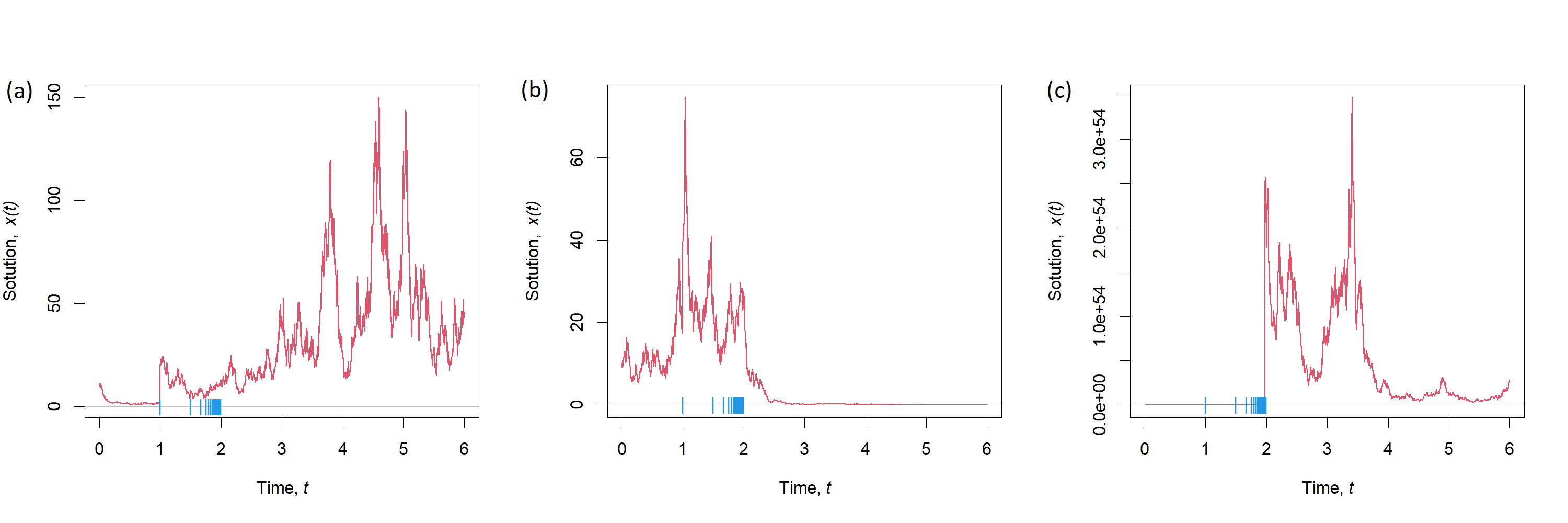

2 Problem statement

On the probabilistic basis [1], [2], we consider a stochastic dynamic system of random structure given by a stochastic differential equation (SDE)

|

|

|

(1) |

with Markov switching

|

|

|

(2) |

and initial conditions

|

|

|

(3) |

Here is a Markov chain with a finite number of states and generator ; is a Markov chain with values in space and with a transition probability matrix ; ; is a -dimensional standard Wiener process; the processes and are independent random processes [1], [2].

We denote by

|

|

|

the minimal -algebra with respect to which and are measured.

Measured by a set of variables functions , , satisfy the boundedness condition and the Lipschitz condition

|

|

|

(4) |

|

|

|

(5) |

|

|

|

(6) |

Consider the case of a point of concentration of jumps, i.e.

|

|

|

Let’s assume that the following relations are true:

|

|

|

(7) |

and

|

|

|

(8) |

The conditions (4)-(8) guarantee the existence of a strong solution to the Cauchy problem (1)-(3) [3].

We denote by

|

|

|

|

|

|

the transition probability of the Markov chain , that determine the solution to the problem (1)-(3) on the -th step.

Definition 1. Discrete Lyapunov operator on a sequence of measurable scalar functions for the SDE (1) with Markov switchings (2) is defined by the equality

|

|

|

|

|

|

(9) |

Here , is a Lyapunov function defined by the following definition.

Definition 2. The Lyapunov function for the system (1)-(3) is a sequence of non-negative functions for whom

-

1.

for all the discrete Lyapunov operator (9) is defined;

-

2.

if

|

|

|

-

3.

if

|

|

|

where and are continuous and monotonic for .

Definition 3. A system with a random structure (1)-(3) is called:

– stable in probability, if for it can specify such that the inequality implies the inequality

|

|

|

(10) |

for all ;

– asymptotically stochastically stable, if it is stable in probability and for any exists such that

|

|

|

(11) |

for all , and .

Definition 4. A system with a random structure (1)-(3) is called:

– mean square stable, if for it can specify the following , that the inequality implies the inequality

|

|

|

(12) |

for all ;

– mean square asymptotically stable, if it is mean square stable for any and

|

|

|

(13) |

If (10)-(13) hold true for all , then the system is stable in the corresponding probabilistic sense on the whole.

For solving the problem (1)-(3) on the intervals , the following estimate is obtained.

Theorem 1.

Let the coefficients of the equation (1) satisfy the condition of uniform boundedness (4), and the condition (6) holds for the function .

Then for all for a strong solution of the Cauchy problem (1)-(3) holds the next inequality

|

|

|

(14) |

We use the same methodology as in [4], [5]. A strong solution of the Cauchy problem (1), (3) for all , can be written in the integral form

|

|

|

(15) |

After squaring the left and right sides of (15), calculating , and applying the Cauchy–Schwarz inequality, we obtain:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

To the last inequality, we apply the conditional mathematical expectation operation with respect to the -algebra and, taking into account the properties of the Ito integral, we obtain

|

|

|

|

|

|

|

|

|

Using the Gronwall inequality, we obtain an estimate of

|

|

|

|

|

|

For the strong solution of the system (1)-(3), obviously, must satisfy the inequality

|

|

|

|

|

|

|

|

|

|

|

|

Combining the last two inequalities, we get the desired estimate (14).

End of proof of Theorem 1.

Remark 1. We will consider the stability of the trivial solution , i.e. the satisfying of (4), if [6], [7], [8].

Remark 2. Note that the Lipschitz condition (5) was not used in the proof of the theorem, i.e. any (not necessarily unique) solution to the problem (1)-(3) satisfies the condition of the theorem.

1) the conditions (4)-(6) are met;

2) the Lyapunov functions and exist, such that, based on the system, the following inequality

|

|

|

(16) |

is correct.

Then the system of random structure (1)-(3) is asymptotically stochastically stable on the whole.

Proof of Theorem 2.

Define by a minimal -algebra, relative to which are measured for all and for . The conditional mathematical expectation is calculated by the formula

|

|

|

|

|

|

(17) |

Then, by the definition of the discrete Lyapunov operator (see (9)) from equality (17), considering (16), we get the inequality

|

|

|

|

|

|

(18) |

From Theorem 1 (because the existence of the second moment implies the existence of the first moment) and from properties of the function follows the existence of a conditional mathematical expectation of the left-hand side of the inequality (18).

Now, using(17), (18), we write the discrete Lyapunov’s operator , which given on the solutions (1)-(3):

|

|

|

|

|

|

(19) |

Then, at the next inequality holds

|

|

|

This means that a sequence of random variables

|

|

|

forms a supermartingale in relation to [9].

Taking the mathematical expectation of both parts of inequality (19), we summarize the obtained expressions for from to , and obviously, we have the next inequality:

|

|

|

|

|

|

|

|

|

(20) |

Since a random variable does not depend on events of -algebra [10], then

|

|

|

(21) |

that is, the inequality (14) also holds for the simple mathematical expectation

|

|

|

Next, we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(22) |

If , then, based on the definition of the Lyapunov function, the next inequality holds:

|

|

|

(23) |

Now let’s use the well-known inequality for nonnegative supermartingales [1], [9] to evaluate the right-hand side of (22):

|

|

|

|

|

|

(24) |

Given inequality (22), inequality (24) make it possible to guarantee the fulfillment of inequality (10) of stability in probability on the whole of the system (1)-(3).

From the inequality (20) follows the estimate

|

|

|

|

|

|

(25) |

for all .

Since the sequence forms Lyapunov functions, there must exist continuous strictly monotone functions and , which are zero if [11] and such that

|

|

|

(26) |

for and .

Thus, from the convergence of the series on the left side of the inequality (25) (which will be convergent in the case of convergence of the series ) follows the convergence of the series for .

Then, taking into account the continuity of and the equality , we have:

|

|

|

(27) |

And from (27) it follows tends to zero in probability of the sequence for for all

So, from the properties of the Lyapunov function, we conclude that the non-negative supermartingale for tends to zero in probability for all realizations of the process and sequence .

Further, the nonnegative bounded supermartingale has a bound with probability 1 [1]. Based on Theorem 1 (inequality (14) for the usual mathematical expectation), we obtain the asymptotic stochastically stability on the whole of the system (1)-(3) by the definition 3 (see (11)). Theorem 2 is proven.

End of proof of Theorem 2.

Theorem 3. Suppose that the conditions of Theorem 2 are satisfied, and the Lyapunov functions satisfy the inequalities

|

|

|

(28) |

|

|

|

(29) |

for some for all

Then the system of random structure (1)-(3) is asymptotically stable in the mean square

Proof of Theorem 3.

Using the inequality (19) for , based on (28) it is easy to obtain an inequality

|

|

|

|

|

|

(30) |

for all and the initial distributions of the random vector .

Hence, by definition 4 (see (12)), it follows a stability in the mean square of the system of random structure (1)-(3).

Using the inequalities (20), (28) and (29), it is possible to obtain an inequality

|

|

|

|

|

|

This inequality guarantees the convergence of the series whose members are for any initial data and initial distributions of the random vector .

Therefore,

|

|

|

which proves Theorem 3.

End of proof of Theorem 3.

Theorem 4. [Corollary]

If the conditions of Theorem 3 are fulfilled and the inequality (28) holds, then the system of random structure (1)-(3) is stable in the mean square on the whole.

3 Computation of the weak infinitesimal operator

Based on the method [12], we will obtain an expression for calculating the explicit form of the weak infinitesimal operator (WIO) based on the system (1)-(3), which plays the role of the Lyapunov operator.

Let be such a scalar integral function, that the sequence

|

|

|

is a Lyapunov function.

It is possible to prove [1] that the pair is a Markov process and it is possible to introduce WIO

|

|

|

|

|

|

(31) |

where , and . It is natural to assume that the function , defined above, belongs to the domain of definition of the operator , if the limit (31) exists in the sense of uniform convergence in some neighborhood of the point uniformly by .

Let’s introduce the operator which is related to Markov switchings (2) at the moment :

|

|

|

(32) |

where is the transition probability of the Markov chain at the -th step, is the indicator of the set .

At the moment of changing of the structure of the parameter of the system there is a jump-like change in the phase vector with transition probability

|

|

|

(33) |

Theorem 5.

The weak infinitesimal operator on the solutions of the system (1)-(3) of the function is calculated by the formula

|

|

|

(34) |

where

|

|

|

(35) |

|

|

|

(36) |

|

|

|

(37) |

Here is scalar product; , is the derivative of the -th coordinate of the vector ; is a matrix of second derivatives; is a trace of the matrix; ; calculated by formula (32); is a function differentiable with respect to , which has derivatives of the 1st and 2nd order by the last argument.

Proof of Theorem 5.

By definition (31)

|

|

|

|

|

|

Next,

|

|

|

|

|

|

|

|

|

Therefore, can be represented as

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Let’s consider each term separately.

The form of the first term is obvious.

Let’s establish the explicit form of the term . Consider a complete group of disjoint events constructed as follows: denote by the event which means that the structure (1) does not change in the interval , i.e. at . Then with an accuracy of we obtain [13]

|

|

|

Next, denote by event, which means that in the interval a change occurs. Then with accuracy up to we have

|

|

|

Denote by and by the increment upon occurrence of the event . Let’s calculate the increments and of the function when events , occur, neglecting terms of order :

|

|

|

(38) |

Here the partial derivatives are calculated at a point , where is the solution of equation (1) with initial condition . Next, for in the case of a change in the structure in the interval we will get an increase

|

|

|

(39) |

with the probability .

The terms that illustrate the possibility of changing the structure of are not included in the last equality and there are no Markov switchings, since after averaging they have the order of and we can ignore them.

To calculate , we use the full probability formula

|

|

|

|

|

|

where the external mathematical expectation on the right-hand side is calculated by the variable at the moment .

Ignoring terms of order , from (38) and (39) we obtain

|

|

|

|

|

|

|

|

|

When calculating the third term, we used the property and the property of the Wiener process with respect to the covariance of the increment [1], [9].

Using division by and passing to the boundary at , we obtain the first, second, and third terms in (34). The idea of calculating the fourth term can be found in [7], pp. 163-164. Theorem 5 is proved.

End of proof of Theorem 5.