Practical algorithms and experimentally validated incentives for equilibrium-based fair division (A-CEEI)

Abstract.

Approximate Competitive Equilibrium from Equal Incomes (A-CEEI) is an equilibrium-based solution concept for fair division of discrete items to agents with combinatorial demands. In theory, it is known that in asymptotically large markets:

-

•

For incentives, the A-CEEI mechanism is Envy-Free-but-for-Tie-Breaking (EF-TB), which implies that it is Strategyproof-in-the-Large (SP-L).

-

•

From a computational perspective, computing the equilibrium solution is unfortunately a computationally intractable problem (in the worst-case, assuming ).

We develop a new heuristic algorithm that outperforms the previous state-of-the-art by multiple orders of magnitude. This new, faster algorithm lets us perform experiments on real-world inputs for the first time. We discover that with real-world preferences, even in a realistic implementation that satisfies the EF-TB and SP-L properties, agents may have surprisingly simple and plausible deviations from truthful reporting of preferences. To this end, we propose a novel strengthening of EF-TB, which dramatically reduces the potential for strategic deviations from truthful reporting in our experiments.

A (variant of) our algorithm is now in production: on real course allocation problems it is much faster, has zero clearing error, and has stronger incentive properties than the prior state-of-the-art implementation.

1. Introduction

Competitive Equilibrium from Equal Incomes (CEEI) (Foley, 1967; Varian, 1974; Thomson and Varian, 1985) is an attempt to leverage the economic efficiency of market equilibria while preserving the ex post fairness properties that come from equal incomes. For complex preferences, however, CEEI does not necessarily exist.

Budish (Budish, 2011) developed a relaxation of CEEI, Approximate CEEI (A-CEEI). He showed that an approximate equilibrium from approximately equal incomes always exists. Budish (Budish, 2011) also showed if the perturbations to agents’ incomes (henceforth budgets) are chosen at random, the mechanism satisfies an Envy-Free-but-for-Tie-Breaking (EF-TB) property, which by (Azevedo and Budish, 2019) implies that it is Strategyproof in the Large (SP-L); i.e. as the number of agents tends to infinity, the mechanism becomes approximately strategyproof.

Budish’s original theoretical work invoked a fixed-point theorem to prove existence. That makes it inherently non-constructive. It was shown in (Othman et al., 2016) that finding an A-CEEI is PPAD-complete, even if we allow constant budget inequality (Rubinstein, 2018). A-CEEI is therefore similar to many other economic equilibria whose existence rely on non-algorithmic proofs, the most famous of which is the Nash equilibrium (Daskalakis et al., 2009; Chen et al., 2009).

Despite this theoretical infeasibility, a heuristic algorithm exists that solves the problem adequately in practice (Budish et al., 2017). The existing heuristic algorithm makes A-CEEI a practical solution concept for settings that require efficiency and fairness but for which the use of real money is impractical or repugnant (Roth, 2007). The setting where A-CEEI has seen the most practical application is in the allocation of courses to students. Student preferences are often quite complex in course allocation. Students typically demand many courses and individual courses could be complements or substitutes depending on the bundle of other courses in a student’s schedule. Course allocation—particularly in professional schools—also tends to be a challenging allocation problem, as the most popular “star courses” tend to have far more demand than supply.

In this paper we explore the course allocation problem experimentally using real data from properly motivated student preferences over schedules of professional school courses, using data from the commercial implementation of A-CEEI fielded by Cognomos.

1.1. Contribution I: A (much) faster heuristic algorithm for computing A-CEEI

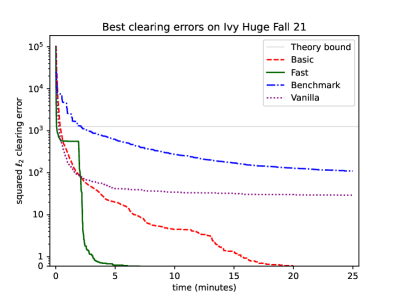

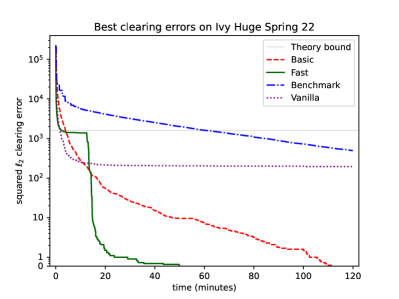

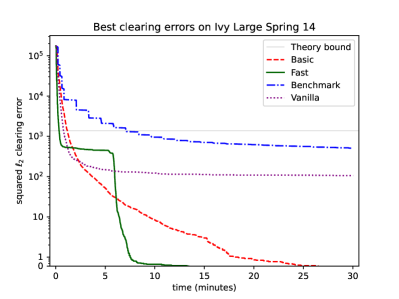

Our first contribution is an improved heuristic algorithm for computing A-CEEI. Our algorithm outperforms the commercial state-of-the-art by several orders of magnitude in both the quality of produced solution as well as runtime on real course allocation problems, see e.g. Figure 1.

We highlight some of our algorithmic findings here, with details in Sections 3 and 4. Further details about the previous state-of-the-art algorithm (henceforth benchmark), can also be found in academic publications (Othman et al., 2010; Budish et al., 2017). At a high level, both our algorithm and the benchmark, perform variants of the classic tatonnement algorithm: increase the price of over-demanded courses, and decrease the prices of under-demanded courses.

One of the main technical innovations introduced in the benchmark algorithm was the use of individual price adjustments: on some iterations, the algorithm can make a larger improvement on the clearing error by adjusting the price of a single course rather than all the courses simultaneously. Based on extensive experiments on randomly generated data (real data from students bidding was not yet available at the time), (Othman et al., 2010) reported that the algorithm was much more likely to find a solution with acceptable clearing error when mixing individual price adjustments and full tatonnement updates. Our first algorithmic insight is to largely reverse this finding of (Othman et al., 2010). We observe that on real world instances, it is in fact much more efficient to use only full tatonnement updates, even when they locally increase the clearing error. We discuss evidence, explanations, and caveats of this finding in Section 4.

Our second (and perhaps more interesting) algorithmic insight focuses on the “end game”, when the algorithm is already close to a reasonable clearing error. Here, we show that making tiny-but-cleverly-optimized perturbations to the budgets (rather than prices) can quickly lead to the holy grail of zero clearing error. Before going into the details, we remark that (i) in the practical benchmark implementation, students budgets are already perturbed at random (and with larger perturbations); (ii) our insight is inspired directly by the non-algorithmic existence proof in (Budish, 2011), which perturbs the students’ budgets twice: once to guarantee a desirable fixed point of the tatonnement correspondence, and a second time to break ties between marginal students at the fixed point.

To describe the budget perturbations, let’s start from the end: we would like to return a vector of course prices and almost-equal student budgets and (ideally) zero clearing error. Towards this, at each iteration of the tatonnement the algorithm solves an (NP-hard but fast in practice) integer program to look for a small budgets perturbation that will nudge students’ demand bundles to zero the overall market clearing error. More generally, at each iteration we can find the optimal budgets perturbation, aka the one that minimizes the clearing error. Since our ultimate goal is to find a price vector that works well with an optimal budget perturbation, we use the clearing error with respect to the optimal budget perturbation to perform the next iteration of tatonnement.

While the idea of using optimal budget perturbations is extremely effective algorithmically, we have to be careful not to open opportunities for manipulability: although budget increases are very small, doing it based on student’s reported course preferences could open an opportunity for strategic reporting. To this end, we encode in our integer program the same EF-TB constraints that guarantee the SP-L (Strategyproof in the Large) condition for the original A-CEEI mechanism. Although this makes the integer program larger, we can solve it very efficiently (see Section 3.1.1 for some optimizations).

1.2. Contribution II: Empirically evaluating the incentives of A-CEEI

In theory, the A-CEEI mechanism has a very desirable property: it is Strategyproof in the Large (SP-L); i.e. the expected utility any student can gain by misreporting their true preferences diminishes as the number of students goes to infinity (Azevedo and Budish, 2019)111The informal intuition is that students who are “price-takers”, i.e. they regard the prices of courses as set “by the market”, receive the optimal schedule they can afford and thus have no incentive to misreport their preferences.. What does this theory guarantee for realistic schools with a finite number of students? Unfortunately, the answer is not much: the formal SP-L convergence guarantee ( (Azevedo and Budish, 2019, Theorem 1)) requires the number of students to be much larger than the number of possible types. For the general A-CEEI mechanism222In practice, students’ reporting language is often more restricted, but still the number of students is always much smaller than the number of possible types., a type consists of a ranking of all possible schedules; the number of possible schedules is exponential in the number of courses, and the number of ways they can be ranked adds another layer of exponentiation. In other words, until the number of students is doubly-exponential in the number of courses, the formal convergence results for SP-L mechanisms are meaningless.

The situation is further complicated by the computational intractability of the A-CEEI problem. A natural approach for dealing with the large number of possible deviations is to directly analyze the way students could manipulate the algorithm’s choice of equilibrium. This has been fruitful in analyzing simple algorithms (Vitercik, 2021; Akbarpour et al., 2020). But because of the PPAD-hardness of the A-CEEI problem we resort to a highly nontrivial heuristic algorithm (see Contribution I). Theoretically analyzing how a possible misreport of preferences would affect the trajectory in price space taken by this algorithm seems far from tractable.

Going beyond intractable theoretical guarantees on students’ incentives, our approach is to empirically evaluate them. Our main question in this part is:

In practice, can students gain in the A-CEEI mechanism by manipulating their reported preferences?

Here, it is paramount that we have our novel fast heuristic algorithm: Previously, it was barely possible to compute one allocation, so re-computing allocations for each possible deviation was completely out of the question. Anecdotally, this is the reason why the computational exploration of the same issue in Budish’s original paper was limited to tiny examples with 2 students and 4 courses (Budish, 2010, Footnote 31).

Still, no matter how fast our equilibrium computation algorithm, we cannot possibly enumerate all possible deviations (again, in theory their number is doubly exponential in the number of courses). However, it is reasonable to expect that computationally- and informationally-bounded students also cannot test every possible deviation. We thus model a strategic student using a simple hill-climbing algorithm that adjusts the single course weights starting from the original truthful report. We also consider different restrictions on the student’s information about the market, as detailed in Definition 2.

In Section 6 we use our manipulation-finding algorithm in combination with our fast A-CEEI finding algorithm to explore the plausibility of effective manipulations for students bidding in A-CEEI. Originally, we had expected that since our mechanism satisfies the EF-TB and SP-L properties, it would at least be practically strategyproof — if even we don’t really understand the way our algorithm chooses among the many possible equilibria, how can a student with limited information learn to strategically bid in such a complex environment?

Indeed, in 2 out of 3 schools that we tested, our manipulation-finding algorithms finds very few or no statistically significant manipulations at all. However, when analyzing the 3rd school, we stumbled upon a simple and effective manipulation for (the first iteration of) our mechanism. We emphasize that although the manipulation is simple in hindsight, in over a year of working on this project we failed to predict it by analyzing the algorithm — the manipulation was discovered by the algorithm.

Inspired by this manipulation, we propose a natural strengthening of envy-free (discussed below), which we call contested-envy free. We encode the analogous contested EF-TB as a new constraint in our algorithm (specifically, the integer program for finding optimal budget perturbations). Fortunately, our algorithm is still very fast even with this more elaborate constraint. And, when we re-run our manipulation-finding experiments, we observe that contested EF-TB significantly reduces the potential for manipulations in practice.

1.3. Contribution III: Contested Envy Free (but for Tie Breaking)

In this section we gradually build towards our new notions of contested-envy free, and contested EF-TB. We begin with the basic notion of Envy-Free (EF): an allocation is said to be envy free if no student prefers the schedule allocated to another student .

In the course allocation problem, due to the challenges of integrality constraint and combinatorial demand, EF allocations rarely exist, but A-CEEI allocations are guaranteed to satisfy important relaxations of EF such as EF-TB (discussed below). In contrast, contested-EF is a strengthening of EF. To motivate the distinction between EF and contested-EF, consider the following anecdote. (This anecdote is for illustration purposes only; in Section 5 we discuss examples of courses and students derived from manipulations found by our algorithm on instances with real preferences.)

Example 0 (Contested envy free).

Eric drives a Honda and Mohammad drives a Porsche. Eric would rather have Mohammad’s Porsche than his Honda. However, Eric doesn’t envy Mohammad, because his kids are in his Honda, and he wouldn’t trade the bundle of for Mohammad’s Porsche (with no kids).

Eric loves his own kids, but nobody else would want them in their car; we thus say that they’re uncontested for understanding the envy between Eric and Mohammad. Formally, in the the specific context of A-CEEI333More generally when prices aren’t available it is natural to extend the notion of “uncontested” to capture under-demanded goods. we say that contested are the goods with strictly positive price, and goods with zero price are uncontested. Considering uncontested goods for the purposes of determining envy is an obvious source of incentive issues: Eric can always report a low value for his kids to claim to envy Mohammad’s allocation. Because they’re uncontested, Eric is still guaranteed to have them in any Pareto optimal allocation.

If we restrict our attention to contested goods, Eric would indeed rather trade his Honda for Mohammad’s Porsche. More generally, we say that Eric contested-envies Mohammad if Eric prefers any subset of over his own allocation. Notice that contested EF is a strengthening of EF.

As mentioned before, EF allocations rarely exist in the course allocation problem. Azevedo and Budish (Azevedo and Budish, 2019) relax the notion of EF to allow tie-breaking (EF-TB): The students are ranked at random444In practice a combination of seniority and random ranking may be used., and the allocation is said to satisfy EF-TB if no student envies any lower-ranked students. (However, may envy higher-ranked students.) EF-TB is not a very satisfying fairness criterion555For fairness, (Budish, 2011) introduced the notion of Envy-Free-up-to-1-good (EF1) and proved that it is satisfied by A-CEEI., but it does imply strategyproof-in-the-large (SP-L) (Azevedo and Budish, 2019).

A-CEEI allocations satisfy EF-TB when the budgets are assigned at random because no student can envy another student with a lower budget (if ’s budget is lower, then ’s schedule must also be affordable for ). When we introduce optimal budget perturbations, we simply encode EF-TB as a constraint in our perturbation-finding integer program: if ’s initial tie breaker is lower than ’s, then the EF-TB constraint is that cannot envy in the perturbed economy. While in theory this approach satisfies SP-L, in practice it can open the door to manipulations; see Sections 5 and 6 for discussion and evidence from experiments.

We can generalize EF-TB to contested EF-TB in the natural way: no student can contested-envy a lower ranked student. We henceforth refer to the EF-TB criterion as classic EF-TB to distinguish it from contested EF-TB.

Note that contested EF-TB is a strengthening of classic EF-TB, so it also implies SP-L. Observe also that if all the budgets respect the random TB rule, then any A-CEEI allocation is contested EF-TB. In our new algorithm, because of the optimal budget perturbations, the budgets may not respect the original TB order; instead, we encode the contested EF-TB constraint in the integer program that optimizes over budget perturbations.

In Section 6 we bring a quantitative analysis of our manipulation-finding algorithm: we give evidence from experiments on real students bids, suggesting that when we enforce contested EF-TB, it is fairly hard to find successful manipulations.

1.4. Limitations of our approach

Modeling students’ valuations

Throughout the paper we take students’ reported preferences as their true valuations. In practice, students do not perfectly report their full preferences (Budish and Kessler, 2022). In fact, students usually have a limited interface, e.g. they may rate courses as “favorite, great, good, fair”, and there is a hand-tuned formula converting those ratings to utilities. Concurrent work by (Soumalias et al., 2022) focuses on the orthogonal direction of better eliciting and modeling of students’ preferences using neural networks. Equilibrium computation is a major bottleneck of their approach, and we leave it to future work to see if our respective algorithms can be combined effectively.

Variance across markets

We are very fortunate to be able to test our algorithms on real data from a few different programs shared with us by Cognomos. There seem to be large variance between instances from different programs. In particular, in one school we find significant manipulations for the no-EF-TB and classic-EF-TB constraints, whereas in others those variants were also hard to manipulate. Running times also vary greatly between instances. However, two trends are consistent between all the instances we tested: (i) our algorithm is much faster than the previous state of the art, and (ii) contested EF-TB seems to have desirable incentive properties. We plan to test on more datasets as they become available.

Limitations of the manipulation finding algorithm

Our algorithm for discovering profitable manipulations is a highly imperfect surrogate to the real question of can real students find robust manipulations? On one hand, students can come up with more complicated manipulations than the ones considered by our algorithm; on the other hand, the algorithm has more information than any single student would normally have. A particular issue is that we run our experiment for exploring profitable deviations with very small sample sizes: even with a very fast algorithm and restriction to very simple manipulations, we have to restrict our experiment to a as few as five samples, which is quite noisy. (We later validate every candidate manipulation with at least 100 iterations.) To make sure that our manipulation-finding algorithm still makes sense, we benchmark it on the HBS mechanism which is known to be manipulable (Budish and Cantillon, 2012); indeed we find significant manipulations are possible with HBS on all instances.

1.5. Conclusion

In this work, we give a significantly faster algorithm for computing A-CEEI. Kamal Jain’s famous formulation “if your laptop cannot find it then neither can the market” (Papadimitriou, 2007) was originally intended as a negative result, casting doubt on the practical implications of many famous economic concepts because of their worst-case computational complexity results. Even for course allocation, where a heuristic algorithm existed and worked in practice, Jain’s formulation seemed to still bind, as solving A-CEEI involved an intense day-long process with a fleet of high-powered cloud servers operating in parallel. The work detailed in this paper has significantly progressed what laptops can find: even the largest and most challenging real course allocation problems we have access to can now be solved in under an hour on a commodity laptop.

This significant practical improvement suggests that the relationship between prices and demand for the course allocation problem—and potentially other problems of economic interest with complex agent preferences and heterogeneous goods—may be much simpler than has been previously believed and may be far more tractable in practice than the worst-case theoretical bounds. Recalling Jain’s dictum, perhaps many more market equilibria can be found by laptops—or, perhaps, Walras’s original and seemingly naive description of how prices iterate in the real world may in fact typically produce approximate equilibria.

Our fast algorithm also opens the door for empirical research on A-CEEI, because we can now solve many instances and see how the solution changes for different inputs. We took it in one direction: empirically investigating the incentives properties of A-CEEI for the first time. For course allocation specifically, this faster algorithm opens up new avenues for improving student outcomes through experimentation. For instance, university administrators often want to subsidize some group of students (e.g., second-year MBA students over first-year MBA students), but are unsure how large of a budget subsidy to grant those students to balance equity against their expectations. Being able to run more assignments with different subsidies can help to resolve this issue.

Remark 1 (Zero vs small clearing error).

We highlight that our algorithm is not only fast - it also finds allocations with zero clearing error. Even the non-algorithmic existence proof of (Budish, 2011) only guarantees a small clearing error.

While the previous heuristic algorithm was able to find adequate allocations in practice, it introduces some additional potential manipulability. That algorithm was a three-stage process. The first stage finds an approximate equilibrium, which equilibrium will tend to have both undersubscription in positive-price courses as well as oversubscription. This is the approximate equilibrium guaranteed to exist by (Budish, 2011). The second stage progressively increases course prices to eliminate all oversubscription. This tends to increase total clearing error but makes the solution implementable, since all of the error comes from underallocating seats in valuable courses. The final stage is a “backfill” process, where students are sequentially allocated extra budget and allowed to spend that budget on courses that are undersubscribed.

While the backfill process substantially reduces the deadweight loss of computed assignments it may have problematic incentive and fairness properties. Students who get first shot at spending that extra budget in the backfill may be able to add an excellent course to their schedule. In particular, the backfill process is not known to satisfy properties like (contested) EF-TB or SP-L. Observe, however, that the backfill process is only necessary because of the clearing error found in the original approximate equilibrium. In contrast, so far our new algorithm has found A-CEEI with zero clearing error on every instance it has encountered. This completely obviates the need for the second and third stages of (Budish et al., 2017): with no clearing error, there are no seats that need to be backfilled.

Remark 2 (Social welfare).

Although our main focus is on improving the algorithmic efficiency and incentives guarantees of the A-CEEI mechanisms, in Appendix C we compare the social welfare of our algorithm and the previous approach. Although the results aren’t as decisive as on other metrics, we observe that our algorithm tends to give better allocations in terms of (utilitarian and Nash) social welfare.

Discussion of additional related work can be found in Appendix A.

2. Preliminaries

Definition 0 (The course allocation market).

A course allocation market consists of:

-

•

courses, where each course has an integral amount of capacity ;

-

•

students, where each student has a utility function over each course bundle.

Definition 0 (Allocation, excess demand, and market-clearing error).

Fix a market , course prices , and student budgets , the allocation function is defined as

We further define the excess demand function as

and the clipped excess demand function as

And we define the market-clearing error as .

Definition 0 (Approximate competitive equilibrium from equal incomes (A-CEEI)).

For constant and market , we say a pair of prices and budgets forms an -CEEI if there is

-

•

small market-clearing error: ;

-

•

small budget perturbation: .

2.1. (Contested) Envy-Free-but-for-Tie-Breaking

We formally define the notions of EF-TB and contested EF-TB. For both, it is important to make the distinction between the initial budgets that are determined exogenously (e.g. at random), and the final budgets which may also depend on the reported preferences. In both cases, students’ initial budgets play a second role in determining the direction in which envy is allowed; in particular the initial budgets are assumed to be distinct (hence “tie-breaking”).

Definition 0 (Envy-Free-but-for-Tie-Breaking (EF-TB)).

Given an initial budget , for a market , price , and budget , the allocation is called EF-TB with respect to budget , if for all student such that , we have for all bundle .

Furthermore, we say that an A-CEEI algorithm is EF-TB, if for any market and any initial budget , the final allocation is always EF-TB with respect to .

Definition 0 (Contested Envy-Free-but-for-Tie-Breaking (Contested EF-TB)).

Given an initial budget , for a market , price , and budget , the allocation is called contested EF-TB with respect to budget and price , if for all student such that , we have for all bundle such that .

Furthermore, we say that an A-CEEI algorithm is contested EF-TB, if for any market and any initial budget , the final allocation is always contested EF-TB with respect to and .

2.2. Utility functions

While the A-CEEI existence works for general ordinal preferences, we focus on the following restricted class of utility functions. This class is consistent with most utilities reported in practice, which are typically taken to be additively-separable utilities, (i) with a preference for schedules satisfying a minimum-number-of-course-units requirements, and (ii) subject to satisfying simple constraints, e.g. timing and curriculum conflicts. Using the language of Operations Research, schedule validity is a hard constraint, while having a schedule meet a student’s requirements is a soft constraint. (The problem remains PPAD-complete in the worst-case when restricted to this class; see Appendix D.)

Formally, every utility function can be described by a tuple , such that for every possible bundle ,

| (1) |

where is some large number such that . The function and also follow some structures so that they can be efficiently represented (e.g., in a mixed-integer program).

3. Our algorithm

In this section we describe our fast heuristic algorithm for computing A-CEEI. We begin with a description of the basic algorithm (Subsection 3.1). We then move to describe some further optimizations that we found helpful when solving larger instances (Subsection 3.2).

3.1. Our Basic Algorithm

All our algorithms take as inputs the students’ reported preferences , the course capacities , and initial budgets that are determined at random, sometimes with a bonus for seniority. Our basic algorithm proceeds as follows: At each iteration, the algorithm looks for the optimal budget perturbation given current prices; then it computes the market clearing error for this optimal budget perturbation; finally, it updates the prices according to tatonnement rule. The algorithm terminates when it reaches zero clearing error666It is also a good idea to enforce a time limit as a solution with zero clearing error is not even guaranteed to exist, but in practice we managed to find solutions with zero clearing error on all the instances we encountered.. The pseudocode is given in Algorithm 1.

-

(1)

Let .

-

(2)

-budget perturbation: find budgets such that the market-clearing error is minimized under the following constraints:

-

(a)

The maximum perturbation ;

-

(b)

Allocation is EF-TB with respect to if , or contested EF-TB with respect to and if .

Furthermore, we shall use as the tie-breaker to guarantee the uniqueness of the solution, i.e., always picking with minimum among all optimal solutions.

-

(a)

-

(3)

If , terminate with .

-

(4)

Otherwise, update , then go back to step 2.

Computing the -budget perturbation.

To compute the -budget perturbation in the second step, we should optimize among all possible budget perturbations so that the resulting clearing error is minimized. Observe that for any fixed price vector, the demand of any student can only change on some budgets that are the sum of some prices; and the sum of prices is always a multiple of the fixed step size .

Therefore, we can always partition the interval of Student ’s possible budgets into sub-intervals , such that ’s demand bundle is constant on each sub-interval:

| (2) |

where s are multiples of in .

Once we compute these arrays, we can solve for the optimal -budget perturbation using the following integer linear program:

| (Budget-Perturb-ILP) | ||||||

| (Minimize clearing error) | ||||||

| s.t. | (Clearing error: ) | |||||

| (Clearing error: ) | ||||||

| (1 schedule per student) | ||||||

| (Integral allocations) | ||||||

We add the following constraint to ensure (contested) EF-TB: For any student such that ’s priority is higher than (i.e. ), and any , if the (contested) EF-TB is violated when student is allocated and student is allocated , i.e. according to Definition 4 and 5, then we prevent simultaneously allocating to student and allocating to student .

| (3) |

Remark 3.

Solving integer programs is NP-hard in general, but we can solve (Budget-Perturb-ILP) quite fast in practice with modern SAT solvers.

Fact 1.

Fix parameters and . For a market and initial budgets , if Algorithm 1 terminates on input , its output forms a -CEEI and the final allocation is EF-TB with respect to if , or contested EF-TB with respect to and if .

3.1.1. Speeding up the search of budget perturbations satisfying EF-TB constraints

The simple implementation of searching EF-TB constraints is that we enumerate all pairs of students with their possible demands and check (3) for all the EF-TB constraints. However, on larger instances this process is very slow because we need to consider pairs of students, each student may receive one of bundles, and finally for each pair of possible bundles checking (3) requires to solve student ’s optimal bundle out of a subset of courses ( for classic EF-TB and for contested EF-TB). For an economy with more than students, it requires to solve for more than million such optimal bundles. Repeating that on each iteration is quite slow! For this issue, we consider two optimizations:

- Two simple sufficient conditions for no-envy::

-

Fixing , we shall use two simple sufficient conditions for proving that allocating and to does not violate the (contested) EF-TB constraints. Because these two conditions are easy to verify, we can reduce the number of times we check (3) a lot and thus save a lot of time. The first condition comes from the reporting language: even if the entire super-bundle is invalid for student , its utility from ’s perspective is no greater than that for , i.e.,

The second condition is from the fact that is the ’s optimal allocation under budget . If the total price of bundle is upper bounded by , .

- Memorize envious pairs of students::

-

Students with very different preferences are likely to never envy each other throughout the run of the algorithm. We take advantage of this idea by only enumerating all pairs of students every 10 iterations, and in the other 9 iterations we only consider pairs of students whose envy constraint was tight in a past iteration. In particular, when the optimal budget perturbation results in a zero-error solution (under a partial enumeration of possible envies), we force the algorithm to recompute the iteration by enumerating all pairs of students. Note that this implementation cannot guarantee that the allocation computed in each iteration satisfies (contested) EF-TB. However, it guarantee the final allocation satisfies (contested) EF-TB.

On an instance with approximately 3000 students, these two optimizations speed up our time-per-iteration (amortized including iterations where we check all pairs) by a factor of about 300.

3.2. Shortcuts in price space

Warm starts.

In the preliminary experiments, we observe the following phenomena when using different step sizes and proper budget perturbation.

-

•

When the step size is small compared to , the algorithm can converge to a zero-error solution. However, for courses that are consistently slightly over-demanded, their prices increase slowly from to their final prices. With these courses, the algorithm needs almost or even more steps to converge.

-

•

On the other hand, when the step size is large, the number of possible budget-demand pairs for each student may not be enough to help the budget perturbation significantly improve the clearing error. However, even if we set to (i.e. we only use discrete tatonnement), the prices found by the algorithm can be quite close to good regions, where prices found with smaller lie, and the algorithm only takes much less time to reach such regions because of the larger step size.

Motivated by these observations, we shall combine discrete tatonnement and our algorithm together to improve the speed. We shall first run discrete tatonnement with a larger step size and with steps, and then turn to our algorithm with a smaller step. In the first warm-start phase we also save time by not computing optimal budget perturbations.

Merge Equivalent Steps.

As discussed above, when we use smaller step sizes, it may take the algorithm many iterations to update some prices. Fortunately, it turns out that for many of those iterations the set of possible demands remains constant across all students for many consecutive iterations. Whenever this is the case, we can save time by binary searching for the next iteration where the excess demand changes. A further more clever optimization considers stretches where the demand sets alternate between only a few possible vectors; again we can binary search for the number of iterations that we need to take to reach a new demand vector.

4. Computational performance of our algorithm

In this section, we discuss the computational performance of our algorithm, in particular in comparison to the previous state of the art. In Subsection 4.1, we describe our experiments comparing the algorithms. Then, in Subsection 4.2 we focus on how the improvements described in Section 3.2 compare to our basic algorithm.

4.1. Comparing with the benchmark

In this subsection we compare our algorithm with the benchmark algorithm. As we will soon see (Figure 2), our algorithm is much faster. To understand why, we also consider two intermediate algorithms. Overall, the algorithms we compare are:

- Benchmark:

-

The (previous) state-of-the-art commercial algorithm; see description in Appendix B.

- Vanilla:

-

Vanilla tatonnement, aka without optimizations such as tabu search, individual price adjustments, or optimal budget perturbations, that are used in other variants that we consider (for pseudocode, see Algorithm 1 with ).

- Basic:

- Fast:

-

Our final algorithm, including optimizations from Subsection 3.2.

Choice of parameters.

All the algorithms perturb the students’ budgets: Benchmark and Vanilla use only random perturbations, while Basic and Fast use a mix of random and optimal budget perturbations. Larger budget perturbations tend to make the algorithmic task of finding an (approximate) equilibrium easier: At one extreme, the existence proof holds even with infinitesimal budget perturbations; at the other extreme, with infinite budget perturbations the mechanism reduces to Random Serial Dictatorship which is computationally trivial.

For the sake of a fair comparison of the algorithms, we ensure the algorithms have the same magnitude of total budget perturbations:

-

•

For Benchmark and Vanilla we draw the budgets uniformly i.i.d. from .

-

•

For Basic and Fast, we draw the base budgets uniformly i.i.d. from , and allow further optimal budget perturbation of magnitude .

In particular, we consider here. We use a large step size of for the warm start of Fast. For the remaining parameters, we replicate that of (Budish et al., 2017) for Benchmark and use the same step size of for all the algorithms (except in the warm start).

Instances.

For the computational experiments, we use the largest instances available to us:

-

•

Law - A law school with about 500 students and 125 classes/sections

-

•

Ivy Large - A large Ivy-league business school with several thousand students and several hundred classes/sections

-

•

Ivy Huge - A large Ivy-league business school with several thousand students and around a thousand classes/sections and lots of challenging constraints

A typical student’s schedule in those instances has around 5 courses, although some schools bid in the fall for the entire year (so around 10 courses total).

Findings

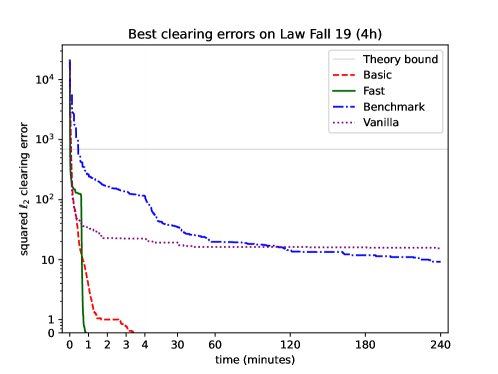

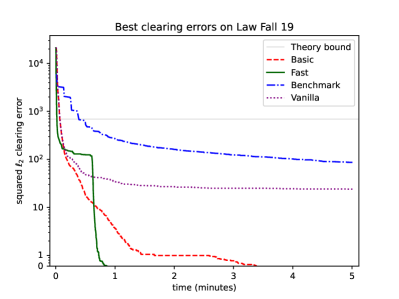

Figure 2 presents the average777 This is an average over different draws of students’ initial budgets; we use 20 runs for Basic and Fast, and 10 runs for the slower Benchmark and Vanilla. best clearing error found by the four algorithms with respect to time.

Observation 1: optimal budget perturbations help, significantly.

From the plot, we can see that the two algorithms with budget perturbation (i.e. Basic and Fast) significantly outperform those without budget perturbation (i.e. Benchmark and Vanilla) on clearing errors — when our basic algorithm terminates with a -CEEI, the average best clearing errors found by Benchmark and Vanilla are still larger than 30. Therefore, we believe budget perturbation is the most important ingredient introduced in our algorithms for clearing the market.

Observation 2: individual price adjustments do not help.

In Figure 2 and 3 it can be observed that Vanilla obtains lower clearing error than Benchmark on all the instances we tested. More precisely if we run both algorithms long enough then Benchmark does eventually catch up (Figure 1), but only at a time scale much larger than our algorithm needs to converge to zero clearing error.

The observation that individual price adjustments slow the algorithm is very surprising since it stands in contrast to the findings of (Othman et al., 2010). It is even more puzzling because in each iteration Algorithm 3 chooses the (myopically) better of updating all the prices or one, so it seems intuitive that individual price adjustments can only help. One simple reason is that the time-per-iteration of Benchmark is significantly slower compared to Vanilla888We note that in the experiments we actually measure a proprietary variant of the benchmark algorithm whose time-per-iteration has been heavily optimized. We also note that when we tried to combine individual price adjustments with optimized budget perturbations, the computational overhead of individual price adjustments was even worse because we had to resolve for optimal budget perturbation for each individual price adjustment.. (In (Othman et al., 2010) this issue did not come up because both algorithms were tested in terms of number of iterations.)

Another interesting piece of this puzzle is that (Othman et al., 2010) thought of tatonnement as computer scientists often do: a direction for a local search algorithm with the objective of minimizing the clearing error (indeed, in some utility models it exactly corresponds to a (sub)-gradient of the clearing error, e.g. (Kelso and Crawford, 1982; Cheung et al., 2020; Leme and Wong, 2020)). When viewed in this way, it may sometimes get stuck in local minima. However, inspired by economics, we view tatonnement as a distributed process where we modify the price of each course simultaneously without worrying about the global clearing error. When used in this way, it may sometimes locally increase the clearing error; but our experiments suggest that it can effectively escape those local minima, leading to better solutions faster. Indeed the clearing error does not monotonically decrease throughout the run of our algorithm.

Observation 3: Our optimized algorithm initially has larger clearing errors than our basic algorithm.

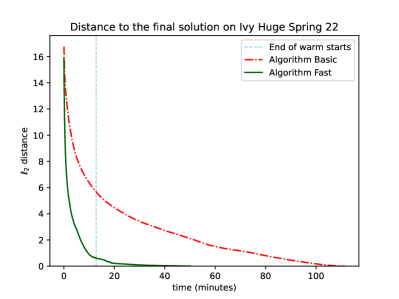

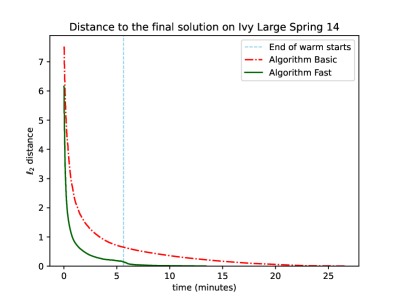

In the plot, it is easy to spot the sharp drop of clearing error for Fast — this is exactly the time when Fast switches from the warm start to the second phase. It may appear that the time we spend on the warm start is too long, but this is in fact not the case, as we discuss in Subsection 4.2.

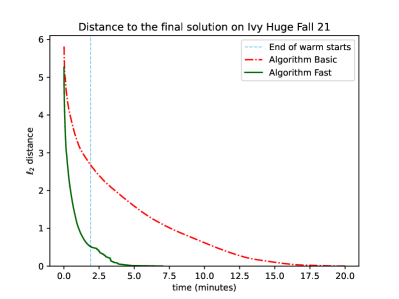

4.2. Our optimized algorithm

As mentioned in Observation 3 above, Fast initially makes slow progress in terms of market clearing error during the warm start compared to Basic. We argue that it still makes important progress towards the eventual equilibrium even if we don’t see that in the clearing error. First, we note that although we did not carefully optimize the cutoff of the warm start (we heuristically set it to approximately , where is the step size), Fast seems to work really well in practice!

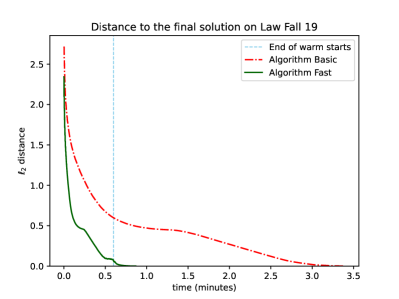

More interestingly, we can measure the progress towards the eventual equilibrium in terms of distance in price space (instead of current clearing error). In Figure 2 and 4, we show that the optimized algorithm approaches an ultimate equilibrium much faster when measured in price space distance. We also observe that at the time that the algorithm switches phases, we’re already quite close in price space, so a more refined (small step size) second phase is appropriate. (Of course we unfortunately only know the distance to eventual equilibrium in hindsight, otherwise this could have made for a great heuristic approach to knowing when to switch phases!)

5. Examples of successful manipulations

How can strategic students manipulate SP-L mechanisms in realistic instances? To really understand the nature of manipulations found by the algorithm, in this section we report insights from our qualitative analysis that zooms in on specific manipulations, one for each variant of our algorithm. Our representation is over simplified with made up student names and courses — but they’re all based on manipulations discovered by our manipulation-finding algorithm on almost-real data (see Remark 4). Of course, each case study may not be representative of all possible manipulations. However, we find this methodology quite helpful for gaining intuition. In particular, we were able to use the case study for classic EF-TB to extract the simple manipulation described in the introduction, and propose the contested EF-TB criterion in response.

All the examples are described in what can be informally thought of as an “almost-large-market”: from the perspective of an individual student, course prices are approximately set by other students, but a student’s reported preferences can nudge them infinitesimally towards a market clearing equilibrium.

Remark 4 (5-additive utilities).

Unfortunately, the original preferences in the true instances are incredibly complicated, mostly due to various constraints imposed by the schools (e.g. avoiding courses with conflicting meeting times, meeting minimum unit requirements, etc). To keep the case study analyses tractable, we repeat the manipulation finding experiments, but on modified preferences that ignore all those constraints and simply assume that the students utility is 5-additive, i.e. each student wants the schedule of 5 courses that maximizes the total weight; here we use the original course weights reported by the students, but ignore all conflicts and requirements. Formally, for every student , the new utility function can be described by tuple where , and for every bundle ,

5.1. A simple manipulation without EF-TB

Example 0 (Manipulation without EF-TB constraints).

Alice and Bob both want only the last seat of CS161. Because of other students’ demand, ECON101 is full but has a low price. With true reporting CS161 could go to either Alice or Bob, depending on the random initial budgets.

Bob can manipulate his preferences to report that he wants ECON101 as his second course (aka Bob’s manipulated preferences are:

Under the manipulated preferences, since ECON101 is cheap, the only way it will not be allocated to Bob is if Bob exhausts his budget on CS161. Even if Alice’s initial budget is higher, the optimal unconstrained budget perturbation will make sure that Bob’s final budget is higher than Alice’s, in which case he gets CS161 and Alice gets nothing — an equilibrium.

For this manipulation to work, Bob had to know that at equilibrium prices ECON101 is already exactly filled by other students — a knowledge he is unlikely to have in realistic bidding. Indeed, suppose that demand for ECON101 was higher this semester, the algorithm raised its price, and now it is missing exactly one student: in this case the optimal budget perturbation would have to ensure that Bob does get into ECON101, which can be achieved by perturbing budgets against Bob and letting Alice grab the last seat in CS161.

However, this manipulation is fairly robust if the price of ECON101 is always very low (“ECON101 tends to have a low price” is a general statistic that a student could plausibly learn from historical bids). In this case, even if ECON101 is missing a student, Bob’s budget may be larger than Alice’s by a sufficient margin to afford both CS161 and ECON101. So when ECON101 is undersubscribed, the budget perturbation could go either way999Alice would have a slight advantage due to our particular tie-breaking rule., but it always goes in favor of the strategic Bob when ECON101 is oversubscribed.

5.2. A simple manipulation with classic EF-TB

Example 0 (Manipulation with classic EF-TB constraints).

Alice and Bob both want the last seat in the popular CS161 course. But Alice is even more excited about taking independent research units with her advisor, of which there is unlimited supply, so the price is always zero (aka this is an uncontested course); she would like to take both. Bob’s second choice is ECON101; because of other students’ demand, ECON101 is full but has a low price.

With true preferences, since ECON101 is cheap, the only way it will not be allocated to Bob is if Bob exhausts his budget on CS161. Thus even if Alice ranks higher, the optimal budget perturbation sets her budget lower than Bob. In this case Alice always gets independent study (only), and Bob always gets CS161 (only) — an equilibrium.

If Alice misreports her preferences to rank independent research units lower than CS161, she would envy Bob whenever he gets the last seat to CS161. Whenever her initial budget is higher, this prevents the optimal budget perturbation from driving it below Bob’s, increasing her chances of getting the last seat in CS161.

Note that ranking the uncontested course (independent research units) lower never hurts Alice. So this manipulation is profitable in expectation for Alice even if she only has very noisy information about her rank and other students’ demand.

Interestingly, this manipulation works because of the EF-TB constraints that we introduce to prevent manipulations!

5.3. A simple manipulation with contested EF-TB

We now discuss a simple manipulation that our algorithm discovered even with the contested EF-TB; while some profitable manipulations may exist in practice, as we show in Section 6 they’re extremely rare.

Example 0 (Manipulation with contested EF-TB constraints).

Many students, including Bob, like to take CS161 and ECON101 together, but they rank ECON101 over CS161. Alice already took ECON101 last semester, so she only wants the last seat in CS161. Because of other students’ demand, ECON101 is full but has a very low price.

With true preferences, if Bob’s budget is higher than Alice’s by a margin greater than the price of ECON101, he could afford both CS161 and ECON101, leaving Alice with nothing.

Alice could manipulate her preferences to report that she wants ECON101 as her second course. Bob always gets ECON101, because it’s cheap and it’s his top priority. Whenever Alice doesn’t get CS161 she has to get ECON101 (because its price is cheap); if both Bob and Alice get ECON101, the course becomes oversubscribed, which would cause a clearing error. Therefore the optimal budget perturbation would make sure Bob’s budget is low enough compared to Alice’s that he can’t afford both courses: he will get ECON101, and Alice will get CS161 - an equilibrium.

As with Example 1, this manipulation does pose some risk — if ECON101 is undersubscribed, the optimal budget perturbation may reduce Alice’s budget below the price of CS161 so that she has to take ECON101. However, if ECON101 is very cheap, there’s always also the small perturbation that increases Alice’s budget so that she can afford both ECON101 and CS161 (while Bob only affords ECON101). So, because of the asymmetry in the prices of CS161 and ECON101, if ECON101 is oversubscribed, this manipulation can increase Alice’s chances of getting into CS161, but if ECON101 is undersubscribed, Alice’s chances aren’t hurt by much.

5.4. Can A-CEEI with random budget perturbation be manipulated?

All the manipulations that we found seemed tied to our optimal budget perturbations procedure. So it is natural to ask whether the original A-CEEI101010For fair comparison, note that the previous state-of-the-art practical implementation augmented the original A-CEEI mechanism with two stages that had other incentive issues (see Remark 1). without optimal budget perturbations can also be manipulated

We speculatively conjecture in practice that manipulations similar to those described in Example 3 can also be profitable without optimal budget perturbations: the simplest way to think about this example is that Alice adding ECON101 to her demand should (slightly) increase the price of ECON101; this makes it less likely for Bob to be able to afford both ECON101 and CS161; this in turn makes it more likely that Alice can get a seat in CS161.

While it seems plausible that such manipulations are profitable in practice, note that for our algorithm with contested EF-TB, our numerical analysis in Section 6 suggests that they are extremely rare. Either way, at this point for A-CEEI without optimal budget perturbations we can only speculate: we could not run our manipulation-finding algorithm with the original A-CEEI algorithm that only uses random budget perturbation because this algorithm is too slow. (The manipulation-finding algorithm needs to make many calls to the A-CEEI algorithm to evaluate different possible deviations for every student.)

6. Quantitative analysis of manipulability

In this section we ask whether in practice strategic students bidding in A-CEEI have an incentive to deviate from truth-telling. To address this question, we model the student’s process for choosing her bids with an optimization algorithm that can try different bid manipulations and test whether they improve the student’s utility.

6.1. The manipulation-finding algorithm

It is still intractable to consider all possible bid-manipulations. This is true both for a student optimizing their bid, and for our algorithms in our experiments. Instead, we restrict attention to a simple hill-climbing algorithm that iteratively looks for a course whose bid-manipulation would increase the utility, in expectation over uncertainty; see Algorithm 2 for details. To validate our approach, we benchmark our manipulation-finding algorithm on a course allocation mechanism that is known to be manipulable (Budish and Cantillon, 2012), which is used at Harvard Business School (we henceforth refer to this mechanism as HBS).

To simplify notations, we explicitly define the notation of randomized mechanism for course allocation problem.

Definition 0 (Randomized mechanism).

A randomized mechanism for course allocation problem can be characterized by a function , which takes the input of the course allocation market and randomness , and outputs an allocation where denotes the bundle that the mechanism allocated to student .

For example, HBS is a randomized mechanism, where the randomness is used to determine the order of students in the random serial dictatorship process. Our A-CEEI algorithm (Algorithm 1) with fixed parameters can also be seen as a randomized mechanism, since an allocation can be uniquely determined based on its output (prices and budgets), and the base budgets are determined by randomness .

Remark 5.

Note that in Definition 1, we do not require the allocation generated by the mechanism to be feasible (i.e., some courses might be oversubscribed). That is because no A-CEEI algorithm can guarantee to always output a price with zero clearing error. Nevertheless, our algorithm was observed to always obtain a feasible solution in all instances we encountered, as mentioned before.

In our experiments on manipulability of a specific mechanism, we iteratively run (a variant of) Algorithm 2 multiple times with respect to different parameters for every student, under the different uncertainty models described later in Definition 2.

-

(1)

Let (or the best manipulation found in previous iterations with different ).

-

(2)

Denote the description for by .

-

(3)

Try to increase or decrease the weight for each course in to obtain new misreports . Each can be described by where for , .

-

(4)

Let

-

(5)

If , terminate with as the best manipulation found when , otherwise return failed.

-

(6)

Otherwise, update and go back to step 2.

Practical optimizations

Since computing the exact expected value in the step 4 is generally intractable, we have to use samples to estimate it. For computational efficiency, we only use 5 samples for each estimation in following experiments, which is a fairly small number. As a result, some profitable manipulations might be missed, and some non-profitable manipulations can be reported incorrectly. Nevertheless, we will use a larger number of samples to test the statistical significance of those manipulations found by Algorithm 2.

We also use another optimization to reduce the number of times we have to solve for an A-CEEI, we search for manipulations in parallel: in each run of Algorithm 2 we actually consider a subset of several students and who are trying out their deviation on the same instance (students subsets are shuffled in each iteration to ensure that the signal corresponds to the deviation by the student and not to particular deviations by their peers).

Handling false positive manipulations

For any manipulation that is profitable on average in the exploration phase (which, as mentioned above is very noisy), we run it for iterations, and then more if it is still profitable. At this point we eliminated manipulations whose profitability did not meet p-value statistical significance.

The original experiments had many false positives, and we expect as many as of them would to survive the p-value test. So for all manipulations that survived the first p-value test, we run additional iterations, and report manipulations that still have p-value .

6.2. Modeling students’ uncertainty

In practice, while students often know the course capacities, they tend to have limited, aggregate information about historical bids; furthermore it is impossible for the students to know the algorithm’s randomness at the time of bidding. We therefore study the students’ decision process under two different models of uncertainty: Resampled randomness is the most conservative model of students’ uncertainty — even if they have perfect knowledge of their peers’ preferences, they never know the randomness of the algorithm (in particular, the random budget perturbation) at the time of bidding. Resampled population adds the students’ uncertainty about their peers’ preferences. See details of both models in Definition 2.

Definition 0 (Profitable manipulation).

For a randomized mechanism , student ’s original utility function and some manipulation , we say the manipulation from to is profitable

-

•

under resampled randomness : profitable in expectation under the market and randomness where , i.e.,

-

•

under resampled population : profitable in expectation under the market and randomness where and , i.e.,

Given a known market , for every student we let be the distribution that re-samples other students, independently and with replacement, from of the true population of other students.

6.3. Experiment set-up

Choice of parameters

For our A-CEEI algorithm (Algorithm 1), we always seek for a -CEEI, where . Same as before, we draw base budgets uniformly i.i.d. from (i.e., ) and allow further optimal budget perturbation of magnitude . We choose different step sizes for different instances to speed up computation. Specifically, we use for Ivy Small, for Biz, and for Small.

For the manipulation-finding algorithm (Algorithm 2), we let the set of local update coefficients be .

The instances

Despite various optimizations, our manipulation-finding ultimately requires solving a very large number of A-CEEI instances, which can require significant computational resources even with our efficient algorithm. Therefore we run this experiment on relatively small instances:

-

•

Small - A small business school with about 150 students and 50 classes/sections (Fall 2021).

-

•

Ivy Small - An Ivy-league business school with about 500 students and 50 classes/sections (Fall 2020).

-

•

Biz - A business school with about 500 students and 50 classes/sections (Fall 2020).

6.4. Statistical findings

Our numerical results are summarized in Table 1. Our algorithm successfully finds profitable manipulations for the benchmark manipulable HBS mechanism on all instances. On instances Small and Biz it finds almost no statistically significant profitable manipulations for any variant of our A-CEEI algorithm. For Ivy Small, it finds that about 7% of the students can gain as much as around 10% from misreporting their preferences with no EF-TB constraints, and somewhat less with classic EF-TB constraints; however with contested EF-TB profitable manipulations were extremely rare.

| Instance | Uncertainty | Mechanism | |||||||

|---|---|---|---|---|---|---|---|---|---|

| No EF-TB | Classic EF-TB | Contested EF-TB | HBS | ||||||

| # | Gain | # | Gain | # | Gain | # | Gain | ||

| Small | Randomness | 1 | 0.04% | 0 | - | 1 | 0.04% | 66 | |

| Population | 0 | - | 0 | - | 0 | - | 63 | ||

| Ivy Small | Randomness | 21 | 15 | 1 | 0.02% | 107 | |||

| Population | 20 | 11 | 0 | - | 117 | ||||

| Biz | Randomness | 0 | - | 0 | - | 0 | - | 87 | |

| Population | 1 | 0.7% | 0 | - | 0 | - | 64 | ||

Remark 6.

We are not sure why profitable manipulations for no EF-TB and classical EF-TB manipulations were found only for Ivy Small and not for the other schools. We observe at equilibrium Ivy Small has two courses that are in very high demand — their price exceeds the entire budgets of some students.

References

- (1)

- Akbarpour et al. (2020) Mohammad Akbarpour, Scott Duke Kominers, Kevin Michael Li, Shengwu Li, and Paul Milgrom. 2020. Investment Incentives in Truthful Approximation Mechanisms. SSRN (2020). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3544100

- Amanatidis et al. (2022) Georgios Amanatidis, Haris Aziz, Georgios Birmpas, Aris Filos-Ratsikas, Bo Li, Hervé Moulin, Alexandros A. Voudouris, and Xiaowei Wu. 2022. Fair Division of Indivisible Goods: A Survey. CoRR abs/2208.08782 (2022). https://doi.org/10.48550/arXiv.2208.08782 arXiv:2208.08782

- Amanatidis et al. (2021) Georgios Amanatidis, Georgios Birmpas, Aris Filos-Ratsikas, Alexandros Hollender, and Alexandros A. Voudouris. 2021. Maximum Nash welfare and other stories about EFX. Theor. Comput. Sci. 863 (2021), 69–85. https://doi.org/10.1016/j.tcs.2021.02.020

- Arunachaleswaran et al. (2022) Eshwar Ram Arunachaleswaran, Siddharth Barman, and Nidhi Rathi. 2022. Fully Polynomial-Time Approximation Schemes for Fair Rent Division. Mathematics of Operations Research 47, 3 (2022), 1970–1998. https://doi.org/10.1287/moor.2021.1196

- Azevedo and Budish (2019) Eduardo M Azevedo and Eric Budish. 2019. Strategy-proofness in the Large. The Review of Economic Studies 86, 1 (08 2019), 81–116. https://doi.org/10.1093/restud/rdy042 arXiv:https://academic.oup.com/restud/article-pdf/86/1/81/27285295/rdy042.pdf

- Aziz (2015) Haris Aziz. 2015. Competitive equilibrium with equal incomes for allocation of indivisible objects. Oper. Res. Lett. 43, 6 (2015), 622–624. https://doi.org/10.1016/j.orl.2015.10.001

- Babaioff et al. (2021) Moshe Babaioff, Noam Nisan, and Inbal Talgam-Cohen. 2021. Competitive Equilibrium with Indivisible Goods and Generic Budgets. Math. Oper. Res. 46, 1 (2021), 382–403. https://doi.org/10.1287/moor.2020.1062

- Barman et al. (2018) Siddharth Barman, Sanath Kumar Krishnamurthy, and Rohit Vaish. 2018. Finding Fair and Efficient Allocations. In Proceedings of the 2018 ACM Conference on Economics and Computation, Ithaca, NY, USA, June 18-22, 2018, Éva Tardos, Edith Elkind, and Rakesh Vohra (Eds.). ACM, 557–574. https://doi.org/10.1145/3219166.3219176

- Boodaghians et al. (2022) Shant Boodaghians, Bhaskar Ray Chaudhury, and Ruta Mehta. 2022. Polynomial Time Algorithms to Find an Approximate Competitive Equilibrium for Chores. In Proceedings of the 2022 ACM-SIAM Symposium on Discrete Algorithms, SODA 2022, Virtual Conference / Alexandria, VA, USA, January 9 - 12, 2022, Joseph (Seffi) Naor and Niv Buchbinder (Eds.). SIAM, 2285–2302. https://doi.org/10.1137/1.9781611977073.92

- Bouveret et al. (2017) Sylvain Bouveret, Katarína Cechlárová, Edith Elkind, Ayumi Igarashi, and Dominik Peters. 2017. Fair Division of a Graph. In Proceedings of the Twenty-Sixth International Joint Conference on Artificial Intelligence, IJCAI 2017, Melbourne, Australia, August 19-25, 2017, Carles Sierra (Ed.). ijcai.org, 135–141. https://doi.org/10.24963/ijcai.2017/20

- Bouveret et al. (2016) Sylvain Bouveret, Yann Chevaleyre, and Nicolas Maudet. 2016. Fair Allocation of Indivisible Goods. In Handbook of Computational Social Choice, Felix Brandt, Vincent Conitzer, Ulle Endriss, Jérôme Lang, and Ariel D. Procaccia (Eds.). Cambridge University Press, 284–310. https://doi.org/10.1017/CBO9781107446984.013

- Brânzei et al. (2015) Simina Brânzei, Hadi Hosseini, and Peter Bro Miltersen. 2015. Characterization and Computation of Equilibria for Indivisible Goods. In Algorithmic Game Theory - 8th International Symposium, SAGT 2015, Saarbrücken, Germany, September 28-30, 2015, Proceedings (Lecture Notes in Computer Science, Vol. 9347), Martin Hoefer (Ed.). Springer, 244–255. https://doi.org/10.1007/978-3-662-48433-3_19

- Brânzei et al. (2016) Simina Brânzei, Yuezhou Lv, and Ruta Mehta. 2016. To Give or Not to Give: Fair Division for Single Minded Valuations. In Proceedings of the Twenty-Fifth International Joint Conference on Artificial Intelligence, IJCAI 2016, New York, NY, USA, 9-15 July 2016, Subbarao Kambhampati (Ed.). IJCAI/AAAI Press, 123–129. http://www.ijcai.org/Abstract/16/025

- Budish (2010) Eric Budish. 2010. The Combinatorial Assignment Problem: Approximate Competitive Equilibrium from Equal Incomes. (2010). https://faculty.chicagobooth.edu/eric.budish/research/budish-approxceei-Aug2010.pdf Working paper version of paper with the same title..

- Budish (2011) Eric Budish. 2011. The Combinatorial Assignment Problem: Approximate Competitive Equilibrium from Equal Incomes. Journal of Political Economy 119, 6 (2011), 1061 – 1103. http://EconPapers.repec.org/RePEc:ucp:jpolec:doi:10.1086/664613

- Budish et al. (2017) Eric Budish, Gérard P. Cachon, Judd B. Kessler, and Abraham Othman. 2017. Course Match: A Large-Scale Implementation of Approximate Competitive Equilibrium from Equal Incomes for Combinatorial Allocation. Oper. Res. 65, 2 (2017), 314–336. https://doi.org/10.1287/opre.2016.1544

- Budish and Cantillon (2012) Eric Budish and Estelle Cantillon. 2012. The Multi-unit Assignment Problem: Theory and Evidence from Course Allocation at Harvard. The American Economic Review 102, 5 (2012), 2237–2271. http://www.jstor.org/stable/41724620

- Budish and Kessler (2022) Eric Budish and Judd B. Kessler. 2022. Can Market Participants Report Their Preferences Accurately (Enough)? Manag. Sci. 68, 2 (2022), 1107–1130. https://doi.org/10.1287/mnsc.2020.3937

- Caragiannis et al. (2019) Ioannis Caragiannis, Nick Gravin, and Xin Huang. 2019. Envy-Freeness Up to Any Item with High Nash Welfare: The Virtue of Donating Items. In Proceedings of the 2019 ACM Conference on Economics and Computation, EC 2019, Phoenix, AZ, USA, June 24-28, 2019, Anna Karlin, Nicole Immorlica, and Ramesh Johari (Eds.). ACM, 527–545. https://doi.org/10.1145/3328526.3329574

- Chaudhury et al. (2022a) Bhaskar Ray Chaudhury, Jugal Garg, Peter McGlaughlin, and Ruta Mehta. 2022a. Competitive Equilibrium with Chores: Combinatorial Algorithm and Hardness. In EC ’22: The 23rd ACM Conference on Economics and Computation, Boulder, CO, USA, July 11 - 15, 2022, David M. Pennock, Ilya Segal, and Sven Seuken (Eds.). ACM, 1106–1107. https://doi.org/10.1145/3490486.3538255

- Chaudhury et al. (2022b) Bhaskar Ray Chaudhury, Jugal Garg, Peter McGlaughlin, and Ruta Mehta. 2022b. On the Existence of Competitive Equilibrium with Chores. In 13th Innovations in Theoretical Computer Science Conference, ITCS 2022, January 31 - February 3, 2022, Berkeley, CA, USA (LIPIcs, Vol. 215), Mark Braverman (Ed.). Schloss Dagstuhl - Leibniz-Zentrum für Informatik, 41:1–41:13. https://doi.org/10.4230/LIPIcs.ITCS.2022.41

- Chaudhury et al. (2021) Bhaskar Ray Chaudhury, Jugal Garg, Kurt Mehlhorn, Ruta Mehta, and Pranabendu Misra. 2021. Improving EFX Guarantees through Rainbow Cycle Number. In EC ’21: The 22nd ACM Conference on Economics and Computation, Budapest, Hungary, July 18-23, 2021, Péter Biró, Shuchi Chawla, and Federico Echenique (Eds.). ACM, 310–311. https://doi.org/10.1145/3465456.3467605

- Chen et al. (2009) Xi Chen, Xiaotie Deng, and Shang-Hua Teng. 2009. Settling the complexity of computing two-player Nash equilibria. Journal of the ACM (JACM) 56, 3 (2009), 1–57.

- Cheung et al. (2020) Yun Kuen Cheung, Richard Cole, and Nikhil R. Devanur. 2020. Tatonnement beyond gross substitutes? Gradient descent to the rescue. Games Econ. Behav. 123 (2020), 295–326. https://doi.org/10.1016/j.geb.2019.03.014

- Daskalakis et al. (2009) Constantinos Daskalakis, Paul W Goldberg, and Christos H Papadimitriou. 2009. The complexity of computing a Nash equilibrium. SIAM J. Comput. 39, 1 (2009), 195–259.

- Diebold et al. (2014) Franz Diebold, Haris Aziz, Martin Bichler, Florian Matthes, and Alexander W. Schneider. 2014. Course Allocation via Stable Matching. Bus. Inf. Syst. Eng. 6, 2 (2014), 97–110. https://doi.org/10.1007/s12599-014-0316-6

- Foley (1967) Duncan K. Foley. 1967. Resource allocation and the public sector. Yale economic essays 7, 1 (1967), 45–98. mit Bibliogr..

- Garg et al. (2021) Jugal Garg, Martin Hoefer, Peter McGlaughlin, and Marco Schmalhofer. 2021. When Dividing Mixed Manna Is Easier Than Dividing Goods: Competitive Equilibria with a Constant Number of Chores. In Algorithmic Game Theory - 14th International Symposium, SAGT 2021, Aarhus, Denmark, September 21-24, 2021, Proceedings (Lecture Notes in Computer Science, Vol. 12885), Ioannis Caragiannis and Kristoffer Arnsfelt Hansen (Eds.). Springer, 329–344. https://doi.org/10.1007/978-3-030-85947-3_22

- Goldman and Procaccia (2014) Jonathan R. Goldman and Ariel D. Procaccia. 2014. Spliddit: unleashing fair division algorithms. SIGecom Exch. 13, 2 (2014), 41–46. https://doi.org/10.1145/2728732.2728738

- Kelso and Crawford (1982) Alexander S. Kelso and Vincent P. Crawford. 1982. Job Matching, Coalition Formation, and Gross Substitutes. Econometrica 50, 6 (1982), 1483–1504.

- Leme and Wong (2020) Renato Paes Leme and Sam Chiu-wai Wong. 2020. Computing Walrasian equilibria: fast algorithms and structural properties. Math. Program. 179, 1 (2020), 343–384. https://doi.org/10.1007/s10107-018-1334-9

- Lipton et al. (2004) Richard J. Lipton, Evangelos Markakis, Elchanan Mossel, and Amin Saberi. 2004. On approximately fair allocations of indivisible goods. In Proceedings 5th ACM Conference on Electronic Commerce (EC-2004), New York, NY, USA, May 17-20, 2004, Jack S. Breese, Joan Feigenbaum, and Margo I. Seltzer (Eds.). ACM, 125–131. https://doi.org/10.1145/988772.988792

- Merting et al. (2019) Sören Merting, Martin Bichler, and Aykut Uzunoglu. 2019. Assigning Course Schedules: About Preference Elicitation, Fairness, and Truthfulness. In Proceedings of the 40th International Conference on Information Systems, ICIS 2019, Munich, Germany, December 15-18, 2019, Helmut Krcmar, Jane Fedorowicz, Wai Fong Boh, Jan Marco Leimeister, and Sunil Wattal (Eds.). Association for Information Systems. https://aisel.aisnet.org/icis2019/data_science/data_science/15

- Othman et al. (2016) Abraham Othman, Christos H. Papadimitriou, and Aviad Rubinstein. 2016. The Complexity of Fairness Through Equilibrium. ACM Trans. Economics and Comput. 4, 4 (2016), 20:1–20:19. https://doi.org/10.1145/2956583

- Othman et al. (2010) Abraham Othman, Tuomas Sandholm, and Eric Budish. 2010. Finding approximate competitive equilibria: efficient and fair course allocation. In 9th International Conference on Autonomous Agents and Multiagent Systems (AAMAS 2010), Toronto, Canada, May 10-14, 2010, Volume 1-3, Wiebe van der Hoek, Gal A. Kaminka, Yves Lespérance, Michael Luck, and Sandip Sen (Eds.). IFAAMAS, 873–880. https://dl.acm.org/citation.cfm?id=1838323

- Papadimitriou (2007) C.H. Papadimitriou. 2007. The complexity of finding nash equilibria. In Algorithmic Game Theory, Noam Nisan, Tim Roughgarden, Éva Tardos, and Vijay V. Vazirani (Eds.). Cambridge University Press, 29–51. https://doi.org/10.1017/CBO9780511800481

- Peters et al. (2022) Dominik Peters, Ariel D. Procaccia, and David Zhu. 2022. Robust Rent Division. In NeurIPS-22: Proc. 36th Annual Conference on Neural Information Processing Systems, 2022.

- Peysakhovich and Kroer (2019) Alexander Peysakhovich and Christian Kroer. 2019. Fair Division Without Disparate Impact. CoRR abs/1906.02775 (2019). arXiv:1906.02775 http://arxiv.org/abs/1906.02775

- Plaut and Roughgarden (2020) Benjamin Plaut and Tim Roughgarden. 2020. Almost Envy-Freeness with General Valuations. SIAM J. Discret. Math. 34, 2 (2020), 1039–1068. https://doi.org/10.1137/19M124397X

- Roth (2002) Alvin E. Roth. 2002. The Economist as Engineer: Game Theory, Experimentation, and Computation as Tools for Design Economics. Econometrica 70, 4 (2002), 1341–1378. https://doi.org/10.1111/1468-0262.00335 arXiv:https://onlinelibrary.wiley.com/doi/pdf/10.1111/1468-0262.00335

- Roth (2007) Alvin E. Roth. 2007. Repugnance as a Constraint on Markets. Journal of Economic Perspectives 21, 3 (September 2007), 37–58. https://doi.org/10.1257/jep.21.3.37

- Rubinstein (2018) Aviad Rubinstein. 2018. Inapproximability of Nash Equilibrium. SIAM J. Comput. 47, 3 (2018), 917–959. https://doi.org/10.1137/15M1039274

- Soumalias et al. (2022) Ermis Soumalias, Behnoosh Zamanlooy, Jakob Weissteiner, and Sven Seuken. 2022. Machine Learning-powered Course Allocation. CoRR abs/2210.00954 (2022). https://doi.org/10.48550/arXiv.2210.00954 arXiv:2210.00954

- Suksompong (2023) Warut Suksompong. 2023. A characterization of maximum Nash welfare for indivisible goods. Economics Letters 222 (2023), 110956. https://doi.org/10.1016/j.econlet.2022.110956

- Thomson and Varian (1985) William Thomson and Hal R. Varian. 1985. Theories of justice based on symmetry. Social goals and social organization : essays in memory of Elisha Pazner (1985), 107–129.

- Varian (1974) Hal R Varian. 1974. Equity, envy, and efficiency. Journal of Economic Theory 9, 1 (1974), 63–91. https://doi.org/10.1016/0022-0531(74)90075-1

- Vitercik (2021) Ellen Vitercik. 2021. Automated algorithm and mechanism configuration. Ph. D. Dissertation. Carnegie Mellon University. http://reports-archive.adm.cs.cmu.edu/anon/2021/abstracts/21-125.html

- Wang et al. (2020) Zihe Wang, Zhide Wei, and Jie Zhang. 2020. Bounded Incentives in Manipulating the Probabilistic Serial Rule. (2020), 2276–2283. https://ojs.aaai.org/index.php/AAAI/article/view/5605

- Wright and Vorobeychik (2015) Mason Wright and Yevgeniy Vorobeychik. 2015. Mechanism Design for Team Formation. In Proceedings of the Twenty-Ninth AAAI Conference on Artificial Intelligence, January 25-30, 2015, Austin, Texas, USA, Blai Bonet and Sven Koenig (Eds.). AAAI Press, 1050–1056. http://www.aaai.org/ocs/index.php/AAAI/AAAI15/paper/view/9902

Appendix A Additional related work

(Wright and Vorobeychik, 2015) consider an adaptation of A-CEEI to team formation games (where agents need to be able to afford all their teammates). They empirically evaluate the gain from a manipulation using a different algorithm than the one we describe in Section 6. They report that on an instance based on 17 students ranking each other, the adapted A-CEEI was significantly more manipulable than the adapted HBS. In contrast, in our experiments for course allocation HBS is always more manipulable.

(Diebold et al., 2014) survey different mechanisms for the course allocation problem. A newer work by (Merting et al., 2019) focuses course allocation via a variant of Probabilistic Serial mechanism; incentives properties of Probabilistic Serial were also recently studied by (Wang et al., 2020).

(Brânzei et al., 2015) study the existence and complexity of exact CEEI with indivisible goods which are either perfect substitutes or complements (unfortunately courses in our instances satisfy neither). (Garg et al., 2021; Boodaghians et al., 2022; Chaudhury et al., 2022a, b) study the problem of designing (approximate or exact) algorithms for computing a CEEI over divisible chores. Interesting variants of CEEI have also been studied by (Aziz, 2015; Brânzei et al., 2016; Peysakhovich and Kroer, 2019; Babaioff et al., 2021).

The fair allocation of indivisible goods has received a lot of attention recently, see for example the recent surveys of (Bouveret et al., 2016) and (Amanatidis et al., 2022). In particular, there is a large body of theoretical work on existence, algorithms, and complexity of allocations satisfying EF1 (as does A-CEEI) or its strengthening EFX (e.g. (Lipton et al., 2004; Bouveret et al., 2017; Barman et al., 2018; Caragiannis et al., 2019; Plaut and Roughgarden, 2020; Amanatidis et al., 2021; Chaudhury et al., 2021; Arunachaleswaran et al., 2022; Suksompong, 2023). Most of those works focus on cases where the agents’ valuation functions satisfy nice properties ranging from additivity to subadditivity; some of these assumptions are applicable in other settings (see e.g. Spliddit (Goldman and Procaccia, 2014)), but for course allocation real-world students utilities are quite complex — they are not sub-additive, and in fact not even monotone.

There has also been a recent body of work on the computation of economic equilibria, which could be considered the most practical application of Alvin Roth’s idea of “The Economist as Engineer” (Roth, 2002). (Peters et al., 2022), similar to our work, provides theoretical grounding and experimental results based on real data for the fair allocation of indivisible goods in a specific context (rent sharing). Works such as (Kelso and Crawford, 1982; Cheung et al., 2020; Leme and Wong, 2020) (and many references therein) provide some theoretical grounding for what we found practically in developing our new search algorithm: that gradient descent-inspired tatonnement may be surprisingly effective for finding approximate equilibria despite worst-case complexity results.

Appendix B The benchmark algorithm

Our benchmark for comparison is the (previous) commercial state of the art algorithm. We provide an overview of the algorithm here, and more details can be found in academic publications (Othman et al., 2010; Budish et al., 2017)111111Our benchmark corresponds to the “first phase” of the algorithm described in (Budish et al., 2017). The remaining two phases are only used to cope with the fact that in practice clearing error is one-sided: undersubscribed courses are undesirable, but oversubscribed courses are absolutely infeasible, due e.g. to safety regulations for room capacities. This is a conservative comparison: we show that our algorithm is already faster than the first phase, and finds assignments with zero clearing error..

-

(1)

Let .

-

(2)

If , terminate with .

-

(3)

Otherwise,

-

•

include all equivalent prices of into the history: ,

-

•

update , and then

-

•

go back to step 2.

-

•