[table]capposition=top

The Emergence of Economic Rationality of GPT

Abstract

As large language models (LLMs) like GPT become increasingly prevalent, it is essential that we assess their capabilities beyond language processing. This paper examines the economic rationality of GPT by instructing it to make budgetary decisions in four domains: risk, time, social, and food preferences. We measure economic rationality by assessing the consistency of GPT’s decisions with utility maximization in classic revealed preference theory. We find that GPT’s decisions are largely rational in each domain and demonstrate higher rationality score than those of human subjects in a parallel experiment and in the literature. Moreover, the estimated preference parameters of GPT are slightly different from human subjects and exhibit a lower degree of heterogeneity. We also find that the rationality scores are robust to the degree of randomness and demographic settings such as age and gender, but are sensitive to contexts based on the language frames of the choice situations. These results suggest the potential of LLMs to make good decisions and the need to further understand their capabilities, limitations, and underlying mechanisms.

1 Introduction

ChatGPT is a sophisticated chatbot application developed by OpenAI, which employs the state-of-the-art Generative Pre-trained Transformer model (hereafter referred to as “GPT”). As one of the most representative examples of large language models (LLMs), GPT uses transformer architecture and deep learning techniques to learn from vast web-based text corpora that contain 175 billion parameters (Vaswani et al., 2017; Brown et al., 2020). Thanks to its massive volume of training data, GPT can generate human-like text with remarkable accuracy and fluency, to the extent that human evaluators find it difficult to distinguish GPT output from text written by humans (Brown et al., 2020). In addition to their natural language-generation capabilities, LLMs have demonstrated impressive abilities in a wide range of domains. For instance, they can generate computer code (Chen et al., 2021), engage in human-like conversations on various topics (Lin et al., 2020), solve university-level math problems (Drori et al., 2022), exhibit theory of mind ability (Kosinski, 2023), and possess psychological characteristics similar to humans (Binz and Schulz, 2023; Park et al., 2023). LLMs have also shown their aptitude in performing high-level reasoning tasks (Webb et al., 2023). The impressive capabilities of LLMs reveal their remarkable potential, which can be likened to the emergence of a new species: “Homo Silicus” (Horton, 2023). Because these achievements signify a major milestone in the development of LLMs, it is important that we understand how GPT performs in various high-level reasoning tasks.

Here we present the first study on the economic rationality of GPT. Rationality has been central to the methodological debate throughout various disciplines and is the fundamental assumption in economics and related social sciences. Here we use a classic notion of economic rationality in revealed preference analysis that captures the extent to which a decision maker maximizes some well-behaved utility functions for the given budget constraints (Afriat, 1967, 1972; Samuelson, 1938; Varian, 1982, 1990; Chambers and Echenique, 2016; Nishimura et al., 2017). Prior studies have computed rationality score based on choice data in risky, intertemporal, and social decision-making in laboratory environments (Andreoni and Miller, 2002; Andreoni and Sprenger, 2012; Ahn et al., 2014; Choi et al., 2007, 2014; Harbaugh et al., 2001; Halevy et al., 2018; Fisman et al., 2007), as well as expenditure data from survey and grocery stores in the field (Blundell et al., 2003, 2008; Echenique et al., 2011; Dean and Martin, 2016). Economic rationality has also been measured in children (Brocas et al., 2019; Harbaugh et al., 2001), monkeys (Chen et al., 2006), rats and pigeons (Kagel et al., 1975). Moreover, it has been proposed as a measure of decision-making quality and linked to a wide range of economic outcomes, such as occupation, income, and wealth differences across individuals, and development gaps across countries (Banks et al., 2019; Cappelen et al., 2023; Carvalho et al., 2016; Choi et al., 2014; Fisman et al., 2017; Kim et al., 2018; Li et al., 2017, 2022). Nevertheless, the rationality of GPT remains unexplored.

We instruct GPT to act as a decision maker to make budgetary decisions in choice environments with varying characteristics. The basic framework contains 25 decision tasks to allocate 100 points between two commodities with different prices, which is commonly used in experimental economics. The rationality of GPT is measured by the consistency of these 25 decisions with the generalized axiom of revealed preference (GARP), a necessary and sufficient condition under which a set of decisions are in accordance with utility maximization (Afriat, 1967, 1972; Varian, 1982, 1990). Therefore, a rationality score is derived from each group of 25 tasks within a given environment. Building on this framework, we construct four environments by specifying the nature of the two commodities—two risky assets; two rewards with one for now and one for one month later; two payments with one for the decision maker and one for another randomly paired subject; and two types of food with meat and tomatoes. Each environment is repeated 100 times, which generates 10,000 tasks for GPT. This design allows us to systematically measure GPT’s rationality in different choice domains. Moreover, we incorporate a series of variations in the randomness of GPT, the framing of decision tasks (Kahneman, 2003), the structure of the choice format (McFadden, 2001), and the demographic settings of GPT (Corbett-Davies and Goel, 2018). In order to compare the economic rationality between GPT and humans, we conduct a parallel experiment with 347 human subjects from a representative US sample.

We find that GPT demonstrates a high level of rationality in all four decision-making tasks concerning risk, time, social, and food, and it outperforms human subjects in the rationality score documented in both our human subject experiment and those reported in the literature. Furthermore, we find that GPT’s rationality scores are consistent across different demographic characteristics and invariant to the specification of the randomness of GPT. However, the level of rationality drops significantly when we employ a different price framing and when we use a discrete choice setting. These findings suggest that GPT obtains high rationality score but has some potential limitations in its decision-making abilities. Moreover, we estimate the preference parameters of GPT and human subjects. We find that the estimated preference parameters of GPT have some minor distinctions from human subjects and show a substantially higher degree of homogeneity.

Taken together, we use tools from revealed preference analysis and experimental economics to study increasingly capable artificial agents. There is growing interest in understanding these agents’ behavior (Rahwan et al., 2019), and ongoing debate about their performance compared with humans (Mitchell and Krakauer, 2023). Even though these artificial agents exhibit surprisingly excellent performance on many cognitive tests, some have expressed concern that such models are still far from achieving human-level understanding of language and semantics and exhibit considerable levels of behavioral bias (Borji, 2023; Chen et al., 2023b). We contribute to the understanding of the capacities and caveats of LLMs, by demonstrating that LLMs can act as if they are rational decision makers. The observed decrease in rationality when alternative price framing or discrete choice are used is line with some studies show that GPT response can be highly sensitive to contexts (Borji, 2023; Mahowald et al., 2023; Horton, 2023; Jones and Steinhardt, 2022; Binz and Schulz, 2023; Brand et al., 2023; Jones and Steinhardt, 2022). Our study also highlights the need for more investigation and refinement of its decision-making mechanisms to ensure reliable and effective decision-making in various domains.

2 Experimental Method

We examine GPT’s decision-making in different environments using the public OpenAI application programming interface (API). Multiple GPT variants are accessible through this API. For our exercise, we focus on the GPT-3.5-Turbo, which powers ChatGPT and is the most popular, stable, and cost-effective model in the GPT family. We use APIs with Python instead of ChatGPT, since APIs enable us to adjust the parameters of the model and conduct massive experiments in an efficient manner.

Below we describe how we ask GPT to “make decisions” by introducing the construction of prompts through which GPT returns a text in response to an input text. We then outline multiple variations of our design to examine the robustness of our results.

2.1 Design of the Baseline Condition

Instruct GPT to “Make Decisions”.

Each input prompt in GPT-3.5-turbo includes the specifications of a role (system, assistant, or user) and corresponding contents. We instruct GPT to make decisions in three steps. First, we specify the system’s role as “a human decision maker” and notify the system that “you should use your best judgment to come up with solutions that you like most”. Second, we explain the role of assistant with respect to the decision format: selecting a bundle of commodities from a standard budget line with varying prices, which will be explained in detail later, without requesting responses for any decision. This assists in storing information about the tasks. Afterward, we assign a series of decision-making tasks to the role of user in order to ask GPT to make decisions.

Moreover, to confirm that GPT has understood the instructions, we ask three testing questions, in which we either directly ask it to recall the decision format or ask about the consequence of certain decision scenarios. For each question, we simulate 25 times and GPT constantly provides correct answers. This confirms that GPT understands the decision environment. Detailed prompts to instruct GPT and obtain GPT responses are provided in Appendix A.

Decision Task.

GPT decision tasks follow a typical budgetary experiment, in which a decision maker (DM) is endowed with 100 points to select a bundle of commodities, commodity and commodity . The prices of the two commodities are based on different exchange rates between points and payoffs. Thus, a decision obtains a tuple whereby a DM selects a bundle under the prices . Since measuring rationality requires a collection of such decisions, we include 25 tasks with randomly generated prices (Choi et al., 2014). After that, we measure the economic rationality of these 25 decisions , based on the extent to which there exists some well-behaved utility functions to rationalize them.

To measure rationality across different preference domains, we vary the commodities in the decision tasks. In the first domain, the two commodities are specified as two contingent securities, in which the decisions capture the DM’s risk preference (Choi et al., 2007). In the second domain, the two commodities are rewards for today and one month later, which are designed to examine the DM’s time preference (Andreoni and Sprenger, 2012). In the third domain, the two commodities are payoffs for the DM and another randomly matched subject, and thus the allocation captures the DM’s social preference (Andreoni and Miller, 2002; Fisman et al., 2007). Finally, in the fourth domain, the two commodities are the amount of meat and tomatoes, which captures the DM’s food preference (Harbaugh et al., 2001).

We incorporate four preference domains of decisions, each consisting of 25 tasks. To examine GPT’s consistency in behavior, we simulate this process 100 times, resulting in 10,000 tasks for GPT. We refer to these 10,000 tasks, the 100 GPT observations in each preferences domain, as the baseline condition. A detailed description of tasks and parameters for prices are provided in Appendix A. We set the temperature parameter to 0 (see the explanation below) and keep the default values for all other parameters.

2.2 Design of Conditions with Variations

To enrich our understanding of GPT’s economic rationality, based on the baseline condition, we introduce variations in the temperature and the decision tasks. We also include demographic information in the text of the prompt as explained below.

Variations of Temperature.

Temperature plays a critical role in regulating the level of stochasticity and creativity in the responses generated by GPT (Goodfellow et al., 2016). It ranges from 0 to 1, with a higher number indicating higher randomness. We set the temperature to be 0 in the baseline condition, in which the model gives deterministic answers (Binz and Schulz, 2023; Horton, 2023; Webb et al., 2023). Some studies on GPT incorporate the variation in temperature to investigate the impact of randomness in creating text (Bommarito II and Katz, 2022; Chen et al., 2021). Following their practice, we conduct two additional sets of conditions, with the parameter set to be 0.5 and 1.

Variations of Decision Task.

We design two variations of decision tasks to change the framing of prices and to switch from continuous to discrete choice, respectively. A detailed description is provided in Appendix A.

In the baseline condition, we use “1 point = X units of commodity” to present price information, which is used in many existing experiments with human subjects (Andreoni and Miller, 2002; Andreoni and Sprenger, 2012; Carvalho et al., 2016; Banks et al., 2019). In the price framing condition, we change it to “Y points = 1 unit of commodity”, which is an alternative framing used in the experimental literature (Drichoutis and Nayga Jr, 2020). Since the budget sets remain constant, this allows us to examine whether framing affects the rationality of GPT.

In the baseline condition, the DM makes choices under the continuous budget sets. In the discrete choice condition, we change these to discrete choices: The DM is presented with 11 discrete options chosen from the budget line and is asked to choose one of them rather than directly choose from the budget line (Chen et al., 2023a; Kim et al., 2018). Specifically, the third prompt changes to: “In this round, there are 11 options, which are , , …, and . Please only tell me your best option in every round”. This allows us to examine whether rationality of GPT is robust to the change from continuous to discrete choice sets.

Response to Demographic Information.

We also investigate whether the rationality exhibited by GPT varies with the embedded demographic information. To achieve this, we include demographic information which varies in gender, age, education level, and minority group status. We change the input content of the system’s role in GPT to be “I want to you to act as a [demographic] decision maker, …”. Variations are gender: “female decision maker” versus “male decision maker”; age: “young child decision maker” versus “elderly decision maker”; education: “decision maker with an elementary school education” versus “decision maker with a college education”; and minority: “Asian decision maker” versus “African American decision maker”. By doing so, we can examine whether GPT is responsive to demographic information and whether it performs differently under different individual characteristics. The responsiveness, if any, is relevant to the discussion about algorithm bias (Corbett-Davies and Goel, 2018).

2.3 Design of the Human Experiment

To obtain a better understanding of the behavior of GPT, we also conduct a human subject experiment with identical decision tasks, in which 347 human subjects from a representative US sample are randomly assigned to the baseline, price framing, and discrete choice conditions.111Variations of temperature are inapplicable among human beings, while variations of demographics can be naturally obtained in a representative sample. We keep the experimental instructions between human subjects and GPT as similar as possible. Appendix B provides the design and instructions of this pre-registered human experiment (AEARCTR-0011750). This experiment was approved by The Institutional Review Board of Finance and Economics Experimental Laboratory in The Wang Yanan Institute of Studies in Economics, Xiamen University (FEEL230701), and all subjects provided informed consent before they started the experiment. Table D1 in Appendix D shows the demographic characteristics of our human subjects.

3 Theoretical Method

3.1 Revealed Preference Analysis

Generalized Axiom of Revealed Preference.

Consider a DM who selects a bundle from a budget line , . A dataset represents a collection of decisions made by the DM. We say that a utility function rationalizes the dataset if for every bundle , we have:

Let be the set of bundles selected by the DM. We say that is directly revealed to be preferred to , denoted by , if the DM chooses when is affordable (i.e., ). We denote as the relation of directly strictly revealed preference. We denote as the transitive closure of , which refers to the revealed preferred relation.

A utility function is well-behaved if it is continuous, concave and strictly increasing. Afriat’s theorem (Afriat, 1967; Varian, 1982) states that a dataset can be rationalized by a well-behaved utility function if and only if the dataset obeys the generalized axiom of revealed preference (GARP):

Apart from GARP, two closely related notions are the weak axiom of revealed preference (WARP): for all and in a dataset , , and the strong axiom of revealed preference (SARP): for all and in a dataset , , which works by exploiting transitivity. In our setting with two goods, checking WARP is equivalent to checking SARP (Rose, 1958). In our discrete setting, Harbaugh et al. (2001) shows that a locally non-satiated, strictly monotonic, continuous, and concave utility may violate GARP and demonstrates the need to use the assumption of strong monotonicity (see also Polisson and Quah (2013) for discussions).

Rationality Score.

Afriat’s theorem provides a powerful tool for analyzing choice behavior. A popular approach for measuring the departure from rationality is the critical cost efficiency index (CCEI) proposed by Afriat (Afriat, 1972). A subject has a CCEI if is the largest number with a well-behaved that rationalizes the data set for every

A CCEI of 1 indicates passing GARP perfectly. A CCEI less than 1—say, 0.95—indicates that there is a utility function for which the chosen bundle is preferred to any bundle that is cheaper than for more than 5%. Put differently, the CCEI can be viewed as the amount by which a budget constraint must be relaxed in order to remove all violations of GARP, because the DM can achieve her utility targets by spending less money (Afriat, 1972; Varian, 1990). We compute CCEI to obtain a score of rationality for each domain with 25 decisions.

In the revealed preference literature, there are several other indices to score rationality (departure from GARP). These indices include the Houtman-Maks index (HMI) (Houtman and Maks, 1985), money pump index (MPI) (Echenique et al., 2011), and minimum cost index (MCI) (Dean and Martin, 2016). We also compute these indices and report the results as robustness checks.

3.2 Structural Estimation for Preferences

In addition to rationality score, we further examine the underlying preferences using structural estimation.

Risk and Time Preferences Estimation.

In the domain of risk preference, suppose that the DM chooses the contingent security , we denote as the high outcome and as the low outcome. In the domain of time preference, suppose that the DM chooses the payment schedule , we denote as the payment for today and as the payment for one month later. For these two domains, we assume that the underlying utility function is given by

where the utility function and . For risk preference, captures the decision weight placed on the better outcome (Gul, 1991; Halevy et al., 2018). When , we have a standard expected utility function and when (), the better outcome is over(under)-weighted relative to the objective probability of 0.5. The parameter captures risk attitude with the parameter being the Arrow-Pratt measure of relative risk aversion.222In our budget set, there is no difference between and , because the DM will choose corner solutions when . Therefore, our estimation is conditional on in all the four preferences domains. SI appendix provides further details about the estimation of corner solutions. For time preference, captures the weight placed on the payment today (Andreoni and Sprenger, 2012). When (), it corresponds to positive (negative) time preference. The parameter is the curvature of the period function. When , the DM allocates all expenditure to the time period with lower price and as decreases, the DM is more desired to smooth payments across periods.

Social and Food Preferences Estimation.

Regarding social preference, suppose that the DM chooses the allocation , we denote as the payment for self and as the payment for the other. In the domain of food preference, assuming that the DM chooses the bundle , we denote as the consumption of meat and as the consumption of tomatoes. Moreover, we assume that the underlying utility function is a member of the CES family and is given by

where and . For social preference, the parameter captures the weight placed on the self’s payment relative to the other’s payment. implies pure selfishness, indicates fair-mindedness, and refers to pure altruistic (Andreoni and Miller, 2002; Fisman et al., 2007). represents the curvature of the indifference curves, which measures equality efficiency orientation. indicates that the two payments are perfectly substitute with , which means that the DM is efficiency orientated. When , the utility function approaches the Cobb–Douglas utility function, and shares of expenditures to self and to the other are constant. When , it approaches to the Leontief utility function , which implies that the two payments are perfectly complemented and the DM is equality orientated (Andreoni and Miller, 2002; Fisman et al., 2007). In a similar vein, the parameter in the food preference domain captures the weight placed on meat relative to tomatoes and the parameter represents the curvature of the indifference curves as that for social preference. We provide further details on estimation methods in Appendix C.1.

4 Results

In this section, we first present the results from the baseline condition, then report whether and how the results change with the variations in the decision tasks.

4.1 Results from the Baseline Condition

Rationality Score.

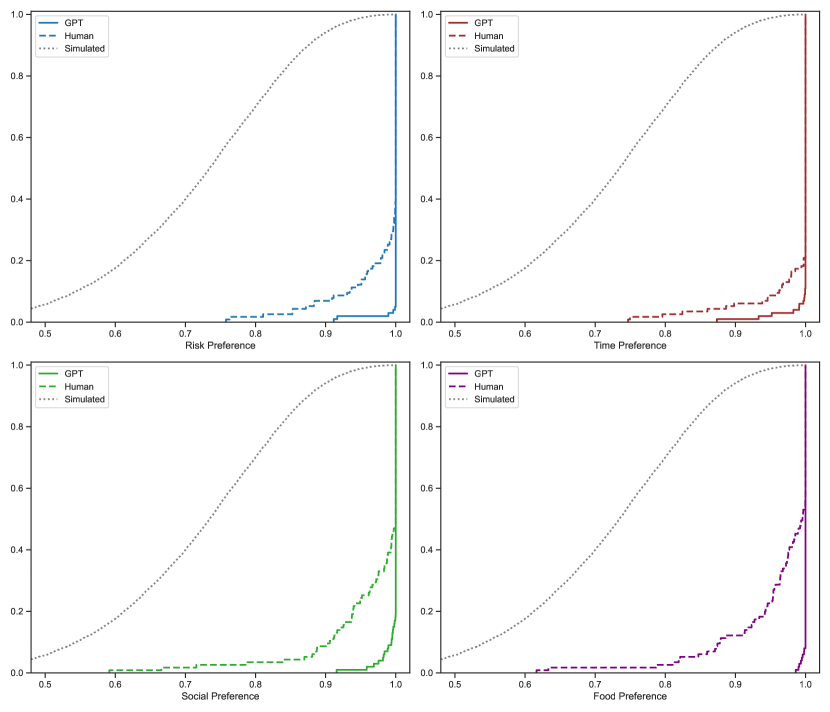

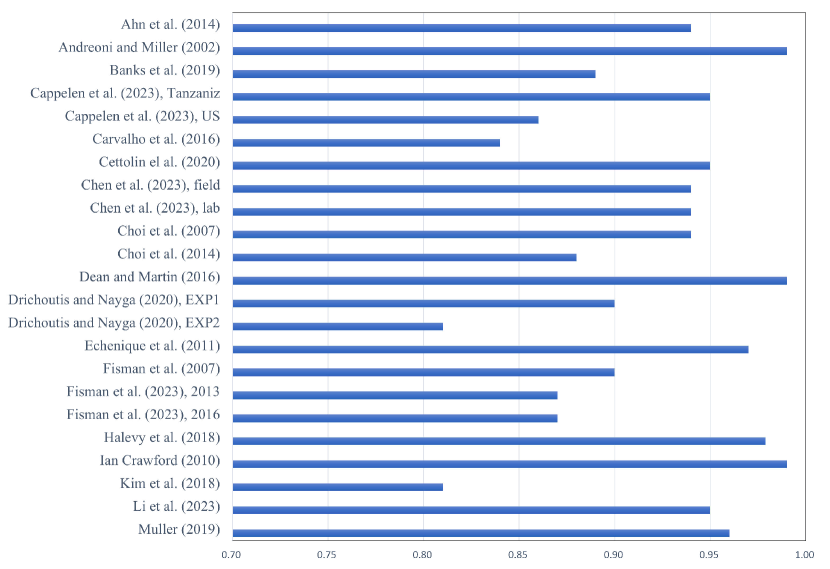

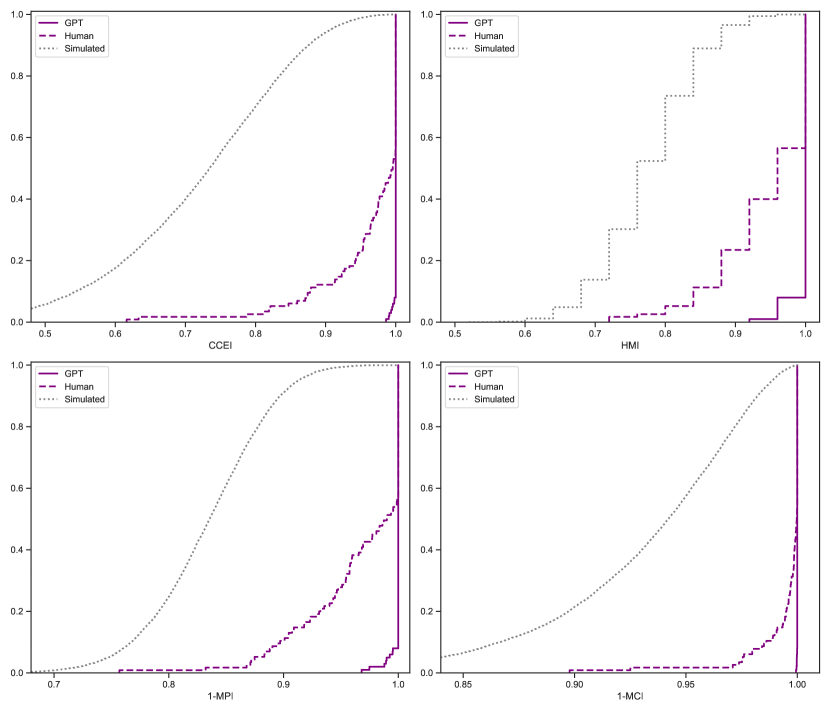

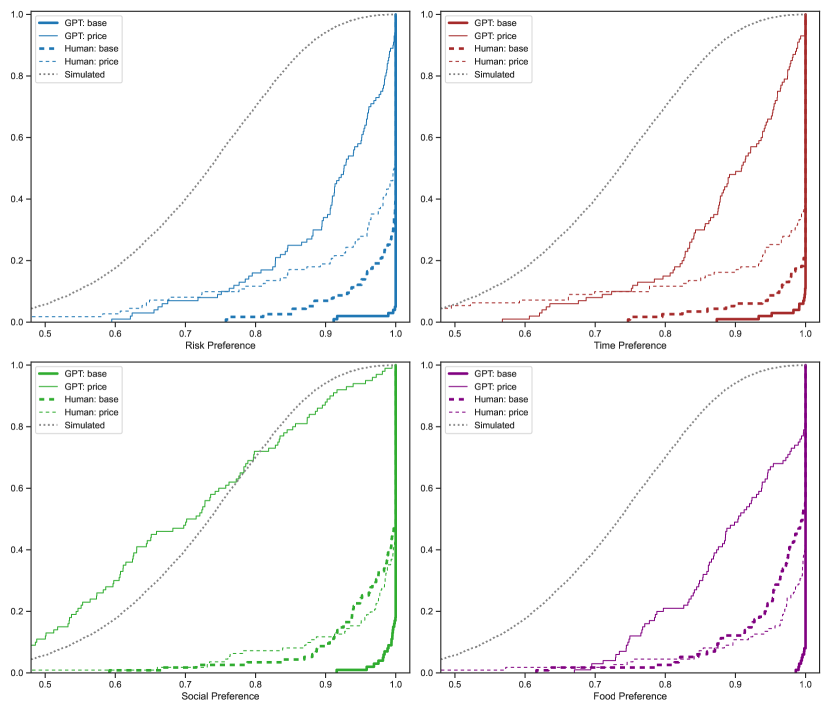

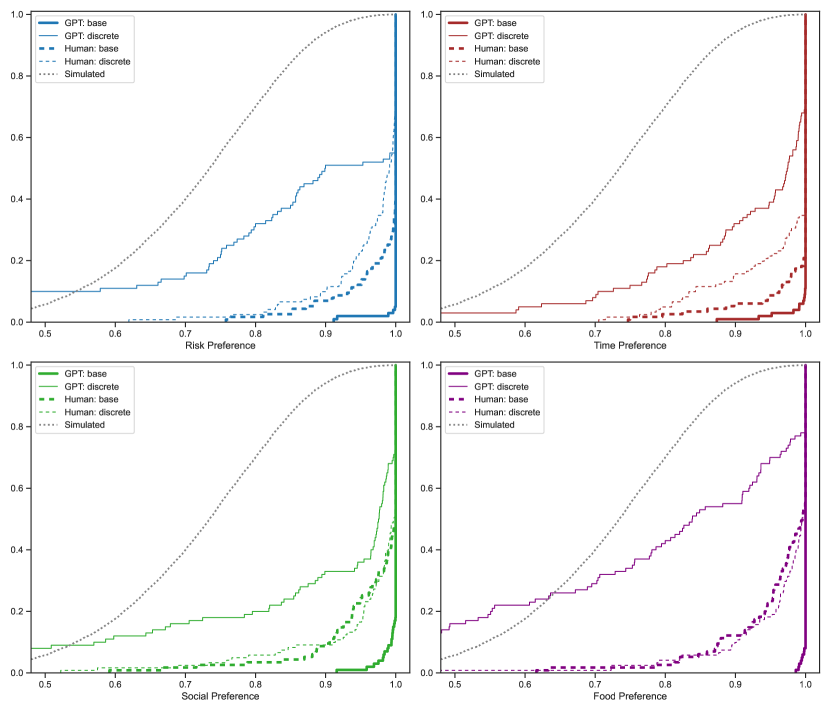

Figure 1 presents the cumulative distributions of CCEI—the rationality score—for each of the four preferences domains. We find that 95, 89, 81, and 92 out of 100 GPT observations for risk, time, social, and food preferences exhibit no violations of GARP; that is, CCEI equals to 1. The average CCEI is 0.998, 0.997, 0.997, and 0.999 for risk, time, social, and food preferences, respectively. Meanwhile, in our human experiment, the average CCEI among human subjects is 0.980, 0.985, 0.967, and 0.963 for risk, time, social, and food preferences, respectively. Figure 1 displays a consistent trend that GPT outperforms human subjects in terms of rationality. In each of the four preferences domains, GPT obtains higher CCEI than human subjects (, two-sided two-sample t-tests). In addition, we summarize studies in the revealed preference literature. Figure D1 in Appendix D plots CCEI values documented in prior studies, which range from 0.81 to 0.99 with an average of 0.918. Consistently, we find that CCEI of GPT also surpasses those of human subjects in all domains (, two-sided one-sample t-tests).

To confirm that our chosen parameters have sufficient power to measure rationality, we adopt the test proposed by Bronars (Bronars, 1987) as a benchmark, in which we generate simulated subjects by uniformly drawing random allocations along each of the budget lines and examine their rationality. We find that 99.9% of simulated subjects violate GARP. Figure 1 shows the cumulative distributions of CCEI of simulated subjects, which are lower than both GPT observations and human subjects. We also conduct the power analysis using the predictive success (Beatty and Crawford, 2011), the Selten score (Dean and Martin, 2016), as well as bootstrapping from the sample of subjects (Andreoni and Miller, 2002). We show that the chosen parameters have the power to detect rationality violations, in support of the empirical validity of our study (see Appendix C.2 for more information).

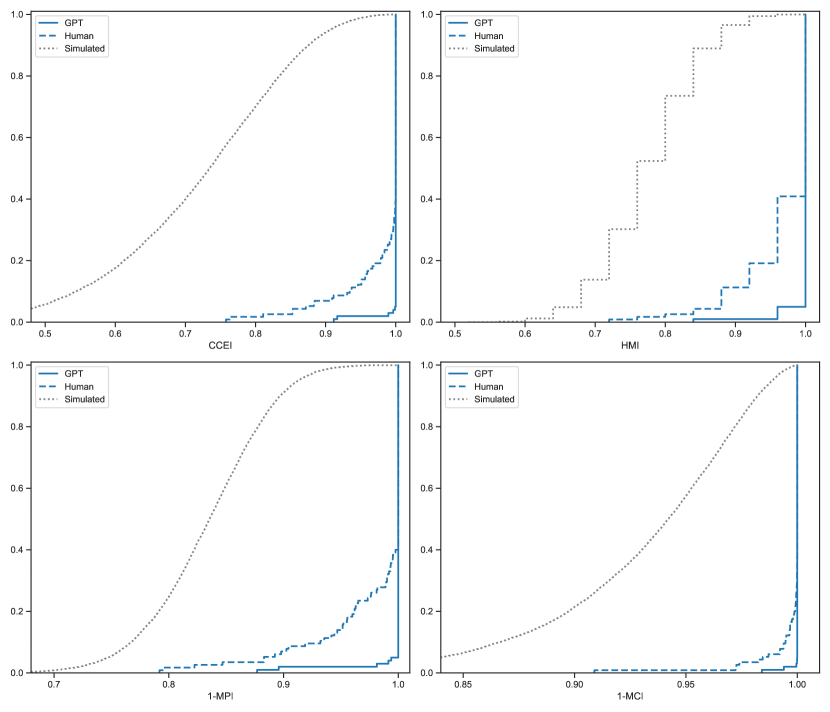

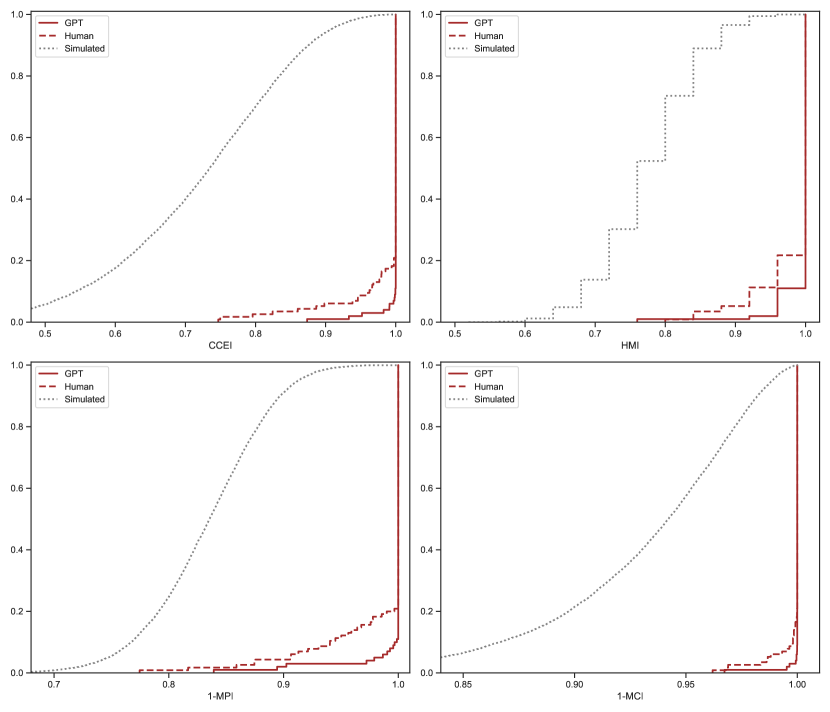

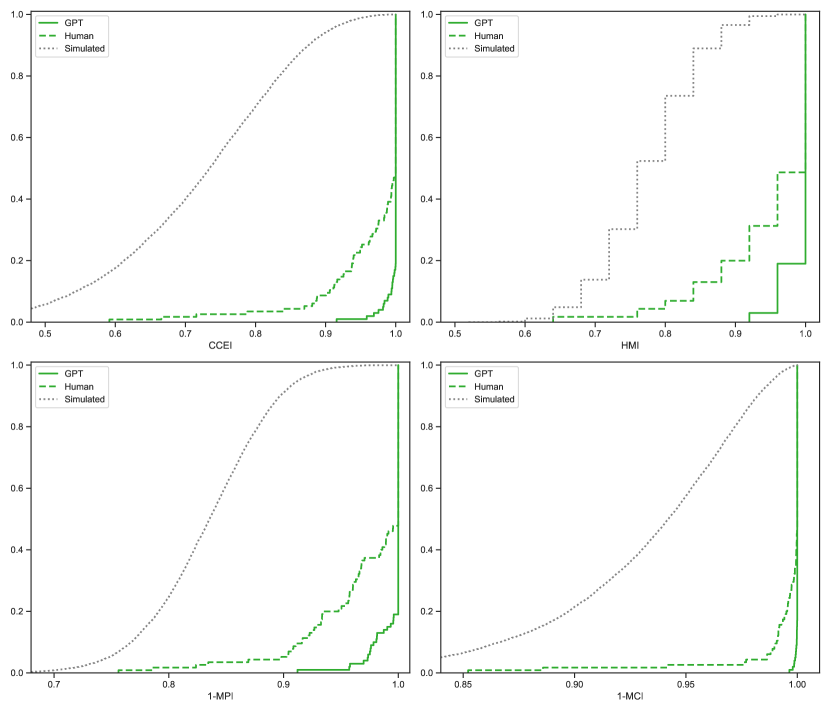

In addition to CCEI, we calculate other indices to measure rationality including the Houtman-Maks index (HMI) (Houtman and Maks, 1985), money pump index (MPI) (Echenique et al., 2011), and minimum cost index (MCI) (Dean and Martin, 2016), and construct cumulative distribution plots for each index of GPT observations, human subjects, and simulated subjects in Figure D2-D5 in Appendix D. Consistent with the observations based on CCEI, results from these indices show that GPT observations exhibit a high level of rationality across the four preferences domains and surpass those of human subjects across all domains (, two-sided two-sample t-tests).

Downward-sloping Demand.

While GPT exhibits a high level of rationality, it is possible that its decisions are simply clustered at the corners or in certain areas. To address such concern, we examine whether GPT behavior respects the property of downward-sloping demand, a fundamental principle in the analysis of consumer behavior whereby the demand for a commodity decreases with its price (Choi et al., 2007; Fisman et al., 2007; Echenique et al., 2023).

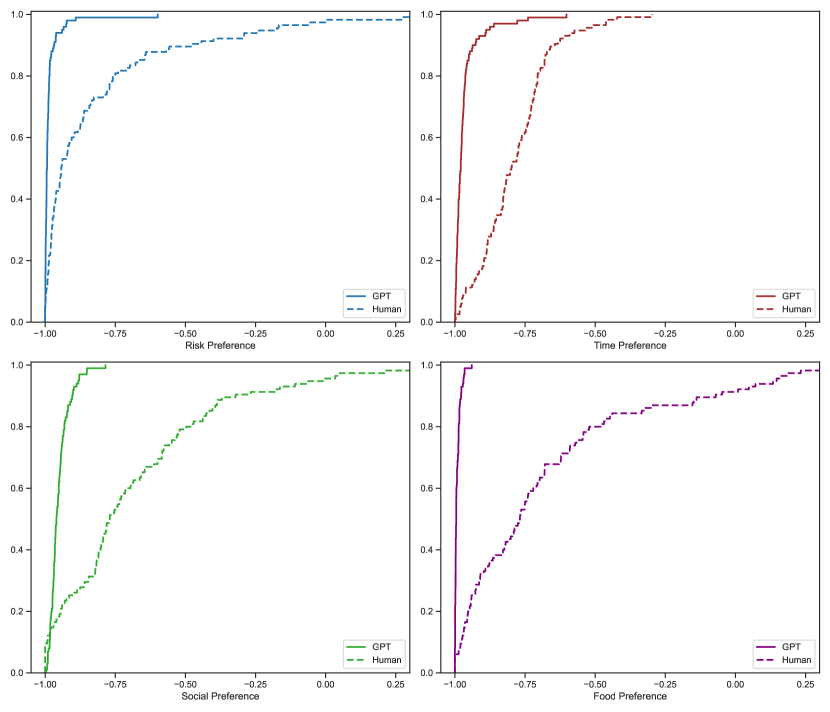

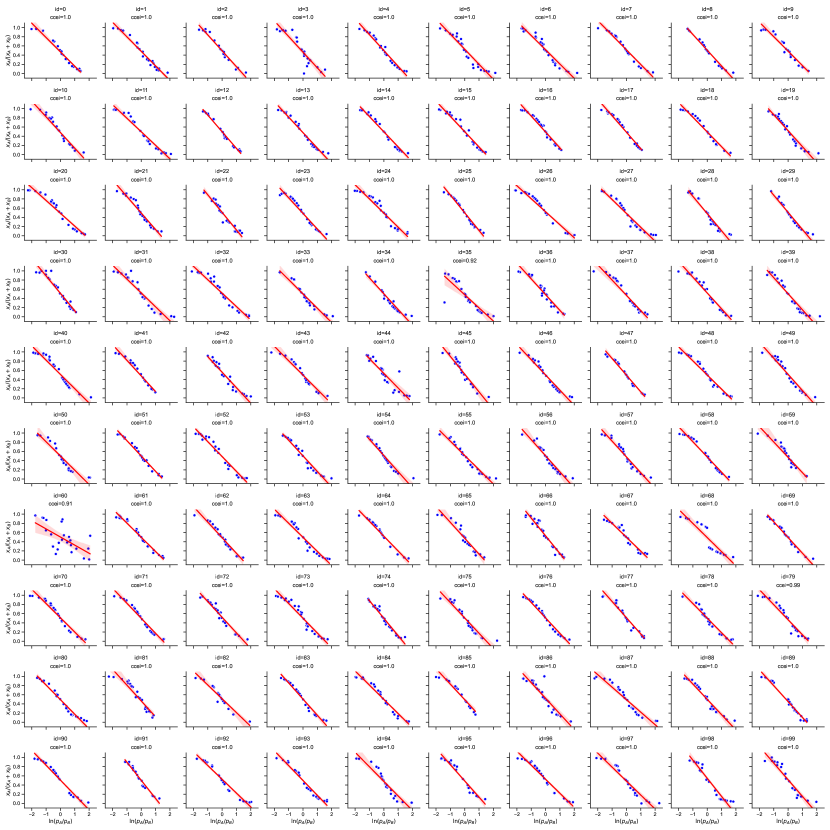

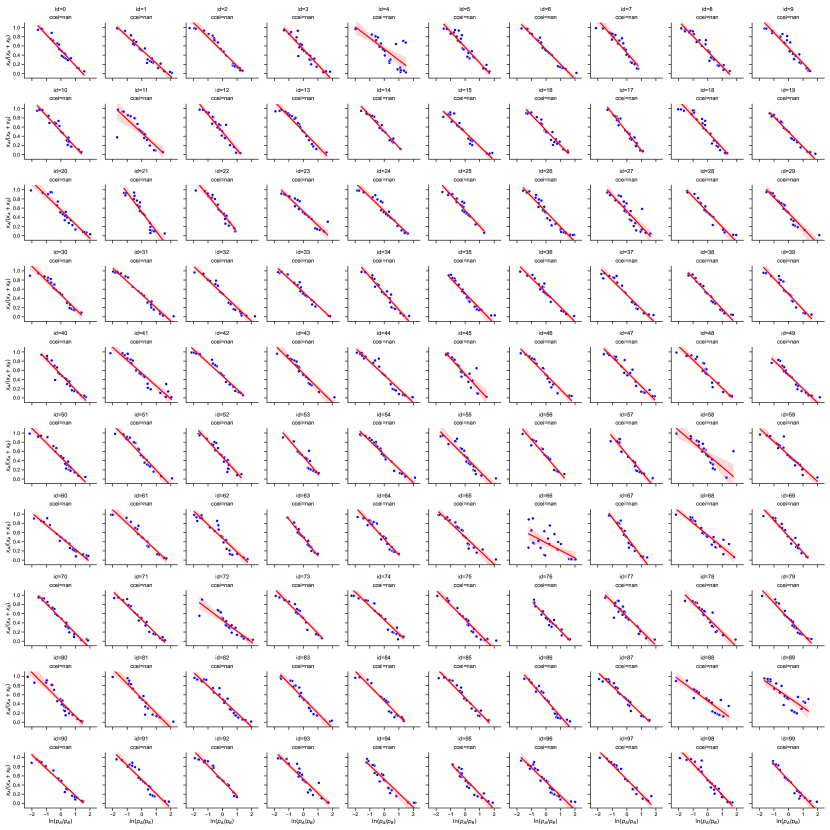

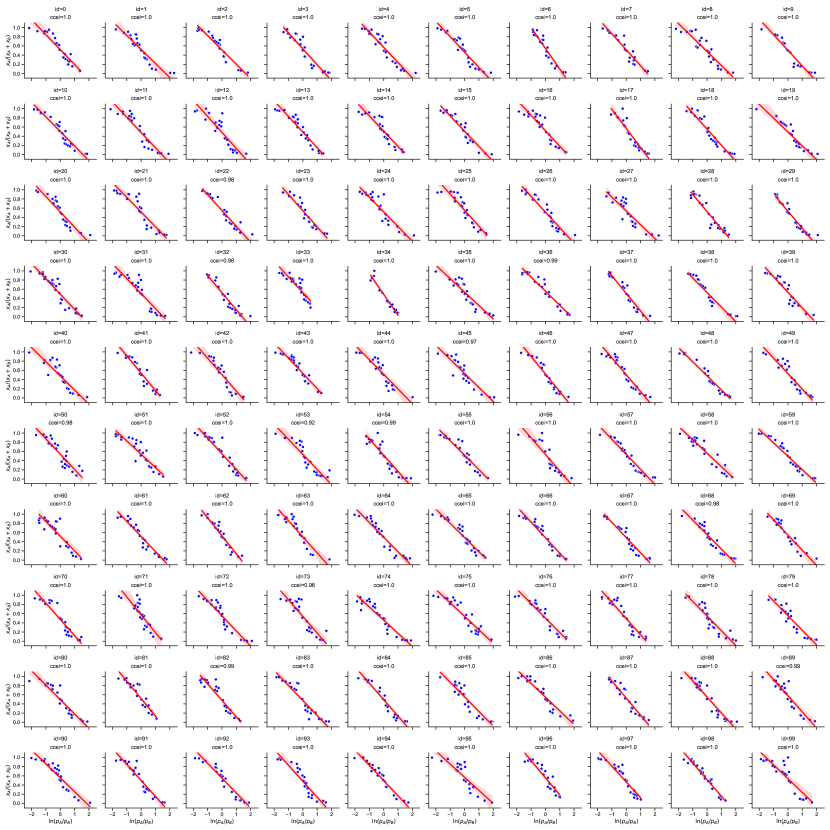

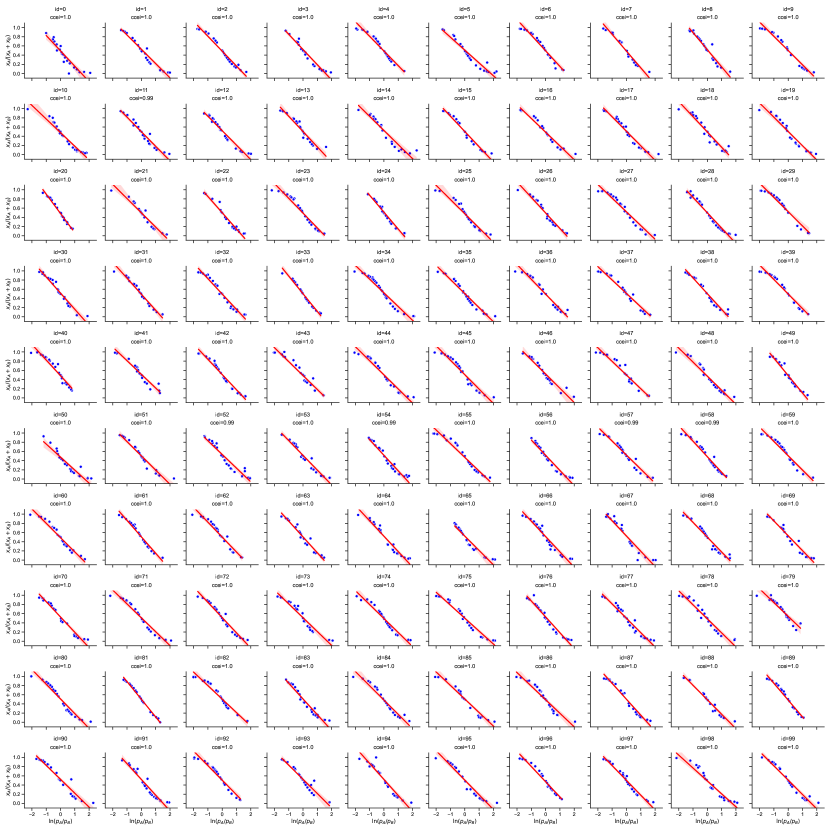

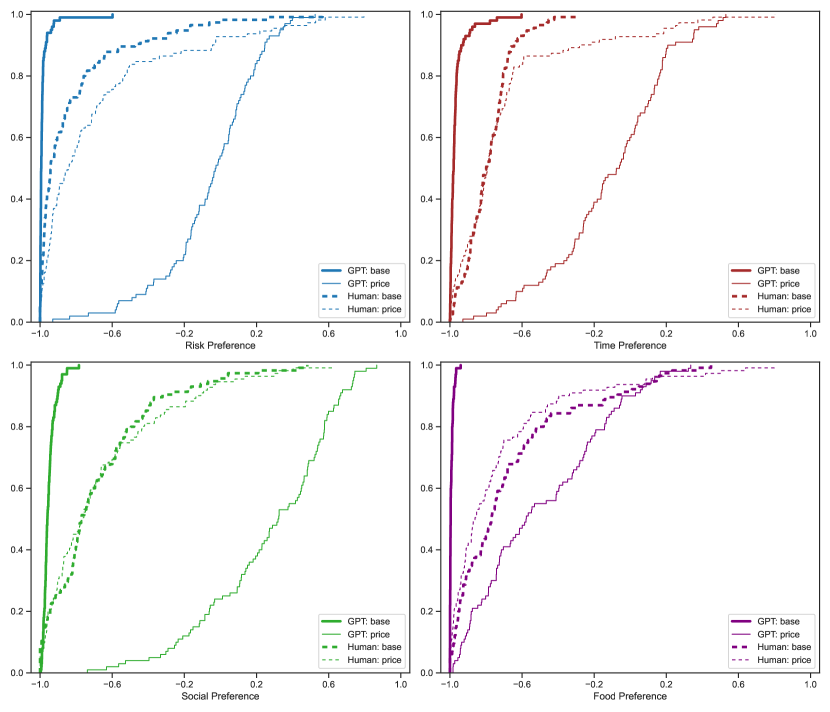

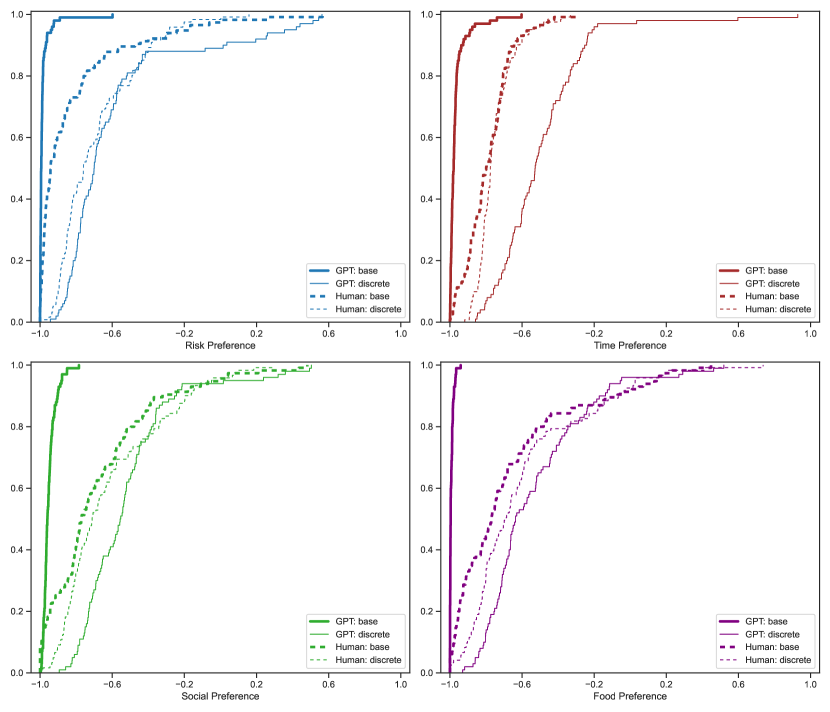

We measure the degree of compliance with downward-sloping demand for GPT observations and human subjects. This principle requires that when the relative price of a commodity increases, the consumer should not increase its consumption. More specifically, we measure whether each DM’s decisions respect this principle by calculating the Spearman’s correlation coefficient of and (Echenique et al., 2023). A negative correlation indicates an appropriate response to price fluctuations, and zero or positive correlation indicates no respond or irregular response to price changes. Note that is not defined in the corners. We adjust corner choices by a small constant, 0.1% of the budget, in each choice (Echenique et al., 2023). We plot the cumulative distribution of the Spearman’s correlation coefficients of and as a proxy for the degree of downward-sloping demand for each of the four preferences domains in Figure 2.

For GPT observations, the coefficients for risk, time, social, and food preferences have a mean of -0.984, -0.966, -0.951, and -0.992, while these are -0.826, -0.788, -0.681, and -0.673 for human subjects, respectively. Overall, GPT is more responsive to price changes than human subjects in each preference domain (, two-sided two-sample t-tests). Figure 2 further illustrates that GPT observations always have a negative Spearman’s correlation coefficients, while human has a lower proportion having a negative Spearman’s correlation coefficients (96.1% on average). This strengthens our findings based on the rationality score and suggests that GPT is more capable of making reasonable responses to the changes in prices than human subjects.

Preference Estimation.

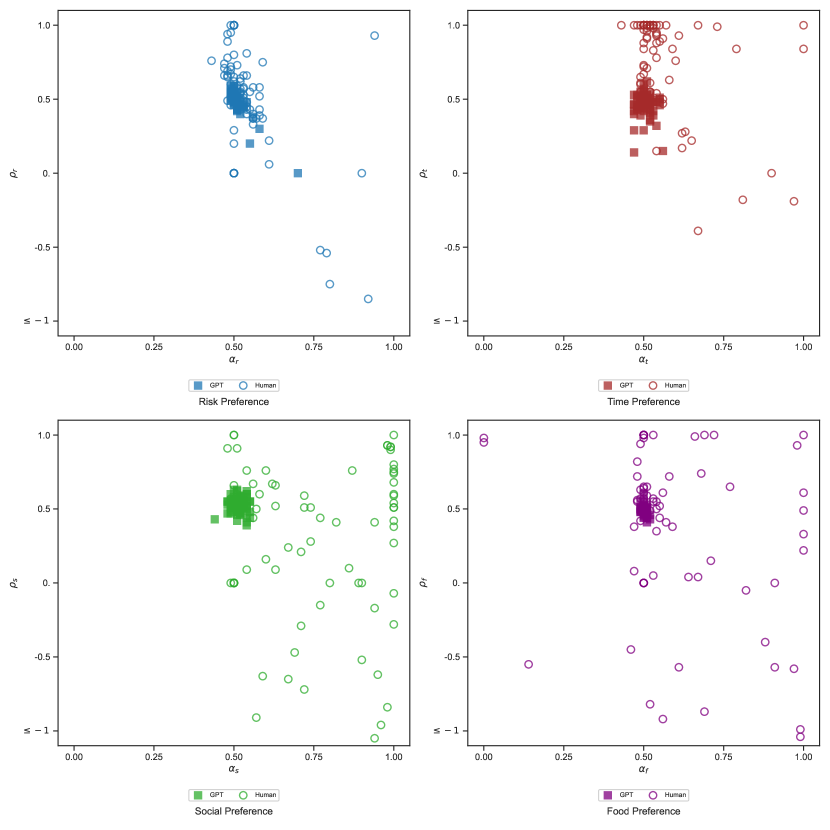

Since choices of GPT and human subjects are mostly consistent with well-behaved utility functions, we proceed to estimate the underlying risk, time, social, and food preferences.333We omit GPT or human individuals with CCEI score below 0.95 (Varian, 1990). In total, we have eight estimated parameters: decision weight of the better outcome () and utility curvature () for risk preference, weight of today () and utility curvature () for time preference, weight for self’s payment () and utility curvature () for social preference, weight for meat () and utility curvature () for food preference. We first estimate the preference parameters at the aggregate level by pooling all responses of GPT observations and human subjects, respectively (Table D2 in Appendix D).

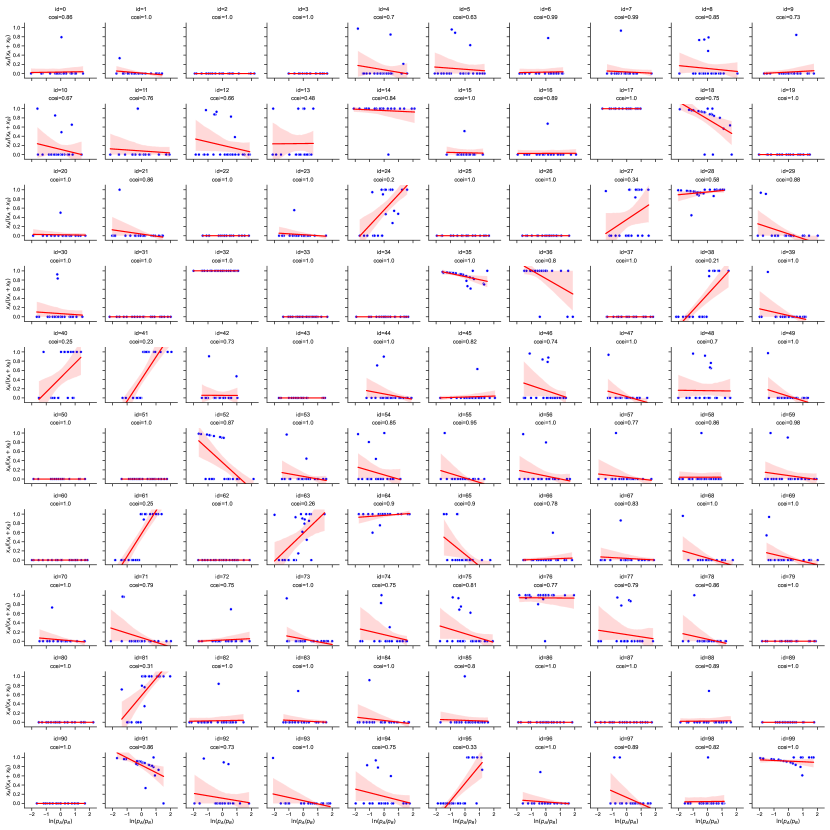

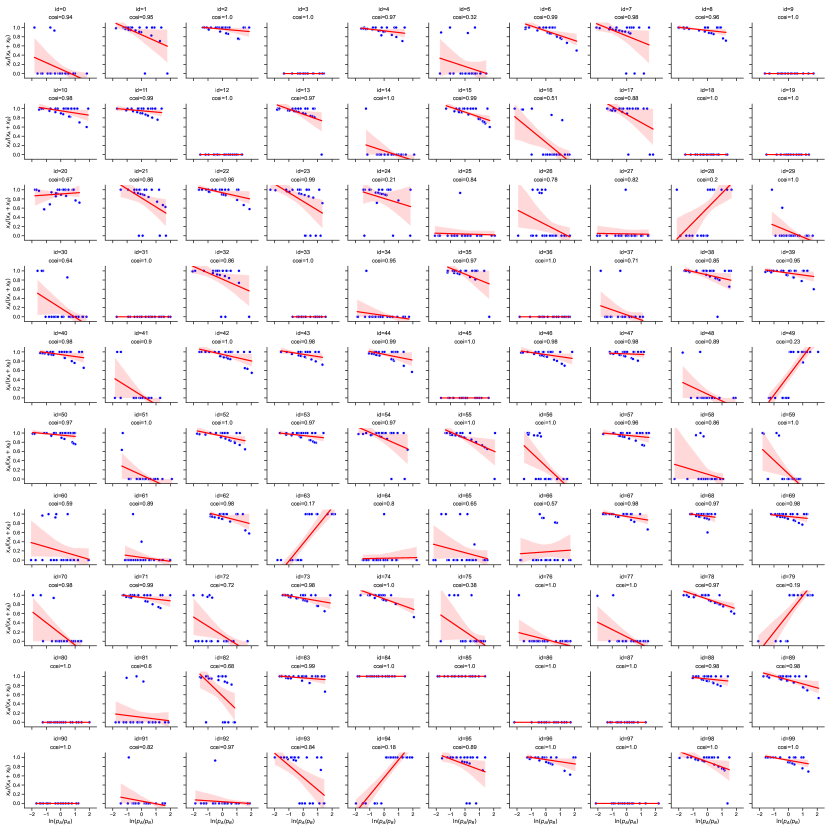

Results show that, compared to human subjects, GPT is closer to an expect-utility maximizer (: 0.618 vs. 0.508 for Human vs. GPT) and has a more linear utility curve (: 0.335 vs. 0.488) in risk preference; is more patient (: 0.513 vs. 0.504) and has a less linear utility curve (: 0.981 vs. 0.466) in time preference; is more other-regarding (: 0.735 vs. 0.512) and more efficiency-orientated (: 0.330 vs. 0.520) in social preference, and is less fond of meat (: 0.583 vs. 0.501) and more efficiency-orientated (: 0.386 vs. 0.491) in food preference. Similar patterns can be observed in the individual-level estimations, in which we estimate preference parameters for each GPT decision maker and human subject, as shown in Figure D3 and Table D3 in Appendix D. Moreover, the scatter plots of human subjects are more dispersed, which suggests a significantly higher level of preference heterogeneity among human subjects than GPT observations.

4.2 Results from the Conditions with Variations

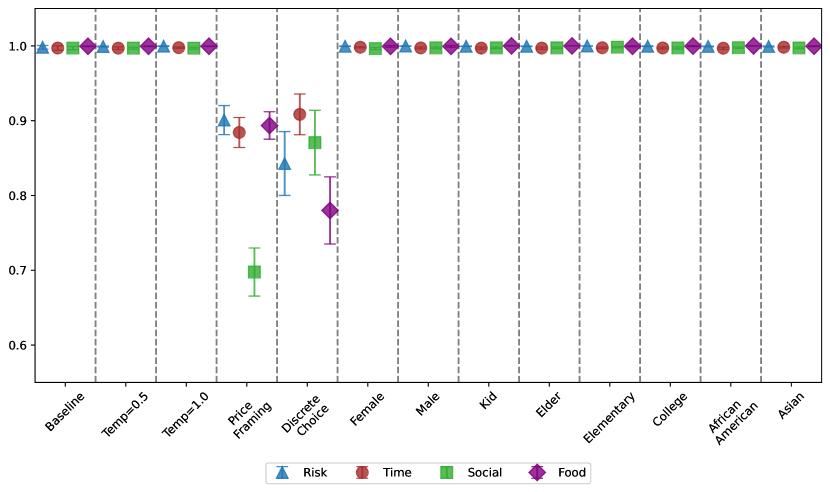

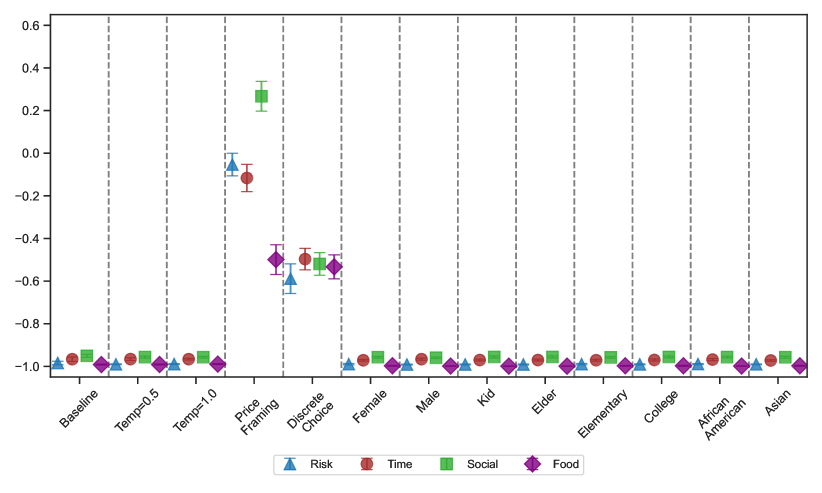

We examine variations in the temperature, decision tasks, and demographic information. Figure 4 presents the mean CCEI values and 95% confidence intervals across variations, and Figure D24 in Appendix D shows the mean Spearman’s correlation coefficients of and and their 95% confidence intervals. We report these results in detail below.

Insensitive to Variations in Temperature.

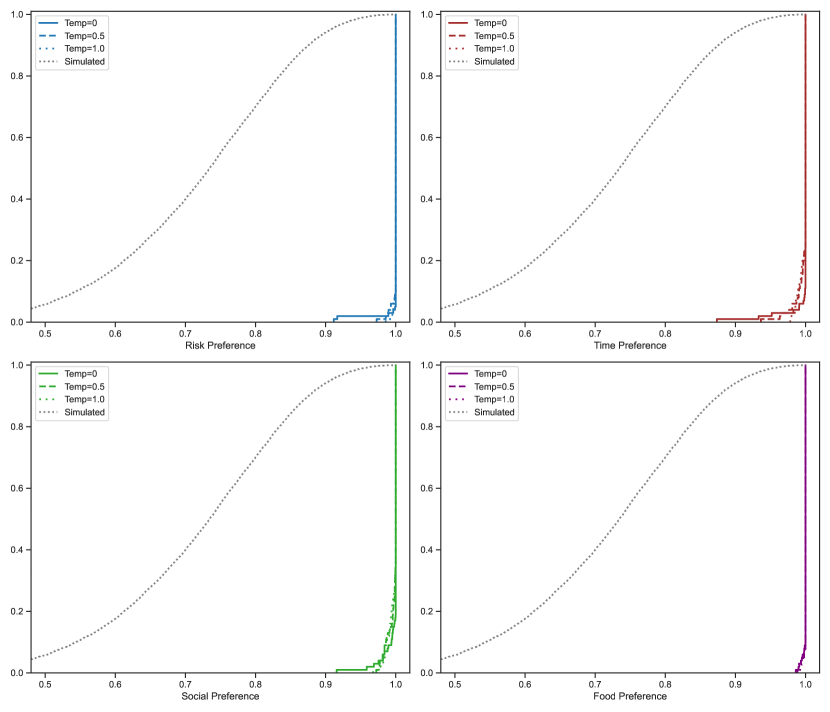

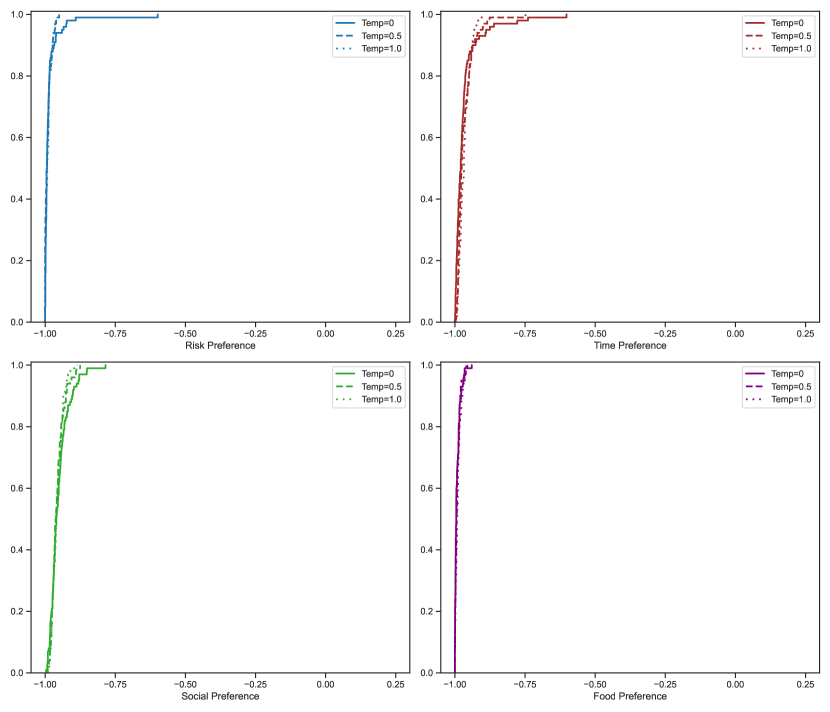

When the temperature increases from 0 to 0.5 and 1, there is a higher number of invalid responses, namely, GPT does not provide an answer to the specified question (invalid response rate is 4.7% for temperature of 0.5 and 9.8% for temperature of 1). Therefore, we analyze the data conditional on those providing valid answers. We find that as the randomness increases, the level of rationality is similar to that in the baseline condition (Figure 4). For each temperature and each preference domain, we plot the cumulative distributions of the CCEI values of GPT observations and simulated subjects for Bronars’ test in Figure D10 in Appendix D and the cumulative distributions of the Spearman’s correlation coefficients in Figure D11 in Appendix D. These findings suggest that randomness increases the stochasticity and creativity in language presentations of GPT, but not the rationality score.

There are no significant differences for the estimated Spearman’s correlation coefficients of and between the baseline and the higher temperature (Figure D24 in Appendix D) at the 10% level (two-sided two-sample t-tests). Similarly, the mean of estimated preference parameters are statistically indifferent to changes in temperature. However, the standard deviations of some parameters increase with temperature (, , , : , two-sample Levene tests), which suggests that high temperature may generate greater heterogeneity in the behavior of GPT.

Sensitive to Variation in the Decision Tasks.

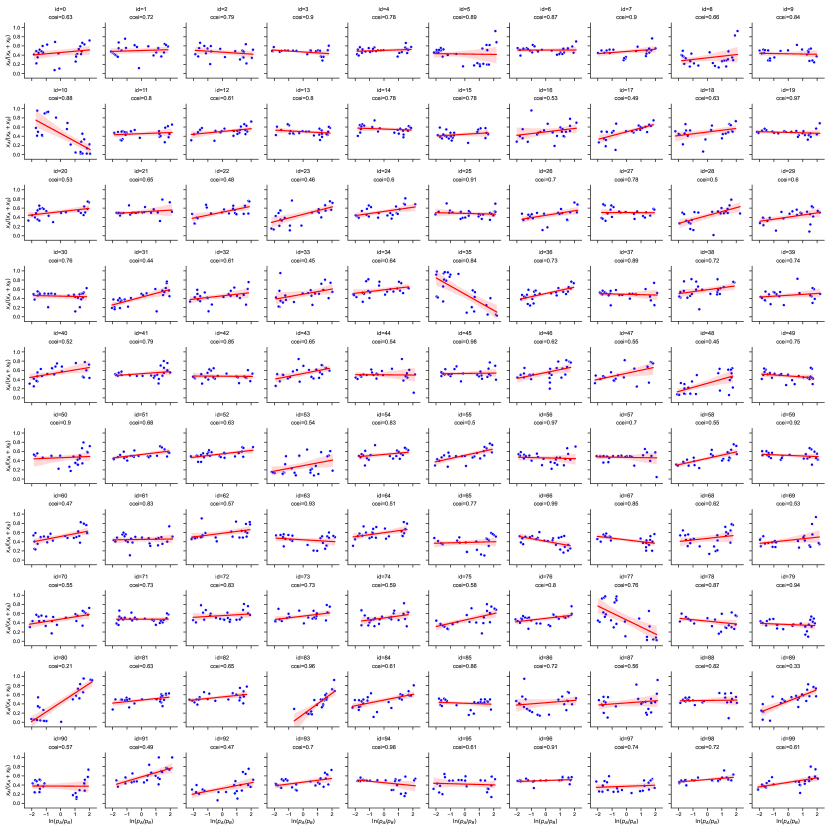

First, we compare the baseline and the price framing conditions. Changing the price framing significantly reduces GPT’s rationality level in all four tasks (Figure 4). Remarkably, the average CCEI for risk preference declines to 0.901, with 34% exhibiting a CCEI below 0.9. These values are 0.884 (48%), 0.698 (88%), and 0.894 (49%) for time, social, and food preferences, respectively.444Given the low level of rationality exhibited by GPT in the price framing condition, we have difficulty in determining that GPT’s decisions are consistent with a well-behaved utility function. Therefore, we refrain from adopting the preference estimation approach under this condition (Varian, 1990). The situation is identical in the discrete choice condition as described below. In each preference domain, CCEI values are significantly higher in the baseline condition than in the price framing condition (, two-sided two-sample t-tests). Moreover, the downward-sloping demand property is impaired under the alternative price framing, with the key Spearman’s correlation coefficients being -0.053, -0.116, 0.267, and -0.499 for risk, time, social, and food preferences, respectively (Figure D24 in Appendix D). Figures D13-D16 in Appendix D show the disordered responses of GPT observations to price changes in the price framing condition, which appear to be flatter compared to those in the baseline condition.

In Figure D17 (Figure D18) in Appendix D, we display the CDFs of CCEI (Spearman’s correlation coefficients) in the four conditions: baseline and price framing conditions in both the GPT experiment and the human experiment. We find that the alternative price framing also reduces the rationality level and the downward-sloping demand property in the human subjects experiment (, two-sided two-sample t-tests in risk and time preferences). However, the figures suggest that these reductions are larger in the GPT experiment than in the human experiment, which is further verified in OLS regression analyses (Table D4 in Appendix D).

Second, we compare the baseline and the discrete choice conditions. When we present GPT with a set of 11 options, we also observe a decrease in rationality levels for discrete choices of GPT observations for all four tasks in Figure 4 (risk: 0.998 vs. 0.843, ; time: 0.997 vs. 0.908, ; social: 0.997 vs. 0.871, ; food: 0.999 vs. 0.780, , two-sided two-sample t-tests). Additionally, 51%, 32%, 33%, and 55% of GPT observations demonstrate a CCEI below 0.9 in risk, time, social, and food preferences, respectively. Figure D19-D22 in Appendix D show the demand curves of GPT observations, which exhibit significantly more corner solutions. Consistently, the Spearman’s correlation coefficients are -0.589, -0.497, -0.519, and -0.533 for risk, time, social, and food preferences (Figure D24 in Appendix D; when compared to the baseline condition, two-sided two-sample t-tests). These suggest that GPT is less responsive to price changes under discrete choices than continuous choices.

Figure D23 (Figure D24) in Appendix D shows the CDFs of the CCEI (Spearman’s correlation coefficients) in baseline and discrete choice conditions in the GPT experiment and human experiment. Human subjects’ rationality level and the downward-sloping demand property reduce in the discrete setting, compared to the baseline condition (, two-sided two-sample t-tests in risk and time preferences). As shown in the figures, these reductions are larger in the GPT experiment than in the human experiment. We also verify this observation through OLS regression analyses (Table D4 in Appendix D). These results suggest that GPT’s decision-making is more significantly affected by both the framing of prices and discrete choices than human subjects.

Insensitive to Demographic Information.

Comparing the baseline condition and variations in demographics in the GPT experiment, we find that CCEI values, Spearman’s correlation coefficients of and , and estimated preference parameters are all insensitive to variations of demographic factors embedded in the prompts to request responses from GPT (Figure 4, Figure D24, Tables D2-D3 in Appendix D).

These are in contrast to results of our human experiment (Tables D5-D6 in Appendix D) and prior studies where rationality score and preference have been shown to differ across demographic groups (Choi et al., 2014; Echenique et al., 2011; Von Gaudecker et al., 2011). The fact that GPT’s decision-making process remains consistent across demographic variables suggests that GPT does not exhibit algorithmic bias in terms of decision-making quality, which provides a measure of reassurance regarding its fairness and consistency across diverse user groups.

5 Discussion

We conduct the first study to assess the rationality of GPT, a popular large language model, using revealed preference analysis. Our findings demonstrate that GPT is able to display a high level of rationality in decision-making related to risk, time, social, and food preferences. We also observe that increasing the randomness of GPT does not significantly impact its performance. Furthermore, our analysis reveals that the level of rationality of GPT remains constant across different demographic characteristics, which indicates that it does not exhibit an algorithm bias. However, we observe a significant drop in rationality when we use a less standard presentation of prices or change the choice set from continuous to discrete. This suggests that GPT may have limitations in terms of sensitivity to contexts and frames.

Our study contributes to the ongoing discussions of the performance of GPT in various domains; these include reasoning, logic, math, language processing, and identifying factual errors (Borji, 2023). In addition to cognitive techniques and practical skills, some researchers have explored whether GPT can exhibit human-like decision-making abilities or perceive others’ thoughts (Horton, 2023; Kosinski, 2023). Our study adds to these parallel studies by subjecting GPT to traditional decision-making tasks and employing a set of measures to systematically describe its behavior. Our work aligns with recent calls to study machine behavior to “reap their benefits and minimize their harms” (Rahwan et al., 2019). By providing insights into GPT’s decision-making capacity, we can better understand how to optimize its performance and address potential limitations.

Our study is situated within the growing literature on AI-based decision support tools. Many researchers have explored the usefulness of leveraging AI in various decision-making domains, such as bail decisions (Kleinberg et al., 2018); clinical diagnosis (Mullainathan and Obermeyer, 2022); work arrangements (Kawaguchi et al., 2021); stock price forecasts (Lopez-Lira and Tang, 2023); job recruitment (Horton, 2017); product or content consumption (Adomavicius et al., 2018; Agrawal et al., 2022); and mathematics development (Davies et al., 2021). Unlike these algorithms, which require data input and training, GPT is a language-based model that provides a direct question-and-answer service for normal users. Given its high level of rationality in decision-making across various domains, our study proves the potential of GPT as a general AI-based decision-support tool. The user-friendly interface and versatility of GPT render it a promising option for individuals and organizations seeking easy-to-use AI-based advice.

Our paper makes contributions to the literature on rationality and experimental methods. First, we demonstrate the effectiveness of experimental economics methods in studying choice behavior of artificial intelligence (Rahwan et al., 2019), which adds earlier studies of children (Brocas et al., 2019; Harbaugh et al., 2001), monkeys (Chen et al., 2006), rats, and pigeons (Kagel et al., 1975). Second, our work highlights the potential of large language models like GPT to streamline experimental research and yield new data and insights (Horton, 2023). Finally, studying the choice behavior of artificial intelligence can provide an important benchmark for understanding natural intelligence. For example, our understanding of how LLMs make decisions could help reveal general principles that govern both language intelligence and decision intelligence (Sejnowski, 2023). By synthesizing insights from these various domains, our paper offers a novel perspective on the nature of rationality and broadens the methods that can be used to study it.

As an initial assessment of the economic rationality of GPT, our study has several limitations. First, our study examines the choice behavior of GPT but does not explore the mechanisms that underlie our observations. For example, we find that GPT responses are highly sensitive to contexts and frames. This may be due to the reflection of biases presented in the existing data (Schramowski et al., 2022; Caliskan et al., 2017),the insufficient training of texts of the alternative contexts and frames (Chen et al., 2021; Drori et al., 2022), or the tendency for LLMs to exploit spurious correlations or statistical irregularities in the data set under dissimilar tasks (McCoy et al., 2019). In particular, McKenna et al. (2023) suggests that a significant source of LLMs bias originates from a corpus-based heuristic using the relative frequencies of words. The “50-50 split” or “equal split” are high-frequency texts in allocation settings, and GPT can adapt this corpus-based heuristic and exhibit the tendency to choose the midpoint under an “unfamiliar” task with the alternative price framework. Similarly, “all or nothing” can be high-frequency texts under the presentation of options context, so GPT exhibits the tendency to choose the first or last option under an “unfamiliar” discrete choice condition. Recent studies have documented similar patterns in different environments (Binz and Schulz, 2023; Brand et al., 2023; Jones and Steinhardt, 2022; Brookins and DeBacker, 2023; Horton, 2023).

In addition, our study reveals that demographic factors do not significantly impact GPT’s rationality or estimated preference parameters. This contrasts with the majority of empirical literature, including our human subject experiment, where demographic factors often play a significant role. The lack of responsiveness to demographics aligns with the concept of hyper-accuracy distortion (Aher et al., 2023), which refers to the distortion resulting from the extensive efforts to align LLMs with human ethics such as the censorship of demographic information to reduce and prevent problematic outputs. In conclusion, with some speculative conjectures, we leave it to future studies to explore the mechanisms that underlie GPT’s choice behavior and open the black-box of this technology.

Second, we focus on economic rationality as defined by revealed preference analysis, whereas rationality is often defined more broadly in the literature to include various decision rules and heuristics (Kahneman, 2003; Simon, 1979; Thaler, 2016). Third, we use a simple experimental environment with only two commodities to present budgetary decisions. However, studying rationality in more realistic settings, such as shopping behavior in a supermarket and portfolio choices in the financial markets would be more challenging yet important. Our study shows that economic rationality can emerge in GPT when decision contexts are simple and framed in specific ways. Future research is needed to investigate the broader applications of artificial intelligent agents as they continue to evolve.

References

- Adomavicius et al. (2018) Adomavicius G, Bockstedt JC, Curley SP, Zhang J (2018). “Effects of online recommendations on consumers’ willingness to pay.” Information Systems Research, 29(1), 84–102.

- Afriat (1967) Afriat SN (1967). “The construction of utility functions from expenditure data.” International Economic Review, 8(1), 67–77.

- Afriat (1972) Afriat SN (1972). “Efficiency estimation of production functions.” International Economic Review, 13(3), 568–598.

- Agrawal et al. (2022) Agrawal K, Athey S, Kanodia A, Palikot E (2022). “Personalized Recommendations in EdTech: Evidence from a Randomized Controlled Trial.” arXiv preprint arXiv:2208.13940.

- Aher et al. (2023) Aher GV, Arriaga RI, Kalai AT (2023). “Using large language models to simulate multiple humans and replicate human subject studies.” In “International Conference on Machine Learning,” pp. 337–371. PMLR.

- Ahn et al. (2014) Ahn D, Choi S, Gale D, Kariv S (2014). “Estimating ambiguity aversion in a portfolio choice experiment.” Quantitative Economics, 5(2), 195–223.

- Andreoni et al. (2013) Andreoni J, Gillen BJ, Harbaugh WT (2013). “The power of revealed preference tests: Ex-post evaluation of experimental design.” Working Paper.

- Andreoni and Miller (2002) Andreoni J, Miller J (2002). “Giving according to GARP: An experimental test of the consistency of preferences for altruism.” Econometrica, 70(2), 737–753.

- Andreoni and Sprenger (2012) Andreoni J, Sprenger C (2012). “Estimating time preferences from convex budgets.” American Economic Review, 102(7), 3333–56.

- Banks et al. (2019) Banks J, Carvalho L, Perez-Arce F (2019). “Education, decision making, and economic rationality.” Review of Economics and Statistics, 101(3), 428–441.

- Beatty and Crawford (2011) Beatty TK, Crawford I (2011). “How demanding is the revealed preference approach to demand?” American Economic Review, 101(6), 2782–95.

- Binz and Schulz (2023) Binz M, Schulz E (2023). “Using cognitive psychology to understand GPT-3.” Proceedings of the National Academy of Sciences, 120(6), e2218523120.

- Blundell et al. (2003) Blundell R, Browning M, Crawford I (2003). “Nonparametric engel curves and revealed preference.” Econometrica, 71(1), 205–240.

- Blundell et al. (2008) Blundell R, Browning M, Crawford I (2008). “Best nonparametric bounds on demand responses.” Econometrica, 76(6), 1227–1262.

- Bommarito II and Katz (2022) Bommarito II M, Katz DM (2022). “GPT takes the bar exam.” arXiv preprint arXiv:2212.14402.

- Borji (2023) Borji A (2023). “A categorical archive of ChatGPT failures.” arXiv preprint arXiv:2302.03494.

- Brand et al. (2023) Brand J, Israeli A, Ngwe D (2023). “Using GPT for market research.” Available at SSRN 4395751.

- Brocas et al. (2019) Brocas I, Carrillo JD, Combs TD, Kodaverdian N (2019). “The development of consistent decision-making across economic domains.” Games and Economic Behavior, 116, 217–240.

- Bronars (1987) Bronars SG (1987). “The power of nonparametric tests of preference maximization.” Econometrica, 55(3), 693–698.

- Brookins and DeBacker (2023) Brookins P, DeBacker JM (2023). “Playing Games With GPT: What Can We Learn About a Large Language Model From Canonical Strategic Games?” Available at SSRN 4493398.

- Brown et al. (2020) Brown T, Mann B, Ryder N, Subbiah M, Kaplan JD, Dhariwal P, Neelakantan A, Shyam P, Sastry G, Askell A, et al. (2020). “Language models are few-shot learners.” Advances in Neural Information Processing Systems, 33, 1877–1901.

- Caliskan et al. (2017) Caliskan A, Bryson JJ, Narayanan A (2017). “Semantics derived automatically from language corpora contain human-like biases.” Science, 356(6334), 183–186.

- Cappelen et al. (2023) Cappelen AW, Kariv S, Sørensen EØ, Tungodden B (2023). “The development gap in economic rationality of future elites.” Games and Economic Behavior, 142, 866–878.

- Carvalho et al. (2016) Carvalho LS, Meier S, Wang SW (2016). “Poverty and economic decision-making: Evidence from changes in financial resources at payday.” American economic review, 106(2), 260–284.

- Castillo and Freer (2018) Castillo M, Freer M (2018). “Revealed differences.” Journal of Economic Behavior & Organization, 145, 202–217.

- Cettolin et al. (2020) Cettolin E, Dalton PS, Kop W, Zhang W (2020). “Cortisol meets GARP: the effect of stress on economic rationality.” Experimental Economics, 23, 554–574.

- Chambers and Echenique (2016) Chambers CP, Echenique F (2016). Revealed preference theory. Cambridge University Press.

- Chen et al. (2023a) Chen M, Liu TX, Shan Y, Zhong S, Zhou Y (2023a). “The Consistency of Rationality Measures.” Working Paper.

- Chen et al. (2021) Chen M, Tworek J, Jun H, Yuan Q, Pinto HPdO, Kaplan J, Edwards H, Burda Y, Joseph N, Brockman G, et al. (2021). “Evaluating large language models trained on code.” arXiv preprint arXiv:2107.03374.

- Chen et al. (2006) Chen MK, Lakshminarayanan V, Santos LR (2006). “How basic are behavioral biases? Evidence from capuchin monkey trading behavior.” Journal of Political Economy, 114(3), 517–537.

- Chen et al. (2023b) Chen Y, Andiappan M, Jenkin T, Ovchinnikov A (2023b). “A Manager and an AI Walk into a Bar: Does ChatGPT Make Biased Decisions Like We Do?” Available at SSRN 4380365.

- Choi et al. (2007) Choi S, Fisman R, Gale D, Kariv S (2007). “Consistency and heterogeneity of individual behavior under uncertainty.” American Economic Review, 97(5), 1921–1938.

- Choi et al. (2014) Choi S, Kariv S, Müller W, Silverman D (2014). “Who is (more) rational?” American Economic Review, 104(6), 1518–50.

- Corbett-Davies and Goel (2018) Corbett-Davies S, Goel S (2018). “The measure and mismeasure of fairness: A critical review of fair machine learning.” arXiv preprint arXiv:1808.00023.

- Crawford (2010) Crawford I (2010). “Habits revealed.” The Review of Economic Studies, 77(4), 1382–1402.

- Crawford and Pendakur (2013) Crawford I, Pendakur K (2013). “How many types are there?” The Economic Journal, 123(567), 77–95.

- Davies et al. (2021) Davies A, Veličković P, Buesing L, Blackwell S, Zheng D, Tomašev N, Tanburn R, Battaglia P, Blundell C, Juhász A, et al. (2021). “Advancing mathematics by guiding human intuition with AI.” Nature, 600(7887), 70–74.

- Dean and Martin (2016) Dean M, Martin D (2016). “Measuring rationality with the minimum cost of revealed preference violations.” Review of Economics and Statistics, 98(3), 524–534.

- Drichoutis and Nayga Jr (2020) Drichoutis AC, Nayga Jr RM (2020). “Economic rationality under cognitive load.” The Economic Journal, 130(632), 2382–2409.

- Drori et al. (2022) Drori I, Zhang S, Shuttleworth R, Tang L, Lu A, Ke E, Liu K, Chen L, Tran S, Cheng N, et al. (2022). “A neural network solves, explains, and generates university math problems by program synthesis and few-shot learning at human level.” Proceedings of the National Academy of Sciences, 119(32), e2123433119.

- Echenique et al. (2023) Echenique F, Imai T, Saito K (2023). “Approximate expected utility rationalization.” Journal of the European Economic Association, 21(5), 1821–1864.

- Echenique et al. (2011) Echenique F, Lee S, Shum M (2011). “The money pump as a measure of revealed preference violations.” Journal of Political Economy, 119(6), 1201–1223.

- Fisman et al. (2015) Fisman R, Jakiela P, Kariv S (2015). “How did distributional preferences change during the great recession?” Journal of Public Economics, 128, 84–95.

- Fisman et al. (2017) Fisman R, Jakiela P, Kariv S (2017). “Distributional preferences and political behavior.” Journal of Public Economics, 155, 1–10.

- Fisman et al. (2023) Fisman R, Jakiela P, Kariv S, Vannutelli S (2023). “The distributional preferences of Americans, 2013–2016.” Experimental Economics, 26(4), 727–748.

- Fisman et al. (2007) Fisman R, Kariv S, Markovits D (2007). “Individual preferences for giving.” American Economic Review, 97(5), 1858–1876.

- Goodfellow et al. (2016) Goodfellow I, Bengio Y, Courville A (2016). Deep learning. MIT press.

- Gul (1991) Gul F (1991). “A Theory of Disappointment Aversion.” Econometrica, 59(3), 667–86.

- Halevy et al. (2018) Halevy Y, Persitz D, Zrill L (2018). “Parametric recoverability of preferences.” Journal of Political Economy, 126(4), 1558–1593.

- Harbaugh et al. (2001) Harbaugh WT, Krause K, Berry TR (2001). “GARP for kids: On the development of rational choice behavior.” American Economic Review, 91(5), 1539–1545.

- Horton (2017) Horton JJ (2017). “The effects of algorithmic labor market recommendations: Evidence from a field experiment.” Journal of Labor Economics, 35(2), 345–385.

- Horton (2023) Horton JJ (2023). “Large language models as simulated economic agents: What can we learn from homo silicus?” NBER Working Paper.

- Houtman and Maks (1985) Houtman M, Maks J (1985). “Determining all maximal data subsets consistent with revealed preference.” Kwantitatieve Methoden, 19(1), 89–104.

- Jones and Steinhardt (2022) Jones E, Steinhardt J (2022). “Capturing failures of large language models via human cognitive biases.” Advances in Neural Information Processing Systems, 35, 11785–11799.

- Kagel et al. (1975) Kagel JH, Battalio RC, Rachlin H, Green L, Basmann RL, Klemm WR (1975). “Experimental studies of consumer demand behavior using laboratory animals.” Economic Inquiry, 13(1), 22–38.

- Kahneman (2003) Kahneman D (2003). “Maps of bounded rationality: Psychology for behavioral economics.” American Economic Review, 93(5), 1449–1475.

- Kawaguchi et al. (2021) Kawaguchi Y, Imoto K, Koizumi Y, Harada N, Niizumi D, Dohi K, Tanabe R, Purohit H, Endo T (2021). “Description and discussion on DCASE 2021 challenge task 2: Unsupervised anomalous sound detection for machine condition monitoring under domain shifted conditions.” arXiv preprint arXiv:2106.04492.

- Kim et al. (2018) Kim HB, Choi S, Kim B, Pop-Eleches C (2018). “The role of education interventions in improving economic rationality.” Science, 362(6410), 83–86.

- Kleinberg et al. (2018) Kleinberg J, Lakkaraju H, Leskovec J, Ludwig J, Mullainathan S (2018). “Human decisions and machine predictions.” The Quarterly Journal of Economics, 133(1), 237–293.

- Kosinski (2023) Kosinski M (2023). “Theory of mind may have spontaneously emerged in large language models.” arXiv preprint arXiv:2302.02083.

- Li et al. (2022) Li J, Casalino LP, Fisman R, Kariv S, Markovits D (2022). “Experimental evidence of physician social preferences.” Proceedings of the National Academy of Sciences, 119(28).

- Li et al. (2017) Li J, Dow WH, Kariv S (2017). “Social preferences of future physicians.” Proceedings of the National Academy of Sciences, 114(48), E10291–E10300.

- Li et al. (2023) Li W, Leng Z, Yi J, Zhong S (2023). “A multifaceted poverty reduction program has economic and behavioral consequences.” Proceedings of the National Academy of Sciences, 120(10), e2219078120.

- Lin et al. (2020) Lin Z, Xu P, Winata GI, Siddique FB, Liu Z, Shin J, Fung P (2020). “Caire: An end-to-end empathetic chatbot.” Proceedings of the AAAI Conference on Artificial Intelligence, 34(09), 13622–13623.

- Lopez-Lira and Tang (2023) Lopez-Lira A, Tang Y (2023). “Can ChatGPT forecast stock price movements? Return predictability and large language models.” arXiv preprint arXiv:2304.07619.

- Mahowald et al. (2023) Mahowald K, Ivanova AA, Blank IA, Kanwisher N, Tenenbaum JB, Fedorenko E (2023). “Dissociating language and thought in large language models: A cognitive perspective.” arXiv preprint arXiv:2301.06627.

- McCoy et al. (2019) McCoy T, Pavlick E, Linzen T (2019). “Right for the wrong Reasons: diagnosing syntactic heuristics in natural language inference.” In “Proceedings of the 57th Annual Meeting of the Association for Computational Linguistics,” pp. 3428–3448.

- McFadden (2001) McFadden D (2001). “Economic choices.” American Economic Review, 91(3), 351–378.

- McKenna et al. (2023) McKenna N, Li T, Cheng L, Hosseini MJ, Johnson M, Steedman M (2023). “Sources of Hallucination by Large Language Models on Inference Tasks.” arXiv preprint arXiv:2305.14552.

- Miao et al. (2021) Miao B, Yang S, Zhong S (2021). “Revealed heterogeneity in risk preference.” Working Paper.

- Mitchell and Krakauer (2023) Mitchell M, Krakauer DC (2023). “The debate over understanding in AI’s large language models.” Proceedings of the National Academy of Sciences, 120(13), e2215907120.

- Mullainathan and Obermeyer (2022) Mullainathan S, Obermeyer Z (2022). “Solving medicine’s data bottleneck: Nightingale open science.” Nature Medicine, 28(5), 897–899.

- Müller (2019) Müller D (2019). “The anatomy of distributional preferences with group identity.” Journal of Economic Behavior & Organization, 166, 785–807.

- Nishimura et al. (2017) Nishimura H, Ok EA, Quah JKH (2017). “A comprehensive approach to revealed preference theory.” American Economic Review, 107(4), 1239–63.

- Park et al. (2023) Park PS, Schoenegger P, Zhu C (2023). “Artificial intelligence in psychology research.” arXiv preprint arXiv:2302.07267.

- Polisson and Quah (2013) Polisson M, Quah JKH (2013). “Revealed preference in a discrete consumption space.” American Economic Journal: Microeconomics, 5(1), 28–34.

- Rahwan et al. (2019) Rahwan I, Cebrian M, Obradovich N, Bongard J, Bonnefon JF, Breazeal C, Crandall JW, Christakis NA, Couzin ID, Jackson MO, et al. (2019). “Machine behaviour.” Nature, 568(7753), 477–486.

- Rose (1958) Rose H (1958). “Consistency of preference: The two-commodity case.” The Review of Economic Studies, 25(2), 124–125.

- Samuelson (1938) Samuelson PA (1938). “A note on the pure theory of consumer’s behaviour.” Economica, 5(17), 61–71.

- Schramowski et al. (2022) Schramowski P, Turan C, Andersen N, Rothkopf CA, Kersting K (2022). “Large pre-trained language models contain human-like biases of what is right and wrong to do.” Nature Machine Intelligence, 4(3), 258–268.

- Sejnowski (2023) Sejnowski TJ (2023). “Large language models and the reverse turing test.” Neural Computation, 35(3), 309–342.

- Selten (1991) Selten R (1991). “Properties of a measure of predictive success.” Mathematical Social Sciences, 21(2), 153–167.

- Simon (1979) Simon HA (1979). “Rational decision making in business organizations.” The American Economic Review, 69(4), 493–513.

- Thaler (2016) Thaler RH (2016). “Behavioral economics: Past, present, and future.” American Economic Review, 106(7), 1577–1600.

- Varian (1982) Varian HR (1982). “The nonparametric approach to demand analysis.” Econometrica, 50(4), 945–973.

- Varian (1990) Varian HR (1990). “Goodness-of-fit in optimizing models.” Journal of Econometrics, 46(1-2), 125–140.

- Vaswani et al. (2017) Vaswani A, Shazeer N, Parmar N, Uszkoreit J, Jones L, Gomez AN, Kaiser Ł, Polosukhin I (2017). “Attention is all you need.” Advances in Neural Information Processing Systems, 30.

- Von Gaudecker et al. (2011) Von Gaudecker HM, Van Soest A, Wengström E (2011). “Heterogeneity in risky choice behavior in a broad population.” American Economic Review, 101(2), 664–694.

- Webb et al. (2023) Webb T, Holyoak KJ, Lu H (2023). “Emergent analogical reasoning in large language models.” Nature Human Behaviour, 7(9), 1526–1541.

- Wooldridge (2010) Wooldridge JM (2010). Econometric analysis of cross section and panel data. MIT press.

Online Appendices

Appendix A Method: GPT Experiment.

In the section, we display the method to prompt GPT to make decisions. In GPT-3.5-turbo, the input prompt must be an array of message objects, each with a role (“system”, “assistant”, or “user”) and content (the message’s content). First, we input the system’s message to set the behavior. Next, we input the assistant’s message to store information about tasks. We use the previous two messages to establish the background, and finally, we use the user’s message to ask understanding testing questions and to give decision tasks.555To confirm that GPT has truly understood our previous instructions, we first ask questions related to the task itself. Based on GPT’s responses, it appears that GPT has understood our instructions. In each preference domain and in each condition, with 25 simulations, we do not encounter any misunderstanding in the testing questions. In each preference domain, the system’s message is fixed, while the assistant’s and users’ messages change across the baseline, price framing, and discrete choice conditions.

A.1 Risk Preference

System’s Message.

I want you to act as a human decision maker. You will be given 25 rounds of decision-making tasks and will be responsible for making decisions. You should use your best judgment to come up with solutions that you like most. My first request is “You must provide your answers in every round.” If you do not provide an answer, I will assume that you make a random choice.666We assign the role of “human decision maker”. In particular, to prevent the possibility that the model returns answers such as “As an AI language model, I am not capable of making decisions on my own…”, we impose the request to provide an answer in every round. In practice, we do encounter cases in which the system refuses to provide an answer, and we simply do not include this outcome in the analyses.

A.1.1 Baseline Condition

Assistant’s Message.

In every round, the decision maker has 100 points that need to be invested between Asset A and Asset B. The decision maker has a 50% chance to get the return from Asset A or the other 50% chance to get the return from Asset B. First please only tell me the number of points for investing Asset A, then please only tell me the number of points for investing Asset B.

User’s Message: Understanding Testing Question 1.

What is the probability you will get a return from Asset A?

-

•

Example of GPT’s responses: “The probability of getting a return from asset A is 50%, and the probability of getting a return from asset B is also 50%.”

User’s Message: Understanding Testing Question 2.

Suppose that you invest 90 points to Asset A, and 10 points to Asset B. In this round, investing every 1 point for Asset A returns 0.8 dollars, and investing every 1 point for Asset B returns 0.2 dollars. What return will you get?

-

•

Example of GPT’s responses: “The total return from Asset A would be 900.8 = 72 dollars, while the total return from Asset B would be 100.2 = 2 dollars. Since there is a 50% chance of getting the return from Asset A, and a 50% chance of getting the return from Asset B, the expected return would be (0.572) + (0.52) = 37. Therefore, the expected return would be 37 dollars.”

User’s Message: Understanding Testing Question 3.

Suppose that you invest 90 points to Asset A, and 10 points to Asset B. In this round, investing every 1 point for Asset A returns 0.8 dollars, and investing every 1 point for Asset B returns 0.2 dollars. Is there a chance to get 72 dollars?

-

•

Example of GPT’s responses: “Yes, there is a chance to get 72 dollars. Investing 90 points in Asset A would give a return of 72 dollars since investing every 1 point in Asset A returns 0.8 dollars. Investing 10 points in Asset B would give a return of 2 dollars since investing every 1 point in Asset B returns 0.2 dollars. So, there is a 50% chance that the return will come from Asset A and a 50% chance that it will come from Asset B. So, there is a chance that the decision maker will get a return of 72 dollars.”

User’s Message: Decision Task.

In this round, investing every 1 point for Asset A returns M dollars, and investing every 1 point for Asset B returns N dollars. What is your allocation?777We repeat the text of the decision task 25 times, where the parameters used in the text differ across rounds, that is . We keep two decimals. To maximize the replicability of our findings and minimize variance in the model’s responses, we send the 25 rounds of questions to the model continuously, without interruption. This method is applicable for the remaining three preference domains under the baseline condition.

A.1.2 Price Framing Condition

Assistant’s Message.

In every round, the decision maker has 100 points that need to be invested between Asset A and Asset B. The decision maker has a 50% chance to get the return from Asset A or the other 50% chance to get the return from Asset B. First please only tell me the number of points for investing Asset A, then please only tell me the number of points for investing Asset B.

User’s Message: Understanding Testing Question 1.

What is the probability you will get a return from Asset A?

-

•

Example of GPT’s responses: “The probability of getting a return from asset A is 50%”

User’s Message: Understanding Testing Question 2.

Suppose that you invest 90 points to Asset A, and 10 points to Asset B. In this round, investing every 1.25 points for Asset A returns 1 dollar, and investing every 5 points for Asset B returns 1 dollar. What return will you get?

-

•

Example of GPT’s responses: “To determine the return, we need to calculate the total return for Asset A and Asset B separately. For Asset A, if investing 1.25 points returns 1 dollar, then investing 90 points would result in a return of 90/1.25=72 dollars. For Asset B, if investing 5 points returns 1 dollar, then investing 10 points would result in a return of 10/5=2 dollars. Therefore, the decision maker will receive a return from either Asset A or Asset B with 50% probability each. The return would be 72 dollars for Asset A or 2 dollars for Asset B.”

User’s Message: Understanding Testing Question 3.

Suppose that you invest 90 points to Asset A, and 10 points to Asset B. In this round, investing every 1.25 points for Asset A returns 1 dollar, and investing every 5 points for Asset B returns 1 dollar. Is there a chance to get 72 dollars?

-

•

Example of GPT’s responses: “In this round, since you have invested 90 points in Asset A and 10 points in Asset B, your total investment is 100 points. For Asset A, every 1.25 points invested returns 1 dollar. So, with 90 points invested, you will get a return of 90/1.25=72 dollars from Asset A. For Asset B, every 5 points invested returns 1 dollar. With 10 points invested, you will get a return of 10/5=2 dollars from Asset B. Since you have a 50% chance of getting the return from either Asset A or Asset B, I will receive $72 from Asset A with 50% probability.”

User’s Message: Decision Task.

In this round, investing every 1/M points for Asset A returns 1 dollar, and investing every 1/N points for Asset B returns 1 dollar. What is your allocation? 888We repeat the text of the decision task 25 times, where the parameters used in the text differ across rounds, that is . We display the numbers 1/M and 1/N directly, and we keep two decimals. To maximize the replicability of our findings and minimize variance in the model’s responses, we send the 25 rounds of questions to the model continuously, without interruption. This method is applicable for the remaining three preference domains under the price framing condition.

A.1.3 Discrete Choice Condition

Assistant’s Message.

In every round, the decision maker will be presented with 11 options, each represented in the form ($M, $N). The decision maker has a 50% chance to get M from Asset A or the other 50% chance to get N from Asset B. Please only tell me about your best option in every round.

User’s Message: Understanding Testing Question 1.

What is the probability you will get a return from Asset A?

-

•

Example of GPT’s responses: “The probability of getting a return from Asset A is 50% in every round.”

User’s Message: Understanding Testing Question 2.

If you choose the option ($72, $2), what return will you get?

-

•

Example of GPT’s responses: “If I choose the option ($72, $2), there is a 50% chance of getting $72 from Asset A and a 50% chance of getting $2 from Asset B. Therefore, the expected return would be the average of the two options, which is ($72 + $2) / 2 = $37.”

User’s Message: Understanding Testing Question 3.

If you choose the option ($72, $2), is there a chance to get 72 dollars?

-

•

Example of GPT’s responses: “Yes, if the option ($72, $2) is chosen, there is a 50% chance of receiving $72 from Asset A.”

User’s Message: Decision Task.

In this round, there are 11 options, which are ($M1,$N1), ($M2,$N2), ($M3,$N3), ($M4,$N4), ($M5,$N5), ($M6,$N6), ($M7,$N7), ($M8,$N8), ($M9,$N9), ($M10,$N10), ($M11,$N11). Which is the best? 999We repeat the text of the decision task 25 times, where the parameters used in the text differ across rounds, that is . We keep two decimals. The numbers are determined by and , for . To maximize the replicability of our findings and minimize variance in the model’s responses, we send the 25 rounds of questions to the model continuously, without interruption. This method is applicable for the remaining three preference domains under the discrete choice condition.

A.2 Time Preference

System’s Message.

I want you to act as a human decision maker. You will be given 25 rounds of decision-making tasks and will be responsible for making decisions. You should use your best judgment to come up with solutions that you like most. My first request is “You must provide your answers in every round.” If you do not provide an answer, I will assume that you make a random choice.

A.2.1 Baseline Condition

Assistant’s Message.

In every round, the decision maker has 100 points that need to be invested between today and one month later. The decision maker will get dollars today from the points invested today and will get check that can be cashed in one month later from the points invested one month later. Please first only tell me the number of points for investing today, then please only tell me the number of points for investing one month later.

User’s Message: Understanding Testing Question 1.

Suppose that you invest 90 points to today, and 10 points to one month later. In this round, investing every 1 point for today returns 0.8 dollars cash today, and investing every 1 point for one month later returns 0.2 dollars check which can be cashed one month later. What return will you get?

-

•

Example of GPT’s responses: “If I invest 90 points today and 10 points one month later, I will get an immediate return of 0.8 dollars for every point invested today, which will be 72 dollars in total (90 0.8 dollars). For the investment of 10 points one month later, I’ll get 0.2 dollars in return for each point invested one month later, that will be a total of 2 dollars (10 0.2 dollars). So, the total return I’ll get if I invest 90 points today and 10 points one month later will be 74 dollars (72 dollars from today’s investment, and 2 dollars from one month later investment).”

User’s Message: Understanding Testing Question 2.

Suppose that you invest 90 points to today, and 10 points to one month later. In this round, investing every 1 point for today returns 0.8 dollars cash today, and investing every 1 point for one month later returns 0.2 dollars check which can be cashed one month later. When can you get just the 2 dollars cash?

-

•

Example of GPT’s responses: “If investing 1 point for today return 0.8 dollars, then investing 90 points for today will return 72 dollars immediately. If investing 1 point for one month later return 0.2 dollars, then investing 10 points for one month later will return 2 dollars check that can be cashed one month later. So, I have a total of 74 dollars (72 dollars from today and 2 dollars after one month). To get just the 2 dollars cash, I will have to wait for one month and then cash the check.”

User’s Message: Understanding Testing Question 3.

In this round, investing every 1 point for today returns 0.8 dollars cash today, and investing every 1 point for one month later returns 0.2 dollars check which can be cashed one month later. What is your allocation? Why?

-

•

Example of GPT’s responses: “I would allocate 75 points for the today return and 25 points for the one-month later return. This allocation would give me an immediate return of 60 dollars (75 points 0.8 dollars/point) and a future return of 5 dollars (25 points 0.2 dollars/point) one month later. I believe this allocation is a good balance between immediate and future returns. Although the return for investing in the one-month later option is lower, it’s still a guaranteed future return. On the other hand, the higher return for the today option is immediate and allows for more flexibility in case of unexpected expenses or emergencies.”

User’s Message: Decision Task.

In this round, investing every 1 point for today returns M dollars today, and investing every 1 point for one month later returns N dollars check which can be cashed in one month later. What is your allocation?

A.2.2 Price Framing Condition

Assistant’s Message.

In every round, the decision maker has 100 points that need to be invested between today and one month later. The decision maker will get dollars today from the points invested today and will get check that can be cashed in one month later from the points invested one month later. Please first only tell me the number of points for investing today, then please only tell me the number of points for investing one month later.

User’s Message: Understanding Testing Question 1.

Suppose that you invest 90 points to today, and 10 points to one month later. In this round, investing every 1.25 points for today returns 1 dollar cash today, and investing every 5 points for one month later returns 1 dollar check which can be cashed one month later. What return will you get?

-

•

Example of GPT’s responses: “Suppose that you invest 90 points to today, and 10 points to one month later. In this round, investing every 1.25 points for today returns 1 dollar cash today, and investing every 5 points for one month later returns 1 dollar check which can be cashed one month later. Based on the given information, if you invest 90 points today, each point will yield 1/1.25 = 0.8 dollars cash today. Therefore, 90 points will yield 0.8 * 90 = 72 dollars cash today. If you invest 10 points one month later, each point will yield 1/5 = 0.2 dollars check. Therefore, 10 points will yield 0.2 * 10 = 2 dollars check that can be cashed one month later. So, in total, the investment will yield 72 dollars cash today and 2 dollars check one month later.”

User’s Message: Understanding Testing Question 2.

Suppose that you invest 90 points to today, and 10 points to one month later. In this round, investing every 1.25 points for today returns 1 dollar cash today, and investing every 5 points for one month later returns 1 dollar check which can be cashed one month later. When can you get just the 2 dollars cash?

-

•

Example of GPT’s responses: “For the 90 points invested today, 1.25 points give 1 dollar cash today. So, 90 points divided by 1.25 equals 72. Hence, I will receive 72 dollars cash today from the investment made today. For the 10 points invested one month later, 5 points give 1 dollar check that can be cashed one month later. So, 10 points divided by 5 equals 2. Therefore, I will receive 2 dollars check one month later from the investment made one month later. To answer your question, I will get the 2 dollars one month later.”

User’s Message: Understanding Testing Question 3.

In this round, investing every 1.25 points for today returns 1 dollar cash today, and investing every 5 points for one month later returns 1 dollar check which can be cashed one month later. What is your allocation? Why?

-

•

Example of GPT’s responses: “In this round, I will allocate 40 points for investing today and 60 points for investing one month later. For investing today, it takes 1.25 points to get 1 dollar cash. Therefore, by investing 40 points today, I would receive 40 / 1.25 = 32 dollars in cash. For investing one month later, it takes 5 points to get 1 dollar check. By investing 60 points one month later, I would receive 60 / 5 = 12 dollars in a check that can be cashed in one month. By allocating more points for investing one month later, I am betting on the potential to earn more returns in the future. However, I am also ensuring some immediate cash by allocating a portion of the points for investing today. This allocation strategy aims to balance the need for immediate liquidity with the opportunity for future gains.”

User’s Message: Decision Task.

In this round, investing every 1/M points for today returns 1 dollar today, and investing every 1/N points for one month later returns 1 dollar check which can be cashed in one month later. What is your allocation?

A.2.3 Discrete Choice Condition

Assistant’s Message.

In every round, the decision maker will be presented with 11 options, each represented in the form ($M, $N). The decision maker will get M dollars today and will get a N dollars check that can be cashed in one month later. Please only tell me about your best option in every round.

User’s Message: Understanding Testing Question 1.

If you choose the option ($72, $2), what return will you get?

-

•

Example of GPT’s responses: “If I choose the option ($72, $2), I will receive $72 immediately and an additional $2 after one month.”

User’s Message: Understanding Testing Question 2.

If you choose the option ($72, $2), when can you get just the 2 dollars cash?

-

•

Example of GPT’s responses: “If I choose the option ($72, $2), I can get just the 2 dollars cash in one month.”

User’s Message: Understanding Testing Question 3.

If you face the options ($40, $10) and ($72, $2), which option will you select? Why?

-

•

Example of GPT’s responses: “I would prefer the option ($40, $10) in this case. While the immediate reward is lower compared to ($72, $2), the $10 received after a month adds value to the overall outcome. The additional $10 compensates for the initial lower amount and makes the total reward more attractive in the long run.”

User’s Message: Decision Task.

In this round, there are 11 options, which are ($M1,$N1), ($M2,$N2), ($M3,$N3), ($M4,$N4), ($M5,$N5), ($M6,$N6), ($M7,$N7), ($M8,$N8), ($M9,$N9), ($M10,$N10), ($M11,$N11). Which is the best?

A.3 Social Preference

System’s Message.

I want you to act as a human decision maker. You will be given 25 rounds of decision-making tasks and will be responsible for making decisions. You should use your best judgment to come up with solutions that you like most. My first request is “You must provide your answers in every round.” If you do not provide an answer, I will assume that you make a random choice.”

A.3.1 Baseline Condition

Assistant’s Message.

In every round, the decision maker is randomly matched with a new anonymous subject and there is no feedback across rounds. The decision maker has 100 points that need to be allocated between him/herself and the other one. The decision maker will get return from the points allocated to him/herself and the other one will get return from the points allocated to him/her. First please only tell me the number of points you want to allocate to yourself, then please only tell me the number of points you want to allocate to the other.

User’s Message: Understanding Testing Question 1.

Suppose that you allocate 90 points to yourself, and 10 points to the other. In this round, allocating every 1 point to yourself returns 0.8 dollars for yourself, and allocating every 1 point to the other returns 0.2 dollars for the other. What return will you get?

-

•