Dynamic Term Structure Models with Nonlinearities using Gaussian Processes

Abstract

The importance of unspanned macroeconomic variables for Dynamic Term Structure Models has been intensively discussed in the literature. To our best knowledge the earlier studies considered only linear interactions between the economy and the real-world dynamics of interest rates in DTSMs. We propose a generalized modelling setup for Gaussian DTSMs which allows for unspanned nonlinear associations between the two and we exploit it in forecasting. Specifically, we construct a custom sequential Monte Carlo estimation and forecasting scheme where we introduce Gaussian Process priors to model nonlinearities. Sequential scheme we propose can also be used with dynamic portfolio optimization to assess the potential of generated economic value to investors. The methodology is presented using US Treasury data and selected macroeconomic indices. Namely, we look at core inflation and real economic activity. We contrast the results obtained from the nonlinear model with those stemming from an application of a linear model. Unlike for real economic activity, in case of core inflation we find that, compared to linear models, application of nonlinear models leads to statistically significant gains in economic value across considered maturities.

1 Introduction

1.1 Term Structure and Macroeconomic Information

A fundamental and economically important argument in macro-finance literature suggests that the current yield curve spans all relevant information for forecasting future yields, returns and bond risk premia. Although the argument is implied by most macro-finance models, recent evidence raises important questions on its validity. In particular, several empirical studies (see, Cooper and Priestley (2009), Ludvigson and Ng (2009), Duffee (2011), Joslin et al. (2014), Cieslak and Povala (2015), Gargano et al. (2019), Bianchi et al. (2021)) provide support for unspanned macroeconomic risks111e.g.: the output gap of Cooper and Priestley (2009), the ‘real’ and ‘inflation’ factors of Ludvigson and Ng (2009), the measures of economic activity and inflation of Joslin et al. (2014) and the long-run inflation expectation of Cieslak and Povala (2015), among others. possessing considerable predictive power above and beyond the yield curve. The vast majority of the extant literature, however, assumes that the relationship between those unspanned macroeconomic factors and the cross section of yields is mostly, if not purely, linear in nature.

Duffee (2011) is the first to comment on the possibility of a nonlinear (albeit, economically weak) relationship between bond risk premia and macroeconomic activity. Only recently, Bianchi et al. (2021) provide evidence on the importance of accounting for nonlinearities in order to detect further information important for forecasting bond risk premia. Due to the rapid increase in the use of machine learning methods, the presence of nonlinearities, relevant for predicting excess returns, has recently attracted attention in the literature. However, we are unaware of any prior research that explores the possibility of an asymmetric/nonlinear relationship between unspanned macroeconomic risks and return predictability in the US bond market within an arbitrage-free pricing model. In this paper, we seek to investigate this relationship, if any, further. With this in mind, we propose a novel class of arbitrage-free Dynamic Term Structure Models (DTSM) that embed nonlinear unspanned macroeconomic risks using Gaussian Processes (Bishop, 2006; Rasmussen and Williams, 2006).

This paper contributes to the literature that studies the linkages between bond risk premia and the macroeconomy. Our first contribution is methodological. Following Joslin et al. (2014), we embed unspanned information coming from (directly observable) macroeconomic risks within a DTSM. The point where our approach deviates from prior studies is that this information is assumed exogenous and is entering the model in a nonlinear fashion without making specific assumption on the manner it affects the yield curve. To do so, we introduce a novel methodological framework that utilises Bayesian non-parametrics within a DTSM, thus staying agnostic about the functional form between macroeconomic activity and bond risk premia. Our setup, also allows us to handle Gaussian Processes sequentially and effectively perform tasks such as sequential parameter estimation and forecasting. Drawing from the work of Chopin (2002) and Del Moral et al. (2006), we allow for a sequential Bayesian treatment of exogeneous macroeconomic information in a nonlinear manner.

Our second contribution is empirical. From a fundamental and economic perspective, the proposed framework seeks to enhance our understanding behind the determinants of bond risk premia. In particular, whether movements in excess bond returns bear any relation to the macroeconomy. Are there important driving forces of bond return predictability that are nonlinear and hard, if not impossible, to summarize utilising information coming solely from linear transformations of the data? Furthermore, we seek to investigate deeper whether such nonlinearities, if any, allow investors to exploit the evident statistical predictability of the resulting models and generate economically significant portfolio benefits to bond investors, out-of-sample.

1.2 Economic Benefits from Nonlinearities

Our results reveal a direct line linking the nonlinear component of the unspanned measures of macroeconomic activity to model performance, especially when it comes to generating additional economic value. In order to scrutinize nonlinear models in a meaningful way, as benchmark we apply a version of the macro-finance DTSM proposed by Joslin et al. (2014), which incorporates unspanned macroeconomic variables in a linear manner. However, we proceed without modeling their underlying dynamics, in order to remain closest possible to the nonlinear setup we propose.

First, we find that nonlinear models provide a competitive edge over linear models in cases where ex-ante nonlinear functions of macroeconomic variables preserve their nonlinear nature ex-post, in the part which is hidden from the yield curve. In this paper, these are specifically the prices, and not the economic activity, which we also consider. We demonstrate that by resorting to risk premium factor decomposition from Duffee (2011).

Second, results in this paper also indicate that for some models, where macroeconomic risk directly affects the level of the yield curve, a nonlinear formulation, like ours which relies on Gaussian Processes, does not necessarily mean outstanding model performance in terms of predictability and economic value gains, however it lets avoid substantial deterioration on that front. In particular, this is the case for macroeconomic variables which in abnormal times, such as the - financial crisis or the more recent COVID- recession, are subject to outliers, like in this paper the economic activity.

1.3 Outline

The remainder of this paper is organized as follows. Section 2 is a brief introduction to Gaussian Processes. Section 3 describes the proposed modelling framework. Section 4 presents the procedure for sequential learning with Gaussian Processes and forecasting, along with the framework for assessing the predictive and economic performance of the resulting models. Section 5 discusses the data and the sample period used and presents the family of models considered in this paper. Section 6 discusses the results both in terms of predictive performance and economic value, including the associated explanatory power where applicable, as well as reveals the links between these results and the hidden nonlinearities. Finally, Section 7 concludes the paper by providing some relevant discussion.

2 Gaussian Processes

In Bayesian non-parametrics a Gaussian Process prior is used to estimate unknown function in supervised learning setting. One does not assume a specific function between some and and instead performs Bayesian inference on the function. Univariate exposition below follows from Bishop (2006), Rasmussen and Williams (2006) and Murphy (2012).

2.1 Gaussian Process Theory

Let be a set and be a set of functions over , for example smooth functions. We observe … … , where , , , satisfying

| (1) |

where and are independent of . Errors have density and usually it is ), being vector of zeros, what further implies that

| (2) |

where . In a Bayes regression we assign prior to and compute the posterior

| (3) |

where is the likelihood. Then can be estimated by its posterior mean.

. Let be a set. A random function is called a Gaussian Process () if for any , has a multivariate normal distribution.

Gaussian Process is characterized by the mean and the covariance kernel . The latter is a positive definite function . If is a with mean and covariance kernel then

| (4) |

where and is matrix with elements such that . There are numerous possibilities when it comes to covariance kernels and their choice depends on the application. For instance, they can be linear kernels

| (5) |

or Gaussian kernels

| (6) |

among others. For details about these and other kernels, and how they can be combined, see Rasmussen and Williams (2006).

2.2 Gaussian Process Regression

For assume that

| (7) |

with

where and are independent and for simplicity one can assume that , what is also a common assumption made in applications.

Marginal distribution of is thus multivariate normal with means and covariances , with . In matrix notation, where denotes the matrix containing all the pairs, we get

| (8) |

Since for each and we have that , the joint distribution of and is

| (9) |

where and is a vector of zeros.

Under such assumptions, by the multivariate normal regression lemma (Durbin and Koopman, 2012), the distribution of is a Gaussian with mean and covariance kernel , which are following

To project based on we need to find the joint distribution of and , given and . To that end, we note that for and we let

to arrive at

| (10) |

Then, by the multivariate normal regression lemma, is a Gaussian with mean and variance such that

Posterior distribution of still depends on unknown vector of parameters consisting of and any hyper-parameters of , for example for squared exponential kernel. In principle, two methods can be used to estimate . We can maximize the marginal likelihood which is a multivariate normal density with mean and covariance matrix . Doing so is denoted empirical Bayes. We can also put a prior on the hyper-parameters and estimate them by their posterior means. Doing this is known as hierarchical Bayes (Bishop, 2006; Murphy, 2012). In what follows, we pursue a pragmatic combination of the two approaches.

3 Dynamic Term Structure Model, Likelihood, and Nonlinear Macros

3.1 Base Case

To start with, consider the no-arbitrage class of discrete-time Affine Term Structure Models (ATSM) (see, Ang and Piazzesi (2003) and Cochrane and Piazzesi (2005)) and in particular the Gaussian case. Under the physical probability measure , let us consider first that a vector of state variables , , evolves according to a first-order Gaussian Vector Autoregressive (VAR) process

| (11) |

where , is a lower triangular matrix, is a vector and is a matrix. Under this initial framework, the one period risk-free interest rate 222Working with monthly data implies that is the 1-month yield. is assumed to be an affine function of the state variables

| (12) |

where is a scalar and is a vector. Absence of arbitrage implies the existence of a pricing kernel specified as

| (13) |

with being the time-varying market prices of risk, which is also assumed to be affine in the state vector

| (14) |

where is a vector and is a matrix. If we assume that the pricing kernel prices all bonds in the economy and we let denote the time-t price of an n-period zero-coupon bond, then the price of the bond is computed from where denotes expectation given the information available up to time . As such, it follows that bond prices are exponentially affine functions of the state vector (see, Duffie and Kan (1996))

| (15) |

with loadings, being a scalar and a vector, satisfying the following recursions

| (16) | ||||

| (17) |

with and . The dynamics of the state vector are given by

| (18) |

where , and . The continuously compounded n-period yield is also an affine function of the state vector

| (19) |

where the loading scalar and the loading vector are calculated using the above recursions as and .

Next, we follow the canonical setup of Joslin et al. (2011) and rotate the vector of unobserved state variables such that they are linear combinations of the observed yields. In particular, we rotate to the first principal components (PCs) of observed yields as

| (20) |

where denotes a matrix containing first PCs’ loadings, is a vector of continuously compounded yields. The vector and the matrix contain model-implied loadings of yields on risk factors, specifically are elements of vector and are transposed rows of matrix . This allows us to re-write the yield equation (19) in vector form

| (21) |

and then as a function of the observable risk factors

| (22) |

where the loadings and , which are derived by applying transformation in (20) to (21), are given below333According to Duffee (2011), outside of knife-edge cases the matrix is invertible, and as such contains the same information as .

| (23) | ||||

| (24) |

Furthermore, the risk-neutral dynamics of are given as

| (25) |

where the risk-neutral measure parameters , and are derived similarly from (18), what leads to

| (26) | ||||

| (27) | ||||

| (28) |

Finally, given the new observable state vector , the one period short rate is also an affine function of given as

| (29) |

with

| (30) | ||||

| (31) |

and the market price of risk specification becomes accordingly

| (32) |

where

| (33) | ||||

| (34) |

We note that dynamics of are of equivalent form to (25) with

| (35) | ||||

| (36) |

where is a vector and is a matrix specified in (33) and (34) respectively, reflecting the market price of risk in terms, as well as with instead of .

Notice also that in (21) and (22), yields are assumed to be observed without any measurement error. Nevertheless, an -dimensional observable state vector cannot perfectly price yields, and as such, we further assume that the bond yields used in the estimation are observed with independent measurement errors. An equivalent way to formulate this is to write

| (37) |

and to consider the dimension of as effectively being . Letting denote a basis of the null space of , the measurement error assumption can be also expressed as

| (38) |

where is a vector (Bauer, 2018).

In our setting, we also follow one of the identification schemes proposed in Joslin et al. (2011) (see, Proposition 1), where the short rate is the sum of the state variables, given as with being a vector of ones, and the parameters and of the state vector’s -dynamics are given as and , where denotes a vector containing the real and distinct eigenvalues of 444Alternative specifications for the eigenvalues are considered in Joslin et al. (2011), however real eigenvalues are found to be empirically adequate..

3.2 Incorporating Unspanned Nonlinear Macros

We further consider an extension of the model presented in the previous section. Our approach resembles the framework of Joslin et al. (2014) in that the model is factorised into a ‘spanned’ component, i.e. risk factors which can be retrieved by the information provided in historical yield curve data, as well as an ‘unspanned’ component that could include background factors such as macroeconomic variables. It is assumed that the latter is not determined by the yield curve, yet it remains highly relevant for the inference and, more importantly, prediction purposes. The points where our approach differs from Joslin et al. (2014) are as follows. First, the unspanned components are regarded as unknown, possibly nonlinear functions, which are to be estimated, of observable macroeconomic variables, rather than just macros entering the model in a linear manner. Having said that, the latter case is considered too, as benchmark in model comparisons, and is henceforth referred to as the linear model. Second, the unspanned components are not assumed endogenous but exogenous.

We thus introduce the following nonlinear model for the -dynamics of the state vector

| (39) |

where and are defined in (35) and (36) respectively. The matrix represents the Cholesky decomposition (i.e. lower triangular with positive diagonal elements) of the covariance matrix , whereas is a vector of error terms that are assumed to be normally distributed with zero mean and , the identity matrix of dimension , as the covariance matrix. The term is of dimension and reflects the impact of (lagged) macros in , a vector, on , with the function being such that . More details are provided in the next section.

3.3 Gaussian Process Mean Ornstein-Uhlenbeck Model

In what follows, we define in more detail the function in (39), and the underlying hyper-parameters. To that end, we follow a Bayesian non-parametric approach using a Gaussian Process with multiple outputs. We focus on a special case of (39) with and , noting that the first three extracted PCs are typically sufficient to capture most of the variation in the yield curve and often correspond to its level, slope, and curvature, respectively (Litterman and Scheinkman, 1991).

For interpretation reasons, we work with models containing macro, and explore their submodels. We believe that it is the natural step to gain the understanding, as to how these models behave, before moving to more complex specifications. Nevertheless, the computational scheme we develop in this paper is capable of handling macros in a single model.

Our starting point is the -dynamics for as in (39) which, for convenience, we simplify to

| (42) |

by setting

| (43) |

Then we assign a Gaussian Process prior on in (42) and denote it as

| (44) |

In the above we assume , what is commonly done in applications (Rasmussen and Williams, 2006). Such a prior assumption about is also reasonable in our context, where we are effectively filtering out s from residuals of a VAR model. Specific choice of kernel is discussed later.

At this point it is worth noting that under these assumptions the term , as backed out from (42) and (43), essentially determines (up to rescaling) the long term mean of the corresponding Ornstein-Uhlenbeck (OU) process that governs . Given that is now a Gaussian Process, the model can be viewed as -dimensional mean OU process. Although according to our notation dimension of in (42) is ), we are able to include Gaussian Process outputs in a single model. For example, if and we introduce two outputs, one in the second and one in the third equation of (42), then it means that the first element of is effectively zero. It is implemented by setting , the first diagonal block of matrix defined in (49) below, to zeros. In the linear model, this would be equivalent to restricting the first row of matrix in (79) to zeros, what is explained in detail in Appendix E.

Without loss of generality for , we adopt the following vector notation

Eventually we consider the concatenated vectors

| (45) |

The distribution of conditional on is then

| (46) |

The next step is to choose a specific kernel for each , . We use the same type of kernel for all the s in the model. Namely, the squared exponential kernel, which is stationary and considered the choice most-widely made to start with in applications (Bishop, 2006; Rasmussen and Williams, 2006; Murphy, 2012). It can be specified as

for some scalars (or vectors) and , where is called the characteristic length-scale and is denoted as signal standard deviation. Squared exponential kernel is infinitely differentiable and thus very smooth, what we welcome here since it is the smooth signal within the rough noise that we are after.

To each we thus assign separate yet the same type of kernel , , what can be expressed as

in covariance terms. Following the assumption made about in (44), it lets us then concretely determine the distribution for each of the s as

| (47) |

where is a vector of zeros and is the matrix shown above.

Finally, in order to specify the distribution of , which in our case is a single input with multiple outputs, we need to make an assumption about the dependence between s. The simplest way, and the one chosen here, is to assume independence between s, what implies the following distribution

| (48) |

with

| (49) |

which is a matrix, and and are a and vector and matrix of zeros, respectively. We collect the hyper-parameters governing covariance matrix , which are and , , in and .

There are also more flexible alternatives for tying up together the s and specifying the covariance of , that is , see for example Alvarez et al. (2012) for a survey of several methods. These include the intrinsic coregionalisation model, the semiparametric latent factor model and the linear model of coregionalisation, among others. Choosing between such models involves considering trade-offs between flexibility, computational cost and interpretability. Here we adopt (49) as a convenient starting point for DTSMs. Consequently, such a single input with multiple inputs is then equivalent to multiple independent single input s with a single output.

Next, using standard properties of Gaussian Processes we can proceed to obtain the conditional distribution of given , the marginal distribution of , by integrating out from (46), and the predictive distribution of , and consequently that of , given all the data up to time including . For reasons mentioned in Section 4.2, in this paper we focus on one-step-ahead predictions. To start with, the marginal distribution of , which nota bene stands behind the -dynamics of , is following

| (50) |

To obtain conditional distribution of given we observe that joint distribution of and is

| (51) |

where for clarity of further exposition we defined

| (52) |

Then, by the multivariate normal regression lemma, we get

| (53) |

To arrive at the predictive distribution of , we first derive the joint distribution of and , using all available macro data, that is . Given the assumption about dependence between s, as it is made in (49), we first note that for

| (54) |

Further, for , we let

to eventually observe that joint distribution of and is as follows

| (55) |

where and , which are and matrices, respectively, are specified as

| (56) |

and

| (57) |

Then, again by the multivariate normal regression lemma, we get the predictive distribution of given all the data up to time including

| (58) |

what translates into the corresponding predictive distribution of as follows

| (59) |

3.4 Likelihood and Risk Price Restrictions

Statistical inference can be performed using the observations and . The likelihood factorizes into two parts stemming from the and respectively. For observable factors, the joint likelihood (conditional on the initial point ) can now be written as

| (60) |

where the -likelihood components are given by (37) and capture the cross-sectional dynamics of the risk factors and the yields, whereas -likelihood components are obtained from (62) below and capture the time-series dynamics of the observed risk factors. The parameter vector is set to and we tune in-sample to fix it out-of-sample at . Details of the tuning procedure are in Appendix D.

For brevity of further exposition, we let and . If all the entries in are free parameters we get the maximally flexible model (model in this paper). Alternative specifications, with some of these entries set to zero, have been proposed in the literature. For details, see the associated discussion with related references in Dubiel-Teleszynski et al. (2022b). Overall, in most models the set of unrestricted parameters is usually a subset of . In this paper, we use restriction set with optimal model performance, in particular with respect to economic value, as evidenced in Dubiel-Teleszynski et al. (2022b). It is also the same restriction set as in Dubiel-Teleszynski et al. (2022a), for reasons mentioned therein. Namely, we only leave unrestricted, as it is in model , here and in the other papers.

Consequently, the likelihood specification of (60) can now be restated as

| (61) |

where is revised accordingly. To obtain -likelihood components above, we resort to Gaussian Process formulation established so far, and exploit the associated marginal distribution of in (50), together with (52), to eventually arrive at the standard log-likelihood representation of in (61), namely

| (62) |

where is matrix determinant and denotes Euclidean norm squared.

4 Sequential Estimation, Learning, and Forecasting

4.1 Sequential Framework with Gaussian Processes

Let denote all bond related data available up to time , such that , and denote all macro data available up to time , such that . Similarly, the likelihood based on data up to time is and is defined in (60). Combined with a prior on the parameters , see the Appendix A for details, it yields the corresponding posterior

| (63) |

where is the model evidence based on data up to time t. Moreover, the posterior predictive distribution, which is the main tool for Bayesian forecasting, is defined as

| (64) |

where is the prediction horizon. As explained further, in Section 4.2, in this paper we focus on . Due to the Gaussian Process formulation, predictions depend computationally on all available data, what is reflected by conditioning on and in the first term under the integral in (64). In theory, it is a potential issue as computational cost of deriving the predictive distribution grows fast. In particular, as new data arrives it becomes more costly to invert covariance matrix in (52). However, given that time series we consider are relatively short, computational time is far from prohibitive. Therefore, it is not a practical concern.

Note also that the predictive distribution in (64) incorporates parameter uncertainty by integrating out according to the posterior in (63). Usually, prediction is carried out by expectations with respect to (64), e.g. but, since (64) is usually not available in closed form, Monte Carlo can be applied in the presence of samples from . This process may facilitate various forecasting tasks; for example forecasting several points, functions thereof, and potentially further ahead in the future. A typical forecasting evaluation exercise requires taking all the consecutive times from the nearest integer of, say, to . In each of these times, serves as the training sample, and points of after are used to evaluate the predictions. Hence, performing such a task requires samples from (64), and thus from , for several times . Note that this procedure can be quite intensive and in some cases not feasible.

Another approach that can also handle forecasting assessment tasks is to use sequential Monte Carlo (see, Chopin (2002) and Del Moral et al. (2006)) to sample from the sequence of distributions for . A general overview of the Iterated Batch Importance Sampling (IBIS) scheme of Chopin (2002), see also Del Moral et al. (2006) for a more general framework, is provided in Algorithm 1.

Initialize particles by drawing independently with importance weights , . For and each time for all :

-

(a)

Calculate the incremental weights from

where the Gaussian Process formulation makes them computationally dependant on all available data, what is reflected by conditioning on and .

-

(b)

Update the importance weights to .

-

(c)

If some degeneracy criterion (e.g. ESS()) is triggered, perform the following two sub-steps:

-

(i)

Resampling: Sample with replacement times from the set of s according to their weights . The weights are then reset to one.

-

(ii)

Jittering: Replace s with s by running MCMC chains with each as input and as output. Set .

-

(i)

The degeneracy criterion is typically defined through the Effective Sample Size () which equals to

| (65) |

and is of the form for some , where is the vector containing the weights.

The IBIS algorithm provides a set of weighted samples, called also particles, that can be used to compute expectations with respect to the posterior distribution, , for all using the estimator . Chopin (2004) shows consistency and asymptotic normality of this estimator as for all appropriately integrable . The same holds for expectations with respect to the posterior predictive distribution, . The weighted samples can be conveniently transformed into weighted samples from by just applying . A very useful by-product of the IBIS algorithm is the ability to compute

which is the criterion for conducting formal Bayesian model choice. Computing the following quantity in step (a) in Algorithm 1 yields a consistent and asymptotically normal estimator of , namely

| (66) |

An additional advantage of SMC is that it provides an alternative when MCMC algorithms are not mixing well and their convergence properties are poor. Generally, it is more robust when the target posterior is problematic, e.g. multimodal.

So as to apply the IBIS output to models and data in this paper, the following adaptations and extensions are implemented. Similar to Dubiel-Teleszynski et al. (2022b), and pursuing motivation therein, we pool together the advantages of data tempering and adaptive tempering (Jasra et al., 2011; Schäfer and Chopin, 2013; Kantas et al., 2014) in a hybrid adaptive tempering scheme which we outline in Appendix C. Because the MCMC algorithm used here is an extended version of Bauer (2018) and so it consists of independence samplers that are known to be unstable, we exploit the IBIS output and estimate posterior moments to arrive at independence sampler proposals; see Appendix B for details, and Dubiel-Teleszynski et al. (2022b) for additional rationale. Under such amended framework, and quite crucially in this paper, we extend the framework presented in Sections 3.3 and 3.4 to handle Gaussian Processes sequentially. In the end, we apply IBIS output in the optimization of a model-driven dynamically rebalanced portfolio of bond excess returns and inspect its economic value, following in the footsteps of Dubiel-Teleszynski et al. (2022b).

In empirical work, we use particles, MCMC steps when jittering, and with regards to minimum we set . The choice of steps at the jittering stage is led by quite well mixing behaviour of the underlying MCMC. We monitored the correlation between particles before and after that stage to realize that performance was already reasonable with this number of iterations.

4.2 Assessing Predictive Performance and Economic Value

Leveraging the evaluation framework summarized in this section, we seek to understand whether macroeconomic information introduced into Gaussian ATSMs in a nonlinear manner using Gaussian Processes lets us predict excess returns better than when macros enter these models linearly. Furthermore, we attempt to explore whether such statistical predictability, if any, can be turned into consistent economic benefits for bond investors.

As explained further in Section 5.1, we use lagged macro data at monthly frequency. Given the limitations to availability of macroeconomic information going forward and its exogenous and not endogenous nature we assume in this paper, what prevents us from associated forecasting further than a month ahead, we concentrate on 1-month prediction horizon. Thus, we refrain from making any assumptions about forward paths of the underlying macros. Consequently, returns we consider in our analysis are non-overlapping.

Along the lines of Dubiel-Teleszynski et al. (2022b), yet with in mind, we define the observed continuously compounded excess return of an -year bond as the difference between the holding period return of the -year bond and the -period yield as

| (67) |

If, instead of taking the observed one, we take the model-implied continuously compounded yield , calculated according to (22), we arrive at the predicted excess return which becomes

| (68) |

where is observed and is a prediction from the model. Our developed framework, see Algorithm 1, allows drawing from the predictive distribution of based on all information available up to time . More specifically, for each particle the -dynamics of can be used to obtain a particle of , which then can be transformed into a particle of via equation (68). Detailed steps are outlined in Algorithm 2.

First, at time , for some and , using , , from IBIS algorithm, iterate over :

- (a)

- (b)

-

(c)

Compute particle prediction of as

Second, since , , is a particle approximation to predictive distribution of , compute point prediction of using particle weights as

Third, repeat above two steps for different .

To assess the predictive ability of the models considered, we compute the associated out-of-sample (), due to Campbell and Thompson (2008). To measure the resulting economic value generated by each model, we consider a Bayesian investor with power utility preferences. Our Bayesian learner solves an asset allocation problem getting optimal portfolio weights which we use to compute the as in Johannes et al. (2014) and Gargano et al. (2019). To that end, we follow the exposition in Dubiel-Teleszynski et al. (2022a), where we refer the reader for further details. Similar to the latter paper, we adopt the Expectations Hypothesis (EH) as initial empirical benchmark, however instead of then looking at the performance relative to model (Dubiel-Teleszynski et al., 2022b), we compare the nonlinear with the corresponding linear models. Again, we only focus on a 1-month prediction horizon.

5 Data and Models

5.1 Yields and Macros

In terms of bond yields, we analyze the same data as these described in Dubiel-Teleszynski et al. (2022a), splitting them in the same training (in-sample) and testing (out-of-sample) periods, thus for further details we refer the reader therein.

When it comes to macroeconomic information about the US, we consider two variables which are well covered in the literature. These include, core555In contrast to Cieslak and Povala (2015), who devise trend inflation by appropriately smoothing core inflation, we use the latter as is to arrive at our own, nonlinear function thereof. inflation () as in Cieslak and Povala (2015), as well as the three-month moving average of the Chicago Fed National Activity Index () from Joslin et al. (2014), which is a measure of current economic conditions. Together they offer parsimonious yet comprehensive enough, for our purposes, description of the US economy. Both macro variables are at a monthly frequency. They are also seasonally adjusted and revised. Unlike , which is a smoothed index in levels, is in percent changes from year ago. The underlying data period is such that it corresponds to this for yields, as discussed above, and also reflects the lagged character assumed for the macros in all models we consider in this paper. Importantly, we standardize the macros only in the nonlinear case and, to that end, we use individual means and standard deviations calculated in-sample for the out-of-sample operations, to avoid look-ahead bias.

5.2 Models and Rationale Behind

In terms of models, we consider several alternatives when it comes to positions the unspanned, nonlinear or linear, macros take in the given model. More specifically, in the nonlinear case these are

| (69) |

and for the linear model we replace with in this notation. In the above, refers to a specific macroeconomic variable, or , introduced in the particular model. For example, for and , that is , index means that macroeconomic impact is allowed in the second and third equation in (39), under the assumption that , and . We only investigate a subset of the available alternative models in greater detail. Investigating and determining which macros, beyond the two included in our analysis, represent best match for specific PCs of the US yield curve, when interacting with the latter in a nonlinear or linear manner, is left for future research.

As result of risk price restrictions (on ) we adopt in this paper from Dubiel-Teleszynski et al. (2022b), without loss of generality for in (69), we define the risk premium factor as

| (70) |

where the first element is similar to Duffee (2011), however in our case its time-varying component, , is a restricted version (only is free) of the risk premium factor defined in Duffee’s paper. The component is in that particular case the first element of the unspanned nonlinear macro . If instead and in (69), then

| (71) |

where the first element, which is related to level risk, equals and is also equivalent to the corresponding factor in model by Dubiel-Teleszynski et al. (2022b) we adopt risk price restrictions from.

Following from Duffee (2011), the time-varying risk premium factor , which in the case therein is a linear combination of the state vector obtained from model shocks to yields, determines the compensation investors require to face fixed-income risk from to , and it contains all information relevant to predicting one-step-ahead, yet not -step-ahead for , excess returns. We instead assume that investors require compensation for level risk stemming from changes to slope only. However, the term in (70), which is a priori unspanned and potentially nonlinear function () of the underlying macroeconomic variable (), affects this compensation. It is important to understand, if this impact is not distorting information relevant to predicting excess returns, already available from alone. One way to achieve this goal is to perform predictability and economic value exercises for the models considered and make appropriate comparisons. Thus, we do so in Section 6.

Different from Duffee (2011), we obtain the state vector from observed yields directly. Nevertheless, for in (69), we are able to similarly define the hidden part of the risk premium factor, as the part unspanned by , in the following way

| (72) | ||||

| (73) |

where is the projection of unspanned nonlinear macros on principal components obtained from observed yields, which is thus spanned by these PCs, and as such not hidden from the yield curve. After Duffee (2011), the hidden can be estimated as residual from a regression of the former on the latter and expressed as

| (74) |

where we take as the mean from its posterior distribution and and are the underlying Ordinary Least Squares parameter estimates. We also note that

and, by rearranging terms in (74), arrive at the following decomposition

| (75) |

of unspanned nonlinear macros , into two orthogonal components. While the first, , which is an affine transformation of the PCs, is by definition not hidden from the yield curve, the second, , duly is.

Then we can examine to what extent assumed nonlinear a priori is actually such a posteriori. More importantly, however, we investigate whether the same can be stated about its hidden component . To that end, we separately regress these, as well as , on the underlying macroeconomic variable and inspect the resulting explanatory powers behind such linear associations, see Section 6.4 for related discussion. By doing so, we can determine whether there is any connection especially between the hidden component of the risk premium factor being nonlinear and the predictability of and economic benefits from nonlinear models we consider in this paper. In what follows, we eventually demonstrate that, when the latter outperform the linear ones on these two important fronts, this is indeed the case.

6 Empirical Results

6.1 Uncovering Nonlinearities

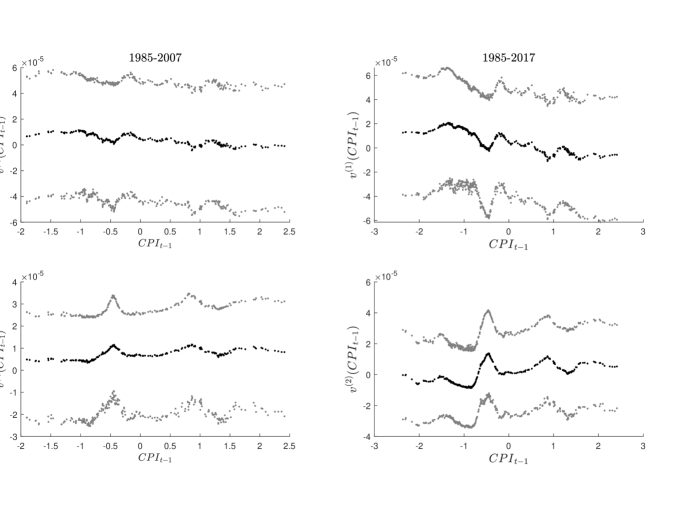

The data contain an important economic event and thus it is interesting to have a look at the plots of individual elements in against , for and , to see how it affects our analysis. These plots are generated from the IBIS output, as described in Section 4.1 and further in Appendix C. In particular, data cover the financial crisis of -. For related discussion, yet focused on principal components as opposed to nonlinear macros, see Dubiel-Teleszynski et al. (2022b). In what follows, we only concentrate on models and , which we also focus on in Section 6.4, for specific reasons mentioned therein.

By inspecting the plots for model , which are shown in Figure 1, we observe that interacts with the yield curve in a nonlinear, rather than linear, manner. This is particularly the case when we look at panels on the right hand side of this figure. In there, distributions of and plotted against are estimated using the entire sample of data, including the recession period. Comparing these two panels with their counterparts on the left hand side in the same figure, which are based on data from the training period only, and thus preclude the recession, we notice that the nonlinear relationship between and the yield curve strengthens in time.

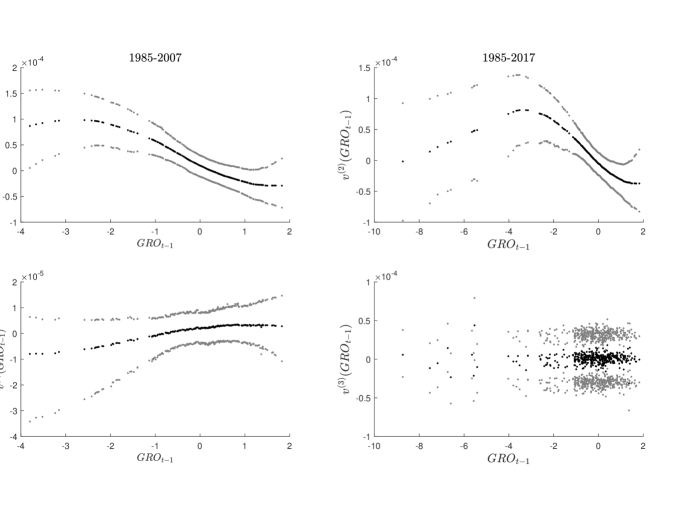

Next, we have a careful look at , where things are quite different. In Figure 2, with associated plots for model , we observe that interacts with the yield curve more in a linear than in a nonlinear manner. It is particularly evident when inspecting the top panel in this figure, which shows the distribution of plotted against . The vast majority of data points in the training period, that is on the left hand side, are located in the part of the graph where the association is linear. The remaining data points constitute the outliers. On the right hand side, that is when the entire data sample is used, the part of the graph which is linear is accompanied by even more outliers. With hindsight, economic activity is heavily affected by outliers due to recession, what can also be noticed by comparing the horizontal axes in these plots between the left and the right hand side panels. Although the functional association of lagged with the yield curve shown in the top panel deteriorates only slightly in time, this presented in the bottom panel for dilutes completely when the entire data sample is involved. Likely, the latter changes in the post-recession period, while the model assumes it is the same, what makes the forecasting exercise we conduct quite challenging but at the same time more realistic.

6.2 Bond Return Predictability

In what follows, we focus on statistical performance. Table 3 reports out-of sample values for all linear (including , the maximally flexible model, and , see Dubiel-Teleszynski et al. (2022b)) and nonlinear models across different bond maturities and at 1-month prediction horizon. The latter means that we only consider non-overlapping excess bond returns. The in-sample (training) period is from January 1985 to the end of 2007 and the out-of-sample (testing) period is from January 2008 to the end of 2018. The latter practically begins with the - financial crisis. Overall, results indicate, as expected and in line with the existing literature (Duffee, 2011; Joslin et al., 2014; Fulop et al., 2019), that models which incorporate macroeconomic information, irrespective of whether in a linear or nonlinear manner, predict well and perform better out-of-sample compared to the EH benchmark, as well as when set against yields-only models. This is confirmed by predictive that are exclusively positive and statistically significant for , across all maturities, and mostly positive and statistically significant for , especially for the short and medium term maturities. Across maturities, they range from to for , whereas for the positive and statistically significant are between to .

Generally, models with macroeconomic variables perform better, in terms of out-of-sample statistical performance, than the yields-only models we consider, namely and . However, there are four notable exceptions in case of , where are practically close to zero. These are linear and nonlinear models with indices and , which either perform as unsatisfactorily as () or worse, and as such similar to (, and ). What they interestingly have in common is that, in these models macroeconomic information interacts with the yield curve through the observed level, meaning that it is included in the equation governing the real-world dynamics of the first PC. This deterioration in statistical performance translates further into correspondingly poor economic value results, especially for linear models, what we discuss in the next section.

Selected results on explanatory power for the nonlinear models with specifically listed above, which are presented in Table 2 (see fourth panel) for model , reveal that, contrary to the out-of-sample statistical performance results, there are statistically significant benefits from including , when explaining the variability of excess bond returns. It is particularly evident when compared to what we observe for the corresponding nonlinear function of lagged . For , such gains decrease at longer maturities and range from at 2-year, through at 5-year, to at 10-year maturity. For , these gains are considerably smaller and amount to about throughout 2- to 5-year maturities. Related results in Table 1 confirm that similar is true in the linear case. Namely, explanatory power gains for , albeit smaller than in the nonlinear case, range from at 2-year to at 4-year maturity, yet occur only at the short end of the yield curve. Those for are in this case practically negligible. Corresponding results on explanatory power for model are quantitatively and qualitatively alike, thus not shown. The latter also applies to such results for all models with indices , and .

One possible rationale behind the above argument is that , the economic activity, varies more profoundly than , the prices, in the aftermath of the - financial crisis, that is throughout the testing sample. Let us compare the horizontal axes on the left with those on the right hand side in the plots shown in Figures 1 and 2. In Figure 1, is approximately between and over 1985-2007 and from to over 1985-2017. In Figure 2, is approximately between and over 1985-2007 and from to over 1985-2017. Importantly, both variables are standardized over 1985-2017 based on their respective means and standard deviations computed over 1985-2007. Thus, throughout 1985-2017 the variation of hardly moves relative to what happens for , which becomes evidently negatively skewed as result of such adverse economic conditions. On the other hand, these abnormal changes in serve explaining the variability of excess bond returns in these turbulent times well, what is also a sign of possible overfitting.

Nevertheless, if the underlying index does begin with 1 not 0 then these nonlinear models with we specifically mention above, with indices and , tend to significantly improve out-of-sample statistical performance results when compared to linear benchmarks, see Table 4. As such, they reduce the risk associated with out-of-sample predictions based on macroeconomic variables which become negatively skewed in times of economic/financial crises. Interestingly, similar improvements occur for in the specific case of nonlinear model with index .

6.3 Economic Performance

In what comes next, we concentrate on model performance in terms of economic value. Table 5 reports results for the annualized s, calculated using out-of-sample forecasts of bond excess returns across maturities and at 1-month prediction horizon. The in-sample and out-of-sample periods are the same as in the case of predictive performance. The coefficient of relative risk aversion is chosen to be and we do not impose any portfolio constraints666These non-conservative choices are motivated by early exploratory character of the analysis conducted herein. The goal is to find economic value first and in future research examine if it can be exploited when stricter conditions apply.. We find that, in most cases, corresponding s are positive and non-negligible, indicating that DTSMs with unspanned macroeconomic information, introduced in the model in a linear or nonlinear way, not only perform well and in a statistically significant manner when it comes to out-of-sample predictability but also generate economic gains for bond investors relative to the EH benchmark.

For the linear case, this is in line with the existing literature, as numerous studies show (Duffee, 2011; Joslin et al., 2014; Fulop et al., 2019), whereas in case of nonlinear models only recently Bianchi et al. (2021), albeit in a regression and not in a no-arbitrage setting, show that forecasts based on neural networks fed with macroeconomic and yield information jointly, translate into economic gains that are larger than those obtained using yields alone. In line with all that, yields-only DTSMs we are concerned with in this paper, that is and , perform evidently worse in terms of economic value than models with macroeconomic information (see, Table 5). This is also consistent with their relatively inferior out-of-sample statistical performance, which we discuss in the previous section.

In case of results show clear evidence of positive out-of-sample economic benefits for bond investors from introducing information about prices in the model. This is the case across most maturities (especially at 2-, 3- and 7-year) and in particular when is introduced in a nonlinear manner. s for linear models with are not even comparably as statistically significant as the former. For example, in case of they are statistically significant at all maturities and range from (at 5-year) to (at 7-year). In relation to such evidence is less pronounced and results are only statistically significant for selected maturities and for linear and nonlinear models with indices 011 and 010 (at 3-, 4- and 7-year, in both cases), as well as 001 (all maturities but 5-year). The outcome is most positive in this last case and, when statistically significant, s for linear and nonlinear models with index 001 range from (at 3-year, for the linear setup) to (at 7-year, for the nonlinear setup).

When comparing nonlinear models with their linear counterparts, only in case of the former perform significantly better than the latter (see, Table 6). For , and we observe positive and non-negligible values across most maturities, in particular at 2- to 5-year. If statistically significant, they span between and relative to the linear benchmarks. For , where results are overall worse compared to those for , we are not able to identify meaningful, statistically significant cases where nonlinear models outperform their linear benchmarks in terms of economic value. In the next section we provide some rationale why and when it might be so.

Overall, out-of-sample economic value results are consistent with those for predictive performance which we discuss in the previous section. As such, based on results presented in this paper, the puzzling behavior between statistical predictability and out-of-sample economic gains for bond investors cannot be unequivocally confirmed for DTSMs utilizing macroeconomic information, especially in a nonlinear manner. It is also important to note that considerable and statistically significant explanatory power gains (see, Tables 1 and 2), especially from macroeconomic variables which are prone to outliers like , not necessarily translate into corresponding economic performance out-of-sample. Even to the contrary, they may lead to significant losses, especially when economic conditions are changing. It is particularly the case for linear models with indices and (see, Table 5). However, nonlinear models may help limit such losses, e.g. by handling outliers better. In some cases, like for (, and ), they perform consistently better out-of-sample than their linear counterparts in terms of economic value (see, Table 6).

6.4 Benefiting from Hidden Nonlinearities

In this section we shed some light on why and when certain nonlinear models we consider in this paper (with macroeconomic variables like ) outperform their linear counterparts in terms of economic value, whereas other (with macros such as ) do not. To that end, we resort to the results obtained from risk premium factor decomposition, as described in Section 5.2, which are presented in Tables 7 and 8. For pragmatic reasons, related to the tuning procedure (see, Appendix D) which is not always optimal and as such affects the way certain aspects of this decomposition can be effectively demonstrated graphically, in what follows we focus on two particular models. Namely, and .

We choose these two models for several reasons. First, both linear and nonlinear models with and index 110 perform well in terms of out-of-sample predictability, however the nonlinear model performs significantly better across maturities than its linear counterpart - with ranging from to against and for the linear model (see, Table 3). Second, both linear and nonlinear models with and index 011 perform fairly well across most maturities when it comes to out-of-sample predictability - with statistically significant ranging from and for both cases. Third, while nonlinear model with does significantly better in terms of out-of-sample economic performance than its linear counterpart - with relative ranging from to across maturities when statistically significant - it is almost entirely the opposite case for the . There, relative are not statistically significant and vary between and (see, Table 6). This is precisely what we are after to facilitate the argumentation which follows.

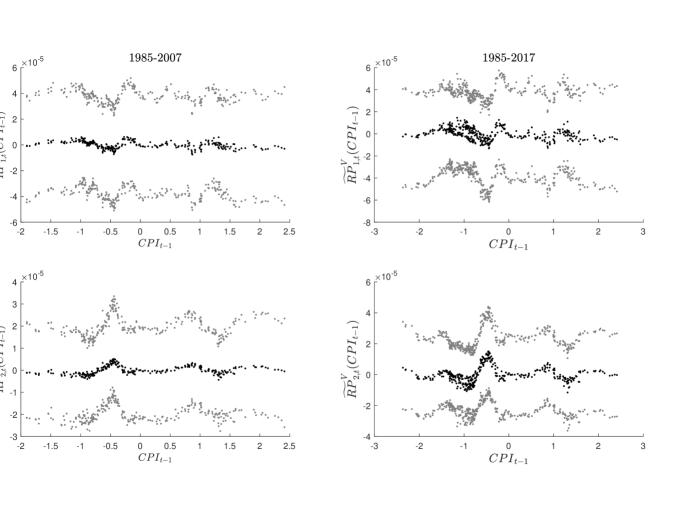

With what we summarised above in mind, we now resort to decomposition in (74) of nonlinear macro into a part about which complete information is contained in the yield curve, that is , and a part which is entirely hidden, that is . We regress individually each of these components on the underlying macro in order to determine the degree to which the resulting relationship is linear, as measured by the associated adjusted . Tables 7 and 8 contain such results for and , respectively. They include related results for all the other models as well, however our focus on these two remains unchanged.

Beginning with , in the third panel of Table 7 we notice that for model both and its part which is not hidden from the yield curve are to large extent linear functions of , as measured by that are equal to and , respectively. At the same time the hidden part, that is , is hardly in a linear relationship with , as indicated by a very low value of equal to only. It is similar in case of where these metrics amount to , and practically , in that order. Hidden parts of in model are thus nonlinear functions of the underlying macroeconomic variable, namely . To realize that it is indeed so, it is sufficient to have a brief look at Figure 3. Therein, we see clearly that functional associations between these hidden parts and lagged are highly nonlinear, stable or become even more pronounced (left versus right hand side). At this point it is safe to state that in this particular case there is a fair reason behind superiority of the nonlinear model, which is implemented using s in this paper, over its linear counterpart. Namely, unspanned information coming from , which is hidden from the yield curve yet it affects its -dynamics, is evidently nonlinear in nature.

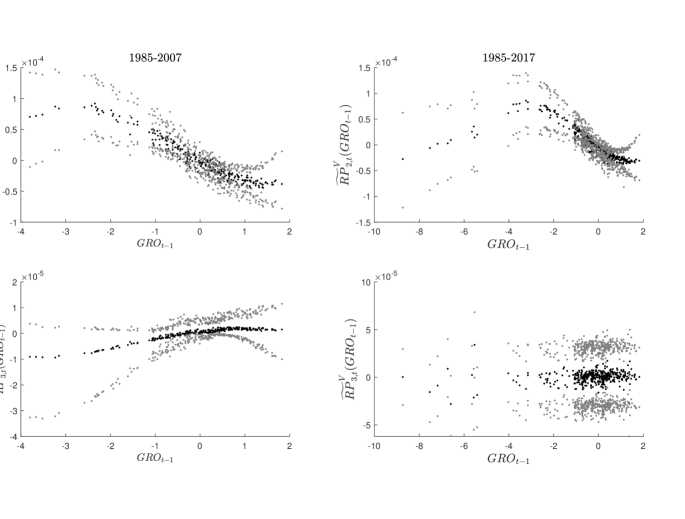

Ending with , in the first panel of Table 8 we observe that, for model , both and its part which is not hidden from the yield curve are to considerable and to moderate extent, respectively, linear functions of , as measured by that are equal to and . What is however different from the case of is that the hidden part, namely , is to larger extent linear in than the part which is not hidden from the yield curve, that is , as indicated by equal to for the former. In case of , these metrics amount to , and , in that order. However, for reasons mentioned in the last paragraph of Section 6.1 and in relation to the tuning procedure (see, Appendix D), which is not always optimal, we also look at the corresponding numbers for model in the first panel of Table 7. They amount to , and , respectively. In this case, the focus of the tuning procedure lies solely on the curvature not slope and curvature together, as in the former model. These latter results correspond more closely to what we observe for in model .

To consolidate the discussion, a careful look at Figure 4 is required. In the top panel, we notice immediately that what adjusted are telling us about in the model of interest is indeed so. Namely, the association between its hidden part and the lagged is visibly more linear than nonlinear. The picture is similar, albeit less pronounced, to this in the corresponding panel in Figure 2, which we discuss in the last paragraph of Section 6.1. On both sides the majority of data points are located in the part of the graph where the association is linear, whereas the remaining data points are the outliers. What happens to in the bottom panel can also be linked to related arguments in the same section. It is thus not surprising that in this case the nonlinear model leads to inferior economic value results, let alone adds such a value, in comparison to the linear benchmark (see, Table 6). In this case and on such front it is evidently hard to beat the linear, more parsimonious model based merely on outliers.

7 Conclusions

We propose a novel methodological framework which combines Bayesian sequential inference with machine learning techniques, in particular Gaussian Processes. It allows us to incorporate unspanned macroeconomic information into Dynamic Term Structure Models in a potentially nonlinear manner. Sequential setup we develop successfully handles real-time adjustments to parameters governing such asymmetric/nonlinear associations. The methodology takes into account parameter uncertainty and provides entire predictive distribution of bond returns, allowing investors to review their beliefs when new information arrives and thus informing their asset allocation in an online manner. The framework is then tested against the Expectations Hypothesis, as well as against the linear benchmark, in a comprehensive out-of-sample exercise involving statistical predictability and economic value, where we assume availability of information about prices and economic activity. To that end, we scrutinize nonlinear models by developing a version of the macro-finance DTSM proposed by Joslin et al. (2014) that incorporates unspanned macroeconomic variables in a linear manner. However, to align with our nonlinear setup we consider them exogenous.

Empirical results confirm that in such an exercise the models with unspanned macroeconomic information, irrespective if it is introduced in a linear or nonlinear manner, perform overall better than the models which are yields-only by construction. Specifically, they also reveal that nonlinear models provide a competitive edge over linear models in cases when a-priori possibly nonlinear functions of macroeconomic variables admit nonlinear character a-posteriori in the parts which are hidden from the yield curve. In this paper it is the case for the prices and not for the economic activity. To demonstrate that, we apply the risk premium factor decomposition from Duffee (2011).

However, results in this paper also indicate that for certain models where macroeconomic information directly affects the yield curve level, using nonlinear formulation might not necessarily lead to superb predictability and economic value gains but it might still mitigate substantial mistakes on those fronts. In particular, it is the case for models with macroeconomic variables which in abnormal times, such as the - financial crisis or the more recent COVID- recession, are subject to outliers like the economic activity. According to our results, Gaussian Processes handle such cases quite well.

Thinking ahead, we acknowledge the limitations of our study where we only consider a set of macroeconomic variables limited to two and Gaussian Processes we apply are of a single-input type and based on one commonly applied nonlinear kernel that we select to use. Verifying what we infer in this paper on a broader set of macroeconomic information, while also using other nonlinear kernels such as Matern kernel or combined kernels, is a possible way going forward. Letting macroeconomic variables interact within a multi-input Gaussian Process framework, for example using ARD (Automatic Relevance Determination) kernels (Rasmussen and Williams, 2006), is also a potentially interesting research avenue to pursue.

References

- (1)

- Alvarez et al. (2012) Alvarez, M. A., Rosasco, L. and Lawrence, N. D. (2012), ‘Kernels for vector-valued functions: A review’, Foundations and Trends® in Machine Learning 4(3), 195–266.

- Ang and Piazzesi (2003) Ang, A. and Piazzesi, M. (2003), ‘A no-arbitrage vector autoregression of term structure dynamics with macroeconomic and latent variables’, Journal of Monetary Economics 50(4), 745–787.

- Bauer (2018) Bauer, M. D. (2018), ‘Restrictions on risk prices in dynamic term structure models’, Journal of Business & Economic Statistics 36(2), 196–211.

- Bianchi et al. (2021) Bianchi, D., Büchner, M. and Tamoni, A. (2021), ‘Bond risk premiums with machine learning’, The Review of Financial Studies 34(2), 1046–1089.

- Bishop (2006) Bishop, C. M. (2006), Pattern Recognition and Machine Learning, Springer.

- Campbell and Thompson (2008) Campbell, J. Y. and Thompson, S. B. (2008), ‘Predicting excess stock returns out of sample: Can anything beat the historical average?’, The Review of Financial Studies 21(4), 1509–1531.

- Chopin (2002) Chopin, N. (2002), ‘A sequential particle filter method for static models’, Biometrika 89(3), 539–552.

- Chopin (2004) Chopin, N. (2004), ‘Central limit theorem for sequential monte carlo methods and its application to bayesian inference’, The Annals of Statistics 32(6), 2385–2411.

- Cieslak and Povala (2015) Cieslak, A. and Povala, P. (2015), ‘Expected returns in treasury bonds’, The Review of Financial Studies 28(10), 2859–2901.

- Cochrane and Piazzesi (2005) Cochrane, J. H. and Piazzesi, M. (2005), ‘Bond risk premia’, The American Economic Review 95(1), 138–160.

- Cooper and Priestley (2009) Cooper, I. and Priestley, R. (2009), ‘Time-varying risk premiums and the output gap’, The Review of Financial Studies 22(7), 2801–2833.

- Del Moral et al. (2006) Del Moral, P., Doucet, A. and Jasra, A. (2006), ‘Sequential monte carlo samplers’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 68(3), 411–436.

-

Dubiel-Teleszynski et al. (2022a)

Dubiel-Teleszynski, T., Kalogeropoulos, K. and Karouzakis, N.

(2022a), On unspanned latent factors

in dynamic term structure models.

Published online.

https://arxiv.org/abs/2205.00098 -

Dubiel-Teleszynski et al. (2022b)

Dubiel-Teleszynski, T., Kalogeropoulos, K. and Karouzakis, N.

(2022b), Sequential learning and

economic benefits from dynamic term structure models.

Forthcoming in Management Science.

https://arxiv.org/abs/2204.10658 - Duffee (2011) Duffee, G. R. (2011), ‘Information in (and not in) the term structure’, The Review of Financial Studies 24(9), 2895–2934.

- Duffie and Kan (1996) Duffie, D. and Kan, R. (1996), ‘A yield-factor model of interest rates’, Mathematical Finance 6(4), 379–406.

- Durbin and Koopman (2012) Durbin, J. and Koopman, S. J. (2012), Time Series Analysis by State-Space Methods, Oxford University Press.

- Fulop et al. (2019) Fulop, A., Li, J. and Wan, R. (2019), ‘Real-time bayesian learning and bond return predictability’, Journal of Econometrics . Forthcoming.

- Gargano et al. (2019) Gargano, A., Pettenuzzo, D. and Timmermann, A. (2019), ‘Bond return predictability: Economic value and links to the macroeconomy’, Management Science 65(2), 508–540.

- Jasra et al. (2011) Jasra, A., Stephens, D. A., Doucet, A. and Tsagaris, T. (2011), ‘Inference for lévy-driven stochastic volatility models via adaptive sequential monte carlo’, Scandinavian Journal of Statistics 38(1), 1–22.

- Johannes et al. (2014) Johannes, M., Korteweg, A. and Polson, N. (2014), ‘Sequential learning, predictability, and optimal portfolio returns’, The Journal of Finance 69(2), 611–644.

- Joslin et al. (2014) Joslin, S., Priebsch, M. and Singleton, K. J. (2014), ‘Risk premiums in dynamic term structure models with unspanned macro risks’, The Journal of Finance 69(3), 1197–1233.

- Joslin et al. (2011) Joslin, S., Singleton, K. J. and Zhu, H. (2011), ‘A new perspective on Gaussian dynamic term structure models’, Review of Financial Studies 24(3), 926–970.

- Kantas et al. (2014) Kantas, N., Beskos, A. and Jasra, A. (2014), ‘Sequential monte carlo methods for high-dimensional inverse problems: a case study for the navier-stokes equations’, SIAM/ASA Journal on Uncertainty Quantification 2, 464–489.

- Litterman and Scheinkman (1991) Litterman, R. B. and Scheinkman, J. (1991), ‘Common factors affecting bond returns’, The Journal of Fixed Income 1(1), 54–61.

- Lütkepohl (2005) Lütkepohl, H. (2005), New introduction to multiple time series analysis, Springer.

- Ludvigson and Ng (2009) Ludvigson, S. C. and Ng, S. (2009), ‘Macro factors in bond risk premia’, The Review of Financial Studies 22(12), 5027–5067.

- Murphy (2012) Murphy, K. P. (2012), Machine Learning: A Probabilistic Perspective, MIT Press.

- Rasmussen and Williams (2006) Rasmussen, C. E. and Williams, C. K. I. (2006), Gaussian processes for machine learning, MIT Press.

- Schäfer and Chopin (2013) Schäfer, C. and Chopin, N. (2013), ‘Sequential Monte Carlo on large binary sampling spaces’, Statistics and Computing 23(2), 163–184.

Appendix A Specification of Priors

In what comes next, we succinctly explain the prior distributions that were not specified in the main body of the paper. For parameters in , , , and , or effectively , priors are constructed in the same manner as in the related appendix in Dubiel-Teleszynski et al. (2022a).

The only exception are parameters in , which have range restricted to positive values. We thus transform them first, so that they have unrestricted range. Specifically, we work in log-scale of . Next, independent normal distributions with zero means and large variances are assigned to each of its components.

Appendix B Markov Chain Monte Carlo Scheme

Following from (61) and (63), and given a prior as described in Appendix A, the posterior can be written in a more detailed manner as

| (76) |

As the above posterior is not available in closed form, methods such as MCMC can be used to draw samples from it using Monte Carlo. Yet, the MCMC output is not assured to lead to precise Monte Carlo calculations since the corresponding Markov chain may have poor mixing and convergence properties, what leads to highly autocorrelated samples.

It is thus necessary to devise a suitable MCMC algorithm that does not exhibit such unfavourable traits. For further details regarding its construction, see the related appendix in Dubiel-Teleszynski et al. (2022b). Such an MCMC scheme is shown in Algorithm 3.

Initialize all values of . Then at each iteration of the algorithm:

-

(a)

Update from its full conditional distribution that can be shown to be an Inverse Gamma distribution with parameters and , such that is and is , where , since prior is assumed diffuse, is a time- residual from (37), and is Euclidean norm squared.

-

(b)

Update using an independence sampler based on the MLE and the Hessian obtained before running the MCMC, using multivariate t-distribution with 5 degrees of freedom as proposal distribution.

-

(c)

Update in a similar manner to (b).

-

(d)

Update in a similar manner to (b).

Appendix C Adaptive Tempering

The aim of adaptive tempering is to smooth peaked likelihoods. For additional information, see the corresponding appendix to Dubiel-Teleszynski et al. (2022b). Implementation of the IBIS scheme with hybrid adaptive tempering steps is outlined in Algorithm 4. It is important to note that, unlike it is presented in Algorithm 1 for the general IBIS case, in the specific case we are dealing here with we initialize the particles by drawing from the posterior instead of the prior . This is done in-sample based on training data, as detailed in Section 5.1.

Although it is straightforward to implement step 4(b) in Algorithm 4 for an independence sampler, adjustments are necessary for a full Gibbs step. It is especially the case for in step (a) in Algorithm 3, see Appendix B. Implementation details are the same as in the corresponding appendix to the paper we mention above.

Initialize particles by drawing independently with importance weights , . For and each time for all :

-

1

Set .

-

2

Calculate the incremental weights from

-

3

Update the importance weights to .

-

4

If degeneracy criterion ESS() is triggered, perform the following sub-steps:

-

(a)

Set and .

-

(b)

While

-

i.

If degeneracy criterion ESS() is not triggered, where , set , otherwise find such that ESS() is greater than or equal to the trigger, where , for example using bisection method, see Kantas et al. (2014).

-

ii.

Update the importance weights to .

-

iii.

Resample: Sample with replacement times from the set of s according to their weights . The weights are then reset to one.

-

iv.

Jitter: Replace s with s by running MCMC chains with each as input and as output, using likelihood given by . Set .

-

v.

Calculate the incremental weights from

-

vi.

Set and .

-

i.

-

(a)

Appendix D Tuning the Gaussian Process

Since we view as tuning parameter we tune it in-sample and fix out-of-sample at . Details about the underlying data are in Section 5.1. To that end, in a manner similar to this in the corresponding appendix in Dubiel-Teleszynski et al. (2022a), we follow a multi-step process which is entirely based on in-sample data. First, as in the base case in Section 3.1, we estimate by maximum likelihood a yields-only DTSM where and, out of , only is left unrestricted to match the risk price restrictions we adopt in this paper. Resulting MLEs let us then obtain , , where refers to in-sample period, from (43).

Second, we formulate an amended version of the likelihood in (61), using only its -likelihood components modified in the following way

| (77) |

where and refer to in-sample data, , , and are the MLEs from the first step, and , with scalar , consists of parameters we estimate by maximum likelihood next. However, before that we parametrize in (77) as

| (78) |

where is a (in accordance with exposition in this paper where we choose ) vector including diagonal elements of the covariance matrix for , and , , are practically as in the first step.

Appendix E Linear Model with Macros

It is straightforward to extend the estimation framework of Bauer (2018), and consequently this in Dubiel-Teleszynski et al. (2022b), to incorporate in a linear manner unspanned macros which are assumed exogenous. It is only the way we handle the -dynamics of in (39) what needs to be adjusted to

| (79) |

where is matrix, which represents the feedback from to .

Following sections C.1 and C.2 in Online Appendix to Bauer (2018) and details from Lütkepohl (2005), to consider coefficients next to in (79) in estimation, it suffices to tackle them jointly with , or in our case with only, to match the risk price restrictions chosen for the nonlinear case in Section 3.4. Adopting notation from Online Appendix to Bauer (2018) to ours where necessary, we can rewrite (79) in vector form as

where , , with adapted , , , with modified , , and amended .

Then, linear constraints after Bauer (2018) are following

where in our case is a selection matrix of zeros and ones, is a vector with and those elements of we decide to leave unrestricted. For example, if our goal it to compare a linear model with a corresponding nonlinear case where and there is no included in the first equation of (42), to allow for a meaningful comparison of results we would restrict the first row in to zeros, in a similar fashion to restricting risk prices in . Finally, . For clarity, contains all elements of , as well as zeros, and in our case and .

After the above modifications the rest is straightforward to conclude and one can easily follow in the footsteps of Bauer (2018) for a Bayesian framework, as well as Dubiel-Teleszynski et al. (2022b) for a corresponding sequential implementation thereof, to eventually arrive at an almost complete estimation framework for a linear model with macros which is comparable to the setup we develop in this paper for the nonlinear case. What is still missing though is the prior specification for . This we choose to be non-informative and thus assign independent normal distribution with zero mean and large variance to each element thereof.

| 2Y | 3Y | 4Y | 5Y | 7Y | 10Y | |

| 4.26 | 3.29 | 3.08 | 2.74 | 2.77 | 3.55 | |

| -0.24 | -0.24 | -0.22 | -0.16 | 0.05 | ||

| 0.08 | -0.21 | -0.17 | ||||

| 4.03 | 3.06 | 2.86 | 2.58 | 2.81 | 3.65 | |

| 6.13 | 4.71 | 3.61 | 2.82 | 2.56 | 3.38 | |

| 2Y | 3Y | 4Y | 5Y | 7Y | 10Y | |

| 4.26 | 3.29 | 3.08 | 2.74 | 2.77 | 3.55 | |

| -0.14 | 0.17 | |||||

| -0.24 | -0.11 | 0.04 | 0.26 | |||

| 0.17 | -0.12 | -0.20 | -0.25 | |||

| 0.11 | -0.15 | -0.25 | -0.25 | |||

| 0.07 | -0.13 | |||||

| 5.71 | 4.40 | 4.23 | 3.93 | 4.07 | 5.39 | |

| 7.94 | 6.43 | 5.86 | 4.95 | 4.90 | 5.73 | |

| 2Y | 3Y | 4Y | 5Y | 7Y | 10Y | |

| -0.04 | -0.06 | -0.05 | -0.04 | -0.02 | -0.01** | |

| 0.01 | 0.03** | 0.03* | 0.02 | 0.02* | 0.04** | |

| 0.03** | 0.04*** | 0.03** | 0.03** | 0.03** | 0.03*** | |

| 0.02* | 0.04** | 0.03** | 0.03* | 0.03* | 0.05*** | |

| 0.03** | 0.05*** | 0.04** | 0.03** | 0.03** | 0.04*** | |

| 0.03** | 0.04*** | 0.03** | 0.03** | 0.03* | 0.04*** | |

| 0.03** | 0.03*** | 0.03** | 0.02** | 0.02** | 0.03*** | |

| 0.06*** | 0.06*** | 0.05*** | 0.04** | 0.04** | 0.04*** | |

| 0.03* | 0.04*** | 0.04** | 0.03** | 0.03** | 0.04*** | |

| 0.05*** | 0.05*** | 0.04*** | 0.04** | 0.03** | 0.04*** | |

| 0.03* | 0.04** | 0.03** | 0.03* | 0.03* | 0.04*** | |

| 0.03** | 0.04*** | 0.04** | 0.03** | 0.03* | 0.04*** | |

| -0.19 | -0.03 | -0.03 | -0.04 | -0.01 | 0.01 | |

| -0.03 | 0.01* | 0.01* | 0.01 | 0.01 | 0.01* | |

| 0.02 | 0.05** | 0.04*** | 0.03** | 0.02* | -0.02 | |

| 0.03* | 0.05** | 0.03** | 0.02** | 0.01 | 0.00 | |

| -0.22 | -0.05 | -0.05 | -0.07 | -0.04 | 0.00 | |

| -0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| 0.01 | 0.05** | 0.03** | 0.02** | 0.02* | -0.01 | |

| 0.03* | 0.05** | 0.03** | 0.02** | 0.01* | 0.00 | |

| 0.03* | 0.04** | 0.04** | 0.04** | 0.03* | 0.03** | |

| 0.03** | 0.04*** | 0.04** | 0.03** | 0.03** | 0.04*** | |

| 2Y | 3Y | 4Y | 5Y | 7Y | 10Y | |

| -0.01 | 0.00 | 0.00 | 0.00 | 0.01 | 0.02* | |

| 0.00 | 0.00 | 0.00 | 0.00 | -0.01 | 0.00 | |

| 0.03** | 0.03** | 0.02* | 0.01 | 0.01 | 0.02* | |

| 0.02** | 0.01 | 0.01 | 0.00 | 0.00 | 0.01 | |

| 0.01 | 0.01* | 0.01 | 0.01 | 0.00 | -0.01 | |

| 0.13* | 0.04 | 0.04 | 0.05* | 0.02 | 0.01 | |

| 0.01 | -0.01 | -0.01 | -0.01 | -0.01 | 0.02 | |

| 0.15** | 0.05* | 0.05 | 0.06* | 0.03 | 0.00 | |

| 0.02 | 0.00 | 0.00 | 0.00 | -0.01 | 0.01 | |

| 0.00 | 0.00 | 0.00 | -0.01 | 0.00 | 0.01 | |

| 2Y | 3Y | 4Y | 5Y | 7Y | 10Y | |

| -10.77 | -11.81 | -10.27 | -8.05 | -3.62 | -7.49 | |

| 2.31 | 1.88 | 1.38 | 0.80 | 2.30 | 2.55 | |

| 1.68 | 1.22 | 1.57 | 1.36 | 3.61** | 1.45 | |

| 3.00* | 2.79* | 2.73 | 2.56 | 4.30* | 3.97* | |

| 2.79* | 2.54* | 2.31 | 1.70 | 3.59 | 2.39 | |

| 3.69** | 3.30** | 2.91* | 2.50 | 4.01* | 3.69* | |

| 0.74 | 0.02 | 0.07 | 0.12 | 2.56* | 0.06 | |

| 4.10** | 3.79** | 3.27 | 2.68 | 3.98 | 2.68 | |

| 2.22* | 2.07 | 2.13 | 2.09 | 4.33** | 2.28 | |

| 4.39*** | 4.29** | 4.09** | 3.67* | 4.94* | 3.69** | |

| 2.40* | 2.29 | 2.01 | 1.71 | 3.25 | 2.67 | |

| 4.14** | 4.43*** | 3.99** | 3.60* | 4.10 | 3.33* | |

| -7.42 | -1.44 | -5.44 | -5.89 | -10.11 | -10.29 | |

| 2.28 | 3.34 | 2.85 | 1.96 | 1.88 | -0.52 | |

| 3.33 | 3.93** | 3.48* | 3.16 | 5.65* | -3.89 | |

| 3.51 | 3.20* | 2.80 | 1.80 | 2.59 | -2.30 | |

| -12.12 | -4.54 | -9.08 | -8.39 | -13.46 | -12.49 | |

| 0.33 | 1.44 | 1.23 | 0.60 | 0.84 | -1.46 | |

| 2.59 | 3.41 | 2.62 | 2.12 | 5.28* | -2.63 | |

| 3.45 | 3.11* | 2.50* | 1.96 | 2.73 | -2.86 | |

| 3.61** | 3.37** | 3.75** | 3.50 | 4.29 | 1.60 | |

| 3.86** | 3.91** | 3.84* | 3.17 | 4.55* | 4.24** | |

| 2Y | 3Y | 4Y | 5Y | 7Y | 10Y | |

| 1.32 | 1.56 | 1.16 | 1.20 | 0.69 | 2.52 | |

| 0.89* | 0.76 | 0.60 | 0.79 | 0.42 | 1.30 | |

| 3.35*** | 3.78*** | 3.19** | 2.55* | 1.41 | 2.62* | |

| 2.16** | 2.21*** | 1.95** | 1.58 | 0.61 | 1.41 | |

| 1.88** | 2.54** | 2.34** | 2.17** | 0.61 | -0.36 | |

| 9.76 | 4.78 | 8.32 | 7.89 | 12.09* | 9.85 | |

| 0.17 | -0.73 | -0.68 | -1.35 | -3.05 | 1.59 | |

| 12.58 | 6.00 | 10.39 | 9.06 | 14.46* | 11.15 | |

| 0.86 | -0.30 | -0.12 | -0.17 | -2.54 | -0.23 | |

| 0.24 | 0.54 | 0.09 | -0.33 | 0.25 | 2.63 | |

| 0.06 | 0.39 | |

| 0.70 | 0.11 | |

| 0.00 | 0.33 | |

| 0.23 | 0.53 | |

| 0.66 | 0.18 | |

| 0.00 | 0.39 | |

| 0.73 | 0.25 | |

| 0.70 | 0.17 | |

| 0.09 | 0.17 | |

| 0.32 | 0.45 | |

| 0.67 | 0.17 | |

| 0.00 | 0.34 | |

| 0.44 | 0.50 | |

| 0.68 | 0.17 | |

| 0.01 | 0.37 | |

| 0.60 | 0.00 | |

| 0.66 | 0.15 | |

| 0.07 | 0.03 | |

| 0.75 | 0.25 | |