Learning Rate Free Sampling

in Constrained Domains

Abstract

We introduce a suite of new particle-based algorithms for sampling in constrained domains which are entirely learning rate free. Our approach leverages coin betting ideas from convex optimisation, and the viewpoint of constrained sampling as a mirrored optimisation problem on the space of probability measures. Based on this viewpoint, we also introduce a unifying framework for several existing constrained sampling algorithms, including mirrored Langevin dynamics and mirrored Stein variational gradient descent. We demonstrate the performance of our algorithms on a range of numerical examples, including sampling from targets on the simplex, sampling with fairness constraints, and constrained sampling problems in post-selection inference. Our results indicate that our algorithms achieve competitive performance with existing constrained sampling methods, without the need to tune any hyperparameters.

1 Introduction

The problem of sampling from unnormalised probability distributions is of central importance to computational statistics and machine learning. Standard approaches to this problem include Markov chain Monte Carlo (MCMC) [76, 11] and variational inference (VI) [96, 41]. More recently, there has been growing interest in particle-based variational inference (ParVI) methods, which deterministically evolve a collection of particles towards the target distribution and combine favourable aspects of both MCMC and VI. Perhaps the most well-known of these methods is Stein variational gradient descent (SVGD) [63], which iteratively updates particles according to a form of gradient descent on the Kullback-Leibler (KL) divergence. This approach has since given rise to several extensions [27, 97, 105, 16] and found success in a wide range of applications [27, 66, 74].

While such methods have enjoyed great success in sampling from unconstrained distributions, they typically break down when applied to constrained targets [see, e.g., 82, 60]. This is required for targets that are not integrable over the entire Euclidean space (e.g., the uniform distribution), when the target density is undefined outside a particular domain (e.g., the Dirichlet distribution), or when the target must satisfy certain additional constraints (e.g., fairness constraints in Bayesian inference [65]). Notable examples include latent Dirichlet allocation [9], ordinal data models [45], regularised regression [15], survival analysis [49], and post-selection inference [88, 54]. In recent years, there has been increased interest in this topic, with several new methodological and theoretical developments [43, 19, 103, 1, 44, 61, 82, 86, 104, 60].

One limitation shared by all of these methods is that their performance depends, often significantly, on a suitable choice of learning rate. In principle, convergence rates for existing constrained sampling schemes (e.g., [1, Theorem 1] or [86, Corollary 1]) allow one to compute the optimal learning rate for a given problem. In practice, however, this optimal learning rate is a function of the unknown target and thus cannot be computed. Motivated by this problem, in this paper we introduce a suite of new sampling algorithms for constrained domains which are entirely learning rate free.

Our contributions We first propose a unifying perspective of several existing constrained sampling algorithms, based on the viewpoint of sampling in constrained domains as a ‘mirrored’ optimisation problem on the space of probability measures. Based on this perspective, we derive a general class of solutions to the constrained sampling problem via the mirrored Wasserstein gradient flow (MWGF). The MWGF includes, as special cases, several existing constrained sampling methods, e.g., mirrored Langevin dynamics [43] and mirrored SVGD (MSVGD) [82]. Using this formulation, we also introduce mirrored versions of several other particle-based sampling algorithms which are suitable for sampling in constrained domains, and study their convergence properties in continuous time.

By leveraging this perspective, and extending the coin sampling methodology recently introduced in [81], we then obtain a suite of learning rate free algorithms suitable for constrained domains. In particular, we introduce mirrored coin sampling, which includes as a special case Coin MSVGD, as well as several other tuning-free constrained sampling algorithms. We also outline an alternative approach which does not rely on a mirror mapping, namely, coin mollified interaction energy descent (Coin MIED). This algorithm can be viewed as the natural coin sampling analogue of the method recently introduced in [60]. Finally, we demonstrate the performance of our methods on a wide range of examples, including sampling on the simplex, sampling with fairness constraints, and constrained sampling problems in post-selection inference. Our empirical results indicate that our methods achieve competitive performance with the optimal performance of existing approaches, with no need to tune a learning rate.

2 Preliminaries

The Wasserstein Space. We will make use of the following notation. For any , we write for the set of probability measures on with finite moment: , where denotes the Euclidean norm. For , we write for the set of measurable with finite . For , we also define . Given and , we write for the pushforward of under , that is, the distribution of when .

Given , the Wasserstein -distance between and is defined according to , where denotes the set of couplings between and . The Wasserstein distance is indeed a distance over [2, Chapter 7.1], with the metric space known as the Wasserstein space. Given a functional , we will write for the Wasserstein gradient of at , which exists under appropriate regularity conditions [2, Lemma 10.4.1]. We refer to App. A for further details on calculus in the Wasserstein space.

Wasserstein Gradient Flows. Suppose that and that admits a density with respect to Lebesgue measure,111In a slight abuse of notation, throughout this paper we will use the same letter to refer to a distribution and its density with respect to Lebsegue measure. where is a smooth potential function. The problem of sampling from can be recast as an optimisation problem over [e.g., 99]. In particular, one can view the target as the solution of

| (1) |

where is a functional uniquely minimised at . In the unconstrained case, , a now rather classical method for solving this problem is to identify a continuous process which pushes samples from an initial distribution to the target . This corresponds to finding a family of vector fields , with , which transports to via the continuity equation

| (2) |

A standard choice is , in which case the solution of (2) is referred to as the Wasserstein gradient flow (WGF) of . In fact, for different choices of , one can obtain the continuous-time limit of several popular sampling algorithms [46, 99, 40, 3, 51, 63, 20]. Unfortunately, it is not straightforward to extend these approaches to the case in which is a constrained domain. For example, the vector fields may push the random variable outside of its support , thus rendering all future updates undefined.

3 Mirrored Wasserstein Gradient Flows

We now outline one way to extend the WGF approach to the constrained case, based on the use of a mirror map. We will first require some basic definitions from convex optimisation [e.g., 77]. Let be a closed, convex domain in . Let be a proper, lower semicontinuous, strongly convex function of Legendre type [77]. This implies, in particular, that and is bijective [77, Theorem 26.5]. Moreover, its inverse satisfies , where denotes the Fenchel conjugate of , defined as . We will refer to as the mirror map and as the dual space.

3.1 Constrained Sampling as Optimisation

Using the mirror map , we can now reformulate the constrained sampling problem as the solution of a ‘mirrored’ version of the optimisation problem in (1). Let us define , with . We can then view the target as the solution of

| (3) |

where now is a functional uniquely minimised by . The motivation for this formulation is clear. Rather than directly solving a constrained optimisation problem for the target as in (1), we could instead solve an unconstrained optimisation problem for the mirrored target , and then recover the target via . This is a rather natural extension of the formulation of sampling as optimisation to the constrained setting.

3.2 Mirrored Wasserstein Gradient Flows

One way to solve the mirrored optimisation problem in (3) is to find a continuous process which transports samples from to the mirrored target . According to the mirror map, this process will implicitly also push samples from to the target . More precisely, we would like to find , where , which evolves on and thus on , through

| (4) |

where should ensure convergence of to . In the case that , we will refer to (4) as the mirrored Wasserstein gradient flow (MWGF) of . The idea of (4) is to simulate the WGF in the (unconstrained) dual space and then map back to the primal (constrained) space using a carefully chosen mirror map. This approach bypasses the inherent difficulties associated with simulating a gradient flow on the constrained space itself.

While a similar approach has previously been used to derive certain mirrored sampling schemes [43, 82, 86], these works focus on specific choices of and , while we consider the general case. Our general perspective provides a unifying framework for these approaches, whilst also allowing us to obtain new constrained sampling algorithms and to study their convergence properties (see App. B). We now consider one such approach in detail.

3.2.1 Mirrored Stein Variational Gradient Descent

MSVGD [82] is a mirrored version of the popular SVGD algorithm. In [82], MSVGD is derived using a mirrored Stein operator in a manner analogous to the original SVGD derivation [63]. Here, we take an alternative perspective, which originates in the MWGF. This formulation is more closely aligned with other more recent papers analysing the non-asymptotic convergence of SVGD [51, 78, 85, 86].

We will require the following additional notation. Let denote a positive semi-definite kernel and the corresponding reproducing kernel Hilbert space (RKHS) of real-valued functions , with inner product and norm . Let denote the Cartesian product RKHS, consisting of elements for . We write for the operator . We assume for , in which case for all [52, Sec. 3.1]. We also define the identity embedding with adjoint . Finally, we define as .

We are now ready to introduce our perspective on MSVGD. We begin by introducing the continuous-time MSVGD dynamics, which are defined by the continuity equation

| (5) |

where for some base kernel . Clearly, this is a special case of the MWGF in (4), in which are defined according to , with . In particular, can be interpreted as the negative Wasserstein gradient of , the KL divergence of the with respect to , under the inner product of .

The key point here is that, given samples from , estimating is straightforward. In particular, if , then, integrating by parts,

| (6) |

To obtain an implementable algorithm, we must discretise in time. By applying an explicit Euler discretisation to (5), we arrive at

| (7) |

where is a step size or learning rate, and is the identity map. This is the population limit of the MSVGD algorithm in [82]. Now, suppose admits a density with respect to the Lebesgue measure. In addition, suppose and . Then, for , if we define

| (8) |

then and in (7) are precisely the densities of and in (8). In practice, these densities are unknown and must be estimated using samples. In particular, to approximate (8), we initialise a collection of particles for , set , and then update

| (9) |

where . This is precisely the MSVGD algorithm introduced in [82] and since also studied in [86].

3.2.2 Other Algorithms

In App. B, we outline several algorithms which arise as special cases of the MWGF. These include existing algorithms, such as the mirrored Langevin dynamics (MLD) [43] and MSVGD [82], and two new algorithms, which correspond to mirrored versions of Laplacian adjusted Wasserstein gradient descent (LAWGD) [20] and kernel Stein discrepancy descent (KSDD) [51]. We also study the convergence properties of these algorithms in continuous time.

4 Mirrored Coin Sampling

By construction, any algorithm derived as a discretisation of the MWGF, including MSVGD, will depend on an appropriate choice of learning rate . In this section, we consider an alternative approach, leading to new algorithms which are entirely learning rate free. Our approach can be viewed as an extension of the coin sampling framework introduced in [81] to the constrained setting, based on the reformulation of the constrained sampling problem as a mirrored optimisation problem.

4.1 Coin Sampling

We begin by reviewing the general coin betting framework [71, 72, 22]. Consider a gambler with initial wealth who makes bets on a series of adversarial coin flips , where denotes heads and denotes tails. We encode the gambler’s bet by . In particular, denotes whether the bet is on heads or tails, and denotes the size of the bet. Thus, in the round, the gambler wins if and loses otherwise. Finally, we write for the wealth of the gambler at the end of the round. The gambler’s wealth thus accumulates as . We assume that the gambler’s bets satisfy , for a betting fraction , which means the gambler does not borrow any money.

In [71], the authors show how this approach can be used to solve convex optimisation problems on , that is, problems of the form , for convex . In particular, [71] consider a betting game with ‘outcomes’ , replacing scalar multiplications by scalar products . In this case, under certain assumptions, they show that at a rate determined by the betting strategy. There are many suitable choices for the betting strategy. Perhaps the simplest of these is , known as the Krichevsky-Trofimov (KT) betting strategy [53, 71], which yields the sequence of bets . Other choices, however, are also possible [72, 22, 70].

In [81], this approach was extended to solve optimisation problems on the space of probability measures. In this case, several further modifications are necessary. First, in each round, one now bets rather than , where is distributed according to some . In this case, viewing as a function that maps , one can define a sequence of distributions as the push-forwards of under the functions . In particular, this means that, if , then .

By using these modifications in the original coin betting framework, and choosing appropriately, [81] show that it is now possible to solve problems of the form . This approach is referred to as coin sampling. For example, by considering a betting game with , [81] obtain a ‘coin Wasserstein gradient descent’ algorithm, which can be viewed as a learning-rate free analogue of Wasserstein gradient descent. Alternatively, setting , one can obtain a learning-rate free analogue of the population limit of SVGD, in which the updates are given by

| (10) |

where, as described above, . In practice, the densities and thus the outcomes are almost always intractable, and will be approximated using a set of interacting particles.

4.2 Mirrored Coin Sampling

By leveraging the formulation of constrained sampling as a ‘mirrored’ optimisation problem over the space of probability measures, we can extend the coin sampling approach to constrained domains. In particular, as an alternative to discretising the MWGF to solve this optimisation problem (Sec. 3.2), we propose instead to use a mirrored version of coin sampling (Sec. 4.1). The idea is to use coin sampling to solve the optimisation problem in the dual space, and then map back to the primal space using the mirror map. In particular, this suggests the following scheme. Let , and . Then, for , update

| (11) |

where and , and where , or some variant thereof. We will refer to this approach as mirrored coin sampling, or mirrored coin Wasserstein gradient descent. In order to obtain an implementable algorithm, we proceed as follows. First, decide on a suitable functional and a suitable . For example, , and . Then, substitute these into (11), and approximate the updates using a set of interacting particles, as in existing ParVIs algorithms.

Following these steps, we obtain a learning rate free analogue of MSVGD [82], which we will refer to as Coin MSVGD. This is summarised in Alg. 2. For different choices of in (11), we also obtain learning rate free analogues of two other mirrored ParVI algorithms introduced in App. B, namely mirrored LAWGD (App. B.3), and mirrored KSDD (App. B.4). These algorithms, which we term Coin MLAWGD and Coin MKSDD, are given in Alg. 6 and Alg. 7 in App. D.

Even in the unconstrained setting, establishing the convergence of coin sampling remains an open problem. In [81], the authors provide a technical sufficient condition under which it is possible to establish convergence to the target measure in the population limit; however, it is difficult to verify this condition in general. In the interest of completeness, in App. C, we provide an analogous convergence result for mirrored coin sampling, adapted appropriately to the constrained setting.

4.3 Alternative Approaches

In this section, we outline an alternative approach, based on a ‘coinification’ of the mollified interaction energy descent (MIED) method recently introduced in [60]. MIED is based on minimising a function known as the mollified interaction energy (MIE) . The idea is that minimising this function balances two forces: a repulsive force which ensures the measure is well spread, and an attractive force which ensures the measure is concentrated around regions of high density. In order to obtain a practical sampling algorithm, [60] propose to minimise a discrete version of the logarithmic MIE, using, e.g., Adagrad [31] or Adam [48]. That is, minimising the function

| (12) |

where , and where is a family of mollifiers [60, Definition 3.1]. This approach can be adapted to handle the constrained case, as outlined in [60]. In particular, if there exists a differentiable such that has Lebesgue measure zero, then one can reduce the constrained problem to an unconstrained one by minimising , where . Meanwhile, if for some differentiable , then one can use a variant of the dynamic barrier method introduced in [37].

Here, as an alternative to the optimisation methods considered in [60], we instead propose to use a learning-rate free algorithm to minimise (12), based on the coin betting framework described in 4.1. We term the resulting method, summarised in Alg. 3, Coin MIED. In comparison to our mirrored coin sampling algorithm, this approach has the advantage that it only requires a differentiable (not necessarily bijective) map.

5 Related Work

Sampling as Optimisation. The connection between sampling and optimisation has a long history, dating back to [46], which established that the evolution of the law of the Langevin diffusion corresponds to the WGF of the KL divergence. In recent years, there has been renewed interest in this perspective [99]. In particular, the viewpoint of existing algorithms such as LMC [23, 24, 33, 34] and SVGD [63, 32] as discretisations of WGFs has proved fruitful in deriving sharp convergence rates [34, 6, 52, 78, 85, 83]. It has also resulted in the rapid development of new sampling algorithms, inspired by ideas from the optimisation literature such as proximal methods [100], coordinate descent [30, 29], Nesterov acceleration [18, 25, 67], Newton methods [68, 84, 98], and coin betting [81, 80].

Sampling in Constrained Domains. Recent interest in constrained sampling has resulted in a range of general-purpose algorithms for this task [e.g., 43, 103, 82, 104, 60]. In cases where it is possible to explicitly parameterise the target domain in a lower dimensional space, one can use variants of classical methods, including LMC [98], rejection sampling [28], Hamiltonian Monte Carlo (HMC) [13], and Riemannian manifold HMC [55, 73]. Several other approaches are based on the use of mirror map. In particular, [43] proposed mirrored Langevin dynamics and its first-order discretisation. [103], and an earlier draft of [43], introduced the closely related mirror Langevin diffusion and the mirror Langevin algorithm, which has since also been studied in [44, 19, 1, 61]. Along the same lines, [82] introduced two variants of SVGD suitable for constrained domains based on the use of a mirror map, and established convergence of these schemes to the target distribution; see also [86]. In certain cases [e.g., 56, 58] one cannot explicitly parameterise the manifold of interest. In this setting, different approaches are required. [12] introduced a constrained version of HMC for this case. Meanwhile, [102] proposed a constrained Metropolis-Hastings algorithm with a reverse projection check to ensure reversibility; this approach has since been extended in [57, 59]. Other, more recent approaches suitable for this setting include MIED [60] (see Sec. 4.3), and O-SVGD [104].

6 Numerical Results

In this section, we perform an empirical evaluation of Coin MSVGD (Sec. 6.1 - 6.2) and Coin MIED (Sec. 6.3). We consider several simulated and real data experiments, including sampling from targets defined on the simplex (Sec. 6.1), confidence interval construction for post-selection inference (Sec. 6.2), and inference in a fairness Bayesian neural network (Sec. 6.3). We compare our methods to their learning-rate-dependent analogues, namely, MSVGD [82] and MIED [60]. We also include a comparison with Stein Variational Mirror Descent (SVMD) [82], and projected versions of Coin SVGD [81] and SVGD [63], which include a Euclidean projection step to ensure the iterates remain in the domain. We provide additional experimental details in App. F and additional numerical results in App. G. Code to reproduce all of the numerical results can be found at https://github.com/louissharrock/constrained-coin-sampling.

6.1 Simplex Targets

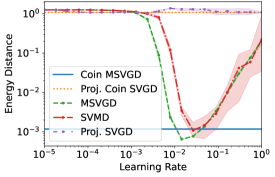

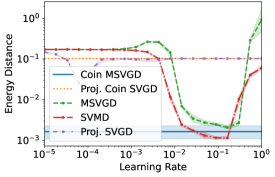

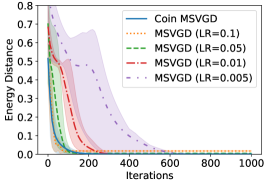

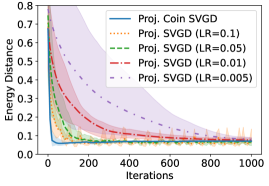

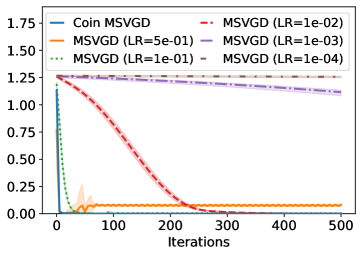

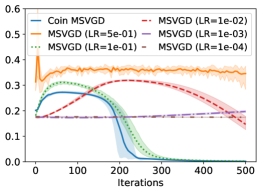

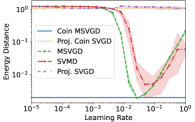

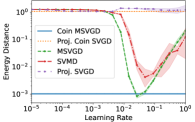

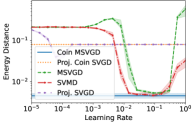

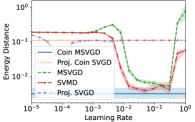

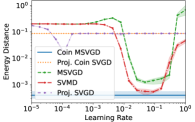

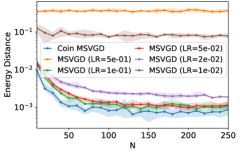

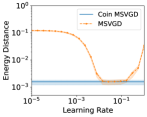

Following [82], we first test the performance of our algorithms on two 20-dimensional targets defined on the simplex: the sparse Dirichlet posterior of [73] and the quadratic simplex target of [1]. We employ the IMQ kernel and the entropic mirror map [7]; and use particles, iterations. In Fig. 1 and Fig. 6 - 7 (App. F.1), we plot the energy distance [87] to a set of surrogate ground truth samples, either obtained i.i.d. (sparse Dirichlet target) or using the No-U-Turn Sampler (NUTS) [42] (quadratic target). After iterations, Coin MSVGD has comparable performance to MSVGD and SVMD with optimal learning rates but significantly outperforms both algorithms for sub-optimal learning rates (Fig. 1). In both cases, the projected methods fail to converge. For the sparse Dirichlet posterior, Coin MSVGD converges more rapidly than MSVGD and SVMD, even for well-chosen values of the learning rate (Fig. 6a in App. F.1). Meanwhile, for the quadratic target, Coin MSVGD generally converges more rapidly than MSVGD but not as fast as SVMD [82], which takes advantage of the log-concavity of the target in the primal space (Fig. 6a in App. F.1).

6.2 Confidence Intervals for Post Selection Inference

We next consider a constrained sampling problem arising in post-selection inference [88, 54]. Suppose we are given data . We are interested in obtaining valid confidence intervals (CIs) for regression coefficients obtained via the randomised Lasso [89], defined as the solution of

| (13) |

where are penalty parameters and is an auxiliary random vector. Let represent the non-zero coefficients of and for their signs. If the support were known a priori, we could determine CIs for using the asymptotic normality of . However, when is based on data, these ‘classical’ CIs will no longer be valid. In this case, one approach is to condition on the result of the initial model selection, i.e., knowledge of and . In practice, this means sampling from the so-called selective distribution, which has support , and density proportional to [e.g., 90, Sec. 4.2]

| (14) |

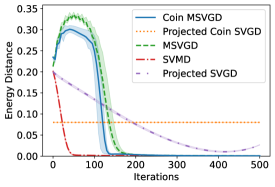

Synthetic Example. We first consider the model setup described in [79, Sec. 5.3]; see App. F.2 for full details. In Fig. 2, we plot the energy distance between samples obtained using Coin MSVGD and projected Coin SVGD, and a set of 1000 samples obtained using NUTS [42], for a two-dimensional selective distribution. Similar to our previous examples, the performance of MSVGD is very sensitive to the choice of learning rate. If the learning rate is too small, the particle converge rather slowly; on the other hand, if the learning rate is too big, the particles may not even converge. Meanwhile, Coin MSVGD converges rapidly to the true target, with no need to tune a learning rate. Similar to the examples considered in Sec. 6.1, the projected methods once again fail to converge to the true target, highlighting the need for the mirrored approach.

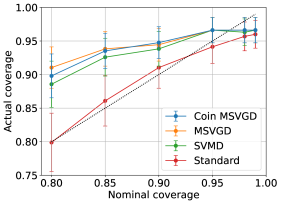

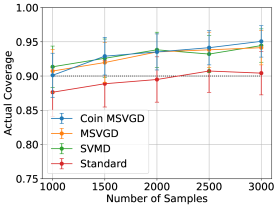

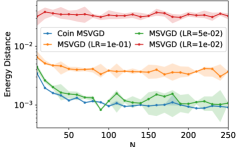

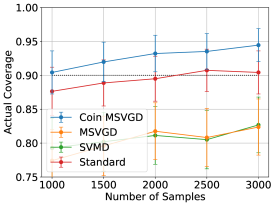

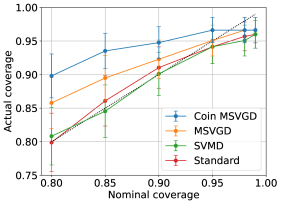

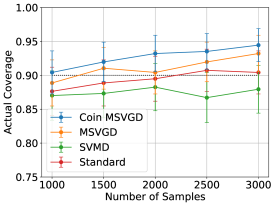

In Fig. 3, we plot the coverage of the CIs obtained using Coin MSVGD, MSVGD, SVMD, and the norejection MCMC algorithm in selectiveInference [91], as we vary the nominal coverage or the total number of samples. For MSVGD and SVMD, we use RMSProp [92] to adapt the learning rate, with an initial learning rate of , following [82]. As the nominal coverage varies, Coin MSVGD achieves similar coverage to MSVGD and SVMD; and significantly higher actual coverage than norejection (Fig. 3a). Meanwhile, as the number of samples varies, Coin MSVGD, MSVGD, and SVMD consistently all obtain a higher coverage than the fixed nominal coverage of 90% (Fig. 3b). This is important for small sample sizes, where the standard approach undercovers. The performance of MSVGD and SVMD is, of course, highly dependent on an appropriate choice of learning rate. In Fig. 11 (App. G.3), we provide additional plots illustrating how the coverage of the CIs obtained using MSVGD and SVMD can deteriorate when the learning-rate is chosen sub-optimally.

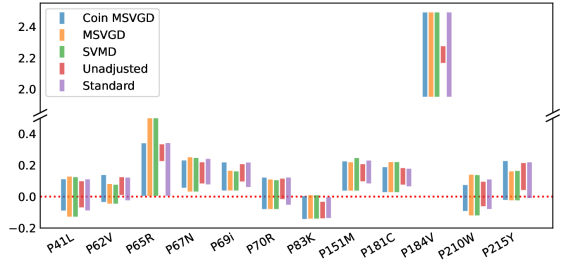

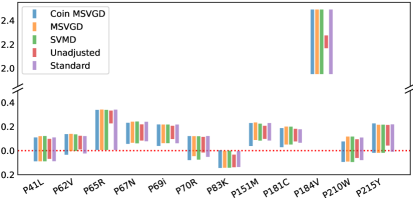

Real Data Example. We next consider a post-selection inference problem involving the HIV-1 drug resistance dataset studied in [75, 8]; see App. F.2 for full details. The goal is to identify statistically significant mutations associated with the response to the drug Lamivudine (3TC). The randomised Lasso selects a subset of mutations, for which we compute 90% CIs using samples and five methods: ‘unadjusted’ (the unadjusted CIs), ‘standard’ (the method in selectiveInference), MSVGD, SVMD, and Coin MSVGD. Our results (Fig. 4) indicate that the CIs obtained by Coin MSVGD are similar to those obtained via the standard approach, which we view as a benchmark, as well as by MSVGD and SVMD (with a well chosen learning rate). Importantly, they differ from the CIs obtained using the unadjusted approach (see, e.g., mutation P65R or P184V in Fig. 4). Meanwhile, for sub-optimal choices of the learning rate (Fig. 4b and Fig. 4c, Fig. 12 in App. G.3), the CIs obtained using MSVGD and SVMD differ substantially from those obtained using the baseline ‘standard’ approach and by Coin MSVGD, once more highlighting the sensitivity of these methods to the choice of an appropriate learning rate.

6.3 Fairness Bayesian Neural Network

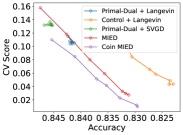

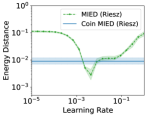

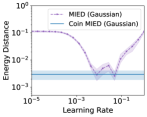

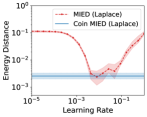

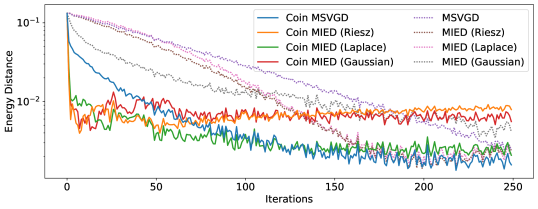

Finally, following [69, 65, 64, 60], we train a fairness Bayesian neural network to predict whether an individual’s income is greater than $50,000, with gender as a protected characteristic. We use the Adult Income dataset [50]. The dataset is of the form , where denote the feature vectors, denote the labels (i.e., whether the income is greater than $50,000), and denote the protected attribute (i.e., the gender). We train a two-layer Bayesian neural network with weights and place a standard Gaussian prior on each weight independently. The fairness constraint is given by for some user-specified . In testing, we evaluate each method using a Calder-Verwer (CV) score [14], a standard measure of disparate impact. We run each method for iterations and use particles.

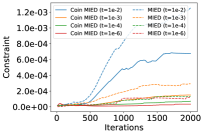

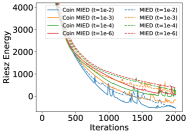

In Fig. 5a, we plot the trade-off curve between test accuracy and CV score, for . We compare the results for Coin MIED, MIED, and the methods in [65], using the default implementations. In this experiment, Coin MIED is clearly preferable to the other methods, achieving a much larger Pareto front. In Fig. 5b and Fig. 5c, we plot the constraint and the MIE versus training iterations for both coin MIED and MIED. Once again, coin MIED tends to outperform MIED, achieving both lower values of the constraint and lower values of the energy.

7 Discussion

Summary. In this paper, we introduced several new particle-based algorithms for constrained sampling which are entirely learning rate free. Our first approach was based on the coin sampling framework introduced in [81], and a perspective of constrained sampling as a mirrored optimisation problem on the space of probability measures. Based on this perspective, we also unified several existing constrained sampling algorithms, and studied their theoretical properties in continuous time. Our second approach can be viewed as the coin sampling analogue of the recently proposed MIED algorithm [60]. Empirically, our algorithms achieved comparable or superior performance to other particle-based constrained sampling algorithms, with no need to tune a learning rate.

Limitations. We highlight three limitations. First, like any mirrored sampling algorithm, mirrored coin sampling (e.g., Coin MSVGD), necessarily depends on the availability of a mirror map that can appropriately capture the constraints of the problem at hand. Second, Coin MSVGD has a cost of per update. Finally, even in the population limit, establishing the convergence of mirrored coin sampling under standard conditions (e.g., strong log-concavity or a mirrored log-Sobolev inequality) remains an open problem. We leave this as an interesting direction for future work.

Acknowledgements

LS and CN were supported by the UK Research and Innovation (UKRI) Engineering and Physical Sciences Research Council (EPSRC), grant number EP/V022636/1. CN acknowledges further support from the EPSRC, grant number EP/R01860X/1.

References

- [1] Kwangjun Ahn and Sinho Chewi. Efficient constrained sampling via the mirror-Langevin algorithm. In Proceedings of the 35th International Conference on Neural Information Processing Systems (NeurIPS 2021), Online, 2021.

- [2] Luigi Ambrosio, Nicola Gigli, and Giuseppe Savaré. Gradient Flows: In Metric Spaces and in the Space of Probability Measures. Birkhäuser, Basel, 2008.

- [3] Michael Arbel, Anna Korba, Adil Salim, and Arthur Gretton. Maximum Mean Discrepancy Gradient Flow. In Proceedings of the 33rd International Conference on Neural Information Processing Systems (NeurIPS 2019), Vancouver, Canada, 2019.

- [4] D Bakry and M Émery. Diffusions hypercontractives. In Jacques Azéma and Marc Yor, editors, Séminaire de Probabilités XIX 1983/84, pages 177–206, Berlin, Heidelberg, 1985. Springer Berlin Heidelberg.

- [5] Dominique Bakry, Ivan Gentil, and Michel Ledoux. Analysis and Geometry of Markov Diffusion Operators. Springer Cham, 2014.

- [6] Krishnakumar Balasubramanian, Sinho Chewi, Murat A. Erdogdu, Adil Salim, and Matthew Zhang. Towards a Theory of Non-Log-Concave Sampling: First-Order Stationarity Guarantees for Langevin Monte Carlo. In Proceedings of the 35th Annual Conference on Learning Theory (COLT 2022), London, UK, 2022.

- [7] Amir Beck and Marc Teboulle. Mirror descent and nonlinear projected subgradient methods for convex optimization. Operations Research Letters, 31(3):167–175, 2003.

- [8] Nan Bi, Jelena Markovic, Lucy Xia, and Jonathan Taylor. Inferactive data analysis. Scandinavian Journal of Statistics, 47(1):212–249, 2020.

- [9] David M. Blei, Andrew Y. Ng, and Michael I. Jordan. Latent Dirichlet Allocation. Journal of Machine Learning Research, 3:993–1022, 2003.

- [10] Sergey G Bobkov. Isoperimetric and Analytic Inequalities for Log-Concave Probability Measures. The Annals of Probability, 27(4):1903–1921, 1999.

- [11] Steve Brooks, Andrew Gelman, Galin Jones, and Xiao-Li Meng. Handbook of Markov Chain Monte Carlo. Chapman and Hall/CRC, 1st edition, 2011.

- [12] Marcus Brubaker, Mathieu Salzmann, and Raquel Urtasun. A Family of MCMC Methods on Implicitly Defined Manifolds. In Proceedings of the 15th International Conference on Artificial Intelligence and Statistics (AISTATS), La Palma, Canary Islands, 2012.

- [13] Simon Byrne and Mark Girolami. Geodesic Monte Carlo on Embedded Manifolds. Scandinavian Journal of Statistics, 40(4):825–845, 2013.

- [14] Toon Calders and Sicco Verwer. Three Naive Bayes Approaches for Discrimination-Free Classification. Data Mining and Knowledge Discovery, 21(2):277–292, 2010.

- [15] Gilles Celeux, Mohammed El Anbari, Jean-Michel Marin, and Christian P Robert. Regularization in Regression: Comparing Bayesian and Frequentist Methods in a Poorly Informative Situation. Bayesian Analysis, 7(2):477–502, 2012.

- [16] Peng Chen and Omar Ghattas. Projected Stein Variational Gradient Descent. In Proceedings of the 34th International Conference on Neural Information Processing Systems (NeurIPS 2020), Vancouver, Canada, 2020.

- [17] Yuansi Chen. An Almost Constant Lower Bound of the Isoperimetric Coefficient in the KLS Conjecture. Geometric and Functional Analysis, 31(1):34–61, 2021.

- [18] Xiang Cheng, Niladri S. Chatterji, Peter L. Bartlett, and Michael I. Jordan. Underdamped Langevin MCMC: A non-asymptotic analysis. In Proceedings of the 31st Annual Conference on Learning Theory (COLT 2018), volume 75, pages 1–24, Stockholm, Sweden, 2018.

- [19] Sinho Chewi, Thibaut Le Gouic, Chen Lu, Tyler Maunu, Philippe Rigollet, and Austin Stromme. Exponential ergodicity of mirror-Langevin diffusions. In Proceedings of the 34th International Conference on Neural Information Processing Systems (NeurIPS 2020), Online, 2020.

- [20] Sinho Chewi, Thibaut Le Gouic, Chen Lu, Tyler Maunu, and Philippe Rigollet. SVGD as a kernelized Wasserstein gradient flow of the chi-squared divergence. In Proceedings of the 34th International Conference on Neural Information Processing Systems (NeurIPS 2020), pages 2098–2109, 2020.

- [21] Kacper Chwialkowski, Heiko Strathmann, and Arthur Gretton. A Kernel Test of Goodness of Fit. In Proceedings of the 33rd International Conference on Machine Learning (ICML 2016), New York, NY, 2016.

- [22] Ashok Cutkosky and Francesco Orabona. Black-Box Reductions for Parameter-free Online Learning in Banach Spaces. In Proceedings of the 31st Annual Conference on Learning Theory (COLT 2018), Stockholm, Sweden, 2018.

- [23] Arnak S Dalalyan. Theoretical guarantees for approximate sampling from smooth and log-concave densities. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 79(3):651–676, 2017.

- [24] Arnak S Dalalyan and Avetik Karagulyan. User-friendly guarantees for the Langevin Monte Carlo with inaccurate gradient. Stochastic Processes and their Applications, 129(12):5278–5311, 2019.

- [25] Arnak S Dalalyan and Lionel Riou-Durand. On sampling from a log-concave density using kinetic Langevin diffusions. Bernoulli, 26(3):1956–1988, 2020.

- [26] Nabarun Deb, Young-Heon Kim, Soumik Pal, and Geoffrey Schiebinger. Wasserstein Mirror Gradient Flow as the Limit of the Sinkhorn Algorithm. arXiv preprint arXiv:2307.16421, 2023.

- [27] Gianluca Detommaso, Tiangang Cui, Alessio Spantini, Youssef Marzouk, and Robert Scheichl. A Stein variational Newton method. In Proceedings of the 32nd International Conference on Neural Information Processing Systems (NIPS 2018), Montreal, Canada, 2018.

- [28] Persi Diaconis, Susan Holmes, and Mehrdad Shahshahani. Sampling from a manifold. Advances in modern statistical theory and applications: a Festschrift in honor of Morris L. Eaton, 10:102–125, 2013.

- [29] Zhiyan Ding, Qin Li, Jianfeng Lu, and Stephen J. Wright. Random Coordinate Langevin Monte Carlo. In Proceedings of the 34th Annual Conference on Learning Theory (COLT 2021), volume 134, pages 1–28, Boulder, CO, 2021.

- [30] Zhiyan Ding, Qin Li, Jianfeng Lu, and Stephen J. Wright. Random Coordinate Underdamped Langevin Monte Carlo. In Proceedings of The 24th International Conference on Artificial Intelligence and Statistics (AISTATS 2021), San Diego, CA, 2021.

- [31] John Duchi, Elad Hazan, and Yoram Singer. Adaptive subgradient methods for online learning and stochastic optimization. Journal of Machine Learning Research, 12(61):2121–2159, 2011.

- [32] Andrew Duncan, Nikolas Nüsken, and Lukasz Szpruch. On the geometry of Stein variational gradient descent. Journal of Machine Learning Research, 24:1–40, 2023.

- [33] Alain Durmus, Szymon Majewski, and Blazej Miasojedow. Analysis of Langevin Monte Carlo via Convex Optimization. Journal of Machine Learning Research, 20(1):2666–2711, 2019.

- [34] Alain Durmus and Éric Moulines. High-dimensional Bayesian inference via the unadjusted Langevin algorithm. Bernoulli, 25(4A):2854–2882, 2019.

- [35] Murat A. Erdogdu and Rasa Hosseinzadeh. On the Convergence of Langevin Monte Carlo: The Interplay between Tail Growth and Smoothness. In Proceedings of the 34th Annual Conference on Learning Theory (COLT 2021), Boulder, CO, 2021.

- [36] Damien Garreau, Wittawat Jitkrittum, and Motonobu Kanagawa. Large sample analysis of the median heuristic. arXiv preprint arXiv:1707.07269, 2017.

- [37] Chengyue Gong, Xingchao Liu, and Qiang Liu. Bi-objective trade-off with dynamic barrier gradient descent. In Proceedings of the 35th International Conference on Neural Information Processing Systems (NeurIPS 2021), Online, 2021.

- [38] Jackson Gorham and Lester Mackey. Measuring Sample Quality with Kernels. In Proceedings of the 34th International Conference on Machine Learning (ICML 2017), Sydney, Australia, 2017.

- [39] T H Gronwall. Note on the Derivatives with Respect to a Parameter of the Solutions of a System of Differential Equations. Annals of Mathematics, 20(4):292–296, 1919.

- [40] Richard Grumitt, Biwei Dai, and Uros Seljak. Deterministic Langevin Monte Carlo with Normalizing Flows for Bayesian Inference. In Proceedings of the 36th International Conference on Neural Information Processing Systems (NeurIPS 2022), New Orleans, LA, 2022.

- [41] Matthew D. Hoffman, David M. Blei, Chong Wang, and John Paisley. Stochastic variational inference. Journal of Machine Learning Research, 14(1):1303–1347, 2013.

- [42] Matthew D Hoffman and Andrew Gelman. The No-U-Turn sampler: adaptively setting path lengths in Hamiltonian Monte Carlo. Journal of Machine Learning Research, 15(1):1593–1623, 2014.

- [43] Ya-Ping Hsieh, Ali Kavis, Paul Rolland, and Volkan Cevher. Mirrored Langevin Dynamics. In Proceedings of the 32nd International Conference on Neural Information Processing Systems (NIPS 2018), Montreal, Canada, 2018.

- [44] Qijia Jiang. Mirror Langevin Monte Carlo: the Case Under Isoperimetry. In Proceedings of the 35th International Conference on Neural Information Processing Systems (NeurIPS 2021), Online, 2021.

- [45] Valen E. Johnson and James H. Albert. Ordinal Data Modeling. Springer, New York, NY, 1999.

- [46] Richard Jordan, David Kinderlehrer, and Felix Otto. The Variational Formulation of the Fokker–Planck Equation. SIAM Journal on Mathematical Analysis, 29(1):1–17, 1998.

- [47] Ravi Kannan, László Lovász, and Miklós Simonovits. Isoperimetric problems for convex bodies and a localization lemma. Discrete & Computational Geometry, 13(3):541–559, 1995.

- [48] Diederik P. Kingma and Jimmy Ba. Adam: a method for stochastic optimisation. In Proceedings of the 3rd International Conference on Learning Representations (ICLR ’15), pages 1–13, San Diego, CA, 2015.

- [49] John P. Klein and Melvin L. Moeschberger. Survival Analysis: Techniques for Censored and Truncated Data. Springer, New York, NY, 2003.

- [50] Ron Kohavi. Scaling up the Accuracy of Naive-Bayes Classifiers: A Decision-Tree Hybrid. In Proceedings of the Second International Conference on Knowledge Discovery and Data Mining, KDD’96, pages 202–207. AAAI Press, 1996.

- [51] Anna Korba, Pierre-Cyril, Aubin-Frankowski, Szymon Majewski, and Pierre Ablin. Kernel Stein Discrepancy Descent. In Proceedings of the 38th International Conference on Machine Learning (ICML 2021), Online, 2021.

- [52] Anna Korba, Adil Salim, Michael Arbel, Giulia Luise, and Arthur Gretton. A Non-Asymptotic Analysis for Stein Variational Gradient Descent. In Proceedings of the 34th International Conference on Neural Information Processing Systems (NeurIPS 2020), Vancouver, Canada, 2020.

- [53] Raphail E Krichevsky and Victor K Trofimov. The performance of universal encoding. IEEE Transactions on Information Theory, 27(2):199–207, 1981.

- [54] Jason D Lee, Dennis L Sun, Yuekai Sun, and Jonathan E Taylor. Exact post-selection inference, with application to the lasso. The Annals of Statistics, 44(3):907–927, 2016.

- [55] Yin Tat Lee and Santosh S Vempala. Convergence Rate of Riemannian Hamiltonian Monte Carlo and Faster Polytope Volume Computation. In Proceedings of the 50th Annual ACM Symposium on the Theory of Computing (STOC 2018), pages 1115–1121, Los Angeles,CA, 2018.

- [56] Tony Lelièvre, Mathias Rousset, and Gabriel Stoltz. Free Energy Computations. Imperial College Press, 2010.

- [57] Tony Lelièvre, Mathias Rousset, and Gabriel Stoltz. Hybrid Monte Carlo methods for sampling probability measures on submanifolds. Numerische Mathematik, 143(2):379–421, 2019.

- [58] Tony Lelièvre and Gabriel Stoltz. Partial differential equations and stochastic methods in molecular dynamics. Acta Numerica, 25:681–880, 2016.

- [59] Tony Lelièvre, Gabriel Stoltz, and Wei Zhang. Multiple projection Markov chain Monte Carlo algorithms on submanifolds. IMA Journal of Numerical Analysis, 43(2):737–788, 2023.

- [60] Lingxiao Li, Qiang Liu, Anna Korba, Mikhail Yurochkin, and Justin Solomon. Sampling with Mollified Interaction Energy Descent. In Proceedings of the 11th International Conference on Learning Representations, Kigali, Rwanda, 2023.

- [61] Ruilin Li, Molei Tao, Santosh S. Vempala, and Andre Wibisono. The Mirror Langevin Algorithm Converges with Vanishing Bias. In Proceedings of the 33rd International Conference on Algorithmic Learning Theory (ALT 2022), Paris, France, 2022.

- [62] Qiang Liu, Jason D. Lee, and Michael Jordan. A Kernelized Stein Discrepancy for Goodness-of-fit Tests. In Proceedings of the 33rd International Conference on Machine Learning (ICML 2016), New York, NY, 2016.

- [63] Qiang Liu and Dilin Wang. Stein Variational Gradient Descent: A General Purpose Bayesian Inference Algorithm. In Proceedings of the 30th Conference on Neural Information Processings Systems (NIPS 2016), Barcelona, Spain, 2016.

- [64] Suyun Liu and Luis Nunes Vicente. Accuracy and fairness trade-offs in machine learning: a stochastic multi-objective approach. Computational Management Science, 19(3):513–537, 2022.

- [65] Xingchao Liu, Xin T. Tong, and Qiang Liu. Sampling with Trustworthy Constraints: A Variational Gradient Framework. In Proceedings of the 35th International Conference on Neural Information Processing Systems (NeurIPS 2021), Online, 2021.

- [66] Yang Liu, Prajit Ramachandran, Qiang Liu, and Jian Peng. Stein Variational Policy Gradient. In Proceedings of the Conference on Uncertainty In Artificial Intelligence (UAI 2017), Sydney, Australia, 2017.

- [67] Yi-An Ma, Niladri S Chatterji, Xiang Cheng, Nicolas Flammarion, Peter L Bartlett, and Michael I Jordan. Is there an analog of Nesterov acceleration for gradient-based MCMC? Bernoulli, 27(3):1942–1992, 2021.

- [68] James Martin, Lucas C Wilcox, Carsten Burstedde, and Omar Ghattas. A Stochastic Newton MCMC Method for Large-Scale Statistical Inverse Problems with Application to Seismic Inversion. SIAM Journal on Scientific Computing, 34(3):1460–1487, 2012.

- [69] Natalia Martinez, Martin Bertran, and Guillermo Sapiro. Minimax Pareto Fairness: A Multi Objective Perspective. In Proceedings of the 37th International Conference on Machine Learning (ICML 2020), Online, 2020.

- [70] Francesco Orabona and Ashok Cutkosky. Tutorial on Parameter-Free Online Learning. In Proceedings of the 37th International Conference on Machine Learning (ICML 2020), Online, 2020.

- [71] Francesco Orabona and David Pal. Coin Betting and Parameter-Free Online Learning. In Proceedings of the 30th Conference on Neural Information Processings Systems (NIPS 2016), Barcelona, Spain, 2016.

- [72] Francesco Orabona and Tatiana Tommasi. Training Deep Networks without Learning Rates Through Coin Betting. In Proceedings of the 31st International Conference on Neural Information Processing Systems (NIPS 2017), Long Beach, CA, 2017.

- [73] Sam Patterson and Yee Whye Teh. Stochastic gradient Riemannian Langevin dynamics on the probability simplex. In Proceedings of the 27th International Conference on Neural Information Processing Systems (NIPS 2013), Lake Tahoe, NV, 2013.

- [74] Yunchen Pu, Zhe Gan, Ricardo Henao, Chunyuan Li, Shaobo Han, and Lawrence Carin. VAE Learning via Stein Variational Gradient Descent. In Proceedings of the 31st International Conference on Neural Information Processing Systems (NIPS 2017), Long Beach, CA, 2017.

- [75] Soo-Yon Rhee, Jonathan Taylor, Gauhar Wadhera, Asa Ben-Hur, Douglas L Brutlag, and Robert W Shafer. Genotypic predictors of human immunodeficiency virus type 1 drug resistance. Proceedings of the National Academy of Sciences, 103(46):17355–17360, 2006.

- [76] Christian P Robert and George Casella. Monte Carlo Statistical Methods. Springer-Verlag, New York, 2 edition, 2004.

- [77] Ralph Tyrrell Rockafellar. Convex Analysis. Princeton University Press, Princeton, NJ, 1970.

- [78] Adil Salim, Lukang Sun, and Peter Richtárik. A Convergence Theory for SVGD in the Population Limit under Talagrand’s Inequality T1. In Proceedings of the 39th International Conference on Machine Learning (ICML 2022), Online, 2022.

- [79] Amir Sepehri and Jelena Markovic. Non-reversible, tuning- and rejection-free Markov chain Monte Carlo via iterated random functions. arXiv preprint arXiv:1711.07177, 2017.

- [80] Louis Sharrock, Daniel Dodd, and Christopher Nemeth. CoinEM: Tuning-Free Particle-Based Variational Inference for Latent Variable Models. arXiv preprint arXiv:2305.14916, 2023.

- [81] Louis Sharrock and Christopher Nemeth. Coin Sampling: Gradient-Based Bayesian Inference without Learning Rates. In Proceedings of the 40th International Conference on Machine Learning (ICML 2023), Honolulu, HI, 2023.

- [82] Jiaxin Shi, Chang Liu, and Lester Mackey. Sampling with Mirrored Stein Operators. In Proceedings of the 10th International Conference on Learning Representations (ICLR 2022), Online, 2022.

- [83] Jiaxin Shi and Lester Mackey. A Finite-Particle Convergence Rate for Stein Variational Gradient Descent. In Proceedings of the 37th International Conference on Neural Information Processing Systems (NeurIPS 2023), New Orleans, LA, 2023.

- [84] Umut Simsekli, Roland Badeau, A. Taylan Cemgil, and Gaël Richard. Stochastic Quasi-Newton Langevin Monte Carlo. In Proceedings of the 33rd International Conference on Machine Learning (ICML 2016), New York, NY, 2016.

- [85] Lukang Sun, Avetik Karagulyan, and Peter Richtarik. Convergence of Stein Variational Gradient Descent under a Weaker Smoothness Condition. In Proceedings of the 26th International Conference on Artificial Intelligence and Statistics (AISTATS 2023), Valencia, Spain, 2023.

- [86] Lukang Sun and Peter Richtárik. A Note on the Convergence of Mirrored Stein Variational Gradient Descent under (L0,L1)-Smoothness Condition. arXiv preprint arXiv:2206.09709, 2022.

- [87] Gábor J. Székely and Maria L. Rizzo. Energy statistics: A class of statistics based on distances. Journal of Statistical Planning and Inference, 143(8):1249–1272, 2013.

- [88] Jonathan Taylor and Robert J Tibshirani. Statistical learning and selective inference. Proceedings of the National Academy of Sciences, 112(25):7629–7634, 2015.

- [89] Xiaoying Tian, Nan Bi, and Jonathan Taylor. MAGIC: a general, powerful and tractable method for selective inference. arXiv preprint arXiv:1607.02630, 2016.

- [90] Xiaoying Tian, Snigdha Panigrahi, Jelena Markovic, Nan Bi, and Jonathan Taylor. Selective sampling after solving a convex problem. arXiv preprint arXiv:1609.05609, 2016.

- [91] Ryan Tibshirani, Rob Tibshirani, Jonatha Taylor, Joshua Loftus, Stephen Reid, and Jelena Markovic. selectiveInference: Tools for Post-Selection Inference, 2019.

- [92] Tijmen Tieleman and Geoffrey E Hinton. Lecture 6.5-rmsprop: divide the gradient by a running average of its recent magnitude. COURSERA: Neural networks for machine learning, 4(2):26–31, 2012.

- [93] Alexandre B. Tsybakov. Introduction to Nonparametric Estimation. Springer, New York, NY, 2009.

- [94] Santosh S. Vempala and Andre Wibisono. Rapid Convergence of the Unadjusted Langevin Algorithm: Isoperimetry Suffices. In Proceedings of the 33rd International Conference on Neural Information Processing Systems (NeurIPS 2019), Vancouver, Canada, 2019.

- [95] Cédric Villani. Optimal Transport: Old and New. Springer-Verlag, Berlin, 2008.

- [96] Martin J Wainwright and Michael I Jordan. Graphical Models, Exponential Families, and Variational Inference. Foundations and Trends in Machine Learning, 1(1-2):1–305, 2008.

- [97] Dilin Wang, Zhe Zeng, and Qiang Liu. Stein Variational Message Passing for Continuous Graphical Models. In Proceedings of the 35th International Conference on Machine Learning (ICML 2018), Stockholm, Sweden, 2018.

- [98] Xiao Wang, Qi Lei, and Ioannis Panageas. Fast Convergence of Langevin Dynamics on Manifold: Geodesics meet Log-Sobolev. In Proceedings of the 34th International Conference on Neural Information Processing Systems (NeurIPS 2020), Vancouver, Canada, 2020.

- [99] Andre Wibisono. Sampling as optimization in the space of measures: The Langevin dynamics as a composite optimization problem. In Proceedings of the 31st Annual Conference on Learning Theory (COLT 2018), Stockholm, Sweden, 2018.

- [100] Andre Wibisono. Proximal Langevin Algorithm: Rapid Convergence Under Isoperimetry. arXiv preprint arXiv:1911.01469, 2019.

- [101] Edwin B Wilson. Probable Inference, the Law of Succession, and Statistical Inference. Journal of the American Statistical Association, 22(158):209–212, 1927.

- [102] Emilio Zappa, Miranda Holmes-Cerfon, and Jonathan Goodman. Monte Carlo on Manifolds: Sampling Densities and Integrating Functions. Communications on Pure and Applied Mathematics, 71(12):2609–2647, 2018.

- [103] Kelvin Shuangjian Zhang, Gabriel Peyré, Jalal Fadili, and Marcelo Pereyra. Wasserstein Control of Mirror Langevin Monte Carlo. In Proceedings of the 33rd Annual Conference on Learning Theory (COLT 2020), Graz, Austria, 2020.

- [104] Ruqi Zhang, Qiang Liu, and Xin T. Tong. Sampling in Constrained Domains with Orthogonal-Space Variational Gradient Descent. In Proceedings of the 36th International Conference on Neural Information Processing Systems (NeurIPS 2022), New Orleans, LA, 2022.

- [105] Jingwei Zhuo, Chang Liu, Jiaxin Shi, Jun Zhu, Ning Chen, and Bo Zhang. Message Passing Stein Variational Gradient Descent. In Proceedings of the 35th International Conference on Machine Learning (ICML 2018), Stockholm, Sweden, 2018.

Appendix A Calculus in the Wasserstein Space

We recall the following from [2, Chapter 10]. Suppose and . Let be a proper and lower semi-continuous functional on . We say that belongs to the Fréchet subdifferential of at and write if, for any ,

| (15) |

where denotes the optimal transport map from to [2, Chapter 7.1]. Under mild conditions [2, Lemma 10.4.1], the subdifferential is single-valued, , and is given by

| (16) |

where denotes the first variation of at , that is, the unique function such that

| (17) |

where , and . We will refer to as the Wasserstein gradient of at .

Appendix B Examples of Mirrored Wasserstein Gradient Flows

In this section, we outline several algorithms which arise as special cases of the MWGF introduced in Sec 3.2, namely

| (18) |

where are vector fields chosen to ensure the convergence of to .

We will assume, throughout this section, that and that . The Monge-Ampere equation determines the relationship between and . In particular, we have [e.g., 43]

| (19) |

Thus, the potential of the mirrored target evaluated at can be expressed in terms of the potential of the original target evaluated at , as

| (20) |

B.1 Mirrored Langevin Dynamics

Suppose that , where, as elsewhere, is the dual target. In addition, let . In this case, it is straightforward to show that [e.g. 2, Chapter 10] . Thus, for this choice of , the MWGF in (18) reads

| (21) |

Substituting , and using the fact that , this can also be written as

| (22) |

This PDE is nothing more than the Fokker-Planck equation describing the evolution of the law of the overdamped Langevin SDE with respect to the mirrored target . In particular, suppose that , , and that and are the solutions of

| (23) |

where is a standard Brownian motion. Then, if we let and denote the laws of and , it follows that and satisfy (22). This is precisely the mirrored Langevin dynamics (MLD) introduced in [43]. We remark that, using (20), the MLD in (23) can also be written as

| (24) |

Remark 1.

It is worth distinguishing between the mirrored Langevin dynamics in (23) and the so-called mirror Langevin diffusion [e.g., 44, Equation 2], which refers to the solution of

| (25) |

These dynamics, and the corresponding Euler-Maruyama discretisation, known as the mirror Langevin algorithm or mirror Langevin Monte Carlo, were first studied in [103], and have since also been analysed in [44, 1, 61]. An alternative time discretisation has also been studied in [19].

In this case, one can show that the law of the solution of the mirror Langevin diffusion in (25) satisfies the Fokker-Planck equation [e.g., 44, App. A.2]

| (26) | ||||

| Recalling that , one can view (26) as a special case of the so-called Wasserstein mirror flow (WMF), defined according to [e.g. 1, App. C] | ||||

| (27) | ||||

The WMF is rather different from the MWGF in (18). In particular, the WMF in (27) describes the evolution of according to the Wasserstein tangent vector , where is a functional minimised at , while the MWGF in (18) describes the evolution of the mirrored according to the tangent vector , where is now a functional minimised at . We refer to [19] for a detailed discussion of the mirror Langevin diffusion from this perspective; and [26] for a more general formulation of the WMF.

B.1.1 Continuous Time Results

We now study the properties of the dynamics in (23) in continuous time, starting with the dissipation of and along the MLD. These results are a natural extension of existing results in the unconstrained case to our setting.

Proposition 1.

The dissipation of along the MWGF in (21) is given by

| (28) |

Proof.

Using differential calculus in the Wasserstein space and the chain rule, we have that

| (29) |

By [43, Theorem 2], we have that . To deal with the term on the RHS, first note that, using the formula for the change of variable in a probability density, we have that

| (30) |

Thus, in particular, if , then we have that

| (31) |

Using this, and the fact that , we can now compute

| (32) | ||||

| (33) | ||||

| (34) | ||||

| (35) | ||||

| (36) | ||||

| (37) |

The conclusion now follows. ∎

Proposition 2.

The dissipation of along the MWGF in (21) is given by

| (38) |

Proof.

The proof is rather similar to the previous one. In this case, using the fact that , we have

We next observe, using now the fact that which follows from (30), that

| (39) | ||||

| (40) |

In addition, based on a very similar argument, we have that

| (41) | ||||

| (42) | ||||

| (43) |

This completes the proof. ∎

Since the RHS of both (28) and (38) are non-positive, these results show that and decrease along the MLD. As an immediate corollary, we have the following continuous time convergence rate for the time-average of and .

Proposition 3.

For any , it holds that

| (44) |

Proposition 4.

For any , it holds that

| (45) |

Proof.

To obtain stronger convergence results, we will require additional assumptions on the target measure. In the first case, we can assume that the target satisfies what we will refer to as a mirrored logarithmic Sobolev inequality (LSI).

Proposition 5.

Assume that satisfies a mirrored LSI with constant . In particular, for all , there exists such that

| (46) |

Then the KL divergence converges exponentially along the MWGF in (21):

| (47) |

Proof.

Alternatively, under the assumption that the target satisfies a mirrored Poincaré inequality (PI), we can obtain exponential convergence in a number of metrics.

Proposition 6.

Assume that satisfies a mirrored PI with constant . In particular, for all locally Lipschitz , there exists such that

| (49) |

Then the total variation distance, Hellinger distance, KL divergence, and the divergence all converge exponentially along the MWGF in (21):

| (50) |

Proof.

Remark 2.

The assumption that satisfies the mirrored LSI in (46) or the mirrored PI in (49) is precisely equivalent to the assumption that the mirrored target satisfies the classical LSI or the classical PI, respectively. The LSI holds, for example, for all strongly log-concave distributions, with constant equal to the reciprocal of the strong convexity constant of the potential [4]. The class of measures satisfying the PI is even larger, including all strongly log-concave measures and, more generally, all log-concave measures [47, 10, 17].

Remark 3.

The mirrored LSI in (46) and the mirrored PI in (49) are distinct from the so-called mirror LSI [44, Assumption 2] and mirror PI [19, Definition 1]. These assumptions are used in [44, Proposition 1] and [19, Theorem 1], respectively, to establish exponential convergence of the mirror Langevin diffusion [e.g., 44, Equation 2], which we recall is distinct from the mirrored Langevin diffusion in (23); see Remark 1.

Remark 4.

In Propositions 5 - 6 above, and also in Proposition 7 below, our assumptions on the target are, in some sense, better viewed as assumptions on the mirrored target . Indeed, by construction, the imposed assumptions are equivalent to the assumptions that the mirrored target satisfies a LSI (Proposition 5, 7), or that the mirrored target satisfies a PI (Proposition 6).

In some sense, it would be preferable to establish such results under more direct assumptions on the target itself. One possibility is to assume that the target is strongly log-concave. In this case, [43, Proof of Theorem 3] guarantees the existence of a mirror map such that the mirrored target is also strongly log-concave. Thus, in particular, the mirrored target satisfies a LSI and a PI or, equivalently, the target satisfies a mirrored LSI and a mirrored PI. Thus, Propositions 5 - 7 all still hold.

B.1.2 Discrete Time Results

In practice, of course, it is necessary to discretise the dynamics in (23) in time. Applying a standard Euler-Maruyama discretisation to (23), or equivalently a forward-flow discretisation to (21) [e.g., 99], one arrives at the mirrored Langevin algorithm (MLA) from [43], viz

| (51) |

where is the step size or learning rate and where are a sequence of i.i.d. standard normal random variables.

Proposition 7.

Suppose that satisfies the mirrored LSI with constant . In addition, suppose that is mirror--smooth.222We say that is mirror--smooth if is -smooth. This holds, in particular, if has Hessian bounded by . Then, if , the iterates in (51) satisfy

| (52) |

Proof.

By [43, Theorem 2], and (32) - (37) in the proof of Proposition 1, if satisfies a mirrored LSI with constant , then satisfies a LSI with the same constant . In addition, by definition, if is mirror--smooth, then is -smooth. Thus, it follows from [94, Theorem 1] that

| (53) |

Finally, using the invariance of the KL divergence under the mirror map [43, Theorem 2], the result follows. ∎

Remark 5.

B.2 Mirrored Stein Variational Gradient Descent

We now turn our attention to the MSVGD dynamics given in Sec. 3.2.1, which we recall are defined by the continuity equation

| (54) |

where, as previously, is the kernel defined according to , given some base kernel .

B.2.1 Continuous Time Results

We now study the convergence properties of the continuous-time MSVGD dynamics. We note that a similar set of results can also found in [82, App. H]. We provide them here to highlight the analogues with the convergence results obtained for the MLD in Sec. B.1.

Proposition 8.

The dissipation of the KL along the mirrored SVGD gradient flow is given by

| (55) |

Proof.

Remark 7.

Similar to before, a straightforward consequence of this result is a continuous time convergence rate for the average of the mirrored stein discrepancy along the continuous-time MSVGD dynamics.

Proposition 9.

For all , it holds that

| (61) |

Proof.

We integrate (55), and use the non-negativity of the KL divergence. ∎

To obtain stronger convergence guarantees, we must once again assume some additional properties on the target. Here, a natural choice is the mirrored Stein LSI, the analogue of the Stein LSI introduced in [32] in the mirrored setting; see also [82, Definition 2].

Proposition 10.

Assume that satisfies the mirrored Stein LSI with constant . In particular, for all , there exists such that

| (62) |

Then the KL divergence converges exponentially along the continuous-time MSVGD dynamics:

| (63) |

Proof.

Remark 8.

The assumption that satisfies the mirrored Stein LSI is equivalent to the assumption that satisfies the classical Stein LSI with kernel . The Stein LSI is rather less well known than the classical LSI, and holds for a much smaller class of targets. In particular, this condition fails to hold if the kernel is too regular with respect to the target , e.g., if has exponential tails and the derivatives of the kernel and the potential grow at most polynomially [32, 52]. It remains an open problem to establish conditions for which this conditions holds.

B.2.2 Discrete Time Results

In discrete time, [86] recently established a descent lemma and a complexity bound for MSVGD in the population limit. For completeness, we recall one of these results here.

Theorem 1 (Corollary 1 in [86]).

Suppose that the following assumptions hold:

-

(1)

The mirror function is strongly -convex.

-

(2)

There exist such that for all , and for all , .

-

(3)

There exist such that .

-

(4)

There exists , , and such that

-

(5)

There exists , such that for any .

Then, provided satisfies [86, Equation 21], then

| (65) |

Remark 9.

The results in [86] are obtained by extending the proofs used to establish convergence of SVGD in [85] to the mirrored setting. In this case, essentially all of the same arguments can be applied (in the dual space), provided suitable assumptions are imposed on the mirrored target . The disadvantage of this approach is that the required assumptions are specified in terms of the mirrored target , rather than the target .

Following a similar approach to [43, Theorem 3], let us show how to recover this result under a standard assumption on itself. Suppose we replace [86, Assumption 4] by the assumption that is strongly log-concave. Under this assumption, [43, Proof of Theorem 3] guarantees the existence of a mirror map such that is also strongly log-concave. By the Bakry-Emery criterion [4], it follows that the inequality is satisfied by the dual target , and thus so too is the inequality. Finally, the inequality is necessary and sufficient for [86, Assumption 4] by [95, Theorem 22.10]. Thus, [86, Corollary 1] holds whenever the target is strongly log-concave.

B.3 Mirrored Laplacian Adjusted Wasserstein Gradient Descent

We now consider the MWGF of the chi-squared divergence; see also [20, Sec. 3] or [2, Theorem 11.2.1] in the unconstrained case. Following similar steps to [20], we will then obtained a mirrored version of the Laplacian Adjusted Wasserstein Gradient Descent (LAWGD) algorithm.

B.3.1 MWGF of the Chi-Squared Divergence

Suppose that with . Setting in (4), we are interested in the following MWGF

| (66) |

Similar to before, we will begin by studying the convergence properties of this MWGF in continuous time.

Proposition 11.

The dissipation of along the MWGF in (66) is given by

| (67) |

Proof.

The proof is essentially identical to the proof of Proposition 2, although the roles of the Lyapunov functional and the Wasserstein gradient are now reversed. In particular, we now have

By Theorem 2 in [43] and (41) - (43) in the proof of Proposition 2, we have that and , from which the conclusion follows. ∎

Proposition 12.

The dissipation of along the MWGF in (66) is given by

| (68) |

Proof.

Similar to before, we can also obtain exponential convergence to the target under a mirrored functional inequality.

Proposition 13.

Assume that satisfies a mirrored PI with constant . In particular, for all locally Lipschitz , there exists such that

| (70) |

Then the KL divergence converges exponentially along the MWGF in (66):

| (71) |

Furthermore, for , the following convergence rate holds:

| (72) |

Proof.

The proof follows closely the proof of [20, Theorem 1]. In particular, substituting the mirrored PI (70) with into (67), we have that

| (73) |

where in the final inequality we have used the fact that (e.g., [93, Sec. 2.4]). The first bound now follows straightforwardly from Grönwall’s inequality.

For the second bound, we will instead use the inequality (e.g., [93, Sec. 2.4]), which implies that . Using this in (73), it follows that

| (74) |

Applying Grönwall’s lemma, we then have that

| (75) |

where in the final line we have used the elementary inequality , for . Finally, observe that if , then . Combining this with the fact that whenever , we have that

| (76) |

for . Alongside the bound in (71), this completes the proof of (72). ∎

B.3.2 Kernelised MWGF of the Chi-Squared Divergence

In [20], the authors provide an interpretation of SVGD as a kernelised WGF of the divergence. Similarly, we can interpret MSVGD as a kernelised MWGF of the divergence; see also [82, App. H]. In particular, observe that [20, Sec. 2.3]

| (77) | ||||

| (78) |

It follows that the continuous-time MSVGD dynamics in (5) or (54) can equivalently be written as

| (79) |

Comparing (79) and (66), it is clear that, up to a factor of two, MSVGD can be interpreted as the MWGF obtained by replacing the gradient of chi-squared divergence, , by . In [82, App. H], the authors obtain continuous-time convergence results for this scheme, under a mirrored Stein PI. Here, we proceed differently, based on the approach in [20].

B.3.3 Mirrored Laplacian Adjusted Wasserstein Gradient Descent (MLAWGD)

Following [20], suppose now that we replace by the vector field . The new dynamics, which we refer to as the mirrored Laplacian adjusted Wasserstein gradient flow (MLAWGF), are then given by

| (80) |

The dynamics in (80) can essentially be viewed as a change of measure of the standard LAWGD dynamics in [20, Sec. 4], designed to converge to the dual target .

Suppose, in addition, that the kernel were chosen such that , where denotes the infinitesimal generator of the Langevin SDE with stationary distribution . Thus, in particular,

| (81) |

where denotes the function , given some base function . Letting , using (20), and then the chain rule, we can rewrite this as

| (82) | ||||

| (83) |

We will denote this kernel . In practice, computing requires computing the spectral decomposition of the operator , which is challenging even in the moderate dimensions. Nonetheless, following [20, Theorem 4], for this choice of kernel we can show that the MLAWGF converges exponentially fast to the target distribution, at a rate independent of the Poincaré constant.

Proposition 14.

Assume that satisfies a mirrored PI with some constant . In addition, suppose that has a discrete spectrum. Then the KL divergence converges exponentially along the MLAWGF, with a rate independent of :

| (84) |

Proof.

Using standard rules for calculus on the Wasserstein space, and the integration by parts formula [e.g., 5], we have

By [43, Theorem 2] and (41) - (43) in the proof of Proposition 2, we have that and , which implies that

| (85) |

where in the final line we have once again used the fact that . The conclusion now follows via Grönwall’s inequality. ∎

To obtain an implementable algorithm, observe that the vector field in the continuity equation can be rewritten as [20]

| (86) |

Next, using a forward Euler discretisation in time, we arrive at

| (87) |

Finally, we approximate the expectations in (87) with samples. In particular, after initialising a collection of particles for , we set for , and then update

| (88) |

This algorithm, which we refer to as the mirrored LAWGD (MLAWGD) algorithm, is summarised in Alg. 4.

B.4 Mirrored Kernel Stein Discrepancy Descent

Finally, we consider the MWGF of the kernel Stein discrepancy (KSD) [62, 21, 38]. In so doing, we will obtain a mirrored version of the kernel Stein discrepancy descent (KSDD) algorithm in [51].

B.4.1 MWGF of the Kernel Stein Discrepancy

We begin by defining , where is the mirrored KSD, which we define as

| (89) |

where is the mirrored Stein kernel, defined in terms of the score of the mirrored target , and the positive semi-definite kernel as

| (90) |

and where, as before, is the kernel defined according to , for some base kernel . The MKSD is nothing more than the KSD between and , with respect to the kernel .

In this case, one can show that [51, Proposition 2]. We can thus define the MKSD gradient flow according to

| (91) |

Similar to the previous sections, we would like to study the properties of this scheme in continuous time.

Proposition 15.

The dissipation of along the MWGF in (91) is given by

| (92) |

Proof.

The result follows straightforwardly using the chain rule. In particular, we have

| (93) | ||||

| (94) |

∎

Remark 10.

Unlike elsewhere (i.e., Propositions 1 - 2, Proposition 8, and Propositions 11 - 12) this dissipation result is given in terms of the mirrored densities and the mirrored target , rather than densities and the target . The crucial difference here is that the objective functional is not equal to , whereas previously it was true that, e.g., or . Nonetheless, it is possible to give a dissipation result in terms of the target .

We begin by rewriting the LHS of (92). Recall that the squared KSD between and is identical to the Stein Fisher information between and [e.g., 62, Theorem 3.6]. This also holds for and in the mirrored space, and thus we have

| (95) |

where in the second equality we have used the result obtained in (57) - (60); see the proof of Proposition 8. Thus, in particular, is equal to the mirrored Stein Fisher information, up to a factor half.

We now turn our attention to the RHS of (92). We would like to simplify , as defined in (B.4.1). Let and . Using the definition of , we have . Using also the chain rule, we have

| (96) |

Similarly, it holds that

| (97) |

Finally, due to (20), we have . Putting everything together, we thus have that

| (98) |

Using (95) and (98) we thus have the following dissipation result for the mirrored Stein Fisher information in terms of the target :

| (99) |

B.4.2 Mirrored Kernel Stein Discrepancy Descent (MKSDD)

To obtain an implementable MKSDD algorithm, it is, of course, necessary to discretise in time and in space. In this case, following [51], we will first discretise in space, replacing the measure by a discrete approximation . This yields, writing ,

| (100) |

The mirrored KSDD algorithm thus takes the following form. Initialise a collection of particles for , and set for . Then, update

| (101) |

Appendix C Convergence of Mirrored Coin Wasserstein Gradient Descent

Proposition 16.

Proof.

First note, using Jensen’s inequality, and [43, Theorem 2], that

| (103) | ||||

| (104) | ||||

| (105) |

where in the final line we have defined . Now, under the assumption that is strongly log-concave, [43, Proof of Theorem 3] guarantees the existence of a mirror map such that the mirrored target is also strongly log-concave. It follows, in particular, that is geodesically convex [e.g., 2, Chapter 9]. Thus, arguing as in the proof of [81, Proposition 3.3], with , it follows that

| (106) |

Finally, once more using the definition of the mirror map and in particular the fact that and , we can rewrite the RHS in (106) as the RHS in (102). This completes the proof. ∎

Appendix D Other Mirrored Coin Sampling Algorithms

In this section, we provide some other mirrored coin sampling algorithms besides Coin MSVGD. Recall, from Sec. 4.2, the general form of the mirrored coin sampling algorithm. Let , and . Then, for , update

| (107) |

where , or some variant thereof. As noted in Sec. 4.2, for different choices of and , one obtains learning-rate free analogues of different mirrored ParVI algorithms.

In Sec. 4.2, we provided the Coin MSVGD algorithm (Alg. 2), which corresponds to and . This can be viewed as the coin sampling analogue of MSVGD (Sec. 3.2.1 and App. B.2). We now provide two more mirrored coin sampling algorithms, which correspond to the coin sampling analogues of MLAWGD (App. B.3) and MKSDD (App. B.4).

D.1 Coin MLAWGD

D.2 Coin MKSDD

Appendix E Adaptive Coin MSVGD

In Sec. 4.1 - 4.2, we described a betting strategy which is valid under the assumption that the sequence of outcomes are bounded by one, in the sense that for all and for all [see also 81, Sec. 3.4]. In practice, this may not be the case. If, instead, for some constant , then one can simply replace by its normalised version, namely in Alg. 2.

If, on the other hand, the constant is unknown in advance, then one can use a coordinate-wise empirical estimate which is adaptively updated as the algorithm runs, following [72] and later [81, App. D].333Here, indexes the particle, and indexes the dimension (see Alg. 8). We provide full details of this version of Coin MSVGD in Alg. 8. One can also obtain an analogous version of Coin MIED; we omit the full details here in the interest of brevity.

Finally, when we use a coin sampling algorithm to perform inference for a (fairness) Bayesian neural network (see Sec. 6.3), we alter the denominator of the betting fraction in Alg. 8 such that it is at least . Thus, the update equation in Alg. 8 (or, analogously, the update equation in the adaptive version of Coin MIED) now reads as

| (108) |

This modification, recommended in [72, Sec. 6], has the effect of restricting the value of the particles in the first few iterations. We should emphasise that these adaptive algorithms, which in practice we use in all experiments, are still free of any hyperparameters which need to be tuned by hand.

Computational Cost. It is worth noting that, in terms of computational and memory cost, the adaptive Coin MSVGD algorithm is no worse than MSVGD when the latter is paired, as is common, with a method such as Adagrad [31], RMSProp [92], or Adam [48]. The computational cost per iteration is , due to the kernelised gradient. Meanwhile, in terms of memory requirements, it is necessary to keep track of the maximum observed absolute value of the gradients (component-wise), the sum of the absolute value of the gradients (component-wise), and the total reward (component-wise). This is similar to, e.g., Adam, which keeps track of exponential moving averages of the gradient and the (component-wise) squared gradient [48].

| (compute SVGD gradient) |

| (update max. observed scale) | ||||

| (update sum of abs. value of gradients) | ||||

| (update total reward) | ||||

| (update the particles) |

Appendix F Additional Experimental Details

In this section, we provide additional details relevant to the experiments carried out in Sec. 6. We implement all methods using Python 3, PyTorch, and TensorFlow. We use the existing implementations of MSVGD and SVMD [82] and MIED [60] to run these methods. We perform all experiments using a MacBook Pro 16" (2021) laptop with Apple M1 Pro chip and 16GB of RAM.

For the experiments in Sec. 6.1 and 6.2, we use the inverse multiquadric (IMQ) kernel due to its favourable convergence control properties (e.g., [38]). Unless otherwise stated, the bandwidth is determined using the median heuristic [63, 36]. For the experiment in Sec. 6.3, following [60], we use the -Riesz family of mollififiers with and .

F.1 Simplex Targets

For both experiments in Sec. 6.1, we initialise all methods with i.i.d samples from a distribution and use the entropic mirror map

| (109) |

We run all methods for iterations using particles. In the interest of a fair comparison, we run all of the learning-rate dependent methods (MSVGD, SVMD, projected SVGD) using RMSProp [92], an extension of the Adagrad algorithm [31], to adapt the learning rates.

Sparse Dirichlet Posterior. We first consider the sparse Dirichlet posterior in [73], which is given by

| (110) |