Option pricing under jump diffusion model

Qian Li111E-mail:lqsx0510@163.com Li Wang222 The corresponding author. E-mail: wangli@mail.buct.edu.cn

College of Mathematics and Physics

Beijing University of Chemical Technology, Beijing 100029, P.R. China

Abstract

We provide an European option pricing formula written in the form of an infinite series of Black–Scholes-type terms under double Lévy jumps model, where both the interest rate and underlying price are driven by Lévy process. The series solution converges with a radius of convergence, and it is complemented by some numerical experiments to demonstrate its speed of convergence.

Key words Lévy jump, measure transformation, Feynman-Kac theorem, option pricing

MSC (2020) 60K40, 91B24, 91B70, 91G20

1 Introduction

Black and Scholes (1973) made a breakthrough by proposing an elegant model with the underlying price following a geometric Brownian motion and deriving an analytical formula for European option prices. Merton(1976) extended the model to the more-general case when the underlying stock returns are generated by a mixture of both continuous and jump processes. However, there are gaps between those models and the market data. One of their main drawbacks is the constant volatility assumption, another is the constant interest rate. Heston (1993) contributed a lot to the literature by incorporating the CIR (Cox–Ingersoll–Ross) model to describe the volatility process and deriving a closed-form pricing formula for European options. Incorporating stochastic interest rate into stock option pricing model is another line of extension. At the earliest, Merton has discussed option pricing under stochastic interest rate, Amin and Jarrow (1992) derived a closed form stock option pricing formula under Merton-type interest rate based on Heath, Jarrow and Morton (1992) framework. Sattayatham and Pinkham (2013) proposed an alternative option pricing model, in which asset prices follow a stochastic volatility Lévy model with stochastic interest rate driven by the Hull–White process. He and Zhu (2017) derived a closed-form pricing formula for European options in the form of an infinite series which is under the Heston model with the interest rate being another random variable following the CIR model.

In conclusion, all the above results, they either assume the asset price or the interest rate has continuous path. So far as we know, there are few results on the both jump case. In our paper, we use jump-extended Black-Scholes model to describe the underlying asset process and jump-extended CIR-model to describe the interest rate regarding the existence of discontinuous jumps in interest rates. Inspired by the idea revealed in Merton(1976), we provide pricing formulas written in the form of an infinite series of Black–Scholes-type terms first for options on a single stock, then for options on basket of stocks. Following a similar method used in He and Zhu (2017), we show that Black–Scholes-type term can also be written in the form of an infinite series a radius of convergence, and it is complemented by some numerical experiments to demonstrate its speed of convergence.

The remainder of the paper is organized as follows. In section 2 we give the models of stock price and the interest rate. The main results and the corresponding proofs are presented in section 3 and section 4. In section 5 we will give data simulations to demonstrate its speed of convergence.

2 The model

2.1 Interest rate model with Lévy jump

The classical term structure of interest rate models, such as the Vasicek (1977) model, the Cox et al. (1985) (CIR) model, the Heath et al. (1992) model, and other extended models for pricing interest rate derivatives (see e.g., the Hull and White (1990) model), all assume that processes of state variables (such as the short-term interest rate, or the long-term interest rate, or others) can be modeled by pure diffusion process. This assumption is inconsistent with many empirical studies (see e.g., [8, 11, 12, 14]) regarding the existence of discontinuous jumps in interest rates. Therefore, the jump-diffusion processes are better model for the interest rate dynamics, since allowing jumps in interest rate model can capture the properties of skewness and excess kurtosis commonly.

In this paper, we assume the term structure of the interest rate is modelled as follows,

| (2.1) |

where is Brownian motion, is a Poisson process with constant intensity rate , and the sequence denotes the magnitudes of jump, which are assumed to be i.i.d. random variables with distribution on nonegative real numbers, . Let be the Poisson random measure corresponding to , then it has intensity . Moreover, and are independent.

2.2 Asset price with Lévy jump

The underlying asset price satisfies the following stochastic differential equation :

where , is Brownian motion, is a Poisson process with constant intensity rate and is a nonnegative variable with distribution and . According to the Itô’s formula which will be given in the next section,

where are independent variables and has the same distribution as . It’s obvious that is strictly positive when .

We further assume that all components of risk in the interest rate and asset prices dynamics, including jump risks, are defined on a filtered complete probability space with information filtration satisfying the usual conditions, is the risk-neutral measure. We assume , , , , and are independent.

3 European option pricing

Under the risk-neutral measure , European call option is actually the expectation of the present value of return,

where represents the strike price. Due to the existence of stochastic interest rate, there are two different random variables in the above formula, which is difficult to calculate. Therefore, in order to obtain the analytical expression of European call option price, we introduce forward measure (for the definition, see Brigo and Mercurio (2006)), then we can get

| (3.1) |

where is the price of a zero-coupon bond with maturity under the risk-neutral measure , which need to be detemined first.

Theorem 3.1

If the interest rate is given by equation (2.1), then the price of a zero-coupon bond with maturity T at time t is

with , where

Proof. Under the risk-neutral measure, the price of a zero-coupon bond with maturity at time is

Let . Then the discounted asset price should be a -martingale (Brigo and Mercurio (2006)), we get the following differential equations,

| (3.5) |

We know from Duffie (2003) that the price of the zero-coupon bond is an exponential affine function of the interest rate, or equivalently, has the following form,

| (3.6) |

Substituting (3.6) into (3.5), we can get

| (3.9) |

By solving (3.9), we can get

Lemma 3.1

Sato (1999): Under measure , is a standard Brownian motion, is a Possion random measure with intensity defined on , and satisfies . There exists a martingale measure which is equivalent to measure , where , and if

then is the standard Brownian motion and is the Possion martingale under measure .

Proposition 3.1

(Girsanov transform) The forward measure is defined by the following equation

Then under measure is a standard Brownian motion and is a Possion martingale.

Proof. By using Itô’s formula and equation (3.9), we obtain

therefore,

where . Then we can get

Under risk-neutral measure , if the interest rate satisfies (2.1), then under the forward measure ,

where

| (3.10) |

and the price of the underlying asset remains the same

In the next section, based on the results obtained in this section, the explicit pricing formula of European options is derived by calculating the expectation of the payment function under the measure .

3.1 Derivation of pricing formula

Under the forward measure , the price of a call option with maturity and strike price can be obtained as follows:

where has been given by Theorem 3.1.

Let , where . According to the Feynman-Kac formula,

| (3.14) |

In order to solve equation (3.14), we introduce the following equations,

| (3.17) |

where has been defined by (3.10) with replaced by . Let be the function defined by

According to the Feynman-Kac formula,

| (3.18) |

Theorem 3.2

4 Options on basket of stocks

Next, we consider options on multi-assets , . The price of the call option with maturity and strike price has payoff . For example, we may take or , with and . For simplicity, we may assume .

Without loss of generality, we assume that the interest rate satisfies equation (2.1) and the stock prices satisfy the following equations,

where , and are independent nonnegative variables with distribution and , respectively, and , . and are two correlated Brownian motions with correlation , while and are two independent Poisson processes with intensity rates and , respectively. Under the forward measure , the price of a call option with maturity and strike price can be obtained as follows,

| (4.1) |

where has been given by Theorem 3.1. Let be the function defined by

where . According to the Feynman-Kac formula,

| (4.2) |

In order to solve equation (4), we introduce the following equations,

where has been defined by (3.10) with replaced by . Let be the function defined by

According to the Feynman-Kac formula,

| (4.4) |

Theorem 4.1

The solution to (4) is

| (4.5) |

where () are independent and identically distributed variables which have the same distribution as (), and ”” is the expectation over the distribution of , and .

The desired result follows.

5 Data simulation

5.1 Series representation for

In this section, we give a series representation for under model (3.17), . For , we just need to replace the dsitribution of by the joint distribution of . Remember that,

Let , denote the probability density function of . By the results in He and Zhu (2017), we can get the following expression of this formula

where

with the characteristic function of . It is clear that in order to obtain an explicit pricing process, we need to derive an analytical expression for the characteristic function of under the forward measure , which results in the following theorem.

Theorem 5.1

If the underlying price follows the dynamics in model (3.17), then the characteristic function has the following form,

| (5.1) |

where

with

The proof is similar to Theorem 2 in He and Zhu (2017), we omit it here. Similarly, we can get that if

| (5.2) |

the series is always convergent. In the next section, matlab will be used for data simulation to test the convergence rate of its series solution.

5.2 Data simulation

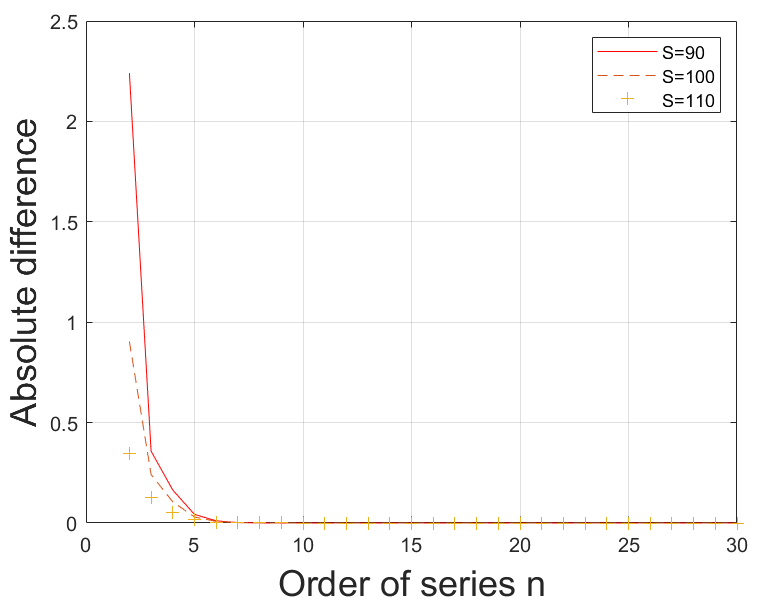

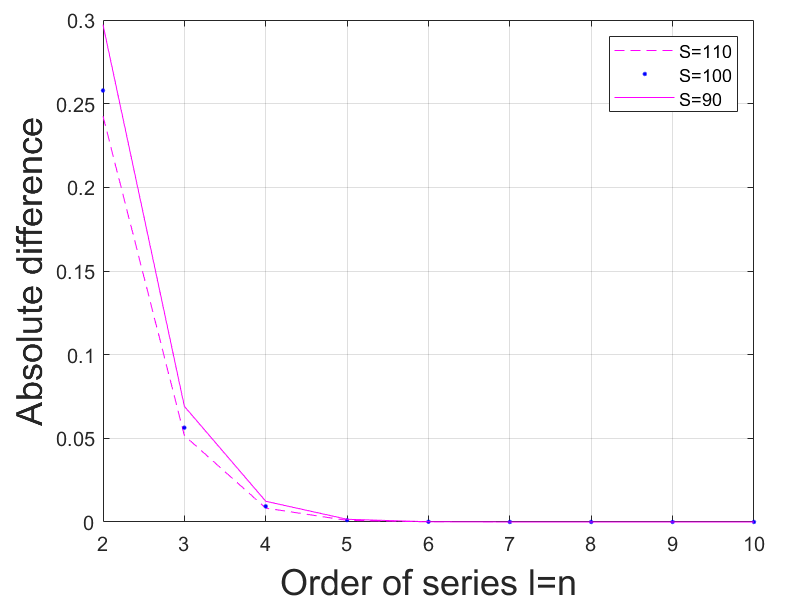

In this section, the speed of convergence of the pricing formula is test with the parameter chosen under condition (5.2), where , , , , , , , and follows an exponential distribution with parameter . a fixed jump amplitude.

More than above, the absolute difference of between -term and -term is of order . When , the absolute difference of between -term and -term is of order , this can certainly show that the -term price can be regarded as the converged option price for the double Lévy jump model.

6 Conclusion

In this paper, we adopt the hybrid model of double Lévy jump, including the underlying asset price with Lévy jump and the CIR interest rate with Lévy jump. The pricing formula for European option in the form of series is given, and the numerical simulation by Matlab proves that our solution indeed converges very fast.

Acknowledgement. I would like to give my sincere thanks to the referee for her or his valuable comments and suggestions.

References

- [1] Aim,K.I. and Jarrow, R.A.(1992). Pricing options on risky assets in a stochastic interest rate economy. Mathematical Finance 4, 217-237.

- [2] Black, F. and Scholes, M. (1973). The pricing of options and corporate liabilities, Journal of Political Economy. 81, 637-659.

- [3] Brigo, D. and Mercurio, F.(2006). Interest Rate Models Theory and Practice[M]. Springer, Berlin, Heidelberg, 27-38.

- [4] Cox, J.C., Ingersoll, J.E. and Ross S.A. (1985). A theory of the term structure of interest rates. Econometrica. 53, 385–406.

- [5] Duffie, D., Filipovi, D. and Schachermayer, W. (2003). Affine processes and applications in finance. Ann. Appl. Probab. 13(3), 984–1053.

- [6] He, X-J and Zhu, S-P. (2017). A closed-form pricing formula for European options under the Heston model with stochastic interest rate.Journal of Computational and Applied Mathematics. 335, 323-333.

- [7] Heath, D., Jarrow, R. and Morton, A.(1992). Bond pricing and the term structure of interest rate: a new methodology for contingent claims Valuation, Econometrica. 60, 77-105.

- [8] Heidari M. and Wu, L.(2010). Market anticipation of Fed policy changes and the term structure of interest rates. Review of Finance. 14, 313–42.

- [9] Heston, S.L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6(2), 327–343.

- [10] Hull, J. and White, A. (1990). Pricing interest-rate derivative securities. Rev. Financ. Stud. 3, 1573–92.

- [11] Johannes, M. (2004). The statistical and economic role of jumps in continuous-time interest rate models. Journal of Finance. 227–60.

- [12] Lin B-H, Yeh Shih-Kuo. (1999). Jump-diffusion interest rate process: an empirical examination. Journal of Business Finance Accounting. 26, 967–95.

- [13] Merton, R.C. (1976). Option pricing when the underlying stock returns are discontinuous. Journal of Financial Economics. 3, 125-144.

- [14] Sattayatham P. and Pinkham. S. (2013). Option pricing for a stochastic volatility Lévy model with stochastic interest rates. Journal of the Korean Statistical Society 42, 25-36.

- [15] Sato, K. (1999). Lvy process and Infinitely Divisible Distributions. Cambridge University Press.

- [16] Vasicek, O. (1977). An equilibrium characterization of the term structure. J Financial Econ. 5, 177–88.