Mean-variance dynamic portfolio allocation with transaction costs: a Wiener chaos expansion approach

Abstract

This paper studies the multi-period mean-variance portfolio allocation problem with transaction costs. Many methods have been proposed these last years to challenge the famous uni-period Markowitz strategy.

But these methods cannot integrate transaction costs or become computationally heavy and hardly applicable. In this paper, we try to tackle this allocation problem by proposing an innovative approach which relies on representing the set of admissible portfolios by a finite dimensional Wiener chaos expansion. This method is able to find an optimal strategy for the allocation problem subject to transaction costs. To complete the study, the link between optimal portfolios submitted to transaction costs and the underlying risk aversion is investigated. Then a competitive and compliant benchmark based on the sequential uni-period Markowitz strategy is built to highlight the efficiency of our approach.

Keywords: multi-period portfolio allocation, mean-variance formulation, Wiener chaos expansion.

Classification: 62L20, 91G10, 91G60, 93E20

1 Introduction

Dynamic portfolio selection is one of the most studied topic in financial economics. The problem consists in allocating the wealth of an investor, among a basket of assets, over time. Finding the optimal portfolio is a difficult challenge since it depends on the objective of the investor. The Markowitz mean-variance formulation represents a first answer to this problem by providing fundamental basics for static portfolio allocation in a uni-period case (see [25]).

Mean-variance framework offers to build a portfolio of assets such that the expected return is maximized for a given level of risk. This method is easy to apply and has the favor of asset managers. Nevertheless, when the time horizon increases, this myopic strategy which cannot see ahead of the next time period, cannot challenge the dynamic optimal portfolio obtained from the multi-period version of the problem.

[26] is one of the first paper studying multi-period portfolio investment in a dynamic programming framework. In this seminal paper, the authors consider a problem with one risky asset

and one risk-free asset. At each date, the investor can re-balance its wealth between the two assets, seeking to maximize an utility of the final time horizon wealth. They derive a simple closed-form expression for the optimal policy when there are no constraint or transaction cost. In a companion paper, [33] derives the discrete-time analog approach. The results presented in those studies and the innovative and promising aspect of the multi-period portfolio selection have stimulated the interest of the related scientific community. In the following years, the literature in multi-period portfolio selection has considerably grown, dominated by maximizing expected utility of terminal wealth of elementary forms as logarithm, exponential or CRRA functions. Dynamic programming techniques turn out to be the most suitable approaches to solve this kind of problems.

However, important difficulties due the non separability of the problem in the sense of dynamic programming, have been reported in finding the optimal portfolio issued from the multi-period mean-variance approach. Nevertheless, [21] and [39] provide explicit formulation for the unconstrained multi-period mean–variance optimal portfolio both in a discrete and continuous time setting. [23] derives the optimal portfolio policy for the continuous-time mean–variance model with no-shorting constraint. [12] extends this work to provide a discrete framework. Even if these last studies have become increasingly realistic, the ignorance of transaction costs, hinders their efficient applications in real life. Transaction costs have a major impact on the optimal policy and cannot be ignored.

The integration of transaction costs has been widely studied in the uni-period mean-var case (see [5], [24], [31], [37], [38]). In a continuous time setting, the problem is not recent, especially when the time horizon is considered infinite (see [14], [15], [17], [27], [28]). In a mean-var and finite time horizon setting, [13] studies the properties of the optimal strategies and boundaries which define the buy, sell and no trade-regions. Discrete time allocation strategies submitted to transaction costs have also been widely pursued. [11] and [19] investigate optimal investment policies with proportional costs, accompanied by fixed costs for the second. They also describe them in terms of a no-trade region in which it is optimal to leave the portfolio allocation unchanged.

But many difficulties have been reported in the literature to design efficient and accurate methods to compute the optimal solutions. Furthermore, when solutions are proposed, they remain computationally heavy and hardly applicable. Some of them tractably solve the problem in several special cases (see [6], [16] and [30]) or search for sub-optimal policies

(see [4], [9], [22] and [35]).

The most prevalent methods to tackle this kind of problem are based on stochastic control techniques. However, they also suffer from the same drawbacks.

In order to limit the dimensionality, [8] uses Chebyshev polynomials to interpolate the value functions on a sparse grid of the space.

Many of other related studies such as [18], [34] and [36] rely on trees for modeling rates of return. [2] goes further by assuming that every future rates of return is known by the investor. Under the same assumption, [7] derives an upper bound to measure and highlight the good performances of heuristic strategies.

[6] performs an ADP (Approximate dynamic programming) by using sub-optimal solutions to approximate value functions. These sub-optimal solutions are issued from a quadratic version of the problem or from MPC method (model predictive control). [10] uses an other sub-optimal solution, called multi-stage strategy to tune the exploring phase of its backward recursion algorithm. This method provides a solution at least, as good as the sub-optimal one. Recently, [32] has also adopted dynamic programming but is forced to handle different cases separately, which makes their method hardly computationally applicable.

In this paper, we attempt to fill this gap by

providing a new computational scheme to solve multi-periods portfolio allocation problem submitted to transaction costs. We address this problem by proposing an innovative approach which relies on representing the set of admissible portfolios by their finite dimensional Wiener chaos expansion. This numerical method estimates optimal portfolios submitted to proportional transaction costs. The policies are computed thanks to a stochastic gradient descent algorithm, and require no exploration framework, which was a major step of the methods based on stochastic control algorithms (see [3]).

Then a competitive benchmark, based on the sequential uni-period Markowitz strategy is built to highlight the efficiency of our approach. This benchmark relies on the independence between the Sharpe ratio and the risk aversion.

The main contribution of this paper is threefold. We introduce an innovative and efficient numerical method to get optimal portfolios submitted to transaction costs. Then, we study the links between risk aversion and multi-period optimal portfolios submitted to transaction costs. Finally, we provide a reliable benchmark with sequential mean-variance uni-period models in the context of transaction costs mentioned above. To the best of our knowledge, our paper is the first to provide this kind of benchmark.

The remaining of this paper is organized as follows. Section 2 is dedicated to describe the mean-variance problem for multi-period portfolio allocation submitted to transaction costs. Our methodology which aims at finding optimal portfolios in this context, is presented in Section 3.

In section 4, the link between risk aversion and optimal solutions is investigated.

Finally, in Section 5, we show the efficiency of our solution and examine the impact of transaction cost by comparing performances of the presented models with benchmark models such as the sequential uni-period Markowitz approach described in Appendix C.

2 Environment

This section defines the environment in which we address the mean-variance allocation problem. In particular, we present the general mean-variance formulation for multi-period portfolio allocation with transaction costs. Then, we specify the dynamics of risky assets and reformulate the initial problem.

2.1 Mean-variance formulation for multi-period portfolio allocation

We define the filtered probability space with , where is a Brownian motion defined on with values in . For , , we introduce the discrete-time grid . Let , be the discrete time filtration generated by the Brownian increments on this grid, for . We denote as

.

We consider a portfolio , of initial wealth , composed of the risky assets and the risk-free asset . An investor, with a risk aversion can re-allocate its portfolio at discrete times . We define (, , the quantities of risky and risk free assets hold in the portfolio, such that . The processes and are assumed to be -predictable. The agent aims to find the strategy (, , such that the generated portfolio , maximizes .

At time , we assume that the owner has all its wealth in cash, ie and .

At time , the investor re-balances his portfolio from to . He pays the transaction costs, proportional to the trade cash volume per asset and equal to

.

The self-financing condition is

The dynamic mean-variance portfolio allocation with transaction costs can be written as

| () | ||||||

| s.t. | ||||||

2.2 Framework and assumptions

For any discrete time process , we write for . Let be the operator which associates its increments process .

We also define the normalized Brownian increments by

for .

We assume that the financial market they represent is complete.

The risk free rate is assumed to be deterministic and , . We assume that the risky assets are defined by

| (1) |

where and are -adapted processes with values in and respectively. The process is called the volatility process and we assume that is a.s. invertible,

and that .

This model implies that knowing , the returns are independent of . Note that local volatility models fit in this framework by considering the Euler scheme of .

Let be the natural filtration of the risky assets, .

Since and are -adapted processes and is a.s. invertible, we can easily prove by induction that .

For we define . Let . We assume that such that the process

is a martingale. Therefore, we know from Girsanov’s theorem that there exists a probability measure equivalent to , defined by

We denote as Let be a -adapted process defined by and

then is a Brownian motion under . Note that

| (2) |

Let , be the discrete time filtration generated by , . We notice that

We can see by induction that we also have .

We use the tilde notation to denote discounting and we notice that is a -martingale under the probability . Lastly, we assume that the process is a.s. invertible and

.

2.3 Reformulation of the problem

With the notations and assumptions of Section2.2, the self-financing condition can be reformulated as

| (3) |

We define the cumulative cost process by

| (4) |

We decide to work with the -martingale under , . Let be the space of squared integrable -martingales under and the sub-space of defined by

is the set of martingales which are a martingale transformations of . The space also represents the space of admissible portfolios in discrete-time. The mean-variance multi-period portfolio allocation problem with transaction costs (), can be reformulated as

| () | ||||||

| s.t. | ||||||

In the next section, we present an innovative approach to solve the dynamic mean-var allocation problem in presence of transaction costs.

3 Main results

The main contribution of this paper is to propose and study a numerically tractable approximation of (). First, we embed the original problem into a more standard stochastic optimization framework (). Then, we use Wiener chaos polynomials to obtain a finite dimensional formulation ().

3.1 Embedding representation

The main difficulty remains to parameterize . We propose to find optimal portfolios on by exploring . Furthermore, the objective function depends on the law of the portfolio value. This non-separable form is not easy to manipulate. In order to solve (), we would like to embed it into a tractable equivalent one.

The proof of Proposition 1 relies on the following Lemma.

Proof (of Lemma 2).

Let be a -adapted process. We define the function

The function is a second order polynomial such that . Then, attains its maximum at a unique point defined by , .

Proof (of Proposition 1).

Let . The projection of on writes as

with -predictable, . Let such that for , . Then we have for ,

| (9) |

By taking , for all , we get . Setting , we have

| (10) |

By developing the expression and using that and are -martingale, we obtain for ,

| (11) |

Then, for ,

| (12) |

Finally, inserting (12) in (10) yields

| (13) |

In the same way, for ,

| (14) |

Then

| (15) |

So

| (16) |

As this equation holds for all , we deduce that solves

Then, we conclude that is defined by (8) and that () can be reformulated as ().

3.2 Wiener chaos parametrization

We will parametrize the elements of through the Wiener chaos expansion of their terminal value. The basic theory of Wiener chaos expansion and the properties used here are presented in Appendix A. According to [1, Theorem 2.1], every element of can be represented by its Wiener chaos expansion as

| (17) |

where

We define the truncated expansion of of order under by such that

It is well-known that

Proposition 21 states that for , , which can be obtained by removing the non -measurable terms from the chaos expansion of . By identifying the martingale with the chaos expansion of its terminal value ,

we slightly abuse the notation

to define the process .

Let’s consider the analog problem for

| () | ||||||

| s.t. | ||||||

The following proposition states that the optimum of () converges to the optimum of (). As a result, we can approach the optimum of () by solving ().

Proposition 3.

The proof of the proposition is based on the following lemmas.

Lemma 5.

Let , then , such that , ,

| (18) |

| (19) |

Proof (of Lemma 19).

Using consecutively Jensen’s inequality and Holder’s inequality with the coefficients and , we have

By recalling that , we find such that

, and obtain (18).

For the second inequality (19), we use Holder’s inequality with the coefficients , , and (18). The constant may change over the inequalities.

The last equality stems from the martingale property of .

Proof (of Lemma 4).

We have

For the first term, we have

Using Lemma 19 and the same arguments as to prove (19), we find , such that

| (20) |

For the second term, we rewrite

Let and . By using the same decomposition and arguments as to prove Lemma 19 and Cauchy Schwartz’ inequality, we find such that

The same result can be obtain for . By using the main assumption of the proposition, and considering the form of and , we find such that

Finally, by using Lemma 19 to bound the term , we find such that

Finally setting gives the result.

Proof (of Proposition 3).

Let be a solution to (). is an admissible solution for (), then

| (21) |

According to Lemma 4, we find independent of such that

| (22) | ||||

We denote as the number of coefficients appearing in the chaos expansion of order , . By identifying the martingale with the coefficients of the chaos expansion of its terminal value , we slightly abuse the notation to write

We can also slightly abuse the definition of the controls in (8). Recalling that define the expansion of , we define

| (23) |

We notice that can be expressed as a linear combination of the chaos coefficients of . Similarly, we also extend the cost function to

| (24) |

Let’s extend in this context, the portfolio value function as

| (25) |

Note that is a positive homogeneous function, ie . We also express the objective function as

| (26) |

Note that is a random function. With these new functions, we can approximate the original problem () by a finite dimensional optimisation problem

| () | ||||||

| s.t. |

The constraint is easily satisfied by setting the first coefficient equal to , .

Proof.

According to Lemma 2, for , always exists and is attained for . Let . We have

By considering the optimums of continuous functions on compact sets, we define

Since the market is assumed to be complete, it is not possible to build a risk free portfolio with risky assets, . Finally, ,

With this inequality, we deduce that The objective function is continuous and , then it attains its maximum. We can conclude that () admits a solution.

4 Resolution

In this section, we describe the numerical framework to solve (). We define the space where optimal strategies are investigated and we study the link between risk aversion and those solutions. In particular, we insure that risk aversion parametrization has no impact on performances. We assume for the numerical resolution that is deterministic (Black-Scholes case).

4.1 Stochastic descent gradient algorithm

We aim to apply a stochastic descent gradient algorithm to solve (). Let’s introduce

is a closed set of of measure null. Elements of this set represents strategies where there is almost surely, no investment, during a time period between and , in a risky asset. These strategies are not realistic, not optimal and therefore are ignored. Optimal strategies are investigated on . It can be shown that is differentiable almost everywhere, on . We refer to Appendix B for a detailed study on differentiability. Furthermore, we have seen that We can then deduce that if is the chaos expansion decomposition of an optimal portfolio then is solution to

| () |

Proof.

4.2 Influence of risk aversion

In this section, we discuss the influence of the risk aversion on optimal multi-period portfolios submitted to transaction costs.

One main result claims that the Sharp ratio of a zeros gradient portfolio submitted to transaction costs is independent from its risk aversion. A second main result affirms that all optimal portfolios have the same Sharp ratio. This study insures that the choice of risk aversion parameter does not influence performances.

In this section, we consider the following formulation of the allocation problem

| () | ||||||

| s.t. |

where . We have seen that solves () if and only if and solves ().

Definition 8.

Definition 9.

Proposition 10.

The risk aversion, the Sharpe ratio and the volatility of a -zero gradient portfolio submitted to transaction costs are related by

| (27) |

Lemma 11.

There exist a -measurable random variable and -adapted processes for and taking values in , such that , for any and

| (28) |

Proof (of Lemma 11).

According to the linearity in of the control functions, defined in (23), there exists a -measurable random variable with values in such that

and , -adapted processes with values in such that ,

By calling , we obtain

, , , so ,

and . And we have , . , then .

Proof (of Proposition 10).

We have seen in () that if is a -zero gradient portfolio, then such that and This equality leads to

We recall that . As is a.s differentiable and using the decomposition of Lemma 11,

| (29) |

We deduce that

Then with

we obtain

We deduce that

Finally,

| (30) |

Corollary 12.

All -optimal portfolios have the same Sharpe ratio.

Proof.

Let be such a -optimal portfolio. As an optimal portfolio, is also a -zero gradient portfolio. Then according to Proposition 10,

Inserting this term in the mean-variance objective function leads to

| (31) |

We deduce that if is another -optimal portfolio then (31) gives . But the two portfolios also attain the same mean-variance value then

With this last equality, we can conclude they have the same variance and as a result, the same Sharpe ratio.

Remark 13.

Maximizing the mean-variance objective function of zero gradient portfolios, is equivalent to maximizing their Sharpe ratio.

Now, let’s prove this important proposition on the impact of the risk aversion.

Proposition 14.

Let , then is a -zero gradient strategy if and only if ( is a -zero gradient strategy.

Proof.

Let be a -zero gradient strategy with the associated chaos coefficients . Then is solution to (). Then with the previous notations

| (32) |

By using the decomposition of Lemma 11, is a.s differentiable on and

| (33) |

Let’s now consider the portfolio

We obtain the following equality

We deduce that

| (34) |

By using the expression (33), we also notice that

| (35) |

Finally, by inserting (34) and (35) in equality (32), we obtain

| (36) |

which finishes the proof.

Corollary 15.

Let , then is a -optimal strategy if and only if ( is a -optimal strategy.

Proof.

Let be a -optimal strategy with the associated chaos coefficients . Then is a solution to (). Firstly, according to Proposition 14, is a solution to with

But as is a positive homogeneous function, ie , then

If such that

then using the previous equality , which is impossible with the optimally of . We deduce that

is a solution to . The converse statement is obvious.

We have seen in (23), that the controls

can be expressed as linear functions of . We can conclude that is an optimal solution for () if and only if ( is an optimal solution for .

Proposition 16.

Let be a -zero gradient strategy and the associated -zero gradient portfolio. Then for all , , where is the portfolio associated to the strategy .

Proof.

By using that is a positive homogeneous function, we have

that finishes the proof.

Proposition 17.

The Sharpe ratio of a zeros gradient portfolio is independent of its risk aversion.

Proposition 18.

Let and be a -zero gradient portfolio. Then there exists and a -zeros gradient portfolio with and with volatility .

Proof.

Proposition 19.

Let s.t. . Let (resp. ) be a -optimal portfolio (resp. -optimal portfolio). Then, .

5 Numerical illustration

In this section, we implement the approach presented above and the sequential uni-period Markowitz model which is used as benchmark, see C.2. We consider the cases where costs are ignored and considered. In order to maximise the rate of return of a portfolio while controlling its volatility at time , an agent consecutively maximizes at time , its uni-period mean-var objective function. We assume that the agent has a uni-period risk aversion parameter . The agent has to consecutively solve for ,

| () | ||||||

| subject to |

Further details on the implemented benchmark model and its link with risk aversion are presented in Appendix C.2.

We assume that the risky assets follow the dynamics (1) with constant parameters. Formally, the drift terms, the volatility matrices and the risk free rate are chosen deterministic and constant, ie. .

Along a first part, we compare the performances by choosing the same risk aversion parameter . As the Sharpe ratios of the estimated portfolios is independent of the aversion parameter (see Propositions 17, 19 , 25, 26), it can be used as an indicator of performance. Then, along a second part, we apply a framework for matching the risk aversion between uni-period and multi-period models. We are able to illustrate and compare the behaviour of our solutions on two realisations.

5.1 Model Parameters

We consider assets, evolving during days. Transactions are only available every days. The model is described in Section 2.2. Instead of specifying a volatility matrix, we fix the marginal volatilities and a correlation matrix as in Tables 1 and 2.

| 0.06 | 0.02 | 0.14 | |

| 0.1 | 0.06 | 0.2 |

| 1 | -0.2 | 0.3 | |

| -0.2 | 1 | -0.2 | |

| 0.3 | -0.2 | 1 |

We fix a constant risk free rate . The initial portfolio wealth is . The implementation parameters are summarized in the following table

| nb.traj. calibration | nb.traj. test | N | p | Chaos degree |

|---|---|---|---|---|

| 368 | 92 | 2 |

We split our sample into two parts. The first part is used to run the descent gradient algorithm to calibrate and to find an optimal portfolio, while the second part is used to compute performance indicators. In presence of costs, we assume that the first position is free of charge.

5.2 Same risk aversion parameter

In this first experiment, we choose the same risk aversion parameter for the different approaches. Since the objective functions are not the same between multi-period and uni-period models, the agents have not the same risk aversion. Therefore volatility and rates of return are not comparable. Nevertheless the Sharpe ratio is a relevant indicator for comparing performances of optimal portfolios based on different risk aversions. Indeed, the Sharpe ratios of estimated portfolios are independent from the risk aversion in every models according to Propositions 17, 19, 25 and 26.

The implementation parameters are summarized in the following table.

| risk aversion | batch size | iteration | learning rate | cost(%) |

|---|---|---|---|---|

| 0.05 | 100 | 1000 | 8.5 | 1 |

We compare five models; two sequential uni-period versions and two multi-period versions, where cost are on one hand ignored and on the other, considered. Moreover, we add in the benchmark the famous equal weight portfolio to measure the performance of the other approaches. We refer to our approach as Multi-period with costs. We refer to Appendix C for further details on the four other benchmark models. Formally, our aim is to evaluate the performance of our method compared to the more basic approaches commonly used. The main results can be found in Table 5.

| rate of return() | vol() | Min-Var | Sharpe ratio | |

|---|---|---|---|---|

| Multi-period ignoring cost | 13.24 | 12.17 | 105.83087 | 1.07939 |

| Multi-period with costs | 12.31 | 11.00 | 106.26365 | 1.11033 |

| Sequential uni-period ignoring cost | 10.44 | 10.00 | 105.43191 | 1.03316 |

| Sequential uni-period with costs | 11.00 | 10.72 | 105.24599 | 1.01606 |

| equal weight | 5.69 | 5.70 | 104.06893 | 0.98125 |

We analyse here, the difference in Sharpe ratios.

By focusing on uni-period models, it is interesting to notice that ignoring costs seems to be better than considering them. The myopic effect, joined with the consideration of costs, may make the optimal strategy rigid and inflexible. The agent’s myopic behavior explains why they do not see the benefit of paying costs for short-term positions.

Therefore considering cost almost freezes the strategy and can explain that performances are not as good as if we have ignored them.

Obviously these remarks, are dependent of the chosen parameter , which determines the weight of costs in transactions.

In contrast, considering costs in the multi-period version is a significant improvement. According to the choices of parameters, a difference of in Sharpe ratio is not negligible.

A multi-period model targets a final value and must adapt its positions according to the variations of the environment. These changes in positions are typically more significant than in myopic strategies, and thus, the impact of costs becomes more critical. Ignoring costs can have a considerable impact on strategies, leading to performance deterioration.

Undoubtedly, the myopic effect has a negative impact on performances. The difference in Sharpe ratios between uni-period and multi-period models is not negligible. Therefore, we advise to use multi-period models, despite their greater complexity. In that case, costs must not be ignored.

5.3 Same risk aversion level

In a second experiment, we want to compare the optimal portfolios submitted to transaction costs in uni-period and multi-period settings with the same level of risk. According to Proposition 18, we can link the risk aversions and in both models to ensure the same level of risk. This experiment aims to illustrate the comparison in terms of rates of returns. We can also directly compare portfolio trajectories.

5.3.1 Performances

Our objective is to obtain a locally optimal multi-period portfolio that carries the same level of risk as the optimal sequential uni-period portfolio. We adopt the approach described in Proposition 18. We use the locally optimal multi-period portfolio estimated in the previous section to build another locally optimal multi-period portfolio with the same volatility as the optimal uni-period portfolio. With a uni-period risk aversion , we have obtained a volatility of for the optimal uni-period portfolio. The locally optimal multi-period portfolio estimated in the previous experiment has a Sharpe ratio equal to . According to Proposition 18, we can build another locally optimal multi-period portfolio with the same Sharpe ratio and a volatility of . To reach this volatility, a multi-period risk aversion parameter is estimated by using (27). The main results can be found in Table 6

| risk aversion | rate of return() | Min-Var | Sharpe ratio | |

|---|---|---|---|---|

| Multi-period with costs | 0.0518 | 11.89 | 105.9372 | 1.11033 |

| Sequential uni-period with costs | 0.0500 | 11.00 | 105.24599 | 1.01606 |

The multi-period model is obviously the most performing. The difference between the rates of return is almost 1%. This difference is important according to a level of risk of 12.72%.

After comparing the performances of the optimal portfolios with the same risk aversion, we illustrate their behaviour by showing trajectories from two different situations, A and B. To ensure consistency, we use the same framework as before to match the risk aversions.

5.3.2 Behaviour on realisation A

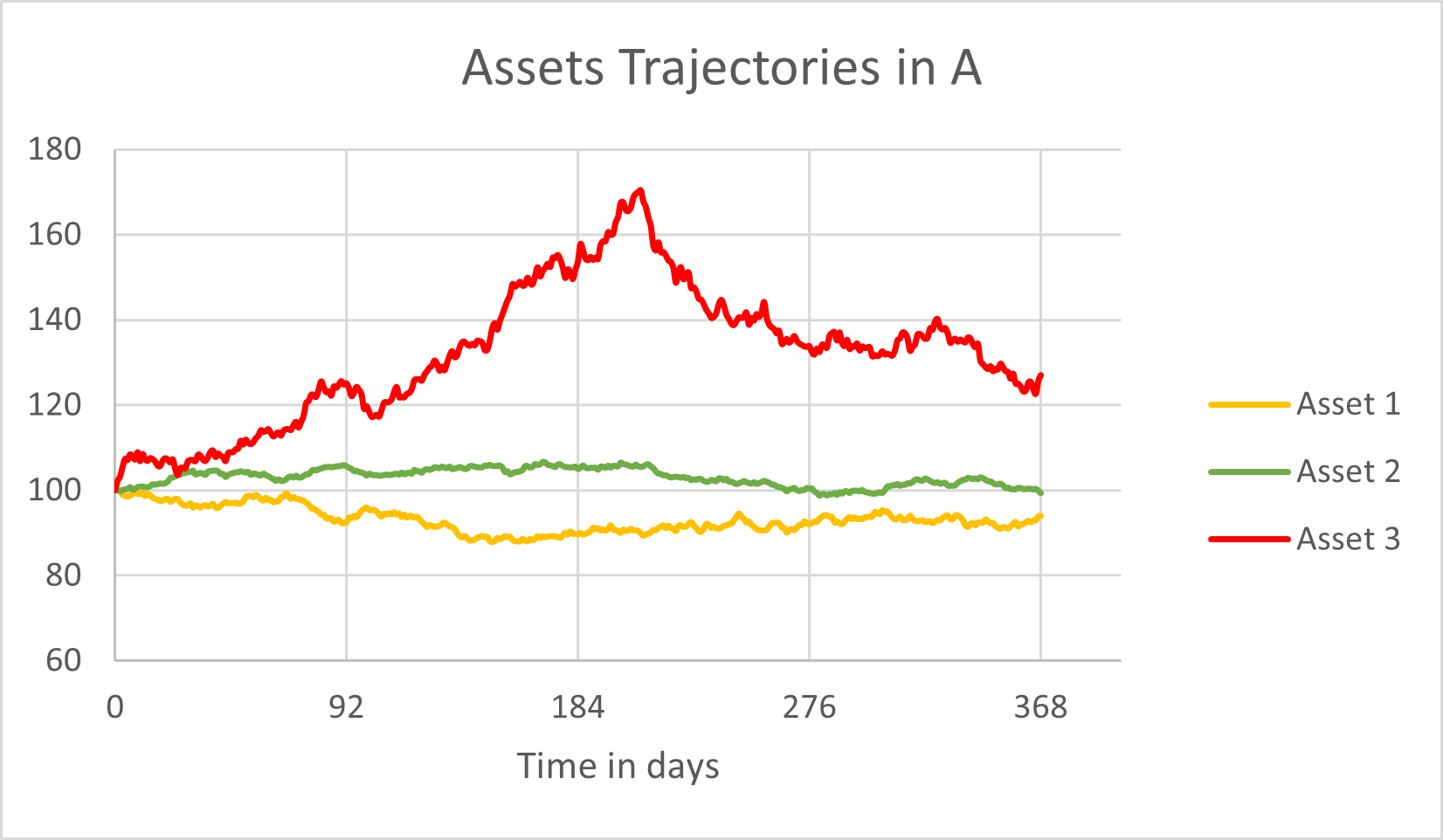

To illustrate the comparison, we present in Figures 1, one particular sample path of assets.

It can be observed that the curves for assets 1 and 2 are relatively flat and symmetric. Asset 2 remains above its initial value. On the other hand, asset 1 remains below its initial value. Asset 3 experiences significant growth, reaching a peak of before collapsing towards the end of the period to finish just above .

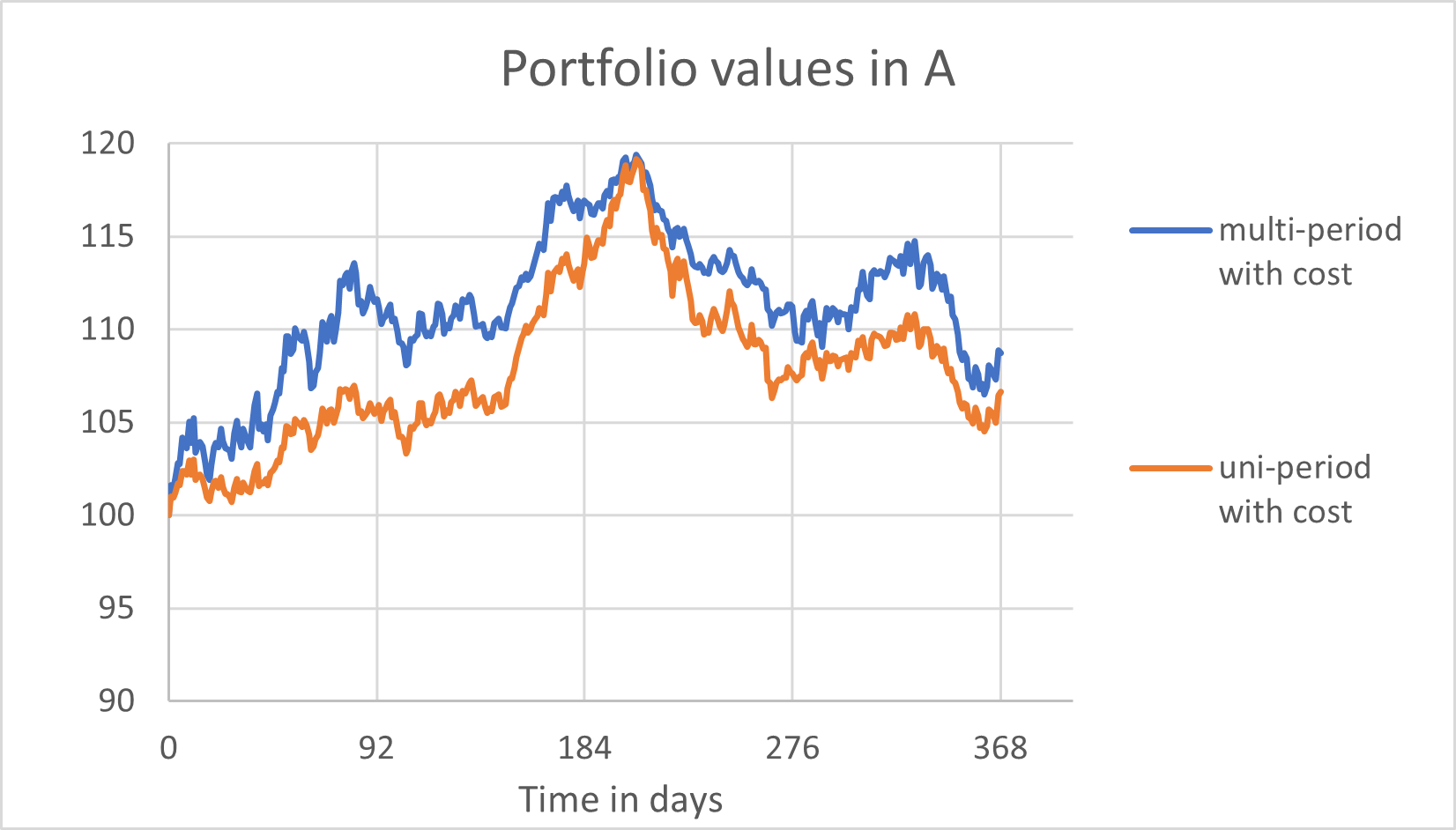

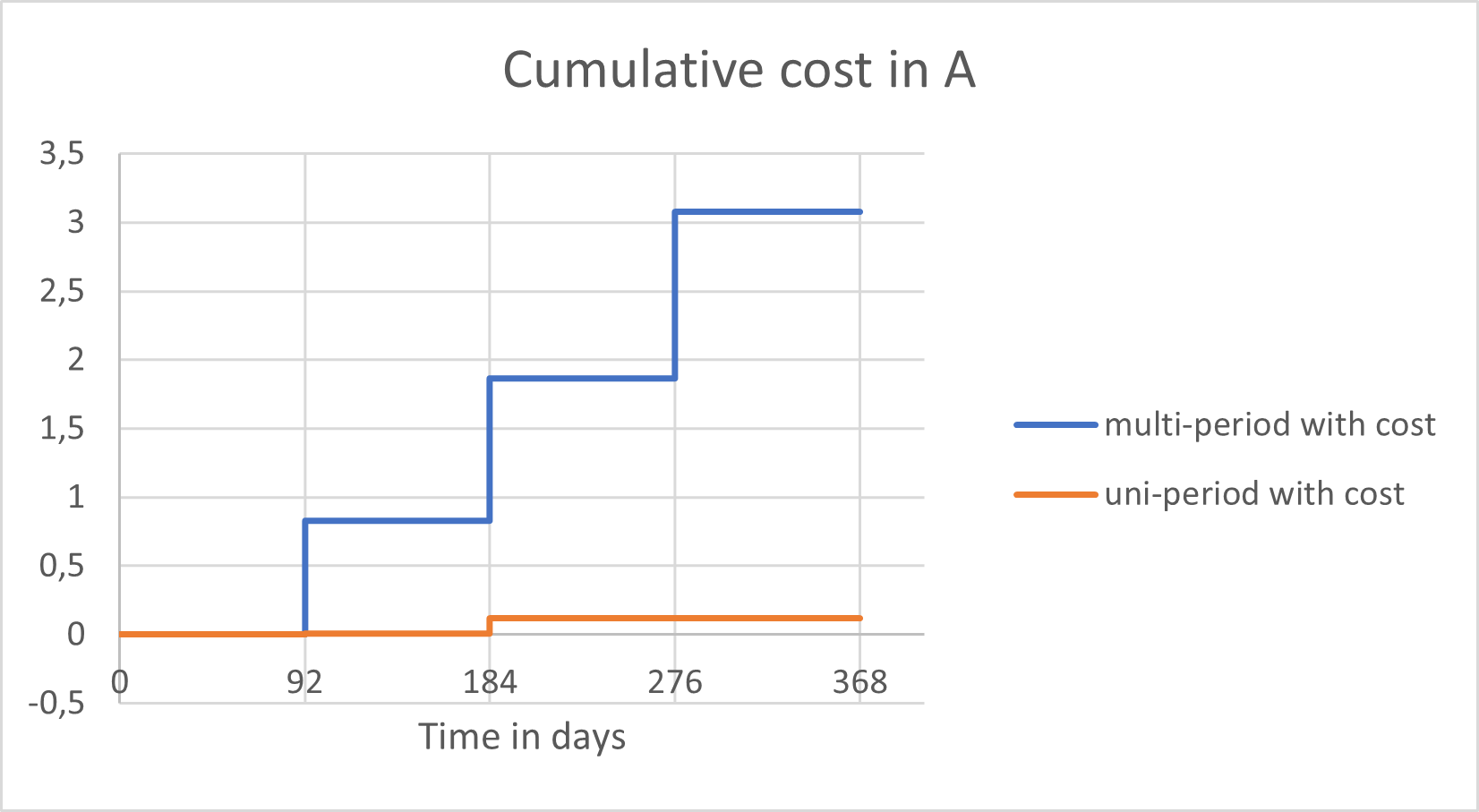

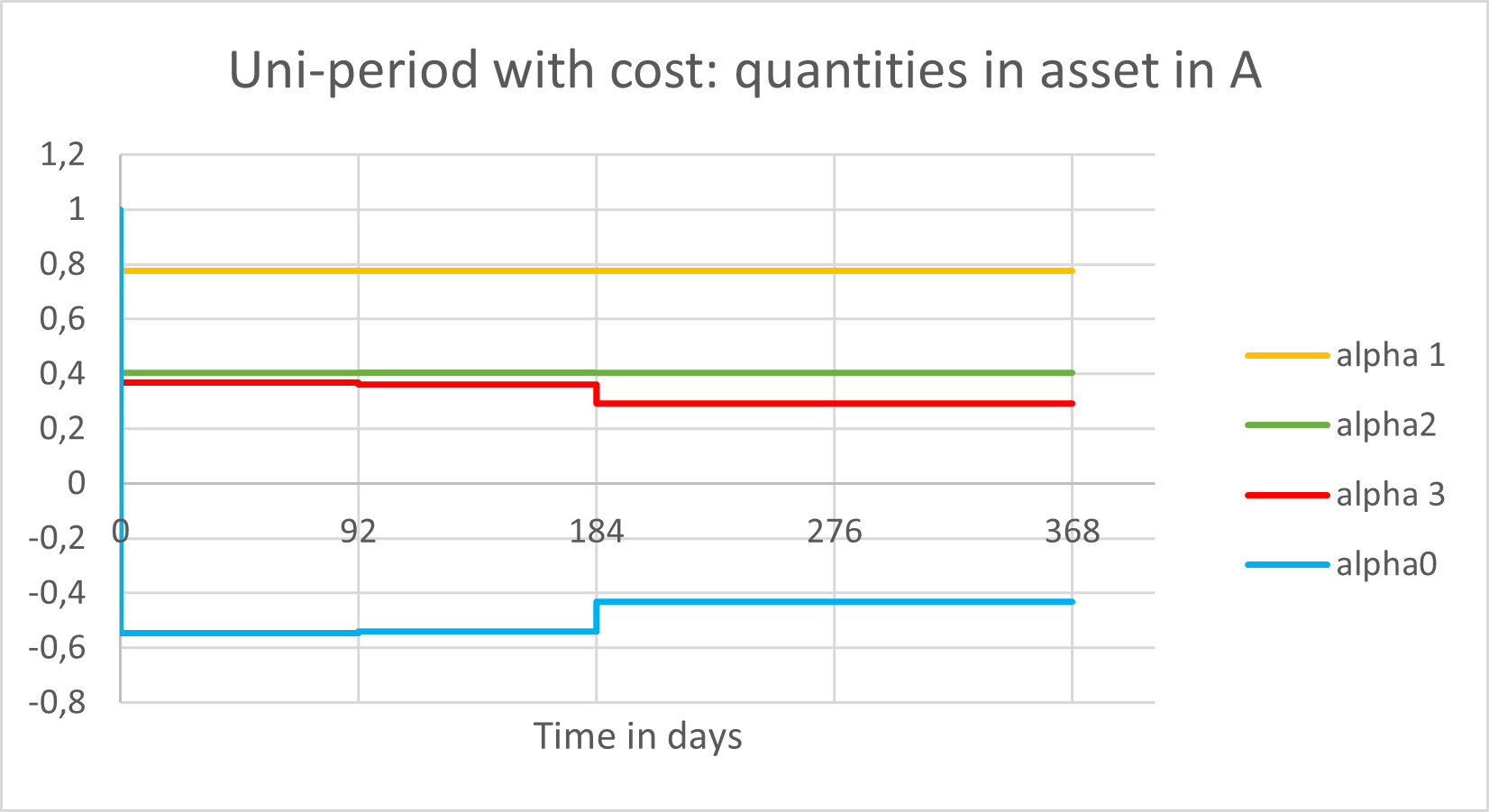

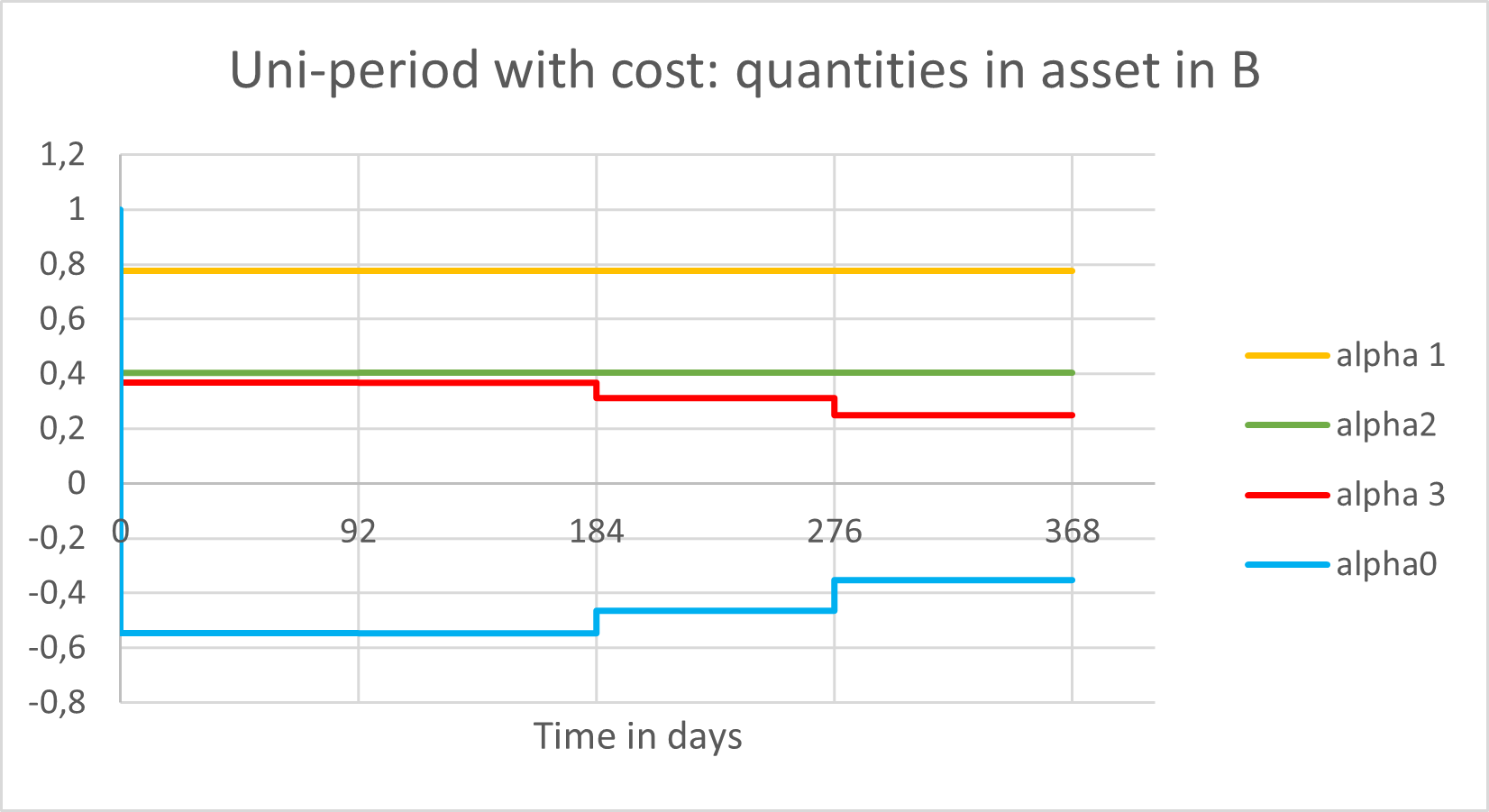

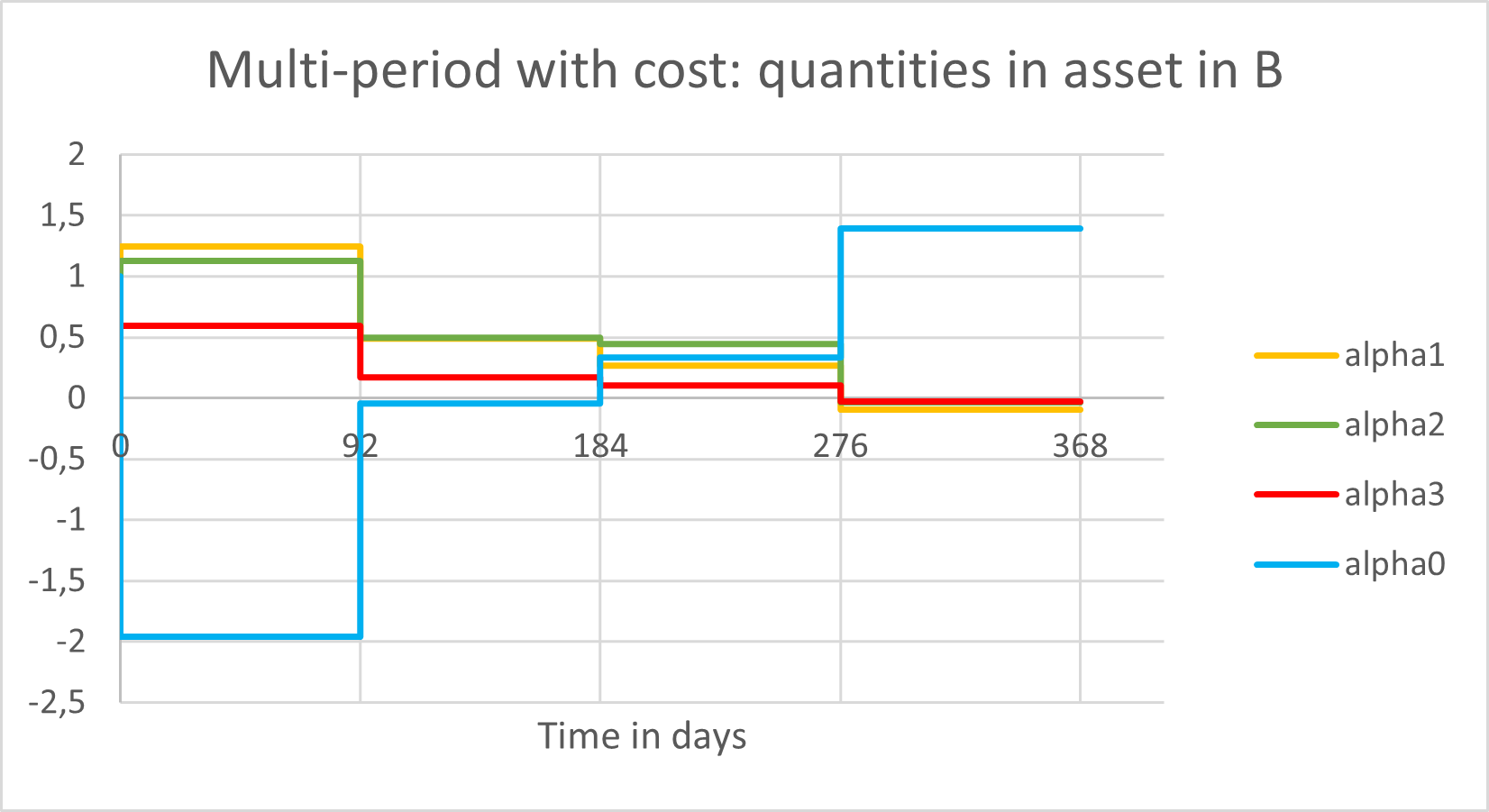

We respectively present in Figures 3, 3, 5, 5, the portfolios values, the cumulative costs and the controls of the uni-period model considering cost against the multi-period model considering cost, whose performances have been presented in Table 6.

By analysing Figure 3, both portfolio trajectories follow the trend of asset 3. This behavior is not surprising given the flat evolution of assets 1 and 2. The multi-period portfolio outperforms at every moment, for this particular realisation.

Figures 3 highlights that the uni-period strategy pays few cost compared to the multi-period one. This can be attributed to the myopic vision of the uni-period strategy, which results in a very flat strategy that is not very sensitive to asset and wealth variations. It can not embrace the benefit of sacrificing money in paying costs to anticipate future evolution.

The high costs required to make a reversal of strategy, further reinforce this inflexibility, which partly explains the low Sharpe ratio estimated in Section 5.2. The long position of this portfolio explains the high dependence with asset 3 and the decline of its value after the middle of the period.

The multi-period portfolio follows a completely different policy. While initially adopting a more aggressive long strategy than the uni-period portfolio, the level of risk taken is significantly higher. The portfolio performs well during the growth of asset 3 until day 276, at which point the strategy begins to reverse as assets are gradually sold. Subsequently, in response to the decline of asset 3, the strategy undergoes another shift, with new asset quantities being purchased.

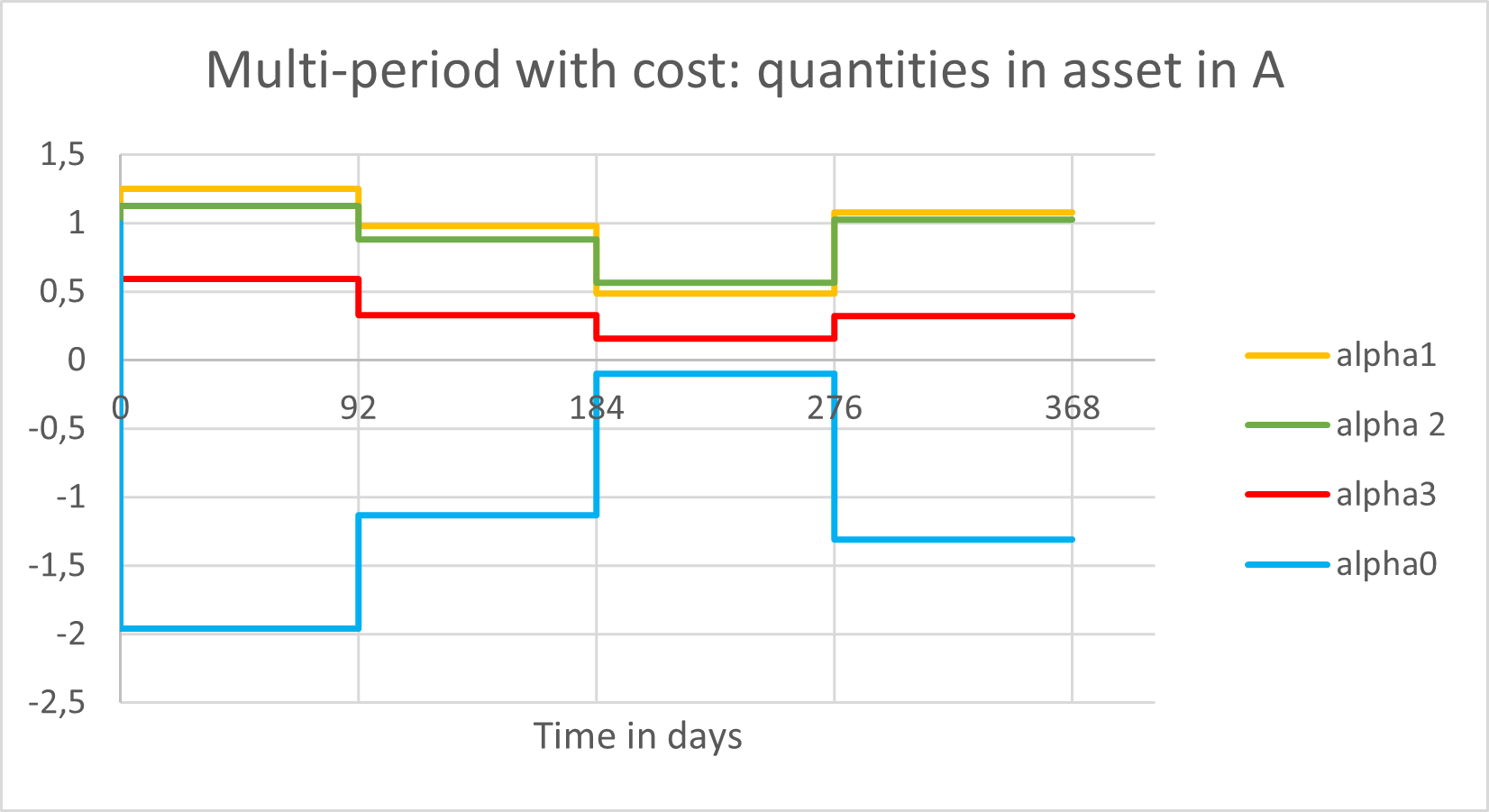

5.3.3 Behaviour on realisation B

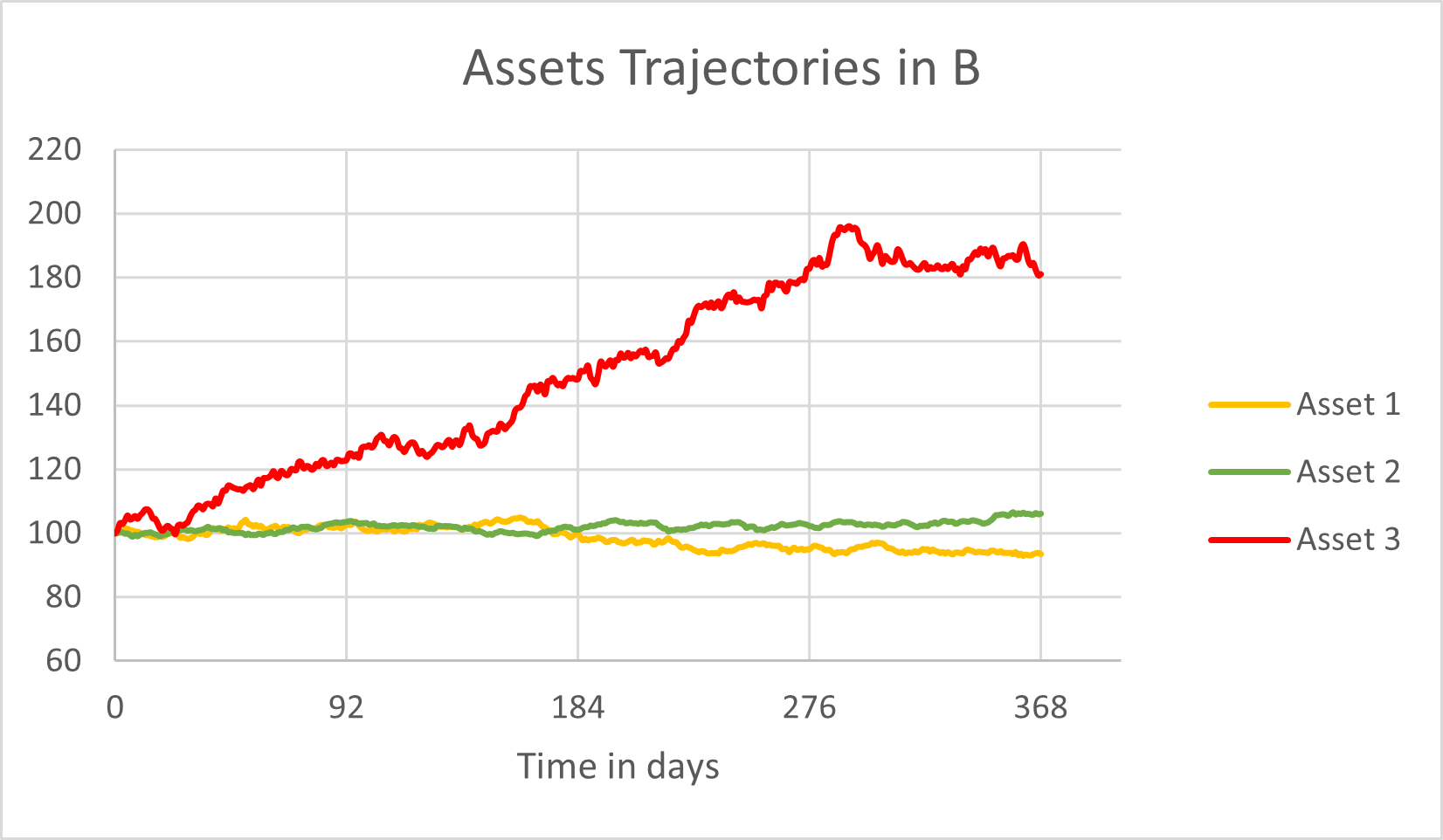

To illustrate the comparison, we present in Figures 6, a new realisation of the assets. This scenario looks like the previous one, as Asset 1 and 2 exhibit minimal changes while Asset 3 experiences a large increase without any significant decrease.

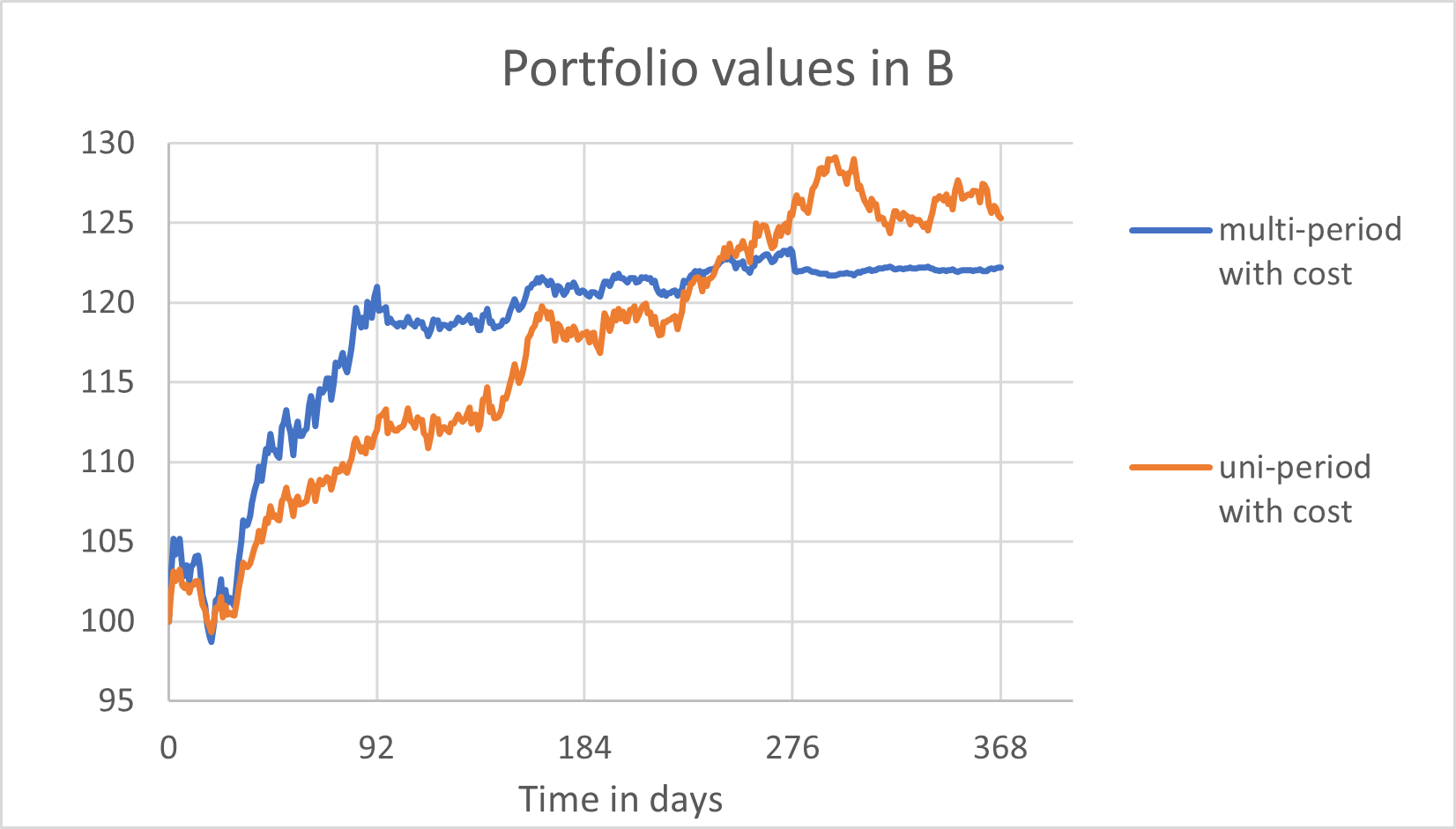

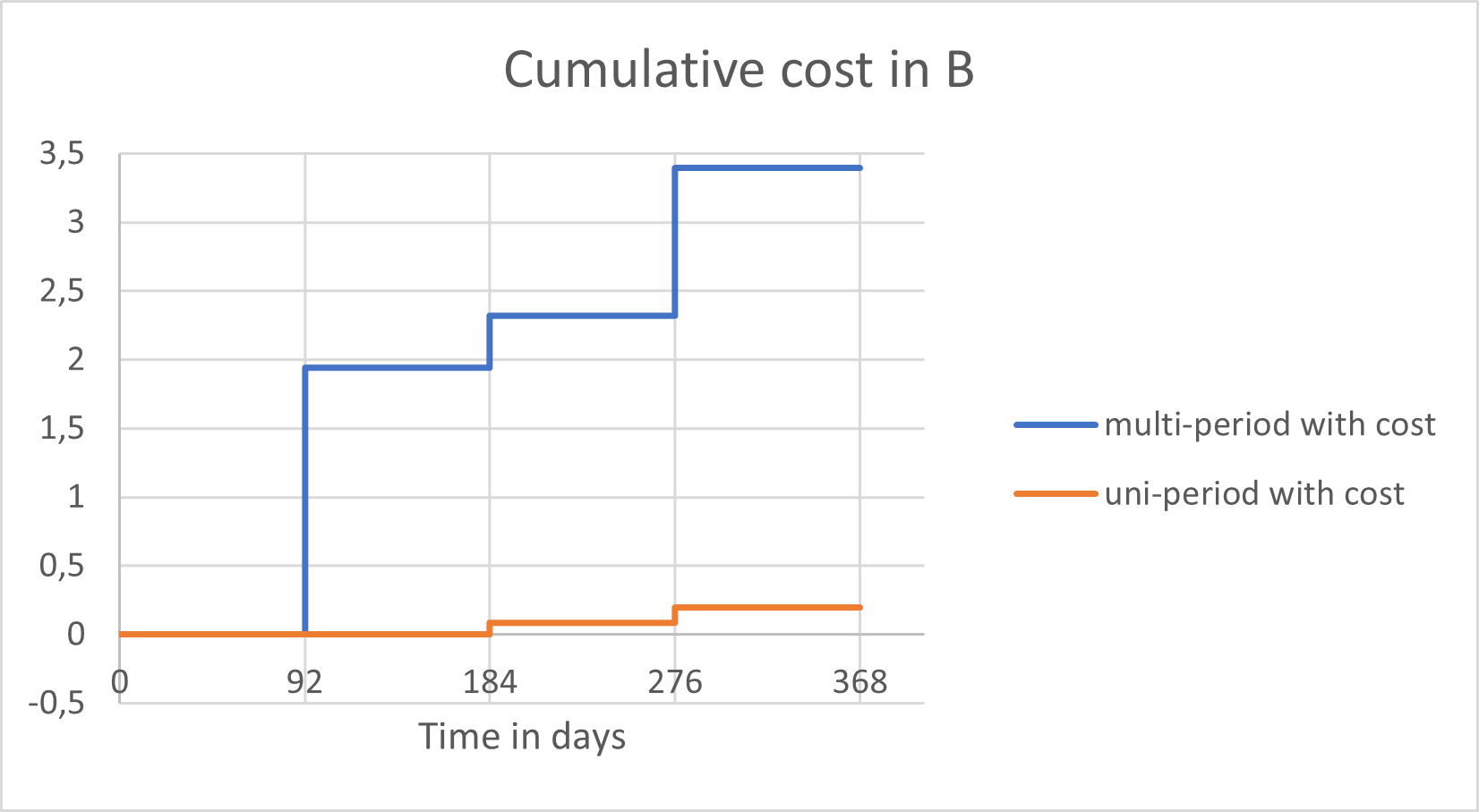

We present respectively in Figures 8, 8, 10, 10, the portfolios values, the cumulative costs and the controls of the uni-period model against the multi-period model with costs, whose performance results have been presented in Table 6.

Although both portfolios experience growth over the period, the uni-period portfolio with costs outperforms the multi-period portfolio at the end. It is important to note that this outcome is specific to this particular trajectory but cannot be generalised. The uni-period portfolio appears to closely track the trend of asset 3, which continues to perform toward the end of the period. As for the realisation A, the positions of the uni-period strategy maintains predominantly long and flat positions. The multi-period strategy is considerably different and more versatile. Following 276 days of long positions, all assets are sold. This reverse of positions explains the plateau reached. After performing , the portfolio eliminates all risk to insure a positive performance. Even if Asset 3 were to continue its upward trend, this approach remains prudent. The portfolio achieves a higher value than anticipated, justifying its wish to protect its gains.

6 Conclusion

In this paper, we have presented an efficient numerical method to solve multi-stage portfolio allocation that involve multiple assets and transaction costs. We applied a stochastic descent gradient algorithm to find the Wiener chaos expansion of an optimal portfolio. The method could be extended to handle realistic constraints as no-shorting and is computationally tractable. We explored the link between risk aversion and optimal portfolios subject to transaction costs, with two findings standing out. Firstly, we have proved that the Sharpe ratio of a locally optimal portfolio with transaction costs does not depend on its risk aversion. Secondly, we have established that all optimal portfolios have the same Sharpe ratio. We have used this result to compare our approach to a competitive benchmark, based on the sequential uni-period mean-variance strategy. We have highlighted the efficiency of our approach and we have showcased our benchmark by analyzing the performance of our models on two selected trajectories. Costs must not be ignored in multi-period setting since reverses of strategy are frequent. On the other hand, considering costs for uni-period models is still a topic of debate. The myopic effect with the consideration of costs may freeze the strategy and negatively impact performance. As expected, the multi-period model is more intricate, but outperforms the uni-period models.

Appendix A Wiener chaos expansion properties

In this Appendix, we present

several fundamental properties on Wiener chaos expansion and Hermite polynomials, use-full in our study. We refer to [1], [20]

[29] for theoretical details.

Let be the -th Hermite polynomial defined by

For , we define

We have the following properties

-

•

For , with .

-

•

For ,

-

•

Let , be two random variables with joint Gaussian distribution such that and . Then , we have

-

•

Let and be a n-multivariate i.i.d standard normal vector. Then we have

-

•

Let , and a n-multivariate i.i.d standard normal vector, then

The following theorem represents the basics of our approach. It provides a discrete-time general representation with a convergent series expansion. This expansion is introduced and proved in [1, Theorem 2.1].

Theorem 20.

Let Y , then the following Wiener chaos expansion holds

We call the truncated expansion of order

We have . Let us define be the number of coefficients appearing in the chaos expansion. We have . We slightly abuse the above definition and also write

Proposition 21.

Let , then

| (37) |

where

The Wiener chaos expansion of the conditional expectation of the variable Y is obtained by truncating the terms which are not -measurable.

Appendix B Differentiability

In this appendix, we study the differentiability of . In our resolution framework, we assume that is deterministic.

Proposition 22.

is almost surely differentiable on .

Proof.

Let us prove that the , . We recall that

Let be the operator which associates to a vector the matrix .

We define

Note that is deterministic and invertible. We slightly abuse of the notation to denote the vector . We have

The term can be expressed as a linear combination of the chaos coefficients of such that

| (38) |

For , we obtain

Note that can be written as

| (39) |

With the definition of , we deduce that .

Let us introduce the following two spaces for ,

We can deduce from (39) that such that . Finally, we conclude that , .

Proposition 23.

The function

is differentiable on .

Proof.

Let and , such that , . According to Lemma 11, we have

Since we have , , we have and . We bound

So . According to Proposition 22, is a.s. differentiable on , then is also a.s. differentiable on . We also have

Following the same arguments, we prove that

We conclude using Cauchy Schwartz’ inequality that . Similarly, we bound

Finally, we apply Lebesgue’s theorem to conclude that is differentiable on and

Appendix C Benchmark models

Here, we present different approaches used to benchmark and challenge the multi-period one, described in Section 3. A first element of comparison is the multi-period approach itself but which ignores transaction costs. A second comparison is done with the sequential uni-period Markowitz framework. We present two versions of this approach, when cost are ignored and considered. We also study the link of risk aversion on optimal solutions for those benchmark models.

C.1 Benchmark: Multi-period allocation Ignoring transaction costs

A natural an simplified approach consists in applying the framework described in Section 3, while ignoring costs. Costs are removed from the portfolio value but do not impact the strategy. Theoretically, we look for an optimal strategy whose costs are refunded. The control , are solution to () by temporally setting during the resolution. Formally, we solve

| () | ||||||

| s.t. | ||||||

Then, the real quantity in risk free asset at stake is deduced with the auto-financing relation and by removing costs generated by the real value of . Formally, after maximizing (), the generated cost is computed and removed to obtain the real portfolio value . This strategy is implemented in order to observe the effect of costs on optimal strategies.

C.2 Benchmark: Sequential Uni-period Markowitz portfolio allocation

In this section, we present an alternative approach, intended to serve as a benchmark. We would like to compare the performance of our method to a method traditionally applied by asset managers. We propose to implement the sequential uni-period mean–variance Markowitz framework. This approach also corresponds to the one-time-step Model Predictive Control (MPC) described in [22]. In order to maximise the rate of return of a portfolio while controlling its volatility at time , an agent consecutively maximizes at time , its uni-period mean-var objective function. We assume that the agent has an uni-period risk aversion parameter . The agent has to consecutively solve for ,

| () | ||||||

| s.t. |

We present two versions of this model. A naive version, where the asset manager pays the cost but does not take the amount into account in its strategy (by ignoring them), is presented in Section C.2.1. In a second version, described in Section C.2.2, the investor consecutively solves () and bases his strategy according to the cost he will have to pay.

C.2.1 Ignoring costs

We aim to propose here, a simplified version of the initial sequential uni-period problem (). The underlying idea is the same as the multi-period version described in Section C.1. At each time step, the agent maximizes its mean-var utility function as though costs are refunded. Costs do not impact the strategy and are just removed from the portfolio value at the end. The agent has to consecutively solve for ,

| () | ||||||

| s.t. |

Let be a solution and , the associated portfolio. The real portfolio is computed after removing the generated costs such that According to the dynamics of the assets, we have for ,

By calling and , We have

| (40) |

Remark 24.

It is equivalent to remove costs at each time step or to remove them at the end because the quantity in the risk free asset does not impact the strategy.

Comparing the multi-period strategy with this framework is a difficult task. The risk aversion parameters and in the two models, do not refer to the same risk aversion for the agent. We need to find a correct matching, or a measure of performance, independent from risk aversion. Obviously, this measure is the Sharpe ratio.

Proposition 25.

The Sharpe ratio of the sequential uni-period Markowitz strategy which ignores costs, does not depend on the risk aversion parameter .

Proof.

We prove by recurrence ,

is true with . We assume true for . We have

By using that , and the form of the solution in (LABEL:eq:uni-withoutcost), we rewrite

We prove by denoting

Using this form we deduce that Finally

which does not depend on .

C.2.2 Taking costs into account

In this version, costs are taken into account in the objective function but the strategy remains myopic.

We recall that the agent has to consecutively solve ().

In the presence of costs, we do not provide an explicit solution of ().

In order to use this model as a benchmark, let us prove an analog result to Proposition 25.

Proposition 26.

The Sharpe ratio of the sequential uni-period Markowitz strategy considering costs, does not depend on the risk aversion parameter .

Proof.

With the notation of the previous section, () can be rewritten as

Let us consider the objective functions

is strictly concave and , then () has an unique solution. We call the solution of (). is differentiable on , where . admits a sub-differential , at any point

We have .

Let us show by recurrence ,

is true with .

We assume true for . If such that then it is sufficient to choose .

If , then

Let us define a -measurable random variable such that . Then with the form of , we have

We can deduce that is not a function of . Therefore is the chosen candidate to be . is then true, and true for all . Then is is easy to check that

which is not a function of .

References

- [1] J. Akahori, T. Amaba, and K. Okuma, A discrete-time clark–ocone formula and its application to an error analysis, Journal of Theoretical Probability, 30 (2017), pp. 932–960.

- [2] M. Al-Nator, S. Al-Nator, and Y. F. Kasimov, Multi-period markowitz model and optimal self-financing strategy with commission, Journal of Mathematical Sciences, 248 (2020), pp. 33–45.

- [3] A. Bachouch, C. Huré, N. Langrené, and H. Pham, Deep neural networks algorithms for stochastic control problems on finite horizon: numerical applications, Methodology and Computing in Applied Probability, (2021), pp. 1–36.

- [4] D. Bertsimas and D. Pachamanova, Robust multiperiod portfolio management in the presence of transaction costs, Computers & Operations Research, 35 (2008), pp. 3–17.

- [5] M. J. Best and J. Hlouskova, An algorithm for portfolio optimization with variable transaction costs, part 1: theory, Journal of optimization theory and applications, 135 (2007), pp. 563–581.

- [6] S. Boyd, M. T. Mueller, B. O’Donoghue, Y. Wang, et al., Performance bounds and suboptimal policies for multi–period investment, Foundations and Trends® in Optimization, 1 (2013), pp. 1–72.

- [7] D. B. Brown and J. E. Smith, Dynamic portfolio optimization with transaction costs: Heuristics and dual bounds, Management Science, 57 (2011), pp. 1752–1770.

- [8] Y. Cai, K. L. Judd, and R. Xu, Numerical solution of dynamic portfolio optimization with transaction costs, tech. rep., National Bureau of Economic Research, 2013.

- [9] G. C. Calafiore, Multi-period portfolio optimization with linear control policies, Automatica, 44 (2008), pp. 2463–2473.

- [10] F. Cong and C. W. Oosterlee, Multi-period mean–variance portfolio optimization based on monte-carlo simulation, Journal of Economic Dynamics and Control, 64 (2016), pp. 23–38.

- [11] G. M. Constantinides, Multiperiod consumption and investment behavior with convex transactions costs, Management Science, 25 (1979), pp. 1127–1137.

- [12] X. Cui, J. Gao, X. Li, and D. Li, Optimal multi-period mean–variance policy under no-shorting constraint, European Journal of Operational Research, 234 (2014), pp. 459–468.

- [13] M. Dai, Z. Q. Xu, and X. Y. Zhou, Continuous-time markowitz’s model with transaction costs, SIAM Journal on Financial Mathematics, 1 (2010), pp. 96–125.

- [14] M. Dai and Y. Zhong, Penalty methods for continuous-time portfolio selection with proportional transaction costs, Available at SSRN 1210105, (2008).

- [15] M. H. Davis and A. R. Norman, Portfolio selection with transaction costs, Mathematics of operations research, 15 (1990), pp. 676–713.

- [16] T. Draviam and T. Chellathurai, Generalized markowitz mean–variance principles for multi–period portfolio–selection problems, Proceedings of the Royal Society of London. Series A: Mathematical, Physical and Engineering Sciences, 458 (2002), pp. 2571–2607.

- [17] B. Dumas and E. Luciano, An exact solution to a dynamic portfolio choice problem under transactions costs, The Journal of Finance, 46 (1991), pp. 577–595.

- [18] G. Gennotte and A. Jung, Investment strategies under transaction costs: The finite horizon case, Management Science, 40 (1994), pp. 385–404.

- [19] H. Holden and L. Holden, Optimal rebalancing of portfolios with transaction costs, Stochastics An International Journal of Probability and Stochastic Processes, 85 (2013), pp. 371–394.

- [20] J. Lelong, Dual pricing of american options by wiener chaos expansion, SIAM Journal on Financial Mathematics, 9 (2018), pp. 493–519.

- [21] D. Li and W.-L. Ng, Optimal dynamic portfolio selection: Multiperiod mean-variance formulation, Mathematical finance, 10 (2000), pp. 387–406.

- [22] X. Li, A. S. Uysal, and J. M. Mulvey, Multi-period portfolio optimization using model predictive control with mean-variance and risk parity frameworks, European Journal of Operational Research, 299 (2022), pp. 1158–1176.

- [23] X. Li, X. Y. Zhou, and A. E. Lim, Dynamic mean-variance portfolio selection with no-shorting constraints, SIAM Journal on Control and Optimization, 40 (2002), pp. 1540–1555.

- [24] M. S. Lobo, M. Fazel, and S. Boyd, Portfolio optimization with linear and fixed transaction costs, Annals of Operations Research, 152 (2007), pp. 341–365.

- [25] H. M. Markowits, Portfolio selection, Journal of finance, 7 (1952), pp. 71–91.

- [26] R. C. Merton, Lifetime portfolio selection under uncertainty: The continuous-time case, The review of Economics and Statistics, (1969), pp. 247–257.

- [27] A. J. Morton and S. R. Pliska, Optimal portfolio management with fixed transaction costs, Mathematical Finance, 5 (1995), pp. 337–356.

- [28] K. Muthuraman and S. Kumar, Multidimensional portfolio optimization with proportional transaction costs, Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 16 (2006), pp. 301–335.

- [29] D. Nualart, The Malliavin calculus and related topics, vol. 1995, Springer, 2006.

- [30] H. Peng, G. Kitagawa, M. Gan, and X. Chen, A new optimal portfolio selection strategy based on a quadratic form mean–variance model with transaction costs, Optimal Control Applications and Methods, 32 (2011), pp. 127–138.

- [31] G. A. Pogue, An extension of the markowitz portfolio selection model to include variable transactions’ costs, short sales, leverage policies and taxes, The Journal of Finance, 25 (1970), pp. 1005–1027.

- [32] C. S. Pun and Z. Ye, Optimal dynamic mean–variance portfolio subject to proportional transaction costs and no-shorting constraint, Automatica, 135 (2022), p. 109986.

- [33] P. A. Samuelson, Lifetime portfolio selection by dynamic stochastic programming, Stochastic optimization models in finance, (1975), pp. 517–524.

- [34] M. C. Steinbach, Markowitz revisited: mean-variance models in financial portfolio analysis, SIAM Review, 43 (2001), pp. 31–85.

- [35] U. Topcu, G. Calafiore, and L. El Ghaoui, Multistage investments with recourse: A single-asset case with transaction costs, in 2008 47th IEEE Conference on Decision and Control, IEEE, 2008, pp. 2398–2403.

- [36] Z. Wang and S. Liu, Multi-period mean-variance portfolio selection with fixed and proportional transaction costs, Journal of Industrial & Management Optimization, 9 (2013), p. 643.

- [37] H.-G. Xue, C.-X. Xu, and Z.-X. Feng, Mean–variance portfolio optimal problem under concave transaction cost, Applied Mathematics and Computation, 174 (2006), pp. 1–12.

- [38] A. Yoshimoto, The mean-variance approach to portfolio optimization subject to transaction costs, Journal of the Operations Research Society of Japan, 39 (1996), pp. 99–117.

- [39] X. Y. Zhou and D. Li, Continuous-time mean-variance portfolio selection: A stochastic lq framework, Applied Mathematics and Optimization, 42 (2000), pp. 19–33.