Confidence sets for Causal Orderings

Abstract.

Causal discovery procedures aim to deduce causal relationships among variables in a multivariate dataset. While various methods have been proposed for estimating a single causal model or a single equivalence class of models, less attention has been given to quantifying uncertainty in causal discovery in terms of confidence statements. The primary challenge in causal discovery is determining a causal ordering among the variables. Our research offers a framework for constructing confidence sets of causal orderings that the data do not rule out. Our methodology applies to structural equation models and is based on a residual bootstrap procedure to test the goodness-of-fit of causal orderings. We demonstrate the asymptotic validity of the confidence set constructed using this goodness-of-fit test and explain how the confidence set may be used to form sub/supersets of ancestral relationships as well as confidence intervals for causal effects that incorporate model uncertainty.

1. Introduction

Inferring causal relations as opposed to mere associations is a problem that is not only of intrinsic scientific interest but also helps predict how an observed system might change under intervention (Peters et al.,, 2017). When randomized controlled trials are infeasible, methods for causal discovery—the problem of estimating a causal model from observational data—become valuable tools for hypothesis generation and acceleration of scientific progress. Examples of applications include systems biology (Sachs et al.,, 2005), neuroscience (Shen et al.,, 2020), and climate modeling (Nowack et al.,, 2020).

Causal models may be represented as a directed acyclic graph (DAG), and—leveraging this representation—causal discovery can be cast as recovering the appropriate DAG. The first step in causal discovery is identification: determining appropriate assumptions under which the causal model can be recovered from population information; see, e.g., Shimizu et al., (2006); Loh and Bühlmann, (2014); Peters et al., (2014). The next step is providing a method to estimate the causal graph from data; see, e.g., Bühlmann et al., (2014); Chen et al., (2019); Wang and Drton, 2020b . Once an estimation procedure is established, it is natural to question the estimation uncertainty. Uncertainty quantification and the ability to test identifying assumptions are essential for trustworthy estimation of causal graphs and help to determine whether key modeling assumptions are appropriate. Nonetheless, the literature on frequentist causal discovery, with a few exceptions (e.g., Strobl et al.,, 2019), only outputs a point estimate in the form of a DAG or single equivalence class.

Given a causal ordering of the variables, causal discovery reduces to variable selection in a sequence of regressions. Thus, the key difficulty lies in inferring the causal ordering; this motivates the issue we address in this paper: developing a procedure that provides a confidence set for causal orderings.

1.1. Setup

We represent a causal model for the random vector with a DAG , where each node in the vertex set indexes a random variable . An edge indicates that has a direct causal effect on , and we say that is a parent of its child . If there exists a directed path in from to , then is an ancestor of its descendant . We denote the sets of parents, children, ancestors, and descendants of node by , , , and , respectively. The models we consider take the form of a recursive structural equation model (SEM) with additive noise:

| (1.1) |

where the are unknown and the errors are mean zero and mutually independent.

In a fully general SEM, the DAG may only be identified from observational data up to a Markov equivalence class—a collection of graphs that imply the same set of conditional independence relations (Spirtes et al.,, 2000). As the different graphs in the equivalence class may have contradicting causal interpretations, it is also of interest to work with restricted SEMs in which the DAG itself becomes identifiable (Maathuis et al.,, 2019, Chap. 18.6.3). Specifically, for the model in (1.1), the DAG becomes identifiable when are non-linear or the errors non-Gaussian. In contrast, the linear Gaussian case, also allowed under (1.1), features the same Markov equivalence classes as the general nonparametric model.

We focus on a causal ordering for the variables in the model given by DAG ; i.e., a total ordering of where variables that appear later have no causal effect on earlier variables. We may identify each possible ordering with a permutation , where yields a causal ordering for if and only if implies that . In general, a causal ordering is not unique, and, letting be the set of all permutations of , we denote the set of all causal orderings

1.2. Contribution

Let be a sample drawn from the SEM in (1.1), and let . We propose a procedure that constructs a confidence set of causal orderings, , where . Specifically, our procedure inverts a goodness-of-fit test for a causal ordering and returns the set of all orderings that are not rejected by the test. Thus, for any :

| (1.2) |

It follows that if has a unique causal ordering (i.e., ), then contains that causal ordering with asymptotic probability at least . If , then our procedure still infers a valid causal ordering—i.e., —with asymptotic probability at least .

The confidence set provides a set of orderings that are not excluded by the data. Different elements of suggest different causal orderings which may, but do not have to, lead to different causal conclusions; we elaborate on this point in Section 4.3. The set being large cautions the analyst against overconfidence in a specific estimated ordering. In contrast, if is small, few causal orderings are compatible with the data under the considered model class. This latter aspect is crucial because may also be empty, indicating that the model class does not capture the data-generating process.

Furthermore, can be post-processed to form other useful objects. Most notably, similar to the problem studied by Strieder et al., (2021), we may form confidence intervals for causal effects that also incorporate model uncertainty. In addition, yields a sub/superset of the true ancestral relationships with some user-defined probability.

Our framework takes a straightforward approach based on goodness-of-fit tests. However, realizing this idea presents significant challenges, and we construct our procedure with careful attention to both statistical and computational aspects. Specifically, our methodology is built using computationally attractive tests for regression models with asymptotic validity under , where is the number of variables and is the sample size. Computationally, we devise the statistical decisions so that we can use a branch-and-bound type procedure to handle problems at a moderate but challenging scale. Despite prioritizing computational tractability, the procedure is asymptotically valid when allowing to grow with , and we establish the asymptotic validity of the confidence set when .

To motivate as an object of interest, we preview the analysis in Section 6.3 of daily stock returns for 12 industry portfolios. DirectLiNGAM (Shimizu et al., 2011a, ) gives a point estimate of the causal ordering where the Utilities industry is first and causally precedes the other 11 industries. The set contains approximately of the possible total orderings, and indeed Utilities is first in every ordering in the confidence set. Nonetheless, many orderings in —i.e., those not rejected by the data—have other causal implications which differ from the point estimate. As shown in Section 6.3, the point estimate is quite far from the Fréchet mean of . Finally, in the estimated causal ordering, Manufacturing precedes Chemicals, so a naive analysis would conclude that the total effect of Chemicals onto Manufacturing is . In contrast, when accounting for model uncertainty, we produce a 90% confidence interval for the total effect of Chemicals onto Manufacturing of .

1.3. Related work

Previous work on uncertainty in causal discovery predominantly focuses on specific parameters within a causal model, rather than uncertainty across the entire model selection procedure. In linear SEMs with equal error variances, Janková and van de Geer, (2019) provide confidence intervals for the linear coefficients and Li et al., (2019) test for absence of edges; Shi et al., (2021) consider the same problem for more general additive noise models. However, this work either assumes a causal ordering is known or requires accurate estimation of a causal ordering to properly calibrate the test. Thus, they are poorly suited for our setting of interest: where the “signal strength” is small or modeling assumptions may be violated. In contrast, Strieder et al., (2021) focus on the equal variance case with bivariate data and form confidence intervals for causal effects that account for model uncertainty.

A confidence set of models has previously been proposed in work such as Hansen et al., (2011) and Lei, (2020), who consider a set of candidate models and remove all models determined to be “strictly worse” than any other candidate in the set. In contrast, Ferrari and Yang, (2015) and Zheng et al., (2019) form confidence sets by including all models that are not rejected when compared to some saturated model.

As an intermediate step, our framework requires a goodness-of-fit test for regression models. This is a classical problem (Breusch and Pagan,, 1979; Cook and Weisberg,, 1983) that has seen renewed interest in recent work such as Sen and Sen, (2014), Shah and Bühlmann, (2018), Berrett and Samworth, (2019), and Schultheiss et al., (2023). In principle, it is possible adopt any of these existing procedures into our proposed framework; however, the high computational cost renders them unusable in all but the smallest problems. Thus, we propose a specific new test that possesses both statistical and computational properties that are particularly advantageous for our goal of targeting causal orderings, which requires us to test a very large number of regression models. We provide a detailed comparison of our proposal and existing work in Section 3 after describing our procedure.

There is a large literature on testing model fit for a specific SEM, particularly in the linear case. Testing model fit is then classically done by comparing empirical and model-based covariances (Bollen and Long,, 1993). However, in some settings, as discussed in Section 1.1, a unique graph may be identified, but simply comparing covariances will fail to falsify graphs in the same Markov equivalence class. Furthermore, the models we consider do not constrain covariances and thus require alternative approaches.

We note that, by their very nature, Bayesian approaches also quantify uncertainty for causal structures and have seen numerous computational advances, e.g., by focusing on causal orderings (Friedman and Koller,, 2003; Niinimäki et al.,, 2016; Kuipers and Moffa,, 2017). This said, nearly all Bayesian causal discovery procedures focus on cases where the graph can only be identified up to an equivalence class. The few exceptions—e.g., Hoyer and Hyttinen, (2009); Shimizu and Bollen, (2014); Chang et al., (2022)—require specifying a likelihood for the data, rather than adopting the semi-parametric approach that we employ. At a more fundamental level, credible intervals differ conceptually from confidence regions that are our focus; especially, since in a complex model selection problem as we consider, there is no Bernstein-von Mises connection between the two concepts.

1.4. Outline

In Section 2, we give background on causal discovery. In Section 3, we propose a computationally attractive goodness-of-fit test for a single causal regression and show in Section 4 that it can be used to test a causal ordering and form the confidence set . We establish theoretical guarantees in Section 5 and examine empirical performance in Section 6.

2. Background on causal discovery

For expository simplicity, we initially focus on the linear SEM in (1.1) where each is linear. Thus, assuming zero means,

| (2.1) |

Collecting and letting denote the matrix of causal effects where if and if , we have the multivariate model . We use to denote the sub-vector corresponding to the elements in . We use bold font to denote the collection of observations; i.e., denotes the th observation of the th variable and and . When we pass sets of observations to a function, it should be interpreted as the function applied to each observation; i.e., and .

For linear SEMs, Shimizu et al., (2006) show that the exact graph can be identified when the errors, , are mutually independent and non-Gaussian. The identification result relies on the following key observation. Let denote the residuals when is regressed—using population values—onto a set of variables . If contains all the parents of but no descendants (i.e., all variables that have a direct causal effect on and no variables that are caused directly or indirectly by ), then the residuals resulting from the population regression are independent of the regressors. Thus, the hypothesis in (2.2) implies the hypothesis in (2.3) where denotes the non-descendants of :

| (2.2) | ||||

| (2.3) |

If contains a descendant of , will still be uncorrelated with . However, if the errors are non-Gaussian then except when takes specific pathological values. Thus, testing the independence of residuals and regressors may falsify the hypothesis in (2.3) and subsequently (2.2).

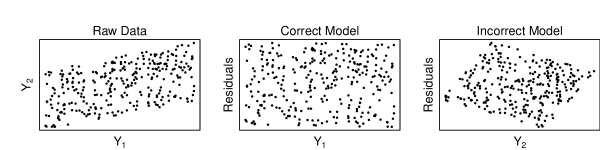

A simple bivariate case is given in Figure 1, where the correct model is . When viewing the raw data (left plot), no specific causal relation is immediately apparent. However, in the middle plot, we have identified the correct model (), and the residuals when regressing onto are independent of the regressor, . On the right-hand side, we have posited the incorrect model . When regressing onto , the residuals remain uncorrelated with , but are no longer independent of .

Of course, we typically do not have access to population values, and the linear coefficients are nuisance parameters that need to be estimated before conducting an independence test. Wang and Drton, 2020b show—in the linear non-Gaussian SEM setting—consistent recovery of the graph is still possible when estimating the nuisance parameters, even in the high-dimensional setting. Thus, to test (2.3) from data, one might naively use least squares regression and directly test whether the residuals, , are independent of . Unfortunately, even when the null hypothesis holds, so and the naive test does not control the Type I error rate. Example A.1 in the appendix provides an illustration. A more careful approach is required for a valid test of (2.3), and this problem has been previously addressed, e.g., by Sen and Sen, (2014). In Section 3, we discuss a procedure that is particularly suited for our setting and contrast our approach with existing procedures.

3. Goodness-of-fit for regression

We now propose a procedure for testing the null hypothesis in (2.3) as a proxy for (2.2); this test will be used as a building block for testing causal orderings as described in Section 4. We first describe how this can be done in the linear SEM setting and then generalize the procedure when may be non-linear.

3.1. Residual bootstrap test for linear models

For some and set , let where denotes the random vector augmented by a term for the intercept and let ; i.e., is the population regression coefficient and is the resulting residual. The quantity and random variable are well defined for all and , and when then coincide with the causal parameters—i.e., —and . Given data, we denote the population residuals as . Furthermore, let be regression coefficients estimated from sample moments, let , and let denote the residuals calculated using .

Our test will require a set of functions, , which we refer to as test functions; these are selected by the analyst and we give practical guidance below. Let

| (3.1) |

Finally, the test statistic aggregates across all . Specifically, let

| (3.2) |

When making statements which refer to both and we will sometimes omit the sub-script and simply use .

By the first order conditions of least squares regression, is always uncorrelated with . Thus, if is a linear function, . Furthermore, in multivariate Gaussians, uncorrelated is equivalent to independent, so for linear Gaussian SEMs, and (2.3) always hold regardless of whether (2.2) holds. We note, however, that this inability to falsify (2.2) is not specific to our approach, but intrinsic to the non-identifiability of linear Gaussian SEMs as previously mentioned. In either of these cases, the Type I error rate of our proposed procedure will be preserved, but the test will have trivial power.

When is a non-linear and the errors are non-Gaussian, we may use (and subsequently ), to assess whether and are truly independent (not just uncorrelated) and ultimately test the hypothesis in and (2.2). Under the null hypothesis, has mean zero, because , and

| (3.3) |

However, when the null hypothesis in (2.2) does not hold, the population regression coefficients are generally not equal to the causal coefficients such that . Letting , with a slight abuse of notation, we define if and otherwise, and similarly let if and otherwise. Then, and is equal to

| (3.4) |

The first term is mean , and the second term is asymptotically mean when is fixed and grows. However, for linear SEMs with non-Gaussian errors, we may select a non-linear which renders so that the third term is . For example, Wang and Drton, 2020a show that for any integer , for generic choices of and th degree moments of the errors. The test will have greater power when is large relative to the variability of the first two terms in (3.4), but selecting a set of test functions with “optimal” power depends on the unknown distribution of the errors and is difficult in practice. Nonetheless, in the simulations, we set and observe that the test exhibits good empirical power when compared to other state-of-the-art tests. In Section 5, we explicitly analyze the power of our proposed testing procedure.

If we had access to new realizations of , we could sample directly from the distribution of and ultimately (conditional on ) by replacing in (3.3) with new draws. Comparing the observed to the distribution of these new realizations would yield an exact finite-sample test. We refer to this distribution as the oracle distribution because, in practice, we cannot resample exactly. Alternatively, conditioning on , the quantity in (3.3) is asymptotically normal under the null hypothesis. Thus, the null distribution could be approximated by samples which replace the in (3.3) with draws from a Gaussian. However, when is not close to a Gaussian, we see drastic improvements by using the residual bootstrap procedure proposed below. We illustrate this explicitly with a simulation study in Section B of the appendix.

Instead, we calibrate our test with a residual bootstrap procedure. For each bootstrap draw, we condition on and replace in (3.3) with where each is drawn i.i.d. from the empirical distribution of . This is equivalent to forming , regressing onto to form the residuals and computing as described in Alg. 1. Similar to before, we thencompute by letting . In the simulations, we use the asymptotically equivalent quantity which divides by instead of . In Section 5, we show that this approximation converges to the oracle distribution in Wasserstein distance when .

Various other procedures, discussed below, have also been proposed for testing goodness-of-fit for a linear model via the hypothesis in (2.3). In theory, these procedures could also be used in the framework we subsequently propose for testing a causal ordering. However, practically speaking and as shown in Section 6, the computational cost of these procedures—save perhaps Schultheiss et al., (2023)—renders them infeasible for our goal of computing confidence sets for causal orderings.

Moreover, beyond the drastic computational benefits, the proposed procedure possesses some statistical advantages, which we briefly discuss now and also empirically demonstrate in Section 6. Sen and Sen, (2014) use the Hilbert-Schmidt Independence Criterion (HSIC) (Gretton et al.,, 2007) to measure dependence between regressors and residuals. They only consider the fixed setting, and the simulations in Section 6 show that the type I error is inflated when is moderately sized compared to . We conjecture this is partly because they bootstrap both the regressors and residuals to approximate the joint distribution rather than conditioning on the regressors and only approximating the distribution of the errors. In contrast, Shah and Bühlmann, (2018) propose Residual Prediction (RP) and Berrett and Samworth, (2019) propose MintRegression, which test the goodness-of-fit conditional on the covariates; however, both procedures calibrate their tests using a parametric bootstrap that assumes the errors are Gaussian. In the supplement, Shah and Bühlmann, (2018) do consider cases where the errors are non-Gaussian and use a residual bootstrap, which shows good empirical performance although they do not provide any theoretical guarantees. Finally, Schultheiss et al., (2023) also propose a goodness-of-fit test for individual covariates in a linear model using a statistic similar to Wang and Drton, 2020b . They show that the statistic is asymptotically normal and calibrate the hypothesis test using an estimate of the limiting distribution. A direct comparison of required conditions is not straightforward because they focus on the high-dimensional sparse linear model; whereas we do not assume sparsity, but require . Nonetheless, for valid testing, they require the number of non-zero coefficients to be ; in contrast, we require .

3.2. Non-linear models via sieves

Using a similar argument with the independence of residuals and regressors, Peters et al., (2014) show that the causal graph may also be identified when the structural equations in (1.1), , are non-linear. The procedure proposed above directly generalizes to this setting.

Let be a basis of functions (e.g., the b-spline or polynomial basis) that take inputs . We approximate with by regressing onto the first elements of —which we will denote by . As in the linear setting where we included an intercept term, we require the constant function to be in the span of . Given the residuals of , the test statistics can then be calculated in the same way as in the linear setting. In this case, to ensure the test statistics are not identically zero, we must select test functions that do not lie in the span of . If we do not know a good basis, , for a priori, we can use a sieve estimator where grows with . Let be the squared error projection of into the span of ; i.e.,

| (3.5) |

In Section 5, we show that even if for any finite , the proposed test is valid as long as decreases appropriately with .

4. Inference for causal orderings

Before discussing details, we first discuss some of the trade-offs involved in our design decisions. Estimating a causal ordering can be seen as a preliminary task when estimating a causal graph and various causal discovery procedures have fruitfully employed a search over causal orderings instead of individual graphs; e.g., Raskutti and Uhler, (2018); Solus et al., (2021). Given a correct causal ordering, estimating the graph simplifies greatly to variable selection in a sequence of regressions (Shojaie and Michailidis,, 2010). Thus, for computational reasons, we focus on confidence sets in the much smaller space of causal orderings rather than all possible graphs. Nonetheless, let be the set of DAGs formed by estimating a graph from each ordering . If—given a correct ordering—the true graph can be recovered with overwhelming probability, then (1.2) trivially implies that is an asymptotically valid confidence set for ; i.e., .

We also choose to form the confidence set by inverting a goodness-of-fit test. If the model assumptions are violated, then all possible orderings may be rejected, resulting in an empty confidence set. Alternatively, one could form a confidence set by considering a neighborhood around , a point estimate of a causal ordering. This would produce a non-empty confidence set even when the model is misspecified and might be preferred if represents a useful “projection” into the considered class of models. However, in practice, it is difficult to know if the misspecification is “mild,” and we argue that observing an empty confidence set is imortant because it alerts the scientist to potentially choose a causal discovery procedure that makes less restrictive identifying assumptions.

Finally, we construct a test for each causal ordering by aggregating several regression tests. Although we only require for asymptotic validity of all individual regression tests, the aggregation requires . Alternatively, a direct test that does not aggregate individual tests might enjoy better statistical properties. However, we trade statistical efficiency for computational efficiency and aggregating individual tests allows for a branch-and-bound type procedure, which in practice drastically decreases computation and enables feasible analysis of “medium-sized” problems. In Section 6.1, we show that this procedure can be applied to problems with .

4.1. Testing a given ordering

For an ordering , let be the set of nodes that precede in . When is a valid ordering for , then for all such that . However, when is not a valid causal ordering, there exists some such that . Thus, testing whether is a valid causal ordering is equivalent to testing

| (4.1) |

To operationalize a test for , we use the procedure from Section 3.1 to test for all such that . Using the residual bootstrap procedure to test produces a p-value, denoted as , which approximates, , the p-value which would result from a test calibrated by the oracle distribution. We propose aggregating the p-values into a single test for (4.1) by taking the minimum p-value. Specifically, let

| (4.2) |

By Lemma 4, the of p-values produced by the oracle procedure, , are mutually independent under the null hypothesis so follows a . Of course we do not have access to , but under conditions described in Section 5, . Thus, to compute a final p-value for , denoted as , we also compare to a distribution.

4.2. Efficient computation

To satisfy (1.2), we construct by including any where is not rejected by a level test; i.e.,

| (4.3) |

Of course, enumerating all permutations is computationally prohibitive, so we propose a branch-and-bound style procedure to avoid unnecessary computation. Pseudocode is given in Alg. 2. For any fixed , we sequentially test for , and we update a running record . Once is less than the quantile of a , we can reject without testing the remainder of the ordering.

Furthermore, we test each ordering in simultaneously rather than sequentially. We first testing all orderings of length . Subsequently, we only consider orderings of length that are formed by appending a node to a set of length that is not already rejected. We repeat this process for increasing . This approach avoids redundant computation because the test of , only depends on the combination of elements included in and not the specific ordering . For example, when , once we have tested for the incomplete ordering we do not need to recompute the test for . In the worst case, when the signal is small and no orderings are rejected, the procedure is still an exhaustive search. Nonetheless, in Section 6, we show that under reasonable signal-to-noise regimes, problems with are feasible.

4.3. Post-processing the confidence set

We now discuss how can be post-processed into other useful objects. Specifically, we consider: (1) confidence intervals for causal effects which incorporate model uncertainty, and (2) sub/super-sets of ancestral relations with confidence.

Strieder et al., (2021) consider a linear SEM with equal variances and provide CIs for causal effects which account for the model uncertainty. With a similar goal, we propose a procedure for the setting of linear SEMs with independent errors. We focus on the total effect of onto — using the do-operator (Pearl,, 2009); a procedure for the direct effect of onto —i.e., —is analogous and discussed in the Section D of the appendix. When , the total effect of on is , and when , the total effect may be recovered by a regression of onto and a set of additional covariates—often called the adjustment set. In particular, letting be the adjustment set yields an unbiased estimate. While adjustment sets which recover the total effect may not be unique, an incorrect adjustment set may bias the estimate; e.g., incorrectly including a descendant of or excluding a parent of from the adjustment set may induce bias. Thus, naively selecting a single adjustment set and calculating a confidence interval for the parameter of interest will not provide nominal coverage when there is considerable uncertainty in a “correct” adjustment set. Robust quantification of uncertainty must also account for uncertainty in the selected adjustment set.

Alg. 3 describes a procedure to calculate CIs for the total effect of onto which account for model uncertainty. Specifically, we consider the adjustment set for each ordering . We then calculate the CI for the regression parameter of interest, conditional on that adjustment set. The final CI is given by the union of all conditional CIs. In practice, if and are fixed in advance, this can be calculated simultaneously with to avoid redundant regressions. This is similar in flavor to the IDA procedure of Maathuis et al., (2009), but we additionally account for uncertainty due to estimating the graph rather than just population level non-identifiability within a Markov equivalence class.

Lemma 1.

Furthermore, may be used to compute a sub/super-set of ancestral relations. Let denote the set of true ancestral relationships in , denote the set of ancestral relations that hold for all , and denote the set of ancestral relations which are implied by at least one . Lemma 2 shows with probability at least . The set is similar to the conservative set of causal predictors given in Peters et al., (2016).

Lemma 2.

Suppose satisfies (1.2). Then,

5. Theoretical guarantees

We now show conditions under which the residual bootstrap procedure is asymptotically valid. We also show that aggregating multiple tests results in a valid test for an entire ordering. Furthermore, we analyze the power of the regression goodness-of-fit test.

5.1. Residual bootstrap

Suppose is a causal ordering of the DAG and consider a fixed . Let denote the distribution of , denote the empirical distribution of , and denote the empirical distribution of the residuals . We allow for non-linear , and recall that is the basis used to model which includes an intercept term. Specializing to linear SEMs, and would simply be linear functions of for and an intercept. Recall that denotes the optimal approximation of within ; i.e.,

Let denote the approximation error such that . If , then .

We examine the distribution of the test statistic under two settings: an oracle distribution of —where we condition on and resample in (3.3) exactly from —and the bootstrap distribution of —where we replace in (3.3) with where . Let denote the Wasserstein-2 distance between the distributions and . In a slight abuse of notation, we will also use to denote when and .

Theorem 1 shows that the oracle distribution and the bootstrapped distribution converge in Wasserstein-2 distance under weak conditions. We consider a sequence of models indexed by , , such that is a graph with vertices and let denote the sample size drawn from . For simplicity, we will suppress the notational dependence on . We will require tail conditions on the errors and test functions which we impose through upper bounds on Orlicz- norms; for , the Orlicz- norm of is . When , has sub-exponential tails, and when for , has been referred to as sub-Weibull (see, e.g., Vladimirova et al., (2020); Götze et al., (2021)). When is sub-exponential, the test functions we use in the simulations, , satisfy for .

Theorem 1.

Suppose that with . Furthermore, there exist constants such that for all and , with , , and for some . Let . Then, for any causal ordering consistent with DAG , with probability , is less than

| (5.1) |

Corollary 1 considers the setting where each belongs to a known finite-dimensional basis . In this case . Corollary 2 considers the setting where a finite basis for is not known a priori, and a sieve estimator for is used so that grows with .

Corollary 1 (Known finite basis).

Suppose that conditions of Theorem 1 are satisfied. If each belongs to a known finite-dimensional basis, then with probability

Corollary 2 (Sieve basis).

Suppose that conditions of Theorem 1 are satisfied. Furthermore, suppose that a finite-dimensional basis for each is not known a priori, but there exists such that for all , , and for some . Letting , we have with probability for some constant which depends on ,

| (5.2) |

Corollary 2 requires that the approximation bias—as measured by —is bounded above by for some . This is satisfied under various more general conditions (Barron and Sheu,, 1991). For example, suppose that where is a univariate function and is its th derivative (i.e., bounded Sobolev norm). Then, letting denote the best polynomial approximation up to degree , we have . Thus, in the additive model where , it follows that . Similar statements hold when has finite support and is approximated by splines or the Fourier basis.

Regardless, whether a finite basis is known or not, Theorem 1 and its corollaries show that for a sequence of models , when fixing and letting , , and grow such that , we have . The convergence in Wasserstein distance, however, does not immediately imply that the p-values from the oracle procedure and the bootstrap procedure converge. Roughly speaking, Lemma 3 shows that when the test statistic does not converge to a point mass, the quantile functions converge uniformly.

Lemma 3.

Let denote the p-value calculated for the test statistic using the CDF . Let denote the p-value calculated using the CDF . Suppose . Then,

| (5.3) |

Lemma 3 implies that the p-values from the idealized and obtainable procedures converge when . This is satisfied when the distribution of is continuous with bounded density. Finally, Lemma 4 shows that, under the null hypothesis in (4.1), the p-values generated by the oracle procedure are mutually independent.

Lemma 4.

Let be a causal ordering for and suppose are p-values calculated using the oracle procedure. Then the elements of are mutually independent.

To test the ordering, , we aggregate the individual p-values into the test statistic and for the oracle and bootstrap procedures, respectively. We then compare and to a to get and , the final p-value for the entire ordering. The following corollary implies that for the final step, if .

Corollary 3.

For a fixed , suppose that the conditions of Theorem 1 hold and . Furthermore, assume that the test statistic has a continuous density bounded above by for all . Then

| (5.4) |

5.2. Power analysis

Recall that denotes the population residuals; i.e., in the linear case where denotes with an added intercept term and . Let , , and

| (5.5) |

Under , for every so that and . Under the alternative, however, when the data is generated by a linear non-Gaussian SEM or non-linear SEM (i.e., when the causal ordering may be identified from data), and for appropriately chosen , the quantity and subsequently are non-zero. Theorem 2 shows that the test for a single regression may have power going to even as grows if and .

Theorem 2.

Suppose and consider a sequence of models where grow, but , and are fixed. Suppose does not hold, then for any fixed level , the hypothesis will be rejected with probability going to if

-

(1)

is jointly sub-Gaussian with Orlicz-2 norm , ,

, and and ; or

-

(2)

is jointly log-concave with Orlicz-1 norm and and ,

where .

When aggregating individual regression tests to test an entire ordering at level , rejecting the null requires that the minimum p-value across the individual tests be less than . Using a crude Bonferroni upper bound, in order to reject the entire ordering with probability going to , we would require to be larger by a factor of ; i.e., in the sub-Gaussian case, we require .

6. Numerical experiments

In Table 1(b) we compare the proposed goodness-of-fit test for a single linear regression to the procedures of Sen and Sen, (2014) (denoted in the table as “S”), RP Test Shah and Bühlmann, (2018) (“RO” for OLS version and “RL” for Lasso version), MINT Berrett and Samworth, (2019) (“M”), and higher-order least squares Schultheiss et al., (2023) (“H”). For our procedure, we use , where each is standardized. We display results for the statistic, and results for the statistic are similar.

For each replication, we construct a graph by starting with edges for all ; for any , is added with probability . For each edge, we sample a linear coefficient uniformly from . We consider settings where all error terms are either uniform, lognormal, gamma, Weibull, or Laplace random variables and a setting—called mixed—where the distribution of each variable in the SEM is randomly selected. We let or . The data is standardized before applying the goodness-of-fit tests. For each setting of , and error distribution, we complete 500 replications.

Table 1(b) shows the computation time for each procedure; the average time is similar across error distribution so we aggregate the results. We display ; similar results for are in the appendix. RP Test is typically the slowest, followed by Sen and Sen, (2014) and MINT. All of these procedures would be prohibitively slow for computing confidence sets of causal orderings. HOLS is the fastest of the existing procedures and is actually faster than our procedure when and . However, across other settings, our proposed procedure is often an order of magnitude faster than HOLS and up to 100-10,000x faster than the other procedures.

In addition to the stark computational benefits, the proposed test also performs well statistically. In Table 1(b), we compare the empirical size and power for tests with nominal level . To measure size we test the (true) ; to measure power we test the (false) . In each setting, if a procedure does not exhibit empirical size within 2 standard deviations of , then we do not display the empirical power.

Our proposed procedure controls size within the nominal rate in every setting. It also has the highest (or comparable) power in many settings where the errors are skewed, but tends to do less well when the errors are symmetric. Sen and Sen, (2014) tends to exceed the nominal size for skewed distributions and performs worse when as opposed to . The OLS variant of Shah and Bühlmann, (2018) performs well across a variety of settings but does not control size when the errors are uniform and ; the Lasso variant generally fails to control the type I error when as the linear model is not sparse. MINT exhibits inflated size when the errors are heavy tailed, but generally has good power in settings where the size is controlled. Finally, HOLS controls empirical size across a wide variety of settings—except the lognormal errors. When , HOLS tends to have good power when the errors are symmetric, but suffers when the errors are skewed.

| p | W | S | RO | RL | M | H | W | S | RO | RL | M | H |

| 10 | .001 | .100 | 2 | 2 | .054 | .004 | .001 | .279 | 19 | 10 | .252 | .005 |

| 20 | .001 | .172 | 9 | 5 | .101 | .007 | .009 | 3 | 195 | 107 | 3 | .011 |

| 45 | .004 | .661 | 73 | 24 | .447 | .018 | .343 | 94 | 3708 | 1403 | 113 | .115 |

| Size | Power | |||||||||||||

| Dist | p | W | S | RO | RL | M | H | W | S | RO | RL | M | H | |

| gamma | 10 | 4 | 5 | 9 | 8 | 11 | 0 | 14 | 7 | 18 | 25 | 14 | 0 | |

| 20 | 9 | 9 | 9 | 8 | 11 | 0 | 26 | 16 | 24 | 35 | 20 | 0 | ||

| 45 | 10 | 19 | 4 | 20 | 19 | 1 | 33 | 33 | 1 | |||||

| laplace | 10 | 5 | 4 | 9 | 8 | 8 | 0 | 5 | 6 | 13 | 9 | 12 | 0 | |

| 20 | 8 | 9 | 8 | 8 | 11 | 0 | 11 | 10 | 12 | 10 | 13 | 0 | ||

| 45 | 8 | 14 | 4 | 16 | 11 | 1 | 14 | 10 | 16 | 1 | ||||

| lognormal | 10 | 6 | 7 | 9 | 8 | 9 | 0 | 23 | 9 | 25 | 24 | 20 | 0 | |

| 20 | 12 | 13 | 4 | 8 | 22 | 0 | 48 | 36 | 41 | 0 | ||||

| 45 | 11 | 20 | 2 | 24 | 51 | 4 | 58 | 49 | 6 | |||||

| mixed | 10 | 6 | 6 | 11 | 7 | 9 | 0 | 11 | 6 | 15 | 19 | 13 | 0 | |

| 20 | 7 | 10 | 6 | 7 | 11 | 0 | 32 | 14 | 24 | 37 | 19 | 0 | ||

| 45 | 10 | 16 | 6 | 18 | 19 | 1 | 44 | 36 | 4 | |||||

| uniform | 10 | 3 | 3 | 10 | 9 | 8 | 0 | 4 | 3 | 9 | 14 | 6 | 0 | |

| 20 | 9 | 7 | 10 | 7 | 8 | 0 | 5 | 6 | 8 | 12 | 5 | 0 | ||

| 45 | 11 | 11 | 10 | 20 | 5 | 1 | 5 | 11 | 10 | 6 | 1 | |||

| weibull | 10 | 5 | 5 | 10 | 11 | 10 | 0 | 24 | 8 | 24 | 30 | 22 | 0 | |

| 20 | 8 | 13 | 5 | 7 | 15 | 0 | 44 | 39 | 48 | 0 | ||||

| 45 | 10 | 17 | 2 | 17 | 26 | 1 | 52 | 47 | 2 | |||||

| gamma | 10 | 7 | 16 | 1 | 8 | 11 | 9 | 86 | 81 | 79 | 92 | 46 | ||

| 20 | 10 | 17 | 0 | 6 | 6 | 12 | 98 | 99 | 100 | 100 | 90 | |||

| 45 | 12 | 14 | 0 | 32 | 7 | 14 | 99 | 100 | 100 | |||||

| laplace | 10 | 9 | 13 | 4 | 11 | 12 | 9 | 34 | 30 | 18 | 18 | 50 | 32 | |

| 20 | 9 | 10 | 0 | 9 | 34 | 9 | 41 | 44 | 31 | 35 | 65 | |||

| 45 | 12 | 10 | 0 | 28 | 52 | 10 | 55 | 55 | 66 | 96 | ||||

| lognormal | 10 | 10 | 26 | 1 | 7 | 44 | 14 | 95 | 88 | 80 | ||||

| 20 | 8 | 18 | 0 | 7 | 74 | 17 | 99 | 100 | 99 | |||||

| 45 | 10 | 18 | 0 | 32 | 98 | 19 | 100 | 100 | ||||||

| mixed | 10 | 9 | 20 | 4 | 10 | 14 | 11 | 83 | 77 | 75 | 61 | |||

| 20 | 12 | 19 | 3 | 8 | 17 | 10 | 96 | 97 | 98 | 97 | ||||

| 45 | 9 | 11 | 7 | 34 | 30 | 13 | 99 | 98 | 99 | |||||

| uniform | 10 | 10 | 10 | 12 | 10 | 1 | 6 | 4 | 15 | 20 | 28 | 6 | 21 | |

| 20 | 11 | 11 | 18 | 10 | 0 | 8 | 14 | 25 | 64 | 0 | 62 | |||

| 45 | 11 | 12 | 33 | 28 | 0 | 8 | 26 | 28 | 0 | 93 | ||||

| weibull | 10 | 8 | 21 | 2 | 10 | 31 | 11 | 92 | 91 | 83 | 75 | |||

| 20 | 11 | 19 | 0 | 6 | 27 | 12 | 99 | 100 | 100 | 99 | ||||

| 45 | 9 | 18 | 0 | 35 | 38 | 15 | 100 | 100 | ||||||

6.1. Confidence sets

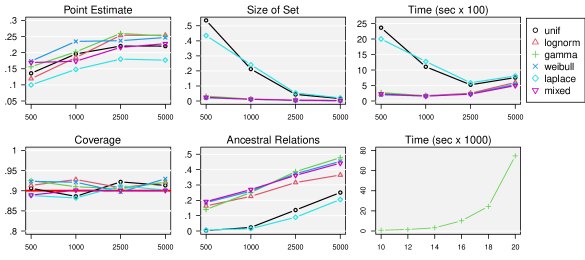

Fig. 2 shows results for replicates when constructing 90% confidence sets using Alg. 2. We fix and let . We generate random graphs and data as before with two changes: for all is included with probability and each linear coefficient is drawn from where is a Rademacher random variable and .

The upper left panel shows the proportion of times that the true causal ordering is recovered by DirectLiNGAM (Shimizu et al., 2011b, ). By construction, the average edge weight decreases with so the causal ordering is not consistently estimated as increases. Nonetheless, the bottom left panel shows that the empirical coverage of the confidence sets are all very close to the nominal rate of . In addition, the upper middle panel shows that the confidence sets are still increasingly informative in that the proportion of all possible orderings which are included in decreases. The proposed procedure is more powerful (i.e., returns a smaller confidence set) for the skewed distributions; however, even with symmetric errors, the confidence sets still contain less than of all orderings when . The bottom middle panel shows the proportion of all pairwise ancestral relationships which are certified into . Again, despite inconsistent estimation of the causal ordering, the proportion of ancestral relations which are recovered increases with .

The top right panel shows the time required to calculate the confidence set when . The computation time is not monotonic with because a larger sample size requires more computation for each considered ordering; however, this may be offset by increased power to reject incorrect orderings so the branch and bound procedure considers fewer orderings. Finally, in the bottom right panel, we show computational feasibility for larger by displaying the median computation time (sec) for replicates with . We consider gamma errors for . We draw random graphs and data as before, except the linear coefficients are selected uniformly from . Although the computational time increases rapidly, the procedure is still feasible for . We note, however, that of the replicates for failed to finish in the allotted hours.

6.2. Confidence intervals with model selection uncertainty

We now consider CIs for causal effects which account for model uncertainty. We draw random graphs and data under the same setup in Section 6.1 with , except we draw the magnitude of the linear coefficients from , so the “signal strength” is fixed instead of decreasing with as before. We compute 80% CIs for the total effect of onto using Alg. 3. We contrast this with a naïve procedure that computes CIs using only the adjustment set implied by , the causal ordering estimated by DirectLiNGAM. Specifically, if , then the naïve procedure uses an adjustment set of and returns the typical 80% CI for the regression coefficient of . When , is estimated to be an non-descendant of , so the returned CI is .

Table 2 compares the empirical coverage and lengths of the proposed CIs and the naïve CIs. The proposed CIs have empirical coverage above the nominal rate. The “Adj” column shows the proportion of times the point estimate yields a valid adjustment set for the total effect. Given that these values are much smaller than , it is unsurprising that the naïve CIs cover well below the nominal rate. Under gamma errors—when the model uncertainty is typically smaller—the proposed CIs have median length that is only 2-3 times larger than the naive procedure. However, in the Laplace setting where model uncertainty is larger, the median length is up to 5 times longer.

| n | Gamma | Laplace | ||||||||||||

| Coverage | Avg Len | Med Len | Adj | Coverage | Avg Len | Med Len | Adj | |||||||

| MU | NV | MU | NV | MU | NV | MU | NV | MU | NV | MU | NV | |||

| 250 | .97 | .67 | .81 | .19 | .55 | .18 | .37 | .99 | .59 | 1.1 | .19 | .74 | .17 | .25 |

| 500 | .96 | .63 | .60 | .14 | .38 | .13 | .42 | .99 | .61 | .86 | .13 | .60 | .12 | .36 |

| 1000 | .97 | .71 | .37 | .10 | .24 | .09 | .51 | .99 | .64 | .68 | .10 | .45 | .09 | .44 |

| 2000 | .94 | .71 | .22 | .07 | .14 | .06 | .61 | .97 | .65 | .46 | .07 | .30 | .06 | .54 |

6.3. Data example

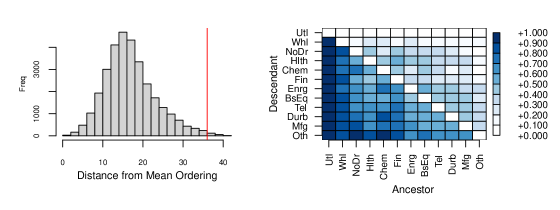

We now analyze data consisting of the daily value-weighted average stock returns for 12 different industry portfolios from 2019 to 2022 ()111Data available at: https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html. Accessed: Jan 2023. All stocks from the NYSE, AMEX, and NASDAQ are placed into one of 12 different industries. Using DirectLiNGAM, the estimated causal ordering is: Utilities, Energy, Manufacturing, Business Equipment, Finance, Other, Telecomm, Consumer Non-Durable, Wholesale, Consumer Durables, Chemicals, Healthcare. The 95% confidence set of causal orderings returned for the data contains approximately of the total orderings. The right panel in Fig. 3 summarizes the pairwise ancestral relationships for all non-rejected orderings, where darker shades of the element indicates that precedes in a larger proportion of non-rejected orderings.

Notably, Utilities is first in every non-rejected ordering so , which agrees with the point estimate. At first glance, this may seem odd; however, Utilities are often viewed as a proxy for bonds and directly capture the effect of changing interest rates and market uncertainty. From 2020 to 2022, the performance of American stock markets was largely driven by uncertainty around COVID-19 and federal monetary interventions. Thus, it makes sense that “Utitilies” are estimated to be an ancestor of all other industries.

Nonetheless, the other orderings in have causal implications which differ from the point estimate. We compute the Fréchet mean of using a distance between two orderings which counts the number of implied ancestral relations present in one ordering but not the other; i.e., The mean ordering is: Utilities, Wholesale, Consumer Non-durables, Healthcare, Chemicals, Finance, Energy, Business Equipment, Telecomm, Consumer Durables, Manufacturing, Other, and the left panel of Fig. 3 shows the distance from the Fréchet mean for all orderings in . The distance of the point estimate is indicated by the vertical line, and we observe that it is actually further from the mean than most other orderings in .

Finally, the naive 90% CI for the total effect of Energy onto Manufacturing is . Furthermore, since Manufacturing precedes Chemicals in the estimated ordering, we would naively conclude that the total effect of Chemicals onto Manufacturing is . In contrast, when accounting for model uncertainty, we produce a 90% CI for the total effect of Energy onto Manufacturing of and a CI for the effect of Chemicals onto Energy of .

7. Discussion

We have proposed a procedure for quantifying uncertainty when estimating the causal structure. Our goodness-of-fit testing framework returns a confidence set that may be informative about the validity of the posited identification assumptions, as well as which causal orderings the identifying assumptions cannot rule out. The confidence set can also be used to compute various other objects of interest. Notably, this includes confidence intervals for causal effects that also account for model uncertainty and a sub/superset of ancestral relations. Our specific goodness-of-fit test is designed for models in which residuals are independent of regressors under the null hypothesis. Future work could extend this procedure to settings where causal sufficiency may not hold (Wang and Drton, 2020a, ).

While we believe the proposed approach has many desirable characteristics, there, of course, also are a few previously mentioned disadvantages which could be addressed in future work. Most notably, the primary disadvantage of our approach is the computational expense required to test the set of all possible orderings. While the proposed branch and bound procedure can handle medium-sized problems and could scale even larger with a careful parallel implementation, the approach is unlikely to scale too far beyond . Nonetheless, we believe that this approach is a useful first step. We believe that this initial method is valuable for practitioners and hope it also spurs further research in statistical methodology for quantifying model uncertainty in estimating causal structures.

References

- Adamczak et al., (2010) Adamczak, R. a., Litvak, A. E., Pajor, A., and Tomczak-Jaegermann, N. (2010). Quantitative estimates of the convergence of the empirical covariance matrix in log-concave ensembles. J. Amer. Math. Soc., 23(2):535–561.

- Barron and Sheu, (1991) Barron, A. R. and Sheu, C.-H. (1991). Approximation of density functions by sequences of exponential families. Ann. Statist., 19(3):1347–1369.

- Bergsma and Dassios, (2014) Bergsma, W. and Dassios, A. (2014). A consistent test of independence based on a sign covariance related to Kendall’s tau. Bernoulli, 20(2):1006–1028.

- Berrett and Samworth, (2019) Berrett, T. B. and Samworth, R. J. (2019). Nonparametric independence testing via mutual information. Biometrika, 106(3):547–566.

- Bickel and Freedman, (1983) Bickel, P. J. and Freedman, D. A. (1983). Bootstrapping regression models with many parameters. A festschrift for Erich L. Lehmann, pages 28–48.

- Bollen and Long, (1993) Bollen, K. A. and Long, J. S. (1993). Testing structural equation models, volume 154. Sage.

- Breusch and Pagan, (1979) Breusch, T. S. and Pagan, A. R. (1979). A simple test for heteroscedasticity and random coefficient variation. Econometrica, 47(5):1287–1294.

- Bühlmann et al., (2014) Bühlmann, P., Peters, J., and Ernest, J. (2014). CAM: causal additive models, high-dimensional order search and penalized regression. Ann. Statist., 42(6):2526–2556.

- Chang et al., (2022) Chang, H., Cai, J., and Zhou, Q. (2022). Order-based structure learning without score equivalence. arXiv preprint arXiv:2202.05150.

- Chen et al., (2019) Chen, W., Drton, M., and Wang, Y. S. (2019). On causal discovery with an equal-variance assumption. Biometrika, 106(4):973–980.

- Cook and Weisberg, (1983) Cook, R. D. and Weisberg, S. (1983). Diagnostics for heteroscedasticity in regression. Biometrika, 70(1):1–10.

- Ferrari and Yang, (2015) Ferrari, D. and Yang, Y. (2015). Confidence sets for model selection by -testing. Statist. Sinica, 25(4):1637–1658.

- Fournier and Guillin, (2015) Fournier, N. and Guillin, A. (2015). On the rate of convergence in wasserstein distance of the empirical measure. Probability Theory and Related Fields, 162(3-4):707–738.

- Friedman and Koller, (2003) Friedman, N. and Koller, D. (2003). Being Bayesian about network structure. A Bayesian approach to structure discovery in Bayesian networks. Machine learning, 50:95–125.

- Götze et al., (2021) Götze, F., Sambale, H., and Sinulis, A. (2021). Concentration inequalities for polynomials in -sub-exponential random variables. Electron. J. Probab., 26:Paper No. 48, 22.

- Gretton et al., (2007) Gretton, A., Fukumizu, K., Teo, C. H., Song, L., Schölkopf, B., and Smola, A. J. (2007). A kernel statistical test of independence. In Platt, J. C., Koller, D., Singer, Y., and Roweis, S. T., editors, Advances in Neural Information Processing Systems 20, Proceedings of the Twenty-First Annual Conference on Neural Information Processing Systems, Vancouver, British Columbia, Canada, December 3-6, 2007, pages 585–592. Curran Associates, Inc.

- Hansen et al., (2011) Hansen, P. R., Lunde, A., and Nason, J. M. (2011). The model confidence set. Econometrica, 79(2):453–497.

- Hoyer and Hyttinen, (2009) Hoyer, P. O. and Hyttinen, A. (2009). Bayesian discovery of linear acyclic causal models. In Proceedings of the Twenty-Fifth Conference on Uncertainty in Artificial Intelligence, pages 240–248.

- Janková and van de Geer, (2019) Janková, J. and van de Geer, S. (2019). Inference in high-dimensional graphical models. In Handbook of graphical models, Chapman & Hall/CRC Handb. Mod. Stat. Methods, pages 325–349. CRC Press, Boca Raton, FL.

- Kuipers and Moffa, (2017) Kuipers, J. and Moffa, G. (2017). Partition MCMC for inference on acyclic digraphs. J. Amer. Statist. Assoc., 112(517):282–299.

- Lei, (2020) Lei, J. (2020). Cross-validation with confidence. J. Amer. Statist. Assoc., 115(532):1978–1997.

- Li et al., (2019) Li, C., Shen, X., and Pan, W. (2019). Likelihood ratio tests for a large directed acyclic graph. Journal of the American Statistical Association, 0(0):1–16.

- Loh and Bühlmann, (2014) Loh, P.-L. and Bühlmann, P. (2014). High-dimensional learning of linear causal networks via inverse covariance estimation. J. Mach. Learn. Res., 15:3065–3105.

- Maathuis et al., (2019) Maathuis, M., Drton, M., Lauritzen, S., and Wainwright, M., editors (2019). Handbook of graphical models. Chapman & Hall/CRC Handbooks of Modern Statistical Methods. CRC Press, Boca Raton, FL.

- Maathuis et al., (2009) Maathuis, M. H., Kalisch, M., and Bühlmann, P. (2009). Estimating high-dimensional intervention effects from observational data. Ann. Statist., 37(6A):3133–3164.

- Niinimäki et al., (2016) Niinimäki, T., Parviainen, P., and Koivisto, M. (2016). Structure discovery in Bayesian networks by sampling partial orders. J. Mach. Learn. Res., 17:Paper No. 57, 47.

- Nowack et al., (2020) Nowack, P., Runge, J., Eyring, V., and Haigh, J. D. (2020). Causal networks for climate model evaluation and constrained projections. Nature communications, 11(1):1–11.

- Pearl, (2009) Pearl, J. (2009). Causality. Cambridge university press.

- Peters et al., (2016) Peters, J., Bühlmann, P., and Meinshausen, N. (2016). Causal inference by using invariant prediction: identification and confidence intervals. J. R. Stat. Soc. Ser. B. Stat. Methodol., 78(5):947–1012. With comments and a rejoinder.

- Peters et al., (2017) Peters, J., Janzing, D., and Schölkopf, B. (2017). Elements of causal inference. Adaptive Computation and Machine Learning. MIT Press, Cambridge, MA. Foundations and learning algorithms.

- Peters et al., (2014) Peters, J., Mooij, J. M., Janzing, D., and Schölkopf, B. (2014). Causal discovery with continuous additive noise models. J. Mach. Learn. Res., 15:2009–2053.

- Pfister et al., (2018) Pfister, N., Bühlmann, P., Schölkopf, B., and Peters, J. (2018). Kernel-based tests for joint independence. J. R. Stat. Soc. Ser. B. Stat. Methodol., 80(1):5–31.

- Raskutti and Uhler, (2018) Raskutti, G. and Uhler, C. (2018). Learning directed acyclic graph models based on sparsest permutations. Stat, 7:e183, 14.

- Sachs et al., (2005) Sachs, K., Perez, O., Pe’er, D., Lauffenburger, D. A., and Nolan, G. P. (2005). Causal protein-signaling networks derived from multiparameter single-cell data. Science, 308(5721):523–529.

- Schultheiss et al., (2023) Schultheiss, C., Bühlmann, P., and Yuan, M. (2023). Higher-order least squares: Assessing partial goodness of fit of linear causal models. Journal of the American Statistical Association, 0(0):1–13.

- Sen and Sen, (2014) Sen, A. and Sen, B. (2014). Testing independence and goodness-of-fit in linear models. Biometrika, 101(4):927–942.

- Shah and Bühlmann, (2018) Shah, R. D. and Bühlmann, P. (2018). Goodness-of-fit tests for high dimensional linear models. J. R. Stat. Soc. Ser. B. Stat. Methodol., 80(1):113–135.

- Shen et al., (2020) Shen, X., Ma, S., Vemuri, P., and Simon, G. (2020). Challenges and opportunities with causal discovery algorithms: application to alzheimer’s pathophysiology. Scientific reports, 10(1):1–12.

- Shi et al., (2021) Shi, C., Zhou, Y., and Li, L. (2021). Testing directed acyclic graph via structural, supervised and generative adversarial learning. arXiv preprint arXiv:2106.01474.

- Shimizu and Bollen, (2014) Shimizu, S. and Bollen, K. (2014). Bayesian estimation of causal direction in acyclic structural equation models with individual-specific confounder variables and non-Gaussian distributions. J. Mach. Learn. Res., 15:2629–2653.

- Shimizu et al., (2006) Shimizu, S., Hoyer, P. O., Hyvärinen, A., and Kerminen, A. (2006). A linear non-Gaussian acyclic model for causal discovery. J. Mach. Learn. Res., 7:2003–2030.

- (42) Shimizu, S., Inazumi, T., Sogawa, Y., Hyvärinen, A., Kawahara, Y., Washio, T., Hoyer, P. O., and Bollen, K. (2011a). Directlingam: A direct method for learning a linear non-Gaussian structural equation model. Journal of Machine Learning Research, 12(Apr):1225–1248.

- (43) Shimizu, S., Inazumi, T., Sogawa, Y., Hyvärinen, A., Kawahara, Y., Washio, T., Hoyer, P. O., and Bollen, K. (2011b). DirectLiNGAM: a direct method for learning a linear non-Gaussian structural equation model. J. Mach. Learn. Res., 12:1225–1248.

- Shojaie and Michailidis, (2010) Shojaie, A. and Michailidis, G. (2010). Penalized likelihood methods for estimation of sparse high-dimensional directed acyclic graphs. Biometrika, 97(3):519–538.

- Solus et al., (2021) Solus, L., Wang, Y., and Uhler, C. (2021). Consistency guarantees for greedy permutation-based causal inference algorithms. Biometrika, 108(4):795–814.

- Spirtes et al., (2000) Spirtes, P., Glymour, C., and Scheines, R. (2000). Causation, prediction, and search. Adaptive Computation and Machine Learning. MIT Press, Cambridge, MA, second edition. With additional material by David Heckerman, Christopher Meek, Gregory F. Cooper and Thomas Richardson, A Bradford Book.

- Strieder et al., (2021) Strieder, D., Freidling, T., Haffner, S., and Drton, M. (2021). Confidence in causal discovery with linear causal models. In de Campos, C. and Maathuis, M. H., editors, Proceedings of the Thirty-Seventh Conference on Uncertainty in Artificial Intelligence, volume 161 of Proceedings of Machine Learning Research, pages 1217–1226. PMLR.

- Strobl et al., (2019) Strobl, E. V., Spirtes, P. L., and Visweswaran, S. (2019). Estimating and controlling the false discovery rate of the pc algorithm using edge-specific p-values. ACM Trans. Intell. Syst. Technol., 10(5).

- Vershynin, (2018) Vershynin, R. (2018). High-dimensional probability, volume 47 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge. An introduction with applications in data science, With a foreword by Sara van de Geer.

- Vladimirova et al., (2020) Vladimirova, M., Girard, S., Nguyen, H., and Arbel, J. (2020). Sub-Weibull distributions: generalizing sub-Gaussian and sub-exponential properties to heavier tailed distributions. Stat, 9:e318, 8.

- (51) Wang, Y. S. and Drton, M. (2020a). Causal discovery with unobserved confounding and non-Gaussian data.

- (52) Wang, Y. S. and Drton, M. (2020b). High-dimensional causal discovery under non-Gaussianity. Biometrika, 107(1):41–59.

- Zheng et al., (2019) Zheng, C., Ferrari, D., and Yang, Y. (2019). Model selection confidence sets by likelihood ratio testing. Statist. Sinica, 29(2):827–851.

Appendix A Example of naive strategy

The following example examines the naive strategy of regressing a parent onto a child and directly testing independence of the residuals and regressors. Specifically, Table 3 shows that the naive procedure does not control the Type I error rate.

Example A.1.

Suppose is generated as

so that the true graph is . We consider two competing hypotheses which suppose for or , and we consider two testing approaches.

Direct approach: Regress onto to form the residuals , and subsequently test using dHSIC (Pfister et al.,, 2018) or (Bergsma and Dassios,, 2014).

Sample splitting: Split the data into a training and test set. Using the training set, regress onto and estimate . Using the test set, form the residuals , and subsequently test .

Table 3 shows the proportion of hypothesis tests that are rejected when the null is true () and when the null is false () for sample sizes of . We see that the naive tests with dHSIC or (both the direct approach or sample splitting) do not control the Type I error rate. Under the direct approach, has a Type I error rate close to the nominal rate when , but when and the test has more power, the Type I error rate is not controlled.

| Direct | Split | Prop | Direct | Split | Prop | |||||

| D | D | D | D | |||||||

| 0.15 | 0.11 | 0.23 | 0.32 | 0.10 | 1.00 | 1.00 | 0.97 | 0.94 | 0.64 | |

| 0.18 | 0.20 | 0.24 | 0.34 | 0.09 | 1.00 | 1.00 | 1.00 | 1.00 | 0.97 | |

Appendix B Calibrating the test with a limiting Gaussian

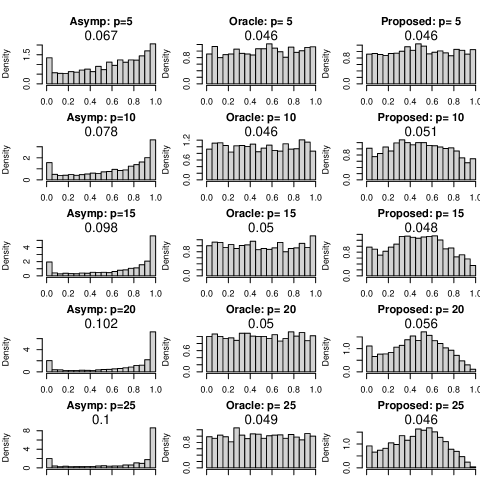

We show that the asymptotic normal distribution of (3.3) may provide a poor approximation when is far from Gaussian. Specifically, we consider log-normal data with and and record the Type I error rate for a nominally test calibrated using the limiting Gaussian with a plug-in estimate of the variance. We see that this test performs quite poorly when compared to the tests calibrated by the oracle and proposed residual bootstrap distributions.

| 10 | 15 | 20 | 25 | ||

| Asymp | 67 (56, 78) | 78 (66, 90) | 98 (84, 111) | 102 (88, 115) | 100 (87, 113) |

| Oracle | 46 (36, 55) | 46 (37, 56) | 50 (40, 60) | 50 (40, 60) | 49 (39, 59) |

| Proposed | 46 (37, 55) | 51 (41, 61) | 48 (39, 58) | 56 (45, 66) | 46 (37, 55) |

We generated data for the simulation in the following way. Let . We draw from a log-normal distribution where with and all off-diagonals . Let denote the matrix where each row denotes an i.i.d observation of with scaled and centered so each column has mean and variance . Furthermore, let denote the matrix augmented with a column of s for the intercept. We use a single test function , and let be the matrix where the th column corresponds to a scaled and centered version of .

We draw where for all and where is also log-normal with so that has mean and variance . We regress onto (including an intercept) and let denote the resulting residuals. We also calculate, , an unbiased estimate of the variance of

For the test calibrated by the asymptotic distribution, we then compare the test statistic to the distribution of

| (B.1) |

where each element of is drawn from . Note that we divide by instead of in the null distribution which should help lower the Type I error rate in finite samples. Indeed, this correction improves performance; however, even with this additional correction the Type I error is inflated.

For the test calibrated by the oracle distribution, we then compare the test statistic to the distribution of

| (B.2) |

where each element of is drawn from with .

This entire procedure is replicated 2000 times with and . In Figure 4, we show the distribution of the resulting p-values for each procedure in each setting.

Appendix C Proofs for Section 4.3

Lemma 1

Let denote the total causal effect of onto . Suppose satisfies (1.2), and is an asymptotically valid confidence interval for the parameter of interest, conditional on being a valid adjustment set. Then, for the confidence interval produced by Alg. 3,

Proof.

If , then for every , . Fix an arbitrary . Let denote the appropriate adjustment set for the effect of interest given and let denote the confidence interval for the effect of interest when using the adjustment set . Then,

| (C.1) |

If , then and there exists a such that . Then,

| (C.2) |

which completes the proof. ∎

Lemma 2

Suppose satisfies (1.2). Then,

Proof.

Suppose so that . Then, by definition, for every . Thus, implies that . Similarly, since for every when , then also implies that . If satisfies Eq. (1.2), then occurs with probability bounded below by as so that

| (C.3) |

Now consider the case where . There exist a pair such that:

-

(1)

For every , we have and

-

(2)

For every , we have and .

Then, for every either or . Thus, the event implies that . Furthermore, for every , . Thus, the event also implies . If satisfies Eq. (1.2), then occurs with probability bounded below by as so that

| (C.4) |

∎

Appendix D Confidence intervals for direct effects

Alg. 4 describes a procedure to calculate confidence intervals for direct effects which also incorporate model uncertainty. When estimating the direct effect of onto , a valid adjustment set is . Thus, this procedure is exactly the same as Alg. 3 except for the definition of .

Appendix E Proofs for Section 5.1

We first give two intermediate lemmas which are needed for the proof of Theorem 1 and then prove Theorem 1.

Lemma 5 is a deterministic statement that decomposes the Wasserstein distance between the oracle distribution of and the residual bootstrap distribution of into the sum of the distance between , the distribution of the errors, and , the empirical distribution of the errors, as well as the distance between and, , the empirical distribution of the residuals. Since we fix , to ease the notational burden, we will drop the and let . For notational simplicity, let denote the matrix that contains the basis functions evaluated on the observations. Let denote the “linear coefficients” of , so that ,

Lemma 5.

For any , , and , let and . When , then

| (E.1) |

Proof.

Under the null hypothesis, the residuals when regressing onto are

| (E.2) | ||||

Thus, for any realization and ,

Let where each element is drawn from , the empirical distribution of , so that the bootstrapped data are . Let denote the estimated coefficients when regressing onto and let denote the corresponding residuals. Then we also have

| (E.3) | ||||

and

Let denote a joint distribution over and , which achieves the Wasserstein lower bound; i.e., . In a slight abuse of notation, we will also use to denote the distribution over and , which is induced by conditioning on and drawing and from . Since preserves the marginal distributions of and , it also preserves the marginal distributions of and for all and .

Let and . For , we have

| (E.4) | ||||

The inequality in (i) holds because of the reverse triangle inequality. Similarly, for , we have

| (E.5) | ||||

Now we examine the quantity for any . Let

so that and . We then have

| (E.6) | ||||

As each draw is independent and , we have . Thus, for the first term in (E.6), we have

since is idempotent. For the second term in (E.6), we have

A similar argument can be made to show that . Combining the last two displays with (E.6), we have

| (E.7) | ||||

By construction, the distribution achieves the Wasserstein-2 lower bound, so . Thus, for all ,

| (E.8) | ||||

Using the triangle inequality to decompose the Wasserstein distance, we have

| (E.9) | ||||

which completes the proof. ∎

Lemma 6 provides a deterministic bound on , which represents the squared Wasserstein distance between the empirical distribution of the errors and the residuals.

Lemma 6.

We have

| (E.10) |

where , denotes the empirical distribution of errors for , and denotes the empirical distribution of residuals for .

Proof.

Let be the th realized error and be the corresponding residual. Then

| (E.11) | ||||

Suppose are drawn from a distribution which is the uniform distribution over the pairs . The marginal distributions of and are and , respectively. Then

| (E.12) | ||||

Since is an idempotent matrix with rank that is independent of , we have , , and . Thus,

| (E.13) |

Since the marginal distributions of and under are and , we have , which completes the proof. ∎

Theorem 1

Suppose that with . Furthermore, there exist constants such that for all and , with , , and for some .

Let . Then, for any causal ordering consistent with DAG , with probability , is less than

| (E.14) |

Proof.

Below we use to denote to evaluated on ; this is similar to our previous use of , but we have added the additional subscript to denote that differs depending on .

Suppose that there exist such that for all :

-

(i)

;

-

(ii)

;

-

(iii)

; and

-

(iv)

.

Then by Lemma 5 and Lemma 6, we have

| (E.15) |

We proceed to show that the above four conditions hold with the desired probability.

Condition (i): Let . Note that is a projection matrix of rank . Therefore, we have , , and . Setting , we have

for some constant using Proposition 1.1 of Götze et al., (2021).

Condition (ii): Theorem 2 of Fournier and Guillin, (2015) states that for any , we have

where the constant depends on . Setting , , and using the union bound, we have

| (E.16) |

Condition (iii): By assumption . Therefore, and, by Corollary 1.4 of Götze et al., (2021),

where is a constant that depends on . Setting and using the union bound, we have

| (E.17) |

Condition (iv): Since is sub-Weibull with Orlicz norm of , so we apply Corollary 1.4 of Götze et al., (2021). Letting , we have by a simple union bound

| (E.18) |

∎

Corollary 1 (Known finite basis)

Suppose that conditions of Theorem 1 are satisfied. If each belongs to a known finite-dimensional basis, then with probability

Proof.

The proof immediately follows from Theorem 1 by setting . ∎

Corollary 2 (Sieve basis)

Suppose that conditions of Theorem 1 are satisfied. Furthermore, suppose that a finite-dimensional basis for each is not known a priori, but there exists such that for all , , and for some . Letting , we have with probability for some constant which depends on ,

| (E.19) |

Lemma 3

Let denote the p-value calculated for the test statistic using the CDF . Let denote the p-value calculated using the CDF . Suppose . Then,

| (E.22) |

Proof.

Suppose two measures are defined on a metric space with Borel -algebra and let denote the respective CDFs. The Lévy-Prokhorov distance is defined as

| (E.23) |

where is the set of all points within of the set . Let so that the calculated p-values are and when using and , respectively.

As shown in (1.4) of (Bickel and Freedman,, 1983), . We now show that . Let and . Then, . In addition, , which implies that . Thus,

| (E.24) |

and . ∎

Lemma 4

Let be a causal ordering for and suppose are p-values calculated using the oracle procedure. Then the elements of are mutually independent.

Proof.

Without loss of generality, let . First, note that for any fixed . Thus, we have , where is the characteristic function of . Then, for any , the characteristic function of is

| (E.25) | ||||

Inductively applying the same argument for yields

| (E.26) |

which shows that the p-values are independent. ∎

Corollary 3

For a fixed , suppose that the conditions of Theorem 1 hold and . Furthermore, assume that the test statistic has a continuous density bounded above by for all . Then

| (E.27) |

Proof.

To show (E.27) it suffices to show that for any fixed causal ordering , the goodness-of-fit test produces a p-value which is asymptotically uniform.

Under the conditions of Theorem 1, when testing any individual level of the ordering the maximum Wasserstein-2 distance between the oracle null distribution and the bootstrap distribution is bounded above by a quantity which is order with probability going to as . Plugging this into Lemma 6, when has a continuous density that is bounded above, then is bounded above by a quantity which is with probability going to as .

Recall that and denote the resulting p-values when comparing and to a . We upper bound the difference between and by

| (E.28) | ||||

so that is bounded above—with probability going to as —by a quantity which is of order . Since , then when .

Lemma 4 implies that the oracle procedure for each individual regression yields p-values which are independent uniform distributions so that is a uniform random variable, and subsequently, is asymptotically a uniform random variable. ∎

Appendix F Proofs for Section 5.2

We first give an intermediate lemma, Lemma 7, which is a deterministic statement about the power of the test. The lemma is then used to prove Theorem 2.

Lemma 7.

Fix an ordering , , and . Let where represents the basis functions evaluated on and let and denote the smallest/largest eigenvalues of . Let and denote the sub-matrices of . Furthermore, let , , and . Suppose and Alg. 1 is used to test . Then the resulting p-value (when sampling an infinite number of bootstrap samples) is bounded above by

| (F.1) |

Proof.

Let be the p-value resulting from Alg. 1, where denotes the probability under the bootstrap distribution conditional on . By Markov’s inequality, for any ,

| (F.2) | ||||

In the remainder of the proof, we let and provide appropriate bounds on and .

Conditioning on the observed data and computing the expectation over the bootstrap draws, we have

For each term, we have

where (i) holds since each element of is independent when conditioning on and , so that , and (ii) holds because is idempotent and , since are the residuals after regressing onto . Thus,

| (F.3) |

For the term , we have

| (F.4) | ||||

For any , we have

| (F.5) | ||||

Let and . By assumption, and are both bounded above by . Following the proof of Wang and Drton, 2020b (, Lemma 1), we have . Furthermore, we have

Since is a sub-matrix of , we have . Similarly . In addition, . Putting these bounds together, we have

| (F.6) | ||||

The result follows by combining (F.3), (F.4), and (LABEL:eq:boundOnAltDeviation). ∎

Theorem 2

Suppose and consider a sequence of models where grow, but , and are fixed. Suppose does not hold, then for any fixed level , the hypothesis will be rejected with probability going to if

-

(1)

is jointly sub-Gaussian with Orlicz-2 norm , , , and and ; or

-

(2)

is jointly log-concave with Orlicz-1 norm and and ,

where .

Proof.

The proof simply requires showing that the numerator in (F.3) can be bounded above by the appropriate quantity with probability going to .

Sub-Gaussian case: Let . Since and are sub-exponential with Orlicz- norm bounded by , we have

| (F.7) | ||||

Additionally, by Exercise 4.7.3 of Vershynin, (2018),

Letting and assuming is large enough so that ,

| (F.8) | ||||

Therefore, with probability at least , the numerator in (F.1) is bounded above by

Thus, when and , the entire quantity in (F.1) goes to .

Log-concave case: Let . Since and have Orlicz- norm bounded by , we have

| (F.9) | ||||

To control , we apply Theorem 4.1 of Adamczak et al., (2010), which states that when are i.i.d. log-concave random vectors in , then for any and constants , when , then with probability at least , we have for the sample covariance ,

Let . The conditions are satisfied when are large enough so that and for the universal constant . Thus,

and with probability at least . Thus, with probability going to , we have that the numerator in (F.1) is bounded above by

Since the denominator is , when and , the entire quantity in (F.1) goes to . ∎

Appendix G Full Simulation Details

We provide the results for the comparison of goodness-of-fit procedures for .

| Size | Power | ||||||||||||

| dist | p | W | S | RO | RL | M | H | W | S | RO | RL | M | H |

| gamma | 10 | 42 | 50 | 92 | 84 | 114 | 0 | 144 | 68 | 182 | 248 | 144 | 0 |

| 15 | 72 | 88 | 76 | 100 | 116 | 0 | 268 | 100 | 262 | 340 | 174 | 0 | |

| 20 | 88 | 90 | 88 | 78 | 114 | 0 | 264 | 156 | 242 | 346 | 200 | 0 | |

| 30 | 98 | 110 | 40 | 86 | 122 | 0 | 322 | 180 | 276 | 490 | 196 | 0 | |

| 45 | 104 | 192 | 36 | 204 | 186 | 10 | 332 | 330 | 14 | ||||

| laplace | 10 | 52 | 38 | 88 | 82 | 76 | 0 | 52 | 60 | 126 | 90 | 122 | 0 |

| 15 | 74 | 60 | 100 | 86 | 80 | 0 | 122 | 98 | 106 | 78 | 130 | 0 | |

| 20 | 80 | 94 | 78 | 78 | 108 | 0 | 112 | 96 | 118 | 98 | 132 | 0 | |