Identification and Estimation of Production Function with Unobserved Heterogeneity††thanks: The first and second authors acknowledge financial support from the Social Sciences and Humanities Research Council while the third author acknowledges financial support from JSPS Grant-in-Aid for Young Scientists (B) No.16K21004 and Grant-in-Aid for Scientific Research (C) No.19K01584. All remaining errors are our own. This paper represents the views of the authors and not necessarily those of the Cabinet Office, the Government of Japan or the institutions they represent.

Abstract

This paper examines the nonparametric identifiability of production functions, considering firm heterogeneity beyond Hicks-neutral technology terms. We propose a finite mixture model to account for unobserved heterogeneity in production technology and productivity growth processes. Our analysis demonstrates that the production function for each latent type can be nonparametrically identified using four periods of panel data, relying on assumptions similar to those employed in existing literature on production function and panel data identification. By analyzing Japanese plant-level panel data, we uncover significant disparities in estimated input elasticities and productivity growth processes among latent types within narrowly defined industries. We further show that neglecting unobserved heterogeneity in input elasticities may lead to substantial and systematic bias in the estimation of productivity growth.

1 Introduction

Estimating a firm’s production function and productivity is a critical topic in empirical economics.111Understanding how the input is related to the output is a fundamental issue in empirical industrial organization (see, for example, Ackerberg et al.,, 2007) while a measure of total factor productivity is necessary to examine the effect of trade policy on productivity and to analyze the role of resource allocation on aggregate productivity (e.g., Pavcnik,, 2002; Kasahara and Rodrigue,, 2008; Kasahara and Lapham,, 2013; Hsieh and Klenow,, 2009). Production function estimation is also important for markup estimation (Hall,, 1988; De Loecker and Warzynski,, 2012; Raval,, 2023). Despite its importance, the standard production function estimation procedures impose an implausible assumption that production functions are common across firms except for separable Hicks-neutral productivity terms (Olley and Pakes,, 1996; Levinsohn and Petrin,, 2003; Wooldridge,, 2009; Ackerberg et al.,, 2015; Gandhi et al.,, 2020). In the presence of identification issues due to the simultaneity problem (Marschak and Andrews,, 1944), the literature on identifying production functions that incorporate unobserved heterogeneity beyond the Hicks-neutral productivity term is scarce but a rapidly growing research area (Li and Sasaki,, 2017; Doraszelski and Jaumandreu,, 2018; Balat et al.,, 2019; Zhang,, 2019; Demirer,, 2020; Chen et al.,, 2021; Raval,, 2023).

This paper establishes the nonparametric identification of production functions from panel data when production functions and productivity growth processes are heterogeneous across firms in unobserved time-varying ways. We consider a finite mixture specification in which there are distinct time-varying production technologies, and each firm belongs to one of the latent types. Econometricians do not observe the latent type of firms. Without making any functional form assumption on production technology and productivity growth processes, we establish nonparametric identification of distinct production functions, productivity processes, and a population proportion of each type under assumptions similar to those used in the existing production function and panel data identification literature. We also address potential measurement errors in labor inputs because of unobserved working hours and labor quality.

Building on our nonparametric identification result and considering computational ease, we propose an estimation procedure for the production function with random coefficients. Under the assumption of Gaussian error terms, we develop a penalized maximum likelihood estimator for a finite mixture model of random coefficient production functions, where the form of the likelihood function is motivated by our identification argument. The EM algorithm is employed to simplify the computational complexity of maximizing the log-likelihood function of the mixture model.

As an empirical application, we investigate the extent of production technology heterogeneity across plants using panel data from Japanese manufacturing plants between 1986 and 2010. We show that the ratios of intermediate cost to sales and intermediate cost to variable cost—averaging from 1986 to 2010 at the plant level—are substantially different across plants within narrowly defined industries. For example, the 90th-10th percentile differences in the intermediate cost shares in variable costs for concrete products and electric audio equipment are large, at 0.27 and 0.67, respectively.222Zhang, (2019) finds considerable heterogeneity in the labor share in sales across firms in the Chinese steel industry. Differences in input levels cannot explain these heterogeneities; that is, a considerable cross-plant variation in the ratio of intermediate cost to sales or variable costs remains after controlling for observable inputs, presenting evidence for persistent and substantial heterogeneity in production technologies across plants.

By employing a finite mixture of random coefficients production functions, we also find substantial differences in estimated input elasticities across latent types within narrowly defined industries. To understand the consequences of neglecting unobserved heterogeneity in input elasticities on productivity growth measurement, we adopt a specification with unobserved heterogeneity as the true model and calculate the bias in productivity growth measurement when using a misspecified production function model that omits unobserved heterogeneity. Our findings indicate that ignoring unobserved heterogeneity in input elasticities can result in substantial and systematic bias in estimated productivity growth, contingent on the heterogeneous parameter estimates and the direction of productivity changes. Additionally, our analysis reveals a significantly stronger correlation between estimated productivity and investment among high capital-intensive latent type firms compared to low capital-intensive type firms, implying that unobserved disparities in input elasticities are vital in plant-level investment decisions.

As first discussed by Marschak and Andrews, (1944), ordinary least squares estimation of production functions is subject to simultaneity bias when firms make input decisions based on their productivity level (Griliches and Mairesse,, 1998). To address the simultaneity issue, Olley and Pakes, (1996) and Levinsohn and Petrin, (2003) develop control function approaches, which have been widely applied in empirical studies (see also Wooldridge,, 2009; Ackerberg et al.,, 2015). Despite their popularity, the control function approach has faced potential identification issues as highlighted in the literature. Bond and Sderbom, (2005) and Ackerberg et al., (2015) discuss identification issues due to collinearity under two flexible inputs (i.e., material and labor) in Cobb-Douglas specification. Furthermore, Gandhi et al., (2020, hereafter GNR) contend that if the firm’s decision follows a Markovian strategy, the moment restriction utilized in the control function approach fails to provide sufficient restriction to identify flexible input elasticities due to a lack of instrumental power.

GNR exploit the first-order condition for flexible input under profit maximization and establish the identification of production functions without making any functional form assumptions. However, their result presumes that production technology is identical across plants, except for the Hicks-neutral productivity term. This paper extends the nonparametric identification approach of GNR to accommodate settings where production technologies exhibit unobserved heterogeneity across plants.

Several papers employ the first-order condition as a restriction to identify heterogenous elasticities of flexible inputs under functional form assumptions (Van Biesebroeck,, 2003; Li and Sasaki,, 2017; Doraszelski and Jaumandreu,, 2018; Balat et al.,, 2019; Zhang,, 2019).333As Solow, (1957) first illustrates, the flexible input elasticities are identified with their input revenue share under the Cobb-Douglas production functions. Doraszelski and Jaumandreu, (2018) develop a framework to identify plant-level time-varying labor-augmenting productivity in addition to Hicks-neutral productivity under the constant elasticity of substitution (CES) production function, allowing for two-dimensional heterogeneity. Zhang, (2019) proposes an estimation method based on the CES production function that accounts for heterogeneity in capital, labor, and material-augmenting efficiency across firms. Li and Sasaki, (2017) use the flexible input cost ratio to construct a control variable for latent technology to identify flexible inputs’ elasticities while imposing the timing assumption suggested by Ackerberg et al., (2015) to identify the labor and capital coefficients under the Cobb-Douglas specification. Balat et al., (2019) also consider the Cobb-Douglas production function with heterogeneity in the efficiency of using skilled and unskilled labor. Demirer, (2020) extends the framework of Doraszelski and Jaumandreu, (2018) by relaxing the parametric assumption of the CES production function but assumes that the labor-augmenting technology is the only additional source of individual-level heterogeneity other than the Hicks neutral productivity. Raval, (2023) demonstrates the importance of accommodating non-neutral productivity differences across firms when estimating markups using flexible inputs. Dewitte et al., (2022) illustrate the significance of accounting for unobserved heterogeneity in productivity growth processes when analyzing export premia and the contributions of exporting firms to aggregate productivity.

These papers identify firm-specific input elasticities, factor-augmenting technologies, or productivity growth processes but impose parametric assumptions or limit the sources of heterogeneity. Our paper complements these studies by establishing nonparametric identification of heterogenous production functions and productivity growth processes without imposing any functional form assumptions or limiting sources of unobserved heterogeneity.

Cheng et al., (2021) extend the k-means clustering approach of Bonhomme and Manresa, (2015) to multi-dimensional clustering in random coefficient production functions in a nonlinear GMM framework, building upon the dynamic panel approach (Arellano and Bond,, 1991; Blundell and Bond,, 1998, 2000). Cheng et al., (2021) consider an asymptotic setting when the time dimension while our identification is based on being fixed. Our identification result with fixed is useful in empirical applications where firm-level panel datasets have limited time dimensions.

Our paper also contributes to the literature on identifying dynamic panel data models with unobserved heterogeneity by relaxing the existing identification conditions. Specifically, Proposition 3 demonstrates that the mixing probabilities and the type-specific time-varying probability distributions across latent types can be identified from panel data with four periods under the Markov assumption and other regularity conditions. This result improves upon the findings of Kasahara and Shimotsu, (2009), who established the identification of dynamic panel data models under the Markov assumption but imposed the stationarity and required panel data with six periods.444Higgins and Jochmans, (2021) point out that the type-specific distribution is identified only up to an arbitrary ordering of the latent types that differs across different points in Kasahara and Shimotsu, (2009). Our argument for identifying a common order of the latent types is based on that of Higgins and Jochmans, (2021). Hu and Shum, (2012) consider a non-stationary case and establish the identification of a continuous mixture dynamic panel data model using a panel dataset with five time periods. However, their result is limited, as they only establish the identification of type-specific distributions for the third to fifth periods, leaving the identification for the first two periods unresolved. In contrast, we identify the type-specific distributions across all four periods from panel data of length four.

A key condition for our identification analysis is that the observed variable must follow a first-order Markov process within the subpopulation specified by latent type. Proposition 2 demonstrates that this Markov assumption is satisfied under our structural model assumptions, including the Markovian investment strategy (Assumption 3(b)) and the monotonicity of flexible input demands for productivity and wage shocks (Assumption 4(b)), both of which are standard assumptions in the production function literature (e.g., Olley and Pakes,, 1996; Levinsohn and Petrin,, 2003). Another identifying condition is a rank condition in Assumption 7 which requires that the changes in the value of the observed vector, , must induce sufficiently different changes in the value of the type specific conditional density function of given the past value across latent types. As illustrated in the Cobb-Douglas example in Appendix B.1, this condition is satisfied when input elasticities are sufficiently different across latent types.

The remainder of this paper is organized as follows. Section 2 presents evidence of heterogeneity in production technologies across plants, using panel data from Japanese manufacturing plants. Section 3 introduces the setup for our production function models and discusses the assumptions. Section 4 provides the main identification results, while Section 5 develops an estimator for the production function using a finite mixture model. In Section 6, we present empirical results based on the Japanese manufacturing plants. Section 7 concludes the paper.

2 Evidence for production technology heterogeneity

In order to underscore the significance of accounting for unobserved heterogeneity in production functions, we first present a set of stylized facts that clearly indicate the presence of heterogeneity beyond Hicks-neutral technology components in production functions. Our analysis employs panel data derived from Japanese manufacturing facilities, spanning the years 1986 to 2010. A comprehensive discussion of the dataset can be found in Section 6.1.

For illustration, consider a plant with the Cobb-Douglas production technology:

where , , , and denote the output, intermediate input, labor, and capital of plant in year , respectively, while represents the total factor productivity (TFP) that follows a first-order Markov process. The superscript in , , and signifies the variation in output elasticities of inputs across different plants.

We assume that firms consider their output and input prices as given, and that the intermediate input and labor are flexibly selected after has been fully observed. Consequently, a plant’s profit maximization implies the following relationships:

| (1) |

where , , and represent the prices of output, intermediate input, and labor, respectively.

In most existing empirical studies, production functions are estimated under the assumption that the coefficients , , and do not vary across plants. This assumption can be tested in light of (1) by examining whether the intermediate input share, , and the ratio of intermediate cost to variable cost (i.e., the sum of intermediate and labor costs), , remain constant across plants. To investigate this, we calculate the plant-level averages over the maximum 25-year period, during which a plant remained in the market between 1986 and 2010, as follows:

Subsequently, we analyze the extent of variation across plants within a narrowly defined industry.

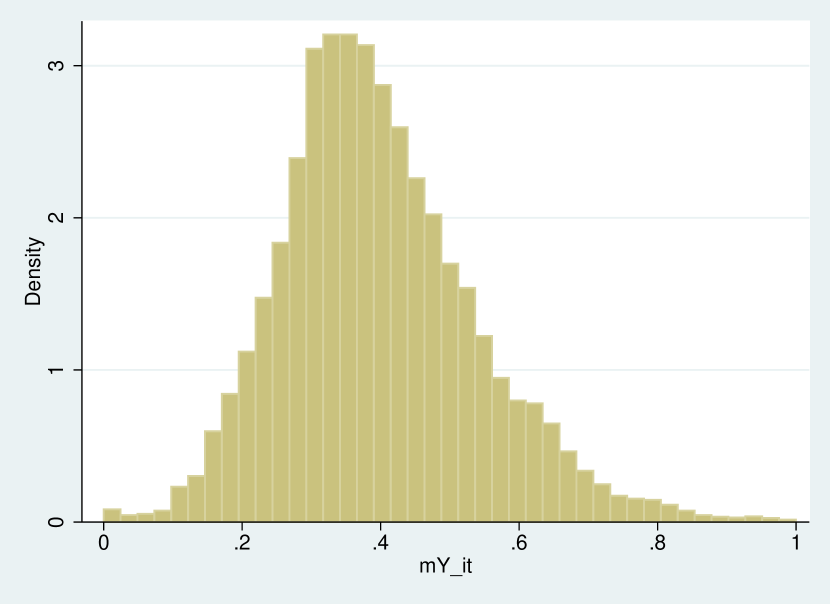

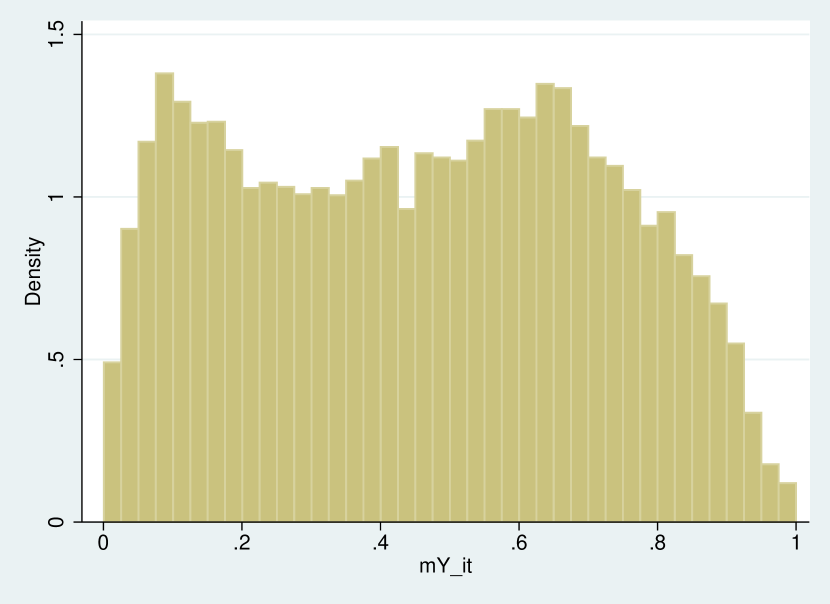

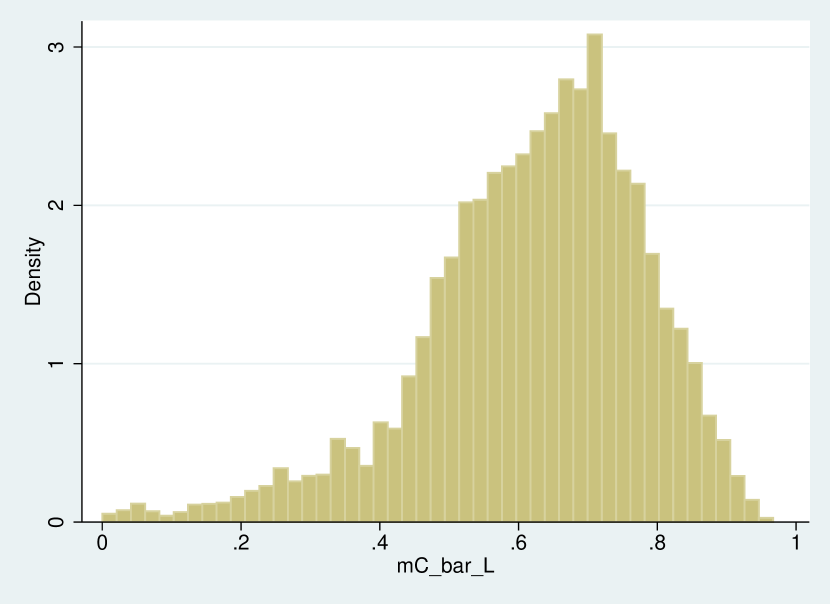

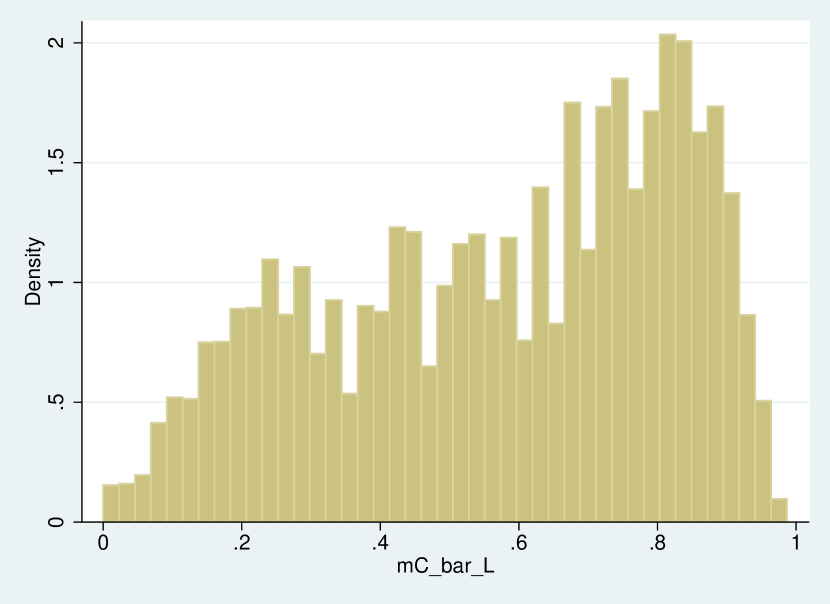

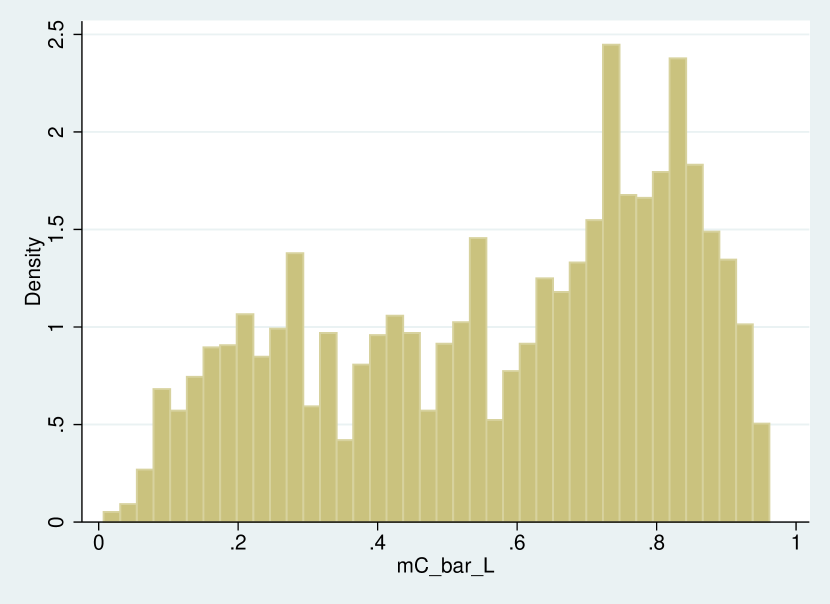

Figure 1 and Figure 1 display histograms illustrating plant-level averages of intermediate input shares, , for all plants within the concrete products and electric audio equipment industries, respectively. Both figures exhibit substantial variation in intermediate shares. The disparity between the 90th and 10th percentiles reaches up to 0.28 for concrete products, an industry typically regarded as having homogeneous technology.

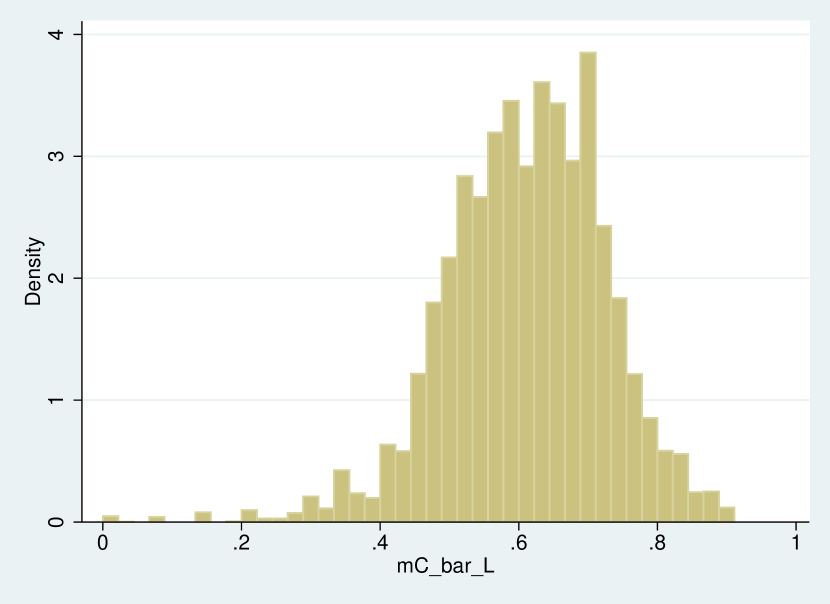

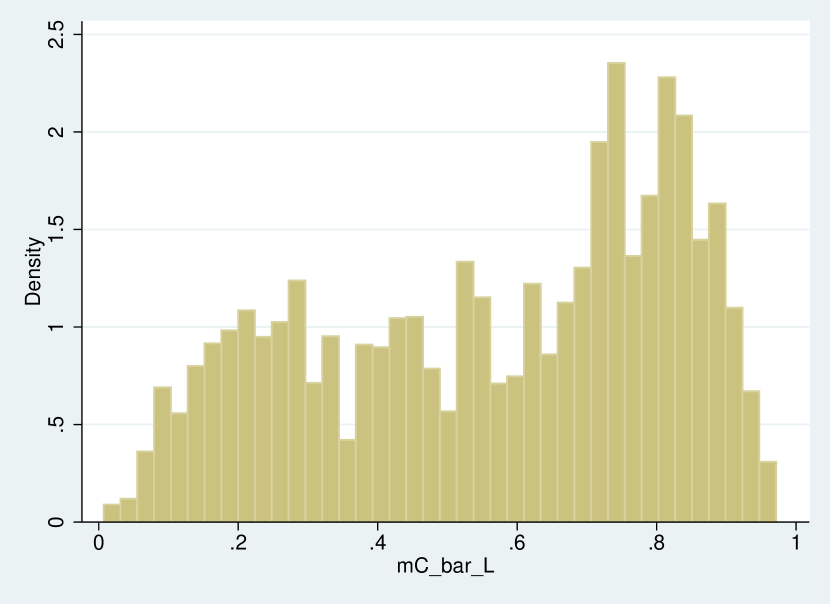

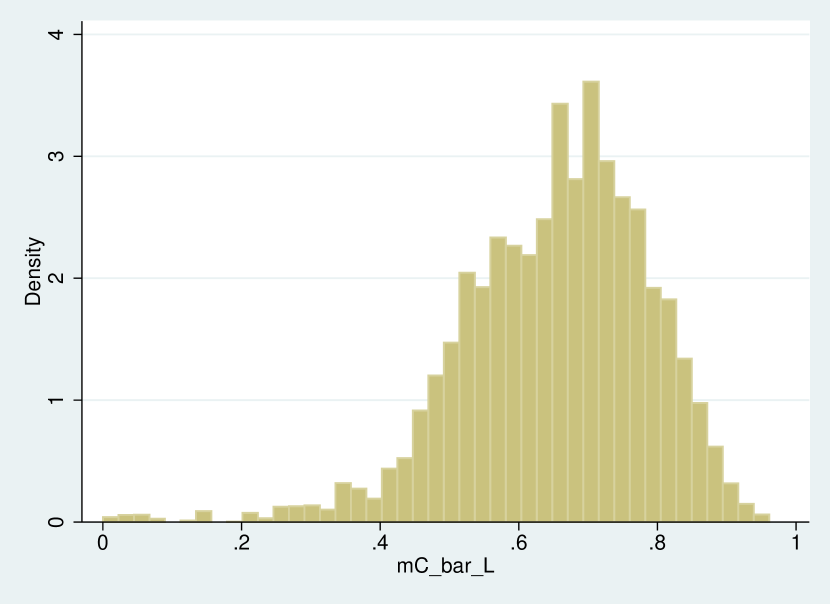

The variation in intermediate shares between plants might be indicative of differences in markups; however, the ratio of intermediate costs to total variable costs is less susceptible to markup discrepancies. Figures 2 and 2 depict histograms of plant-level averages of the ratio of intermediate costs to total variable costs, , for the concrete products and electric audio equipment industries, respectively. The significant variation in intermediate cost shares implies that heterogeneous markups are not the primary explanation for the observed variation in intermediate input shares presented in Figures 1 and 1.

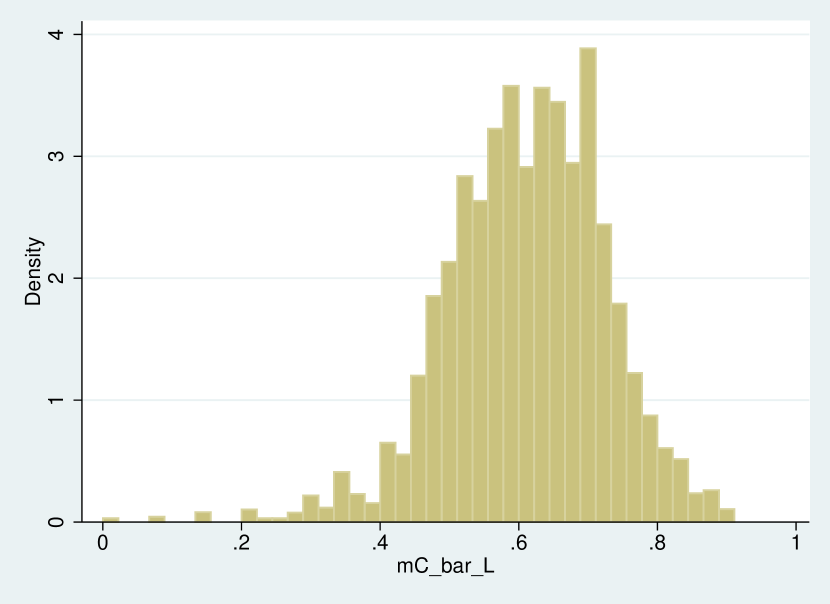

By comparing the degree of dispersion in input shares within the 2-digit industry classification with that within the 3-digit or 4-digit industry classification, we can examine the extent to which classifying industries at a more refined level helps control for heterogeneity in production technology.

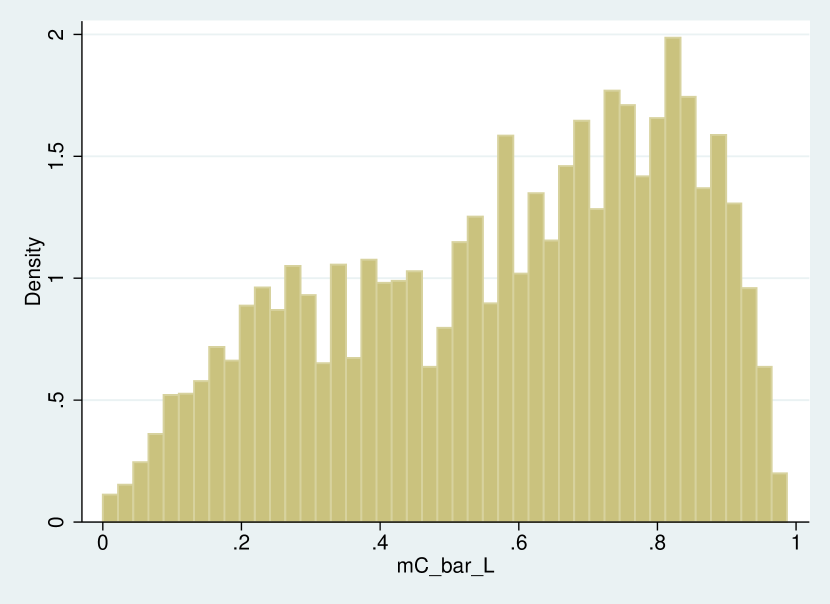

Figures 3, 3, and 3 contrast histograms of plant-level averages of intermediate input shares for ceramics and clay (2-digit), cement products (3-digit), and concrete products (4-digit) industries. These figures suggest that while dispersion decreases somewhat from the 2-digit to the 4-digit level, the degree of heterogeneity remains notably high even at the 4-digit industry classification. Likewise, Figures 4, 4, and 4 reveal that the dispersion of material shares does not decline considerably when transitioning from electric parts, devices, and circuits (2-digit) to electric devices (3-digit) and subsequently to electric audio equipment (4-digit).

As illustrated in Table 1, the 90th-10th percentile difference in intermediate input shares decreases from 0.38 (2-digit) to 0.28 (4-digit) for the ceramics and clay industry. In contrast, the 90th-10th percentile difference for the electric parts industry changes only marginally from 2-digit to 4-digit, ranging from 0.61 to 0.62. Similar patterns are observed for the plant-level averages of intermediate cost shares in variable costs. The 90th-10th percentile differences in intermediate cost shares for concrete products (4-digit) and electric audio equipment (4-digit) are substantial, measuring 0.27 and 0.67, respectively. Therefore, classifying industries at a more refined level does not substantially reduce the heterogeneity in output elasticities with respect to intermediate and labor inputs.

| No. of | 90-10 diff | 90-10 diff in | |

| Industry Code : Name | Obs. | in | |

| 22: Ceramics and Clay | 53,042 | 0.38 | 0.38 |

| 222: Cement Product | 22,834 | 0.35 | 0.32 |

| 2223: Concrete Product | 14,463 | 0.28 | 0.27 |

| 28: Electric Parts/Devise/Circuit | 30,814 | 0.61 | 0.66 |

| 281: Electric Device | 19,901 | 0.62 | 0.66 |

| 2814: Electric Audio Equipment | 11,325 | 0.62 | 0.67 |

| Industry | No. of | Ave. 90-10 diff | Ave. 90-10 diff | Ave. No. |

|---|---|---|---|---|

| Classifications | Industries | in | in | of Obs. |

| 2-digit | 24 | 0.46 | 0.44 | 49,512 |

| (0.08) | (0.11) | |||

| 3-digit | 149 | 0.42 | 0.39 | 7,975 |

| (0.10) | (0.13) | |||

| 4-digit | 479 | 0.38 | 0.35 | 2,481 |

| (0.11) | (0.14) |

Notes: Standard deviations across industries are shown in parentheses.

| Industry | No. of | Ave. 90-10 diff | Ave. 90-10 diff | Ave. No. |

|---|---|---|---|---|

| Classifications | Industries | in for | in for | of Obs. |

| 2-digit | 24 | 0.30 | 0.16 | 49,512 |

| (0.05) | (0.02) | |||

| 3-digit | 149 | 0.28 | 0.14 | 7,975 |

| (0.05) | (0.03) | |||

| 4-digit | 479 | 0.26 | 0.13 | 2,481 |

| (0.06) | (0.04) |

Notes: Standard deviations across industries are shown in parentheses.

Analogous patterns are observed across various industries. Table 2 displays the average differences between the 90th and 10th percentiles for all industries, classified at the 2-digit, 3-digit, and 4-digit levels, with their corresponding standard deviations presented in parentheses. The findings reveal that dispersion decreases only marginally when refining industry classification from the 2-digit to the 4-digit levels. In general, substantial dispersion persists even at the 4-digit classification level, indicating that output elasticities of variable inputs exhibit variation across plants, even when adopting a more detailed industry classification.

The implications in (1) are valid exclusively under the Cobb-Douglas production function. For a more generalized production function, the elasticities of output for inputs are dependent on the levels of material, labor, and capital inputs, even without heterogeneity in production technology. Consequently, we investigate whether the intermediate input cost-to-output value ratio remains similar across firms, even after adjusting for variations in capital, labor, and intermediate inputs. To achieve this, we regress or on second-order polynomials of the natural logarithm of materials, the number of workers, and capital, resulting in residuals denoted by . Subsequently, we compute the plant-level average to assess production technology heterogeneity, conditional on inputs.

Table 3 presents the averages of the 90th-10th percentile differences in for or across all industries, classified at the 2-digit, 3-digit, and 4-digit levels. The findings reveal considerable variation in production technology after accounting for observable inputs, even at the 4-digit industry classification. This provides further evidence supporting the existence of heterogeneity in production technology.

3 The Model

We consolidate the notation as follows. Let stand for ”equal by definition”. Bold letters denote vectors or matrices. For a continuous random variable , a calligraphic letter denotes its support, while its probability density function is represented by for .

Output, capital, intermediate inputs, labor input in effective units of labor, and total wage bills are denoted by , respectively, where , , , , and are the supports of the corresponding variables. We assume that are continuously distributed with strictly positive density on connected supports. We combine capital, intermediate, and labor inputs into a vector as .

We allow firms’ production technologies to differ beyond Hick’s neutral productivity shocks. Specifically, we use a finite mixture specification to capture the unobserved heterogeneity in firms’ production technologies as well as the process through which Hick’s neutral productivity shocks evolve. We assume that there are unobserved types. Define the latent random variable representing the type of firm such that if the production technology of firm is of the -th type. In the following, the superscript indicates that the functions are specific to technology type , while the subscript indicates that the functions are specific to period .

For the -th type of production technology at time , the output is related to inputs as follows:

| (2) |

where is an idiosyncratic productivity shock with its density function , and follows an exogenous first-order stationary Markov process given by:

| (3) |

where is an innovation to the productivity process. As indicated by the subscript in , , , and , production functions and productivity processes differ not only between latent types but also across periods. For example, this reflects type-specific aggregate shocks or type-specific biased technological changes.

We assume that labor input in effective units of labor, , is not directly observable because firms differ in their labor quality and working hours, while we only observe the number of workers. Instead, is related to the number of workers, denoted by , as

| (4) |

Equation (4) imposes a specific structure on how labor input in effective units of labor is related to the observed number of workers, where represents latent worker quality and working hours specific to type . With this specification, measurement errors in observed labor input (i.e., the number of workers) are captured by the latent type-specific value of .

The total wage bills, , are related to the labor input in effective units as follows:

| (5) |

where represents the market wage. The random variable is a transitory wage shock known to firm at the time of choosing intermediate and labor inputs, while is an idiosyncratic wage shock not included in the information set when firm selects these two inputs. Thus, , but .

We assume that firms make flexible choices regarding both and after observing their serially correlated productivity shock, , but before observing . In contrast, is predetermined at the end of the previous period, prior to the observation of the serially correlated productivity shock . Denote the information available to a firm for making decisions on and by .

We present the model assumptions. For continuous random variables and , we denote the probability density function and expectation conditional on as and , respectively. Additionally, we denote the probability density function of conditional on and as . The unconditional probability density function of is denoted by .

Assumption 1.

(a) Each firm belongs to one of the types, where the population probability of belonging to type is given by , and is known to econometricians. (b) A firm knows its type, i.e., .

Assumption 2.

(a) . (b) . (c) For the -th type, and are mean-zero i.i.d. continuous random variables on with its probability density functions and , respectively, while is a mean-zero i.i.d. continuous random variable on with the joint probability density function . (d) The unconditional mean of is zero, i.e., for every .

Assumption 3.

(a) but . (b) the conditional density function of given is type specific and only depends on and , i.e., .

Assumption 4.

(a) and are chosen at time by maximizing expected profit conditional on as

| (6) |

where is a type-specific deterministic function of . (b) For any given , is invertible with respect to with probability one. (c) For any given , the function is continuously differentiable and strictly concave in .

Assumption 5.

(a) A firm is a price taker. (b) The intermediate input price , the output price , and the market wage at time are common across firms. (c) and is known to an econometrician.

Assumption 6.

Labor input in effective unit of labour is not directly observable but is related to the observed number of workers as in (4) with

Assumption 1(a) presumes that the number of types is known. Kasahara and Shimotsu, (2009) and Kasahara and Shimotsu, (2014) discuss nonparametric identification of a lower bound for the number of types. Kasahara and Shimotsu, (2019) and Hao and Kasahara, (2022) develop a likelihood-based testing procedure for the number of types in multivariate and panel data normal mixture models. Assumption 1(b) assumes that a firm is aware of its type.

Assumption 2(a)(b) asserts that is known when and are chosen, while is not known when and are chosen. The presence of the wage shock in (5) provides an additional source of variation for beyond and ; as a result, and are not collinear, avoiding the identification problem discussed by Bond and Sderbom, (2005) and Ackerberg et al., (2015). Assumption 2(c) introduces notation for the probability density function of , , , and , allowing for correlation between and . Assumption 2(d) is a normalization assumption to identify the location of .

Assumption 3(a) presumes that is determined at time , implying that is not known when is chosen. Assumption 3(b) can be explicitly derived from a dynamic model of investment decisions with convex/non-convex adjustment costs under the first-order Markov productivity process (3).

Assumption 4(a) introduces the demand function for and , derived from the static profit maximization problem when and are flexibly chosen in each period. Assumption 4(b) holds when there is a one-to-one relationship between and , except for a set of measure zero conditional on the value of , and is satisfied in the case of a Cobb-Douglas function. Under Assumption 4(c), the first-order condition for the maximization problem (6) characterizes the optimal choice for and .

Assumption 5(a) posits that the firm has no market power. Under Assumption 5(b), the intermediate input price cannot be used for instrumenting . When intermediate prices are exogenous and heterogeneous across firms, the production function could be identified using the intermediate input prices as instruments (Doraszelski and Jaumandreu,, 2018). In Assumption 5(c), an alternative approach assumes that a firm is subject to an idiosyncratic price shock such that, for example, with , then plays a similar role to . We may assume that is not known to the econometrician by treating as parameters to be estimated; in such a case, we can identify the production function up to scale.

Appendix B.2 discusses an alternative assumption to Assumption 5 when a firm produces differentiated products and faces a demand function with constant price elasticity.

Assumption 6 suggests that the quality of workers or the average working hours per worker differ across types and periods, as captured by the parameter , which leads to the systematic difference in the average wage of workers latent types. The assumption that serves as a normalization for identification.

4 Nonparametric identification

Assume that we have panel data for firms over periods consisting of output, capital, intermediate inputs, the number of workers, and total wage bills, denoted by , respectively. For brevity, define . Each firm’s observation is randomly sampled from a population distribution with a density function given by .

Let and be the probability density functions of and , respectively. Under Assumptions 1, 2, 3(a), 4(a), and 5, the first order conditions with respect to and for maximizing the expected static profit in Assumption 4(a) are given by:

| (7) |

where , , , and . Rearranging equations (2), (3), (5), and (7) gives a system of equations:

| (8) | ||||

where

For notational brevity, we drop the subscript in the rest of this section. Because and , there exists a one-to-one relationship between and given under Assumption 5. Therefore, denoting , we consider in place of as our data.

Let . We assume that the population density function, denoted by , is directly identified from the data. We are interested in identifying the model structure

from the population density function given a set of restrictions in (8) under Assumptions 1-6.

We first establish the nonparametric identification of model structure when as follows.

Proposition 1.

Remark 1.

Proposition 1 extends the identification result of GNR to the setting where is contemporaneously determined rather than predetermined.

When , the probability density function of follows an -term mixture distribution

| (9) |

The number of type is defined to be the smallest integer such that the density function of admits the representation (9).

Proposition 2.

Therefore, under the stated model assumption, follows a first order Markov process within subpopulation specified by type. The result of Proposition 2 allows us to establish the nonparametric identification of by extending the argument in Kasahara and Shimotsu, (2009), Carroll et al., (2010), and Hu and Shum, (2012).

We now establish identification when . Define

| (12) | ||||

where , , and .

Assumption 7.

There exists a value that satisfies the following condition: for every , we can find , and such that (a) , , , , and are non-singular, and (b) all the diagonal elements of take distinct values. Furthermore, (c) for every , for .

Proposition 3.

Remark 2.

Remark 3.

Considering serially correlated continuous unobserved variables , Hu and Shum, (2012) analyze the nonparametric identification of the model

Given panel data with , Theorem 1 and Corollary 1 of Hu and Shum, (2012) state that, under their Assumptions 1-4, , , and

are nonparametrically identified, but the identification of , , and remains unresolved.

Our Proposition 3 shows a new identification result that, for a model in which unobserved heterogeneity is discrete and finite, we can nonparametrically identify the type-specific distribution of , including the first two periods of the data, from periods of panel data without imposing stationarity.

Remark 4.

In the identification argument of Kasahara and Shimotsu, (2009), the type-specific distribution is identified only up to an arbitrary ordering of the latent types that differs across different evaluation points in . Our proof of Proposition 3 on the identification of the common order of the latent types is based on Higgins and Jochmans, (2021).

Remark 5.

Assumption 7(a) assumes the rank condition of matrices , , , , and defined in (12), of which elements are constructed by evaluating and at different points. These conditions are similar to the assumption stated in Proposition 1 of Kasahara and Shimotsu (2009), implying that all columns in these matrices must be linearly independent. For example, because each column of represents the type-specific conditional density function of across different values of given , the changes in the value of must induce sufficiently different changes in the values of conditional density function across types. One needs to find only one set of values and one set of and points of and to construct nonsingular , , , , and for each and these rank conditions are not stringent when has continuous support. The identification of and at all other points of , , and follows without any further requirement on the rank condition.

Once the type-specific distribution of is identified, we can use the argument in the proof of Proposition 1 to prove nonparametric identification for the model structure of each type.

Therefore, type-specific production functions, as well as the distribution of unobserved variables, can be identified nonparametrically. In the estimation, we focus on the case where the type-specific production functions are Cobb-Douglas.

Example 1 (Random Coefficients Model).

5 Estimation of production function with finite mixture random coefficients models

In this section, we present a finite mixture model of the random coefficient Cobb-Douglas production function, based on our nonparametric identification analysis and with consideration for computational efficiency. We develop a penalized maximum likelihood estimator for this model.

Let us denote the logarithmic values of using the corresponding lowercase letters, such that , where , and so on. Define and . For estimation purposes, we assume that the data generation follows the parametric assumptions outlined below.

Assumption 8.

(a) is fixed at and . (b) Equation (2) holds with

| (14) |

(c) with , , and , where . Furthermore, we assume in (3) so that

| (15) |

(d) Conditional on being type , given is normally distributed with mean and variance while the distribution of follows a bivariate normal distribution with mean and variance .

Assumption 8(a) posits that the length of panel data is short, while Assumption 8(b) enforces the Cobb-Douglas functional form assumption. Assumptions 8(c) and 8(d) impose Gaussian distribution assumptions under Assumptions 2 and 3, where follows a first-order autoregressive (AR(1)) process.

In equation (14), since , the intercept term encompasses both and . The latter term captures the variation in worker quality across types. The normality assumption in Assumptions 8(c) and 8(d) could potentially be relaxed; for instance, by employing the maximum smoothed likelihood estimator of finite mixture models proposed by Levine et al., (2011), in which the type-specific distribution of and is nonparametrically specified. Additionally, Kasahara and Shimotsu, (2015) develop a likelihood-based procedure to test the number of components in normal mixture regression models.

Suppose we have a random sample of independent observations from the -component mixture model that satisfies Assumptions 1-8. We propose a penalized maximum likelihood estimator (PMLE) that directly maximizes the log-likelihood function of a finite mixture model of production functions. The likelihood function is a parametric version of (11). To address the issue of unbounded likelihood for a normal mixture model (c.f., Hartigan,, 1985), we introduce a penalty term to the log-likelihood function. The maximum likelihood estimator, which leverages distributional information, is consistent even when is small, provided . Given the nonparametric identification result established in Proposition 3, if the parametric assumptions are invalid and the parametric model is misspecified, the parametric maximum likelihood estimator converges in probability to the pseudo-true value of the parameter that minimizes the Kullback-Leibler Information Criterion between the density of the parametric model and the true population density (White,, 1982).

Our estimation procedure is based on the two-stage identification proof from Proposition 3. To address the computational complexity of maximizing the log-likelihood function for the finite mixture model, the EM algorithm is employed.

Under Assumptions 3-6, 8, the first order conditions for the expected profit maximization imply that

| (16) | |||

| (17) |

Collect the model parameter into , and as

where and

for , and .

Denote . Then, under Assumption 8, we may write the probability density function of for type as

| (18) |

where the exact expression for and is derived below.

To deal with the issue of unbounded log-likelihood function of a normal mixture model (Hartigan,, 1985; Hao and Kasahara,, 2022), we estimate the model parameter by a penalized likelihood method proposed by Chen and Tan, (2009). Let be the estimator of for the one-component model with . Then, we consider the following penalized maximum likelihood estimator (PMLE):

| (19) |

where

and

| (20) | ||||

| (21) |

The expression for and are derived below.

To reduce the computational burden of finding the penalized maximum likelihood estimator, we follow a three-stage procedure.

In the first stage, from equations (16)-(17), we can express , , and as a function of , , , and as

| (22) | |||

| (23) |

Then, we estimate by maximizing the log likelihood function as

where, under Assumption 8(b), the likelihood function is given by

In view of equation (24), by a change of variables, we may relate the density function of conditional on and to the density function of , denoted by , as . Then, from (23)-(24) and Assumptions 2-3, we have

| (25) | |||

| (26) | |||

| (27) |

where is the density function of conditional on , is the density function of given , , and

| (28) |

Therefore, under Assumption 8, it follows from (18) and (25)-(27) that

where

Given the first stage estimate , the second stage estimates parameters and by maximizing the log-likelihood function as

Finally, using as an initial value, we obtain the PMLE by maximizing the full-information penalized log-likelihood function as in Equation (19) using the EM algorithm.

Let the true value of the model parameter be denoted by . When the number of types is correctly specified, the Fisher Information matrix is given by

which is positive definite. The following proposition demonstrates that the PMLE is consistent and asymptotically normal.

6 Empirical Application

6.1 Data

We utilize plant-level panel data from the Census of Manufacture of Japan spanning 1986-2010. This dataset encompasses production information for manufacturing plants in Japan. Our analysis focuses on plants with 30 or more employees, as detailed data are consistently available only for these establishments.555The survey employs distinct questionnaires based on plant size: 1. Plants with 30 or more employees; 2. Plants with 4-29 employees; 3. Plants with 1-3 employees. The questionnaire for plants with 30 or more employees provides more comprehensive information. For instance, beginning in 2000, the census collects fixed asset data every five years, rather than annually, for plants with fewer than 30 employees.

At the 4-digit industry classification level accessible in the Census of Manufacture, we identify a total of 276 industries. In our empirical application, we primarily concentrate on concrete products and electric audio equipment for two reasons: 1. Both industries have a substantial number of observations; 2. The former exhibits relatively small variation in intermediate input share, while the latter displays significant variation, as demonstrated in Section 2. Thus, examining these two industries proves useful for assessing the significance of unobserved heterogeneity.

Output () is defined as the sum of shipments, revenue from repair and maintenance services, and revenue from performing subcontracted work. Initial capital value () is determined as the fixed asset value minus land, and subsequent capital values are constructed using the perpetual inventory method. The observed labor input () is represented by the number of employees. The intermediate input () is defined as the sum of material input, energy input, and subcontracting expenses for consigned production.

Flow data, such as shipments and various production costs, pertain to the calendar year. The number of employees refers to the value at the end of the year, while the stock of fixed assets corresponds to the beginning of the period. Table 4 presents summary statistics for the variables employed in our empirical analysis.

| Concrete Products | Electric Audio Equipment | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Obs | Mean | Std. Dev | Min | Max | Obs | Mean | Std. Dev | Min | Max | |

| 13892 | 11.37 | 0.68 | 7.60 | 14.39 | 10913 | 11.24 | 1.78 | 5.51 | 17.35 | |

| 13892 | 3.97 | 0.41 | 3.40 | 6.81 | 10913 | 4.51 | 0.90 | 3.40 | 8.53 | |

| 13892 | 10.91 | 0.86 | 5.22 | 14.06 | 10913 | 10.04 | 1.99 | 1.67 | 16.22 | |

| 13892 | 10.34 | 0.83 | -0.13 | 13.89 | 10913 | 10.37 | 2.31 | 3.27 | 16.89 | |

| 13892 | -0.98 | 0.35 | -1.83 | -0.33 | 10913 | -0.99 | 0.79 | -3.13 | -0.08 | |

| 13892 | -1.47 | 0.43 | -2.39 | -0.50 | 10913 | -1.39 | 0.78 | -3.11 | -0.16 | |

| 13892 | 0.10 | 1.06 | -1.04 | 115.02 | 10913 | 0.34 | 11.49 | -1.28 | 1030.83 | |

6.2 Estimation of Production Function

This section presents estimation results for a random-coefficient Cobb-Douglas production function featuring three technology types and two unobserved labor types within each technology type.

Table 5 and Table 6 present the parameter estimates for the concrete products and electric audio equipment industries, considering both the unobserved heterogeneity case () and the homogeneous case (). The estimated coefficients in both industries demonstrate economically significant differences in output elasticities associated with labor, capital, and intermediate inputs across various firm types.

Comparing the two industries, the variation in across types is more substantial for electric audio equipment than for concrete products, which aligns with the dispersion of intermediate input shares discussed in Section 2. As and also exhibit variation across types, the ratio of output elasticities between capital and labor, , varies as well. For electric audio equipment, the value of ranges from 0.29 (Type 1 and 2) to 1.14 (Type 3 and 4), while for concrete products, it spans from 0.56 to 0.78. As demonstrated below, the value of serves as a crucial determinant of the capital investment response to productivity .

Furthermore, the productivity growth processes display variations across latent types, as indicated by the estimated AR(1) coefficient and standard deviation . In both industries, the estimated AR(1) coefficient for the homogeneous case () is considerably larger than those for the unobserved heterogeneity case (). This suggests that neglecting unobserved heterogeneity may result in an upward bias in the estimates of the AR(1) coefficient for productivity processes.

In various latent types, the returns to scale for concrete products, denoted by , is approximately 0.7, whereas for electrical audio equipment, it ranges between 0.78 and 0.91. When considering the homogeneous case, the returns to scale are comparatively lower at 0.63 and 0.65 for these respective industries. The estimates of indicate the existence of considerable unobserved heterogeneity in labor quality or working hours among manufacturing plants.

| J = 1 | J = 6 | ||||||

|---|---|---|---|---|---|---|---|

| Type 1 | Type 2 | Type 3 | Type 4 | Type 5 | Type 6 | ||

| 0.332 | 0.287 | 0.326 | 0.394 | ||||

| (0.004) | (0.005) | (0.012) | (0.005) | ||||

| 0.224 | 0.263 | 0.220 | 0.186 | ||||

| (0.003) | (0.005) | (0.009) | (0.003) | ||||

| 0.075 | 0.147 | 0.172 | 0.103 | ||||

| (0.015) | (0.036) | (0.034) | (0.014) | ||||

| 0.935 | 0.834 | 0.869 | 0.877 | ||||

| (0.007) | (0.014) | (0.024) | (0.012) | ||||

| 0.155 | 0.137 | 0.248 | 0.114 | ||||

| (0.004) | (0.004) | (0.014) | (0.003) | ||||

| 0.632 | 0.696 | 0.719 | 0.683 | ||||

| 0.336 | 0.558 | 0.780 | 0.556 | ||||

| 6.218 | 5.604 | 5.303 | 5.449 | ||||

| 0.000 | -0.108 | 0.344 | -1.454 | 0.534 | 0.056 | 0.627 | |

| (NA) | (0.086) | (0.090) | (0.339) | (0.081) | (0.085) | (0.088) | |

| 1.000 | 0.174 | 0.240 | 0.051 | 0.119 | 0.263 | 0.152 | |

| (NA) | (0.014) | (0.019) | (0.015) | (0.021) | (0.018) | (0.015) | |

| Obs | 13892 | ||||||

| No. Plants | 914 | ||||||

Notes: Standard errors are reported in parentheses.

| J = 1 | J = 6 | ||||||

|---|---|---|---|---|---|---|---|

| Type 1 | Type 2 | Type 3 | Type 4 | Type 5 | Type 6 | ||

| 0.281 | 0.135 | 0.430 | 0.536 | ||||

| (0.008) | (0.022) | (0.029) | (0.054) | ||||

| 0.296 | 0.496 | 0.163 | 0.195 | ||||

| (0.006) | (0.016) | (0.010) | (0.041) | ||||

| 0.076 | 0.146 | 0.186 | 0.175 | ||||

| (0.016) | (0.031) | (0.027) | (0.049) | ||||

| 0.960 | 0.769 | 0.845 | 0.895 | ||||

| (0.003) | (0.017) | (0.018) | (0.032) | ||||

| 0.378 | 0.457 | 0.376 | 0.135 | ||||

| (0.011) | (0.040) | (0.037) | (0.014) | ||||

| 0.652 | 0.776 | 0.778 | 0.906 | ||||

| 0.256 | 0.294 | 1.140 | 0.893 | ||||

| 6.125 | 5.747 | 4.560 | 2.992 | ||||

| 0.000 | -1.084 | 0.452 | -0.551 | 1.178 | -0.534 | 0.540 | |

| (NA) | (0.249) | (0.080) | (0.062) | (0.109) | (0.390) | (0.146) | |

| 1.000 | 0.278 | 0.168 | 0.163 | 0.098 | 0.109 | 0.184 | |

| (NA) | (0.033) | (0.046) | (0.015) | (0.044) | (0.027) | (0.022) | |

| Obs | 10913 | ||||||

| No. Plants | 907 | ||||||

Notes: Standard errors are reported in parentheses.

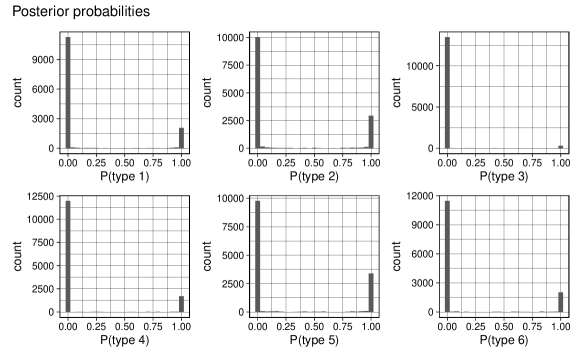

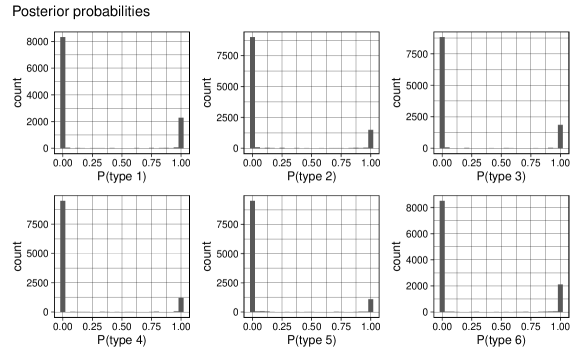

Figures 5 and 6 display the distribution of posterior type probabilities, defined by for , across plants for the model with . The posterior probabilities for each type are concentrated around 0 or 1. In the subsequent analysis, we assign one of the types to each plant based on its posterior type probability that achieves the highest value across the types.

Ignoring unobserved heterogeneity may lead to significant biases in measuring productivity growth. To examine this issue, we consider a specification with as the true model and compute the bias in measuring productivity growth when using a misspecified model with . Specifically, let for be the estimated productivity growth when and let be the estimated productivity growth when , where and denote estimated coefficients when and , respectively. Then, we compute the bias as

The first row of Table 7, labeled as , presents the ratio of the average absolute value of bias to the average productivity growth within each of three subsamples, which are classified by technology types. The magnitude of the bias is around 0.10 for concrete products, while it ranges from 0.23 to 0.35 for electric audio equipment.

The second row of Table 7, denoted by , reports the ratio of the average value of bias to the average productivity growth conditional on positive productivity growth measured by the model with . Note that and . Consequently, the average bias conditional on tends to be positive when . The empirical results confirm this pattern: for both concrete products and electric audio equipment, Types 5-6 have higher than , and thus the estimated bias is positive for these types, while the estimated bias when is negative for Types 1-2 that have lower values of .

These findings imply that neglecting unobserved heterogeneity could lead to significant bias in estimating productivity growth, and the bias is likely to exhibit a systematic pattern depending on the values of .

| Concrete Products | Electric Audio Equipment | |||||

| J = 6 | J = 6 | |||||

| Type 1 - 2 | Type 3 - 4 | Type 5 - 6 | Type 1 - 2 | Type 3 - 4 | Type 5 - 6 | |

| 0.098 | 0.104 | 0.099 | 0.230 | 0.229 | 0.350 | |

| -0.080 | -0.025 | 0.089 | -0.201 | 0.156 | 0.203 | |

| 0.287 | 0.326 | 0.394 | 0.135 | 0.430 | 0.536 | |

As an application of using the estimated productivity growth in empirical analysis, we now investigate whether unobserved heterogeneity, as captured by type-specific production function parameters, is significant for investment decisions. Specifically, for each subsample classified by type, we estimate the following linear investment model:

where represents the ratio of investment to capital stock.

Table 8 displays the OLS estimates of in the first row as well as the quantile regression estimates of at the 10th, 25th, 50th, 75th, and 90th percentiles across different types for and for concrete products. Table 9 presents the same estimates for the electric audio equipment industry. When , the OLS coefficient of is estimated significantly at for concrete products and at for electric audio equipment.

For the model with , the estimated coefficients of differ considerably across different types of plants, indicating that the investment response to a productivity shock varies across plants. Both OLS and quantile regression results show that the estimated coefficients tend to be higher for the types with higher and , suggesting that firms invest more given a positive productivity shock if their production technology features high material shares and high capital-labor ratios. In the case of quantile regressions, this pattern is particularly pronounced for firms with high investment ratios.

Overall, these results highlight the importance of accounting for unobserved heterogeneity in the production function when estimating plant-level productivity and its impact on investment.

| J = 1 | J=6 | ||||||

|---|---|---|---|---|---|---|---|

| Type 1 | Type 2 | Type 3 | Type 4 | Type 5 | Type 6 | ||

Notes: Standard errors are reported in parentheses. The first row presents the OLS estimate, while the second to the sixth rows present the quantile regression estimates at the -th quantile for .

| J = 1 | J=6 | ||||||

|---|---|---|---|---|---|---|---|

| Type 1 | Type 2 | Type 3 | Type 4 | Type 5 | Type 6 | ||

Notes: Standard errors are reported in parentheses. The first row presents the OLS estimate while the second to the sixt rows present the estimates of quantile regressions at the -th quantile for .

7 Conclusion

This paper establishes the nonparametric identifiability of production functions when unobserved heterogeneity exists across firms in the form of latent technology groups. Building on our nonparametric identification analysis and considering computational simplicity, we propose an estimation procedure for the production function with random coefficients employing a finite mixture specification.

Our analysis of Japanese plant-level panel data reveals a substantial degree of variation in estimated input elasticities and productivity growth processes across latent types within narrowly defined industries. We demonstrate that neglecting unobserved heterogeneity in input elasticities can lead to significant and systematic bias in estimated productivity growth. Moreover, we highlight the critical role played by unobserved disparities in input elasticities in plant-level investment decisions. Specifically, we find that the correlation between estimated productivity and investment is notably stronger among high capital-intensive latent type firms than among low capital-intensive type firms.

As future research topics, we may extend our framework in several directions. First, the framework may be extended to explicitly account for plant- or firm-specific biased technological change, which may be continuously distributed. This can be achieved by integrating the structural assumption discussed in Doraszelski and Jaumandreu, (2018), Zhang, (2019), Demirer, (2020), and Raval, (2023) into our framework. The identification approach of this paper—based on panel data with a Markov structure—is different from, but complementary to, the structural approaches of these existing papers. Adopting both identification approaches simultaneously can provide an empirical framework for estimating production functions that incorporates a broader range of unobserved heterogeneity.

Second, although we establish nonparametric identification, we employ a parametric finite mixture model for estimation due to computational complexity. An important research direction would be to relax the parametric assumption and develop a nonparametric estimator for a finite mixture model of the production function. This could be achieved, for instance, by extending the maximum smooth likelihood estimator proposed by Levine et al., (2011) or the estimator presented by Bonhomme et al., (2016).

Finally, the assumption of perfect competition or monopolistic competition with constant price elasticity may not be realistic. If data on quantities and prices are available separately, our framework can be employed to estimate the production function using the quantity of output, instead of relying on sales as a proxy for output. However, it is frequently the case that firm- or plant-level datasets do not contain output quantities and prices separately. Therefore, developing a framework for concurrently identifying the production function and demand structure from revenue data, as demonstrated in the work by Kasahara and Sugita, (2020), while incorporating unobserved heterogeneity, is an important future research topic.

References

- Ackerberg et al., (2007) Ackerberg, D., Benkard, C. L., Berry, S., and Pakes, A. (2007). Econometric tools for analyzing market outcomes. In Handbook of Econometrics, pages 4171–4276. Elsevier, vol. 6, edited by James J. Heckman and Edward E. Leamer. Amsterdam.

- Ackerberg et al., (2015) Ackerberg, D. A., Caves, K., and Frazer, G. (2015). Identification properties of recent production function estimators. Econometrica, 83(6):2411–2451.

- Alexandrovich, (2014) Alexandrovich, G. (2014). A note on the article ‘inference for multivariate normal mixtures’ by j. chen and x. tan. Journal of Multivariate Analysis, 129:245–248.

- Arellano and Bond, (1991) Arellano, M. and Bond, S. (1991). Some tests of specification for panel data: Monte carlo evidence and an application to employment equations. The Review of Economic Studies, 58:277–297.

- Balat et al., (2019) Balat, J., Brambilla, I., and Sasaki, Y. (2019). Heterogeneous firms: Skilled-labor productivity and the destination of exports. mimeo.

- Blundell and Bond, (1998) Blundell, R. and Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1):115–143.

- Blundell and Bond, (2000) Blundell, R. and Bond, S. (2000). GMM estimation with persistent panel data: an application to production functions. Econometric Reviews, 19:321–340.

- Bond and Sderbom, (2005) Bond, S. and Sderbom, M. (2005). Adjustment costs and the identification of cobb douglas production functions. Working paper series no. 05/4, The Institute for Fiscal Studies.

- Bonhomme et al., (2016) Bonhomme, S., Jochmans, K., and Robin, J.-M. (2016). Estimating multivariate latent-structure models. The Annals of Statistics, 44(2):540 – 563.

- Bonhomme and Manresa, (2015) Bonhomme, S. and Manresa, E. (2015). Grouped patterns of heterogeneity in panel data. Econometrica, 83(3):1147–1184.

- Carroll et al., (2010) Carroll, R. J., Chen, X., and Hu, Y. (2010). Identification and estimation of nonlinear models using two samples with nonclassical measurement errors. Journal of Nonparametric Statististics, 22(4):379–399.

- Chen and Tan, (2009) Chen, J. and Tan, X. (2009). Inference for multivariate normal mixtures. Journal of Multivariate Analysis, 100:1367–1383.

- Chen et al., (2021) Chen, Y., Igami, M., Sawada, M., and Xiao, M. (2021). Privatization and productivity in china. RAND Journal of Economics, 52(4):884–916.

- Cheng et al., (2021) Cheng, X., Schorfheide, F., and SHao, P. (2021). Clustering for multi-dimensional heterogeneity.

- De Loecker and Warzynski, (2012) De Loecker, J. and Warzynski, F. (2012). Markups and Firm-Level Export Status. American Economic Review, 102(6):2437–71.

- Demirer, (2020) Demirer, M. (2020). Production function estimation with factor-augmenting technology: An application to markups. mimeo.

- Dewitte et al., (2022) Dewitte, R., Fuss, C., and Theodorakopoulos, A. (2022). Identifying latent heterogeneity in productivity.

- Doraszelski and Jaumandreu, (2018) Doraszelski, U. and Jaumandreu, J. (2018). Measuring the bias of technological change. Journal of Political Economy, 126(3):1027–1084.

- Gandhi et al., (2020) Gandhi, A., Navarro, S., and Rivers, D. (2020). On the identification of gross output production functions. Journal of Political Economy, 128(8):2973–3016.

- Griliches and Mairesse, (1998) Griliches, Z. and Mairesse, J. (1998). Production Functions: The Search for Identification. Cambridge University Press, New York, in econometrics and economic theory in the twentieth century: the ragnar frisch centennial symposium edition.

- Hall, (1988) Hall, R. E. (1988). The Relation between Price and Marginal Cost in US Industry. Journal of Political Economy, 96(5):921–947.

- Hao and Kasahara, (2022) Hao, Y. and Kasahara, H. (2022). Testing the number of components in finite mixture normal regression model with panel data. https://arxiv.org/abs/2210.02824.

- Hartigan, (1985) Hartigan, J. (1985). Failure of log-likelihood ratio test. In Le Cam, L. and Olshen, R., editors, Proceedings of the Berkeley Conference in Honor of Jerzy Neyman and Jack Kiefer, volume 2, pages 807–810, Berkeley. University of California Press.

- Higgins and Jochmans, (2021) Higgins, A. and Jochmans, K. (2021). Identification of mixtures of dynamic discrete choices. TSE Working Papers 21-1272, Toulouse School of Economics (TSE).

- Hsieh and Klenow, (2009) Hsieh, C.-T. and Klenow, P. J. (2009). Misallocation and manufacturing tfp in china and india. Quarterly Journal of Economics, 124(4):1403–1448.

- Hu and Shum, (2012) Hu, Y. and Shum, M. (2012). Nonparametric identification of dynamic models with unobserved state variables. Journal of Econometrics, 171(1):32–44.

- Kasahara and Lapham, (2013) Kasahara, H. and Lapham, B. (2013). Productivity and the decision to import and export: Theory and evidence. Journal of International Economics, 89(2):297–316.

- Kasahara and Rodrigue, (2008) Kasahara, H. and Rodrigue, J. (2008). Does the use of imported intermediates increase productivity? plant-level evidence. Journal of Development Economics, 87(1):106–118.

- Kasahara and Shimotsu, (2009) Kasahara, H. and Shimotsu, K. (2009). Nonparametric identification of finite mixture models of dynamic discrete choices. Econometrica, 77:135–175.

- Kasahara and Shimotsu, (2014) Kasahara, H. and Shimotsu, K. (2014). Non-parametric identification and estimation of the number of components in multivariate mixtures. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 76(1):97–111.

- Kasahara and Shimotsu, (2015) Kasahara, H. and Shimotsu, K. (2015). Testing the number of components in normal mixture regression models. Journal of the American Statistical Association, 110(512):1632–1645.

- Kasahara and Shimotsu, (2019) Kasahara, H. and Shimotsu, K. (2019). Testing the Order of Multivariate Normal Mixture Models. arXiv:1902.02920v1.

- Kasahara and Sugita, (2020) Kasahara, H. and Sugita, Y. (2020). Nonparametric identification of production function, total factor productivity, and markup from revenue data. arXiv:2011.00143v1.

- Levine et al., (2011) Levine, M., Hunter, D. R., and Chauveau, D. (2011). Maximum smoothed likelihood for multivariate mixtures. Biometrika, 98:403–416.

- Levinsohn and Petrin, (2003) Levinsohn, J. and Petrin, A. (2003). Estimating production functions using inputs to control for unobservables. Review of Economic Studies, 70:317–341.

- Li and Sasaki, (2017) Li, T. and Sasaki, Y. (2017). Constructive identification of heterogeneous elasticities in the cobb-douglas production function. mimeo.

- Marschak and Andrews, (1944) Marschak, J. and Andrews, W. H. (1944). Random simultaneous equations and the theory of production. Econometrica, 12(3):4.

- Olley and Pakes, (1996) Olley, G. S. and Pakes, A. (1996). The Dynamics of Productivity in the Telecommunications Equipment Industry. Econometrica, 64(6):1263.

- Pavcnik, (2002) Pavcnik, N. (2002). Trade liberalization, exit, and productivity improvements: Evidence from chilean plants. Review of Economic Studies, 69(1):245–276.

- Raval, (2023) Raval, D. (2023). Testing the Production Approach to Markup Estimation. The Review of Economic Studies. rdad002.

- Solow, (1957) Solow, R. M. (1957). Technical change and the aggregate production function. The Review of Economics and Statistics, 39(3):312–320.

- Van Biesebroeck, (2003) Van Biesebroeck, J. (2003). Productivity dynamics with technology choice: An application to automobile assembly. Review of Economic Studies, 70:167–198.

- White, (1982) White, H. (1982). Maximum likelihood estimation of misspecified models. Econometrica, 50(1):1–25.

- Wooldridge, (2009) Wooldridge, J. M. (2009). On estimating firm-level production functions using proxy variables to control for unobservables. Economics Letters, 104(3):112–114.

- Zhang, (2019) Zhang, H. (2019). Non-neutral technology, firm heterogeneity, and labor demand. Journal of Development Economics, 140:145–168.

Appendix A Appendix

A.1 Proof of Proposition 1

We partition as with and . We drop the superscript and we have and because and under Assumption 6.

We first prove the identification of . Let and let . Because and , we may identify the value of across all observations as and from the second and third equations in (8), and is identified from the identified values of . The marginal density functions of and are also identified as and . Furthermore, because , we may identify as and, similarly, . Given the identification of , , and , we may identify the value of for all observations as , and the identification of follows. is identified as given that and are mean zero random variables. This proves that is identified.

We proceed to show that is identified. Fix such that and . Because and , we have

| (29) |

It follows from (2), (29), , and that

| (30) |

where

Note that, given the identification of , we may identify for each value of .

Substituting the right-hand side of (30) to and rearranging terms give

| (31) |

where the second term on the right hand side only depends on . Fix and let . Then, by taking the conditional expectation given and in (31) and noting that , is identified up to constant as

| (32) |

It follows from the moment restriction with (30) and (32) that we may identify as

Therefore, is identified from (32), and the identification of for follows from (29) given that the first two terms on the right hand side of (29) is identified from and .

Finally, we prove the identification of and . Note that the value of for all observations is identified as for . Thus, we may identify the conditional probability density function of given , denoted by , from the joint distribution of and for . Then, is identified as . Given the identification of , , and , the value of is identified as for all observations and hence the probability density function of is identified. This proves the identification of . ∎

A.2 Proof of Proposition 2

For notational brevity, we drop the subscript from the probability density function by writing, for example, as . The probability density function of for type can be written as

| (33) | ||||

Define . Similarly, define and . Then, we may write a system of equations (8) as

| (34) | ||||

In view of the second and the third equations of (34), because and are i.i.d. under Assumption 2(c), we have

| (35) |

Furthermore,

| (36) | ||||

where the first equality and the last equality hold because there is a one-to-one mapping between and given in view of Assumption 4(b); the third equality follows from Assumptions 2(a) and 3(b); the fifth equality holds because is i.i.d. and, thus, independent of . Therefore, the stated result follows from (33), (35), and (36). ∎

A.3 Proof of Proposition 3

We apply the argument of Kasahara and Shimotsu, (2009), Carroll et al., (2010), and Hu and Shum, (2012) under the assumption that unobserved heterogeneity is permanent and discrete. The proof is constructive.

Consider the case that . For each value of , choose , , and that satisfy Assumption 7. Evaluating (10) for at gives

| (37) | ||||

where , , and . Similarly, evaluating (11) for at gives

| (38) |

Denote and . Evaluating (37) at and gives equations while evaluating (38) at gives equations.

Using matrix notation, we collect these equations as

| (39) |

where , , and are defined in (12) while

| (40) |

Let be the value of as defined in Assumption Assumption 7. For each , choose , , and that satisfy Assumption 7(a)(b). Evaluating (39) at four different points, , , , and gives

Then, following the identification argument in Carroll et al., (2010), under Assumption 7(a)(c), we have

| (41) |

where

| (42) |

We first identify for all up to an unknown permutation matrix. Evaluating (41) at , we have

Because has distinct eigenvalues under Assumption 7(b), the eignvalues of determine the diagonal elements of while the right eigenvectors of determine the columns of up to multiplicative constant and the ordering of its columns. Namely, collecting the right eigenvectors of into a matrix in descending order of their eigenvalues, we identify

where satisfies , is an unknown permutation matrix, and is some diagonal matrix with non-zero diagonal elements.

We can determine the diagonal matrix from the first row of because the first row of is a vector of ones. Then, is determined from and as in view of . Repeating the above argument for all values of , the eigenvalue decomposition algorithm identifies the matrices

| (43) |

where is an unknown permutation matrix that depends on .

Next, we identify permutation matrices that re-arrange in a common order of latent types across different values of using the identification argument in Higgins and Jochmans, (2021). Pre- and post- multiplying (41) by and , respectively, we have

where the last equality uses the fact that is an identity matrix. Because is a permutation matrix, is a matrix obtained by permutating the rows of the diagonal matrix . Therefore, each diagonal element of is identified with the sum of elements in the corresponding column of , and the identification of follows. Then, we may identify as . Therefore, is identified up to a common permutation matrix that does not depend on from (43) as

| (44) |

In the next step, we identify up to a permutation matrix . For this purpose, we evaluate at as

| (45) | ||||

where . Then, evaluating (45) at and collecting them into a vector together with gives

| (46) |

with

where the last equality in (46) follows from (44). Therefore, from (44) and (46), we identify for all values of up to as

| (47) |

where

is a permutation implied by . Furthermore, because and , we may identify from as

| (48) |

Then, we may identify up to as

| (49) |

and is identified from (39), (44), and (49) up to as

| (50) |

where the invertibility of follows from Assumption 7(c).

A.4 Proof of Proposition 4

We first show that and are identified from . Because , we may have for , where is identified from . Then, is identified from as . Once and are identified, then repeating the argument in the proof of Proposition 1 for each type proves the stated result. ∎

A.5 Proof of Proposition 5

Our panel data model belongs to a class of multivariate normal mixture models analyzed in Chen and Tan, (2009). Chen and Tan, (2009) provides the consistency proof under their conditions C1-C3 but Alexandrovich, (2014) identifies a soft spot in the proof of Chen and Tan, (2009) and provides an alternative consistency proof by strengthening the condition C3 of Chen and Tan, (2009).

Let be the variance matrix for the vector of random variables for type , where , , , and . Using our notations, the condition C1-C2 in Chen and Tan, (2009) and the condition C3 strengthned by Alexandrovich, (2014) are stated as follows:

- C1.

-

The penalty function is written as .

- C2.

-

For any fixed with for , we have and . In addition, is differentiable with respect to and as , at any fixed such that for

- C3 by Alexandrovich, (2014).

-

For large enough , , when for some .

The consistency and the asymptotic normality of the PMLE, , follows from Theorems 1 and 2 of Chen and Tan, (2009) and Corollary 3 of Alexandrovich, (2014) if we can show that the above three conditions hold for our penalty function defined in (19). C1 trivially holds with . C2 also holds because for and are for and . For C3, suppose that for . Then, for large . Similarly, we may show that, if , then for large . Therefore, C3 holds. Consequently, satisfies the above three conditions, and the stated result follows follows from Theorems 1 and 2 of Chen and Tan, (2009) and Corollary 3 of Alexandrovich, (2014).

Appendix B Online Appendix

B.1 Assumption 7 under Cobb-Douglas production function

In the following, we discuss the conditions under which Assumption 7 holds when the production function is Cobb-Douglas.

Example 1 (continued).

To simplify our identification analysis, we also assume the followings. First, we fix the value of at, say, so that the variation in the values of ’s and ’s are due the variation in the values of and . Let for and let for . Second, takes the same value at for in the values of ’s and that for in the values of ’s. Third, we assume that the probability density function of does not vary across types, i.e., for all . These assumptions impose restrictions that make it more difficult to satisfy Assumption 7 but help the identification argument to be transparent. Then, in view of Proposition 2, given ,

with

for and , where the dependence of on the value of , , and is implicit.

Therefore, we have

| (54) |

Similarly, given , we have

with

for . Therefore,

For Assumption 7(a), we have and for any when , , , , and for . Note that the value of for and in the element of in (54) represents the value of the probability density function of for the -th type evaluated at . Therefore, the full rank condition of holds if the value of probability density function of changes heterogenously across types when we change the value of . Similarly, the full rank condition of holds if the value of probability density function of changes heterogenously across types when we change the value of .

Assumption 7(b) holds if and for all . Then, we have

Therefore, Assumption 7(c) requires that takes different values across different ’s.

B.2 Constant Price Elasticity of Demand

In place of Assumption 5, we may alternatively consider the case where firms produce differentiated products and face a demand function with constant price elasticity as follows.

Assumption 9 (Constant Demand Elasticity).

(a) A firm faces an inverse demand function with constant elasticity given by , where is an i.i.d. ex-post shock that is not known when is chosen at time . (b) A firm is a price taker for intermediate and labour inputs and the intermediate price and the market wage at time , and , are common across firms. (c) and are not separately observed in the data.

Under Assumption 9, the “revenue” production function is given by , where , , , and . Then, in place of (8), we have

| (55) | ||||

where and . When and are not separately observed in the data, the observable implication of (55) are the same as that of (8). In particular, we cannot separately identify the parameter and the production function . Therefore, we focus on the identification analysis under Assumption 5 although we should be careful in interpreting the empirical result because the unobserved heterogeneity in revenue production function could partly reflect in difference in demand elasticity.