ksdshort=KSD, long=kernel Stein discrepancy \DeclareAcronympdfshort=PDF, long=probability density function \DeclareAcronymrkhsshort=RKHS, long=reproducing kernel Hilbert space \DeclareAcronymmalashort=MALA, long=Metropolis-adjusted Langevin algorithm \DeclareAcronymmcmcshort=MCMC, long=Markov chain Monte Carlo \DeclareAcronymsnisshort=SNIS, long=self-normalised importance sampling \DeclareAcronymgfksdshort=GFKSD, long=gradient-free KSD \DeclareAcronymgarchshort=GARCH, long=generalised auto-regressive moving average

Stein -Importance Sampling

Abstract

Stein discrepancies have emerged as a powerful tool for retrospective improvement of Markov chain Monte Carlo output. However, the question of how to design Markov chains that are well-suited to such post-processing has yet to be addressed. This paper studies Stein importance sampling, in which weights are assigned to the states visited by a -invariant Markov chain to obtain a consistent approximation of , the intended target. Surprisingly, the optimal choice of is not identical to the target ; we therefore propose an explicit construction for based on a novel variational argument. Explicit conditions for convergence of Stein -Importance Sampling are established. For of tasks in the PosteriorDB benchmark, a significant improvement over the analogous post-processing of -invariant Markov chains is reported.

1 Introduction

Stein discrepancies are a class of statistical divergences that can be computed without access to a normalisation constant. Originally conceived as a tool to measure the performance of sampling methods (Gorham and Mackey,, 2015), these discrepancies have since found wide-ranging statistical applications (see the review of Anastasiou et al.,, 2023). Our focus here is the use of Stein discrepancies for retrospective improvement of \acmcmc, and here two main techniques have been proposed: (i) Stein importance sampling (Liu and Lee,, 2017; Hodgkinson et al.,, 2020), and (ii) Stein thinning (Riabiz et al.,, 2022). In Stein importance sampling (also called black box importance sampling), the samples are assigned weights such that a Stein discrepancy between the weighted empirical measure and the target is minimised. Stein thinning constructs a sparse approximation to this optimally weighted measure at a lower computational and storage cost. Together, these techniques provide a powerful set of post-processing tools for \acmcmc, with subsequent authors proposing a range of generalisations and extensions (Teymur et al.,, 2021; Chopin and Ducrocq,, 2021; Hawkins et al.,, 2022; Fisher and Oates,, 2022; Bénard et al.,, 2023).

The consistency of these algorithms has been established in the setting of approximate, -invariant \acmcmc, motivated by challenging inference problems where only approximate sampling can be performed. In these settings, is implicitly an approximation to that is as accurate as possible subject to computational budget. However, the critical question of how to design Markov chains that are well-suited to such post-processing has yet to be addressed. This paper provides a solution, in the form of a specific construction for derived from a novel variational argument. Surprisingly, we are able to demonstrate a substantial improvement using the proposed , compared to the case where and are equal. The paper proceeds as follows: Section 2 presents an abstract formulation of the task and existing results for optimally-weighted empirical measures are reviewed. Section 3 derives our proposed choice of and establishes that Stein post-processing of samples from a -invariant \acmala provides a consistent approximation of . The approach is stress-tested using the recently released PosteriorDB suite of benchmark tasks in Section 4, before concluding with a discussion in Section 5.

2 Background

To properly contextualise our discussion we start with an abstract mathematical description of the task. Let be a probability measure on a measurable space . Let be the set of all probability measures on . Let be a statistical divergence for measuring the quality of an approximation to , meaning that if and only if . In this work we consider approximations whose support is contained in a finite set , and in particular we consider optimal approximations of the form

In what follows we restrict attention to statistical divergences for which such approximations can be shown to exist and be well-defined. The question that we then ask is which states minimise the approximation error ? Before specialising to Stein discrepancies, it is helpful to review existing results for some standard statistical divergences .

2.1 Wasserstein Divergence

Optimal quantisation focuses on the -Wasserstein () family of statistical divergences , where denotes the set of all couplings111A coupling is a distribution whose marginal distributions are and . of , and the divergence is finite whenever and have finite -th moment. Assuming the states are distinct, the corresponding optimal weights are where is the Voronoi neighbourhood222The Voronoi neighbourhood of is the set . of in . Optimal states achieve the minimal quantisation error for ;

the smallest value of the divergence among optimally-weighted distributions supported on at most states. Though the dependence of optimal states on and can be complicated, we can broaden our perspective to consider asymptotically optimal states, whose asymptotic properties can be precisely characterised. To this end, for , let denote the uniform distribution on , and define the universal constant . Suppose that admits a density on . Then the th quantisation coefficient of on , defined as

plays a central role in the classical theory of quantisation, being the rate constant in the asymptotic convergence of the minimal quantisation error; ; see Theorem 6.2 of Graf and Luschgy, (2007). This suggests a natural definition; a collection is called asymptotically optimal if

which amounts to asymptotically attaining the minimal quantisation error . The main result here is that, if are asymptotically optimal, then , where convergence is in distribution and is the distribution whose density is ; see Theorem 7.5 of Graf and Luschgy, (2007). This provides us with a key insight; optimal states are over-dispersed with respect to the intended distributional target. The extent of the over-dispersion here depends both on , a parameter of the statistical divergence, and the dimension of the space on which distributions are defined.

The -Wasserstein divergence is, unfortunately, not well-suited for use in the motivating Bayesian context. In particular, computing the optimal weights requires knowledge of , which is typically not available when is implicitly defined via an intractable normalisation constant. On the other hand, the optimal sampling distribution is explicit and can be sampled (for example using \acmcmc); for discussion of random quantisers in this context see Graf and Luschgy, (2007, Chapter 9), Cohort, (2004, p126) and Sonnleitner, (2022, Section 4.5). The simple form of is a feature of the classical approach to quantisation that we will attempt to mimic in the sequel.

2.2 Kernel Discrepancies

The theory of quantisation using kernels is less well-developed. A kernel is a measurable, symmetric, positive-definite function . From the Moore–Aronszajn theorem, there is a unique Hilbert space for which is a reproducing kernel, meaning that for all and for all and all . Assuming that , we can define the weak (or Pettis) integral

| (1) |

called the kernel mean embedding of in . The kernel discrepancy is then defined as the norm of the difference between kernel mean embeddings

| (2) |

where, to be consistent with our earlier notation, we adopt the convention that is infinite whenever . The second equality in (2) follows immediately from the stated properties of a reproducing kernel. To satisfy the requirement of a statistical divergence, we assume that the kernel is characteristic, meaning that if and only if . In this setting, the properties of optimal states are necessarily dependent on the choice of kernel , and are in general not well-understood. Indeed, given distinct states , the corresponding optimal weights are the solution to the linearly-constrained quadratic program

| (3) |

where and . This program does not admit a closed-form solution, but can be numerically solved. To the best of our knowledge, the only theoretical analysis of approximations based on (3) is due to Hayakawa et al., (2022), who established rates for the convergence of to in the case where states are independently sampled from . The question of an optimal sampling distribution was not considered in that work.

Although few results are available concerning (3), relaxations of this program have been well-studied. The simplest relaxation of (3) is to remove both the positivity () and normalisation () constraints, in which case the optimal weights have the explicit representation . The analysis of optimal states in this context has developed under the dual strands of kernel cubature and Bayesian cubature, where it has been theoretically or empirically demonstrated that (i) if states are randomly sampled, the optimal sampling distribution will be -dependent (Bach,, 2017) and over-dispersed with respect to the distributional target (Briol et al.,, 2017), and (ii) space-filling designs are asymptotically optimal for typical stationary kernels on bounded domains (Briol et al.,, 2019). Analysis of optimal states on unbounded domains appears to be more difficult; see e.g. Karvonen et al., (2021). Relaxation of either the positivity or normalisation constraints results in approximations that behave similarly to kernel cubature (see, respectively, Ehler et al.,, 2019; Karvonen et al.,, 2018). However, relaxation of either constraint can result in the failure of to be an element of , limiting the relevance of these results to the posterior approximation task.

Despite relatively little being known about the character of optimal states in this context, kernel discrepancy is widely used. The application of kernel discrepancies to an implicitly defined distributional target, such as a posterior distribution in a Bayesian analysis, is made possible by the use of a Stein kernel; a -dependent kernel for which for all (Oates et al.,, 2017). The associated kernel discrepancy

| (4) |

is called a \acksd (Chwialkowski et al.,, 2016; Liu et al.,, 2016; Gorham and Mackey,, 2017), and this will be a key tool in our methodological development. The corresponding optimally weighted approximation is the Stein importance sampling method of Liu and Lee, (2017). To retain clarity of presentation in the main text, we defer all details on the construction of Stein kernels to Appendix A.

2.3 Sparse Approximation

If the number of states is large, computation of optimal weights can become impractical. This has motivated a range of sparse approximation techniques, which aim to iteratively construct an approximation of the form , where each is an element from . The canonical example is the greedy algorithm which, at iteration , selects a state

| (5) |

for which the statistical divergence is minimised. In the context of kernel discrepancy, the greedy algorithm (5) has computational cost , which compares favourably333It is difficult to quantify the complexity of numerically solving (3), since this will depend on details of the solver and the tolerance that are used. On the other hand, if we ignore the non-negativity and normalisation constraints, then we can see that the computational cost of solving the -dimensional linear system of equations is . with the cost of solving (3) when . Furthermore, under appropriate assumptions, the sparse approximation converges to the optimally weighted approximation; as with fixed. See Teymur et al., (2021) for full details, where non-myopic and mini-batch extensions of the greedy algorithm are also considered. The greedy algorithm can be viewed as a regularised version of the Frank–Wolfe algorithm (also called herding, or the conditional gradient method), for which a similar asymptotic result can be shown to hold (Chen et al.,, 2010; Bach et al.,, 2012; Chen et al.,, 2018). Related work includes Dwivedi and Mackey, (2021, 2022); Shetty et al., (2022). Since in what follows we aim to retrospectively improve \acmcmc output, where it is not unusual to encounter –, sparse approximation will be important.

This completes our overview of background material. In what follows we seek to mimic classical quantisation by deriving a choice for that is straight-forward to sample using \acmcmc and is appropriately over-dispersed relative to . This should be achieved while remaining in the framework of kernel discrepancies, so that optimal weights can be explicitly computed, and coupled with a sparse approximation that has low computational and storage cost.

3 Methodology

The methods that we consider first sample states using -invariant \acmcmc, then post-process these states using kernel discrepancies (Section 2.2) and sparse approximation (Section 2.3), to obtain an approximation to the target . A variational argument, which we present in Section 3.1, provides a suitable -independent choice for (which agrees with our intuition from Section 2.1 that should be in some appropriate sense over-dispersed with respect to ). Sufficient conditions for strong consistency of the approximation are established in Section 3.3.

3.1 Selecting

Here we present a heuristic argument for a particular choice of ; rigorous theoretical support for Stein -Importance Sampling is then provided in Section 3.3. Our setting is that of Section 2.2, and the following will additionally be assumed:

Assumption 1.

It is assumed that

-

(A1)

-

(A2)

.

Note that (A2) implies that , and thus (1) is in fact a strong (or Bochner) integral.

A direct analysis of the optimal states associated to the optimal weights appears to be challenging due to the fact that the components of are strongly inter-dependent. Our solution here is to instead consider optimal states associated with weights that are near-optimal and whose components are only weakly dependent. Specifically, we will be assuming that is absolutely continuous with respect to (denoted ), and study convergence of \acsnis, i.e. the approximation , , where are independent. Since and , from the optimality of under these constraints we have that . It is emphasised that the \acsnis weights are a theoretical device only, and will not be used for computation; indeed, we can demonstrate that the \acsnis weights perform substantially worse than in general.

The analysis of \acsnis weights is tractable when viewed as approximation of the kernel mean embedding in the Hilbert space . Indeed, recall that where . Then, following Section 2.3.1 of Agapiou et al., (2017), we observe that

| (6) |

The idea is to seek for which the asymptotic variance of is small. Supposing that

| (S1) |

from the weak law of large numbers the denominator in (6) converges in probability to 1. Further supposing that

| (S2) |

from the Hilbert space central limit theorem the numerator in (6) converges in distribution to a Gaussian where is the covariance operator defined via

see Section 10.1 of Ledoux and Talagrand, (1991). Thus, from Slutsky’s lemma applied to (6), we conclude that . Recalling that , and noting that the mean square of the limiting Gaussian random variable is , a natural idea is to select the sampling distribution such that is minimised.

Fortunately, the trace of can be explicitly computed. It simplifies presentation to restrict attention to a Stein kernel , for which , giving , where for convenience we have let . Assuming that and admit densities and on , the variational problem we wish to solve is

| (7) |

where be the set of positive measures on for which (S1-2) are satisfied. To solve this problem, we first relax the constraints (S1-2) and solve the relaxed problem using the Euler–Lagrange equations, which yield

| (8) |

Note that the normalisation constant of is from (1), whose existence we assumed. Then we verify that (S1-2) in fact hold for this choice of . Indeed,

| (S1) | |||

| (S2) |

which shows that we have indeed solved (7). The sampling distribution we have obtained is characterised up to a normalisation constant in (8), so just like we can sample from using techniques such as \acmcmc. The Stein kernel determines the extent to which differs from , as we illustrate next.

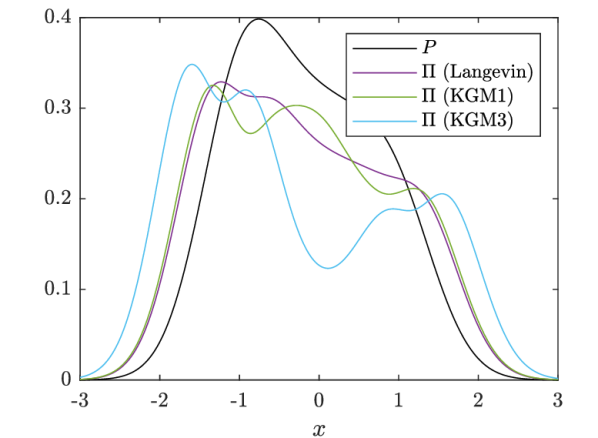

3.2 Illustration

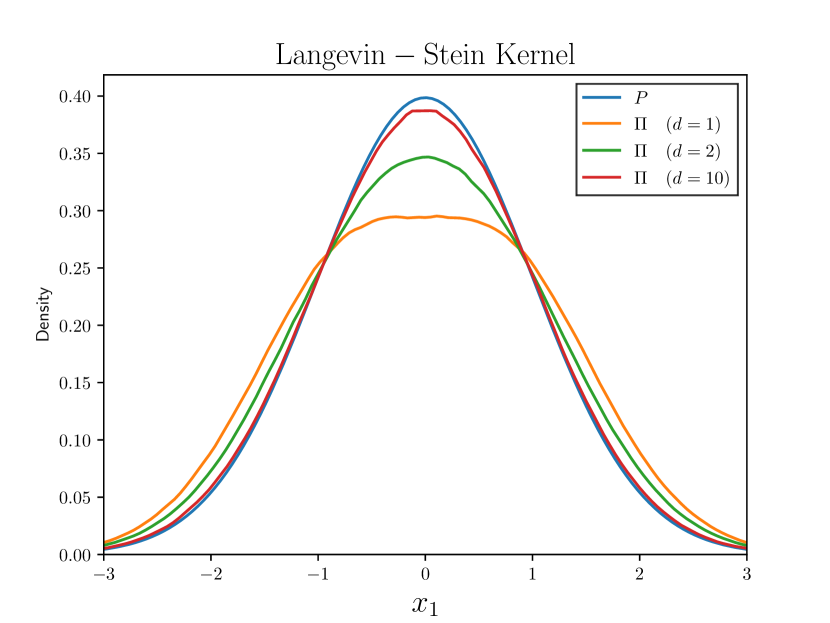

For illustration, consider the univariate target (black curve) in Figure 1(a), a 3-component Gaussian mixture model. Our recommended choice of in (8) is shown for both the Langevin–Stein kernel (purple curve) and the KGM–Stein kernels with (green and blue curves). The Stein discrepancy corresponding to the Langevin–Stein kernel provides control over weak convergence (i.e. convergence of integrals of functions that are continuous and bounded), while the KGM–Stein kernel provides additional control over the convergence of polynomial moments up to order ; full details about the construction of Stein kernels are contained in Appendix A. The Langevin and KGM1–Stein kernels have , while the KGM3–Stein kernel has , in each case as , and thus greater over-dispersion results from use of the KGM3–Stein kernel. This over-dispersion is less pronounced444The same holds for classical quantisation; c.f. Section 2.1. in higher dimensions; see Section D.1.

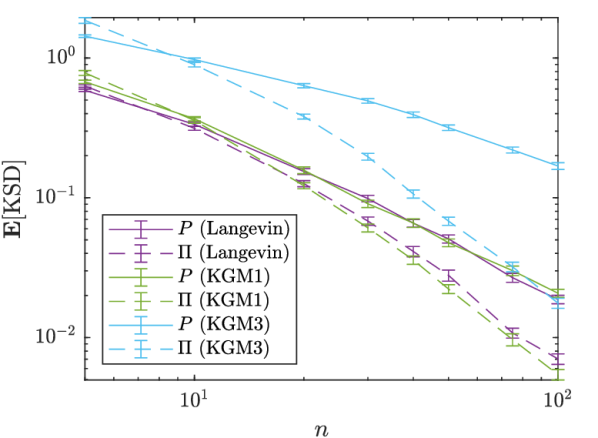

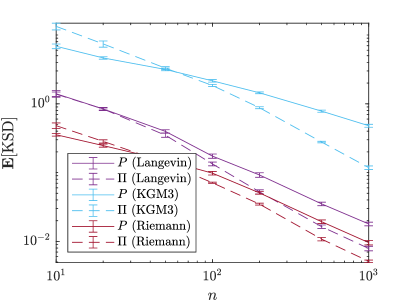

To illustrate the performance of Stein -Importance Sampling, we generated a sequence of independent samples from . For each , the samples were assigned optimal weights by solving (3), and the associated \acksd was computed. As a baseline, we performed the same calculation using independent samples from . Figure 1(b) indicates that, for both Stein kernels, substantial improvement results from the use of samples from compared to the use of samples from . Interestingly, the KGM3–Stein kernel demonstrated a larger improvement compared to the Langevin–Stein kernel, suggesting that the choice of may be more critical in settings where \acksd enjoys a stronger form of convergence control.

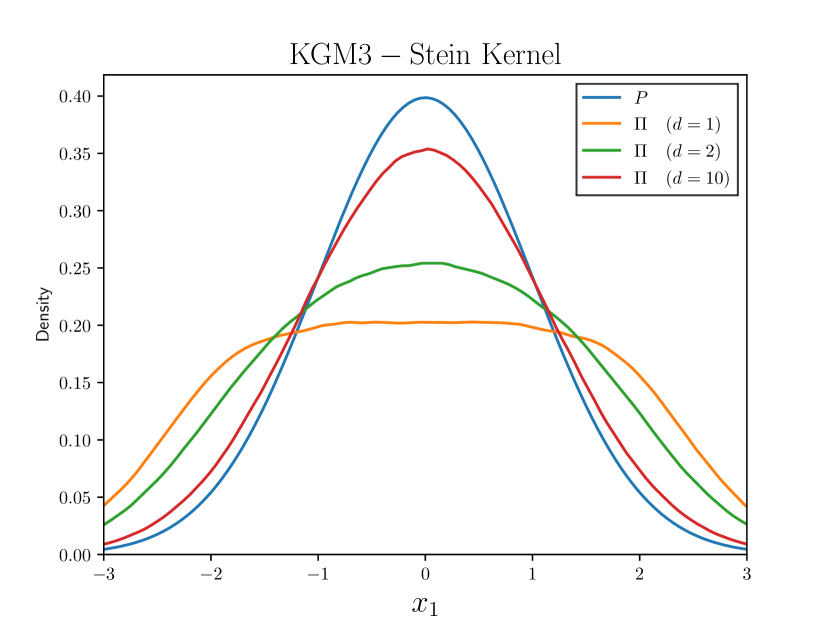

To illustrate a posterior approximation task, consider a simple regression model with , , , with independent . The parameter was assigned a prior . Data were simulated using . The posterior distribution is depicted in the leftmost panel of Figure 2, while our choice of corresponding to the Langevin (centre left), KGM3 (centre right) and Riemann–Stein kernels (right) are also displayed. For the Langevin and KGM3 kernels, the associated target their mass toward regions where varies the most. The reason for this behaviour is clearly seen for the Langevin–Stein kernel since for some ; see Appendix C for detail. The Riemann–Stein kernel can be viewed as a preconditioned form of the Langevin–Stein kernel which takes into account the geometric structure of ; see Appendix A for full detail555The use of geometric information may be beneficial, in the sense that the associated diffusion process may mix more rapidly, and rapid mixing leads to sharper bounds from the perspective of convergence control (Gorham et al.,, 2019). However, the Riemann–Stein kernel is associated with a prohibitive computational cost; it is included here only for academic interest.. Results in Figure S2 demonstrate that Stein -Importance Sampling improves upon the default Stein importance sampling method (i.e. with and equal) for all choices of kernel.

An additional illustration involving a GARCH model with parameters is presented in Section D.4, where the effect of varying the order of the KGM–Stein kernel is explored.

3.3 Theoretical Guarantees

The aim of this section is to establish when post-processing of -invariant \acmcmc produces a strongly consistent approximation of , for our recommended choice of in (8). Our analysis focuses on \acmala (Roberts and Stramer,, 2002), leveraging the recent work of Durmus and Moulines, (2022) to present explicit and verifiable conditions on for our results to hold. In fact, we consider the more general preconditioned form of \acmala, where the symmetric positive definite preconditioner matrix is to be specified. Our results also allow for (optional) sparse approximation, to circumvent direct solution of (3) (c.f. Section 2.3). The resulting algorithms, which we call Stein -Importance Sampling (SIS-MALA) and Stein -Thinning (ST-MALA), are quite straight-forward and contained, respectively, in Algorithms 2 and 3.

Let indicate that is a positive semi-definite matrix for . For a symmetric positive definite matrix let for . Let denote the set of -times continuously differentiable real-valued functions on .

Theorem 1 (Strong consistency of SIS- and ST-MALA).

Let 1 hold where is a Stein kernel, and let denote the associated \acksd. Assume also that

-

(A1)

with

-

(A2)

such that for all

-

(A3)

.

-

(A4)

, such that for all

Let be the result of running Algorithm 2 and let be the result of running Algorithm 3. Let and for some . Then there exists such that, for all step sizes and all initial states , almost surely as .

The proof is in Appendix B. Compared to earlier authors666These earlier results required high-level assumptions on the convergence of \acmcmc, for which explicit sufficient conditions had yet to be derived., such as Chen et al., (2019); Riabiz et al., (2022), a major novelty here is that our assumptions are explicit and can often be verified (see also Hodgkinson et al.,, 2020). (A2) is strong log-concavity of when , while for this condition is slightly stronger than the related distant dissipativity condition assumed in earlier work (Gorham and Mackey,, 2017; Riabiz et al.,, 2022). (A4) holds for the Langevin–Stein kernel (i.e. weak convergence control) and for the KGM1–Stein kernel (i.e. weak convergence control + control over first moments), but not for the higher-order KGM–Stein kernels. Extending our proof strategy to the higher-order KGM–Stein kernels would require further research into the convergence properties of \acmala, and this is expected to be difficult.

4 Benchmarking on PosteriorDB

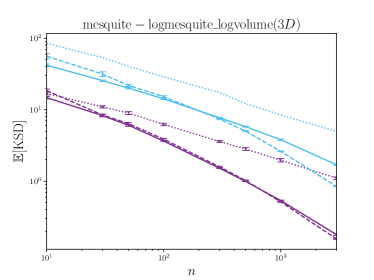

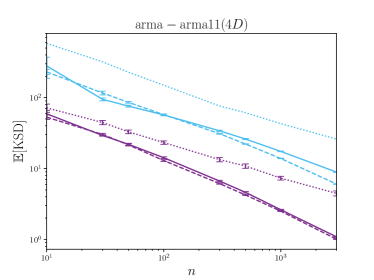

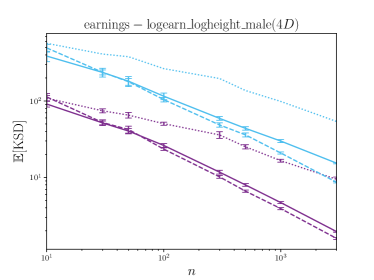

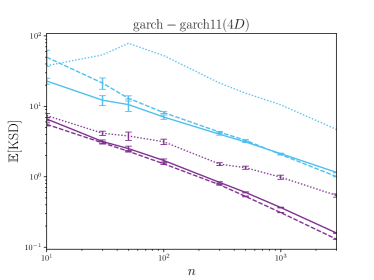

The area of Bayesian computation has historically lacked a common set of benchmark problems, with classical examples being insufficiently difficult and case-studies being hand-picked (Chopin and Ridgway,, 2017). To introduce objectivity into our assessment, we exploited the recently released PosteriorDB benchmark (Magnusson et al.,, 2022). This project is an attempt toward standardised benchmarking, consisting of a collection of posteriors to be numerically approximated. Here, we systematically compared the performance of SIS-MALA against the default Stein importance sampling algorithm (i.e. ; denoted SIS-MALA), and also against unprocessed -invariant \acmala (i.e. uniform weights), reporting results across the breadth of PosteriorDB. The test problems in PosteriorDB are defined in the Stan probabilistic programming language, and so BridgeStan (Roualdes et al.,, 2023) was used to directly access posterior densities and their gradients as required. For all instances of \acmala, an adaptive algorithm was used to learn a suitable preconditioner matrix during the warm-up period; see Section D.3. All experiments that we report can be reproduced using code available at https://github.com/congyewang/Stein-Pi-Importance-Sampling.

| Langevin–Stein Kernel | KGM3–Stein Kernel | ||||||

|---|---|---|---|---|---|---|---|

| Task | MALA | SIS -MALA | SIS -MALA | MALA | SIS -MALA | SIS -MALA | |

| earnings-earn_height | 3 | 1.41 | 0.0674 | 0.0332 | 5.33 | 0.656 | 0.181 |

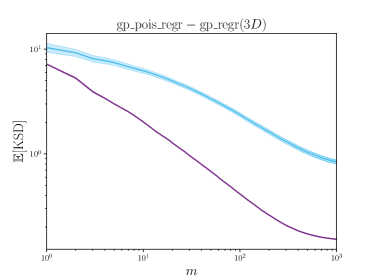

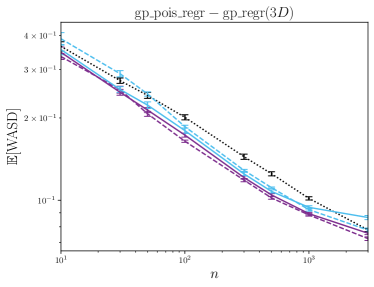

| gp_pois_regr-gp_regr | 3 | 0.298 | 0.0436 | 0.0373 | 1.22 | 0.385 | 0.223 |

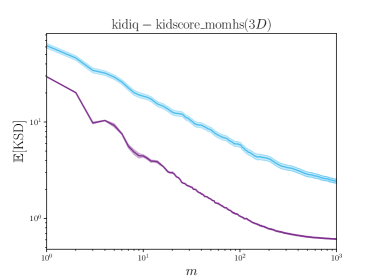

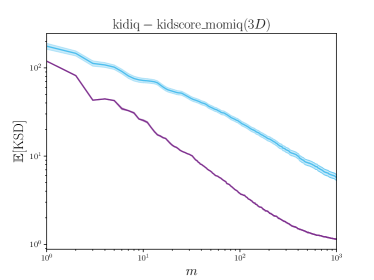

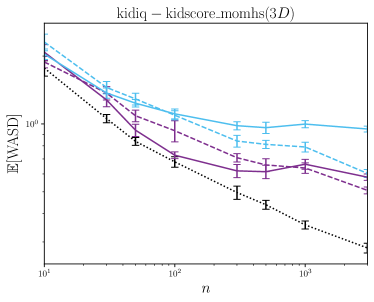

| kidiq-kidscore_momhs | 3 | 1.04 | 0.109 | 0.0941 | 4.66 | 0.848 | 0.476 |

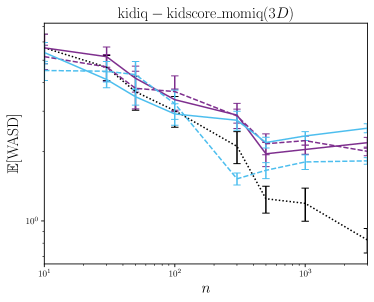

| kidiq-kidscore_momiq | 3 | 5.03 | 0.516 | 0.358 | 25.3 | 4.86 | 1.55 |

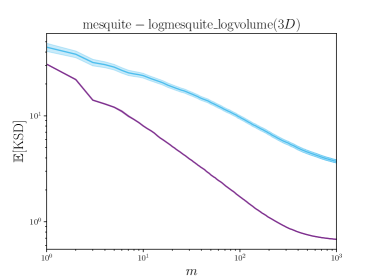

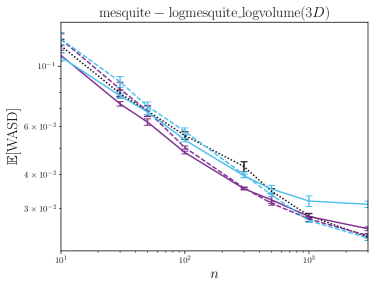

| mesquite-logmesquite_logvolume | 3 | 1.10 | 0.179 | 0.156 | 4.97 | 1.70 | 0.844 |

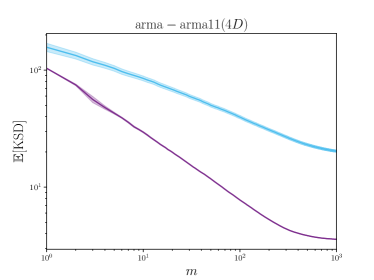

| arma-arma11 | 4 | 4.47 | 1.09 | 1.01 | 26.0 | 8.91 | 6.03 |

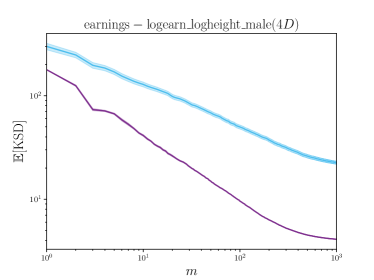

| earnings-logearn_logheight_male | 4 | 9.46 | 1.96 | 1.59 | 53.9 | 15.4 | 8.65 |

| garch-garch11 | 4 | 0.543 | 0.159 | 0.130 | 4.70 | 1.16 | 1.01 |

| kidiq-kidscore_momhsiq | 4 | 5.21 | 0.982 | 0.897 | 29.3 | 7.25 | 5.05 |

| earnings-logearn_interaction_z | 5 | 3.09 | 1.36 | 1.33 | 19.3 | 10.4 | 8.94 |

| kidiq-kidscore_interaction | 5 | 7.74 | 1.65 | 1.79 | 47.8 | 13.2 | 10.1 |

| kidiq_with_mom_work-kidscore_interaction_c | 5 | 1.35 | 0.659 | 0.711 | 7.92 | 4.05 | 4.17 |

| kidiq_with_mom_work-kidscore_interaction_c2 | 5 | 1.38 | 0.689 | 0.699 | 8.09 | 4.24 | 4.25 |

| kidiq_with_mom_work-kidscore_interaction_z | 5 | 1.11 | 0.500 | 0.499 | 6.62 | 2.63 | 3.25 |

| kidiq_with_mom_work-kidscore_mom_work | 5 | 1.07 | 0.507 | 0.545 | 6.70 | 2.63 | 3.04 |

| low_dim_gauss_mix-low_dim_gauss_mix | 5 | 5.51 | 1.87 | 1.76 | 37.5 | 14.7 | 11.3 |

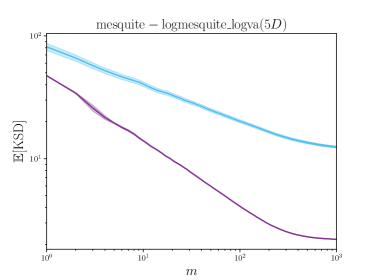

| mesquite-logmesquite_logva | 5 | 1.83 | 0.821 | 0.818 | 12.6 | 5.73 | 5.59 |

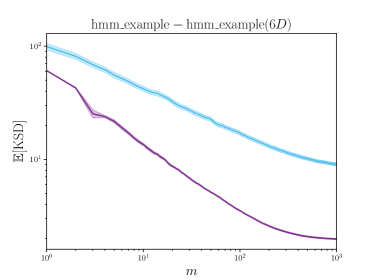

| hmm_example-hmm_example | 6 | 1.99 | 0.578 | 0.523 | 11.6 | 4.13 | 3.40 |

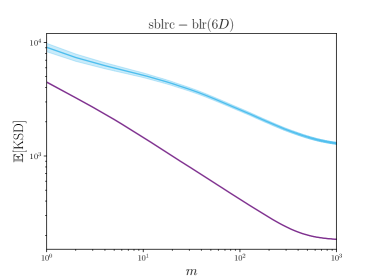

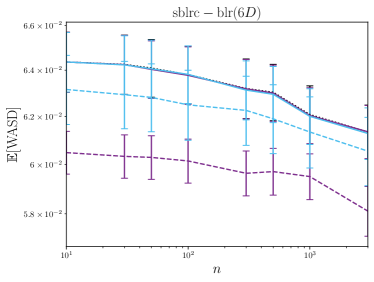

| sblrc-blr | 6 | 479 | 154 | 134 | 3300 | 1100 | 854 |

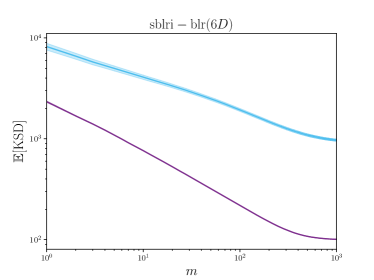

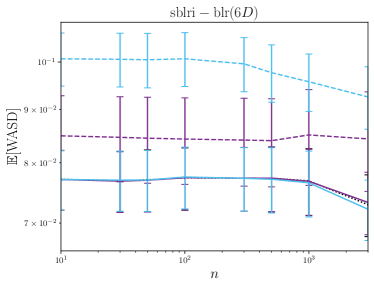

| sblri-blr | 6 | 201 | 66.7 | 60.3 | 1340 | 514 | 595 |

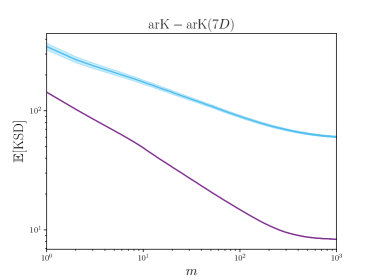

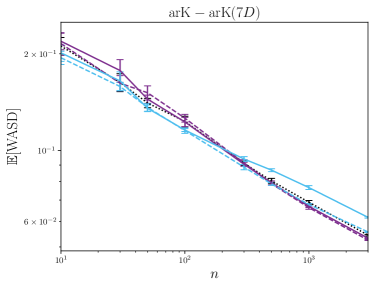

| arK-arK | 7 | 6.87 | 3.39 | 3.16 | 60.4 | 26.4 | 23.0 |

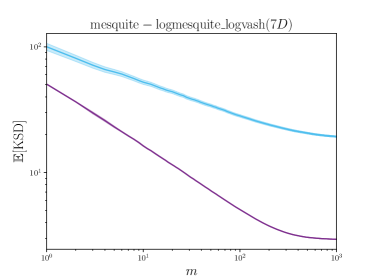

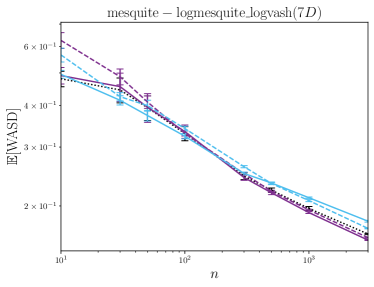

| mesquite-logmesquite_logvash | 7 | 1.89 | 1.18 | 1.23 | 15.5 | 8.88 | 10.1 |

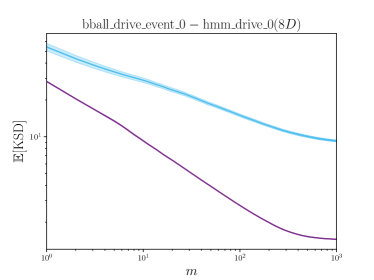

| bball_drive_event_0-hmm_drive_0 | 8 | 1.15 | 0.679 | 0.698 | 8.55 | 4.72 | 3.99 |

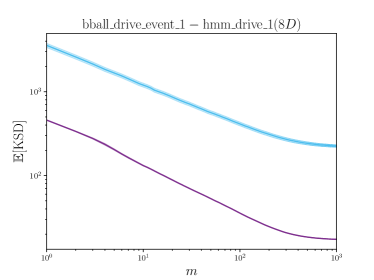

| bball_drive_event_1-hmm_drive_1 | 8 | 42.9 | 11.9 | 12.4 | 285 | 85.6 | 67.8 |

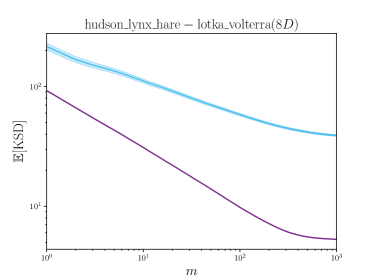

| hudson_lynx_hare-lotka_volterra | 8 | 4.62 | 2.29 | 2.15 | 47.4 | 18.8 | 18.9 |

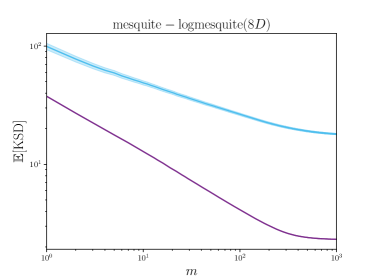

| mesquite-logmesquite | 8 | 1.46 | 1.00 | 1.06 | 13.3 | 8.28 | 9.14 |

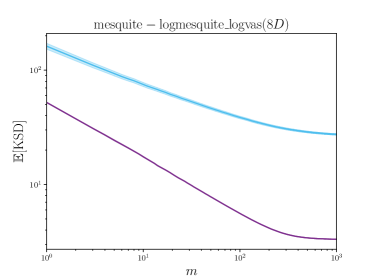

| mesquite-logmesquite_logvas | 8 | 2.02 | 1.31 | 1.35 | 19.2 | 10.8 | 12.2 |

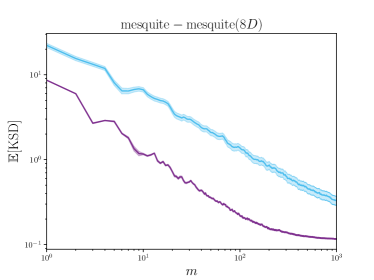

| mesquite-mesquite | 8 | 0.429 | 0.268 | 0.235 | 3.71 | 2.17 | 2.42 |

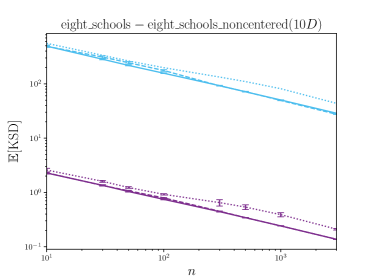

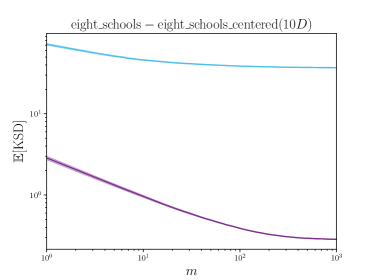

| eight_schools-eight_schools_centered | 10 | 0.526 | 0.100 | 0.182 | 7.53 | 2.15 | 215 |

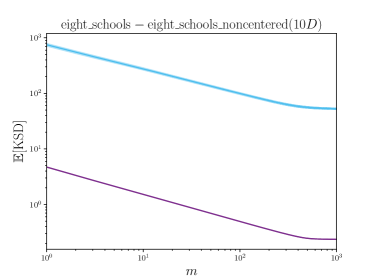

| eight_schools-eight_schools_noncentered | 10 | 0.210 | 0.137 | 0.137 | 43.6 | 28.7 | 27.5 |

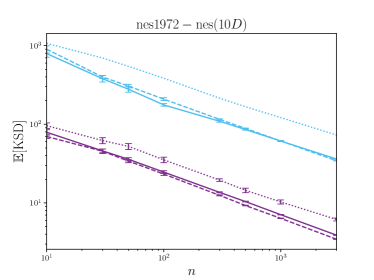

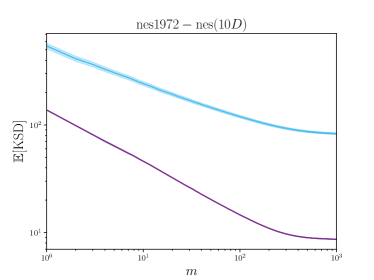

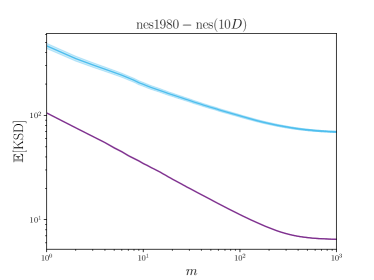

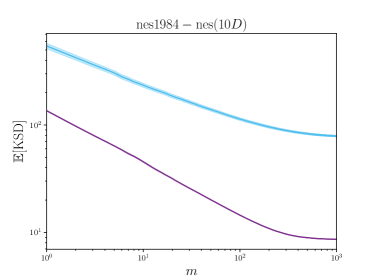

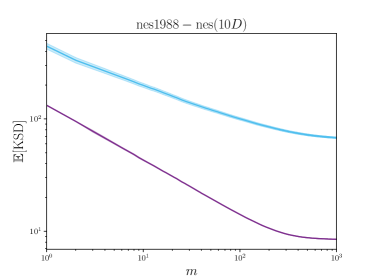

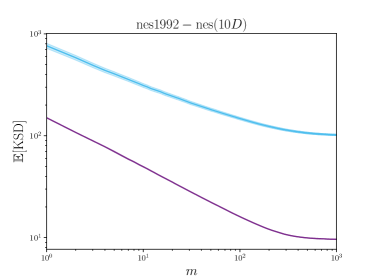

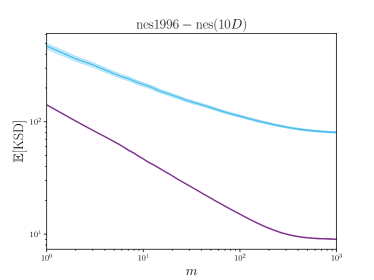

| nes1972-nes | 10 | 6.16 | 3.89 | 3.45 | 72.9 | 36.2 | 34.4 |

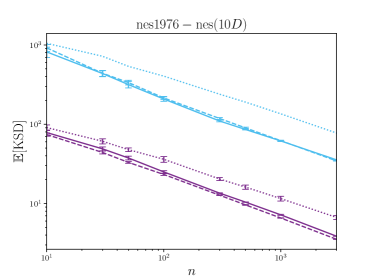

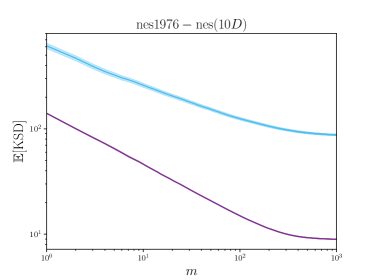

| nes1976-nes | 10 | 6.67 | 3.86 | 3.53 | 77.5 | 35.5 | 34.4 |

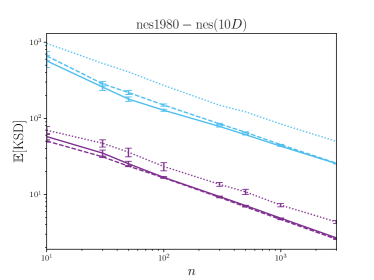

| nes1980-nes | 10 | 4.34 | 2.68 | 2.57 | 49.8 | 25.4 | 25.7 |

| nes1984-nes | 10 | 6.18 | 3.75 | 3.43 | 71.3 | 34.9 | 33.6 |

| nes1988-nes | 10 | 7.40 | 3.70 | 3.27 | 81.4 | 34.6 | 32.4 |

| nes1992-nes | 10 | 7.52 | 4.32 | 3.84 | 89.1 | 39.7 | 37.3 |

| nes1996-nes | 10 | 6.44 | 3.87 | 3.53 | 74.1 | 36.4 | 34.3 |

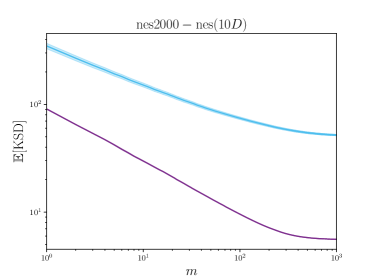

| nes2000-nes | 10 | 3.35 | 2.22 | 2.20 | 38.6 | 21.3 | 22.8 |

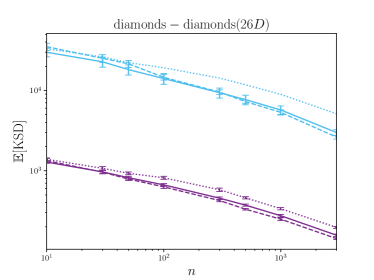

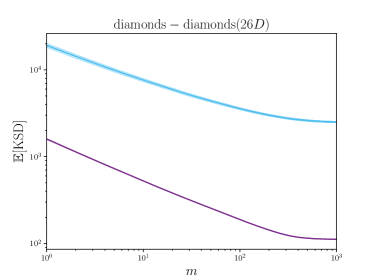

| diamonds-diamonds | 26 | 196 | 157 | 143 | 5120 | 2990 | 2620 |

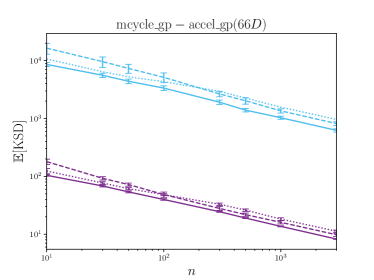

| mcycle_gp-accel_gp | 66 | 11.3 | 8.25 | 9.79 | 960 | 623 | 815 |

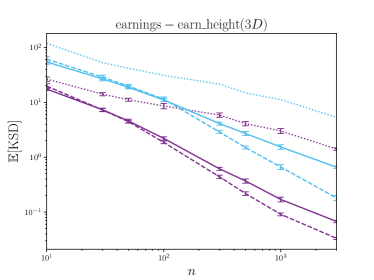

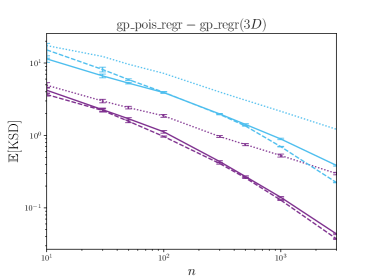

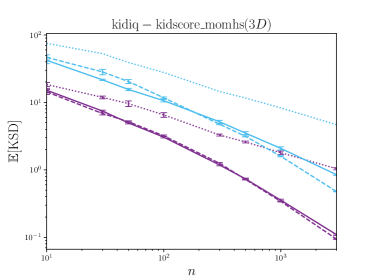

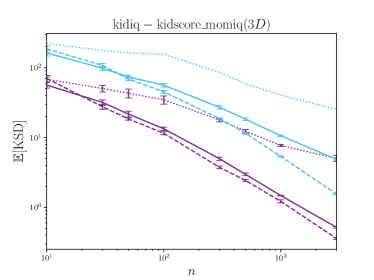

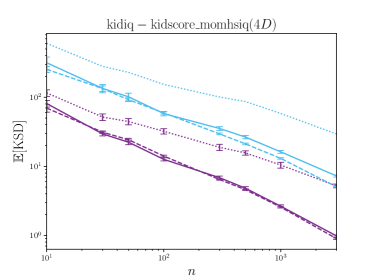

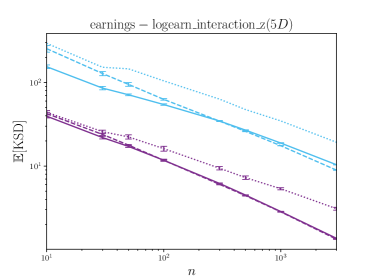

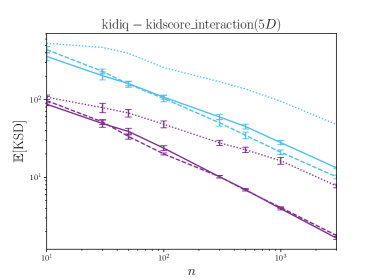

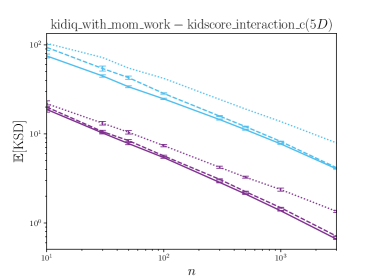

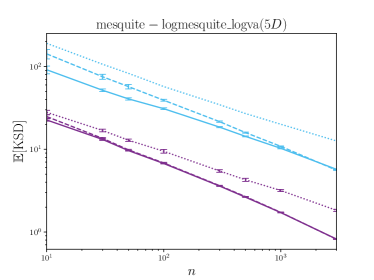

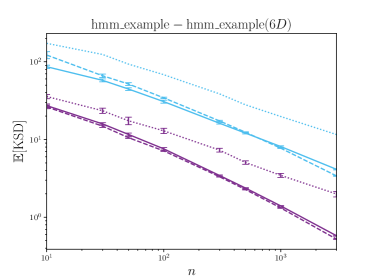

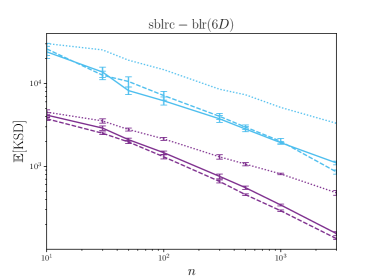

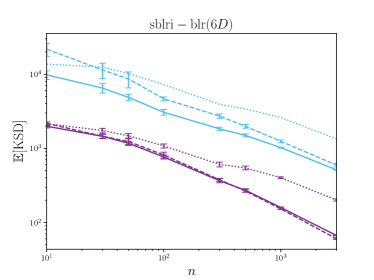

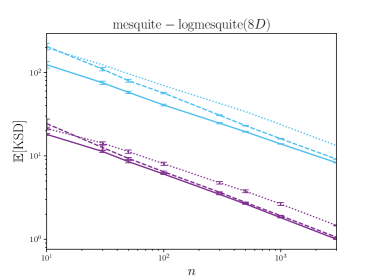

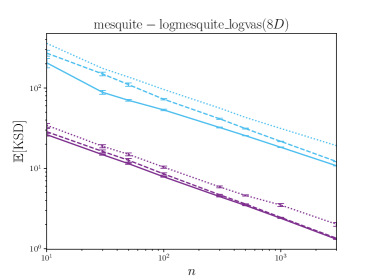

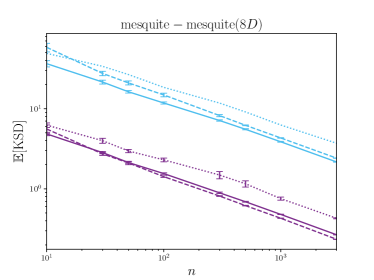

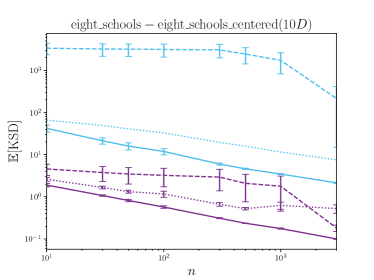

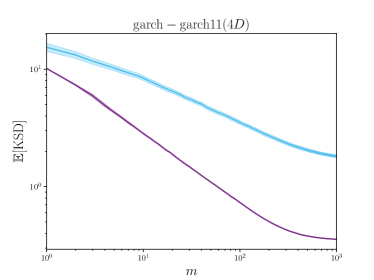

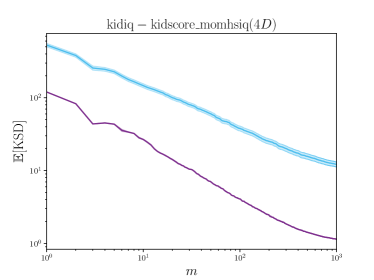

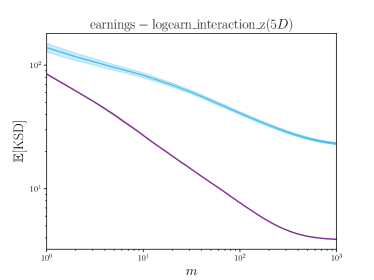

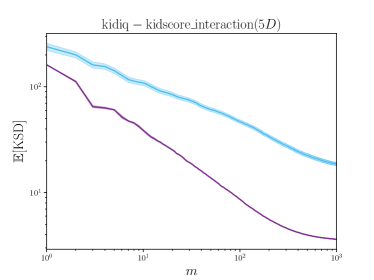

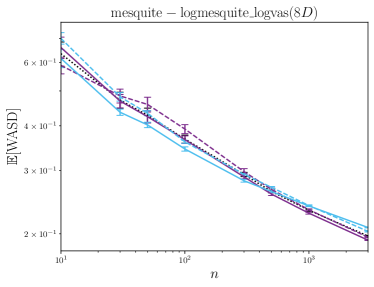

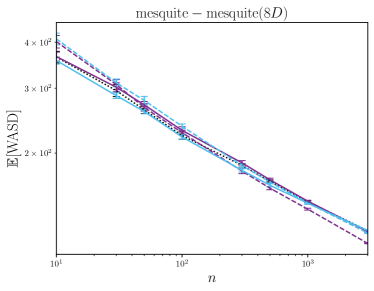

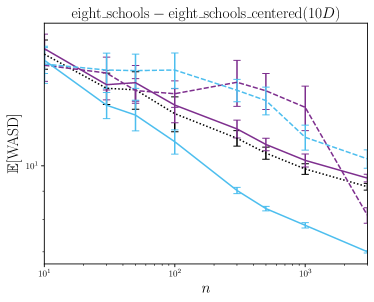

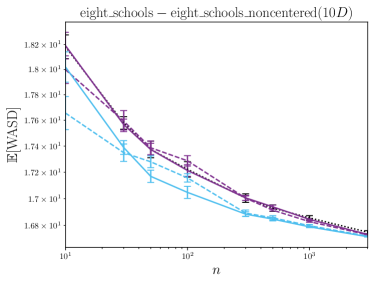

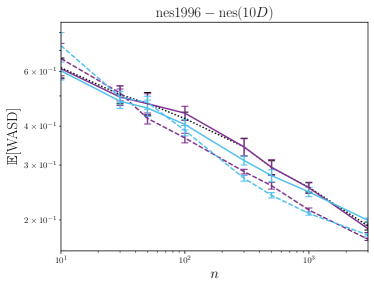

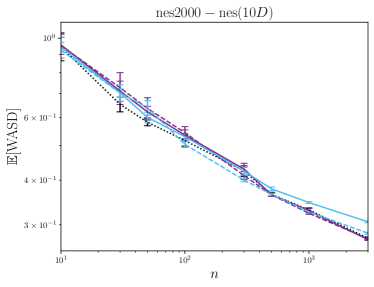

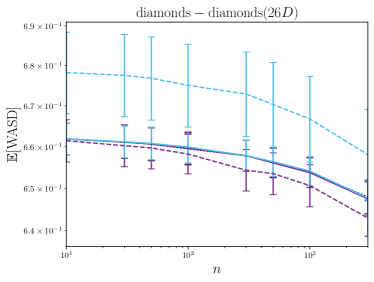

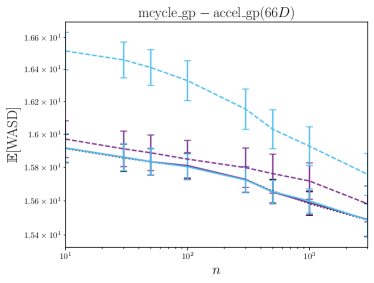

Results are reported in Table 1 for samples from \acmala. These focus on the Langevin–Stein kernel, for which our theory holds, and the KGM3–Stein kernel, for which it does not. There was a significant improvement of SIS-MALA over SIS-MALA in 73% of test problems for the Langevin–Stein kernel and in 65% of test problems for the KGM3–Stein kernel. Compared to unprocessed \acmala, a significant improvement occurred in 100% and 97% of cases, respectively for each kernel. However, the extent of improvement decreased when the dimension of the target increased, supporting the intuition that we set out earlier and in Section D.1. An in-depth breakdown of results, including varying the number of samples that were used, and the performance ST-MALA, can be found in Sections D.5 and D.6.

Our focus is on the development of algorithms for minimisation of \acpksd; the properties of \acpksd themselves are out of scope for this work777The interested reader is referred to Gorham and Mackey, (2017); Barp et al., 2022b ; Kanagawa et al., (2022).. Nonetheless, there is much interest in better understanding the properties of \acpksd, and we therefore also report performance of SIS-MALA in terms of 1-Wasserstein divergence in Section D.7. The main contrast between these results and the results in Table 1 is that, being score-based, \acpksd suffer from the blindness to mixing proportions phenomena which has previously been documented in Wenliang and Kanagawa, (2021); Koehler et al., (2022); Liu et al., (2023). Caution should therefore be taken when using algorithms based on Stein discrepancies in the context of posterior distributions with multiple high probability regions that are spatially separated. This is also a failure mode for \acmcmc algorithms such as \acmala, and yet there are still many problems for which \acmala has been successfully used.

The alternative choice , with , which provides a generic form of over-dispersion and is optimal for approximation in 1-Wasserstein divergence (c.f. Section 2.1), was also considered. Results in Section D.8 indicate that, while yields an improvement compared to the baseline of using itself, may be less effective than our proposed when is skewed.

5 Discussion

This paper presented Stein -Importance Sampling; an algorithm that is simple to implement, admits an end-to-end theoretical treatment, and achieves a significant improvement over existing post-processing methods based on \acksd. On the negative side, second order derivatives of the statistical model are required. For models for which access to second order derivatives is impractical, our methodology and theoretical analysis are directly applicable to gradient-free \acksd (Fisher and Oates,, 2022), and this would be an interesting direction for future work.

Acknowledgements

CW was supported by the China Scholarship Council. HK and CJO were supported by EP/W019590/1.

References

- Agapiou et al., (2017) Agapiou, S., Papaspiliopoulos, O., Sanz-Alonso, D., and Stuart, A. M. (2017). Importance sampling: Intrinsic dimension and computational cost. Statistical Science, 32(3):405–431.

- Anastasiou et al., (2023) Anastasiou, A., Barp, A., Briol, F.-X., Ebner, B., Gaunt, R. E., Ghaderinezhad, F., Gorham, J., Gretton, A., Ley, C., Liu, Q., Mackey, L., Oates, C. J., Reinert, G., and Swan, Y. (2023). Stein’s method meets statistics: A review of some recent developments. Statistical Science, (38):120–139.

- Bach, (2017) Bach, F. (2017). On the equivalence between kernel quadrature rules and random feature expansions. The Journal of Machine Learning Research, 18(1):714–751.

- Bach et al., (2012) Bach, F., Lacoste-Julien, S., and Obozinski, G. (2012). On the equivalence between herding and conditional gradient algorithms. In Proceedings of the 29th International Conference on Machine Learning.

- Barbour, (1988) Barbour, A. D. (1988). Stein’s method and poisson process convergence. Journal of Applied Probability, 25(A):175–184.

- Barbour, (1990) Barbour, A. D. (1990). Stein’s method for diffusion approximations. Probability Theory and Related Fields, 84(3):297–322.

- (7) Barp, A., Oates, C. J., Porcu, E., and Girolami, M. (2022a). A Riemann–Stein kernel method. Bernoulli, 28(4):2181–2208.

- (8) Barp, A., Simon-Gabriel, C.-J., Girolami, M., and Mackey, L. (2022b). Targeted separation and convergence with kernel discrepancies. arXiv preprint arXiv:2209.12835.

- Bénard et al., (2023) Bénard, C., Staber, B., and Da Veiga, S. (2023). Kernel stein discrepancy thinning: A theoretical perspective of pathologies and a practical fix with regularization. arXiv preprint arXiv:2301.13528.

- Briol et al., (2017) Briol, F.-X., Oates, C. J., Cockayne, J., Chen, W. Y., and Girolami, M. (2017). On the sampling problem for kernel quadrature. In Proceedings of the 34th International Conference on Machine Learning, pages 586–595.

- Briol et al., (2019) Briol, F.-X., Oates, C. J., Girolami, M., Osborne, M. A., and Sejdinovic, D. (2019). Probabilistic integration: A role in statistical computation (with discussion and rejoinder). Statistical Science, 34(1):1–22.

- Carmeli et al., (2006) Carmeli, C., De Vito, E., and Toigo, A. (2006). Vector valued reproducing kernel Hilbert spaces of integrable functions and mercer theorem. Analysis and Applications, 4(04):377–408.

- Chen et al., (2019) Chen, W. Y., Barp, A., Briol, F.-X., Gorham, J., Girolami, M., Mackey, L., and Oates, C. J. (2019). Stein point Markov chain Monte Carlo. In Proceedings of the 36th International Conference on Machine Learning, pages 1011–1021.

- Chen et al., (2018) Chen, W. Y., Mackey, L., Gorham, J., Briol, F.-X., and Oates, C. J. (2018). Stein points. In Proceedings of the 35th International Conference on Machine Learning, pages 844–853.

- Chen et al., (2010) Chen, Y., Welling, M., and Smola, A. (2010). Super-samples from kernel herding. In Proceedings of the 26th Conference on Uncertainty in Artificial Intelligence, pages 109–116.

- Chopin and Ducrocq, (2021) Chopin, N. and Ducrocq, G. (2021). Fast compression of MCMC output. Entropy, 23(8):1017.

- Chopin and Ridgway, (2017) Chopin, N. and Ridgway, J. (2017). Leave pima indians alone: Binary regression as a benchmark for Bayesian computation. Statistical Science, 32(1):64–87.

- Chwialkowski et al., (2016) Chwialkowski, K., Strathmann, H., and Gretton, A. (2016). A kernel test of goodness of fit. In Proceedings of the 33rd International Conference on Machine Learning, pages 2606–2615.

- Cohort, (2004) Cohort, P. (2004). Limit theorems for random normalized distortion. The Annals of Applied Probability, 14(1):118–143.

- Durmus and Moulines, (2022) Durmus, A. and Moulines, É. (2022). On the geometric convergence for MALA under verifiable conditions. arXiv preprint arXiv:2201.01951.

- Dwivedi and Mackey, (2021) Dwivedi, R. and Mackey, L. (2021). Kernel thinning. In Proceedings of 34th Conference on Learning Theory, pages 1753–1753.

- Dwivedi and Mackey, (2022) Dwivedi, R. and Mackey, L. (2022). Generalized kernel thinning. In Proceedings of the 10th International Conference on Learning Representations.

- Ehler et al., (2019) Ehler, M., Gräf, M., and Oates, C. J. (2019). Optimal Monte Carlo integration on closed manifolds. Statistics and Computing, 29(6):1203–1214.

- Fisher and Oates, (2022) Fisher, M. A. and Oates, C. J. (2022). Gradient-free kernel Stein discrepancy. arXiv preprint arXiv:2207.02636.

- Girolami and Calderhead, (2011) Girolami, M. and Calderhead, B. (2011). Riemann manifold Langevin and Hamiltonian Monte Carlo methods. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 73(2):123–214.

- Gorham et al., (2019) Gorham, J., Duncan, A. B., Vollmer, S. J., and Mackey, L. (2019). Measuring sample quality with diffusions. The Annals of Applied Probability, 29(5):2884–2928.

- Gorham and Mackey, (2015) Gorham, J. and Mackey, L. (2015). Measuring sample quality with Stein’s method. In Proceedings of the 29th Conference on Neural Information Processing Systems, pages 226–234.

- Gorham and Mackey, (2017) Gorham, J. and Mackey, L. (2017). Measuring sample quality with kernels. In Proceedings of the 34th International Conference on Machine Learning, pages 1292–1301.

- Gotze, (1991) Gotze, F. (1991). On the rate of convergence in the multivariate CLT. The Annals of Probability, pages 724–739.

- Graf and Luschgy, (2007) Graf, S. and Luschgy, H. (2007). Foundations of Quantization for Probability Distributions. Springer.

- Hawkins et al., (2022) Hawkins, C., Koppel, A., and Zhang, Z. (2022). Online, informative MCMC thinning with kernelized Stein discrepancy. arXiv preprint arXiv:2201.07130.

- Hayakawa et al., (2022) Hayakawa, S., Oberhauser, H., and Lyons, T. (2022). Positively weighted kernel quadrature via subsampling. In Proceedings of the 35th Conference on Neural Information Processing Systems.

- Hodgkinson et al., (2020) Hodgkinson, L., Salomone, R., and Roosta, F. (2020). The reproducing Stein kernel approach for post-hoc corrected sampling. arXiv preprint arXiv:2001.09266.

- Kanagawa et al., (2022) Kanagawa, H., Gretton, A., and Mackey, L. (2022). Controlling moments with kernel Stein discrepancies. arXiv preprint arXiv:2211.05408.

- Karvonen et al., (2021) Karvonen, T., Oates, C. J., and Girolami, M. (2021). Integration in reproducing kernel Hilbert spaces of Gaussian kernels. Mathematics of Computation, 90(331):2209–2233.

- Karvonen et al., (2018) Karvonen, T., Oates, C. J., and Sarkka, S. (2018). A Bayes–Sard cubature method. In Proceedings of the 32nd Conference on Neural Information Processing Systems.

- Kent, (1978) Kent, J. (1978). Time-reversible diffusions. Advances in Applied Probability, 10(4):819–835.

- Koehler et al., (2022) Koehler, F., Heckett, A., and Risteski, A. (2022). Statistical efficiency of score matching: The view from isoperimetry. In Proceedings of the 36th Conference on Neural Information Processing Systems.

- Ledoux and Talagrand, (1991) Ledoux, M. and Talagrand, M. (1991). Probability in Banach Spaces: Isoperimetry and Processes, volume 23. Springer Science & Business Media.

- Liu and Lee, (2017) Liu, Q. and Lee, J. (2017). Black-box importance sampling. In Proceedings of the 20th International Conference on Artificial Intelligence and Statistics, pages 952–961.

- Liu et al., (2016) Liu, Q., Lee, J., and Jordan, M. (2016). A kernelized Stein discrepancy for goodness-of-fit tests. In Proceedings of the 33rd International Conference on Machine Learning, pages 276–284.

- Liu et al., (2023) Liu, X., Duncan, A., and Gandy, A. (2023). Using perturbation to improve goodness-of-fit tests based on kernelized Stein discrepancy. In Proceedings of the 40th International Conference on Machine Learning.

- Magnusson et al., (2022) Magnusson, M., Bürkner, P., and Vehtari, A. (2022). PosteriorDB: A set of posteriors for Bayesian inference and probabilistic programming. https://github.com/stan-dev/posteriordb.

- Meyn and Tweedie, (2012) Meyn, S. P. and Tweedie, R. L. (2012). Markov Chains and Stochastic Stability. Springer Science & Business Media.

- Oates et al., (2017) Oates, C. J., Girolami, M., and Chopin, N. (2017). Control functionals for Monte Carlo integration. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79(3):695–718.

- Riabiz et al., (2022) Riabiz, M., Chen, W., Cockayne, J., Swietach, P., Niederer, S. A., Mackey, L., and Oates, C. J. (2022). Optimal thinning of MCMC output. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 84(4):1059–1081.

- Roberts and Rosenthal, (1998) Roberts, G. O. and Rosenthal, J. S. (1998). Optimal scaling of discrete approximations to Langevin diffusions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 60(1):255–268.

- Roberts and Stramer, (2002) Roberts, G. O. and Stramer, O. (2002). Langevin diffusions and Metropolis–Hastings algorithms. Methodology and Computing in Applied Probability, 4:337–357.

- Roualdes et al., (2023) Roualdes, E., Ward, B., Axen, S., and Carpenter, B. (2023). BridgeStan: Efficient in-memory access to Stan programs through Python, Julia, and R. https://github.com/roualdes/bridgestan.

- Shetty et al., (2022) Shetty, A., Dwivedi, R., and Mackey, L. (2022). Distribution compression in near-linear time. In Proceedings of the 10th International Conference on Learning Representations.

- Sonnleitner, (2022) Sonnleitner, M. (2022). The Power of Random Information for Numerical Approximation and Integration. PhD thesis, University of Passau.

- Teymur et al., (2021) Teymur, O., Gorham, J., Riabiz, M., and Oates, C. J. (2021). Optimal quantisation of probability measures using maximum mean discrepancy. In Proceedings of the 24th International Conference on Artificial Intelligence and Statistics, pages 1027–1035.

- Wenliang and Kanagawa, (2021) Wenliang, L. K. and Kanagawa, H. (2021). Blindness of score-based methods to isolated components and mixing proportions. In Proceedings of “Your Model is Wrong” @ the 35th Conference on Neural Information Processing Systems.

Supplement

This supplement contains supporting material for the paper Stein -Importance Sampling. The mathematical background on Stein kernels is contained in Appendix A. The proof of Theorem 1 is contained in Appendix B. For implementation of Stein -Importance Sampling without the aid of automatic differentiation, various explicit derivatives are required; the relevant calculations can be found in Appendix C. The empirical protocols and additional empirical results are presented in Appendix D.

Appendix A Mathematical Background

This appendix contains mathematical background on reproducing kernels and Stein kernels, as used in the main text. Section A.1 introduces matrix-valued reproducing kernels, while Section A.2 specialises to Stein kernels by application of a Stein operator to a matrix-valued kernel. A selection of useful Stein kernels are presented in Section A.3.

A.1 Matrix-Valued Reproducing Kernels

A matrix-valued kernel is a function , that is both

-

1.

symmetric; for all , and

-

2.

positive semi-definite; for all and .

Let . For vector-valued functions , defined by and , define an inner product

| (9) |

There is a unique Hilbert space of such vector-valued functions associated to , denoted ; see Proposition 2.1 of Carmeli et al., (2006). This space is characterised as

where here the closure is taken with respect to the inner product in (9). It can be shown that is in fact a \acrkhs which satisfies the reproducing property

for all and . Matrix-valued kernels are the natural starting point for construction of \acpksd, as described next.

A.2 Stein Kernels

A general construction for Stein kernels is to first identify a matrix-valued \acrkhs and an operator for which for all . Such an operator will be called a Stein operator. The collection inherits the structure of an \acrkhs, whose reproducing kernel

| (10) |

is a Stein kernel, meaning that where is the kernel mean embedding from (1); see Barp et al., 2022b . Explicit calculations for the Stein kernels considered in this work can be found in Appendix C.

For univariate distributions, Barbour, (1988) proposed to obtain Stein operators from infinitessimal generators of -invariant continuous-time Markov processes; see also Barbour, (1990); Gotze, (1991). The approach was extended to multivariate distributions in Gorham and Mackey, (2015). The starting point is the -invariant Itô diffusion

| (11) |

where is the density of , assumed to be positive, is a symmetric matrix called the diffusion matrix, and is a standard Wiener process (Kent,, 1978; Roberts and Stramer,, 2002). Here the notation indicates the divergence operator applied to each row of the matrix . The infinitessimal generator is

Substituting for , we obtain a Stein operator

| (12) |

called the diffusion Stein operator (Gorham et al.,, 2019). This is indeed a Stein operator, since under mild integrability conditions on , the divergence theorem gives that for all ; for full details and a proof see Barp et al., 2022b .

A.3 Selecting a Stein Kernel

There are several choices for a Stein kernel, and which we should use depends on what form of convergence we hope to control (Gorham and Mackey,, 2017; Gorham et al.,, 2019; Hodgkinson et al.,, 2020; Barp et al., 2022b, ; Kanagawa et al.,, 2022). Section A.3.1 describes the Langevin–Stein kernel for weak convergence control, Section A.3.2 describes the KGM–Stein kernels for additional control over moments, and Section A.3.3 presents the Riemann–Stein kernel, whose convergence properties have to-date been less well-studied.

All of the kernels that we consider have length scale parameters that need to be specified, and some also have location parameters to be specified. As a reasonably automatic default we define

as a location and a matrix of characteristic length scales for that will be used throughout. These values can typically be obtained using gradient-based optimisation, which is usually cheaper to perform compared to full approximation of . It is assumed that is positive definite in the sequel.

A.3.1 Weak Convergence Control with Langevin–Stein Kernels

The first kernel we consider, which we called the Langevin–Stein kernel in the main text, was introduced by Gorham and Mackey, (2017). This Stein kernel was developed for the purpose of controlling the weak convergence of a sequence to . Recall that a sequence is said to converge weakly (or in distribution) to if for all continuous bounded functions . This convergence is denoted in shorthand.

The problem considered in Gorham and Mackey, (2017) was how to select a combination of matrix-valued kernel (and, implicitly, a diffusion matrix ) such that the Stein kernel in (10) generates a \acksd in (4) for which implies . Their solution was to combine the inverse multi-quadric kernel with an identity diffusion matrix;

for . Provided that has a density for which is Lipschitz, and that is distantly dissipative (see Definition 4 of Gorham and Mackey,, 2017), the associated \acksd enjoys weak convergence control. Technically, the results in Gorham and Mackey, (2017) apply only when , but Theorem 4 in Chen et al., (2019) demonstrated that they hold also for any positive definite . Following the recommendation of several previous authors, including Chen et al., (2018, 2019); Riabiz et al., (2022), we take throughout.

A.3.2 Moment Convergence Control with KGM–Stein Kernels

Despite its many elegant properties, weak convergence can be insufficient for applications where we are interested in integrals for which the integrand is unbounded. In particular, this is the case for moments of the form , . In such situations, we may seek also the stronger property of moment convergence control. The development of \acpksd for moment convergence control was recently considered by Kanagawa et al., (2022), and we refered to their construction as the KGM–Stein kernels in the main text. (For convenience, we have adopted the initials of the authors in naming the KGM–Stein kernel.)

A sequence is said to converge to in the th order moment if . To establish convergence of moments, we need an additional condition on top of weak convergence control: uniform integrability control. A sequence of measures is said to have uniformly integrable th moments if for any , we can take such that

This condition essentially states that the tail decay of the measures is well-controlled (so that it has a convergent moment). The \acksd convergence implies uniform integrability if for any , we can take and such that

| (13) |

i.e., the Stein-modified \acrkhs can approximate the (norm-weighted) indicator function arbitrarily well. Such a function can be explicitly constructed (while not guaranteed to be a member of the \acrkhs). Specifically, the choice satisfies (13) under an appropriate dissipativity condition, where is a differentiable indicator function vanishing outside a ball, and . This motivated Kanagawa et al., (2022) to introduce the th order KGM–Stein kernel, which is based on the matrix-valued kernel and diffusion matrix

where is a universal kernel (see Barp et al., 2022b, , Theorem 4.8). For comparability of our results, we take to be the inverse multi-quadric , and

Here the normalised linear kernel ensures , while the universal kernel allows approximation of ; see Kanagawa et al., (2022).

A.3.3 Exploiting Geometry with Riemann–Langevin–Stein Kernels

For academic interest only, here we describe the Riemann–Stein kernel that featured in Figure 2 of the main text. This Stein kernel is motivated by the analysis of Gorham et al., (2019), who argued that the use of rapidly mixing Itô diffusions in Stein operators can lead to sharper convergence control. The Riemann–Stein kernel is based on the class of so-called Riemannian diffusions considered in Girolami and Calderhead, (2011), who proposed to take the diffusion matrix in (11) to be , the inverse of the Fisher information matrix, , regularised using the Hessian of the negative log-prior, . For the two-dimensional illustration in Section 3.2, this leads to the diffusion matrix

where we recall that , where the are independent with , and the prior is . For the presented experiment we paired the above diffusion matrix with the inverse multi-quadric kernel for . The Riemann–Stein kernel extends naturally to distributions defined on Riemannian manifolds ; see Barp et al., 2022a and Example 1 of Hodgkinson et al., (2020).

Unfortunately, the Riemann–Stein kernel is prohibitively expensive in most real applications, since each evaluation of requires a full scan through the size- dataset. The computational complexity of Stein -Thinning with the Riemann–Stein kernel is therefore , which is unfavourable compared to the complexity in the case where the Stein kernel is not data-dependent. Furthermore, the convergence control properties of the Riemann–Stein kernel have yet to be established. For these reasons we included the Riemann–Stein kernel for illustration only; further groundwork will be required before the Riemann-Stein kernel can be practically used.

Appendix B Proof of Theorem 1

This appendix is devoted to the proof of Theorem 1. The proof is based on the recent work of Durmus and Moulines, (2022), on the geometric convergence of \acmala, and on the analysis of sparse (greedy) approximation of kernel discrepancies performed in Riabiz et al., (2022); these existing results are recalled in Section B.1. An additional technical result on preconditioned \acmala is contained in Section B.2. The proof of Theorem 1 itself is contained in Section B.3.

B.1 Auxiliary Results

To precisely describe the results on which our analysis is based, we first need to introduce some notation and terminology. Let and, for a function and a measure on , let

Recall that a -invariant Markov chain with step transition kernel is -uniformly ergodic (see Theorem 16.0.1 of Meyn and Tweedie,, 2012) if and only if such that

| (14) |

for all initial states and all .

Although \acmala (Algorithm 1) is classical (Roberts and Stramer,, 2002), until recently explicit sufficient conditions for ergodicity of \acmala had not been obtained. The first result we will need is due Durmus and Moulines, (2022), who presented the first explicit conditions for -uniform convergence of \acmala. It applies only to standard \acmala, meaning that the preconditioning matrix appearing in Algorithm 1 is the identity matrix. The extension of this result to preconditioned \acmala will be handled in Section B.2.

Theorem 2.

Let admit a density, , such that

-

(DM1)

there exists with

-

(DM2)

is twice continuously differentiable with

-

(DM3)

there exists and such that for all .

Then there exists such that for all step sizes , standard -invariant \acmala (i.e. with ) is -uniformly ergodic for .

Proof.

This is Theorem 1 of Durmus and Moulines, (2022). ∎

The next result that we will need establishes consistency of the greedy algorithm applied to samples from a Markov chain that is -invariant.

Theorem 3.

Let with . Let be a Stein kernel and let denote the associated \acksd. Consider a -invariant, time-homogeneous Markov chain such that

-

(R+1)

is -uniformly ergodic, such that

-

(R+2)

-

(R+3)

there exists such that .

Let be the result of running the greedy algorithm in (5). If and for some , then almost surely as .

Proof.

This is Theorem 3 of Riabiz et al., (2022). ∎

B.2 Preconditioned \acmala

In addition to the auxiliary results in Section B.1, which concern standard \acmala (i.e. with ), we require an elementary fact about \acmala, namely that preconditioned \acmala is equivalent to standard \acmala under a linear transformation of the state variable. Recall that the -preconditioned \acmala algorithm is a Metropolis–Hastings algorithm whose proposal is the Euler–Maruyama discretisation of the Itô diffusion (11).

Proposition 1.

Let for a symmetric positive definite and position-independent matrix . Let admit a \acpdf for which the -invariant diffusion , given by setting in (11), is well-defined. Then under the change of variables ,

| (15) |

where for all .

Proof.

Let and be the distributions referred to in Proposition 1, whose \acppdf are respectively and . Proposition 1 then implies that the -preconditioned \acmala algorithm applied to (i.e. Algorithm 1 for ) is equivalent to the standard \acmala algorithm (i.e. ) applied to . This fact allows us to generalise the result of Theorem 2 as follows:

Corollary 1.

Consider a symmetric positive definite matrix . Assume that conditions (DM1-3) in Theorem 2 are satisfied. Then there exists and such that for all step sizes , the -preconditioned -invariant \acmala is -uniformly ergodic for .

Proof.

From Theorem 2 and Proposition 1, the result follows if we can establish (DM1-3) for , since -preconditioned \acmala is equivalent to standard \acmala applied to . For a matrix , let and respectively denote the minimum and maximum eigenvalues of . For (DM1) we set and observe that

For (DM2) we have that

For (DM3) we have that

where , which holds for all , and in particular for all where . Thus (DM1-3) are established for . ∎

Remark 1.

The choice , which sets the preconditioner matrix equal to the inverse of the length scale matrix used in the specification of the kernel (c.f. Section A.3), leads to the elegant interpretation that Stein -Importance Sampling applied to -preconditioned \acmala is equivalent to the Stein -Importance Sampling applied to standard \acmala (i.e. with ) for the whitened target with \acpdf . For our experiments, however, the preconditioner matrix was learned during a warm-up phase of \acmala, since in general the curvature of (captured by ) and the curvature of (captured by ) may be different.

B.3 Proof of Theorem 1

The route to establishing Theorem 1 has three parts. First, we establish (DM1-3) of Theorem 2 with , to deduce from Corollary 1 that -invariant -preconditioned \acmala is -uniformly ergodic. This in turn enables us to establish conditions (R+1-3) of Theorem 3, again for , from which the strong consistency of ST-MALA is established. Finally, we note that , since the support of is contained in the support of , and the latter is optimally weighted, whence also the strong consistency of SIS-MALA.

Establish (DM1-3)

First we establish (DM1-3) for . Fix . For (DM2), first recall that the range of is where , from 1. Since has bounded second derivatives on , there is a constant such that

Thus, using compactness of the set ,

| (16) |

Now, is twice differentiable as it is the product of twice differentiable functions and from (A1) and (A3), and moreover

so (DM2) is satisfied. For (DM3), first note from the chain and product rules that for all

| (17) |

Thus, for all ,

| (18) |

as required. The same argument establishes (DM1); from (18) we have , and since is a continuously differentiable density there must exist an at which is locally minimised. Thus we have established (DM1-3) for and we may conclude from Corollary 1 that there is an and such that, for all , the -invariant -preconditioned \acmala chain is -uniformly ergodic for (since if a Markov chain is -uniformly ergodic, then it is also -uniformly ergodic).

Establish (R+1-3)

The aim is now to establish conditions (R+1-3) of Theorem 3 for . By construction , where and were defined in 1, so that . It has already been established that is -uniformly ergodic, and further

for all , which establishes (R+1). Let and denote constants for which the -uniform ergodicity property (14) is satisfied. From -uniform ergodicity, the integral exists and

which establishes (R+2). Fix . By construction , and thus

where . Since we have assumed that is continuous with, from (A4),

we may take such that , so that and in particular

which establishes (R+3). Thus we have established (R+1-3) for , so from Theorem 3 we have strong consistency of ST-MALA (i.e. ) provided that with for some . The latter condition is equivalent to for some , which we used for the statement. Since , the strong consistency of SIS-MALA is also established.

Appendix C Explicit Calculation of Stein Kernels

This appendix contains explicit calculations for the Langevin–Stein and KGM–Stein kernels , which are sufficient to implement Stein -Importance Sampling and Stein -Thinning. These calculations can also be performed using automatic differentiation, but comparison to the analytic expressions is an important step in validation of computer code.

To proceed, we observe that the diffusion Stein operator in (12) applied to a matrix-valued kernel is equivalent to the Langevin–Stein operator applied to the kernel . In the case of the Langevin–Stein and KGM–Stein kernels we have for some and for some . Thus where

and

following the calculations in Oates et al., (2017). To evaluate the terms in this formula we start by differentiating , to obtain

These expressions involve gradients of , and explicit formulae for these are presented for the choice of corresponding to the Langevin–Stein kernel in Section C.1, and to the KGM–Stein kernel in Section C.2.

To implement Stein -Thinning we require access to both and , the latter for use in the proposal distribution and acceptance probability in \acmala. These quantities will now be calculated. In what follows we assume that is continuously differentiable, so that partial derivatives with respect to and can be interchanged. Then

so that

| (19) |

Let and . Now we can differentiate (19) to get

| (20) |

In what follows we also derive explicit formulae for , and , and hence for , and , for the case of the Langevin–Stein kernel in Section C.1, and the KGM–Stein kernel in Section C.2.

C.1 Explicit Formulae for the Langevin–Stein Kernel

The Langevin–Stein kernel from Section A.3.1 corresponds to the choice and the inverse multi-quadric kernel, so that

Evaluating on the diagonal:

so that , , . Differentiating these formulae, , , .

C.2 Explicit Formulae for the KGM–Stein Kernel

The KGM kernel of order from Section A.3.2 corresponds to the choice

for which we have

Evaluating on the diagonal:

so that

Differentiating these formulae:

These complete the analytic calculations necessary to compute the Stein kernel and its gradient.

Appendix D Empirical Assessment

This appendix contains full details of the empirical protocols that were employed and the additional empirical results described in the main text. Section D.1 discusses the effect of dimension on our proposed . Additional illuatrative results from Section 3.2 are contained in Section D.2. The full details for how \acmala was implemented are contained in Section D.3. An additional illustration using a \acgarch model is presented in Section D.4. The full results for SIS-MALA are contained in Section D.5, and in Section D.6 the convergence of the sparse approximation provided by ST-MALA to the optimal weighted approximation is investigated. Finally, the performance of \acpksd is quantified using the 1-Wasserstein divergence in Section D.7.

D.1 The Effect of Dimension on

The improvement of Stein -Importance Sampling over the default Stein importance sampling algorithm (i.e. ) can be expected to reduce as the dimension of the target is increased. To see this, consider the Langevin–Stein kernel

| (21) |

for some ; see Appendix C. Taking , for which the length scale matrix appearing in Section A.3 is , we obtain

However, the sampling distribution defined in (8) depends on only up to an unspecified normalisation constant; we may therefore equally consider the asymptotic behaviour of . Let . Then is a -independent constant, and

as . This shows that converges to a constant function in , and thus for “typical” values of in the effective support of ,

so that in the limit. This intuition is borne out in simulations involving both the Langevin–Stein kernel (as just discussed) and also the KGM3–Stein kernel. Indeed, Figure S1 shows that as the dimension is increased, the marginal distributions of become increasingly similar to those of .

D.2 2D Illustration from the Main Text

Section 3.2 of the main text contained a 2-dimensional illustration of Stein -Importance Sampling and presented the distributions corresponding to different choices of Stein kernel. Here, in Figure S2, we present the mean \acpksd for Stein -Importance Sampling performed using the Langevin–Stein kernel (purple), the KGM3–Stein kernel (blue), and the Riemann–Stein kernel (red), corresponding to the sampling distributions displayed in Figure 2 of the main text.

For this experiment, exact sampling from both and was performed using a fine grid on which all probabilities were calculated and appropriately normalised. Results are in broad agreement with the 1-dimensional illustration contained in the main text, in the sense that in all cases Stein -Importance Sampling provides a significant improvement over the default Stein importance sampling method with equal to .

D.3 Implementation of \acmala

For implementation of \acmala in Algorithm 4 we are required to specify a step size and a preconditioner matrix . In general, suitable values for both of these parameters will be problem-dependent. Standard practice is to perform some form of manual or automated tuning to arrive at parameter values for which the average acceptance rate is close to 0.57, motivated by the asymptotic analysis of Roberts and Rosenthal, (1998). Adaptive \acmcmc algorithms, which seek to optimise the parameters of \acmcmc algorithms such as \acmala during the warm-up period, provide an appealing solution, and was the approach taken in this work.

The adaptive \acmala algorithm which we used is contained in Algorithm 4, where we have let denote the output from the preconditioned \acmala with initial state , step size , preconditioner matrix , and chain length , described in Algorithm 1. In Algorithm 4, we use to denote the sample covariance matrix. The algorithm monitors the average acceptance rate and increases or decreases it according to whether it is below or above, respectively, the 0.57 target. For the preconditioner matrix, the sample covariance matrix of samples obtained from the penultimate tuning run of \acmala is used. For all experiments that we report using \acmala, we set , , , and . The warm-up epoch lengths were and the final epoch length was . The samples from the final epoch are returned, and constituted output from \acmala for our experimental assessment.

To sample from instead of , we used Algorithm 4 we formally set for all , which recovers as the target.

D.4 Illustration on a GARCH Model

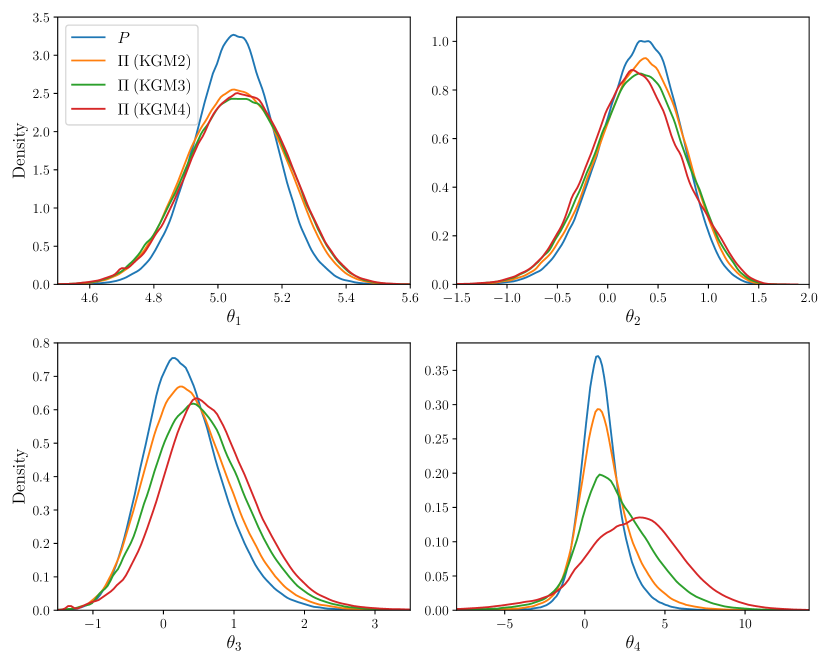

This appendix contains an additional illustrative experiment, concerning a \acgarch model that is a particular instance of a model from the PosteriorDB database discussed in Section 4. The purpose of this illustration is to facilitate an empirical investigation in a slightly higher dimension () and to explore the effect of changing the order of the KGM–Stein kernel defined in Section A.3.2.

First we describe the \acgarch model that was used. These models are widely-used in econometrics to describe time series data in settings where the volatility process is assumed to be time-varying (but stationary). In particular, we consider the GARCH(1,1) model

where , , , and are the model parameters, constrained to a subset of . For ease of sampling, a change of variables is performed in such a way that the parameter is unconstrained. Assuming an improper flat prior on , the log-posterior density for is given up to an additive constant by

where is the Jacobian determinant of .

For this illustration, real data were provided within the model description of PosteriorDB, for which the estimated maximum a posteriori parameter is . The marginal distributions of corresponding to the KGM–Stein kernels of orders are compared to the marginals of in Figure S3. It can be seen that higher orders correspond to greater over-dispersion of ; this makes intuitive sense since larger corresponds to a more stringent \acksd (controlling the convergence of moments up to order ) which places greater emphasis on how the tails of are approximated. Further, for the final skewed marginal of , we note that the distribution exaggerates the skew, placing more of its mass in the tail of the direction which is positively skewed. Further discussion of skewed targets is contained in Section D.8.

D.5 Stein -Importance Sampling for PosteriorDB

To introduce objectivity into our assessment, we exploited the PosteriorDB benchmark (Magnusson et al.,, 2022). This ongoing project is an attempt toward standardised benchmarking, consisting of a collection of posteriors to be numerically approximated. The test problems in PosteriorDB are defined in the Stan probabilistic programming language, and so BridgeStan (Roualdes et al.,, 2023) was used to directly access posterior densities and their gradients as required. The ambition of PosteriorDB is to provide an extensive set of benchmark tasks; at the time we conducted our research, PosteriorDB was at Version 0.4.0 and contained 149 models, of which 47 came equipped with a gold-standard sample of size , generated from a long run of Hamiltonian Monte Carlo (the No-U-Turn sampler in Stan). Of these 47 models, a subset of 40 were found to be compatible with BridgeStan, which was at Version 1.0.2 at the time this research was performed. The version of Stan that we used was Stanc3 Version 2.31.0 (Unix). Thus we used a total of 40 test problems for our empirical assessment.

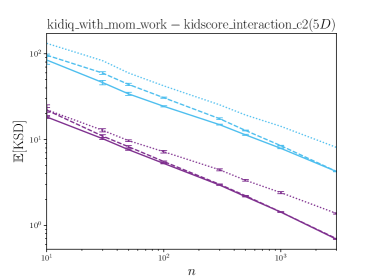

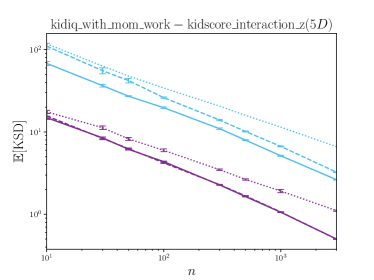

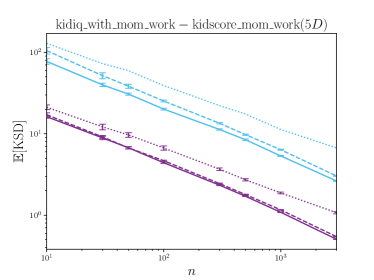

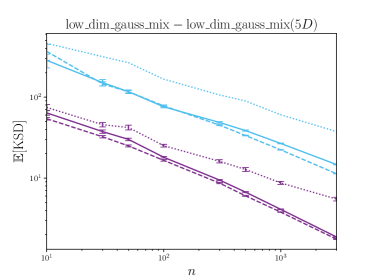

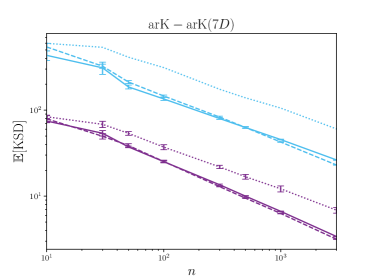

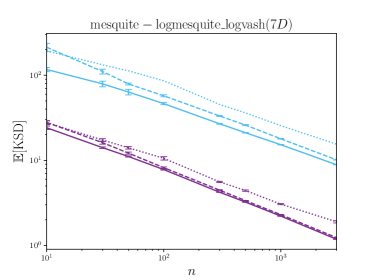

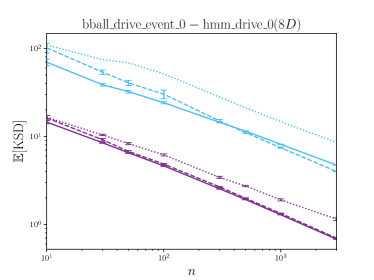

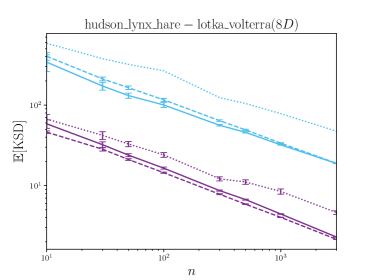

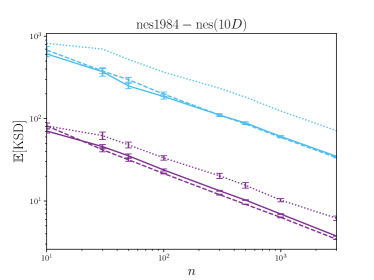

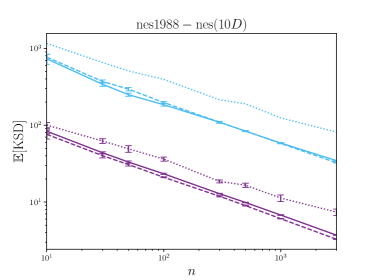

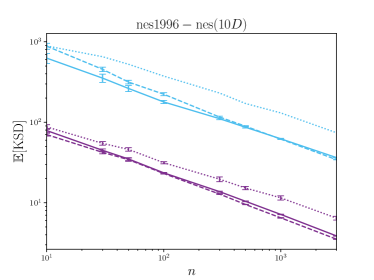

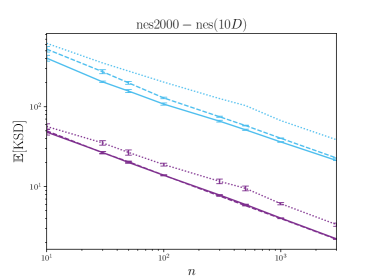

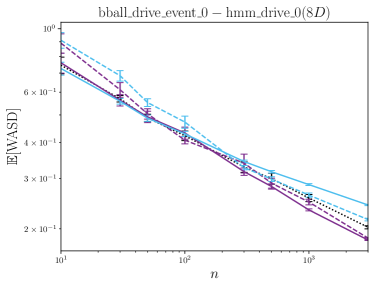

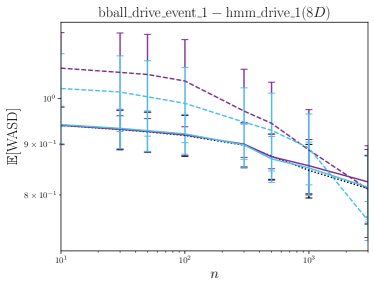

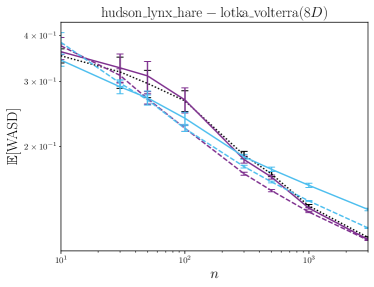

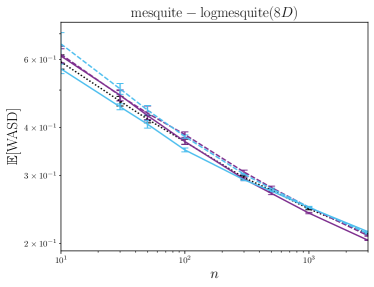

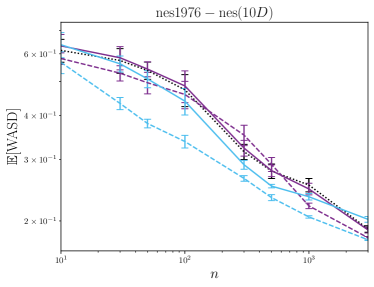

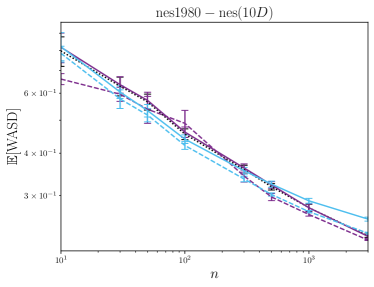

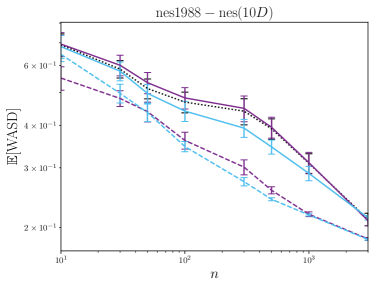

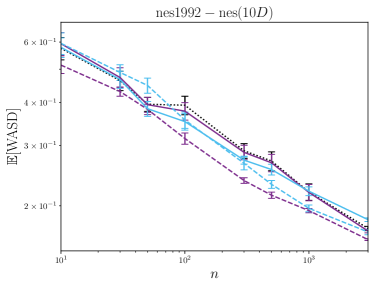

For each test problem, a total of 10 replicate experiments were performed and standard errors were computed. A sampling method was defined as being significantly better for approximation of a given target, compared to all other methods considered, if had lower mean \acksd and the standard error bar did not overlap with the standard error bar of any other method. Table 1 in the main text summarises the performance of SIS-MALA, fixing the number of samples to be . In this appendix, full empirical results are provided.

For sampling from \acmala, we used the adaptive algorithm described in Section D.3 with a final epoch of length . Then, whenever a set of consecutive samples from \acmala are required for our experimental assessment, these were obtained by selecting at random a consecutive sequence of length from the total chain of length . This ensures that the performance of unprocessed \acmala that we report is not negatively affected by burn-in, in so far as is practical to control.

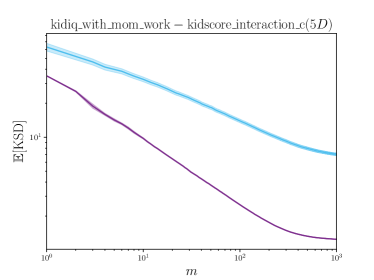

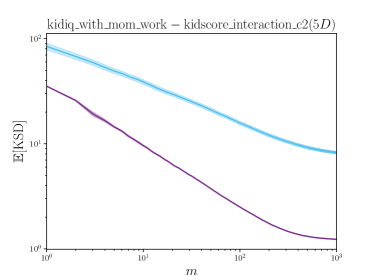

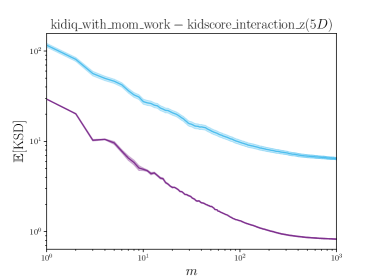

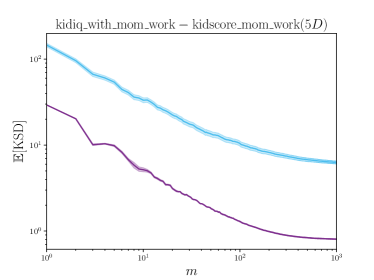

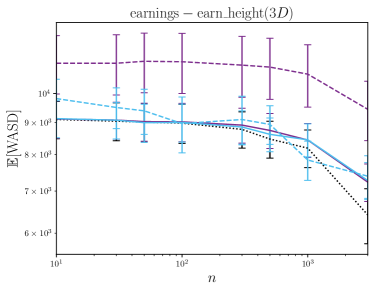

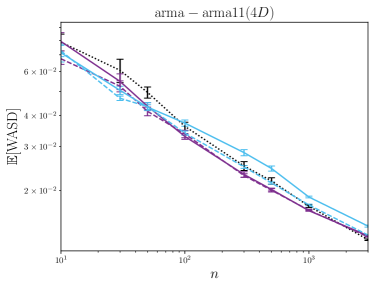

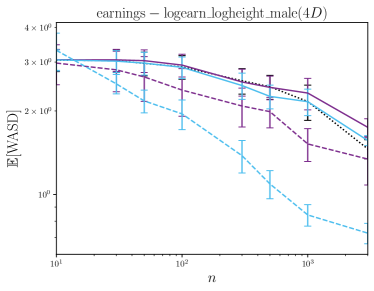

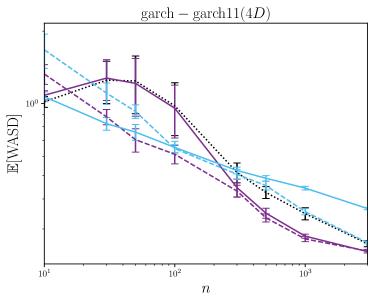

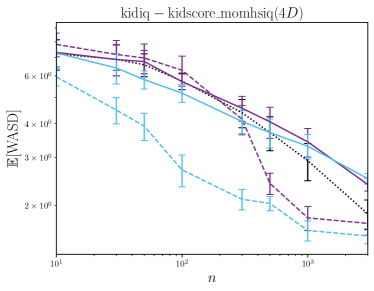

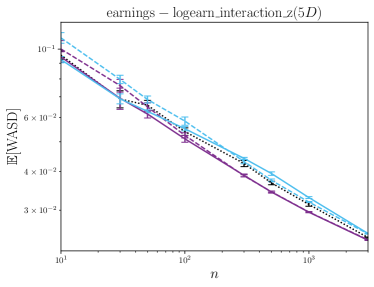

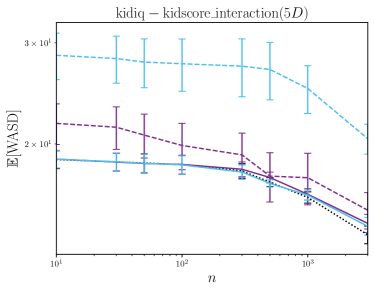

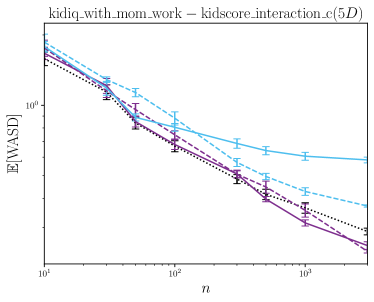

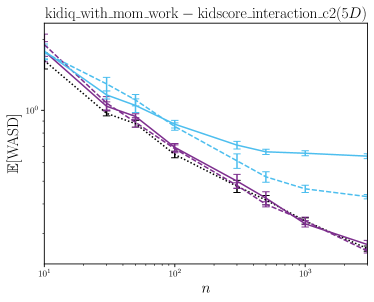

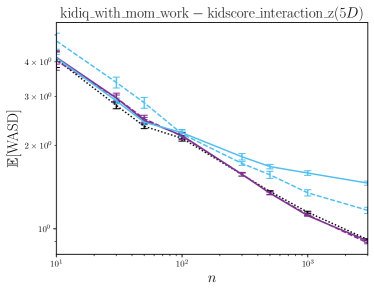

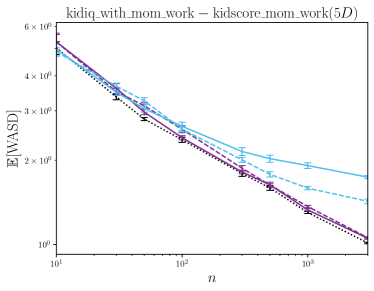

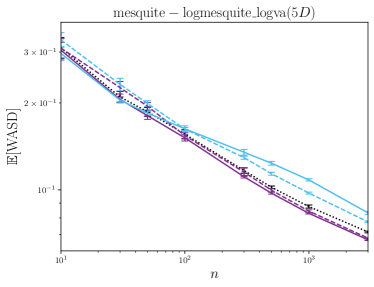

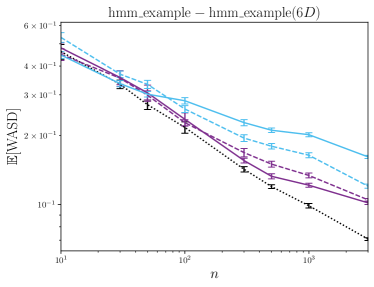

Full results are presented in Figure S4. These results broadly support the interpretation that SIS-MALA usually outperforms SIS-MALA, or otherwise both methods provide a similar level of performance, for the sufficiently large sample sizes considered. The sample size threshold at which SIS-MALA outperforms SIS-MALA appears to be dimension-dependent. A notable exception is panel 29 of Figure S4, a dimensional task for which SIS-MALA provided a substantially worse approximation in \acksd for the range of values of considered.

D.6 Stein -Thinning for PosteriorDB

The results presented in the main text concerned samples from \acmala, which is near the limit at which the optimal weights can be computed in a few seconds on a laptop PC. For larger values of , sparse approximation methods are likely to required. In the main text we presented Stein -Thinning, which employs a greedy optimisation perspective to obtain a sparse approximation to the optimal weights at cost , where are the number of greedy iterations performed. Explicit and verifiable conditions for the strong consistency of the resulting ST-MALA algorithm were established in Section 3.3. The purpose of this appendix is to empirically explore the convergence of ST-MALA using the PosteriorDB test bed.

In the experiments we report the number of \acmala samples was fixed to and the number of greedy iterations was varied from to . The results, in Figure S5, indicate that for most models in PosteriorDB the minimum value of \acksd is approximately reached when is anywhere from to , representing a modest but practically significant reduction in computational cost compared to SIS-MALA. This agrees with the qualitative findings reported in the original Stein thinning paper of Riabiz et al., (2022).

D.7 Performance of Stein Discrepancies

The properties of Stein discrepancies was out of scope for this work. Nonetheless, there is much interest in better understanding the properties of KSDs, and in this appendix the performance of SIS-MALA in terms of 1-Wasserstein divergence is reported. This was made possible since PosteriorDB supplies a set of posterior samples obtained from a long run of Hamiltonian Monte Carlo (the No-U-Turn sampler in Stan) which we treat as a gold standard.

Full results are presented in S6. Broadly speaking, for most models the minimisation of \acksd seems to be associated with minimisation of 1-Wasserstein distance, however there are some models for which minimisation of \acksd is loosely, if at all, related to minimisation of 1-Wasserstein divergence. In these cases, we attribute this performance to the blindness to mixing proportions phenomena, described in Wenliang and Kanagawa, (2021); Koehler et al., (2022); Liu et al., (2023). Convergence in 1-Wasserstein is equivalent to weak convergence plus convergence of the first moment, so the KGM–Stein kernels of order control convergence in 1-Wasserstein. In Section 2.3 we proved that SIS-MALA is strongly consistent in \acksd for the KGM–Stein kernel in the case , so we can expect strong consistency in 1-Wasserstein divergence for SIS-MALA in this case as well. It is interesting to observe that better 1-Wasserstein quantisations tend to be provided by SIS-MALA compared to SIS-MALA when either the Langevin–Stein or KGM–Stein kernel are used.

The development of improved Stein discrepancies is an active area of research, and we emphasise that the methodology developed in this work can be applied to any \acpksd, including potentially \acpksd with better or more direct control over standard notions of convergence (such as 1-Wasserstein) that in the future may be developed.

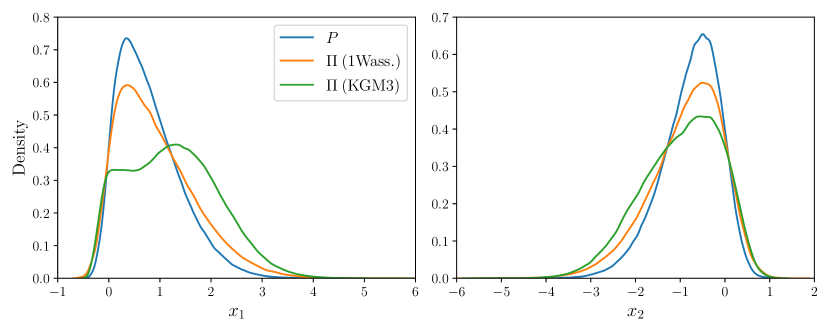

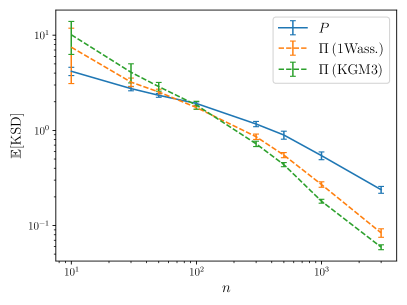

D.8 Investigation for a Skewed Target

This final appendix contrasts the 1-Wasserstein optimal sampling distribution (c.f. Section 2.1), with the choice of that we recommended in (8). In particular, we focus on the KGM3–Stein kernel under a heavily skewed , for which and can be markedly different.

For this investigation a bivariate skew-normal target was constructed, where the density is given by , with and respectively denoting the density and distribution functions of a standard Gaussian. The density of , together with the marginal densities of and , are plotted in Figure S7. It can be seen that, while both and are over-dispersed with respect to , our recommended assigns proportionally more mass to the tail that is positively skewed.

The performance of Stein -Importance Sampling based on and is compared in Figure S8. Though both choices lead to an improvement relative to Stein importance sampling algorithm with , the use of leads to a significant further reduction (on average) in \acksd compared to . Based on our investigations, this finding seems general; the use of does not realise the full potential of Stein -Imporance sampling when the target is skewed.