Evaluating Dynamic Conditional Quantile Treatment Effects with Applications in Ridesharing

Abstract

Many modern tech companies, such as Google, Uber, and Didi, utilize online experiments (also known as A/B testing) to evaluate new policies against existing ones. While most studies concentrate on average treatment effects, situations with skewed and heavy-tailed outcome distributions may benefit from alternative criteria, such as quantiles. However, assessing dynamic quantile treatment effects (QTE) remains a challenge, particularly when dealing with data from ride-sourcing platforms that involve sequential decision-making across time and space. In this paper, we establish a formal framework to calculate QTE conditional on characteristics independent of the treatment. Under specific model assumptions, we demonstrate that the dynamic conditional QTE (CQTE) equals the sum of individual CQTEs across time, even though the conditional quantile of cumulative rewards may not necessarily equate to the sum of conditional quantiles of individual rewards. This crucial insight significantly streamlines the estimation and inference processes for our target causal estimand. We then introduce two varying coefficient decision process (VCDP) models and devise an innovative method to test the dynamic CQTE. Moreover, we expand our approach to accommodate data from spatiotemporal dependent experiments and examine both conditional quantile direct and indirect effects. To showcase the practical utility of our method, we apply it to three real-world datasets from a ride-sourcing platform. Theoretical findings and comprehensive simulation studies further substantiate our proposal.

Keywords: A/B testing, policy evaluation, quantile treatment effect, ridesourcing platform, spatialtemporal experiments, varying coefficient models.

1 Introduction

Online experiments, often referred to as A/B testing in computer science literature, are widely utilized by technology companies (e.g., Google, Netflix, Microsoft) to assess the effectiveness of new products or policies in comparison to existing ones. These companies have developed in-house A/B testing platforms for evaluating treatment effects and providing valuable experimental insights. Take ridesourcing platforms like Uber, Lyft, and Didi as examples. These platforms operate within intricate spatiotemporal ecosystems, dynamically matching passengers with drivers (see, for instance, Wang and Yang, 2019; Qin et al., 2020; Zhou et al., 2021). They implement online experiments to explore various order dispatch policies and customer recommendation initiatives. These innovative products hold the potential to enhance passenger engagement and satisfaction, diminish pickup waiting times, and boost driver earnings, ultimately leading to a more efficient and user-friendly transportation system.

In this study, we address the fundamental question of how to evaluate the difference between the quantile return of a new product (treatment) and that of an existing one. Although the average treatment effect (ATE) is widely used in the literature to quantify the difference between two policies (Imbens and Rubin, 2015; Wang and Tchetgen Tchetgen, 2018; Kong et al., 2022), it only considers the average effect and does not account for variability around the expectation. In applications with skewed and heavy-tailed outcome distributions, decision-makers are more interested in the quantile treatment effect (QTE), which offers a more comprehensive characterization of distributional effects beyond the mean and is robust to heavy-tailed errors (see e.g., Abadie et al., 2002; Chernozhukov and Hansen, 2006; Chen and Hsiang, 2019). For example, in ridesourcing platforms, policymakers may want to determine which policy more effectively raises the lower tail of driver income. Furthermore, developing valid inferential tools for QTE can reveal how treatment effects differ by quantile and provide valuable information about the entire distribution.

Addressing the problem mentioned earlier presents two significant challenges. The first challenge involves efficiently inferring the dynamic QTE (quantile treatment effect), which is defined as the difference between the quantiles of cumulative outcomes under the new and old policies, in long horizon settings with weak signals. In contrast to single-stage decision-making, policy makers for ridesourcing platforms assign treatments sequentially over time and across various locations. Existing estimators, such as those based on (augmented) inverse probability weighting (see e.g., Wang et al., 2018, Section 4), are subject to the curse of horizon, as described by (Liu et al., 2018). This means their variances increase exponentially with respect to the horizon (i.e., the number of decision stages). Such approaches are inadequate in our context, where the horizon typically spans 24 or 48 stages and most policies improve key metrics by only 0.5% to 2% (Qin et al., 2022). Furthermore, unlike the average cumulative outcome, which can be broken down into the sum of individual outcome expectations, the quantile of cumulative outcomes generally does not equal the sum of individual quantiles. This makes estimating our causal effect extremely challenging. Existing efficient evaluation methods designed for mean return, such as those proposed by Kallus and Uehara (2022) and Liao et al. (2022), cannot be easily adapted to our situation.

The second challenge arises from handling the interference effect caused by temporal and spatial proximities in spatiotemporal dependent experiments. This interference effect results in a treatment applied at one location influencing not only its own outcome, but also the outcomes at other locations. Additionally, the current treatment is likely to affect both present and future outcomes. Neglecting these effects would produce a biased QTE estimator. As far as we are aware, there is no existing test capable of concurrently addressing both challenges.

1.1 Related work

A/B testing has been extensively researched in the literature, as evidenced by the works of Yang et al. (2017) and Zhou et al. (2020), among other references. In contrast to most existing A/B testing methods that focus on the Average Treatment Effect (ATE), Quantile Treatment Effects (QTE) have received less attention. Among the few available studies, Liu et al. (2019) proposed a scalable method to test QTE and construct associated confidence intervals. Moreover, Wang and Zhang (2021) developed a nonparametric method to estimate QTEs at a continuous range of quantile locations, including point-wise confidence intervals. More broadly, the estimation and inference of (conditional) QTEs have been considered in the causal inference literature, as seen in the works of Chernozhukov and Hansen (2006), Firpo (2007), and Blanco et al. (2020). However, these methods predominantly address single-stage decision-making. To the best of our knowledge, this paper represents the first attempt to explore QTE in temporally and/or spatially dependent experiments.

Our paper is closely related to the rapidly expanding body of literature on off-policy evaluation in sequential decision-making. The majority of existing studies primarily concentrate on inferring the expected return under a fixed target policy or a data-dependent estimated optimal policy (Zhang et al., 2013; Shi et al., 2020; Kallus and Uehara, 2022). In recent years, several papers have explored policy evaluation beyond averages (Wang et al., 2018; Kallus et al., 2019; Qi et al., 2022; Xu et al., 2022). These works propose using (augmented) inverse probability weighted estimators to evaluate specific robust metrics under a given target policy. As noted previously, these methods are subject to the curse of horizon and become less effective in long-horizon settings. Most notably, policy evaluation in spatiotemporal dependent experiments remains unexplored in the aforementioned studies.

Recent proposals have investigated causal inference with temporal or spatial interference, including studies by Savje et al. (2021) and Hu et al. (2022), among others. However, these methods primarily focus on the average effect. Furthermore, our paper is closely related to the literature on distributional reinforcement learning (see e.g., Zhou et al., 2020). Despite this connection, these studies primarily concentrate on the policy learning problem, and uncertainty quantification of a target policy’s quantile value remains unexplored.

Lastly, our paper is connected to a line of research on quantitative analysis of ridesharing across various fields such as economics, operations research, statistics, and computer science (see e.g., Shi et al., 2022; Zhao et al., 2022). Nevertheless, quantile policy evaluation has not been examined in these papers.

1.2 Contributions

Our proposal offers three valuable contributions to existing literature. First, we present a framework for deducing dynamic conditional Quantile Treatment Effects (QTE), defined as dynamic QTE dependent on market features, irrespective of treatment history. While unconditional QTE may be of interest, as previously noted, it assumes a highly complex form in long horizon settings and is extremely challenging to identify when the signal is weak. In contrast, we demonstrate that under certain modeling assumptions, the proposed dynamic conditional QTE (CQTE) is equal to the sum of individual CQTE at each spatiotemporal unit, even though the conditional quantile of cumulative rewards does not necessarily equate to the sum of conditional quantiles of individual rewards. This finding significantly streamlines the estimation and inference processes for our causal estimand, making our proposal easily implementable in practice. Additionally, the estimated CQTE can exhibit a smaller variance compared to that of the unconditional counterpart.

Second, we introduce an innovative framework to test dynamic CQTE while accounting for the interference effect. We propose two Varying Coefficient Decision Process (VCDP) models, enabling the application of classical quantile regression (Koenker and Hallock, 2001) for parameter estimation and subsequent inference. We then develop a two-step method for estimating CQTE, along with a bootstrap-assisted procedure for testing CQTE. We further extend our proposal to analyze spatiotemporally dependent data and to test Conditional Quantile Direct Effects (CQDE) and Conditional Quantile Indirect Effects (CQIE).

Third, we thoroughly examine the theoretical and finite sample properties of our methods. Theoretically, we prove the consistency of our proposed test procedure, allowing the horizon to diverge with the sample size. Notably, classical weak convergence theorems (Van Der Vaart and Wellner, 1996) necessitate a fixed horizon and are not directly applicable. Empirically, we apply our proposed method to real datasets obtained from a leading ridesourcing platform to assess the dynamic quantile treatment effects of new policies.

1.3 Organization of the paper

The paper’s structure is as follows: Section 2 describes data from online randomized experiments. Section 3 covers temporally dependent experiments, the proposed model, and estimation and inference procedures. Section 4 extends the proposal to spatiotemporally dependent data. Section 5 decomposes CQTE into CQDE and CQIE. Section 6 presents the proposed CQTE test’s asymptotic results. Section 7 evaluates ridesourcing dispatching and repositioning policies, and Section 8 assesses our methods’ finite sample performance using real-data-based simulations.

2 Data Description

The purpose of this paper is to analyze three real datasets collected from Didi Chuxing, one of the world’s leading ride-sharing companies. One dataset was collected during a time-dependent A/B experiment conducted in a city from December 10, 2021 to December 23, 2021. The goal of this experiment was to evaluate the performance of a newly designed order dispatching policy, which aimed to increase the number of fulfilled ride requests and boost drivers’ total revenue. To protect privacy, we will not disclose the city name and the specific policy used. During the experiment, each day was divided into 24 equally spaced non-overlapping time intervals. The new policy (B) and the old policy (A) were alternated and assigned to these intervals every day. On the first day, we used an alternating sequence of ABAB, and on the second day, we used BABA. Thereafter, we switched between A and B every two days, ensuring that each policy was used with equal probability at each time interval, meeting the positivity assumption. For more details, see Section 3.1. It is worth noting that such an alternating-time-interval design is commonly used in industries to reduce the variance of treatment effect estimators, as discussed in Section 6.2 of Shi et al. (2022). For further information, please refer to the article by Lyft on experimentation in a ride-sharing marketplace at https://eng.lyft.com/experimentation-in-a-ridesharing-marketplace-b39db027a66e.

The second dataset comes from a spatiotemporal-dependent experiment conducted in another city between February 19, 2020, and March 13, 2020. Each day is divided into 48 non-overlapping, equal time intervals, and the city is partitioned into 12 distinct, non-overlapping regions. On the first day of the experiment, the initial policy in each region is independently set to either the new or old policy with a probability. The temporal alternation design for time-dependent experiments is then applied in each region.

In addition to the two datasets from A/B experiments mentioned earlier, we also analyze a third dataset collected from an A/A experiment. In this case, the two policies being compared are identical, and the treatment effect is zero. The experiment took place in a specific city from July 13, 2021 to September 17, 2021. This analysis serves as a sanity check to examine the size property of the proposed test. We expect that our test will not reject the null hypothesis when applied to this dataset, as the true effect is zero.

The ridesharing system dynamically connects passengers and drivers in real-time. All three datasets include the number of call orders and the total online time of drivers for each time interval. These metrics represent the supply and demand in this two-sided market. The platform’s outcomes include the drivers’ total income, the answer rate (the number of call orders responded to), and the completion rate (the number of call orders completed) for each time interval. In our study, we are interested in determining whether the new policy improves drivers’ total income at various quantile levels.

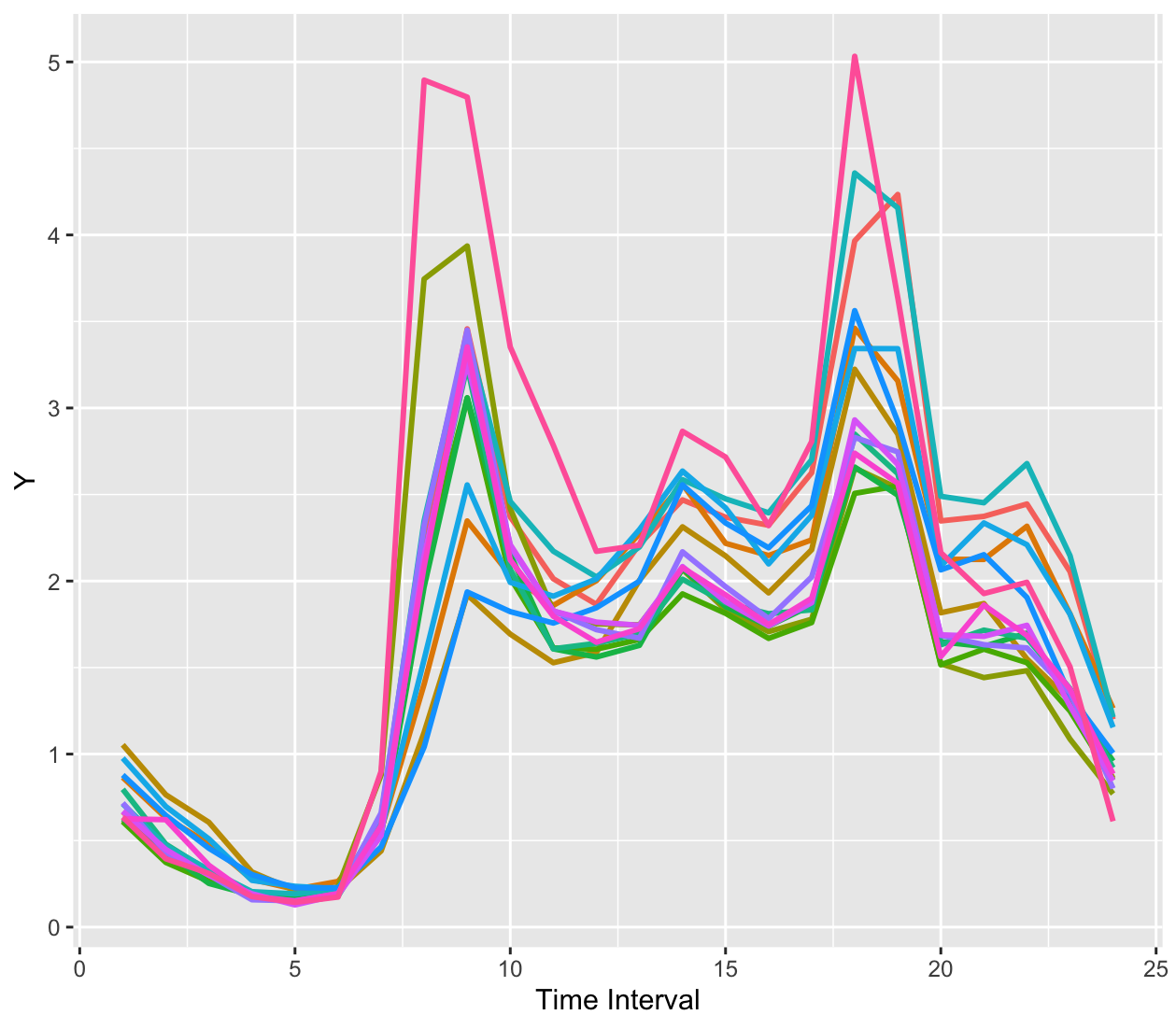

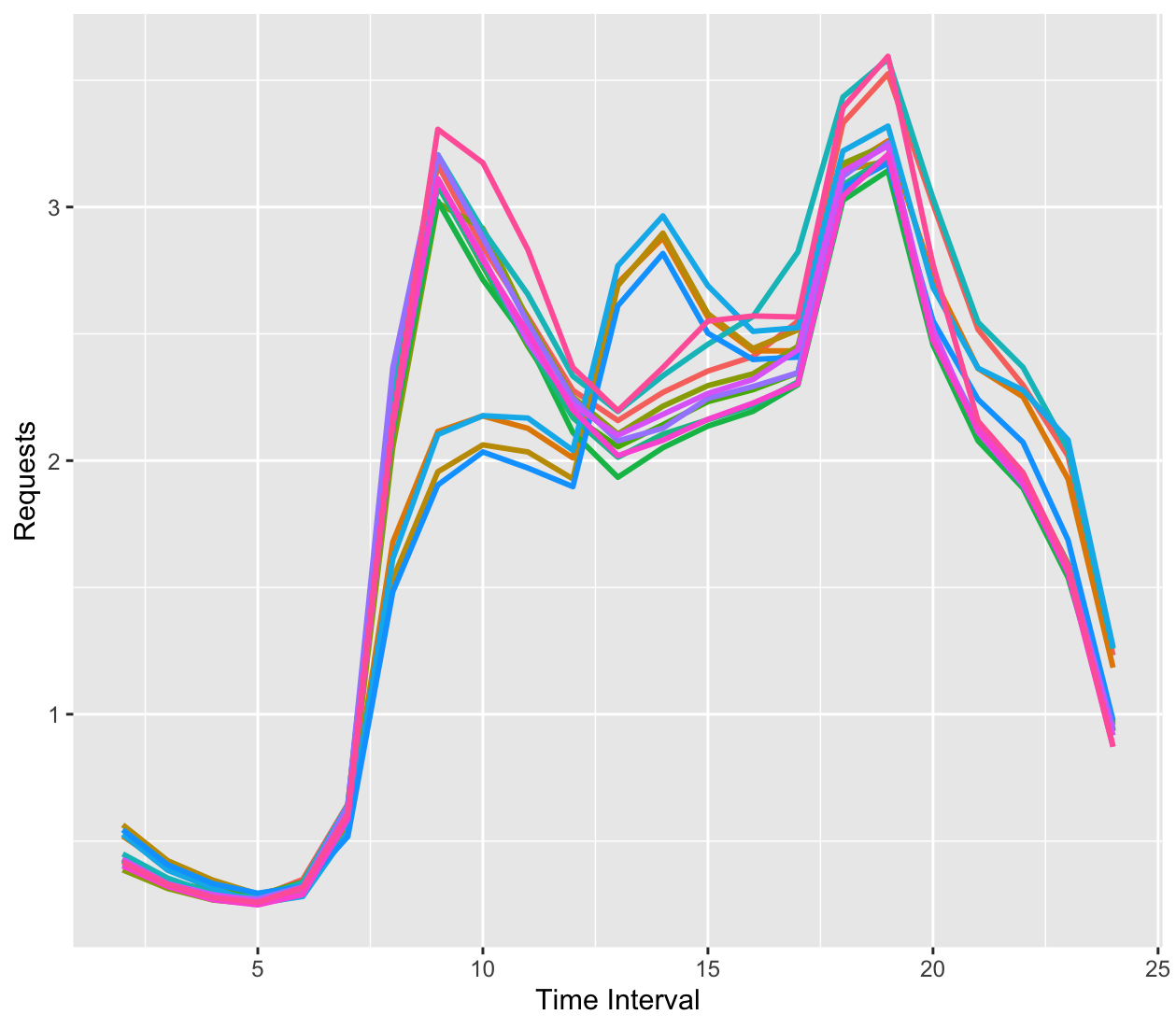

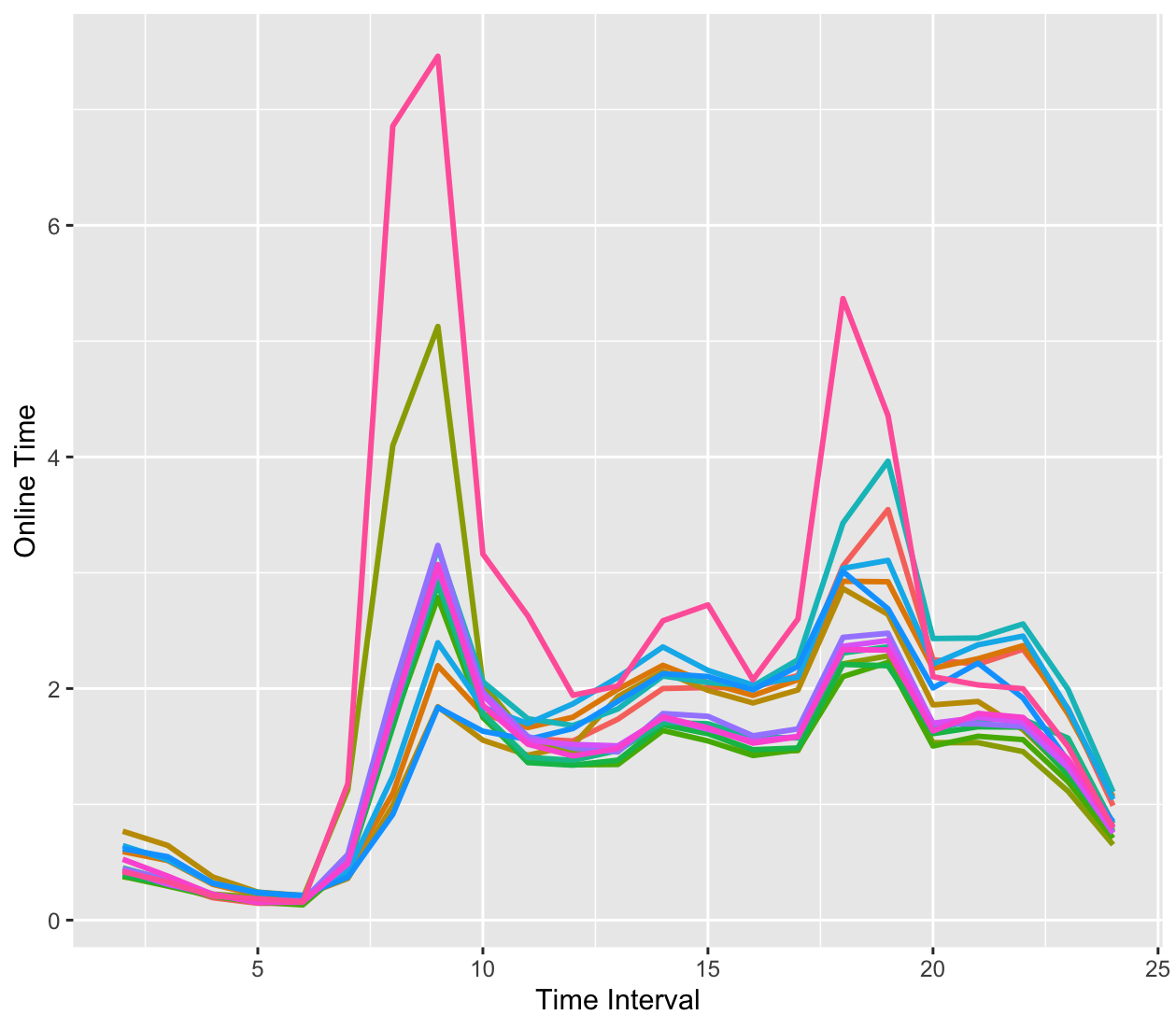

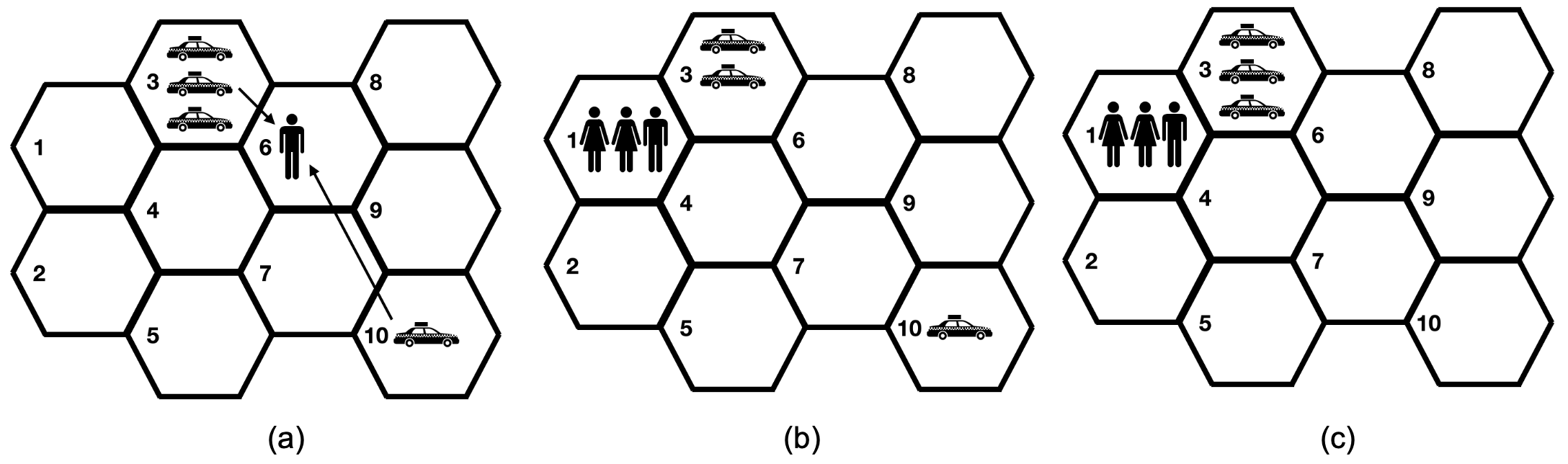

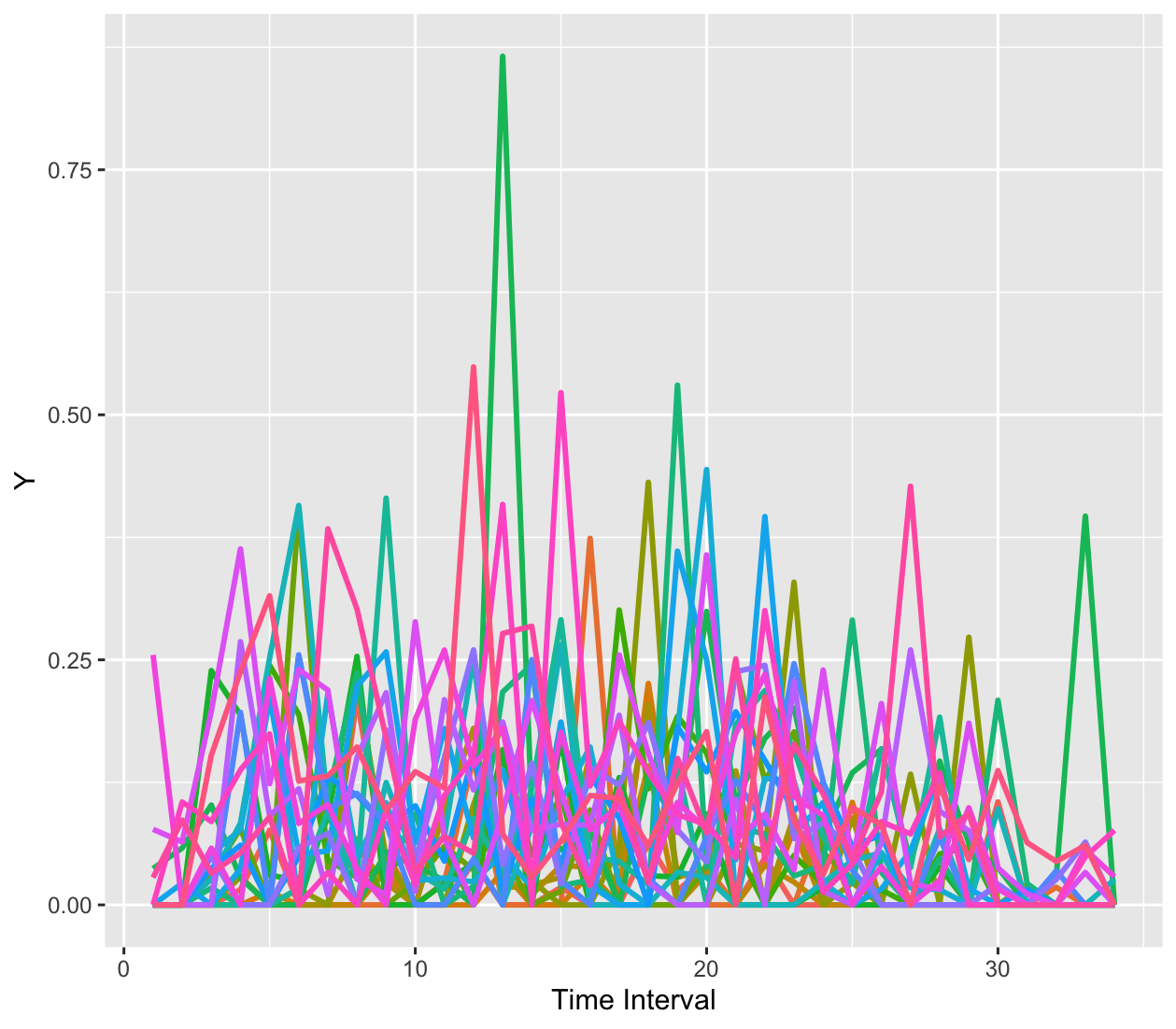

The datasets exhibit four distinct characteristics. First, the horizon duration is typically much longer (e.g., 24 or 48) than the experiment duration, while the treatment effect is usually weak (e.g., 0.5%-2%). Second, both supply and demand are spatiotemporal networks that interact across time and location, as observed in panels (a) and (b) of Figure 1, which display drivers’ online time and the number of call orders. Third, the outcome of interest follows a non-normal and heavy-tailed distribution, illustrated in panels (c) and (d) of Figure 1. Finally, there are interference effects over time and space, demonstrated in Figure 2, with temporal interference effects occurring when past actions impact future outcomes.

We focus on answering three key questions in these datasets:

(Q1) How can we quantify treatment effects across various quantile levels for the time-dependent A/B experiment data in order to gain a comprehensive understanding of the new policy’s effects within the city?

(Q2) How to evaluate the quantile treatment effects for the above spatiatemporal dependent experiment data?

(Q3) How to determine whether or not to replace the old policy with the new one?

These questions drive the methodological development outlined in Sections 3 and 4.

3 Testing CQTE in temporal dependent experiments

In this section, we explicitly state the test hypotheses for our first research question (Q1) and explore the primary challenge encountered in experiments exhibiting temporal dependence. Subsequently, we detail the key technical assumptions that enable the cumulative quantile treatment effect (CQTE) to be equivalent to the sum of individual CQTEs. Finally, to address the third research question (Q3), we present the proposed estimation and testing strategies for our investigation.

3.1 CQTE, test hypotheses and assumptions

We consider the temporal alternation design with a sequence of treatments over time. Specifically, we divide each day into non-overlapping intervals. The platform can implement either one of the two policies at each time interval. For any , let denote the policy implemented at the th time interval where represents exposure to the new policy and represents exposure to the old policy. Let and denote the state (e.g., the supply and demand) and the outcome at time , respectively.

To formulate our problem, we adopt a potential outcome framework (Rubin, 2005). Specifically, we define as the treatment history up to time . We also define and as the counterfactual state and counterfactual outcome, respectively, that would have occurred had the platform followed the treatment history . Our primary interest lies in quantifying the difference between the th quantile of the cumulative outcomes under the new policy and that under the old policy, denoted as the quantile treatment effect (QTE):

where and are vectors of 1s and 0s of length , respectively, and denotes the quantile function at the th level.

However, learning such an unconditional dynamic QTE from our experimental dataset is highly challenging. Remember that in our A/B experiment, the old and new policies are assigned alternately over the time intervals. Nevertheless, the target policy we aim to evaluate corresponds to the global policy, which allocates the new or old policy globally throughout each day. This leads to an off-policy setting where the target policy differs from the behavior policy that generates the data. Existing off-policy quantile evaluation methods based on inverse probability weighting, such as those presented by Wang et al. (2018), are inefficient in our setting with a moderately large . Off-policy evaluation (OPE) methods, including Shi et al. (2020), Liao et al. (2021), and Kallus and Uehara (2022), are semiparametrically efficient111Shi et al. (2020) and Liao et al. (2021) proposed to use the direct method based on linear sieves or kernels. However, the resulting estimators are semiparametrically efficient as well. in long-horizon settings. Despite this, these methods primarily focus on the mean return, making it difficult to adapt them for quantile evaluation due to the nonlinear quantile function . To illustrate, note that there is no guarantee that in general. This observation motivates us to seek an alternative definition for QTE.

Second, let represent the set of features (e.g., extreme weather events) that have an impact on the outcomes up to time , but are not influenced by the treatment history. This means that for any treatment history , the potential outcome of these features remains the same, i.e., . By definition, is an element of , which ensures that is non-empty for any . We introduce CQTE as follows:

| (1) |

The CQTE is a reasonable measure because the set of conditioning variables remains consistent under both new and old policies. When , this definition reduces to the one used in single-stage decision-making, as discussed in previous literature, such as Chernozhukov and Hansen (2006).

Conditioning has several benefits. Firstly, it offers a more convenient way to estimate the dynamic Quantile Treatment Effect (QTE) by aggregating individual QTEs over time. This approach simplifies the estimation process and reduces computational complexity. Secondly, conditioning can also help to reduce the variance of the resulting QTE estimator by removing the need to account for variability in the relevant characteristics. By conditioning on certain variables, researchers can effectively control for confounding factors and produce more accurate estimates of treatment effects.

Third, we introduce the concept of Summed Conditional Quantile Treatment Effects (SCQTE), which represents the sum of individual Conditional Quantile Treatment Effects (CQTE) over time. The SCQTE is defined as follows:

Compared to CQTE, SCQTE is easier to learn from observed data. For example, one can fit a quantile regression model at each stage, estimate individual CQTE values, and then sum these estimators together. Although the quantile function is not additive, we demonstrate in the following proposition that SCQTE is equal to CQTE under specific modeling assumptions.

Proposition 1.

Suppose that for any time point , follows the structural quantile model for a specific deterministic function and a uniformly distributed random variable , which is independent of . Furthermore, assume that and are strictly increasing functions of for any . Under these conditions, we find that .

Proposition 1 establishes the equivalence between CQTE and SCQTE and serves as a fundamental building block for our proposal. It allows us to focus on SCQTE, which is a simplified version of CQTE. This simplification greatly facilitates the estimation and inference procedures that follow, which rely on fitting a quantile regression model at each time point to learn the SCQTE. For more details, see Sections 3.2 and 3.3. Moreover, the proposed model in Proposition 1 is related to the structural quantile model in the quantile regression literature (Chernozhukov and Hansen, 2005, 2006). These models assume that, conditional on the covariate , the potential outcome for and , where is strictly increasing in . The uniformly distributed variable serves as a rank variable that characterizes the heterogeneity of the outcome across different quantile levels. Under the monotonicity constraint, the th conditional quantile of can be shown to equal . Proposition 1 motivates us to focus on testing the following hypotheses for each quantile level :

| (2) |

These hypotheses test whether the treatment effect at the th quantile is non-negative or positive, respectively.

In this study, we utilize the consistency assumption (CA), sequential ignorability assumption (SRA), and positivity assumption (PA) to identify the causal estimand. These assumptions are frequently used in the dynamic treatment regime literature for learning optimal dynamic treatment policies (Gill and Robins, 2001). The consistency assumption (CA) states that the potential state and outcome, given the observed data history, should align with the actual observed state and outcome. The sequential ignorability assumption (SRA) demands that the action be conditionally independent of all potential variables, given the past data history. In our application, the SRA is inherently satisfied as the policy is assigned according to the alternating-time-interval design, independent of data history. The positivity assumption (PA) necessitates that the probability of , given the observed data history, must be strictly between zero and one for any . Under the alternating-time-interval design, this probability is equal to 0.5, which satisfies the PA automatically. It is essential to note that the combination of CA, SRA, and PA enables the consistent estimation of the potential outcome distribution using the observed data.

3.2 VCDP models

Suppose that the experiment is conducted over consecutive days. Let be the state-treatment-outcome triplet measured at the th time interval of the th day for and . We assume that these triplets are independent across different days, but may be dependent within each day over time.

We begin by introducing two varying coefficient decision process models, one for the outcome and the other for the state. The first model characterizes the conditional quantile of the outcome and is given by

| (3) |

where , is a vector of time-varying coefficients, and is the rank variable. Model (3) extends the idea of using rank variables to represent unobserved heterogeneity across different quantiles in a single-stage study to sequential decision making.

The second model characterizes the conditional mean of the observed state variables and is given by:

| (4) |

where and are -dimensional vectors, is a matrix of autoregressive coefficients, and is a coefficient matrix. The term is a random error term whose conditional mean given equals zero. In addition, are independent over time. Therefore, the conditional expectation of given is:

It is worth noting that models (3) and (4) belong to the class of varying-coefficient regression models. The existing literature on this topic mainly focuses on estimating the relationships between scalar predictors and scalar responses (Sherwood and Wang, 2016), or between scalar predictors and functional responses (Zhang et al., 2022), or between longitudinal predictors and responses (Wang et al., 2009). However, to the best of our knowledge, none of these works have utilized varying-coefficient regression models for policy evaluation in sequential decision making.

Furthermore, the temporal independence between ’s implies that the state vector satisfies the Markov property, i.e., is independent of the past data history given for any and . However, the immediate outcomes are conditionally dependent due to the existence of the rank variable . Consequently, the resulting data generating process does not fall under the classical Markov decision processes (MDPs, see e.g., Puterman, 2014). Moreover, models (3) and (4) are valid when the potential outcomes satisfy similar assumptions in the quantile varying coefficient models. Please refer to (19) and (20) in the supplementary material for more details.

If the residual is independent of the treatment history and , we can define as . Under this condition, the assumptions in Proposition 1 are satisfied. Hence, under the proposed VCDP models, CQTE is equivalent to SCQTE. Next, we introduce the following function:

The subsequent proposition offers a closed-form formula for CQTE.

Proposition 2.

Proposition 2 enables us to estimate CQTE through SCQTE under certain assumptions. Among these, the monotonicity assumption can be satisfied under various conditions. For example, it holds when , , and all elements in are strictly increasing in , and , all elements in , and are positive. Additionally, when and for any , it suffices to require and to be strictly increasing in .

To evaluate policy value, we need to estimate the model parameters , , , and . Notice that under the conditions of Proposition 2, we have that:

| (6) |

where , and its conditional -th quantile given equals zero. Therefore, we can employ ordinary quantile regression to learn and . Meanwhile, since the residuals s are independent over time, ordinary least-squares regression is applicable to the state regression model to estimate and . We detail our estimating procedure in the next section.

3.3 Estimation and inference procedures

In this subsection, we outline the procedures for estimating and testing CQTE based on the results in Proposition 2. We first estimate the regression coefficients in models (6) and (4). We then plug these estimates into (5) to estimate CQTE. Finally, we develop a bootstrap-assisted procedure to test CQTE.

Let , , and denote the -th entries of , , and , respectively. Let and denote the -th rows of and , respectively. It follows from (4) that:

We propose a two-step procedure to estimate and . In the first step, we minimize the following functions:

| (7) | |||||

| (8) |

These one-step estimates can be computed easily but suffer from large variances as they rely solely on observations at time . In the second step, we employ kernel smoothing to reduce the variances of these initial estimators and identify weak signals (Zhu et al., 2014). Specifically, for a given kernel function , the second-step estimators and are defined as:

| (9) | |||||

| (10) |

where is the weight function and denotes the kernel bandwidth. The use of kernel smoothing allows us to estimate the varying coefficients and for any real-valued . Given and , we can compute the following CQTE estimator:

| (11) |

To test (2), we use the test statistic , which is set to . Under the null hypothesis, is expected to be negative or close to zero. Therefore, we reject the null hypothesis for a large value of . However, deriving the limiting distribution of for large is complicated due to the complex dependence of on the estimated model parameters. To address this issue, we use the bootstrap method to simulate the distribution of under the null hypothesis. Specifically, we modify the bootstrap method proposed by Horowitz and Krishnamurthy (2018) and adapt it to our setting as follows. Horowitz and Krishnamurthy (2018) proposed to resample the estimated residuals to infer the conditional quantile function in a nonparametric quantile regression model. In our case, to handle the dependence over time, we resample the entire error process (see Step 3 below for details).

The bootstrap method for is implemented as follows:

- •

-

•

Step 2. Estimate the residuals by for and for .

-

•

Step 3. For each , generate i.i.d. random variables by randomly sampling with replacement. Similarly, generate by randomly sampling with replacement. Next, generate pseudo outcomes and as follows,

(12) - •

-

•

Step 5. For each , compute the bootstrapped statistic .

-

•

Step 6. Repeat Steps 3-5 times. Given a significance level , reject (see 2) if the statistic exceeds the upper th empirical quantile of .

In the supplementary material, we present Theorem 1, which rigorously establishes the consistency of the aforementioned bootstrap method. It’s worth noting that the bootstrap consistency theory elaborated in Horowitz and Krishnamurthy (2018) isn’t readily applicable to our context, where can increase along with the sample size.

4 Extension to spatiotemporal dependent experiments

In this section, we aim to address (Q2) and expand upon the method proposed in Section 3 to analyze data from spatiotemporal dependent experiments involving multiple non-overlapping regions receiving distinct treatments in a sequential manner over time. Let represent the number of these non-overlapping regions. As previously discussed, these experiments are not only subject to temporal interference effects but also exhibit spatial interference, whereby the policy implemented in one location may influence the outcomes in other locations. We begin by defining the test hypotheses, followed by an introduction to our models and the suggested procedures.

4.1 Test hypotheses

For the -th region, we use to denote its treatment history up to time . Let represent the treatment history across all regions. Similarly, define and as the potential observation and outcome for the -th region, respectively. The set of potential observations at time is denoted as .

In the spatiotemporal context, our focus is on the cumulative quantile treatment effects, aggregated over all regions. Specifically, we define CQTE and SCQTE at the -th quantile level as:

respectively, where denotes the set of characteristics independent of the treatment history up to time across all regions. For a given quantile level , our goal is to test whether a new policy outperforms the old one as follows:

| (13) |

Compared to the testing problem in (2), (13) focuses on global treatment effects aggregated over time and regions. We assume the consistency assumption holds. Similar to Section 3, under the spatial alternating-time-interval design, one can show that the sequential ignorability assumption and the positivity assumption are automatically satisfied, ensuring that CQTE is identifiable from the observed data.

4.2 Spatiotemporal VCDP models

Suppose that the experiment last for days, and each day is divided into time intervals. For , , and , let represent the state-treatment-outcome triplet measured from the th region at the -th time interval of the -th day. For each , denotes the neighbouring regions of . To model the quantiles of and , we extend the two VCDP models in Section 3 to two spatialtemporal VCDP (STVCDP) models in this section.

The first STVCDP model describes the quantile structure of the outcome. It assumes the following form:

| (14) | ||||

where denotes the average of , , and . Model (14) is based on two key assumptions. Firstly, it is assumed that the effect of treatments in other regions on the conditional quantile of is limited to those of its neighboring regions, as long as each experimental region is large enough. This is because drivers can only travel between neighboring regions in one time unit, meaning that treatments in non-neighboring regions are not expected to impact . Secondly, it is assumed that the influence of treatments in neighboring regions on the conditional quantile of is only through the mean of the treatments. This is a common mean-field assumption used to model spillover effects (e.g., Hudgens and Halloran, 2008; Shi et al., 2022) and can be tested using observed data (Shi et al., 2022).

The second STVCDP model models the conditional distribution of the next state given the current state-action pair as follows:

| (15) | ||||

where and is a matrix of autoregressive coefficients. The conditional mean of each entry in the error process given is zero. The error process is required to be independent over time, although it may be dependent across different locations. Additionally, the varying coefficients are required to be smooth over the entire spatial domain, which will help to reduce the variances of the model estimators and improve the accuracy of the CQTE estimator. The models (14) and (15) hold under the assumption that the potential outcomes satisfy the quantile varying coefficient models, as described in the supplementary material (models (21) and (22)).

The following proposition provides a closed-form expression for and proves that . Let

where and the product when .

Proposition 3.

Proposition 3 provides a foundation for constructing a plug-in estimator for . This forms the basis of the proposed inference procedure, which we discuss in more detail in the next section. Additionally, from models (14) and (15), we can obtain the expression for as:

where is the residual term, defined as , and its conditional -th quantile given is equal to zero. It is worth mentioning that these models can be further extended to incorporate the effects of states from neighboring regions on the immediate outcome by including another mean-field term where . In this case, the closed-form expression for can be similarly derived.

4.3 Estimation and inference procedures

In this subsection, we outline the estimation and testing procedures for .

Firstly, we calculate raw estimators of the unknown coefficients in the two STVCDP models. For each region , we employ standard quantile regression and linear regression as shown in (7) and (8) to the data subsets and to obtain the initial estimators and for and , respectively. Next, we apply kernel smoothing techniques as illustrated in (9) and (10) to refine these initial estimators over time. We denote the resulting estimators as and .

Secondly, we further refine these raw estimators by employing kernel smoothing to borrow information across space. Specifically, we define

where is the th column of and is a normalized kernel function with bandwidth parameter . The kernel function is given by

where represents the longitude and latitude of region . Consequently, regions with smaller spatial distances contribute more significantly.

Thirdly, we estimate by substituting the refined estimators and and use the resulting estimator as the test statistic .

Finally, we introduce a bootstrap method to test (13). During each iteration, we resample the estimated error processes to obtain the bootstrap estimates , , and the bootstrapped statistic . We reject in (13) if exceeds the upper th empirical quantile of . As this approach is highly similar to the one presented in Section 3.3, we omit further details for brevity.

5 Direct and indirect effects

Recall that Proposition 2 provides the closed-form expression of , which is

Consequently, we can divide the quantile treatment effect into two components. Specifically, the first term of represents the direct effect of the treatment on the immediate outcome, expressed as

Observe that for each , the two potential outcomes and differ in the treatment received at time , but they share the same treatment history. The second term quantifies the carryover effects of past treatments on the current outcome, defined as

Similar decompositions have been considered in Li and Wager (2022) and Shi et al. (2022).

The corresponding testing hypotheses are given by

| (16) | |||

| (17) |

Testing these hypotheses not only enables us to determine whether the new policy is significantly better than the old one or not, but also helps us understand how the new (or the old) policy outperforms the other.

To test (16) and (17), we use the two-step estimators in (9) and (10) to construct the plug-in estimators and for CQDE and CQIE, respectively. Next, we employ the bootstrap method in Section 3.3 to approximate the limiting distributions of and under the null hypotheses. We note that although has a tractable limiting distribution and is asymptotically normal, estimating its asymptotic variance without using bootstrap remains challenging.

Finally, we can similarly define the direct effect and indirect effect in the spatiotemporal design as follows,

The estimation and inference procedures can be derived similarly.

6 Asymptotic Properties

In this section, we investigate the theoretical properties of the proposed test statistics for CQTE. Firstly, we provide an upper error bound as a function of and to measure the approximation error of the proposed bootstrap method in temporal dependent experiments.

Theorem 1.

Under the conditions specified in Theorem 1, the error bound delineated in Theorem 1 tends towards zero. When the null hypothesis holds true, we derive that where the little- term uniformly applies to and . When the alternative hypothesis is true and the QTE signal satisfies QTE, the power of the proposed test method approaches (refer to the proof of Theorem 1 for more details). Consequently, the consistency of the proposed test is demonstrated.

There are two significant challenges in establishing Theorem 1: (i) the non-differentiable nature of the checkloss function, and (ii) the allowance for to diverge with . In order to address the first challenge, we utilize classical M-estimation theory from the literature to obtain a Bahadur representation of the proposed estimator (see, for instance, Koenker and Portnoy, 1987). To tackle the second challenge, we draw from arguments similar to those from the high-dimensional multiplier bootstrap theorem (Chernozhukov et al., 2013) to generate a nonasymptotic error bound that explicitly characterizes the dependence of the bootstrap approximation error on .

Secondly, we establish the consistency of the proposed test procedure in spatiotemporal dependent experiments.

Theorem 2.

Based on Theorem 2, we can demonstrate that the proposed test effectively controls the type-I error and its power tends towards when QTE. More details can be found in the proof of Theorem 2. Furthermore, we have provided additional theoretical properties of the proposed test statistics for CQDE and CQIE in Section C of the supplementary material.

7 Real Data Analysis

To address (Q1)-(Q3), we apply the proposed test procedures to the three real datasets obtained from Didi Chuxing introduced in Section 2.

Firstly, we examine the dataset from a temporally dependent A/B experiment conducted from Dec 10, 2021 to Dec 23, 2021. As detailed in Section 2, two order dispatch policies are tested in alternating one-hour time intervals. The new policy, in comparison to the old one, is designed to fulfill more call orders and elevate drivers’ total income. We set drivers’ total income as the outcome, and the observation variables include the number of call orders and drivers’ total online time. To address question (Q1), we apply model (3) to elucidate the correlation structure between supply and demand and model (4) to elucidate the temporal interference effects. For question (Q3), we utilize the testing procedure described in Section 3.3 for these temporally dependent experiments. As a means to validate the proposed test, we also apply our procedure to the A/A dataset outlined in Section 2, where a single order dispatch strategy is employed. We anticipate that our test will not reject the null hypothesis when applied to this dataset.

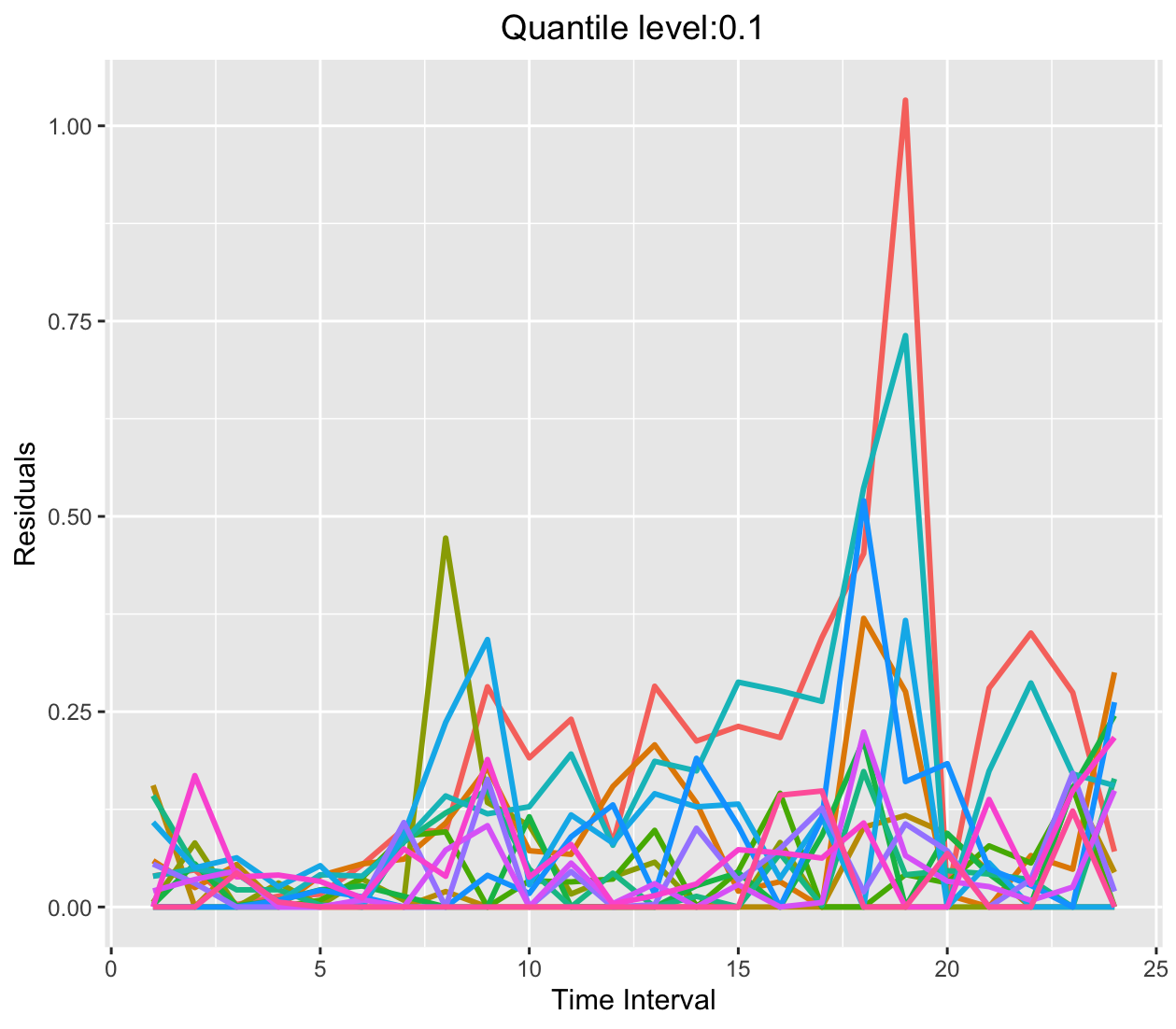

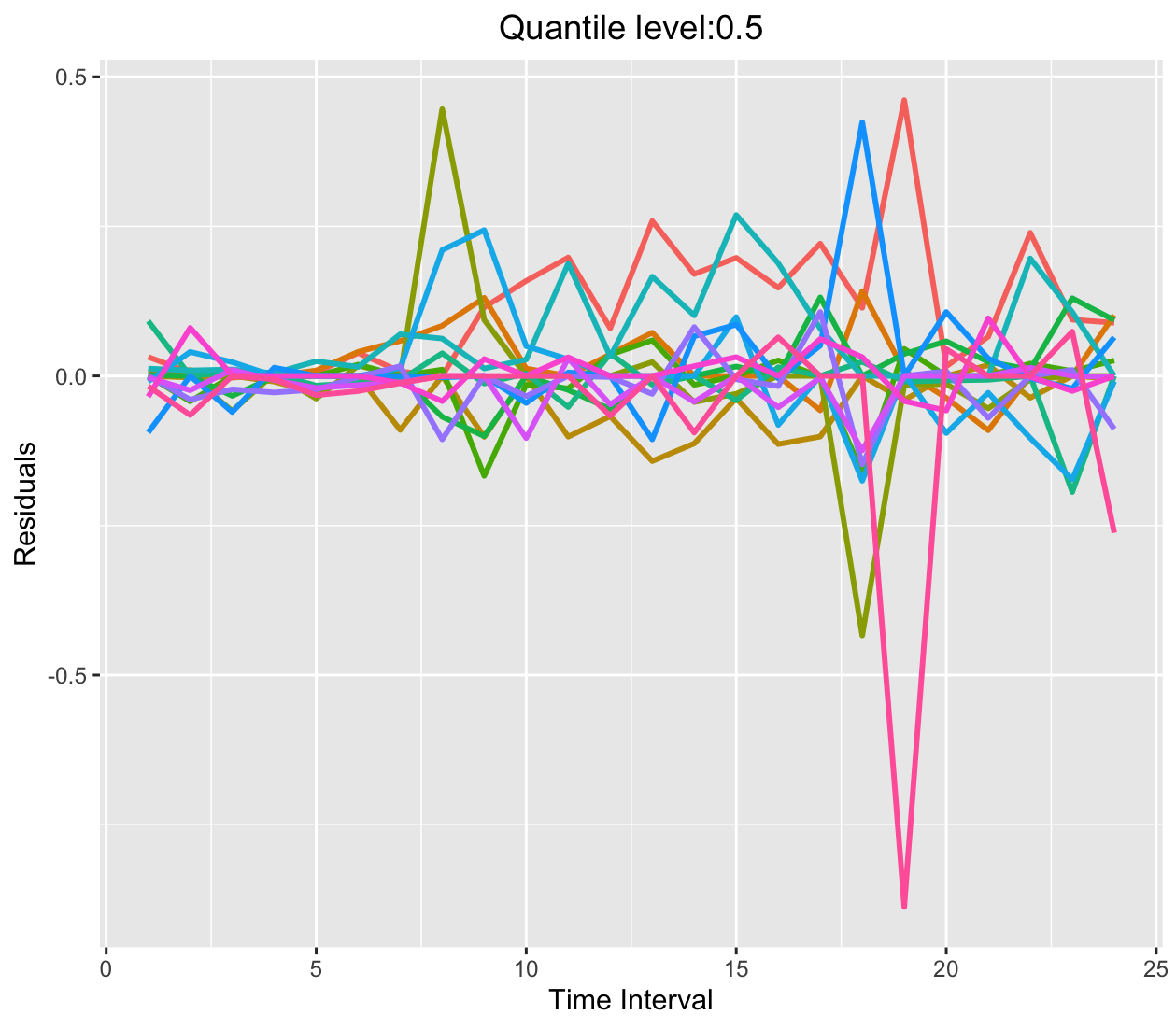

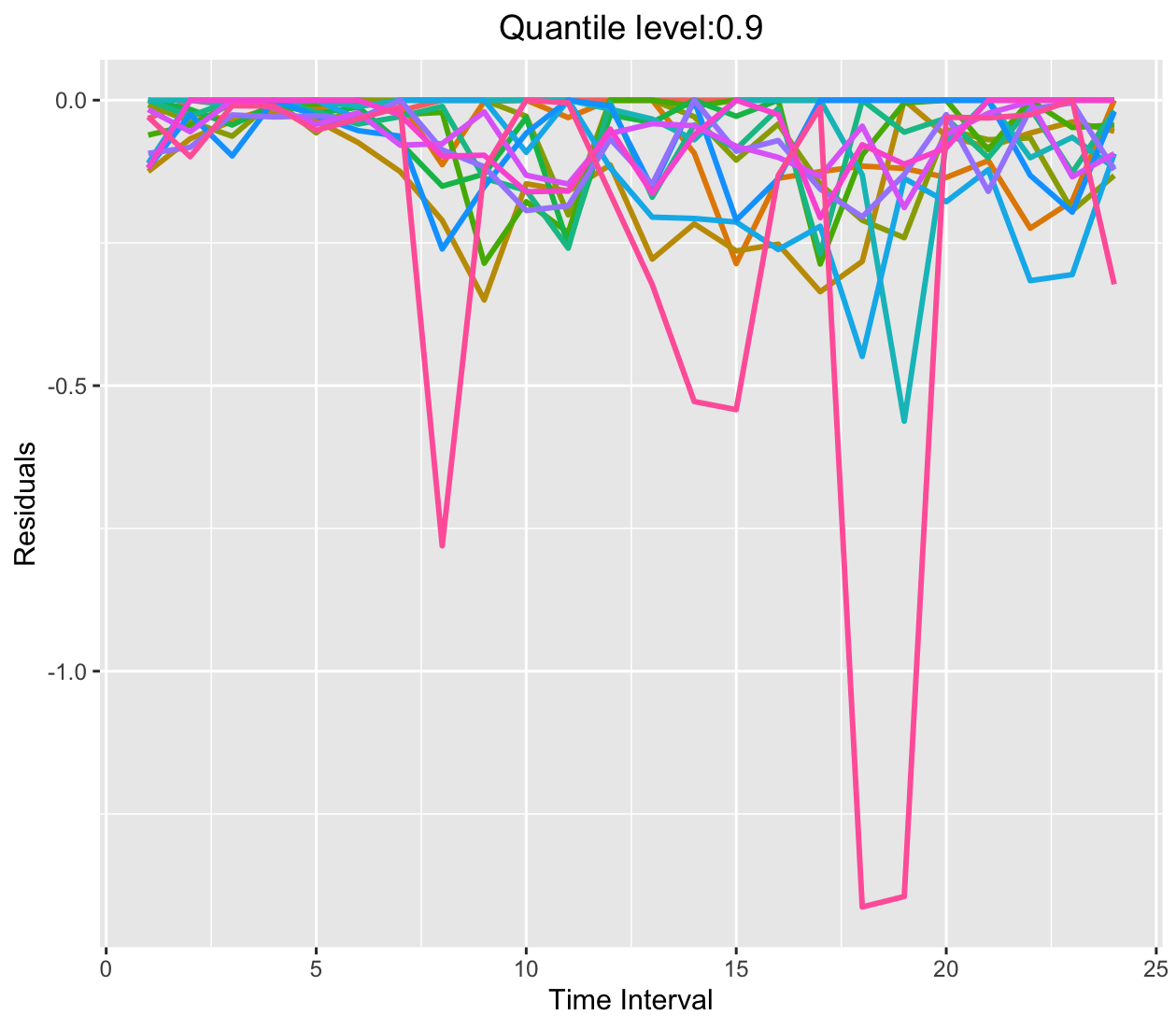

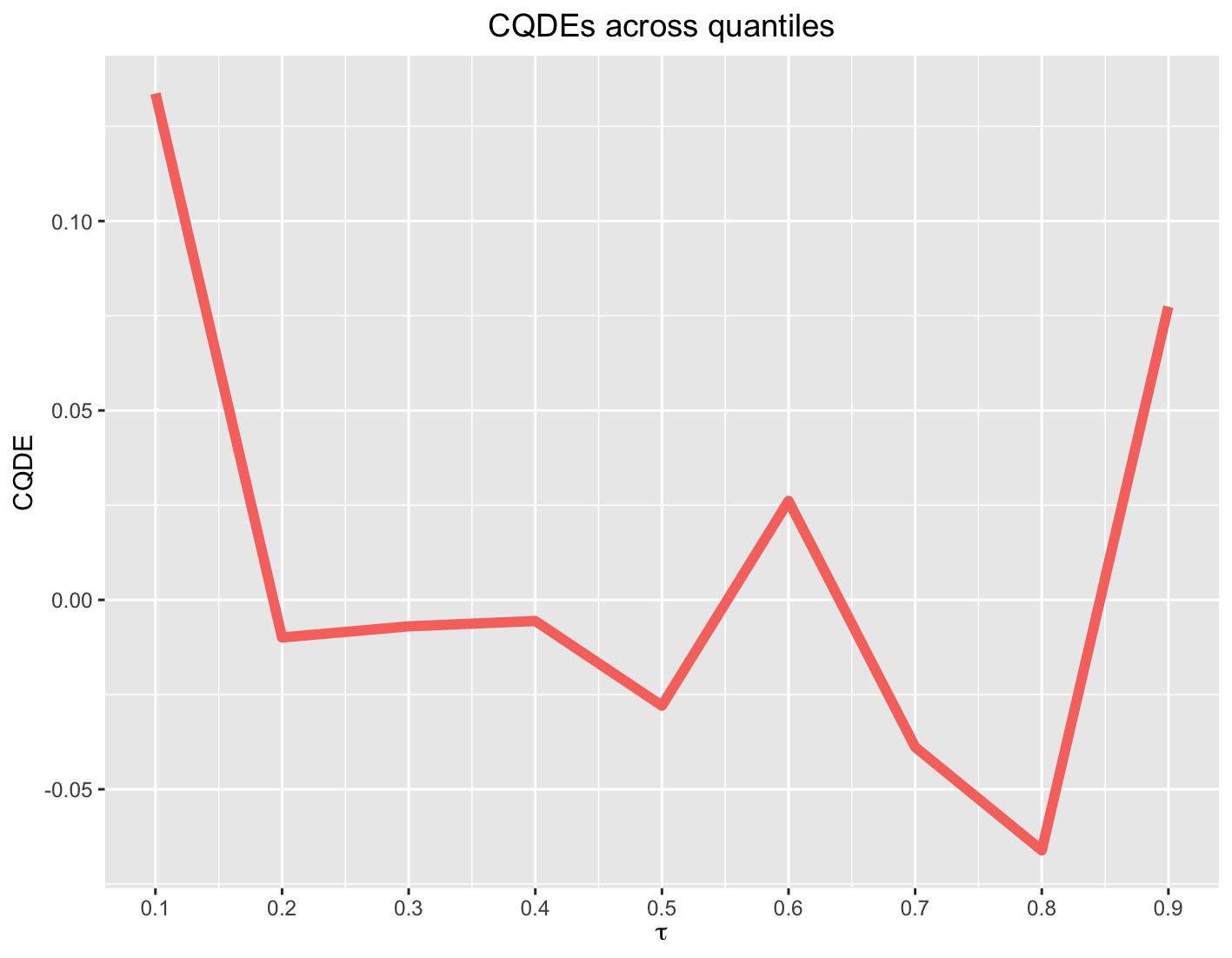

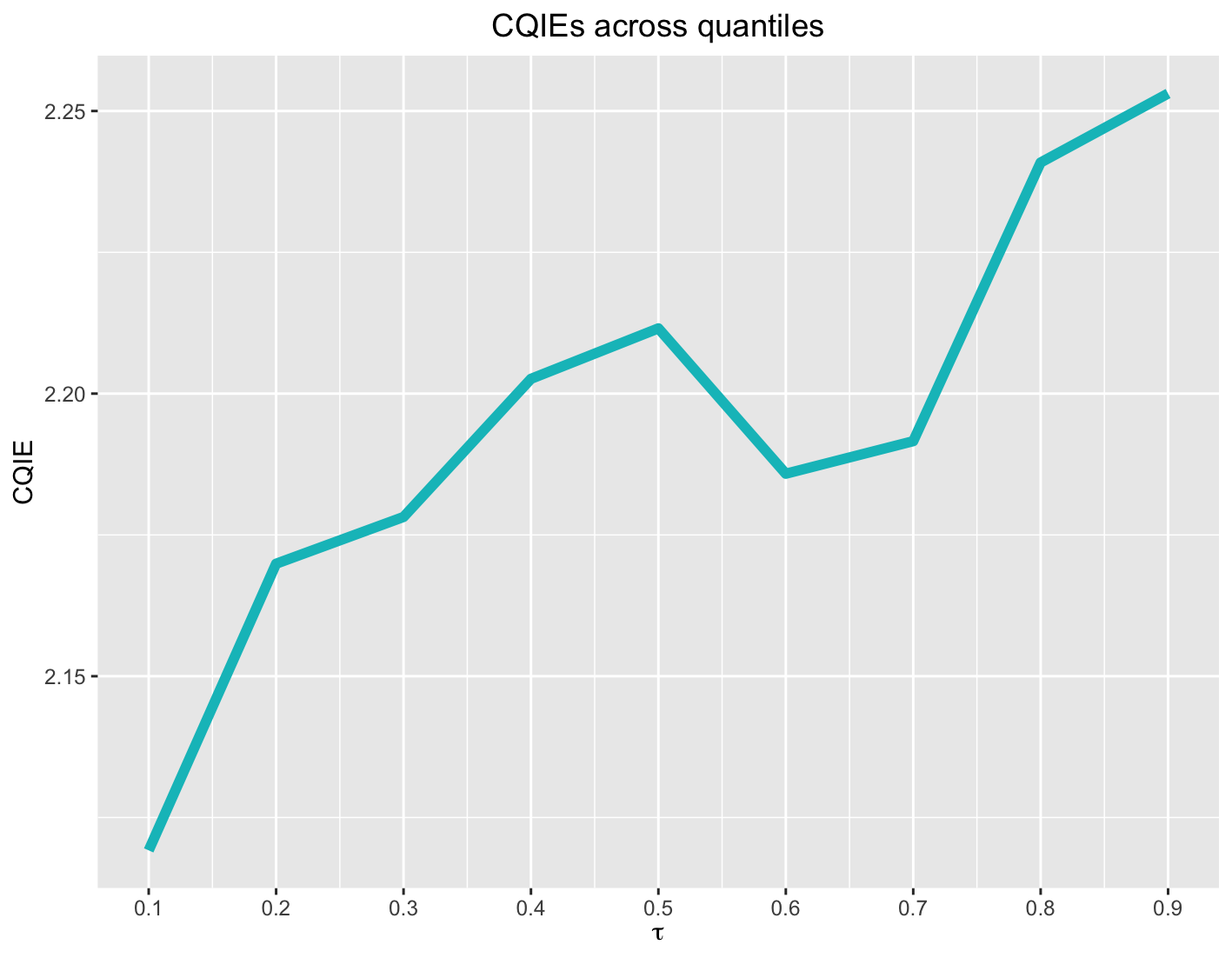

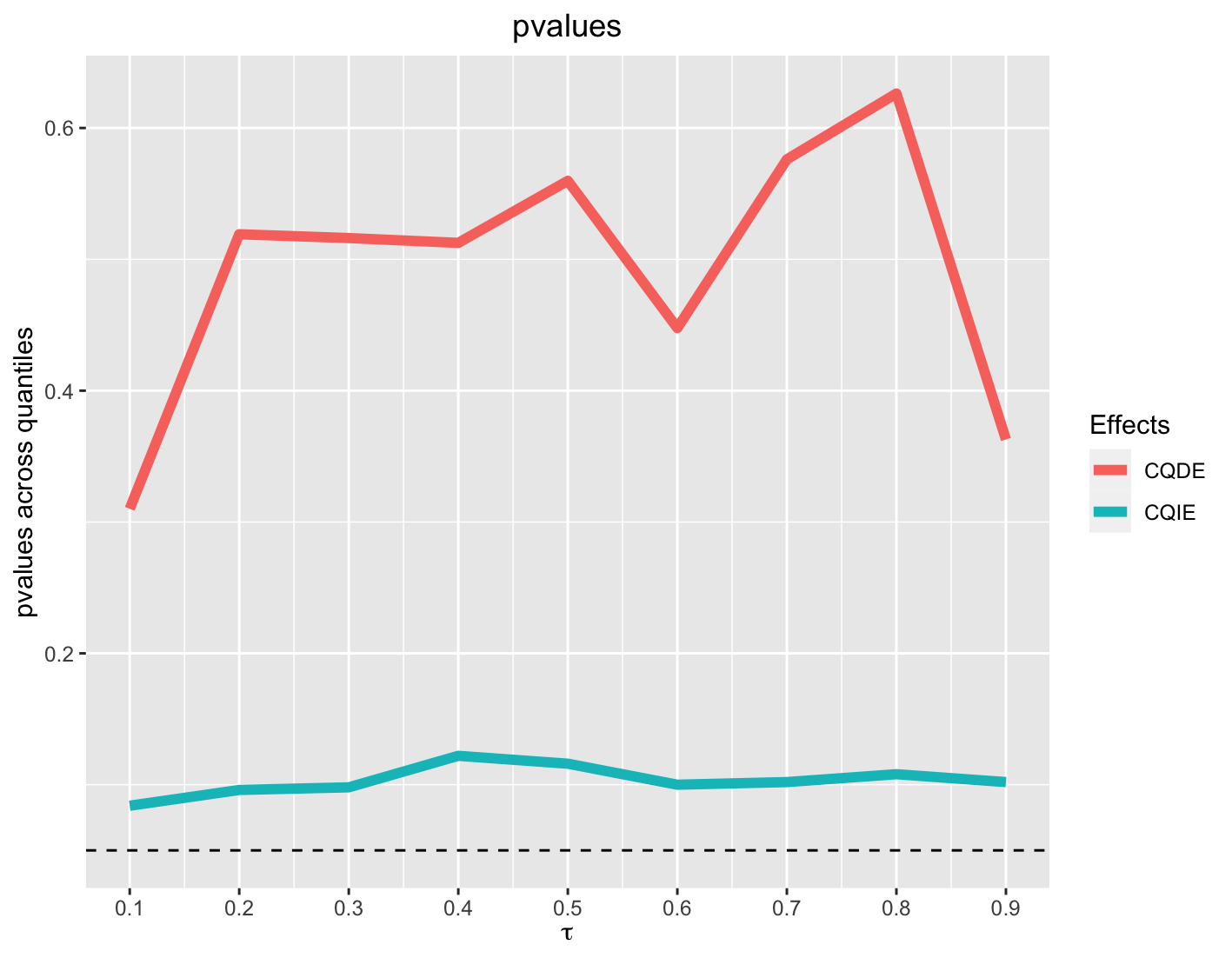

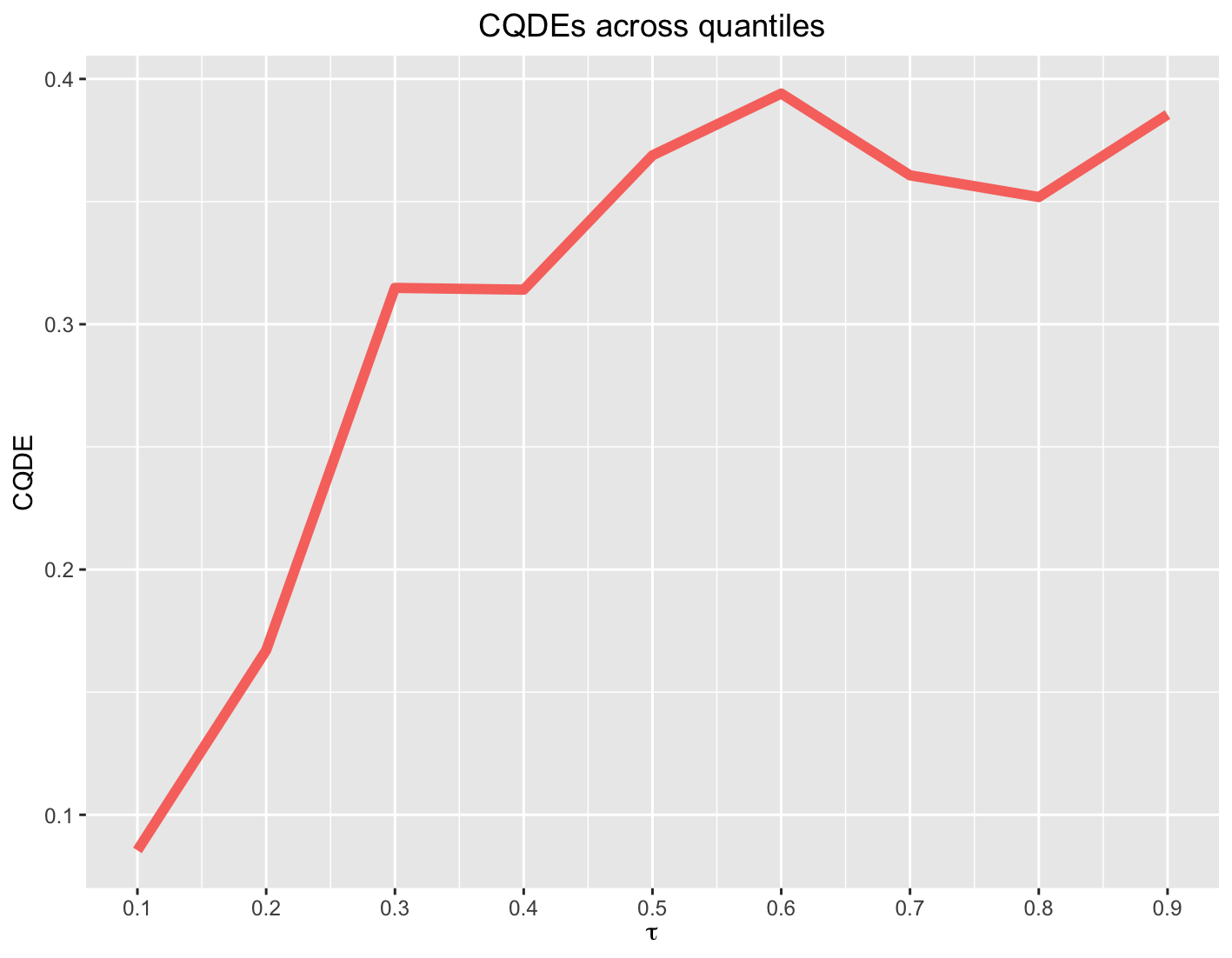

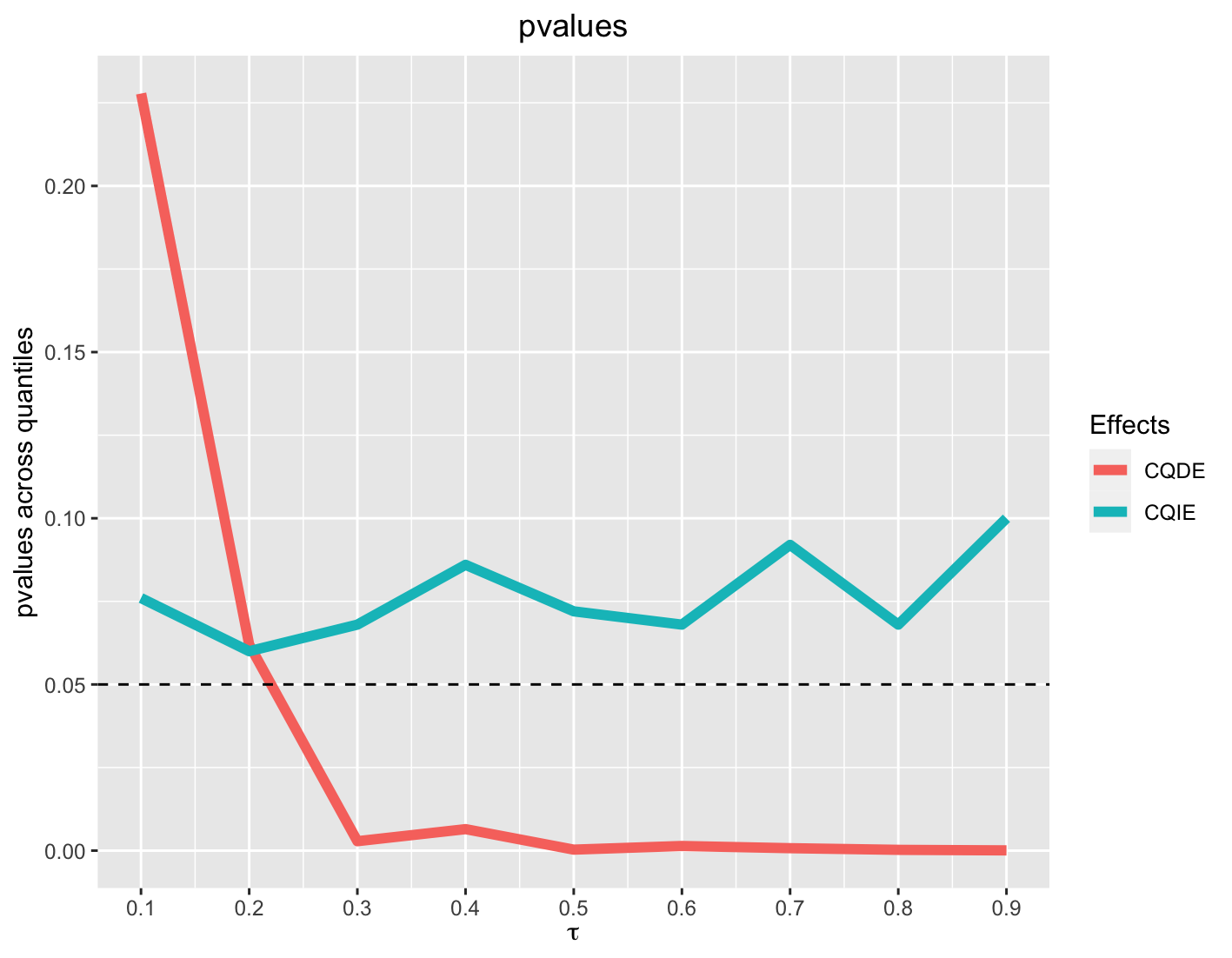

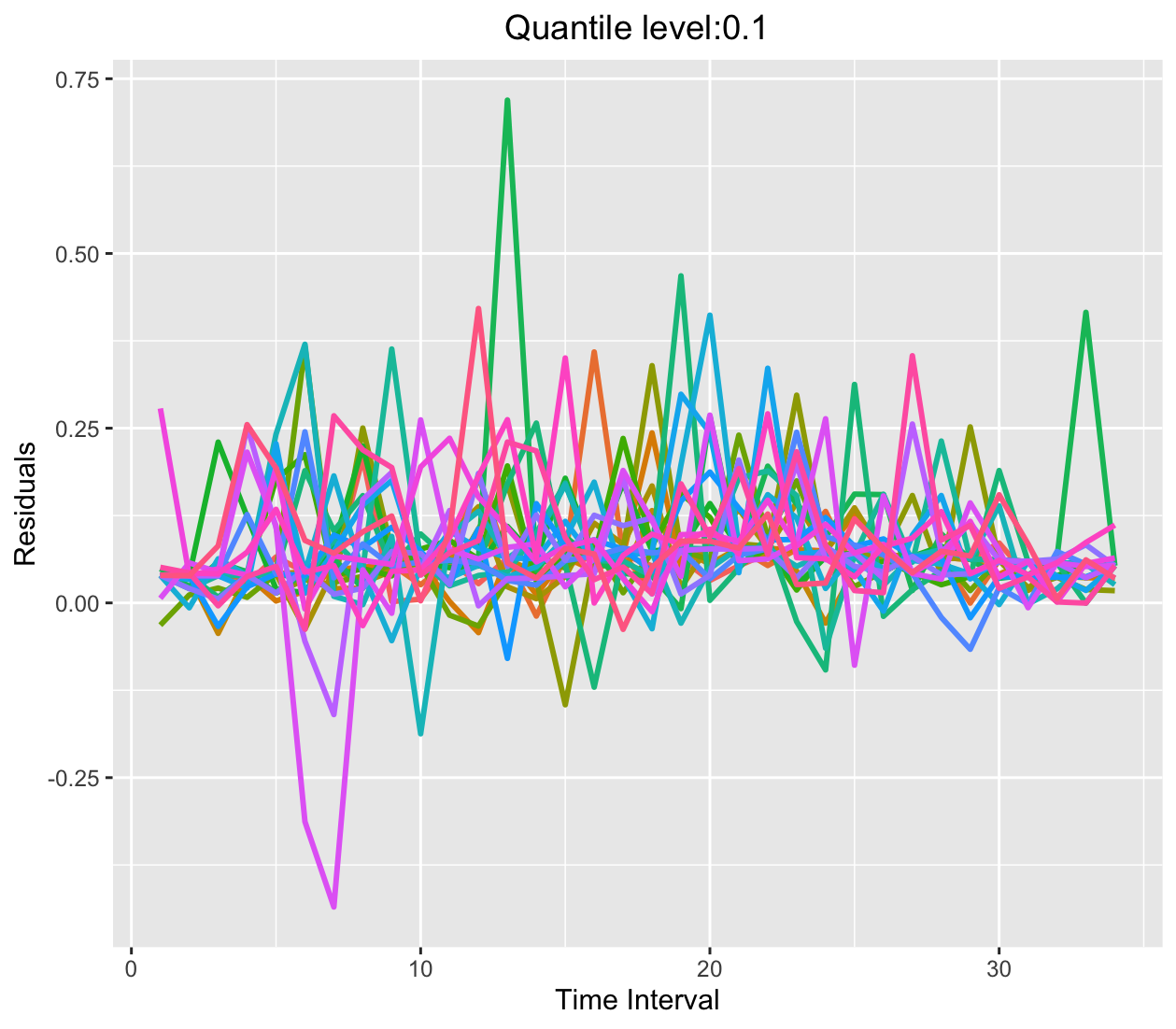

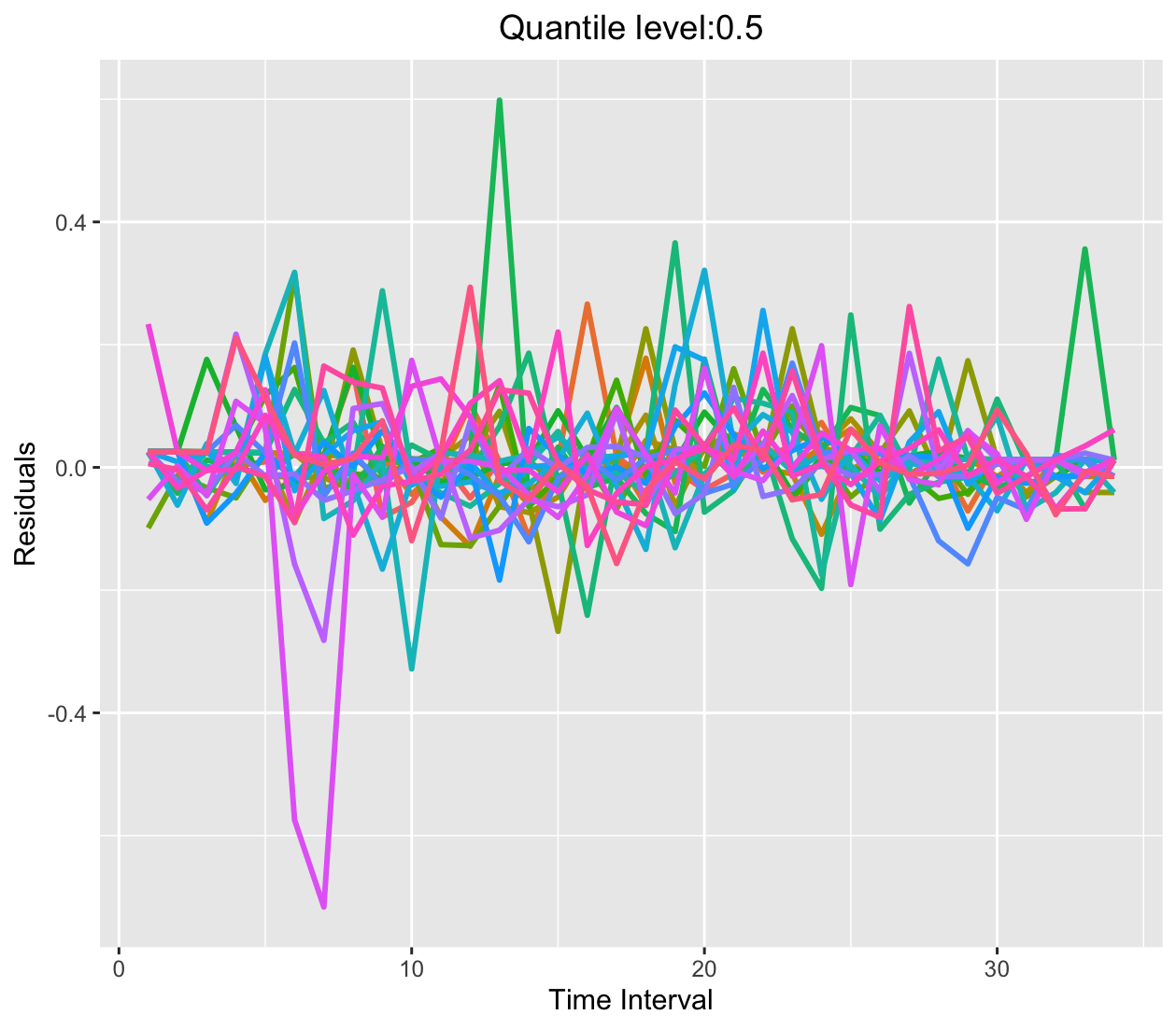

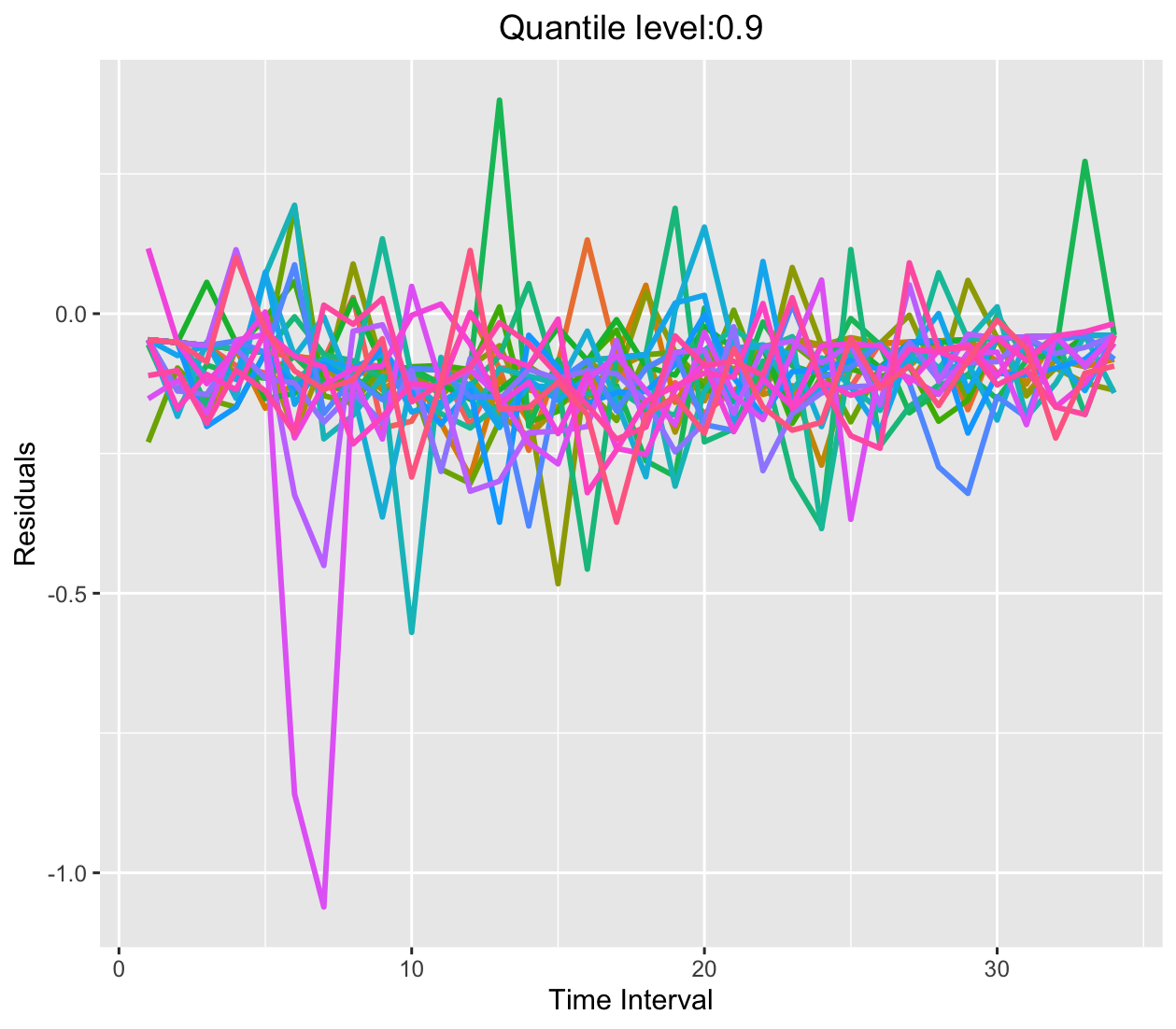

In Figure 3, we display the estimated residuals of the outcome over time for . As can be seen from Figure 3, some residuals are significantly larger than others, suggesting that the outcome likely originates from heavy-tailed distributions. This reinforces the use of quantile treatment effects for policy evaluation. Table 1 presents the -values of the proposed test for CQTEτ, CQDEτ, and CQIEτ, respectively. Furthermore, Figure 4 illustrates the estimated treatment effects and the p-values across various quantiles. As expected, the proposed test does not reject the null hypothesis at any quantile level when applied to the A/A experiment. However, when applied to the A/B experiment, the new policy demonstrates significant quantile direct effects on the business outcome at most quantile levels. In contrast, the indirect effects are not significant.

| pvalues for AA | pvalues for AB | ||||

|---|---|---|---|---|---|

| CQIEτ | |||||

| 0.1 | 0.286 | 0.084 | 0.208 | 0.076 | |

| 0.2 | 0.522 | 0.096 | 0.080 | 0.060 | |

| 0.3 | 0.53 | 0.098 | 0.002 | 0.068 | |

| 0.4 | 0.568 | 0.122 | 0.010 | 0.086 | |

| 0.5 | 0.536 | 0.116 | 2e-4 | 0.072 | |

| 0.6 | 0.464 | 0.100 | 0.002 | 0.068 | |

| 0.7 | 0.548 | 0.102 | 7e-4 | 0.092 | |

| 0.8 | 0.606 | 0.108 | 2e-4 | 0.068 | |

| 0.9 | 0.322 | 0.102 | 7e-5 | 0.100 | |

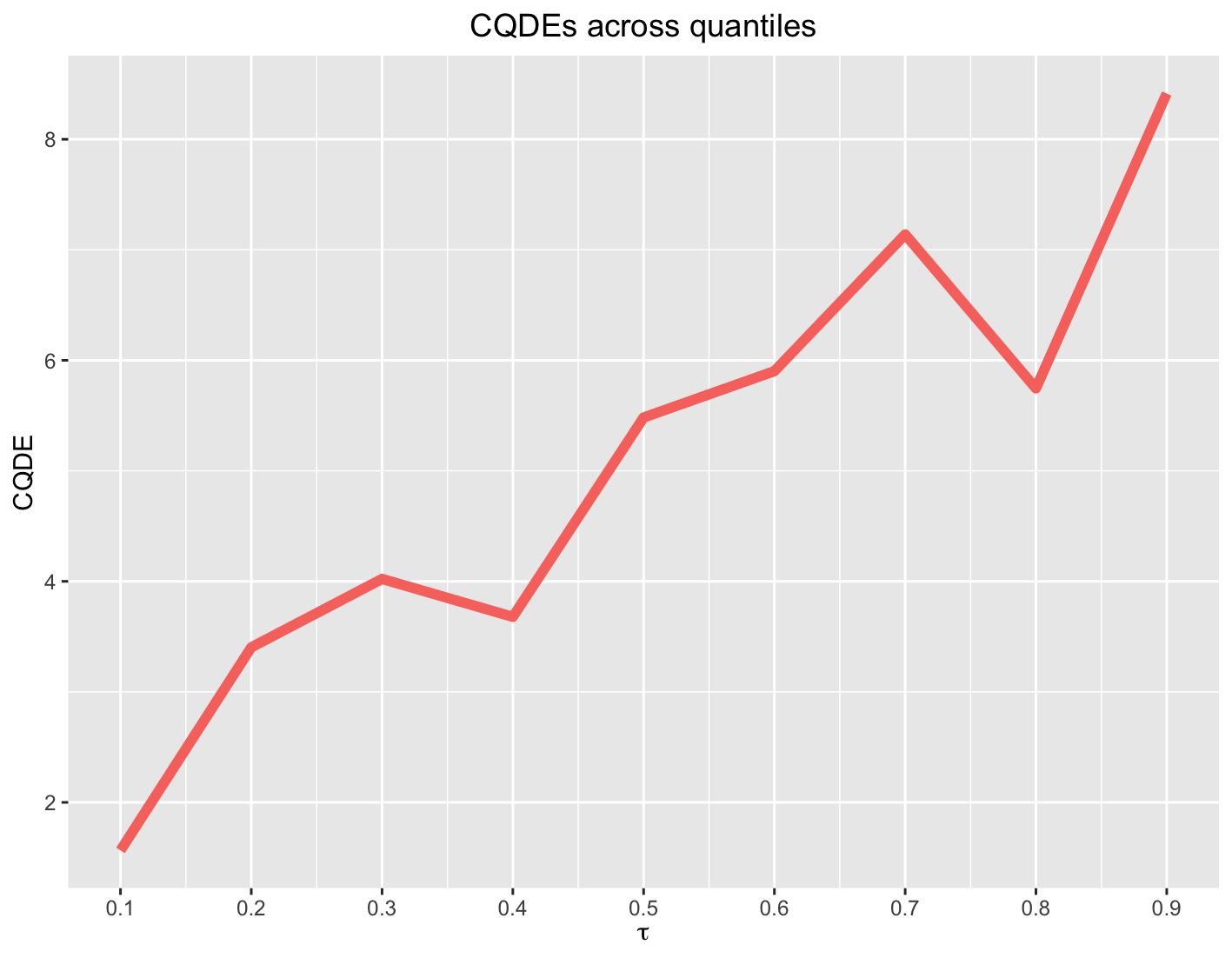

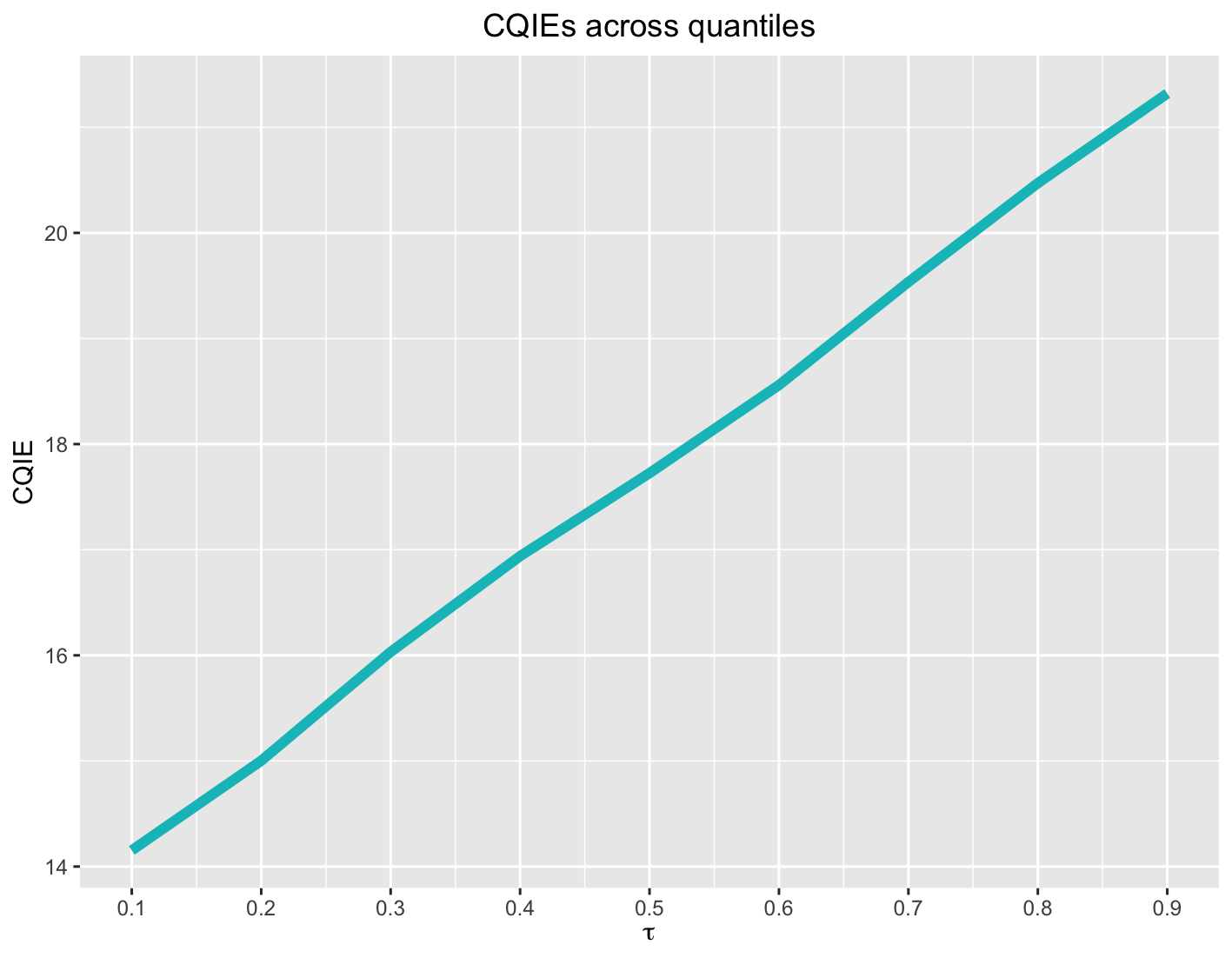

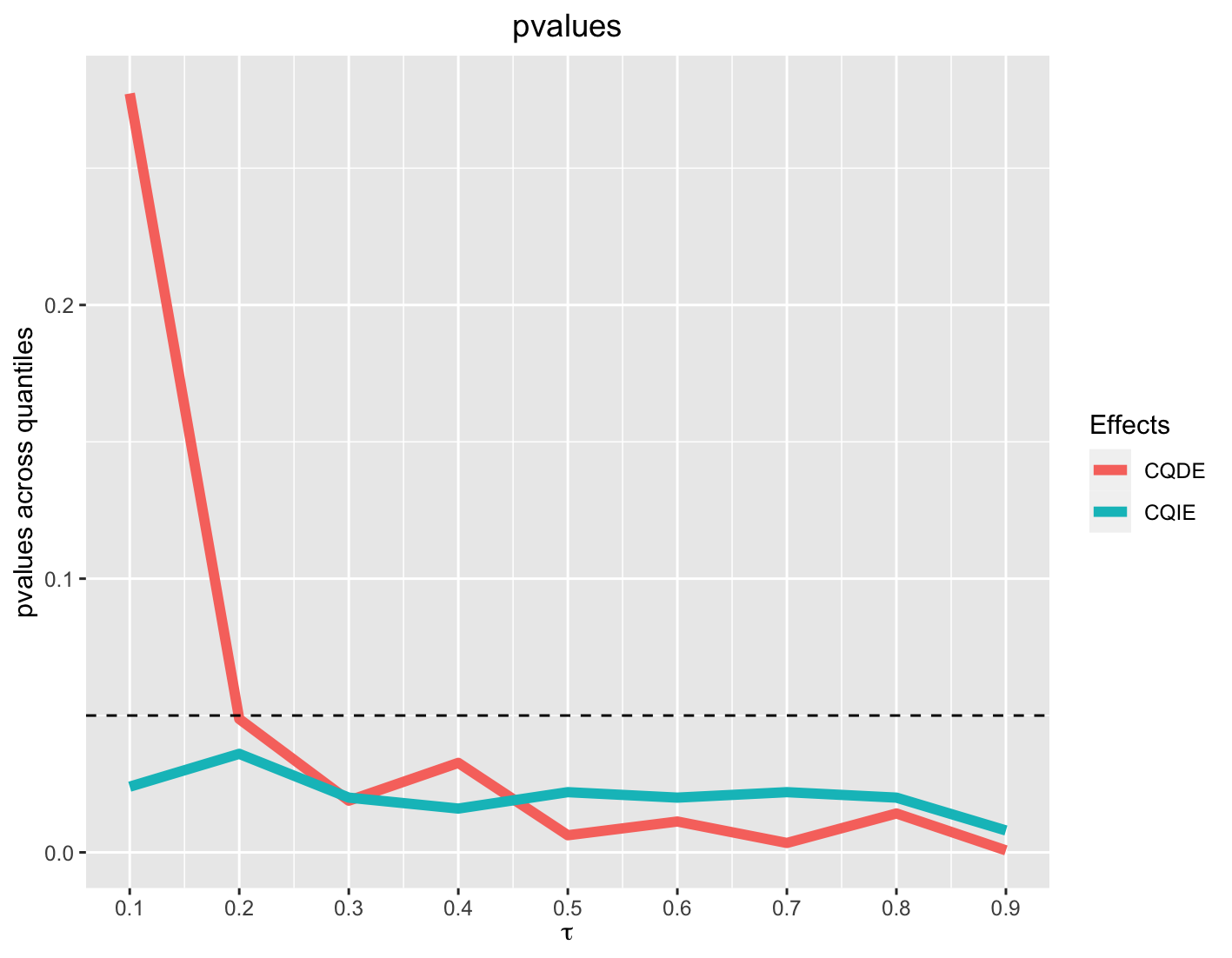

Secondly, we analyze the dataset from the spatiotemporal dependent experiment as described in Section 2. Recall that in this experiment, the city is divided into 12 regions. Policies are implemented based on alternating 30-minute time intervals within each region. We concentrate on a data subset collected from 7 am to midnight each day, as there are relatively few order requests from midnight to 7 am. The drivers’ total income and the number of call orders are designated as the outcome and state variable, respectively. We fit the spatiotemporal VCDP models (14) and (15) to address (Q2), and apply the testing procedure from Section 4.3 to address (Q3) for this spatiotemporal dependent experiment. Our aim is to determine whether the new policy has significant treatment effects on drivers’ total income across various quantile levels.

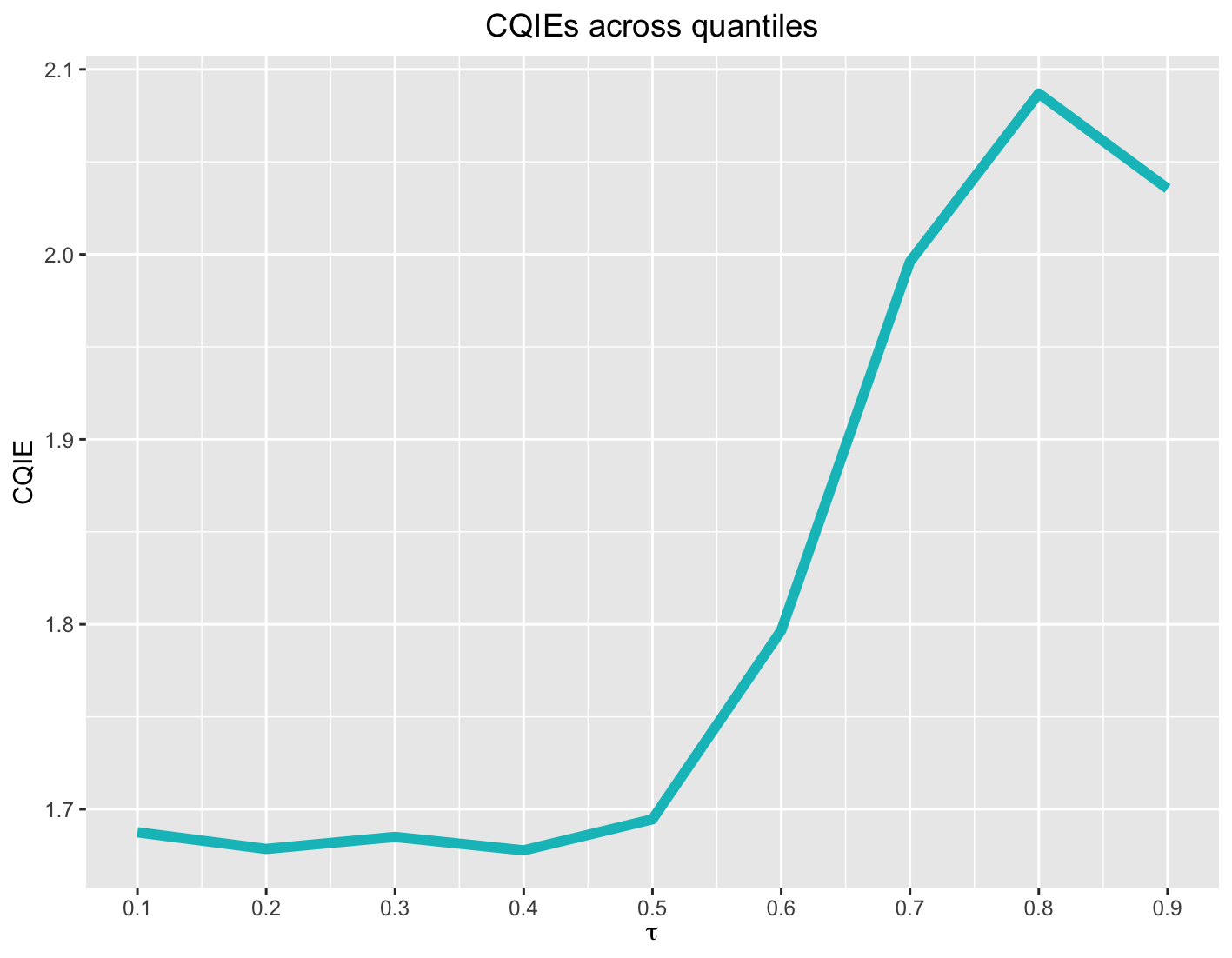

For each quantile level, we implement the proposed estimation and testing procedures on the data. The values are generated through the bootstrap procedure outlined in Section 4, utilizing 500 bootstrap samples. The estimation and testing results for CQDEτst and CQIEτst are summarized in Table 2 and Figure 5. The treatment effects are significant at most quantile levels, and both the estimated direct and indirect effects are positive across all quantiles. Generally, these effects escalate with the quantile level. However, the new policy doesn’t seem to boost the lower quantile of the outcome (e.g., ). These results underline the heterogeneous effects of the new policy across different quantile levels.

Finally, we display the scaled outcomes, and residuals for the representative region 5 over time, with , in Figure 6. It is evident that there may be several outliers in the data. This observation further supports the use of quantiles as the evaluation metric. Similar patterns are observed for other regions as well.

| pvalue | pvalue | |||

|---|---|---|---|---|

| 0.1 | 0.290 | 0.024 | 1.566 | 14.153 |

| 0.2 | 0.072 | 0.036 | 3.403 | 15.002 |

| 0.3 | 0.026 | 0.020 | 4.022 | 16.032 |

| 0.4 | 0.032 | 0.016 | 3.678 | 16.939 |

| 0.5 | 0.010 | 0.022 | 5.482 | 17.725 |

| 0.6 | 0.004 | 0.020 | 5.902 | 18.559 |

| 0.7 | 0.004 | 0.022 | 7.139 | 19.535 |

| 0.8 | 0.006 | 0.014 | 5.746 | 20.473 |

| 0.9 | 7e-4 | 0.008 | 8.414 | 21.320 |

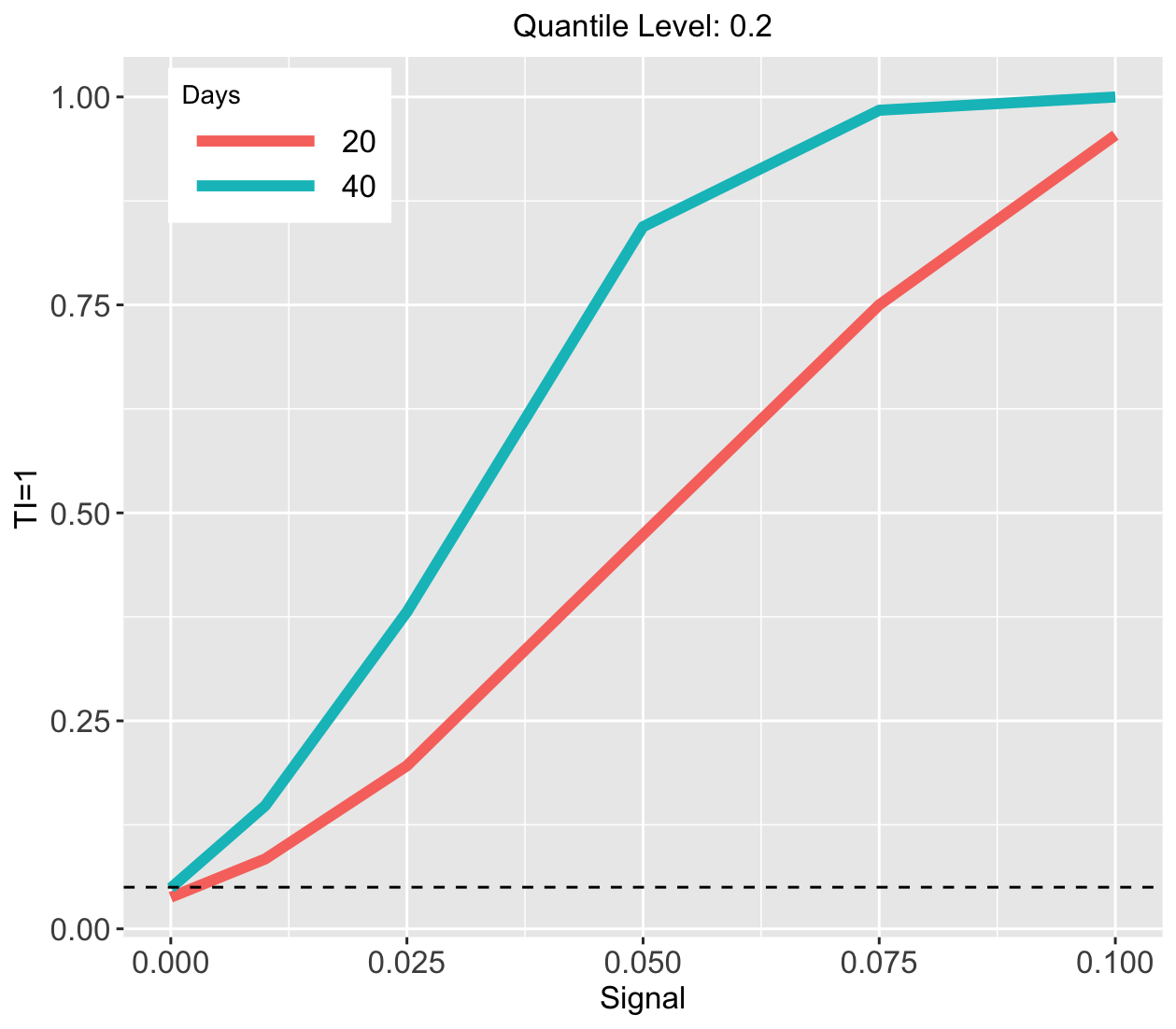

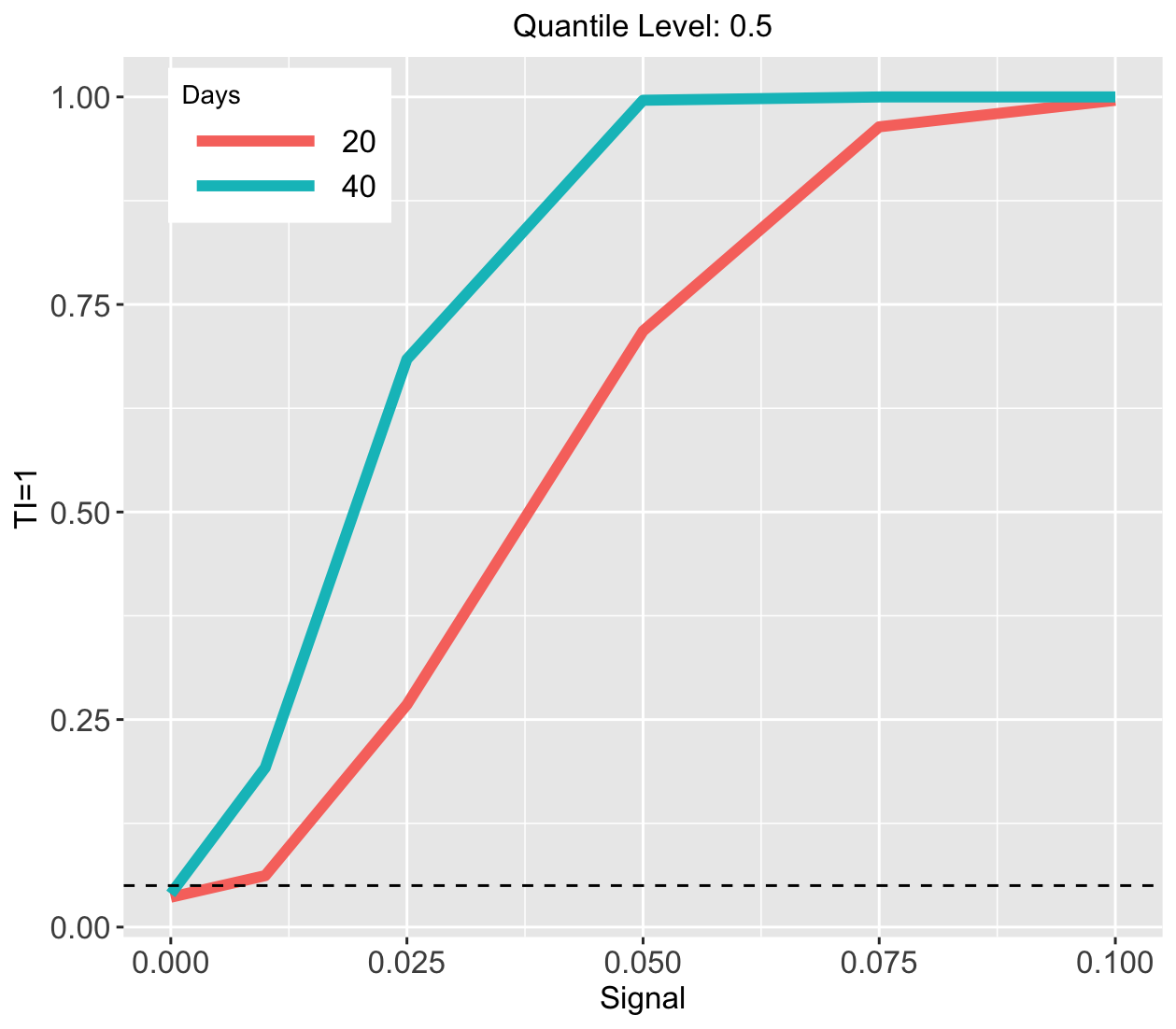

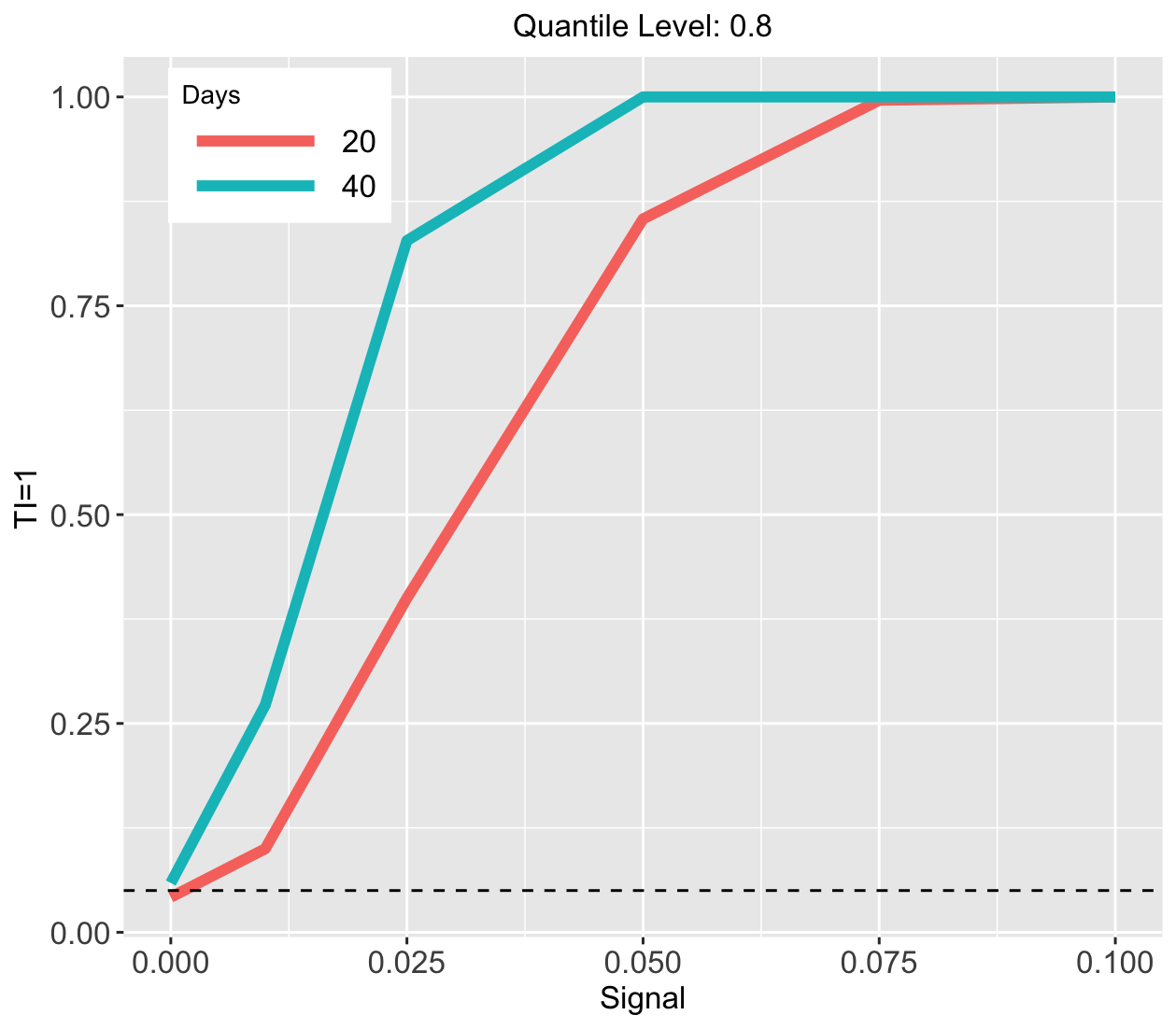

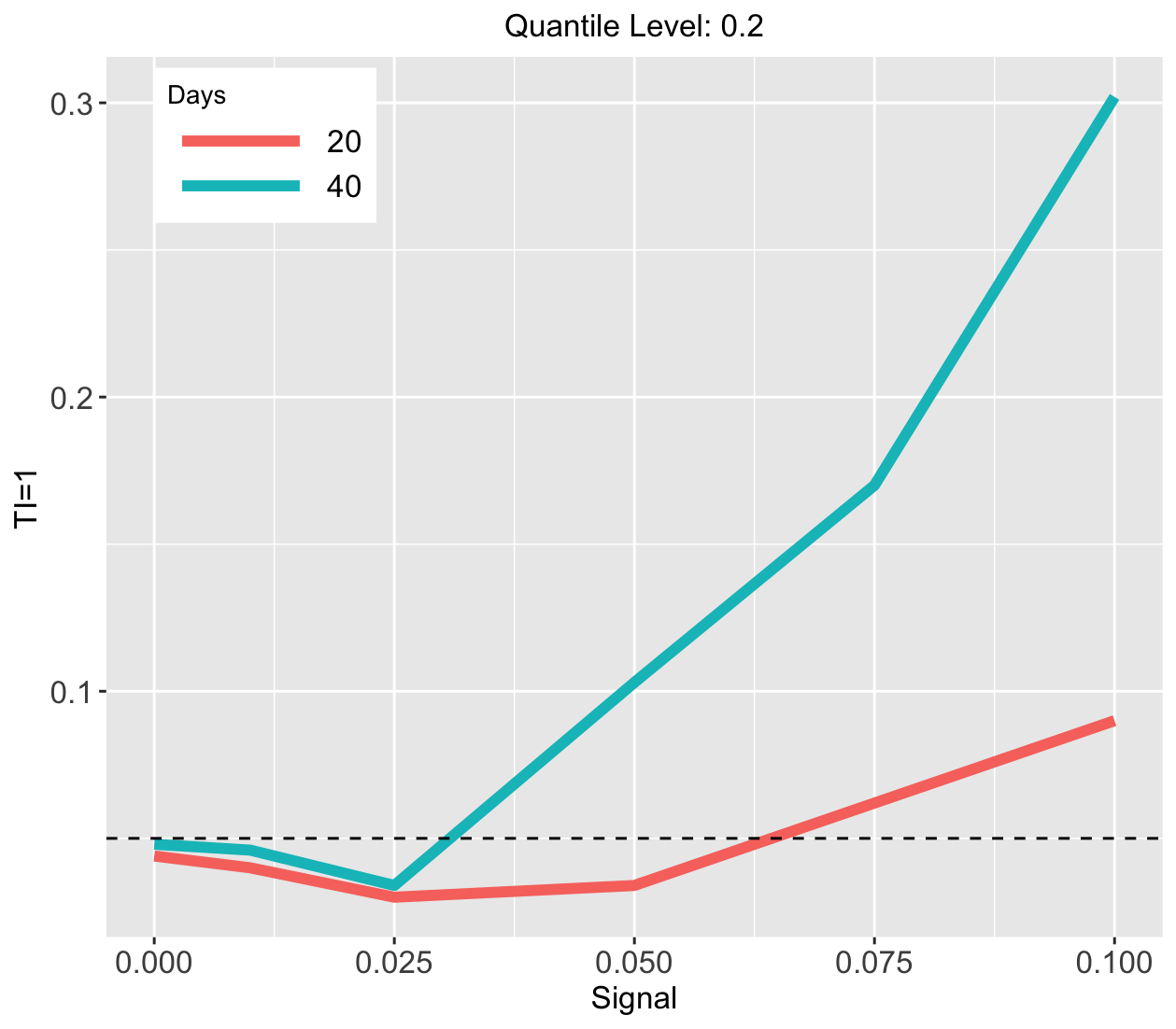

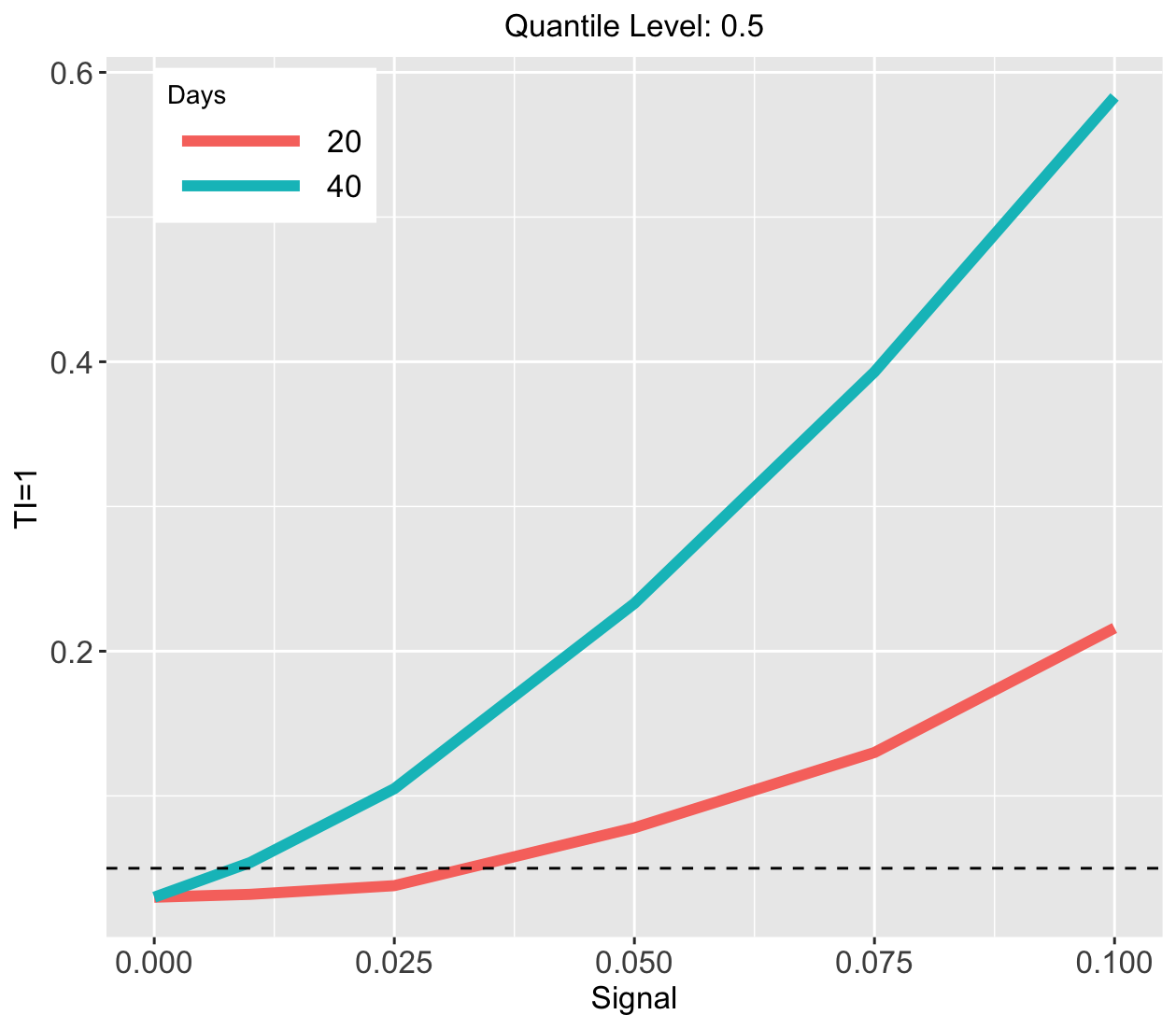

8 Real data based simulations

In this section, we evaluate the finite sample performance of the proposed estimation and testing procedures through simulations. Simulation experiments are conducted based on the real dataset collected from the A/A experiment described in Section 2. Recall that one hour is defined as a time unit, and drivers’ total income within each time unit is set as the outcome of interest. The observation variables correspond to the number of call orders and drivers’ total online time. These variables characterize the demand and supply of the ridesharing platform and have a substantial impact on the outcome.

Next, we outline the simulation environment. For a given quantile level , we fit the proposed VCDP models (3) and (4) to the data by setting = 0, since the two policies being compared are essentially the same. This enables us to obtain the estimated model parameters , , , and and the estimated error processes and for and . To simulate data, we set and for some constant , where and denote the (elementwise) empirical -th quantile of and empirical mean of , respectively. Under this formulation, the coefficients are allowed to vary across different quantiles, and the constant controls the strength of CQTE. Specifically, no CQTE exists if , and the new policy is better if .

Thirdly, we employ the bootstrap method for data generation. Specifically, in each simulation run, we randomly sample initial observations and error processes with replacement. Then, we generate days of data according to the proposed VCDP models:

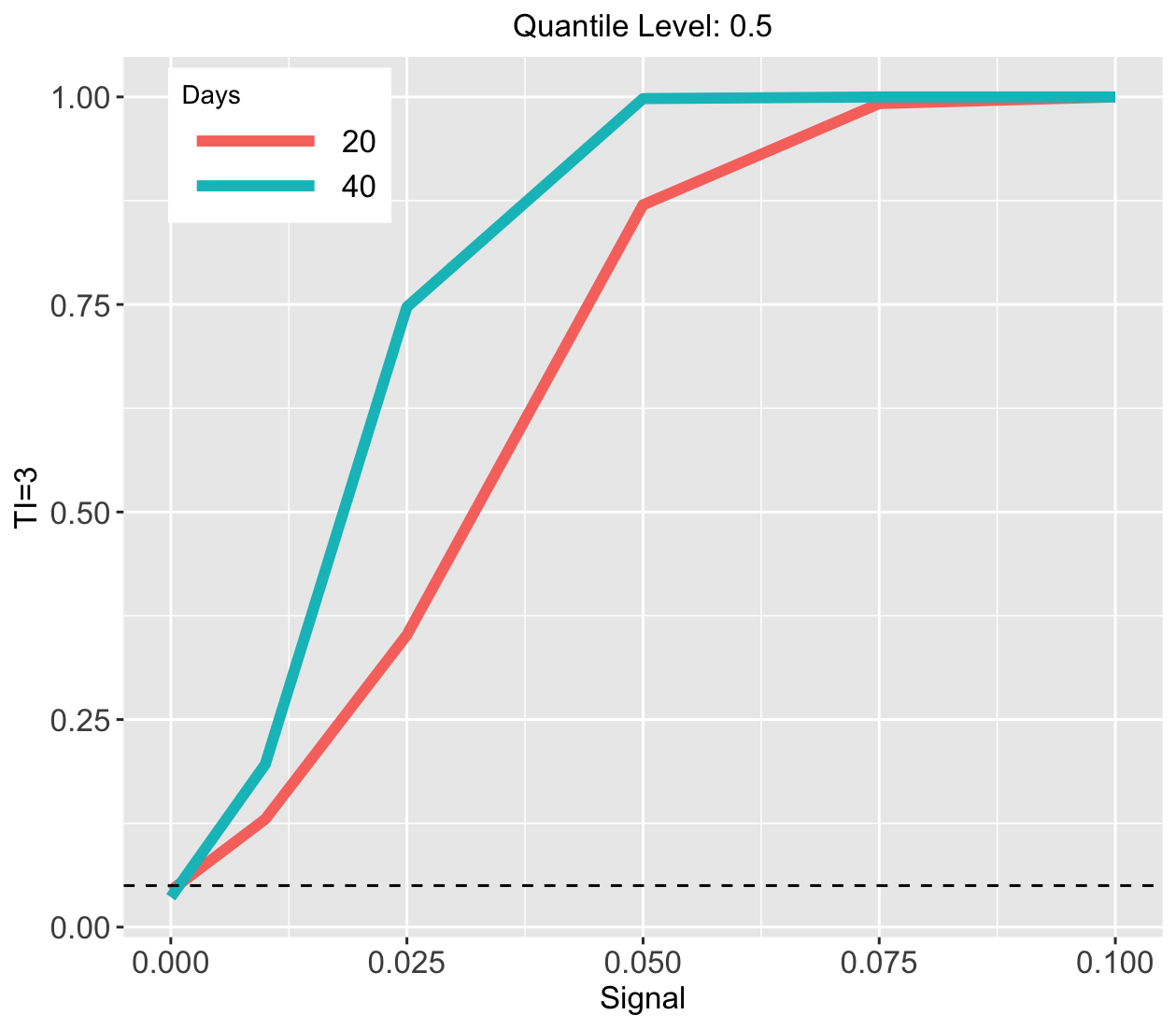

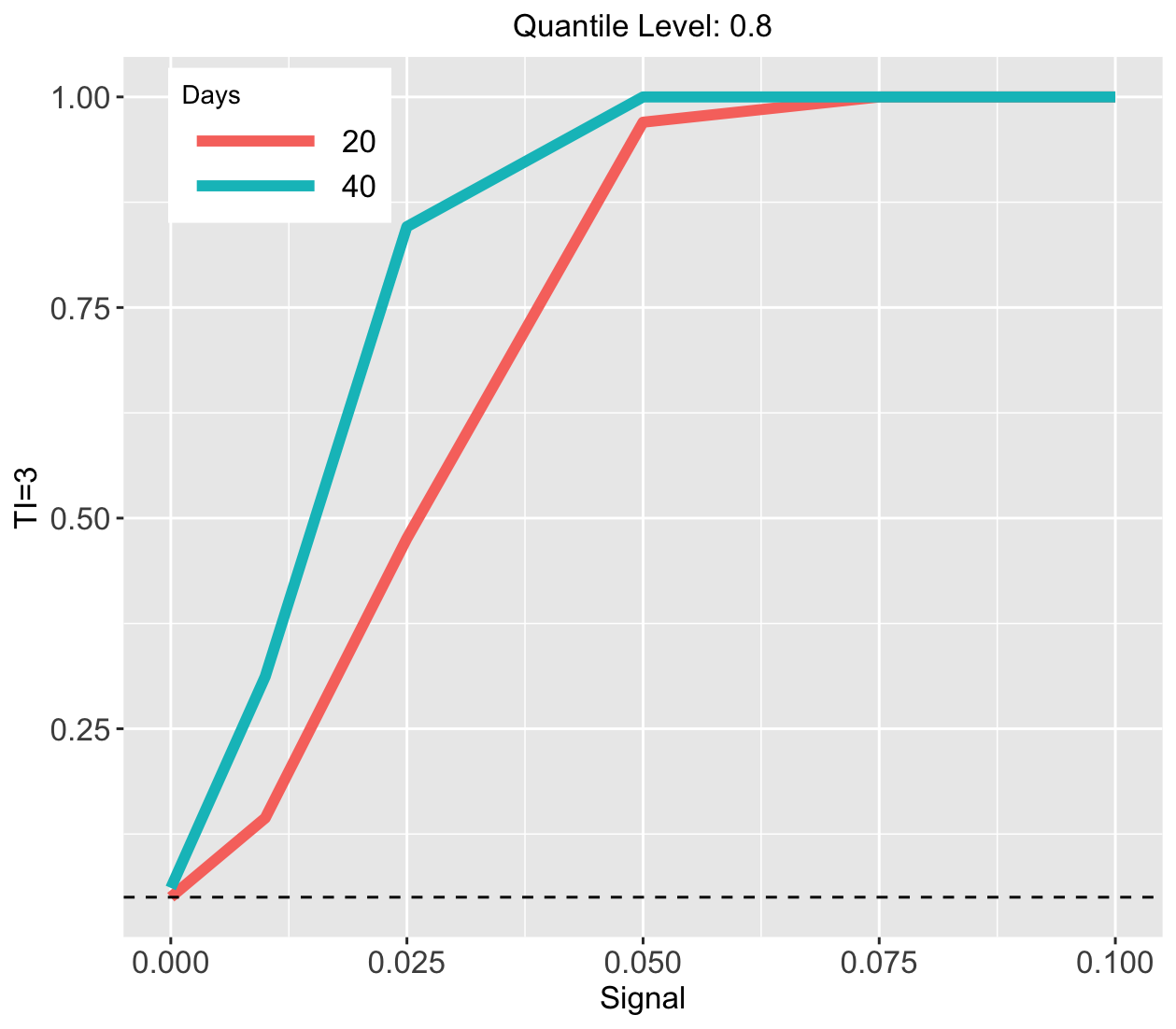

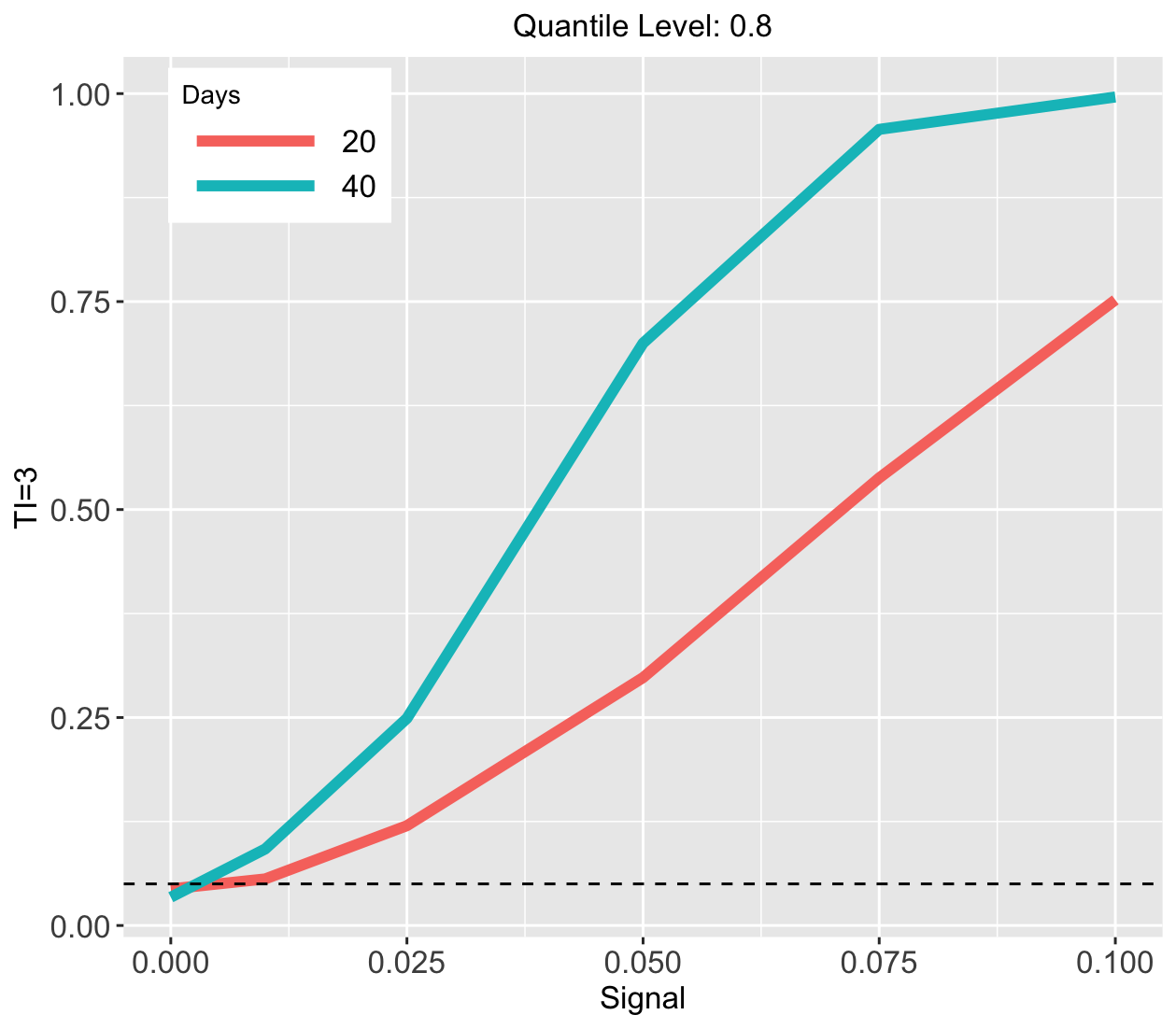

based on these samples and the estimated model parameters. The treatments are generated according to the temporal alternation design. Specifically, we first implement one policy for TI time units, then switch to the other policy for another TI time units, and alternate between the two policies. We consider a wide range of simulation settings by setting , , TI , and . For each scenario, we generate 500 simulation runs to compute the empirical type-I error rate and power. The significance level is fixed at 5% throughout the simulation.

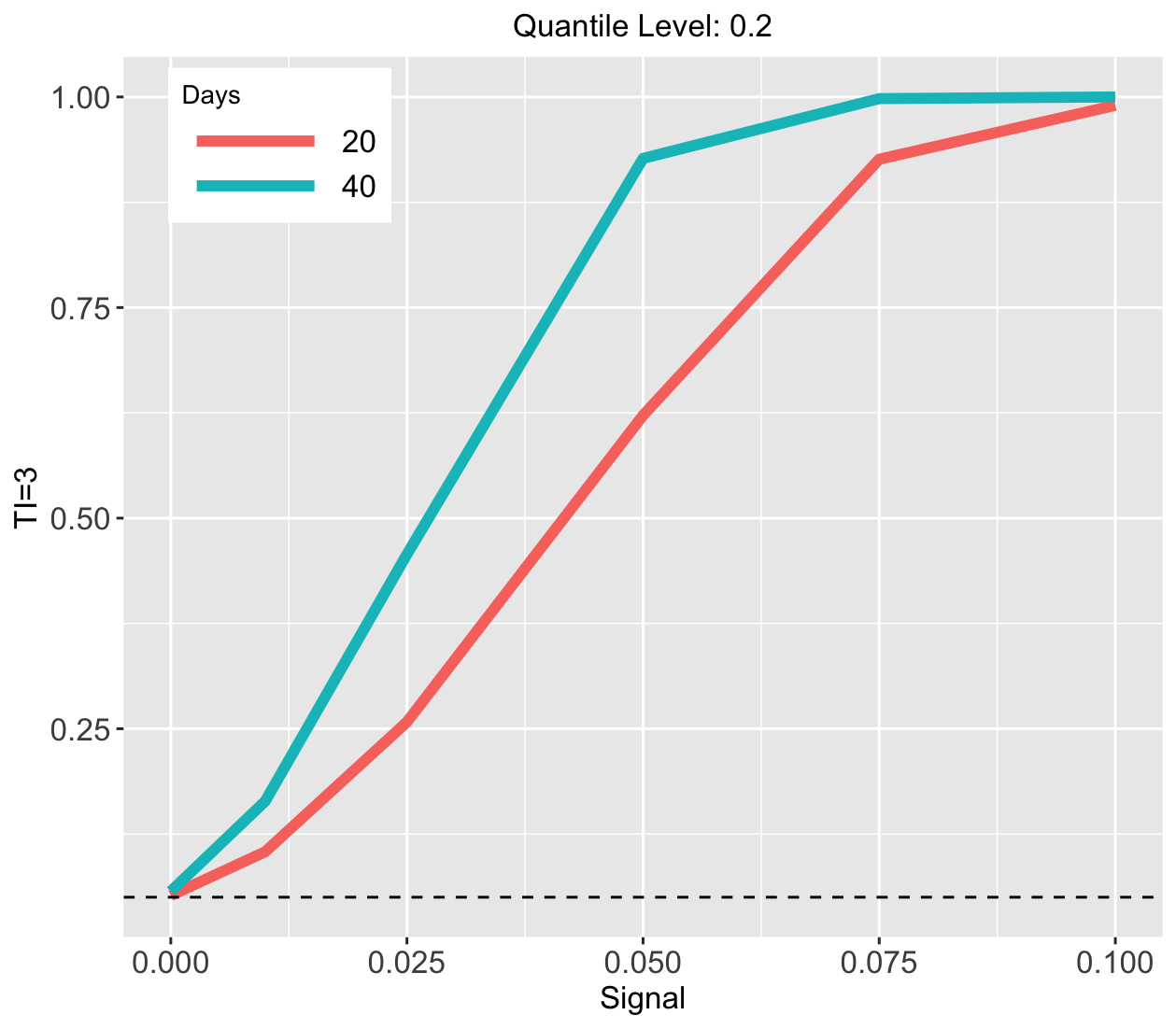

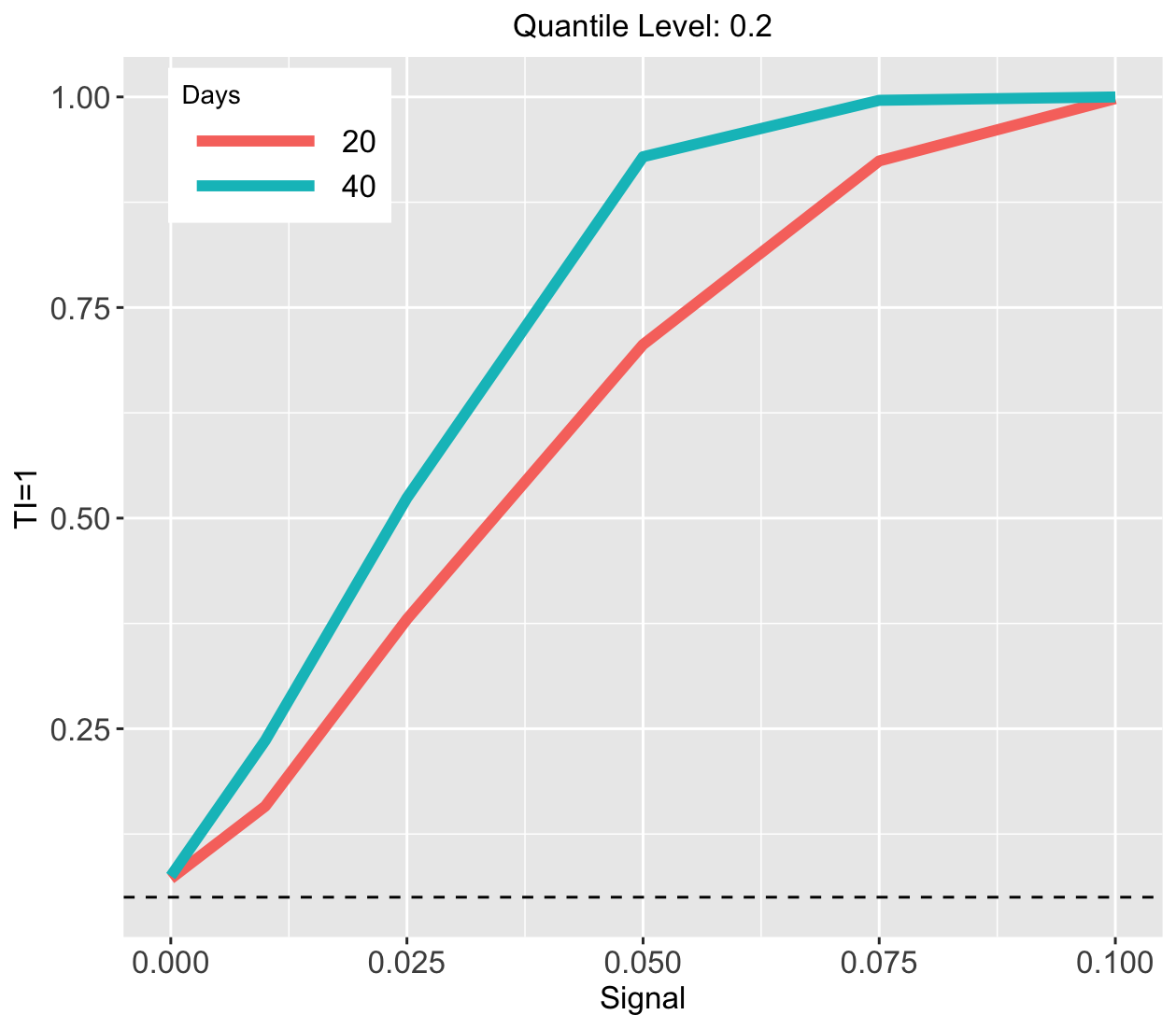

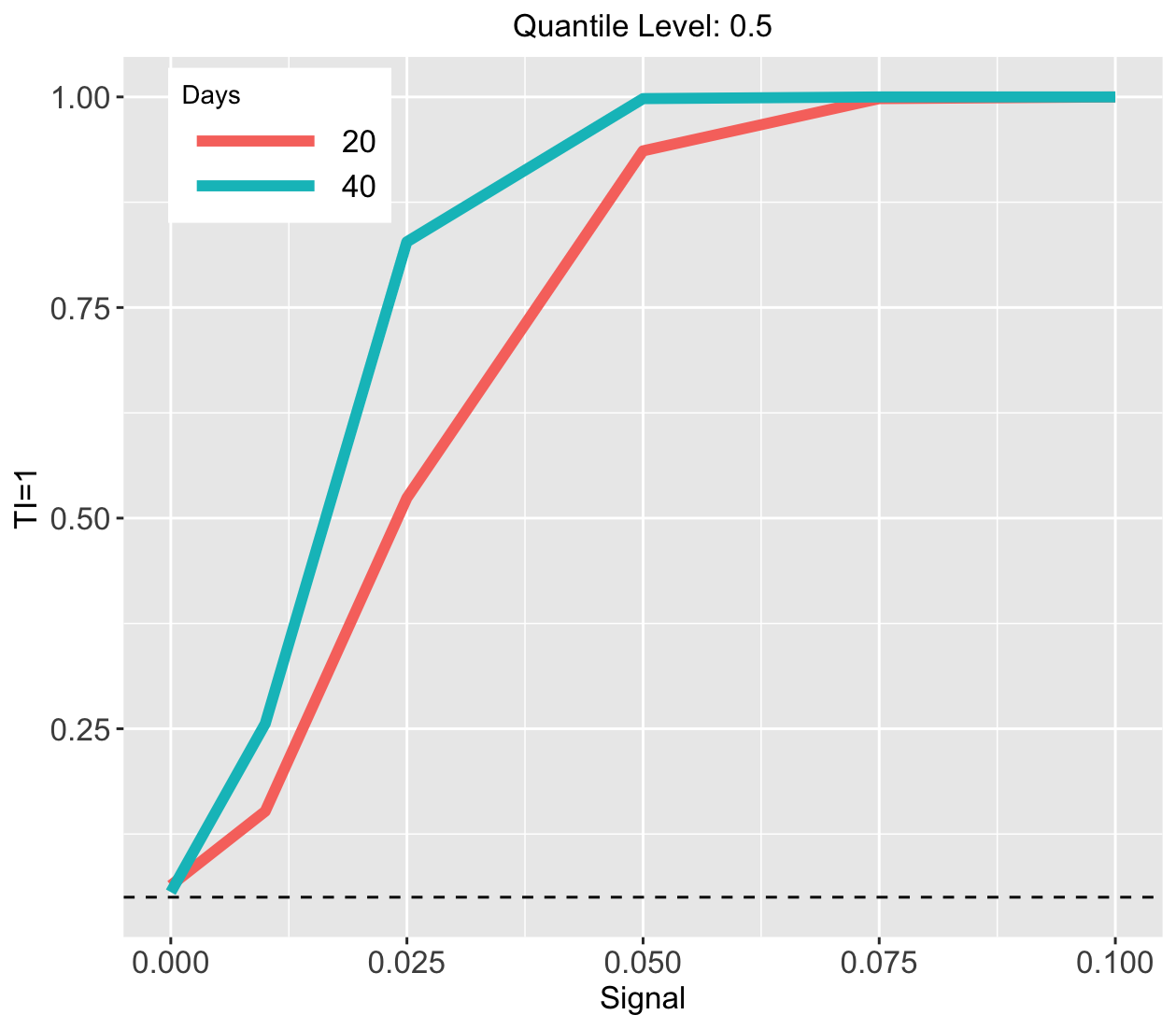

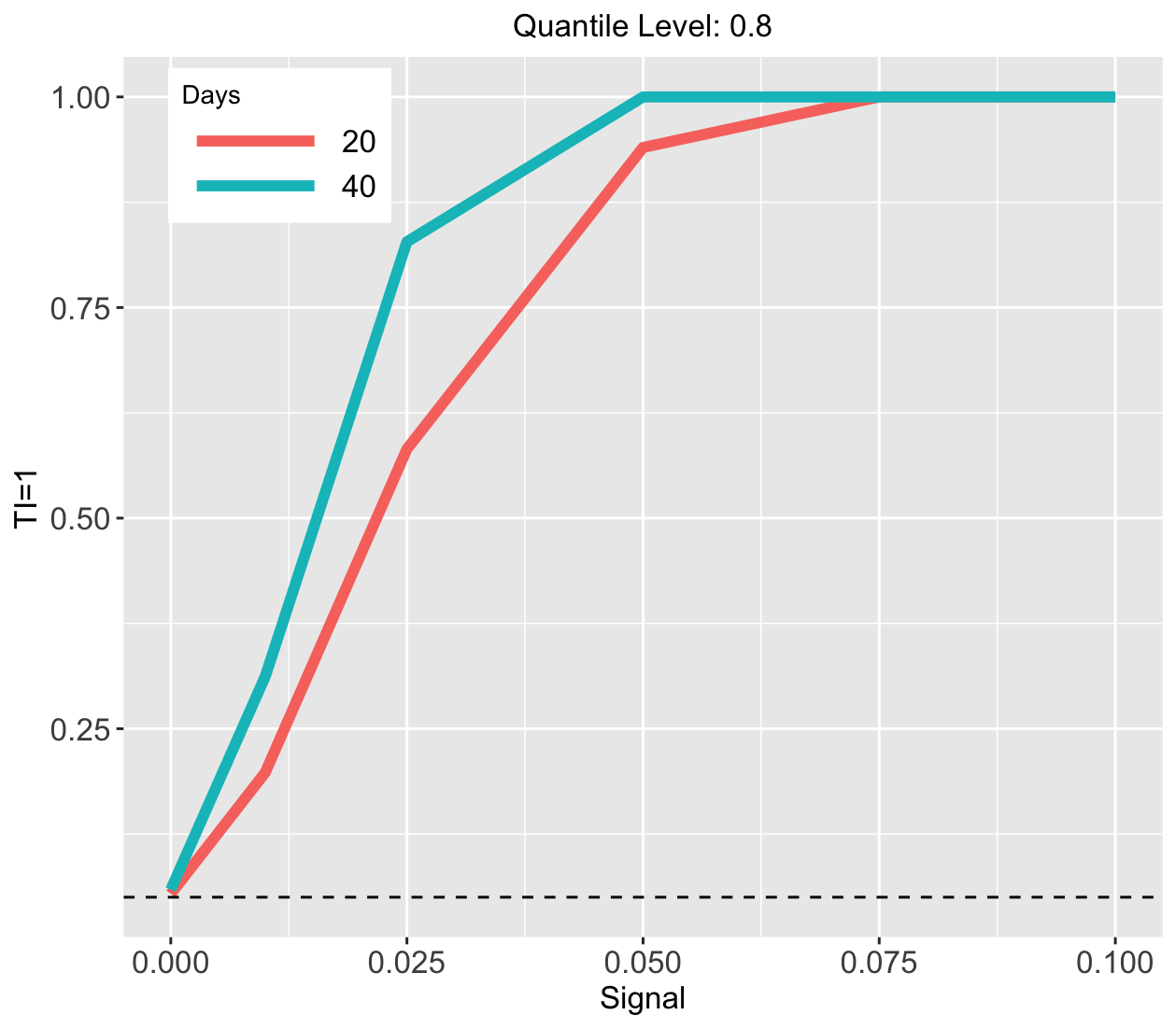

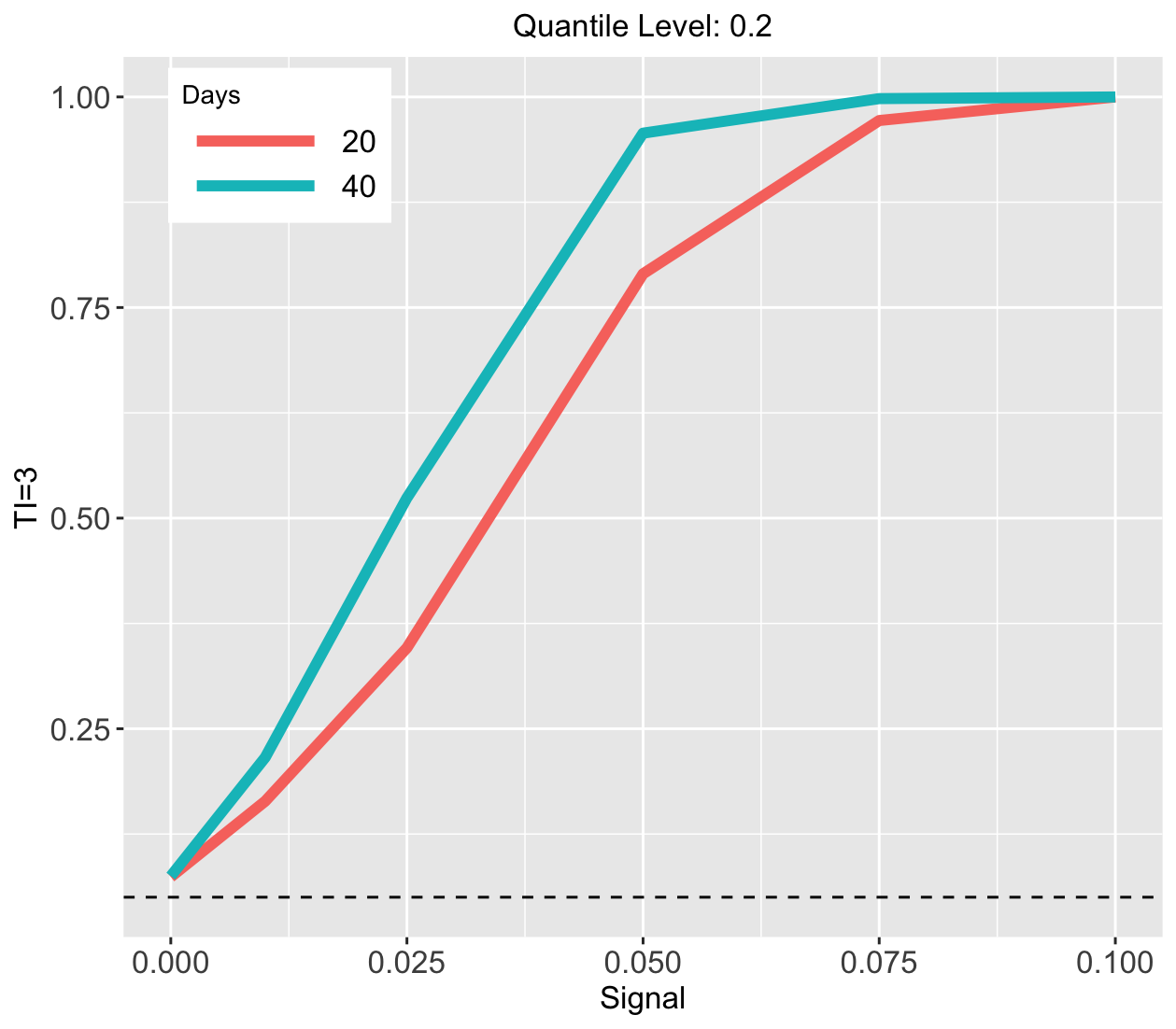

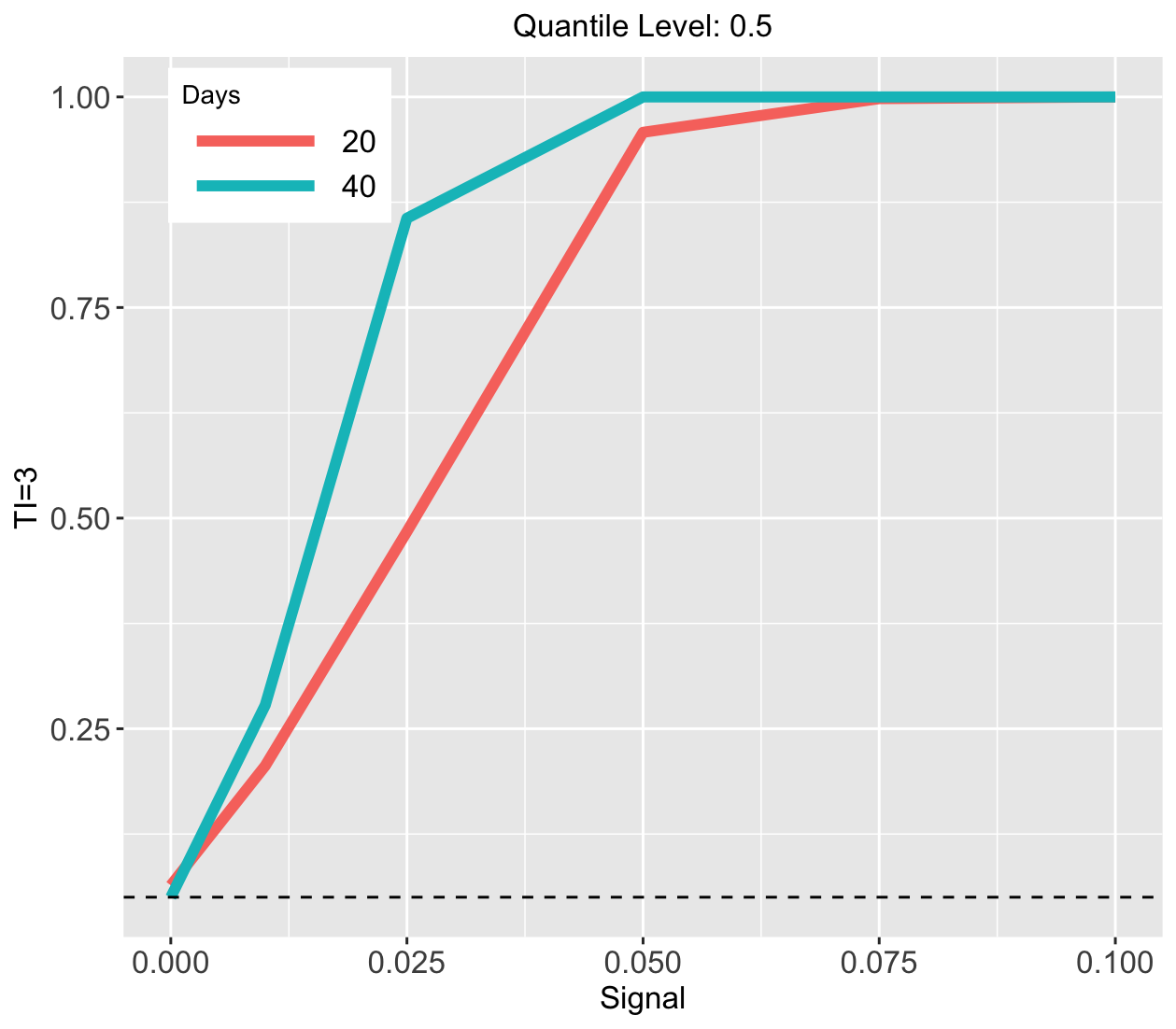

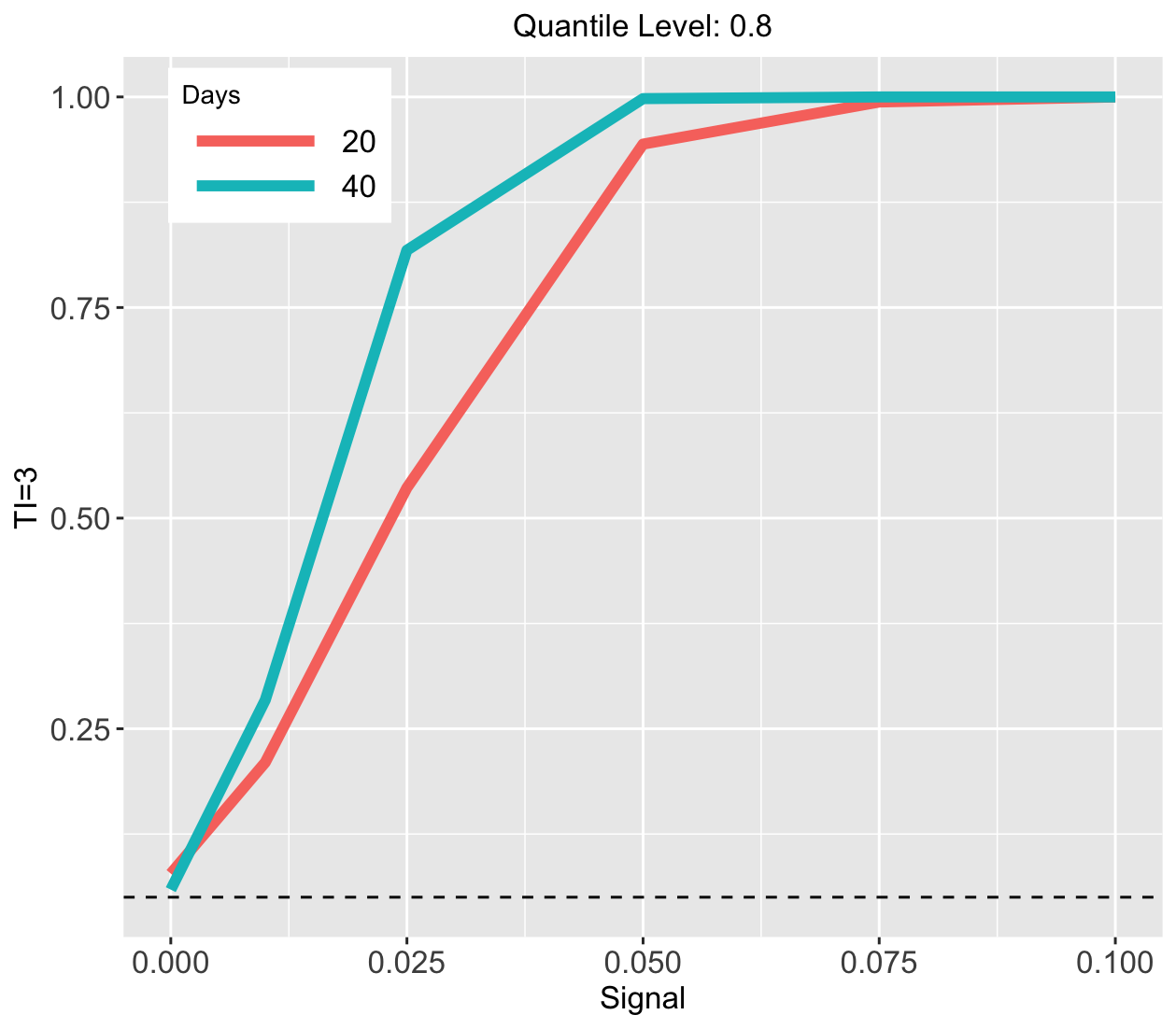

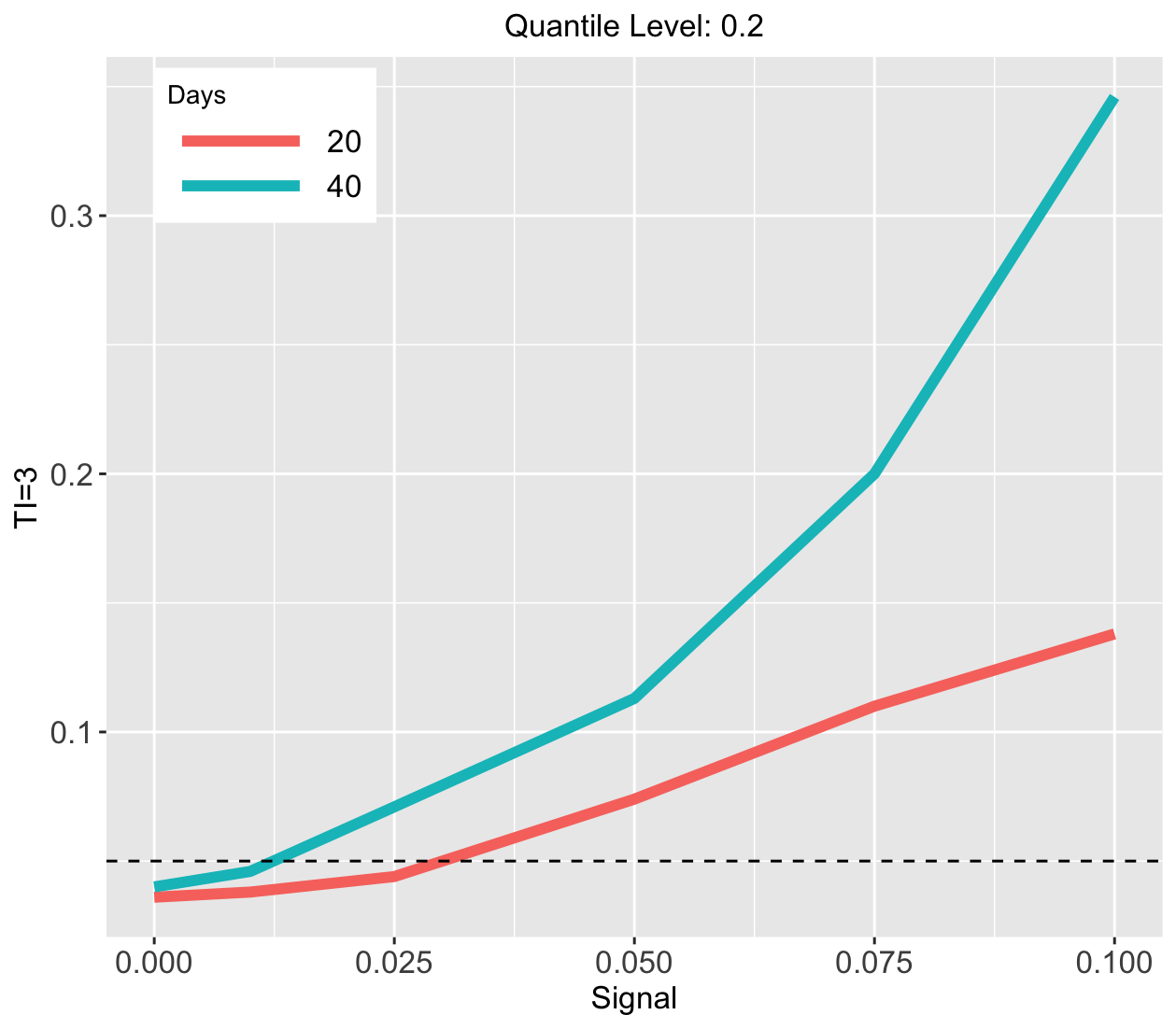

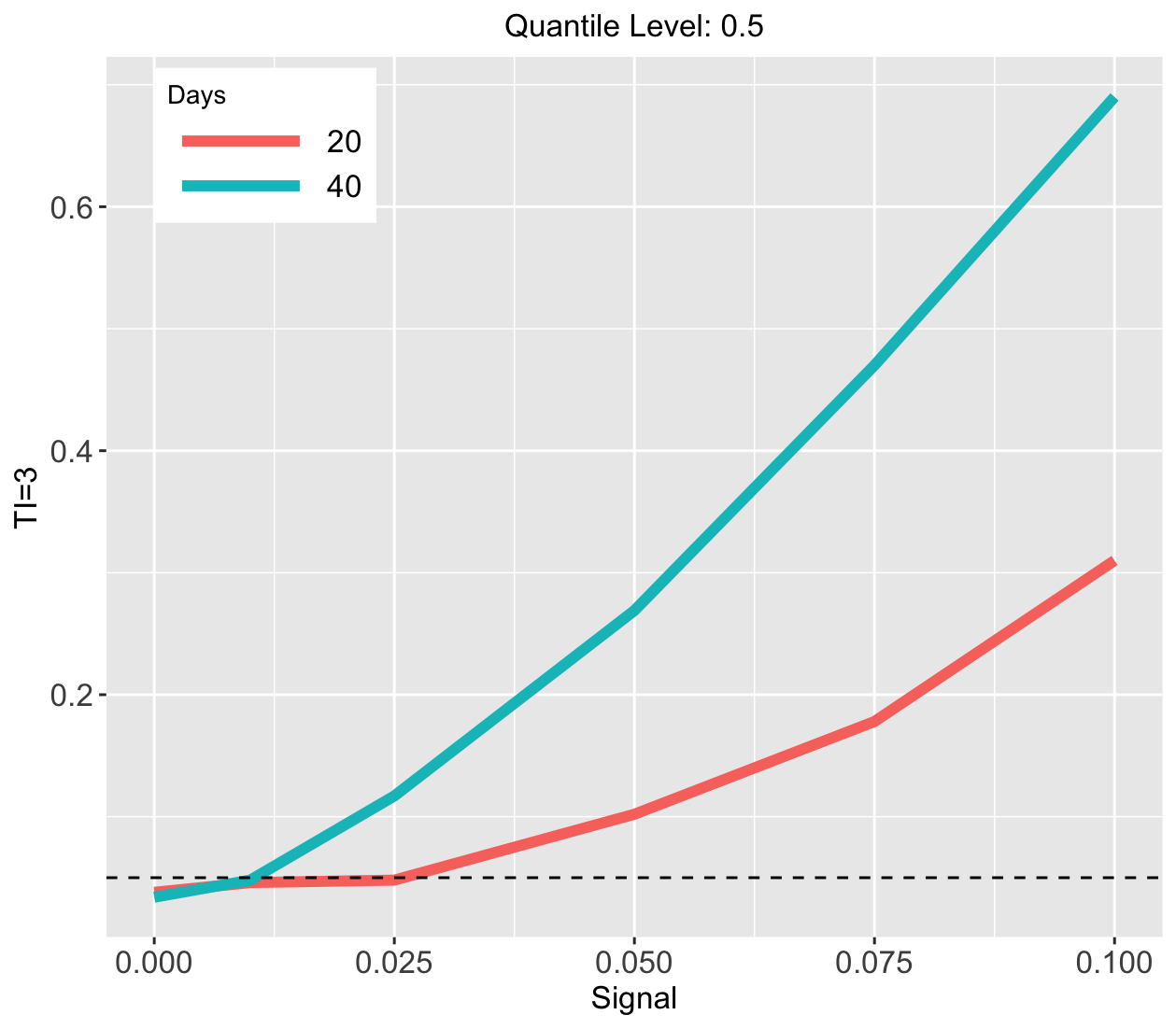

Finally, we discuss the simulation results. Figure 7 presents the empirical rejection rates of the proposed test for CQTE (refer also to Table 3 in the supplementary material). The type-I error is approximately at the nominal level in all cases. The empirical power generally increases with the sample size and approaches as the signal strength increases to . Furthermore, the empirical power increases with the quantile level , which is expected since are set to be proportional to , whose values increase with the quantile level. These results validate our theoretical assertions. We also report the empirical rejection rates of the proposed test for CQDE and CQIE in Figures 8 and 9 of the supplementary material, respectively. The results are very similar to those of CQTE. It is worth noting that the power for CQDE is generally larger than that of CQTE, whereas the power for CQIE is generally smaller than that for CQTE. This is because the test statistics of CQIE have much larger variances than those of CQDE.

9 Discussion

Motivated by the policy evaluation of A/B testing, we proposed a framework for inferring dynamic CQTE on market features, demonstrating that under certain conditions, the CQTE equals the sum of individual CQTE. This significantly simplifies the estimation and inference procedures by focusing on the CQTE at each spatiotemporal unit. To address the interference effect, we proposed two VCDP models for parameter estimation and inference. We developed a two-step method and a bootstrap-based testing procedure for the inference of CQTE. Further, we extended the proposed procedure to accommodate spatiotemporal data, decomposing the CQTE into the sum of CQDE and CQIE. We established consistency results for parameter estimation and the test procedure. Through the analysis of real datasets obtained from DiDi Chuxing, we demonstrated that our proposed method is a valuable statistical tool for assessing the dynamic QTE of new policies.

References

- Abadie et al. (2002) Abadie, A., J. Angrist, and G. Imbens (2002). Instrumental variables estimates of the effect of subsidized training on the quantiles of trainee earnings. Econometrica 70(1), 91–117.

- Blanco et al. (2020) Blanco, G., X. Chen, C. A. Flores, and A. Flores-Lagunes (2020). Bounds on average and quantile treatment effects on duration outcomes under censoring, selection, and noncompliance. Journal of Business & Economic Statistics 38(4), 901–920.

- Brockwell and Davis (2009) Brockwell, P. J. and R. A. Davis (2009). Time series: theory and methods. Springer science & business media.

- Cai and Xiao (2012) Cai, Z. and Z. Xiao (2012). Semiparametric quantile regression estimation in dynamic models with partially varying coefficients. Journal of Econometrics 167(2), 413–425.

- Cao et al. (2015) Cao, H., D. Zeng, and J. P. Fine (2015). Regression analysis of sparse asynchronous longitudinal data. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 77(4), 755–776.

- Chen and Hsiang (2019) Chen, J.-E. and C.-W. Hsiang (2019). Causal random forests model using instrumental variable quantile regression. Econometrics 7(4), 49.

- Chernozhukov et al. (2013) Chernozhukov, V., D. Chetverikov, and K. Kato (2013). Gaussian approximations and multiplier bootstrap for maxima of sums of high-dimensional random vectors. The Annals of Statistics 41(6), 2786–2819.

- Chernozhukov and Hansen (2005) Chernozhukov, V. and C. Hansen (2005). An IV model of quantile treatment effects. Econometrica 73(1), 245–261.

- Chernozhukov and Hansen (2006) Chernozhukov, V. and C. Hansen (2006). Instrumental quantile regression inference for structural and treatment effect models. Journal of Econometrics 132(2), 491–525.

- Feng et al. (2011) Feng, X., X. He, and J. Hu (2011). Wild bootstrap for quantile regression. Biometrika 98(4), 995–999.

- Firpo (2007) Firpo, S. (2007). Efficient semiparametric estimation of quantile treatment effects. Econometrica 75(1), 259–276.

- Gill and Robins (2001) Gill, R. D. and J. M. Robins (2001). Causal inference for complex longitudinal data: the continuous case. The Annals of Statistics 29(6), 1785–1811.

- Horowitz and Krishnamurthy (2018) Horowitz, J. L. and A. Krishnamurthy (2018). A bootstrap method for constructing pointwise and uniform confidence bands for conditional quantile funtions. Statistica Sinica 28(4), 2609–2632.

- Hu et al. (2022) Hu, Y., S. Li, and S. Wager (2022). Average direct and indirect causal effects under interference. Biometrika 109(4), 1165–1172.

- Hudgens and Halloran (2008) Hudgens, M. G. and M. E. Halloran (2008). Toward causal inference withinterference. Journal of the American Statistical Association 103(482), 832–842.

- Imbens and Rubin (2015) Imbens, G. W. and D. B. Rubin (2015). Causal inference in statistics, social, and biomedical sciences. Cambridge University Press.

- Kallus et al. (2019) Kallus, N., X. Mao, and M. Uehara (2019). Localized debiased machine learning: Efficient inference on quantile treatment effects and beyond. arXiv preprint arXiv:1912.12945.

- Kallus and Uehara (2022) Kallus, N. and M. Uehara (2022). Efficiently breaking the curse of horizon in off-policy evaluation with double reinforcement learning. Operations Research 70(6), 3035–3628.

- Koenker (2005) Koenker, R. (2005). Quantile Rregression. Cambridge University Press.

- Koenker and Hallock (2001) Koenker, R. and K. F. Hallock (2001). Quantile regression. Journal of Economic Perspectives 15(4), 143–156.

- Koenker and Portnoy (1987) Koenker, R. and S. Portnoy (1987). L-estimation for linear models. Journal of the American statistical Association 82(399), 851–857.

- Kong et al. (2022) Kong, D., S. Yang, and L. Wang (2022). Identifiability of causal effects with multiple causes and a binary outcome. Biometrika 109(1), 265–272.

- Li and Wager (2022) Li, S. and S. Wager (2022). Network interference in micro-randomized trials. arXiv preprint arXiv:2202.05356.

- Liao et al. (2021) Liao, P., P. Klasnja, and S. Murphy (2021). Off-policy estimation of long-term average outcomes with applications to mobile health. Journal of the American Statistical Association 116(533), 382–391.

- Liao et al. (2022) Liao, P., Z. Qi, R. Wan, P. Klasnja, and S. A. Murphy (2022). Batch policy learning in average reward markov decision processes. The Annals of Statistics 50(6), 3364–3387.

- Liu et al. (2019) Liu, M., X. Sun, M. Varshney, and Y. Xu (2019). Large-scale online experimentation with quantile metrics. arXiv preprint arXiv:1903.08762.

- Liu et al. (2018) Liu, Q., L. Li, Z. Tang, and D. Zhou (2018). Breaking the curse of horizon: infinite-horizon off-policy estimation. In Proceedings of the 32nd International Conference on Neural Information Processing Systems, pp. 5361–5371.

- Luo et al. (2022) Luo, S., Y. Yang, C. Shi, F. Yao, J. Ye, and H. Zhu (2022). Policy evaluation for temporal and/or spatial dependent experiments in ride-sourcing platforms. arXiv preprint arXiv:2202.10887.

- Ma et al. (2019) Ma, H., T. Li, H. Zhu, and Z. Zhu (2019). Quantile regression for functional partially linear model in ultra-high dimensions. Computational Statistics & Data Analysis 129, 135–147.

- Puterman (2014) Puterman, M. L. (2014). Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons.

- Qi et al. (2022) Qi, Z., J.-S. Pang, and Y. Liu (2022). On robustness of individualized decision rules. Journal of the American Statistical Association (Accepted).

- Qin et al. (2020) Qin, Z., X. Tang, Y. Jiao, F. Zhang, Z. Xu, H. Zhu, and J. Ye (2020). Ride-hailing order dispatching at didi via reinforcement learning. Informs Journal on Applied Analytics 50(5), 272–285.

- Qin et al. (2022) Qin, Z. T., H. Zhu, and J. Ye (2022). Reinforcement learning for ridesharing: An extended survey. Transportation Research Part C: Emerging Technologies 144, 103852.

- Rubin (2005) Rubin, D. B. (2005). Causal inference using potential outcomes: Design, modeling, decisions. Journal of the American Statistical Association 100(469), 322–331.

- Savje et al. (2021) Savje, F., P. M. Aronow, and M. G. Hudgens (2021). Average treatment effects in the presence of unknown interference. The Annals of Statistics 49(2), 673–701.

- Sherwood and Wang (2016) Sherwood, B. and L. Wang (2016). Partially linear additive quantile regression in ultra-high dimension. The Annals of Statistics 44(1), 288–317.

- Shi et al. (2020) Shi, C., W. Lu, and R. Song (2020). Breaking the curse of nonregularity with subagging—inference of the mean outcome under optimal treatment regimes. Journal of Machine Learning Research 21(176), 1–67.

- Shi et al. (2022) Shi, C., R. Wan, G. Song, S. Luo, R. Song, and H. Zhu (2022). A multi-agent reinforcement learning framework for off-policy evaluation in two-sided markets. arXiv preprint arXiv:2202.10574.

- Shi et al. (2022) Shi, C., X. Wang, S. Luo, H. Zhu, J. Ye, and R. Song (2022). Dynamic causal effects evaluation in A/B testing with a reinforcement learning framework. Journal of the American Statistical Association (Accepted).

- Shi et al. (2020) Shi, C., S. Zhang, W. Lu, and R. Song (2020). Statistical inference of the value function for reinforcement learning in infinite horizon settings. arXiv preprint arXiv:2001.04515.

- Tsybakov (2008) Tsybakov, A. (2008). Introduction to Nonparametric Estimation. Springer.

- Van Der Vaart and Wellner (1996) Van Der Vaart, A. W. and J. A. Wellner (1996). Weak convergence and empirical processes. Springer.

- Wang and Yang (2019) Wang, H. and H. Yang (2019). Ridesourcing systems: A framework and review. Transportation Research Part B: Methodological 129, 122–155.

- Wang et al. (2009) Wang, H. J., Z. Zhu, and J. Zhou (2009). Quantile regression in partially linear varying coefficient models. The Annals of Statistics 37(6B), 3841–3866.

- Wang and Tchetgen Tchetgen (2018) Wang, L. and E. Tchetgen Tchetgen (2018). Bounded, efficient and multiply robust estimation of average treatment effects using instrumental variables. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 80(3), 531–550.

- Wang et al. (2018) Wang, L., Y. Zhou, R. Song, and B. Sherwood (2018). Quantile-optimal treatment regimes. Journal of the American Statistical Association 113(523), 1243–1254.

- Wang and Zhang (2021) Wang, W. and X. Zhang (2021). Conq: Continuous quantile treatment effects for large-scale online controlled experiments. In Proceedings of the 14th ACM International Conference on Web Search and Data Mining, pp. 202–210.

- Xu et al. (2022) Xu, Y., C. Shi, S. Luo, L. Wang, and R. Song (2022). Quantile off-policy evaluation via deep conditional generative learning. arXiv preprint arXiv:2212.14466.

- Yang et al. (2017) Yang, F., A. Ramdas, K. G. Jamieson, and M. J. Wainwright (2017). A framework for multi-A (rmed)/B (andit) testing with online FDR control. Advances in Neural Information Processing Systems 30.

- Zhang et al. (2013) Zhang, B., A. A. Tsiatis, E. B. Laber, and M. Davidian (2013). Robust estimation of optimal dynamic treatment regimes for sequential treatment decisions. Biometrika 100(3), 681–694.

- Zhang et al. (2022) Zhang, Z., X. Wang, L. Kong, and H. Zhu (2022). High-dimensional spatial quantile function-on-scalar regression. Journal of the American Statistical Association 117(539), 1563–1578.

- Zhao et al. (2022) Zhao, Z., X. Chen, X. Zhang, and Y. Zhou (2022). Dynamic car dispatching and pricing: Revenue and fairness for ridesharing platforms. arXiv preprint arXiv:2207.06318.

- Zhou et al. (2021) Zhou, F., S. Luo, X. Qie, J. Ye, and H. Zhu (2021). Graph-based equilibrium metrics for dynamic supply–demand systems with applications to ride-sourcing platforms. Journal of the American Statistical Association 116(536), 1688–1699.

- Zhou et al. (2020) Zhou, F., J. Wang, and X. Feng (2020). Non-crossing quantile regression for distributional reinforcement learning. Advances in Neural Information Processing Systems 33, 15909–15919.

- Zhou et al. (2021) Zhou, X., L. Kong, R. Karunamuni, and H. Zhu (2021). Quantile regression with varying coefficients for functional responses. Working paper.

- Zhou et al. (2020) Zhou, Y., Y. Liu, P. Li, and F. Hu (2020). Cluster-adaptive network A/B testing: From randomization to estimation. arXiv preprint arXiv:2008.08648.

- Zhu et al. (2014) Zhu, H., J. Fan, and L. Kong (2014). Spatially varying coefficient model for neuroimaging data with jump discontinuities. Journal of the American Statistical Association 109(507), 1084–1098.

- Zhu et al. (2012) Zhu, H., R. Li, and L. Kong (2012). Multivariate varying coefficient model for functional responses. The Annals of Statistics 40(5), 2634–2666.

Appendix A Tables for simulation results

We report Tables 3 to 5 in this section. These tables contain empirical rejection rates of the proposed tests for CQTE, CQDE and CQIE in simulation studies, respectively, based on 500 simulation replications. Figures 8 and 9 depict the empirical rejection rates for CQDE and CQIE.

| TI | 0 | 0.001 | 0.025 | 0.050 | 0.075 | 0.100 | ||

|---|---|---|---|---|---|---|---|---|

| 0.2 | 1 | 20 | 0.038(0.009) | 0.084(0.012) | 0.196(0.018) | 0.474(0.022) | 0.750(0.019) | 0.954(0.009) |

| 40 | 0.049(0.010) | 0.148(0.016) | 0.381(0.022) | 0.844(0.016) | 0.984(0.006) | 1.000(0.000) | ||

| 3 | 20 | 0.052(0.010) | 0.104(0.014) | 0.258(0.020) | 0.622(0.022) | 0.926(0.012) | 0.990(0.004) | |

| 40 | 0.057(0.010) | 0.164(0.017) | 0.457(0.022) | 0.927(0.012) | 0.998(0.002) | 1.000(0.000) | ||

| 0.5 | 1 | 20 | 0.036(0.008) | 0.062(0.011) | 0.268(0.020) | 0.718(0.020) | 0.964(0.008) | 0.996(0.003) |

| 40 | 0.040(0.009) | 0.192(0.018) | 0.684(0.021) | 0.996(0.003) | 1.000(0.000) | 1.000(0.000) | ||

| 3 | 20 | 0.044(0.009) | 0.130(0.015) | 0.352(0.021) | 0.870(0.015) | 0.992(0.004) | 1.000(0.000) | |

| 40 | 0.036(0.008) | 0.196(0.018) | 0.747(0.019) | 0.998(0.002) | 1.000(0.000) | 1.000(0.000) | ||

| 0.8 | 1 | 20 | 0.042(0.009) | 0.100(0.013) | 0.400(0.022) | 0.854(0.016) | 0.996(0.003) | 1.000(0.000) |

| 40 | 0.059(0.011) | 0.272(0.020) | 0.828(0.017) | 1.000(0.000) | 1.000(0.000) | 1.000(0.000) | ||

| 3 | 20 | 0.050(0.010) | 0.144(0.016) | 0.476(0.022) | 0.970(0.008) | 1.000(0.000) | 1.000(0.000) | |

| 40 | 0.061(0.011) | 0.312(0.021) | 0.846(0.016) | 1.000(0.000) | 1.000(0.000) | 1.000(0.000) |

| TI | 0 | 0.001 | 0.025 | 0.050 | 0.075 | 0.100 | ||

|---|---|---|---|---|---|---|---|---|

| 0.2 | 1 | 20 | 0.072(0.012) | 0.158(0.016) | 0.380(0.022) | 0.706(0.020) | 0.924(0.012) | 0.998(0.002) |

| 40 | 0.075(0.012) | 0.236(0.019) | 0.524(0.022) | 0.929(0.011) | 0.996(0.003) | 1.000(0.000) | ||

| 3 | 20 | 0.074(0.012) | 0.164(0.017) | 0.346(0.021) | 0.790(0.018) | 0.972(0.007) | 1.000(0.000) | |

| 40 | 0.075(0.012) | 0.216(0.018) | 0.524(0.022) | 0.957(0.009) | 0.998(0.002) | 1.000(0.000) | ||

| 0.5 | 1 | 20 | 0.064(0.011) | 0.152(0.016) | 0.524(0.022) | 0.936(0.011) | 0.998(0.002) | 1.000(0.000) |

| 40 | 0.056(0.010) | 0.256(0.020) | 0.828(0.017) | 0.998(0.002) | 1.000(0.000) | 1.000(0.000) | ||

| 3 | 20 | 0.064(0.011) | 0.206(0.018) | 0.484(0.022) | 0.958(0.009) | 0.998(0.002) | 1.000(0.000) | |

| 40 | 0.050(0.010) | 0.278(0.020) | 0.856(0.016) | 1.000(0.000) | 1.000(0.000) | 1.000(0.000) | ||

| 0.8 | 1 | 20 | 0.054(0.010) | 0.198(0.018) | 0.582(0.022) | 0.940(0.011) | 1.000(0.000) | 1.000(0.000) |

| 40 | 0.059(0.011) | 0.312(0.021) | 0.828(0.017) | 1.000(0.000) | 1.000(0.000) | 1.000(0.000) | ||

| 3 | 20 | 0.078(0.012) | 0.210(0.018) | 0.536(0.022) | 0.944(0.010) | 0.994(0.003) | 1.000(0.000) | |

| 40 | 0.059(0.011) | 0.284(0.020) | 0.818(0.017) | 0.998(0.002) | 1.000(0.000) | 1.000(0.000) |

| TI | 0 | 0.001 | 0.025 | 0.050 | 0.075 | 0.100 | ||

|---|---|---|---|---|---|---|---|---|

| 0.2 | 1 | 20 | 0.044(0.009) | 0.040(0.009) | 0.030(0.008) | 0.034(0.008) | 0.062(0.011) | 0.090(0.013) |

| 40 | 0.048(0.010) | 0.046(0.009) | 0.034(0.008) | 0.103(0.014) | 0.170(0.017) | 0.302(0.021) | ||

| 3 | 20 | 0.036(0.008) | 0.038(0.009) | 0.044(0.009) | 0.074(0.012) | 0.110(0.014) | 0.138(0.015) | |

| 40 | 0.040(0.009) | 0.046(0.009) | 0.071(0.011) | 0.113(0.014) | 0.200(0.018) | 0.346(0.021) | ||

| 0.5 | 1 | 20 | 0.030(0.008) | 0.032(0.008) | 0.038(0.009) | 0.078(0.012) | 0.130(0.015) | 0.216(0.018) |

| 40 | 0.030(0.008) | 0.054(0.010) | 0.105(0.014) | 0.233(0.019) | 0.393(0.022) | 0.583(0.022) | ||

| 3 | 20 | 0.038(0.009) | 0.046(0.009) | 0.048(0.010) | 0.102(0.014) | 0.178(0.017) | 0.310(0.021) | |

| 40 | 0.034(0.008) | 0.048(0.010) | 0.117(0.014) | 0.269(0.020) | 0.470(0.022) | 0.690(0.021) | ||

| 0.8 | 1 | 20 | 0.038(0.009) | 0.032(0.008) | 0.078(0.012) | 0.186(0.017) | 0.400(0.022) | 0.564(0.022) |

| 40 | 0.034(0.008) | 0.072(0.012) | 0.209(0.018) | 0.625(0.022) | 0.879(0.015) | 0.982(0.006) | ||

| 3 | 20 | 0.044(0.009) | 0.056(0.010) | 0.120(0.015) | 0.298(0.020) | 0.538(0.022) | 0.752(0.019) | |

| 40 | 0.034(0.008) | 0.092(0.013) | 0.249(0.019) | 0.700(0.020) | 0.957(0.009) | 0.996(0.003) |

Appendix B Regularity assumptions

In this section, we present the assumptions for studying the asymptotic properties of the estimators. First, we introduce some notations. Let and denote the probability distribution and density function of the error process. We rescale the time and set for . It follows that . In temporal dependent experiments, we define

In spatiotemporal dependent experiments, we also set for such that . We define , , and

Second, we list the following assumptions to guarantee the theoretical results of the proposed test in temporal dependent experiments. Notice that we allow to grow with .

Assumption 1.

The kernel function is a symmetric probability density function defined over the interval . It is Lipschitz continuous and satisfies the condition , signifying its finiteness under the integral of its absolute derivative.

Assumption 2.

The probability density function is strictly positive and continuously varies as a function of . It is twice differentiable at any , possessing a second-order derivative that is both continuous and uniformly bounded. Similarly, the joint probability density function is strictly positive and continuously varies as a function of . It is twice differentiable at any pair , maintaining a second-order derivative that is continuous and uniformly bounded.

Assumption 3.

The covariates are drawn independently and identically from a sub-Gaussian process. Furthermore, for any integer within the range , the smallest eigenvalue of the expected value matrix remains greater than zero.

Assumption 4.

All components of and possess second-order derivatives with respect to that are not only bounded but also continuous for each .

Assumption 5.

For any in the interval [0, 1], there exist constants , , and such that , , and .

Assumption 1, which is often found in the literature on varying coefficient models and kernel smoothing, pertains to regular conditions in kernel methods (see e.g., Zhu et al., 2012, 2014; Cao et al., 2015). Assumption 2 addresses the distribution function of the error process, a condition frequently stipulated in the quantile regression literature (Koenker and Hallock, 2001; Cai and Xiao, 2012; Ma et al., 2019). This assumption is crucial for establishing the necessary conditions on the distribution and density functions of the error process. Assumption 3 ensures the well-defined nature of the first-step estimators, essentially guaranteeing the positive definiteness of the moment of the design matrix. Assumption 4 is a common requirement in the varying coefficient literature. It mandates the smoothness of the varying coefficients (Zhu et al., 2012, 2014; Zhou et al., 2021). Finally, Assumption 5 is put forth to ensure the stationarity of the observation vector. This type of condition is frequently imposed in the time series literature (see e.g., Brockwell and Davis, 2009).

Finally, we present technical assumptions that establish the consistency of the proposed test in a spatiotemporal dependent experiment. We allow both and to grow with .

Assumption 6.

The probability density function is strictly positive, continuous as a function of , and twice differentiable at any with continuous and uniformly bounded second-order derivative. Moreover, the joint probability density function is strictly positive, continuous at , and twice differentiable at any with continuous and uniformly bounded second-order derivative.

Assumption 7.

The covariate s are independently and identically distributed from a sub-Gaussian process. Furthermore, for and , the minimum eigenvalue of is bounded away from zero.

Assumption 8.

All components of and have bounded and continuous second-order derivatives with respect to for each .

Assumption 9.

There exist some constants , such that , and .

Appendix C Asymptotic properties of the test procedures

In this section, we establish the asymptotic properties of the proposed test procedures in Section 5. We first establish the asymptotic normality of the one-step and second-step estimators, and in the temporal dependent experiment, and prove the validity of the test procedure for QDEτ.

Let’s define , and as an matrix where the th entry equals . Furthermore, we define

| (18) |

These two matrices represent the asymptotic covariance matrices of the one-step and two-step estimators, respectively.

Theorem 3.

Suppose is bounded away from zero. Under Assumptions 1–4 of the supplement material, for any -dimensional nonzero vectors and with unit norm, we have as , , ,

-

(i)

.

-

(ii)

, where the bias .

-

(iii)

Suppose and . Then the conditional distribution of given the observed data weakly converges to the null limit distribution of .

-

(iv)

If further Assumption 5 of the supplement material holds and , for some , then with probability approaching , there exist some constant and some positive constant such that

Part (i) of Theorem 3 is established using standard arguments in the quantile regression literature (see e.g., Koenker and Hallock, 2001). This part of the theorem provides the limit normal distribution of the raw estimators. Part (ii) further shows that the smoothing step introduces only a negligible bias and reduces the asymptotic covariance by a factor of . These two results imply that the proposed test statistic for CQDE is asymptotically normal. However, as noted earlier, consistently estimating its asymptotic variance remains a challenge due to its complex form. Part (iii) of Theorem 3 validates the proposed bootstrap procedure for CQDE. Instead of using the empirical quantile of the bootstrapped statistics to determine the critical value, our test procedure relies on normal approximation and uses bootstrapped statistics to estimate the variance. Part (iv) validates the bootstrap method for CQIE, which directly follows from the bootstrap consistency for CQTE in Theorem 1.

Appendix D Proofs of the theorems

For any two positive sequences and , the notation implies that there exists some constant such that for any . We use to denote some generic constant whose value is allowed to change from place to place.

Proof of Proposition 1.

Under the assumption of monotonicity, it is immediately evident that is a strictly increasing function of when or . The independence between and leads to the following:

when or . By definition, we know that , which yields:

This leads to the conclusion that:

With these steps, the proof is completed. ∎

Proof of Proposition 2.

Proof of Proposition 3.

Proof of Theorem 1.

First, we provide a sketch of the proof, which is divided into three parts. In the initial step, we acquire a uniform Bahadur representation of the first-stage estimator, which is detailed in Lemma 1. In the second step, we dissect the difference between the distributions of the proposed statistic and the bootstrap statistic. These differences are subsequently bounded by employing the technique of comparison of distributions, as elaborated in Chernozhukov et al. (2013). Finally, we investigate the power properties of the proposed test.

We next detail each of the step. Recall that . According to the uniform Bahadur representation in Lemma 1, we have

where and the big- term is uniform in and .

Let and . Similarly, we can represent as

where .

Let and . It follows that

For simplicity, let be the operator that reshapes a matrix into a vector by stacking its columns on top of one another. Define

| (23) |

For any , let be randomly selected samples (with replacement) from . We next define

| (24) |

We also define be the empirical Gaussian analogs of such that where are i.i.d standard normal random variables, and

| (25) |

Let

We remark that the term represents the difference between the estimators and the true smoothed coefficients in terms of the error processes, while the term represents the difference between the bootstrap estimators and the obtained estimators, and is the Gaussian analogy of .

Define the following functions

To verify the proposed bootstrap procedure, we aim to provide an upper error bound for

where and . Notice that and can be represented by

respectively.

Define , , . It follows that . Therefore,

| (26) |

where , and denote the above three components, respectively.

Define the event

Under the sub-Gaussian condition, it follows from Bonferroni’s inequality that for some constant . This probability approaches 1 as diverges to infinity. We can derive the desired result by showing that on the event , .

On the event , similar to the proofs of Lemma 3 and Theorem 2 in Luo et al. (2022, Section D), we can prove that there exits some constant such that

| (27) | ||||

| (28) |

This yields the upper error bounds for and .

To bound , we introduce the following notations. Let be the empirical Gaussian analogs of such that where is the same for ) in (D), and

It follows from triangle inequality that

| (29) |

Similar to the derivation of Lemma 3 in Luo et al. (2022), one can deduce that

| (30) |

As for , notice that

Denote

Notice that . On the event , we have

due to the sub-Gaussian property of and that . Similarly, for we have that

We can deduce that , where

Similar to the steps of deriving the orders of in (32), we can obtain that

On the event , conditional on the data, and are Gaussian random variables, according to Lemma 3.1 in Chernozhukov et al. (2013),

Plugging (30) and (D) into (D), we obtain that . Together with equations (D), (27) and (28), we come to the desired assertion.

Finally, we show that the proposed test has good power properties. Under the alternative that and according to (27), we have

where is the critical value. If we can show that , then it follows that approaches one.

Direct calculations lead to where

Recall that are Sub-Gassuain random vectors. It is straightforward to show that . Define the event

where

On the event , define we can obtain that

Since the sequence is convergent, we have . Meanwhile, denote , then

By the Sub-Gaussian property of and , one can obtain that .

Hence, we have

| (32) | |||||

where the last inequality follows from the fact that , according to the Borell TIS inequality and Lemma 2.2.10 in Van Der Vaart and Wellner (1996). This completes the proof. ∎

Proof of Theorem 2.

Proof of Theorem 3.

The proof involves four parts. In part (i), we present the proof of the asymptotic normality of the first-stage estimator . In part (ii), we give the proof of the asymptotic normality of the second-stage estimator . In parts (iii) and (iv), we give the proofs of the bootstrap consistency of the testing procedures with respect to and , respectively.

For part (i), we use the Bahadur representation for ordinary quantile regression to derive the asymptotic normality of . Specifically, according to Koenker and Portnoy (1987), for a given quantile level , we have

| (33) |

where and .

We need to verify the covariance structure of and for any . According to the Bahadur representation in (33), the asymptotic covariance of and equals

| (34) |

Specifically, we can show

so (34) is equal to

Therefore, we can prove the asymptotic normality of by using some standard arguments in the quantile regression literature (Koenker, 2005).

For part (ii), we establish the limiting distribution of by using

We assume the existence of a function such that . This function is used to derive the bias. The calculation can be as follows:

| (35) | |||||

Since the time grids are prefixed and equally spaced, we have

Noticing that for any , , direct calculations lead to

where the last equality follows from Taylor expansion and Assumptions 1 and 4.

Furthermore, by applying a change of variables and considering Assumptions 1 and 4, we obtain the following:

Hence, for the fixed time grids, we have

| (36) |

Similarly, one can show that

It is easy to derive that by using standard kernel smoothing techniques (Tsybakov, 2008). It leads to

| (38) |

For the asymptotic co-variance of and , direct calculations lead to

where . There also exists some function such that . Then we can have

where and denote the above two terms, respectively.

Denote , one gets

If has bounded and continuous second derivatives, following similar arguments of the proofs for Lemma 4 in Zhu et al. (2012), it is easy to derive that

Meanwhile, we can obtain

It is easy to see that is the leading term of by noticing that is of lower order of according to . Because , one can obtain

The smoothing step reduces of the variance.

With the preparations above, it is easy to calculate that for any vector with unit norm,

By checking the Lindeberg condition, we can establish the asymptotic normality of .

It is not hard to find that is a linear transformation of . Recall the Bahadur representation of , one can deduce that

where with each corresponds to a vector with dimension . Observing that

holds for any according to the Chebyshev’s inequality. Then the Lindeberg condition follows such that

for any .

(iii) As for the bootstrap consistency of the bootstrap procedures for testing QDE, it suffices to establish the Bahadur representation of the bootstrap estimators parallel to (33) such that

| (40) |

where is the bootstrap error. We use to denote “convergence in probability” conditional on the data. Note that .

Recall that . The bootstrap estimates is obtained by minimizing the following loss function with respect to the bootstrap sample

It is easy to see that is globally minimized at . Similar to the steps in Feng et al. (2011), according to the Sub-Gaussian assumption of the covariates and the error process, we have that

uniformly on any compact set of . Thus, in probability.

Now consider

Following equation (2) in the supplementary material of Feng et al. (2011), we can obtain that

Now we calculate the explicit form of . Notice that , this implies

where the last equality follows from the Taylor’s expansion. Direct calculations lead to