Balancing Risk and Reward: An Automated Phased Release Strategy

Abstract

Phased releases are a common strategy in the technology industry for gradually releasing new products or updates through a sequence of A/B tests in which the number of treated units gradually grows until full deployment or deprecation. Performing phased releases in a principled way requires selecting the proportion of units assigned to the new release in a way that balances the risk of an adverse effect with the need to iterate and learn from the experiment rapidly. In this paper, we formalize this problem and propose an algorithm that automatically determines the release percentage at each stage in the schedule, balancing the need to control risk while maximizing ramp-up speed. Our framework models the challenge as a constrained batched bandit problem that ensures that our pre-specified experimental budget is not depleted with high probability. Our proposed algorithm leverages an adaptive Bayesian approach in which the maximal number of units assigned to the treatment is determined by the posterior distribution, ensuring that the probability of depleting the remaining budget is low. Notably, our approach analytically solves the ramp sizes by inverting probability bounds, eliminating the need for challenging rare-event Monte Carlo simulation. It only requires computing means and variances of outcome subsets, making it highly efficient and parallelizable.

1 Introduction

Phased release, also known as staged rollout, is a widely used strategy in the technology industry that involves gradually releasing a new product or update to larger audiences over time [17, 30]. For example, Apple’s App Store offers a phased release option where application updates are released over a 7-day period on a fixed schedule [1]. Google Play Console provides a similar feature with more flexibility in the release schedule [16]. Typically, the audiences are randomly selected at each stage from the set of all customers, and so phased releases can be thought of as a sequence of A/B tests (or randomized experiments) in which the proportion of units assigned to the treatment group changes until either the product or update is fully launched or deprecated [26, 18, 3, 33, 6]. The process of combining phased releases with A/B tests is often called controlled rollout or iterative experiments and provides companies with an important mechanism to gather feedback on early product versions [30, 20, 5].

The key advantage of phased release is its ability to mitigate risks associated with launching a new product or update directly to all users. The potential impact of faulty features is limited by releasing the update first to a small percentage of the users (i.e., the treatment group). However, this risk-averse approach introduces an opportunity cost for slowly launching beneficial features, which quickly adds up for companies that release thousands of features yearly [34]. Therefore, when designing a phased release schedule, it is important to determine the release percentage (known as ramp schedule) at each stage that balances the need to control risk while maximizing the speed of ramp-up.

This paper proposes an algorithm to address this challenge by automatically determining the release percentage for the next phase based on observations from previous stages. Specifically, we frame the challenge as a budget-constrained batched bandit problem. For each batch, we aim to determine the assignment probabilities of newly arrived users while keeping the probability of depleting a pre-specified experimental budget, where the experiment’s cost is the cumulative treatment effect that are not directly observed. Formally, we derive recursive relations that decompose the risk of ruin (depleting the budget) of a phased release to the individual stages in the sense that the risk of ruin of the entire experiment is controlled if stage-wise ruin probabilities are controlled. Our algorithm is Bayesian in the sense that it learns from past observations by computing the posteriors of a conjugate Gaussian model and uses these parameters to infer the remaining budget and other cost-related quantities. However, the algorithm is robust to misspecifications and works well even when underlying outcomes are far from Gaussian by law of large number and central limit theorem; nevertheless, in Appendix E, we provide an extension to non-Gaussian outcomes. Finally, the next stage’s assignment probabilities are derived from the posterior distribution and the stage-wise risk tolerances. Notably, our approach solves ramp sizes analytically from inverting the ruin probability upper bounds, avoiding challenging rare-event Monte-Carlo simulation for budget depletion events and data imputation procedures for unobserved counterfactual outcomes.

1.1 Literature review

While many firms have guidelines on how to conduct a phased release process, these guidelines are often ad-hoc and qualitative, making it difficult to create executable ramp schedules. The SQR framework in [34] is the first attempt to address this problem by providing quantitative guidance. Our work differs significantly from SQR. Our algorithm adopts a fully Bayesian approach, enabling us to incorporate prior information on the risk of a feature in a probabilistic manner when initiating a ramp. Additionally, unlike SQR, our approach introduces a “shared budget” over the entire phased release, allowing the budget to be sequentially adjusted based on the observations from prior iterations. Finally, our algorithm is robust to modifications made to the treatment during experiments and different outcome models.

Our work is notably distinct from the risk-averse multiarmed bandit approaches considered in previous research [19, 14, 35, 28, 23, 10, 8]. In these approaches, the agent considers the expected variability in expected rewards to identify and avoid less predictable (and therefore risky) actions, without considering a budget constraint. A related literature focuses on batched and Bayesian variants of these methods in multi-stage clinical trials [4, 27, 21, 24, 2]. While this literature also aims to determine treatment assignment for each stage of the experiment, it differs from our setting in two key aspects: (i) the objective is to maximize treatment effect while balancing exploration of treatment arms, rather than rapidly ramping up experiments, and (ii) to the best of our knowledge, no clinical trials paper has addressed the imposition of a budget for potential adverse treatment effects. Hence, bandit approaches developed for clinical trials cannot be directly applied to our setting. To illustrate the difference, we present a numerical simulation of a Thompson sampling-based Bayesian bandit from [27] and highlight that budget spent and the aggressiveness of the ramp-up schedule depends on model tuning in a very unpredictable way, making the ramp-up schedule far from ideal. Another related literature is budgeted multiarmed bandits [32, 31, 9, 29, 12]. However, most budgeted bandit algorithms are developed for settings very different from ours and do not consider risk-of-ruin control or handle unobserved costs. Therefore, these algorithms cannot be directly applied to our specific scenario.

Notation.

Let be the set of non-negative integers and . Let denote the set of real numbers and positive real numbers respectively. for . is the generated -algebra. if random variable is measurable to . denotes a random variable with distribution for a random variable and -algebra .

2 Risk-of-ruin-constrained experiment

Consider a scenario in which a single feature is released to a sequence of subpopulations consisting of units at stages , where is not necessarily fixed. At each stage, we randomly assign treatment to a group of units denoting the indexing set , while the control group with indexing set . The size of the treatment group at stage is and the size of the control group is .

Our paper adopts the Neyman-Rubin framework for causal inference [22, 25, 7], where the potential outcome of each unit during experiment stage under control and treatment are denoted by and , respectively111We are implicitly assuming that there is no interference between experimental units, that is, each unit’s outcomes do not depend on any other unit’s assignments [11].. Appendix E provides the extension to multivariate outcomes. The treatment assignment of unit at stage is denoted by . Since each unit only receives a single treatment at each stage, we only observe during the experiment, not the counterfactual (we are explicitly assuming that there is full compliance).

Let be the -algebra generated by the treatment assignment and the observed experiment outcome in the first stages, with representing the trivial -algebra. In our setting, the experimenter aims to ramp up the experiment to the "max-power stage" (50% of the population placed in treatment) as quickly as possible while avoiding the risk of a large negative business impact (or cost). We define the cost of the experiment as the treatment effect on the treated. See generalized cost in Appendix E.

Definition 2.1 (Experiment cost).

The cost of the experiment from stage is , where if . The cumulative cost is .

Throughout, corresponds to a negative business impact; our goal is to control the experiment cost by setting a budget and imposing the cost constraint . Since the outcomes are stochastic, we require this cost constraint to be satisfied with probability at least for some set before the experiment. Our goal is then to adaptively determine the size of the treatment group based on the observed data while satisfying our risk constraint. We refer to such an experiment as a risk-of-ruin-constrained (RRC) experiment.

Definition 2.2 (RRC experiment).

Fix any . A -RRC experiment running for stages selects the size of before -th stage of the experiment such that .

3 Model and the algorithm

3.1 Decompose the risk of ruin

Our experimental design is based on the following theorem, which identifies a sequence of sufficient conditions for a sequential experiment to be -RRC. We defer its proof to Appendix A.

Theorem 3.1.

Fix and . For any stopping time , let be a budget sequence, such that , and be a risk tolerance sequence, such that and . Then, if is chosen such that for ,

| (1) |

and for any , almost surely,

| (2) |

then This inequality is tight when – are all equalities and almost surely. Furthermore, if we set , (1), (2) always hold.

Recall, denotes the budget and is our risk tolerance that controls the risk of ruin (i.e., the probability of exceeding the budget); both need to be fixed a priori. In general, smaller leads to more conservative experimentation and slower releases. The sequence “rations” the budget: setting at stage reserves budget for later stages, which may be beneficial when the released feature is expected to undergo modifications during the experiment [20]. To quickly scale the experiment, we can set . The sequence distributes the overall tolerance to individual stages by allowing us to customize the tolerance for individual stages. If is fixed a priori, we can uniformly distribute the tolerance by setting .

Theorem 3.1 breaks the risk constraint into stage-wise constraints in the form of (1),(2). The idea is to control current-stage cumulative experiment cost given past observations and determine the treatment assignment based on posterior inference of the remaining budget. In our setting, the goal is to maximize subject to (1),(2). Note that the first line in (2) stops the experiment when the model estimates that the budget is exhausted, while the second line sets the stage cost below the remaining budget with high probability. We require assumptions on the data-generating model to derive an explicit algorithm, which we present in the next sections.

Generally, the total number of stages , stage-wise budget and tolerance , can be determined dynamically during the process. That is, we can define and just before stage as long as and . If we plan to terminate the experiment after stage , we can define such that and is attained in which case . If is also possible to have and . For example, choosing where is the unique solution of on (cf. [13, Eq. (1)]) satisfy our condition.

Note that the decomposition scheme in Theorem 3.1 is formulated such that is tight if inequalities (i)—(iv) are tight. Practically, this means that the ramp-up schedules obtained through this approach are typically not overly conservative, unlike approaches that leverage a union-bound for risk decomposition. Finally, Theorem 3.1 holds for a general definition of the cost such that if , making it useful in other budgeted online problems beyond our setting.

3.2 Gaussian outcome model

For this subsection, make the following model assumptions on the outcomes distribution; appendix E provides the extension to general outcome models.

Definition 3.1 (Conjugate Gaussian outcomes).

Let the unknown model parameters satisfy the prior for independently, where are hyperparameters. The experiment outcome of unit at stage are distributed independently and identically as

| (3) |

where are hyperparameters.

The unknown parameters and represent the intrinsic quality of the feature before and after the update, as measured by a specific metric. If , the feature update is likely to have a negative business impact, i.e., .

To derive the posterior distribution we need the following statistics. For

| (4) | ||||

and for

| (5a) | |||

| (5b) | |||

| (5c) | |||

where and are the cumulative number of users in the treatment and control groups up to stage , respectively. In (5a), and represent the cumulative sum of outcomes for in the treatment and control groups up to stage , while and represent the sum of outcomes at stage . In equation (5b), represents the posterior mean of , while in equation (5c), represents the posterior variance of , for . When lacking prior information, we suggest using a non-informative priors by setting and sufficiently large.

The model parameters and at stage can be estimated using unbiased and consistent estimators. For let

| (6) |

For , some prior estimate can be used, either from a similar experiment or from a small-scale pretrial run.

3.3 An algorithm for the sample size in a -RRC experiment

We now derive an explicit algorithm from Theorem 3.1 that to outputs , the treatment group size at stage , such that, the experiment is -RRC. Recall that for an experiment to be -RRC, it suffices that (1), (2) holds for each . Under Definition 3.1, we have that (i) are exchangeable random variables (ii) for any , almost surely for any choice of . Combining these observations, we get that (1), (2) hold if for each ,

| (7) |

Lemma 3.2 provides an upper bound of the left hand size of (7); the proof is in Appendix B.

Lemma 3.2 (Stochastic domination).

Assume the outcomes are generated as in Definition 3.1. For any , almost surely,

| (8) | ||||

Using Lemma 3.2, for (1) and (2) to hold, it suffices to choose any such that

| (9) |

and set if such does not exist. From posterior-predictive formulas for the conjugate Gaussian model in Definition 3.1 (see (15e), (15f) in Appendix C), we have where

| (10a) | |||

| (10b) | |||

Combining the above with (9) yields the following Lemma.

Lemma 3.3.

Assume the outcomes are generated as in Definition 3.1. For each , the inequality (9) holds if and only if

| (11) |

where denotes inverse CDF of the standard normal distribution.

Replace the inequality in (11) with equality and square both sides gives us the quadratic equation where

| (12) | ||||

Algorithm 1 finds the floor transform of the solutions of this equation and chooses as the largest, positive integer that satisfies (11). If such a solution cannot be found, then either we do not have enough budget or the cost of the experiment is negligible (this accrues when ), and the inequality in (11) will be strict for any choice of . In the former case, Algorithm 1 sets ; in the latter case, it sets . Therefore, by construction, the sequence output by Algorithm 1 guarantees that (1) and (2) hold, thereby defining a -RRC experiment. Note that this approach directly solves for from the quadratic equation , bypassing the challenging task of estimating tail probabilities for potential choices of through Monte-Carlo methods. By Algorithm 1, we can also conduct posterior inference on treatment effect after stage using and estimate the remaining budget by .

Theorem 3.2.

Assume the outcomes are generated as in Definition 3.1. The experiment by Algorithm 1 is -RRC.

Even though our algorithms is derived from the conjugate Gaussian model we have found that it remains effective for broader outcome models. This is because the learning occurs essentially through computation of the first and second moments of past outcomes as in (5), (6), and Algorithm 1 tends to be successful so long as they are predictive of the outcome moments in future stages. The risk of ruin control remains approximately valid due to the law of large numbers and standard central limit theorem under specific conditions; see next section.

Finally, in Algorithm 1, the assumption is made that the population size for the next stage is known to ensure that does not exceed . In practice, we recommend estimating and using the model output to calculate the assignment probability , the allows the experimenter to assign each incoming user to the treatment group with a probability of .

3.4 Robustness to non-identically distributed and non-Gaussian outcomes

We now derive conditions for the validity of Algorithm 1 under the assumption that experiment outcomes are independent.

Definition 3.4.

The experiment outcomes are independent across different units and experiment stage .

Definition 3.4 allows and to be dependent and/or discrete-valued (e.g., binary outcomes). In addition, the outcome distribution can differ across ; for instance, treatment effect may be non-stationary. The validity of Algorithm 1 under Definition 3.4 is now given in Theorem 3.3; we defer the proof to Appendix D.

Theorem 3.3.

Assume the outcomes satisfy Definition 3.4. The experiment by Algorithm 1 is -RRC if, for each stage where , the following conditions hold

| (13) |

where

We expect the first condition in (13) to hold as a consequence of central limit theorem for independent but non-identical random variables. Suppose (i.e., ). By law of large number for independent but non-identical random variables, the second condition in (13) holds if (i) we have chosen prior and model parameters conservatively such that

and (ii) if the treatment effects increase or stay roughly constant throughout the experiments

and our variance estimates are accurate or conservative in the sense that

In summary, under Definition 3.4, the validity of Algorithm 1 depends on the accuracy and conservatism of the model’s estimates based on past stages for the true treatment effect and volatility in the next stage. The algorithm’s effectiveness may be compromised when there is a sudden decrease in treatment effect or a surge in outcome volatility in the next stage; see discussion in Appendix D.

4 Numerical and empirical experiments

Simulated ramp schedule

We now examine the following three experimental scenarios, for each are iid sampled from (3) with variance and means given below:

-

i)

PTE: Positive treatment effect, with , ;

-

ii)

NTE: Negative treatment effect, with and ;

-

iii)

NPTE: Negative to positive treatment effect, with .

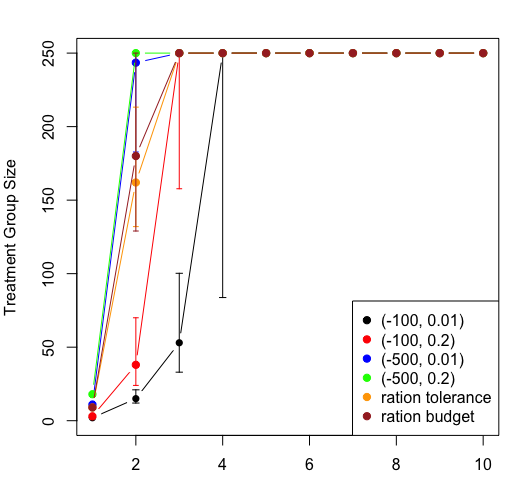

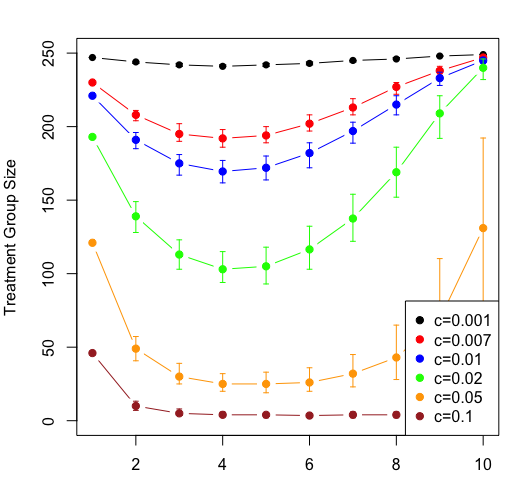

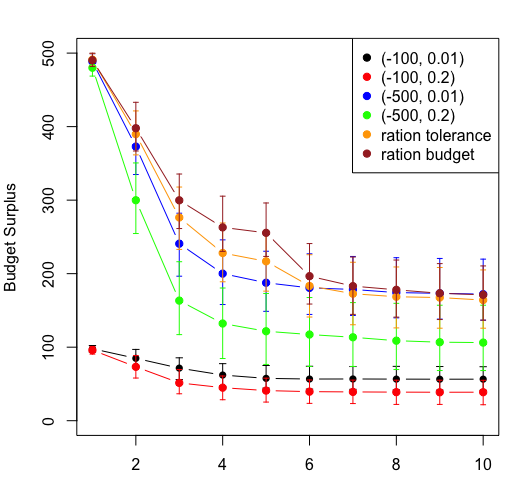

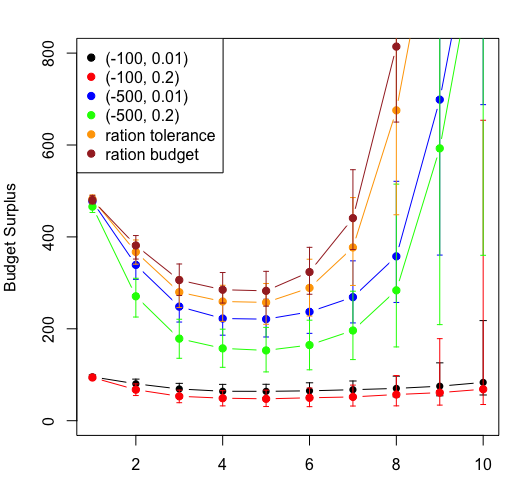

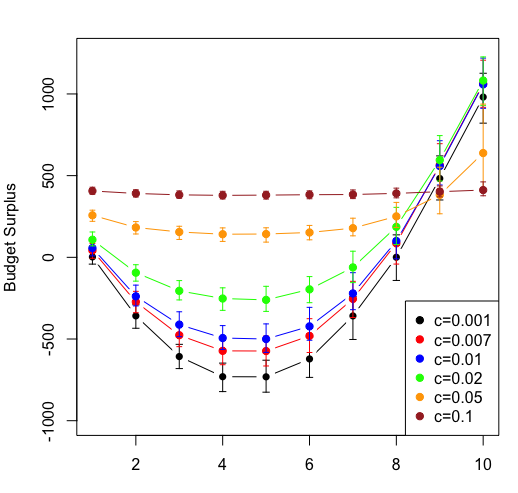

For each scenario, we set with and we choose non-informative prior . We assume model variance is known; however, using (6) to estimate the variance gives similar results. We repeat each scenario 500 times. Figure 1 (a)—(c) show median, 25% and 75% quantile of the simulated ramp schedules and (g),(h) show the budget surpluses produced given different choices of .

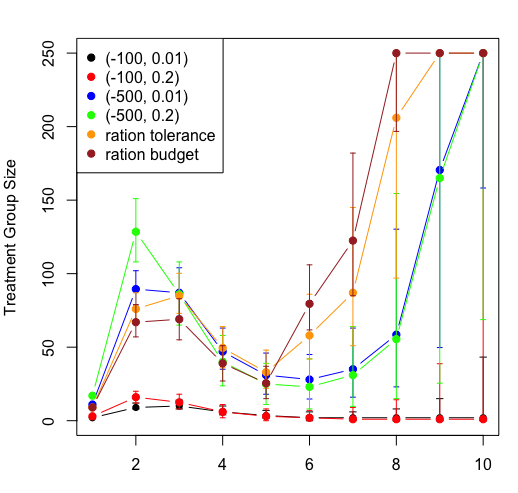

Across the various scenarios, our model gives a reasonable ramp schedule. Large typically leads to more treated units and faster ramp-up. For the NPTE scenario, inadequate budget and low ruin tolerance can result in a failure to ramp up to 50% (). We also found that reserving the budget for later stages by decreasing or in the initial stages leads to a faster ramp-up because more budget is available to support a swift increase when the treatment effect turns positive. This suggests that the experimenter may want to consider reserving some budget for later stages if the treatment effect has not stabilized.

For PNTE scenario, we compare our method to a Thompson-sampling bandit with tuning parameters and prior (see [27] and Appendix G for details). The prior is chosen so that the bandit can initialize conservatively depending on . It can be seen in Figure 1 (e),(i) that the ramp schedule generated is rather sub-optimal and does not respect the budget. It also follows a rigid pattern where with small , the ramp-up initializes too aggressively, and for large , the ramp-up proceeds too conservatively. These results demonstrate that our approach significantly outperforms the main existing alternative.

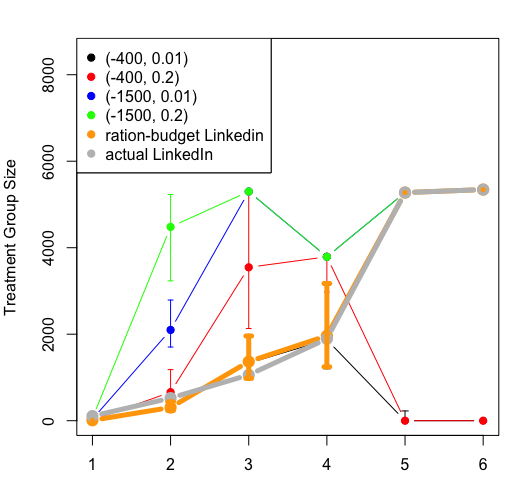

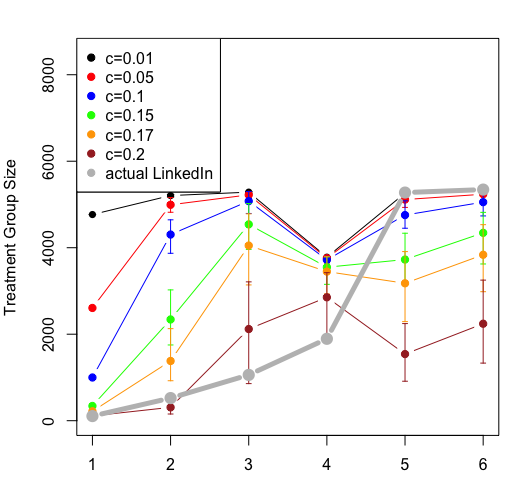

Semi-real LinkedIn ramp schedule comparison

Appendix F gives group-level statistics from a 6-stage phased release run at LinkedIn. Due to privacy constraints, the individual-level data is not available and is simulated from (4) using stage-wise (both unobserved). The ramp-up schedules for different tuning parameters are shown in Figure 1,(d). It is noteworthy that the ramp-up schedule employed by LinkedIn’s data scientists, which was chosen without considering a specific budget, is roughly consistent with the budget-rationing schedule denoted as "ration-budget Linkedin" in the caption. Our results suggest that deducing the budget and risk tolerance associated with an experiment retroactively using our method is possible. We also run the experiment using Thompson sampling Bayesian bandit with the same prior as for NPTE above. In Figure 1(f), we again observe the rigidity issue: with small , the ramp-up initializes too aggressively, and for large , the ramp-up proceeds too conservatively.

Budget-spent distribution

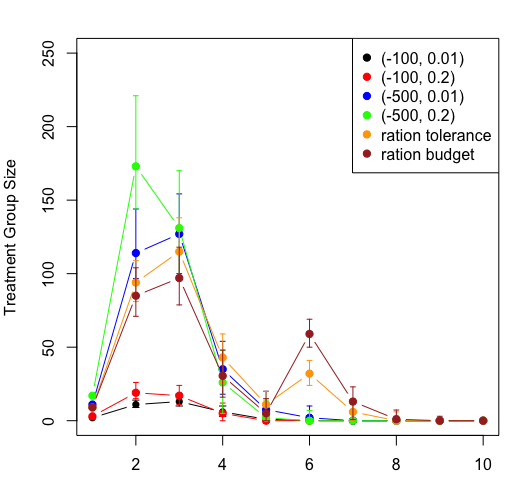

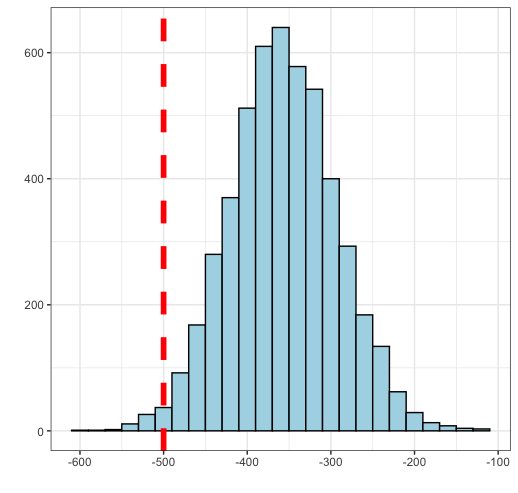

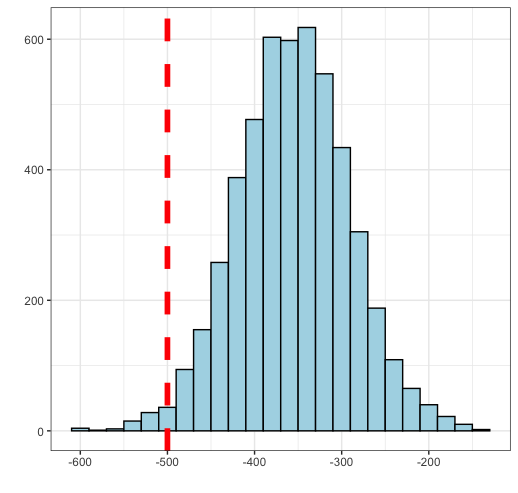

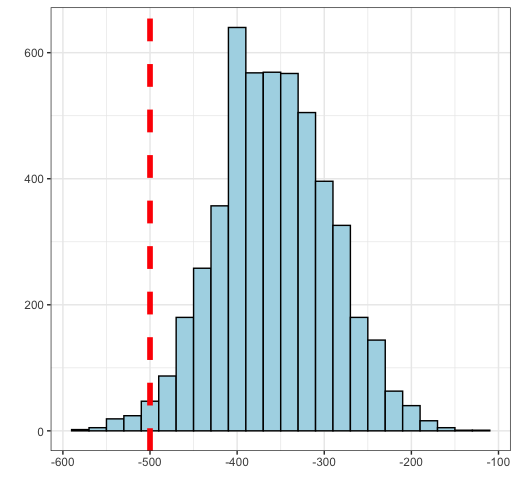

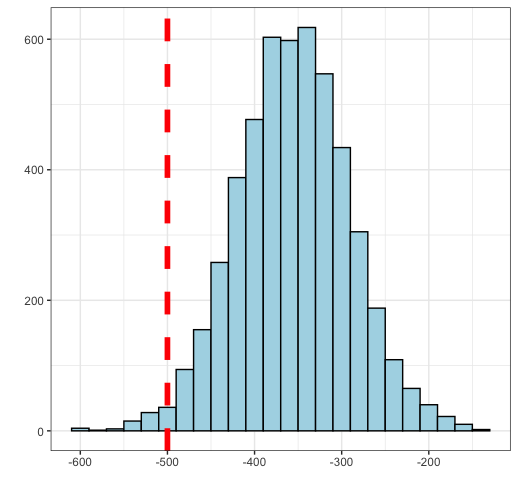

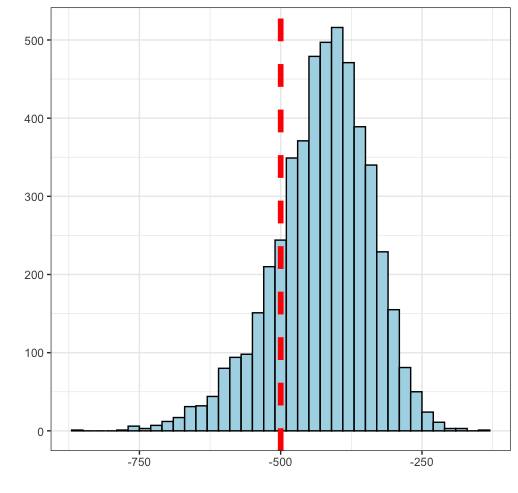

To explore how our algorithms controls the risk of ruin and budget spending, we simulate following experiments for 5,000 times and plot distribution of the budget spent in Figure 2: (i)norm: are sampled iid from (3) with ; (ii) corr: same as norm except that for each , is correlated with with correlation coefficient 0.8 (iii) bern: and ; (iv) fat: and 222Where is a Student-t distribution with 4 degrees of freedom. (v) dec: same as norm except . Note that (iii), (iv) is configured so that . For all the above experiments, we run stages with and we use non-informative prior .

As shown in Figure 2, the model successfully controls risk of ruin for (i)—(iv). The actual ruin risk is at a reasonable level (%) compared to the ruin tolerance given (%). Note that the actual ruin risk are close for different outcome distribution. This is a consequence of central limit theorem and law of large numbers as discussed in Section 3.4. The model fails to control risk of ruin for (v) as expected since the treatment effect keeps decreasing and the model assigns treatment based on past stages which leads to higher-than-expected costs (cf. Section 3.4).

References

- [1] Apple. App store: Release a version update in phases, 2023.

- [2] Maryam Aziz, Emilie Kaufmann, and Marie-Karelle Riviere. On multi-armed bandit designs for dose-finding clinical trials. The Journal of Machine Learning Research, 22(1):686–723, 2021.

- [3] Eytan Bakshy, Dean Eckles, and Michael S Bernstein. Designing and deploying online field experiments. In Proceedings of the 23rd international conference on World wide web, pages 283–292, 2014.

- [4] Donald A Berry. Modified two-armed bandit strategies for certain clinical trials. Journal of the American Statistical Association, 73(362):339–345, 1978.

- [5] Iavor Bojinov and Somit Gupta. Online experimentation: Benefits, operational and methodological challenges, and scaling guide. Harvard Data Science Review, 4(3), 2022.

- [6] Iavor Bojinov and Karim R. Lakhani. Experimentation at yelp. Harvard Business School Case 621-064, 2020.

- [7] Iavor Bojinov and Neil Shephard. Time series experiments and causal estimands: Exact randomization tests and trading. Journal of the American Statistical Association, page Forthcoming, 2019.

- [8] Asaf Cassel, Shie Mannor, and Assaf Zeevi. A general approach to multi-armed bandits under risk criteria. In Conference on learning theory, pages 1295–1306. PMLR, 2018.

- [9] Semih Cayci, Atilla Eryilmaz, and Rayadurgam Srikant. Budget-constrained bandits over general cost and reward distributions. In International Conference on Artificial Intelligence and Statistics, pages 4388–4398. PMLR, 2020.

- [10] Joel QL Chang and Vincent YF Tan. A unifying theory of thompson sampling for continuous risk-averse bandits. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 36, pages 6159–6166, 2022.

- [11] David. R. Cox. Planning of Experiments. John Wiley & Sons, New York, 1958.

- [12] Debojit Das, Shweta Jain, and Sujit Gujar. Budgeted combinatorial multi-armed bandits. arXiv preprint arXiv:2202.03704, 2022.

- [13] WF Eberlein. On euler’s infinite product for the sine. Journal of Mathematical Analysis and Applications, 58(1):147–151, 1977.

- [14] Nicolas Galichet, Michele Sebag, and Olivier Teytaud. Exploration vs exploitation vs safety: Risk-aware multi-armed bandits. In Asian Conference on Machine Learning, pages 245–260. PMLR, 2013.

- [15] Andrew Gelman, John B Carlin, Hal S Stern, and Donald B Rubin. Bayesian data analysis. Chapman and Hall/CRC, 1995.

- [16] Google. Play console help: Release app updates with staged rollouts, 2023.

- [17] Jez Humble and David Farley. Continuous delivery: reliable software releases through build, test, and deployment automation. Pearson Education, 2010.

- [18] Ron Kohavi, Alex Deng, Brian Frasca, Toby Walker, Ya Xu, and Nils Pohlmann. Online controlled experiments at large scale. In Proceedings of the 19th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 1168–1176, 2013.

- [19] Odalric-Ambrym Maillard. Robust risk-averse stochastic multi-armed bandits. In Algorithmic Learning Theory: 24th International Conference, ALT 2013, Singapore, October 6-9, 2013. Proceedings 24, pages 218–233. Springer, 2013.

- [20] Jialiang Mao and Iavor Bojinov. Quantifying the value of iterative experimentation. arXiv preprint arXiv:2111.02334, 2021.

- [21] Vianney Perchet, Philippe Rigollet, Sylvain Chassang, and Erik Snowberg. Batched bandit problems. The Annals of Statistics, pages 660–681, 2016.

- [22] Donald B Rubin. Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of educational Psychology, 66(5):688, 1974.

- [23] Amir Sani, Alessandro Lazaric, and Rémi Munos. Risk-aversion in multi-armed bandits. Advances in neural information processing systems, 25, 2012.

- [24] Sama Shrestha and Sonia Jain. A bayesian-bandit adaptive design for n-of-1 clinical trials. Statistics in Medicine, 40(7):1825–1844, 2021.

- [25] Jerzy Splawa-Neyman, Dorota M Dabrowska, and TP Speed. On the application of probability theory to agricultural experiments. essay on principles. section 9. Statistical Science, pages 465–472, 1990.

- [26] Diane Tang, Ashish Agarwal, Deirdre O’Brien, and Mike Meyer. Overlapping experiment infrastructure: More, better, faster experimentation. In Proceedings of the 16th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 17–26, 2010.

- [27] Peter F Thall and J Kyle Wathen. Practical bayesian adaptive randomisation in clinical trials. European Journal of Cancer, 43(5):859–866, 2007.

- [28] Sattar Vakili and Qing Zhao. Risk-averse multi-armed bandit problems under mean-variance measure. IEEE Journal of Selected Topics in Signal Processing, 10(6):1093–1111, 2016.

- [29] Ryo Watanabe, Junpei Komiyama, Atsuyoshi Nakamura, and Mineichi Kudo. Kl-ucb-based policy for budgeted multi-armed bandits with stochastic action costs. IEICE Transactions on Fundamentals of Electronics, Communications and Computer Sciences, 100(11):2470–2486, 2017.

- [30] Tong Xia, Sumit Bhardwaj, Pavel Dmitriev, and Aleksander Fabijan. Safe velocity: a practical guide to software deployment at scale using controlled rollout. In 2019 IEEE/ACM 41st International Conference on Software Engineering: Software Engineering in Practice (ICSE-SEIP), pages 11–20. IEEE, 2019.

- [31] Yingce Xia, Wenkui Ding, Xu-Dong Zhang, Nenghai Yu, and Tao Qin. Budgeted bandit problems with continuous random costs. In Asian conference on machine learning, pages 317–332. PMLR, 2016.

- [32] Yingce Xia, Haifang Li, Tao Qin, Nenghai Yu, and Tie-Yan Liu. Thompson sampling for budgeted multi-armed bandits. arXiv preprint arXiv:1505.00146, 2015.

- [33] Ya Xu, Nanyu Chen, Addrian Fernandez, Omar Sinno, and Anmol Bhasin. From infrastructure to culture: A/b testing challenges in large scale social networks. In Proceedings of the 21th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 2227–2236, 2015.

- [34] Ya Xu, Weitao Duan, and Shaochen Huang. Sqr: balancing speed, quality and risk in online experiments. In Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 895–904, 2018.

- [35] Qiuyu Zhu and Vincent Tan. Thompson sampling algorithms for mean-variance bandits. In International Conference on Machine Learning, pages 11599–11608. PMLR, 2020.

Appendix A Decompose risk-of-ruin to individual stages

Proof of Theorem 3.1.

The last claim is trivial: it is easy to verify that (1) and (2) hold if we let for all . Now we prove the first and the second claim. The case for is trivial. We assume . For any , we have that

where used that and that , which implies that almost surely

and used that , which implies that almost surely

Rearranging this, we obtain a recurrence relation: for any ,

| (14) |

Using the recurrence relation repeatedly for all , we obtain

as required. To prove the second claim, observe that equality is attained in all of the above inequalities if equality is attained in (14), and , and that equality is attained in (14) if equality is attained in and . Finally, note that equality in is attained if and equality in is attained if equality is attained in and . ∎

Appendix B Stochastic domination

Lemma B.1 (Stochastic domination under truncation).

For any two independent real random variable and real number such that , we have that

Proof of Lemma B.1 .

Assume that , or else the proof is trivial. We first claim that . Note that this holds if and only if

The above holds since its lhs and rhs satisfies

It then follows from law of total probability that

as required. ∎

Proof of Lemma 3.2.

If , (8) holds with equality since . So, assume from now on. By (15f) and the conditional distributions of multivariate Gaussian, we have

where is independent of conditioned on and are defined in (15f). Here, we used that since by Definition 3.1, and . Using the above and that , we have

Since in the above, using also that and that is independent of , (8) follows from Lemma B.1. ∎

Appendix C Derivation of the decision rule

Proof of these facts follows from standard Bayesian analysis (see e.g. [15])

Lemma C.1 (Posterior distributions).

We have for

| (15a) | |||

| (15b) | |||

| (15c) | |||

| (15d) | |||

| (15e) | |||

| (15f) | |||

where

Appendix D Validity for non-identically distributed outcomes

Proof of Theorem 3.3.

To show the experiment by Algorithm 1 is -RRC under Definition 3.4, it suffices to show that (1), (2) hold for each . Since (1), (2) hold for each if , we only need to show that for each , if , almost surely

| (16a) | |||

| (16b) | |||

Note that for each , if ,

where we used first inequality in (13) in (a), second inequality in (13) in (b), and (11) in (c).

We now show (16a) by induction. For , if , Algorithm 1 ensures that

by construction, which implies that

almost surely. If , then since . This proves the base case. For the inductive case, if , Algorithm 1 ensures that

by construction, which implies that

almost surely. If , we have that

from inductive hypothesis. This shows (16a).

To show (16b), note that under Definition 3.4,

On the rhs, is independent of

and that . It follows from these, (16a) and Lemma B.1 that

Therefore, for each , if ,

as required. This concludes the proof. ∎

When are (13) satisfied

Fix any where . Note that

The summands on the rhs are independent random variables under Definition 3.4. We thus expect that when or are sufficiently large,

by central limit theorem under mild moment-growth conditions (e.g. Lyapunov’s conditions). We thus expect that first condition in (13) holds when or are sufficiently large for each .

We now focus on the second condition in (13). Suppose that , which implies by (11). Note that we can write

and

For ,

and

So, second condition in (13) holds for if we have chosen prior and model parameters such that

This corresponds to that we choose prior and model parameters conservatively in the sense that we do not overestimate treatment effect or underestimate its variability. Now fix any . From the law of large number, we expect that for sufficiently large

So if the treatment effects increase or stay roughly constant throughout the experiments

and our variance estimates are accurate or conservative in the sense that

the second condition in (13) holds for each and the experiment produced by Algorithm 1 is -RRC.

Appendix E Algorithm for general Bayesian models and costs

The following outcome model is a generalization of Definition 3.1. Here, experiment outcomes are allowed to be multivariate with each coordinate corresponds a different business metric.

Definition E.1 (General Bayesian model).

Fix . The model parameter is generated from certain prior . The experiment outcome of unit at stage are distributed independently and identically as

where and is a probability distribution on .

The following is a generalization of Definition 2.1. It allows for general experiment cost beyond treatment effect. The cost of treating unit is now for some function chosen by the user. For instance, can be chosen to compute the worst treatment effect across multiple business metrics.

Definition E.2 (General experiment cost).

For each , let the experiment cost from stage- and treated unit be where is any user-chosen function. Then define . We let if . Define the cumulative experiment cost up to stage as .

We now move to derive an explicit algorithm Algorithm 1 from Theorem 3.1 that output such that the experiment is -RRC. Compared to Algorithm 1, the algorithm developed in this section will require Monte-Carlo simulations and generally gives more conservative ramp schedule.

We first review the Cantelli’s inequality, which is an improved version of the well-known Chebyshev’s inequality for one-sided tail bounds.

Lemma E.3 (Cantelli’s inequality).

For any , and real-valued random variable with finite variance,

Given that (i) and that (ii) , a direct application of Cantelli’s inequality shows that

where denotes trivial -algebra.

Our strategy to construct an algorithm that selects ramp size such that (1), (2) hold is as follows: we first verify that condition (i) holds; if not, set and otherwise find such that the following two inequalities hold

| (17a) | |||

| (17b) | |||

To accomplish this, note that by exchangeability of the outcomes under Definition E.1,

| (18) | ||||

and

| (19) | ||||

We thus require a Monte-Carlo procedure to output estimates for the following posterior quantities on the rhs of (18), (19)

where denote costs from treating two units at stage . Recall that under (…), the outcome of the units are exchangeable. So simply refers to any two distinct units. These quantities will be used to construct estimates of and as functions of chosen.

We now outline a procedure to construct . Firstly, suppose that we can obtain samples from the posterior distribution

| (20) |

from certain MCMC algorithms. The specific details of the MCMC algorithm will depend on the Bayesian model used, but generating posterior-predictive samples while imputing unobserved data, as required in (20), is a common objective of such algorithms (see e.g. [15, Chapter 18]). Let us denote the samples as

| (21) |

These will give us samples from as follows:

Then we can estimate by

Let

which denotes the subset of the Monte-Calor samples for which the budgets are not depleted.

If , we can simply out since this corresponds to the case that the condition (i) does not hold, i.e. . Otherwise, we continue to construct as follows:

| (22) | ||||

From (18), (19) and the Monte-Carlo estimates above, we then have estimators for

in terms of as follows

The two inequalities in (17) then become

| (23a) | |||

| (23b) | |||

respectively. Assume that or else set directly. Observe that (23b) can be written as, with ,

where

| (24) | ||||

Then one can choose to be the largest, positive integer in the range defined by

If the range does not contain any positive integer, we set . Note that the range can be easily identified after solving the quadratic equation . Algorithm 2 gives the algorithm that outputs ramp sizes adaptively. Note that by construction, it gives a -RRC experiments if the Monte-Carlo estimators are sufficiently accurate.

We have conducted preliminary simulations of the proposed procedure for a multivariate Gaussian outcome model with Gaussian-inverse-Wishart prior, and observed satisfactory results. However, we defer presenting numerical results until future work when a more systematic investigation of Monte-Carlo based procedures can be conducted.

Appendix F Linkedin experiment data

In Table 1 below, are sample statistics from the actual LinkedIn experiment. are incoming population size reduced by factor for tractability on a personal computer.

| Stages | 1 | 2 | 3 | 4 | 5 | 6 |

|---|---|---|---|---|---|---|

| 0.3648 | 0.3780 | 0.3752 | 0.2317 | 0.4009 | 0.3930 | |

| 0.3659 | 0.3788 | 0.3754 | 0.2317 | 0.4010 | 0.3941 | |

| 2.0993 | 2.2769 | 2.0909 | 1.1165 | 2.2705 | 2.3982 | |

| 2.0923 | 2.2248 | 2.0135 | 1.0526 | 2.2476 | 2.4430 | |

| 10,756 | 10,460 | 10,598 | 7,580 | 10,550 | 10,688 |

Appendix G Thompson-sampling based Bayesian bandit

This algorithm is developed in [27, Section 4] for clinical trials. The algorithm assigns a user at stage to treatment with probability

for tuning parameter . Under Definition 3.1, by (15d), we have that