Game Theory with Simulation of Other Players

Abstract

Game-theoretic interactions with AI agents could differ from traditional human-human interactions in various ways. One such difference is that it may be possible to simulate an AI agent (for example because its source code is known), which allows others to accurately predict the agent’s actions. This could lower the bar for trust and cooperation. In this paper, we formalize games in which one player can simulate another at a cost. We first derive some basic properties of such games and then prove a number of results for them, including: (1) introducing simulation into generic-payoff normal-form games makes them easier to solve; (2) if the only obstacle to cooperation is a lack of trust in the possibly-simulated agent, simulation enables equilibria that improve the outcome for both agents; and however (3) there are settings where introducing simulation results in strictly worse outcomes for both players.

1 Introduction

Game theory is in principle agnostic as to the nature of the players: besides individual human beings, they can be households, firms, countries, and indeed AI agents. Nevertheless, throughout most of the development of the field, game theorists have had in mind players that were either humans or entities whose decisions were taken by humans; and as with any theory, the examples one has in mind while developing that theory are likely to affect its focus. If we try to re-develop game theory specifically with AI agents in mind, how might the theory turn out different? Of course, theorems in traditional game theory will not suddenly become false just because of the change in focus. Instead, we would expect any difference to consist in the kinds of settings and phenomena for which we develop models, analysis, and computational tools.

In this paper, we focus on one specific phenomenon that is more pertinent in the context of AI agents: agents being able to simulate each other. If an agent’s source code is available, another agent can simulate what the former agent will do, which intuitively appears to significantly change the game strategically. We consider settings in which one agent can simulate another, and if they do so, they learn what the other agent will do in the actual game; however, simulating comes at a cost to the simulator, and therefore it is not immediately clear whether and when simulation will actually be used in equilibrium. In particular, we are interested in understanding whether and when the availability of such simulation results in play that is more cooperative. For example, in settings where trust is necessary for cooperative behavior (Berg et al., 1995), one may expect that the ability to simulate the other player can help to establish this trust. But does this in fact happen in equilibrium? And if so, does the ability to simulate foster cooperation in all games, or are there games where it backfires? Are we even able to compute equilibria of games with the ability to simulate?

In terms of related work, our setting is similar to the one of credible commitment (von Stackelberg, 1934), except that one needs to decide whether to pay for allowing the other player to commit. Another perspective is that we study program equilibria (Tennenholtz, 2004), except that only one player’s program can read the other’s source code, and has to pay a cost to do so. For further discussion and references, see Section 7.

In the remainder of this introduction, we describe a specific example of a trust game and use it to overview the technical results presented later. We also give several examples that illustrate how simulation can lead to different results when moving beyond trust games. For a quick overview, the key takeaways are in Section 1.1, highlighted in italics.

1.1 Overview and Illustrative Examples

Trust Game

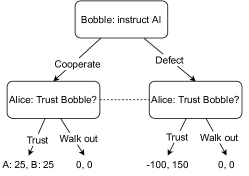

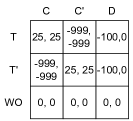

As a motivation, consider the following Trust Game (cf. Figure 1; our TG is a variation on the traditional one from Berg et al. (1995)). Alice has $100k in savings, which are currently sitting in her bank account at a 0% interest rate. She is considering hiring an AI assistant from the company Bobble to manage her savings instead. If Bobble and its AI cooperate with her, the collaboration generates a profit of $50k, to be split evenly between her and Bobble. However, Alice is reluctant to trust Bobble, which might have instructed the AI to defect on Alice by pretending to malfunction, while siphoning off all of the $150k. In fact, the only Nash equilibria of this scenario are ones where Bobble defects on Alice with high probability, and Alice, expecting this, walks out on Bobble.

Adding simulation

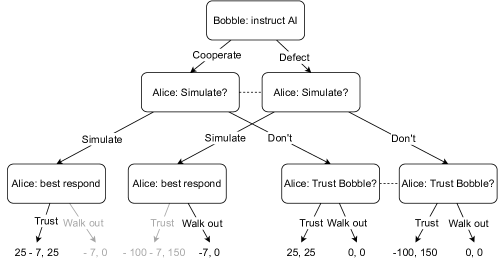

Dismayed by their inability to make a profit, Bobble decides to share with Alice a portion of the AI’s source code. This gives Alice the ability to spend $7k on hiring a programmer, to simulate the AI in a sandbox and learn whether it is going to cooperate or defect. Crucially, we assume that the AI either does not learn whether it has been simulated or is unable to react to this fact. We might hope that this will ensure that Alice and Bobble can reliably cooperate. However, perhaps Alice will try to save on the simulation cost and trust Bobble blindly instead — and perhaps Bobble will bet on this scenario and instruct their AI to defect.

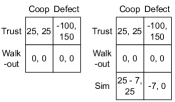

To analyze this modified game , note that when Alice simulates, the only sensible followup is to trust Bobble if and only if the simulation reveals they instructed the AI to cooperate. As a result, the normal-form representation of is equivalent to the normal form of the original game TG with a single added action for Alice (Fig. 2). Analyzing reveals that it has two types of Nash equilibria. In one, Bobble defects with high probability and Alice, expecting this, walks out without bothering to simulate. In the other, Bobble still sometimes defects (), but not enough to stop Alice from cooperating altogether. In response, Alice simulates often enough to stop Bobble from outright defection (), but also sometimes trusts Bobble blindly (). In expectation, this makes Alice and Bobble better off by $16.25k, resp. $25k relative to the (defect, walk-out) equilibrium.

More generally, we can also consider , a parametrization of where simulation costs some . As shown in Figure 2, the equilibria of are similar to the special case for a wide range of c.

| simulation cost | NE of , given as the probs. of (trust, walk-out, simulate) and (cooperate, defect) | ||

|---|---|---|---|

| (simulate, cooperate) | |||

| and | walk-out and | (walk-out, defect) | |

| walk-out and | (walk-out, defect) | ||

Bottom: The extremal equilibria of . The non-extremal NE are precisely the convex combinations of the last two columns.

Top right: The cooperation probability and utilities under each of these NE. The non-extremal NE are light red, the dashed lines illustrate the NE trajectories from Proposition 11. Note that all the red NE (i.e., with ) yield .

Generalizable properties of the trust game

The analysis of Figure 2 illustrates several trends that hold more generally: First, when simulation is subsidized, the simulation game turns into a “pure commitment game” where the simulated player is the Stackelberg leader (Prop. 7 (i)). Conversely, when simulation is prohibitively costly, the simulation game is equivalent to the original game (Prop. 7 (ii)). Third, the simulation game has a finite number of breakpoints between which individual equilibria change continuously — more specifically, the simulator’s strategy does not change at all while the simulated player’s strategy changes linearly in c (Prop. 11). Informally speaking, simulation games have piecewise constant/linear equilibrium trajectories. A corollary of this observation is that it is not the case that as simulation gets cheaper, the simulator must use it more and more often (Fig. 2). Fourth, the indifference principle implies that when the simulator simulates with a nontrivial probability (i.e., neither nor ), the value of information of simulating must be precisely equal to the simulation cost. This also implies that any pure NE of the original game is also a NE of the simulation game for any (Prop. 12). Finally, we saw that at , the outcome of the simulation game becomes deterministic despite the strategy of the simulator being stochastic. (For example, in the NE where Bobble always cooperates, Alice always ends up trusting him — either directly or after first simulating.) In Section 5, we show that this result holds quite generally but not always: By Theorem 2, the equilibria of generic normal-form games with cheap simulation can be found in linear time.

Different effects of simulation

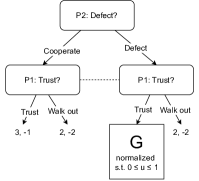

There are games where simulation behaves similarly to the Trust Game above. Indeed, in Theorem 5, we prove that simulation leads to a strict Pareto improvement in generalized trust games with generic payoffs (defined in Section 6). However, simulation can also affect games quite differently from what we saw so far. For example, simulation can benefit either of the players at the cost of the other, or even be harmful to both of them. Indeed, simulation benefits only the simulator in zero-sum games (Prop. 22), benefits only the simulated player in the Commitment Game (Fig. 3), and harms both if cooperation is predicated upon the simulated player’s ability to maintain privacy (Ex. 24). In fact, there are even cases where the Pareto optimal outcome requires simulation to be neither free nor prohibitively expensive (Ex. 28). Finally, with multiple, incompatible ways to cooperate, a game might admit multiple simulation equilibria (i.e., multiple NE with ; cf. Fig. 3).

Right: A variant of Trust Game with multiple simulation NE.

1.2 Outline

The remainder of the paper is structured as follows. First, we recap the necessary background (Section 2). In Section 3, we formally define simulation games and describe their basic properties. In Section 4, we prove several structural properties of simulation games; while these are instrumental for the subsequent results, we also find them interesting in their own right. Afterwards, we analyze the computational complexity of solving simulation games (Section 5) and the effects of simulation on the players’ welfare (Section 6). Finally, we review the most relevant existing work (Section 7), summarize our results, and discuss future work (Section 8). The detailed proofs are presented in the appendix (which is only available in the arXiv version of the paper).

2 Background

A two-player normal-form game (NFG) is a pair where is a finite set of actions and is the utility function. We use P1 and P2 as shorthands for “player one” and “player two”. For finite , denotes the set of all probability distributions over . A strategy (or policy) profile is a pair of strategies . We denote the set of all strategies as . is pure if it has support of size . We identify such strategy with the corresponding action.

For , is the expected utility of . is said to be a best response to if ; denotes the set of all pure best responses to . Since the best-response utility “” is uniquely determined by , we denote it as . (The analogous definitions apply for P2 and .) A Nash equilibrium (NE) is a strategy profile under which each player’s strategy is a best response to the strategy of the other player. We use to denote the set of all Nash equilibria of .

A pure-commitment equilibrium (cf. von Stackelberg (1934)) is, informally, a subgame-perfect equilibrium of the game in which the leader first commits to a pure action, after which the follower sees the commitment and best-responds, possibly stochastically. Since our formalism will assume that P1 is the simulator, we naturally encounter situations where P2 acts as the leader. Formally, we will use to denote all pairs where the optimal commitment and P1’s best-response policy satisfy .

Below, we sometimes restrict the analysis to particular classes of NFGs. To motivate the first one, recall that a property is said to be generic (typical) if it holds for almost all elements of a set (Rudin, 1987, 1.35)

Definition 1 (Generic games).

We say that a statement holds for games with generic payoffs if, among games whose payoffs are sampled i.i.d. from the uniform distribution over , P holds with probability 1.

Since different joint actions in a generic-payoff NFG necessarily yield different payoffs, these games are a special case of the following more general class:

Definition 2 (No best-response utility tiebreaking).

An NFG is said to admit no best-response utility tiebreaking by P1 if for every pure strategy of P2, any two pure best-responses give P2 the same utility, i.e. .

Note that if satisfies Def. 2, any pure-commitment equilibrium can be identified with a joint action s.t. and .

3 Simulation Games

In this section, we formally define simulation games and describe their basic properties. To streamline this initial investigation of simulation games, we assume that when the simulator learns the other agent’s action, they always best-respond to it — that is, they will not execute non-credible threats (Shoham and Leyton-Brown, 2008). (However, this assumption somewhat limits the applicability of the results, and we consider moving beyond it a worthwhile future direction.)

Notation 3.

For a two-player NFG , , resp. , is the set of all stochastic, resp. pure best-response policies.

Definition 4 (Simulation game).

(1) For a simulation cost , the simulation game is defined as the NFG that is identical to , except that P1 additionally has access to “simulation” actions , , s.t. , .

(2) For a fixed , denotes the game where P1 has a single additional action with , .

We refer to P1 as the simulator and to P2 as the simulated player. When the exact value of c is unspecified or unimportant, we write instead of .

3.1 Basic Properties

In the remainder of this paper, we will only study simulation games in the context of a fixed best-response policy. To justify this decision, note that the variants (1) and (2) of Definition 4 are equivalent for most games:

Lemma 5.

If (and only if) admits no best-response utility tiebreaking by P1, and are identical up to the existence of duplicate actions.

Moreover, the problem of solving general simulation games can be reduced to the problem of solving simulation games for a fixed best-response policy:

Lemma 6.

(i.e., the new NE introduced by adding simulation) can be written as a disjoint union .

The next observation we make (Proposition 7) is that if simulation is too costly, then it is never used and the simulation game becomes strategically equivalent to the original game . Conversely, if simulation is subsidized (i.e., a negative simulation cost), then P1 will always use it, which effectively turns into a pure-commitment game with P2 moving first. (The situation is similar when simulation is free but not subsidized, except that this allows for additional equilibria where the simulation probability is less than .)

Proposition 7 (Equilibria for extreme simulation costs).

In any simulation game , we have:

-

(i)

For , simulating is a strongly dominant action.

In particular, .111 If we allowed P1 to consider all possible best-response policies, would turn into equality. -

(ii)

For ,

S is a strictly dominated action.In particular, .

3.2 Information-Value of Simulation

The following definition measures the extra utility that the simulator can gain by using the knowledge of the other player’s strategy:

Definition 8 (Value of information of simulation).

The value of information of simulation for is

Lemma 9.

.

Lemma 9 implies that always lies between and the difference between maximum possible and P1’s maxmin value. Moreover, to make P1 simulate with a non-trivial probability, P2 needs to pick a strategy whose value of information is equal to the simulation cost:

Lemma 10 ( is equal to simulation cost).

(1) For any , we have . (2) Moreover, unless admits multiple optimal commitments of P2 that do not have a common best-response, any has .

(Where, in (2), a set of actions having a common best-response means that .)

4 Structural Properties

We now review several structural properties that appear in simulation games because of the special nature of the simulation action.These results will prove instrumental when determining the complexity of simulation games (Sec. 5) and predicting the impact of simulation on the players’ welfare (Sec. 6). Moreover, we find these results interesting in their own right.

The first of these properties is that a change of the simulation cost typically results in a very particular change in a Nash equilibrium of the corresponding game: The strategy of the simulating player (P1) doesn’t change at all, while the simulated player’s strategy changes linearly. However, to be technically accurate, we need to make two disclaimers. First, there is a finite number of “atypical” values of c, called breakpoints, where the nature of the NE strategies changes discontinuously.222 While all of the non-breakpoint equilibria extend to the corresponding breakpoints as limits (Definition 13), the breakpoints might also admit additional non-limit equilibria, typically convex combinations of the limits (cf. Figure 2). Second, there can be multiple equilibria, which complicates the formal description of the result.

Proposition 11 (Trajectories of simulation NE are piecewise constant/linear).

For every , there is a finite set of simulation-cost breakpoint values such that the following holds: For every and every , there is a linear mapping such that and for every .

Since we were not able to find any existing result that would immediately imply this proposition, we provide our own proof in the appendix. However, a related result in the context of parameterized linear programming appears in (Adler and Monteiro, 1992, Prop. 2.3). As an intuition for why this result holds, recall that in an equilibrium, each player uses a strategy that makes the other player indifferent between the actions in their support. Since P2’s payoffs are not affected by c, P1 should keep their strategy constant to keep P2 indifferent, even when c changes. Similarly, increasing c linearly decreases P1’s payoff for the simulate action, so P2 needs to linearly adjust their strategy to bring P1’s payoffs back into equilibrium.

A particular corollary of Proposition 11 is that while one might perhaps expect simulation will gradually get used more and more as it gets more affordable, this is in fact not what happens — instead, the simulation rate is dictated by the need to balance the unchanging tradeoffs of the other player.

The second structural property of simulation games is the following refinement of Proposition 7:

Proposition 12 (Gradually recovering the NE of ).

Let be a NE of . Then , as a strategy in with , is a NE precisely when .

In particular, is a breakpoint of .

Together, these two results imply that with , may have no NE in common with . As we increase c, the NE of gradually appear in as well, while the simulation equilibria of (i.e., those with ) gradually disappear, until eventually .

4.1 Equilibria for Cheap Simulation

By combining the concept of value of information with the piecewise constancy/linearity of simulation equilibria, we are now in a position to give a more detailed description of Nash equilibria of games where simulation is cheap. First, we identify the equilibria of with that might be connected to the equilibria for :

Definition 13 (Limit equilibrium of ).

A policy profile is a limit equilibrium (at ) of if it is a limit of some where .

As witnessed by the Trust Game (and Table 2 in particular), not every NE of is a limit equilibrium. Note that this definition automatically implies a stronger condition:

Lemma 14.

For any limit equilibrium of , there is some and such that for every , is a NE of .

The following result shows that cheap-simulation equilibria have a very particular structure. Informally, every such NE corresponds to a “baseline” limit equilibrium and P2’s “deviation policy” . As the simulation cost increases, P2 gradually deviates away from their baseline, which forces P1 to randomize between their baseline and simulating. While the technical formulation can seem daunting, all of the conditions in fact have quite intuitive interpretations that can be used for locating the simulation equilibria of small games by hand.

Lemma 15 (Structure of cheap-simulation equilibria).

Let and suppose that admits no best-response utility tiebreaking by P1. Then any with is of the form , where

and the following holds:

-

(i)

For every , .

-

(ii)

is some baseline policy that satisfies:

-

(B1)

every action in the support of is a best-response to every action from ;

-

(B2)

every action in the support of is an optimal commitment by P2 conditional on P2 only using strategies that satisfy (B1).

-

(B1)

-

(iii)

is some deviation policy that satisfies:

-

(D1)

No lies in for all .

-

(D2)

Every satisfies one of

-

(D3)

If satisfies , resp. ,

it maximizes the attractiveness ratio , resp.among all that satisfy , resp. .

-

(D1)

In a generic game, these conditions even imply that both the baseline and deviation policies are pure.

Theorem 1 (Equilibria with binary supports).

Let be a game with generic payoffs and . Then all NE of are either pure or have supports of size two.

5 Computational Aspects

We now investigate the difficulty of solving simulation games. Since many of the results hold for multiple solution concepts, we formulate them using the phrase “solving a game”, with the understanding that this refers to either finding all Nash equilibria, or a single NE, or a single NE with a specific property (e.g., one with the highest social welfare). For a specific game , we will also use to denote the breakpoints of (given by Proposition 11). First, note that the number of -s could be exponential:

Proposition 16 (Games can have exponentially many breakpoints).

For every , there is a two-player NFG with such that has at least breakpoints.

As an upper bound on the complexity of solving simulation games, their definition immediately yields that:

Proposition 17 (Simulation games are no harder than general games).

Solving is at most as difficult as solving a normal-form game where P1 has one more action than in .

For extreme values of c, Prop. 7 implies the following:

Proposition 18 (Solving for extreme c).

(i) For , the time complexity of solving is .

(ii) For , the time-complexity of solving is the same as the time-complexity of solving .

In contrast with Proposition 18 (ii), finding the equilibria at low simulation costs is straightforward if we restrict our attention to generic-payoff NFGs:

Theorem 2 (Cheap-simulation equilibria in generic games).

Let be a NFG with generic payoffs and . Then the time complexity of finding all equilibria of is .

However, without generic payoffs, simulation games can be as hard to solve as fully general games.

Theorem 3 (Solving general simulation games is hard).

For an NFG whose utilities lie in , let be as in Figure 5. Then for , can be identified with . Moreover, whenever has some NE with , , must have some NE strategy with , .

Finally, it is also generally difficult to determine whether simulation is beneficial or not:

Theorem 4.

For a general NFG and , it is co-NP-hard to determine whether there is s.t. .

6 Effects on Players’ Welfare

As we saw in Theorem 4, there is no simple method for determining whether introducing simulation into a general game will be socially beneficial. However, this does not rule out the possibility of identifying particular sub-classes of games where simulation is useful or harmful. We now first confirm the hypothesis that simulation is beneficial in settings where the only obstacle to cooperation is the missing trust in the simulated player. We then give specific examples to illustrate that in general games, simulation can also benefit either player at the cost of the other, or even be harmful to both.

6.1 Simulation in Generalized Trust Games

We now show that when the only obstacle to cooperation is the lack of trust in the possibly-simulated player, simulation enables equilibria that improve the outcome for both players.

Definition 19 (Generalized trust games).

A game is said to be a generalized trust game if any pure-commitment equilibrium (where P2 is the leader) is a strict Pareto improvement over any .

Theorem 5 (Simulation in trust games helps).

Let be a generalized trust game that admits no best-response utility tiebreaking by P1. Then for all sufficiently low c, admits a Nash equilibrium with that is a strict Pareto improvement over any NE of .

Proof sketch.

We construct a NE where P2 mixes between their optimal commitment (from the pure-commitment equilibrium corresponding to ) and some deviation while P1 mixes between their best-response to and simulating. We show that forms the baseline policy of this simulation equilibrium, which implies that as , this NE eventually strictly Pareto-improves any NE of . (And the fact that cannot be a NE of ensures the existence of a suitable .) ∎

6.2 Simulation in General Games

We now investigate the relationship between simulation cost and the players’ payoffs in general games. We start by listing the two general trends that we are aware of.

The first of the general results is that for the extreme values of c, the situation is always predictable: For , P1 always simulates (Prop. 7) and making simulation cheaper will increase their utility without otherwise affecting the outcome. Similarly, when c is already so high that P1 never simulates, any further increase of c makes no additional difference.

Second, if P2 could choose the value of c, they would generally be indifferent between all the values within a specific interval . Indeed, this follows from Proposition 11, which implies that P2’s utility remains constant between any two breakpoints of .

The Examples 20-24 illustrate that the players might both agree and disagree about their preferred value of c, and this value might be both low and high.

Example 20 (Both players prefer cheap simulation).

In the Alice and Bobble game from Figure 2, each player’s favoured NE exists for .

Example 21 (Only simulator prefers cheap simulation).

Consider the “unfair guess-the-number game” where each player picks an integer between and . If the numbers match, P2 pays to P1. Otherwise, P1 pays to P2. In this game, P2 clearly prefers simulation to be prohibitively costly while P1 prefers as low c as possible.

In fact, Example 21 extends to all zero-sum games:

Proposition 22.

If a zero-sum has NE utilities , then : , .

Example 23 (Only simulator prefers expensive simulation).

In the commitment game (Figure 3), introducing free simulation creates a second NE in which P1 is strictly worse off and stops the original NE from being trembling-hand perfect. If simulation were subsidized, the original simulator-preferred NE would disappear completely. (In fact, with that is not prohibitively costly, the situation is similar to the case.) In summary, this shows that simulation can hurt the simulator, even when using it is free (or even subsidized) and voluntary.

Example 24 (Both players prefer expensive simulation).

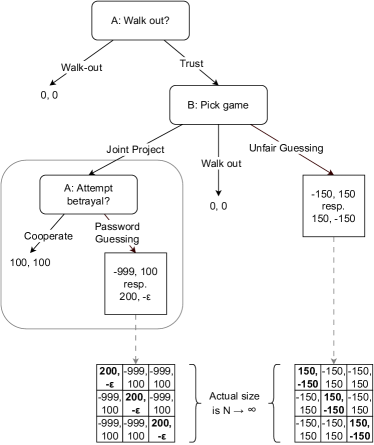

Consider a Joint Project game where P1 proposes that P2 collaborates with them on a startup. If P2 accepts, their business will be successful, yielding utilities . P2 then picks a secure password () and puts their profit in a savings account protected by that password. Finally, P1 can either do nothing or try to guess P2’s password () and steal their money. Successfully guessing the password would result in utilities , , where the comes from opportunity costs. However, if P1 guesses wrong, they will be caught and sent to jail, yielding utilities , (Smith et al., 2009).

Without simulation, the NE of this game is for the players to collaborate and for P1 to not attempt to guess the password. However, with cheap enough simulation, P1 would simulate P2’s choice of password and steal their money — and P2, expecting this, would not agree to the collaboration in the first place. As a result, both players would prefer simulation to be prohibitively expensive.

Example 25 (The preferences depend on equilibrium selection).

Consider various mixed-motive games such as the Threat Game (e.g., (Clifton, 2020, Sec. 3-4)), Battle of the Sexes, or Chicken (e.g., Shoham and Leyton-Brown (2008)). Generally, these games have one pure NE that favours P1, a second pure NE that favours P2, and a mixed NE that is strictly worse than either of the pure equilibria for both P1 and P2. By introducing subsidized simulation into such a game, we eliminate both the simulator-favoured pure NE and the dispreferred mixed NE. This can be bad, neutral, or even good news for the simulator, depending on which of the NE would have been selected in the original game. Somewhat relatedly, introducing subsidized simulation destroys the suboptimal equilibria in Stag Hunt and Coordination Game (e.g., Shoham and Leyton-Brown (2008)).

Beyond the examples above, players might even prefer neither nor but rather something inbetween:

Example 26 (The preferred c is non-extreme).

Informally, the underlying idea behind the example is that the game should have the potential for a positive-sum interaction, but also be unfair towards P1 if they never simulate and unfair towards P2 if P1 always simulates. If we then give each player the option to opt out, the only way either of the players can profit is if simulation is neither free nor prohibitively expensive. For a detailed proof, see Example 28 in Appendix A.

7 Related Work

In terms of the formal framework, our work is closest to the literature on games with commitment (Conitzer and Sandholm, 2006; von Stengel and Zamir, 2010). This is typically modelled as a Stackelberg game (von Stackelberg, 1934), where one player commits to a strategy while the other player only selects their strategy after seeing the commitment. In particular, Letchford et al. (2014) investigates how much the committing player can gain from committing. Commitment in a Stackelberg game is always observed. (An exception is Korzhyk et al. (2011), which assumes a fixed chance of commitment observation.) In contrast, the simulation considered in this paper would correspond to a setting where (1) one player pays for having the other player make a (pure) commitment and (2) the latter player does not know whether their commitment is observed, as the probability of it being observed is a parameter controlled by the observer. Ultimately, these differences imply that the Stackelberg game results are highly relevant as inspiration, but they are unlikely to have immediate technical implications for our setting (except for when ).

In terms of motivation, the setting that is the closest to our paper is open-source game theory and program equilibria [McAfee 1984; Howard 1988; Rubinstein 1998, Sect. 10.4; Tennenholtz 2004]. In program games, two (or more) players each choose a program that will play on their behalf in the game, and these programs can read each other. To highlight the connection to the present paper, note that one approach to attaining cooperative play in this formalism is to have the programs simulate each other (Oesterheld, 2019). The setting of the program equilibrium literature differs from ours in two important ways. First, the program equilibrium literature assumes that both players have access to the other player’s strategy. (Much of the literature addresses the difficulties of mutual simulation or analysis, e.g., see Barasz et al. (2014); Critch (2019); Critch et al. (2022); Oesterheld (2022) in addition to the above.) Second, with the exception of time discounting as studied by Fortnow (2009), the program equilibrium formalism assumes that access to the other player’s code is without cost.

Another approach to simulation is game theory with translucent players (Halpern and Pass, 2018). This framework assumes that the players tentatively settle on some strategy from which they can deviate, but doing so has some chance of being visible to the other player. In our terminology, this corresponds to a setting where each player always performs free but unreliable simulation of the other player.

The literature on Newcomb’s problem (Nozick, 1969) in decision theory also studies problems in which one agent can predict another’s choices. For example, Newcomb’s problem itself and Parfit’s hitchhiker Parfit’s hitchhiker [Parfit 1984; Barnes 1997] can be viewed as a variant of the trust game with simulation and various other scenarios in that literature can be viewed as zero-sum games with the ability to predict similar to Example 21 [Gibbard and Harper 1981, Section 11; Spencer and Wells 2017; Oesterheld and Conitzer 2021]. However, in this literature the predictor is generally not strategic. Instead, the predictor’s behavior is assumed to be fixed (e.g, always simulate and best respond to the observed strategy). The game-theoretic, mutually strategic nature of our simulation games is essential to the present paper. The literature on Newcomb’s problem instead focuses on more philosophical issues of how an agent should choose when being the subject of prediction.

8 Discussion

Summary

In this paper, we considered how the traditional game-theoretic setting changes when one player obtains the ability to run an accurate but costly simulation of the other. We established some basic properties of the resulting simulation games. We saw that (between breakpoint values of which there can be only finitely many), their equilibria change piecewise constantly/linearly (for P1/P2) with the simulation cost. Additionally, the value of information of simulating is often equal to the simulation cost. These properties had strong implications for the equilibria of games with cheap simulation and allowed us to prove several deeper results. Our initial hope was that simulation could counter a lack of trust — and this turned out to be true. However, we also saw that the effects of simulation can be ambiguous, or even harmful to both players. This suggests that before introducing simulation to a new setting (or changing its cost), one should determine whether doing so is likely to be beneficial or not. Fortunately, our analysis revealed that for the very general class of normal-form games with generic payoffs, this can be done cheaply.

Future Work

The future work directions we find particularly promising are the following: First, the results on generic-payoff NFGs cover the normal-form representations of some, but not all, extensive-form games. Extending these results to EFGs thus constitutes a natural next step. Second, we saw that the cost of simulation that results in the socially-optimal outcome varies between games. It might therefore be beneficial to learn how to tailor the simulation cost to the specific game, and to what value. Third, we assumed that simulation predicts not only the simulated agent’s policy, but also the result of any of their randomization — i.e., their precise action. Whether this assumption makes sense depends on the precise setting, but in any case, by considering mixtures over behavioral strategies (Halpern and Pass, 2021), it might be possible to go beyond this assumption while recovering most of our results. Finally, our work assumes that simulation is perfectly reliable, captures all parts of the other agent, and is only available to one agent but not the other. Ultimately, it will be necessary to go beyond these assumptions. We hope that progress in this direction can be made by developing a framework that encompasses both our work and some of the formalisms discussed in Section 7 (and in particular the work on program equilibria).

Limitations

The simulation approach to cooperation has various limitations. Apart from the obstacles implied by the future work above, there is the issue of making sure that the agent we are simulating is the same as the agent we end up interacting with — for example, the other party might try to feed us fake source code, or change it after sharing it. Moreover, the simulated party needs to be willing to its policy, which might be in tension with retaining privacy, trade secrets, etc. Finally, the simulation approach relies on the simulated agents being unable to differentiate between simulation and reality. This might be difficult to achieve as the relevant situations become more complicated and AI agents grow in capability.

Acknowledgments

We are grateful to Emanuel Tewolde for pointing out the connection between Proposition 11 and parametrized linear programming, Zuzana Kovarikova for help with Lemma 14, Lewis Hammond for discussions and feedback on an earlier version of the text, and Emin Berker for feedback on the camera-ready version. We would also like to thank an anonymous IJCAI reviewer for their suggestions regarding the definition of simulation games and inspiring questions regarding the difficulty of determining the usefulness of simulation. We thank the Cooperative AI Foundation, Polaris Ventures (formerly the Center for Emerging Risk Research) and Jaan Tallinn’s donor-advised fund at Founders Pledge for financial support.

References

- Adler and Monteiro [1992] Ilan Adler and Renato DC Monteiro. A geometric view of parametric linear programming. Algorithmica, 8(1):161–176, 1992.

- Barasz et al. [2014] Mihaly Barasz, Paul Christiano, Benja Fallenstein, Marcello Herreshoff, Patrick LaVictoire, and Eliezer Yudkowsky. Robust cooperation in the prisoner’s dilemma: Program equilibrium via provability logic. arXiv preprint arXiv:1401.5577, 2014.

- Barnes [1997] R. Eric Barnes. Rationality, dispositions, and the newcomb paradox. Philosophical Studies: An International Journal for Philosophy in the Analytic Tradition, 88(1):1–28, 10 1997.

- Berg et al. [1995] Joyce Berg, John Dickhaut, and Kevin McCabe. Trust, reciprocity, and social history. Games and economic behavior, 10(1):122–142, 1995.

- Clifton [2020] Jesse Clifton. Cooperation, conflict, and transformative artificial intelligence: A research agenda. Effective Altruism Foundation, March, 4, 2020.

- Conitzer and Sandholm [2006] Vincent Conitzer and Tuomas Sandholm. Computing the optimal strategy to commit to. In Proceedings of the 7th ACM conference on Electronic commerce, pages 82–90, 2006.

- Conitzer and Sandholm [2008] Vincent Conitzer and Tuomas Sandholm. New complexity results about nash equilibria. Games and Economic Behavior, 63(2):621–641, 2008.

- Critch et al. [2022] Andrew Critch, Michael Dennis, and Stuart Russell. Cooperative and uncooperative institution designs: Surprises and problems in open-source game theory. arXiv preprint arXiv:2208.07006, 2022.

- Critch [2019] Andrew Critch. A parametric, resource-bounded generalization of Löb’s theorem, and a robust cooperation criterion for open-source game theory. Journal of Symbolic Logic, 84(4):1368–1381, 12 2019.

- Fortnow [2009] Lance Fortnow. Program equilibria and discounted computation time. In Proceedings of the 12th Conference on Theoretical Aspects of Rationality and Knowledge, pages 128–133, 2009.

- Gibbard and Harper [1981] Allan Gibbard and William L. Harper. Counterfactuals and two kinds of expected utility. In William L. Harper, Robert Stalnaker, and Glenn Pearce, editors, Ifs. Conditionals, Belief, Decision, Chance and Time, volume 15 of The University of Western Ontario Series in Philosophy of Science. A Series of Books in Philosophy of Science, Methodology, Epistemology, Logic, History of Science, and Related Fields, pages 153–190. Springer, 1981.

- Halpern and Pass [2018] Joseph Y Halpern and Rafael Pass. Game theory with translucent players. International Journal of Game Theory, 47(3):949–976, 2018.

- Halpern and Pass [2021] Joseph Y Halpern and Rafael Pass. Sequential equilibrium in games of imperfect recall. ACM Transactions on Economics and Computation, 9(4):1–26, 2021.

- Howard [1988] J. V. Howard. Cooperation in the prisoner’s dilemma. Theory and Decision, 24:203–213, 5 1988.

- Korzhyk et al. [2011] Dmytro Korzhyk, Vincent Conitzer, and Ronald Parr. Solving stackelberg games with uncertain observability. In AAMAS, pages 1013–1020, 2011.

- Letchford et al. [2014] Joshua Letchford, Dmytro Korzhyk, and Vincent Conitzer. On the value of commitment. Autonomous Agents and Multi-Agent Systems, 28(6):986–1016, 2014.

- McAfee [1984] R. Preston McAfee. Effective computability in economic decisions. https://vita.mc4f.ee/PDF/EffectiveComputability.pdf, 1984. Accessed: 2022-12-14.

- Nozick [1969] Robert Nozick. Newcomb’s problem and two principles of choice. In Nicholas Rescher et al., editor, Essays in Honor of Carl G. Hempel, pages 114–146. Springer, 1969.

- Oesterheld and Conitzer [2021] Caspar Oesterheld and Vincent Conitzer. Extracting money from causal decision theorists. The Philosophical Quarterly, 2021.

- Oesterheld [2019] Caspar Oesterheld. Robust program equilibrium. Theory and Decision, 86(1):143–159, 2 2019.

- Oesterheld [2022] Caspar Oesterheld. A note on the compatibility of different robust program equilibria of the prisoner’s dilemma. arXiv preprint arXiv:2211.05057, 2022.

- Parfit [1984] Derek Parfit. Reasons and Persons. Oxford University Press, 1984.

- Rubinstein [1998] Ariel Rubinstein. Modeling Bounded Rationality. Zeuthen Lecture Book Series. The MIT Press, 1998.

- Rudin [1987] Walter Rudin. Real and Complex Analysis. Mathematics. McGraw.. HiII, 1987.

- Shoham and Leyton-Brown [2008] Yoav Shoham and Kevin Leyton-Brown. Multiagent systems: Algorithmic, game-theoretic, and logical foundations. Cambridge University Press, 2008.

- Smith et al. [2009] Richard H Smith, Caitlin AJ Powell, David JY Combs, and David Ryan Schurtz. Exploring the when and why of Schadenfreude. Social and Personality Psychology Compass, 3(4):530–546, 2009.

- Spencer and Wells [2017] Jack Spencer and Ian Wells. Why take both boxes? Philosophy and Phenomenological Research, 99(1):27–48, 7 2017.

- Tennenholtz [2004] Moshe Tennenholtz. Program equilibrium. Games and Economic Behavior, 49(2):363–373, 11 2004.

- von Stackelberg [1934] Heinrich von Stackelberg. Marktform und Gleichgewicht. Springer, 1934.

- von Stengel and Zamir [2010] Bernhard von Stengel and Shmuel Zamir. Leadership games with convex strategy sets. Games and Economic Behavior, 69(2):446–457, 2010.

Appendix A Proofs

See 5

Proof.

This immediately follows from Definition 2 and Definition 4. ∎

See 6

Proof.

Let and suppose that is not in . This means that must put a non-zero probability on at least one of the simulate actions and we have As a result, we can define a (possibly stochastic) best-response policy and use it to construct a policy for as , for , . By definition of and , the utility of any potential deviation from in is the same as the utility of the corresponding deviation from in . This implies that is a NE in .

In the opposite direction, any , corresponds to a unique in — this is because every stochastic best-response policy can be uniquely written as a convex combination of deterministic best-response policies. Since is an equilibrium, P2 will have no incentive to deviate from either (because the utilities in would be identical to the utilities in ). The same will be true for P1’s potential deviations to . Finally, while replacing by some deterministic best-response policy could change the utilities of P2, it will not make a difference to P1’s utilities over , so such actions cannot lead to a profitable deviation either. This shows that will be a NE of . ∎

See 7

Proof.

In (i), the dominance claim hold because for every . As a result, when P1 simulates with probability , P2 gets utility for some best-response policy . As a result, P2 must select an action which maximises this value. And since P1 realises the utility by playing according to , we can identify this equilibrium with some pure Stackleberg equilibrium of where P2 is the leader.

In (ii), S is strongly dominated by P1’s min-max policy. In particular, S cannot be played in any NE. ∎

See 9

Proof.

Let be a policy in . Recall that is defined as the difference between and P1’s best-response utility against . In other words, we have

∎

This result immediately yields the following:

Corollary 27.

Let be a game in which . Then all trembling-hand-perfect NE of satisfy . In particular, the set of trembling-hand-perfect NE of can be identified with the set of pure Stackelberg equilibria of .

See 10

Proof.

(1) This proposition straightforwardly follows from Lemma 9. Indeed, if , the equation implies that deviating to S would decrease P1’s utility, and thus S cannot be in the support of . If , simulation would give strictly higher utility (against ) than any action from the original game, so simulation would have to be the only action in the support of . Consequently, the only case when the support of can include both S and some other action is when .

(2) Suppose that is a NE of with . By Lemma 9, this means that simulating is a strongly dominant action for P1 and . Subsequently, any action from the support of must be an optimal commitment against . However, the definition of implies that there can be no single action of P1 which would give maximum utility against all actions from the support of . In other words, must have optimal commitments of P2 that do not share a best response. This concludes the proof. ∎

See 12

Proof.

Let be a NE of . Proposition 10 implies that when , cannot be a NE of (since S is not in the support of ). Conversely, when , Lemma 9 implies that P1 isn’t incentivised to unilaterally switch to S. Moreover, since is a NE of , no player is incentivised to switch to any other actions. As a result, is a NE of for any . ∎

See 14

Proof.

Let be the first breakpoint of that is higher than . Let be a limit equilibrium of and let be a sequence of strategies for which , , . By Proposition 11, each lies on some line segment , where is the direction the line goes in and for each . The set is necessarily bounded in (otherwise would be unbounded in — i.e., it wouldn’t lie ). Using a compactness argument, we can assume that converges to some . Denote by the line segment . Since the set is closed, satisfies for every . Denoting and concludes the proof. ∎

See 15

Proof.

Let , , and be as in the assumptions of the lemma. To prove the statement, we first identify and the policies and , and then we show that they have the desired properties.

Finding is trivial — we simply and observe that must be a valid policy for P1. To find , , and , we can use Proposition 11. Indeed, this proposition implies that there is some linear function for which . (Once we define the desired properties, this proves the condition (i).) To define the baseline policy of P2, we simply set . To define the deviation policy, we first project onto by setting (where the inequality holds pointwise). We then set and define . Finally, by setting , we get the desired “slope” for which . (This holds because the functions on both sides of this equation are linear and they coincide at and .)

As a side-product of the previous paragraph, we already have (i). To prove the lemma, it remains to prove that satisfies (B1-2) and satisfies (D1-3).

(ii) (B1): By Lemma 10, must be . This implies that any action in the support of must be a best-response to any action from the support of — i.e., we have (B1).

(B2): Since admits no best-response tie-breaking by P1, (B1) implies that playing any with is guaranteed to yield the same utility

As a result, any from the support of must satisfy

Indeed, if it did not, P2 could increase their utility by switching to an action that does satisfy this equality, thus contradicting the fact that is a NE of . This shows that satisfies (B2).

(iii): To prove this part, consider for some .

(D1): Suppose there was a single action of P1 that was a best response to both all actions from and all actions from . Then P1 could gain utility by unilaterally switching to that action (since and ). This in particular implies that no action from can have this property.

(D2): First, suppose some satisfied both and . Then P2 could gain utility by unilaterally deviating to , contradicting the fact that is a Nash equilibrium. The same would be true if some satisfied these formulas with and or with and . Conversely, any action of P2 that satisfies these formulas with and , and , or and is dominated (against ) by playing and therefore cannot be played in equilibrium.

(D3): Denote by , resp. the sets of actions that satisfy , resp. ; these are the actions for which P2 would Like P1 to Simulate, resp. would Like them to play their Baseline strategy.

First, we will consider some and determine the simulation probability that would make P1 indifferent between and . To determine , we first observe that and . This yields

Denote the right-hand side of the last line as

| (A.1) |

Clearly, is a strictly increasing function of the deviation attractiveness ratio

(Intuitively, captures the tradeoffs P2 faces when deviating and hoping they will not be caught by the simulator.) Since is of the type that causes P2 to prefer over simulation, this implies that P2 would deviate to for , be indifferent for , and switch to D for . Finally, denote .

Considering the same equation for , we get

| (A.2) |

Clearly is a strictly decreasing function of inverse ratio

(In contrast to , this ratio captures the tradeoffs P2 faces when deviating and hoping they will be caught by the simulator.) Finally, denote .

Using these calculations, we are not only able to conclude the proof, but we have in fact also determined the values of that are compatible with : If was strictly lower than , P2 would deviate towards some for which . If it was strictly higher than , P2 would deviate towards some for which . (In particular, we must have — otherwise, could not be a limit equilibrium in .) This shows that if there is some action that satisfies , can take any value from . For to contain some action , must be equal to and must satisfy . (Which gives the “” part of (D3).) And analogously, for to contain some action , must be equal to and must satisfy . (Which gives the “” part of (D3).) This concludes the whole proof. ∎

See 1

Proof.

First, we observe several implications of the assumption that has generic payoffs.

-

(0)

In a generic game, no two payoffs are the same.

-

(1)

For every action of P1, P1 only has a single best response. With a slight abuse of notation, we denote this action as .

-

(1’)

The same applies for P2.

-

(2)

By (1), there is a unique action of P2 for which

(A.3) -

(3)

Any two distinct actions , of P2 must also have distinct attractiveness ratios , from (D3) of Lemma 15. (Indeed, if the payoffs of are i.i.d. samples from the uniform distribution over , the probability two of these ratios coinciding is .)

- (3’)

We now proceed with the proof by separately considering the cases , , and .

: If P1 simulated with probability , P2 could respond be playing actions that satisfy (A.3). By (2), there is only one such action; call it . However, this would mean that P1 could gain additional c utility by switching from S to , contradiction the assumption that is an equilibrium. As a result, a generic game with cheap simulation will never have an equilibrium where P1 simulates with probability .

: Suppose that is a NE of for some . We will show that must be pure.

Let be some linear function (given by Proposition 11) for which holds for every c. Since the S is not in the support of , must be equal to (otherwise P1 could gain by deviating to S for , and would not be a NE of ). This means that there must exist some that is a best-response to every from . However, recall that (1) implies that P1 only has a single best response for every action of P2. As a result, is the only action in the support of . By (1’), this means that for every — and for in particular — must also be pure.

: Let be a NE of for some . By Lemma 15, can be expressed as a convex combination of some baseline policy and simulation (for P1), resp. of and some deviation policy (for P2). Combining the condition (B1-2) from Lemma 15 with (1) and (2), we get that must be pure.

Let be some element of and consider the three cases listed in (D2). If satisfies , (0) implies that it must be equal to , and thus not count against the size of . Moreover, to avoid contradicting (D1), must also contain some other action that does not satisfy . If satisfies or , the probability must be equal to , resp. . (We observed this in the last paragraph of the proof of Lemma 15.) By (3’), it is impossible for this to be true for two different actions at the same time. Together with being pure, this shows that and concludes the proof. ∎

See 16

Proof.

Let and let be the Cafés in Paris coordination game with payoffs , , (Figure 4). We will show that for every , has a Nash equilibrium with , where denotes the harmonic mean

and . Once we have proved this result, the conclusion immediately follows from Proposition 12, since for a generic choice of , different subsets yield different values .

Let and denote

First, note that the following formula defines a Nash equilibrium with :

Indeed, this formula ensures that P1’s payoff for playing any is , and similarly for P2. Calculating the expected utility reveals that this strategy yields

However, if P1 was able to best-respond after seeing P1’s choice of action, they would instead get

By definition of (Definition 8), this shows that . This concludes the proof ∎

See 17

Proof.

This trivially follows from the assumption that simulation games are modelled as the original normal-form game with the added simulate action S. ∎

See 18

Proof.

(i): First, suppose that is a game with no best-response tie-breaking (i.e., P1’s choice of best response never affects P2’s utility). By Proposition 7(iii), simulation strongly dominates all other actions when . Consequently, all that is needed to solve is for P2 to search through for the action with the highest best-response value . As a result, the complexity of solving is dominated by the complexity of determining the best-response utilities corresponding the simulate action (which is ).

If allows best-response tie-breaking for P1, the complexity might be higher because P1 could have multiple ways of responding after simulation. However, for the purpose of the paper, we were assuming that this policy (for how to respond after simulation) is fixed. As a result, the argument from the previous paragraph applies to this case as well.

(ii): By Proposition 7(i), S will never be played (in a NE) for high enough c. As a result, solving becomes equivalent to solving . ∎

See 2

Proof.

By Theorem 1, all NE of are either pure or have . (This straightforwardly implies that we could find all NE of in time, by trying all possible supports of size one and two. The purpose of the theorem is, therefore, to show that the task can even be done in linear time.)

First, note that since has generic payoffs, doesn’t have any equilibria with and all of its equilibria with are pure. (This is not hard to see directly. For a detailed argument, see the proof of Theorem 1.) As a result, these two cases can be handled in time.333 Recall that to find all pure NE of an NFG in linear time, we can: First, find all best-responses of P1 to every action of P2. Then find all best-responses of P2 to every action of P1. And finally use these findings to identify all joint actions that form a mutual best response; these coincide with all pure NE.

Second, consider the case when satisfies . From Theorem 1, we know that P1 will be mixing between some and S and P2 will be mixing between some and , where is the baseline strategy satisfying (B1-2) from Lemma 15 and is the deviation strategy satisfying (D1-3) from Lemma 15. If a triplet satisfies (B1-2) and (D1-3), we will call it “suitable”.

To find all NE of , we can use the following procedure: (1a) For each , find the (unique) best response of P2. (1b) For each , find the (unique) best response of P1. (2) Find all suitable triplets . (3) For every suitable triplet from (2), find the unique NE with and , or learn that no such NE exists. (The uniqueness follows from (D1) and (D2).) To prove that the steps (1-3) can be performed in time, we will use the following claims: (I) Each of the steps (1a) and (1b) can be performed in . (II) There are at most suitable, and it is possible to find all of them in time. (III) Performing (3) for a single suitable triplet takes time.

Clearly, the combination of (I), (II), and (II) yields the conclusion of the theorem. Moreover, (I) is elementary and (III) follows from the fact that performing (2) only requires solving the 2-by-2 game with actions and checking that none of the remaining actions is a profitable deviation. To prove the theorem, it remains to prove the claim (II). We do this in two steps: First, we show that there are at most pairs that might be a part of some suitable triplet . Second, we show that for any pair , there are at most two actions for which the triplet is suitable.

For the first step, note that for every , the only pair that might satisfy the condition (B1) is . Therefore, there are at most pairs that might be a part of some suitable triplet . Moreover, for every , there will only be a single that satisfies the condition (B2) (i.e., the condition that maximizes among the actions for which ). Therefore, there are at most pairs that might be a part of some suitable triplet . Combining the two bounds shows that the number of pairs that might be a part of a suitable triplet is .

For the second step, note that in a generic game, the only action that satisfies for is . Moreover, the genericity of implies that either the set of actions satisfying is empty, or there is exactly one action that satisfies and maximizes the attractiveness ratio from (D3). Analogously, there will be at most one action that satisfies and maximizes the inverse attractiveness ratio from (D3). This shows that for any from the previous step, there are at most two actions for which the triplet is suitable. Since this proves completes the proof of (II), we have concluded the whole proof. ∎

See 3

Proof.

Let be a NFG. We will assume that has utilities in — otherwise, we can rescale the utilities without changing the sets of NE. Let be as in Figure 5 and fix some . We will show that a strategy in with is a NE of if and only if it has P1 mixing between simulating and and P2 mixing between cooperating and , where and , . ( also has “non-simulation” equilibria where P1 always walks out and P2 defects with high probability. These will not be relevant for our proof.)

Before proceeding with the proof, observe that for any in , we have

As a result, if P2 attempts to defect while P1 simulates, P1 will best-respond by walking out, which results in the worst possible utility for P2. This shows that for any in , we have

| & | ||||

| & |

(Indeed, the first inequality holds because T is already a best-response to C and . The second holds because no matter what strategy is used in , P1 would be willing to pay utility to walk out instead of playing . The third holds by our initial observation, and finally the fourth holds because no matter what strategy is used in , P2 always prefers playing to cooperating.) These inequalities show that for any fixed , P1 can make P2 indifferent between C and by mixing between S and , and P2 can make P1 indifferent between S and by mixing between C and . Moreover, the probabilities for which the players are indifferent will be unique — we denote them as for P1 and for P2.444 The exact formulas can be derived as in the proof of Theorem 5. However, they only become relevant for the “moreover” part of the proposition, so we avoid deriving them for now.

To prove the main part of the proposition, we now show that can be identified with .

Let be a NE of for which . We will show that is of the form

where is a NE of and , . (1) First, note that P2 must play both C and D. Indeed, if P2 only cooperated, P1 would strictly prefer T over S. Conversely, if P2 only defected, P1 would strictly prefer WO over S. (2) Second, we show that P1 is indifferent between S and T and strictly prefers both of these actions over WO. Indeed, if was such that (and , P2 would strictly prefer C over D, contradicting (1). If P1 was indifferent between all three actions, would have to satisfy . However, solving these equations in particular gives , which is impossible for . (3) Third, by the initial observation about indifference, we know that must be of the desired form — as a result, it only remains to show that is a NE of . (4) Finally, suppose that was not a Nash equilibrium of . Since is of the desired form, we have

Since only the third term depends on , we see that if was not a best response to in , P1 could unilaterally increase their utility by replacing by . Analogously, we have

where only the third term depends on , and therefore must be a best-response to in . This shows that must be a NE of and concludes the proof of “”.

Conversely, let . To prove the “” part of the proposition, it suffices to show that

is a NE of . However, the calculations performed so far already imply that this choice of makes P1 indifferent between S and T and P2 between C and D, and gives no player an incentive to replace by any other policy in . To show that is a NE of , it remains to show that P1 has no incentive to deviate by playing WO — in other words, that . We already know that P1 cannot be indifferent about WO (since this only happens for . Therefore, since , it suffices to show that does not depend on c (and therefore as ). Since we will obtain this independence of on c as a by-product of the last step of our proof, the proof of the main part of the proposition is finished for now.

To conclude the whole proof, it remains to show the “moreover” part of the proposition. We will do this by deriving the exact formulas for and . (This part of the proof is essentially identical to the calculations from the proof of Theorem 5.)

For , we have

For , we have

This concludes the whole proof. ∎

In , the players first simultaneously announce whether they wish to play or not, with being played only if both agree to do so. The top-left corner payoff for P2’s is defined as , which causes voting for playing to be a dominant action for P2. The top-left corner payoff for P1 is a free parameter of .

See 4

Proof.

First, note that the problem := “given an NFG and real number , decide whether has a Nash equilibrium with ” is known to be NP-hard [Conitzer and Sandholm, 2008, Corollary 8]. To prove the theorem, it therefore suffices, for every , to reduce from the complement of to the problem “given a game , decide whether the game has a NE with that is a Pareto-improvement over every NE of ”. We first consider the case where (A) and then (B) extend the solution to .

A) : We construct as follows (Figure 7). First, the players simultaneously announce whether they wish to play . If both agree to play , they play . If neither agrees, P1 receives payoff and P2 receives payoff . If only P1 agrees, both players receive a very large negative payoff (intuitively: ; formally: ). If only P2 agrees, P1 receives a very large negative payoff while P2 receives a very large positive payoff (intuitively: ; formally: ).

First, note that the dominant action in is for P2 to vote for , causing P1 to do the same. Therefore, the equilibria of can be identified with the equilibria of , and they yield the same utilities. Second, note that in , P1 will always simulate (because makes this a dominant course of action). This incentivizes P2 to always vote against playing , resulting in utilities and for P2. P2 will always prefer this over playing , which shows that introducing simulation to is guaranteed to lead to a Pareto-improvement if and only if has no NE with .

B) : We start with a game which is defined identically to from the case “”, except that when the players play the top and left strategy, P1 receives utility (instead of ). However, we also consider a second game, , which works as the traditional Rock-Paper-Scissors game with utilities , except that P1’s payoffs are multiplied by and P2’s payoffs are multiplied by . Finally, game is the game where the players play the games and in parallel (or one after the other; this does not make a difference).

Because of the inclusion of , any NE of will involve P1 simulating with probability . (Indeed, simulating causes them to lose c utility by paying the simulation cost and gaining utility for being able to always win the game. Therefore, against any NE strategy of the opponent, P1 will always simulate.) As before, this incentives P2 to always vote against playing , which in turn makes P1’s best response to also vote against playing . This results in utilities and

As in the previous case, this implies that introducing simulation to is guaranteed to lead to a Pareto-improvement if and only if has no NE with . ∎

See 5

Proof.

Let be a generalised trust game that does not admit best-response tie-breaking by P1, and suppose that is sufficiently low (to be specified later in the proof). We will prove that

-

(A)

either has a NE where and P2 randomizes over all of their optimal commitments

-

(B)

or has a NE where P1 mixes between simulating and some “baseline policy” that only includes “universal best responses” to P2’s optimal commitments and P2 mixes between (all of) their optimal commitments and some “deviation policy” .

Note that (B) should be understood in the context of Lemma 15 — in particular, the probability of P2 deviating will go towards as . Since is a generalized trust game, the outcome corresponding to any optimal commitment and is strict Pareto improvement over any NE of . Moreover (since the set is compact), this further implies that for low enough c, the same holds for . This shows that once we prove that either (A) or (B) holds, we will have proven the conclusion of the whole theorem.

Notation for (A): During the proof, we will use the following notation: By the value of the pure-commitment game given by . By , we denote the set of optimal commitments of P2. For any set of actions , will denote the set of P1’s actions that work as a universal best response to . For a finite set , denotes the uniformly random distribution over

Proof of (A): If there is no universal best-response for all optimal commitments (i.e., if ), we define and . To see that is a Nash equilibrium, note that P2 does not have any profitable deviation (since P1 is simulating with probability and all actions from OC give the maximum utility against S). Similarly, no single action of P1 works as a best-response against every , so we have . By Lemma 9, this means that for , P1 does not have any profitable way of deviating from . This shows that is a NE satisfying (A), and concludes the proof of this case.

Notation for (B): For any and , we use to denote the attractiveness ratio from Lemma 15

We will also consider the following auxiliary game:

Intuitively, is a game where P2 aims to equalize P1’s regrets for playing various actions instead of simulating and P1 aims to equalize the attractiveness ratios of P2’s deviations.

Proof of (B): Let be some NE of and denote , , . First, note that to prove (B), it suffices to show that for sufficiently low c, has a NE of the form

where and do not depend on c. Second, note that to prove the has a NE of this form, it suffices to prove the following claims:

-

(i)

P1 can make P2 indifferent between and by mixing between and S.

-

(ii)

For low enough , P2 can make P1 indifferent between and S by mixing between and .

-

(iii)

The mixing probabilities from (i) and (ii) are uniquely determined by and c, P1’s probability in fact does not depend on c, and P2’s probability depends on c as some , .

-

(iv)

For low enough c, P1 has no incentive to deviate from the strategy determined by (i-iii).

-

(v)

P2 has no incentive to deviate from the strategy determined by (i-iii).

In the remainder of the proof, we focus on showing that (i-v) holds.

Proof of (i): To show (i), it suffices to prove that

To see the first inequality, recall first that , so . Conversely, , so . To see the second inequality, recall that is a generalised trust game, so cannot be a NE of (otherwise could not be a strict improvement to P2’s utility). As a result, P2 must have some for which (since is a best response to ). By definition of and the fact that , this implies that the same holds for .

Proof of (ii): To show (ii), it suffices to prove that for sufficiently low , we have

The first inequality holds because every is already a best response to every , so . To prove the second inequality, first note that any must have . (Indeed, this holds because cannot be a NE of (otherwise wouldn’t be a generalized trust game), so one player must have some profitable deviation — and it cannot be P1, since is already a best response to . As a result, if some had , P2 could unilaterally increase their utility in by deviating to the action with , and would not be a NE of .) This shows that for any , cannot be a best-response to . (Indeed, suppose that was a best-response to . This lead to a contradiction, since we would then have both — because admits no best-response utility tiebreaking by P1 — and — since .) Consequently, the following quantity is necessarily strictly positive:

Finally, by applying the definition of , we get the desired inequality for :

This concludes the proof of (ii).

Proof of (iii): The uniqueness holds because the inequalities in (i) and (ii) are strict. The fact that does not depend on c follows from the fact that P2’s utility does not depend on it. The fact that the probability mass that assigns to is of the form , where does not depend on c, can be verified by solving the equation

Since this calculation is exactly the same as the analogous calculation in the proof of Lemma 15, we skip it.

Proof of (iv): By (iii), we have , which implies that

As a result, for low enough c, any that aims to have must be a best response to each of the strategies . Since all such actions are contained in , it suffices — to prove (iv) — to check that P1 has no incentive to deviate towards some . To prove this, note that for , we have

However, in this formula, only the term depends on the choice of — and since is a NE of , there can be no for which this term would be strictly higher than for the actions from . This concludes the proof of (iv).

Proof of (v): Applying the definition of , we see the utility of any in is equal to ’s “attractiveness ratio” (from Lemma 15):

Using the terminology from Lemma 15, admits no profitable deviation that satisfies or — indeed, this is because P2’s baseline only consists of optimal commitments (which rules out ) and P1’s baseline consists of best-responses to any action that satisfies (so any profitable deviation satisfying would contradict (D1)). Therefore, as a result of Lemma 15 and the choice of in (i), any profitable deviation of P2 would need to have a strictly higher attractiveness ratio than the actions from the support of . However, the existence of such action would contradict the fact that is a Nash equilibrium of . This concludes the proof of (v), and therefore the proof of the whole theorem as well. ∎

See 22

Proof.

For any , we have , which proves the inequality for P1.

To prove the inequality for P2, note that we can write as , where is a best-response (in ) to . Since is zero-sum, we have ∎

Example 28 (Optimal simulation cost is non-trivial).

Consider the game depicted in Figure 8. First, both Alice and Bob have an option to walk out and not play (). If Alice chooses to trust Bob and play, Bob gets to decide which game to play. One option is the Unfair Guessing game (Example 21), where Alice needs to guess an integer that Bob is thinking, else she ends up transferring utility to Bob. If she guesses correctly, Bob transfers to her instead. (This game is parametrized by , the highest integer that Bob is allowed to pick. Since the game is biased in Bob’s favor, the corresponding expected utilities converge to as . Since the precise numbers are not important for our conclusions, we will, for the purpose of this example, treat them as exactly equal to .) The other option available to Bob is to play the Joint Project game (Example 24). In this game, Alice can either Cooperate with Bob () or attempt to betray him by guessing his password and stealing all his profits. A successful betrayal results in utilities , , while an unsuccessful one sends Alice to prison (, ). (This game is also parametrized by , such that when Bob picks his password uniformly at random, the outcomes converge to , . To simplify the notation, we treat them as equal to these numbers.)

We first discuss how the game works before simulation enters the picture. In this simulation, Alice would prefer to Bob to pick the Joint Project game and she would cooperate if Bob did pick this game. However, Bob would rather play the Unfair Guessing game, which is virtually guaranteed to make him better off. Realizing this, Alice decides to walks out instead, and the only equilibrium outcome is .

Conversely, if simulation is free, the Unfair Guessing game becomes unfavourable to Bob — he would get if he picked it. However, simulating would also allow Alice to betray Bob in the Joint Project game, making him worse off than if he didn’t play at all. As a result, when c is equal to , Bob always walks out and the only equilibrium outcome is , as before.

However, consider the case where , such that simulation is cheap enough to be justified by the fear of the Unfair Guessing game, but expensive enough to not be justified by the greed in the Joint Project game. Intuitively, we might hope that this will cause Bob to pick the Joint Project game, in which Alice will cooperate — and this is mostly what actually ends up happening. The only wrinkle is that Alice needs to make the decision about simulation before knowing Bob’s choice of game — and if she never simulates, Bob would switch to always selecting the Unfair Guessing game instead. As a result, the actual equilibrium (given below) will have Bob sometimes deviating towards Unfair Guessing and Alice sometimes simulating. As a by-product, this will sometimes lead to Alice betraying Bob in the Joint Project Game (when she simulates and he doesn’t deviate). However, even with these drawbacks, the resulting outcome is still much better than the default . Indeed, it is not hard to verify that has an equilibrium where Alice simulates with probability and trusts Bob otherwise, while Bob picks the Unfair Guessing game with probability and selects the Joint Project game otherwise, and the resulting utilities are , . (Note that – somewhat counterintuitively – making the Unfair Guessing game riskier for Bob would make the overall outcome better for him, because Alice would not need to simulate with so high probability to disincentivize deviation.)

By adjusting the payoffs in this game, we can obtain examples where the players prefer various values of c that are strictly higher than , yet induce equilibria where simulation happens with non-zero probability.

Appendix B Proof of Proposition 11: Linear Adjustment of P1’s Payoffs Have Constant/Linear Effects on NE

In the main text, we used the following result:

See 11

Proof.

With the exception of the claim about being equal to , the result is an immediate corollary the more general Lemma 30 listed below. The claim about being a breakpoint and about the non-existence of any breakpoints in immediately follows from Proposition 7 (i). ∎

In this section, we prove a more general version of Proposition 11 using the following setting:

Definition 29 (Auxiliary).

A game with linearly adjustable payoffs is any pair where is a two-player normal-form game and is a vector of adjustments for P1’s actions. For a cost-scaling factor , denotes the NFG with actions and utilities , .

The connection between this notion and our setting is that any simulation game can be expressed as , where is the original game with one additional P1 action S that yields utilities (where we fix some for every ).

The piecewise constant/linear phenomenon that we observed on the motivating example of simulation in Trust Game (Figure 2) in fact holds more generally — for every game with linearly adjustable payoffs. The goal of this section is to build up to the proof of the following result, which immediately gives our desired result – Proposition 11 as a corollary:

Lemma 30 (Games with linearly adjustable payoffs have piecewise constant/linear NE trajectories).

For every , there is a finite set of breakpoint values such that the following holds: For every and every , there is a linear mapping such that and for every .

B.1 Background: Linear Programming

Before proceeding with the proof, we recall several results from linear programming. (Since these results are standard, they will be given without a proof. For a detailed exposition of using LPs for solving normal-form games, see for example [Shoham and Leyton-Brown, 2008].)

First, if we can guess the support of a Nash equilibrium, the strategy itself can be found using a linear program:

Observation 31 (Indifference sets of NE).

Every NE of satisfies . As a result, we can write the set of NE in as a (possibly overlapping) union

Lemma 32 (NE as solutions of LP).