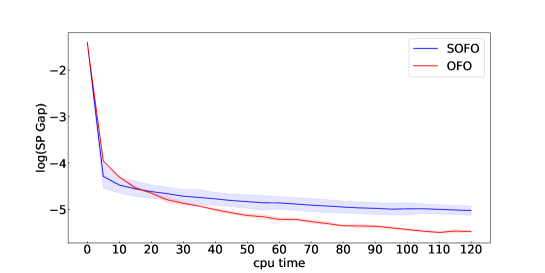

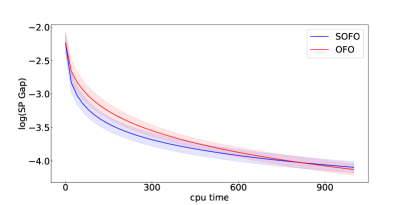

Figure 2 plots the convergence speed between the SOFO-based and OFO-based approaches. The SOFO-based approach obtains the solution with a small SP gap () faster than the OFO-based approach, while OFO eventually achieves a better solution. This result highlights the limitations of our work in the regime where a very accurate solution, i.e., a small value of is desired. This result also follows the commonly recognized trend that stochastic gradient methods perform better early on, but full gradient methods perform better after enough computation time.

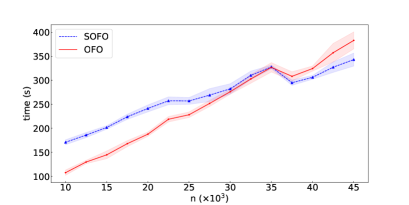

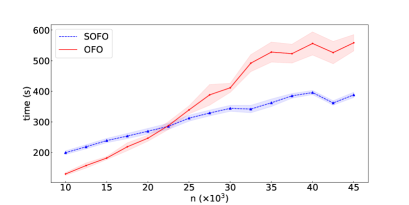

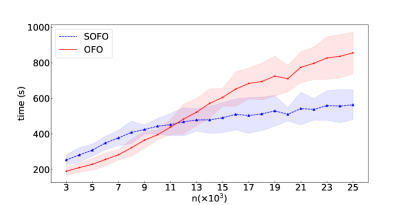

Figure 3 plots the average solve times in seconds for SOFO-based and OFO-based approaches across different values of . When , we randomly sample samples from the dataset for every simulation. Since the OFO-based approach does not use the early termination criterion (by computing the SP gap), we also exclude this feature from our SOFO-based approach; although we expect that including the early termination criterion would improve our overall computation times with proper parameter settings. As our theory suggests, SOFO scales better than OFO in for both and . Additionally, we observe that SOFO outperforms OFO as the value of increases when increases from 174 to 300. However, we see that the SOFO-based approach still has a modest linear grown trend in in both cases. This comes from the update of the cumulative distribution of , which we use when random sampling an index from distribution parameter . Although it is possible to resolve this issue in theory by using a tree structure to update the variables, for the problems we consider, using the tree structure in our implementation is inefficient compared to updating the cumulative distribution of the variables using well-optimized libraries. Thus, instead we use the efficient update scheme proposed in Appendix 8.4.

Table 2 and Table 3 display the total iterations, average solve time, and final saddle point gap for and , respectively. Firstly, observe that the total iteration count is nearly unaffected by the dimensions of and , which aligns with our theoretical findings. Moreover, by comparing the seconds per-iteration for both SOFO-based and OFO-based approaches, we can appreciate the scalability of the SOFO method with respect to both and . For example, in both tables, OFO achieves a smaller overall solve time when whereas SOFO achieves a smaller overall solve time when . Notably, the most significant difference in overall solve time occurs in the largest problem size considered, and , in which case OFO requires about one and half times more solve time than SOFO. While both approaches achieve a final SP gap below the desired level of approximate solution (), we can observe that the OFO-based approach achieves a smaller gap. This result can likely be attributed to the reduced variance inherent in deterministic algorithms, such as the OFO-based approach. On the other hand, it is again notable that our SOFO-based approach excels in overall solve time, primarily due to its cheaper iterations and further highlighting the efficiency and scalability of our proposed method.

| Total Iterations | Solve Time (s) | Seconds Per-Iteration (s) | Final SP Gap | ||

|---|---|---|---|---|---|

| SOFO | 20000 | 121853 | 241.4068 | 0.00198 | 0.00647 |

| OFO | 20000 | 22664 | 187.8148 | 0.00829 | 0.00324 |

| SOFO | 45000 | 120489 | 343.0915 | 0.00284 | 0.00547 |

| OFO | 45000 | 22611 | 383.0715 | 0.01694 | 0.00312 |

| Total Iterations | Solve Time (s) | Seconds Per-Iteration (s) | Final SP Gap | ||

|---|---|---|---|---|---|

| SOFO | 20000 | 129005 | 269.68359 | 0.00209 | 0.00671 |

| OFO | 20000 | 25278 | 246.83508 | 0.00976 | 0.00330 |

| SOFO | 45000 | 127561 | 388.28495 | 0.00304 | 0.00536 |

| OFO | 45000 | 25224 | 558.37625 | 0.02214 | 0.00282 |

4.2 Personalized Parameter Selection in Large-Scale Social Network

In this section, we present another experimental setting for personalized parameter selection in a large-scale social network. This experiment is adopted from Basu and Nandy (2019). Social network companies may set certain “parameters,” such as the gap between different ad displays on the news feed, for different users in order to personalize the experience for each user and subsequently achieve goals with respect to performance metrics. Clearly, choosing a global parameter for all the customers might not be the optimal solution. Instead, we consider dividing our customer base into different cohorts and estimate the optimal parameter for each cohort. Let us assume that the parameter can take possible values, and there are metrics that we consider. Among these metrics, revenue is the primary metric that we would like to maximize, and the other metrics, such as click-through rates (CTR), will appear as constraints in our problem. Let our decision variable denote the probability of assigning the -th treatment to the th cohort. Also, we define as , which is a dimension of our decision variable , and define a random vector as , where represents the casual effect when treatment is applied to a cohort for a metric . We assume that with some distribution . Suppose we have samples of , where th sample is denoted as , for all . Then can be expressed as . Our goal is to find an optimal allocation that maximizes revenue under distributionally robust constraints, hence the problem formulation is:

| (16) | ||||||

| s.t. | ||||||

In our experiment, we solve the feasibility version of (16), where the objective function is changed to an inequality , rather than solving the decision problem itself. We use synthetically generated data for our experiment, where the generation process is described in Appendix 9.3.1. Unless stated otherwise, we set the tolerance level to . Details of other parameter settings can be found in Appendix 9.3.2

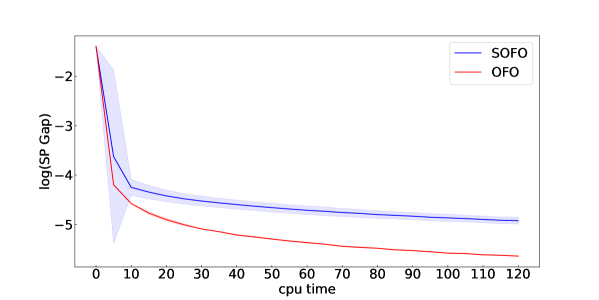

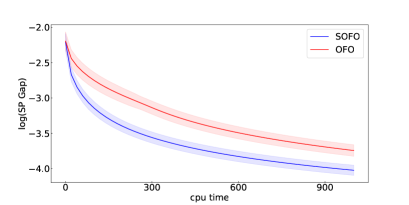

Figure 8 plots the average log duality gap against the CPU-time. Parameter settings are the same as in the previous experiment, except that we fixed the per-iteration sample size to 100, and we set the tolerance level to in this experiment. Similarly to Figure 2, we see that SOFO arrives at the small SP gap solution faster than OFO but, eventually, OFO catches up when . However, when , there is no intersection between the SOFO and OFO curves even after more than 900 seconds.

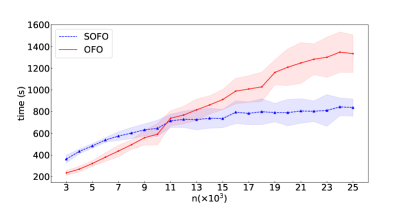

Figure 4 plots the average solve times in seconds for the SOFO-based approach and the OFO-based approach for different . We set for to have a larger feasibility region and . The early termination condition is used to maximize the efficiency of Algorithm 2. As our theory suggests, in the large regime (), the SOFO curve becomes flat, while the solve time of the OFO-based approach increases linearly in . Lastly, Table 4 shows the average total iterations and seconds per iteration for the OFO-based approach and the SOFO-based approaches. We can see that the average iterations of the SOFO-based approach is four times higher than that of the OFO-based approach. Also, we see that the seconds per-iteration scales better in the SOFO-based approach than in the OFO-based approach with respect to .

| Total Iterations | Seconds Per-Iteration | ||

|---|---|---|---|

| SOFO | 5000 | 208445 | 0.0023 |

| OFO | 5000 | 55996 | 0.0058 |

| SOFO | 25000 | 180120 | 0.0046 |

| OFO | 25000 | 57219 | 0.023 |

4.3 Multi-item Newsvendor with Conditional Value at Risk Constraint

Finally, we consider a multi-item newsvendor problem with conditional value at risk (CVaR) constraint. In the multi-item newsvendor problem, the demand for multiple perishable products is uncertain. Any sold item produces revenue, and any inventory replenishment incurs an ordering/production cost. Also, any unsatisfied demand incurs back-order costs, and we can sell any left-over items at their salvage prices. Our goal is to decide the optimal order quantity of items to minimize the loss while satisfying CVaR and budget constraints. Suppose there are items and vectors respectively represent production cost, retail price, salvage price and back-order cost of the items and denote a random demand vector. It is natural to assume that and , and this implies that the optimal order quantities of the items are equal to , where the minimization function is applied element-wise. Under this notation, we can express our loss function as

As we assumed , is a convex, and in fact piece-wise linear, function of . Conditional Value at Risk (CVaR) at level is a widely used risk measure interpreted as the expectation of the 100 worst outcomes of the loss distribution. We assume that the seller is risk-averse so that the seller wants CVaR at level lower than some specified value . We define CVaR at level with respect to distribution as

Incorporating this into the DRO formulation, we require the order portfolio to satisfy

Then, the DRO formulation of this problem is:

| (17) | ||||||

| s.t. | ||||||

The set represents the budget limit in the order portfolio. A similar model has been studied by Hanasusanto et al. (2015), where they instead considered a Lagrangian formulation that moves the CVaR constraint into the objective function. We instead consider directly solving the constrained form as given in (17).

In this experiment, we use a synthetically generated data set. We provide the data generation procedure in Appendix 9.4.1. In contrast to the previous experiments, we solve the optimization problem (17) itself by solving feasibility problems and also utilize the early stopping termination by calculating the SP gap. To speed up both SOFO and OFO-based approaches, we use a warm startup technique, which uses the output and of the previous feasibility iteration to initialize and for the current feasibility problem. Later in this section, we present results that show the effectiveness of the warm startup.

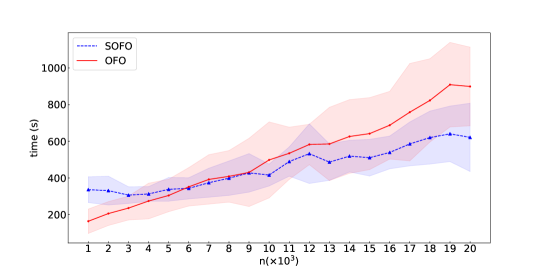

We set to be for SOFO and to be for OFO in the first feasibility iteration. To maximize the efficiency of the warm startup strategy, we set to for SOFO and for OFO after the first feasibility iteration. Lastly, we set our tolerance level to 0.03 and run 20 instances for each setting. Details of other parameters can be found in Appendix 9.4.2. After running a similar test as in the previous experiments, we choose to be 50. Figure 5 plots the average solve times in seconds against different . Similar to the previous experiments, we see that OFO is more sensitive than SOFO to the increasing scale of .

Lastly, we conclude this experiment by showcasing the effectiveness of the warm start strategy. Table 5 displays the solve times for SOFO and OFO with and without warm startup, where WS stands for warm starting.

| SOFO w/ WS | SOFO w/o WS | OFO w/ WS | OFO w/o WS | |

|---|---|---|---|---|

| 5000 | 337 | 565 | 304 | 422 |

| 10000 | 415 | 769 | 498 | 654 |

Observe that the solve times for both SOFO and OFO are reduced when using warm starting. In particular, it is apparent that SOFO has a slight advantage in relative speedup due to warm starting as compared to OFO.

5 Conclusion

We provided a new stochastic first-order meta-algorithm for constrained distributionally robust feasibility problems. To address the issue of calculating stochsatic gradients in the presence of multiple constraints, we propose a new stochastic first-order method called -SMD. We demonstrate the scalability of -SMD, and we also develop specialized results for -divergence set to improve the scalability even further. We numerically validate the improved performance of our meta-algorithm by comparing it with its deterministic counterpart (Ho-Nguyen and Kılınç-Karzan 2018), and we observe that, especially for large , our stochastic meta-algorithm obtains a solution with a small optimality gap in a reasonable time. There are several directions for future research, including developing specialized methods and results for ambiguity sets beyond the -divergence set and considering problems with more intricate stochastic constraints (e.g., chance constraints).

This work was supported, in part, by NSF AI Institute for Advances in Optimization Award 2112533.

References

- Akhtar et al. (2021) Akhtar Z, Bedi AS, Rajawat K (2021) Conservative stochastic optimization with expectation constraints. IEEE Transactions on Signal Processing 69:3190–3205.

- ApS (2019) ApS M (2019) MOSEK Optimizer API for Python 10.0.45. URL https://docs.mosek.com/latest/pythonapi/design.html.

- Asuncion and Newman (2007) Asuncion A, Newman D (2007) Uci machine learning repository.

- Basu and Nandy (2019) Basu K, Nandy P (2019) Optimal convergence for stochastic optimization with multiple expectation constraints. arXiv preprint arXiv:1906.03401 .

- Ben-Tal et al. (2013) Ben-Tal A, Den Hertog D, De Waegenaere A, Melenberg B, Rennen G (2013) Robust solutions of optimization problems affected by uncertain probabilities. Management Science 59(2):341–357.

- Ben-Tal et al. (2015a) Ben-Tal A, Den Hertog D, Vial JP (2015a) Deriving robust counterparts of nonlinear uncertain inequalities. Mathematical programming 149(1):265–299.

- Ben-Tal et al. (2009) Ben-Tal A, El Ghaoui L, Nemirovski A (2009) Robust optimization (Princeton university press).

- Ben-Tal et al. (2015b) Ben-Tal A, Hazan E, Koren T, Mannor S (2015b) Oracle-based robust optimization via online learning. Operations Research 63(3):628–638.

- Bertsimas et al. (2011) Bertsimas D, Brown DB, Caramanis C (2011) Theory and applications of robust optimization. SIAM review 53(3):464–501.

- Bertsimas et al. (2018) Bertsimas D, Gupta V, Kallus N (2018) Data-driven robust optimization. Mathematical Programming 167(2):235–292.

- Biddle (2017) Biddle D (2017) Adverse impact and test validation: A practitioner’s guide to valid and defensible employment testing (Routledge).

- Blanchet et al. (2019) Blanchet J, Kang Y, Murthy K (2019) Robust wasserstein profile inference and applications to machine learning. Journal of Applied Probability 56(3):830–857.

- Blanchet et al. (2022) Blanchet J, Murthy K, Zhang F (2022) Optimal transport-based distributionally robust optimization: Structural properties and iterative schemes. Mathematics of Operations Research 47(2):1500–1529.

- Bonettini et al. (2016) Bonettini S, Benfenati A, Ruggiero V (2016) Scaling techniques for -subgradient methods. SIAM Journal on Optimization 26(3):1741–1772.

- Borwein (1982) Borwein J (1982) A note on -subgradients and maximal monotonicity. Pacific Journal of Mathematics 103(2):307–314.

- Chen et al. (2019) Chen Z, Sim M, Xu H (2019) Distributionally robust optimization with infinitely constrained ambiguity sets. Operations Research 67(5):1328–1344.

- Cormen et al. (2009) Cormen TH, Leiserson CE, Rivest RL, Stein C (2009) Introduction to algorithms (MIT press).

- Delage and Ye (2010) Delage E, Ye Y (2010) Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations research 58(3):595–612.

- Diamond and Boyd (2016) Diamond S, Boyd S (2016) Cvxpy: A python-embedded modeling language for convex optimization. The Journal of Machine Learning Research 17(1):2909–2913.

- Duchi et al. (2008) Duchi J, Shalev-Shwartz S, Singer Y, Chandra T (2008) Efficient projections onto the l 1-ball for learning in high dimensions. Proceedings of the 25th international conference on Machine learning, 272–279.

- Duchi et al. (2021) Duchi JC, Glynn PW, Namkoong H (2021) Statistics of robust optimization: A generalized empirical likelihood approach. Mathematics of Operations Research 46(3):946–969.

- Duchi and Namkoong (2021) Duchi JC, Namkoong H (2021) Learning models with uniform performance via distributionally robust optimization. The Annals of Statistics 49(3):1378–1406.

- Gao (2022) Gao R (2022) Finite-sample guarantees for wasserstein distributionally robust optimization: Breaking the curse of dimensionality. Operations Research .

- Gao et al. (2022) Gao R, Chen X, Kleywegt AJ (2022) Wasserstein distributionally robust optimization and variation regularization. Operations Research .

- Gotoh et al. (2021) Gotoh Jy, Kim MJ, Lim AE (2021) Calibration of distributionally robust empirical optimization models. Operations Research 69(5):1630–1650.

- Hanasusanto et al. (2015) Hanasusanto GA, Kuhn D, Wallace SW, Zymler S (2015) Distributionally robust multi-item newsvendor problems with multimodal demand distributions. Mathematical Programming 152(1):1–32.

- Hazan et al. (2016) Hazan E, et al. (2016) Introduction to online convex optimization. Foundations and Trends® in Optimization 2(3-4):157–325.

- Ho-Nguyen and Kılınç-Karzan (2018) Ho-Nguyen N, Kılınç-Karzan F (2018) Online first-order framework for robust convex optimization. Operations Research 66(6):1670–1692.

- Hu and Hong (2013) Hu Z, Hong LJ (2013) Kullback-leibler divergence constrained distributionally robust optimization. Available at Optimization Online 1(2):9.

- Jin et al. (2021) Jin J, Zhang B, Wang H, Wang L (2021) Non-convex distributionally robust optimization: Non-asymptotic analysis. Advances in Neural Information Processing Systems 34:2771–2782.

- Juditsky et al. (2011) Juditsky A, Nemirovski A, et al. (2011) First order methods for nonsmooth convex large-scale optimization, i: general purpose methods. Optimization for Machine Learning 30(9):121–148.

- Kiwiel (2004) Kiwiel KC (2004) Convergence of approximate and incremental subgradient methods for convex optimization. SIAM Journal on Optimization 14(3):807–840.

- Kuhn et al. (2019) Kuhn D, Esfahani PM, Nguyen VA, Shafieezadeh-Abadeh S (2019) Wasserstein distributionally robust optimization: Theory and applications in machine learning. Operations research & management science in the age of analytics, 130–166 (Informs).

- Levy et al. (2020) Levy D, Carmon Y, Duchi JC, Sidford A (2020) Large-scale methods for distributionally robust optimization. Advances in Neural Information Processing Systems 33:8847–8860.

- Mohajerin Esfahani and Kuhn (2018) Mohajerin Esfahani P, Kuhn D (2018) Data-driven distributionally robust optimization using the wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming 171(1-2):115–166.

- Mutapcic and Boyd (2009) Mutapcic A, Boyd S (2009) Cutting-set methods for robust convex optimization with pessimizing oracles. Optimization Methods & Software 24(3):381–406.

- Namkoong and Duchi (2016) Namkoong H, Duchi JC (2016) Stochastic gradient methods for distributionally robust optimization with f-divergences. NIPS, volume 29, 2208–2216.

- Nemirovski et al. (2009) Nemirovski A, Juditsky A, Lan G, Shapiro A (2009) Robust stochastic approximation approach to stochastic programming. SIAM Journal on optimization 19(4):1574–1609.

- Qi et al. (2021) Qi Q, Guo Z, Xu Y, Jin R, Yang T (2021) An online method for a class of distributionally robust optimization with non-convex objectives. Advances in Neural Information Processing Systems 34:10067–10080.

- Raghavan et al. (2020) Raghavan M, Barocas S, Kleinberg J, Levy K (2020) Mitigating bias in algorithmic hiring: Evaluating claims and practices. Proceedings of the 2020 conference on fairness, accountability, and transparency, 469–481.

- Shafieezadeh Abadeh et al. (2015) Shafieezadeh Abadeh S, Mohajerin Esfahani PM, Kuhn D (2015) Distributionally robust logistic regression. Advances in Neural Information Processing Systems 28.

- Shalev-Shwartz et al. (2011) Shalev-Shwartz S, et al. (2011) Online learning and online convex optimization. Foundations and trends in Machine Learning 4(2):107–194.

- Staib and Jegelka (2019) Staib M, Jegelka S (2019) Distributionally robust optimization and generalization in kernel methods. Advances in Neural Information Processing Systems 32.

- Taskesen et al. (2020) Taskesen B, Nguyen VA, Kuhn D, Blanchet J (2020) A distributionally robust approach to fair classification. arXiv preprint arXiv:2007.09530 .

- Taskesen et al. (2021) Taskesen B, Yue MC, Blanchet J, Kuhn D, Nguyen VA (2021) Sequential domain adaptation by synthesizing distributionally robust experts. International Conference on Machine Learning, 10162–10172 (PMLR).

- Tong et al. (2016) Tong X, Feng Y, Zhao A (2016) A survey on neyman-pearson classification and suggestions for future research. Wiley Interdisciplinary Reviews: Computational Statistics 8(2):64–81.

- Wainwright (2019) Wainwright MJ (2019) High-dimensional statistics: A non-asymptotic viewpoint, volume 48 (Cambridge University Press).

- Wang et al. (2021) Wang J, Gao R, Xie Y (2021) Sinkhorn distributionally robust optimization. arXiv preprint arXiv:2109.11926 .

- Wiesemann et al. (2014) Wiesemann W, Kuhn D, Sim M (2014) Distributionally robust convex optimization. Operations Research 62(6):1358–1376.

- Zafar et al. (2017) Zafar MB, Valera I, Rogriguez MG, Gummadi KP (2017) Fairness constraints: Mechanisms for fair classification. Artificial intelligence and statistics, 962–970 (PMLR).

- Zhu et al. (2020) Zhu JJ, Jitkrittum W, Diehl M, Schölkopf B (2020) Kernel distributionally robust optimization. arXiv preprint arXiv:2006.06981 .

6 Additional Results and Discussion

In this appendix, we provide some additional results and provide complete discussion of several points that were mentioned in the main text.

6.1 Generalization to Dependent Case

In this section, we show that we can reduce an -feasibility problem with dependent random variables , to a -feasibility problem with independent random variables. Let be a joint probability distribution of random variables and define an uncertainty set of the joint distribution as . Then, we can interpret as a marginal distribution of . Let denote a projection matrix that projects the joint distribution to a marginal distribution for each :

This setting allows us to capture the dependency between random variables . If for all are mutually independent, then we set as with and , where the first elements represent and the next elements represent and so on. Let denote matrix that all elements are 0 and denote dimensional identity matrix. Then, in the independent case, we set to be

where only th matrix block is equal to , otherwise . Let us return to the dependent setting and define a vector-valued function as for all . Under our newly introduced notations, we have

Then we can express -approximate version of distributionally robust feasibility problem as:

| (18) |

The main structural difference between -feasibility problem and (18) is that there is a common variable inside the max function over in (18), while there are separate variables inside the max function over in -feasibility problem. However, we can reduce the dependent case to the independent case by generating independent copies of . Suppose be an independent copy of , and be a copy of uncertainty set , for all . Then, we have

| (19) |

Using (19), we can reduce the dependent case to the independent case.

Remark 6.1

We can easily convert the case where for all are not independent to the independent case by defining a new random variable , which is an independent copy of a random variable of a joint distribution of .

It is natural to ask why we need to work on the independent structure instead of the dependent structure, as converting the dependent case to the independent case increases the distribution parameter’s dimension at most times. Let us assume dependence between the random variables and consider solving (18) to answer this question. Notice that we can still apply Theorem 2.1 for the dependent case. However, it is not well studied how to generate a sequence that satisfies termination condition

with the convex-non-concave function . Also, even if we know the way to generate such a sequence by using non-convex optimization methods, usually those methods requires strong assumption on the function such as strong convexity to guarantee convergence. However, by assuming the independence between the random variables, we can use online convex optimization (OCO) tools to solve -feasibility problem with a mild assumption on the function .

6.2 Saddle Point Gap Computation

In this section, we explain methods to compute the SP gap as defined in (3). In order to compute the SP gap, we need to solve and . In general, we have

| (20) |

and we have to solve independent convex optimization with linear objective to solve (20). The complexity of solving each convex optimization largely depends on the structure of the convex set . However, in some cases such as being -divergence uncertainty set, (Namkoong and Duchi 2016) showed that we are able to obtain the explicit solution of (20) in .

To calculate , we use KKT conditions to derive closed-form solution for . As shares the same stucture for all , we only need to consider solving . For simplicity, we omit the constraint index here. We change to and derive its closed-form solution. Notice that is a th element of a vector . We define Lagrangian function as

| (21) |

where and . Using KKT conditions and strict complementary slackness, we get

| (22) |

where . Substituting into equation (21), we have

As is a concave function of , is a non-increasing function of . We define a set . Then, is like:

We use bisection search to find such that . We input to (22) and get .

To solve , we need to solve the following convex optimization:

| (23) | ||||||

| s.t. |

The complexity of solving (23) largely depends on the structure of function . However, in most of the applications, would be in a tractable form such as a linear or quadratic function of , and we can solve (23) by using state-of-the-art convex optimization solvers such as Gurobi or Mosek.

6.3 High-Probability Convergence of SMD

In this section, we introduce the high-probability convergence of online SMD. This is a minor extension of Nemirovski et al. (2009). Let us consider the following online setting. We have a finite time horizon , compact and convex domain and in each time period we have a convex loss function and weight such that . At every iteration , the player must make a decision and suffer a loss , where is unknown to the player beforehand. We want to minimize the weighted regret

by using SMD for an update of . We assume that the set follows the mirror descent setup (Assumption 3.4) and our problem satisfies the following light tail assumption. {assumption}[light tail] Let be given and be a given stochastic subgradient of that we can obtain from stochastic subgradient oracle. There exists such that:

| (24) |

Then, the online SMD has a high-probability convergence guarantee.

Proposition 6.2 (Extension of proposition 2.2 of Nemirovski et al. (2009))

Let be a sequence generated by online stochastic mirror descent (online SMD) with as a stochastic subgradient of at and with diminishing step size

| (25) |

Suppose, the light tail assumption (24) holds with constant and be the normalization of . For any , we have

where .

Proof 6.3

Proof. Let us define as and as . As , for any , we have

| (26) |

Summing from to and dropping a negative term , we have

| (27) |

As implies , we have

| (28) |

By (28), we have

| (29) | |||

Let us define as . Then, by the convexity of the exponential function, we have

Using Markov inequality, we have

Now, we work on . Let us define . Then, we have

By (29), we have

| (30) |

Using martingale technique (see Appendix of Nemirovski et al. (2009)), we have

| (31) |

Combining (27), (6.3), and (31), we have

For , we have

Setting , inputting diminishing step-size (25), and dividing by , for , we have

Setting to , we obtain the desired result. \Halmos

6.4 Lower Bound of Per-Iteration Sample Size

In Section 3.1, we mentioned that if a per-iteration sample size has a low dependency on and satisfies , for all , then Algorithm 4 has much lower per-iteration cost than SMD for solving -feasibility problem. Indeed, is a key factor that determines the complexity of -SMD and the parameters of the approximation condition and . Our goal in this section is to find that satisfies the approximation condition with and , and show that such is almost independent of . In particular, we show that has a low dependency on but is more related to the distribution of random variable , where .

Proposition 6.4

For given , if we have such that , then satisfies the approximation condition with and

Proof 6.5

Proof. This can be shown using Hoeffding’s inequality (Wainwright 2019). Under our assumption, there exists such that for all and for each constraint . Let . Then, by Hoeffding’s inequality, we have

| (32) |

Using union bound and (32), we have

| (33) |

By (33), for to satisfy the approximation condition with and , must satisfy and this is equivalent to . \Halmos

For given and , let us define . Then satisfies the approximation condition with and by Proposition 6.4. Also, we observe that has low dependency on our total iteration , the number of constraints , and probability as all these parameters are inside the log term.

We derive another condition for to satisfy the approximation condition using Bennet’s inequality (Wainwright 2019).

Proposition 6.6

Let be given and be an index random sampled from the distribution for all . Also, we assume that for all , we have have,

Then, for given , if we have such that

where , for , then satisfies the approximation condition with and .

We omit the proof as it is almost same as the proof of Proposition 6.4. The only difference is that we are using different concentration inequality. We define as . Notice that is also independent of and has lower dependency on than . We want to point out that and are independent of and more related to the distribution information of the random variable. Also, there is a high chance of being smaller than if the function has a low variance and the is set to a moderate level (around 0.01 to 0.001). Although Proposition 6.4 and Proposition 6.6 give us theoretical guarantees of to satisfy the approximation condition, it is generally hard to find that satisfies the approximation condition in practice. So, in our experiments, we relax the condition of the approximation condition and use that satisfies for 60% of the total iterations. Our experimental results (section 4 show that we are still able to obtain a solution with a small optimality gap with such .

7 Proofs for Sections 2 and 3

7.1 Proof for Theorem 2.3

Proof 7.1

Proof. For simplicity, we use to denote and use to denote for all By Assumption 2.2, we have

Then we have:

7.2 Proof for Lemma 3.3

Proof 7.2

Proof. For given , let us define as . Suppose Otherwise, we have . Because holds for all , we have

The second inequality comes from the definition of and and our condition , for all . The third inequality can be derived by for given and . The last inequality comes from our condition , for all . Eventually we get

| (34) |

Suppose such that is given. Then we have

By (34), we have . Then we have

Finally using and , we have

This implies . \Halmos

7.3 Bounds related to

Let be given. Then, we have

The first inequality comes from Cauchy-Schwarz inequality and the second inequality comes from . Let us define as . By assuming , we have . In short, we have

| (35) |

Also, we derive an upper bound of . First of all, we have and for any , we have

| (36) |

Using (36), we have

| (37) | ||||

7.4 Proof for Theorem 3.5

Proof 7.3

Proof. In this theorem, as we are discussing the update of , we simplify to for clarity in the proof. To show the high-probability convergence of -SMD, there are two major challenges. First, we need to show that the light tail assumption (Assumption 6.3) holds for the update gradient . Secondly, we need to extend Proposition 6.2 to the case where we use -subgradients.

The first thing can be done by finding a uniform bound of . That is, if there exists such that for a given random vector , then our gradient estimator satisfies the light tail assumption with constant .

Let , and such that be given. As is a -Lipshcitz function from our assumption, this implies for any such that satisfies

As a result, the light tail assumption holds for with constant for all .

Now we extend the proof of Proposition 6.2 to when is a -subgradient of at by adding to the right-hand side of (26). Similary to the proof of Proposition 6.2, define as and as . By the approximation condition (Definition 3.2), we condition on when (7) holds and let be defined as . As by Lemma 3.3, for any and , we have

The rest of the proof follows the same as the proof of Proposition 6.2. Eventually, we get

This implies

Using the approximation condition, we have

The first inequality comes from

for given events and . \Halmos

7.5 Proof for Lemma 3.8

Proof 7.4

Proof. Under the approximation condition, we have

with probability at least . Then following the similar technique that we used in the proof of Lemma 3.3, we get

with probability at least . \Halmos

7.6 Proof for Theorem 3.9

Proof 7.5

Proof. Let . According to Proposition 3.7, if , then becomes -feasible certificate of -feasibility problem and if , then we declare that the problem is infeasible. Now, we consider the following cases.

7.7 Proof for Proposition 3.10

Proof 7.6

Proof. Similar to the proof of Theorem 3.5, we first need to find a constant that satisfies the light tail assumption for the gradient estimator by finding a uniform bound of . Let us assume , , and be given. Also, suppose such that for all , be given. As is a 1-sparse vector and and , we easily get

by (35) and this implies that the gradient estimator satisfy the light tail assumption with constant , for all . We also have upper bound of by (37). We get the desired result by inputting and to Proposition 6.2. \Halmos

7.8 Proof for Theorem 3.11

Proof 7.7

Proof. As does not hold for , we need to slightly modify Theorem 3.5. The only thing that is changed is the constant that satisfies the light tail assumption (Assumption 6.3) for gradient estimator in Algorithm 4. Let , and such that be given. As does not hold for anymore, is now random sampled from the normalized distribution and we modify our function to according to this change. As is a -Lipshcitz function from our assumption, is a -Lipschitz function with by (35). This implies for any such that satisfies

As a result, the light tail assumption holds for with constant for all . So replacing with in Theorem 3.5, we obtain the high-probability convergence result of -SMD under -divergence set. In fact, for any , we have

| (38) | ||||

After combining (38), Theorem 2.3 and Proposition 3.10, we get the desired result. \Halmos

8 Efficient Updates for Bandit Mirror Descent

In this section, we study the per-iteration complexity of Algorithm 6. Even our gradient estimator is 1-sparse, complexity of the projection step of Algorithm 6 could be . (Namkoong and Duchi 2016) show that the complexity of Algorithm 6 is by using a balanced tree structure, where is a tolerance level that we define shortly. In this section, we present a slightly improved version of their work. We show that we can perform each step of Algorithm 6 in .

First of all, we can implement the index random sampling step (line 3) in using the balanced tree structure. We refer our readers to (Cormen et al. 2009), (Duchi et al. 2008), (Namkoong and Duchi 2016) for the detail implementation of the balanced tree structure. Also, the computation of the gradient estimator and the update of can be implemented in a constant time because is 1-sparse. In the rest of this section, we show that the complexity of the projection step is .

As the projection step is identical for all the constraints and iterations, we omit the constraint index and the iteration index unless it is confusing. Initially, we define Lagrangian function as

| (39) |

where and . The problem satisfies Slater condition as is an interior point of . Also, is a strongly convex function on . So, using KKT conditions and strict complementary slackness, we get

| (40) |

where . Substituting into equation (39), we have

Our primary goal is to find such that and input to to obtain . Let us define a set . Then is like: