Dynamic Matrix Recovery

Abstract

Matrix recovery from sparse observations is an extensively studied topic emerging in various applications, such as recommendation system and signal processing, which includes the matrix completion and compressed sensing models as special cases. In this work, we propose a general framework for dynamic matrix recovery of low-rank matrices that evolve smoothly over time. We start from the setting that the observations are independent across time, then extend to the setting that both the design matrix and noise possess certain temporal correlation via modified concentration inequalities. By pooling neighboring observations, we obtain sharp estimation error bounds of both settings, showing the influence of the underlying smoothness, the dependence and effective samples. We propose a dynamic fast iterative shrinkage-thresholding algorithm that is computationally efficient, and characterize the interplay between algorithmic and statistical convergence. Simulated and real data examples are provided to support such findings.

Keywords: compressed sensing, local smoothing, low rank, matrix completion

1 Introduction

Matrix recovery from sparse observations has been extensively studied in a wide range of problems, such as signal processing (Li et al., 2019), recommendation system (Koren et al., 2009) and the quantum state tomography (Gross et al., 2010). The classical model is to link the response with the random matrix via

| (1) |

to recover the low-rank matrix from the independent observations , where is the trace of a matrix, is a mean zero random error and denotes the sample size, which is typically much smaller than (i.e., ). By imposing different assumptions on , the model includes a variety of matrix recovery models, in which matrix completion and compressed sensing are two important cases. Most existing works assume that the target matrix is static (Klopp, 2011; Koltchinskii & Xia, 2015; Fan et al., 2021; Xia & Yuan, 2021). However, there are various scenarios where is dynamic and observed at multiple time points, such as in time-varying user interests in recommendation systems (Xu et al., 2020), temporally-changed graph models (Qiu et al., 2017) and dynamic quantum dot matrices (Csurgay et al., 2000). To formulate a general framework accounting the dynamic changes in numerous applications, we propose investigating the recovery of the dynamic matrix as follows,

| (2) |

where is the timestamp, is the tuple of the response, the design matrix and the noise at time , respectively, and is a dynamic matrix which is assumed smooth across time with a low-rank structure.

A prevalent line of research for solving the classical static model (1) is to impose strict low-rank constraints based on matrix factorization. For instance, Keshavan et al. (2009) proposed singular value decomposition to make the recovery, Zhao et al. (2015) used QR decomposition instead, and Zheng & Lafferty (2016) adopted Burer-Monteiro factorization for rectangle matrix completion. Another stream is the convex approaches, thanks to Candès & Recht (2009) that first relaxed the non-convex rank restriction to nuclear norm for efficient optimization. A variety of convex algorithms and theoretical results are further established (Recht et al., 2010; Candes & Plan, 2011; Agarwal et al., 2012). Though in (2) can be recovered by adopting the static matrix recovery at each time , these single-stage estimates are less desirable, as they only use data at time to reconstruct and fail to take advantage of the neighboring observations and smoothness of the underlying matrix. Related work also includes tensor regression to rebuild , which views the dynamic model (2) from a static perspective by letting be a three order tensor whose th element is the th element of . Gandy et al. (2011) and Liu et al. (2012) proposed algorithms for tensor completion and Zhang et al. (2020) considered the low-rank tensor trace regression via the importance sketching algorithm. We mention that their low-rank assumption of is different from model (2) that is dynamically and smoothly evolving along time . Consequently, one needs to process the whole data to recover in tensor regression setting, which is time- and space-consuming.

A more efficient approach is to adopt the dynamic modeling/algorithm that avoids computing the whole data for update and has been adopted in some relevant problems. Lois & Vaswani (2015) designed a memory-saving algorithm for batch robust principle component analysis; Gao & Wang (2018) studied dynamic robust principal component analysis and proposed a fast iterative algorithm; Hu & Yao (2022) proposed a unified framework to directly estimate dynamic principal subspace in high dimension. The dynamic algorithm for matrix recovery has been explored in Xu & Davenport (2016), which assumed that are independently and identically distributed (i.i.d.) zero-mean Gaussian error and imposed a parametric assumption on structure of the underlying matrix, , where are i.i.d. zero-mean Gaussian noises. Another line of work, namely the dynamic tensors, also finds extensive applications in various domains, and several works have been noted in this direction. For instance, Zhang et al. (2021) proposed a time-varying coefficient model for temporal tensor factorization, employing a polynomial spline approximation, and Zhou et al. (2013) introduced a family of rank-R generalized linear tensor regression models. Most of the current research on dynamic tensors relies on tensor decomposition techniques and assumes that only certain decomposition factors or coefficients are changing (Zhang et al., 2021; Bi et al., 2021; Koren, 2009; Wang et al., 2016).

Different from the existing work, we consider the general scenario where the dynamics are not limited to decomposition components or a parametric structure priori. There exist two major challenges. First, one needs to maintain the low-rank structure in the whole procedure of dynamic algorithm. Second, the combination of neighboring information often inflates the estimation error when the observations are correlated along time. To resolve these, we utilize local smoothing which has the advantages that the manifold structure of low-dimensional matrices can be approximately retained and temporal dependence has less influence when increases. Based on these considerations, we propose a dynamic matrix recovery algorithm without imposing structural assumption besides smoothness and allowing the measurement error and/or design matrix to be possibly dependent across time. The idea is to pool together the observations that lie in the local window to estimate . Noting that is low-rank, we set the target function composed of a locally weighted loss function and the nuclear norm penalty of and propose a Dynamic Fast Iterative Shrinkage-Thresholding Algorithm (DFISTA) for optimization.

The main contributions of this work are summarized as follows. First, we establish a general framework for dynamic matrix recovery with theoretical guarantees. We allow the underlying matrix varying smoothly under the low-rank constraint and allow the observations to be dependent across time, which has more flexibility and applicability. While existing works only study the estimation error bounds for specific problems such as matrix completion and compressed sensing (Koltchinskii et al., 2011a; Negahban & Wainwright, 2011; Xu & Davenport, 2016; Fan et al., 2021), we derive the error bounds under this general framework, which can be readily adopted to such matrix recovery problems. Second, the proposed method attains a faster convergence rate than classical static methods in the following sense. Take the matrix completion for instance. The ratio of error bounds of the proposed estimator compared to the classical one (i.e., single-stage estimates at each ) is , where is the number of observations at time and (”” indicates the greater of two quantities). When the observations are sparse in the sense that , the ratio becomes . Specifically, the dynamic method uses only observations to attain the same convergence rate as the static method using observations. Last but not least, a computationally efficient algorithm is devised for dynamic matrix recovery. This algorithm iterates only a subset of the data to update the estimate at each step. By using the estimate of the last step as the initial of the current optimization procedure, the algorithm converges faster than the single-stage recovery. Specifically, the ratio of computational complexities of our algorithm compared to the single-stage recovery is .

The rest of the paper is organized as follows. In Section 2, we present the proposed method and algorithm for dynamic matrix recovery, and establish theoretical guarantees in Section 3 for both independent and dependent observations with algorithmic analysis. Finally, we conduct simulation and real data experiments in Section 4 and 5 to show the favorable performance of the proposed dynamic method/algorithm compared with other existing methods. Additional theoretical results and technical proofs are deferred to an online Supplementary Material due for space economy.

2 Methodology and Algorithm

We consider the general framework in the form of dynamic trace regression whose coefficient matrix is changing smoothly along time. Specifically, at time , we observe following model (2),

where is the time-varying coefficient matrix, and are design matrices and zero-mean noises, respectively, (given ) are mutually independent across subject and (given ) may be correlated across time. Parallel to the static model (1), the dynamic trace regression includes several problems such as dynamic matrix completion and dynamic compressed sensing that can be applied to dynamic recommendation systems and video signal processing as illustrated in numerical experiments of Section 5.

Example 1

(Dynamic matrix completion). For each , suppose that the design matrices are i.i.d. uniformly distributed on the set

| (3) |

where are the canonical basis vectors in and then forms an orthonormal basis in the space . Then estimating is equivalent to the problem of matrix completion under uniform sampling at random (USR).

Example 2

(Dynamic compressed sensing). For each , suppose that the design matrices are i.i.d. replicates of a random matrix such that is a sub-gaussian random variable for any . In this work, we focus on the concrete example that each design matrix is a random matrix whose elements are independent mean-zero sub-gaussian random variables with variance . Moreover, if the design is homogeneous across , we denote the variance as .

We first briefly review the classical static method in the context of dynamic modeling, i.e., adopting the static method at each time , which is referred to as the single-stage estimates in the sequel. Define the matrix inner product by . Koltchinskii et al. (2011a) proposed to incorporate the knowledge of the distribution of and estimate by

| (4) |

where is a convex set of matrices, is a regularization parameter and is the nuclear norm of . They proved that in the setting of matrix completion in Example 1, if is appropriately set, with probability at least ,

where and is the Frobenius norm of matrix . Though they have proved that the rate is optimal up to logarithmic factors comparing to the minimax lower bounds in classical trace regression, this approach fails to incorporate temporal information and hence is not efficient in multi-stage case.

A direct modification is to utilize the two-step procedure that first obtains the single-stage estimates and then applies local smoothing to to achieve the final estimate as follows,

| (5) |

where the local smoothing weights with the kernel function and bandwidth . The two-step estimation approach computes a weighted average of low-rank matrices that have been estimated at distinct time points. However, this method encounters a significant challenge when dealing with sparse observations. In such scenarios, the estimated matrix for each time point could potentially disrupt the true low-rank structure, displaying significant deviation from the actual value. Unfortunately, this disparity cannot be corrected through smoothing techniques.

Motivated by the observation that the manifold structure of low-rank matrices can be approximately preserved locally without matrix factorization, we design the dynamic target function with nuclear norm penalty, i.e.,

| (6) |

which combines the observations across time and employs local smoothing for incorporating the temporal information. It is worth noting that in many applications including our Examples 1 and 2, the distribution of is known, and yet this information has not been exploited in empirical risk. Thus we may utilize the distribution knowledge by substituting the empirical form with true values . The temporal smoothness of guarantees that information in adjacent time points can be utilized to reduce the estimation error. We mention that the classical estimate in (4) can be regarded as a special case of the proposed local estimate in (6) as the bandwidth . By choosing appropriately, our estimate pools more observations to reduce the estimation variance while controlling the bias caused by the varying of , as discussed in detail in Section 3.

For implementation, we adopt the Fast Iterative Shrinkage-Thresholding Algorithm (FISTA) which is an accelerated proximal method proposed by Beck & Teboulle (2009). It improves traditional proximal methods and terminates in iterations with a -optimal solution. To handle with the trace norm penalty optimization problem (6), we use the matrix form FISTA established by Ji & Ye (2009) and Toh & Yun (2010). Define the objective function in (6) as , where

We mention that the gradient function of is equipped with Lipschitz constant presented in Section 3.4, and that is a continuous convex function. Then the matrix form FISTA can be applied to solve the dynamic trace regression problem

Note that need to be calculated for a sequence . The algorithm is accelerated at time by utilizing the estimate from the timestamp . Specifically, suppose that at time we apply the matrix form FISTA for iteration times to numerically approximate the estimate denoted by . Then input as the initial matrix in the procedure of estimating at time . Such initialization method accelerates the algorithm, as demonstrated in Section 3.4. We summarize the implementations of the proposed DFISTA in Algorithm 2. In the algorithm, “svd” means calculating the single value decomposition components for a matrix and “” means the threshold operator such as where . The learning rate is updated according to Nesterov (1983).

Algorithm 1 Dynamic Low-Rank Matrix Recovery

Unlike most factorization based algorithms that are challenging to analyze for their convergence properties, we are able to analyze the error bounds of the algorithm’s results with respect to the true value. This analysis helps bridge the gap between the statistical estimator and the estimator obtained from the algorithm, as discussed in detail in Section 3.4.

3 Theoretical Guarantees

In this section, we study both the statistical properties of the estimation error and the algorithmic convergence of the proposed method. We first present the error bound of the estimate for general dynamic trace regressions. Then we derive the explicit expressions of the upper bound of when and are independent across and when and are -mixing processes, respectively. Noting that and/or may be unbounded, the assumptions for classical concentration inequalities are violated (Merlevède et al., 2009, 2011; Hang & Steinwart, 2017). We thus modify the Talagrand’s inequalities and adopt truncation technique appropriately to derive the convergence rate for the dependent setting. In both scenarios, we shall explain how the number of time points , the smoothness of and the dependence of and across time influence the estimation error explicitly.

In the sequel, we denote , , , and as the rank, nuclear norm, Frobenius norm, maximum singular value of and the trace of , respectively.

3.1 General error bounds

Let be the vectorization of and define the second moment matrix of by such that

It is necesary to guarantee the identifiability of matrix recovery that the positive semi-definite matrix is invertible. To simplify, we consider the homogeneous scenario such that at each time point , the design have the same second moment matrix as stated below.

Assumption 1

There exists a positive definite matrix with smallest eigenvalue such that .

We remark that in the heterogeneous situation, the convergence rate can be derived similarly, which is at the same order as the homogeneous setting with a more tedious presentation. An important indication of Assumption 1 is that, for all and ,

which is a standard assumption in matrix recovery. The interpretation is that the smallest eigenvalue determines the information contained in the design matrix . Intuitively, the larger is, the more information is revealed by data, thus the more precise the estimator is. In most cases, can be calculated directly. For instances, in matrix completion of Example 1, the smallest eigenvalue of is , and in compressed sensing of Example 2, is the smallest variance of elements in , which is equal to under Assumption 1.

For brevity, we further denote and

The following theorem gives the general upper bound of estimation error .

Theorem 1

The term corresponds to the bias caused by kernel smoothing which is affected by kernel and the bandwidth , and corresponds to the variance term caused by the effective samples in the local window and the measurement error . When , the result in Theorem 1 coincides with the classical result of Corollary 1 in Koltchinskii et al. (2011a) such that when ,

| (9) |

Compared to (9), the bound (8) replaces the error term by the smoothed version at the cost of the bias .

To obtain an explicit expression of the error bound that may be used for bandwidth selection, we further investigate the properties of and . Assumption 2 and 3 are standard conditions for temporal smoothness and the kernel function.

Assumption 2

There exists a matrix function supported on , satisfying that

-

1.

for any , and , for some constants and ;

-

2.

the first and second derivatives are continuous and bounded by some constants and , respectively.

Assumption 3

The kernel function is a symmetric probability density function on [-1, 1] and satisfies that

| (10) |

Define the norm for random variable with as

and Then we impose the following assumption on the distributions of and .

Assumption 4

The designs and noises at the same time point are mutually independent for each fixed and there exists constants that for any

-

1.

is sub-exponential distribution with ;

-

2.

is sub-gaussian distribution with ,

-

3.

There exists such that .

The tail distributions of and are both sub-exponential when satisfy Assumption 4. Denote as the distribution set of satisfying Assumption 4. We remark that is indeed general enough for applications. In the matrix completion problem of Example 1, are bounded with . Then the distributions of lie in as long as the noises follow sub-exponential distributions with . In the compressed sensing problem of Example 2, from Theorem 4.4.5 in Vershynin (2018), we can set to be sub-guassian distributed with and . Then the distributions of lie in if noises follow a sub-guassian distributions with .

Next we consider the temporal dependence between and that decays when the distance between time points and increases. To characterize the structure of such dependence, we impose the strongly dependent assumption that and are -mixing processes across . Our definition of -mixing is the same as in Doukhan (2012), and the detail definition is given in Supplementary Material S.4. In the following subsections, we first derive the estimation error bound in the ideal case that and are independent across time , and then extend to the dependent case. These two settings are described in the following assumptions, respectively.

Assumption 5

(Independent case) The designs and noises are mutually independent across for each , .

Assumption 6

(-mixing processes) There exist two independent sequences of -fields and such that

The -fields and , are both -mixing with coefficients and , satisfying that

3.2 Independent case

The theorem below states the upper bound of under the independent case when the distributions of belong to . For conciseness, we assume that the numbers of observations have the same order denoted by , i.e., for . The conclusions for of different orders can be derived similarly. In the following, the notations , and mean that the ratio approaches to 0, infinity and a constant, respectively, and “” denotes the ceiling function.

Theorem 2

We remark that is the number of samples used in a local window and the condition is the requirement for the effective sample size to guarantee the upper bound (11) tending to zero. The error bound (11) is a trade-off between the bias and variance which is controlled by the bandwidth . When , we can choose the optimal bandwidth

| (12) |

where is a constant. When , we choose which is degenerate to the classical situation with the convergence rate .

We focus on a large enough value for in the subsequent discussion, which allows us to omit the ceiling operator . For situations where is small, we can simply choose , which yields the same results as static methods. With an appropriately selected , we have the following corollary.

Corollary 1

The bound requirement for is composed of two terms: the first is to make hold when takes the form (12), and the second is to guarantee the optimal bandwidth (12) tends to 0 as . In (13), the upper bound is proportional to where is the total sample size. This indicates that our dynamic method makes efficient use of information from adjacent time points to improve the estimation quality. The number of observations in a single time point and the number of time points complement each other to reduce the upper bound (13). When the samples are extremely sparse at each time point, it is infleasible for the classical static method to reconstruct the eigenvalues and eigenvectors of . However, the proposed method can still control the estimation error to a desirable level, as long as there are sufficient time points. We also mention that the two-step smoothing method performs poorly, because the first-step estimate and the reconstruction of eigen-subspace at each time point are far from satisfaction, which cannot be fixed by the second smoothing step regardless how dense the time points are. We emphasize that Theorem 2 and Corollary 1 can be applied directly to any dynamic trace regression problems as long as and lie in . Taking dynamic matrix completion for example, we have the following corollary. The corresponding result for dynamic compressed sensing can be derived similarly, which is presented in Corollary S.3 of the Supplement.

Corollary 2

Recall that the classical static result for the error bound of matrix completion in Koltchinskii et al. (2011a) is

The dynamic method provides a sharper upper bound than the classic one. In other words, when the sample size in each single time point is sparse, our method can borrow information from adjacent time points to improve the estimation, as long as the number of time points is sufficiently large.

3.3 Dependent case

In parallel to the independent case, we derive the bounds of when are -mixing processes, as stated in Theorem 3 below.

Theorem 3

We use and to measure the temporal dependence of design matrices and noises , respectively, where larger and mean stronger dependence. When , it indicates that are independent across and the bound (16) is the same as (11) in Theorem 2 in the independent case. When , if we choose

| (17) |

where , then we have the following corollary.

Corollary 3

When and/or have strong long-term dependence across , becomes large and inflates the bound (18), which means that the convergence rate of is usually slower than that in independent case. Note that the bound for the single-stage estimates at each using static method can also be derived from Theorem 2 by using a degenerated kernel , given by

Then when

| (19) |

our dynamic method yields a sharper bound than the static one though strong dependence across time exists. With the expression of in (17), the condition (19) is equal to . Note that corresponds to the effective time points used in estimation at each . This implies that as the number of effective time points increases, the negative effect caused by temporal correlation would be offset to some extent. For space economy, the applications of Theorem 3 and Corollary 3 to dynamic matrix completion and dynamic compressed sensing are presented as Corollary S.2 and Corollary S.4 in Supplementary Material.

3.4 Empirical error and complexity analysis

Recall that the sequence generated by the iteration of Algorithm 2 at time are denoted by , where is the output matrix after -th iteration and is the initial input matrix. In practice, we use the output to approximate for a certain . Thus, we derive the upper bound of the empirical error in the following theorem, which takes both the algorithmic error between and and the estimation error between and into account.

Theorem 4

The empirical error bound in Theorem 4 has an additional term compared to the estimation error bound (7) in Theorem 1, which is the so-called algorithmic error. The optimal choice is to stop iterating when the algorithmic error attains the same order as the estimation error. Let be the minimal number of iteration steps needed to attain the desired order. From the expression of the algorithmic error, depends on the distance between the initial value and the target , denoted by . Since less iterations are required for a smaller initial distance, the naive strategy to initialize randomly at each time would lead a large . Noting that is close to , we thus make use of the neighboring information in the initialization to reduce computation cost. Hence we propose to use the output matrix at time as the initial value for estimating at time , i.e. . Take the dependent case in Section 3.3 for instance. Recall that the optimal estimation error bound is derived in Corollary 3 with appropriate choice of the bandwidth . Then desired empirical error bound for Theorem 4 can be derived by

| (20) |

To quantify the improvement of our initialization strategy, in Corollary 4, we compute the total number of iteration steps to attain the bound (20) at each , and compare with that of the random initialization. The result for independent case can be derived similarly, which is presented in Corollary S.5 of Supplementary Material for space economy.

Corollary 4

From Corollary 4, once the total number of iterations of random initialization attains the level and that of Algorithm 2 attains , the error is bounded by (20). Then the ratio of computational cost of our proposed algorithm compared to the random initialization method is . We finally mention that the classical static method need iterations to attain the optimal rate for each , and hence the single-stage method (at all times) need iterations in total. Therefore the ratio of computational cost of Algorithm 2 compared to the single-stage method is , which leads to the conclusion that our algorithm is computationally more efficient than the random initial method and the classical static methods.

4 Simulation Studies

We take the dynamic matrix completion as the instance to verify the usefulness of our method. To demonstrate the advantages, we compare the proposed estimates with three benchmark methods: (i) the classical static estimator defined as in (4), abbreviated as Static; (ii) the two-step smoothing estimator given in (5), abbreviated as TwoStep; (iii) the low-rank tensor completion estimator, abbreviated as Tensor,

where is the projection to the observation subspace , Y is the observed data tensor with element

for , and is the mode- unfolding of tensor which is a matrix that arranges the mode- fibers to be columns. We use matrix form FISTA algorithm in Toh & Yun (2010) to approximate , and has a closed form solution. In Tensor, we use AMD-TR(E) algorithm in Gandy et al. (2011) to numerically approximate .

We set and the matrix function in Assumption 2 is constructed by with

where , are composed of standard orthogonal basis. Here we consider the situation that each is the same, i.e., . Denote the rate of observation samples as and the density of time points as . We use a 5-fold cross validation to select in the numerical experiments. Please refer to Section S.9.4 of the Supplement for more details.

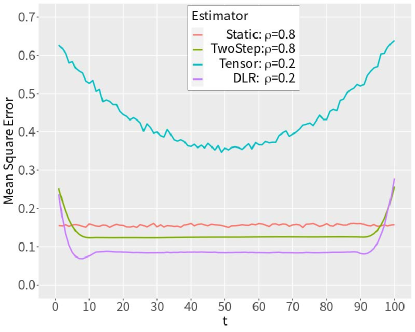

For the independent case, we sample from defined in (3) independently with uniform probabilities, and let i.i.d follow the normal distribution , where and . We use the Epanechnikov kernel and set the bandwidth by the optimal selection form (14) in which we approximate by mean of the top 10% largest and by . We set for our proposed dynamic low-rank (DLR) and Tensor methods. In Static and TwoStep, and fail to recover the matrix structure under the same setting , so we set for feasibility. Figure 1 illustrates the mean square errors

| (21) |

for . For the proposed DLR and TwoStep methods, the MSEt floats up at the boundaries due to slight edge effect. The average MSE, i.e., for the DLR estimate is and for Tensor is when . This implies that the tensor recovery is not effective at least when the temporal structure is smooth. For Static and TwoStep, when , the average MSE is and respectively. That is, these two methods with four times data still perform worse than the proposed DLR method. This verifies the theoretical finding that when the sample size at a single time point is small, the classical trace regression fails to estimate , while our dynamic method can borrow adjacent information to improve the estimation quality.

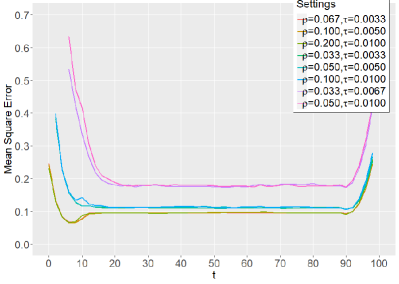

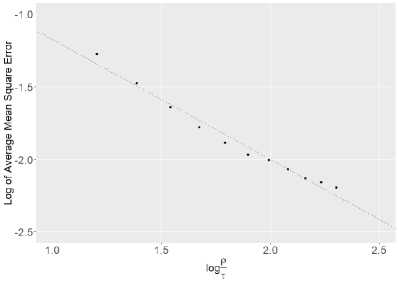

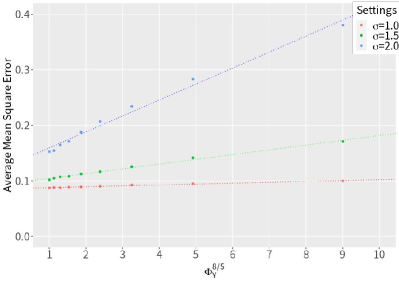

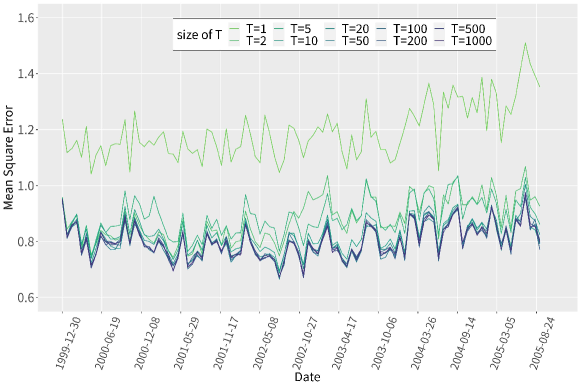

Now we study the empirical influence of and on the estimation results. One can see from (15) that given the underlying matrix, the bound of MSE is in proportion to . We set eight different values for which can be divided into three groups, i.e. . The across under these settings are shown in the left panel of Figure 2, which indicates that given the matrix dimension, the empirical MSE depends on . We further plot the logarithm of average MSE across time versus the logarithm of in the right panel of Figure 2, which reveals the linear relationship of the slope -4/5 between them. This further validates the conclusion (15).

We also investigate the influence of the dependent noise on the proposed estimator. The noises are generated by

| (22) | ||||

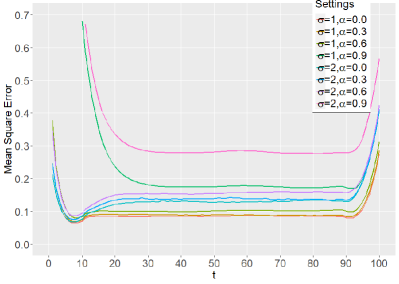

where generates the random matrix whose elements are i.i.d. normal with mean zero and variance . The larger is, the stronger dependence exists among . The other parameters are set are the same as those in the independent case. Then and can be calculated from (4) which is larger than 1 when . We apply the proposed method to recover for under the combinations of and . As illustrated in the left panel of Figure 3, the MSE increases as and/or enlarge(s). Note that according to (S.26) in Supplement, the MSE is proportional to given . We plot the average MSE versus under different in the right panel of Figure 3 which verifies the conclusion.

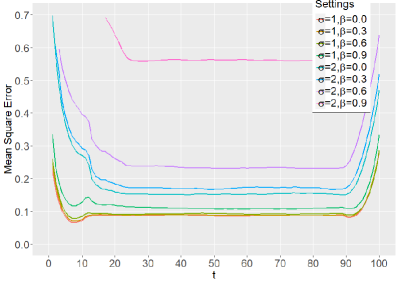

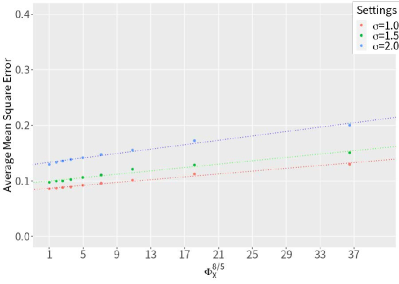

Finally we study the influence of the dependence of design matrices on the estimation. We sample from with uniform probabilities independently and generate by preserving elements randomly in and choosing new elements i.i.d. from . Then the dependence of design matrices across time becomes stronger as increases. We set the remaining parameters the same as those in the independent case and have , , where the equality holds if and only if . We plot the across time under different and and verify the linear relationship between the average MSE and in Figure 4. We remark that the slopes of linear relationships in the right panels of Figure 3 and 4 are different. This is because the bound (S.26) in Supplement is obtained by the technique that . Hence the curves of the average MSE versus become sharper as increases, as shown in the right panel of Figure 3, while the slopes of the average MSE versus under different in the right panel of Figure 4 are similar.

5 Real Data Examples

In this section, we apply the proposed method to two real data examples for the dynamic matrix completion and compressed sensing problems, respectively.

The first example is the Netflix Prize Dataset (Netflix, 2006), in which users ratings for movies received by Netflix were collected from October 1998 to December 2005 and can be downloaded at https://www.kaggle.com/datasets/netflix-inc/netflix-prize-data. The ratings are integer-valued from 1 to 5. We preprocess the dataset to remove those movies which are watched less than 25000 times.

For user selection, we consider two different filters. Filter 1 is to choose users whose rating times are more than 700 because users who watch a larger number of movies tend to offer more reliable ratings and make better comparisons across different movies due to their broader exposure. There remain users and movies with total 2337997 ratings. We split the observations into time intervals in chronological order, then randomly choose of them in each interval as training data and set the rest as test data. The observations within each time interval is collapsed as observed on a time point. At each time point , there exists an underlying matrix to be recovered, where the rows represent users and the columns represent movies. The observed sparse matrix has elements at position , representing the rating given by user to movie at time point , or zero if no rating is available. Thus we can convert it to the trace regression model. The average sample size at each time point is about and thus the rate of observation samples in each time point is . We use again the Epanechnikov kernel and select the bandwidth in the same way as in the simulations. Filter 2 is to select users whose rating times are more than 30 because those users can represent the target groups of users who often using Netflix to watch movies. Then we conduct a random selection of 3000 individuals from the pool of eligible users for ease of computation.

We use 5-fold cross validation to choose tuning parameter and evaluate the performance of by calculating

| (23) |

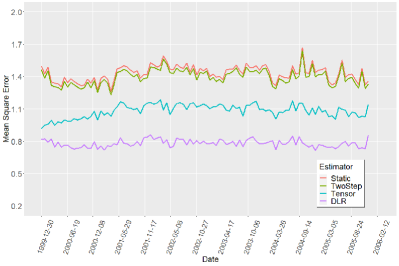

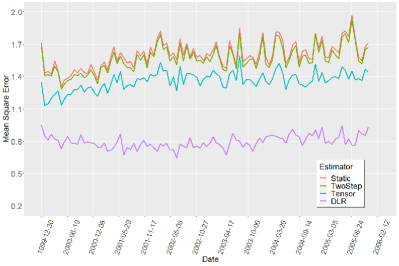

using the test data. To investigate the influence of different values of , we conduct an experiment in which is varied from 1 to 1000. Detailed information about this experiment is presented in Supplement S.9.1. The results indicate that for sufficiently large , the variation in has a negligible impact while when is too small, increasing its value leads to a reduction in estimation error. This observation also corresponds to the dynamic nature inherent in the underlying low-rank matrix, signifying its dynamic essence rather than a static state. Then we set as usual and compare the proposed method with those three benchmarks mentioned in Section 4. Figure 5 shows that our dynamic method is more accurate than those benchmarks across the time domain. And the average MSE∗, i.e. , of our dynamic method and benchmarks Static, TwoStep and Tensor methods are compared in Table 1

| Setting | DLR | Static | TwoStep | Tensor |

|---|---|---|---|---|

| Filter 1 MSE∗ | 0.781 | 1.431 | 1.397 | 1.082 |

| Filter 2 MSE∗ | 0.796 | 1.601 | 1.565 | 1.360 |

Another example is the compression and recovery of videos. We use the lion video from Davis 2017 dataset (Pont-Tuset et al., 2017) and treat each frame as a matrix at each time point.The dataset is publicly available at https://davischallenge.org/davis2017/code.html#unsupervised. For compression, we first separate the matrices into the sparse part and the low-rank part using robust principal component analysis (Candès et al., 2011). The design matrices are the convolution kernel matrices with random centers , i.e., . It is straightforward to verify that the distributions of satisfy Assumption 4. Then we compress the low-rank part to obtain corresponding output . For recovery, we use the dynamic trace regression to reconstruct the low-rank part, denoted as . Then we recover each frame by , while the sparse part is retained. We emphasize that we only need store the centers , the output and the nonzero part of to recover the matrices , which is considerably space-saving compared to storing the whole video. In the lion video, each frame has pixels. We generate with the rate of observation samples and the file volume is reduced by 70% after compression. Here we use Static and TwoStep mentioned in Section 4 to reconstruct and recover , as benchmarks. Figure 6 shows the original frames and the estimates at different time points. The background and the smooth motions of all three lions are recovered well by the proposed DLR method, which can be seen visually better than two benchmark methods. Recall the definition (23), the average MSE is for our dynamic method while is and for the two benchmarks Static and TwoStep repsectively.

References

- (1)

- Agarwal et al. (2012) Agarwal, A., Negahban, S. & Wainwright, M. J. (2012), ‘Noisy matrix decomposition via convex relaxation: Optimal rates in high dimensions’, The Annals of Statistics 40(2), 1171–1197.

- Beck & Teboulle (2009) Beck, A. & Teboulle, M. (2009), ‘A fast iterative shrinkage-thresholding algorithm for linear inverse problems’, SIAM journal on imaging sciences 2(1), 183–202.

- Bi et al. (2021) Bi, X., Tang, X., Yuan, Y., Zhang, Y. & Qu, A. (2021), ‘Tensors in statistics’, Annual review of statistics and its application 8, 345–368.

- Candès et al. (2011) Candès, E. J., Li, X., Ma, Y. & Wright, J. (2011), ‘Robust principal component analysis?’, Journal of the ACM (JACM) 58(3), 1–37.

- Candes & Plan (2011) Candes, E. J. & Plan, Y. (2011), ‘Tight oracle inequalities for low-rank matrix recovery from a minimal number of noisy random measurements’, IEEE Transactions on Information Theory 57(4), 2342–2359.

- Candès & Recht (2009) Candès, E. J. & Recht, B. (2009), ‘Exact matrix completion via convex optimization’, Foundations of Computational mathematics 9(6), 717–772.

- Csurgay et al. (2000) Csurgay, Á. I., Porod, W. & Lent, C. S. (2000), ‘Signal processing with near-neighbor-coupled time-varying quantum-dot arrays’, IEEE Transactions on Circuits and Systems I: Fundamental Theory and Applications 47(8), 1212–1223.

- Doukhan (2012) Doukhan, P. (2012), Mixing: properties and examples, Vol. 85, Springer Science & Business Media.

- Fan et al. (2021) Fan, J., Wang, W. & Zhu, Z. (2021), ‘A shrinkage principle for heavy-tailed data: High-dimensional robust low-rank matrix recovery’, Annals of statistics 49(3), 1239.

- Gandy et al. (2011) Gandy, S., Recht, B. & Yamada, I. (2011), ‘Tensor completion and low-n-rank tensor recovery via convex optimization’, Inverse problems 27(2), 025010.

- Gao & Wang (2018) Gao, P. & Wang, M. (2018), Dynamic matrix recovery from partially observed and erroneous measurements, in ‘2018 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP)’, IEEE, pp. 4089–4093.

- Gross et al. (2010) Gross, D., Liu, Y.-K., Flammia, S. T., Becker, S. & Eisert, J. (2010), ‘Quantum state tomography via compressed sensing’, Physical review letters 105(15), 150401.

- Hang & Steinwart (2017) Hang, H. & Steinwart, I. (2017), ‘A bernstein-type inequality for some mixing processes and dynamical systems with an application to learning’, The Annals of Statistics 45(2), 708–743.

- Hu & Yao (2022) Hu, X. & Yao, F. (2022), ‘Dynamic principal component analysis in high dimensions’, Journal of the American Statistical Association pp. 1–12.

- Ji & Ye (2009) Ji, S. & Ye, J. (2009), An accelerated gradient method for trace norm minimization, in ‘Proceedings of the 26th annual international conference on machine learning’, pp. 457–464.

- Keshavan et al. (2009) Keshavan, R., Montanari, A. & Oh, S. (2009), ‘Matrix completion from noisy entries’, Advances in neural information processing systems 22.

- Klopp (2011) Klopp, O. (2011), ‘Rank penalized estimators for high-dimensional matrices’, Electronic Journal of Statistics 5, 1161–1183.

- Koltchinskii (2011b) Koltchinskii, V. (2011b), ‘Von neumann entropy penalization and low-rank matrix estimation’, The Annals of Statistics 39(6), 2936–2973.

- Koltchinskii et al. (2011a) Koltchinskii, V., Lounici, K. & Tsybakov, A. B. (2011a), ‘Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion’, The Annals of Statistics 39(5).

- Koltchinskii & Xia (2015) Koltchinskii, V. & Xia, D. (2015), ‘Optimal estimation of low rank density matrices.’, J. Mach. Learn. Res. 16(53), 1757–1792.

- Koren (2009) Koren, Y. (2009), Collaborative filtering with temporal dynamics, in ‘Proceedings of the 15th ACM SIGKDD international conference on Knowledge discovery and data mining’, pp. 447–456.

- Koren et al. (2009) Koren, Y., Bell, R. & Volinsky, C. (2009), ‘Matrix factorization techniques for recommender systems’, Computer 42(8), 30–37.

- Li et al. (2019) Li, X. P., Huang, L., So, H. C. & Zhao, B. (2019), ‘A survey on matrix completion: Perspective of signal processing’, arXiv preprint arXiv:1901.10885 .

- Liu et al. (2012) Liu, J., Musialski, P., Wonka, P. & Ye, J. (2012), ‘Tensor completion for estimating missing values in visual data’, IEEE transactions on pattern analysis and machine intelligence 35(1), 208–220.

- Lois & Vaswani (2015) Lois, B. & Vaswani, N. (2015), Online matrix completion and online robust pca, in ‘2015 IEEE International Symposium on Information Theory (ISIT)’, IEEE, pp. 1826–1830.

- Merlevède et al. (2009) Merlevède, F., Peligrad, M. & Rio, E. (2009), Bernstein inequality and moderate deviations under strong mixing conditions, in ‘High dimensional probability V: the Luminy volume’, Institute of Mathematical Statistics, pp. 273–292.

- Merlevède et al. (2011) Merlevède, F., Peligrad, M. & Rio, E. (2011), ‘A bernstein type inequality and moderate deviations for weakly dependent sequences’, Probability Theory and Related Fields 151(3), 435–474.

- Negahban & Wainwright (2011) Negahban, S. & Wainwright, M. J. (2011), ‘Estimation of (near) low-rank matrices with noise and high-dimensional scaling’, The Annals of Statistics 39(2), 1069–1097.

- Nesterov (1983) Nesterov, Y. E. (1983), A method of solving a convex programming problem with convergence rate , in ‘Doklady Akademii Nauk’, Russian Academy of Sciences, pp. 543–547.

- Netflix (2006) Netflix (2006), ‘Netflix prize data’, http://netflixprize.com/index.html.

- Pont-Tuset et al. (2017) Pont-Tuset, J., Perazzi, F., Caelles, S., Arbeláez, P., Sorkine-Hornung, A. & Van Gool, L. (2017), ‘The 2017 davis challenge on video object segmentation’, arXiv:1704.00675 .

- Qiu et al. (2017) Qiu, K., Mao, X., Shen, X., Wang, X., Li, T. & Gu, Y. (2017), ‘Time-varying graph signal reconstruction’, IEEE Journal of Selected Topics in Signal Processing 11(6), 870–883.

- Recht et al. (2010) Recht, B., Fazel, M. & Parrilo, P. A. (2010), ‘Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization’, SIAM review 52(3), 471–501.

- Samson (2000) Samson, P.-M. (2000), ‘Concentration of measure inequalities for markov chains and phi-mixing processes’, The Annals of Probability 28(1), 416–461.

- Toh & Yun (2010) Toh, K.-C. & Yun, S. (2010), ‘An accelerated proximal gradient algorithm for nuclear norm regularized linear least squares problems’, Pacific Journal of optimization 6(615-640), 15.

- Vershynin (2018) Vershynin, R. (2018), High-dimensional probability: An introduction with applications in data science, Vol. 47, Cambridge university press.

- Wang et al. (2016) Wang, X., Donaldson, R., Nell, C., Gorniak, P., Ester, M. & Bu, J. (2016), Recommending groups to users using user-group engagement and time-dependent matrix factorization, in ‘Proceedings of the AAAI Conference on Artificial Intelligence’.

- Watson (1992) Watson, G. A. (1992), ‘Characterization of the subdifferential of some matrix norms’, Linear algebra and its applications 170(0), 33–45.

- Xia & Yuan (2021) Xia, D. & Yuan, M. (2021), ‘Statistical inferences of linear forms for noisy matrix completion’, Journal of the Royal Statistical Society Series B 83(1), 58–77.

- Xu & Davenport (2016) Xu, L. & Davenport, M. (2016), ‘Dynamic matrix recovery from incomplete observations under an exact low-rank constraint’, Advances in Neural Information Processing Systems 29.

- Xu et al. (2020) Xu, X., Dong, F., Li, Y., He, S. & Li, X. (2020), Contextual-bandit based personalized recommendation with time-varying user interests, in ‘Proceedings of the AAAI Conference on Artificial Intelligence’, Vol. 34, pp. 6518–6525.

- Zhang et al. (2020) Zhang, A. R., Luo, Y., Raskutti, G. & Yuan, M. (2020), ‘Islet: Fast and optimal low-rank tensor regression via importance sketching’, SIAM journal on mathematics of data science 2(2), 444–479.

- Zhang et al. (2021) Zhang, Y., Bi, X., Tang, N. & Qu, A. (2021), ‘Dynamic tensor recommender systems’, The Journal of Machine Learning Research 22(1), 3032–3066.

- Zhao et al. (2015) Zhao, T., Wang, Z. & Liu, H. (2015), ‘A nonconvex optimization framework for low rank matrix estimation’, Advances in Neural Information Processing Systems 28.

- Zheng & Lafferty (2016) Zheng, Q. & Lafferty, J. (2016), ‘Convergence analysis for rectangular matrix completion using burer-monteiro factorization and gradient descent’, arXiv preprint arXiv:1605.07051 .

- Zhou et al. (2013) Zhou, H., Li, L. & Zhu, H. (2013), ‘Tensor regression with applications in neuroimaging data analysis’, Journal of the American Statistical Association 108(502), 540–552.

Supplementary Material for

“Dynamic Matrix Recovery”

S.1 Proof of Theorem 1

We need the following lemma for proving Theorem 1.

Lemma S.1

Let be a positive definite matrix with the smallest eigenvalue . Then the following inequality

| (S.1) |

holds for any with .

Proof of Lemma S.1: Note that for a fixed ,

Let be the eigenvalues of satisfying . Using the representation where are orthogonal eigenvectors corresponding to , we have

Consider the minimization problem

This is a convex problem with

and

With Karush-Kuhn-Tucker condition, we have minimum values satisfying that only one of is equal to and others are all zero, which means that

Proof of Theorem 1: For brevity, we denote

for all . With the definition of ,

holds for any . With the identity

we have

Using , one can obtain

Under the assumption that , we have

Set , then

With the identity

we have

| (S.2) |

If , we can maintain the bound

| (S.3) |

If , with Assumption 1, we know that

| (S.4) |

So (S.2) can be expressed as

From Lemma S.1,

| (S.5) | ||||

Thus we have

By solving this inequality, we have

| (S.6) |

| (S.7) |

Because is the minimizer of (6), there exists a sub-gradient matrix satisfying that for all ,

which equals to that there exists satisfying that

It is equivalent to

where .

Denote that with support . have representation from Watson (1992):

We choose a subject to

With the monotonicity of sub-gradients, we have . So

Using the identity

and the inequality

we have

| (S.8) | ||||

With identity

we have that

With

and

we have

| (S.9) |

Also we have

| (S.10) | ||||

With (LABEL:eq_proof_error_bound_1), (S.9) and (S.10),

With ,

Set , so

With the identity

we have

If , we maintain the bound

| (S.11) |

If , using (S.4) and Lemma S.1, we know that

| (S.12) | ||||

So we have

| (S.13) |

Combining (S.11) and (S.13), we have

| (S.14) |

S.2 Proofs of Theorem 2 and Corollary 1, 2

Proposition 1

Under Assumption 2 and 3, if and as , then

Proof of Proposition 1: Note that . The conclusion follows from the classical nonparametric results (of fixed design) that

Now we prove two lemmas which are needed to finish the proofs Lemma S.4 and Theorem 2. For brevity, define that . We extend proposition 2 in Koltchinskii (2011b) to obtain the following Lemma S.2.

Lemma S.2

Let be independent, mean-zero random variables satisfying that

Let and . There exists a constant such that, for all , with probability at least

| (S.15) |

Proof of Lemma S.2:

We follow the proof of proposition 2 in Koltchinskii (2011b) here.

Let

We know that if and only if . Therefore,

and

To bound , we use independence and Golden-Thompson inequality

By induction, we have

It remains to bound the norm . Using Taylor expansion and , we have

Therefore, for all we have

Let

we have

So when

and is chosen to be

which can directly deduce (S.15).

Lemma S.3

If X,Y are random variables with , , and there exists that , then we have

| (S.16) |

Proof of Lemma S.3: Using Young’s inequality we know that for all

Thus we have

where we choose by .

So we have

We construct the following theorem to bound and Lemma S.4 is an immediate result of the following theorem. For brevity, we denote .

Theorem S.1

Under Assumption 4-5, for all , with probability at least ,

where

and constants with respect to such that

Proof of Theorem S.1: Because that

| (S.17) | ||||

Lemma S.4

Under Assumption 4 and 5, if and as , , then with probability at least ,

| (S.21) |

where is a constant independent to such that

in which and

with .

Proof of Lemma S.4:

Define that

Recall the definition of that we have that

and

With the assumption , for , when , the first terms in (S.18), (S.19) and (S.20) dominate those bounds which gives

By setting , we can deduce Lemma S.4 directly.

Proof of Theorem 2: With Lemma S.4 and Theorem 1, we have

which leads to the following conclusion. From Lemma S.4, we know that for all , with probability at least ,

Choose that

If , than

From Proposition 1

With Theorem 1, so

holds with probability at least .

Proof of Corollary 1: Plug in the upper bound of in Lemma S.4, Corollary 1 can be obtained immediately.

Proof of Corollary 2:

From the distribution of and Assumption 4, we have that

and

Then it can be obtained that

Then . Note that , when , the first term in (S.21) dominates the bound. Apply Theorem 2 and Corollary 1 and the proof is finished.

S.3 Heterogeneous Scenario

Consider the heterogeneous assumption first.

Assumption S.1

(Heterogeneous Assumption) The second moment matrix of is positive definite with smallest eigenvalue for .

Here we provide the corresponding results of Theorem 1, Theorem 2 and Corollary 1 under the heterogeneous scenario. The key difference between homogeneous and heterogeneous scenarios is that the covariance matrix used for time points is in homogeneous case and in heterogeneous case. Define , and the difference is using to replace in each theorems and corollaries for the upper bound of .

Theorem S.2

Proof In the Proof of Theorem 1, the whole proof is not changed but changing (S.5) as

and changing (LABEL:eq:homo2) as

Theorem S.3

(Heterogeneous Theorem 2) Under Assumption 1-5, let , and as , when

where and are defined in Lemma S.4 of Supplementary Material, then with probability at least ,

| (S.24) |

where is defined in (10) and in Assumption 2.

Corollary S.1

(Heterogeneous Corollary 1) Under assumptions of Theorem S.3, when

with probability at least ,

| (S.25) |

where .

S.4 Definition of mixing

The dependence of two -field and is measured by

And for a sequence of -field , the -coefficients is defined as

If , the sequence of -field is said to be -mixing.

S.5 Proofs of Theorem 3 and Corollary 3, S.2

Lemma S.5

Under Assumption 4 and 6, if as , and , with probability at least ,

where is a constant independent to .

Proof of Lemma S.5 and Theorem 3: Denote . We know that . Define such that , then

where . So we know that , which means that

Let and . Using Lemma S.2, we know that

Denote the bounded function

we know that

With the tail distribution assumptions for , when , we have the inequalities

And when , we have that

Meanwhile we have the bound

Similar to Theorem 3 in Samson (2000), with the matrix value function and norm

when .

Thus we have

when and .

And similarly

when and .

When

choose

If

we have that

Meanwhile, when

choose

If

we have that .

Thus when

and

the inequality

holds where

Similarly, we choose and

holds when and

And choose , we have

holds when and .

Summarizing the above results with , we know that when and , there exists a constant , with probability at least ,

Choose

and using Theorem 1 and proof of Theorem 2, we have that

Note that when , we can represent the condition and as and respectively.

Corollary S.2

Under assumptions of Theorem 3, when are i.i.d. uniformly distributed on , are independently follow sub-exponential mean-zero distributions, and , then with probability at least ,

When and , we select

then

| (S.26) |

where are the same constants as above.

The proofs of Corollary 3 and S.2 are similar to those of Corollary 1 and 2, which we do not repeat.

S.6 Application to Compressed Sensing

Corollary S.3

(Independent case) Under Assumption 1-5, when are random matrices with independent mean-zero sub-gaussian elements with variance , are independently follow sub-gaussian distributions, , and as , with probability at least ,

When , let

then

| (S.27) |

where and are the same constants as above.

Theorem 6 in Koltchinskii (2011b) presented the error bound for static matrix compressed sensing which is

Similarly to the matrix completion, when , our dynamic method gives a sharper bound than the static method.

From Corollary 2 and Corollary S.3, when the variances of observation errors are small enough comparing to the variances of , i.e., in matrix completion setting and in compressed sensing setting, the upper bound (15) and (S.27) have the same order such that

Proof of Corollary S.3: Because , we know that and (b) in (S.17) becomes zero. From the distribution of and Assumption 4, we know that and by Theorem 4.4.5 in Vershynin (2018). Also, it is easy to check that . With that

and with Lemma S.3

we have that .

Then it can be obtained that

Apply Theorem 2 and Corollary 1, the proof is completed.

Corollary S.4

(Dependent case.) Under assumptions of Theorem 3, when are random matrices with independent mean-zero sub-gaussian elements with variance and are independently follow sub-gaussian distributions, and , with probability at least ,

When and , we select

then

where and are the same constants as above.

S.7 Proof of Theorem 4

Proof of Theorem 4: First we know that

This gives

Define that , Toh & Yun (2010) proved that for any ,

| (S.28) |

Note that (S.28) focuses on the convergence rate of object function instead of .from (S.28) we know

for any . Therefore, we have

With the assumption that , we use the similar methods in proof of Theorem 1 and immediately know that

Next, we consider with the decomposition

where with support , and

Using the convexity of , we have that for all and ,

| (S.29) |

and

| (S.30) |

where . Because is the minimizer of , there exists a matrix satisfies that for all ,

which means that there exists

| (S.31) |

satisfying that

| (S.32) |

Set .

- a.

-

b.

Similarly, we know that for all

holds for all

Choose , so

which means that

(S.34) -

c.

Similarly, we have that for all

holds for all

with

So we have

Then

which means that

(S.35) -

d.

The result is similar to (S.35) as

(S.36)

Using (S.30), (S.33), (S.34), (S.35), (S.36), we know that

| (S.37) | ||||

Meanwhile, we can easily check that hold for all , so we have

| (S.38) |

With (S.28), (S.37), (S.38) and set , we have that

Finally, with Theorem 1, the proof is finished.

S.8 Proof of Corollary 4

Proof of Corollary 4: From (18), under the conditions in Corollary 3, with probability at least ,

When satisfies

then

and thus

Similarly, for in the random initial, we have

In the proposed initial strategy, for , when

we have

which gives

Choosing

and the proof is finished.

For independent case, we need to obtain the error bound

| (S.39) |

and the parallel result is

Corollary S.5

Under assumptions of Theorem 2, to attain (S.39) for each , the total iteration step of random initial choice satisfies

and total iteration step of the proposed initial strategy satisfies

The proof of Corollary S.5 and is similar to that of Corollary 4 and hence we omit it here.

S.9 Additional Numerical Results

S.9.1 Netflix Dataset with varying the choosing of number of time intervals

We conduct a numerical analysis using Netflix data, encompassing 1034 movies that were viewed more than 25000 times. We sample 3000 users from those whose ratings occurred more than 30 times in the dataset. The analysis focus on the first 500000 ratings recorded from October 1998 to November 2005. These ratings are randomly divided, with assigned as training data and the remaining as test data. To explore the impact of varying while keeping constant, we consider 10 different values of ranging from 1 to 1000 and split the observations into time intervals in chronological order. After applying our method, results are presented in Figure S.1 and Table S.1.

The results indicate that for sufficiently large (in this case, ), the variation in has a negligible impact. Conversely, when is too small (for instance, ), increasing its value leads to a reduction in estimation error. This observation also corresponds to the dynamic nature inherent in the underlying low-rank matrix, signifying its dynamic essence rather than a static state.

| MSE* | 1.194 | 0.881 | 0.886 | 0.825 | 0.812 | 0.800 | 0.803 | 0.802 | 0.801 | 0.802 |

|---|

S.9.2 Netflix Dataset with Link Function

In the real data experiment with Netflix dataset, each rating is a discrete integer from to . Here we add experiment results with link function for the Netflix dataset. We assume that each user possesses a latent rating to each movie. Given the rating system’s constraint of integer values ranging from 1 to 5, we consider the observed rating derived from a transformation on the corresponding latent rating , and assume that users typically tend to choose integer values in proximity to their latent ratings with a certain probability as their final ratings, i.e.,

where follow independent Bernoulli distributions with probability to take value 1 and is the floor operator. And we estimate by

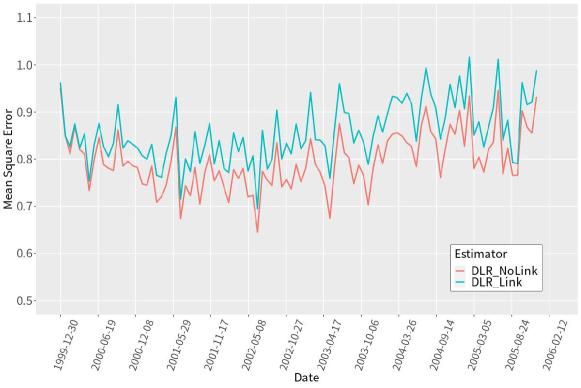

We followed a similar procedure and conducted new experiments with results presented in Figure S.2. It is interesting to note that the inclusion of this link function performs worse. One possible reason might be that the link function may not accurately reflect the true mechanism of users’ ratings. Thus, in this example, we opted to not use such a link function to illustrate the proposed method. However, this does not necessarily imply a link function is not needed in general, e.g., a more flexible form of link function by nonparametric techniques can be considered for future research.

S.9.3 Image Classification

An experiment was conducted utilizing the CIFAR-10 dataset to assess the efficacy of the trace regression framework in improving subsequent image-related tasks, such as classification or regression. The CIFAR-10 dataset is publicly available at https://www.cs.toronto.edu/ kriz/cifar.html. This evaluation is particularly relevant when the original dataset is plagued by incomplete information and noise. Employing a similar approach as detailed in the real-world example involving video data processing, we treated each image’s individual channel as a matrix denoted by . Subsequently, we employed the Robust Principal Component Analysis (RPCA) method to acquire the sparse () and low-rank () components, respectively. For the purpose of dataset generation, we randomly preserved a subset of elements from the low-rank component (), subjecting these elements to perturbation using i.i.d. normal noises. The recovery process involved applying our method to retrieve the low-rank component from the saved subset of elements in and subsequently adding the sparse component . We compared the performance of directly using the compressed data with utilizing the data obtained after image recovery based on the trace regression framework. For the classification tasks, we utilized LeNet and ResNet18 models. The corresponding results are presented in Table S.2. In the table, represents the compression rate, and Acc denotes the classification accuracy in the test dataset. The findings suggest that prior image recovery before classification can lead to an enhancement in classification accuracy by approximately to for the aforementioned compressed datasets.

| Network | No recovery Acc | Recovery Acc | |

|---|---|---|---|

| LeNet | |||

| ResNet | |||

| LeNet | |||

| ResNet | |||

| LeNet | |||

| ResNet | |||

| LeNet | |||

| ResNet |

S.9.4 The selection of and other parameters in the FISTA algorithm

We first remark that the optimal tuning parameter can be chosen for each time points . The penalty term can be relaxed to depend on , and the theoretical analysis is still valid with slight modification. In practice, based on our experience with extensive numerical studies, the universal chosen would not produce similarity in the low-rank structure in terms of ranks and estimated eigen-space, and can substantially reduce the computational cost associated with tuning hyper-parameters. Theoretically, considering the heterogeneous case in Assumption S.1 as an example and assuming that the change of over is not very large, i.e. there exist to bound such that with constants . With the same order assumption for sample size , and has the optimal selection from Theorem 2 and (17) for each by

| (S.40) |

where and are related to . With regularity and smoothness assumption 2, there exist to bound as their change is also not very large. So we can choose a universal bandwidth and tuning parameter with the error bound for optimal up to a constant scalar.

Next, we present the detailed parameters in the FISTA algorithm of the simulation. In our proposed method, we set the tolerance (tor) to around , which is a commonly used for the termination of optimization. For the initial time point , we employ the following strategy,

Then the output of last time is used as the initial matrix for current time , i.e.,

The Lipchitz constant here has an upper bound which can be calculated directly as

and the detail proof can be found in Supplementary S.6. These parameters are set in the same way for the benchmark, independent and dependent cases.

We employ a 5-fold cross-validation (CV) approach to select the tuning parameter in both independent and dependent settings. In our empirical findings, we observed that the results exhibit minimal differences when falls within a certain suitable range. To mitigate computational complexity in tuning the parameter, we suggest employing a coarse grid to estimate a rough range for and subsequently using a finer grid to make the final selection. When altering the matrix size, sample size, or the number of simulation points, it is not necessary to re-select using CV. Instead, we can rely on the theoretical relationship to adjust the new accordingly, i.e.,