SAMoSSA: Multivariate Singular Spectrum Analysis with Stochastic Autoregressive Noise

Abstract

The well-established practice of time series analysis involves estimating deterministic, non-stationary trend and seasonality components followed by learning the residual stochastic, stationary components. Recently, it has been shown that one can learn the deterministic non-stationary components accurately using multivariate Singular Spectrum Analysis (mSSA) in the absence of a correlated stationary component; meanwhile, in the absence of deterministic non-stationary components, the Autoregressive (AR) stationary component can also be learnt readily, e.g. via Ordinary Least Squares (OLS). However, a theoretical underpinning of multi-stage learning algorithms involving both deterministic and stationary components has been absent in the literature despite its pervasiveness. We resolve this open question by establishing desirable theoretical guarantees for a natural two-stage algorithm, where mSSA is first applied to estimate the non-stationary components despite the presence of a correlated stationary AR component, which is subsequently learned from the residual time series. We provide a finite-sample forecasting consistency bound for the proposed algorithm, SAMoSSA, which is data-driven and thus requires minimal parameter tuning. To establish theoretical guarantees, we overcome three hurdles: (i) we characterize the spectra of Page matrices of stable AR processes, thus extending the analysis of mSSA; (ii) we extend the analysis of AR process identification in the presence of arbitrary bounded perturbations; (iii) we characterize the out-of-sample or forecasting error, as opposed to solely considering model identification. Through representative empirical studies, we validate the superior performance of SAMoSSA compared to existing baselines. Notably, SAMoSSA’s ability to account for AR noise structure yields improvements ranging from 5% to 37% across various benchmark datasets.

1 Introduction

Background. Multivariate time series have often been modeled as mixtures of stationary stochastic processes (e.g. AR process) and deterministic non-stationary components (e.g. polynomial and harmonics). To handle such mixtures, classical time series forecasting algorithms first attempt to estimate and then remove the non-stationary components. For example, before fitting an Autoregressive Moving-average (ARMA) model, polynomial trend and seasonal components must be estimated and then removed from the time series. Once the non-stationary components have been eliminated111Note that Autoregressive Integrated Moving-average (ARIMA) and Seasonal ARIMA models use differencing in conjunction with unit root tests to remove stochastic non-stationary components, and are not suited for the model we consider., the ARMA model is learned. This estimation procedure often relies on domain knowledge and/or fine-tuning, and theoretical analysis for such multiple-stage algorithms is limited in the literature.

Prior work presented a solution for estimating non-stationary deterministic components without domain knowledge or fine-tuning using mSSA [3]. This framework systematically models a wide class of (deterministic) non-stationary multivariate time series as linear recurrent formulae (LRF), encompassing a wide class of spatio-temporal factor models that includes harmonics, exponentials, and polynomials. However, mSSA, both algorithmically and theoretically, does not handle additive correlated stationary noise, an important noise structure in time series analysis. Indeed, all theoretical results of mSSA are established in the noiseless setting [16] or under the assumption of independent and identically distributed (i.i.d.) noise [4, 3].

On the other hand, every stable stationary process can be approximated as a finite order AR process [8, 26]. The classical OLS procedure has been shown to accurately learn finite order AR processes [17]. However, the feasibility of identifying AR processes in the presence of a non-stationary deterministic component has not been addressed.

In summary, despite the pervasive practice of first estimating non-stationary deterministic components and then learning the stationary residual component, neither an elegant unified algorithm nor associated theoretical analyses have been put forward in the literature.

A step towards resolving these challenges is to answer the following questions: (i) Can mSSA consistently estimate non-stationary deterministic components in the presence of correlated stationary noise? (ii) Can the AR model be accurately identified using the residual time series, after removing the non-stationary deterministic components estimated by mSSA, potentially with errors? (iii) Can the out-of-sample or forecasting error of such a multi-stage algorithm be analyzed?

In this paper, we resolve all three questions in the affirmative: we present SAMoSSA, a two-stage procedure, where in the first stage, we apply mSSA on the observations to extract the non-stationary components; and in the second stage, the stationary AR process is learned using the residuals.

Setup. We consider the discrete time setting where we observe a multivariate time series at each time index where 222if , we divide the time series into sets of time series where this condition will hold.. For each , and each timestep , the observations take the form

| (1) |

where denotes the non-stationary deterministic component, and is a stationary AR noise process of order (). Specifically, each is governed by

| (2) |

where refers to the per-step noise, modeled as mean-zero i.i.d. random variables, and are the parameters of the -th process.

Goal. For each , our objective is threefold. The first is estimating from the noisy observations for all . The second is identifying the AR process’ parameters . The third is out-of-sample forecasting of for .

Contributions. The main contributions of this work is SAMoSSA, an elegant two-stage algorithm, which manages to learn both non-stationary deterministic and stationary stochastic components of the underlying time series. A detailed summary of the contributions is as follows.

(a) Estimating non-stationary component with mSSA under AR noise. The prior theoretical results for mSSA are established in the deterministic setting [16] or under the assumption of i.i.d. noise [4, 3]. In Theorem 4.1, we establish that the mean squared estimation error scales as under AR noise – the same rate was achieved by [3] under i.i.d. noise. Key to this result is establishing spectral properties of the “Page” matrix of AR processes, which may be of interest in its own right (see Lemma A.2).

(b) Estimating AR model parameters under bounded perturbation. We bound the estimation error for the OLS estimator of AR model parameters under arbitrary and bounded observation noise, which could be of independent interest. Our results build upon the recent work of [17] which derives similar results but without any observation noise. In that sense, ours can be viewed as a robust generalization of [17].

(c) Out-of-sample finite-sample consistency of SAMoSSA. We provide a finite-sample analysis for the forecasting error of SAMoSSA– such analysis of two-stage procedures in this setup is nascent despite its ubiquitous use in practice. Particularly, we establish in Theorem 4.4 that the out-of-sample forecasting error for SAMoSSA for the time-steps ahead scales as with high probability.

(d) Empirical results. We demonstrate superior performance of SAMoSSA using both real-world and synthetic datasets. We show that accounting for the AR noise structure, as implemented in SAMoSSA, consistently enhances the forecasting performance compared to the baseline presented in [3]. Specifically, these enhancements range from 5% to 37% across benchmark datasets.

Related Work. Time series analysis is a well-developed field. We focus on two pertinent topics.

mSSA. Singular Spectrum Analysis (SSA), and its multivariate extension mSSA, are well-studied methods for time series analysis which have been used heavily in a wide array of problems including imputation [4, 3], forecasting [18, 2], and change point detection [22, 6]. Refer to [16, 15] for a good overview of the SSA literature. The classical SSA method consists of the following steps: (1) construct a Hankel matrix of the time series of interest; (2) apply Singular Value Decomposition (SVD) on the constructed Hankel matrix, (3) group the singular triplets to separate the different components of the time series; (4) learn a linear model for each component to forecast. mSSA is an extension of SSA which handles multiple time series simultaneously and attempts to exploit the shared structure between them [18]. The only difference between mSSA and SSA is in the first step, where Hankel matrices of individual series are “stacked” together to create a single stacked Hankel matrix. Despite its empirical success, mSSA’s classical analysis has mostly focused on identifying which time series have a low-rank Hankel representation, and defining sufficient asymptotic conditions for signal extraction, i.e., when the various time series components are separable. All of the classical analysis mostly focus on the deterministic case, where no observation noise is present.

Recently, a variant of mSSA was introduced for the tasks of forecasting and imputation [3]. This variant, which we extend in this paper, uses the Page matrix representation instead of the Hankel matrix, which enables the authors to establish finite-sample bounds on the imputation and forecasting error. However, their work assumes the observation noise to be i.i.d., and does not accommodate correlated noise structure, which is often assumed in the time series literature [26]. Our work extends the analysis in Agarwal et al. [3] to observations under AR noise structure. We also extend the analysis of the forecasting error by studying how well we can learn (and forecast) the AR noise process with perturbed observations.

Estimating AR parameters. AR processes are ubiquitous and of interest in many fields, including time series analysis, control theory, and machine learning. In these fields, it is often the goal to estimate the parameters of an AR process from a sample trajectory. Estimation is often carried out through OLS, which is asymptotically optimal [11]. The asymptotic analysis of the OLS estimator is well established, and recently, given the newly developed statistical tools of high dimensional probability, cf. [31, 29], various recent works have tackled its finite-time analysis as well. For example, several works established results for the finite-time identification for general first order vector AR systems [20, 19, 27, 24, 21]. Further, González et al. [17] provides a finite-time bound on the deviation of the OLS estimate for general processes. To accommodate our setting, we extend the results of [17] in two ways. First, we extend the analysis to accommodate any sub-gaussian noise instead of assuming gaussianity; Second, and more importantly, we extend it to handle arbitrary bounded observation errors in the sampled trajectory, which can be of independent interest.

2 Model

Deterministic Non-Stationary Component. We adopt the spatio-temporal factor model of [3, 6] described next. The spatio-temporal factor model holds when two assumptions are satisfied: the first assumption concerns the spatial structure, i.e., the structure across the time series ; the second assumption pertains to the “temporal” structure. Before we describe the assumptions, we first define a key time series representation: the Page matrix.

Definition 2.1 (Page Matrix).

Given a time series , and an initial time index , the Page matrix representation over the entries with parameter is given by the matrix with for .

In words, to construct the Page matrix of the entries , partition them into segments of contiguous entries and concatenate these segments column-wise (see Figure 1). Now we introduce the main assumptions for .

Assumption 2.1 (Spatial structure).

For each , for some and .

Assumption 2.1 posits that each time series can be described as a linear combination of “fundamental” time series. The second assumption relates to the temporal structure of the fundamental time series , which we describe next.

Assumption 2.2 (Temporal structure).

For each and for any , .

Assumption 2.2 posits that the Page matrix of each “fundamental” time series has finite rank. While this imposed temporal structure may seem restrictive at first, it has been shown that many standard functions that model time series dynamics satisfy this property [4, 3]. These include any finite sum of products of harmonics, low-degree polynomials, and exponential functions (refer to Proposition 2.1 in [3]).

Stochastic Stationary Component. We adopt the following two assumptions about the AR processes . We first assume that these AR processes are stationary (see Definition H.4 in Appendix H).

Assumption 2.3 (Stationarity and distinct roots).

is a stationary process . That is, let , denote the roots of . Then, . Further, , the roots of are distinct.

Further, we assume the per-step noise are i.i.d. sub-gaussian random variables (see Definition H.1 in Appendix H).

Assumption 2.4 (Sub-gaussian noise).

For , are zero-mean i.i.d. sub-gaussian random variables with variance .

Model Implications. In this section, we state two important implications of the model stated above. The first is that the stacked Page matrix defined as

is low-rank. Precisely, we recall the following Proposition stated in [3].

Proposition 2.1 (Proposition 2 in [3] ).

Throughout, we will use the shorthand and 333We will use the same shorthand for the stacked page matrices of and : namely, and .. The second implication is that there exists a linear relationship between the last row of and its top rows. The following proposition establishes this relationship. First, Let denote the -th row of and let denote the sub-matrix that consist of the top rows of .

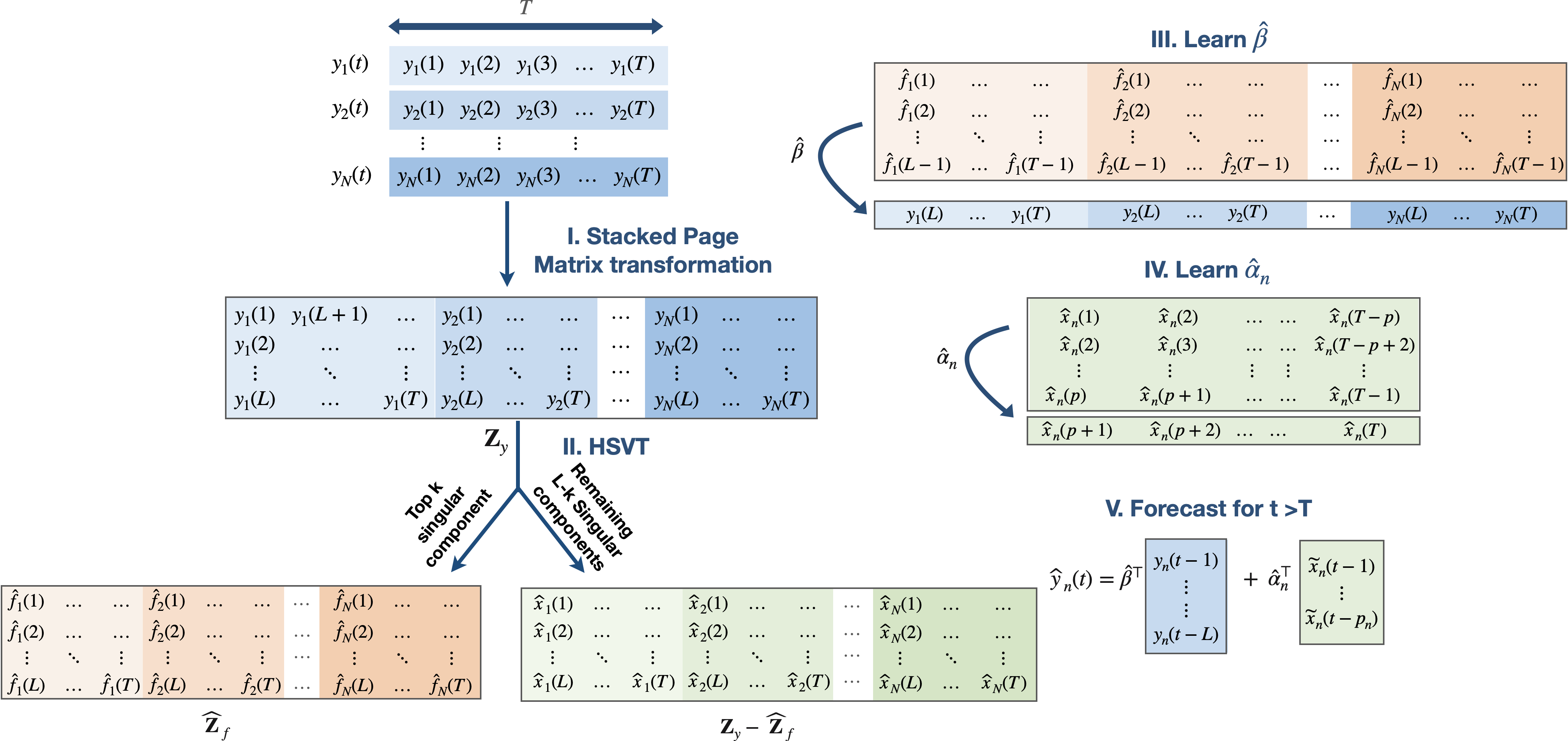

3 Algorithm

The proposed algorithm provides two main functionalities. The first one is decomposing the observations into an estimate of the non-stationary and stationary components for . The second is forecasting for , which involves learning a forecasting model for both and .

Univariate Case. For ease of exposition, we will first describe the algorithm for the univariate case (). The algorithm has the following parameters: , and (refer to Appendix B.2 for how to choose these parameters). For clarity, we will assume, without loss of generality, that is chosen such that is an integer444 Otherwise, one can apply this algorithm to the two ranges and .. In the first step of the algorithm, we transform the observations into the Page matrix . We will use the shorthand henceforth.

Decomposition. We compute the SVD where denote its ordered singular values, and denote its left and right singular vectors, respectively, for . Then, we obtain by retaining the top singular components of (i.e., by applying Hard Singular Value Thresholding (HSVT) with threshold ). That is,

We denote by and the estimates of and respectively. We read off the estimates directly from the matrix using the entry that corresponds to . More precisely, for , equals the entry of in row and column , while .

Forecasting. To forecast for , we produce a forecast for both and . Both forecasts are performed through linear models ( for and for .) For , we first learn a linear model defined as

| (3) |

where for 555 In the forecasting algorithm, the estimates are obtained by applying HSVT on a sub-matrix of which consists of its first rows. This is done to establish the theoretical results as it helps us avoid dependencies in the noise between and for . We then use and the lagged observations to produce . That is where .

For , we first estimate the parameters for the process. Specifically, define the -dimensional vectors 666Note that we assume knowledge of the true parameter (and in the multivariate case).. Then, define the OLS estimate as,

| (4) |

Then, let for any , 777Note the subtle difference between and – precisely, for , is an estimate of before observing (i.e., a forecast), whereas is an estimate of after observing . . We then use and the lagged entries of to produce . That is where . Finally, produce the forecast

Multivariate Case. The key change for the case is the use of the stacked Page matrix , which is the column-wise concatenation of the Page matrices induced by individual time series. Specifically, consider the stacked Page matrix defined as

| (5) |

Decomposition. The procedure for learning the non-stationary component for is similar to that of the univariate case. Specifically, we perform HSVT with threshold on to produce . Then, we read off the estimate of from . Specifically, for , and , let refer to sub-matrix of induced by selecting only its ] columns. Then for , equals the entry of in row and column . We then produce an estimate for as .

Forecasting. To forecast for , as in the univariate case, we learn a linear model defined as

| (6) |

where is the -th component of , and corresponds to the vector formed by the entries of the first rows in the th column of 888 To be precise, here is the truncated SVD of a sub-matrix of which consist of its first rows. for . We then use to produce , where again is the vector of the lags of . That is .

Then, for each , we estimate , the parameters for the -th process. Let denote the OLS estimate defined as

| (7) |

Then, produce a forecast for as where again . Finally, produce the forecast for as . For a visual depiction of the algorithm, refer to Figure 1.

4 Results

In this section, we provide finite-sample high probability bounds on the following quantities:

1. Estimation error of non-stationary component . First, we give an upper bound for the estimation error of each one of for . Specifically, we upper bound the following metric

| (8) |

where are the estimates produced by the algorithm we proposed in Section 3.

2. Identification of AR parameters. Second, we analyze the accuracy of the estimates produced by the proposed algorithm. Specifically, we upper bound the following metrics

| (9) |

where .

3. Out-of-sample forecasting error. Finally, we provide an upper bound for the forecasting error of for . Specifically, we upper bound the following metric

| (10) |

where are the forecasts produced by the algorithm we propose in Section 3. Before stating the main results, we state key additional assumptions.

Assumption 4.1 (Balanced spectra).

Let denote the stacked Page matrix associated with all time series for their consecutive entries starting from . Let , and let denote the -th singular value for . Then, for any , is such that for some absolute constant .

This assumption holds whenever the the non-zero singular values are “well-balanced”, a standard assumption in the matrix/tensor estimation literature [3, 6]. Note that this assumption, as stated, ensures balanced spectra for the stacked Page matrix of any set of consecutive entries of .

Finally, we will impose an additional necessary restriction on the complexity of the time series for (as is done in [3, 5]). Let denote the matrix formed using the top rows of . Further, for any , let denote the matrix formed using the top rows of . For any matrix , let denote the subspace spanned by the its columns. We assume the following property.

Assumption 4.2 (Subspace inclusion).

For any , .

This assumption is necessary as it requires the stacked Page matrix of the out-of-sample time series to be only as “rich” as that of the stacked Page matrix of the “in-sample” time series .

4.1 Main Results

First, recall that is defined in Assumption 2.1, in Assumption 2.2, is in Proposition 2.1, while is defined in Assumption 4.1. Further, recall that for are the roots of the characteristic polynomial of the -th AR process, as defined in Assumption 2.3. Throughout, let and be absolute constants, , , , and denote a constant that depends only (polynomially) on model parameters and . Last but not least, define the key quantity

where and is a constant that depends only on 999 See Appendix A for an explicit expression of .. Note that is a key quantity that we use to bound important spectral properties of AR processes, as Lemma A.2 establishes.

4.1.1 Estimation Error of Non-Stationary Component

Theorem 4.1 (Estimation error of ).

4.1.2 Identification of AR Processes

Theorem 4.2 (AR Identification).

Recall that is estimated using , a perturbed version of the true AR process . This perturbation comes from the estimation error of , which is a consequence of . Hence, it is not surprising that shows up in the upper bound. Indeed, the upper bound we provide here consists of two terms: the first, which scales as is the bound one would get with access to the true AR process , as shown in [17]. The second term characterizes the contribution of the perturbation caused by the estimation error, and it scales as , which we show is with high probability in Theorem 4.1. Also, note that the theorem holds when the estimation error is sufficiently small (). This condition ensures that the perturbation arising from the estimation error remains below the lower bound for the minimum eigenvalue of the sample covariance matrix associated with the autoregressive processes. Note that and are quantities that relate to the parameters of the processes and their “controllability Gramian” as we detail in Appendix A.1. The proof of Theorem 4.2 is in Appendix D.

4.1.3 Out-of-sample Forecasting Error

We first establish an upper bound on the error of our estimate .

Theorem 4.3 (Model Identification ()).

This shows that the error of estimating (in squared euclidean norm) scales as .

Theorem 4.4.

This theorem establishes that the forecasting error for the next time steps scales as with high probability. Note that the term is a function of only, as it is a consequence of the error incurred when we estimate each . Recall that we estimate separately for using the available (perturbed) observation of each process. The term on the other hand is a consequence of the error incurred when learning and forecasting , which is done collectively across the time series. Finally, Theorem 4.4 implies that when , the forecasting error scales as . The proof of Theorems 4.3 and 4.4 are in Appendix F and G, respectively.

5 Experiments

In this section, we support our theoretical results through several experiments using synthetic and real-world data. In particular, we draw the following conclusions:

-

1.

Our results align with numerical simulations concerning the estimation of non-stationary components under AR stationary noise and the accuracy of AR parameter estimation (Section 5.1).

-

2.

Modeling and learning the autoregressive process in SAMoSSA led to a consistent improvement over mSSA. The improvements range from 5% to 37% across standard datasets (Section 5.2).

5.1 Model Estimation

Setup. We generate a synthetic multivariate time series () that is a mixture of both harmonics and an AR noise process. The AR process is stationary, and its parameter is chosen such that is one of three values . Refer to Appendix B.1 for more details about the generating process. We then evaluate the estimation error and the AR parameter estimation error as we increase from to .

Results. Figure 2(a) visualizes the mean squared estimation error of , while Figure 2(b) shows the AR parameter estimation error. The solid lines in both figures indicate the mean across ten trials, whereas the shaded areas cover the minimum and maximum error across the ten trials. We find that, as the theory suggests, the estimation error for both the non-stationary component and the AR parameter decay to zero as increases. We also see that the estimation error is inversely proportional to , which is being reflected in the AR parameter estimation error as well.

5.2 Forecasting

We showcase SAMoSSA’s forecasting performance relative to standard algorithms. Notably, we compare SAMoSSA to the mSSA variant in [3] to highlight the value of learning the autoregressive process.

| Traffic | Electricity | Exchange | Synthetic | |

|---|---|---|---|---|

| SAMoSSA | 0.776 | 0.829 | 0.731 | 0.476 |

| mSSA | 0.747 | 0.605 | 0.674 | 0.366 |

| ARIMA | 0.723 | <-10 | 0.756 | 0.305 |

| Prophet | 0.462 | 0.197 | <-10 | -0.445 |

| DeepAR | 0.824 | 0.764 | 0.579 | 0.323 |

| LSTM | 0.821 | -1.261 | -1.825 | 0.381 |

Setup. The forecasting ability of SAMoSSA was compared against (i) mSSA [3], (ii) ARIMA, a very popular classical time series prediction algorithm, (iii) Prophet [28], (iv) DeepAR [23] and (v) LSTM [14]on three real-life datasets and one synthetic dataset containing both deterministic trend/seasonality and a stationary noise process (see details in Appendix B). Each dataset was split into train, validation, and test sets (see Appendix B.1). Each dataset has multiple time series, so we aggregate the performance of each algorithm using the mean score. We use the score since it is invariant to scaling and gives a reasonable baseline: a negative value indicates performance inferior to simply predicting the mean.

Results. In Table 1 we report the mean for each method on each dataset. We highlight that, across all datasets, SAMoSSA consistently performs the best or is otherwise very competitive with the best. The results also underscore the significance of modeling and learning the autoregressive process in real-world datasets. Notably, learning the autoregressive model in SAMoSSA consistently led to an improvement over mSSA, with the increase in values ranging from 5% to 37%. We note that this improvement is due to the fact that mSSA, as described in [3], overlooks any potential structure in the stochastic processes and assumes i.i.d.mean-zero noise process. While in SAMoSSA, we attempt to capture the structure of through the learned AR process.

6 Discussion and Limitations

We presented SAMoSSA, a two-stage procedure that effectively handles mixtures of deterministic non-stationary and stationary AR processes with minimal model assumptions. We analyze SAMoSSA’s ability to estimate non-stationary components under stationary AR noise, the error rate of AR system identification via OLS under observation errors, and a finite-sample forecast error analysis.

We note that our results can be readily adapted to accommodate (i) approximate low-rank settings (as in the model by Agarwal et al [3]); and (ii) scenarios with incomplete data. We do not discuss these settings to focus on our core contributions, but they represent valuable directions for future studies.

Our analysis reveals some limitations, providing avenues for future research. One limitation of our model is that it only considers stationary stochastic processes. Consequently, processes with non-stationary stochastic trends, such as a random walk, are not incorporated. Investigating the inclusion of such models and their interplay with the SSA literature is a worthy direction for future work. Second, our model assume non-interaction between the stationary processes . Yet, it might be plausible to posit the existence of interactions among them, possibly through a vector AR model (VAR). Examining this setting represents another compelling direction for future work.

References

- [1] Y. Abbasi-yadkori, D. Pál, and C. Szepesvári. Improved algorithms for linear stochastic bandits. In J. Shawe-Taylor, R. Zemel, P. Bartlett, F. Pereira, and K. Weinberger, editors, Advances in Neural Information Processing Systems, volume 24. Curran Associates, Inc., 2011.

- [2] A. Agarwal, A. Alomar, and D. Shah. tspdb: Time series predict db. In NeurIPS 2020 Competition and Demonstration Track, pages 27–56. PMLR, 2021.

- [3] A. Agarwal, A. Alomar, and D. Shah. On multivariate singular spectrum analysis and its variants. ACM SIGMETRICS Performance Evaluation Review, 50(1):79–80, 2022.

- [4] A. Agarwal, M. J. Amjad, D. Shah, and D. Shen. Model agnostic time series analysis via matrix estimation. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 2(3):1–39, 2018.

- [5] A. Agarwal, D. Shah, and D. Shen. On principal component regression in a high-dimensional error-in-variables setting. arXiv preprint arXiv:2010.14449, 2020.

- [6] A. Alanqary, A. Alomar, and D. Shah. Change point detection via multivariate singular spectrum analysis. Advances in Neural Information Processing Systems, 34:23218–23230, 2021.

- [7] A. Alexandrov, K. Benidis, M. Bohlke-Schneider, V. Flunkert, J. Gasthaus, T. Januschowski, D. C. Maddix, S. Rangapuram, D. Salinas, J. Schulz, et al. Gluonts: Probabilistic time series models in python. arXiv preprint arXiv:1906.05264, 2019.

- [8] T. W. Anderson. The statistical analysis of time series. John Wiley & Sons, 2011.

- [9] F. Chollet. keras. https://github.com/fchollet/keras, 2015. Online; accessed 25 February 2020.

- [10] C. Davis and W. M. Kahan. The rotation of eigenvectors by a perturbation. iii. SIAM Journal on Numerical Analysis, 7(1):1–46, 1970.

- [11] J. Durbin. Estimation of parameters in time-series regression models. Journal of the royal statistical society: Series B (Methodological), 22(1):139–153, 1960.

- [12] Facebook. Prophet. https://github.com/facebook/prophet, 2020.

- [13] M. Gavish and D. L. Donoho. The optimal hard threshold for singular values is . IEEE Transactions on Information Theory, 60(8):5040–5053, 2014.

- [14] F. A. Gers, J. Schmidhuber, and F. Cummins. Learning to forget: Continual prediction with lstm. 1999.

- [15] N. Golyandina, A. Korobeynikov, and A. Zhigljavsky. Singular spectrum analysis with R. Springer, 2018.

- [16] N. Golyandina, V. Nekrutkin, and A. A. Zhigljavsky. Analysis of time series structure: SSA and related techniques. Chapman and Hall/CRC, 2001.

- [17] R. A. González and C. R. Rojas. A finite-sample deviation bound for stable autoregressive processes. In Learning for Dynamics and Control, pages 191–200. PMLR, 2020.

- [18] H. Hassani and R. Mahmoudvand. Multivariate singular spectrum analysis: A general view and new vector forecasting approach. International Journal of Energy and Statistics, 1(01):55–83, 2013.

- [19] Y. Jedra and A. Proutiere. Sample complexity lower bounds for linear system identification. In 2019 IEEE 58th Conference on Decision and Control (CDC), pages 2676–2681. IEEE, 2019.

- [20] Y. Jedra and A. Proutiere. Finite-time identification of stable linear systems optimality of the least-squares estimator. In 2020 59th IEEE Conference on Decision and Control (CDC), pages 996–1001. IEEE, 2020.

- [21] Y. Jedra and A. Proutiere. Finite-time identification of linear systems: Fundamental limits and optimal algorithms. IEEE Transactions on Automatic Control, 2022.

- [22] Microsoft. nimbusml package, ssa class, 2020. https://docs.microsoft.com/en-us/python/api/nimbusml/nimbusml.timeseries.ssachangepointdetector.

- [23] D. Salinas, V. Flunkert, J. Gasthaus, and T. Januschowski. Deepar: Probabilistic forecasting with autoregressive recurrent networks. International Journal of Forecasting, 2019.

- [24] T. Sarkar and A. Rakhlin. Near optimal finite time identification of arbitrary linear dynamical systems. In International Conference on Machine Learning, pages 5610–5618. PMLR, 2019.

- [25] S. Seabold and J. Perktold. statsmodels: Econometric and statistical modeling with python. In 9th Python in Science Conference, 2010.

- [26] R. H. Shumway, D. S. Stoffer, and D. S. Stoffer. Time series analysis and its applications, volume 3. Springer, 2000.

- [27] M. Simchowitz, H. Mania, S. Tu, M. I. Jordan, and B. Recht. Learning without mixing: Towards a sharp analysis of linear system identification, 2018.

- [28] S. J. Taylor and B. Letham. Forecasting at scale. The American Statistician, 72(1):37–45, 2018.

- [29] R. Vershynin. Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027, 2010.

- [30] R. Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- [31] M. J. Wainwright. High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge university press, 2019.

- [32] P.-Å. Wedin. Perturbation bounds in connection with singular value decomposition. BIT Numerical Mathematics, 12(1):99–111, 1972.

- [33] P.-Å. Wedin. Perturbation theory for pseudo-inverses. BIT Numerical Mathematics, 13:217–232, 1973.

Appendix A Concentration inequalities for AR processes

In this section, we present two important lemmas that are central to the main results. Before stating the two lemmas, we start with key important quantities of AR Processes.

A.1 Controllability Gramian of AR Processes

In this section, we explain the notation of key quantities used in the main results. First, note that the process in (2) can be written in matrix-vector form by defining a transition matrix and input vector

where is the column vector of zeroes. Then, with ,

With this setup, we define two important matrices,

| (14) |

where is known as the controllability Gramian of the -th process . For a positive semi-definite matrix , let and be its maximum and minimum eigenvalues, respectively. We define and . We also define and analogously for .

A.2 Key Lemmas

Now, we present two important lemmas that are central to the main results. The first lemma states that a vector of consecutive entries of a stationary autoregressive process is a sub-gaussian vector with variance proxy .

Lemma A.1.

This lemma, along with the well known bound on the norm of sub-gaussian vectors, is key to the bounds presented in Section 4.1. Further, this Lemma, along with an -net argument, allows us to bound the operator norm of the stacked Page matrix of the AR processes . Specifically, we establish next that its operator norm grows as with high probability.

Lemma A.2.

Next, we prove Lemma A.1 and Lemma A.2. Before stating the proofs, we start with the important helper Lemma A.3.

Lemma A.3 ( representation of an process).

Let be a stationary process defined as

Assume that the roots of its characteristic polynomial are distinct. Then, has the representation

with , .

Proof.

First, note that that we can write in lag operator form as

| (15) |

Here, is a lag operator such that . Note that since we have assumed the AR process to be stationary, all the roots of lie inside the unit circle [26]. Using the roots of , (15) can be written as,

Further, using the partial fraction decomposition we can write the process as

where,

Recall that we can expand each fraction as

Thus, finally, we can write as,

with . ∎

A.3 Proof of Lemma A.1

Proof.

First, let be the vector of interest. Let , then using Lemma A.3, we can write as

Note that is clearly a sub-gaussian vector with variance proxy . Further note that the sum of two sub-gaussian random vectors, not necessarily independent, is also a sub-gaussian random vector. To see this, suppose and are both sub-gaussian vectors with variance proxies and . Then for any ,

Thus, , for any , is also a sub-gaussian random vector with variance proxy

Now we are interested in bounding . To do so, first recall that where , denote the roots of and . Let and . Then, we can bound as

Thus, with

| (16) |

Hence, is a sub-gaussian random vector with variance proxy . ∎

A.4 Proof of Lemma A.2

Proof.

Let . We will find an upper bound on the operator norm by following two steps: (i) we will represent each as an process; then, (ii) we will bound the operator norm of the stacked Page matrix of this processes.

Step 1: representation for .

As a direct application of Lemma A.3, we can write as,

with ,

Step 2: Bound the Page matrix for the Page matrix.

First, let’s consider, without loss of generality, the case when . That is, let’s consider . To get the desired bound, we will first obtain a high probability bound on the Euclidean norm of for any vector . Then, we will bound the operator norm using this and an -net argument.

Note that by step (1), we have

Now define as the analogous stacked Page matrix for for . Observe that are simply identically distributed (but not independent) matrices of i.i.d. sub-gaussian random variables. Then we can write

| (17) |

where is a diagonal matrix with the -th diagonal . Then

It is easy to verify that is a sub-gaussian random vector (see Definition H.3) with variance proxy , because for any we have (using as a shorthand for )

Using the above, is . Since is a sum of sub-gaussian random vectors, it is also a sub-gaussian random vector with variance proxy as we showed in the proof of Lemma A.1.

Using Lemma H.2, we get, with probability at least ,

Equivalently, for , it holds that

Now we have shown that for any fixed , the quantity grows as with high probability. What remains is to apply the union bound over an -net to extend this to the maximum over , i.e. the operator norm of .

Let be a maximal -net of , i.e. a set of points in spaced at least from each other such that no other point can be added without violating this property. Now consider such that . Since is maximal, there is some within of . Since

and

we have that

i.e. taking the maximum over is equivalent to doing so over up to a factor of two. Using the fact that for some absolute constant , the fact that , and using a sufficiently large absolute constant we have

where and are absolute constants. Recalling that concludes the proof for the operator norm.

Finally, we show that each row in the stacked page matrix is a sub-gaussian vector with variance proxy . Consider, without loss of generality, the first row . Using (17), we have for any

note that is , and hence, using the same argument for the sum of dependent sub-gaussian random variables used in the proof above, we have . ∎

Appendix B Experiment details

In Appendix B.1, we detail the datasets used. In Appendix B.2, we explain the implementations and hyperparameter choices for our method and benchmark algorithms. In Appendix B.3, we describe our hyperparameter tuning strategy.

B.1 Datasets

In the model estimation experiments, we generate a synthetic multivariate time series () that is a mixture of both harmonics and an process. The harmonics are generated as follow: we first generate fundamental time series of the form for , where and are uniformly randomly sampled on the ranges , respectively. We then sample the series using for , where the mixture coefficients are independent standard normal random variables. The AR process is stationary, and its parameter is chosen such that is set to one of . The noise of the process has a variance .

In the forecasting experiments, we evaluate our method and benchmark algorithms on three real-world datasets and one synthetic dataset. The preprocessing steps and setup of each dataset are described below.

Traffic Dataset. This public dataset obtained from the UCI repository shows the occupancy rate of traffic lanes in San Francisco. The data is sampled every 15 minutes but to be consistent with previous work, we aggregate the data into hourly data and use the first 10248 time-points for training, the next 48 points for validation, and another 48 points for testing in the forecasting experiments. Specifically, in our testing period, we do 1-hour ahead forecasts for the next 48 hours.

Electricity Dataset. This is a public dataset obtained from the UCI repository which shows the 15-minutes electricity load of 370 households. We aggregate the data into hourly intervals and use the first 25824 time-points for training, the next 48 points for validation, and another 48 points for testing in the forecasting experiments. Specifically, in our testing period, we do 1-hour ahead forecasts for the next 48 hours.

Exchange Dataset. This is a dataset containing the daily exchange rates of eight foreign currencies, including those of Australia, the UK, Canada, Switzerland, China, Japan, New Zealand and Singapore, between 1990 and 2016. We standardize each time series to have zero mean and unit variance since the range of typical exchange rates varies greatly across the currencies. We use the first 7528 time-points for training, the next 30 for validation, and the final 30 for testing. All forecasts are made 1-day ahead.

Synthetic Dataset. We generate fundamental time series of the form for , where , , and are uniformly randomly sampled on the ranges , , and respectively. We then sample mixtures of the form for , where the mixture coefficients are independent standard normals. We then inject autoregressive noise to each series to produce for , where are independent processes, each with a fixed autoregressive coefficient and noise variance . We fix the coefficient to ensure that each time series has significantly autocorrelated noise that can be exploited to improve predictions.

| Dataset | No. time series | Training period | Validation period | Test period |

|---|---|---|---|---|

| Traffic | 963 | 1 to 10248 | 10249 to 10296 | 10296 to 10344 |

| Electricity | 370 | 1 to 25824 | 25825 to 25872 | 25872 to 25919 |

| Exchange | 8 | 1 to 7528 | 7529 to 7558 | 7559 to 7588 |

| Synthetic | 25 | 1 to 10000 | 10001 to 10025 | 10026 to 10050 |

B.2 Algorithms

In this section, we discuss the implementations used and hyperparameter tuning details for each algorithm that was evaluated.

SAMoSSA & mSSA. Since mSSA is a special case of SAMoSSA where the second stage – fitting autoregressive models – is skipped, we use one in-house implementation to evaluate both algorithms. The relevant hyperparameters are as follows:

-

1.

The number of retained singular values, . This hyperparameter is relevant for both algorithms. We select using one of three methods: (i) the data-driven procedure suggested in [13] which computes a threshold based on the shape and median singular value of the page matrix; (ii) picking as the minimum number of singular values required to capture of the spectral energy of the page matrix; (iii) picking a fixed low rank, specifically .

-

2.

The shape parameter of the stacked Page matrix. This is the ratio between the number of columns and rows of the stacked Page matrix used to carry out the matrix estimation procedure. While our theoretical analysis fixes this value to (recall that we set ), in practice we have found that a slightly wider Page matrix can improve performance. This parameter is chosen from .

-

3.

The number of autoregressive lag coefficients, . This hyperparameter is only relevant for SAMoSSA. While each time series does not necessarily need to use the same value, we enforce this to be the case for computational efficiency. We choose , i.e., the model is allowed to not fit a residual model if it brings no apparent benefit, corresponding to the case of .

Prophet. We use Prophet’s Python library with the parameters selected using a grid search of the following parameters as suggested in [12]:

-

1.

Changepoint prior scale. This parameter determines how much the trend changes at the detected trend changepoints. We choose this parameter from .

-

2.

Seasonality prior scale. This parameter controls the magnitude of the seasonality. We choose this parameter from .

-

3.

Seasonality Mode. We choose between an “additive” and “multiplicative” seasonality term.

The parameters for each time series are chosen independently.

ARIMA. We used the ARIMA implementation of the Python library statsmodels [25]. The hyperparameters are grid searched independently for each time series, and are as follows:

-

1.

Autoregressive order. This is the number of autoregressive lag coefficients fitted, chosen from .

-

2.

Differencing order. This denotes the number of times the time series is differenced before a model is fitted, and we choose between 0 (no differencing) and 1.

-

3.

Moving average order. This is the number of moving average lag coefficients, chosen from .

LSTM. We use Keras implementation [9]. We perform a grid search on the number of layers .

DeepAR. We use the implementation provided by the GluonTS package [7]. We use the default parameters.

B.3 Parameter Selection

We tune hyperparameters for all algorithms evaluated using rolling cross validation. During the validation step, each model is fitted only once on the training set; then, it repeatedly makes one-step-ahead forecasts and is afterwards provided with the realized value, in order to use the updated data to make the next forecast. During test time, the model is fitted on the training and validation sets, and similarly repeatedly makes one-step-ahead forecasts with the fitted parameters. For the models that choose one set of hyperparameters for all time series, the mean score over all time series on the validation set predictions is the metric of choice.

Appendix C Proof of Theorem 4.1

In this section, we provide the proof for Theorem 4.1. While the analysis generally follows the argument for the imputation error in [3], we adapt it for our different assumptions and metric of interest. Metric. First, recall that our metric of interest is

| (18) |

Recall that is the stacked Page matrix of , and is the stacked Page matrix of . To bound this error, we first establish a deterministic bound through a general lemma for Hard Singular Value Thresholding (HSVT).

C.1 Deterministic Bound

We state the following result, a more general version of which is stated in [3].

Lemma C.1 ([3]).

For , let with . Let and denote the top k singular components of the SVD of and respectively. Then, the HSVT estimate is such that for all ,

Proof.

First, note that

where by definition. Note that the vector is in the span of a subspace orthogonal to , and hence we have by the Pythagorean theorem,

| (19) |

C.2 Deterministic To High-Probability

Next, we convert the bound in (24) to a bound in expectation (as well as one in high-probability) for . In particular, we establish

Theorem C.1.

Proof.

We start by identifying certain high probability events. Subsequently, using these events and (24), we will conclude the proof.

High Probability Events. Let be the number of columns in the stacked page matrix , and let be some positive absolute constant. Define

Lemma C.2.

For some positive constant and large enough in definitions of and ,

Proof.

We bound the probability of events above below.

Bounding . This is an immediate consequence of Lemma A.2.

Bounding .

Recall that we assume .

Observe that for any matrix , .

Thus using the argument to bound , concludes the proof.

Bounding . Let be the orthonormal basis for . Then, consider for ,

where . As shown in Lemma A.1, is a sub-gaussian vector with variance proxy . Using Lemma H.4, we have

Therefore, for choice of with large enough constant , we have,

Recalling that , and taking a union bound over all , we have that

∎

The following is an immediate corollary of the above stated bounds.

Corollary C.1.

Let . Then,

| (26) |

where is an absolute positive constant.

| (27) |

This completes the proof of Theorem C.1. Finally, now we are ready to bound . First, let be the set of columns in the stacked Page matrix that belongs to the -th time series . Note that

Choosing , and using , we get,

Finally and setting concludes the proof. ∎

Appendix D Proof of Theorem 4.2

In this section, we prove Theorem 4.2, which bounds the estimation error . First, recall the OLS estimate defined as

| (28) |

where . Alternatively, the OLS estimate can be defined as,

| (29) |

where is the row-wise concatenation of for , and . Further, consider the OLS estimate with access to the true series . Precisely, let defined as

| (30) |

where is the row-wise concatenation of for , and .

In what follows, as we do the analysis for one process , we drop the subscript . We note that the analysis holds for all . First, note that,

| (31) |

To bound , we use Corollary E.2 which states that with probability ,

| (32) |

Next, to bound , let denote the Moore–Penrose inverse of a matrix . Further, let , and , i.e., is the row-wise concatenation of for . Then, with ,we have

| (33) |

Where Lemma H.6 is used in the last inequality. Note that,

| (34) |

| (35) |

Using (33), (34), (35), and the theorem conditions, we get

| (36) |

Using Corollary E.1 we get that with probability

| (37) |

Now, note that , and

| (38) |

Recall that , which we will refer to herein as as we drop the dependence on . Therefore, we have,

| (39) | |||

| (40) |

Finally, using Lemma H.4, with probability at least it holds for an absolute constant ,

| (41) |

First, note that, using (37) and (39), we have

| (42) |

for sufficiently small such that . Now using (36), (37), (39), (40), (41), and (42) we have,

Therefore,

| (43) |

| (44) |

which completes the proof of Theorem 4.2.

Appendix E Identification of AR processes

In this section, we state key theorems for the identification of AR processes without the perturbation we consider in this paper. The theorems in this section and their proofs follow closely the ones in [17], we modify them to accommodate general sub-gaussian noise and state them fully for completeness.

First, consider the stationary process defined by the transition matrix

| (45) |

where is the column vector of zeroes, and input vector

| (46) |

Then, with , the AR process is described as

| (47) |

With being a sub-gaussian random variable with variance proxy With this setup, we define two important matrices,

| (48) | ||||

| (49) |

where is known as the controllability Gramian.

Theorem E.1.

Consider the process described in (47), is an i.i.d. mean-zero sub-gaussian noise with variance . Given , define the following quantities:

where and are constants that depends only on the process coefficients . Then, for and all valid values of such that , we have

Remark E.1.

To get , one must choose a sufficiently small such that . Using Weyl’s inequality, we have

| (50) |

This suggest that yields . For example, a choice of will yield . Note that this ensures , since and as can be seen from

Proof.

First, write

Expanding the summand using the process dynamics yields

Now, defining , we can sum the expression above over to get

This is called a Lyapunov equation, and due to the stability of the process it has solution . The key step is to argue that converges to with high probability, which will allow us to show that converges to . To do this, we will split the terms in into three groups, handling them separately. For some , we will bound the probability of the following events:

where denotes the spectral radius of a matrix.

Lemma E.1.

With the setup above, it holds that

for some absolute constant .

Proof.

Note that

so, considering the fact that and are identically distributed by stationarity, it suffices to upper bound the probability of

First, recall that is a sub-gaussian vector with variance proxy (see Lemma A.2). Thus, using Lemma H.2, for

where in the last inequality, we used the assumption . Finally, note that . Recalling that concludes the proof. ∎

Lemma E.2.

Continuing with the setup above, it holds that

Proof.

Since the spectral radius of is unity, is equivalent to the complement of the event

Since is sub-gaussian with variance proxy , is sub-exponential with parameter . Thus, Lemma H.5 applies, and therefore,

| (51) |

∎

Lemma E.3.

With the same setup, we have

as long as

Proof.

Recall the definition

For the sake of a variational analysis of the spectral radius, consider any vector such that . For notational simplicity. Then

Next, we aim to bound . First note that only the first column of is nonzero which evaluates to

| (52) |

Therefore, we have , which implies that for any unit vector ,

Therefore, we will bound by

| (53) |

First note that each term can be upper bounded by where and for where is the -th standard basis vector. Using Lemma H.7 and choosing and , we have that

and thus

What is left is to bound Using Lemma H.2, we get,

| (54) |

Choosing and yields

Which implies, that for , we have,

| (55) |

for some absolute constants . Now, note that

Thus, using (55) and (53), we have

| (56) | ||||

| (57) | ||||

| (58) |

Using the condition concludes the proof. ∎

Now we argue that the sum of the probabilities deduced from lemmas (E.1), (E.2), and (E.3) can be expressed in the simple form of as defined above. First, from lemma (E.1) we have

From lemma (E.2), and we get

Lastly, lemma (E.3) says, for ,

Thus we can write

Where in the statement we set . Using lemmas (E.1), (E.2), and (E.3) and the subadditivity of the spectral radii of symmetric matrices, we get with probability at least that

∎

Finally, we establish the following corollary, which is an immediate consequence of Theorem E.1.

Corollary E.1.

Consider the process described in (A.1). Let such that . Then, for sufficiently large such that , we have that with probability ,

| (59) | |||

| (60) |

where , are constants and , (the controllability Gramian) and are defined in (14).

Proof.

Note that according to Theorem E.1, Weyl’s inequality (see Lemma H.3), and using we have, with probability ,

| (61) | ||||

| (62) | ||||

| (63) |

Also,

| (64) | ||||

| (65) |

What is left is to check the condition on and . Note that Theorem E.1 requires , which with our choice of implies . To see that the choice of is valid, note that , which validates the choice of . ∎

Theorem E.2.

Proof.

Lemma E.4.

Let be a filtration. Let be a real-valued stochastic process such that is -measurable and is conditionally sub-gaussian with variance proxy . Further, let be an -valued stochastic process such that is -measurable. Consider any positive definite matrix . For any , define

Then for any , with probability at least for all ,

We will apply this result to bound the second term above. Choosing , , and , we have with probability at least

Now further condition on the event of Theorem E.1, which occur together with the condition above with probability at least . Recall, then, that , and so . This means that

Finally, it is clear that under the conditions in Theorem E.1 we have . ∎

Corollary E.2.

Let , where is as defined in Theorem (E.1). Then, for such that we have

Proof.

First, note that with the choice of we have,

| (66) |

Hence, . Further,

| (67) |

where the last inequality holds with probability using Theorem E.1. Finally, consider

| (68) |

Note that, again by our assumed condition on ,

| (69) |

| (70) |

Appendix F Proof of Theorem 4.3

F.1 Setup

Recall as defined in Proposition 2.2, and its estimate defined as

| (74) |

To establish this bound, we first define (and recall) the following notations,

-

•

Recall that is the stacked Page matrix of .

-

•

Let be the stacked Page matrix of .

-

•

Let be the stacked Page matrix of . That is, .

-

•

Let , be the sub-matrix obtained by dropping the -th row from the stacked Page matrix . Define and analogously.

-

•

Let denote the SVD of .

-

•

let and be matrices of orthonormal basis vectors that span the null space of and , respectively.

-

•

Let denote the top k singular components of the SVD of , while denote the remaining components such that .

-

•

Let be the HSVT estimate of with parameter . That is .

F.2 Deterministic Bound

First, given the notation above, the solution for (74), can be written as,

| (75) |

Then, let’s consider the following expansion for ,

| (76) |

where the last equality follow from the fact that . Now, consider the first term in (F.2), and note that ,

| (77) |

Next, by Wedin Theorem (see [10, 32]) we have:

| (78) |

That is,

| (79) |

What is left is bounding . To that end, first consider

| (80) |

Also, consider

| (81) |

| (82) |

First, recall that , and that by definition, . Then the term can be bounded as follows. First, consider

| (83) |

Note that , and , thus,

| (84) |

The term can be further decomposed as

Using Wedin Theorem,

Therefore,

| (85) |

F.3 High probability bound

Let be the number of columns in the stacked page matrix , and let be some positive absolute constant. Define

Lemma F.1.

For some positive constant and large enough in definitions of and ,

Proof.

We bound the probability of events above below.

Bounding and . Note that is a sub-matrix of , and its operator norm is bounded by that of . Hence, as the probability is an immediate consequence of Lemma A.2. The second event probability follow from the fact that .

Bounding . First, recall that is a -dimensional sub-gaussian vector with variance proxy . That is, for any unit vector , . Now, recall that is a set of orthonormal vectors . Let . Clearly, . Therefore, is a -dimensional vector with dependent sub-gaussian entries with variance proxy . Using Lemma H.4, we have

Therefore, for choice of with large enough constant , we have,

Recalling that , and , concludes the proof. ∎

Let . Then, under event , and using (F.2), we have, with probability ,

which concludes the proof of Theorem 4.3.

Appendix G Proof of Theorem 4.4

In this section, we prove an upper bound on the forecasting error,

where , where . First, recall that for ,

where , and . Then, we have,

Now, we will bound each error term separately.

G.1 Bounding Forecasting Error of f

To bound the forecasting error of , we use the following Lemma.

Lemma G.1.

Let the conditions of Theorem 4.1 hold. Then, with probability

where is an absolute constant, and denotes a constant that depends only (polynomially) on model parameters .

Proof.

The proof of this lemma is similar to that in [3], but we adapt it for our different settings. First, note that, where we assume that is an integer,

In what follows, we provide an upper bound for the inner sum for all . Next, we show, without loss of generality, the case for . To establish this bound, we first define (and recall) the following notations,

-

•

Recall that is the stacked Page matrix of for .

-

•

Similarly, let denote the stacked Page matrix of the out-of-sample observations for , i.e., .

-

•

Let be the stacked Page matrix of for , and be the stacked Page matrix of for .

-

•

Similarly, let and be defined similarly but for .

-

•

Let , be the a sub-matrix obtained by dropping the -th row from the stacked Page matrix . Define , , , , and analogously.

-

•

Let and denote the SVD of and respectively.

-

•

let and be matrices of orthonormal basis vectors that span the null space of and , respectively. Define and similarly for the matrix .

-

•

Let denote the top singular components of the SVD of , while denote the remaining components such that .

-

•

Similarly, Let denote the top k singular components of the SVD of , while denote the remaining components such that .

-

•

Let and .

Recall that we are interested in a high-probability bound for the following out-of-sample prediction error:

| (87) |

Recall that and hence we can rewrite (87) as

| (88) | ||||

| (89) |

Next, we derive a deterministic upper found for the expression above.

Deterministic Bound. Through adding and subtracting and triangle inequality, we have

| (90) |

Next, we proceed to bound each of the two terms on the right hand side.

First term: .

| (91) |

Note that equals the -th singular value of . Using Weyl’s inequality (see Lemma H.3), and recalling that , and that the rank of is , we can bound the -th singular value of by the operator norm of . That is,

| (92) |

Next, we bound the term .

| (93) |

Further expanding the first term,

Where in the first equality we use the fact that , i.e., lives in the column space of (Assumption 4.2).

| (95) |

Second term: . To bound the second term, we follow a similar proof to that shown in [5].

| (96) |

Next, we bound the term .

| (97) | ||||

| (98) | ||||

| (99) |

Next, we bound . Recall that spans the column space of . Thus , therefore,

| (100) |

Now recall that we denote the top left singular vectors of by , then consider

| (103) |

| (105) |

For some absolute constant .

High probability bound. With our choice , Let be the number of columns in the stacked page matrix and subsequently to be the number of columns in the stacked page matrix . Let be some positive absolute constant, and be a constant that depends only on model parameters and . Define

| (106) | ||||

| (107) | ||||

| (108) | ||||

| (109) | ||||

| (110) | ||||

| (111) | ||||

| (112) |

First, with is an absolute constant, recall from Lemma F.1,

Further, note that is a sub-matrix of , hence its operator norm is bounded by that of . Therefore, as an immediate consequence of Lemma A.2,

The probability of event is bounded by Theorem 4.3 as

Finally, as an immediate results of Corollary C.1 and its consequence in (27), we have

Now consider the event . Then, under event , and using (G.1), we have, with probability ,

| (113) | ||||

| (114) |

Recalling , , and Assumption 4.1, we get,

| (115) |

Therefore, with probability ,

| (116) | |||

| (117) |

Further, note that the same argument can be used to bound the sum for all . Thus, with probability , we have,

| (118) |

∎

G.2 Bounding Forecasting Error of x

Now, we bound the error of forecasting . First, recall , and let and . Now, let , and , all in , be the row-wise concatenations of , , and for .

Then, we have, where

| (119) | ||||

| (120) | ||||

| (121) | ||||

| (122) | ||||

| (123) |

First note that

| (124) | ||||

| (125) | ||||

| (126) |

Therefore,

| (127) | ||||

| (128) |

High probability bound. For the high probability bound, consider the event where

| (129) | ||||

| (130) | ||||

| (131) |

Note that using Theorems 4.2, 4.1 and the the union bound. Further, note that using both Lemma G.1 and Theorem 4.1. Further, note that according to Corollary E.1, with probability , we have

| (132) |

Therefore, under , and recalling , we have with probability ,

| (133) | ||||

| (134) | ||||

| (135) |

where therefore, with probability , we have

| (136) | |||

| (137) | |||

| (138) |

which completes the proof.

Appendix H Helper Lemmas and Definitions

Definition H.1 (Sub-gaussian random variable [30, 31]).

A zero-mean random variable is said to be sub-gaussian with variance proxy (denoted as ) if its moment generating function satisfies

Definition H.2 (Sub-exponential random variable [30, 31]).

A zero-mean random variable is said to be sub-exponential with parameter (denoted as ) if its moment generating function satisfies

Definition H.3 (Sub-gaussian vector).

A random vector is a sub-gaussian random vector with parameter if

where .

Lemma H.2 (Norm of sub-gaussian vector).

Let be a sub-gaussian random vector with parameter . Then, with probability at least for :

This implies that for any ,

with probability at least .

Definition H.4 (Stationary process [26]).

A process is said to be stationary if its expectation does not depend on and its autocovariance function depend only on the time difference. That is,

Lemma H.3 (Weyl’s inequality).

Given , let and be the -th singular values of and , respectively, in decreasing order and repeated by multiplicities. Then for all ,

Lemma H.4.

Let where each is a sub-gaussian (not necessarily independent) random variable with variance proxy and . Then with probability at least ,

| (139) |

Proof.

From Lemma H.1, we can see that is sub-exponential with parameter . Let , then

| (140) |

Choosing , , and , we get,

| (141) | ||||

| (142) | ||||

| (143) |

where the last inequality follows from the fact the second moment of is bounded by its variance proxy up to a multiplicative constant. ∎

Lemma H.5.

Let be sub-exponential random variables with parameter . Let . Then

| (144) |

Proof.

Recall that the sum of n sub-exponential random variables is also a sub-exponential random variable with parameter (see Lemma H.1). Thus, using the definition of sub-exponential random variable, we have

| (145) |

Choosing , we get,

| (146) | ||||

| (147) |

Applying the same inequality to completes the proof. ∎

Lemma H.6.

Lemma H.7.

[Lemma 4.2 of [27]] Let be a filtration, and and be real-valued processes adapted to and respectively. Moreover, assume is mean zero and -sub-gaussian. Then, for any positive real numbers we have

| (148) |