On Consistency of Signatures Using Lasso ††thanks: Ruixun Zhang and Chaoyi Zhao are corresponding authors. The authors are ordered alphabetically.

Abstract

Signature transforms are iterated path integrals of continuous and discrete-time time series data, and their universal nonlinearity linearizes the problem of feature selection. This paper revisits the consistency issue of Lasso regression for the signature transform, both theoretically and numerically. Our study shows that, for processes and time series that are closer to Brownian motion or random walk with weaker inter-dimensional correlations, the Lasso regression is more consistent for their signatures defined by Itô integrals; for mean reverting processes and time series, their signatures defined by Stratonovich integrals have more consistency in the Lasso regression. Our findings highlight the importance of choosing appropriate definitions of signatures and stochastic models in statistical inference and machine learning.

1 Introduction

Signature transform.

Originally introduced and studied in algebraic topology [4, 5], the signature transform, sometimes referred to as the path signature or simply signature, has been adopted and further developed in rough path theory [13, 31]. Given any continuous or discrete time series, the signature transform produces a vector of real-valued features that extract rich and relevant information [27, 32]. It has been proven an attractive and powerful tool for feature generation and pattern recognition with state-of-the-art performance in a wide range of domains, including handwriting recognition [38, 40, 41], action recognition [25, 39, 42], medical prediction [21, 33, 34], and finance [1, 15, 18, 28, 30]. Comprehensive reviews of successful and potential applications of the signature transform in machine learning can be found in [6] and [27].

Most of the empirical success and theoretical studies of the signature transform are built upon its most striking universal nonlinearity property. It states that every continuous function of the time series may be approximated arbitrarily well by a linear function of its signature (see Section 2.1 for details). This nonlinearity property makes the signature a computationally efficient tool; it also cements the prominent role of regression analysis for time series data thanks to the linearization of the feature space by the signature. When learning nonlinear relationships between variables, utilizing linear regression models after applying the signature transform can yield significantly improved out-of-sample prediction performance compared to modeling without the signature transform [24].

Signatures are iterated path integrals of time series, and there are multiple definitions of integrals adopted for signatures. Given the successful application of the signature transform and the rapidly growing literature on its probabilistic characteristics, it is time to understand and systematically study the statistical implications of these different forms of signatures on a given time series data.

Consistency of Lasso.

In practice, feature selection methods like the Lasso [35] are commonly used to identify a sparse set of features from a universe of all signatures [6, 24, 26, 27]. One of the well-documented and extensively studied issues concerning linear models is the consistency in feature selections by Lasso [2, 37, 43]. Consistency is an important metric for out-of-sample model performance. Given the different definitions of signatures, the natural starting point is the consistency issue for Lasso regression models under different signature transforms.

Main results.

This paper studies the consistency issue of Lasso for signature transforms. It focuses on two definitions of signatures: Itô and Stratonovich. It chooses two representative classes of Gaussian processes: multi-dimensional Brownian motion and Ornstein–Uhlenbeck (OU) process, and their respective discrete-time counterparts, i.e., random walk and autoregressive (AR) process. These processes have been widely applied in a number of domains [1, 19, 24, 27, 36].

To analyze the consistency of Lasso regressions, correlation structures of signatures are first studied for these processes. For Brownian motions, its correlation structure is shown to be block diagonal if its signatures are defined by Itô integrals (Propositions 1–2), and to have a special odd–even alternating structure if its signatures are defined by Stratonovich integrals (Propositions 3–4). In contrast, the OU process exhibits this odd–even alternating structure by either definition of the integral (Proposition 5).

Based on the correlation structures of signatures, we investigate the consistency of Lasso regressions for different processes (Propositions 6–8). For time series and processes that are closer to Brownian motion and with weaker inter-dimensional correlations, the Lasso regression is more consistent for their feature selection by Itô signatures; for mean reverting time series and processes, Stratonovich signatures yield more consistency for the Lasso regression.

Contribution.

Our study takes the first step toward understanding the statistical properties of the signature transform for regression analysis. It fills one of the gaps between the theory and the practice of signature transforms in machine learning. Our work highlights the importance of choosing appropriate signature transforms and stochastic models for feature selections and for general statistical analysis.

2 The framework

In this section, we present the framework for studying the consistency of feature selections in Lasso via signature. All proofs are given in Appendix F.

2.1 Review of signatures and their properties

Consider a -dimensional continuous-time stochastic process , , and its signature or signature transform defined as follows:

Definition 1 (Signature).

For and , the -th order signature of the process with index from time 0 to is defined as

| (1) |

In addition, the 0-th order signature of from time 0 to is defined as for any .

In other words, the -th order signature of given by Equation (1) is its -fold iterated path integral along the indices . For a given order , there are choices of indices , therefore the number of all -th order signatures is .

The integral in Equation (1) can be specified differently. For example, if is a deterministic process, it can be defined via the Riemann/Lebesgue integral. If is a multi-dimensional Brownian motion, it is a stochastic integral that can be defined either by the Itô integral or by the Stratonovich integral. For clarity, we write

when considering the Itô integral, and

for the Stratonovich integral.

Throughout the paper, for ease of exposition, we refer to the signature of as the Itô (the Stratonovich) signature if the integral is defined in the sense of the Itô (the Stratonovich) integral.

Signatures enjoy several nice probabilistic properties. First, all expected signatures of a stochastic process together can characterize the distribution of the process [7, 8]. Second, the signatures uniquely determine the path of the underlying process [3, 16, 22].

One of the most striking properties of the signature transform is its universal nonlinearity [12, 20, 23, 24, 27]. It is of particular relevance for feature selections in machine learning or statistical analysis, where one needs to find or learn a (nonlinear) function that maps time series data to a target label . By universal nonlinearity, any such function can be approximately linearized by the signature of in the following sense: for any , under some technical conditions, there exists and a linear function such that

| (2) |

where represents all signatures of from time 0 to truncated to some order . This universal nonlinearity lays the foundation for learning the relationship between the time series and a target label using a linear regression model. Table 1 summarizes different statements of the universal nonlinearity of signatures in the literature.111Appendix A provides the precise statement of universal nonlinearity. The time augmentation is discussed in Section 5 and Appendix E.

| Path | With time augmentation | Integral | Literature |

|---|---|---|---|

| Càdlàg rough path | Yes | Rough | [10] |

| Continuous semimartingale | Yes | Stratonovich | [9] |

| Continuous rough path | Yes | Stratonovich | [1, 29] |

| Continuous rough path | No | Itô/Stratonovich | [24] |

| Bounded variation path | No | Riemann/Lebesgue | [12, 20, 27] |

In the next section, we study feature selections via Lasso regression by signature transform.

2.2 Feature selection using Lasso with signatures

Suppose that one is given pairs of samples, , where is the -th time series, for . Given a fixed order , consider the following regression model:

| (3) |

where represents samples, and are independent and identically distributed errors. Here the number of predictors, i.e., the signature of various orders, is , including the 0-th order signature , whose coefficient is . It has been documented that including signatures up to a small order as predictors in a linear regression model usually suffices to achieve good performances in practice [27, 32].

The goal of Lasso is to identify the true predictors/features among all the predictors included in the linear regression model (3). We use to represent the set of all signatures of order with nonzero coefficients in Equation (3). Given any (nonlinear) function that one needs to learn, let us define the set of true predictors222True predictors are predictors with nonzero coefficients in Equation (3). by

| (4) |

Here, we begin the union with to include the 0-th order signature for notational convenience.

Given a tuning parameter and samples, we adopt the following Lasso estimator to identify the true predictors:

| (5) |

where is the vector containing all coefficients , and denotes the -norm. Here, represents the standarized version of across samples by the -norm, i.e., for any index ,

We perform this standardization for two reasons. First, the Lasso estimator is sensitive to the magnitudes of the predictors, and standardization helps prevent the domination of predictors with larger magnitudes in the estimation process [17]. Second, the magnitudes of the signatures vary as the order of the signature changes [31], therefore standardization is necessary to ensure that the coefficients of different orders of signatures are on the same scale and can be compared directly. Furthermore, the covariance matrix is now equivalent to the correlation matrix, allowing us to focus on the correlation structure of the signatures in the subsequent analysis.

2.3 Consistency and the irrepresentable condition of Lasso

Our goal is to study the consistency of feature selections via signatures using the Lasso estimator in Equation (5). We use the concept of (strong) sign consistency, a custom definition of consistency for Lasso proposed in [43].

Definition 2 (Consistency).

In other words, sign consistency requires that a pre-selected can be used to achieve consistent feature selection via Lasso.

The following irrepresentable condition is nearly a necessary and sufficient condition for the Lasso to be sign consistent [43].

Definition 3 (Irrepresentable condition).

The feature selection in Equation (3) satisfies the (strong) irrepresentable condition if there exists a positive constant vector such that

where is given by Equation (4) and the complement of , () represents the covariance matrix333In this paper, in line with [43], all covariances and correlation coefficients are defined to be uncentered. Specifically, for random variables and , we define their covariance as , and their correlation coefficient as . One can easily extend our results to the centered case. between all predictors in and ( and ), represents a vector formed by beta coefficients for all predictors in , is an all-one vector, calculates the absolute values of all entries, and the inequality “” holds element-wise.

This irrepresentable condition uses the population covariance matrix instead of the sample covariance matrix in [43]. Nevertheless, similar to [43], it means that the irrelevant predictors in cannot be sufficiently represented by the true predictors in , implying weak collinearity between the predictors.

By the signature transform, predictors in our linear regression model (3) are correlated and have special correlation structures that differ from earlier studies [2, 37, 43]. We will show in the following section that their correlation structures vary with the underlying process , hence leading to different consistency performances for different processes. Moreover, these correlation structures depend on the choice of integrals used in Equation (1).

3 Correlation structure of signatures

To study the consistency of Lasso using signatures, let us investigate the correlation structure of Itô and Stratonovich signatures for two representative Gaussian processes with different characteristics: the Brownian motion and the OU process.

3.1 Correlation structure for multi-dimensional Brownian motion

Definition 4 (Brownian motion).

is a -dimensional Brownian motion if it can be expressed as:

| (6) |

where are mutually independent standard Brownian motions, and is a matrix independent of . In particular, with , where is the volatility of , and is the inter-dimensional correlation between and .

Now we study the correlation structure of Itô and Stratonovich signatures respectively.

3.1.1 Itô signatures for Brownian motion

The following proposition gives the moments of Itô signatures of a -dimensional Brownian motion.

Proposition 1.

Let be a -dimensional Brownian motion given by Equation (6). For and , we have:

With Proposition 1, the following result explicitly characterizes the correlation structure of Itô signatures for Brownian motions.

Proposition 2.

Let be a -dimensional Brownian motion given by Equation (6). If we arrange the signatures in recursive order (see Definition A.1 in Appendix B), the correlation matrix for Itô signatures of with orders truncated to is a block diagonal matrix:

| (7) |

whose diagonal block represents the correlation matrix for all -th order signatures, which is given by:

| (8) |

and , where represents the Kronecker product, and

Proposition 2 reveals several important facts about Itô signatures for Brownian motions. First, signatures of different orders are mutually independent, leading to a block diagonal correlation structure. Second, the correlation between signatures of the same order has a Kronecker product structure determined by the inter-correlation () between different dimensions of .

3.1.2 Stratonovich signatures for Brownian motion

The moments and correlation structure for Stratonovich signatures of Brownian motions are more complicated. We first provide the moments of Stratonovich signatures.

Proposition 3.

The following result explicitly characterizes the correlation structure of Stratonovich signatures for Brownian motions.

Proposition 4.

Let be a -dimensional Brownian motion given by Equation (6). The correlation matrix for all Stratonovich signatures of with orders truncated to has the following odd–even alternating structure:

| (9) |

where is the correlation matrix between all -th and -th order signatures, which can be calculated using Proposition 3. In particular, if we re-arrange the indices of the signatures by putting all odd-order signatures and all even-order signatures together respectively, the correlation matrix has the following block diagonal form:

where and are given respectively by

| (10) |

Propositions 2 and 4 reveal a striking difference between Itô and Stratonovich signatures for Brownian motions. Specifically, Itô signatures of different orders are uncorrelated, leading to a block diagonal correlation structure; Stratonovich signatures, in contrast, are uncorrelated only if they have different parity, leading to an odd–even alternating structure. This difference has significant implications for the consistency of the two types of signatures, which will be discussed in Section 4.

3.2 Correlation structure for multi-dimensional OU process

Definition 5 (OU process).

is a -dimensional Ornstein–Uhlenbeck (OU) process if it can be expressed as:

| (11) |

where is a matrix independent of , and are mutually independent OU processes driven by the following stochastic differential equations:

for . Here , and are independent standard Brownian motions.

The parameter of the OU process controls the speed of mean reversion of the process , and a higher implies a stronger mean reversion. When , reduces to a standard Brownian motion.

The following proposition shows that the odd–even alternating structure we observe in Proposition 4 holds for both Itô and Stratonovich signatures of the OU process.

Proposition 5.

Proposition 5 can be regarded as a generalization of the correlation structures for Itô and Stratonovich signatures of the Brownian motion in Propositions 2 and 4. In particular, for Itô signatures of the Brownian motion, all off-diagonal blocks in the odd–even alternating structure reduce to zero, as we observe in Proposition 2. However, the calculation of moments for the OU process is much more complicated than that for the Brownian motion, which we discuss in Appendix B.

4 Consistency of signatures using Lasso

This section investigates the consistency of feature selection in Lasso using signatures for both classes of Gaussian processes: the Brownian motion and the OU process. We also provide results for their discrete-time counterparts: the random walk and the AR process, respectively.

4.1 Consistency of signatures for Brownian motion and random walk

The following propositions characterize when the irrepresentable condition holds for signatures of Brownian motion.

Proposition 6.

For a multi-dimensional Brownian motion given by Equation (6), the irrepresentable condition holds if and only if it holds for each block in the block-diagonal correlation matrix. In particular, for Itô signatures this is true when the irrepresentable condition holds for each in Equation (8); for Stratonovich signatures this is true when the irrepresentable condition holds for both and in Equation (10).

Proposition 7.

Proposition 6 demonstrates both the similarity and difference between Itô signatures and Stratonovich signatures for Brownian motions. In particular, the difference in the block structure of their correlation matrices leads to the difference in the consistency of their feature selections.

Proposition 7 provides a sufficient condition for Itô signatures that can be easily used in practice: the Lasso is consistent when different dimensions of the multi-dimensional Brownian motion are not strongly correlated, with a sufficient bound by Equation (12).

Empirically, it has been documented that a small suffices to provide a reasonable approximation in applications [27, 32]. Therefore, this bound can be fairly easy to satisfy.

The consistency study for Stratonovich signatures reveals a different picture: the irrepresentable condition may fail even when all dimensions of are mutually independent, as shown in the following example.

Example 1.

Consider a two-dimensional process , where and are independent standard Brownian motions. Suppose that one includes all Stratonovich signatures of orders up to in the Lasso regression given by Equation (5), and the true model given by Equation (3) has beta coefficients , , , , , , , and . Then, by Proposition 3,

which does not satisfy the irrepresentable condition defined in Definition 3 because .

Example 1 distinguishes the consistency of Itô and Stratonovich signatures using Lasso. Since the irrepresentable condition is almost necessary and sufficient for the consistency of Lasso [43], it suggests that the statistical properties of Lasso may be worse for Stratonovich signatures.

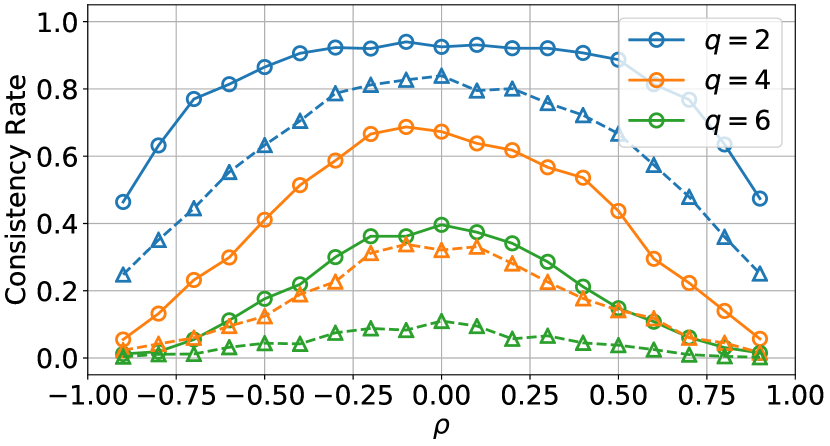

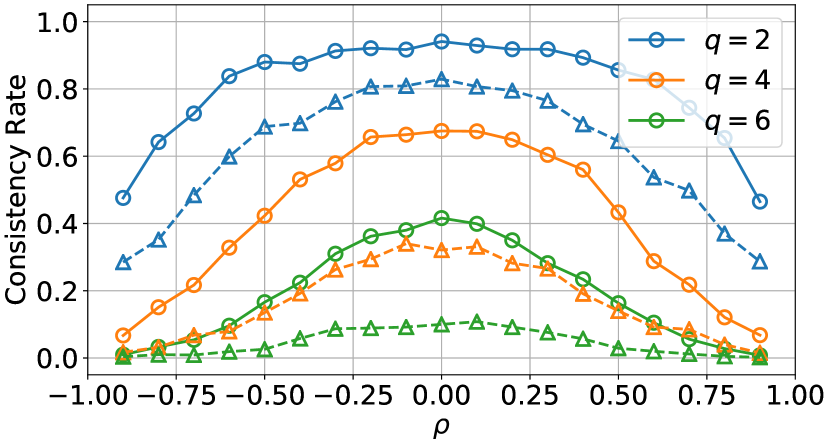

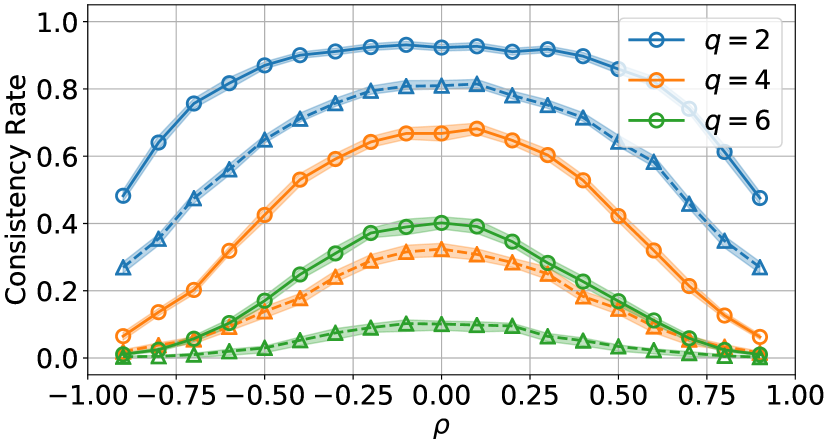

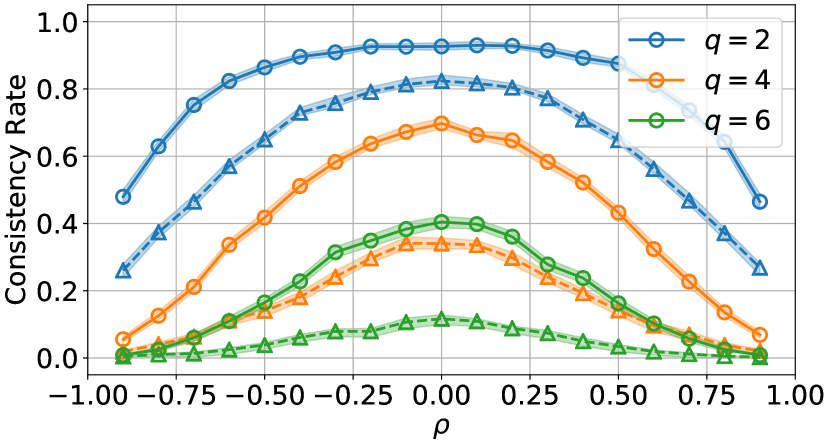

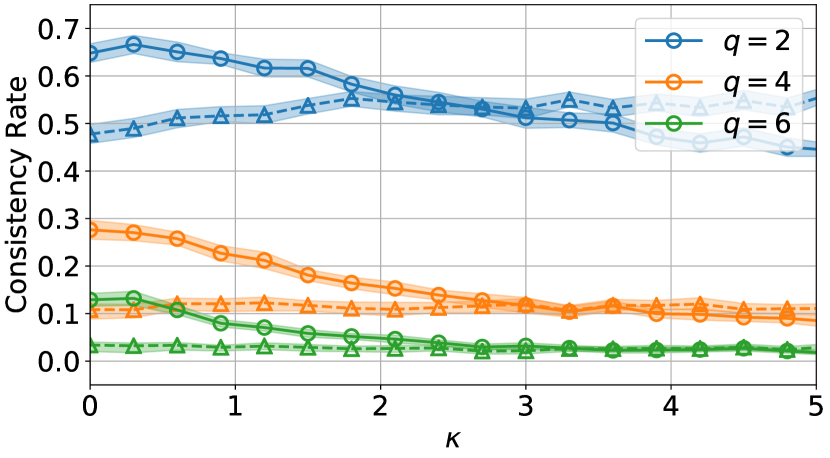

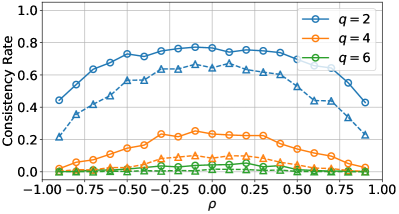

Simulations further confirm this implication.444Appendix C reports more details for the simulations including its computational cost and robustness checks. Consider a two-dimensional () Brownian motion with inter-dimensional correlation ; assume that there are true predictors in the true model (3), and all of these predictors are signatures of orders no greater than . Now, first randomly choose true predictors from all signatures; next randomly set each beta coefficient of these true predictors from the standard normal distribution; next generate 100 samples from this true model with error term drawn from a normal distribution with mean zero and standard error 0.01; then run a Lasso regression given by Equation (5) to select predictors based on these 100 samples; and finally check whether the Lasso is sign consistent according to Definition 2. Repeat the above procedure by 1,000 times and calculate the consistency rate, which is defined as the proportion of consistent results among these 1,000 experiments.

Figure 1 shows the consistency rates for different values of inter-dimensional correlation, , and different numbers of true predictors, . Figure 1(a) shows the results for the Brownian motion, and Figure 1(b) for its discrete version—the random walk. First, signatures for both Brownian motion and random walk are similar: they both exhibit higher consistency rates when the absolute value of is small, i.e., when the inter-dimensional correlations of the Brownian motion (random walk) are weak; as the number of true predictors increases, both consistency rates decrease; and finally, consistency rates for Itô signatures are consistently higher than those for Stratonovich signatures, holding other variables constant ( and ). All these findings are consistent with our theoretical results.

4.2 Consistency of signatures for OU processes and AR processes

For both the Itô and the Stratonovich signatures of the OU process, we have the following necessary and sufficient condition for the irrepresentable condition. However, it appears difficult to derive the analogue of Proposition 7 for OU processes.

Proposition 8.

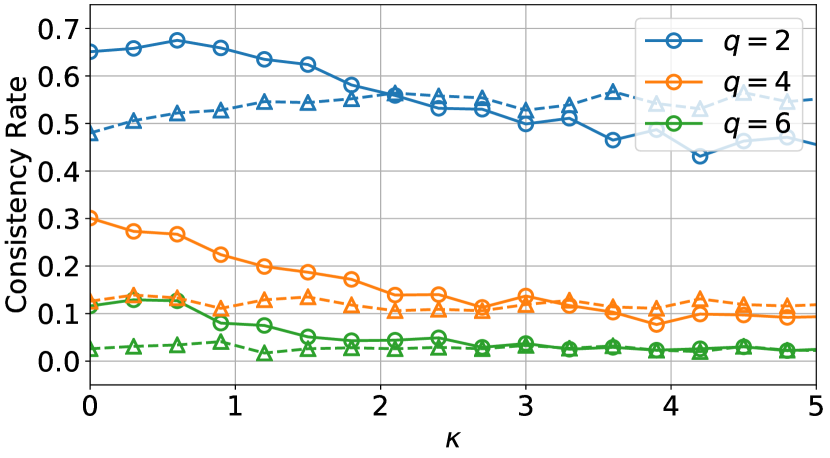

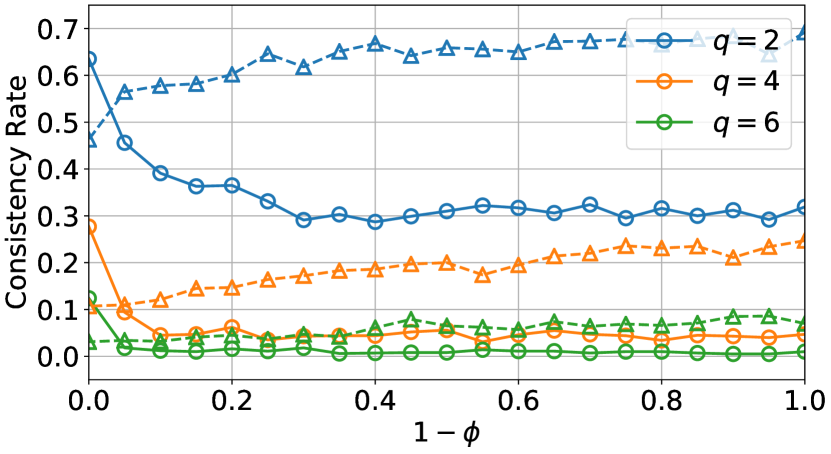

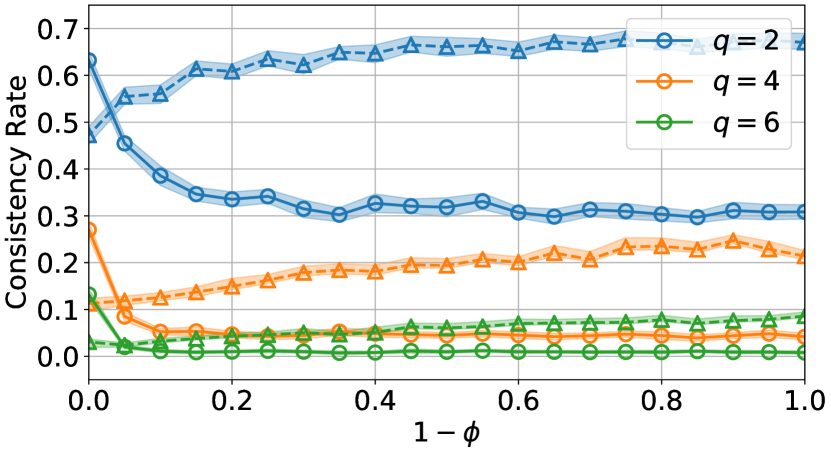

Now we study the impact of different degrees of mean reversion on the consistency of Lasso, for both the OU process and its discrete version—the autoregressive AR(1) model with parameter . Recall that higher values of for the OU process and lower values of for the AR(1) model imply stronger levels of mean reversion. We consider two-dimensional OU processes and AR(1) processes, with both dimensions sharing the same parameters ( and ). The inter-dimensional correlation matrix is randomly drawn from the Wishart distribution. Other simulation setups are the same as in Section 4.1.

Figure 2 shows the simulation results for the consistency rates of both processes. First, the Itô signature reaches the highest consistency rate when and approach , which correspond respectively to a Brownian motion and a random walk. Second, when the process is sufficiently mean reverting, Stratonovich signatures have higher consistency rates than Itô signatures. Finally, as observed in Section 4.1, Lasso gets less consistent when the number of true predictors increases.

5 Discussion

Consistency and universal nonlinearity.

We have adopted the sign consistency of Lasso [43], defined as whether the Lasso can select all true predictors with correct signs. This restrictive notion of consistency may be relaxed in the context of signatures because the true model is approximated by the linear combination of signatures with some error according to Equation (2). Extensions of the sign consistency for signatures are given in Appendix D. Overall, a lower sign consistency implies poorer performances when using other metrics to measure the performance of feature selections using Lasso, such as the out-of-sample mean squared error. This highlights the significant and practical relevance to study the statistical properties of the signature transform.

Time augmentation.

Other feature selection techniques.

While Lasso is a popular feature selection technique, there are also other commonly used techniques, such as the ridge regression [17]. The research on the consistency of signatures using other feature selection techniques is left for further investigation.

6 Conclusion

This paper studies the statistical consistency of Lasso regression for signatures. It finds that consistency is highly dependent on the definition of the signatures and the characteristics of the underlying processes. These findings call for further statistical studies for signature transform before its potential for machine learning can be fully realized.

References

- [1] Imanol Perez Arribas. Derivatives pricing using signature payoffs. arXiv preprint arXiv:1809.09466, 2018.

- [2] Peter J Bickel, Ya’acov Ritov, and Alexandre B Tsybakov. Simultaneous analysis of Lasso and Dantzig selector. The Annals of Statistics, pages 1705–1732, 2009.

- [3] Horatio Boedihardjo, Hao Ni, and Zhongmin Qian. Uniqueness of signature for simple curves. Journal of Functional Analysis, 267(6):1778–1806, 2014.

- [4] Kuo-Tsai Chen. Iterated integrals and exponential homomorphisms. Proceedings of the London Mathematical Society, 3(1):502–512, 1954.

- [5] Kuo-Tsai Chen. Integration of paths, geometric invariants and a generalized Baker–Hausdorff formula. Annals of Mathematics, pages 163–178, 1957.

- [6] Ilya Chevyrev and Andrey Kormilitzin. A primer on the signature method in machine learning. arXiv preprint arXiv:1603.03788, 2016.

- [7] Ilya Chevyrev and Terry Lyons. Characteristic functions of measures on geometric rough paths. Annals of Probability, 44(6):4049–4082, 2016.

- [8] Ilya Chevyrev and Harald Oberhauser. Signature moments to characterize laws of stochastic processes. Journal of Machine Learning Research, 23(176):1–42, 2022.

- [9] Christa Cuchiero, Guido Gazzani, and Sara Svaluto-Ferro. Signature-based models: theory and calibration. arXiv preprint arXiv:2207.13136, 2022.

- [10] Christa Cuchiero, Francesca Primavera, and Sara Svaluto-Ferro. Universal approximation theorems for continuous functions of càdlàg paths and Lévy-type signature models. arXiv preprint arXiv:2208.02293, 2022.

- [11] Omar El Euch, Masaaki Fukasawa, and Mathieu Rosenbaum. The microstructural foundations of leverage effect and rough volatility. Finance and Stochastics, 22:241–280, 2018.

- [12] Adeline Fermanian. Embedding and learning with signatures. Computational Statistics & Data Analysis, 157:107148, 2021.

- [13] Peter K Friz and Nicolas B Victoir. Multidimensional Stochastic Processes as Rough Paths: Theory and Applications, volume 120. Cambridge University Press, 2010.

- [14] Jim Gatheral, Thibault Jaisson, and Mathieu Rosenbaum. Volatility is rough. Quantitative Finance, 18(6):933–949, 2018.

- [15] Lajos Gergely Gyurkó, Terry Lyons, Mark Kontkowski, and Jonathan Field. Extracting information from the signature of a financial data stream. arXiv preprint arXiv:1307.7244, 2013.

- [16] Ben Hambly and Terry Lyons. Uniqueness for the signature of a path of bounded variation and the reduced path group. Annals of Mathematics, pages 109–167, 2010.

- [17] Trevor Hastie, Robert Tibshirani, Jerome H Friedman, and Jerome H Friedman. The Elements of Statistical Learning: Data Mining, Inference, and Prediction, volume 2. Springer, 2009.

- [18] Jasdeep Kalsi, Terry Lyons, and Imanol Perez Arribas. Optimal execution with rough path signatures. SIAM Journal on Financial Mathematics, 11(2):470–493, 2020.

- [19] Patrick Kidger, Patric Bonnier, Imanol Perez Arribas, Cristopher Salvi, and Terry Lyons. Deep signature transforms. Advances in Neural Information Processing Systems, 32, 2019.

- [20] Franz J Király and Harald Oberhauser. Kernels for sequentially ordered data. Journal of Machine Learning Research, 20, 2019.

- [21] Andrey Kormilitzin, Kate EA Saunders, Paul J Harrison, John R Geddes, and Terry Lyons. Detecting early signs of depressive and manic episodes in patients with bipolar disorder using the signature-based model. arXiv preprint arXiv:1708.01206, 2017.

- [22] Yves Le Jan and Zhongmin Qian. Stratonovich’s signatures of Brownian motion determine Brownian sample paths. Probability Theory and Related Fields, 157(1-2):209–223, 2013.

- [23] Maud Lemercier, Cristopher Salvi, Theodoros Damoulas, Edwin Bonilla, and Terry Lyons. Distribution regression for sequential data. In International Conference on Artificial Intelligence and Statistics, pages 3754–3762. PMLR, 2021.

- [24] Daniel Levin, Terry Lyons, and Hao Ni. Learning from the past, predicting the statistics for the future, learning an evolving system. arXiv preprint arXiv:1309.0260, 2016.

- [25] Chenyang Li, Xin Zhang, and Lianwen Jin. LPSNet: a novel log path signature feature based hand gesture recognition framework. In Proceedings of the IEEE International Conference on Computer Vision Workshops, pages 631–639, 2017.

- [26] Terry Lyons. Rough paths, signatures and the modelling of functions on streams. arXiv preprint arXiv:1405.4537, 2014.

- [27] Terry Lyons and Andrew D McLeod. Signature methods in machine learning. arXiv preprint arXiv:2206.14674, 2022.

- [28] Terry Lyons, Sina Nejad, and Imanol Perez Arribas. Numerical method for model-free pricing of exotic derivatives in discrete time using rough path signatures. Applied Mathematical Finance, 26(6):583–597, 2019.

- [29] Terry Lyons, Sina Nejad, and Imanol Perez Arribas. Non-parametric pricing and hedging of exotic derivatives. Applied Mathematical Finance, 27(6):457–494, 2020.

- [30] Terry Lyons, Hao Ni, and Harald Oberhauser. A feature set for streams and an application to high-frequency financial tick data. In Proceedings of the 2014 International Conference on Big Data Science and Computing, pages 1–8, 2014.

- [31] Terry J Lyons, Michael Caruana, and Thierry Lévy. Differential Equations Driven by Rough Paths. Springer, 2007.

- [32] James Morrill, Adeline Fermanian, Patrick Kidger, and Terry Lyons. A generalised signature method for multivariate time series feature extraction. arXiv preprint arXiv:2006.00873, 2020.

- [33] James Morrill, Andrey Kormilitzin, Alejo Nevado-Holgado, Sumanth Swaminathan, Sam Howison, and Terry Lyons. The signature-based model for early detection of sepsis from electronic health records in the intensive care unit. In 2019 Computing in Cardiology (CinC). IEEE, 2019.

- [34] James H Morrill, Andrey Kormilitzin, Alejo J Nevado-Holgado, Sumanth Swaminathan, Samuel D Howison, and Terry J Lyons. Utilization of the signature method to identify the early onset of sepsis from multivariate physiological time series in critical care monitoring. Critical Care Medicine, 48(10):e976–e981, 2020.

- [35] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288, 1996.

- [36] George E Uhlenbeck and Leonard S Ornstein. On the theory of the Brownian motion. Physical Review, 36(5):823, 1930.

- [37] Martin J Wainwright. Sharp thresholds for high-dimensional and noisy sparsity recovery using -constrained quadratic programming (Lasso). IEEE Transactions on Information Theory, 55(5):2183–2202, 2009.

- [38] Daniel Wilson-Nunn, Terry Lyons, Anastasia Papavasiliou, and Hao Ni. A path signature approach to online arabic handwriting recognition. In 2018 IEEE 2nd International Workshop on Arabic and Derived Script Analysis and Recognition (ASAR), pages 135–139. IEEE, 2018.

- [39] Weixin Yang, Lianwen Jin, and Manfei Liu. DeepWriterID: An end-to-end online text-independent writer identification system. IEEE Intelligent Systems, 31(2):45–53, 2016.

- [40] Weixin Yang, Lianwen Jin, Hao Ni, and Terry Lyons. Rotation-free online handwritten character recognition using dyadic path signature features, hanging normalization, and deep neural network. In 2016 23rd International Conference on Pattern Recognition (ICPR), pages 4083–4088. IEEE, 2016.

- [41] Weixin Yang, Lianwen Jin, Dacheng Tao, Zecheng Xie, and Ziyong Feng. DropSample: A new training method to enhance deep convolutional neural networks for large-scale unconstrained handwritten Chinese character recognition. Pattern Recognition, 58:190–203, 2016.

- [42] Weixin Yang, Terry Lyons, Hao Ni, Cordelia Schmid, and Lianwen Jin. Developing the path signature methodology and its application to landmark-based human action recognition. In Stochastic Analysis, Filtering, and Stochastic Optimization: A Commemorative Volume to Honor Mark HA Davis’s Contributions, pages 431–464. Springer, 2022.

- [43] Peng Zhao and Bin Yu. On model selection consistency of Lasso. The Journal of Machine Learning Research, 7:2541–2563, 2006.

Supplementary Material

Appendix A Technical details for universal nonlinearity of signatures

There are different statements of universal nonlinearity of signatures in the literature, which we summarize in Table 1 in the main paper. The following theorem gives the precise statement of universal nonlinearity proposed in [27].

Theorem 1 (Universal nonlinearity, Theorem 3.1 of [27]).

Let be a -valued continuous path with -variation, and let be a compact subset of signature paths of from time 0 to . Assume that is a continuous function. Then, for any , there exists some linear functional such that for every :

Appendix B Technical details and examples for the calculation of correlation matrices

This appendix provides details and examples for calculating the correlation structures of signatures. Appendices B.1 and B.2 discuss the Brownian motion and the OU process, respectively.

B.1 Brownian motion

Itô signature.

Propositions 1–2 in the main paper give explicit formulas for calculating the correlation structure of Itô signatures for Brownian motions. The “recursive order” mentioned in Proposition 2 is defined as follows.

Definition A.1 (Recursive Order).

Consider a -dimensional process . We order the indices of all of its 1st order signatures as:

Then, if all -th order signatures are ordered as:

we define the orders of all -th order signatures as:

For example, for a dimensional process, the recursive order of its signatures is:

-

•

1st order:

-

•

2nd order:

-

•

3rd order:

-

•

…

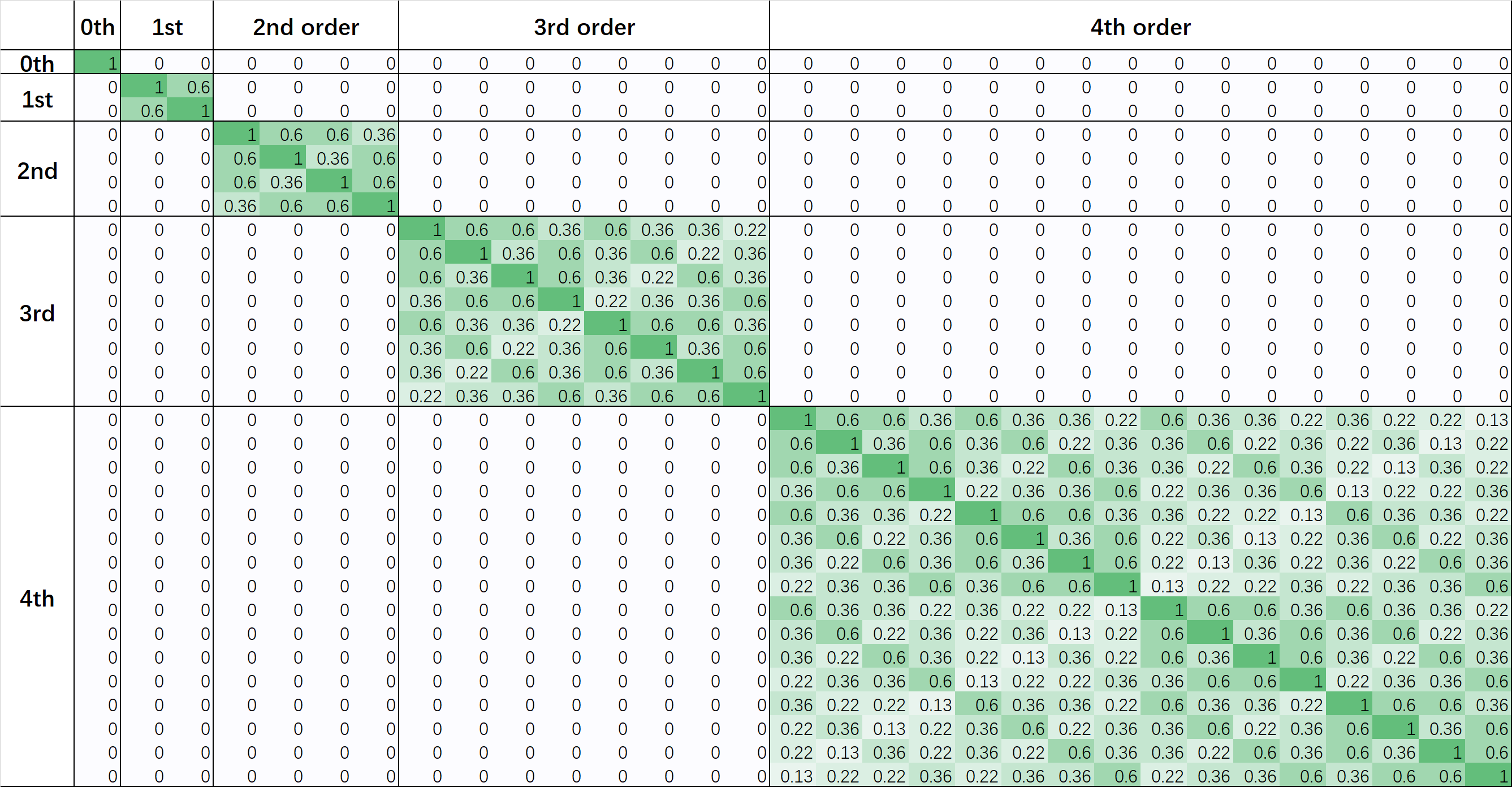

To provide intuition for Propositions 1–2 in the main paper, the following two examples show the correlation structures of Itô signatures for 2-dimensional Brownian motions with inter-dimensional correlations and , respectively.

Example A.1.

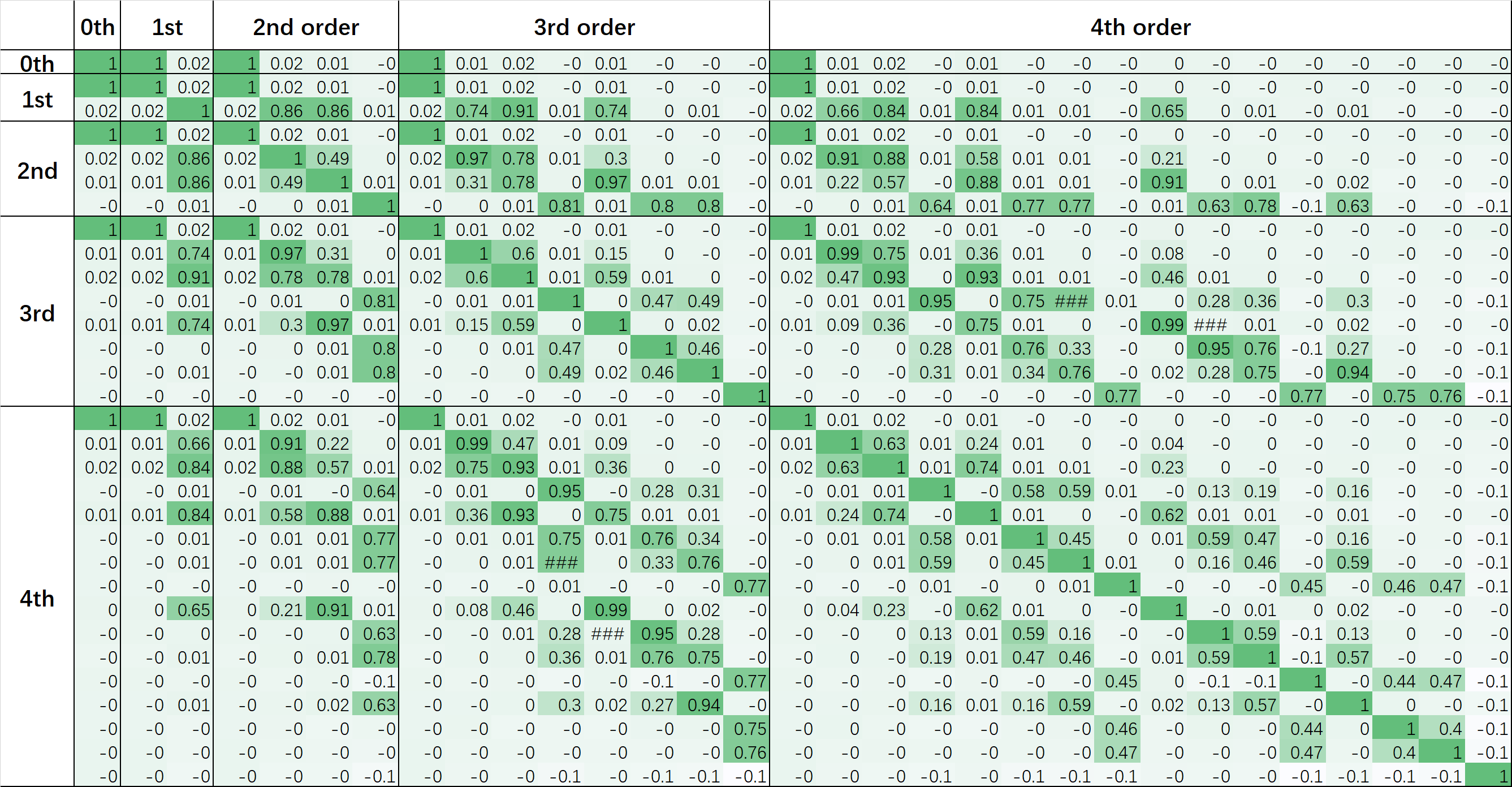

Consider a 2-dimensional Brownian motion given by Equation (6) with inter-dimensional correlation . Figure A.1 shows the correlation matrix of its Itô signatures with orders truncated to 4 calculated using Proposition 1. The figure illustrates Proposition 2—the correlation matrix has a block diagonal structure, and each block of the matrix is the Kronecker product of the inter-dimensional correlation matrix .

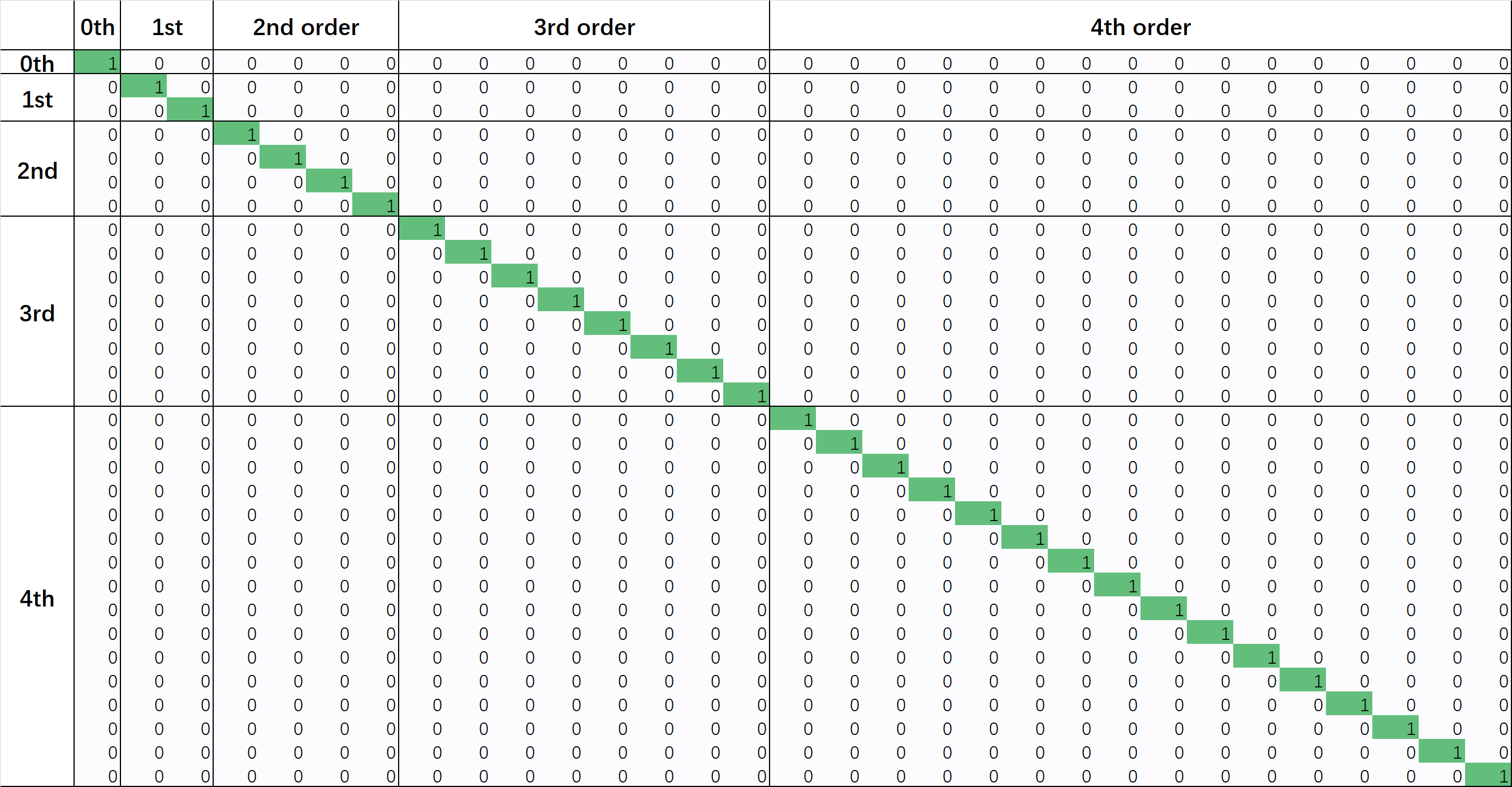

Example A.2.

Consider a 2-dimensional Brownian motion given by Equation (6) with inter-dimensional correlation . Figure A.2 shows the correlation matrix of its Itô signatures with orders truncated to 4 calculated using Proposition 1. When , the block diagonal correlation matrix reduces to an identity matrix, indicating that all of its Itô signatures are mutually uncorrelated.

Stratonovich signature.

Propositions 3–4 in the main paper provide formulas for calculating the correlation structure of Stratonovich signatures for Brownian motions. The following proposition gives recursive formulas for calculating and , which extends Proposition 3 in the main paper.

Proposition A.1.

Let be a -dimensional Brownian motion given by Equation (6). For any and , define , we have:

| (A.1) | ||||

| (A.2) |

with initial conditions

| (A.3) | ||||

| (A.4) |

In addition, define , we have:

| (A.5) | ||||

| (A.6) |

with initial conditions

| (A.7) | ||||

| (A.8) |

Here, represents the smaller value between and .

The following two examples show the correlation structures of Stratonovich signatures for 2-dimensional Brownian motions with inter-dimensional correlations and , respectively, calculated using Propositions 3–4 in the main paper and Proposition A.1.

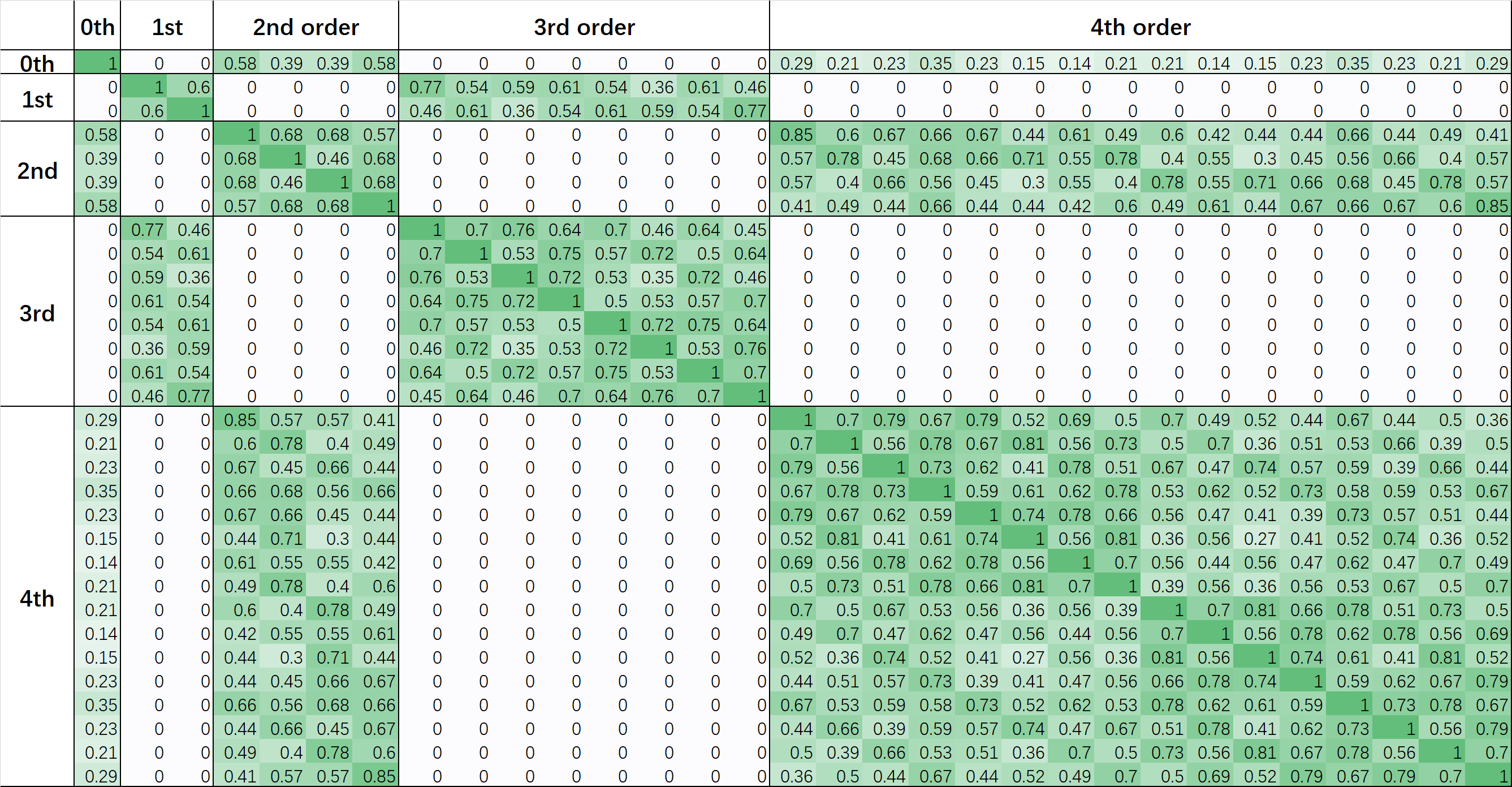

Example A.3.

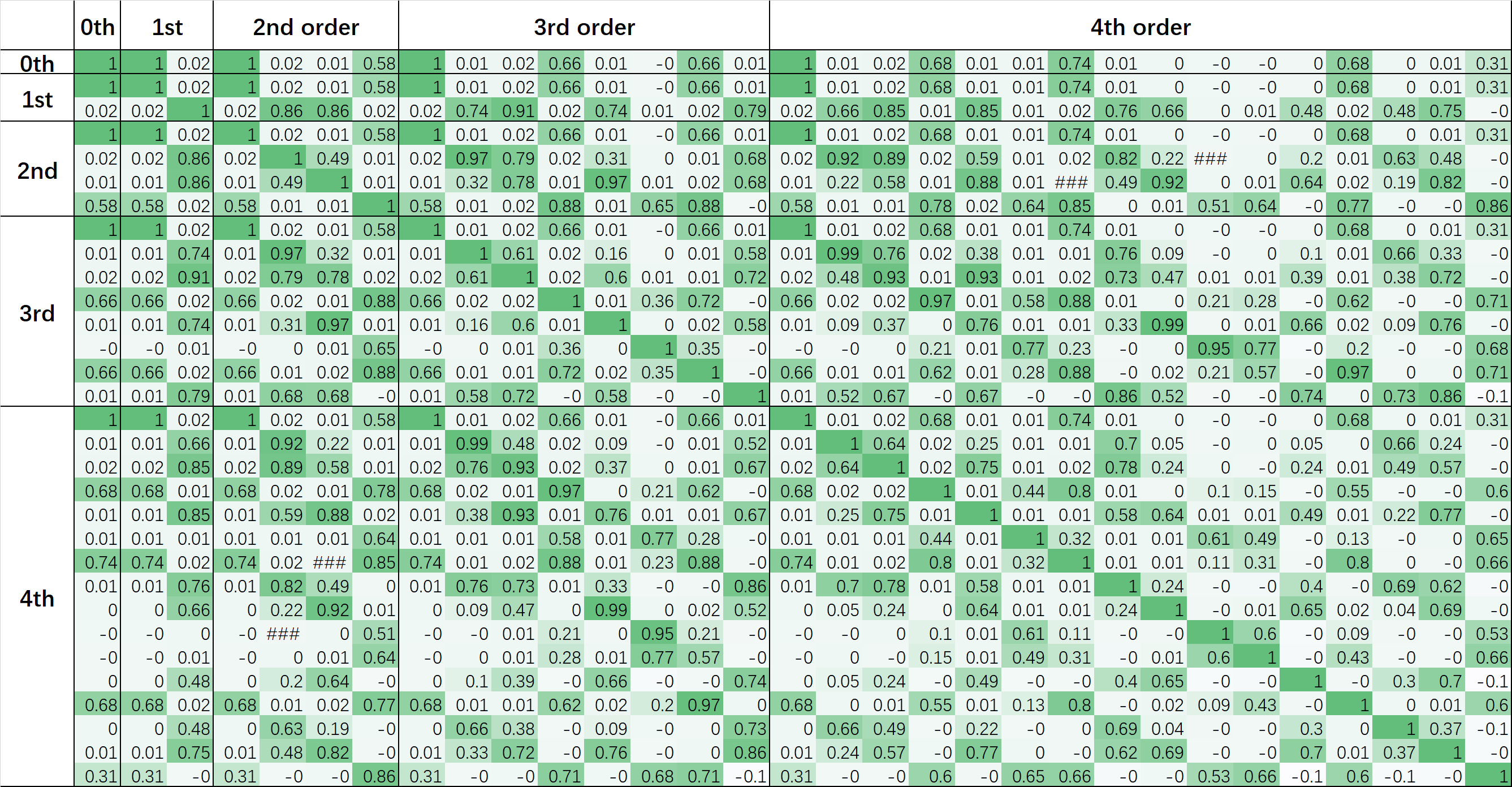

Consider a 2-dimensional Brownian motion given by Equation (6) with inter-dimensional correlation . Figure A.3 shows the correlation matrix of its Stratonovich signatures with orders truncated to 4 calculated using Propositions 3 and A.1. The figure illustrates that the correlation matrix has an odd–even alternating structure.

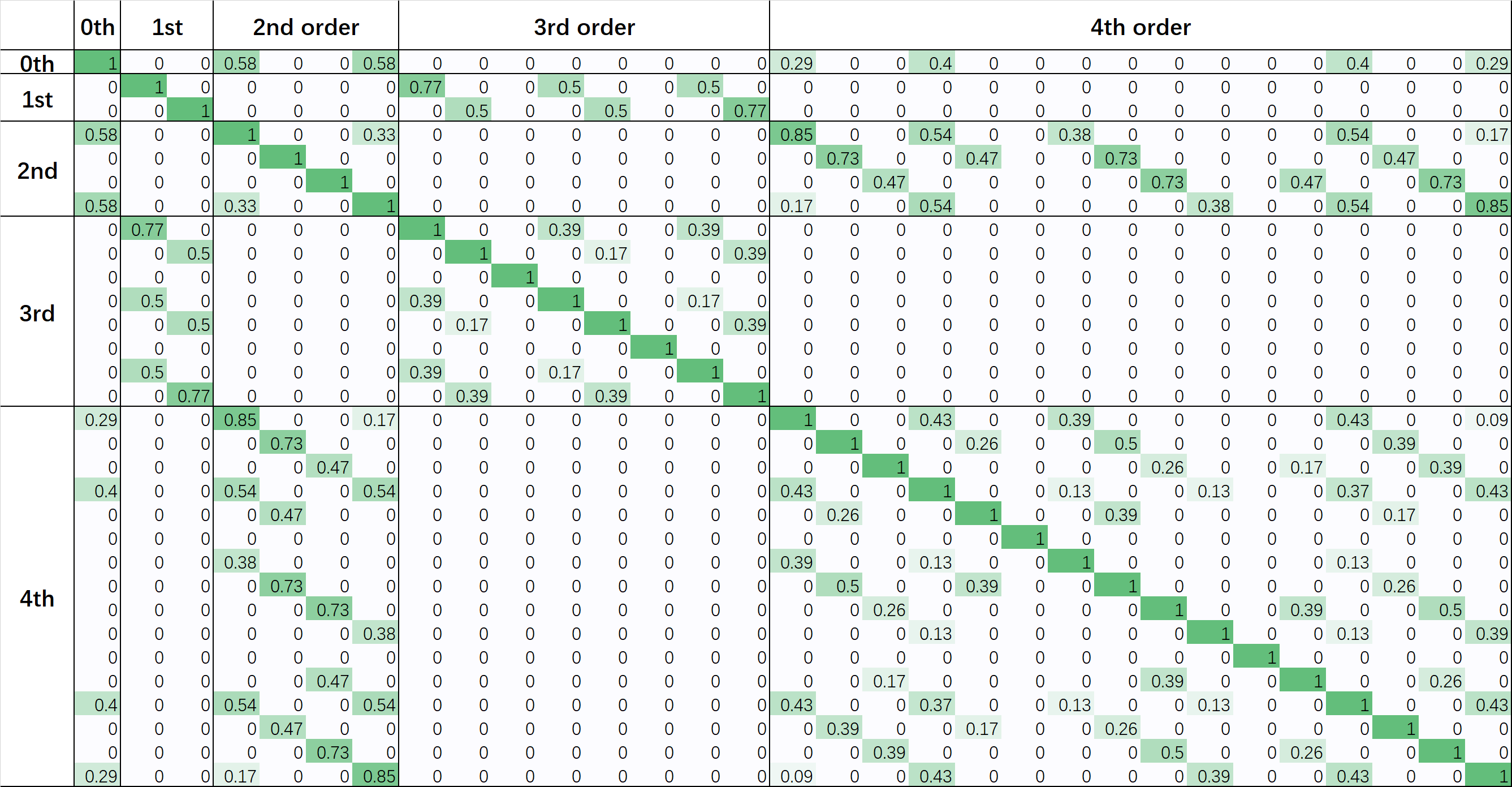

Example A.4.

Consider a 2-dimensional Brownian motion given by Equation (6) with inter-dimensional correlation . Figure A.4 shows the correlation matrix of its Stratonovich signatures with orders truncated to 4 calculated using Propositions 3 and A.1. The figure demonstrates that the correlation matrix has an odd–even alternating structure, even though different dimensions of the Brownian motion are mutually independent (). This is different from the result for Itô signatures shown in Example A.2, where all Itô signatures are mutually uncorrelated. Note that this example has the same setup as Example 1 in the main paper.

B.2 OU process

Deriving explicit formulas for calculating the exact correlation between signatures of OU processes (both Itô and Stratonovich) is complicated. Here we provide an example to show the general approach for calculating the correlation. The proof of this example is given in Appendix F, and one can use a similar routine to compute the correlation for other setups of OU processes.

Example A.5.

Consider a 1-dimensional OU process with a mean reversion speed :

| (A.9) |

The correlation coefficients between its 0-th order and 2nd order signatures are

for Itô and Stratonovich signatures, respectively. The proof is provided in Appendix F.

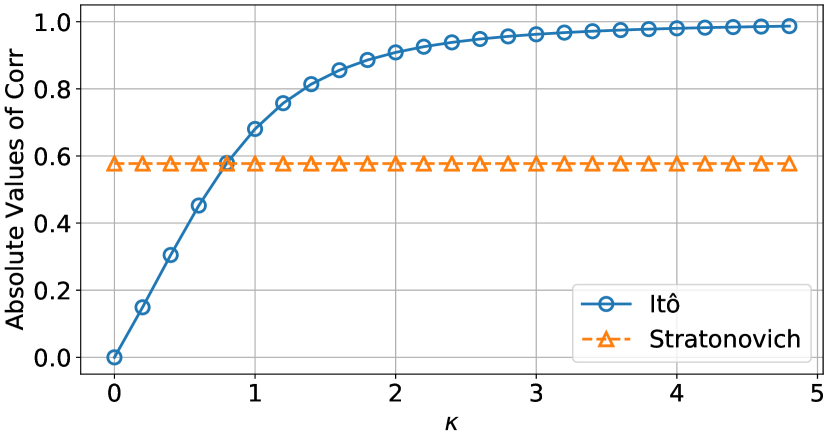

Figure 5(a) shows the absolute values of correlation coefficients between the 0-th order and 2nd order signatures calculated using the formulas above under different values of . Notably, the correlation for Itô signatures rises with , while the correlation for Stratonovich signatures remains fixed at .

We further perform simulations to estimate the correlation coefficients for higher-order signatures of the OU process. We generate 10,000 sample paths of the OU process using the methods discussed in Appendix C. For each path, we calculate the corresponding signatures and then estimate the sample correlation matrix based on the 10,000 simulated samples. Figure 5(b) shows the simulation results for the absolute values of correlation coefficients between the first four order signatures under different values of . Consistent with the observation in Figure 5(a), the correlation for Itô signatures rises with , while the correlation for Stratonovich signatures remains relatively stable. Notably, the correlations for Itô signatures are zero when , which reduces to a Brownian motion. In addition, when is sufficiently large, the absolute values of correlation coefficients for Itô signatures exceed those for Stratonovich signatures.

Recall that the irrepresentable condition, as defined in Definition 3, illustrates that a higher correlation generally leads to poorer consistency. Therefore, based on Example A.5, we can expect that the Lasso is more consistent when using Itô signatures for small values of (weaker mean reversion), and more consistent when using Stratonovich signatures for large values of (stronger mean reversion). This provides a theoretical explanation for our observations in Section 4.2 of the main paper: When processes are sufficiently rough or mean reverting [11, 14], using Lasso with Stratonovich signatures will likely lead to higher statistical consistency compared to Itô signatures.

Appendix C Details for simulations

This appendix provides additional technical details, computational cost, and robustness checks for the simulations conducted in this paper.

C.1 More technical details

Simulation of processes.

We simulate the -th dimension of the Brownian motion, , and OU process, , by discretizing the stochastic differential equations of the processes using the Euler–Maruyama method:

-

•

Brownian motion: , ;

-

•

OU process: , .

Here, , for any , and are randomly drawn from the standard normal distribution. The number of steps is set to .

The -th dimension of the random walk and AR(1) model, both denoted by , are simulated using the following formulas:

-

•

Random walk: , ;

-

•

AR(1) model: , .

Here, , for any , are randomly drawn from the following distribution:

and are randomly drawn from the standard normal distribution. The number of steps is set to .

After simulating each dimension of the processes, we simulate the inter-dimensional correlation between different dimensions of the processes using the Cholesky decomposition. Specifically, we set the inter-dimensional correlation matrix based on the setups described in the main paper and calculate using the Cholesky decomposition. Finally, we generate using Equations (6) or (11).

In all of our simulations, we set the length of the processes to , and the initial values of the processes to zero. These choices have no impact on the results because the signatures of a path are invariant under a time reparametrization and a shift of the starting point of , see, for example, [6].

Calculation of integrals.

The calculation of Itô and Stratonovich signatures requires the calculation of Itô and Stratonovich integrals. By definition, these integrals are computed using the following schemes:

-

•

Itô integral: ;

-

•

Stratonovich integral: .

Here, we set and for any .

C.2 Computational details

-

•

The simulations are implemented using Python 3.7.

-

•

The simulations are run on a laptop with an Intel(R) Core(TM) i7-9750H CPU @ 2.60GHz.

-

•

The random seed is set to 0 for reproducibility.

-

•

The Lasso regressions are performed using the sklearn.linear_model.lars_path package.

-

•

Each individual experiment, including generating 100 paths, calculating their signatures, and performing the Lasso regression, can be completed within one second.

C.3 Robustness checks

To show the robustness of our simulations shown in Figures 1 and 2 in Section 4 of the main paper, we present Figures A.6 and A.7, which include confidence intervals (shaded regions) for the estimated consistency rates of the Brownian motion/random walk and OU process/AR(1) model, respectively.

In Figures A.6 and A.7, we estimate the consistency rate by repeating the procedure described in Section 4 100 times, and this process is repeated 30 times to obtain the confidence interval for the estimation. Thus, these confidence intervals are based on 30 estimations of the consistency rate, with each estimation calculated using 100 experiments.

Appendix D Extensions of the definition of consistency

As remarked in Section 5 of the main paper, the sign consistency may be too restrictive and can be relaxed in the context of signatures. This appendix provides numerical experiments that explore several extensions of consistency measures for signatures.

D.1 Precision, recall, and F1-score

One possible approach for extending the definition of consistency is to use precision, recall, and the F1-score to evaluate the performance of the Lasso regression in selecting true predictors.

In particular, for a given tuning parameter in the Lasso regression, Equation (5), let denote the set of selected predictors based on the Lasso:

where are beta coefficients estimated using Equation (5). The true predictor set, , is defined in Equation (4). We can calculate the true positive (TP), false positive (FP), true negative (TN), and false negative (TN) counts as follows:

where and represent the complements of and , respectively. The precision, recall, and F1-score can then be defined as:

We can then examine the maximum values of precision, recall, and F1-score as we vary the tuning parameter in the Lasso. These maximum values reflect the best performance in terms of feature selection by the Lasso.

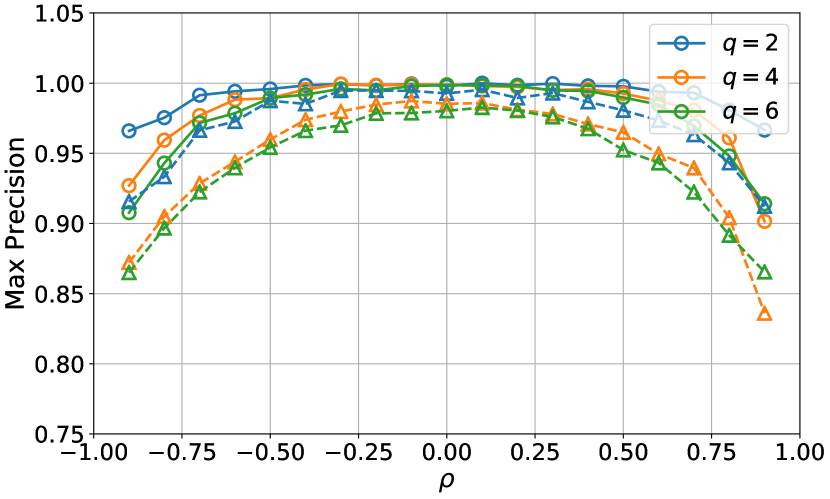

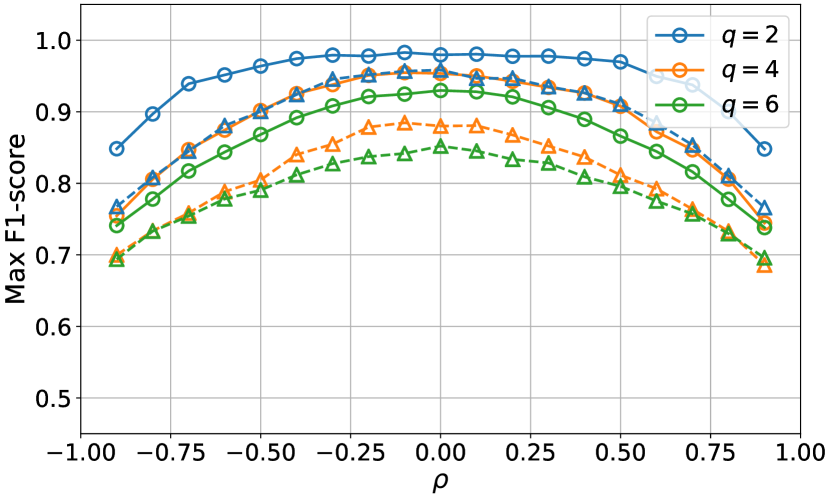

To assess these measures of consistency, we conducted simulations similar to those in Section 4.1 for the Brownian motion. Figure A.8 shows the maximum values of precision, recall, and F1-score for the Brownian motion with different inter-dimensional correlation values () and numbers of true predictors (), averaged over 1,000 experiments. The results demonstrate that, similar to the findings in Figure 1, the maximum precision (Figure 8(a)) and F1-score (Figure 8(c)) reach their highest values when , and decrease as the dimensions of the Brownian motion become more correlated. It is also observed that the results for Itô signatures consistently outperform those for Stratonovich signatures. In addition, compared to Figure 1, these alternative measures of consistency exhibit a less pronounced decrease in performance as the absolute value of increases.

It is worth noting that the maximum recall rate (Figure 8(b)) remains close to 1 under different parameters. This occurs because none of the predictors are selected by the Lasso when the tuning parameter is extremely large. As a result, is zero, and is equal to 1. Consequently, the maximum recall rate is not an appropriate measure of consistency in the context of signatures when using the Lasso.

D.2 Out-of-sample

The out-of-sample is a commonly used measure of model performance in machine learning. It generalizes the notion of consistency as it considers the performance of the model on out-of-sample data, rather than solely focusing on the selection of true predictors by the Lasso. This aligns well with practical applications. Furthermore, it is consistent with the concept of universal nonlinearity in signatures, as described by Equation (2). Universal nonlinearity suggests that the true model can be approximated by a linear combination of signatures, without requiring the exact selection of true predictors by the Lasso regression.

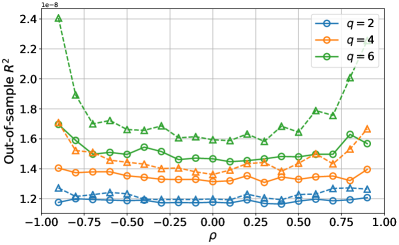

We conduct simulations to study the out-of-sample in the context of signatures using Lasso. Consider a two-dimensional () Brownian motion with inter-dimensional correlation ; assume that there are true predictors in the true model (3), and all of these predictors are signatures of orders no greater than . Now, first randomly choose true predictors from all signatures; next randomly set each beta coefficient of these true predictors from the standard normal distribution; next generate 200 samples from this true model with error term drawn from a normal distribution with mean zero and standard error 0.0001. We divide the 200 samples into a training set and a test set, with 100 samples assigned to each. Then, we run a Lasso regression given by Equation (5) to select predictors based on the training set. The tuning parameter is chosen using 5-fold cross-validation. Finally, we calculate the out-of-sample using the chosen on the test set. We repeat the above procedure by 1,000 times and calculate the average out-of-sample .

Figure A.9 shows the out-of-sample for different values of inter-dimensional correlation, , and different numbers of true predictors, . We can find that, first, Lasso exhibits lower out-of-sample when the absolute value of is small, i.e., when the inter-dimensional correlations of the Brownian motion are weak. Second, as the number of true predictors increases, the out-of-sample increases. Finally, Itô signatures have lower out-of-sample than those for Stratonovich signatures, holding other variables constant ( and ).

All these findings are consistent with our analysis of sign consistency in the main paper. A higher consistency rate corresponds to a higher precision, a higher F1-score, and a lower out-of-sample . This consistency across different metrics reinforces the applicability of our theoretical results when using alternative measures to evaluate the performance of Lasso in the context of signatures. It confirms that the theoretical insights derived from sign consistency extend to other evaluation metrics, demonstrating the robustness and broad applicability of our findings.

Appendix E Time augmentation

Time augmentation is a widely used technique in signature-based analysis, which involves adding a time dimension to the original time series, [6, 27]. In this section, we consider the time-augmented Brownian motion defined as follows:

Definition A.2 (Time-augmented Brownian motion).

is a -dimensional time-augmented Brownian motion if it can be expressed as:

| (A.10) |

where is a -dimensional Brownian motion given by Equation (6) in the main paper. For notational simplicity, let , then

Now we discuss the correlation structure of signatures and the consistency of signatures using Lasso for the time-augmented Brownian motion.

E.1 Correlation structure of signatures for time-augmented Brownian motion

The following proposition shows the moments of Itô signatures for the time-augmented Brownian motion. Note that an index of 0 corresponds to the time dimension, .

Proposition A.2.

Let be a -dimensional time-augmented Brownian motion given by Equation (A.10). For any and , can be calculated recursively by:

with initial conditions

The following proposition shows the moments of Stratonovich signatures for the time-augmented Brownian motion.

Proposition A.3.

Let be a -dimensional time-augmented Brownian motion given by Equation (A.10). For any and , can be calculated recursively by:

with initial conditions

The following example shows the correlation structures of Itô and Stratonovich signatures for a (1+1)-dimensional time-augmented Brownian motion .

Example A.6.

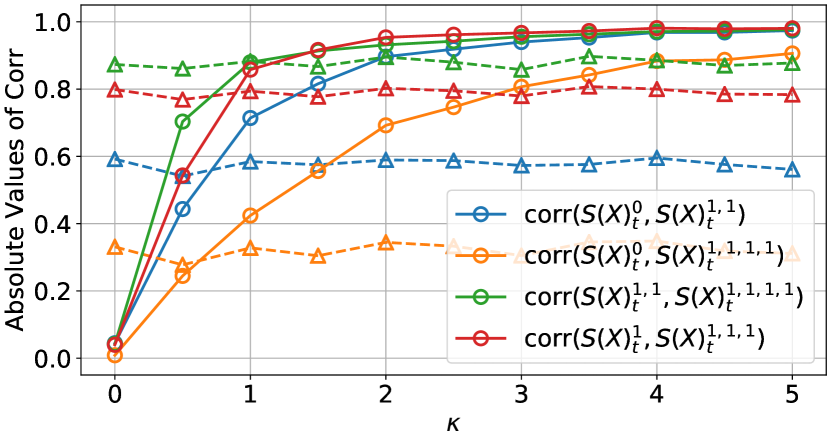

Consider a (1+1)-dimensional time-augmented Brownian motion . Figures A.10 and A.11 show the correlation structures of Itô and Stratonovich signatures of , respectively, calculated through simulations. In particular, we first simulate 10,000 paths of , then calculate the signatures of each path, and finally calculate the sample correlation matrix of the signatures.

From the figures, we can observe that the correlation matrix of the time-augmented Brownian motion does not exhibit the same special structures (block diagonal or odd–even alternating) we observe in the main paper. In addition, the correlation between Stratonovich signatures is generally stronger than that between Itô signatures.

E.2 Consistency of signatures for time-augmented Brownian motion

We conduct simulations to study the consistency of signatures using Lasso for the time-augmented Brownian motion.

Consider a (2+1)-dimensional time-augmented Brownian motion , which is the time-augmented version of a 2-dimensional Brownian motion X. The inter-dimensional correlation of X is . We perform the same experiment as conducted in Section 4.1 for .

Figure A.12 shows the consistency rates for different values of inter-dimensional correlation, , and different numbers of true predictors, . The observations are similar to the results for Brownian motion without time augmentation (Figure 1(a)). In addition, the consistency rates are generally lower when there exists time augmentation (Figure A.12) compared to the case without time augmentation (Figure 1(a)). This is consistent with Example A.6 because time augmentation tends to increase the correlation between signatures, which results in a lower consistency rate.

In summary, our simulation shows that time augmentation lowers the consistency rate of Lasso.

Appendix F Proofs

This appendix provides the proofs of all theoretical results in this paper.

Proof of Proposition 1.

For the expectation, we have

| (A.11) |

because the expectation of an Itô integral is zero.

Next we prove for by induction. Without loss of generality, we assume that . When , for any , we have

where the second equality uses the Itô isometry and the third equality uses Equation (A.11). Now assume that for , we have . Then,

This proves .

We finally prove by induction. When , we have

Then, assume that . We have

Therefore, . This completes the proof. ∎

Proof of Proposition 2.

By Proposition 1, for any , we have

implying that

and

This proves the Kronecker product structure given by Equation (8).

Proposition 1 also implies that, for any ,

This proves that Itô signatures with different orders are uncorrelated and, therefore, the correlation matrix is block diagonal. This completes the proof. ∎

Proof of Proposition 3.

Proof of Proposition 5.

We only need to prove that, for an odd number and an even number , we have

for any and taking values in . Here the signatures can be defined in the sense of either Itô or Stratonovich.

Consider the reflected OU process, . By definition, is also an OU process with the same mean reversion parameter. Therefore, the signatures of and should have the same distribution. In particular, we have

| (A.12) |

Now we consider the definition of the signatures:

where the integral can be defined in the sense of either Itô or Stratonovich. We therefore have

Similarly, we have

Therefore,

and combining this with Equation (A.12) leads to the result. ∎

Proof of Proposition 7.

Proof of Proposition A.1.

By the relationship between the Stratonovich integral and the Itô integral, we have

where represents the quadratic covariation between processes and from time 0 to . Furthermore, by properties of the quadratic covariation,

Therefore,

For any and , define

Then, by Fubini’s theorem,

This proves Equations (A.1) and (A.5). In addition, by Itô isometry and Fubini’s theorem,

Now we prove the initial conditions. First, by the definition of 0-th order signatures, , which proves Equation (A.3). Second,

because the expectation of an Itô integral is zero, which proves Equation (A.4). Third,

which proves Equation (A.7). Fourth, by Itô isometry,

In addition, by using Equation (A.1) recursively, we can obtain that

Therefore,

which proves Equation (A.8). This completes the proof. ∎

Proof of Proposition A.2.

When and , by Fubini’s theorem,

When and , by Fubini’s theorem,

When and , we can similarly obtain

When and , by Itô isometry,

The initial conditions can be easily verified using Proposition 1. This completes the proof. ∎

Proof of Proposition A.3.

Proof of Example A.5.

The solution to stochastic differential equation (A.9) can be explicitly expressed as

where is a standard Brownian motion. Therefore, by Itô isometry, is a Gaussian random variable with mean 0 and variance

Now we calculate the correlation coefficient for its Itô and Stratonovich signatures, respectively.

Itô signatures.

By the definition of signatures and Equation (A.9), we have

| (A.13) |

For the second moment, by Itô isometry, we have

It is easy to calculate Term (c):

| (A.14) |

To derive Term (a), we need to calculate . Assume that and denote , we have , and therefore

Because is a Gaussian random variable with mean 0 and variance

and has independent increments, we further have

when . One can similarly write the corresponding formula for the case of and therefore obtain that

| (a) | |||

For Term (b), note that

we therefore need to calculate for . To do this, by Itô’s Lemma, we have

which implies that

Therefore, for , with the help of Itô isometry and Equation (A.14), we have

and taking derivatives of both sides leads to

By solving this ordinary differential equation with respect to with initial condition , we obtain that

Therefore,

Finally, we obtain that

| (A.15) |

Therefore, for Itô signature, we have

where we use the fact that the 0-th order signature is defined as 1.

Stratonovich signatures.

The Stratonovich integral and the Itô integral are related by

Therefore, for Stratonovich signatures, we have

and

where we use the fact that and . Now we can use our results for the Itô signatures, Equations (A.13) and (A.15), to obtain that

and

Therefore, for the Stratonovich signature, we have

This completes the proof. ∎